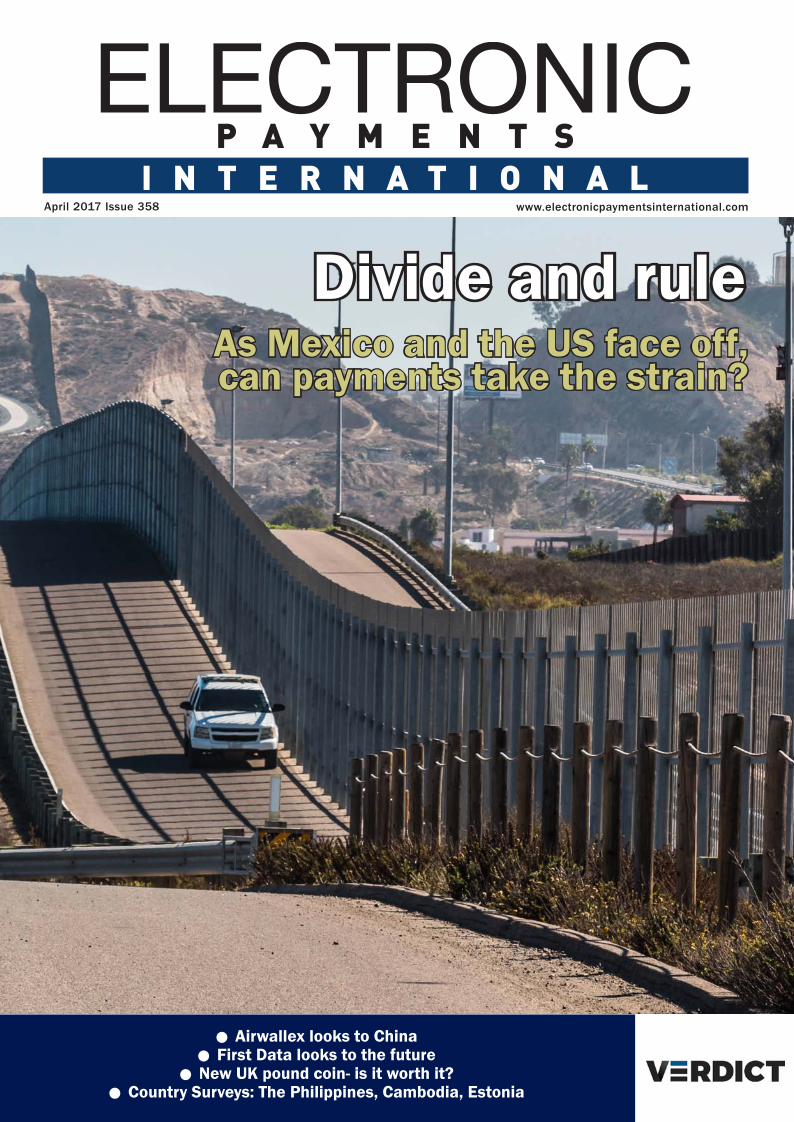

divide and rule - electronic payments international

TRANSCRIPT

•Airwallex looks to China

•First Data looks to the future

•New UK pound coin- is it worth it?

•Country Surveys: The Philippines, Cambodia, Estonia

April 2017 Issue 358 www.electronicpaymentsinternational.com

As Mexico and the US face off, can payments take the strain?

Divide and rule

EPI 358.indd 1 11/04/2017 11:45:13

Intelligent Environments is an international provider of innovative mobile and online solutions for fi nancial services providers. Our mission is to enable our clients to deliver a simple, secure and effortless digital experience to their own customers.

We do this through Interact®, our single software platform, which enables secure customer acquisition, engagement, transactions and servicing across any mobile and online channel and device. Today these are predominantly focused on smartphones, PCs and tablets. However Interact® will support other devices, if and when they become mainstream.

We provide a more viable option to internally developed technology, enabling our clients with a fast route to market whilst providing the expertise to manage the complexity of multiple channels, devices and operating systems. Interact® is a continuously evolving technology that ensures our clients keep pace with the fast moving digital landscape.

We are immensely proud of our achievements, in relation to our innovation, our thought leadership, our industrywide recognition, our demonstrable product differentiation, the diversity of our client base, and the calibre of our partners.

For many years we have been the digital heart of a diverse range of fi nancial services providers including Atom Bank, Generali Wealth Management, HRG, Ikano Retail Finance, Lloyds Banking Group, MotoNovo Finance, Think Money Group and Toyota Financial Services.

To fi nd out more please visit:

www.intelligentenvironments.com

Simple, secure and effortless digital solutions for fi nancial services organisations

@IntelEnviro

IE Adverts - 2017.indd 1IE Adverts - 2017.indd 1 21/12/2016 11:53:1221/12/2016 11:53:12

www.electronicpaymentsinternational.com April 2017 y 1

NEW

S

EDITOR’S LETTER

UK payments regulators take a grilling at annual plan launch event

Financial News Publishing, 2012Registered in the UK No 6931627

ISSN 0956-5558Unauthorised photocopying is illegal. The contents of this publication, either in whole or part, may not be reproduced, stored in a data retrieval system or transmitted by any form or means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of the publishers

Editor: Anna MilneTel: +44 (0)20 7406 6701Email: [email protected]

Group Editor: Douglas BlakeyTel: +44 (0)20 7406 6523Email: [email protected]

Reporter: Patrick BrusnahanTel: +44 (0)20 7406 6526Email: [email protected]

Group Publisher: Ameet PhadnisTel: +44 (0)20 7406 6561Email: [email protected]

Sub-editor: Nick Midgley

Director of Events: Ray GiddingsTel: +44 (0)20 3096 2585Email: [email protected]

Head of Subscriptions: Alex AubreyTel: +44 (0)20 3096 2602Email: [email protected]

Sales Executive: Harry HookerTel: +44 (0)20 3096 2622 Email: [email protected]

Customer Services:Tel: +44 (0)20 3096 2636 or +44 (0)20 3096 2622Email: [email protected]

For more information on Verdict, visit our website at www.verdict.co.uk.

As a subscriber you are automatically entitled to online access to Electronic Payments International. For more information, please telephone +44 (0)20 7406 6536 or email [email protected].

London Office71-73 Carter Lane London EC4V 5EQ

Asia Office1 Finlayson Green, #09-01Singapore 049246Tel: +65 6383 4688Fax: +65 6383 5433Email: [email protected]

The UK’s Payment Systems Regula-tor (PSR) lined itself up for quite the bashing as it set out its reviewed objectives for the year ahead. To its

credit, it took it on the chin, putting itself very much in the firing line with an open Q&A, graciously fielding the ensuing onslaught that came from the audience.

Stoic? Not much. Most of the difficult questions were deferred to the FCA (not in attendance) or deflected using the conveni-ent buffer of collective regulatory responsi-bility – that is to say that to address many of the concerns raised, collaboration among the different regulatory bodies is required, namely the FCA and international regula-tors. Collective responsibility, collective blame.

Dominic Thorncroft, chair of the Asso-ciation of UK Payment Institutions (AUKPI) said a large amount of the 1,000-plus firms regulated by the FCA are not able to access payment systems. “We heard yesterday that Raphaels Bank, which was meant to come in and provide some service, will not actually be doing that.

“As things stand there are no banks allow-ing access to these many payments firms, so your aspirations to deliver competition in the market will come to nothing unless this can be addressed properly, and I’m afraid at the moment we are not making any progress at all.” Scathing stuff.

Another disgruntled punter argued: “Basic access to bank accounts are not being pro-vided to institutions that provide payments across the country. It is a case of inclusivity

in accessing banking accounts, not necessar-ily indirect access. Banks are averse to pro-viding accounts to APIs and institutions.”

But that’s fair enough. Everyone loves to harangue a regulator, yet they all turn very much to the regulator for support during anxious times.

It was pretty clear, given the questions asked by attendees, that payment industry stakeholders want the PSR to become more of a spokesperson for their concerns in the next couple of years, around Brexit and around incoming European regulation, Pay-ment Services Directive, mark 2 (PSD2).

And within that, the main concern, speak-ing to stakeholders, is around data protec-tion. Incoming GDPR regulation is very much at the forefront of business strategy.

While they are not worried about commer-cial opportunities, or indeed being phased out, they are to a certain extent floundering as to how to reconfigure their operations. New regulation stipulates what they cannot do; it’s up to them to figure out what they can. And how.

The complaints, however, were put over with the decorum befitting a parliamentary select committee- exasperation aside, cor-diality, deferentiality and diplomacy holds sway.

And it must be said, the good grace with which the PSR endeavours to maintain the dialogue, does illustrate a certain commit-ment to the cause. Payments industry people, hats off to you all. < ANNA MILNE, [email protected]

CONTENTSNEWS

2: NEWS ANALYSIS

3: NEWS DIGEST

FEATURE

6: AIRWALLEX Melbourne-based Airwallex plans to be the first e-commerce gateway into China. Anna Milne caught up with its global head of partnerships to talk about cracking China, disrupting SWIFT, and leveraging WeChat

8: FIRST DATA What are the main concerns for merchants and issuers these days? Security, digital strategy and e-commerce. Anna Milne speaks to Glenn Fodor from international processor and acquirer First Data

10: MEXICAN Latin America’s third-largest economy could slip into recession if US President Donald Trump’s toxic cocktail of threats come true. However, Mexican banks are – at least for now – unconcerned, writes Ivan Castano

SURVEY

13: THE PHILIPPINES

14: CAMBODIA

15: ESTONIA

COMMENT

12: THE NEW POUND COIN

16: GLOBALDATA FINANCIAL SERVICES

EPI 358.indd 1 11/04/2017 11:45:16

2 y April 2017

NEW

S

www.electronicpaymentsinternational.com

At $89.6bn, Brazil’s total balance outstanding on credit cards was surpassed only by the US in 2015, with $733bn. It was followed by

Canada ($74.7bn) and Mexico ($22.2bn).A significant factor contributing to this

reality is the popularity of instalment cred-it at point of sale, in which retailers allow customers to repay credit in up to 60 instal-ments, with many retailers advertising items by the monthly payment rather than the total cost. This has encouraged consumers

to spend beyond their means and, therefore, accumulate more debt.

