cybercom group annual report 2004 · 2014-09-19 · management and a project that involves system...

TRANSCRIPT

Cybercom Group Annual Report 2004

Forthcoming reports

Dates when fi nancial reports are published:• January–March, published on: Thursday, 21 April 2005

• January–June, published on: Wednesday, 17 August 2005

• January–September, published on: Thursday, 20 October 2005

• Year-end 2005, published on Tuesday, 7 February 2006

Annual general meeting (AGM)The AGM of Cybercom Group Europe AB will be held on Friday, 22 April 2005 at 3 p.m. at the company’s new head-quarters on Fleminggatan 20 in Stockholm. Participant regis-tration starts at 2 p.m.

Shareholders who wish to participate in the AGM must:

• Be registered in the VPC AB share database by Tuesday, 12 April 2005.

• Have sent notifi cation (and the number of participants) to the company’s headquarters by Friday, 15 April 2005 by 5 p.m. at the latest. Shareholders, whose shares are regis- tered through banks or other managers, must temporarily register the shares in their own names if they want to participate in the AGM. This type of registration must be fi led with VPC AB in suffi cient time before 12 April.

Notifi cationNotifi cation of attendance must be submitted in writing to Cybercom Group Europe AB, Box 7574, SE-103 93 Stockholm, Sweden (write AGM notifi cation on the envelope). Notifi cation of attendance can also be made by phone: +46 8 578 646 00, fax: +46 8 578 646 10, or e-mail: [email protected].

Specify all names, addresses, phone numbers, Swedish civil registration numbers (or corporate IDs), and number of shares.

Welcome!

Alfred Berg StockholmKarl Berglund+46 8-723 58 00

Cazenove & CoLondonGorm Thomassen+44 20 7588 2828

Cheuvreux NordicLondonMartin Persson +44 20 7621 5176

Danske Bank CopenhagenPeter Trigarszky+45 33 44 04 49

D.Carnegie & CoStockholmCharlotte WidmarkTomas Öqvist+46 8-676 88 00

Analysts who regularly monitor Cybercom and its industry

Enskilda SecuritiesStockholm Lars Sveder +46 8-522 29 500

Handelsbanken Capital MarketsStockholm Stefan Wård+46 8-701 10 00

Kaupthing Bank StockholmDaniel Djurberg+46 8-791 48 00

Redeye StockholmJonas Elofsson+46 8-545 013 30

United BrokersStockholm David Lindström+46 8-506 520 20

Contents

2004 in brief. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Business concept, goals, and strategies . . . . . . . . . . . . . 2

Cybercom’s offerings . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Directors’ report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3– The operation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3– Sales and income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3– Important events in 2004. . . . . . . . . . . . . . . . . . . . . . . 4– Personnel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5– Market trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6– Business areas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8– Internal resources. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9– The Cybercom share . . . . . . . . . . . . . . . . . . . . . . . . . 10– Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12– Liquidity and cash fl ow. . . . . . . . . . . . . . . . . . . . . . . . 12– Financial position . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12– Parent company . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12– Incentive program . . . . . . . . . . . . . . . . . . . . . . . . . . . 12– Corporate governance . . . . . . . . . . . . . . . . . . . . . . . . 12– Transition to IFRS . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14– Risk and sensitivity analyses . . . . . . . . . . . . . . . . . . . . 15– Outlook . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15– Proposed treatment of accumulated loss . . . . . . . . . . 15– Financial performance summary . . . . . . . . . . . . . . . . . 16– Defi nitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16– Profi t and loss statement: Group and parent company 18– Cash fl ow analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . 19– Balance sheet: Group and parent company . . . . . . . . 20– Changes in shareholder equity . . . . . . . . . . . . . . . . . . 22– Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

Auditors’ report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Board and executives . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Addresses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

1

Jan.–Dec. Jan.–Dec. Q4 Q4 Q3 Q2 Q1 2004 2003 2004 2003 2004 2004 2004

Sales, SEK million (MSEK) 405.3 309.7 113.8 84.0 89.7 98.6 103.2

Operating profi t/loss EBITA, MSEK 15.1 –2.2 6.4 –7.8 2.6 2.5 3.6

Margin, % 3.7 –0.7 5.7 –9.3 2.9 2.6 3.5

Operating profi t/loss EBIT, MSEK 8.0 –111.9 4.2 –8.4 0.8 1.1 1.9

Operating margin, % 2.0 –36.1 3.7 –10.0 0.9 1.0 1.8

Return on equity, % 2.7 Neg

Return on capital employed, % 7.1 Neg

Profi t/loss per share, SEK 0.41 –11.7

Cash fl ow per share, SEK 1.04 0.55

Equity/assets ratio, % 65.2 54.1

No. of employees at period’s end 375 375 375 375 371 366 359

2004 in brief• Strong growth and increased profi tability.

• The Swedish operation is organised into one business area (BA) that targets telecom and selected technologies. The Group’s international subsidiaries are already organised under the International BA.

• Growth in telecom is strong and demand for Cybercom’s services increased sharply, especially in the Öresund region (southern Sweden), where Cybercom has established a strong position.

• Integration with Consafe Infotech is succeeding as planned and is leading to new business. For example, Cybercom wins strategically important assignments within device management and a project that involves system tests and verifi cations of mobile phone platforms for Ericsson Mobile Platforms.

• Cybercom is increasing its commitments with all key customers; it is signing new frame agreements with Ericsson, Teracom, TeliaSonera, and SEB – to name a few.

• Sales of CyberMate are starting.

• JCE Group AB, Magellan B.V, and J Christer Ericsson personally become Cybercom’s largest shareholders in December 2004.

2 Business ConceptCybercom creates business success by using leading-edge technologies.

VisionTo be the preferred partner for delivery of mission-critical solutions in telecom and leading-edge technologies.

Goals and objectivesCybercom will be an established, international solution provi-der within telecom.

Its fi nancial objective is to generate SEK 750 million in sales during 2006; 25% will come from outside Sweden. The company will have an 8% operating margin, and 40–60% of its revenue will come from total project assignments.

Business concept, goals, and strategies2004 objectives and their fulfi lmentIn 2004, Cybercom continued to develop the operation with a focus on telecom. The company reported profi table 31% growth; Q4 2004 growth in its telecom operation increased 48% compared with Q4 2003. Investments in the fi nance sector did not have the desired breakthrough, so it was liquidated and integrated with other operations with focus on telecom and key customers in other segments. Solution-based assignments represent about 40% of sales in 2004, which gives Cybercom a stable revenue stream. Consafe Infotech, which was acquired in 2003, was successfully integrated; this led to increased capacity and new projects.

StrategyCybercom will realise its objectives by focusing on telecom, technology, and growth. Its growth objective of SEK 750 mil-lion in sales by year-end 2006 will be reached by:

1. Focusing operations on three key areas; portals and mobile solutions, e-commerce and billing, and embedded solu-tions.

2. Broadening the customer base and increasing internation-alisation towards Nordic telecom operations.

3. Organic growth combined with acquired growth.

4. Develop spin-off businesses outside telecom, in areas where Cybercom has unique technological expertise.

Cybercom is a specialised IT consulting company that focuses on mobile solutions. Its services primarily target the telecom sector and key customers in other sectors. Cybercom’s of-ferings fall into three areas: embedded systems, portals and mobile solutions, and e-commerce and billing.

Embedded systemsCybercom develops and builds applications and communica-tion software for mobile phones, network simulators, and communication equipment.

Portals and mobile solutionsCybercom designs, develops, and operates portals, and it builds services and offerings that are linked to the portals.

Cybercom’s offeringsE-commerce and billingCybercom delivers solutions for all business processes in the entire e-commerce value chain for B2B, B2E, and B2C. Besides billing solutions linked to e-commerce, Cybercom develops specifi c billing modules for telecom operators.

Application management and projectsIn addition to development and solution sales, Cybercom offers application management (AM) services, which involve system maintenance and further development.

TechnologyCybercom’s consultants are specialists in solutions that use these technologies: Java, .Net, WebSphere, Oracle, J2EE, and Akamai. Mastering the underlying technology is the founda-tion for being able to select, implement, and build the best solutions.

3

Directors’ reportThe board and president of Cybercom Group Europe AB (publ.), corporate ID 556544-6522, hereby submit their annual report for the 1 January 2004–31 December 2004 period.

This report covers the: • Board’s report.

• Consolidated and parent company profi t and loss statement.

• Consolidated and parent company balance sheet.

• Cash fl ow analysis.

• Notes.

All amounts are reported in SEK thousands unless otherwise specifi ed. Numbers enclosed in parentheses ( ) refer to the previous year.

THE OPERATION

The Cybercom Group is a high-tech consulting company that offers business-critical IT solutions mainly in telecom and selec-ted technologies. Cybercom was founded in Sweden in 1995 and has been listed on the Stockholm stock exchange (Stock-holmsbörsen) since 1999. The Group has customers worldwide and offi ces in Denmark, Norway, Sweden, and the UK. It has 375 employees; its consultants have an average of 13 years of industry experience.

Cybercom’s customers are important international players that operate with leading-edge technologies and seek speciali-sed partners. Consequently, Cybercom’s unsurpassed position, with operations know-how and technological expertise won their trust. The company’s largest customers are Ericsson, Sony Ericsson, TeliaSonera, Nokia, Reuters, AFA, ASSA ABLOY, and SEB. In 2004, Cybercom increased its commitments with all of them.

Cybercom develops, integrates, tests, verifi es, and runs app-lication management projects within these areas:

• Portals and mobile solutions.

• E-commerce and billing.

• Embedded systems.

In 2004, Cybercom was commissioned for several new pro-jects such as:

• Upgrading Suntel’s CRM and billing system (an operator in Sri Lanka).

• Delivering a billing solution for TeliaSonera; the solution is used for invoicing electronic refi ll cards that are distributed via retailers.

• Managing a system testing and verifi cation centre for Ericsson Mobile Platforms.

• Managing applications and developing Sony Ericsson’s consumer portal worldwide.

• Developing and integrating ASSA ABLOY’s internal purcha-sing portal for use worldwide.

• Implementing an Akamai solution for the SKF portal.

• Several IBM WebSphere e-commerce projects.

• Solutions for device management of embedded systems.

• Customer life-cycle management-related solution for Telia Mobile Denmark.

• Improvement of a wireless platform for Real Time in Den-mark.

• Wireless communication system for credit card transactions at Clear Channel in Norway.

Cybercom also signed new, larger frame agreements with Ericsson, the Government Offi ces of Sweden (Regeringskans-liet), SEB, TeliaSonera, and Teracom.

SALES AND INCOME

Compared with 2003, sales in 2004 increased 31% to SEK 405.3 million (309.7). The operation reported strong profi t. Before goodwill amortisation, operating profi t reached SEK 15.1 million (–2.2), which yields a 3.7% (–0.7) margin.

