fill copy - world bank documents

TRANSCRIPT

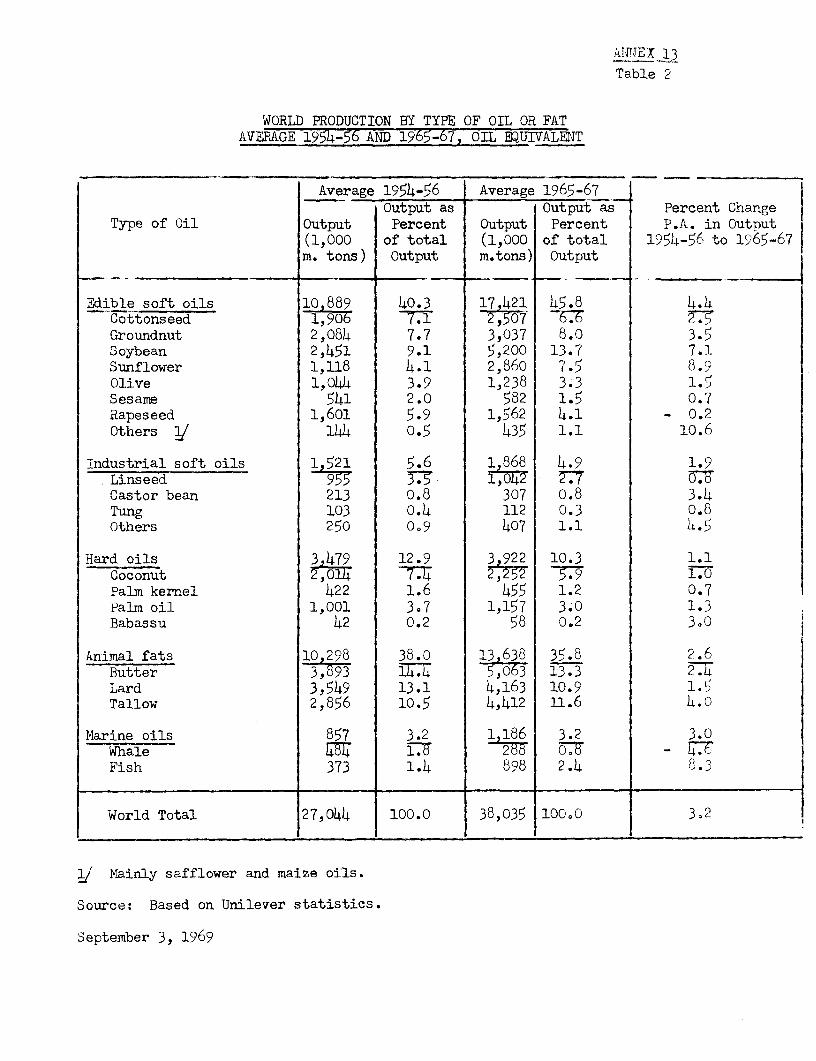

RESTRICTED

FIlL COPY Report No. PA-53

This report was prepared for use within the Bank and its affiliated organizations.They do not accept responsibility for its accuracy or completeness. The report maynot be published nor may it be quoted as representing their views.

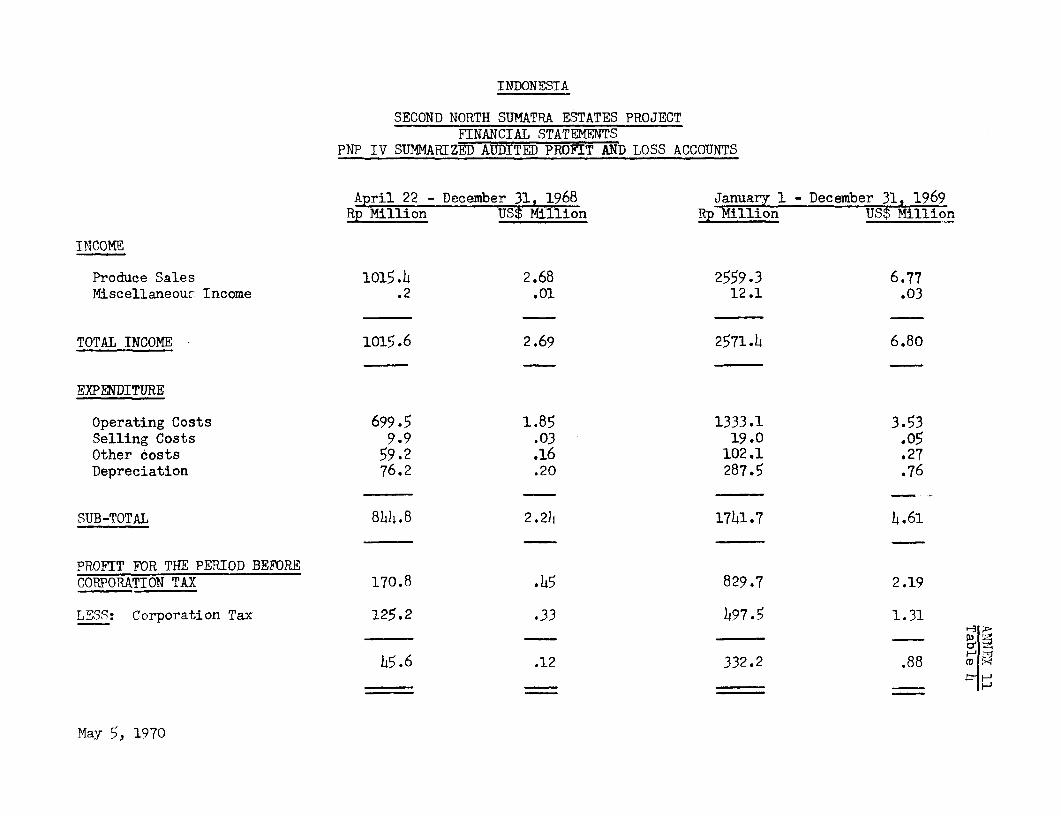

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

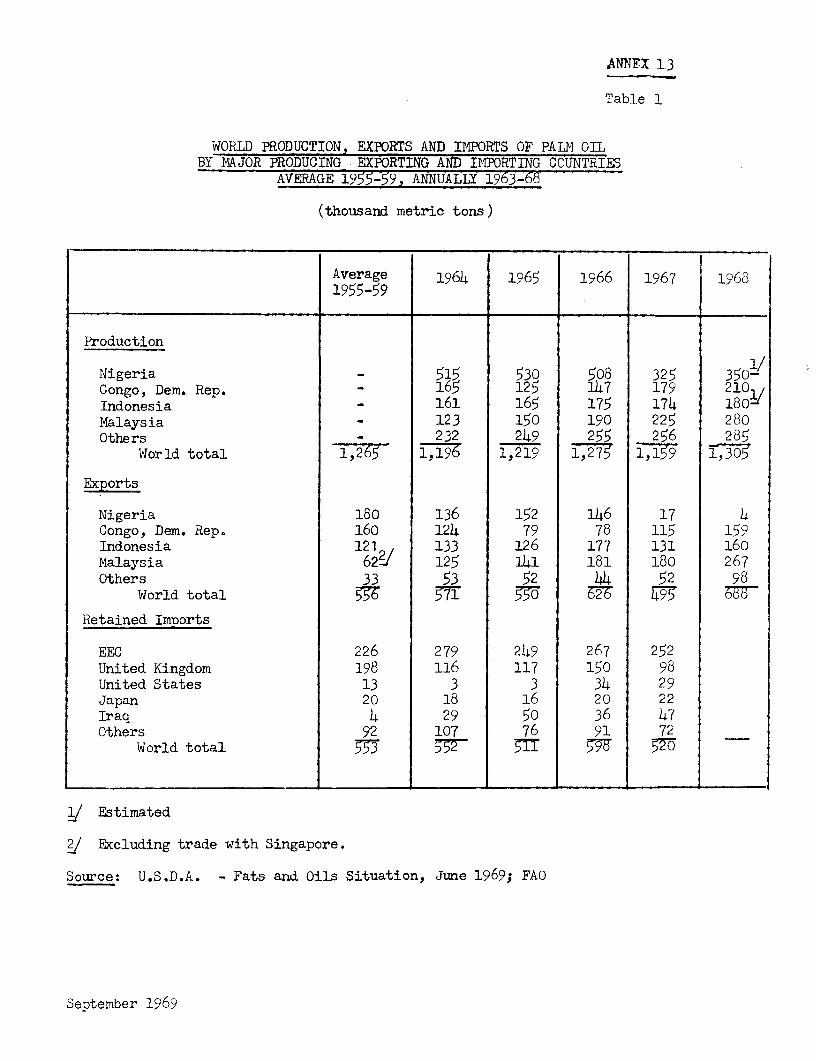

INTERNATIONAL DEVELOPMENT ASSOCIATION

SECOND NORTH SUMATRA ESTATES PROJECT

INDONESIA

May 12, 1970

Agriculture Projects Department

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

US$ 1 Rp 3781 &Upiah 3 US$ 0.0026

WEIGHTS AND MhASURES(Metric System)

1 hectare - 2.47 acres1 square kilometer (km2) - 0.386 square miles1 metric ton - 1,000 kilograms (kg) - 2,205 pounds1 kilometer (km) = 0.62 miles1 millimeter (m) - 0.04 inches

INITIALS AND ACRONYMS

FNP: Perusahan Negara Perkebunan(State-owned Estate Ehterprise),

RISPA: Research Institute of the Sumatran PlantersAssociation

PT: Perseroan Terbatas (Corporate entity operatingunder the Commercial Code)

JMO: Joint Marketing OfficeFFB: Fresh Fruit Bunches (oil palm)

INDONESIA

SECOND NORTH SUMATRA ESTATES PROJECT

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS ...... .........................

I. INTRODUCTION ..................... 1

II. BACKGROUND ..

A. General .,1B. The Estate Industry . ., 2C. Government-Owned Estate Industry .... ............. 3

D. First North Sumatra Estates Project (CreditNo. 155-IND) ... ,.. 4

III. THE PROJECT AREA AND PROJECT ENTITIES. 5

IV. THE PROJECT. 7

A. Project Description. 7B. Estate Development. 8C. Processing Facilities .11D. Technical Assistance .13E. Agricultural Research .13F. Export Duties, Taxes and Exchange Rates 14C. Cost Estimates .14H. Proposed Financing, Disbursement and Procurement . 16

