canada's balance of international payments and international

TRANSCRIPT

StatistiqueCanada

StatisticsCanada

Catalogue no. 67-506-XIE

Canada's Balance of International Payments and International Investment Position

Concepts, Sources, Methods and Products

How to obtain more information...

Specific inquiries about this product and related statistics or services should be directed to: Balance of PaymentsDivision, Statistics Canada, Ottawa, Ontario, K1A 0T6 (telephone: (613) 951-1855).

For information on the wide range of data available from Statistics Canada, you can contact us by calling one of our toll-free numbers. You can also contact us by e-mail or by visiting our Web site.

National inquiries line 1 800 263-1136National telecommunications device for the hearing impaired 1 800 363-7629Depository Services Programinquiries 1 800 700-1033Fax line for Depository Services Program 1 800 889-9734E-mail inquiries [email protected] site www.statcan.ca

Ordering and subscription information

This product, Catalogue no. 67-506-XPE, is published occasionally as a standard printed publication at a price of CDN$45.00 per issue. The following additional shipping charges apply for delivery outside Canada:

Single issue

United States CDN $ 6.00Other countries CDN $ 10.00

This product is also available free in electronic format on the Statistics Canada Internet site as Catalogue no. 67-506-XIE. To obtain a single issues, visit our Web site at www.statcan.ca, and select Products and Services.

All prices exclude sales taxes.

The printed version of this publication can be ordered by

• Phone (Canada and United States)1 800 267-6677• Fax (Canada and United States) 1 877 287-4369• E-mail [email protected]• Mail Statistics Canada

Dissemination DivisionCirculation Management120 Parkdale AvenueOttawa, Ontario K1A 0T6

• And, in person at the Statistics Canada Regional Centre nearest you, or from authorized agents and bookstores.

When notifying us of a change in your address, please provide both old and new addresses.

Standards of service to the public

Statistics Canada is committed to serving its clients in a prompt, reliable and courteous manner and in the official lan-guage of their choice. To this end, the Agency has developed standards of service which its employees observe in ser-ving its clients. To obtain a copy of these service standards, please contact Statistics Canada toll free at 1 800 263-1136.

Statistics CanadaBalance of Payments Division

System of National Accounts

Canada’s Balance of International Payments and International Investment PositionConcepts, Sources, Methods and Products

Published by authority of the Ministerresponsible for Statistics Canada

© Minister of Industry, 2000

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without prior written permission from Licence Services, Marketing Division, Statistics Canada, Ottawa, Ontario, Canada K1A 0T6.

July 2000

Catalogue no. 67-506-XPE

Frequency: Occasional

ISBN 0-660-18175-4

Ottawa

La version française de cette publication est disponible sur demande (no 67-506-XPF au catalogue).

Note of appreciation

Canada owes the success of its statistical system to a long-standing partnership between Statistics Canada, the citizens of Canada, its businesses and governments and other institutions. Accurate and timely statistical information could not be produced without their continued co-operation and goodwill.

The paper used in this publication meets the minimumrequirements of American National Standard forInformation Sciences – Permanence of Paper forPrinted Library Materials, ANSI Z39.48 – 1984.

8

Canadian Cataloguing in Publication Data

Main entry under title:

Canada’s balance of international payments andinternational investment position : concepts, sources,methods and products

(System of National Accounts)Issued also in French under title: La balance des paiementsinternationaux et le bilan des investissements internationauxdu Canada.ISBN 0-660-18175-4CS67-506-XPE

1. Balance of payments – Canada – Statistics.2. Balance of trade – Canada – Statistics.3. Investments, Foreign – Statistics.I. Statistics Canada. Balance of Payments Division.II. Title. III. Series.

HG3883.C3 C36 2000 382.'17'0971021C00-988010-0

Table of contents

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue no. 67-506-XIE iii

TABLE OF CONTENTS

Page

PREFACE ................................................................................................................................................................................ xiii

ACKNOWLEDGEMENTS......................................................................................................................................................xv

INTRODUCTION.......................................................................................................................................................................1

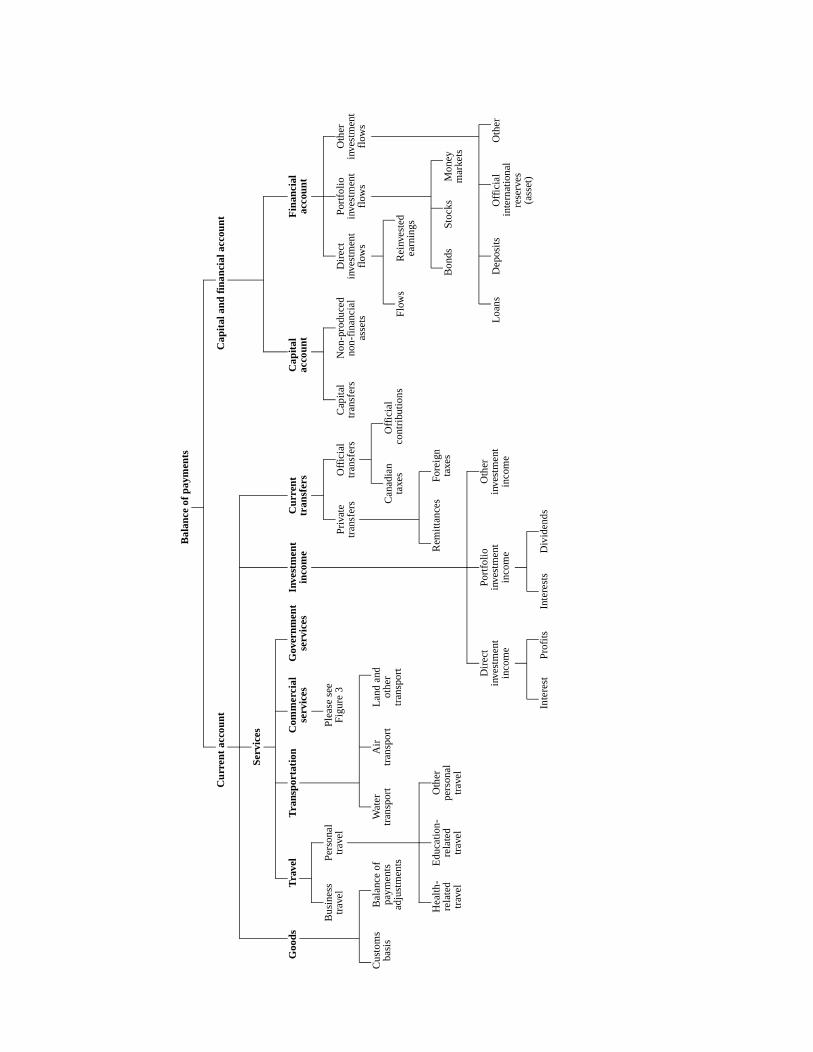

PART I: BALANCE OF INTERNATIONAL PAYMENTS....................................................................................................5

CHAPTER 1 Conceptual Framework of the Balance of Payments .......................................................................................7

CHAPTER 2 The Current Account ......................................................................................................................................17

CHAPTER 3 Goods..............................................................................................................................................................19

CHAPTER 4 Travel..............................................................................................................................................................31

CHAPTER 5 Transportation.................................................................................................................................................35

CHAPTER 6 Commercial Services......................................................................................................................................41

CHAPTER 7 Government Services......................................................................................................................................55

CHAPTER 8 Investment Income .........................................................................................................................................57

CHAPTER 9 Current Transfers ............................................................................................................................................61

CHAPTER 10 The Capital and Financial Account ................................................................................................................63

CHAPTER 11 Capital Account ..............................................................................................................................................65

CHAPTER 12 Direct Investment Flows.................................................................................................................................67

CHAPTER 13 Portfolio Investment Flows ............................................................................................................................71

CHAPTER 14 Other Investment Flows .................................................................................................................................79

PART II: INTERNATIONAL INVESTMENT POSITION..................................................................................................83

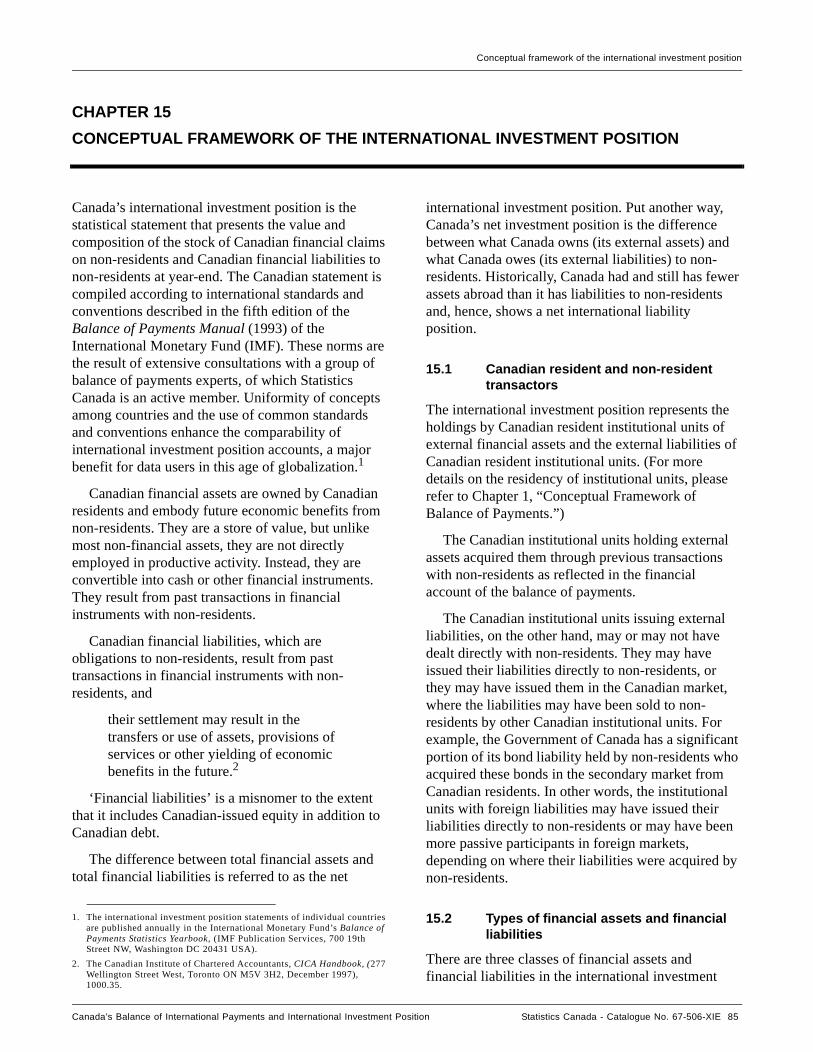

CHAPTER 15 Conceptual Framework of the International Investment Position..................................................................85

CHAPTER 16 Direct Investment Position .............................................................................................................................89

CHAPTER 17 Portfolio Investment Position .........................................................................................................................97

CHAPTER 18 Other Investment Position ............................................................................................................................103

PART III: OVERVIEW OF THE STATISTICAL FRAMEWORK..................................................................................107

CHAPTER 19 Implementation of International Standards ..................................................................................................109

CHAPTER 20 Data Sources.................................................................................................................................................123

CHAPTER 21 Processing Systems ......................................................................................................................................129

CHAPTER 22 Products ........................................................................................................................................................137

CHAPTER 23 Looking Ahead .............................................................................................................................................143

APPENDICES ..........................................................................................................................................................................153

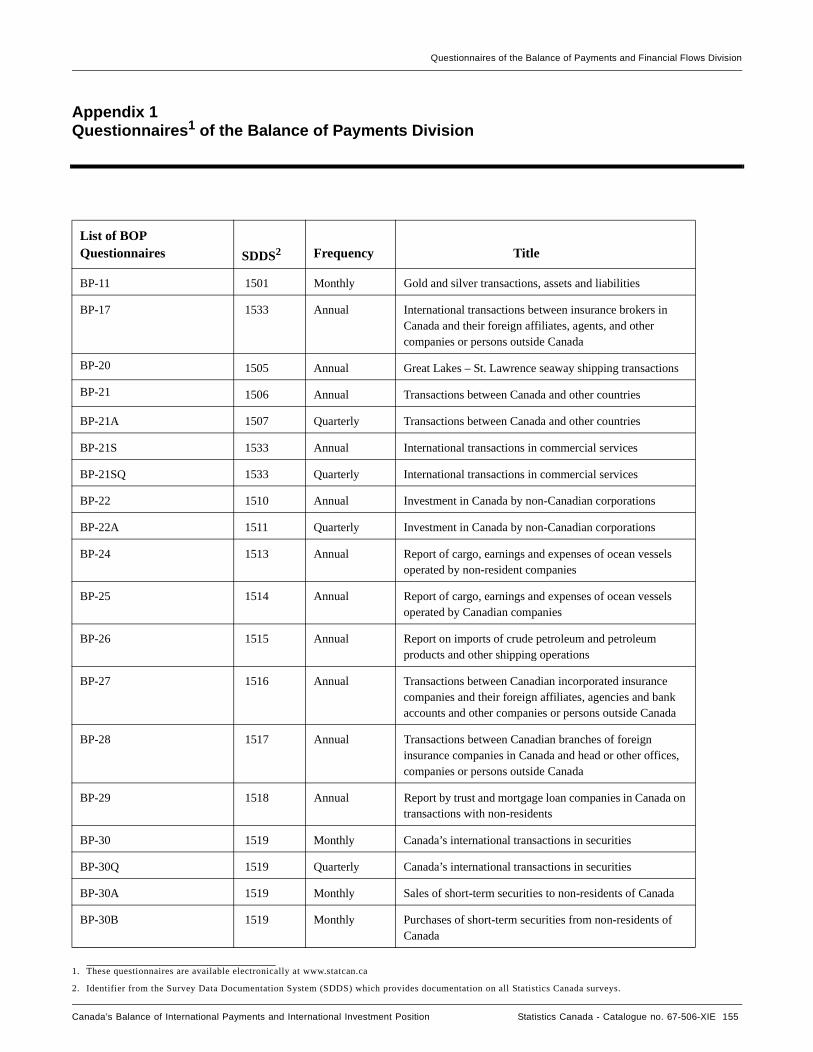

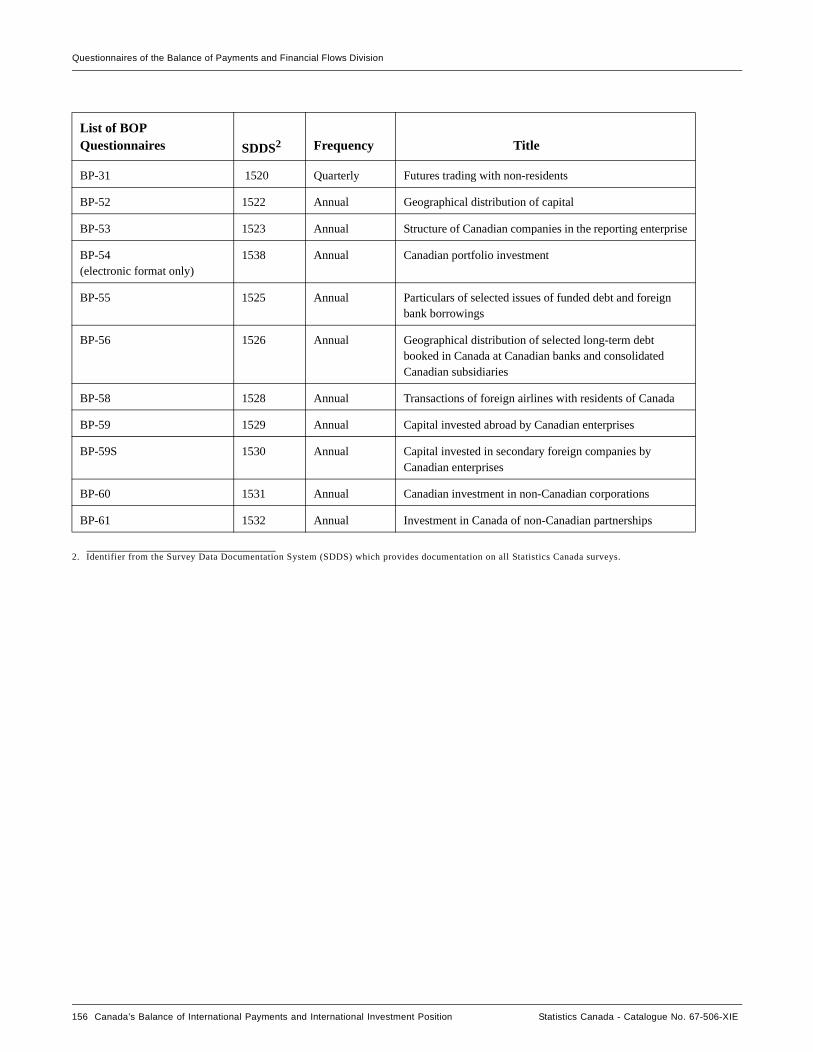

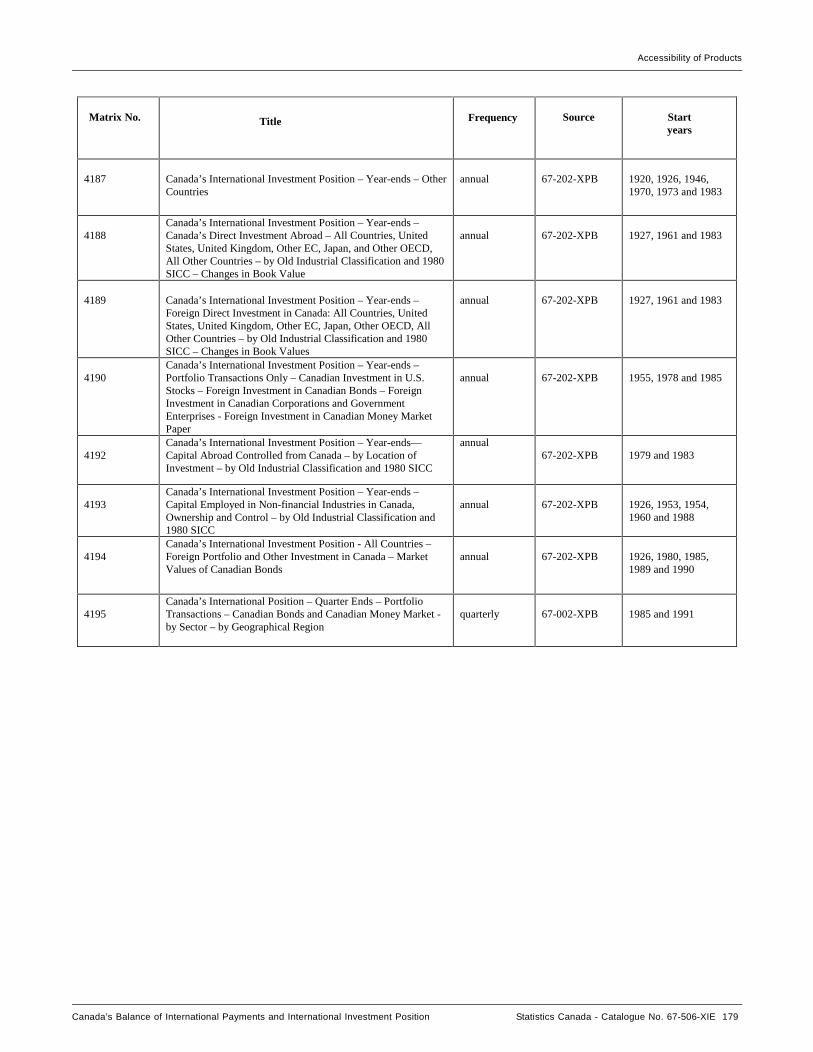

Appendix 1 List of Questionnaires of the Balance of Payments Division ..................................................................155

