communication sector performance for the quarter ending

TRANSCRIPT

Communication Sector Performance

for the Quarter ending December 2017

1

By the Economic Regulation Unit

Legal Disclaimer

The information and figures contained herein were obtained from licensees’ submissions

to the Commission and other sources available to the Commission. It is intended to

provide a communications market overview to the industry, prospective entrants,

Government, Academia and other stakeholders. We do not give any kind of warranty and

may not be liable for any loss or damage arising from its use or misuse.

2 By the Economic Regulation Unit

Introduction

This review presents the performance of the Post, Broadcasting and

Telecommunications industry market Report for the period ending

December 2017. It covers the following;

1. Highlights in Telecommunication Market space.

2. Trends in service growth and penetration.

3. Product and pricing movements in the industry.

4. Mobile Financial services.

5. Internet & Data services.

6. The Broadcasting services.

7. Postal services.

8. Consumer affairs.

3 By the Economic Regulation Unit

Highlights in Telecommunications

Telecommunications

The global telecommunications market

place in the year 2017 was associated

with news of early commercial trials in

5G technology across major markets

across Asia and Europe. With the US

expected to see its commercial launch

in late 2018.

The none standalone 5G new radio

(NSA 5G NR) specifications were

officially approved in December 2017

hence completing the standardization

of 5G.

The early adopters like Ericsson and

Nokia purport that the technology shall

among others deliver;

- Higher speeds

- Better in building penetration

- reduced intra cell multi user

interference

Artificial Intelligence

Leading telcos in the world have

embraced the benefits of artificial

Intelligence which is dominated by

big tech players in the US such as

Google, Amazon, Apple, Facebook, Microsoft & IBM as well

as Chinese Baidu, Alibaba &

Tencent. (source: GSMA)

4 By the Economic Regulation Unit

5

Uganda’s Telecommunication Sector at a Glance

Dec -16 Mar – 17 June- 17 Sept 17 Dec 17

PIP 24 23 23 23 23

PSP Voice and Data 36 33 33 33 33

Pay TV

Subscriptions 1,159,345 1,618,913 1,691,634 1,634,067 1,627,594

Fixed Lines

subscription

368,243

369,237

384,503

263,963

262,286

Mobile Subscriptions 22,838,486 23,665,556 23,608,610 24,361,551 24,948,878

Tele-density 63.4 63.8 63.7 65.4 66.9

Population est: 37,673,800 (UBOS)

By the Economic Regulation Unit

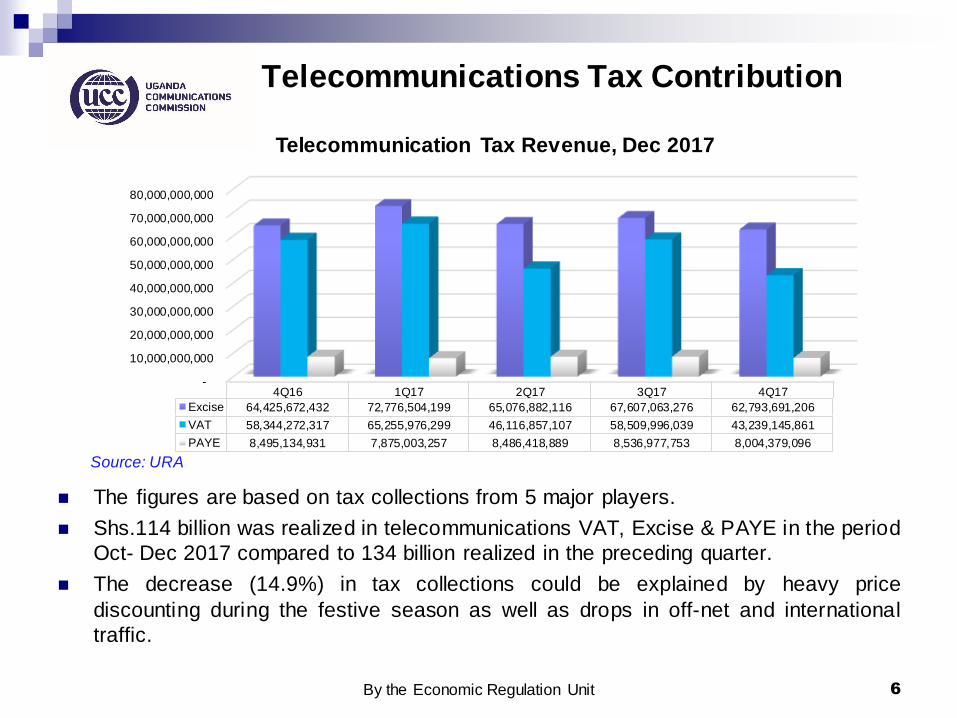

Telecommunications Tax Contribution

The figures are based on tax collections from 5 major players.

