audited project financial statements phi: senior high school

TRANSCRIPT

Audited Project Financial Statements

The audited project financial statements are documents owned by the borrower. The views expressed herein do not necessarily represent those of ADB’s Board of Directors, Management, or staff. These documents are made publicly available in accordance with ADB’s Public Communications Policy 2011 and as agreed between ADB and the Department of Education.

Project Number: 45089-002 Loan Number: 3237 Period covered: 01 January – 31 December 2016

PHI: Senior High School Support Program

Prepared by: Department of Education

For the Asian Development Bank Date received by ADB: 21 August 2017

Republic of the Philippines

COMMISSION ON AUDIT

Commonwealth Ave., Quezon City

CONSOLIDATED

ANNUAL AUDIT REPORT

on the

DEPARTMENT OF EDUCATION

For the Year Ended December 31, 2016

i

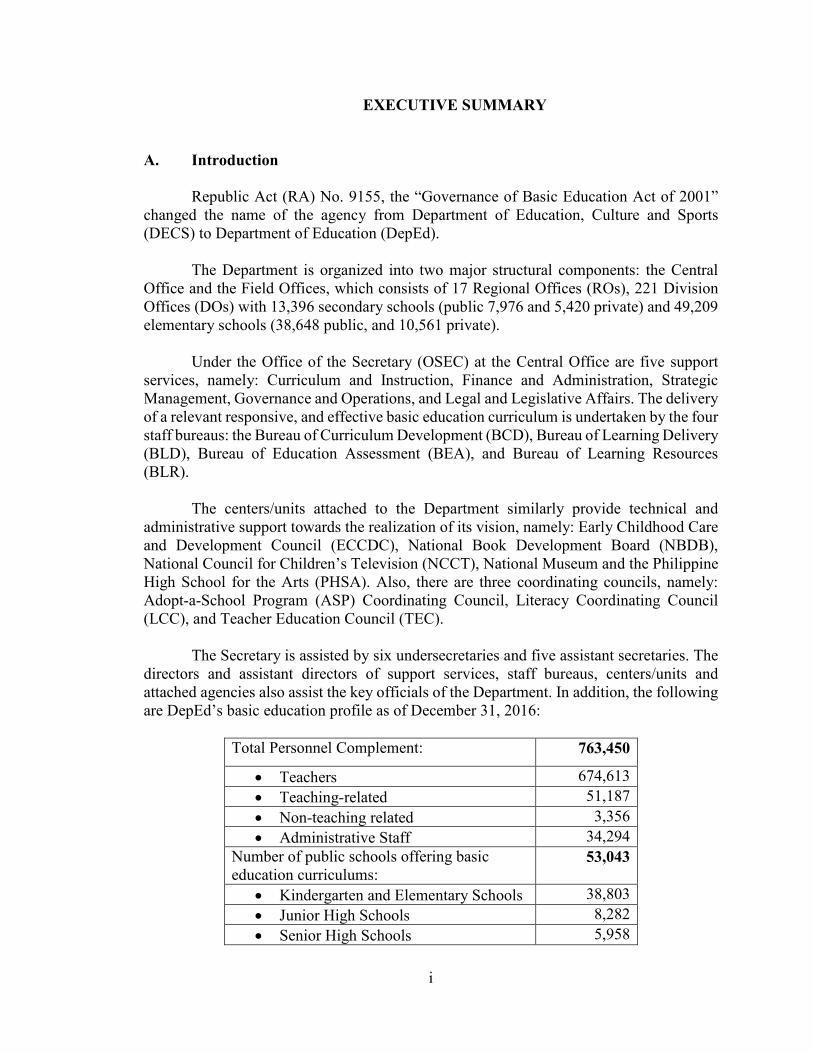

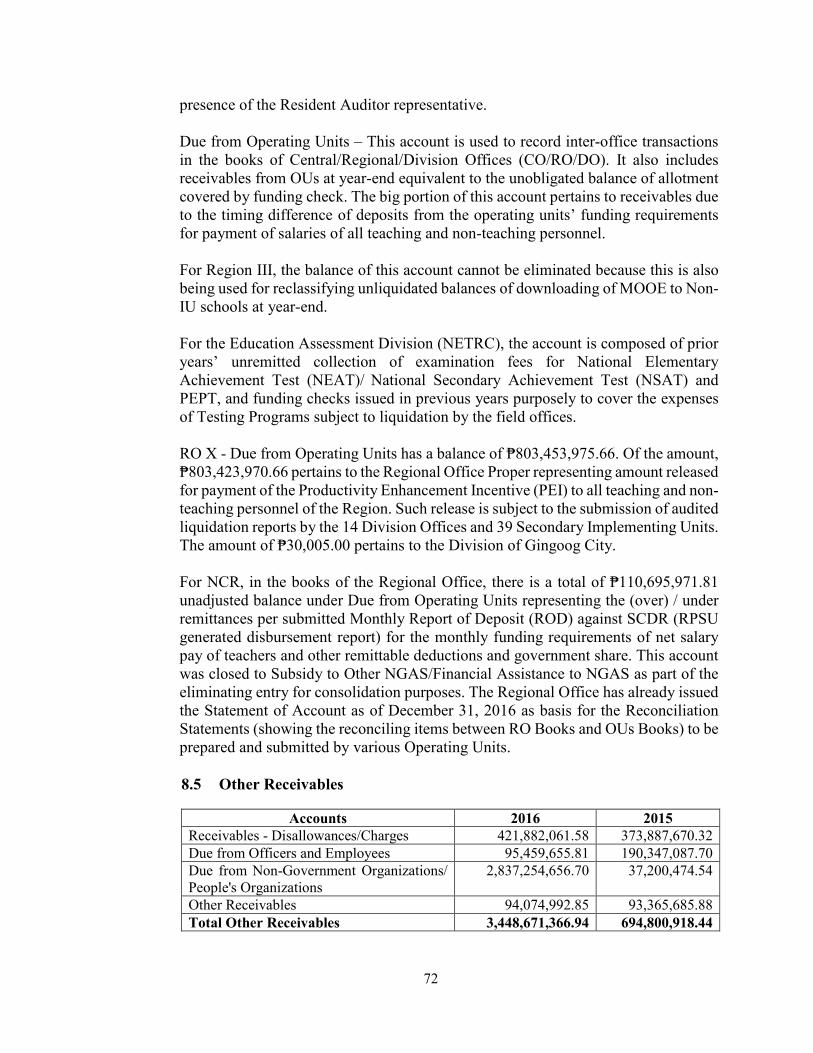

EXECUTIVE SUMMARY

A. Introduction

Republic Act (RA) No. 9155, the “Governance of Basic Education Act of 2001”

changed the name of the agency from Department of Education, Culture and Sports

(DECS) to Department of Education (DepEd).

The Department is organized into two major structural components: the Central

Office and the Field Offices, which consists of 17 Regional Offices (ROs), 221 Division

Offices (DOs) with 13,396 secondary schools (public 7,976 and 5,420 private) and 49,209

elementary schools (38,648 public, and 10,561 private).

Under the Office of the Secretary (OSEC) at the Central Office are five support

services, namely: Curriculum and Instruction, Finance and Administration, Strategic

Management, Governance and Operations, and Legal and Legislative Affairs. The delivery

of a relevant responsive, and effective basic education curriculum is undertaken by the four

staff bureaus: the Bureau of Curriculum Development (BCD), Bureau of Learning Delivery

(BLD), Bureau of Education Assessment (BEA), and Bureau of Learning Resources

(BLR).

The centers/units attached to the Department similarly provide technical and

administrative support towards the realization of its vision, namely: Early Childhood Care

and Development Council (ECCDC), National Book Development Board (NBDB),

National Council for Children’s Television (NCCT), National Museum and the Philippine

High School for the Arts (PHSA). Also, there are three coordinating councils, namely:

Adopt-a-School Program (ASP) Coordinating Council, Literacy Coordinating Council

(LCC), and Teacher Education Council (TEC).

The Secretary is assisted by six undersecretaries and five assistant secretaries. The

directors and assistant directors of support services, staff bureaus, centers/units and

attached agencies also assist the key officials of the Department. In addition, the following

are DepEd’s basic education profile as of December 31, 2016:

Total Personnel Complement: 763,450

• Teachers 674,613

• Teaching-related 51,187

• Non-teaching related 3,356

• Administrative Staff 34,294

Number of public schools offering basic

education curriculums: 53,043

• Kindergarten and Elementary Schools 38,803

• Junior High Schools 8,282

• Senior High Schools 5,958

ii

Total Learners: 24,881,246

• Kindergarten 1,814,713

• Elementary pupils 14,100,290

• Junior High School students 7,521,136

• Senior High School students 1,445,107

B. Operational Highlights

The DepEd reported the following major accomplishments per Major Final Output

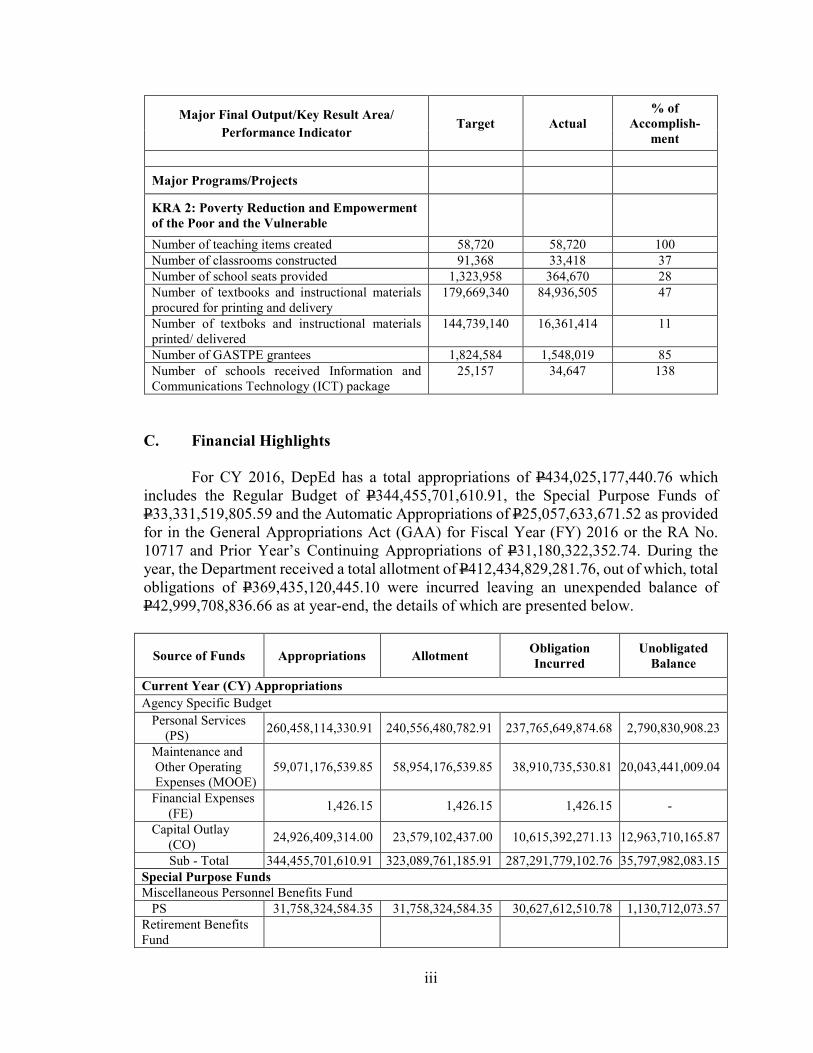

(MFO)/Key Result Area (KRA) and Performance Indicator for Calendar Year (CY) 20161:

Major Final Output/Key Result Area/

Performance Indicator Target Actual

% of

Accomplish-

ment

Operations

MFO 1: Basic Education Policy Services

Number of plans and policies formulated,

reviewed, issued and disseminated

Percentage of policies updated over the last three

years

4

25%

8

26%

200

104

MFO 2: Basic Education Services

Phase 1: Public Kindergarten and Elementary

Education

Number of learners ages 5-11 years old enrolled in

kindergarten and elem. Education

Percentage of learners who completed the school

year

13,600,329

83%

13,048,563

83%

96

100

Phase 2: Public Secondary Education

Number of learners ages 12-15 years old enrolled

in secondary education

Percentage of learners who completed the school

year

4,521,418

80%

4,915,676

74%

109

92.50

Phase 3: Alternative Learning System

Number of learners above 15 years old served

thru Alternative Learning System (ALS) Program

332,888

469,623

141

MFO 3: Regulatory & Devt’l Services

Number of GASTPE grantees 1,824,584 855,449 47

1DepEd Physical Report of Operation as of 31 December 2016

iii

Major Final Output/Key Result Area/

Performance Indicator Target Actual

% of

Accomplish-

ment

Major Programs/Projects

KRA 2: Poverty Reduction and Empowerment

of the Poor and the Vulnerable

Number of teaching items created 58,720 58,720 100

Number of classrooms constructed 91,368 33,418 37

Number of school seats provided 1,323,958 364,670 28

Number of textbooks and instructional materials

procured for printing and delivery

179,669,340 84,936,505 47

Number of textboks and instructional materials

printed/ delivered

144,739,140 16,361,414 11

Number of GASTPE grantees 1,824,584 1,548,019 85

Number of schools received Information and

Communications Technology (ICT) package

25,157 34,647 138

C. Financial Highlights

For CY 2016, DepEd has a total appropriations of P434,025,177,440.76 which

includes the Regular Budget of P344,455,701,610.91, the Special Purpose Funds of

P33,331,519,805.59 and the Automatic Appropriations of P25,057,633,671.52 as provided

for in the General Appropriations Act (GAA) for Fiscal Year (FY) 2016 or the RA No.