V. ORGANIZATION AND MANAGEMENT .18

VI. PRODUCTION MARKETING AND FINANCIAL RESULTS .21

A. Yields and Production .21B. Marketing and Prices .22C. Financial Aspects .25

VII. BENEFITS AND JUSTIFICATION .. 26

VIII. RECOMMENDATIONS .28

ANNEXES

1. The Estate Industry

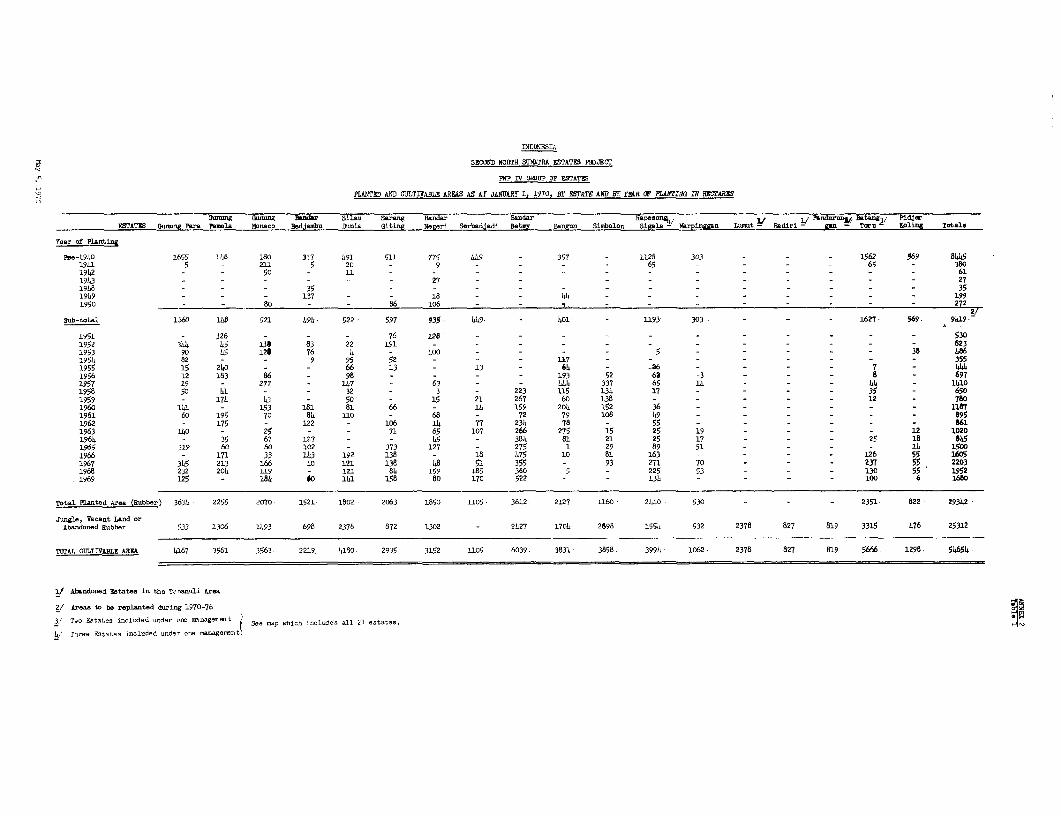

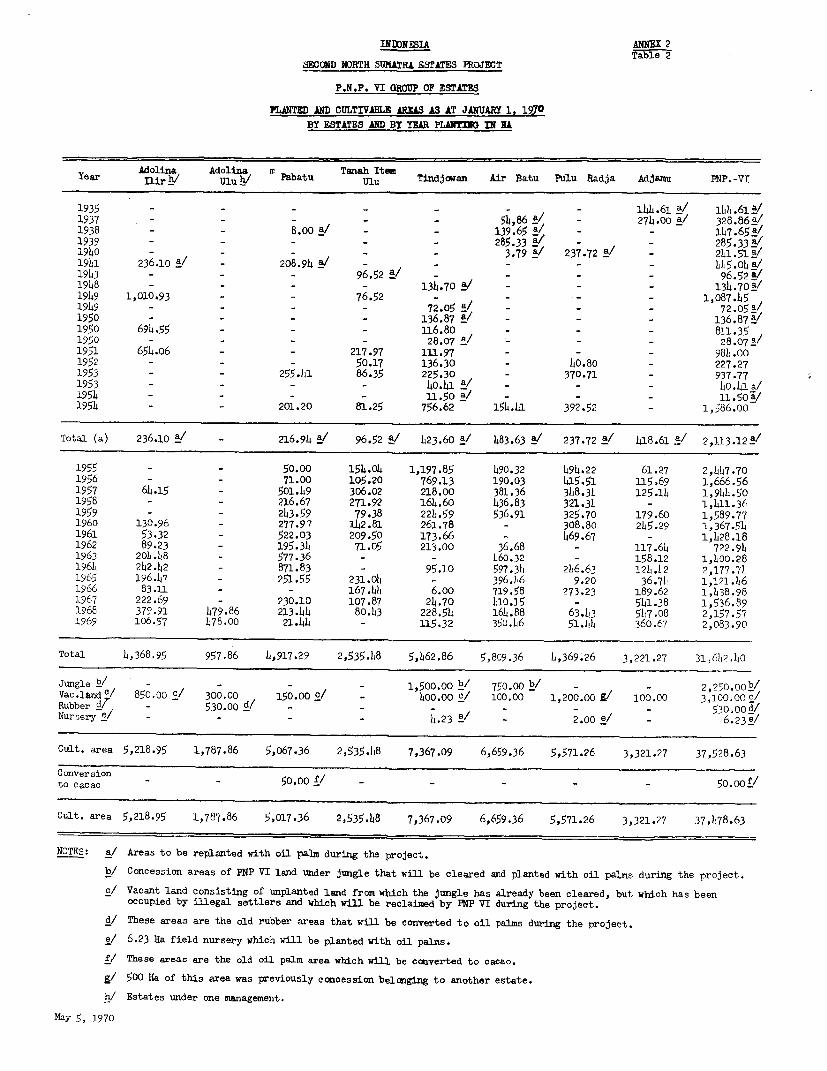

2. PNP IV and PNP VI Planted and Cultivable Areas

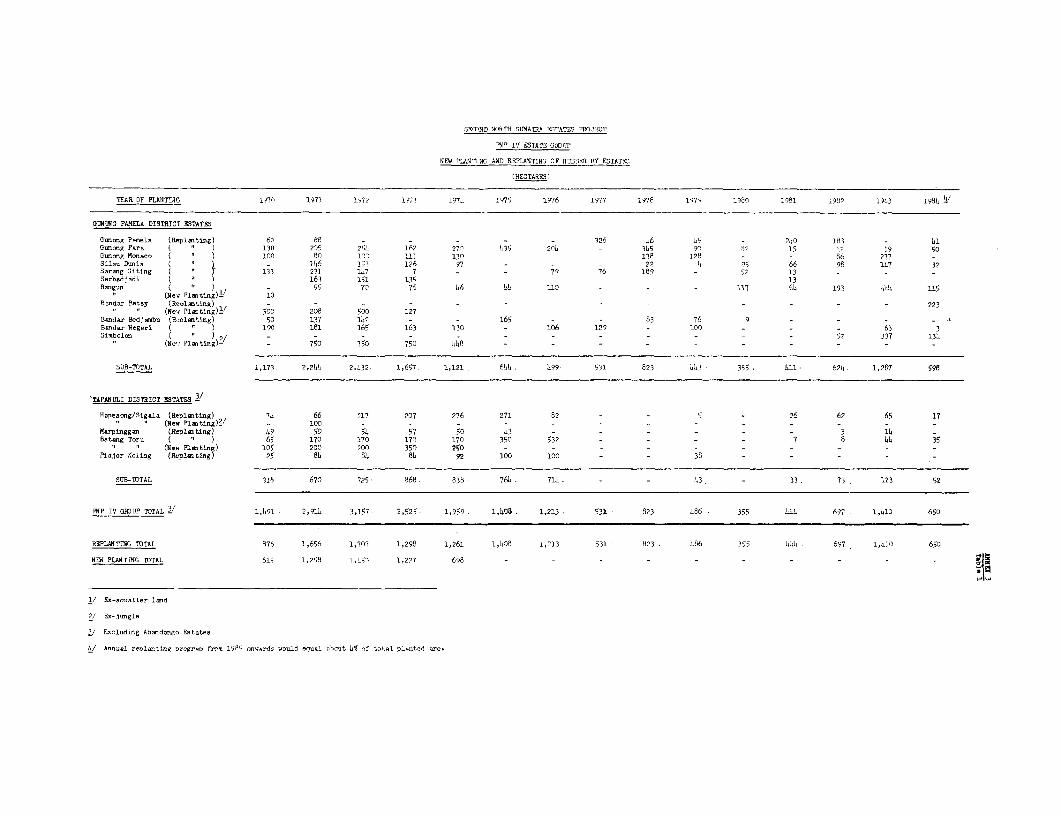

3. Planting Program

4. Plant Breeding and Planting Material

5. Foliar Analysis and the Fertilizer Investment Program

6. PNP IV Rubber Processing Facilities

7. PNP VI Oil Palm Processing Facilities

8. Project Cost Estimates

9. Disbursement Schedule

10. PNP IV and PNP VI Organization Chart

11. PNP IV and PNP VI Financial Statements

12. Yield Assumptions

13. Market Prospects for Palm Oil and Palm Kernels

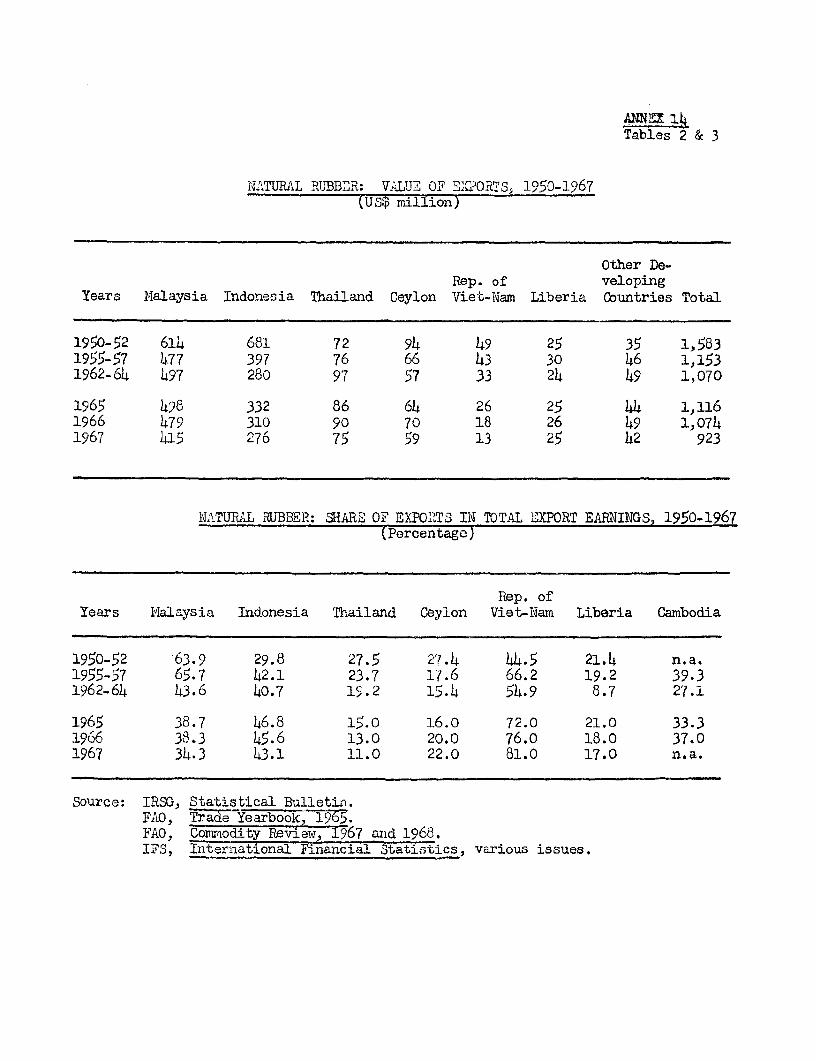

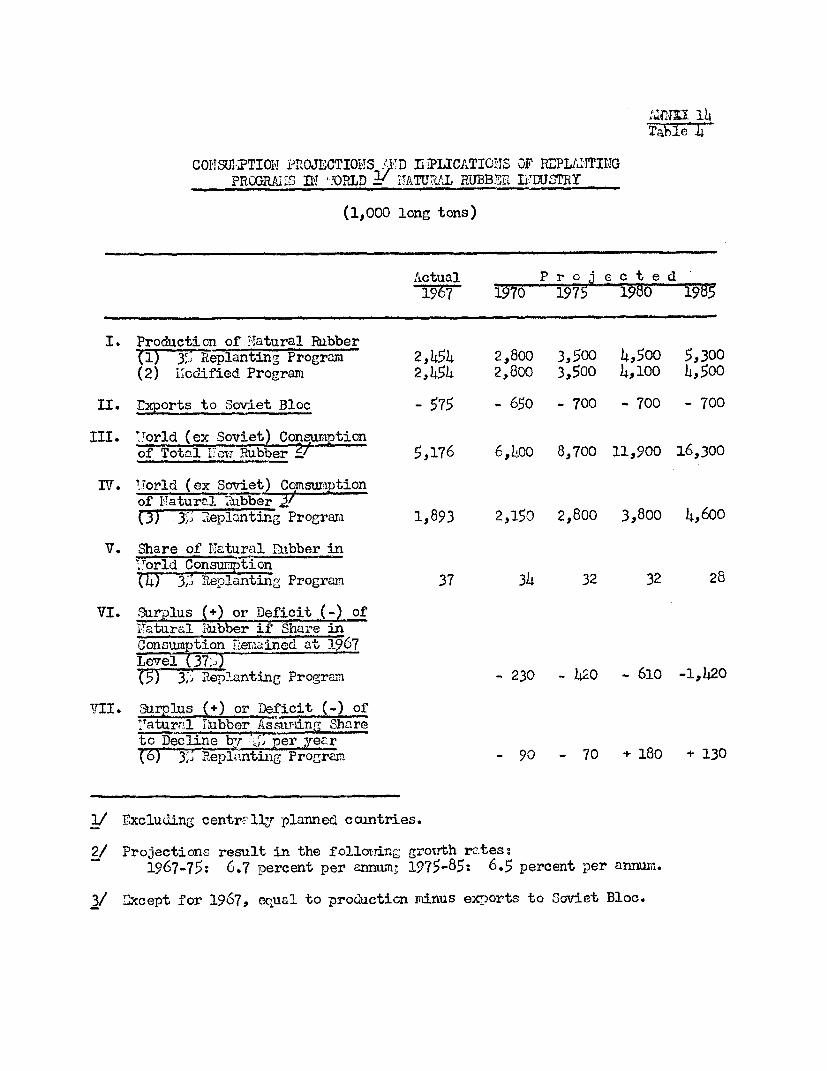

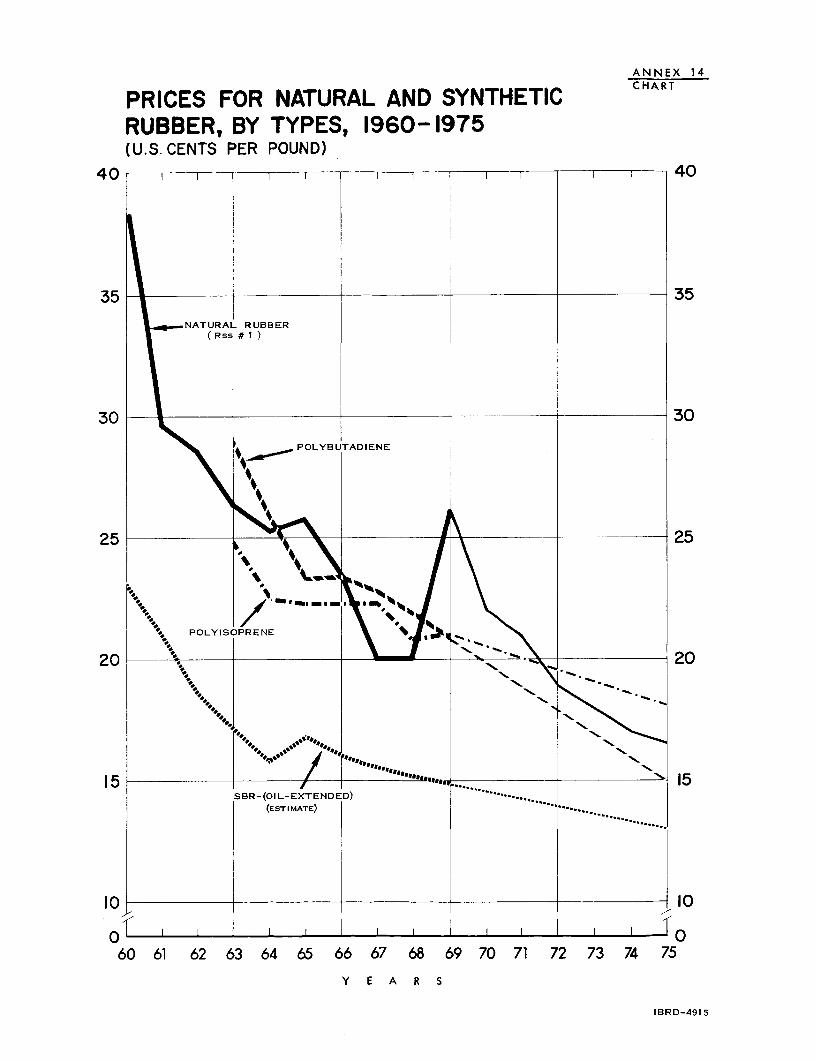

14. Market Prospects for Natural Rubber

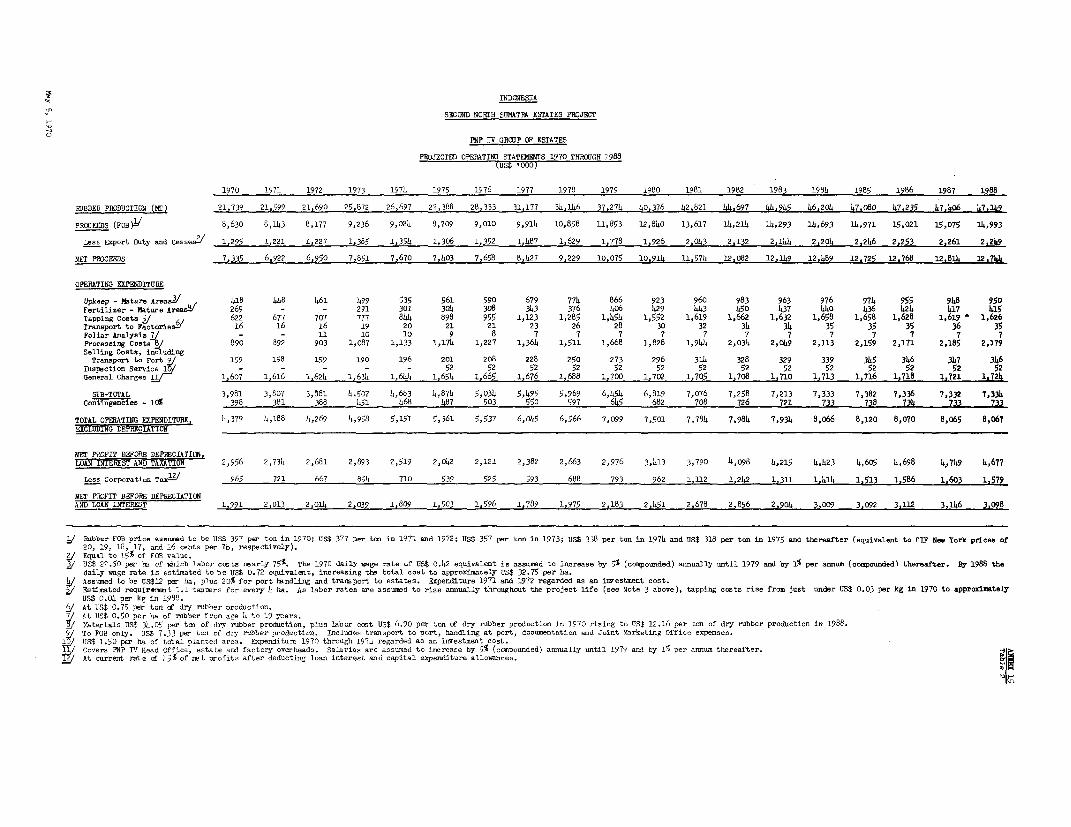

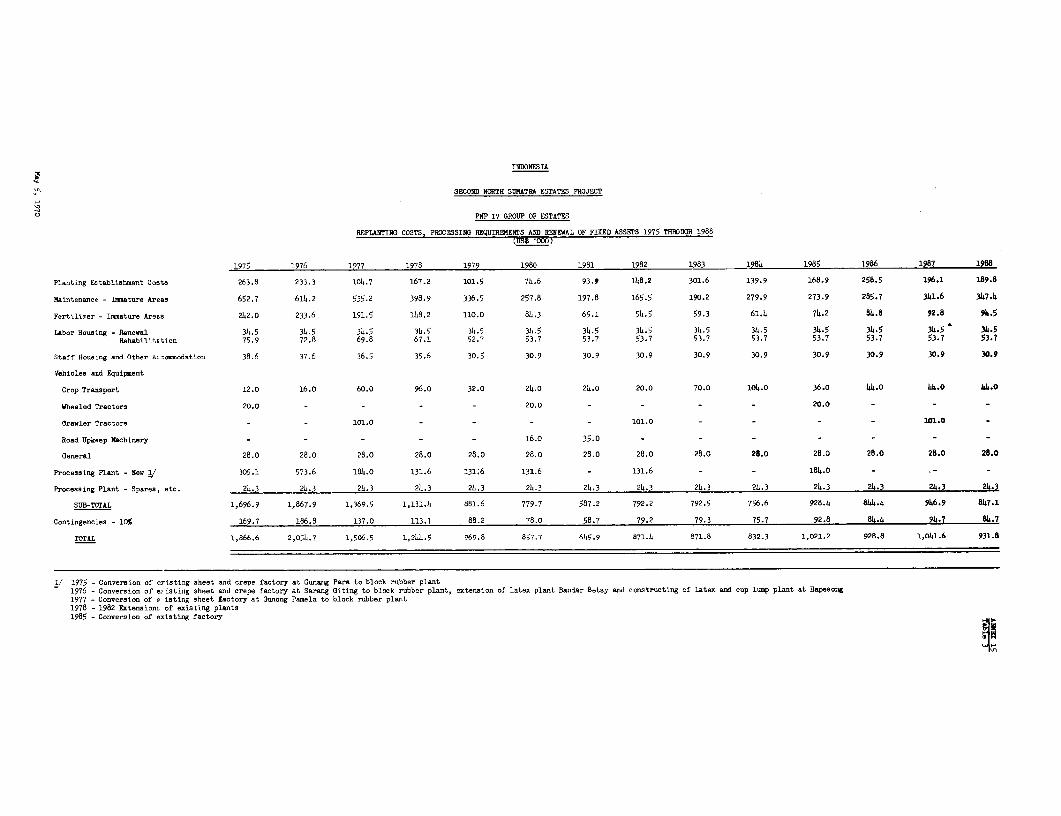

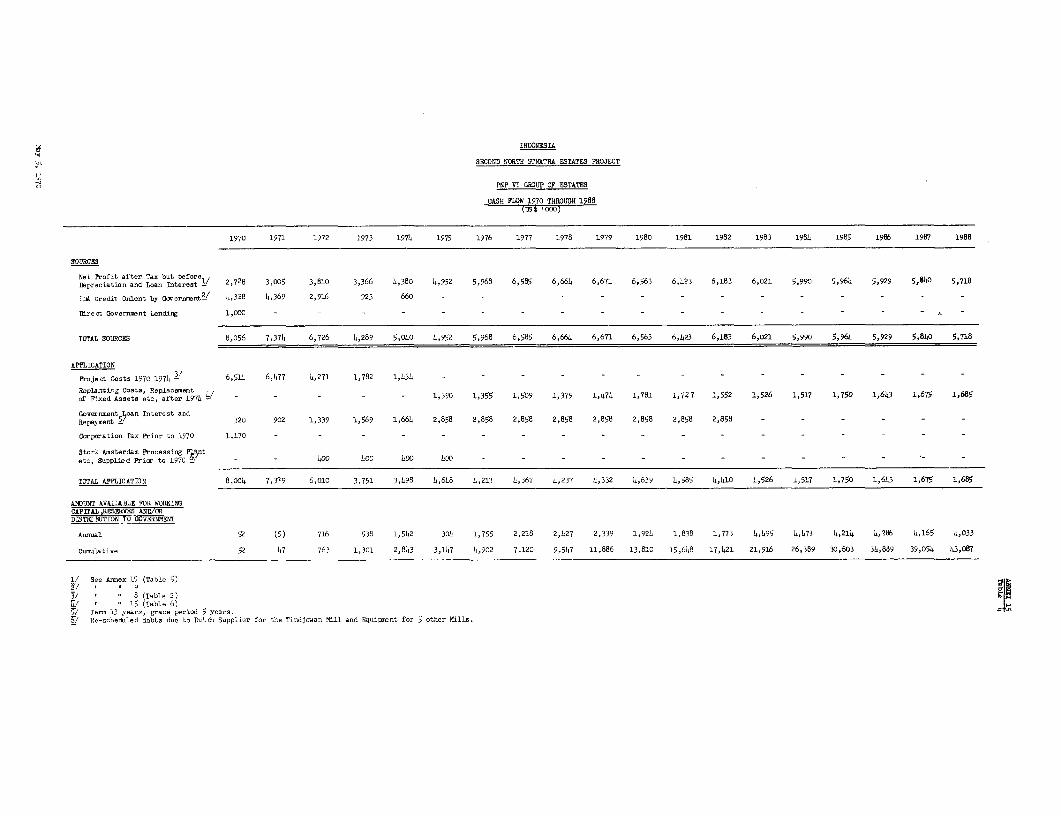

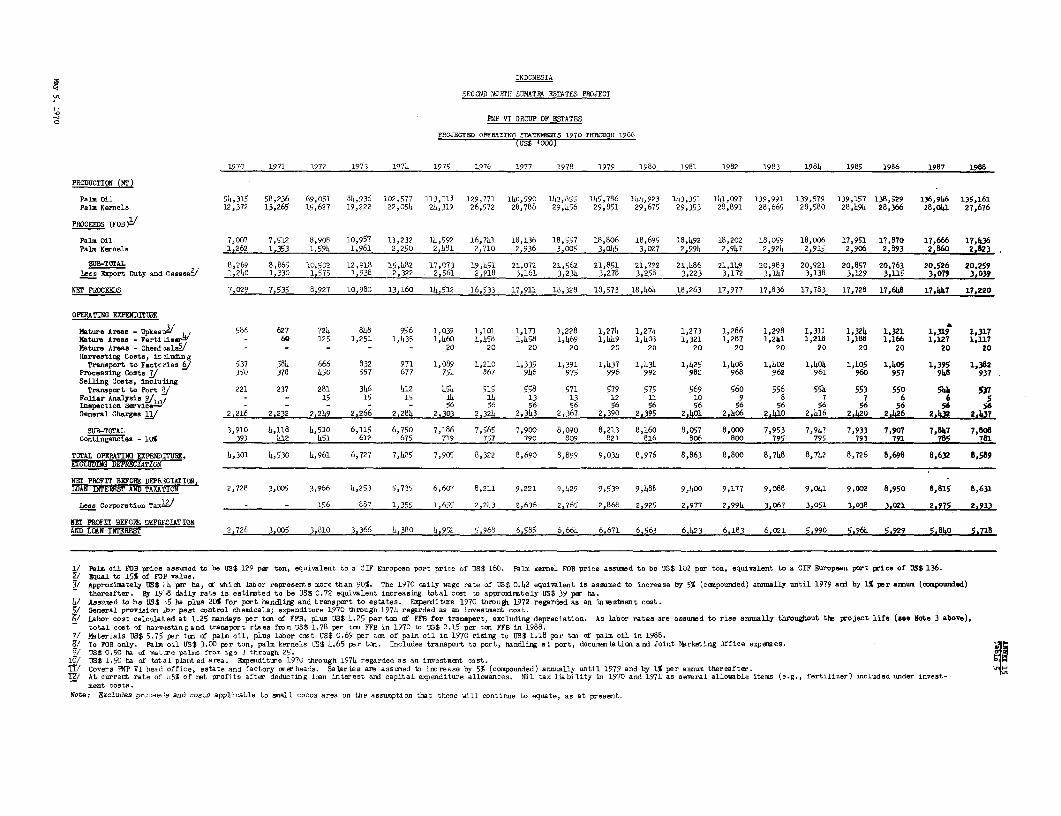

15. Projected Cash Flows and Operating Statements

16. Effect of the project on the Government's Budgetary Position

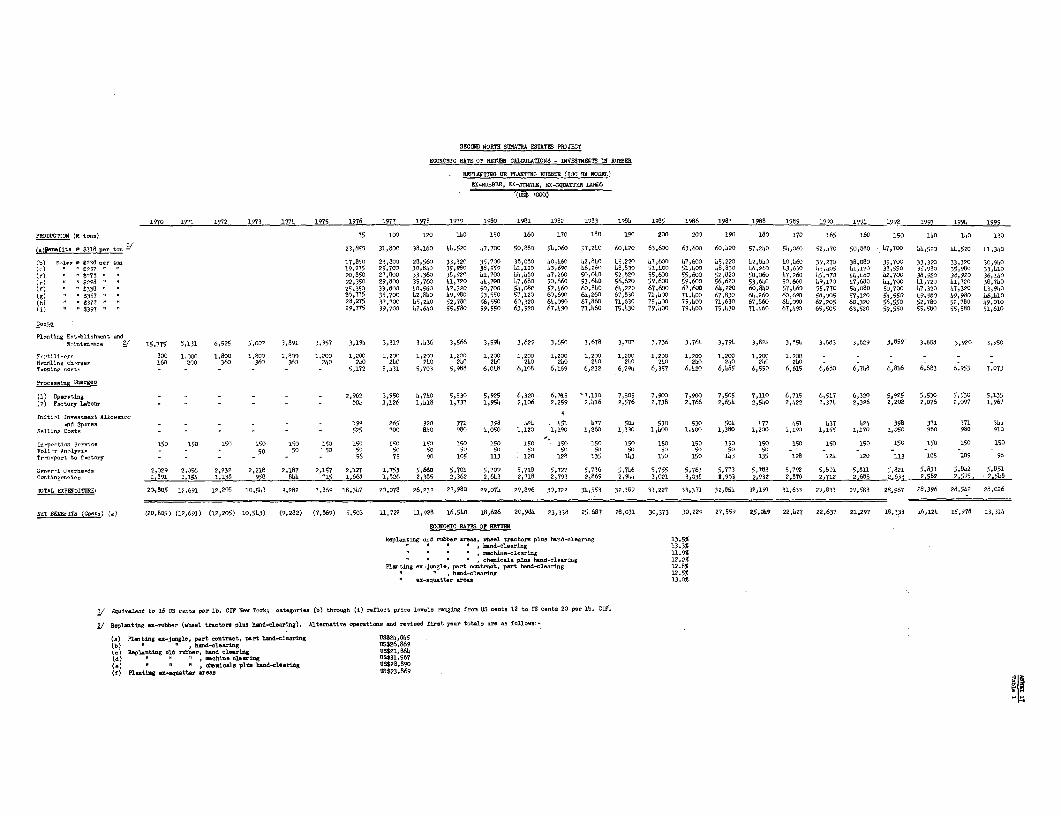

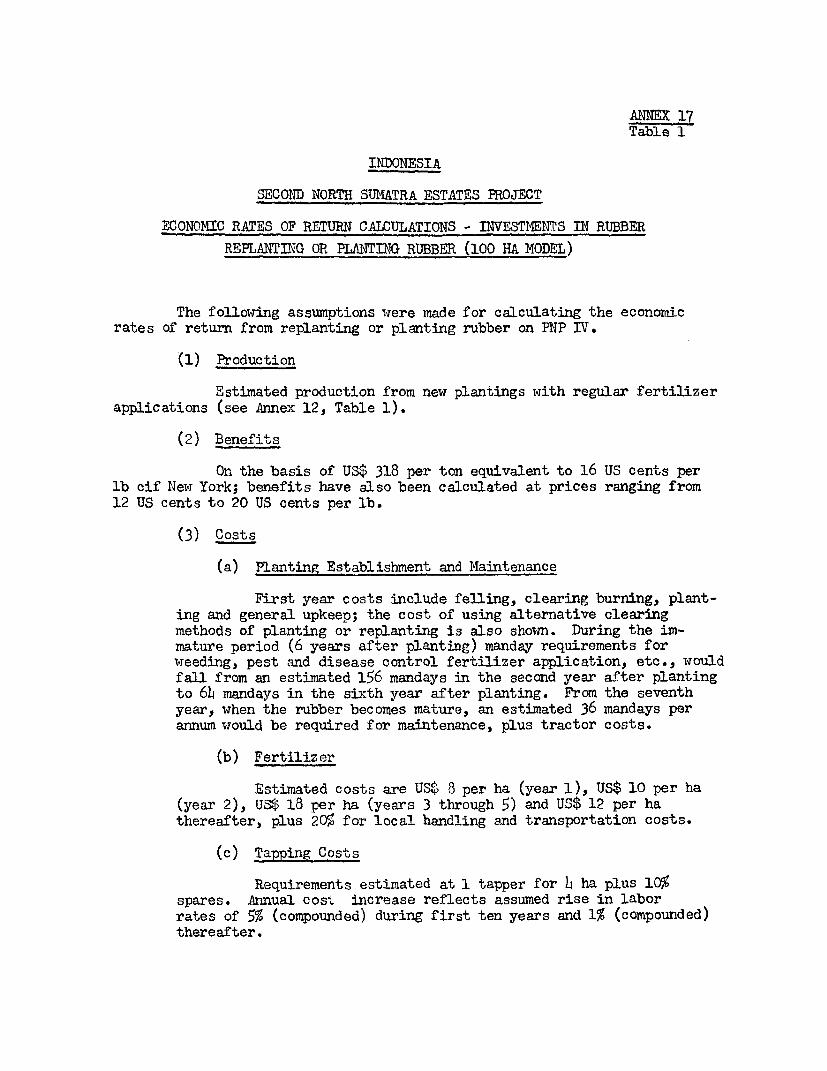

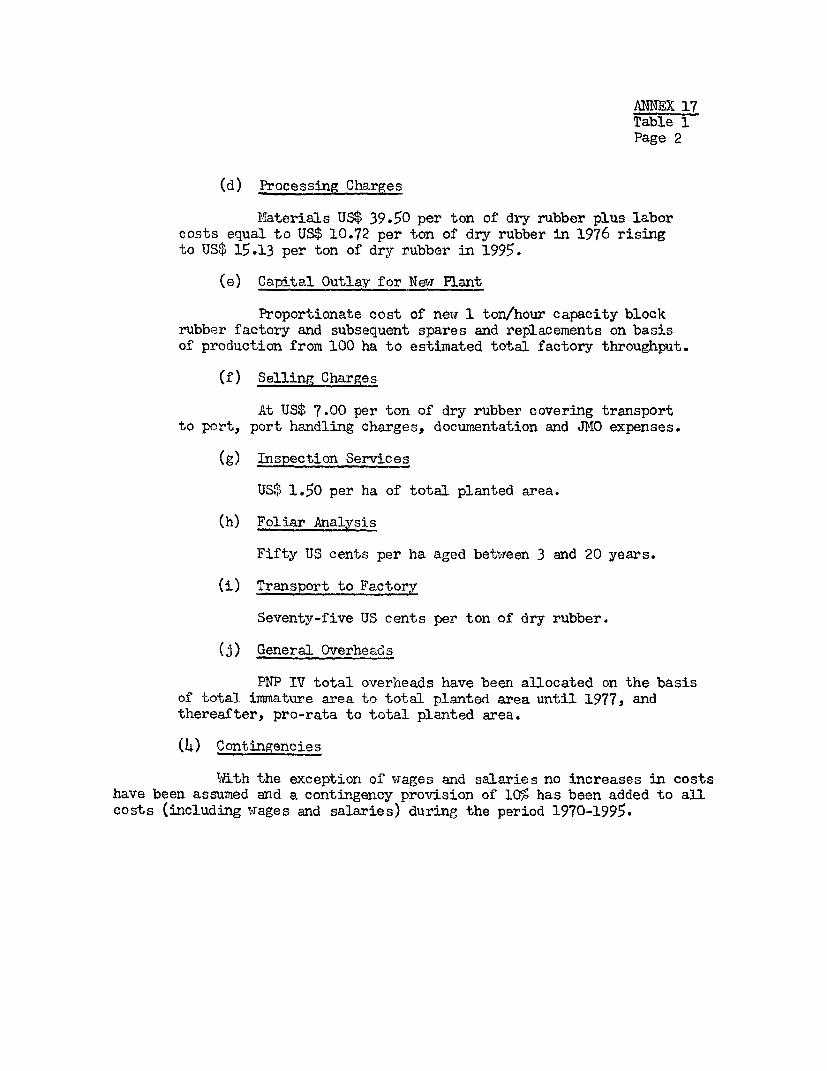

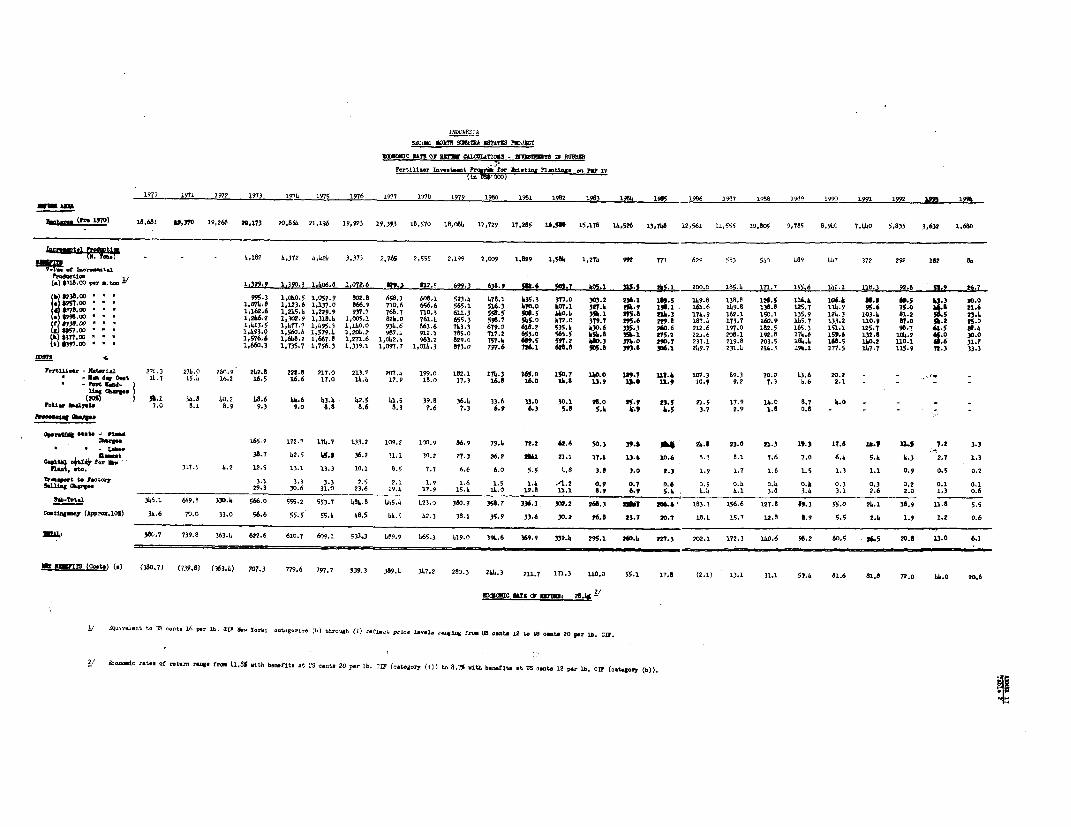

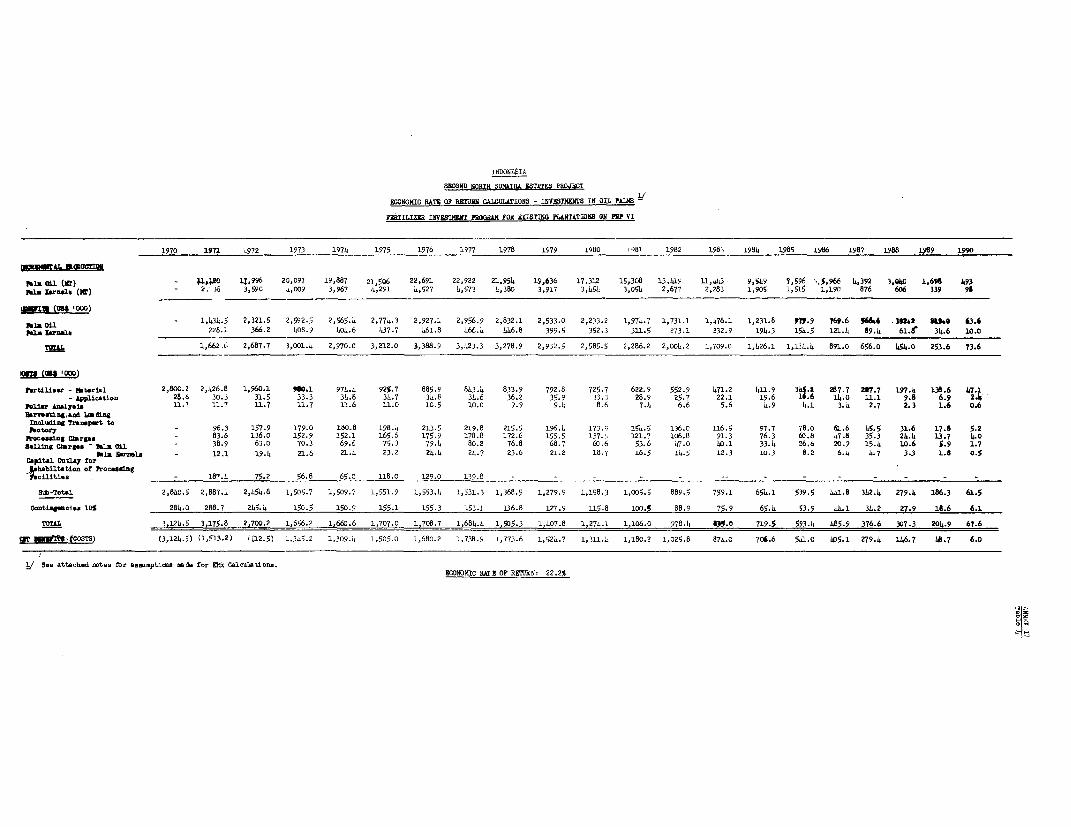

17. Economic Rate of Return Calculations and Sensitivity Analysis.

MAP

INDONESIA

SECOND NORTH SUMATRA ESTATES PROJECT

SUMMARY AND CONCLUSIONS

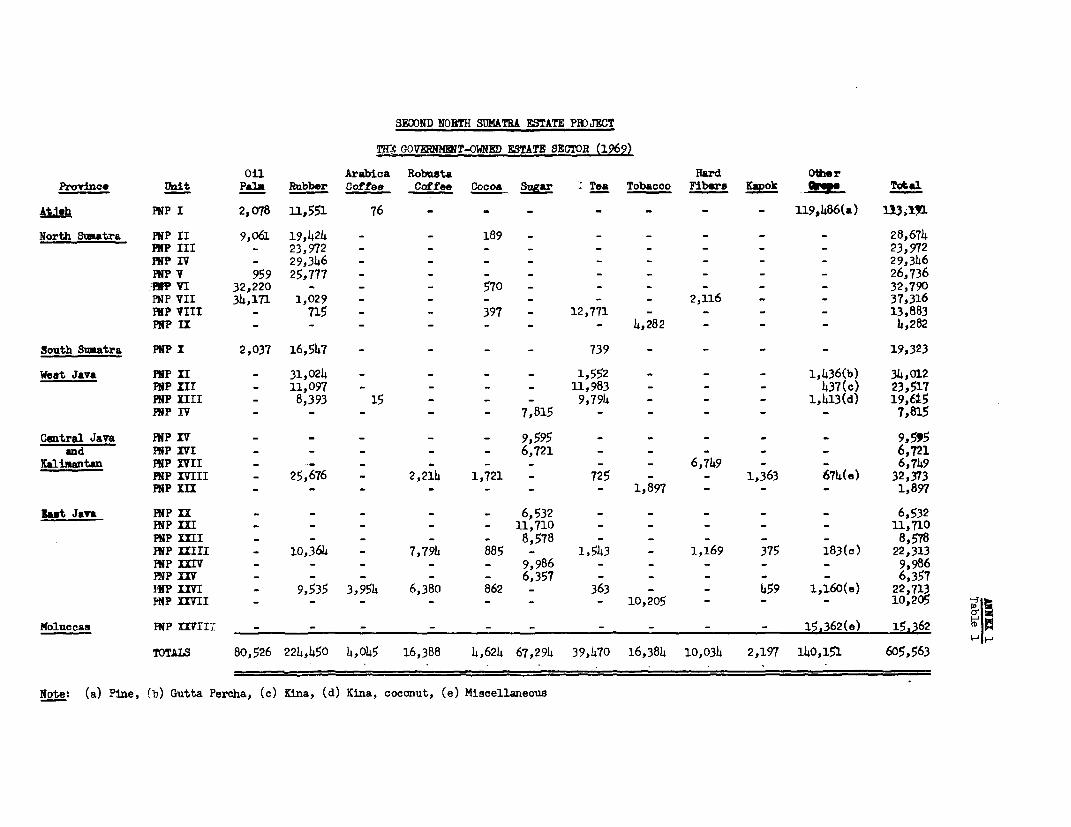

i. This report appraises a second project for the rehabilitation andexpansion of Government-owned estate groups in Indonesia. An IDA credit ofUS$17.0 million is proposed. The estate industry is one of Indonesia'slargest earners of foreign exchange, accounting for some 20% of exports interms of value. Since 1940 the industry has suffered severely, as havemost other sectors, from the political instability, corruption and extremeinflation that have been endemic in Indonesia until recently; and as aresult the contribution of the estates to the economy has declined. Involumetric terms estates now produce less than 50% of their production in1938, when they contributed 60% of exports. The fall in production reflectslow productivity as much as a decrease in the area under estates which hasdeclined by about 25%. The Government which took over in 1966 recognizesthe importance of the estates and in particular their ability to providemuch needed foreign exchange, and is taking measures both to rehabilitatethe estates which it owns, some 606,000 ha, and to create a climate in whichthe productivity of some 122,000 ha of foreign owned estates will improve.

ii. Two Government-owned estate groups in Sumatra, Perusahaan NegaraPerkebunan (PNP) IV and PNP VI, would be rehabilitated and expanded. Theformer comprises 18 estates with a total planted area of 29,300 ha of rub-ber which produced 18,000 tons of rubber in 1969. The latter is a group of7 estates growing 31,600 ha of oil palms and which in 1969 produced 70,000tons of palm oil and kernels. The project consists of planting or replant-ing some 12,000 ha of rubber and 8,000 ha of oil palms; bringing a further9,800 ha of immature rubber and 7,200 ha of immature oil palms into bear-ing; rehabilitating more than 19,000 ha of mature rubber, and 28,000 ha ofmature oil palms; and rehabilitating, replacing and expanding processingfacilities, estate transportation, buildings, workshop and agriculturalmachinery. The management of the two PNPs would be reorganized and strength-ened by the employment of advisers and inspectorate services.

iii. Project costs are estimated at US$31.7 million, of which aboutUS$17.0 million, or 54% would be the foreign exchange component. SomeUS$16.4 million of the proposed IDA credit would be onlent to the two PNPstogether with US$3.0 million of Government funds in the form of loans bear-ing interest at 12%, the Government's current lending rate to public sectorenterprises. The remainder of the credit would be used by Government toimprove agricultural and research facilities. The balance of project costswould be met by the PNPs from self-generated funds and by the Government.All goods to be financed from tne IDA credit would be procured through inter-national competitive bidding.

- ii -

iv. Most of the rubber and oil palm products produced under the proj-ect would be exported, although the local demand for palm oil is expectedto increase. At peak production in the early 1980's, net incremental annualforeign exchange earnings after expenditure on imported goods and serviceswould reach some US$14.0 million, and incremental reVenues accruing to theGovernment (from duties, taxes, and revenues) would reaeh some US$9.0 mil-lion. The estimated rates of return to the economy from planting and re-planting rubber and oil palm and carrying out fertilizer investment programsrange from about 12% to 30% at prices projected by the Bank's Economics De-partment for rubber and oil palm products on world markets.

v. The project would have similar characteristics to the First NorthSumatra Estates Project which is progressing satisfaetorily.

vi. The project is suitable for an IDA credit of US$17.0 million toIndonesia.

INDONESIA

SECOND NORTH SUMATRA ESTATES PROJECT

I. INTRODUCTION

1.01 In June 1969, approval was given for an IDA credit 1/ of US$16.0million to the Government of Indonesia to help finance the rehabilitationana development of two Governiment-owned estate groups in North Sumatra; Per-usahaan Negara Perkebunan Antan (PNP) V 2/, growing rubber, and PNP VII,growing oil palm. Fuller details of the First Estates Project are givenin paragraph 2.10.

1.02 The Government of Indonesia applied, in October 1969, for anotherIDA credit to finance part of the costs of rehabilitating and developingtwo more of the 28 Government-owned estate groups in Indonesia. A BankEconomic Mission to Indonesia in 1969 supported the priority given by Gov-ernment to this sector 3/ and in August/September 1969 Mr. Phillips of theBank's Resident Staff in Indonesia assisted the Government in preparing aproject for the rehabilitation and development of PNP IV, specializing inrubber, and PNP VI, specializing in oil palm, both in North Sumatra.

1.03 This report is based on the findings of an IDA appraisal mission,comprising Messrs. Wadsworth, Gold, Harris (FAO) and Bek-Nielson, Leach andWhiting (Consultants) which visited Indonesia in November/December 1969,and which was assisted by Mr. Phillips of the Bank's Resident Staff inIndonesia.

II. BACKGROUND

A. General

2.01 With its 3,000 islands and a total land surface of 1.9 millionkm2, Indonesia is the world's largest archipelago. Its population is about118 million and the population growth rate, which is increasing, is atpresent 2.4% per annum.

2.02 Indonesia's per capita gross domestic product is about US$80. Theislands of Java (population, 75 million) and Sumatra (population, 19 million)are the most important economically, followed by Sulawesi (population 8.5million) and Kalimantan (population 5 million). The economic developmentof the smaller islands is Just starting. Agriculture plays a dominant role

1/ President's Report No. P-709; Appraisal Report No. PA-19.

2/ Perusahaan Negara Perkebunan Antan V. State-owned Estate EnterpriseUnit V.

3/ Asia Department Report No. EAP-lOa of November 14, 1969 - CurrentEconomic Position and Prospects of Indonesia.

- 2 -

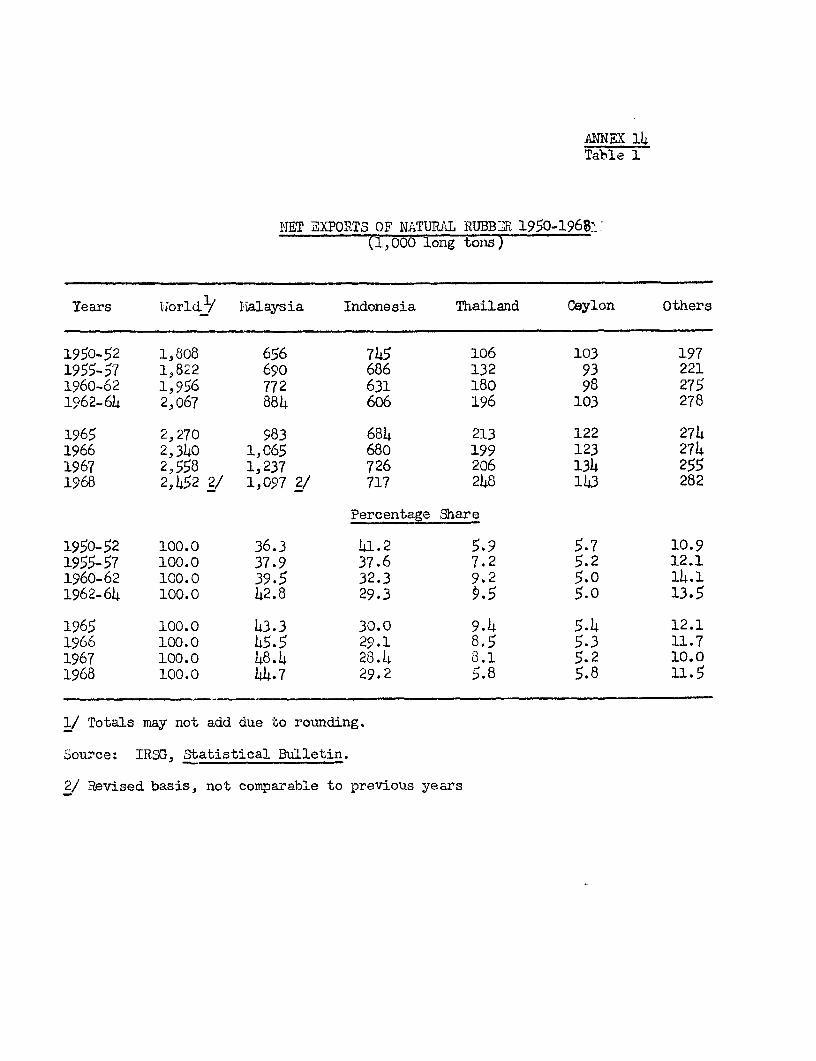

in the Indonesian economy, accounting for nearly h lf of the net domesticproduct, employing approximately 70% of the labor force, and contributingaround 75% of merchandise exports. The major export crop is rubber, whichis produced both by estates and smallholders, and which in 1968 accountedfor 27% of exports.

2.03 A war for independence, internal conflicts, nationalization ofmost foreign-owned enterprises, corruption, and a severe inflation havecurtailed economic development since World War 11. Agricultural exportsdeclined in the last decade and food imports increased.

