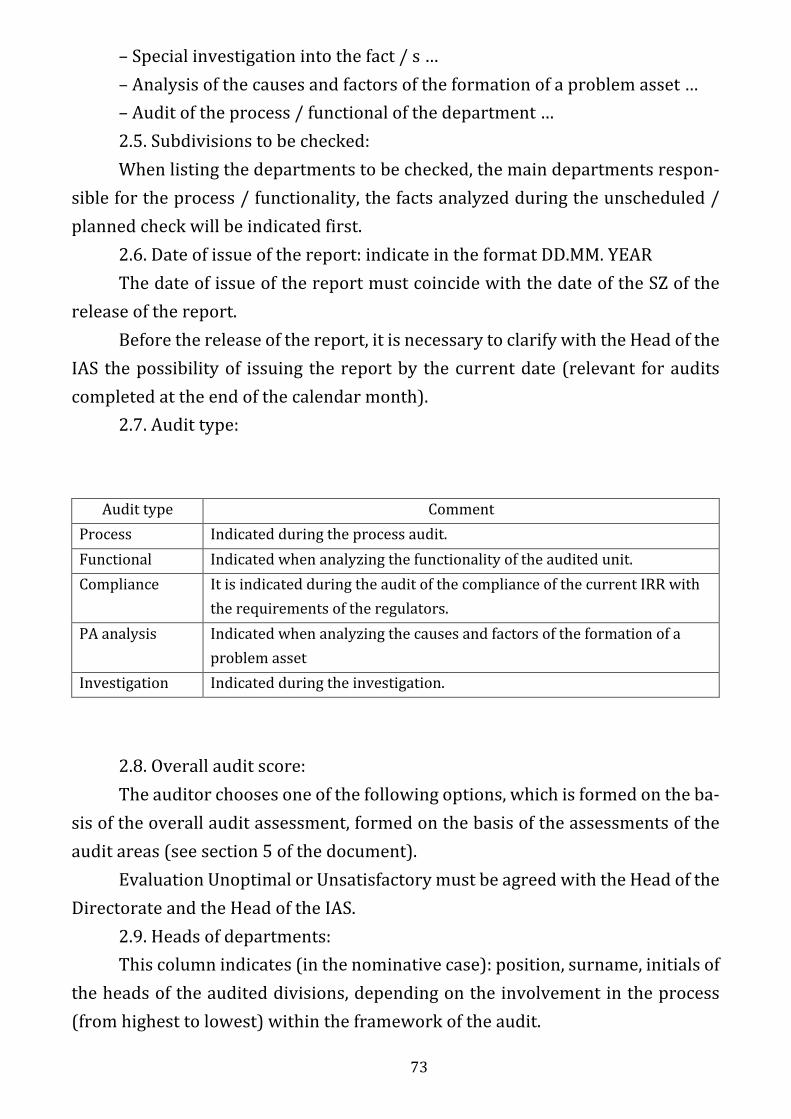

organising issues of operative system of internal control in

TRANSCRIPT

RyabovO.V.

OrganisingIssuesofOperativeSystemofInternalControlinBankingSector

Monograph

ISBN 978-5-4480-0344-8

St.Petersburg

2021

ukonf.com/mon 9 785448 003448

RyabovO.V.OrganisingIssuesofOperativeSystemofInternalControlinBankingSector:

Monograph.MinistryofEducationandScience,North-WestInstituteofManage-ment,branchofRANEPA.St.Petersburg:ConsultingcompanyUcom,2021.114p.

ISBN 978-5-4480-0344-8 https://ukonf.com/doc/mon.2021.04.02.pdf Rev i ewers : AlekseyShipitsyn,CandidateofEconomicSciencesProjectmanagementLlc.,St.PetersburgThe Au to r : OlegRyabov,CandidateofEconomicSciences,associateProfessorNorth-WestInstituteofManagement,branchofRANEPA,St.PetersburgThe information about published Monograph is given to the RISQ

system(contract№856-08/2013K)Monograph.Format60´84/16.Printedsides7,13ConsultingcompanyUcom392000,Tambov,PObox44Circulation500pcs.E-mail:[email protected]

ã2021,RyabovO.V.

3

CONTENTS

Introduction..................................................................................................................4

Chapter1.Theoreticalbasisofinternalaudit.........................................................................6

1.1.Theessenceofinternalaudit:concept,goals,objectivesandrights.............61.2.Theroleofinternalauditinthemanagementsystem

ofaneconomicentity.........................................................................................................91.3.Theplaceofinternalauditintheorganization's

managementsystemanditsimportance................................................................15

Chapter2.Basicsoforganizingthefunctioningoftheinternalcontrolsystemincreditinstitutions..................................................................37

2.1.Financialauditandcompliancecontrolasmethodsofinternalcontrol.............................................................................................................37

2.2.Themainmethodsforassessingthequalityoftheinternalcontrolsystem....................................................................................................................45

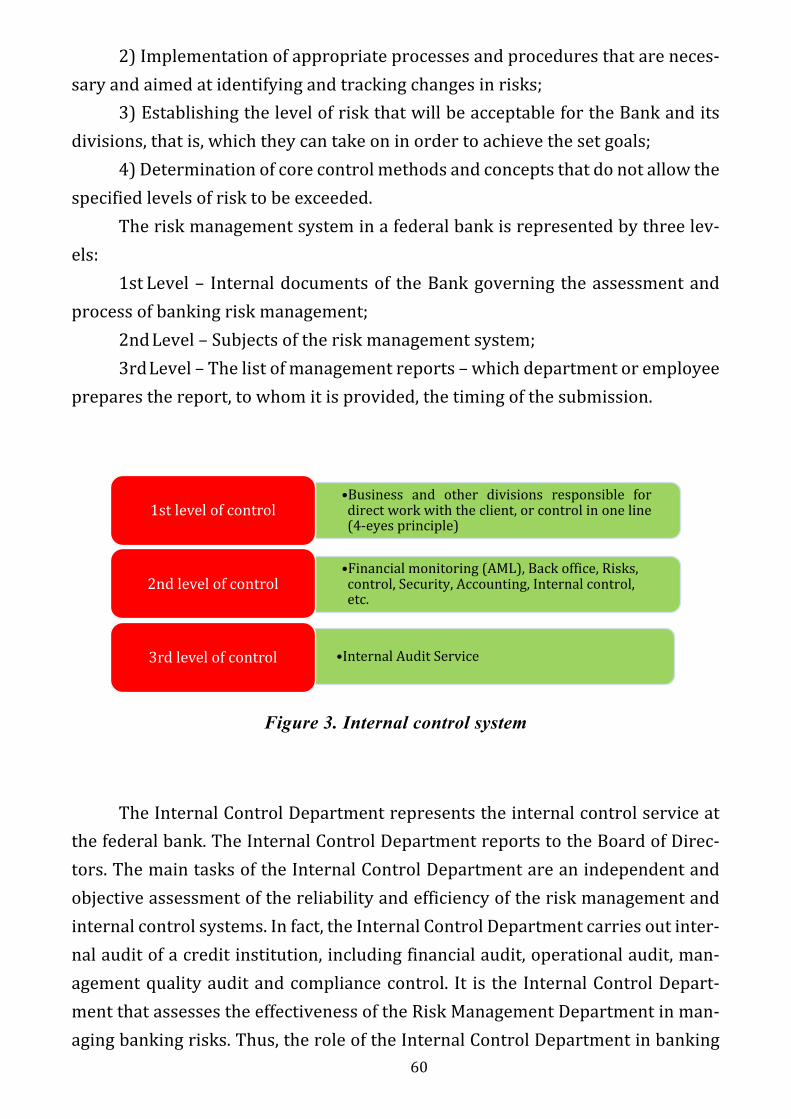

Chapter3.OrganizationoftheinternalcontrolsystemandtheimportanceofICS......................................................................................53

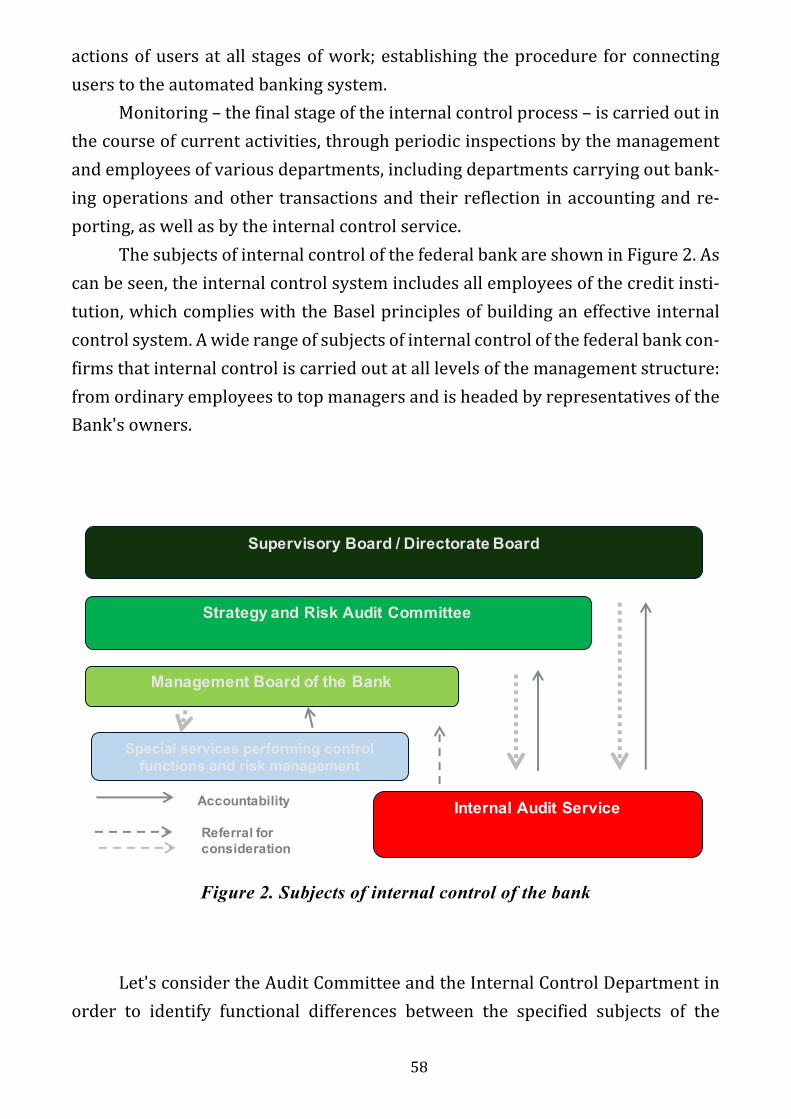

3.1.OrganizationoftheinternalcontrolsystemontheexampleofRussianbanks................................................................................................................53

3.2.Recommendationsforbuildinganinternalcontrolserviceincreditinstitutions.........................................................................................................64

3.3.Methodologicalapproachestotheformationoftheauditor'sreport........72

Conclusion................................................................................................................107

Listofreferences....................................................................................................110

4

Introduction

Thebankingsectorisconsidereduniqueamongothersectorsoftheecon-

omy,asitisasupplieroffinancialresourcesandamanagerofsettlementsbetweenbusinessentities.Improvingthequalityofmanagementofacreditinstitutionisaprerequisiteforincreasingthecompetitivenessofthebank,whichguaranteesthesuccessfuldevelopmentofthebankingbusinessinthelongterm.Theresultsoftheinternal auditors have becomemore visible to themanagement of commercialbanks,asthequalityoftheinternalauditstaff,internalcontrolandriskservicelifewasEC–useofsupervisoryauthoritiestoassessthecontrolenvironmentandthedecisionontheamountofcontributionstothedepositinsurancesystem.

Oneofthemosteffectivetoolsfor identifyingopportunitiesfor improvingtheefficiencyofactivities,thequalityofbankmanagement,and,therefore,oneofthecompetitiveadvantagesofacreditinstitutioncanbeaneffectiveinternalcon-trolsystem.Thevalueofsuchasystemisduetothefollowing.

