week 1: overview of financial institutions and financial markets by: asmadi mohamed naim, phd

TRANSCRIPT

Week 1: Overview of Financial Institutions and

Financial Markets

By:

Asmadi Mohamed Naim, PhD

Overview of Financial Institutions and Financial Markets

he objectives of this chapter are to :

• Discuss the functions and types of financial markets

• Enumerate the concept of surplus spending units and deficit spending units

• Enable the students to discuss about the role played by financial intermediaries.

• Explore the background of the Malaysian Financial Institutions.

Introduction….what is market?

• With the development of markets, the exchange of goods and services was made easier.

• The introduction of money into the exchange process further enhanced the efficiency with which transactions could take place.

• The use of money value also made market-based transactions easier for individuals to save and to accumulate wealth.

• Accumulated savings were available for use by others to finance their investment projects/ and or consumption spending.

Introduction…..cont.

• So, the role of market is to facilitate the exchange of things of value.

• The ‘things’ that are exchanged can be goods, services, financial assets or real ‘physical’ assets.

• Though exchanges can take place without the existence of formal marketplaces, non-market exchanges can be very time consuming and difficult to carry out.

• Just as the exchange of goods and services can be carried out more efficiently through organised markets, so too can the exchange of money between surplus entities (savers) and deficit entities (borrowers).

• Financial markets have developed to facilitate the exchange of money between providers of funds and users of funds.

Introduction……..what is instrument?

• When a financial transaction takes place, that is, financial instruments or contracts, it is claims on future cash-flows that are being bought and sold.

• Eg: When shares (ownership) in a company are bought, what is being acquired is a claim on the company’s future profits.

• Eg.: When an individual or institution buys government bonds (debt), it acquires a claim on the future revenue of the government in the form of interest payments and principal repayment.

• The role of financial markets is to bring together the lenders (savers that buy financial instruments) and the users of funds (borrowers that issues financial instruments.

Suppliers of fund: surplus (savings) units

Demanders of fund:

Deficit unit

are are

Lenders:

Household

Companies,

Governments

Rest of the world

Borrowers:

Household

Companies,

Governments

Rest of the world

Who give RM

and

receive in return financial assets or instrument

Financial markets Who

who

received RM

and

issue financial instrument

Financial markets and flow of funds relations

Functions of the financial systemIntroduction..• It is useful to think of every asset that is purchased, whether

it be a real asset or a financial asset, as being a package of four attributes:

i. return or yieldii. Riskiii. Liquidityiv. Time-pattern of the return• Eg. With a real asset, for example a car, return can be

thought of as the performance and the quality of the ride given; risk relates to variation in the performance and quality of the ride (including the possibility of complete breakdown); the liquidity of the car is the ease with which it can be sold at near to the publish market price of a car of its age and state of repair; and time-pattern of the return can be controlled by switching the car on or off.

Continue……• In the case of financial asset, say a share (ownership) in

a corporation, return consists of the dividends received, and the capital

gains made through movement in the price of the share; risk is measured by variability of the return ( and, in the

extreme, the possibility of the company failing and going into bankruptcy);

the liquidity of the share relates to the ease of selling the share on the share market at the recently publicised price of shares in that company;

and the time pattern of the return (or cash-flow) expected from the share depends upon profitability, and dividend policy, of the company.

The major function of financial market is

• To facilitate the process of portfolio structuring and restructuring through the creation and exchange of suitable types of financial instruments. The financial system (financial institutions, instruments and markets) provides the potential suppliers of funds with the combinations of risk, return, liquidity and cash-flow patterns that best suit each saver’s particular needs.

A well-functioning financial system serves the following important functions within the economy.

• It encourages and allocates savings to competing users by providing financial instruments (asset) that posses a range of mixes of the attributes of risk, return, liquidity and time-pattern of return (cash flows).

Financial Instruments

• There are numerous types of instruments traded on financial markets.

• The distinction between these instruments is based on the mix of risk, return, liquidity and the time-pattern of return or cash flows.

• Its is usual to divide instruments into three broad categories:

1. Equity2. Debt3. Derivatives

1. Equity

• More commonly known as shares.• Equity represents ownership interest in a business.• An equity holders claims are to profits of the

business and, in the event of the failure of the business, to the residual value of the assets after the claims of all other entitled parties are met.

• The principal form of equity is ordinary shares.• Preference shares are another category of equity that

is referred to a equity hybrid. • Quasi-equity instruments are becoming increasingly

important and include convertible notes. These instrument are discuss in detail later.

