bringing a dsge model into policy environment in colombia

TRANSCRIPT

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 1/42

Bringing a DSGE Model into PolicyEnvironment in Colombia

Franz Hamann, Julián Pérez and Diego RodríguezBanco de la República de Colombia

http://www.banrep.gov.co

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 2/42

Monetary Policy in Colombia

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 3/42

Decision Making

■ Policy decision is taken by the Board of Governors

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 3/42

Decision Making

■ Policy decision is taken by the Board of Governors■ A single policy recommendation by the Deputy Governor

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 3/42

Decision Making

■ Policy decision is taken by the Board of Governors■ A single policy recommendation by the Deputy Governor■ The policy recommendation uses a battery of technical tools

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 3/42

Decision Making

■ Policy decision is taken by the Board of Governors■ A single policy recommendation by the Deputy Governor■ The policy recommendation uses a battery of technical tools■ Board decides whether to follow or not the recommendation

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 3/42

Decision Making

■ Policy decision is taken by the Board of Governors■ A single policy recommendation by the Deputy Governor■ The policy recommendation uses a battery of technical tools■ Board decides whether to follow or not the recommendation■ Governor communicates decision by Press Release

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 3/42

Decision Making

■ Policy decision is taken by the Board of Governors■ A single policy recommendation by the Deputy Governor■ The policy recommendation uses a battery of technical tools■ Board decides whether to follow or not the recommendation■ Governor communicates decision by Press Release■ In a TV broadcasted presentation explains the decision

(every quarter)

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 4/42

The Technology

■ The process to produce a policy recommendation is similarto other Central Banks

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 4/42

The Technology

■ The process to produce a policy recommendation is similarto other Central Banks

■ Quarterly policy and forecasting rounds (with monthlyreviews)

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 4/42

The Technology

■ The process to produce a policy recommendation is similarto other Central Banks

■ Quarterly policy and forecasting rounds (with monthlyreviews)

■ Tools for policy recommendation:◆ Assessment of current/future economic conditions◆ Conventional econometric techniques (VARS, SVARS,

VECS, etc.);◆ Subjective forecasting and sectoral experts;◆ Core Macroeconomic Model (small and semi-structural);◆ Other models: financial programming, balance of

payments, financial stability, among others;

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 4/42

The Technology

■ The process to produce a policy recommendation is similarto other Central Banks

■ Quarterly policy and forecasting rounds (with monthlyreviews)

■ Tools for policy recommendation:◆ Assessment of current/future economic conditions◆ Conventional econometric techniques (VARS, SVARS,

VECS, etc.);◆ Subjective forecasting and sectoral experts;◆ Core Macroeconomic Model (small and semi-structural);◆ Other models: financial programming, balance of

payments, financial stability, among others;■ Judgment plays a prominent for the policy recommendation

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 5/42

The Demand

■ There is a demand for improving the structure of the currentCore Model

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 5/42

The Demand

■ There is a demand for improving the structure of the currentCore Model

■ The model does not consider important shocks: productivity,terms of trade shocks, remittances, etc.

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 5/42

The Demand

■ There is a demand for improving the structure of the currentCore Model

■ The model does not consider important shocks: productivity,terms of trade shocks, remittances, etc.

■ Need to understand the macroeconomic effects of theseshocks...

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 5/42

The Demand

■ There is a demand for improving the structure of the currentCore Model

■ The model does not consider important shocks: productivity,terms of trade shocks, remittances, etc.

■ Need to understand the macroeconomic effects of theseshocks...

■ And their impact on monetary policy, given the mandate tocontrol inflation.

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 5/42

The Demand

■ There is a demand for improving the structure of the currentCore Model

■ The model does not consider important shocks: productivity,terms of trade shocks, remittances, etc.

■ Need to understand the macroeconomic effects of theseshocks...

■ And their impact on monetary policy, given the mandate tocontrol inflation.

■ The result: need a structural model taylored to theColombian Economy.

Monetary Policy in Colombia

● Decision Making

● The Technology

● The Demand

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 5/42

The Demand

■ There is a demand for improving the structure of the currentCore Model

■ The model does not consider important shocks: productivity,terms of trade shocks, remittances, etc.

■ Need to understand the macroeconomic effects of theseshocks...

■ And their impact on monetary policy, given the mandate tocontrol inflation.

■ The result: need a structural model taylored to theColombian Economy.

■ Notice that there is also a lot of judgment here too!!