Shs.114 billion was realized in telecommunications VAT, Excise & PAYE in the period

Oct- Dec 2017 compared to 134 billion realized in the preceding quarter.

The decrease (14.9%) in tax collections could be explained by heavy price

discounting during the festive season as well as drops in off-net and international

traffic.

6

-

10,000,000,000

20,000,000,000

30,000,000,000

40,000,000,000

50,000,000,000

60,000,000,000

70,000,000,000

80,000,000,000

4Q16 1Q17 2Q17 3Q17 4Q17

Excise 64,425,672,432 72,776,504,199 65,076,882,116 67,607,063,276 62,793,691,206

VAT 58,344,272,317 65,255,976,299 46,116,857,107 58,509,996,039 43,239,145,861

PAYE 8,495,134,931 7,875,003,257 8,486,418,889 8,536,977,753 8,004,379,096

Telecommunication Tax Revenue, Dec 2017

Source: URA

By the Economic Regulation Unit

Fixed Subscriptions

Dec-16 Mar-17 Jun-17 Sep-17 Dec-17

368,243 369,237

384,503

263,963 262,286

-0.64% quarter to quarter

decline in fixed line

subscriptions.

7 By the Economic Regulation Unit

Fixed Line Penetration, Dec 2017

8

10.1 9.8 10.2

7.0 6.9

-

2.0

4.0

6.0

8.0

10.0

12.0

D E C -16 MAR -17 JU N -17 S E P -17 D E C -17

Fixed lines per 1000 Ugandans

Graph above represents the number of fixed lines for every 1000 people in the country.

By the Economic Regulation Unit

Mobile Subscriptions, Dec 2017

587,327 new mobile subscriptions in the

period October –

December 2017.

This largely on account

of seasonality variations

associated with the

festive season.

