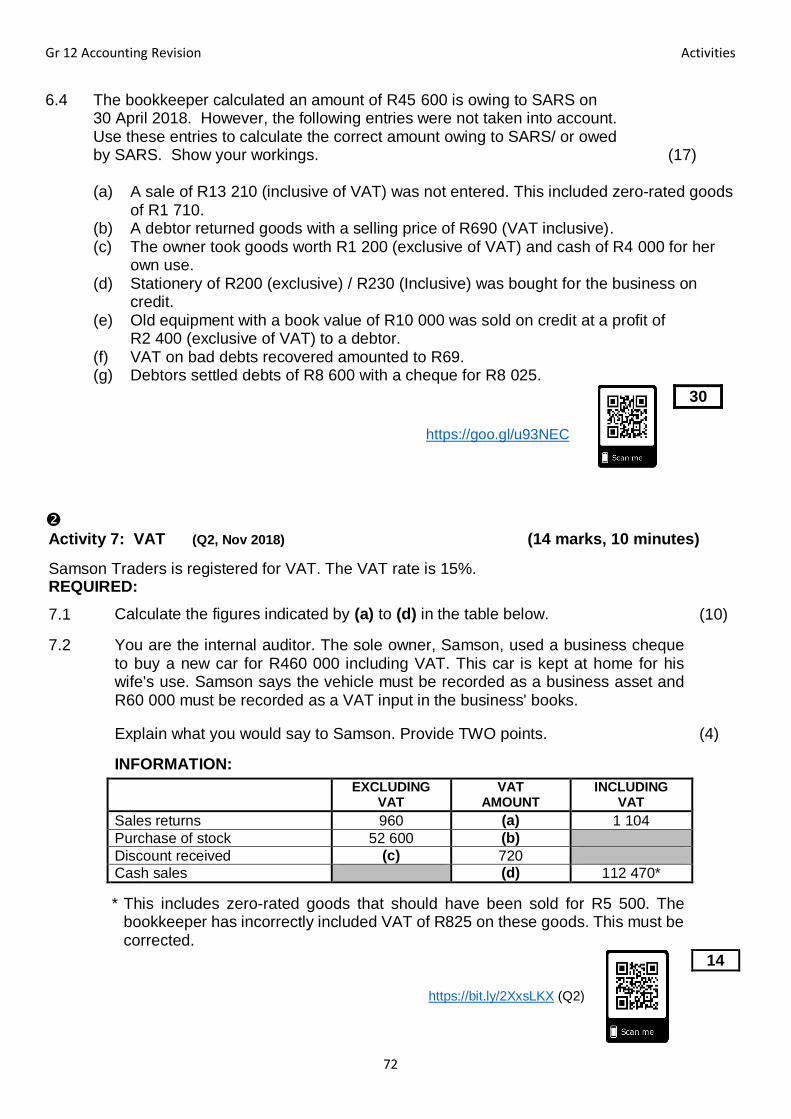

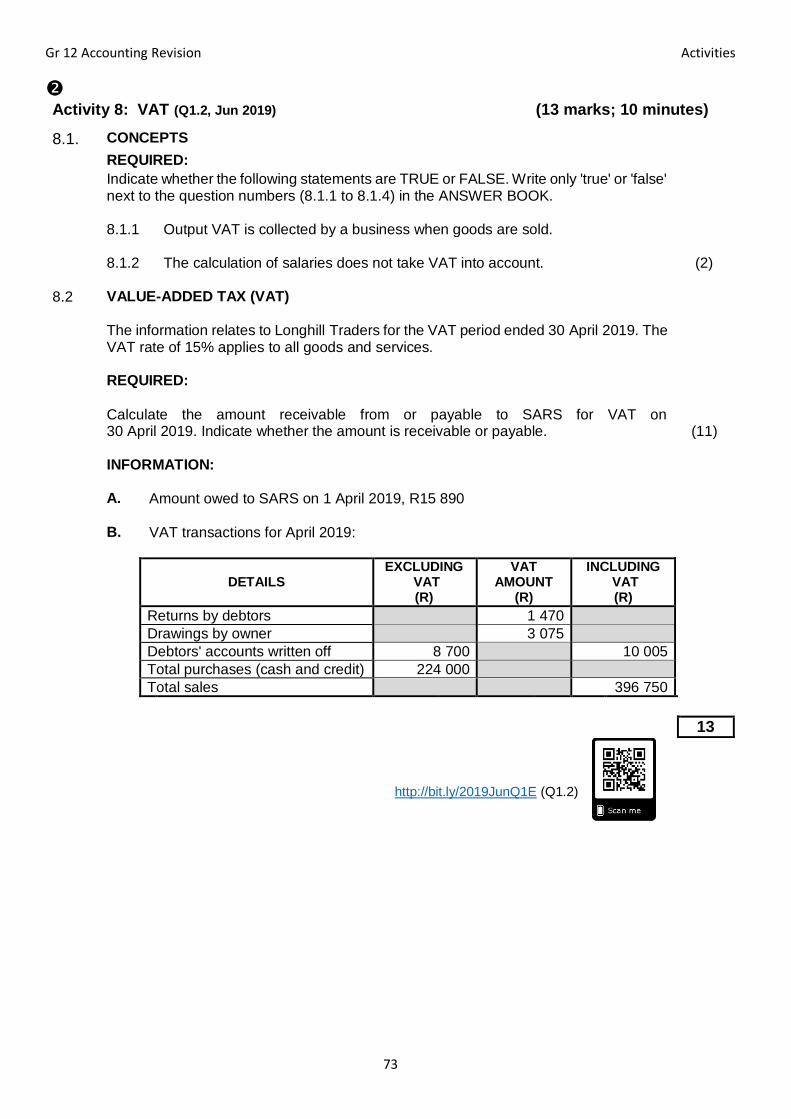

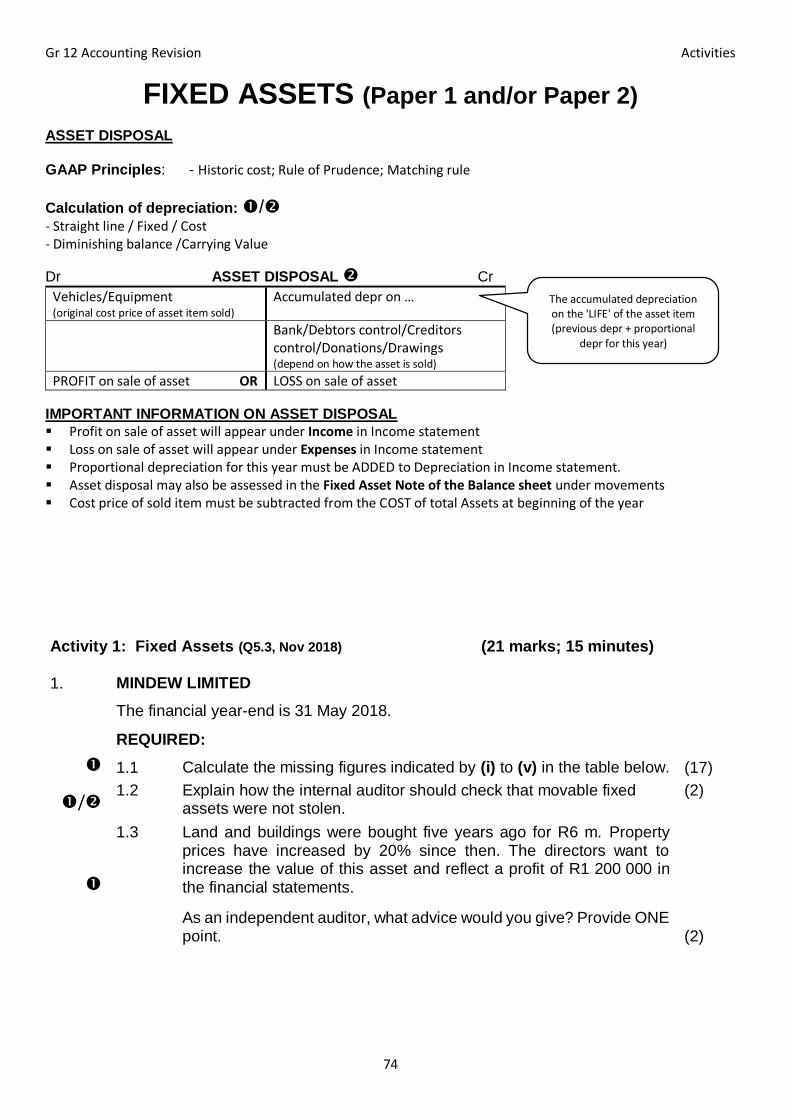

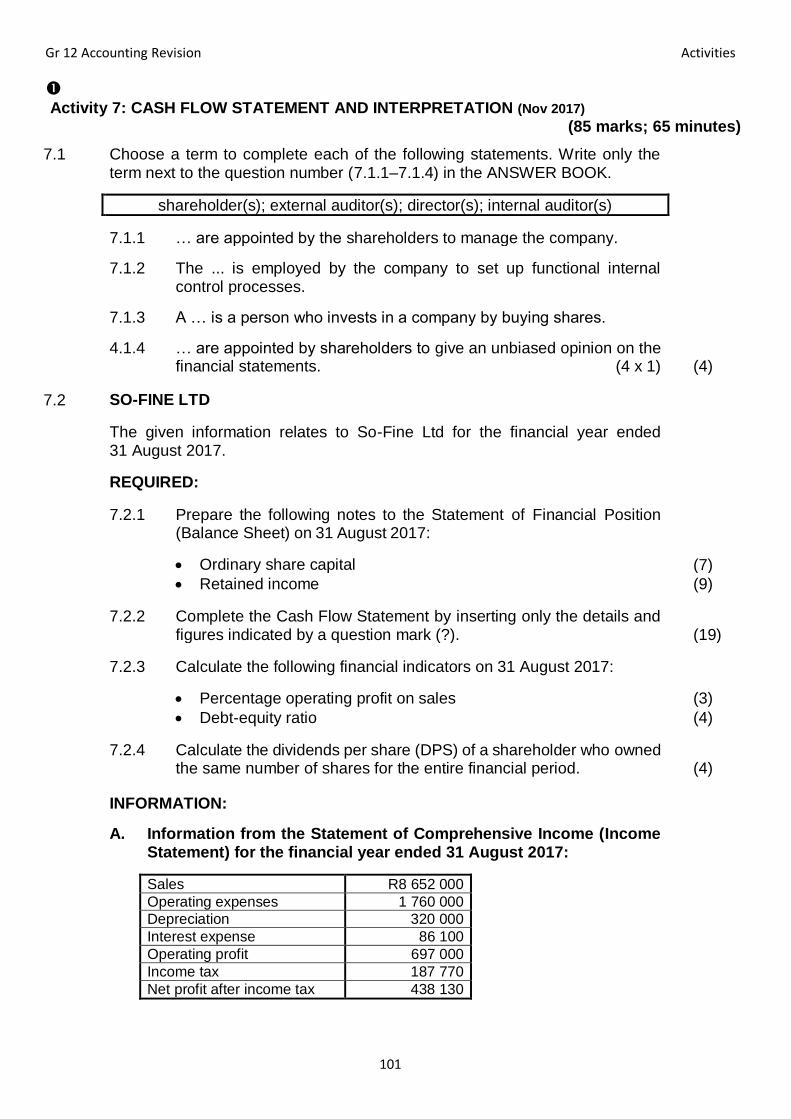

activities - holy cross high school

TRANSCRIPT

Directorate: Curriculum FET

ACCOUNTING

Gr 12

Revision

ACTIVITIES

Gr 12 Accounting Revision Activities

2

INDEX

TOPIC Page No.

Inventory Core notes 4

Activities 1 - 7 5 - 17

Reconciliations Core notes: Bank-, Creditors-, Debtors reconciliation 18 - 20

Activities 1 - 8 20 - 33

Manufacturing Core notes 34

Activities 1 - 7 35 - 48

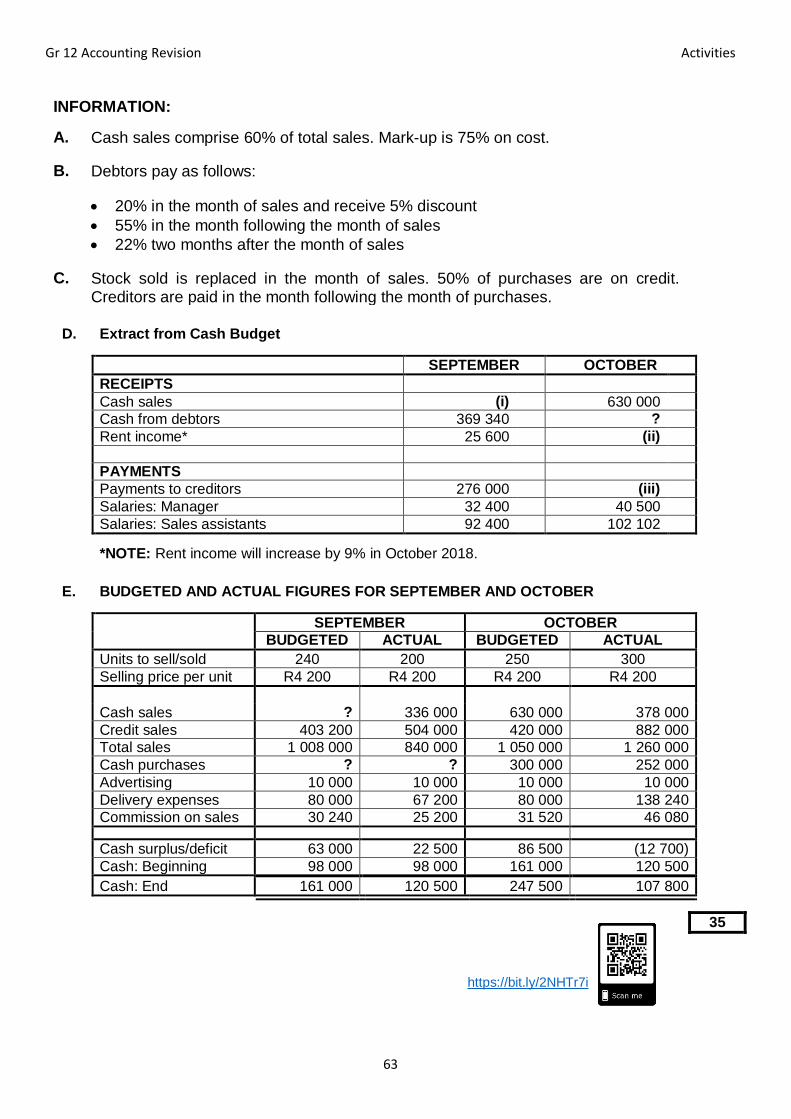

Budgets Core notes 49

Activities 1 - 8 50 - 65

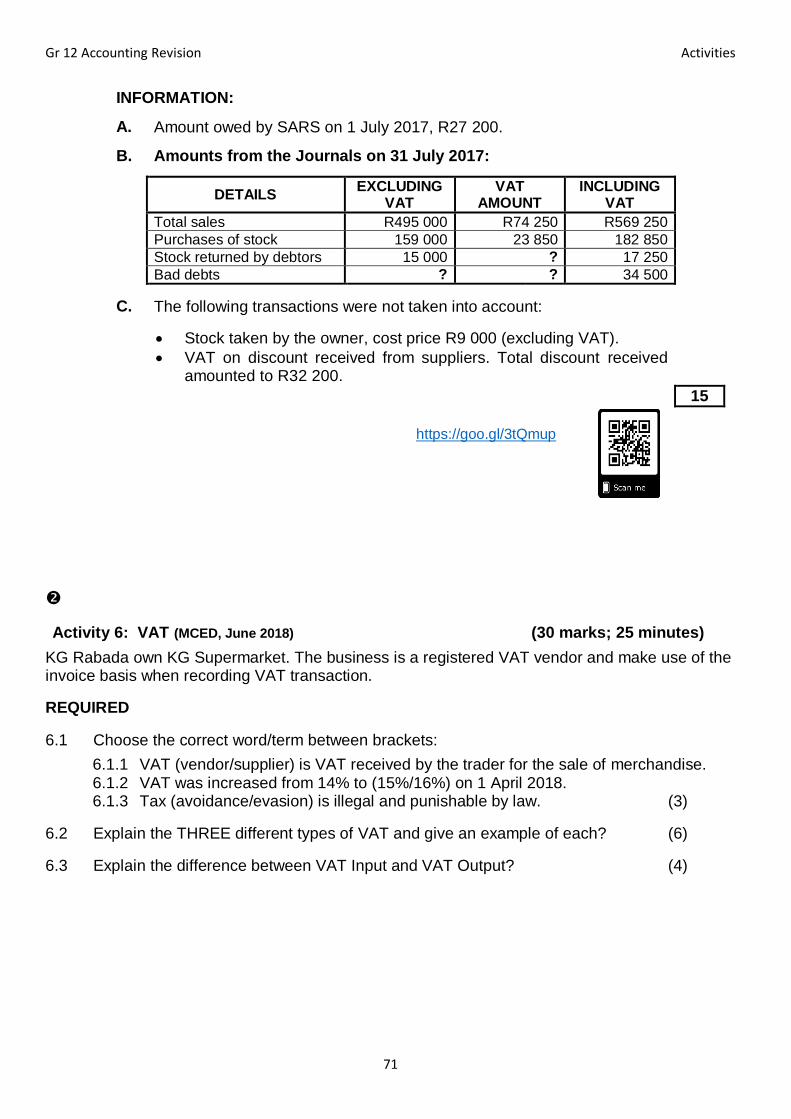

VAT Core notes 66

Activities 1 - 8 66 - 73

Fixed Assets Core notes; Activity 1 74 -75

Companies (Fixed Assets are included in some of these activities)

Core notes: Company accounts; Statement of Comprehensive Income (Income statement); Statement of Financial Position (Balance Sheet); Cash Flow Statement; Analysis and Interpretation (Ratio analysis)

76 - 83

Activities 1 - 12 84 - 119

Dear Gr 12 Accounting learner

The revision activities in this booklet have been selected to ensure all content is covered so that you will be well

prepared for exams if you work through it with dedication. As you will be writing the new 2020 two-paper Exam

format, the TIME ALLOCATED for each activity in this manual (from past Gr 12 exam papers) have been adapted

to include the time advantage you will have in the two-paper format. The content remains the same, but it has

been split to accommodate the two papers. See page 3 for details.

In your preparation focus on:

- the core notes/tips for each topic that highlight what can be expected in exam questions. It also includes

formats and basic information to strengthen your basic knowledge of the particular topic.

- the time allocated to each activity. Use this allocation to practice how to manage your exam time. Try to

adopt time saving methods in order to work more effectively through an activity/exam question.

- Work EVERY DAY on one or more activity to build your exam confidence.

- Other exam tips that you could practice regularly and apply when you write the exam:

ALWAYS read the instructions carefully before answering the question. ONLY do what is required.

Answer the questions that you know best first, e.g. start with Manufacturing (some easy marks are available in this topic) to boost your confidence.

Do not struggle with a question, move on and if you have time come back to it.

If something doesn’t balance, don’t make it balance. Balancing is only about 1 or 2 marks.

Underline certain words in all your questions, so that you know exactly what the examiner expects from you, e.g. quote figures.

SHOW ALL CALCULATIONS CLEARLY. You may use subheadings to label your calculations, e.g. 'depreciation'.

Your positive attitude and the will to succeed supported by hard work will ensure your success in Accounting.

The WCED Accounting team

Gr 12 Accounting Revision Activities

3

Two-paper classification for questions and/or sub-questions in this Activity book

/

Paper 1 Paper 2 Can be in both

papers

MID-YEAR, TRIAL AND FINAL EXAMS

(two papers) (on 2 different days)

Paper 1 Paper 2

150 marks; 2 hours 150 marks; 2 hours

Topics: Discipline 1

Recording, reporting, evaluating

Topics: Discipline 2

Internal management and control processes

Gr 12 Formula sheets included

Gr 12 Formula sheets included

NEW

Gr 12 Accounting Revision Activities

4

INVENTORY (P1 & P2) [Paper 1: Inventory valuation for preparing / reporting in financial statements]

[Paper 2: Stock systems; valuation and internal control/management of stock] Basic concepts

Difference between perpetual and periodic stock systems

Perpetual stock system: Cost of sales is calculated at point of sale Periodic stock system: Cost of sales is calculated at end of financial year after physical stock taking

Difference between stock valuation methods

FIFO Weighted average Specific identification - Based on the assumption that stock bought first will be sold first. Suitable for business selling separate items, e.g. computers, TVs, etc. - Stock with a limited shelf life may also be valued by this method.

- Used when selling large volumes (numbers) of identical small items, e.g. T-shirts, chocolates. - The average cost price of stock is used at all times.

- Used when selling small quantities where the cost of each item can be easily identified (looked up) in a register/ catalogue. - Stock values are realistic as it is based on actual cost price of each item.

Calculation of closing stock

FIFO Weighted average Specific identification Work from bottom up; Add carriage on purchases and subtract goods returned

Opening stock (R) + Purchases (R) – Returns + Carriage Opening units + Purchases (units) – Returns (units) = Answer X closing stock (units) = R…

Actual price of each unit on hand

Other calculations

Periodic Perpetual

Cost of sales Opening stock + Purchases + Carriage - Returns - Closing stock

Based on mark-up % at point of sale

Gross Profit Sales - Cost of sales

Stolen goods Opening units + Purchases units – Returns - Sold units - Closing units

Financial indicators (Paper 1 OR Paper 2)

Mark-up % (Sales - Cost of sales) x 100 Cost of sales 1

Answer given as:

… %

Stock turnover rate Cost of sales Average stock OR ½(Opening stock + Closing stock)

... times

Period/Days of stock on hand

Average stock x 365 Cost of sales 1

… days

GAAP principles for inventories (Paper 1) - Historical cost; - Rule of prudence

Internal control of stock (Paper 2) Division of duties; Documentation; Authorisation; Physical measures

