msm – industry update and the road ahead - wikileaks

TRANSCRIPT

0- Confidential -

MSM – Industry Update and the Road aheadMan Jit Singh

10 June 2013

1- Confidential -

� Multi-Screen Media – 5 year outlook 2

― Advertising Market Overview 4

― Update on Distribution & Digitization 9

� Market developments

― Impact of New Media 16

― Market landscape and Competition Update 19

― Regulatory Update 29

� The Road Ahead 33

� Strategic New Initiatives 39

� Recap – Putting it all together 95

Agenda

2- Confidential -

Multi-Screen Media – 5 year outlook

3- Confidential -

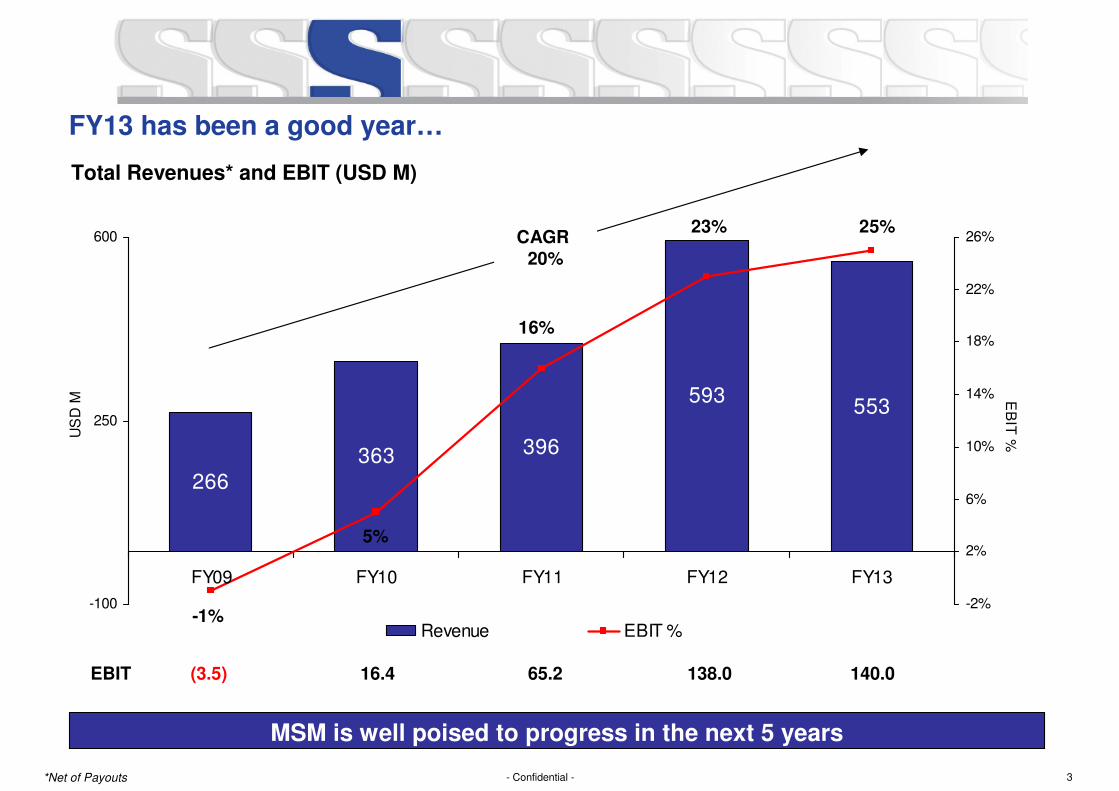

FY13 has been a good year…

MSM is well poised to progress in the next 5 years

*Net of Payouts

Total Revenues* and EBIT (USD M)

266

396

553

363

593

25%

5%

23%

16%

-1%-100

250

600

FY09 FY10 FY11 FY12 FY13

US

D M

-2%

2%

6%

10%

14%

18%

22%

26%

EB

IT %

Revenue EBIT %

EBIT (3.5) 65.216.4 138.0

CAGR

20%

140.0

4- Confidential -

Advertising Market Overview

5- Confidential -

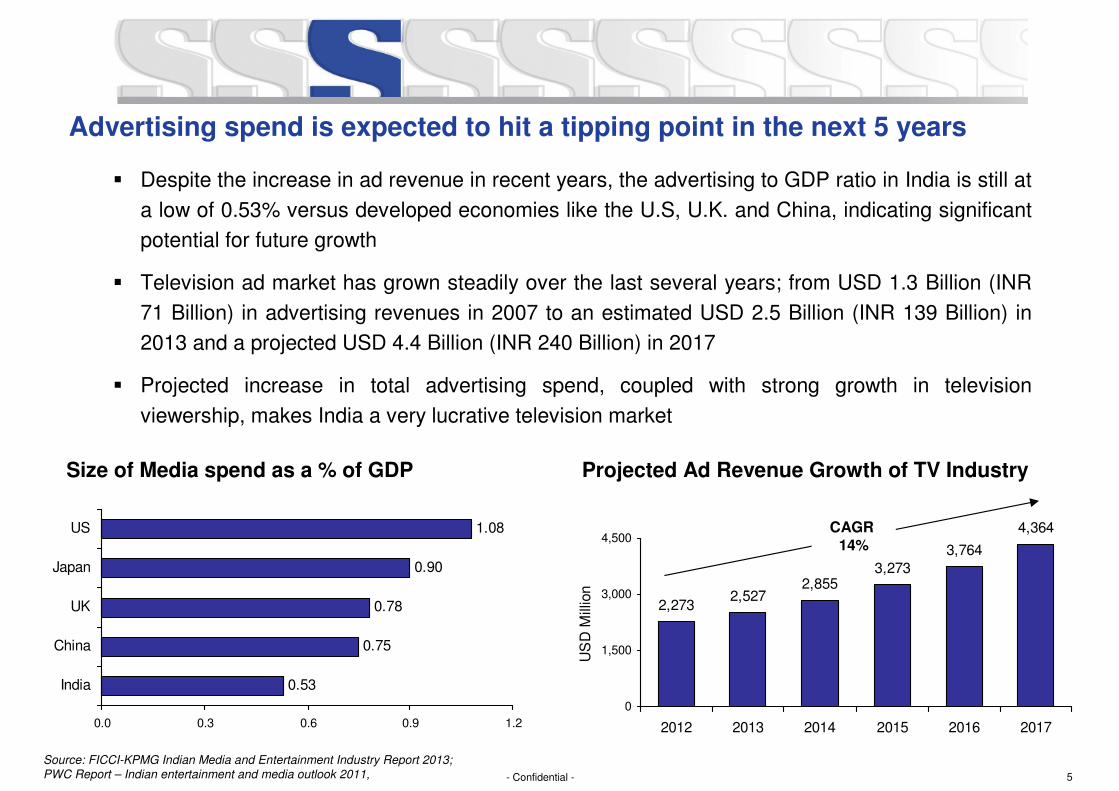

Advertising spend is expected to hit a tipping point in the next 5 years

� Despite the increase in ad revenue in recent years, the advertising to GDP ratio in India is still at

a low of 0.53% versus developed economies like the U.S, U.K. and China, indicating significant

potential for future growth

� Television ad market has grown steadily over the last several years; from USD 1.3 Billion (INR

71 Billion) in advertising revenues in 2007 to an estimated USD 2.5 Billion (INR 139 Billion) in

2013 and a projected USD 4.4 Billion (INR 240 Billion) in 2017

� Projected increase in total advertising spend, coupled with strong growth in television

viewership, makes India a very lucrative television market

2,2732,527

2,8553,273

3,764

4,364

0

1,500

3,000

4,500

2012 2013 2014 2015 2016 2017

US

D M

illio

n

Projected Ad Revenue Growth of TV IndustrySize of Media spend as a % of GDP

CAGR 14%

Source: FICCI-KPMG Indian Media and Entertainment Industry Report 2013;

PWC Report – Indian entertainment and media outlook 2011,

0.53

0.75

0.78

0.90

1.08

0.0 0.3 0.6 0.9 1.2

India

China

UK

Japan

US

6- Confidential -

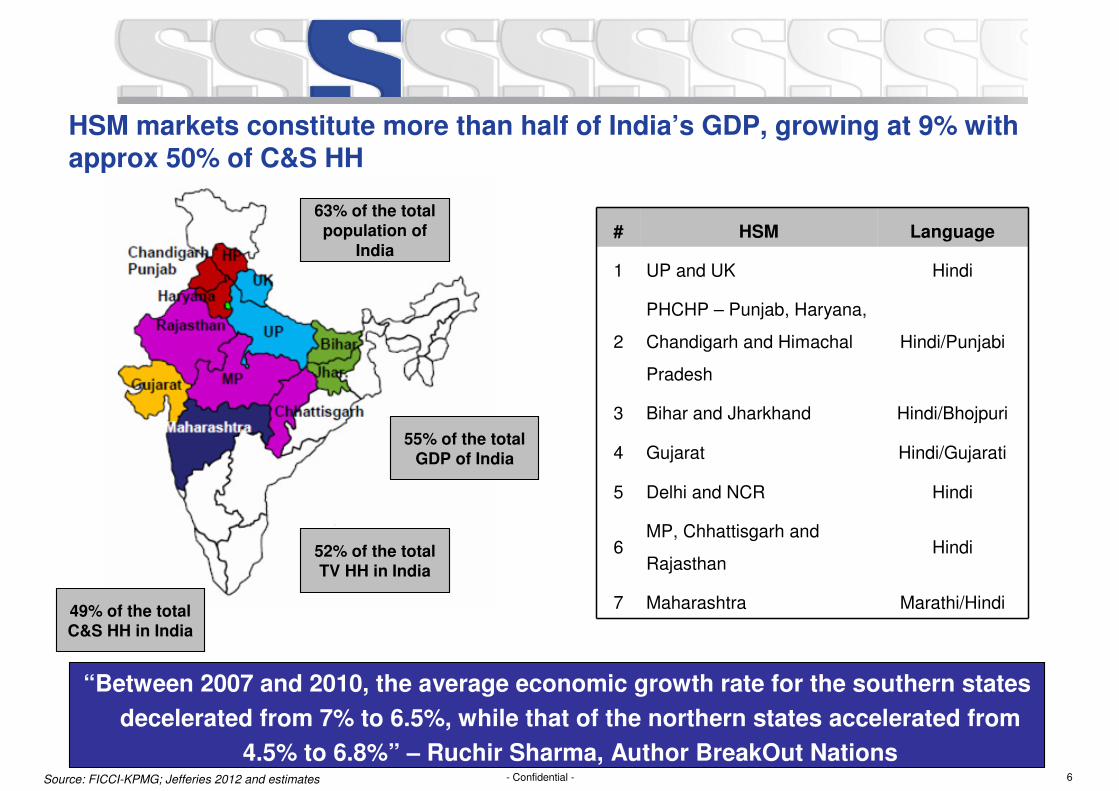

HSM markets constitute more than half of India’s GDP, growing at 9% with approx 50% of C&S HH

“Between 2007 and 2010, the average economic growth rate for the southern states

decelerated from 7% to 6.5%, while that of the northern states accelerated from

4.5% to 6.8%” – Ruchir Sharma, Author BreakOut Nations

HindiDelhi and NCR5

Hindi/GujaratiGujarat4

Maharashtra

MP, Chhattisgarh and

Rajasthan

Bihar and Jharkhand

PHCHP – Punjab, Haryana,

Chandigarh and Himachal

Pradesh

UP and UK

HSM

7

6

3

2

1

# Language

Hindi

Hindi/Punjabi

Hindi/Bhojpuri

Hindi

Marathi/Hindi

63% of the total

population of

India

55% of the total

GDP of India

52% of the total

TV HH in India

49% of the total

C&S HH in India

Source: FICCI-KPMG; Jefferies 2012 and estimates

7- Confidential -

2,6121,709

468

1,788

3969

2334

7104

3,342

2,154

726

2,688

5596

3083

9973

0

4,000

8,000

12,000

UP and UK PHCHP Bihar and

Jharkhand

Gujarat Delhi NCR MP, Chhattisgarh

and Rajasthan

Maharashtra

INR

Crs

Adex 2012 Adex 2015

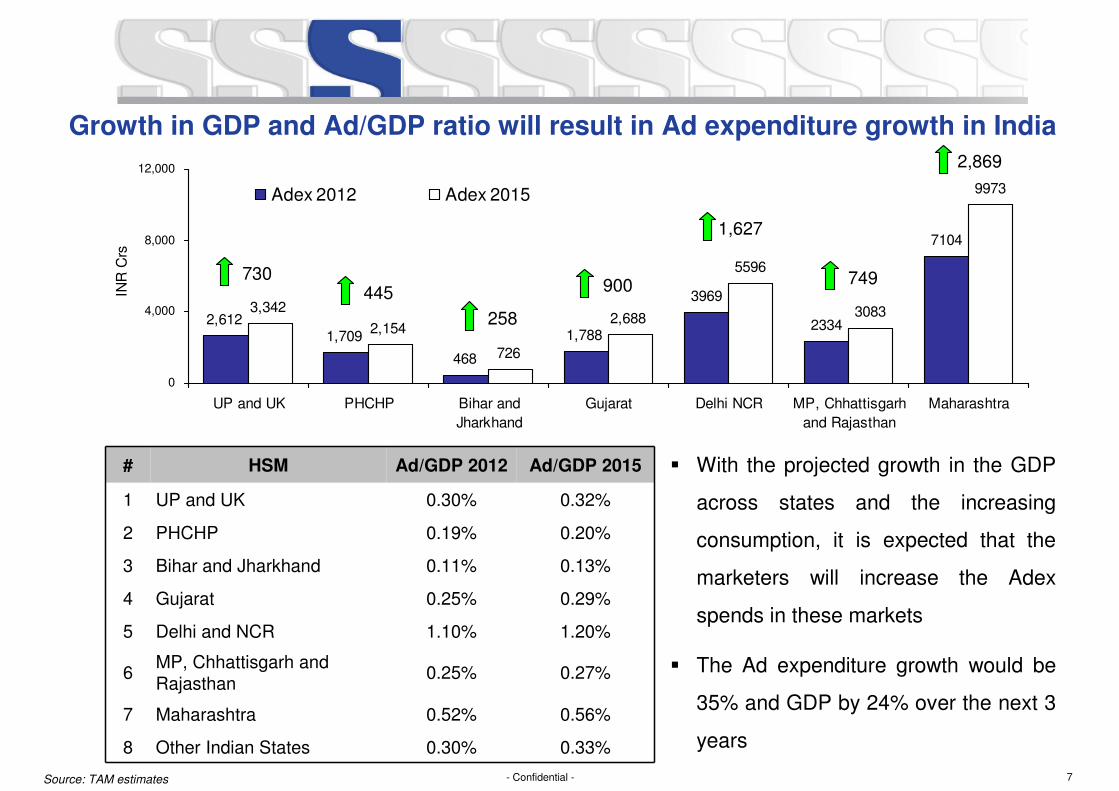

Growth in GDP and Ad/GDP ratio will result in Ad expenditure growth in India

0.30%

0.52%

0.25%

1.10%

0.25%

0.11%

0.19%

0.30%

Ad/GDP 2012

0.56%Maharashtra7

0.33%Other Indian States8

1.20%Delhi and NCR5

0.29%Gujarat4

MP, Chhattisgarh and Rajasthan

Bihar and Jharkhand

PHCHP

UP and UK

HSM

6

3

2

1

# Ad/GDP 2015

0.32%

0.20%

0.13%

0.27%

� With the projected growth in the GDP

across states and the increasing

consumption, it is expected that the

marketers will increase the Adex

spends in these markets

� The Ad expenditure growth would be

35% and GDP by 24% over the next 3

years

730445

258

900

1,627

749

2,869

Source: TAM estimates

8- Confidential -

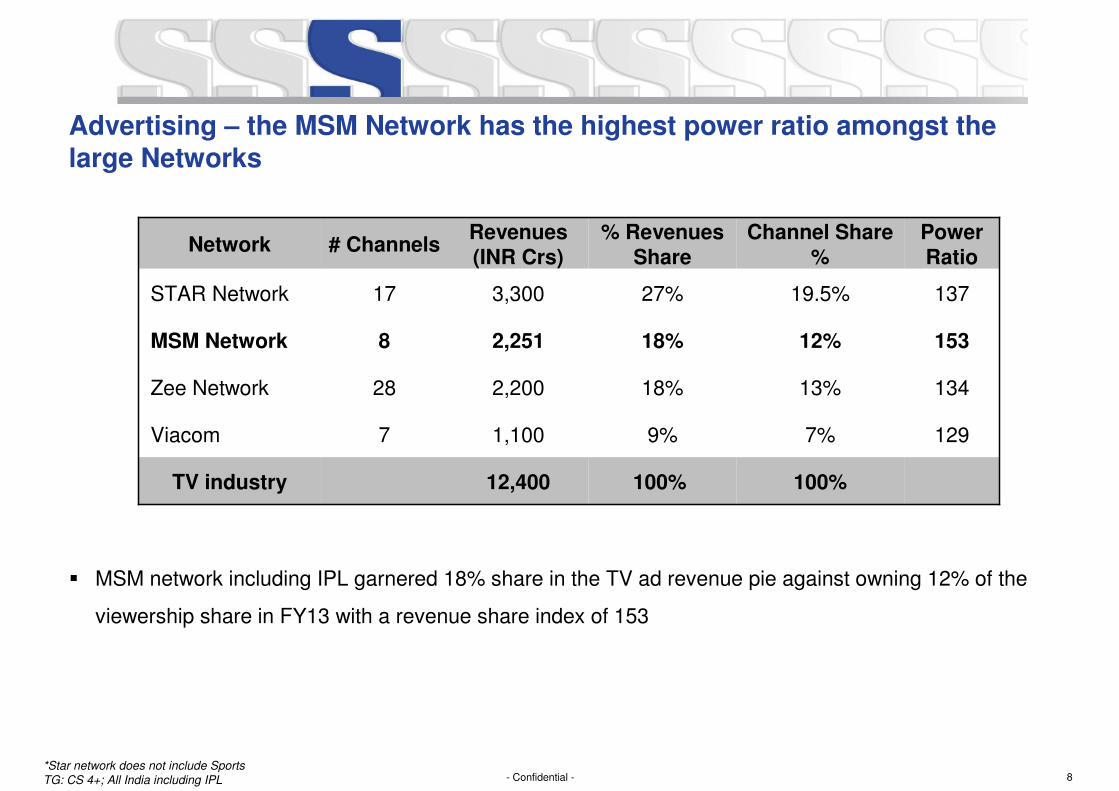

Advertising – the MSM Network has the highest power ratio amongst the large Networks

� MSM network including IPL garnered 18% share in the TV ad revenue pie against owning 12% of the

viewership share in FY13 with a revenue share index of 153

15312%18%2,2518MSM Network

Network # ChannelsRevenues (INR Crs)

% Revenues Share

Channel Share %

Power Ratio

STAR Network 17 3,300 27% 19.5% 137

Zee Network 28 2,200 18% 13% 134

Viacom 7 1,100 9% 7% 129

TV industry 12,400 100% 100%

*Star network does not include Sports

TG: CS 4+; All India including IPL

9- Confidential -

Update on Distribution & Digitization

10- Confidential -

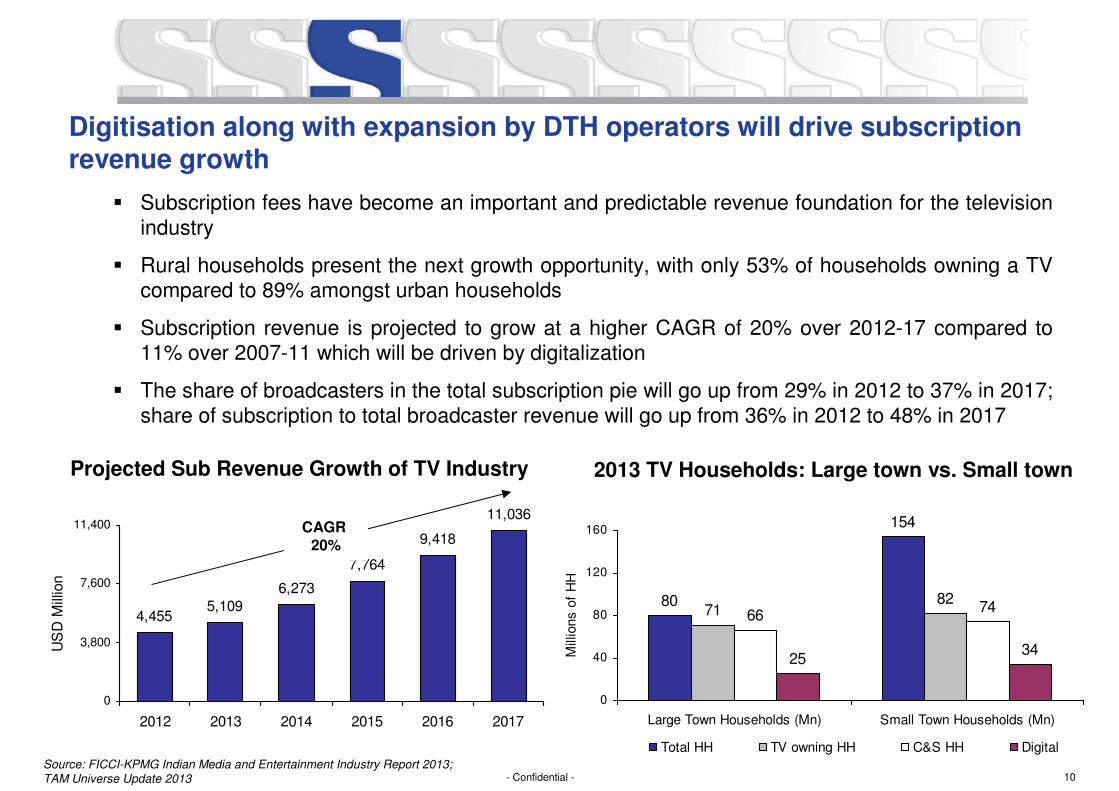

Digitisation along with expansion by DTH operators will drive subscription revenue growth

� Subscription fees have become an important and predictable revenue foundation for the television industry

� Rural households present the next growth opportunity, with only 53% of households owning a TV compared to 89% amongst urban households

� Subscription revenue is projected to grow at a higher CAGR of 20% over 2012-17 compared to 11% over 2007-11 which will be driven by digitalization

� The share of broadcasters in the total subscription pie will go up from 29% in 2012 to 37% in 2017; share of subscription to total broadcaster revenue will go up from 36% in 2012 to 48% in 2017

Source: FICCI-KPMG Indian Media and Entertainment Industry Report 2013;

TAM Universe Update 2013

80

154

7182

6674

3425

0

40

80

120

160

Large Town Households (Mn) Small Town Households (Mn)

Mill

ions o

f H

H

Total HH TV owning HH C&S HH Digital

Projected Sub Revenue Growth of TV Industry 2013 TV Households: Large town vs. Small town

4,4555,109

6,273

7,764

9,418

11,036

0

3,800

7,600

11,400

2012 2013 2014 2015 2016 2017

US

D M

illio

n

CAGR 20%

11- Confidential -

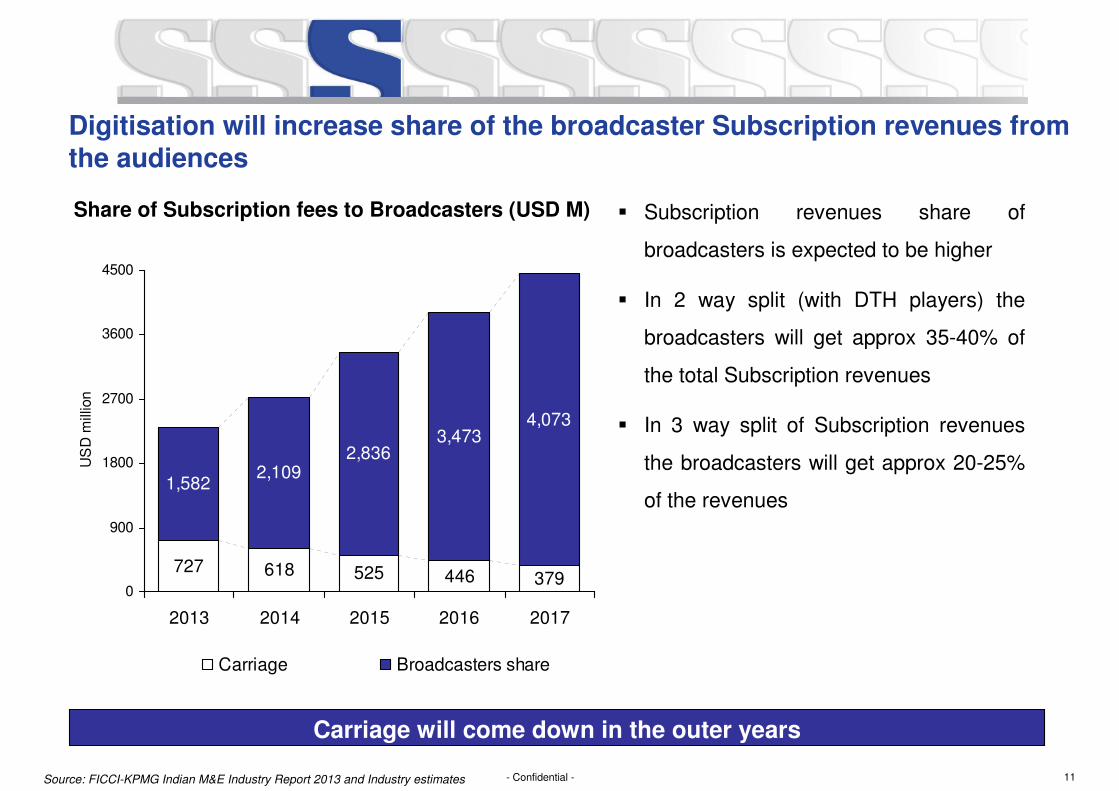

Digitisation will increase share of the broadcaster Subscription revenues from the audiences

Share of Subscription fees to Broadcasters (USD M) � Subscription revenues share of

broadcasters is expected to be higher

� In 2 way split (with DTH players) the

broadcasters will get approx 35-40% of

the total Subscription revenues

� In 3 way split of Subscription revenues

the broadcasters will get approx 20-25%

of the revenues

618 525 446 379

1,5822,109

2,8363,473

4,073

727

0

900

1800

2700

3600

4500

2013 2014 2015 2016 2017

US

D m

illio

n

Carriage Broadcasters share

Carriage will come down in the outer years

Source: FICCI-KPMG Indian M&E Industry Report 2013 and Industry estimates

12- Confidential -

Digital Addressable System (DAS) - Current On Ground Reality

� There are still a few gaps for seeding boxes -

― Phase 1 - 90-92% of Delhi/Mumbai and Kolkata are covered, while only 25-30% of Chennai

has been covered

― Phase 2 - 60-65% of the 38 cities have been seeded

� Unencrypted Analog signals are still accessible – Addressability of subscribers continues to be a

concern area, hence actual numbers are not yet reported and leading to piracy

� Only 35% of the Customer Relationship Forms (CRF) received from the end households, hence

complete clarity on actual subscriber numbers is still pending

� MSOs are still not ready with packages / backend infrastructure

� ARPUs have not increased – lack of packages, CRFs. The on ground customer not willing to pay

extra

� Unavailability of institutional finance to MSOs

� Court stay orders have hindered the roll out in certain states AP, MP where the order has now been

lifted

� MIB / TRAI pressure tactics to force operator deals - under threat of 6 months status quo

13- Confidential -

Digital Addressable System (DAS) – the Ideal Scenario for LC1 and FTA Channels

� No more constraint of Bandwidth with the MSO

� FTA and Niche channels will be greatest benefactor

� MSOs can offer higher number of channels at no extra cost

� MSO entering these markets will improve the quality and variety in the customer offering

� With LC1 falling in Phase 4 of digitization, the MSO focus has already started shifting towards these

towns in terms of acquisition

14- Confidential -

What is Competition doing in LC1 markets?

