m\u0026a market in vietnam's transition economy

TRANSCRIPT

Electronic copy available at: http://ssrn.com/abstract=1608223

Electronic copy available at: http://ssrn.com/abstract=1608223

Journal of Economic and Policy Research

Vol : 5 Oct 2009 – March 2010 No : 1

Contents

Research Papers

★ Mergers & Acquisitions Market in Vietnam’sTransition Economy

VUONG, Quan-Hoang, TRAN, Tri Dung & NGUYEN, Thi Chau Ha ......... 1

★ China’s Evolving Industrial Policy Strategies and Instruments :Lessons for Development (Part-I)

Daniel Poon ..........................................................................................55

★ Keeping Slovenian Public Finances on a Sustainable Path

Pierre Beynet & Willi Leibfritz ..........................................................100

★ De-centralized Rural Welfare Schemes : Information Dynamicsand Endogenous Institutional Change

A.Udayaaditya & Anjula Gurtoo .......................................................151

Mergers & Acquisitions Market in Vietnam’sTransition Economy

1

Mergers & Acquisitions Market inVietnam’s Transition Economy

VUONG, Quan-Hoang*, TRAN, Tri Dung** & NGUYEN, Thi Chau Ha***

This paper is the first major and a thorough study on the Merger & Acquisition (M&A)activities in Vietnam’s emerging market economy, covering almost entirely the M&A historyafter the launch of Doi Moi. The surge in these activities since mid-2000s by no meansincidentally coincides with the jump in FDI and FPI inflows into the nation. M&Aindustry in Vietnam has its socio-cultural traits that could help explain economic happenings,with anomalies and transitional characteristics, far better than even the most complete setof empirical data. Proceeds from the sales of existing assets and firms have mainly flowed intothe highly speculative industries of securities, banking, non-bank financials, portfolio investmentsand real estates. The impact of M&A on Vietnam’s long-term prosperity is thus highlyquestionable. An observable high degree of volatility in the M&A processes would likely blowout the high ex ante expectations by many speculators, when ex post realizations finally arrive.The effect of the past M&A evolution in Vietnam has been indecisively positive or negative,with significant presence of rent-seeking and likelihood of causing destructive entrepreneurship.From a socio-economic and cultural view, the degree of positive impacts may result in domesticentrepreneurship which will perhaps be the single most important indicator.

* VUONG, Quan-Hoang, Centre Emile Bernheim,Université Libre de Bruxelles, CP 145/01, 50Ave. F.D. Roosevelt, B-1050, Belgium.

** TRAN, Tri Dung, Dan Houtte, Vuong &Partners, Economic Research, 6/80 Le Trong Tan,Hanoi, Vietnam.

*** NGUYEN, Thi Chau Ha, Dan Houtte, Vuong& Partners, Economic Research, 6/80 Le TrongTan, Hanoi, Vietnam.

1. Background

Since mid-1990s, Vietnam has beenemerging as a new market economy. Ithas been a member of the Associationof Southeast Asian Nations (ASEAN)since 1995, then the World TradeOrganization (WTO) since 2007. Thecountry is situated in Indochina Penin-sula with an area of 3,30,000 squarekilometres and has a population of over

86 million, according to a national cen-sus in 2009. After its victory in theAmerican war which had led the col-lapse of the South Vietnam regime in1975, the re-unified Vietnam, nowwith the name of the Socialist Repub-lic of Vietnam, followed the Sovietcentrally planned economic modeluntil an extensive reform programmelaunched in 1986 by the ruling

The authors thank their colleagues at DHV&P,Phuong Thi Giang and Nguyen Khanh Ly, fortheir effort in preparing the M&A dataset forthis research. This research is funded in part bythe Strategy Research Project commissioned by theBIDV Securities Co., (BSC). The authors wouldlike to express their gratitude for the generoussupport by Mr.Do Huy Hoai, Director of BSC.

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

2

Communist Party of Vietnam at its SixthNational Congress, usually referred toas Doi Moi, by both Vietnamese andinternational communities (Vuong,2004). The country has since embarkedon a process of gradually building newregulatory framework for a marketeconomy to operate smoothly, newinstitutions and installing foundationsfor functional markets and the so-calledmarket mechanism. More importantly,perhaps, the country has taken boldsteps in reinforcing its solid transfor-mation to a full-blown version of amarket economy.

1.1 Doi Moi – Vietnam’s ExtensiveEconomic Programme

The traits of the Vietnamese centrallyplanned economy before Doi Moi,notably in the struggling period 1976-86,was characterized by the economists asone with economic inefficiencies,bureaucratism, overwhelming institu-tional rigidity and without functionalmarket and market price system. Pri-vate property rights, especially produc-tive physical assets, were not formallyaccepted by laws and regulations. Thecountry had remained to be a memberof the Least Developed Countries(LDCs) even a decade after Doi Moi.Vietnam’s national economy was insevere financial strait, with backwarddistribution system and relying heavilyon Soviet-bloc financial assistance andaids in kind. When the country was first

selected to open a door to the New Eco-nomic Program (NEP) and adopted amarket economic gradualism, its percapita Gross Domestic Product (GDP)stood at a low level of US$202 and thetotal GDP of Vietnam in dollar termswas only approximately US$11 billion(Pham & Vuong, 2009). The signal of‘fence-breaking’ (or by-passing theexisting cumbersome and rigid economicmanagement regulations) and a need foran overhaul of the national economycould be traced back in the early worksby Dam and Le (1981), Ton-That(1984) and Kimura (1986).

Vietnam’s economic reforms broughtabout by Doi Moi (Vuong, 2004)started with a fairly radical epistemo-logical advance of recognizing legiti-mate rights of private properties, theprivate economic sector. Simulta-neously, the need of removing eco-nomic inefficiencies, rigidity and dys-functional market and distribution sys-tems became apparent and imperative.Market forces came in place and theeconomy gradually abolished the old-styled centrally planned economy,which had previously operated based onthe principles of bureaucratic orders,financial and physical subsidies fromthe state and the Soviet vertical pricingsystem. At this point, a shift to a marketeconomy has already been determinedby political leaders and advocated bymajor economic scholars and localgovernmental policy-makers. In the years

Mergers & Acquisitions Market in Vietnam’sTransition Economy

3

following Doi Moi, the issuance of Lawon Foreign Investment in 1987 and itsamendments in 1990, 1992, 1996,2000 and 2005, together with theamendment of the Constitution ofVietnam in 1992, created morefavourable conditions to attract ForeignDirect Investment (FDI) inflows intothe newborn market economy of Viet-nam (Riedel, 1997, Vuong, 2004(a),Pham & Vuong, 2009). The economicconditions have improved significantlydue largely to a substantial economicexpansion under the open-door policy(Nghiep & Quy, 1999).

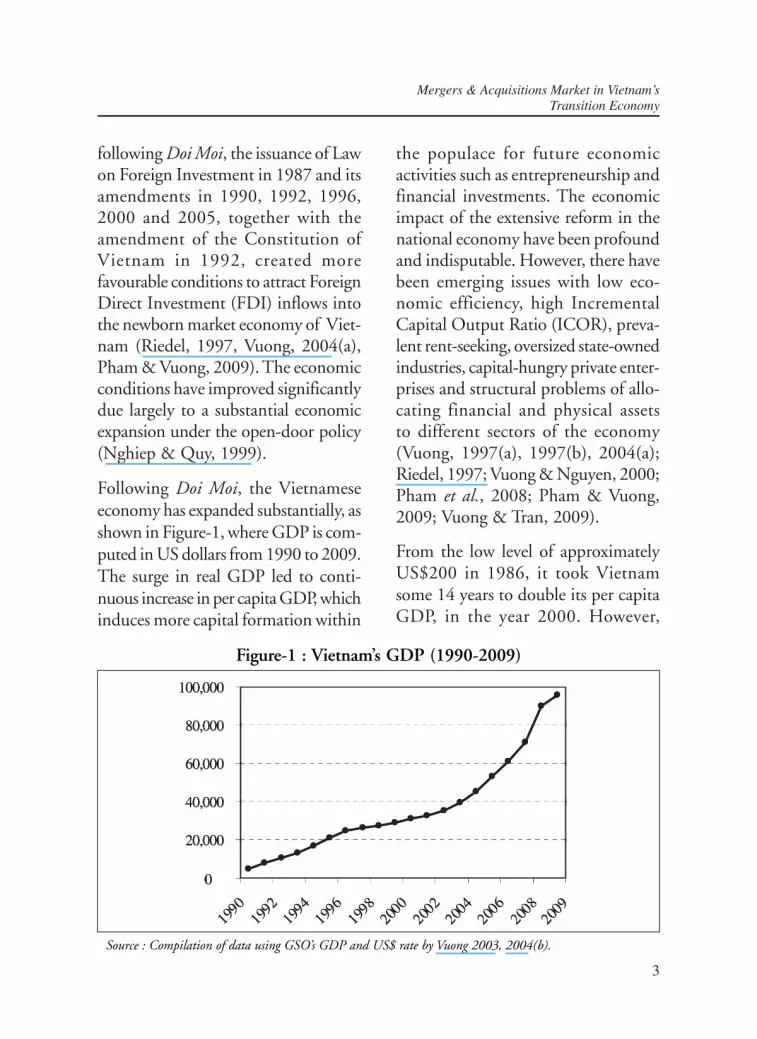

Following Doi Moi, the Vietnameseeconomy has expanded substantially, asshown in Figure-1, where GDP is com-puted in US dollars from 1990 to 2009.The surge in real GDP led to conti-nuous increase in per capita GDP, whichinduces more capital formation within

the populace for future economicactivities such as entrepreneurship andfinancial investments. The economicimpact of the extensive reform in thenational economy have been profoundand indisputable. However, there havebeen emerging issues with low eco-nomic efficiency, high IncrementalCapital Output Ratio (ICOR), preva-lent rent-seeking, oversized state-ownedindustries, capital-hungry private enter-prises and structural problems of allo-cating financial and physical assetsto different sectors of the economy(Vuong, 1997(a), 1997(b), 2004(a);Riedel, 1997; Vuong & Nguyen, 2000;Pham et al., 2008; Pham & Vuong,2009; Vuong & Tran, 2009).

From the low level of approximatelyUS$200 in 1986, it took Vietnamsome 14 years to double its per capitaGDP, in the year 2000. However,

Figure-1 : Vietnam’s GDP (1990-2009)

Source : Compilation of data using GSO’s GDP and US$ rate by Vuong 2003, 2004(b).

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

4

by the end of 2007, the fast-movingeconomy of Vietnam had an opportu-nity to double the per capita GDP in2000, taking only half the time for the1986-level to double (Pham & Vuong,2009). It is expected that the figure islikely to attain US$1,200 in 2010.

1.2 FDI – A Panorama

FDI is not the only source of growthin the reforming economy of Vietnam.Nonetheless, it does serve as a majordriving force of the economy and hasgradually become a leading source ofexternal financing for the Vietnameseeconomy after Doi Moi, coming inunder the form of either greenfieldinvestment or M&As. Equally impor-tant, FDI enterprises have brought in ser-vices and manufacturing technologies,

connections with international marketsand created much needed jobs for theeconomy.

