credit and working capital: a study of impact for strengthening micro, small and medium business...

TRANSCRIPT

Credit and Working Capital: A Study of Impact for Strengthening Micro, Small and

Medium Business Capital And Regional Economy In Banten Province, Indonesia

Bambang DS *)

Abstract

Loans extended to SMEs has not shown significant improvement in the economy, in this case the

PAD in Banten Province. This can be proved by the addition of low labor, and at least

unemployment that can be absorbed by the SMEs. If the acceleration of growth of SMEs, will be

able to hold 99.45 percent of the total workforce. Based on the issues identified above, the

problem is as follows (a) the difficulty of access to capital experienced by almost all SMEs, (b)

management of SMEs in Banten Province is not well ordered. Based on the above, the research

problem can be formulated as follows, (a) What are the variables that affect the implementation

of credit programs and the strengthening of capital to SMEs in Banten Province? (b) What is the

effectiveness of policies related to credit and capital strengthening program for SMEs in Banten

province to act as a mediator? (c) What is the impact of the implementation of the credit and

capital strengthening program for SMEs in Banten Province? Variables examined included: (1)

the factors that affect the implementation of credit programs and the strengthening of capital to

SMEs in Banten; (2) policies related to credit and capital strengthening program for SMEs in

Banten; and (3) the impact of the implementation of the loan program and the strengthening of

capital to SMEs in the province of Banten. The unit of analysis in this study is the Micro, Small

and Medium Enterprises (SMEs) in the province of Banten. Analytical methods used are: (1)

Descriptive Analysis. This analysis is used to illustrate clearly the characteristics of survey

respondents and the variables in the form of a percentage (%), and the average value (mean)

(Santosa, 2009), and (2) regression analysis to predict the impact of the credit program and

strengthen media venture capital small for the regional economy. Processing data using statistical

software SPSS for Windows version 20. Role of Micro, Small and Medium Enterprises (SMEs)

in creating jobs in a category quite well with the average value (mean) of 3:38. (2) Its role in

reducing unemployment and reducing poverty are also included in the category quite well with

the average value (mean), respectively (3.12) and (2.95), and (3) The Role of Small and Medium

Enterprises (SMEs) in improving economy areas, including in both categories with the average

value (mean) of 3.55. This suggests that the role of SMEs should be maintained and enhanced on

an ongoing basis. The role of SMEs in the indicator still less would have to be increased, for

example in terms of reducing poverty, and unemployment.

Keywords: Credit, Working Capital, Impact Strengthening, SMEs, Banten Economy

*)Korespondensi: Bambang DS, Program Studi Manajemen, Sekolah Tinggi Ilmu Ekonomi Banten, email:[email protected],

mobile:08772638803, 081380554478.

1. Background

The role of MSMEs (Micro, Small and Medium Enterprises) has been recognized quite large

parties in the national economy. Some of the strategic role of SMEs according to Bank

Indonesia (2012), among others: (a) large numbers and found in every sector of the economy;

(b) absorb a lot of labor and every investment to create more employment opportunities; (c)

have the ability to utilize local raw materials and produce goods and services needed by the

public at affordable prices. The same issue was also raised by Malik and Siringo-Ringo,

(2008) that there are a number of common problems faced by SMEs include: a) lack of

working capital and investment, b) difficulties in marketing, c) the distribution and

procurement of raw materials and other inputs , d) limited access to information on market

opportunities and others, e) the limitations of high-skilled workers (low quality of human

resources) and technology capabilities, f) communication limitations and high costs due to

administrative and bureaucratic procedures are complex, especially in obtaining a business

license and uncertainty due to regulations and policies that are not clear. One of the sources

of financing are known and used to support the economy, including SMEs, in Banten

province, namely the banking sector. Unfortunately, the amount of loan funds disbursed to

SMEs is still relatively small compared to the provinces in Java lainnya.Ketersediaan funds

from banks to enterprises, leading sectors, as well as SMEs in Banten province will spur

growth in existing businesses. The amount of loan funds disbursed to SMEs have yet to

indicate a significant improvement in the economy, in this case the PAD in Banten Province.

This can be evidenced by the addition of low employment, and the least amount of

unemployment that can be absorbed by the SMEs. If the accelerated growth of SMEs, will be

able to hold 99.45 percent of the total workforce. Based on the problems identified above, the

existing problems are as follows:

a. The difficulty of access to capital experienced by almost all SMEs.

b. Management of SMEs in the province of Banten which not well ordered.

The research question Based on the above, the research problem can be formulated as

follows.

a. Variabel affecting the implementation of credit programs and the strengthening of capital

to SMEs in Banten Province?

b. How is the effectiveness of policies related to credit and capital reinforcement programs to

SMEs in Banten province acts as a mediator?

c. How does the impact of the implementation of the program of credit and capital

strengthening of MSMEs in Banten Province?

2. Theoretical Framework

Loan

The non-Marxian economists, generally follow the definition above, while Marx uses the

term capital to refer to a completely different concept. Capital is not the stuff, but the

relationship (production) that manifest themselves as social goods. Talking about the issue of

capital means talking about how to make money, make money assets which embodies the

special relationship between the owner and a non-owner such that it is not just that the money

is made, but also that private property relations that gave birth to the process in consequential

being conserved (Bottmore, 1983). Thus, capital is an abstract concept that can manifest in

the form of goods or money. Thus, the concept of Marx, capital elements can be

distinguished according to two kinds of criteria. First, the working process of the criteria that

are objective factors such as production facilities, and a subjective factor labor. Secondly, in

terms of the determination of value, ie fixed capital and variable capital. The concept of

credit is a financial facility that allows a person or business entity to borrow money to buy

the product and pay it back within the specified time period. Law No. 10 of 1998 states that

credit is the provision of cash or equivalent, based on agreements between bank lending and

other parties who require the borrower to repay the debt after a certain period of time with

interest. Creditor (the creditor) can examine whether the prospective borrower entered into

Disgraced Persons List (DOT) or not. For that creditors can also examine his bio and

information from their business environment (Malik and Siringoringo, 2008). Collateral is

required for in case the debtor can not repay their loans. Economic conditions that need to be

considered include problems purchasing power, wider markets, competition, technological

developments, raw materials, capital markets, and so forth (Malik and Siringoringo, 2008).

Micro Enterprise

In accordance with PBI Number: 7/39 / PBI 2005 dated October 18, 2005, is a micro-

enterprise is a family-owned productive enterprises or individual citizen (Indonesian citizen),

individually or in a cooperative and have the results of individual sales at most Rp

100,000,000.00 (one hundred million rupiah) per year. As for the characteristics possessed by

micro enterprises, namely: (1) the business is run by his family members, so there is no

separation of households and businesses; (2) the relatively small-scale enterprises, and

generally there are no records of business activities; (3) the source of funding is local, labor

intensive and use simple technology; (4) the lack of a business license (informal) and limited

information (credit history); (5) is a multi-income activities; and (6) the value of assets

(collateral) is relatively low (unmarketable).

Small Business

In accordance with PBI Number: 7/39 / PBI 2005 dated October 18, 2005 is the small

business is the economic activity of the people are small-scale and meet the following

criteria. (1) Has a net worth of at most Rp 200,000,000.00 and excluding land and building a

business stay, or have the proceeds of Rp. 1,000,000,000.00 (one billion dollars). (2) Stand

alone, not subsidiaries or branches of companies owned, controlled or affiliated directly or

indirectly with a medium, or large business. (3) Form of individual businesses, business

entity that is not incorporated or incorporated business entities, including cooperatives.

medium-sized businesses In accordance with PBI No. 7/39/2005 dated October 18, 2005,

which meant Medium enterprises are businesses with the following criteria: (1) It has a

wealth of more than Rp 200,000,000.00 (two hundred million dollars) to a maximum of USD

10,000 .000.000,00 (ten billion dollars), not including the land and building. (2) Owned

Indonesian Citizen (WNI). (3) Stand alone and not a subsidiary owned, controlled or

berfiliasi either directly or indirectly with a great effort. (4) Shaped individual business, a

business entity that is not a legal entity or business entity with legal status.

The role of SMEs in Indonesia Economic Development Progressive development of SMEs is

expected to play a role in the Indonesian economy which is based on reality, among others:

1) SMEs are the economic sectors that have been published; evidence supporting the tough

and last and save the Indonesian economy from bankruptcy; 2) very strong SME sector in the

face of a prolonged economic crisis that has not been recovered; and 3) the type of business

that is not incorporated hukumini will be the driving force of economic development of

traditional maupunregional. The general conditions of SMEs in Indonesia can be drawn from

a population of 2012 there were 49.8 million units which is equal to 99.9% of its Indonesian

unit. While employment = 88.7 million which is equal to 96.9% of all Indonesian workers

(Wiryanto, 2012). Tambunan (2002) including Munizu (2012) suggests that aspects of the

strengths and weaknesses of SMEs are: (1) human factors; consisting of strong motivation,

labor supply, work ethic, work productivity, and quality of labor; and (2) economic factor /

business; which includes raw materials, access to financial resources, economic value, and

market segments served.

Previous Research Relevant

Here are presented some previous research relevant to ini.Tujuannya research is to find out

where are the previous research has been carried out, so that the visible elements of novelty

of this study compared to previous studies. The role of SMEs in Reducing Poverty

Research Wiryanto (2012) found that micro, small and medium enterprises (SMEs) play a

role as a strategic force and have an important position, not only in the employment and

welfare of the people in the region, in many cases they become adhesive and stabilize social

imbalances. SMEs have the flexibility to face the storm of crisis, this is partly due to the high

content in their production factors, in particular on the use of raw materials.

The role of SMEs in Reducing Unemployment Sepiantini (2010) in his study concluded that

the People's Business Credit assistance program in the Village / Village Dalung District of

North Kuta said to be quite effective to 75.5 percent and a positive impact on increasing

income and employment opportunities of SMEs.

Credit Role in Improving Welfare

Setyari (2010) in conducting research on the evaluation of the impact of microcredit on the

welfare of the tanga in Indonesia: Panel Data Analysis, concluded that there is a strong result

to say that microcredit has a positive significant impact on the level of household welfare in

Indonesia in view of the increasing the amount of spending per capita and labor supply of

household beneficiaries Purwati Lestarini, (2013), in conducting a study entitled "The Effect

of Credit SPP (Save-Loan Group Women) PNPM-MP TerhadapPendapatan Society,"

concludes that there is a positive effect between SPP Credit (Save-Loan Group Women)

PNPM-MP with income Lanji villagers Subdistrict Patebon Kendal.

