handouts dam 2015 2016

TRANSCRIPT

DATA ANALYSIS

for

MANAGERS

MScBA

Instituto Universitário de Lisboa (ISCTE-IUL)

JOSÉ DIAS [email protected]

2015/2016

i Contents

Contents

1 Math introductory concepts 11.1 The real numbers system . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2 The concept of sets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.3 Relations and functions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.3.1 Linear function . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.3.2 Exponential function . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41.3.3 Logarithmic function . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51.3.4 Functions of two or more independent variables . . . . . . . . . . . . . . . . 51.3.5 The concepts of derivative and elasticity . . . . . . . . . . . . . . . . . . . . 5

1.4 Matrices and vectors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61.5 Descriptive statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61.6 How to prepare a le for statistical analysis . . . . . . . . . . . . . . . . . . . . . . 71.7 Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1.7.1 Investment Bank 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91.7.2 Investment Bank 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91.7.3 Derivative and Elasticity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91.7.4 Operations involving matrices . . . . . . . . . . . . . . . . . . . . . . . . . . 91.7.5 Descriptive statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2 Statistical and distribution theory 112.1 Random variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2.1.1 Discrete random variables (drv) . . . . . . . . . . . . . . . . . . . . . . . . . 112.1.2 Continuous random variables (crv) . . . . . . . . . . . . . . . . . . . . . . . 122.1.3 Properties of the Expected value of a rv . . . . . . . . . . . . . . . . . . . . 132.1.4 The Correlation Coecient . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.1.5 Properties of the Variance of a rv . . . . . . . . . . . . . . . . . . . . . . . . 142.1.6 Properties of the Covariance . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.1.7 Moments of a rv . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142.1.8 Conditional distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152.1.9 Independence and correlation . . . . . . . . . . . . . . . . . . . . . . . . . . 15

2.2 Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 162.2.1 The properties of estimators . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

2.3 Probability distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.3.1 Normal or Gaussian distribution . . . . . . . . . . . . . . . . . . . . . . . . . 172.3.2 The Chi-square distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . 202.3.3 The Student's t distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . 202.3.4 F distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

2.4 Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212.4.1 Probabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212.4.2 Discrete random variable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212.4.3 Continuous random variable . . . . . . . . . . . . . . . . . . . . . . . . . . . 212.4.4 Normal distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

José Dias Curto Data Analysis for Managers - MScBA

ii Contents

3 Statistical inference: a brief review 233.1 The Hypothesis Testing Methodology: a brief review . . . . . . . . . . . . . . . . . 233.2 Statistical Tests Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

3.2.1 One sample t test . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243.2.2 One Sample Kolmogorov-Smirnov Test (nonparametric test) . . . . . . . . . 263.2.3 Characteristics and limitations of the Kolmogorov-Smirnov test . . . . . . . 263.2.4 Test statistic and signicance . . . . . . . . . . . . . . . . . . . . . . . . . . 263.2.5 Two independent samples . . . . . . . . . . . . . . . . . . . . . . . . . . . . 293.2.6 Analysis of Variance (ANOVA) . . . . . . . . . . . . . . . . . . . . . . . . . 31

4 Correlation and simple linear regression 354.1 Types of data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 354.2 Correlation Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 364.3 Simple Regression Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

5 The multiple linear regression model (MLRM) 425.1 Assumptions of the MLRM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 425.2 Ordinary Least Squares Method (OLS) . . . . . . . . . . . . . . . . . . . . . . . . . 435.3 Properties of OLS estimators . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 445.4 Ohlson Empirical Application . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

5.4.1 Coecient of Determination: R-Square (Quadrado de R) . . . . . . . . . . . 465.4.2 The Standard Error of Regression (Erro-padrão da Regressão) . . . . . . . . 495.4.3 The Unstandardized Coecients . . . . . . . . . . . . . . . . . . . . . . . . . 495.4.4 The Standardized Coecients . . . . . . . . . . . . . . . . . . . . . . . . . . 495.4.5 F test . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 515.4.6 t test . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 515.4.7 Information Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

6 Assumptions of the MLRM: Normality and Multicollinearity 546.1 Normality Tests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

6.1.1 Skewness and Kurtosis coecients . . . . . . . . . . . . . . . . . . . . . . . . 546.2 The Jarque-Bera (JB) Test . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 566.3 The Kolmogorov-Smirnov (KS) Test . . . . . . . . . . . . . . . . . . . . . . . . . . 566.4 Cobb-Douglas Application . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 576.5 Multicollinearity Consequences . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 596.6 Multicollinearity Diagnostic . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

6.6.1 Tolerance and Variance Ination Factor . . . . . . . . . . . . . . . . . . . . . 606.6.2 Matrix Condition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 616.6.3 Variance Decomposition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

6.7 Solutions for Multicollinearity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 626.8 Application: Electric Utility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

7 Assumptions of the MLRM: heteroskedasticity 657.1 The Generalized Least Squares (GLS) Method . . . . . . . . . . . . . . . . . . . . . 667.2 Heteroskedasticity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

José Dias Curto Data Analysis for Managers - MScBA

iii Contents

7.2.1 Detecting Heteroskedasticity . . . . . . . . . . . . . . . . . . . . . . . . . . . 697.2.2 Corrective Measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

7.3 Applications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 757.3.1 Income-Sales-Workforce . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 757.3.2 Ohlson Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

8 Assumptions of the MLRM: AUTOCORRELATION 848.1 The consequences of autocorrelation . . . . . . . . . . . . . . . . . . . . . . . . . . . 858.2 First order autocorrelation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 858.3 How to detect the errors' autocorrelation . . . . . . . . . . . . . . . . . . . . . . . . 88

8.3.1 Graphical representation of residuals . . . . . . . . . . . . . . . . . . . . . . 888.3.2 Hypotheses Testing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

8.4 Solutions for autocorrelation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 928.4.1 The Cochrane-Orcutt (CORC)(1949) iterative procedure . . . . . . . . . . . 928.4.2 The iterative procedure of Hildreth-Lu (HL) . . . . . . . . . . . . . . . . . . 938.4.3 Heteroskedasticity and Autocorrelation Consistent Estimators (HAC) . . . . 93

8.5 Application: GDP and PC (USA) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

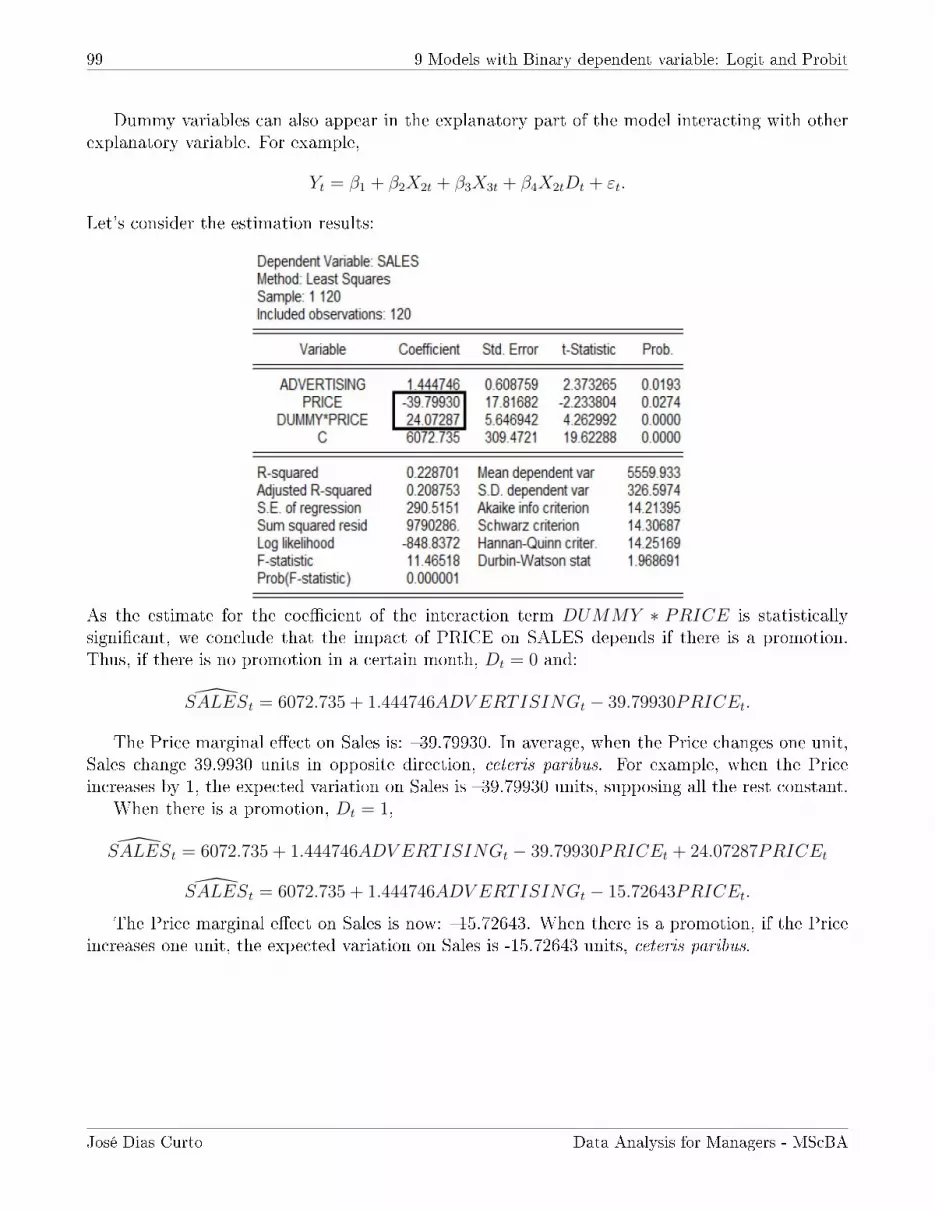

9 Models with Binary dependent variable: Logit and Probit 989.1 Application: Credit Scoring . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

José Dias Curto Data Analysis for Managers - MScBA

1 1 Math introductory concepts

1 Math introductory concepts

The purpose of these rst two lectures is to present a brief review of math introductory conceptslike functions, derivative, elasticity, logarithm, etc.