2.04 The present Government took over in 1966 and has already succeeded,to a large extent, in stabilizing the currency; the rate of ±.flation wasbrought down from 85% in 1968 to 9% in 1969. Furthermore, the Governmenthas given the highest sector priority to agriculture, and particularly torice production in view of the major influence that the CU5pp7q of rice hason internal economic stabilization and the balance of paymen,s of the coun-try. An IDA credit of US$5.0 million to raise rice production through therehabilitation of irrigation works was made in 1969 (Credit No. 127-IND);the costs of this project have proved to be about three times the estimatesmade during appraisal, which was not preceded by a full feasibility study,on the other hand physical progress is satisfactory and the economic bene-fits of the project are ample to justify the increased expenditures. Afterrice, the Government is giving particular attention to the rehabilitationof estates, in order to increase foreign exchange earnings. An IDA creditof US$16.0 million was made in 1969 (Credit No. 155-IND) for the First NorthSumatra Estates Project; progress of this project is described in paras.2.10 through 2.15.

B. The Estate Industry

2.05 The background of the private and Government-owned estate industry,which was given in the First North Sumatra Estates Project appraisal report(Credit No. 155-IND), is detailed in Annex 1.

2.06 Over the last two years Government has taken positive steps to-wards stabilizing ownership, organization and management in the estate indus-try. The nationalized, previously Dutch-owned, estates are to remain underGovernment ownership and management. Some 90,000 ha of estates have beenreturned to their foreign owners -- Goodyear, Uni-Royal (American) andHarrisons and Crosfield (British) are some of the larger companies involved-- and are, and will continue to be managed by their owners. One estatecompany, SOCFIN (Belgian), has entered into a joint ownership and managementventure with Government for the 30,600 ha of rubber and oil palm which itpreviously owned outright.

- 3 -

C. Government-Owned Estate Industry

2.07 In 1969, Government-owned estates comprised a planted area of605,600 ha including some 224,500 ha of rubber and 80,500 ha of oil palm.Annex 1 contains further details.

2.08 While there have been improvements during the past three years,there is a long way to go before pre-war standards can be re-attained andsurpassed. This task would be formidable under any conditions, and whilethe economic, fiscal and political climates of Indonesia are improving,elements remain which constrain progress. Contacts abroad are being in-creasingly resumed, however, and substantial efforts are being made to up-grade research and to absorb modern techniques and management know-how.The Government, however, remains extremely short of cash and the relativelylarge investments needed to rehabilitate the industry must, therefore, con-tinue to come from abroad if the industry is to play its full part in theeconomy in the near future. To date, in addition to Credit 155-IND, otherfinancial assistance received by the Government estate industry has beenan Asian Development Bank credit of US$2.3 million, to rehabilitate some11,500 ha of oil palms on PNP II, and bi-lateral aid from the Federal Repub-lic of Germany for the supply of potash fertilizers.

2.09 Each PNP unit has a Board of Directors located on the estatesthemselves, though many important powers are reserved to the Minister ofAgriculture; these include appointment of senior staff; approval of budgetestimates and financial statements; approval of main lines of operations;and powers to give instructions to the Boards concerning the general dis-charge of their functions. The Minister exercises these powers throughthe Directorate General of Estates within the Ministry. These arrangementswere modified at the suggestion of IDA for PNP V and PNP VII, the two unitsfinanced under Credit 155-IND, and at that time it was thought that thesearrangements would serve as a model for a further degree of decentraliza-tion to be followed by other PNPs at a later date. For the proposed SecondNorth Sumatra Estates Project a further modification is suggested in thelight of experience gained, see para 5.04. It is anticipated that as bothprojects move ahead, they will fully demonstrate the advantages of furtherdecentralization based on more orthodox commercial principles. The Govern-ment is committed to placing its estate enterprises on a commercial basis,and has passed legislation (Government Regulation No. 12 of 1969) enablingPNP to move a stage further towards commercial autonomy by enabling them,as appropriate and when commercially viable, to be converted into a differ-ent type of enterprise - Perseroan Terbatas (PT) (see para 5.07). It ismandatory for PT to operate under the commercial code of Indonesia.

- 4 -

D. First North Sumatra Estates Pro4ect(Credit No. 155-IND)

The Protect

2.10 The project financed by Credit 155-IND is for the renabilitationand development of estate groups PNP V and PNP VII, growing respectivelyrubber and oil palms. Tne project involves planting or replanting 6,550ha of rubber and 13,670 ha of oil palms; bringing a further 7,070 ha ofimmature rubber and 5,750 ha of immature oil palms into bearing, rehabili-tating 9,660 ha of mature rubber and 23,990 ha of mature oil palms; andrehabilitating, replacing and expanding processing facilities, estate trans-portation, buildings, workshops and agricultural machinery. u-ortantly,the project involves the restructuring of the management of the two groupsand the provision of advisory and inspection services to assist management,as well as other technical assistance.

Comparison of Forecast and Actual Performance

2.11 The credit was signed in June 1969 but it did not become effectiveuntil December due to legal difficulties. In the meantime, however, therecruitment of management advisers and inspection services went ahead andcontracts have been signed between PNP V and N.V. Rubber Cultuur MaatschappijAmsterdam (RCMA), and between PNP VII and Societe Financiere des Caoutchoucs(SOCFIN) and Harrisons Fleming Advisory Services (HFAS). 1969 plantings andreplantings were as scheduled, and a total of 5,735 ha of rubber and oilpalms were established. The 1970 budgets and planting programs of the twoPNPs were reviewed by IDA in late 1969 and, following some changes, wereagreed with the Government. These provide for similar planting and replant-ing targets as envisaged at the time of appraisal. There has been no signi-ficant progress in other physical aspects of the project. It was agreed atthe time of appraisal that the procurement of new and replacement equipment,and the design and construction of new processing facilities would be pre-pared with the assistance of the management advisers and Inspection Services.

2.12 Terms of reference have been agreed between the Government and IDAfor the employment of oil palm and rubber plant breeding consultants, andqualified individuals and agencies have been approached. Terms of referencehave also been agreed for a survey of rubber smallholders in North Sumatra;for a survey of other Government-owned estates, and for studies of the mar-keting organization. Qualified consultants are now being contacted fcr thepurpose of carrying out these surveys and studies.

2.13 Insufficient data are available at this stage to compare actualwith forecast costs. In the Second Estates Project, however, higher laborcosts have been used as it appears that these may be increasing more rapidlythan originally forecast. To date, international procurement has been re-stricted to fertilizers, and no problems have arisen; US$212,000 have beendisbursed for the supply of fertilizers.

- 5 -

2.14 In compliance with terms of the Credit Agreement, new Boards ofDirectors have been appointed for PNP V and PNP VII, and a General Manager,Production Manager, and Commercial Manager have been appointed to eachestate group. All appointments to the Boards, and to management, were madefollowing consultation with IDA.

2.15 While the project is in a relatively early stage of development,the rapid progress made by Government and estate managements in the last sixmonths in implementing the terms of the Credit Agreement, and their adherenceto the project outline contained in the appraisal report justifies consider-able optimism for the future of the project.