� Competition (Star) entered the LC1 markets 2-3 years ago for first mover advantage

� Have on ground presence – 300-400 resources (on rolls/contract) in these market to monitor

competition and crack new deals

� Star is willing to spend on carriage. Focus on channel placement within the EPG

� Star Utsav presence on DD Direct ensured reach within the LC1 market. Currently delivers more reach

than Star Plus in LC1

15- Confidential -

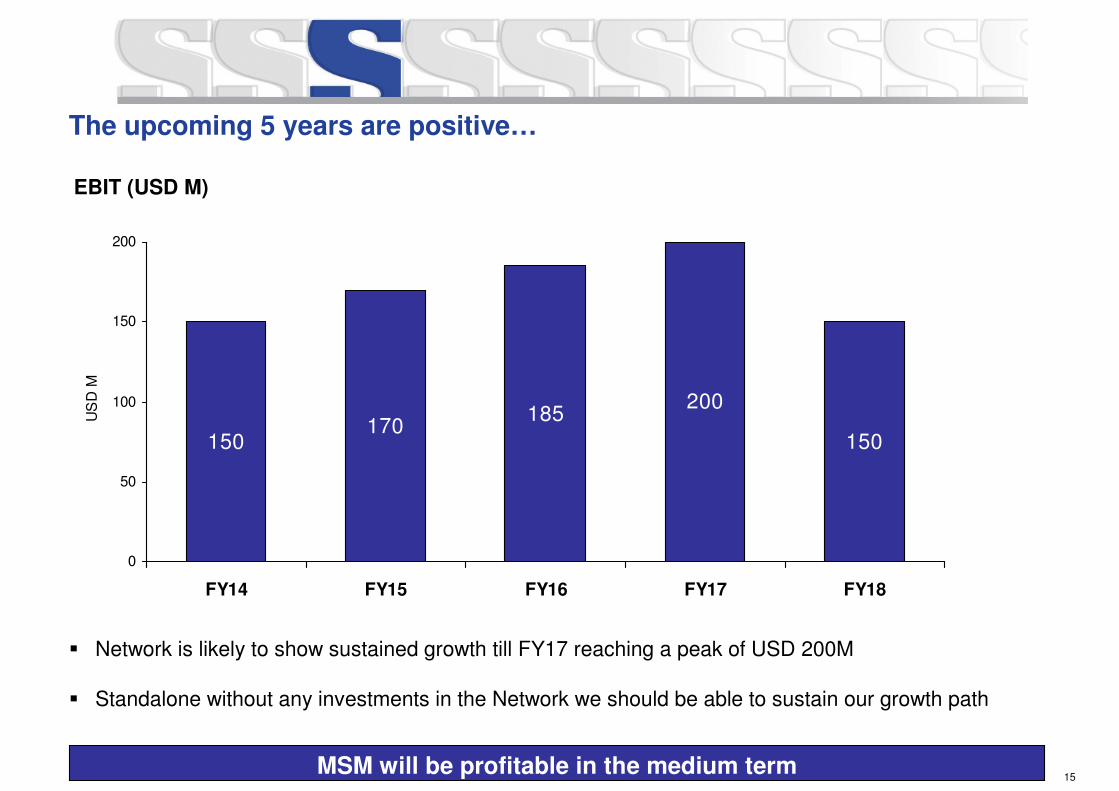

The upcoming 5 years are positive…

� Network is likely to show sustained growth till FY17 reaching a peak of USD 200M

� Standalone without any investments in the Network we should be able to sustain our growth path

150170

185200

150

0

50

100

150

200

FY14 FY15 FY16 FY17 FY18

US

D M

EBIT (USD M)

MSM will be profitable in the medium term

16- Confidential -

Impact of New Media

17- Confidential -

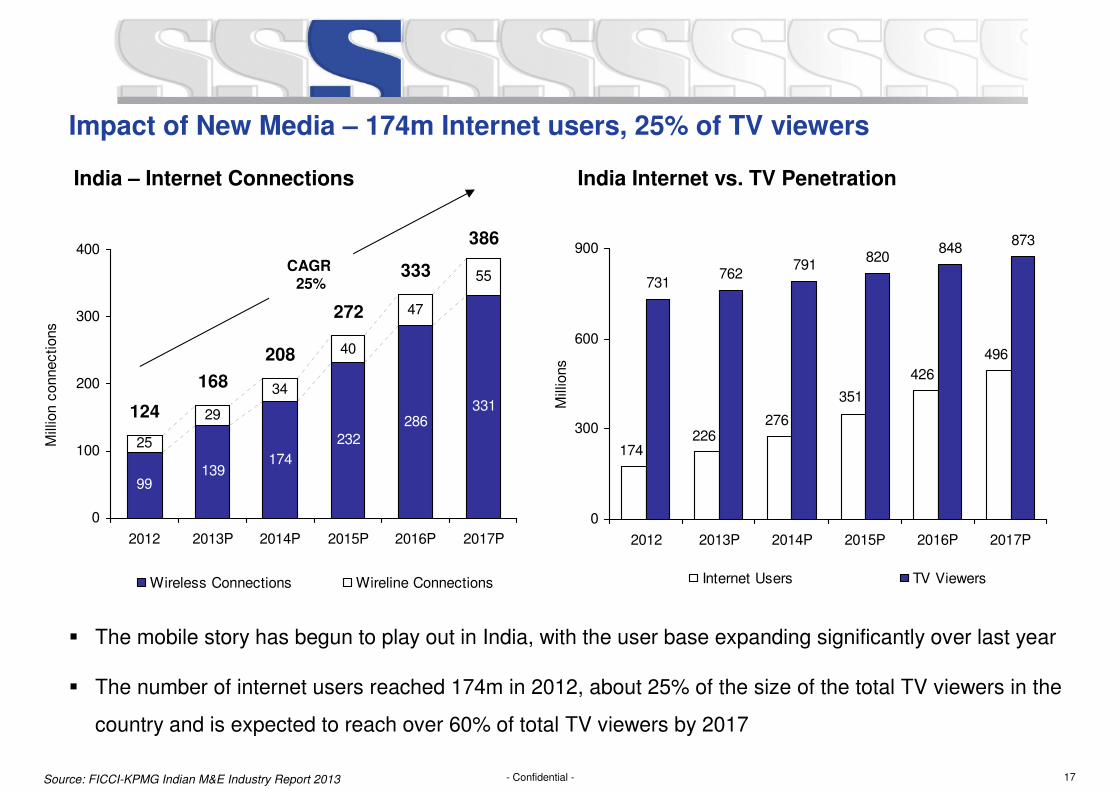

Impact of New Media – 174m Internet users, 25% of TV viewers

� The mobile story has begun to play out in India, with the user base expanding significantly over last year

� The number of internet users reached 174m in 2012, about 25% of the size of the total TV viewers in the

country and is expected to reach over 60% of total TV viewers by 2017

India – Internet Connections India Internet vs. TV Penetration

139174

232286

331

25

29

34

40

47

55

99

272

333

386

168

124

208

0

100

200

300

400

2012 2013P 2014P 2015P 2016P 2017P

Mill

ion c

onnections

Wireless Connections Wireline Connections

CAGR 25% 731

762791

820848

873

496

426

351

276226

174

0

300

600

900

2012 2013P 2014P 2015P 2016P 2017P

Mill

ions

Internet Users TV Viewers

Source: FICCI-KPMG Indian M&E Industry Report 2013

18- Confidential -

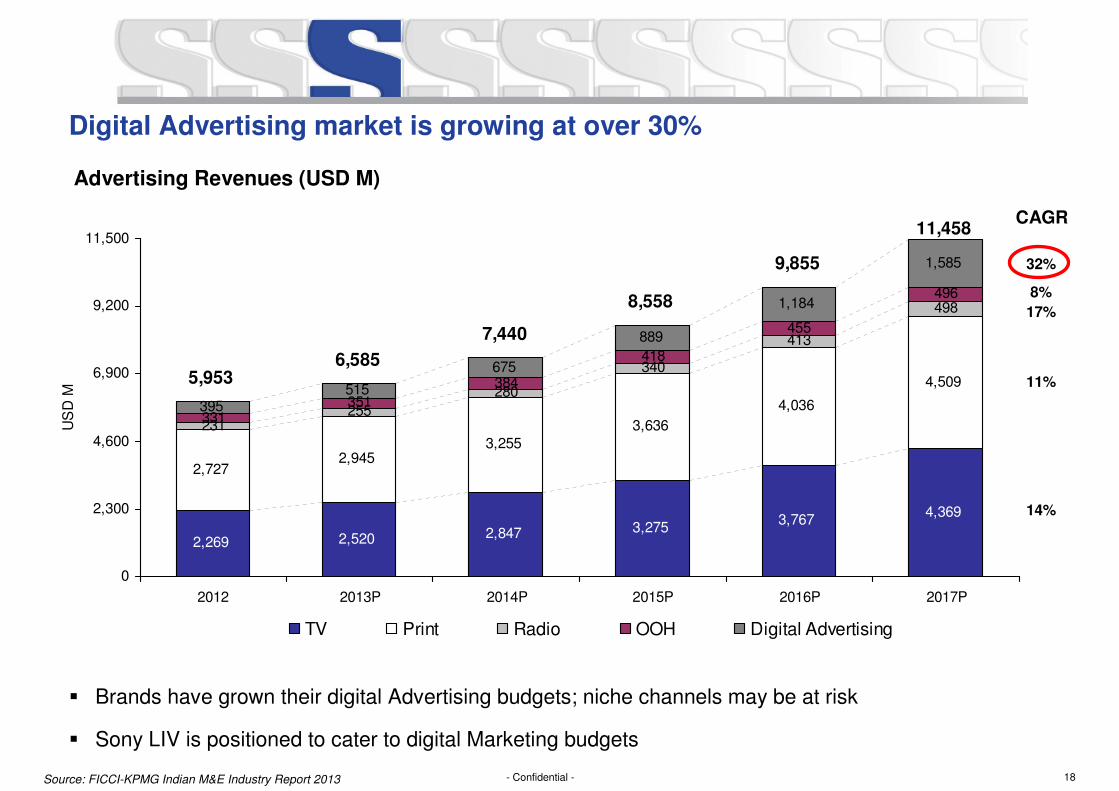

Digital Advertising market is growing at over 30%

� Brands have grown their digital Advertising budgets; niche channels may be at risk

� Sony LIV is positioned to cater to digital Marketing budgets

Advertising Revenues (USD M)

2,520 2,847 3,2753,767

4,369

2,7272,945

3,2553,636

4,036

4,509

231255

280

340

498

331351

384

418

496

395515

675

1,184

2,269

413455

889

1,585

8,558

9,855

11,458

6,5855,953

7,440

0

2,300

4,600

6,900

9,200

11,500

2012 2013P 2014P 2015P 2016P 2017P

US

D M

TV Print Radio OOH Digital Advertising

17%

32%

CAGR

11%

14%

8%

Source: FICCI-KPMG Indian M&E Industry Report 2013

19- Confidential -

Market landscape and Competition Update

20- Confidential -

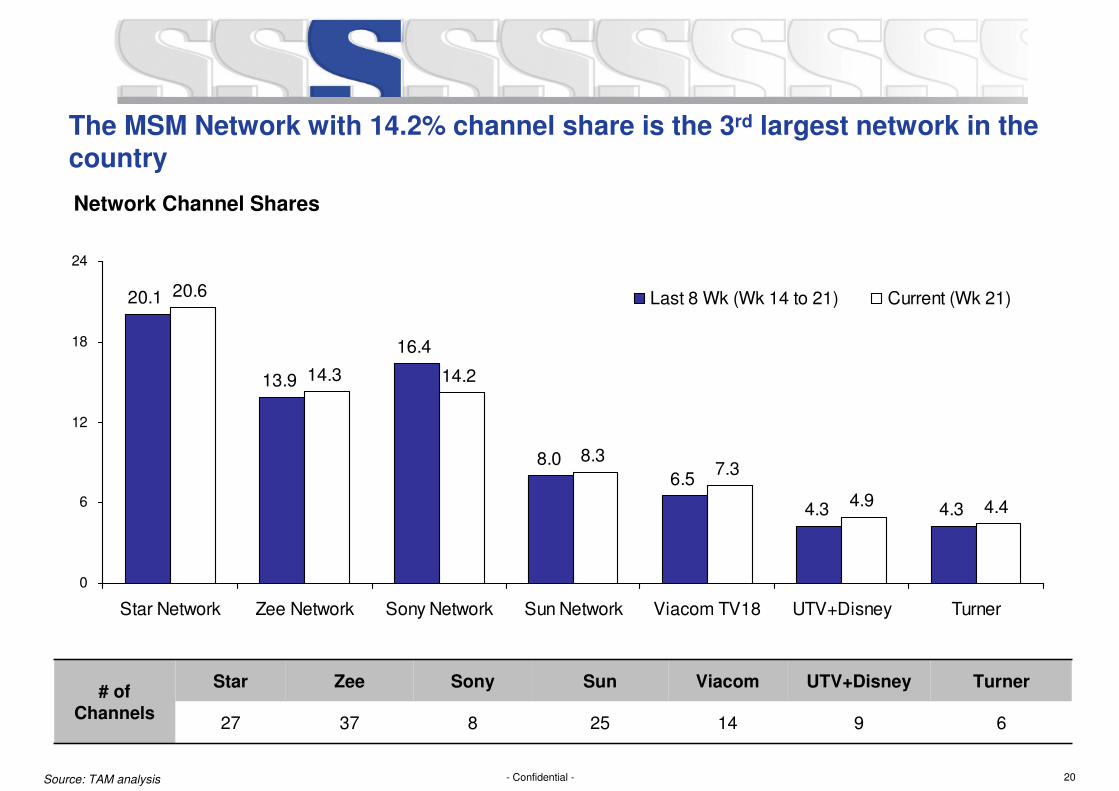

The MSM Network with 14.2% channel share is the 3rd largest network in the country

Network Channel Shares

20.1

13.9

16.4

8.06.5

4.3 4.3

20.6

14.3 14.2

8.37.3

4.9 4.4

0

6

12

18

24

Star Network Zee Network Sony Network Sun Network Viacom TV18 UTV+Disney Turner

Last 8 Wk (Wk 14 to 21) Current (Wk 21)

# of

Channels

Star Zee Sony Sun Viacom UTV+Disney Turner

27 37 8 25 14 9 6

Source: TAM analysis

21- Confidential -

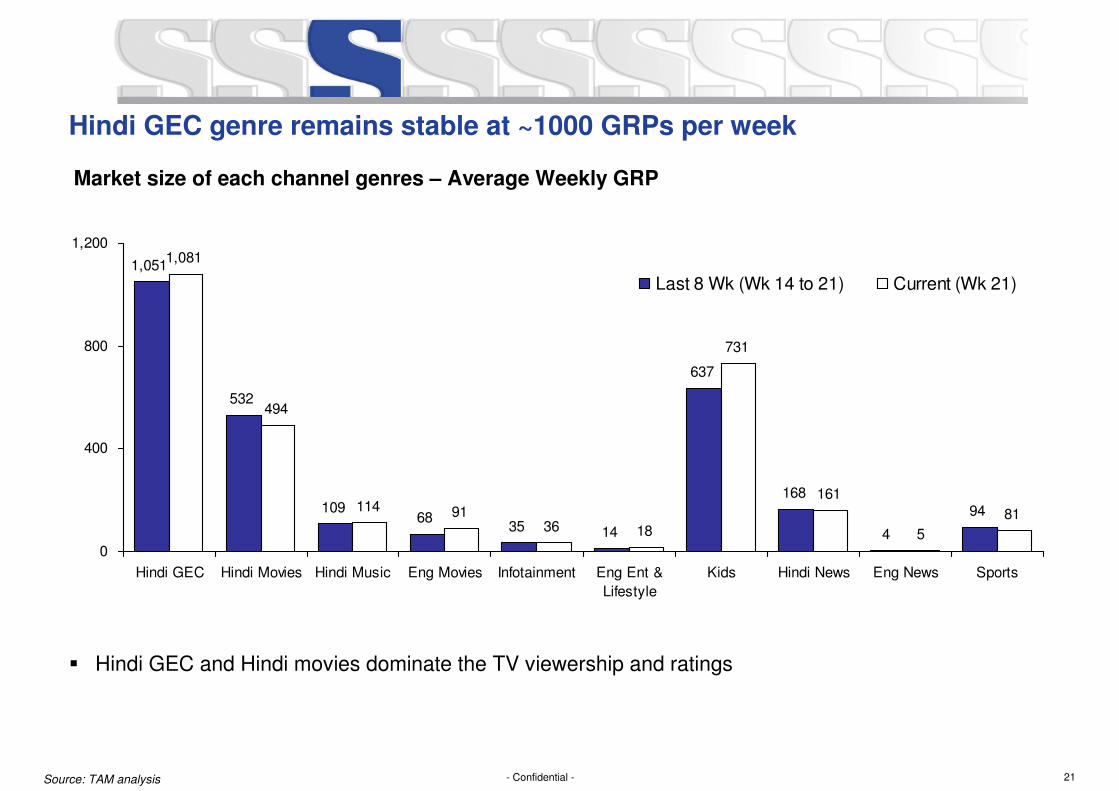

Hindi GEC genre remains stable at ~1000 GRPs per week

1,051

532

10968

35 14

637

168

4

94

1,081

494

114 9136 18

731

161

5

81

0

400

800

1,200

Hindi GEC Hindi Movies Hindi Music Eng Movies Infotainment Eng Ent &

Lifestyle

Kids Hindi News Eng News Sports

Last 8 Wk (Wk 14 to 21) Current (Wk 21)

Market size of each channel genres – Average Weekly GRP

� Hindi GEC and Hindi movies dominate the TV viewership and ratings

Source: TAM analysis

22- Confidential -

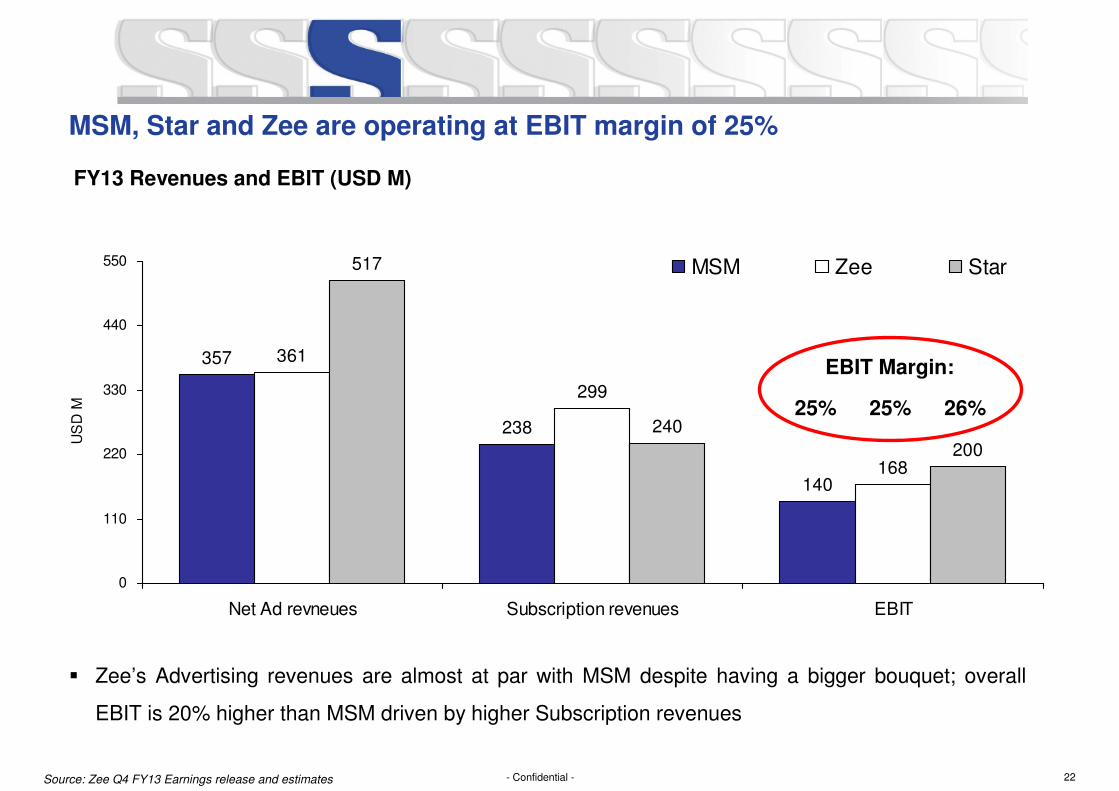

MSM, Star and Zee are operating at EBIT margin of 25%

357

238

140

361

299

168

517

240

200

0

110

220

330

440

550

Net Ad revneues Subscription revenues EBIT

US

D M

MSM Zee Star

FY13 Revenues and EBIT (USD M)

Source: Zee Q4 FY13 Earnings release and estimates

� Zee’s Advertising revenues are almost at par with MSM despite having a bigger bouquet; overall

EBIT is 20% higher than MSM driven by higher Subscription revenues

25% 25% 26%

EBIT Margin:

23- Confidential -

Updates from General Entertainment (GEC) Genre (1 of 2)

Colors

Programming:

� Has launched a number of fiction shows with limited

success

� Channel’s viewership dependant on old shows like

‘Balika Vadhu’ and ‘Uttaran’

� Has invested heavily in big ticket non-fiction properties

� Large number of events and blockbuster movie

premieres, which the channel regularly airs

� Upcoming highlights include a new comedy reality

show ‘Comedy Nights with Kapil’ as well as a new

fiction ‘Mrs Pammi Pyarelal’

Marketing:

� Aggressive player in promoting their properties,

especially their non-fiction ones

� Targets a similar audience profile to Sony and typically

uses its celebrities to push for recall like Madhuri Dixit,

Salman Khan etc

Star Plus

Programming:

� Only GEC to start primetime as early as 6:30pm

� Offering a key non-fiction property ‘Master Chef India’

on weekdays (8pm)

� Hasn’t seen much success with weekend properties

� Upcoming mythological ‘Mahabharat’ as well as ‘Junior

Master Chef’

Marketing:

� Road shows using TV stars across 4-5 key states once

the LC1 markets opened

� Associate on-ground sponsorship on IPL this season

with extensive branding in the stadiums

� Continue to use Bollywood stars on their channel in the

form of movie integrations and/or award events

� Big ticket fiction launches like Mahabharat will probably

see huge spends in promotion

24- Confidential -

Updates from General Entertainment (GEC) Genre (2 of 2)

Life OK

Programming:

� Largely dependent on a single show ‘Mahadev’ for its

growth. Periodic special episodes of the show on

Sundays have helped the channel add to ratings spurts

� Number of fiction launches at frequent intervals but

with only a few being successful

� Has launched a number of alternative genre shows

similar to Sony’s popular space of crime and detective

series; ‘Savdhan India’ and ‘Shapath’ have added to

additional sampling of the channel

� Non-fiction shows has seen limited success, but still

experimenting with format shows including ‘Welcome’

(based on the format ‘Come Dine with Me’)

� Upcoming Shows: Another International format show

‘Bachelorette India’ and ‘Police Dial 100’

Marketing:

� Marginal promotions centred around new show

launches or on Mahadev (flagship show)

� Planning to use Bollywood star Mallika Sherawat to

propel new show “The Bachelorette” and the channel

Zee

Programming:

� Continues to keep weekday fiction programming as its

backbone

� Weekend non-fiction properties have been well

established over many seasons including ‘Saregama’,

‘Dance India Dance’

� Launched new non-fiction format this year - ‘India’s

Best Dramebaaz’

� Has experimented with other alternative fiction

properties like ‘Fear Files’ and recently launched

‘Connected Hum Tum’

� Upcoming highlights for the channel include a epic

show ‘Jodha Akbar’

Marketing:

� Loyal base among lower SEC audiences and smaller

towns in North India

� Communicates effectively with its audiences using low

cost media outreach vehicles

� Extensive promotion for movie premieres across

platforms

25- Confidential -

Update on Hindi Movies genre

� Digitisation is building a level playing field for all Movie channels, increasing dependency on

compelling content for GRPs

� The bulk of viewership comes from Non-Metros and smaller towns

� Marquee titles are being distributed across Networks

� Competition is spending large budgets to lock big stars in long-term deals

26- Confidential -

Update on English Entertainment genre

� Launch of Genre focussed channels

― Star has launched a Genre focused channel – Star Movies Action. Strategy is to defray

content costs across 2 channels

� Launch of Premium services

― HBO is evaluating a Subscription based channel, after launching HBO Defined and HBO Hits

� Times has output deal with Fox and could launch a channel

� There are talks of another Eng GEC/Movie channel entering the space

� PIX is evaluating a SVOD platform, with increasing competition from VOD

27- Confidential -

Update on Music genre

� Genre stands to gain both reach and time spent (TS) from complete digitization roll out, similar to

DAS 1 wherein Music genre’s quantum viewership growth was the highest among all genres

� While TRAI’s mandate of phasing out all commercial inventory in excess of 12 minutes from October

does challenge Advertising revenue, the genre’s viewership stands to benefit considering present

FCT levels are anywhere between 19 to 28 minutes in a clock-hour

� The proposed copyright law may challenge MIX’s proposition of offering the widest spectrum of

music as retro songs in particular face uncertainty over content ownership

� Considering the amendments in the new copyright law, wherein content authors stand to benefit

from revenue share, music labels offering contemporary music are expecting increase in valuation of

libraries

28- Confidential -

138

18

(120)

380

223

-150

-100

-50

0

50

100

150

200

250

300

350

400

Net Ad

revenues

Sub

revenues

Other

income Total

License

fees EBIT

US

D M

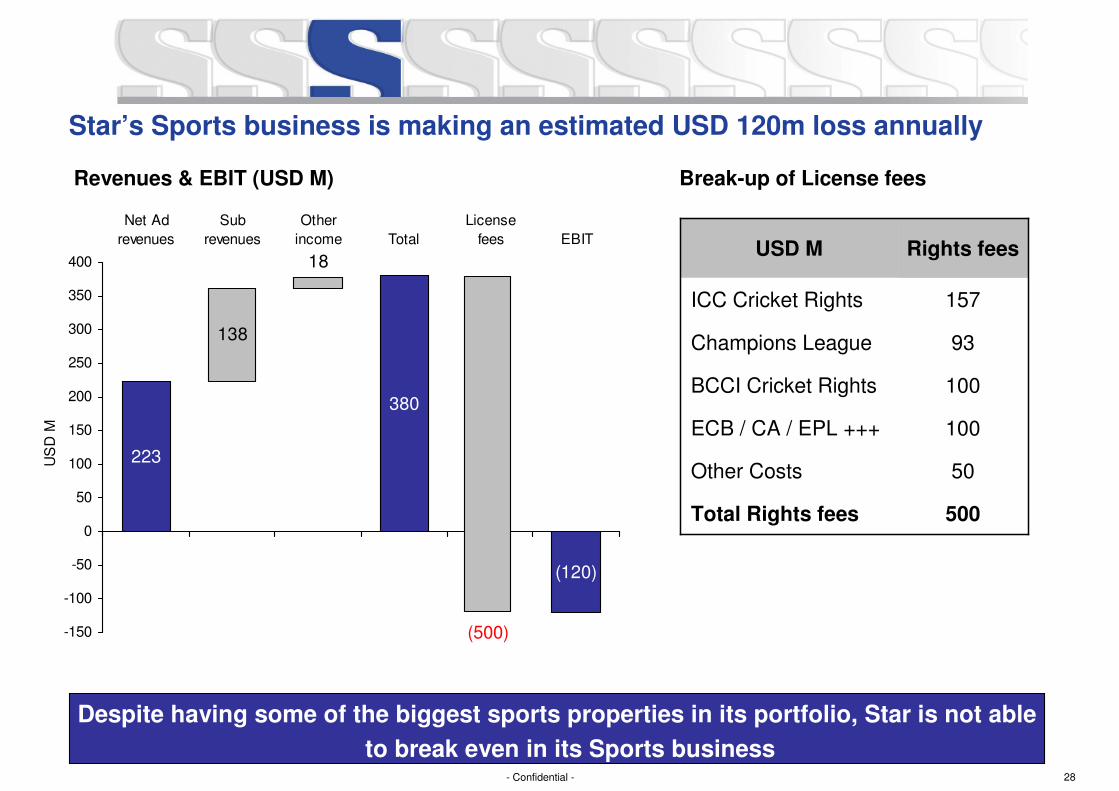

Star’s Sports business is making an estimated USD 120m loss annually

Revenues & EBIT (USD M) Break-up of License fees

500

50

100

100

93

157

Rights feesUSD M

ICC Cricket Rights

Champions League

BCCI Cricket Rights

ECB / CA / EPL +++

Other Costs

Total Rights fees

Despite having some of the biggest sports properties in its portfolio, Star is not able

to break even in its Sports business

(500)

29- Confidential -

Regulatory Update

30- Confidential -

Emerging Regulatory Landscape (1 of 3)

� TRAI: New Regulator and an “aggressive” position on Broadcasting. Proposals by TRAI include:

― Containing “monopolies” in Cable Distribution

― Establishing a national level “independent” rating agency across platforms: digital and

terrestrial

― Restricting ad-sales to 12 minutes per “clock” hour across all genres

― Making “Must carry” mandatory for all digital headends/MSO’s

� Competition Commission of India (CCI)

― Becoming more active

― Investigates “restrictive” trade practices

― An investigation by CCI has found no cartelization in the case related to MediaPro, a 50:50

content distribution JV between Star Den Media Services Pvt. Ltd and Zee Turner Ltd

― CCI has also given green signal to Reliance Industries' acquisition of stake in the Raghav Bahl

promoted media firms Network 18 and TV18 Broadcast

� Order against BCCI

― BCCI held to be “dominant” in cricket

― Fined for monopolistic practice. Tenor of licences for Media Rights not > 5 years

31- Confidential -

Emerging Regulatory Landscape (2 of 3)

� Content Regulation

― “Self Regulation” for GEC working well – points of friction remain

― New Certification process proposed for Films – could impact satellite rights exploitation

� New Media

― New copyrights law introduced, making content costs remain high for film/song based content

― Liability of intermediaries limited

― Safe harbour provisions strengthened

― Enforcing anti-piracy law remains a big issue

� Implementation of Companies Bill

― Constitute a CSR committee and make a CSR policy. Spend 2% of average Net Profits of

preceding three years on CSR activities

― Develop and implement a risk management policy including identification of elements of risks

that threaten existence of the company

― Ensure a resident Director is appointed while reconstituting the Board

32- Confidential -

Emerging Regulatory Landscape (3 of 3)

� FDI in Broadcasting

― Sectoral limit in distribution excluding analogue raised to 74% (up to 49% “automatic”)

― Majority control for foreigners in Cable Distribution now permissible as part of Digitalisation

― Upto 49% in analogue (“automatic”); 100% in Uplinking/Downlinking (non-news)

33- Confidential -

The Road ahead…

34- Confidential -

Where are we today as a Network…

� TAM’s introduction of LC1 Markets in the panel, has resulted in the ratings of the flagship channels to

fall, along with reach and TSV

� The MSM bouquet doesn't have any presence in the Regional space (except Sony Aath)

� Key competition – Star, Zee and Colors have a well established presence in the regional space and

Star and Zee’s flagship channels are performing better in the GEC genre

� Absence of regional channels in the bouquet is a clear gap in the network's genre reach

� Key competition, has a far more “Pan-India” offering both in terms of genre spread and ratings

� Competition has a strategic advantage with presence in carriage. Both Star & Zee have presence in

ground distribution (Star DEN, Tata Sky & Dish)

MSM currently doesn’t have a “complete package” offering for advertisers and

distributors

35- Confidential -

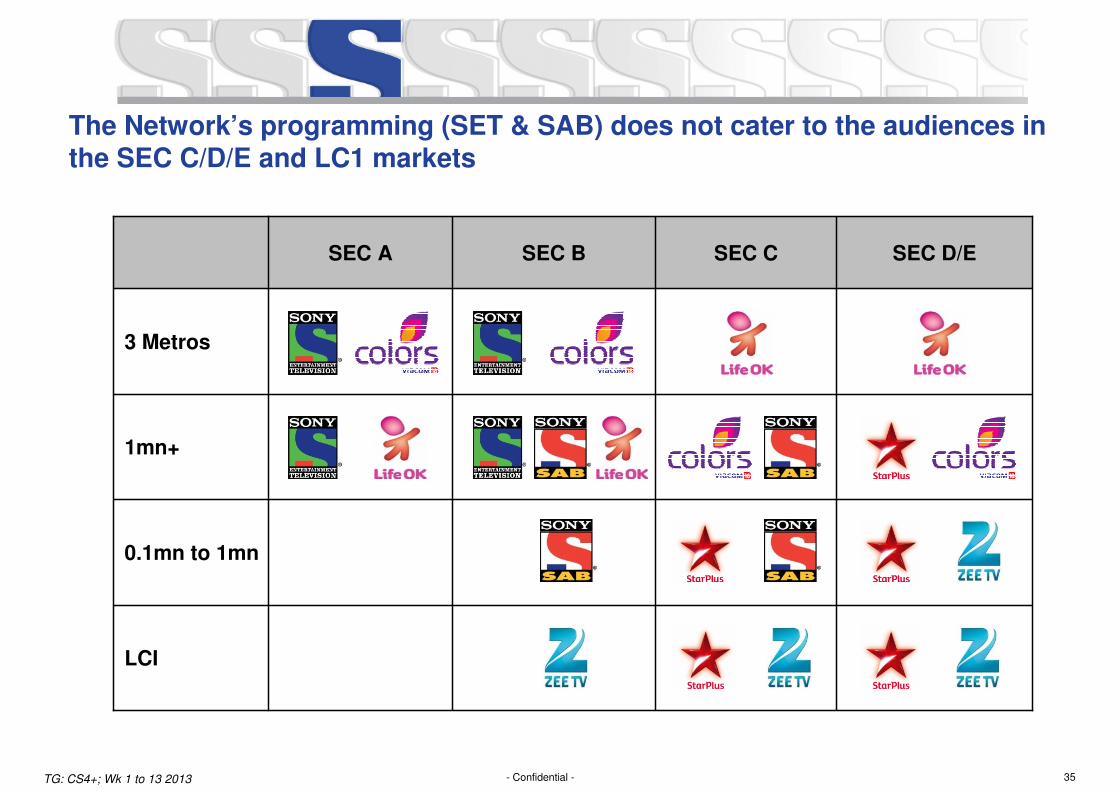

The Network’s programming (SET & SAB) does not cater to the audiences in the SEC C/D/E and LC1 markets

TG: CS4+; Wk 1 to 13 2013

SEC A SEC B SEC C SEC D/E

3 Metros

1mn+

0.1mn to 1mn

LCI

36- Confidential -

The Potential implications…

� With programming not targeted to female audiences in small towns, the introduction of TAM meters

and further expansion, in Rural markets may result in further drop in ratings

� We also run the risk of being dropped by operators due to gaps in our bouquet offering and also for

strategic reasons, which may further fuel a decline in reach and ratings

� Flagship channel’s falling Reach and TSV, may result in Advertisers reducing the premium on the

channel

� The Network is over reliant on SET for driving revenues and EBIT. Falling ratings of the channel is a

risk to Network profitability

The network should aim to target all SECs, markets, across both genres to reduce

the risk of being ignored by media planners and also potentially losing presence

on ground

37- Confidential -

With Business-as-Usual, there is a potential loss of USD 1,045m (INR 5,670 Crs) to USD 1,353m (INR 7,344 Crs) between Years 5 and 10