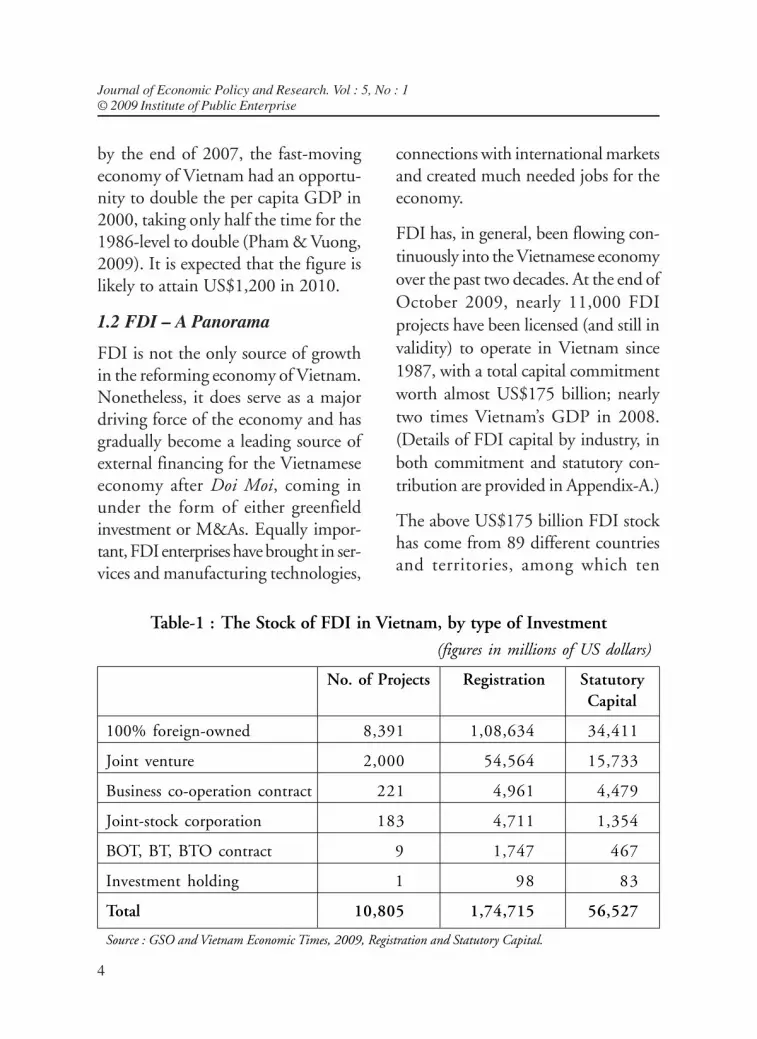

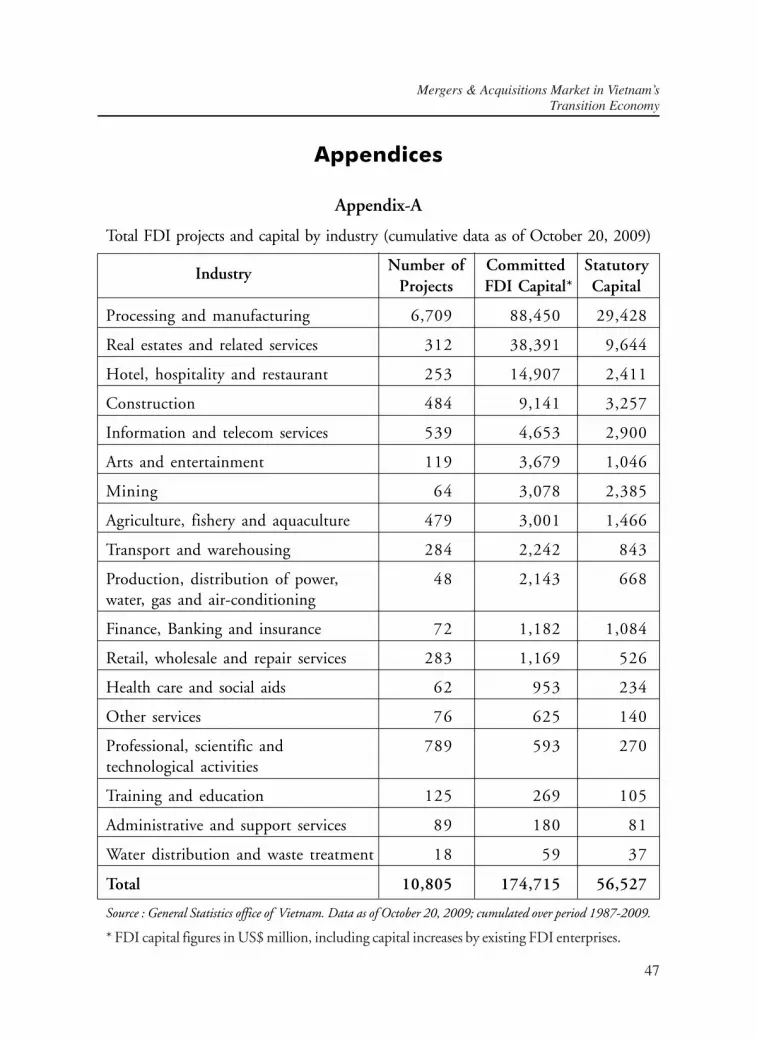

FDI has, in general, been flowing con-tinuously into the Vietnamese economyover the past two decades. At the end ofOctober 2009, nearly 11,000 FDIprojects have been licensed (and still invalidity) to operate in Vietnam since1987, with a total capital commitmentworth almost US$175 billion; nearlytwo times Vietnam’s GDP in 2008.(Details of FDI capital by industry, inboth commitment and statutory con-tribution are provided in Appendix-A.)

The above US$175 billion FDI stockhas come from 89 different countriesand territories, among which ten

Table-1 : The Stock of FDI in Vietnam, by type of Investment

(figures in millions of US dollars)

No. of Projects Registration StatutoryCapital

100% foreign-owned 8,391 1,08,634 34,411

Joint venture 2,000 54,564 15,733

Business co-operation contract 221 4,961 4,479

Joint-stock corporation 183 4,711 1,354

BOT, BT, BTO contract 9 1,747 467

Investment holding 1 98 83

Total 10,805 1,74,715 56,527

Source : GSO and Vietnam Economic Times, 2009, Registration and Statutory Capital.

Mergers & Acquisitions Market in Vietnam’sTransition Economy

5

most important in terms of FDI regis-tration are shown in Figure-2. It is notdifficult to observe that regional econo-mies (ASEAN and Taiwan, HongKong) have by far been the mostimportant direct investors in Vietnam,followed by major world economicplayers, the United States (US) and Japan.A substantial portion of FDI also comesfrom the familiar tax-havens, Caymanand British Virgin Islands (BVI).

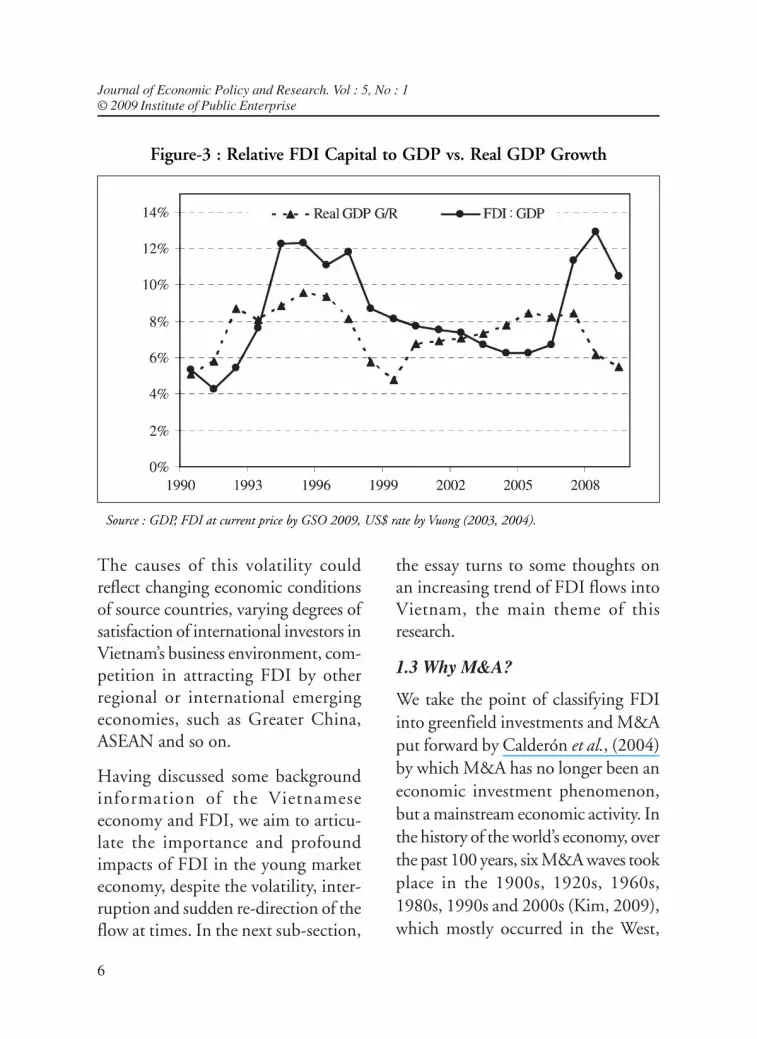

With respect to FDI economic flow,Figure-3 provides us with more insightsabout the relative contribution of realFDI disbursement into the economy.The solid line represents FDI-to-RealGDP statistic (FDI : GDP), where bothare measured in US dollars. The dash

line shows growth rate of GDP (RealGDP G/R). These data run from 1990to 2009, with 2009 data being reason-ably an accurate estimate.

Figure-3 helps us to realize that theannual flow of FDI capital to theeconomy is always substantial in realdollar terms since the beginning ofVietnam’s economic reform, whichnever falls below 4 per cent. Over thepast two decades of reform, there existonly two sub-periods, 1991-93 and2003-07, when the relative FDI-to-GDPratio is lower than real GDP growth ofthe country. However, the flow of FDIcapital to Vietnam exhibits a substan-tial volatility in some periods.

Source : Vietnam Economic Times, 2009. (Data point : Country; Cumulated FDI registration; Relativecontribution in percentage)

Figure-2 : Major FDI Sources

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

6

The causes of this volatility couldreflect changing economic conditionsof source countries, varying degrees ofsatisfaction of international investors inVietnam’s business environment, com-petition in attracting FDI by otherregional or international emergingeconomies, such as Greater China,ASEAN and so on.

Having discussed some backgroundinformation of the Vietnameseeconomy and FDI, we aim to articu-late the importance and profoundimpacts of FDI in the young marketeconomy, despite the volatility, inter-ruption and sudden re-direction of theflow at times. In the next sub-section,

the essay turns to some thoughts onan increasing trend of FDI flows intoVietnam, the main theme of thisresearch.

1.3 Why M&A?

We take the point of classifying FDIinto greenfield investments and M&Aput forward by Calderón et al., (2004)by which M&A has no longer been aneconomic investment phenomenon,but a mainstream economic activity. Inthe history of the world’s economy, overthe past 100 years, six M&A waves tookplace in the 1900s, 1920s, 1960s,1980s, 1990s and 2000s (Kim, 2009),which mostly occurred in the West,

Figure-3 : Relative FDI Capital to GDP vs. Real GDP Growth

Source : GDP, FDI at current price by GSO 2009, US$ rate by Vuong (2003, 2004).

Mergers & Acquisitions Market in Vietnam’sTransition Economy

7

where the economies had for long beenin a more advanced technological andeconomic conditions.

East Asian economies have participatedin this M&A trend since mid-1980sfollowing the trend of financial libera-lization and investment de-regulation,happening in almost every corner of theworld’s market economies, after FDIgreenfield investments in the regionaleconomy had become familiar andsome advanced economies of the EastAsian region had attained higher levelof development, led by Japan, SouthKorea, Taiwan and Hong Kong. TheAsian financial crisis also contributedto the surge of M&A activities in theregion, since this has shown some posi-tive perspective of financing duringpost-crisis projects and this is whatdebt-ridden economies need to do thefixing (Mody & Negishi, 2000).

Since Vietnam embarked on the FDIgame later than most regional econo-mies, M&A only appeared recently,only at the beginning of 1990s andwithout clear trend in the first ten years.However, with a deepening of thefinancial sector and much more openeconomy to international investors,both greenfield and M&A activitiesincreased significantly. From a handfulof deals in the early 2000s, M&Aactivities recorded more than 100 suc-cessful transactions in 2007. The trend

in Vietnam per se is consistent with thesuggestion by Lall (2002) which con-jectures that M&A would be an increa-singly important form of FDI and soonbecome the single most importantcomponent.

In international economic literature,studies on M&A activity has been well-documented and voluminous, at boththe global and regional scale of whichkeen attention has also been paidtoward M&As in the developing andtransition economies, including Easternand Central Europe, Asia and LatinAmerica (for instance, Katz et al.,1997; Lall, 2002; Bertrand & Zuniga,2006; Pop, 2006; Chand, 2009, justto name a few). While these literatureworks have brought light to ourunderstandings of M&A in variouseconomies, regions and industries of theworld, it is unfortunate that there hasbeen little discussion and virtually nosignificant research work devoted toM&A industry in Vietnam. Despitethe strong relation between and thegreat importance of both M&A andgreenfield FDI, we could hardly finddetailed studies discussing the connec-tion between M&As and FDI in theeconomy. This is probably because Viet-nam market is just in its infancy andthe chronic lack of reliable informationand economic data deterred scholarsfrom researching relevant academicquestions and producing sound work.

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

8

In Wang and Wong (2004), we realizethat both FDI and M&A requireappropriate policy-making process,adequacy of human capital and fullrecognition of related issues. These canbecome a direct motivation for thisresearch because M&A, as will be dis-cussed later in this article, has alreadybecome a trend, increasing one, withsimilar effects, negative or positive, tothe overall economy and the businesssector’s performance, in particular.

From the seller’s point of view, achronic disease in the economy is short-age of capital, both debt and equity.Even with the existence of Vietnamstock market in recent years, the situa-tion has not changed significantly, due

to low liquidity of the market and thestructural issue of the Vietnameseeconomy remains in favour of bankcredit and other types of finance thannew-issued equity. The capital shortageespecially for private sector firms hasbeen apparent and well-documented inmany studies such as Vuong (1997(a),1997(b), Vuong and Nguyen (2000)and Pham and Vuong (2009), althougha number of alternative financingoptions had been searched for, forinstance, financial leasing, unsecuredproject lending, corporate bond andmicrofinance (Vuong, 2004(a)). Natu-rally, one would have a question of therole of M&A in this emerging marketeconomy.

Figure-4 : Vietnam’s M&A Value by Seller (1991-98)

Source : United Nations Conference on Trade and Development Report (UNCTAD), 1999.

