budget use and managerial performance

TRANSCRIPT

Journal of Accounting ResearchVol. 16 No. 1 Spring 1978

Printed in V.SA.

Budget Use and ManagerialPerformance

DAVID T. OTLEY*

The effectiveness of a management accounting system depends notonly on the appropriateness of its technical characteristics to theparticular organizational and environmental circumstances to whichit is applied, but also on the way in which organizational participantsmake use of the information that it provides. It is a commonplace thataccounting information is often ignored, sometimes manipulated, andeven falsified by those to whom it is provided. Many of the reportedexamples (see Rosen and Sneck [1967], Lowe and Shaw [1968], Mintz-berg [1975], and Yetton [1976]) indicate that dysfunctional behaviorfrequently stems from the fact that the information provided by theaccounting system does not adequately match the complexity of theunderlying organizational and economic events; but it is also evidentthat distortion of information can occur even when the accoimtingsystem itself is technically adequate. Such distortion is a consequenceof the divergence of individual goals from those of the organizationand most commonly manifests itself in attempts to make accountingreports refiect more favorably on an individual's contribution tooverall organizational performance. Although evidence in anecdotalform abounds (for example, Dearden [1960] and Schiff and Lewin[1970]), little consideration has been given to the type of circumstancesin which manipulation of accounting data occurs.

It is important to know whether distortion of accounting informationis inevitable and can therefore be limited only by ever stricter methods

* Lecturer, University of Lancaster. I wish to acknowledge financial support fromthe Foundation for Management Education and the Social Science Research Counciland the help and advice of faculty and students at the Manchester Business School. Anearlier version of this paper was presented at the Conference on Accounting held by theEuropean Institute for Advanced Studies in Management in Brussels, November 1976.[Accepted for publication April 1977.]

122

Copyright O, Institute of Professional Accounting 1978

BUDGET USE AND MANAGERIAL PERFORMANCE 123

of audit and control, or whether it depends upon precisely howaccounting information is used within an organization. Unfortunately,previous work (Hopwood [1972], Dew and Gee [1973]) has tended toconfound inadequacies in the technical characteristics of the account-ing system with the way in which managers use the accountinginformation provided; although Ansari [1976] has performed an exper-iment designed to investigate the joint effect of leadership style andthe specification of an accounting system. The present study wasdesigned to eliminate technical failings in the accounting system, asfar as possible, by observing the operation of a well-designed systemin a type of organization that was well suited for the application ofbudgetary control. In this way, attention could be directed primarilyto the effects produced by the differential use of budget information.The focus of the study is on the evaluation of managerial performance,because this is both an important organizational function often servedby accounting information and one which is of central importance tothe individual manager being evaluated. It is therefore likely that theuse made of budgetary information in performance evaluation willhave a considerable impact upon managers' reactions te such infor-mation and upon their subsequent performance. Particular attentionwas paid to assessing performance in addition to the interveningvariables of a manager's inner states, attitudes, and feelings.

The Use of Budgetary Data in Managerial PerformanceEvaluation

In order te evaluate managerial performance, it is necessary to havesome form of standard against which measures of performance can beassessed. Ideally, this involves considerations of both effectiveness(i.e., whether the manager is doing the right thing) and efficiency(i.e., whether he is doing what he does with a minimum expenditureof resources). However, an essential component of managerial work isthe exercise of discretion (Jaques [1961]), in that the content of what amanager ought to do and the way in which he ought to do it cannot bespecified in advance.' Thus, for this type of activity, the most that cansensibly be done is te set standards for outputs (i.e., goals, objectives,targets) and to determine appropriate schedules for the inputs thatare deemed necessary for task performance. However, because themanagerial task involves the exercise of discretion and judgment, sothe setting of standards for task performance is also an essentiallyjudgmental activity (see Vickers [1965]). Therefore, the evaluation ofmanagerial performance is, in itself, a managerial task which cannot

' Jaques himself goes considerably beyond this position by claiming that themeasurement of the time span of a manager's discretion is a good measure of the level ofthe work he undertakes and is related to the recompense he considers equitable.Although this extension is controversial, the basic premise that truly managerial workinvolves the exercise of discretion is well accepted.

124 JOURNAL OF ACCOUNTING RESEARCH, SPRING 1978

be precisely predetermined, and which different managers will carryout in different ways.

Budgetary data may play an important role in this process, for abudget can be used to represent standards of both effectiveness andefficiency. It represents a standard of effectiveness insofar as itspecifies a set of desired outputs and a standard of efHciency to theextent that it details the inputs deemed necessary to produce thespecified outputs,^ Data on actual performance may then be used, bycomparison with the budget standard, to evaluate certain dimensionsof managerial performance. Despite the fact that a budgetary systemmay not be designed primarily as a means of performance evaluation,there is evidence that it will almost inevitably be used for thispurpose, whether formally sanctioned or not (see Ridgway [1956] andHofstede [1968] for examples), as it provides what is often the onlyquantitative information relating to managerial performance. Wherebudget information is used as a basis for performance evaluation, it islikely that the effects of such use will predominate in determining howa manager responds to the accounting information, because of theimmediate and personal impact that results. As the distribution oforganizational rewards will be connected with the results of theevaluation process, so behavior will be oriented toward obtainingthose rewards considered desirable by the manager,

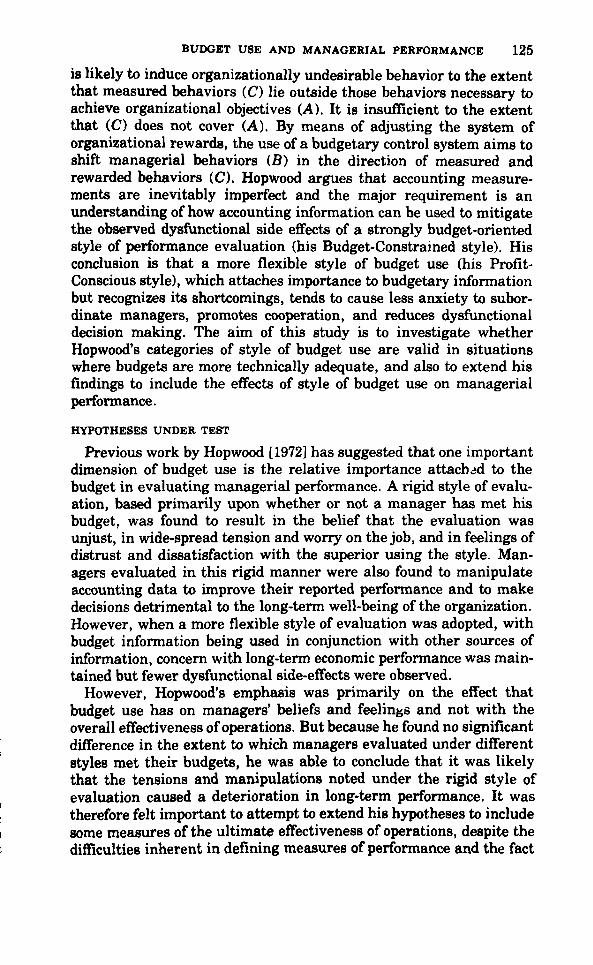

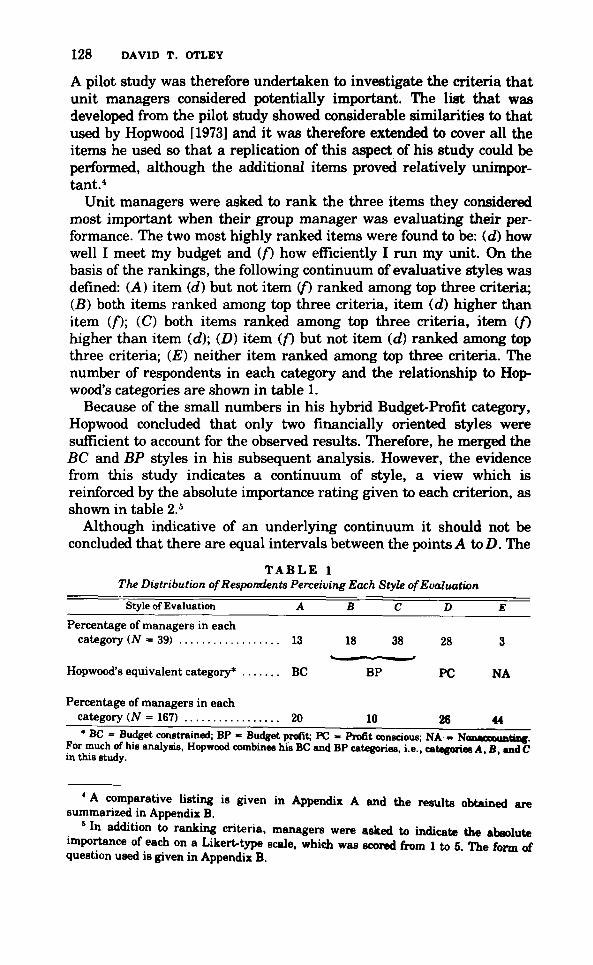

Hopwood [1973] has indicated the possibilities for dysfunctionaldecision making and distortion of information by the (slightly adapted)diagram shown in figure 1, The accounting system is inadequate and

Organizationalpurposes

System of Formal performanceorganizational > measurement

rewards systems

Individual manager'sgoals

FIG. 1. - T h e measurement-reward process with imperfect measurement. A = behav-ior necessary to achieve organizational purposes; B = behavior actually engaged in byindividual manager; C = behavior formally measured by control system.

" In addition, it can be tailored to suit the degree of discretion appropriate to eachmanagerial level by adjusting the level of detail included. For example, a seniormanager may be held responsible only for the attainment of an overall profit figure; amore junior manager may be held responsible for the way a profit figure is made up interms of specified revenue and cost headings.

BUDGET USE AND MANAGERIAL PERFORMANCE 125

is likely to induce organizationally undesirable behavior to the extentthat measured behaviors (C) lie outside those behaviors necessary toachieve organizational objectives (A). It is insufficient to the extentthat (C) does not cover (A). By means of adjusting the system oforganizational rewards, the use of a budgetary control system aims toshift managerial behaviors (B) in the direction of measured andrewarded behaviors (C). Hopwood argues that accounting measure-ments are inevitably imperfect and the major requirement is anunderstanding of how accounting information can be used to mitigatethe observed dysfunctional side effects of a strongly budget-orientedstyle of performance evaluation (his Budget-Constrained style). Hisconclusion is that a more flexible style of budget use (his Profit-Conscious style), which attaches importance to budgetary informationbut recognizes its shortcomings, tends to cause less anxiety to subor-dinate managers, promotes cooperation, and reduces dysfunctionaldecision making. The aim of this study is to investigate whetherHopwood's categories of style of budget use are valid in situationswhere budgets are more technically adequate, and also to extend hisfindings to include the effects of style of budget use on managerialperformance.

