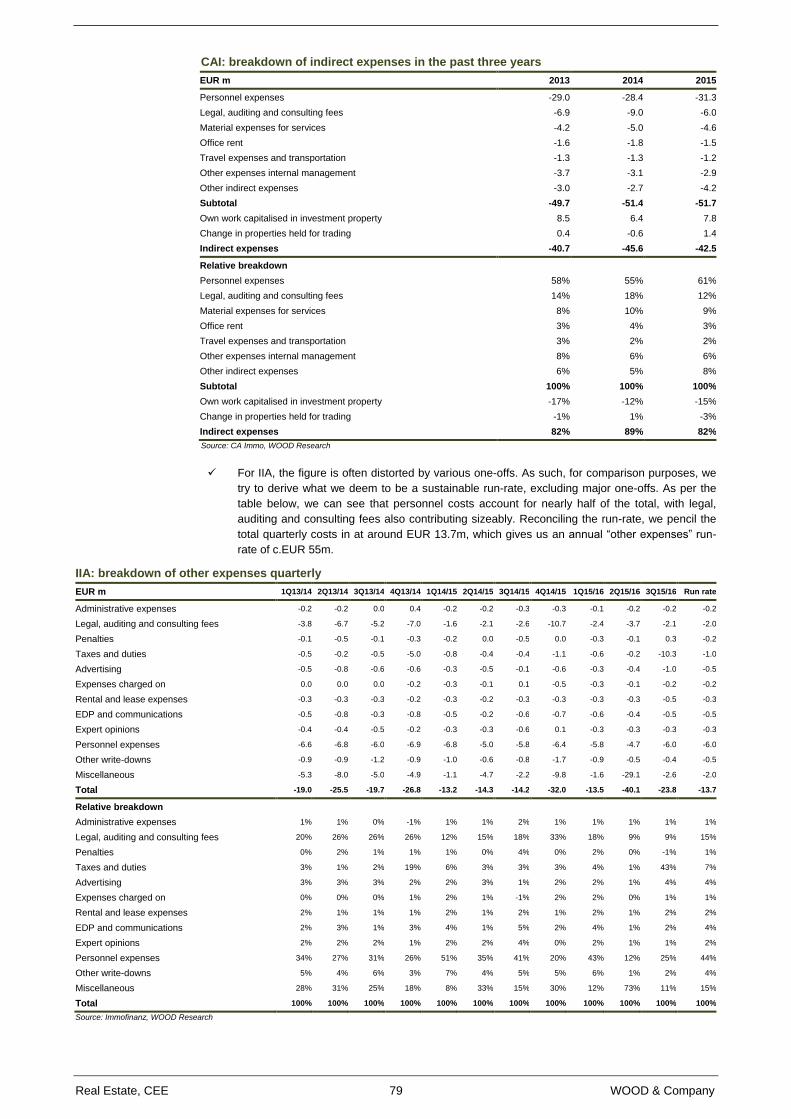

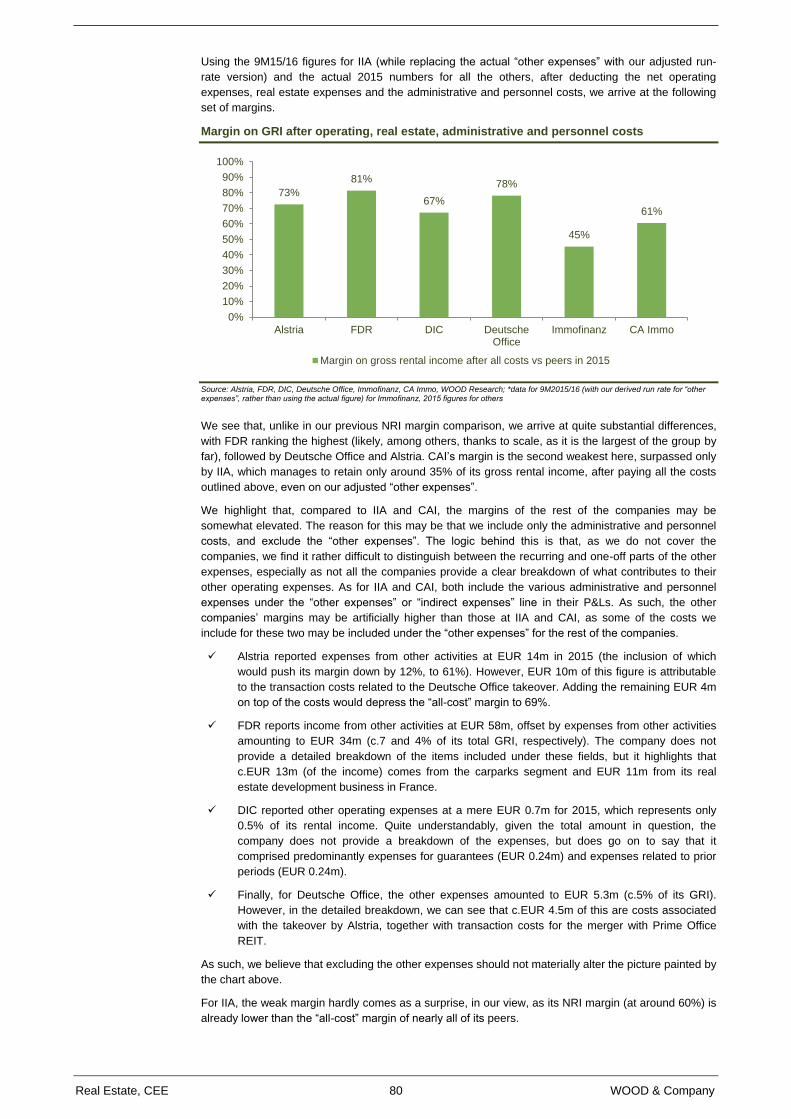

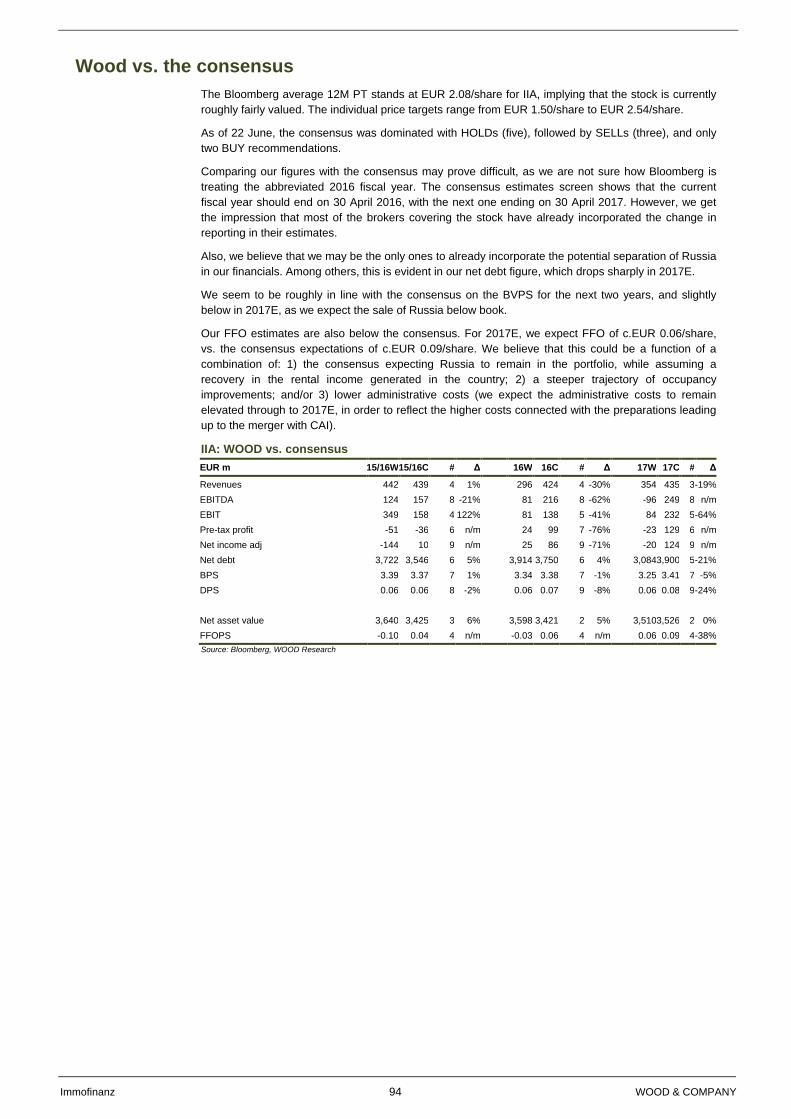

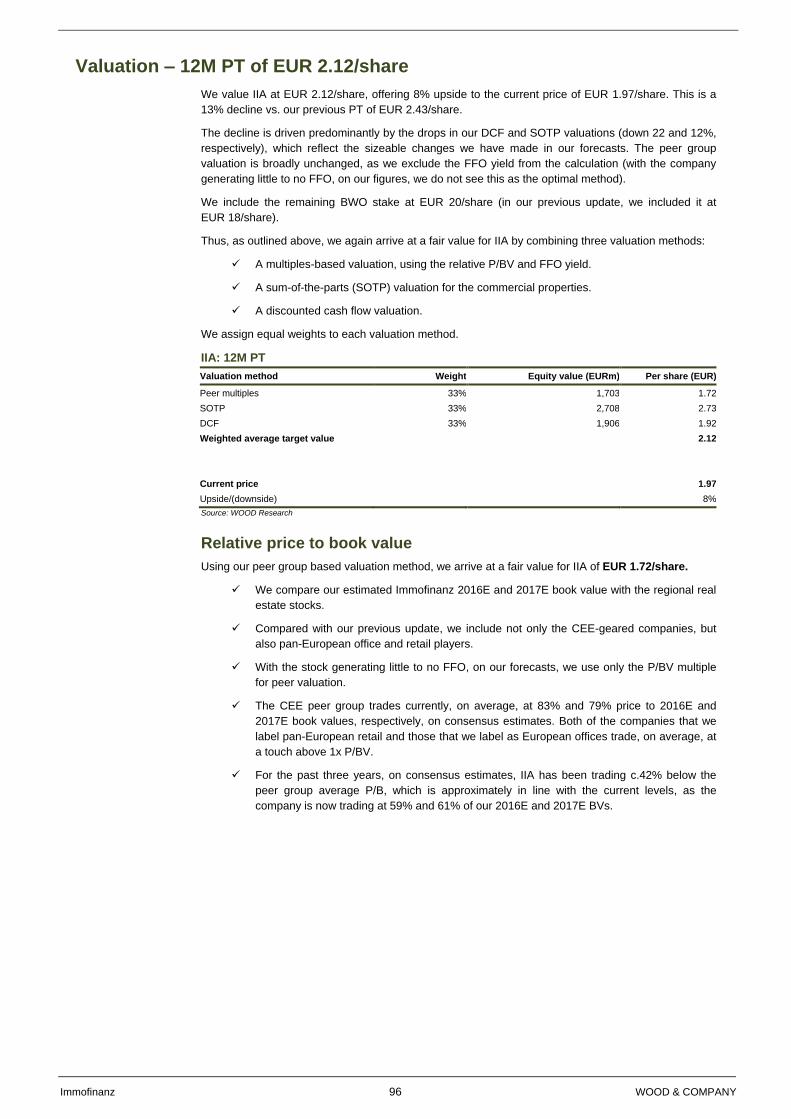

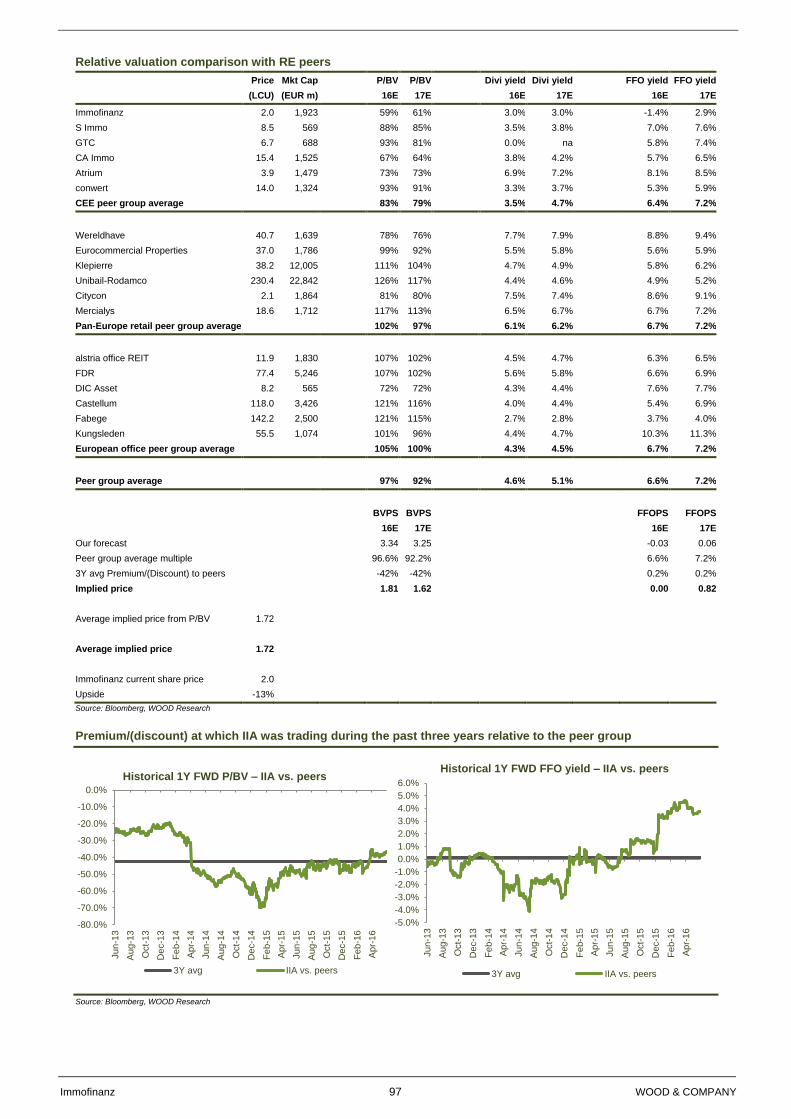

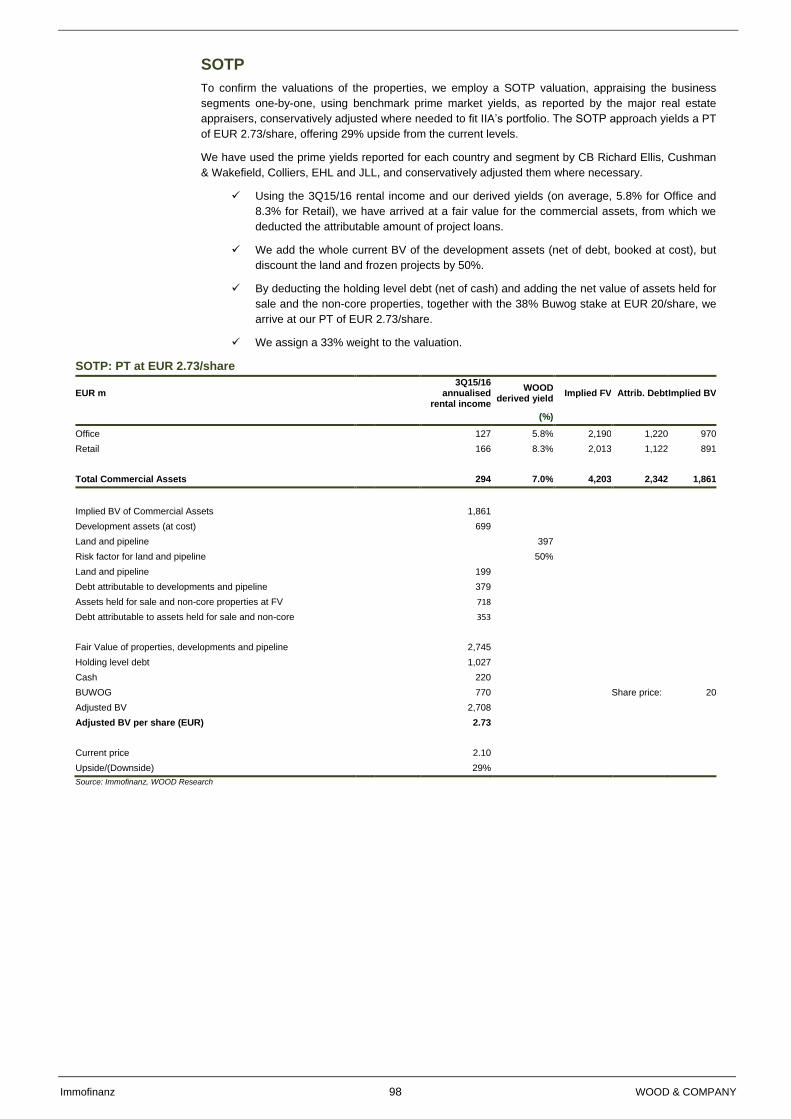

immofinanz/ca immo - wood & company

TRANSCRIPT

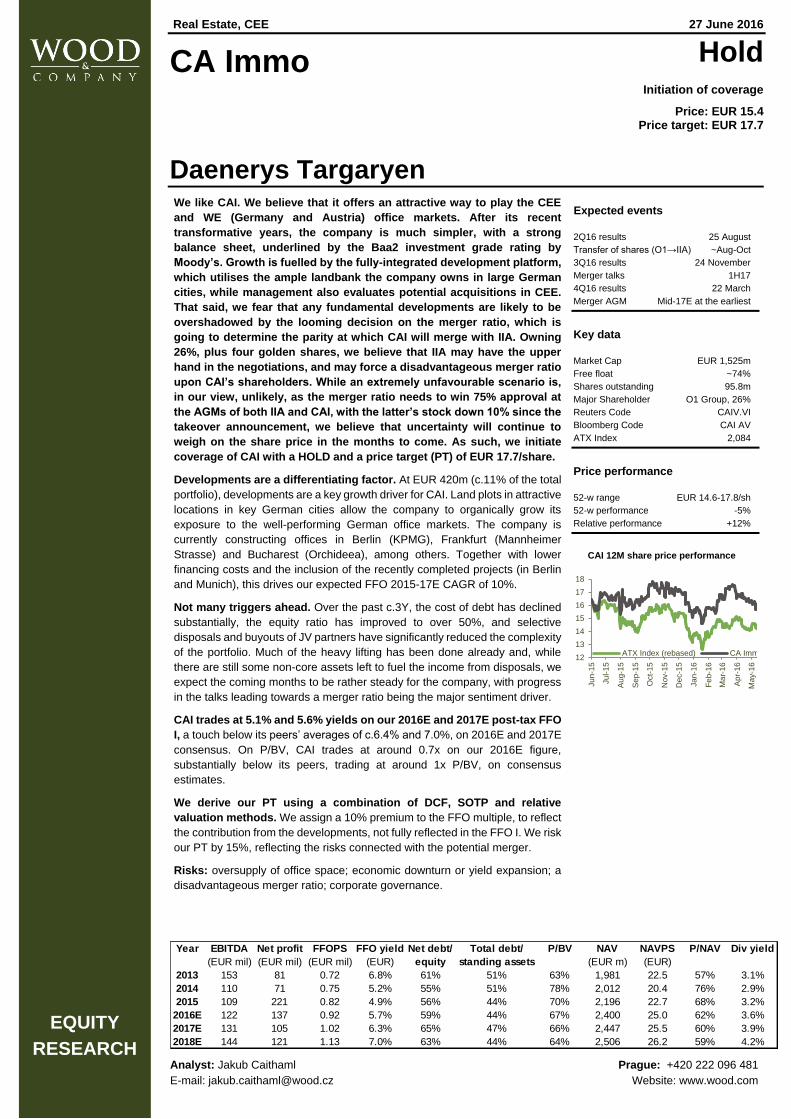

Real Estate, CEE 27 June 2016

Immofinanz/CA Immo Sector report

Deadlocked on the way to wedlock

Price Upside Mkt Cap FFO yield P/BV

Rating target potential (EUR m) YTD Perf 2016E 2017E 2018E 2016E 2017E 2018E

CA Immo HOLD 17.7 14% 1923 -8% 5.7% 6.3% 7.0% 67% 66% 64%

Immofinanz HOLD 2.12 8% 1525 -6% n/m 2.9% 5.7% 59% 61% 59%

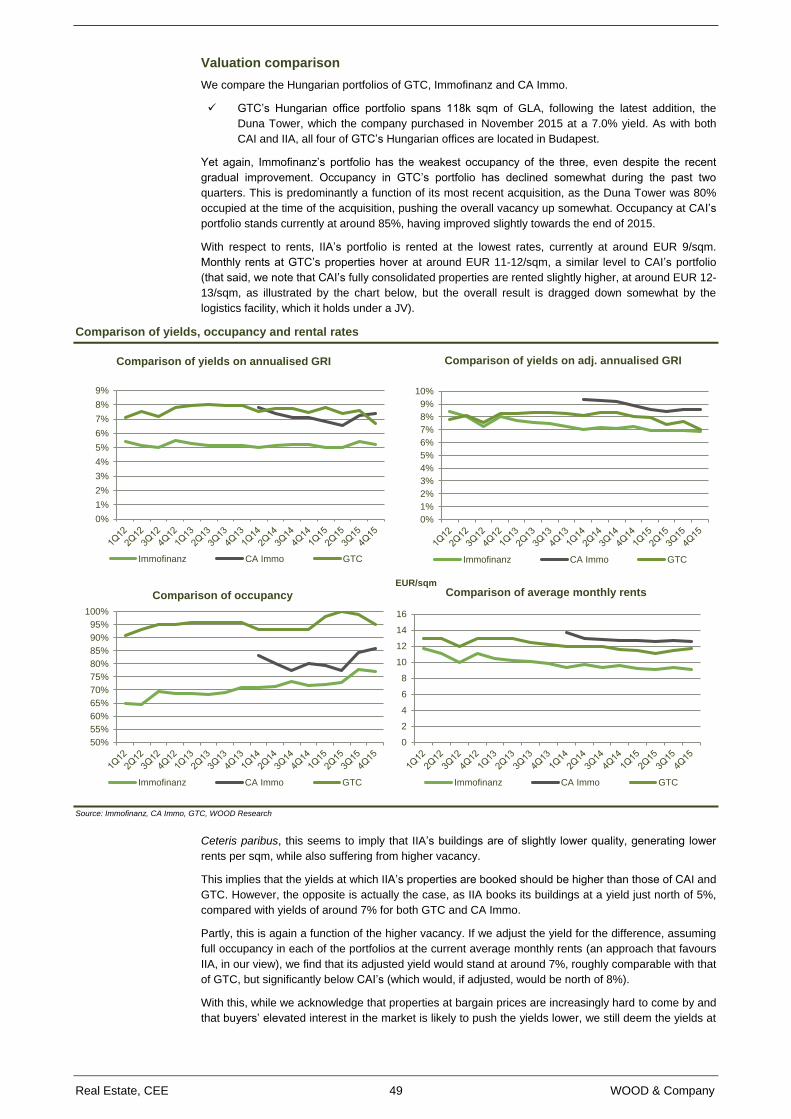

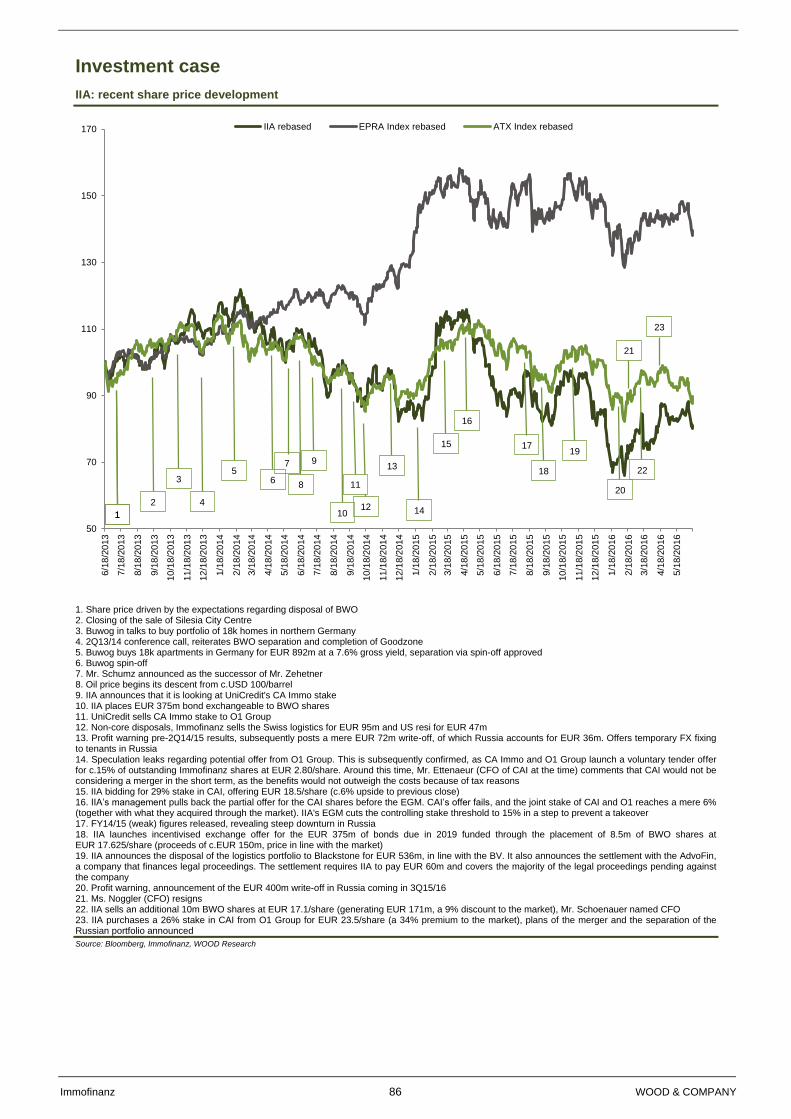

It appears that the, at times rather bumpy, road to the merger of the

two largest CEE Real Estate companies has finally been cleared. With

a substantial regional overlap in the office portfolios, we believe that

the combination of CA Immo (CAI) and Immofinanz (IIA) could lead to

a larger, more cost-efficient and significantly less complex entity.