III. THE PROJECT AREA AND PROJECT ENTITIES

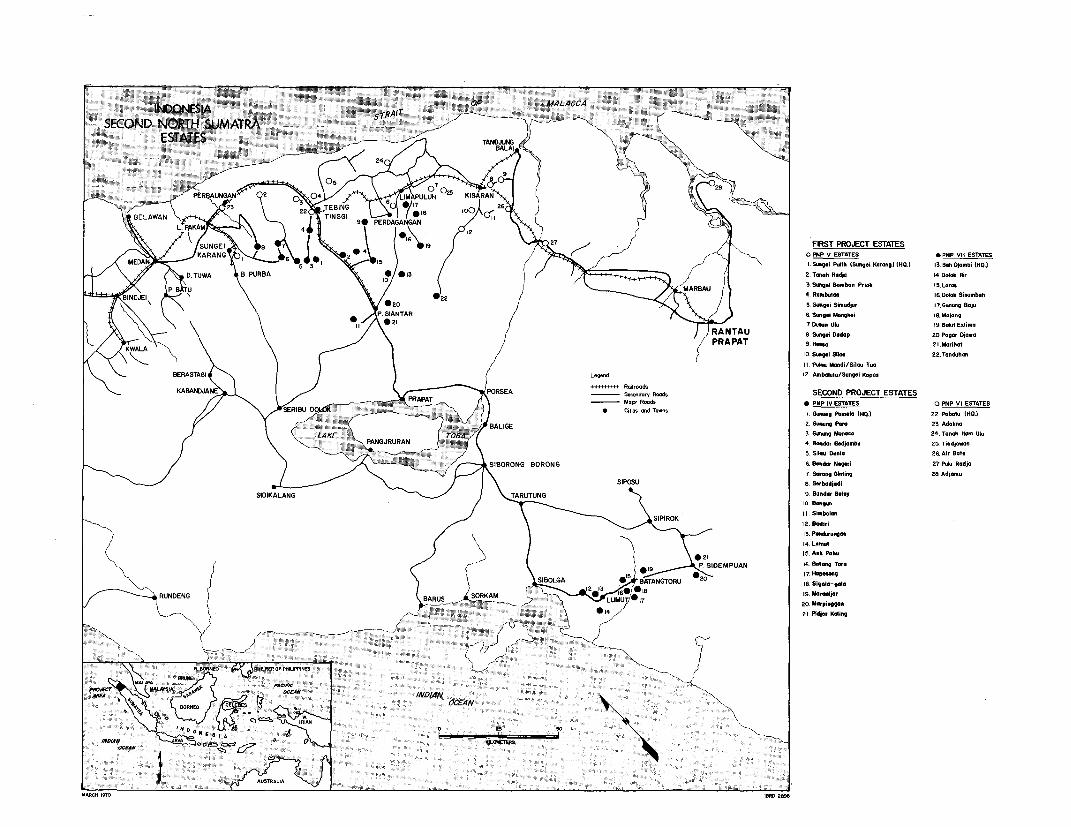

General

3.01 The PNP IV and PNP VI groups of estates lie within the provinceof North Sumatra (see Map). PNP IV has 18 operational estates with a totalplanted area of about 29,300 ha of rubber, and 3 other estates which havebeen abandoned completely. PNP VI comprises 7 estates growing 31,600 ha ofoil palms and 570 ha of cocoa. Currently, PNP VI manages and finances thelosses of Karang Inoue estate of the PNP I group of estates located in theprovince of Atjeh. Government has agreed that such responsibility willterminate shortly and during negotiations assurances were obtained from theGovernment to this effect; such termination would be a condition of effec-tiveness of the proposed credit. Annex 1 provides information on all otherPNPs and Annex 2 details of each estate on PNP IV and PNP VI.

3.02 There are about 300,000 ha of estates in the province of NorthSumatra. Government owns about 197,000 ha of these, private Indonesianssome 40,000 ha, a Government/private joint venture 31,000 ha, and variouswell-known international companies the remainder. In addition, there aresome 200,000 ha of smallholder rubber, and substantial areas of virginjungle.

Climate and Soils

3.03 The mean temperature is 270 C, sunshine averages six hours dailyand annual rainfall ranges from 1,700 mm to 3,500 mm, and is well distri-buted. Soil types vary between PNP IV estates, but all are suitable forrubber cultivation. The soils of PNP VI estates are ideal for growing oilpalms, but four estates situated on alluvial flats adjacent to the SilauTua, Balai, Ular and Barumun rivers are affected by seasonal flooding, someof which is serious. The estuaries of these rivers have not been dredgedfor 30 years, and in this same period the maintenance of outlet drains tothe sea throughout the area has been almost non-existent, see para 4.14.

- 6 -

Location of PNP IV and PNP VI Estates and Communications

3.04 PNP IV. PNP IV group headquarters are at Gunung Pamela, about120 km from the provincial capital of Medan (see Map). Of the operatingestates 11, totalling about 23,000 ha are within a radius of 70 km fromGunung Pamela, and the remaining seven, about 6,000 ha, are located in theTapanuli district and lie between 350 and 400 km from headquarters. Metal-led roads, in poor-to-good condition, lInk PNP IV estates with Miecan, andthe port of Belawan. The production of the Gunung Pamela estates is movedan average of 130 km (range 86-168 km) to Be7awan by the State railwaySystem, which connects with all factories. In Tapanuli, however, presentproduction is sold ex-estate and the buyer is responsible for transportation,which is by road.

3.05 PNP VI. Group headquarters of PNP VI are at Pabatu, some 90 kmfrom Medan, and all but one of the seven estates are within a radius of 100km from headquarters. The remaining estate, Adjamu, is 326 km away. AllPNP VI estates are served by road, and with the exception of Adjamu, byrailway. Road communications with Adjamu are poor, however, in particularthe Rantau Prapat-Adjamu section, which is impassable in wet weather. Dur-ing negotiations assurances were obtained from Government that the RantauPrapat to Adjamu road and all other roads to be used by project estate trans-port for the carrying out of the pro4ect, would be improved and maintainedfor use by ordinary estate vehicles. The evacuation of produce from Adjamupresents a considerable problem, and at the moment it must be transportedto Belawan either by road, by sea or by sea to Tandjung Balai and then byroad or rail to Belawan. To overcome the problem provision is made underthe project for a seagoing palm oil barge to ply between Adjamu and Belawan.

3.06 All project imports and exports would be handled through NorthSumatra's sole major port -- Belawan. While the design capacity of Belawanis adequate to handle existing traffic of about 2,000 ship calls annually,the port infrastructure and shiD-servicing facilities are in poor condition,due to unsatisfactory maintenance and repair. Additionally, heavy siltingand some shortfall in maintenance dredging restrict shipping to freightersof about 15,000 tons, while bulk tankers of higher tonnage would be the mosteconomic means of exporting palm oil. In general, however, the port canhandle present traffic and its improvement is high on the list of Governmentrehabilitation projects. A Dutch consulting firm (NEDECO) has been commis-sioned to study port improvement requirements, including those needed forBelawan, and it is anticipated that action will be taken by the Governmentto implement recommendations made by the consultants, and that the portwill continue to be able to handle North Sumatra estate production. BothPNPs have experienced excessive delays in the port and rail handling of theirproduction and supplies, particularly the turn-around and availability ofrail tankers transporting liquid latex and palm oil from the estates toBelawan. During negotiations assurances were obtained from Government thatsteps would be taken to eliminate delays in handling PNP production and toeffect such improvements as are required to facilitate the export of projectproduction. A specific assurance on this issue was not obtained when Credit155-IND was negotiated since it was believed at that time that improvementswould take place more rapidly than has proved to be the case.

- 7 -

3.07 There is no road or rail link between North and South Sumatra,consequently air services are the only means of rapid transportation betweenMedan and Djakarta. Regular commercial air services connect Medan with otherSumatran towns, Dajakarta on the island of Java, and Penang (Malaysia).

Labor

3.08 The supply of labor in the project area is adequate and is wellable and prepared to work on estates. The majority of estates employ morelabor than required and an expansion in the labor force would not be re-quired to implement the project. If labor shortages should occur, workerscould be recruited from Java, without much difficulty, as in the past. Dueto severe inflation in the recent past the estates follow the general policyof paying a large proportion of wages in kind, such as rice, cloth and kero-sene. The present wage level for estate workers is Rp. 22.50 per day plusRp. 137.50 in kind, equivalent to just under US$0.42. This rate is very lowcompared with those in other countries with a major estate industry. TheGovernment is anxious to return to solely monetary wages, but this has notyet proved possible.

IV. TIIE PROJECT

A. Project Description

4.01 The Project is the rehabilitation and development over the fiveyears 1970 - 1974 of two groups of Government-owned estates, PNP IV andPNP VI, and involves:

- planting or replanting about 12,000 ha of rubber and8,000 ha of oil palms;

- bringing to maturity the above areas and about 9,800ha of immature rubber and 7,200 ha of immature oil palmsplanted prior to 1970-

- rehabilitating 19,400 ha of mature rubber and 28,100ha of mature oil palms by means of a fertilizer program;

- rehabilitating about 9,100 ha of mature oil palms,7,200 ha of immature oil palms and 300 ha of immaturerubber through special programs of weed and diseasecontrol, drainage and selective felling of uneconomicpalms;

- constructing a test laboratory, one new block rubberfactory, and converting an existing sheet factory toblock rubber production;

-8-

rehabilitating seven existing palm oil mills;

rehabilitating and expanding estate agriculturalequipment, transportation services and buildings;

rehabilitating existing estate roads and bridges;

providing machinery for land clearing, and upkeepof estate roads and drains;

- providing technical and management assistance, in-volving an estate and factory inspection service,technical and financial advisers and the purchaseof foliar (leaf) analysis services; and

- rehabilitation and improvement of RISPA after employ-ment of consultants to submit proposals for reorgani-zation and a long-term research and development program.

The physical and organizational components of the project would be similarto those of the First Estates Project, amended as necessary in the light ofexperience gained in carrying out the latter.

B. Estate Development

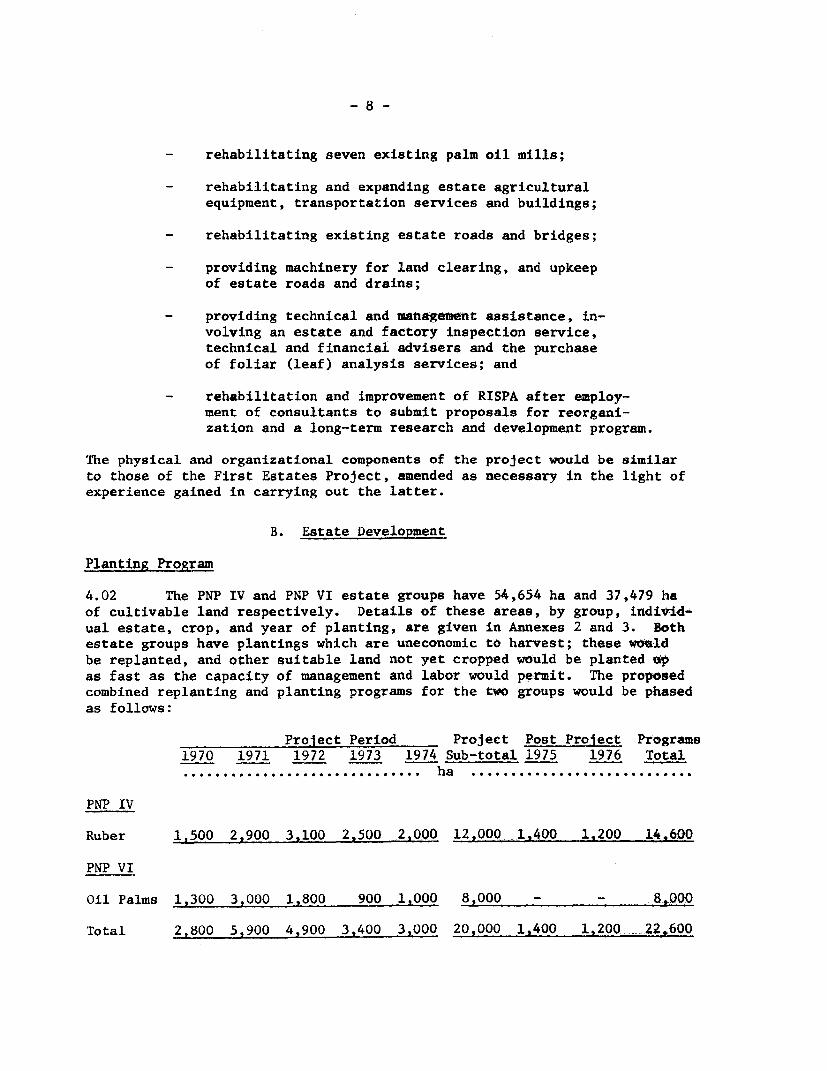

Planting Program

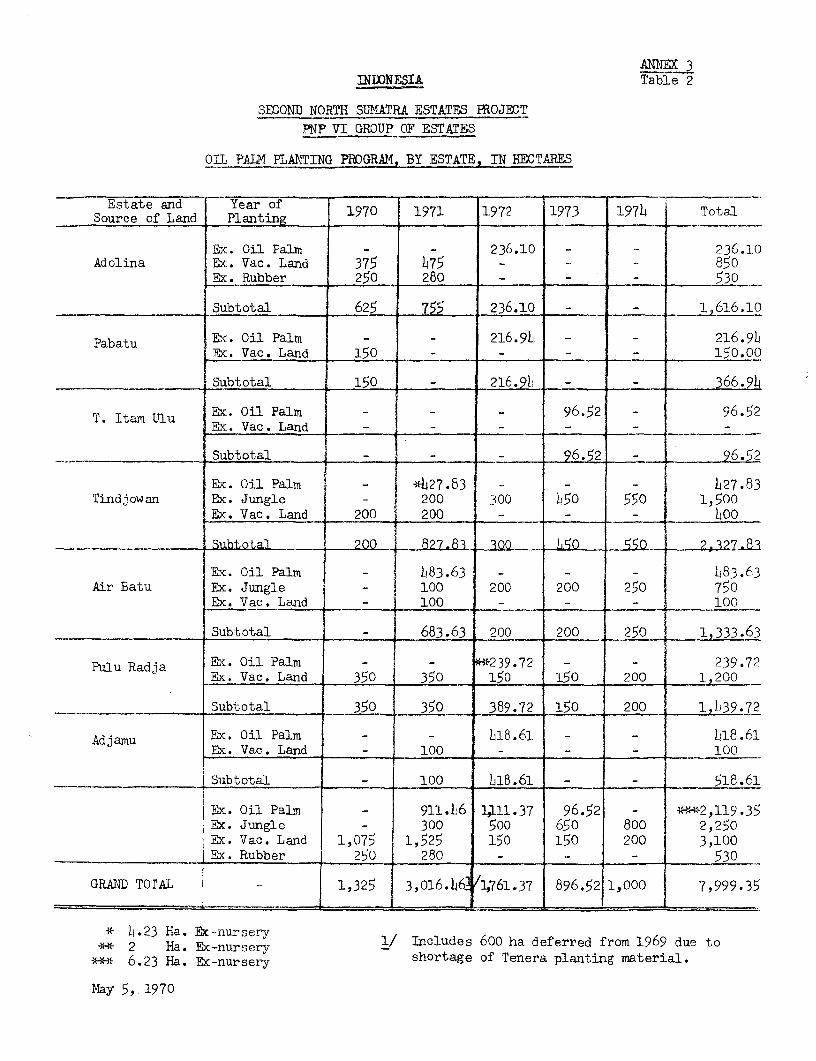

4.02 The PNP IV and PNP VI estate groups have 54,654 ha and 37,479 haof cultivable land respectively. Details of these areas, by group, individ-ual estate, crop, and year of planting, are given in Annexes 2 and 3. Bothestate groups have plantings which are uneconomic to harvest; these wouldbe replanted, and other suitable land not yet cropped would be planted upas fast as the capacity of management and labor would permit. The proposedcombined replanting and planting programs for the two groups would be phasedas follows:

Project Period Project Post Project Programs1970 1971 1972 1973 1974 Sub-total 1975 1976 Total.. . . .ha ............................

PNP IV

Ruber 1,500 2,900 3,100 2,500 2,000 12,000 1,400 1,200 14.600

PNP VI

Oil Palms 1,300 3,000 1,800 900 1,000 8,000 - - 8.000

Total 2,800 5,900 4,900 3,400 3,000 20,000 1,400 1,200 _22,600

4.03 The 14,600 ha PNP IV program would comprise replanting 9,400 hanow under rubber of between 25 and 50 years old, and planting up 3,900 haof jungle and 1,300 ha of land now occupied by illegal squatters but whichwould be recovered through compensating such squatters (see para 4.13).

4.04 The PNP VI program of 8,000 ha would include the replanting of2,100 ha of old and low yielding oil palms, and the planting with oil palmsof 500 ha in old rubber, 2,300 ha under jungle and 3,100 ha of vacant landto be recovered from illegal squatters (see para 4.13).

Routine Replanting

4.05 It is standard estate practice to use a 30-year replanting cyclefor oil palms, and a 25-year cycle for rubber. Replanting carried out underthe above programs would clear up the existing backlog of replanting. From1974 PNP VI would adopt a standard 30-year replanting cycle, and PNP IV a25-year cycle from 1976.

Planting Material

4.06 Both estate groups would produce their own supplies of high-yieldpotential planting material 1/. The only exception would be that for its1971 plantings PNP VI would have to import about half of its oil palm seedrequirements from Malaysia. Annex 4 gives details of the planting materialavailable and the plant breeding situation in Indonesia. In the First NorthSumatra Estates Project the Government undertook to implement suitable plantbreeding programs for all Government-owned estates in North Sumatra, and toappoint oil palm and rubber plant breeding consultants, acceptable to IDA,to oversee these programs. During negotiations, assurances were obtainedfrom the Government that all material used for project oil palm and rubberplanting programs from 1971 through 1974 would be subject to the recommen-dation of these plant breeding consultants. These plant breeding consult-ants are expected to be appointed shortly; and a condition of effectivenessof the proposed credit would be that the plant breeding consultants had beenappointed and were working in Indonesia.

Fertilizer Investment Program

4.07 Economic fertilizer programs can be determined only by scientificanalysis techniques, such as foliar (leaf) analysis which is described inAnnex 5. Foliar analysis services will not be available locally untilsometime during 1971, and provision is made in the project for obtaininganalysis services from abroad through contracts with suitable researchagencies. PNP VI made appropriate arrangements with a Malaysian agencyin 1969, and PNP IV will make similar arrangements in the latter half of1970. Consequently, scientifically based fertilizer programs will stsrtin 1970 in the case of PNP VI and in 1971 in that of PNP IV.

1/ PNP VI would produce oil palm seed from selected mother palms whichwould be pollinated artificially with pollen from selected male parents,

and PNP IV would obtain rubber seeds required for rootstocks from seedgardens, and bud wood from its bud wood nurseries.

- 10 -

4.08 The yields of all Indonesian estates, including those of PNP IVand PNP VI, are seriously depressed due to the lack for many years ofbalanced fertilizer applications. If maximum yield potential is to berealized mature areas on PNP IV and PNP VI must be properly fertilized asquickly as possible, although yield responses to the initial applicationswould not be significant until the second or third year following such ap-plications (see Annex 5). The cost of the initial applications is consider-ed a capital Item and it is proposed to finance them under the project.Thus fertilizer for application to mature PNP IV rubber would be financedin 1971 and 1972; and fertilizer for mature PNP VI oil palms in 1970 (somefoliar analysis results are available), 1971 and 1972. Fertilizer for im-mature areas 1/, which in estate accounting is normally regarded as a capitalitem, would be financed throughout the project period.

Special Rehabilitation

4.09 Many of the estates of PNP IV and PNP VI are in arrears with weed-ing programs, and this backlog of poor maintenance is adversely affectingrubber and oil palm growth in immature areas and yields in mature areas.Additionally, PNP VI is in arrears with disease control and drainage pro-grams and the selective felling of uneconomic oil palms. These programswould be brought up to date in 1970 and 1971, and this special rehabilita-tion would be included in the project. After 1971, the areas rehabilitatedin this way would be covered by routine annual maintenance programs.

Buildings

4.10 Cash shortages over many years have resulted in the wholly inade-quate maintenance of estate buildings, particularly of workers' housing.On many estates much of the workers' accommodation is sub-standard and shouldbe replaced. It is proposed to include in the project the cost of rehabili-tation, maintenance and replacement of estate housing. During the period1970 through 1974 provision has been made for PNP IV and PNP VI to replace125 and 850 double housing units respectively, and for each PNP to rehabili-tate about 50% of the remaining workers' housing units. No additional hous-ing would be required. General provisions have also been made for replace-ment and rehabilitation of staff housing, offices and other buildings.Annual plans for the replacement and rehabilitation of buildings would becarried out only after the Inspection Services had commented on the proposals(see para 5.12).

Vehicles and Equipment

4.11 All PNP IV produce is transported from field to processingfactories by road. PNP VI has an estate rail system, and only a smallproportion of road haulage takes place. The number of vehicles, locomo-

1/ The development period from planting or replanting until the treescome into bearing: 3-4 years for oil palms, 6-7 years for rubber.

- 11 -

tives and rolling stock on both PNPs is substantial, although efficientutilization is precluded due to age and consequent high repair incidence,shortage of spares, and poor organization. Other machinery and equipmentused by the estates, and which is generally in a state of disrepair, in-cludes wheeled and crawler tractors, road upkeep machinery, crop transportand general vehicles.

4.12 Under the project obsolete and irreparable equipment such aslocomotives, rolling stock, wheeled and crawler tractors, road graders,trucks and personnel vehicles (buses, cars, jeeps, and motorcycles) wouldbe replaced; and additional equipment purchased to handle the increasedproduction expected to be generated by the project. Requirements havebeen estimated on the basis of better utilization which would result fromimproved management, see Chapter V.

4.13 The PNP IV and PNP VI planting programs include some 4,400 hawhich are at present illegally occupied by squatters; Government regulationsrequire such squatters to be compensated in accordance with an agreed scalefor crops and housing which may be lost when the land is planted and projectcosts include compensation payable during the period 1970 through 1972.This would not be financed under the IDA credit. During negotiations assur-ances were obtained from the Government that such squatters would be removedin time to prevent any disruption of the agreed planting program.

4.14 Four of the PNP VI estates, and particularly Tanah Itam Ulu estate,are affected by seasonal flooding as river estuaries have not been dredgedand outlet drains to the sea have not been maintained for many years (seepara 3.03). To alleviate the flooding problems Government assurances wereobtained during negotiations that the blocked outlet drain to the sea whichcauses severe flooding at Tanah Itam Ulu estate would be rehabilitated notlater than June 30, 1971, and that other major outlet drains to the seaaffecting other PNP estates within the project would be rehabilitated andproperly maintained, see para 4.31.

C. Processing Facilities

PNP IV

4.15 The current PNP rubber crop of about 18,000 tons per annum is pro-cessed into sheet and crepe rubber 1/ by PNP IV factories and those of Indone-sian remillers, and into concentrated latex at a plant owned and operated bythe Goodyear Company. The 11 PNP IV plants, which are in a generally satis-factory condition, comprise five-sheet and crepe rubber plants, four-sheetrubber plants and two-crepe rubber plants; there are.also two additionalsheet-rubber plants which are only used for sheet drying during peak crop-

I/ The main characteristics of the various types of rubber produced aredescribed in Annex 6.

- 12 -

ping periods. In order to meet competition from synthetic rubbers, and toobtain the long-term marketing advantages of block rubber over sheet andcrepe rubber, the project provides for conversion of PNP IV factories toblock rubber manufacture as and when present facilities or arrangements be-come inadequate to deal with the crop harvested. At least three of the ex-isting sheet and crepe factories would be held in reserve following theintroduction of block rubber processing facilities.

4.16 PNP IV crops are expected to increase to about 47,000 tons by themid 1980's. To provide for the additional crop and conversion of existingfactories when crops exceed present capacity the prbject includes:

- the construction of a new block rubber factory atBandar Betsy;

- conversion to block rubber of an existing sheet rubberfactory at Bangun;

- establishment of a rubber testing laboratory at PNP IVheadquarters in 1970; and

- additional drying facilities at Bandar Negeri and SarangGiting.

