a billion plus… - rawbank.cd · mance, we can see our efforts turning ... 61 ng bi nak l reai t...

TRANSCRIPT

20

15

20

09

20

13

20

11

A N N U A L R E P O R T 2 0 1 5

A B I L L I O N P L U S …

D E M O C R A T I C R E P U B L I C O F C O N G O

USD

MIL

LIO

NS

1,086

total assets

733

deposits

92,3

net banking income

800

1,000

600

400

200

0

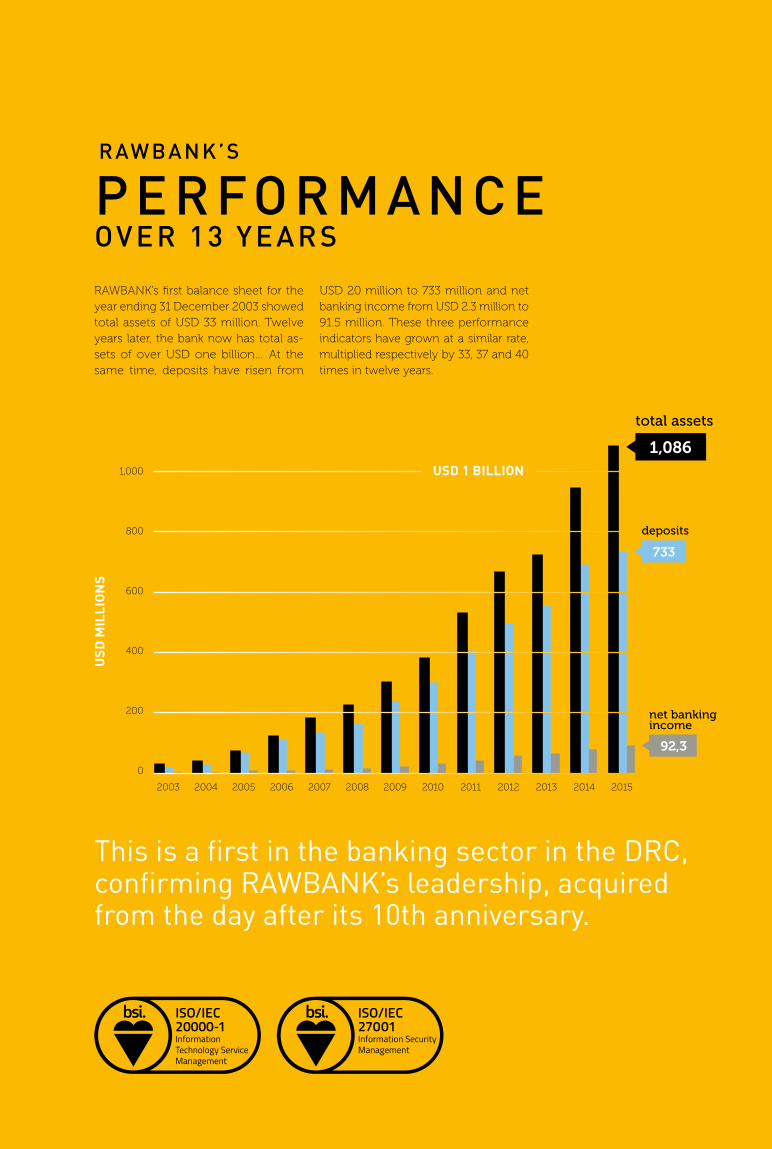

RAWBANK’s first balance sheet for the year ending 31 December 2003 showed total assets of USD 33 million. Twelve years later, the bank now has total as-sets of over USD one billion… At the same time, deposits have risen from

PE R FO R MANCE OVER 13 YEARS

2003 2005 2007 20112009 20132004 2006 2008 20122010 2014 2015

This is a first in the banking sector in the DRC, confirming RAWBANK’s leadership, acquired from the day after its 10th anniversary.

USD 20 million to 733 million and net banking income from USD 2.3 million to 91.5 million. These three performance indicators have grown at a similar rate, multiplied respectively by 33, 37 and 40 times in twelve years.

USD 1 BILLION

R AW BANK’S

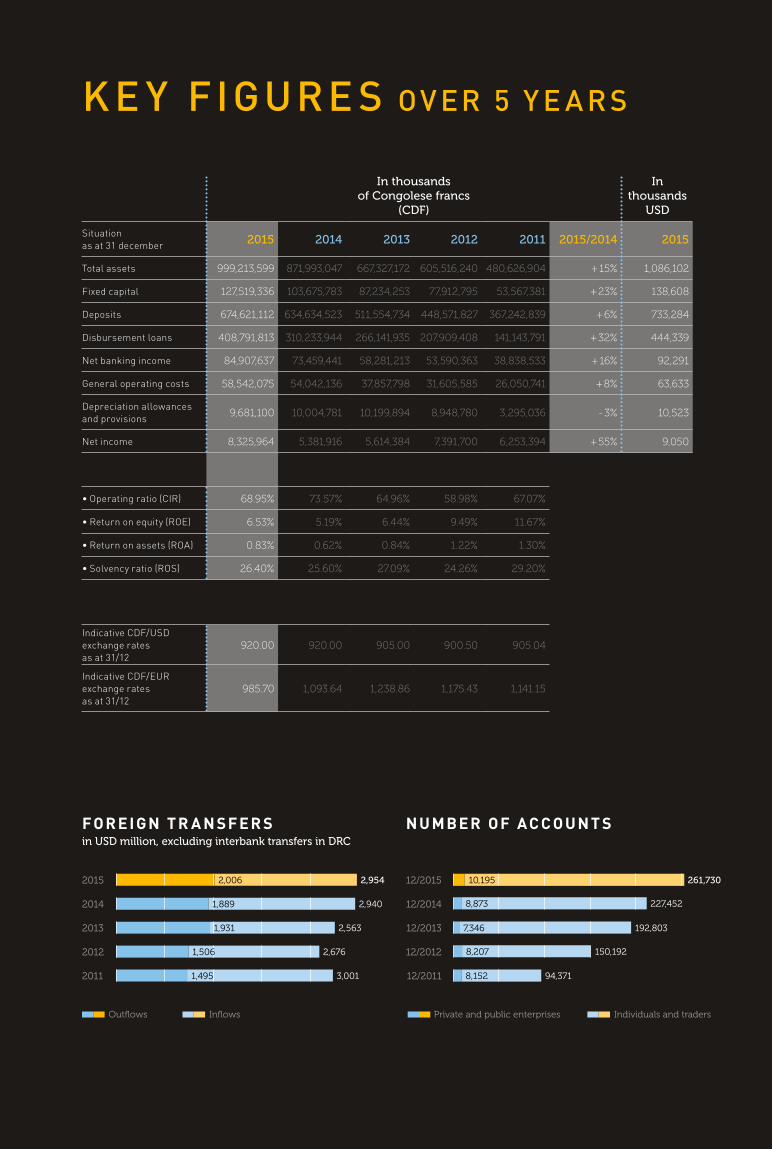

In thousands of Congolese francs

(CDF)

In thousands

USD

Situation as at 31 december 2015 2014 2013 2012 2011 2015/2014 2015

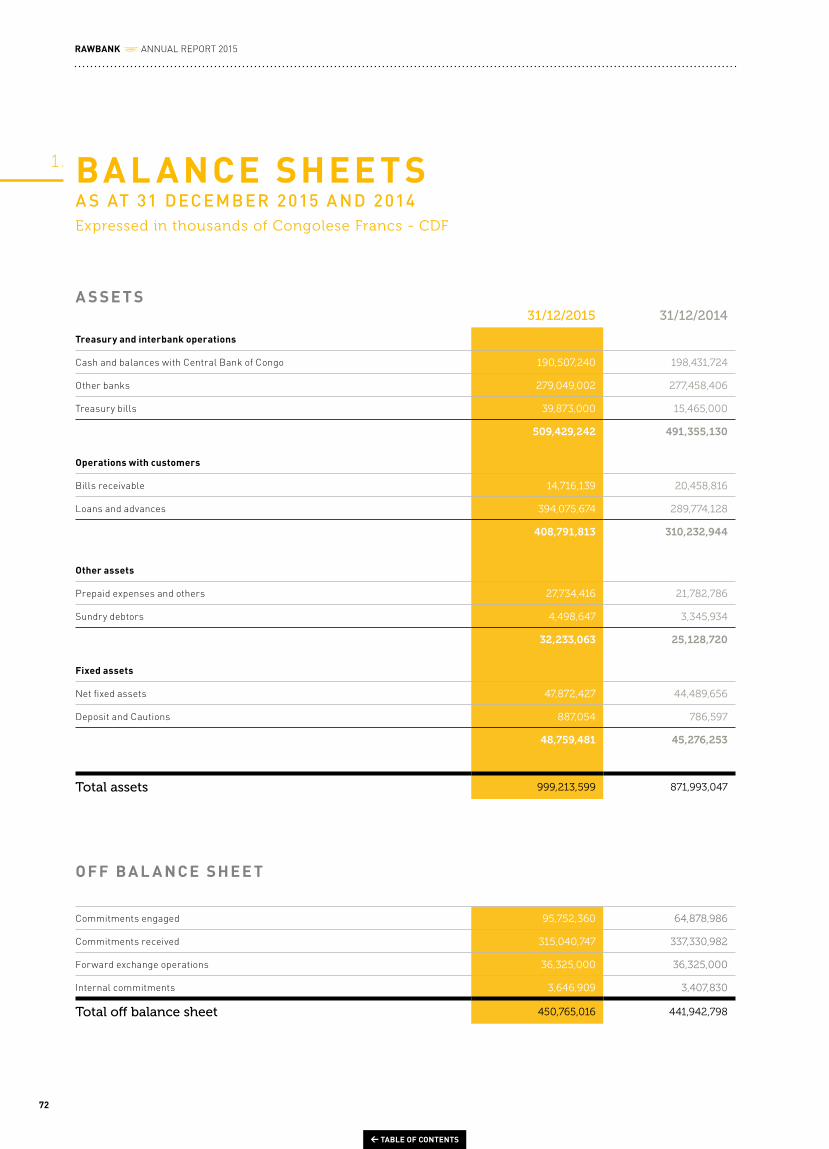

Total assets 999,213,599 871,993,047 667,327,172 605,516,240 480,626,904 + 15% 1,086,102

Fixed capital 127,519,336 103,675,783 87,234,253 77,912,795 53,567,381 + 23% 138,608

Deposits 674,621,112 634,634,523 511,554,734 448,571,827 367,242,839 + 6% 733,284

Disbursement loans 408,791,813 310,233,944 266,141,935 207,909,408 141,143,791 + 32% 444,339

Net banking income 84,907,637 73,459,441 58,281,213 53,590,363 38,838,533 + 16% 92,291

General operating costs 58,542,075 54,042,136 37,857,798 31,605,585 26,050,741 + 8% 63,633

Depreciation allowances and provisions 9,681,100 10,004,781 10,199,894 8,948,780 3,295,036 - 3% 10,523

Net income 8,325,964 5,381,916 5,614,384 7,391,700 6,253,394 + 55% 9,050

• Operating ratio (CIR) 68.95% 73.57% 64.96% 58.98% 67.07%

• Return on equity (ROE) 6.53% 5.19% 6.44% 9.49% 11.67%

• Return on assets (ROA) 0.83% 0.62% 0.84% 1.22% 1.30%

• Solvency ratio (ROS) 26.40% 25.60% 27.09% 24.26% 29.20%

Indicative CDF/USD exchange rates as at 31/12

920.00 920.00 905.00 900.50 905.04

Indicative CDF/EUR exchange rates as at 31/12

985.70 1,093.64 1,238.86 1,175.43 1,141.15

N U MBE R O F AC C O U N T S

K E Y FIGURE S OV ER 5 Y E A R S

FO R E I G N T R A N SF E R S in USD million, excluding interbank transfers in DRC

