132117730 transfer prices

DESCRIPTION

Transfer Prices & Parallel ValuationTRANSCRIPT

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Transfer Prices in

Release 4.0

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Target Audience

Course participants

Project members implementing SAP R/3 in a group

SAP consultants and partners who work with groups

Requirements

Thorough understanding of the integrated value flows in MM,

PP, FI, CO and EC-PCA

Hands-on experience of the SAP R/3 System

Length of course: 1 day

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

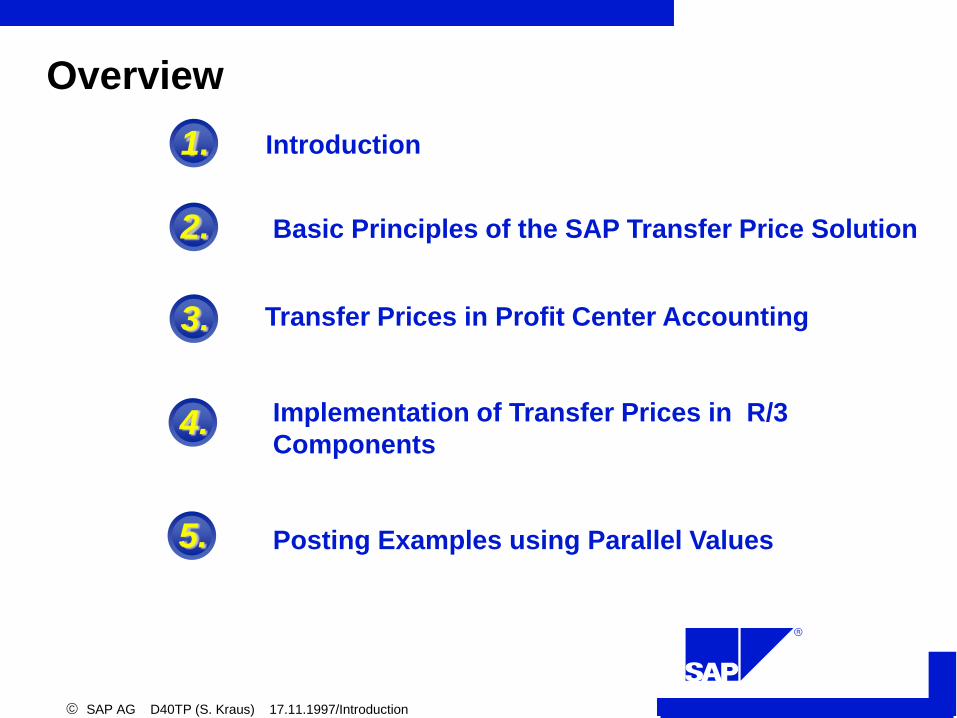

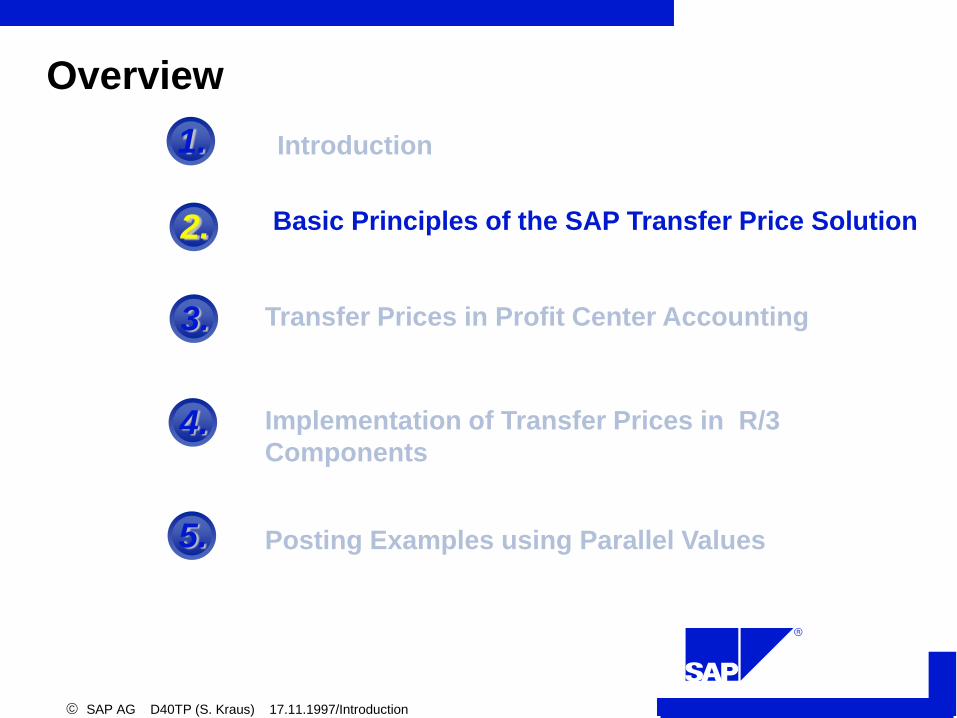

Overview

1.

2.

3.

4.

Transfer Prices in Profit Center Accounting

5.

Introduction

Basic Principles of the SAP Transfer Price Solution

Implementation of Transfer Prices in R/3

Components

Posting Examples using Parallel Values

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Overview

1. Introduction

2. Basic Principles of the SAP Transfer Price Solution

4.

5.

Implementation of Transfer Prices in R/3

Components

Posting Examples using Parallel Values

3. Transfer Prices in Profit Center Accounting

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

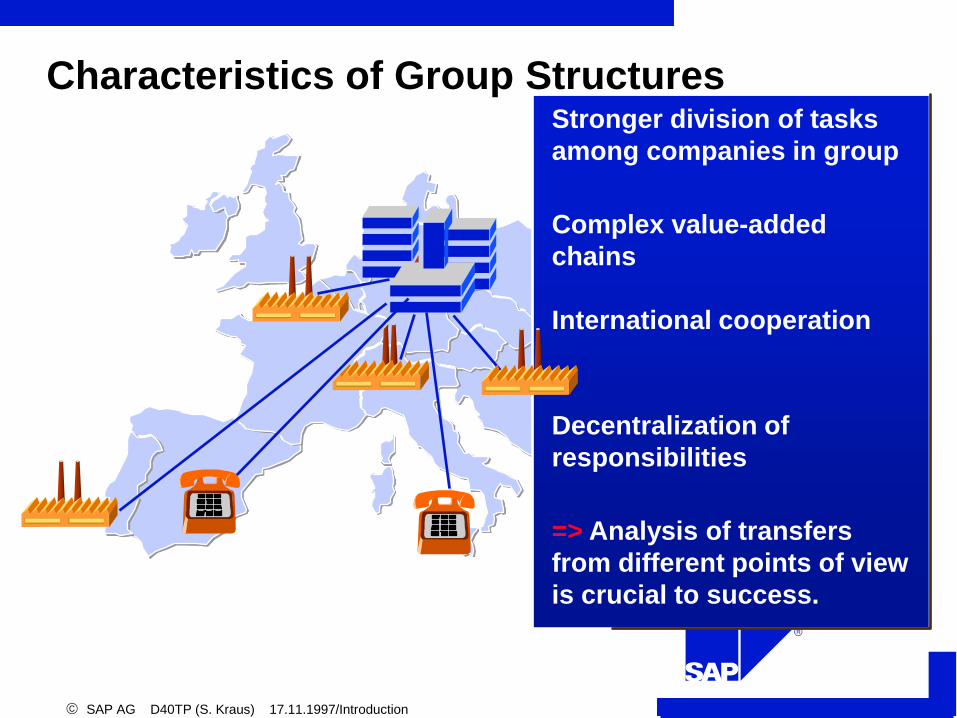

Characteristics of Group Structures Stronger division of tasks

among companies in group

Complex value-added

chains

International cooperation

Decentralization of

responsibilities

=> Analysis of transfers

from different points of view

is crucial to success.

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

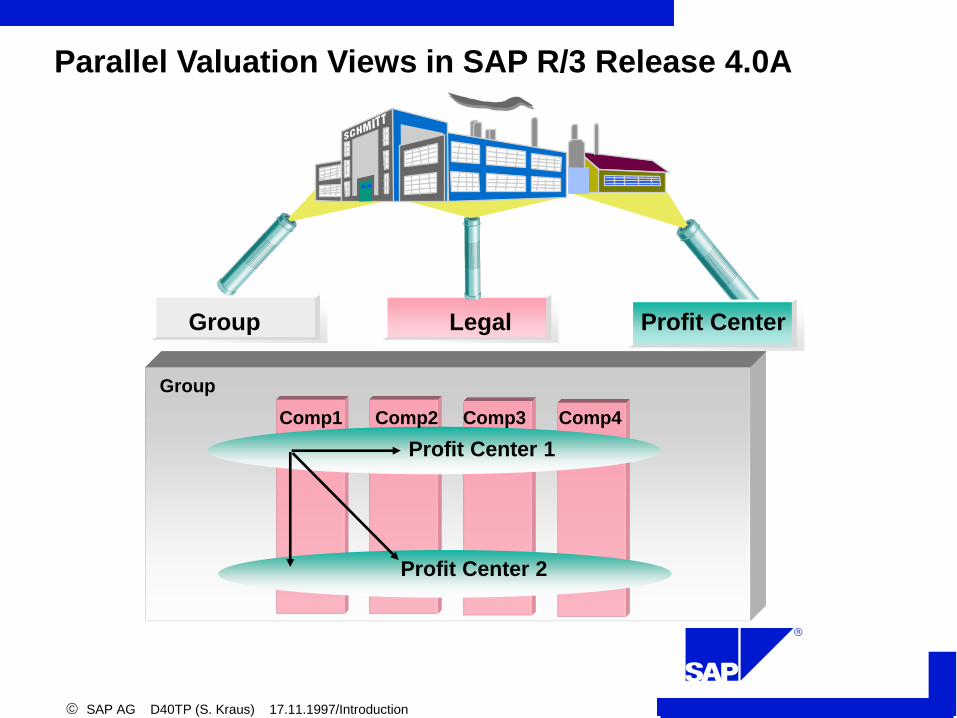

Parallel Valuation Views in SAP R/3 Release 4.0A

Profit Center 1

Profit Center 2

Group Legal Profit Center

Comp1 Comp2 Comp3 Comp4

Group

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

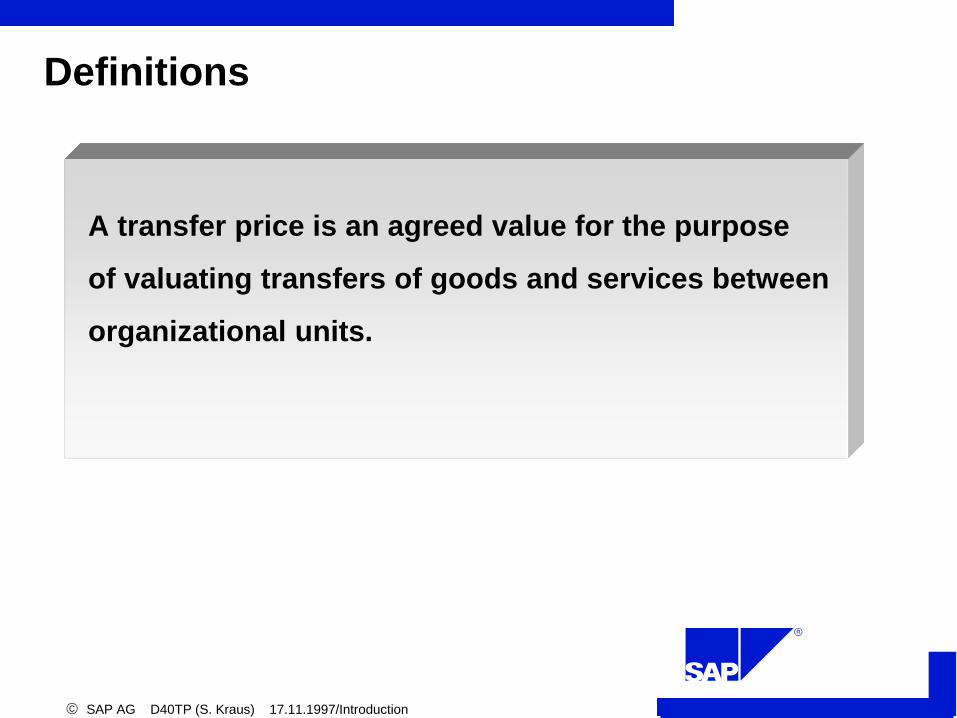

Definitions

A transfer price is an agreed value for the purpose

of valuating transfers of goods and services between

organizational units.

