amandla resource development consortium (ardc) generic presentation bt… · who are; “amandla...

TRANSCRIPT

Amandla Resource Development Consortium

(ARDC)

Presentation

“Solid Biomass to Renewable Energy

(BTRE) ”

www.amandlaresources.com [email protected] 1

Who are; “Amandla Resource

Development Consortium”? • ARDC & its direct associates are active in Renewable Energy &

Local Community Development.

• Mainly in KZN, for 12 years, since 1998.

• Mission : “Renewable Energy, Community & Sustainable Project Development”.

• Amandla: “Empowerment” - through Renewable Energy!

2

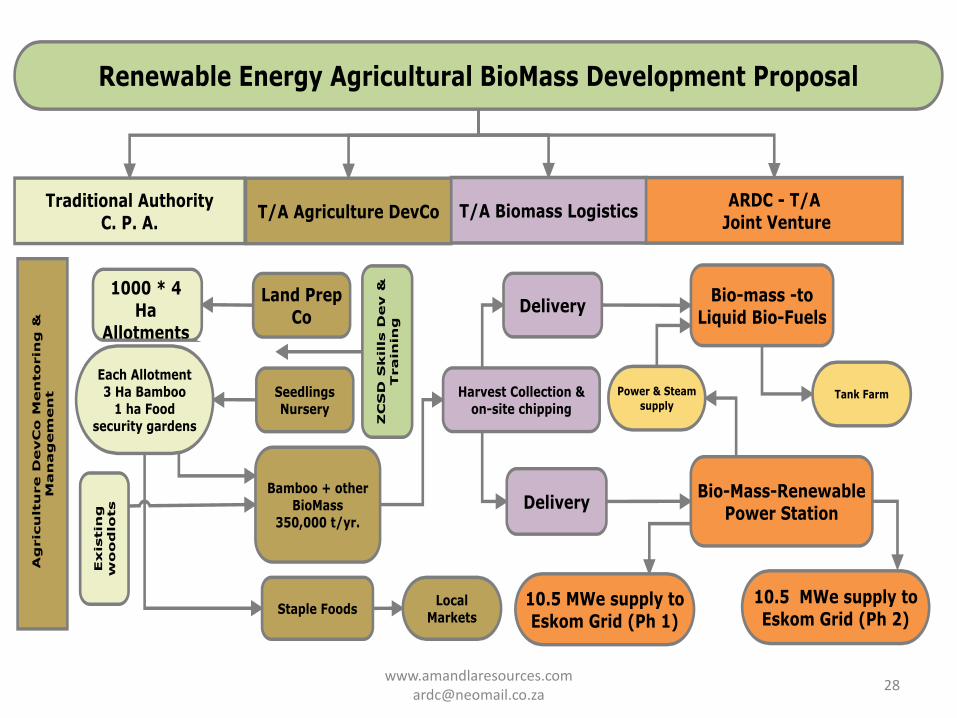

ARDC Biomass Types - REFIT • Forestry:

• Currently unutilised Forest Brushwood, post-harvest toppings, stumps etc. √ for NERSA “Solid Biomass”

• Forest smaller diameter logs (arising from more-efficient whole tree harvesting). √ for NERSA “Solid Biomass”

• Sugar Cane: (not Bagasse that is already delivered to a mill acceptable for COFIT not REFIT).

• Post-harvest Sugar Cane tops & Trash √ for NERSA “Solid Biomass”.

• General Agricultural Biomass residues:

• Vine clippings, Orchard prunings, Stover and cobs, Bush-clearing waste residues, Alien plant eradication biomass, Animal wastes etc. √ for NERSA “Solid Biomass”

• Short-rotation Energy Crops:

• (Bamboo, Moringa, Miscanthus etc that can be ‘out-grown’). √ for NERSA “Solid Biomass”

• Municipal: In compliance with NEMA and Waste Act

• Green biomass (garden) waste. √ for NERSA “Solid Biomass”

• Dried sewage plant sludge, dried abattoir waste/ effluent.

• General Municipal house-hold garbage (can only be processed in specialised equipment).

• Landfill site solid bio-degradable mass (can only be processed in specialised equipment).

