indodairy - squarespace

TRANSCRIPT

IndoDairy Activity 1.5.1: Identify and analyse inclusive business models (IBMs)

between smallholder farmers and private companies

July 2020

The Centre for Global Food and Resources

1 | P a g e

Acknowledgements

This report and underlying analysis were funded by the Australian Centre for International Agricultural Research (ACIAR), whose overarching research project AGB/2012/099 titled ‘Improving milk supply, competitiveness and livelihoods in smallholder dairy chains in Indonesia’ (IndoDairy) is led by the University of Adelaide’s Centre for Global Food and Resources (GFAR) and collaborates with Indonesian institutes, including IPB University, the Indonesian Center for Animal Research for Development (ICARD) and the Center for Agricultural Socio Economic Policy Studies (ICASEPS). The overarching IndoDairy project targets a 25 percent increase in milk production, coupled to increased quality, for 3,000 smallholders by 2020. Under Objective 1, the project will identify and recommend strategies and policies to support development of sustainable, profitable and smallholder-inclusive dairy supply chains. This report aims to “Identify and analyse inclusive business models (IBMs) between smallholder farmers and private companies” and constitutes Activity 1.5.1 of IndoDairy.

The authors thank and acknowledge the project team, in particular Dr Arief Daryanto and Dr Sahara of IPB for analysis and field work and Dr. Erwidodo from ICASEPS for his contributions to the analysis. Additionally, a special thanks to the farmers and the staff of dairy cooperatives, processing companies and retailers for their considerable efforts to supply the information that is the foundation of this report on whole-of-chain opportunities for investment by industry and Government.

For more information:

Contact Professor Wendy Umberger, Project Leader – [email protected]

Visit the project website – www.indodairy.net

2 | P a g e

Table of Contents

Acknowledgements ........................................................................................................................ 1

Executive summary ......................................................................................................................... 3

1.0 Introduction .......................................................................................................................... 4

2.0 Inclusive business principles................................................................................................... 6

3.0 Why inclusive business principles in the agricultural sector? .................................................. 8

4.0 Thesis of this report ............................................................................................................... 9

5.0 Case studies - analysis of key relationships in dairy sector value chains, in East and West Java 10

5.1 Case studies - the examples .......................................................................................................... 12

5.2 Case studies - commercial and relationship analyses ..................................................................... 14 5.2.1 KPS Bogor- West Java ...................................................................................................................................... 14 5.2.2 PT Nestlé Indonesia - East Java (Kejayan) ........................................................................................................ 15 5.2.3 PT Greenfields - East Java ................................................................................................................................ 18 5.2.4 PT Cimory - West Java ..................................................................................................................................... 20 5.2.5 KPBS Pangalengan - West Java ........................................................................................................................ 23 5.2.6 Contract farming model .................................................................................................................................. 26

6.0 Gap analysis - IBM models in East Java compared with KPS Bogor, West Java ...................... 29

6.1 Model comparison ............................................................................................................................ 29

6.2 Impacts on and benefits to smallholder farmers ................................................................................ 35

6.3 Framework for an inclusive and commercially viable dairy sector ....................................................... 37

6.4 Broadening inclusive principles to social inclusion ............................................................................. 39

7.0 Conclusions and recommendations ...................................................................................... 42

Recommendations ................................................................................................................................. 44

References .................................................................................................................................... 45

3 | P a g e

Executive summary

Public investment and policy support are essential to build a viable dairy industry in tropical countries

like Indonesia when exposed to free global competition, especially imports of dairy products from

temperate zones. Indisputably, the aspirational national expansion of smallholder dairying in Indonesia

depends on significant government support. Central to these national goals are import substitution and

the livelihoods of the smallholder communities, that despite serious challenges, already contribute 77

percent of raw milk produced in Indonesia – or 13 percent of the country’s total demand for dairy

products. More targeted government support with clear delineations of the roles of national, provincial

and local bodies will significantly increase smallholder milk production.

In this context, contrasting and diverse case studies of smallholder dairying on the island of Java were

analysed using (1) inclusive business modelling of the triangle of engagement and power relationships

among smallholders, industry and the public (or state) sector; and (2) flows of inputs, outputs, services

and information along dairy chains. Key weaknesses in these value chains were addressed in strategies

to:

• maximise social and economic uplift at the level of the rural household — the “grass roots”;

• increase profitability, confidence and stability to all the value chain;

• revamp existing and under-performing dairy value chains;

• guide sustainable foundations for dairying in new regions of the country; and

• underpin national production goals.

Additional and ongoing state investment in extension services, policy and dairy infrastructure is critical

to maintain a dairy sector in Indonesia. Investment often incorporates repayment of loans, including

those to cooperatives for physical assets and to smallholders for farm improvements. Private processors

may invest in smallholder cooperatives, with a case history in this report demonstrating successful

outcomes for both parties. Further research on scaling out such beneficial relationships is required.

Intensive private investment is generally restricted to smaller regions than those covered by state

entities with national or provincial mandates and with a role in public spending.

A wide range of information on best practices for dairying and associated principles of entrepreneurship

can now be delivered, using multiple formats, to a broad community of farmers’ associations and

cooperatives, processors, marketers and consumers. Information technology and digital tools for on-

farm decision-making and many other on-farm innovations, can stimulate active participation of young

farmers. For deeper engagement of women in smallholder dairying, issues of animal-based products,

nutrition and family welfare can be powerful points of contact. Some specific pilot activities for catalysing

this broad dairying coalition for Indonesia are identified and include competitive grants for audio visual

presentations using existing model dairy farms. With more than 30 local and foreign-controlled dairy

processing companies competing for market share, Indonesia’s downstream industries are well

developed. For the challenge of harnessing and harmonising the diversity of the national dairying sector,

analysis of value chains and inclusive business models proved powerful tools to formulate specific

recommendations on whole-of-chain opportunities for industry and government for advancing

smallholder livelihoods.

4 | P a g e

1.0 Introduction

The Indonesian dairy sector consists of large multinationals, local milk processors, village level dairy

farmer cooperatives (KUD – Koperasi Unit Desa) and many smallholder farmers, the majority of whom

are KUD members (with some non-KUD supply groupings emerging). Since the 1970s, cooperatives

have been central to the national government’s drive to enhance dairy value chains and empower

smallholders (Sulastri & Maharjan 2002). Collective bargaining and representation, through

cooperatives, can successfully buffer the essential inequality of smallholder negotiations with large and

powerful conglomerates. However, governance of dairy farmer cooperatives is unwieldy and

complicated by responsibilities to three Ministries: Cooperatives, Agriculture and Industry. Wijers (2019)

noted that “The Ministries’ national and regional activities vary in effectiveness”. Limitations in defining

logical institutional roles in the transfer of technology and extension are further exacerbated by a lack

of cohesion between provincial and district services. The umbrella organisation, the Union of Indonesian

Dairy Cooperatives (GKSI) is a semi-government coalition focused on the cooperatives, with board

representation from the larger ones. GKSI has a national and regional presence and participates in both

the dairying components within community-based KUDs as well as the dedicated dairy KUDs.

Indonesian milk is produced on two very distinctly different scales: 1) A small, yet growing group of

modern, productive, and integrated dairy companies own about ten percent of the dairy herd yet

contribute 23 percent of fresh milk production; and 2) Smallholders with typically only three to five cows.

The integrated dairy companies average 5,000 lactating cows per farm and are driving modest growth

in milk production. In general, output on these farms is 20 litres per animal per day, with one large

company yielding more than 30 litres. Calving intervals for the companies range between 13 to 14

months. Although 99 percent of production occurs on Java, where the processors are located, new

farms have been established on Sumatera Island. By contrast, smallholder production units are

characteristically inefficient, yielding on average less than 10 litres per animal per day, and with calving

intervals between 18 to 20 months. Study of economic returns to smallholder dairying is ongoing in

ACIAR’s IndoDairy project. Profitability is sufficiently low from dairying to trigger cow culling by

smallholders when beef prices are high. Nonetheless, the somewhat fragile base of small farms delivers

77 percent of Indonesia’s milk production and is therefore pivotal to reducing imports of dairy products.

To serve the aims of both producing more milk and improving rural livelihoods, this report addresses

optimising benefits to smallholders from Indonesia’s diverse dairy value chains.

Most smallholder farmers are dairy cooperative members, who produce milk for processors, however

in addition to the dairy cooperatives, other supply groups are emerging in the market through which

smallholders are able to access buyers. Processors usually pay producers through the cooperatives in

accordance with quality parameters (protein and fat content, and bacterial count). The cooperatives

deduct management fees, animal health and artificial insemination services and feed costs. The GKSI

estimates that only 30 percent of their members own land to produce forage for animals, and only 10

percent provide sufficient forage to their dairy cows. Large cooperatives have tried to overcome this

systemic shortfall in forage by collaborating with state plantation companies to plant forage on adjacent

and available fallow land. Recently, however, the plantations revoked the cooperative’s use of the land.