3.Metodologi

Research Design

This study includes a survey research. The variables examined included: (1) the factors that

affect the implementation of credit programs and the strengthening of capital to SMEs in

Banten Province; (2) policies related to credit programs and strengthening of SMEs in the

capital of the province of Banten; and (3) the impact of the implementation of credit

programs and strengthening capital to SMEs in the province of Banten. The unit of analysis

in this study is the Micro, Small and Medium Enterprises (MSMEs) in the province of

Banten.

Population Research

The study population was recorded in the BPS SMEs Banten Province. Determination of

sample size using purposiverandom sampling technique (purposive sampling). This

technique is used because it is relatively homogeneous population (Cooper and Emory, 1999;

Sugiyono, 2008). Determination of priority factors deciding the performance of SMEs, and

SMEs performance improvement strategy formulation involving all stakeholders, namely:

government, business, NGOs, and universities. Selection of respondents / informants also

done by purposive sampling (Sekaran, 2004; Arikunto, 2005).

Data type

There are two types of data to be collected for this study, the primary data and the data

collected through interviews sekunder.Data primer directly to the respondents. Secondary

data came from: SMEs, BPS, Bapeda, Mass Media, in the form of reports / documents /

tabloid / news that has been published, in the form of relevant documents or published by the

relevant agencies.

Data Collection Techniques

Data collection were interviews, observation, documentation, and FGD (focus group

discussion) .Instrument used were interview, observation guidelines, and FGD guide.

Data Analysis Techniques

Analytical methods used are: (1) Descriptive Analysis. This analysis is used to describe

clearly the characteristics of survey respondents and the variables in the form of a percentage

(%), and the average value (mean) (Santosa, 2009), and (2) regression analysis to predict the

impact of credit programs and strengthening small business capital medium to the local

economy. Data processing using statistical software SPSS for Windows version 19 o'clock.

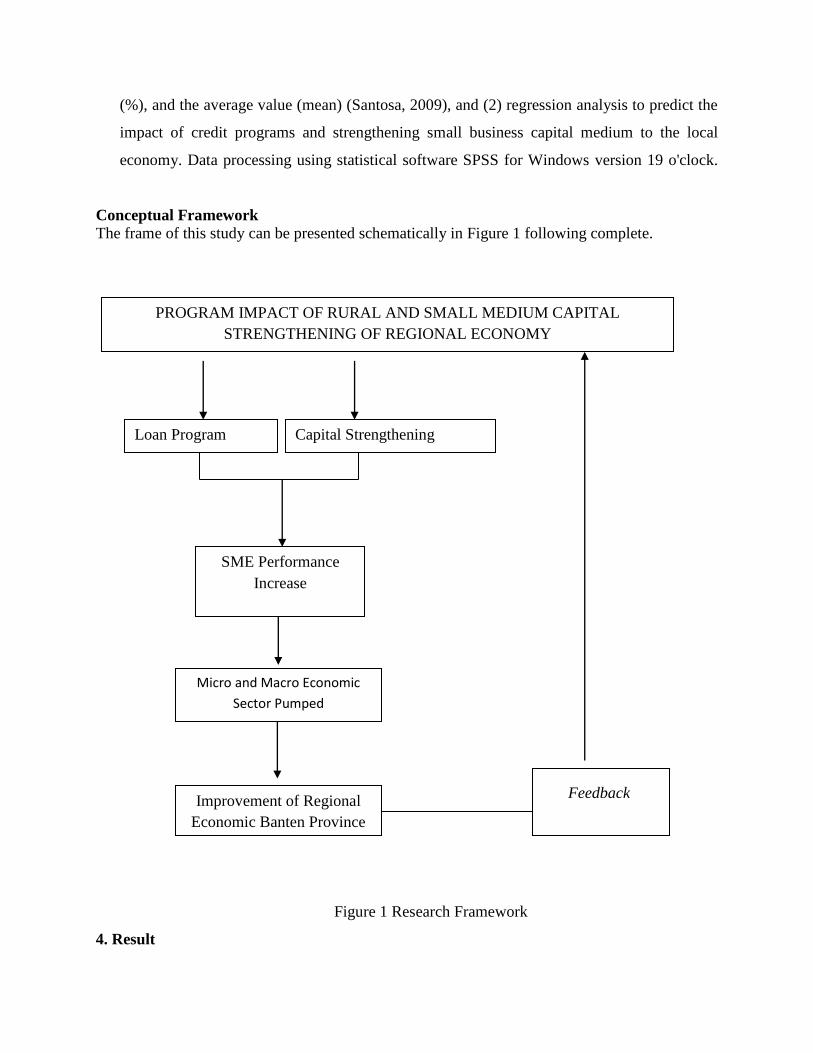

Conceptual Framework The frame of this study can be presented schematically in Figure 1 following complete.

Figure 1 Research Framework

4. Result

PROGRAM IMPACT OF RURAL AND SMALL MEDIUM CAPITAL

STRENGTHENING OF REGIONAL ECONOMY

Capital Strengthening

Program

Loan Program

SME Performance

Increase

Micro and Macro Economic

Sector Pumped

Feedback Improvement of Regional

Economic Banten Province

Factors Population and Labor Force Conditions in Banten Province until now, the socio-

economic development of the province of Banten faced with the problems of quantity and

quality of human resources is still low. The number of human resources available in the new

Bantam reach 5,398,644 jiwa.SDM unevenly spread in 8 districts / kota. Human Resource

Development (HRD) most are in the city of Tangerang (2,960,474 inhabitants) and the least

was in Cilegon 385 720 inhabitants. Quality of HRD Banten still relatively low, at least when

viewed from the side of health and education as well as productivity. If the comparability

between districts / cities, South Tangerang City was only the productivity of their human

resources in excess of two million per month. Achievements The labor productivity of HR

South Tangerang City in 2010 was 27.52 million / year. Lowest labor productivity (5.55

million per year) experienced by HR Lebak District. Factor Number of Small Industries in

Banten Province. If it is seen that there are a small number of industries in Banten Province

until the year 2010 vary widely, ranging from leather industry, wood, precious metals, fabrics,

food, minuma, buffer tourism industry (travel tour packages, restaurants, KAVE, bars, pup,

karaoke, shopping center, spa, beauty salon, cinema, billiards), fish farming, and fish catch.

The whole thing will be explained in detail below. Factors Development Cooperative and

Financial Institutions in the Banten Province

Information cooperative development and financial institutions are as follows:

a. number of active cooperatives in the province of Banten in 2012 there were as many as

3,999 units, while it was in 2013terdapat many as 4,160 units (up sebanuak 161 units).

b. The number of cooperatives that are not active in the province of Banten in 2012 there were

as many as 1,673 units, while in 2013 there were 1,670 units (down 3 units).

c. Overall, in 2013 there were as many as Banten 5,830 cooperatives, with the details as much

as 4,160 active cooperatives, not as many as 1,670 active cooperatives. The development of

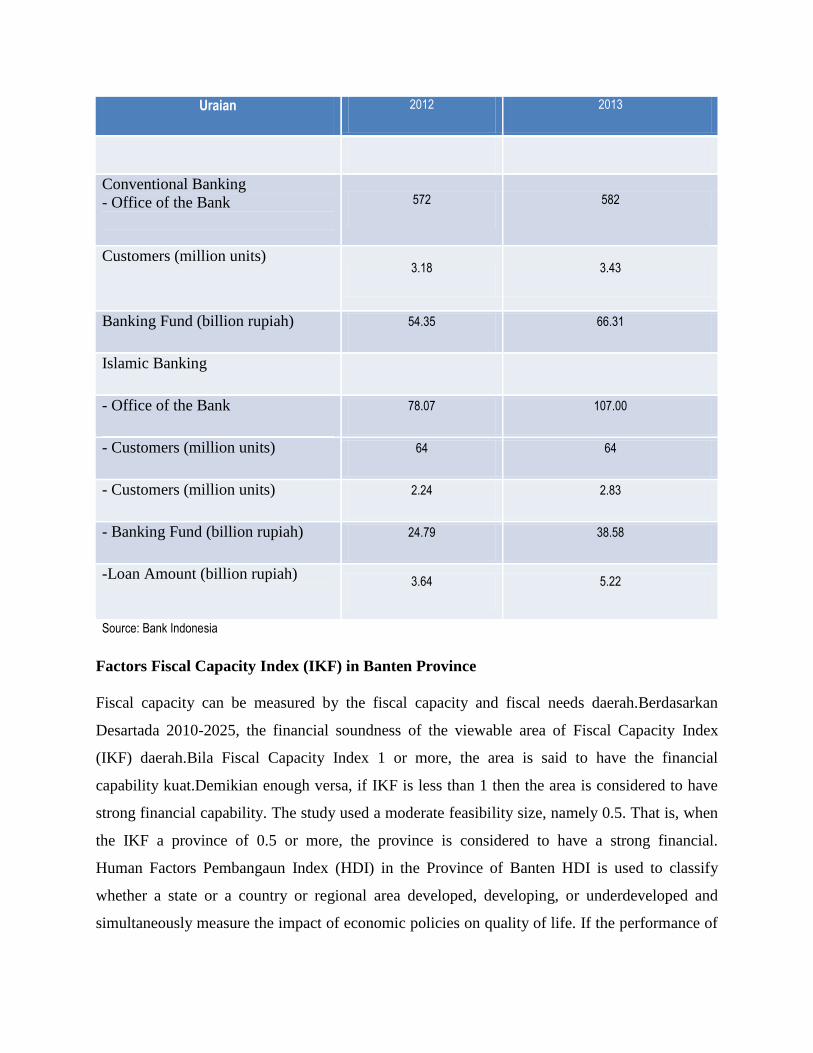

financial institutions in Banten good judging from the number of banks, the number of

customers, number of customer lending in Banten province in 2010 and 2011 can be seen in

the following table.