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Purposes of Transfer Prices

optimize tax payments and distribution of profits

calculate the profit or loss of organizational units

coordinate and guide unit managers

enable cost estimates to be used as basis for

decisions affecting the entire group

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

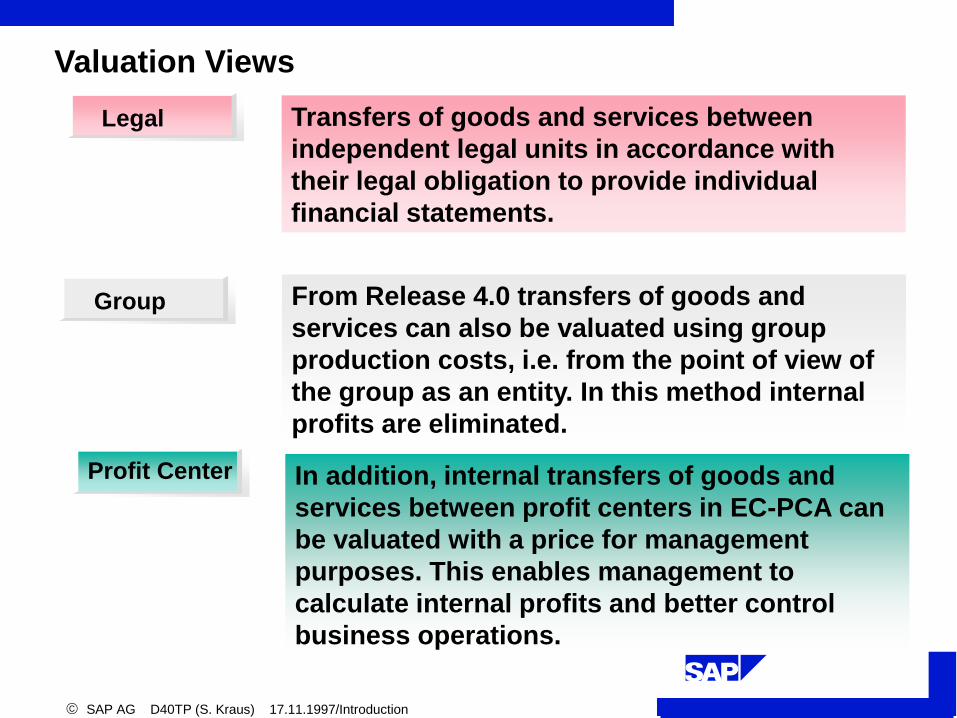

Group

Valuation Views

Legal

Profit Center

Transfers of goods and services between

independent legal units in accordance with

their legal obligation to provide individual

financial statements.

From Release 4.0 transfers of goods and

services can also be valuated using group

production costs, i.e. from the point of view of

the group as an entity. In this method internal

profits are eliminated.

In addition, internal transfers of goods and

services between profit centers in EC-PCA can

be valuated with a price for management

purposes. This enables management to

calculate internal profits and better control

business operations.

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Definition: Transfer Prices in SAP R/3

Group

EC-

PCA

FI

CO

Profit center

Legal units

(Company

codes)

Controlling

area

Organizational

units

1

2

3

4

(1) Transfer price from group point of view = group prod. costs

(2) Transfer price from profit center view = management price

(3) Internal price for activities exchanged between cost centers

(4) Transfer price from legal point of view = sales and purchase price

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Illustration of Need for Parallel Approaches

Prod.

order

Distribution

center Sales

order

Finished

products

Raw

materials

Prod.order

Cost center

Semi

finished

product

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Illustration of Need for Parallel Approaches

Semi-

finished

product

Prod.

order

Distribution

center Sales

order

Finished

product

Raw

materials

Prod.order

Company Code 1

PrCtr1 PrCtr2 PrCtr3 PrCtr4

Cost center

L 70.-

G 70.-

P 70.-

75.-- L 70.-

G 70.-

P 75.-

L 70.-

G 70.-

P 75.-

L 120.-

G 90.-

P 140.-

L 120.-

G 90.-

P 140.-

100.-

120.-

CCtr 20.-

L 220.-

G 90.-

P 240.-

- +

Assumption: Plan = Act => No variance

220.-

240.-

Company Code 2 Company Code 3

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Overview

2. Basic Principles of the SAP Transfer Price Solution

3.

Posting Examples using Parallel Values

4. Implementation of Transfer Prices in R/3

Components

Transfer Prices in Profit Center Accounting

5.

1. Introduction

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

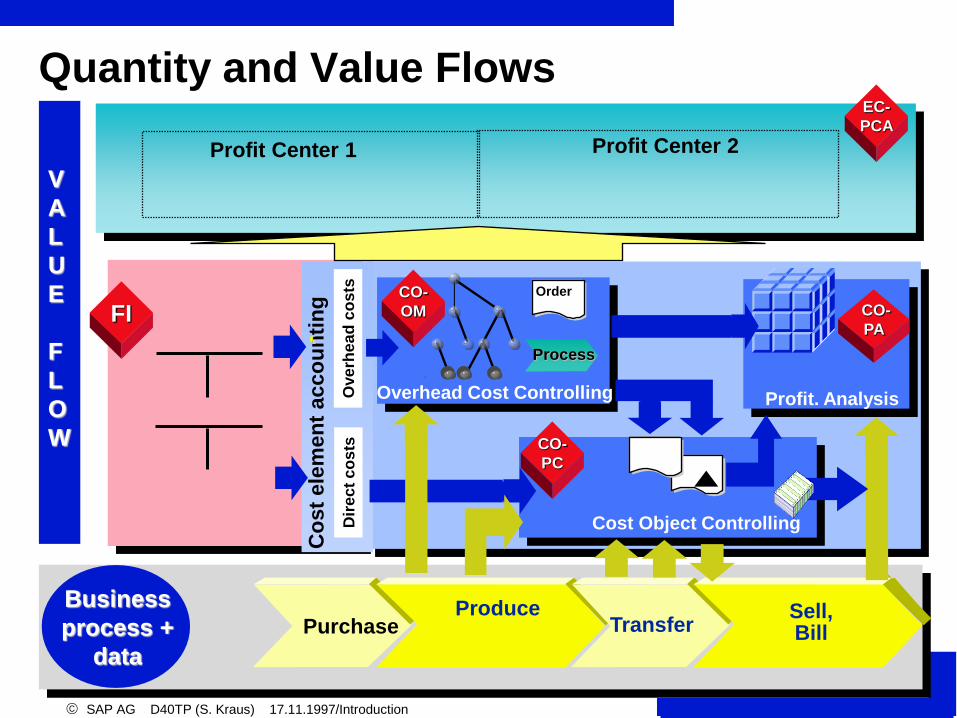

Business

process +

data

EC-

PCA

Profit Center 1 Profit Center 2

Quantity and Value Flows

FI

CO-

PC

CO-

OM CO-

PA

Produce Transfer

Sell, Bill Purchase

Cost Object Controlling

Profit. Analysis Overhead Cost Controlling

Order

Process

Co

st

ele

men

t acco

un

tin

g

D

ire

ct

co

sts

O

ve

rhe

ad

co

sts

V

A

L

U

E

F

L

O

W

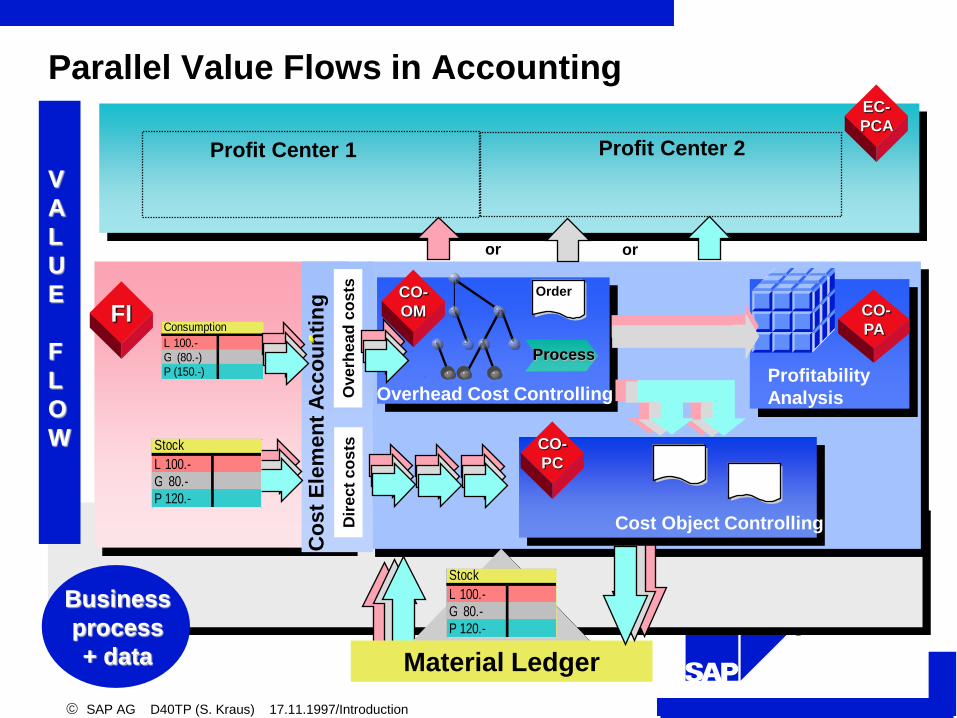

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

EC-

PCA

Profit Center 1 Profit Center 2

Parallel Value Flows in Accounting

FI CO-

OM CO-

PA

Profitability

Analysis Overhead Cost Controlling

Order

Process

Co

st

Ele

men

t A

cco

un

tin

g

D

ire

ct

co

sts

O

ve

rhe

ad

co

sts

Consumption

L 100.-

G (80.-)

P (150.-)

Stock

L 100.-

G 80.-

P 120.-

Material Ledger

CO-

PC

Cost Object Controlling

or or

Business

process

+ data

V

A

L

U

E

F

L

O

W Stock

L 100.-

G 80.-

P 120.-

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Additional Dimension: Valuation View

Currency

types

Valuation

view

Group

Legal 0

1

2

Company code currency

Controlling area currency

Group currency

...

10 20 30

The currency and valuation profile determines which valuation

views are to be stored with which currencies in the system.

X

X

X PrCtr

10

Leg.

30

PrCtr.

30

Grp

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Rule I: Parallel Value Flows in Accounting

The valuation approaches defined in

the currency and valuation profile

are stored in parallel in the system.

A maximum of

3 parallel valuation views in

2 currencies

can be stored in the system!

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Rule II: The valuation of stock occurs in

parallel!

The Material Ledger is the sub-

ledger for materials and stores

parallel stock values.

Stock valuation is carried

out in the SAP system at plant

or company code level.

Stocks of a material in the

same plant belong to the same

profit center.