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 6/42

Stylized Facts

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 7/42

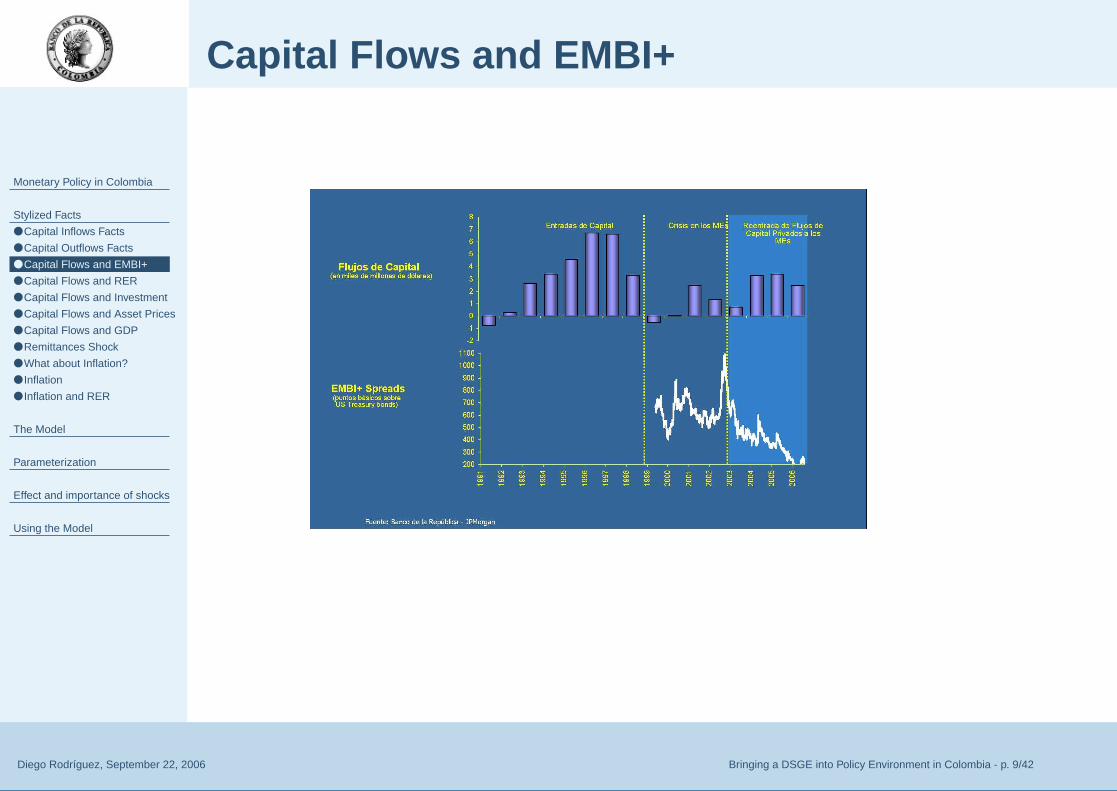

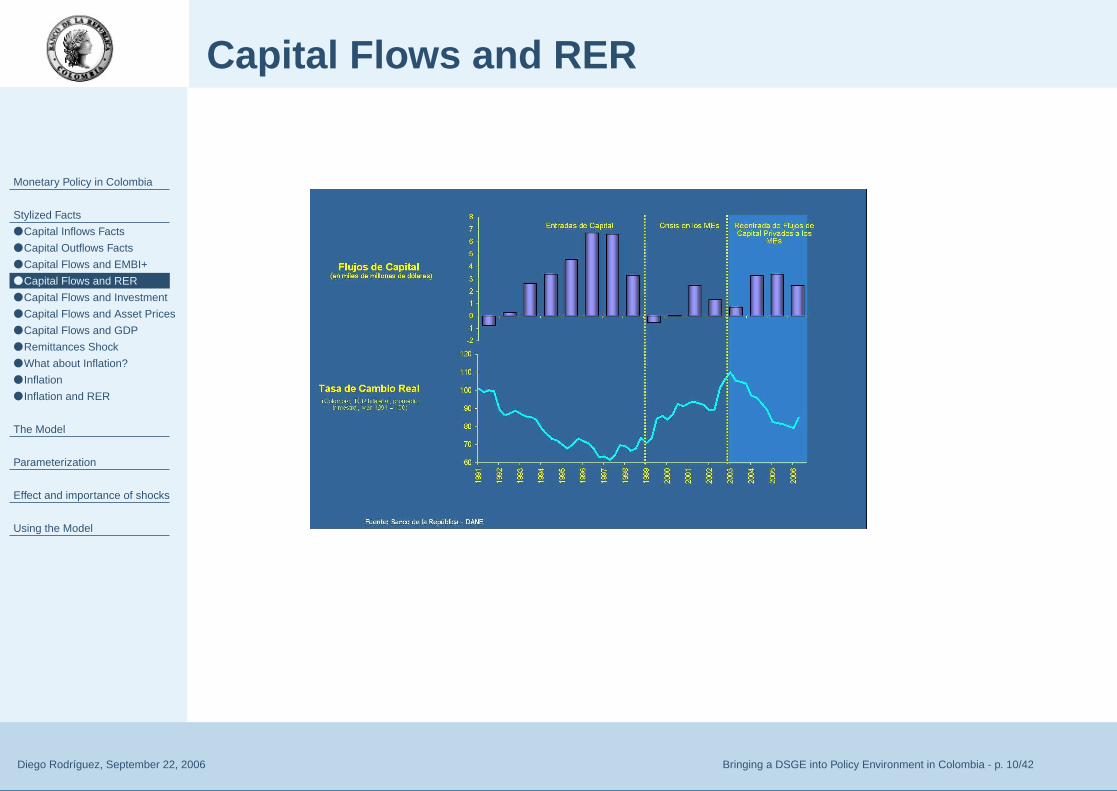

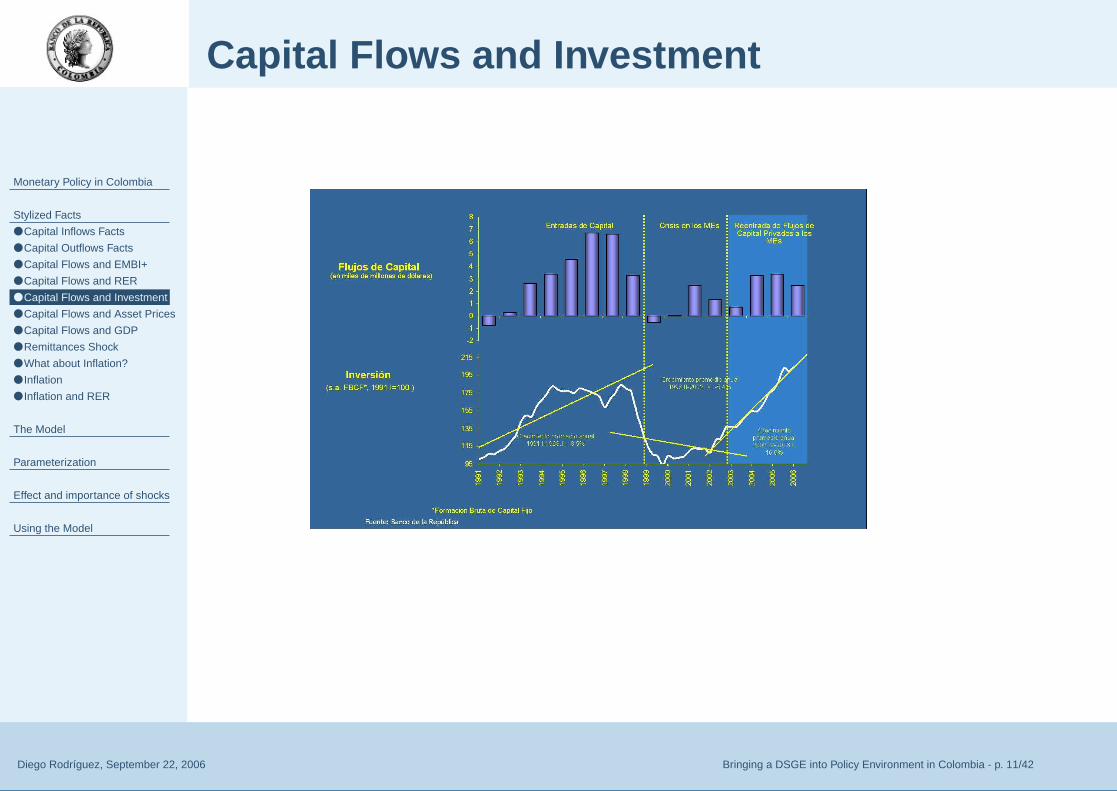

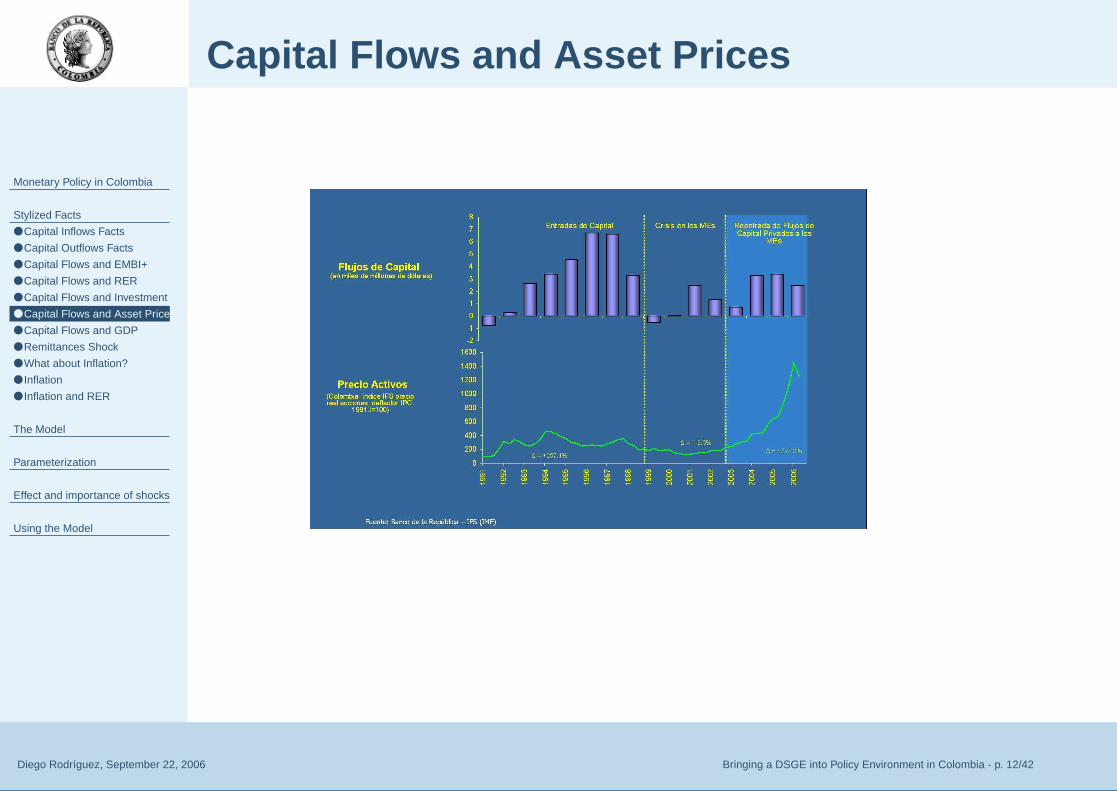

Capital Inflows Facts

■ In Colombia, capital inflows have been accompanied by:

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 7/42

Capital Inflows Facts

■ In Colombia, capital inflows have been accompanied by:■ a significant nominal and real exchange rate appreciation

combined with low sovereign spreads,

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 7/42

Capital Inflows Facts

■ In Colombia, capital inflows have been accompanied by:■ a significant nominal and real exchange rate appreciation

combined with low sovereign spreads,■ a boom in total credit (to the private and/or the public sector)

and domestic demand (consumption and investment),

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 7/42

Capital Inflows Facts

■ In Colombia, capital inflows have been accompanied by:■ a significant nominal and real exchange rate appreciation

combined with low sovereign spreads,■ a boom in total credit (to the private and/or the public sector)

and domestic demand (consumption and investment),■ rapid growth in asset prices, not only stocks or financial

assets, but also non-traded assets (like house prices) and

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 7/42

Capital Inflows Facts

■ In Colombia, capital inflows have been accompanied by:■ a significant nominal and real exchange rate appreciation

combined with low sovereign spreads,■ a boom in total credit (to the private and/or the public sector)

and domestic demand (consumption and investment),■ rapid growth in asset prices, not only stocks or financial

assets, but also non-traded assets (like house prices) and■ increased economic activity and employment.

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 8/42

Capital Outflows Facts

■ In Colombia, capital outflows have been accompanied by:

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 8/42

Capital Outflows Facts

■ In Colombia, capital outflows have been accompanied by:■ a significant nominal and real exchange rate depreciation

combined with high sovereign spreads,

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 8/42

Capital Outflows Facts

■ In Colombia, capital outflows have been accompanied by:■ a significant nominal and real exchange rate depreciation

combined with high sovereign spreads,■ a sharp reduction in total credit (to the private and/or the

public sector) and domestic demand (consumption andinvestment),

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 8/42

Capital Outflows Facts

■ In Colombia, capital outflows have been accompanied by:■ a significant nominal and real exchange rate depreciation

combined with high sovereign spreads,■ a sharp reduction in total credit (to the private and/or the

public sector) and domestic demand (consumption andinvestment),

■ collapse in asset prices, not only stocks or financial assets,but also non-traded assets (like house prices) and

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 8/42

Capital Outflows Facts

■ In Colombia, capital outflows have been accompanied by:■ a significant nominal and real exchange rate depreciation

combined with high sovereign spreads,■ a sharp reduction in total credit (to the private and/or the

public sector) and domestic demand (consumption andinvestment),

■ collapse in asset prices, not only stocks or financial assets,but also non-traded assets (like house prices) and

■ reduced economic activity and employment.

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 9/42

Capital Flows and EMBI+

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 10/42

Capital Flows and RER

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 11/42

Capital Flows and Investment

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 12/42

Capital Flows and Asset Prices

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 13/42

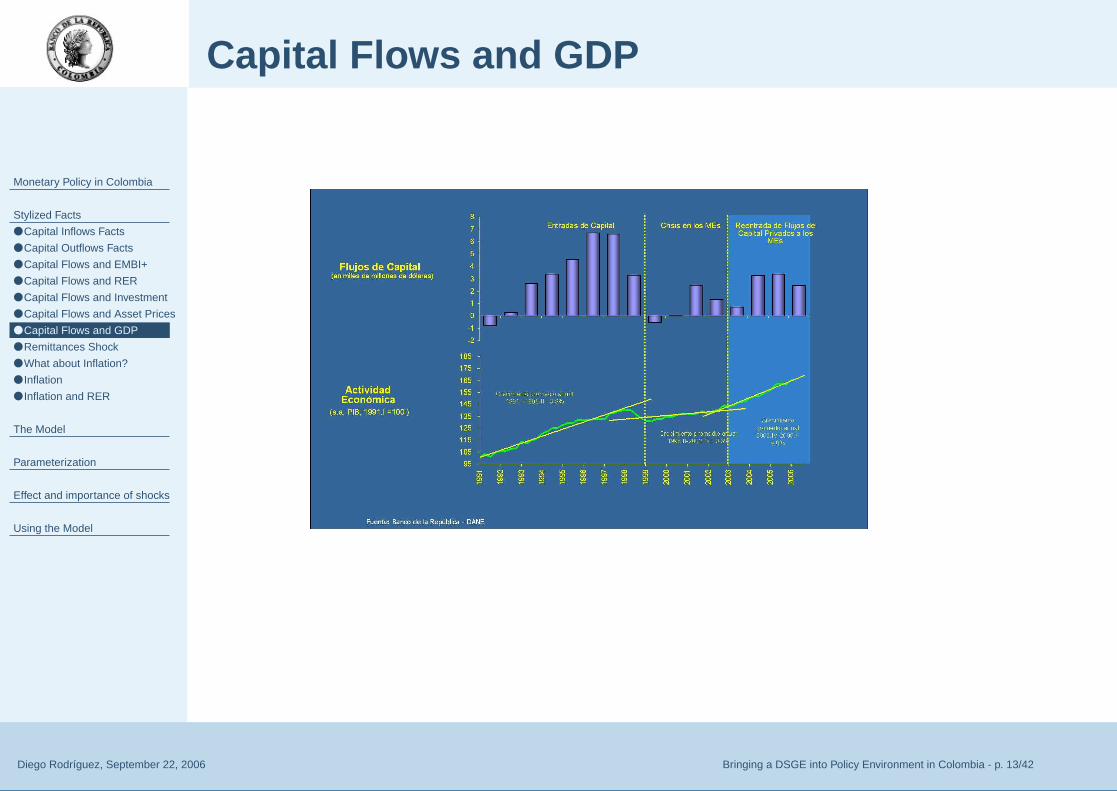

Capital Flows and GDP

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 14/42

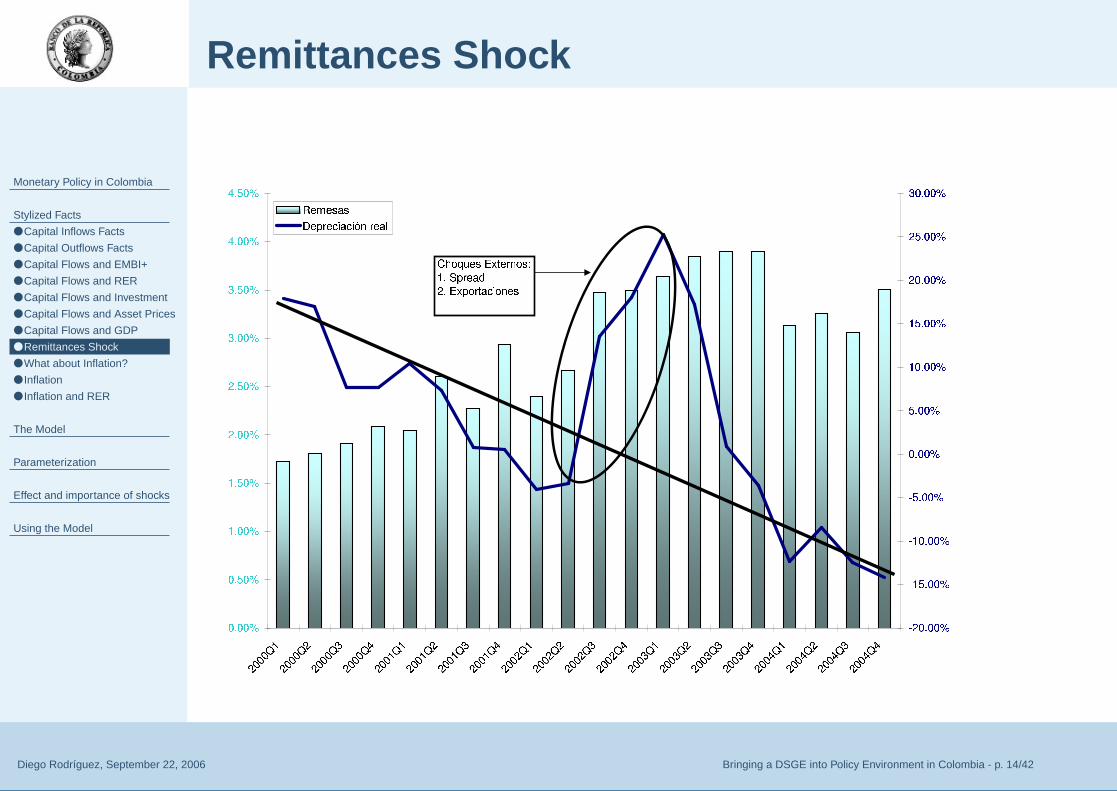

Remittances Shock

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 15/42

What about Inflation?

