© 2013 kpmg, an indian partnership and a member firm of the kpmg network of independent member...

TRANSCRIPT

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

1

Transfer Pricing in India

Vishal Gada

28 November 2013

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

2

Contents

1 Introduction to Transfer Pricing

2 Key components of Transfer Pricing

Methods for determining Arm’s Length Price

Transfer Pricing Documentation & Penalty

4

5

Specified Domestic Transactions 3

Transfer Pricing Issues6

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

3

Contents

7 Base Erosion and Profit Shifting

8 Location Savings

Advanced Pricing Agreement

Safe Harbour

10

11

Economic Scenario9

12 Case Studies and Case Laws

Transfer Pricing (‘TP’) -Introduction

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

5

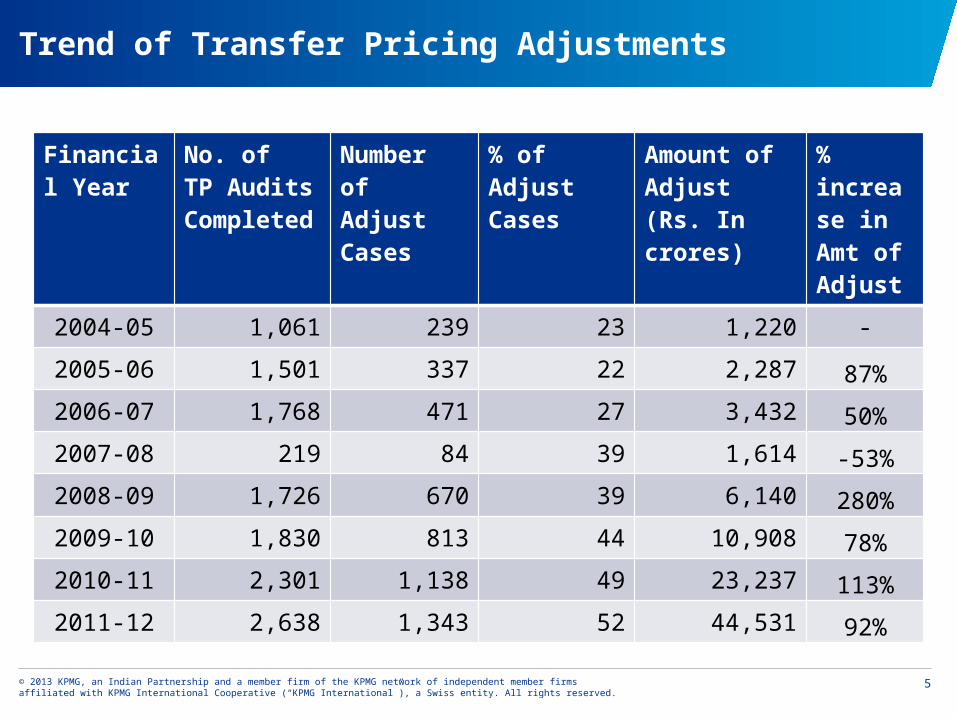

Trend of Transfer Pricing Adjustments

Financial Year

No. of TP Audits Completed

Number of Adjust Cases

% of Adjust Cases

Amount of Adjust (Rs. In crores)

% increase in Amt of Adjust

2004-05 1,061 239 23 1,220 -

2005-06 1,501 337 22 2,287 87%2006-07 1,768 471 27 3,432 50%2007-08 219 84 39 1,614 -53%2008-09 1,726 670 39 6,140 280%2009-10 1,830 813 44 10,908 78%2010-11 2,301 1,138 49 23,237 113%2011-12 2,638 1,343 52 44,531 92%

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

6

2002 2003 2004 2005 2006 2007 2008 2009

0.3 0.6 0.91.7

2.3

5.3

9.3

13.3

TP Adjustments by Revenue(USD bn)**

** Ministry of Finance and Business Standard article dated 11 May 2013

On an average, TP adjustments are made on 54 percent of cases picked up for scrutiny