Firstly, theactivitiesof financial institutionsareprimarilyassociatedwiththeabilitytoattractfundsfromcustomers,whichplaceshigherdemandsonthestability,reliabilityandsafetyofcreditinstitutions.Secondly,theactivitiesoffi-nancialinstitutionsarepredominantlyintangibleinnature.Themaincomponentoftheiractivitiesistheidentification,assessmentandmanagementofeventsthatmayhaveanimpactontheiractivities.Thatis, financialinstitutionshelpclientsachievetheirgoalsbyusingavailableopportunitiesorbyreducingtheimpactofnegativefactors.Atthesametime,thekeytotheeffectiveactivityofacreditinsti-tutionisaconstantchangeintheexistingsetofservicesprovided1.Thirdly,giventhattheactivitiesoffinancialinstitutionsaffectthefinancialstabilityandstabilityoftheirclientsandcounterparties,thestatepaysincreasedattentiontothecontrolandsupervisionofthisarea.Asaresult,specialattentionispaidtothecreationofan internal control system that will adequately assess and manage risks.

1 Malykhin D., Tikhomirov A. Features of the functioning of internal control and audit in banks. // http://www.iia-ru.ru/pu blication

5

Regulationoftheactivitiesoffinancialorganizationsisexpressedinthedevelop-mentofrequirementsthataremandatoryforapplicationincurrentactivities.

Themonographanalyzestheroleoftheinternalcontrolserviceandthein-ternalauditserviceinthemanagementofbankingrisksbyassessingthesystemoforganizinginternalcontrolinthebank.

Therelevanceofthetopicisduetoasignificantincreaseintheimportanceoftheinternalcontrolfunctioninbanksinthecontextoftheongoingglobalfinancialcrisis.Thepracticalsignificanceofthemonographliesinrecommendationsforim-provingtheefficiencyofinternalauditandinternalcontrolservicesincreditinsti-tutions.

Theobjectoftheresearchistheinternalcontrolserviceandtheinternalau-ditservice.

Thesubjectoftheresearchistheprocessofinternalcontrolinabankasatoolthatensurestheeffectivenessofthebank'scontrolinmanagingbankrisks.

ThetheoreticalbasisofthemonographwastheworkofsuchresearchersasR.Adams,A.Daley,B. Stanmeier,Hahn.D., CochranC., BrownL.M.,Russell J.P.,Spencer Pickett K. H., Kiran D.R., Reichmann Th., Utkin E.A., Beloglazova G.N.,KroliveskayaL.P.,SukhanovM.S.,ZemskovV.V.,ZadorozhnayaK.A.,PashkovR.V.,YudenkovYu.N.,LotobaevaG.G.,TavasievA.M.,TarasovI.T.andetc.

Themainpurposeof themonograph is to identify theroleof the internalcontrolserviceandtheinternalauditserviceinthemanagementofbankingrisks.

Inaccordancewiththesetgoal,thefollowingtasksaresolvedinthemono-graph:

–to reveal the essenceof the conceptof internal control of a commercialbank;

–analyzetheexistingregulatoryframeworkfororganizingtheinternalcon-trolofthebank;

–definetheroleandfunctionsoftheinternalcontrolserviceandtheinternalauditserviceinthebank'sinternalcontrolsystem;

–evaluateoptionsfororganizingandforminginternalcontrolandauditser-vicesofthebank;

–givepracticaladviceonthespecificsofconductinginternalaudits;–explainthesubtletiesofwritinganauditreportbyaninternalauditorofa

commercialbankusingspecificexamples.

6

Chapter 1.

Theoretical basis of internal audit

1.1. The essence of internal audit:

concept, goals, objectives and rights

Internalauditisunderstoodasacontrolsystemorganizedbyaneconomicentity,actingintheinterestsofitsmanagementand(or)owners,regulatedbyin-ternaldocuments,overtheobservanceoftheaccountingprocedureandtherelia-bilityoftheinternalcontrolsystem.

Internalauditisanactivityregulatedbytheinternaldocumentsoftheor-ganizationtocontrolthelevelsofmanagementandvariousaspectsofthefunction-ingoftheorganization,carriedoutbyrepresentativesofaspecialcontrolbodyintheframeworkofassistancetothemanagementbodiesoftheorganizationines-tablishingthelegalityofbusinessoperationscarriedoutbyemployeesandtheireconomicfeasibilityfortheenterprise,incompliancewiththeestablishedproce-dureformaintainingaccountingaccounting.Internalauditistheactivityofprovid-ingindependentandobjectiveguaranteesandadviceaimedatimprovingtheeco-nomicactivitiesofanorganization. Ithelpsanorganizationachieve itsgoalsbyusingasystematicandconsistentapproachtoassessandimprovetheeffective-nessofriskmanagement,controlandcorporategovernancesystems.Itisworthnotingthattheorganization,goals,roleandfunctionsofinternalauditaredeter-minedbythemanagementand(or)theowneroftheeconomicentity,dependingontheorganizationalandlegalformandtheexistingmanagementsystem,thecon-tentandspecificsofactivities,thevolumeoffinancialandeconomicactivitiesandthestateofinternalcontrol2.

Theobjectivesoftheorganizationoftheinternalcontrolsystemattheen-terpriseare: implementationoforderlyandefficientactivitiesoftheenterprise,including profitability and protection from losses; ensuring compliance withthemanagementpolicyof eachemployeeof theenterprise; ensuring the safety

2 9. Itkin Yu.M. Problems of the formation of audit. M.: Finance and statistics, 2016, P.13.

7

ofproperty;maintaininggoodrelationshipswithregulatoryauthorities.Sinceex-ternalandinternalcontrolareinterdependent,interdependentcomponentsofaunifiedcontrolsystem,inthedevelopmentoftasksfacinginternalauditors,aswellas in the performance of functions, it is necessary to take into account the im-portantroleoftheaccompanyingaudit,detailedintheFederalLawNo.119-FZ"OnAuditingActivity"services,whichwillallowmorespecifically,withlegislativejus-tification, toassess thepossibilityof implementingsuch internalaudit services,whichshouldbeunderstoodas:accountingandtaxconsulting;analysisofthefi-nancialandeconomicactivitiesoftheorganization,economicandfinancialcon-sulting;managementconsulting,includingthoserelatedtoorganizationrestruc-turing;legaladvice,aswellasrepresentationincourtandtaxauthoritiesontaxandcustomsdisputes;accountingautomationandimplementationofinformationtechnologies; appraisal of property value, appraisal of enterprises as propertycomplexes,aswellasentrepreneurialrisks;developmentandanalysisofinvest-mentprojects,drawingupbusinessplans;marketingresearch;provisionofotherservicesrelated toauditactivities.Toachieve theabovegoalsoforganizing theinternalcontrolsystem,itisnecessarytosolvethefollowingtasks:periodiccon-troloverthefinancialandeconomicactivitiesoftheparentorganizationanditsbranches;analysisofeconomicandfinancialactivitiesandassessmentofeconomicand investment projects, economic security of accounting systems and internalcontroloftheparentorganizationanditsbranches.Thesolutiontothisproblemmakesitpossibletoincreasetheefficiencyoftheactivitiesofindividualseparatedivisionsandtheentireorganizationasawhole,whichwillmakeitpossibletofullyfulfillthemaingoalsetfortheinternalauditservice;seminars,professionaldevel-opmentandtrainingofpersonnel,assistancetotheHRdepartmentintheselectionandtestingofaccountingpersonneloftheparentorganizationanditsbranches;toensurethatthecomputerprogramsthatcontrolthefunctioningoftheaccountingsystem,includingtheformationofprimarydocuments,theiranalysisandpostingtoaccounts,cannotbefalsified;enterprisefundsshouldnotbemisappropriatedorineffectivelyused;internalreportingshouldbepromptlytransferredtopersonsauthorizedtomakemanagementdecisionsforitsoptimaluse;scientificdevelop-ment,publicationofmethodologicalmanualsandrecommendationsonaccount-ing,taxation,analysisoffinancialandeconomicactivities,audit,businesslaw,andinformationservicesfortheheadorganizationanditsbranches;advisingonfinan-

8

cial, tax,bankingandothereconomic legislation, investmentactivities,manage-ment,marketing,taxoptimization,registration,reorganizationandliquidationofenterprises.Anaccountant inchargeofday-to-dayworkmayneedprofessionalhelpinunusualorrareeconomicsituations,aswellasincaseofsignificantchangesinlegislation.Interactionwithexternalauditors,representativesoftaxauthoritiesandotherregulatoryauthorities.

Tosolveproblems,theinternalauditserviceisendowedwithcertainrights:checkingaccountingregistersandprimarydocuments,theavailabilityofmoney,valuablesandsecuritiesatthecashdesk,researchingestimates,plansandotherdocumentsoffinancialandeconomicactivities;acquaintancewithorders,ordersofthehead,decisionsofmeetingsoffounders,shareholders,boardandofficials,already concluded and draft (non-concluded) contractswith organizations andotherdocuments;inspectionofconstructionsites,territories,warehouses,work-shopsandotherproduction,utilityandofficepremises,storageareasforfinishedproducts,equipment,etc.;checkingtheavailability,conditionandsafetyofprop-erty,inventoryitemsfrommateriallyresponsiblepersons;therequirementforafullorpartialinventoryofthepropertyandobligationsoftheorganizationorin-ventorydirectlybytheauditorwiththeparticipationofemployeesoftheorgani-zationinvolvedinthis, ifnecessary,sealingofsafes,cashregisters,warehouses,storerooms,archivesandotherplacesofstorageoffunds;monitoringthecorrect-nessofthereflectionofbusinesstransactionsinaccounting,checkingthecorrect-nessofthecalculationoftaxes,feesandpayments,aswellasthetimelinessoftheirpaymenttothebudgetandoff-budgetfunds;verificationofthereliabilityoftheindicatorsofaccountingandstatisticalreporting,thecorrectnessofthecompila-tionofcalculationsfortaxesandmandatorypayments;therighttoreceivefromtheheadsofstructuraldivisions,specialistsoftheorganizationnecessaryfortheaudit of documents, certificates, calculations, certified copies of documents fortheirattachmenttotheactoropinion,oralandwrittenexplanationsonissuesaris-ingduringtheaudit;examinationoftheeffectivenessofthesegmentmanagementsystemandanalysisofproductionandeconomicactivities,financialcondition,sol-vencyandliquidationoftheorganization;preparationoftheorganizationforex-ternalauditandtaxcontrol;representationoftheorganization'spropertyinter-ests ineconomicdisputes incourtandinanarbitrationcourt;evaluationofthesoftwareusedbytheeconomicentity;special investigationsof individualcases,forexample,suspicionsofabuse;developmentandpresentationofproposalsto

9

eliminate the identified deficiencies and recommendations to improve the effi-ciencyofmanagement3.

Theresponsibilityoftheinternalauditserviceisdeterminedbythreemainpoints: thevalidityand timelinessof submissionofopinionson the stateof ac-countingandreporting,thecomplianceofconstituentdocuments,internalregula-tionswiththecurrentlegislationandthelegalstatusoftheorganization,aswellasconclusionsontheachievedlevelandefficiencyfactorsofproduction,economicandfinancialactivities;thevalidityofthesubmittedproposalsforimprovingtheorganizationofthecontrolsystem,accounting,financialresponsibilityofofficials,programs for the development of activities, projects for optimizing productioncosts,taxablebases,distributionofprofits,creationanduseoffundsandotheris-sues;thecorrectnessoftheconsultationsprovidedtothefounders,headsofde-partments,specialistsandemployeesofthemanagementapparatusontheorgan-izationofproduction,themanagementsystemontheorganizationofproduction,themanagementsystem,accounting,methodsofanalyzingeconomicandfinancialactivities,legalandotherissues.Theobjectivityofinternalauditisensuredbythedegreeof its independence in themanagementstructureofaneconomicentity.This requirement for internal audit is ensuredby the fact that he obeys and isobligedtosubmitreportsonlytothemanagementwhoappointedhimand(or)theownersandindependentoftheheadsoftheauditedbranchesoftheeconomicen-tity,structuraldivisions,internalcontrolbodies,etc.

1.2. The role of internal audit in the management

system of an economic entity

Theprocessofmanaginganeconomicentityandaproperlyorganizedsys-temofinternalcontrolcannotbeseparatedfromeachotherwithoutviolatingtheharmonyandefficiencyoftheentiremanagementsystem,then,asaresult,thereis a need not for the occasional use of an independent external audit, but forapermanentandeffectivestructure,whichispartoftheinternalcontrolsystemasanintegralpartofit4.