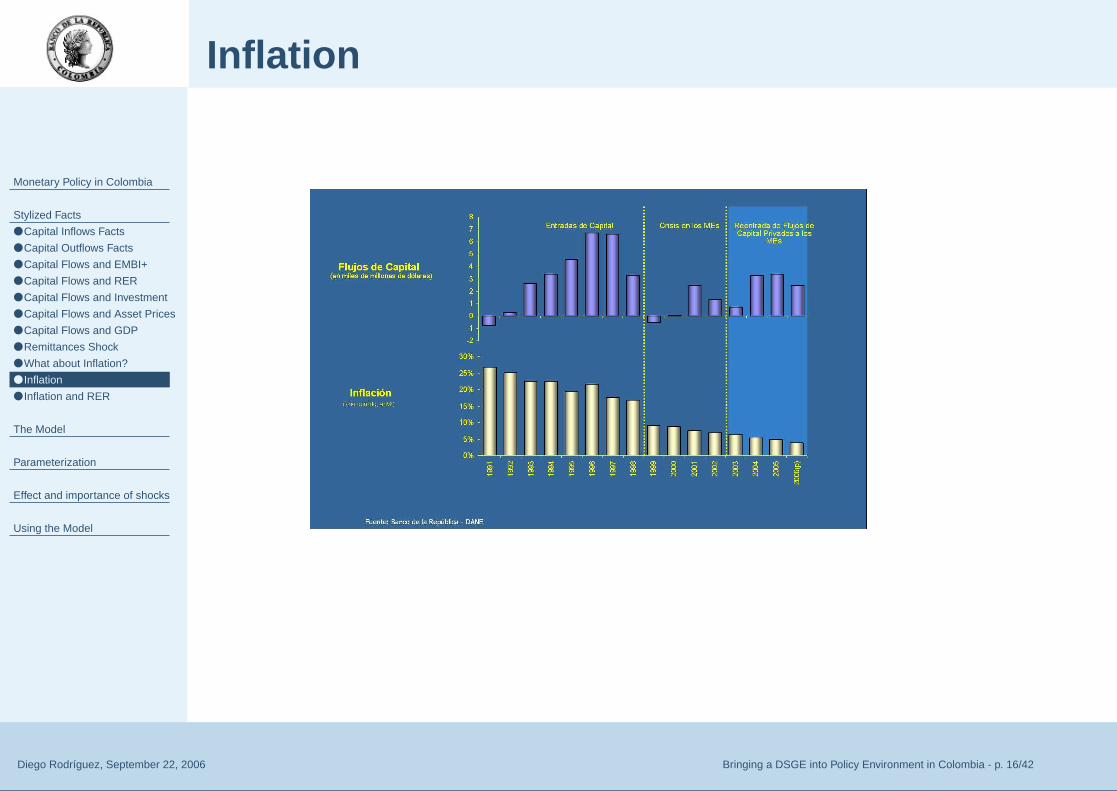

■ Like many LACs, in Colombia inflation drop steadily duringthe nineties.

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 15/42

What about Inflation?

■ Like many LACs, in Colombia inflation drop steadily duringthe nineties.

■ In inflow periods nontradable inflation tends to increaserelative to tradable.

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 15/42

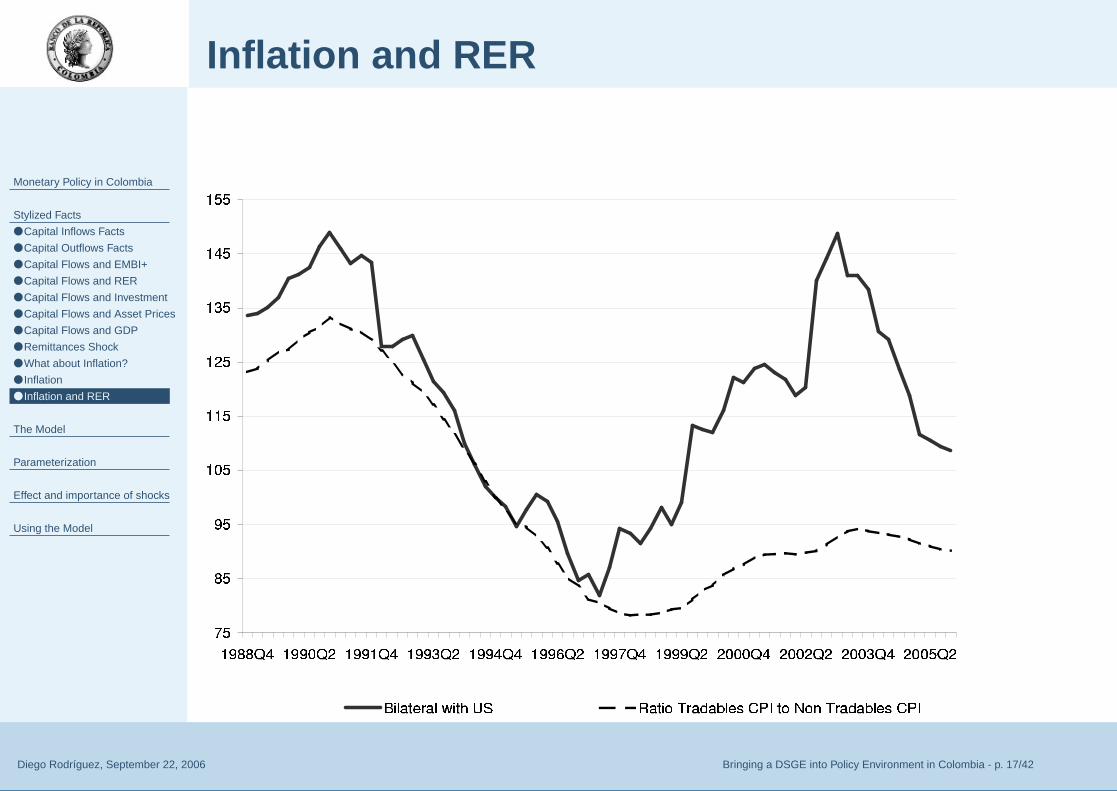

What about Inflation?

■ Like many LACs, in Colombia inflation drop steadily duringthe nineties.

■ In inflow periods nontradable inflation tends to increaserelative to tradable.

■ In outflow periods tradable inflation tends to increase relativeto nontradable.

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 15/42

What about Inflation?

■ Like many LACs, in Colombia inflation drop steadily duringthe nineties.

■ In inflow periods nontradable inflation tends to increaserelative to tradable.

■ In outflow periods tradable inflation tends to increase relativeto nontradable.

■ There is low degree of pass through to total inflation.

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 15/42

What about Inflation?

■ Like many LACs, in Colombia inflation drop steadily duringthe nineties.

■ In inflow periods nontradable inflation tends to increaserelative to tradable.

■ In outflow periods tradable inflation tends to increase relativeto nontradable.

■ There is low degree of pass through to total inflation.■ A full-fledged IT regime started in September 1999

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 16/42

Inflation

Monetary Policy in Colombia

Stylized Facts

● Capital Inflows Facts

● Capital Outflows Facts

● Capital Flows and EMBI+

● Capital Flows and RER

● Capital Flows and Investment

● Capital Flows and Asset Prices

● Capital Flows and GDP

● Remittances Shock

● What about Inflation?

● Inflation

● Inflation and RER

The Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 17/42

Inflation and RER

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 18/42

The Model

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 19/42

A New Core Model

■ Small Open Economy Model with tradable and nontradablesectors.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 19/42

A New Core Model

■ Small Open Economy Model with tradable and nontradablesectors.

■ Firms: export-oriented and nontradables.◆ Mining Exporting Firms (endowment). Perfect competition.◆ Non-mining Exporting Firms. Use capital and labor.

Perfect competition.◆ Nontradable Firms. Use capital and labor. Imperfect

competition.◆ Importing firms (a la Burstein et al.) Perfect competition.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 19/42

A New Core Model

■ Small Open Economy Model with tradable and nontradablesectors.

■ Firms: export-oriented and nontradables.◆ Mining Exporting Firms (endowment). Perfect competition.◆ Non-mining Exporting Firms. Use capital and labor.

Perfect competition.◆ Nontradable Firms. Use capital and labor. Imperfect

competition.◆ Importing firms (a la Burstein et al.) Perfect competition.

■ Households: consume NT and imported goods. Inelasticlabor supply. Choose in which sector to work.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 19/42

A New Core Model

■ Small Open Economy Model with tradable and nontradablesectors.

■ Firms: export-oriented and nontradables.◆ Mining Exporting Firms (endowment). Perfect competition.◆ Non-mining Exporting Firms. Use capital and labor.

Perfect competition.◆ Nontradable Firms. Use capital and labor. Imperfect

competition.◆ Importing firms (a la Burstein et al.) Perfect competition.

■ Households: consume NT and imported goods. Inelasticlabor supply. Choose in which sector to work.

■ Imperfect capital mobility.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 19/42

A New Core Model

■ Small Open Economy Model with tradable and nontradablesectors.

■ Firms: export-oriented and nontradables.◆ Mining Exporting Firms (endowment). Perfect competition.◆ Non-mining Exporting Firms. Use capital and labor.

Perfect competition.◆ Nontradable Firms. Use capital and labor. Imperfect

competition.◆ Importing firms (a la Burstein et al.) Perfect competition.

■ Households: consume NT and imported goods. Inelasticlabor supply. Choose in which sector to work.

■ Imperfect capital mobility.■ Government: nontradable outlays, lump-transfers and Taylor

rule to meet inflation target.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 20/42

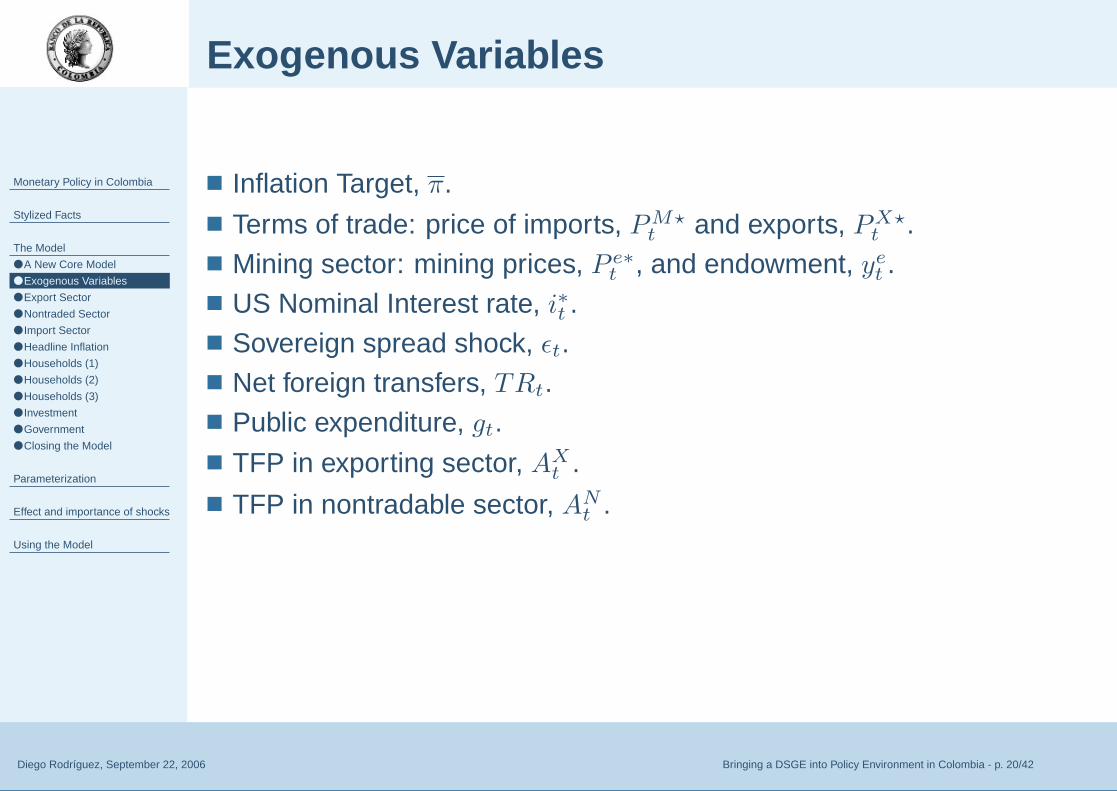

Exogenous Variables

■ Inflation Target, π.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 20/42

Exogenous Variables

■ Inflation Target, π.■ Terms of trade: price of imports, PM?

t and exports, PX?t .

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 20/42

Exogenous Variables

■ Inflation Target, π.■ Terms of trade: price of imports, PM?

t and exports, PX?t .

■ Mining sector: mining prices, P e∗t , and endowment, ye

t .

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 20/42

Exogenous Variables

■ Inflation Target, π.■ Terms of trade: price of imports, PM?

t and exports, PX?t .

■ Mining sector: mining prices, P e∗t , and endowment, ye

t .■ US Nominal Interest rate, i∗t .