HYPOTHESES UNDER TEST

Previous work by Hopwood [1972] has suggested that one importantdimension of budget use is the relative importance attached to thebudget in evaluating managerial performance. A rigid style of evalu-ation, based primarily upon whether or not a manager has met hisbudget, was found to result in the belief that the evaluation wasunjust, in wide-spread tension and worry on the job, and in feelings ofdistrust and dissatisfaction with the superior using the style. Man-agers evaluated in this rigid manner were also found to manipulateaccounting data to improve their reported performance and to makedecisions detrimental to the long-term well-being of the organization.However, when a more flexible style of evaluation was adopted, withbudget information being used in conjunction with other sources ofinformation, concern with long-term economic performance was main-tained but fewer dysfunctional side-effects were observed.

However, Hopwood's emphasis was primarily on the effect thatbudget use has on managers' beliefs and feelings and not with theoverall effectiveness of operations. But because he found no significantdifference in the extent to which managers evaluated under differentstyles met their budgets, he was able to conclude that it was likelythat the tensions and manipulations noted under the rigid style ofevaluation caused a deterioration in long-term performance. It wastherefore felt important to attempt to extend his hypotheses to include8ome measures of the ultimate effectiveness of operations, despite thedifficulties inherent in defining measures of performance and the fact

126 DAVID T. OTLEY

that many of these measures are dependent upon a budget standardwhich is itself open to manipulation. The major hypotheses to betested can be stated as follows.

When a manager perceives that he is evaluated primarily on hisahility to meet his budget (rather than on the basis of a more fiexibleuse of budgetary information), he is more likely to (a) experience job-related and budget-related tension; (6) distrust his superior; (c) beclear about how his performance is evaluated; (d) consider his evalu-ation to be unfair. His response to such feelings will be such that he ismore likely to (e) bias his budget estimates by building in "slack" sothat the budget becomes easier to attain; {f) have a short-term view ofhis job in that his performance measure is short-term; {g) performpoorly, particularly on those aspects of performance which yield onlylong-term benefits.

In order to concentrate on the effect of alternative styles of budgetuse independently of the effect of imperfections in the accountingsystem, a research site was sought that was well suited to theapplication of budgetary control systems. Following Baulmer [1971], asituation where organizational subunits were substantially independ-ent on each other was considered most appropriate for the use ofdefined criteria of performance. Since Bruns and Waterhouse [1975]also suggest that a decentralized and structured organization operat-ing in a stable organizational environment is particularly well suitedto the use of budgetary control, a profile of the optimum situation forbudgetary control was obtained.

Research Site and Methodology

A suitable research site was found in a single, large organizationwhich had a considerable number of production facilities, producingsimilar products, geographically dispersed £U'ound the United King-dom. Marketing and distribution were centrally organized, hut pro-duction units were largely independent on each other, to the extentthat variations in demand were attenuated by stocking in the short-term and by the opening and closing of production units in the longer-term. Production units were allocated to groups under a group man-ager on a geographical basis, and three groups containing forty-oneoperating units were selected for study on the basis of being physicallyand environmentally similar, but having group managers with verydifferent managerial styles.

Therefore, the unit of analysis was the individual unit manager whowas responsible to his group manager for the production of his unit,which typically employed a thousand men and had a turnover ofseveral million pounds sterling per year. A system of budgetarycontrol had been in operation for a number of years under whichproduction units were considered as profit centers. This was reasona-ble insofar as output was largely under the control of the unit

BUDGET USE AND MANAGERIAL PERFORMANCE 127

manager, although price was centrally determined. As productionconsisted of essentially a single product, the budget contained ameasure of output in physical units in addition to the usual statementsof costs and revenues, to yield a bottom-line profit figure. Costs ofcapital employed were allocated and a figure approximating residualincome was computed, but hecause investment was only marginallycontrollable by the unit manager, this figure was not used in themanagerial evaluation process to any significant extent, although itwas relevant to the evaluation of the unit's economic performance.

Monthly reports comparing actual and budgeted outputs, costs, andrevenues were generated for each production unit on a uniform basis.Below the unit-manager level, the control systems employed differedfrom unit to unit, but unit managers were formally held to account atleast on a quarterly basis by their group managers, who were in turnheld formally accountable by central management.

Information for this study was collected by three main methods.First, all forty-one unit managers and the group staff in the linehierarchy above them were interviewed. Second, a questionnaire wasleft with each interviewee for completion and return to the researcherwith follow-up letters being used where necessary. Third, the budget-ary and other records of the organization were used to obtain data onmeasvired performance. This strategy allowed an interview which wasrelatively relaxed smd unstructured so that exploratory work could becarried out and confidence and trust relationships built with themanagers concerned. The questionnaire allowed the collection ofspecific information in a uniform manner and the use of recorded datapermitted most of the performance data recorded by the organizationto be obtained. The methodology restricted the size of sample thatcould be used, but resulted in a gratifying 100-percent response rate,which gives the results increased validity, despite the small sample.The statistical analysis of the data obtained is based on nonparametricstatistics, namely, Kendall's r for correlation between variables andStudent's t (or Mann-Whitney U, where necessary) for differences invalue of variables.'

MEASUREMENT OF THE VARIABLES

Style of Evaluation. The crucial independent variable concerns theway in which a unit manager perceives the budget to be used inevaluating his performance, in relation to other relevant information.

' Significance levels of all results are stated by giving the probability that the statedresult could have occurred by chance (e.g., p = .05 for the conventional 95-percentsigniflcance level). For tests comparing sample means, a two-tailed probability level isstated, whereas correlation coefficients are reported with a sign attached and anassociated one-tailed probability level. Events with a one-tailed probability level greaterthan p = . 10 are reported aa not significant. In this way, it is hoped that the reader willhave adequate information from which to draw his own conclusions based on his ownprior hypotheses.

128 DAVID T. OTLEY

A pilot study was therefore undertaken te investigate the criteria thatunit managers considered potentially important. The list that wasdeveloped from the pilot study showed considerable similarities to thatused by Hopwood [1973] and it was therefore extended to cover all theitems he used so that a replication of this aspect of his study could beperformed, although the additional items proved relatively unimpor-tant."

Unit managers were asked to rank the three items they consideredmost important when their group manager was evaluating their per-formance. The two most highly ranked items were found te be: (d) howwell I meet my budget and {f) how efficiently I run my unit. On thebasis of the rankings, the following continuum of evaluative styles wasdefined: (A) item {d) but not item {f) ranked among top three criteria;{B) both items ranked among top three criteria, item {d) higher thanitem {f); (C) both items ranked among tep three criteria, item (/)higher than item {d); {D) item (/O but not item {d) ranked among topthree criteria; {E) neither item ranked among top three criteria. Thenumber of respondents in each category and the relationship to Hop-wood's categories are shown in table 1.

Because of the small numbers in his hybrid Budget-Profit category,Hopwood concluded that only two financially oriented styles weresufficient to account for the observed results. Therefore, he merged theBC and BP styles in his subsequent analysis. However, the evidencefrom this study indicates a continuum of style, a view which isreinforced by the absolute importance rating given to each criterion, asshown in table 2.*

Although indicative of an underlying continuum it should not beconcluded that there are equal intervals between the points A toD. The

TABLE 1Tfie Distribution of Respondents Perceiving Each Style of Evaluation

Style of Evaluation A B C 5 £

Percentage of managers in eachcategory (N = 39) 13 18 38 28 3

Hopwood's equivalent category* BC BP PC NA

Percentage of managers in eachcategory jN = 167) 20 10 26 44

• BC = Budget constrained; BP - Budget profit; PC = Profit conscious; NA = NonaooiMintinK.For much of his analysis, Hopwood combines his BC and BP categories, i.e., categories A, B and Cin this study.

* A comparative listing is given in Appendix A and the results obtained aresummarized in Appendix B.

' In addition to ranking criteria, managers were asked to indicate the absoluteimportance of each on a Likert-type scale, which was scored from 1 to 5. The form ofquestion used is given in Appendix B.

BUDGET USE AND MANAGERIAL PERFORMANCE 129

T A B L E 2The Absolute Importance of Each Criterion by Perceived Style of Evaluation

Style A B C D ENo. of respondents 5 7 15 11 1(d) How well I meet my budget 5.0 4.9 4.7 3.7 3(/) How efficiently I run my unit 4.3 4.9 5.0 5.0 4Statistical significance of the

difference {d)-ifi p = .01 n.s. .03 .001 n.s.

evidence suggests that points B and C are closer together than theothers, and possibly closer to A than D, which would be consistent withHopwood's amalgamation of points A, B, and C, The nonaccountingstyle, which was of considerable importance in the organization studiedby Hopwood, is virtually nonexistent here,®

In addition, a set of questions based on the Smith and Tannenbaum[1963] control graphs was included to detect the amount of influence amanager considered he had on setting his budgeted level of performancein comparison with other orgamizational levels. This indicates a furtherdimension of the way in which the budgetary system was used.

Intervening Variables. The main intervening variable between howthe budget is perceived to be used in performance evaluation and theindividual manager's response to such use is hypothesized to be hisfeelings of tension and anxiety, A fourteen-item index of job-relatedtension based on the fifteen-item index developed by the Institute forSocial Research at the University of Michigan was used,^ This scale hasbeen extensively used in previous studies and is known to be sensitiveto at least some of the dysfunctional consequences of tension, beingpositively correlated with role conflict and ambiguity and to thepresence of mild neurotic symptoms (Kahn et al, [1964]), Two otheritems were used to measure specifically budget-related tension, whichwas found to be significantly correlated with job-related tension (Ken-dall's T = 0,37; p = ,001),

The trust a manager felt he had in his group manager was measuredby the five-item scale developed by Read [1962] which has been shownto be correlated with accuracy of upward communication. Job ambiguitywas measured by another five-item scale developed by Kahn et al,[1964], with particular attention being paid to the item on ambiguityconcerning evaluation. Finally, an item to measure the manager'sfeelings about the fairness of the evaluation was included.

Performance Measures. In order to compare the relative performanceof two managers, it is not possible directly to contrast their levels of

' Further details of the construction and validation of this measure of evaluativestyle may be found in Otley [1976].

' One item (i,e., "feeling that you are not fully qualified to handle your job") wasomitted as it had little relevance to the managers who had to satisfy stringent legalrequirements concerning their qualifications.