• Ordinary shares differ from debt in that they are ownership claims rather than contractual claims, and thus have the lowest priority in claims on the firm’s income and assets.

• Ordinary shares, being claims on the real assets of firm, have no maturity date.

• The owners of ordinary shares have a voting right in the election of members of the board of the directors of the company.

• Preference shareholders have no voting rights, but are typically entitled to receive specified fixed return out of the firms net earnings before any payment is made to ordinary shareholders.

• Convertible notes are included in the category of equity because, even though they do not constitute an ‘ownership interest’, they give the holder of the instrument the right to acquire shares in the issuing company during a specified future period.

2. Debt• Debt instruments represent a contractual claim on an issuer

(borrower) to make specific payments, such as periodic interest payments and principal repayments, over a defined period.

• The main non-government debt instruments are:i. Debenturesii. Unsecured notesiii. Intercompany loansiv. Commercial billsv. Promissory notesvi. Term loansvii. Overdraftsix. Mortgage loansx. Leases

Categories of debt.

• Debt can be divided into two subcategories on the basis of the nature of the loan contract: secured and unsecured debt.

• Another subdivision of debt is sometimes constructed on the basis of the negotiability (or transferability of ownership) of the debt instrument.

Derivatives• Derivatives are based on, or derived from two types

of physical markets instruments (equity and debt) identified above.

• They include:

i. Futures

ii. Forwards

iii. Options

iv. Swaps

• Essentially a derivative instrument is synthetically designed to provide specific future rights in relation to the underlying debt or equity instruments.

The concept of surplus spending units and deficit spending units

Deficit units- individuals or enterprises which require to borrow (borrowers).

Surplus units- persons or enterprises with funds to lend (lenders).

Relations between surplus units and deficit units

• Primary debt is direct loan from surplus units to deficit units.

• Primary market is in which the flow of funds between borrowers and lenders is direct.

• Secondary debt is indirect loan from surplus unit to deficit units.

• Secondary market is in which the flow is conducted through a financial intermediaries.

Direct flow markets

• The main advantages of direct financing are that:1. it removes the cost of a financial intermediaries.2. it allows a borrower to access different funding

markets and therefore enables diversification of funding sources. This reduces the risk of exposure to a single funding source of market.

3. it enables greater flexibility in the types of funding instruments used for different financing needs.

Some disadvantages that may be associated with direct financing:

• a problem of matching the preferences of borrowers and lenders.

• the liquidity and marketability of the debt instrument (is there an active secondary market on which security may be sold?).

• search and transaction costs associated with direct issues.

• Assessment of the level of risk in a direct issues.

Intermediated flow markets

• Very often the preferences of savers and borrowers differ.

• A lender may be prepared to received a lower rate of return in exchange of maintaining funds at call.

• On the other hand, a borrower may be prepared to pay of higher rate of return, but may want to have the funds available for a numbers of years.

• If only direct financial relationships were possible, it is most likely that both the savers and borrower would be frustrated in meeting their goals.

The benefits of financial intermediation

• receive the saver’s funds as a deposit;

• issue a claim against itself, such as interest-bearing investment account

• use the saver’s funds to extend a loan to a borrower (deficit unit)

• receive, in return, a primary claim against the borrower.