1.1 The real numbers system

The real number system consists of rational and irrational numbers. These numbers may bepositive, zero, or negative. Real numbers may be represented by innite decimals, for example:

9.7243527 . . . ;2

3= 0.6666666 . . . ;

√3 = 1.73205 . . . ; π = 3.14159265 . . .

Natural numbers or Counting numbers: NThese are the numbers that we use to count:N = 1, 2, 3, 4, . . .

Whole numbers: N0

These are the natural numbers plus the number zero:N0 = 0, 1, 2, 3, 4, . . .

The Whole numbers set includes the Natural numbers set (or N is a subset of N0):

N ⊂ N0 or N0 ⊃ N.

Integers: ZThe expanded set of numbers that we get by including negative versions of the counting numbersis called the Integers:Z = . . . ,−4,−3,−2,−1, 0, 1, 2, 3, 4, . . .

N0 ⊂ Z or Z ⊃ N0.

Rational numbers: QA rational number is a number which can be expressed as a ratio of two integers. Non-integerrational numbers (commonly called fractions) are usually written as the vulgar fraction x

y, where

y cannot be zero (but x can). x is called the numerator, and y the denominator.

Q =

x

y, x ∈ Z, y ∈ Z, y 6= 0

where Z denotes the set of integers.

All integers can also be thought of as rational numbers, with a denominator 1:

5 =5

1;−15 =

−15

1.

This means that all the previous sets of numbers (Natural numbers, Whole numbers andIntegers) are subsets of the rational numbers:

N ⊂ N0 ⊂ Z ⊂ Q or Q ⊃ Z ⊃ N0 ⊃ N.

José Dias Curto Data Analysis for Managers - MScBA

2 1.2 The concept of sets

Irrational numbers: IQThese are the numbers that cannot be expressed as a ratio of two integers. The decimals neverrepeat or terminate (rational numbers always do one or the other). Perhaps the most well knownirrational numbers are π and

√2.

Real numbers: RThe real numbers set includes all the rational and irrational numbers. A real number may beexpressed by a point on the real line:

ExamplesConsider the following numbers:

3,−4.3,−7345.22, 1456, 67495.78, 0.25(1

4),√

3 = 1.73205080756

1. Classify each one of the numbers. For example, 3 is a natural number.

2. Is this sentence true: 3 is also a rational number but it is not an integer.

3. Propose a fraction to represent the number −4.3.

4. Suggest real situations where these numbers can be used. For example, 3 can be a family'snumber of children.

1.2 The concept of sets

A set is a collection of distinct objects and sets are one of the most fundamental concepts inmathematics. The sets can be represented in extension or in comprehension:

Extension:A = 5, 6, 7, 8, 9, 10

Comprehension:A = x : x is an integer bigger than 4 and lower than 11

N, N0, Z, Q, IQ and R are all examples of sets where the objects are numbers.

Operations involving setsConsider the sets A, B and C:

A = 1, 2, 3, 4, B = 3, 4, 5, 6, 7 and C = 1, 3, 4, 5, 6, 7

• The union of two sets A and B is the set of elements which are in A or in B or in both andit is denoted by A ∪ B:

A ∪B = 1, 2, 3, 4, 5, 6, 7

José Dias Curto Data Analysis for Managers - MScBA

3 1.3 Relations and functions

• The intersection of sets A and B is the set of all elements common to both A and B and itis denoted by A ∩ B:

A ∩B = 3, 4

• x ∈ A if x belongs to A. For example, 1 ∈ A.

• If B is a subset of C than B is included in C or C contains B:

B ⊂ C or C ⊃ B.

1.3 Relations and functions

In management and economics the quantitative phenomena are usually represented by variables:x, y, z and the mathematical functions are used to establish the relationship between those phe-nomena.

The mathematical concept of a function expresses the dependence between two quantities, oneof which is given (the independent variable, argument of the function, or its input) and the otheris the result (the dependent variable, value of the function, or output):

y = f(x),

where x is the independent variable and y is the dependent one.For example, if y = 2x and x = 4 then y = 8.

1.3.1 Linear function

A linear (strictly speaking, ane) function has the form:

y = f(x) = b+mx,

for two real numbers b and m, where b is the intercept and m is the slope.If y is a linear function its slope is always constant.

ProportionalityWe say that y is (directly) proportional to x if there is a nonzero constant k such that

y = kx,

where k is the constant of proportionality.Let the function g represent the yearly production of car brand A since 1990 (t=0):

y = g(t) = 10000 + 500t,

where 10000 represents the production in 1990 (at t=0) and the slope (500) tells us that theproduction increases by about 500 units per year. We say that g is an increasing function as theslope is positive.

José Dias Curto Data Analysis for Managers - MScBA

4 1.3 Relations and functions

VariationsLet ∆y and ∆x represent the absolute variation in y and x, respectively.

∆y = y2 − y1 and ∆x = x2 − x1,

where the absolute variation in y is always proportional to the absolute variation in x: ∆y = m∆xand the slope is given by m = ∆y

∆x. For example, if ∆t = 5, ∆y = 500× 5 = 2500.

The relative variations in y and x are given by ∆yy1

and ∆xx1, respectively. If the ratio between the

absolute variations is always constant and it is given by the slope, the ratio of relative variationsdepends on the x and y values.

The percentage variation (or the rate of change) is the product of 100 by the relative variation:100× ∆y

y1and 100× ∆x

x1.

Now you are able to answer to APPLICATION 1.7.1 (at the end of this section).

1.3.2 Exponential function

The common form of the exponential function is:

y = f(x) = abx,

where a is the value of y when x = 0, b is the base and x is the exponent. Special cases of theexponential function are:

• a = 1, y = bx;

• a = 1 and b = e, y = ex, where e is a mathematical constant, the base of the naturallogarithm, which equals approximately 2.718281828, and is also known as the Euler's number.

In this function, y increases (b > 1) or decreases (0 < b < 1) at the same rate. Let the relativevariation in y be:

y2 − y1

y1

=abx2 − abx1

abx1=bx2

bx1− 1 = bx2−x1 − 1.

If ∆x = x2 − x1 = 1, then the relative variation in y is given by:

b− 1

and the percentage variation in y is100× (b− 1)

which is constant.Go to APPLICATION 1.7.2.

José Dias Curto Data Analysis for Managers - MScBA

5 1.3 Relations and functions

1.3.3 Logarithmic function

The logarithm of a number x one base a (necessarily positive) is dened as the power y of whichmust be increased the base a to obtain that number: y = loga(x). For example, log2(16) = 4, as 4is the number that should powered 2 to aord 16: 24 = 16.

The logarithm of base e is referred to as the natural logarithm and is represented by ln(x) withno explicit reference to the base. In practice one can also use common logarithms, or logarithms ofbase 10, which are usually represented by log(x). The relationship between the natural logarithmand the logarithm of base 10 is given by:

ln(x) = 2.3026 log(x).

1.3.4 Functions of two or more independent variables

The functions can include more than one independent variable. The usual notation is:

y = f(x1, x2, x3)

and if there is a linear relationship between y and each one of the independent variables, then

y = b+m1x1 +m2x2 +m3x3.

In management and economics the models include usually more than one independent variable.Let yt represents the aggregate consumption of one country in year t, x1t and x2t represent the

interest rates and the GDP, respectively. A function can be used to determine the relationshipbetween the consumption and each one of these independent variables.

1.3.5 The concepts of derivative and elasticity

The derivative is a measurement of how a function changes when the values of their inputs change.Thus, the derivative is the marginal eect of x in y :

dy

dx= Lim

∆x→0

∆y

∆x.

The elasticity (that we represent by η) measures the percentage change in one variable thatresults from a 1% change in another variable. For example, if the price elasticity of demand is −5,when the price rises by 1%, quantity demanded might fall by 5%:

100× ∆yy

100× ∆xx

=∆y

y:

∆x

x=x

y× ∆y

∆x.

When ∆x→ 0, ∆y∆x

= dydx

and η = xy× dy

dx, or,

η =∆y

y:

∆x

x=x

y× ∆y

∆x=x

y× dy

dx.

Go to APPLICATION 1.7.3.

José Dias Curto Data Analysis for Managers - MScBA

6 1.4 Matrices and vectors

1.4 Matrices and vectors

Let m and n be two integer positive numbers. The matrix A is a table with m rows and n columnsand the cells are lled by scalars that usually are real numbers:

A = (aij) =

a11 a12 . . . a1n

a21 a22 . . . a2n...

.... . .

...am1 am2 . . . amn

, (1)

where i = 1, 2, . . . ,m and j = 1, 2, . . . , n.In the following matrix m = 2 and n = 3. The rows and the columns determine the dimension

of the matrix that is 2× 3.

A =

[3 4 62 5 8

].

A vector is a special matrix with just one row (row-vector) or one column (column-vector).The dimension is 1× n and m× 1, respectively.

There are special matrices students must know: Quadratic, Symmetric, Diagonal and Identity.Main operations involving matrices and vectors are: Product, Inverse, Transpose and Deter-

minant. The Excel functions to perform these operations are (in english): MMULT, MINVERSE,

TRANSPOSE, MDETERM.MATRIZ.MULT, MATRIZ.INVERSA, TRANSPOR, MATRIZ.DETERM (in portuguese). In order to

compute these functions,

1. Select the range where the output will appear (for example, if the result is a 4 × 4 matrixyou have to select an Excel range composed by 4 rows and 4 columns);

2. Introduce the function;

3. Press simultaneously the keys <Shift>+ <Ctrl>+<Enter> to get all the matrix elements. Ifyou press just <Enter> only the rst element of the matrix will appear.

Go to APPLICATION 1.7.4.

1.5 Descriptive statistics

Descriptive statistics are used to describe the basic features of the data. Together with simplegraphical analysis, they form the basics of every data quantitative analysis. Descriptive statisticsare usually divided in three main sets:

• Location measures

Central tendency (arithmetic mean, mode and median).The arithmetic mean is probably the most commonly used statistic to describing centraltendency:

X =

∑ni=1 Xi

n.

The median is the score found at the exact middle of the set of values. The mode is themost frequently occurring value in the set of scores.

José Dias Curto Data Analysis for Managers - MScBA

7 1.6 How to prepare a le for statistical analysis

Noncentral tendency (percentiles, deciles and quartiles).

• Dispersion measures (variance, standard deviation, interquartile range, mean absolute devi-ation and coecient of variation).