Gr 12 Accounting Revision Activities

5

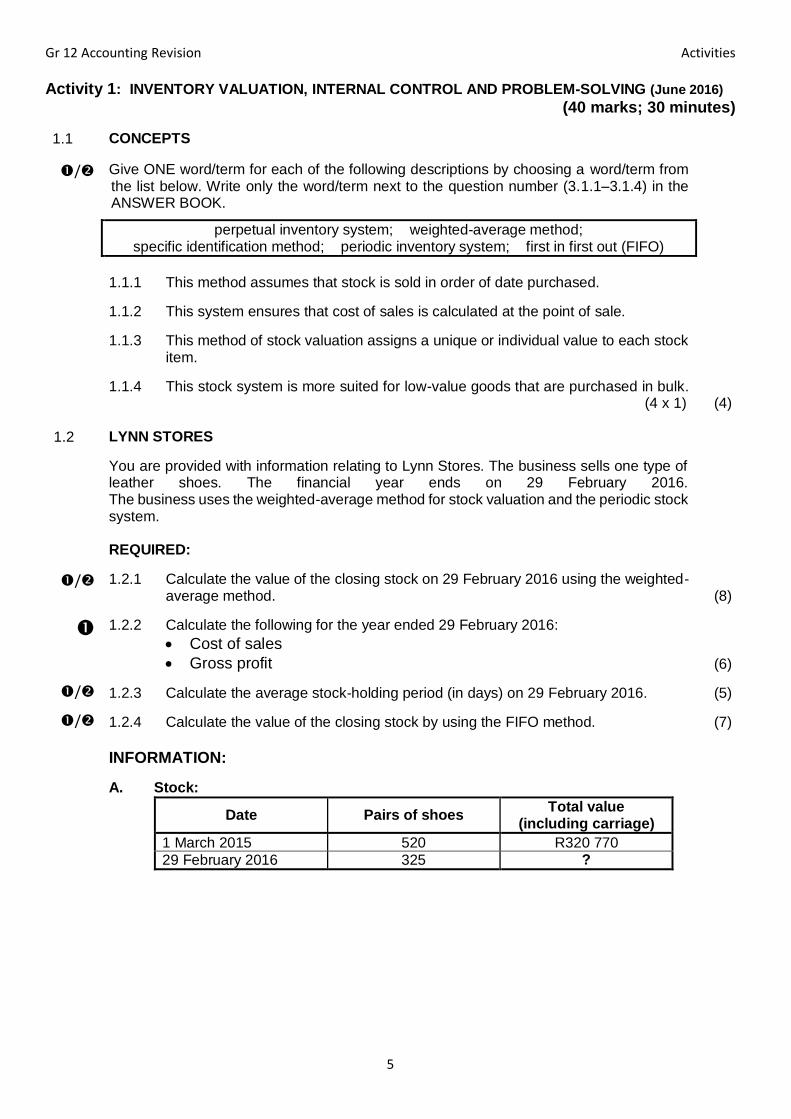

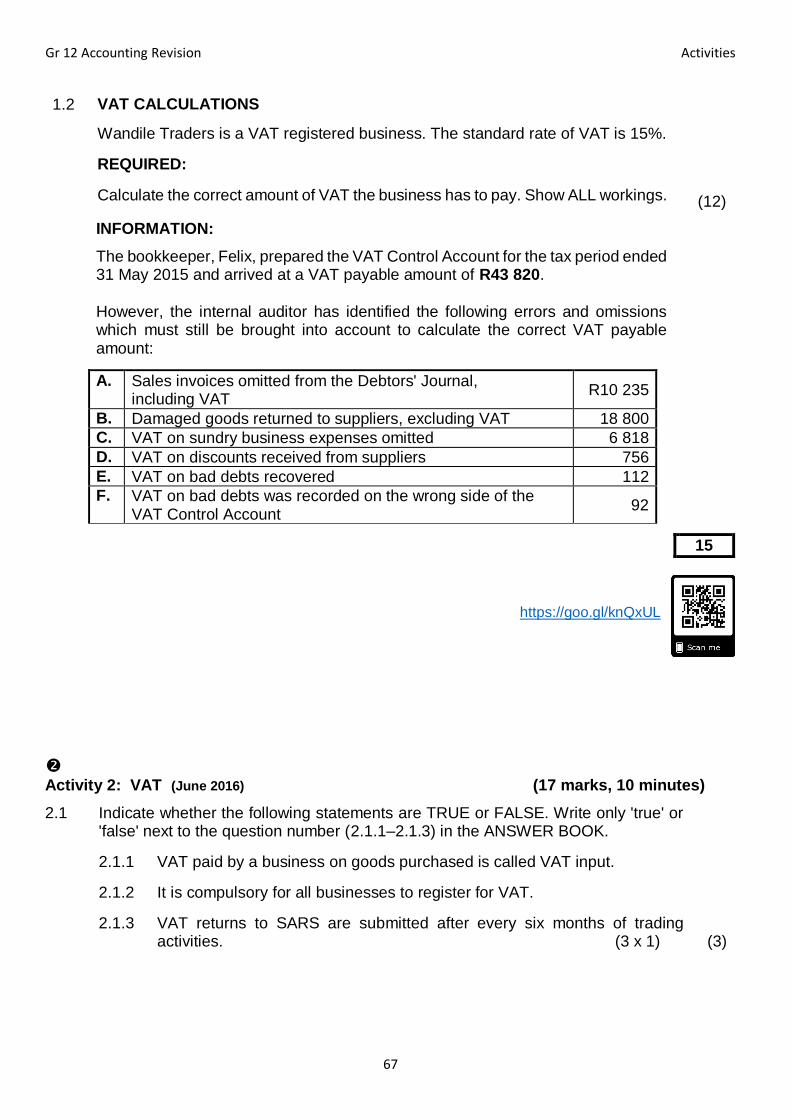

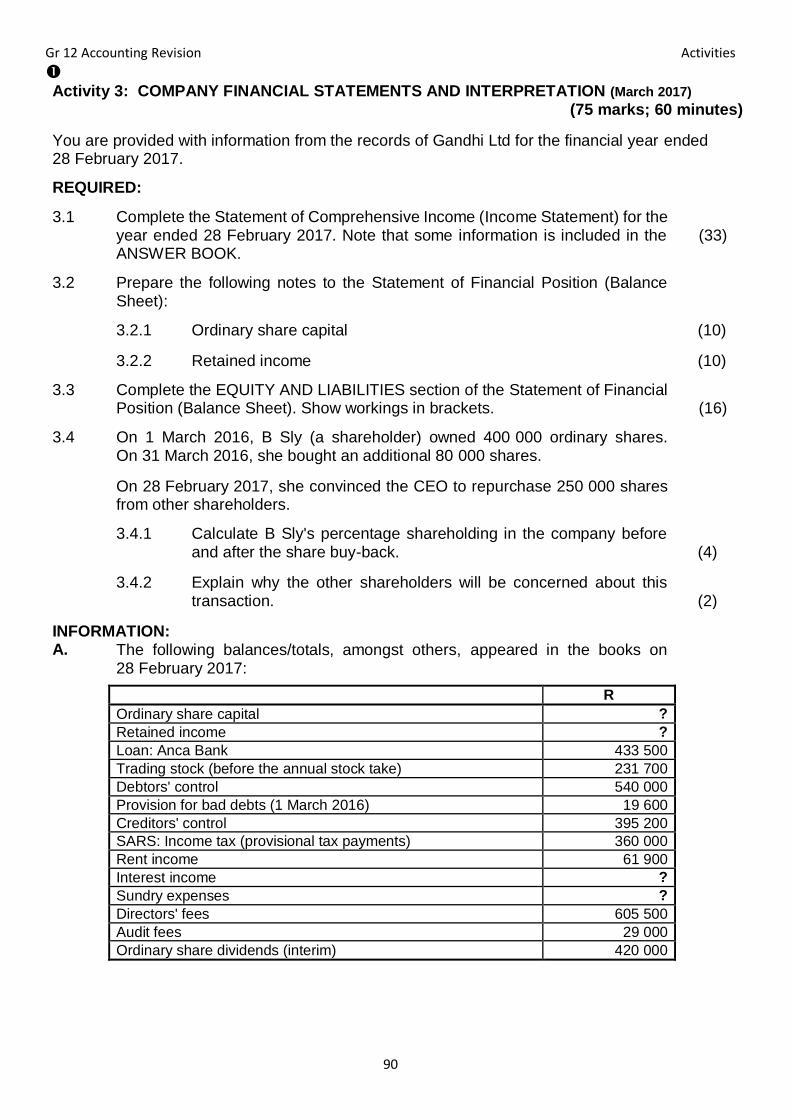

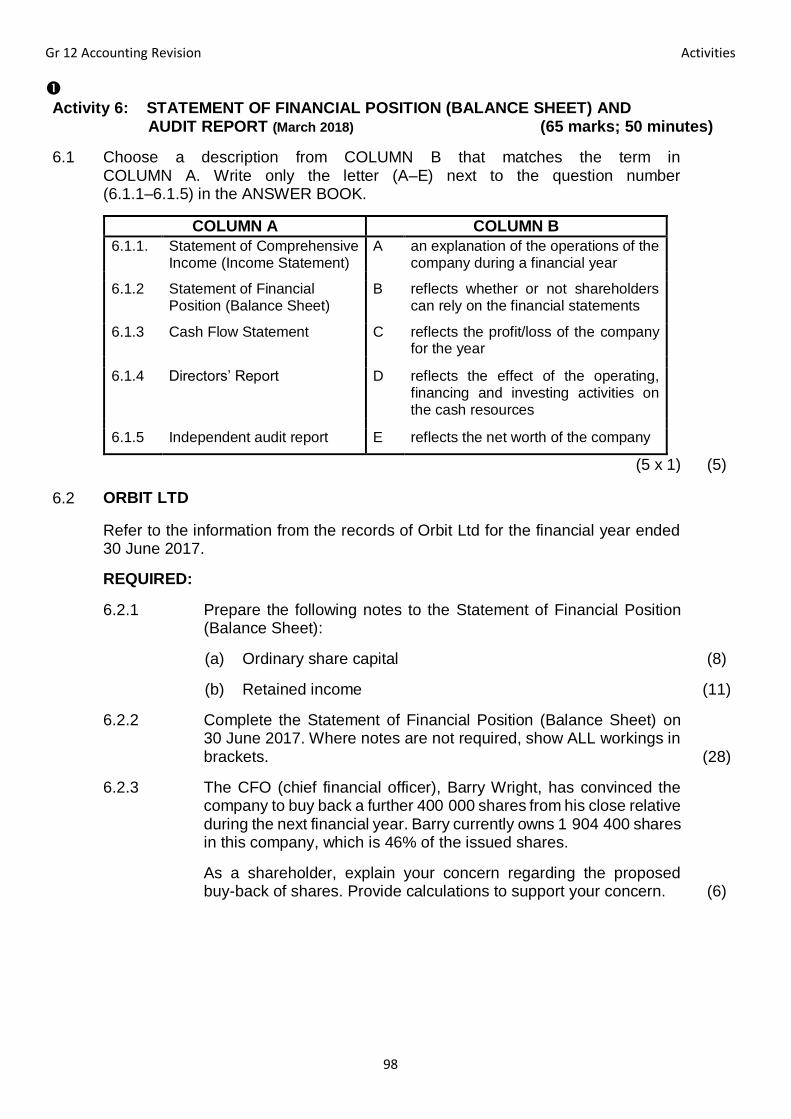

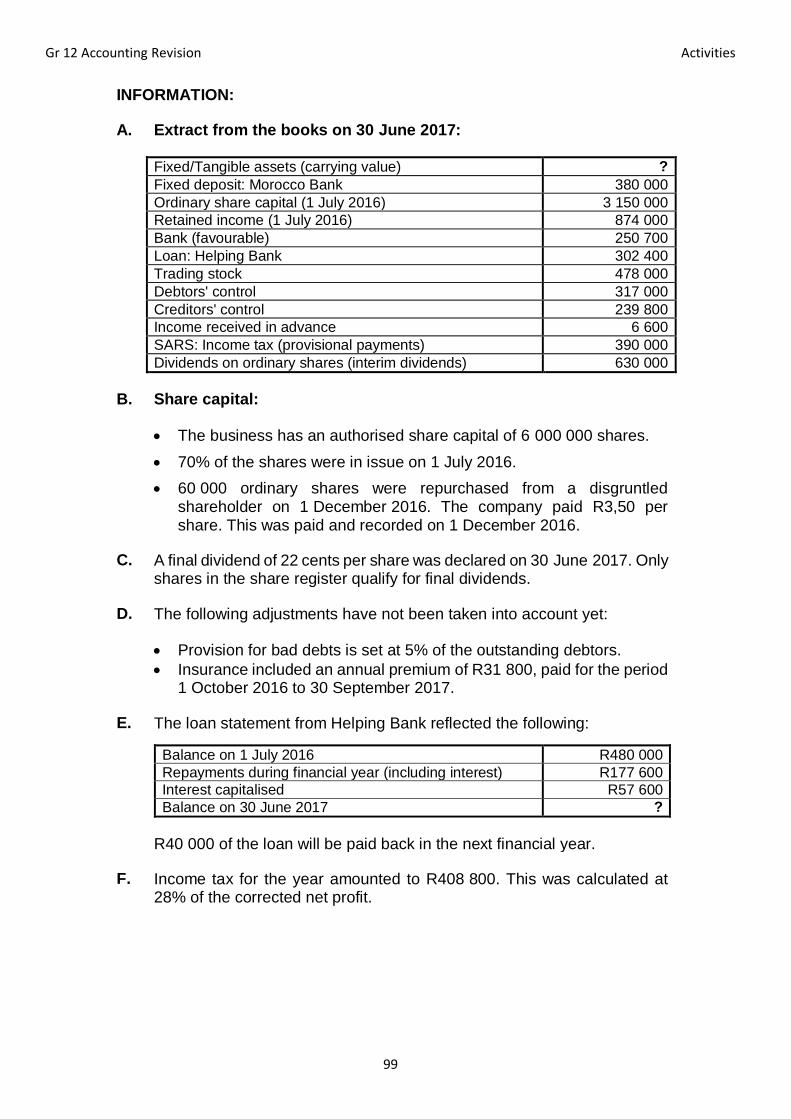

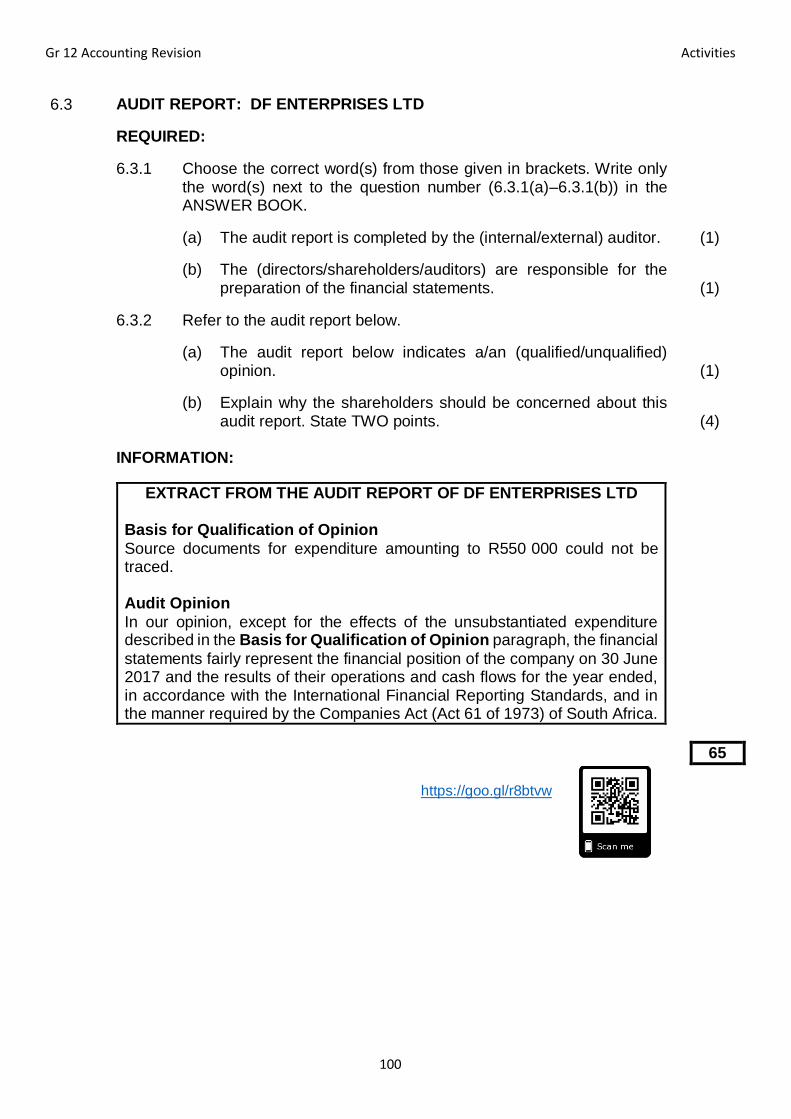

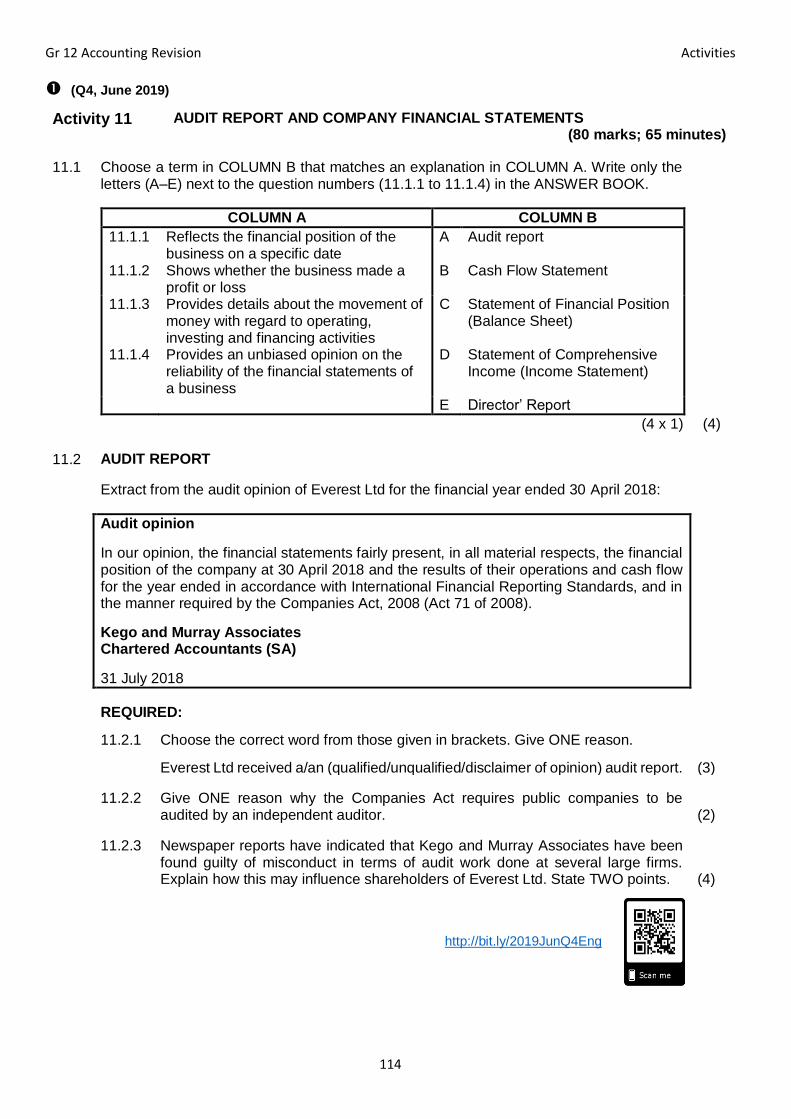

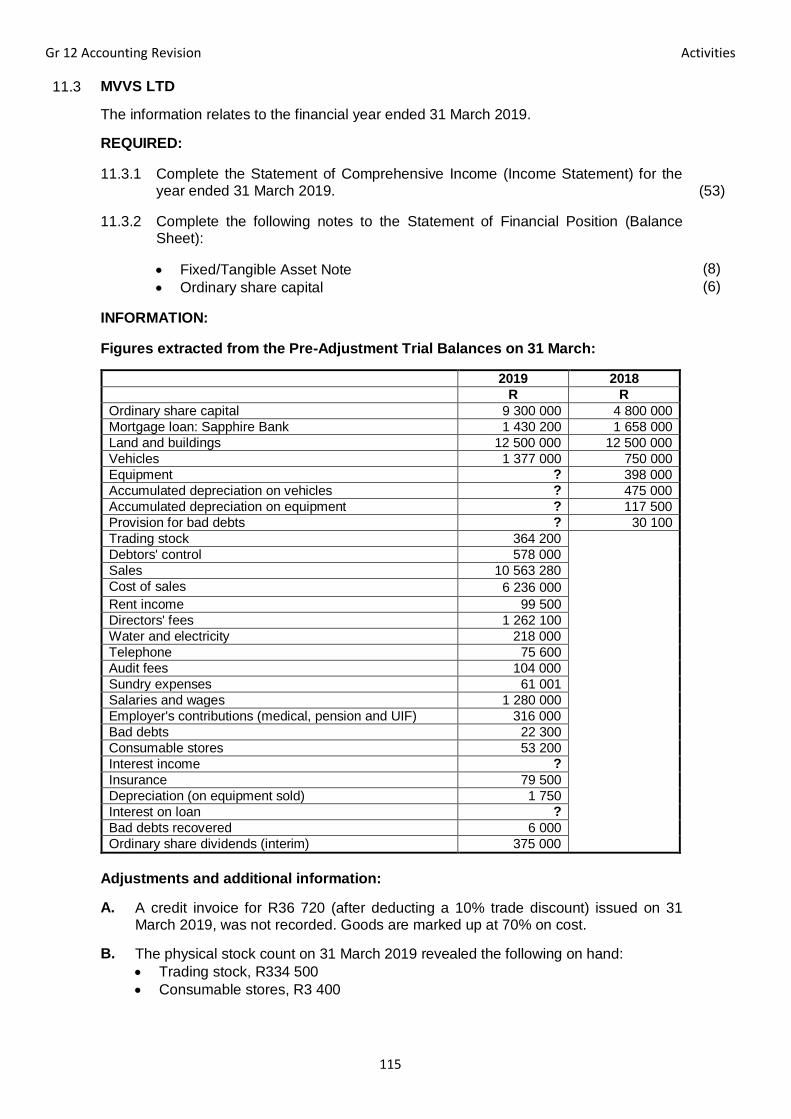

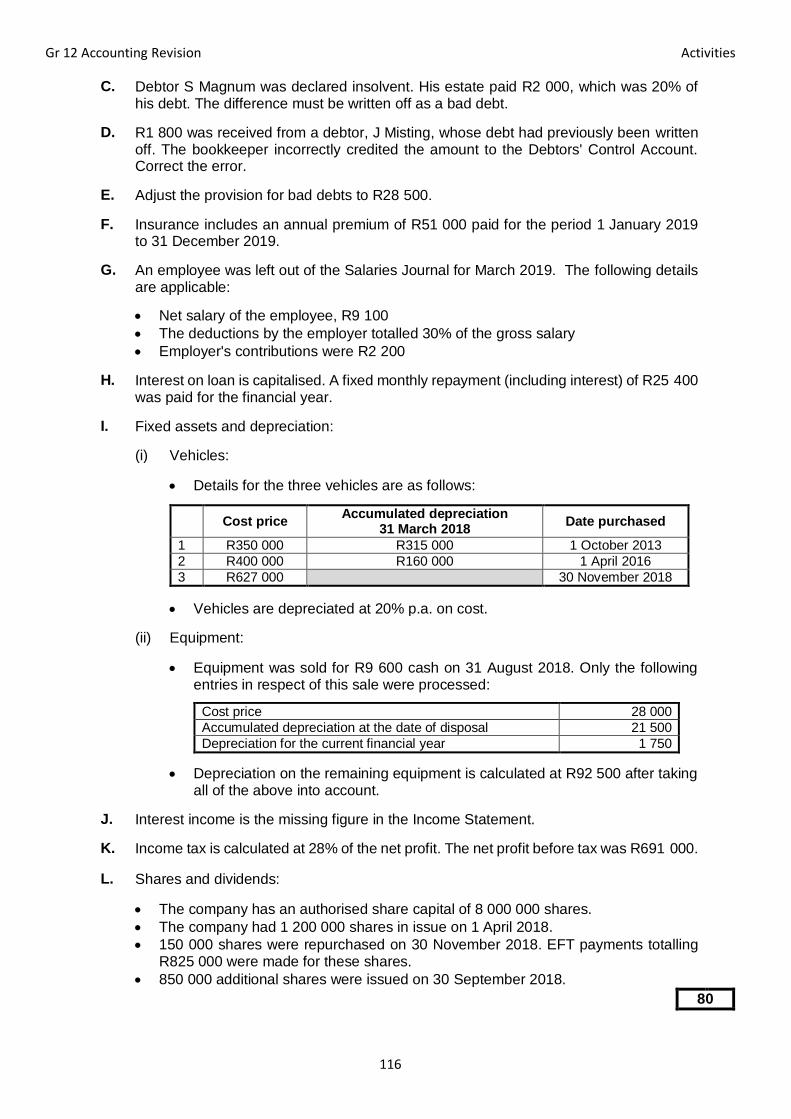

Activity 1: INVENTORY VALUATION, INTERNAL CONTROL AND PROBLEM-SOLVING (June 2016)

(40 marks; 30 minutes)

1.1 CONCEPTS

/ Give ONE word/term for each of the following descriptions by choosing a word/term from the list below. Write only the word/term next to the question number (3.1.1–3.1.4) in the ANSWER BOOK.

perpetual inventory system; weighted-average method; specific identification method; periodic inventory system; first in first out (FIFO)

1.1.1 This method assumes that stock is sold in order of date purchased.

1.1.2 This system ensures that cost of sales is calculated at the point of sale.

1.1.3 This method of stock valuation assigns a unique or individual value to each stock item.

1.1.4 This stock system is more suited for low-value goods that are purchased in bulk. (4 x 1) (4)

1.2 LYNN STORES

You are provided with information relating to Lynn Stores. The business sells one type of leather shoes. The financial year ends on 29 February 2016. The business uses the weighted-average method for stock valuation and the periodic stock system.

REQUIRED:

/ 1.2.1 Calculate the value of the closing stock on 29 February 2016 using the weighted-average method. (8)

1.2.2 Calculate the following for the year ended 29 February 2016:

Cost of sales

Gross profit (6)

/

1.2.3 Calculate the average stock-holding period (in days) on 29 February 2016. (5)

/

1.2.4 Calculate the value of the closing stock by using the FIFO method. (7)

INFORMATION:

A. Stock:

Date Pairs of shoes Total value

(including carriage)

1 March 2015 520 R320 770

29 February 2016 325 ?

Gr 12 Accounting Revision Activities

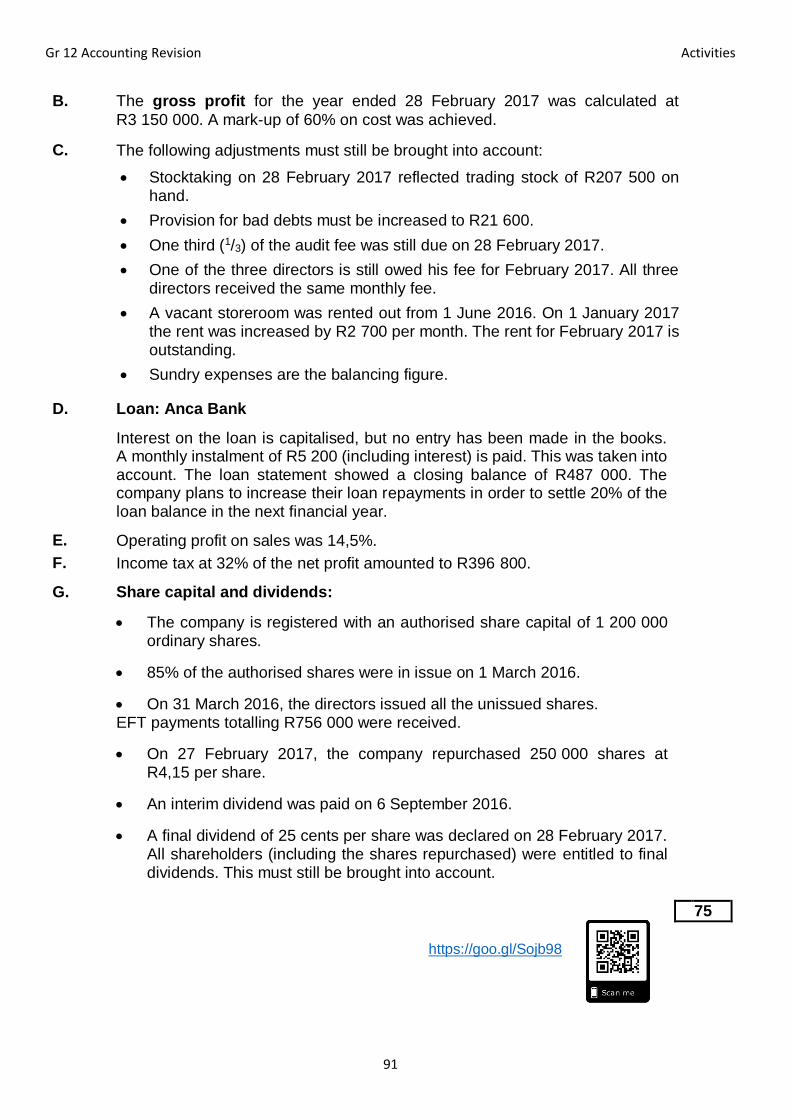

6

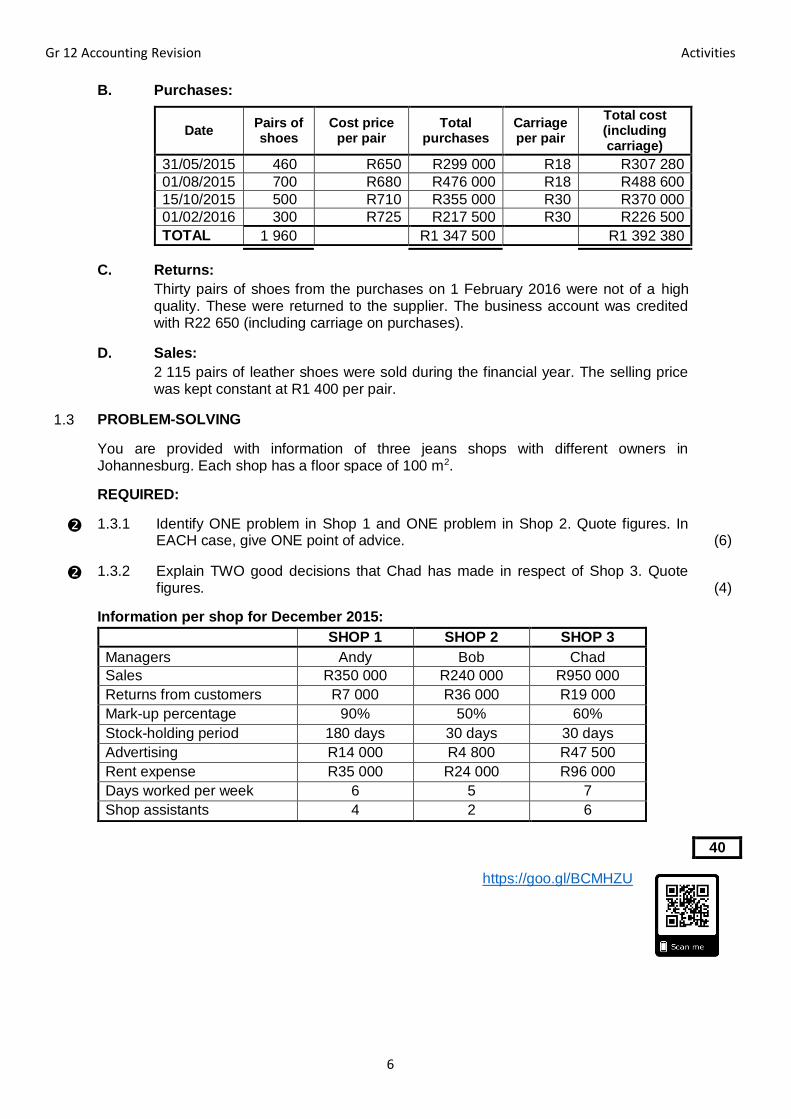

B. Purchases:

Date Pairs of shoes

Cost price per pair

Total purchases

Carriage per pair

Total cost (including carriage)

31/05/2015 460 R650 R299 000 R18 R307 280

01/08/2015 700 R680 R476 000 R18 R488 600

15/10/2015 500 R710 R355 000 R30 R370 000

01/02/2016 300 R725 R217 500 R30 R226 500

TOTAL 1 960 R1 347 500 R1 392 380

C. Returns: Thirty pairs of shoes from the purchases on 1 February 2016 were not of a high

quality. These were returned to the supplier. The business account was credited with R22 650 (including carriage on purchases).

D. Sales: 2 115 pairs of leather shoes were sold during the financial year. The selling price

was kept constant at R1 400 per pair.

1.3 PROBLEM-SOLVING

You are provided with information of three jeans shops with different owners in Johannesburg. Each shop has a floor space of 100 m2.

REQUIRED:

1.3.1 Identify ONE problem in Shop 1 and ONE problem in Shop 2. Quote figures. In EACH case, give ONE point of advice. (6)

1.3.2 Explain TWO good decisions that Chad has made in respect of Shop 3. Quote figures. (4)

Information per shop for December 2015:

SHOP 1 SHOP 2 SHOP 3

Managers Andy Bob Chad

Sales R350 000 R240 000 R950 000

Returns from customers R7 000 R36 000 R19 000

Mark-up percentage 90% 50% 60%

Stock-holding period 180 days 30 days 30 days

Advertising R14 000 R4 800 R47 500

Rent expense R35 000 R24 000 R96 000

Days worked per week 6 5 7

Shop assistants 4 2 6

40

https://goo.gl/BCMHZU

Gr 12 Accounting Revision Activities

7

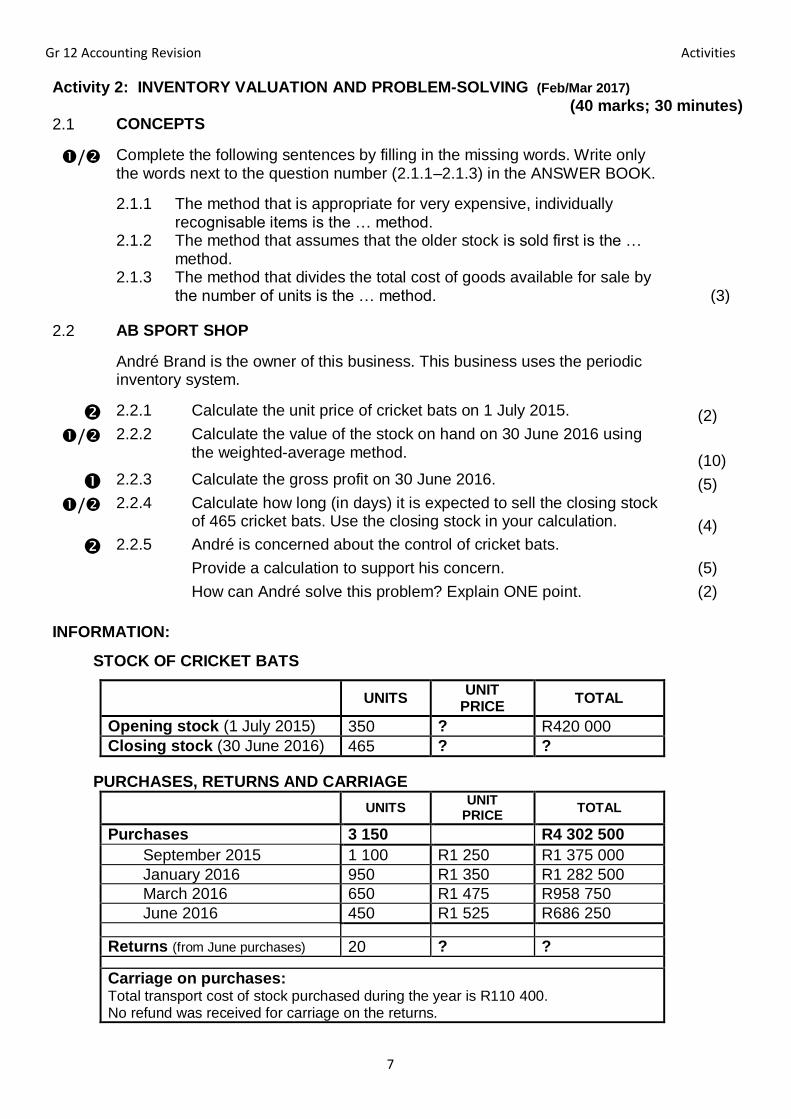

Activity 2: INVENTORY VALUATION AND PROBLEM-SOLVING (Feb/Mar 2017) (40 marks; 30 minutes)

2.1 CONCEPTS

/ Complete the following sentences by filling in the missing words. Write only the words next to the question number (2.1.1–2.1.3) in the ANSWER BOOK.

2.1.1 The method that is appropriate for very expensive, individually recognisable items is the … method.

2.1.2 The method that assumes that the older stock is sold first is the … method.

2.1.3 The method that divides the total cost of goods available for sale by the number of units is the … method.

(3)

2.2 AB SPORT SHOP

André Brand is the owner of this business. This business uses the periodic inventory system.

2.2.1 Calculate the unit price of cricket bats on 1 July 2015. (2)

/ 2.2.2 Calculate the value of the stock on hand on 30 June 2016 using the weighted-average method.

(10)

2.2.3 Calculate the gross profit on 30 June 2016. (5)

/ 2.2.4 Calculate how long (in days) it is expected to sell the closing stock of 465 cricket bats. Use the closing stock in your calculation.

(4)

2.2.5 André is concerned about the control of cricket bats.

Provide a calculation to support his concern.

How can André solve this problem? Explain ONE point.

(5)

(2)

INFORMATION:

STOCK OF CRICKET BATS

UNITS UNIT

PRICE TOTAL

Opening stock (1 July 2015) 350 ? R420 000

Closing stock (30 June 2016) 465 ? ?

PURCHASES, RETURNS AND CARRIAGE

UNITS UNIT

PRICE TOTAL

Purchases 3 150 R4 302 500

September 2015 1 100 R1 250 R1 375 000

January 2016 950 R1 350 R1 282 500

March 2016 650 R1 475 R958 750

June 2016 450 R1 525 R686 250

Returns (from June purchases) 20 ? ?

Carriage on purchases: Total transport cost of stock purchased during the year is R110 400. No refund was received for carriage on the returns.

