alan hayes strategy & sustainability...

TRANSCRIPT

FOLLOW ME ON TWITTER @AlanHayes_IGD November 2016 Birmingham

Alan Hayes

Strategy & Sustainability Manager

We are a research and training charity in the UK

We are food and grocery experts

We have an international membership of over 1,000 companies across the entire supply chain

1. Megatrends and Economic Sentiment

2. How Brexit will affect the retail market

3. How the retail industry has changed

4. What we can expect in the future

Agenda

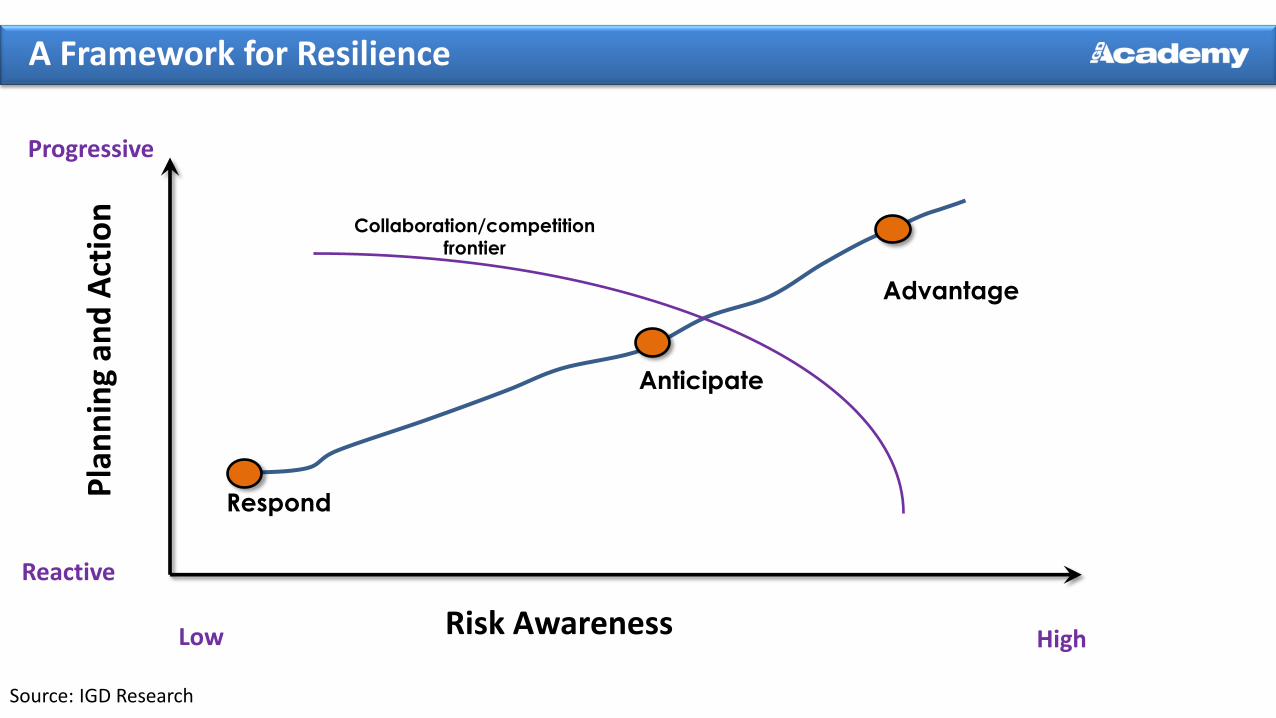

Respond

Advantage

Risk Awareness

Pla

nn

ing

and

Act

ion

Progressive

Low High

Reactive

Anticipate

Collaboration/competition frontier

Source: IGD Research

A Framework for Resilience

1. Megatrends and Economic Sentiment

Digital world

Entrepreneurship

Global marketplace

Urban world

Resourceful planet

Health reimagined

Optimism Pessimism Status Quo

Megatrends and local economic sentiments

interact with each other to create a

complex and changing set of drivers which continue to shape

futures - society and business

Source: IGD Research

Megatrends and Economic Sentiment

• Source: IGD Research, EY Megatrends Digital world

Entrepreneurship

Global marketplac

e

Urban world

Resourceful planet

Health reimagined

Optimism Pessimism Status Quo

They affects economic sentiment for business

and shopper. They do not impact the

existence of megatrends or their

transformative capacity. They are likely to

impact the pace and scale of transformation.