3,001

Outflows Inflows

2015

2014

2013

2012

2011

2,006

2,9401,889

1,931

1,506

2,563

2,676

2,954

1,495

Private and public enterprises Individuals and traders

12/2015

12/2014

12/2013

12/2012

12/2011

10,195 261,730

8,152 94,371

8,207 150,192

7,346 192,803

8,873 227,452

Individuals and traders

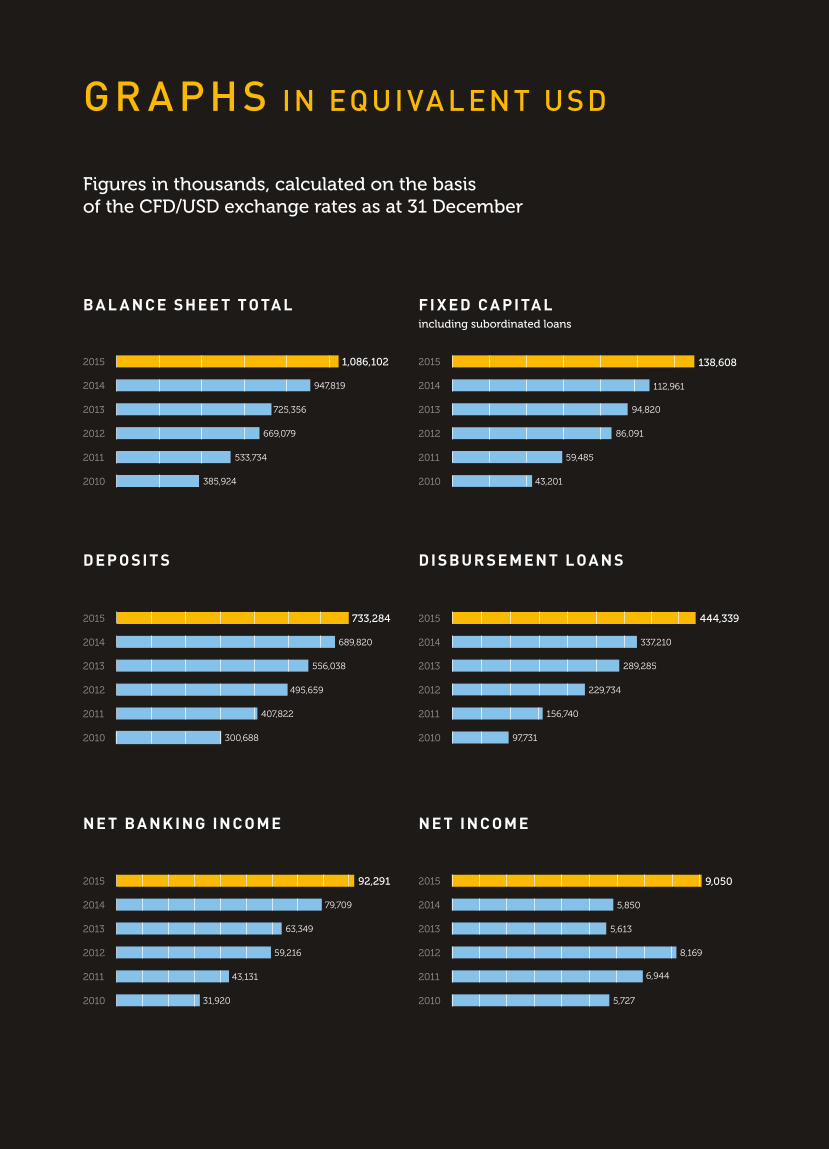

GR A PHS IN EQUI VA LENT USD

B A L A N C E SHE E T T O TA L F I X E D C A P I TA Lincluding subordinated loans

2013

2012

2011

2010

2013

2012

2011

2010

2014

2015

2014

2015

725,356

669,079

533,734

385,924

947,819

1,086,102

94,820

86,091

59,485

43,201

112,961

138,608

DEP O SI T S D I SBU R SE ME N T L OA N S

2013

2012

2011

2010

2013

2012

2011

2010

2014

2015

2014

2015

300,688

407,822

495,659

556,038

689,820

733,284

289,285

229,734

156,740

97,731

337,210

444,339

NE T B A NK IN G IN C O ME

2013

2012

2011

2010

2014

2015

63,349

59,216

43,131

31,920

79,709

92,291

NE T IN C O ME

2013

2012

2011

2010

2014

2015

8,169

6,944

5,727

5,613

5,850

9,050

Figures in thousands, calculated on the basis of the CFD/USD exchange rates as at 31 December

Dear customers, dear readers,

Last year, I invited you to join us “moving to the next level.” If you remember, this was the title of the 2014 Annual Report.

We have got there through the enthusiasm of all our stakeholders, associated with this momentum for growth serving all those involved in economic development. There is still a lot of work to do and effort to be made, because the task never ends. But step by step, while paying attention to quality and controlling risks, and in accordance with our strategy of monitoring perfor-mance, we can see our efforts turning into reality in the figures.

The bank has just exceeded the milestone of one billion dollars in total assets. I am even happier that this growth in the balance sheet is fully in line with our commercial development and our profitability.

These indicators demonstrate the confidence of the Congolese market in the bank. In 13 years, deposits have risen from USD 20 million to USD 733 million. The next step is to achieve deposits of one billion dollars. This will soon occur, due to the confidence of our customers, whom I would like to thank, on behalf of the Board of Directors, the Executive Committee and all our staff.

We have every confidence in the future, even though macro-economic analyses do not indicate encouraging prospects

for 2016. The mining boom – and the growth that it enabled from 2010 to 2014 – has ended. This threat to our economy must spur our leaders to take the most favourable strategic measures possible to achieve accelerated industrialisation of the country by encouraging foreign investment and by promoting the creation of a large number of SMEs in the major growth sectors of the economy. SMEs are the main source of jobs; entrepreneurs should be encouraged by promoting the competitiveness of our companies in the face of global competition.

A sign of the times is that the country is on the right track towards certain economic liberalisation and state-owned companies, which are now commercial companies, are increasingly managed according to measured and monitored performance criteria. There still remain the legal and judicial components of public governance to be brought under control, and efforts must be focused on allowing investors and economic

operators to benefit as much as possible from the DRC’s recent membership of the Organisation for the Harmonisation of Business Law in Africa (OHADA).

In this general context that leaves a few unknowns weighing on the short-term future, I confirm our willingness to contribute more than ever to the development of the Congo. The bank has become the main financial artery of this country to which our destiny is entirely and intimately linked, for the benefit of all market segments.

With this in mind, I am pleased to confirm our “bancassurance” projects. Two insurance companies will be launched in the DRC – our project is ready – one covering the life sector, the other property and casualty, under the same “RAWSUR” brand. The complementary nature of banking and insurance will enable us to quickly roll out a high-qual-ity bancassurance package.

We will achieve our aims by fully con-trolling costs and risks, paying particular attention to our returns and productivity so that, in the end, we are continuously improving our commercial, human, organisational, operational and financial performance.

In this drive towards excellence, our ongoing concern remains “Client Advantage”, in accordance with the strategy that we initiated in 2014.

Yours sincerely,

Mazhar Rawji Chairman of the Board

of Directors

RAWBANK PASSES A NEW MILESTONE

Let us encourage entrepreneurs by promoting the competitiveness of our companies in the face of global competition.

01

ANNUAL REPORT 2015 RAWBANK

05 Chapter 01 RAWBANK 2015 IN PERSPECTIVE07 Strengths and assets in the view of the Chairman of the Executive Committee

09 Business development: continuing growth

11 Corporate & Institutional Banking (CIB)13 Commercial Banking 15 Private Banking16 Retail Banking18 Across all functions: “Customer Experience”

19 The Branch Network: a strategy for strengthening a local presence

22 The Treasury Department: an outstanding nerve centre

25 Chapter 02 A NEW EFFICIENCY STRATEGY26 POINT OF VIEW - Overview by the new Deputy CEO

29 Performance in line with organisational and operating efficiency

30 The IT Department32 In perspective: Mobile Banking34 The Operations Department36 The Organisation Department

39 Chapter 03 CORPORATE GOVERNANCE40 Governance, a long-lasting, effective process40 The Board of Directors42 The Executive Committee44 The specific committees reporting to the Executive Committee45 The bank organisation chart

47 Chapter 04 RISK MANAGEMENT48 RAWBANK’s requirements in terms of risk management

49 Credit risk51 Market risk54 IT risk55 Operational risk 55 Other risk measurement indicators56 At the forefront: fighting money laundering

C O N T E N T S

RAWBANK ANNUAL REPORT 2015

02

59 Chapter 05 HUMAN RESOURCE DEVELOPMENT60 Human resources and career management report

63 The development of the Rawbank Academy

65 RAWBANK, a bank committed to Congolese society

71 Chapter 06 FINANCIAL REPORT72 Balance sheets as at 31 December 2015 and 2014

74 Income statement for the year ended 31 December 2015 and 2014

75 Statement of changes in equity for the year ended 31 December 2015 and 2014

76 Cash flows statement for the year ended 31 December 2015 and 2014

77 Independent accountants’ report

79 Chapter 07 RAWBANK NETWORKS80 Correspondent bank network

80 The Brussels representative office

80 The Shanghai representative office

81 Branch Network in the DRC

83 Postscript: the Rawji Group establishes RAWSUR

Published by General Management of RAWBANK PO Box 2499 – Kinshasa 1 Democratic Republic of Congo

Design and production M&C.M sprl - www.mcmanagement.be

Graphics and layout A collaboration between M&C.M and De Visu - www.devisu.com

Editor Marc-F. Everaert (M&C.M sprl) [email protected] With thanks to the management and staff

Photos M.F. Everaert / RAWBANK / Istock

Printing Imprimerie Artoos | Hayez - Belgium © June 2016

ANNUAL REPORT 2015 RAWBANK

03

04

← TABLE OF CONTENTS

R A W B A N K 2 0 1 5 I N P E R S P E C T I V E

01

07 Strengths and assets in the view of the Chairman of the Executive Committee

09 Business development: continuing growth

11 Corporate & Institutional Banking (CIB)13 Commercial Banking 15 Private Banking16 Retail Banking18 Across all functions: “Customer Experience”

19 The Branch Network: a strategy for strengthening a local presence

22 The Treasury Department: an outstanding nerve centre

C H A P T E R

05

← TABLE OF CONTENTS

Perspective 2017: the Atrium, the Bank’s future Head Office.

In the foreground: Thierry Taeymans, Chairman of the Executive Committee.

06

← TABLE OF CONTENTS

S TRENG TH S A ND A S SE T S IN THE V IE W OF THE CH A IRM A N OF THE E X ECU TI V E C OMMIT TEE

A few highlights deserve particular attention:

What can we learn from 2015?

Our economy has turned the page of several years of growth in which commodity prices were reaching new heights, the mining companies were pulling a significant number of job-creating SMEs along in their wake, the commercial activities of the banks were growing strongly … At the same time, the banking sector stabilised after having experienced the arrival of a large number of new Pan-African players. Some of them have only achieved a break-

through at the price of risks which they had poorly assessed the consequences of, and which they are now suffering from.

Given this, we have continued to maintain a very active – but never aggressive – commercial approach, out of concern for our customers and the market as a whole, while maintaining full control of our operating and credit risks.

RAWBANK confirms its leading position in a market consisting of 18 banks, with an average market share of 21% of total deposits and loans, up 1% compared to 2014. According to the criteria selected, RAWBANK now has a market share of 6 to 8 points more than that of its closest competitors.

The bank now has over one billion dollars in total assets (USD 1.087 billion), or 20% of the total assets of all the banks.

Profitability is in line with GNP of USD 91.5 million and NBI exceeds USD 9 million.

These successful results are spread over the four lines of business of the sales organisation, which are all experiencing excellent market penetration with satisfactory growth rates:

• Corporate & Institutional Banking• Commercial Banking• Private Banking• Retail Banking

The credit rating was confirmed at the beginning of 2015 as ‘stable outlook’. This performance is highly appreciated in the market; it reassures correspondent banks as to RAWBANK’s standing, opens new doors with major groups active in the DRC and enables the bank to have access to new international sources of financing.

For reference, as announced in the 2014 annual report, RAWBANK became the first bank in the Democratic Republic of Congo – and also in the central African region – to obtain a credit rating from Moody’s Investor Services. The grade awarded, B3, is the highest grade a bank can receive in the DRC and is on the same level as the sovereign grade awarded to the DRC for the first time in its history in September 2013.

