bloomberg briefs

TRANSCRIPT

June 25, 2015 Bloomberg Brief Economics 3

INSIDE

Global Growth. Low long rates may imply doldrums for living standards.Page 4

U.S. The economy is in transition and shifting toward domestic-led growth. Page 5

Secular Stagnation. There's a specter haunting dismal scientists.Page 6

Brazil. Latin America's biggest country needs productivity increases. Page 7

Canada. Low productivity and high household debt are constraints. Page 8

Euro Area. The competitiveness gap is wide, as labor costs have diverged.Page 9

Germany. A shrinking working-age population threatens growth potential. Page 10

Cost of heavy labor market France.regulation hinders the economy. Page 11

Spain. A stabilizing housing market and rising real income support growth.Page 12

Italy. Economic inefficiencies could cause the country to lag behind.Page 13

Reduced productivity could be U.K. the new norm.Page 14

. Ethiopia and Morocco are Africabuilding up their manufacturing hubs.Page 15

China. More can be done to hit long-term growth targets.Page 16

Demographic and fiscal Japan. challenges loom as growth rebounds.Page 17

Modi's reforms will increase India. the importance of manufacturing.Page 18

Second-half hopes are South Korea. pinned on overseas sales.Page 19

Southeast Asia. Which countries are most resilient to economic volatility?Page 20

Market Outlook. The impact on U.S. markets from ECB and BOJ easing.Page 21

STORYCHARTGlobal Growth in 2015 Held Back by Emerging Markets

Global growth will be divided in 2015 between developed countries, where systemic risks are on the wane, and the emerging markets, where many countries, especially oil exporters who did not build substantial reserves during the boom years, will contract or see slower growth.

Private sector economists are more optimistic than the IMF for a return to growth in the emerging markets in 2016. Find out more by launching the interactive chart.

— Deirdre Fretz, Bloomberg Brief Editor

StoryCharts are optimized for Chrome. If you have a different default browser, copy the link below and paste it in Chrome:

http://briefs.blpprofessional.com/viz/-Emerging-Markets-Projected-to-Hold-Back-Global-Growth-in-2015/index.html

GLOBAL OUTLOOK JAMIE MURRAY, BLOOMBERG INTELLIGENCE ECONOMIST

Brazil, Russia Exceptions to Global Recovery

Source: IMF's World Economic Outlook 2015

June 25, 2015 Bloomberg Brief Economics 4

GLOBAL OUTLOOK JAMIE MURRAY, BLOOMBERG INTELLIGENCE ECONOMIST

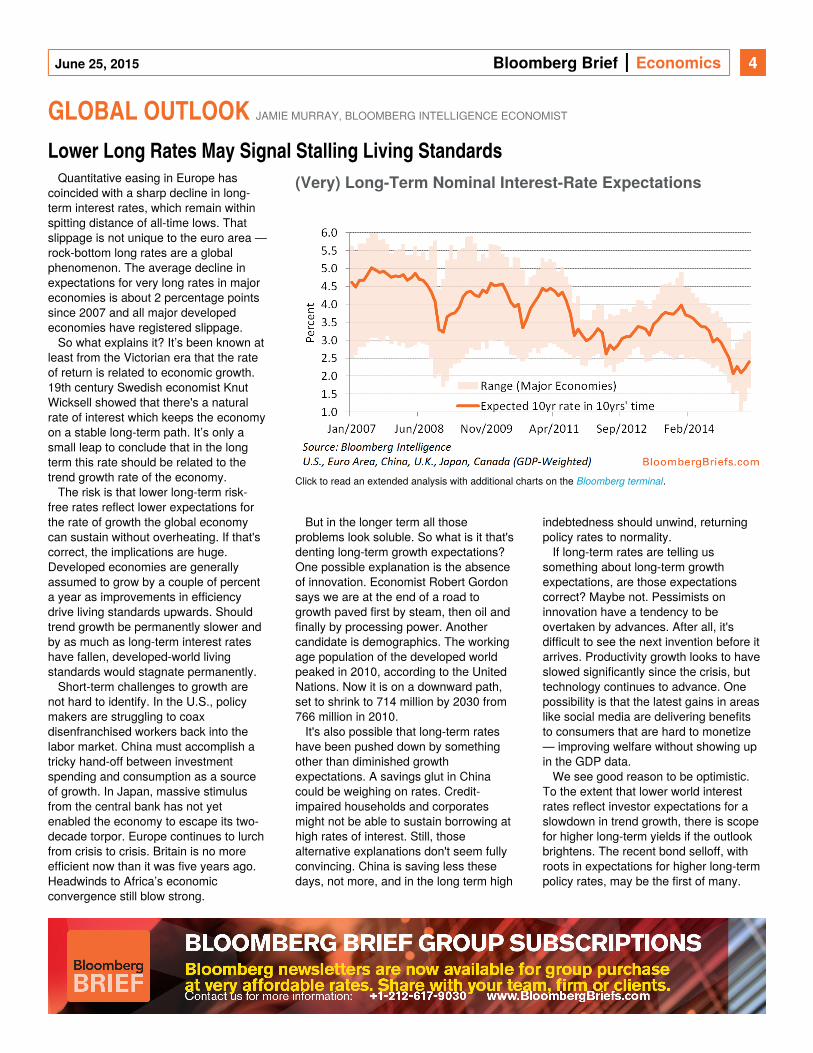

Lower Long Rates May Signal Stalling Living StandardsQuantitative easing in Europe has

coincided with a sharp decline in long-term interest rates, which remain within spitting distance of all-time lows. That slippage is not unique to the euro area — rock-bottom long rates are a global phenomenon. The average decline in expectations for very long rates in major economies is about 2 percentage points since 2007 and all major developed economies have registered slippage.

So what explains it? It’s been known at least from the Victorian era that the rate of return is related to economic growth. 19th century Swedish economist Knut Wicksell showed that there's a natural rate of interest which keeps the economy on a stable long-term path. It’s only a small leap to conclude that in the long term this rate should be related to the trend growth rate of the economy.

The risk is that lower long-term risk-free rates reflect lower expectations for the rate of growth the global economy can sustain without overheating. If that's correct, the implications are huge. Developed economies are generally assumed to grow by a couple of percent a year as improvements in efficiency drive living standards upwards. Should trend growth be permanently slower and by as much as long-term interest rates have fallen, developed-world living standards would stagnate permanently.

Short-term challenges to growth are not hard to identify. In the U.S., policy makers are struggling to coax disenfranchised workers back into the labor market. China must accomplish a tricky hand-off between investment spending and consumption as a source of growth. In Japan, massive stimulus from the central bank has not yet enabled the economy to escape its two-decade torpor. Europe continues to lurch from crisis to crisis. Britain is no more efficient now than it was five years ago. Headwinds to Africa’s economic convergence still blow strong.

Click to read an extended analysis with additional charts on the .Bloomberg terminal

But in the longer term all those problems look soluble. So what is it that's denting long-term growth expectations? One possible explanation is the absence of innovation. Economist Robert Gordon says we are at the end of a road to growth paved first by steam, then oil and finally by processing power. Another candidate is demographics. The working age population of the developed world peaked in 2010, according to the United Nations. Now it is on a downward path, set to shrink to 714 million by 2030 from 766 million in 2010.

It's also possible that long-term rates have been pushed down by something other than diminished growth expectations. A savings glut in China could be weighing on rates. Credit-impaired households and corporates might not be able to sustain borrowing at high rates of interest. Still, those alternative explanations don't seem fully convincing. China is saving less these days, not more, and in the long term high

indebtedness should unwind, returning policy rates to normality.

If long-term rates are telling us something about long-term growth expectations, are those expectations correct? Maybe not. Pessimists on innovation have a tendency to be overtaken by advances. After all, it's difficult to see the next invention before it arrives. Productivity growth looks to have slowed significantly since the crisis, but technology continues to advance. One possibility is that the latest gains in areas like social media are delivering benefits to consumers that are hard to monetize — improving welfare without showing up in the GDP data.

We see good reason to be optimistic. To the extent that lower world interest rates reflect investor expectations for a slowdown in trend growth, there is scope for higher long-term yields if the outlook brightens. The recent bond selloff, with roots in expectations for higher long-term policy rates, may be the first of many.

U.S. CARL RICCADONNA, BLOOMBERG INTELLIGENCE ECONOMIST

(Very) Long-Term Nominal Interest-Rate Expectations

June 25, 2015 Bloomberg Brief Economics 5

U.S. CARL RICCADONNA, BLOOMBERG INTELLIGENCE ECONOMIST

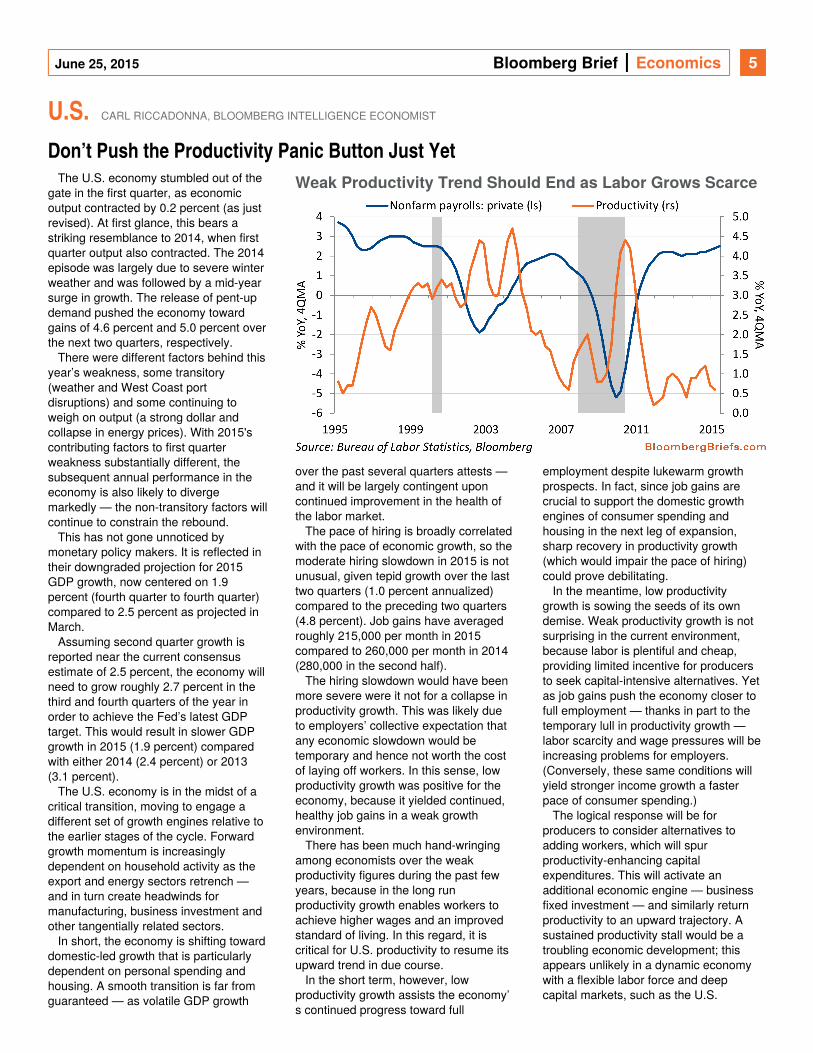

Don’t Push the Productivity Panic Button Just YetThe U.S. economy stumbled out of the

gate in the first quarter, as economic output contracted by 0.2 percent (as just revised). At first glance, this bears a striking resemblance to 2014, when first quarter output also contracted. The 2014 episode was largely due to severe winter weather and was followed by a mid-year surge in growth. The release of pent-up demand pushed the economy toward gains of 4.6 percent and 5.0 percent over the next two quarters, respectively.

There were different factors behind this year’s weakness, some transitory (weather and West Coast port disruptions) and some continuing to weigh on output (a strong dollar and collapse in energy prices). With 2015's contributing factors to first quarter weakness substantially different, the subsequent annual performance in the economy is also likely to diverge markedly — the non-transitory factors will continue to constrain the rebound.

This has not gone unnoticed by monetary policy makers. It is reflected in their downgraded projection for 2015 GDP growth, now centered on 1.9 percent (fourth quarter to fourth quarter) compared to 2.5 percent as projected in March.

Assuming second quarter growth is reported near the current consensus estimate of 2.5 percent, the economy will need to grow roughly 2.7 percent in the third and fourth quarters of the year in order to achieve the Fed’s latest GDP target. This would result in slower GDP growth in 2015 (1.9 percent) compared with either 2014 (2.4 percent) or 2013 (3.1 percent).

The U.S. economy is in the midst of a critical transition, moving to engage a different set of growth engines relative to the earlier stages of the cycle. Forward growth momentum is increasingly dependent on household activity as the export and energy sectors retrench — and in turn create headwinds for manufacturing, business investment and other tangentially related sectors.

In short, the economy is shifting toward domestic-led growth that is particularly dependent on personal spending and housing. A smooth transition is far from guaranteed — as volatile GDP growth

over the past several quarters attests — and it will be largely contingent upon continued improvement in the health of the labor market.

The pace of hiring is broadly correlated with the pace of economic growth, so the moderate hiring slowdown in 2015 is not unusual, given tepid growth over the last two quarters (1.0 percent annualized) compared to the preceding two quarters (4.8 percent). Job gains have averaged roughly 215,000 per month in 2015 compared to 260,000 per month in 2014 (280,000 in the second half).

The hiring slowdown would have been more severe were it not for a collapse in productivity growth. This was likely due to employers’ collective expectation that any economic slowdown would be temporary and hence not worth the cost of laying off workers. In this sense, low productivity growth was positive for the economy, because it yielded continued, healthy job gains in a weak growth environment.

There has been much hand-wringing among economists over the weak productivity figures during the past few years, because in the long run productivity growth enables workers to achieve higher wages and an improved standard of living. In this regard, it is critical for U.S. productivity to resume its upward trend in due course.