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Rule III: No change to posting rules!

Parallel values are posted to the

same accounts in additional data

fields.

Additional accounts are only

necessary in exceptional cases: - To balance accounts payable and

accounts receivable

- For internal revenue und costs

In 4.0A, parallel values can only

be stored for the transfer of goods

but not for services!

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Scenarios: Parallel Valuation Approaches in R/3

as in 3.0 or or Curr.

Leg.

Curr.

Grp PrCtr

Curr. EC-

PCA

Profit Center Accounting

Curr.

Leg.

Curr.

Grp

PrCtr

Curr.

FI

Financial Accounting

Oblig.

Opt.

Opt.

Curr.

Leg.

Curr.

Grp

PrCtr

Curr.

CO- OM

Controlling

see

version

concept

CO- PC

Curr.

Leg.

Curr.

Grp

CO- PA

Opt. Oblig. Opt. Curr.

Leg.

Curr.

Grp PrCtr

Curr. Material Ledger

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Scenario: US Model

Curr.

Grp

EC-

PCA

Profit Center Accounting

Curr.

Leg.

Curr.

Grp

FI

Financial Accounting

Curr.

Leg.

Curr.

Grp

CO- OM

Controlling

CO- PC

Curr.

Leg.

Curr.

Grp

CO- PA

Curr.

Leg.

Curr.

Grp

Material Ledger

Operative

version

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Scenario: Profit Center Model

EC-

PCA

Profit Center Accounting

Curr.

Leg.

PrCtr

Curr.

FI

Financial Accounting

Curr.

Leg.

PrCtr

Curr. CO- OM

Controlling

CO- PC

Curr.

Leg. CO- PA

Curr.

Leg. PrCtr

Curr. Material Ledger

Curr.

PrCtr

Operative

version

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Restrictions I

... General

Services can only be allocated in one valuation.

In Release 4.0A transfer prices can only be implemented by

new customers. Productive customers should contact SAP

directly.

... In Financial Accounting

Parallel valuations must be posted in MM and the Material

Ledger. In Release 4.0A the transfer price concept does not

allow manual entries or corrections to parallel valuations.

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

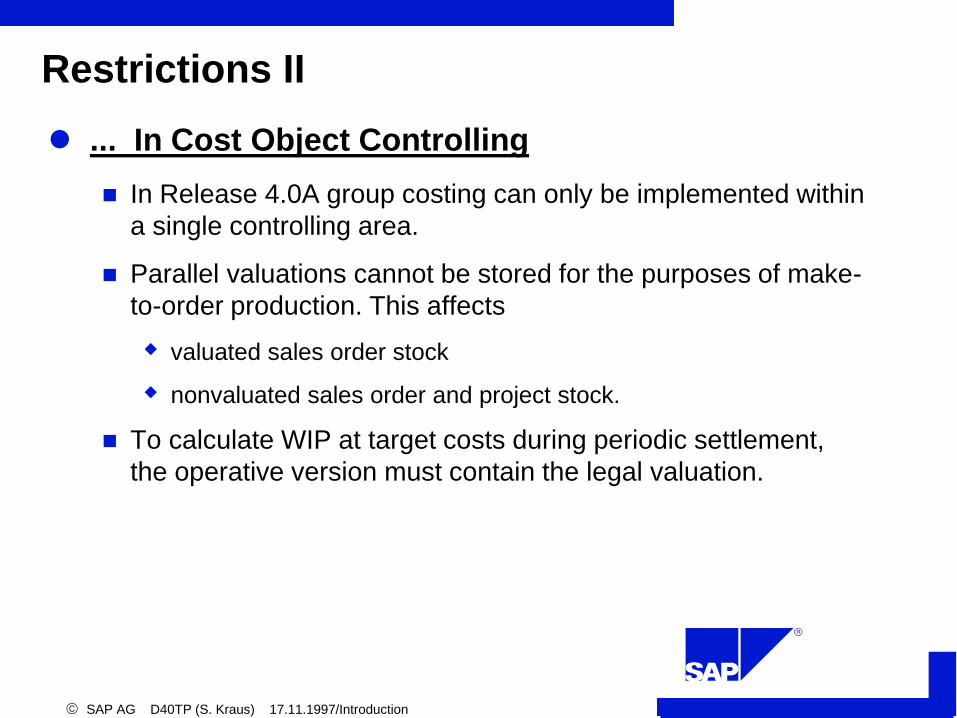

Restrictions II

... In Cost Object Controlling

In Release 4.0A group costing can only be implemented within

a single controlling area.

Parallel valuations cannot be stored for the purposes of make-

to-order production. This affects

valuated sales order stock

nonvaluated sales order and project stock.

To calculate WIP at target costs during periodic settlement,

the operative version must contain the legal valuation.

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

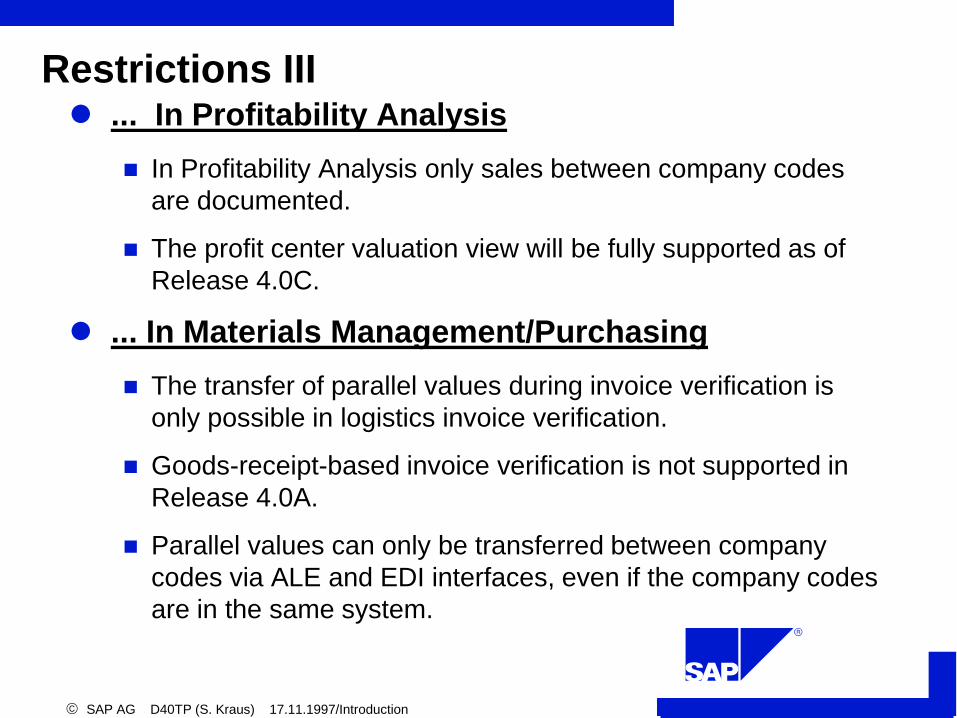

Restrictions III ... In Profitability Analysis

In Profitability Analysis only sales between company codes

are documented.

The profit center valuation view will be fully supported as of

Release 4.0C.

... In Materials Management/Purchasing

The transfer of parallel values during invoice verification is

only possible in logistics invoice verification.

Goods-receipt-based invoice verification is not supported in

Release 4.0A.

Parallel values can only be transferred between company

codes via ALE and EDI interfaces, even if the company codes

are in the same system.

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Overview

2. Basic Principles of the SAP Transfer Price Solution

3.

Posting Examples using Parallel Values

4. Implementation of Transfer Prices in R/3

Components

Transfer Prices in Profit Center Accounting

5.

1. Introduction

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

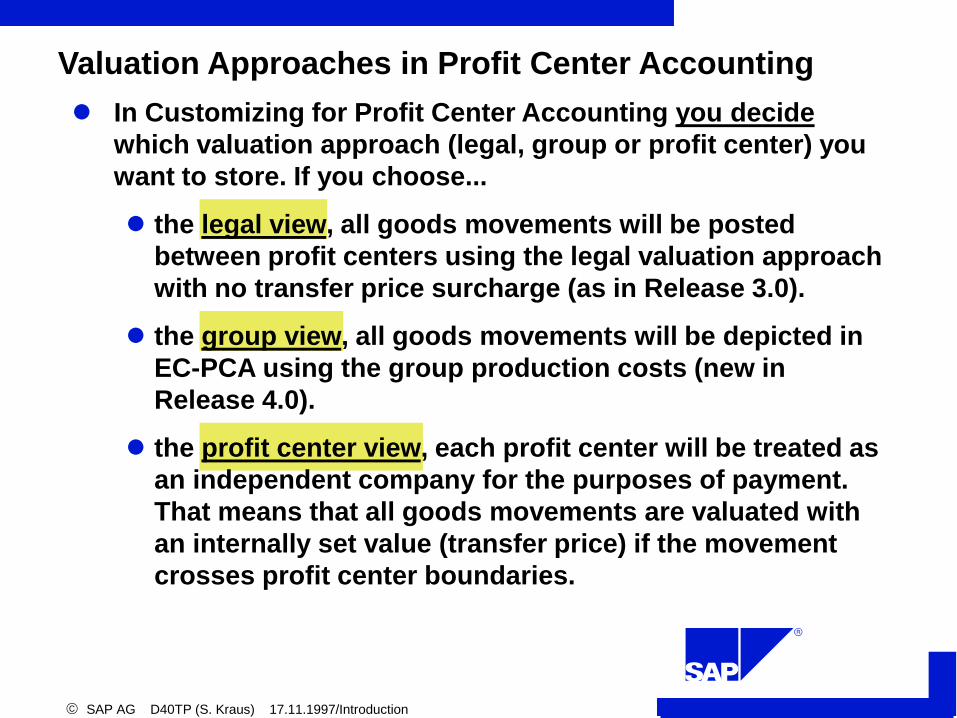

In Customizing for Profit Center Accounting you decide

which valuation approach (legal, group or profit center) you

want to store. If you choose...

the legal view, all goods movements will be posted

between profit centers using the legal valuation approach

with no transfer price surcharge (as in Release 3.0).

the group view, all goods movements will be depicted in

EC-PCA using the group production costs (new in

Release 4.0).

the profit center view, each profit center will be treated as

an independent company for the purposes of payment.

That means that all goods movements are valuated with

an internally set value (transfer price) if the movement

crosses profit center boundaries.