L E A D E R S H I P CONFIRMED

M O O D Y ’ S IN V E S T O R S E R V I C E S

1 .

07

RAWBANK 2015 IN PERSPECTIVE RAWBANK

← TABLE OF CONTENTS

Regardless of the concerns related to changes in the international economic outlook and its consequences for the DRC, and despite the wait-and-see policy due to the forthcoming elections in the country, the Board of Directors and the Executive Committee continue to pursue their vision of long-term development.

To illustrate RAWBANK’s aims, the following are the four main challenges that the bank intends to address successfully during the next two years:

• To extend its branch network in order to strengthen its local-ly-based services and to be able to offer services as quickly as possible in the main towns of the 26 provinces of the DRC

• To extend the penetration of the SME segment in pursuit of the momentum of 2014 and 2015

• To improve operating efficiency through a thoroughly redesigned organisational management strategy and through optimum use of its computing facilities

• To promote the new financial technologies to provide new, cheaper and high quality financial services to all customer segments

These four projects are described in the current annual report.

Two financial partnerships were concluded in 2015. One is with Proparco, amounting to USD10 million to strengthen the bank’s ability to provide loans to SMEs, and the other with Shelter Afrique, amounting to USD10.6 million to enable the bank to offer property loans. These two lines of credit were fully taken up in 2015.

RAWBANK has been certified to ISO/IEC 20000 and ISO/IEC 27001 since 21 August 2015 at the end of a process which began in April 2014.

• ISO/IEC 20000-1:2011 certification covers the system for managing IT services. Compliance with ISO 20000 standards enables IT audit and management to be improved and strengthened to meet the highest requirements in terms of governance of information technology. This optimises IT services management systems in order to reduce the risks and costs they entail.

• ISO/IEC 27001:2013 certification covers the requirements relating to establishing, implementing, updating and the continuous improvement of the information security management system, and for the assessment and treatment of security risks.

These two certifications have been awarded by BSI, an international body accredited by ISO (the International Organisation for Stand-ardisation) for the certification of enterprises using the various ISO standards.

P R O PA R C O SHELTER A F R I Q U E

I S O 2 0 0 0 0 A N D 2 7 0 0 1

R AW B A NK ’S

A IM S

In June 2015, RAWBANK was the only bank in the DRC to have sent two delegates to the week-long certified training programme organised by the International Finance Corporation (IFC) in Abidjan dealing with social and environmental responsibility.

The bank now includes the environmental performance standards adopted by the IFC in its operating procedures with regard to the “Equator Principles” used by the major international banks. These principles take social, societal and environmental criteria into account in the financing of projects.

Another first for RAWBANK in the DRC.

EN V IRONMEN TA L R E S P O N S IB IL I T Y

RAWBANK ANNUAL REPORT 2015

08

← TABLE OF CONTENTS

• On the Corporate & Institutional Banking market, the first half of 2015 was exceptional in terms of growth in deposits, enabling the bank to take two additional market-share points. The collapse in the prices of raw materials, including copper and oil, resulted in a follow-on downturn in deposits of companies active in these sectors during the second half of the year.

• On the SME Commercial Banking market, performance is twofold. Firstly, we have successfully met the challenge of an approach that was spe-cifically focused on small businesses in Kinshasa. We intend to extend this to cover the whole country, beginning in 2016. At the same time, we also intend to strengthen the bank’s market share of the SME segment in all regions. The bank also continues to develop business relationships between its SME customers and large corporations.

BUSINE S S DE V ELOPMENT: C ONTINUING G ROW TH

At 31 December 2015, RAWBANK had a 22% market share of total bank deposits and 19% of total loans in the DRC, confirming its leading position and the confidence of its customers.

Didier Tilman, Commercial Manager and Member of the Executive Committee:

The new sales organisation set up in 2014 is bearing fruit. It has helped to set in motion a new phase of growth, and as a result in 2015 the bank achieved success in all its lines of business.

View Didier Tilman’s message (in French)

(1’50’’)

2 .

09

RAWBANK 2015 IN PERSPECTIVE RAWBANK

← TABLE OF CONTENTS

• In the Private Banking VIP customer segment, the bank is attracting a growing number of carefully selected customers, to whom it offers a high quality, tailor-made service in comfort-able private areas, guaranteeing confi-dentiality, both in Kinshasa – with four points of contact – and in Lubumbashi – with two points of contact.

• In the Retail Banking segment, the number of customers, total deposits and total credits continue the growth that began in previous years. The employees of major corporations who are customers of the bank have their own bank accounts and are eligible for credit facilities, in some cases of up to 15 times their monthly salary, with a repayment period of up to 5 years. In addition, 80,000 civil servants and state employees have accounts with

the bank and 34,000 INSS [National Social Security Institute] pensioners are currently having bank accounts set up.

• The RAWBANK networks are developing in line with this growth.

- The national network is now organised into five regions, each under the supervision of a Sales Manager. They are Kinshasa / West / Centre / East / South, covering all 26 provinces.

- In addition to the Brussels Repre-sentative Office, the international network will soon be extended by the opening of a representation office in Shanghai.

There are four objectives in opening this office in Shanghai:

• To strengthen contact with the parent companies of Chinese companies operating in the DRC

• To develop relationships with Chinese banks and with cor-respondent banks in particular

• To penetrate the market of Congolese merchants estab-lished in China, in particular in Guangzhou, to promote the use of the RAWBANK CHINA UNION PAY payment card

• And, in general, to keep up to date with market trends and business development prospects.

RAWBANK is working on two major projects to strengthen its sales portfolio and the quality of its services. It is optimising the efficiency of its support services and also launching an electronic banking facility.

The success of these two projects will strengthen RAWBANK’s position across the market.

RAWBANK ANNUAL REPORT 2015

10

← TABLE OF CONTENTS

After a significant 14% increase during the first six months of 2015, deposits by major corporations and institutional customers have returned to levels slightly lower than those at the end of 2014. This rarely observed change was caused by two factors: the release, during the second half of the year, of major deposits for investment by certain enterprises which are customers of the bank and, above all, the fall in the price of copper, which has obviously had a significant impact on the reduction of the amounts repatriated by the mining companies.

Despite these external factors, RAWBANK CIB has continued to gain new customers and to strengthen its position with several existing customers, due mainly to the strength of its central-ised sales organisation.

This improved commercial approach has enabled the credit portfolio granted to major corporations to grow signifi-cantly, up by 24% in one year.

This has enabled the bank to maintain its market share of this segment, which is highly sought after by the competition.

T HE NE W BE NE F I T S O F C IB

The new benefits of the CIB line are clearly recognised and appreciated today. They include:

• Centralised management of major accounts, which enables customers whose organisation has rapidly expanded throughout the country to optimise their financial consolidation by providing a cash management service in line with their needs, with the effective support of the bank’s Treasury Department for investments and foreign exchange transactions.

CORP OR ATE & INS T IT U T ION A L BA NK ING (CIB)

Etienne Mabunda, CIB National Manager:

The CIB package offers three key benefits:

The size of the bank’s balance sheet and its financial soundness

Its extensive network, offering a range of services locally

Centralised management of customer accounts

+24%

11

RAWBANK 2015 IN PERSPECTIVE RAWBANK

← TABLE OF CONTENTS

• This centralisation also makes it possible to obtain an in-depth knowledge of customers, due in part to the development of a customised CRM tool, and as a result to be able to recommend the most comprehensive package in line with their needs and business, whether within the country or for import/export.

• The bank’s extended network also provides a locally based service not only for the companies themselves (for raising cash, for example) but also, and in particular, for their staff who appreciate the bank’s range of facilities (payment of salaries into a

bank account, bank cards, savings, personal loans, electronic banking, etc.).

• Assistance by the bank to SME customers and suppliers of major cor-porations to enable them to optimise their business relationships by, for example, tailored ‘distributor loan’ and ‘supplier loan’ packages.

• The enhanced ability of the bank to secure the availability of sizeable loans for major corporations. Given the level of its capital resources (USD130 million), the bank can now offer loans of up to USD25 million per customer.

Although the 2016 financial year is a difficult one, RAWBANK CIB is doing everything possible to support its customers through a high-quality portfolio that has rarely been equalled.

The bank is concentrating its efforts on new business opportunities that have not yet been taken into account by the competition and, at the same time, is strengthening its commercial approach with a comprehensive package which meets all the requirements of its major corporate and institutional customers effectively.

RAWBANK ANNUAL REPORT 2015

12

← TABLE OF CONTENTS

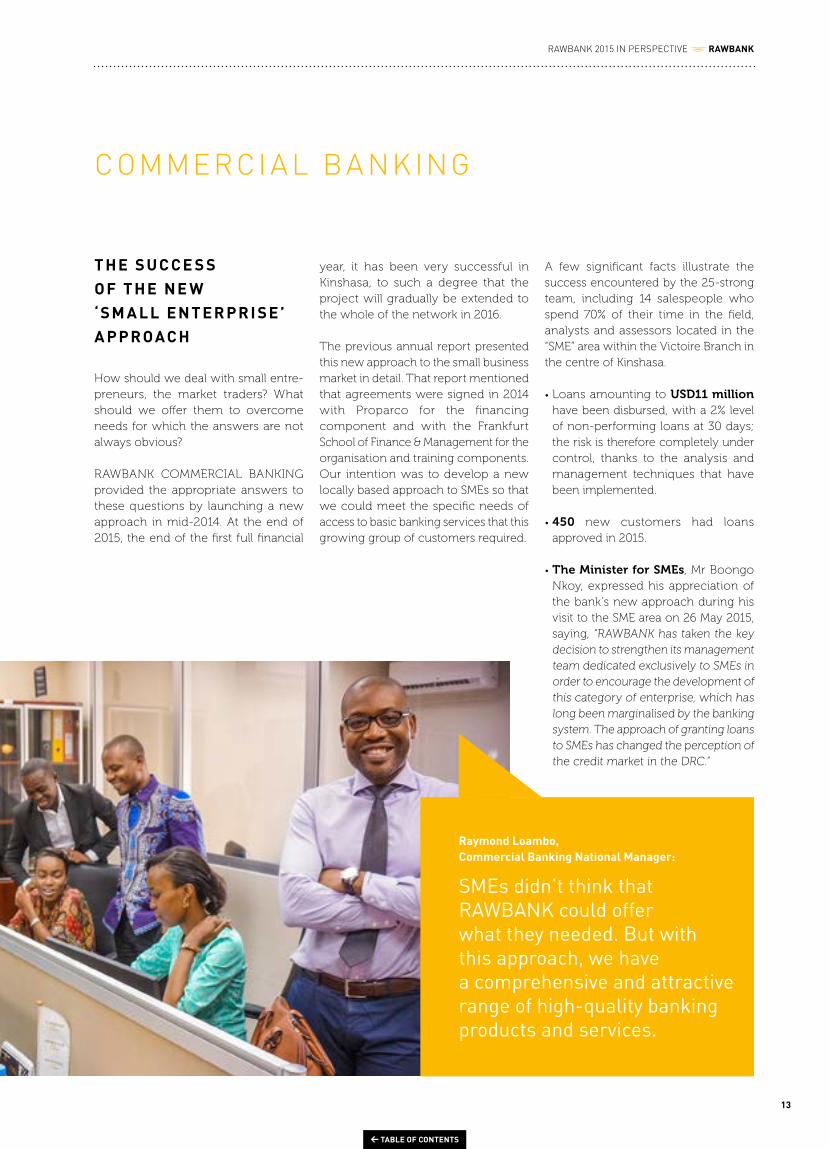

year, it has been very successful in Kinshasa, to such a degree that the project will gradually be extended to the whole of the network in 2016.

The previous annual report presented this new approach to the small business market in detail. That report mentioned that agreements were signed in 2014 with Proparco for the financing component and with the Frankfurt School of Finance & Management for the organisation and training components. Our intention was to develop a new locally based approach to SMEs so that we could meet the specific needs of access to basic banking services that this growing group of customers required.