Variance: S2 =∑n

i=1(Xi−X)2

n;

Standard deviation: S =

√∑ni=1(Xi−X)

2

n;

Coecient of variation: CV = SX× 100.

• Asymmetry and Kurtosis measures.

1.6 How to prepare a le for statistical analysis

The common procedure is to prepare an Excel le with all the data and open it later in SPSS1 orEViews2. Suppose that you want to prepare a le with the information of 10 master students:

where gender 0 is male and gender 1 is female, pincome represents the monthly parents' income,city represents the city of origin, where 1 is Lisbon, 2 is Porto, 3 is Coimbra and 4 is Faro; andnally distance represents the time of travel between home and the university. As one can see,and when it is possible, we introduce numbers instead of labels: for example we couldintroduce male instead of 0! but it is more correct to introduce the number andassociate later the respective designation.

Once the EXCEL le is prepared you must save it. After that, it can be opened in SPSSthrough the usual procedure: File, Open, Data. The SPSS appearance must be:

1The SPSS can be downloaded free from https://dsi.iscte.pt/.2You can access the EVIEWS, in any room or lab, by checking on the Windows button and write:

\\aplicacoes.iul.intra

José Dias Curto Data Analysis for Managers - MScBA

8 1.6 How to prepare a le for statistical analysis

Now you can save the le in SPSS format: name.SAV. The next steps are:

1. Associate the labels Male and Female to the numbers 0 and 1 in the gender variable:

(1) Change from Data View to Variable View, (2) Check on the right dots . . . of None, (3)Introduce the value 0 and the label Male and (4) Check on the button Add. You can dothe same for Female. After this click OK and change again to Data View. If you selectView, Value Labels, the numbers are replaced by the labels introduced before. In spiteof this, the numbers 0 and 1 remain in the le.

2. Apply the same procedure for the variable City.

3. Change again from Data View to Variable View and introduce a longer designation for thevariable pincome: Monthly Parents Income. You have to introduce this on the column Labelon the right side of the variable pincome. Go to APPLICATION 1.7.5

José Dias Curto Data Analysis for Managers - MScBA

9 1.7 Applications

1.7 Applications

1.7.1 Investment Bank 1

The investment bank ALLMONEY has a nancial application with the following characteristics:

• Capital: 500000 euros;

• Duration: 4 years;

• Annual interest rate: 3%;

• Simple interests type;

Based on this information look for a linear function to compute the cumulative amount of capi-tal+interests for each year.

• Represent graphically the resulting function;

• Compute the rate of change in the amount of capital+interests for each year;

1.7.2 Investment Bank 2

Now assume that interests are compounding yearly.

1. Propose a (non-linear) function to compute the cumulative amount of capital+interests foreach year;

2. Compute the rate of change in the amount of capital+interests for each year;

1.7.3 Derivative and Elasticity

Consider the following linear function: y = 20 + 2x. Compute the derivative of y in relation to xand the elasticity of y in relation to x if x = 10.

1.7.4 Operations involving matrices

A company has 4 stores (Lisboa, Porto, Faro and Leiria) where it sells 4 products that we nameby RA, RB, RC and RD. Let the matrix A be composed by the quantities sold in each one of thestores in the last month.

A =

40 50 30 2520 15 60 8090 25 35 4045 30 55 45

If the vector of prices is represented by b,

b =

10152512

,José Dias Curto Data Analysis for Managers - MScBA

10 1.7 Applications

compute the amount of sales per store using the rules of matrices' product.If the company establishes as target the following vector of sales compute the corresponding

prices.

S =

3000400037003825

.1.7.5 Descriptive statistics

The Excel le international.xls includes the saving rate and the per-capita disposable income for50 countries.

1. Import the data from the Excel to the SPPS: FILE, OPEN, Data.

2. Compute and interpret the descriptive statistics for both variables: the saving rate and theper-capita disposable income,ANALYZE, DESCRIPTIVE STATISTICS, Frequencies.STATISTICS Percentile values (Quartiles and Percentiles: 43, 75, 80) Central Tendency(Mean, Median, Mode) Dispersion (Std. deviation, Variance, Minimum, Maximum).CHARTS Histogram with normal curve.

3. Based on the coecient of variation compare the two distributions in terms of dispersion.

REFERENCESChiang, Alpha C. (2005), Fundamental Methods of Mathematical Economics, 4th edition.McClave, James T., Benson, P. G. and Sincich, T. (2012), Statistics for Business and Economics,12th edition.

José Dias Curto Data Analysis for Managers - MScBA

11 2 Statistical and distribution theory

2 Statistical and distribution theory

In this lecture we refer the most important concepts related with probabilities, random variablesand theoretical distributions.

2.1 Random variables

A random variable is a variable that can takes dierent outcomes, each with a probability less thanor equal to 1. A random variable can be described by examining the process which generates itsvalues and this process is called probability distribution. A probability distribution lists all possiblevalues and the probability that each will occur.

ExampleConsider the coin random experiment. The outcomes are: Ω = F,C, where F denotes a cointoss of heads and C is a toss of tails. If the coin is fair and thrown randomly the probability ofheads will be 1

2: P (F ) = P (C) = 1

2. Let the random variable X be the Number of heads. Thus, X

can assume the values 1 and 0 with probability 12.

Based on this, we might dene a random variable as a function that assigns to each outcomeof a random experiment a real number:

F → 1 C → 0.

The random variables (rv) can be distinguished between discrete and continuous rv. A discreterandom variablemay take on only a nite or an innite but countable number of distinct values suchas 0, 1, 2, 3, 4, ... Discrete random variables are usually (but not necessarily) counts. Examples ofdiscrete random variables include the number of children in a family, the Friday night attendanceat a cinema, the number of patients in a doctor's surgery, the number of defective light bulbs in abox of ten.

A continuous random variable can take an innite number of dierent outcomes, for example,any value in the interval [0, 3]. In this case each individual outcome has a probability of zero.Continuous random variables are usually measurements. Examples include height, weight, theamount of sugar in an orange, the time required to run a mile.

2.1.1 Discrete random variables (drv)

If X is a drv then:

• The probability function, f(x) = P (X = x), has the following properties: f(x) ≥ 0 and∑f(x) = 1.

• The distribution function is given by: F (x) = P (X ≤ x).

• The expected value or mean of a drv, often denoted by µ, is dened as: µ = E(X) =∑ni=1 f(xi)xi. The expected value should be distinguished from the sample mean which is

denoted by X and it is the average of the outcomes obtained in a sample.

José Dias Curto Data Analysis for Managers - MScBA

12 2.1 Random variables

• The variance is a weighted average of the squares of the deviations of outcomes on X fromits expected value, with the corresponding probabilities of each outcome serving as weights.It is dened as: σ2 =

∑ni=1 f(xi) [xi − E(X)]2. The variance is in itself an expectation: σ2 =

E [X − E(X)]2. The positive square root of the variance is called the standard deviation.

Example of a drv

x 0 1 2 3 4 5

f(x) 0.15 0.30 0.25 0.15 0.10 0.05F (x) 0.15 0.45 0.70 0.85 0.95 1.00xf(x) 0.00 0.30 0.50 0.45 0.40 0.25E(X) 1.90x2 0 1 4 9 16 25

x2f(x) 0.00 0.30 1.00 1.35 1.60 1.25E(X2) 5.50

x− E(X) -1.90 -0.90 0.10 1.10 2.10 3.10(x− E(X))2 3.61 0.81 0.01 1.21 4.41 9.61

f(x)(x− E(X))2 0.54 0.24 0.00 0.18 0.44 0.48Var(X) 1.89

2.1.2 Continuous random variables (crv)

If Y is a crv then:

• We dene the probability density function (pdf)

f(y) ≥ 0 as P a ≤ Y ≤ b =∫ baf(y)dy.

In a graph P a ≤ Y ≤ b =∫ baf(y)dy is the area under the function f(y) between the points

a and b. Taking the integral of f(y) over all possible outcomes gives∫ +∞−∞ f(y)dy = 1.

• The cumulative density function (cdf) is dened asF (y) = P Y ≤ y =

∫ y−∞ f(u)du, such that f(y) = F ′(y) (the derivative). The cdf has the

property that 0 ≤ F (y) ≤ 1, and is monotonically increasing, i.e., F (y) ≥ F (x) if y > x.

• The expected value or mean is dened as µ = E(Y ) =∫ +∞−∞ yf(y)dy.

• The variance is given by σ2 = V ar(Y ) =∫ +∞−∞ [y − E(Y )]2f(y)dy. Or,

V ar(Y ) = E[(Y − µ)2

]= E

(Y 2 − 2Y µ+ µ2

)= E

(Y 2)−2µE(Y )+µ2 = E

(Y 2)−[E(Y )]2 .

José Dias Curto Data Analysis for Managers - MScBA

13 2.1 Random variables

Next gure shows pdf and cdf of a certain continuous variable

Example of a crvLet X be a crv with the following pdf: f(x) = 1

2x for 0 ≤ x ≤ 2 and f(x) = 0 for other x values.

The cdf is given by: F (x) =∫ x−∞ f(x)dx =

[x2

4

]x0

= x2

4for 0 ≤ x ≤ 2 and F (x) = 0 for other x

values.

The expected value of X is given by:

E(X) =∫ +∞−∞ xf(x)dx = 0 +

∫ 2

0xf(x)dx+ 0 =

[x3

6

]2

0= 8

6.

The variance results from:V ar(X) = E (X2)− [E(X)]2.

As E (X2) = 0 +∫ 2

0x2f(x)dx+ 0 =

[x4

8

]2

0= 2 then

V ar(X) = 2− 86

= 0.22(2)

2.1.3 Properties of the Expected value of a rv

Let X and Y be rv and k be a constant. Then,

• E(k) = k: the expected value of a constant is the constant.

• E(kX) = kE(X);

• E(X + Y ) = E(X) + E(Y );

• E(X − Y ) = E(X)− E(Y );

• E(XY ) = Cov (X, Y ) + E(X)E(Y ) or E(XY ) = E(X)E(Y ) if X and Y are uncorrelatedand Cov (X, Y ) = 0.

The covariance is a measure of the linear relationship between X and Y :Cov (X, Y ) = E [(X − µX) (Y − µY )]

• drv: Cov (X, Y ) =∑n

i=1

∑nj=1 (xi − µX) (yj − µY ) f(xi, yj);

• crv: Cov (X, Y ) =∫ +∞−∞

∫ +∞−∞ (x− µX) (y − µY ) f(x, y)dxdy.