In the short term, however, low productivity growth assists the economy’s continued progress toward full

employment despite lukewarm growth prospects. In fact, since job gains are crucial to support the domestic growth engines of consumer spending and housing in the next leg of expansion, sharp recovery in productivity growth (which would impair the pace of hiring) could prove debilitating.

In the meantime, low productivity growth is sowing the seeds of its own demise. Weak productivity growth is not surprising in the current environment, because labor is plentiful and cheap, providing limited incentive for producers to seek capital-intensive alternatives. Yet as job gains push the economy closer to full employment — thanks in part to the temporary lull in productivity growth — labor scarcity and wage pressures will be increasing problems for employers. (Conversely, these same conditions will yield stronger income growth a faster pace of consumer spending.)

The logical response will be for producers to consider alternatives to adding workers, which will spur productivity-enhancing capital expenditures. This will activate an additional economic engine — business fixed investment — and similarly return productivity to an upward trajectory. A sustained productivity stall would be a troubling economic development; this appears unlikely in a dynamic economy with a flexible labor force and deep capital markets, such as the U.S.

QUICKTAKE CLIVE CROOK, BLOOMBERG VIEW

Weak Productivity Trend Should End as Labor Grows Scarce

June 25, 2015 Bloomberg Brief Economics 6

QUICKTAKE CLIVE CROOK, BLOOMBERG VIEW

Secular Stagnation Now Means 'Nightmare' in EconomeseA specter is haunting dismal scientists,

an economic nightmare with an ugly name. It’s secular stagnation, the proposition that the slow growth plaguing developed economies may be permanent. If true, it means busts won’t turn to booms, tried and true growth policies won’t work, lost jobs won’t be regained. And here’s the really scary part: Future economic expansion may be inseparable from the reckless financial practices that caused the problem in the first place.

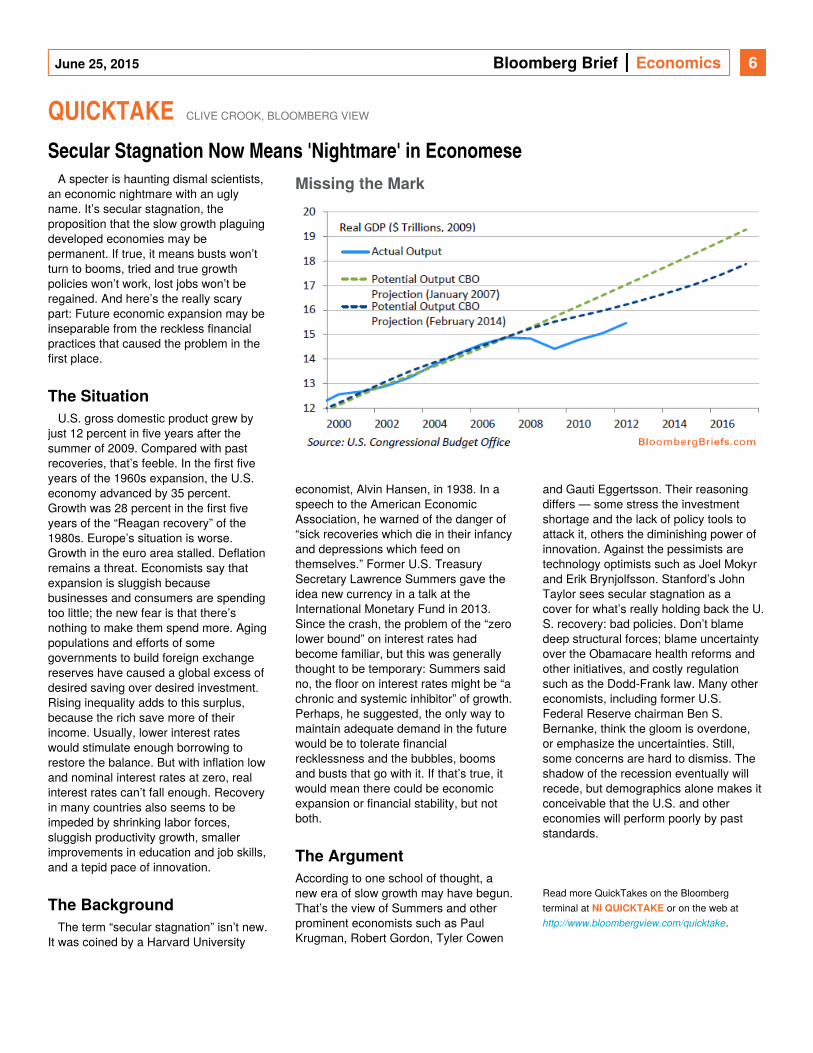

U.S. gross domestic product grew by just 12 percent in five years after the summer of 2009. Compared with past recoveries, that’s feeble. In the first five years of the 1960s expansion, the U.S. economy advanced by 35 percent. Growth was 28 percent in the first five years of the “Reagan recovery” of the 1980s. Europe’s situation is worse. Growth in the euro area stalled. Deflation remains a threat. Economists say that expansion is sluggish because businesses and consumers are spending too little; the new fear is that there’s nothing to make them spend more. Aging populations and efforts of some governments to build foreign exchange reserves have caused a global excess of desired saving over desired investment. Rising inequality adds to this surplus, because the rich save more of their income. Usually, lower interest rates would stimulate enough borrowing to restore the balance. But with inflation low and nominal interest rates at zero, real interest rates can’t fall enough. Recovery in many countries also seems to be impeded by shrinking labor forces, sluggish productivity growth, smaller improvements in education and job skills, and a tepid pace of innovation.

The term “secular stagnation” isn’t new. It was coined by a Harvard University

The Situation

The Background

economist, Alvin Hansen, in 1938. In aspeech to the American Economic Association, he warned of the danger of “sick recoveries which die in their infancy and depressions which feed on themselves.” Former U.S. Treasury Secretary Lawrence Summers gave the idea new currency in a talk at the International Monetary Fund in 2013. Since the crash, the problem of the “zero lower bound” on interest rates had become familiar, but this was generally thought to be temporary: Summers said no, the floor on interest rates might be “a chronic and systemic inhibitor” of growth. Perhaps, he suggested, the only way to maintain adequate demand in the future would be to tolerate financial recklessness and the bubbles, booms and busts that go with it. If that’s true, it would mean there could be economic expansion or financial stability, but not both.

According to one school of thought, a new era of slow growth may have begun. That’s the view of Summers and other prominent economists such as Paul Krugman, Robert Gordon, Tyler Cowen

The Argument

and Gauti Eggertsson. Their reasoning differs — some stress the investmentshortage and the lack of policy tools to attack it, others the diminishing power of innovation. Against the pessimists are technology optimists such as Joel Mokyr and Erik Brynjolfsson. Stanford’s John Taylor sees secular stagnation as a cover for what’s really holding back the U.S. recovery: bad policies. Don’t blame deep structural forces; blame uncertainty over the Obamacare health reforms and other initiatives, and costly regulation such as the Dodd-Frank law. Many other economists, including former U.S. Federal Reserve chairman Ben S. Bernanke, think the gloom is overdone, or emphasize the uncertainties. Still, some concerns are hard to dismiss. The shadow of the recession eventually will recede, but demographics alone makes it conceivable that the U.S. and other economies will perform poorly by past standards.

Read more QuickTakes on the Bloomberg

terminal at or on the web at NI QUICKTAKE

.http://www.bloombergview.com/quicktake

BRAZIL MICHAEL MCDONOUGH, BLOOMBERG INTELLIGENCE ECONOMIST

Missing the Mark

June 25, 2015 Bloomberg Brief Economics 7

BRAZIL MICHAEL MCDONOUGH, BLOOMBERG INTELLIGENCE ECONOMIST

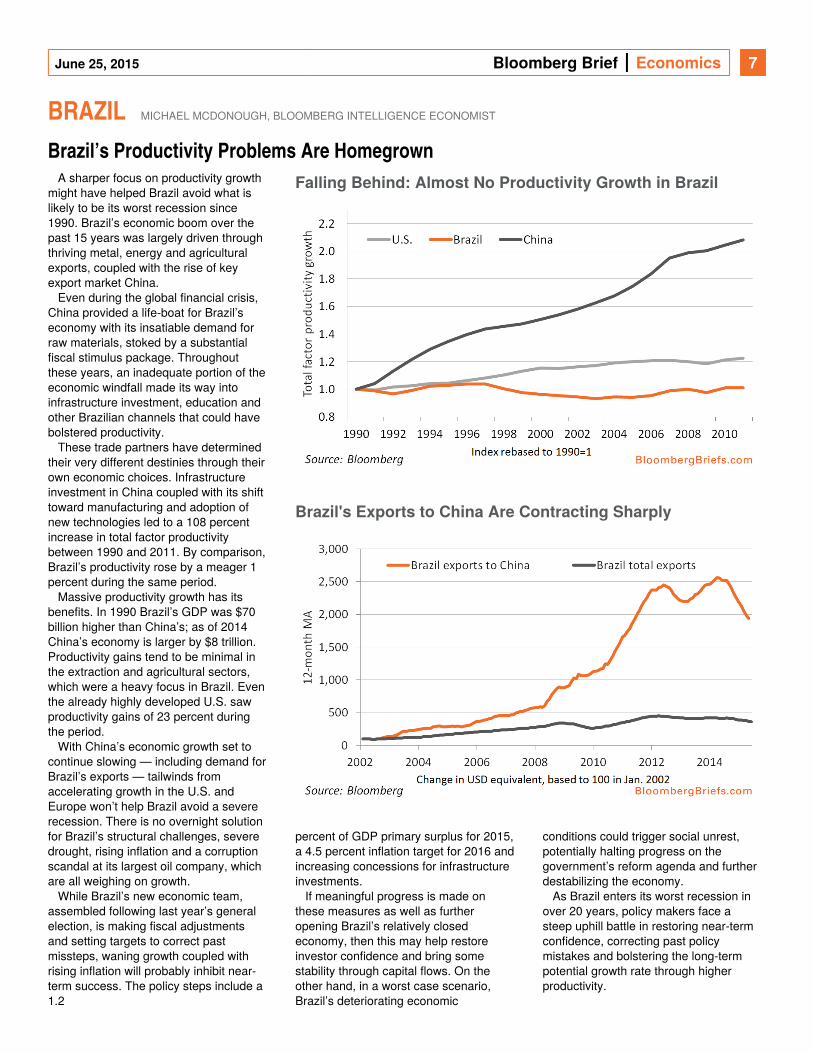

Brazil’s Productivity Problems Are HomegrownA sharper focus on productivity growth

might have helped Brazil avoid what is likely to be its worst recession since 1990. Brazil’s economic boom over the past 15 years was largely driven through thriving metal, energy and agricultural exports, coupled with the rise of key export market China.

Even during the global financial crisis, China provided a life-boat for Brazil’s economy with its insatiable demand for raw materials, stoked by a substantial fiscal stimulus package. Throughout these years, an inadequate portion of the economic windfall made its way into infrastructure investment, education and other Brazilian channels that could have bolstered productivity.

These trade partners have determined their very different destinies through their own economic choices. Infrastructure investment in China coupled with its shift toward manufacturing and adoption of new technologies led to a 108 percent increase in total factor productivity between 1990 and 2011. By comparison, Brazil’s productivity rose by a meager 1 percent during the same period.

Massive productivity growth has its benefits. In 1990 Brazil’s GDP was $70 billion higher than China’s; as of 2014 China’s economy is larger by $8 trillion. Productivity gains tend to be minimal in the extraction and agricultural sectors, which were a heavy focus in Brazil. Even the already highly developed U.S. saw productivity gains of 23 percent during the period.

With China’s economic growth set to continue slowing — including demand for Brazil’s exports — tailwinds from accelerating growth in the U.S. and Europe won’t help Brazil avoid a severe recession. There is no overnight solution for Brazil’s structural challenges, severe drought, rising inflation and a corruption scandal at its largest oil company, which are all weighing on growth.

While Brazil’s new economic team, assembled following last year’s general election, is making fiscal adjustments and setting targets to correct past missteps, waning growth coupled with rising inflation will probably inhibit near-term success. The policy steps include a 1.2

percent of GDP primary surplus for 2015, a 4.5 percent inflation target for 2016 and increasing concessions for infrastructure investments.

If meaningful progress is made on these measures as well as further opening Brazil’s relatively closed economy, then this may help restore investor confidence and bring some stability through capital flows. On the other hand, in a worst case scenario, Brazil’s deteriorating economic

conditions could trigger social unrest, potentially halting progress on the government’s reform agenda and further destabilizing the economy.

As Brazil enters its worst recession in over 20 years, policy makers face a steep uphill battle in restoring near-term confidence, correcting past policy mistakes and bolstering the long-term potential growth rate through higher productivity.