A few significant facts illustrate the success encountered by the 25-strong team, including 14 salespeople who spend 70% of their time in the field, analysts and assessors located in the “SME” area within the Victoire Branch in the centre of Kinshasa.

• Loans amounting to USD11 million have been disbursed, with a 2% level of non-performing loans at 30 days; the risk is therefore completely under control, thanks to the analysis and management techniques that have been implemented.

• 450 new customers had loans approved in 2015.

• The Minister for SMEs, Mr Boongo Nkoy, expressed his appreciation of the bank’s new approach during his visit to the SME area on 26 May 2015, saying, “RAWBANK has taken the key decision to strengthen its management team dedicated exclusively to SMEs in order to encourage the development of this category of enterprise, which has long been marginalised by the banking system. The approach of granting loans to SMEs has changed the perception of the credit market in the DRC.”

COMMERCI A L BA NK ING

Raymond Loambo, Commercial Banking National Manager:

SMEs didn’t think that RAWBANK could offer what they needed. But with this approach, we have a comprehensive and attractive range of high-quality banking products and services.

T HE S U C C E S S O F T HE NE W ‘SM A L L E N T E R P R I SE ’ A P P R OAC H

How should we deal with small entre-preneurs, the market traders? What should we offer them to overcome needs for which the answers are not always obvious?

RAWBANK COMMERCIAL BANKING provided the appropriate answers to these questions by launching a new approach in mid-2014. At the end of 2015, the end of the first full financial

13

RAWBANK 2015 IN PERSPECTIVE RAWBANK

← TABLE OF CONTENTS

T HE BR E A K T HR O U G H O F C O MME RC I A L B A NK IN G IN T HE B A NK ’S BU SINE S S

The Commercial Banking line of business for the SME market is broken down into three parts:

1. Medium-sized enterprises over the bank’s entire network;

2. Small enterprises for which the specific approach described above has proved successful;

3. Lady’s First, a programme established in 2010 with the support of the Inter-national Finance Corporation (IFC) which is effective in promoting the place of women at the very heart of the bank’s customers.

2015 has been an excellent year across all these segments in terms of commercial development, with tight control over costs and risks. The Commercial Banking portfolio has grown by 69% in terms of deposits and by 35% in terms of outstanding credit.

It is RAWBANK’s intention to support the owners of SMEs more than ever in developing their business.

E N C O U R AG IN G P R O SP EC T S

A wait-and-see attitude seems to be prevalent as regards economic devel-opment in 2016. This is not preventing RAWBANK focusing more and more on the key SME segment.

• The sales organisation will be restruc-tured to create a new SME business development team within each branch.

Internal trainers have been trained to organise the Frankfurt School approach in each branch.

• The bank is preparing to implement a new approach to training courses designed by the International Finance Corporation (IFC), called Business Edge. These training programmes are intended for owners of SMEs who want to improve the management of their business and make it more competitive. Several internal trainers have received awareness training and been trained by experts from the IFC to provide these training courses, which are open to all SMEs, whether customers of the bank or not.

• Other innovative products are being prepared and should be launched during 2016 to extend the range of products for SMEs.

.

+69%

RAWBANK ANNUAL REPORT 2015

14

← TABLE OF CONTENTS

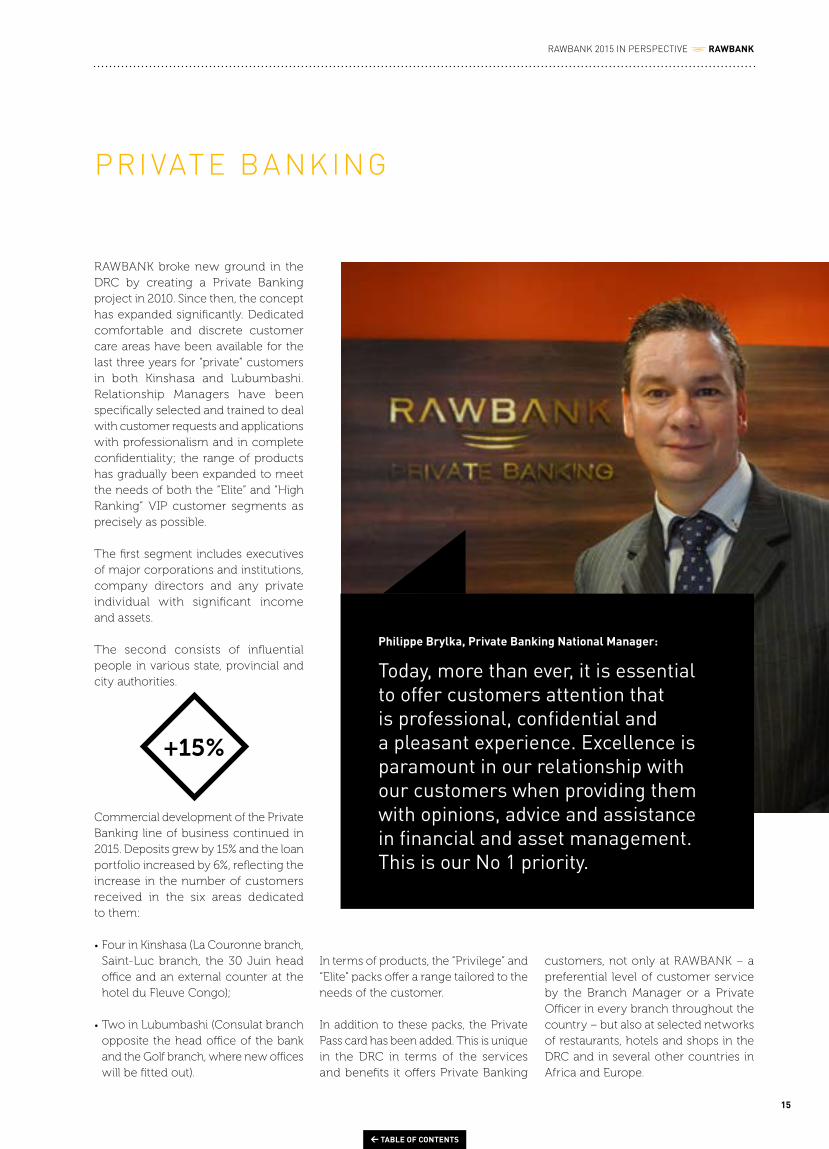

PRI VATE BA NK ING

RAWBANK broke new ground in the DRC by creating a Private Banking project in 2010. Since then, the concept has expanded significantly. Dedicated comfortable and discrete customer care areas have been available for the last three years for “private” customers in both Kinshasa and Lubumbashi. Relationship Managers have been specifically selected and trained to deal with customer requests and applications with professionalism and in complete confidentiality; the range of products has gradually been expanded to meet the needs of both the “Elite” and “High Ranking” VIP customer segments as precisely as possible.

The first segment includes executives of major corporations and institutions, company directors and any private individual with significant income and assets.

The second consists of influential people in various state, provincial and city authorities.

Commercial development of the Private Banking line of business continued in 2015. Deposits grew by 15% and the loan portfolio increased by 6%, reflecting the increase in the number of customers received in the six areas dedicated to them:

• Four in Kinshasa (La Couronne branch, Saint-Luc branch, the 30 Juin head office and an external counter at the hotel du Fleuve Congo);

• Two in Lubumbashi (Consulat branch opposite the head office of the bank and the Golf branch, where new offices will be fitted out).

Philippe Brylka, Private Banking National Manager:

Today, more than ever, it is essential to offer customers attention that is professional, confidential and a pleasant experience. Excellence is paramount in our relationship with our customers when providing them with opinions, advice and assistance in financial and asset management. This is our No 1 priority.

In terms of products, the “Privilege” and “Elite” packs offer a range tailored to the needs of the customer.

In addition to these packs, the Private Pass card has been added. This is unique in the DRC in terms of the services and benefits it offers Private Banking

customers, not only at RAWBANK – a preferential level of customer service by the Branch Manager or a Private Officer in every branch throughout the country – but also at selected networks of restaurants, hotels and shops in the DRC and in several other countries in Africa and Europe.

+15%

15

RAWBANK 2015 IN PERSPECTIVE RAWBANK

← TABLE OF CONTENTS

• Key fact: the sub-segment of so-called “potential” customers has expanded significantly. These customers belong to the middle class, which is gradually expanding in the DRC. Their income, according to the bank’s segmentation criteria, amounts to more than $1000 per month. These customers represent 10% of total retail customers, but their deposits represent 45% of total retail deposits. They use value-added products such as loans and/or savings, bank cards, RawbankOnline, etc. These customers are looked after by customer managers throughout the branch network. The number of managers is expected to increase significantly from 2016.

• The bank has gained some 80,000 civil servants and state employees in a short period of time. Most of them have bank cards, enabling them to use the network of over 300* cash machines throughout country. Some of them have Leopard loans (four times the amount of their monthly salary, repayable in 15 months) which is proving highly popular and indicates the growing interest in the bank’s services by this retail customer sub-segment.

• Several products were highly successful in 2015.

Car and motorcycle loans were popular, particularly at open day events organised by dealers. An “occase-auto” (used car) loan will be launched shortly.

The Habitat loan, launched at the beginning of 2015, did not require media coverage, as demand for it was quickly taken up. The subordi-nated loan of $10.6 million granted by Shelter Afrique for this purpose has been used in full.

Among the savings products, Fidélité continues to be attractive, with 56% of all retail deposits.

LIBERTY PACKS: two new packages intended for the so-called “potential” customer sub-segment seem to be much in demand since their recent launch:

- The Liberty + pack, consisting of a current account, Rapidos Visa Gold card, Travelia, Fidélité account, SMS Banking and RawbankOnline, all for 15,000 Congolese francs per month

- The Liberty pack, consisting of a Fidélité account, SMS Banking and RawbankOnline, all for only 6,000 Congolese francs per month

RE TA IL BA NK ING

For several years, RAWBANK has focused much of its sales efforts on the individual customer segment, which has involved significant development of the branch network and the number of ATMs, providing the best electronic banking products, payment of salaries into a bank account for employees of enterprises that are customers of the bank, and for civil servants and state employees with tailor-made loan packages…

In 2015, the success of this approach was also in line with the amount of effort made, with a significant growth in business.

T HE FO L L O W IN G HI G HL I G H T S A R E IND I C AT I V E O F T HI S G R O W T H

• The number of accounts has increased by 55,000.

• Deposits have increased by 16%; deposits by civil servants and state employees alone have grown spec-tacularly by 43%.

• The credit portfolio has had sound growth of 39%, with the growth of credit to civil servants and state employees peaking at 131%.

• It has been necessary to curb the growth of the retail credit portfolio for the first time, due to the fact that the limit set by the Board of Directors in terms of observing the prudential management ratios was reached before the end of the year. Since then, efforts to increase deposits have been made as a matter of priority.

+39%

* RAWBANK customers have access not only to more than 130 RAWBANK ATMs but also to the ATMs of three other banks: BCDC, ProCredit Bank and FBNBank under the Multipay system.

RAWBANK ANNUAL REPORT 2015

16

← TABLE OF CONTENTS

P R O SP EC T S

In 2016, efforts will be focused above all on improving the level of service that customers receive at the bank counters, on introducing reception desks at the counters to improve traffic flow and so reduce queuing as much as possible, together with ongoing training of staff in how to treat customers, product knowledge, and in the quality of our approach to the way we do business.

The launch of an electronic banking facility (Mobile banking – Mobile Money) will be the finishing touch to the already extensive range of banking products available to individual customers.

Jean-Paul Odent, Retail Banking National Manager*:

Business owners care about how their staff are treated at our branch counters. We are fully aware of this, and we are doing our utmost to provide our customers with the best possible experience by offering a high-quality service and providing first-class banking products, including SMS Banking, which is very much appreciated.

* Effective January 2016, Jean-Paul Odent replaces Michel Brabant, who takes up a new management position at RAWSUR.

17

RAWBANK 2015 IN PERSPECTIVE RAWBANK

← TABLE OF CONTENTS

SE V E R A L SI G NIF I C A N T P O IN T S A R E W O R T H Y O F N O T E .