Large farms supplement local forage with imported lucerne, an option that is unavailable to

smallholders, some of whom do use maize silage, which is also insufficient. The processing companies

arrange low or no interest loans to cooperatives for maintaining milk supplies and upgrading cold chain

infrastructure, collection points, handling equipment and transport vehicles. Some processors also

provide business and production management training for young farmers, the details of which are

described further below.

5 | P a g e

Protective tariffs on imports of milk powder from Australia and New Zealand were removed recently,

underlining that smallholder dairying is increasingly vulnerable to exposure from free global competition,

especially imports of dairy products from countries in temperate zones that are highly mechanised and

capture significant economies of scale.

Long-term and ongoing investments associated with the Bill and Melinda Gates Foundation (BMGF)

through the East Africa Dairy Development initiative (EADD Phase I 2008-13: USD 51 million for Kenya,

Uganda and Rwanda) were lifelines for smallholder dairying in East Africa. In EADD Phase II (USD 26

million; Tanzania, Kenya and Uganda), BMGF partnered with Heifer International, the International

Livestock Research Institute and the World Agroforestry Centre. Without underwriting and investment

by government and/or industry, in a manner comparable both in size and in focus to EADD, dairying is

even less viable in tropical countries like Indonesia, where environmental conditions, chiefly higher

temperatures, are less suitable for dairying than in East Africa. In Vietnam, dairying struggled to become

established except in cooler highland zones. Indisputably, the aspirational national expansion of the

smallholder dairy industry in Indonesia depends on significant government support; or an interventionist

rather than laissez-faire model. Central to the national goals, are import substitution and the

advancement of smallholder communities.

Indonesia’s yearly dairy consumption approaches 4 billion litres, with local production between 600 and

700 million litres, or around 17 percent of total demand (USDA Foreign Agricultural Service 2019) and

annual imports now routinely costing more than US$1 billion to address shortfalls. These trade and

production statistics are consistent with FAO’s (2019) independent estimate of imported dairy products

of 3.2 million metric tons of milk equivalent in 2019.

The growing middle class and changes in lifestyle (Valenta 2018) and diet have fuelled yearly dairy

industry growth of 10 percent. With per capita milk consumption approaching 15 litres per annum

compared with the Philippines and Thailand with 22 and 31 litres respectively, there is a huge potential

for growth of the dairy sector (Valenta 2018). Indonesian smallholders often express concerns about

rates of return from dairying. The average profit by smallholders without costing any household labour

was IDR 1,967 or US 14 cents per litre of milk in a study of four districts in West Java (The Centre for

Global Food and Resources 2020b). Positive non-price stimuli for adopting dairying include a relatively

shorter time to first sales or returns when compared to forestry or perennial crops, an income stream

that is distributed to households throughout the year rather than being aggregated into a short post-

harvest period as for many cropping enterprises and relatively fast payment after delivery.

This report analyses the activities of selected key actors in the dairy industry and their interactions with

the smallholders in the dairy value chains. The key actors include PT Nestlé, and PT Greenfields,

located in East Java and KPBS Pangalengan, PT Cimory, and KPS Bogor in West Java. The

commercial and relationship models between processors and smallholder farmers along with their

influences on household livelihoods, the community, and the economy at large were analysed.

Government inputs to develop the value chains were examined and recommendations were made. The

broad role of government in agriculture in other fast-growing economies was also examined. This

provided insight on the validity of the models for engaging smallholders and processing firms and on

strategies for improving the value chains.

This report also analyses the existing dominant models for engaging smallholders in dairy value

chains, identifies gaps and flaws in these models and then proposes viable business models and

industry strategies. These enhanced models, by embracing principles of inclusiveness, strengthen the

commercial viability of smallholder entities, improve the livelihoods of smallholder households and

communities, and build resilience, quality and productivity in the supply of raw milk. The lessons learnt

6 | P a g e

from dairying in Java will inform decisions regarding expansion of dairying to new regions of the

country.

Snapshots of dairy value chains

Most commonly, smallholders produce raw milk (with limited inputs of feed and forage sourced locally),

deliver to milk collection points (MCPs), are generally operated by local cooperatives (KUDs), and

receive payment directly from processors or through KUDs. Processors primarily purchase the

smallholders’ raw milk, via KUDs, and market either fresh milk or processed products (such as long

shelf-life milk, condensed milk, yoghurt and yoghurt products, confectionery etc.). KUDs have strict

geographic boundaries eliminating competition for markets between them. Alternatives to the dominant

model include PT Greenfields, a joint Australian/Indonesian company which has vertically integrated

milk supply and processing in East Java, and PT Cimory in West Java that invested in large commercial

farms to ensure supply. This report addresses the extent to which the different models integrate

inclusive business principles that benefit the smallholder sector.

In addition to the main supply models, there are a few retail producers, such as Susu Mbok Darmi, in

the city of Bogor, who purchase raw milk directly from several medium-sized farms to produce

sweetened and flavoured, fresh milk products in their own facilities for sale through their network of

street vendors. Although small players in the broader dairy sector, such businesses reflect growing

consumption of fresh milk rather than long shelf-life and processed milk in the market.

2.0 Inclusive business principles

The agricultural industry is highly reliant on investments and improvements in research and

development, productivity and processing. The ability to sustainably source sufficient raw materials that

meet required quality standards is a major goal of global agribusinesses. More than 80 percent of food

consumed in most of the developing world (International Fund for Agricultural Development 2013) is

produced by smallholders who are therefore pivotal to agricultural value chains. Smallholders are

farming households that cultivate or own less than two hectares of land (Rapsomanikis 2015),

depending on the crop and country. Smallholders are often not included in agribusiness and decision-

making for several reasons including their often remote location, high transaction costs of doing

business, information asymmetry and inconsistent production and quality. Asymmetrical information

refers to information deficiencies whereby the buyer and the seller at any point in a value chain have

unequal access to information, especially prices that impact on transactions. Often internationally, small

farmers without access to prices paid by other processors or in other places have been exploited by

processors with whom farmers lose trust. Mobile phone networks supplying such information to farmers

have corrected several instances world-wide of this imbalance. Conversely, information is asymmetrical

when an agribusiness cannot observe and understand farmers’ practices that impinge on the quality of

the product sold.

Around 87 percent of the world’s more than 500 million smallholder farmers live in the Asia Pacific

region (Oxfam 2015). Most of them are geographically scattered and have limited access to modern

farming technology, market access, information, and agribusinesses. Due to the increasing number of

intermediaries in agricultural value chains, smallholder profit margins are continuously being squeezed

and farmers are left in poverty. These issues have driven innovation in sourcing raw materials. For this

report, relevant and contrasting case-studies from the Indonesian dairy industry are analysed using

inclusive business models and reviewed in the light of previous agricultural development in Japan,

China, Taiwan, and South Korea.

7 | P a g e

The Asian Development Bank defines inclusive businesses as generating high development impact by

providing access to goods and services for the ‘base of the pyramid’ and/or providing income and/or

employment opportunities to low income earners as producers, suppliers, distributors, employers and

employees. The ‘base of the pyramid’ is the large proportion of businesses, workers and consumers

who are excluded from normal commercial opportunities through a lack of capital, assets or education.

Smallholders who typically farm small allotments are often excluded from value chains because of

physical remoteness and poor access to markets. As well as geographic isolation, sociological or

cultural differences with traders and the business community may inhibit profitable and harmonious

transactions from developing. Smallholders constitute about 85 percent of farmers globally but earn the

least (Oxfam et al. 2015). In the Indonesian context, a smallholder dairying household would usually

manage six cows or less. A large percentage of smallholder farmers worldwide are illiterate, limiting

access to information on best practices and collaborative opportunities. They are characterised by low

production levels of heterogeneous quality. Their supply is often haphazard and aggregation into a

steady stream of product of constant quality is difficult. Firms are often discouraged from working with

small-scale farmers by the transaction costs associated with aggregation of highly heterogeneous raw

materials (Oxfam et al. 2015). Also, access to information about the farming activities of smallholder

farmers is another constraint that discourages their inclusion.

Smallholders’ inability to secure credit for expansion and intensification is a major constraint that

impedes their scaling up and makes it very hard for them to access new technologies, more efficient

inputs and production requirements of major players in value chains.

From the perspective of buyers and processors, the risks highlighted above (poor access to knowledge,

practices and new technologies) create an equivalent risk to their own businesses. A weak supply chain

delivering inconsistent quality and supply, risks a failure to meet consumer demand, their own quality

standards, and their own profitability. Thus, we can see an interdependence between smallholders and

commercial entities in all agricultural value chains.