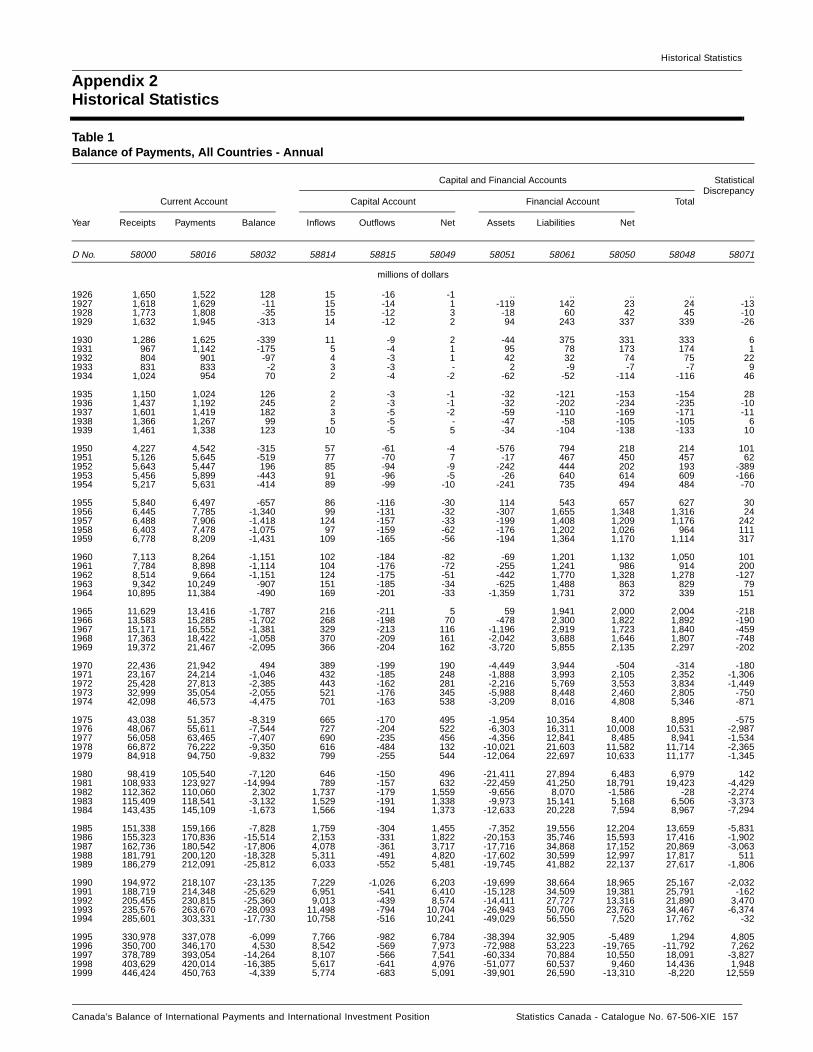

Appendix 2 Historical Statistics .....................................................................................................................................157

Appendix 3 Chronology of Events Affecting the External Sector of the Canadian Economy Since 1944..............163

Appendix 4 Accessibility of Products ............................................................................................................................173

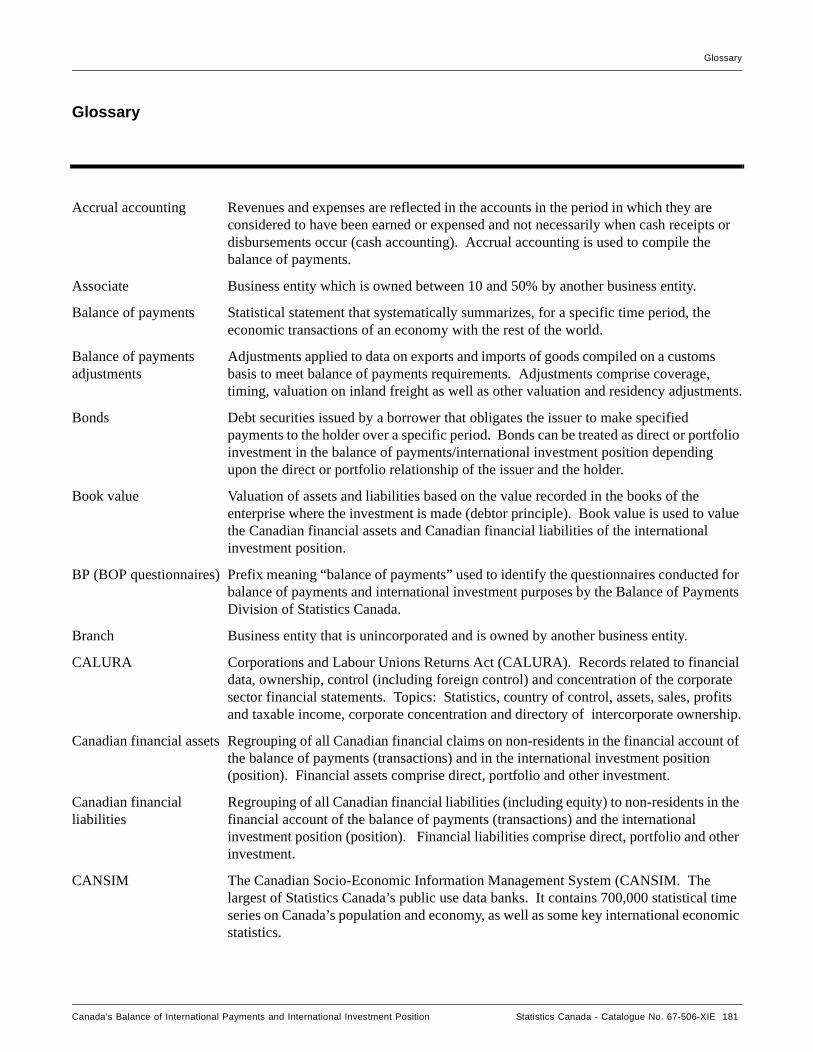

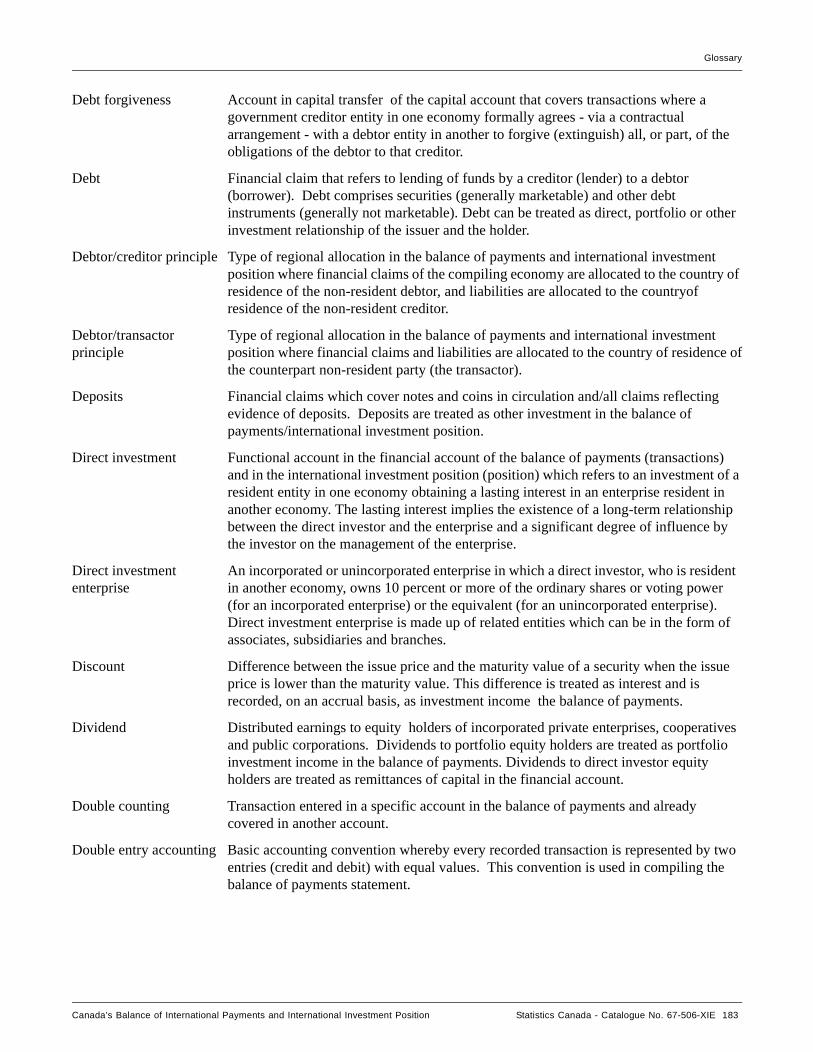

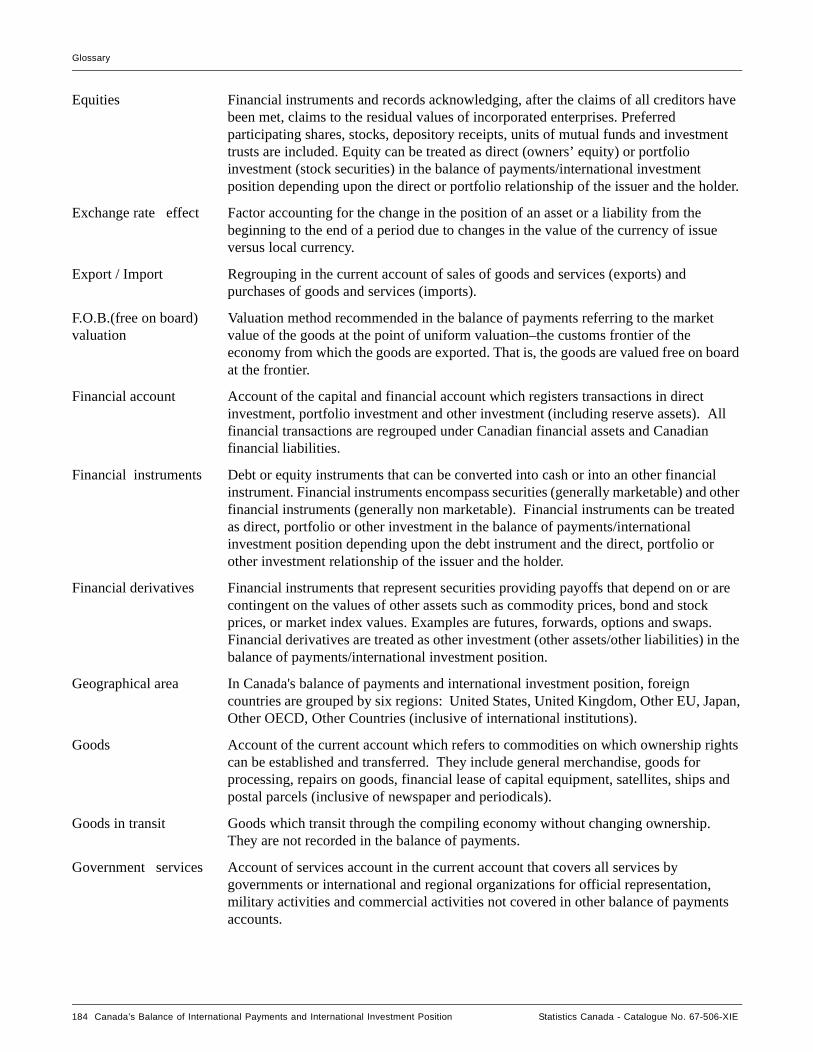

Glossary ....................................................................................................................................................................................181

Bibliography .............................................................................................................................................................................189

Structure of Accounts..............................................................................................................................................................193

Index ..........................................................................................................................................................................................195

Table of contents (detailed)

TABLE OF CONTENTS (detailed)

Page

PREFACE ...................................................................................................................................................................... xiii

ACKNOWLEDGEMENTS......................................................................................................................................................xv

INTRODUCTION.......................................................................................................................................................................1

PART I BALANCE OF INTERNATIONAL PAYMENTS ....................................................................................5

CHAPTER 1 Conceptual Framework of the Balance of Payments .................................................................................7

1.1 Canadian resident transactors and non-resident transactors ...................................................................71.1.1 Persons as Canadian residents .........................................................................................................................71.1.2 Unincorporated businesses, corporations and government enterprises as Canadian residents .......................81.1.3 Various levels of Canadian government as Canadian residents ......................................................................81.1.4 Summary on Canadian residents .....................................................................................................................9

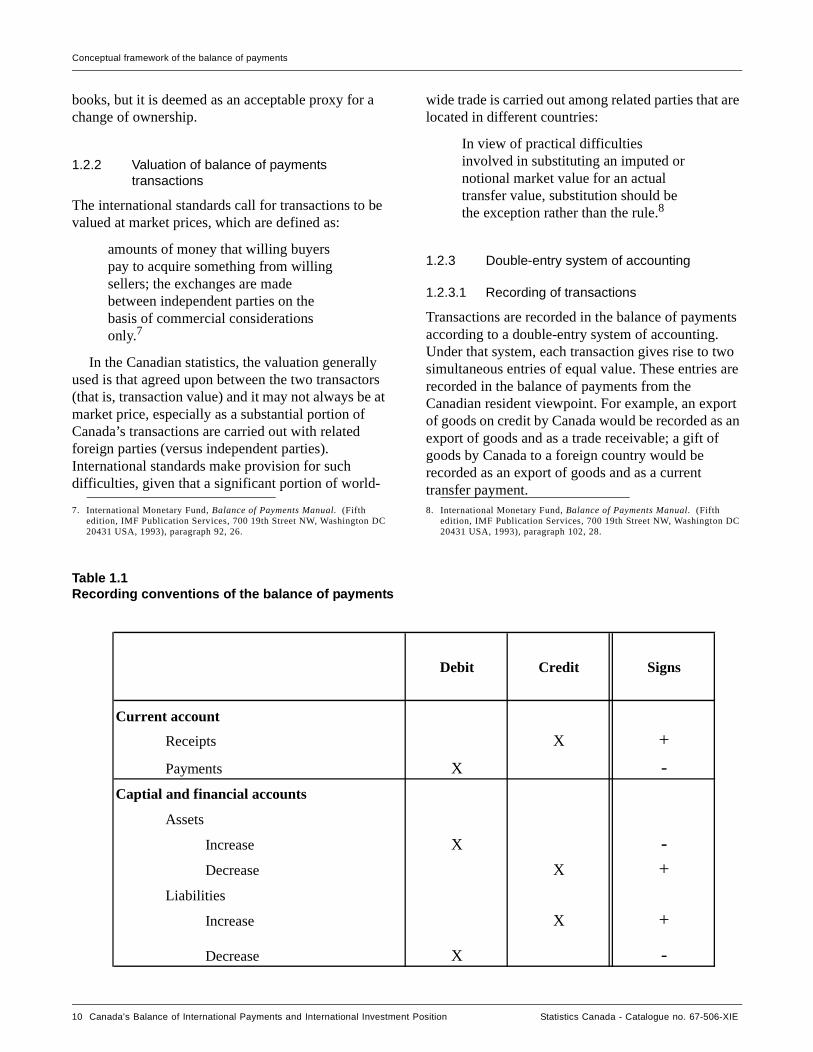

1.2 Balance of payments transactions ................................................................................................................91.2.1 Timing for recording balance of payments transactions .................................................................................91.2.2 Valuation of balance of payments transactions .............................................................................................101.2.3 Double-entry system of accounting ...............................................................................................................101.2.3.1 Recording of transactions ..............................................................................................................................101.2.3.2 Statistical discrepancy ...................................................................................................................................11

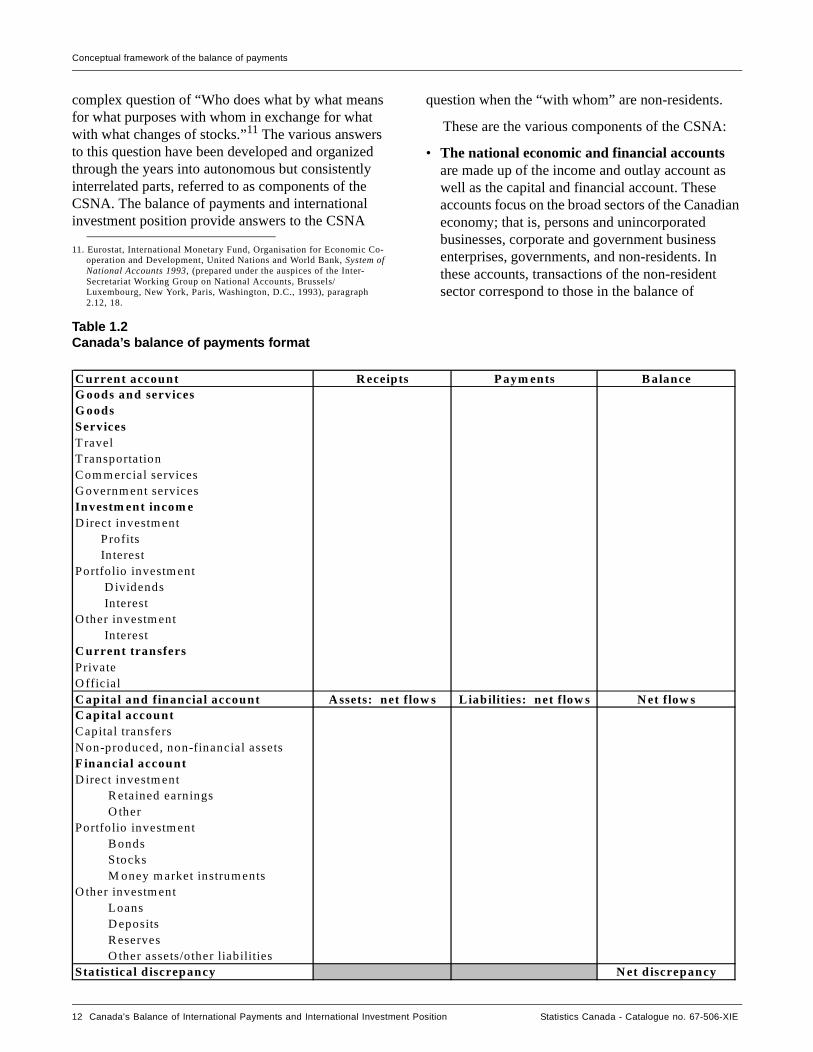

1.3 Format of the balance of payments statement ..........................................................................................11

1.4 Relationship with other statistical systems ................................................................................................111.4.1 Linkages to the Canadian System of National Accounts ..............................................................................111.4.2 Link with balance of payments systems of other countries ...........................................................................13

1.5 Interpretation of balance of payments accounts .......................................................................................131.5.1 Accounting interpretation ..............................................................................................................................131.5.2 Analytical interpretation ................................................................................................................................14

CHAPTER 2 The Current Account ..................................................................................................................................17

2.1 Concepts .......................................................................................................................................................17

2.2 Data sources .................................................................................................................................................17

2.3 Methods ........................................................................................................................................................17

2.4 Products ........................................................................................................................................................172.4.1 Data accuracy ................................................................................................................................................172.4.2 Data accessibility ...........................................................................................................................................17

CHAPTER 3 Goods .............................................................................................................................................................19

3.1 Concepts .......................................................................................................................................................19

3.2 Data sources .................................................................................................................................................213.2.1 General commodity trade system ..................................................................................................................213.2.2 Commodity presentation ...............................................................................................................................213.2.3 Valuation .......................................................................................................................................................223.2.3.1 Transaction value ...........................................................................................................................................223.2.3.2 Valuation at the border ..................................................................................................................................223.2.4 Country attribution ........................................................................................................................................23

3.3 Methods ........................................................................................................................................................ 243.3.1 Exports ...........................................................................................................................................................243.3.1.1 Coverage adjustments ....................................................................................................................................24

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue no. 67-506-XIE v

Table of contents (detailed)