José Dias Curto Data Analysis for Managers - MScBA

14 2.1 Random variables

2.1.4 The Correlation Coecient

The value of the covariance depends on the units in which X and Y are measured. As a result weuse the correlation coecient:

ρXY = −1 ≤ σXYσXσY

≤ +1,

where σXY is the covariance between X and Y , σX and σY represent the standard deviations ofX and Y , respectively.

Unlike covariance, the correlation coecient has been normalized and is scale-free. The value ofthe correlation coecient always lies between −1 and +1. A positive correlation indicates that thevariables tend to move in the same direction, while a negative value implies that they tend to movein opposite directions. A zero value means that variables are linearly independent (uncorrelated).

2.1.5 Properties of the Variance of a rv

Let X and Y be rv and k be a constant. Then,

• V ar(k) = 0.

• V ar(kX) = k2V ar(X);

• V ar(X ± Y ) = V ar(X) + V ar(Y )± 2Cov(X, Y );

2.1.6 Properties of the Covariance

When a, b, c and d are constants, it holds that

Cov(aX + b, cY + d) = acCov(X, Y ).

Further,Cov(aX + bY, Y ) = aCov(X, Y ) + bCov(Y, Y ) =

= aCov(X, Y ) + bV ar(Y ).

It also follows that two variables X and Y are perfectly correlated (ρXY = 1) if Y = kX for somenonzero value of k. If X and Y are correlated, the variance of a linear function of X and Y dependsupon their covariance. In particular,

V ar(aX + bY ) = a2V ar(X) + b2V ar(Y ) + 2Cov(X, Y ).

2.1.7 Moments of a rv

In most cases the distribution of a rv is not completely described by its mean and variance, andwe can dene the k-th central moment as

E[(X − µX)k

], k = 1, 2, 3, . . .

The variance is the second central moment.

José Dias Curto Data Analysis for Managers - MScBA

15 2.1 Random variables

In particular, the third central moment is a measure for skewness, where a value of 0 indicates asymmetric distribution, and the fourth central moment measures kurtosis. It is a measure of thethickness of the tails of the distribution.

2.1.8 Conditional distributions

A conditional distribution describes the distribution of a variable, say Y , given the outcome ofanother variable X. The conditional distribution is implied by the joint distribution of the twovariables. We dene

f(y|X = x) = f(y|x) =f(x, y)

f(x).

If X and Y are independent then

f(y|x) = f(y) and f(x, y) = f(y)f(x).

The conditional expectation and variance of Y given X = x are:

E(Y |X = x) = E(Y |x) =

∫yf(y|x)dy

V ar(Y |x) =

∫[y − E(Y/x)]2 f(y/x)dy.

andV ar(Y |x) = E

(Y 2/x

)− [E(Y |x)]2 .

It holds thatV ar(Y ) = Ex [V ar(Y |X)] + V arx [E(Y |X)] ,

where Ex and V arx denote the expected value and variance, respectively, based upon the marginaldistribution of X.

If Y is conditional mean independent of X it means that

E(Y |X) = E(Y ) = 0.

This is stronger than zero correlation because E(Y |X) = 0 implies that E(Y ) = 0.

2.1.9 Independence and correlation

If two variables X and Y are independent, the covariance between them is zero. However, theresults does not hold in the opposite direction. Two variables may have zero correlation, yet theremay be a dependence between the variables. The key is that covariance and correlation measurelinear dependence; the variables may be related nonlinearly yet have a zero covariance.

Consider the example where Y = X4 and the correlation between Y and X is null:

X -4 -3 -2 -1 0 1 2 3 4Y 256 81 16 1 0 1 16 81 256

José Dias Curto Data Analysis for Managers - MScBA

16 2.2 Estimation

2.2 Estimation

Means, variances and covariances can be measured with certainty only if we know all the possibleoutcomes, i.e., the population. Usually, however, we have only a sample of the population andthose measures have to be estimated. Finding the best estimator for any given sample is a com-plex issue but for the moment assume that the estimator of a parameter yields estimates closelyapproximating that parameter. We would like the estimator to be UNBIASED, i.e., the expectedvalue of the estimator is equal to the parameter itself. Unbiased estimators for:

• The mean: µ = X =∑n

i=1Xi

n;

• The variance: σ2 = S′2 =

∑ni=1(Xi−X)2

n−1;

• The covariance: σ2XY =

∑ni=1(Xi−X)(Yi−Y )

n−1;

• The correlation coecient: ρXY =∑n

i=1(Xi−X)(Yi−Y )√∑ni=1(Xi−X)2

∑ni=1(Yi−Y )2

.

2.2.1 The properties of estimators

Let θ and θ represent the parameter and the estimator, respectively. There are four properties ofestimators that are important:

• Lack of bias: θ is an unbiased estimator if the mean or expected value of θ is equal to the

true value: E(θ)

= θ.

• Eciency: θ is an ecient unbiased estimator if for a given sample size the variance of θ issmaller than the variance of any other unbiased estimators. One estimator is more ecientthan another if it has smaller variance.Thus θ1 is more ecient than θ2 if V ar(θ1) < V ar(θ2), assuming that θ1 and θ2 are bothunbiased.

José Dias Curto Data Analysis for Managers - MScBA

17 2.3 Probability distributions

• Minimum Mean Square Error (MSE): There are many circumstances in which one is forcedto trade o bias and variance of estimators. Sometimes an estimator with very low varianceand some bias may be more desirable than an unbiased estimator with high variance. Onecriterion is to minimize Mean Square Error which is dened as

MSE(θ) = E(θ − θ)2

or

MSE(θ) =[Bias(θ)

]2

+ V ar(θ).

When θ is unbiased, the Bias(θ) = E(θ)− θ = 0 and the MSE and variance of θ are equal.

• Large-sample or asymptotic properties: as the sample size increases we expect that θ ap-proaches θ. Thus, the probability that θ diers from θ becomes very small.

The probability limit of θ (plim θ) is dened as follows:plim θ is equal to θ if, as n goes to innity, the probability that |θ − θ| will be less than anarbitrary small positive number will approach 1:

limn→∞

P(|θ − θ| < δ

)= 1,

for any small positive δ.

Consistency property: θ is a consistent estimator of θ if the probability limit of θ is θ.In an alternative criterion the MSE of the estimator should approach zero as the sample sizeincreases. The MSE criterion implies that:

The estimator is unbiased asymptotically:

limn→∞

E(θ)

= θ,

The estimator is the most ecient asymptotically. Thus, the variance of the estimatorgoes to zero as the sample size gets very large:

limn→∞

V ar(θ)

= 0.

An estimator with a MSE that approaches zero will be a consistent estimator but the reverseneed not be true. However, in the most part of applications consistent estimators have MSEapproaching zero, and the two criteria are used interchangeably.

2.3 Probability distributions

2.3.1 Normal or Gaussian distribution

The normal distribution is a continuous symmetric distribution that can be fully described by itsmean and variance and we write

X ∼ N(µ, σ)

José Dias Curto Data Analysis for Managers - MScBA

18 2.3 Probability distributions

meaning that X is normally distributed with mean µ and variance σ2. The pdf is given by:

f(x) =1

σ√

2πexp

[−(x− µ)2

2σ2

]

Let Z = X−µσ

be the standardization of X, with mean 0 and standard deviation 1. The pdf of Z(the standard normal distribution) is given by:

f(z) =1√2π

exp

(−1

2z2

)

All normal density curves satisfy the following property which is often referred to as the Em-pirical Rule.

• 68.27% of the observations fall within 1 standard deviation of the mean:

P (µ− σ ≤ X ≤ µ+ σ) = 0.6827.

• 95.45% of the observations fall within 2 standard deviations of the mean

P (µ− 2σ ≤ X ≤ µ+ 2σ) = 0.9545.

• 99.73% of the observations fall within 3 standard deviations of the mean:

P (µ− 3σ ≤ X ≤ µ+ 3σ) = 0.9973.

As the normal distribution is fully described by its mean and variance, we need not worryabout other properties such as skewness and kurtosis.

A linear function of a normal variable is also normal. If X ∼ N(µ, σ2) then

(aX + b) ∼ N(aµ+ b, a2σ2).

José Dias Curto Data Analysis for Managers - MScBA

19 2.3 Probability distributions

The cdf of the normal distribution does not have a closed form. Thus

P (X ≤ x) = P

(X − µσ

≤ x− µσ

)= Φ

(x− µσ

)=

∫ (x−µ)/σ

−∞f(z)dz,

where Φ denotes the cdf of the standard normal distribution.The symmetry of the normal distribution implies that:

• Φ(z) = 1− Φ(−z);

• The third central moment of a normal distribution is zero:E[(X − µX)3] = 0.

It can be shown that the fourth central moment of the normal distribution is 3σ4:

E[(X − µX)4] = 3σ4.

The properties of the third and fourth central moments are used in tests against normality (theJarque-Bera test, for example).

More results related with the normal distribution:

• If two (or more) variables have a joint normal distribution, all marginal distributions andconditional distributions are also normal;

• The conditional expectation of one variable given the other(s) is a linear function (with anintercept term);

• If ρXY = 0 it follows that f(y|x) = f(y) so that f(x, y) = f(x)f(y) and X and Y areindependent. Thus, if X and Y have a joint normal distribution with zero correlation thenthey are automatically independent.

• A linear function of normal variables is also normal.If X ∼ N(µX , σ

2X) and Y ∼ N(µY , σ

2Y ) then

(aX + bY ) ∼ N(aµX + bµY , a

2σ2X + b2σ2

Y + 2abσXY).

The Central Limit TheoremIf the random variable X has mean µ and variance σ2 (whatever the distribution is), then thesampling distribution of X becomes approximately normal with mean µ and variance σ2/n as nincreases:

Xa∼ N(µ, σ/

√n).

José Dias Curto Data Analysis for Managers - MScBA

20 2.3 Probability distributions

2.3.2 The Chi-square distribution

The chi square is useful for testing hypothesis that deal with variances of random variables. IfX1, X2, . . . , XK is a set of independent standard normal variables it holds that

Y =K∑i=1

X2i ∼ χ2

K ,

Y has a chi square distribution with K degrees of freedom. If Y ∼ χ2K then E(Y ) = K and

V ar(X) = 2K.Let S2 be the sample variance of n observations drawn from a normal distribution with variance

σ2. Then, it can be shown that:(N − 1)S2

σ2χ2n−1.