During the following ten years to 1985 provision has been made for fo'tr m'orbfactories to be converted to block rubber production, the construction of anew block rubber plant at Hapesong and extension of plant capacity as andwhen required. Further details of existing plants and proposed investmentsare given in Annex 6.

4.17 After 1970 PNP IV processing should be adequate for all PNP IVcrops and the need for outside processing arrangements would be eliminatff8.During negotiations assurances were obtained from the Government that exist-ing and any future outside processing arrangements would be subject to theapproval of IDA and the Joint Marketing Office (JMO), see para 6.03.

PNP VI

4.18 The current PNP VI oil palm crop of about 300,000 tons of FFB perannum is processed in seven mills. The condition of four of the mills isgenerally satisfactory but the mills at Tindjowan (built in 1922 and re-habilitated in 1968), Pulu Radja (built in 1920), and Adjamu (built in1938) operate inefficiently due to poor layout and lack of equipment. Withthe exception of Tindjowan, all mills are operating far below rated capacity.Quality control checks acceptable internationally are carried out by RISPAlaboratories.

- 13 -

4.19 PNP VI crops are expected to increase to about 690,000 tons FFB by1979. Additional mill capacity would not be required but rehabilitation andadditional equipment is necessary to enable each mill to operate efficientlyat full rated capacity. The project provides for substantial rehabilitationand new equipment for the mills at Tindjowan, Pulu Radja and Adja"u, mach-inery spares, incinerators and conveyors for bunch waste disposal (a productof such disposal is valuable potash fertilizer), storage facilities, labora-tory equipment and rehabilitation and improvement of mill workshops. (Annex7 gives further details of existing mills and proposed investments.)

D. Technical Assistance

4.20 Reference has already been made to technical assistance for rubberand oil palm plant breeding programs being provided under Credit 155-IND(paras 2.12 and 4.06). Technical assistance would be provided under theproject to strengthen and up-date the management of both PNP IV and PNP VI(paras 5.06 thru 5.10).

E. Agricultural Research

4.21 The Research Institute of the Sumatran Planters' Association(RISPA) was established early in the century (under the name AVROS) toprovide a common research service for the estate sector, and soon developedworld-wide reputation for the quality of its work. RISPA remains theprincipal research center for rubber, palm oil and tea, but since theexpropriation of Dutch owned estates has been unable to maintain a satis-factory service. The main reasons for this have been shortages of fundsand of qualified staff. Consequently, the estate sector is receiving in-adequate research support, despite the efforts of individual estates toconduct their own research programs.

4.22 The Government recognizes the importance of RISPA and the devel-opment of agricultural research for all sectors. In April 1969 a cess wasintroduced for all export crops to finance research requirements and toprovide other essential services for the export crops sector. Equipmentfor soil and leaf analyses at RISPA is being provided under bilateral aidand IDA assistance has been made available under the First North SumatraEstates credit for periodic visits by foreign plant breeding experts, thetraining of Indonesian personnel, and the purchase of equipment.

4.23 An early improvement in the advisory and product testing servicesprovided by RISPA to the estate sector is considered essential. It is rotpossible to establish in detail RISPA's financial and man-power needs in theabsence of a long-term research and development program for the institute.The preparation of such a program is long overdue, but when the First EstatesProject was being appraised Government's intentions for the future of RISPAwere insufficiently clear to permit IDA to consider providing financial

- 14 -

assistance other than for the services described above. The situation isnow clear, and RISPA will be operated under Government auspices with appro-priate representation by the estates on its management body. Funds wouldbe provided under the project to employ consultants to prepare a researchand development program, and to recommend the organizational and financialarrangements, such as the level of a research cess, required to support it.An amount of US$200,000 would be provided from the proposed credit for thispurpose, and an additional US$400,000 for the procurement of any goods andservices shown by the studies to be urgently required and which could not befinanced readily from RISPA resources. It is estimated that Governmentcounterpart funds equivalent to US$400,000 also would be required. Assur-ances were obtained during negotiations that, to carry out preparation ofthe research and development program the Government and RISPA would employconsultants satisfactory to IDA, on terms and conditions satisfactory toIDA. Assurances were also obtained from the Government that the consultant'sfindings and recommendations would be submitted to IDA to enable agreemeatto be reached on their implementation.

F. Export Duties, Taxes and Exchange Rates

4.24 Export duties and taxes payable to Government by the PNPs amountto 15% of the fob proceeds of rubber and palm produce. The rate of exportduty is currently 10% and agricultural and other taxes account for a further5%. In addition a cess of Rp 1,000 (US$2.65) per ton of production io payableto the Provincial Government for infrastructure maintenance (see para. 7.03).All financial projections in this report are expressed in US dollars andconversions from rupiahs have been made at the rate of US$1 - Rp 378.

G. Cost Estimates

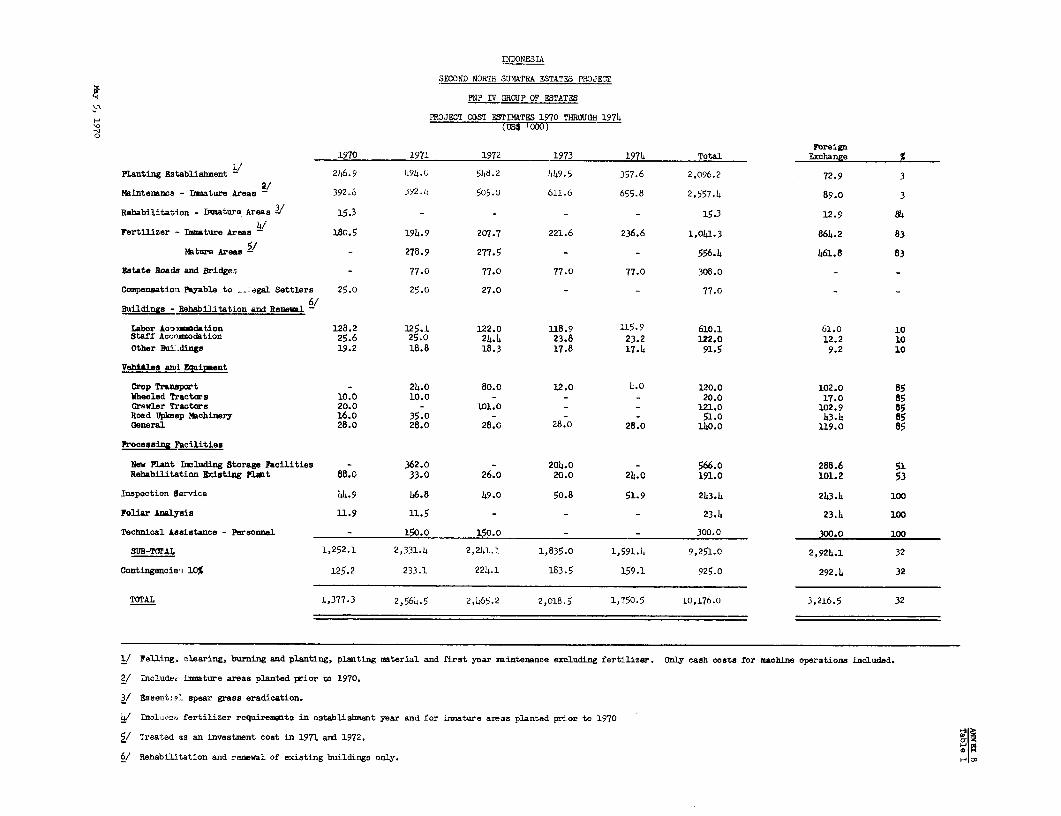

4.25 Total project costs are estimated at US$31.7 million, with aforeign exchange component of US$17.0 million. The following is a summaryof the cost estimates; further details are given in Annex 8.

- 15 -

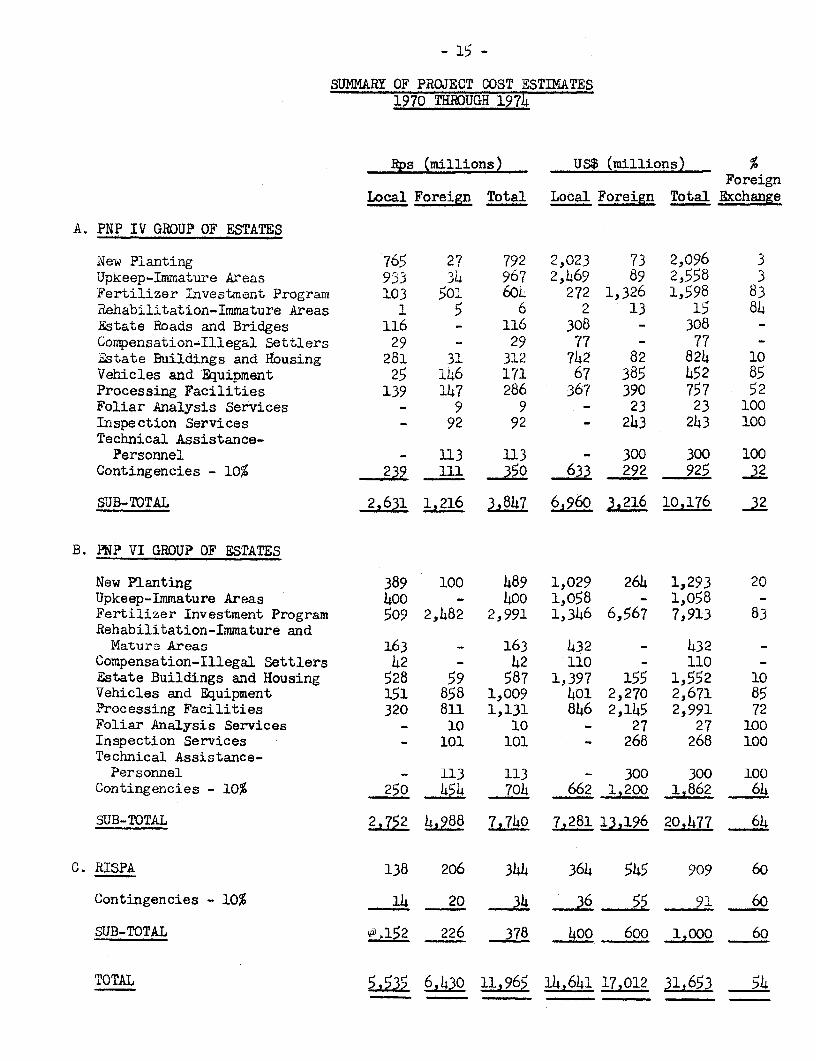

SUMMARY OF PROJECT COST ESTIMATES1970 THROUGH 1974

Rps (millions) US$ (millions) %Foreign

Local Foreign Total Local Foreign Total Exchange

A. PNP IV GROUP OF ESTATES

New Planting 765 27 792 2,023 73 2,096 3Upkeep-Immature Areas 933 34 967 2,469 89 2,558 3Fertilizer investment Program 103 501 604 272 1,326 1,598 83Rehabilitation-Immature Areas 1 5 6 2 13 15 84Estate Roads and Bridges 116 - 116 308 - 308 _Compensation-Illegal Settlers 29 - 29 77 - 77 -Estate Buildings and Housing 281 31 312 742 82 824 10Vehicles and Equipment 25 146 171 67 385 452 85Processing Facilities 139 147 286 367 390 757 52Foliar Analysis Services - 9 9 - 23 23 100Inspection Services - 92 92 - 243 243 100Technical Assistance-Personnel - 113 113 - 300 300 100

Contingencies - 10% 239 111 350 633 292 925 32

SUB-TOTAL 2,631 1,216 3,847 6,960 3,216 10,176 32

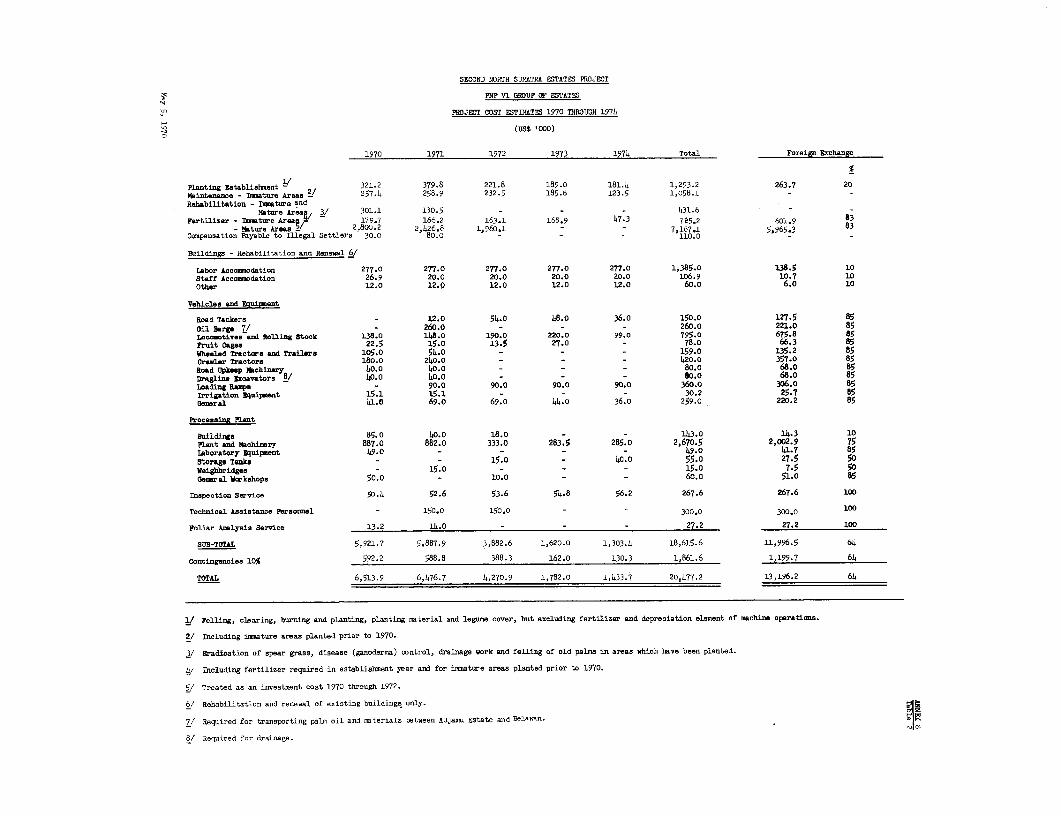

B. PNP VI GROUP OF ESTATES

New Planting 389 100 489 1,029 264 1,293 20Upkeep-Immature Areas 400 - 400 1,058 - 1,058 -Fertilizer Investment Program 509 2,482 2,991 1,346 6,567 7,913 83Rehabilitation-Immature andMature Areas 163 - 163 432 - 432 -

Compensation-Illegal Settlers 42 - 42 110 - 110 -Estate Buildings and Housing 528 59 587 1,397 155 1,552 10Vehicles and Equipment 151 858 1,009 401 2,270 2,671 85Processing Facilities 320 811 1,131 846 2,145 2,991 72Foliar Analysis Services - 10 10 - 27 27 100Inspection Services - 101 101 - 268 268 100Technical Assistance-Personnel - 113 113 - 300 300 100

Contingencies - 10% 250 454 704 662 1,200 1,862 64

SUB-TOTAL 2,752 4,988 7,740 7,281 13,196 20,477 64

C. RISPA 138 206 344 364 545 909 60

Contingencies - 10% 14 20 34 36 55 9 60

SUB-TOTAL @,152 226 378 400 600 1,000 60

TOTAL L^L 6,430 11,965 14,641 17,012 31,653 54

- 16 -

4.26 Although the severe inflation experienced in Indonesia in recentyears has abated during the last twelve months, previous costs are not yeta reliable guide for establishing cost projections. Wherever possible,cost estimates have been calculated on the basis of man-day requirementswhich have then been compounded by the daily wage rate assumed. Increasesof 5% in the wage rate were made at the beginning of both 1969 and 1970,and in the cost projections it has been assumed that wages and salarieswould be increased by 5% per annum (compounded) for a further nine years,until 1979, and that thereafter the annual increase would be 1% for theremainder of the project life. Current daily wage rates are less than50% of those now being paid to estate labor in Malaysia, but the averageIndonesian worker's output is appreciably lower. Productivity improvementsare achievable, as shown by experience in Malaysia where despite increasinglabor costs, costs of production have fallen. Estimates for the rehabilita-tion and replacement of existing buildings, vehicles and equipment have beenarbitrarily assessed as it was not possible to appraise each item, and to'forecast the precise life left in many of the items would be difficult. Itemswould only be purchased, replaced or rehabilitated as required, and in accord-ance with annual budgets approved by PNP Boards which would incorporate thecomments of the Inspection Service (see para. 5.12). The Government hasgranted duty free privileges to projects financed with foreign aid, andthese arrangements would apply to PNP IV and PNP VI for goods required forthe project. A contingency provision of 10% has been applied to all coststhroughout the life of the project as increases have- only been provided forwages and salaries.

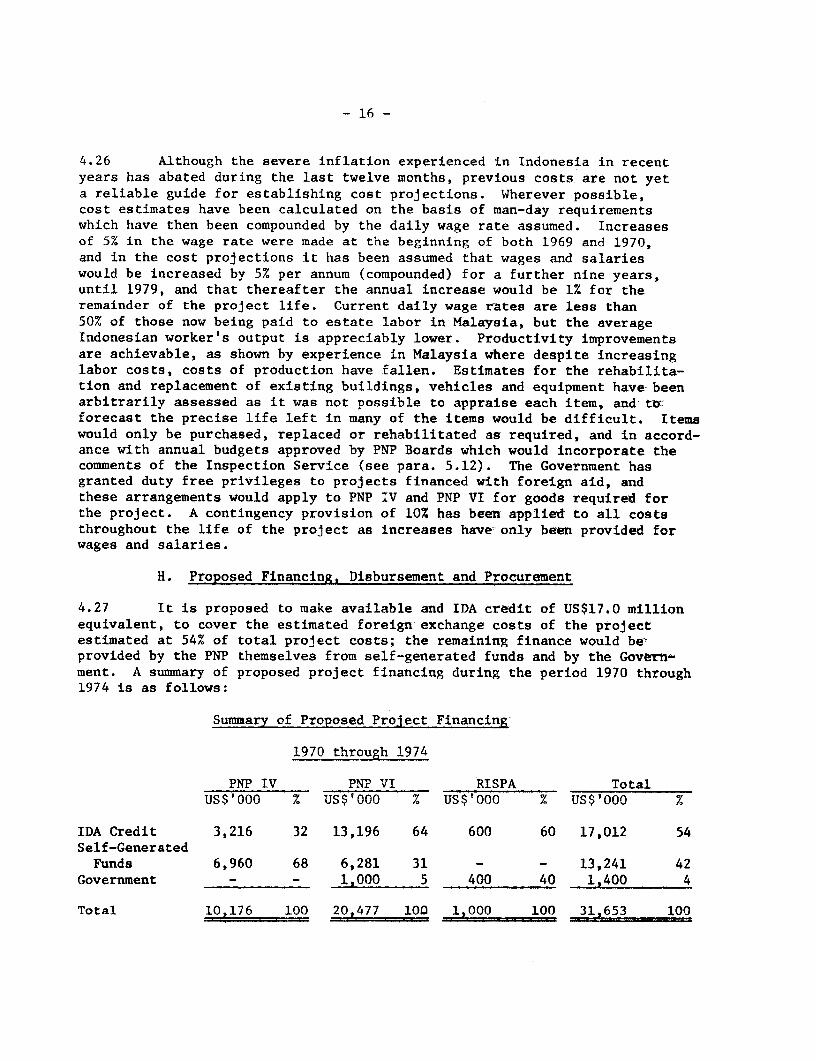

H. Proposed Financing, Disbursement and Procurement

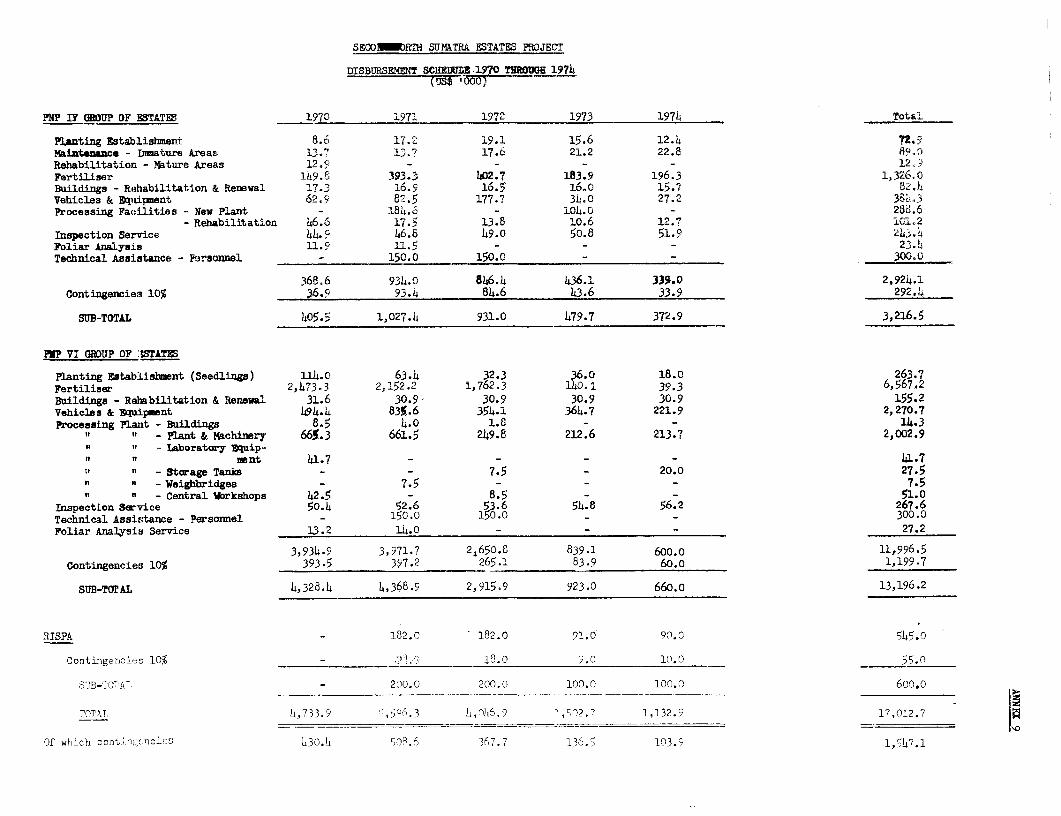

4.27 It is proposed to make available and IDA credit of US$17.0 millionequivalent, to cover the estimated foreign exchange costs of the projectestimated at 54% of total project costs; the remaining finance would bevprovided by the PNP themselves from self-generated funds and by the Govern-ment. A summary of proposed project financing during the period 1970 through1974 is as follows:

Summary of Proposed Project Financing

PNP IV PNP VI RISPA TotalUS$'000 % US$'000 % US$'000 % US$'000 %

IDA Credit 3,216 32 13,196 64 600 60 17,012 54Self-GeneratedFunds 6,960 68 6,281 31 - - 13,241 42

Government - - 1,000 5 400 40 1,400 4

Total 10,176 100 20,477 100 1,000 100 31,653 100

- 17 -

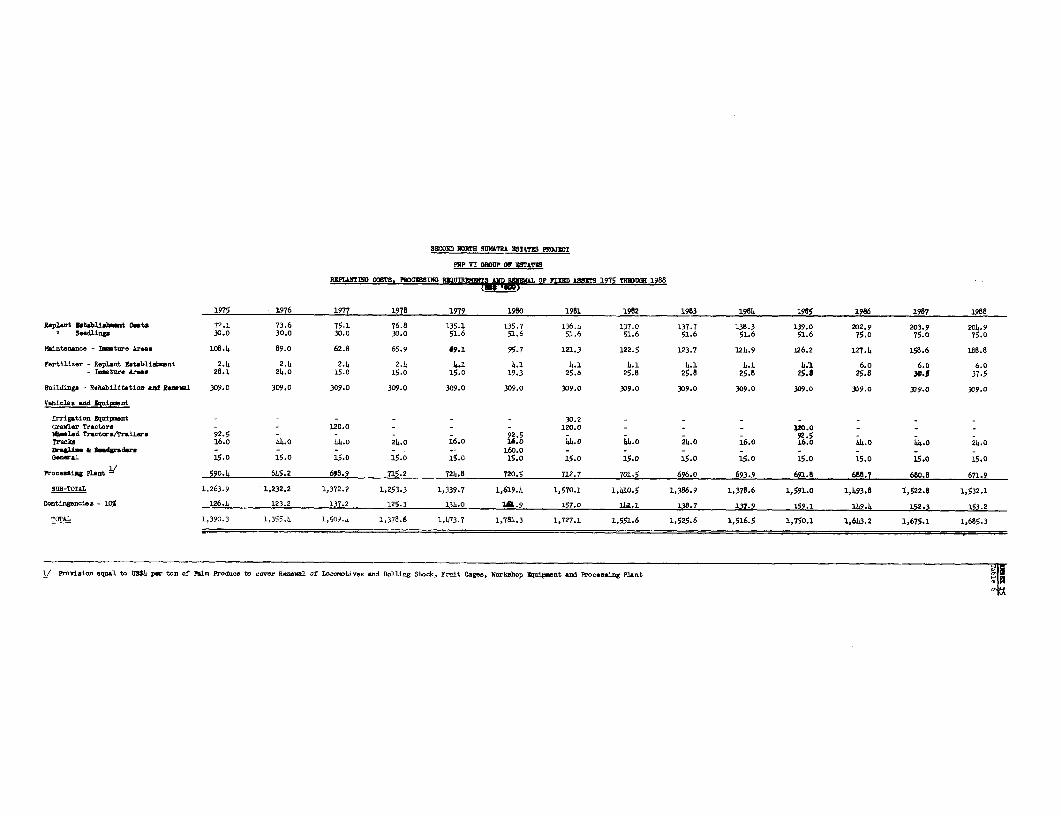

4.28 In addition to the US$1.0 million to be provided for PNP VI byGovernment during the period 1970 - 1974, a further US$2.0 million would berequired by PNP IV in 1975 and 1976 for replanting, processing facilitiesand renewal of fixed assets, which would increase the total Governmentcontribution for the two PNP to US$3.0 million. Government funds requiredfor both PNP IV and PNP VI would be amply covered by export duty andcorporation tax received from the PNP during the period 1970 - 1976 (seeAnnex 16).