Net fi nancial items stood at SEK 2.1 million (1.7). Profi t after net fi nancial items reached SEK 10.1 million (–110.2), which yields a positive 2.5% net margin for all of 2004 (–35.6%).

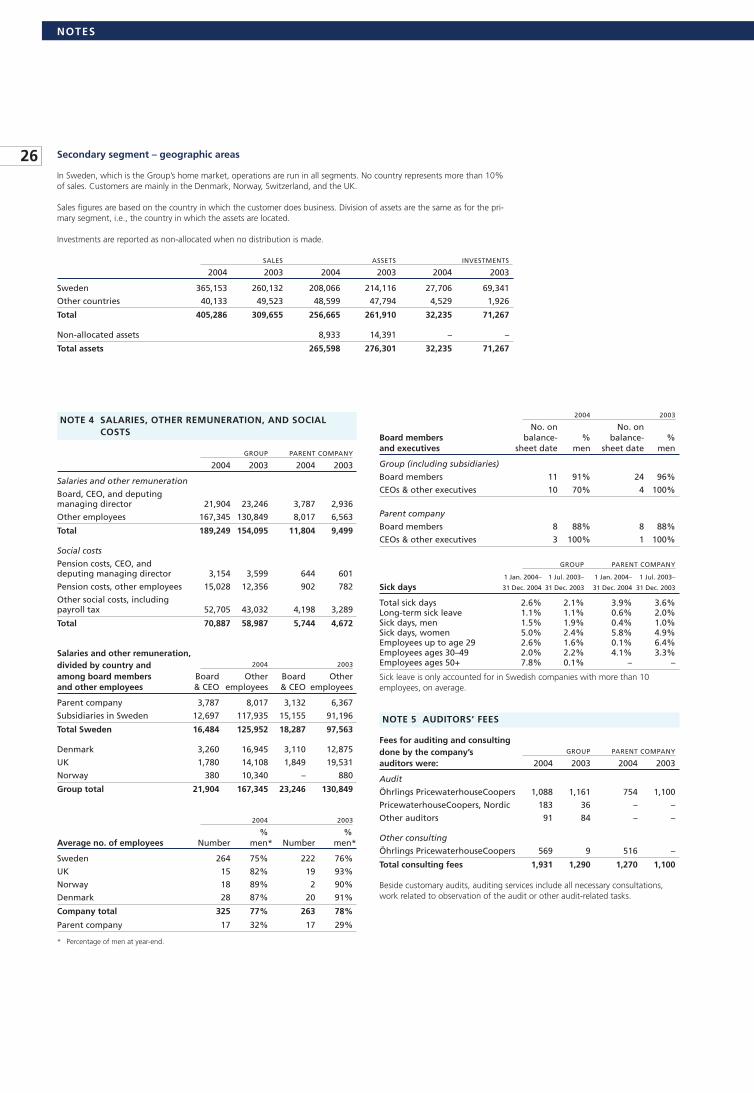

SALES IN 2004 BY INDUSTRY

Telecom, 67%

Finance, 14%

Pharma, 4%

Industry, 5%

Other, 10%

SALES BY INDUSTRY, PER QUARTER

Q1 Q2 Q3 Q4

%

90

80

70

60

50

40

30

20

10

0

Other

Industry

Pharma

Finance

Telecom

SALES IN 2004

Total project assignments, 42%

Other assignments, 58%

4

DIRECTORS’ REPORT

IMPORTANT EVENTS IN 2004

Focus on telecom from December 2004Cybercom strengthened its position within telecom. Sales to this market increased from about 60% in Q1 to 74% in Q4. Cybercom’s capabilities were particularly in demand for em-bedded systems and systems that support them (e.g., device management). The company also worked with the entire e-commerce supply chain; here, Cybercom has unrivalled experience and expertise in billing and in portals with mobile solutions.

In December, Cybercom’s executives decided to further focus the operation in Sweden on telecom and on selected technologies that give Cybercom a unique position that enables successful business deals. The decision is aligned with Cybercom’s growth strategy – to better meet demand for its services and to continue assertive growth.

In 2004, Cybercom’s Financial Services BA carried out ini-tiatives that targeted banking, fi nance, and insurance. Desired results were not achieved, so the BA successively refocused toward selected key customers and selected technology areas that it has in common with the Telecom & Services BA. The Swedish operation is now organised into one BA that targets telecom and technologies that are Cybercom’s strongest suit.

Cybercom’s CyberMate PreHospital product is offered to county councils and other enterprises that offer emergency care in Europe. Several licenses were sold in 2004. The market for med-tech equipment has a long sales cycle. Because of the focus that Cybercom now makes on telecom and selected technologies, a decision was taken regarding the sale of CyberMate and its operation. By selling CyberMate, the product’s long-term development is assured.

Starting 1 January 2005, Cybercom’s operation is reported as two divisions:

• Sweden – operations in Sweden that mainly specialise in telecom and selected technologies.

• International – operations in the Group’s companies in Denmark, Norway, and the UK.

Before and during 2004, Cybercom reported its operations in three BAs:

• Telecom and Services – operations in Sweden that mostly specialise in telecom.

• Financial Services – operations in Sweden that mostly specialise in banking, fi nance, and insurance.

• International – operations in the Group’s companies in Denmark, Norway, and the UK.

Successful integration of Consafe InfotechConsafe Infotech was acquired in 2003 and fully integrated in 2004, which led to substantial business synergy effects. From the start, the main focus of the integration was placed on customers, and the merger resulted in business that neither of the companies would have won on their own. Several projects were staffed with consultants from both operations.

In October 2004, a supplementary purchase price of SEK 18 million was set for the acquired Consafe Infotech; this increased Group goodwill by the same amount. The 8 Decem-ber 2004 extraordinary meeting decided on a new share issue of 523,887 shares directed to the previous majority owners of Consafe Infotech. Minority owners were paid in cash.

During 2004, the acquired operation accounted for 30% of sales in the Telecom & Services BA and 20% of sales in the International BA.

New issue and new ownerIn December, Cybercom decided that a special issue of new shares would fi nance the fi xed supplementary purchase price of the Consafe Infotech acquisition. With this new issue, JCE Group AB, Magellan BV, and J. Christer Ericsson became the largest shareholders in Cybercom Group Europe, with total holdings of 14.3%. This new issue increased the company’s share capital by SEK 10,672,468 to 11,196,355. A total of 523,887 shares were issued with a nominal value of SEK 1 per share, at an issue price per share equal to the latest price paid on 8 December 2004, which was SEK 30.10.

In December, Cybercom’s founders and JCE Group AB reached an agreement regarding share transfer. Through the agreement, JCE Group acquires all the founders’ shares, and on 15 March 2005, JCE Group AB owns 37.8% of all shares in Cybercom.

5

DIRECTORS’ REPORT

PERSONNEL

For all of 2004, the average number of employees in the Gro-up was 325 (263). At year-end, the number of employees in the Group was 375 (375), of which 25% (24) were women. Cybercom has offi ces in Denmark, Norway, Sweden, and the UK. The company has operations in six other countries, including Sri Lanka and Switzerland. Most employees work in Sweden (81%).

Of all Cybercom’s consultants, 91% (87) have a university education. The company’s IT consultants have an average of 13 (13) years of industry experience. Total personnel turnover in the Group was 19.7%; restructuring of Financial Services accounts for most of the turnover. Of the 74 employees who left, 44 were in Financial Services. Remaining turnover was 9%, which is normal for the industry. Absence due to illness was 2.6% (2.1), of which 1.1% (1.1)1 was long-term illnesses.

During 2004, Cybercom hired 74 employees, mainly for telecom; 50 are working in this operation.

1 These fi gures cover the 1 July–31 December 2003 period only.

YEARS OF EMPLOYMENT

< 3 years, 48%

3–5 years, 32%

5–10 years, 20%

INDUSTRY EXPERIENCE

< 5 years, 21%

5–10 years, 29%

10–15 years, 19%

15–20 years, 19%

> 20 years, 12%

EDUCATION

University-trained engineer, 37%

Systems analysts, 16%

Other academic education in technology, 23%

Other academic education, 15%

Other post-secondary studies, 9%

EMPLOYEES’ AGES

ages 21–25, 2%

ages 26–30, 18%

ages 31–35, 27%

ages 36–40, 24%

ages 41–45, 16%

ages > 45, 13%

6

DIRECTORS’ REPORT

MARKET

A Nordic company with an international perspectiveCybercom mainly operates in northern Europe, with establis-hed operations in Denmark, Norway, Sweden, and the UK. In 2004, 90% of sales came from the Swedish operation. Cybercom will mainly expand in the Nordics.

Continued investment upsurges in 2004The IT market gained momentum in 2004, which led to increased activity. In 2002 and 2003, customers put a hold on investments; nearly all investments they made involved cost-cutting measures. This hard-line approach began to loosen up during H2 2003, and it continued into 2004.

Continued strict cost controlThe market for IT services has matured, which has resulted in stricter cost-control requirements from customers. Despite increased investments in 2004, customers’ cost controls continue to be stringent, and cost-saving investments are still the most common. But business development investments for increasing business volume increased. Telecom companies, which are now in an intensive development phase, were espe-cially inclined to make new investments. For these companies, 2004 was the time to grab additional market shares. Swedish exports increased substantially in 2004, mainly because of the very active telecom sector.

New technology drives investmentsNew technology and shifts in technology mainly drive these assertive market investments. This tremendous rate of innova-tion has decreased since the 1990s, and a more long-term balance between technological development and its com-mercial applications was seen in 2004. Many technologies within mobile services have now reached a commercial phase, and development is more and more commercially driven. So it’s important for consultants to complement their specialised technical expertise with expertise in the application area.

Outsourcing of IT system development and administrationCustomers’ tendencies to outsource some services continue to be strong drivers on the IT services market. These services include IT system development and management and testing

operations. Often, customers retain overall control of their systems and only purchase subsystems or solutions for specifi c application areas – and that’s where specialised consultancies like Cybercom enter the picture. Large consultancies, such as IBM, CapGemini, and Accenture often take on larger, far-reaching assignments.

Increased mobility for IT consultantsThe improved IT consultancy market, primarily within telecom, resulted in increased mobility for consultants in 2004. After several years of downsizing and staff reductions, many consultancies need new people. The market for consultants presents a fragmented picture, where the degree of speciali-sation, expertise, and experience determines demand.

Consolidation results in specialisationConsultancy sector consolidation, which has been occurring since 2000, has continued; this indicates that the industry has been split into various segments.

One segment consists of large global companies with very broad capabilities focused on large, complex orders.