• Based on customer satisfaction surveys, there appears to be a satisfaction rate of 90%. Good? Yes, but despite everything not enough! Significant efforts are being made on the basis of the information gathered. For corporate customers, surveys are conducted in the form of individual interviews at management level.

• A network of “Quality” correspond-ents has been established within the bank’s branches and departments, with specific instructions in relation to Quality Control and monitoring. The objective: how small actions can solve small problems which, if allowed to build up, could seize up the works.

• As regards the “alternative channels”, the high level of customer satisfaction to now having access to more than 300 ATMs should be noted. The launch of Multipay (see note at the bottom of the previous page) has proved to be an immediate success; from the very first month, the initial statistics registered 5,000 transactions made by customers of the four banks concerned at cash dispensers of banks they are not customers of. This facility has therefore gone a long way towards meeting customer requirements, and the Multipay project continues to evolve.

• Still regarding the use of ATMs, customers now have the Exchange module, which permits withdrawals in Congolese francs or in dollars regardless of the currency of the account to which the card is linked. More than 10,000 transactions of this type are recorded on average each month.

Across al l f unct ions: “C US TOMER E X PERIENCE”

The Customer Experience Department has existed as part of the Sales Department since 2014 under its original name of Customer Relationship Department. This department acted as a focal point for customer complaints, such as problems in using electronic banking, the service provided at the counters, follow-up on accounting records, waiting times for dealing with applications, or calls for help about problems that cannot be solved, etc.

These complaints enabled the necessary measures to be taken to close certain gaps that users of the bank’s products and services noticed. The aim was 100% customer satisfaction!

This department quickly changed as part of the “Client Advantage” strategic plan; it widened its field of activity and took the name “Customer Experience”.

T HR E E IMP R OV E D BU SINE S S S T R E A M S:

1. Three people are in charge of the quality of the database, satisfaction surveys and complaints, respectively.

2. Five people manage the alternative channels, namely the effective use of ATMs, electronic payment terminals (with regular visits to merchants to ensure they are properly trained and manage potential technical problems) and RawbankOnline.

3. One person is responsible for monitoring the services and the devel-opment of the MoneyGramnetwork.

C O N C LU SIO N

“Client Advantage” is more than ever the theme of the actions of the Customer Experience Department.

A Support Committee has also been set up at senior management level, to ensure that appropriate solutions to any major operational problems or problems due to lack of efficiency that could affect the quality and excellence that the customer is entitled to demand can be provided.

BenefitsCustomer

90%

RAWBANK ANNUAL REPORT 2015

18

← TABLE OF CONTENTS

THE BR A NCH NE T WORK: A S TR ATEGY FOR S TRENG TH-ENING A LOC A L PRE SENCE

3 .

At the end of 2015, RAWBANK had 40 branches and 27 external counters as well as a number of cash desks on the premises of major corporate customers.

New branch at Lodja, in the province of

Sankuru

One of the external counters at Inga, an extension of the Matadi branch

19

RAWBANK 2015 IN PERSPECTIVE RAWBANK

← TABLE OF CONTENTS

O P E NIN G O F 11 BR A N C HE S A ND E X T E R N A L C O U N T E R S IN 2015

Several projects were brought to a successful conclusion in 2015, in accordance with the published devel-opment plan.

• Two branches opened at Lodja and Lusambo in the new province of Sankuru in the centre of the country.

• Nine external counters have been established:

� Three in Kinshasa:

- Ndolo-Aéro, an extension of the 30 Juin branch

- “Kimbanguiste”, an extension of the UPC branch

- ISTM (Higher Institute of Medical Technology), an extension of the Ngaba branch

� One in Kolwezi, in the UAC commercial centre, covering two major districts of the city

� Five in the province of Kongo Central (ex Bas-Congo):

- Kwilu Ngongo, an extension of the Kimpese branch, on the premises of Compagnie Sucrière, plus a unit at Kwilu Ngongo station

- Yema, on the border with Angola, an extension of the Moanda branch, plus a unit in the road toll pay station area

The new external counter of the Kimpese branch at the Kwilu Ngongo factory

- Three external counters as an extension of the Matadi branch: Aidel Ticom (new dry port), Inga and Kinkanda.

The external counters generally consist of at least three people and deal with withdrawals, payments and foreign exchange up to a maximum equivalent to $10,000, as well as MoneyGram transfers.

20

← TABLE OF CONTENTS

O N G O IN G P R O J EC T S A ND P R O SP EC T S

Four branches and external counters will be opened in Kinshasa by the end of the first half of 2016:

• The branches at Bandale, Bayaka and Bon Marché (the “3 Bs”)

• The Matete branches

• Four external counters in Engen filling stations, each consisting of two cash desks and an ATM

At the end of June 2016, RAWBANK will have 35 points of contact in Kinshasa: 17 branches and 18 external counters.

Then, by the end of 2016, and depending on the cyclical trends in the country, it is planned to extend the bank’s presence in some 15 localities throughout the country. The business plans are ready and the installation schedules have been organised.

The objective is to cover the core of the 26 provinces resulting from the recent boundary changes to the country’s provinces as quickly as possible.

R A P ID A ND L I G H T C O N S T RU C T IO N T EC HNIQ U E S

The bank opted for modular construc-tion for some of its new branches and external counters opened in 2015, offering a number of advantages such as lower investment and installation costs, speed of construction and the ability to relocate quickly if new require-ments arise. A set of modules is kept at the bank’s headquarters to be able to respond quickly to any new request.

These modular branches offer com-fortable, high-quality facilities, are constructed of materials that are made to last, and meet the security standards set by the bank’s senior management.

They are the intermediate stage between a large branch built in the traditional way and the small “container” branches such as those used at road toll pay stations.

Counter at Kwilu Ngongo station

At the end

of 2015 there were

40branchesand 27 counters

Modular construction offers several benefits: lower costs, speed of construction and the ability to relocate quickly if new requirements arise.

21

RAWBANK 2015 IN PERSPECTIVE RAWBANK

← TABLE OF CONTENTS

THE TRE A SURY DEPA R TMENT: A N OU T S TA NDING NER V E CENTRE

4.

Antoine Kiala is the Treasury Manager:

One of RAWBANK’s strengths is its ability to respond in real time to any need for cash or liquidity by customers. We continually monitor the bank’s liquidity in conjunction with our representatives in the branches.

RAWBANK ANNUAL REPORT 2015

22

← TABLE OF CONTENTS

As regards managing foreign exchange risk, because the bank opted for the foreign exchange position to be decentralised, each branch manages its position in accordance with its operating limits under the supervision of the General Treasurer. Exchange rates may vary from one city to the next, taking into account local factors that cannot always be effectively managed centrally.

For your information, the USD/CDF exchange rates by city where the bank has a presence are updated daily at www.rawbank.cd.

The outlook for the second half of 2015 was not favourable for the devel-opment of investment and foreign exchange transactions of many large corporations. Oil and mining companies reduced their operations following the sharp decline in the price of their products, and some mining companies even stopped production. Despite this, RAWBANK retains an almost 30% share of the foreign exchange market in the DRC, which reflects its ability to respond effectively and with professionalism to its customers’ needs. The currencies traded are mainly the dollar and the euro, but also the Chinese renminbi, the South African rand, the Swiss franc, the Canadian dollar and the pound sterling.

A highlight of the second half of the year was the need to acquire new deposits to cope with a growing demand for credit, particularly by the Retail Banking sector. By adopting a customer-focused strategy and with the support of the

sales departments, the Treasury has been able to inject new deposits into the bank, while respecting the prudential ratios as regards managing liquidity.

At the same time, faced with interna-tional markets offering low or even negative rates, part of the bank’s cash has been invested in prime quality international bonds that are easily available and offer a yield of 2 to 5%, representing an investment portfolio three times larger than that at the end of 2014.

Vigilance is the watchword for 2016. At the start of this year, the forecasts as to the ability of the Congolese franc to maintain a certain parity with the dollar are uncertain in light of the decline in state revenues related to the reduction in oil and mining activities. In one year, the international reserves fell from USD1.8 to 1.4 billion, the equivalent of approximately five weeks’ imports.

In addition, the ever-growing use of cash machines means that there is a need for a significant supply of new banknotes, in particular in dollars. The bank must export the used banknotes that it receives in the form of payments and import new notes; monthly imports amount to approximately $180 million. This results in costs which must be taken into account in day-to-day management to cushion the impact as much as possible.

With the rapid development of sales activities, the Treasury is increasingly one of the bank’s core nerve centres and a significant profit centre. It is constantly in touch with the treasurers of large corporations, and keeps a watchful eye on the proper conduct of foreign exchange and investment transactions, as well as on the liquidity of the bank as a whole.

23

RAWBANK 2015 IN PERSPECTIVE RAWBANK

← TABLE OF CONTENTS

24

← TABLE OF CONTENTS

A N E W E F F I C I E N C Y S T R A T E G Y

02

26 POINT OF VIEW - Overview by the new Deputy CEO

29 Performance in line with organisational and operating efficiency

30 The IT Department32 In perspective: Mobile Banking34 The Operations Department36 The Organisation Department

C H A P T E R

25

← TABLE OF CONTENTS

P OINT OF V IE W - OV ER V IE W BY THE NE W DEP U T Y CEO

1 .

L O O K IN G FO R WA R D T O L O N G -T E R M G R O W T H

Mustafa Rawji has been Vice-Chairman of the bank’s Executive Committee since the beginning of 2015. In June 2015, he was appointed Deputy CEO, responsible for assisting the General Manager and supervising the Logistical Support, IT, Operations and Organisation Departments. His remit, in coordination with the four managers who lead their departmental teams, is to put in place the operating efficiency tools that will enable RAWBANK to optimise its momentum for growth while reducing the size of its administrative organisation so as to create a lightweight, flexible, efficient and highly reactive tool, driving performance.

This new approach is intended to improve both the cost-to-income ratio and customer satisfaction in the use of RAWBANK products and services. It forms part of the “Client Advantage” Strategic Plan launched in 2014 and presented in the 2013 Annual Report published in May 2014.

Mustafa Rawji, Deputy CEO and Vice-Chairman of the Executive Committee:

We want a lightweight, flexible, efficient and highly reactive tool, driving performance.

From listening to staff, customers and the market as a whole, Mustafa Rawji had proposed and then implemented the “CLIENT ADVANTAGE” strategic project with the assistance of his colleagues. This gave RAWBANK a new lease of life and a new sales impetus in a market that had become hyper-competitive, and in so doing strengthened the bank’s leading position in the DRC, providing customers with better service and added value.

• One of the shareholders in the bank, he understands, assesses and shares the entrepreneurial risk.

• A member of senior management, he is a man of action, keen to drive the company forward as regards performance, and shares his desire for excellence with his colleagues on the Executive Committee, and with the managers and staff of the bank.

On both these counts, in these pages, he gives his point of view on how he sees RAWBANK developing and on its 2014-2016 “Client Advantage” business plan, addressing at the end his vision and his strategy of efficiency for driving long-term development.

RAWBANK ANNUAL REPORT 2015

26

← TABLE OF CONTENTS

1. The sales aspect of “Client Advantage”

“Our strategic plan looks three years ahead, covers all the bank’s activities and involves every department. Imple-menting it has had some immediate effects as a result of the motivation and involvement of members of staff who were informed through and stimulated by an intensive internal communication plan and programme.

One measure has very quickly borne fruit with regard to sales – the new segmentation of customers into four sales departments, each consisting of specifically trained bank professionals who are experienced in their respective fields (see page 8 and following of this report).

This has enabled us to organise and streamline the services we offer to maximum effect by setting up distri-bution channels specifically tailored to the needs and expectations of each of these customer segments. We have done this to the satisfaction of each of our customers, as we can measure and as evidenced by our commercial and financial results.

Among these results, one in particular deserves to be highlighted. It is the result of the new commercial approach that we initiated in September 2014, which focuses on a particularly important market segment in terms of the economic development of the DRC – that of the SMEs.

Our Commercial Banking department set out to conquer a structurally difficult market – the small and medium enterprise market, in which the majority still work in the informal sector and for which credit risk is even greater because it is difficult to assess. Although surrounded by experts, we took a risk as a banker-entrepreneur… and we were

right to do so (see page 12 of the report). It was a real challenge, and a year later we can measure the positive impact not only in terms of the bank’s profits, but, and which is even more important, on the lives of our SME customers, who are growing thanks to our support.”