Gr 12 Accounting Revision Activities

8

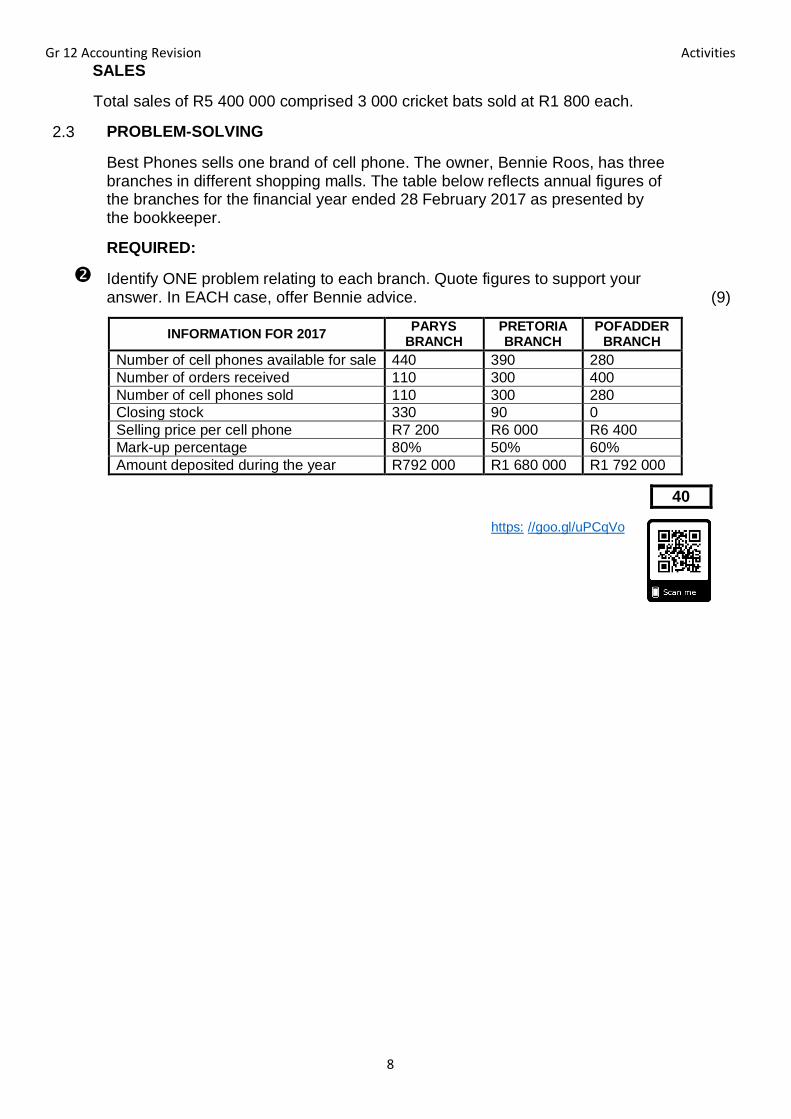

SALES

Total sales of R5 400 000 comprised 3 000 cricket bats sold at R1 800 each.

2.3

PROBLEM-SOLVING

Best Phones sells one brand of cell phone. The owner, Bennie Roos, has three branches in different shopping malls. The table below reflects annual figures of the branches for the financial year ended 28 February 2017 as presented by the bookkeeper.

REQUIRED:

Identify ONE problem relating to each branch. Quote figures to support your answer. In EACH case, offer Bennie advice.

(9)

INFORMATION FOR 2017 PARYS

BRANCH PRETORIA BRANCH

POFADDER BRANCH

Number of cell phones available for sale 440 390 280

Number of orders received 110 300 400

Number of cell phones sold 110 300 280

Closing stock 330 90 0

Selling price per cell phone R7 200 R6 000 R6 400

Mark-up percentage 80% 50% 60%

Amount deposited during the year R792 000 R1 680 000 R1 792 000

40

https: //goo.gl/uPCqVo

Gr 12 Accounting Revision Activities

9

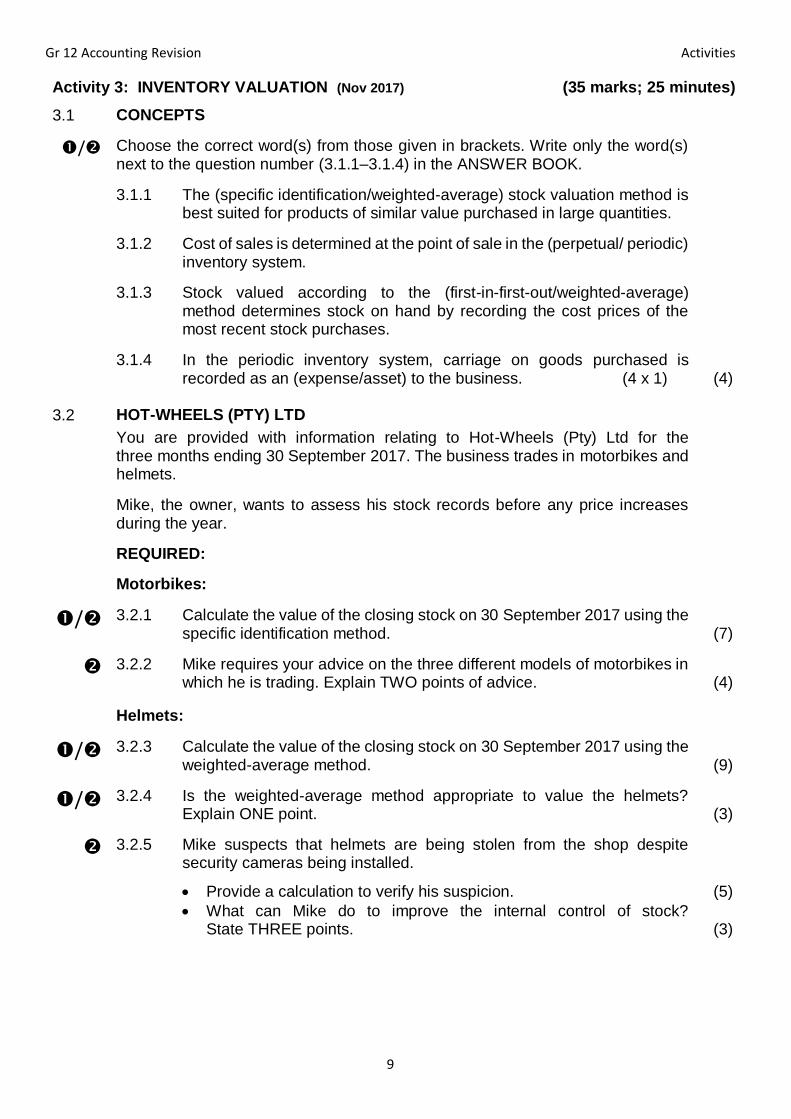

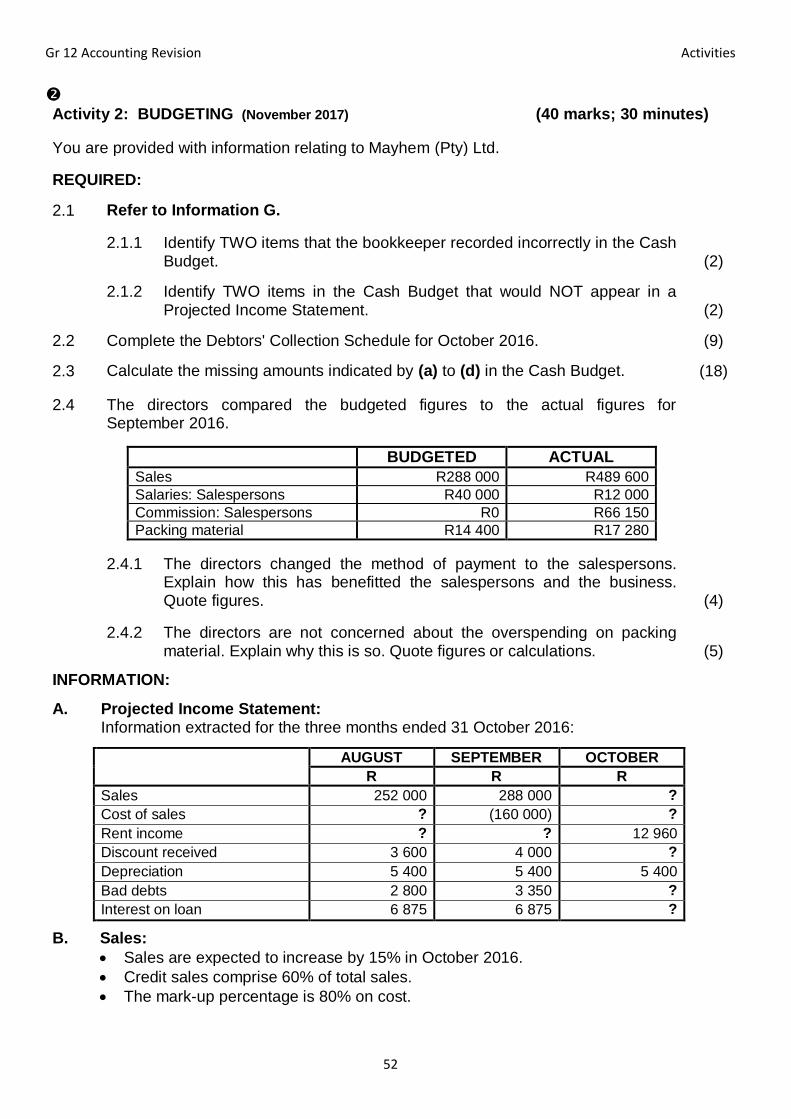

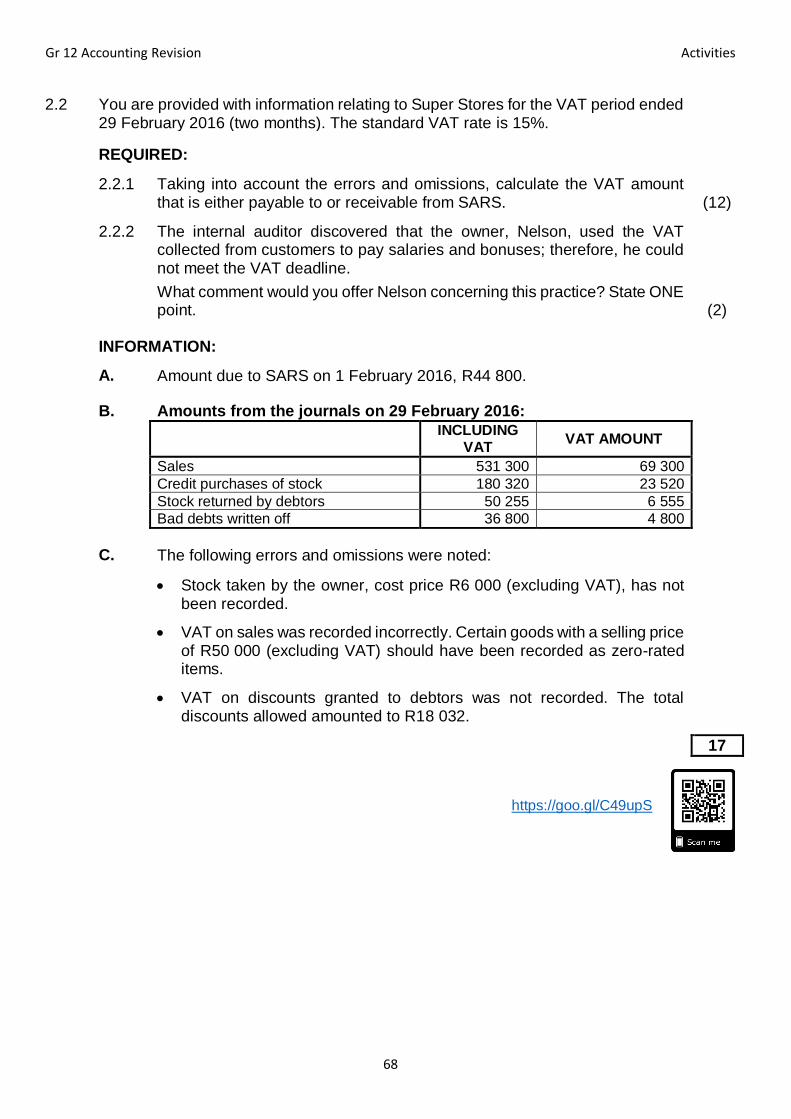

Activity 3: INVENTORY VALUATION (Nov 2017) (35 marks; 25 minutes)

3.1 CONCEPTS

/ Choose the correct word(s) from those given in brackets. Write only the word(s) next to the question number (3.1.1–3.1.4) in the ANSWER BOOK.

3.1.1 The (specific identification/weighted-average) stock valuation method is best suited for products of similar value purchased in large quantities.

3.1.2 Cost of sales is determined at the point of sale in the (perpetual/ periodic) inventory system.

3.1.3 Stock valued according to the (first-in-first-out/weighted-average) method determines stock on hand by recording the cost prices of the most recent stock purchases.

3.1.4 In the periodic inventory system, carriage on goods purchased is recorded as an (expense/asset) to the business. (4 x 1) (4)

3.2 HOT-WHEELS (PTY) LTD

You are provided with information relating to Hot-Wheels (Pty) Ltd for the three months ending 30 September 2017. The business trades in motorbikes and helmets.

Mike, the owner, wants to assess his stock records before any price increases during the year.

REQUIRED:

Motorbikes:

/ 3.2.1 Calculate the value of the closing stock on 30 September 2017 using the specific identification method. (7)

3.2.2 Mike requires your advice on the three different models of motorbikes in which he is trading. Explain TWO points of advice. (4)

Helmets:

/ 3.2.3 Calculate the value of the closing stock on 30 September 2017 using the weighted-average method. (9)

/ 3.2.4 Is the weighted-average method appropriate to value the helmets? Explain ONE point. (3)

3.2.5 Mike suspects that helmets are being stolen from the shop despite security cameras being installed.

Provide a calculation to verify his suspicion. (5) What can Mike do to improve the internal control of stock?

State THREE points. (3)

Gr 12 Accounting Revision Activities

10

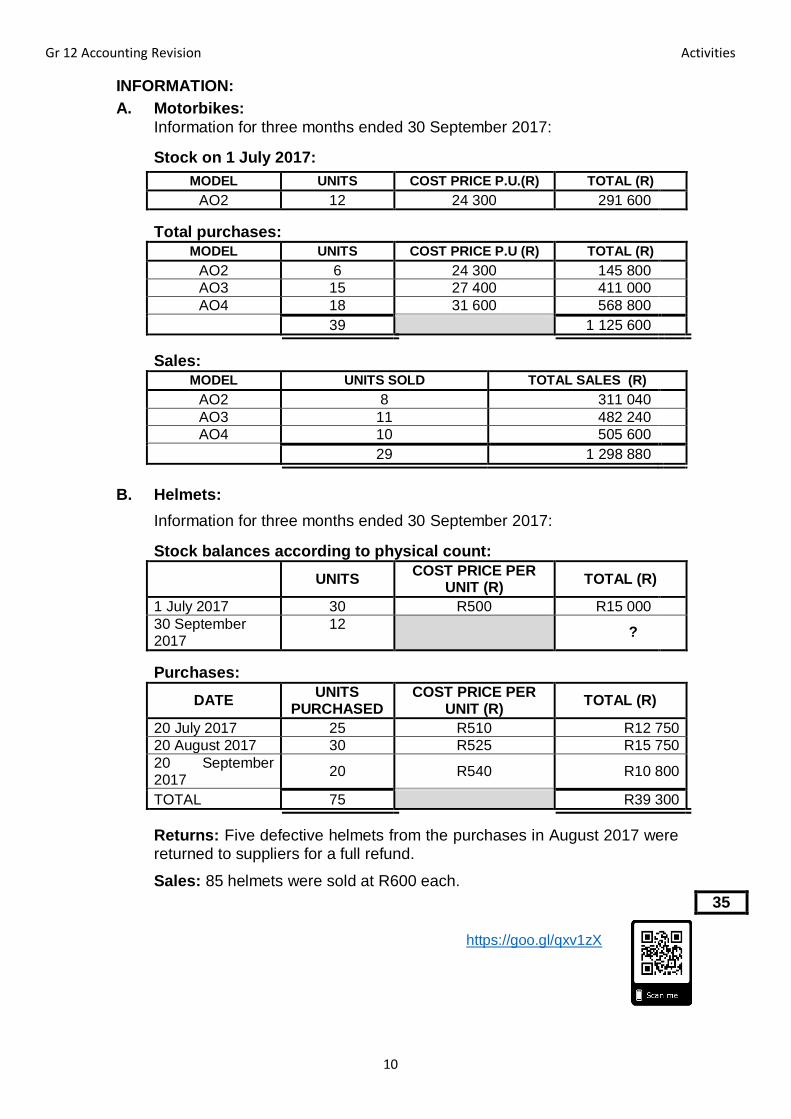

INFORMATION: A. Motorbikes:

Information for three months ended 30 September 2017:

Stock on 1 July 2017:

MODEL UNITS COST PRICE P.U.(R) TOTAL (R)

AO2 12 24 300 291 600

Total purchases:

MODEL UNITS COST PRICE P.U (R) TOTAL (R)

AO2 6 24 300 145 800

AO3 15 27 400 411 000

AO4 18 31 600 568 800

39 1 125 600

Sales:

MODEL UNITS SOLD TOTAL SALES (R)

AO2 8 311 040

AO3 11 482 240

AO4 10 505 600

29 1 298 880

B. Helmets:

Information for three months ended 30 September 2017:

Stock balances according to physical count:

UNITS

COST PRICE PER UNIT (R)

TOTAL (R)

1 July 2017 30 R500 R15 000

30 September 2017

12 ?

Purchases:

DATE

UNITS PURCHASED

COST PRICE PER UNIT (R)

TOTAL (R)

20 July 2017 25 R510 R12 750

20 August 2017 30 R525 R15 750

20 September 2017

20 R540 R10 800

TOTAL 75 R39 300

Returns: Five defective helmets from the purchases in August 2017 were returned to suppliers for a full refund.

Sales: 85 helmets were sold at R600 each.

35

https://goo.gl/qxv1zX

Gr 12 Accounting Revision Activities

11

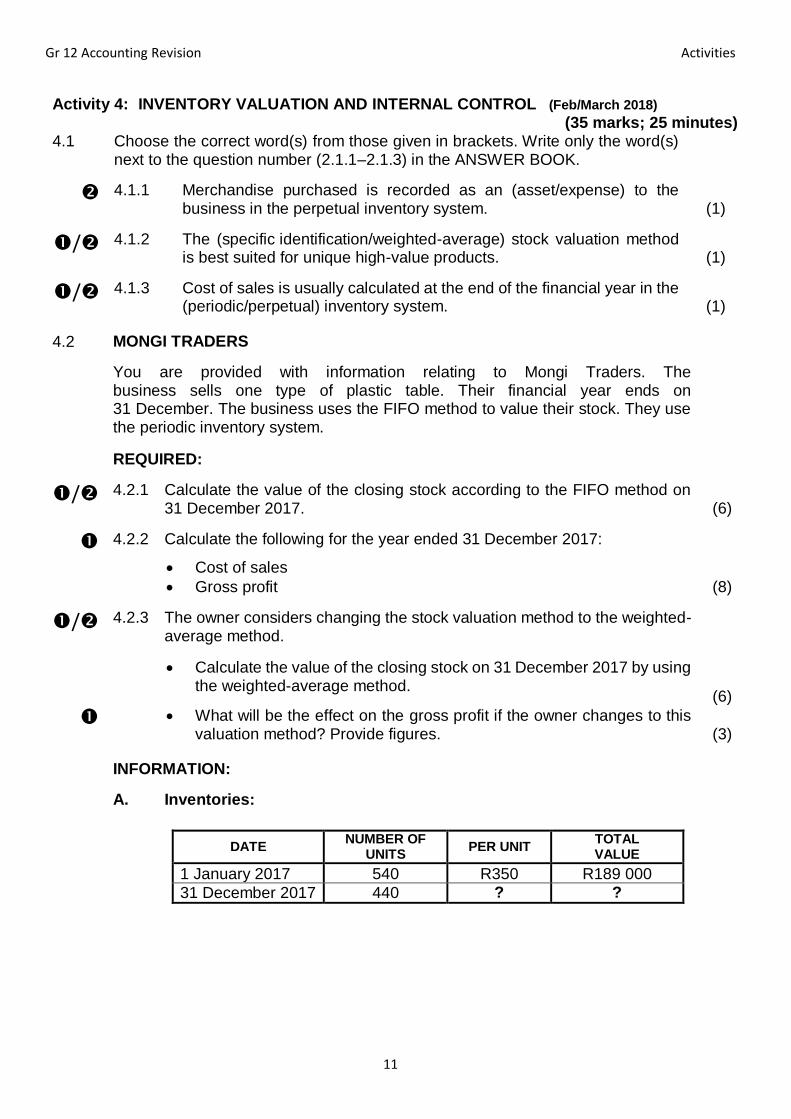

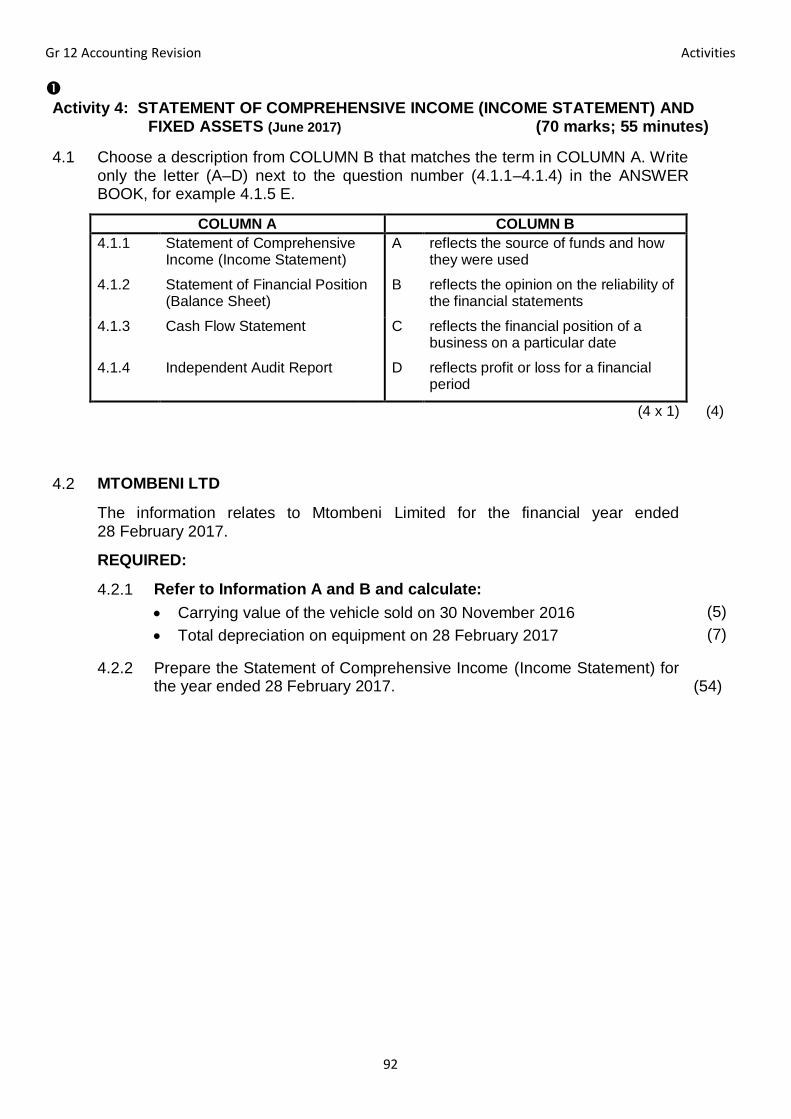

Activity 4: INVENTORY VALUATION AND INTERNAL CONTROL (Feb/March 2018)

(35 marks; 25 minutes) 4.1 Choose the correct word(s) from those given in brackets. Write only the word(s)

next to the question number (2.1.1–2.1.3) in the ANSWER BOOK.

4.1.1 Merchandise purchased is recorded as an (asset/expense) to the business in the perpetual inventory system. (1)

/ 4.1.2 The (specific identification/weighted-average) stock valuation method is best suited for unique high-value products. (1)

/ 4.1.3 Cost of sales is usually calculated at the end of the financial year in the (periodic/perpetual) inventory system. (1)

4.2 MONGI TRADERS

You are provided with information relating to Mongi Traders. The business sells one type of plastic table. Their financial year ends on 31 December. The business uses the FIFO method to value their stock. They use the periodic inventory system.

REQUIRED:

/ 4.2.1 Calculate the value of the closing stock according to the FIFO method on 31 December 2017. (6)

4.2.2 Calculate the following for the year ended 31 December 2017:

Cost of sales

Gross profit (8)

/ 4.2.3 The owner considers changing the stock valuation method to the weighted-average method.

Calculate the value of the closing stock on 31 December 2017 by using the weighted-average method.

(6)

What will be the effect on the gross profit if the owner changes to this valuation method? Provide figures. (3)

INFORMATION:

A. Inventories:

DATE

NUMBER OF UNITS

PER UNIT TOTAL VALUE

1 January 2017 540 R350 R189 000

31 December 2017 440 ? ?

Gr 12 Accounting Revision Activities

12

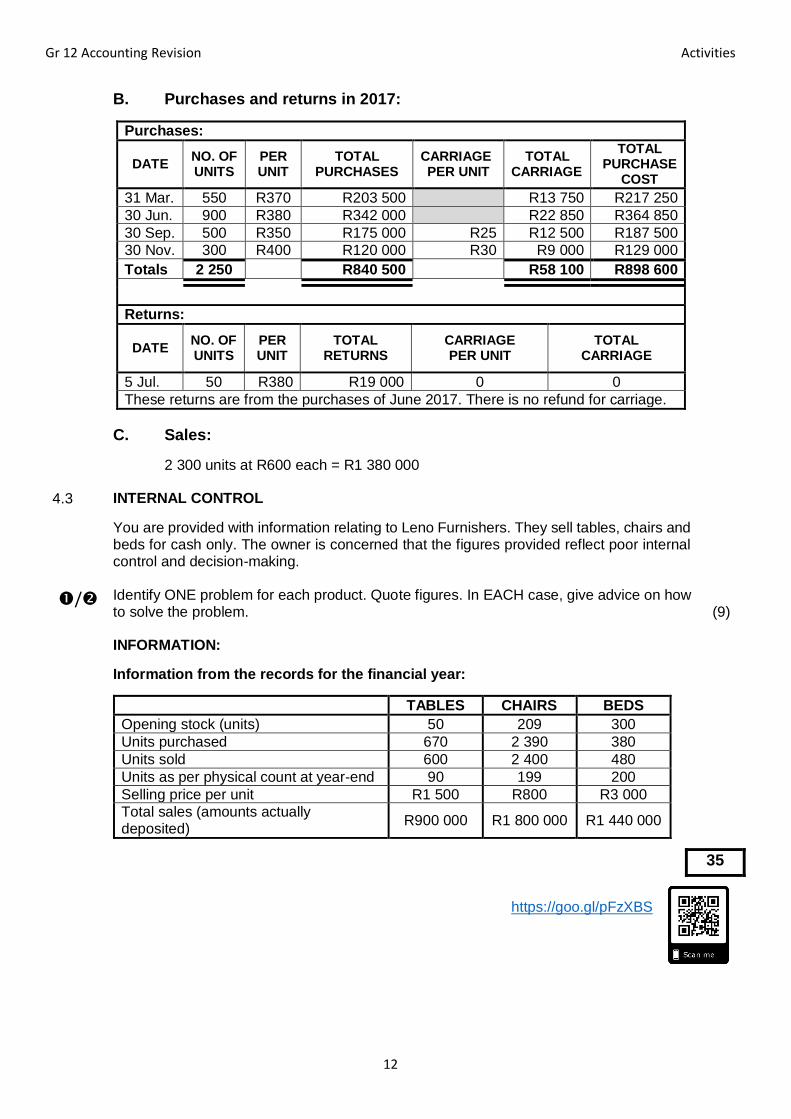

B. Purchases and returns in 2017:

Purchases:

DATE NO. OF UNITS

PER UNIT

TOTAL PURCHASES

CARRIAGE PER UNIT

TOTAL CARRIAGE

TOTAL PURCHASE

COST

31 Mar. 550 R370 R203 500 R13 750 R217 250

30 Jun. 900 R380 R342 000 R22 850 R364 850

30 Sep. 500 R350 R175 000 R25 R12 500 R187 500

30 Nov. 300 R400 R120 000 R30 R9 000 R129 000

Totals 2 250 R840 500 R58 100 R898 600

Returns:

DATE NO. OF UNITS

PER UNIT

TOTAL RETURNS

CARRIAGE PER UNIT

TOTAL CARRIAGE

5 Jul. 50 R380 R19 000 0 0

These returns are from the purchases of June 2017. There is no refund for carriage.

C. Sales:

2 300 units at R600 each = R1 380 000 4.3 INTERNAL CONTROL

/

You are provided with information relating to Leno Furnishers. They sell tables, chairs and beds for cash only. The owner is concerned that the figures provided reflect poor internal control and decision-making. Identify ONE problem for each product. Quote figures. In EACH case, give advice on how to solve the problem.

(9) INFORMATION:

Information from the records for the financial year:

TABLES CHAIRS BEDS

Opening stock (units) 50 209 300

Units purchased 670 2 390 380

Units sold 600 2 400 480

Units as per physical count at year-end 90 199 200

Selling price per unit R1 500 R800 R3 000

Total sales (amounts actually deposited)

R900 000 R1 800 000 R1 440 000

35

https://goo.gl/pFzXBS

Gr 12 Accounting Revision Activities

13

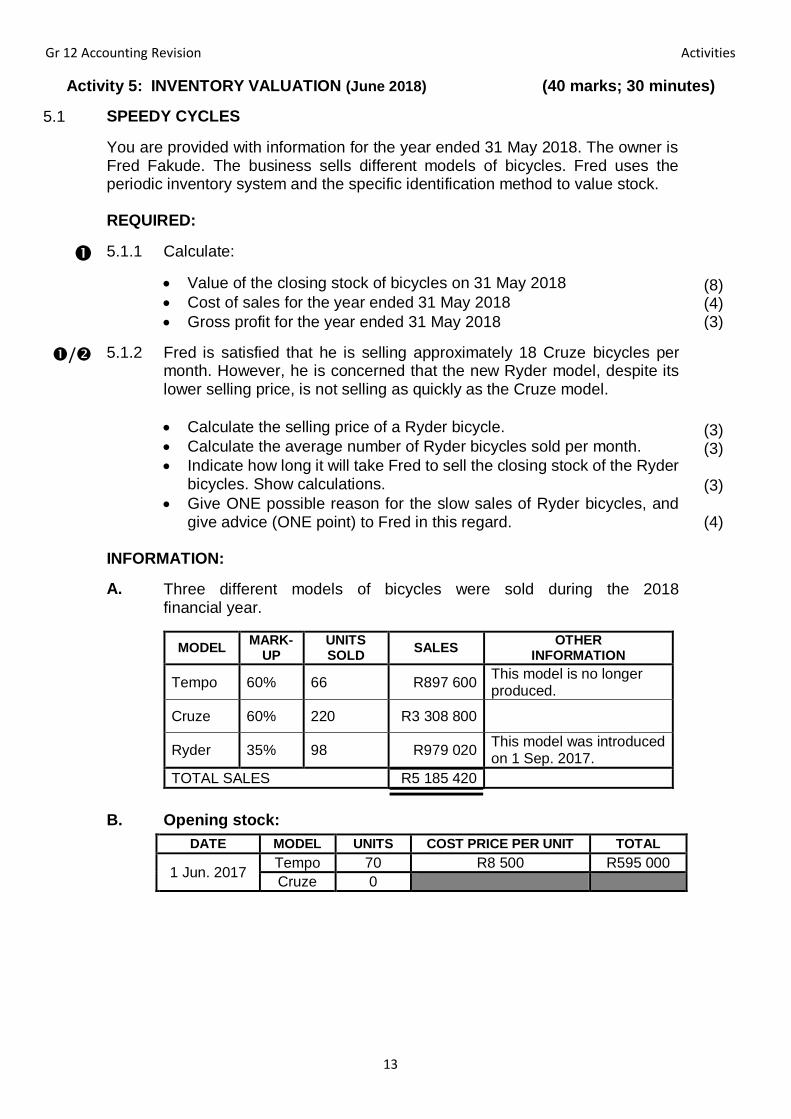

Activity 5: INVENTORY VALUATION (June 2018) (40 marks; 30 minutes)

5.1 SPEEDY CYCLES

You are provided with information for the year ended 31 May 2018. The owner is Fred Fakude. The business sells different models of bicycles. Fred uses the periodic inventory system and the specific identification method to value stock.