Table 1: Statistics of Banking in the Province of Banten Year 2012-2013

Uraian 2012 2013

Conventional Banking

- Office of the Bank

572 582

Customers (million units)

3.18 3.43

Banking Fund (billion rupiah) 54.35 66.31

Islamic Banking

- Office of the Bank 78.07 107.00

- Customers (million units) 64 64

- Customers (million units) 2.24 2.83

- Banking Fund (billion rupiah) 24.79 38.58

-Loan Amount (billion rupiah)

3.64 5.22

Source: Bank Indonesia

Factors Fiscal Capacity Index (IKF) in Banten Province

Fiscal capacity can be measured by the fiscal capacity and fiscal needs daerah.Berdasarkan

Desartada 2010-2025, the financial soundness of the viewable area of Fiscal Capacity Index

(IKF) daerah.Bila Fiscal Capacity Index 1 or more, the area is said to have the financial

capability kuat.Demikian enough versa, if IKF is less than 1 then the area is considered to have

strong financial capability. The study used a moderate feasibility size, namely 0.5. That is, when

the IKF a province of 0.5 or more, the province is considered to have a strong financial.

Human Factors Pembangaun Index (HDI) in the Province of Banten HDI is used to classify

whether a state or a country or regional area developed, developing, or underdeveloped and

simultaneously measure the impact of economic policies on quality of life. If the performance of

a country's HDI is less or equal to 50, then the country is categorized as a country of Human

Development Rate (HDR) is low. Medium HDI countries that achievement is its HDI countries

is in the range of 50.1 to 79.9. As for the state of its HDI attainment over 80 countries

categorized as high HDR. Per capita income Factors Society Provision Bante Expenditure per

capita is one of the parameters to measure the success of development ekonomi.Pengeluaran per

capita reflection of income per capita. Adjusted Income per Capita (PKD) is the highest (638 640

USD / month) in South Tangerang City and lowest PKD (USD 604,110 / month) in Lebak

district can be defined as the gap of development between regions. Socio-economic development

in South Tangerang City is far more advanced than the district / city lainnya.Ketersediaan basic

infrastructure is far more complete than any other district / city. It seems that the future

distribution of development still needs to be improved. Economic Growth Factors Banten

Province regional economic growth in 2012 amounted to 5.45 (Banten in figures, 2012: 1) is the

embodiment of the dynamics of the various sectors of local development. Some areas in Banten

actually have the ability to improve the economic conditions of the region. In 2010, from 8

districts / cities in Metro Manila showed that all districts / cities managed to achieve economic

growth above 5%. Of the eight districts / cities, there are six district / city growth rate is above

the provincial average.

Local Revenue Factors

PAD is earned income that is levied by the Regional Local Regulation. Revenue (PAD) is one

component of the Regional Income dapatdijadikan as performance benchmarks Local

Government in managing and optimizing the region's potential. The economic and financial

aspects of the region, Banten province can optimize the utilization and utilization

sumberdayaekonomi and fiscal resources to support business growth and equity

pembangunan.Provinsi Banten is a region that remains dinamis.Potensi diverse resources is the

driving produksidaerah.

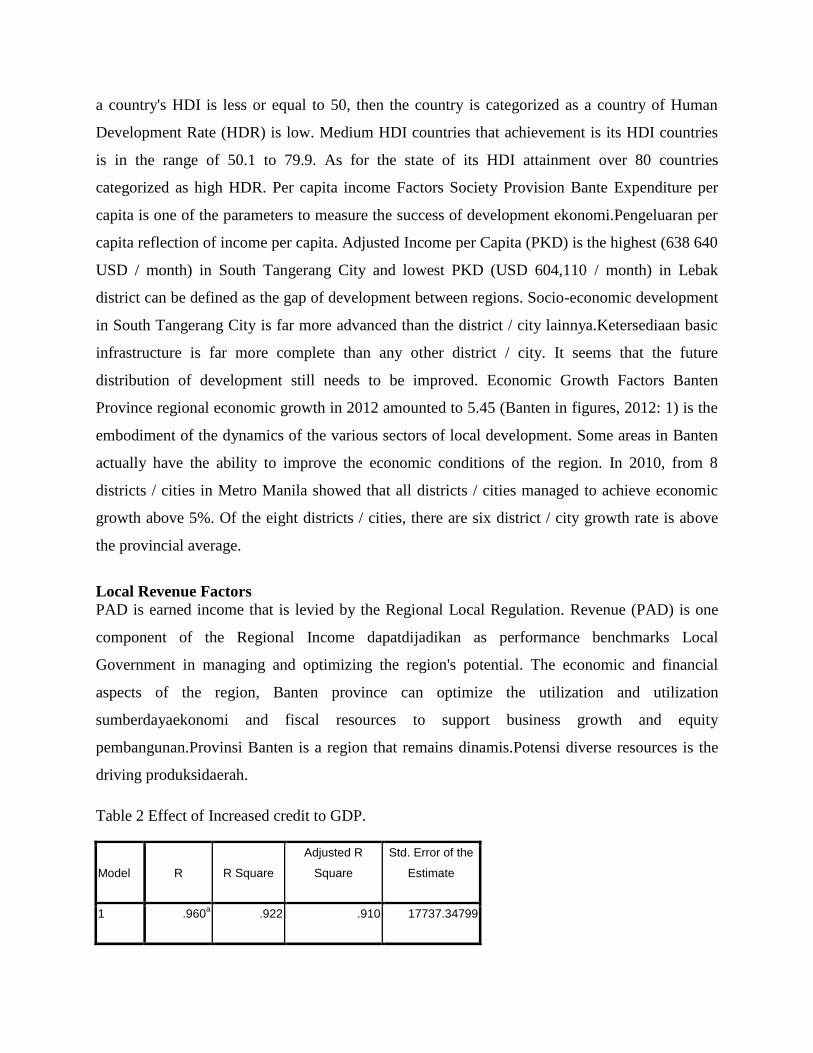

Table 2 Effect of Increased credit to GDP.

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .960a .922 .910 17737.34799

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .960a .922 .910 17737.34799

Predictors: (Constant), sum of loan, 2011

Source: Data processed

Provision of SME loans cumulatively very large impact on GDP is equal 0.960.dengan other

words, credit contributed to a GDP increase of 92.2 per cent, while the remaining 7.8% sebesa

influenced by other factors not accounted for in this analysis.

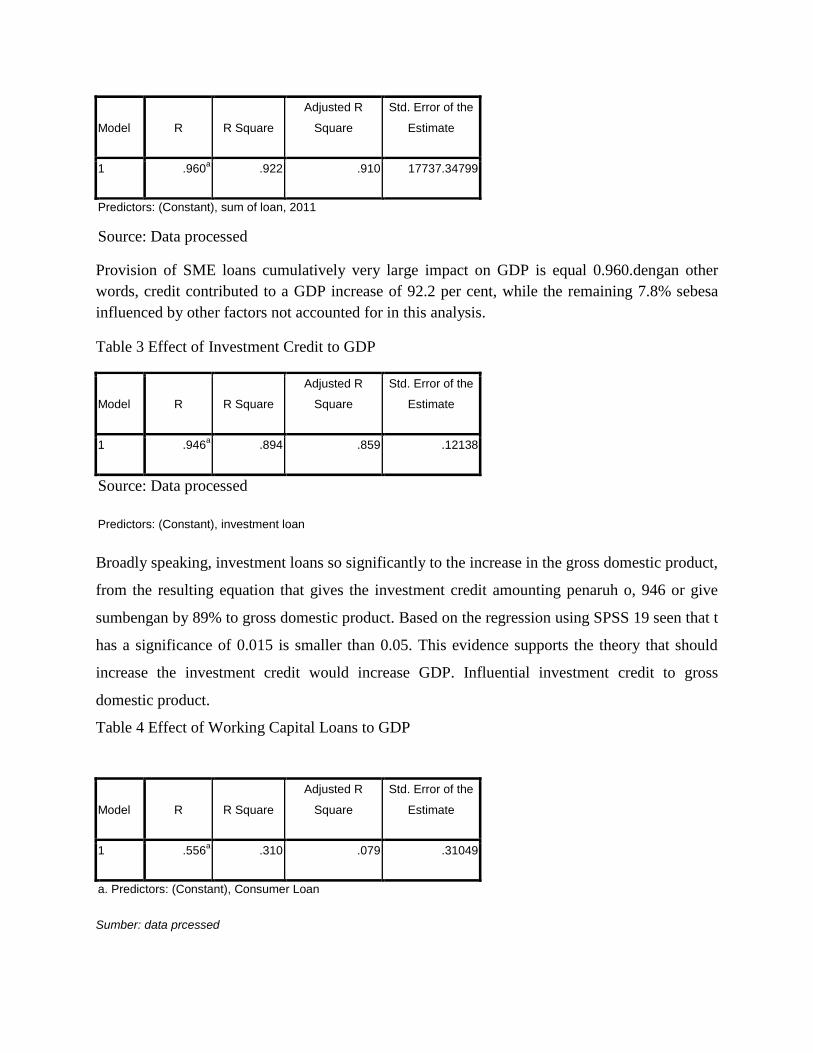

Table 3 Effect of Investment Credit to GDP

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .946a .894 .859 .12138

Source: Data processed

Predictors: (Constant), investment loan

Broadly speaking, investment loans so significantly to the increase in the gross domestic product,

from the resulting equation that gives the investment credit amounting penaruh o, 946 or give

sumbengan by 89% to gross domestic product. Based on the regression using SPSS 19 seen that t

has a significance of 0.015 is smaller than 0.05. This evidence supports the theory that should

increase the investment credit would increase GDP. Influential investment credit to gross

domestic product.

Table 4 Effect of Working Capital Loans to GDP

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .556a .310 .079 .31049

a. Predictors: (Constant), Consumer Loan

Sumber: data prcessed

Based on the equation individually / each working capital loan of 0.556 to give effect to the

increase in the gross domestic product. In other words, consumer credit only contributes 31% to

GDP. This contribution can be said to be very small.