� The MSO/DTH operator drops our channel from the base tier due to a gap in the portfolio:

― If 30% of operators drop SET and SAB from their bouquet then the loss can be USD 524m

(INR 2,842 Crs) in Subscription revenues and USD 830m (INR 4,502 Crs) in Ad revenues due

to subsequent impact on ratings

― There is a potential risk since 35% of our Distribution revenues comes from Competition

controlled MSO/DTH (DEN – 6%, Dish TV – 11%, Tata Sky – 14%, WWIL – 4%)

� TRAI Regulation of 10 minutes (currently our GEC channels are running 14 minutes average per

hour)

― Reduction will be approx 29% in Ad revenues i.e. USD 1,045m (INR 5,670 Crs)

� Drop in ratings due to Programming and LC1 market changes

― If drop in revenue is pro-rata to reduction in ratings then reduction in Ad revenues will be

approx. USD 859m (INR 4,664 Crs) and Subscription revenues will be USD 189m (INR 1,023

Crs)

FX rate: USD 1= INR 54.265

38- Confidential -

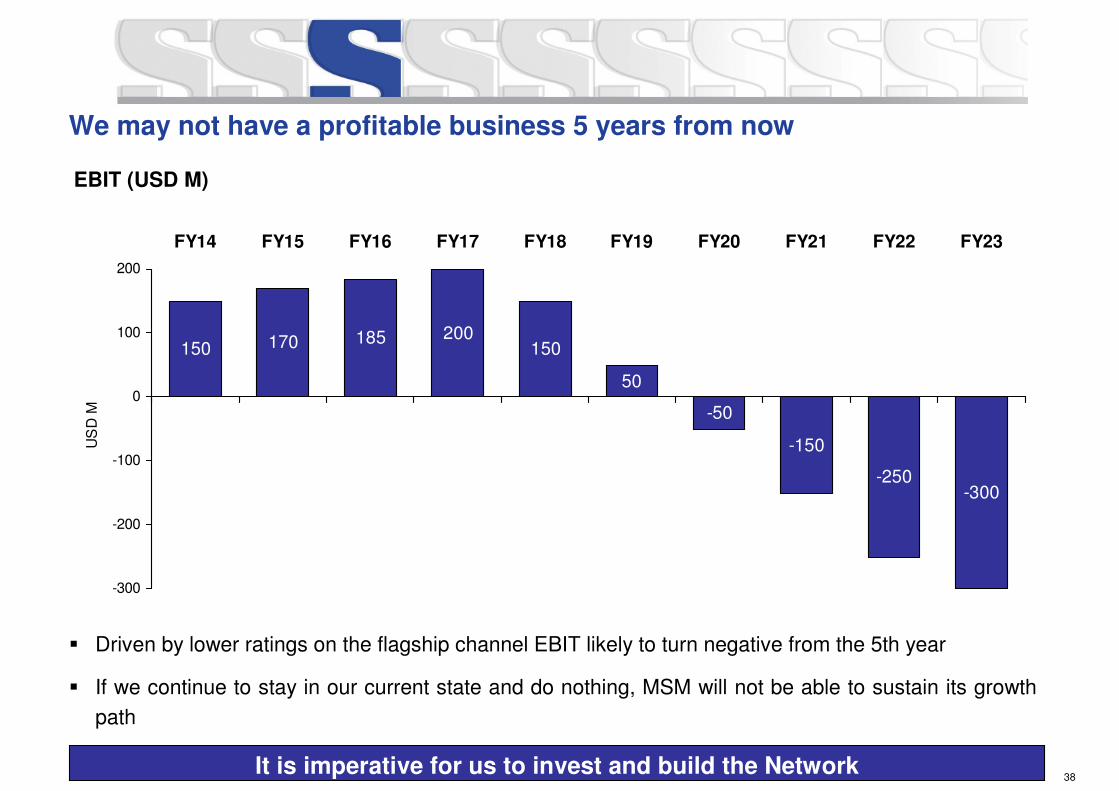

We may not have a profitable business 5 years from now

� Driven by lower ratings on the flagship channel EBIT likely to turn negative from the 5th year

� If we continue to stay in our current state and do nothing, MSM will not be able to sustain its growth

path

150 170 185 200150

50

-50

-150

-250-300

-300

-200

-100

0

100

200

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23

US

D M

EBIT (USD M)

It is imperative for us to invest and build the Network

39- Confidential -

Strategic New Initiatives

40- Confidential -

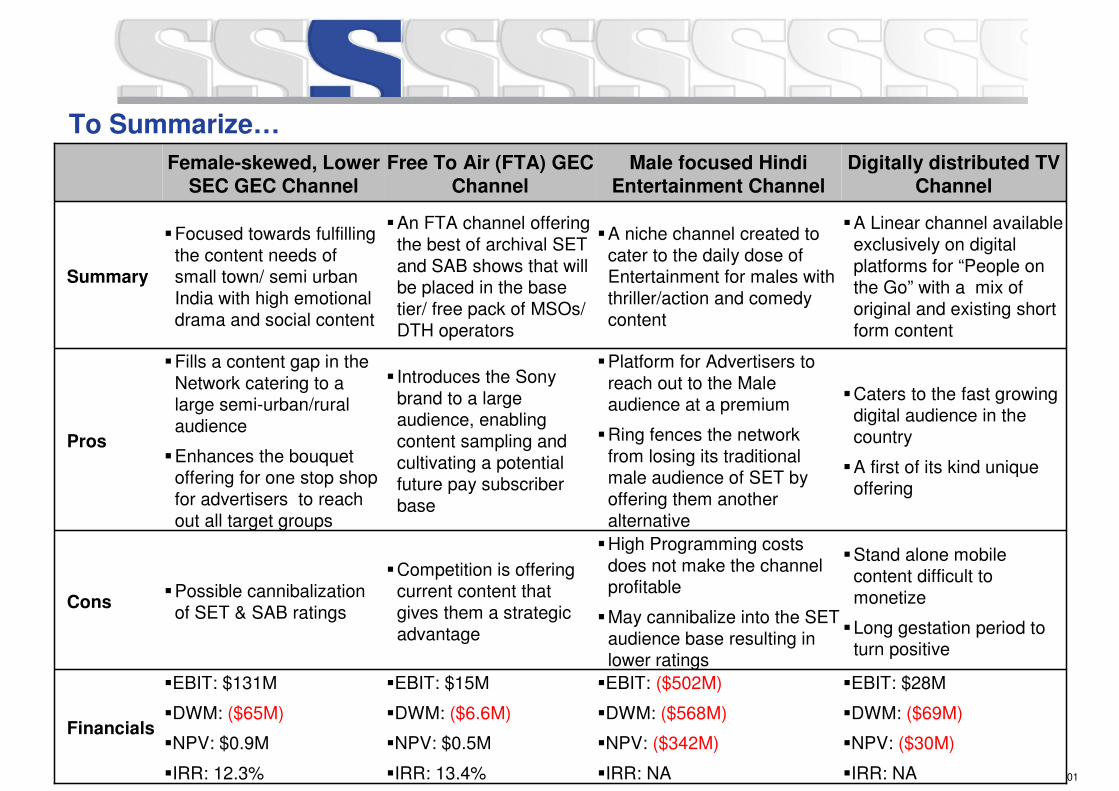

Opportunity 1 – Female-skewed, lower SEC GEC Plan

Strategic New Initiatives

41- Confidential -

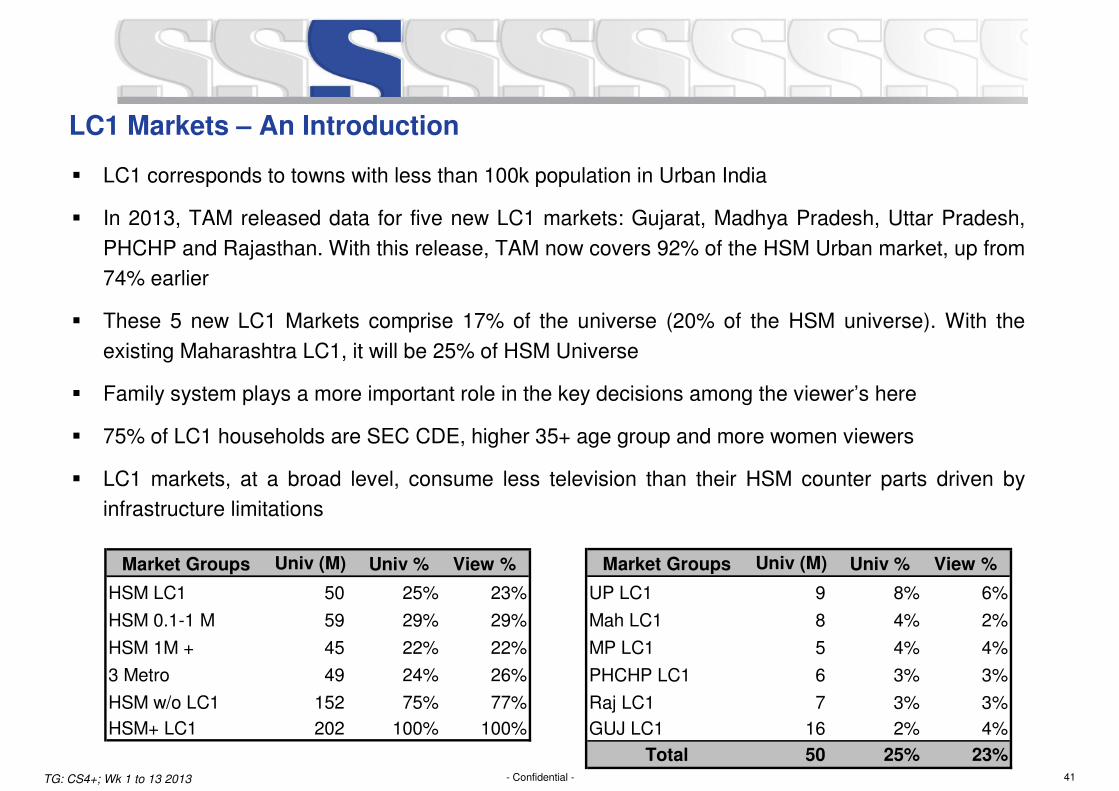

LC1 Markets – An Introduction

� LC1 corresponds to towns with less than 100k population in Urban India

� In 2013, TAM released data for five new LC1 markets: Gujarat, Madhya Pradesh, Uttar Pradesh,

PHCHP and Rajasthan. With this release, TAM now covers 92% of the HSM Urban market, up from

74% earlier

� These 5 new LC1 Markets comprise 17% of the universe (20% of the HSM universe). With the

existing Maharashtra LC1, it will be 25% of HSM Universe

� Family system plays a more important role in the key decisions among the viewer’s here

� 75% of LC1 households are SEC CDE, higher 35+ age group and more women viewers

� LC1 markets, at a broad level, consume less television than their HSM counter parts driven by

infrastructure limitations

TG: CS4+; Wk 1 to 13 2013

Market Groups Univ (M) Univ % View %

HSM LC1 50 25% 23%

HSM 0.1-1 M 59 29% 29%

HSM 1M + 45 22% 22%

3 Metro 49 24% 26%

HSM w/o LC1 152 75% 77%

HSM+ LC1 202 100% 100%

Market Groups Univ (M) Univ % View %

UP LC1 9 8% 6%

Mah LC1 8 4% 2%

MP LC1 5 4% 4%

PHCHP LC1 6 3% 3%

Raj LC1 7 3% 3%

GUJ LC1 16 2% 4%

Total 50 25% 23%

42- Confidential -

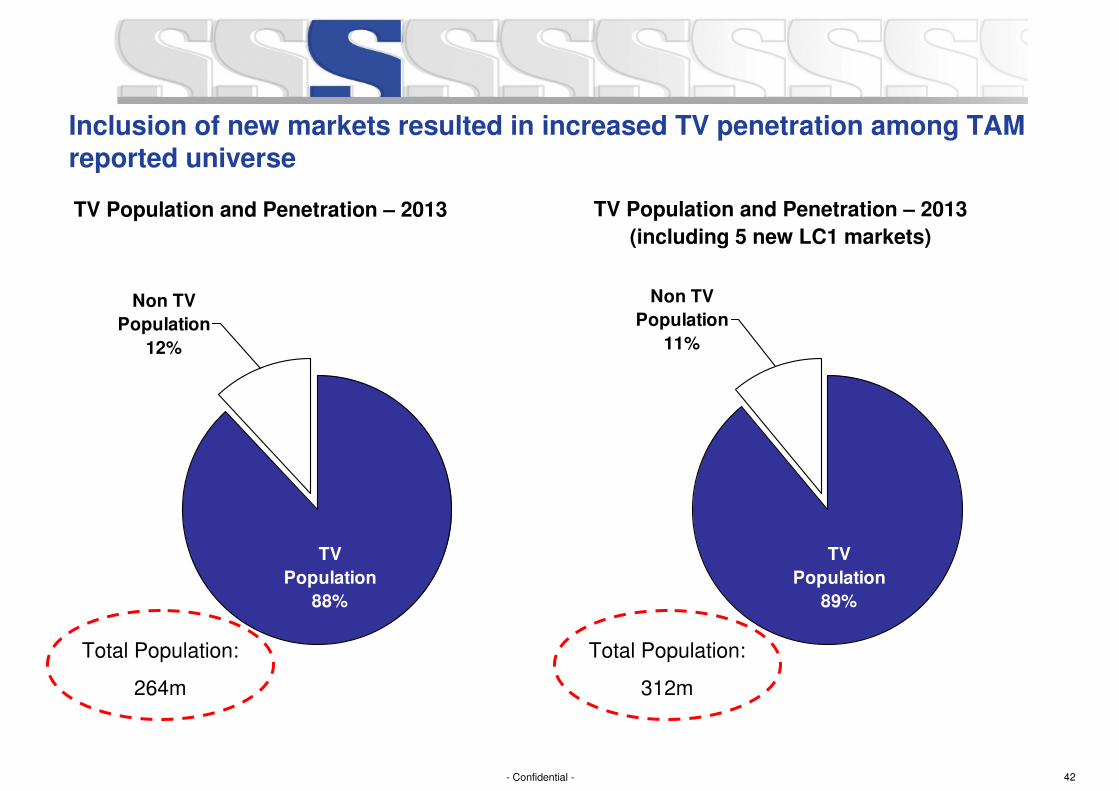

Inclusion of new markets resulted in increased TV penetration among TAM reported universe

Non TV

Population

12%

TV

Population

88%

TV Population and Penetration – 2013 TV Population and Penetration – 2013

(including 5 new LC1 markets)

Non TV

Population

11%

TV

Population

89%

Total Population:

264m

Total Population:

312m

43- Confidential -

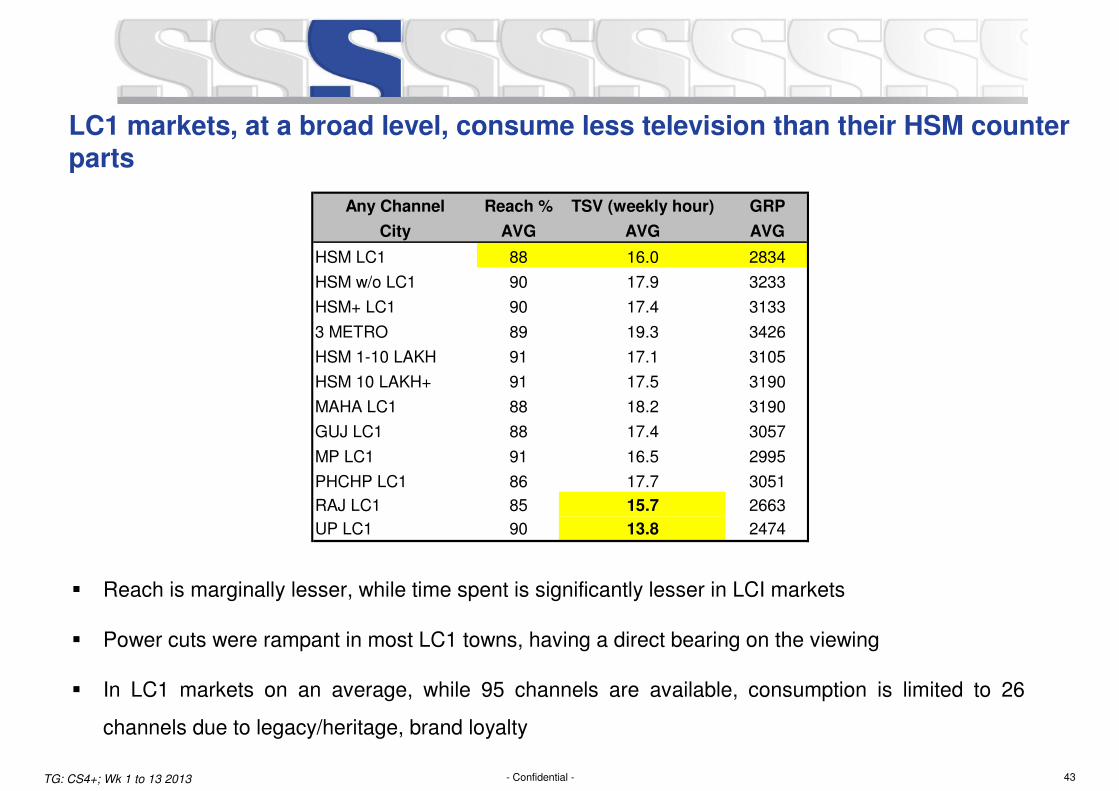

LC1 markets, at a broad level, consume less television than their HSM counter parts

� Reach is marginally lesser, while time spent is significantly lesser in LCI markets

� Power cuts were rampant in most LC1 towns, having a direct bearing on the viewing

� In LC1 markets on an average, while 95 channels are available, consumption is limited to 26

channels due to legacy/heritage, brand loyalty

TG: CS4+; Wk 1 to 13 2013

Any Channel Reach % TSV (weekly hour) GRP

City AVG AVG AVG

HSM LC1 88 16.0 2834

HSM w/o LC1 90 17.9 3233

HSM+ LC1 90 17.4 3133

3 METRO 89 19.3 3426

HSM 1-10 LAKH 91 17.1 3105

HSM 10 LAKH+ 91 17.5 3190

MAHA LC1 88 18.2 3190

GUJ LC1 88 17.4 3057

MP LC1 91 16.5 2995

PHCHP LC1 86 17.7 3051

RAJ LC1 85 15.7 2663

UP LC1 90 13.8 2474

44- Confidential -

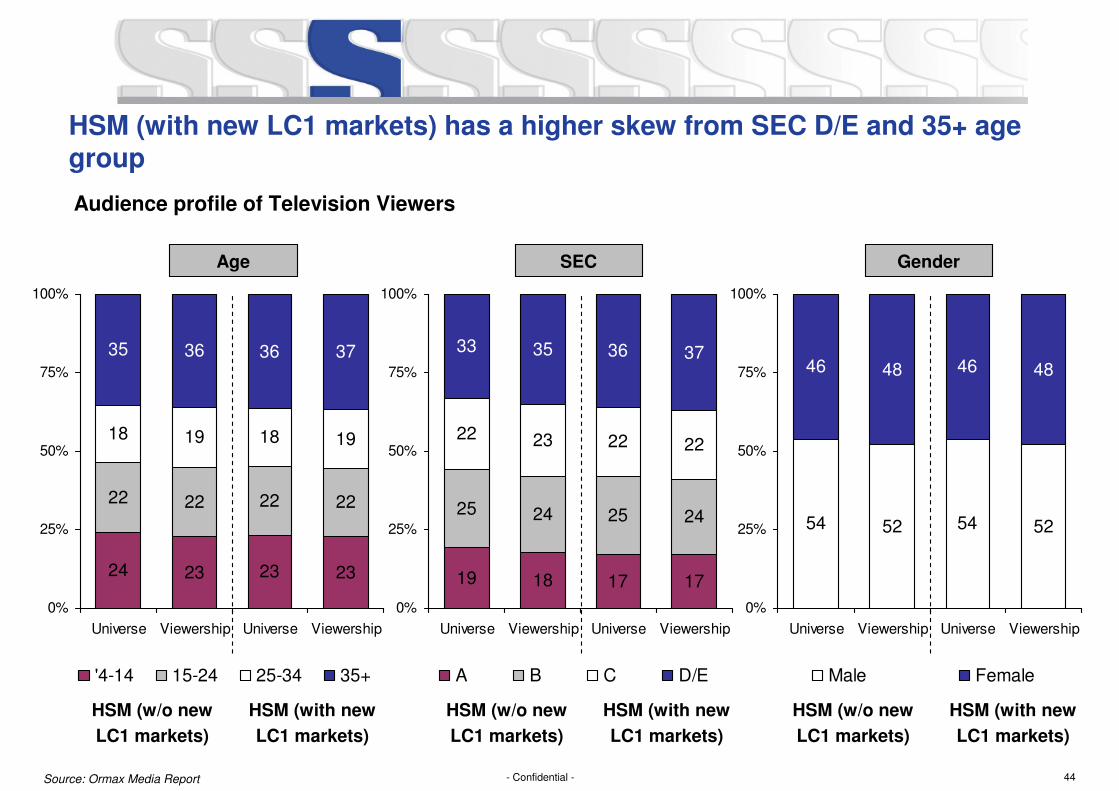

HSM (with new LC1 markets) has a higher skew from SEC D/E and 35+ age group

Audience profile of Television Viewers

23 23 23

22 22 22 22

18 19 18 19

35 36 36 37

24

0%

25%

50%

75%

100%

Universe Viewership Universe Viewership

'4-14 15-24 25-34 35+

18 17 17

25 24 25 24

22 23 22 22

33 35 36 37

19

0%

25%

50%

75%

100%

Universe Viewership Universe Viewership

A B C D/E

54 52 54 52

46 48 46 48

0%

25%

50%

75%

100%

Universe Viewership Universe Viewership

Male Female

Age GenderSEC

HSM (with new

LC1 markets)

HSM (w/o new

LC1 markets)

HSM (with new

LC1 markets)

HSM (w/o new

LC1 markets)

HSM (with new

LC1 markets)

HSM (w/o new

LC1 markets)

Source: Ormax Media Report

45- Confidential -

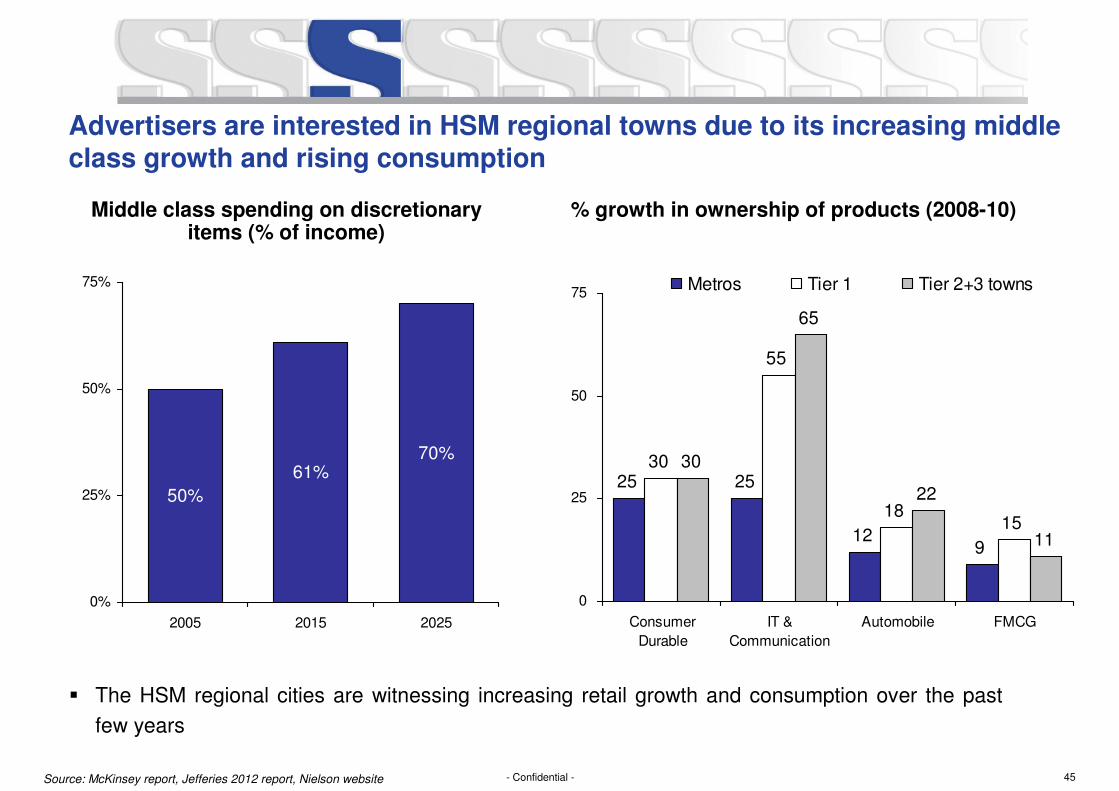

Advertisers are interested in HSM regional towns due to its increasing middle class growth and rising consumption

Middle class spending on discretionary items (% of income)

50%

61%70%

0%

25%

50%

75%

2005 2015 2025

� The HSM regional cities are witnessing increasing retail growth and consumption over the past

few years

% growth in ownership of products (2008-10)

25 25

129

30

55

1815

30

65

22

11

0

25

50

75

Consumer

Durable

IT &

Communication

Automobile FMCG

Metros Tier 1 Tier 2+3 towns

Source: McKinsey report, Jefferies 2012 report, Nielson website

46- Confidential -

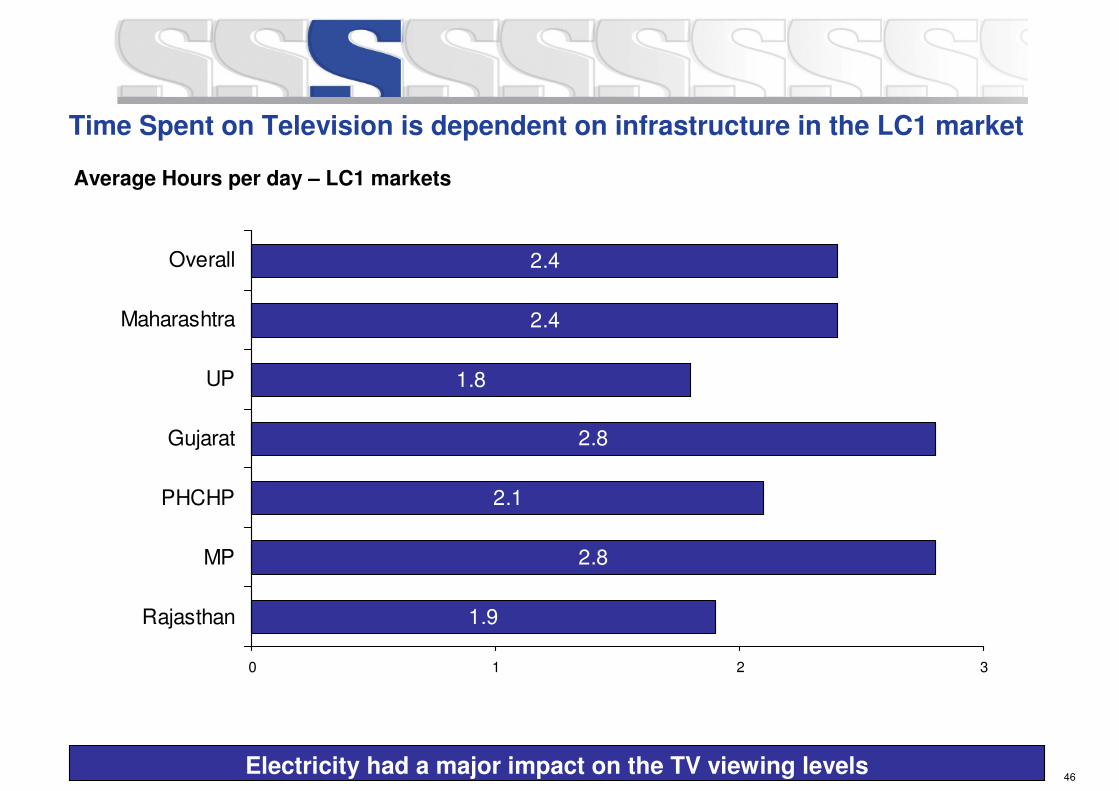

Time Spent on Television is dependent on infrastructure in the LC1 market

Electricity had a major impact on the TV viewing levels

Average Hours per day – LC1 markets

1.9

2.8

2.1

2.8

1.8

2.4

2.4

0 1 2 3

Rajasthan

MP

PHCHP

Gujarat

UP

Maharashtra

Overall

47- Confidential -

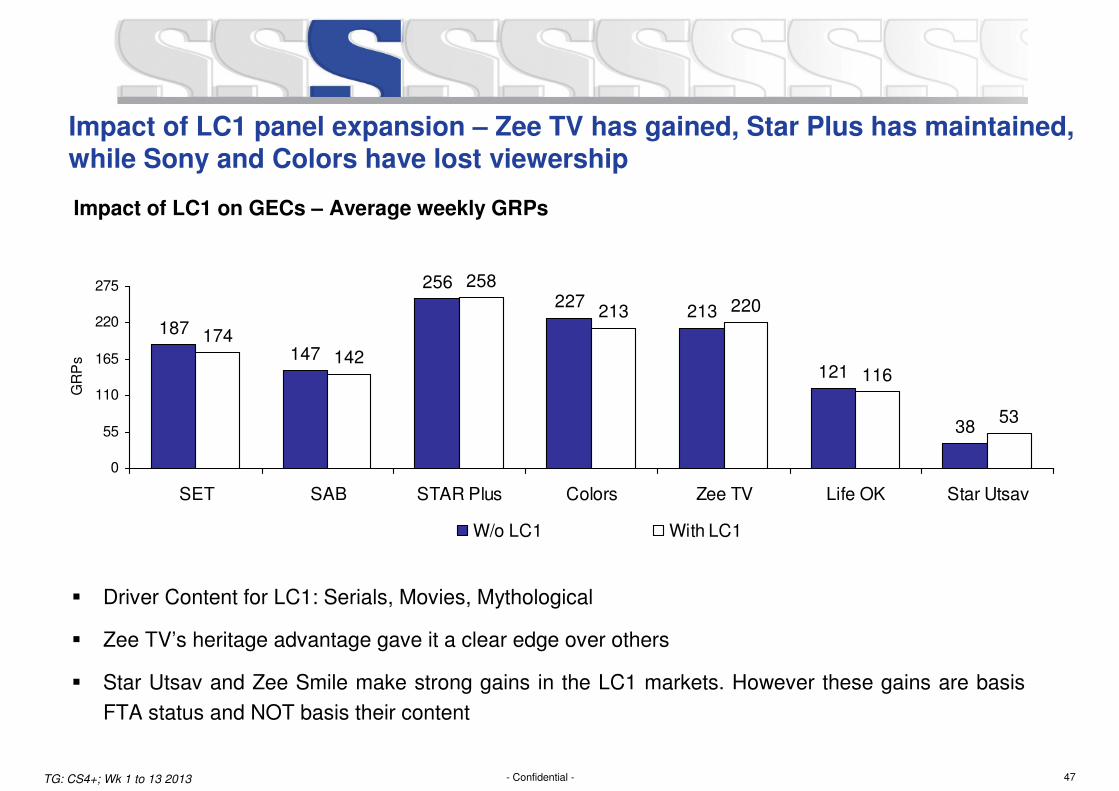

187

147

256227

213

121

38

174142

258

213 220

116

53

0

55

110

165

220

275

SET SAB STAR Plus Colors Zee TV Life OK Star Utsav

GR

Ps

W/o LC1 With LC1

� Driver Content for LC1: Serials, Movies, Mythological

� Zee TV’s heritage advantage gave it a clear edge over others

� Star Utsav and Zee Smile make strong gains in the LC1 markets. However these gains are basis