• Landfill gas extraction (qualifies for a different REFIT tariff rate than solid biomass)

3

ARDC (Solid) Biomass Sources

• Commercial forest owners & companies

• Community forest / wood-lot owners and (rural) Traditional Authority entities

• Commercial Cane-grower consortiums

• Small-scale cane growers (Rural communities)

• Municipalities (for green garden waste & MSW)

• Contract Future energy-crop out-growers

• Other agricultural “waste” i.e. pruning's etc., distilleries and pulp/ paper-mill outflows

4 www.amandlaresources.com [email protected]

Relative Proportions of Tree

Components (Avg. Trees)

www.amandlaresources.com [email protected] 6

• Branch wood & Tops

• Foliage

• Stem wood

• Stump wood

• Root wood

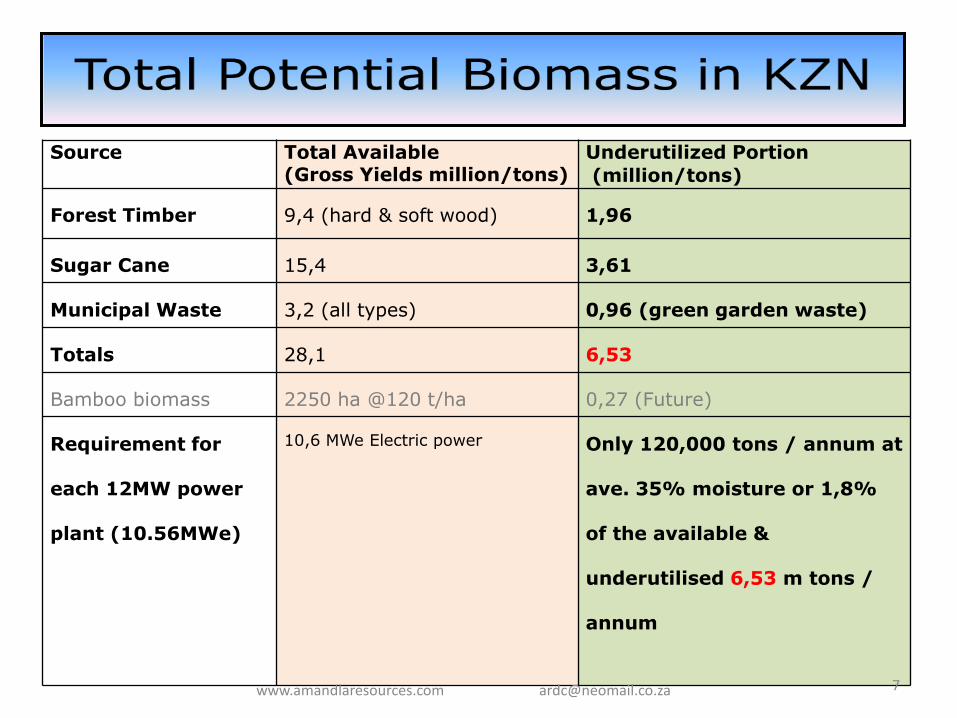

Source Total Available (Gross Yields million/tons)

Underutilized Portion

(million/tons)

Forest Timber 9,4 (hard & soft wood) 1,96

Sugar Cane 15,4 3,61

Municipal Waste 3,2 (all types) 0,96 (green garden waste)

Totals 28,1 6,53

Bamboo biomass 2250 ha @120 t/ha 0,27 (Future)

Requirement for

each 12MW power

plant (10.56MWe)

10,6 MWe Electric power Only 120,000 tons / annum at

ave. 35% moisture or 1,8%

of the available &

underutilised 6,53 m tons /

annum

www.amandlaresources.com [email protected] 7

8 www.amandlaresources.com [email protected]