Mergers & Acquisitions Market in Vietnam’sTransition Economy

9

This study is pioneering to fill out suchgap, through which Vietnam’s M&Adata problem would be addressed at thebeginning of the process. This workaims to provide for a general under-standing of the context, analysis of theeconomic situation and to articulateinsights and implications on thecountry’s featuring M&A. In the nextSection, a substantial survey of theexisting literature on M&A and in part,FDI, is performed to equip us with thenecessary understanding provided bycontemporaneous scholars, before mov-ing on with the analysis of the Viet-namese M&A context.

2. Related Literature of M&A

We have mentioned that the literatureof M&A in the world is well-docu-mented and very large. In what follows,some selected works are going to bereviewed so that we could gain a betterunderstanding of how scholars havelooked into the M&A industries andtheir related issues and what resultscould benefit this research undertaking.

2.1 International Studies on M&A

We start this review with a good accountof details of M&A history which couldbe traced back to the 1890s, docu-mented by Kim (2009). The first waveoccurred in the US and Europe in thelate 19 century and usually formed sometype of monopoly through horizontal

integration within industries. This earlyevolution ended in 1903-05 whenstock markets crashed.

A second wave began as a response tothe enforcement of anti-trust legislationwhich was the result of the public con-cern over large conglomerates andsuper powerhouse in the US economy.This time, firms pursued expansionsthrough vertical integration, generatingthe second wave of M&A, starting inthe late 1910s and ending in 1929 whenthe stock market crashed.

The third wave started in 1965 andended in 1973. Due to the economicdepression and the second world war,no significant activities occurred in thisperiod. The fourth wave was set off bythe so-called environmental transition,such as changes in anti-trust policy,de-regulation of financial sector, newfinancial innovations and markets andrapid advances in technology andapplied sciences. Many hostile take-overs and on-going private transactionstook place in this period, which startedin 1978 and finished in 1989.

The fifth wave started in 1993 alongwith a new economic boom phase andhalted when the bubble burst in 2000.This wave witnessed a largest ever totalglobal value of M&A transactionsworth US$15 trillion, more than fivetimes the combined total of the 1978-89period. Also, during this time, the AsianM&A market started emerging.

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

10

The most recent M&A boom periodbegan in mid-2003, when the increas-ing M&A activities occurred in majoreconomic regions of the US, the EUand East Asia following the economicand financial recovery. China, India andthe Middle East also entered this stageas new major players. Hostile takeoverswere strong in Japan and China. InKim (2009), the fact that many com-panies tried to acquire other companiesthrough M&A without much valueincrease indicates that M&As are pur-sued with a long-term growth purposerather than for chasing short-term pro-fits. As far as cross-border M&A is con-cerned, industrial environment and stra-tegic pursuit, including alliance, repre-sent two major driving factors. Further-more, Öberg and Holtström (2006)add that besides the reasons to mergeor acquire as strategies of the mergingor acquiring parties, M&As are contex-tually driven with the existence ofparallel M&A transaction, for instance,between the customer and the supplierfirms in the economy.

A substantial amount of the world’sM&A value belongs to the powerfulbanking houses and the work of Focarelliet al., (2002) is credited for valuableinsights into the banks’ motivation forthis trend. Banking institutions havelong had motivations behind theirM&A activities being strategic pursuitof diverse banking services. Notably,

before the merger endeavour, the activebuyer bank derived a high share ofincome from services. It might havewanted to offer its innovative productsto the customers of the target bankwhich was currently not providing themto existing clients. Banking M&A dealsmay also be able to help banking firmsto improve immediate quality of assetportfolio and, in many cases, to increasecapital adequacy as risk cushion, whenfacing new reserve requirement. Andimportantly, the authors conclude thatno significant evidence of an improve-ment in profit is found after a mergerand this is different from the ex anteexpectation set out by many executivesor at least in their communication to theshareholders. The results are consistentwith those found when performingtests using the US empirical data.

Within the financial economics litera-ture, a substantial amount of studies isdevoted to empirical investigation onpost-M&A performance, in general andmarket values and abnormal cumula-tive returns of buyer and target firms.An early contribution is Block (1968)which through performing a parametrictest aims to verify the hypothesis ofsignificant differences in stock behavioursof merging and non-merging firms.The result is that in general, the mergereffect on the stock of the acquiringcompanies is somewhat neutral.However, the effect on acquired firms

Mergers & Acquisitions Market in Vietnam’sTransition Economy

11

in terms of stock behaviour is substan-tial and responsive. We could notice anunderstanding that a potential acquiredfirm’s stock many-a-time represents agood investment, while the transactionmay make the acquiring firm lessattractive. Another research effort in thisaspect of M&A is Shick (1972) whichfocuses on measuring the returnsbrought about following a mergertransaction, using the prevailing valua-tion model and empirical data selectedfrom the US chemical industry. Shickestablishes that merger return formulacould be built successfully based oncommon stock valuation model. Usingthis, the empirical evidence suggeststhat a merger could result in positivereturns and the success or failure of amerger could be judged almost instantlyafter the transaction concludes. How-ever, in the recent edited volume onregional M&A perspectives, Chand(2009) re-visits the value creation issue,discussing a number of numerousscenarios under which M&As can createvalue for the acquiring or merging com-panies. It does not assert that all suchattempts would indeed create value inthe end due to the possible complica-tion arising in the transaction process.

In between the two M&A waves of the1960s and the 1980s, Ijiri and Simon(1971) made an attempt in gaugingeffects of M&A activities on businessconcentration. Their empirical results

from their own model for investiga-ting whether Pareto and Gibrat’s Lawshold for the research of 1960s US datasetand hypothetical relationship (equi-librium equations) lead to an impor-tant finding that the concentrationmeasure following M&A activitiesremains, to a large extent unaffected.The result rejects the then widelyaccepted position that mergers wouldlead to increased concentration and,thus, reduce competition. From theother view, Werhane (1988) discussesethical issues following M&A. Twomajor issues that prove to be of pri-mary concern are : (i) the rights ofemployees would likely be affected; and(ii) the responsibilities of shareholdersduring the M&A undertaking. Thisview is also re-affirmed in the recentwork of Chand (2009) which articu-lates that growth of firms can beachieved through organic growth (in-vestment/re-investment in a new plant)or M&As (mergers, acquisitions stra-tegic alliances) under forms of horizon-tal, vertical and conglomerate (i.e.,firms in unrelated industries). Duringand after a M&A transaction, theundertakings have influences on manystakeholders, not just on share value.Thus, other stakeholders in the firmtend to have different priorities.

In a general understanding that amajor portion of M&A transactionsand values are undertaken by powerful

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

12

Trans-national Corporations (TNCs),Lall (2002) studies their implicationson cross-border M&A in the develop-ing countries. The work articulates asimilar point as what was discussed ear-lier that international M&As now be-come “the most important forms ofFDI, far outstripping investment in thenew facilities (greenfield) in terms ofvalue”, citing United Nations Confe-rence or Trade and Development(UNCTAD) and World InvestmentReport’s statistics and estimates thataround 80 per cent of FDI in deve-loped countries have been in the formof cross-border M&A. In less developedeconomies, M&A already reached arecord level of 40 per cent of the totalFDI inflows in 1998.

This work supports the existence of sig-nificant differences between TNCentry by greenfield FDI and M&A, interms of the impacts on host econo-mies, most of which manifest them-selves in the short-term. Lall (2002)empirically rejects the general presump-tion of ‘superiority’ of greenfield invest-ment over M&A, while Raff et al.,(2006) suggests a strong interdepen-dence between different forms of M&A.

Also in the line of research on cross-border M&A and performance ofTNC, theoretical foundations of cross-border M&As are reviewed in Shimizuet al., (2004) in the current context thatempirical results regarding determi-nants of M&A are mixed. Technical

aspects of M&A process such as duediligence exercises and legal verificationcontinue to be financially and time-consuming and still need further litera-ture for our better understanding. Theliterature could help practitioners learnfrom past lessons and derive importantinsights from this complex field ofbusiness, especially with cross-borderM&As. As the importance of andopportunities from cross-border M&Asare likely to increase further in the glo-bal economy, learning from acquisitionexperience could be a critical source ofcompetitive advantage. Countriesdiffer in their institutional contexts and,thus, in the types of corporate gover-nance mechanism utilized. Therefore,governance problems related to M&Asrequire more research efforts.

From an operational view, Rossi andVolpin (2003) study determinants ofM&A activities using empirical data,1992-2002, from 49 target countries,including a bit of Vietnamese data (notsubstantial) which exhibit the volume,the incidence of hostile takeovers, thepattern of cross-border deals, the pre-mium and the method of payment.The work suggests that right protec-tion on M&A and cross-border take-overs could be efficient catalysts forimproving corporate governance,a much desired goal in any re-structur-ing process. Khimizu et al., (2004) alsopresent a similar position on corporate

Mergers & Acquisitions Market in Vietnam’sTransition Economy

13

governance issues which should enablea more favourable and productive eco-nomic transformation.

In a wave of cross-border M&A withinthe developed economies of Organiza-tion for Economic Co-operation andDevelopment (OECD), Bertrand andZuniga (2005) extend their effort to in-vestigate M&A transactions in conjunc-tion with issues in Research and Deve-lopment (R&D) investments in OECDmember economies in 1990s. A mainaddressing of the study is on the ques-tion of whether there exists significantdifference in likely impacts on indus-trial innovations between national andcross-border M&A operations.

The authors use GMM to estimate adynamic linear model for R&D invest-ment and control for market-relatedand technological determinants ofR&D production. Their results showthat the latest M&A wave in OECDhas not resulted in a significant effecton domestic R&D activities at the in-dustrial level. M&A only seems to haveplayed a role in some specific groupsof industries. In addition, results sug-gest that domestic and cross borderM&A differed in their impact on R&Dinvestment. It appears that domesticM&A activities generated positiveimpacts on R&D activities in low-techindustries. Interestingly, they presentthe insight that indicates mainly targetfirms seemed to benefit from M&A

operations in their sample, but notbuyer firms at home countries. Thiswork is basically a counter-argument tothe general public opinion that consi-ders foreign takeovers fearful.

With respect to M&A operation intransition economies, Pop (2006) pre-sents some results obtained from ananalysis of the Romanian case, whereapproximately 500 privatized firmswere targets of takeovers. The studyfocuses the effect of takeovers on thetargets’ performance, mostly listed firmson Romanian RASDAQ, over the1998-2002 period. Empirical results oftheir multivariate regression analysisreject any evidence of significant abnor-mal returns of the target, based on listedstock prices.

In a more national industry-specificstudy using basic computations andsurvey data, Beena (2007) researchesthe performance of post-M&A phar-maceutical firms licensed to operate inthe Indian emerging markets. The studyuses a sample of 32 merging firms ofwhich 20 belong to the domestic sec-tor and 38 merged firms of which 20are domestic. The report shows thatmany merging firms are engaged inmultiple mergers.

Domestic merging with domesticaccounted for 64 per cent of the totalnumber of mergers, foreign with foreignconstituted 26 per cent. Large-sized

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

14

firms accounted for 60 per cent of thetotal mergers, medium-sized 38 percent. More than 85 per cent of themergers in Indian pharmaceutical pro-ducers were horizontal type. In this sur-vey, Beena reports that cross-borderM&A deals account for about 28 percent and foreign-invested firms show aclear trend of acquisitions and strategicalliances, compared to domestic ones.

The result of this survey indicates thatthe merging firms, less than 10 per centof all firms in this industry, their over-all performance has been far better thanthe rest of the Indian pharmaceuticalindustries. The post-merger perfor-mance of the undertaking firms has alsoshown a general improvement com-pared to their own pre-merger periodlevel.

2.2 The Regional and VietnameseLiterature in Relation to FDIand M&A

The M&A markets in Asia have becomeincreasingly important as their share inthe worldwide transactions increasedfrom 8.5 per cent in 1995 to 17.7 percent in 2008. The total value of theM&A transactions also increased from13.3 per cent to 20 per cent during theperiod (Kummer, 2009). The figureper se is adequate to understand the roleof M&A in the financial economicsliterature of the regional economy.

M&A activities are useful for re-struc-turing business firms, at least in the eraof fast-changing economic conditionsand post-crisis consolidation. The roleof cross-border M&As in the Asianeconomic re-structuring, presented byMody and Gegishi (2000) is relevantto our understanding. In East Asia,Korea and Thailand have been attrac-ting large volumes of M&A activitysince 1997. The recent M&A activitiesstem from two distinctive motivations :(i) resolving past problems; and(ii) grasping prospective opportunities.Within the developing countries, LatinAmerica has been the largest targetregion of cross-border M&As, most ofwhich have been through privatizationprogrammes. East Asia is the fastestgrowing target region, growing at anannual average rate of 106 per cent. Inthe world, M&As have been donelargely by selling private firms.