3 Burtsev V.V. Organization of the internal control system of a commercial organization. M.: "Exam", 2020, p.109 4 Dodge R. A Brief Guide to Auditing Standards and Norms: Per. from English; foreword by S.A. Stukov. (Audit: theory and practice). M.: Finance and statistics; UNITY, 2017, p.89

10

Itisknownthatevenatthestageofacquaintancewiththenatureandchar-acteristicsofthefinancialandeconomicactivityofaneconomicentity,theauditormustassessthequalityoftheaccountingsystemsandinternalcontrolofthisen-tity.However,itshouldberememberedthatthevalueforaneconomicentityofanyinformation,includingthatobtainedasaresultofanaudit,isthehigher,thelowerthecostofobtainingit.Atthesametime,anecessaryconditionfortheeffec-tivenessoftheinternalcontrolsystemistheavailabilityofanindependentorgan-izationalstructureforaneconomicentity–aninternalauditservice.

IntheofficialRussianregulationsinthefieldofauditing , internalauditisunderstoodas“…organizedbyaneconomicentity,acting in the interestsof itsmanagementand(or)owners,asystemofcontrolovercompliancewiththeestab-lishedaccountingprocedureandthereliabilityoftheinternalcontrolsystemreg-ulatedbyinternaldocuments"Or"…oneofthewaystocontroltheefficiencyofthelinksinthestructureofaneconomicentity."5

Intheeconomicliterature,theconceptofinternalauditisinterpretedindif-ferentwaysbybothdomesticandforeignauthors.

So,forexample,BychkovaS.M.believesthat"internalauditisanelementoftheinternalcontrolsystem,organizedbythemanagementoftheenterpriseinor-dertoanalyzeaccountingandothercontroldata".6

AccordingtoV.V.Burtsev,"internalauditisanactivityregulatedbythein-ternaldocumentsofanorganizationtocontrolthelevelsofmanagementandvar-iousaspectsofthefunctioningofanorganization,carriedoutbyrepresentativesofaspecialcontrolbodywithintheframeworkofassistancetothemanagementbodiesoftheorganization…"7

FromthepointofviewofA.M.BogomolovandGoloshchapovaN.A.,“internalaudit(internal,internal)isanintegralpartofageneralauditorganizedataneco-nomicentityintheinterestsofitsownersandregulatedbyitsinternaldocuments

5 International Standards on Auditing and the Code of Ethics for Professional Accountants (1999). M.: MTsRSBU, 2018 P.218. 6 International Standards on Auditing and the Code of Ethics for Professional Accountants (1999). M.: MTsRSBU, 2018, P. 21 7 Bogomolov A.M., Goloshchapov N.A. Internal audit. Organization and methodology. M.: "Exam", 2014, P.212

11

tocomplywiththeestablishedprocedureforaccounting,protectionofpropertyandthereliabilityoftheinternalcontrolsystem"8.

ThefamousEnglishscientistR.Dodge,whopresentedoneofthefirstworksrelatedtointernationalauditinRussia,giveshisunderstandingofinternalaudit.“Internalauditisanintegralpartofinternalcontrol;carriedoutbythedecisionofthemanagementbodiesofthecompanyforthepurposesofcontrolandanalysisofeconomicactivity”9

AccordingtothefamousAmericanscientistsE.A.Arens.andLobbekJ.K.,in-ternalaudit isan internalaudit thatprovides theadministrationwith“valuableinformationformakingdecisionsregardingtheeffectivefunctioningoftheirbusi-ness”.10

Fromtheabovedefinitionsdescribingtheconceptofinternalaudit,itfollowsthatitstillhassignificantdifferencesfromexternalaudit,whichcanbeidentifiedas:limitedindependence;ensuringregularcontroloverthefinancialandeconomicactivitiesofaneconomicentity;regularprovisionofinformationforthepurposeofmakingandadjustingpreviouslyadoptedmanagementdecisions.

Beforedefiningtheplaceofinternalauditintheprocessofmanaginganeco-nomicentity,andinparticularintheinternalcontrolsystem,letusconsiderthemaincharacteristicfeaturesofthissystem.

AccordingtotheprovisionsexistinginbothRussianandinternationalprac-tice,theinternalcontrolsystemconsistsofthreemainelements:aproperlyorga-nizedaccountingsystem;controlenvironment;separatecontrols.

Thus,themodernsystemofinternalcontrolofaneconomicentityisacertainpolicyandprocedures(controls)adoptedbythemanagementsystemofthisentitytoachievethegoalsofthemanagementprocess,providingforthedegreeoffeasi-bilityoftheorderlyandefficientconductofthefinancialandeconomicactivitiesofthisentity,includingstrictadherencetothemanagementpolicy,ensuringthesafetyofproperty,detectingandpreventingdistortionsarisingfrombothuninten-tionalactionsandabuse,therelativeaccuracyandcompletenessofaccounting(fi-nancial)information11.

8 Bogomolov A.M., Goloshchapov N.A. Internal audit. Organization and methodology. M.: "Exam", 2014, P.6. 9 Danilevsky Yu.A., Shapiguzov S.M., Remizov N.A., Starovoitova E.V. Audit. M.: ID FBK-PRESS, 2018, P.87. 10 Federal Law of Russia. "On Auditing" No. 119-FZ, P14 11 Kamyshanov P.I. A practical guide to auditing. M.: INFRA-M, 2018, P.49.

12

Analysisoftheabovedefinitionsofinternalaudit,aswellasthemainele-mentsoftheinternalcontrolsystem,allowsustodefineinternalauditasaneffec-tive,multifunctional(integrated)controltoolorganizedbythemanagementofaneconomicentity,designedtoensuretheeffectivenessoftheentireinternalcontrolsystemandoptimizationofmanagementdecisions.

Before determining the feasibility of organizing internal auditwithin anyeconomicentity,itisnecessarytounderstanditsmaingoal,ontheachievementofwhichtheeffectivenessofitsfunctioningdepends.

Sinceinternalauditisaconstituentelementoftheinternalcontrolsystem,itsstrategicfocusshouldbe,firstofall,adequatetothetargetsettingsofthissys-tem.

Ifweproceedfromthisstatement,thenitisnecessarytotakeintoaccountthefactthatthepurposeoftheinternalcontrolsystemistoensurethemanage-mentprocessofaneconomicentitywithvarious,properlyprocessedandanalyzedboth internal and external information flowsnecessary to achieve the strategicgoalsofthefunctioningofaneconomicentity.

Forthisreason,thegoalofinternalauditatthepresentstageofdevelopmentofeconomicrelationscanbedefinedasmultifunctionalassistancetothemanage-mentsystemofaneconomicentityintheimplementationoftheeffectivefunction-ingoftheinternalcontrolsystemand,asaconsequence,optimizationoftheman-agementdecisionstaken.

Atthepresentstage,thetargetsettingofinternalaudithasshiftedfromcon-trol-confirmingtocontrol-regulating,which,inturn,radicallychangedthenatureandscopeofthetasksitsolves,whichcanbeformulatedasfollows:regularcontroloverthefinancialandeconomicactivitiesofaneconomicentityanditsbranches;controlofthetimelinessandcompletenessofthereflectionoffinancialandeco-nomictransactionsinaccounting;controloverthesafetyofthepropertyofaneco-nomic entity and its branches; control over settlement andpaymentdiscipline;controlovercompliancewithlegislationandotherregulatorylegalacts;controlover the timeliness of settlements with the budget of different levels and off-budgetfunds;identificationorpreventionandcontroloverthecorrectionofdis-tortionsinaccountinginformationduetounintentionalerrorsandabuse;checkingtheaccountingofproductioncosts,completenessandcorrectnessofthereflectionofproceedsfromthesaleofproducts,works(services),aswellastheformationoffinancialresultsofaneconomicentityanditsbranches;assessmentofthedegree

13

ofefficiencyofaccountingandinternalcontrolsystemsofaneconomicentityanditsbranches;controlovercompliancewiththepolicyofaneconomicentityandensuringtheeffectivenessofitsfinancialandeconomicactivities;analysisofthefinancialandeconomicactivitiesofaneconomicentityanditsbranches;assess-mentofeconomicsecurity;evaluationofinvestmentandothereconomicprojects;identificationandmobilizationofavailablereservesoflimitedresources;advisingthepersonnelofaneconomicentityanditsbranchesonallaspectsfallingwithinthe competence of internal audit; scientific developments and preparation ofmethodological recommendations and manuals on accounting and other areaswithinitscompetence;computerizationofaccounting,preparationandformationofaccounting(financial)statements,calculationsfortaxation, financialandeco-nomicanalysisandotherareaswithinthecompetenceoftheinternalauditofaneconomicentity;controlovertheexecutionofdecisionstoeliminateidentifieddis-tortionsandothershortcomings;assessmentofthedegreeofreliabilityofthein-formationprovidedto thecontrolsystem;organizationofofficial investigationsintovariousemergenciesandcircumstances;interaction,ifnecessary,withexter-nalauditors,representativesoftaxandotherregulatoryauthorities.

Thegiven,althoughnotclaimingtobecomplete,listoftasksfacingtheinter-nalauditmayvarydependingontheemergingneedinthemanagementprocess.Atthesametime,itsdiversityconfirmsthemultifunctionalcapabilitiesofinternalaudit.Moreover, all these tasks canbe combined intoa generalized concept. Inotherwords,thetaskofinternalauditatthepresentstageofitsdevelopmentistoprovidetheprocessofmanaginganeconomicentitywithsufficientandappropri-atecontrolandregulatoryinformationthatallowsmakingthemosteffectiveman-agementdecisions,aswellaspromptlyandtimelyadjustmentstopreviouslymadedecisions.

Inthiscase,sufficiencyshouldbeunderstoodasthecompletenessofinfor-mationflows,andbyrelevance–theirreliability.

Sincethegoalandobjectivesofanyactivitymainlycharacterizeonlyitsmainfocus,thenforadeeperunderstandingoftheessenceofthisactivity,itisimportanttodeterminethefundamentalprinciplesonwhichitisbased.

Forthisreason,thenext,nolessimportantaspectthatdeterminesthecon-ditions for the functioningof internal audit is the setting and characteristics ofthoseprinciplesthatpredetermineitsfeatureandtherequirementsimposedonitbythemanagementsystemofaneconomicentity.

14

IntheofficialRussianlegislativeandregulatoryactsinthefieldofaudit,in-ternalauditisregulatedonlyintheRules(standards)ofauditingactivitiesand,atthesametime,onlyforthepurposeoftheexternalauditor'sassessmentofthein-ternalcontrolsystemofaneconomicentity.

Thetheoreticalstudiesofscientistsandthepracticalexperienceofauditorsfromcountrieswithdevelopedmarketeconomiesinthedevelopmentandappli-cationof fundamentalprinciplesofauditdefine themasethicalrules,normsorprinciples,theobservanceofwhichmakesitpossibletoincreasethedegreeofcon-fidenceintheresultsofauditactivitiesofinterestedusers.

Theseprinciplesinclude:independence,honesty,honesty,objectivity,confi-dentiality,professionalcompetence,professionalbehavior.

Anyauditor,includinganinternalone,mustrespectthepriorityoftheinter-estsofthesocio-economicsystemthatheservesandmaintainahighreputationforhisprofession.Atthesametime,hisresponsibility:foranimprudent,withinreasonablelimits,assessmentoftheamountofworkrequiredtoachievethegoalssetforhim;forasubjectiveassessmentofthecomplexity,materialityorsignifi-canceofcertainaspectsinrelationtowhichheformshisconclusions;forassessingtheadequacyandeffectivenessofriskmanagement,aswellasaccountingandin-ternal control systems; for the likelihood of significant errors; for the costs in-curredfortheprovidedauditedinformationforthemanagementsystemofaneco-nomicentity, exceeding thepossibleeconomicbenefits frommanagementdeci-sionsthatarenotformedonitsbasis,–shouldbeadequatetothepossibleconse-quenceswithinitscompetence.

Inaddition,theinternalauditorisobligedatallstagesofhisactivity,solvingcertaintasksassignedtohim,toproceedfromawell-knownpositionofprofes-sionalskepticism,realizingthatthereisapossibilitythatallinformationreceivedbyhimfromvarioussourcesmaycarryacertainlevelofunreliability…

Despitethefactthatadherencetotheprinciplesdiscussedaboveincreasesthedegreeofconfidenceininternalaudit,however,thelackofthedevelopmentofcertainrulesgoverningtheprocedurefortheirpracticalapplicationmakesitpos-sible to judge them only as high ethical intentions declared by general moralnorms.