CANADA RICHARD YAMARONE, BLOOMBERG INTELLIGENCE ECONOMIST

Falling Behind: Almost No Productivity Growth in Brazil

Brazil's Exports to China Are Contracting Sharply

June 25, 2015 Bloomberg Brief Economics 8

CANADA RICHARD YAMARONE, BLOOMBERG INTELLIGENCE ECONOMIST

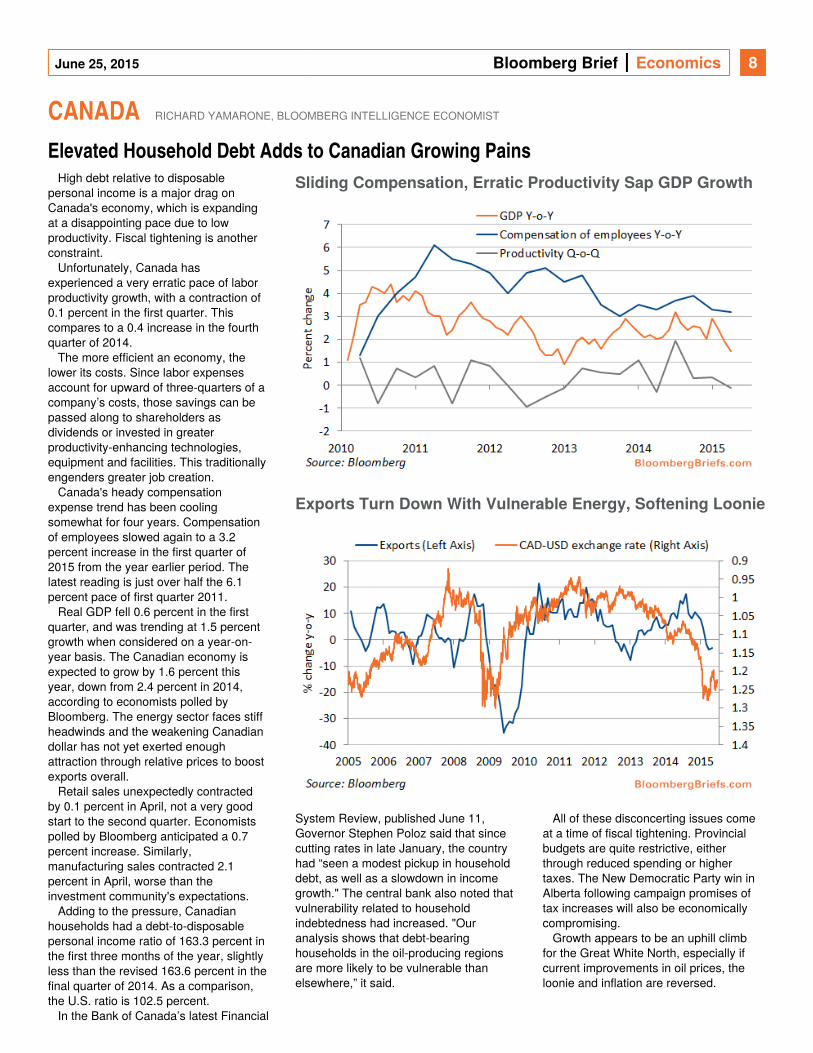

Elevated Household Debt Adds to Canadian Growing PainsHigh debt relative to disposable

personal income is a major drag on Canada's economy, which is expanding at a disappointing pace due to low productivity. Fiscal tightening is another constraint.

Unfortunately, Canada has experienced a very erratic pace of labor productivity growth, with a contraction of 0.1 percent in the first quarter. This compares to a 0.4 increase in the fourth quarter of 2014.

The more efficient an economy, the lower its costs. Since labor expenses account for upward of three-quarters of a company’s costs, those savings can be passed along to shareholders as dividends or invested in greater productivity-enhancing technologies, equipment and facilities. This traditionally engenders greater job creation.

Canada's heady compensation expense trend has been cooling somewhat for four years. Compensation of employees slowed again to a 3.2 percent increase in the first quarter of 2015 from the year earlier period. The latest reading is just over half the 6.1 percent pace of first quarter 2011.

Real GDP fell 0.6 percent in the first quarter, and was trending at 1.5 percent growth when considered on a year-on-year basis. The Canadian economy is expected to grow by 1.6 percent this year, down from 2.4 percent in 2014, according to economists polled by Bloomberg. The energy sector faces stiff headwinds and the weakening Canadian dollar has not yet exerted enough attraction through relative prices to boost exports overall.

Retail sales unexpectedly contracted by 0.1 percent in April, not a very good start to the second quarter. Economists polled by Bloomberg anticipated a 0.7 percent increase. Similarly, manufacturing sales contracted 2.1 percent in April, worse than the investment community's expectations.

Adding to the pressure, Canadian households had a debt-to-disposable personal income ratio of 163.3 percent in the first three months of the year, slightly less than the revised 163.6 percent in the final quarter of 2014. As a comparison, the U.S. ratio is 102.5 percent.

In the Bank of Canada’s latest Financial

System Review, published June 11,Governor Stephen Poloz said that since cutting rates in late January, the country had “seen a modest pickup in household debt, as well as a slowdown in income growth." The central bank also noted that vulnerability related to household indebtedness had increased. "Our analysis shows that debt-bearing

households in the oil-producing regions are more likely to be vulnerable than

elsewhere,” it said.

All of these disconcerting issues come at a time of fiscal tightening. Provincial budgets are quite restrictive, either through reduced spending or higher taxes. The New Democratic Party win in Alberta following campaign promises of tax increases will also be economically compromising.

Growth appears to be an uphill climb for the Great White North, especially if current improvements in oil prices, the loonie and inflation are reversed.

EURO AREA JAMIE MURRAY AND MAXIME SBAIHI, BLOOMBERG INTELLIGENCE ECONOMISTS

Sliding Compensation, Erratic Productivity Sap GDP Growth

Exports Turn Down With Vulnerable Energy, Softening Loonie

June 25, 2015 Bloomberg Brief Economics 9

EURO AREA JAMIE MURRAY AND MAXIME SBAIHI, BLOOMBERG INTELLIGENCE ECONOMISTS

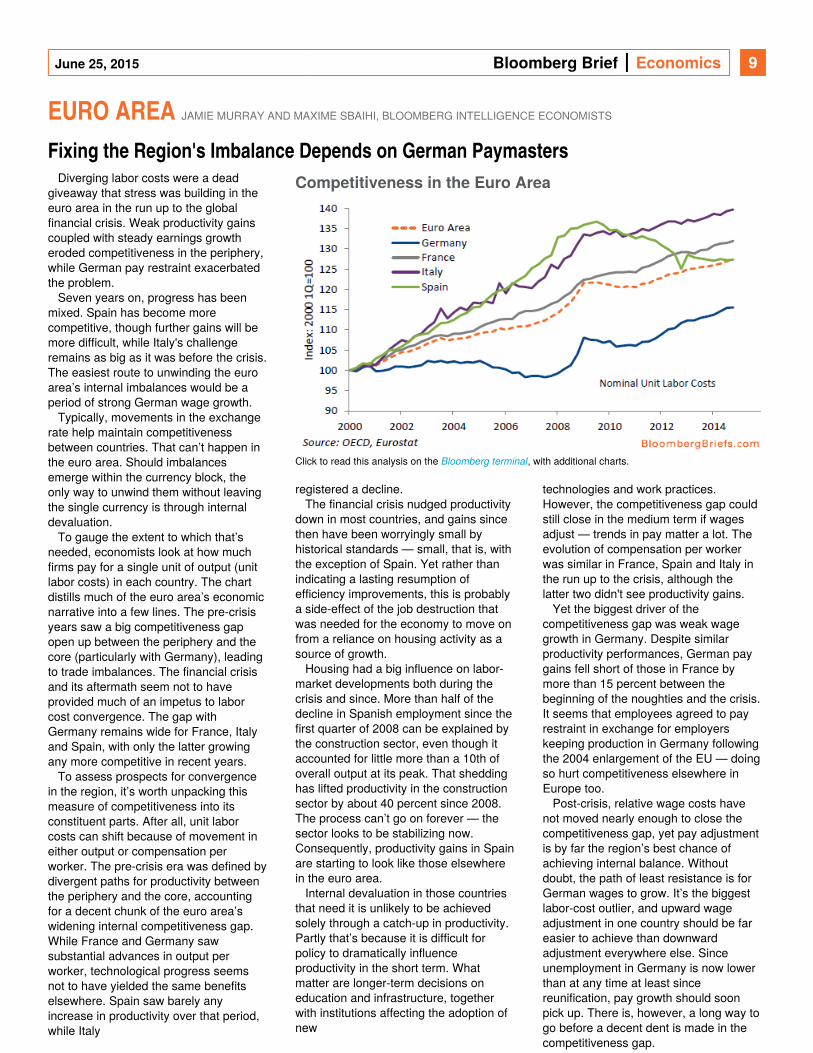

Fixing the Region's Imbalance Depends on German PaymastersDiverging labor costs were a dead

giveaway that stress was building in the euro area in the run up to the global financial crisis. Weak productivity gains coupled with steady earnings growth eroded competitiveness in the periphery, while German pay restraint exacerbated the problem.

Seven years on, progress has been mixed. Spain has become more competitive, though further gains will be more difficult, while Italy's challenge remains as big as it was before the crisis. The easiest route to unwinding the euro area’s internal imbalances would be a period of strong German wage growth.

Typically, movements in the exchange rate help maintain competitiveness between countries. That can’t happen in the euro area. Should imbalances emerge within the currency block, the only way to unwind them without leaving the single currency is through internal devaluation.

To gauge the extent to which that’s needed, economists look at how much firms pay for a single unit of output (unit labor costs) in each country. The chart distills much of the euro area’s economic narrative into a few lines. The pre-crisis years saw a big competitiveness gap open up between the periphery and the core (particularly with Germany), leading to trade imbalances. The financial crisis and its aftermath seem not to have provided much of an impetus to labor cost convergence. The gap with Germany remains wide for France, Italy and Spain, with only the latter growing any more competitive in recent years.

To assess prospects for convergence in the region, it’s worth unpacking this measure of competitiveness into its constituent parts. After all, unit labor costs can shift because of movement in either output or compensation per worker. The pre-crisis era was defined by divergent paths for productivity between the periphery and the core, accounting for a decent chunk of the euro area’s widening internal competitiveness gap. While France and Germany saw substantial advances in output per worker, technological progress seems not to have yielded the same benefits elsewhere. Spain saw barely any increase in productivity over that period, while Italy

Click to read this analysis on the , with additional charts. Bloomberg terminal

registered a decline.The financial crisis nudged productivity

down in most countries, and gains since then have been worryingly small by historical standards — small, that is, with the exception of Spain. Yet rather than indicating a lasting resumption of efficiency improvements, this is probably a side-effect of the job destruction that was needed for the economy to move on from a reliance on housing activity as a source of growth.

Housing had a big influence on labor-market developments both during the crisis and since. More than half of the decline in Spanish employment since the first quarter of 2008 can be explained by the construction sector, even though it accounted for little more than a 10th of overall output at its peak. That shedding has lifted productivity in the construction sector by about 40 percent since 2008. The process can’t go on forever — the sector looks to be stabilizing now. Consequently, productivity gains in Spain are starting to look like those elsewhere in the euro area.

Internal devaluation in those countries that need it is unlikely to be achieved solely through a catch-up in productivity. Partly that’s because it is difficult forpolicy to dramatically influence productivity in the short term. What matter are longer-term decisions on education and infrastructure, together with institutions affecting the adoption of new

technologies and work practices. However, the competitiveness gap could still close in the medium term if wages adjust — trends in pay matter a lot. The evolution of compensation per worker was similar in France, Spain and Italy in the run up to the crisis, although the latter two didn't see productivity gains.

Yet the biggest driver of the competitiveness gap was weak wage growth in Germany. Despite similar productivity performances, German pay gains fell short of those in France by more than 15 percent between the beginning of the noughties and the crisis. It seems that employees agreed to pay restraint in exchange for employers keeping production in Germany following the 2004 enlargement of the EU — doing so hurt competitiveness elsewhere in Europe too.

Post-crisis, relative wage costs have not moved nearly enough to close the competitiveness gap, yet pay adjustment is by far the region’s best chance of achieving internal balance. Without doubt, the path of least resistance is for German wages to grow. It’s the biggest labor-cost outlier, and upward wage adjustment in one country should be far easier to achieve than downward adjustment everywhere else. Since unemployment in Germany is now lower than at any time at least since reunification, pay growth should soon pick up. There is, however, a long way to go before a decent dent is made in the competitiveness gap.

GERMANY DAVID POWELL, BLOOMBERG INTELLIGENCE ECONOMIST

Competitiveness in the Euro Area

June 25, 2015 Bloomberg Brief Economics 10

GERMANY DAVID POWELL, BLOOMBERG INTELLIGENCE ECONOMIST

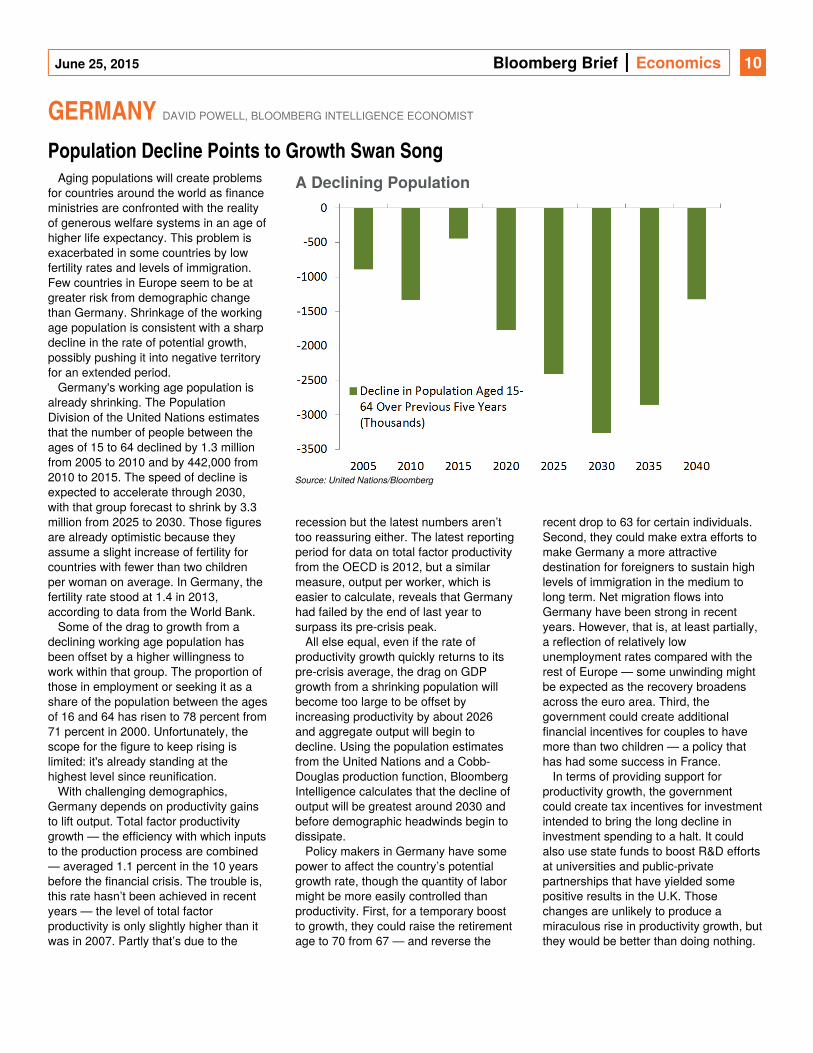

Population Decline Points to Growth Swan SongAging populations will create problems

for countries around the world as finance ministries are confronted with the reality of generous welfare systems in an age of higher life expectancy. This problem is exacerbated in some countries by low fertility rates and levels of immigration. Few countries in Europe seem to be at greater risk from demographic change than Germany. Shrinkage of the working age population is consistent with a sharp decline in the rate of potential growth, possibly pushing it into negative territory for an extended period.