130 DAVID T. OTLEY

output, cost, and revenue, as these are affected by other organizationaland environmental variables, the most important of which is the size ofthe unit being operated. Within the organization, comparisons weremade with the budget standard, and this approach will be adopted here,although it must be clearly recognized that variances from budget mayrepresent both differences in actual performance and differences inbudget difficulty. Budget errors may also be caused by mere variabilityin performance; however, it was found that the greater the averagedeviation from budget, the more likely it was that such a deviation wasof statistical significance, so a simple measure of budget error wascomputed.* This was based on performance over an eighteen-monthperiod prior to the interviews and was calculated as the mean percent-age error in budget estimates over that period, that is:

Mean percentage budget error = 100 x {B - A)/B,

where B is the mean budget value and A the mean actual value.The time perspective of a manager concerning his job w£is measured

by a question relating to the amount of time he spent on matters whichwould affect production more than one year ahead. Other aspects ofperformance that would affect long-term success were measured includ-ing accident rates, voluntary wastage rates, and levels of unauthorizedabsenteeism, although it is known that all of these Eire affected byenvironmental circumstances to a considerable extent.^

Results

THE EFFECT OF STYLE OF EVALUATION ON INTERVENING

VARIABLES

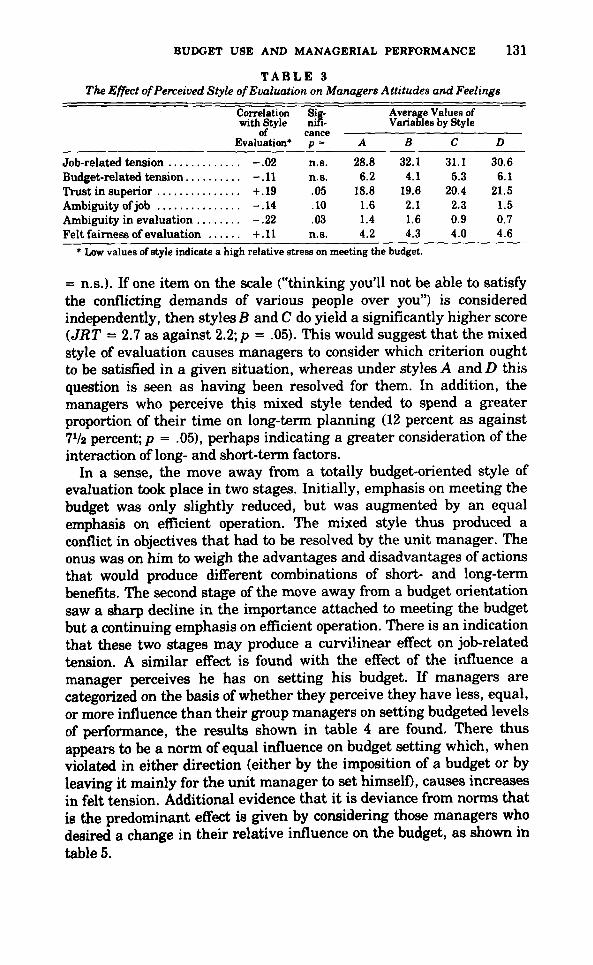

The initial analysis is based on the evaluative styles perceived byunit managers, in terms of the relative importance of various criteria ofevaluation. Examination of table 3 indicates that managers' feelingsabout their method of evaluation do not appear to be strongly related tothe style they perceive to be used.

The effect of style of evaluation on interpersonal trust is significantand in the hj^jothesized direction, but the effect on ambiguity ofevaluation is in the opposite direction with stress on budget increasingambiguity. The effect on job-related tension is insignificant althoughthere is some weak evidence that styles B and C, which involveestablishing a balance between budgetary and efficiency criteria, docause more tension than the other styles {JRT = 31.4 as against 30.0; p

' The results from using a variety of more sophisticated measures are discussed inOtley [1976, pp. 88-95]. As a rough rule of thumb, errors in the output budget in excessof 5 percent are likely to be statistically significant (p = .075).

• Such indirect measures of performance were collected as they represented the onlyquantitative information available to the organization which could be used to comparemanagerial performance independent of budgetary standards.

BUDGET USE AND MANAGERIAL PERFORMANCE 131

T A B L E 3The Effect of Perceived Style of Evaluation on Managers Attitudes and Feelings

Correlation Sig- Average Values ofwith Style nifl- Variables by Style

of canceEvaluation* p = A B C D

Joh-related tension - .02 n.s, 28.8 32.1 31.1 30.6Budget-related tension -.11 n.s. 6.2 4.1 5.3 6.1Trust in superior +.19 .05 18.8 19.6 20.4 21.5Ambiguity of job -.14 .10 1.6 2.1 2.3 1.5Ambiguity in evaluation -.22 .03 1.4 1.6 0.9 0.7Felt fairness of evaluation +.11 n.s. 4.2 4.3 4.0 4.6

* Low values of style indicate a high relative stress on meeting the budget.

= n.s.). If one item on the scale ("thinking you'll not be able to satisfythe confiicting demands of various people over you") is consideredindependently, then styles B and C do yield a significantly higher score{JRT = 2.7 as against 2.2; p = .05). This would suggest that the mixedstyle of evaluation causes managers to consider which criterion oughtto be satisfied in a given situation, whereas under styles A and D thisquestion is seen as having been resolved for them. In addition, themanagers who perceive this mixed style tended to spend a greaterproportion of their time on long-term planning (12 percent as against7V2 percent;/? = .05), perhaps indicating a greater consideration of theinteraction of long- and short-term factors.

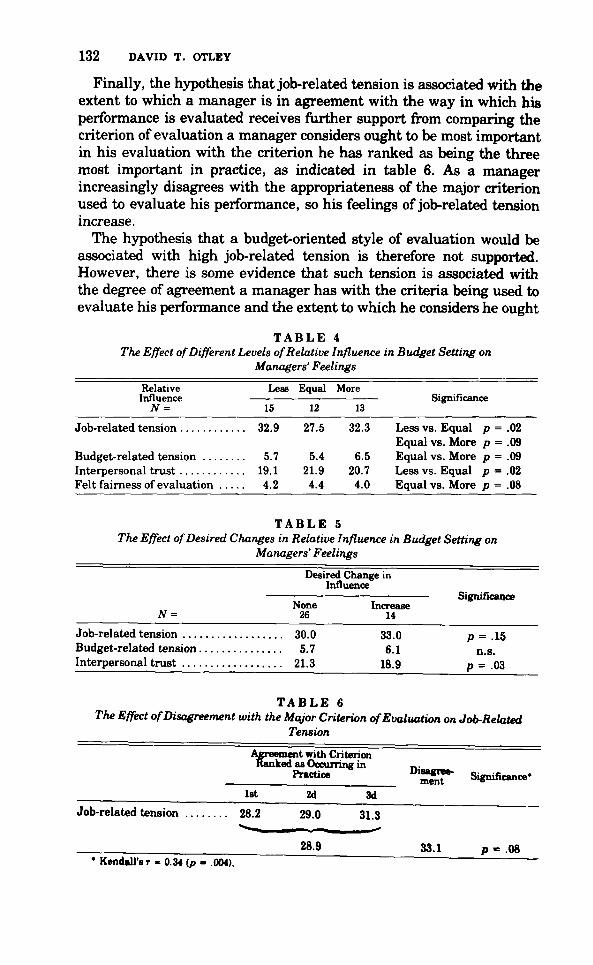

In a sense, the move away from a totally budget-oriented style ofevaluation took place in two stages. Initially, emphasis on meeting thebudget was only slightly reduced, but was augmented by an equalemphasis on efficient operation. The mixed style thus produced aconhict in objectives that had to be resolved by the unit manager. Theonus was on him to weigh the advantages and disadvantages of actionsthat would produce different combinations of short- and long-termbenefits. The second stage of the move away from a budget orientationsaw a sharp decline in the importance attached to meeting the budgetbut a continuing emphasis on efficient operation. There is an indicationthat these two stages may produce a curvilinear effect on job-relatedtension. A similar effect is found with the effect of the infiuence amanager perceives he has on setting his budget. If managers arecategorized on the basis of whether they perceive they have less, equal,or more infiuence than their group managers on setting budgeted levelsof performance, the results shown in table 4 are found. There thusappears to be a norm of equal infiuence on budget setting which, whenviolated in either direction (either by the imposition of a budget or byleaving it mainly for the unit manager to set himself), causes increasesin felt tension. Additional evidence that it is deviance from norms thatis the predominant effect is given by considering those managers whodesired a change in their relative influence on the budget, as shown intable 5.

132 DAVID T. OTLEY

Finally, the hypothesis that job-related tension is associated with theextent to which a manager is in agreement with the way in which hisperformance is evaluated receives further support from comparing thecriterion of evaluation a manager considers ought to be most importantin his evaluation with the criterion he has ranked as being the threemost important in practice, as indicated in table 6. As a managerincreasingly disagrees with the appropriateness of the major criterionused to evaluate his performance, so his feelings of job-related tensionincrease.

The hypothesis that a budget-oriented style of evaluation would beassociatod with high job-related tonsion is therefore not supported.However, there is some evidence that such tension is associated withthe degree of agreement a manager has with the criteria being used toevaluate his performance and the extent to which he considers he ought

TABLE 4The Effect of Different Levels of Relative Influence in Budget Setting on

Managers' Feelings

Relative Less Equal MoreInfluence Signiflcance

N= 15 12 13

Job-related tension 32.9 27.5 32.3 Less vs. Equal p = .02Equ£d vs. More p = .09

Budget-related tension 5.7 5.4 6.5 Equal vs. More p = .09Interpersonal trust 19.1 21.9 20.7 Less vs. Equal p = .02Felt fairness of evaluation 4.2 4.4 4.0 Equal vs. More p = .08

T A B L E 5The Effect of Desired Changes in Relative Influence in Budget Setting on

Managers' Feelings

Desired Change inInfluence

SignificanceNone Increase

N= 26 14

Job-related tension 30.0 33.0 p = .15Budget-related tension 5.7 6.1 n.s.Interpersonal trust 21.3 18.9 p = .03

TABLE 6The Effect of Disagreement with the Major Criterion of Evaluation on Job-Related

Tension

^reement with CriterionRanked as Occurring in p

P « i ^^ST' Significance*

Job-related tension 28.2 29.0 31.3

Kendall'sr - 0.34 {p - .004).

BUDGET USE AND MANAGERIAL PERFORMANCE 133

to participate in setting his own budget. Although fairness of evaluationis associated with low job ambiguity (T = .31; p = .003), stress onmeeting the budget did not reduce ambiguity, as hypothesized. Theseresults indicate that the effects found by Hopwood are conditional onthe organizational context in which the evaluative style is used, withthe prevalent norms and values exerting a significant effect.

THE EFFECTS OF INTERVENING VARIABLES ON PERFORMANCE

The budget for an operating unit contained information on output,costs categorized under a variety of headings, and revenues, with abottom-line profit figure being computed. When managers were askedto indicate the importance of each dimension of performance specifiedby the budget, the majority (71 percent) selected output as mostimportant, with most of the remainder selecting profit (22 percent).Total costs were also considered important, but secondary to the abovetwo summary measures of performance. Thus the succeeding analysisconcentrates on the output budget, with some attention being given tototal costs and profit.

Although data were gathered concerning forty-one managers and theunits under their command, it is inappropriate to associate the perform-ance of units over the eighteen-month period considered with managerswho had not been in the post for a sufficient length of time to haveinfluenced both the budget-setting process and actual performance.This consideration led to twenty manager-unit pairs being eliminated,many from one group with a highly budget-oriented group managerwho also operated on the basis of rotating or replacing his unitmanagers at frequent intervals. However, the correlations of style ofevaluation with the intervening variables were similar for the reducedsample of twenty-one managers and the total sample.'" In addition, thereduced sample differed only slightly in demographic details, beingsomewhat older and more experienced, as would be expected, so it doesnot appear that any great distortion is introduced by this restriction,although the small sample size reduces the significance of the results.