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 20/42

Exogenous Variables

■ Inflation Target, π.■ Terms of trade: price of imports, PM?

t and exports, PX?t .

■ Mining sector: mining prices, P e∗t , and endowment, ye

t .■ US Nominal Interest rate, i∗t .■ Sovereign spread shock, εt.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 20/42

Exogenous Variables

■ Inflation Target, π.■ Terms of trade: price of imports, PM?

t and exports, PX?t .

■ Mining sector: mining prices, P e∗t , and endowment, ye

t .■ US Nominal Interest rate, i∗t .■ Sovereign spread shock, εt.■ Net foreign transfers, TRt.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 20/42

Exogenous Variables

■ Inflation Target, π.■ Terms of trade: price of imports, PM?

t and exports, PX?t .

■ Mining sector: mining prices, P e∗t , and endowment, ye

t .■ US Nominal Interest rate, i∗t .■ Sovereign spread shock, εt.■ Net foreign transfers, TRt.■ Public expenditure, gt.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 20/42

Exogenous Variables

■ Inflation Target, π.■ Terms of trade: price of imports, PM?

t and exports, PX?t .

■ Mining sector: mining prices, P e∗t , and endowment, ye

t .■ US Nominal Interest rate, i∗t .■ Sovereign spread shock, εt.■ Net foreign transfers, TRt.■ Public expenditure, gt.■ TFP in exporting sector, AX

t .

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 20/42

Exogenous Variables

■ Inflation Target, π.■ Terms of trade: price of imports, PM?

t and exports, PX?t .

■ Mining sector: mining prices, P e∗t , and endowment, ye

t .■ US Nominal Interest rate, i∗t .■ Sovereign spread shock, εt.■ Net foreign transfers, TRt.■ Public expenditure, gt.■ TFP in exporting sector, AX

t .■ TFP in nontradable sector, AN

t .

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 21/42

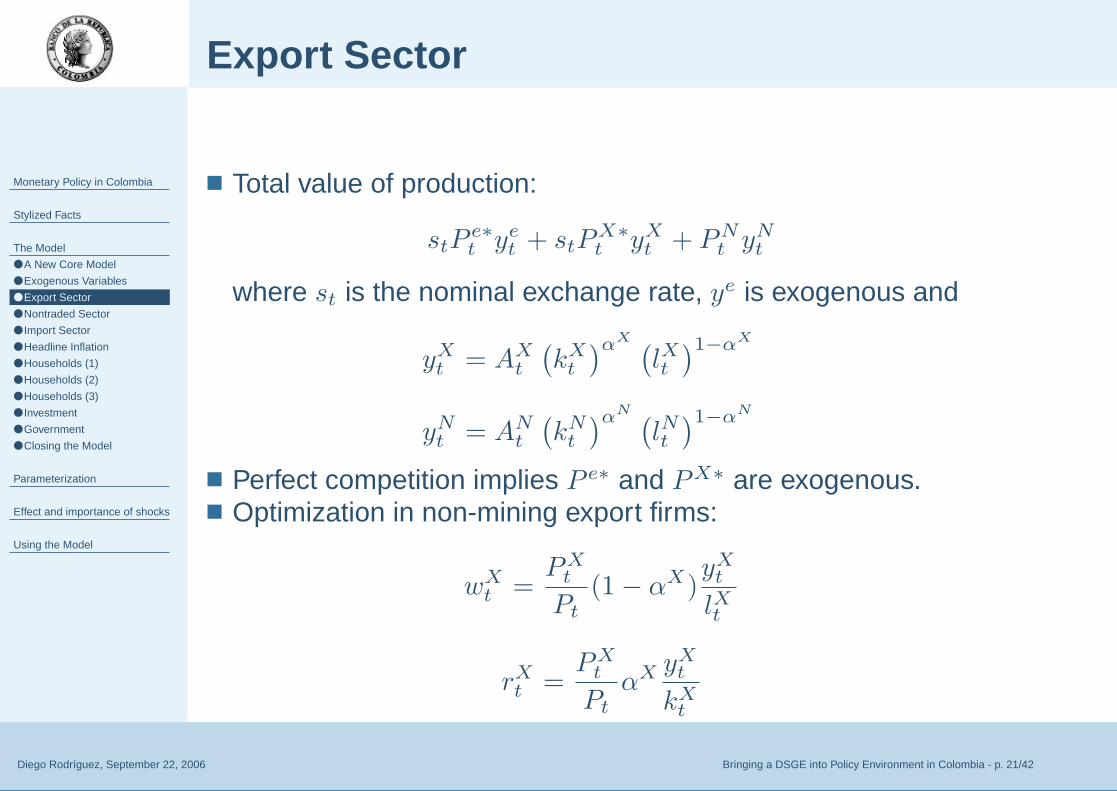

Export Sector

■ Total value of production:

stPe∗t ye

t + stPX∗

t yXt + PN

t yNt

where st is the nominal exchange rate, ye is exogenous and

yXt = AX

t

(kX

t

)αX (lXt)1−αX

yNt = AN

t

(kN

t

)αN (lNt)1−αN

■ Perfect competition implies P e∗ and PX∗ are exogenous.■ Optimization in non-mining export firms:

wXt =

PXt

Pt

(1 − αX)yX

t

lXt

rXt =

PXt

Pt

αX yXt

kXt

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 22/42

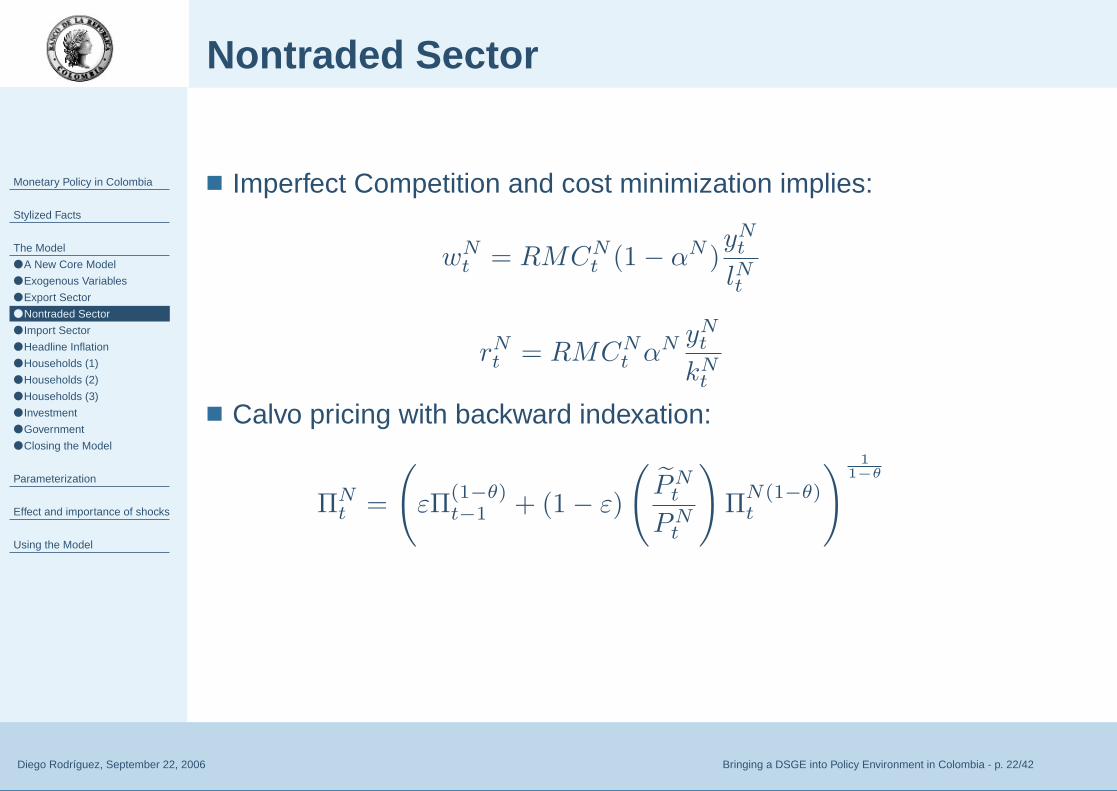

Nontraded Sector

■ Imperfect Competition and cost minimization implies:

wNt = RMCN

t (1 − αN )yN

t

lNt

rNt = RMCN

t αN yN

t

kNt

■ Calvo pricing with backward indexation:

ΠNt =

(εΠ

(1−θ)t−1 + (1 − ε)

(P̃N

t

PNt

)Π

N(1−θ)t

) 1

1−θ

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 23/42

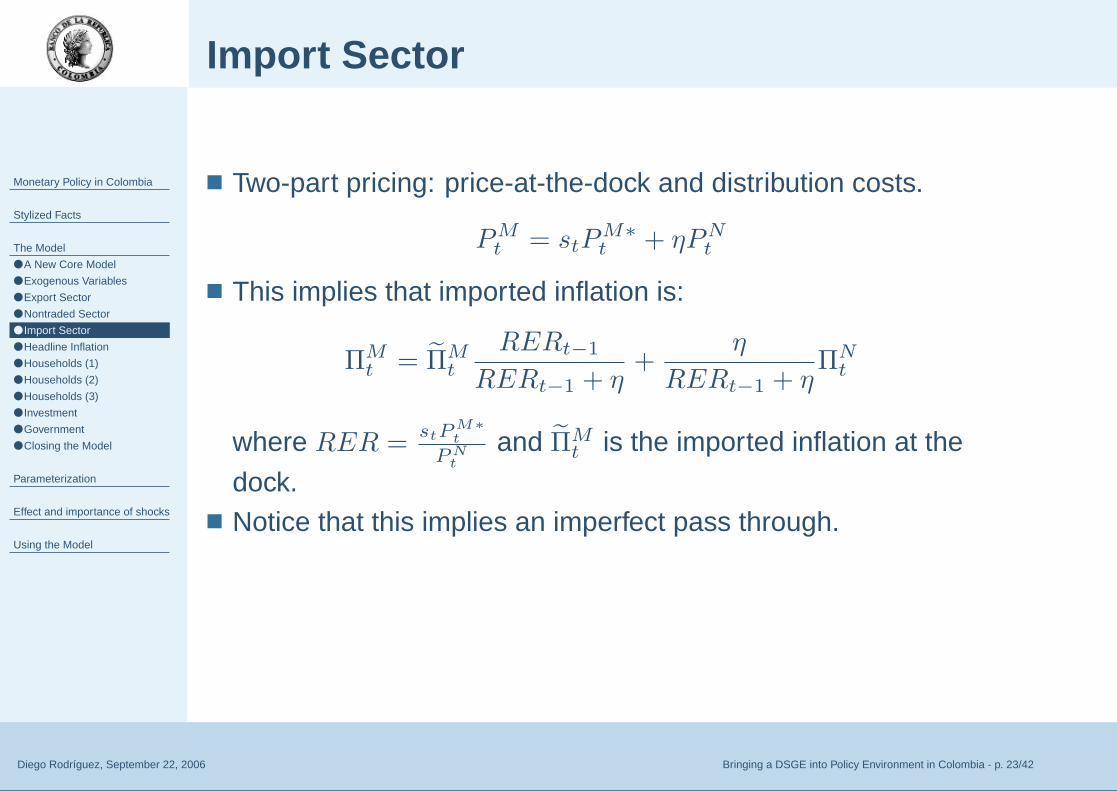

Import Sector

■ Two-part pricing: price-at-the-dock and distribution costs.