The post-crisis economies, especiallythe emerging ones at times, render theirfinancial assets under-valued, togetherwith critical exchange rate depreciationin favour of acquiring the firms’ homecurrencies. Therefore, it is not uncom-mon that M&A activities surged in thepost-crisis recovery phase in the emer-ging markets. Crisis economies also needto improve their policy frameworks inorder to encourage foreign capital byliberalizing their economy, for at leasta medium-term recovery process which

Mergers & Acquisitions Market in Vietnam’sTransition Economy

15

could possibly help their domesticfirms solve the debt payments andre-structuring. After the 1997-98 finan-cial crisis in East Asia, cross-borderM&A activity has largely concentratedin the most troubled sector of the crisiscountries and many regional govern-ments have taken steps to incentivizeM&A for consolidating their financialsystems through both private and regu-latory incentives. Sales of financially dis-tressed firms to foreign entrants willbenefit the host countries, particularly,if ‘fire-sale’ can be prevented using com-petitive auctioning. Foreign acquiringfirms are expected to bring in bothmanagement and financial resourceswhich are necessary conditions for fix-ing target firms’ inefficiencies.

Although there is little evidence to sug-gest that cross-border M&As havemade immediate contributions tore-structuring of the troubled economies,the most significant role of cross-bor-der M&As lies in longer-term re-struc-turing processes such as operationalre-structuring and more productivere-allocation of physical and financialresources in the regional economies.

Ramlee and Said (2009) on trends andpractices in Malaysian financial indus-tries provide some useful insights and,more importantly, may be comparableto the recent M&A trend in Vietnam’sfinancial sector, including noticeable

cross-border transactions, such asHSBC-Techcombank as we will analyzelater. The article reasons that glo-balization, financial de-regulations,advances in technology, cost savings andthe desire for acquiring larger marketshares are forces prompting commer-cial consolidations taking the form ofM&A. Malaysian M&A activities aswith most of its ASEAN neighboursare non-market driven. The 1997 crisisexposed fragilities of the Malaysianbanking sector and economy and thereneeded a push to correct weaknesses inthe banking system. The governmentsaw the development of the bankingsystem as vital in facilitating recovery.This is rationale for the Malaysianbanking to speed up consolidation.

Subsequent relaxing of legal restrictionson foreign participation and the searchfor profit opportunities in the emer-ging economies, have led to the grow-ing presence of foreign-owned finan-cial institutions in domestic bankingsystem. Those who promote consoli-dations by M&A method postulatethat the activities help improve boththe general degree of economic efficien-cies and firm-level competitiveness inparticular. Larger banks also want to belarger because of the belief that thegovernment will not let large banks failas it could lead to panic.

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

16

In the first stage, banking industry wasfragmented but heavily protected andregulated. In the 1980s, banking sys-tem, comprising of many small banks,was poorly diversified geographicallywith inefficient management. In thesecond phase, the banking industry wasde-regulated and interest rate ceilingsand lending rates were left for the banks’determination; central bank just pro-vided guidelines. In phase three, banksexpanded their scope of activities. In theperiod 1999-2000, Malaysia accountedfor 41 per cent of the total deals and38 per cent of the M&A transactionvalue of target firms in ASEAN.

In a research of the Philippines’ marketfor large-scaled bank M&A, Castillo(2009) claims that the M&A activitiesare subject to substantial regulations,despite de-regulation in financial ser-vices industry from the late 1980s. Itprovides context and history of thePhilippines’ banking systems from the1950s to present and discuss regula-tions which are introduced to facilitateor prompt M&A in the banking sec-tor. The current trend in M&A is pos-tulated to have emerged from the mid-1990s consolidation in the financialsector, causing a wave and then fol-lowed by post-1997 monetary crisisconsolidations. It concludes that banksconsider M&A a method to improvetheir financial positions and competi-tiveness, although little empirical

evidence has employed to reach that.Banks also use M&A as a way to fendoff competition by remaining power-ful financial services players in metro-politan hubs. In addition, we could notrule out a high possibility that the pur-poseful consolidations could trigger awave of M&A that could result in anoligopoly structure creating problemsfor the Philippines economy andsociety. Thus, socio-economic impactsof M&A could be double-faced.

Yasumaru (2009) discusses the rationalefor the Japanese Small and MediumEnterprises (SMEs) to adopt M&Ain a recent period of its economicevolution. Typically, there are fourmajor options to further develop ormaintain existing businesses of SMEs :(i) go public : this is not an easy optiondue mainly to strict regulatory criteriaof internal control and observance oflaws which usually incur the highestcosts of expenditure and time; (ii) pass-ing control within the company : thischoice faces a dilemma that founders’offspring normally want to pursue theirown interests while they may not havethe right charisma to take on the job;(iii) liquidation of firm : A choice thatis not considered optimal in terms ofretaining the firm’s long-term corevalues and sustainable employment,conventionally lifetime commitment inJapan; and, (iv) merger : The societyconsiders this a better option because

Mergers & Acquisitions Market in Vietnam’sTransition Economy

17

by undertaking merger, small firmscould have better access to both creditand equity finance, while the firmscould still secure jobs for currentemployees.

In the first Japanese M&A boomperiod, 1989-90, when many Japanesefirms bought American interests andreal estates, thanks to the JPY appre-ciation and abundance of bank liqui-dity, ex ante expectations were not rea-lized later because real estate bubble burstleading to the following down-slopingM&A trend in Japan. The second wavebegan in 1999, fueled by revisions oflaws and tax regulations and the emerg-ing sector of information technologyand telecom. When the tech-bubblefizzled out, the M&A activity quicklyvanished.

The Post-merger Integration (PMI)issue is discussed in Kummer (2009),in which the author aims to articulatethe importance of PMI in a successfulM&A transaction. In this discussion,many M&A transactions are said tohave been unsuccessful, with the typi-cal success rate being a modest 25 percent and in the best case scenario thatprobability only reaching 50 per cent.The author singles out one critical fai-lure factor : the poor PMI result. In theregion, the reasons for this failure areusually inadequate attention to strategymaking for deals, while the earliest steps

have substantial impact on PMI andinappropriate and ineffective due dili-gence process, mostly comprising ofreality check and obtaining actionableinsights. Not less important are cross-cultural issues, especially to cross-bor-der M&A activities, also advocated inShimizu et al. (2004)

Employing the multiple-case researchmethod, Deng (2009) goes on givingus more insights into the reality andreasoning of more Chinese firms com-ing in the game of cross-border M&Aas a means to access and source strate-gic assets, addressing their own com-petitive disadvantages from an institu-tional perspective. In this discussion,the importance of institutional con-straints and prior experiences affectingM&A determination are highlighted.Chinese firms seek to acquire strategicassets which they could not have athome in order to compete in highlycompetitive international markets. Thetrend happens when many globalplayers revise their investment strategy,in many cases using M&A to divestfrom their non-core activities. And thisdiscussion is both compatible and sug-gestive for the case of Vietnam’s M&Aprocess.

The fact that a very large stock of FDIexists in China is also compatible to thesituation of Vietnam, as presented inFigure-3. In both the situations, FDI

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

18

flows also stimulate cross-border M&Atransactions, inward and outward.However, in the current trend of theChinese economy, more Chinese firmsgo overseas to primarily enhance afirm’s critical competence rather thanto exploit existing assets, while this maynot hold for Vietnamese firms. Authorsarticulate that interactions betweenfirms and government can have sub-stantial influence on government poli-cies which is in line with the sugges-tion by Vuong and Tran (2009(b)) forthe contemporaneous socio-culturalcontext in Vietnam.

A final result of this research that maybe highly relevant for Vietnameseenterprises is that domestic firms mightnot find M&A pursuits, inward or out-ward, very productive and financiallyrewarding, if the sole purpose is to seekmarket expansion.

Equipped with the above-discussedresults and suggestions from variousresearch works and authors in this lineof financial economic literature, we nowspearhead our effort to find suitableconnections and research results articu-lated particularly for the Vietnameseemerging market economy.

The first noteworthy point is thatalthough the authors of this article havemade substantial effort in searching foracademic assessment and results whichare directly related to the M&A activities,

the outcome has been very limited.Therefore, a substitution that enlargesthe scope of our review appears to bemore productive and useful. In fact,much of our review, purposefully aim-ing at insights and implications for theVietnamese context of M&A activitiesis performed with the literature ofFDI.

An additional note to our previousopening discussion on FDI in Vietnamis that Vietnam shares much of theChinese experience in regulating theeconomy with a normative temptationthat “the government should do more toset the rules governing FDI and M&A”.This is consistent with a considerationof the rules with a very powerful statealso functioning in the marketplace(Vuong & Tran, 2009(b)). It appearsthat this argument is further bolsteredwhen these young market economiesare faced with economic crisis, finan-cial market meltdown or are adverselyaffected by international market forcesand globally changing conditions (seealso, Vuong & Tran, 2009(a)).

Leproux and Brooks (2004) discuss thenecessity of the continuous flows ofFDI to the Vietnamese transitioneconomy. The point is also supportedby Vuong (2003, 2004(a), 2007) andPham and Vuong (2009). The capacityfor the Vietnamese economy to absorbnew FDI in the future depends much

Mergers & Acquisitions Market in Vietnam’sTransition Economy

19

on how the country addresses theeconomic, political and institutionalweaknesses.

Most economists agree that inward FDIhas important impacts on the Vietna-mese economy, especially in : (i) provi-ding important financial resources;(ii) financing the rapid growth that Viet-nam has experienced over 20 years; and(iii) providing market access for risingexports. Although the impact on emp-loyment has not been as expected, stillthe FDI sector plays an important rolein introducing new ideas and processesin elevating skills and knowhow andproposing models that have beencopied by domestic investors whose eco-nomic background was formed in acentrally planned economy. In addi-tion, in Pham and Vuong (2009), theissue of general level of economic effi-ciency in the Vietnamese economy hasbeen chronic with high ICOR and thestate’s investments overshadowingother sectors of the economy. This maycause both unfair competition in themarketplace and discouragement forthe re-structuring of the state-run firmsand the economy, a major and directmotivation for FDI flows in the formof M&A.

Another important attribute that theeconomy expects from both greenfieldFDI and M&A activities is a generalcondition for improving human capital

and its accumulation process as high-lighted in the result of Wang and Wong(2004). We also realize that at somepoint, there exists the question “Isgreenfield FDI better than M&A?” Lall(2002) and other works find the ques-tion groundless and again Wang andWong (2004) provide a suitable answerfor such consideration in Vietnam thatis the answer lies in an adequate prepa-ration and resource for human capitalaccumulation, not the M&A per se. TeVelde (2001) emphasizes a critical needfor implementing an effective compe-tition policy and this proves to be ofprimary concern in the case of Vietnamwhere the socio-cultural contextfavours some interest groups whichcould undermine the effort of build-ing its market economy in transition(Vuong & Tran, 2009(b)).

Although there are different forms ofFDI in Vietnam’s economy, Raff et al.,(2006) find a strong interdependenceamong different modes, i.e., greenfieldinvestment, acquisition of or mergerwith domestic companies, joint ventureor any other kind of co-operation. Ithas been suggestive that greenfieldinvestment decision has something todeal with export opportunities. Ifgreenfield investment is more profi-table than exporting, this reduces theprice the multinational has to offer toacquire a local firm with the conse-quence that a TNC may prefer M&A

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

20

to greenfield investment. This result isconsistent with real-world practices andconsiderations during M&As in Viet-nam and not only limited to TNCs butit generally holds for mergers amongVietnamese firms and even in case Viet-namese firms acquire part of TNCs.

We also see the relevance of both FDIand M&A with Calderón et al., (2004)which looks closely into the fact thatacquisition of existing assets by M&Ahas grown rapidly since the 1990s.Their results provide us with animportant implication on the likelyeffect of M&A to the politically correctspeaking, ‘equitization’ process in Viet-nam (where state-owned firms becomemulti-ownership through sales of sharesto the management, staff, strategic busi-ness partners and the public). Using thedata from 72 countries from 1987 to2001, Calderon et al., suggest that inall samples, higher M&A is typicallyfollowed by higher greenfield invest-ment, while the reserve is true only forthe countries. In general, FDI inflowsusually induce domestic investments,at some time lag. However, there hasbeen no firm evidence that domesticinvestments would likely cause to FDIflow. FDI inflows do not necessarilyestablish the cause of subsequent eco-nomic growth in the recipient econo-mies but these investments ratherrespond positively to the economies withsignificantly improved growth rates.

In the light of this, we see the consistencyshown by high growth sub-periodsin Vietnam inducing fast-growinginward FDI and a surge in M&A in2006-2007.

We also note that six years after itsinception in July 2000, Vietnam stockmarket started growing quickly in2006, providing a new source of liqui-dity for business firms in Vietnam,including FDI enterprises in variousindustries. Now FDI, M&A and port-folio investments have become moreinterdependent in reality. This point isbrought up also by Tolmunen andTorstila (2005) saying that firms thathave a near plan for listing usuallyinduce more M&A intents and realiza-tions. The reality in Vietnam’s emerg-ing capital market in 2006-2009 hasthus far been consistent with this argu-ment.