REQUIRED:

5.1.1 Calculate:

Value of the closing stock of bicycles on 31 May 2018

Cost of sales for the year ended 31 May 2018

Gross profit for the year ended 31 May 2018

(8) (4) (3)

/ 5.1.2 Fred is satisfied that he is selling approximately 18 Cruze bicycles per month. However, he is concerned that the new Ryder model, despite its lower selling price, is not selling as quickly as the Cruze model.

Calculate the selling price of a Ryder bicycle.

Calculate the average number of Ryder bicycles sold per month.

Indicate how long it will take Fred to sell the closing stock of the Ryder bicycles. Show calculations.

Give ONE possible reason for the slow sales of Ryder bicycles, and give advice (ONE point) to Fred in this regard.

(3) (3)

(3)

(4)

INFORMATION:

A. Three different models of bicycles were sold during the 2018 financial year.

MODEL MARK-

UP UNITS SOLD

SALES OTHER

INFORMATION

Tempo 60% 66 R897 600 This model is no longer produced.

Cruze 60% 220 R3 308 800

Ryder 35% 98 R979 020 This model was introduced on 1 Sep. 2017.

TOTAL SALES R5 185 420

B. Opening stock:

DATE MODEL UNITS COST PRICE PER UNIT TOTAL

1 Jun. 2017

Tempo 70 R8 500 R595 000

Cruze 0

Gr 12 Accounting Revision Activities

14

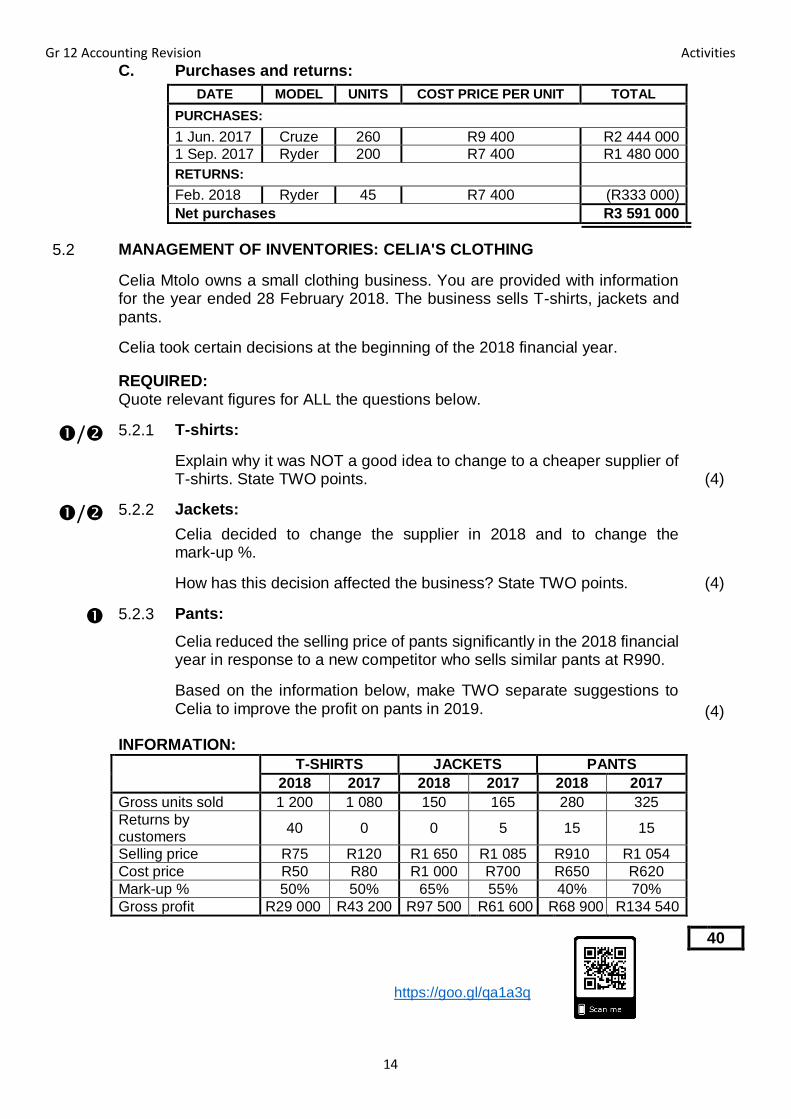

C. Purchases and returns:

DATE MODEL UNITS COST PRICE PER UNIT TOTAL

PURCHASES:

1 Jun. 2017 Cruze 260 R9 400 R2 444 000

1 Sep. 2017 Ryder 200 R7 400 R1 480 000

RETURNS:

Feb. 2018 Ryder 45 R7 400 (R333 000)

Net purchases R3 591 000

5.2 MANAGEMENT OF INVENTORIES: CELIA'S CLOTHING

Celia Mtolo owns a small clothing business. You are provided with information for the year ended 28 February 2018. The business sells T-shirts, jackets and pants.

Celia took certain decisions at the beginning of the 2018 financial year.

REQUIRED: Quote relevant figures for ALL the questions below.

/ 5.2.1 T-shirts:

Explain why it was NOT a good idea to change to a cheaper supplier of T-shirts. State TWO points. (4)

/ 5.2.2 Jackets:

Celia decided to change the supplier in 2018 and to change the mark-up %.

How has this decision affected the business? State TWO points.

(4)

5.2.3 Pants:

Celia reduced the selling price of pants significantly in the 2018 financial year in response to a new competitor who sells similar pants at R990.

Based on the information below, make TWO separate suggestions to Celia to improve the profit on pants in 2019. (4)

INFORMATION:

T-SHIRTS JACKETS PANTS

2018 2017 2018 2017 2018 2017

Gross units sold 1 200 1 080 150 165 280 325

Returns by customers

40 0 0 5 15 15

Selling price R75 R120 R1 650 R1 085 R910 R1 054

Cost price R50 R80 R1 000 R700 R650 R620

Mark-up % 50% 50% 65% 55% 40% 70%

Gross profit R29 000 R43 200 R97 500 R61 600 R68 900 R134 540

40

https://goo.gl/qa1a3q

Gr 12 Accounting Revision Activities

15

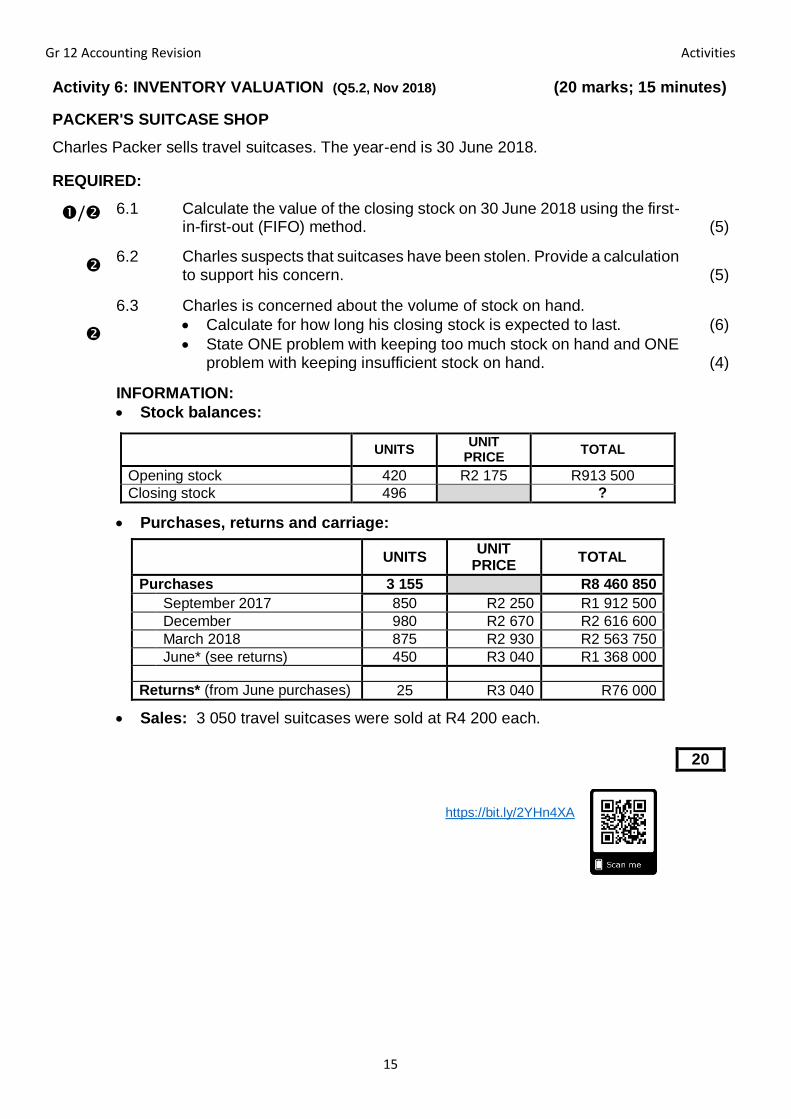

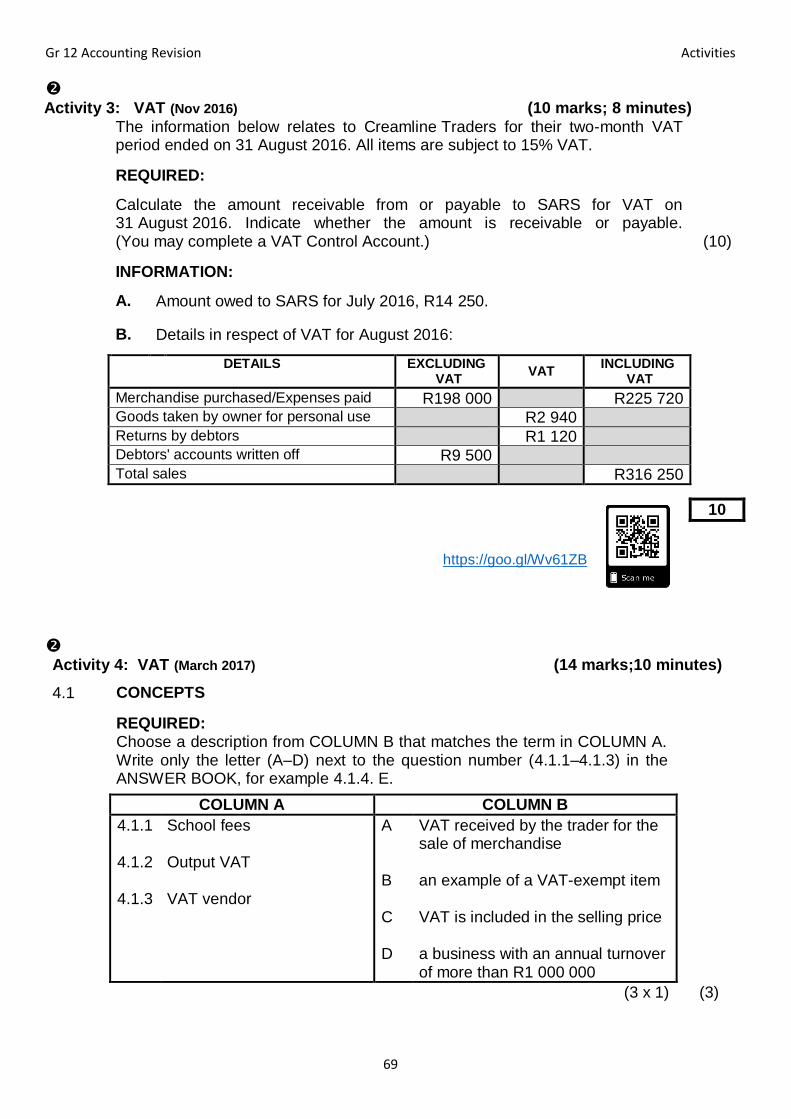

Activity 6: INVENTORY VALUATION (Q5.2, Nov 2018) (20 marks; 15 minutes)

PACKER'S SUITCASE SHOP

Charles Packer sells travel suitcases. The year-end is 30 June 2018.

REQUIRED:

/

6.1 Calculate the value of the closing stock on 30 June 2018 using the first-in-first-out (FIFO) method. (5)

6.2 Charles suspects that suitcases have been stolen. Provide a calculation

to support his concern.

(5)

6.3 Charles is concerned about the volume of stock on hand.

Calculate for how long his closing stock is expected to last. (6) State ONE problem with keeping too much stock on hand and ONE

problem with keeping insufficient stock on hand. (4)

INFORMATION: Stock balances:

UNITS

UNIT PRICE

TOTAL

Opening stock 420 R2 175 R913 500

Closing stock 496 ?

Purchases, returns and carriage:

UNITS

UNIT PRICE

TOTAL

Purchases 3 155 R8 460 850

September 2017 850 R2 250 R1 912 500

December 980 R2 670 R2 616 600

March 2018 875 R2 930 R2 563 750

June* (see returns) 450 R3 040 R1 368 000

Returns* (from June purchases) 25 R3 040 R76 000

Sales: 3 050 travel suitcases were sold at R4 200 each.

20

https://bit.ly/2YHn4XA

Gr 12 Accounting Revision Activities

16

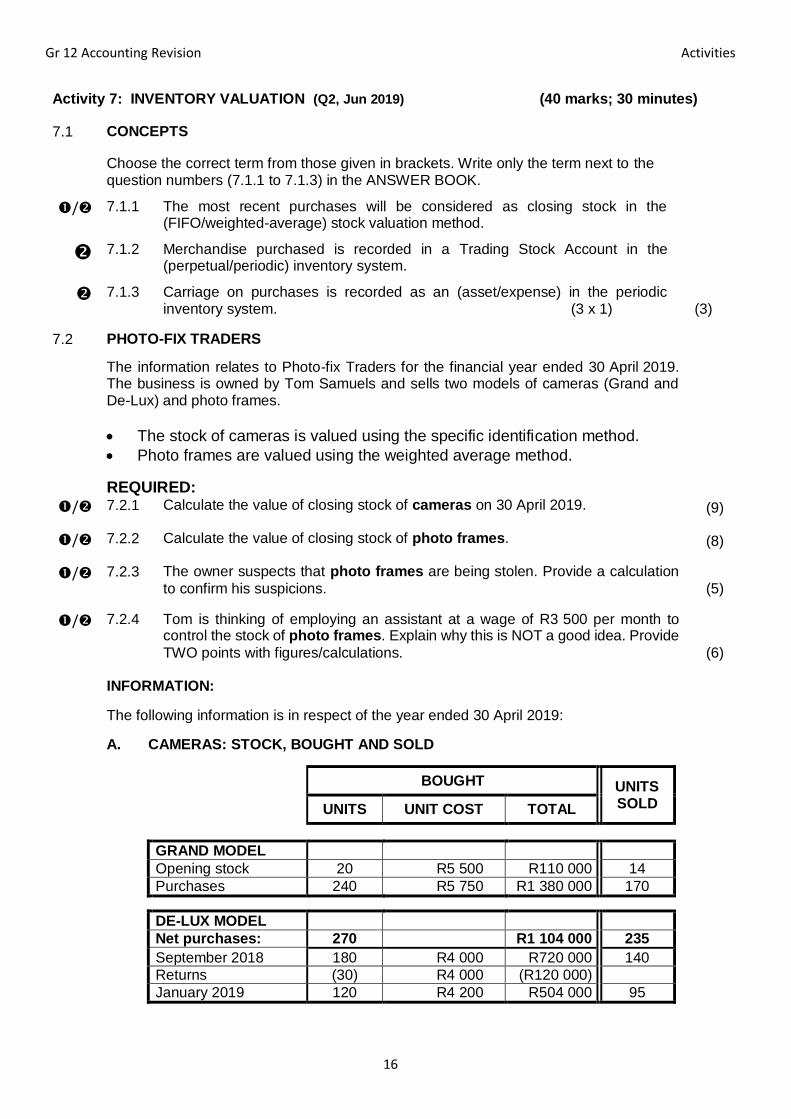

Activity 7: INVENTORY VALUATION (Q2, Jun 2019) (40 marks; 30 minutes)

7.1 CONCEPTS

Choose the correct term from those given in brackets. Write only the term next to the question numbers (7.1.1 to 7.1.3) in the ANSWER BOOK.

/ 7.1.1 The most recent purchases will be considered as closing stock in the (FIFO/weighted-average) stock valuation method.

(3)

7.1.2 Merchandise purchased is recorded in a Trading Stock Account in the (perpetual/periodic) inventory system.

7.1.3 Carriage on purchases is recorded as an (asset/expense) in the periodic inventory system. (3 x 1)

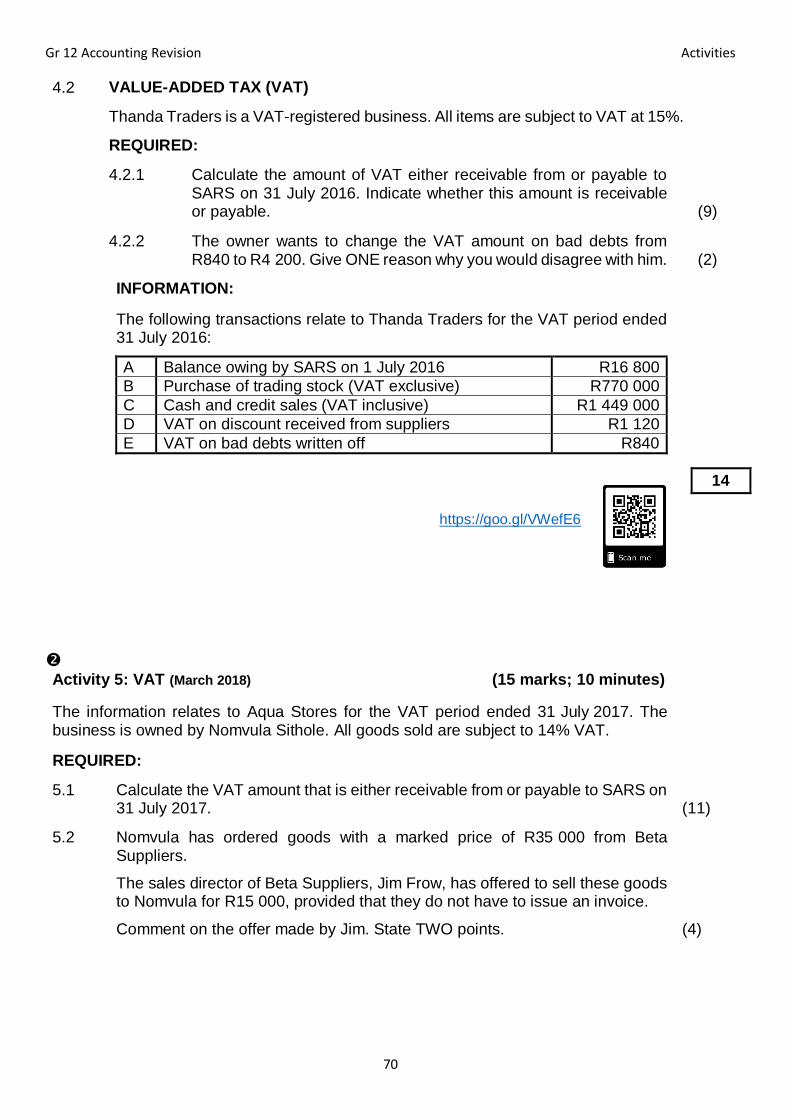

7.2 PHOTO-FIX TRADERS

The information relates to Photo-fix Traders for the financial year ended 30 April 2019. The business is owned by Tom Samuels and sells two models of cameras (Grand and De-Lux) and photo frames.

The stock of cameras is valued using the specific identification method.

Photo frames are valued using the weighted average method.

REQUIRED:

/ 7.2.1 Calculate the value of closing stock of cameras on 30 April 2019. (9)

/ 7.2.2 Calculate the value of closing stock of photo frames. (8)

/ 7.2.3 The owner suspects that photo frames are being stolen. Provide a calculation

to confirm his suspicions. (5)

/ 7.2.4 Tom is thinking of employing an assistant at a wage of R3 500 per month to control the stock of photo frames. Explain why this is NOT a good idea. Provide

TWO points with figures/calculations. (6) INFORMATION:

The following information is in respect of the year ended 30 April 2019:

A. CAMERAS: STOCK, BOUGHT AND SOLD

BOUGHT UNITS

SOLD UNITS UNIT COST TOTAL

GRAND MODEL

Opening stock 20 R5 500 R110 000 14

Purchases 240 R5 750 R1 380 000 170

DE-LUX MODEL

Net purchases: 270 R1 104 000 235

September 2018 180 R4 000 R720 000 140

Returns (30) R4 000 (R120 000)

January 2019 120 R4 200 R504 000 95

Gr 12 Accounting Revision Activities

17

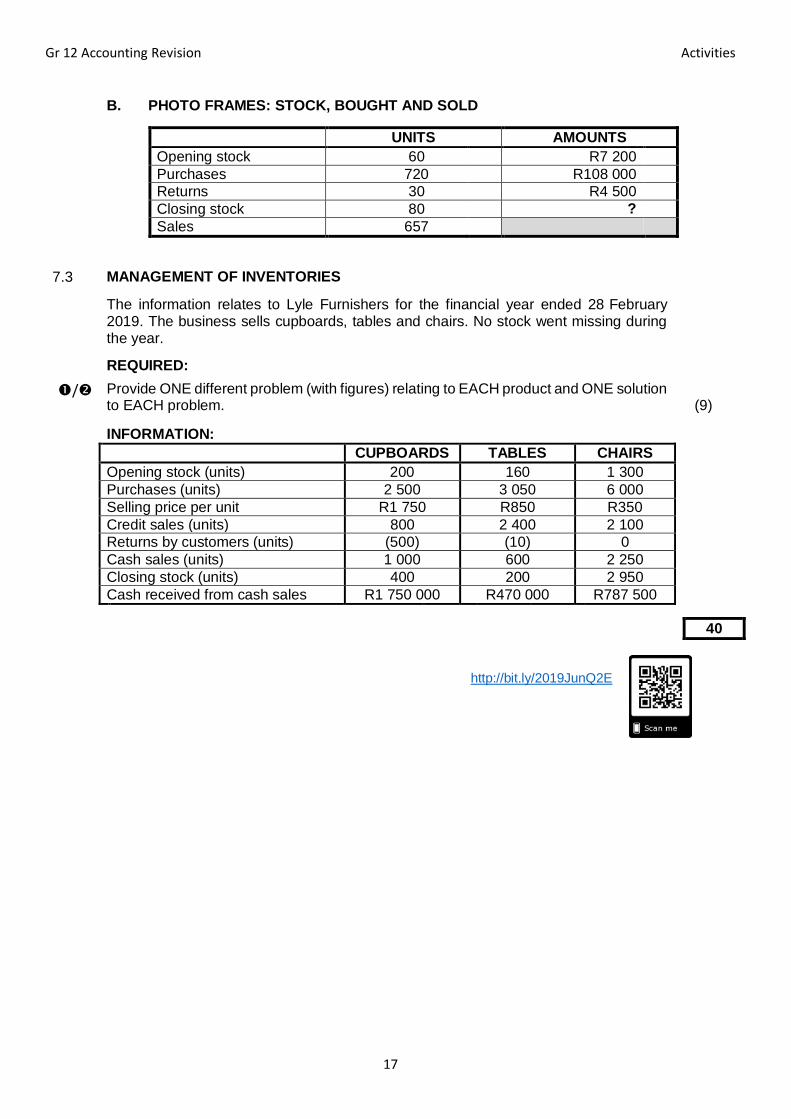

B. PHOTO FRAMES: STOCK, BOUGHT AND SOLD

UNITS AMOUNTS

Opening stock 60 R7 200

Purchases 720 R108 000

Returns 30 R4 500

Closing stock 80 ?

Sales 657

7.3 MANAGEMENT OF INVENTORIES

The information relates to Lyle Furnishers for the financial year ended 28 February 2019. The business sells cupboards, tables and chairs. No stock went missing during the year.

REQUIRED:

/ Provide ONE different problem (with figures) relating to EACH product and ONE solution to EACH problem. (9)

INFORMATION:

CUPBOARDS TABLES CHAIRS

Opening stock (units) 200 160 1 300

Purchases (units) 2 500 3 050 6 000

Selling price per unit R1 750 R850 R350

Credit sales (units) 800 2 400 2 100

Returns by customers (units) (500) (10) 0

Cash sales (units) 1 000 600 2 250

Closing stock (units) 400 200 2 950

Cash received from cash sales R1 750 000 R470 000 R787 500

40

http://bit.ly/2019JunQ2E

Gr 12 Accounting Revision Activities

18

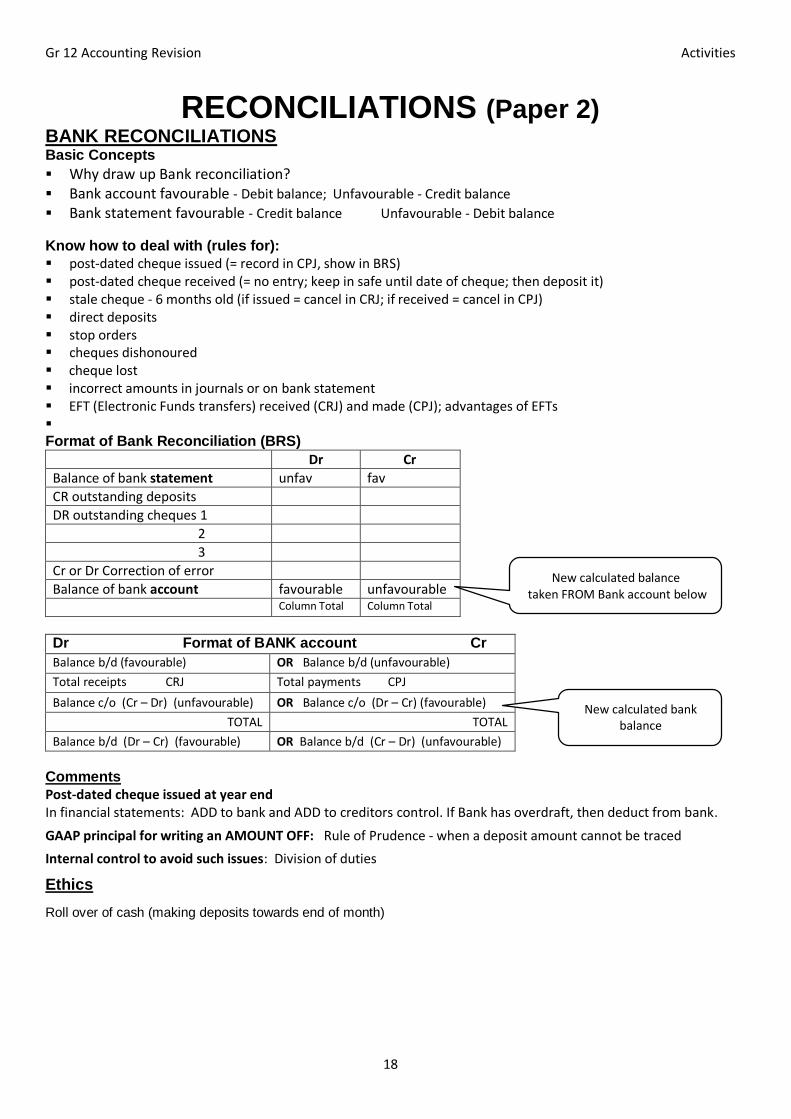

RECONCILIATIONS (Paper 2) BANK RECONCILIATIONS

Basic Concepts

Why draw up Bank reconciliation?

Bank account favourable - Debit balance; Unfavourable - Credit balance

Bank statement favourable - Credit balance Unfavourable - Debit balance

Know how to deal with (rules for):

post-dated cheque issued (= record in CPJ, show in BRS) post-dated cheque received (= no entry; keep in safe until date of cheque; then deposit it) stale cheque - 6 months old (if issued = cancel in CRJ; if received = cancel in CPJ) direct deposits stop orders cheques dishonoured cheque lost incorrect amounts in journals or on bank statement EFT (Electronic Funds transfers) received (CRJ) and made (CPJ); advantages of EFTs Format of Bank Reconciliation (BRS)

Dr Cr

Balance of bank statement unfav fav

CR outstanding deposits

DR outstanding cheques 1

2

3

Cr or Dr Correction of error

Balance of bank account favourable unfavourable

Column Total Column Total

Dr Format of BANK account Cr

Balance b/d (favourable) OR Balance b/d (unfavourable)

Total receipts CRJ Total payments CPJ

Balance c/o (Cr – Dr) (unfavourable) OR Balance c/o (Dr – Cr) (favourable)

TOTAL TOTAL

Balance b/d (Dr – Cr) (favourable) OR Balance b/d (Cr – Dr) (unfavourable)

Comments

Post-dated cheque issued at year end In financial statements: ADD to bank and ADD to creditors control. If Bank has overdraft, then deduct from bank.