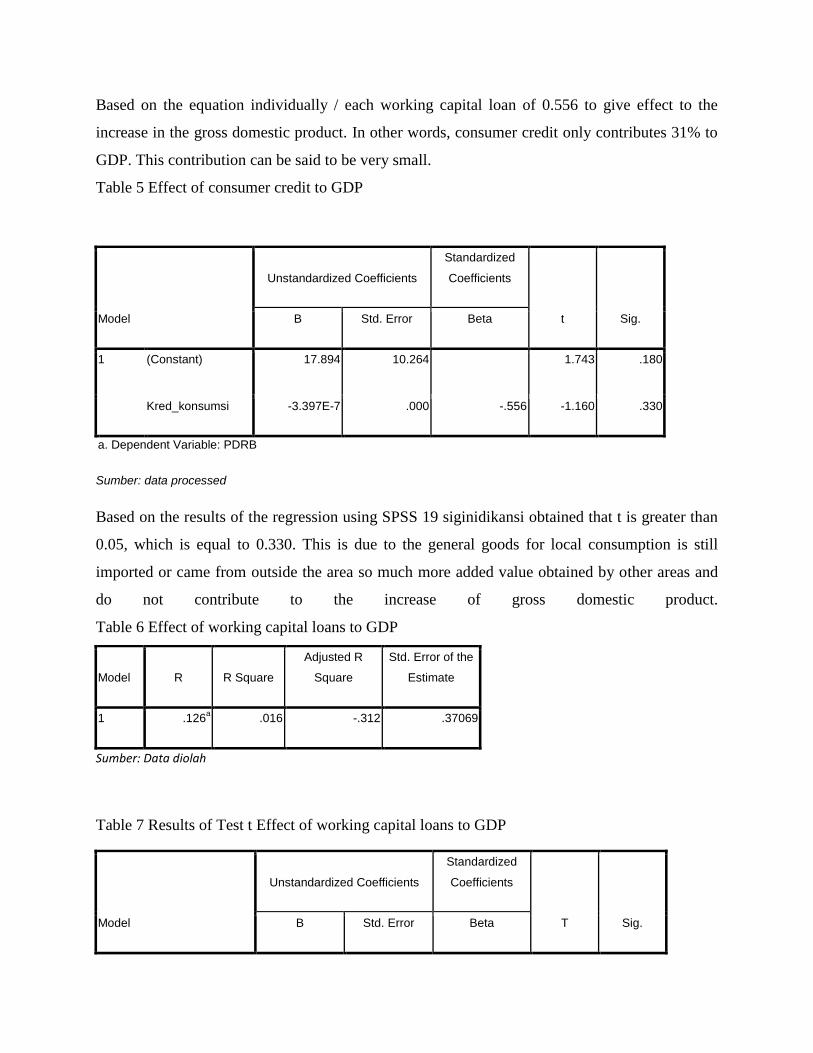

Table 5 Effect of consumer credit to GDP

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) 17.894 10.264 1.743 .180

Kred_konsumsi -3.397E-7 .000 -.556 -1.160 .330

a. Dependent Variable: PDRB

Sumber: data processed

Based on the results of the regression using SPSS 19 siginidikansi obtained that t is greater than

0.05, which is equal to 0.330. This is due to the general goods for local consumption is still

imported or came from outside the area so much more added value obtained by other areas and

do not contribute to the increase of gross domestic product.

Table 6 Effect of working capital loans to GDP

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .126a .016 -.312 .37069

Sumber: Data diolah

Table 7 Results of Test t Effect of working capital loans to GDP

Model

Unstandardized Coefficients

Standardized

Coefficients

T Sig. B Std. Error Beta

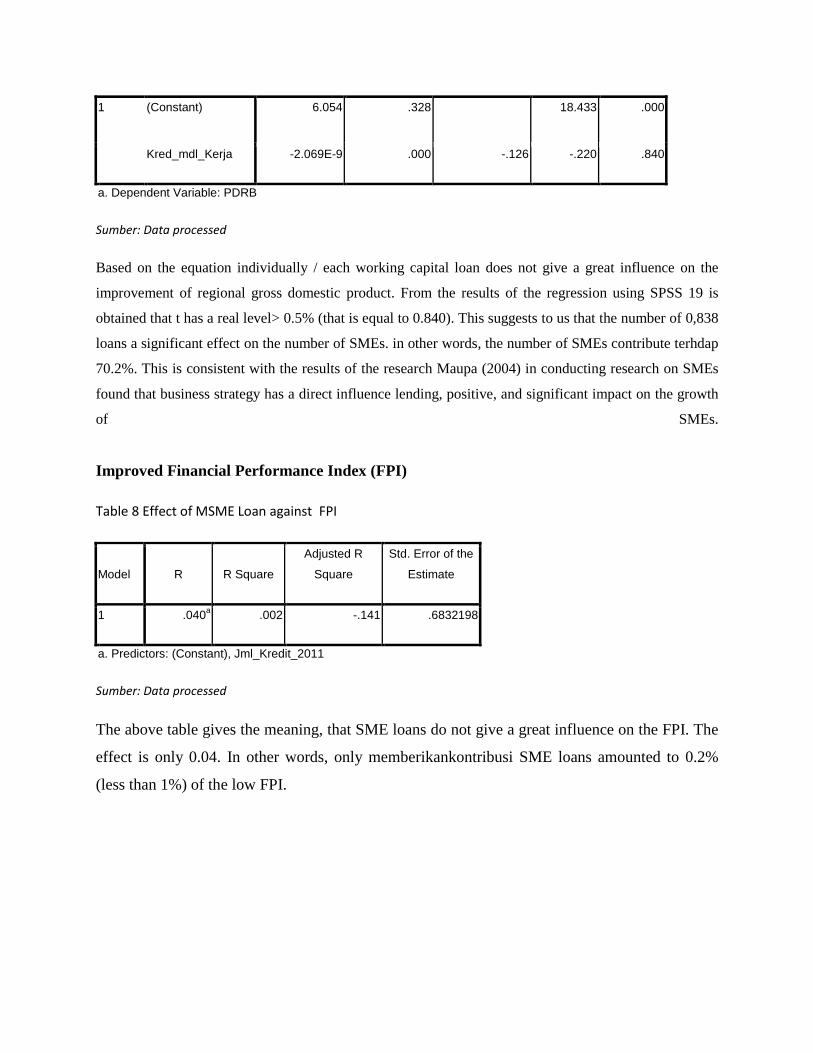

1 (Constant) 6.054 .328 18.433 .000

Kred_mdl_Kerja -2.069E-9 .000 -.126 -.220 .840

a. Dependent Variable: PDRB

Sumber: Data processed

Based on the equation individually / each working capital loan does not give a great influence on the

improvement of regional gross domestic product. From the results of the regression using SPSS 19 is

obtained that t has a real level> 0.5% (that is equal to 0.840). This suggests to us that the number of 0,838

loans a significant effect on the number of SMEs. in other words, the number of SMEs contribute terhdap

70.2%. This is consistent with the results of the research Maupa (2004) in conducting research on SMEs

found that business strategy has a direct influence lending, positive, and significant impact on the growth

of SMEs.

Improved Financial Performance Index (FPI)

Table 8 Effect of MSME Loan against FPI

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .040a .002 -.141 .6832198

a. Predictors: (Constant), Jml_Kredit_2011

Sumber: Data processed

The above table gives the meaning, that SME loans do not give a great influence on the FPI. The

effect is only 0.04. In other words, only memberikankontribusi SME loans amounted to 0.2%

(less than 1%) of the low FPI.

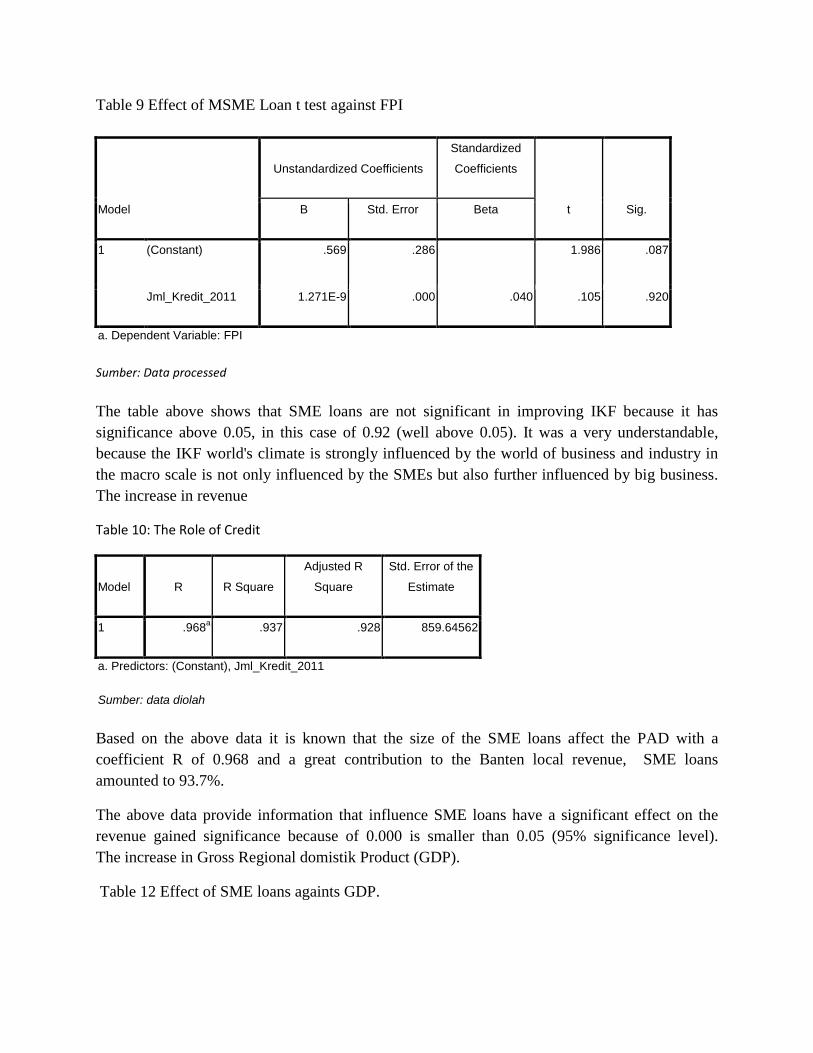

Table 9 Effect of MSME Loan t test against FPI

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) .569 .286 1.986 .087

Jml_Kredit_2011 1.271E-9 .000 .040 .105 .920

a. Dependent Variable: FPI

Sumber: Data processed

The table above shows that SME loans are not significant in improving IKF because it has

significance above 0.05, in this case of 0.92 (well above 0.05). It was a very understandable,

because the IKF world's climate is strongly influenced by the world of business and industry in

the macro scale is not only influenced by the SMEs but also further influenced by big business.

The increase in revenue

Table 10: The Role of Credit

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .968a .937 .928 859.64562

a. Predictors: (Constant), Jml_Kredit_2011

Sumber: data diolah

Based on the above data it is known that the size of the SME loans affect the PAD with a

coefficient R of 0.968 and a great contribution to the Banten local revenue, SME loans

amounted to 93.7%.