Valuation Approaches in Profit Center Accounting

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Quantity flow

Parallel value flow

Logistics

FI/CO

Possible Valuations in EC-PCA

Profit

Center

Accounting

Profit Center 1 Profit Center 2

Internal revenues Internal costs

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Quantity flow

Parallel value flow

Logistics

FI/CO

Transfer Prices from the Profit Center View

Profit

Center

Accounting

Profit Center 1 Profit Center 2

150.-

Calculation

of transfer

price

150.-

120.-

Raw materials Production

order

Example: Profit Center Valuation

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Quantity flow

Parallel value flow

Logistics

FI/CO

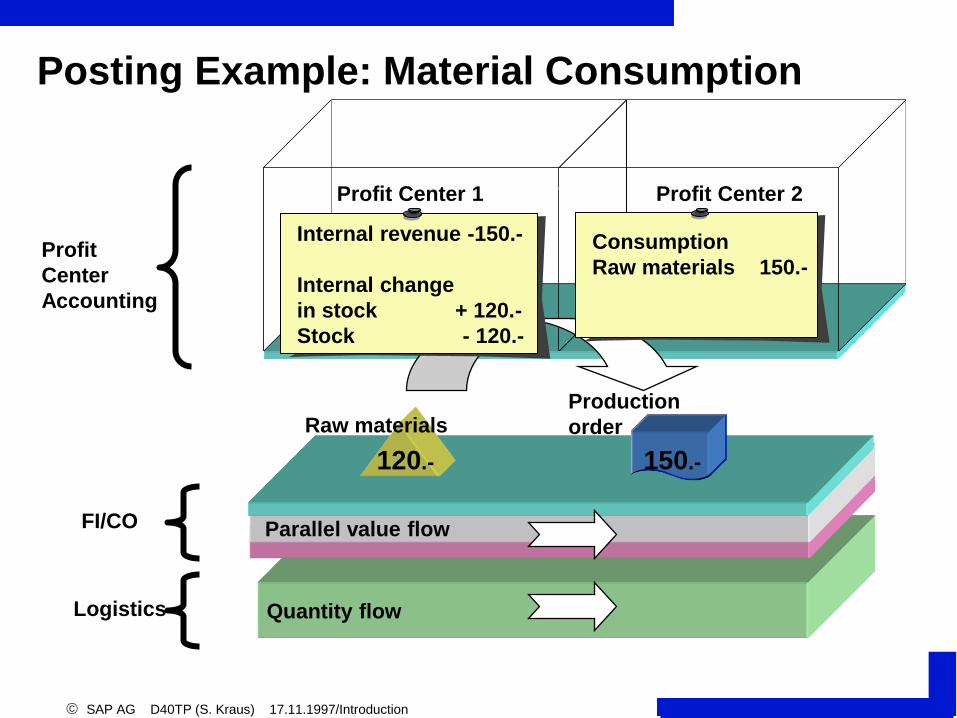

Posting Example: Material Consumption

Profit

Center

Accounting

Profit Center 1 Profit Center 2

150.-

150.-

120.-

Raw materials Production

order

Internal revenue -150.-

Internal change

in stock + 120.-

Stock - 120.-

Consumption

Raw materials 150.-

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

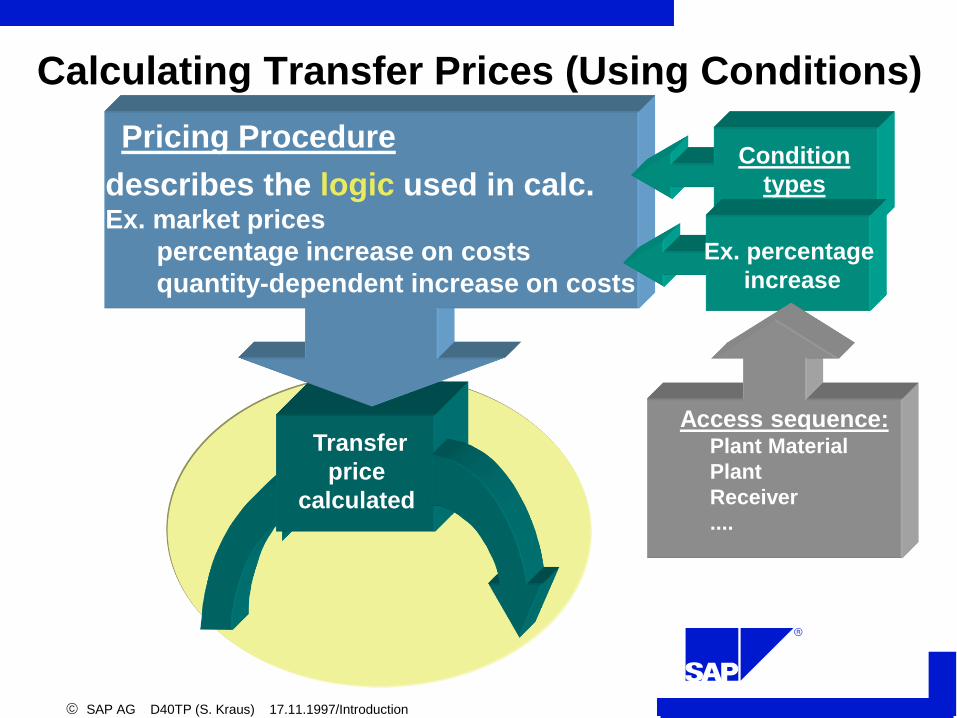

Calculating Transfer Prices (Using Conditions)

Pricing Procedure

describes the logic used in calc. Ex. market prices

percentage increase on costs

quantity-dependent increase on costs

Condition

types

Ex. percentage

increase

Transfer

price

calculated

Access sequence: Plant Material

Plant

Receiver

....

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

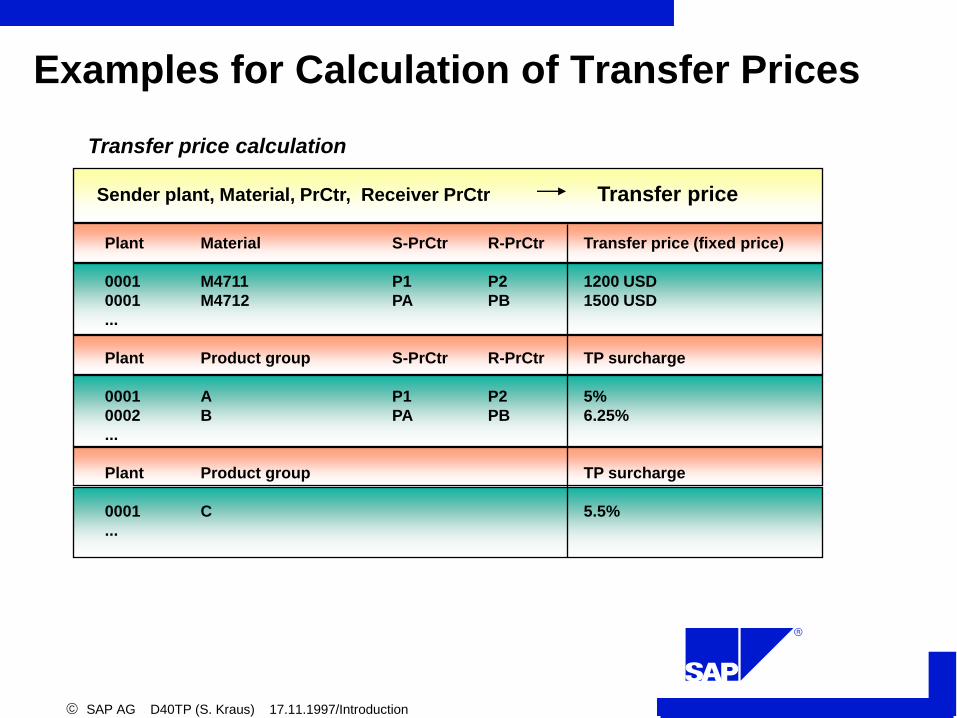

Examples for Calculation of Transfer Prices

Transfer price calculation

Sender plant, Material, PrCtr, Receiver PrCtr Transfer price

Plant Material S-PrCtr R-PrCtr Transfer price (fixed price)

0001 M4711 P1 P2 1200 USD

0001 M4712 PA PB 1500 USD

...

Plant Product group S-PrCtr R-PrCtr TP surcharge

0001 A P1 P2 5%

0002 B PA PB 6.25%

...

Plant Product group TP surcharge

0001 C 5.5%

...

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

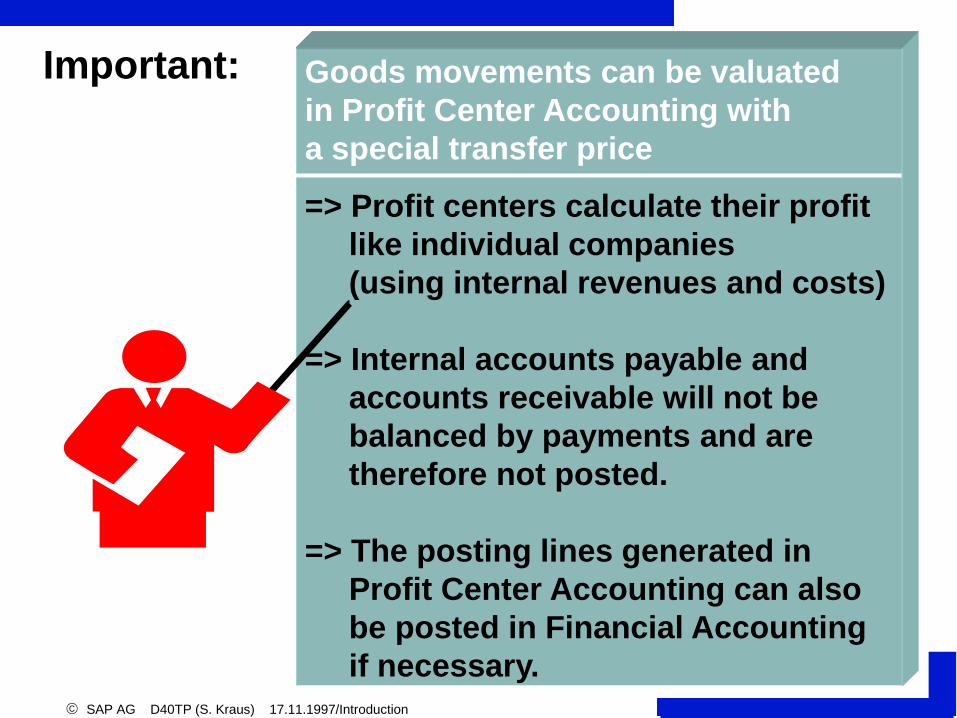

Important: Goods movements can be valuated

in Profit Center Accounting with

a special transfer price

=> Profit centers calculate their profit

like individual companies

(using internal revenues and costs)

=> Internal accounts payable and

accounts receivable will not be

balanced by payments and are

therefore not posted.

=> The posting lines generated in

Profit Center Accounting can also

be posted in Financial Accounting

if necessary.

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Overview

2. Basic Principles of the SAP Transfer Price Solution

3.

Posting Examples using Parallel Values

4. Implementation of Transfer Prices in R/3

Components

Transfer Prices in Profit Center Accounting

5.

1. Introduction

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

PrCtr

Curr.

Material Ledger

Curr.

Leg. Curr.

Grp

Parallel Valuation Approaches for Material Stock

Cost estimate for

material

Inventory

management

Invoice verification

Delivery and

settlement of

production orders

Material

P-100

Material Master Plant 1000

Quantity: 1200 units

Value : 24,000

Financial

Accounting

Information

systems in

Logistics and

Controlling

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

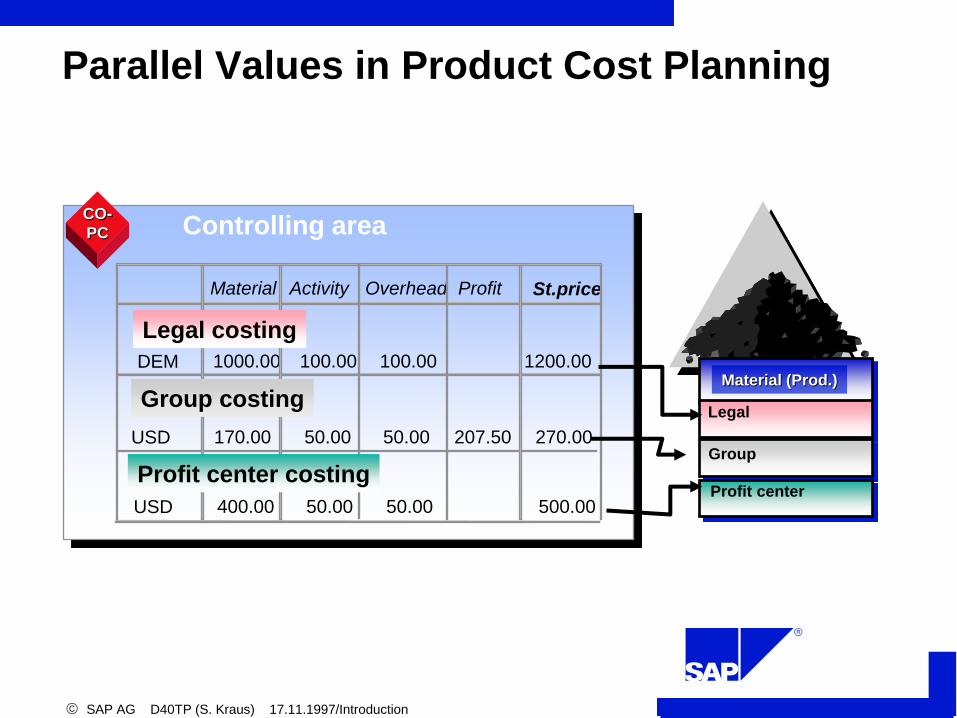

Parallel Values in Product Cost Planning

Material (Prod.)