Source: IGD Research

Brexit, Trump and Megatrends

2. BREXIT and its (potential) impact on retail

• Source: IGD Research European political changes

Economic and fiscal

effects

Labour movement

Regulatory drift

Trade terms

Source: IGD Research

Brexit Implications and Uncertainties

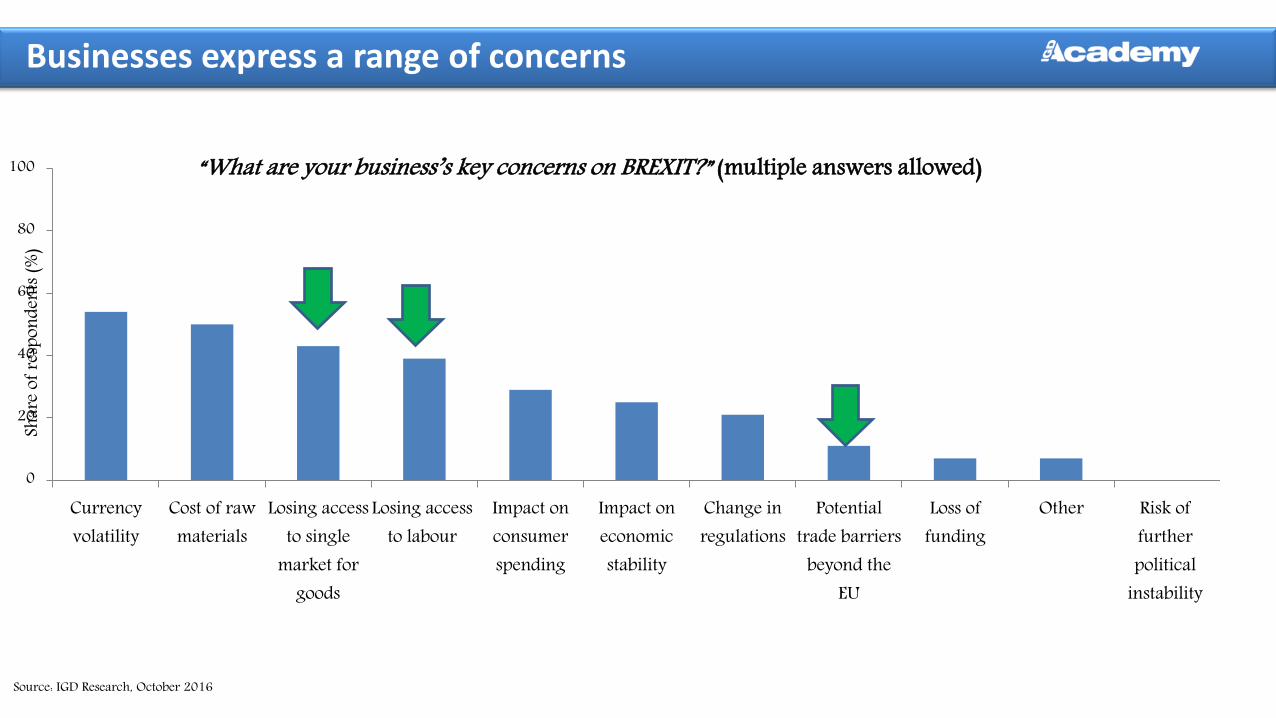

0

20

40

60

80

100

Risk offurtherpolitical

instability

OtherLoss offunding

Potentialtrade barriers

beyond theEU

Change inregulations

Impact oneconomicstability

Impact onconsumerspending

Losing accessto labour

Losing accessto single

market forgoods

Cost of rawmaterials

Currencyvolatility

Shar

e of r

espo

nden

ts (%

)

“What are your business’s key concerns on BREXIT?” (multiple answers allowed)

Source: IGD Research, October 2016

Businesses express a range of concerns

Images: Thinkstockphotos

Welfare and healthcare Will the government be able to meet

its social obligations?