The above data provide information that influence SME loans have a significant effect on the

revenue gained significance because of 0.000 is smaller than 0.05 (95% significance level).

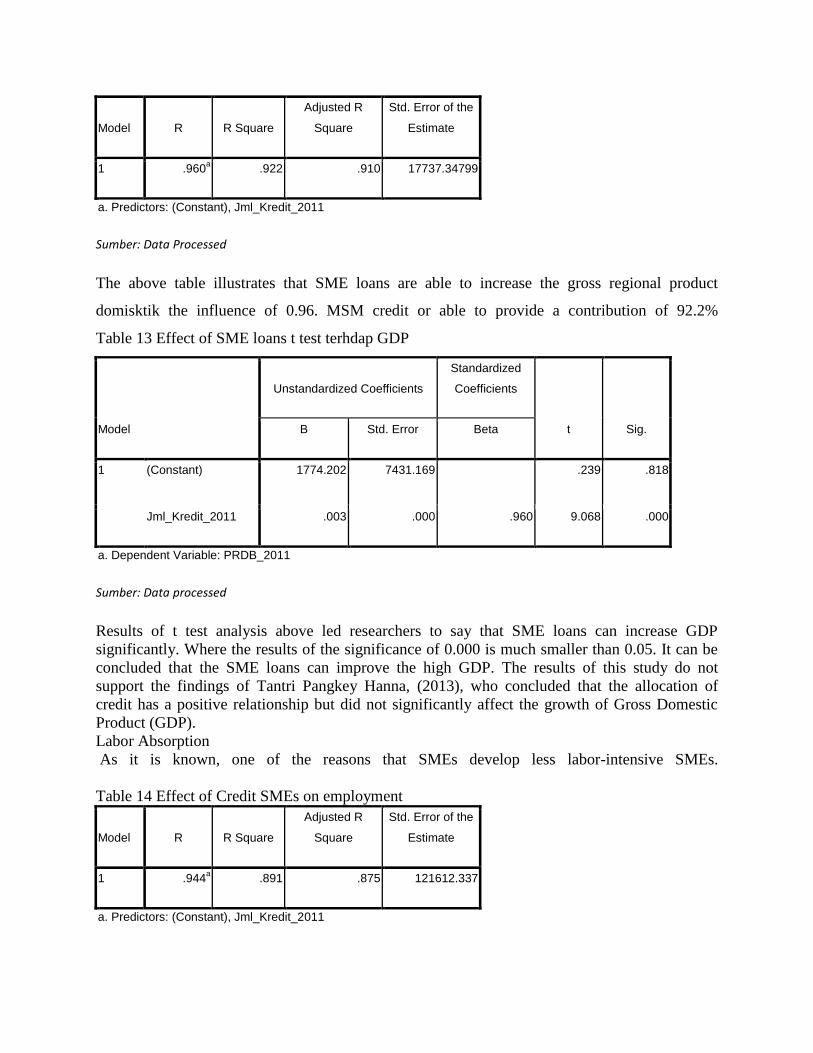

The increase in Gross Regional domistik Product (GDP).

Table 12 Effect of SME loans againts GDP.

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .960a .922 .910 17737.34799

a. Predictors: (Constant), Jml_Kredit_2011

Sumber: Data Processed

The above table illustrates that SME loans are able to increase the gross regional product

domisktik the influence of 0.96. MSM credit or able to provide a contribution of 92.2%

Table 13 Effect of SME loans t test terhdap GDP

Model

Unstandardized Coefficients

Standardized

Coefficients

t Sig. B Std. Error Beta

1 (Constant) 1774.202 7431.169 .239 .818

Jml_Kredit_2011 .003 .000 .960 9.068 .000

a. Dependent Variable: PRDB_2011

Sumber: Data processed

Results of t test analysis above led researchers to say that SME loans can increase GDP

significantly. Where the results of the significance of 0.000 is much smaller than 0.05. It can be

concluded that the SME loans can improve the high GDP. The results of this study do not

support the findings of Tantri Pangkey Hanna, (2013), who concluded that the allocation of

credit has a positive relationship but did not significantly affect the growth of Gross Domestic

Product (GDP).

Labor Absorption

As it is known, one of the reasons that SMEs develop less labor-intensive SMEs.

Table 14 Effect of Credit SMEs on employment

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .944a .891 .875 121612.337

a. Predictors: (Constant), Jml_Kredit_2011

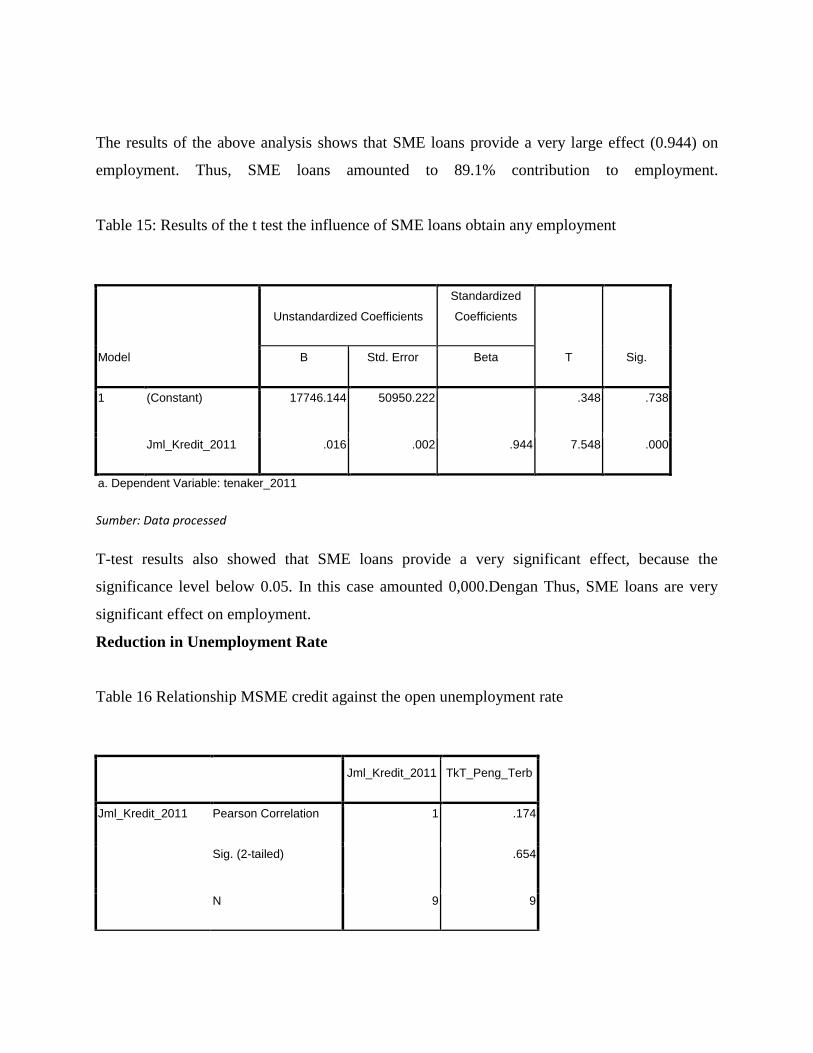

The results of the above analysis shows that SME loans provide a very large effect (0.944) on

employment. Thus, SME loans amounted to 89.1% contribution to employment.

Table 15: Results of the t test the influence of SME loans obtain any employment

Model

Unstandardized Coefficients

Standardized

Coefficients

T Sig. B Std. Error Beta

1 (Constant) 17746.144 50950.222 .348 .738

Jml_Kredit_2011 .016 .002 .944 7.548 .000

a. Dependent Variable: tenaker_2011

Sumber: Data processed

T-test results also showed that SME loans provide a very significant effect, because the

significance level below 0.05. In this case amounted 0,000.Dengan Thus, SME loans are very

significant effect on employment.