FTA status and NOT basis their content

TG: CS4+; Wk 1 to 13 2013

Impact of LC1 panel expansion – Zee TV has gained, Star Plus has maintained, while Sony and Colors have lost viewership

Impact of LC1 on GECs – Average weekly GRPs

48- Confidential -

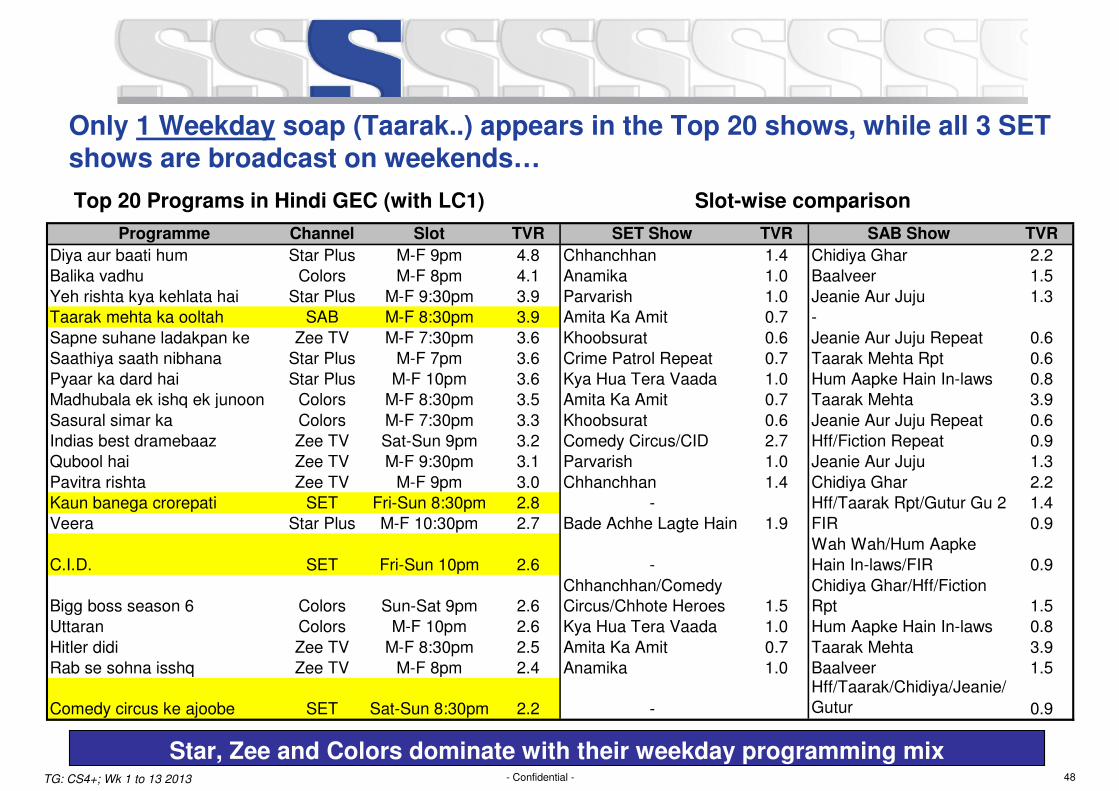

Only 1 Weekday soap (Taarak..) appears in the Top 20 shows, while all 3 SET shows are broadcast on weekends…

Star, Zee and Colors dominate with their weekday programming mixTG: CS4+; Wk 1 to 13 2013

Top 20 Programs in Hindi GEC (with LC1) Slot-wise comparison

Programme Channel Slot TVR SET Show TVR SAB Show TVR

Diya aur baati hum Star Plus M-F 9pm 4.8 Chhanchhan 1.4 Chidiya Ghar 2.2

Balika vadhu Colors M-F 8pm 4.1 Anamika 1.0 Baalveer 1.5

Yeh rishta kya kehlata hai Star Plus M-F 9:30pm 3.9 Parvarish 1.0 Jeanie Aur Juju 1.3

Taarak mehta ka ooltah SAB M-F 8:30pm 3.9 Amita Ka Amit 0.7 -

Sapne suhane ladakpan ke Zee TV M-F 7:30pm 3.6 Khoobsurat 0.6 Jeanie Aur Juju Repeat 0.6

Saathiya saath nibhana Star Plus M-F 7pm 3.6 Crime Patrol Repeat 0.7 Taarak Mehta Rpt 0.6

Pyaar ka dard hai Star Plus M-F 10pm 3.6 Kya Hua Tera Vaada 1.0 Hum Aapke Hain In-laws 0.8

Madhubala ek ishq ek junoon Colors M-F 8:30pm 3.5 Amita Ka Amit 0.7 Taarak Mehta 3.9

Sasural simar ka Colors M-F 7:30pm 3.3 Khoobsurat 0.6 Jeanie Aur Juju Repeat 0.6

Indias best dramebaaz Zee TV Sat-Sun 9pm 3.2 Comedy Circus/CID 2.7 Hff/Fiction Repeat 0.9

Qubool hai Zee TV M-F 9:30pm 3.1 Parvarish 1.0 Jeanie Aur Juju 1.3

Pavitra rishta Zee TV M-F 9pm 3.0 Chhanchhan 1.4 Chidiya Ghar 2.2

Kaun banega crorepati SET Fri-Sun 8:30pm 2.8 - Hff/Taarak Rpt/Gutur Gu 2 1.4

Veera Star Plus M-F 10:30pm 2.7 Bade Achhe Lagte Hain 1.9 FIR 0.9

C.I.D. SET Fri-Sun 10pm 2.6 -

Wah Wah/Hum Aapke

Hain In-laws/FIR 0.9

Bigg boss season 6 Colors Sun-Sat 9pm 2.6

Chhanchhan/Comedy

Circus/Chhote Heroes 1.5

Chidiya Ghar/Hff/Fiction

Rpt 1.5

Uttaran Colors M-F 10pm 2.6 Kya Hua Tera Vaada 1.0 Hum Aapke Hain In-laws 0.8

Hitler didi Zee TV M-F 8:30pm 2.5 Amita Ka Amit 0.7 Taarak Mehta 3.9

Rab se sohna isshq Zee TV M-F 8pm 2.4 Anamika 1.0 Baalveer 1.5

Comedy circus ke ajoobe SET Sat-Sun 8:30pm 2.2 -

Hff/Taarak/Chidiya/Jeanie/

Gutur 0.9

49- Confidential -

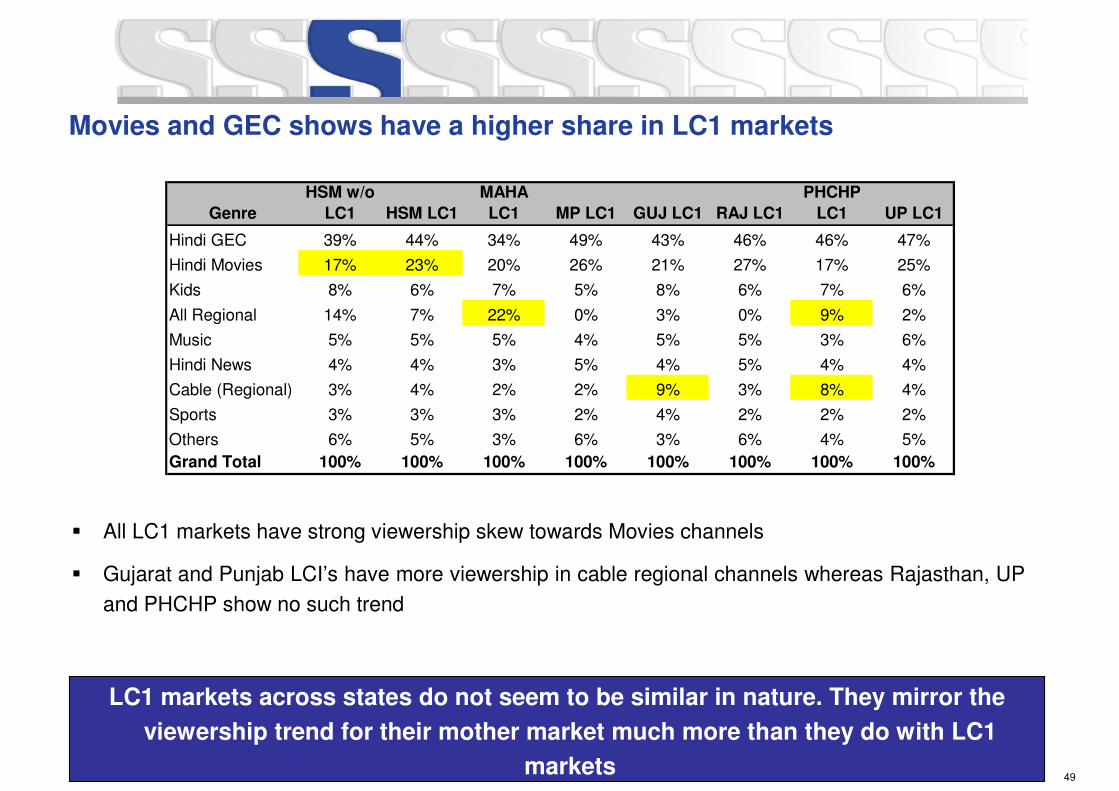

Movies and GEC shows have a higher share in LC1 markets

*CS4+. Wk 1 to 13 2013

LC1 markets across states do not seem to be similar in nature. They mirror the

viewership trend for their mother market much more than they do with LC1

markets

� All LC1 markets have strong viewership skew towards Movies channels

� Gujarat and Punjab LCI’s have more viewership in cable regional channels whereas Rajasthan, UP

and PHCHP show no such trend

Genre

HSM w/o

LC1 HSM LC1

MAHA

LC1 MP LC1 GUJ LC1 RAJ LC1

PHCHP

LC1 UP LC1

Hindi GEC 39% 44% 34% 49% 43% 46% 46% 47%

Hindi Movies 17% 23% 20% 26% 21% 27% 17% 25%

Kids 8% 6% 7% 5% 8% 6% 7% 6%

All Regional 14% 7% 22% 0% 3% 0% 9% 2%

Music 5% 5% 5% 4% 5% 5% 3% 6%

Hindi News 4% 4% 3% 5% 4% 5% 4% 4%

Cable (Regional) 3% 4% 2% 2% 9% 3% 8% 4%

Sports 3% 3% 3% 2% 4% 2% 2% 2%

Others 6% 5% 3% 6% 3% 6% 4% 5%

Grand Total 100% 100% 100% 100% 100% 100% 100% 100%

50- Confidential -

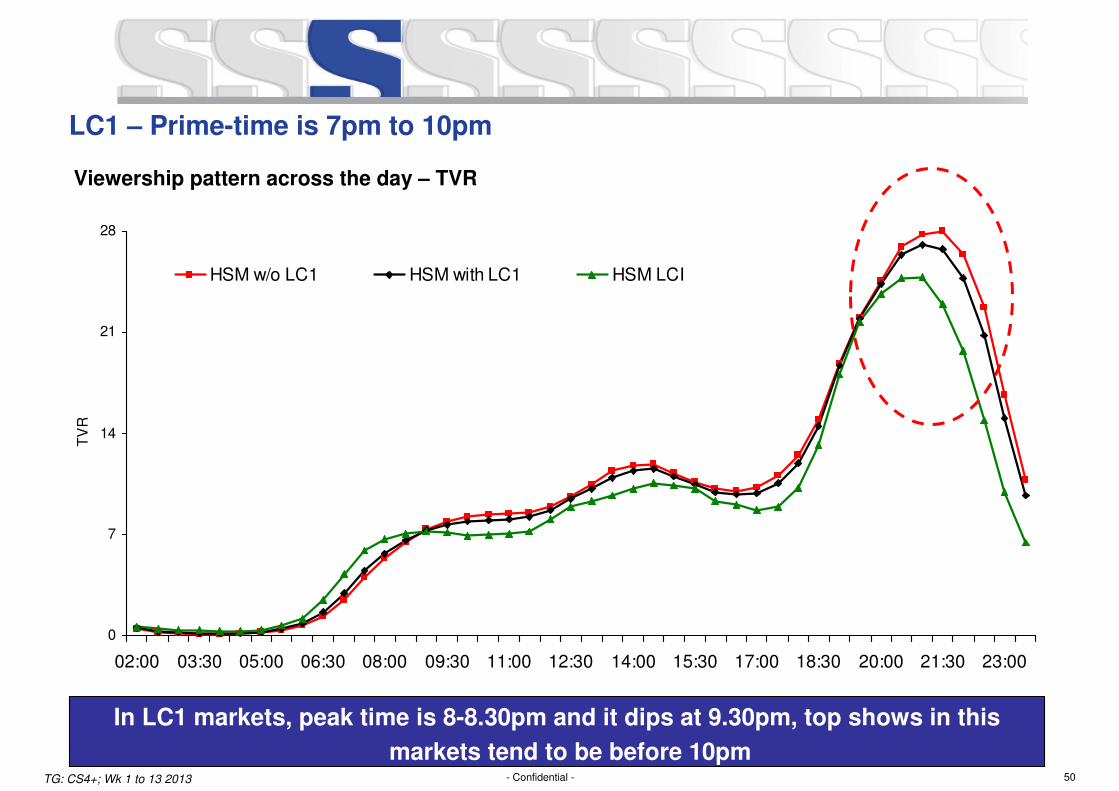

LC1 – Prime-time is 7pm to 10pm

In LC1 markets, peak time is 8-8.30pm and it dips at 9.30pm, top shows in this

markets tend to be before 10pmTG: CS4+; Wk 1 to 13 2013

Viewership pattern across the day – TVR

0

7

14

21

28

02:00 03:30 05:00 06:30 08:00 09:30 11:00 12:30 14:00 15:30 17:00 18:30 20:00 21:30 23:00

TV

R

HSM w/o LC1 HSM with LC1 HSM LCI

51- Confidential -

Key insights from on-ground research in LC1 markets (1 of 2)

Channel Imagery

� Inertia in brand preference

― Heritage brands that are being watched over time, continued to enjoy high equity in these

markets e.g. Zee TV

� Less Variety Seeking Behavior

― While about 50 channels were available, the daily routine included only 4-5 channels at best

� Besides Star Plus and SAB, most other channels were seen as an aggregation of programs or movies

� Given the high weight-age these markets carry, it is prudent to shift the language of all on-air and off-

air communication to Hindi

Viewership Behavior and Lifestyle

� In single TV households, television is watched along with the family so the programme ought to cater

to entire family at a time, also “Parivaarik” movies will be watched rather than romantic movies

� Besides television, only three other touch points emerge for these markets:

― Print (primary off-air medium)

― Mobiles

― Local grocery shops (visited regularly by 60%+)

52- Confidential -

� There were three key influencers of viewing behaviour:

― Viewing companion (whom are they watching TV with?)

― Control over the remote

― Power cuts

� Even at a claimed level, only 1 out of 3 were comfortable with English

Source: Ormax Media Report

Key insights from on-ground research in LC1 markets (2 of 2)

53- Confidential -

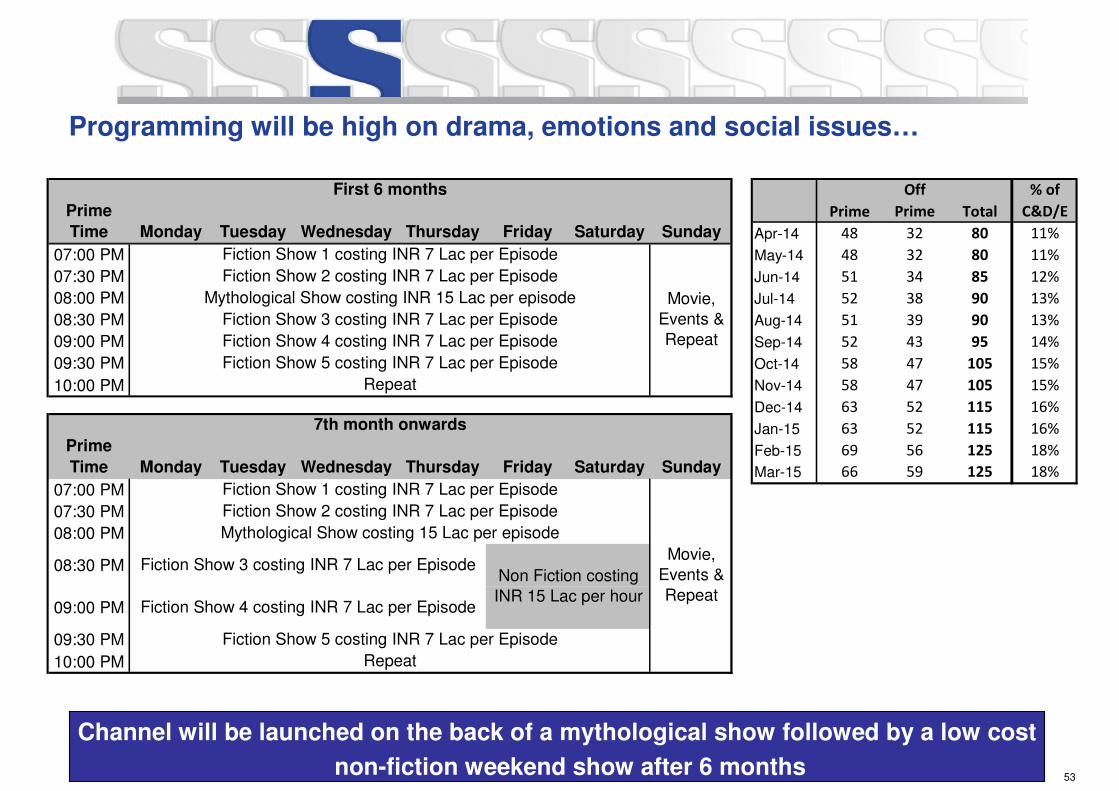

Programming will be high on drama, emotions and social issues…

Channel will be launched on the back of a mythological show followed by a low cost

non-fiction weekend show after 6 months

Prime

Off

Prime Total

% of

C&D/E

Apr-14 48 32 80 11%

May-14 48 32 80 11%

Jun-14 51 34 85 12%

Jul-14 52 38 90 13%

Aug-14 51 39 90 13%

Sep-14 52 43 95 14%

Oct-14 58 47 105 15%

Nov-14 58 47 105 15%

Dec-14 63 52 115 16%

Jan-15 63 52 115 16%

Feb-15 69 56 125 18%

Mar-15 66 59 125 18%

Prime

Time Monday Tuesday Wednesday Thursday Friday Saturday Sunday

07:00 PM

07:30 PM

08:00 PM

08:30 PM

09:00 PM

09:30 PM

10:00 PM

First 6 months

Fiction Show 1 costing INR 7 Lac per Episode

Movie,

Events &

Repeat

Fiction Show 2 costing INR 7 Lac per Episode

Mythological Show costing INR 15 Lac per episode

Fiction Show 3 costing INR 7 Lac per Episode

Fiction Show 4 costing INR 7 Lac per Episode

Fiction Show 5 costing INR 7 Lac per Episode

Repeat

Prime

Time Monday Tuesday Wednesday Thursday Friday Saturday Sunday

07:00 PM

07:30 PM

08:00 PM

08:30 PM

09:00 PM

09:30 PM

10:00 PM

7th month onwards

Fiction Show 1 costing INR 7 Lac per Episode

Movie,

Events &

Repeat

Fiction Show 2 costing INR 7 Lac per Episode

Mythological Show costing 15 Lac per episode

Fiction Show 3 costing INR 7 Lac per EpisodeNon Fiction costing

INR 15 Lac per hourFiction Show 4 costing INR 7 Lac per Episode

Fiction Show 5 costing INR 7 Lac per Episode

Repeat

54- Confidential -

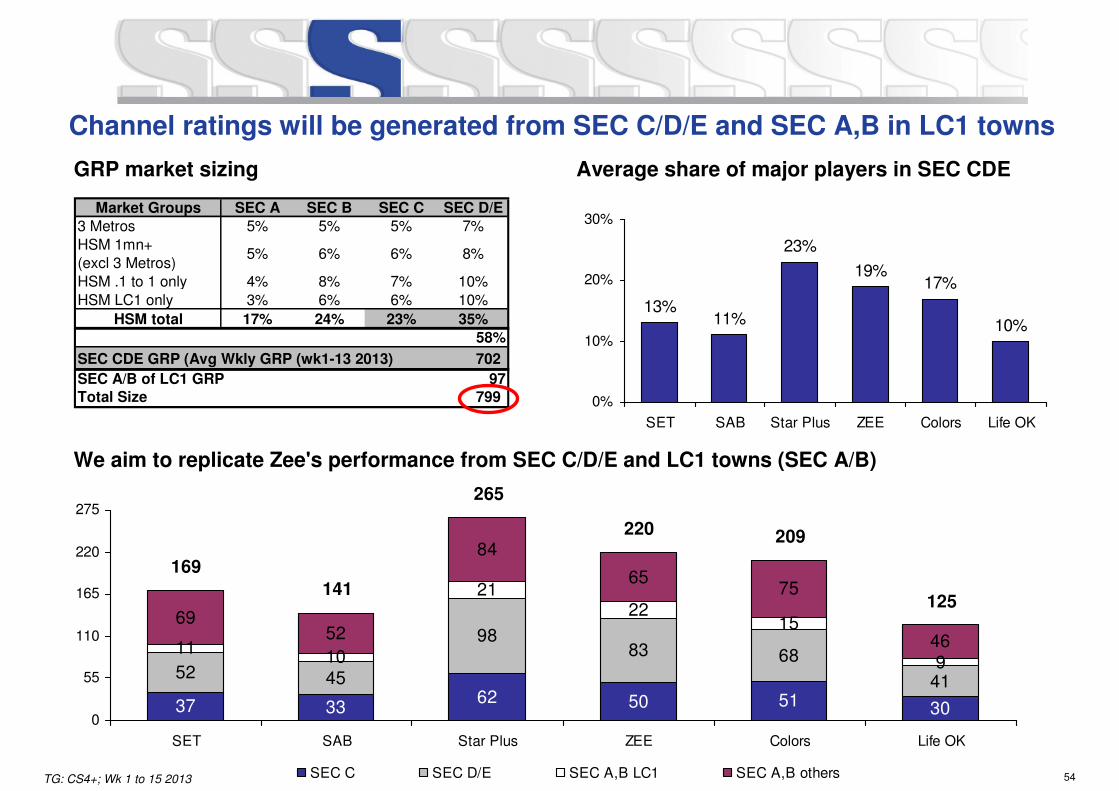

Channel ratings will be generated from SEC C/D/E and SEC A,B in LC1 towns

TG: CS4+; Wk 1 to 15 2013

GRP market sizing Average share of major players in SEC CDE

We aim to replicate Zee's performance from SEC C/D/E and LC1 towns (SEC A/B)

Market Groups SEC A SEC B SEC C SEC D/E

3 Metros 5% 5% 5% 7%

HSM 1mn+ (excl 3 Metros)

5% 6% 6% 8%

HSM .1 to 1 only 4% 8% 7% 10%

HSM LC1 only 3% 6% 6% 10%

HSM total 17% 24% 23% 35%

SEC CDE GRP (Avg Wkly GRP (wk1-13 2013) 702

SEC A/B of LC1 GRP 97

Total Size 799

58%

13%11%

23%

19%17%

10%

0%

10%

20%

30%

SET SAB Star Plus ZEE Colors Life OK

62 50 51 30

45

9883 68

41

10

2122

15

9

6952

84

6575

46

37 33

52

11

265

220 209

125

169

141

0

55

110

165

220

275

SET SAB Star Plus ZEE Colors Life OK

SEC C SEC D/E SEC A,B LC1 SEC A,B others

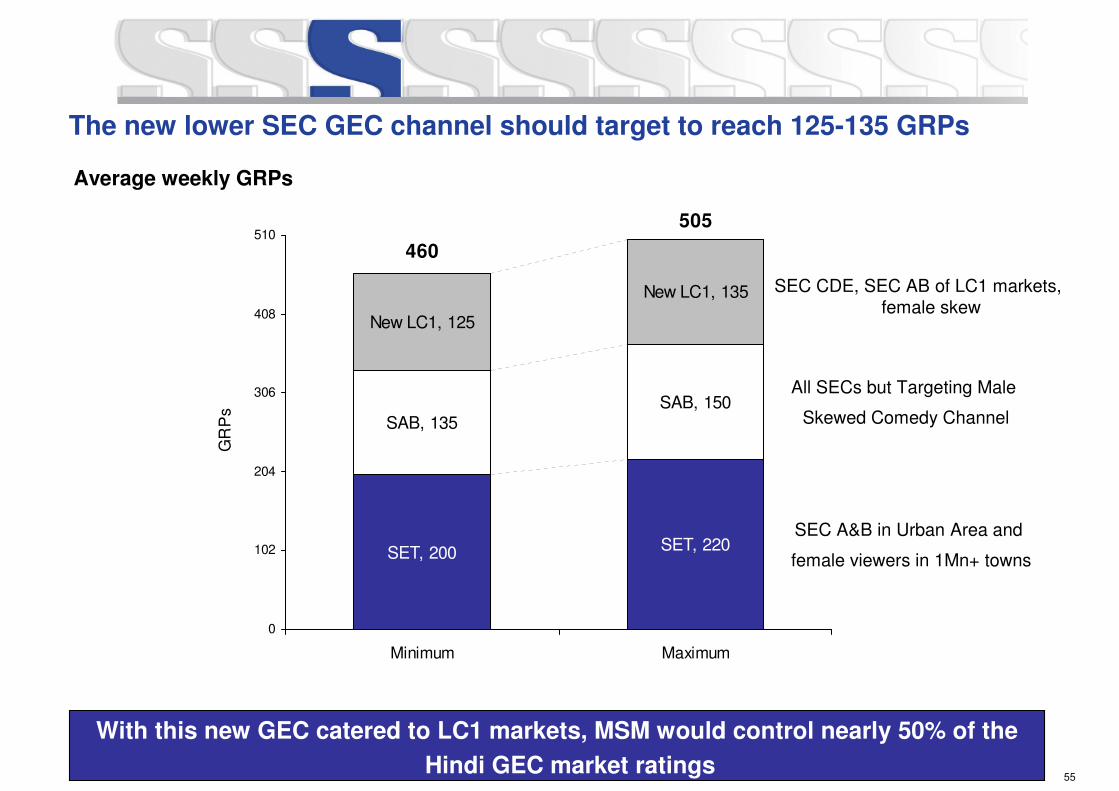

55- Confidential -

SAB, 150

New LC1, 135

SET, 220 SET, 200

SAB, 135

New LC1, 125

505

460

0

102

204

306

408

510

Minimum Maximum

GR

Ps

SEC A&B in Urban Area and

female viewers in 1Mn+ towns

All SECs but Targeting Male

Skewed Comedy Channel

SEC CDE, SEC AB of LC1 markets, female skew

The new lower SEC GEC channel should target to reach 125-135 GRPs

With this new GEC catered to LC1 markets, MSM would control nearly 50% of the

Hindi GEC market ratings

Average weekly GRPs

56- Confidential -

44 50 5766

7688

614

2933

38

44

51

59

2516

3732

25

110

127

146

95

84

31

16

61

73

46

0

50

100

150

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

US

D M

Net Ad Revenues Subscription Revenues

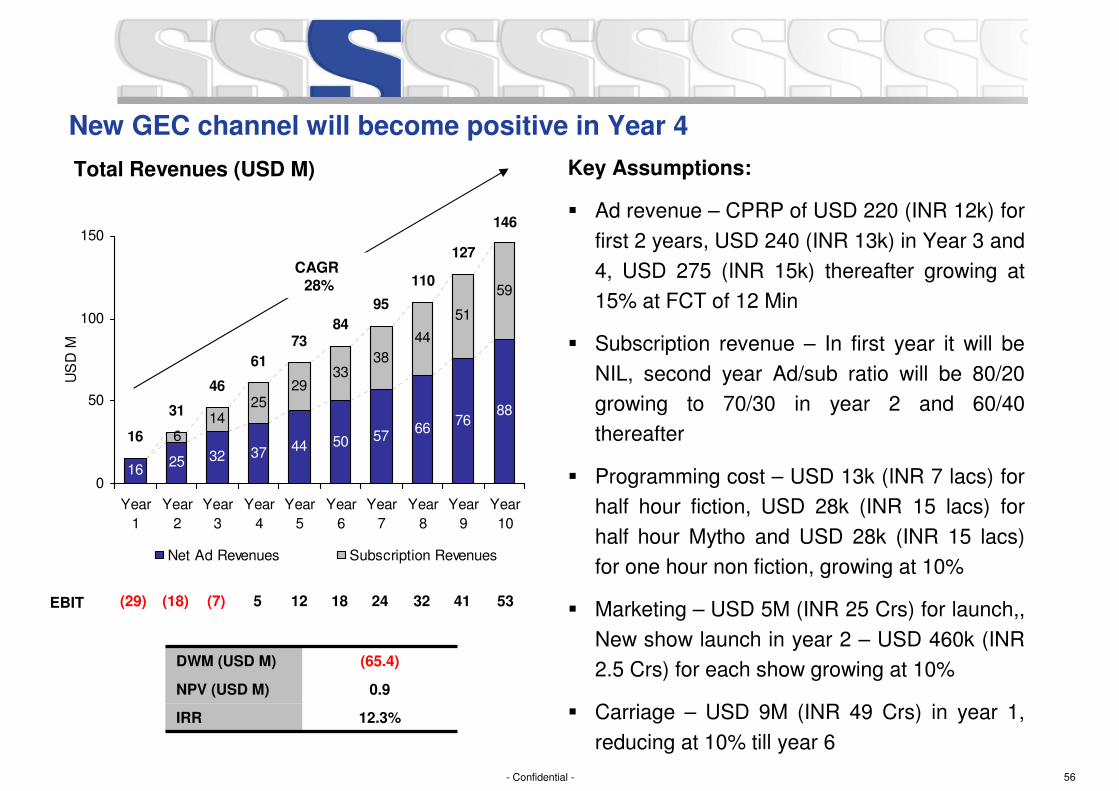

DWM (USD M) (65.4)

NPV (USD M) 0.9

IRR 12.3%

EBIT (29) (18) 53

CAGR 28%

(7) 5 12 18 24 32 41

Total Revenues (USD M)