Wages Will the National Living Wage be

maintained, post-BREXIT?

Skills and training Do UK employees have the skills to

prosperous post-BREXIT?

Pension performance This will be a key question for the

soon-to-retire

House prices Housing is a big cost – but houses are

also key assets

Competitive society UK workers may be more exposed to

global competition

Brexit – likely impact on household economics

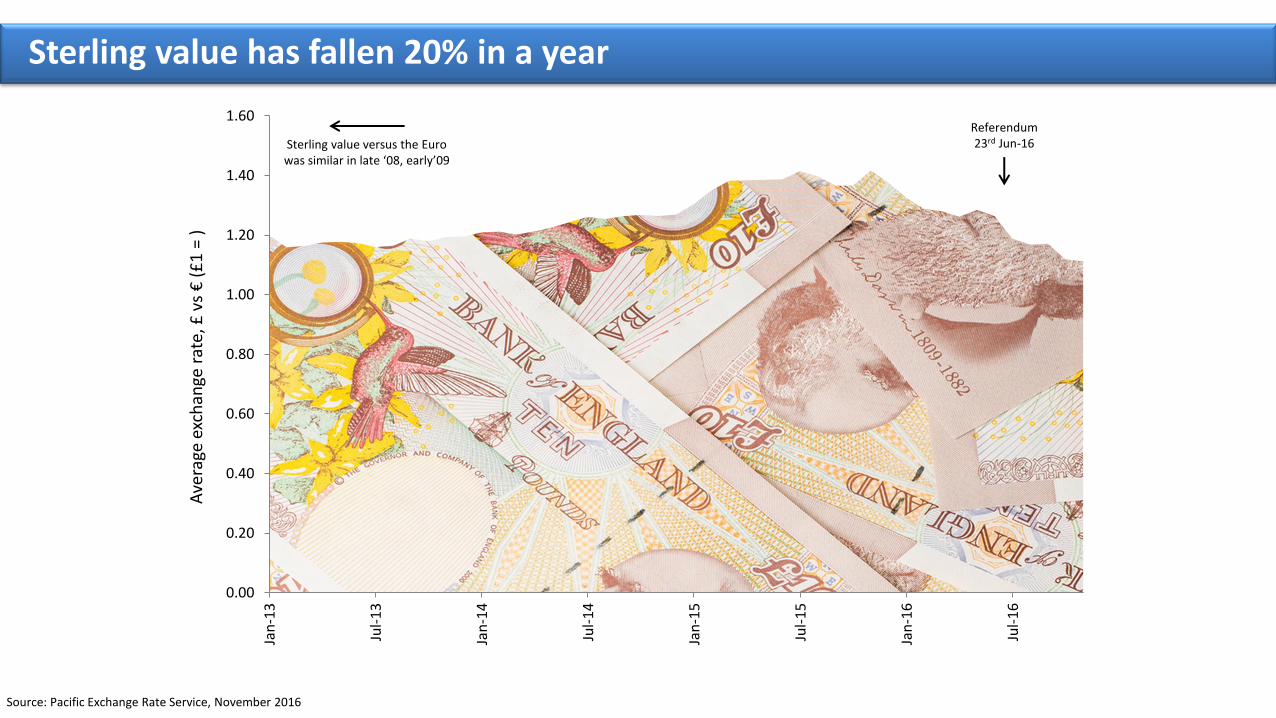

Sterling value has fallen 20% in a year

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Jul-

16

Ave

rage

exc

han

ge r

ate,

£ v

s €

(£

1 =

)