Germany's working age population is already shrinking. The Population Division of the United Nations estimates that the number of people between the ages of 15 to 64 declined by 1.3 million from 2005 to 2010 and by 442,000 from 2010 to 2015. The speed of decline is expected to accelerate through 2030, with that group forecast to shrink by 3.3 million from 2025 to 2030. Those figures are already optimistic because they assume a slight increase of fertility for countries with fewer than two children per woman on average. In Germany, the fertility rate stood at 1.4 in 2013, according to data from the World Bank.

Some of the drag to growth from a declining working age population has been offset by a higher willingness to work within that group. The proportion of those in employment or seeking it as a share of the population between the ages of 16 and 64 has risen to 78 percent from 71 percent in 2000. Unfortunately, the scope for the figure to keep rising is limited: it's already standing at the highest level since reunification.

With challenging demographics, Germany depends on productivity gains to lift output. Total factor productivity growth — the efficiency with which inputs to the production process are combined — averaged 1.1 percent in the 10 years before the financial crisis. The trouble is, this rate hasn’t been achieved in recent years — the level of total factor productivity is only slightly higher than it was in 2007. Partly that’s due to the

recession but the latest numbers aren’t too reassuring either. The latest reporting period for data on total factor productivity from the OECD is 2012, but a similar measure, output per worker, which is easier to calculate, reveals that Germany had failed by the end of last year to surpass its pre-crisis peak.

All else equal, even if the rate of productivity growth quickly returns to its pre-crisis average, the drag on GDP growth from a shrinking population will become too large to be offset by increasing productivity by about 2026 and aggregate output will begin to decline. Using the population estimates

from the United Nations and a Cobb-Douglas production function, Bloomberg

Intelligence calculates that the decline of output will be greatest around 2030 and before demographic headwinds begin to

dissipate.Policy makers in Germany have some

power to affect the country’s potential growth rate, though the quantity of labor might be more easily controlled than productivity. First, for a temporary boost to growth, they could raise the retirement age to 70 from 67 — and reverse the

recent drop to 63 for certain individuals. Second, they could make extra efforts to make Germany a more attractive destination for foreigners to sustain high levels of immigration in the medium to long term. Net migration flows into Germany have been strong in recent years. However, that is, at least partially, a reflection of relatively low unemployment rates compared with the rest of Europe — some unwinding might be expected as the recovery broadens across the euro area. Third, the government could create additional financial incentives for couples to have more than two children — a policy that has had some success in France.

In terms of providing support for productivity growth, the government could create tax incentives for investment intended to bring the long decline in investment spending to a halt. It could also use state funds to boost R&D efforts at universities and public-private partnerships that have yielded some positive results in the U.K. Those changes are unlikely to produce a miraculous rise in productivity growth, but they would be better than doing nothing.

FRANCE MAXIME SBAIHI, BLOOMBERG INTELLIGENCE ECONOMIST

A Declining Population

Source: United Nations/Bloomberg

June 25, 2015 Bloomberg Brief Economics 11

FRANCE MAXIME SBAIHI, BLOOMBERG INTELLIGENCE ECONOMIST

France's Labor Market Impedes One of Its Greatest AssetsFrance is benefiting from a cyclical

recovery, masking deeper structural problems. The overregulation and dismal state of the labor market reflect some of the obstacles standing in the way of better long-term growth prospects. Removing these would allow the country to make the most of one of its greatest strengths for the future: demographics.

Like its euro peers, the French economy is benefiting in 2015 from a cyclical upturn due to lower oil prices and euro levels as well as additional monetary stimulus. Yet so far the recovery has remained jobless. The mainland unemployment rate — calculated by the national statistics office for the International Labour Organization — was 10 percent in the first quarter of the year. That's only 0.1 percentage point down from the 16-year high reached at the end of last year.

High unemployment has established itself as a French tradition. Since 1984, the unemployment rate has fallen below 7 percent only once: during the first quarter of 2008. The youth unemployment rate (calculated for 15-to-24 year-olds) has been above 15 percent since 1990 and continued to rise during the first three months of this year, to stand at 24.1 percent.

The participation rate among 15-to-24 year olds in 2013 remained well below levels seen in Germany and the average of the members of the Organization for Economic Co-operation and Development. That is also true — albeit to a lesser extent — for the overall participation rate.

The structurally high unemployment rate and low participation rate in France reflect a labor market split in two. While outsiders struggle with unemployment or precarious forms of work contracts, insiders often enjoy well-paid, open ended contracts protected by a 3000 page labor code which makes dismissal procedures costly and lengthy. In 2012, these procedures in court lasted 15

Click to view this analysis with more charts on the .Bloomberg terminal

months on average, a recent study by the French Treasury shows. The rigidity discourages employers from hiring while the elevated rate of unemployment probably deters people from entering the labor market. It is also a burden for the French economy since businesses can't adjust their workforce as they please to react to the variations of the economic cycle.

Yet France's problem is chiefly one of work quantity rather than efficiency. Like many other developed economies, productivity has grown only very slowly in France since the financial crisis yet it started from a good position, having posted strong gains in the preceding decade or so. By contrast, France is among the worst OECD members in terms of annual hours worked, with a 2013 average per worker of 1489, compared with 1770 for the OECD as a whole.

There's a lot of vague talk about the need for structural reforms in France but little by way of concrete proposals. A relaxation of the nationwide law enforcing

a 35-hour working week or of the protection of open-ended contracts could, among other ideas, allow insiders to work more hours while giving outsiders a better chance of getting a job. Changing the structure of the labor market to get more people into work should be a priority if France wants to make the most of its demographics, one of its greatest assets for the future.

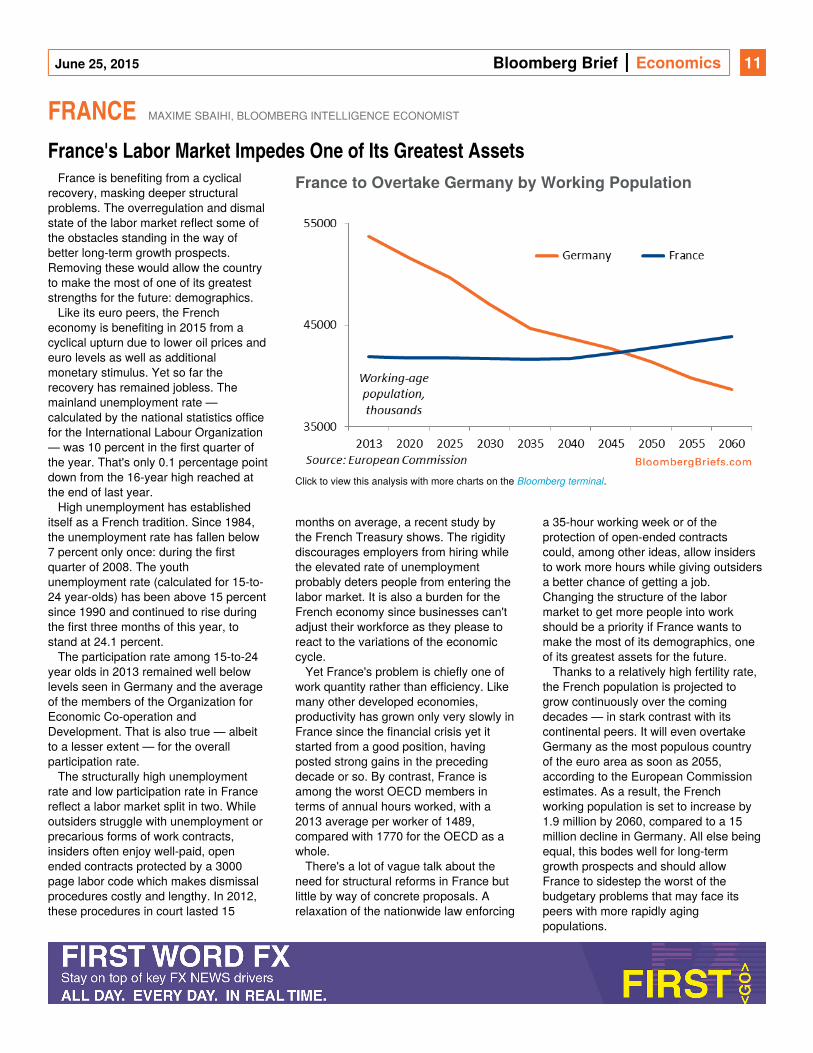

Thanks to a relatively high fertility rate, the French population is projected to grow continuously over the coming decades — in stark contrast with its continental peers. It will even overtake Germany as the most populous country of the euro area as soon as 2055, according to the European Commission estimates. As a result, the French working population is set to increase by 1.9 million by 2060, compared to a 15 million decline in Germany. All else being equal, this bodes well for long-term growth prospects and should allow France to sidestep the worst of the budgetary problems that may face its peers with more rapidly aging populations.

SPAIN DAVID POWELL, BLOOMBERG INTELLIGENCE ECONOMIST

France to Overtake Germany by Working Population

June 25, 2015 Bloomberg Brief Economics 12

SPAIN DAVID POWELL, BLOOMBERG INTELLIGENCE ECONOMIST

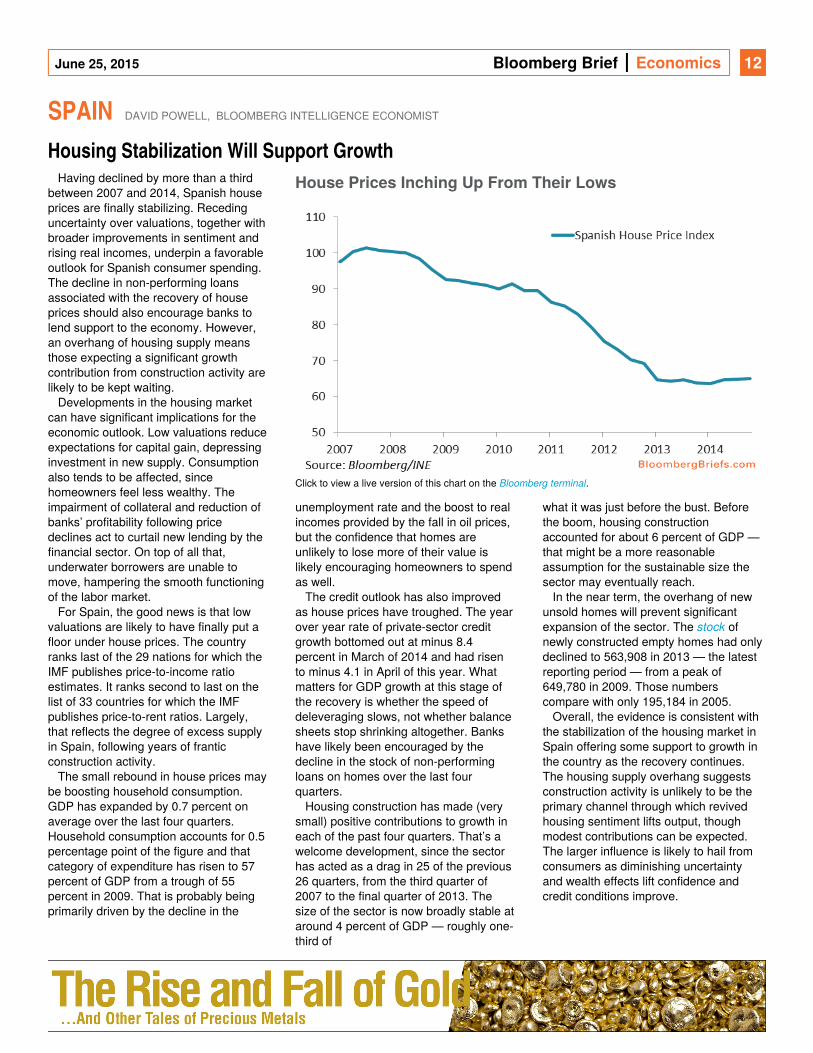

Housing Stabilization Will Support GrowthHaving declined by more than a third

between 2007 and 2014, Spanish house prices are finally stabilizing. Receding uncertainty over valuations, together with broader improvements in sentiment and rising real incomes, underpin a favorable outlook for Spanish consumer spending. The decline in non-performing loans associated with the recovery of house prices should also encourage banks to lend support to the economy. However, an overhang of housing supply means those expecting a significant growth contribution from construction activity are likely to be kept waiting.

Developments in the housing market can have significant implications for the economic outlook. Low valuations reduce expectations for capital gain, depressing investment in new supply. Consumption also tends to be affected, since homeowners feel less wealthy. The impairment of collateral and reduction of banks’ profitability following price declines act to curtail new lending by the financial sector. On top of all that, underwater borrowers are unable to move, hampering the smooth functioning of the labor market.

For Spain, the good news is that low valuations are likely to have finally put a floor under house prices. The country ranks last of the 29 nations for which the IMF publishes price-to-income ratio estimates. It ranks second to last on the list of 33 countries for which the IMF publishes price-to-rent ratios. Largely, that reflects the degree of excess supply in Spain, following years of frantic construction activity.