The above review enables us to formu-late our relevant questions on severalpolicy and technical aspects of theM&A activities in Vietnam which leadto our next Section of organizing datafor further analysis.

3. Data and Methodology

As we mentioned during the reviewingof literature, there exists virtually nosubstantial work directly studyingM&A in Vietnam, although manyauthors did extend their effort to the

Mergers & Acquisitions Market in Vietnam’sTransition Economy

21

academic studies on FDI in Vietnam.Thus, this research uses a unique andperhaps most complete, dataset orga-nized and compiled by the authors withthe assistance from research associatesat DHV&P. We would briefly describethe dataset below and, then, present ourmethods of analysis next.

3.1 Empirical Data on the Viet-namese M&A Market

In this research, we construct a datasetusing various sources of information,namely : (i) press release by firms;(ii) public media analyses where somedetails of M&A transaction are unveiledat times; (iii) direct interviews withreliable sources mainly senior managersat securities firms or buyer/seller firmsin M&A transactions; and (iv) occa-sionally, separate reports by the finan-cial sector.

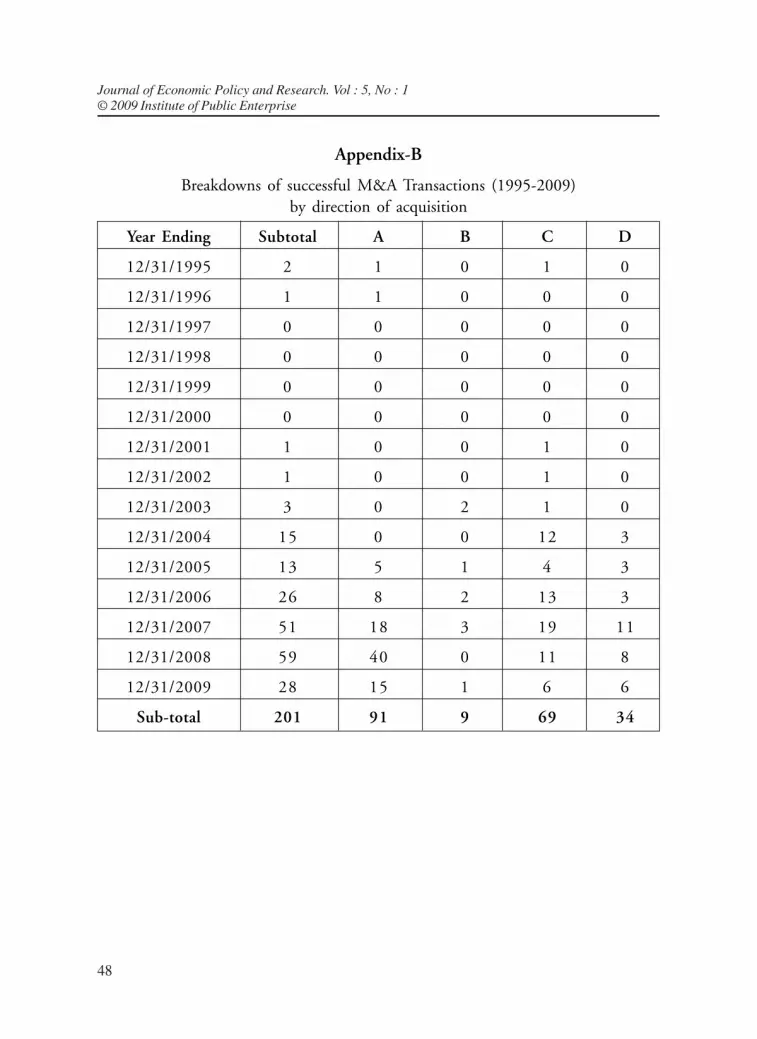

The dataset comprises of 252 entriesfor four categories of M&A : (A) foreignfirms acquiring foreign firms;(B) foreign firms acquiring Vietnamesefirms; (C) Vietnamese firms acquiringforeign firms; and (D) Vietnamesefirms acquiring Vietnamese firms. Assuch, the dataset is not limited to onlycross-border or transactions amongdomestic firms. Almost all data entriesthat could be identified have beenincluded in this set. In the course ofcollecting data with our serious conside-ration of the data integrity, careful check

and a sound judgement on which toinclude or exclude, we have come to areasonable assessment that this datasample of M&A transactions in Viet-nam can de facto represent approxi-mately 40 per cent of the total marketand it is only a sample that we couldgather with an adequate degree of con-fidence to put it in analysis.

Our dataset spans over the period from1990 to 2009 which corresponds toFigure-3 for FDI and GDP data. Thisperiod contains two active sub-periodsof 1993-95 and 2006-08. Although wecould not verify the accuracy of M&Adata provided by the UNCTAD 1999report, but the reality is that there werean increasing number of transactionsoccurring in the 1993-95, due toconsolidations of some investmentfunds and a wave of investments inspeculating the lifting of US tradeembargo against Vietnam that was laterannounced by President Clinton inFebruary 1994.

Each data entry contains useful infor-mation of date, type of M&A (asdescribed above), target and acquiringfirms, industry, status of transaction,value in dollar term and equity stakeof the transaction in percentage. Dueto the absence of a system for trackingM&A transactions, data point mayhave full or only part of the attributesthat we wish to collect. In this dataset,

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

22

the data quality issues constantly lie intwo main data fields of transaction valueand/or the equity stake that is intendedfor in the transaction. Sometimes, thevalues are not unveiled or cannot betracked. In other times, the informa-tion that is accessible turns out notaccurate. To address these issues, we optto leave the values empty in the dataTable, so they are not treated in lateranalysis.

Some caveats with data quality :During the process of data collectingand preliminary assessment, we fre-quently encountered the issue of qua-lity with public media. In many reports,portfolio investments mixed up withM&A activities. In some other cases,reporters may have inferred values oftransactions using nominal price or self-estimated subjective values. Both couldhave led to confusing aggregate valuesreported by different sources. Thus, itis suggested that aggregates in theM&A market in Vietnam should beused with caution and reservation if weare to draw significant conclusions. Thisresearch is, therefore, not relying on theaggregates, but using our dataset withnecessary attention to possible bias dueto incompleteness of data.

3.2 Our Method of Analysis

At this point, we need to state clearlythat although this dataset is to our bestunderstanding and knowledge, the

most up-to-date and complete, the lackof a relevant paradigm for the treatmentof the data makes it almost impossibleto identify a suitable econometricframework and specification. In theabsence of a general hypothesis, it is ourbelief that a better method of analysisis to go for insights from basic treat-ment of data, subject to varying levelsof completeness and judgementalvalues. Therefore, this study mainlyemploys basic statistical analysis com-bined with qualitative judgementstowards hard-to-be-quantified issuessuch as regulatory framework, environ-mental variables, socio-cultural aspectsand subjective public assessments whichcould lead to different behaviours inand form ex ante expectations for eachM&A deal.

The main quantitative analysis focuseson assigning data entries into variousrelevant classifications, trying to capturemeaningful insights from the dataset.The criteria for defining the relevanceof data treatments are the analyticaldepth we wish to obtain to articulatemost useful understanding, be it a veri-fication of an already postulated posi-tion or a new finding. Statistical dis-crepancies and contradictory results,speculations, if appearing during theanalysis, will also be reported forbetter understanding and judgement ofthe practical situation.

Mergers & Acquisitions Market in Vietnam’sTransition Economy

23

Part of the analysis will be in the formof critical reasoning which is usuallyuseful and applicable when data are notvery useful or the use of data may causecontradicting insights. A discussionwith regard to policy and regulationissues will also be included.

Toward the end, the results of analysiswill be discussed in comparison withother works, whenever possible, as thiscould help exhibit both similarities anddifferences between M&A market inVietnam and in the world out there.

4. Analysis and Results

Having stated our principles of analy-sis above, this Section is now movingon to present facts and findings, whichare obtained from our statistical con-siderations and suitable qualitativeassessments.

4.1 Some Statistical Analysis

The dataset contains 252 records ofM&A transactions, announced, pur-sued and realized by both acquiring andtarget firms operating in Vietnam from1995 to 2009. The estimated totalvalue intended for through these M&Atransactions is US$4,003 million,using the verifiable and reliable statistics.However, this aggregate is below thereal total value since individual valuesof nearly 32 per cent of the transactionsthat were successfully completed havenot been accessible1. Also, there are a

number of transactions in type ‘C’ thatare taking place outside Vietnam.Therefore, we could estimate, with rea-sonable accuracy that the M&A mar-ket in Vietnam has a total transactedvalue of approximately US$10 billionin this period (1990-2009).

4.1.1 Market Share

Firstly, we derive Table-4 from the com-plete data sample to investigate the datamore closely. It is noteworthy that themarket belongs to foreign acquiring/merging firms. These firms representedby ‘A’ and ‘C’, account for 79.4 per centof the M&A attempts, be it success,failure or pending (200/252 cases).Thus the trend for the 1990-2009period is clearly seen as foreign firmsproactively acquiring/merging withexisting entities operating in Vietnam.

Now we are able to look at the successrate of M&A deals in the 1990-2009period which were announced andtraceable by different sources of infor-mation with a summary being providedby Table-2. The success rate is very high,above 80 per cent, compared to 6 percent announced failure and nearly14 per cent of transactions pendingwith unclear results. This fact needs anexplanation, the job that we will performin the upcoming discussion sub-sections.

Among different directions of M&Asin the Vietnamese markets, categorizedin Table-2 by ‘A’, ‘B’, ‘C’ and ‘D’,

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

24

Table-3 shows us some useful insightsobtained from the overall data sample.Firstly, the varying degree success ratecan be seen clearly. When foreign firmacquires a domestic equity stake ‘B’, theconfidence of concluding the deal ismuch higher, almost 91 per cent, com-pared to the second best rate of 83 percent for M&A among Vietnamesefirms and nearly 75 per cent for theopposite direction, that is when a Viet-namese firm acquires a foreign one ‘C’.

Our sample shows that failure rate ishigher when the target firm is a domes-tic operation, with both ‘A’ and ‘D’being 7.3 per cent. When the target firmis a foreign entity, failure rate reducessignificantly. For the transactions with

unclear results classified as pending,only transactions among foreign firmsexhibit a substantially higher rate, nearly20 per cent for ‘C’, while the pendingrate for the other three directions runsin a narrow range of 9-12 per cent.

4.1.2 Market Timing

Figure-5 shows a recent trend observedfrom our data sample with the solidline representing a number of M&Aattempts and the dash line, successfultransactions.

Both the numbers of total of transac-tions and successful deals have beenincreasing substantially since 1994.M&A activities mushroomed in 2006,2007 and 2008, with its momentum

Table-2 : Summary Statistics on Transaction Status by Type

No. of Cases A B C D

Success 202 89 10 69 34

Failure 15 8 0 4 3

Pending results 35 11 1 18 5

Total 252 109 11 91 41

Table-3 : Transaction Status in Direction of M&A

A B C D

Success 81.7% 90.9% 75.8% 82.9%

Failure 7.3% 0.0% 4.4% 7.3%

Pending 10.1% 9.1% 19.8% 12.2%

Total 100.0% 100.0% 100.0% 100.0%

Mergers & Acquisitions Market in Vietnam’sTransition Economy

25

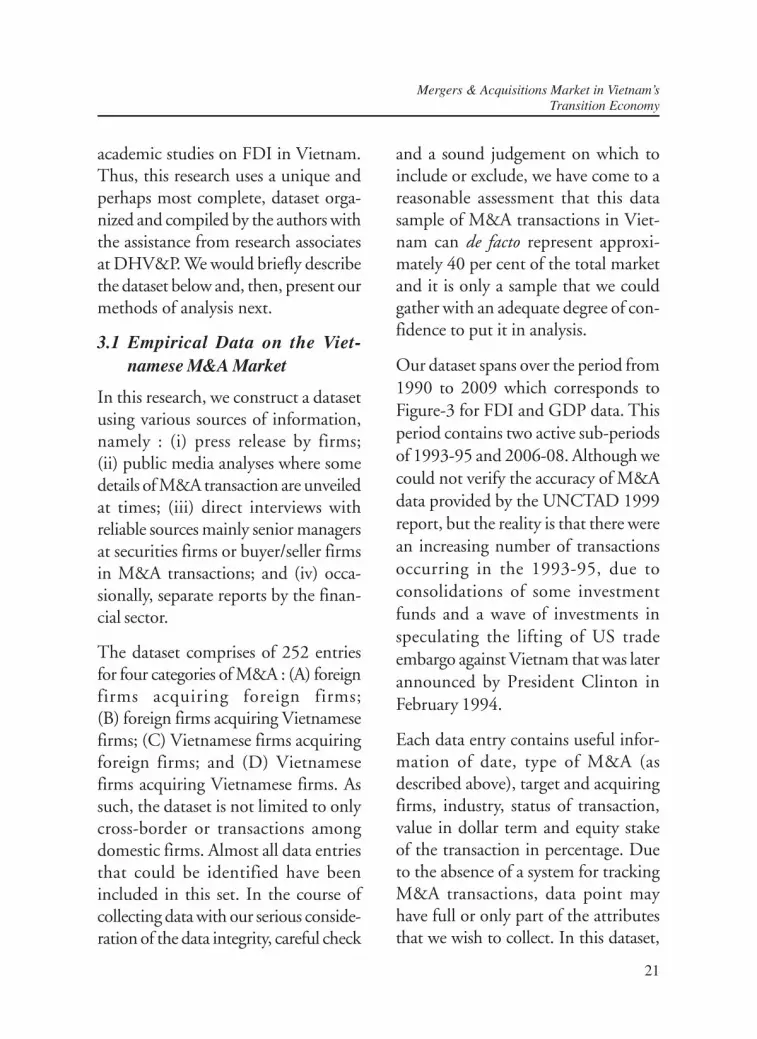

being carried on until 2009. Thepattern of both successful and unsuc-cessful attempts, however, exhibits a highdegree of volatility through largechanges in the number itself and thetiming when attempts are made in theevolution of M&A activities. The cor-relation co-efficient for the two linesin Figure-5 is +99.6 per cent, confirm-ing that the pair of data to be almostperfectly positively correlated.