The chi square starts at the origin, is skewed to the right and has a tail which extends innitelyfar to the right. The distribution becomes more and more symmetric as the number of degreesof freedom gets larger and when the degrees of freedom get very large, the chi square distributionapproximates the normal.

2.3.3 The Student's t distribution

IfX has a standard normal distribution, X ∼ N(0, 1) and Y ∼ χ2K and ifX and Y are independent,

then the ratio

t =X√YK

has a Student's t distribution with K degrees of freedom. Like the normal, the t is symmetric, andit approximates the normal for large sample sizes. For sample sizes of roughly 30 or less the t hasfatter tails than the normal distribution.

2.3.4 F distribution

The F distribution is the distribution of the ratio of two independent chi squared distributedvariables, divided by their respective degrees of freedom:

F =Y1/K1

Y2/K2

,

where Y1 ∼ χ2K1

and Y2 ∼ χ2K2.

When K1 = 1 the F distribution is just the square of a t distribution. If K2 is large thedistribution of

K1F =Y1

Y2/K2

is well approximated by a chi-squared distribution with K1 degrees of freedom. For large K2 thedenominator is thus negligible.

José Dias Curto Data Analysis for Managers - MScBA

21 2.4 Applications

2.4 Applications

2.4.1 Probabilities

Next table presents some information related with ISCTE-IUL master students:

NACIONALITYSEX Portuguese Non-Portuguese TotalMale 200 20 220Female 100 20 120Total 300 40 340

Dene the events related with each one of the cells in the table.Compute the probabilities that a student selected randomly will be:

1. Portuguese;

2. Non-Portuguese;

3. Male;

4. Female;

5. If a student is a female compute the probability that she will be Portuguese.

2.4.2 Discrete random variable

The probability function of points scored per match by a Portuguese football team is as follows:Points 0 1 3f(x) 0.1 25 0.65

1. Is it f(x) a probability function?

2. Interpret the values of the probability function.

3. Compute and represent graphically the distribution function.

4. What is the probability that points scored per match will be higher than 0?

5. Compute the mean and variance of points per match.

2.4.3 Continuous random variable

A random variable X has probability density function (pdf)

f(x) = kx2(1− x) if 0 ≤ x ≤ 1, 0 otherwise.

1. Determine k.

2. Find E(X) and V ar(X).

3. Show that the median m satises the equation 6m4 − 8m3 + 1 = 0.

José Dias Curto Data Analysis for Managers - MScBA

22 2.4 Applications

2.4.4 Normal distribution

Let X ∼ N(µ = 100, σ = 20). Answer to the following questions:

• Compute the following probabilities:P (X < 100), P (X < 65), P (75 < X < 120) and P (X > 130) based on Statistical Tablesand Excel functions.

• Compute x : P (X < x) = 0.975.

• Comment the following sentence: The tails of the normal distribution are thin.

• If Y ∼ N(µ = 80, σ = 40) and X is independent of Y , compute P (X + Y < 160).

REFERENCESPinto, J. C. and Curto, J. D. (2001), Estatística para economia e gestão, Ed. Sílabo.McClave, James T., Benson, P. G. and Sincich, T. (2012), Statistics for Business and Economics,12th edition.

José Dias Curto Data Analysis for Managers - MScBA

23 3 Statistical inference: a brief review

3 Statistical inference: a brief review

Statistical inference allows us to draw conclusions about the population from which the sample hasbeen collected. The main tools of statistical inference are the CONFIDENCE INTERVALS andHYPOTHESES TESTING. Students must be able to deduce and interpret a condence intervaland to formulate and decide on hypothesis testing.

3.1 The Hypothesis Testing Methodology: a brief review

Hypothesis testing is the use of statistics to determine the probability that a given hypothesis(involving parameters or not) is true. Hypothesis testing is sometimes called conrmatory dataanalysis, in contrast to exploratory data analysis. In statistics, a result is called statisticallysignicant if it is unlikely to have occurred by chance. The usual process of hypothesis testingconsists in four steps.

1. The rst step is to specify the null hypothesis (H0) and the alternative hypothesis (H1).Until further decision it is assumed that the null hypothesis is true. If the research concernswhether one production method is better than another, the null hypothesis would most likelybe that there is no dierence between the means of two methods (H0 : µ1 − µ2 = 0) andthe alternative hypothesis would be H1 : µ1 6= µ2. If the research concerned the correlationbetween two variables, the null hypothesis would state that there is no correlation (H0 : ρ = 0)and the alternative hypothesis would be H1 : ρ 6= 0.

2. Identify a test statistic that can be used to assess the truth of the null hypothesis. After all,we intend to investigate whether the sampling results are very or somewhat believable, giventhe conditions postulated in the null hypothesis. This likelihood is quantied in probabilisticterms. For that, it is necessary to know the distribution of the test to be used, which is nomore than a function of sample values.

3. The third step correponds to the determination of the Rejection (or Critical) region (RR)and the Non Rejection (or Acceptance) region (NRR). The critical region comprises a setof values that the test can take for which there is a small plausibility between the sampleinformation and what is postulated in H0, which consequently leads to the rejection of thenull hypothesis. The acceptance region is also formed by a set of values that the test cantake and if the test assumes one of these values the decision should be do not reject H0.

The critical region can be one of two types: unilateral and bilateral. For example, thehypothesis H0 : µ <= b/H1 : µ > b, referring to a right-sided critical region, and thehypotheses H0 : µ >= b/H1 : µ < b suggest a left-sided critical region. The critical regionbilaterally, results from a formulation of hypotheses such as: H0 : µ = b/H1 : µ 6= b.

Associated to the set of values on the critical region there is a probability mass that thesevalues can occur under conditions of H0. This portion of probability is called as signicancelevel (α). In general, the level of signicance more commonly used ranges between 0.01 and0.05, without having a scientic criterion for its determination. Therefore the analyst setsthis value taking into account his experience or the cost of making a bad decision.

If the test value falls in the critical region there is a statistical evidence to doubt aboutthe truth of H0, i.e., if the signicance level is 0.01, for example, it means that under the

José Dias Curto Data Analysis for Managers - MScBA

24 3.2 Statistical Tests Applications

conditions dictated by the null hypothesis, the probability to collect a random sample with acertain size and to obtain results that lead to a test value that belongs to the critical regionis only 0.01 a very low probability, meaning that this is a situation unlikely to occur thuswe are led to doubt seriously about the postulate under the null hypothesis and thereforereject this hypothesis.

4. Test value and decision making. In this step a sample is collected and we assess the plausibil-ity between the results obtained from the sample and what is stated in H0. This evaluationshould be based on the test value that would belong to one of the two predened regions -the critical or the acceptance regions. If the test value belongs to the rst one, the decisionshould be to reject H0; otherwise, if it is included in the other region, the decision should bedo not reject H0.

3.2 Statistical Tests Applications

3.2.1 One sample t test

Test the hypothesis that the parents monthly income is 3000 euros. Apply the methodologypresented before.

1. Hypotheses formulation:

H0 : µ = 3000

H1 : µ 6= 3000;

2. The statistic of the test:X − µ0

s′√n

∼ t(n−1),

where X is the sample mean, µ0 is the µ value under the null hypothesis, s′ is the standarddeviation of the sample income and n is the sample size.

3. Determination of the Rejection (or Critical (CR)) and Non Rejection (NRR) (or Acceptance(AR) regions considering a signicance level of 5%, α = 0.05:

4. Test value and decision making:

t =2888.29− 3000

1210.645√100

= −0.923.

José Dias Curto Data Analysis for Managers - MScBA

25 3.2 Statistical Tests Applications

Since the test value falls in the acceptance region, we do not reject the null hypothesis, giventhe sample and the signicance level.

The decision can be based on the probability associated with the test value. Assuming thatthe null hypothesis is true, what is the probability of observing a value for the test statisticthat is at least as extreme as the value that was actually observed? If the probability islower than or equal to the signicance level, then the null hypothesis is rejected; if theprobability is greater than the signicance level then the null hypothesis is not rejected. Ifthe null hypothesis is rejected, the outcome is said to be statistically signicant, if the nullhypothesis is not rejected then the outcome is said to be not statistically signicant.

In order to compute that probability we can use the EXCEL Student's t function:

= DISTT (0.923; 99; 2) = 0.358 (in Portuguese)

or= TDIST (0.923; 99; 2) = 0.358 (in English).

As the probability is greater than the signicance level (0.05) the null hypothesis is notrejected. Assuming that the null hypothesis is true, there is a high probability of observinga value of −0.923 for the test value.

Do the same test, but now refer directly to SPSS:

José Dias Curto Data Analysis for Managers - MScBA

26 3.2 Statistical Tests Applications

As you can see, the SPSS shows the test value (-0.923) and also the probability associated withit (0.358). Thus, you only need to compare the Sig. (2-tailed) with the signicance level that weconsider (0.05 in our application) in order to decide if we reject or not the null.

3.2.2 One Sample Kolmogorov-Smirnov Test (nonparametric test)

The one-sample Kolmogorov-Smirnov test (Kolmogorov, 1933; Smirnov, 1939) is the best knownsupremum goodness-of-t test for continuous variables due to its simplicity and intuition and it canbe used to test whether or not the sample data is consistent with a specied distribution function.

The K-S statistic examines the maximum vertical deviation between the empirical and thetheoretical distribution functions and is dened as:

D = sup−∞<x<∞

|Fn(x)− F0(x)| , (2)

where F0(x) is the theoretical cumulative distribution being tested which must be a continuousdistribution and it must be fully specied, i.e., the location, scale, and shape parameters cannotbe estimated from the data. The null hypothesis, and the distribution under test, is rejected forlarge values of D.

3.2.3 Characteristics and limitations of the Kolmogorov-Smirnov test

An attractive feature of this test is that the distribution of the K-S test statistic itself does notdepend on the underlying cumulative distribution function being tested. Another advantage isthat it is an exact test (for example, the chi-square goodness-of-t test depends on an adequatesample size for the approximations to be valid).

