company report

TRANSCRIPT

Monday, April 10, 2017

Company Report China Merchants Securities (HK) Co., Ltd.

Hong Kong Equity Research

Please see penultimate page for additional important disclosures. China Merchants Securities (CMS) is a foreign broker-dealer unregistered in the USA. CMS research is prepared by research analysts who are not registered in the USA. CMS research is distributed in the USA pursuant to Rule 15a-6 of the Securities Exchange Act of 1934 solely by Rosenblatt Securities, an SEC registered and FINRA-member broker-dealer. 1

Wonderful Sky (1260 HK) Wonderful PR firm as a leader and innovator

■ With its 21 years of development, Wonderful Sky is the leading

financial PR firm in HK and the only one of its kind being listed. It dominated HK IPO market with 88% market share in 2016

■ Revenue to grow at 1%/9%/8% in FY17E/18E/19E (Mar) with high

core net margin of 32%/33%/34% on the growing number of long-term clients as well as IPO projects

■ Leveraging on its dominating position, we see Wonderful Sky’s

growth trend and high margin to be sustainable. Initiate with BUY & TP of HK$2.51 at 13x FY18E (Mar) P/E, in line with the 5-year avg of its global peers

Leader in HK financial Public Relation (PR) services Wonderful Sky dominated 88% HK IPO market in terms of fund-raising size, covering all the top-10 HK IPO deals in 2016. It provides a full range of financial PR services throughout pre-IPO to post-IPO via its five-in-one platform: 1) financial public relations, 2) financial printing, 3) international roadshow, 4) corporate branding, and 5) investor relations. Moreover, it is the only PR firm serving A+H market listed corporates for IPO, M&A, bond issuance and restructuring. Besides, the company is planning to launch phase I of its online financial service platform “Wonderful Cloud” in late 2017, which could enhance client loyalty and bring synergies throughout its financial PR/IR services.

Stable growth, high margin, new drivers kicking in We expect five factors to drive the company’s growth: 1) more IPOs in HK and China, 2) expansion of its client base, 3) ramp-up of IPO printing, 4) expansion into China and global markets, and 5) extension into eight-in-one service platform. As a result, we expect its revenue to reach HK$737mn in FY19E, implying a stable CAGR of 9% during FY17E-19E. We expect high core net margin of 32-34% within this period.

Strong profitability with high dividend yield Trading at 11x FY18E P/E (Mar year-end), Wonderful Sky’s valuation is at 31% discount to its global peers. We believe the stock is undervalued given its strong core net profit growth of 13% and 5% dividend yield in FY18E. We expect the re-rating door to be unlocked when 1) its number of long-term clients grows rapidly, 2) China govt launches registration-based IPO system with faster IPO process, and 3) phase I of Wonderful Cloud is launched in late 2017.

Financials (Mar year-end)

HK$ mn FY15 FY16 FY17E FY18E FY19E

Revenue 524 619 626 683 737

Growth (%) 14.2% 18.2% 1.0% 9.1% 7.9%

Core net profit 190 198 200 225 253

Growth (%) 28.8% 4.2% 0.7% 12.5% 12.4%

Core EPS (HK$) (excluding after-tax gain/loss from fin. inv)

0.19 0.17 0.17 0.19 0.21

P/E (x) 11.0x 12.4x 12.5x 11.1x 9.9x

Dividend yield (%) 5.2% 5.8% 6.2% 5.4% 6.0%

ROE (%) 26% 16% 15% 16% 17%

Sources: Company data, CMS (HK) estimates

Ryan YU

+852 3189 6268

Angela HAN LEE

+852 3189 6634

WHAT’S NEW

Initiation

BUY

Previous N.A.

Price HK$2.09

12-month Target Price (Potential up/downside)

HK$2.51 (+20%)

Previous N.A.

Price Performance

Source: Bigdata

% 1m 6m 12m

1260 HK (0.5) (12.6) 11.2 HSI 2.5 1.7 19.7

Sector: Media

Hang Seng Index 24,267

HSCEI 10,274

Key Data

52-week range (HK$) 1.70 / 2.43

Market cap (US$ mn) 321

Avg. daily volume (mn) 1.3

BVPS (HK$) 1.0

Shareholding Structure Liu’s family 64%

Value Partners 6%

No. of shares outstanding (mn) 1192 Others 30%

-10

0

10

20

30

Apr/16 Jul/16 Nov/16 Mar/17

(%) 1260 HSI Index

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 2

Investment thesis

Market leader with competitive advantage With its 21 years of development, Wonderful Sky has a dominating position with competitive advantage over its competitors: 1) good reputation, 2) strong bargaining power to suppliers, 3) service specialization, 4) full-range PR/IR services, and 5) the ability to offer A+H financial PR services. Besides, the company is planning to launch phase I of its online financial service platform “Wonderful Cloud” in late 2017, which could enhance client loyalty and bring synergies throughout its financial PR/IR services.

Five investment highlights 1) HK is the largest IPO market and China’s IPO process is

accelerating: HKEx has been the world No.1 stock exchange for IPO fund raised for two consecutive years. Given the improved regulation and approval system, China’s IPO approval process is accelerating with IPO fund raised tripled in 2H16 vs. 1H16.

2) Stable expansion of its client base: the quantity of its long-term clients has been increasing by c.40 per year in the past three financial years, and could grow at an accelerated pace given its leading position and solid reputation in the market.

3) The company is enlarging its lucrative IPO printing business: the company has completed 2 projects in 2015, 4 in 2016 and has 15 projects in the pipeline.

4) Strengthening footprint in China and expanding into Singapore, New York and London with its experienced team in PR services and good reputation.

5) Upgrading to eight-in-one service platform by adding new value-added services: 1) ESG reporting, 2) business consultant, and 3) executive recruiters.

Healthy financial position with high dividend yield Asset-light business with high profitability. Given its 1) stable cash flow from recurring business, and 2) relatively low CAPEX requirements, we expect Wonderful Sky to continue generating strong cash flows and strengthening its cash balance. We estimate its gross margin to remain high at 52-54% and core net margin to reach 32-34% in FY17E-19E.

Dividend payout ratio to remain high at 60%, implying 5% dividend yield in FY18E. Historically, Wonderful Sky has a high dividend payout ratio (60% in FY14/15/16). Given its solid cash position and stable cash flow, we expect that the company will maintain its high dividend policy, which should be loved by high-yield seekers.

Revenue to rebound from the high base effect of roadshow revenue in 1H16. We expect total revenue to grow 1% in FY17E, given 37% YoY decline in roadshow revenue in 1H17. The decline was due to outperformance in 1H16 on 1) larger projects with above-average roadshow revenue, and 2) more IPO projects (15 vs. 11 projects in 1H16/1H17). We expect the roadshow revenue to record -1% YoY, +20% HoH in 2H17 and grow stably with 9% CAGR during FY17E-19E.

We initiate coverage of Wonderful Sky with BUY rating and TP of HK$2.51. Our 12-month TP is based on 13x FY18E P/E, in line with the 5-year historical average of its global peers. Catalysts are: 1) its number of long-term clients grows rapidly, 2) China govt launches registration-based IPO system with faster IPO process, and 3) phase I of Wonderful Cloud is launched in late 2017. Risks include: 1) substantial drop in the number of IPO projects, 2) losing market share to competitors, and 3) negative political changes.

88% market share in HK IPO market in terms of fund raised

Actively expanding the scope of business coverage not only geographically but also in terms of service diversity

60% dividend payout ratio and 5% dividend yield

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 3

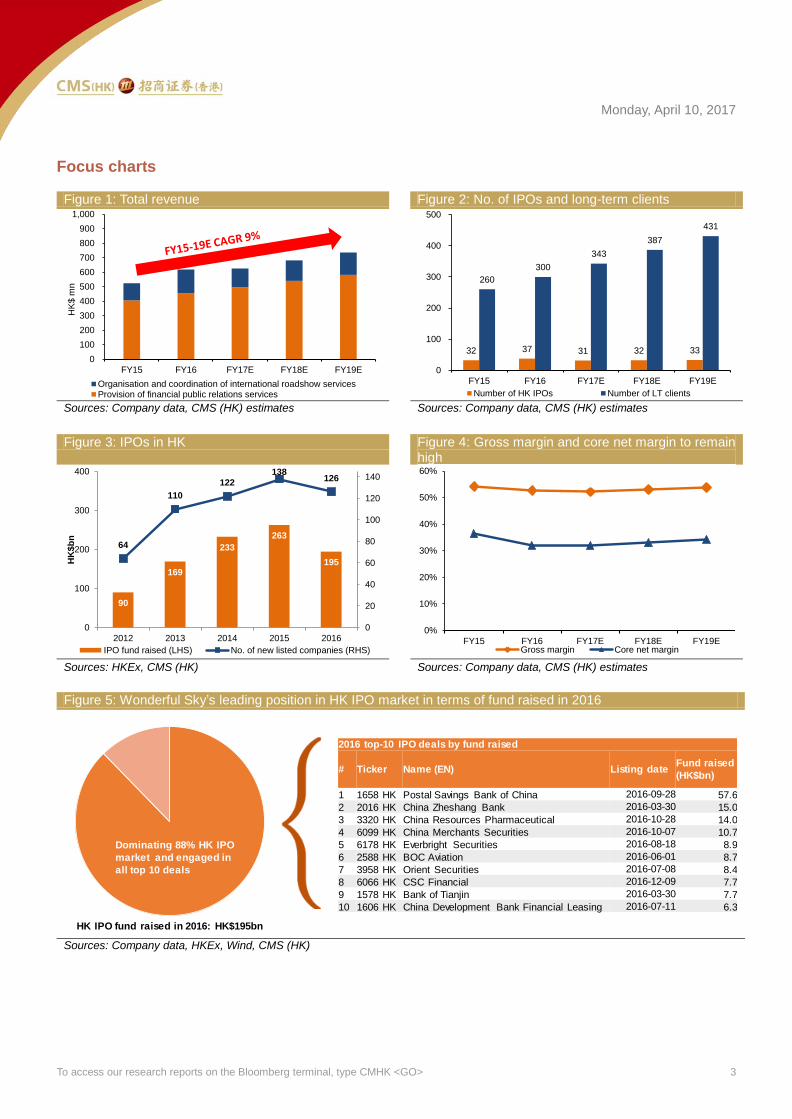

Focus charts

Figure 1: Total revenue Figure 2: No. of IPOs and long-term clients

Sources: Company data, CMS (HK) estimates Sources: Company data, CMS (HK) estimates

Figure 3: IPOs in HK Figure 4: Gross margin and core net margin to remain

high

Sources: HKEx, CMS (HK) Sources: Company data, CMS (HK) estimates

Figure 5: Wonderful Sky’s leading position in HK IPO market in terms of fund raised in 2016

Sources: Company data, HKEx, Wind, CMS (HK)

0

100

200

300

400

500

600

700

800

900

1,000

FY15 FY16 FY17E FY18E FY19E

HK

$ m

n

Organisation and coordination of international roadshow servicesProvision of financial public relations services

32 37 31 32 33

260

300

343

387

431

0

100

200

300

400

500

FY15 FY16 FY17E FY18E FY19E

Number of HK IPOs Number of LT clients

90

169

233

263

195

64

110

122

138126

0

20

40

60

80

100

120

140

0

100

200

300

400

2012 2013 2014 2015 2016

HK

$b

n

IPO fund raised (LHS) No. of new listed companies (RHS)

0%

10%

20%

30%

40%

50%

60%

FY15 FY16 FY17E FY18E FY19EGross margin Core net margin

Dominating 88% HK IPO

market and engaged in

all top 10 deals

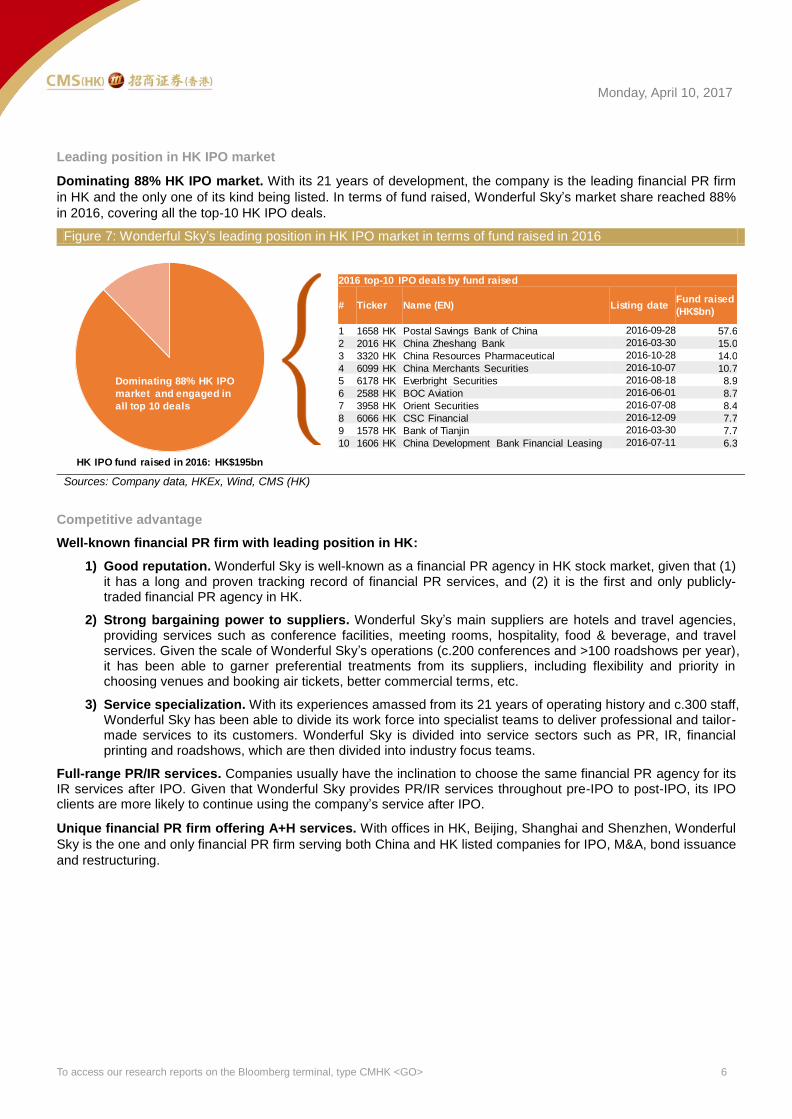

2016 top-10 IPO deals by fund raised

# Ticker Name (EN) Listing dateFund raised

(HK$bn)