Source: Pacific Exchange Rate Service, November 2016

Sterling value versus the Euro was similar in late ‘08, early’09

Referendum 23rd Jun-16

Source: ONS June 2016

-4

-2

0

2

4

6

8

10

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Ch

ange

, 3m

on

sam

e 3

m y

r ag

o (

%)

Non-food retailvol

Food retail vol

Volume has been rising (weakly)

Source: Source: ONS / IGD, June 2016. Impact of inflation calculated by IGD using Fisher equation

-6

-4

-2

0

2

4

6Ja

n-0

6

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Ch

ange

, 3m

on

sam

e 3

m y

r ag

o (

%)

Av weekly earnings, nom Impact of CPI inflation Av weekly earnings, real

Household wealth has been increasing

3. How retail has changed

45% claim to be buying higher quality goods for the same or less money than previously

Our ability to spend will be split across multiple industries

Source: IGD ShopperVista, August 2015

A good time to be a shopper?

Source: IGD ShopperVista, February 2016

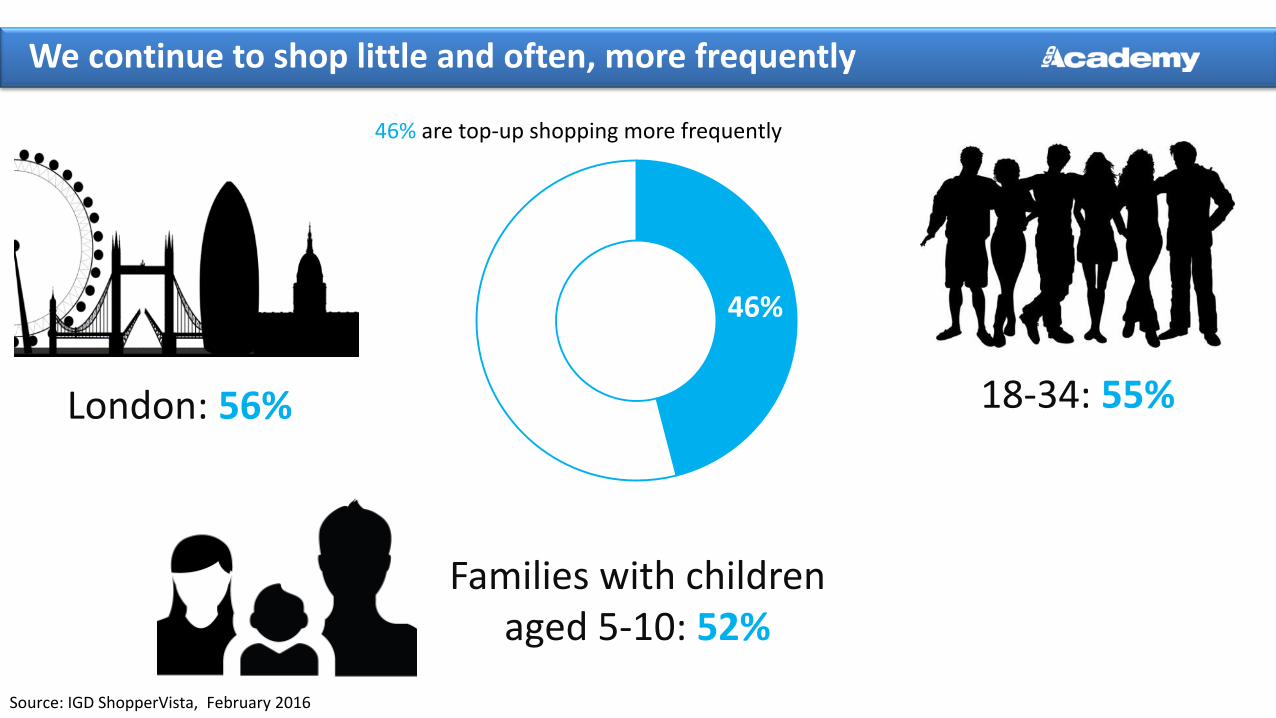

46%

46% are top-up shopping more frequently

London: 56% 18-34: 55%

Families with children aged 5-10: 52%

We continue to shop little and often, more frequently

Value Quality Convenience Health

Four key prevalent shopper truths

No let up in ‘EDLP’ activity from the multiples

Source: Companies

Personalisation

Romantic Marmite for Valentine’s Day

Feb 2016

Brand halo

Magnum ‘pop-up’ shop in London,

August 2016

Digital engagement

McVities augmented reality iKittens

June 2016

Customisation

Nestle cereal cocktails, Westfield Stratford

April 2016

Story telling and demand creation

Higher expectations from shoppers

Online and multichannel

Greater levels of responsiveness

High focus

Low focus

CU

STO

MER

COST Low

efficiency High

efficiency

1 2

3

4 5

6

Economies of scale

Reducing under-utilised assets

Automation of systems and processes

Source: IGD Research

Supply chains continue to evolve

4. What we can expect in the future

Business confidence in the UK is falling …

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

UK

bu

sin

ess

con

fid

ence

ind

ex –

hig

her

sco

res

ind

icat

e gr

eate

r co

nfi

den

ce

Source: UK Business Confidence Monitor, ICAEW, September 2016

Note: loss of confidence seen is recent quarters is recorded across all business types and all regions

Confidence was falling long before the referendum was

announced

UK shopper sentiment is moderate, but stable

Source: ShopperVista, IGD Research, November 2016

Base: 1,000 main shoppers per month; note change in sample method in Sep-16

33 26 24

50 57

52

17 17 24

0

20

40

60

80

100

Sep

-14

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Shar

e o

f re

spo

nd

ents

(%

)

