commercial laws and statutes relating to islamic banking and finance in malaysia by dr. asmadi...

TRANSCRIPT

Commercial laws and statutes relating to Islamic banking and finance in Malaysia

ByDr. Asmadi Mohamed Naim

Objectives

The history and the development of Islamic banking and finance in the globe.

Islamic view on codification of additional law related to administration purposes in Islamic financial system.

Discussion on Islamic Bank Act 1983. Discussion on BAFIA 1989 Discussion on Takaful Act. Issues on laws, which are governing Islamic instruments

in capital market.

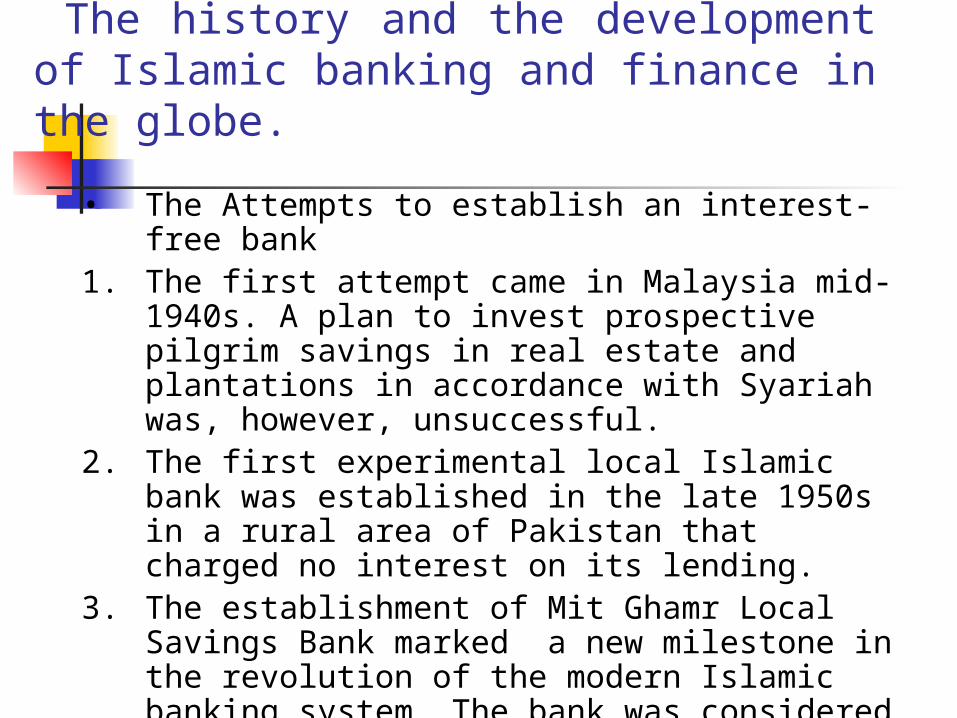

The history and the development of Islamic banking and finance in the globe.

• The Attempts to establish an interest-free bank1. The first attempt came in Malaysia mid-1940s. A plan to

invest prospective pilgrim savings in real estate and plantations in accordance with Syariah was, however, unsuccessful.

2. The first experimental local Islamic bank was established in the late 1950s in a rural area of Pakistan that charged no interest on its lending.

3. The establishment of Mit Ghamr Local Savings Bank marked a new milestone in the revolution of the modern Islamic banking system. The bank was considered to be the most innovative and successful experiment with interest-free banking.

List of Islamic Banks

Name Country Date of Establishment

Nasser Social Bank Egypt 1972

Islamic Development Bank

Saudi Arabia 1975

Dubai Islamic Bank UAE 1975

Faisal Islamic Bank of Egypt

Egypt 1977

Faisal Islamic Bank of Sudan

Sudan 1977

Islamic Banking System International Holding

Luxembourg 1978

Jordan Islam Bank Jordan 1978

Bahrain Islamic Bank Bahrain 1979

Dar al-Mal al-Islami Switzerland 1981

Bahrain Islamic Inv. Company

Bahrain 1981

Cont…Islamic International Bank for Inv. & Development

Egypt 1981

Islamic Investment House

Jordan 1981

Al-Baraka Investment & Development Company

Saudi Arabia 1982

Saudi-Philippine Islamic Development Bank.