We are now ready to ‘decompose’ thedash line of Figure-5 into constituentcomponents as presented in Figure-6where the numbers of successful M&Atransactions are classified into direc-tions of realization. It is noticeable that

before the substantial drop in all direc-tions in 2009, the M&A market inVietnam had appeared to be ‘steady asshe goes’, since 2004.

The steepest curve also belongs to themost active category of transaction, thatis foreign firms acquiring the local firms.And the correlation co-efficient of annualdata series for type ‘A’ transaction andthe total number of successful attemptsis +93.0 per cent, just a marginally lowerthan the correlation statistic reported inFigure-5. Although there did appeartiming for many more transactions ofthe other M&A types to have takenplace, they exhibit almost non-trendedfluctuations.

Figure-5 : Attempts vs. Successes (1995-2009)

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

26

Table-4 reports a changing level of cor-relation for different pairs of databetween total number of successfultransactions and that of each category.The most stable, although not thehighest, is type ‘A’, while the rest clearlydrop in the most active period of M&Ain Vietnam, i.e., from 2004 to 2009.

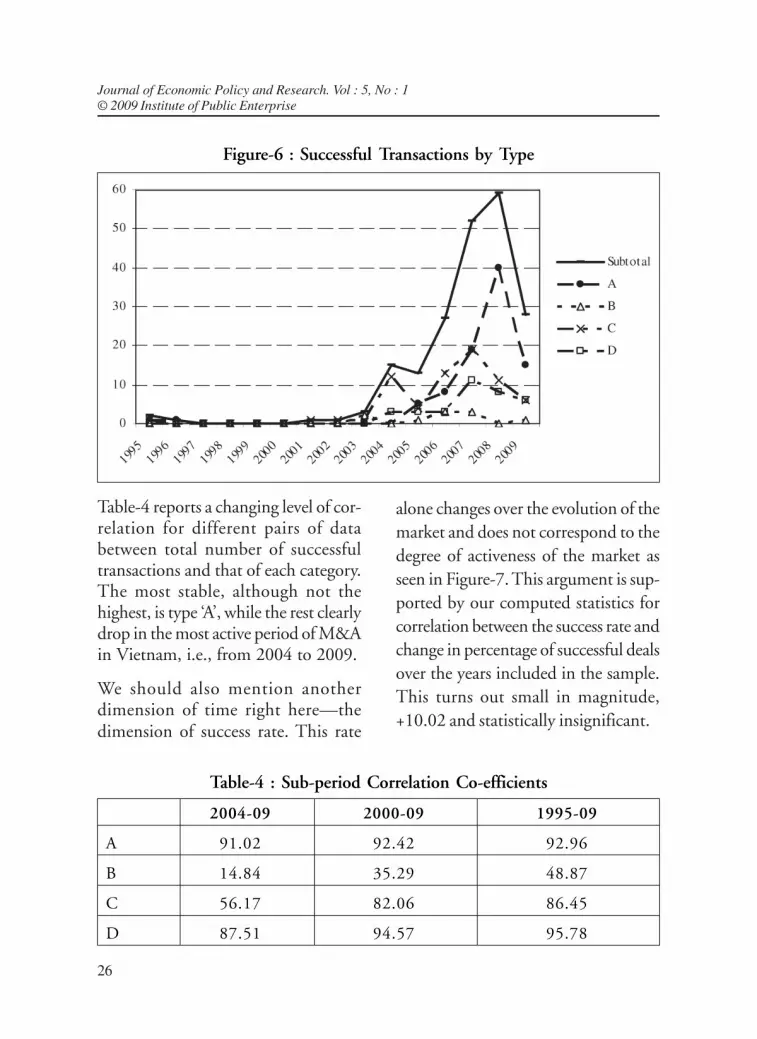

We should also mention anotherdimension of time right here—thedimension of success rate. This rate

alone changes over the evolution of themarket and does not correspond to thedegree of activeness of the market asseen in Figure-7. This argument is sup-ported by our computed statistics forcorrelation between the success rate andchange in percentage of successful dealsover the years included in the sample.This turns out small in magnitude,+10.02 and statistically insignificant.

Figure-6 : Successful Transactions by Type

Table-4 : Sub-period Correlation Co-efficients

2004-09 2000-09 1995-09

A 91.02 92.42 92.96

B 14.84 35.29 48.87

C 56.17 82.06 86.45

D 87.51 94.57 95.78

Mergers & Acquisitions Market in Vietnam’sTransition Economy

27

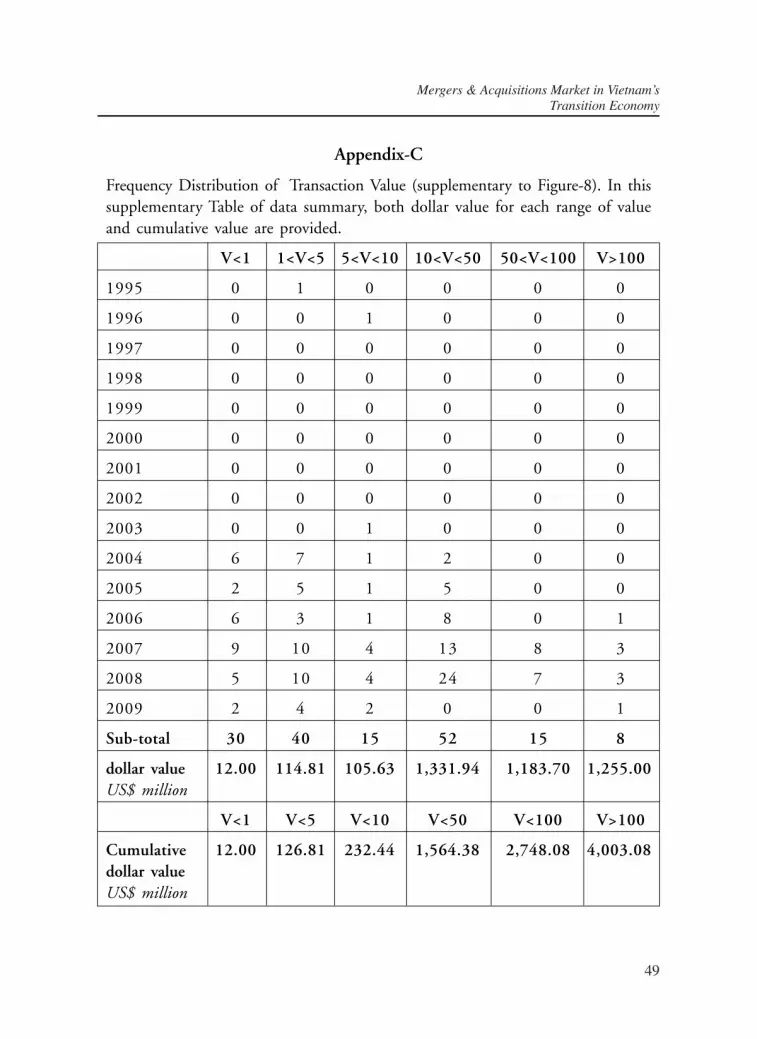

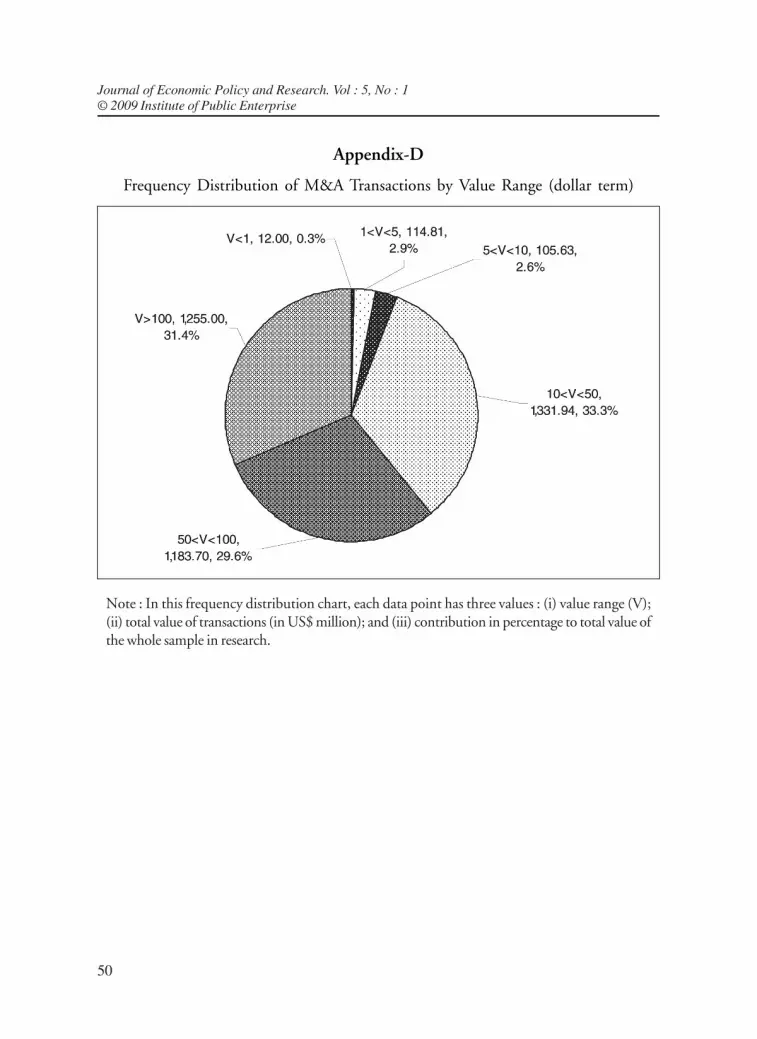

4.1.3 A Distributional Analysis

To understand the monetary values ofM&A transaction in the Vietnamesemarket, Figure-8 provides us with someinsights. It is drawn from a sub-sampleof 160 data entries (out of ourcomplete 252-point sample) which hasa non-zero transaction value. Attachedto each data point are two values. Oneis the range of transaction value weconsider suitable for this distributionalanalysis, the other, the frequency dataentry that appears in the range.(For more detailed information, seeAppendix-C). Let us denote F(X|.) thefrequency that an event appears in our

data sample, then FN(X| X<5) means a

ratio of the number of transactionswith value of less than $5 million tothe total number of transactions of thesample and likewise F

V(X| .) denotes

the ratio but in unit of dollar value oftransaction.

It can be observed directly that transac-tion value of US$10 million is almostidentical to the median of the datasample, below this value the numberof M&A deals account for approxi-mately 53 per cent, that is F

N(X| X<10).

The highest frequency of transactionvalue belongs to the range betweenUS$10 million and US$50 million.

Figure-7 : Evolving Success Rates

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

28

For this value range, all transactions arerecorded for the active period from2004 to 2009 of which nearly 87 percent took place in the three boom years,2006-2008. In addition, for the extremevalue of US$100 million to Vietnamesestandards, the frequency is low, withF

N(X| X>100) = 5 per cent, all occur-

ring in the boom years 2006-2008. Butdue to their large value, total monetaryvalues of seven completed transactionsreach US$1,255 million, showingF

V(X| X>100) = 31.4 per cent of total

value computed from the sample.

Although other value ranges also wit-ness the boom period with higher fre-quency from 2004, no other witnessesthe same pattern.

In dollar terms, the situation is in reverse.This 160-point sample represents atotal value of US$4,003 million, butthe distribution of dollar value fordifferent size range is skewed to larger-size deals. As mentioned, eight transac-tions with top dollar value, each largerthan US$100 million, account for31.4 per cent of total market value.However, the empirical data show that53 per cent of the number of M&Atransactions (85 out of 160), represent-ing all transactions with individualcommercial value of US$10 millioneach, make a total receipt of onlyUS$252 million or a contribution intotal market value of F

V(X| X<10) =

5.8 per cent.