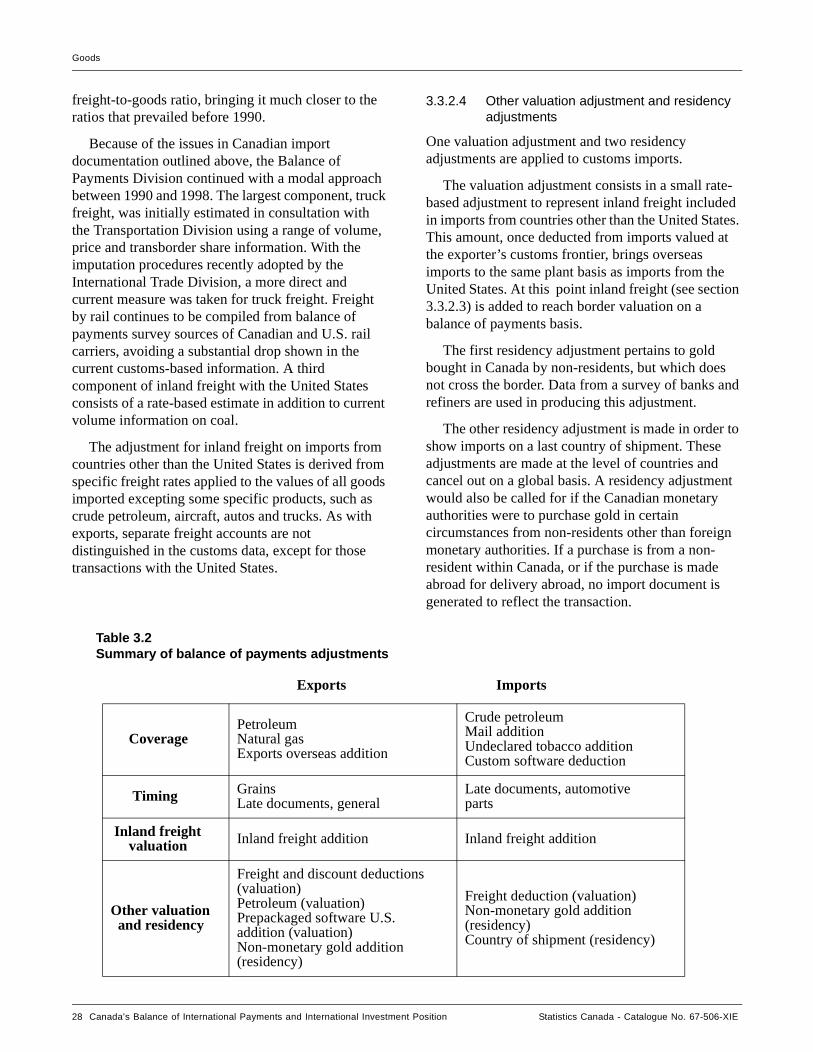

3.3.1.2 Timing adjustments .......................................................................................................................................253.3.1.3 Valuation adjustments for inland freight .......................................................................................................253.3.1.4 Other valuation and residency adjustments ...................................................................................................263.3.1.4.1 Removal of customs-based and additional freight ........................................................................................263.3.1.4.2 Valuation adjustments to prepackaged software ...........................................................................................263.3.1.4.3 Residency adjustments on gold .....................................................................................................................263.3.2 Imports of goods ............................................................................................................................................273.3.2.1 Coverage adjustments ....................................................................................................................................273.3.2.2 Timing adjustment .........................................................................................................................................273.3.2.3 Valuation adjustment for inland freight ........................................................................................................273.3.2.4 Other valuation adjustment and residency adjustments ................................................................................283.3.3 Summary ........................................................................................................................................................29

3.4 Products ........................................................................................................................................................293.4.1 Data accuracy ................................................................................................................................................293.4.2 Data accessibility ...........................................................................................................................................29

CHAPTER 4 Travel ............................................................................................................................................................31

4.1 Concepts .......................................................................................................................................................314.1.1 Business travel ...............................................................................................................................................314.1.2 Personal travel ...............................................................................................................................................314.1.2.1 Health-related travel ......................................................................................................................................314.1.2.2 Education-related travel .................................................................................................................................324.1.2.3 Other personal travel .....................................................................................................................................32

4.2 Data sources .................................................................................................................................................32

4.3 Methods ........................................................................................................................................................334.3.1 General methodology ....................................................................................................................................334.3.2 Extended geographical breakouts ..................................................................................................................33

4.4 Products ........................................................................................................................................................334.4.1 Data accuracy ................................................................................................................................................334.4.2 Data accessibility ...........................................................................................................................................34

CHAPTER 5 Transportation .............................................................................................................................................35

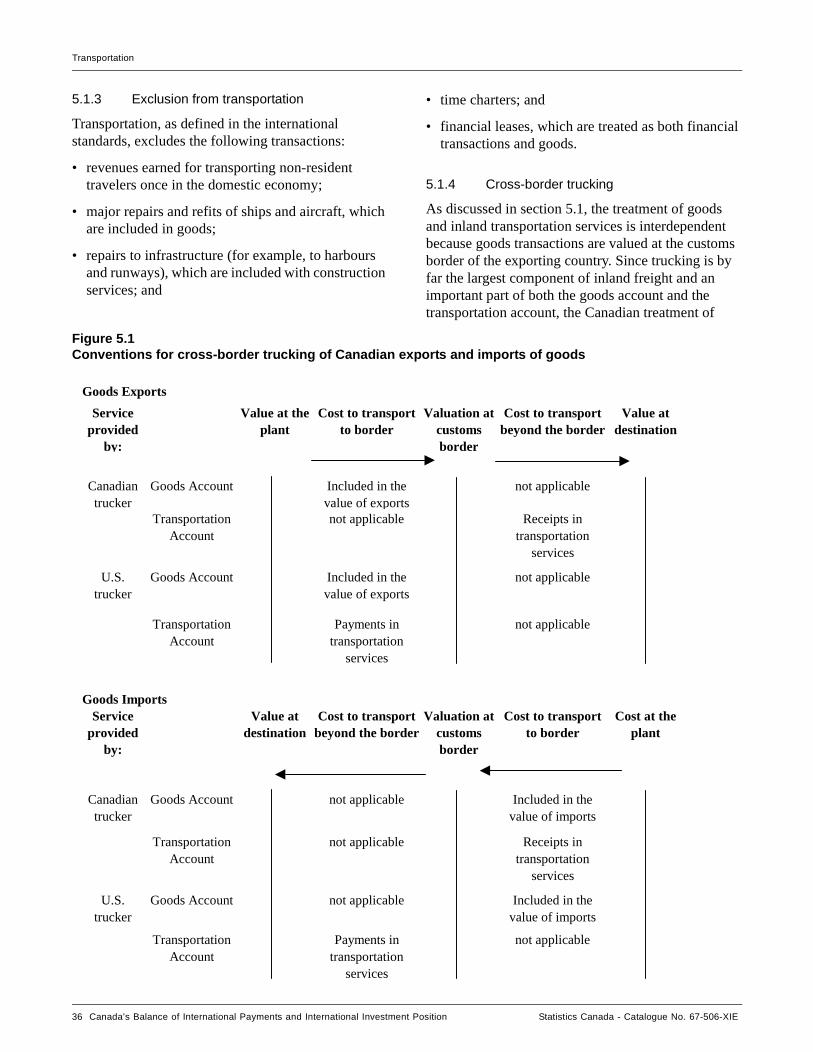

5.1 Concepts ........................................................................................................................................................355.1.1 Receipts .........................................................................................................................................................355.1.2 Payments ........................................................................................................................................................355.1.3 Exclusion from transportation .......................................................................................................................365.1.4 Cross-border trucking ....................................................................................................................................36

5.2 Data sources .................................................................................................................................................375.2.1 Passenger fares ..............................................................................................................................................375.2.2 Transportation of goods .................................................................................................................................37

5.3 Methods ........................................................................................................................................................375.3.1 General methodology ....................................................................................................................................375.3.2 Extended geographical breakouts ..................................................................................................................38

5.4 Products ........................................................................................................................................................385.4.1 Data accuracy ................................................................................................................................................385.4.2 Data accessibility ...........................................................................................................................................39

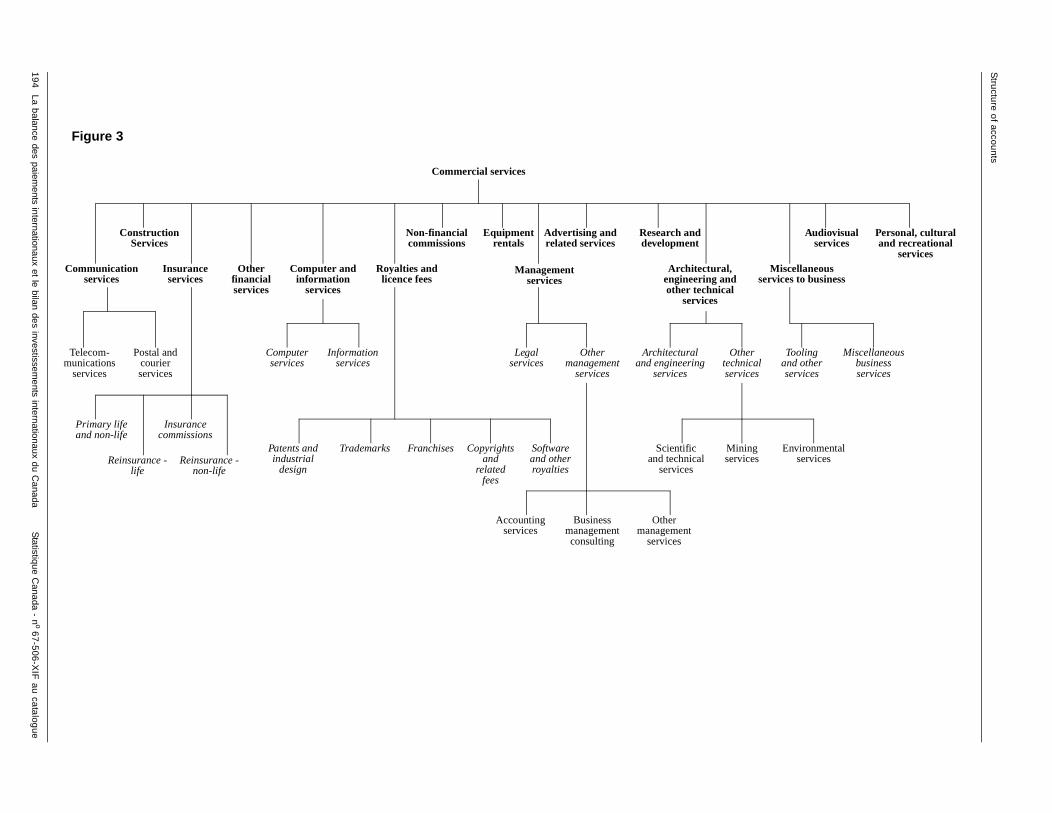

CHAPTER 6 Commercial Services ...................................................................................................................................41

6.1 Concepts .......................................................................................................................................................416.1.1 Transactions ...................................................................................................................................................416.1.2 Transactors ....................................................................................................................................................41

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue no. 67-506-XIE vi

Table of contents (detailed)

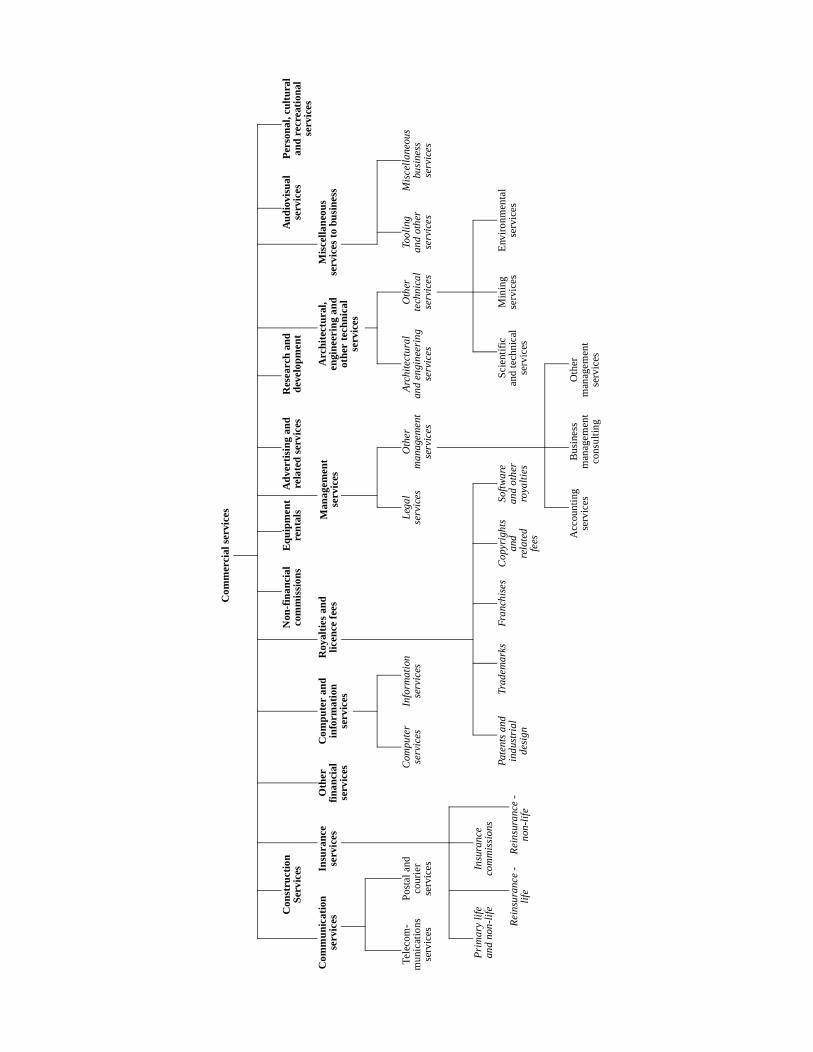

6.2 Data sources .................................................................................................................................................426.2.1 General description ........................................................................................................................................426.2.2 Description and sources by service categories ..............................................................................................436.2.2.1 Communication services ...............................................................................................................................436.2.2.2 Construction services .....................................................................................................................................446.2.2.3 Insurance services ..........................................................................................................................................446.2.2.4 Other financial services .................................................................................................................................456.2.2.5 Computer and information services ...............................................................................................................466.2.2.6 Royalties and licence fees .............................................................................................................................476.2.2.7 Non-financial commissions ...........................................................................................................................476.2.2.8 Equipment rentals ..........................................................................................................................................486.2.2.9 Management services ....................................................................................................................................486.2.2.10 Advertising and related services ....................................................................................................................496.2.2.11 Research and development ............................................................................................................................496.2.2.12 Architectural, engineering and other technical services ................................................................................496.2.2.13 Miscellaneous services to business ...............................................................................................................506.2.2.14 Audiovisual services ......................................................................................................................................516.2.2.15 Personal, cultural and recreational services ...................................................................................................51

6.3 Methods ........................................................................................................................................................516.3.1 General methodology ....................................................................................................................................516.3.2 Extended geographical breakouts ..................................................................................................................52

6.4 Products ........................................................................................................................................................526.4.1 Data accuracy ................................................................................................................................................526.4.2 Data accessibility ...........................................................................................................................................52

CHAPTER 7 Goverment Services .....................................................................................................................................55

7.1 Concepts .......................................................................................................................................................55

7.2 Data sources .................................................................................................................................................55

7.3 Methods ........................................................................................................................................................557.3.1 General methodology ....................................................................................................................................557.3.2 Extended geographical breakouts ..................................................................................................................56

7.4 Products ........................................................................................................................................................567.4.1 Data accuracy ................................................................................................................................................567.4.2 Data accessibility ...........................................................................................................................................56

CHAPTER 8 Investment Income ......................................................................................................................................57

8.1 Concepts .......................................................................................................................................................578.1.1 Direct investment income ..............................................................................................................................578.1.2 Portfolio investment income ..........................................................................................................................578.1.3 Other investment income ...............................................................................................................................57

8.2 Data sources .................................................................................................................................................58

8.3 Methods ........................................................................................................................................................58

8.4 Products ........................................................................................................................................................598.4.1 Data accuracy ................................................................................................................................................598.4.2 Data accessibility ...........................................................................................................................................60

CHAPTER 9 Current Transfers .......................................................................................................................................61

9.1 Concepts .......................................................................................................................................................619.1.1 Receipts .........................................................................................................................................................619.1.2 Payments ........................................................................................................................................................61

9.2 Data sources .................................................................................................................................................62

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue no. 67-506-XIE vii

Table of contents (detailed)

9.3 Methods ........................................................................................................................................................62

9.4 Products ........................................................................................................................................................629.4.1 Data accuracy ................................................................................................................................................629.4.2 Data accessibility ...........................................................................................................................................62

CHAPTER 10 The Capital and Financial Account ...........................................................................................................63

10.1 Concepts .......................................................................................................................................................63

10.2 Data sources .................................................................................................................................................63

10.3 Methods ........................................................................................................................................................63

10.4 Products ........................................................................................................................................................6410.4.1 Data accuracy ................................................................................................................................................6410.4.2 Data accessibility ...........................................................................................................................................64

CHAPTER 11 Capital Account ...........................................................................................................................................65

11.1 Concepts .......................................................................................................................................................65

11.2 Data sources .................................................................................................................................................65

11.3 Methods ........................................................................................................................................................65

11.4 Products ........................................................................................................................................................6611.4.1 Data accuracy ................................................................................................................................................6611.4.2 Data accessibility ...........................................................................................................................................66

CHAPTER 12 Direct Investment Flows .............................................................................................................................67

12.1 Concepts .......................................................................................................................................................67

12.2 Data sources .................................................................................................................................................6712.2.1 Survey sources ...............................................................................................................................................6712.2.2 Administrative sources ..................................................................................................................................6812.2.3 Other sources .................................................................................................................................................68

12.3 Methods ........................................................................................................................................................68

12.4 Products ........................................................................................................................................................6912.4.1 Data accuracy ................................................................................................................................................6912.4.2 Data accessibility ...........................................................................................................................................69

CHAPTER 13 Portforlio Investment Flows .......................................................................................................................71

13.1 Concepts .......................................................................................................................................................7113.1.1 Description ....................................................................................................................................................7113.1.2 Canadian and foreign securities .....................................................................................................................7213.1.3 Transactions in securities ..............................................................................................................................72

13.2 Data sources .................................................................................................................................................7213.2.1 Bonds and stocks ...........................................................................................................................................7213.2.1.1 New issues of bonds and stocks ....................................................................................................................7213.2.1.2 Trade in outstanding bonds and stocks ..........................................................................................................7313.2.1.3 Retirements of bonds and stocks ..................................................................................................................7313.2.2 Canadian money market instruments ............................................................................................................73

13.3 Methods ........................................................................................................................................................7413.3.1 System to process Canadian bonds ................................................................................................................7413.3.1.1 Valuation of bonds ........................................................................................................................................7413.3.1.2 Income calculation of bonds ..........................................................................................................................7513.3.1.3 Transactions in Canadian bonds ....................................................................................................................7513.3.1.4 Reconciliation of positions and flows ...........................................................................................................76

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue no. 67-506-XIE viii

Table of contents (detailed)

13.3.2 Processing of other portfolio securities .........................................................................................................77

13.4 Products ........................................................................................................................................................7713.4.1 Data accuracy ................................................................................................................................................7713.4.2 Data accessibility ...........................................................................................................................................77

CHAPTER 14 Other Investment Flows ..............................................................................................................................79

14.1 Concepts .......................................................................................................................................................7914.1.1 Loan assets and loan liabilities ......................................................................................................................7914.1.2 Deposit assets and deposit liabilities .............................................................................................................7914.1.3 Official reserve assets ....................................................................................................................................7914.1.4 Other assets and other liabilities ....................................................................................................................79

14.2 Data sources .................................................................................................................................................8014.2.1 Loan assets and loan liabilities ......................................................................................................................8014.2.2 Deposit assets and deposit liabilities .............................................................................................................8114.2.3 Official reserve assets ....................................................................................................................................8114.2.4 Other assets and other liabilities ....................................................................................................................81

14.3 Methods ........................................................................................................................................................81

14.4 Products ........................................................................................................................................................8114.4.1 Data accuracy ................................................................................................................................................8114.4.2 Data accessibility ...........................................................................................................................................81