10717 and Prior Year’s Continuing Appropriations of P31,180,322,352.74. During the

year, the Department received a total allotment of P412,434,829,281.76, out of which, total

obligations of P369,435,120,445.10 were incurred leaving an unexpended balance of

P42,999,708,836.66 as at year-end, the details of which are presented below.

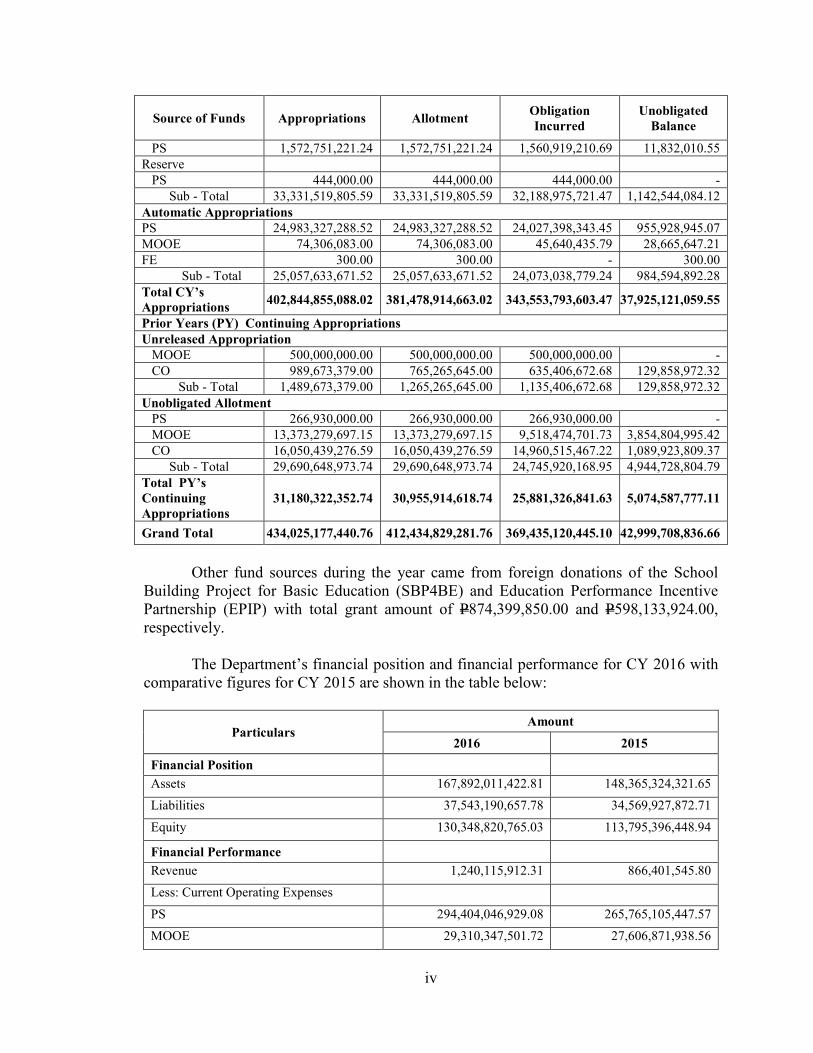

Source of Funds Appropriations Allotment Obligation

Incurred

Unobligated

Balance

Current Year (CY) Appropriations

Agency Specific Budget

Personal Services

(PS) 260,458,114,330.91 240,556,480,782.91 237,765,649,874.68 2,790,830,908.23

Maintenance and

Other Operating

Expenses (MOOE)

59,071,176,539.85 58,954,176,539.85 38,910,735,530.81 20,043,441,009.04

Financial Expenses

(FE) 1,426.15 1,426.15 1,426.15 -

Capital Outlay

(CO) 24,926,409,314.00 23,579,102,437.00 10,615,392,271.13 12,963,710,165.87

Sub - Total 344,455,701,610.91 323,089,761,185.91 287,291,779,102.76 35,797,982,083.15

Special Purpose Funds

Miscellaneous Personnel Benefits Fund

PS 31,758,324,584.35 31,758,324,584.35 30,627,612,510.78 1,130,712,073.57

Retirement Benefits

Fund

iv

Source of Funds Appropriations Allotment Obligation

Incurred

Unobligated

Balance

PS 1,572,751,221.24 1,572,751,221.24 1,560,919,210.69 11,832,010.55

Reserve

PS 444,000.00 444,000.00 444,000.00 -

Sub - Total 33,331,519,805.59 33,331,519,805.59 32,188,975,721.47 1,142,544,084.12

Automatic Appropriations

PS 24,983,327,288.52 24,983,327,288.52 24,027,398,343.45 955,928,945.07

MOOE 74,306,083.00 74,306,083.00 45,640,435.79 28,665,647.21

FE 300.00 300.00 - 300.00

Sub - Total 25,057,633,671.52 25,057,633,671.52 24,073,038,779.24 984,594,892.28

Total CY’s

Appropriations 402,844,855,088.02 381,478,914,663.02 343,553,793,603.47 37,925,121,059.55

Prior Years (PY) Continuing Appropriations

Unreleased Appropriation

MOOE 500,000,000.00 500,000,000.00 500,000,000.00 -

CO 989,673,379.00 765,265,645.00 635,406,672.68 129,858,972.32

Sub - Total 1,489,673,379.00 1,265,265,645.00 1,135,406,672.68 129,858,972.32

Unobligated Allotment

PS 266,930,000.00 266,930,000.00 266,930,000.00 -

MOOE 13,373,279,697.15 13,373,279,697.15 9,518,474,701.73 3,854,804,995.42

CO 16,050,439,276.59 16,050,439,276.59 14,960,515,467.22 1,089,923,809.37

Sub - Total 29,690,648,973.74 29,690,648,973.74 24,745,920,168.95 4,944,728,804.79

Total PY’s

Continuing

Appropriations

31,180,322,352.74 30,955,914,618.74 25,881,326,841.63 5,074,587,777.11

Grand Total 434,025,177,440.76 412,434,829,281.76 369,435,120,445.10 42,999,708,836.66

Other fund sources during the year came from foreign donations of the School

Building Project for Basic Education (SBP4BE) and Education Performance Incentive

Partnership (EPIP) with total grant amount of P874,399,850.00 and P598,133,924.00,

respectively.

The Department’s financial position and financial performance for CY 2016 with

comparative figures for CY 2015 are shown in the table below:

Particulars Amount

2016 2015

Financial Position

Assets 167,892,011,422.81 148,365,324,321.65

Liabilities 37,543,190,657.78 34,569,927,872.71

Equity 130,348,820,765.03 113,795,396,448.94

Financial Performance

Revenue 1,240,115,912.31 866,401,545.80

Less: Current Operating Expenses

PS 294,404,046,929.08 265,765,105,447.57

MOOE 29,310,347,501.72 27,606,871,938.56

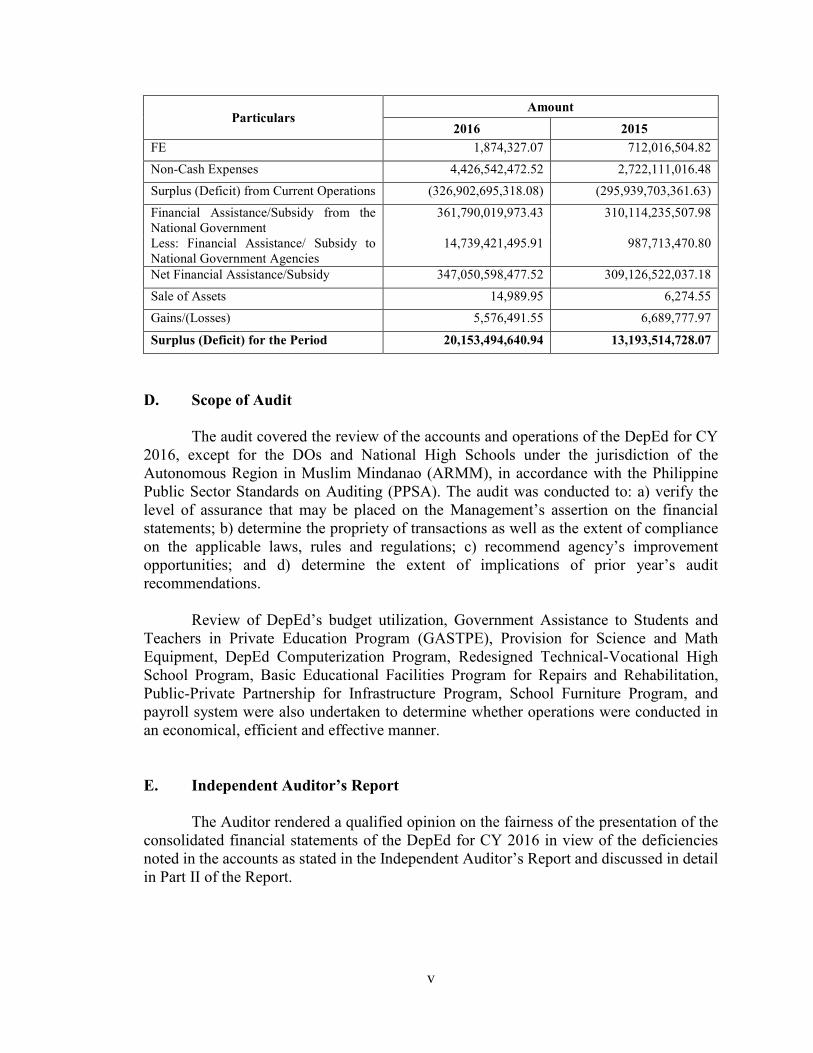

v

Particulars Amount

2016 2015

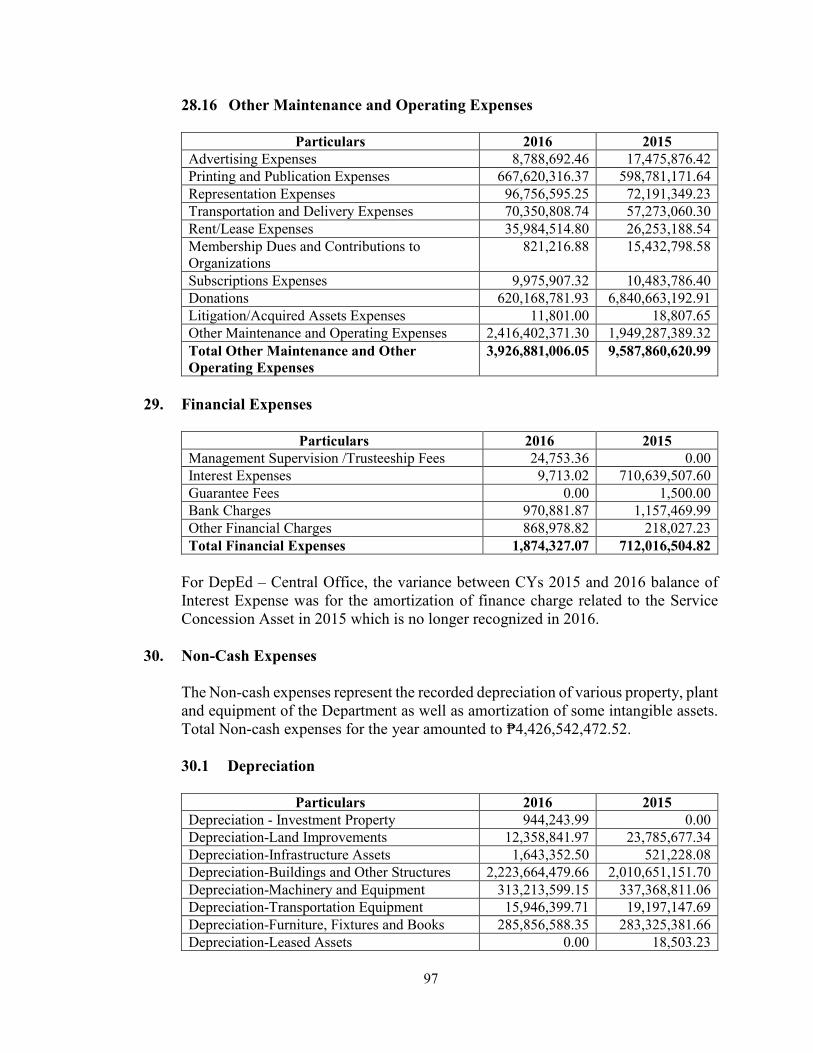

FE 1,874,327.07 712,016,504.82

Non-Cash Expenses 4,426,542,472.52 2,722,111,016.48

Surplus (Deficit) from Current Operations (326,902,695,318.08) (295,939,703,361.63)