PMt = stP

M∗

t + ηPNt

■ This implies that imported inflation is:

ΠMt = Π̃M

t

RERt−1

RERt−1 + η+

η

RERt−1 + ηΠN

t

where RER =stP

M∗

t

P Nt

and Π̃Mt is the imported inflation at the

dock.■ Notice that this implies an imperfect pass through.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 24/42

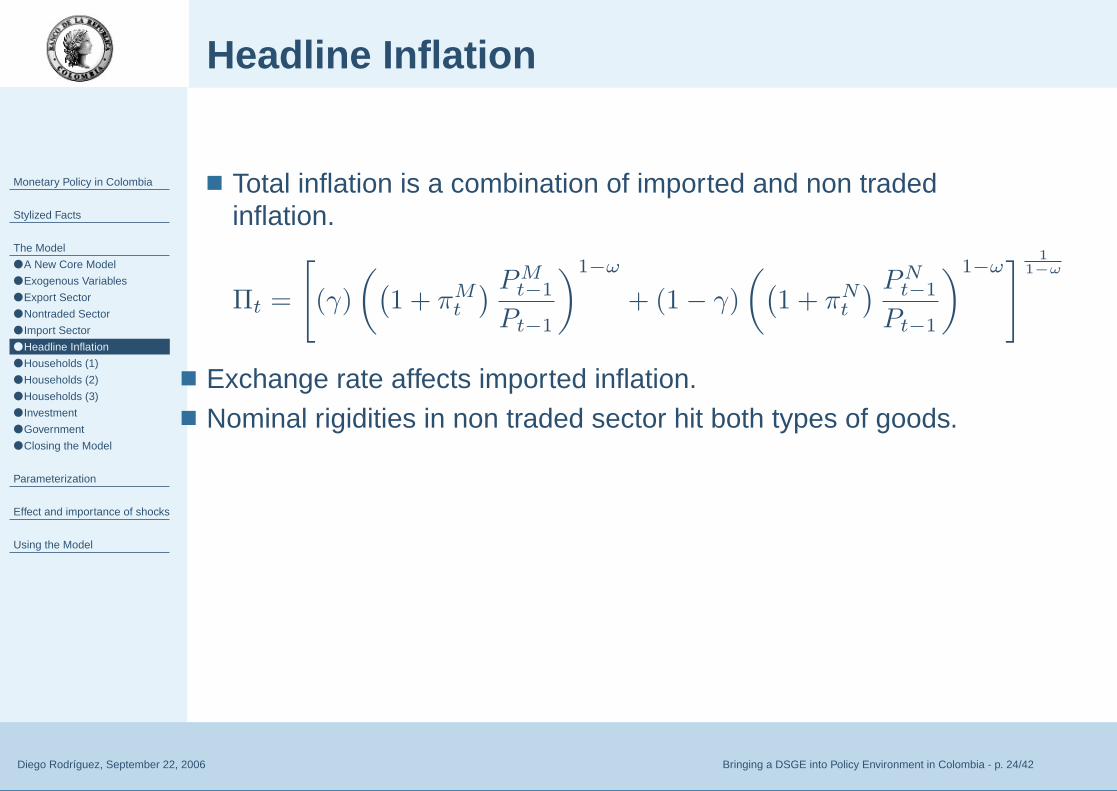

Headline Inflation

■ Total inflation is a combination of imported and non tradedinflation.

Πt =

[(γ)

((1 + πM

t

) PMt−1

Pt−1

)1−ω

+ (1 − γ)

((1 + πN

t

) PNt−1

Pt−1

)1−ω] 1

1−ω

■ Exchange rate affects imported inflation.■ Nominal rigidities in non traded sector hit both types of goods.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 25/42

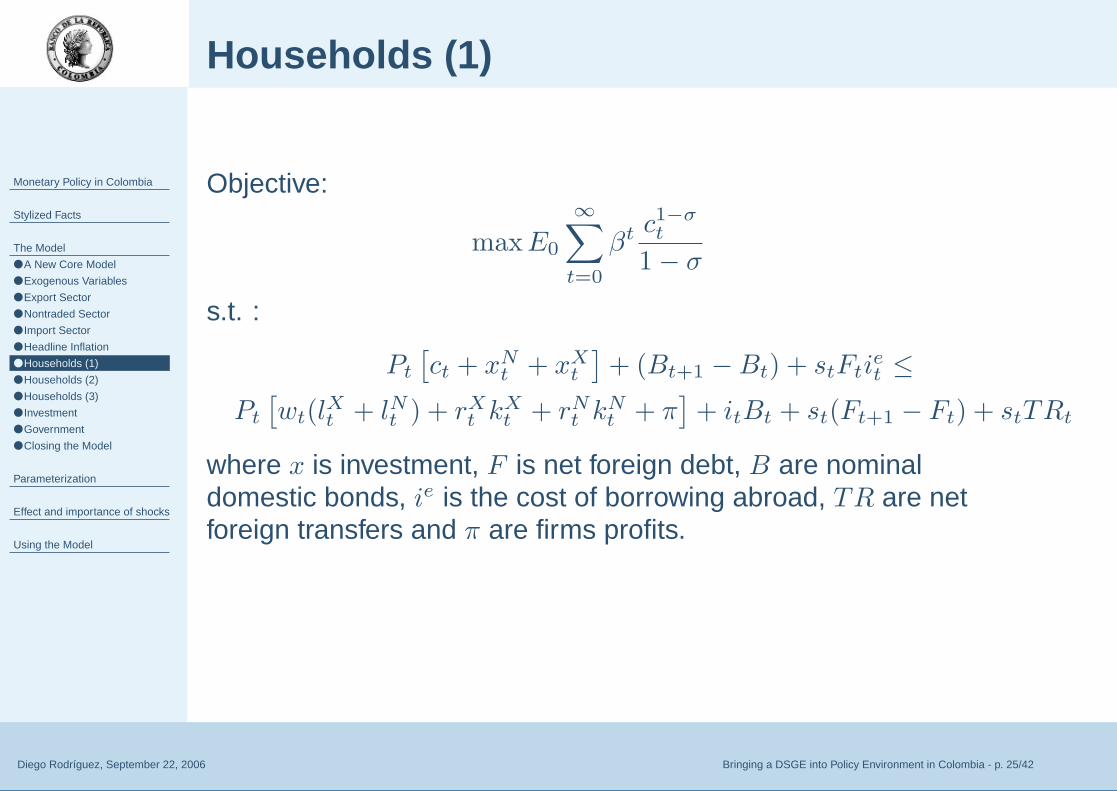

Households (1)

Objective:

maxE0

∞∑

t=0

βt c1−σt

1 − σ

s.t. :

Pt

[ct + xN

t + xXt

]+ (Bt+1 −Bt) + stFti

et ≤

Pt

[wt(l

Xt + lNt ) + rX

t kXt + rN

t kNt + π

]+ itBt + st(Ft+1 − Ft) + stTRt

where x is investment, F is net foreign debt, B are nominaldomestic bonds, ie is the cost of borrowing abroad, TR are netforeign transfers and π are firms profits.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 26/42

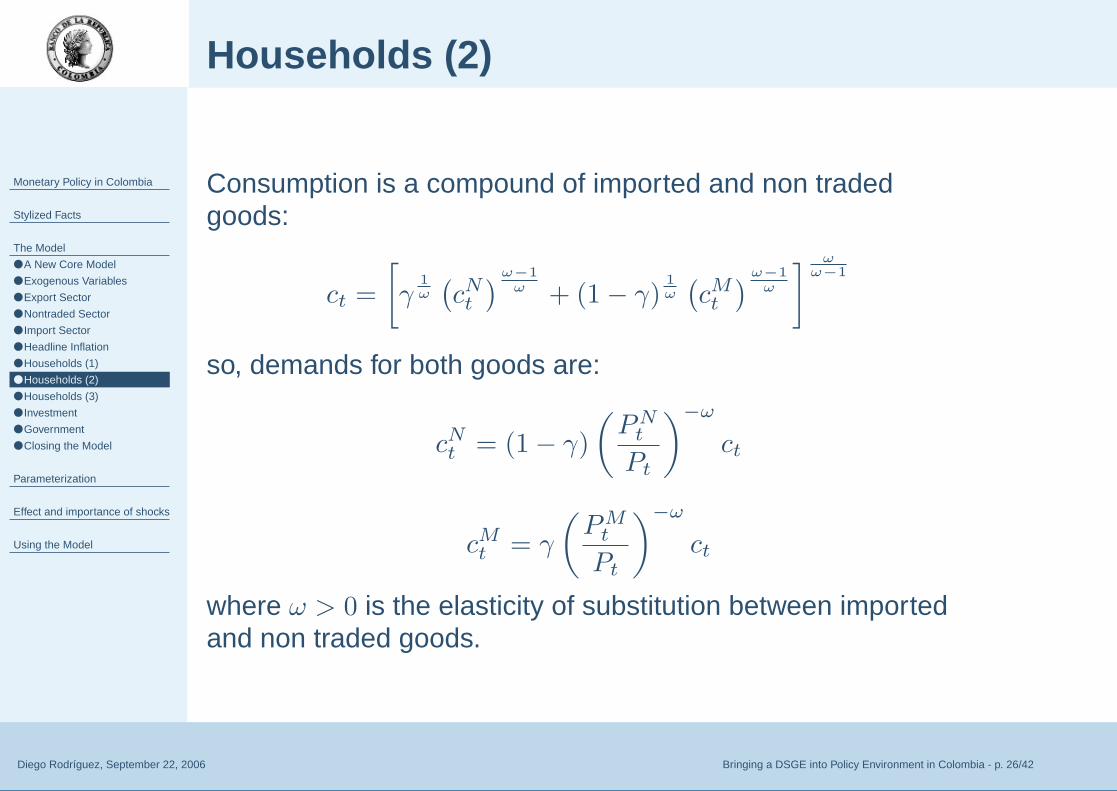

Households (2)

Consumption is a compound of imported and non tradedgoods:

ct =

[γ

1

ω

(cNt)ω−1

ω + (1 − γ)1

ω

(cMt)ω−1

ω

] ωω−1

so, demands for both goods are:

cNt = (1 − γ)

(PN

t

Pt

)−ω

ct

cMt = γ

(PM

t

Pt

)−ω

ct

where ω > 0 is the elasticity of substitution between importedand non traded goods.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 27/42

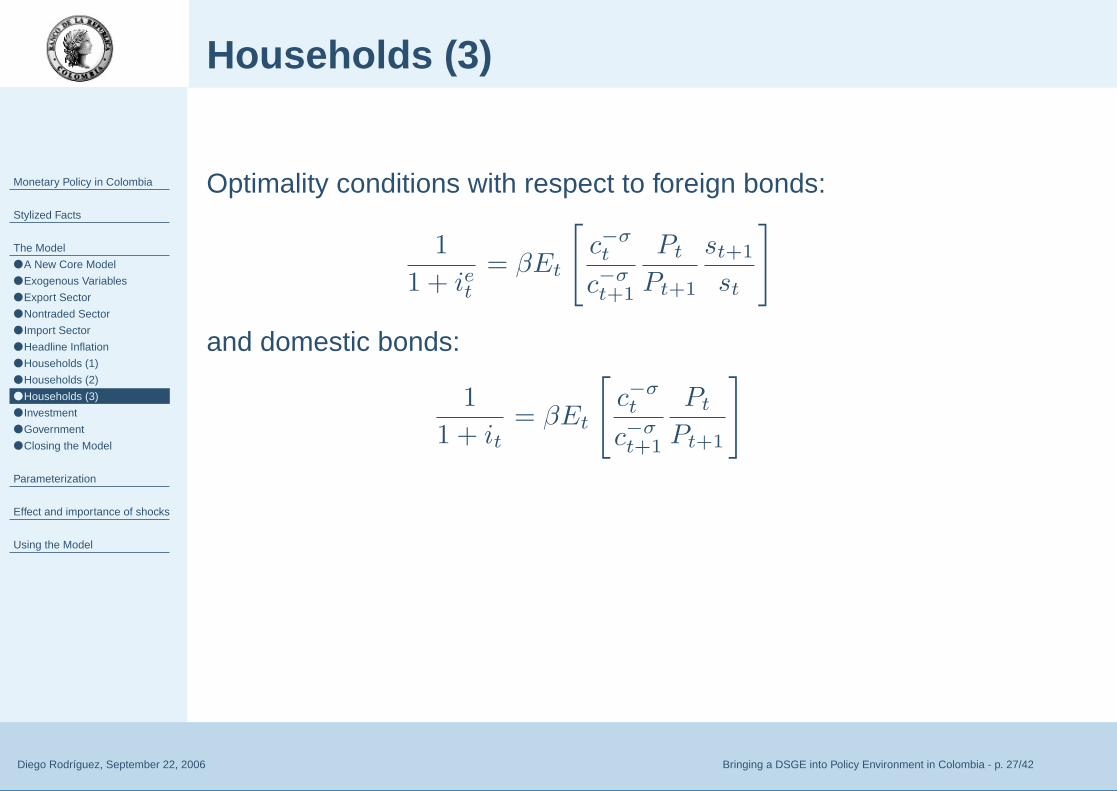

Households (3)

Optimality conditions with respect to foreign bonds:

1

1 + iet= βEt

[c−σt

c−σt+1

Pt

Pt+1

st+1

st

]

and domestic bonds:

1

1 + it= βEt

[c−σt

c−σt+1

Pt

Pt+1

]

