e-banking an introduction

TRANSCRIPT

Report of FIN-5213: E-Commerce & E-Banking

Report On

E-B

an

kin

g: A

n In

trodu

ction

Sk. Alamgir Hossain

Lecturer

Department of Finance

Faculty of Business Studies

Jagannath University, Dhaka

Md. Mehedi Hassan

Representative of the group

Green Wave

MBA 3rd Batch

Department of Finance

Faculty of Business Studies

Jagannath University, Dhaka.

Submitted By

Submitted To

Green Wave

Group Name: Green Wave

Sl. no Name ID

1 Md. Mehedi Hassan M120203044

2 Sharjil Ahmed M120203067

3 Proyiva Talukder M120203055

4 Mohammad Didarul Islam Khan M120203087

5 Mamunur Rashid M120203079

6 Md. Rashedul Islam M120203045

Group Representative: Md. Mehedi Hassan

November 07, 2014

Sk. Alamgir Hossain

Lecturer

Department of Finance

Jagannath University, Dhaka.

Sub: Thanks giving letter to the respective faculty member.

Sir,

We are the student of Department of Finance (3rd batch) of Jagannath University, Dhaka &

also from the group named “Green Wave”. We are very much enthusiastic about our

presentation. We are really happy to have such a presentation of challenging and interesting

like this presentation & also thanks to you for making us worthy for corporate. Our topic is

“E-Banking: An Introduction”. We have learned many things from this topic which will help

us in future to conduct well ethical practices. There were some obstacles we have faced at the

time of collecting information about our topic. But we have overcome all the obstacles by the

endeavor effort by each member of our group and tried our best to give an overview of our

topic.

We the group “Green Wave” tried our best to make this term paper impeccable, interesting,

informative and enjoyable by the help of electronic and print media in association with our

honorable teacher, mentor, counselor, instructor and advocate “Sk. Alamgir Hossain”. We are

really grateful to him. We had limitations at the time preparing presentation. So mistakes may

occur in our demonstration of our presentation. We hope that, you will exempt our mistakes.

Thanking in anticipation,

Yours Fidel,

Md. Mehedi Hassan

Group Representative,

Group-“Green Wave”

MBA 3rd Batch

Department of Finance

Jagannath University,Dhaka.

First of all we would like to thank the Almighty for giving us the strength, and the aptitude to

complete this report within due time. We are deeply indebted to our course teacher, mentor,

and counselor, Sk. Alamgir Hossain for assigning us such an interesting topic named “E-

Banking: An Introduction”. We also express the depth of my appreciation to our honorable

course teacher for his suggestion and guidelines, which helped us in completing this term

paper.

The present age is the age of information technology. Each and every sectors of this world is

now based on information technology. The banking sector is now fully dependent on

information technology. With the help of information technology bank has introduced e

banking and internet banking. Almost all the banks of the world are now continuing their

banking activities with the help of information technology. From account opening to account

closing, deposit to withdrawal, fund transfer to fund collection, customer services,

information services, security etc. are now done by e banking and internet banking. One can

easily get all the banking services not going to bank. Banks have a wide connection with

other banks in the world. So any kind of banking services is quickly received by the clients.

The banks are providing the facilities of ATMs almost every areas, providing virtual money

services with smarts card like debit card , credit cards etc. the cost of banking has been

reduced and the security has been upgraded due to modern technology. Now a person can

have the access with a bank by his personal computer or mobile from every corner of the

world.

Those days are not far away when we will get all the charm of E commerce. To ensure this

we need Bangladesh Telecommunications Regulatory Commission (BTRC) should be

established independently out of the government control. Moreover, VOIP gateway should be

allowed and political commitment to establishment is needed. Beside all of this both of

Ministry of Commerce & Ministry of Science and Information & Communication

Technology should update the act & article regarding to e-commerce in accordance with

global market to put a significant footsteps in the world economy.