That said, we are struggling to find the best way to play the

combination. Of the two, we like CAI better: with its well-capitalised

balance sheet, broadly conservative valuations and ample lucrative

landbank in key German cities, it offers good value, trading currently

at c.0.7x our 2016E BV and a 5-6% 2016E FFO yield. That said, we fear

that the looming decision on the merger ratio is likely to weigh on

CAI’s share price, capping the potential upside, as we believe that IIA

may have the upper hand in the negotiations. Thus, we initiate with a

HOLD, setting our price target (PT) at EUR 17.7/share. At IIA, we

appreciate the disposal of its logistics portfolio and BWO shares, and

the recent improvement in its office occupancy. Going forward, the

sale or spin-off of the Russian assets, or further improvements in

occupancy may trigger a rerating. However, even though we model a

gradual improvement in office occupancy and margins, we do not see

meaningful FFO generation before 2018E. With little visibility on the

likelihood of the disposal of Russia, we do not see a fundamental

case for a rerating, and we reiterate our HOLD rating, adjusting our

PT to EUR 2.12/share.

CAI looks attractive at its current valuation... Over the past three years,

the cost of debt has declined substantially, the equity ratio has improved to

over 50%, and selective disposals and buyouts of JV partners have

significantly reduced the complexity of the portfolio. CAI generates a

healthy FFO yield (c.5-6%), with an additional boost from the fully-

integrated development arm of the business, which allows CAI to

organically increase its exposure to the well-performing German office

markets.

… however, merger ratio likely to cap upside. IIA’s management has

indicated that the merger ratio will be based on NAV parity. Admittedly, the

decision is still at least a year away, and the NAVs may yet evolve (e.g.,

due to new developments or the disposal of Russia). However, as CAI

trades closer to its NAV than IIA, unless IIA rerates substantially, a merger

ratio based on NAV parity (vs. share price parity) would likely be

disadvantageous for CAI’s shareholders (at current prices, the merger ratio

based on the latest NAVs would correspond to CAI’s share price of c.EUR

13-14/share). That said, as the merger ratio will need to win 75% approval

at both companies’ AGMs, the downside should be limited, in our view.

IIA’s profitability likely to remain weak even after the separation of

Russia. Despite modelling gradual improvements in office occupancy and

margins, we see IIA turning positive on FFO only in 2017E, while starting

to generate a FFO yield (at the current price levels) of around 5-6% (in line

with its peers) only from 2018E-on. While the successful disposal of the

Russian assets would be likely to boost sentiment, we believe that a sale

at the current valuation may prove challenging. Combined with what we

deem to be, on balance, a rather aggressive valuation approach, we would

need to see further evidence before we adopt more a bullish view on the

stock.

Immofinanz

HOLD (maintained)

Price: EUR 1.97/share

Price target: EUR 2.12/share

CA Immo

HOLD (initiation of coverage)

Price: EUR 15.4/share

Price target: EUR 17.7/share

EQUITY

RESEARCH Analyst: Jakub Caithaml Prague: +420 222 096 481

E-mail: [email protected] Website: www.wood.com

Real Estate, CEE 2 WOOD & Company

Contents

The merger and the exchange ratio ................................................................................................................ 3

The potential resulting entity .......................................................................................................................... 7

While cheaper on P/BV, peers continue to offer stronger FFO yields ...................................................... 11

Overview of the individual markets .............................................................................................................. 14

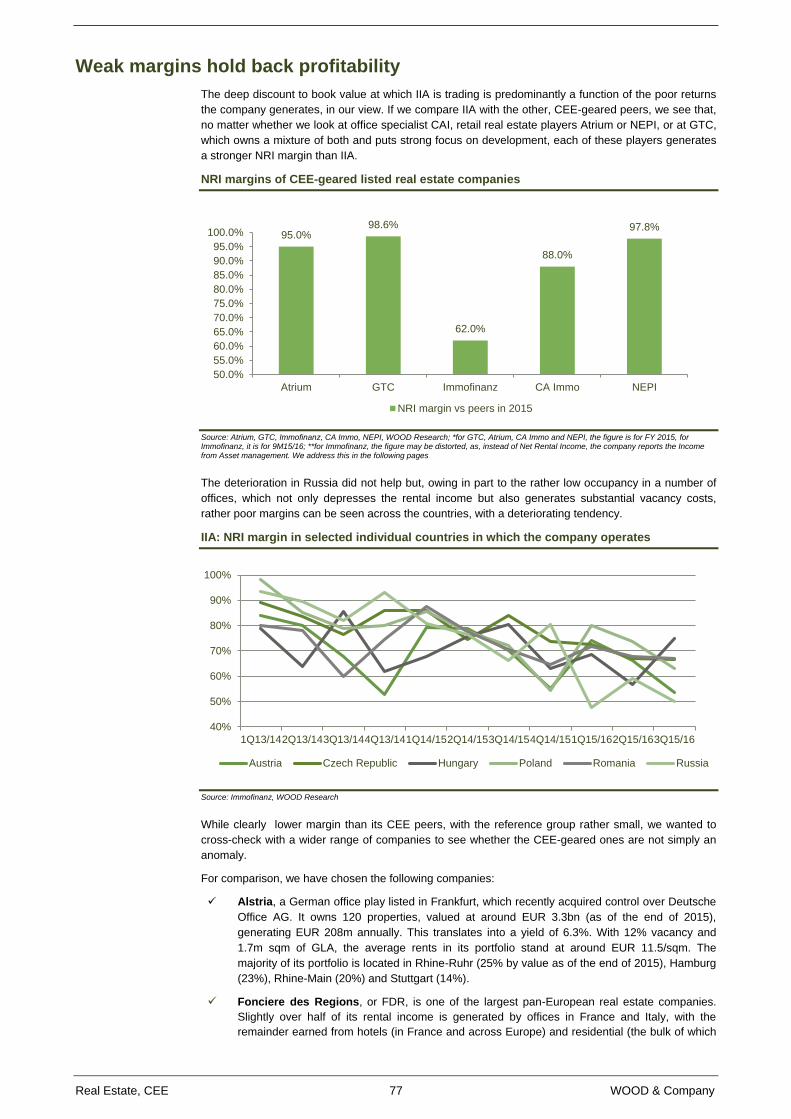

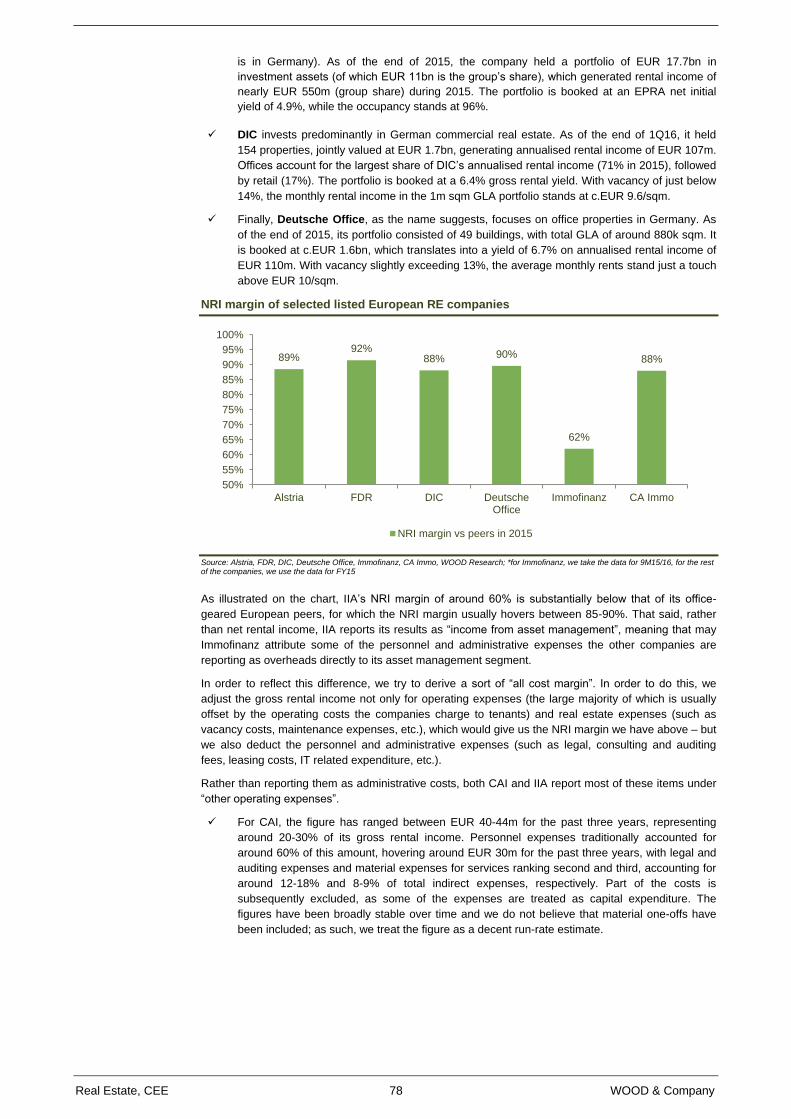

Weak margins hold back profitability ........................................................................................................... 77

Company sections

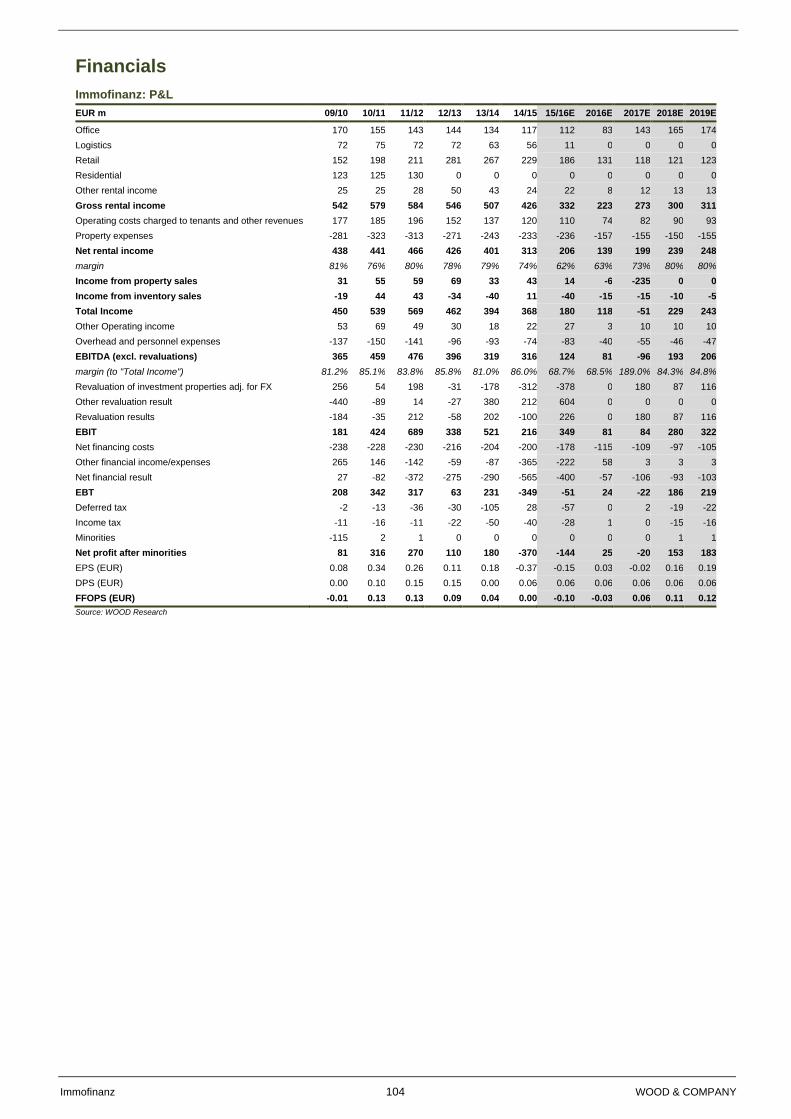

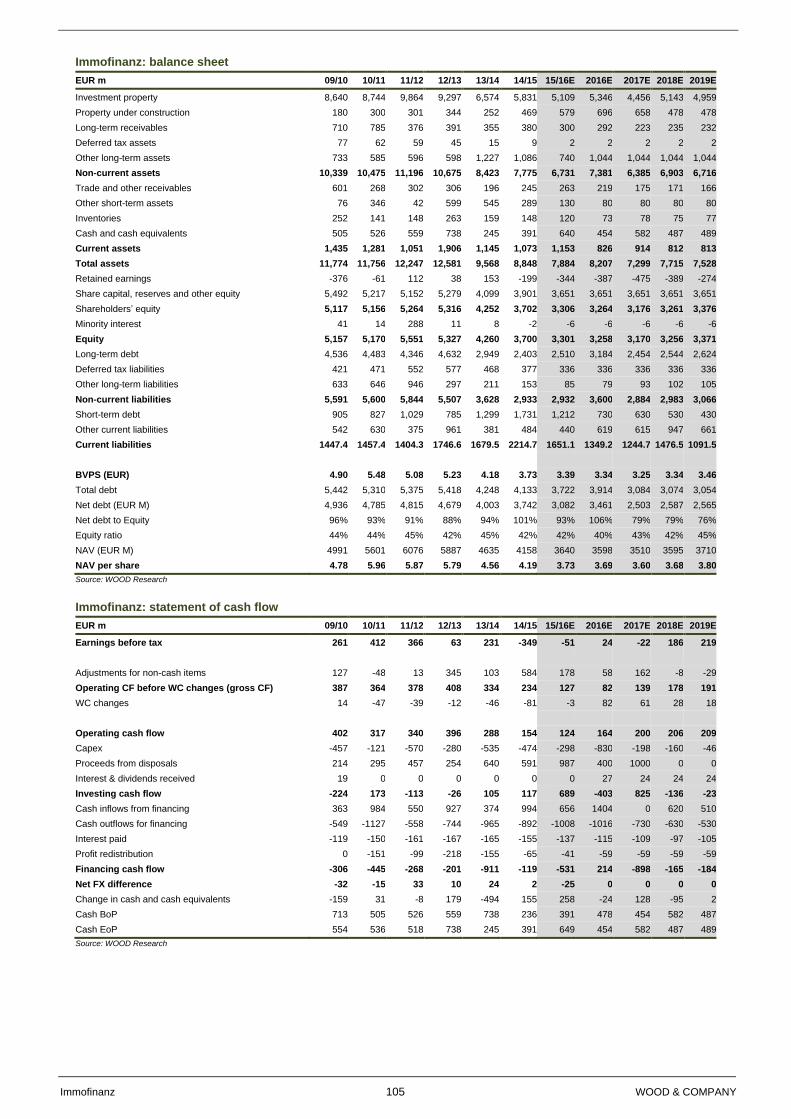

Immofinanz .............................................................................................................................................. 85

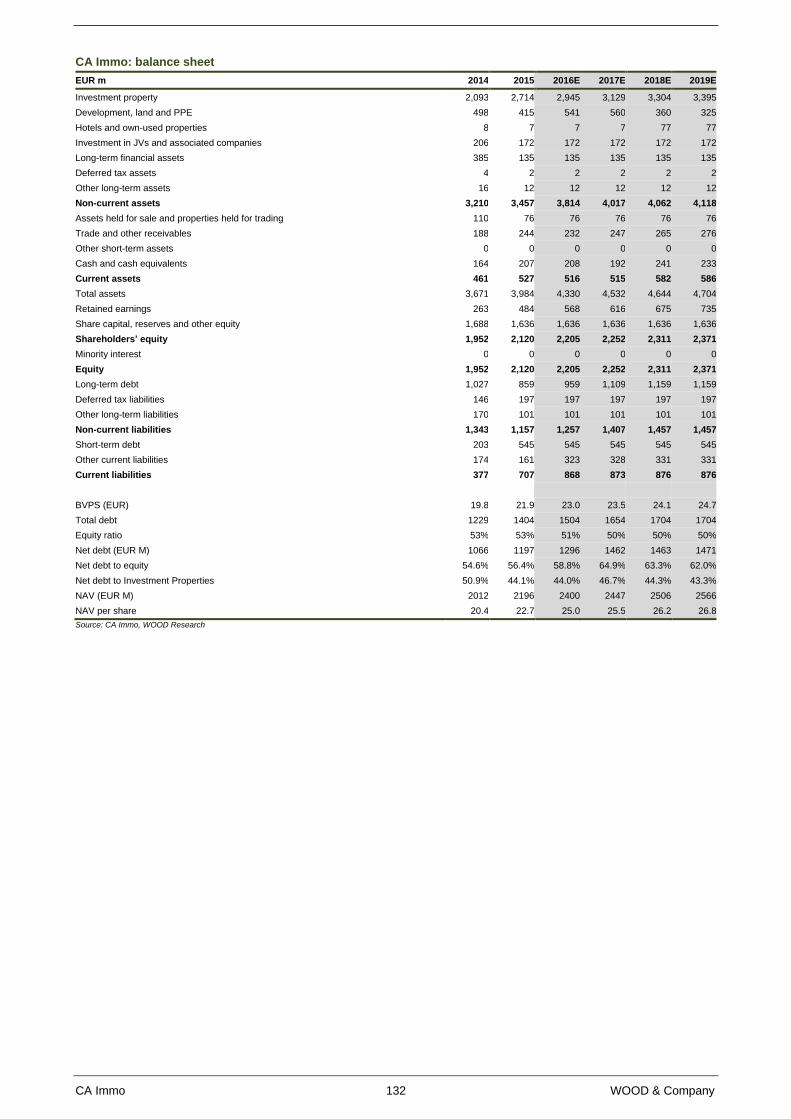

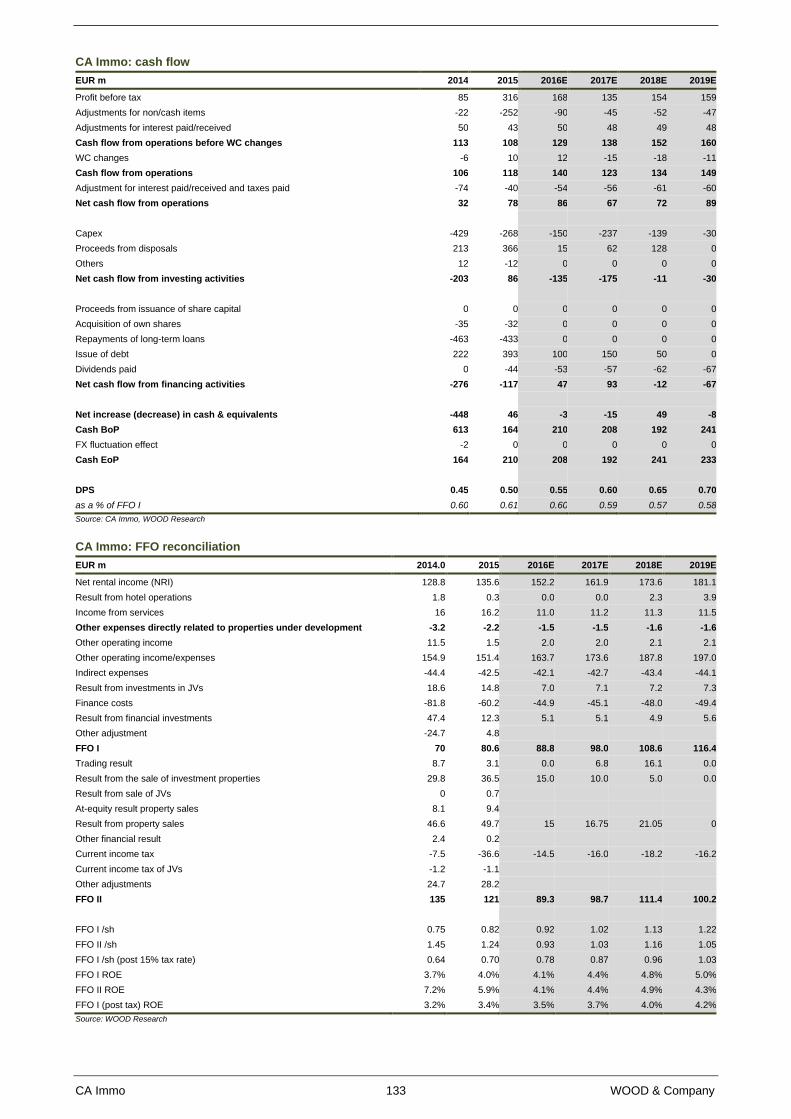

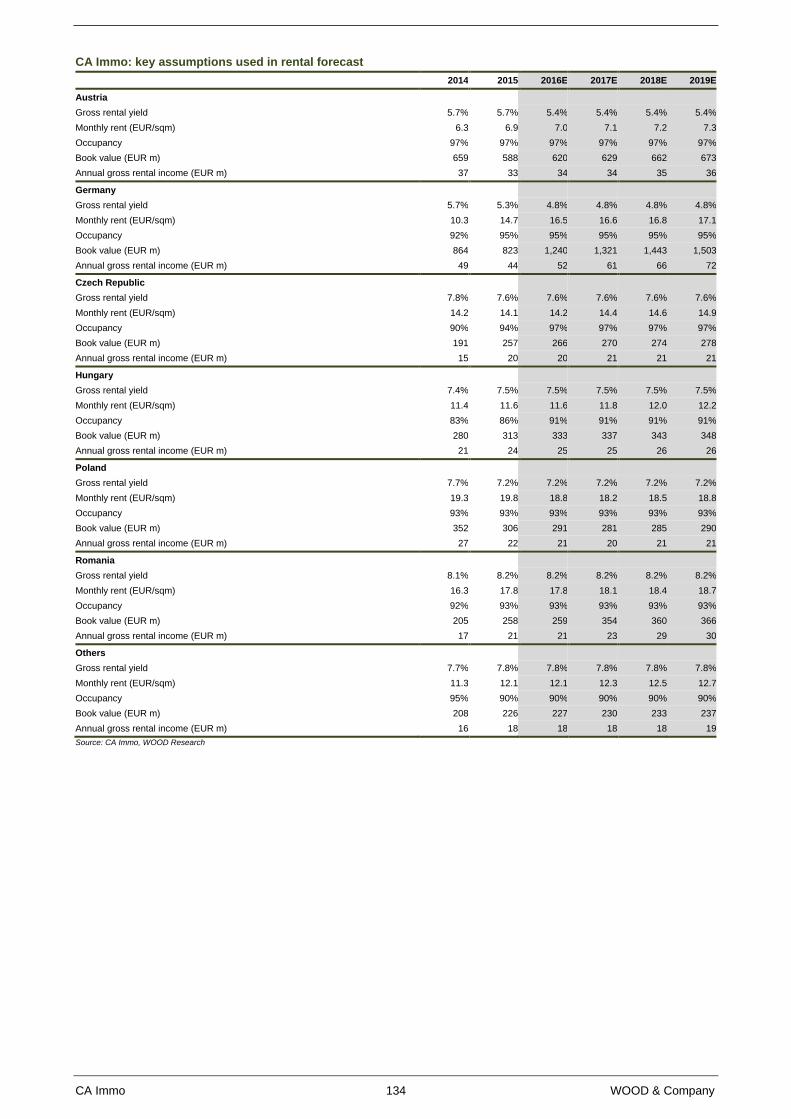

CA Immo ................................................................................................................................................ 107

Important disclosures .................................................................................................................................. 135

Closing Prices as of 24 June 2016

© 2016 by WOOD & Company Financial Services, a.s. All rights reserved. No part of this report may be reproduced or transmitted in any form or by any means electronic or mechanical without written permission from WOOD & Company Financial Services, a.s. This report may not be lent, resold, hired out or otherwise disposed of by way of trade in any form of binding or cover other than that in which it is published without written permission from WOOD & Company Financial Services, a.s. Requests for permission to make copies of any part of this report should be mailed to: WOOD & Company Financial Services a.s. Palladium, Namesti Republiky 1079/1a, 110 00 Prague 1 – Czech Republic tel.: +420 222 096 111 fax: +420 222 096 222 http//:www.wood.cz

Real Estate, CEE 3 WOOD & Company

The merger and the exchange ratio

As its first step towards a full merger, Immofinanz (IIA) announced in mid-April that it had

agreed to purchase a 26% stake in CA Immo (CAI) from O1 Group. If carried out, the merger

would change Immofinanz's profile considerably, creating a CEE Real Estate behemoth, while

shifting the portfolio’s centre of gravity westwards. Even though there is a clear regional

overlap in the office portfolios, and the deal is likely to unlock a number of synergies

(especially stemming from lower overhead costs, in our view), we view the price (EUR

23.5/share, a 34% premium to the market price, or a 3.4% yield on the Bloomberg consensus

2016E FFO for CAI) as rather demanding. In our view, it puts substantial pressure on IIA to

deliver on the merger as, without the synergies, we believe the price would be difficult to

justify.

While the deal may prove value-accretive for IIA eventually, a number of hurdles need to be

overcome first.

We believe the key developments to watch out for on this front in the coming months will be the

disposal or spin-off of the Russian portfolio, along with further information on potential

synergies.

Deal overview

On 18 April, IIA announced that it had purchased 25.7m CAI shares from O1 (a c.26% stake), together

with four registered shares, each of which grants its holder the option to nominate a supervisory board

member.

The price per share is EUR 23.5/share, representing a 34% premium to the closing price the day

before the transaction and a 3.4% discount to CAI’s 2015 EPRA NAV. On the Bloomberg consensus

estimates, the price represents a slight premium to the 2016E BV of EUR 23.0/share and c.3.7%

2016E FFO yield (on the 2016E FFO of EUR 0.88/share).

The O1 Group purchased its stake from UniCredit in 3Q14 for EUR 18.5/share. The current offer

represents 27% upside to the original purchase price.

The total value of the transaction is c.EUR 604m. Initially, Immofinanz planned to fund the purchase via

a combination of additional debt and the issuance of convertible bonds. In the subsequent conference

call, IIA suggested that the company may fund part of the deal also with cash. Following the disposal of

the 18.5m of BWO shares for EUR 19/share, we believe that, instead of the convertible bond, IIA will

use the c.EUR 350m proceeds to fund part of the purchase.

As the next step, IIA is planning a statutory merger of IIA and CAI. In a presentation that explains the

rationale behind the acquisition, IIA cites potential income and cost synergies of EUR 33m annually, of

which synergies of c.EUR 10m per annum are expected to be achieved straight after the stake

acquisition.

Before the statutory merger is completed, IIA plans to dispose of its Russian portfolio.

With respect to timing, the shareholder meetings to approve the statutory merger will not take place

earlier than 2Q17, according to IIA’s presentation.