Reduction in Unemployment Rate

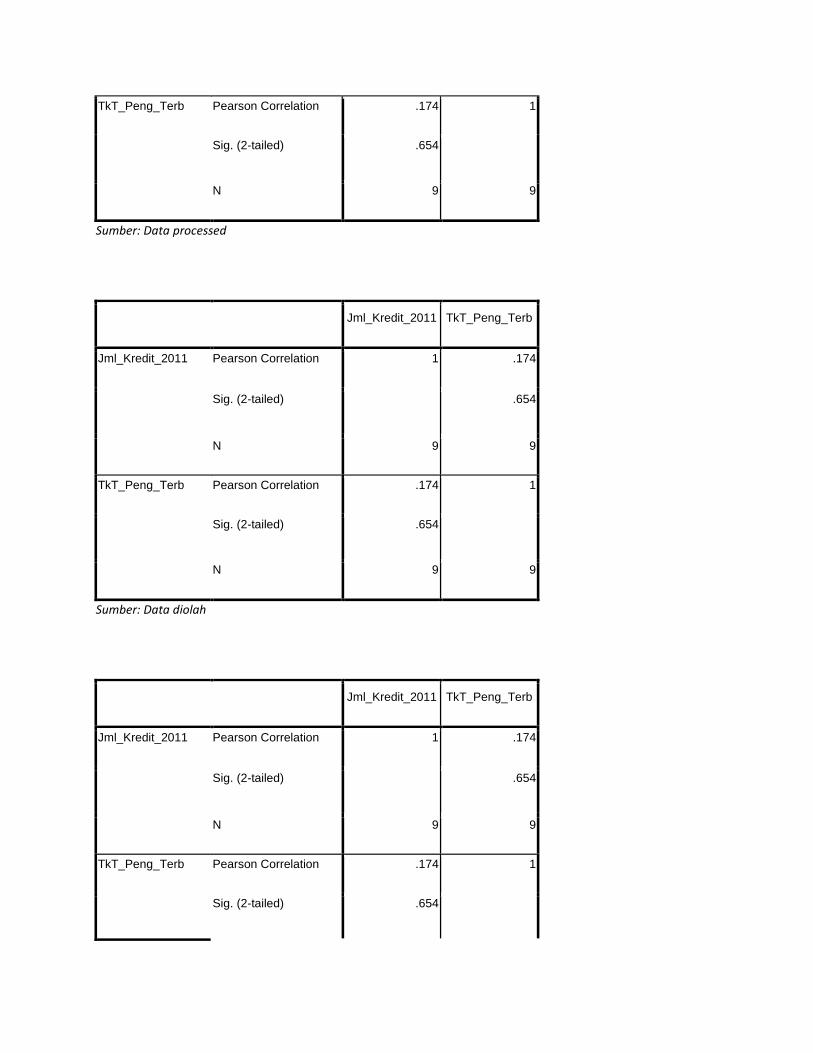

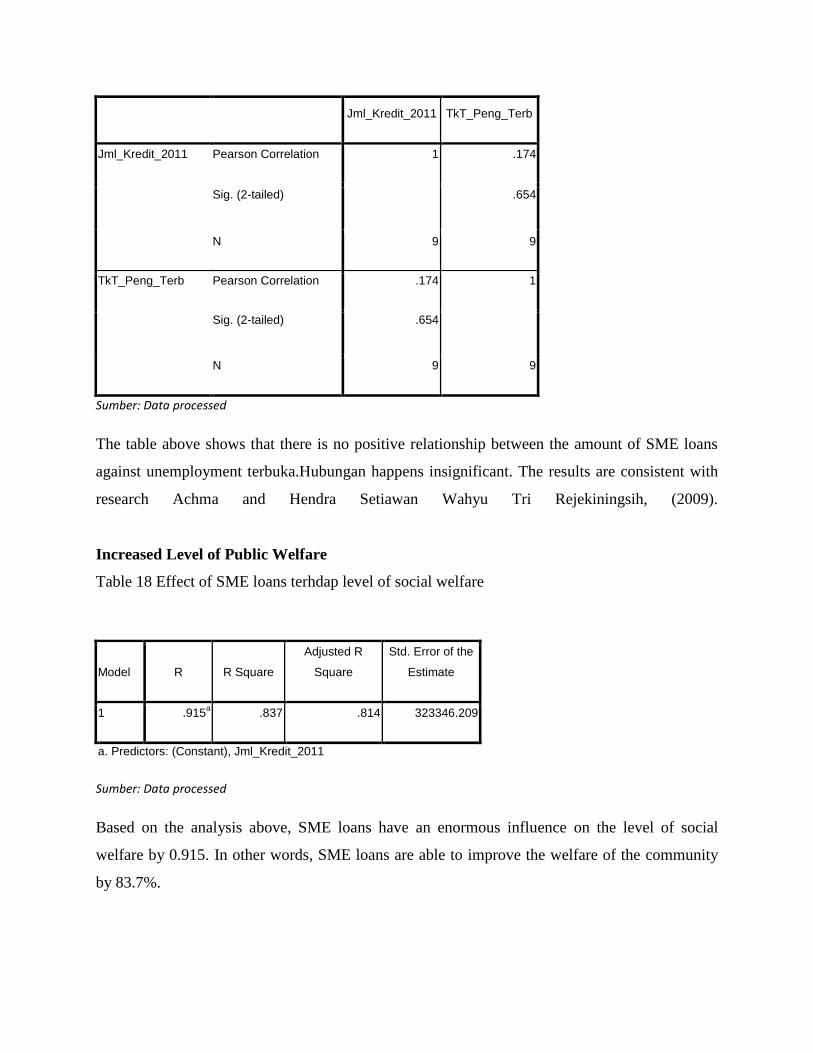

Table 16 Relationship MSME credit against the open unemployment rate

Jml_Kredit_2011 TkT_Peng_Terb

Jml_Kredit_2011 Pearson Correlation 1 .174

Sig. (2-tailed) .654

N 9 9

TkT_Peng_Terb Pearson Correlation .174 1

Sig. (2-tailed) .654

N 9 9

Sumber: Data processed

Jml_Kredit_2011 TkT_Peng_Terb

Jml_Kredit_2011 Pearson Correlation 1 .174

Sig. (2-tailed) .654

N 9 9

TkT_Peng_Terb Pearson Correlation .174 1

Sig. (2-tailed) .654

N 9 9

Sumber: Data diolah

Jml_Kredit_2011 TkT_Peng_Terb

Jml_Kredit_2011 Pearson Correlation 1 .174

Sig. (2-tailed) .654

N 9 9

TkT_Peng_Terb Pearson Correlation .174 1

Sig. (2-tailed) .654

Jml_Kredit_2011 TkT_Peng_Terb

Jml_Kredit_2011 Pearson Correlation 1 .174

Sig. (2-tailed) .654

N 9 9

TkT_Peng_Terb Pearson Correlation .174 1

Sig. (2-tailed) .654

N 9 9

Sumber: Data processed

The table above shows that there is no positive relationship between the amount of SME loans

against unemployment terbuka.Hubungan happens insignificant. The results are consistent with

research Achma and Hendra Setiawan Wahyu Tri Rejekiningsih, (2009).

Increased Level of Public Welfare

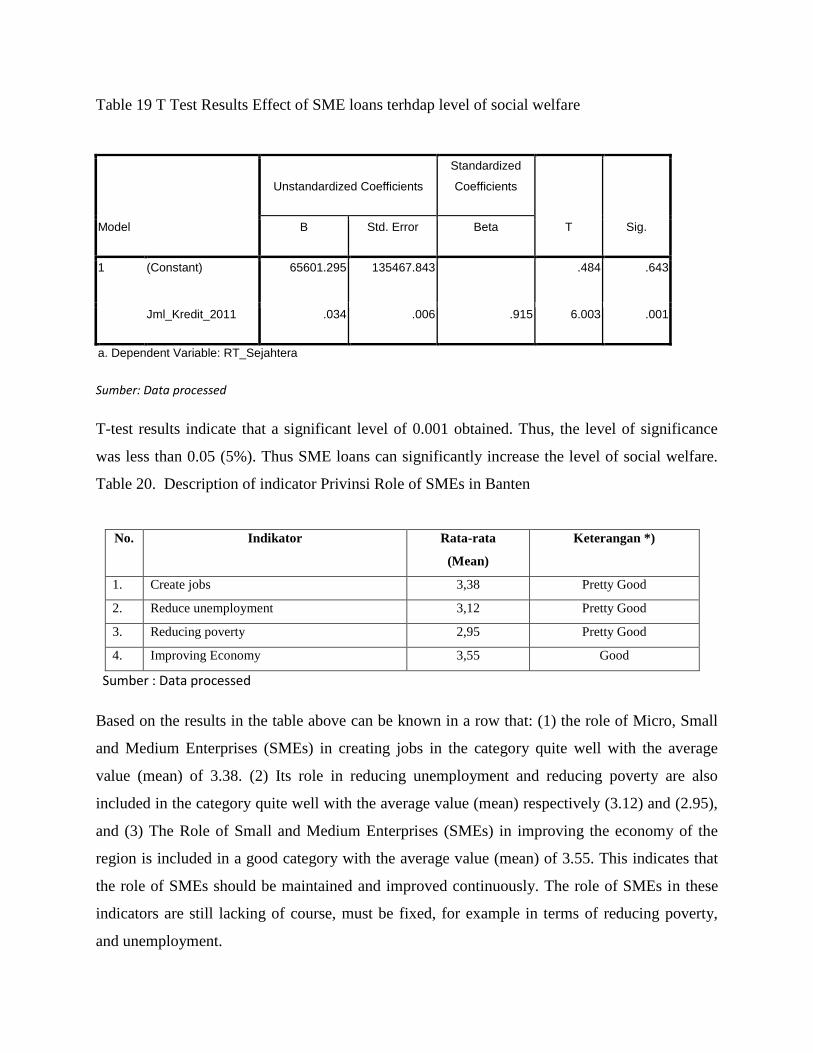

Table 18 Effect of SME loans terhdap level of social welfare

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

1 .915a .837 .814 323346.209

a. Predictors: (Constant), Jml_Kredit_2011

Sumber: Data processed

Based on the analysis above, SME loans have an enormous influence on the level of social

welfare by 0.915. In other words, SME loans are able to improve the welfare of the community

by 83.7%.

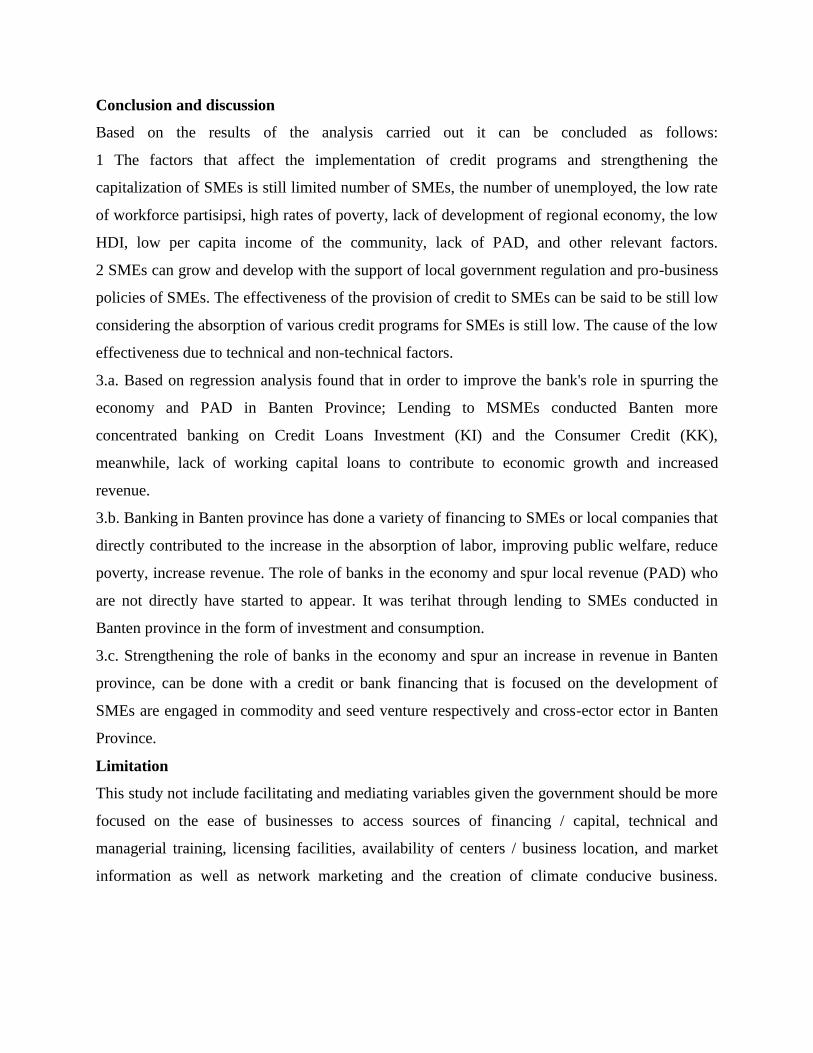

Table 19 T Test Results Effect of SME loans terhdap level of social welfare

Model

Unstandardized Coefficients

Standardized

Coefficients

T Sig. B Std. Error Beta

1 (Constant) 65601.295 135467.843 .484 .643

Jml_Kredit_2011 .034 .006 .915 6.003 .001

a. Dependent Variable: RT_Sejahtera

Sumber: Data processed

T-test results indicate that a significant level of 0.001 obtained. Thus, the level of significance

was less than 0.05 (5%). Thus SME loans can significantly increase the level of social welfare.