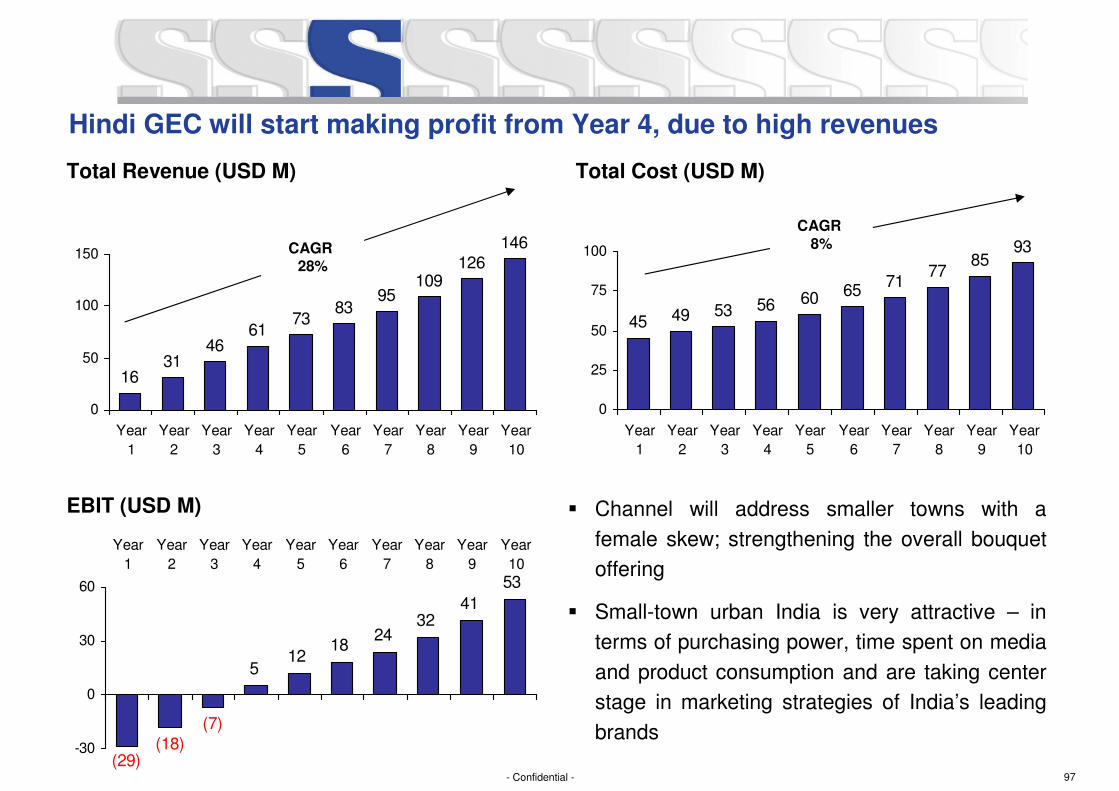

New GEC channel will become positive in Year 4

Key Assumptions:

� Ad revenue – CPRP of USD 220 (INR 12k) for

first 2 years, USD 240 (INR 13k) in Year 3 and

4, USD 275 (INR 15k) thereafter growing at

15% at FCT of 12 Min

� Subscription revenue – In first year it will be

NIL, second year Ad/sub ratio will be 80/20

growing to 70/30 in year 2 and 60/40

thereafter

� Programming cost – USD 13k (INR 7 lacs) for

half hour fiction, USD 28k (INR 15 lacs) for

half hour Mytho and USD 28k (INR 15 lacs)

for one hour non fiction, growing at 10%

� Marketing – USD 5M (INR 25 Crs) for launch,,

New show launch in year 2 – USD 460k (INR

2.5 Crs) for each show growing at 10%

� Carriage – USD 9M (INR 49 Crs) in year 1,

reducing at 10% till year 6

57- Confidential -

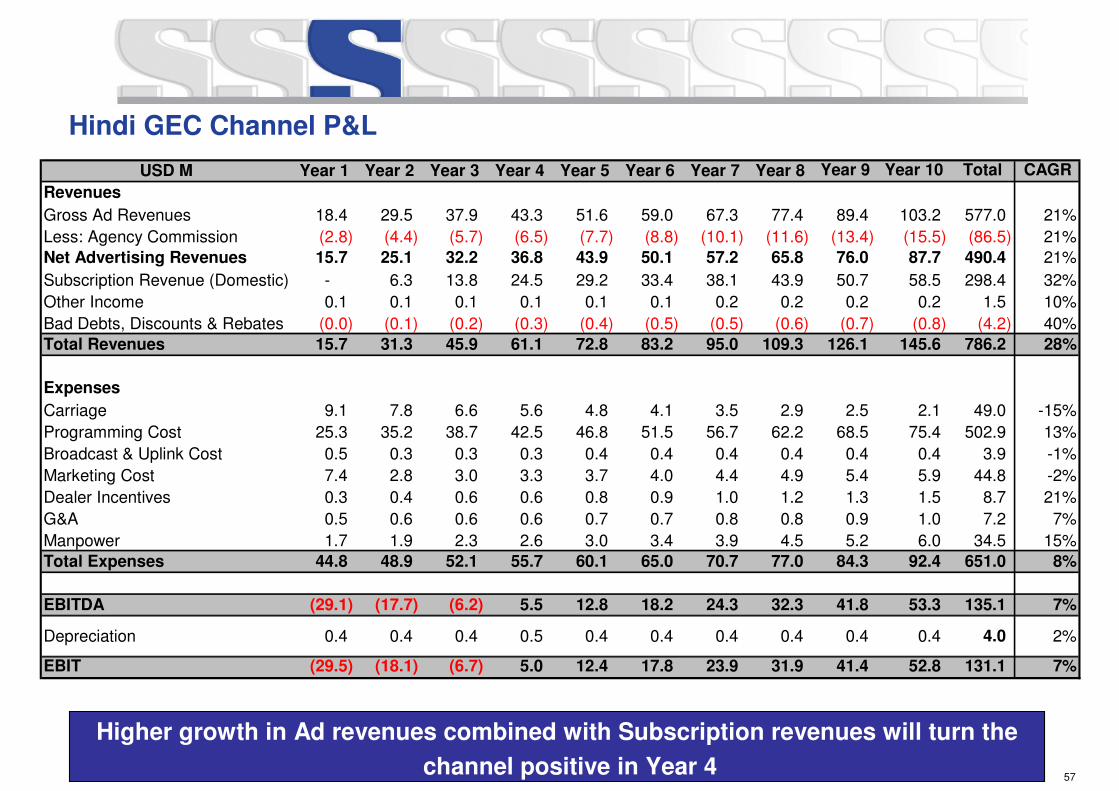

Hindi GEC Channel P&L

Higher growth in Ad revenues combined with Subscription revenues will turn the

channel positive in Year 4

USD M Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Total CAGR

Revenues

Gross Ad Revenues 18.4 29.5 37.9 43.3 51.6 59.0 67.3 77.4 89.4 103.2 577.0 21%

Less: Agency Commission (2.8) (4.4) (5.7) (6.5) (7.7) (8.8) (10.1) (11.6) (13.4) (15.5) (86.5) 21%

Net Advertising Revenues 15.7 25.1 32.2 36.8 43.9 50.1 57.2 65.8 76.0 87.7 490.4 21%

Subscription Revenue (Domestic) - 6.3 13.8 24.5 29.2 33.4 38.1 43.9 50.7 58.5 298.4 32%

Other Income 0.1 0.1 0.1 0.1 0.1 0.1 0.2 0.2 0.2 0.2 1.5 10%

Bad Debts, Discounts & Rebates (0.0) (0.1) (0.2) (0.3) (0.4) (0.5) (0.5) (0.6) (0.7) (0.8) (4.2) 40%

Total Revenues 15.7 31.3 45.9 61.1 72.8 83.2 95.0 109.3 126.1 145.6 786.2 28%

Expenses

Carriage 9.1 7.8 6.6 5.6 4.8 4.1 3.5 2.9 2.5 2.1 49.0 -15%

Programming Cost 25.3 35.2 38.7 42.5 46.8 51.5 56.7 62.2 68.5 75.4 502.9 13%

Broadcast & Uplink Cost 0.5 0.3 0.3 0.3 0.4 0.4 0.4 0.4 0.4 0.4 3.9 -1%

Marketing Cost 7.4 2.8 3.0 3.3 3.7 4.0 4.4 4.9 5.4 5.9 44.8 -2%

Dealer Incentives 0.3 0.4 0.6 0.6 0.8 0.9 1.0 1.2 1.3 1.5 8.7 21%

G&A 0.5 0.6 0.6 0.6 0.7 0.7 0.8 0.8 0.9 1.0 7.2 7%

Manpower 1.7 1.9 2.3 2.6 3.0 3.4 3.9 4.5 5.2 6.0 34.5 15%

Total Expenses 44.8 48.9 52.1 55.7 60.1 65.0 70.7 77.0 84.3 92.4 651.0 8%

EBITDA (29.1) (17.7) (6.2) 5.5 12.8 18.2 24.3 32.3 41.8 53.3 135.1 7%

Depreciation 0.4 0.4 0.4 0.5 0.4 0.4 0.4 0.4 0.4 0.4 4.0 2%

EBIT (29.5) (18.1) (6.7) 5.0 12.4 17.8 23.9 31.9 41.4 52.8 131.1 7%

58- Confidential -

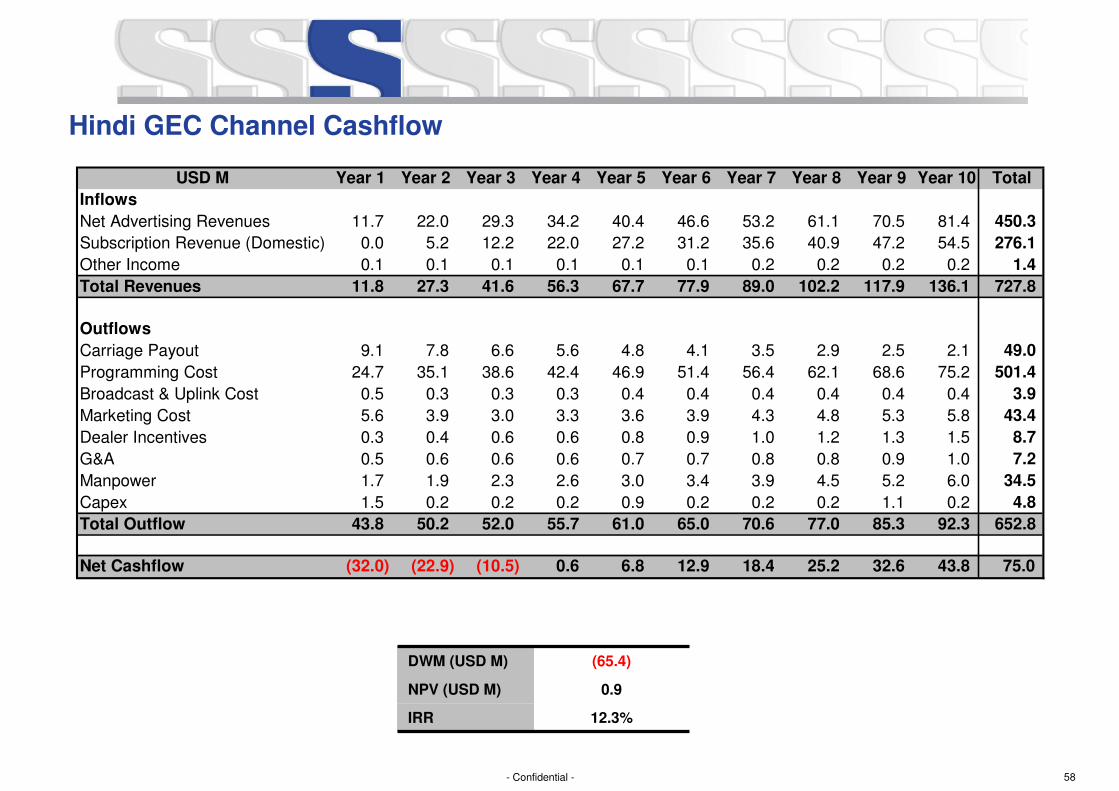

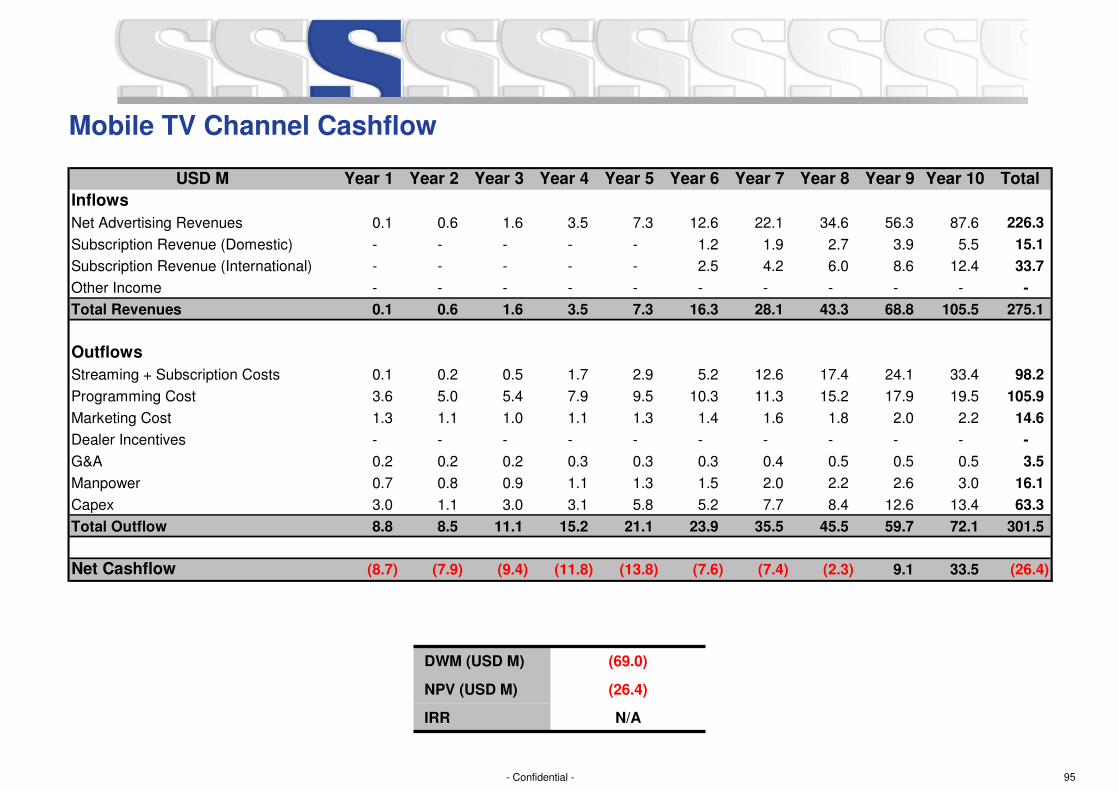

Hindi GEC Channel Cashflow

USD M Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Total

Inflows

Net Advertising Revenues 11.7 22.0 29.3 34.2 40.4 46.6 53.2 61.1 70.5 81.4 450.3

Subscription Revenue (Domestic) 0.0 5.2 12.2 22.0 27.2 31.2 35.6 40.9 47.2 54.5 276.1

Other Income 0.1 0.1 0.1 0.1 0.1 0.1 0.2 0.2 0.2 0.2 1.4

Total Revenues 11.8 27.3 41.6 56.3 67.7 77.9 89.0 102.2 117.9 136.1 727.8

Outflows

Carriage Payout 9.1 7.8 6.6 5.6 4.8 4.1 3.5 2.9 2.5 2.1 49.0

Programming Cost 24.7 35.1 38.6 42.4 46.9 51.4 56.4 62.1 68.6 75.2 501.4

Broadcast & Uplink Cost 0.5 0.3 0.3 0.3 0.4 0.4 0.4 0.4 0.4 0.4 3.9

Marketing Cost 5.6 3.9 3.0 3.3 3.6 3.9 4.3 4.8 5.3 5.8 43.4

Dealer Incentives 0.3 0.4 0.6 0.6 0.8 0.9 1.0 1.2 1.3 1.5 8.7

G&A 0.5 0.6 0.6 0.6 0.7 0.7 0.8 0.8 0.9 1.0 7.2

Manpower 1.7 1.9 2.3 2.6 3.0 3.4 3.9 4.5 5.2 6.0 34.5

Capex 1.5 0.2 0.2 0.2 0.9 0.2 0.2 0.2 1.1 0.2 4.8

Total Outflow 43.8 50.2 52.0 55.7 61.0 65.0 70.6 77.0 85.3 92.3 652.8

Net Cashflow (32.0) (22.9) (10.5) 0.6 6.8 12.9 18.4 25.2 32.6 43.8 75.0

DWM (USD M) (65.4)

NPV (USD M) 0.9

IRR 12.3%

59- Confidential -

Opportunity 2 – Free to Air GEC Plan

Strategic New Initiatives

60- Confidential -

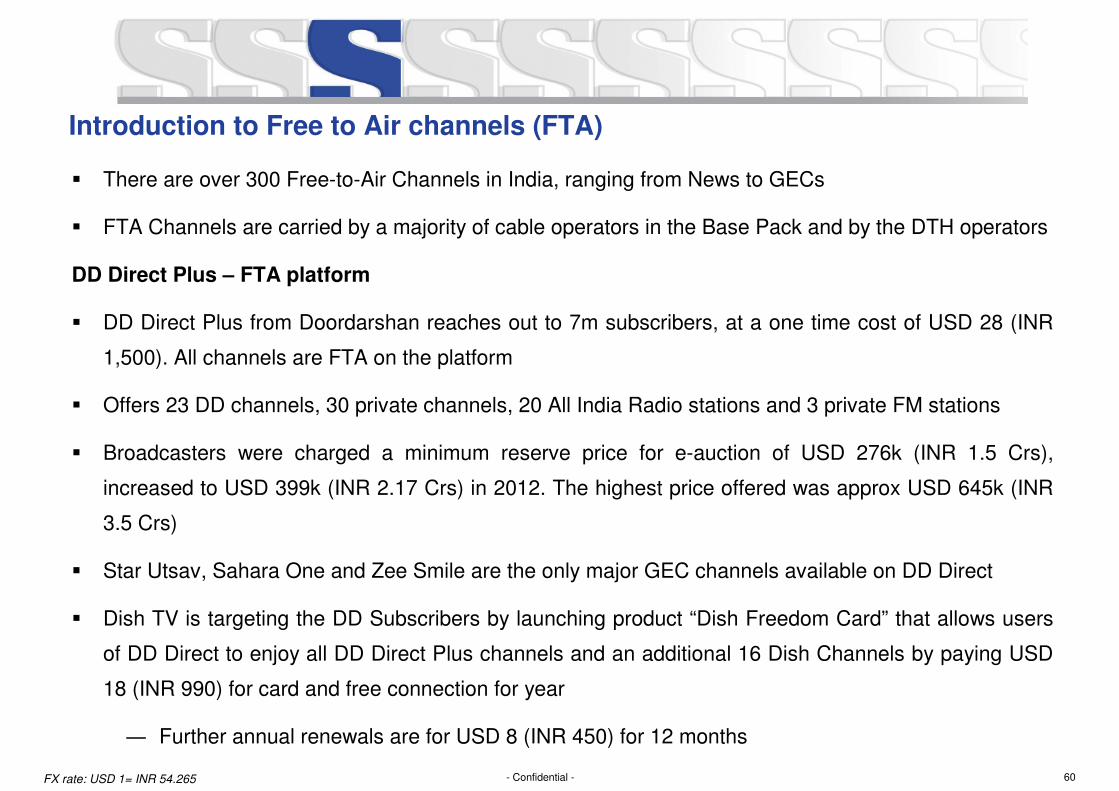

Introduction to Free to Air channels (FTA)

FX rate: USD 1= INR 54.265

� There are over 300 Free-to-Air Channels in India, ranging from News to GECs

� FTA Channels are carried by a majority of cable operators in the Base Pack and by the DTH operators

DD Direct Plus – FTA platform

� DD Direct Plus from Doordarshan reaches out to 7m subscribers, at a one time cost of USD 28 (INR

1,500). All channels are FTA on the platform

� Offers 23 DD channels, 30 private channels, 20 All India Radio stations and 3 private FM stations

� Broadcasters were charged a minimum reserve price for e-auction of USD 276k (INR 1.5 Crs),

increased to USD 399k (INR 2.17 Crs) in 2012. The highest price offered was approx USD 645k (INR

3.5 Crs)

� Star Utsav, Sahara One and Zee Smile are the only major GEC channels available on DD Direct

� Dish TV is targeting the DD Subscribers by launching product “Dish Freedom Card” that allows users

of DD Direct to enjoy all DD Direct Plus channels and an additional 16 Dish Channels by paying USD

18 (INR 990) for card and free connection for year

― Further annual renewals are for USD 8 (INR 450) for 12 months

61- Confidential -

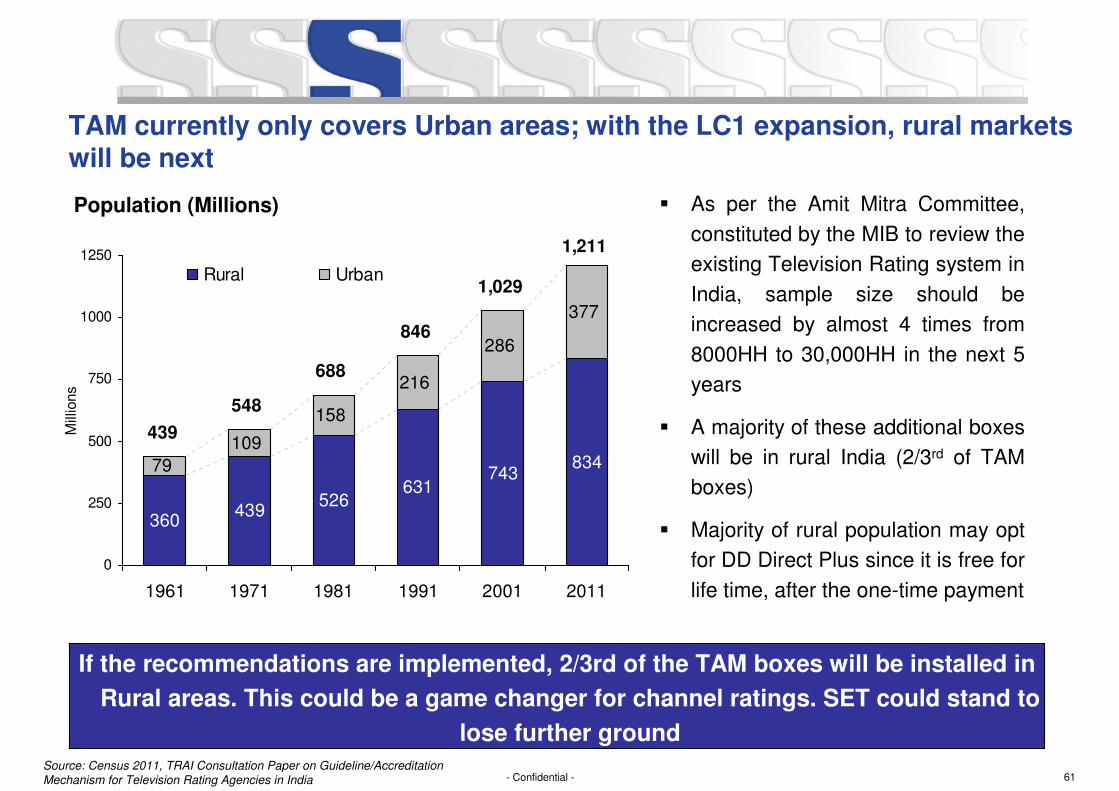

TAM currently only covers Urban areas; with the LC1 expansion, rural markets will be next

If the recommendations are implemented, 2/3rd of the TAM boxes will be installed in

Rural areas. This could be a game changer for channel ratings. SET could stand to

lose further ground

� As per the Amit Mitra Committee,

constituted by the MIB to review the

existing Television Rating system in

India, sample size should be

increased by almost 4 times from

8000HH to 30,000HH in the next 5

years

� A majority of these additional boxes

will be in rural India (2/3rd of TAM

boxes)

� Majority of rural population may opt

for DD Direct Plus since it is free for

life time, after the one-time payment

Source: Census 2011, TRAI Consultation Paper on Guideline/Accreditation

Mechanism for Television Rating Agencies in India

743834

109

158

286

377

439360

631526

216

79

1,211

548

439

846

1,029

688

0

250

500

750

1000

1250

1961 1971 1981 1991 2001 2011

Mill

ions

Rural Urban

Population (Millions)

62- Confidential -

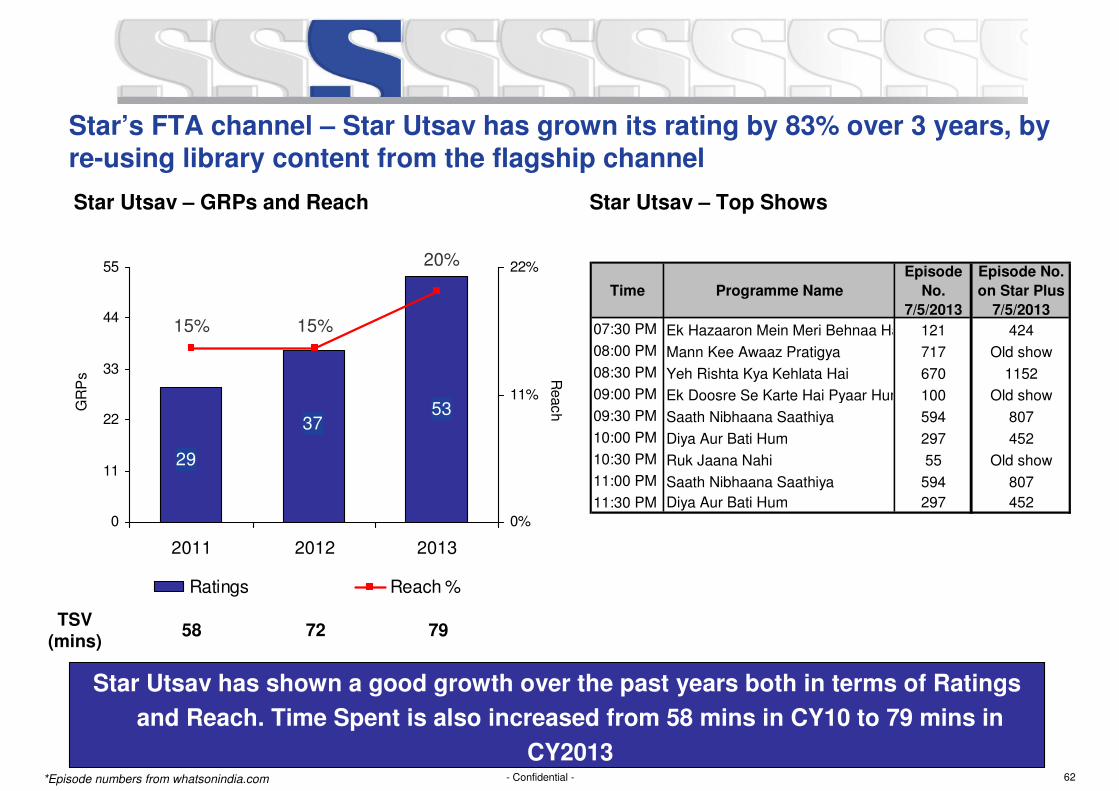

Star’s FTA channel – Star Utsav has grown its rating by 83% over 3 years, by re-using library content from the flagship channel

5337

29

15%

20%

15%

0

11

22

33

44

55

2011 2012 2013

GR

Ps

0%

11%

22%

Reach

Ratings Reach %

Time Programme Name

Episode

No.

7/5/2013

Episode No.

on Star Plus

7/5/2013

07:30 PM Ek Hazaaron Mein Meri Behnaa Hai 121 424

08:00 PM Mann Kee Awaaz Pratigya 717 Old show

08:30 PM Yeh Rishta Kya Kehlata Hai 670 1152

09:00 PM Ek Doosre Se Karte Hai Pyaar Hum 100 Old show

09:30 PM Saath Nibhaana Saathiya 594 807

10:00 PM Diya Aur Bati Hum 297 452

10:30 PM Ruk Jaana Nahi 55 Old show

11:00 PM Saath Nibhaana Saathiya 594 807

11:30 PM Diya Aur Bati Hum 297 452

*Episode numbers from whatsonindia.com

Star Utsav has shown a good growth over the past years both in terms of Ratings

and Reach. Time Spent is also increased from 58 mins in CY10 to 79 mins in

CY2013

Star Utsav – GRPs and Reach Star Utsav – Top Shows

TSV

(mins)58 72 79

63- Confidential -

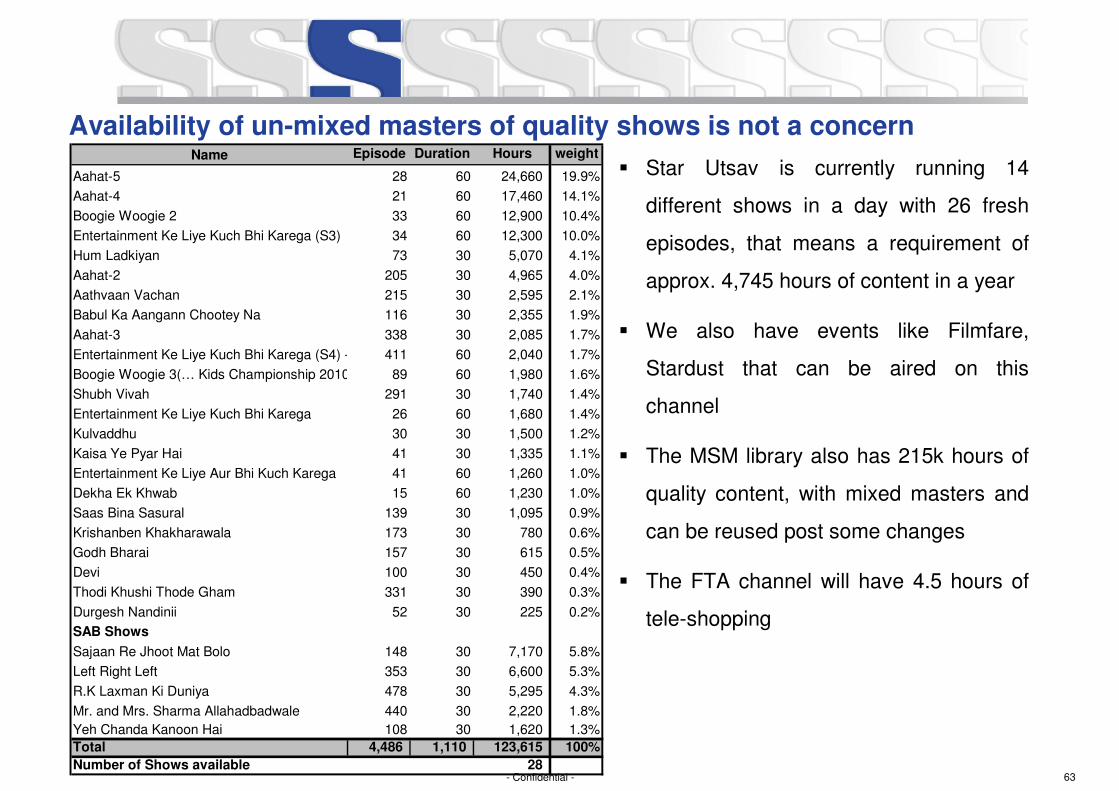

� Star Utsav is currently running 14

different shows in a day with 26 fresh

episodes, that means a requirement of

approx. 4,745 hours of content in a year

� We also have events like Filmfare,

Stardust that can be aired on this

channel

� The MSM library also has 215k hours of

quality content, with mixed masters and

can be reused post some changes

� The FTA channel will have 4.5 hours of

tele-shopping

Name Episode Duration Hours weight

Aahat-5 28 60 24,660 19.9%

Aahat-4 21 60 17,460 14.1%

Boogie Woogie 2 33 60 12,900 10.4%

Entertainment Ke Liye Kuch Bhi Karega (S3) 34 60 12,300 10.0%

Hum Ladkiyan 73 30 5,070 4.1%

Aahat-2 205 30 4,965 4.0%

Aathvaan Vachan 215 30 2,595 2.1%

Babul Ka Aangann Chootey Na 116 30 2,355 1.9%

Aahat-3 338 30 2,085 1.7%

Entertainment Ke Liye Kuch Bhi Karega (S4) - Eps 40 & 41 - 2 hrs each411 60 2,040 1.7%