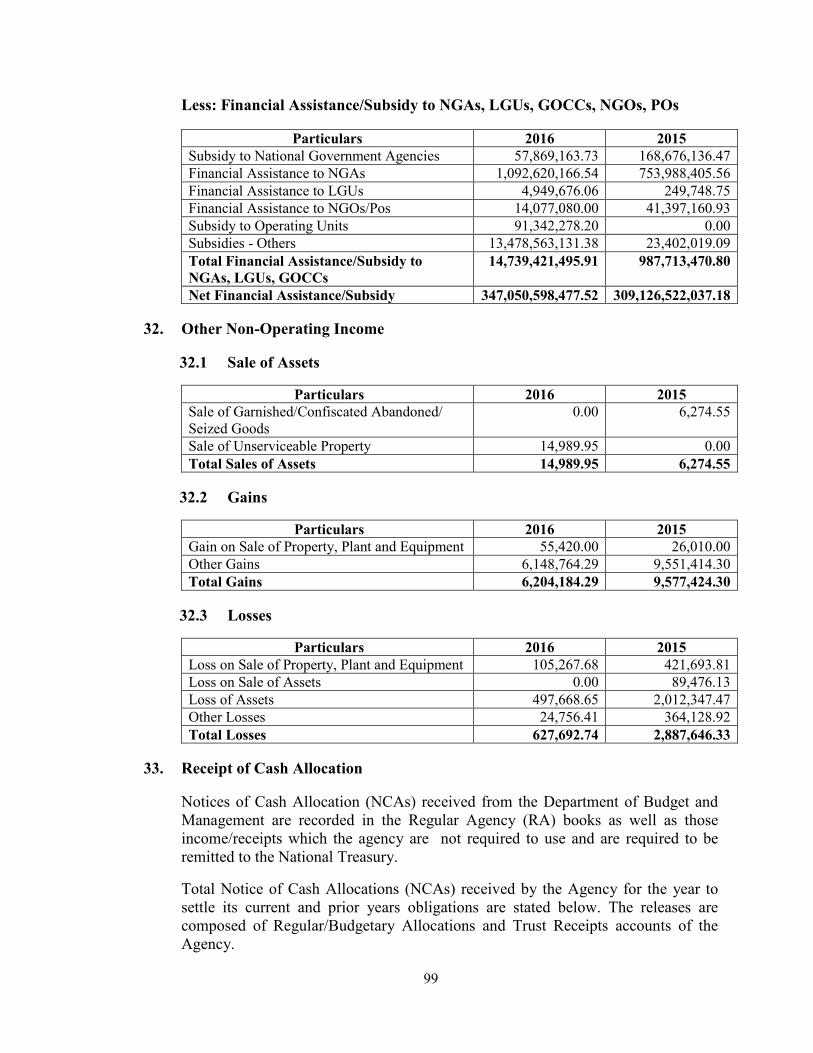

Financial Assistance/Subsidy from the

National Government

361,790,019,973.43 310,114,235,507.98

Less: Financial Assistance/ Subsidy to

National Government Agencies

14,739,421,495.91 987,713,470.80

Net Financial Assistance/Subsidy 347,050,598,477.52 309,126,522,037.18

Sale of Assets 14,989.95 6,274.55

Gains/(Losses) 5,576,491.55 6,689,777.97

Surplus (Deficit) for the Period 20,153,494,640.94 13,193,514,728.07

D. Scope of Audit

The audit covered the review of the accounts and operations of the DepEd for CY

2016, except for the DOs and National High Schools under the jurisdiction of the

Autonomous Region in Muslim Mindanao (ARMM), in accordance with the Philippine

Public Sector Standards on Auditing (PPSA). The audit was conducted to: a) verify the

level of assurance that may be placed on the Management’s assertion on the financial

statements; b) determine the propriety of transactions as well as the extent of compliance

on the applicable laws, rules and regulations; c) recommend agency’s improvement

opportunities; and d) determine the extent of implications of prior year’s audit

recommendations.

Review of DepEd’s budget utilization, Government Assistance to Students and

Teachers in Private Education Program (GASTPE), Provision for Science and Math

Equipment, DepEd Computerization Program, Redesigned Technical-Vocational High

School Program, Basic Educational Facilities Program for Repairs and Rehabilitation,

Public-Private Partnership for Infrastructure Program, School Furniture Program, and

payroll system were also undertaken to determine whether operations were conducted in

an economical, efficient and effective manner.

E. Independent Auditor’s Report

The Auditor rendered a qualified opinion on the fairness of the presentation of the

consolidated financial statements of the DepEd for CY 2016 in view of the deficiencies

noted in the accounts as stated in the Independent Auditor’s Report and discussed in detail

in Part II of the Report.

vi

F. Audit Observations and Recommendations

The following is a summary of significant observations and recommendations,

among others, the details of which are discussed in Part II-Observations and

Recommendations of the Report:

1. For CY 2016, DepEd has unobligated allotment of P42,999,708,837.00, of

which, the Central Office (CO) has 70 percent share amounting to

P30,153,331,186.00; while the Regional Offices (ROs) have

P12,846,377,651.00 or 30 percent. The unobligated balance includes lapsed

CY 2015 allotments from CO of P3,230,719,122.00 and from the ROs of

P1,843,868,656.00 that were automatically reverted to the General Fund at

the end of CY 2016.

Whereas, CO received total allotments of P60,515,744,274.00 from the

current year’s appropriations, wherein P14,269,308,867.00 thereof was sub-

allotted to ROs/Division Offices (DOs) for the implementation of various

programs/ projects; while P19,323,823,343.00 was obligated out of the

available allotment of P46,246,435,407.00, thereby, leaving an unobligated

balance of P26,922,612,064.00 at year-end. The deficiency in the budget

utilization attributable to some gaps noted in carrying out the required

processes/procedures in the program planning and implementation affected

the DepEd’s timely delivery of its physical targets desired for basic education

services. (Observation No. 1)

We recommended that Management require the concerned offices to:

a. re-assess CO’s process to effect sub-allotment of funds, procurement

planning, as well as the procedures for review and approval of

documents to properly address the causes of the delays in the delivery

or performance targets/outputs; and

b. strengthen the monitoring of allotments to immediately respond to

issues causing non-utilization thereof so that other options/strategies

could be considered to ensure its optimum utilization, thus, realize

agency commitments towards delivery of the programs/projects’

objectives.

2. The multi million contract of fund transfer ranging from P100 million to P163

million annually entered into by the DepEd in previous years with the Fund

for Assistance to Private Education (FAPE) as a service provider, and now

with the Private Education Assistance Committee (PEAC) as the trustee of

FAPE, for the implementation of the GASTPE programs, over the years had

restricted the COA’s audit authority due to uncertain information as to the

legal personality of FAPE and PEAC, which from the start had created an

impression to be a private entity, where in fact, it is a public entity according

to its creation, and is likewise vested with authority to perform public

functions.

vii

Moreover, the Irrevocable Trust Fund (ITF) created under EO 156, the FAPE

to be managed by PEAC, as trustee, and chaired by the DepEd Secretary, with

a reported year-end equity of P184,378,049.692 has not been accounted as

government funds, and was not subjected to COA audit, hence, the validity of

the charges made to the fund since its creation has not been validated.

(Observation No. 2)

We recommended that the DepEd Secretary, in her capacity as

Chairman of PEAC, and with reference to Sandiganbayan decision on

Criminal Case No. SB-12-CRM-0134,:

a. initiate the opening of the books and records pertaining to all receipts

of and uses of funds and properties of PEAC/FAPE for the audit and

examination of COA for transparency and public accountability;

b. direct preservation of all PEAC/FAPE funds and properties

including the financial reports, records and documents from the time

it has been in operation;

c. immediately submit complete set of financial statements including the

necessary schedules, for FAPE’s Account 00022594 TA 01, as well as

financial reports on other funds, investments or financial interests of

PEAC/FAPE for the CYs 2014 to 2016, to COA for audit/

examination; and

d. instruct the officers concerned to submit other documents and

records when needed in the course of audit to establish unaccounted

government funds and property entrusted to PEAC/FAPE.

3. The Public Secondary School’s unreadiness to accommodate the expected

number of SHS entrants, that necessitated the utilization of Private Secondary

Schools facilities/resources to accommodate the projected 1,445,107

enrollees nationwide, ensures the latter a guaranteed revenue, as 90 percent

of their senior high enrollees are Senior High School (SHS VP) grantees. On

the part of DepEd, it incurred an additional expenses of P33,000,000.00 due

to the corresponding increase in the administration cost to pay PEAC/FAPE.

Further, the student’s financial capacity was not considered to qualify for the

SHS VP and likewise, as recipient of other scholarship grants/programs, to

conform with the provision of Section 22 of RA No. 10533. Thus, students

enrolled in prestigious/high paying private schools/universities who are

financially capable even without government’s financial assistance, were also

SHS VP grantees.

2 FAPE’s “Account 00022594 TA 01 Agent” Statement of Financial Position as of December 31, 2013

viii

Moreover, DepEd did not closely monitor and supervise the implementation

of the GASTPE Program to ensure the wise utilization of the funds and the

effectiveness of the Program to address any deficiencies noted in the period

of implementation. (Observation No. 3)

We recommended that Management:

a. ensure public secondary schools’ readiness to implement the SHS

Program by closely monitoring and timely addressing issues/

deficiencies encountered so as not to rely on the capability and

resources of private/non-DepEd schools and therefore funds set aside

to support these institutions could be allocated to sustain and enhance

the basic education services in public schools;

b. provide concrete guidelines in assessing the financial capacity of the

grantees in conformance with Section 22 of RA No. 10533 and impose

reasonable limitations on the availment of financial grant;

c. determine reasonableness and propriety of covering those students

that are enrolled in the prestigious high paying schools/universities

and those who are covered with other scholarship programs of the

schools/universities;

d. consider the process that the financial capacity of the Junior High

School (JHS) grantees be assessed before enrolment to SHS and not

just for the initial (one-time) assessment; and

e. establish strategy to validate and monitor compliance to rules and

procedures of the program and to assess PEAC/FAPE performance

at least annually.

4. Out of the total allotment of P8,966,176,422.00 for CYs 2014 to 2016

provision for Science and Mathematics Equipment (SME) program consisting

of three projects, P1,220,123,879.00 was not utilized and had lapsed, while

P792,790,343.00 is expected to lapse by end of CY 2017 if problems on

delayed procurement cannot be remedied. Further, the amount of

P2,443,289,053.00 awarded contracts was already due for termination on

account of breach of contract/default of the supplier. In view of these

deficiencies, the program suffers implementation setbacks, depriving the

recipient schools with the needed SMEs as targeted by DepEd.