9

22,838,486

23,665,556 23,608,610

24,361,551

24,948,878

21,500,000

22,000,000

22,500,000

23,000,000

23,500,000

24,000,000

24,500,000

25,000,000

25,500,000

Dec-16 Mar-17 Jun-17 Sep-17 Dec-17

Mobile Subscriptions

2.4%

By the Economic Regulation Unit

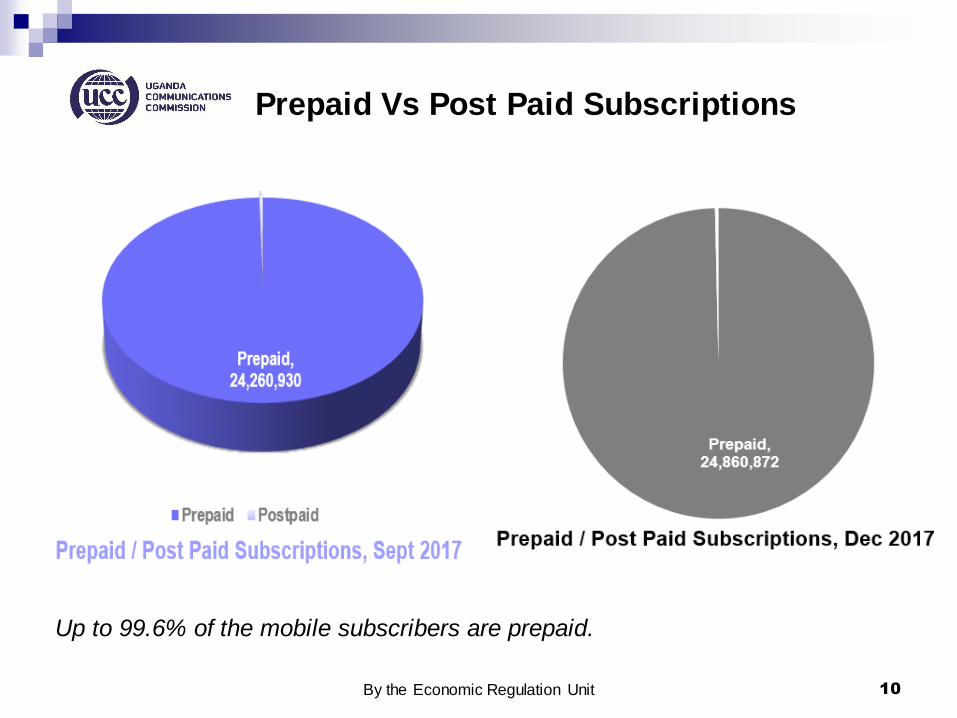

Prepaid Vs Post Paid Subscriptions

10

Up to 99.6% of the mobile subscribers are prepaid.

By the Economic Regulation Unit

Mobile Telephone Access, Dec 2017

11

60.6

62.8 62.7

64.7

66.2

57.0

58.0

59.0

60.0

61.0

62.0

63.0

64.0

65.0

66.0

67.0

D E C -16 MAR -17 JU N -17 S E P -17 D E C -17

Mobile lines per 100 Ugandans

A 1.5% growth in mobile penetration was realized during the quarter.

By the Economic Regulation Unit

Mobile Market Competitiveness, Dec 2017

12

4109.5

4068.0 4064.6

4003.9

3936.3

Dec-16 Mar-17 Jun-17 Sep-17 Dec-17

Mobile Market HHI - Dec 17 (Based on Subscriptions)

HHI

• The downward trend implies increasing mobile market competition.

• This is largely on account of aggressive price and customer acquisition

offerings within the segment

By the Economic Regulation Unit

Aggregate Fixed & Mobile Subscription, Dec 2017

13

The 585,650 growth in mobile subscriptions in the fourth quarter resulted

into a 2.4% increase in tele density.

This growth is credited to the end of year aggressive on net promotions

within the quarter.