The small rebound in house prices may be boosting household consumption. GDP has expanded by 0.7 percent on average over the last four quarters. Household consumption accounts for 0.5 percentage point of the figure and that category of expenditure has risen to 57 percent of GDP from a trough of 55 percent in 2009. That is probably being primarily driven by the decline in the

Click to view a live version of this chart on the .Bloomberg terminal

unemployment rate and the boost to real incomes provided by the fall in oil prices, but the confidence that homes are unlikely to lose more of their value is likely encouraging homeowners to spend as well.

The credit outlook has also improved as house prices have troughed. The year over year rate of private-sector credit growth bottomed out at minus 8.4 percent in March of 2014 and had risen to minus 4.1 in April of this year. What matters for GDP growth at this stage of the recovery is whether the speed of deleveraging slows, not whether balance sheets stop shrinking altogether. Banks have likely been encouraged by the decline in the stock of non-performing loans on homes over the last four quarters.

Housing construction has made (very small) positive contributions to growth in each of the past four quarters. That’s a welcome development, since the sector has acted as a drag in 25 of the previous 26 quarters, from the third quarter of 2007 to the final quarter of 2013. The size of the sector is now broadly stable at around 4 percent of GDP — roughly one-third of

what it was just before the bust. Before the boom, housing construction accounted for about 6 percent of GDP — that might be a more reasonable assumption for the sustainable size the sector may eventually reach.

In the near term, the overhang of new unsold homes will prevent significant expansion of the sector. The of stocknewly constructed empty homes had only declined to 563,908 in 2013 — the latest reporting period — from a peak of 649,780 in 2009. Those numbers compare with only 195,184 in 2005.

Overall, the evidence is consistent with the stabilization of the housing market in Spain offering some support to growth in the country as the recovery continues. The housing supply overhang suggests construction activity is unlikely to be the primary channel through which revived housing sentiment lifts output, though modest contributions can be expected. The larger influence is likely to hail from consumers as diminishing uncertainty and wealth effects lift confidence and credit conditions improve.

ITALY JAMIE MURRAY, BLOOMBERG INTELLIGENCE ECONOMIST

House Prices Inching Up From Their Lows

June 25, 2015 Bloomberg Brief Economics 13

ITALY JAMIE MURRAY, BLOOMBERG INTELLIGENCE ECONOMIST

Italy Owes Its Lost Decade to InefficiencyThe pre-crisis decade was a good one

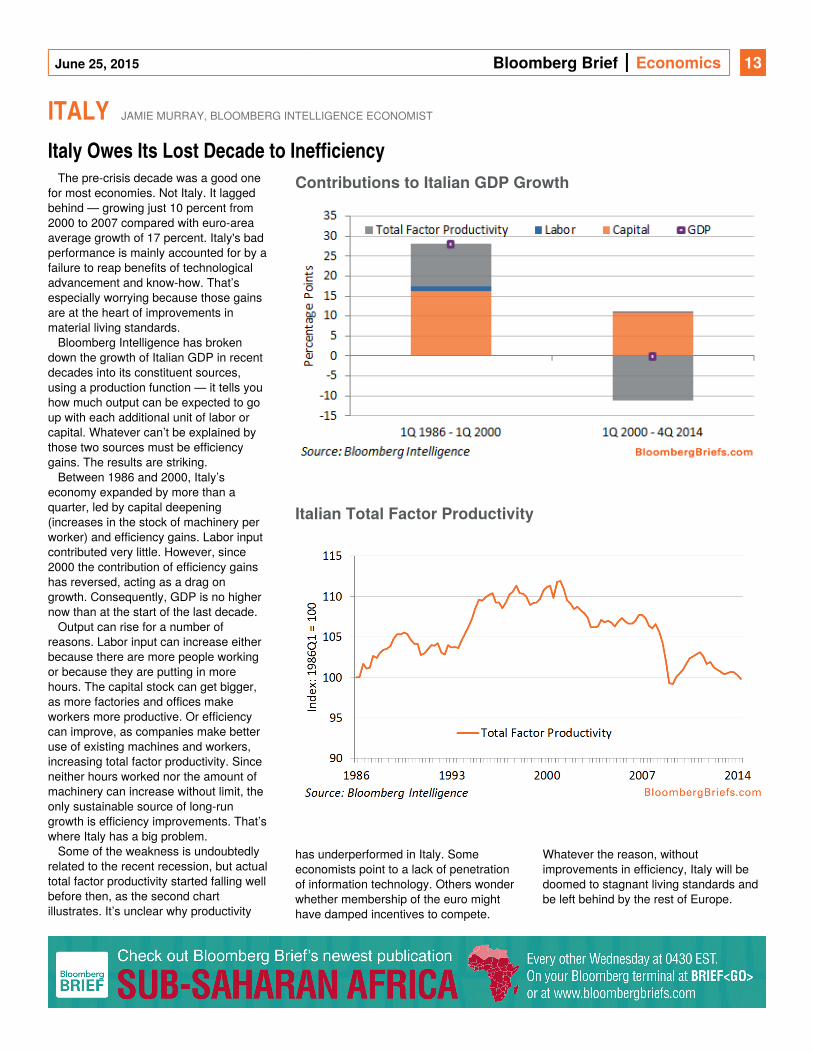

for most economies. Not Italy. It lagged behind — growing just 10 percent from 2000 to 2007 compared with euro-area average growth of 17 percent. Italy's bad performance is mainly accounted for by a failure to reap benefits of technological advancement and know-how. That’s especially worrying because those gains are at the heart of improvements in material living standards.

Bloomberg Intelligence has broken down the growth of Italian GDP in recent decades into its constituent sources, using a production function — it tells you how much output can be expected to go up with each additional unit of labor or capital. Whatever can’t be explained by those two sources must be efficiency gains. The results are striking.

Between 1986 and 2000, Italy’s economy expanded by more than a quarter, led by capital deepening (increases in the stock of machinery per worker) and efficiency gains. Labor input contributed very little. However, since 2000 the contribution of efficiency gains has reversed, acting as a drag on growth. Consequently, GDP is no higher now than at the start of the last decade.

Output can rise for a number of reasons. Labor input can increase either because there are more people working or because they are putting in more hours. The capital stock can get bigger, as more factories and offices make workers more productive. Or efficiency can improve, as companies make better use of existing machines and workers, increasing total factor productivity. Since neither hours worked nor the amount of machinery can increase without limit, the only sustainable source of long-run growth is efficiency improvements. That’s where Italy has a big problem.

Some of the weakness is undoubtedly related to the recent recession, but actual total factor productivity started falling well before then, as the second chart illustrates. It’s unclear why productivity

has underperformed in Italy. Some economists point to a lack of penetration of information technology. Others wonder whether membership of the euro might have damped incentives to compete.

Whatever the reason, without improvements in efficiency, Italy will be doomed to stagnant living standards and be left behind by the rest of Europe.

U.K. DAN HANSON AND JAMIE MURRAY, BLOOMBERG INTELLIGENCE ECONOMISTS

Contributions to Italian GDP Growth

Italian Total Factor Productivity

June 25, 2015 Bloomberg Brief Economics 14

U.K. DAN HANSON AND JAMIE MURRAY, BLOOMBERG INTELLIGENCE ECONOMISTS

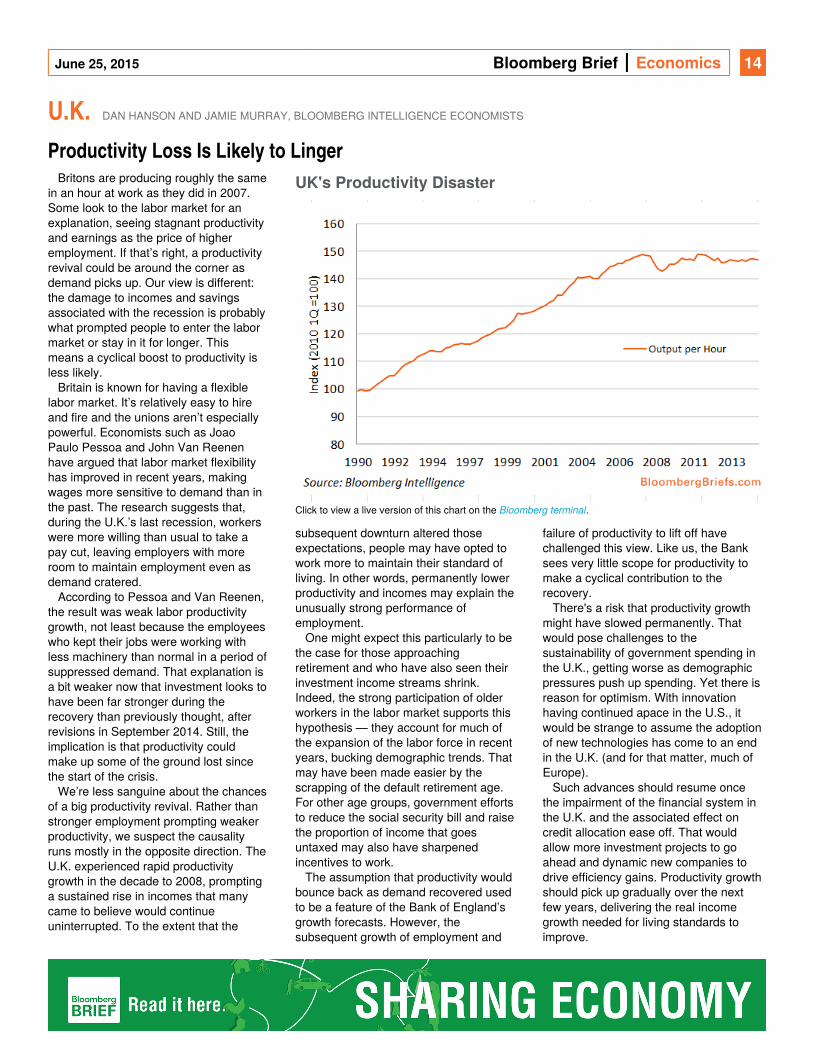

Productivity Loss Is Likely to LingerBritons are producing roughly the same

in an hour at work as they did in 2007. Some look to the labor market for an explanation, seeing stagnant productivity and earnings as the price of higher employment. If that’s right, a productivity revival could be around the corner as demand picks up. Our view is different: the damage to incomes and savings associated with the recession is probably what prompted people to enter the labor market or stay in it for longer. This means a cyclical boost to productivity is less likely.

Britain is known for having a flexible labor market. It’s relatively easy to hire and fire and the unions aren’t especially powerful. Economists such as Joao Paulo Pessoa and John Van Reenen have argued that labor market flexibility has improved in recent years, making wages more sensitive to demand than in the past. The research suggests that, during the U.K.’s last recession, workers were more willing than usual to take a pay cut, leaving employers with more room to maintain employment even as demand cratered.

According to Pessoa and Van Reenen, the result was weak labor productivity growth, not least because the employees who kept their jobs were working with less machinery than normal in a period of suppressed demand. That explanation is a bit weaker now that investment looks to have been far stronger during the recovery than previously thought, after revisions in September 2014. Still, the implication is that productivity could make up some of the ground lost since the start of the crisis.

We’re less sanguine about the chances of a big productivity revival. Rather than stronger employment prompting weaker productivity, we suspect the causality runs mostly in the opposite direction. The U.K. experienced rapid productivity growth in the decade to 2008, prompting a sustained rise in incomes that many came to believe would continue uninterrupted. To the extent that the

Click to view a live version of this chart on the .Bloomberg terminal

subsequent downturn altered those expectations, people may have opted to work more to maintain their standard of living. In other words, permanently lower productivity and incomes may explain the unusually strong performance of employment.

One might expect this particularly to be the case for those approaching retirement and who have also seen their investment income streams shrink. Indeed, the strong participation of older workers in the labor market supports this hypothesis — they account for much of the expansion of the labor force in recent years, bucking demographic trends. That may have been made easier by the scrapping of the default retirement age. For other age groups, government efforts to reduce the social security bill and raise the proportion of income that goes untaxed may also have sharpened incentives to work.

The assumption that productivity would bounce back as demand recovered used to be a feature of the Bank of England’s growth forecasts. However, the subsequent growth of employment and

failure of productivity to lift off have challenged this view. Like us, the Bank sees very little scope for productivity to make a cyclical contribution to the recovery.

There's a risk that productivity growth might have slowed permanently. That would pose challenges to the sustainability of government spending in the U.K., getting worse as demographic pressures push up spending. Yet there is reason for optimism. With innovation having continued apace in the U.S., it would be strange to assume the adoption of new technologies has come to an end in the U.K. (and for that matter, much of Europe).

Such advances should resume once the impairment of the financial system in the U.K. and the associated effect on credit allocation ease off. That would allow more investment projects to go ahead and dynamic new companies to drive efficiency gains. Productivity growth should pick up gradually over the next few years, delivering the real income growth needed for living standards to improve.

AFRICA MARK BOHLUND, BLOOMBERG INTELLIGENCE ECONOMIST

UK's Productivity Disaster

June 25, 2015 Bloomberg Brief Economics 15

AFRICA MARK BOHLUND, BLOOMBERG INTELLIGENCE ECONOMIST

Africa's Struggle for Productivity GrowthFor the vast majority of African

countries, GDP per capita remains a fraction of the figures in developed and many other developing countries. While a rising population and greater investment should support economic growth, increased wealth depends on faster productivity growth. If history is any guide, this will require an expansion of the manufacturing sector. Morocco and Ethiopia are the most recent examples of African countries aiming to become manufacturing hubs, but historical examples and shifts in the global economy illustrate the challenges to such policy drives.

Low GDP per capita is closely tied to poor productivity in African economies, with only the capital-intensive extractive sectors generating output at comparable levels to developed and other emerging markets. In the past century, convergence in developing economies has been stimulated by labor transfers from the low productivity agricultural sector to factories that use more capital and technology.

This was the strategy used by so-called Asian tigers, nations that started at the bottom of the value-added ladder and are now producing more sophisticated goods ranging from smartphones to floating liquefied natural gas vessels.