15

1.3. The place of internal audit in the organization's

management system and its importance

Theemergingmarketrelations,firstofall,representeconomicfreedom.Thefreedomofoneeconomicentityisaccompaniedatthesametimebythefreedomofothereconomicentitiesthathavetheopportunitytobuyornotbuyitsproducts,offer theirprices for it,dictatetheir termsof transactions.At thesametime,allmarketparticipantsentering intoeconomicrelationsstrive, firstofall, for theirownbenefit,fortheprofitoftheircompany,whichcanobjectivelybecomealossforothers,becauseanybusinessentityseekstosurpassitsopponent,attractmoredemandforitsproducts,thusbypushingoutitscompetitorfromthemarket,thesearethelawsofcompetition.Fromtheabove,animportantruleofentrepreneurialbehaviorfollows:nottoavoidrisk,buttoanticipateit,tryingtoreduceittothelowestpossiblelevel.Thisrequiresconstant,effectiveandtimelycontrolovertheactivitiesofemployeesandthefirmasawholethroughaproperlyseteconomicandlegalwork,accountingandreporting,etc.

Controlistheprocessofdeterminingthequalityandadjustingtheworkper-formedbysubordinatesinordertoensurethetasksfacingtheenterprise.Itspur-poseistoidentifyweaknessesanderroneousdecisions,correcttheminatimelymannerandpreventrepetition.Allmaterials,peopleofactionarecontrolled.Mon-itoringallowsyoutodeterminetheeffectivenessandtakethenecessarymeasurestoensurethefulfillmentofthetask.Knowclearlywhointheenterpriseisperson-allyresponsiblefordeviatingfromtargetsandtakingcorrectiveaction.Controlofactivities iscarriedoutbypeople.Toknowwho isresponsible for thesafetyofmaterialand financial resources, their storage, leave,accountingand inventory,preparationofprimarydocuments,deviations fromassignmentsandcorrectiveactions,theremustbecompleteclarityregardingthedistributionofresponsibilitythroughouttheorganization.Anessentialpreconditionforeffectivecontrolistheexistenceofanorganizationalstructure,whichisobjectivelyduetothecreationofaninternalauditserviceinthemanagementapparatus.Thetasksofinternalauditincludethecreationofaninternalcontrolsystemnecessaryfortheimplementa-tionofthecompetence,rightsandresponsibilitiesofmanagementbodiesandoffi-cials,aswellasaclearsystemofeconomicresponsibilityofofficialsandspecialistsoftheenterprise.

16

Internalauditisanimportantmanagementfunctionthatcoversaccounting,financial analysis and control, comparison and assessment of the actual resultsachievedwiththegoalsandobjectivesoftheenterprise.Internalauditsystemati-callymonitorstheactivitiesofallmanagementobjects,identifiesthereasonsfordeviationsfromstandards,deviationsfromthegoalssetforaspecificobject,whichcontributestotheprompteliminationofidentifiedviolations.Organizationofin-ternalauditasafunctionofenterprisemanagementimpliesstrictregulationofitsactivities, determination of the rights, duties and responsibilities of specialists,qualificationrequirements,relationshipswithdepartmentsandpersonneloftheenterprise.Theworkoftheinternalauditserviceattheenterpriseisorganizedinaccordancewithindividualandcalendarworkplans,whichareapprovedbytheheadoftheenterprise.Attheendofanytypeofwork,theinternalauditorsubmitsareporttotheheadoftheenterprisethatallowshimtodrawthehead'sattentiontotheidentifiedorpossibleviolations.Theworkisconsideredcompletedwhentheissuesraisedinthereportsofinternalauditorsareconsideredbytheheadoftheenterpriseandwhenanofficialorderhasbeenissuedontheacceptance(re-jection)oftherecommendationsoftheauditors.

Organizationoftheriskmanagementsystemasasubsystemofinternal

controlThemostfamousschoolinthetheoryoffinancialriskandriskmanagement

since1955istheAmericanschool.AmongitsmodernrepresentativesareD.Galai,H.Groening,A.Damodaran,F.Jorion,J.Kalman,M.Crui,M.McCarthy,R.Mark,T.Flynnandanumberofotherfamousscientists.

H.Grüningmadeasignificantcontributiontothestudyofbankingrisks,cor-porateandfinancialriskmanagement.

A.Damodaranisaspecialistinfinance,anemployeeoftheSternSchoolofBusinessattheUniversityofNewYork(specialistincorporatefinanceandcapitalvaluation).His areas of interest are capital valuation, portfolio capitalmanage-ment,corporatefinanceandstrategicriskmanagement.In1994,BusinessWeekmagazine named him one of the top twelve professors to teach inUS businessschools.HisworkshavebeenpublishedintheJournalofFinancialandQuantitativeAnalysis,JournalofFinance,JournalofFinancialEconomics,ReviewofFinancialStudies.Hisworksaredevotedtoissuesofcapitalvaluation(DamodaranonValu-

17

ation,InvestmentValuationandDarkSideofValuation),aswellascorporatefi-nanceissues(CorporateFinance:TheoryandPractice,AppliedCorporateFinance:AUser'sManual).ThelatestbookbyA.Damodaranisdevotedtotheprinciplesandmethods of strategic risk management: it combines various areas of riskknowledge:theeconomic justificationof itsbehavioralaspects, financialassess-ment,riskmanagementitself,andforthefirsttimeprovidesitscompletepicture;showshowtobuildanorganizationallinkbetweenriskmanagementfunctionsinacompany:strategy,financeandcurrentactivities,sothatthetoolsandresultsofassessmentaredeterminedbythedecision-makingprocess,andnotviceversa;usingpracticalexamples,hearguesthepositiveeffectofrisk,itsusetoincreasethecompany'sprofit.Experienceshowsthatevaluatinginnovativeprojectscausesdifficultiesforcompanies,sincetheircashflowsaredifficulttopredict.Theuseofthemethodofrealoptions,clearlystatedbytheauthor,allowsyoutosolvethisproblem;topmanagerswhomakedecisionsrelatedtorisksanduncertaintieswillbeabletoreasonablychooseanyofthemoderntoolsforassessingrisk:risk-dis-countadjustedrates,options.12Analysisofstudiesofforeignscientificschoolsofriskmanagement,simulationmodeling,scenarioanalysis,VARmethodsandrealoptions.Thisstudywillhelpmanagerstakeadvantageofthepositivecomponentof risksanddevelopaneffectivesystemformanaging themusingvaluepricingmodels.Successfulmanagementisdistinguishedpreciselybytheabilitytoidentifyrisksandmaintainanoptimalbalancebetweenhedgingthem,sharetheresponsi-bilityofriskmanagementwithinvestorsandusethemtoincreasecashflows,and,consequently,thevalueoftheircompanies.Expertsandanalystsseetherelation-shipofriskassessmentstotheholisticpictureofacompany'sriskmanagement.

Dr.J.Kalmanisarenownedspecialistinriskmanagement,riskcontrol,fi-nancingriskandfinancialmanagement.Dr.J.KalmanistheownerofKallmanCon-sultingServices (KCS),whichprovidespractical applications for enterprise riskmanagement.BytheopeningofKCS,J.KalmanwasExecutiveVicePresidentoftheNationalAllianceresponsibleforthecertificationofriskmanagersfortheinterna-tionalprogramoftheAcademyforRiskandInsuranceResearch.Hisresearchfo-cuses on risk management and loss control of project solutions. Dr. J. Kalman

12 Arens A., Lobbek J. Audit: / Ch. series editor prof. I'M IN. Sokolov. (Series on accounting and au-diting). M.: Finance and Statistics, 2017

18

servesonvarious committees for theAmericanRiskand InsuranceAssociationandtheWesternRiskandInsuranceAssociation.13

ManybooksonriskmanagementhavebeenpublishedintheWest.BookofM.Crui,D.GalaiandR.Mark"FundamentalsofRiskManagement"14-oneofthebest,availablenotonlytoriskmanagers,butalsotoawideraudienceinterestedinunderstandingmodernriskmanagement.Attentionispaidnottomodels(whichpresupposes a certain level ofmathematical training), but to the essential andpracticalaspectsofriskmanagement.Therefore, inparticular, it is intended forbothcreative-mindedtopmanagersandcolleaguesofriskmanagerswhoseactiv-itiesare facedwithriskmanagement issues, forexample, internalauditors.Thebookisacompletelyoriginalwork,whichisdifficulttofindananalogueinthelit-eratureonthistopic.Thisisbynomeansamonographoracomprehensivetext-bookonriskmanagement.Theauthorsofthebookarerenownedexpertsinthedevelopment of the theory of riskmanagement, occupying leading positions inwell-known international financialorganizations.Thebookcoversa fairlywiderangeofissues:riskclassification,riskassessmentmethods,forexample,VaR,RA-ROC,etc.,Modernriskmanagementtools.Theauthorsarequitecriticalregardingthepracticeofriskmanagement,itsregulation,thelevelofunderstandingandap-plicationoftherelevantmodelsatthepresentstage.Andthiscriticismisveryuse-ful forallparticipants in theriskmanagementprocess, since it contributes toamore accurate and careful application ofmodern technologies, a change in theprinciplesofriskmanagementandtheirregulation.Itisnocoincidencethatthisbookwas chosen by the Professional RiskManager's International Association(PRMIA)asthemainguideforpreparingfortheentry-levelcertificationexam–AssociateProfessionalRiskManager(APRM).

Research carriedoutbyKPMG topmanagersM.McCarthyandT.Flynn15,highlightshowtoday'sleadingcorporateleadersmanagerisksandcontroltheirimpacton thecorporation, reveals the internal sourcesof themost threateningcorporaterisksandmethodsofneutralizingtheirimpact;waysofmanagingrisks,

13 Bogomolov A.M., Goloshchapov N.A. Internal audit. Organization and methodology. M.: "Exam", 2014 14 Burtsev V.V. Organization of the internal control system of a commercial organization. M.: "Exam", 2020 15 Bychkova S.M. Auditing activity. Theory and practice. (Series "Textbooks for universities. Special literature"). SPb.: Publishing house "Lan", 2021

19

donotinterferewiththeimplementationofcurrentprojects;therelationshipbe-tweentheareasofcorporategovernanceandriskmanagementwiththeincreaseinthevalueofthecompany,analyzestheactionstorecognize,assessandneutral-izetheriskoftoday'scorporate leaders inthefaceofrisk.Therearealsomanyexamples from corporate governance practice and exclusive interviews with anumberofleadingtopmanagersofourtime–theleadersofMicrosoft,Hewlett-Packard,Sprint,MotorolaandothersbelongingtotheFortune500list.Thatis,thisisastudyonoptimizationandriskmanagement,inwhichgiven:provenmethodsofprevention,responseandeffectivereductionofoperational,businessandfinan-cialrisks;strategiestohelpthecompanybecomeanadaptiveorganization–anorganizationthatperceivesriskasanopportunityratherthanaburden;programs,thankstowhichitispossibletomakeriskmanagementtheresponsibilityofalmosteveryemployeeandtointroducethemostimportantconceptsofriskmanagementatalllevelsofmanagement.

F. Jorion, inhisthirdeditionofthis internationalbestseller,addressesthefundamentalchangesinriskmanagementthathavetakenplacearoundtheworldinrecentyears.F.JorionprovidesthelatestinformationneededtounderstandandimplementVARsandmanagefinancialrisk.F. JorionreferstothecalculationofVARandtheuseofmodelstopredictriskandcorrelations:hedescribestheuseofVARforriskcontrolfortrading,investmentmanagement,aswellasforcorporateriskmanagement,andalsopointsoutthekeymistakesofriskmanagement.