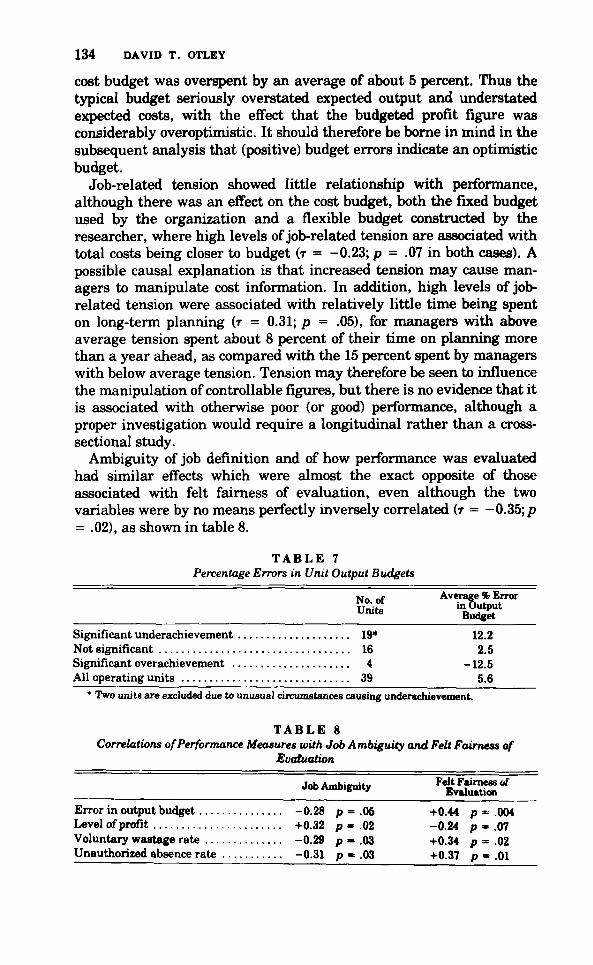

When the data on budget errors was considered, it was immediatelyapparent that the output budget was not met and the cost budget wasexceeded by a considerable margin at most operating units. Some of thevariances from budget were not statistically significant in relation tothe time series from which they were drawn, but a natural break in thedata occurred at thep = .075 (one-tailed) level. On this basis, 48 percentof operating units did not meet their output budget by a significantmargin, whereas only 10 percent exceeded it significantly, the averageerrors being shown in table 7.

A similar situation was found with the (fixed) cost budget, for despitethe output being underattained by an average of about 6 percent, the

'• Again, the only significant effect was a negative correlation with job ambiguityand ambiguity of evaluation.

134 DAVID T, OTLEY

cost budget was overspent by an average of about 5 percent. Thus thetypical budget seriously overstated expected output and understatedexpected costs, with the effect that tlie budgeted profit figure wasconsiderably overoptimistic. It should therefore be borne in mind in thesubsequent analysis that (positive) budget errors indicate an optimisticbudget.

Job-related tension showed little relationship with performance,although there was an effect on the cost budget, both the fixed budgetused by the organization and a fiexible budget constructed by theresearcher, where high levels of job-related tension are associated withtotal costs being closer to budget (T = -0,23; p = ,07 in both cases), Apossible causal explanation is that increased tension may cause man-agers to manipulate cost information. In addition, high levels of job-related tension were associated with relatively little time being spenton long-term planning (T = 0,31; p = ,05), for managers with aboveaverage tension spent about 8 percent of their time on planning morethan a year ahead, as compared with the 15 percent spent by managerswith below average tension. Tension may therefore be seen to influencethe manipulation of controllable figures, but there is no evidence that itis Eissociated with otherwise poor (or good) performance, although aproper investigation would require a longitudinal rather than a cross-sectional study.

Ambiguity of job definition and of how performance was evaluatedhad similar effects which were almost the exact opposite of thoseassociated with felt fairness of evaluation, even although the twovariables were by no means perfectly inversely correlated (T = -0,35;/?= ,02), as shown in table 8,

TABLE 7Percentage Errors in Unit Output Budgets

Kn nf Average % Error

Significant underachievement 19* 12,2Not significant 16 2,5Significant overachievement 4 -12,5All operating units 39 5,6

* Two units are excluded due to unusual circumstances causing underachievement,

T A B L E 8Correlations of Performance Measures with Job Ambiguity and Felt Fairness of

Evaluation

JobAmbiguity

Error in output budget -0,28 p = .05 +0,44 p - .004Level of profit +0,32 p « .02 -0,24 p = ,07Voluntary wastage rate -0.29 p - ,03 +0,34 p = .02Unauthorized absence rate -0,31 p = .03 +0.37 p = ,01

BUDGET USE AND MANAGERIAL PERFORMANCE 135

Therefore, the hj^othesized relationships did not occur in the case offelt fairness of evaluation which was high when performance on all theabove measures was generally poor. Conversely, a high level of jobambiguity was associated with good performance. Both sets of findingstogether indicated that when a unit manager was performing poorly,possibly due to being faced by adverse uncontrollable factors, he feltquite clear about what his job involved and how he was evaluated, andalso felt that his performance was being evaluated fairly by hissuperiors. However, when his performance was relatively good, he feltless sure about what his job involved and how his performance wasevaluated. In these circumstances, he felt that his performance wasevaluated less fairly.

THE EFFECT OF STYLE OF EVALUATION ON PERFORMANCE

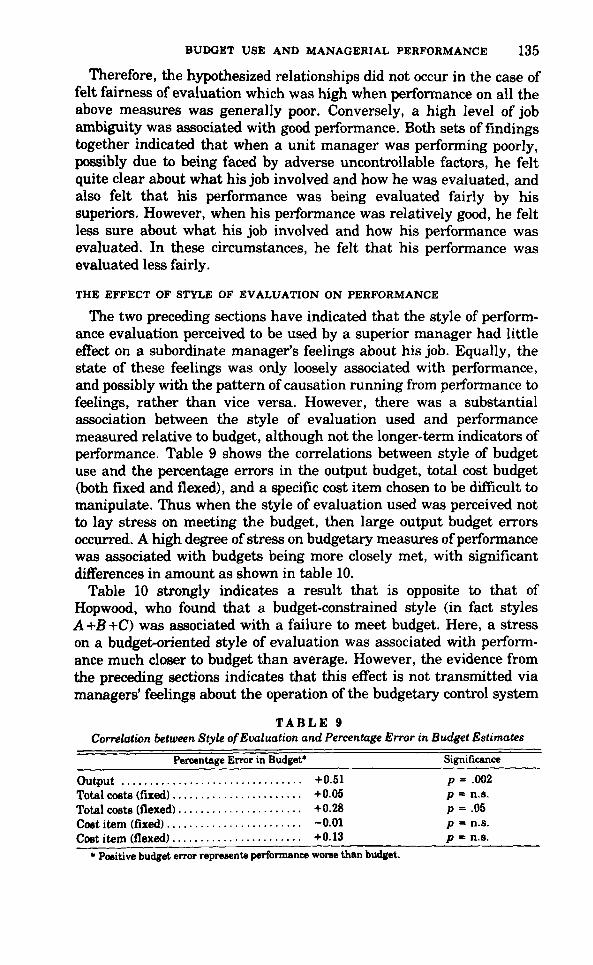

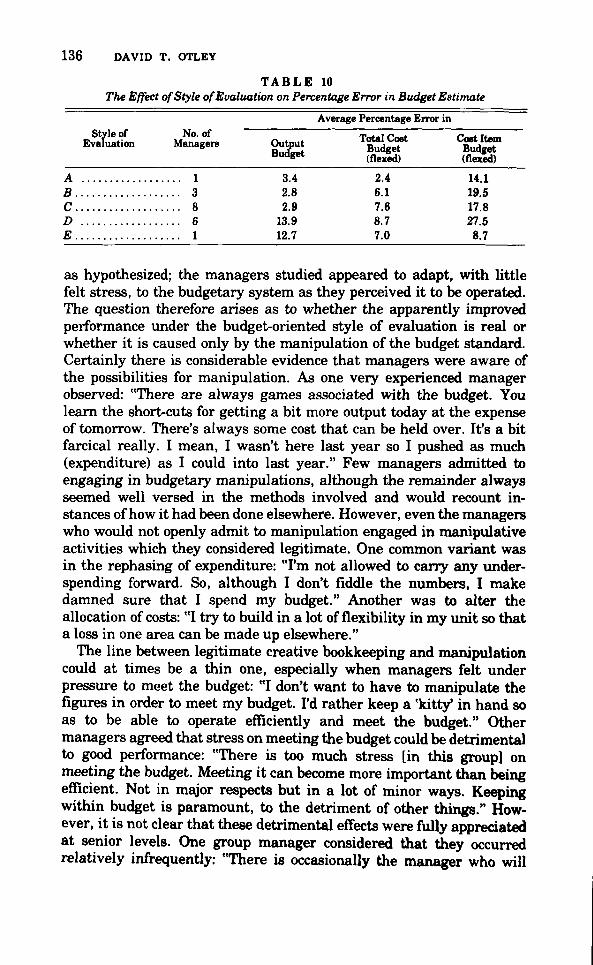

The two preceding sections have indicated that the style of perform-ance evaluation perceived to be used by a superior manager had littleeffect on a subordinate manager's feelings about his job. Equally, thestate of these feelings was only loosely associated with performance,and possibly with the pattern of causation running from performance tofeelings, rather than vice versa. However, there was a substantialassociation between the style of evaluation used and performancemeasured relative to budget, although not the longer-term indicators ofperformance. Table 9 shows the correlations between style of budgetuse and the percentage errors in the output budget, total cost budget(both fixed and fiexed), and a specific cost item chosen to be difficult tomanipulate. Thus when the style of evaluation used was perceived notto lay stress on meeting the budget, then large output budget errorsoccurred. A high degree of stress on budgetary measures of performancewas associated with budgets being more closely met, with significantdifferences in amount as shown in table 10.

Table 10 strongly indicates a result that is opposite to that ofHopwood, who found that a budget-constrained style (in fact stylesA 4-fi +C) was associated with a failure to meet budget. Here, a stresson a budget-oriented style of evaluation was associated with perform-ance much closer to budget than average. However, the evidence fromthe preceding sections indicates that this effect is not transmitted viamanagers' feelings about the operation of the budgetary control system

TABLE 9

Correlation between Style of Evaluation and Percentage Error in Budget Estimates

Percentage Error in Budget* Significance

Output +0.51 p = .002Total costs (fixed) +0.05 p = n.s.Total costs (flexed) +0.28 p = .05Cost item (fixed) -0.01 p = n.s.Cost item (flexed) +0.13 p = n.s.