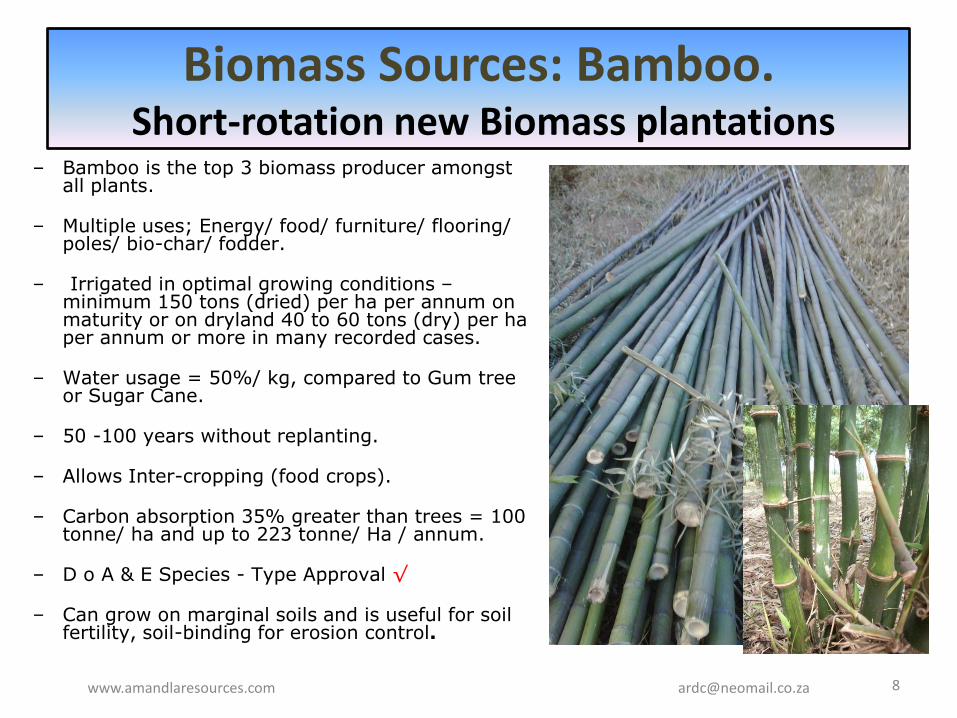

Biomass Sources: Bamboo. Short-rotation new Biomass plantations

– Bamboo is the top 3 biomass producer amongst all plants.

– Multiple uses; Energy/ food/ furniture/ flooring/ poles/ bio-char/ fodder.

– Irrigated in optimal growing conditions – minimum 150 tons (dried) per ha per annum on maturity or on dryland 40 to 60 tons (dry) per ha per annum or more in many recorded cases.

– Water usage = 50%/ kg, compared to Gum tree or Sugar Cane.

– 50 -100 years without replanting.

– Allows Inter-cropping (food crops).

– Carbon absorption 35% greater than trees = 100 tonne/ ha and up to 223 tonne/ Ha / annum.

– D o A & E Species - Type Approval √

– Can grow on marginal soils and is useful for soil fertility, soil-binding for erosion control.

www.amandlaresources.com [email protected]

9

Biomass Sources: Various Short-rotation new Biomass plantations

Clockwise from top left: • Bales of cane tops • Poplar Trees • Casuarina trees • Sweet Sorghum • Forest post-harvest

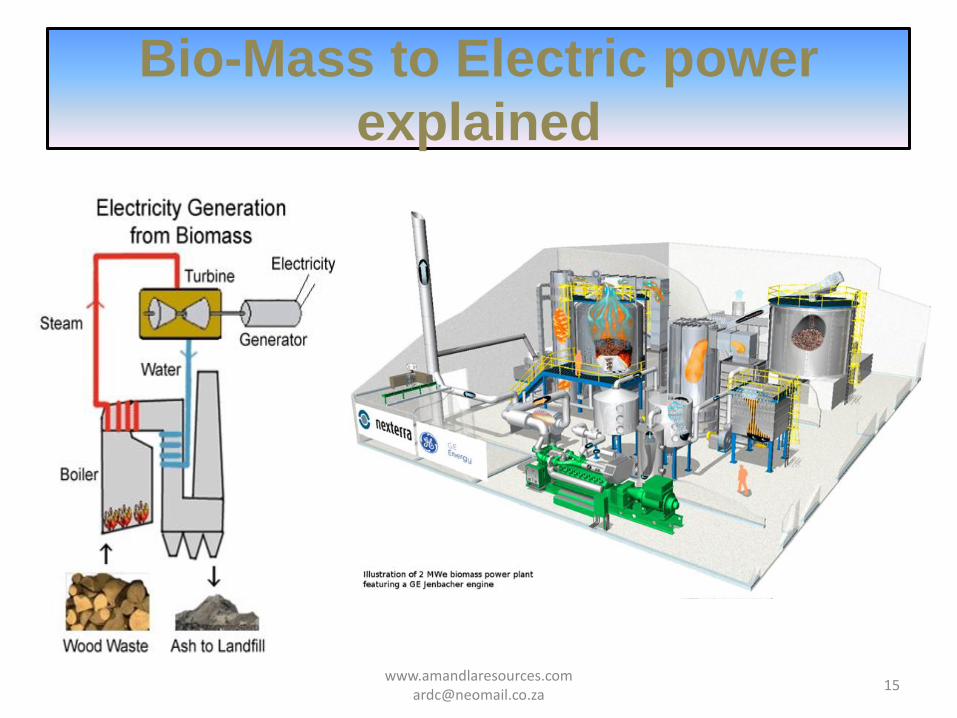

ARDC's Biomass to Renewable Energy

(BTRE) Streams

ARDC has Evaluated Technologies for converting Biomass to;