Table 20. Description of indicator Privinsi Role of SMEs in Banten

No. Indikator Rata-rata

(Mean)

Keterangan *)

1. Create jobs 3,38 Pretty Good

2. Reduce unemployment 3,12 Pretty Good

3. Reducing poverty 2,95 Pretty Good

4. Improving Economy 3,55 Good

Sumber : Data processed

Based on the results in the table above can be known in a row that: (1) the role of Micro, Small

and Medium Enterprises (SMEs) in creating jobs in the category quite well with the average

value (mean) of 3.38. (2) Its role in reducing unemployment and reducing poverty are also

included in the category quite well with the average value (mean) respectively (3.12) and (2.95),

and (3) The Role of Small and Medium Enterprises (SMEs) in improving the economy of the

region is included in a good category with the average value (mean) of 3.55. This indicates that

the role of SMEs should be maintained and improved continuously. The role of SMEs in these

indicators are still lacking of course, must be fixed, for example in terms of reducing poverty,

and unemployment.

Conclusion and discussion

Based on the results of the analysis carried out it can be concluded as follows:

1 The factors that affect the implementation of credit programs and strengthening the

capitalization of SMEs is still limited number of SMEs, the number of unemployed, the low rate

of workforce partisipsi, high rates of poverty, lack of development of regional economy, the low

HDI, low per capita income of the community, lack of PAD, and other relevant factors.

2 SMEs can grow and develop with the support of local government regulation and pro-business

policies of SMEs. The effectiveness of the provision of credit to SMEs can be said to be still low

considering the absorption of various credit programs for SMEs is still low. The cause of the low

effectiveness due to technical and non-technical factors.

3.a. Based on regression analysis found that in order to improve the bank's role in spurring the

economy and PAD in Banten Province; Lending to MSMEs conducted Banten more

concentrated banking on Credit Loans Investment (KI) and the Consumer Credit (KK),

meanwhile, lack of working capital loans to contribute to economic growth and increased

revenue.

3.b. Banking in Banten province has done a variety of financing to SMEs or local companies that

directly contributed to the increase in the absorption of labor, improving public welfare, reduce

poverty, increase revenue. The role of banks in the economy and spur local revenue (PAD) who

are not directly have started to appear. It was terihat through lending to SMEs conducted in

Banten province in the form of investment and consumption.

3.c. Strengthening the role of banks in the economy and spur an increase in revenue in Banten

province, can be done with a credit or bank financing that is focused on the development of

SMEs are engaged in commodity and seed venture respectively and cross-ector ector in Banten

Province.

Limitation

This study not include facilitating and mediating variables given the government should be more

focused on the ease of businesses to access sources of financing / capital, technical and

managerial training, licensing facilities, availability of centers / business location, and market

information as well as network marketing and the creation of climate conducive business.

Reference

Asih, Dewi Nur, 2008, “Analisis Kebijakan Kredit Terhadap Pengembangan Usaha Perikanan

Nelayan Tradisional Di Kabupaten Tojo Una-Una,” Jurnal Agroland Vol 15 No 1Maret

2008

Asnur, Daniel. 2010. ”Penyusunan Instrumen dan Pembangunan Sistem Informasi Data Dasar

Koperasi dan UKM Terpilih.” Jurnal Ekonomi. 2010,Vol.5,No.119–144.

Athesa. 2006. Program Bantuan Mikro Banking dari Bank BRI. Jakarta

Badan Pusat Statistik, 2011, Berita Resmi Statistik No. 28/05/Th. XVI, Jakarta.

Badan Pusat Statistik, 2012, Berita Resmi Statistik No. 26/03/Th. VVII, Jakarta.

BPS Provinsi Banten, 2010, Banten dalam Angka, Banten: BPS

BPS, Sensus Ekonomi 2006, Hasil Pendaftaran Perusahaan Kalimantan Selatan, Jakarta,

November 2007;

Cooper, Donald R. Dan C.William Emory, 1999, Business Research Methods, Fifth Edition,

Richard D. Irwin Inc., Chicago, USA.

Dani, Irwan. 2006. ”Pengkajian Produk Unggulan dalam Meningkatkan Ekspor UKM dan

Pengembangan Ekonomi Lokal.” Jurnal Ekonom. 2006, Vol.1, No.113–123.

Darsana, Ida Bagus. 2010. ”Analisis Faktor-Faktor yang Mempengaruhi Pendapatan Usaha

Mikro Kecil dan Menengah (UMKM) di Kota Denpasar.” Dalam Jurnal Ekonomi

Pembangunan.

Deva. 1989. Keuangan pemerintah Daerah di Indonesia. (Masri Maris, Penerjemah), Jakarta:

Universitas Indonesia.

Doss,Chely R. 2002. Analyzing Technology Adoption Using Micro studies: Limitations,

Challenges and Opportunities For Improvement. World Economics Academics

Research Development.

Gilarso, T. 1998. Ekonomi Indonesia, Sebuah Pengantar. Yogyakarta: Kanisius.

Gilarso. 1992. Pengantar Ilmu Ekonomi Bagian Makro. Yogyakarta: Kanisius

Gopar, Achmad H. 2010. ”Analisis Biaya Transaksi pada Kredit Usaha Rakyat.” Jurnal

Ekonomi. 2010, Vol. 5, No. 74–98.

Gujarati, Damodar. 1997. Ekonometrika Dasar. Jakarta: Erlangga.

Haeruman, H, 2000, Peningkatan Daya Saing UMKM untuk Mendukung Program PEL.

Makalah Seminar Peningkatan Daya Saing, Graha Sucofindo, Jakarta.

Hafsah, Mohammad Jafar, 2004, Upaya Pengembangan Usaha Kecil dan Menengah (UKM),

Infokop 25, 40-44.

Hamdan, Iwan K, dkk, 2013, “Kajian Grand Design Pemekaran Wilayah Banten,” Laporan hasil

Penelitian, Serang: Balitbangda Provinsi Banten

Handayani. 2004. “Peran Dana Kukesra dalam Meningkatkan Pendapatan Usaha.” Tesis,

Program Pasca Sarjana, Universitas Muhammadyah Surakarta.

Hanna Tantri Pangkey, 2013, Pengaruh Alokasi Kredit Sektor-Sektor Ekonomi terhadap

Pertumbuhan Produk Domestik Regional Bruto (PDRB) Sulawesi Utara (Periode

2008.1-2012.3)”, Jurnal EMBA, Vol.1 No.3 September 2013, Hal. 465-475

Hasan, Ishak. 2010. ”Analisis Daya Dukung UMKM dan Koperasi Berbasis Agrobisnis Pasca-

Konflik Aceh dan dalam Menghadapi ACFTA.” Jurnal Ekonomi. 2010, Vol. 5, No. 145–

174.

Hidayat, Wisnu Adi. 2007. Analisis Kredit Macet Usaha Mikro Kecil dan Menengah di Sentra

Konveksi Ulujami Pemalang. Jurnal Ekonomi. 2007, Vol.2, No. 1–78.

http://id.wikipedia.org/wiki/Tujuan_Pembangunan_Milenium

http://www.pustaka-deptan.go.id/publikasi/p3272084.pdf.

Idris, Indra dan Sri Lestari. 2009. ”Kajian Efektifitas Model Promosi Pemasaran Produk Usaha

Mikro Kecil Menengah (UMKM).” Jurnal Ekonomi Pembangunan. 2010, Vol. 4, No.

116–139.

Idris, Indra. 2010. ”Kajian Dampak Kredit Usaha Rakyat (KUR).” Jurnal Ekonomi

pembangunan. 2010, Vol. 5, No. 49-73.

Instruksi Presiden Nomor 3 Tahun 2010 tentang Program Pembangunan yang Berkeadilan.

Irmayanto, Juli, 2004, Bank dan Lembaga Keuangan Lainnya, Jakarta: Universitas Trisakti

Kasmir. 2007. Manajemen Perbankan. Jakarta: PT Raja GrafindoPersada.

Kasmir., 2007. Bank dan Lembaga Keuangan Lainnya. Edisi Keenam. Jakarta: PT Raja Grafindo

Persada

Keijiro Otsuka, Takashi Yamano. 2001. Introduction to the Special Issue on the Role of non

farm Income in Poverty Reduction: Evidence from Asia and East Africa. World

Economics Academics Research Development.

Keputusan Presiden Nomor 127/2001 tentang Bidang/Jenis Usaha yang terbuka untuk

Usaha Menengah atau Besar dengan Syarat Kemitraan.

Kornita, Sri Endang; dan Anthony Mayes, 2010, “Analisis Peran Perbankan Dalam

Perekonomian Di Kabupaten Siak”, Jurnal Ekonomi, Volume 18. Nomor 1 Maret2010

Kuncoro, Mudrajat, 2002, Manajemen Perbankan: Teori dan Aplikasi, Yogyakarta: BPFE

Lembaga Administrasi Negara, 2011, ”Kajian Pengembangan dan Instrumentasi Kebijakan

Pengelolaan Ekonomi Daerah,” Laporan Akhir , Jakarta: LAN

Lesceviva, M, 2004, Rural Entrepreneurship Success Determinant, Unpublished Working

Papers, Eksjo, Latvian: Faculty of Economics, Latvian University of Agriculture.

Malik, Rachmawati dan Hotniar Siringoringo, 2008, “Analisis Pengaruh Kredit, Aset Dan

Jumlah Pegawai Terhadap Pendapatan Usaha Kecil Menengah(Ukm) Penerima Kredit

Bankperkreditan Rakyat,” Hasil penelitian, Depok: Universitas Gunadharma

Mantra, I.B. 2003. Demografi Umum. Yogyakarta: Pustaka Pelajar

Manurung, Mandala dan Prathama Rahardja, Uang, Perbankan, dan Ekonomi Moneter, (Kajian

Kontektual Indonesia), Jakarta: Fakultas Ekonomi Universitas Indonesia.