1 1658 HK Postal Savings Bank of China 2016-09-28 57.6

2 2016 HK China Zheshang Bank 2016-03-30 15.0

3 3320 HK China Resources Pharmaceutical 2016-10-28 14.0

4 6099 HK China Merchants Securities 2016-10-07 10.7

5 6178 HK Everbright Securities 2016-08-18 8.9

6 2588 HK BOC Aviation 2016-06-01 8.7

7 3958 HK Orient Securities 2016-07-08 8.4

8 6066 HK CSC Financial 2016-12-09 7.7

9 1578 HK Bank of Tianjin 2016-03-30 7.7

10 1606 HK China Development Bank Financial Leasing 2016-07-11 6.3

HK IPO fund raised in 2016: HK$195bn

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 4

Contents

Investment thesis ........................................................................................................................................................ 2

Focus charts................................................................................................................................................................. 3

Business overview ...................................................................................................................................................... 5

Five-in-one financial PR/IR 5

Leading position in HK IPO market 6

Competitive advantage 6

“Wonderful Cloud” on the way 7

Driver #1: Rooted in the largest IPO market ............................................................................................................. 8

HK – the world no.1 market of IPO fund raised in 2015/2016 8

China – improving IPO process with huge potential 8

Driver #2: Increasing number of long-term clients .................................................................................................. 9

Stable expansion of long-term client base 9

Even faster growth in the future 9

High contribution from recurring business 9

Driver #3: Ramp-up of IPO printing.......................................................................................................................... 10

Started IPO printing in 2015 10

Financial printing – still a fragmented market 10

Cutting a larger slice from the lucrative pie 10

Driver #4: Geographical expansions ........................................................................................................................ 11

Penetrating into China market 11

Footprints in Singapore 11

Global expansions 11

Driver #5: Eight-in-One Service Platform – adding three more value-added services ....................................... 12

ESG (Environmental, Social and Governance) reporting 12

Business consultant 12

Executive recruiters 12

Financial analysis ...................................................................................................................................................... 13

Revenue and P&L analysis 13

Balance sheet and cash flow analysis 15

Valuation ..................................................................................................................................................................... 16

Peer valuation table ................................................................................................................................................... 17

Risks ........................................................................................................................................................................... 18

Appendix 1: Shareholding structure ....................................................................................................................... 19

Appendix 2: Company history .................................................................................................................................. 19

Appendix 3: Profile of directors ............................................................................................................................... 20

Appendix 4: Wonderful Sky’s IPO projects in Hong Kong since Jan 2016 ......................................................... 21

Financial summary (Mar year-end) .......................................................................................................................... 22

Investment Ratings .................................................................................................................................................... 23

Disclaimer ................................................................................................................................................................... 23

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 5

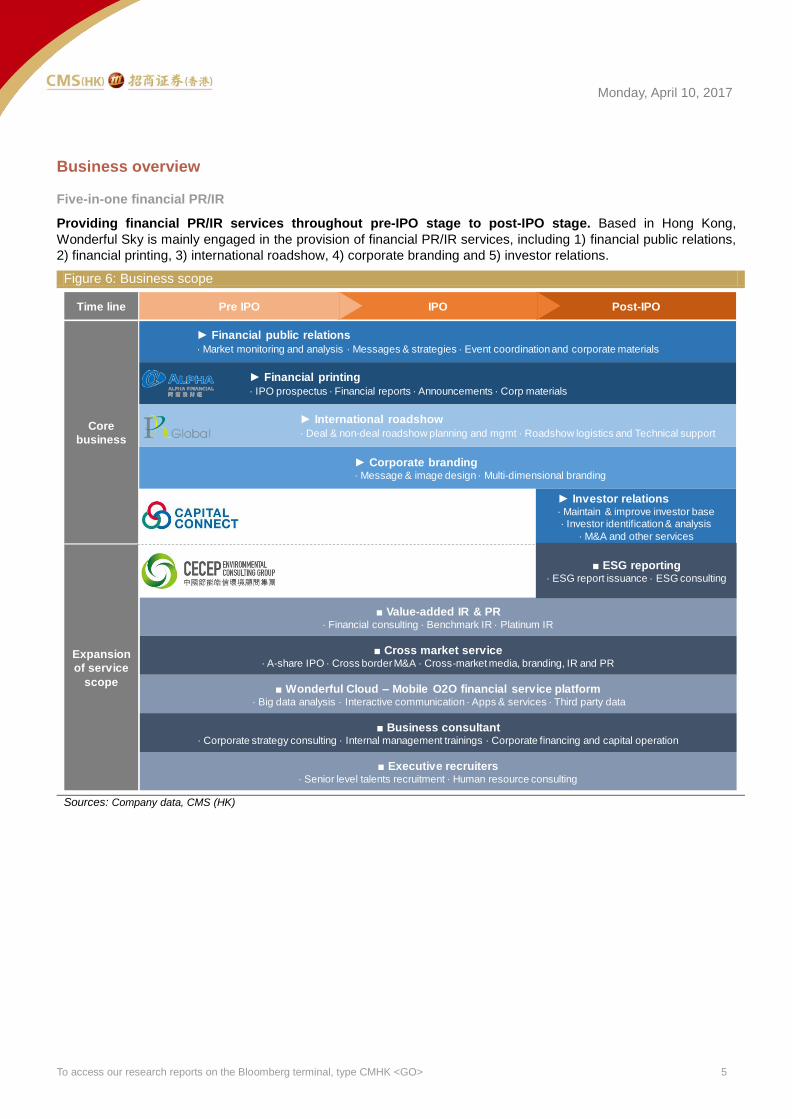

Business overview

Five-in-one financial PR/IR

Providing financial PR/IR services throughout pre-IPO stage to post-IPO stage. Based in Hong Kong,

Wonderful Sky is mainly engaged in the provision of financial PR/IR services, including 1) financial public relations,

2) financial printing, 3) international roadshow, 4) corporate branding and 5) investor relations.

Figure 6: Business scope

Sources: Company data, CMS (HK)

Post-IPO

Financial public relations

· Market monitoring and analysis · Messages & strategies · Event coordination and corporate materials

Financial printing

· IPO prospectus · Financial reports · Announcements · Corp materials

Corporate branding· Message & image design · Multi-dimensional branding

International roadshow

· Deal & non-deal roadshow planning and mgmt · Roadshow logistics and Technical support

Investor relations· Maintain & improve investor base· Investor identification & analysis

· M&A and other services

Time line

Core

business

Expansion

of service

scope

■ Value-added IR & PR· Financial consulting · Benchmark IR · Platinum IR

■ Cross market service· A-share IPO · Cross border M&A · Cross-market media, branding, IR and PR

■ Wonderful Cloud – Mobile O2O financial service platform· Big data analysis · Interactive communication · Apps & services · Third party data

IPOPre IPO

■ ESG reporting· ESG report issuance · ESG consulting

■ Business consultant· Corporate strategy consulting · Internal management trainings · Corporate financing and capital operation

■ Executive recruiters· Senior level talents recruitment · Human resource consulting

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 6

Leading position in HK IPO market

Dominating 88% HK IPO market. With its 21 years of development, the company is the leading financial PR firm

in HK and the only one of its kind being listed. In terms of fund raised, Wonderful Sky’s market share reached 88%

in 2016, covering all the top-10 HK IPO deals.

Figure 7: Wonderful Sky’s leading position in HK IPO market in terms of fund raised in 2016

Sources: Company data, HKEx, Wind, CMS (HK)

Competitive advantage

Well-known financial PR firm with leading position in HK:

1) Good reputation. Wonderful Sky is well-known as a financial PR agency in HK stock market, given that (1) it has a long and proven tracking record of financial PR services, and (2) it is the first and only publicly-traded financial PR agency in HK.

2) Strong bargaining power to suppliers. Wonderful Sky’s main suppliers are hotels and travel agencies, providing services such as conference facilities, meeting rooms, hospitality, food & beverage, and travel services. Given the scale of Wonderful Sky’s operations (c.200 conferences and >100 roadshows per year), it has been able to garner preferential treatments from its suppliers, including flexibility and priority in choosing venues and booking air tickets, better commercial terms, etc.

3) Service specialization. With its experiences amassed from its 21 years of operating history and c.300 staff, Wonderful Sky has been able to divide its work force into specialist teams to deliver professional and tailor-made services to its customers. Wonderful Sky is divided into service sectors such as PR, IR, financial printing and roadshows, which are then divided into industry focus teams.

Full-range PR/IR services. Companies usually have the inclination to choose the same financial PR agency for its IR services after IPO. Given that Wonderful Sky provides PR/IR services throughout pre-IPO to post-IPO, its IPO clients are more likely to continue using the company’s service after IPO.

Unique financial PR firm offering A+H services. With offices in HK, Beijing, Shanghai and Shenzhen, Wonderful

Sky is the one and only financial PR firm serving both China and HK listed companies for IPO, M&A, bond issuance

and restructuring.

Dominating 88% HK IPO

market and engaged in

all top 10 deals

2016 top-10 IPO deals by fund raised

# Ticker Name (EN) Listing dateFund raised

(HK$bn)

1 1658 HK Postal Savings Bank of China 2016-09-28 57.6

2 2016 HK China Zheshang Bank 2016-03-30 15.0

3 3320 HK China Resources Pharmaceutical 2016-10-28 14.0

4 6099 HK China Merchants Securities 2016-10-07 10.7

5 6178 HK Everbright Securities 2016-08-18 8.9

6 2588 HK BOC Aviation 2016-06-01 8.7

7 3958 HK Orient Securities 2016-07-08 8.4

8 6066 HK CSC Financial 2016-12-09 7.7

9 1578 HK Bank of Tianjin 2016-03-30 7.7

10 1606 HK China Development Bank Financial Leasing 2016-07-11 6.3

HK IPO fund raised in 2016: HK$195bn

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 7

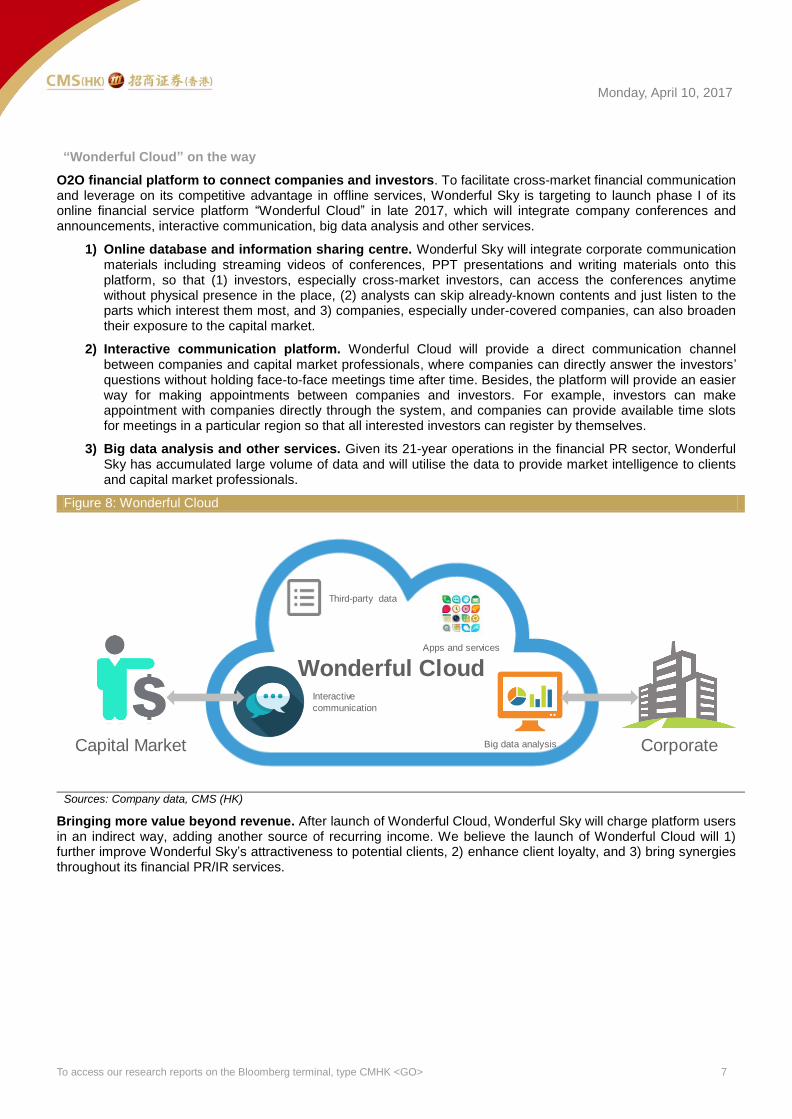

“Wonderful Cloud” on the way

O2O financial platform to connect companies and investors. To facilitate cross-market financial communication and leverage on its competitive advantage in offline services, Wonderful Sky is targeting to launch phase I of its online financial service platform “Wonderful Cloud” in late 2017, which will integrate company conferences and announcements, interactive communication, big data analysis and other services.

1) Online database and information sharing centre. Wonderful Sky will integrate corporate communication materials including streaming videos of conferences, PPT presentations and writing materials onto this platform, so that (1) investors, especially cross-market investors, can access the conferences anytime without physical presence in the place, (2) analysts can skip already-known contents and just listen to the parts which interest them most, and 3) companies, especially under-covered companies, can also broaden their exposure to the capital market.