InastudybyS.Borodina,A.Shvyrkov,withtheparticipationofJ.Bui, thestateofcorporategovernanceinthelargestcountries–Russia,Brazil,India,Chinaand South Africa – was assessed in terms ofmarket infrastructure, ownershipstructure,legalandregulatoryinfrastructure,informationtransparency.16Theau-thorspresentamethodologyforanalyzingcorporatepracticesinsuchaspectsastransparencyofownershipandcontrolstructure,attitudetowardsshareholders,informationdisclosure,efficiencyoftheboardofdirectorsandriskmanagement.Corporategovernancemistakescanbeverycostly.Forexample,therecentfinan-cialcrisis,thecollapseofEnronandothercorporatescandalsearlyinthelastdec-ade,or the1997Asian financialcrisis.Allof themhave thesameprerequisites:poor quality of corporate governance. Companies used false business models,couldnotunderstandtheconsequencesofoff-balancesheettransactionsorhigh-

16 Danilevsky Yu.A. General audit, audit of stock exchanges, off-budget funds and investment insti-tutions. M.: Accounting, 2018

20

riskborrowingpolicies,andhadsignificantforeignexchangerisks.Theresultformanycompanieswasthecollapse,whichturnedintosignificantfinanciallossesforshareholdersandemployees,humiliationanddishonorforthemanagement. In-vestmentsintheBRICScountries.Itissometimesdifficulttounderstandwhatef-fectivecorporategovernanceprovidesatthelevelofday-to-dayactivities.Inde-velopedmarkets,wherecompaniesadheretosimilarstandards,therearenotal-ways visible differences in the cost of capital. But in emergingmarkets,wherestandardsmay differ significantly, these differences becomemore pronounced.Companiesthatdemonstratetheiradherencetocorporategovernancestandardsaregenerallyratedsignificantlyhigherbythemarketthanothercompanies.Asaresult,theytakeadvantageofthelowercostofraisingcapital,thatis,theyincreasetheircompetitiveness.Theideaofthestudyistohighlighttheimportanceofgoodcorporategovernanceforcompanies intheBRICScountries.Effectivecorporategovernancecertainlyrequiresalotofeffort,especiallyintimesofeconomicandfinancialuncertainty,capitalflowsaredirectedtothosecountriesthatarereadytoaccepttheseefforts,andgoodcorporategovernancecanimprovethesituation.

Agreatcontributiontothedevelopmentofthetheoryandpracticeofriskmanagementwasmade byEnglish economists – representatives of the EnglishschoolofriskmanagementT.Andersen,T.Bedford,A.Griffin,A.Zaman,R.Cook,P.Sweeting,P.Hopkin,GermanP.Schroederandothers.17

T.AndersenandP.Schroederbelievethattoday,whencorporatescandalsandmajorfinancialfailuresoccur,therelevanceofeffectiveriskmanagementisincreasing.Lackormismanagementofriskcanhavedevastatingconsequencesforthe organization and the economy as a whole (Barings Bank, Enron, LehmannBrothers,NorthernRock,tonamejustafew).Modernorganizationsandcorporateleadersmustlearnfromsuchfailuresbydevelopingpracticestoeffectivelydealwithrisk.BasedonaEuropeanperspective,thispaperbringstogetherideas,con-ceptsandmethodologiesdevelopedindifferentriskmarketsandacademicfieldstoprovideamuchneededoverviewofdifferentapproachestoriskmanagement.Theauthorscriticize theprevailingenterpriseriskmanagement(ERM)systemsandproposeanappropriatealternative.

T.BedfordandR.Cookinsituationswhereclassicalstatisticalanalysisisdif-ficultor impossibletouse,applyprobabilisticriskanalysistoquantifyrisk.The

17Danilevsky Yu.A., Shapiguzov S.M., Remizov N.A., Starovoitova E.V. Audit. M.: ID FBK-PRESS, 2018

21

bookbyEnglisheconomists–T.BedfordandR.Cook–examinesthefundamentalconceptsofuncertainty,itsrelationshipwithprobability,boundarieswithaquan-titativeassessmentofuncertainty.Drawingonextensiveexperienceinrisktheoryandanalysis,theauthorsfocusedontheconceptualandmathematicalfoundationsthat underpin the quantification, interpretation andmanagement of risk. Theycoverstandardandimportantnewtopicssuchastheuseofexpert judgmentofuncertainty.

A.Griffin,havingextensiveexperienceinmanagingacompany'sreputation,usesspecificexamplestoanalyzetheeffectiveanderroneousactionsofcorpora-tionstocreate,managetheirownreputationandreputationrisks.Corporationsmustnotonlyprotecttheirownreputationunderpressure,strengthenedbythecorporationfromthestateandsociety,butlearntocontrolit.

AccordingtotheDecreeoftheCentralBankoftheRussianFederationdated04.15.2015No.3624-U"Onrequirementsfortheriskmanagementsystemandthecapitalofacreditinstitutionandbankinggroup"theriskmanagementandcapitalmanagementsystemofacreditinstitution(bankinggroup)shouldcoverfactorsofcredit,marketandoperationalrisks,aswellasothersignificantrisks,forexample,interestrateriskandconcentrationrisk.

Theimplementationofriskmanagementinthebankisassignedtotheriskmanagementservice,whiletheinternalauditservicemustverifytheeffectivenessofindividualriskmanagementandtheriskmanagementsystemasawhole.

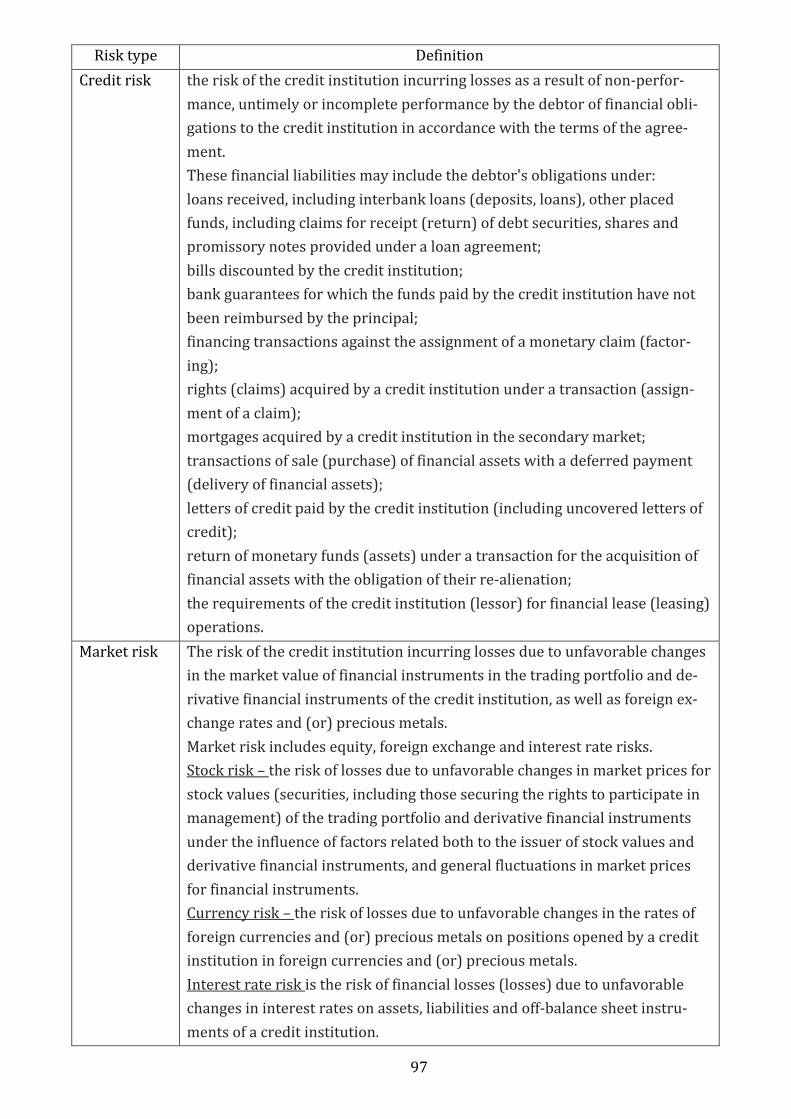

Typicalbankingrisks includefinancialandnon-financialrisksarisingasaresultoftheBank'scorebusiness:

Credit risk is theriskof theBank incurring lossesasa resultof failure tofulfill,untimelyorincompletefulfillmentbythedebtoroffinancialobligationstotheBank.

Withintheframeworkofcreditriskmanagement,industryandcountryrisksaremanaged:

–Industryrisk–theriskoftheBankincurringfinanciallosses(damage)asaresultofthedebtor'sfailuretofulfillhisobligationsasaresultofchangesintheeconomicconditionoftheindustryandthenatureofthesechangesbothwithintheindustryandincomparisonwithotherindustries.

–Countryrisk–theriskoftheBankincurringlossesasaresultofnon-ful-fillmentby foreign counterparties (legal entities and individuals) of obligationsdue to economic, political, social changes, andalsobecause the currencyof the

22

monetaryobligationmaynotbeavailabletothecounterpartyduetothepeculiar-itiesofnationallegislation(regardlessofthefinancialpositionofthecounterpartyitself)

Marketrisk–theriskoftheBankincurringfinanciallosses(losses)duetoanadversechangeinthemarketvalueoffinancialinstrumentsofthetradingport-folioandderivativefinancialinstrumentsoftheBank,aswellasforeignexchangeratesand(or)preciousmetals…Marketriskincludesstock,currencyandinterestraterisks.

Stockrisk–theriskof lossesduetoadversechangesinmarketpricesforstockvalues(securities, includingfixingrightstoparticipateinmanagement)ofthetradingportfolioandderivativefinancialinstrumentsundertheinfluenceoffactorsrelatedtoboththeissuerofstockvaluesandderivativefinancial instru-ments,andgeneralfluctuationsinmarketpricesforfinancialinstruments.

Currencyrisk– theriskof lossesdue toadversechanges in theexchangeratesofforeigncurrenciesand(or)preciousmetalsatopencreditinstitutionpo-sitionsinforeigncurrenciesand(or)preciousmetals.

Interestraterisk–theriskoffinanciallosses(losses)resultingfromadversechangesininterestratesonassets,liabilitiesandoff-balancesheetinstrumentsoftheBank. “Interestrateriskinthebankingbook(IRRBB)gaineditsimportancethrough the regulatory requirements that have been growing and guiding thebankingindustryforthelastcoupleofyears.TheimportanceofIRRBBisshiftingforbanks,awayfrom‘just’aregulatoryrequirementtohavinganimpactontheoverall profitability of a financial institution. Interest Rate Risk in the BankingBookshedslightonthebestpracticesformanagingthisimportanceriskcategoryandprovidesdetailedanalysisofthehedgingstrategies,practicalexamples,andcasestudiesbasedontheauthor’sexperience.ThishandbookisrichinpracticalinsightsonmethodologicalapproachandcontentsofALCOreport,IRRBBpolicy,ICAAP,RiskAppetiteStatement(RAS)andmodeldocumentation.ItisintendedfortheTreasury,RiskandFinancedepartmentandishelpfulinimprovingandopti-mizingtheirIRRBBframeworkandstrategy.BytheendofthisIRRBBjourney,thereaderwillbeequippedwithallthenecessarytoolstobuildaproactiveandcom-pliantframeworkwithinafinancialinstitution”. 18

18 Beata Lubinska. Interest Rate Risk in the Banking Book: A Best Practice Guide to Management and Hedging (Wiley Finance) 1st Edition. John Wiley&Sons, Ltd, 2021, p.248

23

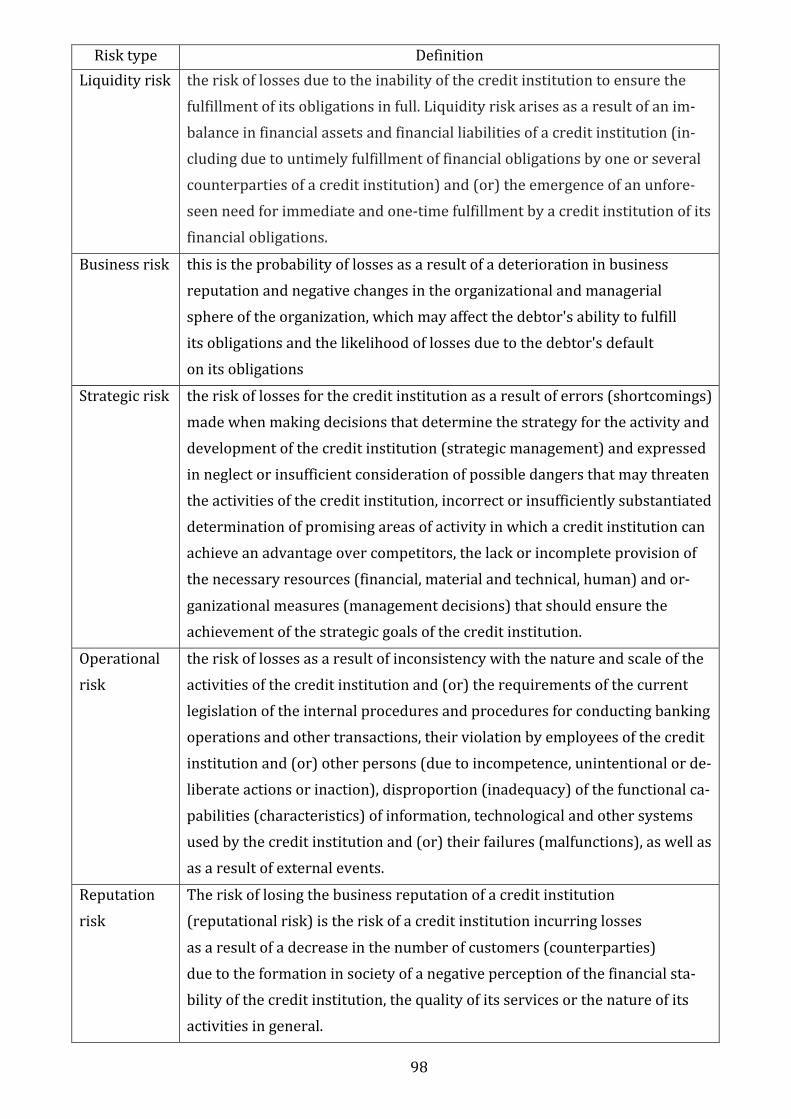

LiquidityriskistheriskoflossesduetotheBank'sinabilitytofullyfulfillitsobligations.LiquidityriskarisesasaresultoftheimbalanceoftheBank'sfinancialassets and financial obligations with respect to the repayment and repaymentterms(includingduetountimelyfulfillmentoffinancialobligationsbyoneormoreoftheBank'scounterparties)and(or)theunforeseenneedfortheBanktoimme-diatelyandimmediatelyfulfillitsfinancialobligations.