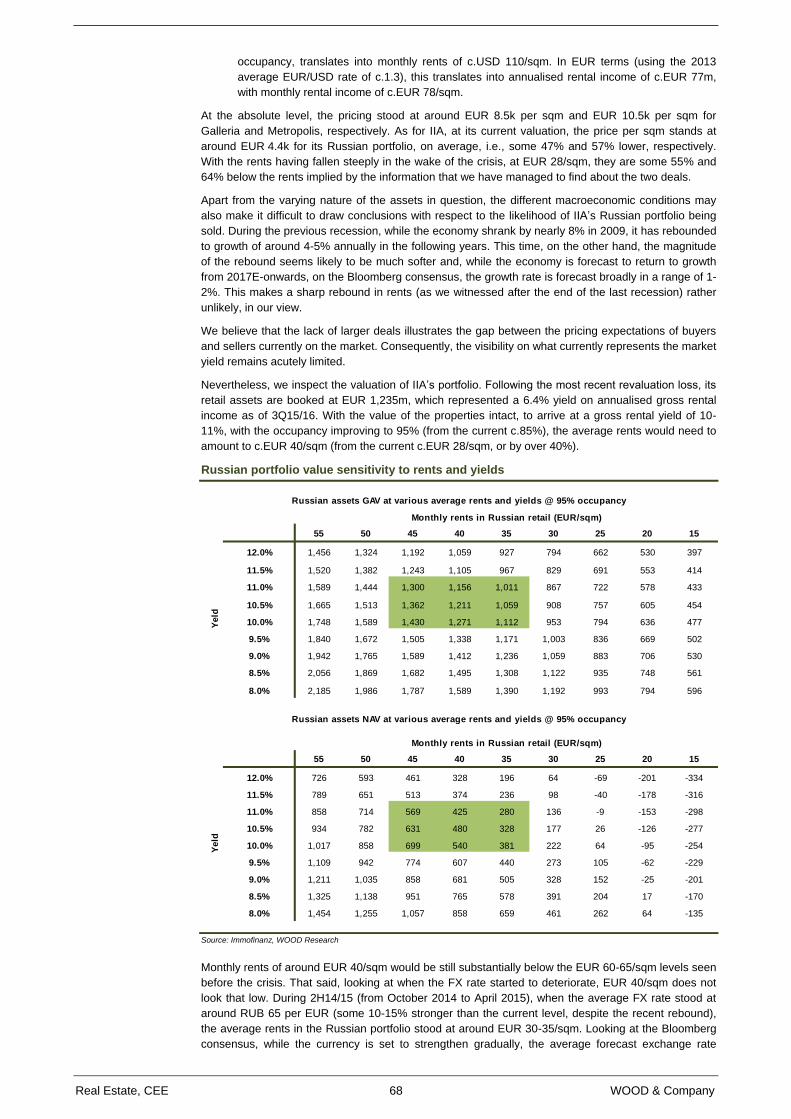

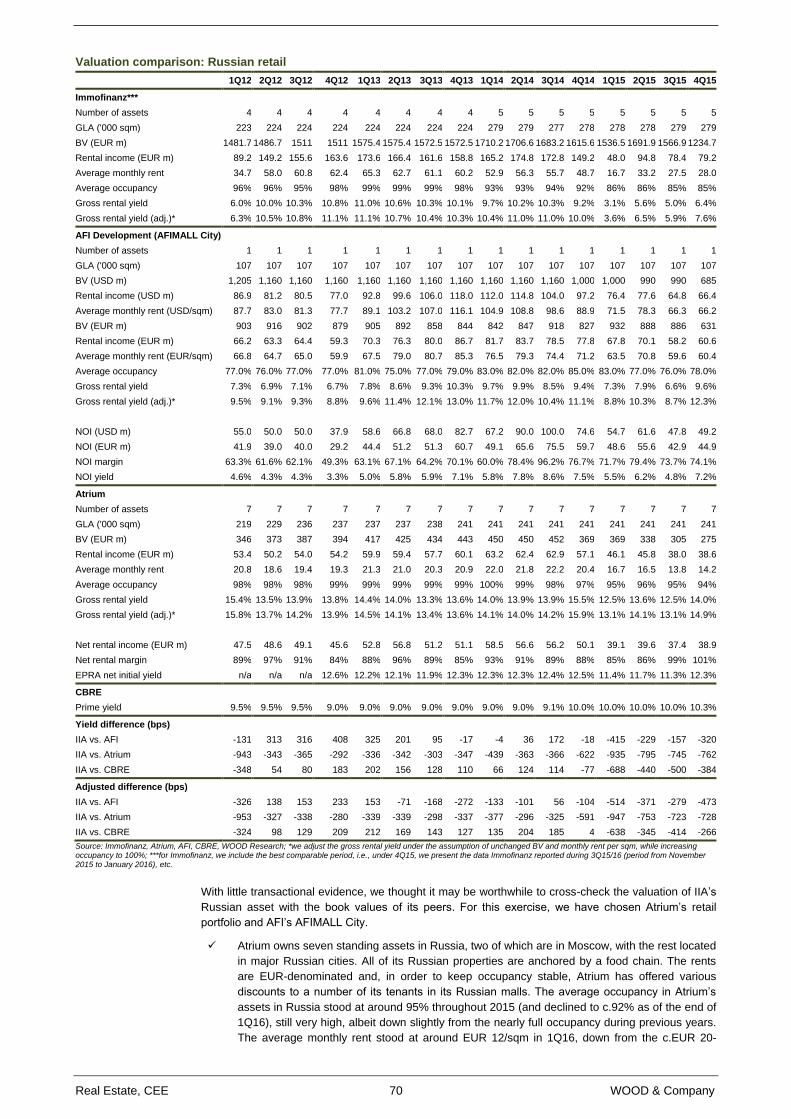

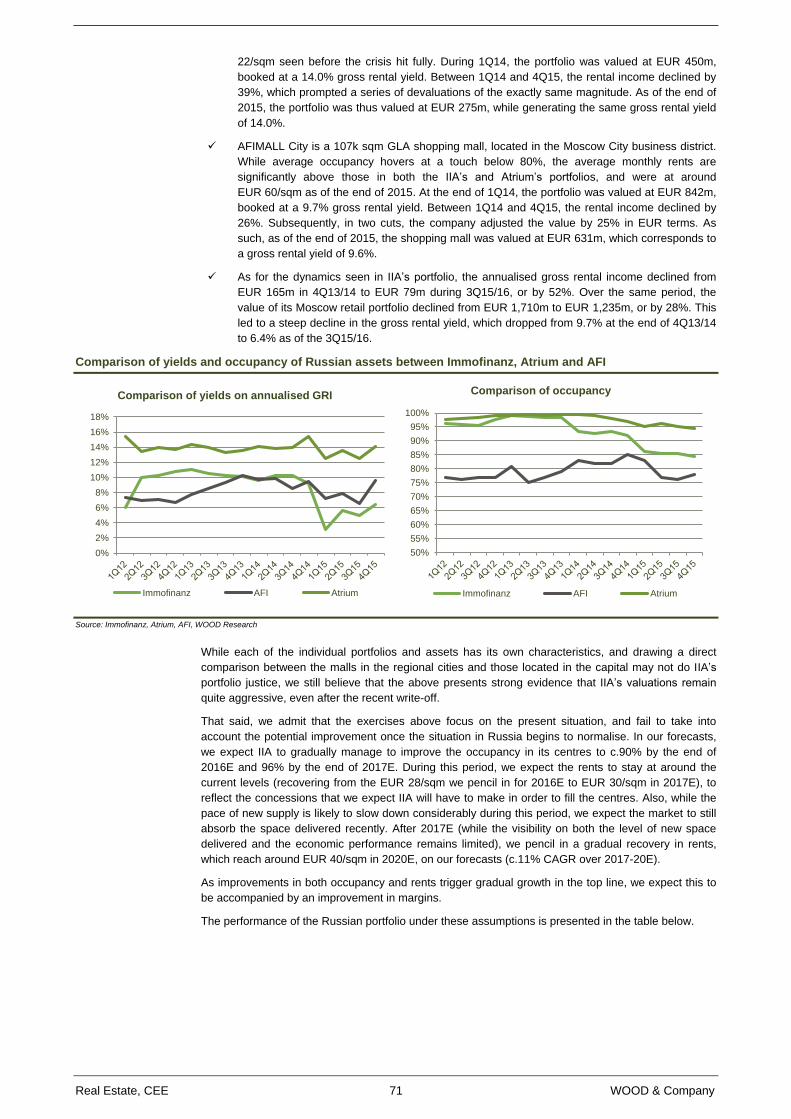

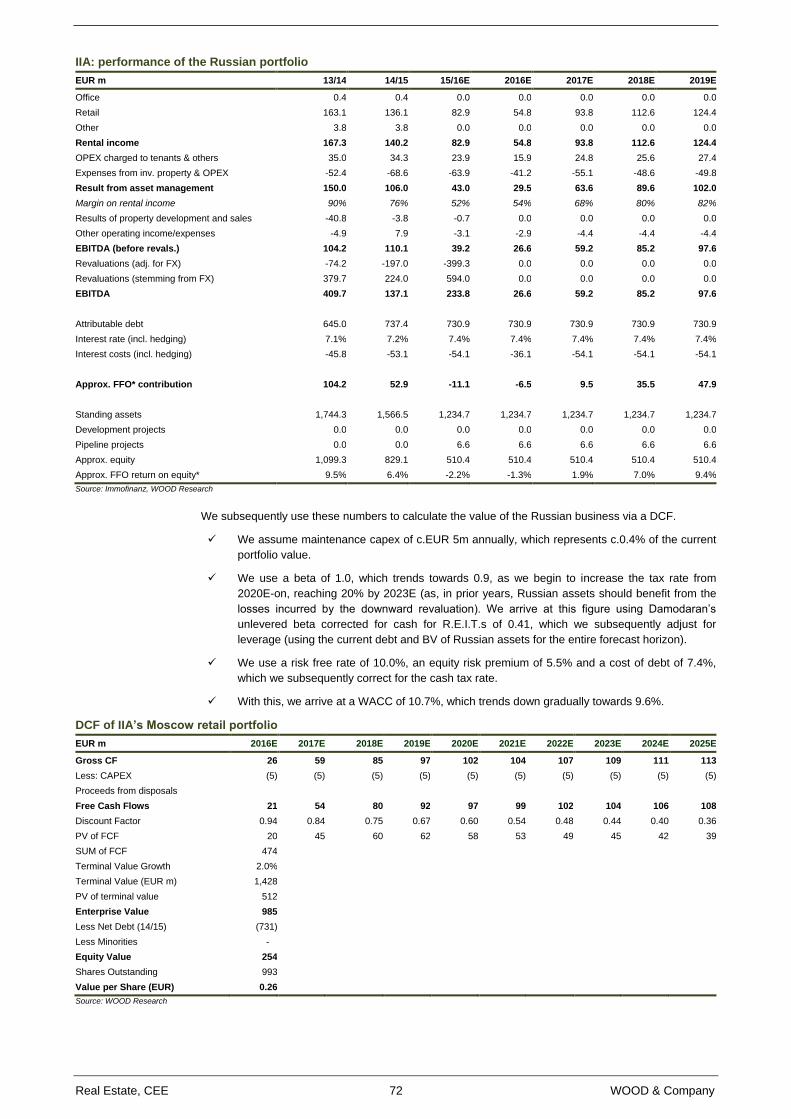

Russia – liquidity slowly returning to the market?

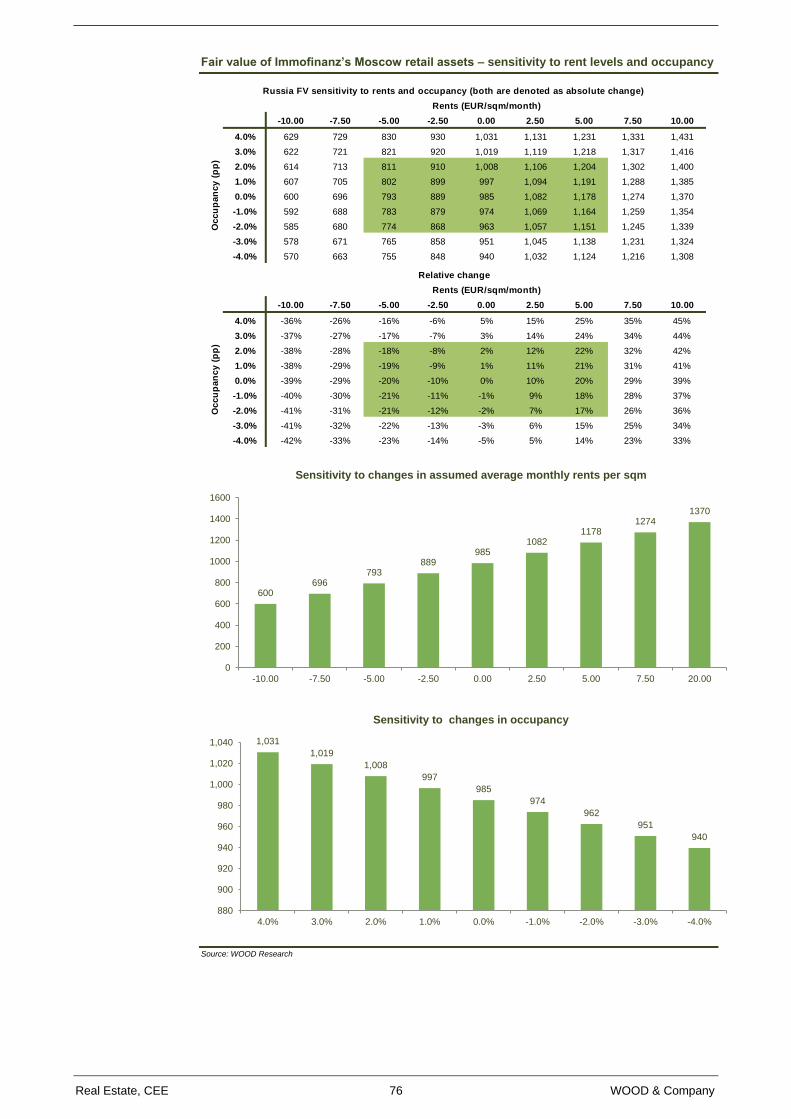

IIA has highlighted that, before the merger can take place, it would either sell or spin-off its Russian

retail portfolio. While the market environment may still change dramatically (the vote on the merger

should take place in 2Q17, at the earliest), we believe that the disposal of the Russian portfolio at its

current valuation may prove challenging. There has been very little transaction evidence for retail

assets in general in Russia since the start of the crisis, and none of the recent transactions has been

even close to the volume we would be looking at here.

That said, following the recent rebound in oil prices, money may be coming back to the market. This

has been visible already in 1Q16, when USD 1.9m was invested into Russian commercial property,

compared with EUR 3.0m for the whole of 2015, as the deferred demand has gradually started to be

realised, with investors beginning to anticipate a recovery. Although we do not believe there is

substantial upside for the oil price in the short to medium term (as a rising price would likely prompt an

increase in US production, thus putting a cap on further growth), we believe that, unless Saudi Arabia

increases production significantly, strong weakness from the current levels is rather unlikely.

As such, even though Russia is currently barely breakeven at the FFO level, we tend to agree with

IIA’s management that it would likely be over-simplistic just to value Russia by applying a yield to the

current, depressed level of rental income. While we still consider the valuation by IIA to be quite

Real Estate, CEE 4 WOOD & Company

aggressive, we believe that it may be possible to sell the Russian assets at some premium to the

volume of debt on the assets.

That said, should management fail to identify a buyer, we believe that IIA may need to invest further

equity into Russia, repaying part of the loan, in order to reduce the burden of interest costs before it

can consider spinning the assets off. We believe that, after the vote on BREXIT, the risk of this

scenario has increased, as the volatility and risk aversion, induced by the unexpected result of the

referendum, may make the investors more cautious, as they may choose to wait and see how the

negotiations begin to play out. As with Buwog, a spin-off of the Russian assets would need to be voted

through at an AGM. Should there be a spin-off, the entity would be listed in Vienna and Warsaw. It

could also potentially list on other exchanges.

We include a more detailed overview in the chapter on Russia in the market overview section of this

report.

Merger ratio – quarrels ahead

The merger needs to be approved by the shareholder meetings of both companies, with majorities of

75% of the votes cast. As there is still a valuation gap between CAI and IIA’s share prices (IIA trades at

around 55% of its latest reported EPRA NAV; CAI trades at 65%), even after the recent decline in

CAI’s share price, reaching a consensus on the resulting exchange ratio may prove challenging.

While IIA’s management has highlighted that it is too early to announce any details on what the

exchange ratio might be, management has strongly highlighted that the merger ratio will be based on a

fundamental valuation, and, as such, any potential difference in the share prices should not play a role.

The result of the valuation will be a range, within which the two management teams should agree on

the final exchange ratio, which will then be presented to the shareholders for approval.

In order to determine how this has been done in the past, we have looked at the IIA and Immoeast

merger, which took place at the turn of 2009/10. According to a presentation we found, the exchange

ratio then (three shares of Immofinanz for two Immoeast shares, or 1.5x) was based on the NAV of

each company as of the agreed valuation due date, 31 October 2009. Furthermore, the agreed

exchange ratio was verified by the discounted cash flow valuations of the companies.

That said, there clearly had to be some adjustments, as we would arrive at an exchange ratio of 1.3x, if

simply comparing the NAV/share of the two entities (vs. the final exchange ratio of (1.5x)). Looking at

the share prices of the two companies prior to the announcement, it seems that the market was

expecting even higher ratio in favour of Immoeast (around 1.65x), as per the table below.

IIA & Immoeast: illustrative calculation of difference between exchange ratio (ER) based

on share price and NAV

NAV* Share price** ER based on NAV/sh ER based on share price Diff.

EUR/sh EUR/sh

IIA 5.62 2.6 0.77 IIA shrs / 1 IEA share 0.60 IIA shrs / 1 IEA share 27%

IEA 7.31 4.3 1.30 IEA shrs / 1 IIA share 1.65 IEA shrs / 1 IIA share -21%

Source: Immofinanz, Immoeast, WOOD Research; *as of end-October 2010; **as of 16 December 2010; a day prior to the announcement of the exchange ratio

If we were to apply the same methodology to IIA and CAI, the table (priced as of the date of the

transaction) would be as follows:

IIA & CAI: illustrative calculation of the difference between exchange ratio (ER) based on

share price and NAV

NAV* Share price** ER based on NAV/sh ER based on share price Diff.

EUR/sh EUR/sh

CAI 24.32 17.44 6.45 IIA shrs / 1 CAI share 8.76 IIA shrs / 1 CAI share -26%

IIA 3.77 1.99 0.16 CAI shrs / 1 IIA share 0.11 CAI shrs / 1 IIA share 36%

Source: Bloomberg, Immofinanz, CA Immo, WOOD Research; *as of the end of Q415 for CA Immo, as of the end of 3Q15/16 for Immofinanz; **as of 15 April 2016

Essentially, if the exchange ratio were to be based on the share prices, it would imply 8.8 IIA shares for

one CAI share (as of the date of the deal announcement). If based solely on NAV (the latest available

as at the date of the announcement of the transaction), the ratio would stand at 6.45 IIA shares for one

CAI share, implying 26% downside for CA Immo. If we calculate the mid-point as a simple arithmetic

average of the two approaches, we arrive at an exchange ratio of 7.61 IIA shares for one CAI share.

This would imply some 15% upside for IIA and some 15% downside for CAI (prices based on the close

before the deal was announced).

Real Estate, CEE 5 WOOD & Company

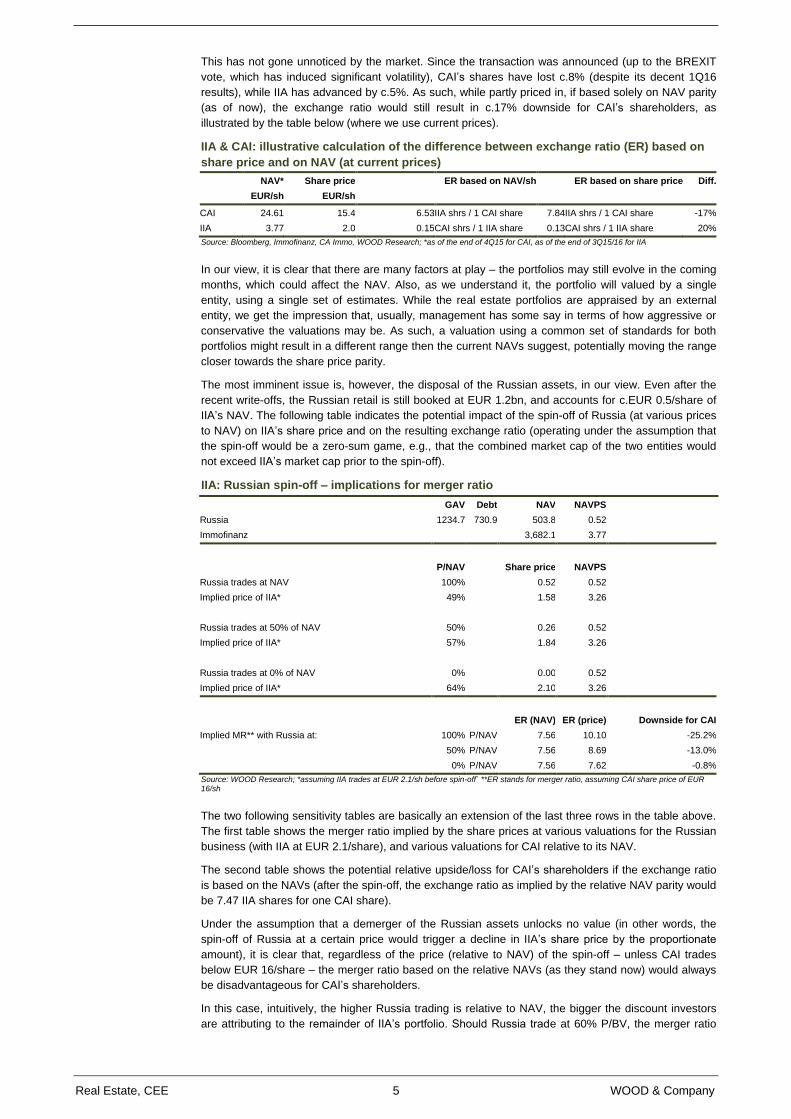

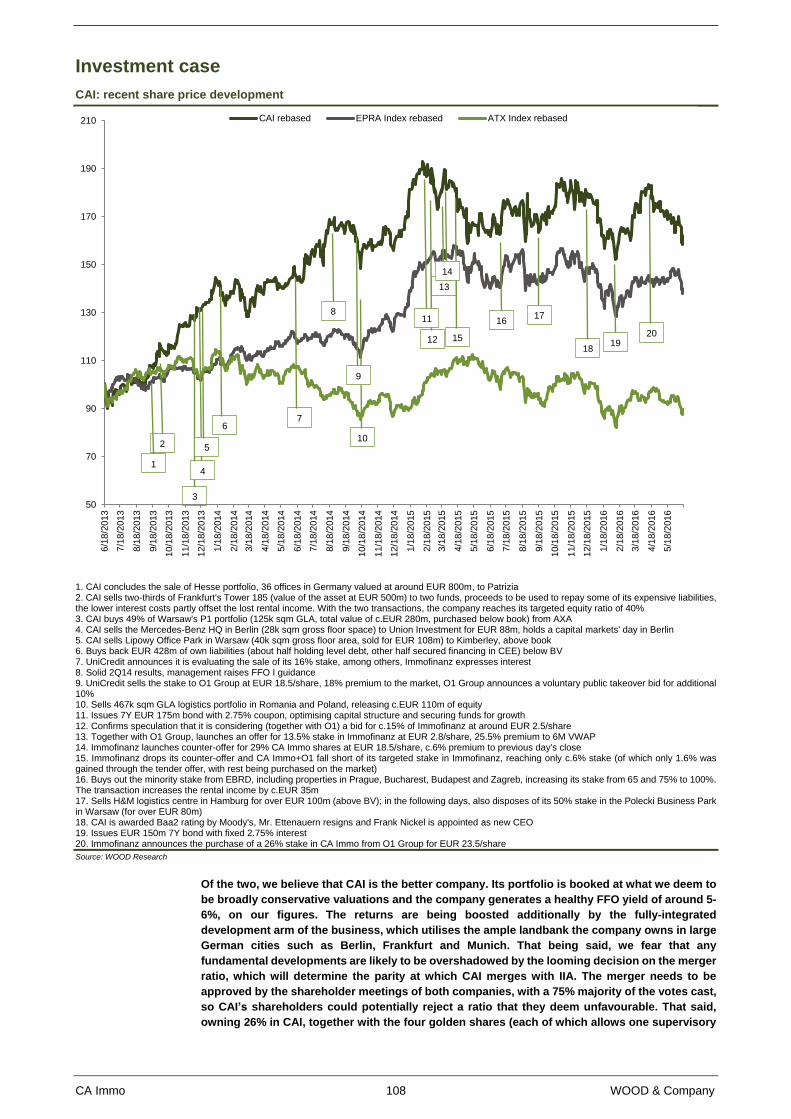

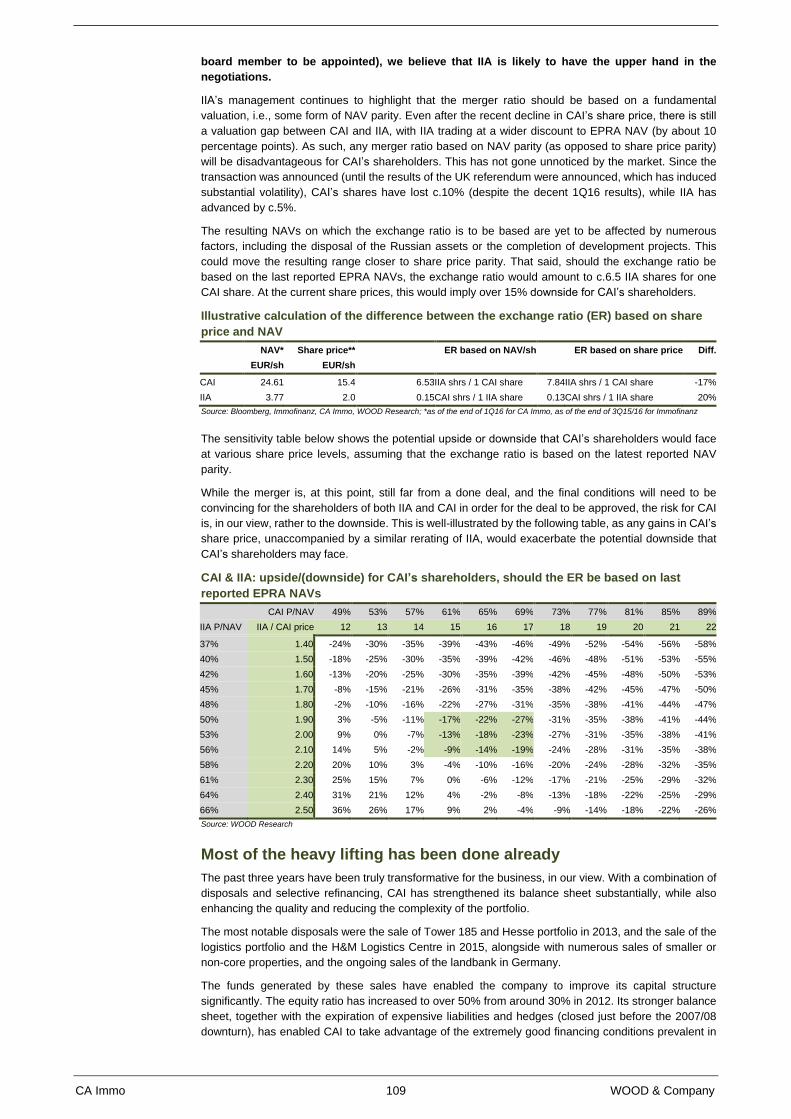

This has not gone unnoticed by the market. Since the transaction was announced (up to the BREXIT

vote, which has induced significant volatility), CAI’s shares have lost c.8% (despite its decent 1Q16

results), while IIA has advanced by c.5%. As such, while partly priced in, if based solely on NAV parity

(as of now), the exchange ratio would still result in c.17% downside for CAI’s shareholders, as

illustrated by the table below (where we use current prices).