2) Interactive communication platform. Wonderful Cloud will provide a direct communication channel between companies and capital market professionals, where companies can directly answer the investors’ questions without holding face-to-face meetings time after time. Besides, the platform will provide an easier way for making appointments between companies and investors. For example, investors can make appointment with companies directly through the system, and companies can provide available time slots for meetings in a particular region so that all interested investors can register by themselves.

3) Big data analysis and other services. Given its 21-year operations in the financial PR sector, Wonderful Sky has accumulated large volume of data and will utilise the data to provide market intelligence to clients and capital market professionals.

Figure 8: Wonderful Cloud

Sources: Company data, CMS (HK)

Bringing more value beyond revenue. After launch of Wonderful Cloud, Wonderful Sky will charge platform users in an indirect way, adding another source of recurring income. We believe the launch of Wonderful Cloud will 1) further improve Wonderful Sky’s attractiveness to potential clients, 2) enhance client loyalty, and 3) bring synergies throughout its financial PR/IR services.

Wonderful Cloud

Capital Market

Interactive

communication

Big data analysis

Third-party data

Apps and services

Corporate

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 8

Driver #1: Rooted in the largest IPO market

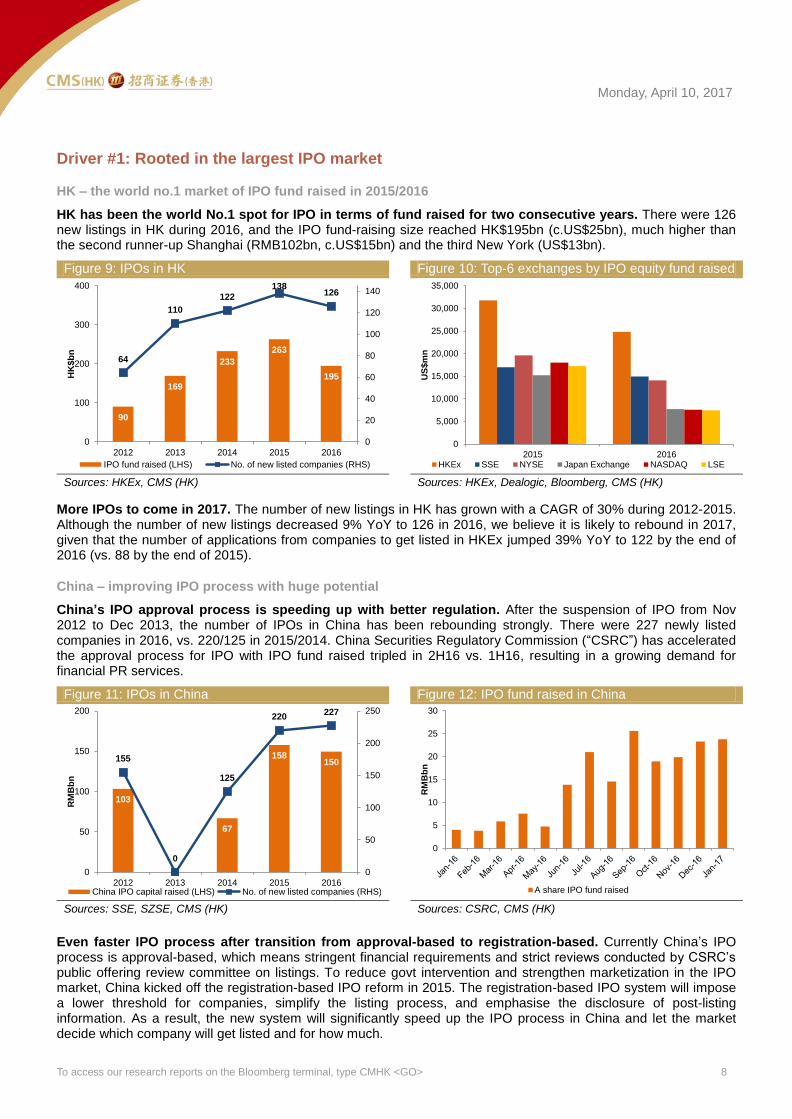

HK – the world no.1 market of IPO fund raised in 2015/2016

HK has been the world No.1 spot for IPO in terms of fund raised for two consecutive years. There were 126 new listings in HK during 2016, and the IPO fund-raising size reached HK$195bn (c.US$25bn), much higher than the second runner-up Shanghai (RMB102bn, c.US$15bn) and the third New York (US$13bn).

Figure 9: IPOs in HK Figure 10: Top-6 exchanges by IPO equity fund raised

Sources: HKEx, CMS (HK) Sources: HKEx, Dealogic, Bloomberg, CMS (HK)

More IPOs to come in 2017. The number of new listings in HK has grown with a CAGR of 30% during 2012-2015. Although the number of new listings decreased 9% YoY to 126 in 2016, we believe it is likely to rebound in 2017, given that the number of applications from companies to get listed in HKEx jumped 39% YoY to 122 by the end of 2016 (vs. 88 by the end of 2015).

China – improving IPO process with huge potential

China’s IPO approval process is speeding up with better regulation. After the suspension of IPO from Nov 2012 to Dec 2013, the number of IPOs in China has been rebounding strongly. There were 227 newly listed companies in 2016, vs. 220/125 in 2015/2014. China Securities Regulatory Commission (“CSRC”) has accelerated the approval process for IPO with IPO fund raised tripled in 2H16 vs. 1H16, resulting in a growing demand for financial PR services.

Figure 11: IPOs in China Figure 12: IPO fund raised in China

Sources: SSE, SZSE, CMS (HK) Sources: CSRC, CMS (HK)

Even faster IPO process after transition from approval-based to registration-based. Currently China’s IPO process is approval-based, which means stringent financial requirements and strict reviews conducted by CSRC’s public offering review committee on listings. To reduce govt intervention and strengthen marketization in the IPO market, China kicked off the registration-based IPO reform in 2015. The registration-based IPO system will impose a lower threshold for companies, simplify the listing process, and emphasise the disclosure of post-listing information. As a result, the new system will significantly speed up the IPO process in China and let the market decide which company will get listed and for how much.

90

169

233

263

195

64

110

122

138126

0

20

40

60

80

100

120

140

0

100

200

300

400

2012 2013 2014 2015 2016

HK

$b

n

IPO fund raised (LHS) No. of new listed companies (RHS)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2015 2016

US

$m

n

HKEx SSE NYSE Japan Exchange NASDAQ LSE

103

67

158150155

0

125

220227

0

50

100

150

200

250

0

50

100

150

200

2012 2013 2014 2015 2016

RM

Bb

n

China IPO capital raised (LHS) No. of new listed companies (RHS)

0

5

10

15

20

25

30

RM

Bb

n

A share IPO fund raised

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 9

Driver #2: Increasing number of long-term clients

Stable expansion of long-term client base

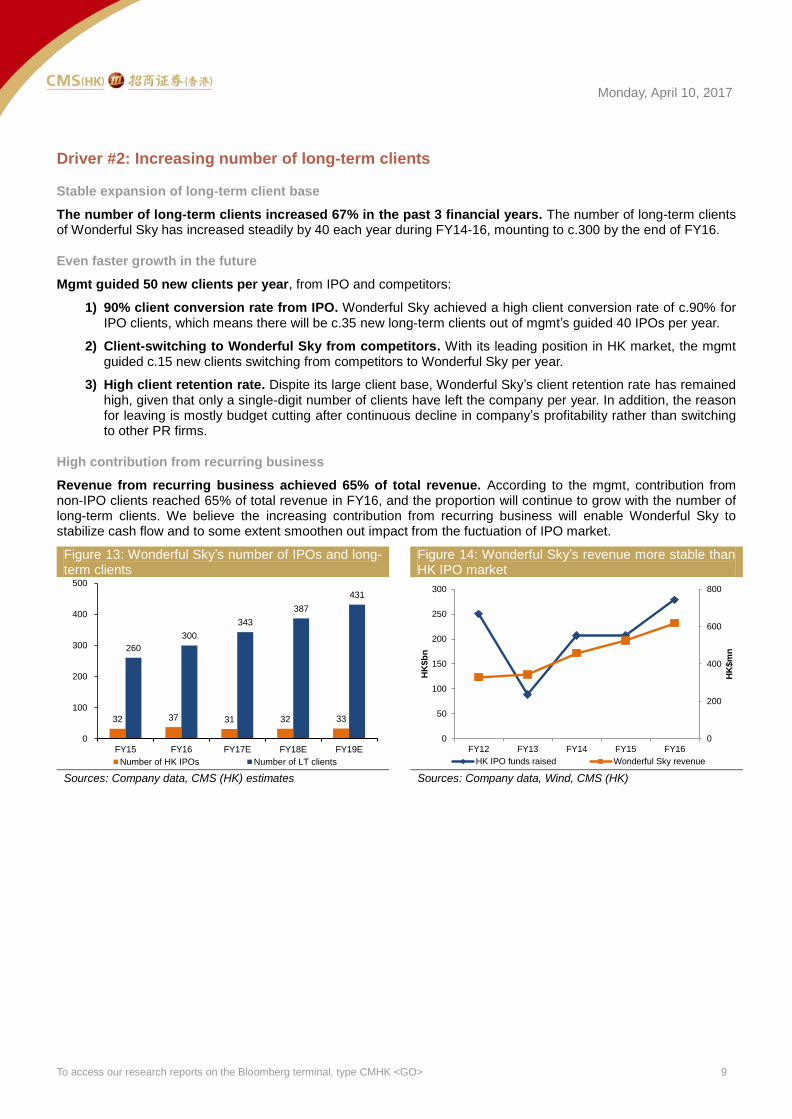

The number of long-term clients increased 67% in the past 3 financial years. The number of long-term clients of Wonderful Sky has increased steadily by 40 each year during FY14-16, mounting to c.300 by the end of FY16.

Even faster growth in the future

Mgmt guided 50 new clients per year, from IPO and competitors:

1) 90% client conversion rate from IPO. Wonderful Sky achieved a high client conversion rate of c.90% for IPO clients, which means there will be c.35 new long-term clients out of mgmt’s guided 40 IPOs per year.

2) Client-switching to Wonderful Sky from competitors. With its leading position in HK market, the mgmt guided c.15 new clients switching from competitors to Wonderful Sky per year.

3) High client retention rate. Dispite its large client base, Wonderful Sky’s client retention rate has remained high, given that only a single-digit number of clients have left the company per year. In addition, the reason for leaving is mostly budget cutting after continuous decline in company’s profitability rather than switching to other PR firms.

High contribution from recurring business

Revenue from recurring business achieved 65% of total revenue. According to the mgmt, contribution from non-IPO clients reached 65% of total revenue in FY16, and the proportion will continue to grow with the number of long-term clients. We believe the increasing contribution from recurring business will enable Wonderful Sky to stabilize cash flow and to some extent smoothen out impact from the fuctuation of IPO market.

Figure 13: Wonderful Sky’s number of IPOs and long-term clients

Figure 14: Wonderful Sky’s revenue more stable than HK IPO market

Sources: Company data, CMS (HK) estimates Sources: Company data, Wind, CMS (HK)

32 37 31 32 33

260

300

343

387

431

0

100

200

300

400

500

FY15 FY16 FY17E FY18E FY19E

Number of HK IPOs Number of LT clients

0

200

400

600

800

0

50

100

150

200

250

300

FY12 FY13 FY14 FY15 FY16

HK

$m

n

HK

$b

n

HK IPO funds raised Wonderful Sky revenue

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 10

Driver #3: Ramp-up of IPO printing

Started IPO printing in 2015

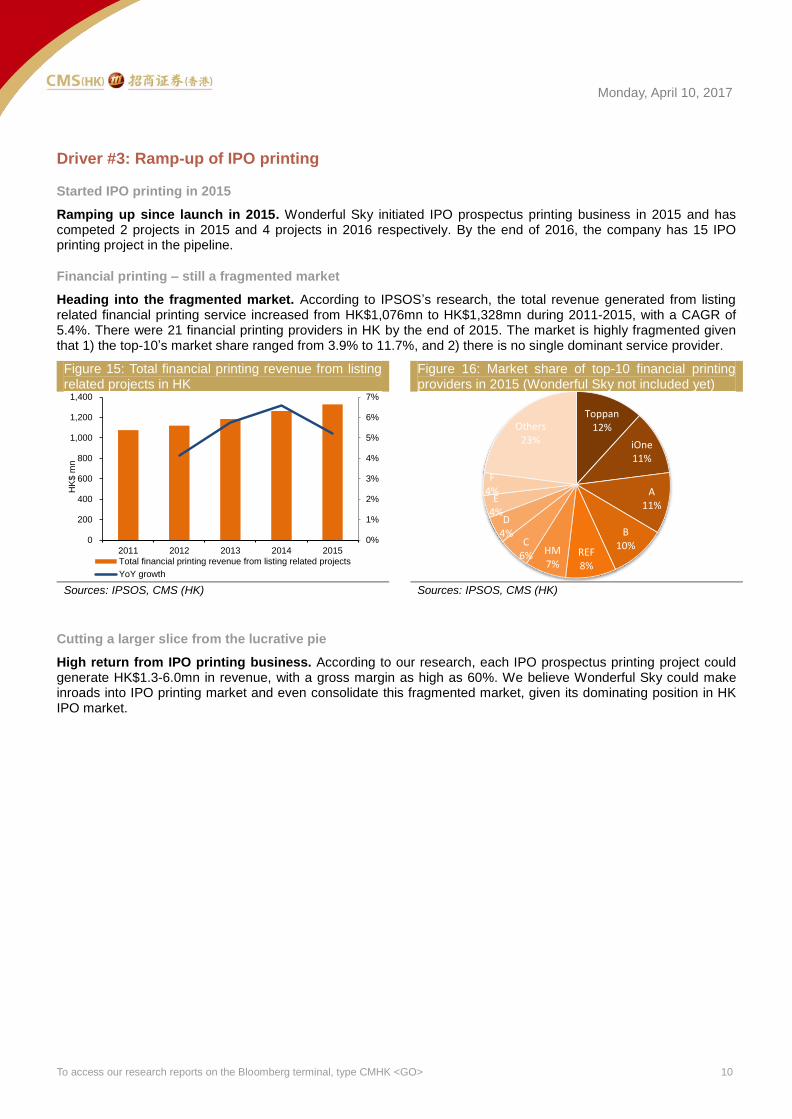

Ramping up since launch in 2015. Wonderful Sky initiated IPO prospectus printing business in 2015 and has competed 2 projects in 2015 and 4 projects in 2016 respectively. By the end of 2016, the company has 15 IPO printing project in the pipeline.