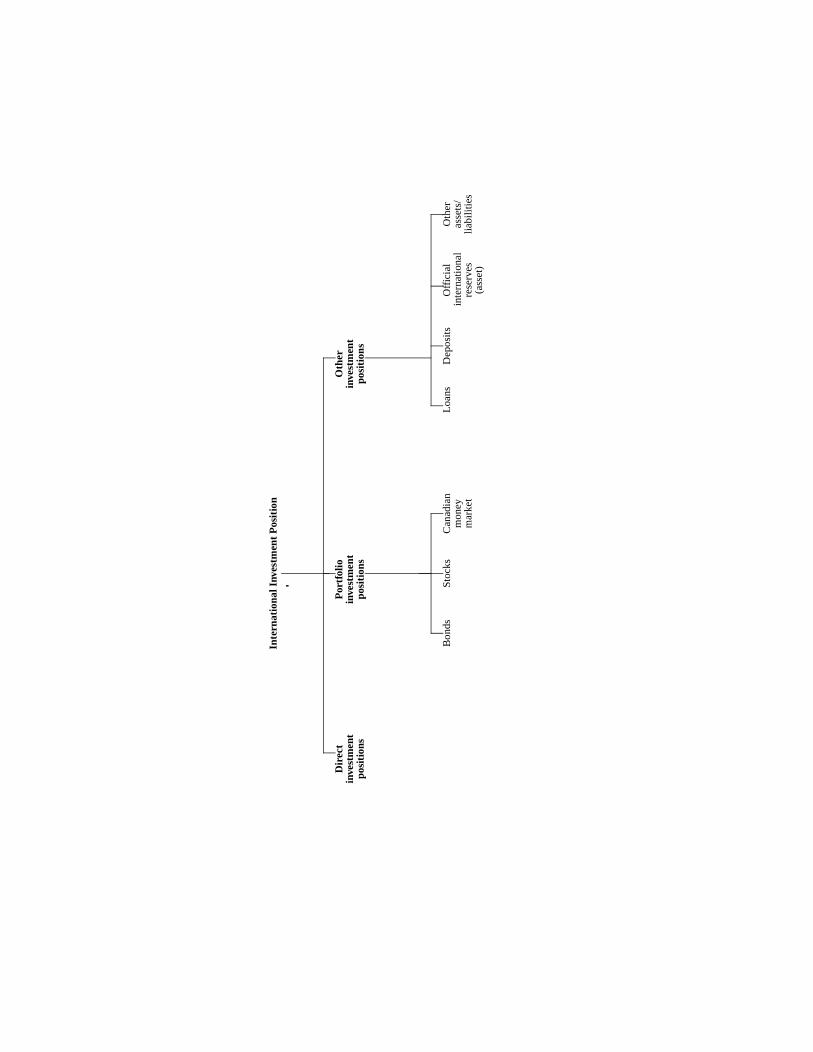

PART II INTERNATIONAL INVESTMENT POSITION ....................................................................................83

CHAPTER 15 Conceptual Framwork of the International Investment Position ...........................................................85

15.1 Canadian resident and non-resident transactors .....................................................................................85

15.2 Types of financial assets and financial liabilities ...................................................................................... 85

15.3 Valuation of international assets and liabilities ........................................................................................86

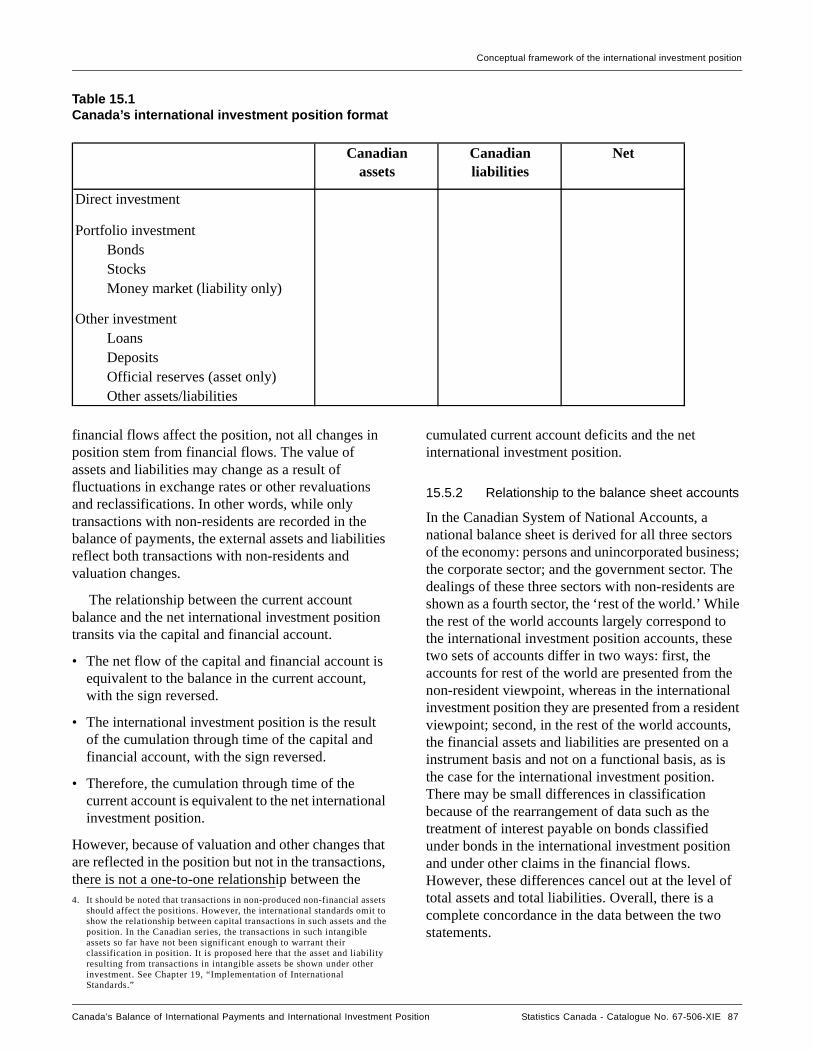

15.4 Format of the international investment position ......................................................................................86

15.5 Relationship to other statistical systems ....................................................................................................8615.5.1 Relationship to the balance of payments .......................................................................................................8615.5.2 Relationship to the balance sheet accounts ...................................................................................................87

15.6 Interpretation of the international investment position ...........................................................................8815.6.1 Accounting interpretation ..............................................................................................................................8815.6.2 Analytical interpretation ................................................................................................................................88

CHAPTER 16 Direct Investment Position ..........................................................................................................................89

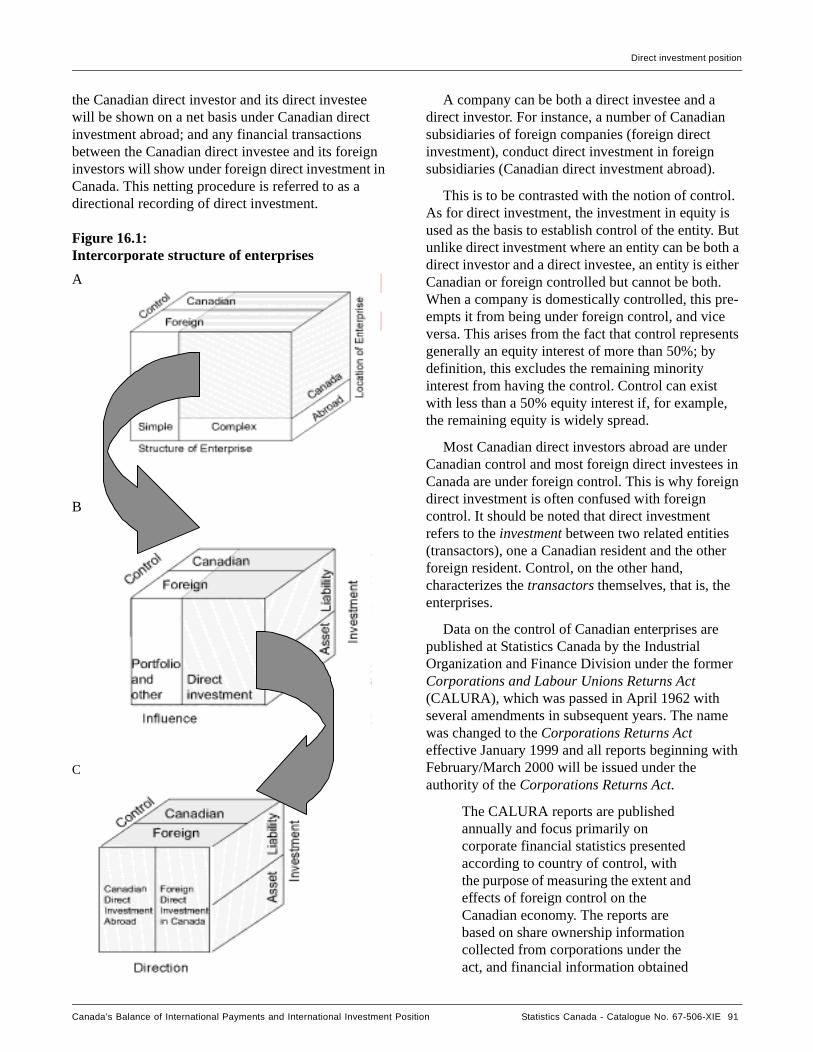

16.1 Concepts .......................................................................................................................................................8916.1.1 Description ....................................................................................................................................................8916.1.2 Valuation .......................................................................................................................................................8916.1.3 Distinction between direct investment and control .......................................................................................8916.1.4 Distinction between company and enterprise ................................................................................................9216.1.5 Distinction between direct investment and other investment ........................................................................92

16.2 Data sources .................................................................................................................................................9316.2.1 Surveys ..........................................................................................................................................................9316.2.1.1 Canadian direct investment abroad ...............................................................................................................9316.2.1.2 Foreign direct investment in Canada .............................................................................................................9416.2.1.3 Consolidating structure of the reporting entity ..............................................................................................9416.2.2 Other sources .................................................................................................................................................94

16.3 Methods ........................................................................................................................................................95

16.4 Products ........................................................................................................................................................95

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue no. 67-506-XIE ix

Table of contents (detailed)

16.4.1 Data accuracy ................................................................................................................................................9516.4.1.1 Canadian direct investment abroad ...............................................................................................................9516.4.1.2 Foreign direct investment in Canada .............................................................................................................9516.4.2 Data accessibility........................................................................................................................................... 95

CHAPTER 17 Portfolio Investment Position .....................................................................................................................97

17.1 Concepts .......................................................................................................................................................9717.1.1 Description ....................................................................................................................................................9717.1.2 Valuation ........................................................................................................................................................97

17.2 Data sources .................................................................................................................................................97

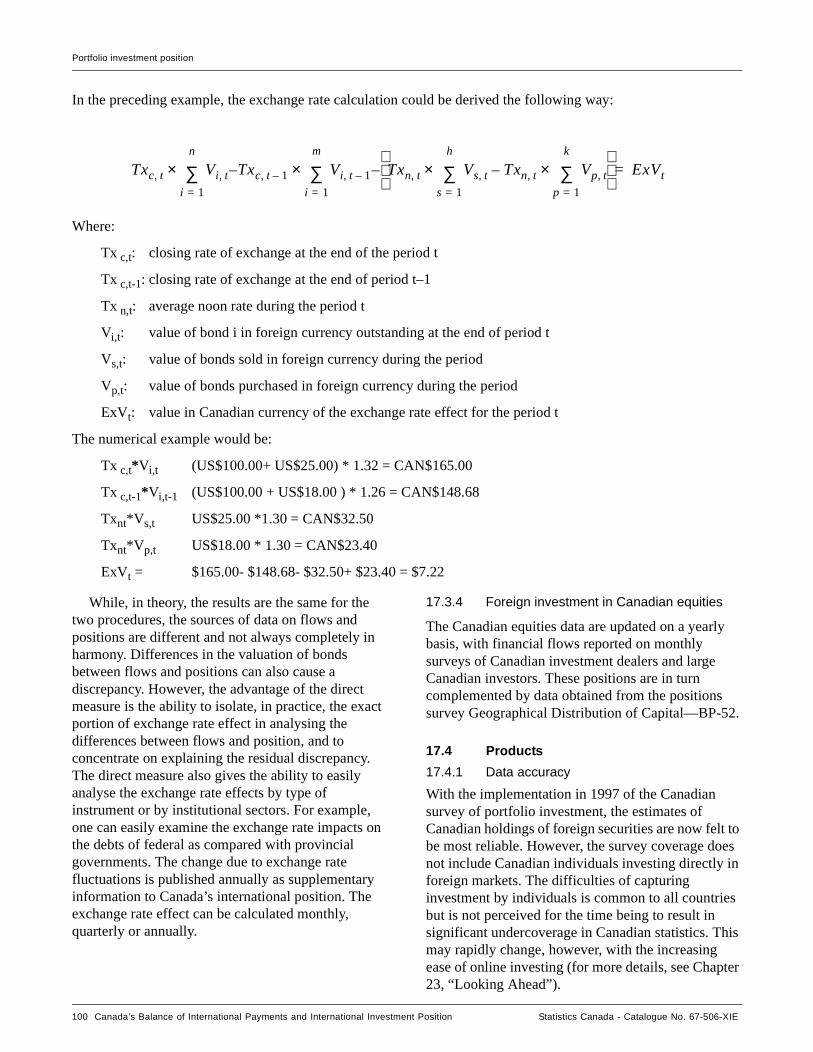

17.3 Methods ........................................................................................................................................................9817.3.1 Canadian portfolio investment abroad ...........................................................................................................9817.3.2 Foreign portfolio investment in Canadian bonds and money market ............................................................9817.3.3 Exchange rate valuation in Canadian bonds ..................................................................................................9817.3.4 Foreign investment in Canadian equities ....................................................................................................100

17.4 Products ......................................................................................................................................................10017.4.1 Data accuracy ..............................................................................................................................................10017.4.2 Data accessibility .........................................................................................................................................101

CHAPTER 18 Other Investment Position ........................................................................................................................103

18.1 Concepts .....................................................................................................................................................10318.1.1 Loan assets and loan liabilities ....................................................................................................................10318.1.2 Deposit assets and deposit liabilities ...........................................................................................................10318.1.3 Official international reserves .....................................................................................................................10318.1.4 Other assets and other liabilities .................................................................................................................104

18.2 Data sources ...............................................................................................................................................10518.2.1 Loan assets and loan liabilities ....................................................................................................................10518.2.2 Deposit assets and deposit liabilities ...........................................................................................................10518.2.3 Official international reserves .....................................................................................................................10518.2.4 Other assets and other liabilities ..................................................................................................................105

18.3 Methods ......................................................................................................................................................106

18.4 Products ......................................................................................................................................................10618.4.1 Data accuracy ..............................................................................................................................................10618.4.2 Data accessibility .........................................................................................................................................106

PART III OVERVIEW OF THE STATISTICAL FRAMEWORK ......................................................................107

CHAPTER 19 Implementation of International Standards ...........................................................................................109