However, GlobalData’s Credit Card Cus-tomer Analytics revealed that Brazil reported the lowest average balance outstanding per credit card from these countries at $545 in 2015, behind Mexico with $799, Canada with $1,127, and the US with $1,191.

At the same time, at 24.5% Brazil had the lowest share of credit card holders who revolve at least some part of their monthly balance from the above-mentioned countries.

This suggests that despite the higher amounts outstanding, Brazilian consumers are highly concerned about the debt they hold, and are keen to repay their debts.

In 2015, the share of credit card holders who repaid the balance in full gained 10 per-centage points to reach over 75%.

This increasing level is largely explained by credit card issuers in Brazil normally charg-ing very high interest rates; for example, the Central Bank of Brazil reported that interest rates on credit card debt had reached 482% in December 2016.

Given the substantial revenue that can be earned from outstanding balances, it comes as very little surprise that the majority of issuer revenue in Brazil is derived from inter-est rates, in addition to interchange on pur-chase volumes.<

Accessing the underserved segment could significantly extend Pay-Pal’s customer reach while also providing an efficient tool to com-

pete with banks for serving this increas-ing global population.

PayPal has announced it will acquire TIO Networks for C$304m ($233mn) and on closure of the acquisition, TIO will operate as an integrated service within PayPal.

Speaking about the expected strategic benefits of the acquisition, Hamed Shahbazi, Chairman and CEO of TIO said the compa-ny’s mission harmonises with PayPal’s vision to democratise money by giving consumers more convenient and affordable ways to pay their bills.

As a leading multi-channel North Ameri-can bill payment processor, TIO processed

over $7bn in customer bill payments in fis-cal year 2016 and serves 14m customer bill pay accounts. The company has more than 10,000 biller partners, including some of the largest telecoms, wireless, cable and utility companies, enabling it to efficiently process bill payments for its customers.

The acquisition will help PayPal enter the bill payments market and gain scale due to

both TIO’s presence and partnerships in the North American market. It will also attract a new segment of customers by offering bill payments to current PayPal customers.

While bill payments increasingly become digitalised, the acquisition can also help PayPal extend its value proposition by pro-viding TIO’s service to PayPal’s customers within its online and mobile product port-folio.

Since many of TIO’s services target the underserved segment, the acquisition can be an even larger market opportunity for PayPal to serve more than 33 million US households, and two billion people globally.

This is a segment that has been tradi-tionally difficult for PayPal to access, since its accounts are largely funded by bank accounts or payment cards. <

ANALYSIS Electronic Payments International

Paypal targets bill payments and the underserved through the acquisition of TIO

n IN 2015, THE SHARE OF CREDIT CARD HOLDERS WHO REPAID THE BALANCE IN FULL GAINED 10 POINTS TO REACH OVER 75%

Balance paid in full75.5%

Over half10.1%

Around half4.7%

Less than half5.3%

Minimumpayment 2.7%

No payment1.7%

Source: GlobalData

High interest rates on credit cards continue to drive revenues for issuers in Brazil

Payments giant PayPal is to acquire Canada-based bill-payment company TIO, aiming to develop its customer value proposition and extend its market reach through accessing the global underserved segment. GlobalData Financial Services analyses the deal

According to GlobalData’s Payment Cards Analytics, Brazil reported the second-largest level of balances outstanding on credit cards in the Americas in 2015, largely due to the size of the market and the trend among local retailers and issuers to offer repayments in instalments

EPI 358.indd 2 11/04/2017 11:45:21

www.electronicpaymentsinternational.com April 2017 y 3

NEW

S

DIGESTElectronic Payments InternationalElectronic Payments International

STRATEGY

JPMorgan Chase to take on Apple and Android Pay with MCX m-payment systemJPMorgan Chase has reached an agreement to acquire Merchant Customer Exchange (MCX)’s payments technology to help expand Chase Pay, the smartphone-based payment system that enables Chase custom-ers to pay retailers using mobile devices.

The transaction, which is likely to con-clude in the coming weeks, will enable Chase Pay to better compete with Apple Pay and Android Pay in the US’s growing mobile-payments market.

MCX, a network of America’s largest mer-chants such as Walmart, Target, Best Buy and Shell, acted as premier launch partner for Chase Pay in October 2015.

On completion of the deal, major mer-chants that are part of the MCX consortium, as well as non-MCX merchants, will be able to easily integrate Chase Pay as a digital pay-ment option.

Chase Pay head Jennifer Roberts said: “When we think about fintech, we go through a build-buy-partner evaluation to decide how we can get to market most efficiently.“MCX has been an important partner, and

their technology complements ours, so we’re thrilled to deepen our relationships with the merchant community through the purchase of this technology. This will help us get to market faster.”

In December 2016, Chase announced an investment in LevelUp to offer an “order ahead, pay ahead” facility for customers at quick-service restaurants. <

STRATEGY

PayPal invests in South Korean money transfer app TossPayPal has made an undisclosed minor-ity investment in South Korean fintech startup Viva Republica, the devel-oper of money transfer app Toss, in a $48m series C funding led by venture capital firm Goodwater Capital.

Bessemer Venture Partners, Altos Ventures and Partech Ventures also participated in the funding round.

Viva Republica intends to use the fund to expand its fintech product range and become a full financial services platform.

Launched in February 2015, the peer-to-peer payments app now supports cards

issued by nearly all major South Korean banks.

Modeled after mobile pay-ment services such as Venmo and Square Cash, the app has, to date,

been downloaded more than six million times.

By the end of 2016, the app had facili-tated the transfer of around $3bn, and cur-rently processes over $400m in payments each month. <

REGULATION

Japanese and UK regulators sign fintech co-operation agreementThe Financial Services Agency of Japan (JFSA) and the UK’s Financial Conduct Authority (FCA) have signed an agreement to expand co-operation on fintech.

The regulators will refer to each other innovator businesses that would like to oper-ate in the other authority’s jurisdiction.

Once a referral is received, the regulators will help fintech firms to understand regula-tory requirements, and minimise regulatory uncertainty and the time to market.

The two regulators also committed to share information about emerging fintech trends and regulatory issues pertaining to innovation.

JFSA vice-commissioner for international affairs Shunsuke Shirakawa commented:

“This is our first case in creating a pro-fin-tech co-operation framework with any other country.“We believe that this exchange of letters

strengthens the relationship between the JFSA and the FCA and promotes innovation in our respective markets.”

FCA executive director of strategy and competition Christopher Woolard said:

“Today’s exchange of letters with the JFSA will help break down barriers to entry both in Japan and in the UK for firms with inter-esting new services and products.” <

REGULATION

Singapore and Abu Dhabi regulators team up on fintechThe Monetary Authority of Singapore (MAS) and Abu Dhabi Global Market (ADGM) have signed a co-operation agree-ment to support growth of fintechs in the two jurisdictions.

The two regulators will help startups to gain insights into the regulatory regimes in their jurisdictions, and offer support during the application and authorisation process.

The watchdogs will also explore joint innovation projects covering technology such as digital and mobile payments, block-chain and distributed ledgers, and big data.

MAS chief fintech officer Sopnendu Mohanty commented: “The agreement will open up new avenues and create opportuni-ties for fintech firms in Singapore and Abu Dhabi looking to expand into each other’s markets.“We look forward to greater knowledge

exchange and deeper financial cooperation with the FSRA that will nurture a vibrant fintech global ecosystem.”

ADGM Financial Services Regulatory Authority CEO Richard Teng said: “Asia and the MENA regions have immense growth potential and a large underserved financial sector. “We hope that through closer collaboration

with like-minded fintech hubs, we are able to leverage the strengths and expertise of our markets to more efficiently address the immediate needs of the industry in respective regions, and anticipate the demands of the future.” <

EPI 358.indd 3 11/04/2017 11:45:23

www.electronicpaymentsinternational.com 4 y April 2017

NEW

SDIGEST Electronic Payments International

LAUNCH

Beta version of Samsung Pay launches in SwedenSouth Korean electronics giant Samsung has launched a beta version of its mobile payment solution, Samsung Pay, in Sweden. The move makes Sweden the first Nordic coun-try to support Samsung Pay.

Initially, debit and credit card providers including MasterCard, MasterCard SAS, Visa and Eurocard, and banks Nordea and SEB have extended support for Samsung Pay. Entercard, Handelsbanken, ICA Banken, Rikskuponger, and Swedbank will support the Samsung contactless mobile pay-ment service in the near future.

Nordea Bank has announced that its cus-tomers can use Samsung Pay to make

in-store payments with mobile phones.

The service can be accessed by all Nordea customers in Sweden who own an active credit or debit card and a compatible Samsung phone.The Nordea Wallet app

automatically registers custom-ers’ Visa and MasterCard debit or

credit cards in the Samsung Pay app. Users can then use Samsung Pay to pay by phone in most stores in Sweden. Samsung Pay is currently compatible with the Galaxy

A5, Galaxy S7 and Galaxy S7 Edge devices in Sweden. Samsung Pay beta will also work on the recently launched Galaxy A5.