Moreover, the Management through the Bids and Awards Committee (BAC)

failed to institute appropriate remedy measures to immediately address the

default in the contractual obligations incurred by Philab Industries Inc. in

Joint Venture agreement with Zacto System Philippines, Inc., and China

Educational Instrument & Equipment Corporation, as the company was able

to participate in the subsequent biddings and was again awarded several

contracts, undermining the possible risks it poses on the program’s

ix

implementation. Besides, two advance payments of P42,916,901.04 and

P211,906,724.01 were granted to the same supplier for the subsequent

awarded projects. (Observation No. 4)

We recommended that the Management undertake the following courses

of action:

For unutilized SME Budget –

a. adhere with the procurement law giving importance to the process of

post qualification on which the DepEd made lapses in determining

the suppliers responsiveness to the project that led to a huge setback

on the SME project;

b. conduct a rigorous market survey to obtain a more objective and

reasonable estimates to encourage more bidders to participate, or

minimize failure of bidding;

c. assess the availability and capabilities of local markets or

manufacturers in the country to supply the needed SMEs;

d. strictly evaluate bidders’ track records in awarding contracts;

e. revisit existing guidelines and procedures in the procurement for

possible enhancement and to consider previous problems

encountered; and

f. consider decentralization of procurement at least at the regional level

or those regions which are already well equipped to handle the

procurement.

For breach of contract by Philab Industries Inc. –

a. conduct investigation on the validity and propriety of the awarded

contracts to Philab Industries Inc. and its Joint Venture Partners and

institute appropriate sanctions against responsible officers/employees

when warranted;

b. institute forfeiture of performance bonds/securities and immediately

demand for the return of the advance payments of P254,823,625.05;

c. impose administrative penalty against the Philab Industries Inc. and

its Joint Venture partners as provided under Rule XXIII of the

Revised IRR of RA No. 9184; and

x

d. require National Science Testing Instrumentation Center (NSTIC)

monitoring teams in coordination with the Asset Management

Division to strictly monitor suppliers compliance to contractual

commitments, especially for contracts under massive projects that

will significantly affect the achievement of the Agency’s goals/

mandate and address the issues causing the inefficient delivery of the

project.

5. The CYs 2014 and 2015 delivered SMEs to various recipient schools were

not fully utilized due to non-readiness of the recipients to accept the deliveries

for lack of suitable classrooms or laboratories, non/late/partial delivery of

SME items in the package/kit allotted per recipient schools, lack of training

and the reported missing or unaccounted items. Further, non-compliance with

the DepEd Order No. 45, s. 2006 had resulted in unaccounted delivered SMEs

in the books of the recipient DOs/IUs. (Observation No. 5)

We recommended that the CO and the officers of concerned DOs:

a. strengthen coordination and monitoring and ensure readiness of

recipient schools in terms of facilities to ensure proper utilization of

SMEs and to secure proper storage and safety;

b. comply strictly with the provisions of DepEd Order No. 45 s. 2006

regarding the submission of required reports on the delivery,

inspection, acceptance and recording of the SMEs;

c. coordinate with and inform in writing the concerned CO Officials

regarding the undelivered packages of the SME Kits and those

delivered with deficiencies. Monitor the delivery of the remaining

undelivered packages;

d. observe the issuance of Property Acknowledgment Receipts and

Inventory Custodian Slips by the Property Custodian upon release of

the items to coordinators and teachers, and maintenance of a log book

to monitor the borrowings and returns of the said items; and

e. establish proper accountability on the missing and/or unaccounted

items as noted during inspection by the Audit Team. In case of

neglect of duty, impose appropriate sanction against the erring

personnel for the loss of the delivered items.

6. The implementation of CY 2015 DepEd Computerization Program (DCP)

with allocated budget of P7,400,223,434.82 was not fully attained due to

extended timelines in the performance of some procurement activities and

inability of the awarded suppliers to comply with the targeted delivery period,

thus, the information and communication technology (ICT) equipment was

not made available to the intended beneficiaries at the most opportune time.

xi

Moreover, to address the perennial delay encountered in the program

implementation, the DepEd transferred P2,800,639,480.00 to United Nations

Development Programme (UNDP) to handle the procurement of ICT

equipment covering the CYs 2015 and 2016 budgets. (Observation No. 6)

We recommended that the Management require the concerned offices to:

a. re-assess the existing procurement process and address the

underlying causes for the delayed awarding of contracts and concerns

that are within the DepEd’s control;

b. strictly observe the timelines provided in RA No. 9184 in the

performance of procurement activities especially in contract

approval or signing;

c. strictly adhere to the Government Accounting Manual with regard to

financial reporting compliance;

d. advise ICTS to submit a justification for the grant of contract

extension of the two identified suppliers, otherwise, it is

recommended that the Accounting Division should impose the

corresponding liquidated damages;

e. consider decentralization of procurement in selected areas in line

with the fiscal responsibility principle for an efficient and effective

functioning of the DepEd’s procurement system;

f. for fund transfer made to UNDP, provide necessary documents, such

as the cost-benefit analysis, detailed breakdown of items to be

procured including other components chargeable out of the

transferred funds to UNDP, operating guidelines to include

accounting and reporting requirements for the settlement thereof, to

establish the propriety that the support services of UNDP is more

advantageous to the DepEd and the government as a whole; and

g. designate or assign specific unit which shall coordinate with UNDP

regarding the transfer of ownership for the ICTS equipment and

instruct the Accounting Division and Asset Management Division

(AMD) to coordinate and effect appropriate adjustment in the books.

7. Aside from the delayed procurement and deliveries to recipient schools, other

factors adversely affecting the implementation of DCP such as non-utilization

due to unreadiness of recipient schools, loss ICT packages, and defective poor

after sale assistance from suppliers were also reported that resulted in non-

utilization and eventual deterioration of the ICT Equipment. (Observation No.

7)

xii

We recommended that the Management require the concerned officers

to:

a. assess the readiness of the intended school recipients particularly

infrastructure requirements before including them as beneficiaries of

the ICT packages;

b. consider the allocation of budget for the construction of computer

classrooms especially for those without funds for the purpose;

c. revisit the guidelines and procedure on the implementation of DCP at

all levels, review the process involved in the recording of deliveries

and establishing accountability over the ICT packages;

d. strictly enforce the warranty and after sales support provision of the

contracts against the suppliers by charging liquidated damages or

blacklisting the same from other DCP procurement; and

e. impose appropriate sanctions under RA No. 9184 on suppliers who

refused to rectify defects or replace missing/incomplete/damaged

units/parts on delivered items.

8. The Repair and Rehabilitation of School Building Project in 12 Regions with

an aggregate contract amount of at least P718,331,308.56 had reported several

implementation lapses/deficiencies that affected the early achievement of the

project’s physical target of increasing the provision of safe and structurally

stable school facilities conducive to learning. (Observation No. 8)

We recommended that the Management require concerned offices to:

a. exercise close monitoring and strict supervision on the

implementation of repairs and rehabilitation of school building

projects to immediately resolve issues and lapses that will affect the

delivery of DepEd’s physical targets of addressing resource gap in

school facilities and the provision of adequate, safe, comfortable and

functional facilities conducive to learning and teaching;

b. validate as necessary the status of accomplishments of repair/

rehabilitation projects through the Region/Division Engineers to

ensure that projects are on schedule, that repair works are performed

in accordance with the approved Program of Works (POW) and that

defects, if there are any, will be rectified accordingly; and

c. comply with applicable provisions of RA No. 9184 and its Revised

IRR in all phases of procurements activities, and with reporting

requirements prescribed by DepEd policies and COA rules and

regulations.

xiii

9. Structural and other identified defects that were not rectified/fixed in the

school buildings implemented under the Public-Private Partnership for

School Infrastructure Programs (PSIP) resulted in either idle or structurally

unstable/defective school facilities in Regions II, IV-A and VI. Likewise,

there were noted documentary requirements of the National Building Code of

the Philippines (NBCP) that were not yet submitted in Region IV-A.

(Observation No. 9)

We recommended that the Management of concerned DOs in Regions II,

IV-A and VI:

a. immediately notify the Division Physical Facilities Engineer on the

defects identified for proper coordination and reporting with

appropriate DepEd office in charged with PSIP to ensure that the

Proponent comply with its obligation to repair or rectify, at its own

cost, all defects and deficiencies on project’s compliance with the

Minimum Performance Standards and Specifications (MPSS) for the

safety of the students/teachers; and

b. ascertain compliance with the PD No. 1096, the 1997 NBCP and other

relevant rules and regulations related to construction.

10. The late release of Sub-AROs by the CO for the implementation of the School

Furniture Program (SFP), delay in the execution of procurement activities and

the inability of suppliers to meet delivery dates had compromised the

availability of school furnitures amounting to at least P153,353,807.69 in six

Regions, in disregard of the urgent nature of the program to timely address

the need for school furniture. Other deficiencies such as: (a) noted

defects/inferior quality/non-compliance with the technical specifications of at

least 2,043 delivered school furniture; (b) delay in the completion of new

school buildings intended to accommodate the deliveries in 27 recipient

schools; and (c) inconsistency/omission of the actual delivery dates in the

DRs and non-compliance with documentary requirements contributed to the

program’s unsatisfactory implementation. (Observation No. 10)

We recommended and the concerned Management agreed to:

a. make representation with the DepEd CO to facilitate the

downloading of funds and issuance of the authority to procure to

ensure the timely implementation of the SFP;

b. observe timelines in the execution of procurement activities and

ensure the proper utilization of the procured school furniture to meet

the objective of the program;

xiv

c. coordinate and/or discuss with the DepEd CO and the Department of

Public Works and Highways (DPWH) to synchronize timelines in the

construction of school buildings and provision of school furniture, to

ensure timely completion of the new school buildings and utilization

of the school furniture, and eventually address the needs of the

students;

d. report deliveries with defects/inferior quality to procuring DepEd

Office to require the supplier the repair or replacement of damaged

school furniture covered within the Warranty Period;

e. consider the actual dates of delivery indicated by the recipient schools

in imposing liquidated damages. For future deliveries, require the

designated Property Custodians/authorized school representatives to

indicate the actual dates of deliveries before signing the Delivery

Receipts (DRs) to properly determine supplier’s compliance with the

delivery timelines and to ensure that liquidated damages, if there are

any, are accurately computed;

f. require the submission of the DRs, Inspection and Acceptance Report

(IAR), Certificate of Acceptance and other relevant supporting

documents to determine the completeness of deliveries, to establish

the propriety of claim/s for payment by the supplier and for proper

recording by the Accounting and Property/Supply Divisions; and

g. direct the concerned RO and DO personnel to strengthen the

monitoring of the program implementation and inspection of the

deliveries to ensure faithful performance by the contractors of their

contractual obligation and ultimately address the urgent need of

school furniture.

11. The Redesigned Technical-Vocational High School Program for SY 2016-

2017 was not implemented as planned in eight Regions in view of the: (a) late

releases of Sub-ARO by the CO; (b) the delayed/non delivery of the Technical

Vocational and Livelihood (TVL) tools, materials and equipment costing at

least P218,431,506.66; and (c) non/limited use of the delivered items in at

least 70 schools due to, among others, the defects in the items/specification,

the schools’ unreadiness for the program, and lack of enrollees on TVL tracks.

Further, a number of delivered TVL items were unutilized and still in sealed

boxes and/or found stored separately in vacant rooms and hallways exposing

these property to harmful elements and risk of being damaged or loss thru

theft. (Observation No. 11)

xv

We recommended that the Management of the CO and the respective

ROs and DOs:

a. establish proper coordination among the CO, RO and DO to ensure

timely release of funds;

b. require the School Heads of Senior High Schools (SHSs) to closely

coordinate with their respective DOs and the ROs regarding the

specific requirements of the TVL tracks offered by their schools

particularly the need for a technical-vocational laboratory, qualified

teachers with expertise in the TVL courses, quantity and technical

specifications of the TVL equipment and point of delivery;

c. require the SHSs designated Property Custodians to monitor the

completeness of the deliveries and to report to their respective DOs

and/or ROs goods delivered that are not in accordance with the

technical specifications and/or damaged to facilitate their

replacement by the concerned supplier;

d. strictly enforce supplier’s compliance with the delivery period, and

require them to immediately deliver all the remaining items and

impose liquidated damages equivalent to one half of one percent of

the cost of unperformed portion for every day of delay, as stipulated

in the contract. See to it that the DRs are duly accomplished and

indicate therein the actual date of receipt of deliveries by the recipient

schools; and

e. check proper accounting recognition of the TVL materials, tools and

equipment and the corresponding depreciation where appropriate,

immediately upon advice of the ROs on the transfer of accountability.