Manurung, Romulus.1996. Dampak Kredit Bank Perkreditan Rakyat Dalam Meningkatkan

Perekonomian Pedesaan (studikasus di wilayah Jawa Barat, Jawa Timur dan Bali).

Jakarta: Jurnal Keuangandan Moneter Vol 2. No 2 Juni 1996.

Mardiasmo. 2000. Pengelolaan Keuangan Daerah yang Berorientasi pada Kepentingan Publik.

Yogyakarta: Andi Offset.

Marimbo. 2008. Ayo ke Bank dapatkan Kredit UMKM. Jakarta: PT Ela Media Komputindo

Maupa, Haris, 2004, “Faktor-Faktor yang Menentukan Pertumbuhan Usaha Kecil di Sulawesi

Selatan.” Disertasi, Program Pascasarjana Unhas. Tidak dipublikasikan.

Mulyono, Sri, 2000, Teori Pengambilan Keputusan, Lembaga Penerbit FEUI, Jakarta.

Munizu, Musran, 2010, Pengaruh Faktor-Faktor Eksternal dan Internal Terhadap Kinerja Usaha

Mikro dan Kecil (UMK) di Sulawesi Selatan, Jurnal Manajemen dan Kewirausahaan 12,

33-41.

Munizu, Musran, 2012, “Strategi Peningkatan Kinerja dan Peran Usaha Kecil dan Menengah

(UKM) Pengolah Produk Berbasis Pangan di Kota Makassar,” Hasil Penelitian, Fakultas

Ekonomi dan Bisnis Unhas (FEB-Unhas) Makassar dalam [email protected]

MurjanaYasa, I Gusti Wayan. 1993. ”Jam Kerja, Pendapatan dan Pengeluaran Pekerja

Migran di Daerah Wisata Kuta Bali.” Tesis” Program Pascasarjana UGM.

Oemar, Mohammad. 2006. Kajian Faktor-faktor yang Mempengaruhi Perkembangan Usaha

UKM di Provinsi Sumatra Utara. Jurnal Ekonomi. 2006, Vol. 1, No. 1–12.

Panggabean, Riana. 2010. Kajian Pengembangan UMKM di Sentra Klaster Rotan Kabupaten

Cierebon. Jurnal Ekonomi. 2010, Vol. 5, No. 99–118.

Panji Anoraga. 1997. Uang dan Perbankan. Jakarta: Rineka Cipta

Peraturan Menteri BUMN No. PER-05/MBU/2007 tentang Program Kemitraan BUMN

dengan Usaha Kecil dan Program Bina Lingkungan.

Peraturan Presiden Nomor 5 Tahun 2010 tentang Rencana Pembangunan Jangka Menengah

Nasional 2010-2014

Peraturan Pemerintah Nomor 44 Tahun 1997 tentang Kemitraan

Prima, Dwi. 2009. ”Efektivitas Kredit Tanpa Agunan (KTA) Dalam Peningkatan Volume

Produksi Usaha Mikro Kecil dan Menengah (UMKM) di Kota Denpasar.” Skripsi.

Fakultas Ekonomi Universitas Udayana. Denpasar.

Purwati Lestarini, 2013, “Pengaruh Kredit SPP (Simpan-Pinjam Kelompok Perempuan) PNPM-

MP Terhadap Pendapatan Masyarakat, Jurnal Pendidikan Ekonomi IKIP Veteran

Semarang Vol. 01 No. 01, Juni 2013

Putra, Edy. 2009. ”Efektivitas Program Pemberian Bantuan Dana Bergulir pada UMKM di

Kabupaten Badung.” Skripsi. Fakultas Ekonomi Universitas Udayana. Denpasar.

Rangkuman Diskusi Dialog Strategis Pengambilan Kebijakan untuk Mewujudkan Target

Millenium Development Goals 2015, Jakarta, 15 Agustus 2011;

Rival Veithzalm, dkk. 2007, Bank and Financial Instution Management Conventional & Sharia

System, Jakarta: Rajagrafindo Persada

Robert, N. 2006. Economics Analysis of the Spatial Integration of Plantain Markets in

Cameroon: how Equilibrium Between Supply and Demand Affect Food Supply. African

Economics Research Consortium (AERC).

Santoso, Singgih, 2009, SPSS Statistik Multivariate, Jakarta: Elex Media Komputindo

Sekaran, Uma, 2004, Research Methods For Business: A Skill-Bulding Approach, New York,

USA: John Wiley & Sons.

Sepiantini, Ni Komang. 2010. ”Efektivitas Program Bantuan Kredit Usaha Rakyat Terhadap

Peningkatan Pendapatan dan Kesempatan Kerja Usaha Mikro Kecil dan Menengah di

Desa/Kelurahan Dalung Kecamatan Kuta Utara.” Skripsi. Fakultas Ekonomi

Universitas Udayana. Denpasar.

Setiawan, Achma Hendra dan Tri Wahyu Rejekiningsih, 2009, “Dampak Program Dana

Bergulir Bagi Usaha Kecil dan Menengah (UKM),” ASET, September 2009, Vol. 11 No.

2 hal. 109-115

Setyari, Ni Putu Wiwin, (2010) dalam melakukan penelitian tentang evaluasi dampak kredit

mikro terhadap kesejahteraan rumah tanga di Indonesia: Analisis data Panel,” JEKT, Vol

5 No 2 Hal 141-150

Setyobudi, Andang, 2007, Peran Serta Bank Indonesia dalam Pengembangan Usaha Mikro,

Kecil dan Menengah (UMKM), Buletin Hukum Perbankan dan Kebanksentralan 5, 29-

35.

Siamat, Dahlan, 2004, Manajemen Lembaga Keuangan, Jakarta: Lembaga Penerbit Fakultas

Ekonomi Universitas Indonesia

Simanjuntak, Payaman, J. 2001. Pengantar Ekonomi Sumber Daya Manusia. Jakarta: FEUI.

SMECDA. 2006. “Kajian Dampak Program Perkreditan dan Perkuatan Permodalan Usaha Kecil

Menengah terhadap Perekonomian Daerah.” Jurnal Pengkajian Koperasi dan UKM No.

1 Tahun I –2006.

Subagyo, Ahmad Wito. 2000. Efektivitas Program Penanggulangan Masyarakat Pedesaan.

Yogyakarta: UGM.

Sugiyono, 2008, Metode Penelitian Bisnis, Bandung: Alfabeta.

Sulaeman, Suhendar, 2004, Pengembangan Usaha Kecil dan Menengah dalam Menghadapi

Pasar Regional dan Global, Infokop 25, 113-120.

Suryadharma, Ali. 2008. “Menkop: Indonesia Bangkrut Kalau UMKM diabaikan.” Antara News,

Senin 22 Desember.

Susilo, Y Sri, Sigit Triandaru, A. Totk Budi Santoso, 2000, Bank dan Lembaga Keuangan Lain,

Jakarta: Salemba Empat.

Sutojo, Siswanto. 1995, ”Kredit Usaha Rakyat (KUR) Kupedes.” Handout. Jakarta: Devisi

Bisnis Mikro KP BRI.

Sutojo, Siswanto. 1995. Analisis Kredit Bank Umum: Konsep dan Teknik. Jakarta: Pustaka

Binaman Pressindo.

Syarif, Teuku dan Budhiningsih, Etty. 2009. ”Kajian Kontribusi Kredit Bantuan Perkuatan

Dalam Mendukung Permodalan UMKM.” Jurnal Ekonomi. 2009,Vol. 4, No. 62–87.

Syarif, Teuku. 2009. ”Kajian Pengembangan Formalisasi UMKM.” Jurnal Ekonomi. 2009, Vol.

4, No. 18–36.

Tambunan, Tulus T.H., 2002, Usaha Kecil dan Menengah di Indonesia: Beberapa Isu Penting,

Jakarta: Salemba Empat

Temtime, Zelealem T., and J. Pansiri, 2004, Small Business Critical Succes/Failure Factors in

Developing Economies: Some Evidence From Bostwana, American Journal of Applied

Sciences 1, 18-25.

Todaro, Michael P. 2000. Pembangunan Ekonomi di Dunia ketiga. Jilid I. Edisi ketujuh. Jakarta:

Erlangga.

Undang-Undang Nomor 20 Tahun 2008 tentang Usaha Mikro, Kecil dan Menengah.

Utomo, Cahyo Trio dan Achma Hendra Setiawan, 2013, “Analisis Peran Kredit Mikro Dari Pd

Bpr Bkk Kebumen Cabang Kutowinangun Dalam Upaya Mengembangkan Usaha Mikro

Di Wilayah Kerjanya” Diponegoro Journal Of Economics, Volume 2, Nomor 1, Tahun

2013, Halaman 1-10

Wiryanto, Wisber, 2012, ”Pemberdayaan Usaha Kecil dan Menengah di Kota Banjarbaru dalam

Rangka Millenium Development Goals 2015,” Hasil Penelitian, Jakarta: Pusat Kajian

Administrasi Internasional, Lembaga Administrasi Negara

Yoseva, dan Teuku Syarif. 2010. ”Kajian Kemanfaatan Bantuan Perkuatan Untuk Usaha Mikro,

Usaha Kecil dan Usaha Menengah (UMKM).” Jurnal Ekonomi. 2010, Vol. 5, No. 30–48

Hidayat, Iman Pirman dan Adi Ridwan Fadillah, 2012, “Pengaruh Penyaluran Kredit Usaha

Mikro Kecil Menengah (UMKM) Dan Pendapatan Operasional Terhadap Laba

Operasional (Kasus Pada PT Bank Jabar Banten.” Tbk), http://www.Jurnal.umkm.

Deckiyanto, Firmansyah, 2013, Efektifitas Kebijakan Pemberian Kredit Usaha Rakyat (KUR)

Mikro Berdasarkan Surat Edaran Direksi Nose: S.09c–DIR/ADK/03/2010 Atas

Ketentuan Kredit Usaha Rakyat (KUR) Mikro: (Studi di Bank Rakyat Indonesia Unit

Sleko Cabang Madiun)” Skripsi, FH Univ Brawijaya Malang