Legal

Profit center

Group

Material Activity Overhead Profit St.price

DEM 1000.00 100.00 100.00 1200.00

USD 170.00 50.00 50.00 207.50 270.00

USD 400.00 50.00 50.00 500.00

Controlling area CO-

PC

Legal costing

Group costing

Profit center costing

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Background to Group Costing Member of grp:

Company A

Member of grp:

Company B

Member of grp:

Company C

Key:

DC = Direct costs

POH = Prop. overhead costs

FOH = Fixed overhead costs

P = Profit (Revenue ./. Full costs)

Index A, B, C = Company A, B, C

Grp costing St. costing Grp costing St. costing

DCA

POHA FOHA

PA

DCA

POHA FOHA

DCB

POHB FOHB

DCB

POHB FOHB

DCA

POHA FOHA

DCB

POHB FOHB

PB

DCC

Broken down Total

DCC

POHC FOHC POHC FOHC

PC

DCA

DCB

DCC

POHA FOHA

POHB FOHB

POHC FOHC

PB

PC

DC

P

POH FOH

Group

costing Group = St. costing

PA PA

PB PB

PA

PC

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

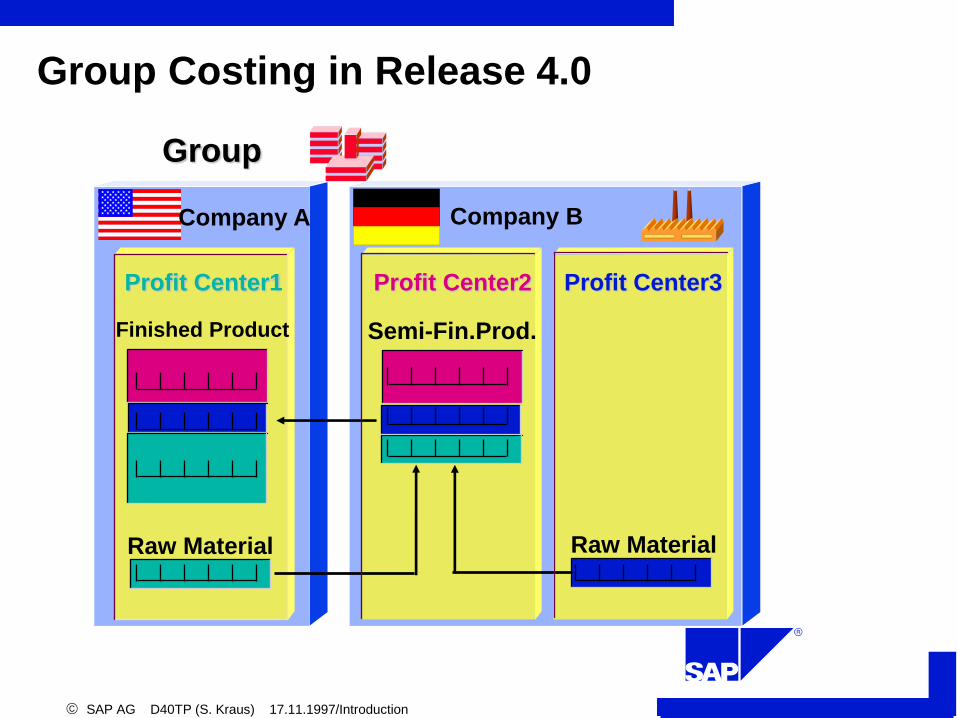

Group

Semi-Fin.Prod.

Raw Material

Profit Center2 Profit Center3 Profit Center1

Finished Product

Raw Material

Group Costing in Release 4.0

Company A Company B

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

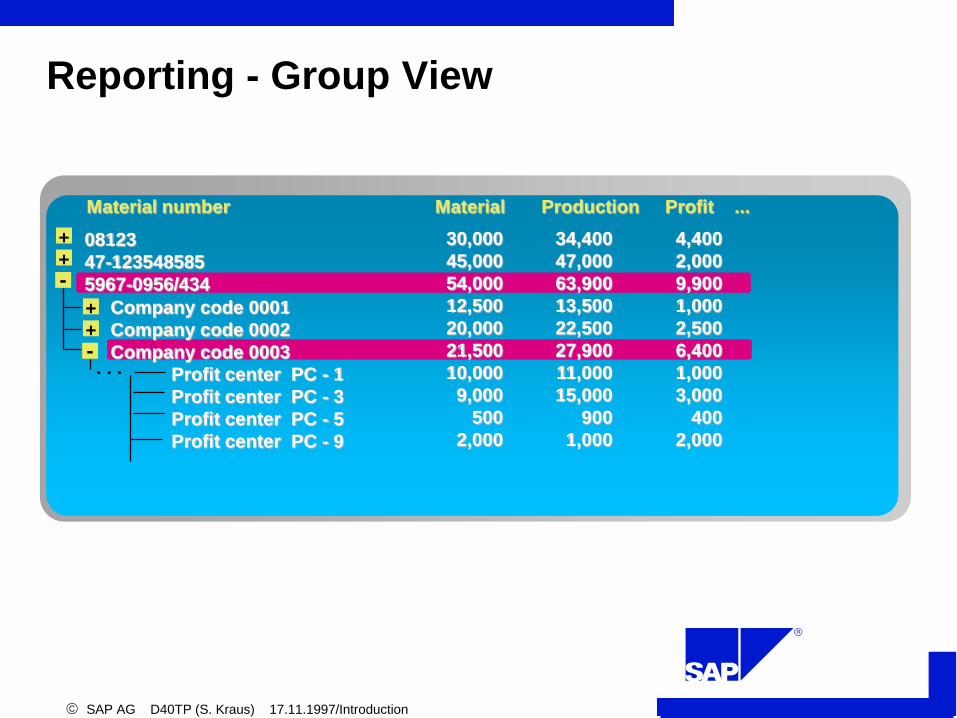

Reporting - Group View

+

- +

+

- +

08123

47-123548585

5967-0956/434

Company code 0001

Company code 0002

Company code 0003

Profit center PC - 1

Profit center PC - 3

Profit center PC - 5

Profit center PC - 9

30,000 34,400 4,400

45,000 47,000 2,000

54,000 63,900 9,900

12,500 13,500 1,000

20,000 22,500 2,500

21,500 27,900 6,400

10,000 11,000 1,000

9,000 15,000 3,000

500 900 400

2,000 1,000 2,000

Material number Material Production Profit ...

. . .

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

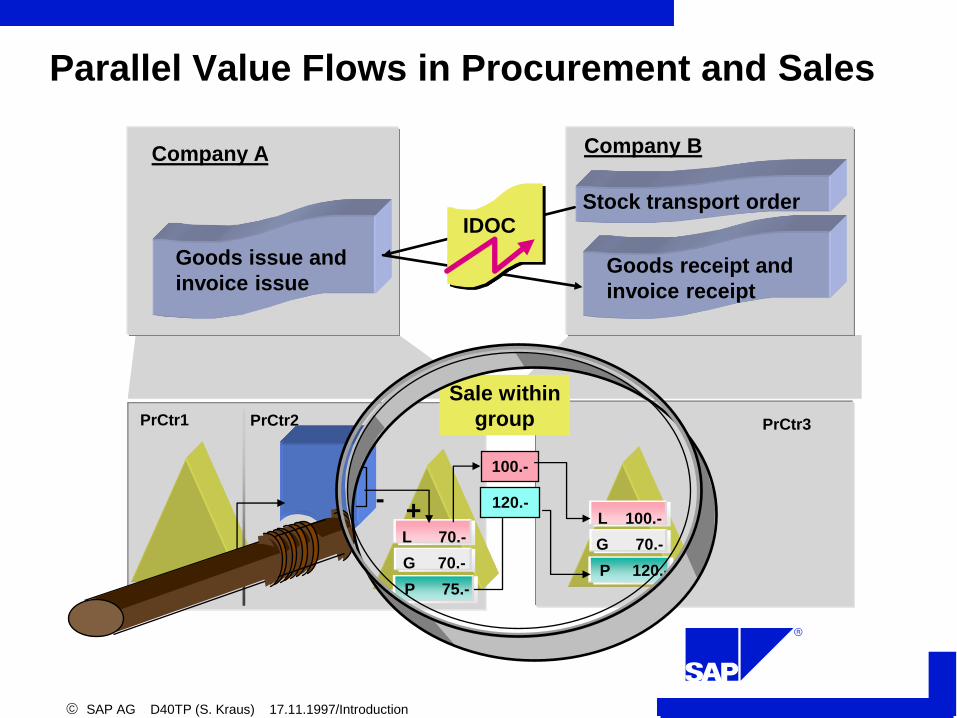

Parallel Value Flows in Procurement and Sales

PrCtr1 PrCtr2 PrCtr3

L 70.-

G 70.-

P 75.-

L 100.-

G 70.-

P 120.-

100.-

120.- - +

Company A Company B

Stock transport order

Goods receipt and

invoice receipt

Goods issue and

invoice issue

IDOC

Sale within

group

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Using Transfer Prices in FI

FI

Company code

Currency and

valuation profile

Group

PrCtr

Legal

Currency

Valuation

Local

currency

Group

currency

10 30

X

In FI, the different valuation approaches are stored in the “old”

currency fields and updated in the general ledger.

FI doc. - curr1

- curr2

- curr3

. .

X

X

General

ledger

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

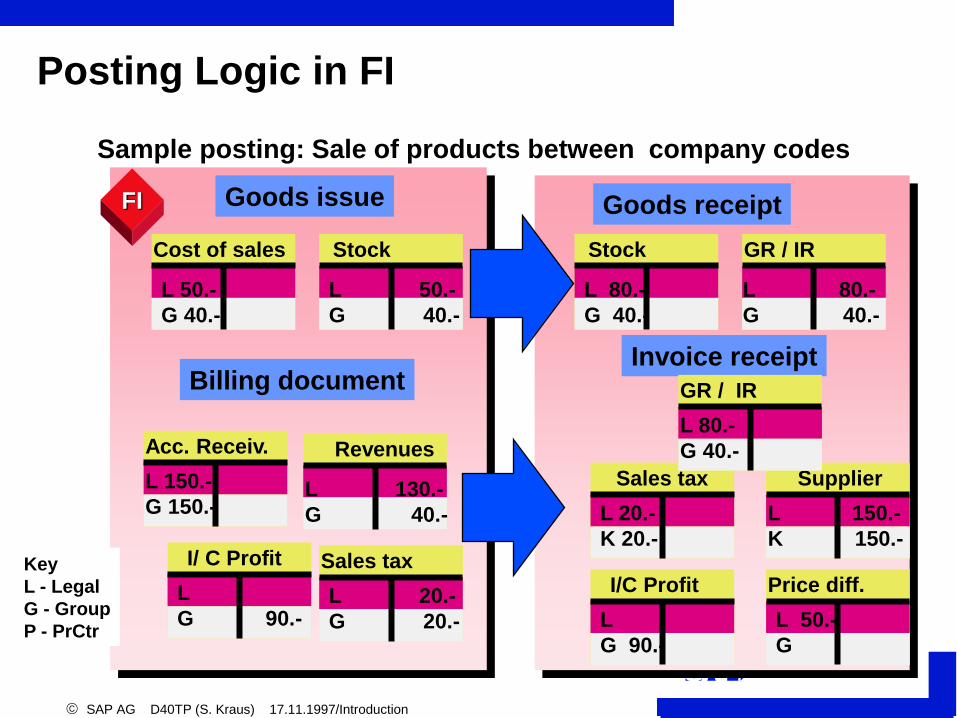

FI

Sample posting: Sale of products between company codes

Key

L - Legal

G - Group

P - PrCtr

Cost of sales

L 50.-

G 40.-

Acc. Receiv.