– Pellets & Briquettes, – Bio-Gas, – Process Steam – Electricity – and Bio-Fuels such as

• Fuel-grade Alcohol, • Bio-Diesel & • Bio-GTL Diesel

• It Concluded that the focus should be on Electricity and Diesel • This presentation is mainly based on Electricity output • ARDC has several smaller projects in preparation also for Bio-GTL Diesel.

www.amandlaresources.com

www.amandlaresources.com [email protected]

14

Biomass to Liquid Bio-Fuel

Processing Plants

Input Bio mass Agricultural waste MSW (municipal solid waste) Domestic / community waste All Plastics Animal residues Crude oils residues Waste oils & Fats Sludge waste Processed & Cut materials

Output • Bio-GTL EN 590 clean Diesel fuel • Distilled water • Ash = Fertilizer (1-3%)

• CO 2 (Re-entered in the process)

Biomass Technical Specs

Bio Mass Type %

Dry Basis

Sugar Cane

Saligna Grandis

Saligna

(Grandis)

Bamboo Wattle Other

Garden Waste

Variety Post Harvest

Tops & Trash

Post Harvest residues

Estimates

Round-log wood chip

Bambusa Culms

Chipped

Round-log woodchip

Chipped

Energy Value [Dry Basis]

Mj/ Kg

17 to18.5

17 to19 19.41 17.0 to 18.5 *

18.99 14-16

Ash * % 4.3% +2% 0.53% >2% 0.41% 2-5%

Sulphur % 0.1% 0.30% 0.24% 0% to 0.1%

0.03% 0.2%

Kg/ Gj 0.05 0.15 0.12 0 to 0.05 0.15 0.09

Volatiles % 79% 80% 83.19% 76% 84.86% 80%+ Kg/ Gj 42.2

Moisture Content (ex field)

% 15%

Sun-Dried

30% as received

6.43% min ***

30% ave

12%

Sun-Dried

6.46% Min***

30% ave

Variable

www.amandlaresources.com [email protected]

16

ARDC BTE Project Sites

• Mainly in Rural KZN but also in E Cape and southern Mpumalanga provinces.

• Next to / close to existing Eskom Sub stations.

• Will contribute to decentralised grid stability.

• Have access to water or specialised water recycling and treatment plants.

• Have advanced or In–progress Environmental approvals.

• Situated at epicentres of bulk biomass supplies.

• Contribute to job-creation, SMMEs and BBBEE development. www.amandlaresources.com [email protected] 17

ARDC Biomass Pricing Objectives

• BTE (Electricity) Plants should generate electricity continuously, without need for excessive storage & must contribute to decentralised base-load grid-stability.

• Should provide Incentives to; – Recover & Deliver currently underutilised biomass to BTEs

– Grow new energy crops such as Bamboo/ Moringa/ Poplar

– Create long-term sustainable employment in this process

– Establish new SMME & BBBEE entities as service entities

– Provide Training & Mentorship for all the above

18 www.amandlaresources.com [email protected]