Dani Rodrik, a development economist, has shown empirically that economic transformation has been different in Africa. Agricultural laborers have tended to migrate to the services sector or smaller manufacturing firms rather than factories. Both tend to be less efficient than large manufacturing companies, which benefit from economies of scale

Rodrik and other economists have also pointed out that developing countries tend to start de-industrializing at much earlier levels of development than in the past, which could be due to technological advances reducing the manpower needed in manufacturing. This implies that African countries may have to pursue a growth model different from prior "economic miracles" based on industrialization, in order to attain higher sustainable growth.

Undeterred, Ethiopia and Morocco are taking a new crack at ramping up economic growth via industrialization.

Reflecting their different levels of economic development, the two countries are targeting different points on the value chain.

Ethiopia is pitching at the lower end. It hopes to utilize its production of input materials such as cotton and leather to develop a textile industry.

Meanwhile, Morocco already has manufacturing experience; the new Tangier-Med port has improved its transport links and it has close cultural ties to France. This has helped it attract investment from French car manufacturers looking to cut costs through outsourcing more labor-intensive work, similar to the way German rivals shifted production to Eastern Europe.

While the Ethiopian and Moroccan governments have both shown an awareness of the importance of supply chains in modern manufacturing, questions remain over how they will foster employment beyond their already targeted industries.

Textiles has traditionally been the entry point into manufacturing for developing countries. From this base they can move up the value chain fairly rapidly by attracting investment from other industries, as Vietnam is doing. Moving into higher value-added industries, such as electronics, is dependent on fitting into regional supply chains.

While Ethiopia is in the process of upgrading its infrastructure through rail and transport links with Djibouti and other ports, it does not easily fit into any regional network of production. The transport of sub-components from other production locations would probably be slow and costly. This means that Ethiopia is likely to find it harder to develop value added industries than Asean nations or East European countries.

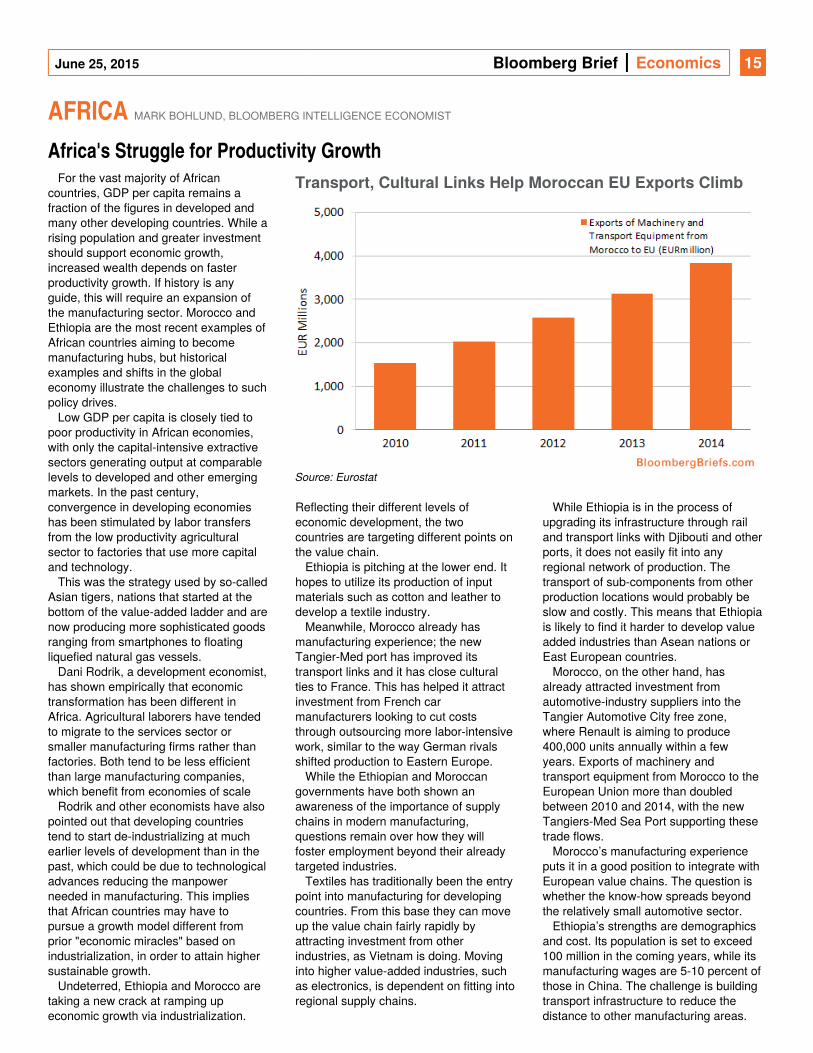

Morocco, on the other hand, has already attracted investment from automotive-industry suppliers into the Tangier Automotive City free zone, where Renault is aiming to produce 400,000 units annually within a few years. Exports of machinery and transport equipment from Morocco to the European Union more than doubled between 2010 and 2014, with the new Tangiers-Med Sea Port supporting these trade flows.

Morocco’s manufacturing experience puts it in a good position to integrate with European value chains. The question is whether the know-how spreads beyond the relatively small automotive sector.

Ethiopia’s strengths are demographics and cost. Its population is set to exceed 100 million in the coming years, while its manufacturing wages are 5-10 percent of those in China. The challenge is building transport infrastructure to reduce the distance to other manufacturing areas.

CHINA TOM ORLIK AND FIELDING CHEN, BLOOMBERG INTELLIGENCE ECONOMISTS

Transport, Cultural Links Help Moroccan EU Exports Climb

Source: Eurostat

June 25, 2015 Bloomberg Brief Economics 16

CHINA TOM ORLIK AND FIELDING CHEN, BLOOMBERG INTELLIGENCE ECONOMISTS

Short-Term Gain, Long-Term Pain for GrowthChina’s economy enters the second

half of 2015 with hopes that stimulus efforts have arrested the slowdown in growth, and fears that reforms will be insufficient to restore lost luster.

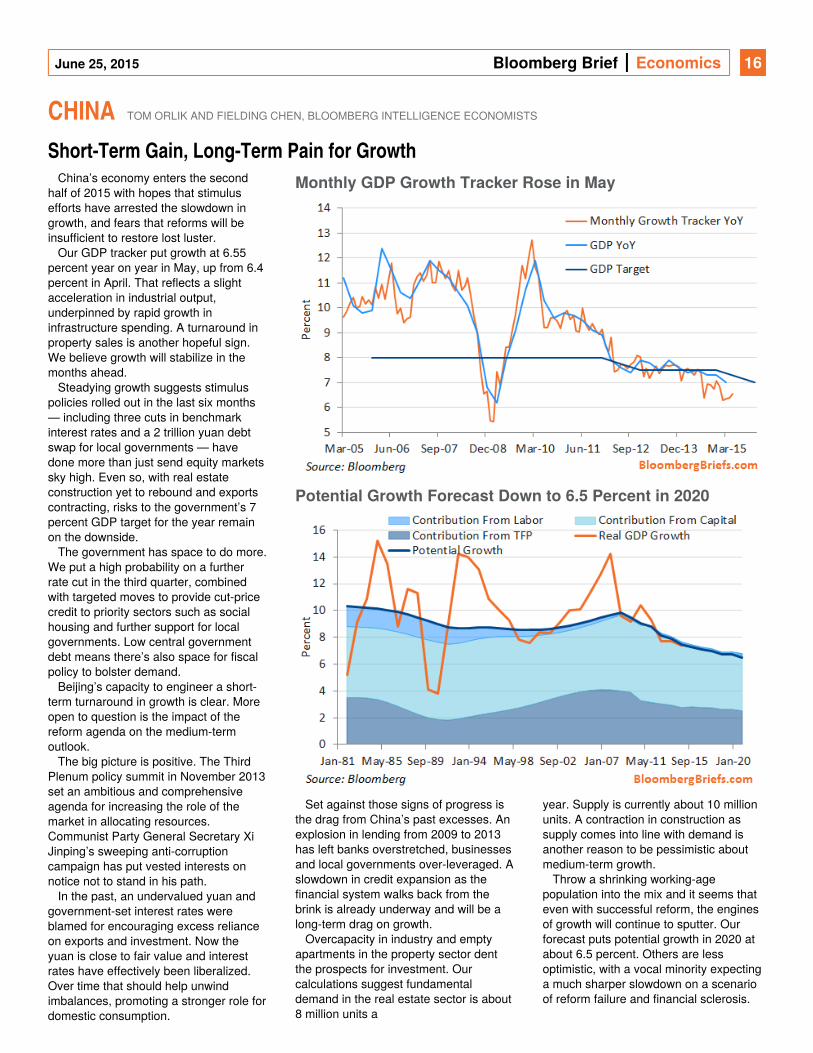

Our GDP tracker put growth at 6.55 percent year on year in May, up from 6.4 percent in April. That reflects a slight acceleration in industrial output, underpinned by rapid growth in infrastructure spending. A turnaround in property sales is another hopeful sign. We believe growth will stabilize in the months ahead.

Steadying growth suggests stimulus policies rolled out in the last six months — including three cuts in benchmark interest rates and a 2 trillion yuan debt swap for local governments — have done more than just send equity markets sky high. Even so, with real estate construction yet to rebound and exports contracting, risks to the government’s 7 percent GDP target for the year remain on the downside.

The government has space to do more. We put a high probability on a further rate cut in the third quarter, combined with targeted moves to provide cut-price credit to priority sectors such as social housing and further support for local governments. Low central government debt means there’s also space for fiscal policy to bolster demand.

Beijing’s capacity to engineer a short-term turnaround in growth is clear. More open to question is the impact of the reform agenda on the medium-term outlook.

The big picture is positive. The Third Plenum policy summit in November 2013 set an ambitious and comprehensive agenda for increasing the role of the market in allocating resources. Communist Party General Secretary Xi Jinping’s sweeping anti-corruption campaign has put vested interests on notice not to stand in his path.

In the past, an undervalued yuan and government-set interest rates were blamed for encouraging excess reliance on exports and investment. Now the yuan is close to fair value and interest rates have effectively been liberalized. Over time that should help unwind imbalances, promoting a stronger role for domestic consumption.

Set against those signs of progress is

the drag from China’s past excesses. An explosion in lending from 2009 to 2013 has left banks overstretched, businesses and local governments over-leveraged. A slowdown in credit expansion as the financial system walks back from the brink is already underway and will be a long-term drag on growth.

Overcapacity in industry and empty apartments in the property sector dent the prospects for investment. Our calculations suggest fundamental demand in the real estate sector is about 8 million units a

year. Supply is currently about 10 million units. A contraction in construction as supply comes into line with demand is another reason to be pessimistic about medium-term growth.

Throw a shrinking working-age population into the mix and it seems that even with successful reform, the engines of growth will continue to sputter. Our forecast puts potential growth in 2020 at about 6.5 percent. Others are less optimistic, with a vocal minority expecting a much sharper slowdown on a scenario of reform failure and financial sclerosis.

JAPAN TOM ORLIK, BLOOMBERG INTELLIGENCE ECONOMIST

Monthly GDP Growth Tracker Rose in May

Potential Growth Forecast Down to 6.5 Percent in 2020

June 25, 2015 Bloomberg Brief Economics 17

JAPAN TOM ORLIK, BLOOMBERG INTELLIGENCE ECONOMIST

Growth Rebound Short-Lived as Challenges LoomJapan’s economy heads into the

second half of 2015 with growth back on track and 2014’s mini-recession fading into memory. That should be enough to keep monetary policy on hold, even though inflation remains below target. Longer term, demographic and fiscal challenges loom and structural reforms — required to fire the engines of growth — remain largely undone.

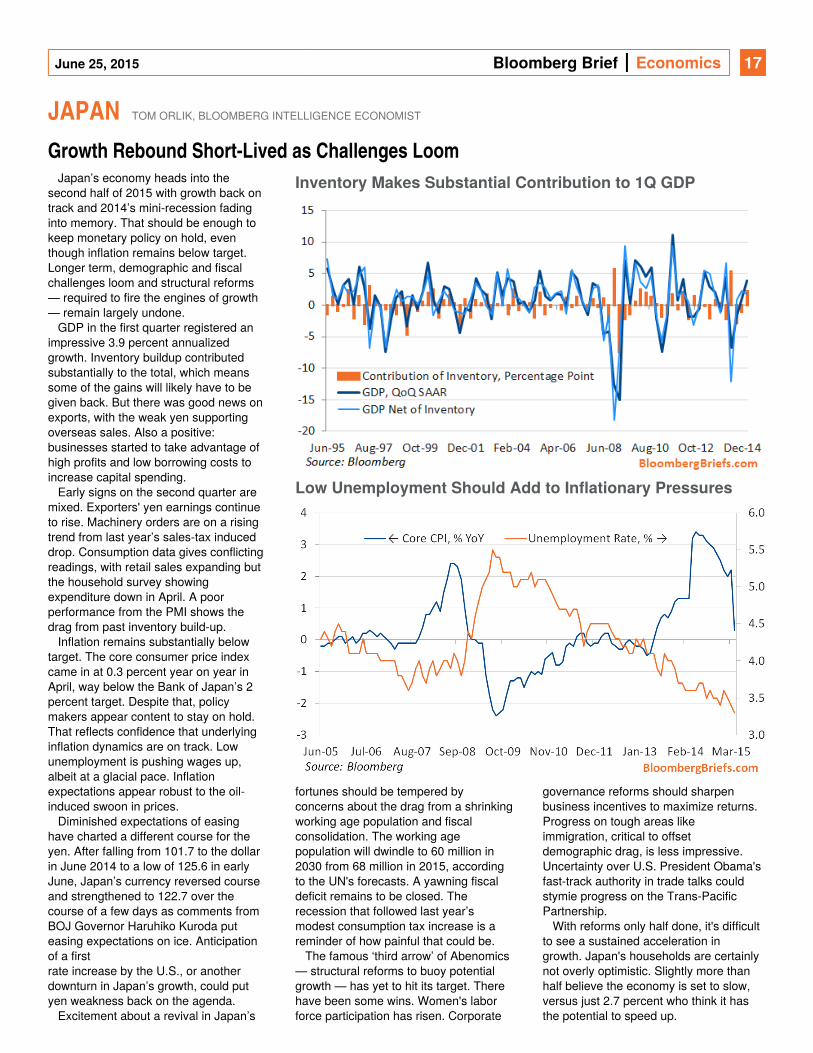

GDP in the first quarter registered an impressive 3.9 percent annualized growth. Inventory buildup contributed substantially to the total, which means some of the gains will likely have to be given back. But there was good news on exports, with the weak yen supporting overseas sales. Also a positive: businesses started to take advantage of high profits and low borrowing costs to increase capital spending.