L 150.-

G 150.-

Revenues

L 130.-

G 40.-

Sales tax

L 20.-

G 20.-

Billing document

Goods issue

Stock

L 50.-

G 40.-

Stock

L 80.-

G 40.-

GR / IR

L 80.-

G 40.-

I/ C Profit

L

G 90.-

I/C Profit

L

G 90.-

Price diff.

L 50.-

G

Sales tax

L 20.-

K 20.-

Supplier

L 150.-

K 150.-

Goods receipt

Invoice receipt

GR / IR

L 80.-

G 40.-

Posting Logic in FI

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

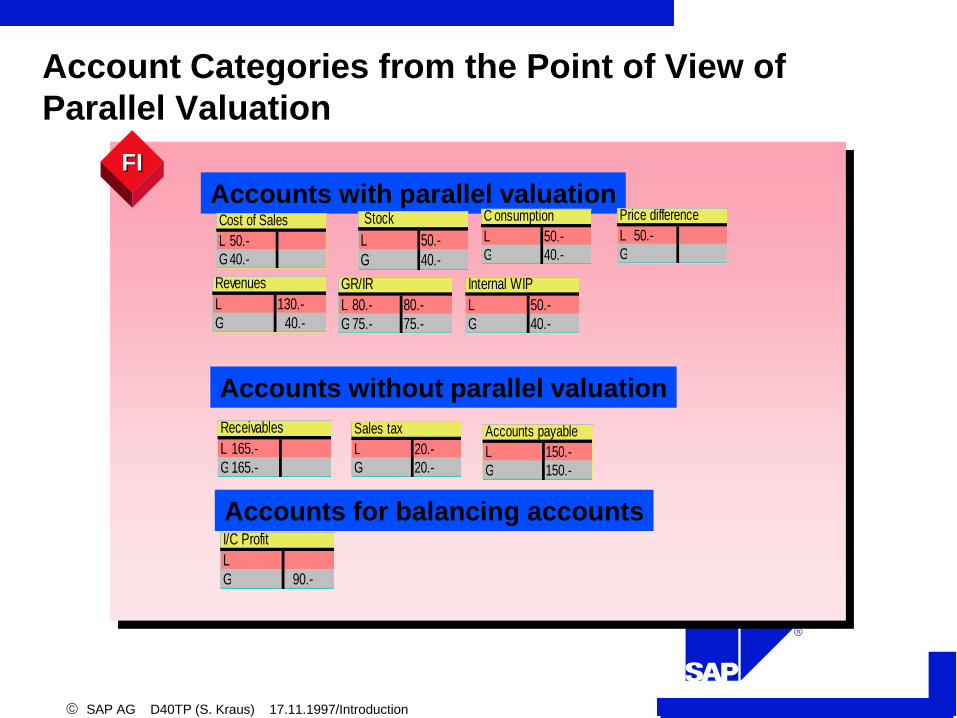

Account Categories from the Point of View of

Parallel Valuation

FI

I/C Profit

L

G 90.-

Accounts with parallel valuation

Accounts without parallel valuation

Accounts for balancing accounts

GR/IR

L 80.- 80.-

G75.- 75.-

Revenues

L 130.-

G 40.-

Internal WIP

L 50.-

G 40.-

Stock

L 50.-

G 40.-

C onsumption

L 50.-

G 40.-

Price difference

L 50.-

G

Cost of Sales

L 50.-

G40.-

Receivables

L 165.-

G165.-

Sales tax

L 20.-

G 20.-

Accounts payable

L 150.-

G 150.-

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Transfer Prices in AA: Settling an Order to an Asset

AA IM

Cap. invest. order

L 50.-

G (40.-)

P (60.-)

Depreciation areas

Curr. type Area

50.- 01 01

50.- 11 31

50.- 21 32

Settlement

to asset

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

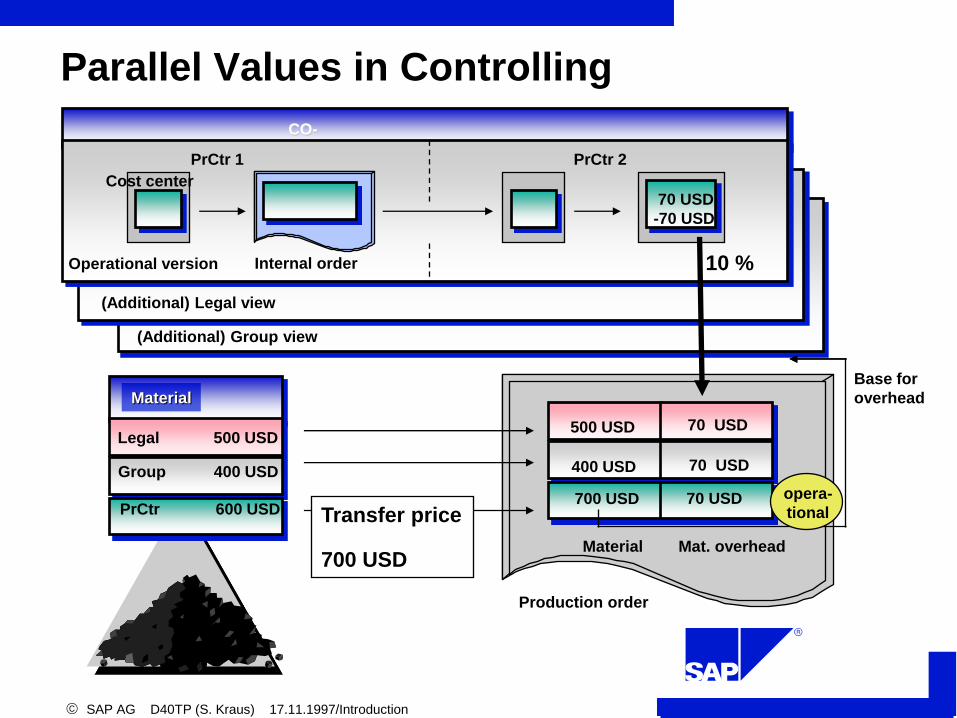

Parallel Versions in Controlling

-300 USD

Material

Legal 500 USD

PrCtr 600 USD

Group 400 USD

Transfer price

700 USD Material Mat. overhead

700 USD 70 USD

Production order

400 USD

70 USD

500 USD

70 USD

70 USD

Profit Center 1

Profit Center 2

opera-

tive

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

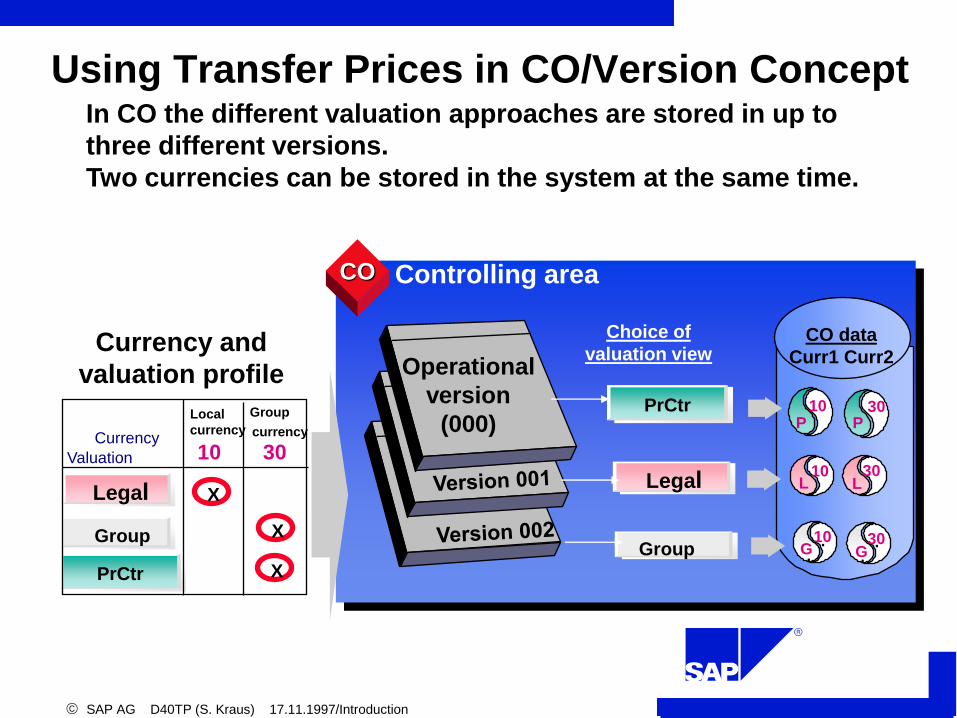

Using Transfer Prices in CO/Version Concept In CO the different valuation approaches are stored in up to

three different versions.

Two currencies can be stored in the system at the same time.

Currency and

valuation profile

Group

PrCtr

Legal

Currency

Valuation

Local

currency

Group

currency

X

CO Controlling area

Operational

version

(000)

Choice of

valuation view

Legal

Group

PrCtr

10 30

CO data

Curr1 Curr2

X

X

. .

30 10

30 10

10 . . 30

P P

L

G G

L

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Parallel Values in Controlling

Material

Legal 500 USD

PrCtr 600 USD

Group 400 USD

Production order

Transfer price

700 USD

700 USD

400 USD

Material Mat. overhead

70 USD

70 USD

70 USD

Base for

overhead

500 USD

CO-

OM PrCtr 1

PrCtr 2

70 USD

-70 USD

Cost center

Internal order Operational version

(Additional) Legal view

(Additional) Group view

10 %

opera-

tional

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

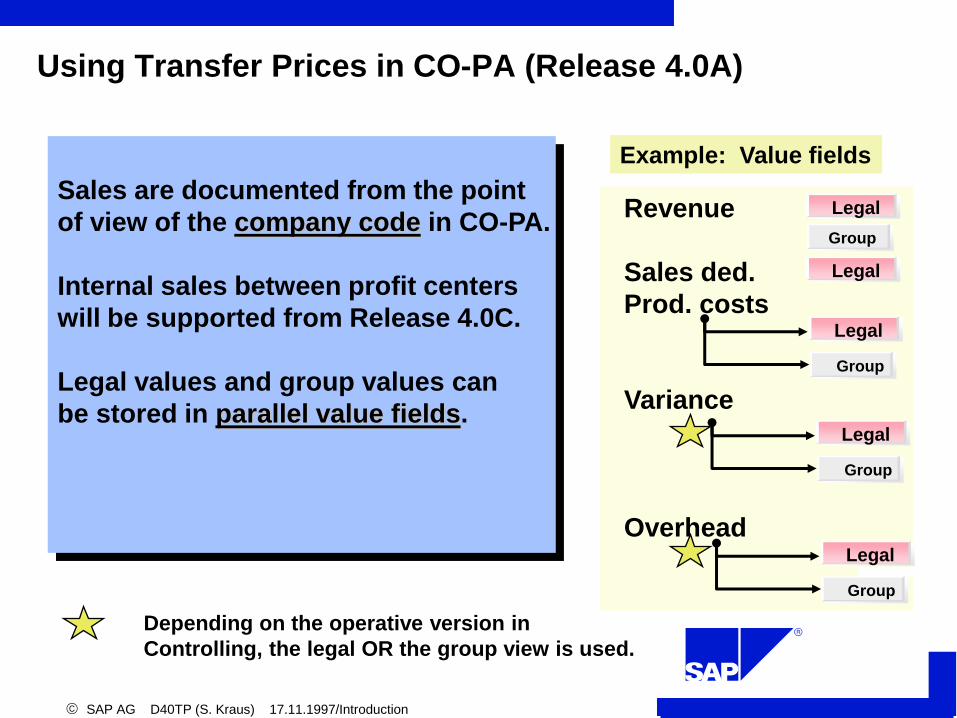

Revenue

Sales ded.