Financial printing – still a fragmented market

Heading into the fragmented market. According to IPSOS’s research, the total revenue generated from listing related financial printing service increased from HK$1,076mn to HK$1,328mn during 2011-2015, with a CAGR of 5.4%. There were 21 financial printing providers in HK by the end of 2015. The market is highly fragmented given that 1) the top-10’s market share ranged from 3.9% to 11.7%, and 2) there is no single dominant service provider.

Figure 15: Total financial printing revenue from listing related projects in HK

Figure 16: Market share of top-10 financial printing providers in 2015 (Wonderful Sky not included yet)

Sources: IPSOS, CMS (HK) Sources: IPSOS, CMS (HK)

Cutting a larger slice from the lucrative pie

High return from IPO printing business. According to our research, each IPO prospectus printing project could generate HK$1.3-6.0mn in revenue, with a gross margin as high as 60%. We believe Wonderful Sky could make inroads into IPO printing market and even consolidate this fragmented market, given its dominating position in HK IPO market.

0%

1%

2%

3%

4%

5%

6%

7%

0

200

400

600

800

1,000

1,200

1,400

2011 2012 2013 2014 2015

HK

$ m

n

Total financial printing revenue from listing related projects

YoY growth

Toppan12%

iOne11%

A11%

B10%

REF8%

HM7%

C6%

D4%

E4%

F4%

Others23%

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 11

Driver #4: Geographical expansions

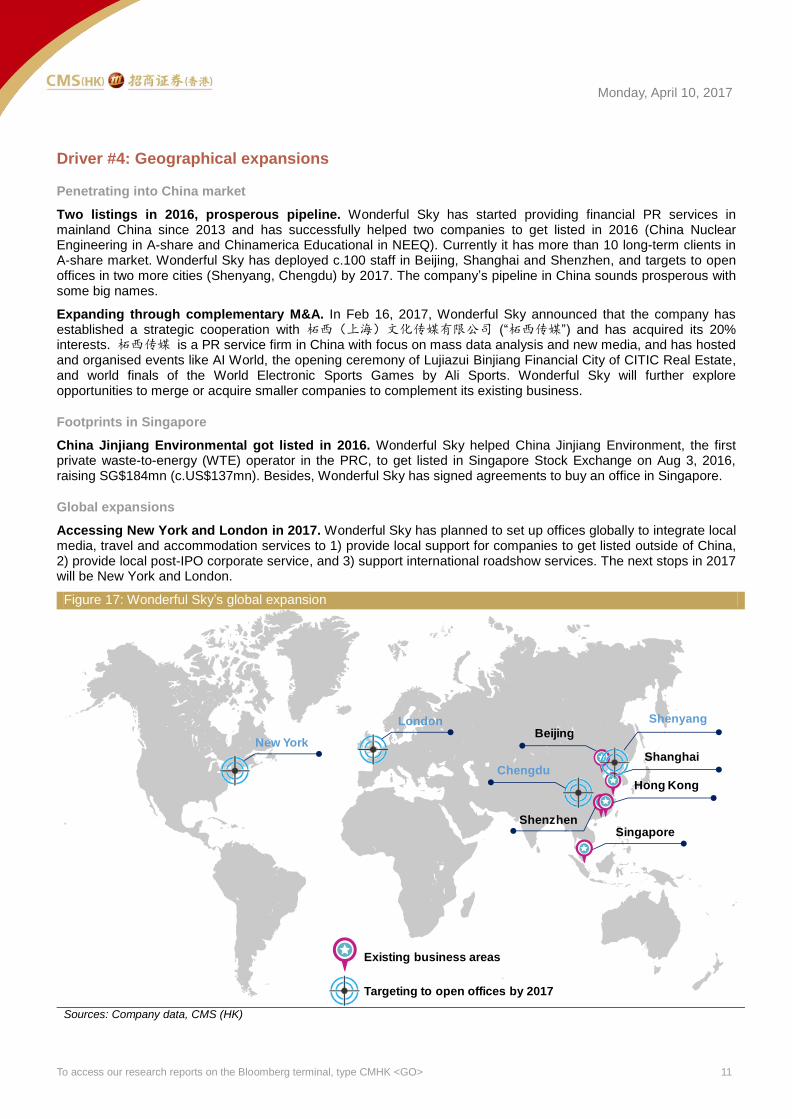

Penetrating into China market

Two listings in 2016, prosperous pipeline. Wonderful Sky has started providing financial PR services in mainland China since 2013 and has successfully helped two companies to get listed in 2016 (China Nuclear Engineering in A-share and Chinamerica Educational in NEEQ). Currently it has more than 10 long-term clients in A-share market. Wonderful Sky has deployed c.100 staff in Beijing, Shanghai and Shenzhen, and targets to open offices in two more cities (Shenyang, Chengdu) by 2017. The company’s pipeline in China sounds prosperous with some big names.

Expanding through complementary M&A. In Feb 16, 2017, Wonderful Sky announced that the company has established a strategic cooperation with 柘西(上海)文化传媒有限公司 (“柘西传媒”) and has acquired its 20% interests. 柘西传媒 is a PR service firm in China with focus on mass data analysis and new media, and has hosted and organised events like AI World, the opening ceremony of Lujiazui Binjiang Financial City of CITIC Real Estate, and world finals of the World Electronic Sports Games by Ali Sports. Wonderful Sky will further explore opportunities to merge or acquire smaller companies to complement its existing business.

Footprints in Singapore

China Jinjiang Environmental got listed in 2016. Wonderful Sky helped China Jinjiang Environment, the first private waste-to-energy (WTE) operator in the PRC, to get listed in Singapore Stock Exchange on Aug 3, 2016, raising SG$184mn (c.US$137mn). Besides, Wonderful Sky has signed agreements to buy an office in Singapore.

Global expansions

Accessing New York and London in 2017. Wonderful Sky has planned to set up offices globally to integrate local media, travel and accommodation services to 1) provide local support for companies to get listed outside of China, 2) provide local post-IPO corporate service, and 3) support international roadshow services. The next stops in 2017 will be New York and London.

Figure 17: Wonderful Sky’s global expansion

Sources: Company data, CMS (HK)

Hong Kong

Shanghai

Beijing

ShenzhenSingapore

London

New York

Targeting to open offices by 2017

Existing business areas

Shenyang

Chengdu

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 12

Driver #5: Eight-in-One Service Platform – adding three more value-added services

Leveraging on its large client base, 21-year experience and professional workforce, Wonderful Sky is expanding its service scope from five-in-one to eight-in-one, by adding 1) ESG reporting, 2) business consultant and 3) executive recruiters.

ESG (Environmental, Social and Governance) reporting

Upgraded requirements on environment KPIs in ESG reporting. According to the "Consultation Conclusions on Review of the Environmental, Social and Governance Reporting Guide" published in Dec 2015, for a listed company with financial year starting from Jan 1, its FY17 ESG report must include all the information required under the "Environmental" KPIs or give considered reasons, which used to be voluntary disclosure for companies.

Set up joint venture – CECEP Environmental Consulting Group (“the JV”). In 2016, together with ShineWing International (“ShineWing”) and CECEP (Hong Kong) Investments (“CECEPHK”), Wonderful Sky set up the JV in which it holds 30% interests. The JV’s business includes 1) ESG report writing, 2) ESG consultancy services and 3) governance system building.

Business consultant

The company plans to initiate corporate consulting business, offering consultancy services on 1) corporate strategy consultancy, 2) internal management and training, and 3) corporate financing and capital operation.

Executive recruiters

The company will further offer human resource consultancy services, which include 1) senior level talents recruitment, and 2) human resource consultancy.

Figure 18: Wonderful Sky’s Eight-in-One Service Platform

Sources: Company data

Financial Public

Relations

Investor Relations

Int’l Roadshow

Business Consultant

Executive Recruiters

Corporate Branding

ESG Report

Financial Printing

• Issuance of ESG Report

According to Requirements

• Governance System Building

among Environment, Society &

Company

• Corporate Strategy Consulting

• Internal Management Trainings

• Corporate Financing and

Capital Operation

• Senior Level Talents Recruitment

• Human Resources Consulting

Eight-in-One

Service Platform,

The most integrated

service chain in industry

• Investor Identification and Analysis

• M&A and Proxy Solicitation

• Investors and Analysts Roadshow

• Optimize Shareholding Structure

• Market Monitoring and Analysis

• Messages & Strategies Design and Delivery

• Event Coordination

• Corporate Materials Design

• Deal & Non-deal Roadshow

Planning and Management

• Roadshow Logistics

• Technical Support

• Design, Typesetting, Translation

and Production of Prospectus

• Financial Reports

• Circulars

• Announcements

• Corporate Materials

• Message & Image Design

• Develop Multi-dimensional

Branding Strategies

• Financial Market Branding Actions

• New Media & Individual Media

Promotion

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 13

Financial analysis

Revenue and P&L analysis

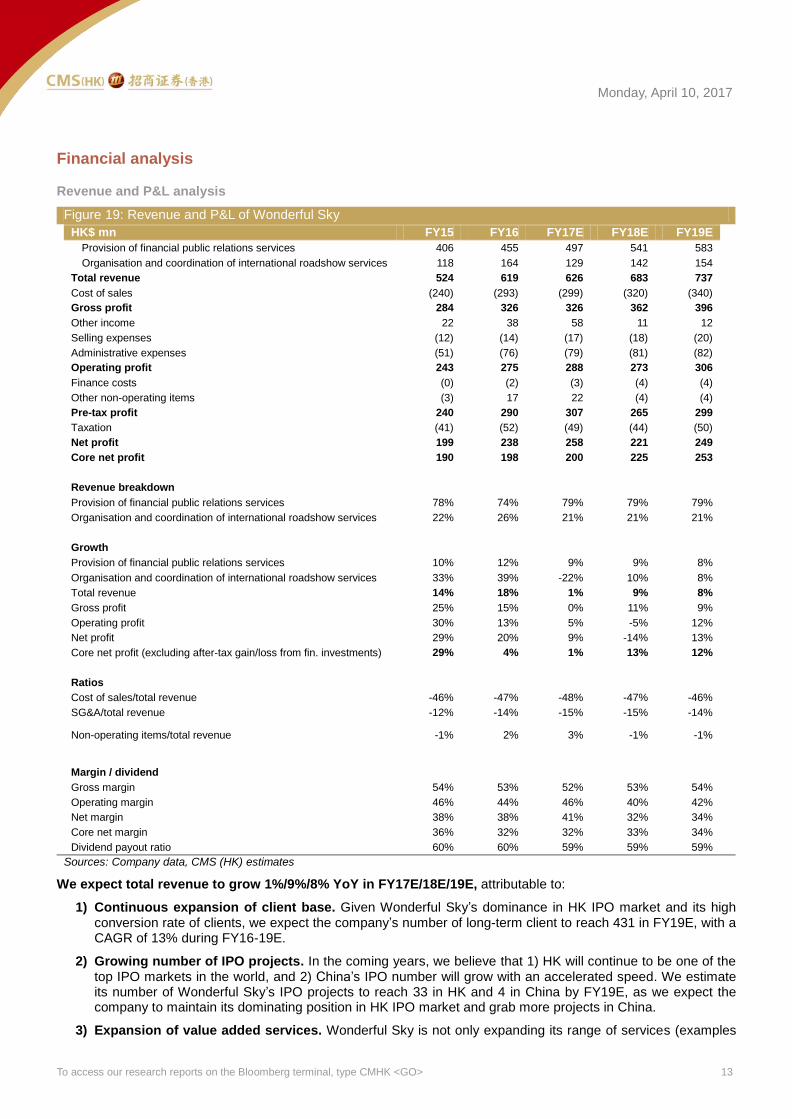

Figure 19: Revenue and P&L of Wonderful Sky

HK$ mn FY15 FY16 FY17E FY18E FY19E

Provision of financial public relations services 406 455 497 541 583

Organisation and coordination of international roadshow services 118 164 129 142 154

Total revenue 524 619 626 683 737

Cost of sales (240) (293) (299) (320) (340)

Gross profit 284 326 326 362 396

Other income 22 38 58 11 12

Selling expenses (12) (14) (17) (18) (20)

Administrative expenses (51) (76) (79) (81) (82)

Operating profit 243 275 288 273 306

Finance costs (0) (2) (3) (4) (4)

Other non-operating items (3) 17 22 (4) (4)

Pre-tax profit 240 290 307 265 299

Taxation (41) (52) (49) (44) (50)

Net profit 199 238 258 221 249

Core net profit 190 198 200 225 253

Revenue breakdown

Provision of financial public relations services 78% 74% 79% 79% 79%

Organisation and coordination of international roadshow services 22% 26% 21% 21% 21%

Growth

Provision of financial public relations services 10% 12% 9% 9% 8%

Organisation and coordination of international roadshow services 33% 39% -22% 10% 8%

Total revenue 14% 18% 1% 9% 8%

Gross profit 25% 15% 0% 11% 9%

Operating profit 30% 13% 5% -5% 12%

Net profit 29% 20% 9% -14% 13%

Core net profit (excluding after-tax gain/loss from fin. investments) 29% 4% 1% 13% 12%

Ratios

Cost of sales/total revenue -46% -47% -48% -47% -46%

SG&A/total revenue -12% -14% -15% -15% -14%

Non-operating items/total revenue -1% 2% 3% -1% -1%

Margin / dividend

Gross margin 54% 53% 52% 53% 54%

Operating margin 46% 44% 46% 40% 42%

Net margin 38% 38% 41% 32% 34%

Core net margin 36% 32% 32% 33% 34%

Dividend payout ratio 60% 60% 59% 59% 59%

Sources: Company data, CMS (HK) estimates

We expect total revenue to grow 1%/9%/8% YoY in FY17E/18E/19E, attributable to:

1) Continuous expansion of client base. Given Wonderful Sky’s dominance in HK IPO market and its high conversion rate of clients, we expect the company’s number of long-term client to reach 431 in FY19E, with a CAGR of 13% during FY16-19E.