Nordea Bank head of personal bank-ing Topi Manner said: “Sweden is the first Nordic country where Samsung Pay is made available, and Sweden is also a leading coun-try when it comes to using mobile payment services.“Smartphone penetration is very high and

many of our customers are using a Samsung mobile device.”

Samsung Pay is currently available in 11 markets: South Korea, the US, China, Spain, Singapore, Australia, Brazil, Puerto Rico, Russia, Thailand and Malaysia. <

STRATEGY

Misys to merge with D+H in $2.2bn collaborationPrivate equity firm Vista Equity Partners has agreed to acquire D+H, a Canada-based pro-vider of financial software solutions.

Vista intends to merge D+H with UK soft-ware company Misys, which it acquired for £1.27bn ($2bn) in 2012.

The merger of D+H and Misys would cre-ate a fintech firm with $2.2bn in revenue, around 10,000 employees, and more than 9,000 customers in 130 countries, including 48 of the top 50 banks, Vista said.

Commenting on the deal, D+H CEO Ger-rard Schmid said: “By combining D+H with Misys, Vista will be creating a global leader in financial technology with a broad array of products to serve customers.

“D+H brings depth in North America and leadership in payments and lending, while Misys has a strong market position in Europe, the Middle East, Africa and Asia, and leader-ship capabilities in banking, capital markets, investment management and risk solutions.“I believe this transaction is beneficial to

our customers, shareholders and employees. We look forward to working closely with Vista and the leadership team at Misys to complete this transaction.”

Misys CEO Nadeem Syed said: “By com-ing together, we have the opportunity to cre-ate a global fintech powerhouse, positioning us to lead the corporate banking software space, accelerate our cloud-based offerings,

and expand our footprint in North America.”Vista Equity Partners co-founder and pres-

ident Brian Sheth said: “D+H is an outstand-ing company with impressive talent and deep experience, providing technology solutions to financial institutions worldwide.“Over the last five years we have worked

closely with the Misys management team to transform and grow its global business; this is a great next step in that process.“Together, Misys and D+H have the prom-

ise to shape and lead the future of financial software.”

The combined entity will be privately held on completion of the transaction at the end of the third calendar quarter 2017. <

STRATEGY

MasterCard and Unilever to promote digital payments among SMES in emerging markets

MasterCard and Unilever have reached a strategic partnership to launch joint ini-tiatives targeted at empowering small and micro businesses in emerging markets.

The agreement will enable technology resources to be utilised to drive inclusive growth at greater scale.

To achieve this objective, Unilever’s net-work of distributors in developing countries will be integrated with digital payment and acceptance solutions from MasterCard.

MasterCard and Unilever will look at ways to enable better access to formal finan-cial tools for smaller retail outlets, while also developing entrepreneurship capacity, par-ticularly for women and girls.

Both companies will also concentrate to strengthen the use of electronic payments at both wholesale and retail locations.

MasterCard president and CEO Ajay Banga said: “Too many small merchants and micro entrepreneurs are stuck, like their cus-tomers, in a cash economy that doesn’t work for them.“With Unilever, we can bring a unique com-

bination of technology and know-how to help these shop owners build a better future, and serve their customers who are them-selves on a path towards financial inclusion,” Banga added.

Initially, MasterCard and Unilever have launched their first pilot project in Kenya, with an aim to enable sustainable growth for small retail entrepreneurs. <

EPI 358.indd 4 11/04/2017 11:45:26

www.electronicpaymentsinternational.com April 2017 y 5

NEW

S

DIGESTElectronic Payments InternationalElectronic Payments International

RESEARCH

MasterCard: Consumers keen on biometric m-payment securityNearly half of consumers worldwide (43%) have expressed an interest in biometrics and other forms of authentication to improve digital payment security, and 51% of those discussions were driven by advances in facial and fingerprint recognition, reveals a new study by MasterCard.

The MasterCard Digital Payments Study was conducted by the company in partner-ship with Prime Research and social listening platform Synthesio. It analysed 3.5 million conversations from the past year on several social media channels, including Facebook, Twitter, Instagram and Weibo.

Consumer enthusiasm towards new biom-etric and authentication technologies in Asia-Pacific, particularly in India, led to a 66% positive sentiment for safety and security discussions.

The study found that digital wallets domi-nated 75% of online discussions around pay-ments, and that use of in-store digital pay-ments received two million mentions.

The activation of newer technology such as home assistants and artificial intelligence was the second-most-popular payment-related topic of last year, while Internet of Things-enabled payments grew significantly in North America and Europe.

Commenting on the study, MasterCard vice-president of digital communications Marcy Cohen said: “Technology is making the promise and the potential of a less-cash life a reality for more people every day.“This year’s study notes a change in the

level of interest for new ways to shop and pay that only a few years ago would have seemed far-fetched.” <

LAUNCH

Samsung Pay early access begins in India ahead of full launchSamsung has announced an early access pro-gramme for its Samsung Pay digital payment service in India, ahead of its full launch.

Samsung Pay enables owners of specific Samsung Galaxy devices to use the phones to make payments virtually at any location that accepts swipe card payments.

Additionally, the mobile payment system supports both contactless payment systems and magnetic secure transmission (MST) technology.

Samsung said owners of the Galaxy Note5, the Galaxy S7 and S7 Edge, the Galaxy S6

Edge+, and the Galaxy A7 and A5 smart-phone devices will initially be offered access to Samsung Pay.

The company has announced that interest-ed users can now “register for early access” on its India website; however, it has not yet revealed the launch date of the digital wallet in India.

At present, Samsung provides support for MasterCard and Visa credit and debit cards from Axis, HDFC, ICICI, SBI and Standard Chartered banks, with support for Citibank expected in the near future. <

DATA

UK card spending rises in 2016UK consumers spent £647bn ($808bn) through the use of payment cards in 2016, an increase of 4% compared to the total card spend of £620bn a year ago, according to the latest figures released by the UK Cards Association.

Overall, 2016 recorded 14.8bn card trans-actions, with debit cards accounting for the majority, £461bn, of the card spending.

Contactless payments contributed £25bn of spending, a surge from £7.75bn in 2015. In total, 2.9 billion contactless transactions were conducted in 2016.

Retail spending on cards stood at £298bn in 2016, compared to £290bn in 2015. Pay-ment cards accounted for 76.4% of overall retail spending in 2016.

The UK Cards Association’s CEO, Gra-ham Peacop, said: “Cards are the preferred way to pay for millions of consumers, and underpin the retail economy.“Contactless cards are increasingly becom-

ing the payment method of choice for eve-ryday, low-value purchases, with a quarter of card payments now contactless,” Peacop added. <

LAUNCH

Android Pay lands in BelgiumTech giant Google has launched mobile payment service Android Pay in Belgium, allowing users to pay for purchases using an Android-based smartphone.

Belgium is the 10th country in which Google has launched its contactless mobile payment solution. Android smartphone owners in Belgium can now make in-store payments using their devices at over than 85,000 retail locations, including McDon-ald’s, Carrefour, Media Markt, Medi-Mar-ket, H&M and Quick.

Android Pay in Belgium will initially be supported by MasterCard and Visa credit cards issued by BNP Paribas Fortis, Fintro and Hello bank. Support for debit cards from the three banks, as well as CBC/KBC will follow soon.

Android Pay can be used to shop online through its own app, as well as supporting apps including Deliveroo, TransferWise, Fancy, Vueling, Hotel Tonight, Sit, Uber, Touchnote and Showroomprive.com. <

LAUNCH

Apple Pay arrives in IrelandApple has launched its Apple Pay mobile payment service in Ireland, allowing users to pay for goods by tapping their phone on a contactless reader.

Visa and MasterCard-branded credit and debit cards issued by the KBC and Ulster Bank can be used with Apple Pay in the country; the system will also work with Wirecard’s Boon prepay system.

Participating retailers in Ireland include Aldi, Amber Oil, Applegreen, Boots, Burger King, Centra, Dunnes Stores, Harvey Nor-man, Lidl, Marks and Spencer, PostPoint and SuperValu.

Apple Pay is already available in the US, the UK, China, Australia, Canada, Switzer-land, France, Hong Kong, Russia, Singapore, Japan, New Zealand and Spain.

Wirecard executive vice-president for con-sumer solutions Georg von Waldenfels said:

“By launching boon with Apple Pay in Ire-land, even more users in Europe can experi-ence a new level of mobile payments without being a customer of a specific bank.”

Apple Pay is now gearing up to launch in Taiwan, where seven banks have recently secured regulatory permission from the Financial Supervisory Commission to pro-vide the payment service. <

EPI 358.indd 5 11/04/2017 11:45:26

www.electronicpaymentsinternational.com 6 y April 2017

“We would like to be the first cross border e - commerce gateway into mainland China, and we think we might well

be that,” says Joe McGuire, head of sales and partnerships at Airwallex.

China has had a lot of problems with peo-ple taking money out of the country – take the Sydney and Melbourne property mar-ket for starters. And McGuire should know. Based in Melbourne, he can see first-hand the evidence of huge outflows of money from China.

The People’s Bank of China (PBOC) is particularly careful around how people are spending their money and where their money is going. Not only does it have reason to be, due to past experiences, it also has good rea-son to take control of what it has now – and to be wise to the growing affluence in the country and the ever-burgeoning economy.

A recent McKinsey report stated that dis-posable income in urban parts of China will equal that of South Korea by 2020. Things have very much shifted in China over the last ten years from an export-driven economy to a consumer-driven economy.