Boogie Woogie 3(… Kids Championship 2010) 89 60 1,980 1.6%

Shubh Vivah 291 30 1,740 1.4%

Entertainment Ke Liye Kuch Bhi Karega 26 60 1,680 1.4%

Kulvaddhu 30 30 1,500 1.2%

Kaisa Ye Pyar Hai 41 30 1,335 1.1%

Entertainment Ke Liye Aur Bhi Kuch Karega 41 60 1,260 1.0%

Dekha Ek Khwab 15 60 1,230 1.0%

Saas Bina Sasural 139 30 1,095 0.9%

Krishanben Khakharawala 173 30 780 0.6%

Godh Bharai 157 30 615 0.5%

Devi 100 30 450 0.4%

Thodi Khushi Thode Gham 331 30 390 0.3%

Durgesh Nandinii 52 30 225 0.2%

SAB Shows

Sajaan Re Jhoot Mat Bolo 148 30 7,170 5.8%

Left Right Left 353 30 6,600 5.3%

R.K Laxman Ki Duniya 478 30 5,295 4.3%

Mr. and Mrs. Sharma Allahadbadwale 440 30 2,220 1.8%

Yeh Chanda Kanoon Hai 108 30 1,620 1.3%

Total 4,486 1,110 123,615 100%

Number of Shows available 28

Availability of un-mixed masters of quality shows is not a concern

64- Confidential -

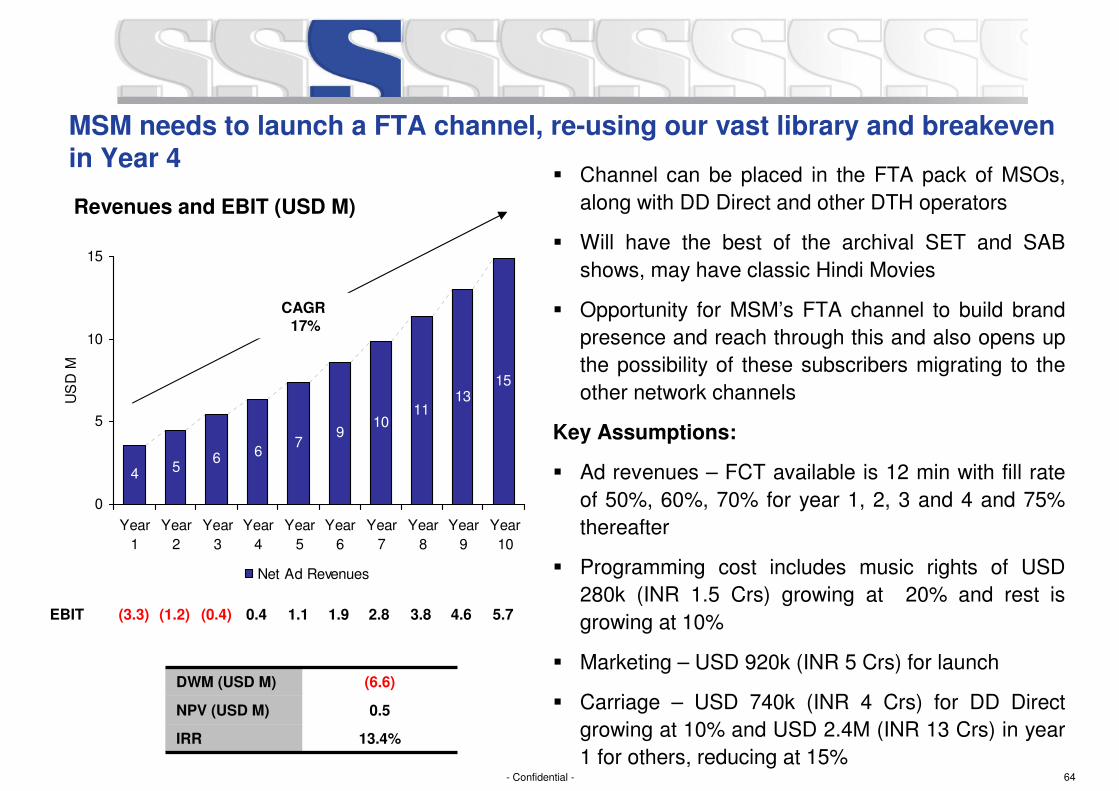

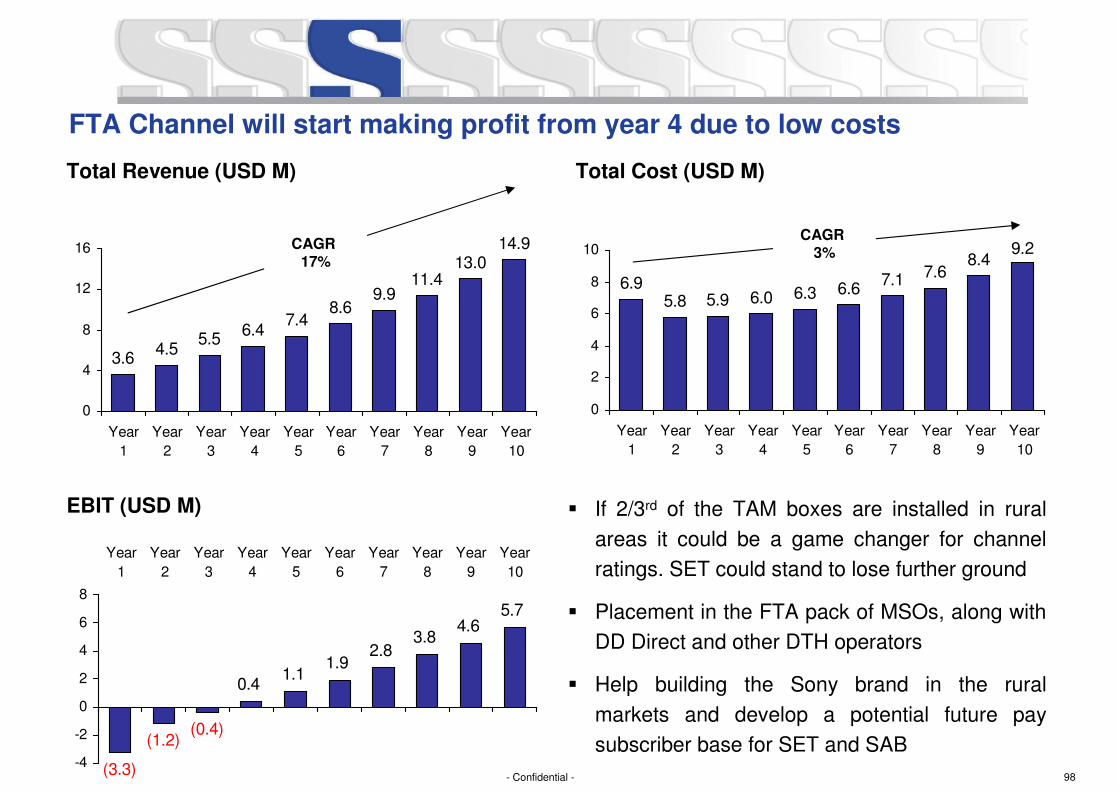

MSM needs to launch a FTA channel, re-using our vast library and breakeven in Year 4

79

1011

1315

54

66

0

5

10

15

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

US

D M

Net Ad Revenues

DWM (USD M) (6.6)

NPV (USD M) 0.5

IRR 13.4%

EBIT (3.3) (1.2) 5.7

CAGR 17%

(0.4) 0.4 1.1 1.9 2.8 3.8 4.6

Revenues and EBIT (USD M)

� Channel can be placed in the FTA pack of MSOs,

along with DD Direct and other DTH operators

� Will have the best of the archival SET and SAB

shows, may have classic Hindi Movies

� Opportunity for MSM’s FTA channel to build brand

presence and reach through this and also opens up

the possibility of these subscribers migrating to the

other network channels

Key Assumptions:

� Ad revenues – FCT available is 12 min with fill rate

of 50%, 60%, 70% for year 1, 2, 3 and 4 and 75%

thereafter

� Programming cost includes music rights of USD

280k (INR 1.5 Crs) growing at 20% and rest is

growing at 10%

� Marketing – USD 920k (INR 5 Crs) for launch

� Carriage – USD 740k (INR 4 Crs) for DD Direct

growing at 10% and USD 2.4M (INR 13 Crs) in year

1 for others, reducing at 15%

65- Confidential -Ad revenues even with low ERs are sufficient to cover up costs

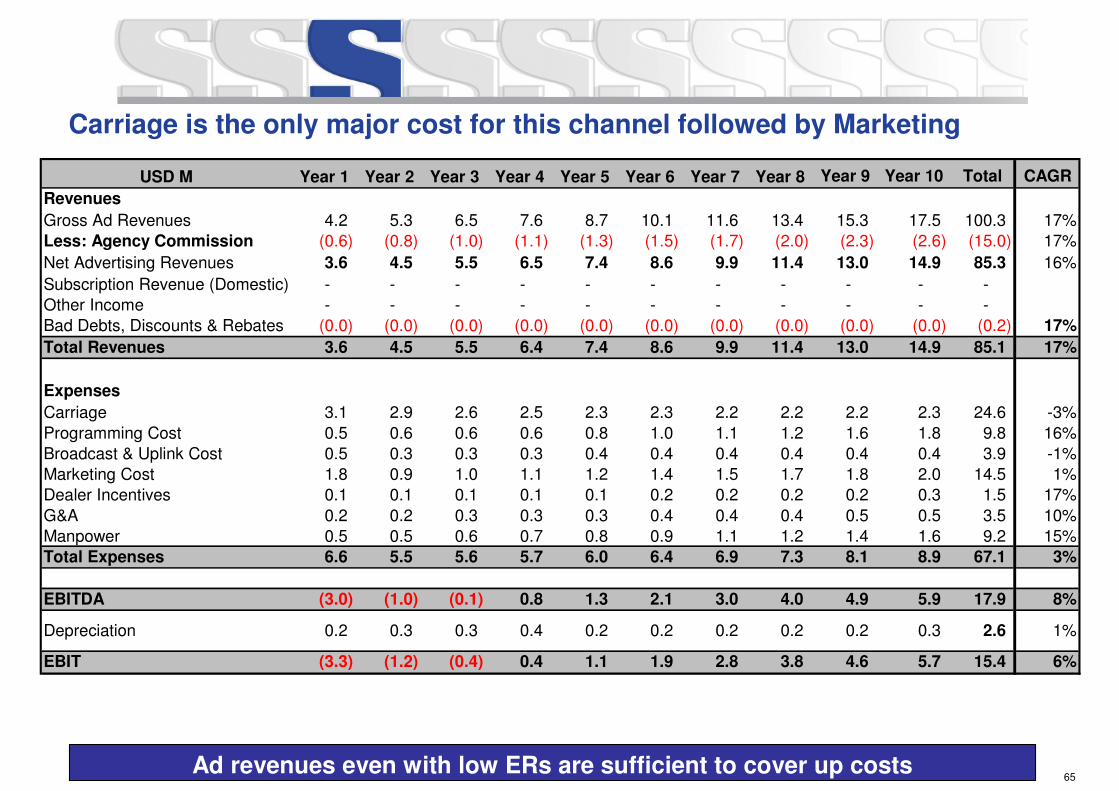

Carriage is the only major cost for this channel followed by Marketing

USD M Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Total CAGR

Revenues

Gross Ad Revenues 4.2 5.3 6.5 7.6 8.7 10.1 11.6 13.4 15.3 17.5 100.3 17%

Less: Agency Commission (0.6) (0.8) (1.0) (1.1) (1.3) (1.5) (1.7) (2.0) (2.3) (2.6) (15.0) 17%

Net Advertising Revenues 3.6 4.5 5.5 6.5 7.4 8.6 9.9 11.4 13.0 14.9 85.3 16%

Subscription Revenue (Domestic) - - - - - - - - - - -

Other Income - - - - - - - - - - -

Bad Debts, Discounts & Rebates (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.0) (0.2) 17%

Total Revenues 3.6 4.5 5.5 6.4 7.4 8.6 9.9 11.4 13.0 14.9 85.1 17%

Expenses

Carriage 3.1 2.9 2.6 2.5 2.3 2.3 2.2 2.2 2.2 2.3 24.6 -3%

Programming Cost 0.5 0.6 0.6 0.6 0.8 1.0 1.1 1.2 1.6 1.8 9.8 16%

Broadcast & Uplink Cost 0.5 0.3 0.3 0.3 0.4 0.4 0.4 0.4 0.4 0.4 3.9 -1%

Marketing Cost 1.8 0.9 1.0 1.1 1.2 1.4 1.5 1.7 1.8 2.0 14.5 1%

Dealer Incentives 0.1 0.1 0.1 0.1 0.1 0.2 0.2 0.2 0.2 0.3 1.5 17%

G&A 0.2 0.2 0.3 0.3 0.3 0.4 0.4 0.4 0.5 0.5 3.5 10%

Manpower 0.5 0.5 0.6 0.7 0.8 0.9 1.1 1.2 1.4 1.6 9.2 15%

Total Expenses 6.6 5.5 5.6 5.7 6.0 6.4 6.9 7.3 8.1 8.9 67.1 3%

EBITDA (3.0) (1.0) (0.1) 0.8 1.3 2.1 3.0 4.0 4.9 5.9 17.9 8%

Depreciation 0.2 0.3 0.3 0.4 0.2 0.2 0.2 0.2 0.2 0.3 2.6 1%

EBIT (3.3) (1.2) (0.4) 0.4 1.1 1.9 2.8 3.8 4.6 5.7 15.4 6%

66- Confidential -

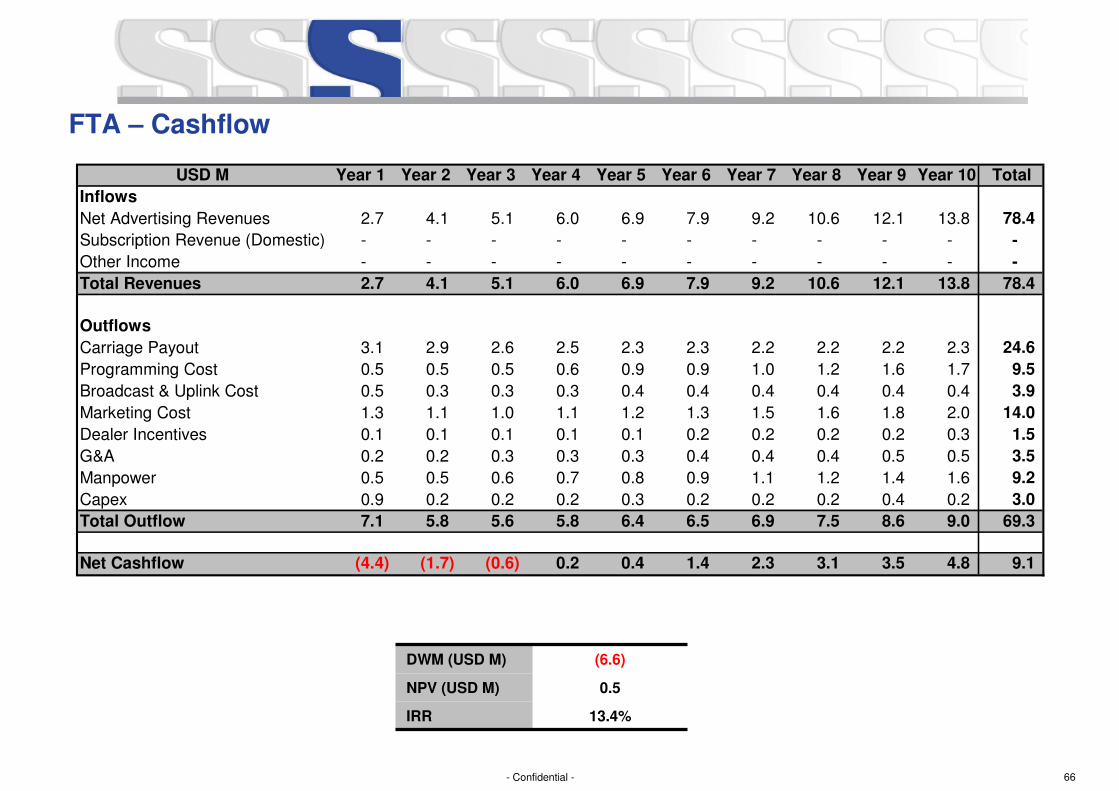

FTA – Cashflow

USD M Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Total

Inflows

Net Advertising Revenues 2.7 4.1 5.1 6.0 6.9 7.9 9.2 10.6 12.1 13.8 78.4

Subscription Revenue (Domestic) - - - - - - - - - - -

Other Income - - - - - - - - - - -

Total Revenues 2.7 4.1 5.1 6.0 6.9 7.9 9.2 10.6 12.1 13.8 78.4

Outflows

Carriage Payout 3.1 2.9 2.6 2.5 2.3 2.3 2.2 2.2 2.2 2.3 24.6

Programming Cost 0.5 0.5 0.5 0.6 0.9 0.9 1.0 1.2 1.6 1.7 9.5

Broadcast & Uplink Cost 0.5 0.3 0.3 0.3 0.4 0.4 0.4 0.4 0.4 0.4 3.9

Marketing Cost 1.3 1.1 1.0 1.1 1.2 1.3 1.5 1.6 1.8 2.0 14.0

Dealer Incentives 0.1 0.1 0.1 0.1 0.1 0.2 0.2 0.2 0.2 0.3 1.5

G&A 0.2 0.2 0.3 0.3 0.3 0.4 0.4 0.4 0.5 0.5 3.5

Manpower 0.5 0.5 0.6 0.7 0.8 0.9 1.1 1.2 1.4 1.6 9.2

Capex 0.9 0.2 0.2 0.2 0.3 0.2 0.2 0.2 0.4 0.2 3.0

Total Outflow 7.1 5.8 5.6 5.8 6.4 6.5 6.9 7.5 8.6 9.0 69.3

Net Cashflow (4.4) (1.7) (0.6) 0.2 0.4 1.4 2.3 3.1 3.5 4.8 9.1

DWM (USD M) (6.6)

NPV (USD M) 0.5

IRR 13.4%

67- Confidential -

Opportunity 3 – Male focused Hindi Entertainment Channel

Strategic New Initiatives

68- Confidential -

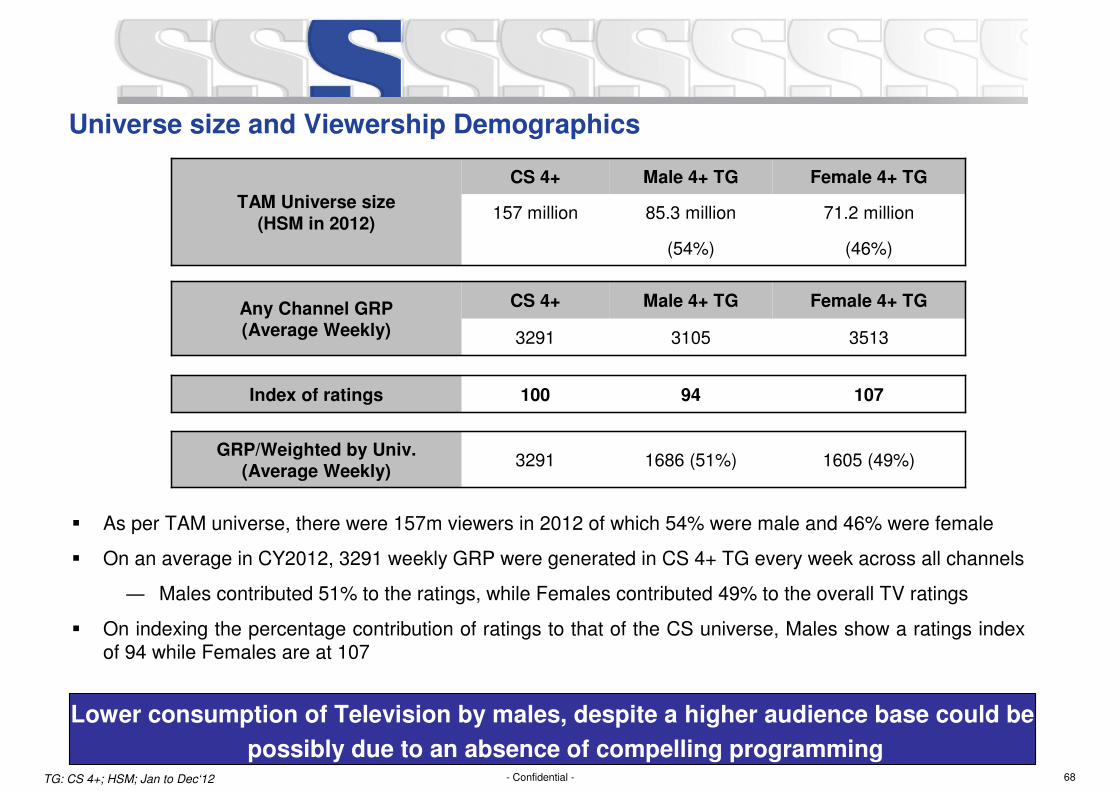

Universe size and Viewership Demographics

� As per TAM universe, there were 157m viewers in 2012 of which 54% were male and 46% were female

� On an average in CY2012, 3291 weekly GRP were generated in CS 4+ TG every week across all channels

― Males contributed 51% to the ratings, while Females contributed 49% to the overall TV ratings

� On indexing the percentage contribution of ratings to that of the CS universe, Males show a ratings index of 94 while Females are at 107

TG: CS 4+; HSM; Jan to Dec‘12

TAM Universe size

(HSM in 2012)

CS 4+ Male 4+ TG Female 4+ TG

157 million 85.3 million 71.2 million

(54%) (46%)

Any Channel GRP (Average Weekly)

CS 4+ Male 4+ TG Female 4+ TG

3291 3105 3513

Index of ratings 100 94 107

GRP/Weighted by Univ.(Average Weekly)

3291 1686 (51%) 1605 (49%)

Lower consumption of Television by males, despite a higher audience base could be

possibly due to an absence of compelling programming

69- Confidential -

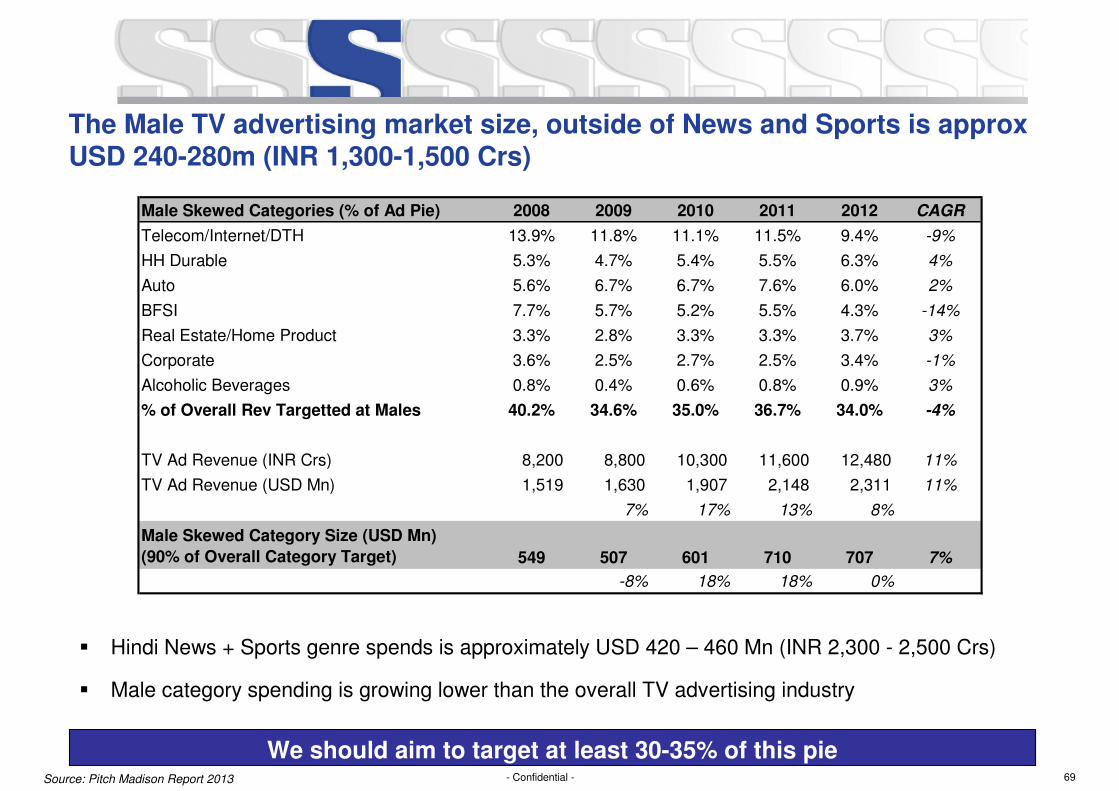

� Hindi News + Sports genre spends is approximately USD 420 – 460 Mn (INR 2,300 - 2,500 Crs)

� Male category spending is growing lower than the overall TV advertising industry

The Male TV advertising market size, outside of News and Sports is approx USD 240-280m (INR 1,300-1,500 Crs)

Source: Pitch Madison Report 2013

We should aim to target at least 30-35% of this pie

Male Skewed Categories (% of Ad Pie) 2008 2009 2010 2011 2012 CAGR

Telecom/Internet/DTH 13.9% 11.8% 11.1% 11.5% 9.4% -9%

HH Durable 5.3% 4.7% 5.4% 5.5% 6.3% 4%

Auto 5.6% 6.7% 6.7% 7.6% 6.0% 2%

BFSI 7.7% 5.7% 5.2% 5.5% 4.3% -14%

Real Estate/Home Product 3.3% 2.8% 3.3% 3.3% 3.7% 3%

Corporate 3.6% 2.5% 2.7% 2.5% 3.4% -1%

Alcoholic Beverages 0.8% 0.4% 0.6% 0.8% 0.9% 3%

% of Overall Rev Targetted at Males 40.2% 34.6% 35.0% 36.7% 34.0% -4%

TV Ad Revenue (INR Crs) 8,200 8,800 10,300 11,600 12,480 11%

TV Ad Revenue (USD Mn) 1,519 1,630 1,907 2,148 2,311 11%

7% 17% 13% 8%

Male Skewed Category Size (USD Mn)

(90% of Overall Category Target) 549 507 601 710 707 7%

-8% 18% 18% 0%

70- Confidential -

Others

8%Z Classic

4%

UTV Action

7%

Star Gold

18%

Z Action

3%

Movies OK

10%

Z Cinema

20%

MAX

20%

UTV Movies

8%

FILMY

2%

Youth and

Music

5%

Sports

4%

Hindi GEC

37%

Hindi Movies

21%

Hindi News

6%

Others

11%

Maharashtra

Regional

6%

Bangla

Regional

4%

Infotainment

2%Kids

4%

Sahara

One

3%

Others

2%DD

National

2%

SET

16%

SAB

12%

Zee

15%

Colors

16%

Star Plus

19%Star Utsav

4%

Life OK

11%

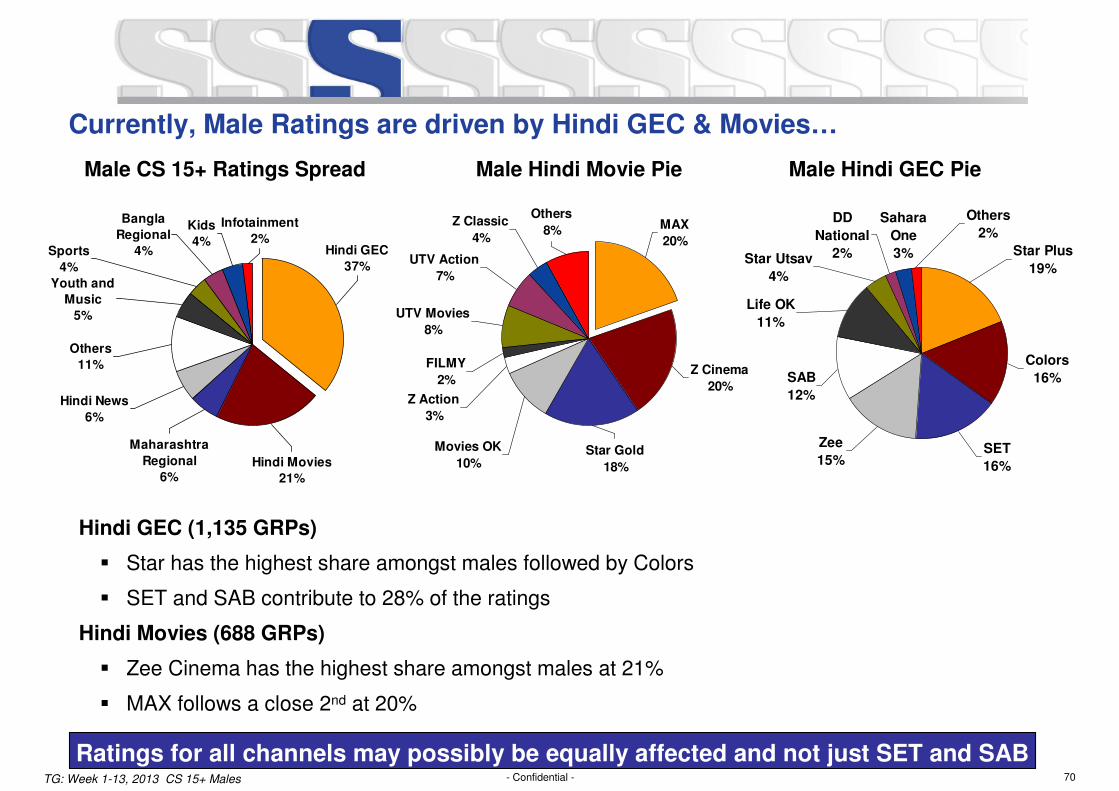

Hindi GEC (1,135 GRPs)

� Star has the highest share amongst males followed by Colors

� SET and SAB contribute to 28% of the ratings

Hindi Movies (688 GRPs)

� Zee Cinema has the highest share amongst males at 21%

� MAX follows a close 2nd at 20%

Currently, Male Ratings are driven by Hindi GEC & Movies…

Male CS 15+ Ratings Spread Male Hindi Movie Pie Male Hindi GEC Pie

TG: Week 1-13, 2013 CS 15+ Males

Ratings for all channels may possibly be equally affected and not just SET and SAB