2) Growing number of IPO projects. In the coming years, we believe that 1) HK will continue to be one of the top IPO markets in the world, and 2) China’s IPO number will grow with an accelerated speed. We estimate its number of Wonderful Sky’s IPO projects to reach 33 in HK and 4 in China by FY19E, as we expect the company to maintain its dominating position in HK IPO market and grab more projects in China.

3) Expansion of value added services. Wonderful Sky is not only expanding its range of services (examples

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 14

of new services: IPO printing, “Wonderful Cloud”, ESG reporting), but also broadening its geographical coverage of services by providing cross-market PR/IR services. We remain relatively conservative on its new services and estimate the revenue contribution from new services to reach 5% of total revenue in FY19E.

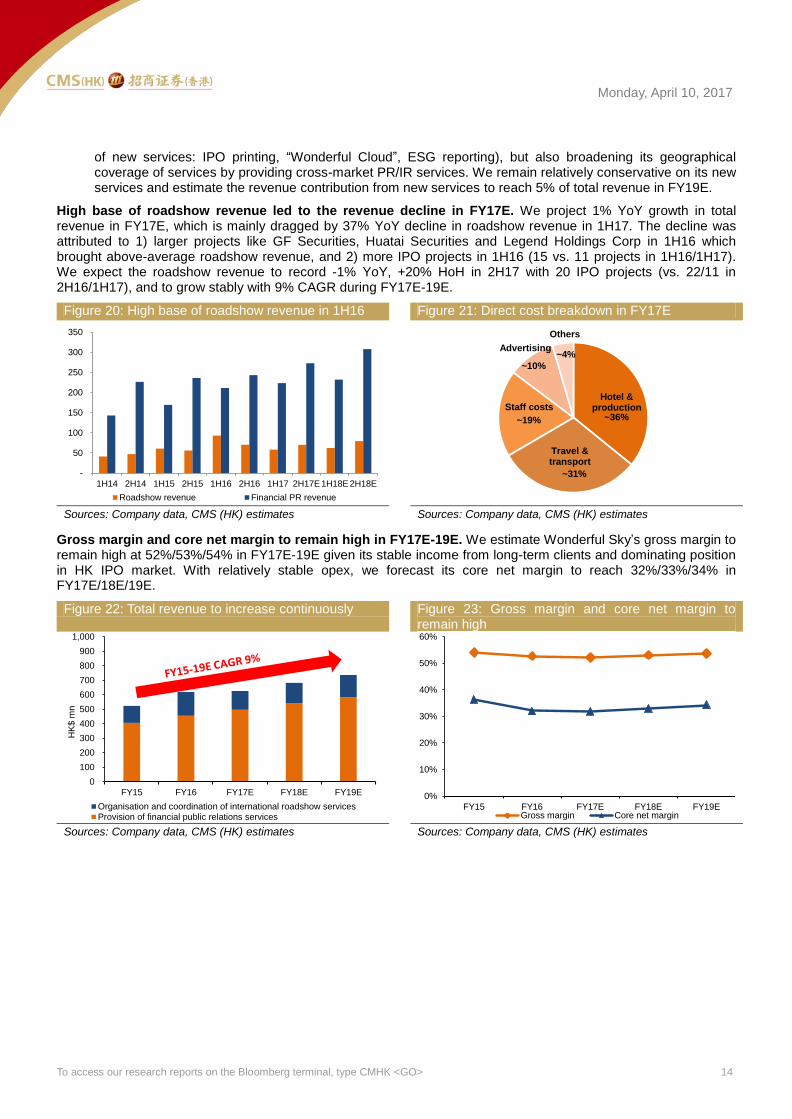

High base of roadshow revenue led to the revenue decline in FY17E. We project 1% YoY growth in total revenue in FY17E, which is mainly dragged by 37% YoY decline in roadshow revenue in 1H17. The decline was attributed to 1) larger projects like GF Securities, Huatai Securities and Legend Holdings Corp in 1H16 which brought above-average roadshow revenue, and 2) more IPO projects in 1H16 (15 vs. 11 projects in 1H16/1H17). We expect the roadshow revenue to record -1% YoY, +20% HoH in 2H17 with 20 IPO projects (vs. 22/11 in 2H16/1H17), and to grow stably with 9% CAGR during FY17E-19E.

Figure 20: High base of roadshow revenue in 1H16 Figure 21: Direct cost breakdown in FY17E

Sources: Company data, CMS (HK) estimates Sources: Company data, CMS (HK) estimates

Gross margin and core net margin to remain high in FY17E-19E. We estimate Wonderful Sky’s gross margin to remain high at 52%/53%/54% in FY17E-19E given its stable income from long-term clients and dominating position in HK IPO market. With relatively stable opex, we forecast its core net margin to reach 32%/33%/34% in FY17E/18E/19E.

Figure 22: Total revenue to increase continuously Figure 23: Gross margin and core net margin to remain high

Sources: Company data, CMS (HK) estimates Sources: Company data, CMS (HK) estimates

-

50

100

150

200

250

300

350

1H14 2H14 1H15 2H15 1H16 2H16 1H17 2H17E 1H18E 2H18E

Roadshow revenue Financial PR revenue

Hotel & production

Travel & transport

Staff costs

Advertising

Others

~31%

~36%~19%

~10%

~4%

0

100

200

300

400

500

600

700

800

900

1,000

FY15 FY16 FY17E FY18E FY19E

HK

$ m

n

Organisation and coordination of international roadshow servicesProvision of financial public relations services

0%

10%

20%

30%

40%

50%

60%

FY15 FY16 FY17E FY18E FY19EGross margin Core net margin

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 15

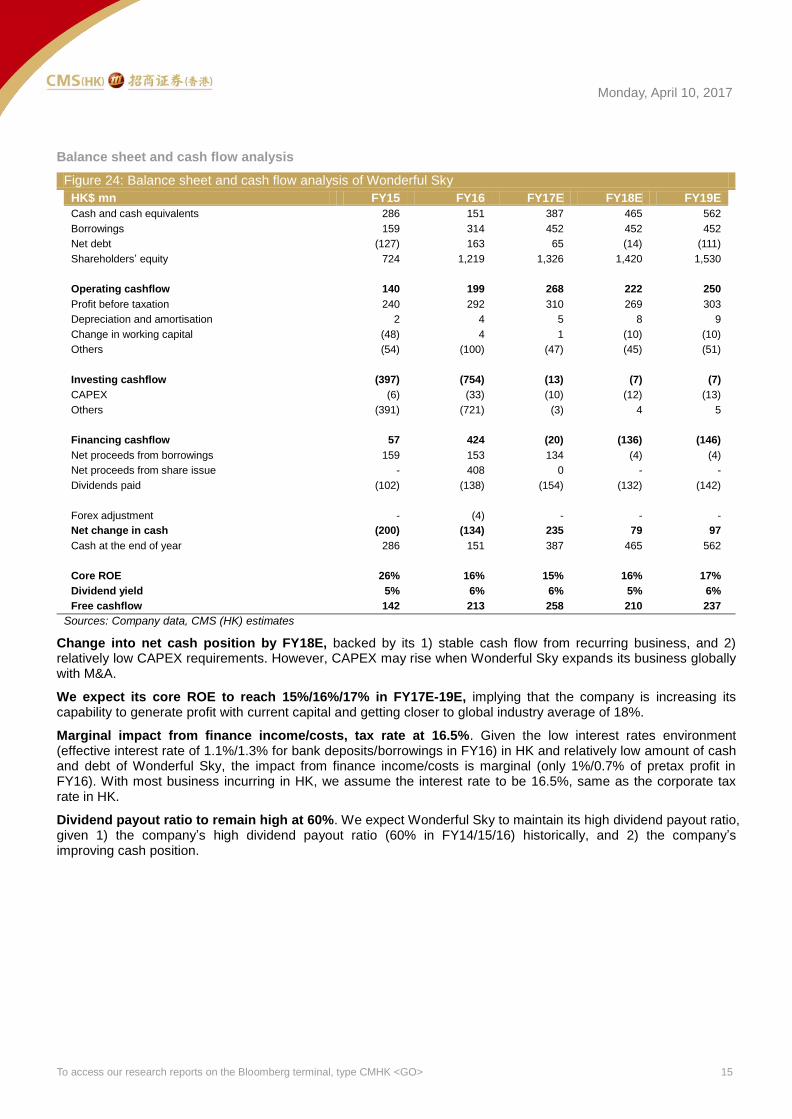

Balance sheet and cash flow analysis

Figure 24: Balance sheet and cash flow analysis of Wonderful Sky

HK$ mn FY15 FY16 FY17E FY18E FY19E

Cash and cash equivalents 286 151 387 465 562

Borrowings 159 314 452 452 452

Net debt (127) 163 65 (14) (111)

Shareholders’ equity 724 1,219 1,326 1,420 1,530

Operating cashflow 140 199 268 222 250

Profit before taxation 240 292 310 269 303

Depreciation and amortisation 2 4 5 8 9

Change in working capital (48) 4 1 (10) (10)

Others (54) (100) (47) (45) (51)

Investing cashflow (397) (754) (13) (7) (7)

CAPEX (6) (33) (10) (12) (13)

Others (391) (721) (3) 4 5

Financing cashflow 57 424 (20) (136) (146)

Net proceeds from borrowings 159 153 134 (4) (4)

Net proceeds from share issue - 408 0 - -

Dividends paid (102) (138) (154) (132) (142)

Forex adjustment - (4) - - -

Net change in cash (200) (134) 235 79 97

Cash at the end of year 286 151 387 465 562

Core ROE 26% 16% 15% 16% 17%

Dividend yield 5% 6% 6% 5% 6%

Free cashflow 142 213 258 210 237

Sources: Company data, CMS (HK) estimates

Change into net cash position by FY18E, backed by its 1) stable cash flow from recurring business, and 2) relatively low CAPEX requirements. However, CAPEX may rise when Wonderful Sky expands its business globally with M&A.

We expect its core ROE to reach 15%/16%/17% in FY17E-19E, implying that the company is increasing its capability to generate profit with current capital and getting closer to global industry average of 18%.

Marginal impact from finance income/costs, tax rate at 16.5%. Given the low interest rates environment (effective interest rate of 1.1%/1.3% for bank deposits/borrowings in FY16) in HK and relatively low amount of cash and debt of Wonderful Sky, the impact from finance income/costs is marginal (only 1%/0.7% of pretax profit in FY16). With most business incurring in HK, we assume the interest rate to be 16.5%, same as the corporate tax rate in HK.

Dividend payout ratio to remain high at 60%. We expect Wonderful Sky to maintain its high dividend payout ratio, given 1) the company’s high dividend payout ratio (60% in FY14/15/16) historically, and 2) the company’s improving cash position.

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 16

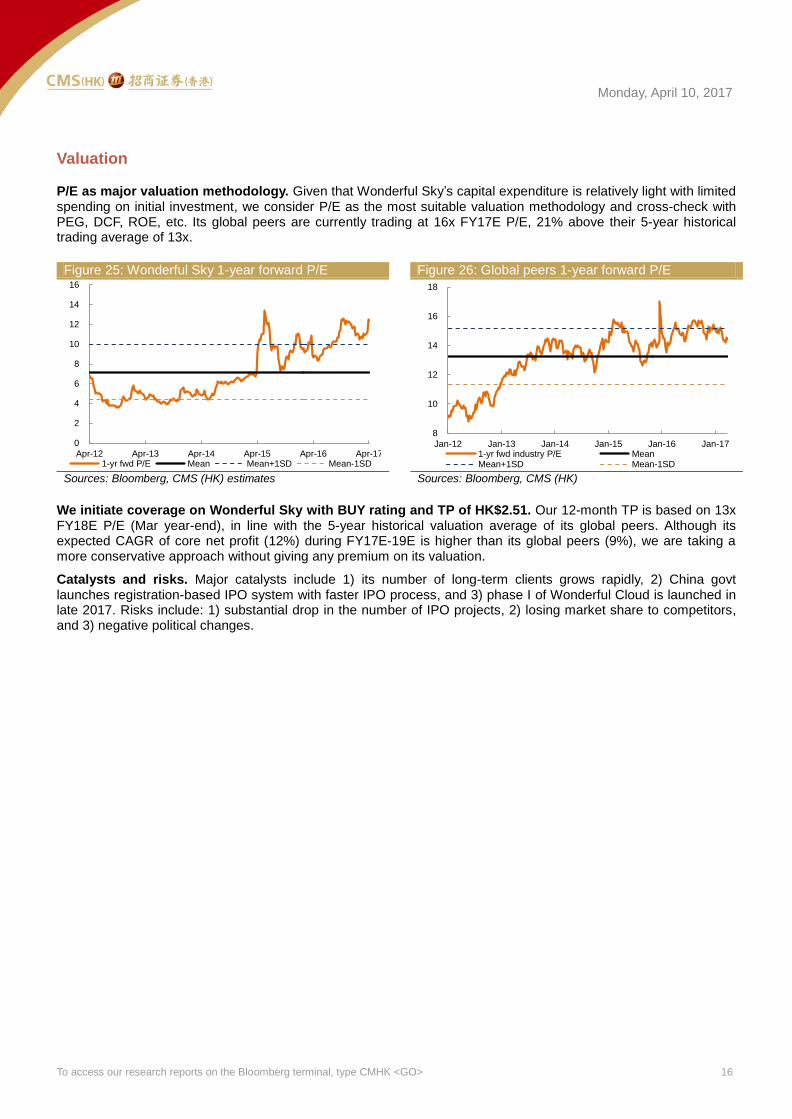

Valuation

P/E as major valuation methodology. Given that Wonderful Sky’s capital expenditure is relatively light with limited spending on initial investment, we consider P/E as the most suitable valuation methodology and cross-check with PEG, DCF, ROE, etc. Its global peers are currently trading at 16x FY17E P/E, 21% above their 5-year historical trading average of 13x.