All this, coupled with significant chal-lenges around historical corruption in China, the current government is highly focused on stamping out corruption and making sure that people are not unduly taking money out of the country. “They are very risk-averse about it, and

yet small businesses in China would be very interested in having a gateway to be able to export out of the country,” explains McGuire.

“For businesses outside China, to sell direct into China is of massive appeal.”

Enter Airwallex, a company which was founded between late 2015 and early 2016 by Jack Zhang and Lucy Liu.

It all started because Zhang owned and ran a cafe alongside his role at a bank build-ing foreign exchange (FX) payment systems. He struggled to purchase stock such as coffee cups from China with a fair FX rate, so he created this business to give the opportunity to SMEs with a lot of international trade but which were not getting a fair price from the Australian banks – fair being better than 3.3%, the average transaction rate, accord-ing to McGuire.

Zhang and Liu pitched Gobi Partners, the venture capital fund for Alibaba, on the concept with a prototype and raised €3m ($3.2m). After the seed-round funding, the business grew to over 30 people.“We have built an FX product for importers

and exporters but really the focus is on two products, which are based on a number of

APIs [Application Programming Interfaces].”“Being a fintech business is really expen-

sive. A lot of that money was used for legal purposes, and we hired the head of compli-ance from AIG Singapore, which didn’t come cheap,” says McGuire. “We have an Australian financial services

licence, the equivalent in New Zealand and Hong Kong, and most importantly we were able to get access to the cross-border third-party and foreign-currency licence in China.”

It took Zhang and Liu a lot of groundwork to crack this, and being Chinese came at a massive advantage – in fact it was “abso-lutely crucial”.

They spent a great deal of time working with contacts and partners in China to build that trust.

This licence is a huge barrier to entry for other people trying to do the same. There are 28 licences across the globe to take money in and out of China, issued by the PBOC, and Airwallex is not in the least bit complacent about having access to one of these

A lot of those are actually dormant, say ten, because they are held by institutions such as tax offices, etc. “Of the 15-18 that are left, we have access

to one,” McGuire explains. “Effectively, we have a licence to use

that licence and we are very careful with it because it is so hard to come across.

We are very careful around who we are working with and the reasons why they are sending it, and making sure they are within the cap the PBOC has set on money being taken out of the country and it not being used for gambling or investments, etc.”

FEAT

URE

AIRWALLEX Electronic Payments International

Melbourne-based Airwallex has ambitious plans to be the first e-commerce gateway into China, and by all accounts is on course to do so. Anna Milne caught up with its global head of partnerships to find out how hard it was to crack China, disrupting SWIFT, and why he thinks the future of many things is WeChat

Cracking China from Down Under

“We’re building it to effectively disrupt SWIFT”Joe McGuire, Airwallex

EPI 358.indd 6 11/04/2017 11:45:30

www.electronicpaymentsinternational.com April 2017 y 7

FEAT

URE

AIRWALLEXElectronic Payments International

Two products: acquiring and distributionThe acquiring product is around accepting all the new forms of payment coming out of China, such as WeChat; the other product is enabling businesses globally to distribute things cheaply.

The acquiring product is to get WeChat acceptance mainly, but also all the Chinese forms of payment, accepted in Europe for the Chinese tourists coming over. “The acquiring product is pretty simple.

Think Stripe – Stripe is an acquiring API. Its focus is on developers, winning over develop-ers with really beautiful API documentation: ten lines of code to plug into a website to change from .com to .ch so that you can sell directly to the Chinese consumer.“We want to do Stripe directly into China

– cross-border, into China. The reason why Stripe hasn’t done that is lack of a licence.”

Currently, if you want to sell direct to the Chinese customer there are only really two options: Alibaba, which has a number of sites, or a local distributor.

In both instances if you’re a brand that cares about price point, about who is buy-ing your product, how it’s being sold, neither of those are good propositions as an online merchant.

“It’s interesting because in China no one has Visa or MasterCard, so the majority of payments there are through WeChat Pay, Ali-pay, and some other mobile payment solu-tions, such as UnionPay, which is actually a very small percentage of the transactions in the country, 10-12%.”

The second product is a distribution prod-uct, involving a number of APIs.“SWIFT has 11,000 financial institutions

plugged in, in every jurisdiction. They have been very important for global trade – but a commonly held view is that they haven’t kept up with changes in technology,” says McGuire.

To compete – because Airwallex doesn’t have the funds to build its own payments network or payment rails, nor the financial

connections, Zhang and team have built a piece of machine learning, which sits atop several different payment rails that they’re connecting into the system. “I can’t tell you just yet who they are, but

there are six or seven companies also trying to disrupt SWIFT and beat them at their own game, and they’re building payment rails off SWIFT for transactions. “What we’re doing is really simple: We are

going to connect them all together. Our piece of machine learning will, per transaction, funnel transactions through the cheapest and fastest rail, depending on the jurisdiction it’s going into,” McGuire continues. “There are a few people trying to disrupt

SWIFT by building payment rails and all of them are doing a really good job in certain jurisdictions, but none of them have the glob-al reach of SWIFT. “We think we will be able to send money

anywhere in the world within a day within the next six to 12 months. And that’s a direct transaction. Currently SWIFT goes through correspondent bank networks, with a fee of around 3-5%, and takes three to four days.”

McGuire says that for the majority of busi-nesses, Airwallex’ service would mean a 90% reduction in transaction fees. The team cur-rently stands at 20 developers, and is relying on a series A funding round in the pipeline.

If Airwallex is going to be the first cross-border e-commerce gateway into China, does it expect more will follow?“Stripe is doing some things with UnionPay

and Alibaba, leveraging its licence to get in there. I’m not 100% sure of this but we are certainly going to be one of the first cross-

border e-commerce gateways into China. Other people have been trying to do it for a long period of time; they just don’t have a licence.”

Airwallex is already looking to expand its reach, hopeful of garnering some space in one of Barclays’ innovation labs in London.

Where to from here?“We’ll hire a couple of staff, and then when summer hits we’ll be ready to go,” says McGuire.“Alipay is doing a really good job in terms

of getting memoranda of understanding with the right businesses here, but really the future is not Alipay, it’s WeChat Pay. “A huge proportion of Chinese people

– 85%, don’t quote me– have WeChat Pay. Users spend on average about an hour a day on it. Once they start to roll that out glob-ally, it will take over as the biggest form of payment.“People who buy stuff on Alibaba have Ali-

pay, but most people would use WeChat for P2P payments,” McGuire adds.“It’s such a rich app in terms of function-

ality, it’s going to really take over the West as well I think; it’s going to be huge. People do everything on it; it’s Facebook, it’s Tinder, it’s booking flights, hotels, doctor appoint-ments, Didi Chuxing, the Chinese equivalent of Uber. “Alibaba will still be really important and

Alipay will always have a place, but I think WeChat will dominate – it’s what everyone uses,” says McGuire.“I think the next generation of kids will be

on WeChat as opposed to Facebook.” <

“Users spend on average about an hour a day on WeChat – once it starts to roll that out globally, it will take over as the

biggest form of payment”Joe McGuire, Airwallex

“If Uber is the biggest cab company in the world without owning taxis, we want to be the biggest payments company in the world that doesn’t own rails”Joe McGuire, Airwallex

EPI 358.indd 7 11/04/2017 11:45:35

www.electronicpaymentsinternational.com 8 y April 2017

Digital projections

There is no doubt the payments world is fast-changing, which has led to not a small amount of con-cern among payment outfits large

and small about carving out a new niche.Without meaning to imply the business

world is all about exploitation and profiteer-ing on others’ weaknesses, it would be wrong not to highlight the fact that the changing payments landscape, and the fear and trepi-dation it can inspire among its stakeholders vis-à-vis their future relevance in it, is a rich source of revenue for the likes of massive global processors.

All this talk about the opportunity for banks and new payment and account service providers is secondary to the palpable oppor-tunity for those with the nous, wherewithal and mettle to be the first to offer guidance on navigating the new waters, and to offer new digital services that keep the regulators, if not at bay, at least adequately placated.

With the advent of digital, and therein the lightning pace at which this new scene is being set, ripe pickings are there for the taking in the form of consultancy and com-pliance advisory services. And seeing as the new scene is being driven in part by Euro-pean regulators and the second Payment Services Directive (PSD2), and will resonate across the Atlantic, who are we to decry such opportunistic enterprise? But do not take it from us; take it from the horse’s mouth: Glenn Fodor, SVP, head of strategic intelli-

gence at First Data.“Disruption is good for the industry

because then providers which can’t figure this out on their own are going to come to their processor or technology provider for answers and technology solutions to figure all this out,” Fodor explains.

“Confusion is good for us at the end of the day. It causes merchants and banks to come to us and ask, ‘What are you seeing? How can you help us?’

“That’s a conversation we’d like to have all day long. If you’re a bank, you are think-ing, ‘How do I manage the fintech landscape on one hand against the regulatory oversight landscape that I have on the other?’ That’s fair game whether you’re a US bank, or a European or beyond bank.”

Most of First Data’s, and indeed Fodor’s time is spent with merchants or issuers. They

all look to the processors to understand what to expect from PSD2 and the landscape in general. They want to check they have the right approach, the right online banking and mobile setup, and the right products and ser-vices. They look to the processors for these answers.

“If you listen to the conference calls of First Data’s peers and competitors, everybody is of the view we’re going to figure this out.

“Security is the underpinning of every con-versation: How do we keep this secure? How do we keep it locked down? Protecting the customer data – again, that’s another conver-sation we love to have, because we think we have the best security solutions, be they for merchant or issuer.”