4.29 The IDA credit be on-lent by the Government to the PNP. Boththe IDA credit and the direct Government contributions to PNP IV and PNP VIwould be lent under Subsidiary Loan Agreements, which would be similar tothose executed between the Government and the PNP financed under the FirstNorth Sumatra Estates project. The subsidiary loans would bear interest at12% per annum, the standard Government lending rate for all State enterprises.The term of the PNP IV subsidiary loan would be 16 years, including a 9 yeargrace period; the PNP VI loan would be for 13 years, with a grace period offive years. The terms of these sub-loans are largely determined by thecapacity of the PNP to meet loan interest and repayments, (see paras. 6.12through 6.14). During negotiations assurances were obtained from the Govern-ment that draft Subsidiary Loan Agreements would be submitted to IDA forapproval. Signature of the Subsidiary Loan Agreements would be a conditionof effectiveness of the proposed credit.

Procurement

4.30 During negotiations assurances were obtained from Governmentthat goods to be imported under the project, and to be financed by IDA,would be procured following international competitive bidding procedures,and that for all contracts in excess of US$50,000 draft tender documentswould be submitted to IDA for approval together with analyses of bids beforecontracts are awarded. The Inspection Services would assist the PNP toprepare bid documents and specifications and to evaluate tenders.

Disbursement

4.31 IDA funds would be disbursed against full CIF documentation forfertilizers and chemicals amounting to about US$8.5 million, processing andother machinery amounting to some US$2.8 million and transporation equip-ment totalling US$3.0 million. Disbursements would be made against foreignexchange payments for the purchase of foliar analysis and inspection servicesand the cash cost of employing technical assistance personnel would be re-imbursed in full. No disbursements would be made for goods and services forRISPA until the consultants' recommendations for the RISPA research programhave been discussed and agreed with IDA (see para. 4.23), or for Tanah ItamUlu estate until rehabilitation of the outlet drain has been completed (seepara. 4.14). A disbursement schedule is at Annex 9. Should any savings bemade the resultant balance of the IDA credit would be cancelled.

- 18 -

V. ORGANIZATION AND MANAGEMENT

5.01 Until recently, Government-owned estates have been isolated frominternational developments in estate technology and management, and theintroduction of modern crop production and processing techniques and manage-ment skills is urgently required. The first North Sumatra Estates Projectprovided for a restructuring of the Boards of Directors and managements ofthe two estate groups involved, as well as for a greater decentralizationof authority, appointment of expatriate management advisers, and employmentof foreign estate companies to make regular inspections of all estates.These arrangements were agreed by IDA as the existing day to day managementof the estates was regarded as generally satisfactory.

5.02 The revised directorate and management arrangements under thefirst North Sumatra Estates Project have only been in operation for a shortperiod. Generally they appear to be working well, and it is proposed thatsimilar arrangements should be introduced for PNP IV and PNP VI.

Boards of Directors

5.03 The Boards of Directors for PNP IV and PNP VI would have powerssimilar to the Boards of Directors of commercial companies, including fullauthority for hiring and dismissing managers and staff and for determiningand implementing all administrative, financial, technical and commercialpolicies and programs. Each Board would consist of a Chairman and at leastthree other members who would be appointed for an initial period of fiveyears by the President of Indonesia acting on the reconmendation of theMinister of Agriculture. In each case the Director General of Estates, ora senior member of his staff nominated by him, would serve as an ex-officiomember. The Director General is a civil servant responsible to the Ministerof Agriculture for all matters pertaining to the estate industry, as such hehas broad experience of PNP operations. The other members of the Boardswould be Indonesians with experience in estate business and management, bank-ing, commerce or some related field. The Boards would not be responsiblefor day to day management (see para. 5.04). During negotiations assuranceswere obtained from the Government that such new boards of Directors forPNP IV and PNP VI would be established, and that all appointments to theBoards would be subject to prior consultation with IDA. Establishment ofthe two Boards, and the filling of their positions would be a condition ofeffectiveness of the proposed credit.

Day to Day Management

5.04 Day to day management is now in the hands of the three Directorswho make up the existing Boards of Directors of PNP IV and PNP VI. Theseare, a First Director, Production Director and Commercial Director. Underthe project these directorships would be abolished, and their managementfunctions would be exercised respectively by a General Manager, ProductionManager and Commercial Manager appointed by the Minister of Agriculture onthe recommendations of the new Boards of Directors. This would be similarto the arrangements agreed by IDA for the First North Sumatra Estate Proj-

- 19 -

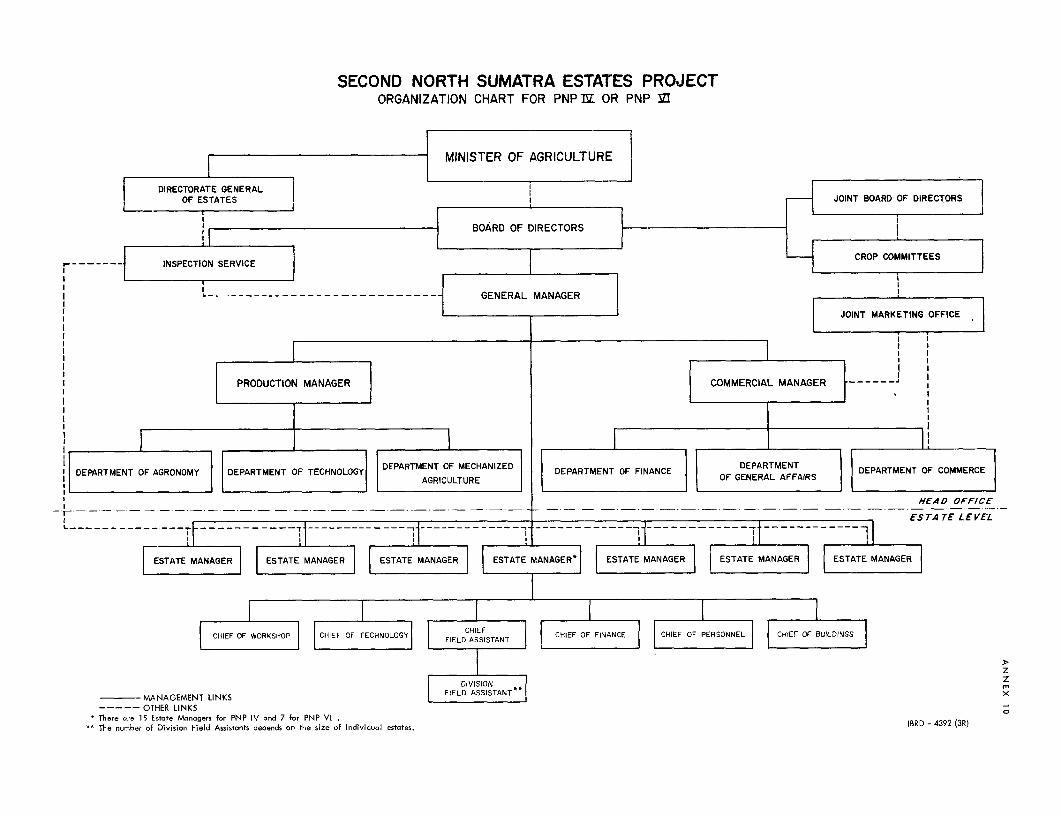

ect which appear to work well. A change under the second project would bethat the Director of Estates, or his representative, would be an ex-officiomember of the two Boards and would assist them in making managerial appoint-ments and, additionally, ensure close cooperation between the PNPs and theDirectorate of Estates. Initial appointments to the three key managerialpositions of PNP VI would be almost certainly the three present Directorsbut changes are considered desirable for PNP IV. Assurances were obtainedfrom the Government during negotiations that such managerial appointmentswould be made only after prior consultation with IDA, and appointment ofthe six managers would be a condition of effectiveness of the proposedcredit. Management organization below group level would remain unchanged.Managers of individual estates would be responsible to the group managersand the latter would be assisted at Head Office by a Department of Agronomyand Technology (reporting to the Production Manager) and a Department ofFinance, Commerce and General Affairs (reporting to the Commercial Manager).Marketing is organized through a Joint Marketing Office (see para. 6.03).An organization chart for the reorganized PNP IV and PNP VI is shown atAnnex 10.

5.05 Existing Government regulations for the dismissal of employeespreclude the effective operation of incentive payment schemes, which wouldimprove productivity, but might result in some redundancy. Increasedproductivity is essential for the success of the project and assuranceswere obtained from the Government that the Boards and Managements of PNP IVand PNP VI would be fully authorized to hire and dismiss project personnelas required. Assurances were also obtained from the Government that theexisting wage premium system in use by the PNPs would be improved and,wherever possible, future wage and salary increases would be linked toincentive payments systems.

5.06 In order to ensure the strengthening and consolidation of themanagement of PNP IV and PNP VI, assurances were obtained during negotia-tions that no changes would be made in the management responsibilities andstructure of the two PNPs without IDA's approval during the disbursementperiod of the proposed credit or without prior consultation with IDA there-after. IDA financing of the PNPs, and the introduction of foreign advisersand inspectors should lessen interference by the military in the affairsof these estate groups, which has, and still does occur, particularly inthe case of PNP IV. This assumption is based on the experience in caseswhere foreign companies have recovered the management control of theirestates.

5.07 The Government is presently considering a new form of corporateentity, Purusahaan Perseroan Terbatas (PT), for the operation of PNP estategroups and other Government-owned enterprises. Only profitable enterpr1seswould be converted to PT which mandatoriy would operate under the Commer-cial Code. In such cases share capital of the PT would be issued to theGovernment with the Minister of Finance making appointments to a Board ofManagement and a Supervisory Board.

- 20 -

Inspection Service

5.08 As in the case of the First Estates Project, PNP IV and PNP VImanagements would be assisted and strengthened by their each employing anexperienced plantation company or companies to provide an InspectionService for an initial period of at least five years. The service wouldentail at least semi-annual visits of highly experienced estate managers,accountants, agriculturists and engineers to each individual estate andfactory the purpose of which would be to review the operations of thepreceding six months, to compare performance with Board policy directivesand approved budgets, and to prepare proposals for future operations. TheInspection Service would also report on general standards of technical andfinancial management, and comment on draft annual budgets prior to theirapproval by the Board. The service would be directly responsible to thePNP Board and copies of its reports would be sent to the Minister of Agri-culture. During negotiations assurances were obtained from the Governmentthat an experienced plantation company or companies satisfactory to IDAwould be engaged by PNP IV and PNP VI for an initial period of about fiveyears to provide inspection services on terms and conditions satisfactoryto IDA; these appointments would be a condition of effectiveness of theproposed credit. Companies qualified to provide the necessary serviceswould need to have considerable first-hand experience of the developmentand management of rubber and oil palm plantations, including up-to-dateexperience of modern field and factory technology and of marketing. Theterms of reference of the inspection service would also provide for thein-service training of selected Indonesians who would subsequently assumethese duties, as well as for assistance to the PNP in the preparation oftender documents, and the analysis of bids, for goods and services to bepurchased under the project.

Management Advisers

5.09 PNP IV and PNP VI would each appoint a financial adviser for aninitial period of about two years. The adviser would assist and instructhis PNP in utilizing the mass of financial data that is now being producedand collated at all levels, but which is not being used for financial con-trol, and for making management decisions. The financial system now inuse was introduced by the former Dutch owners of the PNP but detailedanalysis of the material was carried out in the Netherlands; thus whilethe material is still being collected PNP financial personnel have inade-quate experience to make use of it. In addition, the adviser would reviewthe PNP financial management structure and assist in the revaluation ofassets necessitated by the severe inflation of past and recent years.

5.10 Each PNP would also engage for about a two year period an estatemanagement specialist to advise the General Manager in all aspects of estatemanagement, and an agricultural specialist to advise the Production Ma)sger,and train estate managers and field assistants in modern rubber and oil palmproduction practices. Close cooperation between advisers and Inspection

- 21 -

Service personnel would be essential, and for this reason assurances wereobtained from Government during negotiations that the companies providingthe Inspection Services would supply advisers under the same contract.

Accounts and Audit

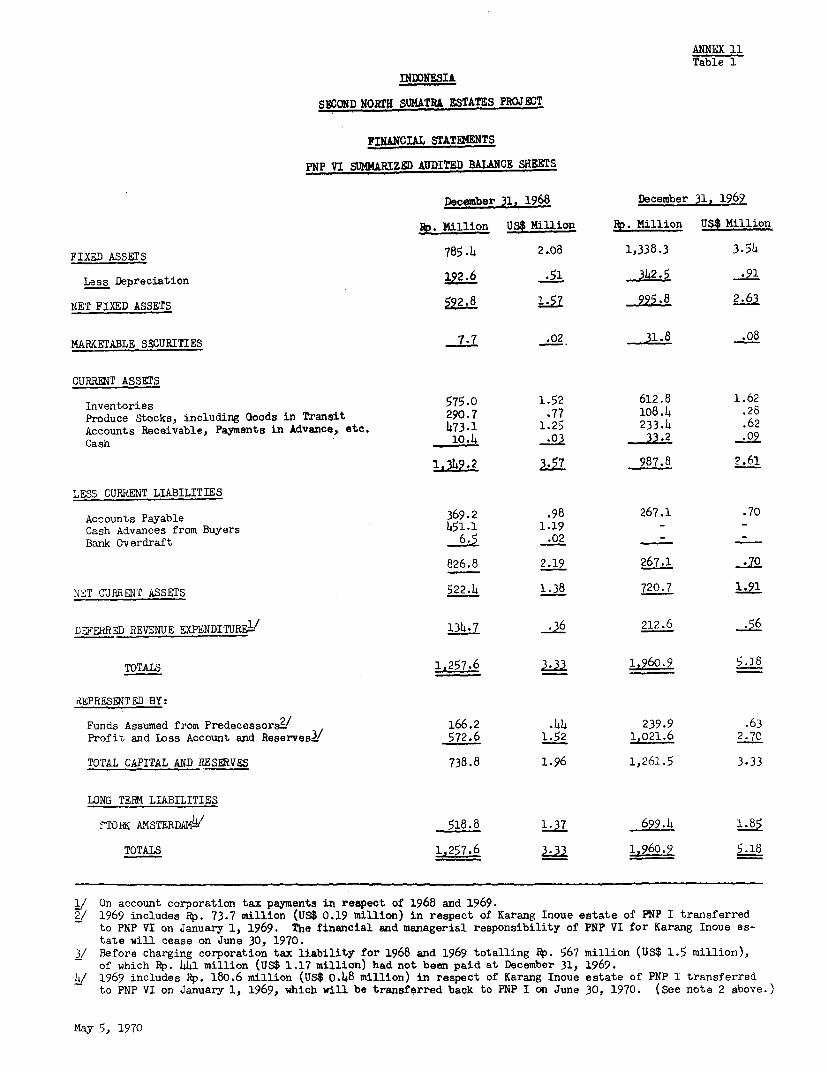

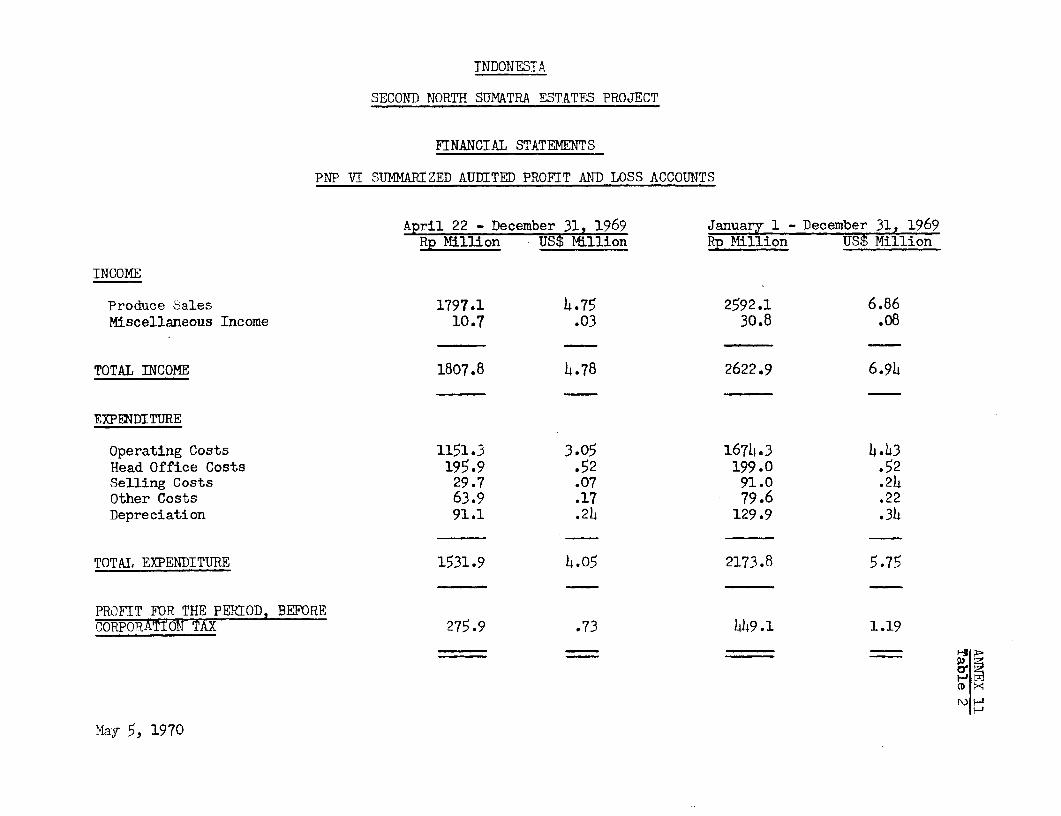

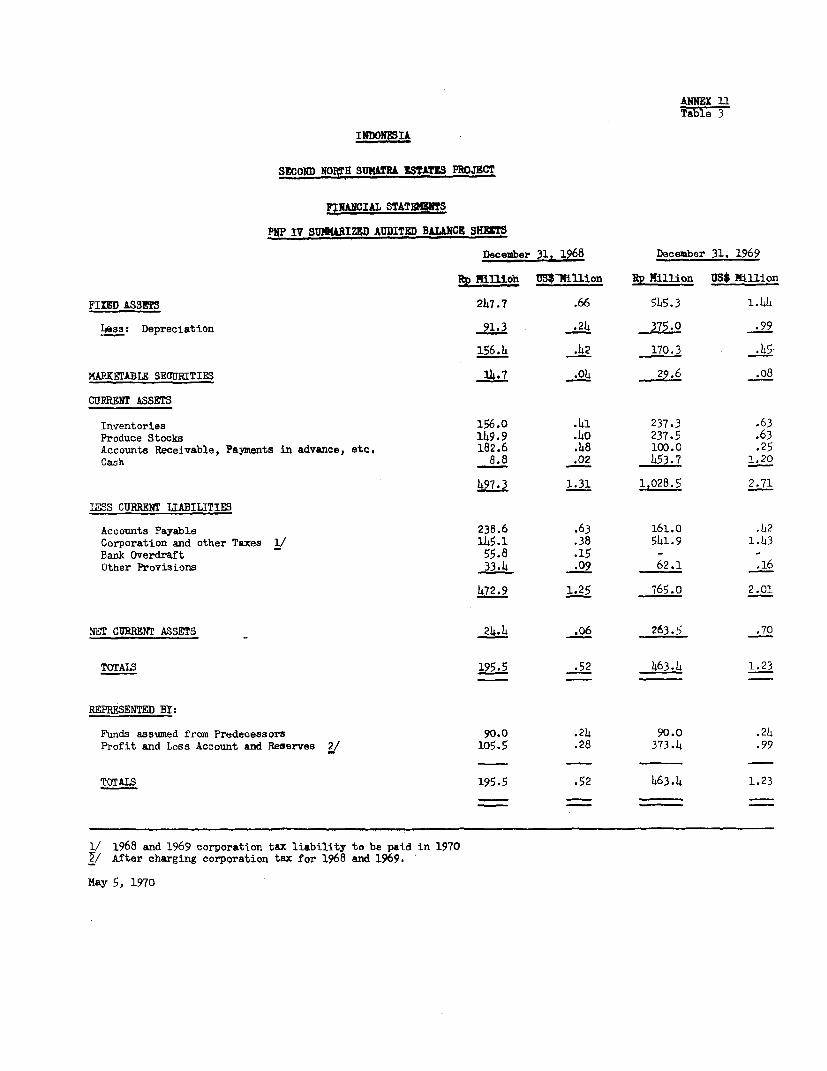

5.11 Audited accounts of PNP IV and PNP VI for the periods ended Decem-ber 31, 1968 and 1969 are summarized in Annex 11. Audits are now carriedout by Government auditors, but these arrangements are not considered satis-factory and thus assurances were obtained from the Government during negotia-tions that independent auditors satisfactory to IDA, as in the case of theFirst Estates Project, would be appointed to audit the accounts of PNP IVand PNP VI, and that audited accounts would be submitted to IDA within fourmonths of the close of the financial year.

Annual Budgets

5.12 Annual budgets prepared by PNP IV and PNP VI would incorporatethe comments of the Inspection Services and would be approved by the res-pective Boards. Approval by IDA of the planting program included in theannual budget, and of any material changes made subsequently is considereddesirable and during negotiations assurances to this effect were obtainedfrom the Government. Assurances were also obtained that annual budgetsand any material changes made subsequently, would be submitted to IDA forcomment not later than 30 days prior to their adoption.