* Poeitive budget error represents performance worse than budget.

136 DAVID T. OTLEY

TABLE 10The Effect of Style of Evaluation on Percentage Error in Budget Estimate

Stvle ofEvaluation

ABcDE

No. ofManagers

13861

OutputBudget

3.42.82.9

13.912.7

Average Percentage Error in

Total CoetBudget(flexed)

2.46.17.68.77.0

Cost ItemBudget(flexed)

14.119 517.827.58.7

as h3^othesized; the managers studied appeared to adapt, with littlefelt stress, to the budgetary system as they perceived it to be operated.The question therefore arises as to whether the apparently improvedperformance under the budget-oriented style of evaluation is real orwhether it is caused only by the manipulation of the budget standard.Certainly there is considerable evidence that managers were aware ofthe possibilities for manipulation. As one very experienced managerobserved: "There are always games associated with the budget. Youlearn the short-cuts for getting a bit more output today at the expenseof tomorrow. There's always some cost that can be held over. It's a bitfarcical really. I mean, I wasn't here last year so I pushed as much(expenditure) as I could into last year." Few managers admitted toengaging in budgetary manipulations, although the remainder alwaysseemed well versed in the methods involved and would recount in-stances of how it had been done elsewhere. However, even the managerswho would not openly admit to manipulation engaged in manipulativeactivities which they considered legitimate. One common variant wasin the rephasing of expenditure: "I'm not allowed to carry any under-spending forward. So, although I don't fiddle the numbers, I makedamned sure that I spend my budget." Another was to alter theallocation of costs: "I try to build in a lot of flexibility in my unit so thata loss in one area can be made up elsewhere."

The line between legitimate creative bookkeeping and manipulationcould at times be a thin one, especially when managers felt underpressure to meet the budget: "I don't want to have to manipulate thefigures in order to meet my budget. I'd rather keep a 'kitty* in hand soas to be able to operate efficiently and meet the budget." Othermanagers agreed that stress on meeting the budget could be detrimentalto good performance: "There is too much stress [in this group] onmeeting the budget. Meeting it can become more important than beingefficient. Not in msgor respects but in a lot of minor ways. Keepingwithin budget is paramount, to the detriment of other things." How-ever, it is not clear that these detrimental effects were fully appreciatedat senior levels. One group manager considered that they occurredrelatively infrequently: "There is occasionally the manager who will

BUDGET USE AND MANAGERIAL PERFORMANCE 137

meet his budget by doing things he shouldn't. I don't rate this veryhighly." However, one of the more blatant examples of manipulation bythe phasing of expenditure into periods other than those in which it wasincurred came from his group:

"Take [a cost item] as an example of how the budget makes you operate. I ordered[item] at the end of last financial year because I knew that I'd need it in the comingyear, and I was above my profit forecast. It came, but it was the wrong kind andhad to be returned to the [group stores]. I was given a credit for last year, makingmy profit even higher, but it put me in the red for this year. I got on to [stores] andthey eventually agreed to charge it to me in nine monthly installments because Iargued the mistake was their fault."

The above example was kept covert, possibly because it involvedengaging in an accounting practice which was not sanctioned by theorganization and possibly because secrecy was necessary for the man-ager to be able to exert pressure, based on not revealing the errors ofother members of the organization. But another manager had no suchinhibitions: "I know that people at [group] wonder how the [****] at[this unit] gets so consistent an output. As I see it their job isn't toworry about it as long as I get it. So I let them know all is well byreporting a consistent figure, even if it's not exactly what I got today."

Yet, despite the comments above, many unit managers still felt thata certain degree of emphasis on meeting the budget could be useful. Asone conscientious manager put it: "I think that the budget level has areal effect on efficiency and relationships at a unit. For instance, Ispend a considerable amount of time controlling my expenditure onmaterials. I try to get some slack in the budget to take the pressure off."Another manager made a similar point, but emphasized that the budgethad to be applied with some care: "The trouble is that we're not bloodyhonest. I say we'll get an output of 2,800. They say 2,900 in the budget.So what happens? I get 2,900 for six months and then 2,600 for the restof the year. It does no one any good." However, it should be noted thatthese findings are derived from a sample of managers who had been intheir present position for at least two and one-half years and who hadbeen managers of similar units for an average of eleven years. Sincemanagers who had been unit managers longest perceived least stress onbudgetary means of evaluation (T = 0.25; p = .02), if budgetarymanipulation does occur when the budget is stressed for these managersthe effect is likely to be more pronounced, if less observable, than fornewer managers who have not been at a unit for long enough for theirperformance to be analyzed by the techniques used here.

PROFITABILITY AND THE BUDGET STANDARD

In general, it has been shown that where a unit manager perceivedthat the most important aspect of his evaluation concerns how well hemeets his budget, he is more likely to meet his budget (interpreted in aflexible rather than a rigid manner) than would otherwise he the case.

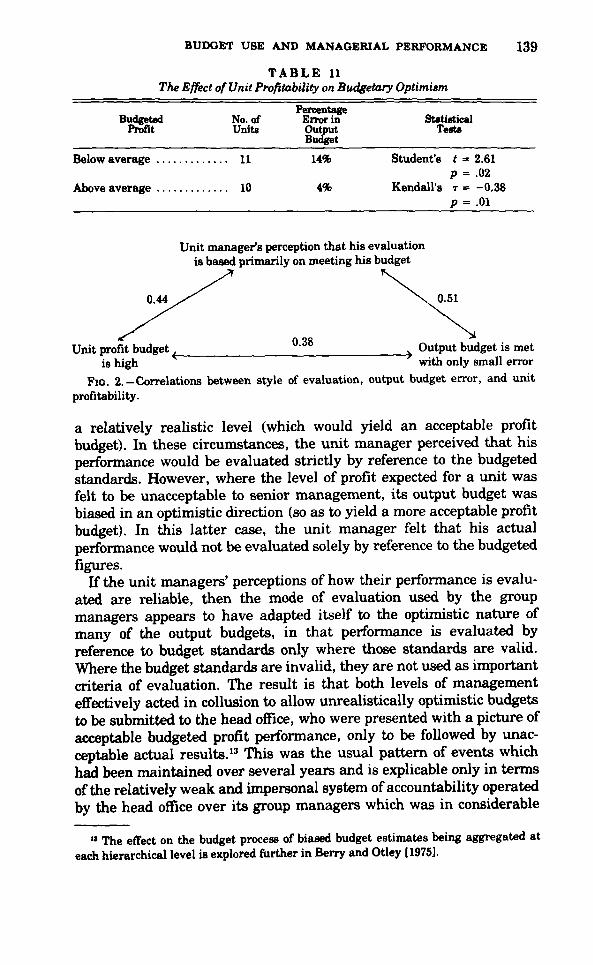

138 DAVID T. OTLEY

The question therefore arises as to whether this tendency to meet thebudget is caused by better actual performance or by manipulation of thebudget estimates, or possibly the actual results reports. Some light maybe thrown on this question by considering the profit record of eachoperating unit.

There is a strong correlation (T = -0.55; p = .001) between actualprofit and the perceived style of performance evaluation. That is, strongstress on meeting the budget was associated with relatively high levelsof profit. However, as there was a similar correlation with output (T =-0.48; p = .002) and a lesser one with manpower (T = -0.28; p = .05), itis evident that unit size effects the perceived style of evaluation." Thismay well be because group managers stressed budgetary measures ofperformance to a greater extent at lsirge and therefore, to them, moreimportant operating units.

However, there is also a high correlation between actual profit andthe percentage error in the output budget (T = 0.54; p = .001), indicatingthat high levels of profit were associated with exceeding the outputbudget. This was not merely a refiection of the random effect that mightbe expected, as there was nearly as large a correlation betweenbudgeted profit and percentage error in the output budget (T = 0.38; p= .01). That is, when the profit budget was relatively high, the outputbudget was more nearly attained; when it was relatively low, the outputbudget was significantly underachieved. This result strongly suggeststhat the budgetary standard is manipulated in an optimistic directionwhen expected profits are low.

An indication of the size of this effect can be obtained by comp£iringthose units having budgeted profits that were below average, with thosehaving above profit budgets, as shown in table 11. This analysis is crudein that it confounds size and profitability, but if the effect of size isremoved by constructing a measure of profit per man employed, thecorrelation coefficient is only slightly reduced (T = —0.32; p = .02),confirming the assertion that optimistic output budgets were submittedwhen profitability was considered te be unacceptable.'^

It therefore appears that a major reason for performance being closerte budget when budgetary means of evaluation are stressed is not somuch that performance improves, but that the budget is set at morerealistic levels. Such reahsm in budgets is also associated with perform-ance that is acceptable in terms of profitability, giving the triad ofrelationships shown in figure 2.

This set of relationships cannot be explained in terms of a singlecausal path, but is consistent with an interpretation along the followinglines. Where a unit was thought likely to achieve a level of profit whidiwould be acceptable te senior management, its output budget was set at

" A similar effect was noted by Hopwood [1973, p. 170]." There is some evidence that the level of unacceptability is, roughly, the point at

which profit becomes loss.

BUDGET USE AND MANAGERIAL PERFORMANCE 139

TABLE 11The Effect of Unit Profitability on Budgetary Optimism

BudgetedProfit

No. ofUnits

PercentageError inOutputBudget

StatiaticalTests

Below average

Above average

11

10

14%

4%

Student's ( = 2.61p = .02

Kendall's T = -0.38p = .01

Unit manager's perception that his evaluationis based primarily on meeting his budget

0.44 0,51

Unit profit budget 0.38 Output budget is metwith only small erroris high

FIG, 2,-Correlations between style of evaluation, output budget error, and unitprofitability,

a relatively realistic level (which would yield an acceptable profitbudget). In these circumstances, the unit manager perceived that hisperformance would be evaluated strictly by reference to the budgetedstandards. However, where the level of profit expected for a unit wasfelt to be unacceptable to senior management, its output budget wasbiased in an optimistic direction (so as to yield a more acceptable profitbucket). In this latter case, the unit manager felt that his actualperformance would not be evaluated solely by reference to the budgetedfigures.

If the unit managers' perceptions of how their performance is evalu-ated are reliable, then the mode of evaluation used by the groupmanagers appears to have adapted itself to the optimistic natiire ofmany of the output budgets, in that performance is evaluated byreference to budget standards only where those standards are valid.Where the budget standards are invalid, they are not used as importantcriteria of evaluation. The result is that both levels of managementeffectively acted in collusion to allow unrealistically optimistic budgetsto be submitted to the head office, who were presented with a picture ofacceptable budgeted profit performance, only to be followed by unac-ceptable actual results,'' This was the usual pattern of events whichhad been maintained over several years and is explicable only in termsof the relatively weak and impersonal system of accountability operatedby the head office over its group managers which was in considerable

'• The effect on the budget process of biased budget estimates being aggregated ateach hierarchical level is explored further in Berry and Otley [1975],

140 DAVID T. OTLEY

contrast to the strict and personal accountability operated withingroups.