IIA & CAI: illustrative calculation of the difference between exchange ratio (ER) based on

share price and on NAV (at current prices)

NAV* Share price ER based on NAV/sh ER based on share price Diff.

EUR/sh EUR/sh

CAI 24.61 15.4 6.53 IIA shrs / 1 CAI share 7.84 IIA shrs / 1 CAI share -17%

IIA 3.77 2.0 0.15 CAI shrs / 1 IIA share 0.13 CAI shrs / 1 IIA share 20%

Source: Bloomberg, Immofinanz, CA Immo, WOOD Research; *as of the end of 4Q15 for CAI, as of the end of 3Q15/16 for IIA

In our view, it is clear that there are many factors at play – the portfolios may still evolve in the coming

months, which could affect the NAV. Also, as we understand it, the portfolio will valued by a single

entity, using a single set of estimates. While the real estate portfolios are appraised by an external

entity, we get the impression that, usually, management has some say in terms of how aggressive or

conservative the valuations may be. As such, a valuation using a common set of standards for both

portfolios might result in a different range then the current NAVs suggest, potentially moving the range

closer towards the share price parity.

The most imminent issue is, however, the disposal of the Russian assets, in our view. Even after the

recent write-offs, the Russian retail is still booked at EUR 1.2bn, and accounts for c.EUR 0.5/share of

IIA’s NAV. The following table indicates the potential impact of the spin-off of Russia (at various prices

to NAV) on IIA’s share price and on the resulting exchange ratio (operating under the assumption that

the spin-off would be a zero-sum game, e.g., that the combined market cap of the two entities would

not exceed IIA’s market cap prior to the spin-off).

IIA: Russian spin-off – implications for merger ratio

GAV Debt NAV NAVPS

Russia 1234.7 730.9 503.8 0.52

Immofinanz

3,682.1 3.77

P/NAV

Share price NAVPS

Russia trades at NAV 100%

0.52 0.52

Implied price of IIA* 49%

1.58 3.26

Russia trades at 50% of NAV 50%

0.26 0.52

Implied price of IIA* 57%

1.84 3.26

Russia trades at 0% of NAV 0%

0.00 0.52

Implied price of IIA* 64%

2.10 3.26

ER (NAV) ER (price)

Downside for CAI

Implied MR** with Russia at: 100% P/NAV 7.56 10.10

-25.2%

50% P/NAV 7.56 8.69

-13.0%

0% P/NAV 7.56 7.62 -0.8%

Source: WOOD Research; *assuming IIA trades at EUR 2.1/sh before spin-off` **ER stands for merger ratio, assuming CAI share price of EUR 16/sh

The two following sensitivity tables are basically an extension of the last three rows in the table above.

The first table shows the merger ratio implied by the share prices at various valuations for the Russian

business (with IIA at EUR 2.1/share), and various valuations for CAI relative to its NAV.

The second table shows the potential relative upside/loss for CAI’s shareholders if the exchange ratio

is based on the NAVs (after the spin-off, the exchange ratio as implied by the relative NAV parity would

be 7.47 IIA shares for one CAI share).

Under the assumption that a demerger of the Russian assets unlocks no value (in other words, the

spin-off of Russia at a certain price would trigger a decline in IIA’s share price by the proportionate

amount), it is clear that, regardless of the price (relative to NAV) of the spin-off – unless CAI trades

below EUR 16/share – the merger ratio based on the relative NAVs (as they stand now) would always

be disadvantageous for CAI’s shareholders.

In this case, intuitively, the higher Russia trading is relative to NAV, the bigger the discount investors

are attributing to the remainder of IIA’s portfolio. Should Russia trade at 60% P/BV, the merger ratio

Real Estate, CEE 6 WOOD & Company

based on NAV would, for CAI’s shareholders, be equivalent to CAI’s share price dropping to around

EUR 13.5/share.

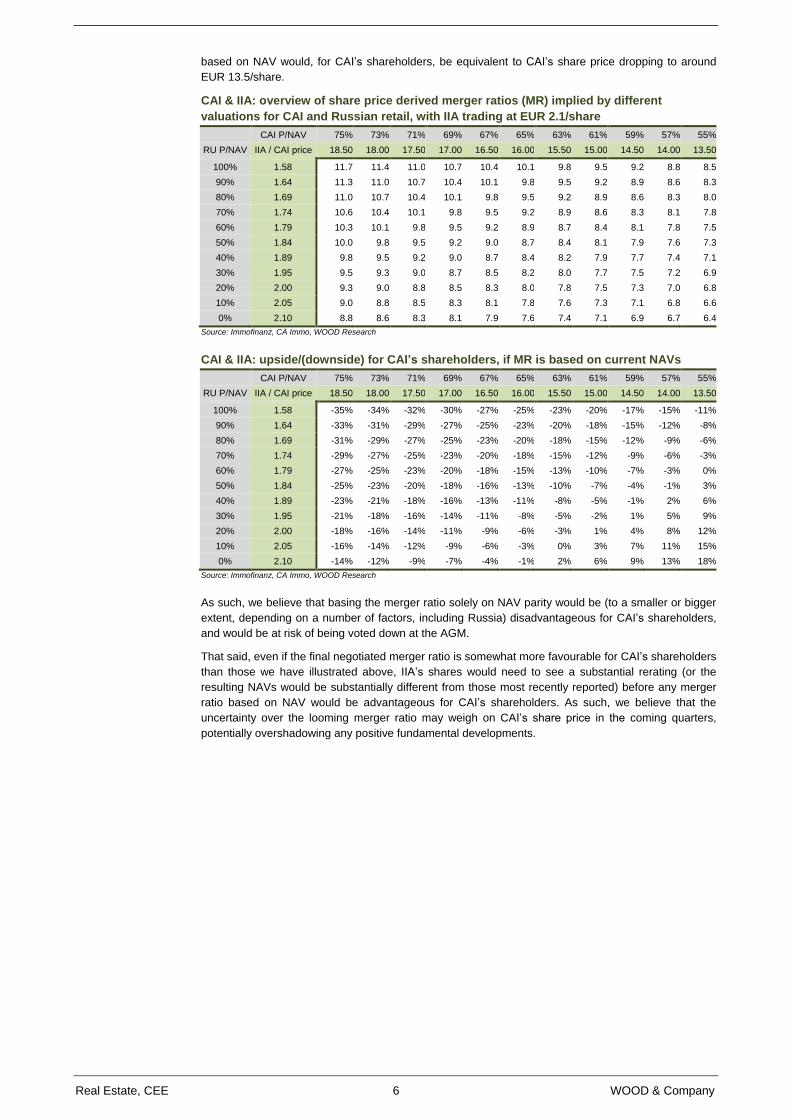

CAI & IIA: overview of share price derived merger ratios (MR) implied by different

valuations for CAI and Russian retail, with IIA trading at EUR 2.1/share

CAI P/NAV 75% 73% 71% 69% 67% 65% 63% 61% 59% 57% 55%

RU P/NAV IIA / CAI price 18.50 18.00 17.50 17.00 16.50 16.00 15.50 15.00 14.50 14.00 13.50

100% 1.58 11.7 11.4 11.0 10.7 10.4 10.1 9.8 9.5 9.2 8.8 8.5

90% 1.64 11.3 11.0 10.7 10.4 10.1 9.8 9.5 9.2 8.9 8.6 8.3

80% 1.69 11.0 10.7 10.4 10.1 9.8 9.5 9.2 8.9 8.6 8.3 8.0

70% 1.74 10.6 10.4 10.1 9.8 9.5 9.2 8.9 8.6 8.3 8.1 7.8

60% 1.79 10.3 10.1 9.8 9.5 9.2 8.9 8.7 8.4 8.1 7.8 7.5

50% 1.84 10.0 9.8 9.5 9.2 9.0 8.7 8.4 8.1 7.9 7.6 7.3

40% 1.89 9.8 9.5 9.2 9.0 8.7 8.4 8.2 7.9 7.7 7.4 7.1

30% 1.95 9.5 9.3 9.0 8.7 8.5 8.2 8.0 7.7 7.5 7.2 6.9

20% 2.00 9.3 9.0 8.8 8.5 8.3 8.0 7.8 7.5 7.3 7.0 6.8

10% 2.05 9.0 8.8 8.5 8.3 8.1 7.8 7.6 7.3 7.1 6.8 6.6

0% 2.10 8.8 8.6 8.3 8.1 7.9 7.6 7.4 7.1 6.9 6.7 6.4

Source: Immofinanz, CA Immo, WOOD Research

CAI & IIA: upside/(downside) for CAI’s shareholders, if MR is based on current NAVs

CAI P/NAV 75% 73% 71% 69% 67% 65% 63% 61% 59% 57% 55%

RU P/NAV IIA / CAI price 18.50 18.00 17.50 17.00 16.50 16.00 15.50 15.00 14.50 14.00 13.50

100% 1.58 -35% -34% -32% -30% -27% -25% -23% -20% -17% -15% -11%

90% 1.64 -33% -31% -29% -27% -25% -23% -20% -18% -15% -12% -8%

80% 1.69 -31% -29% -27% -25% -23% -20% -18% -15% -12% -9% -6%

70% 1.74 -29% -27% -25% -23% -20% -18% -15% -12% -9% -6% -3%

60% 1.79 -27% -25% -23% -20% -18% -15% -13% -10% -7% -3% 0%

50% 1.84 -25% -23% -20% -18% -16% -13% -10% -7% -4% -1% 3%

40% 1.89 -23% -21% -18% -16% -13% -11% -8% -5% -1% 2% 6%

30% 1.95 -21% -18% -16% -14% -11% -8% -5% -2% 1% 5% 9%

20% 2.00 -18% -16% -14% -11% -9% -6% -3% 1% 4% 8% 12%

10% 2.05 -16% -14% -12% -9% -6% -3% 0% 3% 7% 11% 15%

0% 2.10 -14% -12% -9% -7% -4% -1% 2% 6% 9% 13% 18%

Source: Immofinanz, CA Immo, WOOD Research

As such, we believe that basing the merger ratio solely on NAV parity would be (to a smaller or bigger

extent, depending on a number of factors, including Russia) disadvantageous for CAI’s shareholders,

and would be at risk of being voted down at the AGM.

That said, even if the final negotiated merger ratio is somewhat more favourable for CAI’s shareholders

than those we have illustrated above, IIA’s shares would need to see a substantial rerating (or the

resulting NAVs would be substantially different from those most recently reported) before any merger

ratio based on NAV would be advantageous for CAI’s shareholders. As such, we believe that the

uncertainty over the looming merger ratio may weigh on CAI’s share price in the coming quarters,

potentially overshadowing any positive fundamental developments.

Real Estate, CEE 7 WOOD & Company

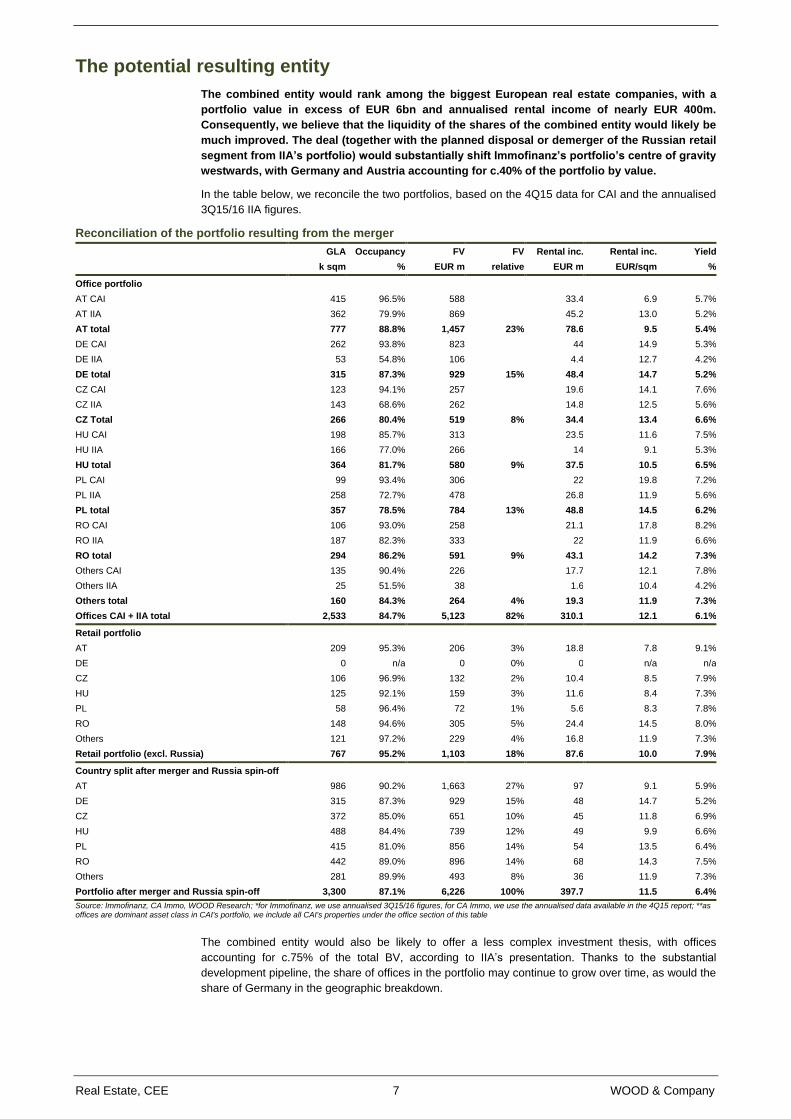

The potential resulting entity

The combined entity would rank among the biggest European real estate companies, with a

portfolio value in excess of EUR 6bn and annualised rental income of nearly EUR 400m.

Consequently, we believe that the liquidity of the shares of the combined entity would likely be

much improved. The deal (together with the planned disposal or demerger of the Russian retail

segment from IIA’s portfolio) would substantially shift Immofinanz’s portfolio’s centre of gravity

westwards, with Germany and Austria accounting for c.40% of the portfolio by value.

In the table below, we reconcile the two portfolios, based on the 4Q15 data for CAI and the annualised

3Q15/16 IIA figures.

Reconciliation of the portfolio resulting from the merger

GLA Occupancy FV FV Rental inc. Rental inc. Yield

k sqm % EUR m relative EUR m EUR/sqm %

Office portfolio

AT CAI 415 96.5% 588

33.4 6.9 5.7%

AT IIA 362 79.9% 869

45.2 13.0 5.2%

AT total 777 88.8% 1,457 23% 78.6 9.5 5.4%

DE CAI 262 93.8% 823

44 14.9 5.3%

DE IIA 53 54.8% 106

4.4 12.7 4.2%

DE total 315 87.3% 929 15% 48.4 14.7 5.2%

CZ CAI 123 94.1% 257

19.6 14.1 7.6%

CZ IIA 143 68.6% 262

14.8 12.5 5.6%

CZ Total 266 80.4% 519 8% 34.4 13.4 6.6%

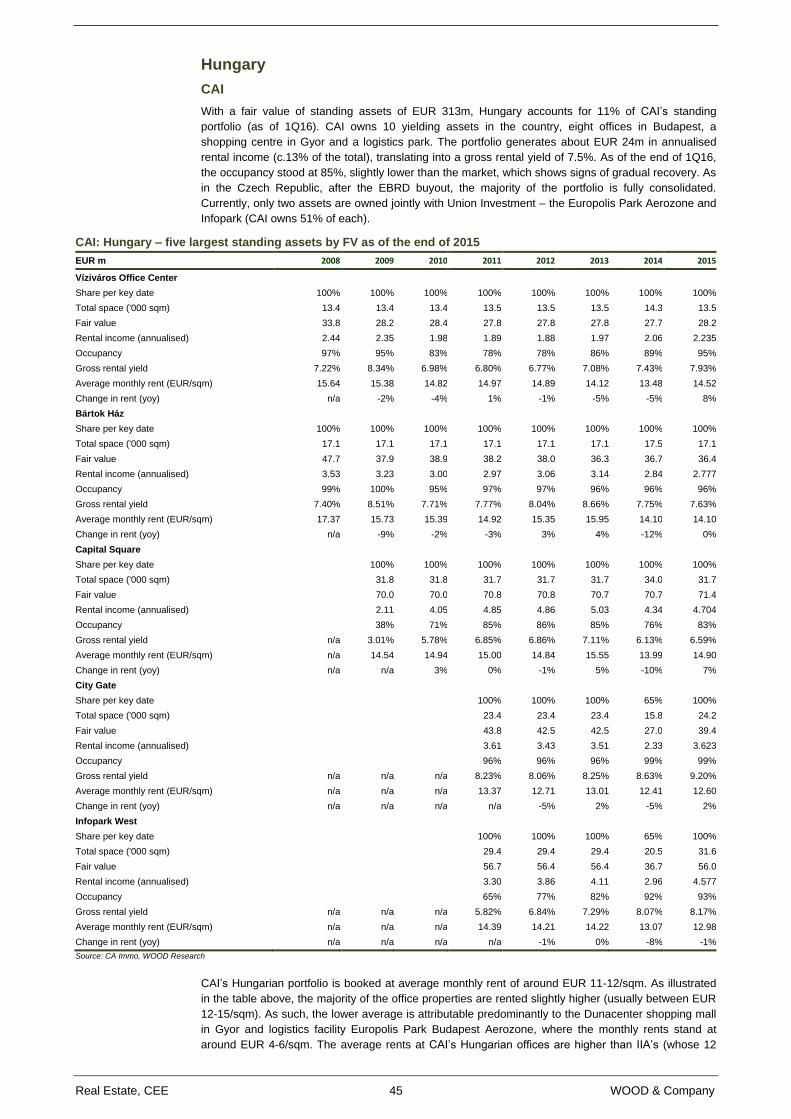

HU CAI 198 85.7% 313

23.5 11.6 7.5%

HU IIA 166 77.0% 266

14 9.1 5.3%

HU total 364 81.7% 580 9% 37.5 10.5 6.5%

PL CAI 99 93.4% 306

22 19.8 7.2%

PL IIA 258 72.7% 478

26.8 11.9 5.6%

PL total 357 78.5% 784 13% 48.8 14.5 6.2%

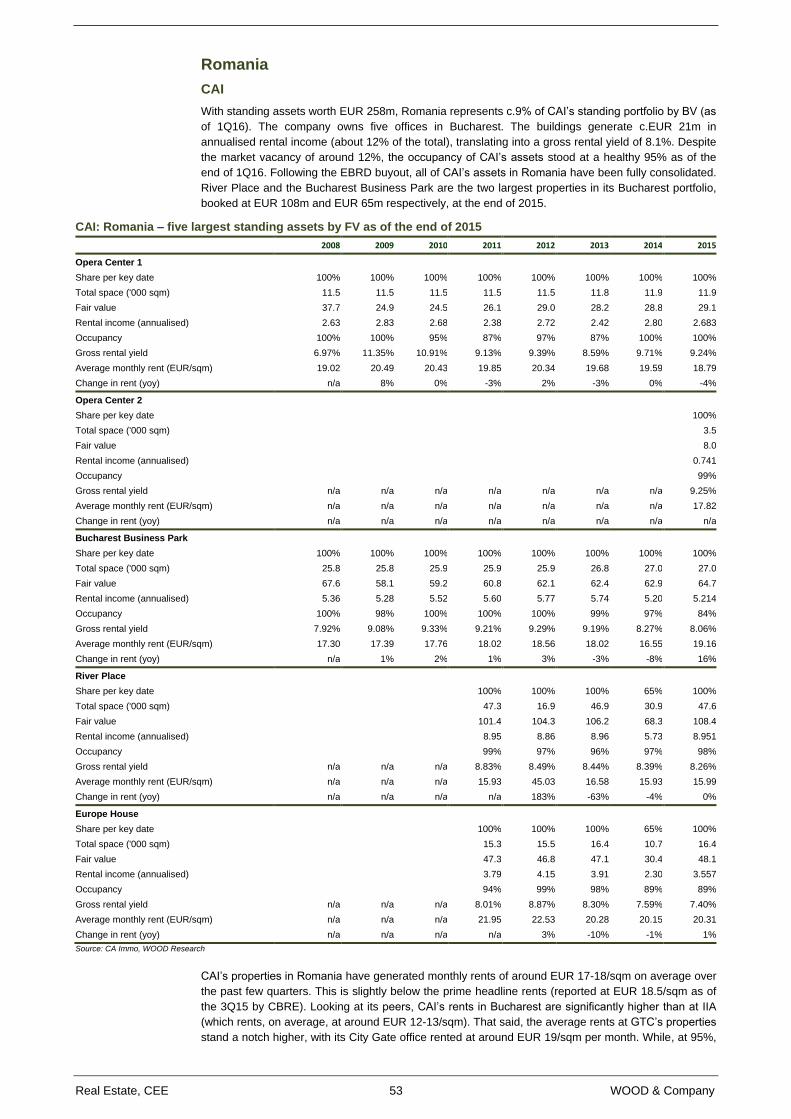

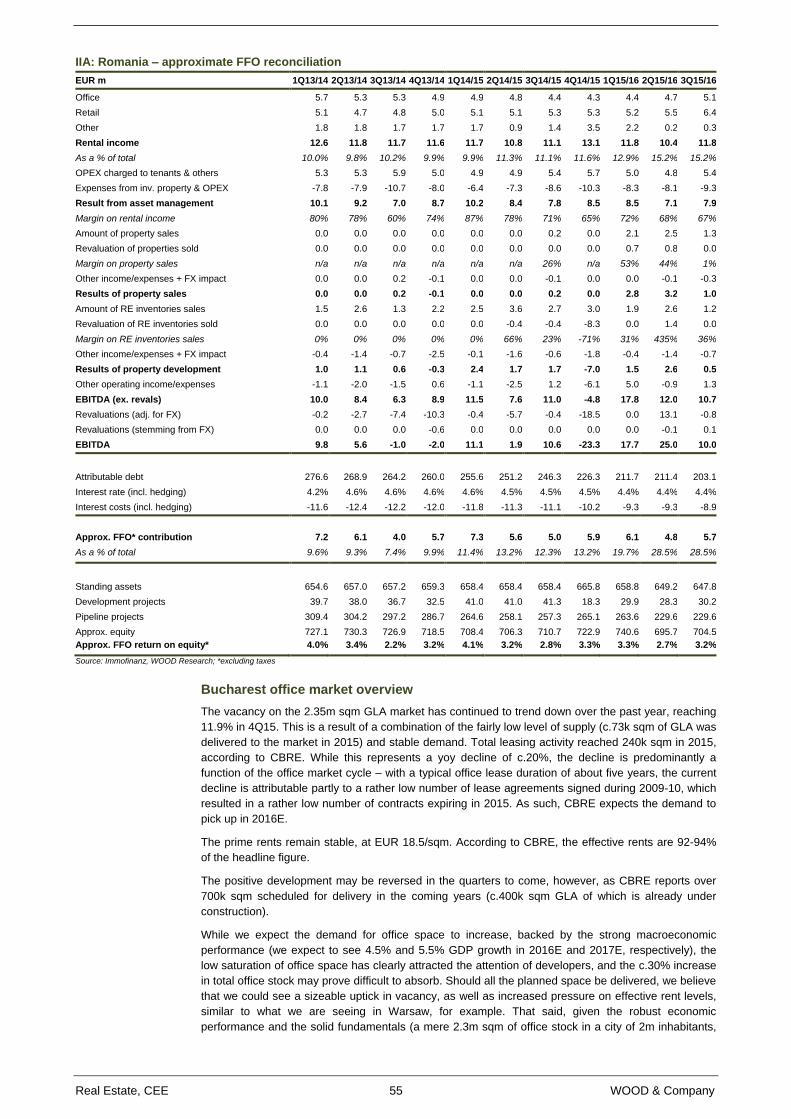

RO CAI 106 93.0% 258

21.1 17.8 8.2%

RO IIA 187 82.3% 333

22 11.9 6.6%

RO total 294 86.2% 591 9% 43.1 14.2 7.3%

Others CAI 135 90.4% 226

17.7 12.1 7.8%

Others IIA 25 51.5% 38

1.6 10.4 4.2%

Others total 160 84.3% 264 4% 19.3 11.9 7.3%

Offices CAI + IIA total 2,533 84.7% 5,123 82% 310.1 12.1 6.1%

Retail portfolio

AT 209 95.3% 206 3% 18.8 7.8 9.1%

DE 0 n/a 0 0% 0 n/a n/a

CZ 106 96.9% 132 2% 10.4 8.5 7.9%

HU 125 92.1% 159 3% 11.6 8.4 7.3%

PL 58 96.4% 72 1% 5.6 8.3 7.8%

RO 148 94.6% 305 5% 24.4 14.5 8.0%

Others 121 97.2% 229 4% 16.8 11.9 7.3%

Retail portfolio (excl. Russia) 767 95.2% 1,103 18% 87.6 10.0 7.9%

Country split after merger and Russia spin-off

AT 986 90.2% 1,663 27% 97 9.1 5.9%

DE 315 87.3% 929 15% 48 14.7 5.2%

CZ 372 85.0% 651 10% 45 11.8 6.9%

HU 488 84.4% 739 12% 49 9.9 6.6%

PL 415 81.0% 856 14% 54 13.5 6.4%

RO 442 89.0% 896 14% 68 14.3 7.5%

Others 281 89.9% 493 8% 36 11.9 7.3%

Portfolio after merger and Russia spin-off 3,300 87.1% 6,226 100% 397.7 11.5 6.4%

Source: Immofinanz, CA Immo, WOOD Research; *for Immofinanz, we use annualised 3Q15/16 figures, for CA Immo, we use the annualised data available in the 4Q15 report; **as offices are dominant asset class in CAI's portfolio, we include all CAI's properties under the office section of this table

The combined entity would also be likely to offer a less complex investment thesis, with offices

accounting for c.75% of the total BV, according to IIA’s presentation. Thanks to the substantial

development pipeline, the share of offices in the portfolio may continue to grow over time, as would the

share of Germany in the geographic breakdown.