Personal financial expectations, next 12m

Worse off Same Better off

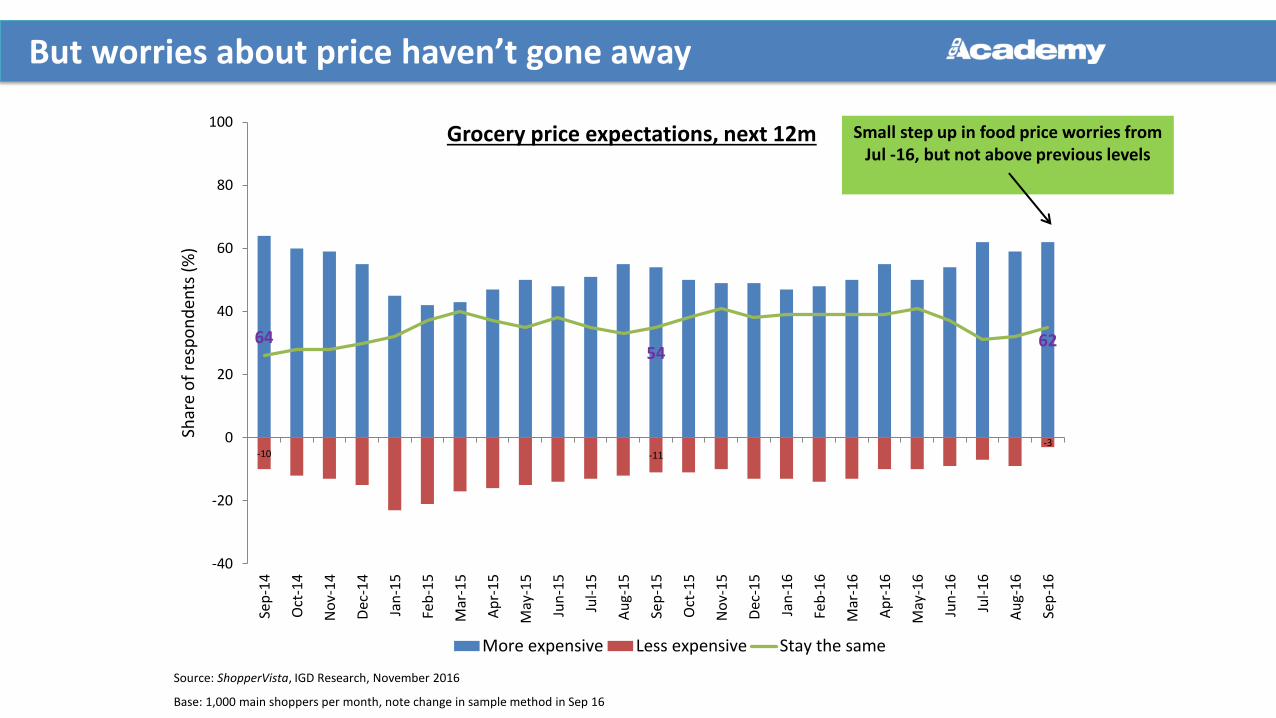

But worries about price haven’t gone away

Source: ShopperVista, IGD Research, November 2016

Base: 1,000 main shoppers per month, note change in sample method in Sep 16

64 54

62

-10 -11 -3

-40

-20

0

20

40

60

80

100

Sep

-14

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Shar

e o

f re

spo

nd

ents

(%

)

Grocery price expectations, next 12m

More expensive Less expensive Stay the same

Small step up in food price worries from Jul -16, but not above previous levels

163.8 169.1 175.0 177.4 178.0 179.1 181.6 184.8 188.6 192.8 196.9

4.7%

3.2% 3.5%

1.3%

0.4% 0.6%

1.4% 1.8%

2.1% 2.2% 2.1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

50

100

150

200

250

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

YOY

Gro

wth

(%

)

Gro

cery

ret

ail m

arke

t si

ze (

£b

n)

Source: IGD Research, Grocery Retail forecast 2016 - 2021)

Grocery retail market forecast

Source: IGD Research, Grocery Retail forecast 2016 - 2021)

£179.1

£196.9

£2.3

£7.3

£8.1

170

175

180

185

190

195

200

2016 Inflation Volume 2021

Gro

cery

ret

ail m

arke

t si

ze (

£b

n)

Grocery - growth contributors

+0.2%

£0.1bn

+0.8%

£0.7bn

+39.5%

£7.1bn

+11.7%

£4.4bn

+68.3%

£7.2bn

Hypermarket Supermarkets Discount Convenience Online

Source: IGD Research, Grocery Retail forecast 2016 - 2021)

Larger stores stable amidst discount and online growth