Operationalrisk– theriskof lossesresulting from inconsistencywith thenatureandextentoftheBank'sactivitiesand(or)therequirementsofapplicablelaw,internalproceduresandproceduresforbankingoperationsandothertrans-actions,theirviolationbytheBank'semployeesand(or)otherpersons(duetoin-competence,unintentionalorintentionalactionsorinaction),disproportion(in-sufficiency) of functionality (characteristics) of information, technological andothersystemsusedbytheBankand(whether)theirfailures(malfunctions),aswellasfromexternalevents.«ОperationalRiskManagementinFinancialServicesalsofeaturesresultsfrompollstakenbyriskpractitionerswhichprovideasnap-shotofcurrentpracticesandallowthereadertobenchmarkthemselvesagainstotherfirms.Thisistheessentialguideforprofessionalslookingtoderivevalueoutofoperationalriskmanagement,ratherthanapplyingacompliance'tickbox'ap-proach19».

Strategicrisk–theriskoftheBankincurringlossesasaresultoferrors(de-ficiencies)madewhenmakingdecisionsthatdeterminetheBank'sactivityandde-velopmentstrategy(strategicmanagement)andexpressedinthefailuretotakeintoaccountor insufficientconsiderationofpossibledangersthatmaythreatentheBank'sactivities,incorrectorinsufficientareasonabledeterminationofprom-isingareasofactivityinwhichtheBankcanachieveanadvantageovercompeti-tors,theabsenceorpartialprovisionofnecessaryresources(financial,material,technical,human)andorganizationalmeasures(administrativedecisions),whichshouldensuretheachievementofthestrategicobjectivesoftheBank.

Legalrisk–theriskoftheBankincurringdirectlossesorlossesintheformoflostprofitdueto:

–non-compliancebytheBankwiththerequirementsofregulatorylegalactsandconcludedagreements;

19 Elena Pykhova Operational Risk Management in Financial Services: A Practical Guide to Estab-lishing Effective Solutions 1st Edition. Kogan Page Ltd, United Kingdom, 2021, p.364

24

–legalerrorsmadeincarryingoutactivities(incorrectlegaladviceorincor-rectpreparationofdocuments,includingwhenconsideringdisputedissuesinthejudiciary);

–imperfectionsofthelegalsystem(inconsistencyoflegislation,lackoflegalnormstoregulatecertainissuesarisinginthecourseoftheBank'sactivities);

–violationbycounterpartiesofnormativelegalacts,aswellasthetermsofcontracts.

TheriskoflossoftheBank'sbusinessreputation(reputationalrisk)istheriskoftheBankincurringlossesasaresultofadecreaseinthenumberofcustom-ers(counterparties)duetotheformationinthecompanyofanegativeideaoftheBank'sfinancialstability,thequalityofitsservicesorthenatureofitsactivitiesingeneral.

Additionalrisksincludethoserisksthatariseasaresultofvariousprofes-sionalactivitiesbytheBankinthesecuritiesmarket,aswellasrisksthatmayarisewhentheseprofessionalactivitiesarecombined.

Theriskmanagementprocessincludesthefollowingsteps:–riskidentificationandidentification;–riskassessment(quantitative,qualitative);–restriction(minimization)ofrisk;–monitoringandcontrollingthelevelofrisk.Riskidentificationistheestablishmentofinternalandexternalfactors,the

effectofwhichhasaninfluenceontheriskoftheemergenceandestablishmentofoperationsand/orprocesses,whichresultintheoccurrenceandimplementationofthisrisk.

Riskidentificationistheassignmentofrisktoaspecifictypeoftypicalriskinordertoimplementspecificmeasurestolimitthelevelofrisk.

RiskassessmentisdeterminationofthelikelyconsequencesthattheBankmayhaveintheeventoftheimplementationofexternaland/orinternalriskfac-tors during the commission of any transaction. Due to the fact that the conse-quences canbepresentednot only in the formof a certain amount of possiblelosses,butalsointheformofotherconsequencesfortheBank'sactivities,theriskassessmentcanbequantitativeandqualitative.

QuantitativeriskassessmentinvolvesthedeterminationandanalysisoftheamountoflossesthattheBanksufferedasaresultoftheimplementationofanytypeofrisk.

25

Aqualitativeassessmentinvolvesananalysisofanemergencysituation,de-terminingthereasonsfortheimplementationoftherisk,aswellasdeterminingmethodsandtoolstoeliminatetheconsequencesoftherisk,aswellasthewaystopreventtheimplementationoftheriskinthefuture.

Risk restriction (minimization) – a set ofmeasures to develop limits andotherrestrictionsaimedatpreventingtheimplementationoftherisk.

Themainmethodsoflimiting(minimizing)bankingrisksinclude:–riskpooling–amethodaimedatreducingriskbyturningrandomlosses

intorelativelysmallfixedcosts;–riskdistribution–amethod inwhichtheriskofprobabledamage isdi-

videdbetweentheparticipantsinsuchawaythatthepossiblelossesofeacharerelativelysmall;

–limiting–amethodofminimizingrisks,involvingthedevelopmentofde-tailedstrategicdocumentationestablishingthemaximumpermissiblelevelofrisk,acleardistributionoffunctionsandresponsibilitiesofpersonnel;

–diversification–amethodof reducingriskby formingagroupofassetswhoseincomesareweaklycorrelatedwitheachother;

–hedging–abalancingtransactionaimedatminimizingrisk;–assetsecuritization–theissueandsubsequentsaleoftheBank'ssecurities

backedbyhomogeneousassetsgeneratingstablecashflows.Riskmonitoringandcontrol–asetofmeasurestomonitorthelevelofeach

specifictypeofriskandtotalbankingriskingeneral,aimedatmaintainingbankingrisksatanacceptablelevel.

Monitoringandcontroliscarriedoutonadynamicbasis,takingintoaccounta retrospective and prospective analysis of bank portfolios, events and perfor-mancefeaturesofkeyriskindicators.Monitoringandcontroloftheriskleveliscarriedoutonaperiodicbasis,itsresultsareusedtomakeadequatemanagementdecisionsinorderto:

–achievecomplianceoftheamountofformedreserveswiththelevelofac-ceptedrisks;

–preventingadecreaseintheBank'sequity;–preventofviolationsofestablishedriskrestrictions;–preventthelong-termexposureoftheBanktoexcessiverisk;–increasetheprofitabilityofthebankingbusiness;–optimizetheorganizationalstructureoftheBank;

26

–improvetheinformationandtechnologicalsystems.Credit riskThebasicprinciplesof theBank'screditactivitiesof theorganization, the

mainprinciplesoftheBank'screditactivityorganization,strategyandtacticsofcreditriskmanagementaredefinedintheCreditpolicy.

Creditpolicyisenshrinedbythefollowingmanagementsystemelementsofcreditrisk:

–alistofoperationsandtransactions,theimplementationofwhichmaybeaccompaniedbytherealizationofcreditrisks;

–generalapproachestocreditriskmanagement(toolsformanagingcreditrisk,asystemoflimitsandrestrictionsoncreditrisk,theauthorityofsubjectsofcredit riskmanagement andmulti-step decision-making on credit transactions,risklevelcontrol);

–functionunitsofthecreditinstitutionintheprocessofanalysis,evaluation,monitoringandcontroloflevelofcreditriskwithintheframeworkdevelopedbytheconstraintsofthesystem.

AssessmentoftheBank'screditriskforthetotalportfolioofloanandequiv-alentdebtiscarriedoutinaccordancewiththevaluesofmandatorystandardses-tablishedintheInstructionoftheCentralBankoftheRussianFederationNo.180-I,aswellasinaccordancewithindicatorsofthequalityoftheloanportfolioandthedegreeofconcentrationofrisksforassetsestablishedrequirementsoftheCen-tralBankoftheRussianFederationNo.3277-U.

Thelevelofcreditrisksforloans,debtandequivalentdebt,aswellasthedeterminationofthequalitycategoryofloanandequivalentdebtiscarriedoutinaccordancewiththerequirementsoftheRegulationoftheCentralBankoftheRus-sianFederationNo.590-P.

Thelevelofcreditrisksforcontingentliabilitiesofacreditnature,aswellasforanumberofotherinstruments,isdeterminedinaccordancewiththerequire-mentsdefinedintheRegulationoftheCBRNo.611-P.

Assessmentofcreditrisksofborrowers(groupsofrelatedborrowers)iscar-riedouttakingintoaccountindustryrisks.Theanalysisiscarriedoutinthecon-textoflong-termandshort-termindustryrisks.

Whenassessingindustryrisksinthelongterm,thefollowingindicatorsareused:

27

–industrysensitivitytomacroeconomicconditions;–averageleverageofanindustryenterprise.Asfactorsofshort-termindustryrisksareconsidered:–productiondynamicsintheshortandmediumterm;–thedynamicsoftheEntrepreneurialConfidenceIndex;–dynamicsofinventories.Keyeventsthathaveoccurredorareexpectedtochangetheindustry'sen-

vironment.Asaresultoftheanalysisofindustryrisks,thepreferredorpromisinglend-

ingareasfortheBankaredetermined.Aspartofcreditriskmanagement,countryriskmanagementiscarriedout.

Intheprocessofestablishing(revising)limitsoncounterparties,thefollowingin-formationistakenintoaccount:

–thetotalamountof limitsonresidentcounterpartiesofonecountryandtheriskstakenbytherespectivecountryfortheaggregateofalloperationsoftheBankwithcounterparties;

–assessments of international rating agencies of the country where thecounterpartyislocated;

–macroeconomic indicatorsbycountries(budgetdeficit,publicdebt,GDPgrowthrate,inflationrate,unemploymentrate);

–theamountofstatesupportallocatedtothebankingsector;–TheresultsofstresstestingofthebankingsectorconductedbytheEuro-

peanBankingOrganization(hereinafter–EBA)amongEuropeanbanksandtheFederalReserveSystem(hereinafter–theFed)oftheUnitedStates.

Managementreportingoncreditriskassessmentincludesanumberofana-lyticaltables:

–thestructureofloanandequivalentdebtfortheBankasawhole,bytypesofcreditrequirementsandcurrencies,overtimeforthereportingperiod;

–thestructureoftheBank'sloanportfoliobycreditqualitycategoriesindi-catingtheamountoftheformedreserveforpossiblelosses;

–tablesforassessingtheconcentrationofcreditrisk;–assessmentoflong-termindustryrisks;–loanportfoliostructurebyindustry;–analysisoftheindustrystructureoftheBank'sportfoliowithdata.

28

Market riskThemarketriskmanagementprocessisregulatedbyinternaldocumentsof

theBank.Forexample:Regulationonmanagingrisksarisingintheoperationswithfinancialinstruments;Regulationonforeignexchangemanagement;Regulationoninterestmanagement.