Figure 25: Wonderful Sky 1-year forward P/E Figure 26: Global peers 1-year forward P/E

Sources: Bloomberg, CMS (HK) estimates Sources: Bloomberg, CMS (HK)

We initiate coverage on Wonderful Sky with BUY rating and TP of HK$2.51. Our 12-month TP is based on 13x FY18E P/E (Mar year-end), in line with the 5-year historical valuation average of its global peers. Although its expected CAGR of core net profit (12%) during FY17E-19E is higher than its global peers (9%), we are taking a more conservative approach without giving any premium on its valuation.

Catalysts and risks. Major catalysts include 1) its number of long-term clients grows rapidly, 2) China govt launches registration-based IPO system with faster IPO process, and 3) phase I of Wonderful Cloud is launched in late 2017. Risks include: 1) substantial drop in the number of IPO projects, 2) losing market share to competitors, and 3) negative political changes.

0

2

4

6

8

10

12

14

16

Apr-12 Apr-13 Apr-14 Apr-15 Apr-16 Apr-171-yr fwd P/E Mean Mean+1SD Mean-1SD

8

10

12

14

16

18

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-171-yr fwd industry P/E MeanMean+1SD Mean-1SD

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 17

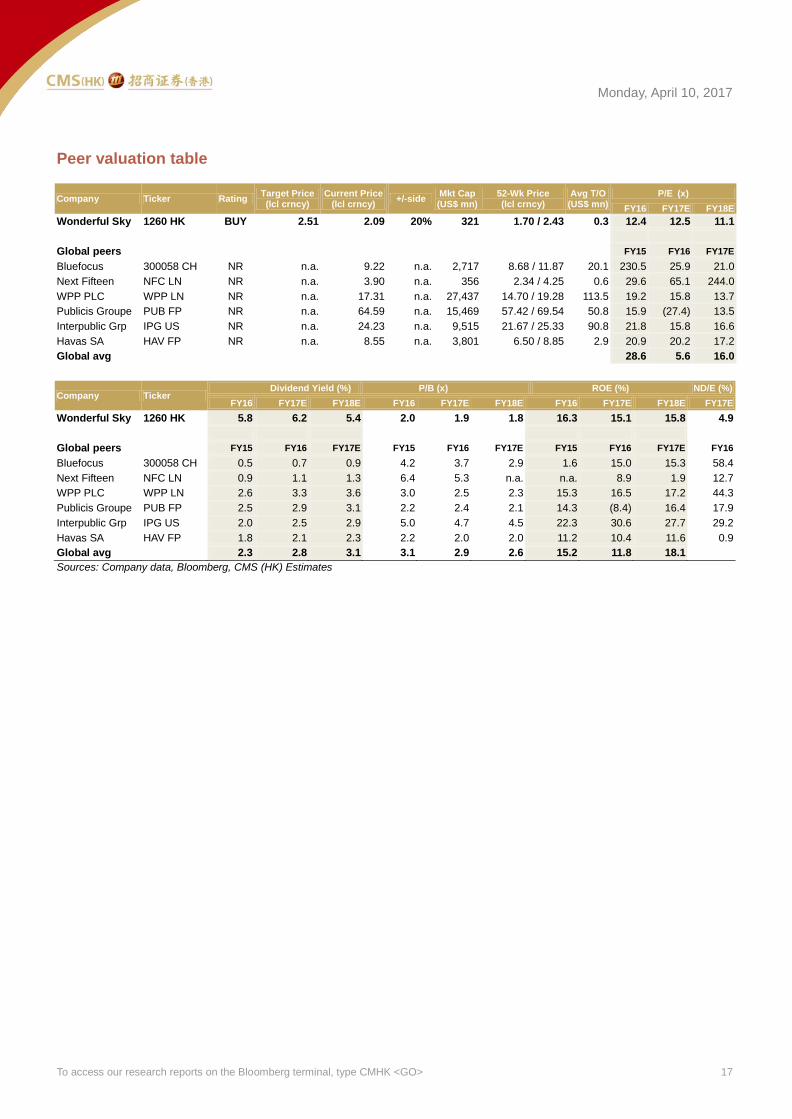

Peer valuation table

Company Ticker Rating Target Price (lcl crncy)

Current Price (lcl crncy)

+/-side

Mkt Cap (US$ mn)

52-Wk Price (lcl crncy)

Avg T/O (US$ mn)

P/E (x)

FY16 FY17E FY18E

Wonderful Sky 1260 HK BUY 2.51 2.09 20% 321 1.70 / 2.43 0.3 12.4 12.5 11.1

Global peers FY15 FY16 FY17E

Bluefocus 300058 CH NR n.a. 9.22 n.a. 2,717 8.68 / 11.87 20.1 230.5 25.9 21.0

Next Fifteen NFC LN NR n.a. 3.90 n.a. 356 2.34 / 4.25 0.6 29.6 65.1 244.0

WPP PLC WPP LN NR n.a. 17.31 n.a. 27,437 14.70 / 19.28 113.5 19.2 15.8 13.7

Publicis Groupe PUB FP NR n.a. 64.59 n.a. 15,469 57.42 / 69.54 50.8 15.9 (27.4) 13.5

Interpublic Grp IPG US NR n.a. 24.23 n.a. 9,515 21.67 / 25.33 90.8 21.8 15.8 16.6

Havas SA HAV FP NR n.a. 8.55 n.a. 3,801 6.50 / 8.85 2.9 20.9 20.2 17.2

Global avg

28.6 5.6 16.0

Company Ticker Dividend Yield (%) P/B (x) ROE (%) ND/E (%)

FY16 FY17E FY18E FY16 FY17E FY18E FY16 FY17E FY18E FY17E

Wonderful Sky 1260 HK 5.8 6.2 5.4 2.0 1.9 1.8 16.3 15.1 15.8 4.9

Global peers FY15 FY16 FY17E FY15 FY16 FY17E FY15 FY16 FY17E FY16

Bluefocus 300058 CH 0.5 0.7 0.9 4.2 3.7 2.9 1.6 15.0 15.3 58.4

Next Fifteen NFC LN 0.9 1.1 1.3 6.4 5.3 n.a. n.a. 8.9 1.9 12.7

WPP PLC WPP LN 2.6 3.3 3.6 3.0 2.5 2.3 15.3 16.5 17.2 44.3

Publicis Groupe PUB FP 2.5 2.9 3.1 2.2 2.4 2.1 14.3 (8.4) 16.4 17.9

Interpublic Grp IPG US 2.0 2.5 2.9 5.0 4.7 4.5 22.3 30.6 27.7 29.2

Havas SA HAV FP 1.8 2.1 2.3 2.2 2.0 2.0 11.2 10.4 11.6 0.9

Global avg

2.3 2.8 3.1 3.1 2.9 2.6 15.2 11.8 18.1

Sources: Company data, Bloomberg, CMS (HK) Estimates

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 18

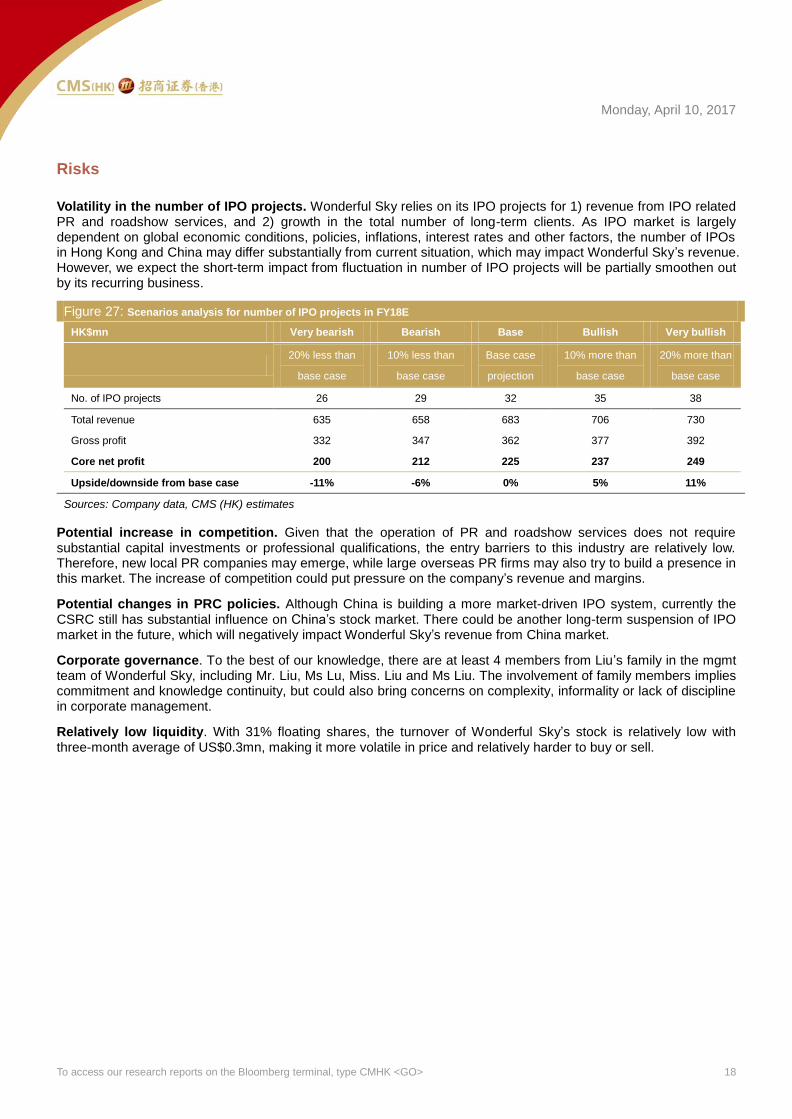

Risks

Volatility in the number of IPO projects. Wonderful Sky relies on its IPO projects for 1) revenue from IPO related PR and roadshow services, and 2) growth in the total number of long-term clients. As IPO market is largely dependent on global economic conditions, policies, inflations, interest rates and other factors, the number of IPOs in Hong Kong and China may differ substantially from current situation, which may impact Wonderful Sky’s revenue. However, we expect the short-term impact from fluctuation in number of IPO projects will be partially smoothen out by its recurring business.

Figure 27: Scenarios analysis for number of IPO projects in FY18E

HK$mn Very bearish Bearish Base Bullish Very bullish

20% less than

base case

10% less than

base case

Base case

projection

10% more than

base case

20% more than

base case

No. of IPO projects 26 29 32 35 38

Total revenue 635 658 683 706 730

Gross profit 332 347 362 377 392

Core net profit 200 212 225 237 249

Upside/downside from base case -11% -6% 0% 5% 11%

Sources: Company data, CMS (HK) estimates

Potential increase in competition. Given that the operation of PR and roadshow services does not require substantial capital investments or professional qualifications, the entry barriers to this industry are relatively low. Therefore, new local PR companies may emerge, while large overseas PR firms may also try to build a presence in this market. The increase of competition could put pressure on the company’s revenue and margins.

Potential changes in PRC policies. Although China is building a more market-driven IPO system, currently the CSRC still has substantial influence on China’s stock market. There could be another long-term suspension of IPO market in the future, which will negatively impact Wonderful Sky’s revenue from China market.

Corporate governance. To the best of our knowledge, there are at least 4 members from Liu’s family in the mgmt team of Wonderful Sky, including Mr. Liu, Ms Lu, Miss. Liu and Ms Liu. The involvement of family members implies commitment and knowledge continuity, but could also bring concerns on complexity, informality or lack of discipline in corporate management.

Relatively low liquidity. With 31% floating shares, the turnover of Wonderful Sky’s stock is relatively low with three-month average of US$0.3mn, making it more volatile in price and relatively harder to buy or sell.