Security and e-commerceMerchants are worried about the shift from

FEAT

URE

FIRST DATA Electronic Payments International

What are the main concerns for merchants and issuers these days? Security, digital strategy and e-commerce. Anna Milne speaks to Glenn Fodor, SVP and

head of strategic intelligence at international processor and acquirer First Data

First Data’s projections for payments in 2017• Investments in digital payments will accelerate as

both merchants and banks fight for their share of the consumer wallet.

• Banks are seeing a strong macro environment and favourable industry tailwinds

• Collaboration will continue for banks and fintechs

• Faster payments will take hold in 2017; blockchain will be a longer journey

• E-commerce continues its path to ubiquity, but so does fraud

• Amazon’s ambitions will continue to challenge

EPI 358.indd 8 11/04/2017 11:45:39

www.electronicpaymentsinternational.com April 2017 y 9

FEAT

URE

FIRST DATAElectronic Payments International

offline to online. Is their online strategy coherent? Do they have the right solutions in place?

Security presents possibly the largest chal-lenge to businesses, and with that, the great-est opportunity for the likes of First Data. And there has been an exponential growth in e-commerce.

Put simply, given the rate at which fraud-sters are developing and getting better, stronger and more powerful, can First Data and its competitors keep up?

“We think we can and we think we do. We’ve spent a lot of money investing; we have a crack team. We’ve hired people from the National Security Agency, the CIA, the Department of the Treasury, and the Depart-ment of Defense. We think we’re ahead of the curve here, and it’s one of our fastest-growing product segments,” Fodor confirms.

“As I like to say, ‘No good deed goes unpunished,’ because with this fast growth in commerce comes super-fast growth in fraud and mishaps like that,” counters Fodor.

He goes on to explain fraud and bad behaviour are growing, and that the dol-lar amount of fraud is growing faster than e-commerce overall.

“So, again, a good place for us to be, because that’s where we come in and provide them the security solutions. That’s, first and foremost, what merchants are asking about,” says Fodor.

Connected commerceOne of the major themes in First Data’s 2017 rhetoric is connected commerce. How soon are things going to get ever more connected?

“Now. People ask me what’s the next big thing in payments. I say connected com-merce, that’s the next big thing. That’s the e-commerce of tomorrow.”

The burning question therefore is can the banks compete? It is a tired question accord-ing to Fodor, and he does, of course, have a vested interest. Banks are going to be phased out “not at all”.

Fodor adds: “People like to talk about that time and time again. If, by chance, the regula-tory environment eases and interest rates go up, that’s going to help banks.

“It’s going to drive more operating profit at the end of the day, thanks to interest rates – again, perhaps free up some compliance spending. All this leaves more money for investments. Digital is going to be one of the key differentiating factors for banks in the new age.

“That applies to all things digital. In the past when you look at how banks competed, they competed on services, interest rates, price, high-touch interactions with their cus-tomers. All of this defined and allowed them

to differentiate themselves.”The new differentiator these days, it seems,

is digital prowess. It is true, most consumer banking surveys show that 60% plus of them prefer to work with a bank in an online or global channel.

Having that robust online banking system, global banking system, integrated mobile payments offering, loyalty and rewards offer-ing, is keys to setting themselves apart from the other banks.

“We are seeing that in the merchant world. For example, in the US there’s a merchant called Panera, a boutique sandwich shop, probably one of the first merchants of its kind which came out on its earnings call to Wall Street. When they come out on a Wall Street earnings call, you know they’re for real, because they’re on the stage for all their investors to see.

“Our digital strategy and our digital prow-ess are allowing us to take share from our competitors,” Fodor notes.

“In the early 1990s Bill Gates said, ‘Banks are dinosaurs, they can be displaced.’ Fast-forward about 20 years and, having invested in a fintech startup, came his quip of, ‘I vastly underestimated how complex banking was.’ He came around to the realisation that it’s really tough to unseat these folk.

“Banks have plenty of things to worry about, but they’ve shown time and time again that they can fend off the competition. As long as they have a coherent strategy, and are in touch with the market and the trends, they can eke out a very good, if not fantastic, existence.

“There is something to be said for having

the money and the trust.“At the height of the financial crisis sur-

veys were taken of banks, and still when asked who they trust with their money, con-sumers answered, ‘I trust my bank’,” Fodor explains.

“There was the headline stuff concerning hatred towards banks, but the consumer mindset was, ‘At the end of the day, if I have to put my money somewhere, when every-thing goes to hell, I know it’s going to be safe with the bank.’ So, we love [banks’] chances, and love working with them. About half our business comes from the banking side.”

In terms of social commerce and how important it is to focus on the upcoming generation, Fodor explains that, in the main, doing everything on digital is a “leap of faith” for consumers, likely to be adopted by the 18-30 age group and “not a chance” by the 30-plus age group.

He argues that all the wealth and spend-ing is in the 30-plus category, so while keep-ing an eye on the upcoming demographic is important, the priority is to keep the main revenue group sweet.

“Do we need to make a big bet this moment? No. The beauty of what we do and how we build our systems is that the core infrastructure can be transported to new emerging technologies. So you build once and scale it across other interfaces.

“I’m not saying there won’t be another dollar investment if social commerce takes off, but nothing changes the essence of our scaled bedrock foundation of platforms; we go about our business doing the processing as we always do.” <

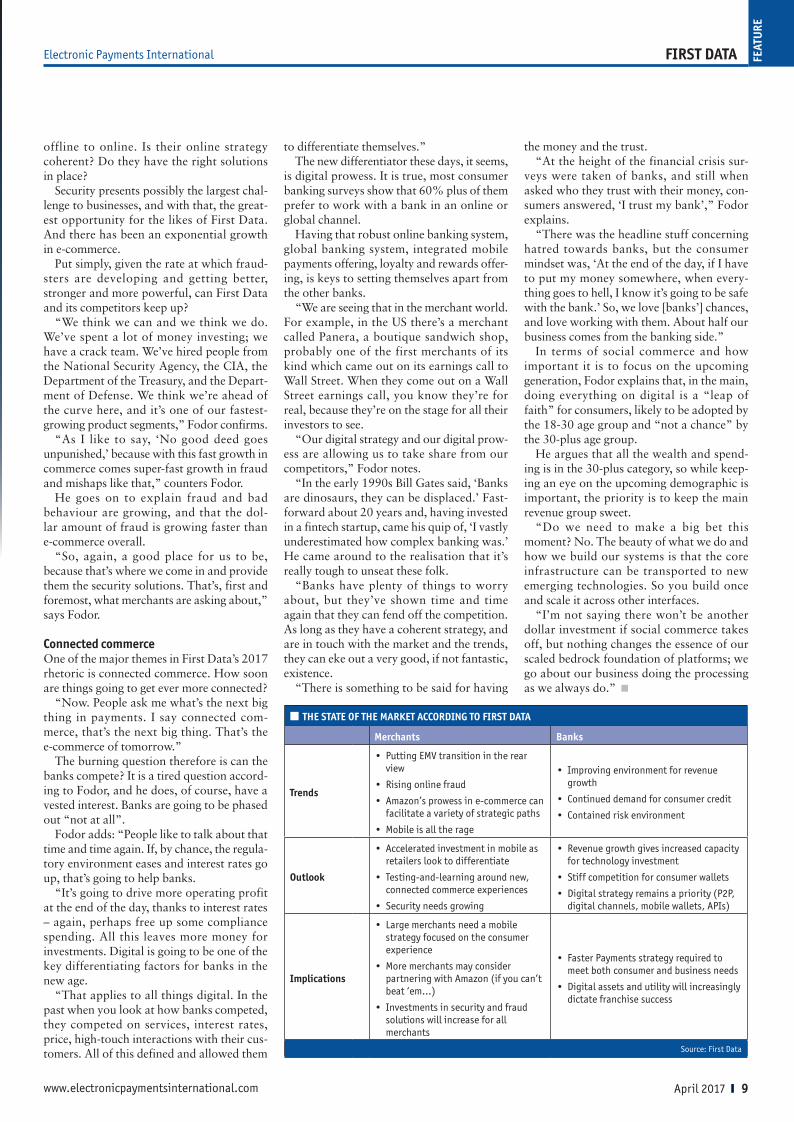

n THE STATE OF THE MARKET ACCORDING TO FIRST DATA

Merchants Banks

Trends

• Putting EMV transition in the rear view

• Rising online fraud

• Amazon’s prowess in e-commerce can facilitate a variety of strategic paths

• Mobile is all the rage

• Improving environment for revenue growth

• Continued demand for consumer credit

• Contained risk environment

Outlook

• Accelerated investment in mobile as retailers look to differentiate

• Testing-and-learning around new, connected commerce experiences

• Security needs growing

• Revenue growth gives increased capacity for technology investment

• Stiff competition for consumer wallets

• Digital strategy remains a priority (P2P, digital channels, mobile wallets, APIs)

Implications

• Large merchants need a mobile strategy focused on the consumer experience

• More merchants may consider partnering with Amazon (if you can’t beat ‘em…)

• Investments in security and fraud solutions will increase for all merchants

• Faster Payments strategy required to meet both consumer and business needs

• Digital assets and utility will increasingly dictate franchise success

Source: First Data

EPI 358.indd 9 11/04/2017 11:45:40

www.electronicpaymentsinternational.com 10 y April 2017

MEXICO Electronic Payments International

Latin America’s third-largest economy could slip into recession if US President Donald Trump’s toxic cocktail of threats to upend the North American Free Trade Agreement or impose heavy tariffs on Mexican exports come true. However, Mexican banks are – at least for now – unconcerned. Ivan Castano writes

Mexico’s payments sector is shrug-ging off concerns that US Presi-dent Donald Trump’s protection-ist threats could hit its fortunes,

forecasting strong revenues despite moni-toring portfolios more closely.“So far, we haven’t taken any provisions,”

says Miguel Angel Laurencio de La Vega, investor relations director at Banorte, which with roughly 2m customers is Mexico’s third-largest bank.“Overall, consumption remains strong and

there are no [portfolio] deterioration signs, despite future uncertainty.”