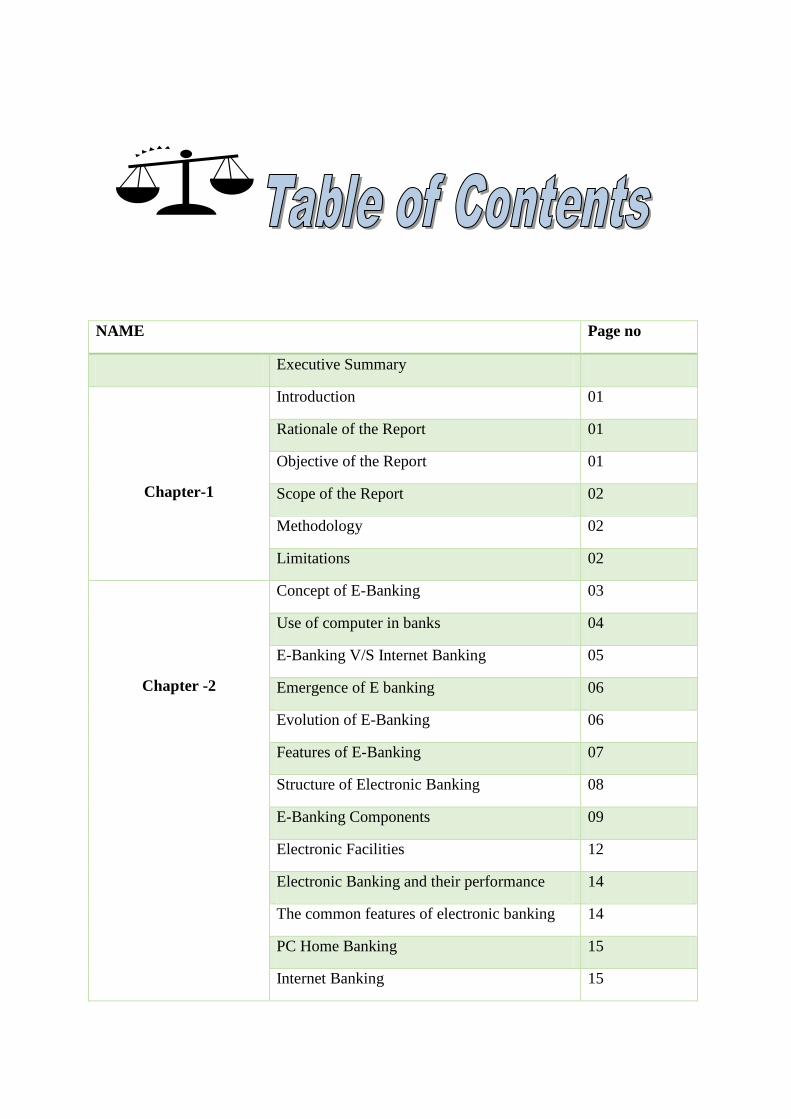

NAME Page no

Executive Summary

Chapter-1

Introduction 01

Rationale of the Report 01

Objective of the Report 01

Scope of the Report 02

Methodology 02

Limitations 02

Chapter -2

Concept of E-Banking 03

Use of computer in banks 04

E-Banking V/S Internet Banking 05

Emergence of E banking 06

Evolution of E-Banking 06

Features of E-Banking 07

Structure of Electronic Banking 08

E-Banking Components 09

Electronic Facilities 12

Electronic Banking and their performance 14

The common features of electronic banking 14

PC Home Banking 15

Internet Banking 15

Factors That Drive Bank’s Strategy 16

Types of Internet Banking 17

Internet Banking Risks 18

E-Banking and its Challenges 21

Chapter -3 Findings of the Report 23

Reference 23

Chapter- 01

Introduction

E-banking is defined as the automated delivery of new and traditional banking products and

services directly to customers through electronic, interactive communication channels. E-

banking includes the systems that enable financial institution customers, individuals or

businesses, to access accounts, transact business, or obtain information on financial products

and services through a public or private network, including the Internet. Customers access e-

banking services using an intelligent electronic device, such as a personal computer (PC),

personal digital assistant (PDA), automated teller machine (ATM), kiosk, or Touch Tone

telephone. While the risks and controls are similar for the various e-banking access channels,

this booklet focuses specifically on Internet-based services due to the Internet's widely

accessible public network. Accordingly, this booklet begins with a discussion of the two

primary types of Internet websites: informational and transactional.

In this term paper we tried to show how E-Banking conduct their operation & understand it.