VI. PRODUCTION MARKETING AND FINANCIAL RESULTS

A. Yields and Production

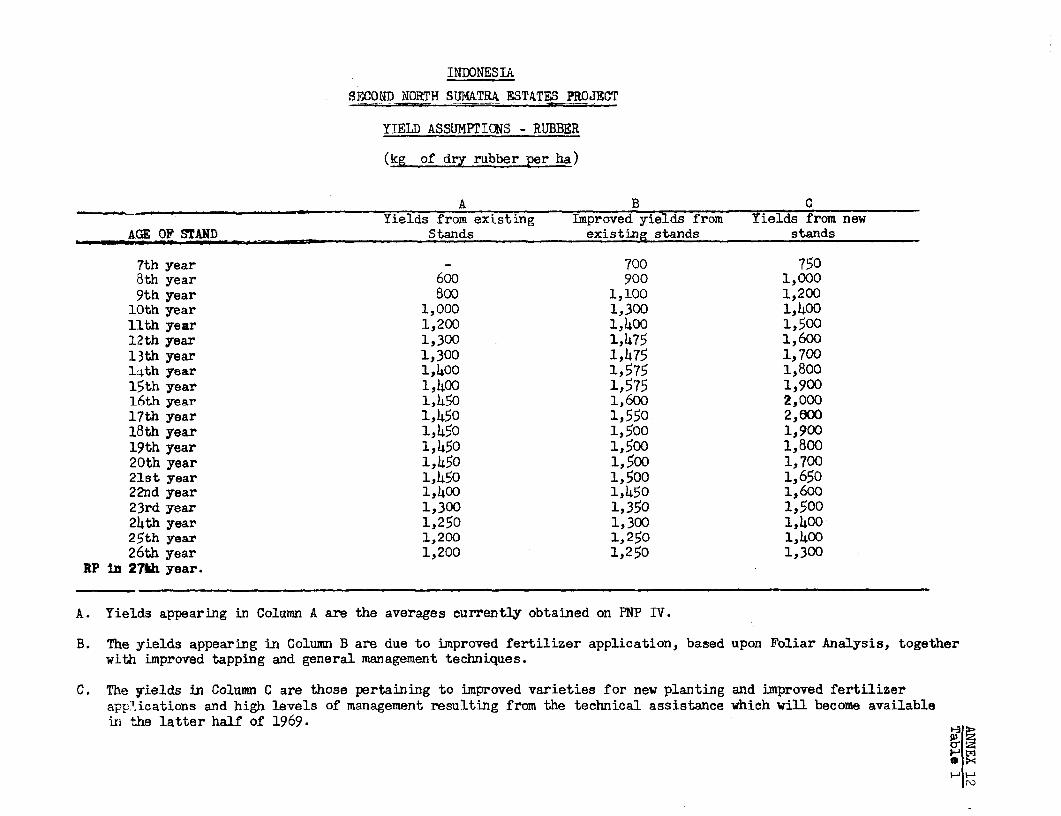

6.01 Growing conditions for rubber and oil palm in the project areamong the best in the world. Yield projections used for plantings underthe project for the period up to peak production are as follows:

Rubber ------------------- Ha------------------------

Year after planting: 7 8 9 10 11 12 13 14/16

Kg of dry rubber 750 1,000 1,200 1,400 1,500 1,600 1,700 1,800/2,000

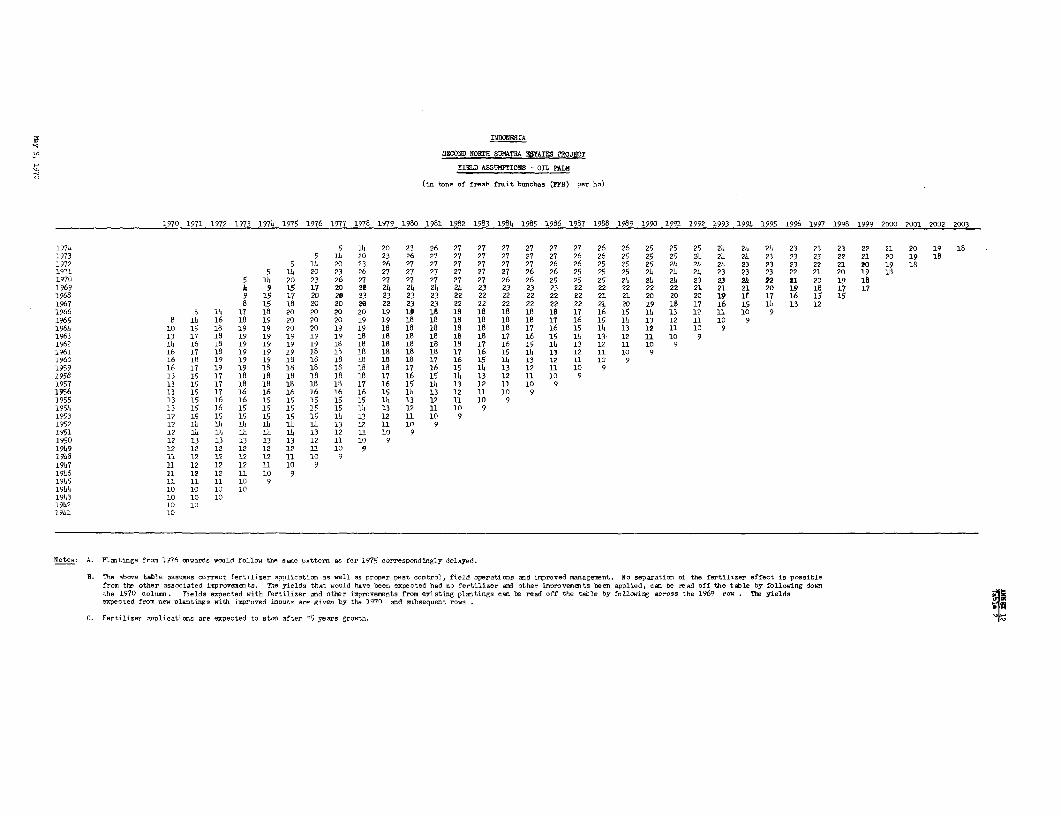

Oil Palm

Year after planting: 4 5 6 7 8 9

Tons of FFB 5 14 20 23 26 27

Oil extraction rate (x) 16 18 19 20 22 22

- 22 -

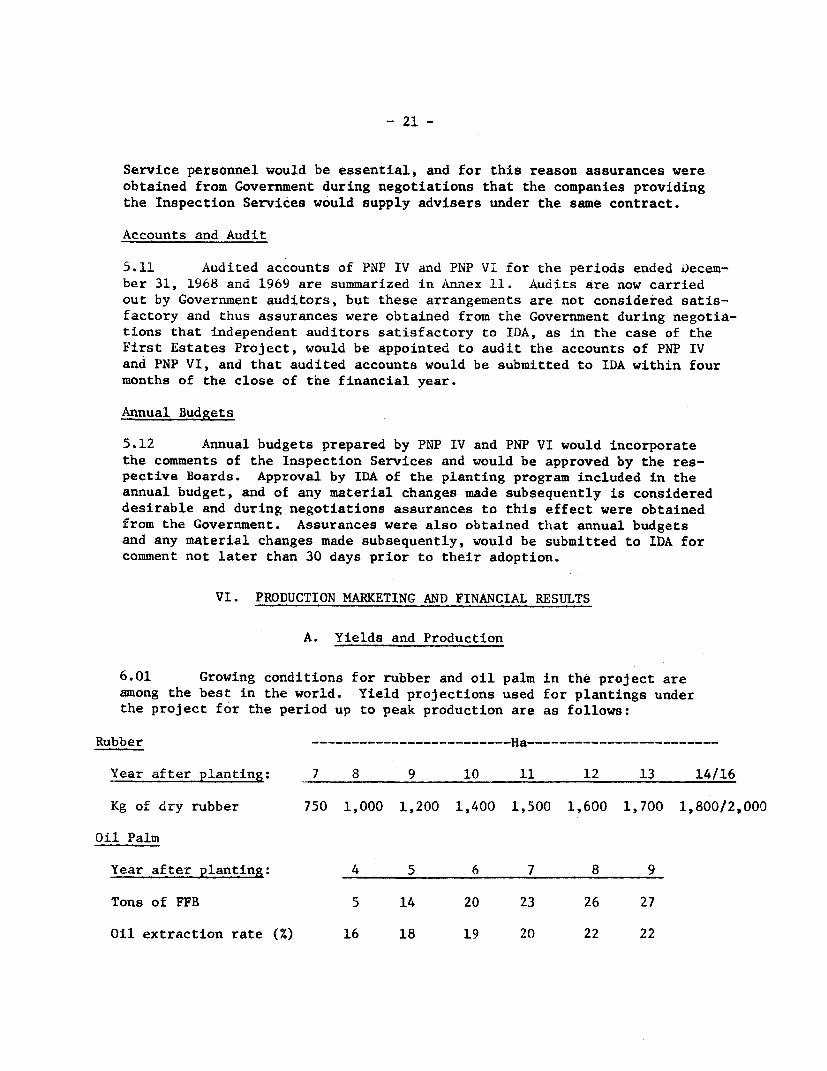

Further details are given in Annex 12 together with the expected decline inyields after the years of peak production, and incremental yields from exist-ing mature areas as a result of the fertilizer investment program. Theyields used in project estimates are similar to those obtained in Malaysiaon soils classed as of average suitability for oil palm and rubber, andunder average management efficiency. Climatic conditions of project estatesare similar to Malaysia, soils tend to be superior and under the project,management should be equivalent.

6.02 Total annual production of PNP IV is estimated to rise from approxi-mately 18,000 tons of rubber in 1969 to a peak of abut 47,000 tons in 1985.For PNP VI annual production is estimated to rise from about 56,500 tons ofpalm oil and 13,500 tons of palm kernels in 1969 to a peak of nearly 146,000tons of palm oil and 30,000 tons of palm kernels in 1979. Peak incrementalproduction amounts to some 29,000 tons of rubber, 89,500 tons of palm oiland 16,500 tons of kernels.

B. Marketing and Prices

Joint Marketing Office

6.03 The nine PNP's in Atjeh and North Sumatra (PNP's I through IX)sell all export produce through a Joint Marketing Office (JMO) with head-quarters in Medan. The JMO is headed by a Managing Director appointed bythe Minister of Agriculture and control is vested in a Joint Board ofDirectors in which each of the nine PNP's is represented by its FirstDirector or General Manager. Separate committees comprising the directorsdirectly concerned with the marketing of each crop meet every fortnightand establish the JMO policy for that crop.

6.04 Most of the major rubber buyers are represented directly, or byagents, in Medan, and much of the dry rubber for export is marketed by JMOunder a local auction system. Buyers of concentrated latex are limited andsales are usually made under negotiated forward contracts. Palm oil andpalm kernels are sold by a system of continuous worldwide offers and bidscarried out directly between the JMO and purchasers. PNP produce isexported to East and West Europe, Japan, Pakistan and the USA.

6.05 Except for PNP V and PNP VII, local sales of rubber are madedirectly by the PNP's without proper bidding procedures, which is unsatis-factory. Under the first North Sumatra Estate project (Credit 155-IND) theGovernment agreed that all PNP V and PNP VII rubber for local sale wouldbe handled by the JMO using its standard procedures. Local palm oil salesare satisfactorily handled by JMO, prices being determined on the basis ofaverage prices obtained for recent exports, and at present all palm kernelsare exported. During negotiations assurances were obtained from Governmentthat rubber, palm oil and palm kernels produced by PNP IV and PNP VI wouldbe marketed by the JMO using its standard procedures.

- 23 -

6.06 In 1960 a jointly-owned selling agency company (Indoham) wasformed in Hamburg between the Government and German commodity trading andbusiness interests to handle all PNP produce sold in Germany and much ofthe PNP production sold elsewhere in Europe. The company maintains con-tacts with European buyers, submits buyers' offers to JMO for approval,deals with documentation, payment procedures and claims, and supplies salesrecommendations, marketing advice and information to the JMO. The Boardof Directors consists of one resident Indonesian transferred from JMO, anda representative of the German shareholders. Indoham receives 1% of theFOB sales it handles from which is paid total operating costs, includingthe salaries and expenses of the directors and a small locally recruitedstaff; any profit remaining is paid to the German shareholders. The JMOhas no other overseas agents or representation.

6.07 The JMO needs restructuring to give the PNP's strong and reliablemarketing services. Coordination between the JMO and the individual PNP'sis often weak and greater autonomy and flexibility is required for JMOoperations. The first North Sumatra Estates Project provided technicalassistance for consultants to carry out with JMO's assistance, a marketsurvey for oil palm and rubber products and to recommend the marketingmethods to be adopted; and consultants to advise the Managing Director onJMO's internal organization and procedures. The JMO would also retainmarketing consultants to give marketing advice as and when required. Invi-tations will shortly be circulated to a selected list of consultants. Theconsultants finally appointed and the terms and conditions of appointmentmust be satisfactory to IDA in accordance with assurances received underCredit 155-IND.

Market Prospects - Oil Palm Products

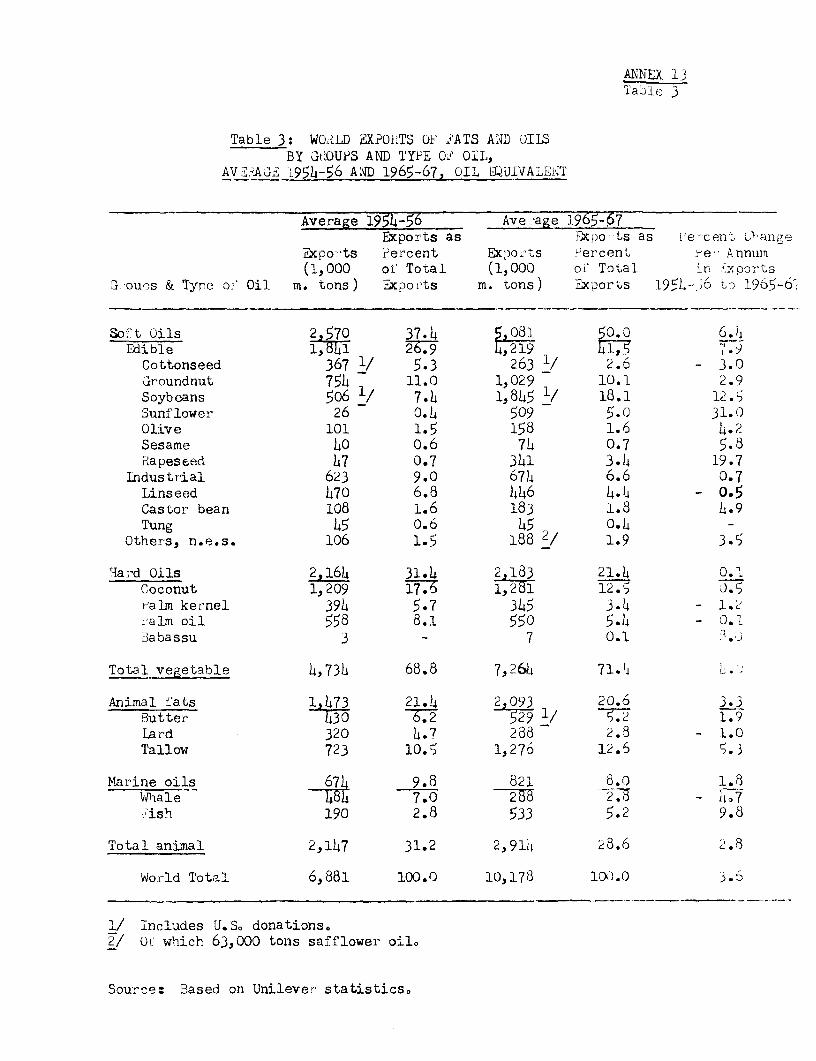

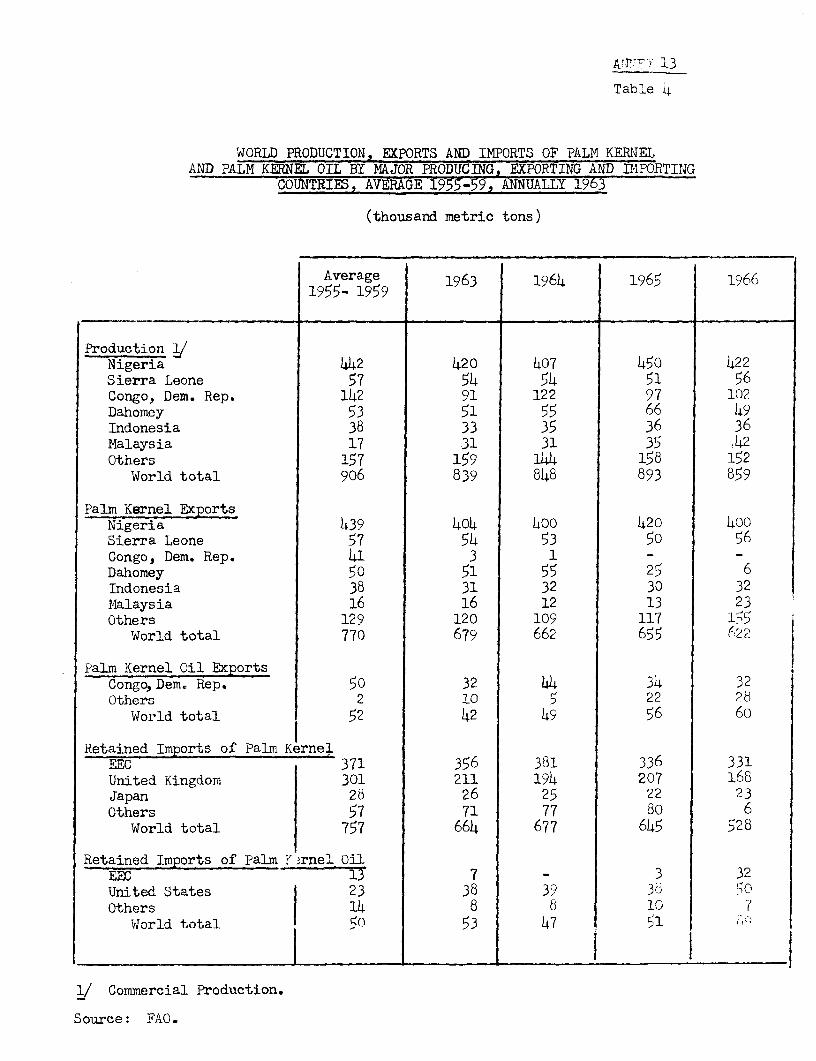

6.08 Current production of palm oil in Indonesia is about 175,000 tonsper annum of which more than 80% is exported, the remainder being used bylocal soap manufacturers. In addition to an increase in soap consumptionit is expected that demand for palm oil as an edible fat, in substitutionfor decreasing coconut oil supplies, will increase considerably as thereare no alternative local sources of edible oil other than palm oil. Assum-ing a continued population growth of 2.4% per annum, that annual per capitaconsumption of edible fats and oils remains at about 4 kg and that coconutoil cannot supply the increased demand, local sales of palm oil for ediblepurposes could increase to some 150,000 tons by 1980 plus approximately50,000 tons for soap manufacture, a total of 200,000 tons. By 1980 projectproduction would be approximately 146,000 tons and total Indonesian produc-tion might be in the region of about 400,000 tons. Under these assumptionsexports would therefore increase from their present level of 150,000 tonsto some 200,000 tons. While this is necessarily a somewhat speculativeprojection, it does indicate that oil palm development under this projectis unlikely to significantly affect world trade patterns in the long term.

- 24 -

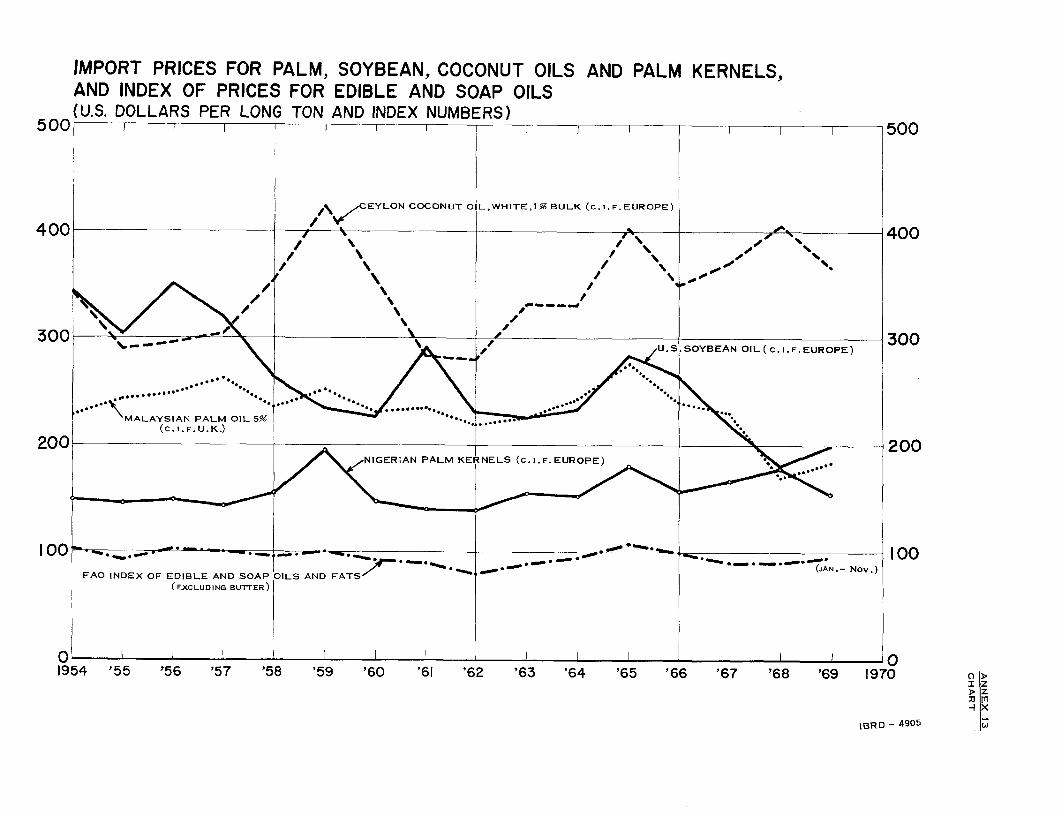

6.09 Annex 13 examines market prospects for palm oil and kernels onthe world market. Until recently the growth rate in the supply of palmoil was low compared with other fats and oil amounting to only 1.3% duringthe 14 year period to 1967. New plantings, particularly in Malaysia, areexpected to increase the annual growth rate to more than 5% by 1970 andto raise the share of palm oil production in total fats and oils fromabout 3% in 1965/67 to 5% by 1980. Much of the additional world suppliesof palm oil will be exported and absorbed by the international market. Al-lowing for an expected decline in world market prices for nearly all majorfats and oils, and the need for palm oil to increase its share of totalusage, it is estimated that palm oil prices will fall by the mid-1970'sfrom the average 1969 price of US$181 cif per ton into a price range ofUS$155 - US$165 per ton cif; palm kernels are expected to range betweenUS$135 - US$138 per ton cif compared with an average price for 1969 ofUS$153 per ton cif. For the purpose of making economic and financialprojections in this report cif prices of palm oil are assumed to beUS$160 per ton and for palm kernels US$136 per ton.

Market Prospects - Rubber

6.10 Indonesia exports most of its rubber and will continue to do sofor the foreseeable future. Over the last 20 years annual net exports ofrubber from Indonesia have been fairly constant at nearly 700,000 tons butduring the same period world production has risen by more than 30% andIndonesia's share has fallen from 41% to 29%.