12. Weakness in the procedures of the centralized payroll system and the leniency

in budgeting, resulted in:

a) presence of excess remittances of required contributions to Government

Service Insurance System (GSIS) amounting to P25,999,282.27 by the

DOs/IUs of their payroll requirements to Regional Office Proper (ROP)

to avoid the lapsing of Notice of Cash Allocations (NCAs) at the same

time with under remittances of P103,754,171.82 due to insufficient

allotment to cover the required remittance, which led to the improper use

of the over remittances to augment the funding requirement of other

DOs/IUs with budget deficit;

xvi

b) discrepancies between the payroll amount of P7,326,577,385.85 and

deposits/remittances of P7,291,997,632.75 per books of the NCR (ROP)

and its DOs/IUs as well as the unidentified/unreconciled lump sum and

abnormal negative balances of Due from Operating Units of

P865,846,694.45 and P166,275,346.28, respectively, in Region V;

c) non-deduction and remittance of P92,905,087.58 required contribution

for GSIS and P3,002,417.57 in favor of Pag-Ibig in Region XI; and

over/double payment of salaries amounting to P1,172,558.40 in Regions

I and X. (Observation No. 12)

We recommended that the Management undertake the following:

a. simplify the processing, paying and recording of payroll transactions

by decentralizing the same to the respective DOs/IUs. The DOs/IUs

should implement the School-based payroll in accordance with

DepEd Order No. 30 s. 2011 dated March 24, 2011;

b. strictly require the DOs/IUs to: a) transfer funds based on the actual

monthly payroll requirements/Summary of Cash Disbursement

Report (SCDR) and return the excess to the BTr; b) for those with

deficient payroll requirements, submit to the DBM an updated

plantilla to ensure realistic budget/appropriations for Personnel

Services; and c) regularly provide the ROP with a copy of deposit

slips to facilitate recording and reconciliation of financial records/

reports on payrolls;

c. direct the ROPs to reconcile its records with those of the DOs/IUs in

order to correct the discrepancies between the reciprocal accounts

Due from Operating Units and Due to Regional Office and require

DepEd NCR to refrain from closing the net balance of the said

reciprocal accounts in the Subsidy to Other National Government

Agencies or Financial Assistance to National Government Agencies;

d. require the settlement/refund of the overpaid salaries in Regions I

and X. Strictly ensure no duplication of records of employees in the

payroll data base to avoid double payment of salaries and deduct in

the payroll all monetary value of leaves without pay using the formula

prescribed under Civil Service Commission (CSC) Circular No. 08 s.

2014 and DepEd Memorandum No.78 s. 2016;

e. draw journal entry to correct the inappropriate take up of payroll

deductions in Region VIII; and

xvii

f. ensure that authorized deductions are done in the order of preference

in Region XI as prescribed in the GAA and the full implementation

of the ATM payroll system in Region XIII to avoid the risk of possible

loss or misapplication of public funds.

The foregoing audit observations and recommendations were communicated

through Audit Observation Memoranda (AOM) and discussed during the Exit Conference

with concerned DepEd officials and employees on June 23, 2017. Their comments were

incorporated in this Report, where appropriate.

G. Status of Settlement of Audit Suspensions, Disallowances and Changes

Out of total suspensions and disallowances of P5,727,522,060.64 and

P285,539,345.14, respectively, issued in Central/Regional/Division Offices, Bureaus and

attached Agencies of DepEd, only a total of P2,504,831,042.85 was settled leaving a

balance of P3,245,024,248.50 and P263,206,114.43, respectively, as of year-end.

H. Status of Implementation of Prior Year’s Audit Recommendations

Out of the 82 prior years’ audit recommendations, 22 of which were fully

implemented and 60 were partially implemented as shown below. The details are discussed

in Part III of this Report.

Status of Implementation Number Percentage

Fully Implemented

Partially Implemented

22

60

27

73

Total 82 100

We enjoin Management to ensure full implementation of all partially implemented

audit recommendations in prior years to improve the operational as well as financial

efficiency of the agency.

Republic of the Philippines

COMMISSION ON AUDIT Commonwealth Avenue, Quezon City

INDEPENDENT AUDITOR’S REPORT

Honorable Secretary LEONOR M. BRIONES Department of Education

Meralco Avenue, Pasig City

We have audited the accompanying consolidated financial statements of the Department

of Education which comprise the Consolidated Statement of Financial Position as at

December 31, 2016, and the Consolidated Statements of Financial Performance, Changes

in Net Assets/Equity, Cash Flows, Comparison of Budget and Actual Amounts, and

Notes to Financial Statements comprising a summary of significant accounting policies

and other explanatory information.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial

statements in accordance with Philippine Public Sector Accounting Standards (PPSAS),

and for such internal control as management determines is necessary to enable the

preparation of financial statements that are free from material misstatement, whether due

to fraud or error

Auditor’s Responsibility

Our responsibility is to express an opinion on these consolidated financial statements

based on our audit. We conducted our audit in accordance with Philippine Public Sector

Standards on Auditing (PPSSA). Those standards require that we comply with ethical

requirements and plan and perform the audit to obtain reasonable assurance about

whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the financial statements. The procedures selected depend on the auditor’s

judgment, including the assessment of the risks of material misstatement of the financial

statements, whether due to fraud or error. In making those risk assessments, the auditor

considers internal control relevant to the entity’s preparation and fair presentation of the

financial statements in order to design audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing an opinion on the effectiveness of

2

the entity’s internal control. An audit also includes evaluating the appropriateness of

accounting policies used and the reasonableness of accounting estimates made by

management, as well as evaluating the overall presentation of the consolidated financial

statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to

provide a basis for our audit opinion.

Basis for Qualified Opinion

As discussed in Part II of the Report, our audit disclosed the following audit observations

which affected the fair presentation of the consolidated financial statements:

1. Misstatements in Cash and Cash Equivalents due to discrepancy of

P497,652,480.71 between the Cash account balance and as confirmed by the

bank; and erroneous/unrecorded transactions amounting to P497,558.34;

2. Unreliable Receivables balance due to:

a. Past due Loans Receivable of P34,452,935.68 that have been outstanding for

more than one to 15 years;

b. The account Due from National Government Agencies-DBM-PS with an

unreconciled variance of P6,274,537,959.00 with DBM-PS account balance;

dormant and long outstanding accounts of P4,897,365,764.00; and

overstatement of P2,079,402,100.00 for settled items delivered that were not

derecognized;

c. Inclusion in the Inter-Agency and Other Receivables balances of past due

outstanding accounts in the amount of P310,457,780.00 aged over one year to

more than 10 years pertaining to unliquidated fund transferred to various

government agencies and non-government organizations;

3. Doubtful validity of Inventory accounts due to: (a) presence of dormant balance

amounting to P279,206,604.67 without details and schedules to validate its

existence; and (b) non-recognition/adjustment of damaged/lost textbooks

amounting to P5,890,310.38 still recognized in the books for more than five years,

and issuances of inventories and recorded purchases of supplies and materials not

yet delivered in total amount of P15,783,450.62;

4. Inaccurate balance of Property, Plant and Equipment due to: (a) unreconciled

difference of P23,414,327,275.25 between the accounting and property records;

(b) non-performance of physical inventory to verify existence and completeness

of reported assets in aggregate amount of P20,565,319,146.52; and (c) various

errors and omissions in recording transactions affecting PPE accounts like

inclusion of semi-expendable items costing at least P154,068,245.61, unrecorded

unserviceable/demolished/razed by fire/losses/transferred/disposed PPEs

3

amounting to P125,870,052.52, unrecorded properties of P628,900,400.34,

completed school buildings still in Construction in Progress account of

P532,714,034.49; and existence of unsubstantiated balances in total amount of

P757,710,107.68;

5. Doubtful validity of Advances due to existence of outstanding accounts in total

amount of P2,070,618,524.64 granted to officers and employees which remained

unliquidated as of year-end, hence, the corresponding expenses incurred out of the

cash advances were not recognized in the proper accounting period; and

erroneous/misclassified transactions in the amount of P157,876,747.84; and

6. Misstatements in the Liabilities due to: (a) net overstatement of

P1,404,934,265.19 for non-reversion of undocumented payables of

P1,047,087,873.75 and long outstanding payables without existing valid claims of

P365,737,390.70, and erroneous recording/omission of entries in the amount of

P7,890,999.26; and (b) liability accounts in aggregate amount of

P1,129,423,831.96 not supported by subsidiary ledgers to validate their existence.

Opinion

In our opinion, except for the effects on the consolidated financial statements of the

matters described in the Basis for Qualified Opinion paragraph, the consolidated financial

statements present fairly, in all material respects, the consolidated financial position of

the Department of Education as at December 31, 2016, and its financial performance,

changes in net assets/equity, cash flows, comparison of budget and actual amounts, and

notes to financial statements for the year then ended in accordance with PPSAS.

COMMISSION ON AUDIT

By:

MARIVEL C. BROÑOLA State Auditor V Supervising Auditor

DepEd Audit Group A1

28 June 2017

11

DEPARTMENT OF EDUCATION

Notes to Consolidated Financial Statements For the year ended December 31, 2016

1. General Information /Agency Profile

The consolidated financial statements of the Department of Education (DepEd) were

authorized for issue on March 31, 2017 as shown in the Statement of Management

Responsibility for Financial Statements signed by Ms. Victoria Catibog,

Undersecretary for Finance Disbursements and Accounting.

The DepEd is the primary agency of the government responsible to provide the

framework for the governance of basic education, which shall set the general

directions for educational policies, standards, established authority, accountability

and responsibility for achieving higher learning outcomes. It shall also fulfill the

mandate embodied in the Constitution per Article XVI, Section 1, which provides

that: “The State shall protect and promote the right of all citizens to quality education

at all levels and shall take steps to make such education accessible to all.” Its mission

is to provide quality education that is equitably accessible to lay the foundation for

holistic, life-long learning through critical and creative thinking. Its ultimate aim is

to develop Filipinos to be functionally literate, economically secure, socially and

morally responsible and nationalistic citizens who will contribute to sustain global

development.

On August 11, 2001, Republic Act (RA) No. 9155 or the “Basic Education

Governance Act of 2001” came into law and on August 22, 2012, the then DepEd

Secretary Edilberto C. De Jesus signed the Implementing Rules and Regulations

(IRR) of RA No. 9155.

RA No. 9155 renamed among others, the Department of Education, Culture and

Sports (DECS) to the Department of Education wherein the functions and programs

related to sports competition was transferred to the Philippine Sports Commission

(PSC) but the programs for school sports and physical fitness still forms part of basic

education curriculum. RA No. 9155 put emphasis on the decentralization of functions

and governance in basic education through the school based management framework

and mechanisms and stresses the principles of “shared governance.” The Act and its

IRR also call for an equitable, direct, immediate release of resources to field offices

and assuring that financial resources are within the reach of the schools. The

Department of Budget and Management (DBM) and the DepEd issued Joint Circular

(JC) No. 2004-1 dated January 1, 2004 which covers the release of funds to DepEd-

Central Office (CO), Regional Offices (RO) s, Division Offices (DO) and Secondary

Schools (SS) for their respective regular operating requirements, locally-funded and

foreign-assisted projects and the nationwide/region-wide lump-sum appropriations

as provided in the General Appropriations Act (GAA).

12

RA No. 10533, the Enhanced Basic Education Act of 2013, was signed by President

Benigno S. Aquino III on May 15, 2013 and its IRR was promulgated on

September 3, 2013. Under RA No. 10533, the enhanced basic education program

encompasses at least one year kindergarten education, six years elementary

education, six years secondary education wherein in the secondary education

includes four years of Junior High School (JHS) and two years Senior High School

(SHS). The K to 12 Program under RA No. 10533 envisions to provide sufficient

time for mastery of concepts and skills, develop lifelong learners, and prepare

graduates for tertiary education, middle-level skills development, employment, and

entrepreneurship.

The Agency registered office is located at DepEd Complex, Meralco Avenue Pasig

(formerly University of Life Complex).