Rationale of Report

The term paper is assigned by our honorable teacher Sk. Alamgir Hossain as a part of our “E

Commerce & E-Banking” course. The topic of this paper is “E-Banking: An Introduction”.

By conducting this report we can enrich our knowledge regarding E-Banking and make

ourselves proficient in both our professional life as well as higher educational life. The paper

has given us a chance to raise our proficiency in E-Banking. By doing so, we can boost

our acceptability in job market and develop our real life knowledge.

Objective of the Report

Primary objective

The main objective of the report is to know about E-Banking business procedure in

Bangladesh.

Secondary objective:

The report has some following objectives:-

Business types of E-Banking and relationship with the customers and clients involved.

International method of payment & local payment.

Risk & overcome to E-Banking.

Support from related parties to establish E-Banking in Bangladesh.

Scope

There were huge scopes to work in the area of this Report. Considering the dead line, and

exposure of the paper has been wide-ranging. The report “E-Banking: An Introduction” has

covered details scenario of E-banking market in the world. Beside this it has covered

operations of E-banking, procedure, support form parties, & future of its in Bangladesh. It

deals E-market scenario of Bangladesh. By preparing this report, we have got a chance to

work on modern & high tech upcoming banking era

Methodology

We have used the concept of the course, information of several banking corporations

who operate e-banking in Bangladesh from their own website and regulation, act &

other different legal information is being gathered from Bangladesh Bank

Sources of Data

Here the secondary sources of information were used. The secondary sources are:

Website of Ministry of Commerce & Ministry of Science and Information &

Communication Technology.

Websites of different e-commerce website like Amazon.com, eBay, etc.

Limitations

Although it has been tried on the level best to make this report based on facts and complete

information available, there are some limitations that are inevitable. They are following:

Deficiencies in data required for the report.

There were some restrictions to have access to the information confidential by

concern authority.

The time which we got was not enough to gather practical knowledge and prepare a

report on a topic like this one. As the tenure of the report preparation was limited, it

was not possible to highlight everything deeply

Inaccurate or contradictory information.

Too much sensitive information for any organization.