Saudi Arabia 1982

Faisal Islamic Bank Kibris Turkey 1982

BIMB Malaysia 1983

Islami Bank Bangladesh Ltd

Bangladesh 1983

Islamic Bank International

Denmark 1983

Tadoman Islamic Bank Sudan 1983

Qatar Islamic Bank Qatar 1983

Development of Islamic Banking system in Malaysia

Year Remark

1980 Formal request to set-up Islamic Bank was made during the Bumiputera Economic Congress

July 30, 1981

The Government appointed National Steering Committee on Islamic Banking. The secretarial functions were given to the Pilgrimage Board of Malaysia. This committee studied both operations of the Faisal Islamic Bank of Egypt and The Faisal Islamic Bank of Sudan.

July 5, 1982

Among the recommendations made by the committee in its report:

i. The Government should establish an Islamic bank whose operations are in accordance to the principles of Syariah.

ii. The proposed bank is to be incorporated as a company under the auspices of the Companies Act, 1965.

iii. A new Islamic banking act must be introduced to license and supervise the Islamic bank.

iv. The Islamic bank is to establish its own Shariah Supervisory Board whose function is to ensure that the operations of Islamic bank are in accordance to the Shariah.

Cont…Mac 1, 1983

BIMB was incorporated and commenced operations on July 1, 1983.

March 10, 1983

The Islamic Banking Act was gazette.

April 7, 1983

The Islamic Banking Act came into effect.

July 1, 1983

BIMB commenced operations.

1983 The Government introduced The Government Investment Act in 1983 to enable the government to issue Government Investment Certificates, which are government bonds issued in accordance to Islamic principles.

March 4, 1993

Central Bank has introduced a scheme known as ‘Skim Perbankan Tanpa Faedah’ or ‘Interest-free Banking Scheme’ (Often known as ‘Islamic windows). Under this scheme, all commercial banks, merchant banks and finance companies are given an opportunity to introduce Islamic banking products and services. The pilot phase of the scheme involved the three largest commercial banks in Malaysia.

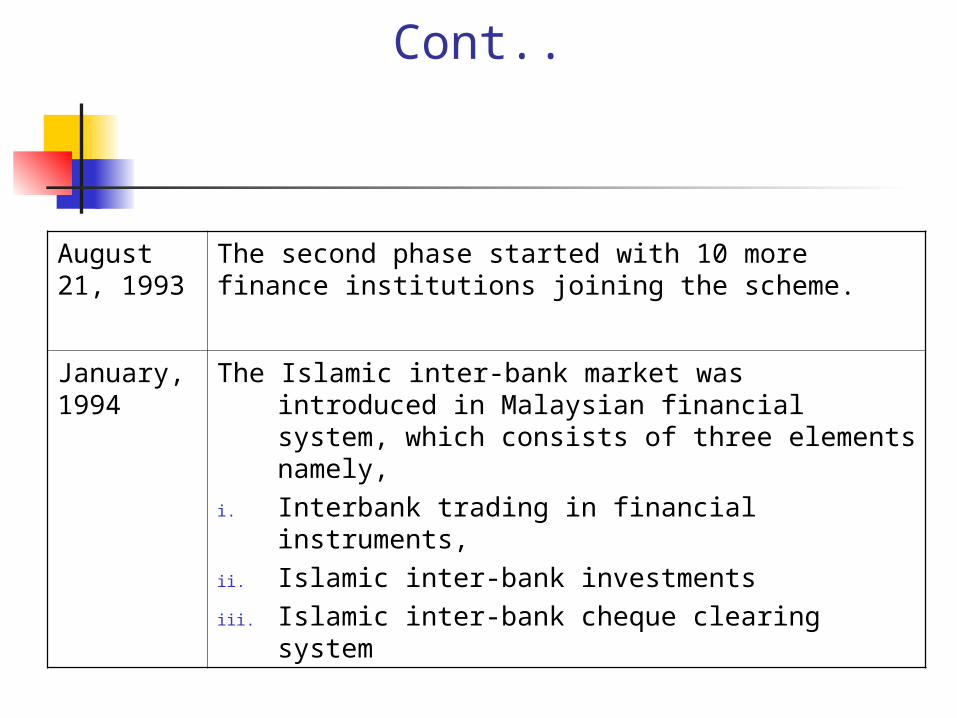

Cont..