Early signs on the second quarter are mixed. Exporters' yen earnings continue to rise. Machinery orders are on a rising trend from last year’s sales-tax induced drop. Consumption data gives conflicting readings, with retail sales expanding but the household survey showing expenditure down in April. A poor performance from the PMI shows the drag from past inventory build-up.

Inflation remains substantially below target. The core consumer price index came in at 0.3 percent year on year in April, way below the Bank of Japan’s 2 percent target. Despite that, policy makers appear content to stay on hold. That reflects confidence that underlying inflation dynamics are on track. Low unemployment is pushing wages up, albeit at a glacial pace. Inflation expectations appear robust to the oil-induced swoon in prices.

Diminished expectations of easing have charted a different course for the yen. After falling from 101.7 to the dollar in June 2014 to a low of 125.6 in early June, Japan’s currency reversed course and strengthened to 122.7 over the course of a few days as comments from BOJ Governor Haruhiko Kuroda put easing expectations on ice. Anticipation of a firstrate increase by the U.S., or another downturn in Japan’s growth, could put yen weakness back on the agenda.

Excitement about a revival in Japan’s

fortunes should be tempered by concerns about the drag from a shrinking working age population and fiscal consolidation. The working age population will dwindle to 60 million in 2030 from 68 million in 2015, according to the UN's forecasts. A yawning fiscal deficit remains to be closed. The recession that followed last year’s modest consumption tax increase is a reminder of how painful that could be.

The famous ‘third arrow’ of Abenomics — structural reforms to buoy potential growth — has yet to hit its target. There have been some wins. Women's labor force participation has risen. Corporate

governance reforms should sharpen business incentives to maximize returns. Progress on tough areas like immigration, critical to offset demographic drag, is less impressive. Uncertainty over U.S. President Obama's fast-track authority in trade talks could stymie progress on the Trans-Pacific Partnership.

With reforms only half done, it's difficult to see a sustained acceleration in growth. Japan's households are certainly not overly optimistic. Slightly more than half believe the economy is set to slow, versus just 2.7 percent who think it has the potential to speed up.

INDIA TAMARA HENDERSON, BLOOMBERG INTELLIGENCE ECONOMIST

Inventory Makes Substantial Contribution to 1Q GDP

Low Unemployment Should Add to Inflationary Pressures

June 25, 2015 Bloomberg Brief Economics 18

INDIA TAMARA HENDERSON, BLOOMBERG INTELLIGENCE ECONOMIST

Focused Reforms Set Stage for Strong GrowthIndia’s growth is poised to pick up from

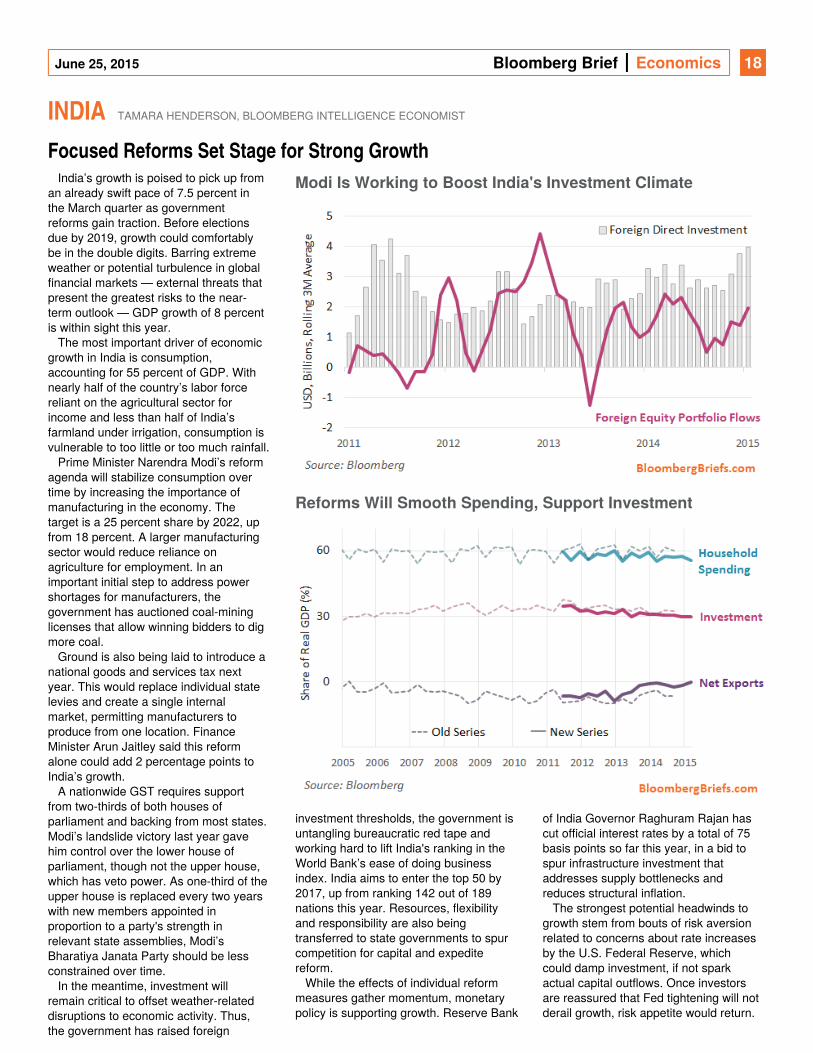

an already swift pace of 7.5 percent in the March quarter as government reforms gain traction. Before elections due by 2019, growth could comfortably be in the double digits. Barring extreme weather or potential turbulence in global financial markets — external threats that present the greatest risks to the near-term outlook — GDP growth of 8 percent is within sight this year.

The most important driver of economic growth in India is consumption, accounting for 55 percent of GDP. With nearly half of the country’s labor force reliant on the agricultural sector for income and less than half of India’s farmland under irrigation, consumption is vulnerable to too little or too much rainfall.

Prime Minister Narendra Modi’s reform agenda will stabilize consumption over time by increasing the importance of manufacturing in the economy. The target is a 25 percent share by 2022, up from 18 percent. A larger manufacturing sector would reduce reliance on agriculture for employment. In an important initial step to address power shortages for manufacturers, the government has auctioned coal-mining licenses that allow winning bidders to dig more coal.

Ground is also being laid to introduce a national goods and services tax next year. This would replace individual state levies and create a single internal market, permitting manufacturers to produce from one location. Finance Minister Arun Jaitley said this reform alone could add 2 percentage points to India’s growth.

A nationwide GST requires support from two-thirds of both houses of parliament and backing from most states. Modi’s landslide victory last year gave him control over the lower house of parliament, though not the upper house, which has veto power. As one-third of the upper house is replaced every two years with new members appointed in proportion to a party's strength in relevant state assemblies, Modi’s Bharatiya Janata Party should be less constrained over time.

In the meantime, investment will remain critical to offset weather-related disruptions to economic activity. Thus, the government has raised foreign

investment thresholds, the government is untangling bureaucratic red tape and working hard to lift India's ranking in the World Bank’s ease of doing business index. India aims to enter the top 50 by 2017, up from ranking 142 out of 189 nations this year. Resources, flexibility and responsibility are also being transferred to state governments to spur competition for capital and expedite reform.

While the effects of individual reform measures gather momentum, monetary policy is supporting growth. Reserve Bank

of India Governor Raghuram Rajan has cut official interest rates by a total of 75 basis points so far this year, in a bid to spur infrastructure investment that addresses supply bottlenecks and reduces structural inflation.

The strongest potential headwinds to growth stem from bouts of risk aversion related to concerns about rate increases by the U.S. Federal Reserve, which could damp investment, if not spark actual capital outflows. Once investors are reassured that Fed tightening will not derail growth, risk appetite would return.

Modi Is Working to Boost India's Investment Climate

Reforms Will Smooth Spending, Support Investment

June 25, 2015 Bloomberg Brief Economics 19

investment limits. To encourage take-up of the higher

SOUTH KOREA FIELDING CHEN, BLOOMBERG INTELLIGENCE ECONOMIST

June 25, 2015 Bloomberg Brief Economics 20

SOUTH KOREA FIELDING CHEN, BLOOMBERG INTELLIGENCE ECONOMIST

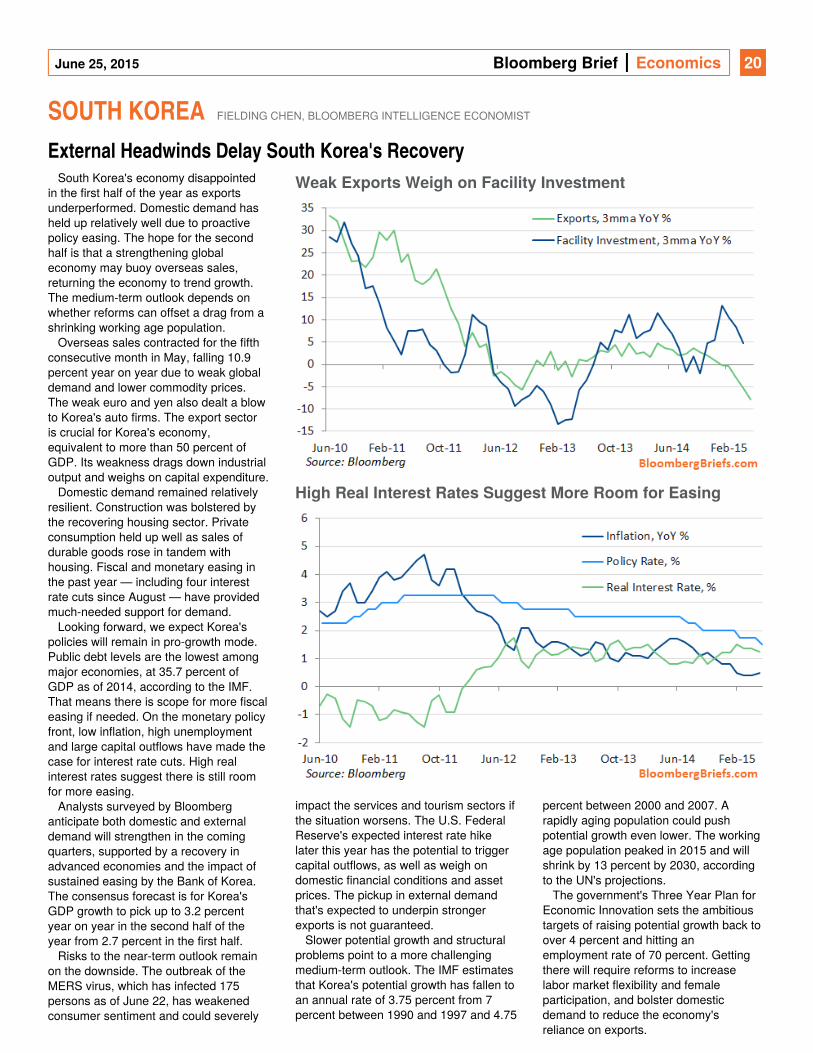

External Headwinds Delay South Korea's RecoverySouth Korea's economy disappointed

in the first half of the year as exports underperformed. Domestic demand has held up relatively well due to proactive policy easing. The hope for the second half is that a strengthening global economy may buoy overseas sales, returning the economy to trend growth. The medium-term outlook depends on whether reforms can offset a drag from a shrinking working age population.

Overseas sales contracted for the fifth consecutive month in May, falling 10.9 percent year on year due to weak global demand and lower commodity prices. The weak euro and yen also dealt a blow to Korea's auto firms. The export sector is crucial for Korea's economy, equivalent to more than 50 percent of GDP. Its weakness drags down industrial output and weighs on capital expenditure.

Domestic demand remained relatively resilient. Construction was bolstered by the recovering housing sector. Private consumption held up well as sales of durable goods rose in tandem with housing. Fiscal and monetary easing in the past year — including four interest rate cuts since August — have provided much-needed support for demand.

Looking forward, we expect Korea's policies will remain in pro-growth mode. Public debt levels are the lowest among major economies, at 35.7 percent of GDP as of 2014, according to the IMF. That means there is scope for more fiscal easing if needed. On the monetary policy front, low inflation, high unemployment and large capital outflows have made the case for interest rate cuts. High real interest rates suggest there is still room for more easing.

Analysts surveyed by Bloomberg anticipate both domestic and external demand will strengthen in the coming quarters, supported by a recovery in advanced economies and the impact of sustained easing by the Bank of Korea. The consensus forecast is for Korea's GDP growth to pick up to 3.2 percent year on year in the second half of the year from 2.7 percent in the first half.

Risks to the near-term outlook remain on the downside. The outbreak of the MERS virus, which has infected 175 persons as of June 22, has weakened consumer sentiment and could severely

impact the services and tourism sectors if the situation worsens. The U.S. Federal Reserve's expected interest rate hike later this year has the potential to trigger capital outflows, as well as weigh on domestic financial conditions and asset prices. The pickup in external demand that's expected to underpin stronger exports is not guaranteed.

Slower potential growth and structural problems point to a more challenging medium-term outlook. The IMF estimates that Korea's potential growth has fallen to an annual rate of 3.75 percent from 7 percent between 1990 and 1997 and 4.75

percent between 2000 and 2007. A rapidly aging population could push potential growth even lower. The working age population peaked in 2015 and will shrink by 13 percent by 2030, according to the UN's projections.