71- Confidential -

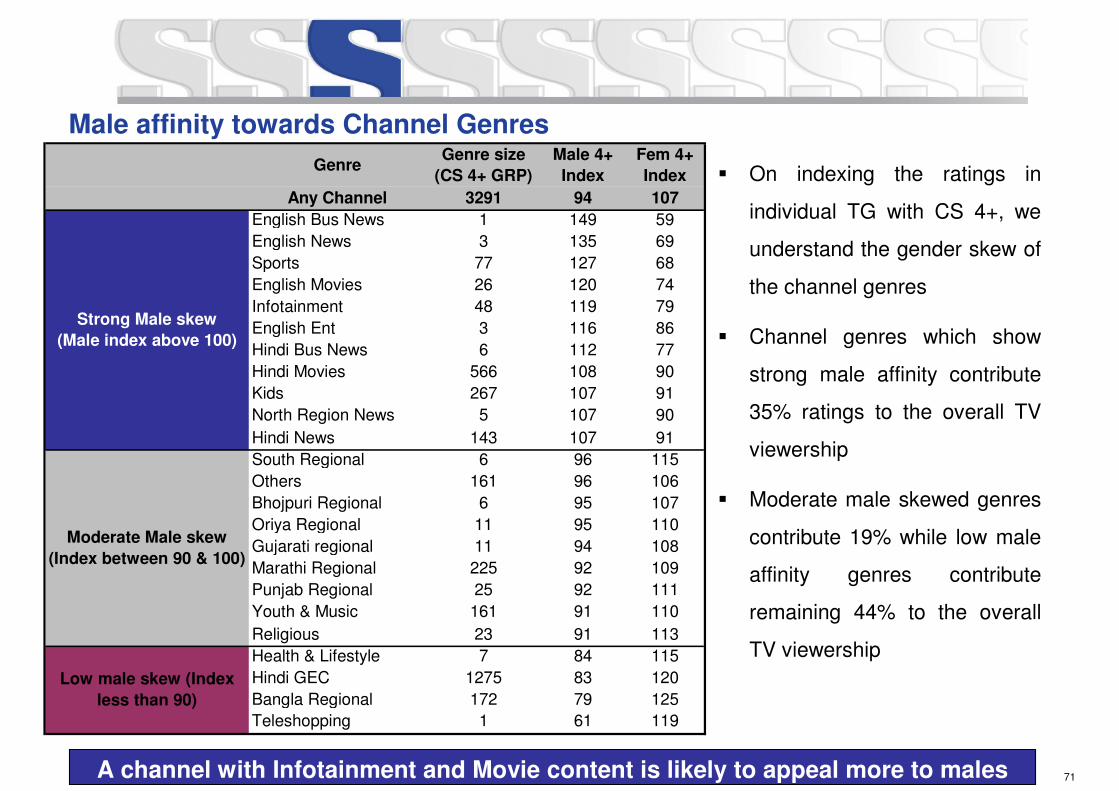

Male affinity towards Channel Genres

� On indexing the ratings in

individual TG with CS 4+, we

understand the gender skew of

the channel genres

� Channel genres which show

strong male affinity contribute

35% ratings to the overall TV

viewership

� Moderate male skewed genres

contribute 19% while low male

affinity genres contribute

remaining 44% to the overall

TV viewership

GenreGenre size

(CS 4+ GRP)

Male 4+

Index

Fem 4+

Index

Any Channel 3291 94 107

English Bus News 1 149 59

English News 3 135 69

Sports 77 127 68

English Movies 26 120 74

Infotainment 48 119 79

English Ent 3 116 86

Hindi Bus News 6 112 77

Hindi Movies 566 108 90

Kids 267 107 91

North Region News 5 107 90

Hindi News 143 107 91

South Regional 6 96 115

Others 161 96 106

Bhojpuri Regional 6 95 107

Oriya Regional 11 95 110

Gujarati regional 11 94 108

Marathi Regional 225 92 109

Punjab Regional 25 92 111

Youth & Music 161 91 110

Religious 23 91 113

Health & Lifestyle 7 84 115

Hindi GEC 1275 83 120

Bangla Regional 172 79 125

Teleshopping 1 61 119

Strong Male skew

(Male index above 100)

Moderate Male skew

(Index between 90 & 100)

Low male skew (Index

less than 90)

A channel with Infotainment and Movie content is likely to appeal more to males

72- Confidential -

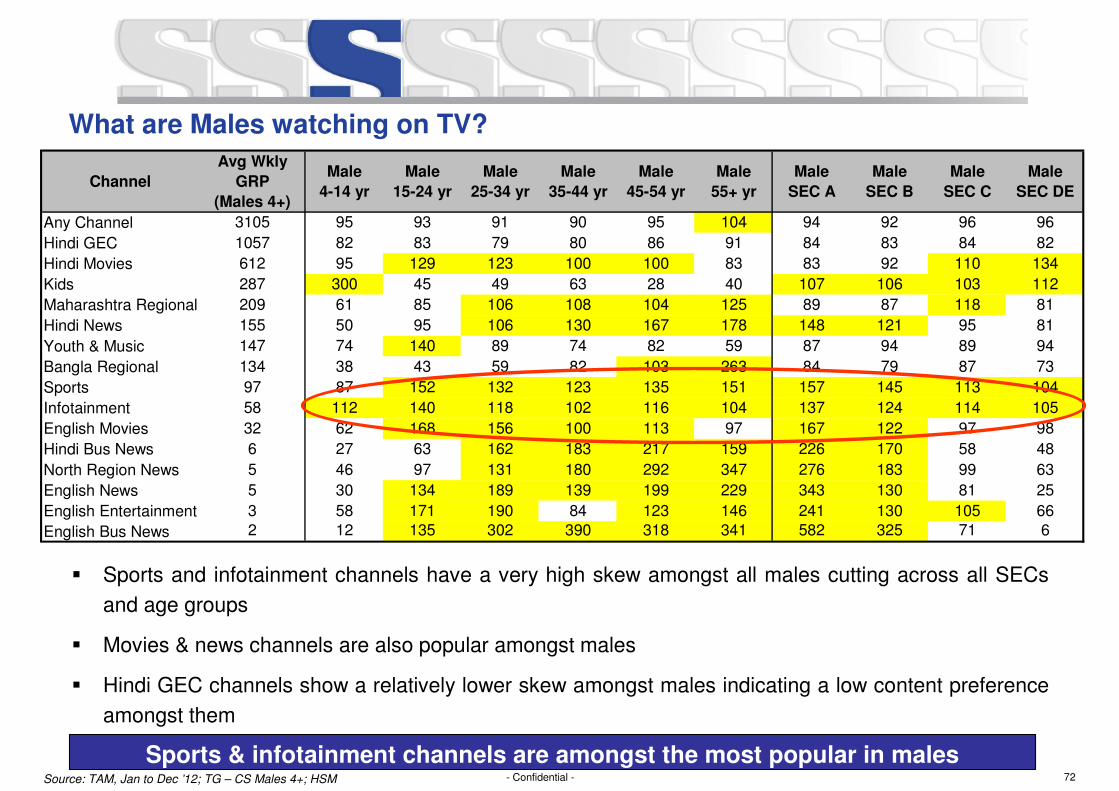

What are Males watching on TV?

� Sports and infotainment channels have a very high skew amongst all males cutting across all SECs

and age groups

� Movies & news channels are also popular amongst males

� Hindi GEC channels show a relatively lower skew amongst males indicating a low content preference

amongst them

Source: TAM, Jan to Dec ’12; TG – CS Males 4+; HSM

Channel

Avg Wkly

GRP

(Males 4+)

Male

4-14 yr

Male

15-24 yr

Male

25-34 yr

Male

35-44 yr

Male

45-54 yr

Male

55+ yr

Male

SEC A

Male

SEC B

Male

SEC C

Male

SEC DE

Any Channel 3105 95 93 91 90 95 104 94 92 96 96

Hindi GEC 1057 82 83 79 80 86 91 84 83 84 82

Hindi Movies 612 95 129 123 100 100 83 83 92 110 134

Kids 287 300 45 49 63 28 40 107 106 103 112

Maharashtra Regional 209 61 85 106 108 104 125 89 87 118 81

Hindi News 155 50 95 106 130 167 178 148 121 95 81

Youth & Music 147 74 140 89 74 82 59 87 94 89 94

Bangla Regional 134 38 43 59 82 103 263 84 79 87 73

Sports 97 87 152 132 123 135 151 157 145 113 104

Infotainment 58 112 140 118 102 116 104 137 124 114 105

English Movies 32 62 168 156 100 113 97 167 122 97 98

Hindi Bus News 6 27 63 162 183 217 159 226 170 58 48

North Region News 5 46 97 131 180 292 347 276 183 99 63

English News 5 30 134 189 139 199 229 343 130 81 25

English Entertainment 3 58 171 190 84 123 146 241 130 105 66

English Bus News 2 12 135 302 390 318 341 582 325 71 6

Sports & infotainment channels are amongst the most popular in males

73- Confidential -

Language-GenresWkly

GRP

Male

4-14 yr

Male

15-24 yr

Male

25-34 yr

Male

35-44 yr

Male

45-54 yr

Male

55+ yr

Male

SEC A

Male

SEC B

Male

SEC C

Male

SEC DE

Hindi-Serials 534 72 73 69 71 79 89 75 72 75 74

Hindi-Feature Films 479 95 124 115 94 95 80 82 89 107 125

Hindi-Comedies 131 131 102 82 92 96 81 104 112 104 89

Hindi-Action/Thriller 126 82 97 107 99 94 95 90 95 97 96

Dubbed Hindi-Feature Films 120 97 142 133 96 97 78 82 94 115 141

English-Cricket Match 109 87 140 133 129 129 140 147 139 112 104

Marathi-Serials 79 56 77 97 92 95 132 86 80 109 73

Hindi-Film Songs 72 71 123 93 79 87 65 76 89 85 101

Bengali-Serials 61 35 36 45 69 80 241 67 68 74 65

Hindi-Mythos/Costume Dramas 46 80 87 85 86 101 132 90 91 96 89

Hindi-Talent Search/Feats 46 83 100 84 80 94 78 97 89 88 80

Marathi-Feature Films 37 78 97 116 114 86 92 75 88 131 94

Hindi-Reality Shows 29 63 111 83 68 95 86 116 93 83 60

Marathi-News Bulletin 20 51 98 127 139 143 150 112 106 129 91

Hindi-Events/Concerts/Awards 18 79 89 79 79 90 85 95 87 82 73

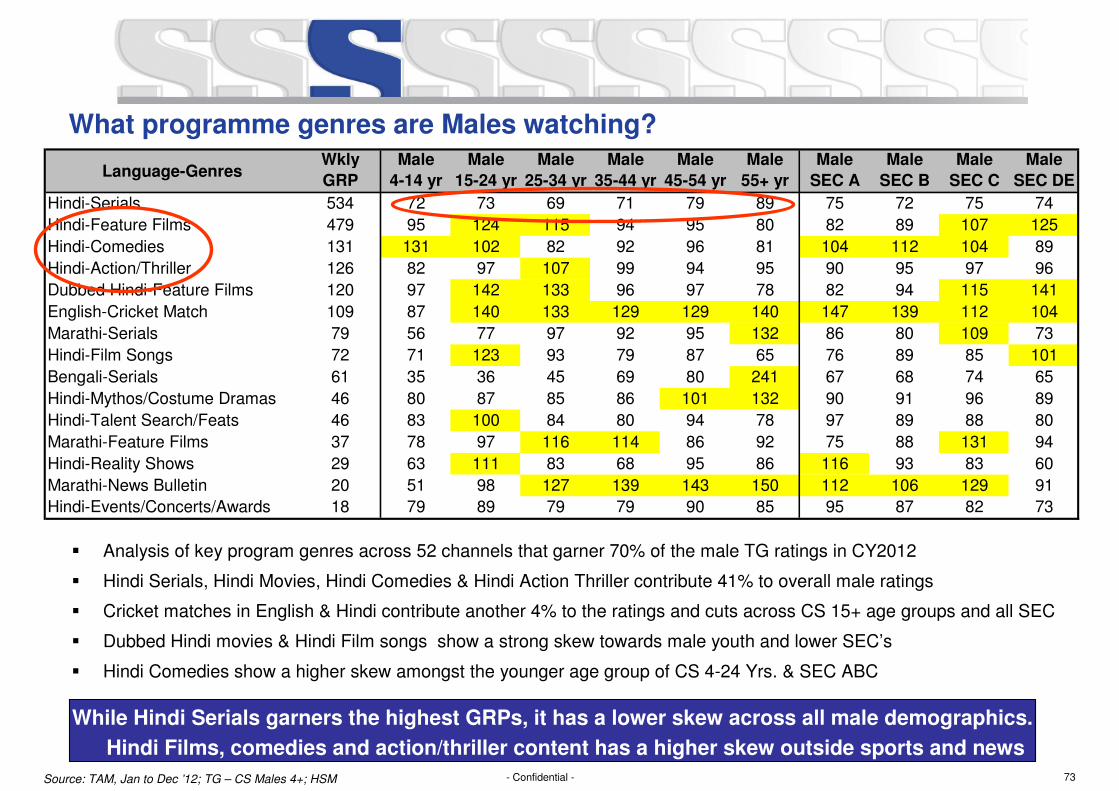

What programme genres are Males watching?

� Analysis of key program genres across 52 channels that garner 70% of the male TG ratings in CY2012

� Hindi Serials, Hindi Movies, Hindi Comedies & Hindi Action Thriller contribute 41% to overall male ratings

� Cricket matches in English & Hindi contribute another 4% to the ratings and cuts across CS 15+ age groups and all SEC

� Dubbed Hindi movies & Hindi Film songs show a strong skew towards male youth and lower SEC’s

� Hindi Comedies show a higher skew amongst the younger age group of CS 4-24 Yrs. & SEC ABC

Source: TAM, Jan to Dec ’12; TG – CS Males 4+; HSM

While Hindi Serials garners the highest GRPs, it has a lower skew across all male demographics.

Hindi Films, comedies and action/thriller content has a higher skew outside sports and news

74- Confidential -

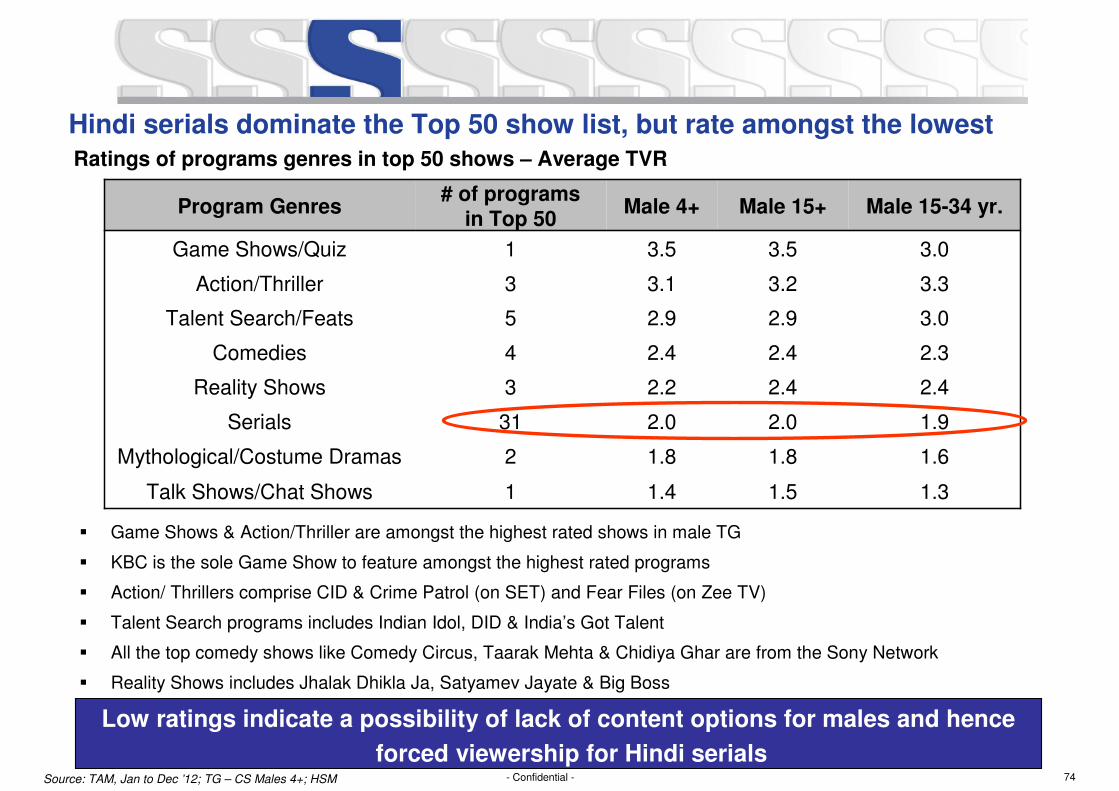

Hindi serials dominate the Top 50 show list, but rate amongst the lowest

Source: TAM, Jan to Dec ’12; TG – CS Males 4+; HSM

Ratings of programs genres in top 50 shows – Average TVR

Program Genres# of programs

in Top 50Male 4+ Male 15+ Male 15-34 yr.

Game Shows/Quiz 1 3.5 3.5 3.0

Action/Thriller 3 3.1 3.2 3.3

Talent Search/Feats 5 2.9 2.9 3.0

Comedies 4 2.4 2.4 2.3

Reality Shows 3 2.2 2.4 2.4

Serials 31 2.0 2.0 1.9

Mythological/Costume Dramas 2 1.8 1.8 1.6

Talk Shows/Chat Shows 1 1.4 1.5 1.3

� Game Shows & Action/Thriller are amongst the highest rated shows in male TG

� KBC is the sole Game Show to feature amongst the highest rated programs

� Action/ Thrillers comprise CID & Crime Patrol (on SET) and Fear Files (on Zee TV)

� Talent Search programs includes Indian Idol, DID & India’s Got Talent

� All the top comedy shows like Comedy Circus, Taarak Mehta & Chidiya Ghar are from the Sony Network

� Reality Shows includes Jhalak Dhikla Ja, Satyamev Jayate & Big Boss

Low ratings indicate a possibility of lack of content options for males and hence

forced viewership for Hindi serials

75- Confidential -

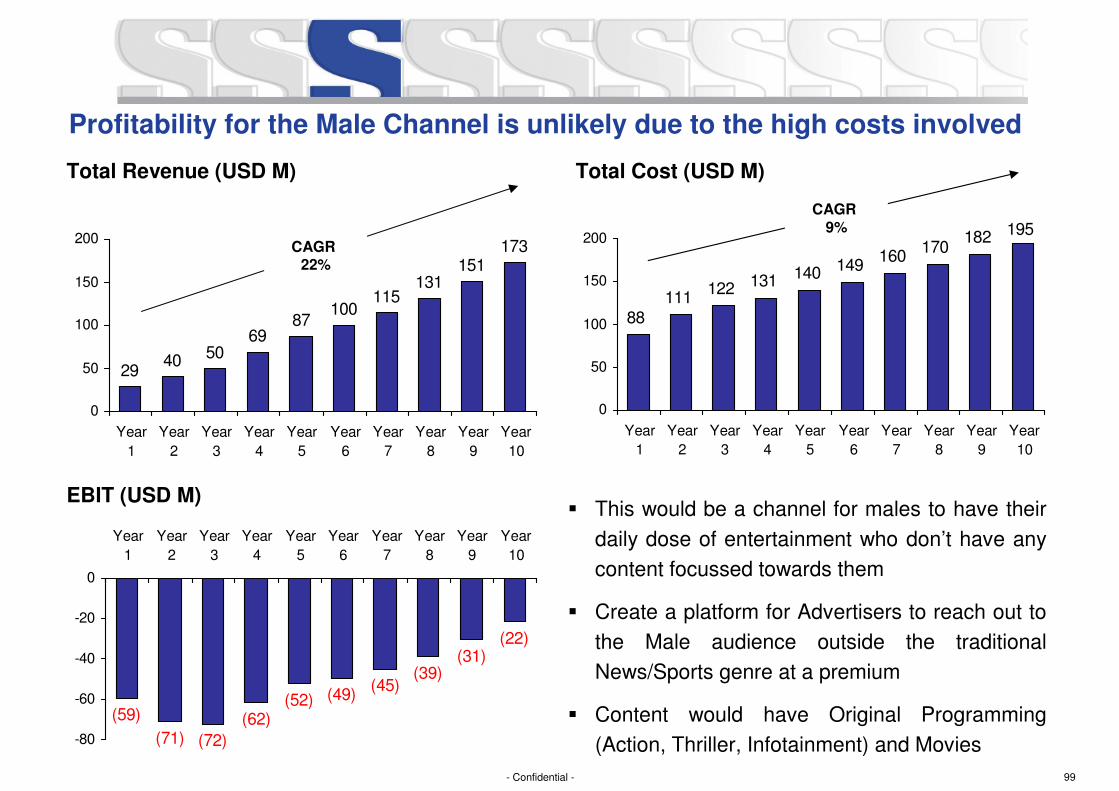

The Average male doesn’t have one dedicated Entertainment channel catered to his needs…

� Channel for the 15+ Males in the HSM Markets

� Content would be a mix of Original Programming (Action, Thriller, Infotainment) and Movies

� Male audiences don’t have content focused towards them. This would be a channel for them to

have their daily dose of entertainment

� Sports & News command higher ERs for reaching out to this audience

� Create a platform for Advertisers to reach out to the Male audience outside the traditional News/

Sports genre and charge a premium for this

Create a new GEC channel targeted to the Hindi speaking males

76- Confidential -

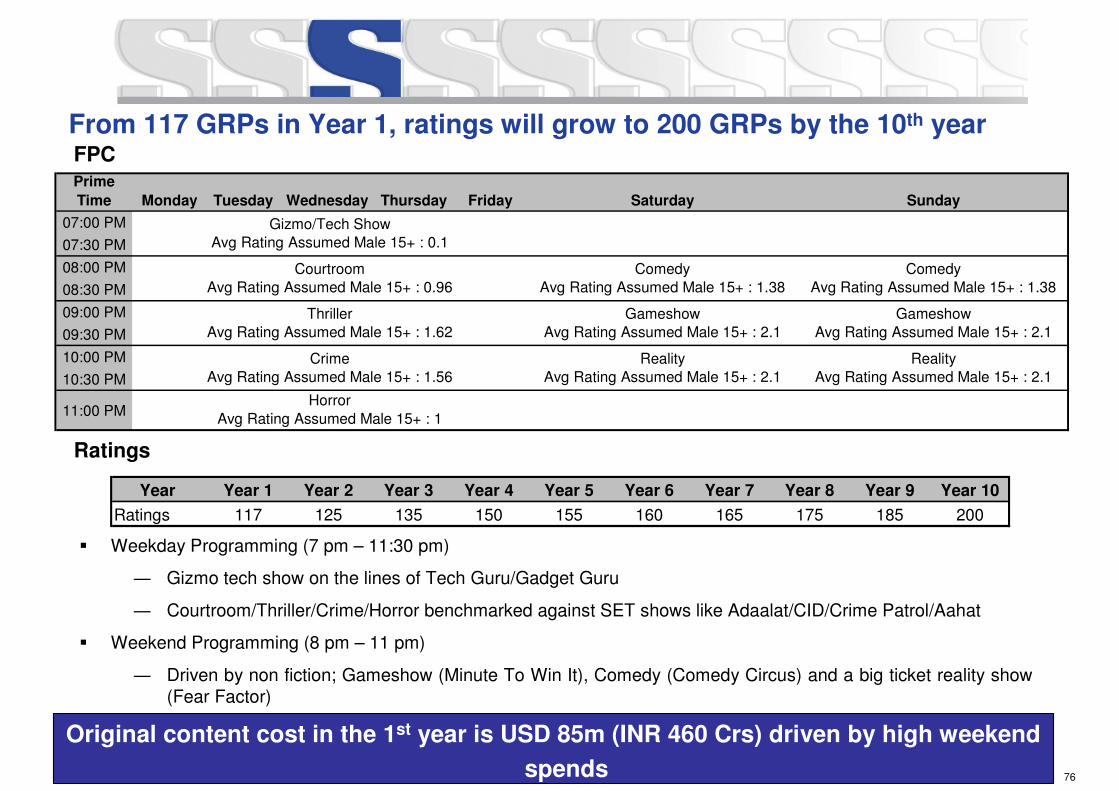

� Weekday Programming (7 pm – 11:30 pm)

― Gizmo tech show on the lines of Tech Guru/Gadget Guru

― Courtroom/Thriller/Crime/Horror benchmarked against SET shows like Adaalat/CID/Crime Patrol/Aahat

� Weekend Programming (8 pm – 11 pm)

― Driven by non fiction; Gameshow (Minute To Win It), Comedy (Comedy Circus) and a big ticket reality show (Fear Factor)

From 117 GRPs in Year 1, ratings will grow to 200 GRPs by the 10th yearFPC

Original content cost in the 1st year is USD 85m (INR 460 Crs) driven by high weekend

spends

Year Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Ratings 117 125 135 150 155 160 165 175 185 200

Ratings

Prime

Time Monday Tuesday Wednesday Thursday Friday Saturday Sunday

07:00 PM

07:30 PM

08:00 PM

08:30 PM

09:00 PM

09:30 PM

10:00 PM

10:30 PM

11:00 PMHorror

Avg Rating Assumed Male 15+ : 1

Thriller

Avg Rating Assumed Male 15+ : 1.62

Gameshow

Avg Rating Assumed Male 15+ : 2.1

Gameshow

Avg Rating Assumed Male 15+ : 2.1

Crime

Avg Rating Assumed Male 15+ : 1.56

Reality

Avg Rating Assumed Male 15+ : 2.1

Reality

Avg Rating Assumed Male 15+ : 2.1

Gizmo/Tech Show

Avg Rating Assumed Male 15+ : 0.1

Courtroom

Avg Rating Assumed Male 15+ : 0.96

Comedy

Avg Rating Assumed Male 15+ : 1.38

Comedy

Avg Rating Assumed Male 15+ : 1.38

77- Confidential -

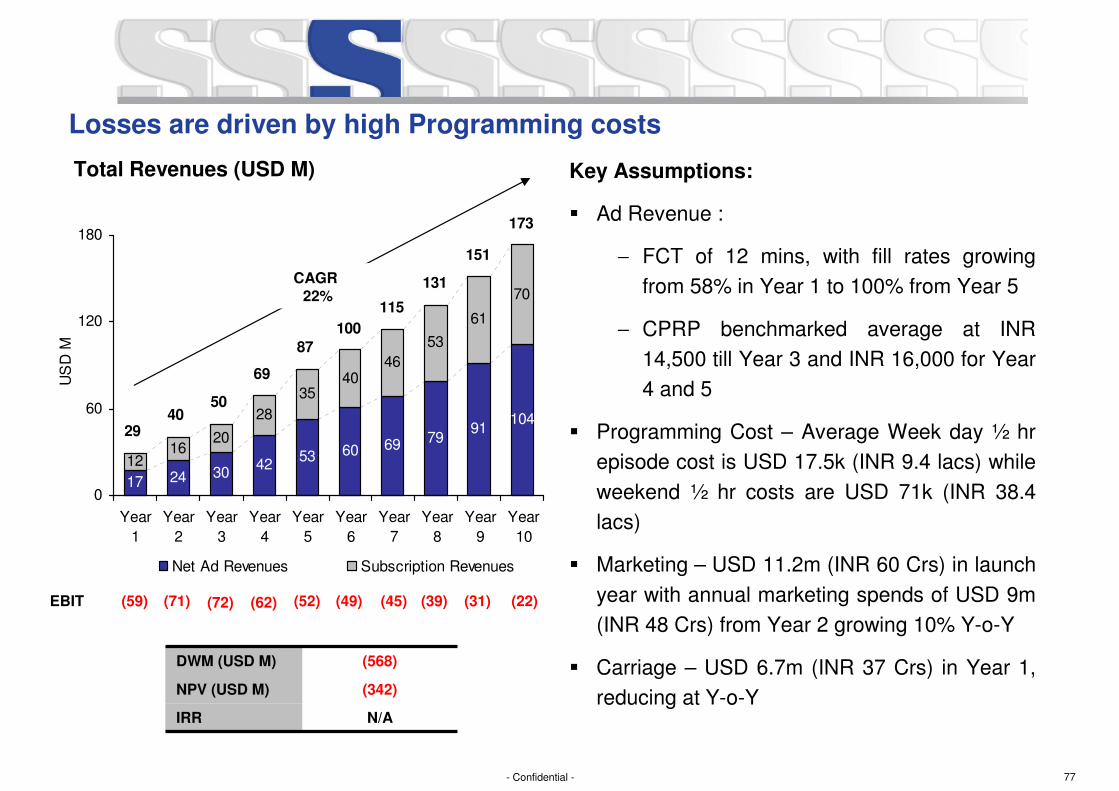

Losses are driven by high Programming costs

53 60 69 7991

104

1620

3540

46

53

61

70

241742

30

28

12

173

151

131

115

100

4029

69

87

50

0

60

120

180

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

US

D M

Net Ad Revenues Subscription Revenues

DWM (USD M) (568)

NPV (USD M) (342)

IRR N/A

EBIT (59) (71)

CAGR 22%

(72) (62) (52) (49) (45) (39) (31)

Key Assumptions:

� Ad Revenue :

− FCT of 12 mins, with fill rates growing

from 58% in Year 1 to 100% from Year 5

− CPRP benchmarked average at INR

14,500 till Year 3 and INR 16,000 for Year

4 and 5

� Programming Cost – Average Week day ½ hr

episode cost is USD 17.5k (INR 9.4 lacs) while

weekend ½ hr costs are USD 71k (INR 38.4

lacs)

� Marketing – USD 11.2m (INR 60 Crs) in launch

year with annual marketing spends of USD 9m

(INR 48 Crs) from Year 2 growing 10% Y-o-Y

� Carriage – USD 6.7m (INR 37 Crs) in Year 1,

reducing at Y-o-Y

(22)

Total Revenues (USD M)

78- Confidential -

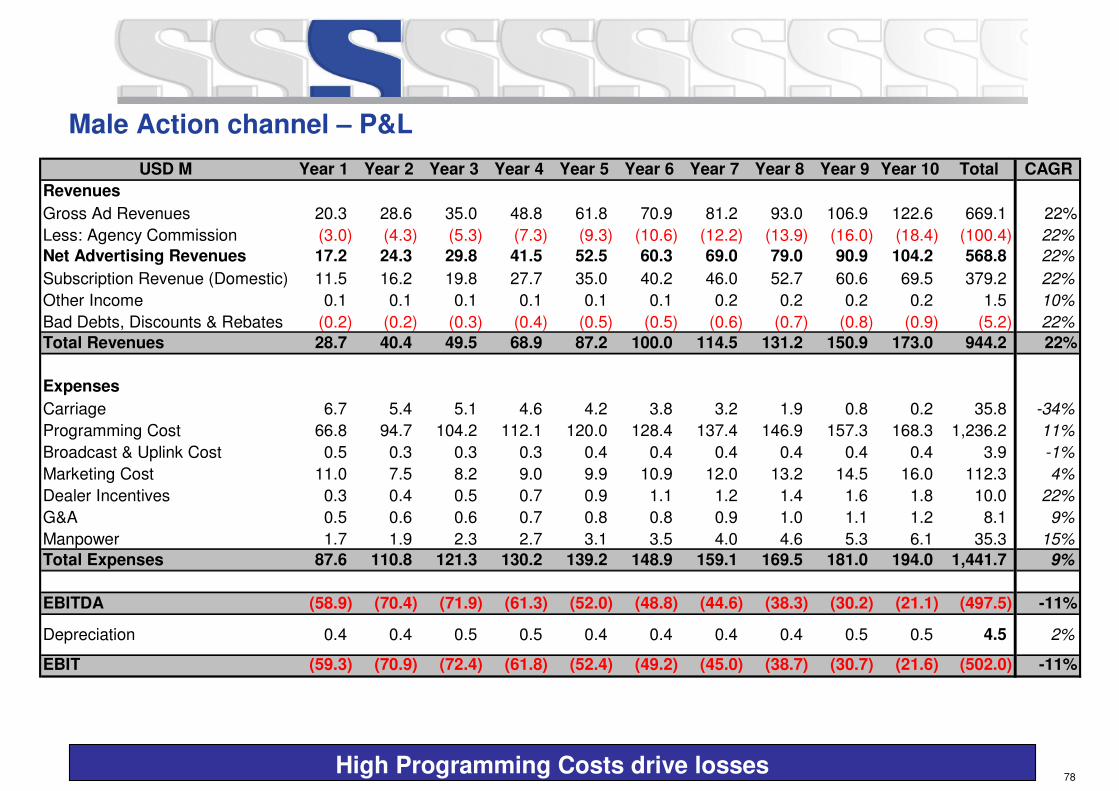

Male Action channel – P&L

High Programming Costs drive losses

USD M Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Total CAGR

Revenues

Gross Ad Revenues 20.3 28.6 35.0 48.8 61.8 70.9 81.2 93.0 106.9 122.6 669.1 22%

Less: Agency Commission (3.0) (4.3) (5.3) (7.3) (9.3) (10.6) (12.2) (13.9) (16.0) (18.4) (100.4) 22%