Real Estate, CEE 8 WOOD & Company

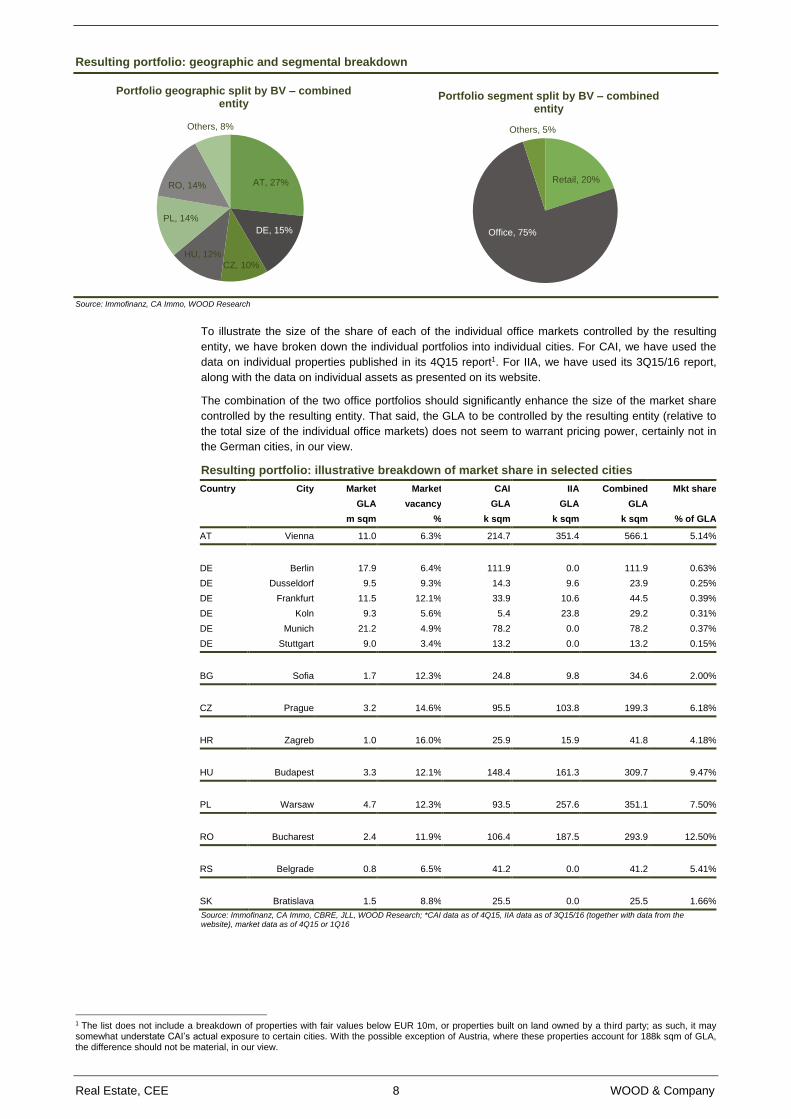

Resulting portfolio: geographic and segmental breakdown

Source: Immofinanz, CA Immo, WOOD Research

To illustrate the size of the share of each of the individual office markets controlled by the resulting

entity, we have broken down the individual portfolios into individual cities. For CAI, we have used the

data on individual properties published in its 4Q15 report1. For IIA, we have used its 3Q15/16 report,

along with the data on individual assets as presented on its website.

The combination of the two office portfolios should significantly enhance the size of the market share

controlled by the resulting entity. That said, the GLA to be controlled by the resulting entity (relative to

the total size of the individual office markets) does not seem to warrant pricing power, certainly not in

the German cities, in our view.

Resulting portfolio: illustrative breakdown of market share in selected cities

Country City Market Market CAI IIA Combined Mkt share

GLA vacancy GLA GLA GLA

m sqm % k sqm k sqm k sqm % of GLA

AT Vienna 11.0 6.3% 214.7 351.4 566.1 5.14%

DE Berlin 17.9 6.4% 111.9 0.0 111.9 0.63%

DE Dusseldorf 9.5 9.3% 14.3 9.6 23.9 0.25%

DE Frankfurt 11.5 12.1% 33.9 10.6 44.5 0.39%

DE Koln 9.3 5.6% 5.4 23.8 29.2 0.31%

DE Munich 21.2 4.9% 78.2 0.0 78.2 0.37%

DE Stuttgart 9.0 3.4% 13.2 0.0 13.2 0.15%

BG Sofia 1.7 12.3% 24.8 9.8 34.6 2.00%

CZ Prague 3.2 14.6% 95.5 103.8 199.3 6.18%

HR Zagreb 1.0 16.0% 25.9 15.9 41.8 4.18%

HU Budapest 3.3 12.1% 148.4 161.3 309.7 9.47%

PL Warsaw 4.7 12.3% 93.5 257.6 351.1 7.50%

RO Bucharest 2.4 11.9% 106.4 187.5 293.9 12.50%

RS Belgrade 0.8 6.5% 41.2 0.0 41.2 5.41%

SK Bratislava 1.5 8.8% 25.5 0.0 25.5 1.66%

Source: Immofinanz, CA Immo, CBRE, JLL, WOOD Research; *CAI data as of 4Q15, IIA data as of 3Q15/16 (together with data from the website), market data as of 4Q15 or 1Q16

1 The list does not include a breakdown of properties with fair values below EUR 10m, or properties built on land owned by a third party; as such, it may somewhat understate CAI’s actual exposure to certain cities. With the possible exception of Austria, where these properties account for 188k sqm of GLA, the difference should not be material, in our view.

AT, 27%

DE, 15%

CZ, 10%

HU, 12%

PL, 14%

RO, 14%

Others, 8%

Portfolio geographic split by BV – combined entity

Retail, 20%

Office, 75%

Others, 5%

Portfolio segment split by BV – combined entity

Real Estate, CEE 9 WOOD & Company

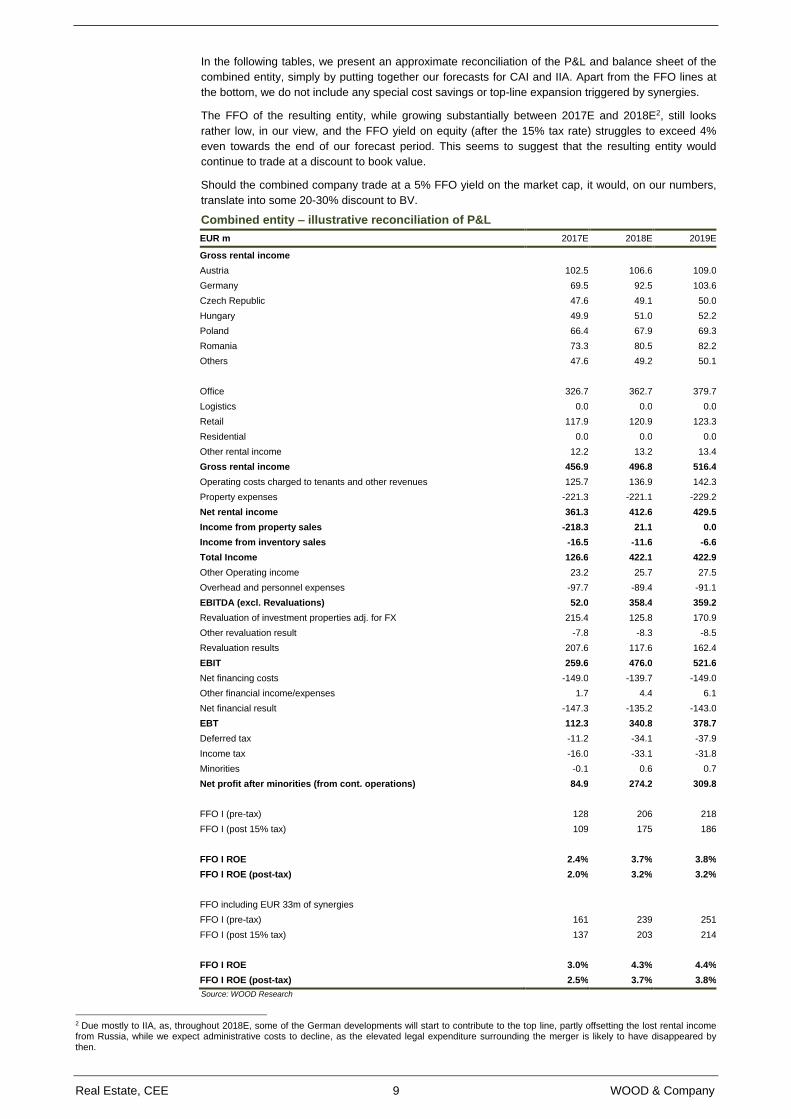

In the following tables, we present an approximate reconciliation of the P&L and balance sheet of the

combined entity, simply by putting together our forecasts for CAI and IIA. Apart from the FFO lines at

the bottom, we do not include any special cost savings or top-line expansion triggered by synergies.

The FFO of the resulting entity, while growing substantially between 2017E and 2018E2, still looks

rather low, in our view, and the FFO yield on equity (after the 15% tax rate) struggles to exceed 4%

even towards the end of our forecast period. This seems to suggest that the resulting entity would

continue to trade at a discount to book value.

Should the combined company trade at a 5% FFO yield on the market cap, it would, on our numbers,

translate into some 20-30% discount to BV.

Combined entity – illustrative reconciliation of P&L

EUR m 2017E 2018E 2019E

Gross rental income

Austria 102.5 106.6 109.0

Germany 69.5 92.5 103.6

Czech Republic 47.6 49.1 50.0

Hungary 49.9 51.0 52.2

Poland 66.4 67.9 69.3

Romania 73.3 80.5 82.2

Others 47.6 49.2 50.1

Office 326.7 362.7 379.7

Logistics 0.0 0.0 0.0

Retail 117.9 120.9 123.3

Residential 0.0 0.0 0.0

Other rental income 12.2 13.2 13.4

Gross rental income 456.9 496.8 516.4

Operating costs charged to tenants and other revenues 125.7 136.9 142.3

Property expenses -221.3 -221.1 -229.2

Net rental income 361.3 412.6 429.5

Income from property sales -218.3 21.1 0.0

Income from inventory sales -16.5 -11.6 -6.6

Total Income 126.6 422.1 422.9

Other Operating income 23.2 25.7 27.5

Overhead and personnel expenses -97.7 -89.4 -91.1

EBITDA (excl. Revaluations) 52.0 358.4 359.2

Revaluation of investment properties adj. for FX 215.4 125.8 170.9

Other revaluation result -7.8 -8.3 -8.5

Revaluation results 207.6 117.6 162.4

EBIT 259.6 476.0 521.6

Net financing costs -149.0 -139.7 -149.0

Other financial income/expenses 1.7 4.4 6.1

Net financial result -147.3 -135.2 -143.0

EBT 112.3 340.8 378.7

Deferred tax -11.2 -34.1 -37.9

Income tax -16.0 -33.1 -31.8

Minorities -0.1 0.6 0.7

Net profit after minorities (from cont. operations) 84.9 274.2 309.8

FFO I (pre-tax) 128 206 218

FFO I (post 15% tax) 109 175 186

FFO I ROE 2.4% 3.7% 3.8%

FFO I ROE (post-tax) 2.0% 3.2% 3.2%

FFO including EUR 33m of synergies

FFO I (pre-tax) 161 239 251

FFO I (post 15% tax) 137 203 214

FFO I ROE 3.0% 4.3% 4.4%

FFO I ROE (post-tax) 2.5% 3.7% 3.8%

Source: WOOD Research

2 Due mostly to IIA, as, throughout 2018E, some of the German developments will start to contribute to the top line, partly offsetting the lost rental income from Russia, while we expect administrative costs to decline, as the elevated legal expenditure surrounding the merger is likely to have disappeared by then.

Real Estate, CEE 10 WOOD & Company

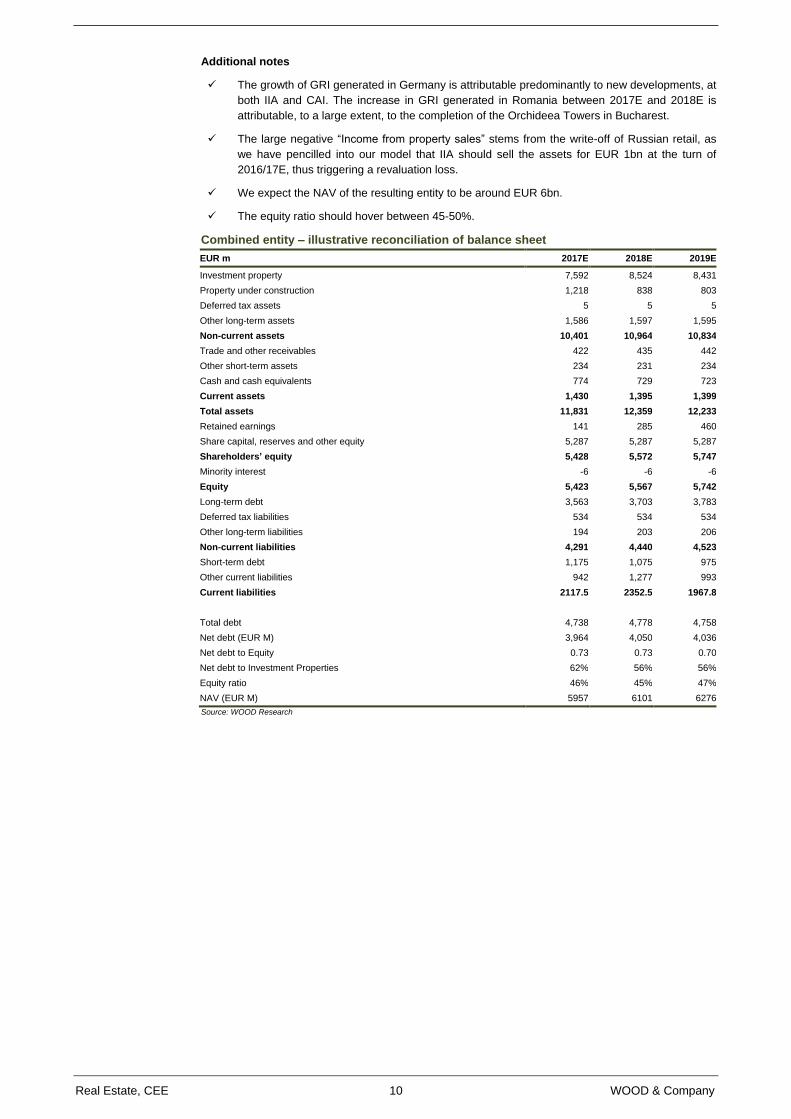

Additional notes

The growth of GRI generated in Germany is attributable predominantly to new developments, at

both IIA and CAI. The increase in GRI generated in Romania between 2017E and 2018E is

attributable, to a large extent, to the completion of the Orchideea Towers in Bucharest.

The large negative “Income from property sales” stems from the write-off of Russian retail, as

we have pencilled into our model that IIA should sell the assets for EUR 1bn at the turn of

2016/17E, thus triggering a revaluation loss.

We expect the NAV of the resulting entity to be around EUR 6bn.

The equity ratio should hover between 45-50%.

Combined entity – illustrative reconciliation of balance sheet

EUR m 2017E 2018E 2019E

Investment property 7,592 8,524 8,431

Property under construction 1,218 838 803

Deferred tax assets 5 5 5

Other long-term assets 1,586 1,597 1,595

Non-current assets 10,401 10,964 10,834

Trade and other receivables 422 435 442

Other short-term assets 234 231 234

Cash and cash equivalents 774 729 723

Current assets 1,430 1,395 1,399

Total assets 11,831 12,359 12,233

Retained earnings 141 285 460

Share capital, reserves and other equity 5,287 5,287 5,287

Shareholders’ equity 5,428 5,572 5,747

Minority interest -6 -6 -6

Equity 5,423 5,567 5,742

Long-term debt 3,563 3,703 3,783

Deferred tax liabilities 534 534 534

Other long-term liabilities 194 203 206

Non-current liabilities 4,291 4,440 4,523

Short-term debt 1,175 1,075 975

Other current liabilities 942 1,277 993

Current liabilities 2117.5 2352.5 1967.8

Total debt 4,738 4,778 4,758

Net debt (EUR M) 3,964 4,050 4,036

Net debt to Equity 0.73 0.73 0.70

Net debt to Investment Properties 62% 56% 56%

Equity ratio 46% 45% 47%

NAV (EUR M) 5957 6101 6276

Source: WOOD Research

Real Estate, CEE 11 WOOD & Company

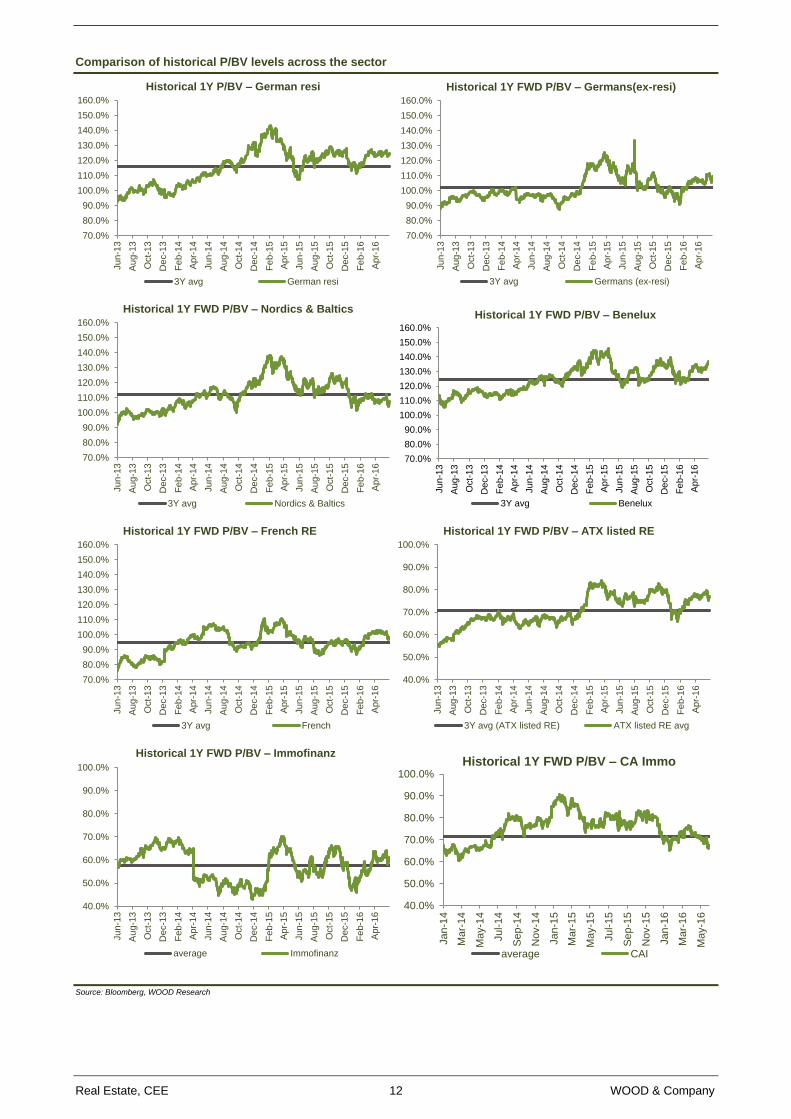

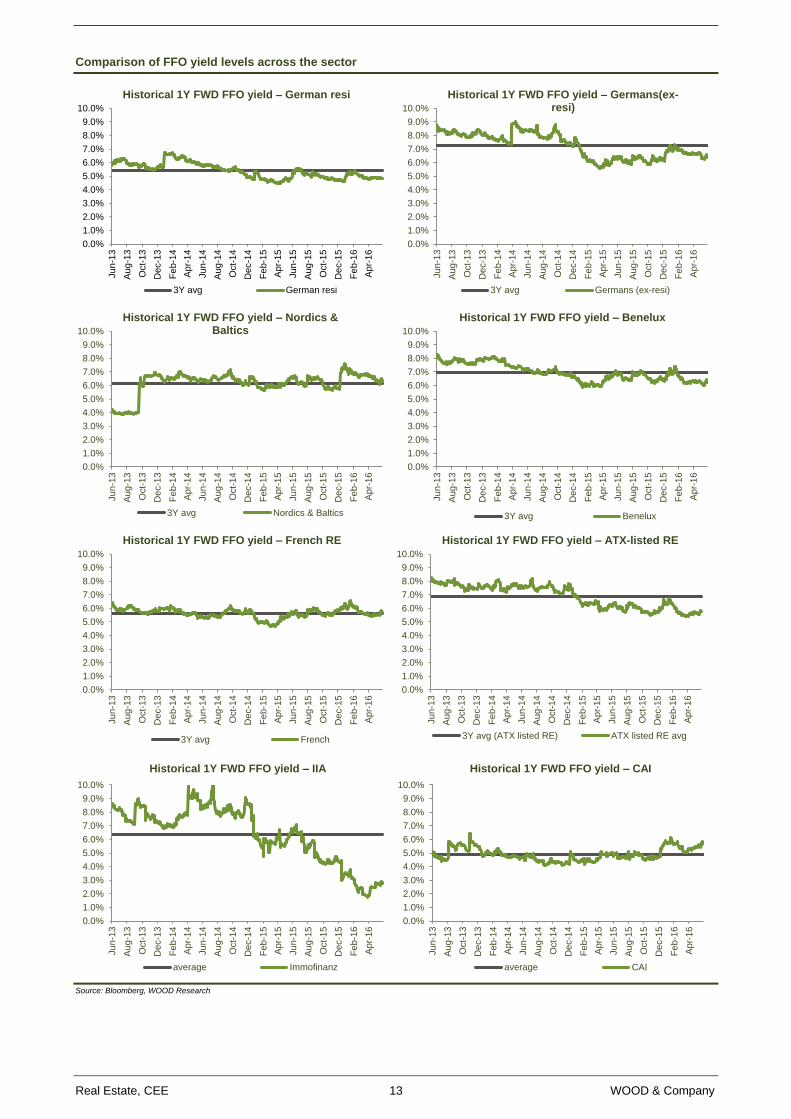

While cheaper on P/BV, peers continue to offer stronger FFO yields

1Y FWD FFO yield: CAI vs. IIA vs. ATX listed RE

Source: Bloomberg, WOOD Research

ATX-listed real estate companies have traded historically at a discount to BV (3Y average 1Y FWD

P/BV of c.0.7x, on the Bloomberg consensus). Recently, some of the stocks have rerated, with conwert

and S-Immo trading at around 1x BV. The average is, however, still being dragged down by stock-

specific issues, with Russian exposure weighing on IIA and Atrium, and, recently, the potential adverse

merger ratio affecting CAI.

Looking at FFO yields, we see that, despite the substantial discount to BV, IIA continues to generate a

very low yield (c.2-3%, on consensus estimates), as Russia and low office occupancy are limiting

profitability. This is likely to limit the potential upside in the mid-term, in our view. On the Bloomberg

consensus, CAI trades currently at close to a 6% 1Y FWD FFO yield, roughly in line with both its

European and ATX-listed peers and slightly above its 3Y average of c.5%. However, the potential

downside from the merger would be likely to limit any strong rerating at CAI, despite the c.10% FFO

CAGR we expect in 2015-17E.

What the charts show and the respective constituents

On the following pages, we present an overview of the relative valuation of IIA and CAI compared to a

number of major European real estate stocks. We have divided the selected stocks from the European

listed universe into several categories, based on where the respective constituents carry out the

majority of their operations. Please note that we actively follow just a fraction of this universe, so some

of the companies may fit better in another peer group (therefore, this division should serve

predominantly for illustrative purposes only).

The FFO yield and P/BV charts on the following pages show where the respective segments have

traded for the past three years on 1Y forward FFO and BV, using the average Bloomberg consensus.

The constituents of the respective groups are broadly those shown below, while excluding a handful of

companies at which the numbers differed dramatically from the rest and thus distorted the average.

The constituents

ATX-listed RE – Conwert; CA Immo; S-Immo; Warimpex; Atrium; Immofinanz

German residential – Annington; Deutsche Wohnen; LEG; Gagfah; Buwog

Pan-Europeans - Aedifica; Vastned Retail; Wereldhave; EuroCommercial Ppty; Klepierre; Hansteen

Holdings; Unibail-Rodamco; Corio; Inmobiliara Colonial S.A.