Another segment consists of specialised consultancies that are also relatively large. These consultancies offer develop-ment and solutions within special niches, often with highly technical content. Cybercom belongs to this segment.

A third segment consists of pure resource consultants that sell their services by the hour, along with a certain amount of functions; here, the degree of specialisation is low, and pricing is very competitive. Companies in this segment often work as subcontractors for companies in the fi rst two seg-ments.

Consolidation continues, which provides good opportuni-ties for acquisition of mostly smaller consultancies that realise they can’t move into the second segment on their own.

Cybercom has different competitors in different areas. The company has won and lost contracts in competition with IBM, Accenture, TietoEnator, Teleca, CapGemini, Sigma, and HiQ.

Telecom leads investmentsPositive market signals are mostly noted within the telecom sector; operators have begun to invest in development of new business areas and services. Revenue from voice traffi c and short message services still dominates, but this revenue

IT COMPANIES’ POSITIONS IN THE VALUE CHAIN

CybercomTeleca, HiQ, Enea,

Sigma

Resource consultants

Cybercom positions itself in the middle of the value chain, so it delivers concepts and specialized solutions in close co-operation with customers.Source: Cybercom

Customers have concepts, buy solutions and system co-ordination

Customers develop in-house, buy blanket-order resources

Customers outsource IT, buy total functionality

IBM, WM-data,Accenture, TietoEnator,

Cap Gemini Ernst & Young

VOLUME

IMPORTANT PARTNERSHIPS

7

DIRECTORS’ REPORT

is decreasing. Interest in investing in new, more sophisticated services has increased. The commercial breakthrough for mobile telephony’s third generation (3G) defi nitely occurred in 2004. Expansion of the 3G network spurred investments, because 3G provides new business opportunities through advanced mobile data services. Gradually, larger portions of a telecom operator’s revenue will come from other types of content services or digital media.

Telecom operators and other companies in telecom offer these services, but content is developed and supplied by the music industry, terminal manufacturers, news agencies, and others. The increased infl uence that content providers have on telecom operators’ service offerings creates a need for new business models and payment functions. Consumers must be able to easily pay for these services, and content providers and telecom operators must be able to collect pay-ments. That’s why new billing solutions and pricing strategies for revenue streams between telecom operators and content providers must be developed.

IP telephony, which links data communication to telepho-ny, has also started to be used on a large scale. Conditions are good for telephony over the Internet to gain momentum. New IP telephony solutions will be implemented, and IT sys-tems will have to be adapted and developed.

Larger customers and fewer vendorsA few large companies dominate the telecom market. Custo-mers of consulting companies have become larger, and the

paring down of purchases has resulted in a transition from dealing with more than 100 different vendors to signing mas-ter contracts with 20–30 selected vendors. These contracts lead to long-term relationships with highly qualifi ed vendors. Size, specialisation, and international presence are critical suc-cess factors for consultancies.

Similar developments in all the Nordic countriesMarket trends in Norway and Denmark signal increased activity, although market players are somewhat more cautious than in Sweden. The Öresund region in southern Sweden enjoyed the strongest upturn. The Danish market differs from the Swedish in that it’s more fragmented and dominated by mid-sized customers, so vendor size isn’t as important. In Norway, the telecom market mostly consists of telecom ope-rators and service providers; here, equipment manufacturers have pretty much disappeared. Finland’s market is similar to Sweden’s, with a few large customers within telecom. Prices in the Nordic countries are stable.

Continued investment-rate escalation Increased investment activities that prevailed in telecom during 2004 are expected to continue in 2005. The upswing in telecom at the end of 2004 is expected to continue for several quarters but at a slower pace. The Öresund region is expected to continue to be the driving force.

Affärsvärlden’s ranking of IT consultancies Sales No. profi table Market value/ Ranking Ranking 2004, Growth years Margin employee Sales/ P/E future stability (MSEK) 5 years, % 2000–2004 20041 (KSEK) employee (2005)3 outlook (fi ve year)2

Tieto Enator 13,725 36 5 12 1,542 1,075 15 4 5

HIQ 513 27 4 10 2,226 959 19 4 4

Semcon 1,289 28 4 4 416 876 11 4 4

Cybercom 405 13 3 2 995 1,080 16 4 4

Teleca 2,728 10 3 –0.2 817 871 18 4 3

Knowit 384 –23 2 3 879 1,110 12 3 3

Sigma 853 –15 2 0.7 834 985 19 4 3

WM-Data 8,160 –38 4 4 982 1,071 18 4 2

ENEA 657 –23 2 0 3,659 1,357 37 3 2

ADDNODE 300 –43 2 5 1,271 1,145 7 3 2

Prevas 178 –25 2 8 1,065 1,053 7 3 2

Acando Frontec 600 –41 2 3 822 1,183 13 3 2

Framfab 326 –78 1 3 1,829 997 29 3 1

LB Icon 568 –67 0 –8 1,146 840 33 2 1

1 Profi t/loss after net fi nancial items & sales. 2 Sales trend, personnel development, dividend. 3 Redeye’s assessment (without WM-data, Enea, Addnode, Prevas, Framfab, and Icon).Source: Affärsvärlden No. 7, 16 February 2005

TOTAL CELL PHONE SALES WORLDWIDE(2002–2008; f=forecast)

2002

GrowthNumber

03 04fSource: Alpha Research-Nordea Markets

05f 06f 07f 08f

billion

1,000

800

600

400

200

0

%

25

20

15

10

5

0

MOBILE INFRASTRUCTURE MARKET(2001–2010 f=forecast)

2001

GrowthMarket value

0302 04f 05f 06f 07f 08f 09f 10f

EUR m

60,000

50,000

40,000

30,000

20,000

10,000

0

%

20

10

0

–10

–20

–30

–40

Source: Alpha Research-Nordea Markets

8

DIRECTORS’ REPORT

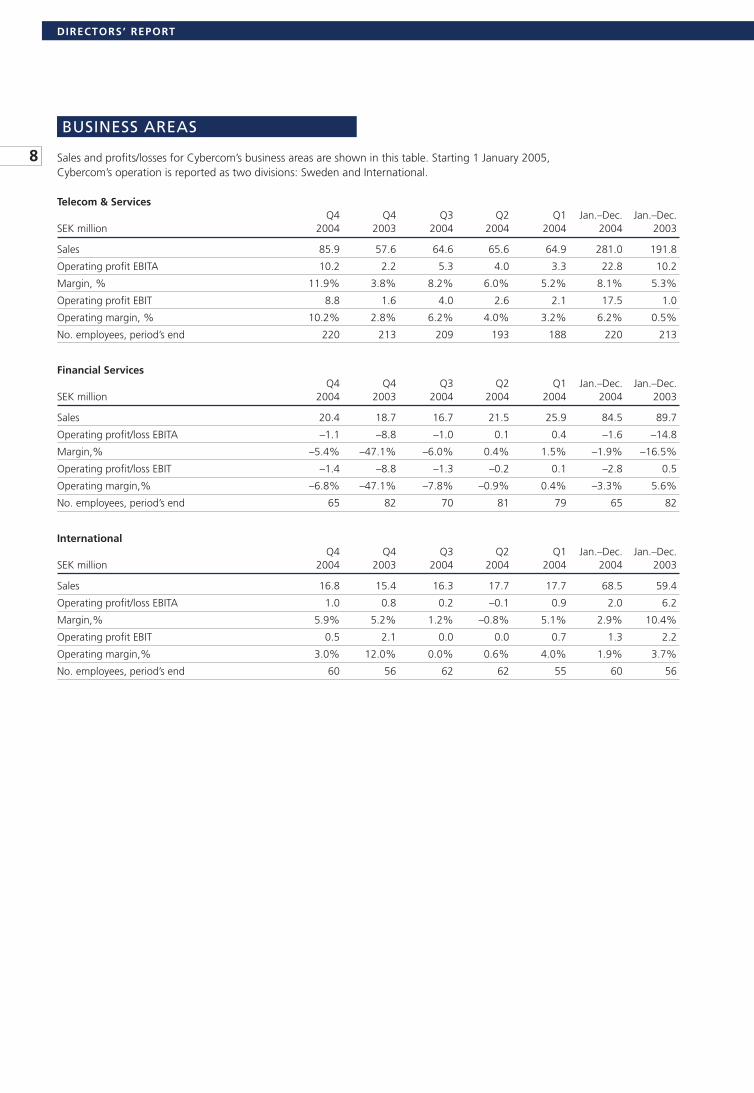

BUSINESS AREAS

Sales and profi ts/losses for Cybercom’s business areas are shown in this table. Starting 1 January 2005, Cybercom’s operation is reported as two divisions: Sweden and International.

Telecom & Services Q4 Q4 Q3 Q2 Q1 Jan.–Dec. Jan.–Dec.SEK million 2004 2003 2004 2004 2004 2004 2003

Sales 85.9 57.6 64.6 65.6 64.9 281.0 191.8

Operating profi t EBITA 10.2 2.2 5.3 4.0 3.3 22.8 10.2

Margin, % 11.9% 3.8% 8.2% 6.0% 5.2% 8.1% 5.3%

Operating profi t EBIT 8.8 1.6 4.0 2.6 2.1 17.5 1.0

Operating margin, % 10.2% 2.8% 6.2% 4.0% 3.2% 6.2% 0.5%

No. employees, period’s end 220 213 209 193 188 220 213

Financial Services Q4 Q4 Q3 Q2 Q1 Jan.–Dec. Jan.–Dec.SEK million 2004 2003 2004 2004 2004 2004 2003

Sales 20.4 18.7 16.7 21.5 25.9 84.5 89.7

Operating profi t/loss EBITA –1.1 –8.8 –1.0 0.1 0.4 –1.6 –14.8

Margin,% –5.4% –47.1% –6.0% 0.4% 1.5% –1.9% –16.5%

Operating profi t/loss EBIT –1.4 –8.8 –1.3 –0.2 0.1 –2.8 0.5

Operating margin,% –6.8% –47.1% –7.8% –0.9% 0.4% –3.3% 5.6%

No. employees, period’s end 65 82 70 81 79 65 82

International Q4 Q4 Q3 Q2 Q1 Jan.–Dec. Jan.–Dec.SEK million 2004 2003 2004 2004 2004 2004 2003

Sales 16.8 15.4 16.3 17.7 17.7 68.5 59.4

Operating profi t/loss EBITA 1.0 0.8 0.2 –0.1 0.9 2.0 6.2

Margin,% 5.9% 5.2% 1.2% –0.8% 5.1% 2.9% 10.4%

Operating profi t EBIT 0.5 2.1 0.0 0.0 0.7 1.3 2.2

Operating margin,% 3.0% 12.0% 0.0% 0.6% 4.0% 1.9% 3.7%

No. employees, period’s end 60 56 62 62 55 60 56

9

DIRECTORS’ REPORT

INTERNAL RESOURCES

Quality process – ISO 9000Cybercom always strives to reach its goals and offers value beyond its contracted requirements. To live up to our own standards, and our customers’ standards, Cybercom works according to the quality management principles that are the cornerstone of the ISO 9000 standard. Our employees use several well-documented processes that compose a system that’s constantly being reviewed. Cybercom follows guidelines from the Swedish Institute for Quality, the European Founda-tion for Quality Management, and Six Sigma.