GAAP principal for writing an AMOUNT OFF: Rule of Prudence - when a deposit amount cannot be traced

Internal control to avoid such issues: Division of duties

Ethics

Roll over of cash (making deposits towards end of month)

New calculated bank balance

New calculated balance taken FROM Bank account below

Gr 12 Accounting Revision Activities

19

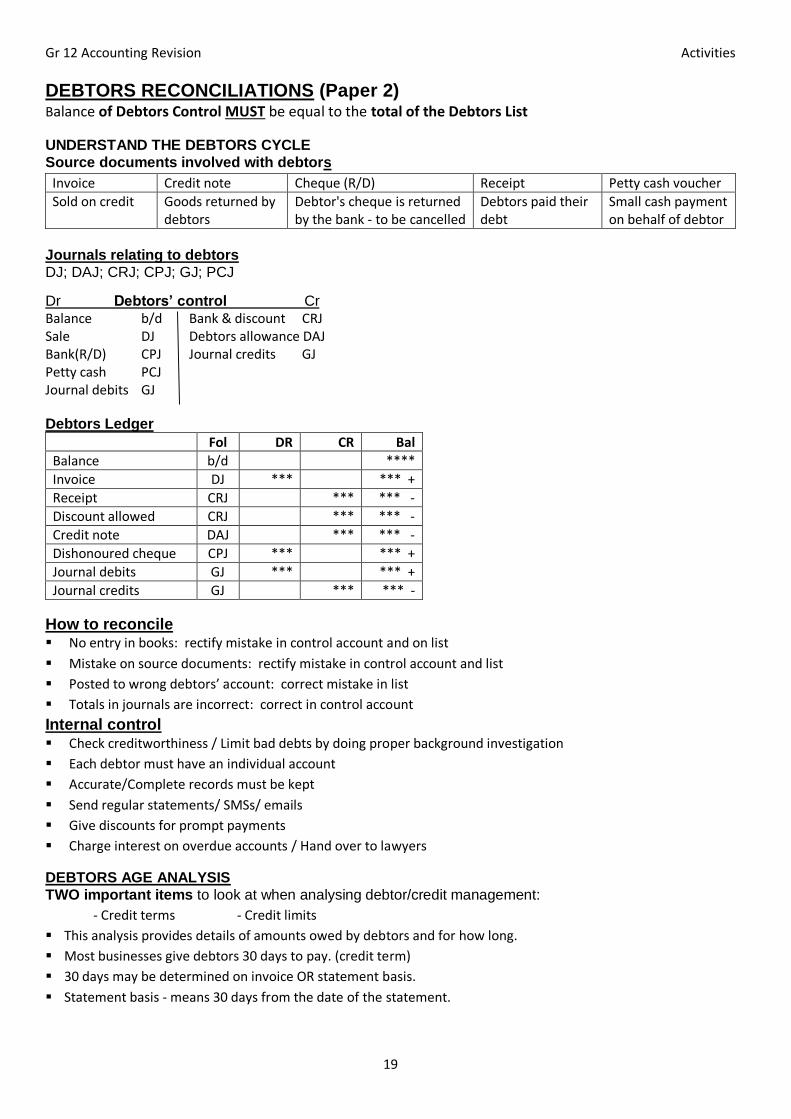

DEBTORS RECONCILIATIONS (Paper 2) Balance of Debtors Control MUST be equal to the total of the Debtors List

UNDERSTAND THE DEBTORS CYCLE

Source documents involved with debtors

Invoice Credit note Cheque (R/D) Receipt Petty cash voucher

Sold on credit Goods returned by debtors

Debtor's cheque is returned by the bank - to be cancelled

Debtors paid their debt

Small cash payment on behalf of debtor

Journals relating to debtors

DJ; DAJ; CRJ; CPJ; GJ; PCJ

Dr Debtors’ control Cr

Balance b/d Bank & discount CRJ Sale DJ Debtors allowance DAJ Bank(R/D) CPJ Journal credits GJ Petty cash PCJ Journal debits GJ Debtors Ledger

Fol DR CR Bal

Balance b/d ****

Invoice DJ *** *** +

Receipt CRJ *** *** -

Discount allowed CRJ *** *** -

Credit note DAJ *** *** -

Dishonoured cheque CPJ *** *** +

Journal debits GJ *** *** +

Journal credits GJ *** *** -

How to reconcile No entry in books: rectify mistake in control account and on list

Mistake on source documents: rectify mistake in control account and list

Posted to wrong debtors’ account: correct mistake in list

Totals in journals are incorrect: correct in control account

Internal control Check creditworthiness / Limit bad debts by doing proper background investigation

Each debtor must have an individual account

Accurate/Complete records must be kept

Send regular statements/ SMSs/ emails

Give discounts for prompt payments

Charge interest on overdue accounts / Hand over to lawyers

DEBTORS AGE ANALYSIS

TWO important items to look at when analysing debtor/credit management:

- Credit terms - Credit limits

This analysis provides details of amounts owed by debtors and for how long.

Most businesses give debtors 30 days to pay. (credit term)

30 days may be determined on invoice OR statement basis.

Statement basis - means 30 days from the date of the statement.

Gr 12 Accounting Revision Activities

20

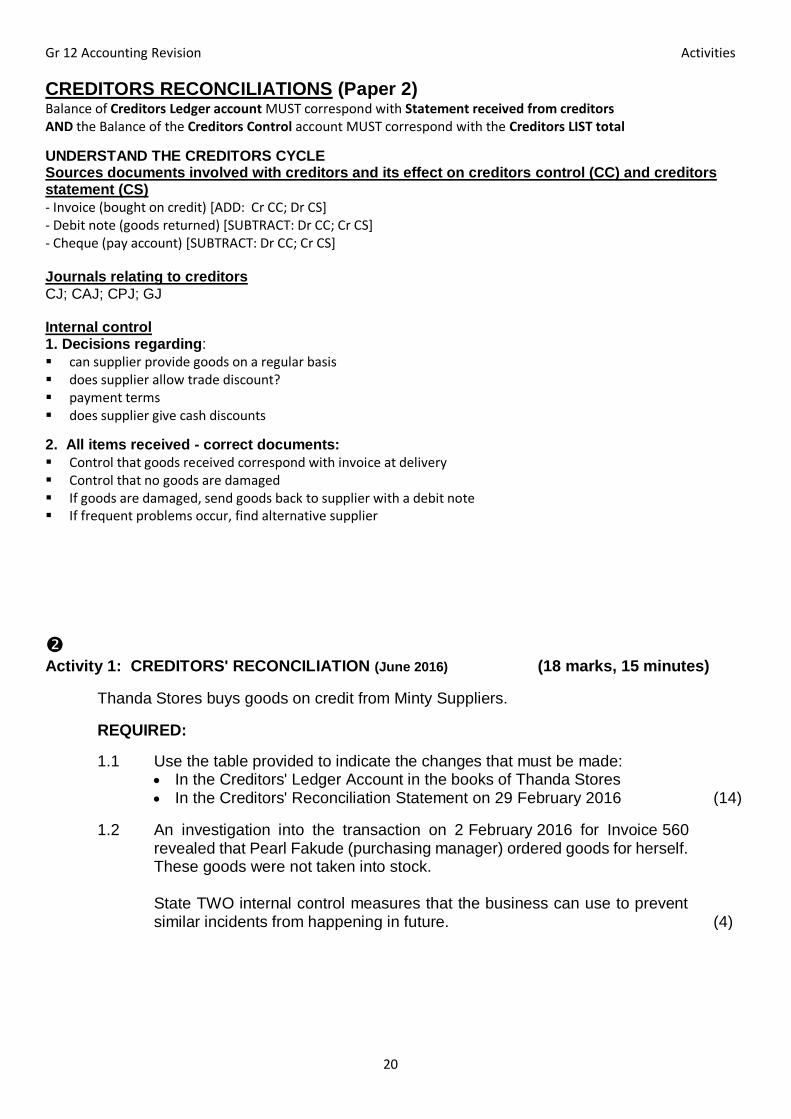

CREDITORS RECONCILIATIONS (Paper 2) Balance of Creditors Ledger account MUST correspond with Statement received from creditors AND the Balance of the Creditors Control account MUST correspond with the Creditors LIST total

UNDERSTAND THE CREDITORS CYCLE Sources documents involved with creditors and its effect on creditors control (CC) and creditors statement (CS)

- Invoice (bought on credit) [ADD: Cr CC; Dr CS] - Debit note (goods returned) [SUBTRACT: Dr CC; Cr CS] - Cheque (pay account) [SUBTRACT: Dr CC; Cr CS] Journals relating to creditors

CJ; CAJ; CPJ; GJ Internal control 1. Decisions regarding:

can supplier provide goods on a regular basis does supplier allow trade discount? payment terms does supplier give cash discounts

2. All items received - correct documents:

Control that goods received correspond with invoice at delivery Control that no goods are damaged If goods are damaged, send goods back to supplier with a debit note If frequent problems occur, find alternative supplier

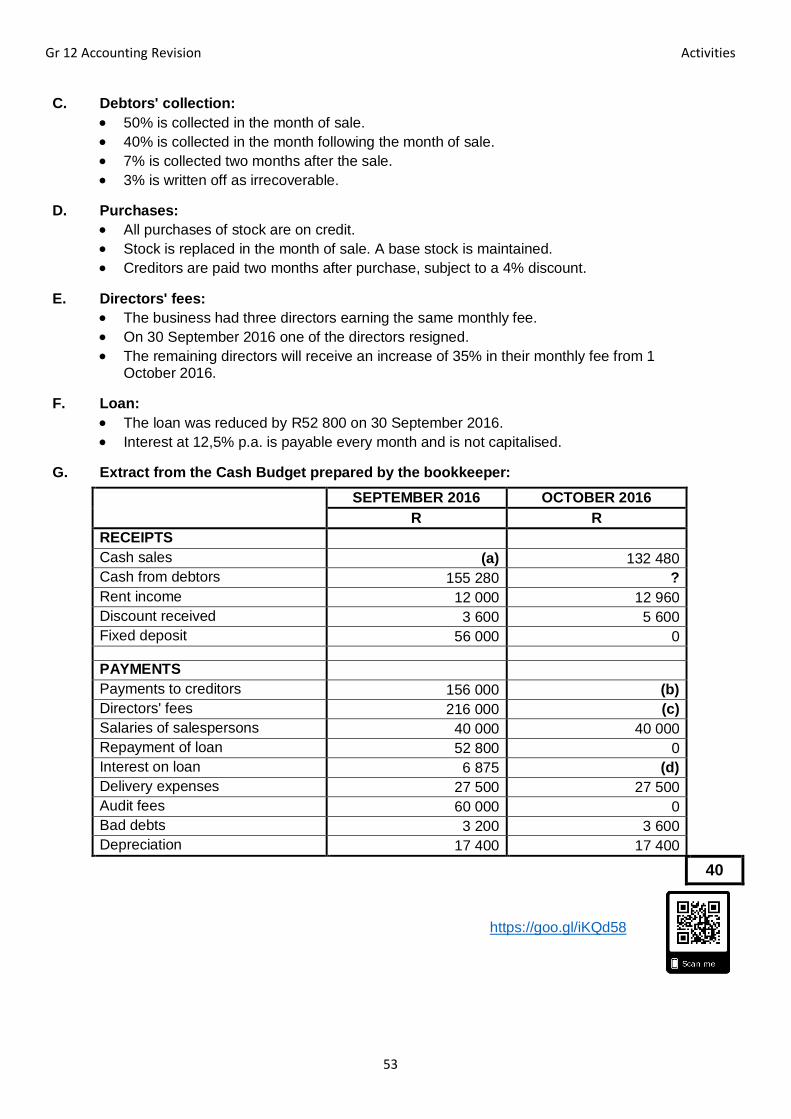

Activity 1: CREDITORS' RECONCILIATION (June 2016) (18 marks, 15 minutes)

Thanda Stores buys goods on credit from Minty Suppliers.

REQUIRED:

1.1 Use the table provided to indicate the changes that must be made: In the Creditors' Ledger Account in the books of Thanda Stores

In the Creditors' Reconciliation Statement on 29 February 2016 (14)

1.2 An investigation into the transaction on 2 February 2016 for Invoice 560 revealed that Pearl Fakude (purchasing manager) ordered goods for herself. These goods were not taken into stock. State TWO internal control measures that the business can use to prevent similar incidents from happening in future. (4)

Gr 12 Accounting Revision Activities

21

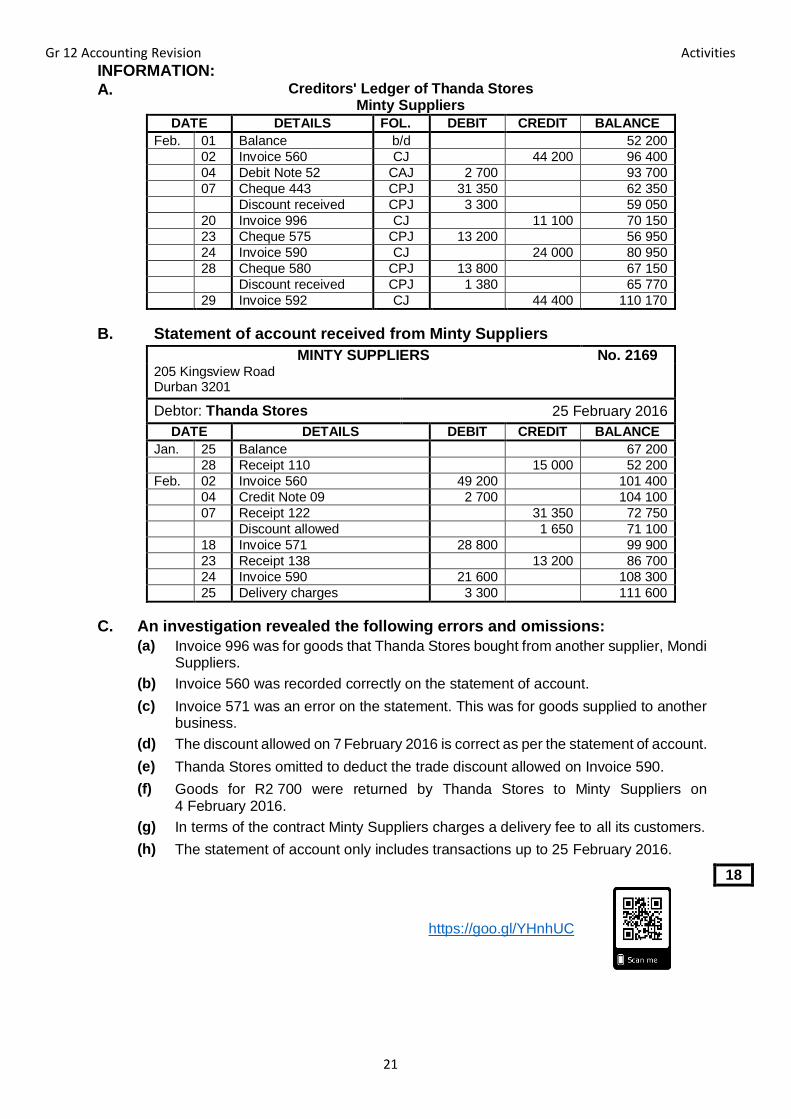

INFORMATION:

A. Creditors' Ledger of Thanda Stores

Minty Suppliers

DATE DETAILS FOL. DEBIT CREDIT BALANCE

Feb. 01 Balance b/d 52 200

02 Invoice 560 CJ 44 200 96 400

04 Debit Note 52 CAJ 2 700 93 700

07 Cheque 443 CPJ 31 350 62 350

Discount received CPJ 3 300 59 050

20 Invoice 996 CJ 11 100 70 150

23 Cheque 575 CPJ 13 200 56 950

24 Invoice 590 CJ 24 000 80 950

28 Cheque 580 CPJ 13 800 67 150

Discount received CPJ 1 380 65 770

29 Invoice 592 CJ 44 400 110 170

B. Statement of account received from Minty Suppliers

MINTY SUPPLIERS No. 2169 205 Kingsview Road

Durban 3201

Debtor: Thanda Stores 25 February 2016

DATE DETAILS DEBIT CREDIT BALANCE

Jan. 25 Balance 67 200

28 Receipt 110 15 000 52 200

Feb. 02 Invoice 560 49 200 101 400

04 Credit Note 09 2 700 104 100

07 Receipt 122 31 350 72 750

Discount allowed 1 650 71 100

18 Invoice 571 28 800 99 900

23 Receipt 138 13 200 86 700

24 Invoice 590 21 600 108 300

25 Delivery charges 3 300 111 600

C. An investigation revealed the following errors and omissions:

(a) Invoice 996 was for goods that Thanda Stores bought from another supplier, Mondi Suppliers.

(b) Invoice 560 was recorded correctly on the statement of account.

(c) Invoice 571 was an error on the statement. This was for goods supplied to another business.

(d) The discount allowed on 7 February 2016 is correct as per the statement of account.

(e) Thanda Stores omitted to deduct the trade discount allowed on Invoice 590.

(f) Goods for R2 700 were returned by Thanda Stores to Minty Suppliers on 4 February 2016.

(g) In terms of the contract Minty Suppliers charges a delivery fee to all its customers.

(h) The statement of account only includes transactions up to 25 February 2016.

18

https://goo.gl/YHnhUC

Gr 12 Accounting Revision Activities

22

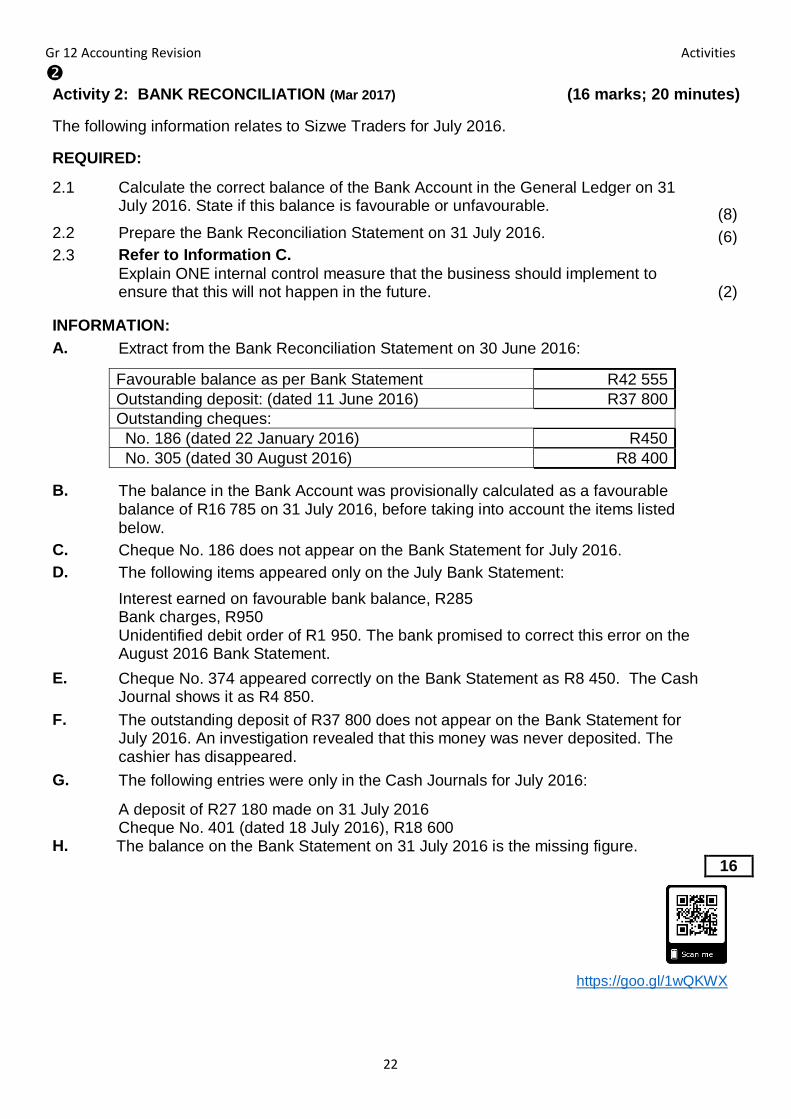

Activity 2: BANK RECONCILIATION (Mar 2017) (16 marks; 20 minutes)

The following information relates to Sizwe Traders for July 2016.

REQUIRED:

2.1 Calculate the correct balance of the Bank Account in the General Ledger on 31 July 2016. State if this balance is favourable or unfavourable.

(8) 2.2 Prepare the Bank Reconciliation Statement on 31 July 2016. (6) 2.3 Refer to Information C.

Explain ONE internal control measure that the business should implement to ensure that this will not happen in the future.

(2)

INFORMATION:

A. Extract from the Bank Reconciliation Statement on 30 June 2016:

Favourable balance as per Bank Statement R42 555

Outstanding deposit: (dated 11 June 2016) R37 800

Outstanding cheques:

No. 186 (dated 22 January 2016) R450

No. 305 (dated 30 August 2016) R8 400

B. The balance in the Bank Account was provisionally calculated as a favourable balance of R16 785 on 31 July 2016, before taking into account the items listed below.

C. Cheque No. 186 does not appear on the Bank Statement for July 2016.

D. The following items appeared only on the July Bank Statement:

Interest earned on favourable bank balance, R285 Bank charges, R950 Unidentified debit order of R1 950. The bank promised to correct this error on the August 2016 Bank Statement.

E. Cheque No. 374 appeared correctly on the Bank Statement as R8 450. The Cash Journal shows it as R4 850.

F. The outstanding deposit of R37 800 does not appear on the Bank Statement for July 2016. An investigation revealed that this money was never deposited. The cashier has disappeared.

G. The following entries were only in the Cash Journals for July 2016:

A deposit of R27 180 made on 31 July 2016 Cheque No. 401 (dated 18 July 2016), R18 600

H. The balance on the Bank Statement on 31 July 2016 is the missing figure.

16

https://goo.gl/1wQKWX

Gr 12 Accounting Revision Activities

23

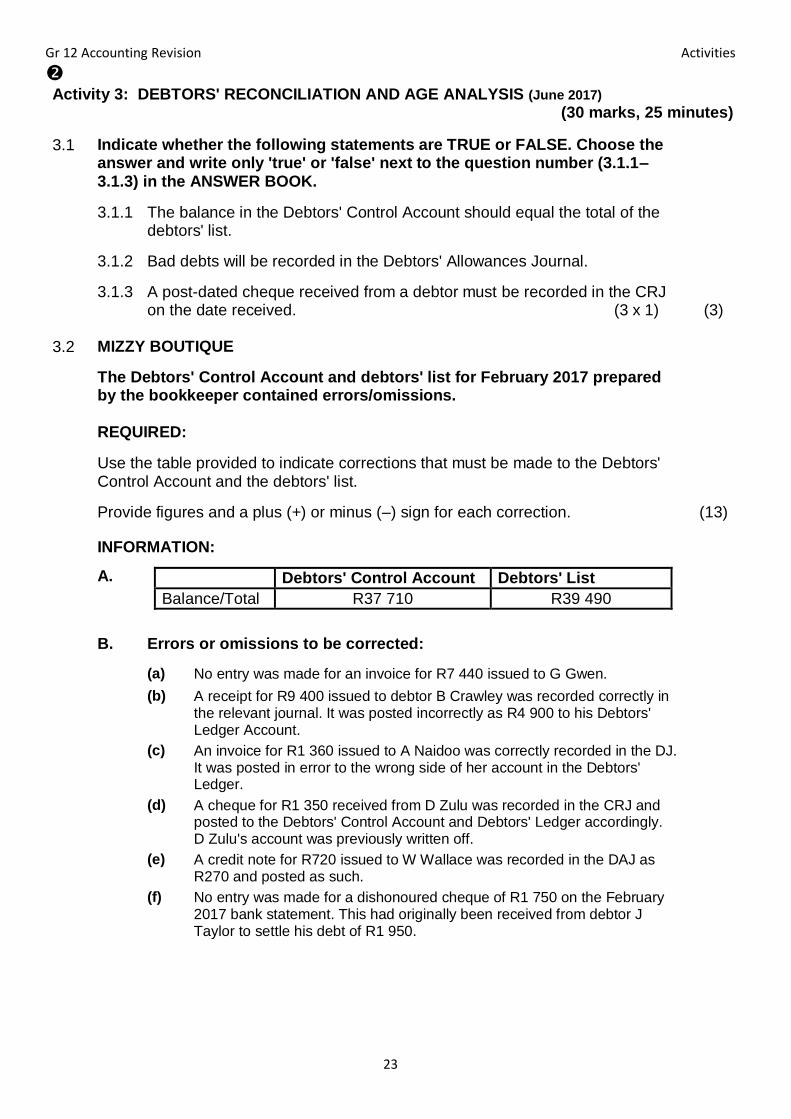

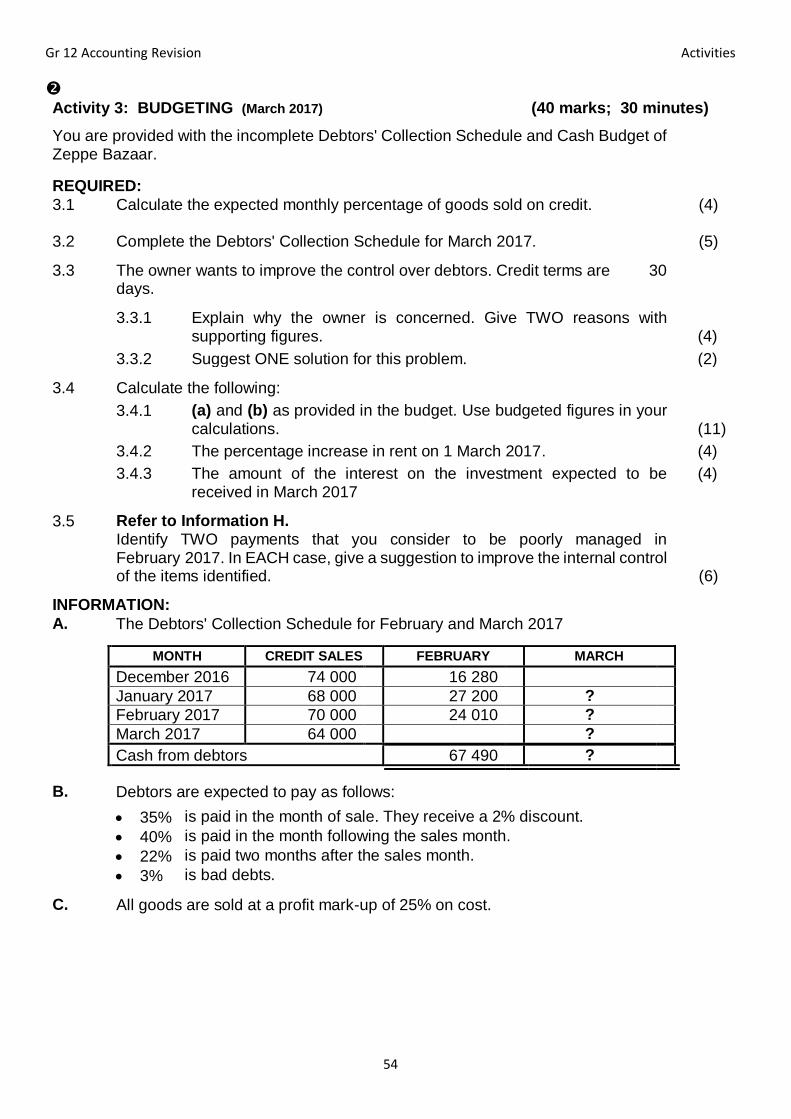

Activity 3: DEBTORS' RECONCILIATION AND AGE ANALYSIS (June 2017) (30 marks, 25 minutes)

3.1 Indicate whether the following statements are TRUE or FALSE. Choose the answer and write only 'true' or 'false' next to the question number (3.1.1–3.1.3) in the ANSWER BOOK.

3.1.1 The balance in the Debtors' Control Account should equal the total of the debtors' list.

3.1.2 Bad debts will be recorded in the Debtors' Allowances Journal.

3.1.3 A post-dated cheque received from a debtor must be recorded in the CRJ on the date received. (3 x 1)

(3)

3.2 MIZZY BOUTIQUE

The Debtors' Control Account and debtors' list for February 2017 prepared by the bookkeeper contained errors/omissions.

REQUIRED:

Use the table provided to indicate corrections that must be made to the Debtors' Control Account and the debtors' list.

Provide figures and a plus (+) or minus (–) sign for each correction. (13)

INFORMATION:

A.

Debtors' Control Account Debtors' List

Balance/Total R37 710 R39 490

B. Errors or omissions to be corrected:

(a) No entry was made for an invoice for R7 440 issued to G Gwen. (b) A receipt for R9 400 issued to debtor B Crawley was recorded correctly in

the relevant journal. It was posted incorrectly as R4 900 to his Debtors' Ledger Account.

(c) An invoice for R1 360 issued to A Naidoo was correctly recorded in the DJ. It was posted in error to the wrong side of her account in the Debtors' Ledger.

(d) A cheque for R1 350 received from D Zulu was recorded in the CRJ and posted to the Debtors' Control Account and Debtors' Ledger accordingly. D Zulu's account was previously written off.

(e) A credit note for R720 issued to W Wallace was recorded in the DAJ as R270 and posted as such.

(f) No entry was made for a dishonoured cheque of R1 750 on the February 2017 bank statement. This had originally been received from debtor J Taylor to settle his debt of R1 950.

Gr 12 Accounting Revision Activities

24

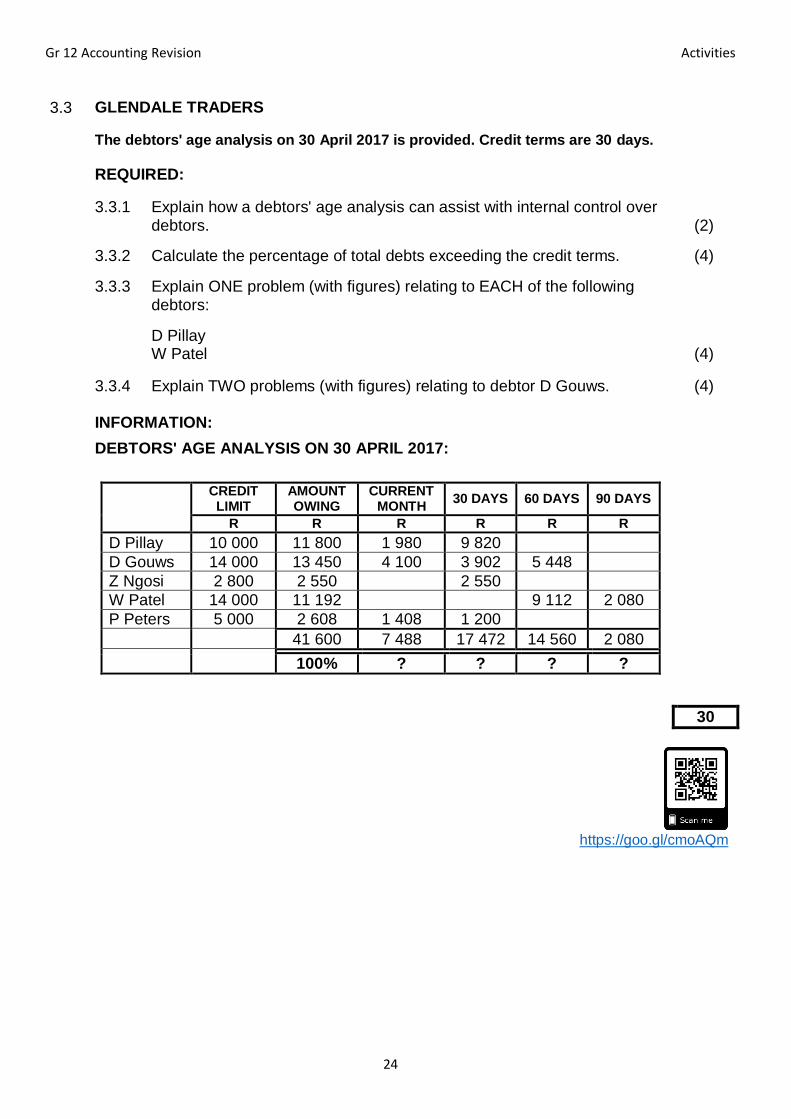

3.3 GLENDALE TRADERS

The debtors' age analysis on 30 April 2017 is provided. Credit terms are 30 days.

REQUIRED:

3.3.1 Explain how a debtors' age analysis can assist with internal control over debtors. (2)

3.3.2 Calculate the percentage of total debts exceeding the credit terms. (4)

3.3.3 Explain ONE problem (with figures) relating to EACH of the following debtors:

D Pillay W Patel (4)

3.3.4 Explain TWO problems (with figures) relating to debtor D Gouws. (4) INFORMATION:

DEBTORS' AGE ANALYSIS ON 30 APRIL 2017:

CREDIT LIMIT

AMOUNT OWING

CURRENT MONTH

30 DAYS 60 DAYS 90 DAYS

R R R R R R

D Pillay 10 000 11 800 1 980 9 820

D Gouws 14 000 13 450 4 100 3 902 5 448

Z Ngosi 2 800 2 550 2 550

W Patel 14 000 11 192 9 112 2 080

P Peters 5 000 2 608 1 408 1 200

41 600 7 488 17 472 14 560 2 080

100% ? ? ? ?