Germans (ex-resi) – Alstria Office; Deutsche EuroShop; DIC Asset AG ;Prime Office AG ; Hamborner

REIT AG

Nordics & Baltics – Castellum; Citycon; DIOS Fastigheter AB; FABEGE; Fastighets AB Balder B;

Hemfosa Fastigheter AB; Hufvudstaden A; Klovern AB; Kungsleden; Norwegian Property ASA;

Technopolis; Sponda Oyj; Wallenstam AB; Wihlborgs Fastigheter

Benelux – Cofinimmo; Intervest Offices & Warehouses; Leasinvest-Sicafi; Nieuwe Steen Inv;

Wereldhave Belgium; Befimmo (Sicafi); Warehouses De Pauw

French – Affine; ANF-Immobilier S.A.; Fonciere Des Regions; Gecina; Icade; Mercialys; Societe de la

Tour Eiffel

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Ju

n-1

3

Ju

l-1

3

Au

g-1

3

Se

p-1

3

Oct-

13

No

v-1

3

De

c-1

3

Ja

n-1

4

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ju

n-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oct-

14

No

v-1

4

De

c-1

4

Ja

n-1

5

Fe

b-1

5

Ma

r-1

5

Ap

r-1

5

Ma

y-1

5

Ju

n-1

5

Ju

l-1

5

Au

g-1

5

Se

p-1

5

Oct-

15

No

v-1

5

De

c-1

5

Ja

n-1

6

Fe

b-1

6

Ma

r-1

6

Ap

r-1

6

Ma

y-1

6

ATX listed RE avg Immofinanz CAI

Real Estate, CEE 12 WOOD & Company

Comparison of historical P/BV levels across the sector

Source: Bloomberg, WOOD Research

70.0%

80.0%

90.0%

100.0%

110.0%

120.0%

130.0%

140.0%

150.0%

160.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y P/BV – German resi

3Y avg German resi

70.0%

80.0%

90.0%

100.0%

110.0%

120.0%

130.0%

140.0%

150.0%

160.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD P/BV – Germans(ex-resi)

3Y avg Germans (ex-resi)

70.0%

80.0%

90.0%

100.0%

110.0%

120.0%

130.0%

140.0%

150.0%

160.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD P/BV – Nordics & Baltics

3Y avg Nordics & Baltics

70.0%

80.0%

90.0%

100.0%

110.0%

120.0%

130.0%

140.0%

150.0%

160.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD P/BV – Benelux

3Y avg Benelux

70.0%

80.0%

90.0%

100.0%

110.0%

120.0%

130.0%

140.0%

150.0%

160.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD P/BV – French RE

3Y avg French

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD P/BV – ATX listed RE

3Y avg (ATX listed RE) ATX listed RE avg

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD P/BV – Immofinanz

average Immofinanz

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Jan-1

4

Mar-

14

May-1

4

Jul-14

Sep-1

4

Nov-1

4

Jan-1

5

Mar-

15

May-1

5

Jul-15

Sep-1

5

Nov-1

5

Jan-1

6

Mar-

16

May-1

6

Historical 1Y FWD P/BV – CA Immo

average CAI

Real Estate, CEE 13 WOOD & Company

Comparison of FFO yield levels across the sector

Source: Bloomberg, WOOD Research

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD FFO yield – German resi

3Y avg German resi

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD FFO yield – Germans(ex-resi)

3Y avg Germans (ex-resi)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD FFO yield – Nordics & Baltics

3Y avg Nordics & Baltics

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD FFO yield – Benelux

3Y avg Benelux

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD FFO yield – French RE

3Y avg French

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD FFO yield – ATX-listed RE

3Y avg (ATX listed RE) ATX listed RE avg

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD FFO yield – IIA

average Immofinanz

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Ju

n-1

3

Au

g-1

3

Oct-

13

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oct-

15

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Historical 1Y FWD FFO yield – CAI

average CAI

Real Estate, CEE 14 WOOD & Company

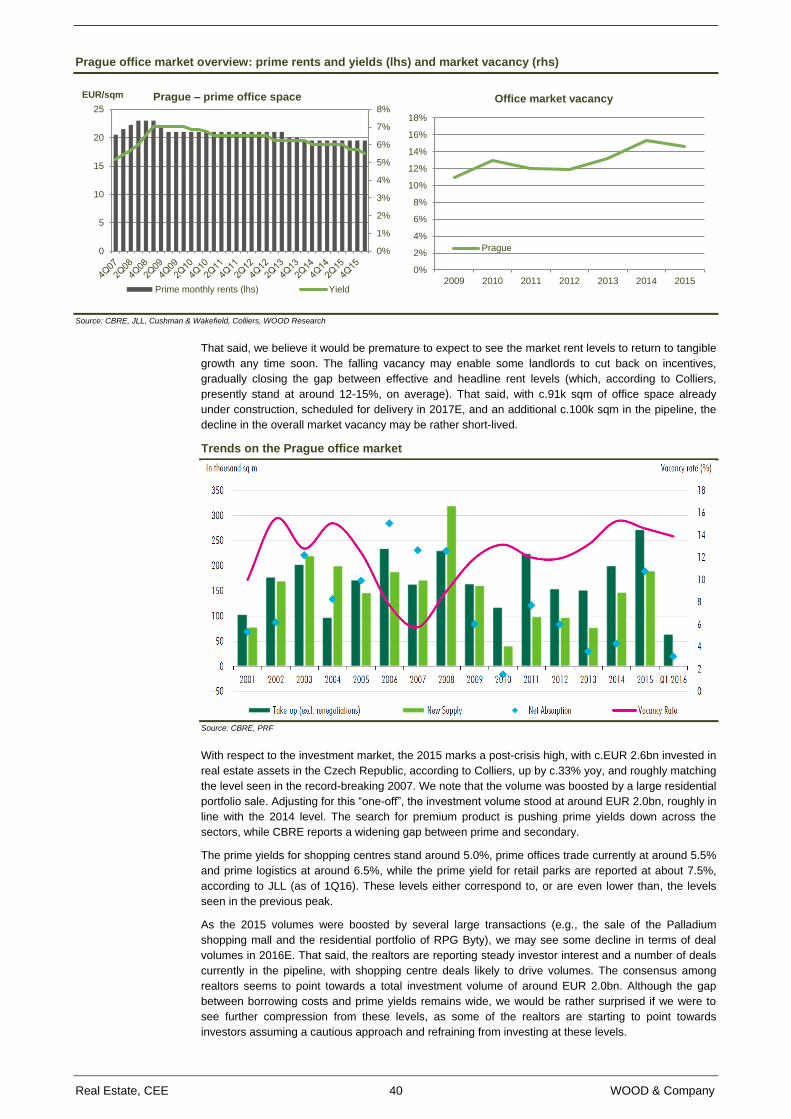

Overview of the individual markets

On the following pages, we analyse the individual markets in which CAI and IIA operate. We believe

the following are the key takeaways.

IIA’s portfolio seems, on balance, to be booked at more aggressive yields than CAI

In a number of the markets we have reviewed, IIA’s properties had higher vacancy and were

leased at lower average monthly rents compared to its competitors. Ceteris paribus, this seems

to imply that IIA’s properties are lower quality. Despite this, IIA’s properties are often booked at

a lower gross rental yield than its peers’ portfolios, which is the case at its Polish, Czech,

Hungarian and Romanian offices. While the gross rental yield is often depressed by sub-

optimal vacancy, even if we adjust for full occupancy while keeping the average rents intact (an

approach that tends to favour IIA, in our view), the resulting adjusted gross rental yields are, in

most cases, still lower than its competitors in the aforementioned markets.

We see little evidence for organic rental growth

Offices: we expect to see rather stable developments in rents in Vienna, Munich and Frankfurt

over the medium term, as these are generally stable, mature markets. The pace of new

completions seems to have slowed down in Prague and, while it is likely to remain a tenants’

market, it is usually spared strong and abrupt changes in rent levels. We see further downside

potential in Warsaw and Bucharest, where a strong wave of supply is likely to push vacancy up

and put rents under pressure. We believe we may see a positive development in Berlin and

Budapest, where a limited supply of new space is coupled with strong demand.

Moscow retail: the performance of IIA’s shopping malls in the city will depend largely on the

future course of oil prices, which seem unlikely to break above USD 50/barrel in the short- to

mid-term, as this would trigger a ramp-up of US production, which would likely cap further

gains, in our view. That said, with the consensus expecting modest GDP growth from 2017E-

on, we expect a gradual improvement in occupancy, followed by a steady recovery of rents. We

note that the Moscow retail market has been flooded with new projects, and the modern retail

space is set to expand by over a third between 2014-16E. As such, the new rent equilibrium will

likely stand substantially below the levels seen pre-2014/15, even if the economy begins to

grow at a significantly higher-than-forecast pace.

Retail elsewhere: IIA classifies about half of its retail portfolio by BV as Quality Shopping

Center/VIVO!, with the other half being the STOP.SHOPs, or other retail parks. Past

performance seems to suggest that the rents in the segments are generally stable. However,

we believe that the upside for potential rental growth is rather limited, especially in the retail

parks segment.

Across the markets, pricing has reached or surpassed historical highs

Total investment volume for CEE (ex. Russia) stood at EUR 10bn in 2015, up 25% yoy

according to CBRE. In Austria, nearly EUR 4bn was transacted during the year (+38 yoy), while

Germany saw a deal volume of a huge EUR 55bn, (up 39% yoy), according to CBRE figures. In

a number of countries, volumes are moving close to historical highs, surpassed only by

2006/07.

The massive volume of capital is driving the yields down across the markets and

sectors, with the prime yields for offices now standing as low as 4% in a number of German

cities. In CEE, 2015 was dominated by retail investment, which represented nearly 50% of the

turnover. The pricing of prime shopping centres in the CE3 capitals stands at around 5.0%, and

we are seeing retail deals close to the 5% mark even outside the capitals in these countries.

This trend is also visible in the office markets. Having hovered at around 6.0% for a number of

years, the prime office yield for both Prague and Warsaw (as reported by CBRE) has declined

recently to 5.5%. Romania and Hungary, while also registering growing demand, still continue

to offer better pricing, with yields at around 7% for offices and retail, but the liquidity is still

rather limited compared to CEE, and concentrated mainly in the capitals. With respect to

Russia, after a weak 2015, volumes have picked up in 2016 ytd, and we see investor interest

picking up. However, there have been no transactions of a similar size to IIA’s portfolio since

the downturn, so the visibility of pricing in the current environment remains limited.

Real Estate, CEE 15 WOOD & Company

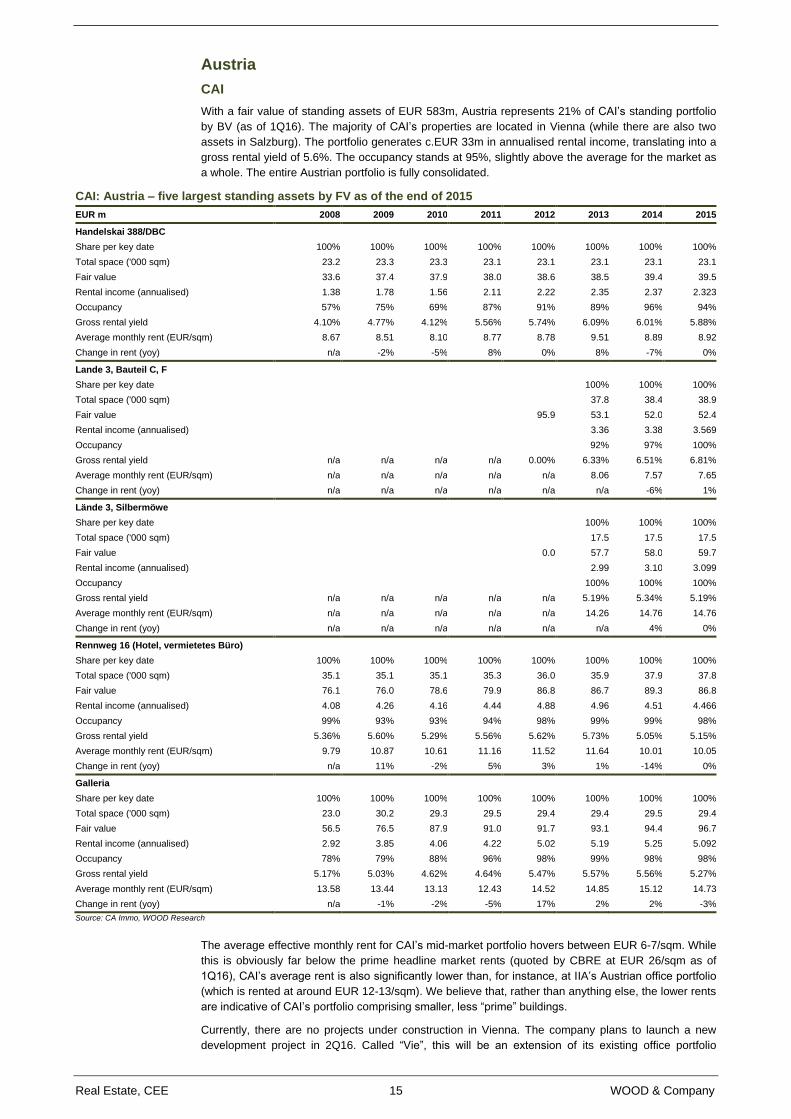

Austria

CAI

With a fair value of standing assets of EUR 583m, Austria represents 21% of CAI’s standing portfolio

by BV (as of 1Q16). The majority of CAI’s properties are located in Vienna (while there are also two

assets in Salzburg). The portfolio generates c.EUR 33m in annualised rental income, translating into a

gross rental yield of 5.6%. The occupancy stands at 95%, slightly above the average for the market as

a whole. The entire Austrian portfolio is fully consolidated.

CAI: Austria – five largest standing assets by FV as of the end of 2015

EUR m 2008 2009 2010 2011 2012 2013 2014 2015

Handelskai 388/DBC

Share per key date 100% 100% 100% 100% 100% 100% 100% 100%

Total space ('000 sqm) 23.2 23.3 23.3 23.1 23.1 23.1 23.1 23.1

Fair value 33.6 37.4 37.9 38.0 38.6 38.5 39.4 39.5

Rental income (annualised) 1.38 1.78 1.56 2.11 2.22 2.35 2.37 2.323

Occupancy 57% 75% 69% 87% 91% 89% 96% 94%

Gross rental yield 4.10% 4.77% 4.12% 5.56% 5.74% 6.09% 6.01% 5.88%

Average monthly rent (EUR/sqm) 8.67 8.51 8.10 8.77 8.78 9.51 8.89 8.92

Change in rent (yoy) n/a -2% -5% 8% 0% 8% -7% 0%

Lande 3, Bauteil C, F

Share per key date

100% 100% 100%

Total space ('000 sqm)

37.8 38.4 38.9

Fair value

95.9 53.1 52.0 52.4

Rental income (annualised)

3.36 3.38 3.569

Occupancy

92% 97% 100%

Gross rental yield n/a n/a n/a n/a 0.00% 6.33% 6.51% 6.81%

Average monthly rent (EUR/sqm) n/a n/a n/a n/a n/a 8.06 7.57 7.65

Change in rent (yoy) n/a n/a n/a n/a n/a n/a -6% 1%

Lände 3, Silbermöwe

Share per key date

100% 100% 100%

Total space ('000 sqm)

17.5 17.5 17.5

Fair value

0.0 57.7 58.0 59.7

Rental income (annualised)

2.99 3.10 3.099

Occupancy

100% 100% 100%

Gross rental yield n/a n/a n/a n/a n/a 5.19% 5.34% 5.19%

Average monthly rent (EUR/sqm) n/a n/a n/a n/a n/a 14.26 14.76 14.76

Change in rent (yoy) n/a n/a n/a n/a n/a n/a 4% 0%

Rennweg 16 (Hotel, vermietetes Büro)

Share per key date 100% 100% 100% 100% 100% 100% 100% 100%

Total space ('000 sqm) 35.1 35.1 35.1 35.3 36.0 35.9 37.9 37.8

Fair value 76.1 76.0 78.6 79.9 86.8 86.7 89.3 86.8

Rental income (annualised) 4.08 4.26 4.16 4.44 4.88 4.96 4.51 4.466

Occupancy 99% 93% 93% 94% 98% 99% 99% 98%

Gross rental yield 5.36% 5.60% 5.29% 5.56% 5.62% 5.73% 5.05% 5.15%

Average monthly rent (EUR/sqm) 9.79 10.87 10.61 11.16 11.52 11.64 10.01 10.05

Change in rent (yoy) n/a 11% -2% 5% 3% 1% -14% 0%

Galleria

Share per key date 100% 100% 100% 100% 100% 100% 100% 100%

Total space ('000 sqm) 23.0 30.2 29.3 29.5 29.4 29.4 29.5 29.4

Fair value 56.5 76.5 87.9 91.0 91.7 93.1 94.4 96.7

Rental income (annualised) 2.92 3.85 4.06 4.22 5.02 5.19 5.25 5.092

Occupancy 78% 79% 88% 96% 98% 99% 98% 98%

Gross rental yield 5.17% 5.03% 4.62% 4.64% 5.47% 5.57% 5.56% 5.27%

Average monthly rent (EUR/sqm) 13.58 13.44 13.13 12.43 14.52 14.85 15.12 14.73

Change in rent (yoy) n/a -1% -2% -5% 17% 2% 2% -3%

Source: CA Immo, WOOD Research

The average effective monthly rent for CAI’s mid-market portfolio hovers between EUR 6-7/sqm. While

this is obviously far below the prime headline market rents (quoted by CBRE at EUR 26/sqm as of

1Q16), CAI’s average rent is also significantly lower than, for instance, at IIA’s Austrian office portfolio

(which is rented at around EUR 12-13/sqm). We believe that, rather than anything else, the lower rents

are indicative of CAI’s portfolio comprising smaller, less “prime” buildings.

Currently, there are no projects under construction in Vienna. The company plans to launch a new

development project in 2Q16. Called “Vie”, this will be an extension of its existing office portfolio

Real Estate, CEE 16 WOOD & Company

Laende 3, in Vienna. However, this building will not increase the size of CAI’s Austrian portfolio, as it is

subject to a forward sale agreement to an Austrian investor.

This is not to say that the composition of the Austrian portfolio will remain intact. We believe the

company may utilise the strong demand and offload some of the smaller properties it holds in Vienna,

thus improving the quality of the portfolio.

The largest building by fair value is the Galleria, a shopping mall with adjacent office space located in

Vienna, on the Landstrasser Hauptstrasse. Generating c.EUR 5m p.a., the building was booked at

EUR 97m, accounting for 16% of the Austrian portfolio and 3% of the total standing portfolio. Jointly,

the five largest buildings, listed in the table above (the mall, three offices and a hotel, Savoyen),

accounted for over half of the Austrian portfolio by BV as of the end of 2015, while c.12% of CAI’s total

standing portfolio.

Booked at gross rental yields between 5.0% and 7.0%, we believe that the valuation of the top-5

buildings in the Austrian portfolio is fairly conservative, considering the steep yield compression across

the city (as of 1Q16, the prime office yield, as reported by CBRE, stood at 4.15%, while high street

retail traded at a yield below 4%, according to the realtor).

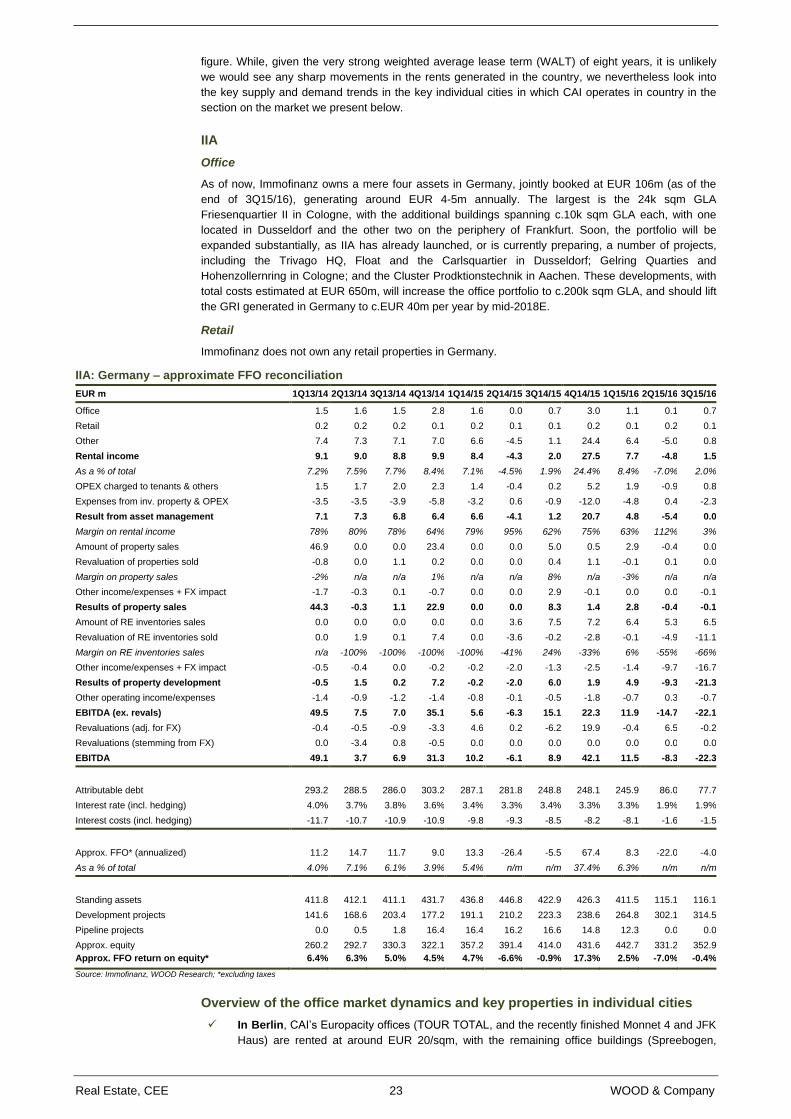

IIA

As illustrated in the table presented below, IIA’s Austrian portfolio generates annualised rental income

of c.EUR 70m, or around 20% of the group’s total. IIA owns a large office portfolio, located

predominantly in the capital, along with a number of smaller retail assets scattered across the country.

The margin on asset management hovers at around 60-70%. In our view, the main reason for the

unimpressive figure is the rather low occupancy in the office portfolio, which IIA is currently trying to

address via an extensive refurbishment programme.

The value of the standing assets is at around EUR 1.1bn, with c.EUR 580m of attributable debt, on

which IIA pays 2.7% (including hedging). Together with a handful of pipeline and development assets

(which together amounted to just around EUR 52m as of the end of 3Q15/16), the attributable equity

stands at c.EUR 560m.

On our simplified calculations (we just subtract calculated interest costs from the results from asset

management for the respective quarter), the Austrian portfolio has generated around EUR 28m of FFO

over the past 12 months. This represents c.25% of the total FFO for the period.

Office

As of the end of 3Q15/16, IIA held 33 office assets in Austria, with a BV of EUR 869m. This accounts

for 37% of its standing office portfolio and 18% of its total standing portfolio. With occupancy at around

80%, the 362k sqm GLA office portfolio generates around EUR 11m every quarter, or c.EUR 45m

annually. As of 3Q15/16, the buildings were booked at a 5.25% yield on annualised gross rental

income.

Similar to CAI, the majority of IIA’s properties are located in Vienna. According to the portfolio

breakdown that the company provides on its website, there are two additional buildings in Salzburg,

and one each in Klagenfurt and St. Polten. The largest assets in IIA’s Austrian portfolio include

Business Park Vienna (168k sqm GLA), the Bösendorferstrasse 4 (29k sqm GLA), City Tower Vienna

(27k sqm GLA) and Office 11 (20k sqm GLA).

Although Vienna is its home market, IIA’s office portfolio in the city suffers from persistently high

vacancy, which hovers at around 20%. We expect that IIA is likely to succeed in gradually increasing

the occupancy in its Austrian offices as well, as part of its broader initiative to improve the occupancy

across its office portfolio. In our forecasts, we have pencilled in a gradual improvement in occupancy to

90% by 2018E. That said, we expect the improvement in occupancy to come at a price: a modest

softening in the average rent level. As such, we have pencilled in the rents to stagnate at around EUR

12.5-13.0/sqm until 2018E, while increasing them on par with inflation afterwards.