This set of results differs from Hopwood's in that he found noassociation between style of evaluation and the degree to which thebudget was met, and was thus able to conclude that, because of theevidence he had obtained concerning dysfunctional activities under hisbudget-constrained style, it was likely that the performance was worseunder this style. The evidence from this study gives little support tosuch hjT)othesis. It seems more likely that the style of evaluation usedis, in part, a reaction to environmental and economic circumstances,thus making comparisons of performance under each style meaningless.In fact, some support seems to be given to the Cherringtons' [1973]result that, where rewards are contingent on meeting the budget,estimation errors are lowest and, in certain circumstances (i.e., imposedbudgets or pseudo-participation in budget setting), performance ishighest.

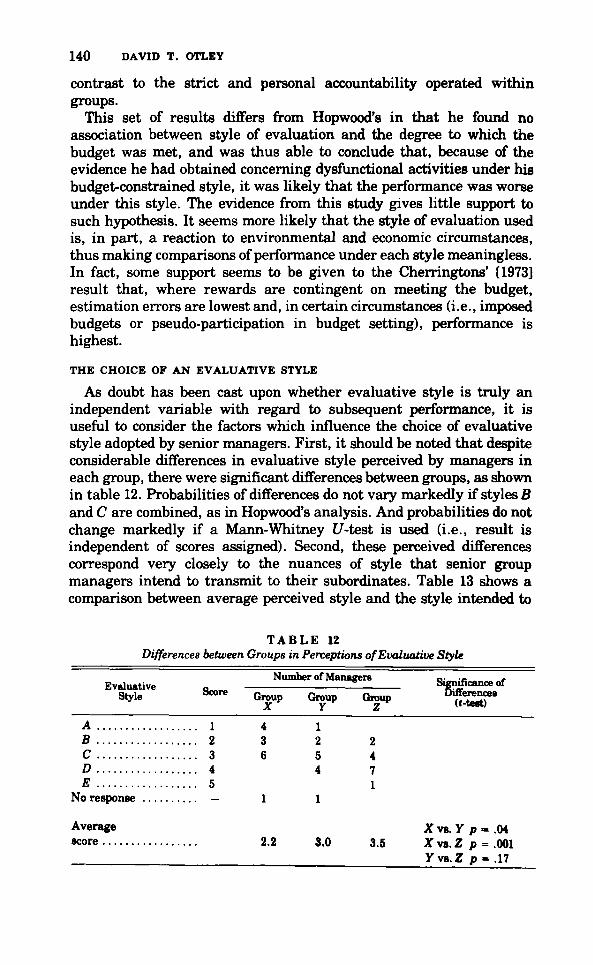

THE CHOICE OF AN EVALUATIVE STYLE

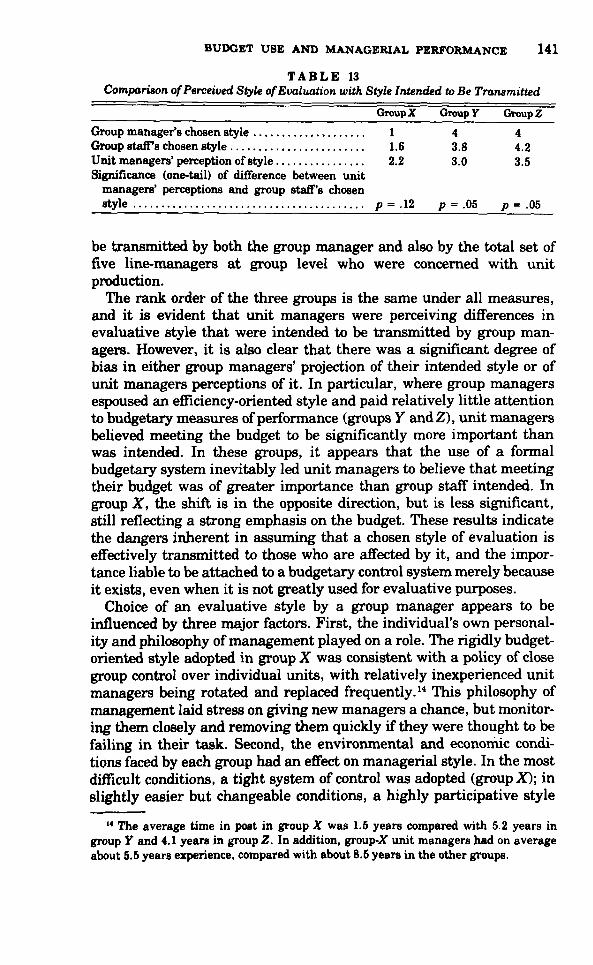

As doubt has been cast upon whether evaluative style is truly anindependent variable with regard to subsequent performance, it isuseful to consider the factors which influence the choice of evaluativestyle adopted by senior managers. First, it should be noted that despiteconsiderable differences in evaluative style perceived by managers ineach group, there were significant differences between groups, as shownin table 12. Probabilities of differences do not vary markedly if styles Band C are combined, as in Hopwood's analysis. And probabilities do notchange markedly if a Mann-Whitney C7-test is used (i.e., result isindependent of scores assigned). Second, these perceived differencescorrespond very closely to the nuances of style that senior groupmanagers intend to transmit to their subordinates. Table 13 shows acomparison between average perceived style and the style intended to

TABLE 12Differences between Groups in Perceptions of Evaluative Style

Style

ABCDE

No response

Averagescore

Score

. 12345

Number of Managers

Group

436

1

2.2

Group

1254

1

3.0

Z

2471

3.5

Significance ofDifferences

((-test)

X vs. y p - .04X vs. Z p = .001yva.Z p = .17

BUDGET USE AND MANAGERIAL PERFORMANCE 141

T A B L E 13Comparison of Perceived Style of Evaluation with Style Intended to Be TransmitUd

^_^_ Group X Group y Group Z

Group manager's chosen style 1 4 4Group 8taff's chosen style 1.6 3.8 4.2Unit managers'perception of style 2.2 3.0 3.5Significance (one-tail) of difference between unit

managers' perceptions and group staff's chosenstyle p = .12 p = .05 p = .05

be transmitted by both the group manager and also by the total set offive line-managers at group level who were concerned with unitproduction.

The rank order of the three groups is the same under all measures,and it is evident that unit managers were perceiving differences inevaluative style that were intended to be transmitted by group man-agers. However, it is also clear that there was a significant degree ofbias in either group managers' projection of their intended style or ofunit managers perceptions of it. In particular, where group managersespoused an efficiency-oriented style and paid relatively little attentionto budgetary measures of performance (groups Y andZ), unit managersbelieved meeting the budget to be significantly more important thanwas intended. In these groups, it appears that the use of a formalbudgetary system inevitably led unit managers to believe that meetingtheir budget was of greater importance than group staff intended. Ingroup X, the shift is in the opposite direction, but is less significant,still reflecting a strong emphasis on the budget. These results indicatethe dangers inherent in assuming that a chosen style of evaluation iseffectively transmitted to those who are affected by it, and the impor-tance liable to be attached to a budgetary control system merely becauseit exists, even when it is not greatly used for evaluative purposes.

Choice of an evaluative style by a group manager appears to beinfluenced by three major factors. First, the individual's own personal-ity and philosophy of management played on a role. The rigidly budget-oriented style adopted in group X was consistent with a policy of closegroup control over individual units, with relatively inexperienced unitmanagers being rotated and replaced frequently.*" This philosophy ofmanagement laid stress on giving new managers a chance, but monitor-ing them closely and removing them quickly if they were thought to befailing in their task. Second, the environmental and economic condi-tions faced by each group had an effect on managerial style. In the mostdifficult conditions, a tight system of control was adopted (group X); inslightly easier but changeable conditions, a highly participative style

'* The average time in post in group X was 1.5 years compared with 5.2 years ingroup Y and 4.1 years in group Z. In addition, group-A' unit managers had on averageabout 5.5 years experience, compared with about 8.5 years in the other groups.

142 DAVID T. OTLEY

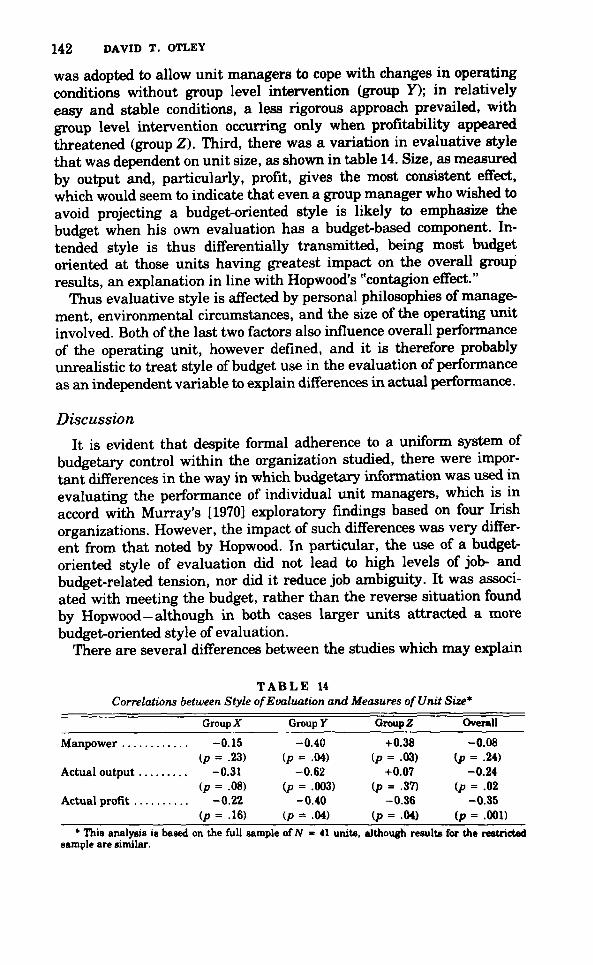

was adopted to allow unit managers to cope with changes in operatingconditions without group level intervention (group Y); in relativelyeasy and stable conditions, a less rigorous approach prevailed, withgroup level intervention occurring only when profitability appearedthreatened (group Z). Third, there was a variation in evaluative stylethat was dependent on unit size, as shown in table 14. Size, as measuredby output and, particularly, profit, gives the most consistent efiFect,which would seem to indicate that even a group manager who wished toavoid projecting a budget-orientod style is likely to emphasize thebudget when his own evaluation has a budget-based component. In-tended style is thus differentially transmitted, being most budgetoriented at those units having greatest impact on the overall groupresults, an explanation in line with Hopwood's "contagion effect."

Thus evaluative style is affected by personal philosophies of manage-ment, environmental circumstances, and the size of the operating unitinvolved. Both of the last two factors also infiuence overall performanceof the operating unit, however defined, and it is therefore probablyunrealistic to treat style of budget use in the evaluation of performanceas an independent variable to explain differences in actual performance.