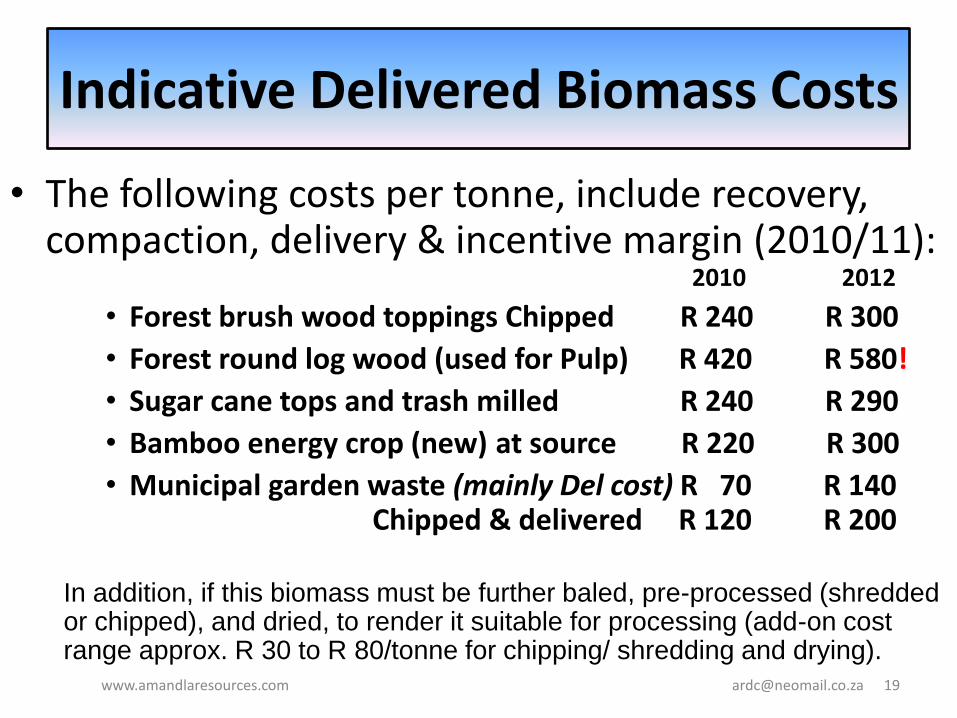

Indicative Delivered Biomass Costs

• The following costs per tonne, include recovery, compaction, delivery & incentive margin (2010/11): 2010 2012

• Forest brush wood toppings Chipped R 240 R 300

• Forest round log wood (used for Pulp) R 420 R 580!

• Sugar cane tops and trash milled R 240 R 290

• Bamboo energy crop (new) at source R 220 R 300

• Municipal garden waste (mainly Del cost) R 70 R 140 Chipped & delivered R 120 R 200

In addition, if this biomass must be further baled, pre-processed (shredded or chipped), and dried, to render it suitable for processing (add-on cost range approx. R 30 to R 80/tonne for chipping/ shredding and drying).

19 www.amandlaresources.com [email protected]

ARDC Biomass Power Plant Costs: per KWh

• Biomass feedstock 40,1%

• Salaries & Wages 15,5%

• Other factory expenses 10,6%

• Sub total 66,2%

• Fixed asset repayments 33,8%

• Total cost break down 100.00%

20 www.amandlaresources.com [email protected]

ARDC Employment, SMME / BBBEE Opportunities

• Each 12 MW (10.5MWe) plant, including plant operation, biomass supply side logistics, biomass growing & recovery will create 1,200 jobs (including 12 SMME / BEEs each employing 10 persons) in the complete supply-chain.

• Capital investment cost per job – R 365,000 averaged • These jobs are sustainable for 12 months of the year , for

the full operational life of the project(s). • Excludes plant manufacturing construction & build costs

that create additional, interim project-development employment.

21 www.amandlaresources.com [email protected]

www.amandlaresources.com [email protected]

22

Category Per 12 MWe CAPEX R’m

Cost/ new job R’000

Per 24 MW CAPEX R’m

Cost/ new job R’000

BTE Plant Operation 117 328 2,800 138 647 4,688

Supply Side Logistics & harvesting 181 21 116 350 42 120

Biomass Plantation 1200 ha 302 89 295 604 175 290

Total Direct Jobs 600 438 730 1092 864 791

Add Indirect Jobs (Source TH/CSIR)* 600 1092

Total Jobs per BTE 1200 438 365 2184 864 396

Total ARDC Jobs (2X12 & 2X 24MWe) 2400 4368

All BTEs - 2400 plus 4368 = 6768

Cost per Job

SMME / BEE Opportunities 12 24

SMME / BEE Jobs 112 224

ARDC Employment: (2) SMME / BBBEE Opportunities

Potential ARDC Customers for

Electricity & Bio-GTL Diesel

• Major Corporates*

• Transport Companies*

• Forestry Companies*

• Municipalities*

• Eskom (via NERSA) –next tender round 03/2012

• Oil Companies* • * = Already engaged

www.amandlaresources.com

(ZCSD) a Section 21, Not-for-Profit NGO

• Permaculture and organic farming

• Food Gardens & food processing

• Alternative energy and appropriate technology

• Integrated waste management systems

• Composting

• Craft from waste

• Growing of traditional medicinal plants and herbs

• Aquaculture and Aquaponics

• Ecotourism

www.amandlaresources.com [email protected]

24

ZCSD Community Development

www.amandlaresources.com [email protected]

25

Pictures Clockwise from Top Left: 1. Craft-making / skills development 2. Working for Water: Rural housing/Water tanks/ Toilets

3. Rural Sanitation CWP projects 3. Cement Block –making projects

ARDC Project Economics & Returns

• CAPEX for 12 MW plant is approx R340m (2011)

• IRR of 17 to20% & ROE of 20 to 29% where equity is 30% of CAPEX.