Impact may multiply with widening of definition of the term ‘International Transaction’ and application of Specified Domestic Transactions to domestic related party transactions

Transfer Pricing Litigation Scenario in India

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

7

Transfer Pricing: A Global Overview

New and expanding transfer pricing legislation and rules are in trend in many countries

Levy of Harsh penalties

Stepped up enforcement globally in the form of:

• More auditors, better training

• Increasingly sophisticated

• Change in scrutiny mechanism

Complex issues and transactions are picked up for scrutiny and increasingly challenged

India, China, Australia, Korea and Japan have all recently seen an increase in number of cases picked up for scrutiny

Other tax authorities have signaled intent to step up TP compliance and field audit work

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

8

Why Transfer Pricing?

Finance Minister’s speech on the rationale for introducing Transfer Pricing Regulations

“The presence of multinational enterprises in India and

their ability to allocate profits in different jurisdictions

by controlling prices in intra-group transactions has

made the issue of transfer pricing a matter of serious

concern. I had set up an Expert Group in November 1999

to examine the detailed structure for transfer pricing

legislation. Necessary legislative changes are being made

in the Finance Bill based on these recommendations.”

-Mr. Yashwant Sinha Finance Minister, Government of India

February 28, 2001

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

9

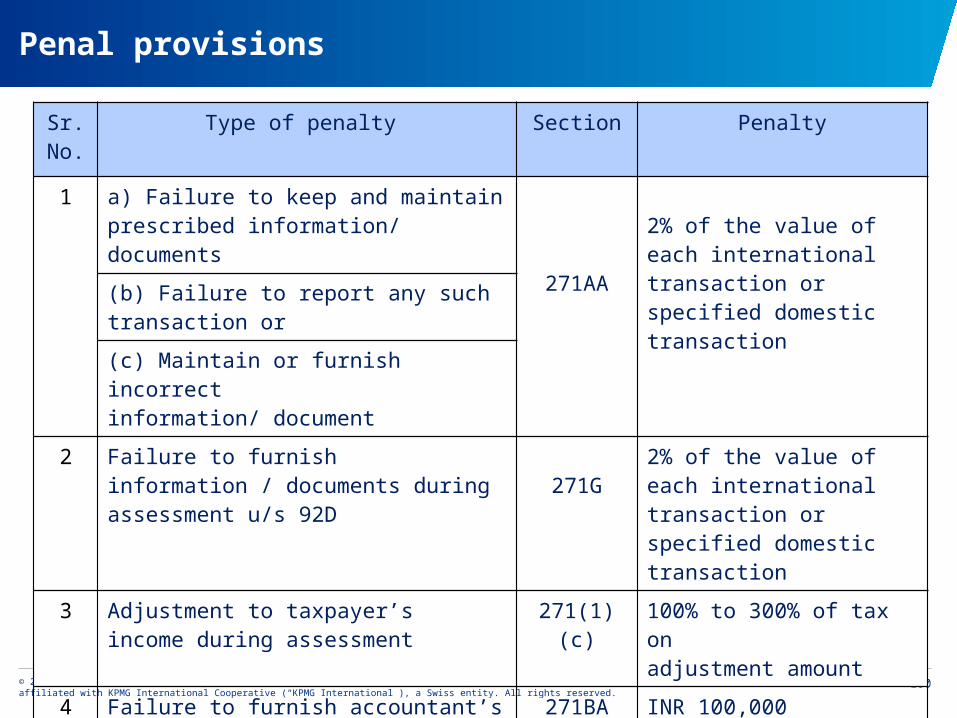

Provision Section / Rules Reference

Computation of Income from international transaction having regard to Arms Length Price

Section 92

Associated Enterprises Section 92A

International Transactions Section 92B

Specified Domestic TransactionSection 92BA / Section 40A(2)(b) / Section 80A / Section 80-IA / Section 10AA