DepEd Management Structure

To carry out its mandates and objectives, the Department is organized into two major

structural components. The Central Office maintains the overall administration of

basic education at the national level. The Field Offices are responsible for the

regional and local coordination and administration of the Department’s mandate. RA

9155 provides that the Department should have no more than four Undersecretaries

and four Assistant Secretaries with at least one Undersecretary and one Assistant

Secretary who are career service officers chosen among the staff of the Department.

In 2015, the Department underwent a restructuring of its office functions and staffing.

The result of which was the Rationalization Plan for the new organizational structure.

Details of the new structure are further explained in DepEd Order No. 52, s. 2015,

also known as the New Organizational Structures of the Central, Regional, and

Schools Division Offices of the Department of Education.

At present, the Department operates with four Undersecretaries in the following

areas:

• Curriculum and Instruction

• Finance and Administration

• Governance and Operations

• Legal and Legislative Affairs

Four Assistant Secretaries are assigned in the following areas:

• Curriculum and Instruction

• Finance and Administration

• Governance and Operations

• Legal and Legislative Affairs

13

Supporting the Office of the Secretary (OSEC) at the Central Office are the different

strands, services, bureaus, and divisions.

There are five strands under OSEC:

• Curriculum and Instruction

• Finance and Administration

• Governance and Operations

• Legal and Legislative Affairs

• Strategic Management

Five attached agencies:

• Early Childhood Care and Development (ECCD) Council

• National Book Development Board (NBDB)

• National Council for Children's Television (NCCT)

• National Museum

• Philippine High School for the Arts

Three coordinating councils:

• Adopt-a-School Program (ASP) Coordinating Council

• Literacy Coordinating Council (LCC)

• Teacher Education Council (TEC)

At the sub-national level, the Field Offices consist of the following:

• Seventeen Regional Offices, and the Autonomous Region in Muslim Mindanao

(ARMM*), each headed by a Regional Director (a Regional Secretary in the

case of ARMM).

• Two hundred twenty-one Provincial and City Schools Divisions, each headed

by a Schools Division Superintendent. Assisting the Schools Division Offices

are 2,602 School Districts, each headed by a District Supervisor.

Under the supervision of the Schools Division Offices are 62,605 schools, broken

down as follows:

• 49,209 elementary schools (38,648 public and 10,561 private)

• 13,396 secondary schools (7,976 public and 5,420 private)

*ARMM is included in the budget of the Department on the following: creation of

teaching and non-teaching positions; funding for newly-legislated high schools;

regular School Building Program; and certain foreign-assisted and locally-funded

programs and projects.

14

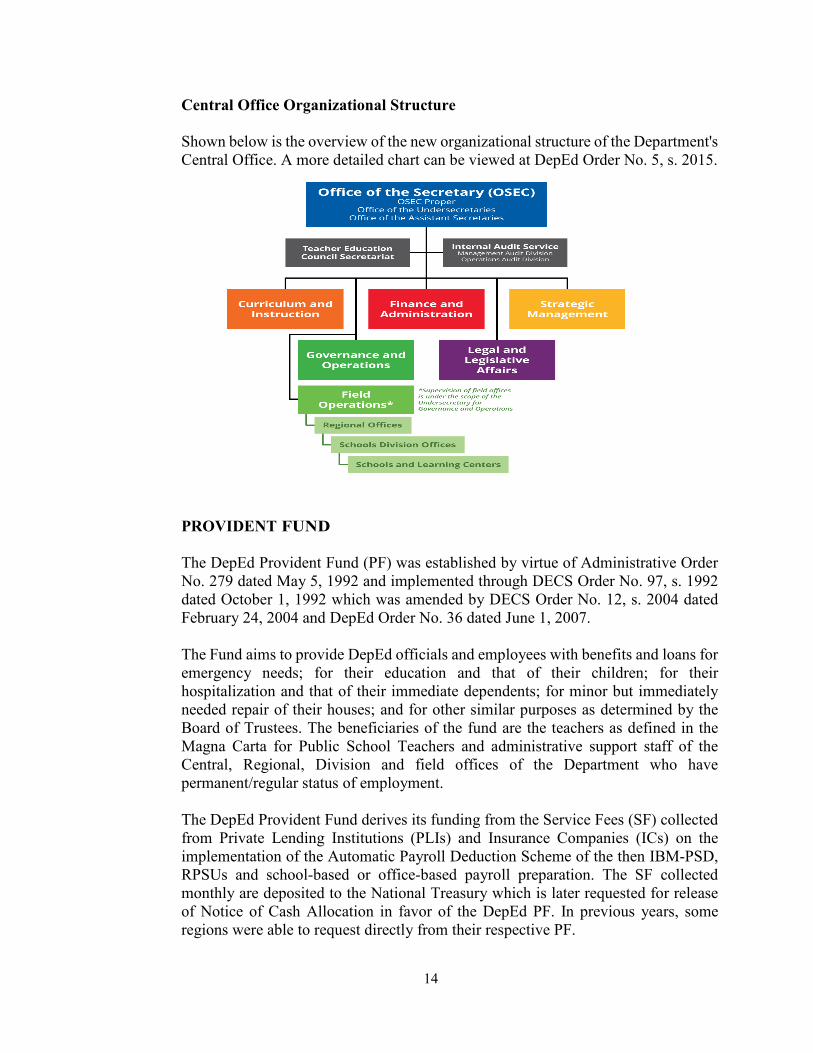

Central Office Organizational Structure

Shown below is the overview of the new organizational structure of the Department's

Central Office. A more detailed chart can be viewed at DepEd Order No. 5, s. 2015.

PROVIDENT FUND

The DepEd Provident Fund (PF) was established by virtue of Administrative Order

No. 279 dated May 5, 1992 and implemented through DECS Order No. 97, s. 1992

dated October 1, 1992 which was amended by DECS Order No. 12, s. 2004 dated

February 24, 2004 and DepEd Order No. 36 dated June 1, 2007.

The Fund aims to provide DepEd officials and employees with benefits and loans for

emergency needs; for their education and that of their children; for their

hospitalization and that of their immediate dependents; for minor but immediately

needed repair of their houses; and for other similar purposes as determined by the

Board of Trustees. The beneficiaries of the fund are the teachers as defined in the

Magna Carta for Public School Teachers and administrative support staff of the

Central, Regional, Division and field offices of the Department who have

permanent/regular status of employment.

The DepEd Provident Fund derives its funding from the Service Fees (SF) collected

from Private Lending Institutions (PLIs) and Insurance Companies (ICs) on the

implementation of the Automatic Payroll Deduction Scheme of the then IBM-PSD,

RPSUs and school-based or office-based payroll preparation. The SF collected

monthly are deposited to the National Treasury which is later requested for release

of Notice of Cash Allocation in favor of the DepEd PF. In previous years, some

regions were able to request directly from their respective PF.

15

However, as the DepEd Central Office move to standardize operations, such

procedure is no longer allowed. Instead, certifications of deposits from the National

Treasury are submitted to the Central Office as integral document for issuance of

Notice of Cash Allocations (NCAs) from the DBM and subsequently allocated to the

Regional Offices following certain criteria and procedures.

The following is the manner of allocation and distribution of service fee (which form

part of the additional equity/capital of the PF) per Resolution No. 01, s. 2010 issued

by the National Board:

• Twenty percent of the service fee collections shall be transferred to the National

Common Fund;

• Fifty percent of the amount of service fee collected by the concerned regional

implementing units shall be returned to them; and

• The remaining balance shall be distributed among the regional implementing

units based on equity and performance on a 60/40 ratio.

The types of loan that can be availed by the borrowers with six percent per annum

interest add-on and straight computation is stated below:

A. Regular loans – for emergency needs of the teachers/employees, or immediate

and other members of his/her family up to the fourth degree of consanguinity

and affinity (up to P100,000.00)

• Hospitalization and/or medical expenses resulting from an accident/

illness;

• Death of immediate and /or other members of his/her family;

• Minor but immediately needed repair of the house of the teacher/

employee;

• Educational loans;

• Other emergency expenses to be specified by the teacher/employee-

applicant;

B. Additional loan (up to P100,000.00) can be granted at the discretion of the

Secretary to teachers and non-teaching employees, suffering from extreme

financial difficulty because of an immediate need for financial assistance and

whose final recourse is the DepEd Provident Fund;

C. Calamity loan (maximum of P20,000.00) may be availed in areas and

provinces declared under State of Calamity.

The accumulated interests earned from the lending operations over the years also

work as a revolving fund for continuous loaning operations. Administrative expenses

to support the operations are allowed but not to exceed 20% of the current year

interest income earned.

16

The fund is being managed by the (1) National Board of Trustees which promulgate

rules and policies governing operations of the Fund, (2) the Regional Board of

Trustees which implement the policies, rules and regulations promulgated by the

National Board and supervises the Fund operations to their respective regions,

(3) and along with them are the designated Secretariats of the National/Regional

Boards that serve as the implementing arm of the Fund. Currently, the Chairman for

the National Board of Trustees is Undersecretary Victoria M. Catibog and Assistant

Secretary Jesus L.R. Mateo sits as Vice-Chairman of the Board.

DEPARTMENT OF EDUCATION - REGIONAL EDUCATION CENTERS

(RELC)

The Department of Education has incomes derived from business-type activities

operating under the Revolving Fund concept. The incomes are derived from the

rentals and use of DepEd facilities, such as the Regional Education Learning Centers

(RELC), The Ecological Technology Livelihood Community Center (Ecotech

Center), Baguio Teacher’s Camp, the National Educators Academy of the

Philippines (NEAP), Applied Nutrition Center (ANC) and the National Science

Teacher Instrumentation Centers (NSTIC). Most of the Regional Offices have

operating RELCs except for Region IV-B; the Ecotech Center, ANC and NSTIC are

located in Cebu City; as the name implies, the Baguio Teacher’s Camp is situated in

Baguio City.

• Regional Educations Learning Centers (RELC)

RELCs have been established under the Program for Decentralized Educational

Development (PRODED) to sustain the capability of the regions to effectively

and efficiently manage their staff. As envisioned, this center was designed to

meet the educational needs of school officials and teachers in the regions in

relation to education innovations and program implementation. On March 25,

1987, DECS Order No. 30, s. 1997 – Guidelines for the Effective Utilization of

the Regional Educational Learning Centers was issued.

• National Educator’s Academy of the Philippines (NEAP)

Letter of Instruction No. 1487 dated December 10, 1985 created the National

Education Learning Center (NELC). This is to sustain gains derived from the

Program for Decentralized Educational Development (PRODED). It mainly

addressed concerns related to the improvement of the curricula and

development of better instructional materials, the reorientation and retraining

of teachers and the improvement of the management capabilities of

superintendents, supervisors and administrators at the elementary level. On

May 27, 1992, Administrative Order No. 282 was issued renaming NELC to

National Educators’ Academy of the Philippines (NEAP).

17

• Ecological Technology Livelihood and Community Center (Ecotech)

The Ecological Technology Livelihood Community Center, usually referred to

as “ECOTECH CENTER” is an inter-agency project by and between the

Department of Education and the defunct Ministry of Human Settlements.

The center was established in 1978 and acquired by DECS on August 25, 1989

from the Strategic Development Corporation (SIDCOR) as stipulated in a Deed

of Assignment executed by both parties on August 9, 1989 for a considerable

amount of P9,055,594.00. The lot where the center is situated was donated by

the Provincial Government of Cebu and was transferred in the name of DepEd

on February 8, 1999 per TCT No. 150266.

• Baguio Teacher’s Camp

The Baguio Teachers’ Camp is a year-round center for conferences, seminar-

workshops, and training and human resource development program for the

Department of Education (DepEd). Whenever possible, the Camp is also open

for the housing and conference needs of other government agencies, student and

professional organizations holding conferences in Baguio City. It also

accommodates teachers, school officials and other DepEd personnel and their

guests who are vacationing in Baguio City. This is a privilege extended to

teachers as a fitting tribute to their role in education in the country.

The Camp, with an area of 23.7 hectares, has 12 dormitories that can

accommodate 1,208 guests, 47 cottages with a bed capacity of 446, seven

conference halls and other facilities such as the water system. The Camp

provides the upkeep and maintenance of these facilities, including its grounds

and gardens. A staff of very competent personnel attends to these various areas.