Testing systems for best possible quality assuranceToday, product development has more technical content and a shorter life cycle, while stringent demands are put on pro-ductivity, security, and quality. Cybercom uses modern tools and methods for system development, project management, and testing – to assure that all requirements are met. This includes established commercial tools and custom-developed tools. We have lots of experience with recognised methods such as Agile, Extreme Programming, RUP, PPS, and PROPS. Cybercom’s consultants are certifi ed in these methods.

The company has developed project and testing meth-ods for information systems called X-pert and X-act – for implementing and securing successful projects and testing in a structured, effi cient, and consistent manner. X-pert divides the project into three phases: preparation, production, and close-down (wind-up). Each phase defi nes which activities are included, which decision points (milestones) arise, and which documents are required. X-pert supports daily project work by providing concepts, procedures, templates, and checklists. The same goes for X-act. Cybercom’s high standards in its test management projects have led to independent projects in which Cybercom performs system tests and verifi cations of mobile telephone platforms.

Application management – maintenance and development of operational systemsDeveloping and running IT projects takes a lot of time and money. To stay within a budget, it’s important to have control over costs. Cybercom offers a service called applica-tion management (AM), which guarantees high quality and service levels at a fi xed price. With AM, Cybercom takes on maintenance and development of IT systems that are in operation. This service can include customised and third-party applications. The concept clarifi es responsibilities, activities, and costs related to support, development, and operation of a system or an application. Cybercom’s AM concept focuses

on all key business processes that demand maximum use of applications – from business development and management to technical support. It’s a structured way of working that enables contracted service levels and facilitates accurate cost forecasting. Each AM service is driven by one or more service level agreements. Cybercom’s management, together with customer and supplier representatives, regularly follow up on the AM services.

Information security policyInformation and data are the most important resources we have, and they are invaluable. Operational procedures are well documented in the information security policy and the business support system. Cybercom works actively, systemati-cally, and continuously to protect information and information systems from assessed threats and to ensure that current laws and regulations are followed.

Environment policyCybercom works actively to improve its operation from an ecological perspective by prioritising environment-related issues in its operations. The company ensures that hardware suppliers comply with TCO 95 and TCO 99 (environmental regulations) and that material is marked to enable effective recycling. Cybercom also strives to select the best products from energy-effi ciency and environmentally friendly perspec-tives. The company is not subject to reporting obligations established by the Swedish Environmental Protection Agency.

Professional developmentCybercom has a strategy for professional development in which management decides which business areas, services, and products should be prioritised. Based on these priorities, annual reviews are done where decisions on comprehensive, company-wide professional development areas are made. An-nual performance appraisals are signifi cant, because employ-ees and managers together design individual development plans. The plans are based on Cybercom’s strategy and each individual’s development needs. Professional development at Cybercom occurs in customer projects, expert groups, and through external training. Costs for external training in 2004 amounted to about SEK 718,500. Besides pure professional development, Cybercom also runs a series of seminars that emphasise the business culture and technical interests within the Group.

Research and developmentThe company does not run an R&D operation.

10

DIRECTORS’ REPORT

THE CYBERCOM SHARE

Share capitalOn 31 December 2004, Cybercom’s share capital stood at SEK 11,196,355, which was divided among an equal number of shares. The share’s nominal value is SEK 1. All shareholders have an equal right to a share in the company’s assets and profi ts.

Price trend and turnoverOn 1 December 1999, Cybercom B shares were listed on the Stockholm Stock Exchange’s O list.

In August 2000, Cybercom’s A shares (not issued) and B shares were reclassifi ed as shares without classifi cation. Since then, Cybercom has just one type of share. One round lot consists of 500 shares. During 2004, Cybercom’s share price was unchanged. The SX-IT index, which includes Cybercom’s share, rose 47%, and the SX All-Share index rose 16%.

At year-end, the share price was SEK 30.40, which yields a stock market value of SEK 323 million. The price has fl uctuated between SEK 22.10 (12 August) and SEK 38.80 (9 February). On average, 33,031 shares were traded daily during 2004; this is comparable to SEK 0.9 million per stock-exchange day.

ShareholdersAt year-end, there were 5,301 shareholders (5,720), of which 73% (75) of these shareholders owned 500 shares or fewer. Large institutional shareholders owned 24.0% (25.2); the company’s board members (including the company’s foun-ders) owned 24.5% (28.5); company executives owned 0.7% (0.3); and other shareholders owned 37.4% (46.0). Foreign shareholders owned 12.0% (15.6).

Dividend policyThe board set a goal of securing Cybercom’s continued growth. Regard must always be made to the Group’s invest-

ment needs and fi nancial position before dividend-related decisions are made. The board proposes to the annual general meeting that no dividend be given for the 2004 fi nancial year.

WarrantsDuring the year, the 500,000 warrants in warrant program 6 expired; at that time, the share’s market value was lower than the subscription rate, so warrants weren’t exercised. During January and February 2005, the 162,483 warrants in warrant program 8 will expire at a subscription rate of SEK 33.50. The 200,000 warrants in warrant program 9, with the 16 August 2006–16 January 2007 subscription period and a subscription price of SEK 32.92, were in Cybercom’s possession as of 31 December 2004.

Acquisitions and new issuesAt an extraordinary meeting of Cybercom Group Europe on 8 December, it was decided to fi nance the fi xed supplemen-tary purchase price of the acquired Consafe Infotech through a directed share issue according to the board’s proposal. This new issue increased the company’s share capital of SEK 10,672,468 by SEK 523,887 to SEK 11,196,355. A total of 523,887 shares were issued with a nominal value of SEK 1 per share at an issue price per share that is equal to the latest price paid on 8 December 2004, which was SEK 30.10.

Those entitled to subscribe for the newly issued shares are the JCE Group, Magellan B.V, J Christer Ericsson, and Per Edlund, which deviates from other shareholders’ preferential rights. Because Per Edlund is on Cybercom’s board, it’s requi-red that the emission be approved by a decision in which at least nine-tenths of the votes cast and those shares represen-ted at the meeting approve the issue, according to statute 1987:646 on directed issues in stock market companies. The meeting’s decision was unanimous.

Source: Ecovision

THE CYBERCOM SHARE

0

500

1,000

1,500

2,000

2,500

3,000

No. (000s)

0

50

100

150

200

250

SEK

2000 2001 2002 2003 2004

Cybercom SX-All-Share SX-IT Traded shares in 000s

11

DIRECTORS’ REPORT

Share capital trends Nominal Future no. Total Share capital- Total shareYear Transaction amount, SEK of shares Price, SEK shares increase, SEK capital, SEK

1997 Company construction 100 1,000 – 1,000 100,000 100,000

1998 Split 5000:1 0.02 4,999,000 – 5,000,000 – 100,000

1998 New issue directed to Intertech Ltd, Torsten Jungner, & Melina AB 0.02 515,000 13.60 5,515,000 10,300 110,300

1998 New issue directed to Peter Törnquist and Lars Ahlman 0.02 110,300 16.32 5,625,300 2,206 112,506

1998 New issue directed to Peter Törnquist and Peter Karaszi 0.02 57,575 16.32 5,682,875 1,152 113,658

1999 Bonus (share dividend) issue 1 – – 5,682,875 5,569,218 5,682,875

1999 New issue directed to Pir New World Media AB 1 300,000 35.00 5,982,875 300,000 5,982,875

1999 New issue directed to Lingfi eld AB 1 100,000 40.00 6,082,875 100,000 6,082,875

1999 New issue directed to the 6th AP fund 1 100,000 45.00 6,182,875 100,000 6,182,875

1999 New issue 1 1,700,000 62.00 7,882,875 1,700,000 7,882,875

2000 New issue directed to shareholders of Intra-X Data AB 1 111,428 210.00 7,994,303 111,428 7,994,303

2000 New issue after exercise of warrants – warrant programme (WP 1) 1 350,000 23.50 8,344,303 350,000 8,344,303

2000 New issue after exercise of warrants (WP 2) 1 95,500 41.50 8,439,803 95,500 8,439,803

2001 New issue after exercise of warrants (WP 2) 1 53,000 41.50 8,492,803 53,000 8,492,803

2001 New issue directed to shareholders of StreamIT AB 1 101,521 98.50 8,594,324 101,521 8,594,324

2001 New issue directed to shareholders of Intra-X Data AB 1 145,455 87.00 8,739,779 145,455 8,739,779

2001 New issue after exercise of warrants (WP 3) 1 17,500 51.50 8,757,279 17,500 8,757,279

2002 New issue directed to shareholders of Intra-X Data AB 1 227,274 32.90 8,984,553 227,274 8,984,553

2002 New issue directed to shareholders of Stratum PM Ltd 1 267,224 34.61 9,251,777 267,224 9,251,777

2003 New issue directed to shareholders of Mobility Partner Europe AB 1 200,000 16.55 9,451,777 200,000 9,451,777

2004 New issue directed to shareholders of Consafe Infotech 1 1,220,691 26.50 10,672,468 1,220,691 10,672,468

2004 New issue directed to the JCE Group with Christer Ericsson as largest owner 1 523,887 30.10 11,196,355 523,887 11,196,355

2005 Fully subscribed warrants (WP 8) 1 162,483 33.50 11,358,838 162,483 11,358,838

2007 Fully subscribed warrants (WP 9) 1 200,000 32.92 11,558,838 200,000 11,558,838

Subscription of the new shares was done on a special sub-scription list by 15 December 2004. With this new issue, the JCE Group, Magellan B.V, and J Christer Ericsson became the largest shareholders in Cybercom Group Europe, with total holdings of 14.3%.

In December 2004, an agreement was also reached regar-ding a share transfer between the JCE Group and Cybercom’s founder who has also been the principal owner of the company until now. Through this share transfer agreement, the JCE Group acquired 2,628,050 shares from two compa-nies that were controlled by Per Bergström and Pekka Seitola, Cybercom’s previous principal owners. The price per share was SEK 33. The shares will be issued in two instalments: 50% on 17 January 2005 and 50% on 15 March 2005.

The new issue increases the collective holdings of the JCE Group, Magellan B.V and J Christer Ericsson to a total of 1,602,429 shares in Cybercom, which corresponds to 14.3% of the total number of shares and votes.