Computation of Arm’s Length Price Section 92C read with Rule 10B and 10C

Power of Assessing Officer and Transfer Pricing Officer Section 92C / Section 92CA

Power of Board to make safe harbour rules Section 92CB

Advance Pricing Agreement Section 92CC / Section 92CD

Reference to Dispute Resolution Mechanism Section 144C

Documentation Requirements Section 92D / Rule 10D

Accountant’s Report Section 92E / Rule 10E and Form 3CEB

PenaltiesSection 271 (1) (c), Section 271AA, Section 271BA and Section 271G

Income escaping assessment Section 147

Definition Section 92F / Rule 10A

Statutory Regulations pertaining to TP in India

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

10

Background – What is Transfer Pricing?

Unrelated parties Transaction Price

Related parties Transaction Transfer Price

Transaction includes goods, services or finance

Implicit Assumption: Due to special relationship between related parties, high possibility of transfer price being different than the price that would have been agreed between the unrelated parties.

And such price charged between unrelated parties in uncontrolled conditions is referred to as the “arm’s length” price (ALP)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

11

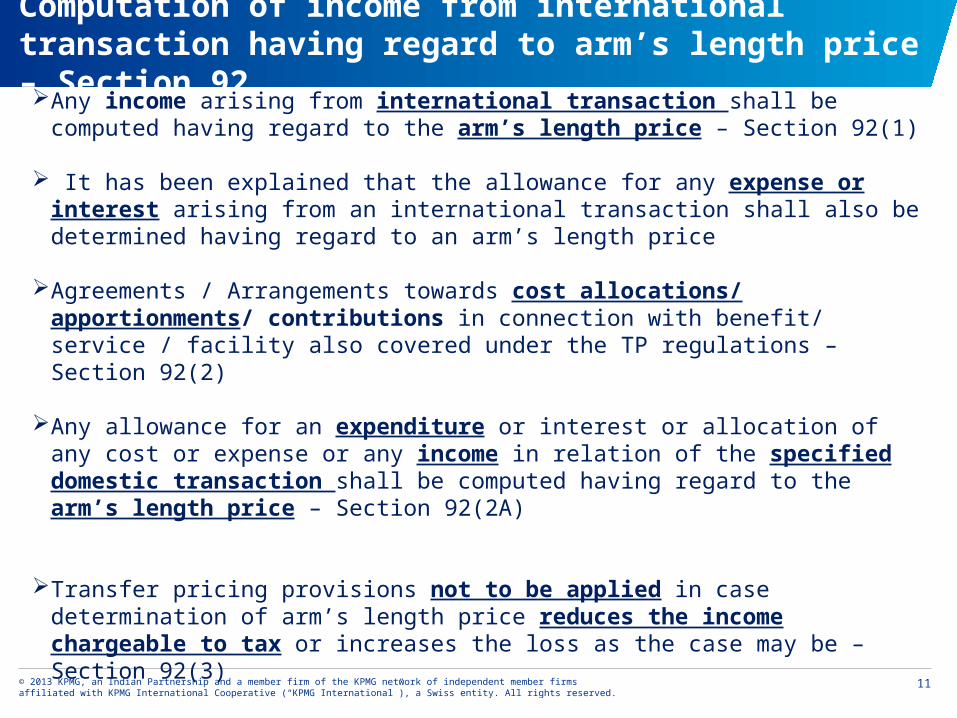

Computation of income from international transaction having regard to arm’s length price – Section 92

Any income arising from international transaction shall be computed having regard to the arm’s length price – Section 92(1)

It has been explained that the allowance for any expense or interest arising from an international transaction shall also be determined having regard to an arm’s length price

Agreements / Arrangements towards cost allocations/ apportionments/ contributions in connection with benefit/ service / facility also covered under the TP regulations – Section 92(2)