• National Science Teaching Instrumentation Center (NSTIC)

The National Science Teaching Instrumentation Center (NSTIC) is part of the

Science Teaching Improvement Project (STIP), which started in 1989. The

project was implemented by DECS-EDPITAF and GTZ, the German Agency

for Technical Cooperation. On July 1993, President Fidel V. Ramos

institutionalized the Center through Executive Order No. 112 mandated to

undertake the following tasks:

• to develop prototypes of science teaching equipment using locally available

materials and technology;

• to develop user’s and experimentation manuals;

• to facilitate technology transfer to the private sector that will mass-produce

the science equipment developed by the Center;

• to provide training programs for science teachers;

18

• to undertake quality control; and

• to implement a system of repair and maintenance for the science equipment

• School Health and Nutrition Center

The Department of Education, through the School Health and Nutrition Center

(SHNC), established in 1975 four nutrition centers nationwide to oversee the

implementation of the nutrition and health activities throughout the country.

These centers were named Applied Nutrition Center (ANC).

The facilities are not only for the learning centers of the Department but also compete

in the market for affordable venues for conferences, seminars, workshops and trainings

and other related activities. Not only the trainings and workshops of the Department

are held in these facilities but other Government Agencies and Private Entities as well

appreciate and choose the decent services that these Centers can offer.

I. Basic Education Profile

The Department of Education manages a considerable number of schools, personnel,

and learners which act as the software and hardware of delivering quality basic

education to every Filipino. For the year 2016, DepEd ensured to provide for the basic

necessities and requirements needed to facilitate continuous learning and over-all

development of Filipino learners across the nation.

Our schools

Nationwide, there are 221 school divisions and 2,683 school districts. The table below

summarizes the number of schools offering the basic education curriculums:

Out of the above mentioned schools, the following table shows the number of schools

offering special curricular program.

Particulars Number of Schools

Secondary schools offering Special Programs 2,480

Regular schools with Special Education (SPED) centers 278

Schools operating solely as SPED centers 7

Special Science Elementary Schools 304

Sector

Number of Schools Offering

Kindergarten &

Elementary Schools

Junior High

School

Senior High

School Total

Public 38,803 8,282 5,958 53,043

Private 11,680 5,935 4,373 21,988

LUCs & SUCs 42 243 226 511

Total 50,525 14,460 10,557

19

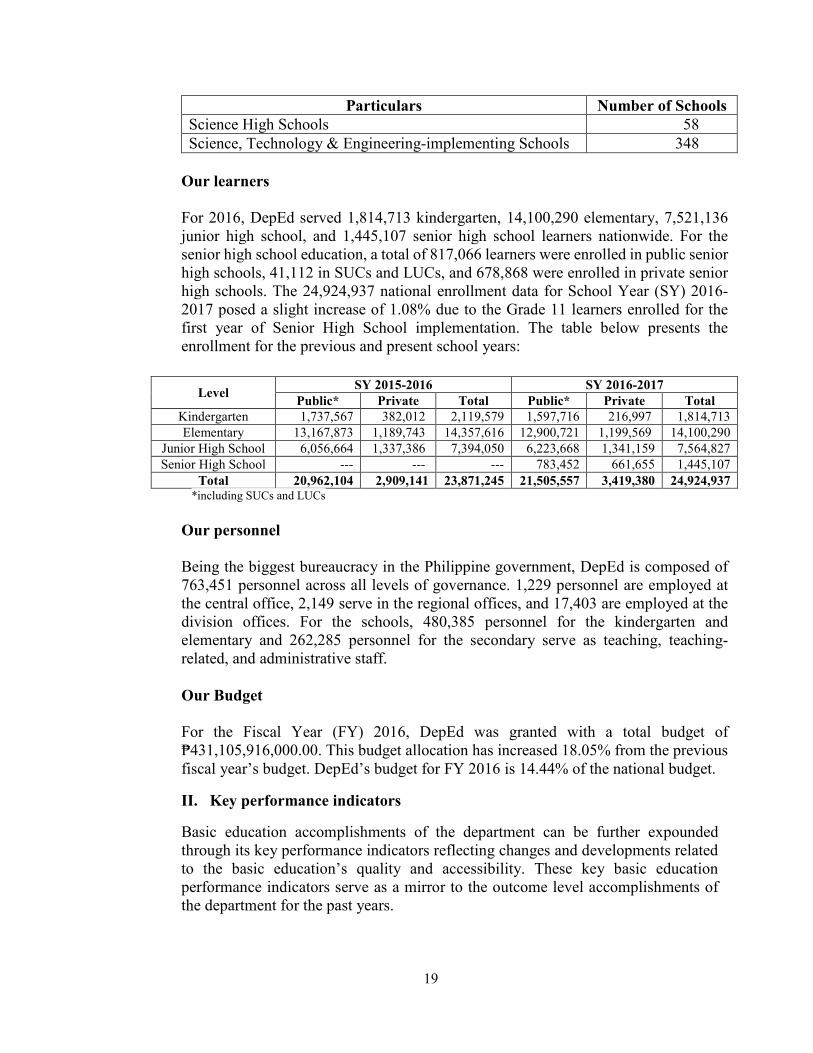

Particulars Number of Schools

Science High Schools 58

Science, Technology & Engineering-implementing Schools 348

Our learners

For 2016, DepEd served 1,814,713 kindergarten, 14,100,290 elementary, 7,521,136

junior high school, and 1,445,107 senior high school learners nationwide. For the

senior high school education, a total of 817,066 learners were enrolled in public senior

high schools, 41,112 in SUCs and LUCs, and 678,868 were enrolled in private senior

high schools. The 24,924,937 national enrollment data for School Year (SY) 2016-

2017 posed a slight increase of 1.08% due to the Grade 11 learners enrolled for the

first year of Senior High School implementation. The table below presents the

enrollment for the previous and present school years:

Level SY 2015-2016 SY 2016-2017

Public* Private Total Public* Private Total

Kindergarten 1,737,567 382,012 2,119,579 1,597,716 216,997 1,814,713

Elementary 13,167,873 1,189,743 14,357,616 12,900,721 1,199,569 14,100,290

Junior High School 6,056,664 1,337,386 7,394,050 6,223,668 1,341,159 7,564,827

Senior High School --- --- --- 783,452 661,655 1,445,107

Total 20,962,104 2,909,141 23,871,245 21,505,557 3,419,380 24,924,937 *including SUCs and LUCs

Our personnel

Being the biggest bureaucracy in the Philippine government, DepEd is composed of

763,451 personnel across all levels of governance. 1,229 personnel are employed at

the central office, 2,149 serve in the regional offices, and 17,403 are employed at the

division offices. For the schools, 480,385 personnel for the kindergarten and

elementary and 262,285 personnel for the secondary serve as teaching, teaching-

related, and administrative staff.

Our Budget

For the Fiscal Year (FY) 2016, DepEd was granted with a total budget of

₱431,105,916,000.00. This budget allocation has increased 18.05% from the previous

fiscal year’s budget. DepEd’s budget for FY 2016 is 14.44% of the national budget.

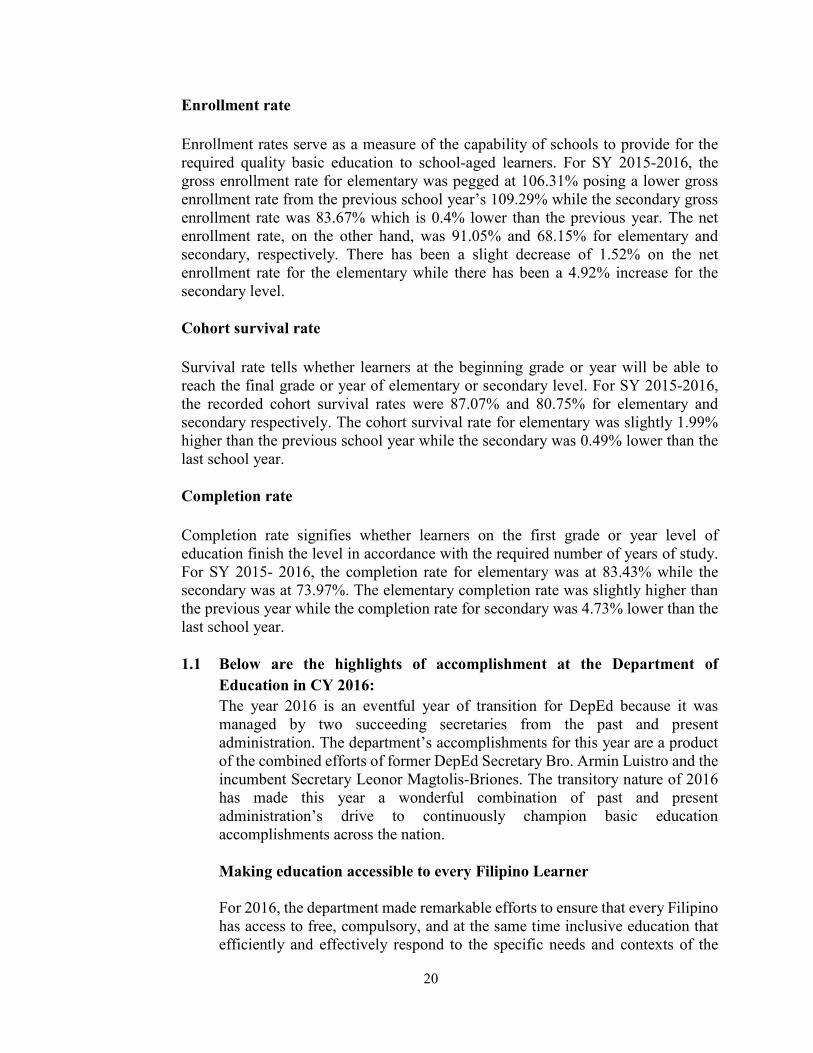

II. Key performance indicators

Basic education accomplishments of the department can be further expounded

through its key performance indicators reflecting changes and developments related

to the basic education’s quality and accessibility. These key basic education

performance indicators serve as a mirror to the outcome level accomplishments of

the department for the past years.

20

Enrollment rate

Enrollment rates serve as a measure of the capability of schools to provide for the

required quality basic education to school-aged learners. For SY 2015-2016, the

gross enrollment rate for elementary was pegged at 106.31% posing a lower gross

enrollment rate from the previous school year’s 109.29% while the secondary gross

enrollment rate was 83.67% which is 0.4% lower than the previous year. The net

enrollment rate, on the other hand, was 91.05% and 68.15% for elementary and

secondary, respectively. There has been a slight decrease of 1.52% on the net

enrollment rate for the elementary while there has been a 4.92% increase for the

secondary level.

Cohort survival rate

Survival rate tells whether learners at the beginning grade or year will be able to

reach the final grade or year of elementary or secondary level. For SY 2015-2016,

the recorded cohort survival rates were 87.07% and 80.75% for elementary and

secondary respectively. The cohort survival rate for elementary was slightly 1.99%

higher than the previous school year while the secondary was 0.49% lower than the

last school year.

Completion rate

Completion rate signifies whether learners on the first grade or year level of

education finish the level in accordance with the required number of years of study.

For SY 2015- 2016, the completion rate for elementary was at 83.43% while the

secondary was at 73.97%. The elementary completion rate was slightly higher than

the previous year while the completion rate for secondary was 4.73% lower than the

last school year.

1.1 Below are the highlights of accomplishment at the Department of

Education in CY 2016:

The year 2016 is an eventful year of transition for DepEd because it was

managed by two succeeding secretaries from the past and present

administration. The department’s accomplishments for this year are a product

of the combined efforts of former DepEd Secretary Bro. Armin Luistro and the

incumbent Secretary Leonor Magtolis-Briones. The transitory nature of 2016

has made this year a wonderful combination of past and present

administration’s drive to continuously champion basic education

accomplishments across the nation.

Making education accessible to every Filipino Learner

For 2016, the department made remarkable efforts to ensure that every Filipino

has access to free, compulsory, and at the same time inclusive education that

efficiently and effectively respond to the specific needs and contexts of the

21

learners. The Department of Education strengthened its commitment to make

education accessible to every Filipino learner. In this regard, the department is

committed to ensure that there is inclusion of all learners in education through

reaching out and catering to all types of learners regardless of age, gender,

religion, and capacity.