2. Managing talent – the cor-nerstone of the business plan

“To support this large-scale commercial roll-out, we needed talented people who are capable of meeting our aims and, above all, an HR organisation in tune with this enormous project, whose long-term future we want to ensure.

Today, our Human Resources Department, renamed “Human Capital” and reporting directly to the General Manager, is split into three sections:

• “HR Business Partner” focuses on managing job and skill requirements so that the organisation can respond at any time and anywhere to the need for skilled staff, whether in terms of reacting quickly to a specific need or organising a planned development.

• “HR Recruitment” takes a continuously proactive approach towards recruiting the best talented people the organ-isation needs to ensure that it can support our development efficiently across all departments.

• “HR Administration” deals with the day-to-day operations which are required so that everyone working for the organisation can function smoothly and efficiently.

What is our objective?

To offer our staff a work environment within which we intend to give them the means to be trained, as a result primarily of the smooth running of the Rawbank Academy, and to be motivated, to flourish and to find enjoyment in their work so that, in the end, they satisfy the CUSTOMER, who occupies a key position in the organisation.”

3. Focus on operations management

“The developments we have just spoken about only make sense if they are backed up by first-class financial, organisational and operations management. There are two main reasons for this. Both financial performance measurement tools and decision-making instruments in terms of growth must be available.

Financial performance is dependent on strict control over and monitoring of operating costs. Optimising costs also enables the company to be better positioned in an extremely aggressive competitive market. How can we react effectively to this aggressive-ness if control over costs cannot be guaranteed? If cost rationalisation cannot be reconciled with productivity measurement? If the measurement tools do not enable the most appropriate decisions to be taken? It is all a question of financial management analysis which we are working on in order to refine our tools as quickly as possible.

At the same time, we have redeployed our Organisation Department as a strategic tool in the ongoing search to optimise our processes. More than ever before, these processes must be flexible, while retaining complete control over operational risks, but always with

27

A NEW EFFICIENCY STRATEGY RAWBANK

← TABLE OF CONTENTS

the aim of achieving efficiency and profitability. Within this department, an “Operational Efficiency” section has been created, whose remit is to analyse the processes, to simplify them as far as possible, and to reduce the unproduc-tive use of time and resources as much as possible. In short, to put intelligence and creativity to use to help with the organisational process. And to do this with the CUSTOMER in mind at all times.”

4. In Perspective

“In the next two years, we intend to focus our attention and efforts in the Executive Committee on the efficiency of the organisation. We have decided to focus on consolidating our gains after several years of rapid growth which, since the bank’s tenth anniversary almost three years ago, have made us market leader.

However, we do not intend to curb either our initiatives and spirit of innovation, or our growth. On the contrary, we want to keep on being involved with our customers and to respond to requests by continually releasing innovative products such as, for example, “electronic banking”

which we are ready for and which will fundamentally turn banking product usage habits upside down.

But we must take care that we do not get too carried away and ensure that we are capable of expanding in line with short, medium and long-term needs by strengthening every aspect – financial, human, technical, organisational, commercial and administrative – as much as possible.

The Board and the Executive Committee are overseeing this because we want to be a modern, efficient and competitive bank, able to serve a million customers tomorrow in a market we believe in, especially as our family has been involved in it for almost a hundred years.”

These initiatives form part of an ongoing medium and long-term thought process: would we be capable of managing a bank with a network of 200 branches? Would we be able to absorb rapid growth without causing an imbalance in our organisational and financial structure? Because the market could change very quickly…

RAWBANK ANNUAL REPORT 2015

28

← TABLE OF CONTENTS

T O WA R D S A NE W D IME N SIO N IN S U P P O R T SE R V I C E S

How can we facilitate growth and avoid bottlenecks in support services? Or how can we optimise the management of all the flows within the bank to improve returns, and therefore efficiency and productivity? Or yet again, how can we raise “internal customer” satisfaction, knowing that, at the end of the day, end-customer satisfaction depends on the sum of internal added value?

To put the tools in place that will enable these questions to be answered with a vision and long-term perspective of the bank’s development and its performance, the organisation chart of the main support services has been reviewed to enable each individual to focus on their core activities, coor-dinated by the Deputy CEO, who is responsible for this to the Board.

• The Resources Department takes the new name of Logistical Support Department and will focus on the development and maintenance of the network, logistics services and document management.

• The IT Department retains its operating structure but works in ever closer collaboration with the Organi-sation Department in particular.

• The Operations Department is in the process of optimising how operations entrusted to us by the customer are processed to simplify the procedures as much as possible and to free up many administrative tasks which can then be redirected to front-facing customer services.

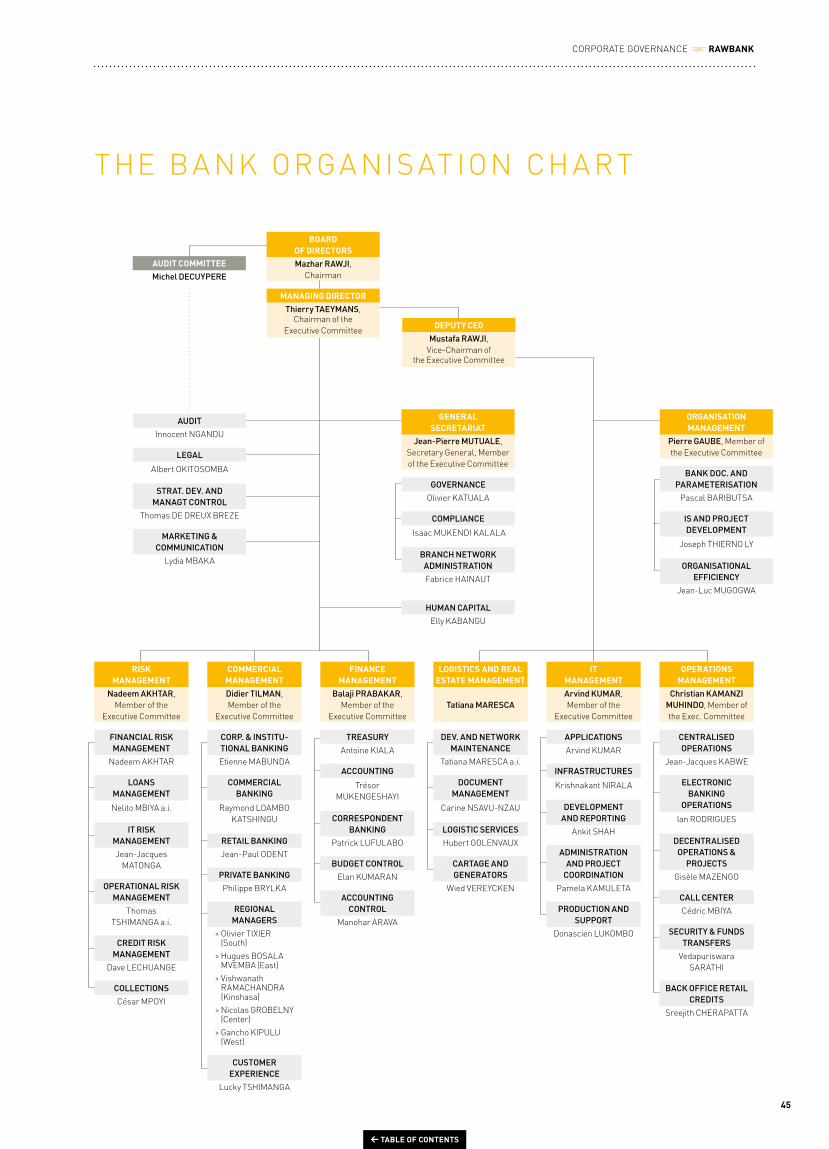

These three departments are on the same line in the new organisation chart (see page 45).

• The Organisation Department, which was formerly the Resources Department, comes under staff insofar as it does not form part of operating activities but is located in the management, analysis and strategic planning centre with three depart-ments – banking documentation and specifications, information system development and projects, studies and organisational efficiency.

PERFORM A NCE IN L INE W ITH ORGA NIS ATION A L A ND OPER ATING EFFICIENCY

2 .

A glance at three key departments at the centre of the new process of efficiency: IT, Operations and Organisation.

The organisation chart of the main support services has been revised to enable each individual to focus on their core activities.

29

A NEW EFFICIENCY STRATEGY RAWBANK

← TABLE OF CONTENTS

A few significant highlights should be mentioned with regard to IT develop-ment in 2015.

I S O C E R T IF I C AT IO N

RAWBANK has been certified to ISO/IEC 20000 and ISO/IEC 27001 since 21 August 2015 at the end of a process which began in April 2014.

ISO/IEC 20000-1:2011 certification covers the system for managing IT services. Compliance with ISO 20000 standards enables IT audit and management to be improved and strengthened to meet the highest requirements in terms of governance of information technology. This optimises IT services management systems in order to reduce the risks and costs they entail.

ISO/IEC 27001:2013 certification covers the requirements relating to establish-ing, implementing, updating and the continuous improvement of the data security management system, and for assessing and dealing with security risks.

These two certifications are both new guarantees of rigorousness and quality in the way internal processes are dealt with and in the provision of the bank’s services to its customers.

They were awarded by BSI, an inter-national body accredited by ISO (the International Organisation for Standardi-sation) for the certification of enterprises using the various ISO standards.

THE IT DEPA RTMEN T

RAWBANK is the first bank in Central Africa to be ISO 20000 and ISO 27001 certified simultaneously.

What could be more reassuring for all RAWBANK’s partners and stakeholders than to work with an organisation which has robust data security policies validated by a body with a world-wide reputation?

T HE MI G R AT IO N T O A MP L I T U D E V10

RAWBANK has updated its integrated core banking system in migrating to version 10 of the Sopra Banking Amplitude solution. This migration, which ended successfully in October 2015, enables the performance of the bank’s activities and the optimisation of the customer relationship to be enhanced, thus accelerating growth. Carried out in close collaboration with the Organisation Department and the Operations Department, this project required some 4,000 man-days.

RAWBANK ANNUAL REPORT 2015

30

← TABLE OF CONTENTS

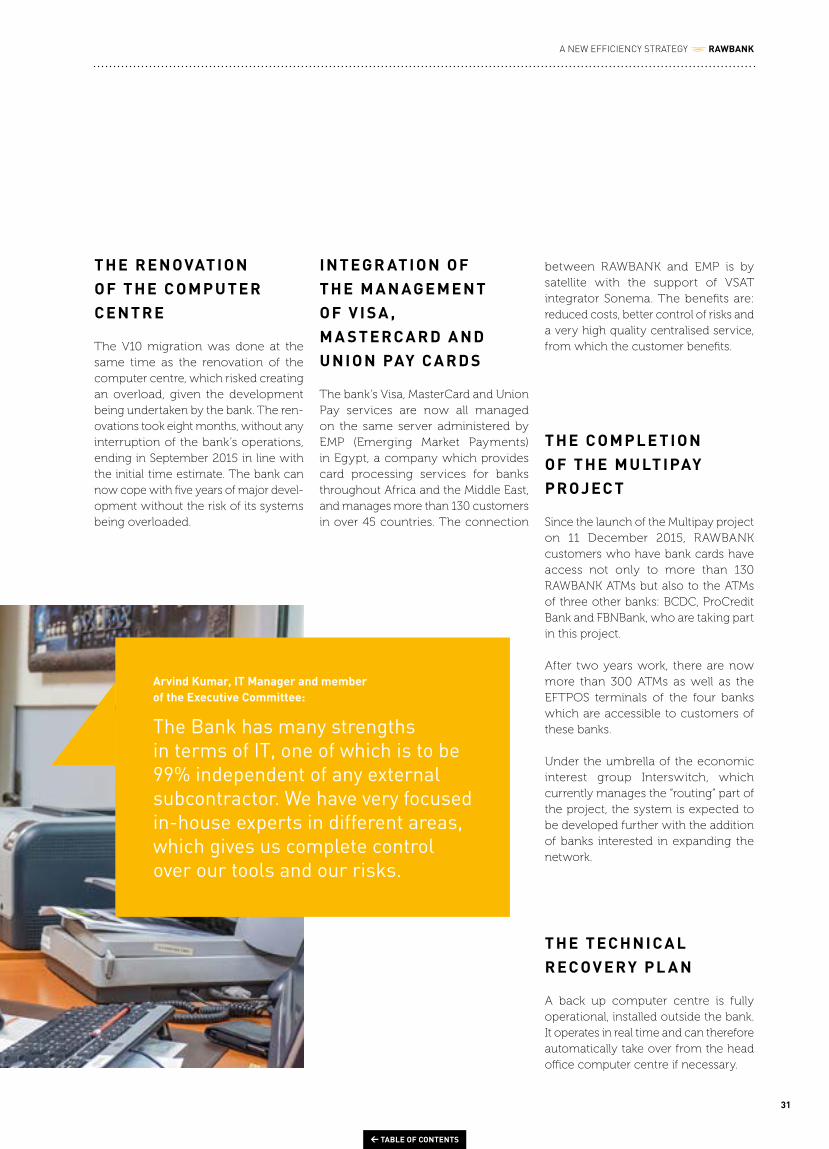

T HE R E N OVAT IO N O F T HE C O MP U T E R C E N T R E

The V10 migration was done at the same time as the renovation of the computer centre, which risked creating an overload, given the development being undertaken by the bank. The ren-ovations took eight months, without any interruption of the bank’s operations, ending in September 2015 in line with the initial time estimate. The bank can now cope with five years of major devel-opment without the risk of its systems being overloaded.