Any allowance for an expenditure or interest or allocation of any cost or expense or any income in relation of the specified domestic transaction shall be computed having regard to the arm’s length price – Section 92(2A)

Transfer pricing provisions not to be applied in case determination of arm’s length price reduces the income chargeable to tax or increases the loss as the case may be – Section 92(3)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

12

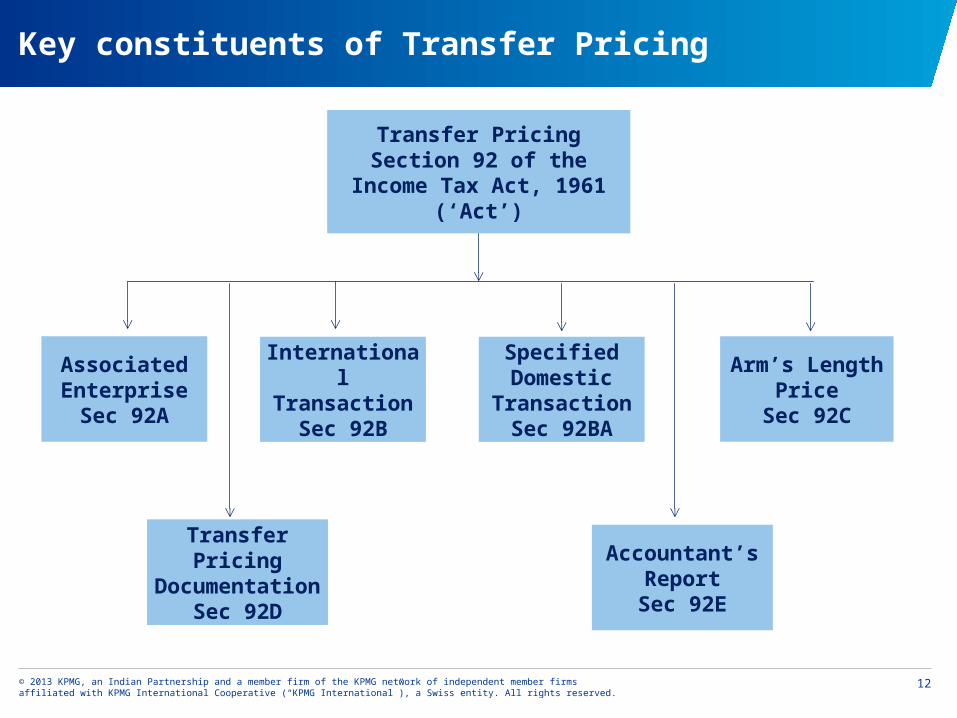

Key constituents of Transfer Pricing

Transfer PricingSection 92 of the Income Tax

Act, 1961 (‘Act’)

Associated EnterpriseSec 92A

International Transaction

Sec 92B

Specified Domestic

TransactionSec 92BA

Arm’s Length Price

Sec 92C

Transfer Pricing Documentation

Sec 92D

Accountant’s Report

Sec 92E

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

13

International Transaction - Section 92B(1)

Components of International transaction :

• Transaction;

• Between two or more associated enterprises;

• Either or both of whom are non-residents

Supply of goods / services

India Singapore

Parent Co.Resident

Subsidiary Co.

Non Resident

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

14

What is an International Transaction?