August 21, 1993

The second phase started with 10 more finance institutions joining the scheme.

January, 1994

The Islamic inter-bank market was introduced in Malaysian financial system, which consists of three elements namely,

i. Interbank trading in financial instruments,ii. Islamic inter-bank investmentsiii. Islamic inter-bank cheque clearing system

Islamic view on codification of additional law related to administration purposes in Islamic financial system.

Shari’ah consists two main characteristics in its law:1. Thabat /Constancy2. Mutaghayyirat/ changeable

There are many issues which are unchangeable in Islamic law such as:

i. Faithii. Issues regarding to worshipiii. Hududiv. Islamic financial contract principles.v. Other regulations.

Mutaghayyirat/ Changeable

The penalties under the rule of Ta’zir. Issues which relate to the customs and cultures of

the society. Legal maxim: The changing of rules are not to be

denial because of the changing of eras and places..

Legal maxim: Custom is arbitrator/ arbiter. Thus, codification of additional law related to

administration purposes in Islamic financial system is welcome by Shari’ah as long as the regulation are not contradicted with the teaching of Islam.

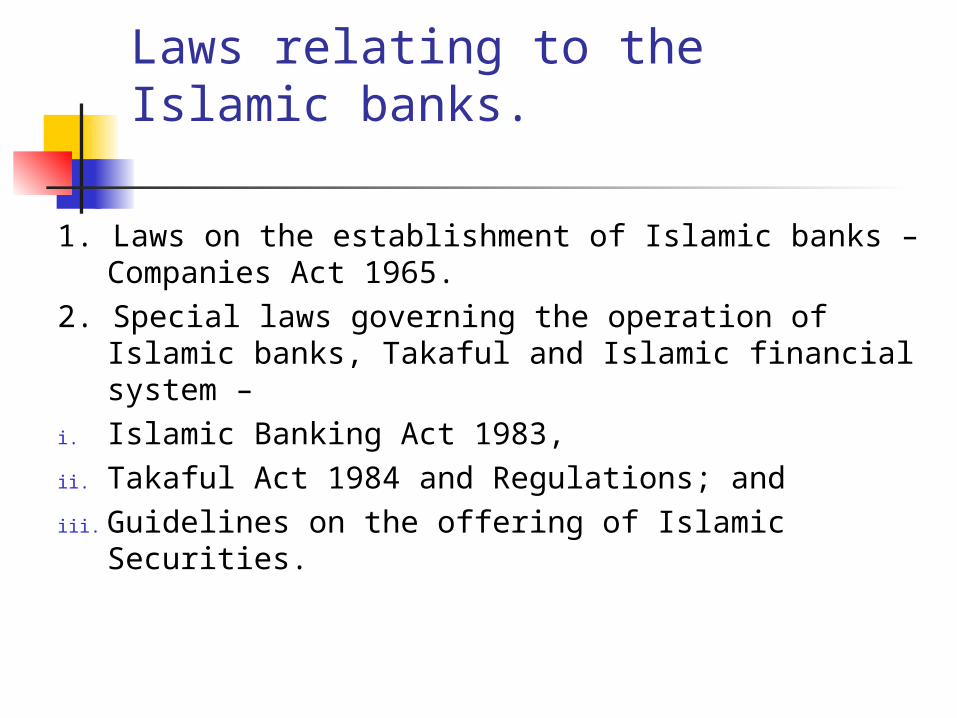

Laws relating to the Islamic banks.

1. Laws on the establishment of Islamic banks – Companies Act 1965.

2. Special laws governing the operation of Islamic banks, Takaful and Islamic financial system –

i. Islamic Banking Act 1983, ii. Takaful Act 1984 and Regulations; andiii. Guidelines on the offering of Islamic Securities.