Prod. costs

Variance

Overhead

Using Transfer Prices in CO-PA (Release 4.0A)

Sales are documented from the point

of view of the company code in CO-PA.

Internal sales between profit centers

will be supported from Release 4.0C.

Legal values and group values can

be stored in parallel value fields.

Legal

Group

Legal

Legal

Example: Value fields

Group

Legal

Group

Legal

Group

Depending on the operative version in

Controlling, the legal OR the group view is used.

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Overview

2. Basic Principles of the SAP Transfer Price Solution

3.

Posting Examples using Parallel Values

4. Implementation of Transfer Prices in R/3

Components

Transfer Prices in Profit Center Accounting

5.

1. Introduction

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

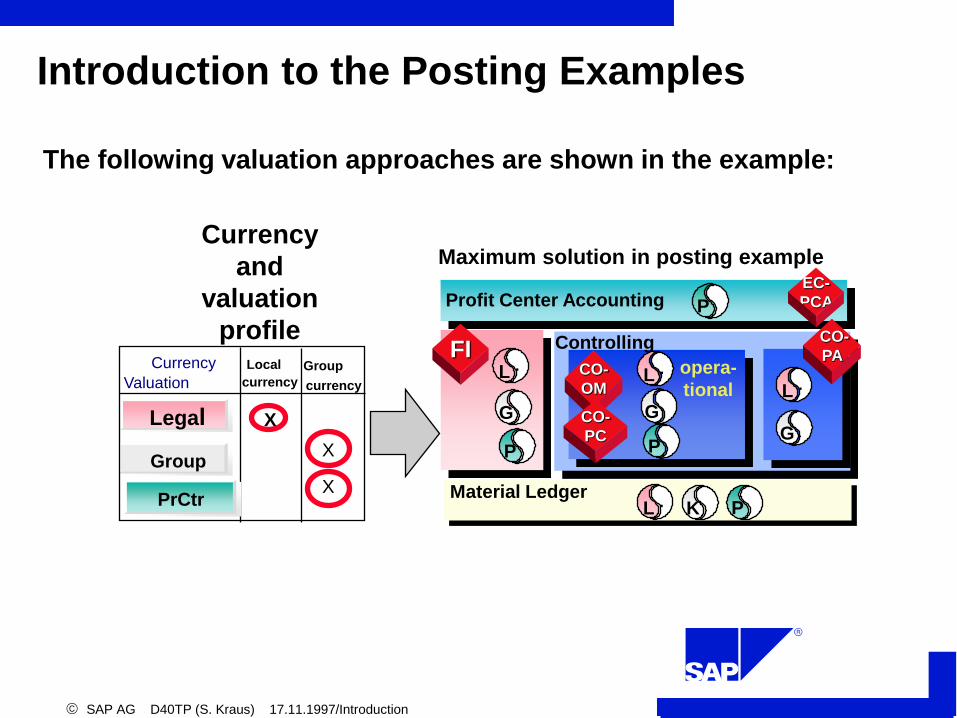

Introduction to the Posting Examples

Currency

and

valuation

profile

Group

Legal

Currency

Valuation

Local

currency

Group

currency

X

X

X

PrCtr

The following valuation approaches are shown in the example:

Profit Center Accounting

CO-

OM

CO-

PA Controlling FI

Material Ledger

. L

G

P

CO-

PC

. L K P

. L

G

P

. L

G

opera-

tional

Maximum solution in posting example EC-

PCA

P

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Business

process +

data

EC-

PCA

Internal WIP

P 120.-

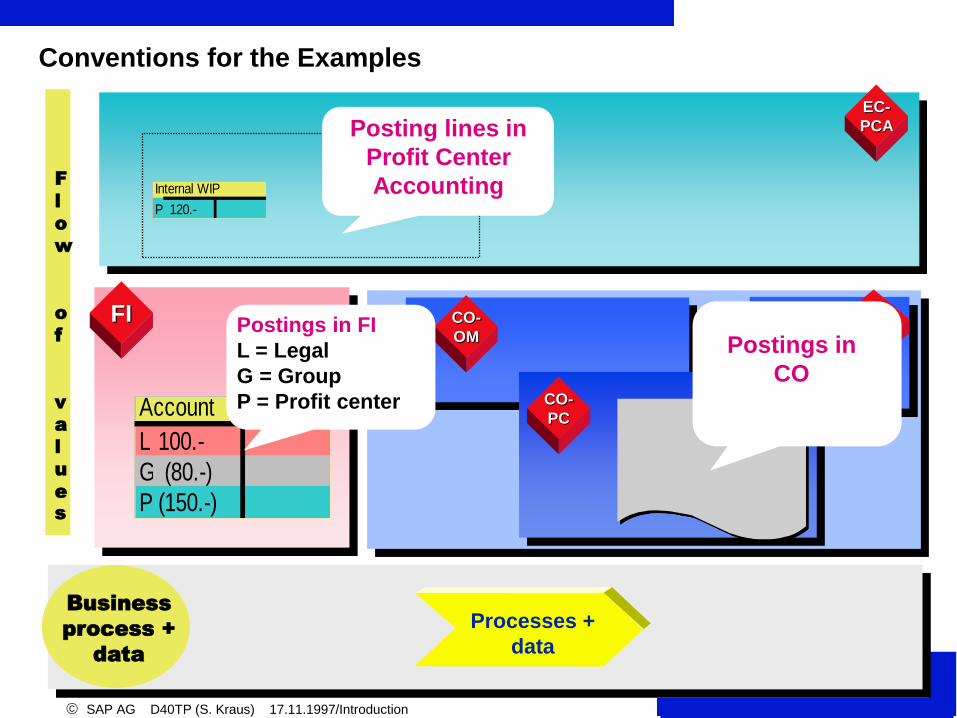

Conventions for the Examples

F

l

o

w

o

f

v

a

l

u

e

s

FI

Account

L 100.-

G (80.-)

P (150.-)

CO-

PC

CO-

OM

CO-

PA

Processes +

data

Postings in

CO

Postings in FI

L = Legal

G = Group

P = Profit center

Posting lines in

Profit Center

Accounting

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Business

process +

data

Material

withdrawal

EC-

PCA

PrCtr1

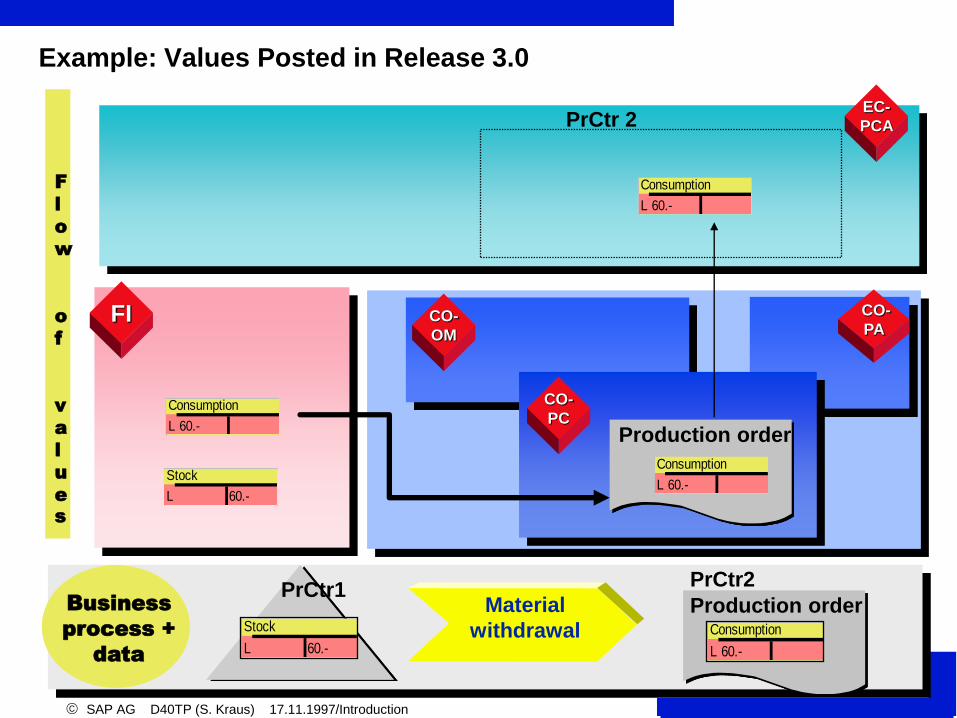

Example: Values Posted in Release 3.0

F

l

o

w

o

f

v

a

l

u

e

s

FI

CO-

PC

CO-

OM

CO-

PA

PrCtr2

Production order Stock

L 60.-

Consumption

L 60.-

Stock

L 60.-

Consumption

L 60.- Production order

Consumption

L 60.-

Consumption

L 60.-

PrCtr 2

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Business

process +

data

EC-

PCA

Int. change in stock

P 120.-

PrCtr 1

Stock

P 120.-

Internal revenues

P 150.-

Material stock

L 100.-

G 80.-

P 120.-

Material Withdrawal for Production Order

F

l

o

w

o

f

v

a

l

u

e

s

FI

CO-

PC

CO-

OM

CO-

PA

Price => 150.00 USD

Withdrawal for

production

order

Production order Usage raw mat.

L 100.-

G 80.-

P 150.-

Production order

Usage raw mat.

P 150.-

PrCtr 2

PrCtr 1 PrCtr 2

Usage rawmaterial

L 100.-

G (80.-)

P (150.-)

Stock

L 100.-

G (80.-)

P (120.-)

Transfer price = 150.00

Usage raw mat.