Purchase, sale or lease of tangible or intangible property; or

Provision of services; or

Lending or borrowing money; or

Any other transaction having a bearing on the profits, income, losses or assets of such enterprises; or

A mutual agreement or arrangement for the allocation or apportionment of, or any contribution to, any cost or expense incurred or to be incurred in connection with a benefit, service or facility provided or to be provided to any one or more of such enterprises

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

15

Deemed International Transaction - Section 92B(2)

As per section 92B(2), transaction

undertaken with any person other than

associated enterprise shall be deemed

to be an International transaction if :

there exists a prior agreement

between such person and the

associated enterprise; or

the terms of the relevant

transaction are determined in

substance between such person

and the associated enterprise

A’s Parent 3rd party

A

Prior agreement

Services100%

A’s Parent 3rd party

A

Determination of terms

Services100%

A & the 3rd Party to be regarded as AEs

A & the 3rd Party to be regarded as AEs

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

16

International Transaction – Definition Expanded – Finance Act 2012

Non reported transactions? • Guarantee

• Excess credit period

• Advance for services

Financing Transactions covered • Capital Financing

Business restructuring / reorganization covered

• Covered transactions even if related profit/ loss on future date

• Very wide coverage

Intangible properties defined • Marketing related intangible assets (customer list, customer contracts etc.)

• Human capital related intangible assets (organized and trained work force)

• Other property deriving value from intellectual content rather than physical attributes

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

17

AE – Section 92A(1)

Section 92A (1) of the Income-tax Act states as under :

Associated Enterprise in relation to other enterprise, means an enterprise-

Which participates, directly or indirectly, or through one or more intermediaries, in the management or control or capital of the other enterprise; or

In respect of which one or more persons who participate, directly or indirectly, or through one or more intermediaries, in its management or control or capital, are the same persons who participate, directly or indirectly, or through one or more intermediaries, in the management or control or capital of the other enterprise.