This interdependence between smallholders and processors therefore creates a synergistic

relationship, one where improvements in smallholder access to knowledge and techniques leads to

improved reliability and consistency of supply for processors.

Thus, we can see that models of relationships between supplier and processor that improve the

productivity and quality of supply, benefit both processors profitability, while improving the productivity

and livelihoods of smallholders. While not the only principle implicit in inclusive business models, a fair

and balanced relationship between buyer and seller is fundamental to inclusive business models and is

the main focus of this report.

In the context of the Indonesian dairy sector, those at the bottom of the pyramid are typically small

farmers supplying raw milk, and with whom value chains begin. Empowering these farmers to innovate,

through extension and other inputs, is central to building robust value chains. One approach to

implementing smallholder extension work aims to target as many farmers from communities as possible

– an extensive model – as opposed to an intensive model in which “champion farmers” are identified

for education on emerging farm practices and operations, mainly by processors and other buyers, and

provided with a comprehensive perspective and first-hand experience of the operation of their value

chain as well as familiarity with potential providers of extension by government and private entities. In

fact, in many instances of the broader community, targeting natural leaders also emerges to play a

larger and more catalytic role in implementing technology advances than their peers. While Indonesia

is culturally diverse and heterogeneous, peer learning from the “champion farmers” has generally been

associated with a rapid advance in capacity of those at the bottom of the pyramid. Judicious

8 | P a g e

identification of key individuals, who are respected and lead communities by example, was credited with

highly effective transfer of technology in ACIAR’s forestry projects in Indonesia, e.g. FST/2016/141 –

that broke new ground through appointing a female champion farmer – and FST/2015/040. Networking

is a key ingredient of the “champion” approach that seems more flexible than mass education in linking

to diverse and often restricted government agencies for assistance and collaboration.

3.0 Why inclusive business principles in the agricultural sector?

Historically in developing countries, and particularly East Asia after the Second World War,

strengthening agricultural capacity and output was critical in developing robust market economies

(Studwell 2013). Studwell (2013) discusses how agricultural development and land reform formed one

of three central planks in the economic development of Taiwan, Japan and South Korea following the

Second World War, and in China after 1975.

In Taiwan, Japan and South Korea state interventions for smallholders through land reform, technical

assistance and financing was critical in forming a regulated buffer between small landholders and larger

commercial interests (e.g. large landholders leasing land to individual households). This buffering and

protection of smallholders stimulated agricultural growth through households leveraging their own

labour and maximising outputs from small plots of land (often around one hectare per family).

Inclusive business principles focus on providing commercial value to those at the ‘base of the pyramid’

through goods and services. Inclusive agribusiness models can target all segments of the value chain

from production to market access and creating access to inputs, finance and extension, in the countries

noted above. In South Korea, the protection of smallholders was implemented by land reform which

resulted in a subsequent increase in farmland ownership from 5 percent to 70 percent and a reduction

in land tenancy from 95 to an average of 10 percent (Boyer & Man Ahn 1991). With tenancy issues

resolved, most smallholders focused on other vital factors for increasing productivity and profitability.

The transformation of farmers from tenants to owners stimulated increased efficiency and productivity

and sparked major economic surpluses from these agricultural sectors in East Asia.

Inclusive business principles in the agricultural sector provide smallholder farmers access to

information, improved inputs and technology, land, better markets, and shortens the longer chains of

intermediaries, whose participation decreases returns farmers. Equipping farmers with these resources

reduces poverty, develops agriculture and industry and improves food security and economic growth.

In some instances of economic uplift, smallholder communities evolve to employ their own advisers.

This interventionist development model for emerging economies is contrary to the tenets of the laissez-

faire economics that dominated international development and aid agencies in the 1980s and 1990s

and favours reduced government participation. By contrast, Studwell (2013) asserts that intervention to

reinforce the role of smallholders, improving their productivity, profitability, and livelihoods, not only

improves the economic well-being of a large proportion of the rural poor during the growth of the

agricultural sector, but also contributes significantly to the national economy through increased

agricultural output. National, regional and district policies which fail to recognise the importance of the

smallholder production in the economy, jeopardise shaping a strong, viable and growing agricultural

sector from the ground up. A government role is critical to expanding the base of production of an

emerging agricultural sector and there can be significant synergies between private sector investment

(in this report through larger commercial companies in the dairy sector) and government policy that

supports and invests in smallholder farmers. Regional and district policies matter and the skills

9 | P a g e

associated with decentralisation are evolving in the public sector. This government/public sector role is

the third key component analysed.

4.0 Thesis of this report

By studying various commercial models for the relationships between smallholders and the agricultural

supply chains in the dairy sector in Indonesia, we assess the relative balance between smallholder

farmers, larger commercial and corporate players (e.g. processors or large vertically integrated

companies) and the state (in various forms of intervention).

Where there is a clear state role (normally public funding of extension programs or a similar structure),

the balance of the market power and economic benefits may be more evenly distributed across the

value chain than when the state role is diminished. State investment is not the only mechanism for

achieving equitable benefits and, in one case history, a balanced distribution of benefits results from a

commercial entity (PT Nestlé) investing in smallholders. Especially as Indonesia is ranked as having

the sixth worst inequality of wealth in the world, it is prudent that scrutiny for any evidence of larger

companies gaining undue market control should continue, such that the balanced relationships with

smallholders as typified by the Nestlé example become the norm. Fortunately, today there are major

commitments by companies globally so that consumers’ concerns regarding food safety and ethical

behaviour are addressed by audits of supply chains that reach back to the farm. Dairy sectors in

developed and developing countries have played a key pioneering role in auditing supply chains, with

carbon emissions and environmental sustainability now scrutinised with respect to global public good in

the very broadest international contexts.

The successful application of models with balanced benefits for processors and smallholders requires

one of two pre-conditions:

• State support for increasing smallholder productivity, through investment in extension training,

infrastructure, and support for solutions for market barriers (e.g. supply of forage and silage, or

quality animals). The state provides inherent support to farmers through the KUD structure as

the governance, accreditation, monitoring, and reporting requirements provide a level of

collective market power and accountability to the KUDs. This is built into our assessment of state

support in the system. We also note that the KUD structure provides a strong framework for the

strengthening of the market position of smallholders, but it is not necessarily sufficiently well-

funded to provide the required infrastructure support.

• Strong commercial operators that channel investment in financial and extension support to

smallholder organisations, resulting in stronger commercial returns for both sides of the

transaction (commercial company and the smallholders), and therefore returning macro-

economic benefits such as improved productivity, and improved livelihoods for smallholders and

improved tax revenues, reduced reliance on imports and increased export opportunities. A

deterrent to corporate investment, in support to smallholders, has been identified as an absence

of confidence that those farmers who receive support will not shift allegiance and sell to other

commercial enterprises for higher short-term prices on offer.

With their wider breadth of vision, state extension services are more able than local institutions to

leverage relevant cross-cutting information from other regions of Indonesia and abroad for local dairying

enterprises. For example, the findings from the ACIAR project targeting smallholder beef fattening

systems based on forage tree legumes on calcareous soils in eastern Indonesia and northern Australia

(Project no. LPS/2008/054) can provide innovations for dairying. Silage production, information on

10 | P a g e

forage quality as well as the commercial potential for association with forestry and larger farmers for

forage production can also be strengthened by government-wide connectivity. Similarly, there is a

wealth of information to be gleaned from many sources on catalysing women’s engagement in

smallholder agribusiness.

Active support for organisations such as the independent youth-focused dairy network, PERPAMI and

gender-focused programs, will provide secondary support and strengthening for emerging

entrepreneurial business models. Such entrepreneurship and associated inclusive business activities

require specifically targeted policy support. We emphasise the need for more active support and

engagement for networks like PERPAMI that can catalyse youth and gender involvement in the

agricultural sector, and the need for structured policy that can build this support directly. Social evolution

is the enabling environment for technology transfer. Currently, major disincentives for youth

engagement in agriculture include drudgery of operations, limited opportunities, and a poor social image

of subsistence and smallholder farmers. Further specific actions, including support for professional

development through travel that address the disincentives, are detailed in section 6.4 of this report.

Our thesis is that where smallholder and inclusive-focused models are supported (principally by some

state intervention linked to other government policies such as food security and rural development, but

also commercial investment), economic benefits accrue broadly to establish a more robust agricultural

sector. This in turn builds a more resilient economy with a strong foundation of small landholders. In

models where the state involvement is diminished, economic benefits may tend to accrue to the

corporate players in the value chain, with fewer broad gains in the wider economy. There is a worldwide

trend to reduced state funding of extension, especially for mature industries in developed countries. In

Bangladesh, however, the Department of Agricultural Extension remains that country’s largest institution

and, in the case of Indonesia, the fledgling dairy industry that is part of the government’s aspirations for

rural development will fail without public support for extension.