Through an agreement with both of the principal owners regarding acquisition of shares, the JCE Group is further increasing its holdings to 4,230,479 shares. So after 15 March 2005, the JCE Group, Magellan B.V, and J Christer Ericsson, all else being equal, together own shares in Cybercom equiva-lent to 37.8% of the total number of shares.

The number of shares – at full dilution of 362,483 warrants and including the new issue of 523,887 shares – amounted to 11,558,838 at year-end.

Ownership structure as of 31 December 2004 No. of shares Share ofName and capital votes in, %

Per Bergström via company 1,314,025 11.74

Pekka Seitola via company 1,314,025 11.74

MAGELLAN BV* 949,501 8.48

JCE GROUP* 622,894 5.56

AMF PENSION FUND – SMALL COMPANY 459,700 4.11

SIS Segaintersettle AG 354,350 3.16

Carlson Small Company Fund 191,000 1.71

Östersjöstiftelsen 142,700 1.27

MORGAN STANLEY & CO INTL LTD, W8IMY 140,000 1.25

NORDEA BANK S A 119,850 1.07

Total for the 10 largest owners 5,608,045 50.1

Other 5,588,310 49.9

Total** 11,196,355 100.0

* Company controlled by J Christer Ericsson, total 14%.** 523,887 newly issued shares were registered with PRV on 29 December but were registered in the owners’ names in January 2005.

Holdings as of 31 December 2004 SHARES OWNERS

Size Quantity % Quantity %

1 – 100 120,773 1.1% 1,995 37.6%

101 – 500 565,693 5.1% 1,852 34.9%

501 – 1,000 630,250 5.6% 697 13.1%

1,001 – 5,000 1,480,208 13.2% 609 11.5%

5,001 – 10,000 464,857 4.2% 64 1.2%

10,001 – 50,000 1,272,395 11.4% 62 1.2%

50,001 – 100,000 739,634 6.6% 9 0.2%

100,001 – 5,922,545 52.9% 13 0.2%

11,196,355 100% 5,301 100%

12

DIRECTORS’ REPORT

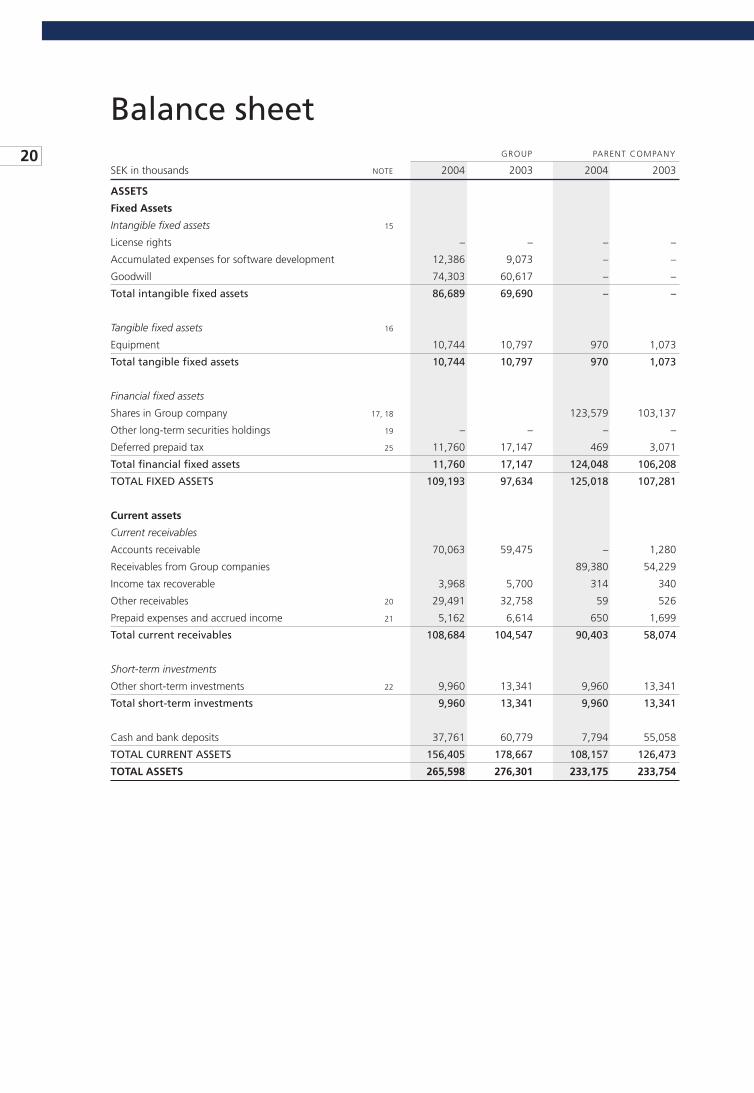

INVESTMENTS

In 2004, tangible, fi xed-asset investments reached SEK 5.6 million (3.6). Total intangible-asset investments reached SEK 26.6 million (63.0), of which goodwill accounts for SEK 20.8 million (57.3). Besides goodwill related to Consafe Infotech, executives in Cyber Com Consulting A/S exercised their warrants to purchase an additional 3.3% of the shares in the Danish subsidiary. During Q2 2004, the Group bought back these shares for SEK 2.4 million, which led to a SEK 2.2 million goodwill item.

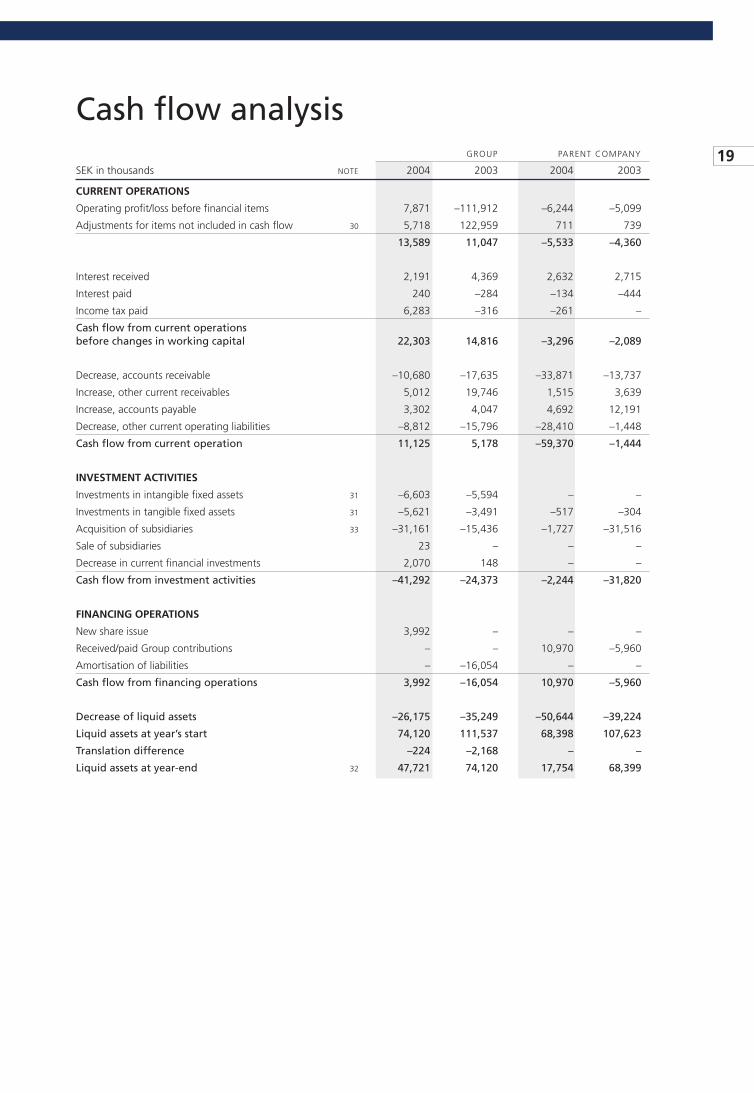

LIQUIDITY AND CASH FLOW

On 31 December 2004, the Group’s liquid assets were worth SEK 47.7 million (74.1 million on 31 December 2003).

Cash fl ow from the operation was SEK 11.1 million for all of 2004 (5.3). During 2004, SEK –26.5 million affected the in-vestment operation’s results because of earlier acquisitions: (1) SEK –18 million for redemption of loan notes from Stratum, Cybercom’s UK company, and (2) SEK –8.5 million, which was paid after year-end 2004 for Consafe Infotech.

FINANCIAL POSITION

As of 31 December 2004, shareholders’ equity stood at SEK 173.2 million (149.5), which yields a 65.2% (54.1%) equity/assets ratio. Shareholders’ equity per share reached SEK 15.47 (14.01).

THE PARENT COMPANY

Parent company operations primarily support Group functions (e.g., fi nance, communications, marketing, administration, HR, and internal systems). Sales in 2004 reached SEK 29.0 million (27.1). Operating loss was SEK 6.2 million (–4.9). Loss after fi nancial items was SEK 5.4 million (–145.1). On 31 De-cember 2004, the parent company’s cash fl ow stood at SEK 17.8 million (68.4). Investments worth SEK 0.5 million (0.3), in computers and other equipment, were made during 2004. At year-end, the parent company employed 25 (24) persons, of which 5 were on leave of absence. The average number of employees during the year stood at 18 (17).

INCENTIVE PROGRAM

During 2004, 500,00 options (warrant programme 6) expired. There are now 362,483 options outstanding, all directed to employees in the UK operation: 162,483 expire during January–February 2005 and 200,000 during August 2006–January 2007. See note 23.

CORPORATE GOVERNANCE

Cybercom’s board has briefl y evaluated the new Swedish code for corporate governance that the Stockholm stock exchange is expected to add to its regulations. This evaluation led to the conclusion that Cybercom’s governance meets the require-ments of the code and that no changes will be made for the time being. The board intends to comply with the code as soon as it’s adopted by a larger regulatory entity, such as the Stockholm Stock Exchange.

Shareholder and board representationCybercom’s board and executive team work diligently with corporate governance issues. Three of the largest sharehol-ders are represented on the board. The company’s nomination committee requires that board members have the appropriate expertise. A remuneration committee strives to create the best possible conditions for reasonable compensation and bonus levels. The audit committee consists of all board members who work closely with the company’s auditors. Individual sha-reholders may submit proposals to the committees, via regular mail, to Cybercom’s headquarters in Stockholm.

Annual general meeting (AGM)The AGM is the decision-making body in which all sharehol-ders can participate. At the AGM, developments in the com-pany are presented and decisions are made on several central items, such as dividends, remuneration for the board and auditors, changes to the articles of association, the appoint-ment of auditors, discharge from liability for board members, and election of the board for the coming 12 months.