Despite these advantages, the K-S test has several drawbacks. First, it only applies to contin-uous distributions. Second, it tends to be more sensitive near the center of the distribution thanat the tails, which makes it more conservative. Finally, and perhaps the most serious limitation,the distribution under the null must be fully specied. That is, if location, scale, and shape pa-rameters are estimated from the data, the critical region of the K-S test is no longer valid. Dueto the rst two limitations, many analysts prefer to use the Anderson-Darling goodness-of-t testin the presence of heavy-tailed distributions. However, this test is only available for a few specicdistributions.

3.2.4 Test statistic and signicance

The table of critical values for D when testing continuous distributions with known parameters ispresented next.

José Dias Curto Data Analysis for Managers - MScBA

27 3.2 Statistical Tests Applications

Level of signicance (α)

n 0.20 0.15 0.10 0.05 0.01

1 0.900 0.925 0.950 0.975 0.995

2 0.684 0.726 0.776 0.842 0.929

3 0.565 0.597 0.642 0.708 0.828

4 0.494 0.525 0.564 0.624 0.733

5 0.446 0.474 0.510 0.565 0.669

6 0.410 0.436 0.470 0.521 0.618

7 0.381 0.405 0.438 0.486 0.577

8 0.358 0.381 0.411 0.457 0.543

9 0.339 0.360 0.388 0.432 0.514

10 0.322 0.342 0.368 0.410 0.490

11 0.307 0.326 0.352 0.391 0.468

12 0.295 0.313 0.338 0.375 0.450

13 0.284 0.302 0.325 0.361 0.433

14 0.274 0.292 0.314 0.349 0.418

15 0.266 0.283 0.304 0.338 0.404

16 0.258 0.274 0.295 0.328 0.392

17 0.250 0.266 0.286 0.318 0.381

18 0.244 0.259 0.278 0.309 0.371

19 0.237 0.252 0.272 0.301 0.363

20 0.231 0.246 0.264 0.294 0.356

25 0.210 0.220 0.240 0.270 0.320

30 0.190 0.200 0.220 0.240 0.290

35 0.180 0.190 0.210 0.230 0.270

over 35 1.07/√n 1.14/

√n 1.22/

√n 1.36/

√n 1.63/

√n

Two common but incorrect uses of these critical values occur 1) when they are used to evaluatet of discrete distributions with known parameters despite their continuous distributions purposeand 2) when the parameters are unknown and they have to be estimated from sample data. Inboth cases the incorrect critical values (based on the distribution of the test for known parameters)biases the test toward acceptance of the theoretical distribution under the null. Due to this lastissue, Lilliefors (1967) proposed the corrected critical values when the distribution parameters haveto be estimated.

We can proceed by testing the normality of the Parents Monthly Income computing theKolmogorov-Smirnov test (in SPSS) with critical values proposed by Lilliefors: Analyse, DescriptiveStatistics, Explore and next proceed as it is shown in the gure:

José Dias Curto Data Analysis for Managers - MScBA

28 3.2 Statistical Tests Applications

The obtained results are presented next:

As one can see, the SPSS also shows the Shapiro-Wilk normality test (it is more appropriate forsmall samples). In the null of the tests we assume that the Parents Monthly Income distributionis normal. As one can see, the signicance associated with the test values is lower than 0.05 inboth tests. Thus, based on this sample and the 0.05 signicance level, there is statistical evidenceto reject the normality of the variable.

José Dias Curto Data Analysis for Managers - MScBA

29 3.2 Statistical Tests Applications

3.2.5 Two independent samples

Suppose that we want to test if the means of parents' income are statistically dierent betweenmale and female students.

1. Hypotheses formulation:H0 : µ1 = µ2 or µ1 − µ2 = 0

H1 : µ1 6= µ2 or µ1 − µ2 6= 0,

where 1 and 2 represent male and female students, respectively.

2. The statistic of the test can assume three dierent forms:

(a) For two populations with normal distributions with known variances (σ21, σ

22), the statis-

tic of the test is:(X1 − X2)− (µ1 − µ2)√

σ21

n1+

σ22

n2

∼ N(0; 1);

(b) For two populations with normal distribution with unknown but equal variances,

(X1 − X2)− (µ1 − µ2)0√(n1−1)S′2

1 +(n2−1)S′22

n1+n2−2

√1n1

+ 1n2

∼ t(n1+n2−2)

(c) For two normal populations with unknown variances,

(X1 − X2)− (µ1 − µ2)0√S′21

n1+

S′22

n2

∼t(v),

where 1v

=(

c2

n1−1

)+[

(1−c)2n2−1

]and c =

(S′21

n1

)/[S′21

n1+

S′22

n2

].

For big samples, and even if the distributions are not normal,

(X1 − X2)− (µ1 − µ2)0√S′21

n1+

S′22

n2

a∼ N(0; 1).

In order to test the equality of variances (H0 : σ21 = σ2

2) we can perform the Levene's test:Analyse, Compare Means, Independent-Samples T Test,

José Dias Curto Data Analysis for Managers - MScBA

30 3.2 Statistical Tests Applications

The results are shown in step 4. As one can see, the probability associated with the Levene'stest is 0.000 (lower than 0.05). Thus we reject the null and we cannot assume that thevariances are equal. SPSS computes the statistics of the test (b) and (c) and we interpretthe test value in the rst or second row depending on the Levene's test decision. In our case,as we reject the null, we should interpret the test value in the second row which results fromthe statistic of the test (c), the one which has exactly a Student's t distribution in spite ofthe sample size.

3. Determination of the Rejection (CR) and Acceptance regions (AR) considering a signicancelevel of 5%, α = 0.05.

As 1v

=(

c2

n1−1

)+[

(1−c)2n2−1

]and c =

(S′21

n1

)/[S′21

n1+

S′22

n2

]then v = 94.990. Based on these

degrees of freedom, we can determine the critical values from the Student's t distribution byusing the EXCEL functions:

= INV T (0.05; 94.990) = 1.9855 (in Portuguese)

or= TINV (0.05; 94.990) = 1.9855 (in English).

Thus,CR =]−∞;−1.9855] ∪ [1.9855;−∞[ AR =]− 1.9855; 1.9855[.

4. Test value and decision making:

José Dias Curto Data Analysis for Managers - MScBA

31 3.2 Statistical Tests Applications

t =(1707.68− 3815.91)− 0√

453.8632

44+ 697.0992

56

= −18.24.

Since the test value falls in the rejection region, we reject the null hypothesis, given thesample and the signicance level. Thus, we can conclude that the income means dierenceis statistically signicant.

In order to compute the probability associated to the test value, we can use the EXCELStudent's t function:

= DISTT (18.24; 94.99; 2) = 0.000 (in Portuguese)

or= TDIST (18.24; 94.99; 2) = 0.000 (in English).

As the probability is lower than the signicance level (0.05), then the null hypothesis is re-jected. Assuming that the null hypothesis is true, there is a very low probability of observinga value of −18.24 for the test value.

3.2.6 Analysis of Variance (ANOVA)

The parametric ANALYSIS OF VARIANCE is an appropriate statistical procedure to test theequality of means (µ1, µ2, . . . , µk) of the same variable, named dependent variable (Y ), in two ormore populations and based on the same number of samples. The null hypothesis is the equalityof means:

H0 : µ1 = µ2 = . . . = µk,

and in the alternative hypothesis there are at least two populations in which the means are dierent:

H1 : µi 6= µj with i 6= j.

The hypothesis that the samples come from populations with the same mean, can be testedassuming the verication of the following conditions:

José Dias Curto Data Analysis for Managers - MScBA

32 3.2 Statistical Tests Applications

• The elements in the samples are randomly selected and the samples are independent of eachother;

• The dependent variable must be normally distributed in each population. This condition isnot mandatory when big samples are available;

• All populations have equal variances: σ2.

Starting from this last condition, the decision about the equality of means is based on thecomparison of two estimates for the variance of populations, an estimate that results from thevariation among sample means: S2

B and a second resulting from the variation of the dependentvariable within each group: S2

W .

σ21 = S2

B =

k∑j=1

nj(Yj − Y

)2

k − 1, σ2

2 = S2W =

k∑j=1

nj∑i=1

(Yji − Yj

)2

n− k,

Where:

• k is the number of samples or groups (each category of the explanatory variable denes agroup of observations);

• nj is the number of the dependent variable observations in the sample j;

• Yj is the mean of the dependent variable in the sample j;

• Yji is the observation i of the dependent variable in the sample j;

• Y is the overall mean of the dependent variable;

• n is the total number of observations (all samples):

If the k samples (groups) with nj (j = 1, . . . , k) observations were randomly collected from knormal populations with equal variance, and if the hypothesis of equal means is true, the ratiobetween the two estimators for the variance of the population has a F -Snedecor distribution withk − 1 and n − k degrees of freedom, i.e., the degrees of freedom associated with each of the twosample variances:

F =S2B

S2W

∼ F(k−1;n−k).