Dec-16 Mar-17 Jun-17 Sep-17 Dec-17

fixed & mobile subs 23,206,729 24,034,793 23,993,113 24,625,514 25,211,164

Teledensity 63.4 63.8 63.7 65.4 66.9

63.4 63.8 63.7

65.4

66.9

61.0

62.0

63.0

64.0

65.0

66.0

67.0

68.0

22,000,000

22,500,000

23,000,000

23,500,000

24,000,000

24,500,000

25,000,000

25,500,000

By the Economic Regulation Unit

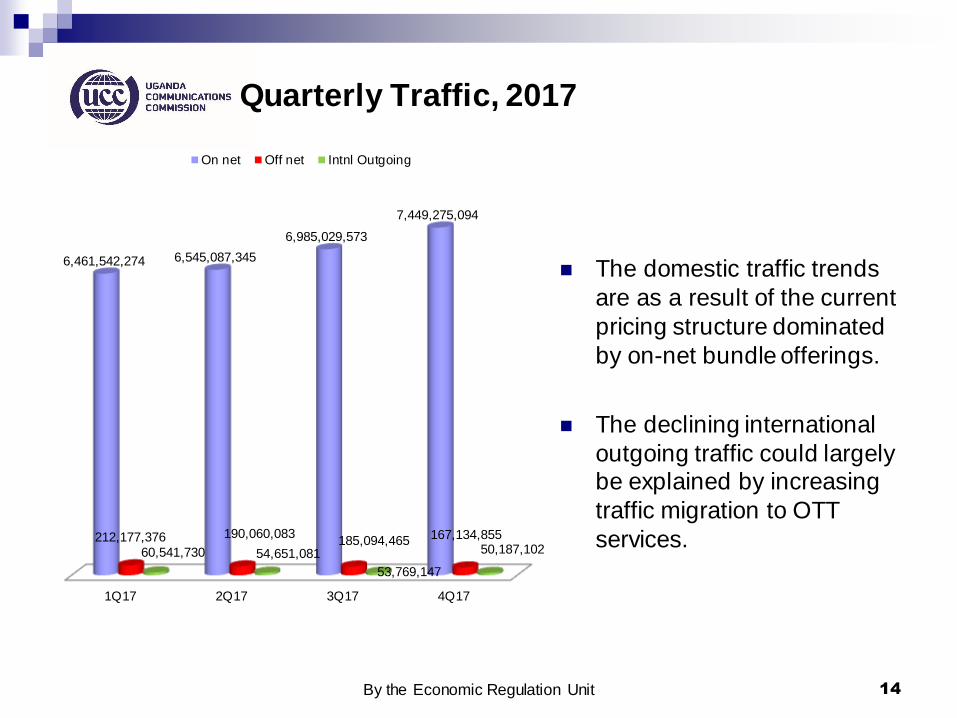

Quarterly Traffic, 2017

1Q17 2Q17 3Q17 4Q17

6,461,542,274 6,545,087,345

6,985,029,573

7,449,275,094

212,177,376 190,060,083 185,094,465 167,134,855

60,541,730 54,651,081

53,769,147

50,187,102

On net Off net Intnl Outgoing

The domestic traffic trends

are as a result of the current

pricing structure dominated

by on-net bundle offerings.

The declining international

outgoing traffic could largely be explained by increasing

traffic migration to OTT

services.

14 By the Economic Regulation Unit

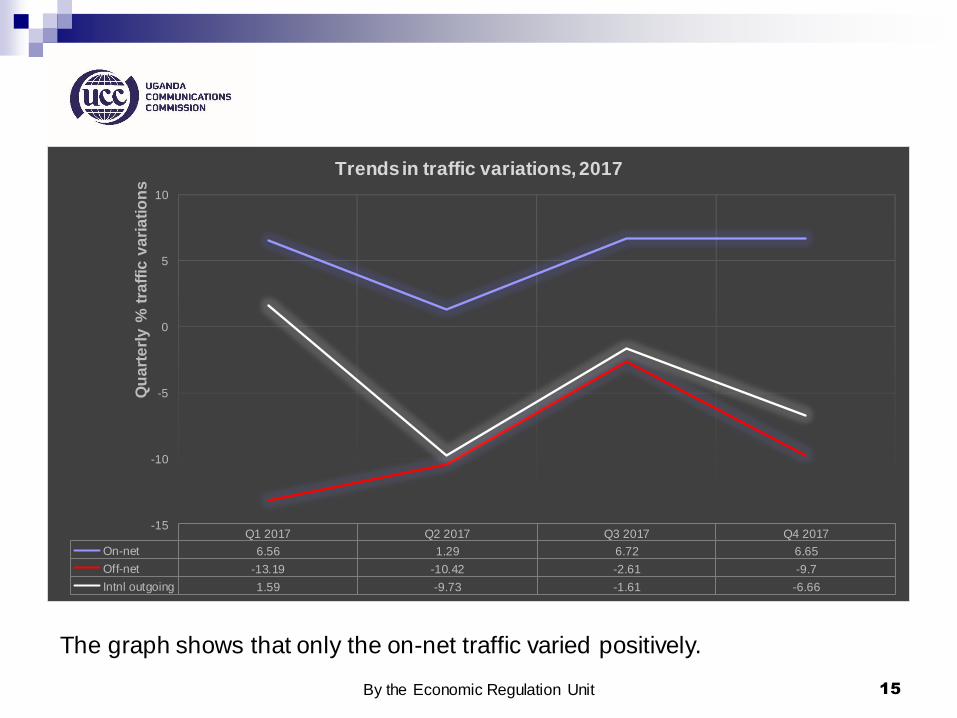

15

Q1 2017 Q2 2017 Q3 2017 Q4 2017

On-net 6.56 1.29 6.72 6.65

Off-net -13.19 -10.42 -2.61 -9.7

Intnl outgoing 1.59 -9.73 -1.61 -6.66

-15

-10

-5

0

5

10

Qu

art

erl

y %

tra

ffic

va

ria

tio

ns

Trends in traffic variations, 2017

The graph shows that only the on-net traffic varied positively.