Arvind Kumar, IT Manager and member of the Executive Committee:

The Bank has many strengths in terms of IT, one of which is to be 99% independent of any external subcontractor. We have very focused in-house experts in different areas, which gives us complete control over our tools and our risks.

IN T EG R AT IO N O F T HE M A N AG E ME N T O F V I S A , M A S T E RC A R D A ND U NIO N PAY C A R D S

The bank’s Visa, MasterCard and Union Pay services are now all managed on the same server administered by EMP (Emerging Market Payments) in Egypt, a company which provides card processing services for banks throughout Africa and the Middle East, and manages more than 130 customers in over 45 countries. The connection

between RAWBANK and EMP is by satellite with the support of VSAT integrator Sonema. The benefits are: reduced costs, better control of risks and a very high quality centralised service, from which the customer benefits.

T HE C O MP L E T IO N O F T HE M U LT IPAY P R O J EC T

Since the launch of the Multipay project on 11 December 2015, RAWBANK customers who have bank cards have access not only to more than 130 RAWBANK ATMs but also to the ATMs of three other banks: BCDC, ProCredit Bank and FBNBank, who are taking part in this project.

After two years work, there are now more than 300 ATMs as well as the EFTPOS terminals of the four banks which are accessible to customers of these banks.

Under the umbrella of the economic interest group Interswitch, which currently manages the “routing” part of the project, the system is expected to be developed further with the addition of banks interested in expanding the network.

T HE T EC HNI C A L R EC OV E RY P L A N

A back up computer centre is fully operational, installed outside the bank. It operates in real time and can therefore automatically take over from the head office computer centre if necessary.

31

A NEW EFFICIENCY STRATEGY RAWBANK

← TABLE OF CONTENTS

RAWBANK ANNUAL REPORT 2015

32

The Board and the Executive Committee are of the opinion that electronic banking is the way forward for the bank. It is particularly important because the retail banking market is far from being saturated, as the major corporation banking market may be. But easy, flexible solutions must be available to continue the penetration of this market effectively in a country as big as the DRC.

IN PERSPECTIVE:

MOBILE BA NK ING

Mikhail Rawji, Project Manager:

The approach initiated by RAWBANK is part of an ongoing strategy of developing electronic banking tools. We want to retain control of the professions which are ours but, in order to do this, we need to move forward quickly in terms of electronic technology and think about banking being completely electronic in order to meet the challenge of mobile operators who are today challenging the banks.

RAWBANK intends to maintain its state-of-the-art position and remain at the forefront of technology so that it meets the needs of the market.

← TABLE OF CONTENTS

A NEW EFFICIENCY STRATEGY RAWBANK

33

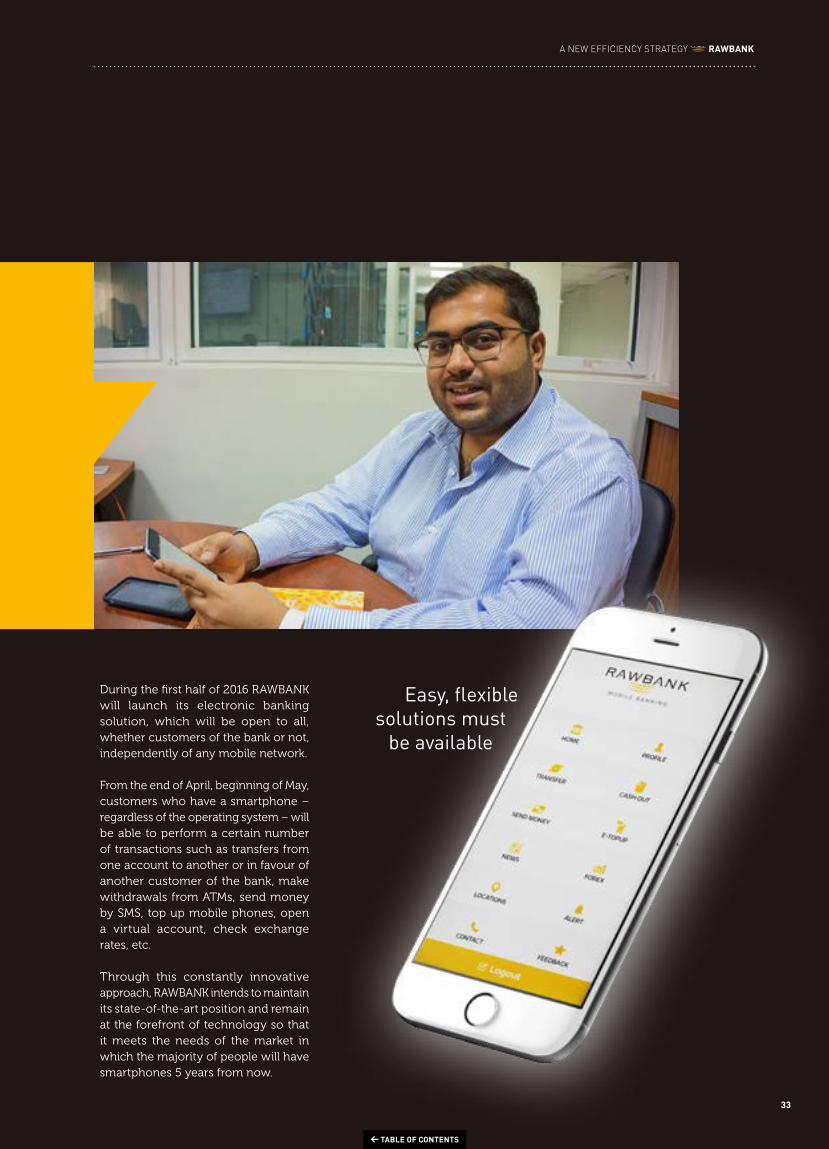

During the first half of 2016 RAWBANK will launch its electronic banking solution, which will be open to all, whether customers of the bank or not, independently of any mobile network.

From the end of April, beginning of May, customers who have a smartphone – regardless of the operating system – will be able to perform a certain number of transactions such as transfers from one account to another or in favour of another customer of the bank, make withdrawals from ATMs, send money by SMS, top up mobile phones, open a virtual account, check exchange rates, etc.

Through this constantly innovative approach, RAWBANK intends to maintain its state-of-the-art position and remain at the forefront of technology so that it meets the needs of the market in which the majority of people will have smartphones 5 years from now.

Easy, flexible solutions must

be available

← TABLE OF CONTENTS

Overall, Operations account for some 60% of the bank’s staff, including those working in branches. This makes a total of almost 800 people who look after customer requests and instructions.

In this respect, RAWBANK is highly regarded for the speed with which it processes transactions; any instruction given to the bank between 8am and 3.30pm must be processed the same day provided, of course, that it fulfils the required conditions.

Reliability is also one of the bank’s assets, as confirmed, for example, by the Euro STP Excellence Award presented in 2013 by the corresponding bank KBC.

In 2015, the Operations Department worked in close collaboration with the IT Department responsible for migrating the banking software package Amplitude to version 10. This migration makes the tool more efficient, more flexible and streamlined, and makes it possible to process many operations more quickly.

T O WA R D S G R E AT E R O P ER AT IO N A L E F F I C IE N CY

This new tool is the first stage in the “Operational efficiency” approach which will take place during 2016 and 2017 under the direction of the Deputy CEO and will result in optimising the management of financial flows within the bank and to improved performance and therefore improved efficiency and productivity.

This is increasingly important since the number of transactions processed is increasing significantly, as the figures show.

THE OPER ATIONS DEPA RTMEN T

Christian Kamanzi, Operations Manager and member of the Executive Committee:

We attach great importance to the ongoing training given to operations staff. This is what it takes to ensure the quality of their work, and we are developing training programmes in close collaboration with the Rawbank Academy, which organises not only theoretical training courses but practical ones as well to respond very quickly to needs.

RAWBANK ANNUAL REPORT 2015

34

← TABLE OF CONTENTS

C O N T R O L A ND C O MP L I A N C E

Control of operations and observance of the rules of compliance form part of the strict management rules implemented by the bank for a long time, reviewed on a regular basis and modified in line with changes to regulations and to internal criteria and management standards.

Prudence is also vital and is to the customer’s advantage.

The following two examples illustrate this prudential approach:

• No cheque can be paid in at bank counters if it equals or exceeds 15,000 dollars in value without the agreement of the issuer, confirmed by telephone.

• An SMS is sent to confirm that a debit or credit transaction has occurred and to log every Visa or MasterCard transaction. This enables customers to react in the event of receiving information about a transaction that they themselves did not initiate.

With regard to compliance, new tools and new databases provide improved automated analyses of data before transactions are finally logged. (See also page 56)

Reliability is also one of the bank’s strengths, as confirmed, for example, by the Euro STP Excellence Award presented in 2013 by the correspondent bank KBC.

The number of transactions processed has increased significantly.

2013 2014 2015

6,077,894

5,339,8824,810,526

+26%in 2 years

35

A NEW EFFICIENCY STRATEGY RAWBANK

← TABLE OF CONTENTS

The Organisation Department is an offshoot of the Resources Department, which it was part of until Q4 2015. Its staff report directly to the Deputy CEO in order to focus efforts on the new “Operational efficiency” strategy already described in the previous pages, which endeavours to provide the bank with the efficiency tools that will enable it to improve its performance in the coming years.

In its new configuration, the Organ-isation Department consists of three departments.

T HE “B A NK D O C U -ME N TAT IO N A ND I S PA R A ME T E R I S AT IO N ” D EPA R T MEN T

This department provides first level support to the other departments of the bank in terms of formalising and

optimising the processes underlying RAWBANK’s activities and their impli-cations for the information system.

The IS parameterisation Department is responsible for the production of new banking software or modules (or features of the latter). Its mission extends, also and perhaps above all, to corrective maintenance (resolution of everyday problems encountered by users) and preventive maintenance (anticipation of potential concerns).

It keeps the data needed for the information system to function up to date on a daily basis. This involves the authorisation of users, definition in the system of new operations or their pricing, creation of new products, etc.

The remit of the Bank Documenta-tion Department is to analyse, produce and develop the processes governing the activities of the bank. In addition, it is also responsible for “setting in stone” all of the bank’s documentation – its procedures, instructions, its security notices and various circulars. It plays an active part in ensuring that every Rawbanker is fully committed to this documentation and supports the opening of new branches.

1

THE ORGA NIS AT ION DEPA RTMEN T

The management of the organisation is putting a lot of effort into the new “operational efficiency” strategy, which endeavours to provide the bank with the efficiency tools that will enable it to improve its performance.