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 28/42

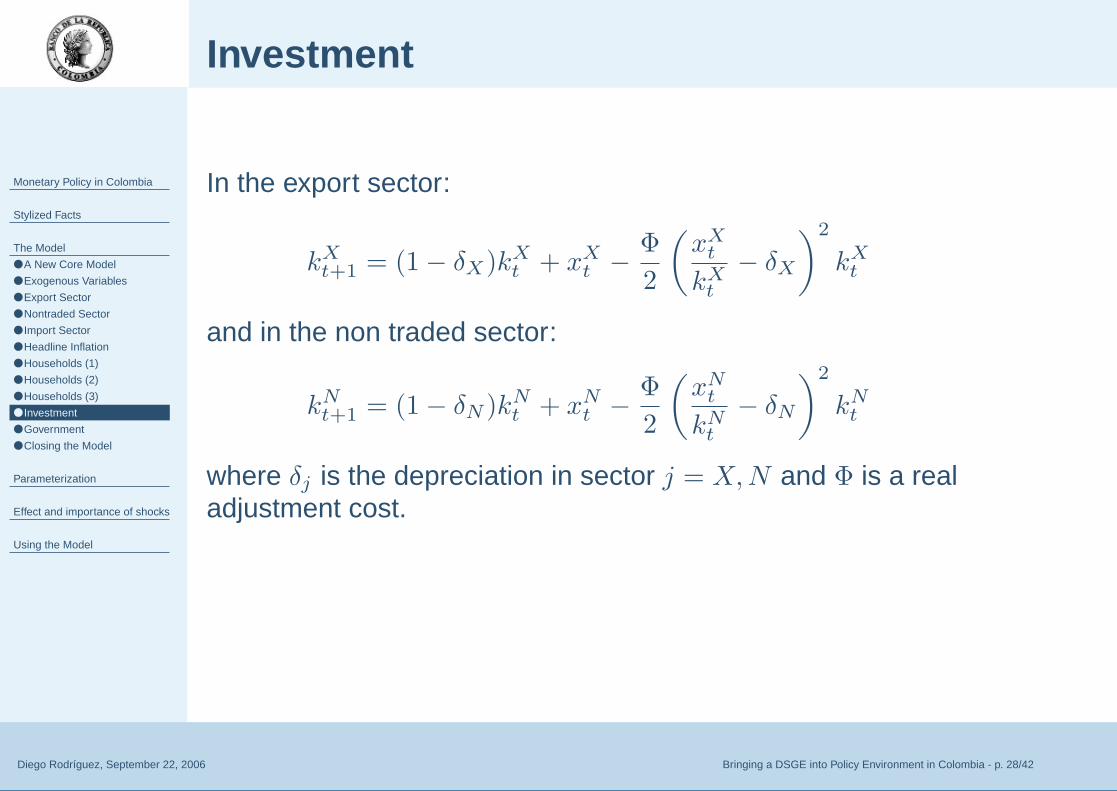

Investment

In the export sector:

kXt+1 = (1 − δX)kX

t + xXt −

Φ

2

(xX

t

kXt

− δX

)2

kXt

and in the non traded sector:

kNt+1 = (1 − δN )kN

t + xNt −

Φ

2

(xN

t

kNt

− δN

)2

kNt

where δj is the depreciation in sector j = X,N and Φ is a realadjustment cost.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 29/42

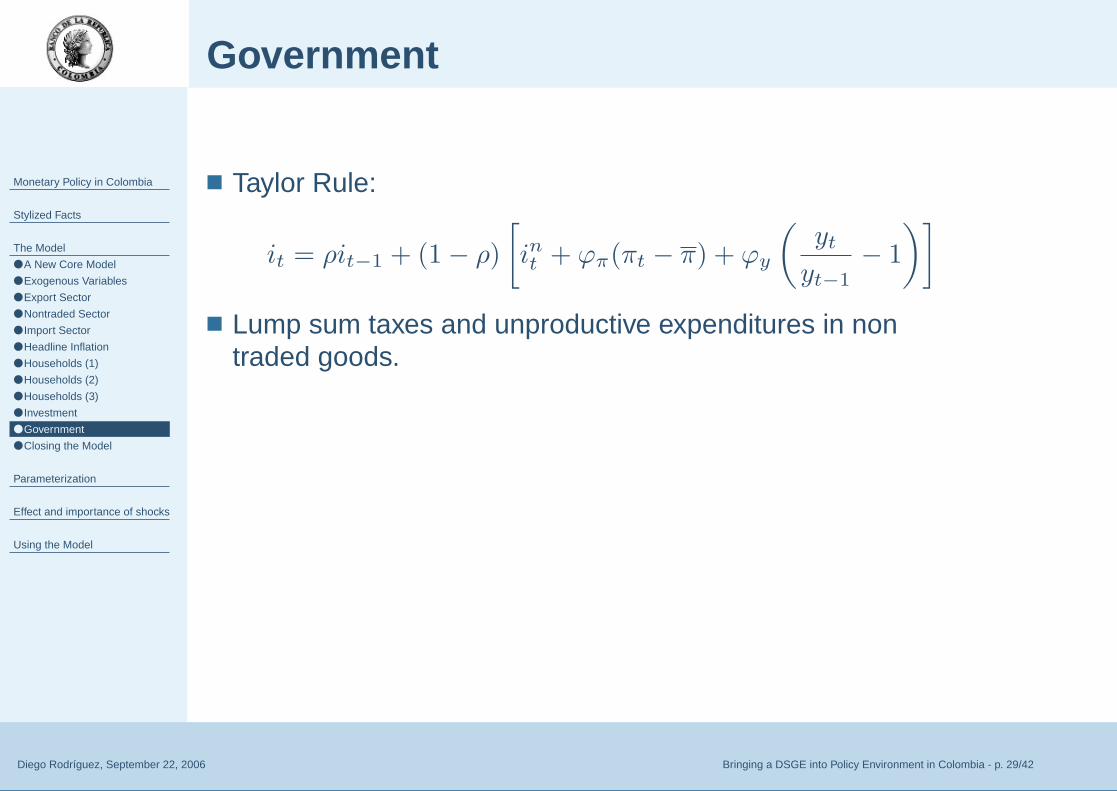

Government

■ Taylor Rule:

it = ρit−1 + (1 − ρ)

[int + ϕπ(πt − π) + ϕy

(yt

yt−1− 1

)]

■ Lump sum taxes and unproductive expenditures in nontraded goods.

Monetary Policy in Colombia

Stylized Facts

The Model

● A New Core Model

● Exogenous Variables

● Export Sector

● Nontraded Sector

● Import Sector

● Headline Inflation

● Households (1)

● Households (2)

● Households (3)

● Investment

● Government

● Closing the Model

Parameterization

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 30/42

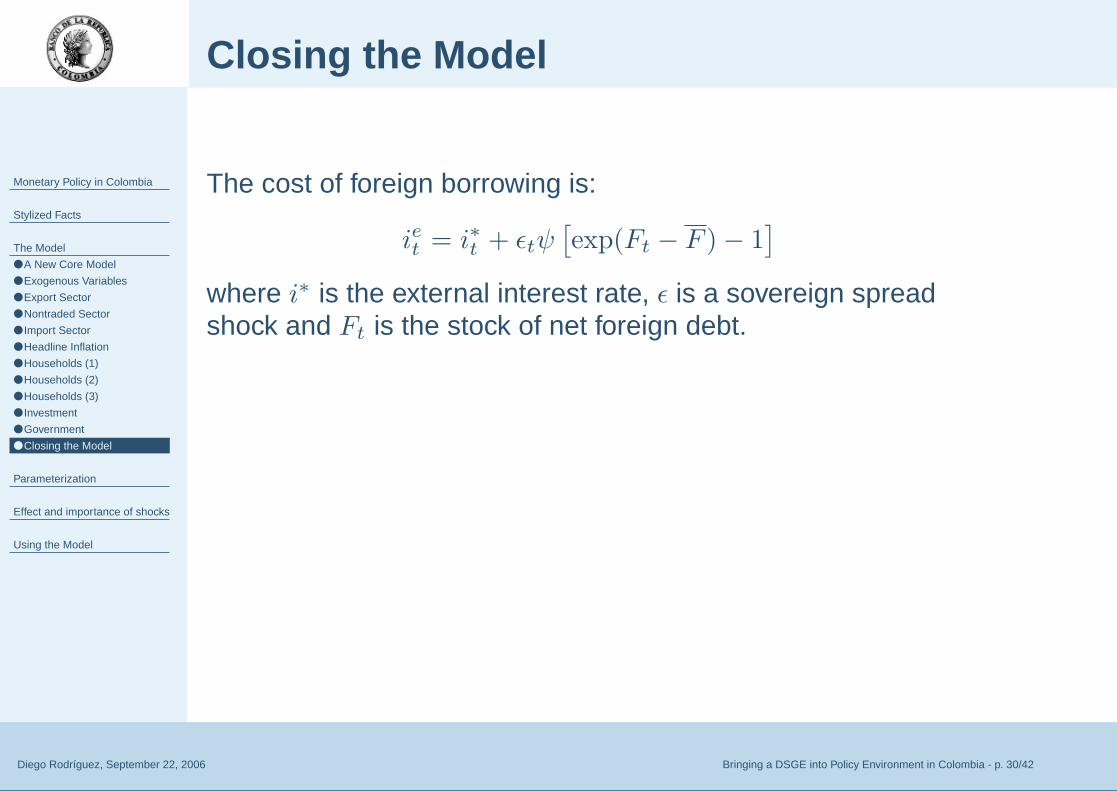

Closing the Model

The cost of foreign borrowing is:

iet = i∗t + εtψ[exp(Ft − F ) − 1

]

where i∗ is the external interest rate, ε is a sovereign spreadshock and Ft is the stock of net foreign debt.

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 31/42

Parameterization

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 32/42

Calibration

■ Set parameters to be consistent with long run restrictionsimplied by the model and the data.

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 32/42

Calibration

■ Set parameters to be consistent with long run restrictionsimplied by the model and the data.

■ Build a model-consistent database (National Accounts to 3sector database)

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 32/42

Calibration

■ Set parameters to be consistent with long run restrictionsimplied by the model and the data.

■ Build a model-consistent database (National Accounts to 3sector database)

■ Compute model-consistent great ratios and detrend timeseries

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 32/42

Calibration

■ Set parameters to be consistent with long run restrictionsimplied by the model and the data.

■ Build a model-consistent database (National Accounts to 3sector database)

■ Compute model-consistent great ratios and detrend timeseries

■ Set parameters to match great ratios and volatility ofinvestment and current account

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 33/42

Bayesian estimation

■ For a given set of parameters we find the state transitionequation

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 33/42

Bayesian estimation

■ For a given set of parameters we find the state transitionequation

■ Add a measurement equation to the model dynamics to getits state space representation

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 33/42

Bayesian estimation

■ For a given set of parameters we find the state transitionequation

■ Add a measurement equation to the model dynamics to getits state space representation

■ Use Kalman filter to obtain the likelihood function of themodel

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 33/42

Bayesian estimation

■ For a given set of parameters we find the state transitionequation

■ Add a measurement equation to the model dynamics to getits state space representation

■ Use Kalman filter to obtain the likelihood function of themodel

■ Combine the likelihood function with the prior distribution ofthe parameters to compute the posterior density

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 33/42

Bayesian estimation

■ For a given set of parameters we find the state transitionequation

■ Add a measurement equation to the model dynamics to getits state space representation

■ Use Kalman filter to obtain the likelihood function of themodel

■ Combine the likelihood function with the prior distribution ofthe parameters to compute the posterior density

■ Using numerical optimization compute the mean of theposterior density and use a Metropolis-Hasting algorithm toget the posterior distribution of the parameters

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

● Calibration

● Bayesian estimation

● Prior and Posterior Distributions

Effect and importance of shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 34/42