By the Economic Regulation Unit

Voice Traffic Distribution, 2017

Jan- June 2017 July- Dec 2017

16

On net 96%

3% off net Intnl

Outgoing 1%

Voice Traffic Distribution Jan-June 17

On net 97%

Off net 2%

Intnl Outgoing

1%

Voice Distribution July - Dec 17

By the Economic Regulation Unit

International Incoming Traffic, 2017

International incoming minutes

continued to grow from 117 million

minutes recorded in the preceding

quarter to 122 million minutes for

the quarter ending December 2017.

This therefore represents a 4.6%

growth from the previous quarter.

17

1Q17 2Q17 3Q17 4Q17

98,475,931

113,135,755

117,391,241

122,751,990

Intnl incoming on Mobile

Intnl incoming on Mobile

By the Economic Regulation Unit

Roaming Minutes

The fourth quarter registered a

total of 20.8 million roaming

minutes in foreign networks

compared to 17.3 million minutes

realized in the previous quarter. Roaming by foreign networks

dropped from 13 million to 12.5

million minutes during the quarter.

This translates to a respective

20.6% growth and 4.2% drop in

roaming minutes.

18

1Q17 2Q17 3Q17 4Q17

16,924,997

18,689,670

17,276,576

20,844,138

7,396,734

9,029,534

13,040,778 12,488,448

Roaming Traffic, Dec 17

Roaming Minutes in Foreign networks

Roaming Minutes by Foreign networks

By the Economic Regulation Unit

SMS Traffic Growth

There was a drop of 7.1% in total

SMS traffic in the fourth quarter of

2017.

This drop is accredited to the

growing popularity and added

functionality of Over The Top (OTT) messaging services.

The On net SMS again dominated

the sms market accounting for 98

% of all SMSs sent, while off net accounted for only 1.5% of SMSs.

19

-

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

1Q17 2Q17 3Q17 4Q17

Onnet Sms 1,207,976, 1,012,684, 1,557,364, 1,444,287,

Off net Sms 23,240,984 20,311,965 20,972,939 21,469,994

Int'nal Out 3,909,315 3,601,890 3,695,974 3,691,904

Incoming Intn'l SMS 22,296,239 13,203,520 16,309,013 12,588,164

Quarterly SMS Traffic Growth, Dec 2017

By the Economic Regulation Unit

Tariffs

Post broadcasting & telecommunication plans are available on the two

UCC accredited price comparison websites;

By the Economic Regulation Unit 20

Mobile Money Services

21 By the Economic Regulation Unit

Mobile Money Services

For the first time since the

inauguration of Mobile money service in Uganda in 2009,

the Industry has realized a

1.5% drop in mobile money

subscriptions.

22

1Q17 2Q17 3Q17 4Q17

Number of Mobilemoney subscribers

22,532,144 22,893,648 23,726,352 23,362,532.0

growth in MM subs 4.4 1.6 3.6 (1.5)

4.4

1.6

3.6

(1.5)

(2.0)

(1.0)