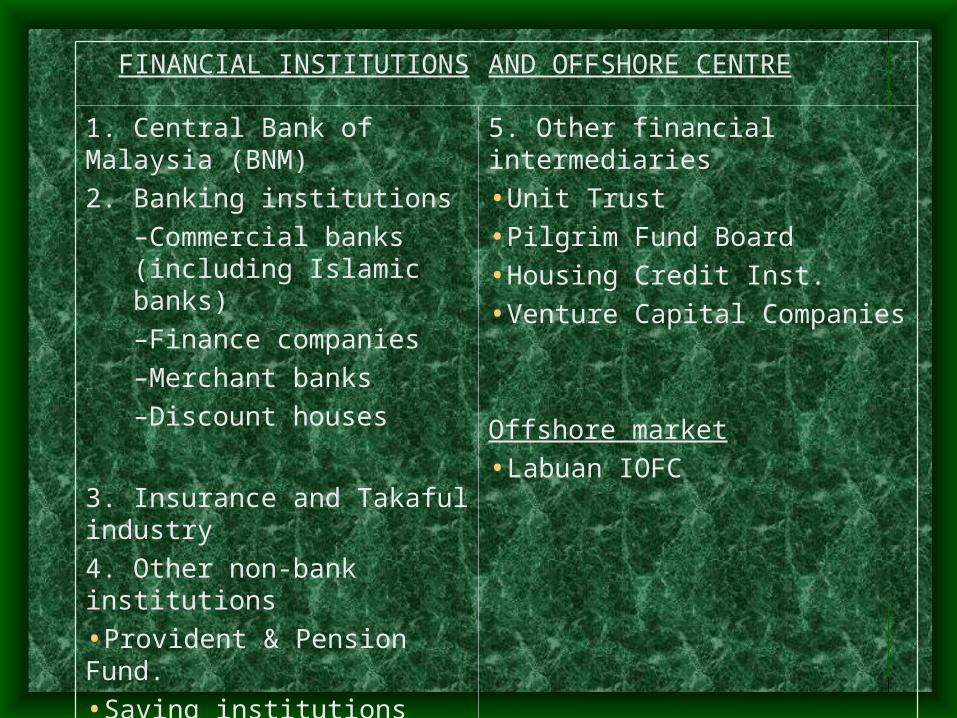

Overview of the Malaysian Financial Institutions

FINANCIAL INSTITUTIONS AND OFFSHORE CENTRE

1. Central Bank of Malaysia (BNM)

2. Banking institutions

–Commercial banks (including Islamic banks)

–Finance companies

–Merchant banks

–Discount houses

3. Insurance and Takaful industry

4. Other non-bank institutions

•Provident & Pension Fund.

•Saving institutions

•Co-operatives

5. Other financial intermediaries

•Unit Trust

•Pilgrim Fund Board

•Housing Credit Inst.

•Venture Capital Companies

Offshore market

•Labuan IOFC

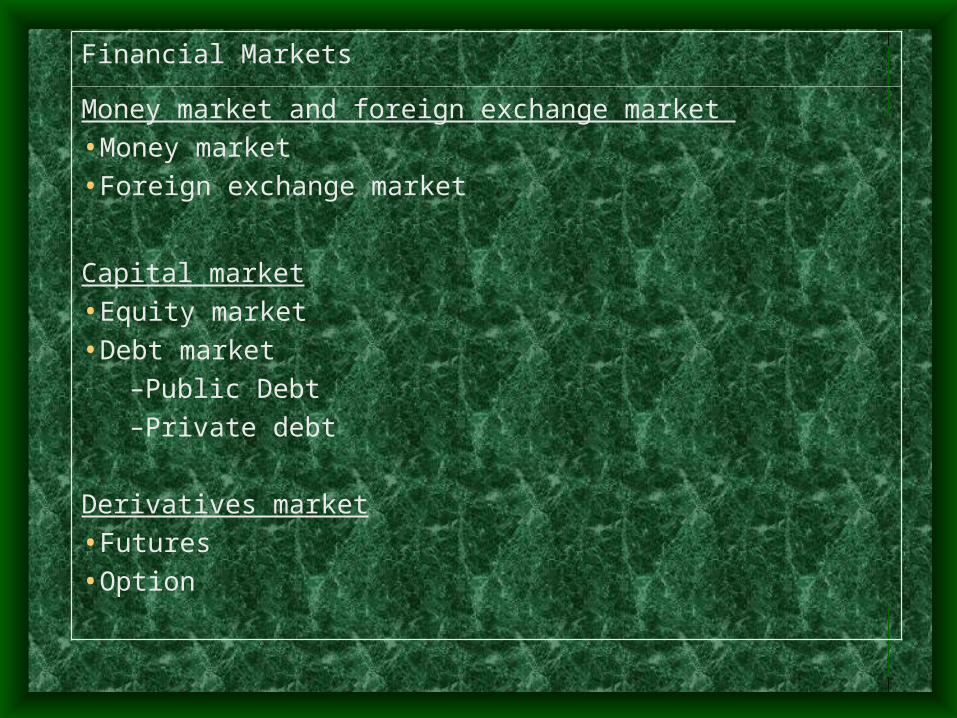

Financial Markets

Money market and foreign exchange market

•Money market

•Foreign exchange market

Capital market

•Equity market

•Debt market

–Public Debt

–Private debt

Derivatives market

•Futures

•Option

• There are two types of institutions in the Malaysian banking system:1. Banking institutions

(BNM, commercial bank, merchant banks, finance companies, discount houses)2. Non-Bank Financial Intermediaries

(Development finance institutions, saving institutions, co-operative societies, provident and pension funds, insurance and takaful companies, etc).