• Installed cost per MW $3,2 to 3,7 m

• Internal plant usage is 1,4 MW (Parasitic Load).

• Electricity available to grid or private customer 10,6 MWe

• Build period up to 3 yrs – EIA dependant Where land and EIA issues already concluded, build-time is 24 months

26 www.amandlaresources.com [email protected]

Typical Equity Structure for a

BTE Project

• Biomass Suppliers private & TAs 20%

• ARD Consortium 6%

• Strategic “Technical” Equity Partner SEP 26%

• BEE Partner “major” some identified 18%

• IDC includes minor / local BEE 30%

• Total Equity 100%

www.amandlaresources.com [email protected]

27

Additional Benefits to Economy

• Decentralised Grid-stability in remote / rural areas • Continuous power output - without need of storage • Environmental benefits from less in-field/ post-

harvest burning-off of ‘wasted’ resources • Additional community / SMME income from

currently wasted resources = Substantial new job / SMME / BBBEE creation

• Rural economic development that will provide security of supply for the needed feedstocks for the plant(s).

• Uplifted rural communities that can also drive and grow food-security.

29 www.amandlaresources.com [email protected]

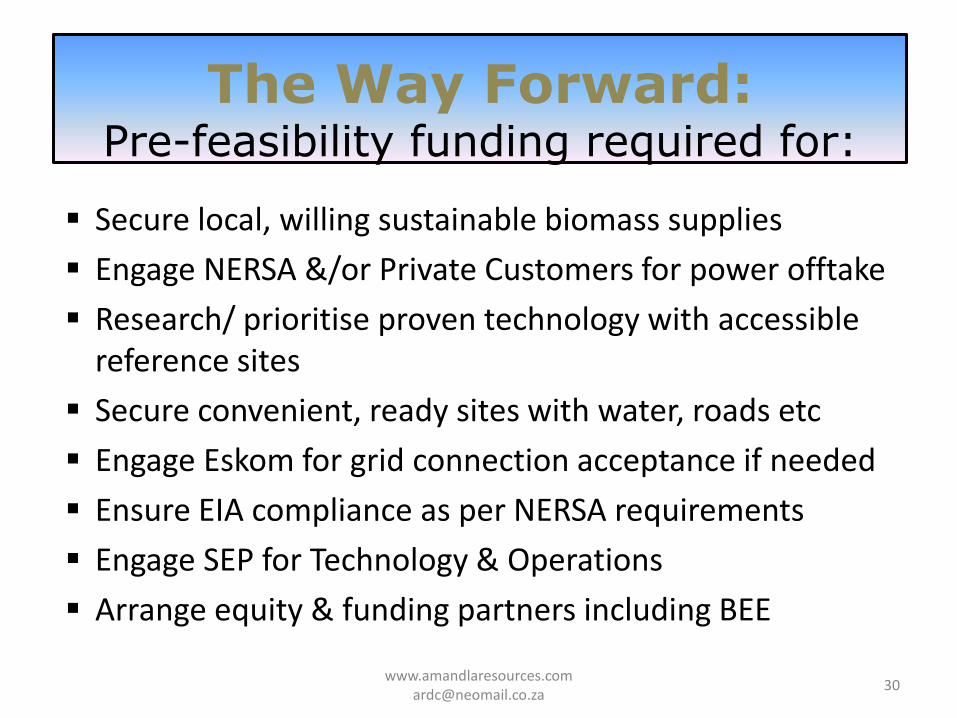

Secure local, willing sustainable biomass supplies

Engage NERSA &/or Private Customers for power offtake

Research/ prioritise proven technology with accessible reference sites

Secure convenient, ready sites with water, roads etc

Engage Eskom for grid connection acceptance if needed

Ensure EIA compliance as per NERSA requirements

Engage SEP for Technology & Operations

Arrange equity & funding partners including BEE

www.amandlaresources.com [email protected]

30

The Way Forward:

Pre-feasibility funding required for:

Realising Africa’s Natural Potential, through Renewable Resource Management

Amandla Resource Development Associates:

Zululand Centre for Sustainable Development [ZCSD]

Section 21 co.

Ecosystems cc.

Rainbow Millennium Power Corporation

Envirovest Bioproducts (Pty) Ltd; Bamboo development

Various Biomass grower-suppliers:

Commercial/ Local Community and Traditional Authorities that have already signed cooperation agreements

www.amandlaresources.com [email protected]