Internaldocumentsonmanagementofmarketrisksaresecuredbythefol-lowingmanagementsystemelementsofcreditrisk:

–alistofoperationsandtransactions,theimplementationofwhichmaybeaccompaniedbytheimplementationofmarketrisks;

–sourcesofmarketrisksandtypesoflossesresultingfromtheimplementa-tionofmarketrisks;

–approachestomanagingstock,currencyandinterestraterisks(manage-menttools,asystemoflimitsandrestrictions,thepowersofmarketriskmanage-mententitiesandtheprocedureformakingdecisionsontheconductofrelevantoperationsandtransactions,monitoringthelevelofrisk);

–functionsofstructuralunitsoftheBankintheprocessofmarketriskman-agement.

AggregateassessmentofmarketriskiscarriedoutinaccordancewiththeRegulationoftheCentralBankoftheRussianFederationNo.511-PandisincludedinthecalculationofthemandatorystandardsoftheBankinaccordancewiththeInstructionoftheCentralBankoftheRussianFederationNo.180-I.

Liquidity riskLiquidityriskmanagementisregulatedbyinternaldocumentsinacreditin-

stitution.Externalsourcesofliquidityriskinclude:–theinstabilityoftheeconomicandpoliticalsituationinthecountryandin

theregion;–significantchangesinthelegalregulationofbankingactivities;–thecapacityofmarkets,includingfinancial,notmeetingtheinterestsofthe

bank;–forcemajeurecircumstances.–Internalcausesofliquidityriskinclude:–imbalanceofclaimsandobligationsbythetermsofreturnandrepayment;–poorassetquality;

29

–diversionoffundstolong-termprojects;–significantinvestmentinrealestate;–instabilityandhighconcentrationoftheresourcebase.Methodsforidentifyingliquidityriskinclude:–analysisofthecapacityandprofitabilityofthemarketsinwhichtheBank

operates;–analysisofchangesinthevaluesofmandatoryliquidityratios;–studyoftheBank'scustomerbaseforitsstability,analysisofthestability

oftheBank'sliabilities;–analysisofthestateoftheBank'sassets,especiallywithoverduematuri-

ties;–analysis of concentration of credit risk and concentration of borrowed

funds;–analysisofliquidityusingascenario-baseddevelopmentapproach;–theidentificationofanextraordinaryconflictofinterestbetweenliquidity

andprofitability.Asindicatorsforassessingtheliquidityrisklevel,theBankusesthemanda-

torystandardsestablished in the Instructionof theCentralBankof theRussianFederationNo.180-I(standardsfor instant,currentand long-termliquidity),aswellastherelevantindicatorsestablishedintheInstructionoftheCentralBankoftheRussianFederationNo.3277-U(indicatorsofassetliquidity,liquidityindica-torsandstructureofliabilities,indicatorsofthegeneralliquidityofthebank,riskindicatorsforlargecreditorsanddepositors;theaboveindicatorsareincludedinthecalculationofthegeneralizedresultfortheindicatorsliquiditymarket(RGL)).

LiquidityassessmentiscarriedoutbytheBankbasedonthecalculationandanalysisofliquiditygaps(maturityofassetsandliabilities),forecastsoftheade-quacyofliquidityreserves,theBank'spaymentposition,andinterbankloanmar-ketcapacity.

Methodstominimizeliquidityriskinclude:–forecastingthelevelofliquidity,drawinguppaymentcalendars;–developmentofdecision-makingproceduresformobilizingliquidassets,

attractingadditionalresourcesincaseofaliquidityshortage;–thedevelopmentofdifferentscenariosincaseofworseningconditionsac-

tivitiesofcreditorganization;

30

–developmentofanactionplantorestoreandmaintainliquidityatthere-quiredlevel.

Themostcommonriskminimizationtoolsincludelimitsandrestrictionsonoperations,forecasts,andpaymentcalendars.

TheBankcanconsideredonlyfourpossiblescenariosofthecurrentcondi-tion and liquidity forecast, to determine which uses data analysis of paymentschedulesandtheliquiditygap,"Optimistic","Standard","Alarm"and"Crisis".

In order tomake adequatemanagement decisions, liquidity risk ismoni-tored.ThemonitoringresultisthemaintenanceoftheoptimalratiobetweenthevolumeoftheBank'sliabilitiesandthevolumeofliquidityreserves,whichensureshighprofitabilityofbankingoperationswhileensuringtheproperlevelofliquidityindicators.

Themanagementreportingonliquidityriskassessmentisthefollowingre-porting(withacertainfrequencyofpreparationandprovision):

–standardsN2andN3,structuralbalance;–aforecastplanforoperationsontheBank'scorrespondentaccountsforthe

day,receipts-write-offsontheBank'scorrespondentaccounts,largebalancesoncustomeraccounts;

–theBank'spaymentpositionasofmorningandapromisingpaymentposi-tion(timehorizonof7-15days).

–forecastvaluesofthestandardsN2andN3;–liquidity status report: current liquidity scenario, volume, structure and

adequacyofliquidityreserves;opportunitiestoattractfundsfromthebudgetandtheBankofRussia,thesizeoftheinterbankloanmarket;

–forecastofliquidityreservesforthenextthreemonths.–reportonliquiditygaps;–reportonliquidityreserves:currentliquidityscenario;volume,structure

andadequacyofliquidityreserves;refinancingopportunities.OperationalriskOperational risk management is regulated by an internal document of a

creditinstitution.Thefollowingelementsoftheoperationalriskmanagementsystemshould

bedescribedindetailinthisinternaldocument:

31

–the procedure for implementing the basic principles of operational riskmanagement;

–sourcesandcausesofoperationalrisks;–waystoidentifyandidentifyoperationalrisks;–procedureforassessing(quantitativeandqualitative)thelevelofopera-

tionalrisks;–thesystemofkeyindicatorsofoperationalriskinallareasoftheBank's

business;–theprocedurefortheformationandupdatingofthedatabaseofexternal

andinternaldataonoperationaleventsandlosses;–methodsandtoolstominimizeoperationalrisks;–procedureformonitoringoperationalrisks;–internalreportingsystemforoperationalriskmanagement;–theprocedureforconductingself-assessmentandquestionnairesonoper-

ationalriskmanagement;–separationofpowersandresponsibilitiesintheprocessofoperationalrisk

management.AnimportantcomponentofensuringthecontinuityoftheBank'soperations

incaseofemergencysituationsisthepresenceoftheBank'sinternaldocumentsset,fixingthegoals,objectives,procedures,methodsandtimingoftheimplemen-tationofapackageofmeasuresforthepreventionortimelyliquidationofconse-quencesofapossibleviolationofthenormalfunctioningoftheBank.

ThemanagementbodyofthecreditinstitutionapprovestheBusinessconti-nuityand/orrestorationplan,hereinafterreferredtoastheBCRPlan.

Thesetofmeasuresprovidedby theBCRPlanhelpsminimize theBank'soperationalandreputationalrisks,aswellasliquidityrisks.

Legal risk Riskmanagementisregulatedbyaninternaldocumentofacreditorganiza-

tion.Themainobjectiveoflegalriskmanagementistomaintainthelegalriskas-

sumedbytheBankataleveldeterminedbytheBankinaccordancewithstrategicobjectives.Thepriorityistoensuremaximumsafetyofassetsandcapitalonthebasisofreducingandpossiblelosses.

32

ThespecifiedinternaldocumentoftheBankmaydescribeindetailthefol-lowingcontrolsystemelementsofthelegalrisk:

–externalandinternalfactorsofthelegalrisk;–theprocedureforassessingthelevelofthelegalriskandasystemofindi-

catorsofthelegalrisk;–thelegalriskmonitoring;–methodsandtoolstominimizethelegalrisk;–internalreportingsystemforoperationalriskmanagement;–theprocedureforconductingself-assessmentsandquestionnairesonthe

legalriskmanagementissues;–separationofpowersandresponsibilitiesintheprocessofmanaginglegal

risks.Goodwillrisk(reputationalrisk)Reputational riskmanagement is regulated by an internal document of a

creditorganization.ThemainobjectivesoftheBank'sreputationriskmanagementare:–ensuringthemaximumsafetyoftheBank'sassetsandcapitalbyprevent-

ingorreducingpossiblelossesoftheBankduetotherealizationofreputationalrisk;

–maintainingandmaintainingtheBank'sbusinessreputationwithcustom-ersandcounterparties,founders(participants),participantsinthefinancialmar-ket,stateauthoritiesandlocalgovernments,bankingunions(associations),self-regulatoryorganizationsofwhichtheBankisaparticipant.

ThespecifiedinternaldocumentoftheBankmaydescribethefollowingcon-trolsystemelementsofthereputationrisk:

–externalandinternalfactorsofoccurrenceofthereputationrisk;–procedureforassessingthelevelofreputationalriskandasystemofindi-

catorsofthereputationalrisk;–thereputationriskmonitoring;–methodsandtoolstominimizereputationrisk;–thesystemofinternalreportingonthereputationriskmanagement;–theprocedureforconductingself-assessmentsandquestionnairesonis-

suesofreputationriskmanagement;

33

–differentiationofpowersandresponsibilitiesintheprocessofmanagingreputationrisks.

Strategic risk The main sources of the strategic risk of the Bank are: – the Bank's lack of a strategic development plan for the near and medium term; – insufficiency of taking into account global trends (including possible dangers)

in the development of the banking system of the Russian Federation and the global fi-nancial system;

– complete or partial lack of necessary resources from the Bank, including finan-cial, logistical and human, to achieve the goals set in the strategic development plan;

– the Bank's lack of well-developed and effective approaches to making manage-rial decisions ensuring the achievement of strategic business goals.

Assessment of the strategic risk is carried out on the basis of professional moti-vated judgment, formed on the result of analysis in the framework of identifying strate-gic risk.

When forming a motivated judgment on the level of the strategic risk, the follow-ing are analyzed:

– results of a SWOT analysis of the external and internal factors of the Bank's activity with the aim of determining the level of its competitiveness in the market.

– Bank development strategy, trends in increasing the volume and range of oper-ations and services;

– the compliance of the values of the planned indicators established by the stra-tegic plan for the Bank as a whole, and differentiated by business units, to the actual values of these indicators (periodicity – quarterly, semi-annual and annual);

– reasons for a significant deviation of actual indicators; – existing opportunities to compensate for failure to meet planned targets. – Minimization of strategic risk is achieved by improving the quality of the stra-

tegic planning process in the Bank due to: – monitoring the macroeconomic situation and the environment; – monitoring the implementation of strategic objectives by the Bank; – timely adjustments to the strategic development plan; – compliance of annual corporate (business and financial) plans with a long-term

strategy; – making collegial decisions in the face of multivariate development of the busi-

ness environment;

34

– assessment of the Bank's market position and comparative analysis of compet-itors;

– professional development of top managers of the Bank involved in the devel-opment of the Bank's strategy and its implementation.

Interaction in the strategic risk management process. The strategic development plan of the Bank is approved by the governing body

of the credit organization. Monitoring the implementation of the strategic development plan of the Bank, within its powers, is carried out by the executive bodies of the credit organization.

Directorate of Planning and Financial Control: – organizes the process of development and approval of a strategic plan; –providestheauthorizedmanagementbodiesoftheBankwiththeneces-

saryinformationonthecurrentperformanceofindicatorsdefinedbythestrategy;–possibleanalyzespossiblesourcesofstrategicrisk;–makesapreliminaryassessmentofstrategicriskandofferswaystomini-

mizestrategicrisk.20ThestructuraldivisionsoftheBankcarryouttheirfunctionsandsolveprob-

lemswithintheframeworkoftheapprovedRegulationsandthetargetsspecifiedfortheimplementation.

Assessmentandmanagementoftheaggregatebankingrisk.Theaggregatebankingriskistheriskoflossesanddamagesintheactivities

ofacredit institution for theentiresetofacceptedrisks,aswellas therisksofcombiningprofessionalactivities.Thestructureoftheaggregatebankingriskde-pendsonthetypesandvolumesofoperationscarriedoutbytheBankandonthequalityofmanagingspecificrisks,includinganeffectiveapproachtolimitingtheserisks.Thestructureoftheaggregatebankingriskisusuallydominatedbytheriskassociatedwithactiveoperations,whichhavethelargestshareintheBank'snetassets.Otherbankingrisksofafinancialandnon-financialnaturemaysignificantlyaffecttheaggregatebankingrisk.