Definition of bank

• Under BAFIA 1989, the business of banking is defined as the business of

i. Receiving deposits

ii. Paying and collecting cheques

iii. Provision of finance; and

iv. Such other business as BNM with the approval of the Minister may prescribe

Commercial banks

• Commercial banks were brought under BNM supervision through Banking Act, 1973, but this was subsequently replaced by the BAFIA in 1989.

• Under this Act, a bank is defined as “ any person who carries on banking business” that is, “the business of receiving money on current or deposit account, paying and collecting cheques drawn or paid in by customers, and making advances to customers and includes such other business as the Central Bank, with the approval of the Finance Minister.

Finance companies

• Finance companies were initially brought within the ambit of BNM’s supervisory control through the enactment of Borrowing Companies Act 1969 (later renamed the Finance Companies Act 1969).

• This was replaced in 1989 with enactment of the comprehensive Banking and Financial Institutions Act 1989 (BAFIA 1989).

• Finance company business is defined as:i. the business of receiving deposits on deposits account, saving account or other similar account;ii. the lending of money;iii. Leasing business or the business of hire-purchase; andiv. Any such business as BNM with the approval of the Minester may prescribe

Merchant banks

• Merchant banks emerged in the Malaysian banking scene in the 1970s.

• Unlike the commercial banks, which depend on their large deposit base to fund their loan and investment portfolios, the merchant banks have been envisaged to function primarily as specialist financial intermediaries in money and capital markets, with particular expertise in the provision of basically fee-based services.

• They play a role in the short-term money market and capital arising activities including financing, specialising in syndication; corporate finance and management advisory services, arranging for the issue and listing of shares, as well as investment portfolio management.

Discount Houses• Discount houses began operations in Malaysia since

1963. As at end-June 1999, there are seven discount houses.

• Generally, these discount houses specialise in short-term money market operations and mobilise deposits from financial institutions and corporations in the form of money at call, overnight money, and short-term deposits.

• The funds mobilised are invested in the Malaysian Treasury bills (TB), Malaysian Government Securities (MGS), bankers acceptances (BA), negotiable instruments of deposits (NID) and Cagamas bonds.

• The discount houses also actively trade these securities in the secondary market.

Money and Foreign Exchange Market.

• The money and foreign exchange markets are intermediaries for short-term funds.

• They are integral to the functioning of the banking system,

i. firstly, in providing financial institutions with the facility for funding and adjusting portfolios over the short term.

ii. And secondly, serving as a channel for a transmission of monetary policy.

• The main difference between the two is that in the money market financial assets traded are denominated in domestic currency, whereas in the foreign exchange market trading is conducted in foreign currencies.

• In the money market, those with surplus funds would want to lend and earn some return rather than holding them either in non-interest earning demand deposits or currency notes and coins.

• At the same time, those who are in need of fund could raise them in the market either by borrowing or selling their holdings of short-term negotiable financial instrument, such as Treasury bills, bankers acceptances, negotiable certificates of deposits, Cagamas notes and bonds, Khazanah bonds and Malaysian Government securities.

• The major participants in the money market are the commercial banks, merchant banks, finance companies, discounts houses, insurance companies, large corporations, pension funds and money brokers.

Foreign exchange Market

• Foreign exchange Market is essentially a wholesale interbank market for the sale and purchase of foreign currencies including purchases by importers to pay for their imports and sale of ringgit by exporters arising from receipt of export proceeds.

Capital market

• The capital market in Malaysia comprise the conventional and Islamic markets for medium-term and long-term financial assets.

• The conventional markets consist of two main markets, namely the equity market dealing with corporate stocks and shares, and the bonds market dealing in public and private debt securities with maturities exceeding one year.

Derivatives Markets

• Accompanying the upsurge in the demand for capital and the development of the capital markets, was emergence of the need for risk management facilities and hence, derivatives offering additional financial products.

• In Malaysia, the Malaysia Derivatives Exchange Berhad (MDEX) exemplifies the Futures Exchange, offering both futures and options contract.

IOFC- International Offshore Financial Centre

• An IOFC is basically a small territory or jurisdiction that imposes low or no taxes on income, profit, dividend and interest earned or derived from the offshore business activities or transactions carried out by offshore multinational corporations (MNCs) in or from those jurisdiction.

• Activities promoted:1. Offshore banking operation2. Trust and fund management3. Offshore insurance and offshore insurance-related business and,4. Offshore investment holding companies

Main references

• The Central Bank And The Financial System in Malaysia, A Decade of Change 1989-1999. Kuala Lumpur: Bank Negara Malaysia.

• McGrath, Michael (2000). Financial Institutions, Instruments and Markets. Australia: McGraw- Hill Book Company Australia Pty Limited.