DiscussionIt is evident that despite formal adherence to a uniform system of

budgetary control within the organization studied, there were impor-tant differences in the way in which budgetary information was used inevaluating the performance of individual imit managers, which is inaccord with Murray's [1970] exploratory findings based on four Irishorganizations. However, the impact of such differences was very differ-ent from that noted by Hopwood. In particular, the use of a budget-oriented style of evaluation did not lead to high levels of job- andbudget-related tension, nor did it reduce job ambiguity. It was associ-ated with meeting the budget, rather than the reverse situation foundby Hopwood—although in both cases larger units attracted a morebudget-oriented style of evaluation.

There are several differences between the studies which may explain

TABLE 14Correlations between Style of Evaluation and Measures of Unit Size*

Group X Group y Group Z Overall

Manpower -0.15(p = .23)

Actual output -0.31(p = .08)

Actual profit -0.22(p = .16)

* ThiB analysis is based on the full sample of N - 41 units, although results for the restrictedsample are similar.

-0.40(p = .04)

-0.62(p = .003)

-0.40(p = .04)

+0.38(p = .03)

+0.07(p = .37)

-0.36(p = .04)

-0.08(p = .24)

-0.24(p = .02

-0.35(p = .001)

BUDGET USE AND MANAGERIAL PERFORMANCE 143

the conflicting results. The organizational units studied here were profitcenters that were substantially independent of each other, whereasHopwood's units were cost centers in an integrated manufacturingplant. Several studies, including those by Baulmer [1971] and Brunsand Waterhouse [1975], indicate that whereas budgetary control islikely to be appropriate in the case studied here, it will be lessappropriate in an interdependent situation and liable to cause dysfunc-tional side effects. This difference may also explain the considerablygreater range of evaluative styles found to be used in Hopwood's study,in particular the number of managers who adopted a nonaccountingstyle.

A partial explanation for the different impact of evaluative style onhow well the budget is met may be found in the application ofexpectancy theory, along the lines developed by Ronen and Livingstone[1975], who extend House's [1971] theory of motivation by postulating

i \lVa + SP2i • EVi ,Motivation = IVb + Pi \lVa + SP2i • EVi , where

is the intrinsic valence associated with successful task per-formance;is the intrinsic valence associated with goal-directed behav-ior;

i are the extrinsic valences associated with extrinsic rewardscontingent on work-goal accomplishment;

Pi is the expectancy that goal-directed behavior will accomplishthe work goal;

Pa is the expectancy that work-goal accomplishment will lead toreward.

The adoption of a budget>oriented style of evaluation by the superiorcan be seen as affecting both EVi and Pa, thus increasing the subordi-nate's motivation to achieve the goal. However, this depends on P,being the same in both circumstances; but it is noted that P, can beaffected by the superior by his being supportive to the subordinate'sefforts, thus increasing the likelihood of successful task performance. Itwas noted in the organization studied that group staff exhibited behav-ior that was highly supportive te unit managers, thus allowing abudget-oriented evaluative style te lead te budgets being more closelymet. There is some evidence from Hopwood's study that supportivebehavior was negatively correlated with a rigid style of budget use;certeunly there is an implication that the budget-constrained style wasprimarily punitive in its ethos, which may have given a net resultwhich was counterproductive.

The difference in the impact of evaluative style on how closely thebudget was met may also be explained by differences in the operatingenvironment. Unit managers tended to pitch their budget estimates at

144 DAVID T, OTLEY

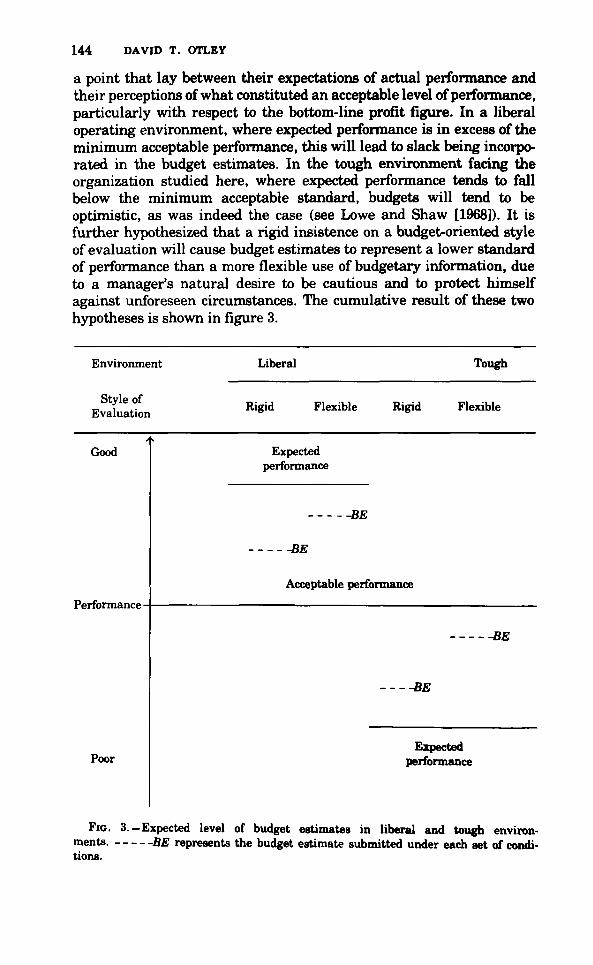

a point that lay between their expectations of actual performance andtheir perceptions of what constituted an acceptable level of performance,particularly with respect to the bottom-line profit figure. In a liberaloperating environment, where expected performance is in excess of theminimum acceptable performance, this will lead to slack being incorpo-rated in the budget estimates. In the tough environment facing theorganization studied here, where expected performance tends to fallbelow the minimum acceptable standard, budgets will tend to beoptimistic, as was indeed the case (see Lowe and Shaw [1968]), It isfurther hypothesized that a rigid insistence on a budget-oriented styleof evaluation will cause budget estimates to represent a lower standardof performance than a more fiexible use of budgetary information, dueto a manager's natural desire to be cautious and to protect himselfagainst unforeseen circumstances. The cumulative result of these twohypotheses is shown in figure 3,

Environment

Style ofEvaluation

Liberal Tough

Rigid Flexible Rigid Flexible

>Good

Poor

Expectedperformance

BE

Acceptable

SE

performance

BE

BE

Expectedperformance

FIG, 3.-Expected level of budget estimates in liberal and t o u ^ environ-ments. BE represents the budget estimate submitted under each set of condi-tions.

BUDGET USE AND MANAGERIAL PERFORMANCE 145

The overall effect is that the move from a flexible style of budget useto a rigidly budget-oriented style differs in the two postulated environ-mental conditions. In a liberal environment, the most accurate budgetestimate occurs under a flexible style of budget use; but in a toughenvironment, it occurs under a rigid style of use. Thus, if budgetestimates are required to be close to expected performance, a differentstyle of budget use is called for, contingent upon the nature of theoperating environment. This hypothesis obviously requires furthertesting under a wider variety of conditions than those observed here,and it needs to be borne in mind that actual performance may differfrom that expected by a systematic as well as a random error, an effectthat can be exploited by a manager in a liberal environment deliber-ately attaining only his (slack) budget estimate.

The essence of the control problem outlined here is that there is adegree of uncertainty in what constitutes an appropriate standard ofperformance for an organizational unit, but that this uncertainty isoften greater to the superior than to the subordinate, who is moreclosely involved. As the evaluation of operating performance cannot besatisfactorily separated from the budgetary standard, the mode ofoperation of the budgetary system is of central importance. The so-called game of budget control (Hofstede [1968]) is played in the area ofuncertainty that lies between a superior's knowledge of a specificsituation and that possessed by his subordinate. Since the budget hasbeen seen to be used as a tool to enforce an organizational rationalityupon the individual, it is not surprising that it can also be used in thereverse direction with the subordinate attempting to influence hissuperior's behavior by the provision of appropriate budgetary informa-tion. Whether such confiict develops into a game or a battle will dependcrucially on each individual's perceptions of the fairness and equity ofthe eventual outcomes, and is thus linked to the prevailing norms andvalues—both those internal to the organization and those more gener-ally held in society at large. The importance of having the budgetaryprocesses used within an organization command widespread acceptancecannot therefore be overstressed, and the much-discussed concept ofparticipation may be seen as but one means to such an end. An objectiveof the budgetary processes is to resolve conflict and to assist in theformulation of expectations; insensitively implemented, a budget sys-tem may promote conflict and lead to a variety of organizationally (andpossibly individually) undesirable effects. Thus, further work in thisarea must pay attention to the cultural norms and values that underpinthe operation of control systems.

Summary and Conclusions

The measure of the way in which senior managers use budgetaryinformation in evaluating their subordinates' performance devised by

146 DAVID T. OTLEY

Hopwood [1972] has been successfully adapted for use in a differentorganization, although the results indicate that an underlying contin-uum for style of budget use is more appropriate than a dichotomy.However, contrary to the initial hypotheses, style of budget use did notafTect job- or budget-related tension, nor did a budget-oriented styledecrease job ambiguity or ambiguity of evaluation. These differencesfrom Hopwood's results may be explained in terms of the appropriate-ness of the budgetary measures of performance for the independentoperating units studied. Job-related tension increased when a managerdisagreed with the way in which budgets were set or his performancewas evaluated, rather than being uniformly associated with any partic-ular style.

The use of a particular style of evaluation by group managers wasconditioned partly by their own managerial philosophy, but varied fromunit to unit according to the toughness of its operating environmentand its size and profitability. Senior managers thus acted in a waywhich suggests that no uniformly best style exists, but that style ofbudget use should be matched to circumstances.

The style of budget use adopted had a marked effect on the accuracyof budget estimates, with a budget-oriented style being £issociated withrelatively high budget accuracy, the reverse of Hopwood's finding. Atentative explanation of this difference is put forward, based on whetherthe operating environment is tough or liberal. There is little evidence toindicate that style of budget use affected actual performance, althoughthis is a most elusive relationship to capture in a field study. But it wasfound that there were considerable interactions between style of budgetuse, budget accviracy, and unit profitability. A situation had evolvedwhere profitable units produced accurate budgets which were subse-quently used as a basis for evaluation, whereas unprofitable unitsproduced optimistic budgets which gave the impression of profitability,but which were not then used in evaluating unit and managerialperformance. In these circumstances, the style of budget use is not anindependent variable by which differences in performance might beexplained, but style of budget use and performance both depend uponthe state of the economic environment. Thus, it is invalid to usedifferences in style of budget use to explain differences in performance.

It can be seen that the way in which a budget system is operated bythe line managers involved is as important in its effects as the technicaldesign of the system. Particular methods of budget use are likely toaffect managerial behavior significantly, but not in any uniform man-ner, differences being caused by variations in shared norms and valuesboth internal to and external to the organization concerned. Theseresults point toward the need to develop a more contingent theory ofbudgetary control based on differences in organizational types, theenvironmental circumstances in which they operate, and the norms andvalues current both within the organization itself and within the societyin which it is set.