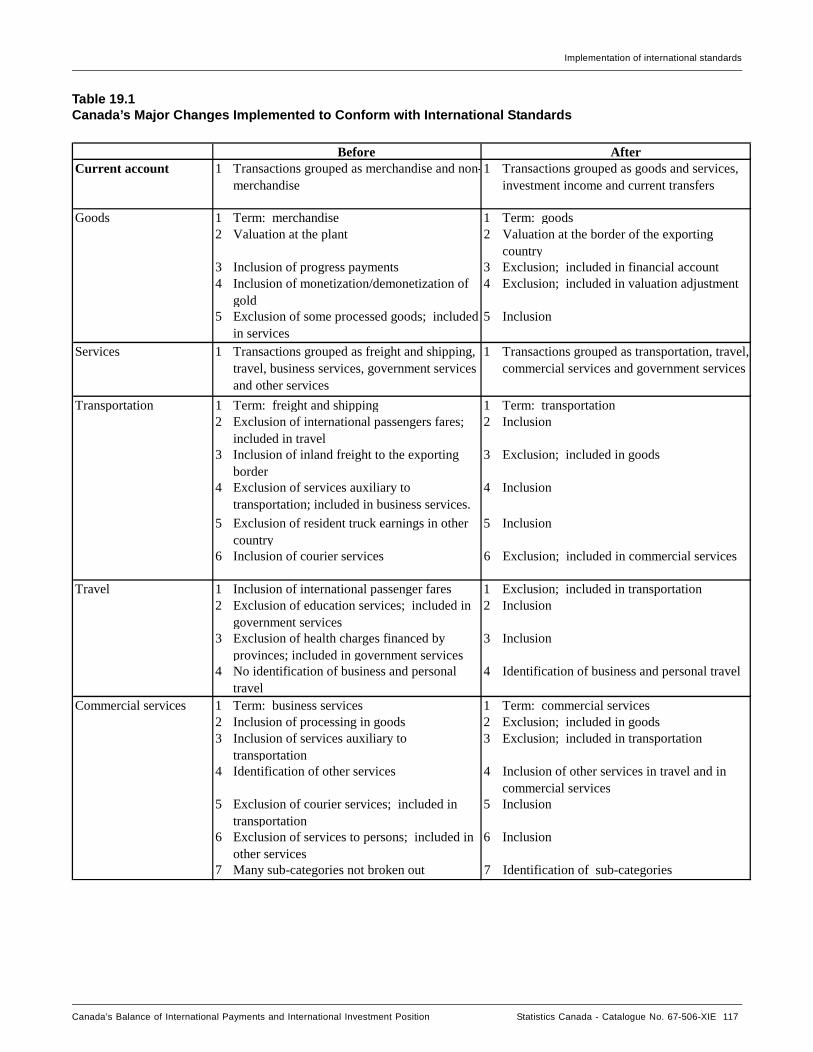

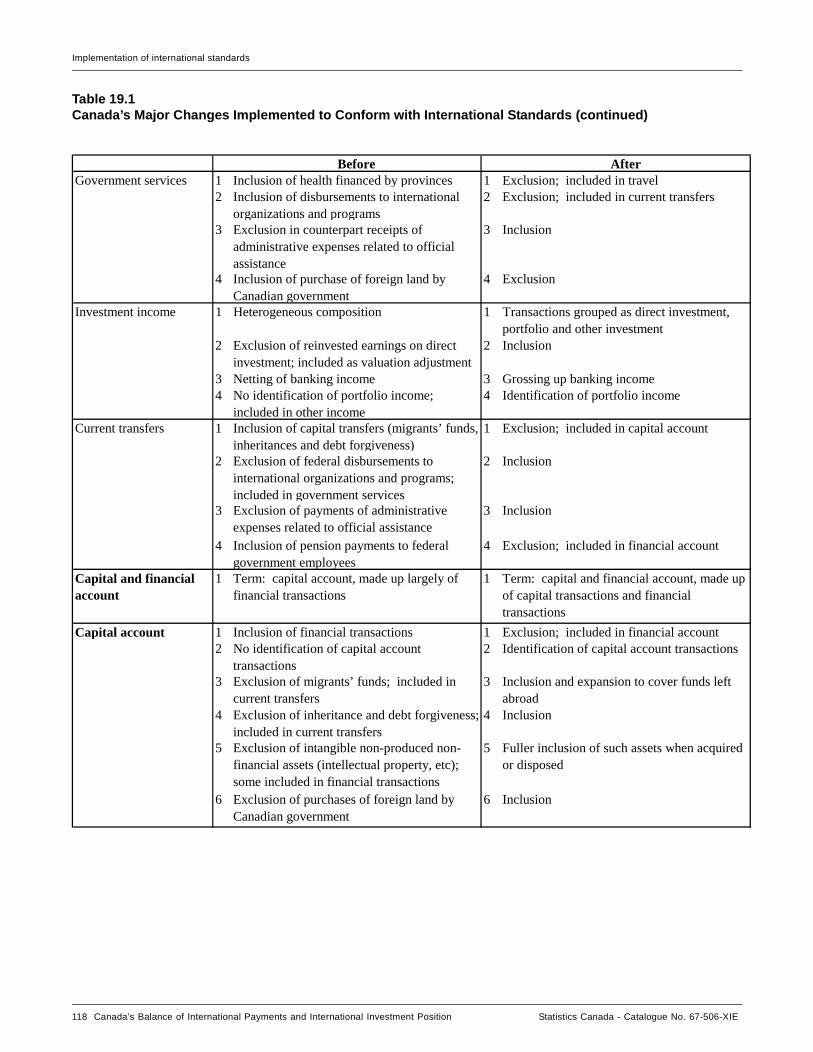

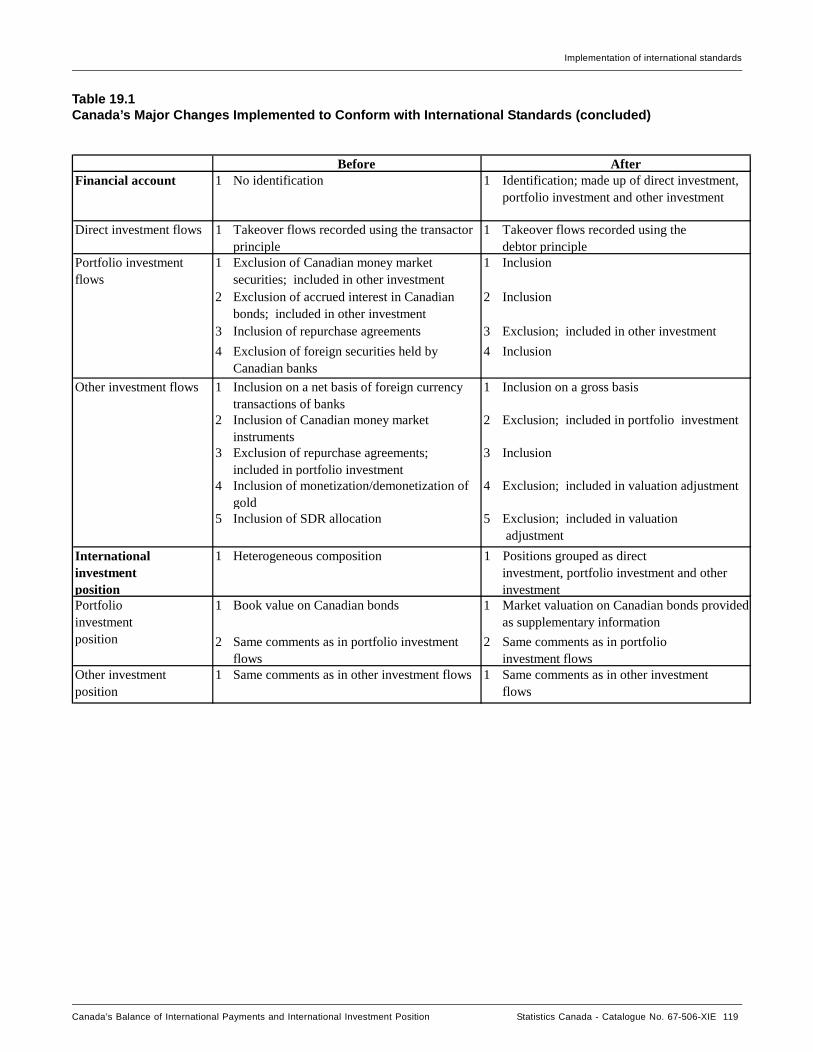

19.1 Major changes made to implement international standards .................................................................10919.1.1 Balance of payments ....................................................................................................................................10919.1.1.1 Current account ...........................................................................................................................................11019.1.1.2 Capital and financial account ......................................................................................................................11119.1.1.2.1 Capital account ............................................................................................................................................11119.1.1.2.2 Financial account .........................................................................................................................................11119.1.2 International investment position ................................................................................................................112

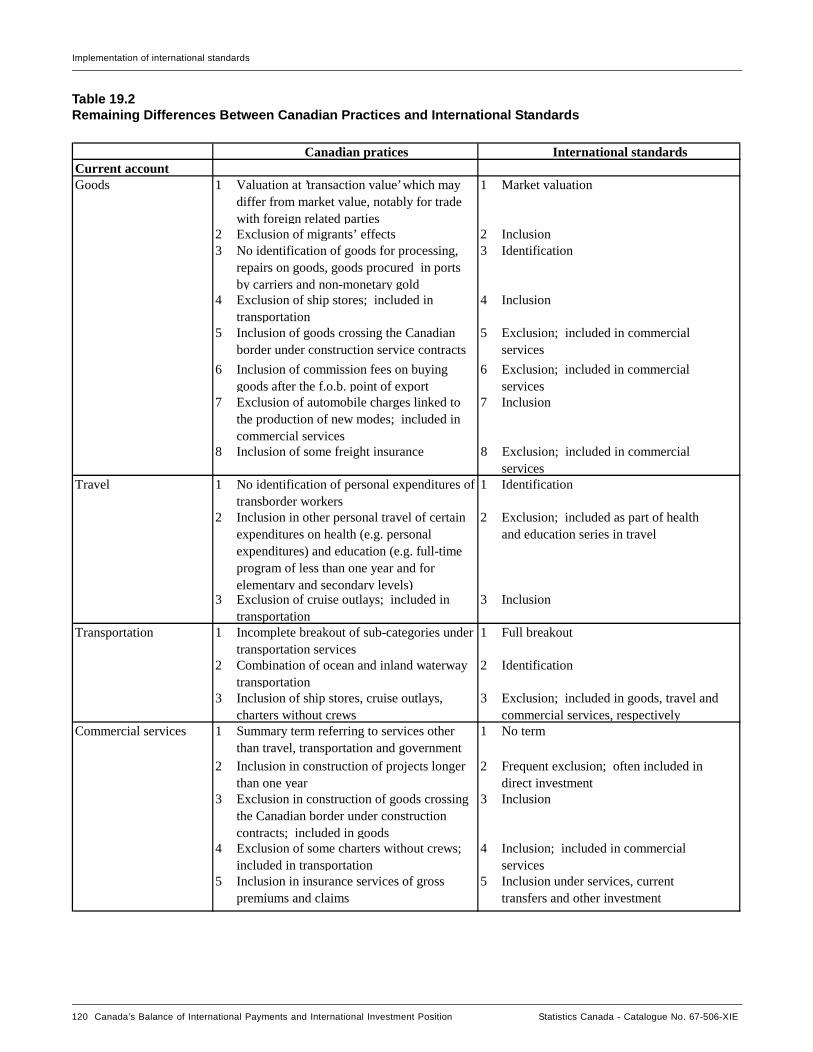

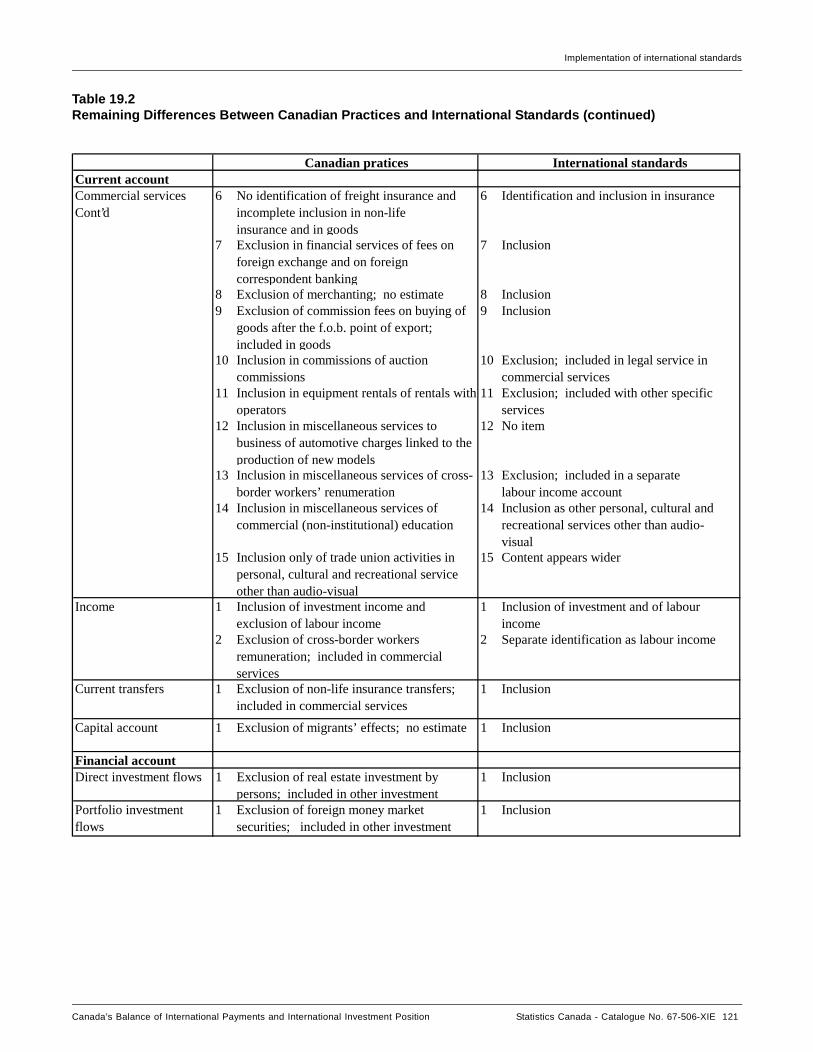

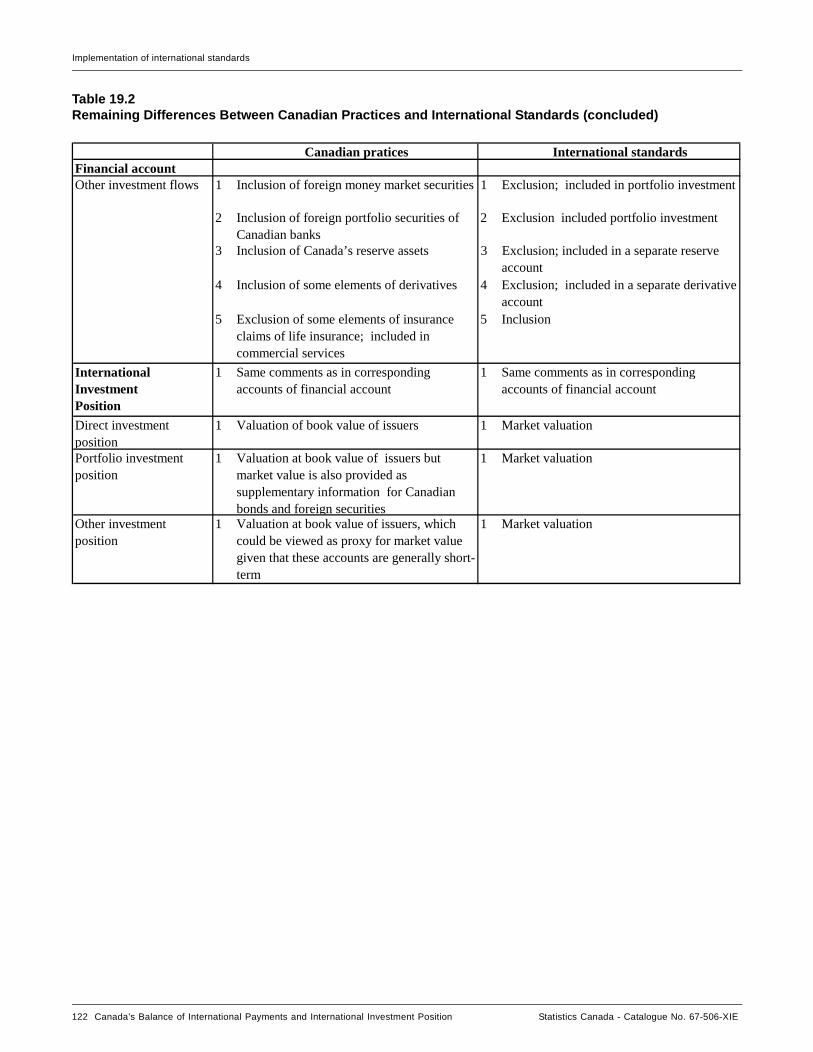

19.2 Remaining differences with international standards .............................................................................11319.2.1 Balance of payments ....................................................................................................................................11319.2.1.1 Current account ...........................................................................................................................................11319.2.1.2 Financial account .........................................................................................................................................11519.2.2 International investment position ................................................................................................................115

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue no. 67-506-XIE x

Table of contents (detailed)

.1

.......129

.......129

........130

.......132

....134

......137

.......137

...140

.....143

.......143

.......144

.......145

.......145

.......147

........147

........149

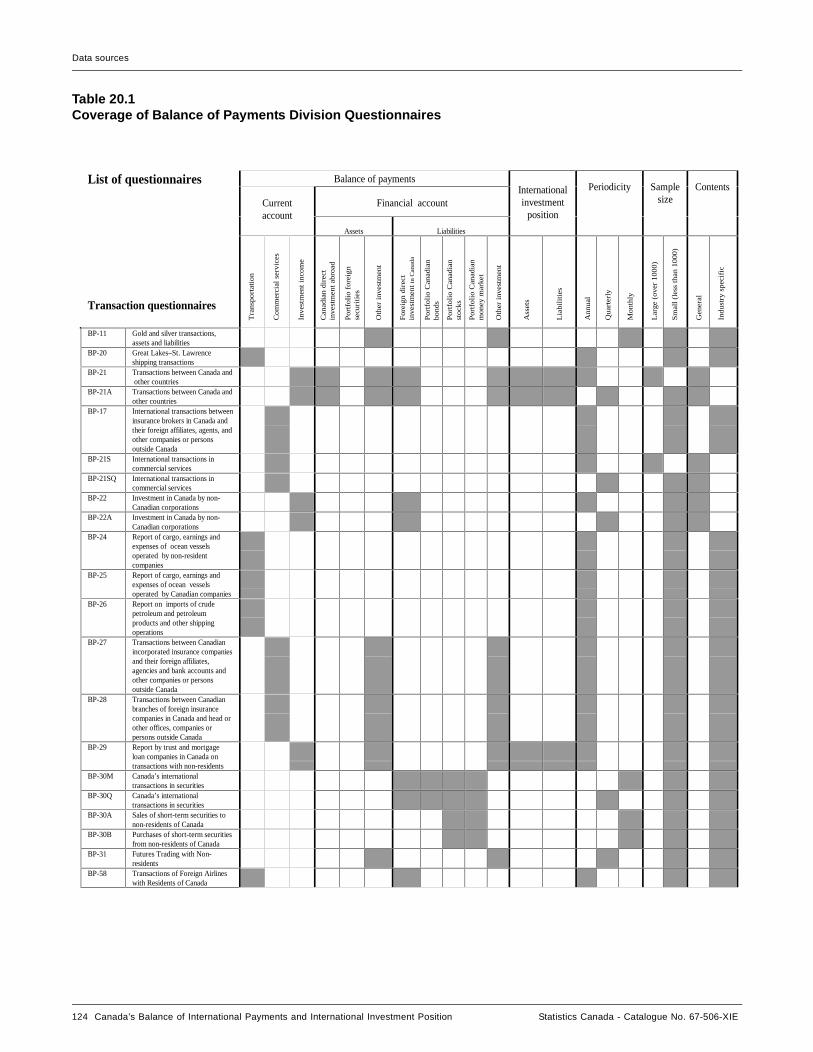

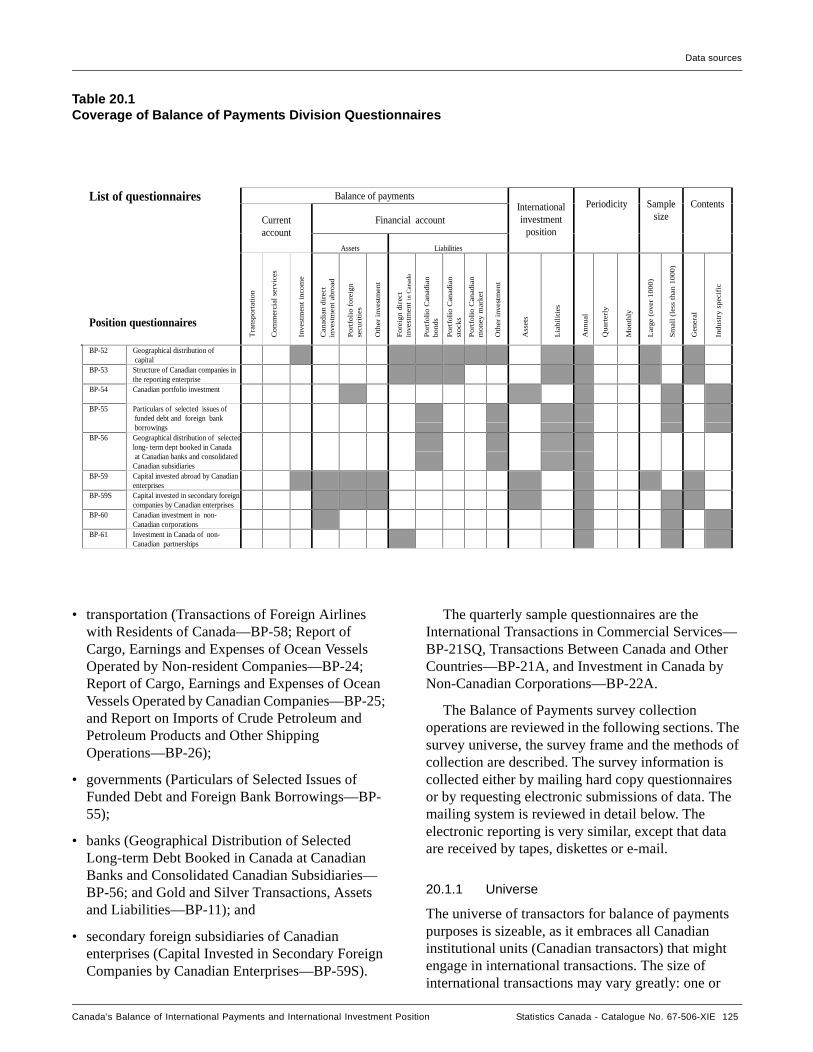

CHAPTER 20 Data Sources ...............................................................................................................................................123

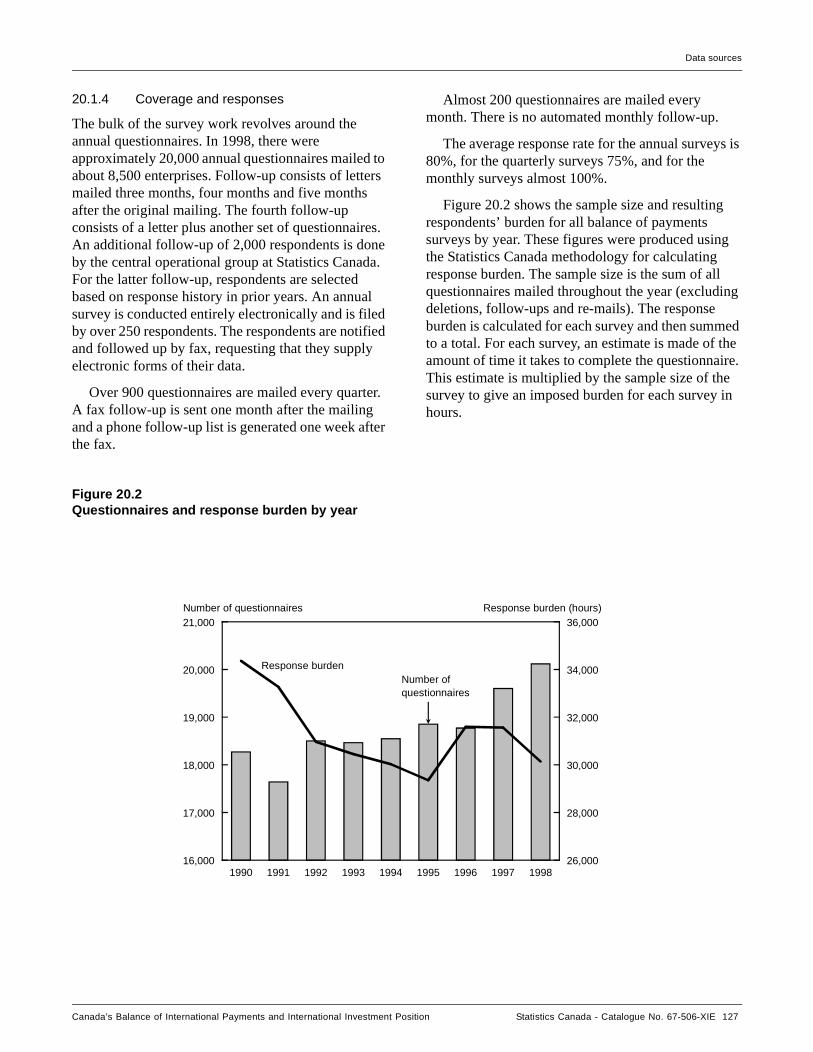

20.1 Balance of Payments Division surveys .....................................................................................................12320.1.1 Universe .......................................................................................................................................................12520.1.2 Balance of payments survey frame ..............................................................................................................12620.1.3 Survey Collection System ...........................................................................................................................12620.1.4 Coverage and responses .............................................................................................................................126

20.2 Canada–United States current account reconciliation .........................................................................28

CHAPTER 21 Processing Systems .............................................................................................................................