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 19

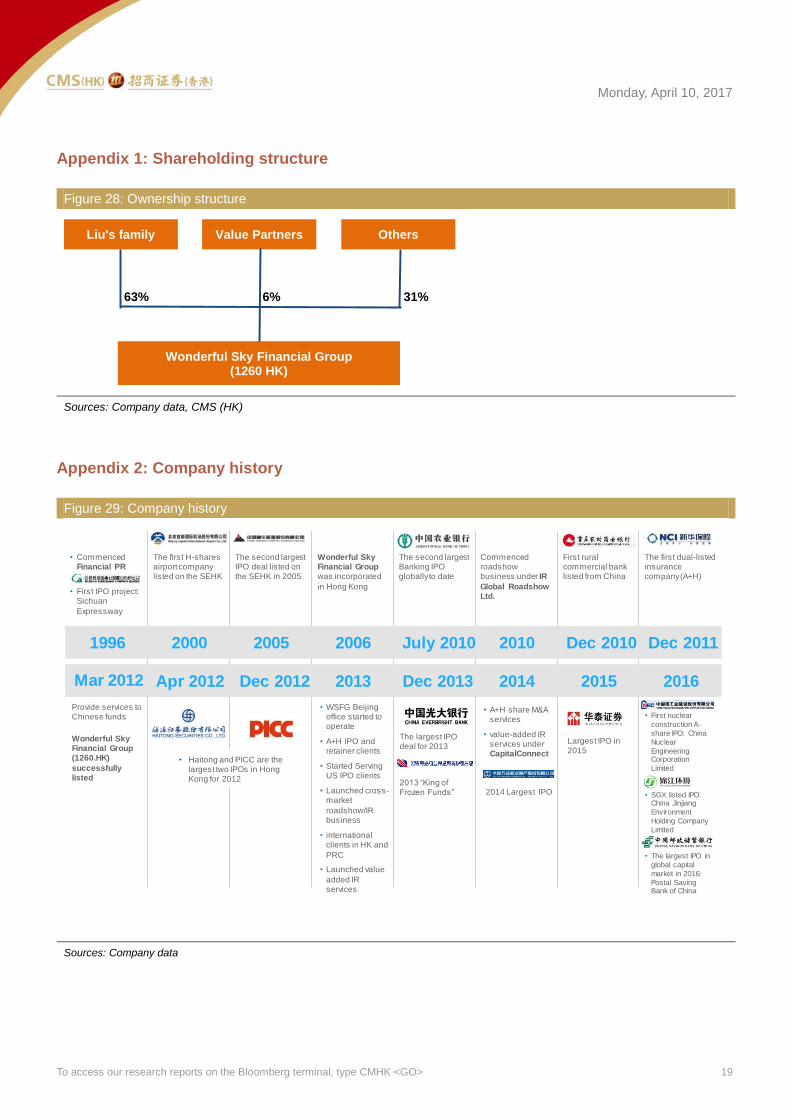

Appendix 1: Shareholding structure

Figure 28: Ownership structure

Sources: Company data, CMS (HK)

Appendix 2: Company history

Figure 29: Company history

Sources: Company data

Liu's family

Wonderful Sky Financial Group(1260 HK)

Value Partners Others

63% 6% 31%

• Commenced Financial PR business

• First IPO project: Sichuan

Expressway

1996 2000 2005 2006 July 2010 2010 Dec 2010 Dec 2011

2014 2015

The first H-shares airport company listed on the SEHK

The second largest IPO deal listed on the SEHK in 2005

Wonderful Sky Financial Group was incorporated

in Hong Kong

The second largest Banking IPO globally to date

Commenced roadshow business under IR

Global Roadshow Ltd.

First rural commercial bank listed from China

The first dual-listed insurance company (A+H)

Mar 2012 Apr 2012 Dec 2012 2013

Provide services to Chinese funds

Wonderful Sky Financial Group (1260.HK)

successfully listed

• Haitong and PICC are the largest two IPOs in Hong Kong for 2012

• WSFG Beijing office started to operate

• A+H IPO and retainer clients

• Started Serving US IPO clients

• Launched cross-market

roadshow/IR business

• international clients in HK and

PRC

• Launched value

added IR services

Dec 2013

The largest IPO deal for 2013

2013 “King of Frozen Funds”

• A+H share M&A services

• value-added IR services under CapitalConnect

Largest IPO in 2015

2014 Largest IPO

2016

• First nuclear

construction A-

share IPO: China

Nuclear

Engineering Corporation

Limited

• SGX listed IPO: China Jinjiang

Environment

Holding Company

Limited

• The largest IPO in

global capital

market in 2016:

Postal Saving Bank of China

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 20

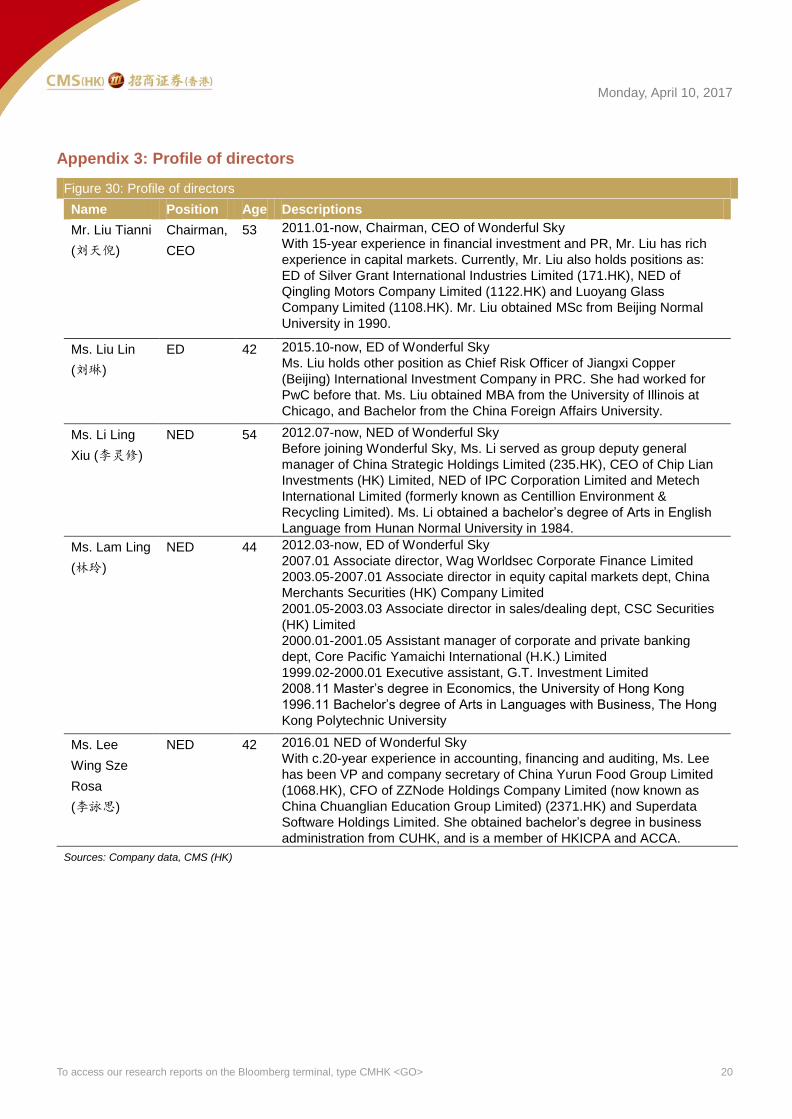

Appendix 3: Profile of directors

Figure 30: Profile of directors

Name Position Age Descriptions

Mr. Liu Tianni

(刘天倪)

Chairman,

CEO

53 2011.01-now, Chairman, CEO of Wonderful Sky

With 15-year experience in financial investment and PR, Mr. Liu has rich

experience in capital markets. Currently, Mr. Liu also holds positions as:

ED of Silver Grant International Industries Limited (171.HK), NED of

Qingling Motors Company Limited (1122.HK) and Luoyang Glass

Company Limited (1108.HK). Mr. Liu obtained MSc from Beijing Normal

University in 1990.

Ms. Liu Lin

(刘琳)

ED 42 2015.10-now, ED of Wonderful Sky

Ms. Liu holds other position as Chief Risk Officer of Jiangxi Copper

(Beijing) International Investment Company in PRC. She had worked for

PwC before that. Ms. Liu obtained MBA from the University of Illinois at

Chicago, and Bachelor from the China Foreign Affairs University.

Ms. Li Ling

Xiu (李灵修)

NED 54 2012.07-now, NED of Wonderful Sky

Before joining Wonderful Sky, Ms. Li served as group deputy general

manager of China Strategic Holdings Limited (235.HK), CEO of Chip Lian

Investments (HK) Limited, NED of IPC Corporation Limited and Metech

International Limited (formerly known as Centillion Environment &

Recycling Limited). Ms. Li obtained a bachelor’s degree of Arts in English

Language from Hunan Normal University in 1984.

Ms. Lam Ling

(林玲)

NED 44 2012.03-now, ED of Wonderful Sky

2007.01 Associate director, Wag Worldsec Corporate Finance Limited

2003.05-2007.01 Associate director in equity capital markets dept, China

Merchants Securities (HK) Company Limited

2001.05-2003.03 Associate director in sales/dealing dept, CSC Securities

(HK) Limited

2000.01-2001.05 Assistant manager of corporate and private banking

dept, Core Pacific Yamaichi International (H.K.) Limited

1999.02-2000.01 Executive assistant, G.T. Investment Limited

2008.11 Master’s degree in Economics, the University of Hong Kong

1996.11 Bachelor’s degree of Arts in Languages with Business, The Hong

Kong Polytechnic University

Ms. Lee

Wing Sze

Rosa

(李詠思)

NED 42 2016.01 NED of Wonderful Sky

With c.20-year experience in accounting, financing and auditing, Ms. Lee

has been VP and company secretary of China Yurun Food Group Limited

(1068.HK), CFO of ZZNode Holdings Company Limited (now known as

China Chuanglian Education Group Limited) (2371.HK) and Superdata

Software Holdings Limited. She obtained bachelor’s degree in business

administration from CUHK, and is a member of HKICPA and ACCA.

Sources: Company data, CMS (HK)

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 21

Appendix 4: Wonderful Sky’s IPO projects in Hong Kong since Jan 2016

Figure 31: Wonderful Sky’s IPO projects in Hong Kong since Jan 2016

Listing date Ticker English name Chinese name GICS sector name IPO fund raised

(HK$mn)

2017-03-31 2281 HK Luzhou Xinglu Water Group 兴泸水务 Utilities 494

2017-03-13 8423 HK Chi Ho Development 潪㵆发展 Industrials 80

2017-03-10 3395 HK Persta Resources PERSTA Energy 220

2017-02-28 6169 HK China Yuhua Education 宇华教育 Consumer Discretionary 1,538

2017-01-18 1518 HK New Century Healthcare 新世纪医疗 Health Care 883

2017-01-12 6122 HK Jilin Jiutai Rural Commercial Bank 九台农商银行 Financials 3,461

2016-12-15 1357 HK Meitu 美图公司 Information Technology 4,879

2016-12-15 8342 HK Vixtel Technologies 飞思达科技 Information Technology 76

2016-12-09 6066 HK CSC Financial 中信建投证券 Financials 7,697

2016-12-05 1635 HK Shanghai Dazhong Public Utilities 大众公用 Utilities 1,921

2016-11-25 6189 HK Guangdong Adway Construction 爱得威建设 Industrials 274

2016-11-15 1272 HK Datang Environment Industry 大唐环境 Industrials 2,145

2016-11-11 1458 HK Zhou Hei Ya International 周黑鸭 Consumer Staples 2,496

2016-11-08 3689 HK Guangdong Kanghua Healthcare 康华医疗 Health Care 974

2016-11-01 1610 HK COFCO Meat 中粮肉食 Consumer Staples 1,951

2016-10-31 3306 HK JNBY Design 江南布衣 Consumer Discretionary 800

2016-10-28 3320 HK China Resources Pharmaceutical 华润医药 Health Care 14,043

2016-10-20 8407 HK CISI FIN 兴证国际 Financials 1,330

2016-10-07 6099 HK China Merchants Securities 招商证券 Financials 10,695

2016-10-07 2166 HK Smart-Core 芯智控股 Information Technology 229

2016-09-28 1658 HK Postal Savings Bank of China 邮储银行 Financials 57,627

2016-08-18 6178 HK Everbright Securities 光大证券 Financials 8,928

2016-07-15 1589 HK China Logistics Property 中国物流资产 Real Estate 3,557

2016-07-15 2278 HK Hailan 海蓝控股 Real Estate 297

2016-07-13 1579 HK Yihai International 颐海国际 Consumer Staples 881

2016-07-12 2869 HK Greentown Service 绿城服务 Industrials 1,780

2016-07-12 1586 HK China Leon Inspection 中国力鸿 Energy 98

2016-07-11 1606 HK CDB Leasing 国银租赁 Financials 6,285

2016-07-08 3958 HK Orient Securities 东方证券 Financials 8,371

2016-06-27 8280 HK China Digital Video 中国数字视频 Consumer Discretionary 295

2016-06-01 2588 HK BOC Aviation 中银航空租赁 Industrials 8,745

2016-03-30 2016 HK China Zheshang Bank 浙商银行 Financials 15,028

2016-03-30 1578 HK Bank of Tianjin 天津银行 Financials 7,678

2016-03-30 2239 HK SMIT 国微技术 Information Technology 284

2016-01-15 1565 HK Virscend Education 成实外教育 Consumer Discretionary 2,013

2016-01-07 3773 HK NNK 年年卡 Information Technology 115

Sources: Company data, Wind, CMS (HK)

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 22

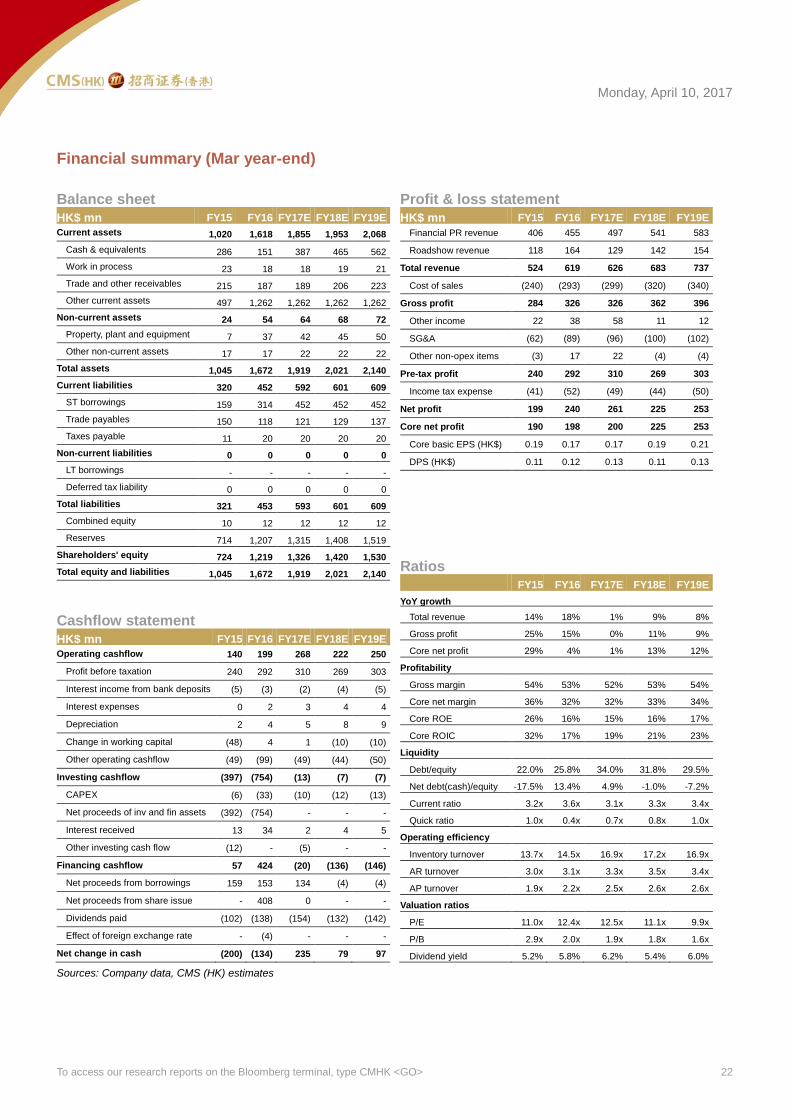

Financial summary (Mar year-end)