Share will continue to shift

0

10

20

30

40

50

Hypermarkets Supermarkets Convenience Discount Online Other

Val

ue

shar

e o

f U

K g

roce

ry r

etai

l mar

ket

(%)

2016

2021

Source: IGD Research, November 2016

Channel value forecasts based on “main case”, “discount” includes grocery component of High St discount retail

Like our stuff? Now subscribe!

Technology will continue to reshape retail

Wearable technology

Semi- automatic replenishment

Buy buttons on websites

Has Amazon found the killer in Echo?

Image: Amazon.com

Renewable energy Especially local and small scale

New manufacturing eg: 3D printing

Novel foods eg: test tube meat, no-cow milk

Indoor agriculture eg: hydroponics

Virtual reality Making travel less necessary, esp

business travel

AI and robotics Making cheap labour less necessary

Image: Thinkstockphotos

New technologies will be driven by megatrends

Considerations

1. Are you evaluating the impact of the most relevant risks to your business, not just BREXIT related uncertainty?

2. What planning horizons are you using when evaluating these?

3. How will you make, implement and review your decisions in this unprecedented period ahead?

4. Does your management team have the capabilities to fail fast and learn quickly, especially in such uncertain times?

5. Have you recalibrated your expectations for future value and volume growth?

6. Is your business financially resilient to an extended period of UK economic weakness?