20 Risk From the CEO and Board Perspective: What All Managers Need to Know About Growth in a Turbulent World Hardcover – Illustrated, 2003 by Mary Pat McCarthy, Tim Flynn.

35

Themainindicatorforassessingthe leveloftheaggregatebankingrisk ismandatorystandardN1“Capitaladequacyratio”establishedintheCBRinstruc-tionNo.180-I.Whencalculatingthisindicator,thelevelofcredit,marketandop-erationalrisksistakenintoaccount.TheimpactontheBank'scapitaladequacyofothertypicalbankingrisksisassessedonthebasisofprofessionalreasonedjudg-ment.

Asadditionalindicatorsinassessingthetotalbankingrisk,theindicatorsusedarethoseestablishedintheCentralBankoftheRussianFederationNo.3277-U.

Methods for limiting aggregate banking risk. Since the aggregate bankingriskisanintegralindicator,themethodsoflimitingitarethemethodsoflimitingindividualriskcomponents.

InteractionofstructuraldivisionsoftheBankinassessingthe leveloftheaggregatebankingrisk.

Specific management decisions regarding the limitation of the aggregatebankingriskaremadebytheBank'sgoverningbodies–theGeneralMeetingofShareholders,theSupervisoryBoard,theManagementBoardoftheBankwithinthepowersdefinedbytheBank'sCharter,theRegulationontheSupervisoryCoun-cilandtheManagementBoard.Tomakemanagerialdecisions,theBank'smanage-mentbodiesconsidertheresultsoftheassessmentoftheaggregatebankingrisk,methodsandtoolstominimizethem,proposedbytherelevantcollegialmanage-mentbodies.21

TheBank'sInternalAuditServiceperformsacontrolfunctiontoverifythecorrectapplicationofBankofRussiaregulatorydocumentsandtheBank'sinternaldocumentsregulatingthemanagementofcertaintypesof typicalbankingrisks,andalsoevaluatestheeffectivenessofbankriskmanagement.

RiskManagementReports.Basedontheresultsofriskmanagement,aRiskManagementReportissub-

mitted.Thereportispreparedintermsofthecompetenceoftherespectiveunits,summarized and submitted for consideration to themanagement bodies of thecreditorganization22.

21 Investments in the BRICS Countries: Assessing Risk and Corporate Governance in Brazil, Russia, India, China and South Africa M.: Alpina Publishers, 2010. 356 p. 22 Panfilova E.A. The concept of risk: a variety of approaches and definitions // Economic analysis: theory and practice. 2017. No. 95 (143).

36

Inaddition,thefinalstatementscontainingcertainaspectsoftheBank'sriskmanagementinclude:

–Reportsoftheauditorofaprofessionalparticipantinthesecuritiesmarketontheworkdonefortheperiod;

–Reportsoftheauditoroftheexchangeintermediaryontheworkdonefortheperiod;

–ReportsonmonitoringtheinternalcontrolsystemandtheworkoftheIn-ternalControlServicefortheperiod;

–Report on the implementation of the Internal Control Rules in order tocounterthelegalization(laundering)ofproceedsfromcrimeandthefinancingofterrorism,includingitsimplementationprogramsfortheyear.

Theprocedure forpreparingandpresentingthesereports isregulatedbytherelevantinternaldocumentsoftheBank,whichdeterminetheseareasofactiv-ityandriskmanagement.

37

Chapter 2.

Basics of organizing the functioning of the internal control system in

credit institutions

2.1. Financial audit and compliance control

as methods of internal control

AccordingtotheRegulationoftheBankofRussiadatedDecember16,2003,No.242-P"Ontheorganizationofinternalcontrolincreditinstitutionsandbank-inggroups",thereare4possiblewaystocarryoutinspectionsbytheinternalauditservice:

1)financialaudit,thepurposeofwhichistoassessthereliabilityofaccount-ingandreporting;

2)verificationofcompliancewiththelegislationoftheRussianFederation(banking,onthesecuritiesmarket,oncounteringthelegalization(laundering)ofproceedsfromcrimeandthefinancingofterrorism,ontaxesandfees,etc.)andotheractsofregulatoryandsupervisorybodies,internaldocumentsofthecreditinstitutionandthemethods,programs,rules,proceduresandproceduresestab-lishedbythem,thepurposeofwhichistoassessthequalityandconformityofthesystemscreatedinthecredit institutiontoensurecompliancewiththerequire-mentsofthelegislationoftheRussianFederationandotheracts;

3)operationalaudit,thepurposeofwhichistoassessthequalityandcon-formity of systems, processes and procedures, analysis of organizational struc-turesandtheiradequacytoperformtheassignedfunctions;

4)qualitycontrolofmanagement,thepurposeofwhichistoassessthequal-ityoftheapproachesofthemanagementbodies,divisionsandemployeesofthecredit institution tobankingrisksandmethodsofcontrolover themwithin theframeworkoftheobjectivesofthecreditinstitution.

AccordingtoRegulationNo.242-P,theinternalauditservicemustdevelopanauditplan,whichincludesaschedulefortheimplementationofaudits.Thisplanmustbeapprovedbytheboardofdirectors(supervisoryboard)ofthecreditin-stitution.

38

Planningtheupcomingwork,drawingupaprogramofinspectionspresentsa certaindifficulty for thebank's internalauditdepartment.Theauditprogramshouldcontaintheobjectivesoftheauditandidentifykeybankingrisksandmech-anismstoensurethecompletenessandeffectivenessofcontrolintheauditedareaofbankingactivities.Consequently,thefrequencyandscopeofinspectionsoftheactivitiesofvariousdepartmentsandtheeffectivenessofthebank'sproductsareusuallydetermineddependingon their inherentrisk. It is thepossiblerisk thataffectsthevalueofmateriality,whichinturndeterminesthescopeofauditproce-dures.Theauditschedulingcanbeviewedasasequenceofthefollowingsteps23:

1)determinationofthetypesofactivitiesandproductsofthebanktobever-ified;

2)assessmentofintra-businessrisk,riskofcontrolsforthebank'sdivisionsandproducts;

3)rankingtheriskvaluesofthebank'sdivisionsandproducts;4)determinationofobjectsandfrequencyofinspections,distributionofin-

ternalauditresourcesinthecontextofinspections;5)monitoringandadjustingat leastannually theriskvaluesof thebank's

divisionsandproducts.Theriskofabankunit(product)includestwocomponents–intra-business

riskandcontrolrisk24.Thetableshowstheriskassessmentofadivision(bankingproduct)dependingontheassessmentofcontrolsandthelevelofinherentriskonascalefrom0(lowrisk)to4(highrisk).Therefore,theriskwillbeminimalifthelevelofinherentriskisassessedaslow.

Table3.Division(product)riskassessmentmatrix

Controlrisk Intra-businessrisklevelShort Average High

Short Belowaverage-1 Aboveaverage-3 High-4Average Low-0 Medium-2 Aboveaverage-3High Low-0 Belowaverage-1 Medium-2

23 Posokhov I.M. Analysis of the content of the concept of risk and scientific approaches regarding the essence of risk // Actual problems of economics. 2018. No. 17. S. 25-32. 24 Utkin E.A., Sukhanov M.S. Banking audit. M.: TEIS, 2003. 223 p.

39

Whenassessingrisk,thefollowingfactorsareusuallytakenintoaccount:1)quantitative characteristicsof transactions (for example, thevolumeof

transactions);2)qualitativecharacteristicsofoperations(complexity,economicandlegal

conditions);3)internalcontrolprocedures,security,appliedinformationsystems;4)personnelcharacteristics(competence,turnover);Thelistofriskfactorsandtheprinciplesofitsassessmentareenshrinedin

aseparatedocument,whichincludes,amongotherthings:one)scaleofriskvalues(low,medium,high;scoresfrom1to10,etc.);2)thedurationoftheinternalauditcycledependingonthemagnitudeofthe

risk:forexample,sixmonthsforhigh-riskactivities,1yearforactivitieswithme-diumrisk,over1yearforactivitieswithlowrisk;

3)theconditionsunderwhichtheriskassessmentmaynotbetakenintoac-count,thelistofpersonsauthorizedtomakesuchdecisions(boardofdirectors,auditcommittee,managementoftheinternalauditunit),aswellasrequirementsfordocumentingdecisions.Ignoringriskassessmentshouldbetheexceptionra-therthantherule;

4)thefrequencyofriskassessmentforeachdivisionandproduct.Riskas-sessmentisimportanttocarryoutannually,butitcanbecarriedoutmoreoftenifthebankorbankingproductisdevelopingrapidly;

5)minimumdocumentationrequirementsforriskassessment;Theinternalauditserviceneedstoconstantlymonitorauditobjects,riskval-

ues,adjustthevolumeandstructureofauditprocedures,itisalsousefultokeepcardfilescontainingriskassessment,descriptionofauditobjectsandthedurationoftheauditcycleforeachdivisionandproductofthebank.

BasedonthemainmethodsofICSchecksproposedbytheCentralBankoftheRussianFederationinAppendix3toRegulationNo.242-p,thefollowingtypesof internalauditcanbedistinguished,dependingonthecontentofauditproce-dures:

1)Financialauditinvolvescheckingthereliabilityofthebank'saccountingandreportingsystem.Whenconductingthistypeofaudit,externalauditstandardscanbeappliedregardingthelevelofmaterialityandauditrisk,sampling,studyingtheaccountingsystem,andothers.

40

2)Complianceauditchecksthecomplianceofthebank'sactivitieswithleg-islation,bylaws,andinternalregulations.

3)Operational audit evaluates the effectiveness of operations and proce-dures,analyzesthecomplianceoftheorganizationalstructure,methodsofworkandresourcesofthebankwiththesetgoals.

4)Management audit evaluates the quality of management in order toachievethegoalsofthebank.

Considerafinancialauditaspartoftheinternalcontrolofacreditinstitu-tion.AccordingtotheFederalrules(standards)ofauditing25,thepurposeoftheaudit is to express an opinion on the reliability of financial (accounting) state-ments.Thus,whenconductingfinancialaudits,internalauditorscanrelyonexter-nalauditstandards.

Samplingisakeypartofaninternalaudit.Themeaningofthesampleisthatnottheentiresetofoperationsistested,butonlyapartofit.Theresultsoftestingapartofthepopulationwithasufficientdegreeofreliabilitywillmakeitpossibletojudgethepopulationasawhole.Therationalefortheneedforsamplingandthesamplingmethod,adescriptionoftheproceduresfordisseminatingthesamplingresultstotheentirepopulationshouldbeclearlyspelledoutintheworkprogramsandinternalauditreports.

According to theRussianstandardofauditingactivityNo.16"Audit sam-pling",theauditorshouldtrytoformarepresentativepopulationbyselectingsam-pleelementsthathavecharacteristicstypicalofthegeneralpopulation.26

Havingreceivedthefinalresult,theauditorshouldmakesurethattheerrorintheauditedpopulationdoesnotexceedtheallowablevalue.Todothis,theau-ditorcomparesthepopulationerrorobtainedthroughthepropagationwiththeacceptableerror.Ifthefirsterrorturnedouttobemorepermissible,theinternalauditorshouldre-assessthesamplingrisks,andifheconsidersthemunacceptable,thentherangeofauditproceduresshouldbeexpandedorauditproceduresshouldbeappliedthatarealternativetothosealreadycarriedout.

Let'sconsidercomplianceauditasanintegralpartofinternalauditincreditinstitutions.

25 Starostina A. A. Risk management: Theory and practice: [textbook. manual] / A. A. Starostina, V. A. Kravchenko. M.: Kondor, 2017. 200 p. 26 Federal rules (standards) of auditing from 23.09.2002, as amended. Resolutions of the Government of the Russian Federation of 04.07.2003, No. 405.

41

As noted earlier, compliance control is control over the compliance of acreditinstitution'sactivitieswithlegalrequirementsandinternalregulations.

Theneedforcompliancecontrolisduetothefollowingreasons27:–highmarketrequirementsforthereliabilityandsafetyofthebank;–ahighdegreeofregulationofthebank'soperationsbysupervision;–theneedforaclearformalizationofmostofthefunctionsinthebank;–thecomplexityoftheinternalstructureofthebank;–theimportanceofthehumanfactorinthehigh-qualityexecutionofopera-

tions.Compliancecontrolisapreventivemeasureinrelationtotheriskofcompli-