Real Estate, CEE 17 WOOD & Company

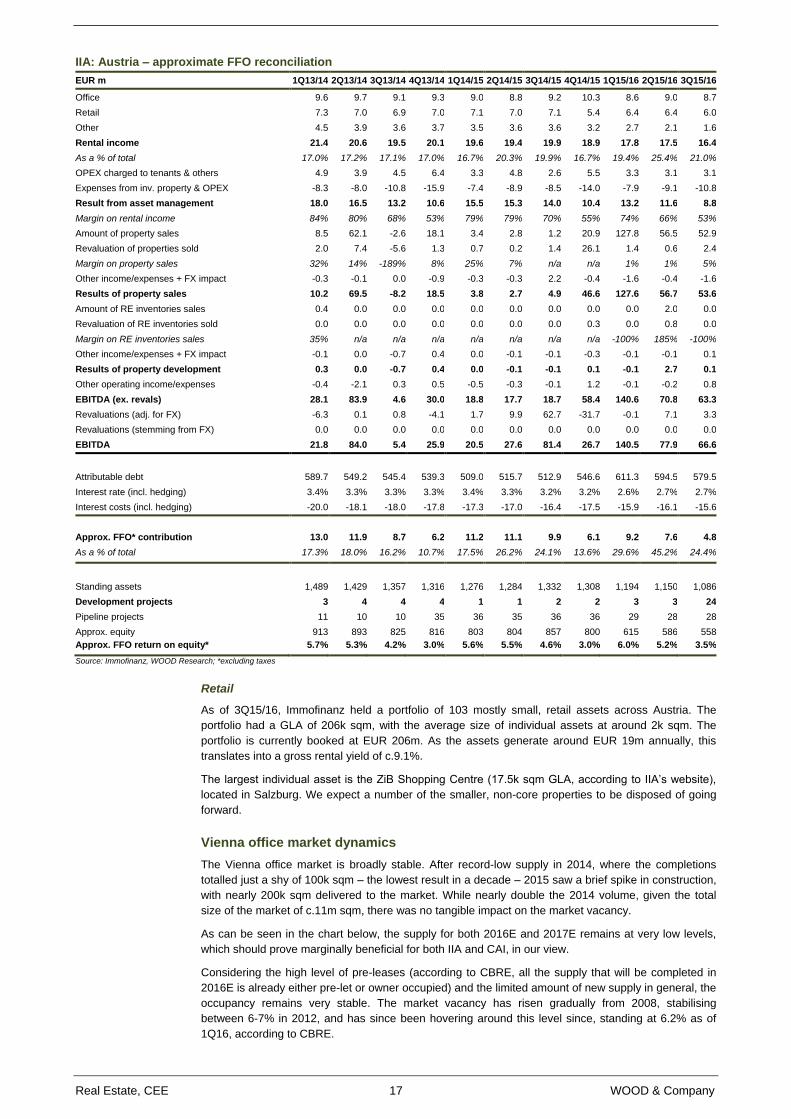

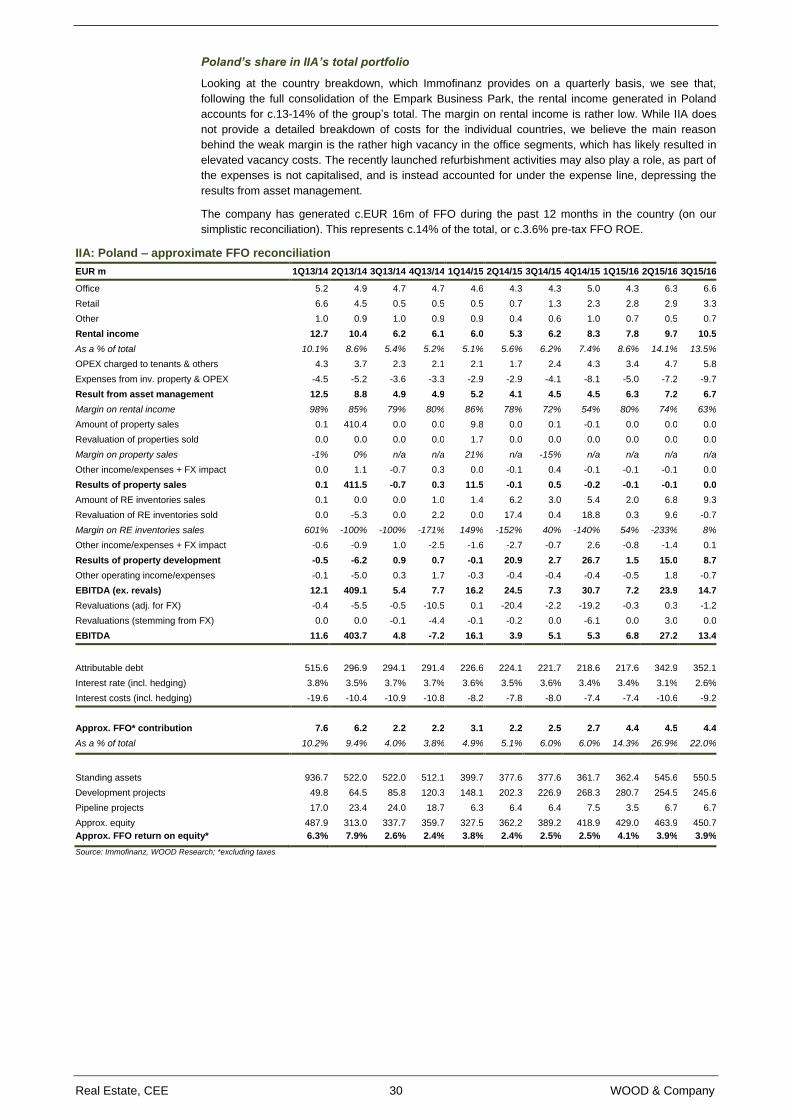

IIA: Austria – approximate FFO reconciliation

EUR m 1Q13/14 2Q13/14 3Q13/14 4Q13/14 1Q14/15 2Q14/15 3Q14/15 4Q14/15 1Q15/16 2Q15/16 3Q15/16

Office 9.6 9.7 9.1 9.3 9.0 8.8 9.2 10.3 8.6 9.0 8.7

Retail 7.3 7.0 6.9 7.0 7.1 7.0 7.1 5.4 6.4 6.4 6.0

Other 4.5 3.9 3.6 3.7 3.5 3.6 3.6 3.2 2.7 2.1 1.6

Rental income 21.4 20.6 19.5 20.1 19.6 19.4 19.9 18.9 17.8 17.5 16.4

As a % of total 17.0% 17.2% 17.1% 17.0% 16.7% 20.3% 19.9% 16.7% 19.4% 25.4% 21.0%

OPEX charged to tenants & others 4.9 3.9 4.5 6.4 3.3 4.8 2.6 5.5 3.3 3.1 3.1

Expenses from inv. property & OPEX -8.3 -8.0 -10.8 -15.9 -7.4 -8.9 -8.5 -14.0 -7.9 -9.1 -10.8

Result from asset management 18.0 16.5 13.2 10.6 15.5 15.3 14.0 10.4 13.2 11.6 8.8

Margin on rental income 84% 80% 68% 53% 79% 79% 70% 55% 74% 66% 53%

Amount of property sales 8.5 62.1 -2.6 18.1 3.4 2.8 1.2 20.9 127.8 56.5 52.9

Revaluation of properties sold 2.0 7.4 -5.6 1.3 0.7 0.2 1.4 26.1 1.4 0.6 2.4

Margin on property sales 32% 14% -189% 8% 25% 7% n/a n/a 1% 1% 5%

Other income/expenses + FX impact -0.3 -0.1 0.0 -0.9 -0.3 -0.3 2.2 -0.4 -1.6 -0.4 -1.6

Results of property sales 10.2 69.5 -8.2 18.5 3.8 2.7 4.9 46.6 127.6 56.7 53.6

Amount of RE inventories sales 0.4 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 2.0 0.0

Revaluation of RE inventories sold 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.3 0.0 0.8 0.0

Margin on RE inventories sales 35% n/a n/a n/a n/a n/a n/a n/a -100% 185% -100%

Other income/expenses + FX impact -0.1 0.0 -0.7 0.4 0.0 -0.1 -0.1 -0.3 -0.1 -0.1 0.1

Results of property development 0.3 0.0 -0.7 0.4 0.0 -0.1 -0.1 0.1 -0.1 2.7 0.1

Other operating income/expenses -0.4 -2.1 0.3 0.5 -0.5 -0.3 -0.1 1.2 -0.1 -0.2 0.8

EBITDA (ex. revals) 28.1 83.9 4.6 30.0 18.8 17.7 18.7 58.4 140.6 70.8 63.3

Revaluations (adj. for FX) -6.3 0.1 0.8 -4.1 1.7 9.9 62.7 -31.7 -0.1 7.1 3.3

Revaluations (stemming from FX) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

EBITDA 21.8 84.0 5.4 25.9 20.5 27.6 81.4 26.7 140.5 77.9 66.6

Attributable debt 589.7 549.2 545.4 539.3 509.0 515.7 512.9 546.6 611.3 594.5 579.5

Interest rate (incl. hedging) 3.4% 3.3% 3.3% 3.3% 3.4% 3.3% 3.2% 3.2% 2.6% 2.7% 2.7%

Interest costs (incl. hedging) -20.0 -18.1 -18.0 -17.8 -17.3 -17.0 -16.4 -17.5 -15.9 -16.1 -15.6

Approx. FFO* contribution 13.0 11.9 8.7 6.2 11.2 11.1 9.9 6.1 9.2 7.6 4.8

As a % of total 17.3% 18.0% 16.2% 10.7% 17.5% 26.2% 24.1% 13.6% 29.6% 45.2% 24.4%

Standing assets 1,489 1,429 1,357 1,316 1,276 1,284 1,332 1,308 1,194 1,150 1,086

Development projects 3 4 4 4 1 1 2 2 3 3 24

Pipeline projects 11 10 10 35 36 35 36 36 29 28 28

Approx. equity 913 893 825 816 803 804 857 800 615 586 558

Approx. FFO return on equity* 5.7% 5.3% 4.2% 3.0% 5.6% 5.5% 4.6% 3.0% 6.0% 5.2% 3.5%

Source: Immofinanz, WOOD Research; *excluding taxes

Retail

As of 3Q15/16, Immofinanz held a portfolio of 103 mostly small, retail assets across Austria. The

portfolio had a GLA of 206k sqm, with the average size of individual assets at around 2k sqm. The

portfolio is currently booked at EUR 206m. As the assets generate around EUR 19m annually, this

translates into a gross rental yield of c.9.1%.

The largest individual asset is the ZiB Shopping Centre (17.5k sqm GLA, according to IIA’s website),

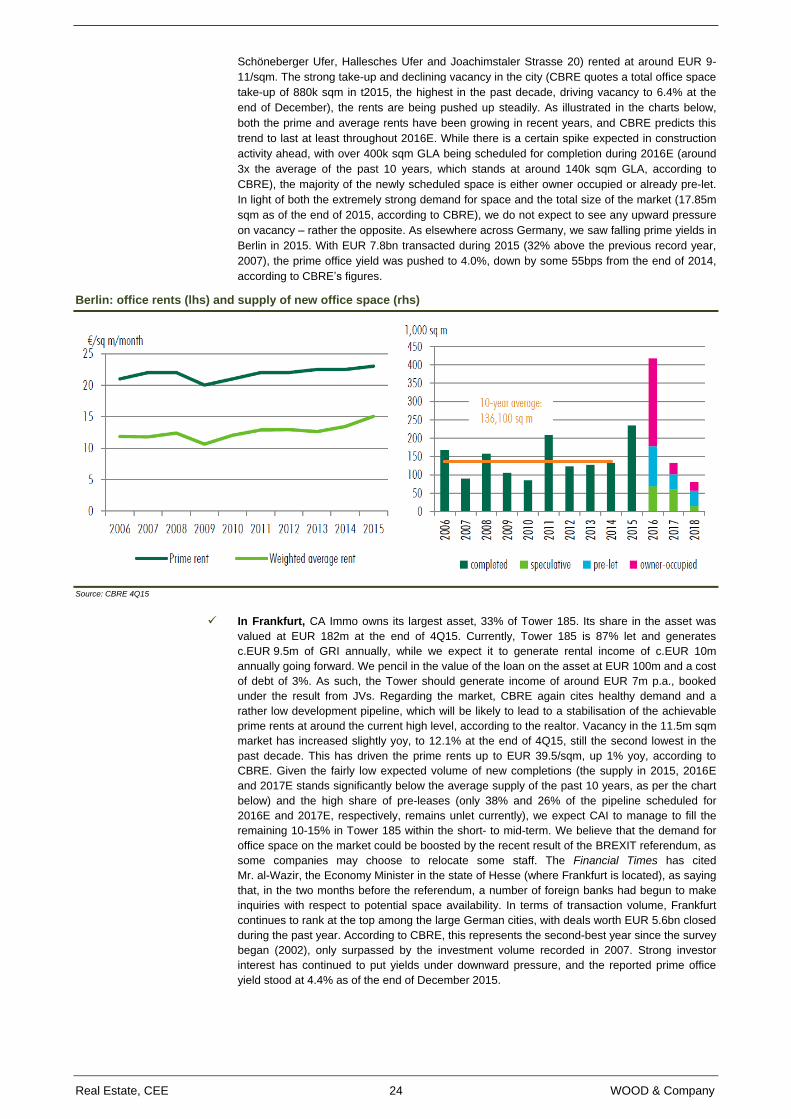

located in Salzburg. We expect a number of the smaller, non-core properties to be disposed of going

forward.

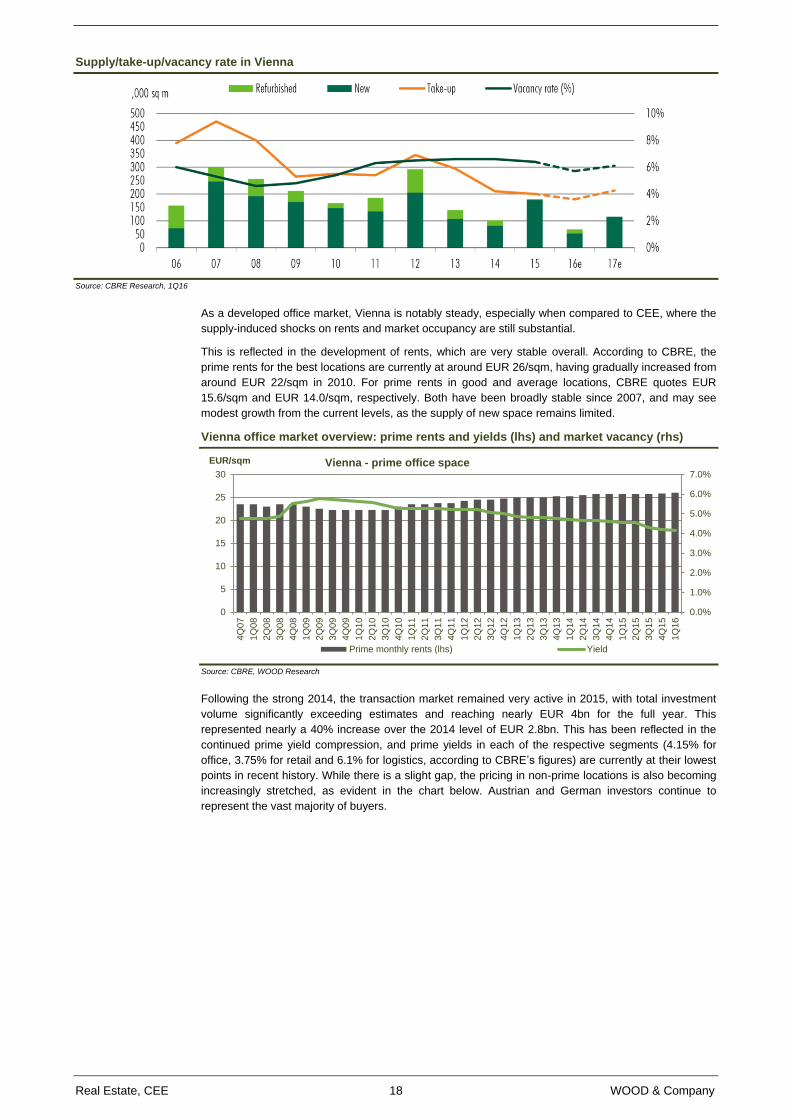

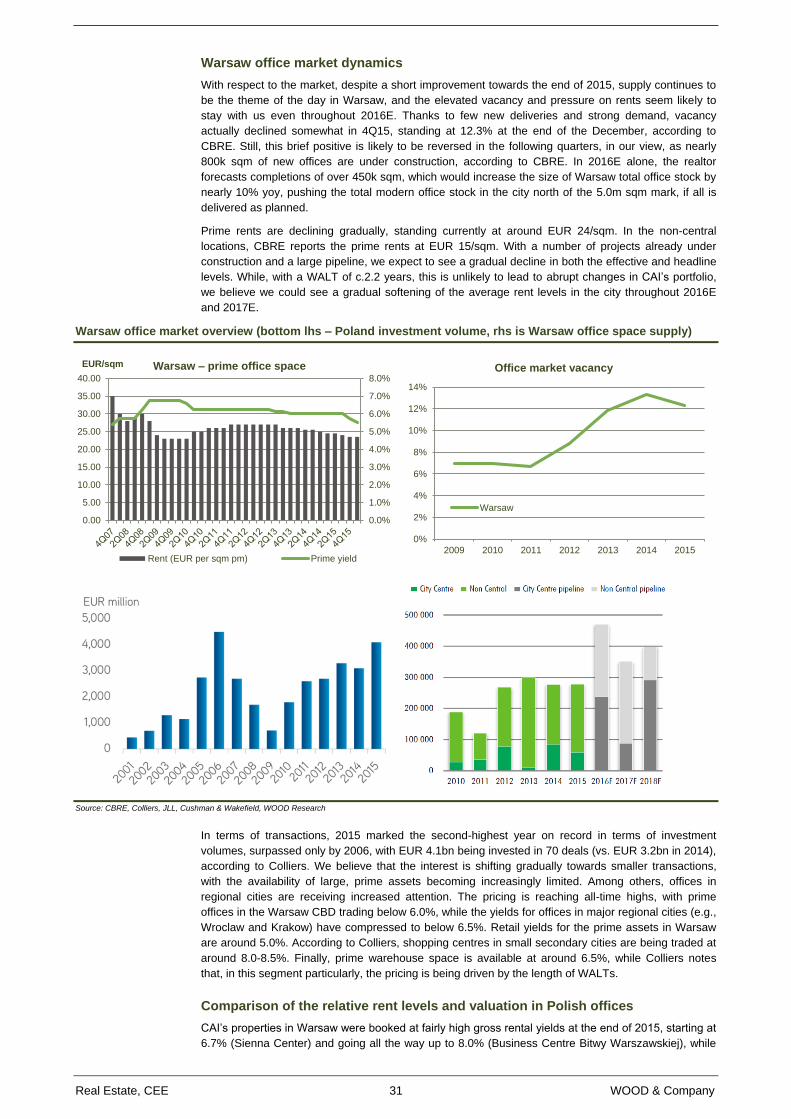

Vienna office market dynamics

The Vienna office market is broadly stable. After record-low supply in 2014, where the completions

totalled just a shy of 100k sqm – the lowest result in a decade – 2015 saw a brief spike in construction,

with nearly 200k sqm delivered to the market. While nearly double the 2014 volume, given the total

size of the market of c.11m sqm, there was no tangible impact on the market vacancy.

As can be seen in the chart below, the supply for both 2016E and 2017E remains at very low levels,

which should prove marginally beneficial for both IIA and CAI, in our view.

Considering the high level of pre-leases (according to CBRE, all the supply that will be completed in

2016E is already either pre-let or owner occupied) and the limited amount of new supply in general, the

occupancy remains very stable. The market vacancy has risen gradually from 2008, stabilising

between 6-7% in 2012, and has since been hovering around this level since, standing at 6.2% as of

1Q16, according to CBRE.

Real Estate, CEE 18 WOOD & Company

Supply/take-up/vacancy rate in Vienna

Source: CBRE Research, 1Q16

As a developed office market, Vienna is notably steady, especially when compared to CEE, where the

supply-induced shocks on rents and market occupancy are still substantial.

This is reflected in the development of rents, which are very stable overall. According to CBRE, the

prime rents for the best locations are currently at around EUR 26/sqm, having gradually increased from

around EUR 22/sqm in 2010. For prime rents in good and average locations, CBRE quotes EUR

15.6/sqm and EUR 14.0/sqm, respectively. Both have been broadly stable since 2007, and may see

modest growth from the current levels, as the supply of new space remains limited.

Vienna office market overview: prime rents and yields (lhs) and market vacancy (rhs)

Source: CBRE, WOOD Research

Following the strong 2014, the transaction market remained very active in 2015, with total investment

volume significantly exceeding estimates and reaching nearly EUR 4bn for the full year. This

represented nearly a 40% increase over the 2014 level of EUR 2.8bn. This has been reflected in the

continued prime yield compression, and prime yields in each of the respective segments (4.15% for

office, 3.75% for retail and 6.1% for logistics, according to CBRE’s figures) are currently at their lowest

points in recent history. While there is a slight gap, the pricing in non-prime locations is also becoming

increasingly stretched, as evident in the chart below. Austrian and German investors continue to

represent the vast majority of buyers.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0

5

10

15

20

25

30

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

EUR/sqm Vienna - prime office space

Prime monthly rents (lhs) Yield

Real Estate, CEE 19 WOOD & Company

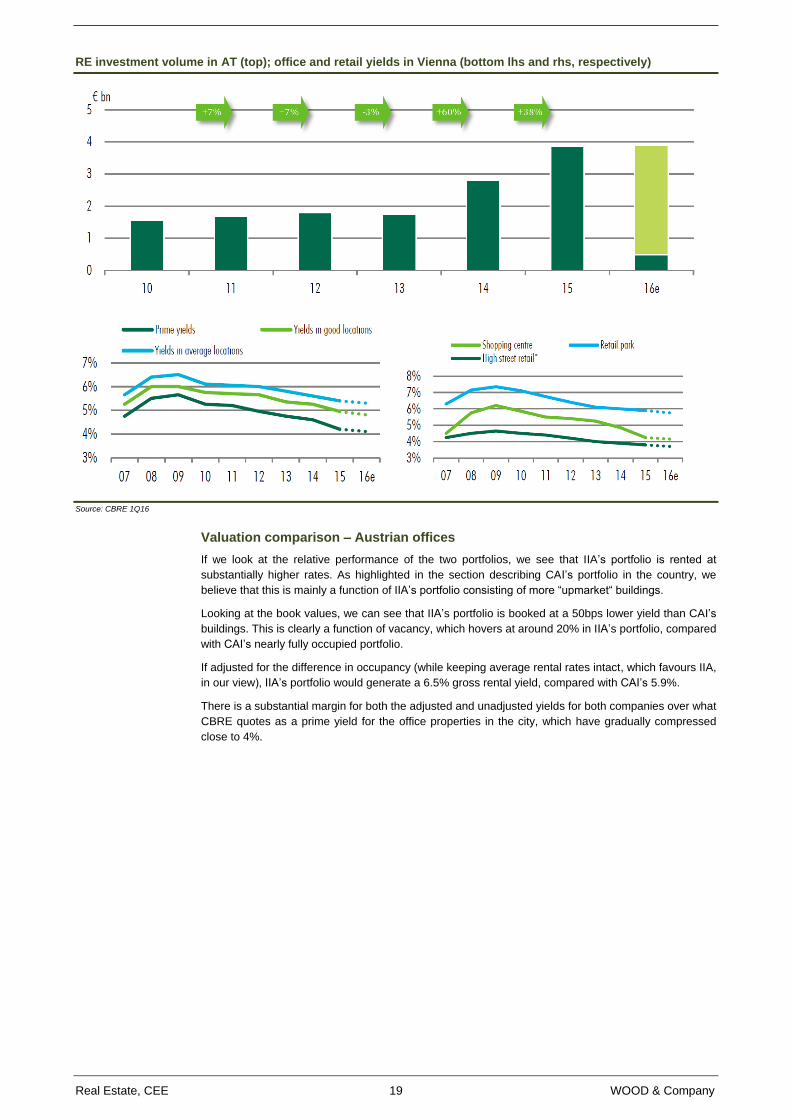

RE investment volume in AT (top); office and retail yields in Vienna (bottom lhs and rhs, respectively)

Source: CBRE 1Q16

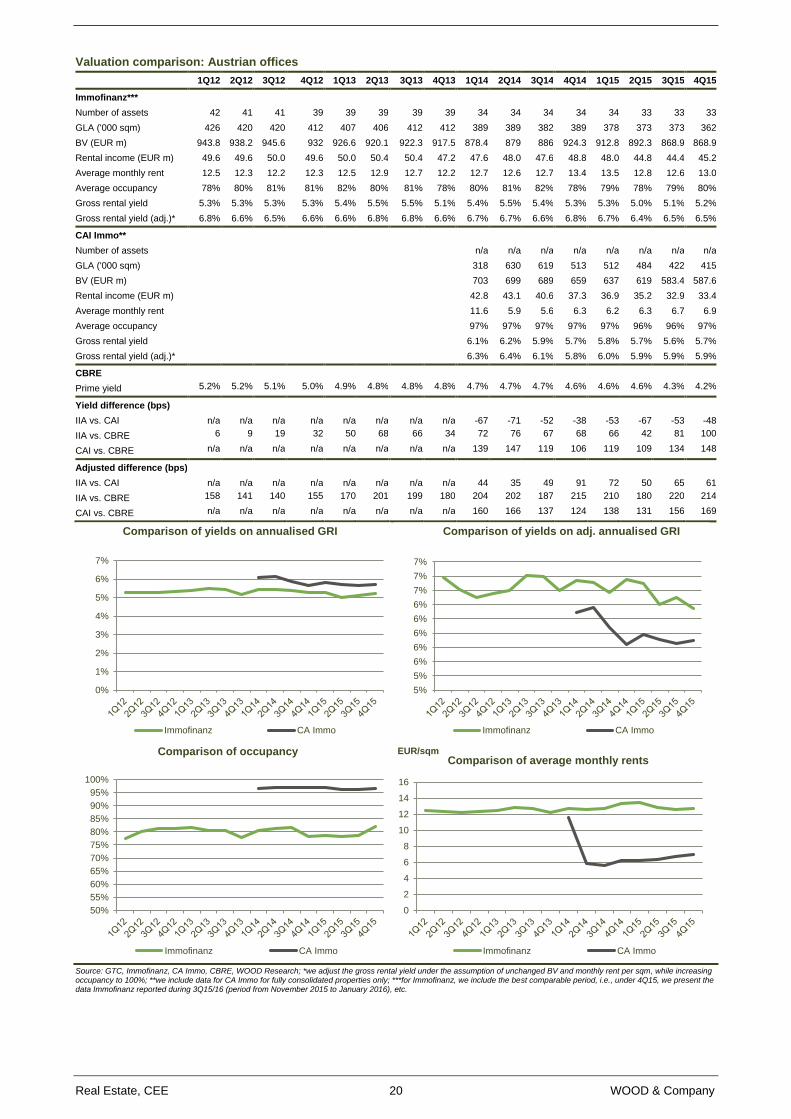

Valuation comparison – Austrian offices

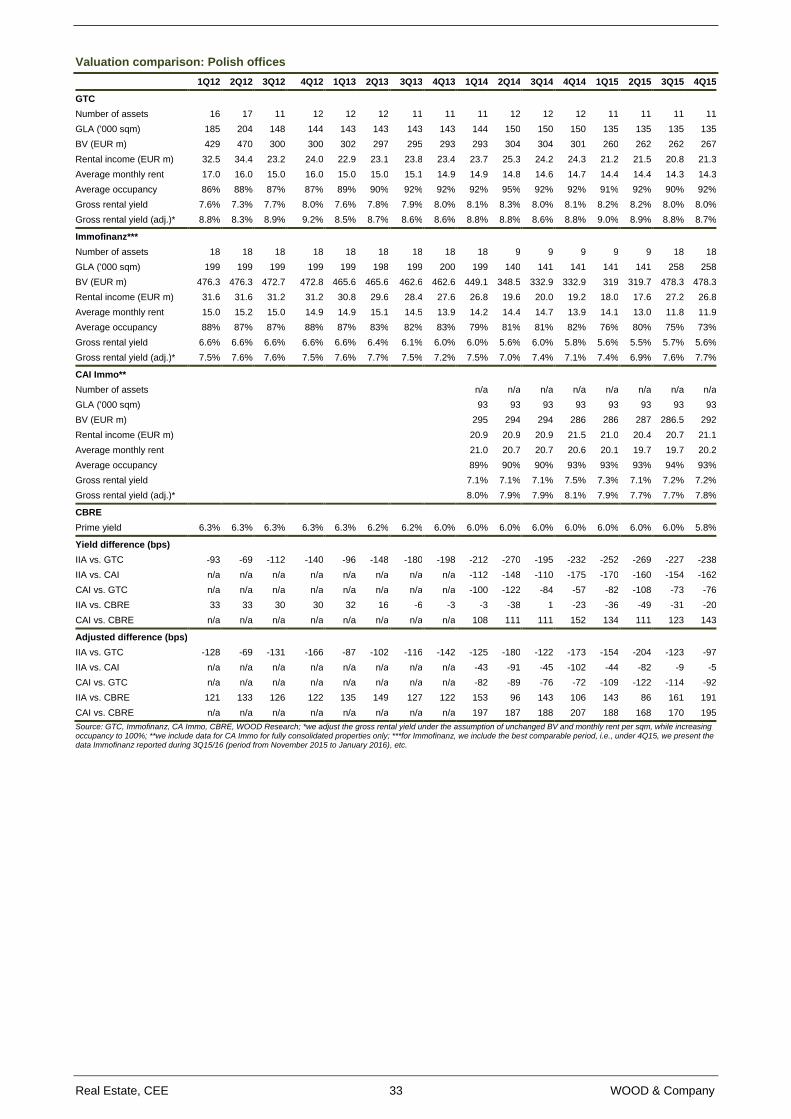

If we look at the relative performance of the two portfolios, we see that IIA’s portfolio is rented at

substantially higher rates. As highlighted in the section describing CAI’s portfolio in the country, we

believe that this is mainly a function of IIA’s portfolio consisting of more “upmarket“ buildings.