30

https://goo.gl/cmoAQm

Gr 12 Accounting Revision Activities

25

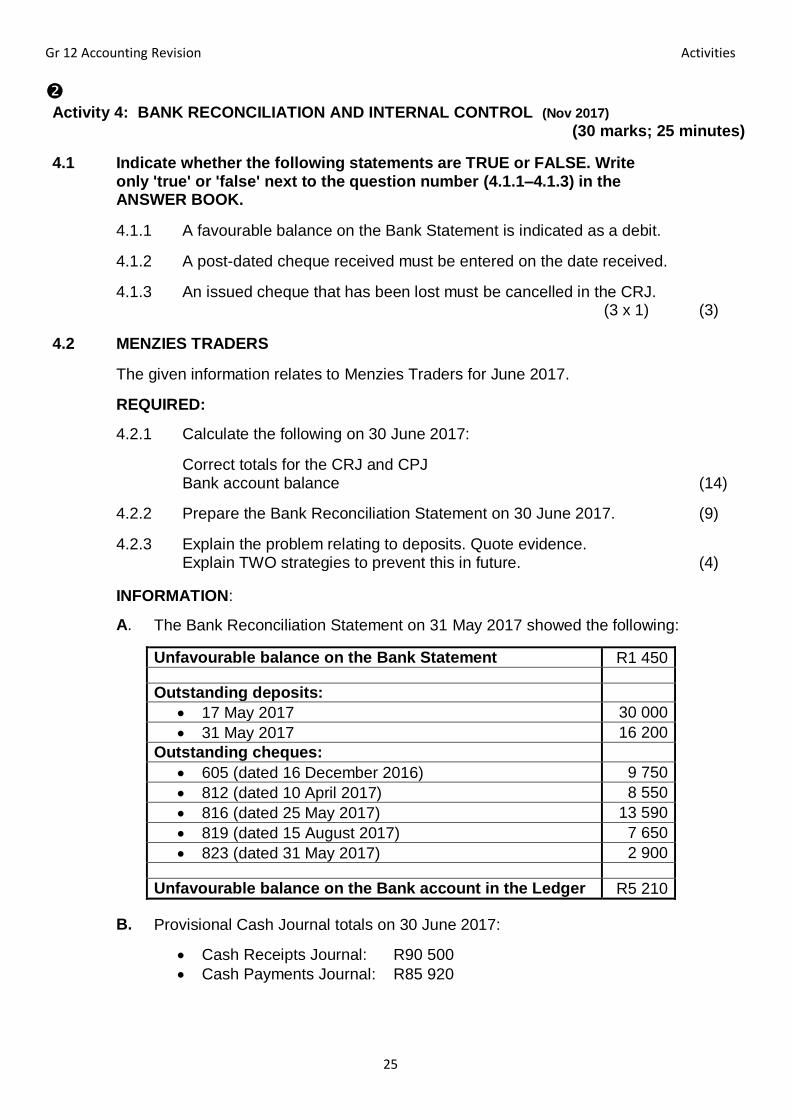

Activity 4: BANK RECONCILIATION AND INTERNAL CONTROL (Nov 2017) (30 marks; 25 minutes)

4.1 Indicate whether the following statements are TRUE or FALSE. Write only 'true' or 'false' next to the question number (4.1.1–4.1.3) in the ANSWER BOOK.

4.1.1 A favourable balance on the Bank Statement is indicated as a debit.

4.1.2 A post-dated cheque received must be entered on the date received.

4.1.3 An issued cheque that has been lost must be cancelled in the CRJ. (3 x 1) (3)

4.2 MENZIES TRADERS

The given information relates to Menzies Traders for June 2017.

REQUIRED:

4.2.1 Calculate the following on 30 June 2017:

Correct totals for the CRJ and CPJ Bank account balance (14)

4.2.2 Prepare the Bank Reconciliation Statement on 30 June 2017. (9)

4.2.3 Explain the problem relating to deposits. Quote evidence. Explain TWO strategies to prevent this in future.

(4)

INFORMATION:

A. The Bank Reconciliation Statement on 31 May 2017 showed the following:

Unfavourable balance on the Bank Statement R1 450

Outstanding deposits:

17 May 2017 30 000

31 May 2017 16 200

Outstanding cheques:

605 (dated 16 December 2016) 9 750

812 (dated 10 April 2017) 8 550

816 (dated 25 May 2017) 13 590

819 (dated 15 August 2017) 7 650

823 (dated 31 May 2017) 2 900

Unfavourable balance on the Bank account in the Ledger R5 210

B. Provisional Cash Journal totals on 30 June 2017:

Cash Receipts Journal: R90 500

Cash Payments Journal: R85 920

Gr 12 Accounting Revision Activities

26

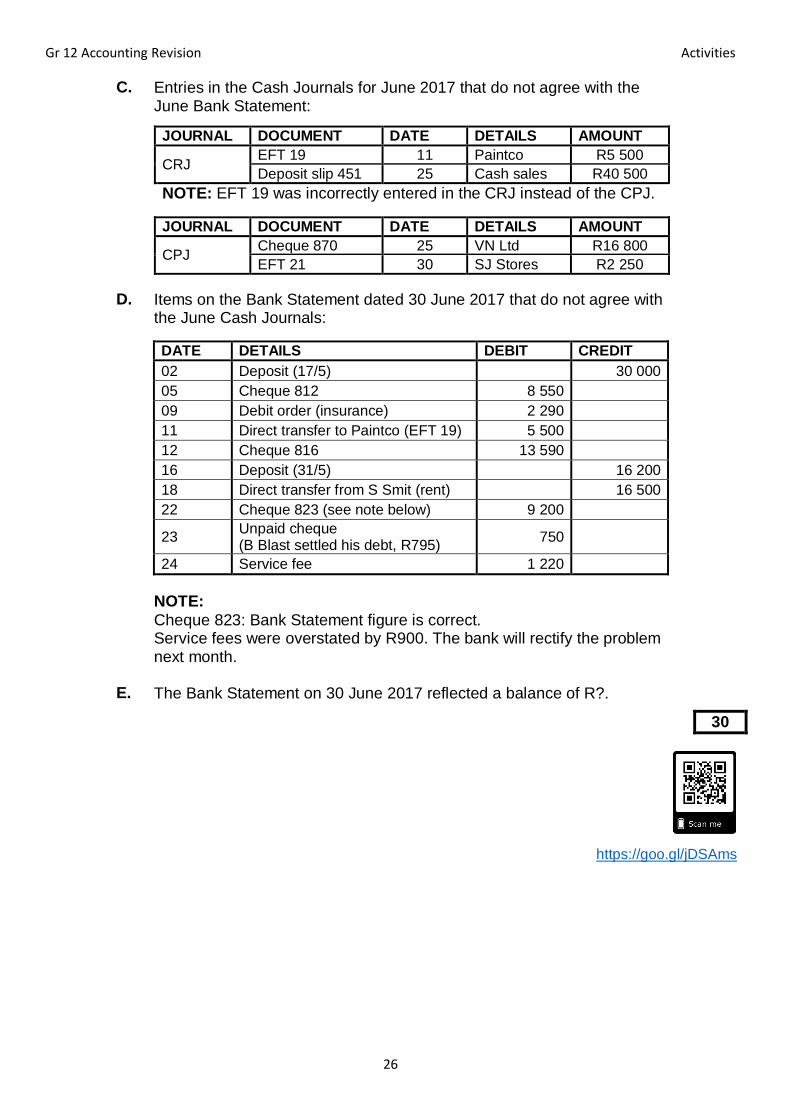

C. Entries in the Cash Journals for June 2017 that do not agree with the June Bank Statement:

JOURNAL DOCUMENT DATE DETAILS AMOUNT

CRJ EFT 19 11 Paintco R5 500

Deposit slip 451 25 Cash sales R40 500

NOTE: EFT 19 was incorrectly entered in the CRJ instead of the CPJ.

JOURNAL DOCUMENT DATE DETAILS AMOUNT

CPJ Cheque 870 25 VN Ltd R16 800

EFT 21 30 SJ Stores R2 250

D. Items on the Bank Statement dated 30 June 2017 that do not agree with the June Cash Journals:

DATE DETAILS DEBIT CREDIT

02 Deposit (17/5) 30 000

05 Cheque 812 8 550

09 Debit order (insurance) 2 290

11 Direct transfer to Paintco (EFT 19) 5 500

12 Cheque 816 13 590

16 Deposit (31/5) 16 200

18 Direct transfer from S Smit (rent) 16 500

22 Cheque 823 (see note below) 9 200

23

Unpaid cheque (B Blast settled his debt, R795)

750

24 Service fee 1 220

NOTE:

Cheque 823: Bank Statement figure is correct. Service fees were overstated by R900. The bank will rectify the problem next month.

E. The Bank Statement on 30 June 2017 reflected a balance of R?.

30

https://goo.gl/jDSAms

Gr 12 Accounting Revision Activities

27

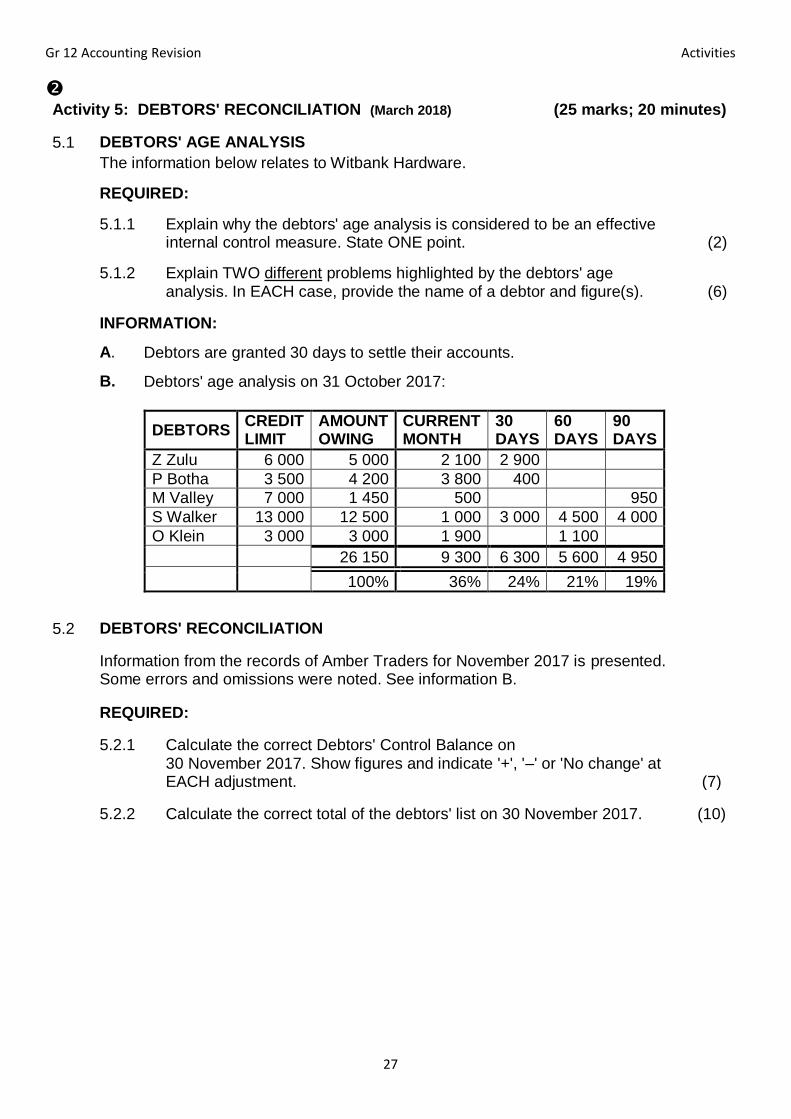

Activity 5: DEBTORS' RECONCILIATION (March 2018) (25 marks; 20 minutes)

5.1 DEBTORS' AGE ANALYSIS

The information below relates to Witbank Hardware.

REQUIRED:

5.1.1 Explain why the debtors' age analysis is considered to be an effective internal control measure. State ONE point. (2)

5.1.2 Explain TWO different problems highlighted by the debtors' age analysis. In EACH case, provide the name of a debtor and figure(s). (6)

INFORMATION:

A. Debtors are granted 30 days to settle their accounts.

B. Debtors' age analysis on 31 October 2017:

DEBTORS CREDIT LIMIT

AMOUNT OWING

CURRENT MONTH

30 DAYS

60 DAYS

90 DAYS

Z Zulu 6 000 5 000 2 100 2 900

P Botha 3 500 4 200 3 800 400

M Valley 7 000 1 450 500 950

S Walker 13 000 12 500 1 000 3 000 4 500 4 000

O Klein 3 000 3 000 1 900 1 100

26 150 9 300 6 300 5 600 4 950

100% 36% 24% 21% 19%

5.2 DEBTORS' RECONCILIATION

Information from the records of Amber Traders for November 2017 is presented. Some errors and omissions were noted. See information B.

REQUIRED:

5.2.1 Calculate the correct Debtors' Control Balance on 30 November 2017. Show figures and indicate '+', '–' or 'No change' at EACH adjustment. (7)

5.2.2 Calculate the correct total of the debtors' list on 30 November 2017. (10)

Gr 12 Accounting Revision Activities

28

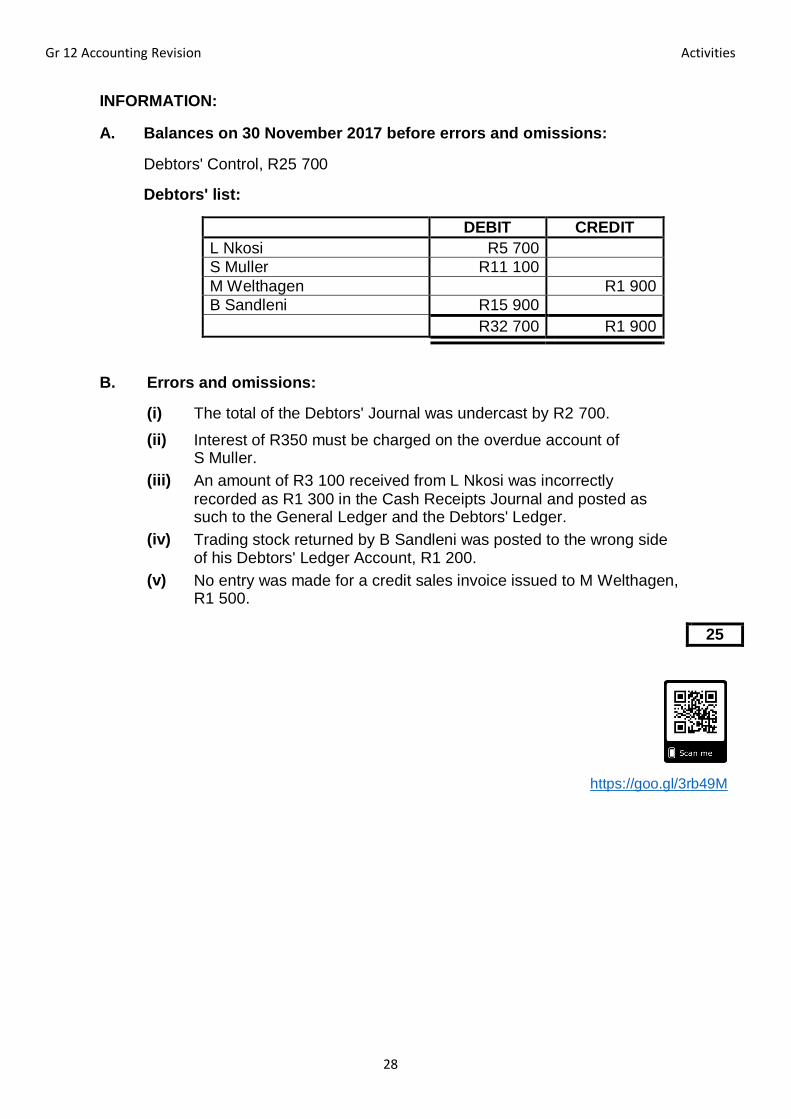

INFORMATION:

A. Balances on 30 November 2017 before errors and omissions:

Debtors' Control, R25 700

Debtors' list:

DEBIT CREDIT

L Nkosi R5 700

S Muller R11 100

M Welthagen R1 900

B Sandleni R15 900

R32 700 R1 900

B. Errors and omissions:

(i) The total of the Debtors' Journal was undercast by R2 700.

(ii) Interest of R350 must be charged on the overdue account of S Muller.

(iii) An amount of R3 100 received from L Nkosi was incorrectly recorded as R1 300 in the Cash Receipts Journal and posted as such to the General Ledger and the Debtors' Ledger.

(iv) Trading stock returned by B Sandleni was posted to the wrong side of his Debtors' Ledger Account, R1 200.

(v) No entry was made for a credit sales invoice issued to M Welthagen, R1 500.

25

https://goo.gl/3rb49M

Gr 12 Accounting Revision Activities

29

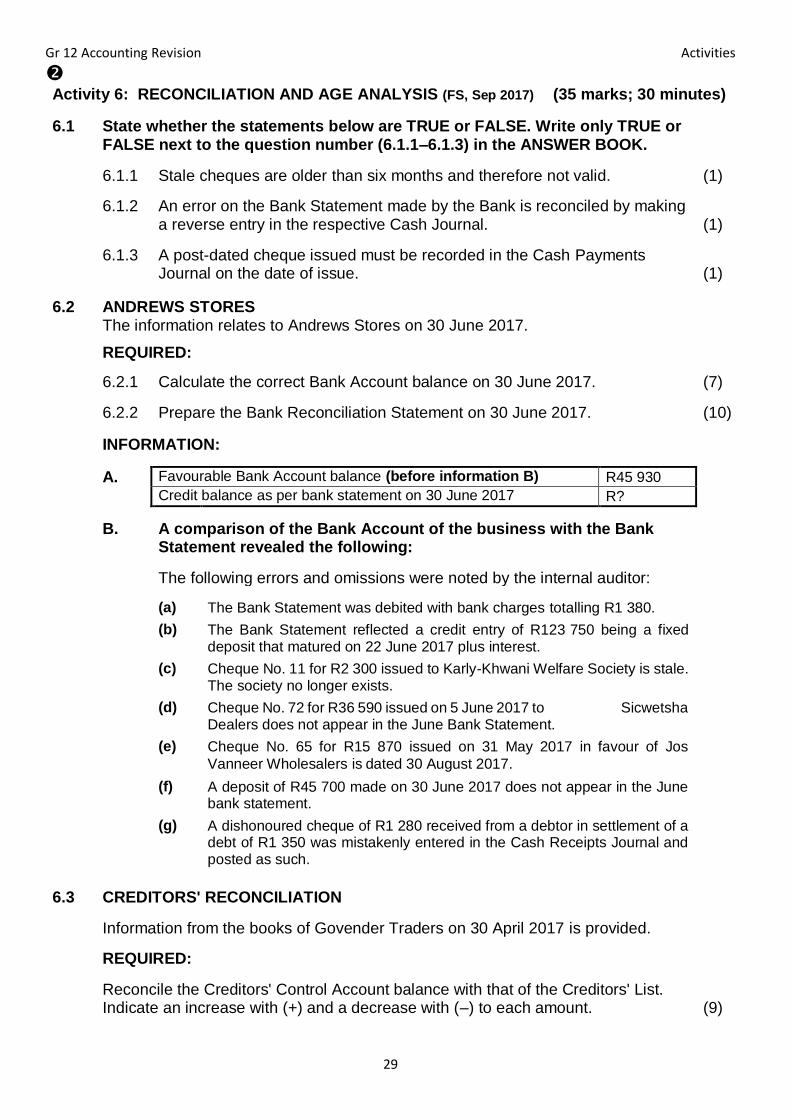

Activity 6: RECONCILIATION AND AGE ANALYSIS (FS, Sep 2017) (35 marks; 30 minutes)

6.1 State whether the statements below are TRUE or FALSE. Write only TRUE or FALSE next to the question number (6.1.1–6.1.3) in the ANSWER BOOK.

6.1.1 Stale cheques are older than six months and therefore not valid. (1)

6.1.2

An error on the Bank Statement made by the Bank is reconciled by making a reverse entry in the respective Cash Journal.

(1)

6.1.3 A post-dated cheque issued must be recorded in the Cash Payments Journal on the date of issue.

(1)

6.2 ANDREWS STORES The information relates to Andrews Stores on 30 June 2017.

REQUIRED:

6.2.1 Calculate the correct Bank Account balance on 30 June 2017. (7)

6.2.2 Prepare the Bank Reconciliation Statement on 30 June 2017. (10)

INFORMATION:

A. Favourable Bank Account balance (before information B) R45 930

Credit balance as per bank statement on 30 June 2017 R?

B. A comparison of the Bank Account of the business with the Bank Statement revealed the following:

The following errors and omissions were noted by the internal auditor:

(a) The Bank Statement was debited with bank charges totalling R1 380.

(b) The Bank Statement reflected a credit entry of R123 750 being a fixed deposit that matured on 22 June 2017 plus interest.

(c) Cheque No. 11 for R2 300 issued to Karly-Khwani Welfare Society is stale. The society no longer exists.

(d) Cheque No. 72 for R36 590 issued on 5 June 2017 to Sicwetsha Dealers does not appear in the June Bank Statement.

(e) Cheque No. 65 for R15 870 issued on 31 May 2017 in favour of Jos

Vanneer Wholesalers is dated 30 August 2017.

(f) A deposit of R45 700 made on 30 June 2017 does not appear in the June bank statement.

(g) A dishonoured cheque of R1 280 received from a debtor in settlement of a debt of R1 350 was mistakenly entered in the Cash Receipts Journal and posted as such.

6.3 CREDITORS' RECONCILIATION

Information from the books of Govender Traders on 30 April 2017 is provided.

REQUIRED:

Reconcile the Creditors' Control Account balance with that of the Creditors' List. Indicate an increase with (+) and a decrease with (–) to each amount.

(9)

Gr 12 Accounting Revision Activities

30

INFORMATION:

A. Balances and totals on 30 April 2017 (before information B).

Creditors' Control Account in the General Ledger R184 870

Creditors' list total R170 490

B. Errors and omissions:

(a) The Creditors' Allowances Journal was incorrectly totaled as R15 400 instead of R18 500.

(b) An invoice for R20 000 for trading stock bought from a creditor, CRP Suppliers was correctly entered in the respective journal. The bookkeeper forgot to post this to the supplier's account in the Creditors’ Ledger. Take into account that a deposit of 20% was paid on this invoice.

(c) The bookkeeper posted a debit note for R2 360 to the wrong side of a creditor's account. Posting to the General Ledger was done correctly.

(d) A credit balance of R27 000 from the debtors' ledger account of SK Traders must be transferred to their account in the creditors' ledger.

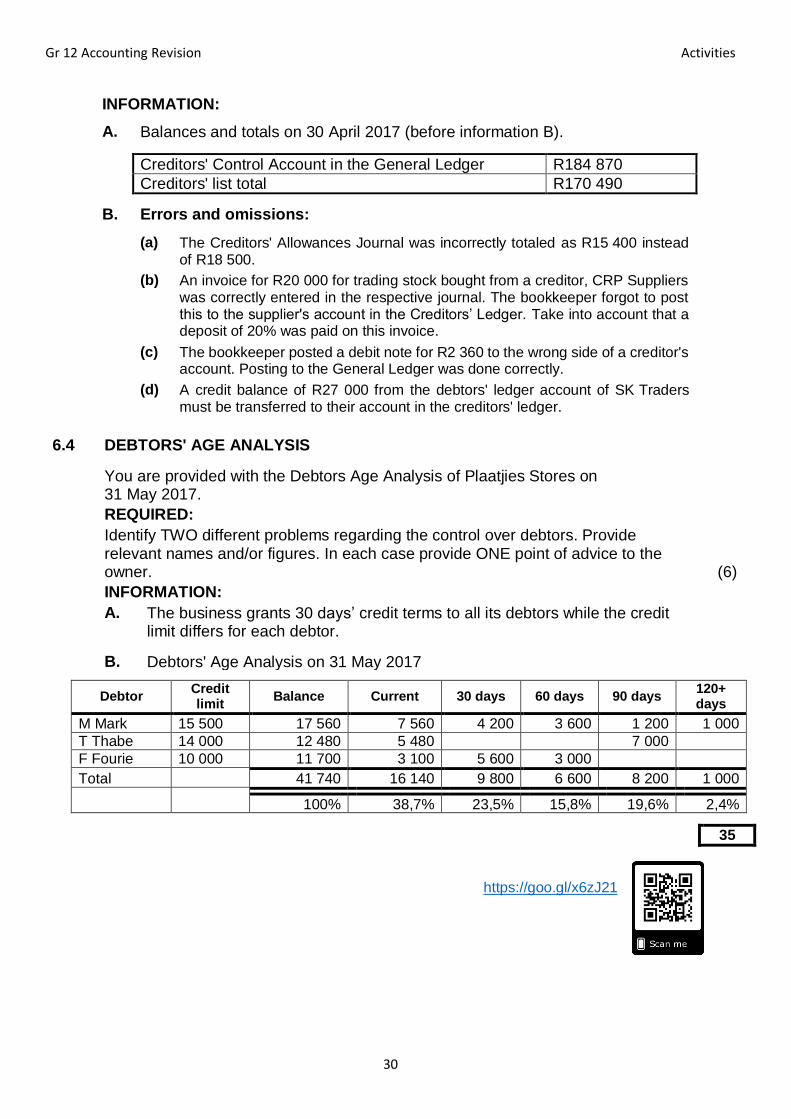

6.4 DEBTORS' AGE ANALYSIS

You are provided with the Debtors Age Analysis of Plaatjies Stores on 31 May 2017.

REQUIRED:

Identify TWO different problems regarding the control over debtors. Provide relevant names and/or figures. In each case provide ONE point of advice to the owner.

(6)

INFORMATION:

A. The business grants 30 days’ credit terms to all its debtors while the credit limit differs for each debtor.

B. Debtors' Age Analysis on 31 May 2017

Debtor Credit limit

Balance Current 30 days 60 days 90 days 120+ days

M Mark 15 500 17 560 7 560 4 200 3 600 1 200 1 000

T Thabe 14 000 12 480 5 480 7 000

F Fourie 10 000 11 700 3 100 5 600 3 000

Total 41 740 16 140 9 800 6 600 8 200 1 000

100% 38,7% 23,5% 15,8% 19,6% 2,4%

35

https://goo.gl/x6zJ21

Gr 12 Accounting Revision Activities

31

Activity 7: CREDITORS' RECONCILIATION (Q2.2, Nov 2018) (21 marks, 15 minutes)

7. CREDITORS' RECONCILIATION

Claire Traders buys goods on credit from Mariti Suppliers.

REQUIRED: 7.1 Use the table provided to indicate changes to the:

Creditors' Ledger Account in the books of Claire Traders

Creditors' Reconciliation Statement on 31 July 2018

(13)

7.2 The internal auditor insists that direct payments (EFTs) must be used to pay suppliers. Explain:

ONE reason to support his decision

ONE internal procedure to ensure control over this system (2) (2)

7.3 Refer to Invoice 301. It was discovered that the store manager, Vernon, had signed a fictitious order form and took the goods for himself when they arrived. Besides dismissing Vernon, provide:

ONE suggestion for action to be taken against him

ONE suggestion to prevent this problem in future (4)

INFORMATION:

A. Creditors' Ledger of Claire Traders

MARITI SUPPLIERS (CL5)

DEBIT CREDIT BALANCE

2018 1 Balance b/d 67 500

July 10 Invoice 209 81 000

EFT 33 750

17 Debit Note 674 8 640

Invoice 282 40 950

Invoice 301 25 000

21 Invoice 360 50 250

24 Debit Note 995 8 100

27 Journal Voucher 570 5 400

31 Cheque and discount 77 190 147 820

B. Statement of account from Mariti Suppliers

MARITI SUPPLIERS

Claire Traders 108 Kruger Road

25 July 2018

DEBIT CREDIT BALANCE

2018 1 Balance 67 500

July 10 Invoice 209 81 000

Receipt 695 33 750

17 Credit Note 741 6 840

Invoice 301 25 000

21 Invoice 360 20 250

24 Credit Note 811 8 100 145 060

Gr 12 Accounting Revision Activities

32

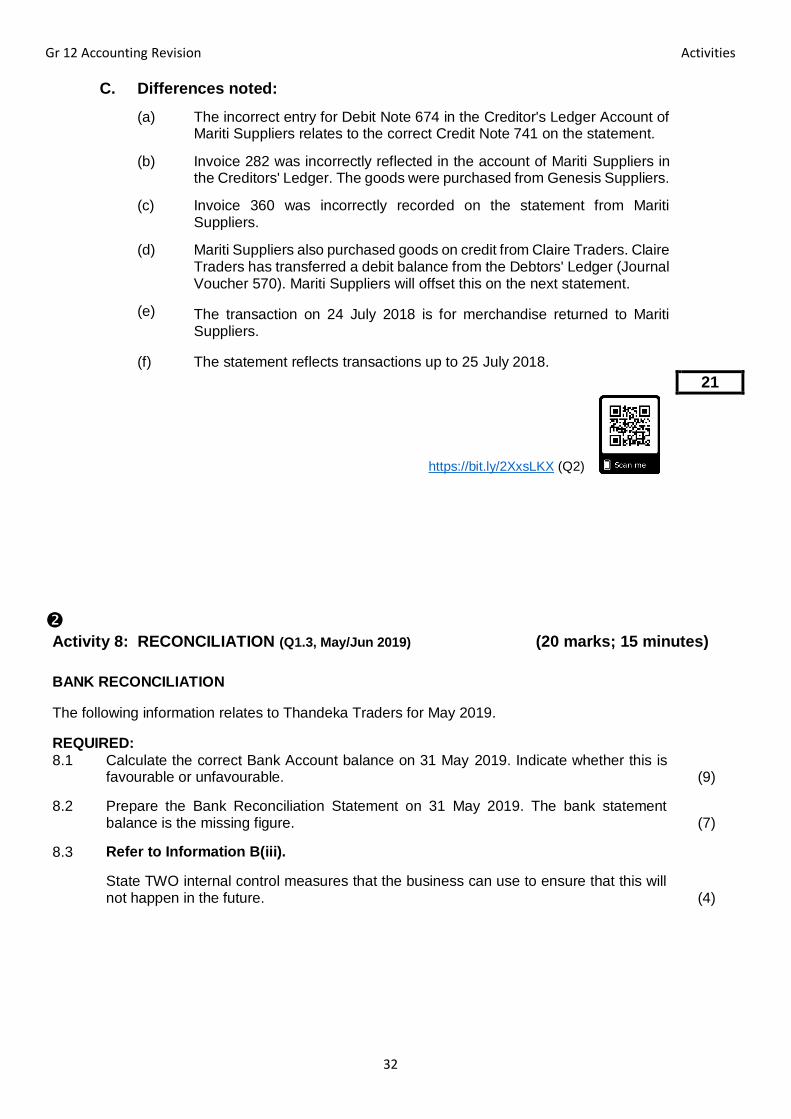

C. Differences noted:

(a) The incorrect entry for Debit Note 674 in the Creditor's Ledger Account of

Mariti Suppliers relates to the correct Credit Note 741 on the statement.