José Dias Curto Data Analysis for Managers - MScBA

33 3.2 Statistical Tests Applications

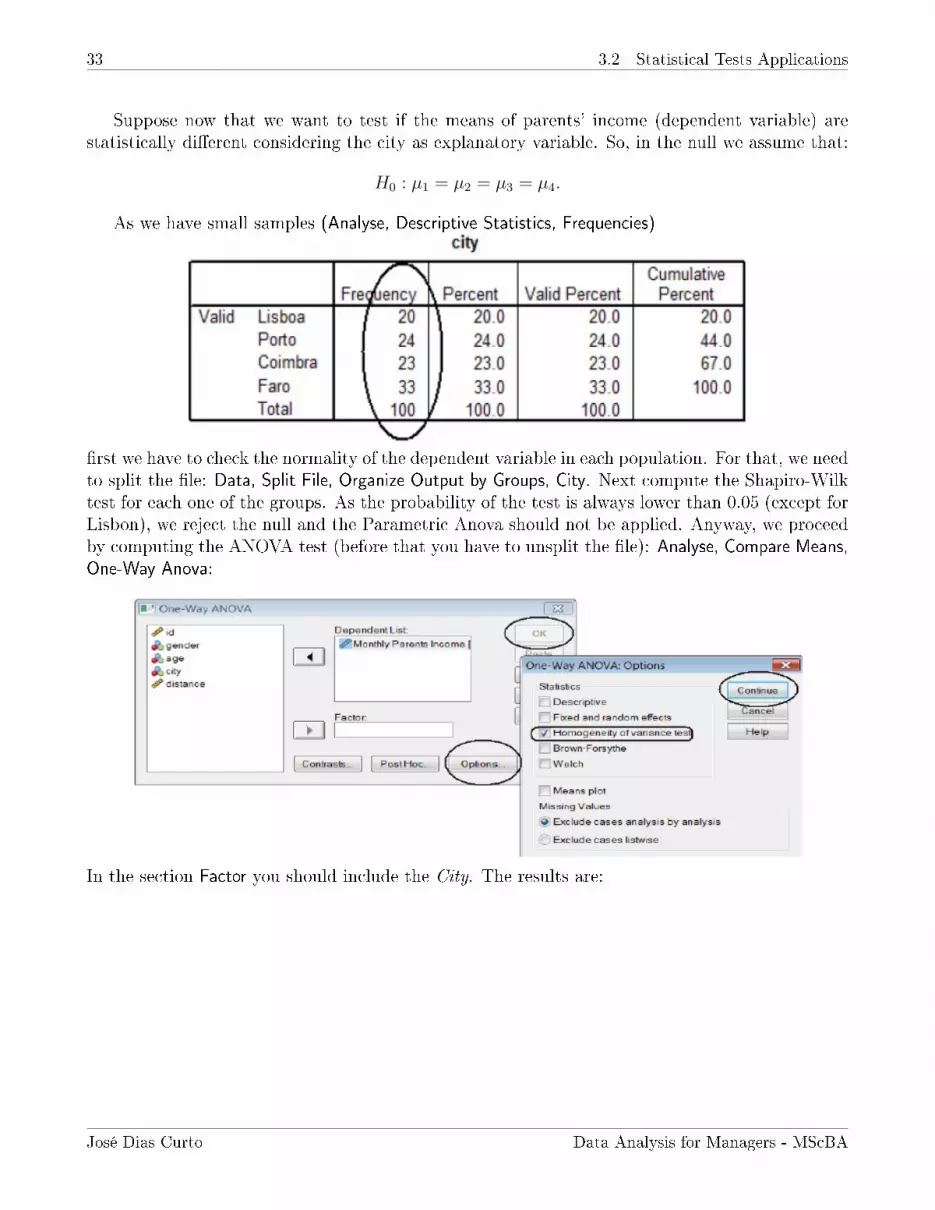

Suppose now that we want to test if the means of parents' income (dependent variable) arestatistically dierent considering the city as explanatory variable. So, in the null we assume that:

H0 : µ1 = µ2 = µ3 = µ4.

As we have small samples (Analyse, Descriptive Statistics, Frequencies)

rst we have to check the normality of the dependent variable in each population. For that, we needto split the le: Data, Split File, Organize Output by Groups, City. Next compute the Shapiro-Wilktest for each one of the groups. As the probability of the test is always lower than 0.05 (except forLisbon), we reject the null and the Parametric Anova should not be applied. Anyway, we proceedby computing the ANOVA test (before that you have to unsplit the le): Analyse, Compare Means,One-Way Anova:

In the section Factor you should include the City. The results are:

José Dias Curto Data Analysis for Managers - MScBA

34 3.2 Statistical Tests Applications

As the probability associated with the ANOVA F-test (0.768) is higher than 0.05, we don't rejectthe null and the equality of means can be assumed. However, as the normality assumption is re-jected and the sample size is small, this conclusion is statistically limited. In this case you shouldapply a nonparametric test.

REFERENCESPinto, J. C. and Curto, J. D. (2001), Estatística para economia e gestão, Ed. Sílabo.McClave, James T., Benson, P. G. and Sincich, T. (2012), Statistics for Business and Economics,12th edition.

José Dias Curto Data Analysis for Managers - MScBA

35 4 Correlation and simple linear regression

4 Correlation and simple linear regression

Correlation analysis can be used to quantify the linear association between two variables. Simplelinear regression is used to establish the linear relationship between a dependent and one explana-tory variable. Students must be able to interpret the scatter diagram, to compute and interpretthe linear correlation coecient and to estimate the parameters of the simple linear regressionmodel.

When quantitative variables are involved, the correlation and regression analyzes are suitableto quantify the relationship between those variables. The regression analysis is more complete andallows us to determine the equation that describes, in average terms, that relationship.

4.1 Types of data

The data that support correlation and regression analyzes can be classied into three categories:

• Data which describe the movement of a variable over time are called time-series data and maybe hourly, daily, weekly, monthly, quarterly or annual. In nance, time series observationscan also be recorded with elapsed time lower that one hour (the price of a stock ve-by-veminutes, for example);

• Data which describe the activities of individual persons, rms, or other units at a given pointin time are called cross-section data;

• Panel data, which combine time-series and cross-section data, may be used to study thebehavior of a group of rms over time.

Examples

• Time series dataXt The sales of EDP in the last 10 years, t = 1, 2, . . . 10.Xt The BCP quarterly income in the last 5 years, t = 1, 2, . . . 20.

• Cross section dataYi The sales of the Portuguese Stock Index listed rms in 2014,i = 1, 2, . . . , 20.Yi The stock prices of the NASDAQ listed rms at the end of 2014, i = 1, 2, . . . , 100.

• Panel dataZit The yearly closing price of PT, EDP, and BCP since 2000,i = 1, 2, 3 and t = 1, 2, . . . , 8.Zit The sales of the PSI20 listed rms in the last 10 years,i = 1, 2, . . . 20 and t = 1, 2, . . . , 10.

t, i and it are used to represent a particular observation from time-series, cross-section and pooleddata, respectively. We represent by T , n and nT the total of observations for each kind of data.

José Dias Curto Data Analysis for Managers - MScBA

36 4.2 Correlation Analysis

4.2 Correlation Analysis

The main tools from correlation analysis are: the scatter diagram, the covariance and the simplelinear correlation coecient. The scatter diagram is a graph, the sample covariance and linearcorrelation coecient are given by:

SXY = SY X =n∑i=1

(Xi − X

) (Yi − Y

)n− 1

,

−1 ≤ rXY = rY X = r =

n∑i=1

(Xi−X)(Yi−Y )

n−1√n∑

i=1(Xi−X)2

n−1

√n∑

i=1(Yi−Y )2

n−1

=SXYSXSY

≤ +1,

where n is the sample size, SXY is the sample covariance, rXY is the sample linear correlationcoecient, X and Y are the sample means and SX and SY are the sample standard deviations ofvariables X and Y , respectively.

Work le: Data1.xls. The le includes information about the stock market price (PRICE), theBook Value of Equity per share (BVEPS) and the Net Income per share (NIPS) of several Euro-pean rms.

1. Open the le in Excel;

2. To construct the scatter diagram between PRICE and BVEPS, select the rst 51 rows (in-cluding the name of the variables) and proceed as presented next: INSERT, Scatter.

The result must be the graph:

José Dias Curto Data Analysis for Managers - MScBA

37 4.2 Correlation Analysis

The scatter diagram suggests a positive linear association between PRICE and BVEPS: whenthe BVEPS increases/decreases the PRICE tends also to increase/decrease. They tend tomove in the same direction.

More: nonlinear relationship, negative linear association and no linear association.

3. To compute the covariance and the linear correlation coecient we can use the Excel func-tions: COVAR and CORREL. Introduce in the blank cells I1 and J1 the functions:

= COV AR(E2 : E51;F2 : F51)and = CORREL(E2 : E51;F2 : F51).

The results must be 117.79349 and 0.8134, respectively. The value of the linear correlationcoecient conrms the strong positive linear association between PRICE and BVEPS.

To test if the sample linear correlation coecient is statistically signicant, we can performthe following test: H0 : ρ = 0 against H1 : ρ 6= 0, where ρ is the population linear correlationcoecient. The statistic of the test is given by:

r√(1− r2)/(n− 2)

=r√n− 2√

1− r2∼ t(n−2).

This test is valid only if the variables are normally distributed and the samples are independent.When big samples are available, and despite the variables' distribution,

r√n− 2√

1− r2

a∼ N (0, 1) .

To test the signicance of the sample correlation coecient, open the le Data1.xls in SPSS.Then Analyse, Correlate, Bivariate. In the opened window proceed as follows:

José Dias Curto Data Analysis for Managers - MScBA

38 4.3 Simple Regression Analysis

The correlation coecient is also named by Pearson correlation coecient due to its author,the statistician Karl Pearson. The obtained results are summarized next:

The test value is given by:

t =0.8√

13371− 2√1− 0.82

= 154.1659

and the associated probability (Sig. (2-tailed)) is obtained from the Excel function

= DISTT (154.1659; 13369; 2) = 0.000 (in Portuguese)

or= TDIST (154.1659; 13369; 2) = 0.000 (in English).

Based on this signicance (0.000) we reject the null. Thus, we conclude that the sample linearcorrelation coecient between PRICE and BVEPS is statistically signicant, in accordance to thesample and the 5% signicance level.

4.3 Simple Regression Analysis

The equation for the simple linear regression model is given by:

Yi = β1 + β2X2i + εi

José Dias Curto Data Analysis for Managers - MScBA

39 4.3 Simple Regression Analysis

where Y is the dependent variable, β1 and β2 are the parameters or coecients of the model andε is the error term. If we exclude ε, we have the equation of a straight line.

The index i is used to represent a cross section data: information for dierent companiesreferred to a single period of time. See section 4.1 for more on types of data.

To obtain the equation that represents, in average terms, the relationship between PRICE andBVEPS we can do that directly on the scatter diagram. Go back to the Excel.

1. Check with the right button of the mouse in any point of the scatter diagram. In the openedwindow select Add Trend Line (Adicionar Linha de Tendência):

More: nonlinear relationships.

José Dias Curto Data Analysis for Managers - MScBA

40 4.3 Simple Regression Analysis

2. Next proceed as follows:

And the result must be:

You can use the mouse to move the equation for any position in the graph.