Nomination committeeAt the AGM, a nomination committee is elected and charged with submitting proposals regarding possible board mem-bers, choice of auditors, remuneration, and associated issues before the next AGM. The nomination committee makes up a profi le of requirements and ensures that the company’s board members have expertise relevant to Cybercom’s operation. Committee members before the 2005 AGM are Gert Schybor-ger (chairman), John Örtengren, representative for minority shareholders (via the Swedish Shareholders’ Association), and Per Bergström, representative for the company’s larger share-holders in 2004. Per Edlund was a co-opted member for the meetings that were held after the contract went into effect regarding share transfer from the previous main owners. The nomination committee works closely with the shareholders and meets three times a year.

The boardThe board is responsible for the Group’s organisation and management according the Swedish Companies Act. A fi xed programme regulates the distribution of responsibilities bet-ween the board and Cybercom’s CEO. According to this pro-gramme, the board takes decisions on the CEO appointment, the main organisation, long-term fi nancial planning, opera-tion plans, the budget, and annual reports. The programme

13

DIRECTORS’ REPORT

is considered and fi xed annually. The board formulates CEO and reporting instructions, and Cybercom’s CEO is responsible for planning and implementing initiatives according to board decisions and the company’s ongoing administration.

The board consists of eight members who represent a broad range of expertise in IT, telecom, business development, and other areas. Three of the largest owners are represented on the board; they represent a total of 37.2% of the votes in Cybercom. During 2004, the board met nine times. According to the corporate bylaws, Cybercom’s board can select three deputies. The nomination committee and the board decided to exercise that right for another year, because it’s a good way to phase-in future board members. The nomination commit-tee reviews and evaluates the board’s work and contributions of individual members.

Remuneration committeeCybercom’s remuneration committee sets salaries for the CEO, vice president, and other executives. The remuneration committee strives to create the best possible conditions so that benefi t issues are treated comprehensively and carefully. The remuneration committee met three times during 2004; its members are:1. Gert Schyborger, Cybercom’s board chairman.

2. Kerstin Ryer, board member and CEO of HumanPartner AB. She was the HR director of If Skadeförsäkring AB. She has extensive experience in developing remuneration prin-ciples for salary setting and other terms of employment.

3. Pekka Seitola, one of Cybercom’s founders, board mem-ber, and representative for larger shareholders.

Audit committeeThe audit committee consists of all board members and is charged with proposing auditors and approving their fees. Ulf Pettersson, Öhrlings PricewaterhouseCoopers, was elected as auditor through 2008. During the year, the board receives presentations from the company’s auditor, who ensures that the company’s internal and external reports fulfi l the require-ments of a company listed on the stock exchange.

AuditorsAuditors are appointed at the AGM every fourth year; the last appointment was done at the AGM held in 2004. The auditor’s job is to audit the company’s annual report, its accounting records, and the asset management activities of the board and the CEO on behalf of the shareholders. The auditors report continuously to the board.

Group managementThe CEO supervises the Group’s managing directors and orga-nises and develops the business in such a way that the goals established by the board regarding profi tability and direction are reached. Written instructions determine the work distribu-tion between the board and the CEO. The CEO submits a

monthly report to the board. The work distribution rules also regulate the CEO’s fi nancial framework.

During 2004, Cybercom has strengthened Group mana-gement to better refl ect the company’s focus on telecom and its international growth strategy. The management group increased from four to ten persons during the year. In the an-nual budget process, the board and Group management set the framework for the operation and lay the groundwork for a strong decentralisation of the Group’s operation. Common policy documents set the framework for management and follow-up.

Finance policyThe fi nance policy regulates the division of fi nancial responsi-bilities and authority between the board, the CEO, the CFO, and the subsidiary managers. The fi nance policy includes cur-rency and cash handling, and fi nances.

Management of business areasThe Cybercom Group’s managing directors report to their respective business area managers. At the end of 2004, there were two business areas whose managers report to the CEO, who in turn reports to the board. Each month, the subsidia-ries submit reports that contain:

• New and existing customer business.

• Customers or jobs lost.

• New sales.

• Workload.

• Threats and opportunities.

Internal controlManagement and internal control follow the Group’s com-mon reporting structure, fi nance policy, and other policies established by the parent company’s board. Internal reporting procedures are audited during the annual audit. The audi-tors also draw up an annual risk analysis for the Group. The auditors’ review of internal controls and risks is presented in a report that is submitted to the board.

CommunicationCybercom’s intends to increase interest in Cybercom shares with existing and potential investors. This will be done by actively and quickly furnishing the market with relevant and current information. Openness and a high level of service are also part of Cybercom’s ambition to develop trust in the com-pany on the stock exchange. During the year, Cybercom met regularly with investors and capital market companies. On the company’s website (www.cybercomgroup.se), you will fi nd all published information on the Group’s development, stock exchange information, and other important information. All external contact with the market is made by the board chair-man, the CEO or the communications manager.

14

DIRECTORS’ REPORT

TRANSITION TO INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS)

From 1 January 2005, the company will issue fi nancial reports according to the IFRS. The interim report for Q1 2005 will be the company’s fi rst IFRS report. Through 2004, the company used the Swedish Financial Accounting Standards Council’s recommendations. Provided that the transition date is 1 January 2004, the transition to IFRS is reported according to IFRS 1: First-time Adoption of International Financial Reporting Standards. IFRS 1 stipulates that the 2004 compa-rison year must also be reported according to IFRS. Financial information referring to fi nancial years before 2004 are not recalculated. The principal rule states that all applicable IFRS and IAS standards that take effect and are approved by the EU as of 31 December 2005 must be applied retroactively. But IFRS 1 contains some exceptions to the principal rule that the company can choose to follow.

The changes in accounting principles that this transi-tion entails and the transition effects on the Group’s profi t and loss statements and balance sheets are presented here. The exceptions to complete retroactive application that the company chose to apply are also explained. These effects are preliminary and may change because the revision of certain IAS/IFRS standards are still in progress and further information from the IFRIC can be expected during 2005. It’s possible that new standards with an application date of 1 January 2006 might have to be implemented in advance.

Here are the most important changes that affect Cybercom in connection with the transition to IFRS:

• IFRS 3: company acquisitions. IFRS 3 (Business Combina-tions) requires that goodwill and other intangible assets with an undetermined useful life should no longer be written off, but should be tested for depreciation when transitioning to IFRS on 1 January 2004, and annually or more often – if there are indications of a decrease in value. Such an asset is depreciated if the reported value exceeds the recoverability value. The company performed deprecia-tion tests as of 1 January 2004 and 30 September 2004. According to these tests, there is no need for depreciation requirements. According to Swedish accounting principles, all intangible assets, including goodwill, are written off during the assessed useful life. This change doesn’t affect shareholders’ equity at the time of transition because goodwill amortisation before 1 January 2004 will not be cancelled. As a consequence of the transition to IFRS, goodwill amortisation for 2004 that was reported ac-cording to Swedish accounting principles (SEK 7.1 million) was cancelled.

Another effect of the transition to IFRS 3 is a change in rules regarding distribution of purchase prices for company acquisitions, where it’s required that the purchase price, to a greater extent than what Swedish accounting principles stipulate, is allocated to intangible assets in the acquired company before the residual can be classifi ed as goodwill. The transition rules in IFRS 1 require that allocation of purchase prices according to IFRS 3 be done for all com-

pany acquisitions made after 1 January 2004. Acquisitions before 1 January 2004 need not be recalculated according to IFRS 1. Cybercom did not acquire companies during 2004, so recalculation need not be done.

• IFRS 5: sale of assets. Fixed assets or sold groups that fulfi l criteria for being classifi ed as holdings to be sold must be assessed at the lowest reported value and the actual value minus selling costs. These assets must not be written off during the period when the asset is classifi ed as a holding to be sold until it’s disposed of. According to the transition rules, companies should apply this recommendation begin-ning 1 January 2005. During Q4 2004, Cybercom decided to sell CyberMate PreHospital, which is an intangible asset. There are no effects resulting from the transition to IFRS 5, because the reported value falls below the actual value minus the selling costs.

• IAS 32 and 39: fi nancial instruments. Reporting and valuation were applied starting 1 January 2005. With the support of IFRS 1, the company chose to not recalculate corresponding fi gures for 2004, which relate to fi nancial instruments, according to IAS 39 principles. A reclas-sifi cation and revaluation of the assets and liabilities to be reported according to IAS 39 were implemented on 1 January 2005. So fi nancial instruments are reported in corresponding fi gures for 2004 according to previously applied principles. The difference between reported values, according to IAS 39, and previously applied principles will be reported in the 1 January 2005 balance sheet directly against equity capital according to IFRS 1 transition rules. Effect from the transition to IAS 39 is expected to be SEK –0.6 million, which will be reported directly against shareholders’ equity for 2005. A revaluation of short-term investments in bonds and currency futures will be done.

The transition’s fi nancial effectsThe table illustrates the way in which recalculating the 2004 corresponding fi gures preliminarily affect the Group’s income and balance sheet.

SEK million Equity Profi t/loss

Opening balance, 1 January 2004 149.5

Opening balance à la IFRS 149.5

Income statement

Profi t after tax, 2004 4.3 4.3

Equity, net change, 2004 19.4

IFRS 3 acquisition 7.1

Deferred tax –0.3

Adjusted profi t for the year 6.8 6.8

Closing balance according to IFRS 180.0

Closing balance à la Swedish accounting, 31 Dec. 2004 173.2

All information above is preliminary and may change because the new recommendations are still being implemented.

15

DIRECTORS’ REPORT

RISK AND SENSITIVITY ANALYSES

Business risks

Market changesA few large companies dominate the telecom sector. This trend has meant that customers of consulting companies have gone from working with more than 100 vendors to signing master contracts with 20–30 select vendors. These contracts lead to long-term relationships with highly qualifi ed vendors. Size, specialisation, and an international presence have become increasingly important for consultancies. Cybercom currently has master contracts with about 11 companies that together represent 71% of Cybercom’s sales.

Business-cycle sensitivityThe market and customers are basing their businesses and IT investments on the business cycle. That’s why Cybercom positioned itself so that cycle swings will have minimal effect on business and revenue. Cybercom offers total solutions and works closely with customers.

AcquisitionsPart of Cybercom’s growth strategy involves acquisition of other operations. Cybercom has developed a method for suc-cessfully integrating these operations as quickly and effecti-vely as possible.

CustomersCybercom’s 10 largest customers account for 73% of its sales. Cybercom has long-term relationships with many customers.

CompetitorsA turbulent market means that players, offerings, and pricing models constantly change. It’s becoming increasingly impor-tant for companies to create niches and position themselves in relation to their market players to create their own custo-mer space. Cybercom has clear offerings for its niches.