Accordingly, for the development of the dairying sector the recommended approach (below and with

specific recommendations in 7.0) includes strong support through infrastructure investments and

extension training programs, and policies that increase the quality, consistency, and reliability of supply

of raw product. This will improve the productivity of both smallholder producers, and downstream

processors in the supply chain. Notwithstanding that some companies invest as part of their commercial

strategy, the support should come primarily from increased state involvement and not be left to the

private sector to carry the load in emerging and developing industry sectors, as the dairy sector is

currently positioned. Since the 1970s, dairy cooperatives have been central to the Indonesian

government’s drive for dairy value chain improvement (Wijers 2019), to the extent that KUDs dominate

the current dairy landscape – but not to the exclusion of others – and with smallholders supplying 77

percent of the milk produced in the country. Beyond that, partitioning the “success” of smallholder

dairying between government and commercial investment is beyond the scope of this report, but in the

case studies that follow, viable value chains are associated either with commercial investment or

significant levels of foreign aid.

5.0 Case studies - analysis of key relationships in dairy sector value chains, in

East and West Java

As noted, this report focuses on analysing existing value chains East Java, identifying the strengths of

these models, describing benefits associated with inclusive business practices, and through a gap

11 | P a g e

analysis of value chains in West Java (near the city of Bogor), determine the necessary pre-conditions

for applying the inclusive business principles to the existing value chains.

The analysis assesses the relationships between three key actors in the value chains: smallholder

farmers (and women and young members of farming households); commercial operators (mostly

processors and large vertically integrated farms); and public institutions (referred to as the ‘state’: i.e.

policy settings, public infrastructure investment, organisations supporting cooperatives, and national or

international development donors or investments).

For each model under analysis, we present two figures describing these relationships. The first is a

simple value chain analysis with the key players identified inside the circles, connected by arrows

indicating the flow of product (inputs as well as milk) from one to another. The smaller curved arrows

indicate a flow of beneficial goods from one to another, normally from a processor back to the

smallholder in the form of service over and above money. For example, Nestle provides finance and

training to smallholders as well as purchasing their product.

The second figure determines the balance of the relationship between three parties: the public goods

provided by state support (infrastructure, financing, regulation etc), the corporate sector (processors)

and the smallholders. The size of the circle for each party indicates a high-level assessment of the role

played by each party in the relationship, with the arrow indicating net flow of benefits. For example, in

a balanced relationship between processor and farmers, the farmers supply a necessary input to the

processors, and are paid for it, and the processors may invest in extension training to secure a reliable

supply of quality input, and the public sector (state) gains through increased domestic production and

tax receipts. In this situation, both parties gain, and the relationship is balanced. In an unbalanced

relationship, the processor may leverage an external milk supply (imported) to drive the supply price to

farmers downwards, minimising the benefits for the farmers, maximising benefits for processors, but

also, in turn, increasing import volumes, and reducing doestic food security at a national level.

Dashed lines connecting parties in the figures indicate an indirect link, for example, between Greenfields

main product line of fresh milk, and their secondary line of lower quality milk which is used for processed

milk products. In the case of the three-way relationship model, where one party (eg processors) may

dominate, it can have the effect of weakening the link between the farmers and the state, indicating that

this relationship requires strengthening.

This relationship analysis allows ranking of the examples in terms of the relative degree of inclusiveness

implied in the models, providing two preferred examples to be used for the gap analysis comparison

with KPS Bogor.

For business models to be considered successful in terms of integrating inclusive business principles,

value (commercial, financial, market influence, etc.) needs to be distributed fairly between the two

commercial entities, farmers and commercial operators. If this is the case, it can be argued that the less

powerful actors (particularly women, and young farmers) are provided with a commercial framework

that gives them voice in negotiations, market influence, and protection of their interests. Ideally, the

beneficial gains of the value chain would be distributed upwards through the economy through broader

macro-economic gains for the nation resulting in better access to export markets, reductions in imports,

and a reduction in poverty. These last elements, can be considered as the fundamental elements of a

robust, market-based development model (Studwell 2013). Inclusive business principles will therefore

fundamentally benefit the least powerful players in the value chains and, within agricultural industries,

support the participation of smallholders in the national economy. Models that partition equitable

benefits from the value chains to smallholders, dairying businesses and the state are considered

successful.

12 | P a g e

Figure 1. A ‘Balanced Relationship’ using the inclusive business principles.

Figure 1 presents a balanced or ideal relationship between the three value chain actors, against which

the value chains of the case histories are compared. The analytical tool overlays each real value chain

– or case history – on the ideal model to help capture the distribution of benefits. Figure 2 depicts an

unbalanced relationship that constrains implementing inclusive business principles, with the relative

size of the processors in the model reflecting their greater market influence, for example, unilaterally

setting prices for buying milk from smallholders and on-selling to other processors; while providing no

incentives nor support to enhance productivity. Such skewing of power towards processors typically

precludes an equitable distribution of benefits right along the value chain and fails with respect to

inclusive business principles.

Figure 2. An 'Unbalanced Relationship' using inclusive business principles.

5.1 Case studies - the examples

For this study, the IndoDairy team visited examples of dairy value chains in East Java and West Java:

State

ProcessorsSmallholder

farmers

Balanced relationship

State

ProcessorsSmall-holder

farmers

Unbalanced relationship

13 | P a g e

1. PT Nestlé Indonesia

2. PT Greenfields Indonesia

3. PT Cisarua Mountain Dairy (Cimory)

4. KPS Bogor (‘Dairy Production Cooperative of Bogor’; -- KUD)

5. KPBS Pangalengan (‘Dairy Farmer Cooperative of South Bandung, Pangalengan’; -- KUD)

KPS Bogor provides the baseline for the gap analysis, as the broader IndoDairy research specifically

identified KPS Bogor, and the West Java KUDs in general, as underperforming in comparison with the

value chains of East Java. (Nonetheless, KPBS Pangalengan in West Java is considered a success

story in Indonesia’s dairying history and the comparisons below between KPS Bogor and KPBS

Pangalengan, the latter with a significant long-term contribution from Dutch aid, highlight the

differences.)

In addition, two small start-up businesses targeting the consumer markets of Bogor and the owner of a

medium-sized farm near Bogor who convenes a youth-focused farmers’ network, PERPAMI, were

interviewed:

6. Susu Mbok Darmi (‘Mrs Darmi’s Milk’)1

7. Rumah Kopi Ranin (‘Ranin Coffee House’)2

8. PERPAMI (’Indonesian Association of Young Livestock Farmers’)3

The last three interviews provided a framework for broader inclusiveness in the supply chains.

The key question that this report addresses is whether inclusive principles from highly performing value

chains in East Java can be applied in such as KPS Bogor. The remaining four examples (Nestlé,

Greenfields, KPBS Pangalengan and Cimory) are therefore assessed in terms of their relative success

at implementing inclusive business principles, using the analysis described above.

We then compare the baseline model for KPS Bogor with these models, the gaps in the value chain are

subsequently highlighted, enabling us to better understand what is required to successfully apply

successful models, as well as further strengthen these with policy recommendations to improve the

value chain rating for inclusiveness and balance.

Table 1 lists the case studies modelled using KPS Bogor as a baseline as well as contract farming, for

which an hypothetical model is considered.

Table 1. Case studies and the KPS Bogor baseline

Model Location Description

KPS Bogor Bogor, West Java Underperforming KUD in Bogor

PT Nestlé Surabaya, East Java Private processor and privately

funded extension program

PT Greenfields Malang, East Java Vertically integrated large-scale

farming and processing

operation

1 https://www.facebook.com/Susu-Mbok-Darmi-385946975099091/ 2 http://rumahkopiranin.com/ 3 https://www.facebook.com/perpami/

14 | P a g e

PT Cimory Bogor, West Java Private processor and privately

funded model farm program

KPBS Pangalengan Bandung, West Java Foreign government funded

program through KUD

Contract farming No examples visited Generic contract farming model

discussed

5.2 Case studies - commercial and relationship analyses

Each of the examples above are analysed in terms of firstly, the commercial structure between the key

actors as a high-level value chain analysis following the flow of money and product. Then secondly, as

a ‘relationship analysis’, to determine the relative power relations, between the actors, and assessing

the relative benefits to each actor, reflecting the implied application of inclusive business principles

(initially in commercial terms only, not social or environmental).

5.2.1 KPS Bogor- West Java

The KUD structure of KPS Bogor provides the baseline for scope improvement analysis .