(b) Invoice 282 was incorrectly reflected in the account of Mariti Suppliers in

the Creditors' Ledger. The goods were purchased from Genesis Suppliers.

(c) Invoice 360 was incorrectly recorded on the statement from Mariti

Suppliers.

(d) Mariti Suppliers also purchased goods on credit from Claire Traders. Claire

Traders has transferred a debit balance from the Debtors' Ledger (Journal Voucher 570). Mariti Suppliers will offset this on the next statement.

(e) The transaction on 24 July 2018 is for merchandise returned to Mariti

Suppliers.

(f) The statement reflects transactions up to 25 July 2018.

21

https://bit.ly/2XxsLKX (Q2)

Activity 8: RECONCILIATION (Q1.3, May/Jun 2019) (20 marks; 15 minutes)

BANK RECONCILIATION

The following information relates to Thandeka Traders for May 2019.

REQUIRED: 8.1

Calculate the correct Bank Account balance on 31 May 2019. Indicate whether this is favourable or unfavourable.

(9)

8.2 Prepare the Bank Reconciliation Statement on 31 May 2019. The bank statement balance is the missing figure.

(7)

8.3 Refer to Information B(iii).

State TWO internal control measures that the business can use to ensure that this will not happen in the future.

(4)

Gr 12 Accounting Revision Activities

33

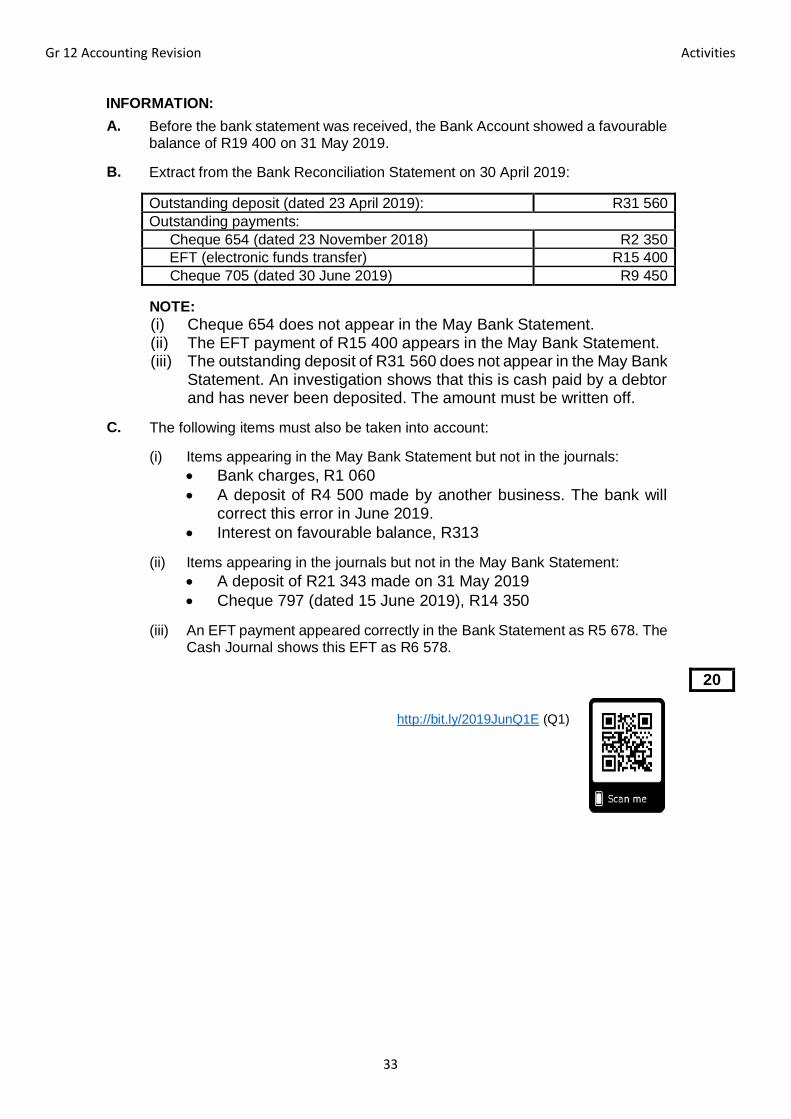

INFORMATION: A. Before the bank statement was received, the Bank Account showed a favourable

balance of R19 400 on 31 May 2019.

B. Extract from the Bank Reconciliation Statement on 30 April 2019:

Outstanding deposit (dated 23 April 2019): R31 560

Outstanding payments:

Cheque 654 (dated 23 November 2018) R2 350

EFT (electronic funds transfer) R15 400

Cheque 705 (dated 30 June 2019) R9 450

NOTE: (i) Cheque 654 does not appear in the May Bank Statement.

(ii) The EFT payment of R15 400 appears in the May Bank Statement.

(iii) The outstanding deposit of R31 560 does not appear in the May Bank Statement. An investigation shows that this is cash paid by a debtor and has never been deposited. The amount must be written off.

C. The following items must also be taken into account:

(i) Items appearing in the May Bank Statement but not in the journals:

Bank charges, R1 060

A deposit of R4 500 made by another business. The bank will correct this error in June 2019.

Interest on favourable balance, R313

(ii) Items appearing in the journals but not in the May Bank Statement:

A deposit of R21 343 made on 31 May 2019

Cheque 797 (dated 15 June 2019), R14 350

(iii) An EFT payment appeared correctly in the Bank Statement as R5 678. The Cash Journal shows this EFT as R6 578.

20

http://bit.ly/2019JunQ1E (Q1)

Gr 12 Accounting Revision Activities

34

MANUFACTURING (Paper 2)

Basic concepts and calculations

Direct material cost (DMC) Opening stock + Purchases + Carriage on purchases - Closing stock = Raw materials used

Direct labour cost (DLC) Normal wages (no. of workers x no. of hours x rate) ADD Overtime (no. of workers x no. of hours x rate) ADD UIF/Medical/Pension contributions

Factory / Manufacturing overheads (FOHC)

Indirect material (Opening stock + Purchases - Closing stock) Indirect labour (Cleaners, security, foreman) ADD contributions UIF/Pension Depreciation - Factory equipment Water & Electricity (Factory) All other factory expenses

Unit costs Total cost divided by number of units produced

Fixed cost FOHC + Admin costs (AC)

Variable cost DMC + DLC + Selling&Distribution costs (DC)

FORMAT OF THE PRODUCTION COST STATEMENT FORMAT OF THE ABRIDGED INCOME STATEMENT (short format)

Direct material cost Sales

+Direct labour cost Less Cost of Sales (Cos) (…….)

=Prime cost Gross profit

+Factory overhead cost Selling & Distribution costs

=Total cost of production Administration costs

+Work in process beg year Net profit

-Work in process end year ( )

=Total cost of production of finished goods CoS

ANALYSING PRODUCTION COSTS STATEMENTS Calculating the cost per unit of certain cost items will reveal:

= which costs are higher/ lower as the budgeted costs, = which items are exceptionally high and need to be controlled carefully = how costs compare to previous years.

Calculate the break-even point (BEP):

= BEP determines the quantity produced where no profit or loss is shown; = Income is only enough to cover costs. = FORMULA: TOTAL FIXED costs = .... Number of products/units (selling price per unit - variable costs per unit)

POSSIBLE IDEAS TO SAVE/DECREASE/CUT PRODUCTION COSTS:

- Bulk buying (buy in large quantities) to receive bulk discount - Cash purchases to receive cash discounts - Use alternative suppliers that offer more promising buying conditions - Do a work study in the factory to determine whether the factory is using efficient production methods, e.g.

reduce wastage of materials and labour time

Gr 12 Accounting Revision Activities

35

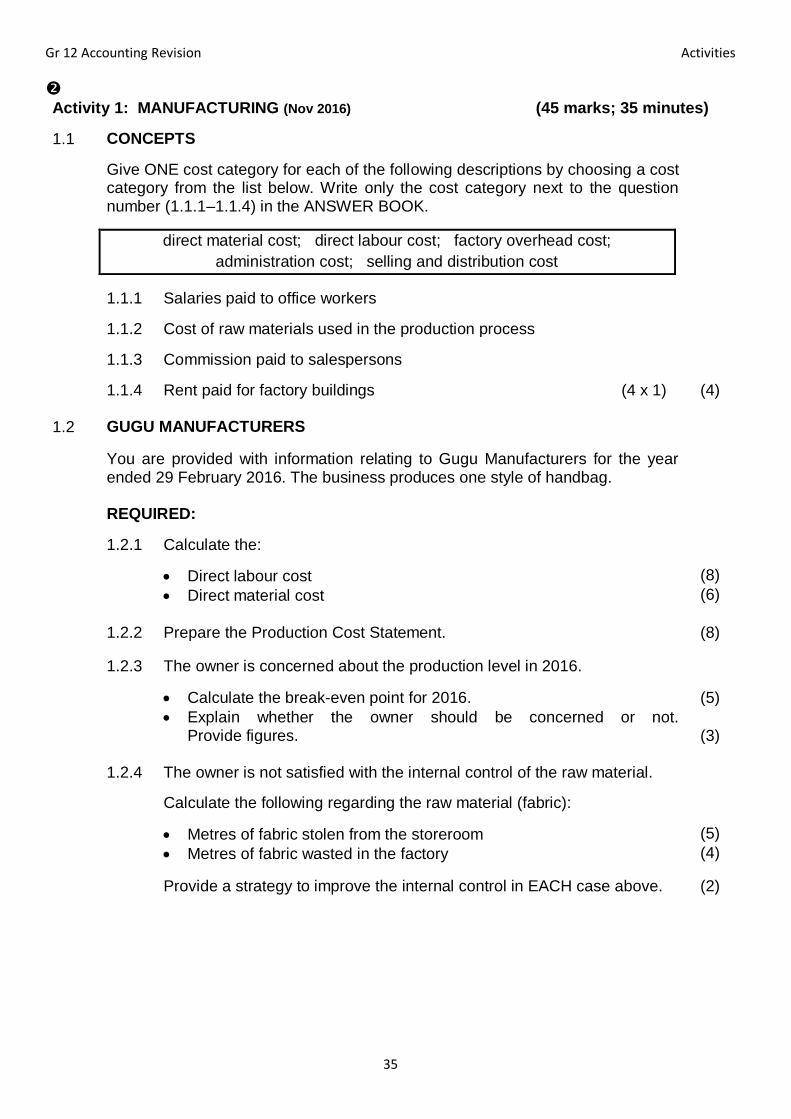

Activity 1: MANUFACTURING (Nov 2016) (45 marks; 35 minutes)

1.1 CONCEPTS

Give ONE cost category for each of the following descriptions by choosing a cost category from the list below. Write only the cost category next to the question number (1.1.1–1.1.4) in the ANSWER BOOK.

direct material cost; direct labour cost; factory overhead cost;

administration cost; selling and distribution cost

1.1.1 Salaries paid to office workers

1.1.2 Cost of raw materials used in the production process

1.1.3 Commission paid to salespersons

1.1.4 Rent paid for factory buildings (4 x 1) (4) 1.2 GUGU MANUFACTURERS

You are provided with information relating to Gugu Manufacturers for the year ended 29 February 2016. The business produces one style of handbag.

REQUIRED:

1.2.1 Calculate the:

Direct labour cost (8)

Direct material cost (6)

1.2.2 Prepare the Production Cost Statement. (8)

1.2.3 The owner is concerned about the production level in 2016.

Calculate the break-even point for 2016. (5) Explain whether the owner should be concerned or not.

Provide figures. (3) 1.2.4 The owner is not satisfied with the internal control of the raw material.

Calculate the following regarding the raw material (fabric):

Metres of fabric stolen from the storeroom (5)

Metres of fabric wasted in the factory (4)

Provide a strategy to improve the internal control in EACH case above. (2)

Gr 12 Accounting Revision Activities

36

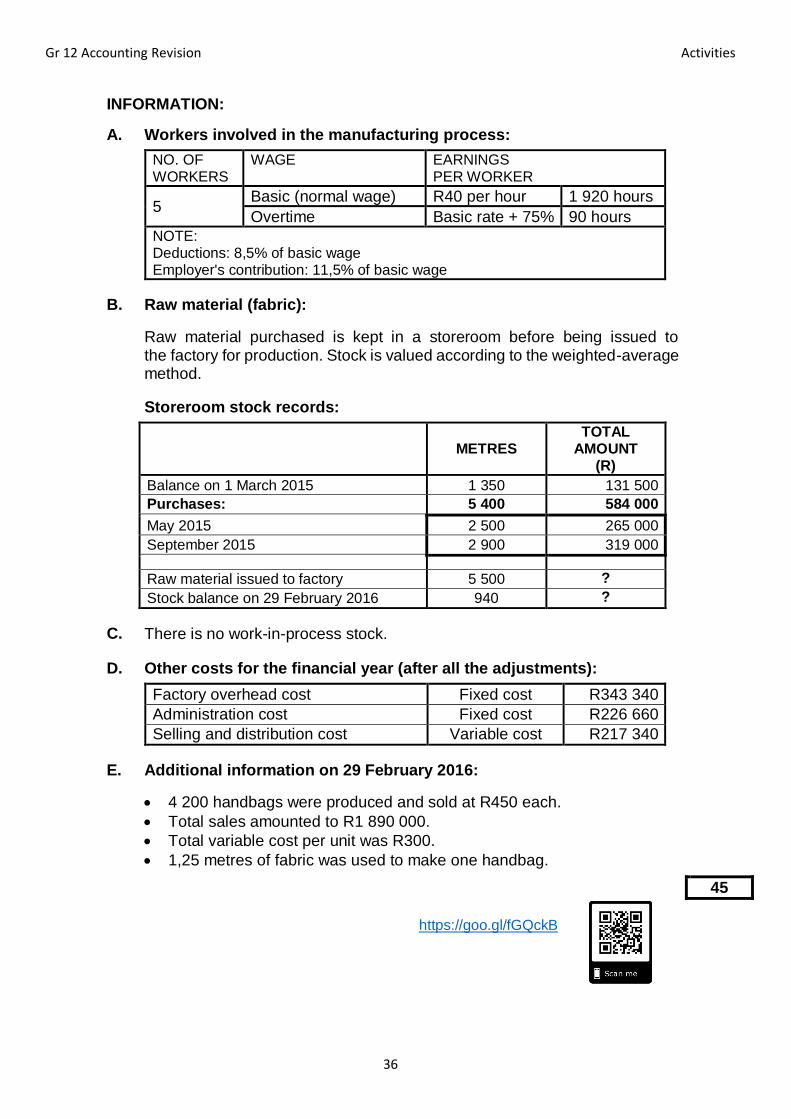

INFORMATION:

A. Workers involved in the manufacturing process:

NO. OF WORKERS

WAGE EARNINGS PER WORKER

5 Basic (normal wage) R40 per hour 1 920 hours

Overtime Basic rate + 75% 90 hours

NOTE: Deductions: 8,5% of basic wage Employer's contribution: 11,5% of basic wage

B. Raw material (fabric):

Raw material purchased is kept in a storeroom before being issued to the factory for production. Stock is valued according to the weighted-average method.

Storeroom stock records:

METRES

TOTAL AMOUNT

(R)

Balance on 1 March 2015 1 350 131 500

Purchases: 5 400 584 000

May 2015 2 500 265 000 September 2015 2 900 319 000

Raw material issued to factory 5 500 ? Stock balance on 29 February 2016 940 ?

C. There is no work-in-process stock.

D. Other costs for the financial year (after all the adjustments):

Factory overhead cost Fixed cost R343 340

Administration cost Fixed cost R226 660

Selling and distribution cost Variable cost R217 340

E. Additional information on 29 February 2016:

4 200 handbags were produced and sold at R450 each.

Total sales amounted to R1 890 000.

Total variable cost per unit was R300.

1,25 metres of fabric was used to make one handbag.

45

https://goo.gl/fGQckB

Gr 12 Accounting Revision Activities

37

Activity 2: MANUFACTURING (June 2016) (50 marks; 40 minutes)

2.1 ABE ACCESSORIES

Abe Accessories manufactures cell phone covers. The information below is in respect of the financial year ended 29 February 2016.

REQUIRED: 2.1.1 Prepare the Factory Overhead Cost Note. Show ALL calculations in brackets. (15)

2.1.2 Prepare the Production Cost Statement for the year ended 29 February 2016. (8)

INFORMATION: A.

Stock balances: 29 FEBRUARY 2016 1 MARCH 2015

Work-in-process stock R9 320 R30 640

B. Transactions for the year ended 29 February 2016:

Consumable stores used in the factory R129 300

Salaries and wages:

Production wages ?

Other factory workers R97 500

Administration R250 000

Sales department R130 000

Sundry expenses:

Factory R31 500

Offices R28 000

Water and electricity R50 000

Insurance R24 000

C. Additional information and adjustments

The factory cleaner was omitted from the salaries and wages list for February 2016. Her details are as follows:

Gross salary Deductions Net salary Employer's

Contribution

R3 800 R420 R3 380 R380

The employer's contribution is added to the salaries and wages.

An amount of R4 000 is still outstanding for water and electricity for February 2016. The factory uses 60% of the water and electricity.

Insurance has been paid from 1 March 2015 to 30 June 2016. This expense must be allocated to the factory, administration and sales departments in the ratio 3 : 2 : 1 respectively.

D. The business manufactured 10 500 cell phone covers at a cost of R82,40 per unit.

Gr 12 Accounting Revision Activities

38

2.2 NEW FASHION MANUFACTURERS This business is owned by Gloria Smit. She makes and sells dresses. The

financial year ends on 29 February 2016.

REQUIRED:

2.2.1 Gloria is concerned about the wastage of direct materials. Calculate the number of metres of fabric that was wasted. (5)

Gloria feels that the wastage is significant. Give a calculation to support her opinion. (3)

2.2.2 Give TWO possible reasons for this wastage and, in EACH case, give advice to prevent this from happening in future. (4)

2.2.3 Break-even point and production: Calculate the break-even point for the year ended 29 February 2016. (4) Explain why the business should be satisfied with the number of units

made during the current financial year. State TWO points. (4)

2.2.4 The direct material used to make the dresses is purchased locally at a cost of R150 per metre. Gloria is considering importing the fabric, as it will cost R120 per metre (all costs included). If she decides to import the fabric:

What effect will it have on the production cost of a dress? Provide a calculation to support your answer. (3)

State TWO other consequences of importing the direct material. (4)

INFORMATION:

A. Direct materials:

2,5 metres of fabric is used for each dress.

Number of metres of fabric

Opening stock 525

Purchases 12 450

Raw materials issued to factory ?

Closing stock 1 475

B. Production levels:

2016 2015

Total number of units produced and sold 4 500 3 800

Break-even point ? 3 200

C. Additional information:

Total Per unit

Sales R2 925 000 R650

Fixed cost R900 000 R200

Variable cost R1 575 000 R350

50

https://goo.gl/kU6nnf

Gr 12 Accounting Revision Activities

39

Activity 3: MANUFACTURING (Nov 2017) (55 marks; 45 minutes)

3.1 GEVEN MANUFACTURERS

The business produces wooden tables.

REQUIRED:

Prepare the following for the year ended 28 February 2017:

3.1.1 Production Cost Statement (14)

3.1.2 Abridged Income Statement (14)

INFORMATION:

A. Stock on hand: 28 FEBRUARY 2017 1 MARCH 2016

Work-in-process ? R160 000

Finished goods 400 tables, valued using

FIFO method 1 200 tables at R280

= R336 000

B. Production and sales for the year:

7 200 tables were produced at a unit cost of R330 each.

8 000 tables were sold for R4 080 000.

C. Costs (before adjustments):

Administration R148 400

Factory overheads R487 200

Direct materials R1 050 000

Direct labour ?

Selling and distribution R422 000

Adjustments:

Payment to EZ Transport, R102 000, was incorrectly allocated to Selling and Distribution. This was actually meant for delivering wood to the factory.

The cleaning contract for the year, R126 000, was shared between Factory and Administration in the ratio 2 : 1. However, 80% should have been allocated to Factory.

D. Prime cost: R1 800 000 (after adjustments)

3.2 GYMWEAR MANUFACTURERS

Gymwear Manufacturers is owned by Jan Fiks. They produce shoes and shirts for gym training. Jan requires assistance in interpreting his 2017 results. Note that one pair of shoes comprises one unit.

Gr 12 Accounting Revision Activities

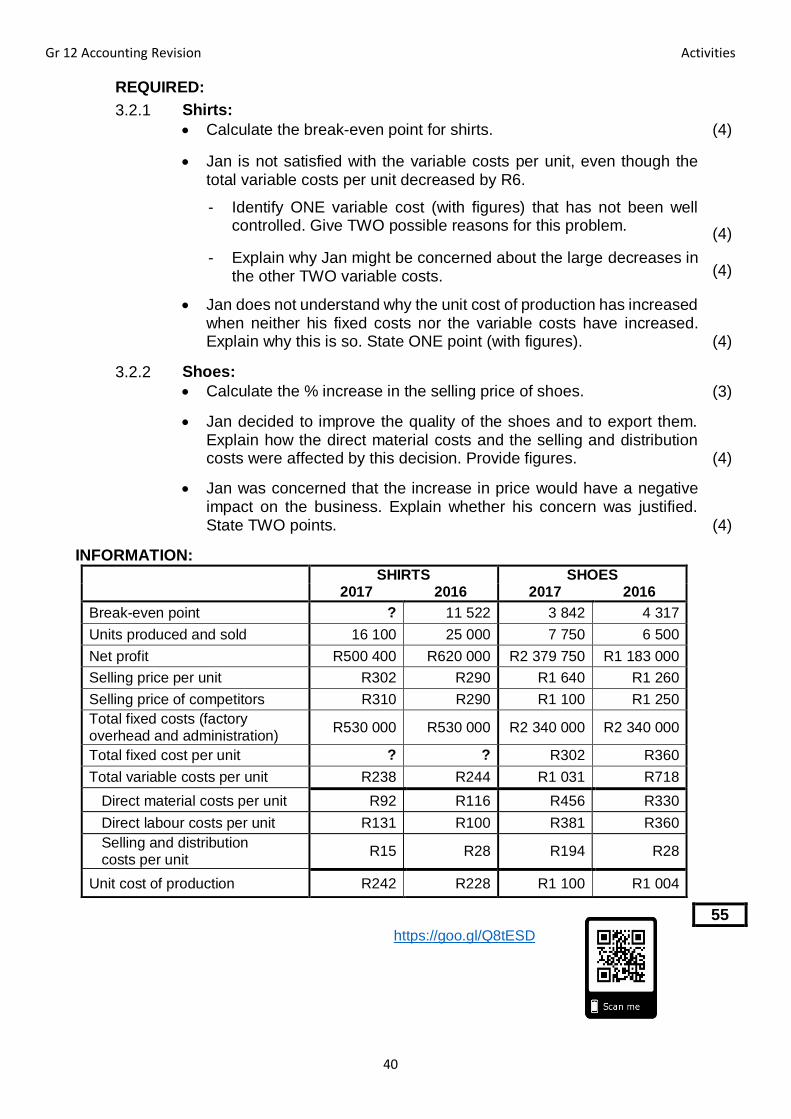

40

REQUIRED:

3.2.1 Shirts:

Calculate the break-even point for shirts. (4)

Jan is not satisfied with the variable costs per unit, even though the total variable costs per unit decreased by R6.

- Identify ONE variable cost (with figures) that has not been well controlled. Give TWO possible reasons for this problem.

- Explain why Jan might be concerned about the large decreases in the other TWO variable costs.

(4) (4)

Jan does not understand why the unit cost of production has increased when neither his fixed costs nor the variable costs have increased. Explain why this is so. State ONE point (with figures).

(4)

3.2.2 Shoes: Calculate the % increase in the selling price of shoes. (3)

Jan decided to improve the quality of the shoes and to export them. Explain how the direct material costs and the selling and distribution costs were affected by this decision. Provide figures.

(4)

Jan was concerned that the increase in price would have a negative impact on the business. Explain whether his concern was justified. State TWO points.

(4)

INFORMATION:

SHIRTS SHOES 2017 2016 2017 2016

Break-even point ? 11 522 3 842 4 317

Units produced and sold 16 100 25 000 7 750 6 500

Net profit R500 400 R620 000 R2 379 750 R1 183 000

Selling price per unit R302 R290 R1 640 R1 260

Selling price of competitors R310 R290 R1 100 R1 250

Total fixed costs (factory overhead and administration)

R530 000 R530 000 R2 340 000 R2 340 000

Total fixed cost per unit ? ? R302 R360

Total variable costs per unit R238 R244 R1 031 R718

Direct material costs per unit R92 R116 R456 R330

Direct labour costs per unit R131 R100 R381 R360

Selling and distribution costs per unit

R15 R28 R194 R28

Unit cost of production R242 R228 R1 100 R1 004

55

https://goo.gl/Q8tESD

Gr 12 Accounting Revision Activities

41

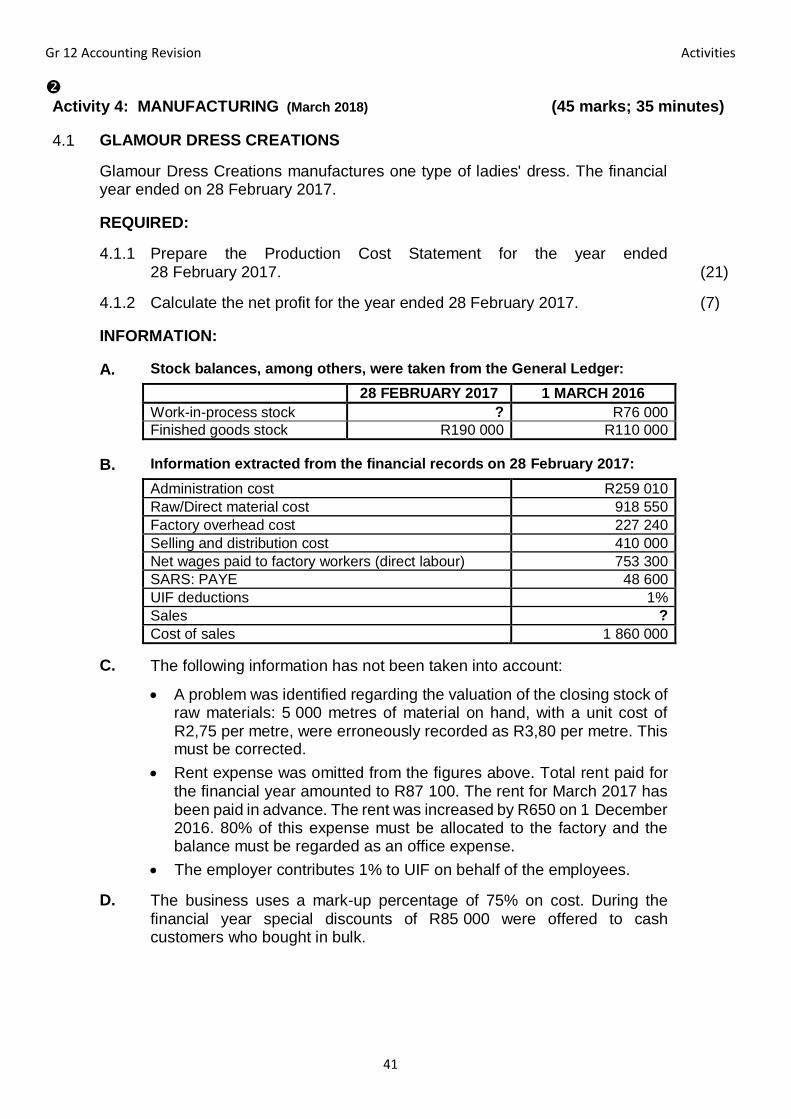

Activity 4: MANUFACTURING (March 2018) (45 marks; 35 minutes)

4.1 GLAMOUR DRESS CREATIONS

Glamour Dress Creations manufactures one type of ladies' dress. The financial year ended on 28 February 2017.

REQUIRED:

4.1.1 Prepare the Production Cost Statement for the year ended 28 February 2017. (21)

4.1.2 Calculate the net profit for the year ended 28 February 2017. (7)

INFORMATION:

A. Stock balances, among others, were taken from the General Ledger:

28 FEBRUARY 2017 1 MARCH 2016

Work-in-process stock ? R76 000

Finished goods stock R190 000 R110 000

B. Information extracted from the financial records on 28 February 2017:

Administration cost R259 010

Raw/Direct material cost 918 550

Factory overhead cost 227 240

Selling and distribution cost 410 000

Net wages paid to factory workers (direct labour) 753 300

SARS: PAYE 48 600

UIF deductions 1%

Sales ?

Cost of sales 1 860 000

C. The following information has not been taken into account:

A problem was identified regarding the valuation of the closing stock of raw materials: 5 000 metres of material on hand, with a unit cost of R2,75 per metre, were erroneously recorded as R3,80 per metre. This must be corrected.

Rent expense was omitted from the figures above. Total rent paid for the financial year amounted to R87 100. The rent for March 2017 has been paid in advance. The rent was increased by R650 on 1 December 2016. 80% of this expense must be allocated to the factory and the balance must be regarded as an office expense.

The employer contributes 1% to UIF on behalf of the employees.

D. The business uses a mark-up percentage of 75% on cost. During the financial year special discounts of R85 000 were offered to cash customers who bought in bulk.

Gr 12 Accounting Revision Activities

42

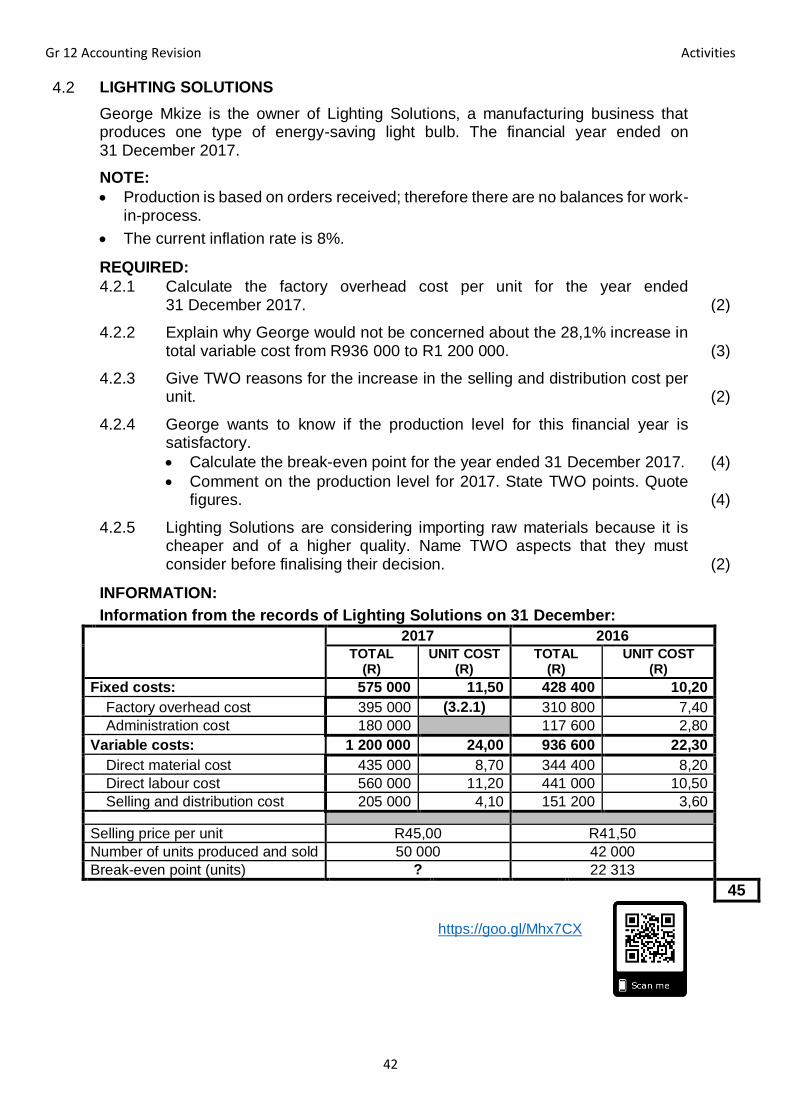

4.2 LIGHTING SOLUTIONS

George Mkize is the owner of Lighting Solutions, a manufacturing business that produces one type of energy-saving light bulb. The financial year ended on 31 December 2017.