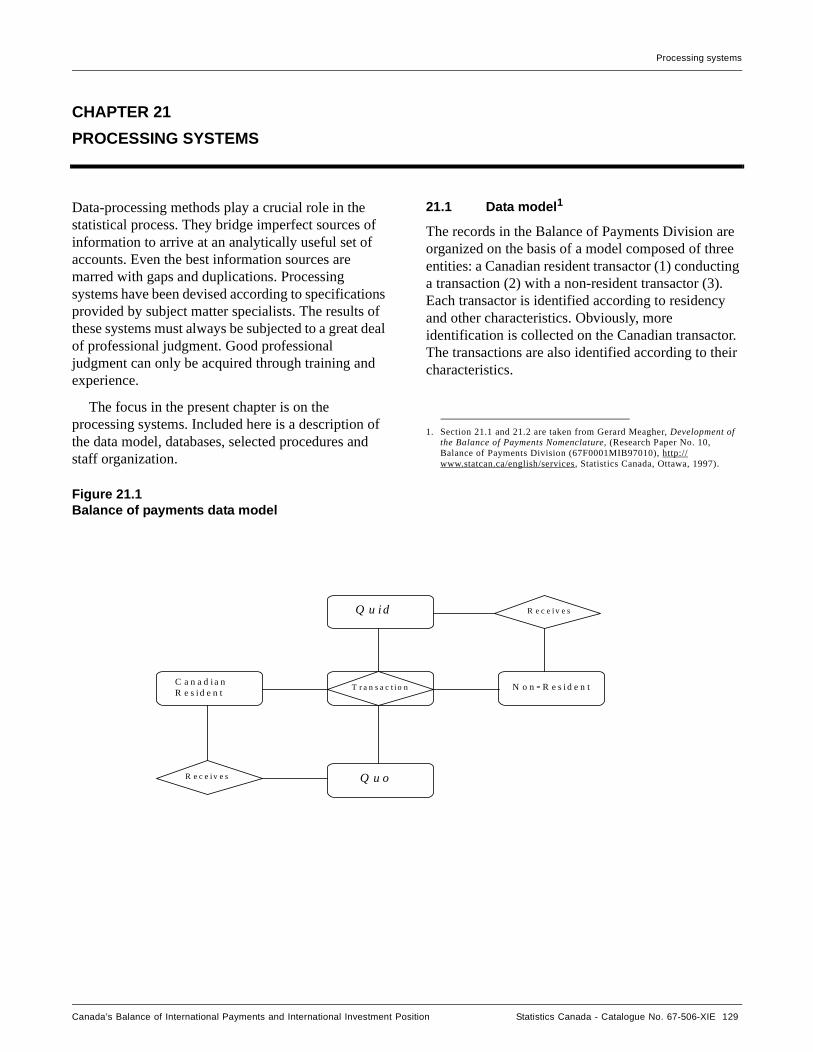

21.1 Data model ..........................................................................................................................................

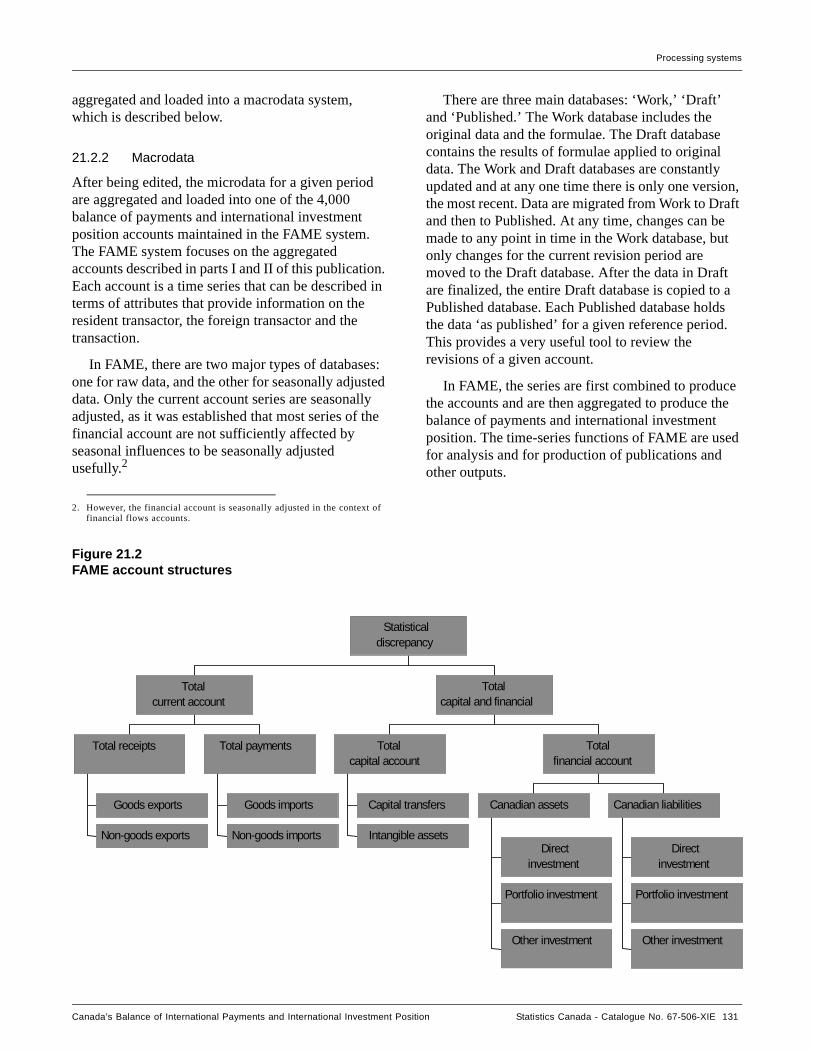

21.2 Databases ............................................................................................................................................21.2.1 Microdata .....................................................................................................................................................13021.2.2 Macrodata ....................................................................................................................................................131

21.3 Selected procedures ............................................................................................................................21.3.1 Quarterly and annual estimates ...................................................................................................................13221.3.2 Flows and position estimates .......................................................................................................................13221.3.3 Geographical distribution ............................................................................................................................13221.3.3.1 Principles of geographical allocation ..........................................................................................................13221.3.3.2 Published geographical distribution ............................................................................................................13321.3.3.3 Historical geographical allocation ...............................................................................................................13321.3.4 Industrial classification ................................................................................................................................133

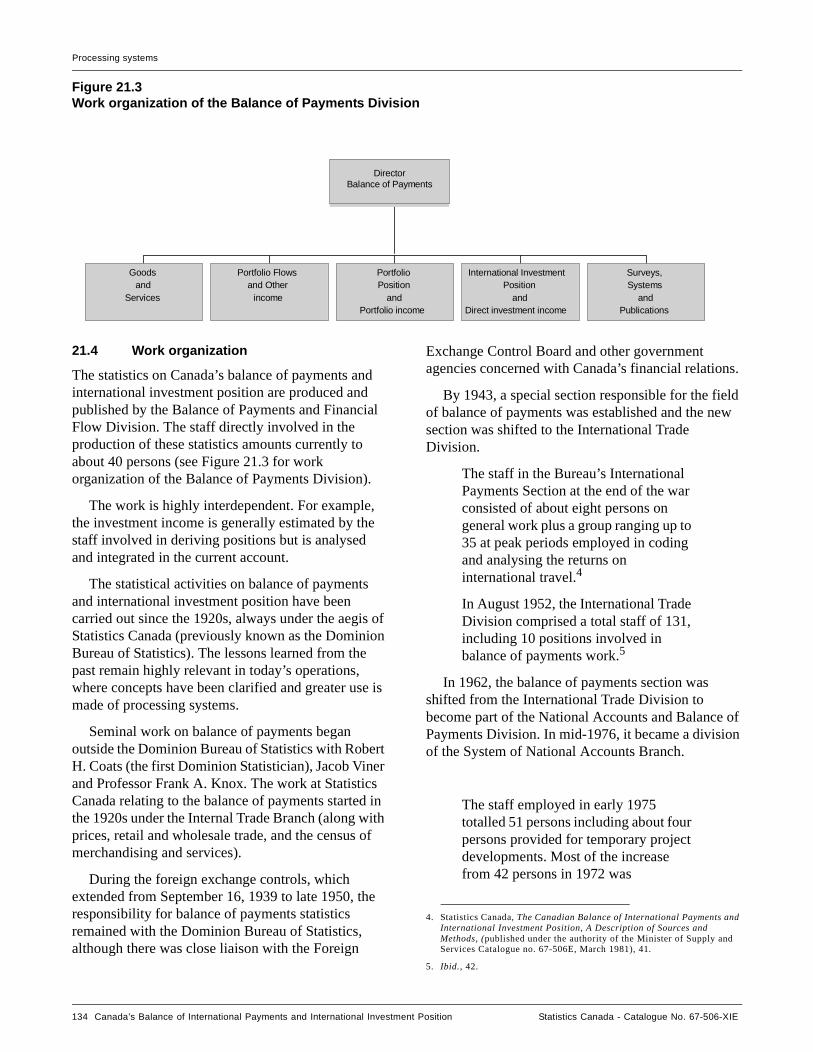

21.4 Work organization .................................................................................................................................

CHAPTER 22 Products ................................................................................................................................................

22.1 Products ...............................................................................................................................................22.1.1 Overview of regular programs .....................................................................................................................13722.1.2 Analytical papers .........................................................................................................................................13822.1.3 Other products .............................................................................................................................................139

22.2 Historical continuity of time series ..........................................................................................................139

22.3 Supranational organizations as major users ........................................................................................

CHAPTER 23 Looking Ahead ......................................................................................................................................

23.1 Concepts ..............................................................................................................................................

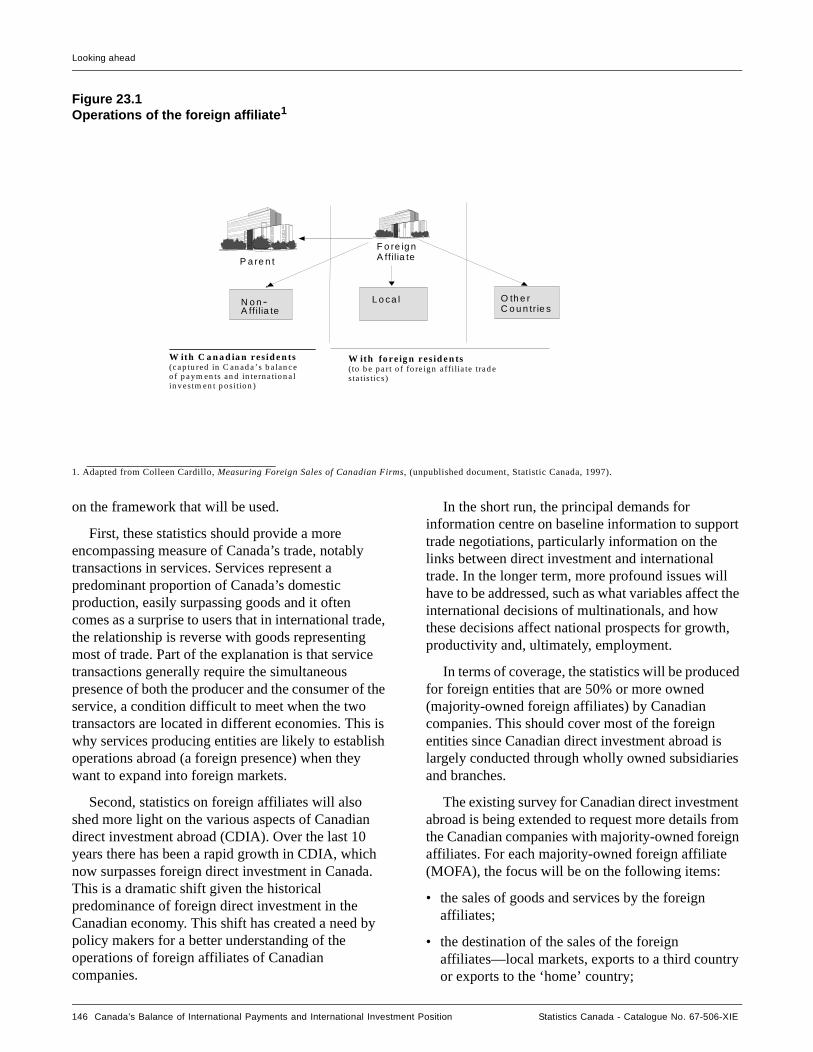

23.2 Data sources ........................................................................................................................................23.2.1 Electronic trade ............................................................................................................................................14423.2.2 Business data from other areas of Statistics Canada ...................................................................................14423.2.3 Tax data .......................................................................................................................................................14523.2.4 Partner countries’ data ..........................................................................................................................23.2.5 Foreign affiliate trade ...........................................................................................................................

23.3 Methods ......................................................................................................................................................14723.3.1 Time series FAME system ...................................................................................................................23.3.1.1 Operational nomenclature ...................................................................................................................23.3.1.2 Positions, flows and investment income links .............................................................................................14723.3.2 Portfolio system (BP-2000) .........................................................................................................................14723.3.2.1 Foreign investment in Canadian stock ........................................................................................................14823.3.2.2 Canadian investment in foreign securities ...................................................................................................14823.3.2.3 An all-encompassing domestic and foreign portfolio investment ...............................................................148

23.4 Products ......................................................................................................................................................14823.4.1 Ongoing description of the statistical infrastructure ...................................................................................14823.4.2 Data developments ..............................................................................................................................

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue no. 67-506-XIE xi

Table of contents (detailed)

23.4.3 Descriptive Analysis ....................................................................................................................................15023.4.4 Analysis of emerging trends ........................................................................................................................15023.4.5 Management of analysis ..............................................................................................................................150

23.5 Conclusion ..................................................................................................................................................151

APPENDICES ......................................................................................................................................................................153

Appendix 1 Questionnaires of the Balance of Payments Division .............................................................................155