Recruitment and skillsQualifi ed consultants are a requirement for enabling the com-pany to implement successful projects and to satisfy custo-mers. During recruitment, Cybercom puts stringent demands on experience and expertise. The company continuously strives to ensure that it has the right skills mix.

Financial risks

Credits, interest, and liquid assetsCybercom has no external credits. Liquid assets are placed in risk-free interest-bearing funds.

Credit institutes’ ratingsThe Cybercom Group’s parent company has an AA rating with D&B (previously called Duhn & Bradstreet), a credit institute.

Currency effectSubsidiaries in Denmark, Norway, and the UK generate sales equal to 16% of the Group’s total sales. The subsidiaries’ net assets are exposed to translation risk. For larger exposures in foreign currency, the Group uses derivative instruments to secure the exposure.

TaxPrepaid tax can be used against future tax on profi ts for the operations in Denmark, Norway, and Sweden and can thus lower future tax. The company isn’t involved in a tax dispute.

Personnel expensePersonnel expense is the company’s largest fi nancial item, which is about 64% of total expenses, excluding goodwill.

Table:These items show effects from a 1% change in operating profi t, calculated on the outcome for 2004

+/– 1% MSEK

Price paid by customer 3.1

Amount/degree of invoicing 2.2

No. of consultants 0.5

HR expenses 2.6

These effects are independent of each other and are depen-dent on other factors not changing.

To lower sensitivity to the above factors, Cybercom restruc-tured its operation to accommodate solution-based assign-ments. So its capabilities and effi ciency in delivering solutions affect profi tability more than hourly rates, invoicing rates, and the number of consultants.

OUTLOOK

The outlook for Cybercom’s services in telecom and selected technologies is positive. Cybercom intends to grow organically and through acquisition and to strengthen its international presence.

The company’s fi nancial goal before year-end 2006 is to generate sales worth SEK 750 million, of which 25% come from outside Sweden. It still targets an 8% operating margin.

PROPOSAL FOR TREATMENT OF ACCUMULATED LOSS

The board proposes that the accumulated loss of SEK 103,694,180 be covered by offsetting it against the share premium reserve.

According to the consolidated balance sheet, the Group’s accumulated loss is SEK 99,787,313. Appropriation of restric-ted reserves has not been proposed.

16 Profi t and loss statement, SEK million 2004 2003 2002 2001 2000 1999

Sales 405.3 309.7 344.8 396.2 357.6 191.9Operating expense* –382.0 –401.0 –338.6 –368.9 –320.6 –178.6Scheduled depreciation –8.2 –7.0 –5.8 –6.2 –6.2 –3.8Items affecting comparability – – – – –4.1 –Operating profi t/loss before goodwill 15.1 –98.3 0.4 21.1 26.7 9.5

Goodwill amortisation –7.1 –13.6 –12.9 –8.9 –6.4 –0.7Operating profi t/loss 8.0 –111.9 –12.5 12.2 20.3 8.8

Financial income 4.2 2.6 5.4 4.8 3.3 6.2Financial expenses –2.1 –0.9 –1.1 –5.2 –0.2 –0.5Profi t/loss after fi nancial items 10.1 –110.2 –8.2 11.8 23.4 14.5

Tax –5.8 –0.5 –1.2 –6.9 –8.5 0.0

Profi t/loss for the year 4.3 –110.7 –9.4 4.9 14.9 14.5

Shareholder equity/share, SEK 15.47 14.01 25.02 25.52 23.15 17.43

Balance sheet, SEK million 2004 2003 2002 2001 2000 1999

Assets Intangible fi xed assets 86.7 69.7 121.0 83.3 75.9 9.3Tangible fi xed assets 10.7 10.8 9.9 11.3 11.3 10.3Financial fi xed assets 11.8 14.4 3.7 2.9 5.6 1.8Total other current assets 108.7 107.3 70.7 91.2 89.9 50.0Liquid assets 47.7 74.1 111.5 120.8 111.9 107.3

Total assets 265.6 276.3 316.8 309.5 294.6 178.7

Shareholders’ equity and liabilities Shareholders’ equity 173.2 149.5 231.5 223.5 195.4 137.4Provisions 4.5 14.8 4.3 6.1 20.1 0.9Interest-bearing liabilities 0.4 0.3 11.2 0.0 0.0 0.0Non-interest-bearing liabilities 87.5 111.7 69.8 79.9 79.1 40.4

Total shareholders’ equity and liabilities 265.6 276.3 316.8 309.5 294.6 178.7

Cash fl ow, SEK million 2004 2003 2002 2001 2000 1999

Cash fl ow from current activities 11.1 5.2 7.0 31.4 28.7 7Cash fl ow from investment activities –41.3 –24.4 –17.1 –23.4 –44.1 –13.2Cash fl ow from fi nancing activities 4.0 –16.0 1.4 0.9 20.0 107.6Change in liquid assets –26.2 –35.2 –8.7 8.9 4.6 101.4

Liquid assets at year’s start 74.1 111.5 120.8 111.9 107.3 5.9Translation difference –0.2 –2.2 –0.6 – – –

Liquid assets at year’s end 47.7 74.1 111.5 120.8 111.9 107.3

* Including goodwill write-off.

Group fi nancial performance summary

Acid-test ratioCurrent assets excluding stock divided by current liabilities.

Asset turnover rateNet sales divided by average balance sheet total.

Ave. no. of consultantsAverage number of employed consultants based on monthly fi gures and adjusted for part-time employment.

Ave. no. of employeesAverage number of employees based on monthly fi gures and adjusted for part-time employment.

Average number of sharesCalculated as a weighted average for each year according to the Swedish Society of Financial Analysts’ recommendations.

Capital employedBalance sheet total minus non-interest-bearing liabilities.

Defi nitions

EBITEarnings before interest and taxes.

EBITAEarnings before interest, taxes, and amortisation.

Employee turnoverNumber of employees that terminated employ-ment divided by the average number of em-ployees for the period.

Equity/assets ratioShareholders’ equity as a percentage of the balance sheet total.

Interest coverage ratioProfi t/loss after fi nancial items plus fi nancial expenses divided by fi nancial expenses.

Net debt/equity ratioNet interest-bearing liabilities divided by share-holders’ equity.

Cash fl ow per shareCurrent cash fl ow divided by average number of shares after full dilution.

Capital turnover rateNet sales divided by an average balance sheet total.

Debt/equity ratioInterest-bearing liabilities divided by shareholders’ equity.

Earnings per shareProfi t after fi nancial items minus tax divided by average number of shares.

Earnings per share after full dilutionEarnings per share is calculated as though war-rants had already been exercised. Net profi t/loss is credited on an estimated 4% return on subscrip-tion liquidity minus 28% tax after which the adjusted profi t/loss is divided by the average number of shares after warrants are exercised.

17

GROUP FINANCIAL PERFORMANCE SUMMARY

Key fi gures 2004 2003 2002 2001 2000 1999

Total capital, SEK million 265.6 276.3 314.5 309.5 294.6 178.7Capital employed, SEK million 178.1 164.6 247.0 229.3 215.5 138.3Shareholders’ equity, SEK million 173.2 149.5 231.5 223.5 195.4 137.4

Return on total capital, % 4.5% Neg Neg 5.6% 10.0% 13.6%Return on employed capital, % 7.1% Neg Neg 7.6% 13.4% 19.5%Return on shareholders’ equity, % 2.7% Neg Neg 2.3% 9.0% 19.3%

Operating margin before goodwill and items affecting comparability, % 3.7% Neg 0.1% 5.3% 7.5% 5.0%Operating margin, % 2.0% Neg Neg 3.1% 5.7% 4.6%Net margin, % 2.5% Neg Neg 3.0% 6.6% 7.6%

Acid test ratio 1.8 1.6 2.7 2.6 2.6 3.9Equity/assets ratio, % 65.2% 54.1% 73.6% 72.2% 66.3% 76.9%Debt/equity ratio 0.0 0.0 0.0 0.0 0.0 0.0Net debt/equity ratio Neg Neg Neg Neg Neg NegShare of risk-bearing capital, % 66.9% 55.9% 75.0% 74.2% 73.2% 77.4%Interest coverage ratio 6.3 Neg Neg 3.3 82.9 30.3Working capital in relation to net sales, % 5.2% Neg 0.3% 2.8% 3.0% 5.0%Capital turnover rate, multiple 1.5 1.2 1.1 1.3 1.5 1.7Investments, SEK million 32.2 71.3 54.0 24.5 42.2 19.3

Ave. no. of employees 325 263 289 312 310 185No. of employees at year’s end 375 375 280 300 285 270Ave. no. of consultants 265 215 236 252 263 157Net sales per employee, SEK thousand 1,247 1,177 1,193 1,270 1,153 1,037Net sales per consultant, SEK thousand 1,529 1,440 1,461 1,572 1,360 1,222Value added per employee, SEK thousand 811 3921) 715 742 722 756Salaries and remunerations excluding social security costs, SEK million 189.2 154.1 167.0 162.4 150.7 97.0

Share data 2004 2003 2002 2001 2000 1999

No. of shares at year-end 11,196,355 10,672,4682) 9,251,777 8,757,279 8,439,803 7,882,875No. of shares at year-end, full dilution 11,196,355 10,672,4682) 9,251,777 9,384,553 9,417,032 8,532,875Shareholders’ equity per share, SEK 15.47 14.01 25.02 25.52 23.15 17.43Shareholders’ equity per share after full dilution, SEK 15.47 14.01 25.02 23.82 20.75 16.10Ave. no. of shares 10,716,125 9,470,197 9,169,361 8,696,703 8,212,315 5,991,208Ave. no. of shares after full dilution 10,716,125 9,470,197 9,169,361 8,757,279 9,198,839 6,553,708Profi t/loss per share, SEK 0.41 –11.7 –1.03 0.56 1.82 2.42Profi t/loss per share after full dilution, SEK 0.41 –11.7 –1.03 0.65 1.73 2.21Cash fl ow per share after full dilution, SEK 1.04 0.55 0.76 3.34 3.13 1.07Dividend per share, SEK 0.00 0.00 0.00 0.00 0.00 0.001) Includes one-time goodwill write-down of SEK 96.1 million, see note 15.2) Includes new issue for the Consafe Infotech acquisition.

Dilution effects are only considered in instances when profi t per share or shareholders’ equity per share declines.

Net interest-bearing liabilitiesInterest-bearing liabilities minus interest-bearing assets.

Net marginProfi t/loss after fi nancial items as a percentage of net sales.

Net sales per employee/consultantNet sales for the period divided by the average number of employees or consultants.

Number of employees at period’s endNumber of persons with an employment contract on the last day of the period.

Operating expensesOperating expenses including goodwill amortisa-tion.

Operating marginOperating profi t/loss as a percentage of net sales.