Looking at the book values, we can see that IIA’s portfolio is booked at a 50bps lower yield than CAI’s

buildings. This is clearly a function of vacancy, which hovers at around 20% in IIA’s portfolio, compared

with CAI’s nearly fully occupied portfolio.

If adjusted for the difference in occupancy (while keeping average rental rates intact, which favours IIA,

in our view), IIA’s portfolio would generate a 6.5% gross rental yield, compared with CAI’s 5.9%.

There is a substantial margin for both the adjusted and unadjusted yields for both companies over what

CBRE quotes as a prime yield for the office properties in the city, which have gradually compressed

close to 4%.

Real Estate, CEE 20 WOOD & Company

Valuation comparison: Austrian offices

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Immofinanz***

Number of assets 42 41 41 39 39 39 39 39 34 34 34 34 34 33 33 33

GLA ('000 sqm) 426 420 420 412 407 406 412 412 389 389 382 389 378 373 373 362

BV (EUR m) 943.8 938.2 945.6 932 926.6 920.1 922.3 917.5 878.4 879 886 924.3 912.8 892.3 868.9 868.9

Rental income (EUR m) 49.6 49.6 50.0 49.6 50.0 50.4 50.4 47.2 47.6 48.0 47.6 48.8 48.0 44.8 44.4 45.2

Average monthly rent 12.5 12.3 12.2 12.3 12.5 12.9 12.7 12.2 12.7 12.6 12.7 13.4 13.5 12.8 12.6 13.0

Average occupancy 78% 80% 81% 81% 82% 80% 81% 78% 80% 81% 82% 78% 79% 78% 79% 80%

Gross rental yield 5.3% 5.3% 5.3% 5.3% 5.4% 5.5% 5.5% 5.1% 5.4% 5.5% 5.4% 5.3% 5.3% 5.0% 5.1% 5.2%

Gross rental yield (adj.)* 6.8% 6.6% 6.5% 6.6% 6.6% 6.8% 6.8% 6.6% 6.7% 6.7% 6.6% 6.8% 6.7% 6.4% 6.5% 6.5%

CAI Immo**

Number of assets

n/a n/a n/a n/a n/a n/a n/a n/a

GLA ('000 sqm)

318 630 619 513 512 484 422 415

BV (EUR m)

703 699 689 659 637 619 583.4 587.6

Rental income (EUR m)

42.8 43.1 40.6 37.3 36.9 35.2 32.9 33.4

Average monthly rent

11.6 5.9 5.6 6.3 6.2 6.3 6.7 6.9

Average occupancy

97% 97% 97% 97% 97% 96% 96% 97%

Gross rental yield

6.1% 6.2% 5.9% 5.7% 5.8% 5.7% 5.6% 5.7%

Gross rental yield (adj.)* 6.3% 6.4% 6.1% 5.8% 6.0% 5.9% 5.9% 5.9%

CBRE

Prime yield 5.2% 5.2% 5.1% 5.0% 4.9% 4.8% 4.8% 4.8% 4.7% 4.7% 4.7% 4.6% 4.6% 4.6% 4.3% 4.2%

Yield difference (bps)

IIA vs. CAI n/a n/a n/a n/a n/a n/a n/a n/a -67 -71 -52 -38 -53 -67 -53 -48

IIA vs. CBRE 6 9 19 32 50 68 66 34 72 76 67 68 66 42 81 100

CAI vs. CBRE n/a n/a n/a n/a n/a n/a n/a n/a 139 147 119 106 119 109 134 148

Adjusted difference (bps)

IIA vs. CAI n/a n/a n/a n/a n/a n/a n/a n/a 44 35 49 91 72 50 65 61

IIA vs. CBRE 158 141 140 155 170 201 199 180 204 202 187 215 210 180 220 214

CAI vs. CBRE n/a n/a n/a n/a n/a n/a n/a n/a 160 166 137 124 138 131 156 169

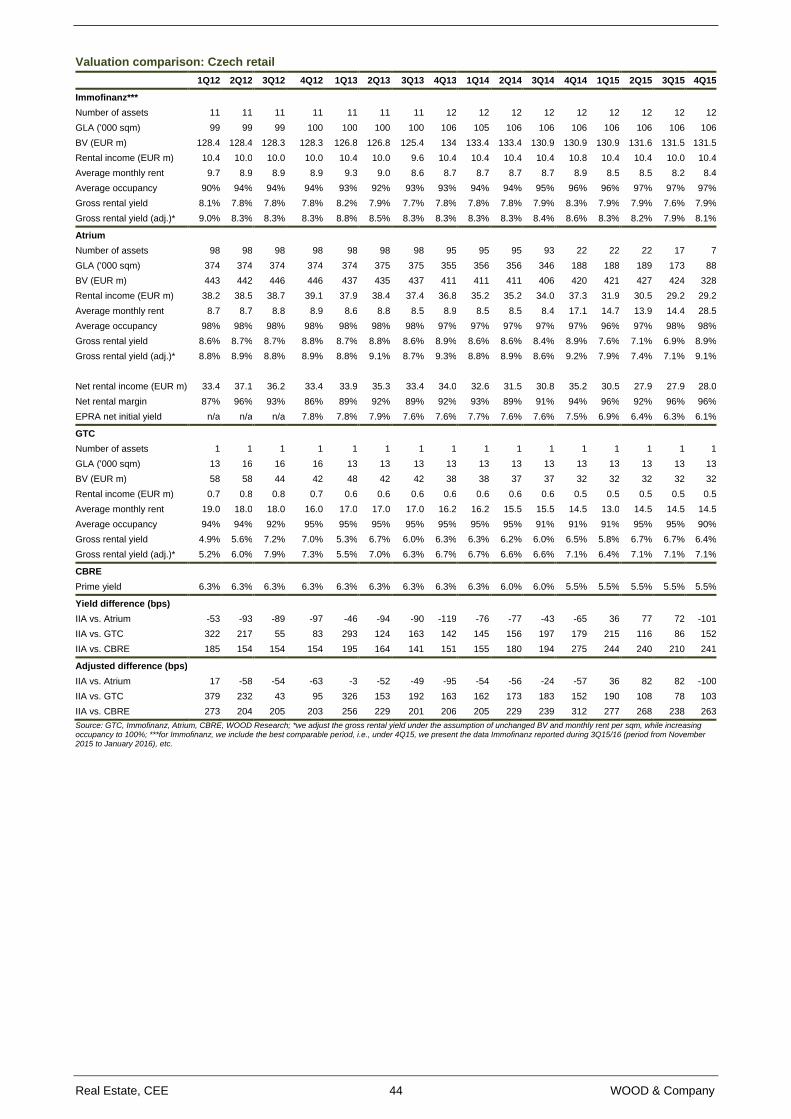

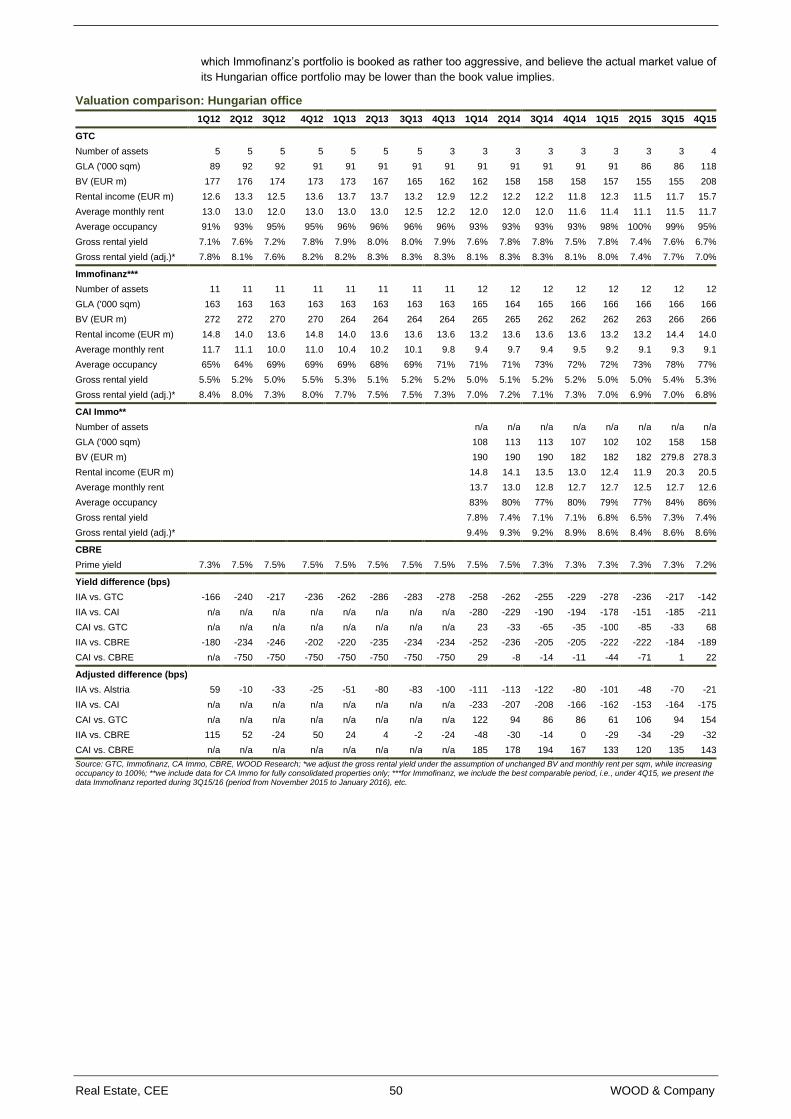

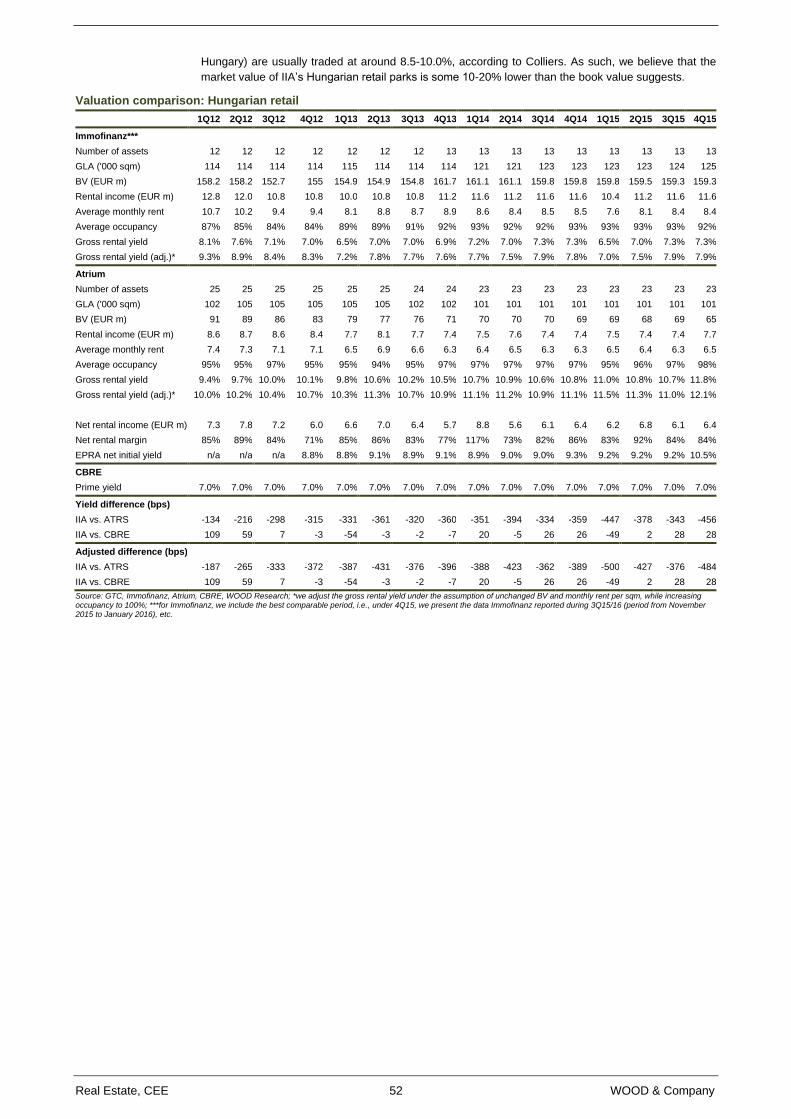

Source: GTC, Immofinanz, CA Immo, CBRE, WOOD Research; *we adjust the gross rental yield under the assumption of unchanged BV and monthly rent per sqm, while increasing occupancy to 100%; **we include data for CA Immo for fully consolidated properties only; ***for Immofinanz, we include the best comparable period, i.e., under 4Q15, we present the data Immofinanz reported during 3Q15/16 (period from November 2015 to January 2016), etc.

0%

1%

2%

3%

4%

5%

6%

7%

Comparison of yields on annualised GRI

Immofinanz CA Immo

5%

5%

6%

6%

6%

6%

6%

7%

7%

7%

Comparison of yields on adj. annualised GRI

Immofinanz CA Immo

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Comparison of occupancy

Immofinanz CA Immo

0

2

4

6

8

10

12

14

16

EUR/sqmComparison of average monthly rents

Immofinanz CA Immo

Real Estate, CEE 21 WOOD & Company

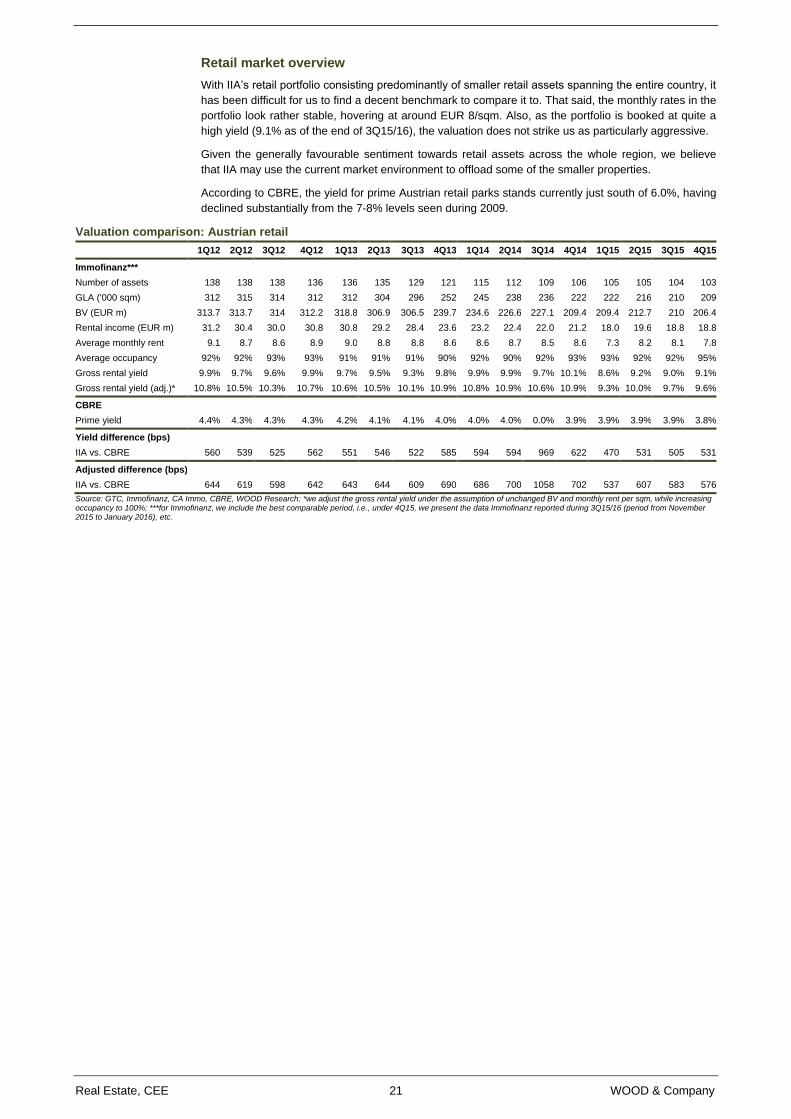

Retail market overview

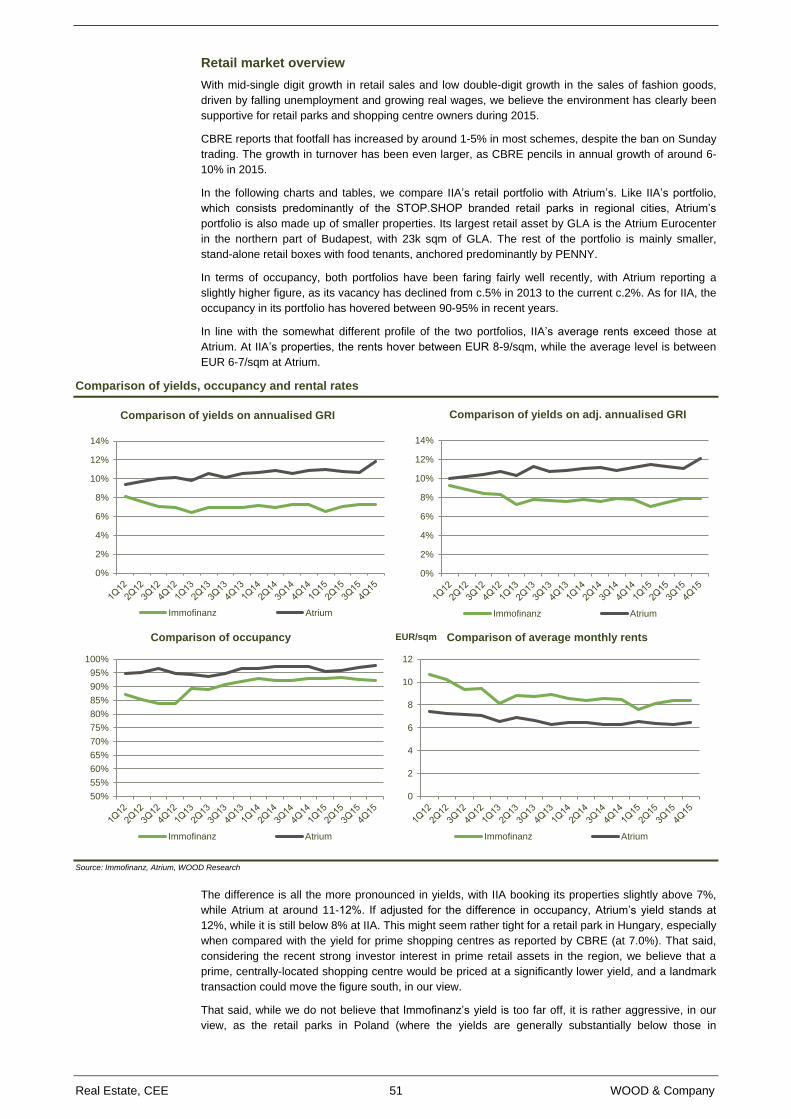

With IIA’s retail portfolio consisting predominantly of smaller retail assets spanning the entire country, it

has been difficult for us to find a decent benchmark to compare it to. That said, the monthly rates in the

portfolio look rather stable, hovering at around EUR 8/sqm. Also, as the portfolio is booked at quite a

high yield (9.1% as of the end of 3Q15/16), the valuation does not strike us as particularly aggressive.

Given the generally favourable sentiment towards retail assets across the whole region, we believe

that IIA may use the current market environment to offload some of the smaller properties.

According to CBRE, the yield for prime Austrian retail parks stands currently just south of 6.0%, having

declined substantially from the 7-8% levels seen during 2009.

Valuation comparison: Austrian retail

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Immofinanz***

Number of assets 138 138 138 136 136 135 129 121 115 112 109 106 105 105 104 103

GLA ('000 sqm) 312 315 314 312 312 304 296 252 245 238 236 222 222 216 210 209

BV (EUR m) 313.7 313.7 314 312.2 318.8 306.9 306.5 239.7 234.6 226.6 227.1 209.4 209.4 212.7 210 206.4

Rental income (EUR m) 31.2 30.4 30.0 30.8 30.8 29.2 28.4 23.6 23.2 22.4 22.0 21.2 18.0 19.6 18.8 18.8

Average monthly rent 9.1 8.7 8.6 8.9 9.0 8.8 8.8 8.6 8.6 8.7 8.5 8.6 7.3 8.2 8.1 7.8

Average occupancy 92% 92% 93% 93% 91% 91% 91% 90% 92% 90% 92% 93% 93% 92% 92% 95%

Gross rental yield 9.9% 9.7% 9.6% 9.9% 9.7% 9.5% 9.3% 9.8% 9.9% 9.9% 9.7% 10.1% 8.6% 9.2% 9.0% 9.1%

Gross rental yield (adj.)* 10.8% 10.5% 10.3% 10.7% 10.6% 10.5% 10.1% 10.9% 10.8% 10.9% 10.6% 10.9% 9.3% 10.0% 9.7% 9.6%

CBRE

Prime yield 4.4% 4.3% 4.3% 4.3% 4.2% 4.1% 4.1% 4.0% 4.0% 4.0% 0.0% 3.9% 3.9% 3.9% 3.9% 3.8%

Yield difference (bps)

IIA vs. CBRE 560 539 525 562 551 546 522 585 594 594 969 622 470 531 505 531

Adjusted difference (bps)

IIA vs. CBRE 644 619 598 642 643 644 609 690 686 700 1058 702 537 607 583 576

Source: GTC, Immofinanz, CA Immo, CBRE, WOOD Research; *we adjust the gross rental yield under the assumption of unchanged BV and monthly rent per sqm, while increasing occupancy to 100%; ***for Immofinanz, we include the best comparable period, i.e., under 4Q15, we present the data Immofinanz reported during 3Q15/16 (period from November 2015 to January 2016), etc.

Real Estate, CEE 22 WOOD & Company

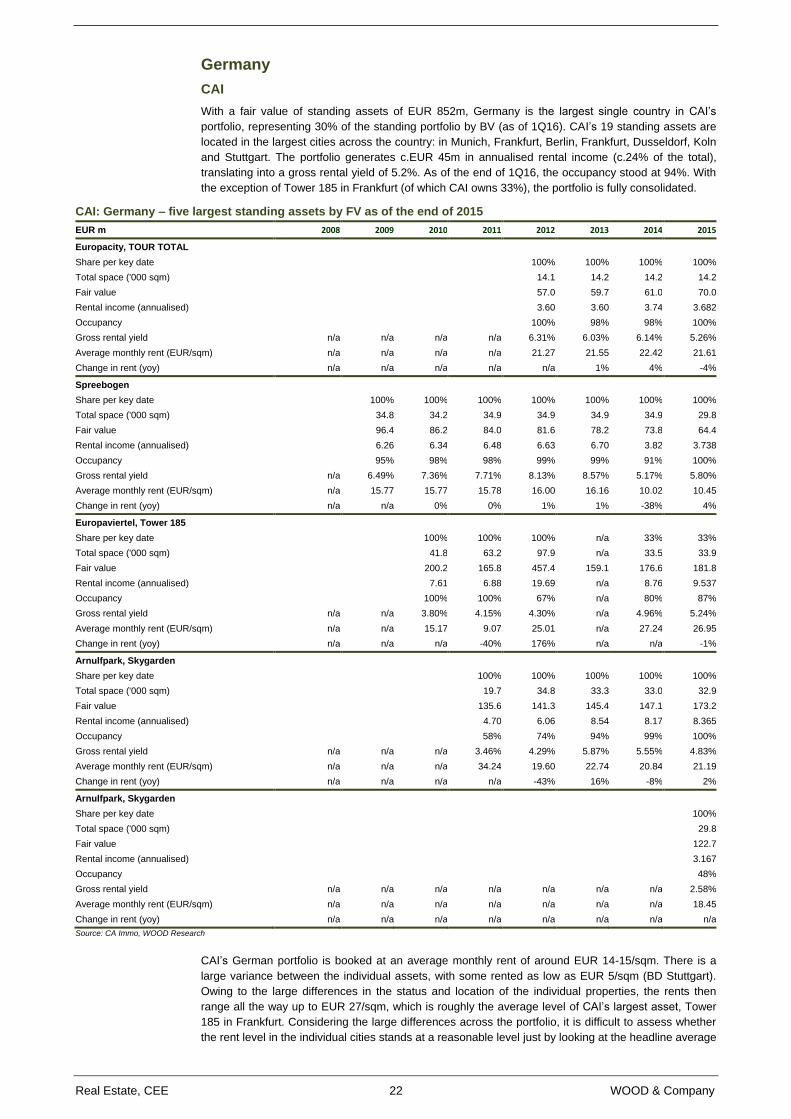

Germany

CAI

With a fair value of standing assets of EUR 852m, Germany is the largest single country in CAI’s

portfolio, representing 30% of the standing portfolio by BV (as of 1Q16). CAI’s 19 standing assets are

located in the largest cities across the country: in Munich, Frankfurt, Berlin, Frankfurt, Dusseldorf, Koln

and Stuttgart. The portfolio generates c.EUR 45m in annualised rental income (c.24% of the total),

translating into a gross rental yield of 5.2%. As of the end of 1Q16, the occupancy stood at 94%. With

the exception of Tower 185 in Frankfurt (of which CAI owns 33%), the portfolio is fully consolidated.

CAI: Germany – five largest standing assets by FV as of the end of 2015

EUR m 2008 2009 2010 2011 2012 2013 2014 2015

Europacity, TOUR TOTAL

Share per key date

100% 100% 100% 100%

Total space ('000 sqm)

14.1 14.2 14.2 14.2

Fair value

57.0 59.7 61.0 70.0

Rental income (annualised)

3.60 3.60 3.74 3.682

Occupancy

100% 98% 98% 100%