Balance sheet

HK$ mn FY15 FY16 FY17E FY18E FY19E

Current assets 1,020 1,618 1,855 1,953 2,068

Cash & equivalents 286 151 387 465 562

Work in process 23 18 18 19 21

Trade and other receivables 215 187 189 206 223

Other current assets 497 1,262 1,262 1,262 1,262

Non-current assets 24 54 64 68 72

Property, plant and equipment 7 37 42 45 50

Other non-current assets 17 17 22 22 22

Total assets 1,045 1,672 1,919 2,021 2,140

Current liabilities 320 452 592 601 609

ST borrowings 159 314 452 452 452

Trade payables 150 118 121 129 137

Taxes payable 11 20 20 20 20

Non-current liabilities 0 0 0 0 0

LT borrowings - - - - -

Deferred tax liability 0 0 0 0 0

Total liabilities 321 453 593 601 609

Combined equity 10 12 12 12 12

Reserves 714 1,207 1,315 1,408 1,519

Shareholders' equity 724 1,219 1,326 1,420 1,530

Total equity and liabilities 1,045 1,672 1,919 2,021 2,140

Cashflow statement

HK$ mn FY15 FY16 FY17E FY18E FY19E

Operating cashflow 140 199 268 222 250

Profit before taxation 240 292 310 269 303

Interest income from bank deposits (5) (3) (2) (4) (5)

Interest expenses 0 2 3 4 4

Depreciation 2 4 5 8 9

Change in working capital (48) 4 1 (10) (10)

Other operating cashflow (49) (99) (49) (44) (50)

Investing cashflow (397) (754) (13) (7) (7)

CAPEX (6) (33) (10) (12) (13)

Net proceeds of inv and fin assets (392) (754) - - -

Interest received 13 34 2 4 5

Other investing cash flow (12) - (5) - -

Financing cashflow 57 424 (20) (136) (146)

Net proceeds from borrowings 159 153 134 (4) (4)

Net proceeds from share issue - 408 0 - -

Dividends paid (102) (138) (154) (132) (142)

Effect of foreign exchange rate - (4) - - -

Net change in cash (200) (134) 235 79 97

Sources: Company data, CMS (HK) estimates

Profit & loss statement

HK$ mn FY15 FY16 FY17E FY18E FY19E

Financial PR revenue 406 455 497 541 583

Roadshow revenue 118 164 129 142 154

Total revenue 524 619 626 683 737

Cost of sales (240) (293) (299) (320) (340)

Gross profit 284 326 326 362 396

Other income 22 38 58 11 12

SG&A (62) (89) (96) (100) (102)

Other non-opex items (3) 17 22 (4) (4)

Pre-tax profit 240 292 310 269 303

Income tax expense (41) (52) (49) (44) (50)

Net profit 199 240 261 225 253

Core net profit 190 198 200 225 253

Core basic EPS (HK$) 0.19 0.17 0.17 0.19 0.21

DPS (HK$) 0.11 0.12 0.13 0.11 0.13

Ratios

FY15 FY16 FY17E FY18E FY19E

YoY growth

Total revenue 14% 18% 1% 9% 8%

Gross profit 25% 15% 0% 11% 9%

Core net profit 29% 4% 1% 13% 12%

Profitability

Gross margin 54% 53% 52% 53% 54%

Core net margin 36% 32% 32% 33% 34%

Core ROE 26% 16% 15% 16% 17%

Core ROIC 32% 17% 19% 21% 23%

Liquidity

Debt/equity 22.0% 25.8% 34.0% 31.8% 29.5%

Net debt(cash)/equity -17.5% 13.4% 4.9% -1.0% -7.2%

Current ratio 3.2x 3.6x 3.1x 3.3x 3.4x

Quick ratio 1.0x 0.4x 0.7x 0.8x 1.0x

Operating efficiency

Inventory turnover 13.7x 14.5x 16.9x 17.2x 16.9x

AR turnover 3.0x 3.1x 3.3x 3.5x 3.4x

AP turnover 1.9x 2.2x 2.5x 2.6x 2.6x

Valuation ratios

P/E 11.0x 12.4x 12.5x 11.1x 9.9x

P/B 2.9x 2.0x 1.9x 1.8x 1.6x

Dividend yield 5.2% 5.8% 6.2% 5.4% 6.0%

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 23

Investment Ratings

Industry Rating Definition

OVERWEIGHT Expect sector to outperform the market over the next 12 months

NEUTRAL Expect sector to perform in-line with the market over the next 12 months

UNDERWEIGHT Expect sector to underperform the market over the next 12 months

Company Rating Definition

BUY Expect stock to generate 10%+ return over the next 12 months

NEUTRAL Expect stock to generate +10% to -10% over the next 12 months

SELL Expect stock to generate loss of 10%+ over the next 12 months

Analyst Disclosure

The analysts primarily responsible for the preparation of all or part of the research report contained herein hereby certify that: (i) the views expressed in this research report accurately reflect the

personal views of each such analyst about the subject securities and issuers; and (ii) no part of the analyst’s compensation was, is, or will be directly or indirectly, related to the specific

recommendations or views expressed in this research report.

Regulatory Disclosure

Please refer to the important disclosures on our website http://www.newone.com.hk/cmshk/en/disclosure.html or http://www.cmschina.com.hk/Research/Disclosure.

Disclaimer

This document is prepared by China Merchants Securities (HK) Co., Limited (“CMS HK”). CMS HK is a licensed corporation to carry on Type 1 (dealing in securities), Type 2 (dealing in futures),

Type 4 (advising on securities), Type 6 (advising on corporate finance) and Type 9 (asset management) regulated activities under the Securities and Futures Ordinance (Chapter 571). This

document is for information purpose only. Neither the information nor opinion expressed shall be construed, expressly or impl iedly, as an advice, offer or solicitation of an offer, invitation,

advertisement, inducement, recommendation or representation of any kind or form whatsoever to buy or sell any security, financial instrument or any investment or other specific product. The

securities, instruments or strategies discussed in this document may not be suitable for all investors, and certain investors may not be eligible to participate in some or all of them. Certain

services and products are subject to legal restrictions and cannot be offered worldwide on an unrestricted basis and/or may not be eligible for sale to all investors. CMS HK is not registered as a

broker-dealer in the United States and its products and services are not available to U.S. persons except as permitted under SEC Rule 15a-6.

The information and opinions, and associated estimates and forecasts, contained herein have been obtained from or are based on sources believed to be reliable. CMS HK, its holding or

affiliated companies, or any of its or their directors, officers or employees (“CMS Group”) do not represent or warrant, expressly or impliedly, that it is accurate, correct or complete and it should

not be relied upon. CMS Group will not accept any responsibility or liability whatsoever for any use of or reliance upon this document or any of the content thereof. The contents and information

in this document are only current as of the date of their publication and will be subject to change without prior notice. Past performance is not indicative of future performance. Estimates of

future performance are based on assumptions that may not be realized. The analysis contained herein is based on numerous assumptions. Different assumptions could result in materially

different results. Opinions expressed herein may differ or be contrary to those expressed by other business divisions or other members of CMS Group as a result of using different assumptions

and/or criteria.

This document has been prepared without regard to the individual financial circumstances and investment objectives of the persons who receive it. Use of any information herein shall be at the

sole discretion and risk of the user. Investors are advised to independently evaluate particular investments and strategies, take financial and/or tax advice as to the implications (including tax) of

investing in any of the securities or products mentioned in this document, and make their own investment decisions without relying on this publication.

CMS Group may have a long or short position, make markets, act as principal or agent, or engage in transactions in securities of companies referred to in this document and may also perform

or seek to perform investment banking services or provide advisory or other services for those companies. This document is for the use of intended recipients only and this document may not

be reproduced, distributed or published in whole or in part for any purpose without the prior consent of CMS Group. CMS Group will not be liable for any claims or lawsuits from any third parties

arising from the use or distribution of this document. This document is for distribution only under such circumstances as may be permitted by applicable law. This document is not directed at you

if CMS Group is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available to you. In particular, this document is only made available to certain US

persons to whom CMS Group is permitted to make available according to US securities laws, but cannot otherwise be made available, distributed or transmitted, whether directly or indirectly,

into the US or to any US person. This document also cannot be distributed or transmitted, whether directly or indirectly, into Japan and Canada and not to the general public in the People’s

Republic of China (for the purpose of this document, excluding Hong Kong, Macau and Taiwan).

Monday, April 10, 2017

To access our research reports on the Bloomberg terminal, type CMHK <GO> 24

Important Disclosures for U.S. Persons

This research report was prepared by CMS HK, a company authorized to engage in securities activities in Hong Kong. CMS HK is not a registered broker-dealer in the United States and,

therefore, is not subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. This research report is provided for distribution solely to “major

U.S. institutional investors” in reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Any U.S. recipient of this research report wishing to effect any transaction to buy or sell securities or related financial instruments based on the information provided in this research report

should do so only through Rosenblatt Securities Inc, 40 Wall Street 59th Floor, New York, NY 10005, a registered broker dealer in the United States. Under no circumstances should any

recipient of this research report effect any transaction to buy or sell securities or related financial instruments through CMS HK. Rosenblatt Securities Inc. accepts responsibility for the contents

of this research report, subject to the terms set out below.

The analyst whose name appears in this research report is not registered or qualified as a research analyst with the Financial Industry Regulatory Authority (“FINRA”) and may not be an

associated person of Rosenblatt Securities Inc. and, therefore, may not be subject to applicable restrictions under FINRA Rules on communications with a subject company, public appearances

and trading securities held by a research analyst account.

Ownership and Material Conflicts of Interest

Rosenblatt Securities Inc. or its affiliates does not ‘beneficially own,’ as determined in accordance with Section 13(d) of the Exchange Act, 1% or more of any of the equity securities mentioned

in the report. Rosenblatt Securities Inc, its affiliates and/or their respective officers, directors or employees may have interests, or long or short positions, and may at any time make purchases

or sales as a principal or agent of the securities referred to herein. Rosenblatt Securities Inc. is not aware of any material conflict of interest as of the date of this publication.

Compensation and Investment Banking Activities

Rosenblatt Securities Inc. or any affiliate has not managed or co-managed a public offering of securities for the subject company in the past 12 months, nor received compensation for

investment banking services from the subject company in the past 12 months, neither does it or any affiliate expect to receive, or intends to seek compensation for investment banking services

from the subject company in the next 3 months.

Additional Disclosures

This research report is for distribution only under such circumstances as may be permitted by applicable law. This research report has no regard to the specific investment objectives, financial

situation or particular needs of any specific recipient, even if sent only to a single recipient. This research report is not guaranteed to be a complete statement or summary of any securities,

markets, reports or developments referred to in this research report. Neither CMS HK nor any of its directors, officers, employees or agents shall have any liability, however arising, for any

error, inaccuracy or incompleteness of fact or opinion in this research report or lack of care in this research report’s preparation or publication, or any losses or damages which may arise from

the use of this research report.

CMS HK may rely on information barriers, such as “Chinese Walls” to control the flow of information within the areas, units, divisions, groups, or affiliates of CMS HK.

Investing in any non-U.S. securities or related financial instruments (including ADRs) discussed in this research report may present certain risks. The securities of non-U.S. issuers may not be

registered with, or be subject to the regulations of, the U.S. Securities and Exchange Commission. Information on such non-U.S. securities or related financial instruments may be limited.

Foreign companies may not be subject to audit and reporting standards and regulatory requirements comparable to those in effect within the United States.

The value of any investment or income from any securities or related financial instruments discussed in this research report denominated in a currency other than U.S. dollars is subject to

exchange rate fluctuations that may have a positive or adverse effect on the value of or income from such securities or related financial instruments.

Past performance is not necessarily a guide to future performance and no representation or warranty, express or implied, is made by CMS HK with respect to future performance. Income from

investments may fluctuate. The price or value of the investments to which this research report relates, either directly or indirectly, may fall or rise against the interest of investors. Any

recommendation or opinion contained in this research report may become outdated as a consequence of changes in the environment in which the issuer of the securities under analysis

operates, in addition to changes in the estimates and forecasts, assumptions and valuation methodology used herein.

No part of the content of this research report may be copied, forwarded or duplicated in any form or by any means without the prior consent of CMS HK and CMS HK accepts no liability

whatsoever for the actions of third parties in this respect.

Hong Kong

China Merchants Securities (HK) Co., Ltd.

Address: 48/F, One Exchange Square, Central, Hong Kong

Tel:+852 3189 6888 Fax:+852 3101 0828