Figure-8 : Frequency Distribution of Transaction Value

Mergers & Acquisitions Market in Vietnam’sTransition Economy

29

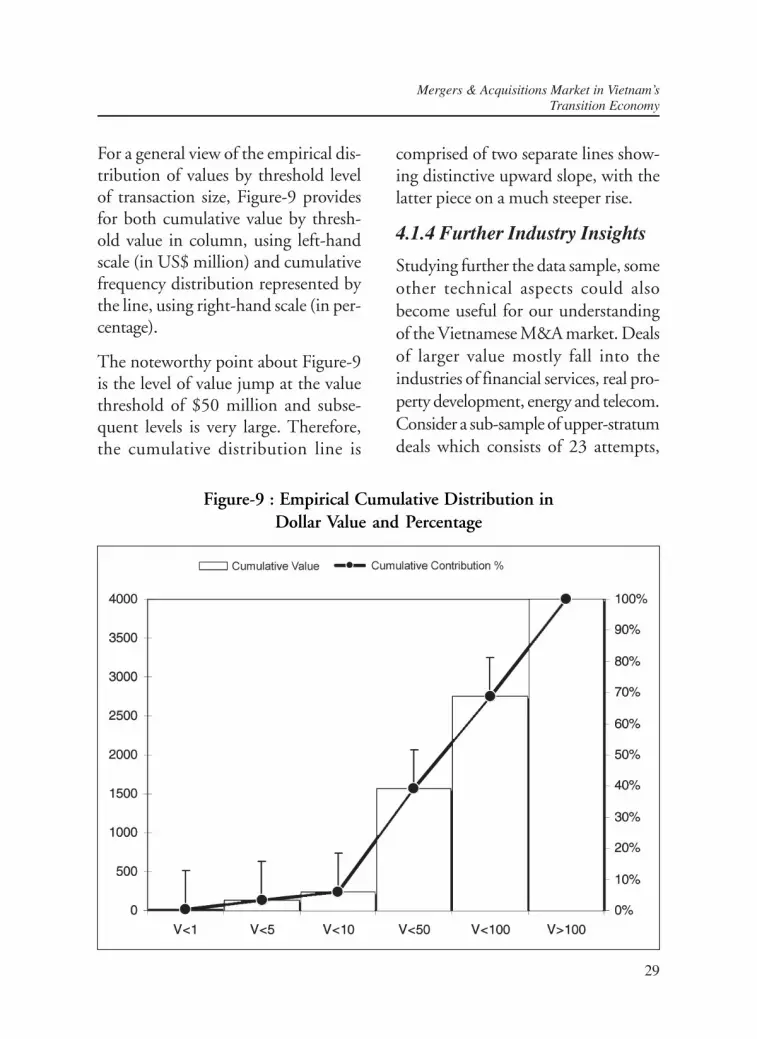

For a general view of the empirical dis-tribution of values by threshold levelof transaction size, Figure-9 providesfor both cumulative value by thresh-old value in column, using left-handscale (in US$ million) and cumulativefrequency distribution represented bythe line, using right-hand scale (in per-centage).

The noteworthy point about Figure-9is the level of value jump at the valuethreshold of $50 million and subse-quent levels is very large. Therefore,the cumulative distribution line is

comprised of two separate lines show-ing distinctive upward slope, with thelatter piece on a much steeper rise.

4.1.4 Further Industry Insights

Studying further the data sample, someother technical aspects could alsobecome useful for our understandingof the Vietnamese M&A market. Dealsof larger value mostly fall into theindustries of financial services, real pro-perty development, energy and telecom.Consider a sub-sample of upper-stratumdeals which consists of 23 attempts,

Figure-9 : Empirical Cumulative Distribution inDollar Value and Percentage

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

30

each leading to monetary exchange ofUS$50 million and above. 12/23 dealsare M&A in banking industry, happen-ing in the years 2007 and 2008. Withbanking as an example, it is observedthat the majority of transactions takeplace in a limited number of industrieswhich we should be able to look intomore deeply now with the dataset athand.

In the boom period from 2005-2008,the industries where most M&A dealswere conducted in Vietnam are :

• Banking services

• Non-Bank financial services (in-cluding securities brokerage andinsurance)

• Portfolio investments

• Business real estates and hotelbusiness

• Construction and materials

• Steel

• Mining and mineral processing

• Home appliances

• Foods and foodstuff

In the course of economic developmentand building market institutions inVietnam, the importance of a commer-cially viable financial sector has alwaysbeen an emphasis for both policy-makers

and the business community. A greatdeal of funds and effort has been spenton this sector and our data also unveilsthat trend. Among the nine industrieslisted above, the first three belong tofinancial products and services whichrepresent both the primary publicemphasis concern, in general and a criti-cal portion of the M&A market, in par-ticular. Vietnam’s two-pronged strategyfor an efficient transition towards a full-fledged economy has explicitly reliedon : (i) re-forming the state-run enter-prises sector; and (ii) re-vamping itsnascent financial economy, currentlydominated by a large number of com-mercial banks (56), including five state-run banking super-powerhouses. Thereare same stories in Malaysia (Ramlee &Said, 2009) and the Philippines(Castillo, 2009).

The economy of Vietnam alreadyexperienced a period of collapse in thelate 1980s when a nation-wide chainof ‘credit co-operatives’ abruptly becametechnically or completely bankrupt,wiping out the lifetime savings ofmillions of people and causing anextremely high degree of financialuncertainty in the economy. Althoughmore than 20 years have passed, thememory is still alive to a large portionof the populace and the credibility ofthe domestic banking sector has notbeen restored fully.

Mergers & Acquisitions Market in Vietnam’sTransition Economy

31

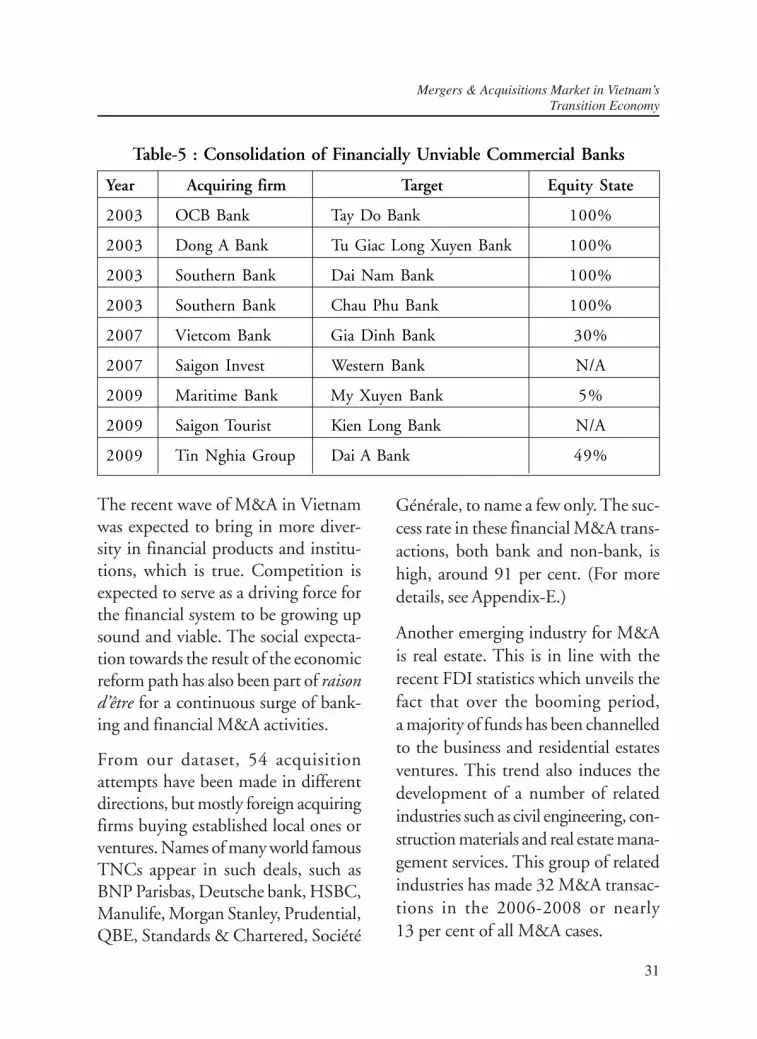

The recent wave of M&A in Vietnamwas expected to bring in more diver-sity in financial products and institu-tions, which is true. Competition isexpected to serve as a driving force forthe financial system to be growing upsound and viable. The social expecta-tion towards the result of the economicreform path has also been part of raisond’être for a continuous surge of bank-ing and financial M&A activities.

From our dataset, 54 acquisitionattempts have been made in differentdirections, but mostly foreign acquiringfirms buying established local ones orventures. Names of many world famousTNCs appear in such deals, such asBNP Parisbas, Deutsche bank, HSBC,Manulife, Morgan Stanley, Prudential,QBE, Standards & Chartered, Société