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

18

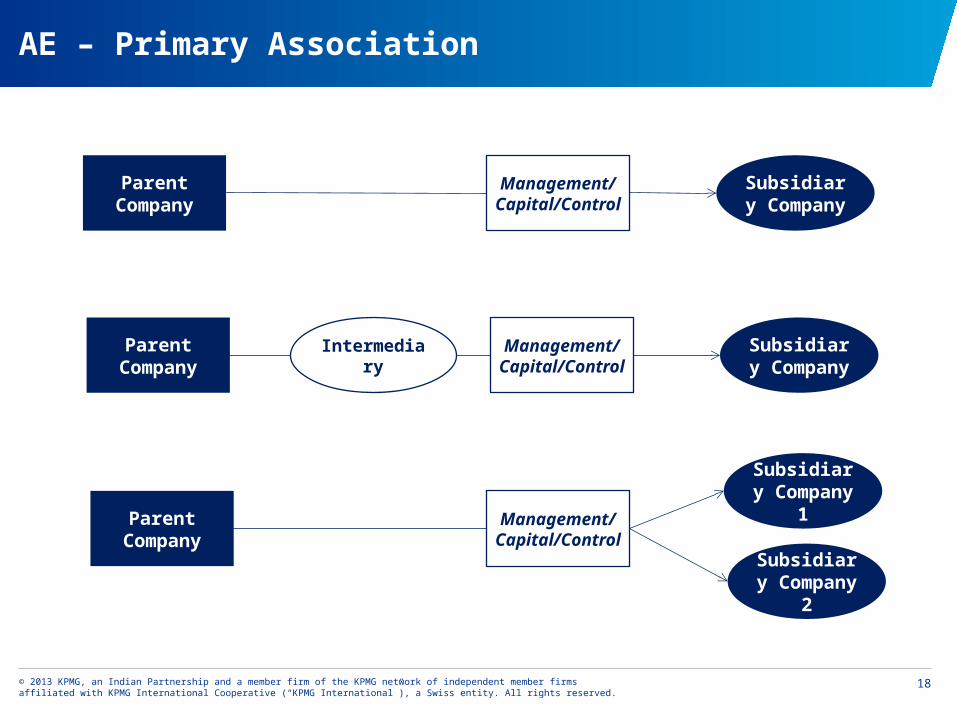

AE – Primary Association

Parent Company

Subsidiary Company

Management/ Capital/Control

Parent Company

Subsidiary Company

Management/ Capital/Control

Intermediary

Parent Company

Subsidiary Company 1

Management/ Capital/Control

Subsidiary Company 2

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

19

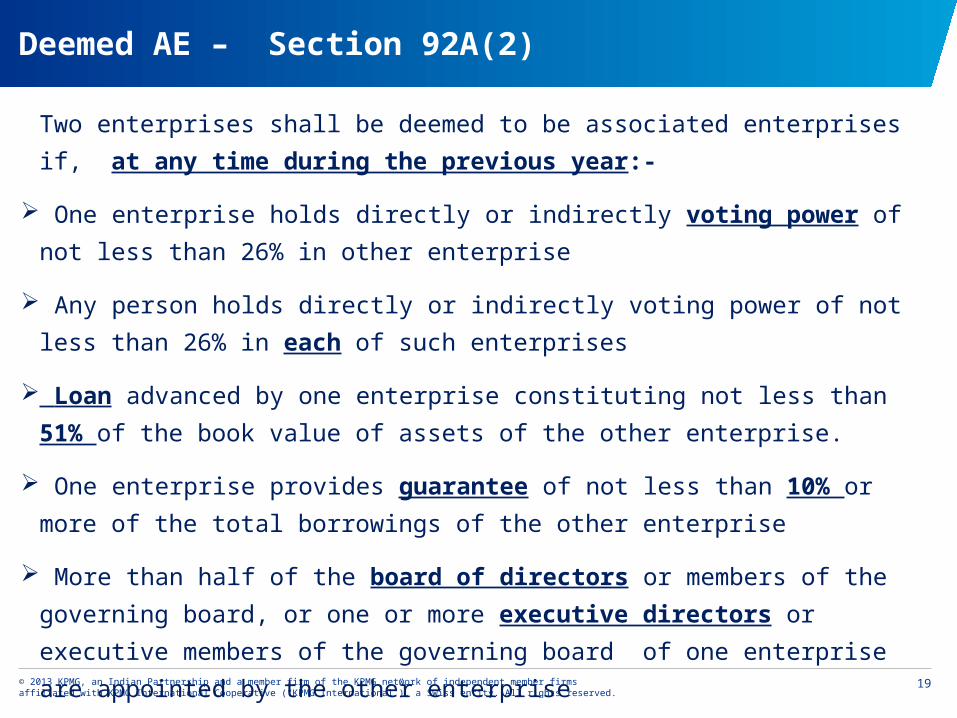

Two enterprises shall be deemed to be associated enterprises if, at any time

during the previous year:-

One enterprise holds directly or indirectly voting power of not less than 26% in

other enterprise

Any person holds directly or indirectly voting power of not less than 26% in each of

such enterprises

Loan advanced by one enterprise constituting not less than 51% of the book value

of assets of the other enterprise.

One enterprise provides guarantee of not less than 10% or more of the total

borrowings of the other enterprise

More than half of the board of directors or members of the governing board, or

one or more executive directors or executive members of the governing board of

one enterprise are appointed by the other enterprise

Deemed AE – Section 92A(2)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

20

Same person/s appoints more than half of directors on board or one executive

director in each of the two enterprises

One enterprise is wholly dependent on the knowhow, patents, copyrights, trade

marks, licenses, franchises or any other business or commercial rights of similar

nature of the other enterprise

90 percent of the raw materials consumed for the manufacture or processing of

goods and articles carried out by one enterprise is supplied by the other enterprise.