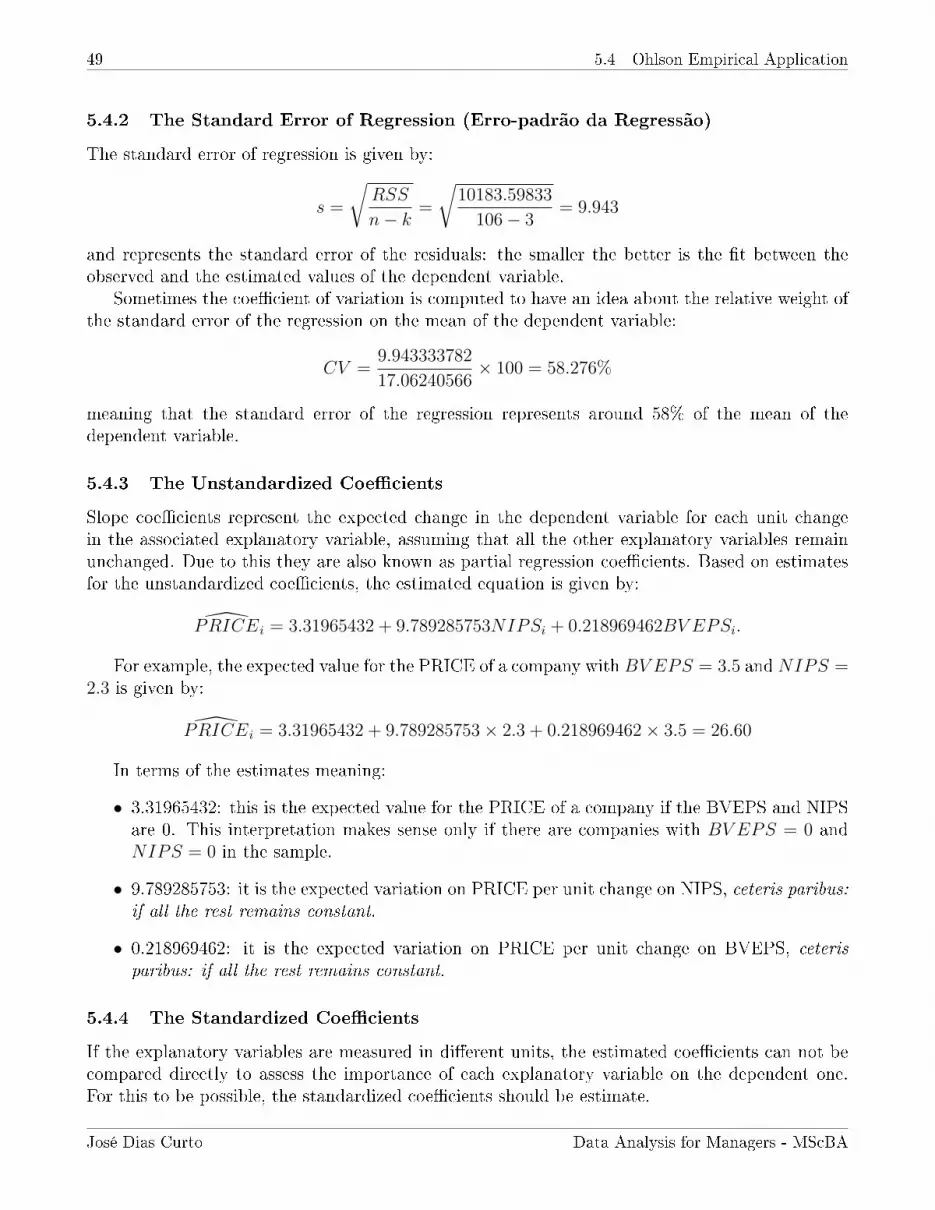

The equation of the straight line is given by:

Yi = 6.7232 + 1.2332Xi or P ricei = 6.7232 + 1.2332BV EPSi.

The hat means predicted instead of observed. In terms of the estimates for the parameters:

• 6.7232 is the expected value for the PRICE of a company if the BVEPS is 0. This interpre-tation makes sense only if there are companies with BV EPS = 0 in the sample.

• 1.2332 is the expected variation on price per unit change on BVEPS, ceteris paribus: if allthe rest remains constant.

José Dias Curto Data Analysis for Managers - MScBA

41 4.3 Simple Regression Analysis

The Excel presents also the R2, the Coecient of determination, and it represents the per-centage of the total variation of the dependent variable that is explained by the variation of theexplanatory variables in the sample. In the simple linear regression model, the coecient of de-termination is the square of the linear correlation coecient: R2 = 0.81342. Thus, on this sample,66% of the total variation on price is explained by the variation on BVEPS. This result conrmsthe strong linear association between PRICE and BVEPS.

REFERENCEWooldridge, Jerey M. (2015), Introductory Econometrics: A Modern Approach, South-Western,5th Edition

José Dias Curto Data Analysis for Managers - MScBA

42 5 The multiple linear regression model (MLRM)

5 The multiple linear regression model (MLRM)

Multiple linear regression is used to establish the linear relationship between a dependent and morethan one explanatory variables; it is a generalization of the simple model. Students must be ableto understand how the Ordinary Least Squares (OLS) method works, to compute and interpretthe R2, the adjusted R2, the standard error of the regression, the F -test, the t-tests and condenceintervals for the parameters.

The multiple linear regression model allows us to establish a linear relationship between adependent variable and more than one explanatory variables. The main purpose is to estimatehow the variation in each of the explanatory variables impacts on the dependent one. The equationof the model is given by (for cross section data):

Yi = β1 + β2X2i + . . . , βkXki + εi

The error term is included because we can not expect that changes in the explanatory variablesfully explain the variation in the dependent one. Therefore, the error term represents the variationin the dependent variable that is not associated, or does not result, from the variations in theexplanatory variables.

The number of parameters is k+1 including k coecients (βj) plus the variance of the errors: σ2ε .

The explanatory variables can be a linear (or a nonlinear) transformation of the other explanatoryvariables but the relationship between the dependent and the explanatory variables must be linearin the parameters βj.

The MLRM equation can be presented for each observation i:Y1 = β1 + β2X21 + β3X31 + . . .+ βkXk1 + ε1

Y2 = β1 + β2X22 + β3X32 + . . .+ βkXk2 + ε2

. . . . . . . . .Yn = β1 + β2X2n + β3X3n + . . .+ βkXkn + εn.

and it can be represented by using matrices and vectors:

y = Xβ + ε,

where:

y =

Y1

Y2...Yn

, X =

1 X21 X31 Xk1

1 X22 X32 Xk2...

......

...1 X2n X3n Xkn,

, β =

β1

β2...βk

, ε =

ε1

ε2...εn

.y and ε are n × 1 vectors, β is a k × 1 vector and X is a n × k matrix. Each X elementhas two indexes: the rst one refers to the column (variables) and the second one to the row (ob-servation). X2i, for example, represents the observation i for the explanatory variable X2. EachX column represents a vector with n observations for each of the explanatory variables.

5.1 Assumptions of the MLRM

The assumptions of the MLRM can be presented in terms of matrices and vectors:

1. The specication of the model is given by: y = Xβ + ε;

José Dias Curto Data Analysis for Managers - MScBA

43 5.2 Ordinary Least Squares Method (OLS)

2. E (ε) = 0;

3. The covariance matrix (ε) of the errors is given by: E (εε′) = σ2I (Homoskedasticity andNo Autocorrelation assumptions), where I is a n× n identity matrix:

E (εε′) =

E (ε2

1) E (ε1ε2) . . . E (ε1εn)E (ε2ε1) E (ε2

2) . . . E (ε2εn)...

......

...E (εnε1) E (εnε2) . . . E (ε2

n)

=

=

Var (ε1) Cov (ε1, ε2) . . . Cov (ε1, εn)

Cov (ε2, ε1) Var (ε2) . . . Cov (ε2, εn)...

......

...Cov (εn, ε1) Cov (εn, ε2) . . . Var (εn)

.Since Var (εi|X2, X3, ..., Xk) = σ2 and Cov (εi, εj) = E (εiεj) = 0 for i 6= j then,

E (εε′) = σ2I = σ2

1 0 . . . 00 1 . . . 0...

......

...0 0 . . . 1

;

4. The errors are normally distributed: ε ∼ (0, σ2I) ;

5. The X elements are non random and the rank of X is k, the number of X columns. If therank of matrix X is k, the explanatory variables are not perfectly correlated (No Multi-collinearity assumption). Thus, we can conclude that X′X is a regular symmetric matrixwhose determinant is dierent from 0;

6. E (X′ε) = 0, according to the last assumption and since that E (ε) = 0.

5.2 Ordinary Least Squares Method (OLS)

The objective of the Ordinary Least Squares method is to nd the estimator β that minimize theResidual Sum of Squares (RSS):

Min RSS =n∑i=1

e2i =

n∑i=1

ε2i = ε′ε = e′e,

where e is the vector of ordinary residuals: e = y − y and y = Xβ is the OLS estimator for themean of the vector y: Xβ.

To obtain the OLS estimators, we simplify rst the Residual Sum of Squares:

e′e =(y −Xβ

)′ (y −Xβ

)= y′y − β

′X′y − y′Xβ + β

′X′Xβ =

= y′y − 2β′X′y + β

′X′Xβ, (3)

Considering that:

José Dias Curto Data Analysis for Managers - MScBA

44 5.3 Properties of OLS estimators

• The transpose of the product of matrices is the product of transposes considering the inverse

order of the original product(Xβ)′

= β′X′,

• The transpose of a scalar is the scalar itself, y′Xβ =(y′Xβ

)′= β

′X′y.

The rst order conditions to minimize the RSS are:

∂RSS

∂β= −2X′y + 2X′Xβ = 0,

considering the derivative of a quadratic form:

∂(β′X′Xβ

)/∂β = 2X′Xβ.

Based on this it is possible to deduce the normal equations :

(X′X) β = X′y

and the vector of the Ordinary Least Squares estimators is given by:

β = (X′X)−1

(X′y) .

5.3 Properties of OLS estimators

If the assumptions of the MLRM hold, the OLS estimators β are the most ecient from the set ofthe linear unbiased estimators for β, i.e., they are the ones with the smallest (minimum) varianceand we conclude that OLS estimators are BLUE : Best Linear Unbiased Estimators (by theGauss-Markov theorem).

We show next that β is an unbiased estimator for β. As,

β = (X′X)−1

(X′Y) = (X′X)−1

X′ (Xβ + ε) =

= (X′X)−1

X′Xβ + (X′X)−1

X′ε = β + (X′X)−1

X′ε = β + Aε,

where A = (X′X)−1 X′ and, therefore,

E(β)

= β + AE (ε) = β.

The OLS estimators are normally distributed as β is a linear function of ε and, by assumption,ε has normal distribution.

Next we deduce the variances and covariances of the individual estimators βj:

var(β)

= E

[(β − β

)(β − β

)′]=