Employment continues to grow, with the nation adding 500,000 jobs in the past year, De La Vega says. Unemployment stood at 3.6% in January, down 4.2% year-on-year according to the latest data from statistics institute Inegi. “If unemployment rises that would give

us a reason to act, but so far our past due portfolio remains at 5%, which matches the industry’s, with an improving outlook,” De La Vega adds.

Banorte, which intends to double its pay-ments market share to over 16% by 2022, matching arch-rival Citigroup’s Citiban-amex, expects card revenues to climb 14% to MXN8.2bn ($435m) this year, helped by soaring interest rates in Mexico.

The central Bank of Mexico has stepped up benchmark rates six times to 5.25%

since Trump swept into the White House, in a move aimed at shoring up the plummet-ing peso and combatting soaring inflation, which is currently hovering at 5% – well over its 2% target.

The actions have boosted variable credit card rates, lifting margins for the top three bank issuers: Spain’s BBVA Bancomer, Citi-group’s Banamex, and Santander.

The increases will add 200 basis points to the 28% average rate that Banorte charges for its silver, platinum and gold products, offsetting a slight decrease in its portfolio growth. “This year, we will probably grow less in

our portfolio but more in revenues,” says De La Vega, adding that last year its outstanding balance grew by 10% to roughly MXN26bn.

Despite rising margins, Mexico’s economy is set to cool this year, with the government recently cutting GDP growth projections to 1.3-1.5%, down from a previous estimate of 2.5%.

Latin America’s third-largest economy could slip into recession, however, if Trump’s toxic cocktail of threats to upend the North American Free Trade Agreement (NAFTA) – a 23-year-old free-trade agreement that has largely modernised Mexico – or impose heavy tariffs on Mexican exports come true, triggering a trade war between the two nations. The US president also wants to tax remittances – money Mexicans send to

families south of the border, a huge economic driver – to build his $15bn border wall, and has expanded immigration laws to expel as many as 3m Mexicans.

The deepening uncertainties are putting investors and businesses on tenterhooks, trig-gering a sharp fallout in foreign direct invest-ment that is unlikely to recover until the two governments tentatively wrap up negotia-tions to modify NAFTA by the summer.

Amid such risks, Banorte will focus on growing business with existing clients, and largely shunning new ones or entering new market segments until Mexico’s future pros-pects become clearer.“We will be more cautious and seek to grow

similarly to last year. We will not be launch-ing any new products or targeting new mar-ket segments aggressively,” De La Vega notes. “Many of our customers use our cards very

little, so the plan is to increase this through reward programmes and promotions.”

Others are also being cautious. BBVA Bancomer, which leads Mexico’s banking sector, has begun lowering card limits and more closely monitoring its accounts, ana-lysts say; much smaller Inbursa, which belongs to telecoms tycoon Carlos Slim, is also becoming more selective, they add.

Jorge Benitez, an analyst with broker GBM, has a sanguine outlook for 2017. He says issuers continue to enjoy high margins and improving credit quality, with interest

FEAT

URE

High altitude, higher stakes?

EPI 358.indd 10 11/04/2017 11:45:41

www.electronicpaymentsinternational.com April 2017 y 11

rates hovering at 26.4%. This, coupled with an expected 9% rise in plastic issuance this year, will drive revenues up 11% to MXN-94bn.

“We are not that negative,” Benitez says. “We don’t see signals of deterioration because consumer demand remains strong.”

That said, if the economy were to decline by more than expected in the second half – something economists expect if a trade war erupts – lenders could suffer amid rising unemployment and defaults. “We could see a small decrease in employ-

ment which would affect banks’ portfolios and they would stop issuing credit,” Benitez explains.

To protect themselves, institutions could cut risky personal loans and raise their expo-sure to safer direct deposit credits, he adds.

However, even if that happens, the pay-ment sector’s long-term prospects look bright, largely as a result of Mexico’s low banking penetration. “Credit cards represent 33% of the

MXN4.3trn banking sector, where penetra-tion is about 4% of GDP,” Benitez says.

Enrique Mendoza, an analyst at broker Actinver, is more pessimistic, adding that a sharp economic downturn could severely hit issuers. “Banks would have to provision very rapid-

ly, even if there is a small default change from one institution or if credit bureau reports worsen,” Mendoza notes.

Joel Cortes, co-founder of consumer card-comparison site Kardmatch, says issu-ers would struggle to pass on higher inter-est rates to customers who would likely fall behind on payments.

Leading retailers Coppel, Liverpool and Walmart, which cater to the nation’s vast majority of low- and middle-income con-sumers, would be worst hit in this scenario.

By targeting the less-wealthy shoppers whom banks typically shun, the firms have made a fortune, offering customers a cornu-copia of store cards with ‘months-without-interest’ instalments.

And in the last five years, other depart-ment stores such as luxury chain El Palacio de Hierro, Saks Fifth Avenue Mexico and Sears de Mexico have followed suit, issuing ludicrously long, 12-18-month zero-interest credits, fuelling fears that they have over-hedged themselves.“There is a bubble risk for these retailers,”

warns Cortes. “Of course, they are betting this won’t happen, but falling incomes will increase the probability of defaults.”

Liverpool and Coppel have buffered against these risks by charging higher prices for merchandise sold on credit or charging above-market interest rates, however.

Cortes agrees that the payments market remains healthy. However, like Banorte, most issuers are concentrating on their exist-ing pool of good-credit customers and cast-ing “a strong eye” on portfolios.

They have also cut purchasing rewards sharply. “No one is talking about this, but rewards have fallen around 40% since 2012 [when the economy was growing at more robust rates] so now you have to spend 70% more to accumulate the same number of points,” Cortes reveals.

Cortes adds that 2017 “will be very bor-ing” for new plastic launches or product innovation, except perhaps in the digital arena where online and mobile purchasing is growing strongly.

He highlights Banregio, a tiny lender in Northern Mexico, as this year’s top innova-tor after it launched a platinum card offering 1% cashback, 5% interest and no annual fee.

“You hardly see cards with such high rewards and low interest rates,” he notes, adding that the bank has an innovative online application feature. “Banregio has an interesting philosophy,

which is sort of populist because it wants to be seen to be offering a product that won’t break your finances,” Cortes says.

That could chime well with impoverished Mexicans who have boycotted US brands Starbucks, McDonalds and Walmart to decry Trump’s calls that Mexico pay for his bor-der wall, on top of his well-publicised insults against its population.

However, Cortes says the actions have not hurt the likes of Visa, Mastercard or Ameri-can Express, which has a $2.2bn exposure that analysts believe it is looking to trim.

“Each bank has customer complaints or issues, but nothing has changed because of Trump itself,” Cortes adds.

Meanwhile, De La Vega says Banorte is keen to grow its digital business as Mexico’s e-commerce market is growing rapidly amid falling mobile data rates, catching up with leading markets in Brazil and Chile.

It recently incorporated a selfie identifica-tion feature to its mobile banking app, which it says is unique in the market, for example.

Banorte hopes to bring similar innovations to the fore to grow its card segment, which accounts for MXN55bn of its MXN559bn consumer loan portfolio. “We want to develop our cards business to

mirror the 14% market share we have for our other loan products,” De La Vega con-cludes. <

FEAT

URE

MEXICOElectronic Payments International

Separate ways? The Trump presidency could redefine US-Mexican relationships

EPI 358.indd 11 11/04/2017 11:45:45

www.electronicpaymentsinternational.com 12 y April 2017

COM

MEN

TTHE NEW POUND COIN Electronic Payments International

New quid on the block- a sterling effort?