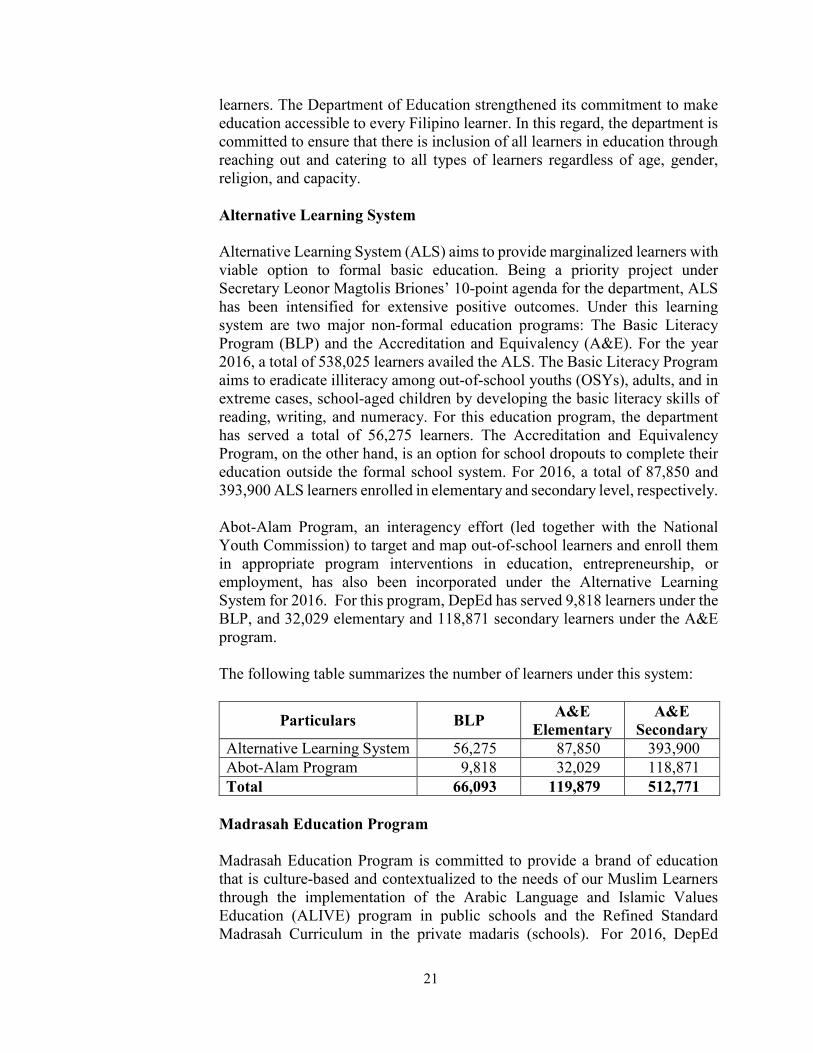

Alternative Learning System

Alternative Learning System (ALS) aims to provide marginalized learners with

viable option to formal basic education. Being a priority project under

Secretary Leonor Magtolis Briones’ 10-point agenda for the department, ALS

has been intensified for extensive positive outcomes. Under this learning

system are two major non-formal education programs: The Basic Literacy

Program (BLP) and the Accreditation and Equivalency (A&E). For the year

2016, a total of 538,025 learners availed the ALS. The Basic Literacy Program

aims to eradicate illiteracy among out-of-school youths (OSYs), adults, and in

extreme cases, school-aged children by developing the basic literacy skills of

reading, writing, and numeracy. For this education program, the department

has served a total of 56,275 learners. The Accreditation and Equivalency

Program, on the other hand, is an option for school dropouts to complete their

education outside the formal school system. For 2016, a total of 87,850 and

393,900 ALS learners enrolled in elementary and secondary level, respectively.

Abot-Alam Program, an interagency effort (led together with the National

Youth Commission) to target and map out-of-school learners and enroll them

in appropriate program interventions in education, entrepreneurship, or

employment, has also been incorporated under the Alternative Learning

System for 2016. For this program, DepEd has served 9,818 learners under the

BLP, and 32,029 elementary and 118,871 secondary learners under the A&E

program.

The following table summarizes the number of learners under this system:

Particulars BLP A&E

Elementary

A&E

Secondary

Alternative Learning System 56,275 87,850 393,900

Abot-Alam Program 9,818 32,029 118,871

Total 66,093 119,879 512,771

Madrasah Education Program

Madrasah Education Program is committed to provide a brand of education

that is culture-based and contextualized to the needs of our Muslim Learners

through the implementation of the Arabic Language and Islamic Values

Education (ALIVE) program in public schools and the Refined Standard

Madrasah Curriculum in the private madaris (schools). For 2016, DepEd

22

served a total number of 938,966 elementary and 253,435 secondary muslim

learners. 2,368 of these learners benefitted from the private madaris provided

with financial assistance and 1,046 azatids (teachers) were provided with

compensation, allowance, and were trained during the in-service training.

Indigenous Peoples Education Program

Indigenous Peoples Education Program (IPEd) offers indigenous peoples (IP)

with a context-based education that considers their indigenous beliefs,

practices, and cultures and at the same time promote the knowledge translation

across generations. A total of 2,251,765 elementary and 678,072 secondary

learners were enrolled in the IPEd program in 2016. The number of IP learners

for 2016 increased by 20% from the previous year. Efforts were also made to

ensure that the IP cultures and traditions were incorporated in the development

and implementation of the K to 12 curriculum.

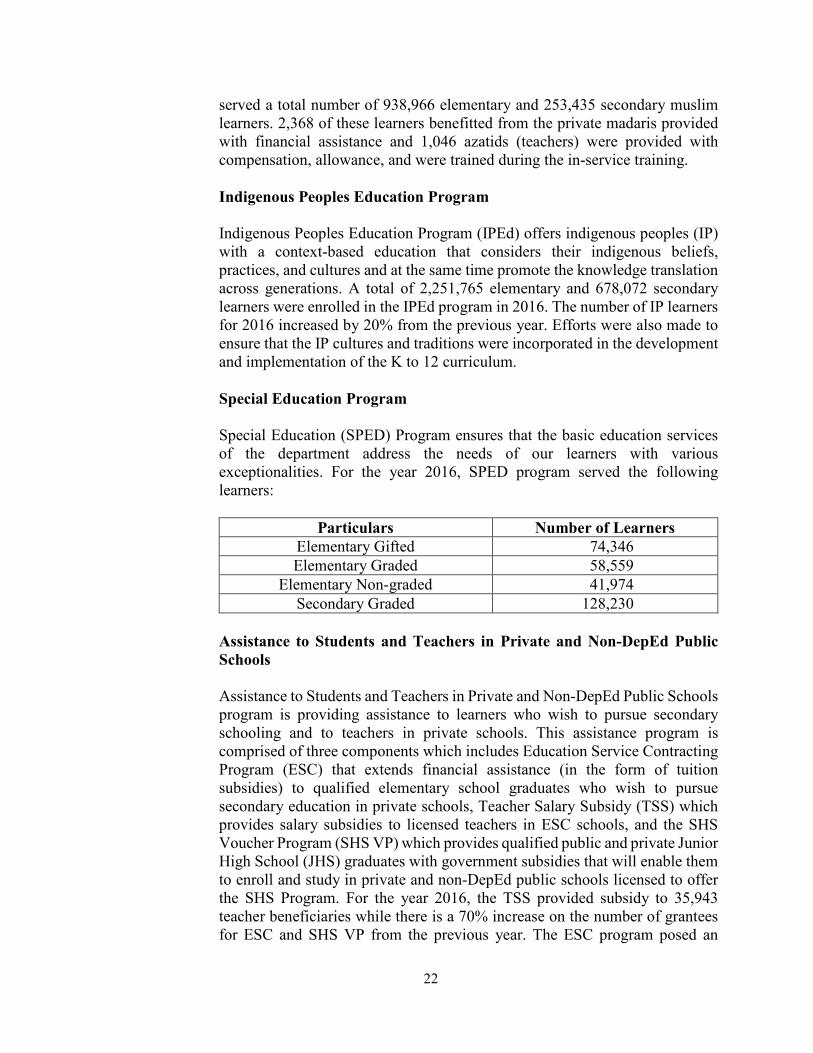

Special Education Program

Special Education (SPED) Program ensures that the basic education services

of the department address the needs of our learners with various

exceptionalities. For the year 2016, SPED program served the following

learners:

Particulars Number of Learners

Elementary Gifted 74,346

Elementary Graded 58,559

Elementary Non-graded 41,974

Secondary Graded 128,230

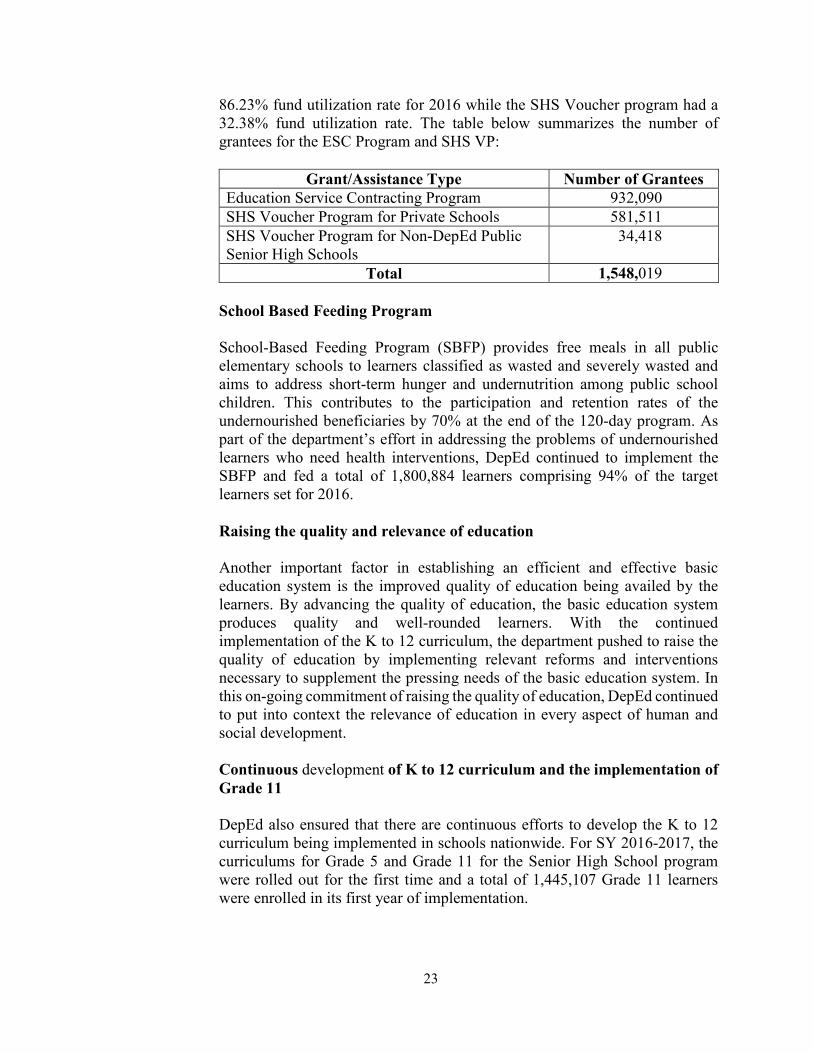

Assistance to Students and Teachers in Private and Non-DepEd Public

Schools

Assistance to Students and Teachers in Private and Non-DepEd Public Schools

program is providing assistance to learners who wish to pursue secondary

schooling and to teachers in private schools. This assistance program is

comprised of three components which includes Education Service Contracting

Program (ESC) that extends financial assistance (in the form of tuition

subsidies) to qualified elementary school graduates who wish to pursue

secondary education in private schools, Teacher Salary Subsidy (TSS) which

provides salary subsidies to licensed teachers in ESC schools, and the SHS

Voucher Program (SHS VP) which provides qualified public and private Junior

High School (JHS) graduates with government subsidies that will enable them

to enroll and study in private and non-DepEd public schools licensed to offer

the SHS Program. For the year 2016, the TSS provided subsidy to 35,943

teacher beneficiaries while there is a 70% increase on the number of grantees

for ESC and SHS VP from the previous year. The ESC program posed an

23

86.23% fund utilization rate for 2016 while the SHS Voucher program had a

32.38% fund utilization rate. The table below summarizes the number of

grantees for the ESC Program and SHS VP:

Grant/Assistance Type Number of Grantees

Education Service Contracting Program 932,090

SHS Voucher Program for Private Schools 581,511

SHS Voucher Program for Non-DepEd Public

Senior High Schools

34,418

Total 1,548,019

School Based Feeding Program