Return on capital employedProfi t/loss after fi nancial items plus fi nancial ex-penses as a percentage of the average capital employed.

Return on shareholders’ equityProfi t/loss after fi nancial items minus tax as a percentage of average shareholders’ equity.

Return on total capitalProfi t/loss after fi nancial items plus fi nancial ex-penses as a percentage of the average balance sheet total.

Share of risk-bearing capitalShareholders’ equity plus deferred tax (including minority) as a percentage of the balance sheet total.

Shareholders’ equityShareholders’ equity includes 72% of the un-taxed reserves.

Shareholders’ equity per shareShareholders’ equity divided by the number of shares at the period’s end.

Total project assignmentsOutsourcing, application management (AM) assignments or projects in which Cybercom has management and staffi ng responsibilities.

Value added per employeeOperating profi t/loss plus labour costs divided by the average number of employees. Labour costs are salary expenses plus a standard 35% for social security costs.

Working capitalCurrent assets minus liquid assets and current liabilities.

18

Profi t and loss statement GROUP PARENT COMPANY

SEK in thousands NOTE 2004 2003 2004 2003

Operating income

Sales 34, 3 405,131 309,059 28,984 26,658

Other operating income 155 596 822 491

Total operating income 405,286 309,655 29,806 27,149

Operating expense

Other external expenses 34, 5, 7 –123,631 –89,218 –18,793 –16,805

Personnel expenses 4, 26, 34 –258,092 –215,163 –16,637 –14,201

Depreciation and write-downs of tangible and intangible assets 15, 16 –15,287 –116,699 –613 –777

Other operating expenses 6 –242 –487 –7 –465

Total operating expense –397,252 –421,567 –36,050 –32,248

Operating profi t/loss 8,034 –111,912 –6,244 –5,099

Profi t/loss from fi nancial investments

Loss from shares in Group company 8 –163 – –1,048 –142,296

Profi t/loss from other securities and receivables 9 – –182 – –

Interest income and similar income items 10 4,261 2 542 3,792 2,764

Interest expenses and similar items 11 –1,938 –682 –1,891 –444

Total profi t/loss from fi nancial items 2,160 1,678 853 –139,976

Profi t/loss after fi nancial items 10,194 –110,234 –5,391 –145,075

Tax on the year’s income 12 –5,845 –540 470 963

PROFIT/LOSS FOR THE YEAR 4,349 –110,774 –4,921 –144,112

Share information GROUP

Amount in SEK 2004 2003

Before dilution

Profi t/loss per share, SEK 0.41 –11.70

Shareholders’ equity/share, SEK 15.47 14.01

No. of shares at period’s end 11,196,355 10,672,468

Ave. no. of shares 10,716,125 9,470,197

After dilution

Profi t/loss per share, SEK 0.41 –11.70

Shareholders’ equity/share, SEK 15.47 14.01

No. of shares at period’s end 11,196,355 10,672,468

Ave. no. of shares 10,716,125 9,470,197

Dilution effects are only considered in instances when profi t per share or shareholders’ equity per share declines.

19

Cash fl ow analysis GROUP PARENT COMPANY

SEK in thousands NOTE 2004 2003 2004 2003

CURRENT OPERATIONS

Operating profi t/loss before fi nancial items 7,871 –111,912 –6,244 –5,099

Adjustments for items not included in cash fl ow 30 5,718 122,959 711 739

13,589 11,047 –5,533 –4,360

Interest received 2,191 4,369 2,632 2,715

Interest paid 240 –284 –134 –444

Income tax paid 6,283 –316 –261 –

Cash fl ow from current operationsbefore changes in working capital 22,303 14,816 –3,296 –2,089

Decrease, accounts receivable –10,680 –17,635 –33,871 –13,737

Increase, other current receivables 5,012 19,746 1,515 3,639

Increase, accounts payable 3,302 4,047 4,692 12,191

Decrease, other current operating liabilities –8,812 –15,796 –28,410 –1,448

Cash fl ow from current operation 11,125 5,178 –59,370 –1,444

INVESTMENT ACTIVITIES

Investments in intangible fi xed assets 31 –6,603 –5,594 – –

Investments in tangible fi xed assets 31 –5,621 –3,491 –517 –304

Acquisition of subsidiaries 33 –31,161 –15,436 –1,727 –31,516

Sale of subsidiaries 23 – – –

Decrease in current fi nancial investments 2,070 148 – –

Cash fl ow from investment activities –41,292 –24,373 –2,244 –31,820

FINANCING OPERATIONS

New share issue 3,992 – – –

Received/paid Group contributions – – 10,970 –5,960

Amortisation of liabilities – –16,054 – –

Cash fl ow from fi nancing operations 3,992 –16,054 10,970 –5,960

Decrease of liquid assets –26,175 –35,249 –50,644 –39,224

Liquid assets at year’s start 74,120 111,537 68,398 107,623

Translation difference –224 –2,168 – –

Liquid assets at year-end 32 47,721 74,120 17,754 68,399

20

Balance sheet GROUP PARENT COMPANY

SEK in thousands NOTE 2004 2003 2004 2003

ASSETS

Fixed Assets

Intangible fi xed assets 15

License rights – – – –

Accumulated expenses for software development 12,386 9,073 – –

Goodwill 74,303 60,617 – –

Total intangible fi xed assets 86,689 69,690 – –

Tangible fi xed assets 16

Equipment 10,744 10,797 970 1,073

Total tangible fi xed assets 10,744 10,797 970 1,073

Financial fi xed assets

Shares in Group company 17, 18 123,579 103,137

Other long-term securities holdings 19 – – – –

Deferred prepaid tax 25 11,760 17,147 469 3,071

Total fi nancial fi xed assets 11,760 17,147 124,048 106,208

TOTAL FIXED ASSETS 109,193 97,634 125,018 107,281

Current assets

Current receivables

Accounts receivable 70,063 59,475 – 1,280

Receivables from Group companies 89,380 54,229

Income tax recoverable 3,968 5,700 314 340

Other receivables 20 29,491 32,758 59 526

Prepaid expenses and accrued income 21 5,162 6,614 650 1,699

Total current receivables 108,684 104,547 90,403 58,074

Short-term investments

Other short-term investments 22 9,960 13,341 9,960 13,341

Total short-term investments 9,960 13,341 9,960 13,341

Cash and bank deposits 37,761 60,779 7,794 55,058

TOTAL CURRENT ASSETS 156,405 178,667 108,157 126,473

TOTAL ASSETS 265,598 276,301 233,175 233,754

21

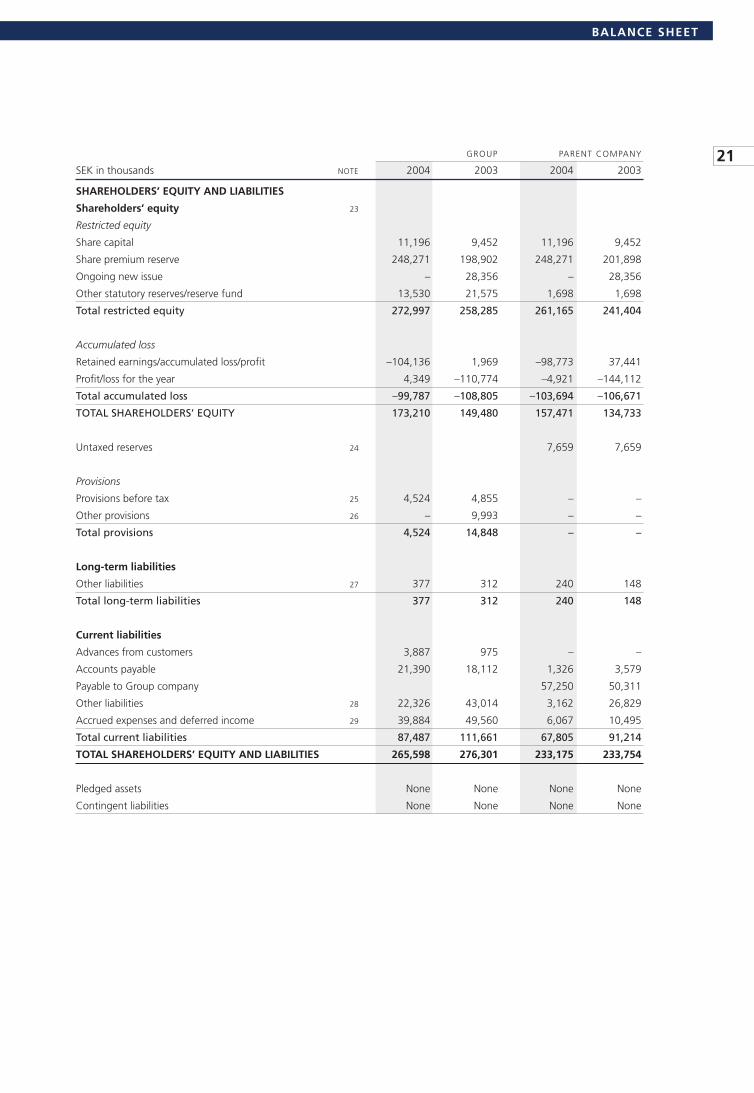

BALANCE SHEET

GROUP PARENT COMPANY

SEK in thousands NOTE 2004 2003 2004 2003

SHAREHOLDERS’ EQUITY AND LIABILITIES

Shareholders’ equity 23

Restricted equity

Share capital 11,196 9,452 11,196 9,452

Share premium reserve 248,271 198,902 248,271 201,898

Ongoing new issue – 28,356 – 28,356

Other statutory reserves/reserve fund 13,530 21,575 1,698 1,698

Total restricted equity 272,997 258,285 261,165 241,404

Accumulated loss

Retained earnings/accumulated loss/profi t –104,136 1,969 –98,773 37,441

Profi t/loss for the year 4,349 –110,774 –4,921 –144,112

Total accumulated loss –99,787 –108,805 –103,694 –106,671

TOTAL SHAREHOLDERS’ EQUITY 173,210 149,480 157,471 134,733

Untaxed reserves 24 7,659 7,659

Provisions

Provisions before tax 25 4,524 4,855 – –

Other provisions 26 – 9,993 – –

Total provisions 4,524 14,848 – –

Long-term liabilities

Other liabilities 27 377 312 240 148

Total long-term liabilities 377 312 240 148

Current liabilities

Advances from customers 3,887 975 – –

Accounts payable 21,390 18,112 1,326 3,579

Payable to Group company 57,250 50,311

Other liabilities 28 22,326 43,014 3,162 26,829

Accrued expenses and deferred income 29 39,884 49,560 6,067 10,495

Total current liabilities 87,487 111,661 67,805 91,214

TOTAL SHAREHOLDERS’ EQUITY AND LIABILITIES 265,598 276,301 233,175 233,754