Discussion on Islamic Bank Act 1983

Islamic Banking Act 1983 (IBA 1983) was gazetted on 10th. March 1983.

It is the Act to provide for licensing and regulation of Islamic banking business.

This act consists 60 sections, divided to eight parts as follows:

1. Preliminary.2. Licensing of Islamic Banks.3. Financial requirements and duties of

Islamic banks4. Ownership, control and management of

Islamic banks.

Cont’

5. Restriction on business.6. Powers of supervision and control

over Islamic banks.7. Miscellaneous8. Consequential Amendment This act consists 60 sections.

1. Preliminary This part discusses about title,

commencement, application, and interpretation.

Under Section 2: Interpretation. This section consists the interpretation of :

- Branch - Central bank- Company - Corporation- Depositor - Islamic bank- Islamic banking business- Investment account

liabilities- Licence - Other deposit liabilities- Public company - Saving account liabilities- Share - Sight liabilities- Subsiadiary - Time liabilities

Definition

Section 2 of Central Bank of Malaysia Act 1958 defines ‘bank’, in relation to Malaysia, as a licensed bank as defined in the BAFIA 1989 or an Islamic bank.

Under BAFIA 1989: a bank is defined as “ any person who carries on banking business” that is, “the business of receiving money on current or deposit account, paying and collecting cheques drawn or paid in by customers, and making advances to customers and includes such other business as the Central Bank, with the approval of the Finance Minister”.

See Section 124: Islamic banking and finance business.

Definition Under IBA 1983:‘Islamic bank’ means any companies which

carries on Islamic banking business and holds a valid licence; and all the offices and branches in Malaysia of such bank shall be deemed to be one bank.

‘Islamic banking business’ means banking business whose aims and operations do not involve any element which is not approved by the Religion of Islam.

2. Licensing of Islamic banking

Islamic banking business to be transacted only by licensed Islamic bank. (Sect. 3)

Minister may vary or revoke condition of licence. (Sect. 4) Licence not to be granted in certain cases. (Sect. 5) Opening of new branch (Sect. 7) Islamic bank may establish correspondent banking relation with

bank outside Malaysia. (Sect. 8) Licence fee (Sect.9) Restriction of use of certain words in an Islamic bank’s name.

(Sect.10) Revocation of licence. (Sect. 11) Effect of revocation of licence. (Sect. 12) Publication of list of Islamic banks. Sect. 13) Advice of Syariah Advisory Council. (Sect.14)

3. Financial requirement & duties of Islamic bank Maintenance of capital funds. Maintenance of reserve funds. Percentage of liquid assets. Auditor and auditor’s report. Audited balance sheet. Statistics to be published. Information on foreign branches.

4. Ownership, control and management of Islamic banks.

Information on change in control of Islamic banks.

Sanction for reconstruction, etc, of bank required.

Disqualification of directors and employees of banks.

5. Restrictions on Business24. Restriction on payment of dividends and

grant of advance and loans.25. Prohibition of loan, etc., of bank required.26. Restriction on grant of loan, advance or

credit facility under section 25 (4).27. Restriction of credit to single customer.27A. Control of credit limits.28. Disclosure of interests by directors.29. Limitation on credit facility for purpose of

financing the purchase or holding of shares.

30. Proof of compliance with sections 24, 25, 26, 27 and 29.

Powers of supervision and control over Islamic Banks. Investigation of bank Special investigation of bank. Production of books and documents. Banking secrecy. Action to be taken if advances are against

interests of depositors. Banks unable to meet obligations to inform

Central Bank. Action by Central Bank if bank unable to meet

obligations or conducting business to the detriment of depositors.

Effect of removal of office of director or appointment of a director of a bank by Central Bank.

Cont’… Control of Islamic bank by Central

Bank. Islamic bank under control of Central

Bank to co-operate with Central Bank. Extension of jurisdiction to

subsidiaries of banks. Moratorium. Amendment of bank’s constitution.

7. Miscellaneous

8. Consequential amendments