-

1.0

2.0

3.0

4.0

5.0

21,800,000

22,000,000

22,200,000

22,400,000

22,600,000

22,800,000

23,000,000

23,200,000

23,400,000

23,600,000

23,800,000

24,000,000

Mobile Money Subscriptions and growth rates, Dec, 2017

By the Economic Regulation Unit

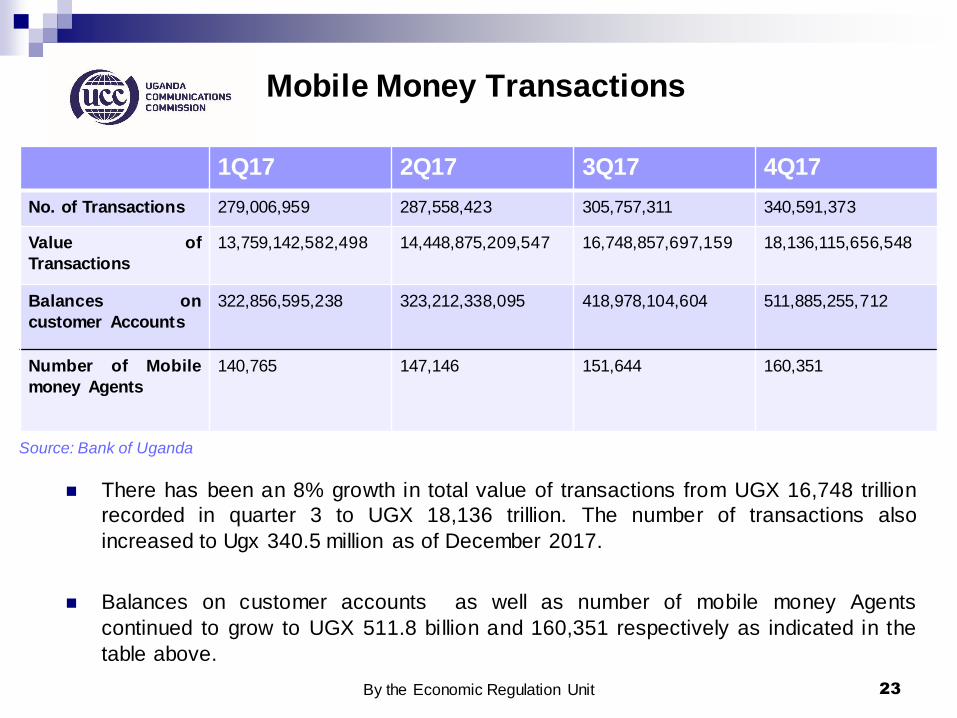

Mobile Money Transactions

1Q17 2Q17 3Q17 4Q17

No. of Transactions 279,006,959 287,558,423 305,757,311 340,591,373

Value of

Transactions

13,759,142,582,498 14,448,875,209,547 16,748,857,697,159 18,136,115,656,548

Balances on

customer Accounts

322,856,595,238 323,212,338,095 418,978,104,604 511,885,255,712

Number of Mobile

money Agents

140,765 147,146 151,644 160,351

There has been an 8% growth in total value of transactions from UGX 16,748 trillion

recorded in quarter 3 to UGX 18,136 trillion. The number of transactions also

increased to Ugx 340.5 million as of December 2017.

Balances on customer accounts as well as number of mobile money Agents

continued to grow to UGX 511.8 billion and 160,351 respectively as indicated in the

table above.

23

Source: Bank of Uganda

By the Economic Regulation Unit

Communications Infrastructure.

The number of Base

Transceiver Stations (BTSs)

increased during the quarter

by 3% from 4,286 to 4,418.

The number of PIPs remained

the same as of the previous

quarter at 23.

By the Economic Regulation Unit 24

International Bandwidth

By the end of December 2017,

Total international bandwidth had

risen to 75,879.7 mbps from

68,360.1 mbps at the end of

September 2017. (see chart on the right)

85% of the available bandwidth is

provided by sea cables at the East

African Coast such as TEAMS,

ESSAY, Seacom

This has encouraged data usage

leading to declining internet

prices.

25

Mar-17 Jun-17 Sep-17 Dec-17

Total Bandwidth(mbps)

55,482.6 61,585.6 68,360.1 75,879.7

Bandwidth per1,000,000inhabitants

1,472.7 1,634.7 1,814.5 2,014.1

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2,000.0

2,200.0

-

10,000.0

20,000.0

30,000.0

40,000.0

50,000.0

60,000.0

70,000.0

80,000.0

Bandwidth Growth, Dec 2017

By the Economic Regulation Unit

Internet Services

26 By the Economic Regulation Unit

Internet Subscriptions & Usage

27

16,484,312

17,102,456

18,148,923

18,825,254

Mar-17 Jun-17 Sep-17 Dec-17

Estimated internet users, Dec 2017

Estimated internet users

8,583,536 9,077,326

9,637,568 10,028,847

153,150 158,000 162,850 167,700

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

As of March2017

As of June2017

As of Sept2017

As of Dec2017

Estimated Internet subscription (Mobile)

Estimated Internet subscription (Fixed)

By the Economic Regulation Unit

Mobile Internet Access

The mobile broadband subscriptions grew to 10 million while fixed internet

subscriptions were 167,700 at the end of December 2017.

The growth in subscriptions resulted in an estimated 18.8 million internet

users translating into a penetration of 49 persons per 100.

Internet growth in subscriptions is largely due to price reduction in internet

bundles as well as increasing availability of data enabled handsets.