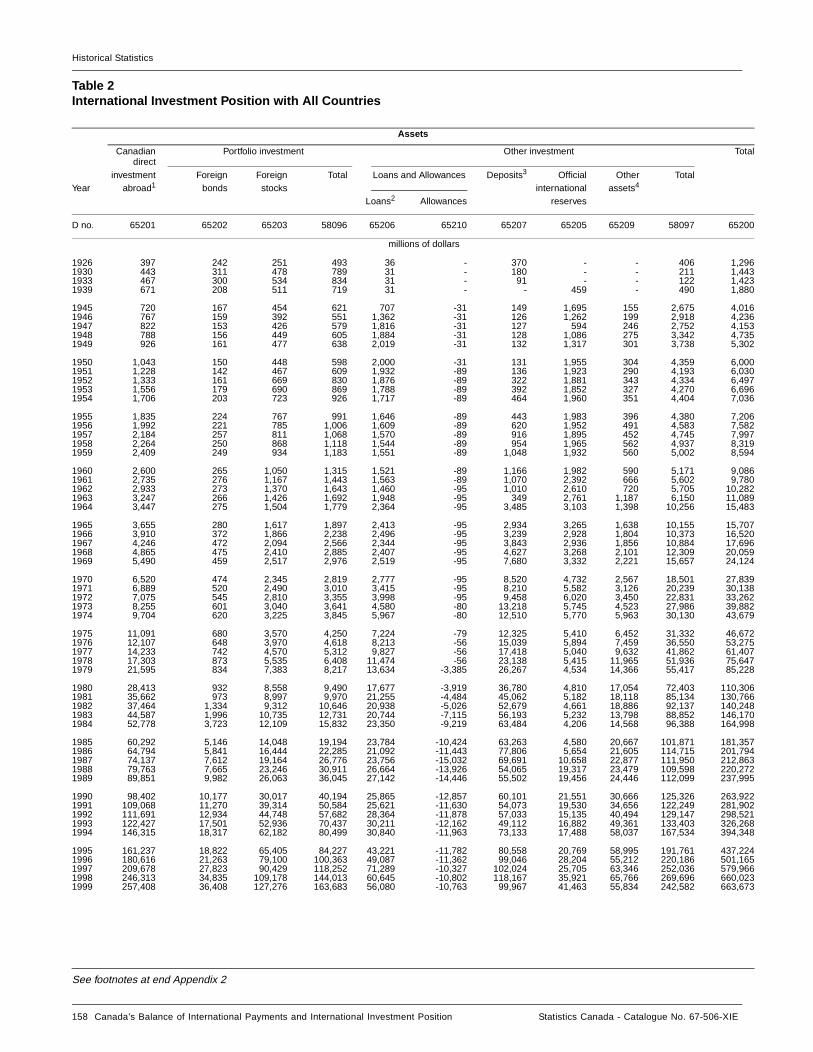

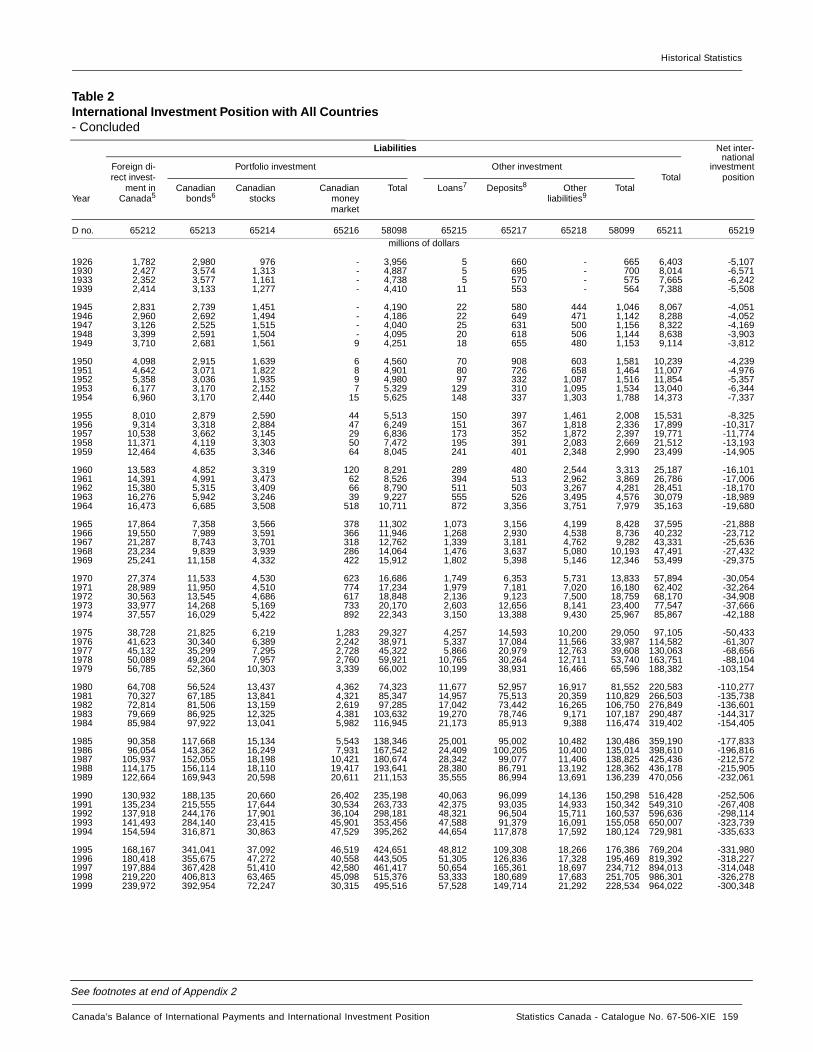

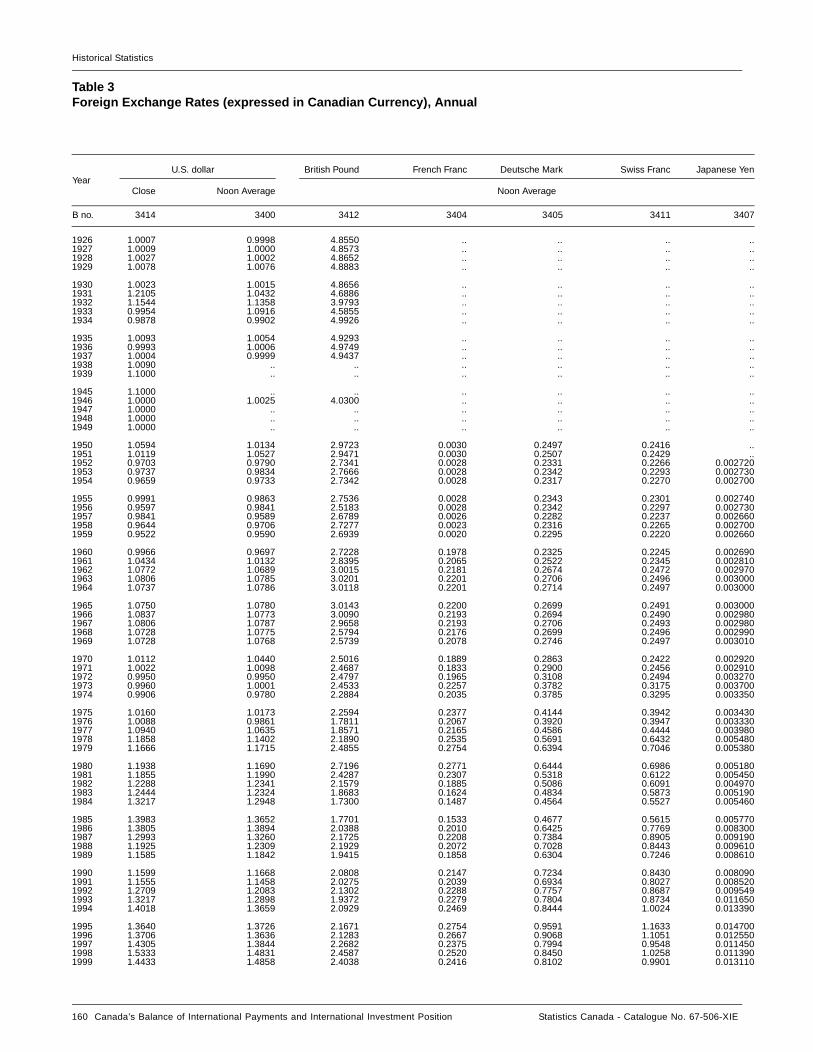

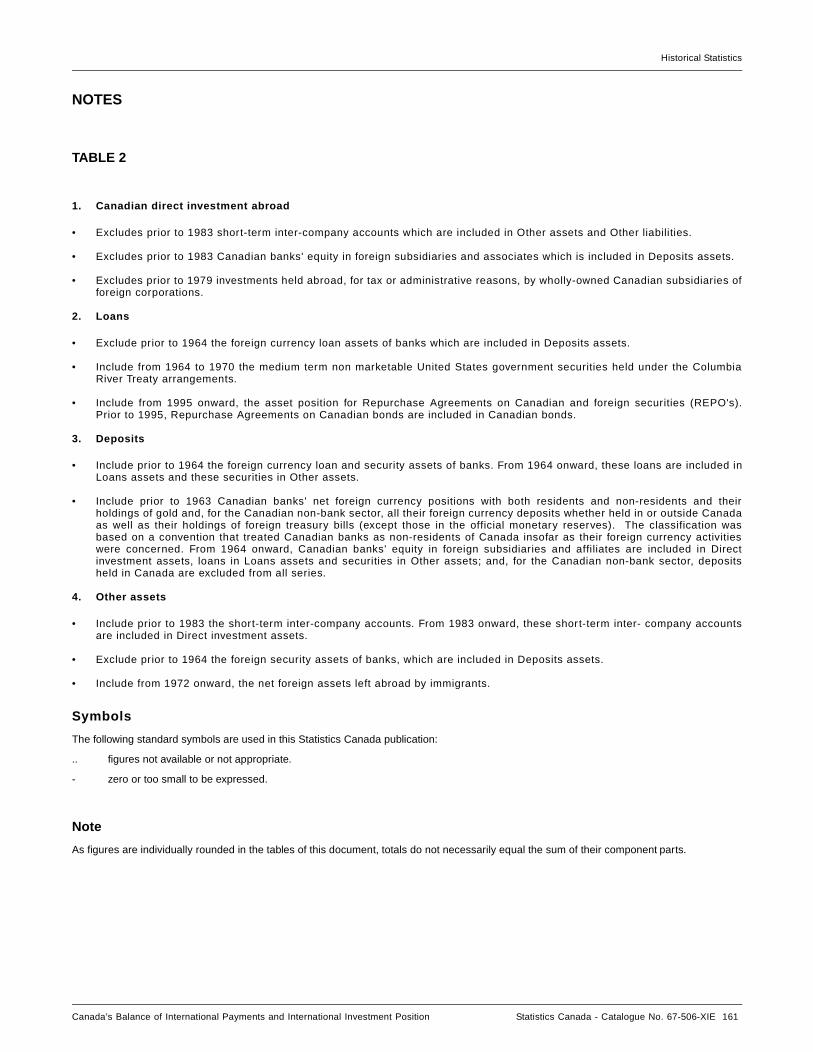

Appendix 2 Historical Statistics ....................................................................................................................................157

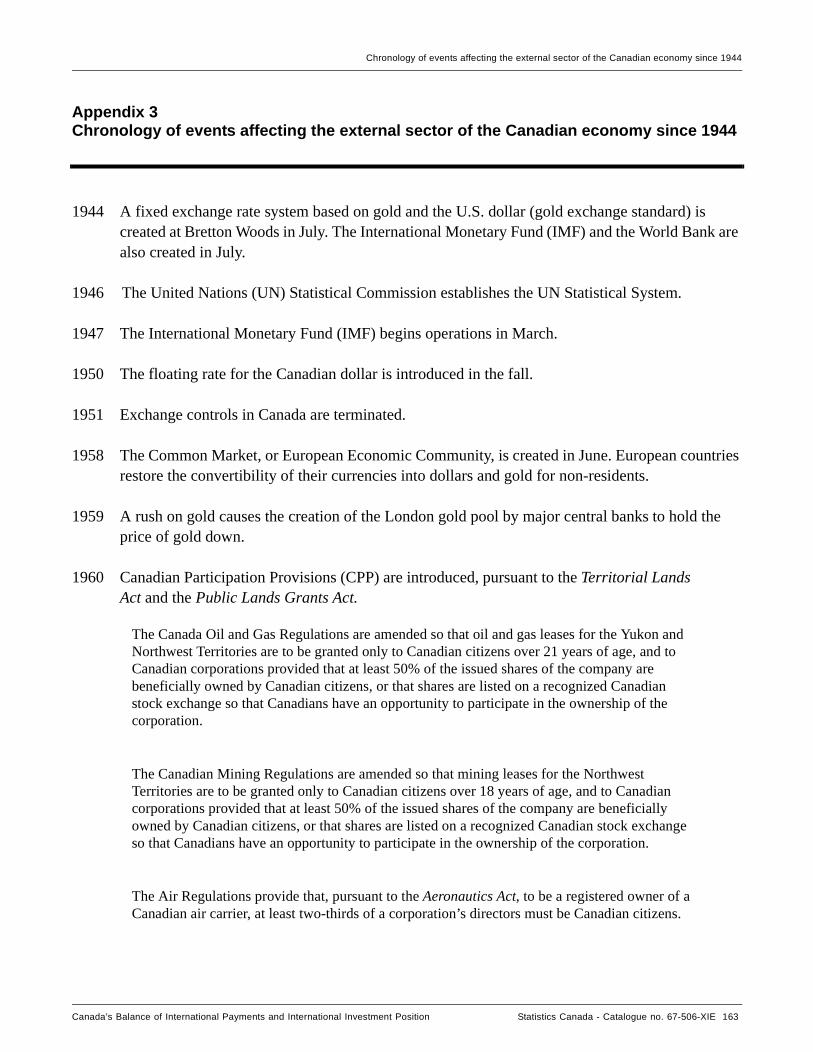

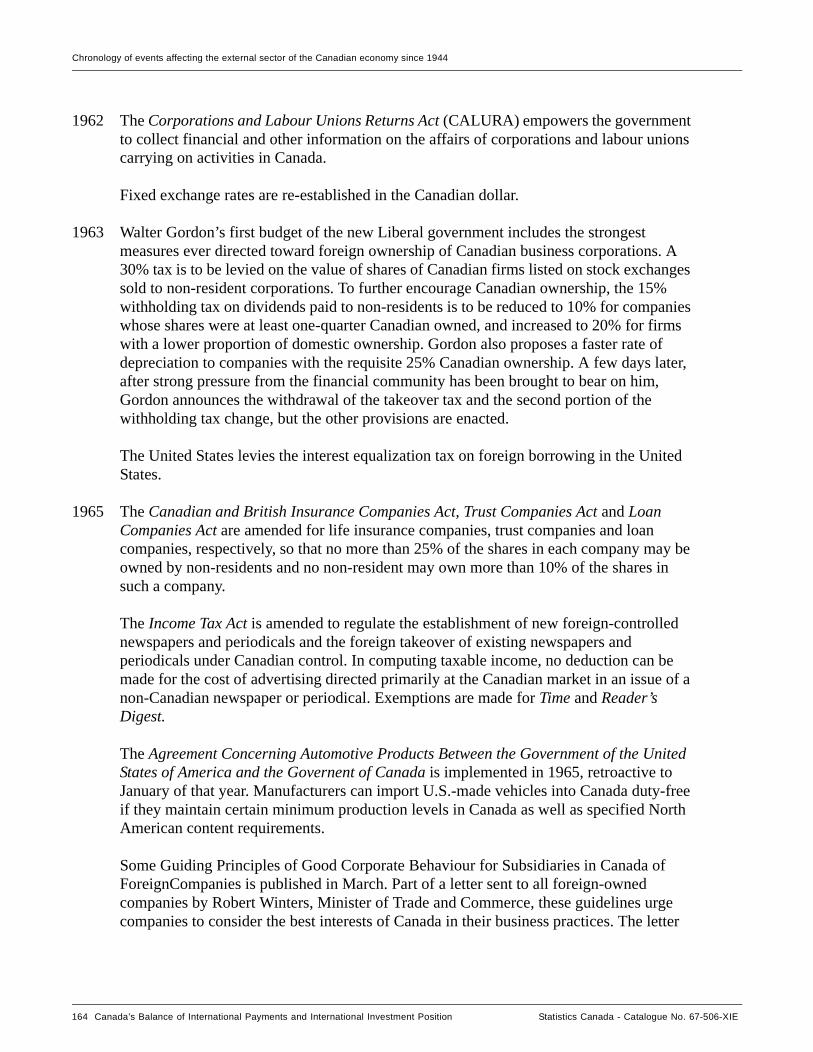

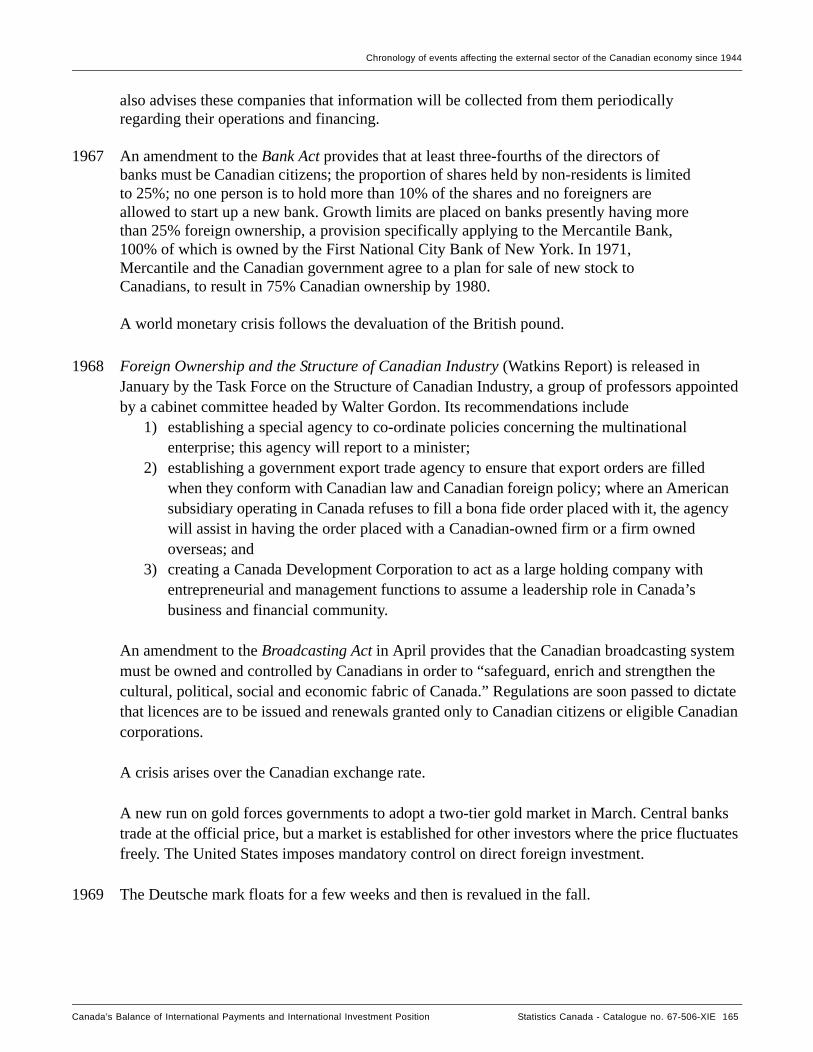

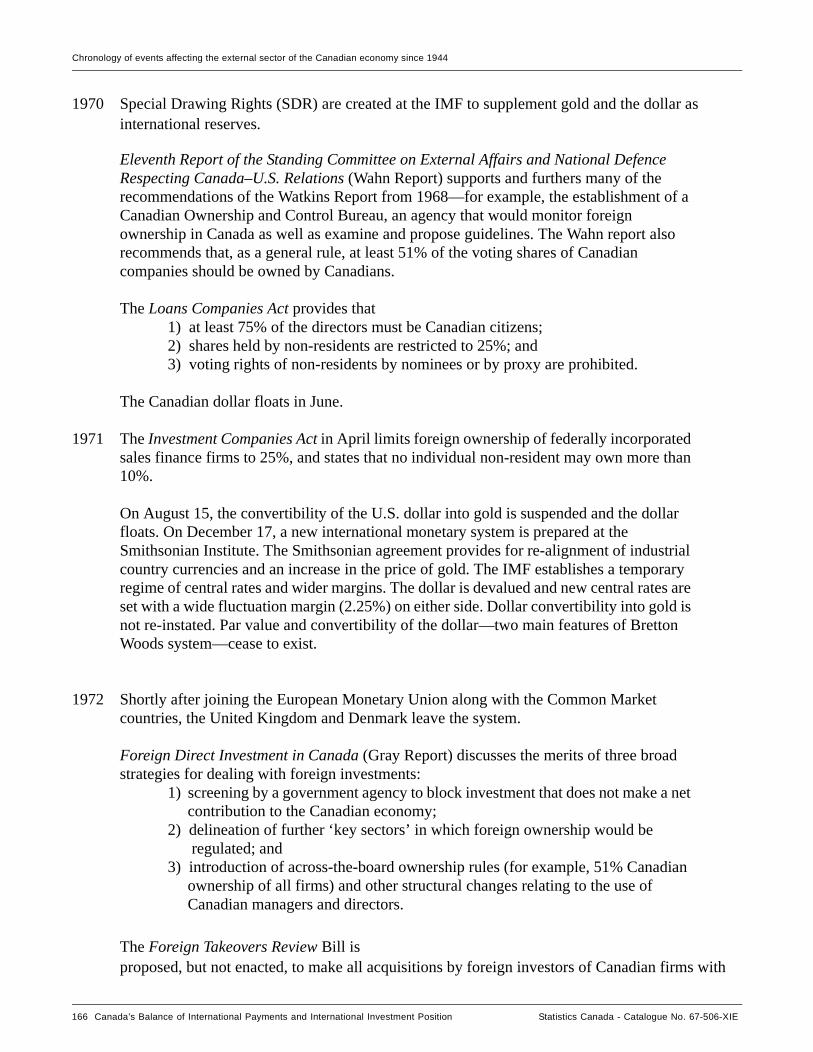

Appendix 3 Chronology of Events Affecting the External Sector of the Canadian Economy Since 1944 .............163