Net Advertising Revenues 17.2 24.3 29.8 41.5 52.5 60.3 69.0 79.0 90.9 104.2 568.8 22%

Subscription Revenue (Domestic) 11.5 16.2 19.8 27.7 35.0 40.2 46.0 52.7 60.6 69.5 379.2 22%

Other Income 0.1 0.1 0.1 0.1 0.1 0.1 0.2 0.2 0.2 0.2 1.5 10%

Bad Debts, Discounts & Rebates (0.2) (0.2) (0.3) (0.4) (0.5) (0.5) (0.6) (0.7) (0.8) (0.9) (5.2) 22%

Total Revenues 28.7 40.4 49.5 68.9 87.2 100.0 114.5 131.2 150.9 173.0 944.2 22%

Expenses

Carriage 6.7 5.4 5.1 4.6 4.2 3.8 3.2 1.9 0.8 0.2 35.8 -34%

Programming Cost 66.8 94.7 104.2 112.1 120.0 128.4 137.4 146.9 157.3 168.3 1,236.2 11%

Broadcast & Uplink Cost 0.5 0.3 0.3 0.3 0.4 0.4 0.4 0.4 0.4 0.4 3.9 -1%

Marketing Cost 11.0 7.5 8.2 9.0 9.9 10.9 12.0 13.2 14.5 16.0 112.3 4%

Dealer Incentives 0.3 0.4 0.5 0.7 0.9 1.1 1.2 1.4 1.6 1.8 10.0 22%

G&A 0.5 0.6 0.6 0.7 0.8 0.8 0.9 1.0 1.1 1.2 8.1 9%

Manpower 1.7 1.9 2.3 2.7 3.1 3.5 4.0 4.6 5.3 6.1 35.3 15%

Total Expenses 87.6 110.8 121.3 130.2 139.2 148.9 159.1 169.5 181.0 194.0 1,441.7 9%

EBITDA (58.9) (70.4) (71.9) (61.3) (52.0) (48.8) (44.6) (38.3) (30.2) (21.1) (497.5) -11%

Depreciation 0.4 0.4 0.5 0.5 0.4 0.4 0.4 0.4 0.5 0.5 4.5 2%

EBIT (59.3) (70.9) (72.4) (61.8) (52.4) (49.2) (45.0) (38.7) (30.7) (21.6) (502.0) -11%

79- Confidential -

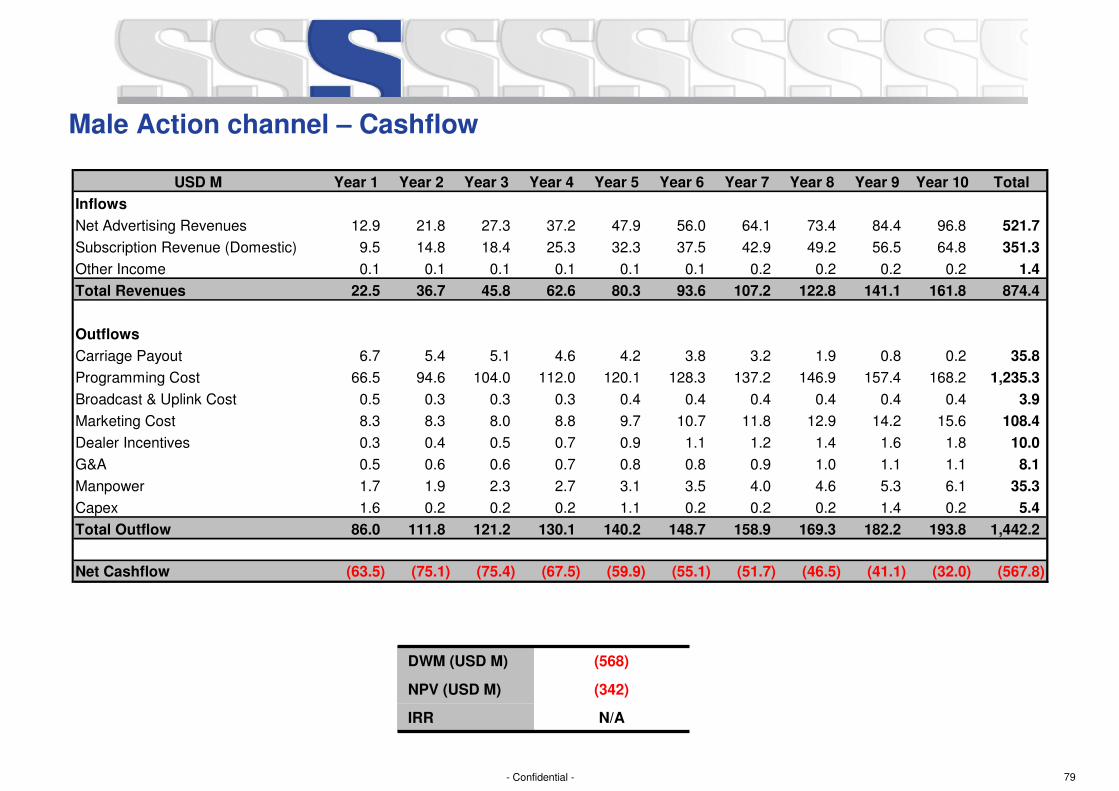

Male Action channel – Cashflow

USD M Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Total

Inflows

Net Advertising Revenues 12.9 21.8 27.3 37.2 47.9 56.0 64.1 73.4 84.4 96.8 521.7

Subscription Revenue (Domestic) 9.5 14.8 18.4 25.3 32.3 37.5 42.9 49.2 56.5 64.8 351.3

Other Income 0.1 0.1 0.1 0.1 0.1 0.1 0.2 0.2 0.2 0.2 1.4

Total Revenues 22.5 36.7 45.8 62.6 80.3 93.6 107.2 122.8 141.1 161.8 874.4

Outflows

Carriage Payout 6.7 5.4 5.1 4.6 4.2 3.8 3.2 1.9 0.8 0.2 35.8

Programming Cost 66.5 94.6 104.0 112.0 120.1 128.3 137.2 146.9 157.4 168.2 1,235.3

Broadcast & Uplink Cost 0.5 0.3 0.3 0.3 0.4 0.4 0.4 0.4 0.4 0.4 3.9

Marketing Cost 8.3 8.3 8.0 8.8 9.7 10.7 11.8 12.9 14.2 15.6 108.4

Dealer Incentives 0.3 0.4 0.5 0.7 0.9 1.1 1.2 1.4 1.6 1.8 10.0

G&A 0.5 0.6 0.6 0.7 0.8 0.8 0.9 1.0 1.1 1.1 8.1

Manpower 1.7 1.9 2.3 2.7 3.1 3.5 4.0 4.6 5.3 6.1 35.3

Capex 1.6 0.2 0.2 0.2 1.1 0.2 0.2 0.2 1.4 0.2 5.4

Total Outflow 86.0 111.8 121.2 130.1 140.2 148.7 158.9 169.3 182.2 193.8 1,442.2

Net Cashflow (63.5) (75.1) (75.4) (67.5) (59.9) (55.1) (51.7) (46.5) (41.1) (32.0) (567.8)

DWM (USD M) (568)

NPV (USD M) (342)

IRR N/A

80- Confidential -

Opportunity 4 – Digitally distributed TV Channel

Strategic New Initiatives

81- Confidential -

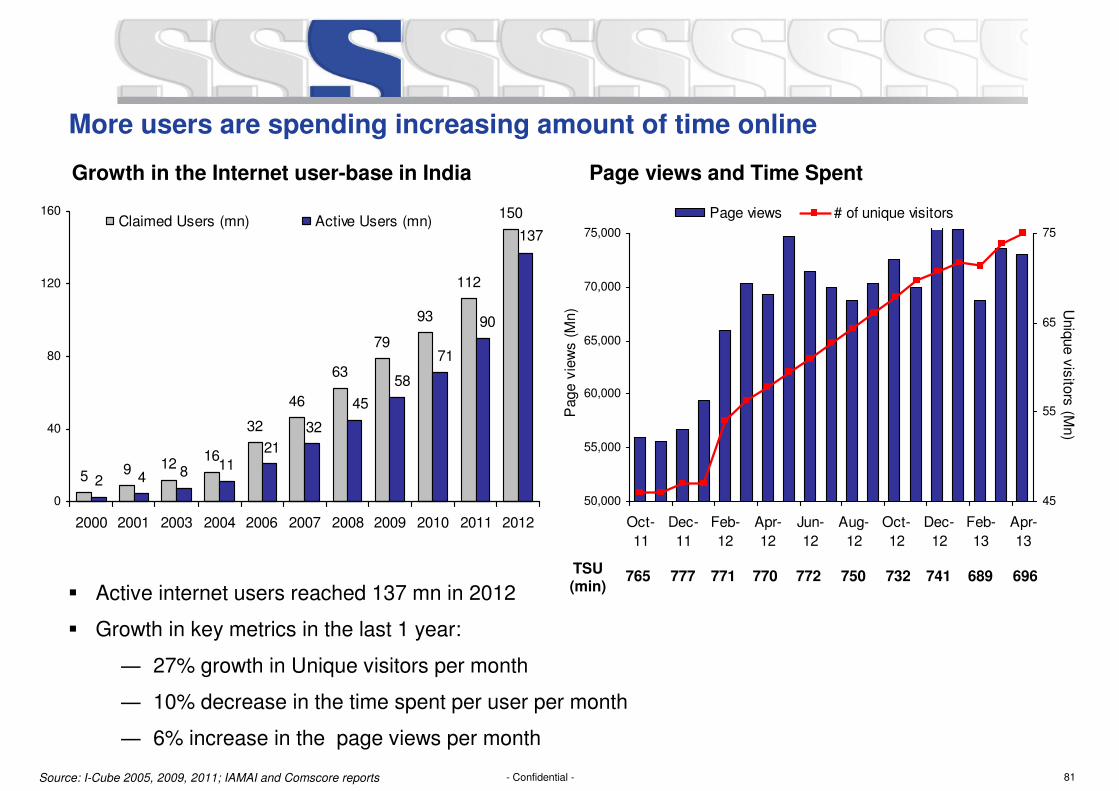

More users are spending increasing amount of time online

Growth in the Internet user-base in India

� Active internet users reached 137 mn in 2012

� Growth in key metrics in the last 1 year:

― 27% growth in Unique visitors per month

― 10% decrease in the time spent per user per month

― 6% increase in the page views per month

Source: I-Cube 2005, 2009, 2011; IAMAI and Comscore reports

5 9 1216

32

46

63

79

93

112

150

2 4 8 11

137

21

32

45

58

71

90

0

40

80

120

160

2000 2001 2003 2004 2006 2007 2008 2009 2010 2011 2012

Claimed Users (mn) Active Users (mn)

50,000

55,000

60,000

65,000

70,000

75,000

Oct-

11

Dec-

11

Feb-

12

Apr-

12

Jun-

12

Aug-

12

Oct-

12

Dec-

12

Feb-

13

Apr-

13

Page v

iew

s (

Mn)

45

55

65

75

Uniq

ue v

isito

rs (M

n)

Page views # of unique visitors

765TSU (min)

777 771 770 772 750

Page views and Time Spent

741 696732 689

82- Confidential -Source: FICCI KPMG 2013

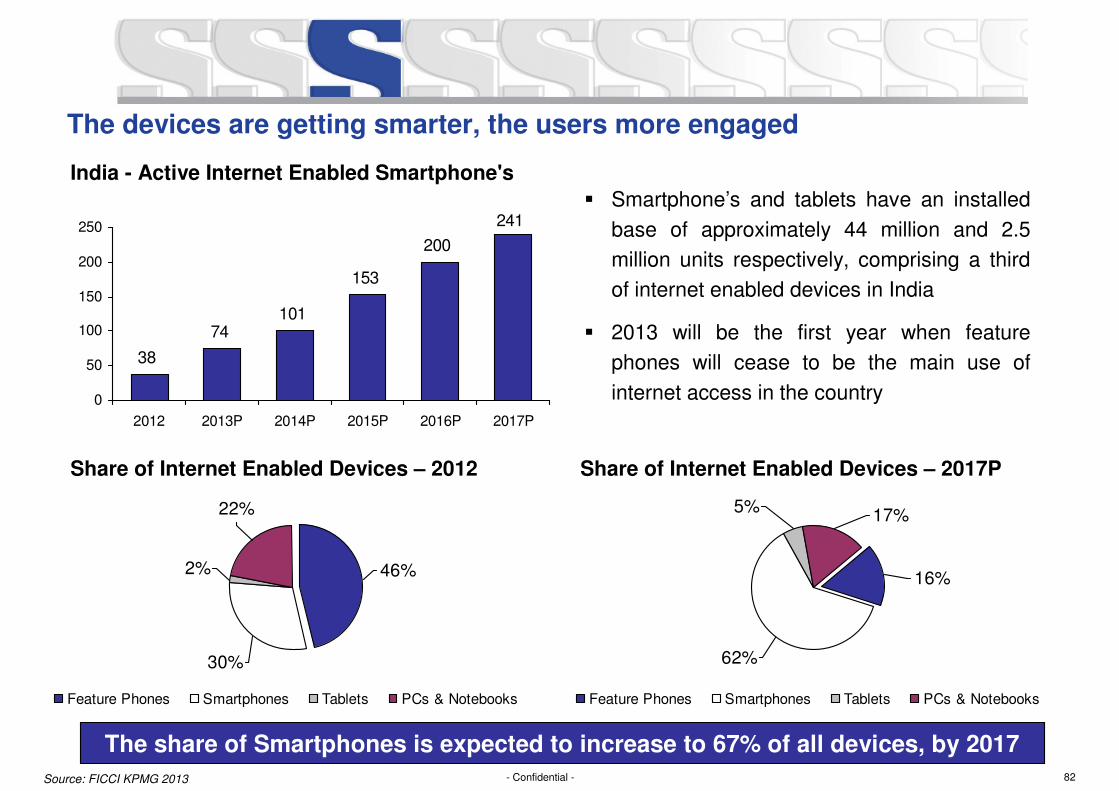

The devices are getting smarter, the users more engaged

� Smartphone’s and tablets have an installed

base of approximately 44 million and 2.5

million units respectively, comprising a third

of internet enabled devices in India

� 2013 will be the first year when feature

phones will cease to be the main use of

internet access in the country

2%

22%

30%

46%

Feature Phones Smartphones Tablets PCs & Notebooks

38

74101

153

200

241

0

50

100

150

200

250

2012 2013P 2014P 2015P 2016P 2017P

India - Active Internet Enabled Smartphone's

Share of Internet Enabled Devices – 2012 Share of Internet Enabled Devices – 2017P

5%17%

62%

16%

Feature Phones Smartphones Tablets PCs & Notebooks

The share of Smartphones is expected to increase to 67% of all devices, by 2017

83- Confidential -

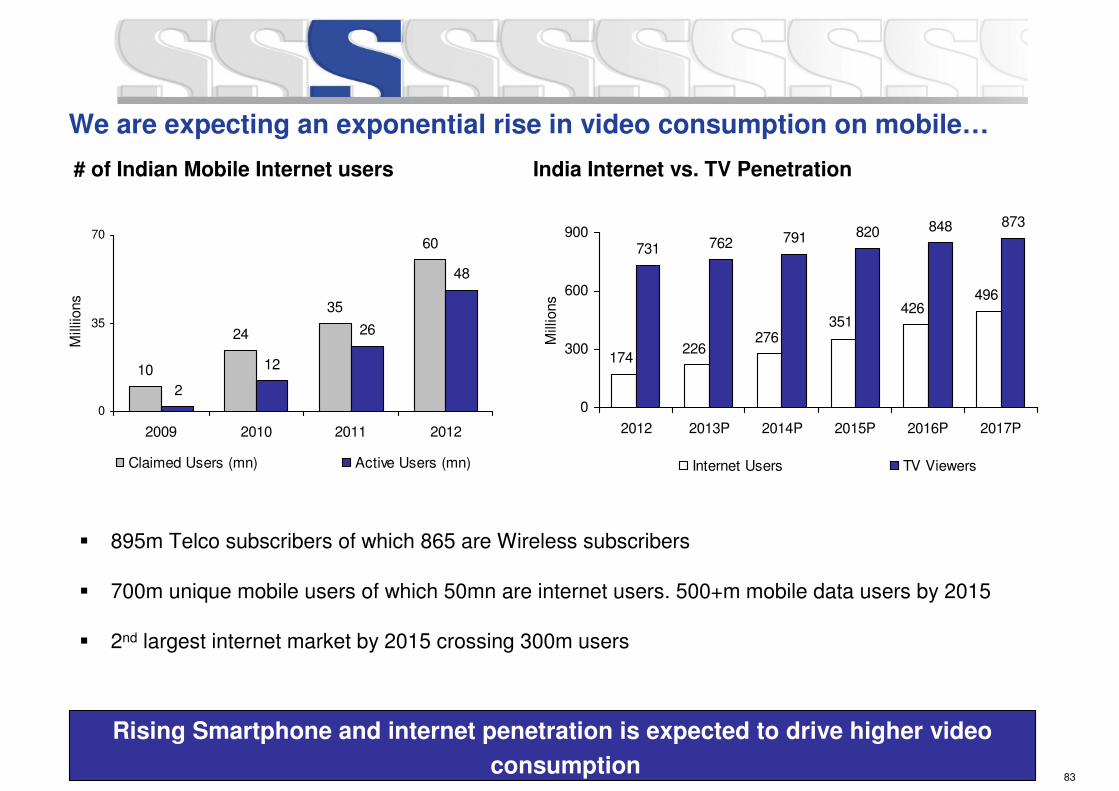

10

24

35

60

2

12

26

48

0

35

70

2009 2010 2011 2012

Mill

iions

Claimed Users (mn) Active Users (mn)

We are expecting an exponential rise in video consumption on mobile…

Rising Smartphone and internet penetration is expected to drive higher video

consumption

� 895m Telco subscribers of which 865 are Wireless subscribers

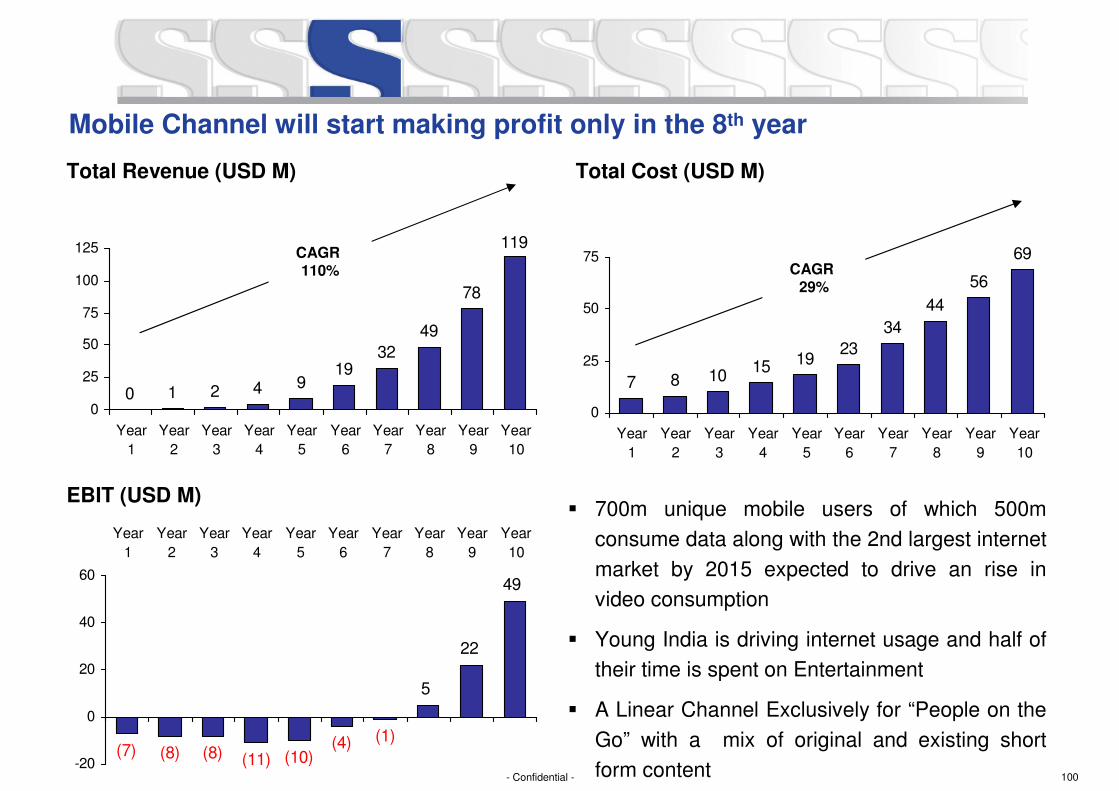

� 700m unique mobile users of which 50mn are internet users. 500+m mobile data users by 2015

� 2nd largest internet market by 2015 crossing 300m users

# of Indian Mobile Internet users India Internet vs. TV Penetration

731 762 791 820 848 873

496426

351276

226174

0

300

600

900

2012 2013P 2014P 2015P 2016P 2017P

Mill

ions

Internet Users TV Viewers

84- Confidential -

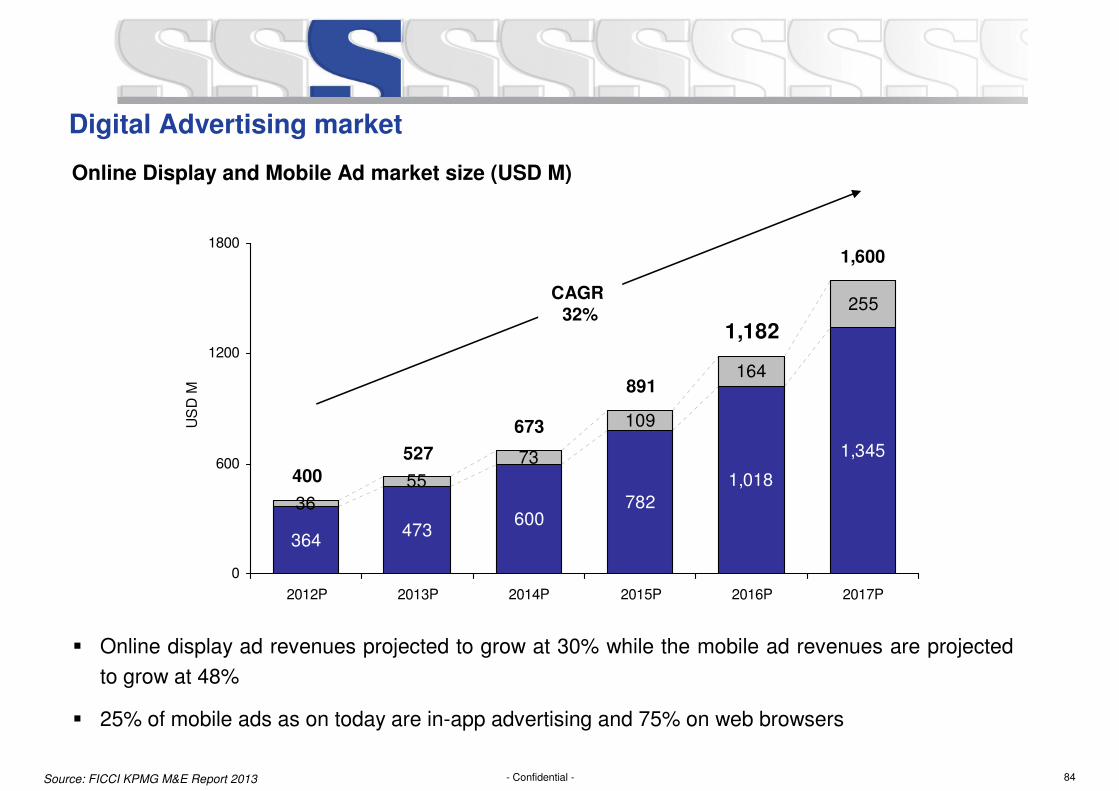

Digital Advertising market

Online Display and Mobile Ad market size (USD M)

782

1,018

1,345

55

73

109

164

255

600473

364

36

1,600

673

527

400

891

1,182

0

600

1200

1800

2012P 2013P 2014P 2015P 2016P 2017P

US

D M

� Online display ad revenues projected to grow at 30% while the mobile ad revenues are projected

to grow at 48%

� 25% of mobile ads as on today are in-app advertising and 75% on web browsers

CAGR

32%

Source: FICCI KPMG M&E Report 2013

85- Confidential -

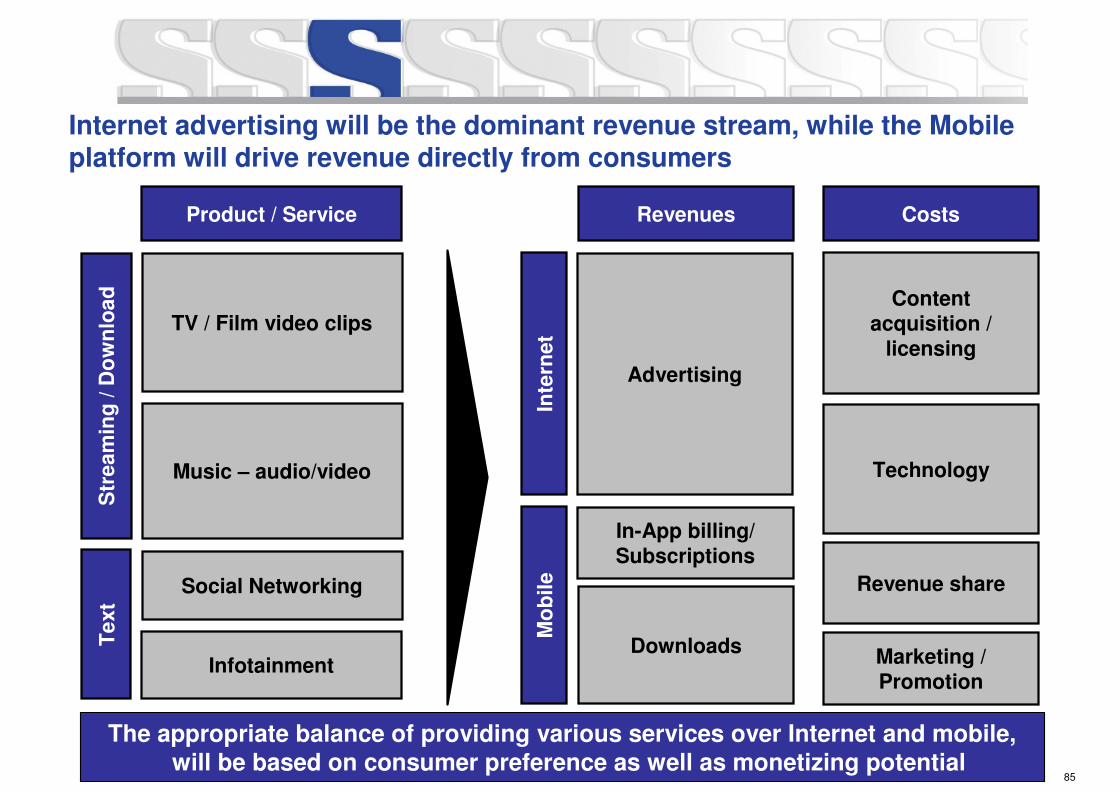

Internet advertising will be the dominant revenue stream, while the Mobile platform will drive revenue directly from consumers

The appropriate balance of providing various services over Internet and mobile, will be based on consumer preference as well as monetizing potential

Revenues Costs

Advertising

In-App billing/ Subscriptions

Downloads

Inte

rnet

Mo

bile

Content acquisition /

licensing

Technology

Revenue share

Marketing / Promotion

Product / Service

TV / Film video clips

Music – audio/video

Social Networking

Str

ea

min

g / D

ow

nlo

ad

Te

xt

Infotainment

86- Confidential -

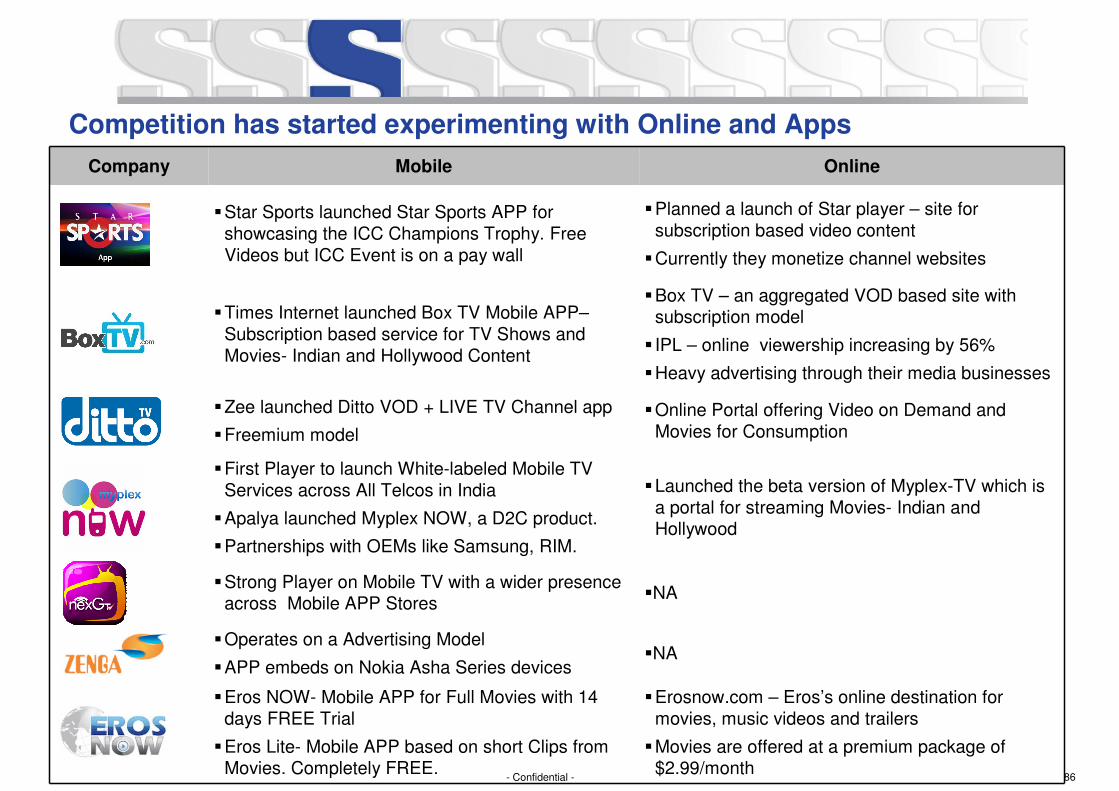

Competition has started experimenting with Online and Apps

Company Mobile Online

�Star Sports launched Star Sports APP for showcasing the ICC Champions Trophy. Free Videos but ICC Event is on a pay wall

�Planned a launch of Star player – site for subscription based video content

�Currently they monetize channel websites

�Times Internet launched Box TV Mobile APP–Subscription based service for TV Shows and Movies- Indian and Hollywood Content

�Box TV – an aggregated VOD based site with subscription model

� IPL – online viewership increasing by 56%

�Heavy advertising through their media businesses

�Zee launched Ditto VOD + LIVE TV Channel app

�Freemium model

�Online Portal offering Video on Demand and Movies for Consumption

�First Player to launch White-labeled Mobile TV Services across All Telcos in India

�Apalya launched Myplex NOW, a D2C product.

�Partnerships with OEMs like Samsung, RIM.