T HE “ I S & P R O J EC T S DE V EL O P MEN T ” DEPA R T MEN T

The IS Development Department works in close collaboration with the IT Department and focuses on the installa-tion of new modules in the system and on updating and increasing the functionality of existing modules. For example, the new version V10 of the banking software package enables several management modules to be implemented, offering the benefit of new features improving the speed and productivity of processing operations by the various departments of the bank. Many modules are currently in the testing phase and will be implemented in line with changes to users’ needs.

The Projects Department works on the development and management of projects regardless of their nature provided they can be classified as management optimisation, whether in terms of organisational efficiency or for the benefit of the customer.

2

RAWBANK ANNUAL REPORT 2015

36

← TABLE OF CONTENTS

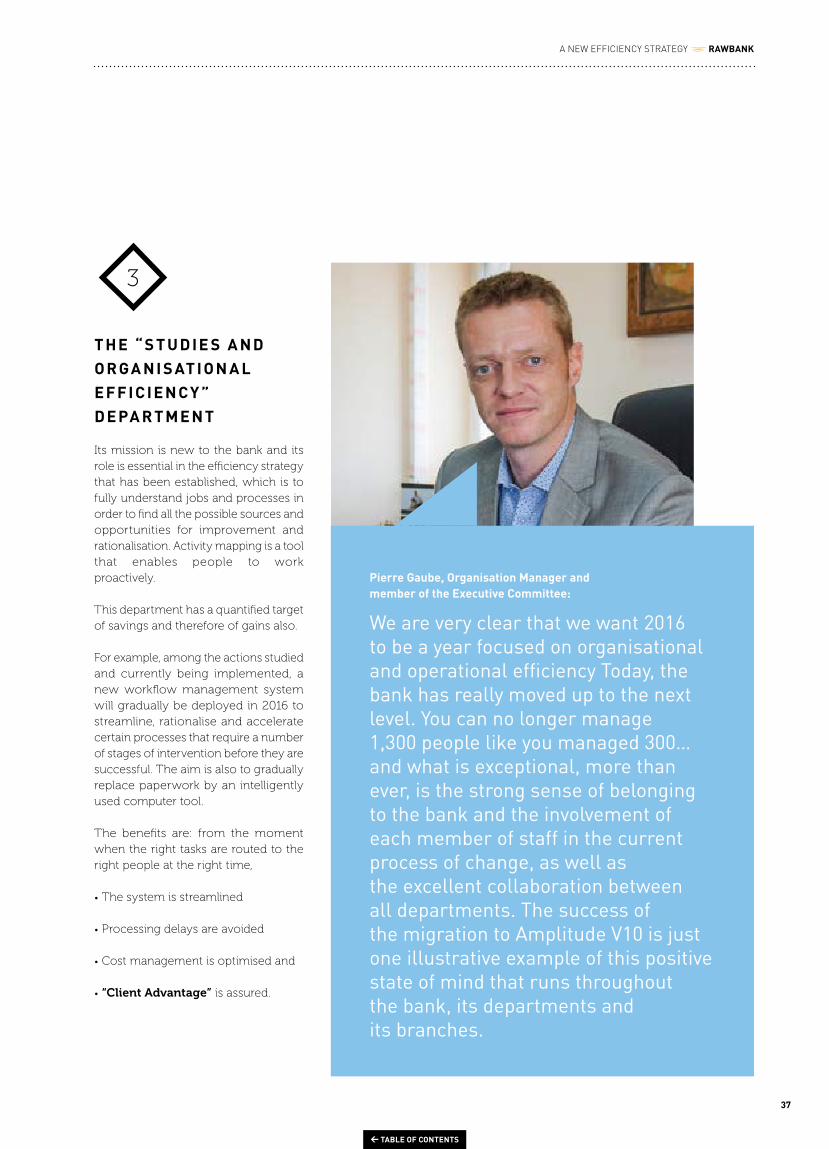

Pierre Gaube, Organisation Manager and member of the Executive Committee:

We are very clear that we want 2016 to be a year focused on organisational and operational efficiency Today, the bank has really moved up to the next level. You can no longer manage 1,300 people like you managed 300… and what is exceptional, more than ever, is the strong sense of belonging to the bank and the involvement of each member of staff in the current process of change, as well as the excellent collaboration between all departments. The success of the migration to Amplitude V10 is just one illustrative example of this positive state of mind that runs throughout the bank, its departments and its branches.

T HE “S T U D IE S A ND O RG A NI S AT IO N A L E F F I C IE N CY ” DEPA R T MEN T

Its mission is new to the bank and its role is essential in the efficiency strategy that has been established, which is to fully understand jobs and processes in order to find all the possible sources and opportunities for improvement and rationalisation. Activity mapping is a tool that enables people to work proactively.

This department has a quantified target of savings and therefore of gains also.

For example, among the actions studied and currently being implemented, a new workflow management system will gradually be deployed in 2016 to streamline, rationalise and accelerate certain processes that require a number of stages of intervention before they are successful. The aim is also to gradually replace paperwork by an intelligently used computer tool.

The benefits are: from the moment when the right tasks are routed to the right people at the right time,

• The system is streamlined

• Processing delays are avoided

• Cost management is optimised and

• “Client Advantage” is assured.

3

37

A NEW EFFICIENCY STRATEGY RAWBANK

← TABLE OF CONTENTS

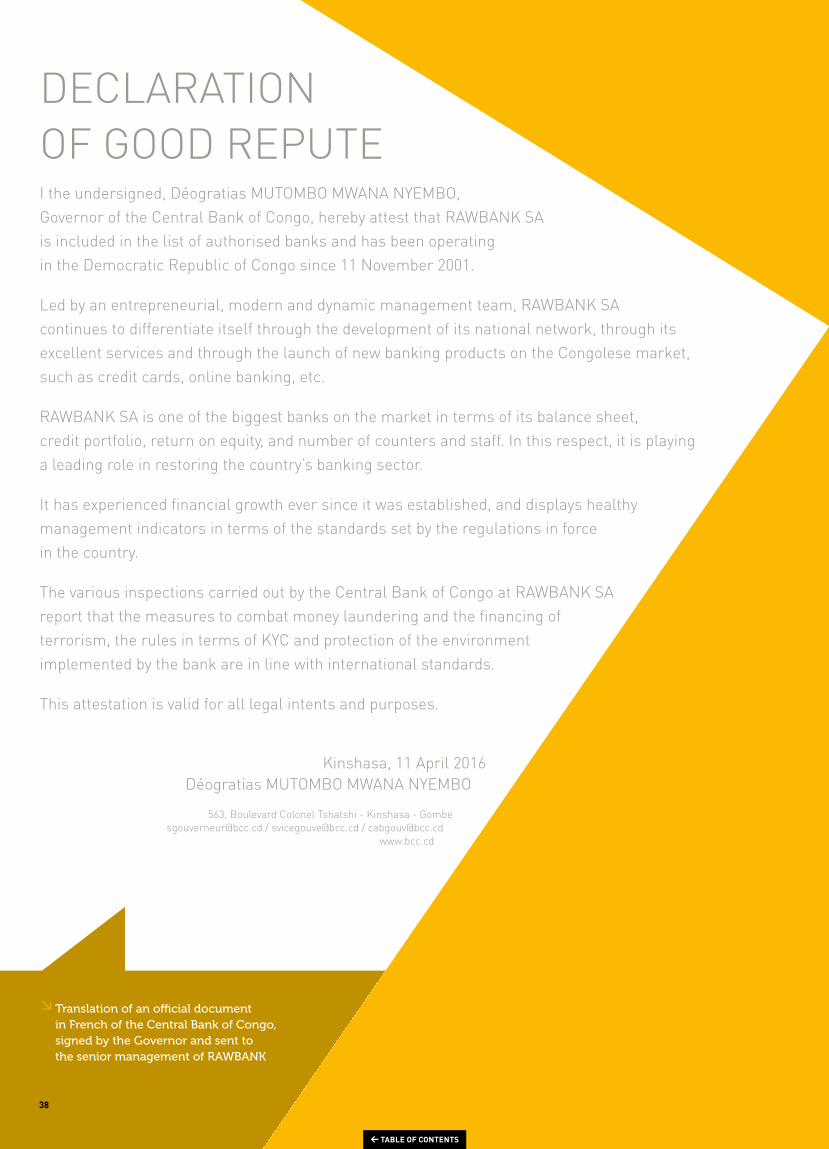

DECLARATION OF GOOD REPUTE I the undersigned, Déogratias MUTOMBO MWANA NYEMBO, Governor of the Central Bank of Congo, hereby attest that RAWBANK SA is included in the list of authorised banks and has been operating in the Democratic Republic of Congo since 11 November 2001.

Led by an entrepreneurial, modern and dynamic management team, RAWBANK SA continues to differentiate itself through the development of its national network, through its excellent services and through the launch of new banking products on the Congolese market, such as credit cards, online banking, etc.

RAWBANK SA is one of the biggest banks on the market in terms of its balance sheet, credit portfolio, return on equity, and number of counters and staff. In this respect, it is playing a leading role in restoring the country’s banking sector.

It has experienced financial growth ever since it was established, and displays healthy management indicators in terms of the standards set by the regulations in force in the country.

The various inspections carried out by the Central Bank of Congo at RAWBANK SA report that the measures to combat money laundering and the financing of terrorism, the rules in terms of KYC and protection of the environment implemented by the bank are in line with international standards.

This attestation is valid for all legal intents and purposes.

Kinshasa, 11 April 2016 Déogratias MUTOMBO MWANA NYEMBO

563, Boulevard Colonel Tshatshi - Kinshasa - Gombe [email protected] / [email protected] / [email protected]

www.bcc.cd

↘ Translation of an official document in French of the Central Bank of Congo, signed by the Governor and sent to the senior management of RAWBANK

38

← TABLE OF CONTENTS

C O R P O R A T E G O V E R N A N C E

03C H A P T E R

40 Governance, a long-lasting, effective process

40 The Board of Directors42 The Executive Committee44 The specific committees reporting to the Executive Committee45 The bank organisation chart

39

← TABLE OF CONTENTS

GOV ERN A NCE , A LONG -L A S TING, EFFEC TI V E PROCE S S

THE BOA RD OF DIRECTOR S

Corporate governance defines the system formed by all the processes, reg-ulations, laws, rules and management and behavioural options for regulating the way in which an enterprise is admin-istered, managed and supervised, while at the same time ensuring that there is a harmonious relationship between all the stakeholders.

Governance is described in several charters that determine how the Board of Directors and the Executive Committee work. These standards of governance comply with the instructions of the Central Bank of Congo (instructions 15, 17 and 22) and satisfy internationally recognised banking management criteria.

In terms of the Board of Directors:

• The memorandum of good governance

• The charter of the Board of Directors• The charter of the Audit and Perfor-

mance Committee

In terms of the Executive Committee:

• The executive management charter• The charter of professional conduct• The compliance charter• The internal control charter• The internal audit charter• The social and environmental risk

management policy

RAWBANK meets all the requirements of the Central Bank of Congo and of all other regulatory and supervisory authorities in this respect, and is developing in accordance with the strategic standards specified by its Board of Directors. The Board also attaches particular importance to the principles of ethics, compliance,

transparency, independence and responsibility through the adoption of responsible behaviour throughout the bank, in order to ensure a long-lasting and effective process of added value consistent with the expectations of all stakeholders.

The Board of Directors is the corporate body with the widest powers for managing the bank and for producing its financial, organisational and commercial strategy to achieve its corporate purpose. It sets the guidelines for the bank’s business and ensures that they are implemented. It examines all issues concerning the running of the bank and, through its deliberations, sets the policy for those matters which relate to the bank.

The Board has various remits, which are described in the memorandum of good governance. These are restated below.

• To determine the values of the organ-isation (codes of conduct, ethical and other values) and to ensure that the executive management ensures that they are adhered to, and that all bank staff comply with all legal requirements.

• To determine the strategic direction of the bank, ideally in conjunction with the executive management, and to ensure that it is implemented.

• To reinforce the power of the executive management and provide it with legitimacy and support.