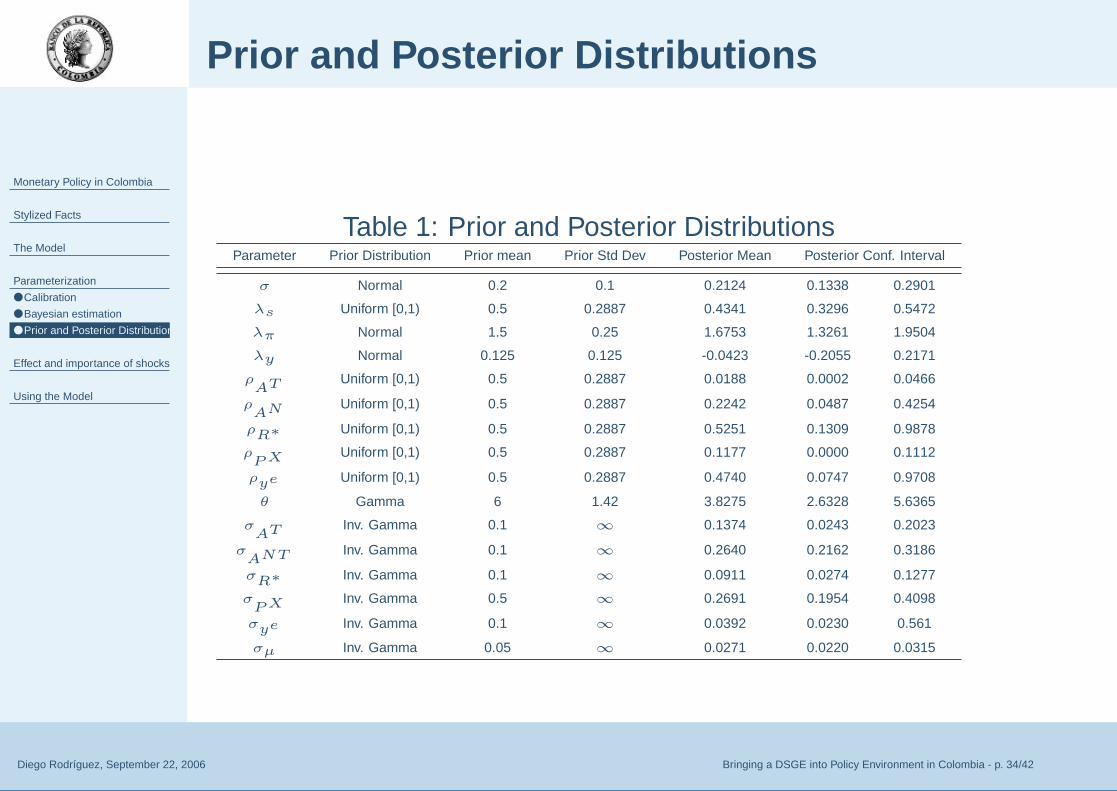

Prior and Posterior Distributions

Table 1: Prior and Posterior DistributionsParameter Prior Distribution Prior mean Prior Std Dev Posterior Mean Posterior Conf. Interval