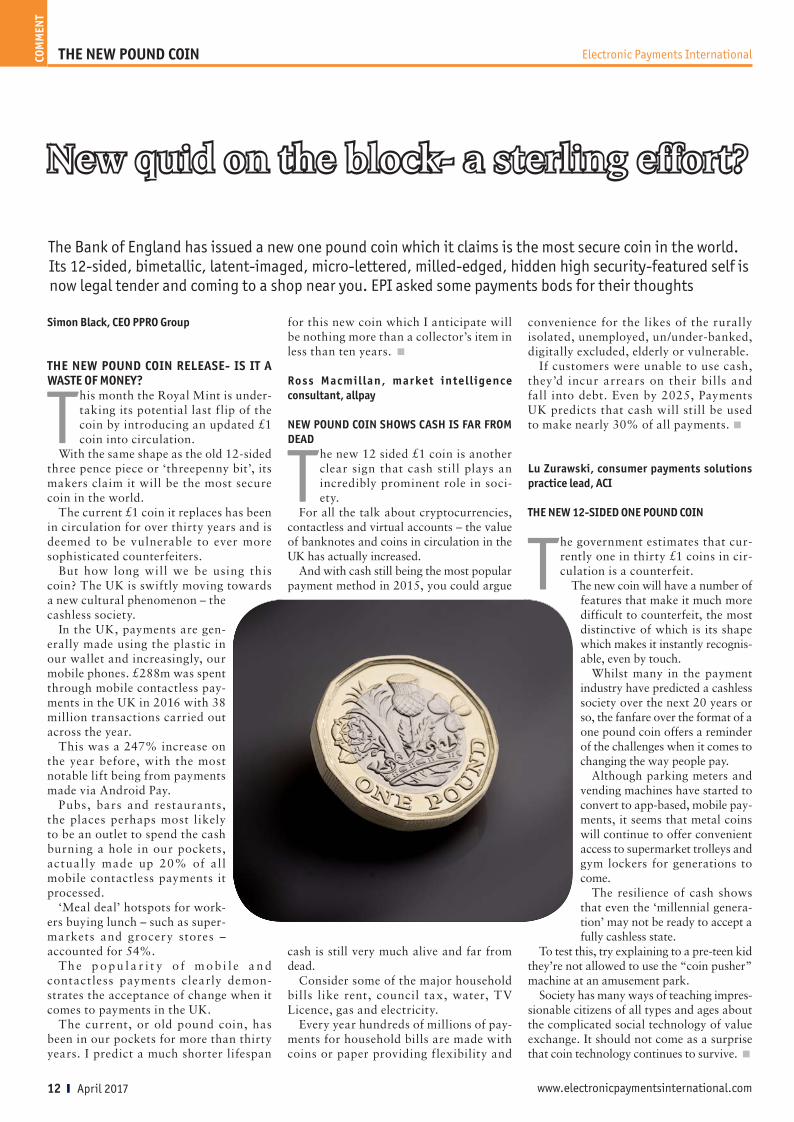

The Bank of England has issued a new one pound coin which it claims is the most secure coin in the world. Its 12-sided, bimetallic, latent-imaged, micro-lettered, milled-edged, hidden high security-featured self is now legal tender and coming to a shop near you. EPI asked some payments bods for their thoughts

Simon Black, CEO PPRO Group

THE NEW POUND COIN RELEASE- IS IT A WASTE OF MONEY?

This month the Royal Mint is under-taking its potential last flip of the coin by introducing an updated £1 coin into circulation.

With the same shape as the old 12-sided three pence piece or ‘threepenny bit’, its makers claim it will be the most secure coin in the world.

The current £1 coin it replaces has been in circulation for over thirty years and is deemed to be vulnerable to ever more sophisticated counterfeiters.

But how long will we be using this coin? The UK is swiftly moving towards a new cultural phenomenon – the cashless society.

In the UK, payments are gen-erally made using the plastic in our wallet and increasingly, our mobile phones. £288m was spent through mobile contactless pay-ments in the UK in 2016 with 38 million transactions carried out across the year.

This was a 247% increase on the year before, with the most notable lift being from payments made via Android Pay.

Pubs, bars and restaurants, the places perhaps most likely to be an outlet to spend the cash burning a hole in our pockets, actually made up 20% of al l mobile contactless payments it processed.

‘Meal deal’ hotspots for work-ers buying lunch – such as super-markets and grocery stores – accounted for 54%.

Th e p o p u l a r i t y o f m o b i l e a n d contactless payments clearly demon-strates the acceptance of change when it comes to payments in the UK.

The current, or old pound coin, has been in our pockets for more than thirty years. I predict a much shorter lifespan

for this new coin which I anticipate will be nothing more than a collector’s item in less than ten years. <

Ross Macmillan, market intell igence consultant, allpay

NEW POUND COIN SHOWS CASH IS FAR FROM DEAD

The new 12 sided £1 coin is another clear sign that cash still plays an incredibly prominent role in soci-ety.

For all the talk about cryptocurrencies, contactless and virtual accounts – the value of banknotes and coins in circulation in the UK has actually increased.

And with cash still being the most popular payment method in 2015, you could argue

cash is still very much alive and far from dead.

Consider some of the major household bills like rent, council tax, water, TV Licence, gas and electricity.

Every year hundreds of millions of pay-ments for household bills are made with coins or paper providing flexibility and

convenience for the likes of the rurally isolated, unemployed, un/under-banked, digitally excluded, elderly or vulnerable.

If customers were unable to use cash, they’d incur arrears on their bills and fall into debt. Even by 2025, Payments UK predicts that cash will still be used to make nearly 30% of all payments.<

Lu Zurawski, consumer payments solutions practice lead, ACI

THE NEW 12-SIDED ONE POUND COIN

The government estimates that cur-rently one in thirty £1 coins in cir-culation is a counterfeit.

The new coin will have a number of features that make it much more difficult to counterfeit, the most distinctive of which is its shape which makes it instantly recognis-able, even by touch.

Whilst many in the payment industry have predicted a cashless society over the next 20 years or so, the fanfare over the format of a one pound coin offers a reminder of the challenges when it comes to changing the way people pay.

Although parking meters and vending machines have started to convert to app-based, mobile pay-ments, it seems that metal coins will continue to offer convenient access to supermarket trolleys and gym lockers for generations to come.

The resilience of cash shows that even the ‘millennial genera-tion’ may not be ready to accept a fully cashless state.

To test this, try explaining to a pre-teen kid they’re not allowed to use the “coin pusher” machine at an amusement park.

Society has many ways of teaching impres-sionable citizens of all types and ages about the complicated social technology of value exchange. It should not come as a surprise that coin technology continues to survive. <

EPI 358.indd 12 11/04/2017 11:45:48

www.electronicpaymentsinternational.com April 2017 y 13

Cash continues to be the most popu-lar consumer payment instrument in the Philippines, particularly in rural areas.

Cash accounts for 99.5% of the country’s total payment transaction volume, due pri-marily to a lack of banking infrastructure, limited public awareness of electronic pay-ments and low acceptance at retailers.

However, cash’s share is anticipated to decline gradually over the forecast period (2017–2021), as a result of the central bank’s financial inclusion program.

The emergence of contactless technology is also expected to support payment card mar-ket growth.

The unbanked – a large untapped marketThe percentage of the Philippine population aged 15 or above with a bank account was 34.3% in 2016. The government has taken a number of initiatives, in the form of pro-grams and policies, to bring a greater pro-portion of the population into the formal banking system.

The government also introduced the Phil-ippine Development Plan 2011–2016; this includes the promotion and delivery of finan-cial services in rural areas, the promotion of financial literacy and consumer education, and the development of loan and banking products to meet the needs of women, and low-income and disabled individuals.

As part of the government’s financial inclu-sion plan, a number of micro-banking offic-es, electronic money, microfinance providers, pawnshops, and remittance agents are being employed to provide access to financial ser-vices in un- or underserved areas.

Rising remittances drive debit card useRemittances form a key part of the Philip-pines’ economy, accounting for 10% of the country’s GDP.

Remittances also play an important role in driving growth in the debit cards mar-ket, with many Filipinos emigrating. Inward remittances rose from $24.6bn (PHP1.0trn) in 2012 to $27.9bn in 2016, and are expected to grow as more Filipinos seek work abroad.

As migration rises, banks are increasingly offering bank accounts and debit cards that facilitate the transfer of money to beneficiar-ies back home. For instance, in September 2015 Land Bank of the Philippines formed

a partnership with Trans-Fast Remittance, a provider of multicurrency cross-border pay-ments solutions, to enable remittance trans-fers for Trans-Fast customers.

The partnership enables Filipinos in the US and Canada to use Trans-Fast to make real-time instant transfers into Land Bank of the Philippines accounts, which can be with-drawn using a debit card.

Robust credit card market growthDebit cards remained the largest card type in terms of transaction value with an 81.7% share, which is expected to grow over the forecast period as more of the unbanked population are brought into the formal bank-ing system.

Though small in size, the credit cards market registered robust review-period (2012–2016) growth both in terms of trans-action value and volume. The growth can be attributed to economic growth and a steady rise in the middle-class and young working populations.

Also driving credit card transactions are monthly instalment facilities and pricing benefits such as annual fee waivers, reward programs and cashback.

The enactment of the central bank’s Inter-bank Debt Relief Program to control credit card debt, and the arrival of global credit bureaux are expected to further strengthen the country’s credit card market. <

Cash’s dominance of the payments landscape in the Philippines is verging on total, with much of the population unbanked and consumer awareness of electronic payments limited. Initiatives by the central bank, and migrants’ increasing use of electronic payments to send money home could be catalysts for change, however

n PHILIPPINE CARD TRANSACTION VALUES BY CHANNEL ($ BILLION), 2012–2021

ATM POS

2012 47.3 16.0

2013 53.9 18.2

2014 57.9 19.3

2015 61.9 20.9

2016 (estimate) 64.9 22.2

2017 71.3 24.7

2018 77.8 27.4

2019 84.6 30.3

2020 91.5 33.3

2021 97.7 36.3

Source: EPI

n PHILIPPINE PAYMENT CARDS BY TYPE (MILLION), 2012–2021

Debit Cards Pay Later Cards

2012 36.8 7.2

2016 (estimate) 50.8 9.2

2017 54.4 9.8

2021 68.6 12.1

Source: EPI

n PHILIPPINE CARD TRANSACTION VOLUMES BY CHANNEL (MILLION), 2012–2021

ATM POS

2012 747.5 227.7

2013 837.5 254.1

2014 925.0 277.1

2015 1,005.2 301.6

2016 (estimate) 1,086.5 327.6

2017 1,171.0 355.0

2018 1,258.2 384.1

2019 1,347.6 414.3

2020 1,438.0 445.6

2021 1,525.1 477.5

Source: EPI

n NUMBER OF ATMS AND POS TERMINALS IN THE PHILIPPINES (THOUSAND), 2012–2021

ATM POS

2012 12.2 134.7

2013 14.5 150.1

2014 15.7 165.7

2015 17.3 187.0

2016 (estimate) 18.8 204.7

2017 20.2 223.0

2018 21.5 242.2

2019 22.5 262.1

2020 23.3 281.6

2021 23.9 298.8

Source: Central Bank of the Philippines, EPI

The Philippines

THE PHILIPPINESElectronic Payments International COU

NTR

YSU

RVEY

EPI 358.indd 13 11/04/2017 11:45:50

www.electronicpaymentsinternational.com 14 y April 2017

Cambodia’s government and banks are focusing on providing financial access to the unbanked population, expanding banking infrastructure

such as ATMs, and introducing agent banking, in a move to reduce the coun-try’s high dependence on cash.