The government's Three Year Plan for Economic Innovation sets the ambitious targets of raising potential growth back to over 4 percent and hitting an employment rate of 70 percent. Getting there will require reforms to increase labor market flexibility and female participation, and bolster domestic demand to reduce the economy's reliance on exports.

SOUTHEAST ASIA TAMARA HENDERSON, BLOOMBERG INTELLIGENCE ECONOMIST

Weak Exports Weigh on Facility Investment

High Real Interest Rates Suggest More Room for Easing

June 25, 2015 Bloomberg Brief Economics 21

SOUTHEAST ASIA TAMARA HENDERSON, BLOOMBERG INTELLIGENCE ECONOMIST

Malaysia, Philippines May Lead Asean Growth Higher The second half of 2015 may bring new

twists to the first half's Fed-watching and inflation stories. Within Southeast Asia, Malaysia and the Philippines appear better suited to navigate the choppy external cross-currents, while Singapore and Thailand may struggle as political uncertainty provides additional headwinds.

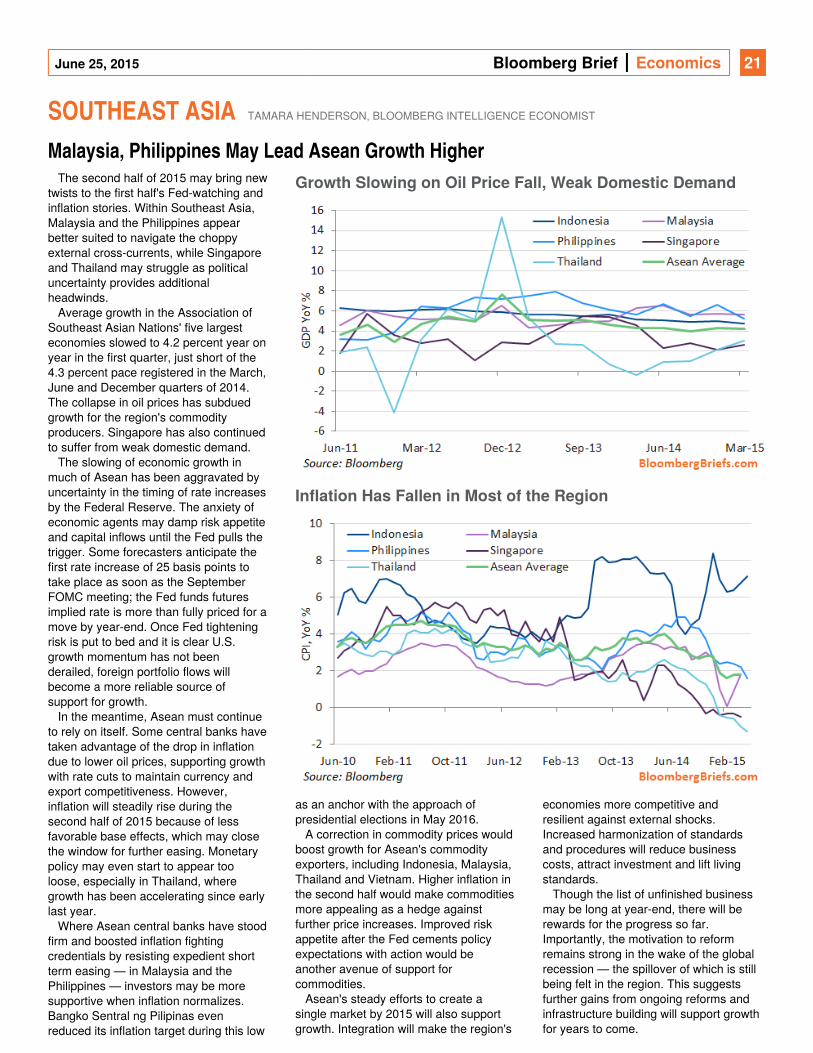

Average growth in the Association of Southeast Asian Nations' five largest economies slowed to 4.2 percent year on year in the first quarter, just short of the 4.3 percent pace registered in the March, June and December quarters of 2014. The collapse in oil prices has subdued growth for the region's commodity producers. Singapore has also continued to suffer from weak domestic demand.

The slowing of economic growth in much of Asean has been aggravated by uncertainty in the timing of rate increases by the Federal Reserve. The anxiety of economic agents may damp risk appetite and capital inflows until the Fed pulls the trigger. Some forecasters anticipate the first rate increase of 25 basis points to take place as soon as the September FOMC meeting; the Fed funds futures implied rate is more than fully priced for a move by year-end. Once Fed tightening risk is put to bed and it is clear U.S. growth momentum has not been derailed, foreign portfolio flows will become a more reliable source of support for growth.

In the meantime, Asean must continue to rely on itself. Some central banks have taken advantage of the drop in inflation due to lower oil prices, supporting growth with rate cuts to maintain currency and export competitiveness. However, inflation will steadily rise during the second half of 2015 because of less favorable base effects, which may close the window for further easing. Monetary policy may even start to appear too loose, especially in Thailand, where growth has been accelerating since early last year.

Where Asean central banks have stood firm and boosted inflation fighting credentials by resisting expedient short term easing — in Malaysia and the Philippines — investors may be more supportive when inflation normalizes. Bangko Sentral ng Pilipinas even reduced its inflation target during this low

as an anchor with the approach of presidential elections in May 2016.

A correction in commodity prices would boost growth for Asean's commodity exporters, including Indonesia, Malaysia, Thailand and Vietnam. Higher inflation in the second half would make commodities more appealing as a hedge against further price increases. Improved risk appetite after the Fed cements policy expectations with action would be another avenue of support for commodities.

Asean's steady efforts to create a single market by 2015 will also support growth. Integration will make the region's

economies more competitive and resilient against external shocks. Increased harmonization of standards and procedures will reduce business costs, attract investment and lift living standards.

Though the list of unfinished business may be long at year-end, there will be rewards for the progress so far. Importantly, the motivation to reform remains strong in the wake of the global recession — the spillover of which is still being felt in the region. This suggests further gains from ongoing reforms and infrastructure building will support growth for years to come.

Growth Slowing on Oil Price Fall, Weak Domestic Demand

Inflation Has Fallen in Most of the Region

June 25, 2015 Bloomberg Brief Economics 22

inflation period, which could pay extra dividends

MARKET OUTLOOK MICHAEL R. ROSENBERG, SENIOR BLOOMBERG CONSULTANT

June 25, 2015 Bloomberg Brief Economics 23

MARKET OUTLOOK MICHAEL R. ROSENBERG, SENIOR BLOOMBERG CONSULTANT

How QE in Europe and Japan Affects U.S. Financial MarketsThe debate on the global

consequences of quantitative easing is likely to shift from the U.S. QE programs — which have played a dominant role in the global financial markets since their start in November 2008 — to the QE programs by the European Central Bank and the Bank of Japan.

A recent Bank of England study anticipates combined ECB and BOJ purchases of around $125 billion per month, “equivalent in value to all of the net (bond) issuance by (all) advanced economy governments over the next 18 months.” This large injection of liquidity will occur at a time when the Federal Reserve will likely be following through on the long-awaited normalization of its policy rate. These conflicting monetary policies could come to loggerheads, potentially limiting the effectiveness of or compromising the conduct of central bank actions in either the U.S. on the one hand, or the euro area and Japan on the other.

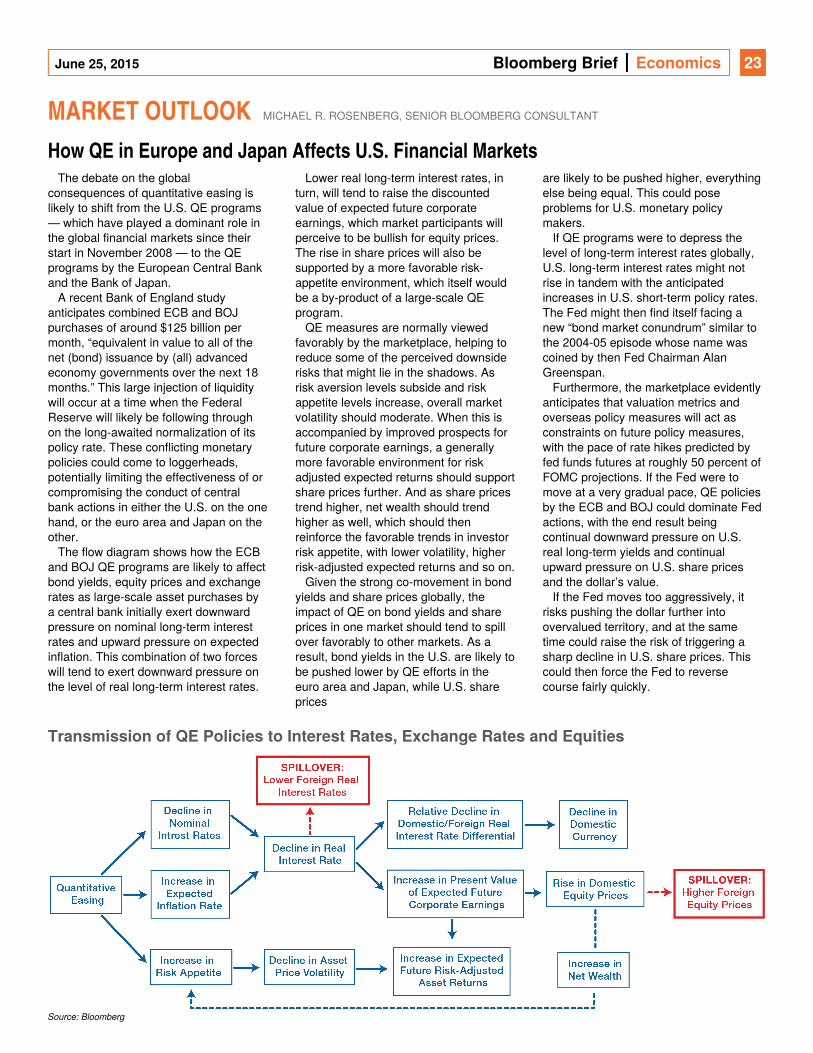

The flow diagram shows how the ECB and BOJ QE programs are likely to affect bond yields, equity prices and exchange rates as large-scale asset purchases by a central bank initially exert downward pressure on nominal long-term interest rates and upward pressure on expected inflation. This combination of two forces will tend to exert downward pressure on the level of real long-term interest rates.

Lower real long-term interest rates, in turn, will tend to raise the discounted value of expected future corporate earnings, which market participants will perceive to be bullish for equity prices. The rise in share prices will also be supported by a more favorable risk-appetite environment, which itself would be a by-product of a large-scale QE program.

QE measures are normally viewed favorably by the marketplace, helping to reduce some of the perceived downside risks that might lie in the shadows. As risk aversion levels subside and risk appetite levels increase, overall market volatility should moderate. When this is accompanied by improved prospects for future corporate earnings, a generally more favorable environment for risk adjusted expected returns should support share prices further. And as share prices trend higher, net wealth should trend higher as well, which should then reinforce the favorable trends in investor risk appetite, with lower volatility, higher risk-adjusted expected returns and so on.

Given the strong co-movement in bond yields and share prices globally, the impact of QE on bond yields and share prices in one market should tend to spill over favorably to other markets. As a result, bond yields in the U.S. are likely to be pushed lower by QE efforts in the euro area and Japan, while U.S. share prices

are likely to be pushed higher, everything else being equal. This could pose problems for U.S. monetary policy makers.

If QE programs were to depress the level of long-term interest rates globally, U.S. long-term interest rates might not rise in tandem with the anticipated increases in U.S. short-term policy rates. The Fed might then find itself facing a new “bond market conundrum” similar to the 2004-05 episode whose name was coined by then Fed Chairman Alan Greenspan.

Furthermore, the marketplace evidently anticipates that valuation metrics and overseas policy measures will act as constraints on future policy measures, with the pace of rate hikes predicted by fed funds futures at roughly 50 percent of FOMC projections. If the Fed were to move at a very gradual pace, QE policies by the ECB and BOJ could dominate Fed actions, with the end result being continual downward pressure on U.S. real long-term yields and continual upward pressure on U.S. share prices and the dollar’s value.

If the Fed moves too aggressively, it risks pushing the dollar further into overvalued territory, and at the same time could raise the risk of triggering a sharp decline in U.S. share prices. This could then force the Fed to reverse course fairly quickly.

Transmission of QE Policies to Interest Rates, Exchange Rates and Equities

Source: Bloomberg

June 25, 2015 Bloomberg Brief Economics 24

CONTACTS

June 25, 2015 Bloomberg Brief Economics 25

CONTACTS

Bloomberg Briefs

Bloomberg Brief Managing Editor

Jennifer Rossa

+1-212-617-8074

Economics Newsletter Editors

Alex Brittain

Anne Riley

Ben Baris

Jennifer Bernstein

Justin Jimenez

Paul Smith

Rebecca Spong

Scott Johnson

William C. Johnsen

Economics Terminal Sales

Matthew Traum

+1-212-617-4671

Newsletter Business Manager

Nick Ferris

+1-212-617-6975

Advertising

Adrienne Bills

+1-212-617-6073

Reprints & Permissions

Lori Husted

+1-717-505-970

Bloomberg Intelligence

Chief Economist

Michael McDonough

Chief U.S. Economist

Carl Riccadonna

U.S. Economist

Josh Wright

U.S. Economist

Richard Yamarone

Chief EMEA Economist

Jamie Murray

Chief Euro-Area Economist

David Powell

Africa and Middle East Economist

Mark Bohlund

U.K. Economist

Dan Hanson

Europe Economist

Maxime Sbaihi

Europe Economist

Niraj Shah

Chief Asia Economist

Tom Orlik

Asia Economist

Tamara Henderson

Asia Economist

Fielding Chen

Bloomberg News

Executive Editor

Marco Babic

Head of Economic Surveys

Joshua Robinson

QuickTakes Editor-at-Large

Leah Harrison

QuickTakes

Jonathan Landman

© 2015 Bloomberg LP. All rights reserved. This newsletter and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Please contact our reprints group listed left for more information.