σ Normal 0.2 0.1 0.2124 0.1338 0.2901

λs Uniform [0,1) 0.5 0.2887 0.4341 0.3296 0.5472

λπ Normal 1.5 0.25 1.6753 1.3261 1.9504

λy Normal 0.125 0.125 -0.0423 -0.2055 0.2171

ρAT Uniform [0,1) 0.5 0.2887 0.0188 0.0002 0.0466

ρAN Uniform [0,1) 0.5 0.2887 0.2242 0.0487 0.4254

ρR∗ Uniform [0,1) 0.5 0.2887 0.5251 0.1309 0.9878

ρP X Uniform [0,1) 0.5 0.2887 0.1177 0.0000 0.1112

ρye Uniform [0,1) 0.5 0.2887 0.4740 0.0747 0.9708

θ Gamma 6 1.42 3.8275 2.6328 5.6365

σAT Inv. Gamma 0.1 ∞ 0.1374 0.0243 0.2023

σANT Inv. Gamma 0.1 ∞ 0.2640 0.2162 0.3186

σR∗ Inv. Gamma 0.1 ∞ 0.0911 0.0274 0.1277

σP X Inv. Gamma 0.5 ∞ 0.2691 0.1954 0.4098

σye Inv. Gamma 0.1 ∞ 0.0392 0.0230 0.561

σµ Inv. Gamma 0.05 ∞ 0.0271 0.0220 0.0315

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

● Oil shock

● Terms of trade shock

● Monetary policy shock

● Importance shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 35/42

Effect and importance of shocks

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

● Oil shock

● Terms of trade shock

● Monetary policy shock

● Importance shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 36/42

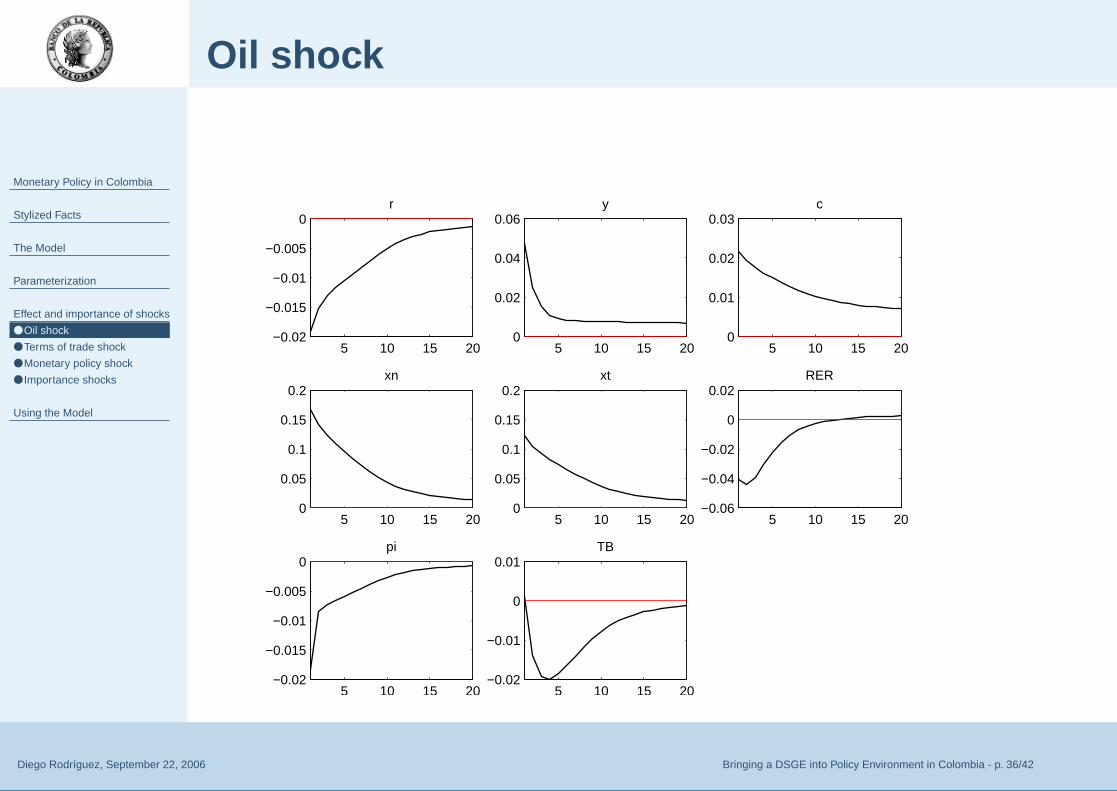

Oil shock

5 10 15 20−0.02

−0.015

−0.01

−0.005

0r

5 10 15 200

0.02

0.04

0.06y

5 10 15 200

0.01

0.02

0.03c

5 10 15 200

0.05

0.1

0.15

0.2xn

5 10 15 200

0.05

0.1

0.15

0.2xt

5 10 15 20−0.06

−0.04

−0.02

0

0.02RER

5 10 15 20−0.02

−0.015

−0.01

−0.005

0pi

5 10 15 20−0.02

−0.01

0

0.01TB

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

● Oil shock

● Terms of trade shock

● Monetary policy shock

● Importance shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 37/42

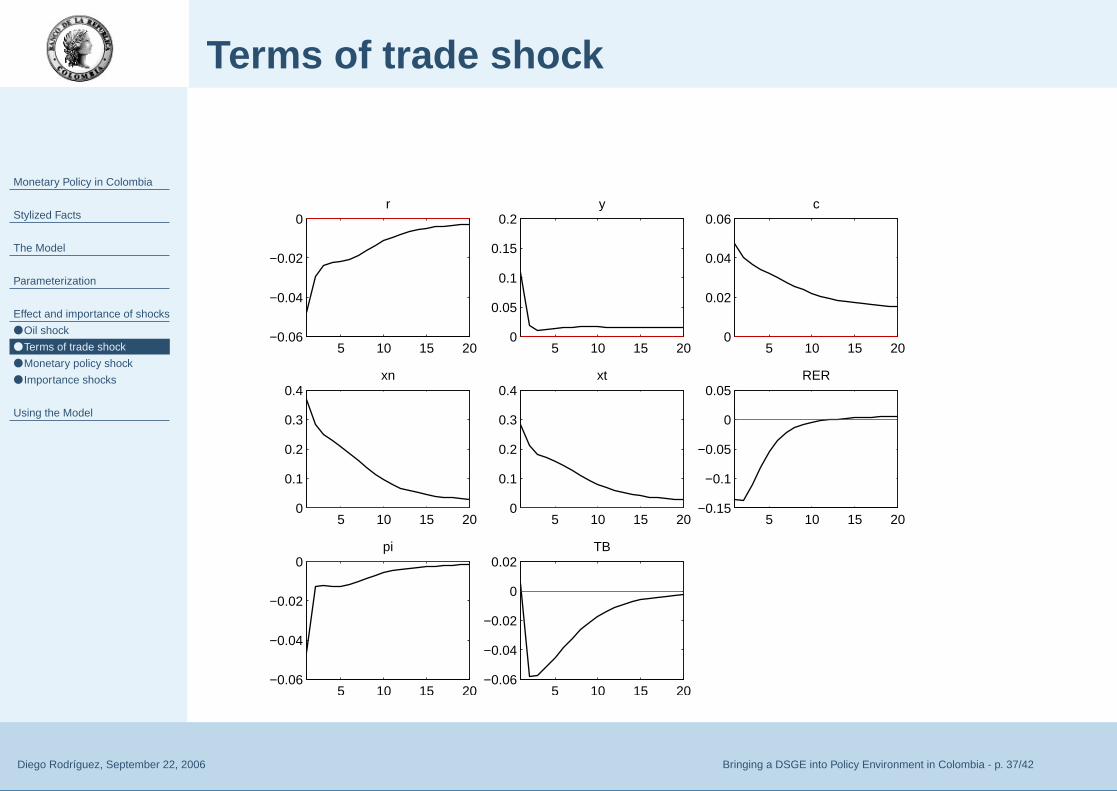

Terms of trade shock

5 10 15 20−0.06

−0.04

−0.02

0r

5 10 15 200

0.05

0.1

0.15

0.2y

5 10 15 200

0.02

0.04

0.06c

5 10 15 200

0.1

0.2

0.3

0.4xn

5 10 15 200

0.1

0.2

0.3

0.4xt

5 10 15 20−0.15

−0.1

−0.05

0

0.05RER

5 10 15 20−0.06

−0.04

−0.02

0pi

5 10 15 20−0.06

−0.04

−0.02

0

0.02TB

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

● Oil shock

● Terms of trade shock

● Monetary policy shock

● Importance shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 38/42

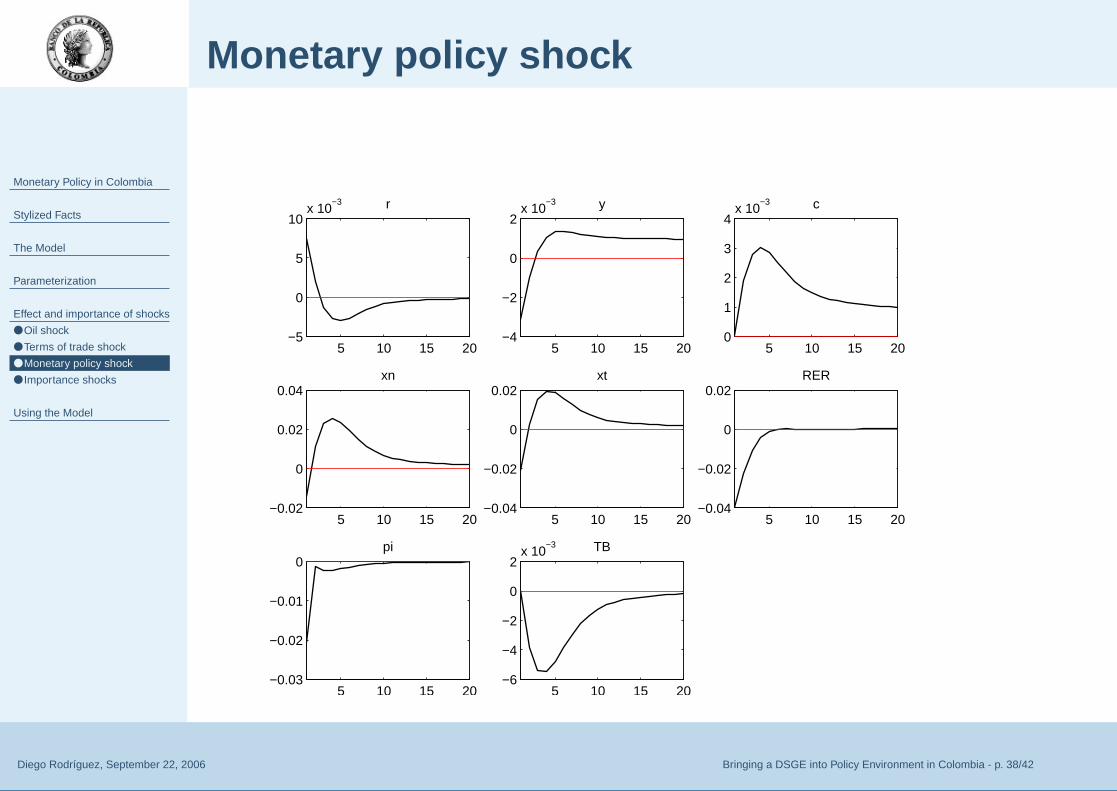

Monetary policy shock

5 10 15 20−5

0

5

10x 10

−3 r

5 10 15 20−4

−2

0

2x 10

−3 y

5 10 15 200

1

2

3

4x 10

−3 c

5 10 15 20−0.02

0

0.02

0.04xn

5 10 15 20−0.04

−0.02

0

0.02xt

5 10 15 20−0.04

−0.02

0

0.02RER

5 10 15 20−0.03

−0.02

−0.01

0pi

5 10 15 20−6

−4

−2

0

2x 10

−3 TB

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

● Oil shock

● Terms of trade shock

● Monetary policy shock

● Importance shocks

Using the Model

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 39/42

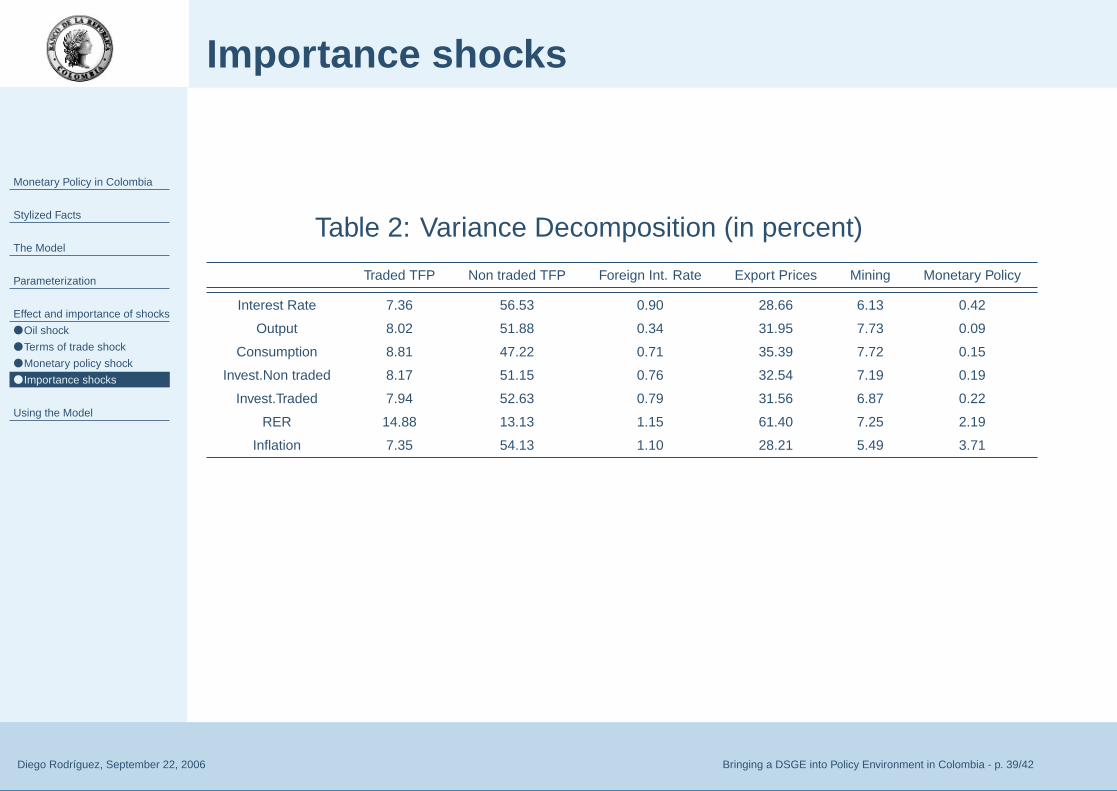

Importance shocks

Table 2: Variance Decomposition (in percent)

Traded TFP Non traded TFP Foreign Int. Rate Export Prices Mining Monetary Policy

Interest Rate 7.36 56.53 0.90 28.66 6.13 0.42

Output 8.02 51.88 0.34 31.95 7.73 0.09

Consumption 8.81 47.22 0.71 35.39 7.72 0.15

Invest.Non traded 8.17 51.15 0.76 32.54 7.19 0.19

Invest.Traded 7.94 52.63 0.79 31.56 6.87 0.22

RER 14.88 13.13 1.15 61.40 7.25 2.19

Inflation 7.35 54.13 1.10 28.21 5.49 3.71

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

● Forecasting Performance(1)

● Forecasting Performance (2)

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 40/42

Using the Model

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

● Forecasting Performance(1)

● Forecasting Performance (2)

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 41/42

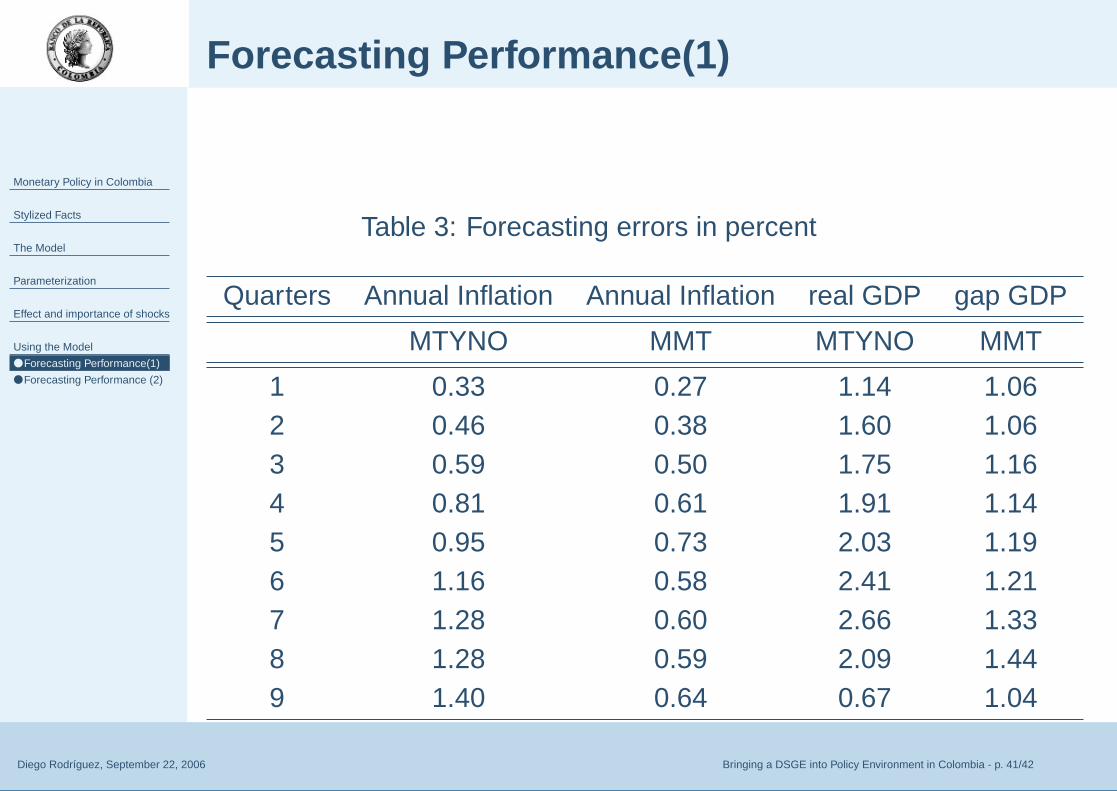

Forecasting Performance(1)

Table 3: Forecasting errors in percent

Quarters Annual Inflation Annual Inflation real GDP gap GDP

MTYNO MMT MTYNO MMT

1 0.33 0.27 1.14 1.062 0.46 0.38 1.60 1.063 0.59 0.50 1.75 1.164 0.81 0.61 1.91 1.145 0.95 0.73 2.03 1.196 1.16 0.58 2.41 1.217 1.28 0.60 2.66 1.338 1.28 0.59 2.09 1.449 1.40 0.64 0.67 1.04

Monetary Policy in Colombia

Stylized Facts

The Model

Parameterization

Effect and importance of shocks

Using the Model

● Forecasting Performance(1)

● Forecasting Performance (2)

Diego Rodríguez, September 22, 2006 Bringing a DSGE into Policy Environment in Colombia - p. 42/42

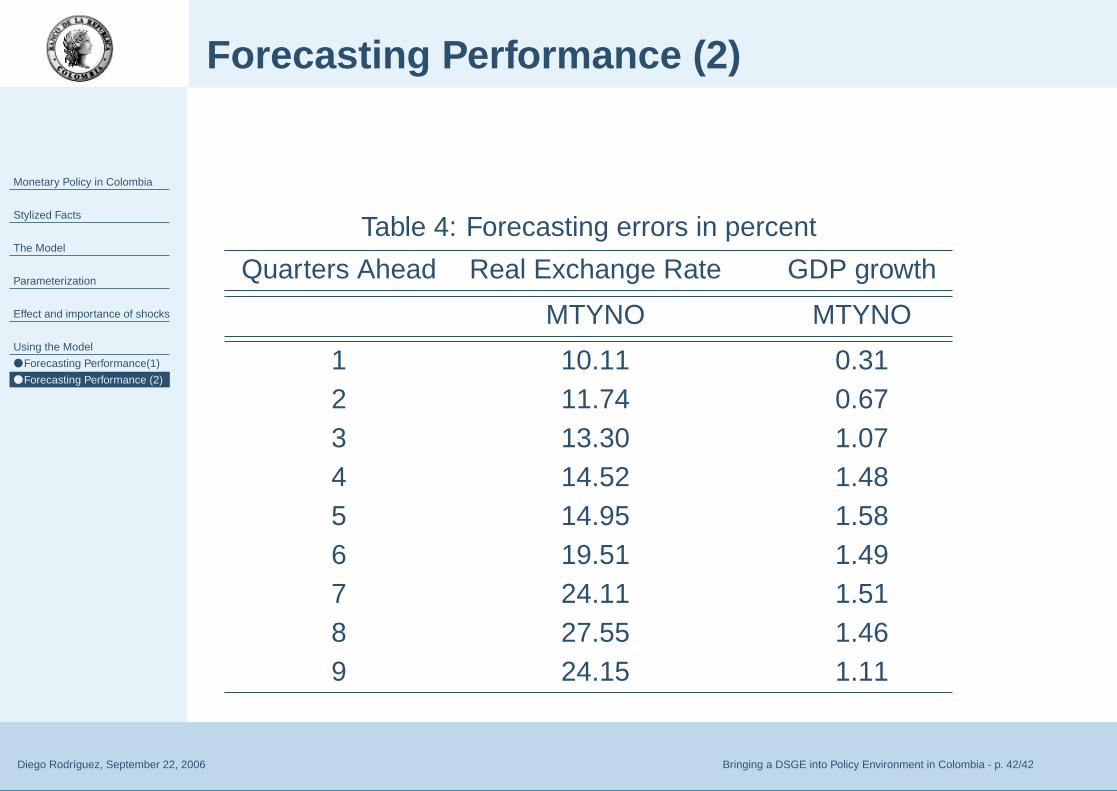

Forecasting Performance (2)

Table 4: Forecasting errors in percent

Quarters Ahead Real Exchange Rate GDP growth

MTYNO MTYNO

1 10.11 0.312 11.74 0.673 13.30 1.074 14.52 1.485 14.95 1.586 19.51 1.497 24.11 1.518 27.55 1.469 24.15 1.11