NOTE: Production is based on orders received; therefore there are no balances for work-

in-process.

The current inflation rate is 8%.

REQUIRED:

4.2.1 Calculate the factory overhead cost per unit for the year ended 31 December 2017. (2)

4.2.2 Explain why George would not be concerned about the 28,1% increase in total variable cost from R936 000 to R1 200 000. (3)

4.2.3 Give TWO reasons for the increase in the selling and distribution cost per unit. (2)

4.2.4 George wants to know if the production level for this financial year is satisfactory.

Calculate the break-even point for the year ended 31 December 2017. (4) Comment on the production level for 2017. State TWO points. Quote

figures. (4)

4.2.5 Lighting Solutions are considering importing raw materials because it is cheaper and of a higher quality. Name TWO aspects that they must consider before finalising their decision. (2)

INFORMATION:

Information from the records of Lighting Solutions on 31 December:

2017 2016

TOTAL (R)

UNIT COST (R)

TOTAL (R)

UNIT COST (R)

Fixed costs: 575 000 11,50 428 400 10,20

Factory overhead cost 395 000 (3.2.1) 310 800 7,40

Administration cost 180 000 117 600 2,80

Variable costs: 1 200 000 24,00 936 600 22,30

Direct material cost 435 000 8,70 344 400 8,20

Direct labour cost 560 000 11,20 441 000 10,50

Selling and distribution cost 205 000 4,10 151 200 3,60

Selling price per unit R45,00 R41,50

Number of units produced and sold 50 000 42 000

Break-even point (units) ? 22 313

45

https://goo.gl/Mhx7CX

Gr 12 Accounting Revision Activities

43

Activity 5: MANUFACTURING (Mar 2017) (45 marks; 35 minutes)

5.1 MOSES MANUFACTURERS

The following information relates to Moses Manufacturers, a small business that manufactures photo frames. The financial year ended on 30 April 2016.

REQUIRED:

5.1.1

Prepare the Production Cost Statement for the year ended 30 April 2016.

(16)

5.1.2 Complete the abridged (shortened) Income Statement to calculate the net profit for the year ended 30 April 2016.

(8)

INFORMATION:

A. Stock records 30 APRIL 2016 30 APRIL 2015

Raw material stock R58 560 R37 600

Work-in-process stock ? R142 000

Purchases of raw materials for the financial year amounted to R555 000.

Defective material valued at R21 000 was returned to suppliers.

B. The business produced 39 000 units at a cost of R45 each.

C. The following information was calculated on 30 April 2016.

R

Direct material cost ?

Direct labour cost 716 960

Factory overhead cost (See D below.) 468 450

Selling and distribution cost (See D below.) 609 850

Administration cost (See D below.) 443 950

Cost of production of finished goods ?

Gross profit 1 250 000

D. The following items must be taken into account:

Administration cost includes the annual insurance premium of R22 750; however, 60% must be allocated to the factory.

Factory overhead cost includes the full amount of rent paid, R36 300. However, this should have been allocated according to floor area. The areas are: factory 400 square metres, office 120 square metres, shop 80 square metres.

Gr 12 Accounting Revision Activities

44

5.2 UNIT COSTS AND BREAK-EVEN ANALYSIS

Bill's Manufacturers is a business that produces pencil cases. Bill is concerned about his cost of production.

REQUIRED:

5.2.1 Explain the difference between fixed cost and variable cost. (2)

5.2.2 Calculate the break-even point for 2017. (5)

5.2.3 Comment on the break-even point and the level of production for 2016 and 2017. Explain why the owner should be satisfied or not.

(6)

5.2.4

Identify the variable cost that should be of great concern to the owner. Explain and provide a calculation to support your answer.

(4)

5.2.5 Despite the fact that there was a decrease in the fixed costs per unit, the owner is still not satisfied with his control over the fixed costs. Explain and provide calculation(s) to support his opinion.

(4)

INFORMATION:

PENCIL CASES UNIT COSTS

2017 2016

Variable costs R11,60 R11,00

Direct material cost 6,03 5,80

Direct labour cost 4,05 3,50

Selling and distribution cost 1,52 1,70

Fixed cost R5,40 R5,50

Factory overhead cost 3,50 3,65

Administration cost 1,90 1,85

Selling price per unit R17,80 R16,50

Units Units

Units produced and sold 80 000 65 000

Break-even units ? 65 000

NOTE: Take the inflation rate of 8% into account.

45

https://goo.gl/CezHbZ

Gr 12 Accounting Revision Activities

45

Activity 6: MANUFACTURING (Q1, Nov 2018) (40 marks; 30 minutes)

6.1

Indicate whether the following statements are TRUE or FALSE. Write only 'true' or 'false' next to the question numbers (6.1.1 to 6.1.3) in the ANSWER BOOK.

6.1.1 Bad debts are an administration cost. 6.1.2 Indirect labour is a factory overhead cost. 6.1.3 Rent expense is a fixed cost. (3)

6.2 KRIGE SHIRTS

The business manufactures shirts. The financial year-end is 31 July 2018.

REQUIRED:

6.2.1 Refer to Information C. Calculate direct labour cost. (9)

6.2.2 Production Cost Statement for the year ended 31 July 2018 (12)

INFORMATION:

A. Work-in-progress stock balance

31 JULY 2018 1 AUGUST 2017

? R35 570

B. Raw materials issued to factory: R528 300 C. Direct labour: Number of factory workers 4

Normal time expected per worker per year 1 960 hours

Normal time rate R90 per hour

Bonuses to workers: 12% of normal wages

NOTE: One worker worked only 1 680 hours and received a reduced bonus of R12 146.

D. Factory overheads were calculated at R360 880 for the year. However,

this excludes insurance of R48 750 paid for the period 1 August 2017 to 31 August 2018. Insurance must be allocated to the factory, administration and sales in the ratio 4 : 3 : 2.

E. Production for the year: 17 500 shirts at a cost of R95 per shirt

Gr 12 Accounting Revision Activities

46

6.3 GEMMA'S MANUFACTURERS

This business manufactures security gates. The financial year-end is 31 August 2018.

REQUIRED:

6.3.1 Calculate the break-even point for the year ended 31 August 2018. (5)

6.3.2 Compare and comment on the break-even point and the production level

achieved over the last two years. Quote figures.

(6)

6.3.3 Give TWO reasons for the increase in direct material cost. Suggest ONE way to control this cost.

(5)

INFORMATION FOR YEAR ENDED 31 AUGUST:

A.

COSTS

2018 2017

TOTAL AMOUNT

UNIT

COST

UNIT

COST

Direct materials

Variable

75 600 R180 R148

Direct labour 105 840 R252 R244

Selling and distribution 60 900 R145 R136

TOTAL VARIABLE COST 242 340 R577

Factory overheads Fixed

67 200 R160 R156

Administration 51 660 R123 R127

B. Additional information:

2018 2017

Total sales R382 200 R475 200

Selling price per unit R910 R880

Units produced and sold 420 units 540 units

Break-even point ? 435 units

40

https://bit.ly/2NGNNIV

Gr 12 Accounting Revision Activities

47

Activity 7: MANUFACTURING (Q3, Jun 2019) (40 marks; 30 minutes)

7.1 Choose the correct term from those given in brackets. Write only the term next to the question numbers (7.1.1 to 7.1.4) in the ANSWER BOOK.

7.1.1 Wages paid to the factory cleaner is considered to be (direct/indirect) labour.

7.1.2 Bad debts must be shown as a (selling and distribution/ factory overhead) cost.

7.1.3 Rent paid for the factory building is regarded as a (fixed/variable) cost.

7.1.4 Carriage on purchases of raw materials is regarded as a/an (direct material/indirect material) cost. (4)

7.2 ZINZI MANUFACTURERS

Information is provided for the financial year ended 31 December 2018. The business manufactures leather jackets according to orders received. There is no work-in-progress stock.

REQUIRED:

7.2.1 Raw material stock:

Calculate: The value of the closing stock using the first-in-first-out stock valuation method (5)

The direct material cost (4)

7.2.2 Refer to Information C.

Calculate the correct factory overhead cost for the year.

(8)

7.2.3 The owner is concerned about the increase in the following:

Total fixed cost per unit Direct labour cost per unit

Provide evidence (figures) to justify his concern. In each case, also give a possible reason for the increase in EACH unit cost, apart from normal inflation.

(6)

7.2.4 Break-even:

Calculate the break-even point on 31 December 2018. (4)

Explain whether or not there was any improvement in the trends of the level of production and the break-even point from one year to the next. Quote figures.

(4)

The owner cannot understand why he is making a better profit this year. Explain how this happened. Provide TWO points. Quote figures.

(5)

INFORMATION:

A. Raw material:

Stock balance: Metres Cost per metre Total amount

1 January 2018 920 R65 R59 800

31 December 2018 1 195 ? ?

Gr 12 Accounting Revision Activities

48

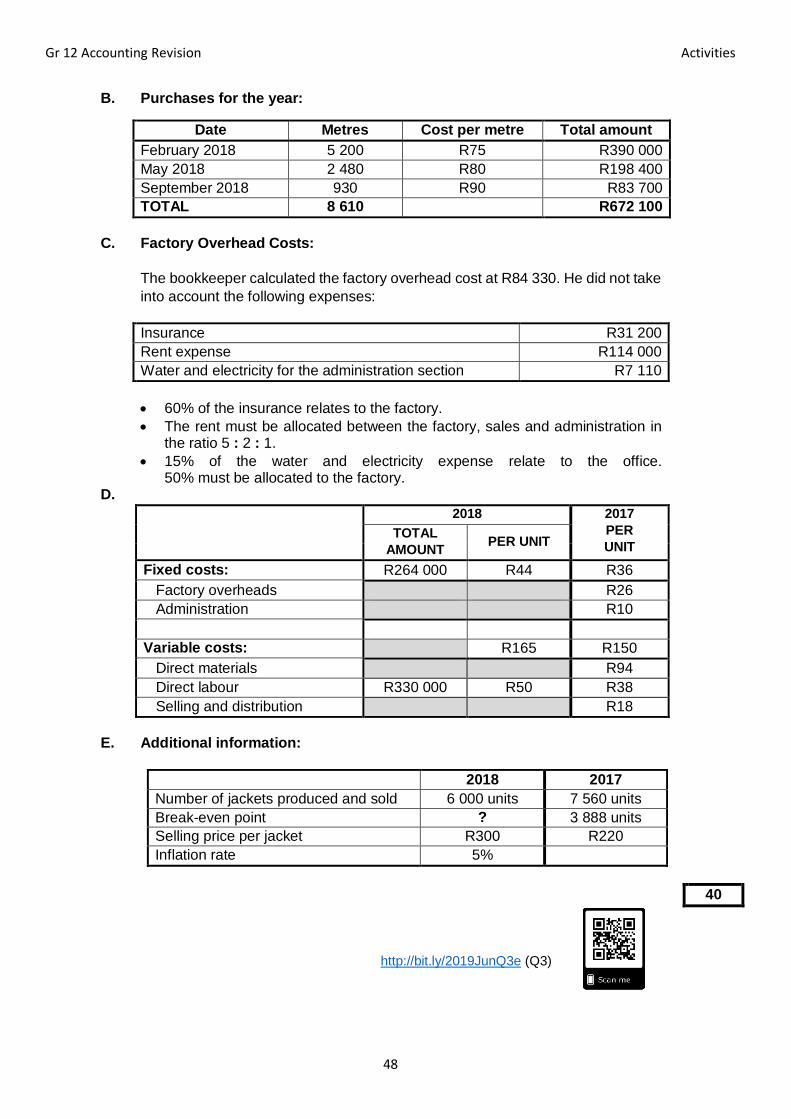

B. Purchases for the year:

Date Metres Cost per metre Total amount

February 2018 5 200 R75 R390 000

May 2018 2 480 R80 R198 400

September 2018 930 R90 R83 700

TOTAL 8 610 R672 100

C. Factory Overhead Costs:

The bookkeeper calculated the factory overhead cost at R84 330. He did not take

into account the following expenses:

Insurance R31 200

Rent expense R114 000

Water and electricity for the administration section R7 110

60% of the insurance relates to the factory.

The rent must be allocated between the factory, sales and administration in the ratio 5 : 2 : 1.

15% of the water and electricity expense relate to the office. 50% must be allocated to the factory.

D.

2018 2017

PER

UNIT TOTAL

AMOUNT PER UNIT

Fixed costs: R264 000 R44 R36

Factory overheads R26

Administration R10

Variable costs: R165 R150

Direct materials R94

Direct labour R330 000 R50 R38

Selling and distribution R18

E. Additional information:

2018 2017

Number of jackets produced and sold 6 000 units 7 560 units

Break-even point ? 3 888 units

Selling price per jacket R300 R220

Inflation rate 5%

40

http://bit.ly/2019JunQ3e (Q3)

Gr 12 Accounting Revision Activities

49

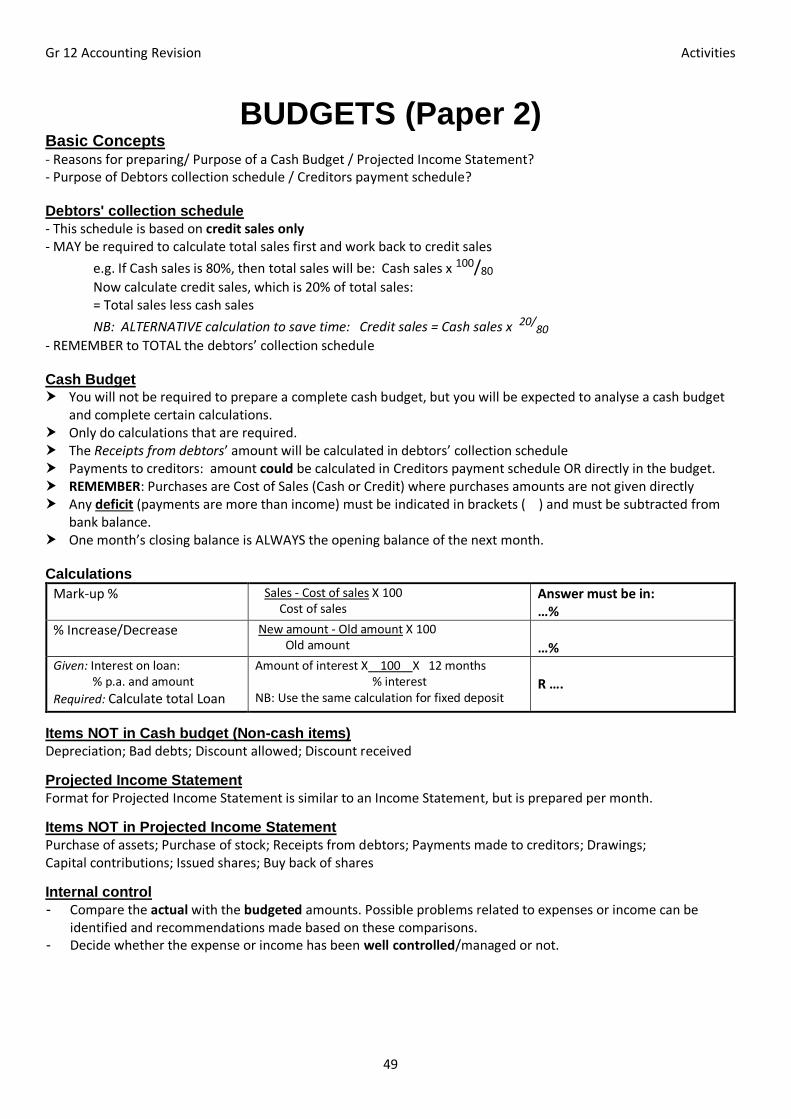

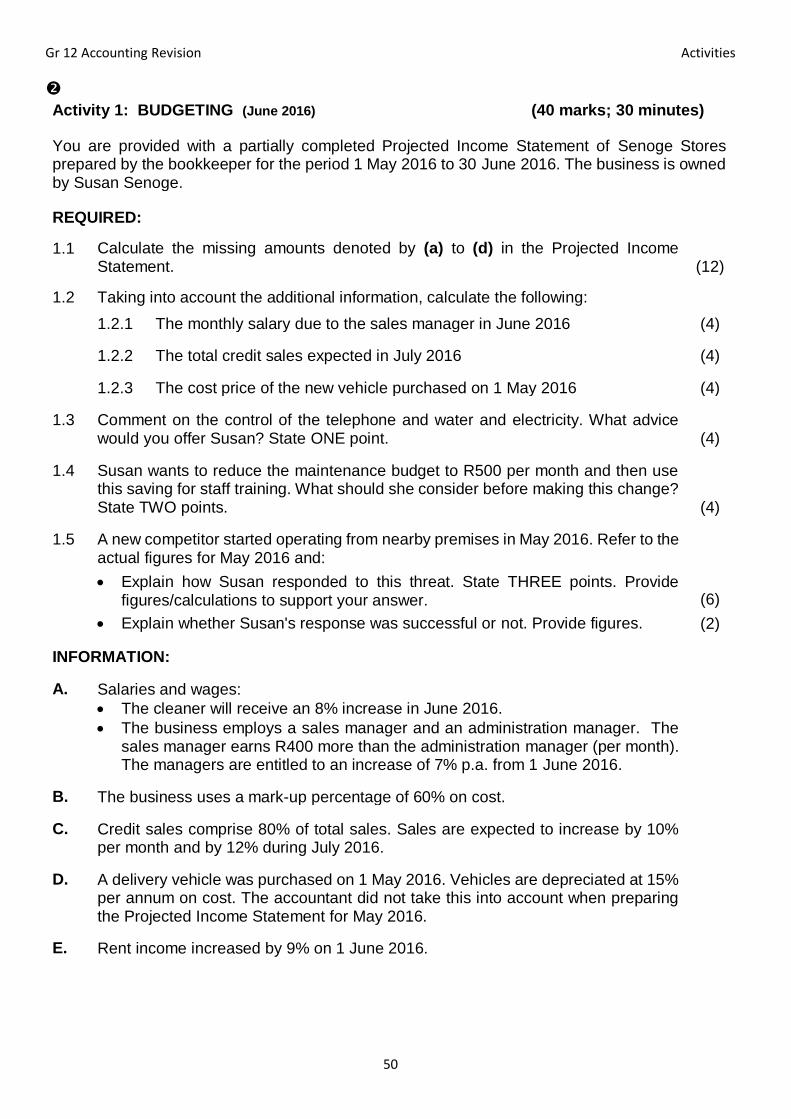

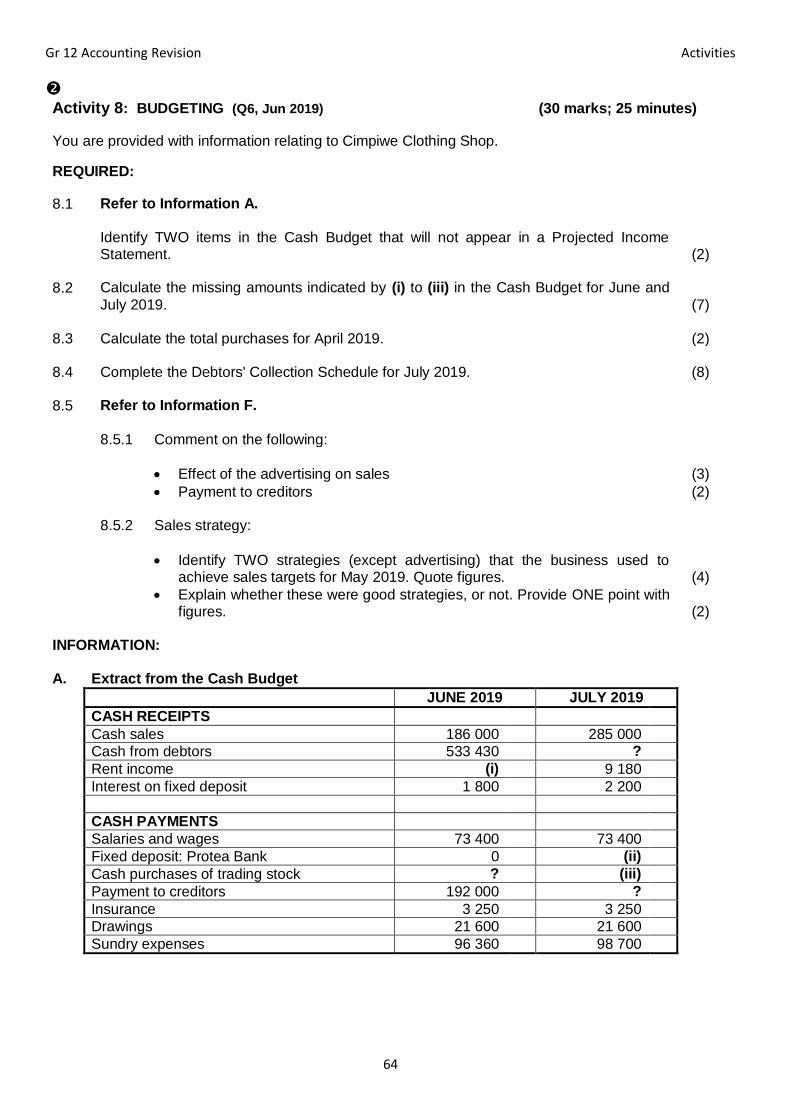

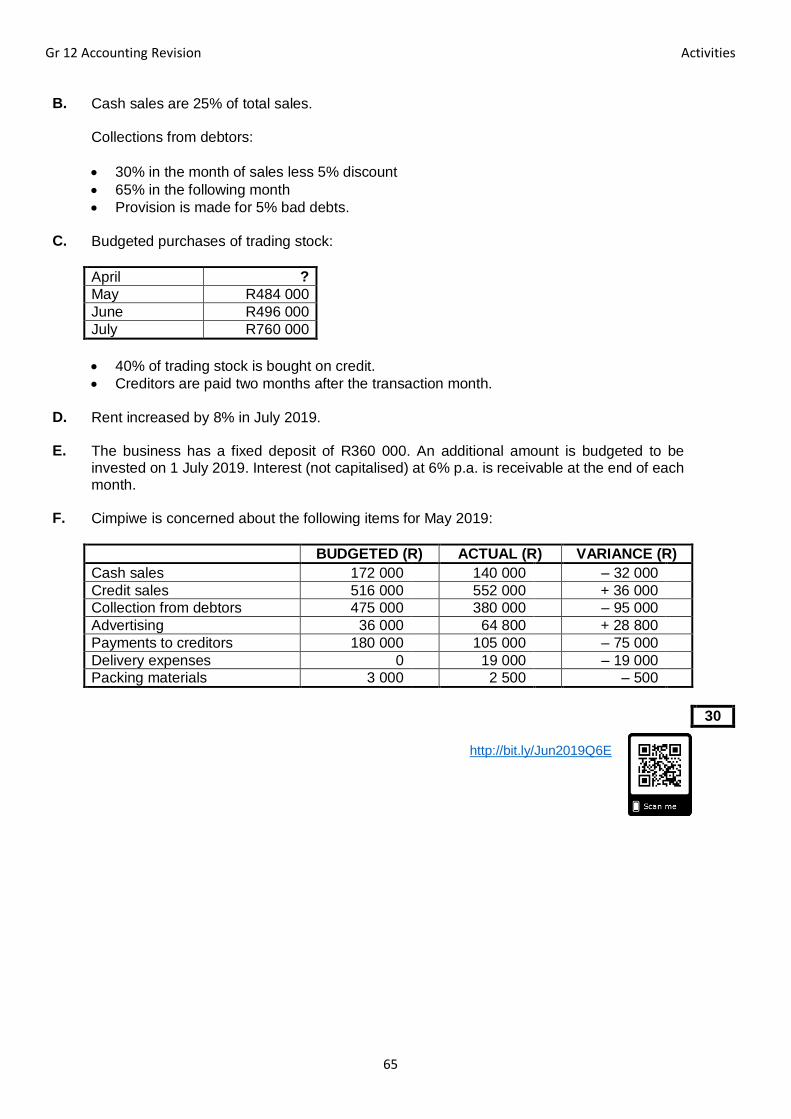

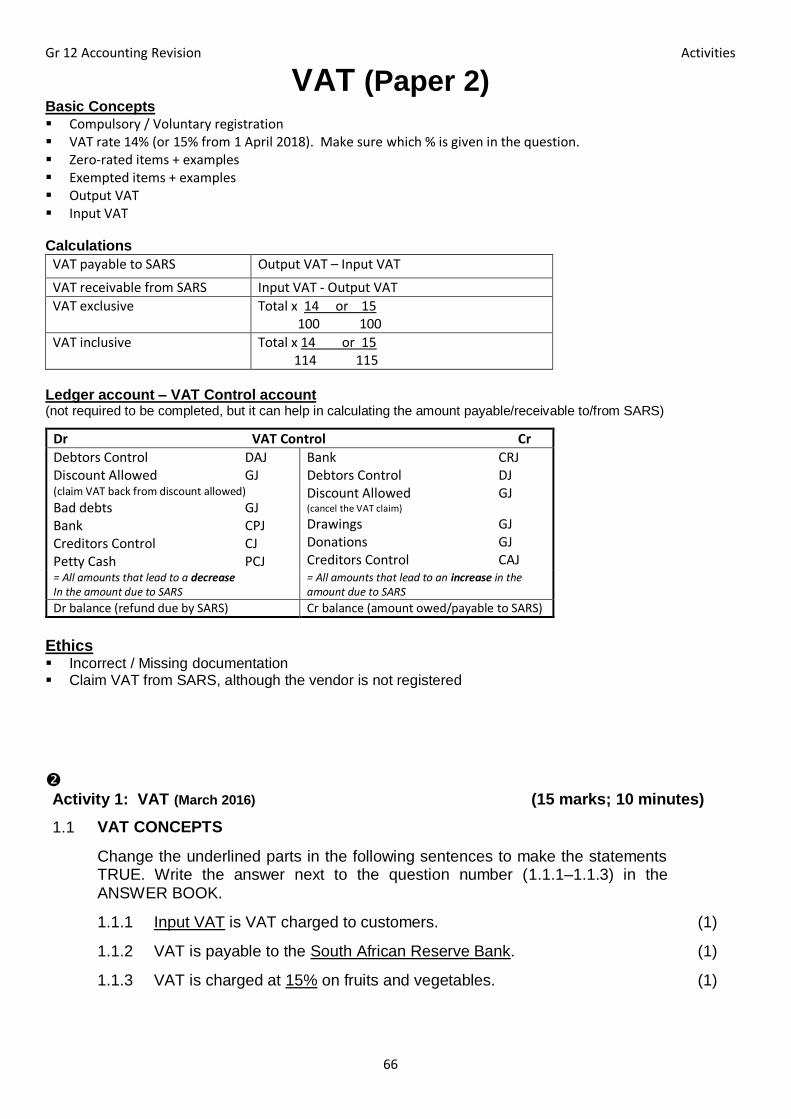

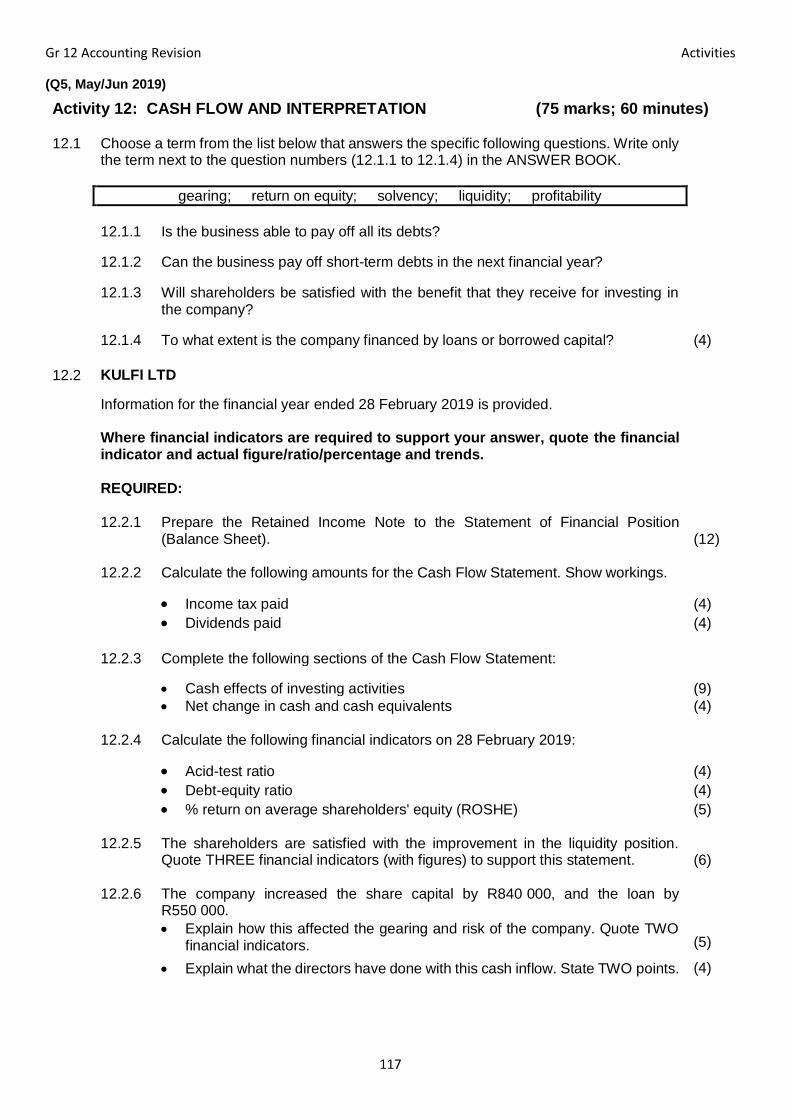

BUDGETS (Paper 2)