One enterprise is controlled by an individual , the other enterprise is also

controlled by such individual or his relative or jointly by such individual and relative

of such individual

Deemed AE – Section 92A(2)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

21

Deemed AE – Secondary Association

Deemed AssociatedEnterprises

Deemed AssociatedEnterprises

Power to appoint more than half of

directors

Loans in excess of

51% of total assets

Common executive director(s)

Guarantees in excess of 10% of total borrowings

Supply of raw materials

(90% or more)

Complete dependence

on IPRs

Existence of common

control

Holding shares carrying 26% or

more of the voting power

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

22

International Transfer Pricing - Genesis

InternationalTransactions

Associated

Enterprises

(‘AEs’)

Not subject to Transfer Pricing

Income / expense to be computed having regard to Arm’s Length Price (‘ALP’)

Specified Domestic Transactions (‘SDT’)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

24

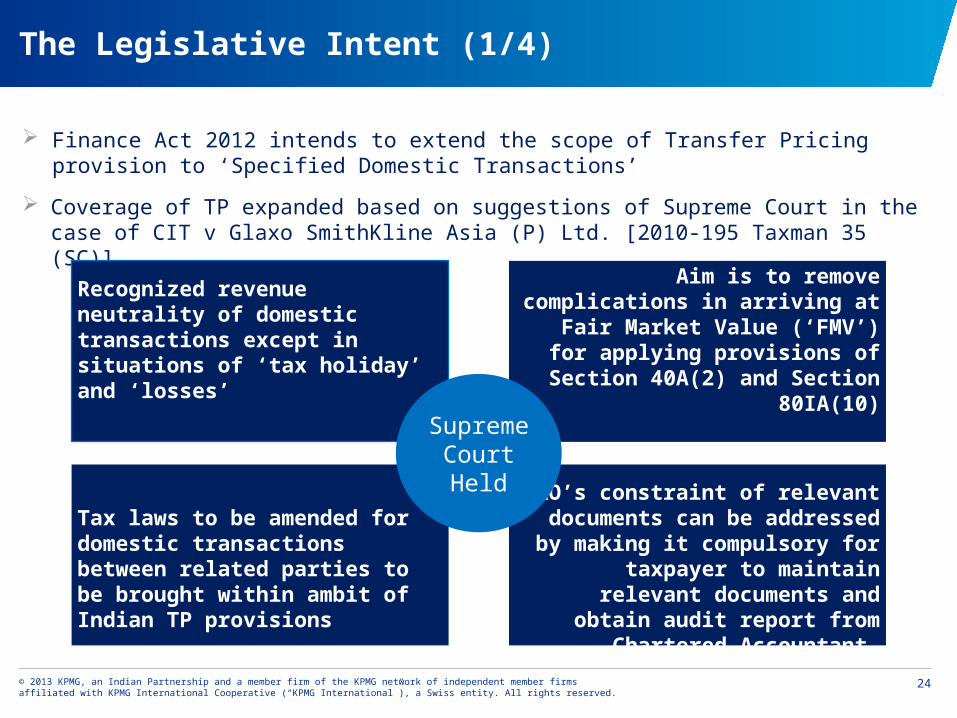

The Legislative Intent (1/4)

Finance Act 2012 intends to extend the scope of Transfer Pricing provision to ‘Specified Domestic Transactions’

Coverage of TP expanded based on suggestions of Supreme Court in the case of CIT v Glaxo SmithKline Asia (P) Ltd. [2010-195 Taxman 35 (SC)]

Recognized revenue neutrality of domestic transactions except in situations of ‘tax holiday’ and ‘losses’

Aim is to remove complications in arriving at Fair Market Value (‘FMV’)

for applying provisions of Section 40A(2) and Section 80IA(10)

Tax laws to be amended for domestic transactions between related parties to be brought within ambit of Indian TP provisions

AO’s constraint of relevant documents can be addressed by

making it compulsory for taxpayer to maintain relevant documents and

obtain audit report from Chartered Accountant

Supreme Court Held

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

25

The Legislative Intent (2/4)