L 100.-

G 80.-

P 150.-

Int. change in stock

L

G

P 120.-

Internal revenues

L

G

P 150.-

EC-PCA

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Business

process +

data

EC-

PCA PrCtr 1

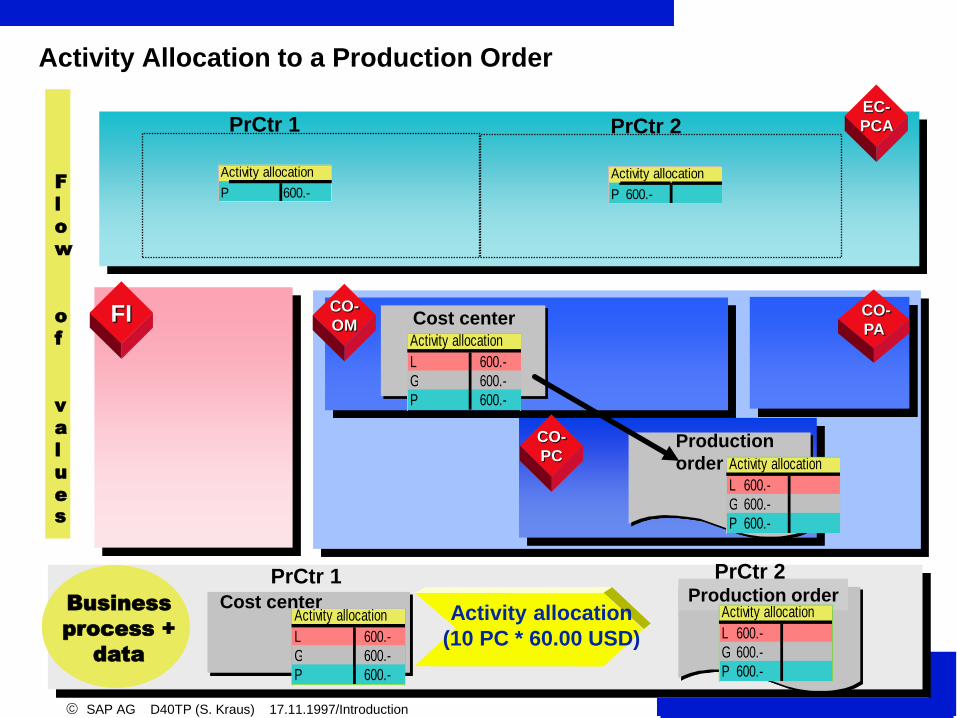

Activity Allocation to a Production Order

F

l

o

w

o

f

v

a

l

u

e

s

FI

CO-

PC

CO-

OM CO-

PA

Activity allocation

(10 PC * 60.00 USD)

Cost center

Cost center Production order Activity allocation

L 600.-

G 600.-

P 600.-

Activity allocation

L 600.-

G 600.-

P 600.-

Production

order

Activity allocation

P 600.-

PrCtr 2

PrCtr 1 PrCtr 2

Activity allocation

L 600.-

G 600.-

P 600.-

Activity allocation

L 600.-

G 600.-

P 600.-

Activity allocation

P 600.-

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Business

process +

data

EC-

PCA

Work in Process

F

l

o

w

o

f

v

a

l

u

e

s

FI

CO-

PC

CO-

OM

CO-

PA

Calculation and

settlement of

work in process

Production order

FI document

PrCtr 1

Stock WIP

L 700.-

G (680.-)

P (750.-)

Changes WIP

L 700.-

G (680.-)

P (750.-)

Production costs

L 700.-

G 680.-

P 750.-

Changes WIP

P 750.-

Stock WIP

P 750.-

Production costs

L 700.-

G 680.-

P 750.-

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Business

process +

data

EC-

PCA

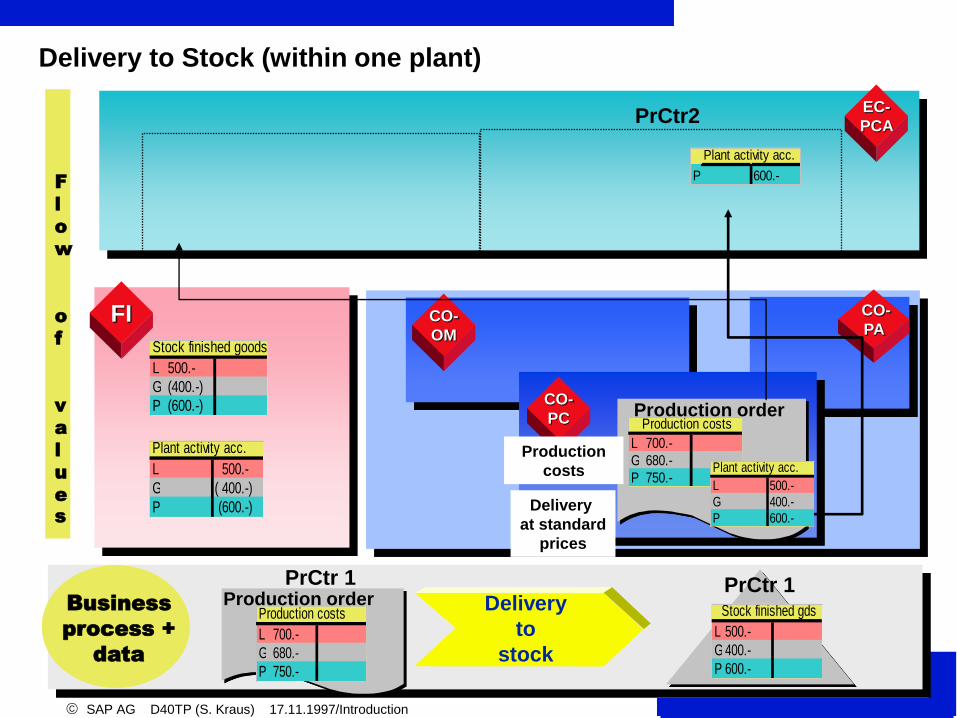

Delivery to Stock (within one plant)

F

l

o

w

o

f

v

a

l

u

e

s

FI

CO-

PC

CO-

OM

CO-

PA

Delivery

to

stock

Production order

Production order

PrCtr 1

Plant activity acc.

L 500.-

G ( 400.-)

P (600.-)

Stock finished goods

L 500.-

G (400.-)

P (600.-)

PrCtr 1

PrCtr2

Plant activity acc.

P 600.-

Production

costs

Delivery

at standard

prices

Production costs

L 700.-

G 680.-

P 750.- Plant activity acc.

L 500.-

G 400.-

P 600.-

Stock finished gds

L 500.-

G400.-

P 600.-

Production costs

L 700.-

G 680.-

P 750.-

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Business

process +

data

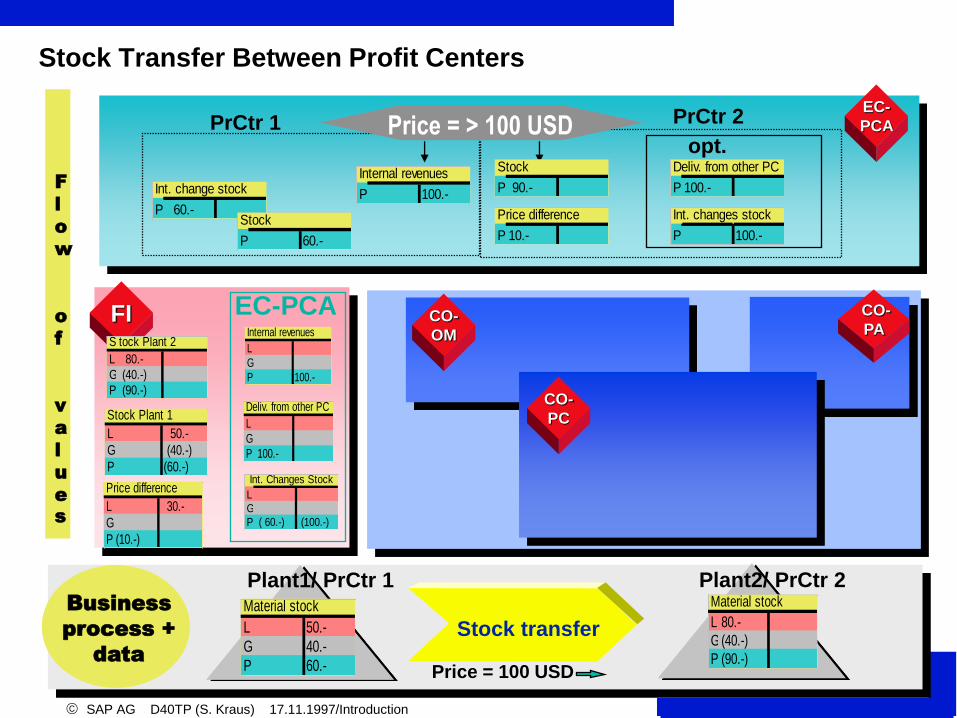

Stock transfer

EC-

PCA

Int. change stock

P 60.-

PrCtr 1

Deliv. from other PC

P 100.-

Stock

P 60.-

Internal revenues

P 100.-

Material stock

L 50.-

G 40.-

P 60.-

Plant1/ PrCtr 1

Stock Transfer Between Profit Centers

F

l

o

w

o

f

v

a

l

u

e

s

CO-

PC

CO-

OM

CO-

PA

Plant2/ PrCtr 2

Price = > 100 USD

Price difference

P 10.-

Stock

P 90.-

PrCtr 2

FI

Stock Plant 1

L 50.-

G (40.-)

P (60.-)

Stock Plant 2tock Plant 2

L 80.-

G (40.-)

P (90.-)

Price difference

L 30.-

G

P (10.-)

Internal revenues

L

G

P 100.-

Deliv. from other PC

L

G

P 100.-

EC-PCA

Int. changes stock

P 100.-

Int. Changes Stock

L

G

P ( 60.-) (100.-)

Material stock

L 80.-

G (40.-)

P (90.-) Price = 100 USD

opt.

SAP AG D40TP (S. Kraus) 17.11.1997/Introduction

Business

process +

data

EC-

PCA

Consultant's bill

P 200.-

PrCtr 2

Consultant's bill

L 200.-

G

P

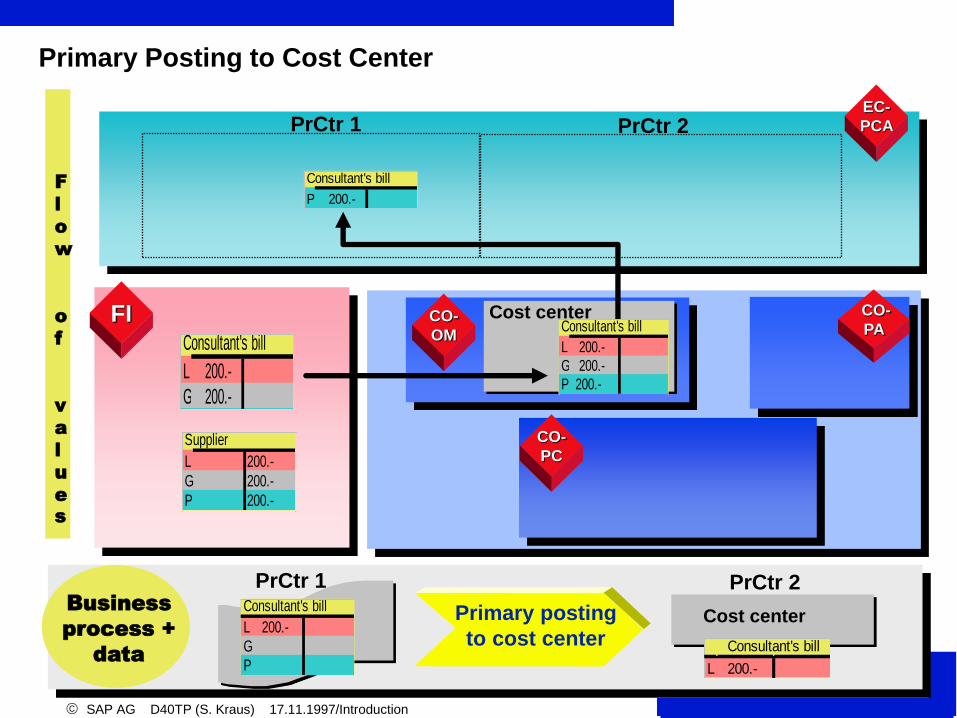

Primary Posting to Cost Center

F

l

o

w

o

f

v

a

l

u

e

s

FI

CO-

PC

CO-

OM

CO-

PA

Primary posting

to cost center Cost center

Cost center

PrCtr 1

PrCtr 1 PrCtr 2

Consultant's bill

L 200.-

G 200.-

Supplier

L 200.-

G 200.-

P 200.-

Consultant's bill

L 200.-

G 200.-

P 200.-

Consultant's bill

L 200.-