KPS Bogor operates a typical structure of KUDs in the dairy industry by operating a number of milk

collection points (MCPs) and purchasing milk from farmers through these MCPs. The KUD sells the

milk to several processors in the region (eg Indolkato and Friesian Fag in South Jakarta), at a IDR1,000

per litre margin on the price paid to the farmers. The processors will pay a higher price for higher quality

milk, based on total plate count (TPC), which is reflected in the process they pay the farmers. This

ranges from IDR4,100/L for a TPC of >1.0Mppm, to IDR5,300/L for a TPC of <500ppm.

Figure 3. Value chain map for KPS Bogor farmers.

The KUD has indicated that the key challenge for their farmers is increasing and maintaining a higher

quality milk supply. To achieve this quality standard consistently (for example a TPC of less than 500

ppm) requires increased skills and training for farmers, improved logistics including the use of stainless

steel pails for transport, improved chilling and storage capacity at the MCPs, and improved access to

new technologies for maintaining healthier animals, better testing of animals and milk, and improved

feed supplies to the farmers. Although the KUD is funded through milk sales, they do not generate the

sort of revenues required to fund these improvements in the supply chain. Farmers express the

frustration of lower prices by trying to increase the volume of their production through more cattle, rather

KPS Bogor MCPs

Farmers deliver Milk Collection Point (MCP)

Smallholder farmers (milk)

PT Friesian Flag

PT

Indolakto

15 | P a g e

than the quality of the product. Local processors hedge against the lower quality of locally supplied milk

by purchasing their inputs from further afield and using the lower quality milk for products other than

high-margin fresh milk.

Thus the driver for change in the supply chain is not driven by the processors, as they can source better

quality milk elsewhere, nor is it being driven by the KUD as their revenues do not provide the capacity

to invest capital where it is needed, and the farmers, through a lack of knowledge and training, cannot

make the changes themselves.

Through this analysis, we can see that market forces alone are not enough to drive change in the

industry in Bogor. If there remains a policy direction to strengthen and improve the domestic dairy

industry, then support needs to be provided to supply basic infrastructure of extension training, farm

inputs, and capital investment in logistics to provide a baseline for the market to build on.

Figure 4. KPBS Bogor relationship model

5.2.2 PT Nestlé Indonesia - East Java (Kejayan)

Commercial and Relationship Analysis

For more than 140 years, Nestlé has been leading the world in nutrition, health, and wellness with their

range of food products. Nestlé is the largest producer of fast-moving consumer goods and has presence

in 189 countries, including Indonesia. To save a neighbours’ child unable to accept breast milk, Henri

Nestlé developed the world’s first milk food for infants. Since then, Nestlé has consistently developed

other milk products with small farmers supplying the value chain. Nestlé commenced dairy operations

in Indonesia in 1970 in West Java. A factory was established in 1971 in West Java and another in

Kejayan, East Java in 1988. Currently Nestlé works via cooperatives with more than 26,000 farmers

owning 70,000 cows.

Public

Processors

Small-holder

farmers

Benefits:

• Few benefits currently flowing to smallholders

Strengths:

• Can source milk from other regions or import;

• No incentive to support local farmers

Benefits:

• Limited direct benefits to national economy;

• No reduction in importation of powdered milk

Support:

• Limited direct state support for farmers.

16 | P a g e

Website: https://www.nestle.co.id/id

Operating principles

The fundamental relationships that Nestlé build with their raw commodity suppliers is a model used in

other parts of Asia in other commodities. It has been successfully used with rice farmers in Malaysia to

improve the farmers productivity, but more critically to improve the supply quality and consistency of

farmers’ raw products. This in turn provides a commercial benefit to Nestlé by creating a more reliable

supply of raw products, where reliance on a smallholder network can put at risk the quality and reliability

of supply.

Nestlé’s goal of reliability of supply is built on the principle of ‘Creating Shared Value’, and involves

investment by Nestlé through assistance with capital purchases, or providing finance for capital

purchases, as well as investment in extension support to farmer networks through co-operatives.

However, while the principle is driven by commercial outcomes and requires a financial commitment,

and corresponding return on investment, the principle recognises the reciprocal nature of accrued

benefits. Nestlé understands that by improving the productivity of their supplier farmers, they not only

improve the livelihoods of the farmers, through an increase in their profitability, but they also improve

their own commercial outcomes, providing a robust platform for responding to increasing product

demand. Daily demand grew from 300 t/day in 2007 to 1150 t/day in 2017 and production of participating

smallholder farmers increased from 9.5 litres/cow to 11.8 litres/cow.

Description of model

Through Nestlé’s ‘Creating Shared Value’ strategy, farmers experience increased productivity and

quality to meet Nestlé’s demands and specifications. Nestlé provides interest-free finance to

cooperatives to setup and manage milk collection centres. Specifications such as time between milking

and chilling, purity, cleanliness, and handling are strictly adhered to by the cooperatives to ensure

consistency in quality of fresh milk. For consistency to be achieved, Nestlé invested in the purchase of

cooling tanks, stainless steel collecting cans and transportation. Investments further down the value

chain have been made by distributing seeds/nurseries of fodder species to cooperatives, developing

fodder farms, and providing water ad-libitum to cowsheds. Extension agents from Nestlé ensure

compliance by farmers with the recommended practices in feeding, milking and handling of animals.

The approach fosters self-reliance and engagement of farmers, rather than a habit of reliance on welfare

payments. Nestlé’s investments have increased the quality of farmers’ milk, strengthened cooperatives

and delivered a reliable source of high-quality milk.

Nestlé purchases milk from a number of KUDs in the vicinity of Kejayan, and pay nominally higher than

KUD prices for the milk, indicating that their investment is not directly recouped through lower farm-gate

prices. They pay IDR5,250/L for TPC of <500K ppm, as compared with IDR4,950/L through KPBS

Pangalengan, and around IDR4,700 ithrough KPS Bogor fo the same quality milk.

17 | P a g e

Figure 5. Value chain map for Nestlé East Java.

Relationship model

Overlaying Nestlé’s operating model on the generic relationship diagram described in the introduction

to this section and analysing the resulting benefits, highlights two significant factors. First, because there

is a well-balanced relationship between smallholders and Nestlé, both benefit economically and mitigate

their risks in the market.

Figure 6. Nestlé East Java relationship model

Nestlé provides extension training, access to finance, logistics and milk handling.

KUDs supports and implements extension training, access to finance, logistics to farmers.

Smallholder farmers

KUD Milk Collection Centres

Nestlé

Other suppliers (Greenfields)

KUDs

State

NestléSmallholder

farmers

Balanced relationship

Benefits: • Access to finance • Access to training and

extension • Improved productivity • Improved livelihoods

Some state role in KUD accreditation and monitoring, but no direct support.

Benefits: • Improved supply quality • Improved productivity

and profits • Increased market share

Strong corporate returns to national economy

• Import reduction • Export opportunity • Poverty reduction

18 | P a g e

Second, there is no significant role played by any state or public entity (other than through the

organisational framework of the KUD structure, accreditation, and monitoring; whereas generally three-

way models reflect the state – through funding, policy, and infrastructure – playing a major role in

positive outcomes). The Nestlé model reflects a balanced relationship between smallholders and Nestlé

(based on the ‘shared value’ concept), strong benefits to all parts of the supply chain and the broader

economy, and little intervention from the state.

5.2.3 PT Greenfields - East Java

Commercial and Relationship Analysis

Australian and Indonesian entrepreneurs founded PT Greenfields’ large-scale dairying operations in

East Java. The first farm was established in the Malang Highland at 1,200 metres above sea level in

1997 and their milk-processing plant came onstream in 2000, producing about 20,000 litres of milk per

day. Construction of Greenfields’ second farm commenced in 2017 at Wlingi. The feed processing and

silage systems of the farms support optimal nutrition, a core component of the package of best practices

in dairy husbandry that is recognised as the hallmark of Greenfields operations. Products include

pasteurised extended shelf life (ESL) and pasteurised ultra-high temperature (UHT) milk that exceeds

the highest international qualities standards, with Greenfield’s products sold in Indonesia, Malaysia,

Hong Kong, the Philippines and other Asian markets. PT Greenfields currently meets 5 percent of the

entire milk demand of Indonesia and will supply a further 6 percent when the second farm reaches full

capacity.

Website: https://greenfieldsdairy.com/

Operating principles

Greenfields sources fresh milk from their two farms but do not process any milk from smallholder

farmers because of quality issues. Nonetheless, Greenfields brokers the purchasing of smallholder milk

through a single, local, independent MCP (not directly through a KUD) for supply to processors including

Nestlé, Indolacto and Real Good. Greenfields has no contractual relationship with KUDs, nor obligations

to follow price floors for smallholders’ milk, nor provide extension. Greenfields has, however, a dairy

institute and a demonstration farm where farmers from across Indonesia are taught best practices. The

institute delivers a common good, namely to improve farmer husbandry, rather than to drive contractual

or commercial compliance with Greenfields’ product standards.