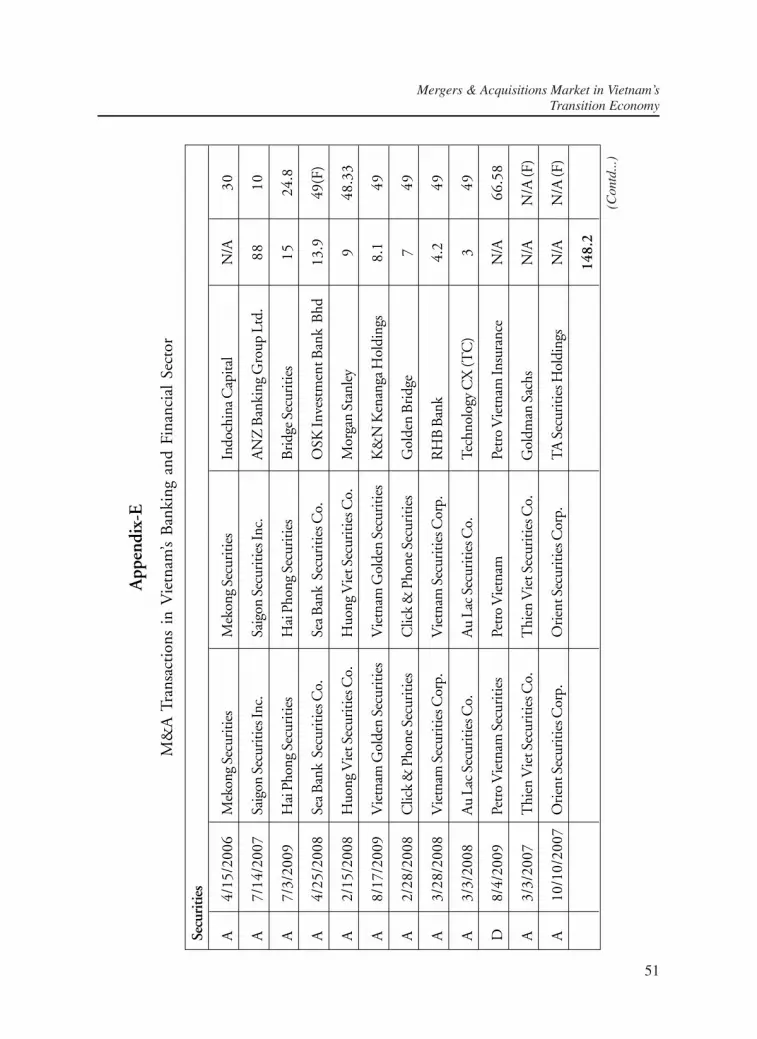

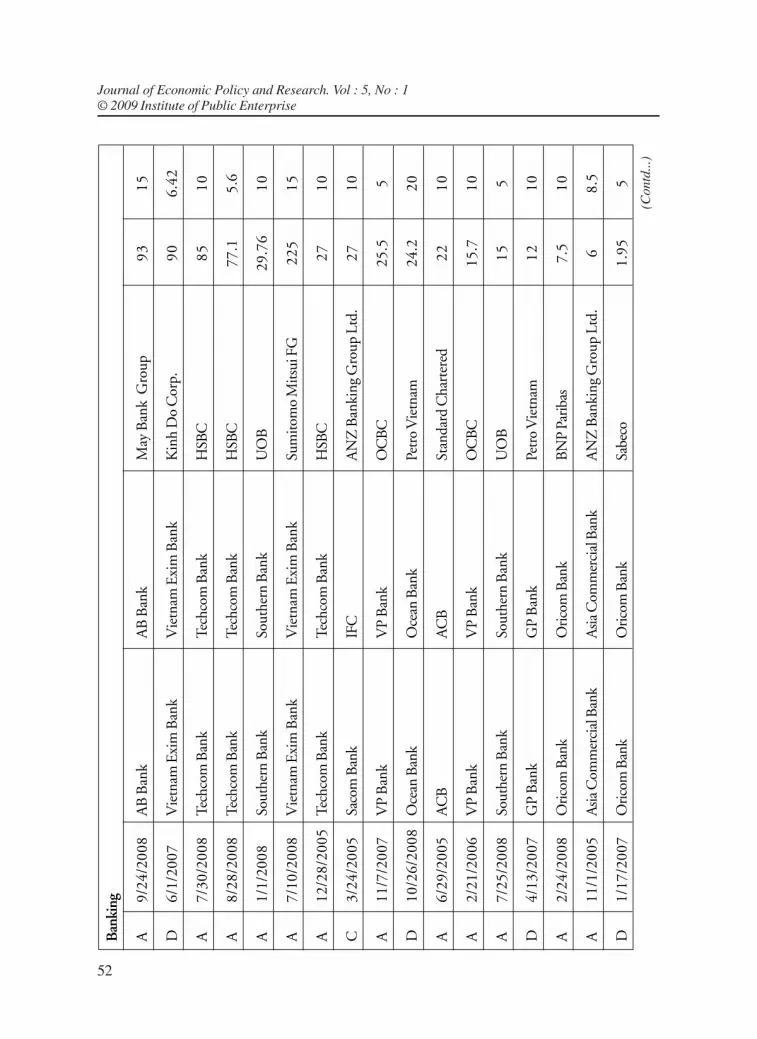

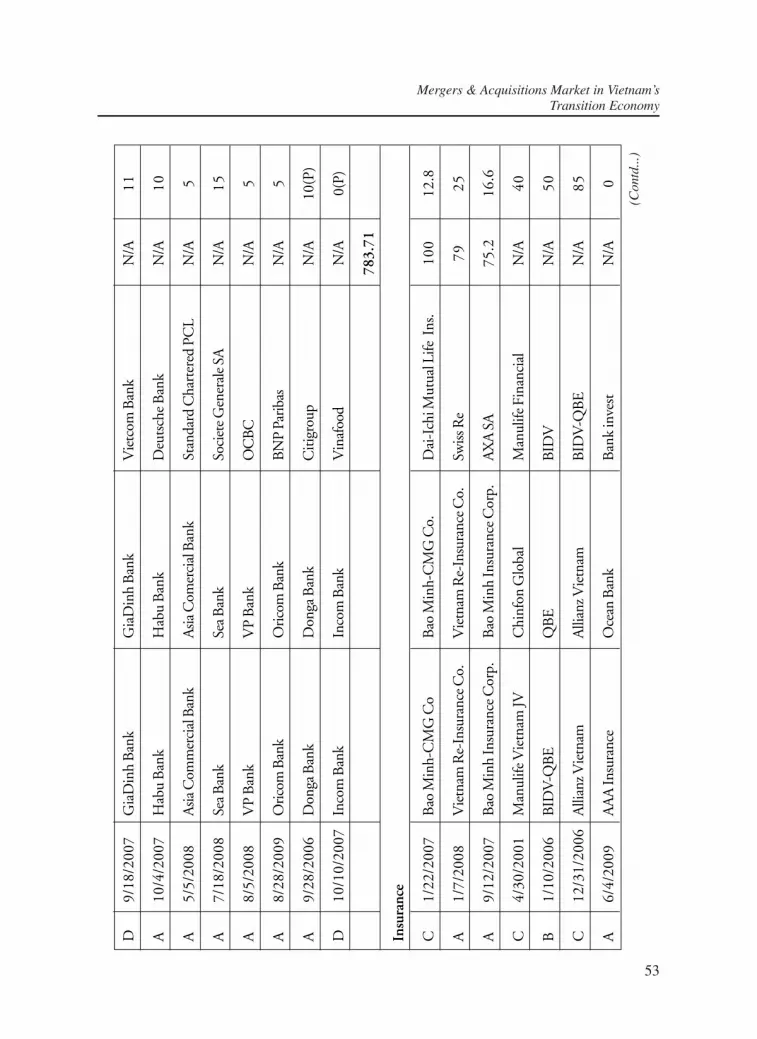

Générale, to name a few only. The suc-cess rate in these financial M&A trans-actions, both bank and non-bank, ishigh, around 91 per cent. (For moredetails, see Appendix-E.)

Another emerging industry for M&Ais real estate. This is in line with therecent FDI statistics which unveils thefact that over the booming period,a majority of funds has been channelledto the business and residential estatesventures. This trend also induces thedevelopment of a number of relatedindustries such as civil engineering, con-struction materials and real estate mana-gement services. This group of relatedindustries has made 32 M&A transac-tions in the 2006-2008 or nearly13 per cent of all M&A cases.

Table-5 : Consolidation of Financially Unviable Commercial Banks

Year Acquiring firm Target Equity State

2003 OCB Bank Tay Do Bank 100%

2003 Dong A Bank Tu Giac Long Xuyen Bank 100%

2003 Southern Bank Dai Nam Bank 100%

2003 Southern Bank Chau Phu Bank 100%

2007 Vietcom Bank Gia Dinh Bank 30%

2007 Saigon Invest Western Bank N/A

2009 Maritime Bank My Xuyen Bank 5%

2009 Saigon Tourist Kien Long Bank N/A

2009 Tin Nghia Group Dai A Bank 49%

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

32

This whole sub-section has beendevoted to making use of our datasetof M&As in the Vietnamese economy.Nonetheless, it is not that this essaymainly emphasizes a ‘number-crunch-ing’ task. The main reason for thislengthy discussion on insights derivedfrom the data is only that in the absenceof a systemic database for various eco-nomic activities in Vietnam, a good useof this dataset per se may be able to pro-vide us with more insights and lead tofurther implications. These will, inturn, help us better discuss some criti-cally important aspects of M&A indus-try as an emergent part of the Vietna-mese economy, in general and for a bet-ter transformation of it into a morevigorous market economy.

4.2 A Socio-Cultural Epistemology

Our view of M&A activities in Viet-nam is that they should be consideredan economic process, not a situation or

a reflection of some equilibrium-analy-sis framework. The role of M&Ashould be understood in the existenceof major transformations of the economy,in the light of growing globalization,re-integration of the Vietnamese of theeconomy, vibrant transformation ofeconomic functions assumed by localentrepreneurs, public investors and thestate. Therefore, this part of the essaydiscussing a socio-cultural epistemo-logy towards M&A in the new andfast-changing, economic setting of Viet-nam should naturally be a sine qua non.

4.2.1 Opportunities, Risks, Profitsand Exits

As reviewed in Kim (2009) the empiri-cal data over 130 years usually recordM&A waves following right after apreceding period of financial crisis andstock market collapse, no matterwhether these crises and collapse areeither the cause or effect of persistingeconomic recession.

Table-6 : Summary of Banking and Financial M&A

Time Deals Value

Securities 2007-09 11 148.2

Insurance 2001-09 9 544.2

Banking 2005-09 24 783.71

NBFI 2007-08 4 460.0

Portfolio 2004-08 6 123.9

Overall Success Rate 90.9% 54 2,060.0

Mergers & Acquisitions Market in Vietnam’sTransition Economy

33

In the case of Vietnam’s emerging mar-ket economy, as discussed in 4.1.2, theperiod 2006-08 witnesses an abruptsurge of M&A transactions amidincreasing activeness of investors andspeculators in an increasingly growingdomestic capital market. At that time,investments in the speculative marketsbecame ‘hot and noisy’, attractingattention of perhaps the majority of thepopulace that has some concern inbuilding up personal wealth2. Thesecombined with M&A wave in Viet-nam have been naturally a socio-culturalprocess and not limited to a pure eco-nomic phenomenon or a transient eco-nomic situation.

One may refer to two major reasonsfor the above-said fact. First, the finan-cial markets in Vietnam have beenbeing in its infancy. Even terminologythat is used among investors and thepublic is both new and, at times, mis-leading. New economic and financialterms started being queried andsearched for by the society when theincreasing degree of capital marketactivities became apparent, showingobserved anomalies (Farber et al., 2006).Although early M&A operation wasrecorded in the Vietnamese economyin the early 1990s, still ‘M&A’ belongsto the bunch of new economic andfinancial terminologies imported intothe Vietnamese economic vocabularywhich appeared more frequently in the

public media at the real boom time ofVietnam stock market at the end of2006 (Pham & Vuong, 2009).

Second, in understanding the under-lying economic motivations for M&Aattempts by the Vietnamese businesspartners, as both seller and buyer, oneshould not shirk their socio-culturaltraits, especially those relevant to thetransformation of entrepreneurship tomature full-blown corporation, wherethe separation of ownership and con-trol turns out critical. Behind the scene,one has to accept the reality that seek-ing profits, a major economic motiva-tion for M&A attempts like themajority of other economic activities,carries with the act much of the herdmentality and rampant rent-seeking, inthe form of taking informational, powerand connection advantages (Vuong &Tran, 2009(b)).

As mentioned earlier in this essay, ourdataset, although believed to be themost complete so far, is still sparse andunsuitable for doing mainstreameconometric analysis on M&A market.Furthermore, in our view, a discussionon socio-economic and cultural traitsof such processes would likely result infar better understanding of the marketevolution in the transitional economy;we will use casestudy discussion herefor further analysis.

Journal of Economic Policy and Research. Vol : 5, No : 1© 2009 Institute of Public Enterprise

34

Now, take the example of the Vietnamstock market before early March 2007to see it more clearly. Ungroundedex ante expectations set by an increasingnumber of new-arriving speculators hadpressurized the Ho Chi Minh Citybourse’s price composite VN-Index.Eventually, this index was pushed up toits pinnacle of 1,171 points in March 12,2007, showing a ‘spectacular’ marketvalue gain of +175.9 per cent over oneyear (VN-Index at 424.5 on March 13,2006) and a geometric annual capitalgain of 198.5 per cent for the2005-2007 period (VN-Index at 237on March 11, 2005). Acting on lackof information, under pressure ofunspecified source of rumours and withvery high ex ante expectations, the Vietna-mese speculators, including corporate,quickly spent money on any stock theycould buy (not an easy job due to vani-shing liquidity in high speculation). The‘foreign factor’ is meaningful in thiscontext. An injection of approximatelyUS$6 billion FPI funds into theVietnamese’s nascent capital markets,in 2006-07 alone, had not been neu-tralized appropriately, first causing adecent type of inflation, for capitalassets. The existence of herd behaviourcombined with a price-fueled increas-ing funds flow triggered a real assetbubble, making an upward spiral inprice formation process of the Viet-namese capital markets.

This overexcitement represents super-abnormal profit opportunities causingmany domestic firms, both entrepre-neurial and well-established, to findways of exploiting them. ‘M&A’ trans-action, together with a fake brandingby using the term ‘strategic alliance’with a foreign firm’s name, turned outtruly fashionable in this context (andstill fashionable today) since that pur-poseful act could stir up further thespeculative mentality and sky-rocketnaïve speculators’ expectations. In a caseof Thien Viet Securities, even anunsuccessful fake M&A transactionwith Goldman Sachs did not preventthe market from investing stock of thisnewborn firm, with a thin equity baseand without professional track record.Its market price was spurred up to itspeak of US$4.38 from US$0.63, fourweeks after the first rumour travellingout of their office, representing amonthly profitability of 600 per cent.When the fake M&A was disclosed inpart in the mass media, this stock valueevaporated in a price free fall down toUS$0.6 over two weeks.

In another case, the short-lived marriagebetween Vietnam’s leading technologyfirm FPT and the US-based TexasPacific Group (TPG) is evidence thateven well-established firms with mosthighly-regarded entrepreneur-corporateleaders are not exempt from this super-abnormal profit seeking. In October 2006,

Mergers & Acquisitions Market in Vietnam’sTransition Economy

35

TPG and Intel Capital became strate-gic partners holding US$36.5million equity in FPT in exchange of1.2 million shares of common stock(market price at US$10.625 then), asannounced in a joint communiqué.This ‘strategic partner’ turned out a veryshort-term price arbitrageur, strikinglynot even with an adequate lock-up term,when they sold them off. Needless tosay, the world tech-giant name of Intelhelped excite the speculators in favourof FPT stock, believing in a genuineM&A success story, which could bringthe already-mighty leading IT firm FPTto a new level, perhaps world-class.When FPT share made its debut on thestock market on December 13, 2006,its share was valued at US$25, repre-senting a huge annualized return of811.8 per cent. In a seemingly unstop-pable price increase, its share attained anew record, still Vienam’s stock pricerecord thus far, of US$41.56 onFebruary 27, 2007. A lucky arbitrageurcould enjoy a 265 per cent annualizedprofit, counting from its listing dateonly. However, aftermath of thedivorce was also huge. Stockholderssaw FPT common stock being valuedat US$2.22, losing 92 per cent of valueexactly two years after the peak time inFebruary 2007.

In the wave of M&A booms in 2006-08,especially into banking, financial andsecurities industries, it is observable that

these are business fields with own fea-tures of profits, risks and exit methods.Capital adequacy, international expe-rience and persuasive performance recordsaltogether do not suffice writing a suc-cess story. In-market human capital,relationship and connection, social capi-tal are also needed to get it up and run-ning, as typical socio-cultural traits inVietnam and also several other EastAsian contexts (Vuong & Tran,2009(b)). Furthermore, the mimick-ing act performed by the investing pub-lic, including corporate entities,towards stocks following M&Atransactions, certainly is not the ‘creativeimitation strategy’ as termed byDrucker, (1986, p. 220).