Payment cards are gradually becoming more accepted, with their use expected to grow over the forecast period (2017–2021) with a CAGR of 12.52% in terms of transac-tion value. However, use of cards is mostly limited to ATM cash withdrawals, with lit-tle use at merchant outlets; POS transactions accounted for only 4% of total card transac-tions in 2016.

A major challenge to the growth of card-based payments in Cambodia is the charging of additional fees by merchants. However, international scheme providers such as Visa and MasterCard, along with commercial banks, are educating customers and mer-chants on the benefits of card payments, and are working to remove surcharging.

Low banking penetration hinders growthDebit card penetration stood at 10.1 per 100 individuals in 2016. The figure is compara-tively low when compared to peer countries such as China (369.8), Malaysia (140.7), Thailand (116.5), Vietnam (114.4), India (60.7), the Philippines (49), Indonesia (48.2) and Pakistan (15.7).

Low banking penetration and limited consumer awareness of the benefits of cards remain the primary reasons for low debit card penetration. As the majority of the population resides in rural areas, exposure to electronic payments is relatively low.

The government and banks are taking vari-ous measures to bring more of the popula-tion into the formal banking system. Local bank Wing is focusing on providing access to financial services to rural and remote locations; the bank has expanded into 25 provinces and operates a network of 5,000 branches. Wing also offers agent banking, with its 3m customers carrying out around 60m transactions annually through agents.

Acleda Bank increased its ATM network from 219 in 2014 to 280 in 2015, and the number of POS terminals from 2,116 to 2,595 over the same period. These initia-tives provided a much-needed push to the government’s financial inclusion program,

and resulted in the proportion of the banked population rising from 10% in 2012 to 33% in 2016.

Scope for growth in credit cardsAs most of Cambodia’s population is lower middle class, and with 90% of the popula-tion residing in rural areas, exposure to credit cards and need of use are very low. Banks therefore focus more on corporate, upper-middle-class, high-income customers, as well as travellers.

The absence of bankruptcy laws also has hindered credit card adoption in the coun-try, as issuers are reluctant to supply cards to consumers without any legal assurance of receiving repayment.

Despite its small size, the credit card mar-ket has grown significantly in terms of both cards in circulation and transaction value.

The Credit Bureau of Cambodia (CBC) was established in 2011 to help develop the country’s credit cards market. The CBC is a private company, regulated and licensed by the NBC, and is responsible for managing credit information and functionality.

Its establishment has provided a frame-work and regulations for the operation of credit cards, building confidence among issu-ers and consumers. Since the CBC’s establish-ment, the credit cards market has registered an average annual growth rate of 17.3%, in terms of transaction value. <

n CAMBODIAN CARD TRANSACTION VALUES BY CHANNEL ($ BILLION), 2012–2021

ATM POS

2012 1.7 0.1

2013 2.0 0.1

2014 2.7 0.1

2015 3.1 0.1

2016 (estimate) 3.6 0.2

2017 4.2 0.2

2018 4.8 0.2

2019 5.4 0.3

2020 6.0 0.3

2021 6.6 0.4

Source: EPI

n CAMBODIAN CARD TRANSACTION VOLUMES BY CHANNEL (MILLION), 2012–2021

ATM POS

2012 23.0 0.9

2013 26.3 1.0

2014 34.3 1.3

2015 38.9 1.6

2016 (estimate) 43.9 1.8

2017 49.2 2.1

2018 54.7 2.4

2019 60.5 2.8

2020 66.4 3.1

2021 72.3 3.5

Source: EPI

n NUMBER OF ATMS AND POS TERMINALS IN CAMBODIA (THOUSAND), 2012–2021

ATM POS

2012 0.7 4.2

2013 0.8 4.8

2014 0.9 5.8

2015 1.1 9.6

2016 (estimate) 1.3 12.5

2017 1.5 14.6

2018 1.7 16.8

2019 1.9 18.8

2020 2.1 20.8

2021 2.3 22.6

Source: Central Bank of Cambodia, EPI

n CAMBODIAN PAYMENT CARDS BY TYPE (MILLION), 2012–2021

Debit Cards Pay Later Cards

2012 23.5 0.3

2016 (estimate) 45.1 0.6

2017 50.6 0.7

2021 74.6 1.2

Source: EPI

CAMBODIA Electronic Payments InternationalCOU

NTR

YSU

RVEY

Cambodia is a largely cash-based society, as a result of low banking penetration, a lack of consumer knowledge of other payment instruments such as payment cards, and limited access to payment infrastructure. However, the small credit card market is receiving support and growing strongly

Cambodia

EPI 358.indd 14 11/04/2017 11:45:54

www.electronicpaymentsinternational.com April 2017 y 15

Card transactions in Estonia record-ed robust growth during the review period (2012–2016), surpassing cash to become the dominant pay-

ment instrument.In terms of transaction volume, payment

cards accounted for 44.3% of the total cards and payments industry in 2016, while cash accounted for 33.6%. Nearly 90% of indi-viduals used payment cards for daily pur-chases in 2015, as compared to only 33% in 2001.

Payment card penetration stood at 1.40 in 2016, higher than in Latvia (1.25) and Lithu-ania (1.24). Estonia’s young population are among the most prolific users of payment cards in the Baltic region. According to a survey conducted by SEB Estonia in 2015, 76% of the Estonian population aged 18-25 years use payment cards for all purchases, in comparison to 59% in Latvia and 40% in Lithuania.

Low levels of card fraud make Estonia a prominent country in the European cards and payments industry. A 2015 report by the European Central Bank indicated that at five instances of fraud per 1,000 people, Estonia was the lowest-ranking nation in the SEPA region, where the average is 20.

Estonia has a robust banking infrastruc-ture. ATM penetration – the number of ATMs per 100 inhabitants – in the country stood at 7.8, lower than its Baltic peers of

Latvia and Lithuania, which had rates of 10.5 and 11.7 respectively. POS terminal penetration stood at 346.9, compared again to Latvia and Lithuania which had respective rates of 335.8 and 536.7.

To increase financial access among the rural population, state postal service Eesti Post launched a cash withdrawal service in May 2015, allowing consumers to withdraw up to €400 ($448) at mobile POS terminals carried by mail delivery personnel.

Highest Baltic debit card penetrationDebit cards remained the most widely used payment card during the review period, and accounted for 91.8% of the total transaction volume and 90.5% of the total value of pay-ment card transactions in 2016.

Debit card penetration in Estonia is the highest in the Baltic region, at 116.3 cards per 100 inhabitants, compared to Latvia with 85.2 and Lithuania with 108.9.

According to the World Bank’s Global Fin-dex survey, banking penetration in Estonia reached 98.1% in 2016; as debit cards are generally supplied as complementary with current accounts, the explanation for their high penetration rate is clear.

In addition to banks, mobile banking ser-vice provider Pocopay launched in Febru-ary 2016, allowing customers to open and operate bank accounts using mobile phones. There are three account types: Poco Power, Poco Basic, and Poco Power Youth.

Poco Basic has no monthly fee, but has limited transaction functionality. The Poco Power account is available for a monthly fee of €2.9 ($3.2), and has no transaction fees. The Poco Power Youth account is designed for individuals aged 18-26, carries a monthly fee of $1, and has the same features as the Poco Power account. All account holders are offered a MasterCard contactless debit card.

Contactless to gain prominenceEurope has the world’s highest adoption of contactless payments. Estonian banks plan to embrace the technology, and all ATMs are expected to be equipped with contactless functionality by 2020, while new POS termi-nals are expected to be contactless by 2017.

To expedite the process, Swedbank, Nordea Bank and LHV Pank have already launched contactless cards; SEB plans to introduce them by the end of 2017. <

n ESTONIAN CARD TRANSACTION VALUES BY CHANNEL ($ BILLION), 2012–2021

ATM POS

2012 4.4 4.6

2013 4.8 5.3

2014 4.9 5.7

2015 4.2 5.2

2016 (estimate) 4.4 5.7

2017 4.5 6.2

2018 4.6 6.7

2019 4.8 7.3

2020 4.9 7.9

2021 5.0 8.4

Source: Central Bank of Estonia, EPI

n ESTONIAN CARD TRANSACTION VOLUMES BY CHANNEL (MILLION), 2012–2021

ATM POS

2012 41.1 214.1

2013 40.1 230.2

2014 38.8 246.3

2015 38.4 264.1

2016 (estimate) 37.8 282.8

2017 37.4 302.2

2018 36.9 322.1

2019 36.6 342.2

2020 36.3 362.5

2021 36.0 383.0

Source: Central Bank of Estonia, EPI

n NUMBER OF ATMS AND POS TERMINALS IN ESTONIA (THOUSAND), 2012–2021

ATM POS

2012 0.9 27.2

2013 0.9 27.5

2014 0.8 28.8

2015 0.8 31.7

2016 (estimate) 0.8 34.7

2017 0.8 37.6

2018 0.7 40.2

2019 0.7 42.5