Description of model

Greenfields aim to provide high quality milk and milk products for the local and international market. In

their bid to achieve this, there has been a conscious or subconscious displacement of smallholder

farmers from the value chain, as Greenfields sources all raw milk from their own production rather than

from smallholder farmers. Their operations have led smallholder to shift from producing milk to selling

forage to the Greenfields dairy.

19 | P a g e

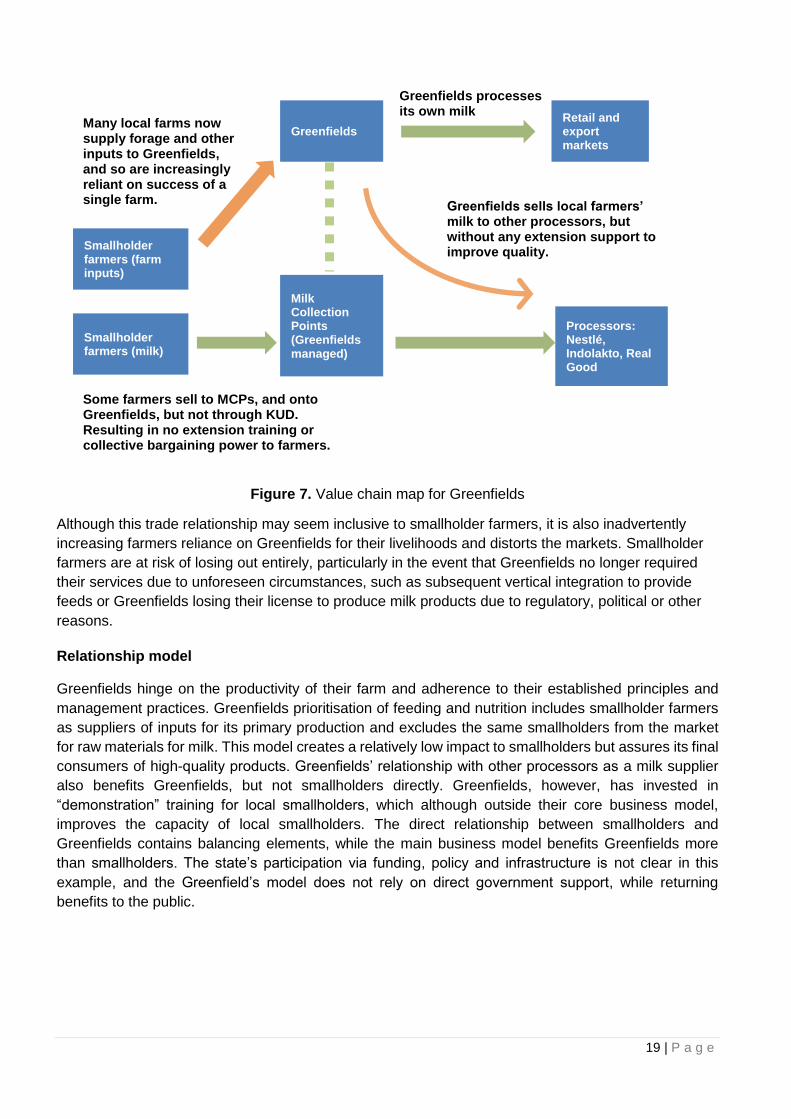

Figure 7. Value chain map for Greenfields

Although this trade relationship may seem inclusive to smallholder farmers, it is also inadvertently

increasing farmers reliance on Greenfields for their livelihoods and distorts the markets. Smallholder

farmers are at risk of losing out entirely, particularly in the event that Greenfields no longer required

their services due to unforeseen circumstances, such as subsequent vertical integration to provide

feeds or Greenfields losing their license to produce milk products due to regulatory, political or other

reasons.

Relationship model

Greenfields hinge on the productivity of their farm and adherence to their established principles and

management practices. Greenfields prioritisation of feeding and nutrition includes smallholder farmers

as suppliers of inputs for its primary production and excludes the same smallholders from the market

for raw materials for milk. This model creates a relatively low impact to smallholders but assures its final

consumers of high-quality products. Greenfields’ relationship with other processors as a milk supplier

also benefits Greenfields, but not smallholders directly. Greenfields, however, has invested in

“demonstration” training for local smallholders, which although outside their core business model,

improves the capacity of local smallholders. The direct relationship between smallholders and

Greenfields contains balancing elements, while the main business model benefits Greenfields more

than smallholders. The state’s participation via funding, policy and infrastructure is not clear in this

example, and the Greenfield’s model does not rely on direct government support, while returning

benefits to the public.

Smallholder farmers (farm inputs)

Milk Collection Points (Greenfields managed)

Greenfields Many local farms now supply forage and other inputs to Greenfields, and so are increasingly reliant on success of a single farm.

Some farmers sell to MCPs, and onto Greenfields, but not through KUD. Resulting in no extension training or collective bargaining power to farmers.

Smallholder farmers (milk)

Greenfields processes its own milk

Retail and export markets

Processors: Nestlé, Indolakto, Real Good

Greenfields sells local farmers’ milk to other processors, but without any extension support to improve quality.

20 | P a g e

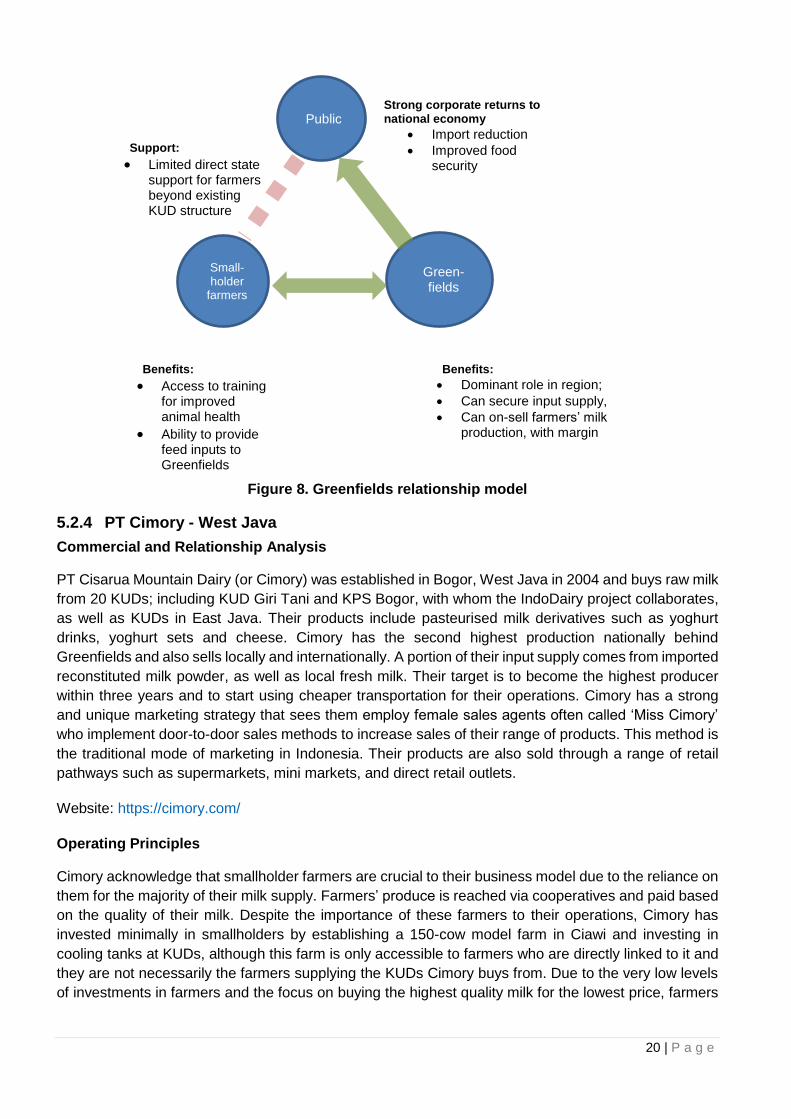

Figure 8. Greenfields relationship model

5.2.4 PT Cimory - West Java

Commercial and Relationship Analysis

PT Cisarua Mountain Dairy (or Cimory) was established in Bogor, West Java in 2004 and buys raw milk

from 20 KUDs; including KUD Giri Tani and KPS Bogor, with whom the IndoDairy project collaborates,

as well as KUDs in East Java. Their products include pasteurised milk derivatives such as yoghurt

drinks, yoghurt sets and cheese. Cimory has the second highest production nationally behind

Greenfields and also sells locally and internationally. A portion of their input supply comes from imported

reconstituted milk powder, as well as local fresh milk. Their target is to become the highest producer

within three years and to start using cheaper transportation for their operations. Cimory has a strong

and unique marketing strategy that sees them employ female sales agents often called ‘Miss Cimory’

who implement door-to-door sales methods to increase sales of their range of products. This method is

the traditional mode of marketing in Indonesia. Their products are also sold through a range of retail

pathways such as supermarkets, mini markets, and direct retail outlets.