BUDGET USE AND MANAGERIAL PERFORMANCE 147

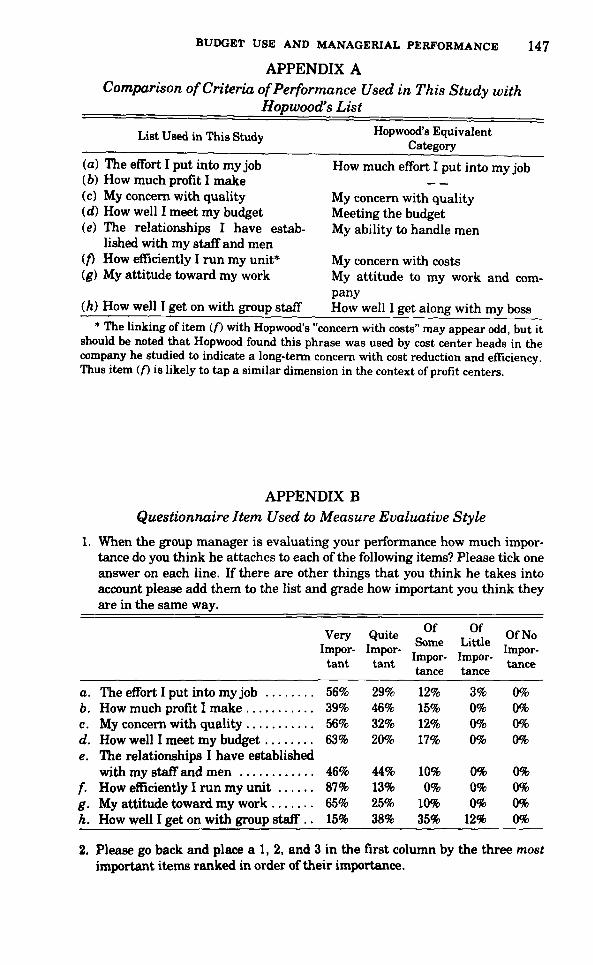

APPENDIX AComparison of Criteria of Performance Used in This Study with

Hopwood's List

List Used in This Study Hopwood's EquivalentCategory

(a) The effort I put into my joh(b) How much profit I make(c) My concern with quality(d) How well I meet my budget(e) The relationships I have estah-

lished with my staff and men(/) How efficiently I run my unit*(g) My attitude toward my work

(h) How well I get on with group staff

How much effort I put into my job

My concern with qualityMeeting the budgetMy ahility to handle men

My concern with costsMy attitude to my work and com-panyHow well I get along with my hoss

* The linking of item (f) with Hopwood's "concern with costs" may appear odd, but itshould be noted that Hopwood found this phrase was used by cost center heads in thecompany he studied to indicate a long-term concern with cost reduction and efficiency.Thus item {f) is likely to tap a similar dimension in the context of profit centers.

APPENDIX BQuestionnaire Item Used to Measure Evaluative Style

1. When the group manager is evaluating your performance how much impor-tance do you think he attaches to each of the following items? Please tick oneanswer on each line. If there are other things that you think he takes intoaccount please add them to the list and grade how important you think theyare in the same way.

Very Quite J^^ . .°^ Of NoT . Some Little ,Impor- Impor- . - Impor-. . . . Impor- Impor- , '^tant tant ^ ^ tancetance tance

a. The effort I put into my job 56% 29% 12% 3% 0%b. How much profit I make 39% 46% 15% 0% 0%c. My concern with quality 56% 32% 12% 0% 0%d. How well I meet my budget 63% 20% 17% 0% 0%e. The relationships I have established

with my staff and men 46% 44% 10% 0% 0%f. How efficiently I run my unit 87% 13% 0% 0% 0%g. My attitude toward my work 65% 25% 10% 0% 0%h. How well I get on with group staff .. 15% 38% 35% 12% 0%

2. Please go back and place a 1, 2, and 3 in the first column by the three mostimportant items ranked in order of their importance.

148 DAVID T. OTLEY

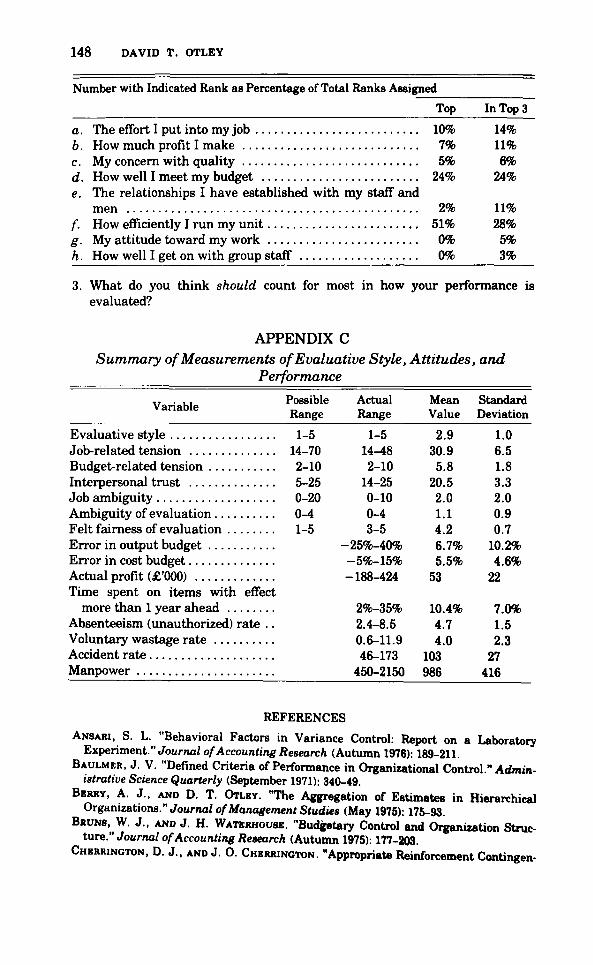

Number with Indicated Rank as Percentage of Total Ranks Assigned

Top In Top 3

a. The effort I put into my job 10% 14%b. How much profit I make 7% 11%c. My concern with quality 5% 6%d. How well I meet my budget 24% 24%e. The relationships I have established with my staff and

men 2% 11%f. How efficiently I run my unit 51% 28%g. My attitude toward my work 0% 5%h. How well I get on with group staff 0% 3%

3. What do you think should count for most in how your performance isevaluated?

APPENDIX CSummary of Measurements of Evaluative Style, Attitudes, and

Performance

.r . ,,, Possible Actual Mean StandardVariable _ _ tr ^ -n • ^•

Range Range Value DeviationEvaluative style 1-5 1-5 2.9 1.0Job-related tension 14-70 14-48 30.9 6.5Budget-related tension 2-10 2-10 5.8 1.8Interpersonal trust 5-25 14-25 20.5 3.3Job ambiguity 0-20 0-10 2.0 2.0Ambiguity of evaluation 0-4 0-4 1.1 0.9Felt fairness of evaluation 1-5 3-5 4.2 0.7Error in output budget -25%-40% 6.7% 10.2%Error in cost budget -5%-15% 5.5% 4.6%Actual profit (£'OOO) -188-424 53 22Time spent on items with effect

more than 1 year ahead 2%-35% 10.4% 7.0%Absenteeism (unauthorized) rate .. 2.4-8.5 4.7 1.5Voluntary wastage rate 0.6-11.9 4.0 2.3Accident rate 46-173 103 27Manpower 450-2150 986 416

REFERENCES

ANSARI, S. L. "Behavioral Factors in Variance Control: Report on a LaboratoryExperiment." Journa/ of Accounting Research (Autumn 1976): 189-211.

BAULMER, J. V. "Defined Criteria of Performance in Organizational Control." Admin-istrative Science Quarterly (September 1971): 340-49.

BERRY, A. J., AND D. T. OTLEY. "The Aggregation of Estimates in HierarchicalOrganizaiiora." Journal of Management Studies (May 1975): 175-93.

BRUNS, W. J., AND J. H. WATBRHOUSE. "Budjfetary Control and Organization Struc-ture." Journa/o/'Accountin^Aesearcli (Autumn 1975): 177-203.

CHERRINGTON, D. J., AND J. O. CHERRINOTON. "Appropriate Reinforcement Contingen-

BUDGET USE AND MANAGERIAL PERFORMANCE 149

cies in the Budgeting Process," Empirical Research in Accounting: Selected Studies,1973. Supplement to Journal of Accounting Research 11: 225-66,

DEASDSN, J , "Problems in Decentralized Profit Responsibility." Harvard BusinessReview (May/June 1960): 72-80.

DEW, R, B , , AND K. P. GEE, Management Control and Information. New York:Macmillan, 1973.

H0F8TEDE, G, H. The Game of Budget Control. London: Tavistock, 1968.HOPWOOD, A, G. "An Empirical Study of the Role of Accounting Data in Performance

Evaluation." Empirical Research in Accounting: Selected Studies, 1972. Supplementto Journal of Accounting Research 10:156-82.

. An Accounting System and Managerial Behaviour. London: Saxon House, 1973.HOUSE, R, J. "A Path-Goal Theory of Leader Effectiveness." Administrative Science

Quarterly (September 1971): 321-38.JAQUES, E . Equitable Payment. New York: Heineman, 1961.KAHN, R. L. , ET AL. Organizational Stress: Studies in Role Conflict and Ambiguity. New

York: Wiley, 1964.LOWE, E . A., AND R. W. SHAW. "An Analysis of Managerial Biasing: Evidence from a

Company's Budgeting Process." Journal of Management Studies (1968): 304-15.MiNTZBERG, H. Impediments to the Use of Management Information. Washington, D.C.:

National Association of Accountants, 1975.MURRAY, W. Management Controls in Action. Dublin: Irish National Productivity

Committee, 1970.OTLEY, D . T. "Budgetary Control and Managerial Performance." Ph.D. dissertation.

University of Manchester, 1976.READ, W. H. "Upward Communication in Industrial Hierarchies." Human Relations

(1%2): 3-16.RIDGWAY, V. F, "Dysfunctional Consequences of Performance Measurements." Admin-

istrative Science Quarterly (September 1956): 240-47.RoNEN, J,, AND J, L. LIVINGSTONE. "An Expectancy Theory Approach to the Motiva-

tional Impact of Budgets." The Accounting Review (October 1975): 671-85.ROSEN, L, S., AND R. E . SNECK. "Some Behavioral Consequences of Accounting

Measurement Systems." Cost and Management (October 1967): 6-16.ScHiFT, M., AND A. Y. LEWIN. "The Impact of People on Budgets." The Accounting

Review (April 1970): 259-68.SMITH, C. G,, AND A. S. TANNENBAUM, "Organizational Control Structure: A Compara-

tive Analysis, "HMmanBe/ations (1963): 299-316.ViCKERS, G. The Art of Judgment. London: Chapmeui and Hall, 1965.YETTON, P. W, "The Interaction between a Standard Time Incentive Payment Scheme

and a Simple Accounting Information System." Accoi/raim^, Organization and Society(1976): 81-87.