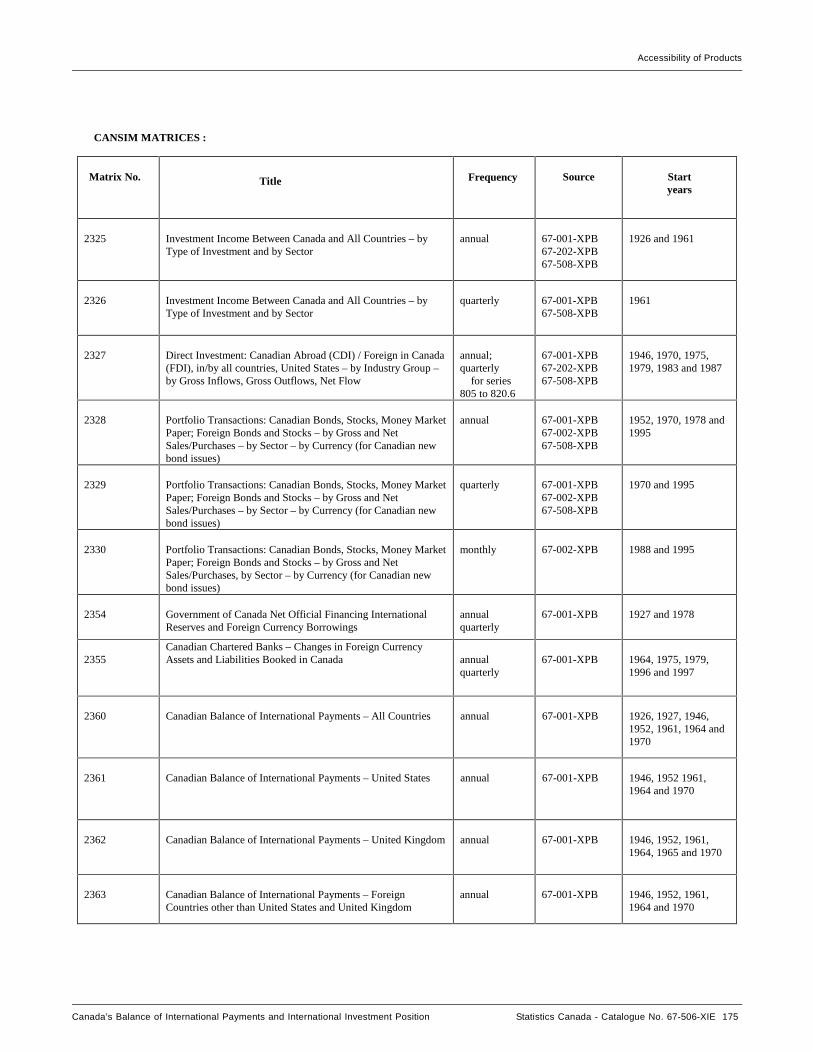

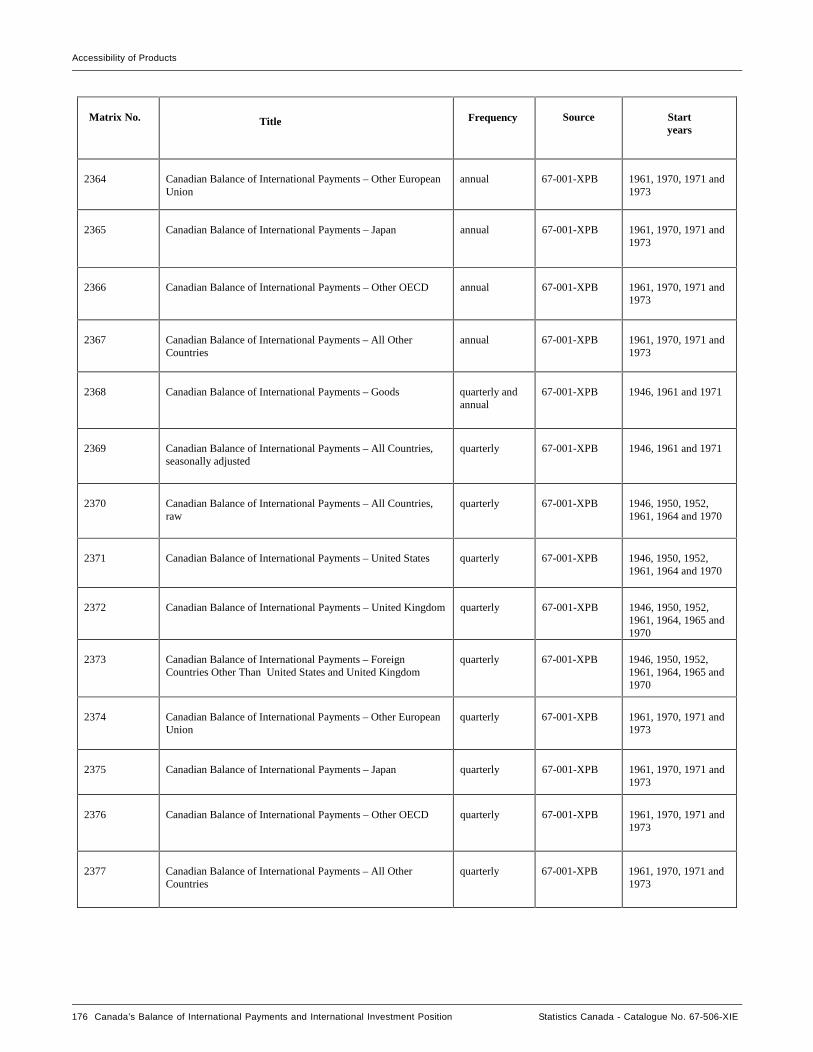

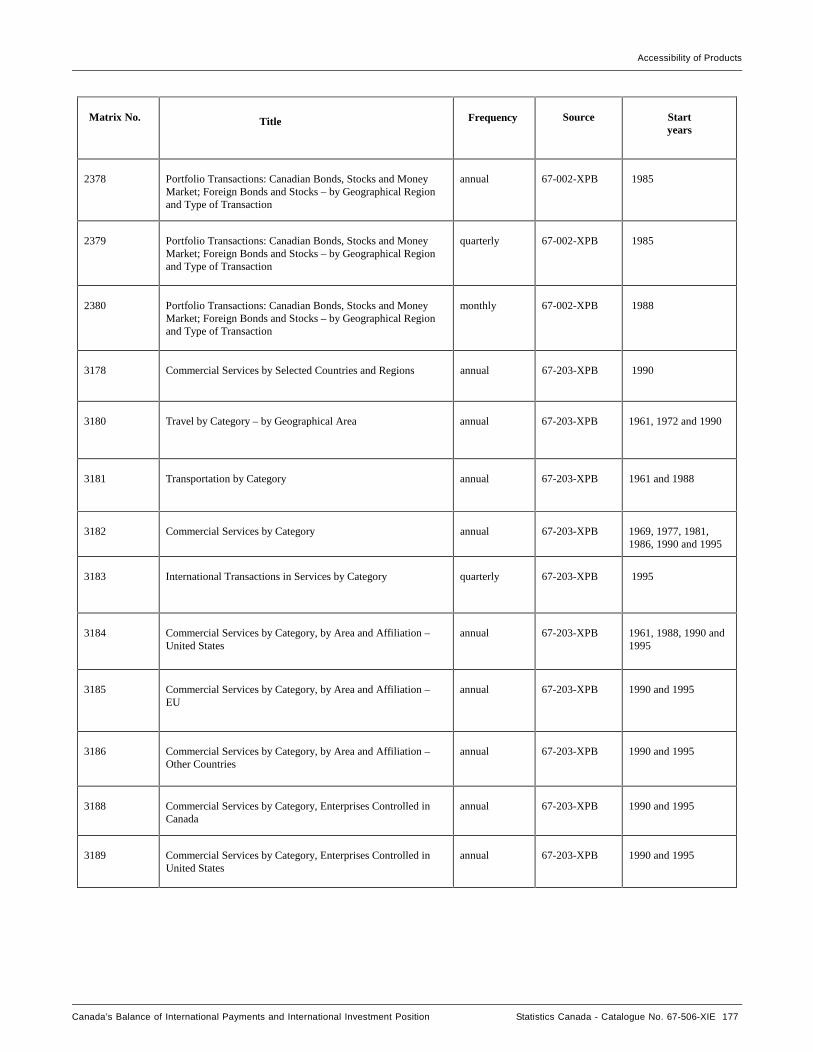

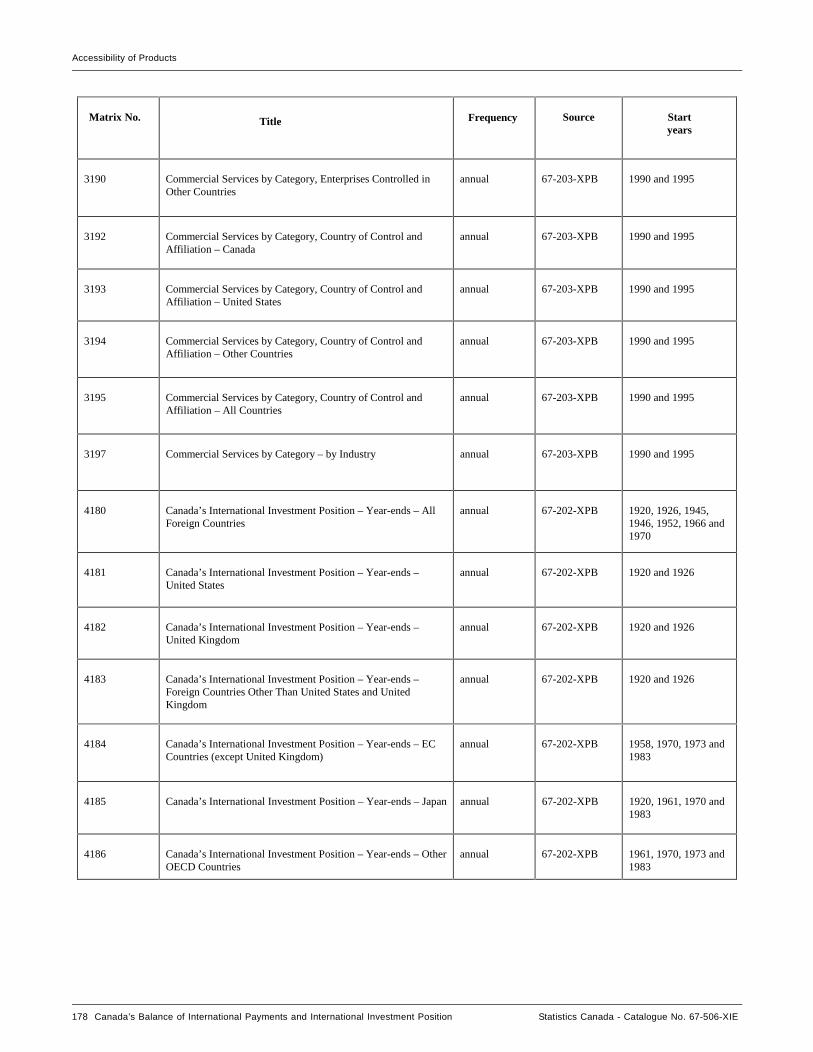

Appendix 4 Accessibility of Products ...........................................................................................................................173

Glossary ......................................................................................................................................................................181

Bibliography ......................................................................................................................................................................189

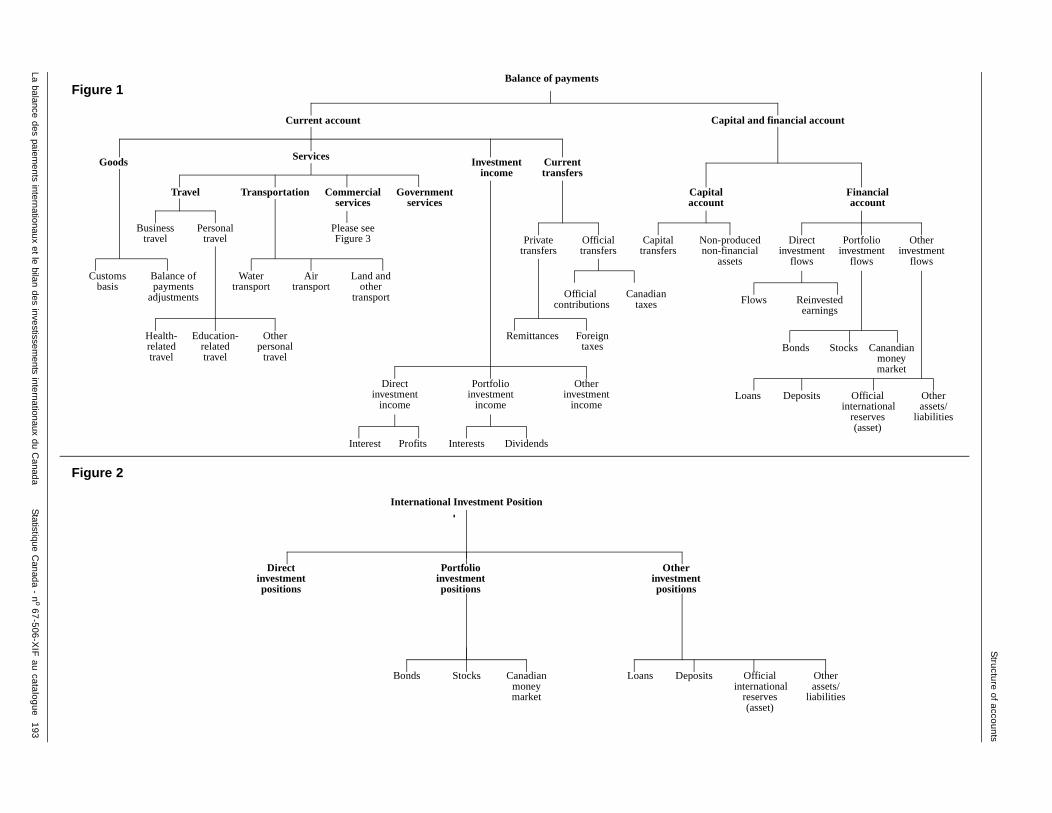

Structure of Accounts .............................................................................................................................................................193

Index ......................................................................................................................................................................195

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue no. 67-506-XIE xii

Preface

PREFACE

, ign trade . ade c at large tions to Co-

n ability of l antial. llowed

the divided urrent

was f ed

46–

e IMF’s two

two of

position engthened,

ith the

Official statistics of Canada’s balance of international payments1 and Canada’s international investment positionwhich began with the reference year 1926, survived the passage of time because of the importance of foreand foreign capital in the Canadian economy, and the relevance of these statistics to a wide range of usersGovernment relies on these statistics for the formulation, implementation and monitoring of financial and trpolicies. They are also used extensively by businesses, the academic community, the media and the publifor both informational and analytical purposes. Finally, they are needed to meet Canada’s statistical obligasupranational organizations, notably the International Monetary Fund (IMF), the Organisation of Economicoperation and Development (OECD) and the World Trade Organization (WTO).

The statistics on Canada’s balance of payments and international investment position are the result of aextensive process where statistical concepts constantly need to be made operational in relation to the availdata sources. Standards and conventions then play a major role in translating the concepts into meaningfustatistics. Over the years, the changes in the real and, particularly, the financial economy have been substWhere those changes have been significant enough to trigger revisions in concepts and data sources, it fothat statistical organizations and methods needed to adapt accordingly.

Since the inception of these statistics in the reference year 1926, the methods employed in constructingCanadian balance of international payments and international investment position estimates can be broadlyinto three periods: the interwar period (1926 to 1938), the period from World War II through 1951, and the cperiod (1952 to the present). The methodology used during the interwar period is described in The Canadian Balance of International Payments, A Study of Methods and Results, published in 1939. With the outbreak of World War II in 1939, Canada introduced exchange controls; this entailed a massive reporting system that incorporated with the methodology employed in the interwar period. This period also saw the emergence ointernational statistical standards for balance of payments under the aegis of the IMF. The methodology usduring this period is described in The Canadian Balance of International Payments 1926–1948, published in 1949. The third main period, which began with the lifting of exchange controls near the end of 1951, involved the more extensive use of survey methods that took into account the experience of the two earlier periods. The first few years of the latest period are described in The Canadian Balance of International Payments in the Postwar Years, 191952, published in 1953, and Canada’s International Investment Position, 1926–1954, published in 1956.

A detailed description of the third period up to the late 1970s was published in 1981 in The Canadian Balance ofInternational Payments and International Investment Position—A Description of Sources and Methods. (At that time, the statistics were constructed according to standards that largely conformed to the third edition of thBalance of Payments Manual, published in 1961.) The 1981 publication also contains an overview of the firstperiods along with the historical evolution in treatment of each account of the balance of payments and international investment position. Its strength is the insight it provides on the history of Canada’s external economic statistics.

Three developments should be noted since the last full account in 1981. First, historical data previously dispersed in various publications over the years were collated into a common framework and presented involumes, with data going back to 1926: the first complete compendium since the mid-1950s on the balancepayments appeared in 1991; and the first compendium since the late 1960s on the international investmentappeared in 1993. Second, the processing systems were computerized and the data management was strresulting in a marked improvement in timeliness. Third, the statistics were fully integrated into the broader Canadian System of National Accounts (CSNA) through the major historical revisions of 1986 and 1997. W

1. Also referred to as ‘balance of payments.’

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue No. 67-506-XIE xiii

Preface

stem of

period ns—ius and

the 98th

1997 historical revision, standards of the fifth edition of the IMF’s Balance of Payments Manual, published in 1993, were implemented as far back as 1926 and published in 1997. In parallel, the 1993 norms for the SyNational Accounts were implemented in the other parts of the CSNA.

The present publication deals with the statistical concepts, sources, methods and products, covering thesince the late 1970s. Special emphasis is given to concepts—and the associated standards and conventiobecause of their central importance as illustrated in the following conversation between the Master ConfucTse-Lu:

Tse-Lu: “The prince of Wei is ready to hand over the reins of government to you. What is the first taskthat you will undertake, master?”

The Master: “Unquestionably, the clarification of concepts.”

Tse-Lu: “How impractical you are. Why care for the clarification of concepts?”

The Master: “How crude you are, Tse-Lu … If concepts are not clear, words do not fit. If words do notfit, the day’s work cannot be accomplished. If the day’s work cannot be accomplished, morals and artdo not flourish. If morals and art do not flourish, punishments are not just. If punishments are not just,the people do not know where to put hand or foot.”2

2. Cited in G. Jaszi, “An Economic Accountant’s Audit” (lecture on economics in government, American Economic Review, Papers and Proceedings of Annual Meeting of the American Economic Association, December 28–30, 1985, New York, Vol. 76, No. 2, May 1986), 22.

xiv Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue No. 67-506-XIE

Acknowledgements

ACKNOWLEDGEMENTS

unior n in

vious . The

t tion on Caron nd

osition an-, Chief urveys e

French

depth ific con- With the , from

This publication has benefited greatly from the work of many people. High on the list is Bower Carty, the author of the preceding publication on sources and methods (The Canadian Balance of International Payments and International Investment Position, A Description of Sources and Methods), a landmark in the history of Canada’sbalance of payments and international investment position statistics. He mentored me when I began as a jeconomist in the Balance of Payments Division in 1973; by the time I left the post of Director of that divisio1998, he had become a personal friend.

The staff of the Balance of Payments Division have contributed significantly through their work, their predocuments on selected aspects of statistics and their helpful comments on drafts of the present publicationfollowing staff members played a major role in the production of this document: Art Ridgeway, Director; PaO’Hagan, Assistant Director; Hugh Henderson, Chief of the Current Account Section (extensive documentathe current account) and from his staff, Wai-yong Yong (compilation guide of the current account) and Denis(adjustments to trade in goods); Barry Mersereau, Chief of the Financial Account Section (portfolio flows) afrom his staff, Robert Théberge and Don Granger; Christian Lajule, Chief of the International Investment PSection (direct investment position) and from his staff, Colleen Cardillo, Rick Murat and Demi Kotsovos; JeFrançois Carbonneau (Canadian portfolio investment abroad position); Éric Boulay (glossary); Frank Chowof the Direct Investment Flows Section (historical facts); and Gerard Meagher, Chief of the Systems and SSection (survey system and processing systems). The following staff merit recognition as producers of thaccounts:

Brian André Marguerite Desnoyers Jeff Maden Chantal RouvroyGaétan Bélanger Peter Escander Paul Mellor Éric SimardJoanne Bonneau Waneta Featherstone Bruce Nichols Denise StrangewaysSean Burrow Rosemary Gleeson Carole Parent Linda TasséClaude Campeau Blair Guy Gisèle Parent Josée ThibeaultAllison Collier Tai Hu Robert Poisson Pierre VincentNicole Charron Asif Husain Francine Rouleau Peter WoodardJohn Côté Ed Joseph Manon Roussell Xiaoyi YanDenise Demers John Kowalski

I also want to thank the members of the editorial and production team who painstakingly worked on the and English versions of this document:

Janis Camelon Elizabeth Irving Francine RouleauMélanie Desjardins John Kowalski Linda Tassé Glen Gagnon Annie Lebeau Yan Thériault

I owe a great deal of gratitude to Art Ridgeway, the Director of the Balance of Payments Division for his in-review of the whole document and his most welcome comments. He questioned my interpretation of speccepts, and redrafted selected sections, such as the definition of resident persons, travel and transportation.very effective assistance of Francine Rouleau, he also ably directed and managed the whole editorial workbeginning to end.

Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue No. 67-506-XIE xv

Acknowledgements

nt.

I am indebted to Kishori Lal, Director General of the System of National Accounts, for his valuable comments on this document, and to Stewart Wells, Assistant Chief Statistician, National Accounts, and Ivan Fellegi, Chief Statistician, for fostering a very stimulating work environment.

I commend Carol Carson, Director of the Department of Statistics of the International Monetary Fund, and her staff for actively promoting common standards among countries.

Finally, I am extremely grateful to Lise Prud’homme, who patiently typed the many drafts of this docume

Lucie LalibertéAssociate Director GeneralSystem of National Accounts

xvi Canada’s Balance of International Payments and International Investment Position Statistics Canada - Catalogue No. 67-506-XIE

Introduction

INTRODUCTION

Canadian ajor non-

nt

urrent nd

ancial they

the

rnational of the of each an be

own ons used d upon at

I ceptual hose of

ercial

duced tment

r e main osition

s s of this f the

Canada’s external economic statistics are measures of economic transactions and investment positions of residents with residents of other countries (non-residents). These external statistics are presented in two mprograms at Statistics Canada1: the balance of payments, which covers economic transactions of Canada withresidents for a specific period of time, on both a quarterly and annual basis; and the international investmeposition, which covers the economic position of Canada with non-residents at the end of a year.

In the balance of payments, economic transactions are presented in two main groups of accounts: the caccount for transactions in goods and services, investment income and current transfers; and the capital afinancial account for capital transactions as well as for financial transactions in direct investment, portfolio investment and other investment. The international investment position groups positions into three main finaccounts: direct investment position, portfolio investment position and other investment position. Although pertain to the country as a whole, these economic accounts are comparable to the financial statements of enterprises: the current account is analogous to the income statement; the capital and financial account, tochanges in financial position; and the international investment position, to the balance sheet.