Website: https://cimory.com/

Operating Principles

Cimory acknowledge that smallholder farmers are crucial to their business model due to the reliance on

them for the majority of their milk supply. Farmers’ produce is reached via cooperatives and paid based

on the quality of their milk. Despite the importance of these farmers to their operations, Cimory has

invested minimally in smallholders by establishing a 150-cow model farm in Ciawi and investing in

cooling tanks at KUDs, although this farm is only accessible to farmers who are directly linked to it and

they are not necessarily the farmers supplying the KUDs Cimory buys from. Due to the very low levels

of investments in farmers and the focus on buying the highest quality milk for the lowest price, farmers

Public

Green- fields

Small- holder

farmers

Benefits:

• Access to training for improved animal health

• Ability to provide feed inputs to Greenfields

Benefits:

• Dominant role in region;

• Can secure input supply,

• Can on-sell farmers’ milk production, with margin

Strong corporate returns to national economy

• Import reduction • Improved food

security

Support:

• Limited direct state support for farmers beyond existing KUD structure

21 | P a g e

are not obliged to supply KUDs that supply Cimory. This makes the constant supply of milk a major

challenge for Cimory as KUDs are always looking forward to selling to the highest bidder.

Description of model

Cimory potentially has two models, one of which invests in cooling tanks and buys from KUDs, the other

is vertically-integrated model and sees the development of their model farms and the subsequent

development of more farms.

Investment in cooling tanks and purchase from KUDs

In this model, farmers supply to KUDs and Cimory purchases from different KUDs in West Java. Cimory

deals with smallholder farmers from different cooperatives. Cimory purchases 250 tonnes of milk per

week from these cooperatives in West Java. The cooperatives place a 20 percent margin on the price

of the milk before selling to Cimory, and the price offered to cooperatives is based on the quality of the

milk they receive. Milk samples with less than 1.0million Total Plate Count (TPC) – a measure of

bacterial contamination – get as much as a 13 percent price premium (paid to the KUD), thus the lower

the TPC, the higher the price. Milk with less than 1.0m TPC is used for fresh milk production while that

which has more than 1.0m is processed into yoghurt. Thirty percent of the milk is processed as fresh

milk while 70 percent is used in the production of yoghurt. On arrival at the MCPs, milk is weighed,

tested and chilled. To retain the milk’s quality, PT Cimory has invested in the procurement and

installation of cooling tanks at the various KUDs from whom it purchases.

This investment, however, favours Cimory and does not benefit the smallholders directly, although

Cimory does pay farmers (via KUDs) a slightly higher price for milk than other models (IDR5,200/L

compared with IDR4,550/L by KPBS Pangalengan and IDR 4,100/L by KPS Bogor (all for <1.0M TPC).

This model helps smallholder farmers to sustain their livelihoods and is somewhat inclusive, but does

not necessarily prioritise them as major stakeholders in the value chain.

We note also that Cimory implement a practice where imported reconstituted dairy product is

reprocessed and marketed as a fresh milk product. This practice is not currently regulated by any

national government policy covering branding and consumer protection, which in turn leaves

smallholders exposed, as this works against their interests. Improved national policy in this area will

help to strengthen the market position for smallholders, and increase the competitiveness of their

product in a globalised market.

Development of a model (‘demo’) farm

Smallholders are fundamental to PT Cimory’s growth as their procurement methods may not be

appealing to big companies. This has spurred investments in the establishment of a farm with 150 cows

to serve as a model farm for farmers. For the farm to run successfully, a partnership has been

established with the Forestry Department to sustainably provide forage for the farm by thinning trees

instead of clear felling, allowing the growth of grass for silage within the forested areas. A drawback of

this model is that many farmers who supply the KUDs, from whom they purchase milk, do not have

access to the farm, therefore limiting the reach and impacts of the farm.

PT Cimory has plans for two more farms in West and Central Java with herds of 500-1,000. These cows

will have an average production of 15-20 litres per cow per day. This investment will most likely reduce

Cimory’s reliance on smallholder milk.

22 | P a g e

Figure 9. Value chain map for PT Cimory in West Java

Relationship model

Although the relationship established from Cimory’s operating model is beneficial, measures can be put

in place to make it even more efficient. Cimory and smallholder farmers face risks in this relationship

model as the price smallholders receive and the availability of milk for Cimory is never assured. Cimory’s

investment in model farms benefits the farmers who are fortunate to be able to access it, although these

farmers are a fraction of those involved in its supply chain. This translates to a partially balanced

relationship between smallholder farmers and Cimory. As is typical in Indonesia, the government plays

no direct significant role in the value chain except for regulation and monitoring of KUDs.

KUD Giri Tani

KPS Bogor

Many farmers sell milk to KUDs who sell to Cimory.

Smallholder farmers (milk)

Cimory

Cimory medium-size model farm- Ciawi

Cimory medium-sized ‘model farms’ supply smallholder extension to improve the milk supply of farmers trading with Cimory, rather than targeting the broad KUD membership.

Retail and export markets

Limited investment by Cimory back to KUDs or farmers for productivity improvements, other than model farms below.

Smallholder farmers (milk)

Individual Large scale dairy farms (milk)

23 | P a g e

Figure 10. Cimory relationship model

From the above, we conclude that Cimory’s model is partially beneficial and requires modification for

full inclusiveness of smallholders.

5.2.5 KPBS Pangalengan - West Java

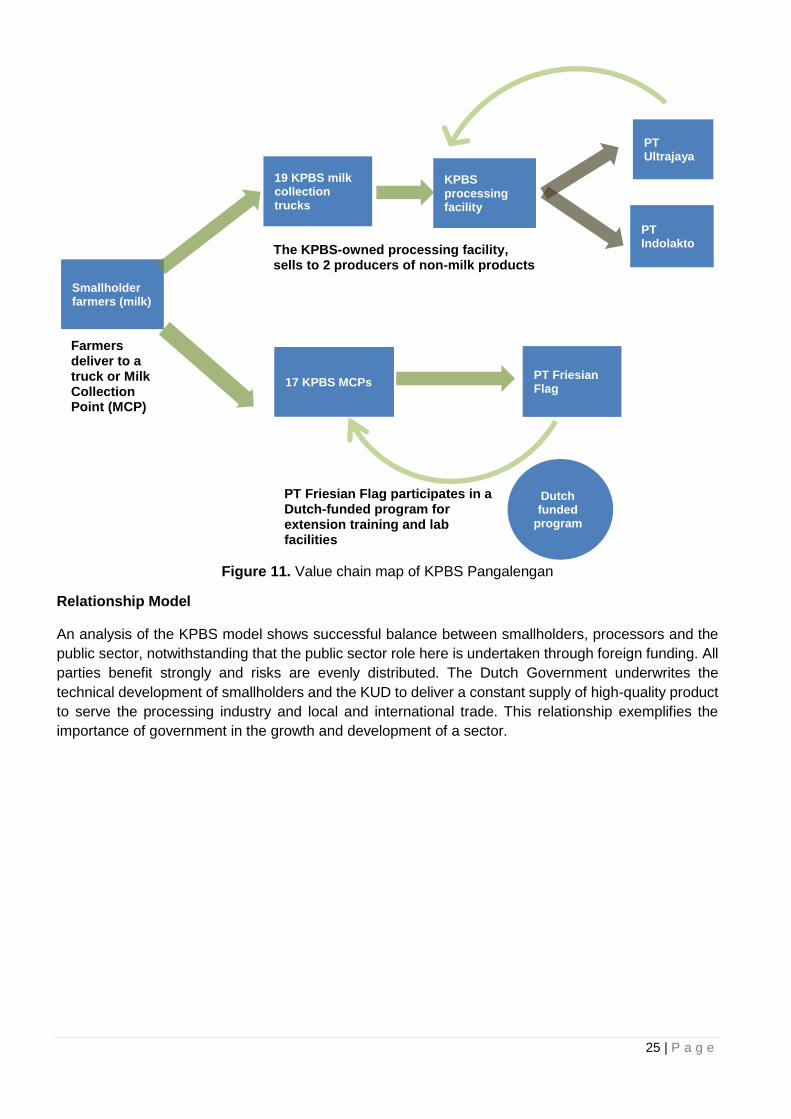

Commercial and Relationship Analysis

KPBS Pangalengan was established in 1969 for smallholder dairy farmers and with current membership

exceeding 2,500, KPBS is considered one of the more successful dairy cooperatives in Indonesia.