28 By the Economic Regulation Unit

Mobile Internet Access

29

30,000

34,500

15,000

35,000

32,000

28,000

- 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000

1GB MTN bundle

Africell 1GB

Airtel 1.25GB bundle

1GB (Vodafone)

smile Lite bundle(1GB)

1GB UTL (GPRS/Edge)

Monthly Mobile Internet capacity based pricing, Dec 2017

By the Economic Regulation Unit

BROADCASTING

30 By the Economic Regulation Unit

PAY TV Landscape

31

Eight Pay Televisions players in the market, of which four broadcast using Satellite, 2

Digital Terrestrial, one uses cable and one uses SMS for broadcasting. The only Country

Wide broadcasting is through satellite mode.

By the Economic Regulation Unit

Station Name Mode of Broadcasting Television Coverage

DSTV Satellite Country wide

ZUKU TV Satellite Country wide

AZAM TV Satellite Country wide

STARTIMES Terrestrial Kampala, Masaka, Entebbe,

Jinja,Mbale, Mbarara, Luweero,

Mukono, Fortportal, Gulu, Ssese

Island

GO TV Terrestrial Kampala, Jinja, Iganga, Mbale,Lira,

Gulu,Arua, Kasese, Mbarara,

Masaka,Wakiso

Kampala SITI Cable Cable Kampala & Jinja

KSSU TV SMS Country wide

NUMBER OF CHANNELS RUN BY EACH PAY TV, 4Q17

32 By the Economic Regulation Unit

PAY TV Subscriptions, Dec 2017

Q1 Q2 Q3 Q4

1,559,913

1,614,404

1,544,615

1,627,594

By the Economic Regulation Unit 33

POST & COURIER SERVICES

34 By the Economic Regulation Unit

Postal & Courier Access

35

Indicator 1Q17 2Q17 3Q17 4Q17

Number of

Permanent

Post Offices

334 334 334 334

Number of

Permanent

Post Offices

connected to

the internet

33 33 49 33

Post Offices

offering public

internet

services

25 25 32 25

Private letter

boxes

82,900 82,900 82,900 82,900

Courier Access

points

846 851 858 867

By the Economic Regulation Unit

Postal distribution in Uganda

36 By the Economic Regulation Unit

Quarterly Postal Mail Volumes

37

1Q17 2Q17 3Q17 4Q17

52,144

39,210

44,460

67,246

1,126 2,605 2,589 6,826

34,076

59,602

32,584

47,045

Domestic Postal Mail Volumes, Dec 17

Domestic Ordinary letter post Domestic Registered Letter Post Domestic EMS

By the Economic Regulation Unit

Quarterly Domestic Courier Volumes

38

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

1Q17 2Q17 3Q17 4Q17

442,177

513,589 530,612

742,857

54,133 63,422 64,960

84,447

Domestic Courier Volumes,Dec 17

Courier items collected & posted within Kla Courier items collected & posted outside Kla

By the Economic Regulation Unit

Select International Postal Traffic, Dec 2017

39

1Q17 2Q17 3Q17 4Q17

6,835 5,312 6,096 6,781

740 1,191

701 1,489

44,519

31,252

41,416

65,464

23,025 22,238

60,178

111,014

Select International Postal Traffic, Dec 2017

East African Letter post East African Letter post European Letter post European Letter post

By the Economic Regulation Unit

Consumer Affairs

Consumers of communication

services when dissatisfied with a

service are required to first lodge

complaints with their respective

service providers. Where a consumer remains dissatisfied, they can then

lodge complaints with UCC, at which

point it becomes a second level

complaint. The data used in this

report represent second level complaints to UCC. However, the

figures may include some first level

complaints from consumers who

claim inability to access their service

providers.

By the Economic Regulation Unit 40

Consumer Empowerment, Dec,2017

41 By the Economic Regulation Unit

Consumer Empowerment, Cont’

Operators are expected to resolve 90% of all complaints received within a

24-hour period.

The data analyzed included tickets for inquiries, queries and complaints.

The ticket items include feedback provided to customers within a call

session of a customer calling the call center. The feedback includes

guidance, advise, information and actual complaint resolution given to a

complainant. It is noted that in several instances a resolution to a complaint may be reached after several customer calls.

42 By the Economic Regulation Unit