6.11 The market prospects and price trends for rubber are reviewedin Annex 14. During the years to 1975 consumption of both natural andsynthetic rubber in non-Centrally Planned countries is estimated to in-crease at 6.5% per annum compared with a rate of 6% per annum during thepast 20 years. Prices for natural rubber must become more competitive withprices of synthetic rubber if natural rubber is to retain its share of themarket. Polyisoprene, a synthetic rubber which is highly competitive withnatural rubber, costs about 21 US cents per lb to produce. A technicalbreakthrough which would reduce production costs is a possibility whichcannot be ignored, and the projected prices for natural rubber used inthis report allow for some reduction in the production costs of syntheticrubber. Consequently, it is assumed that the price of natural rubber wouldfall from an average price of 26.2 cents per lb in 1969, to an average ofabout 20 US cents per lb for 1970 to about 16 US cents per lb by 1975 andin subsequent years, as shown below:

1970 1971 1972 1973 1974 1975 onwards

US cents per lb cif New York 20 19 19 18 17 16

- 25 -

C. Financial Aspects

PNP IV

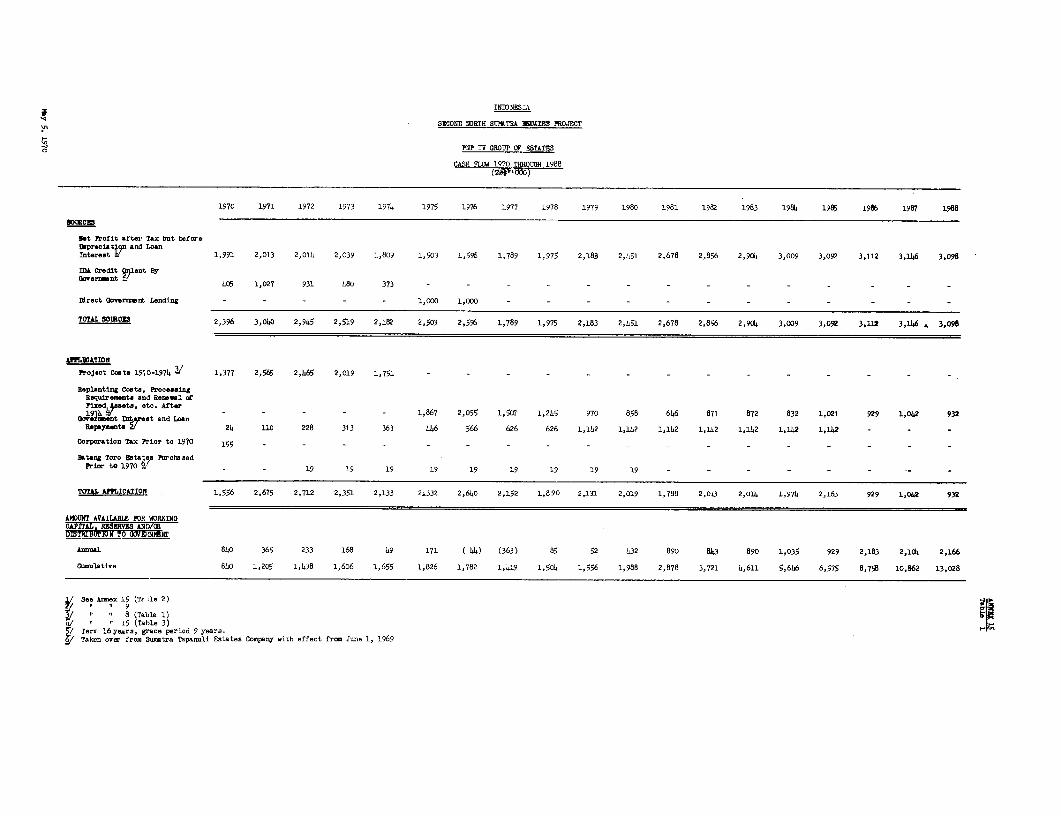

6.12 PNP IV would obtain a loan from Government of about US$5.2 million(of which proceeds of the IDA credit on-lent by Government would be US$3.2million) during the period 1970 through 1976; this would be adequate tocomplete the investment program described in paras. 4.01 and 4.02. There-after, self-generated funds would be sufficient to meet all operating costs,planting and other investment requirements and debt service, even if thepresent high rates of export duty and corporation tax continue. From 1980onwards up to US$1.0 million annually would be available for distributionto Government which would be increased to about US$2.0 million annuallyafter completion of debt service in 1985.

PNP VI

6.13 PNP VI would require a Government loan of about US$14.2 million(of which proceeds of the IDA credit on-lent by Government would be US$13.2million) during the project period 1970 through 1974. Self-generated fundsthereafter would be adequate to cover all operating costs, other invest-ment requirements and repayment of the Government loan which would commencein 1975. From 1976 onwards, an average US$2.0 million annually would beavailable for distribution to Government and this would increase to approxi-mately US$4.0 million annually in 1983 when debt service is completed.

6.14 PNP IV and PNP VI projected cash flows, operating statements, andreplanting costs and other capital expenditure after the project is completedare detailed in Annex 15. The Government onlending terms for PNP IV - 16years with a 9-year grace period - are softer than those for PNP VI, 13 years,including a grace period of 5 years. The terms of these sub-loans are largelydetermined by the draw-down periods, and the capacity of each PNP to meetloan interest and repayments. PNP IV requires loan funds from Governmentfrom 1970 through 1976, two years more than PNP VI, due to the replantingbacklog and other project requirements. During the first 10 years of theproject, immature areas of PNP IV would average more than 30% of the totalplanted area, compared with only 10% for PNP VI, which restricts self-generated funds and requires an extension of the Government loan repaymentand grace periods.

6.15 Annual financial rates of return on capital employed cannot becalculated for the PNPs as the real value of assets employed is not knowndue to the heavy inflation experienced in Indonesia in recent years. Arevaluation of assets would be undertaken as part of the project (see para.5.09). Calculation of the incremental financial rate of return to thePNPs from the project would have little value since it is not possible topredict, without wide margins of error, the financial performance of thetwo PNPs without the project. The financial rates of return to the Govern-ment, as the sole owner of the PNPs, from project activities would besimilar to the economic rates of return shown at para. 7.03.

- 26 -

Government

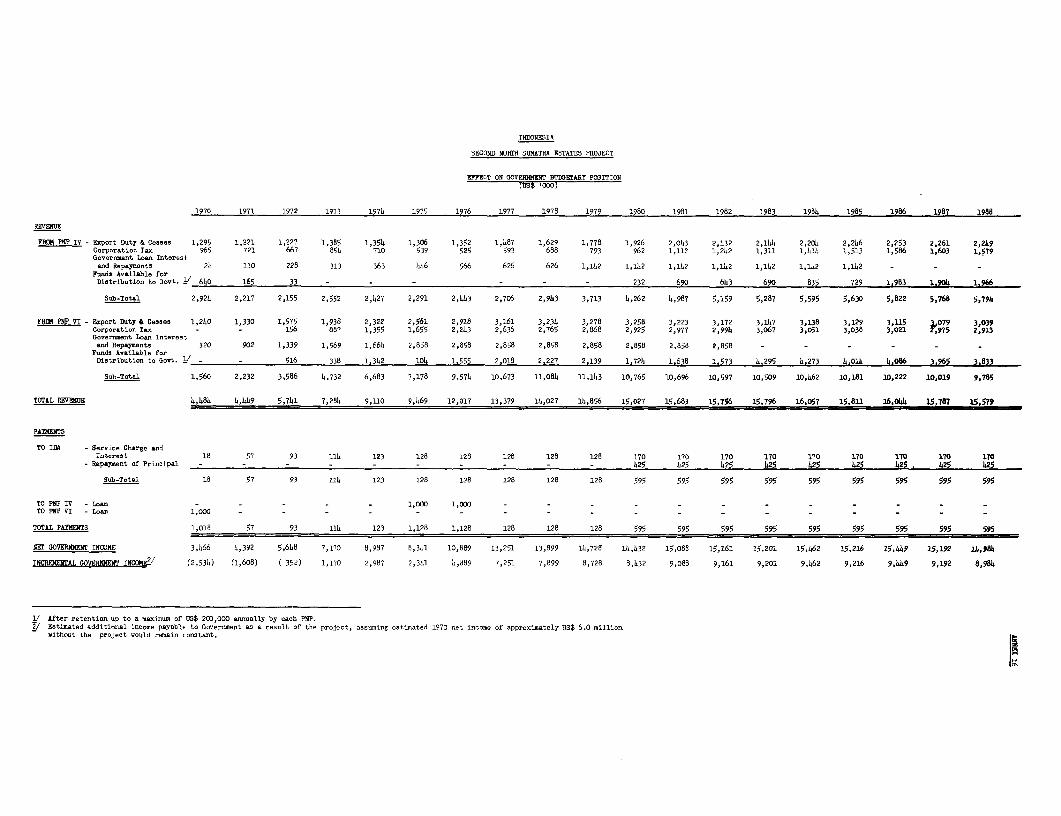

6.16 Annex 16 shows the effect of the PNP IV and PNP VI sub-projectson the Government's budgetary position and assumes that present rates ofexport duty and corporation tax would continue. Import duties and personaltaxation, however, are excluded. Throughout the project life both PNPswould provide a net source of income to the Government since, despite theneed for direct Government loans totalling US$3.0 million during the period1970 through 1976, these would be more than offset by tax revenues. Theestimated additional net income accruing to Government, assuming that thenet income expected in 1970 without the project remains constant, wouldrise from more than US$1.0 million in 1973 to about US$9 million annuallyfrom 1981 onwards. During the life of the project additional net incomeaccruing to Government is estimated at about US$175 million.

VII. BENEFITS AND JUSTIFICATION

7.01 The principal benefits of the project are:

- increased net foreign exchange earnings, rising froma current US$16 million per annum to about US$30 mil-lion by 1981. Insofar as this latter figure may notfully represent exports because of increased localconsumption of palm oil, it would represent foreignexchange savings from import substitution;

- increased budgetary support to the Government, risingfrom a current US$6.0 million per annum to about US$15.0million by 1981;

- improved management arrangements for two Govetnment-owned estate groups;

- maintenance of job opportunities at adequate wage ratesfor some 20,000 workers;

- improved research support both for the estate industryand for small farmers growing export crops; and

- a general improvement in the estate industry which couldhelp to stimulate new investment and reinvestment bythe private sector.

7.02 The project comprises a number of separate programs which aredistinct in terms of costs and benefits. Consequently, individual econemicrates of return have been calculated for each of these rather than anoverall rate of return for the project as a whole, or global rates ofreturn for each of the PNPs. Project benefits accrue both from new invest-ment and past investment which are considered sunk, such as estate infra-

- 27 -

structure and processing facilities. Sunk costs have not been taken intoaccount in calculating rates of return, but the costs of rehabilitating,replacing, and expanding estate infrastructure and processing facilitieshave been apportioned to the individual programs in accordance with theirrequirements.

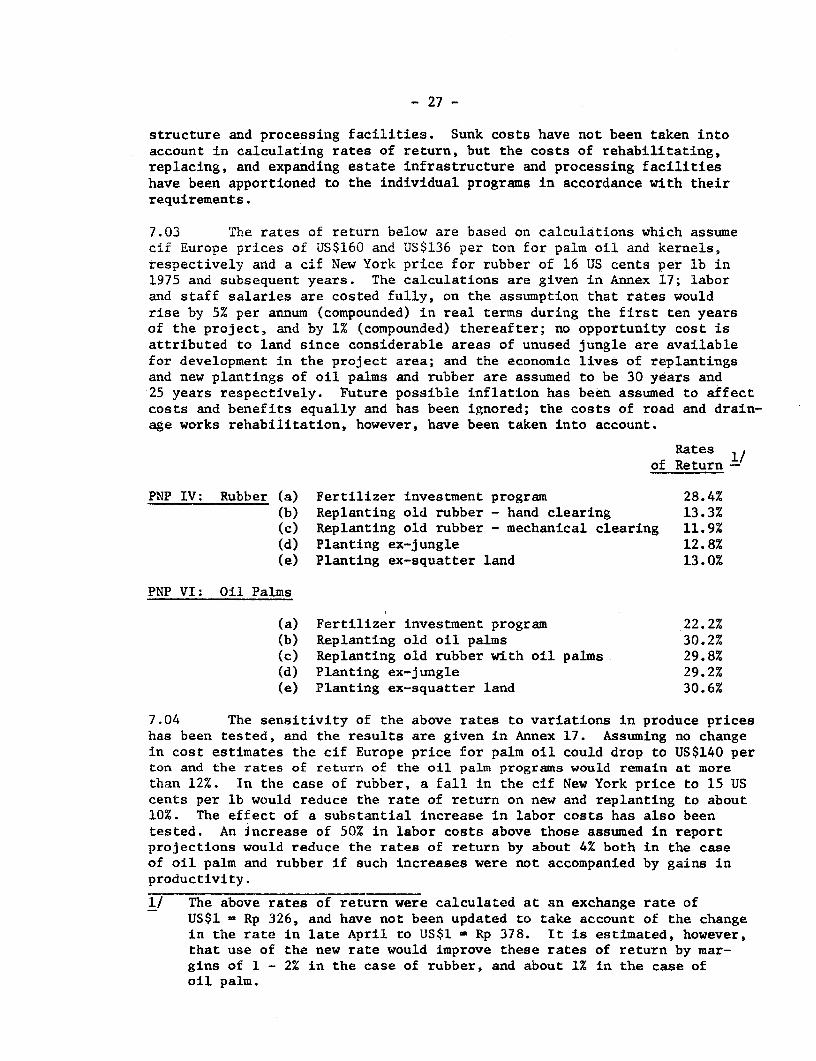

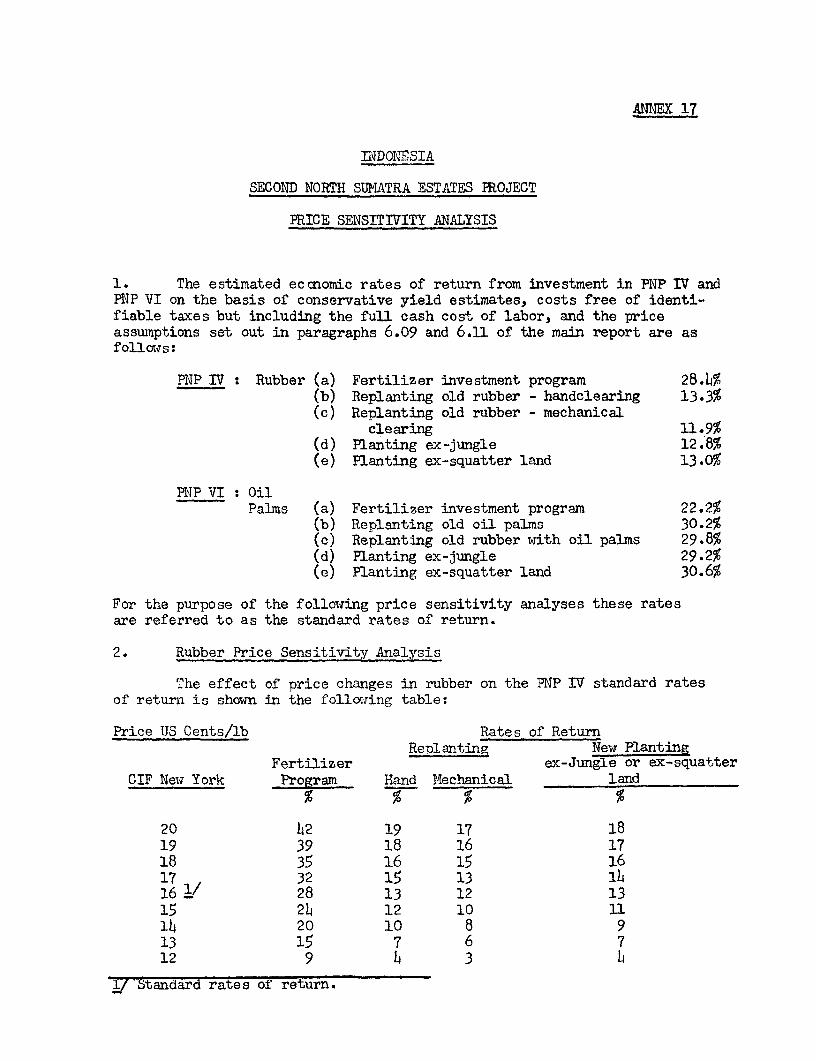

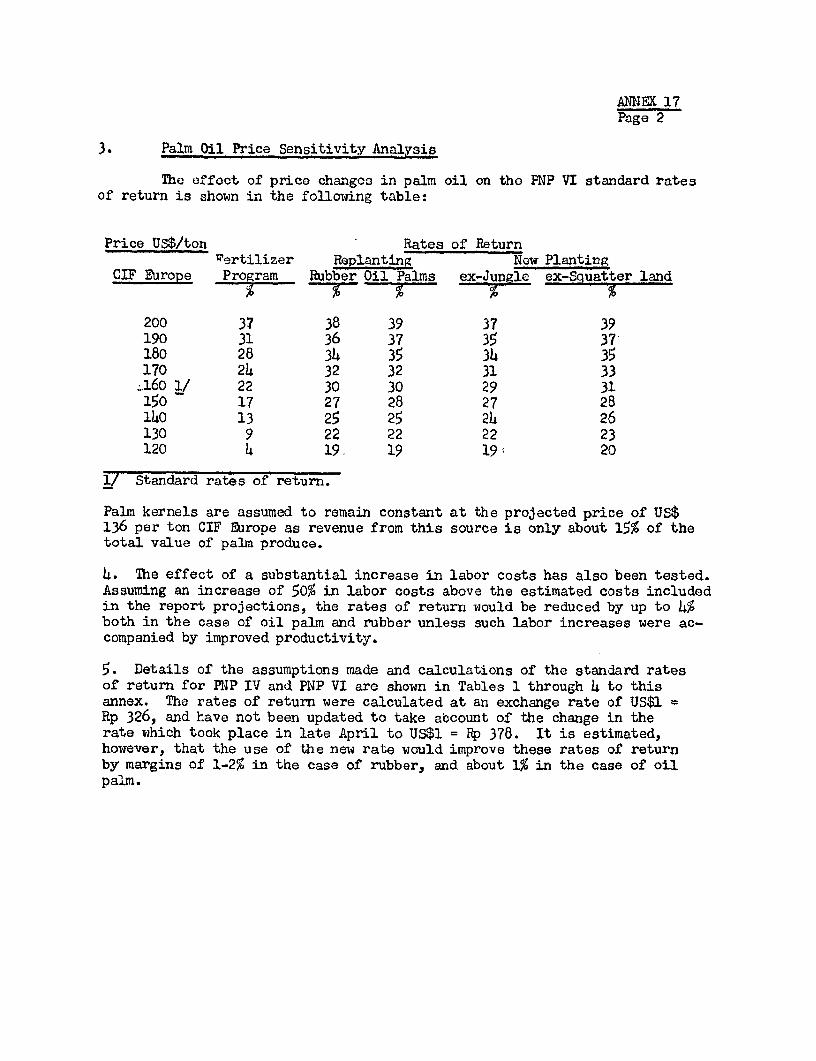

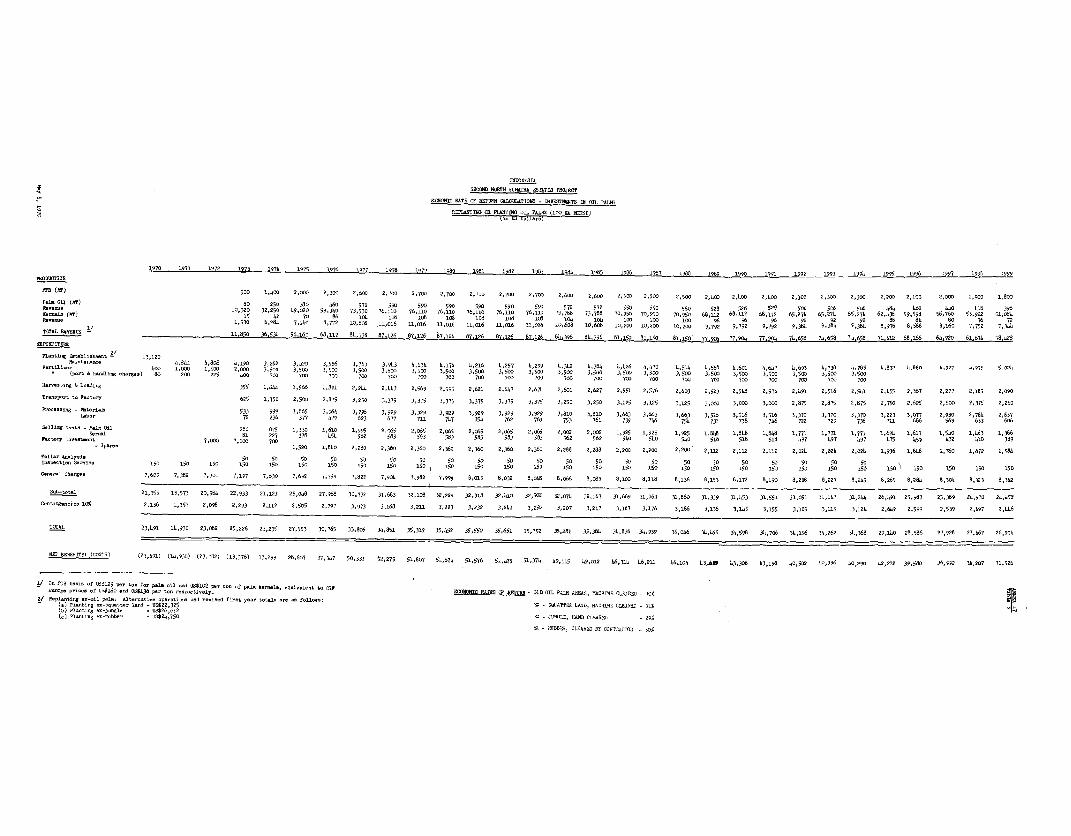

7.03 The rates of return below are based on calculations which assumecif Europe prices of US$160 and US$136 per ton for palm oil and kernels,respectively and a cif New York price for rubber of 16 US cents per lb in1975 and subsequent years. The calculations are given in Annex 17; laborand staff salaries are costed fully, on the assumption that rates wouldrise by 5% per annum (compounded) in real terms during the first ten yearsof the project, and by 1% (compounded) thereafter; no opportunity cost isattributed to land since considerable areas of unused jungle are availablefor development in the project area; and the economic lives of replantingsand new plantings of oil palms and rubber are assumed to be 30 years and25 years respectively. Future possible inflation has been assumed to affectcosts and benefits equally and has been ignored; the costs of road and drain-age works rehabilitation, however, have been taken into account.

Rates 1/of Return -

PNP IV: Rubber (a) Fertilizer investment program 28.4%(b) Replanting old rubber - hand clearing 13.3%(c) Replanting old rubber - mechanical clearing 11.9%(d) Planting ex-jungle 12.8%(e) Planting ex-squatter land 13.0%

PNP VI: Oil Palms

(a) Fertilizer investment program 22.2%(b) Replanting old oil palms 30.2%(c) Replanting old rubber with oil palms 29.8%(d) Planting ex-jungle 29.2%(e) Planting ex-squatter land 30.6%

7.04 The sensitivity of the above rates to variations in produce priceshas been tested, and the results are given in Annex 17. Assuming no changein cost estimates the cif Europe price for palm oil could drop to US$140 perton and the rates of return of the oil palm programs would remain at morethan 12%. In the case of rubber, a fall in the cif New York price to 15 UScents per lb would reduce the rate of return on new and replanting to about10%. The effect of a substantial increase in labor costs has also beentested. An increase of 50% in labor costs above those assumed in reportprojections would reduce the rates of return by about 4% both in the caseof oil palm and rubber if such increases were not accompanied by gains inproductivity.

1/ The above rates of return were calculated at an exchange rate ofUS$1 - Rp 326, and have not been updated to take account of the changein the rate in late April to US$1 - Rp 378. It is estimated, however,that use of the new rate would improve these rates of return by mar-gins of 1 - 2% in the case of rubber, and about 1% in the case ofoil palm.

- 28 -

VIII. RECOMMENDATIONS

8.01 The assurances obtained during negotiations included:

(i) The mangerial and financial responsibility of PNP VIfor Karang Inoue estate of the PNP I group of estateswould be terminated (para. 3.01);

(ii) arrangements would be made by Government for the removalof illegal squatters from project estates in accordancewith the agreed planting program (para. 4.13);

(iii) consultants satisfactory to IDA would be employed by theGovernment and RISPA on terms and conditions satisfactoryto IDA to carry out preparation of a research and develop-ment program for RISPA, and the consultants findings andrecommendations would be promptly submitted to IDA in orderthat agreement can be reached on their implementation (para.4.23);