KPBS operates seven digitally automated MCPs to drive a responsive testing and pricing protocol for

their suppliers and higher quality milk for their buyers. The KPBS fleet of 19 milk collection trucks also

improves farmers’ access to the collection network. Besides supplying fresh milk to PT Friesian Flag

Indonesia (FFI) and other processors, KPBS is also involved in the production of about 18 dairy

products.

Operating principles

The KPBS cooperative operates a beneficial business relationship with their smallholder dairy farmers

to broker low cost credit for equipment updates and to continuously grow their competencies for higher

quality milk supply. KPBS access to both public and private fund streams positions it as a driver of

innovation for smallholder dairies. KPBS is supported by Dutch government aid via FFI - an Indonesian

subsidiary of a Dutch multinational company, FrieslandCampina, to train dairy farmers. FFI continuously

invests in smallholder farmers meeting standards for milk quality and provides farmers with access to

extensionists, a dairy extension manual and trains KUD staff. Cooperation among smallholders,

cooperatives and FFI has occurred for more than 20 years, with FFI’s commitment to smallholder

dairying further consolidated through its MoU signed in 2018 with KPBS and other cooperatives in West

Java. The following activities were included:

State

CimorySmall-holder

farmers

Partially balanced relationship focus on commercial strength by vertically linking model farms with processor

Some state role in KUD accreditation and monitoring, but no direct support

Strong corporate returns to national economy • Import reduction • Export opportunity • Poverty reduction

Benefits: • Access to training

and extension through KUDs and model farm

• Improved livelihoods

Benefits: • Improved supply

quality • Improved

productivity and profits

• Increased market share

24 | P a g e

• sharing knowledge and experience among farmers in Indonesia and in the Netherlands;

• an academy promoting networking among young farmers;

• machinery for automating MCPs;

• a dairying radio program for communication among farmers, the extension service and cooperatives; and

• a dairy village to demonstrate sustainable dairying with cutting-edge technology. Despite the long-term positive relationship between FFI and KPBS Pangalengan, the latter is still

perceived as inefficient rather than a cutting-edge enterprise. The above activities covered in the MOU

largely parallel those of PERPAMI and stimulation of synergies between such like-minded initiatives is

recommended for maximum benefit to the broader rural community. The commercial dairy industry has

often invested in smallholders for philanthropic reasons related more to global public good than to profit.

These contributions, and those of aid programs of developed countries, have dramatically augmented

access to modern technologies for dairying beyond the advances resulting from Indonesian public

investment. The elements for innovation seem to be in place, but often the dynamism engendered by

R&D projects finishes with the project and stagnation seems pervasive, for example as referred to above

with the long-term collaboration between FFI and KPBS Pangalengan.

Description of model

KPBS model focuses on providing extension, finance and ready markets for smallholder dairy farmers.

This has led to an increase in productivity and profitability of their farmer members. KPBS operations

are digital to ensure farmers receive a fair and transparent payment for their produce and the method

of milk collection is flexible and closer to farmers. Through FFI, KPBS is able to invest in farmer training.

Rather than using model farms, FFI deploys extension workers and extension materials to the farmers,

which has led to a high adherence by farmers as they have one-on-one sessions with extension agents

who can help to solve issues unique to them. The provision of inputs such as concentrates and water,

coupled with the extension services, helps to achieve regularity among the members, while the provision

of low-cost finance leaves no farmer lacking basic equipment for production. This inclusive business

model spurs farmers to be active decision-makers but can encourage the reliance on foreign

government for development. KPBS does, however, have the ability to supply their processors and

produce milk products effectively using this model.

KPBS Pangalengan pays farmers on a sliding scale based on TPC, the price increasing from IDR4,550

for 800K-1.0M ppm TPC up to IDR5,250/L for < 100K ppm. Using a quality benchmark of <500K ppm,

the KPBS price (IDR4,950/L) is lower than the price paid ny Nestle (IDR5,250/L).

25 | P a g e

Figure 11. Value chain map of KPBS Pangalengan

Relationship Model

An analysis of the KPBS model shows successful balance between smallholders, processors and the

public sector, notwithstanding that the public sector role here is undertaken through foreign funding. All

parties benefit strongly and risks are evenly distributed. The Dutch Government underwrites the

technical development of smallholders and the KUD to deliver a constant supply of high-quality product

to serve the processing industry and local and international trade. This relationship exemplifies the

importance of government in the growth and development of a sector.

17 KPBS MCPs

19 KPBS milk collection trucks

Farmers deliver to a truck or Milk Collection Point (MCP) atruck

Smallholder farmers (milk)

The KPBS-owned processing facility, sells to 2 producers of non-milk products

KPBS processing facility

PT Friesian Flag

PT Ultrajaya

PT Indolakto

Dutch funded

program

PT Friesian Flag participates in a Dutch-funded program for extension training and lab facilities

26 | P a g e

Figure 12. Relationship model for KPBS Pangalengan

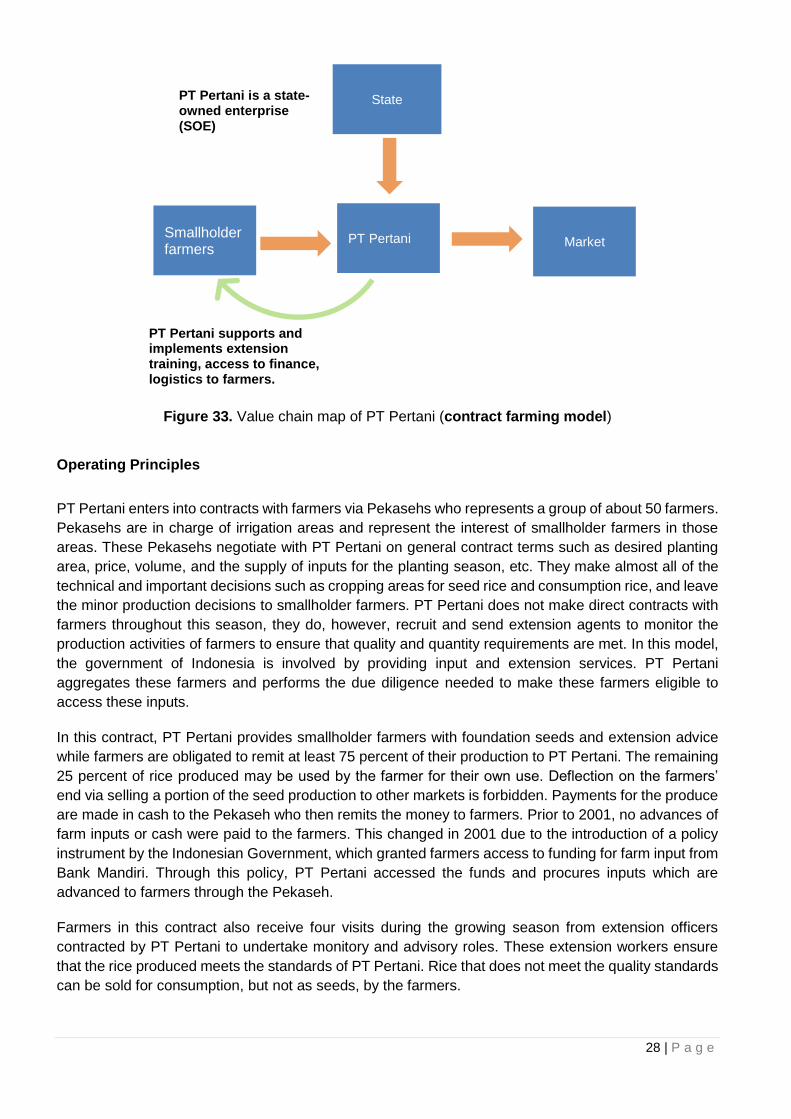

5.2.6 Contract farming model

Commercial and Relationship Analysis

Contract farming has existed for more than 100 years and is increasingly deployed by large agricultural

processors and development practitioners due to a high level of smallholder inclusion and the mutual

benefit provided to both buyers and farmers. Often referred to as an ‘’outgrower scheme’’ (Eaton &

Shepherd 2001), it is defined as a contractual arrangement between a farmer and a firm (buyer) (Rehber

2007), whether oral or written, which provides resources and/or specifies one or more conditions of

production, in addition to one or more marketing condition, for an agricultural product, which is non-

transferable.

There are five different models of contract farming (Eaton & Shepherd 2001), but all share the same

basic structure, which usually involves a buyer and the farmer and sometimes intermediaries such as

government bodies acting as regulators or 3rd party companies who help with sourcing and aggregating

of farmers. These models include: the centralised model where the sponsor purchases crops from a

number of smallholder farmers and processes or packages them into marketable products and are

heavily involved in production where they often take control of most production aspects; the nucleus