Sufficient records, publications

Chapter- 02

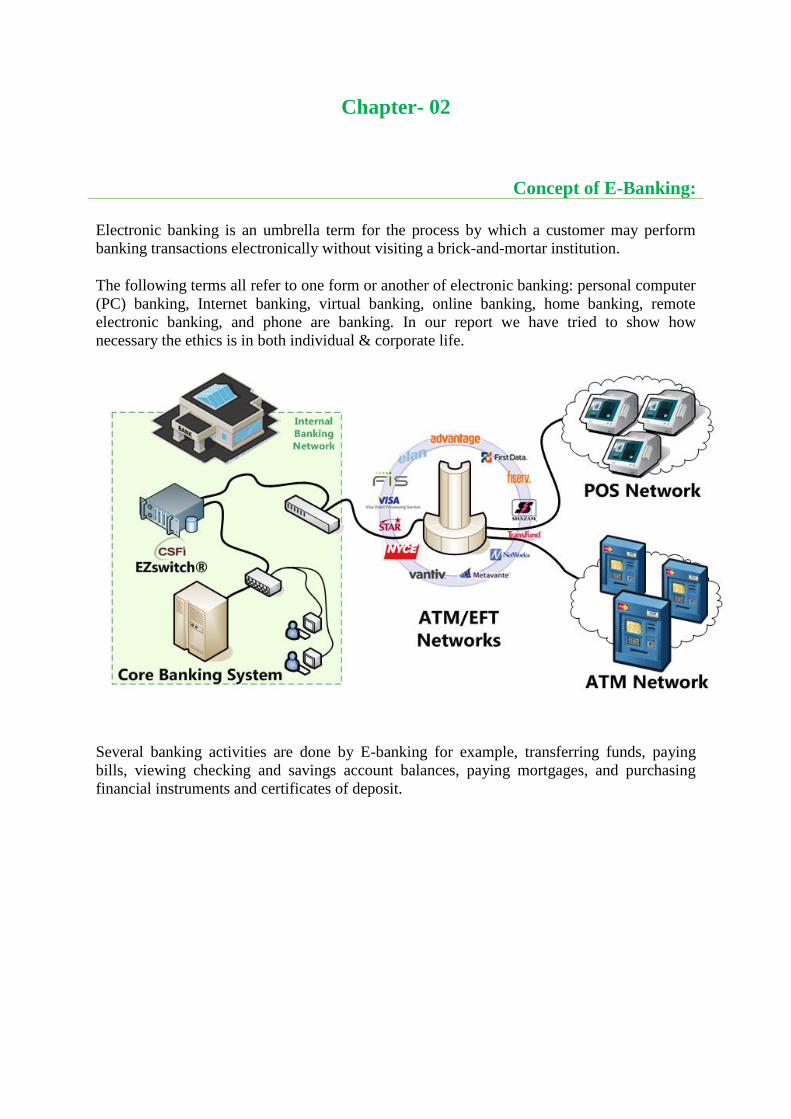

Concept of E-Banking:

Electronic banking is an umbrella term for the process by which a customer may perform

banking transactions electronically without visiting a brick-and-mortar institution.

The following terms all refer to one form or another of electronic banking: personal computer

(PC) banking, Internet banking, virtual banking, online banking, home banking, remote

electronic banking, and phone are banking. In our report we have tried to show how

necessary the ethics is in both individual & corporate life.

Several banking activities are done by E-banking for example, transferring funds, paying

bills, viewing checking and savings account balances, paying mortgages, and purchasing

financial instruments and certificates of deposit.

Use of Computer in Banks

Computer is a blessing for the modern business world specially in banking business. Almost

all the banks in the world use computers in their daily functions.

Account Management

In banking, activities start with banks automating customer accounts, which allows personnel

to create, update and maintain customer records. Banking hardware and software have

enhanced the accuracy of accounts that tellers and other banking personnel process. Banking

software performs customer transactions through a centralized data record system. Account

management is the genesis and backbone of all banking information systems.

Hardware Technology

In the 1960s, bank hardware consisted of a mainframe and a punch card machine. Punch

cards contained customer account information and were read into the main system by a punch

card machine. Midrange and client/server hardware configurations, which are no larger than a

minitower system, can run an entire bank in addition to receiving transactions from affiliated

bank branches. These new hardware technologies can process more transactions than legacy

banking hardware systems. Hardware technologies have enabled advances into wireless

banking and telecommunications banking.

Electronic Transactions

Banking systems must perform electronic transactions. Direct deposit is an example of an

electronic transaction. Computers processing electronic transactions must have hardware and

software encryption capabilities to keep data from being compromised during a transmission.

After the computer performs electronic transmissions, it transfer the information to the main

computer system for processing and updating. Banks have extended electronic transaction

capabilities through landline and cell phones, the Internet and ATMs.

Web-based Banking

Web-based banking systems use a dedicated server through a bank network system. An area

of the banking system is partitioned for Internet applications. Web-based banking systems by

law must include secure servers and authenticated certificates regarding transactions from the

Federal Deposit Insurance Company and the Federal Reserve Board. Customers who choose

to bank online can access their account through a web interface, which integrates with the

main computer. A customer's credentials -- user ID and password -- pass through several

checkpoints before entering the main system to perform a web-based transaction.

E-Banking V/S Internet Banking

The advent of internet has not been beneficial for just getting loads of information; it has

helped enormously in making life easier in all walks of life. One such industry that has

benefited enormously is banking. Internet banking has made lives easier for not only banks; it

has made possible for customers to access their bank accounts without having to go

physically to their banks. Internet banking is also referred to as online banking or e-banking.

A person with a PC and internet connection can log onto his bank account and make

payments or conduct other financial transactions easily and quickly thus saving a lot of time

and money.

For customers, online banking and e-banking have brought a lot of convenience in their wake

but for banks, they are much more than that. Banks switching to online banking have

experienced reduction in operational costs. Earlier customers had to come physically even to

know their account balances and certainly every time to withdraw money from their accounts.

Even when they had to make payments to other accounts from their saving or current

account, they had to come to the bank to deposit Cheques. All this was done by personnel at

the bank which unnecessarily resulted in wastage of time and manpower. But the use of

online banking and e-banking has obliterated the need of personally visiting the bank for such

For total file browse

http://adf.ly/6b2AP skip the ad then E-Learning Papers and Acts> Papers.

It’s free!!!!! free!!!!! free!!!!!