Loss making Unit

Profit making Unit

Shifting of Expenses

Shifting of Income

No tax due to loss

Tax reduced due to profit

shifting

Taxable Unit

Shifting of Income

Tax @ 33%

Tax Holiday Unit

Tax Exemption

Loss to Indian Revenue as a result of the above

Shifting of Expenses

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

26

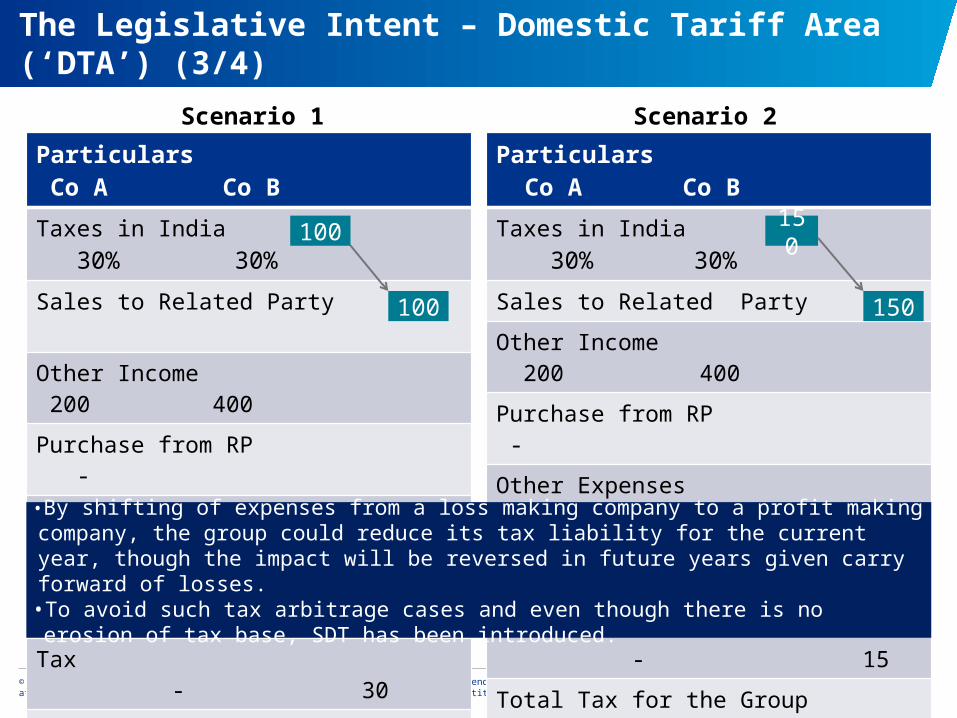

The Legislative Intent – Domestic Tariff Area (‘DTA’) (3/4)

Particulars Co A Co B

Taxes in India 30% 30%

Sales to Related Party

Other Income 200 400

Purchase from RP -

Other Expenses 400 200

Profit/ Loss (100) 100

Tax - 30

Total Tax for the Group 30

Particulars Co A Co B

Taxes in India 30% 30%

Sales to Related Party

Other Income 200 400

Purchase from RP -

Other Expenses 400 200

Profit/ Loss (50) 50

Tax - 15

Total Tax for the Group 15

Scenario 1 Scenario 2

•By shifting of expenses from a loss making company to a profit making company, the group could reduce its tax liability for the current year, though the impact will be reversed in future years given carry forward of losses.•To avoid such tax arbitrage cases and even though there is no erosion of tax base, SDT has been introduced.

100

100

150

150

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

27

The Legislative Intent – DTA and Tax Holiday Unit (4/4)

Scenario 1 Scenario 2

•By shifting of expenses from a tax holiday unit (Power) to a unit in the Domestic Tariff Area, the group could reduce its tax liability by 22.5.

•To avoid such cases Domestic TP has been introduced.

Particulars Tax Holiday

DTA

Taxes in India 0*% 30%

Sales to Related Party

Other Income 300 600

Purchase from RP

Other Expenses 300 300

Profit/ Loss 150 150

Tax * - 45

Total Tax for the Group 45

Particulars Tax Holiday

DTA

Taxes in India 0*% 30%

Sales to Related Party

Other Income 300 600

Purchase from RP

Other Expenses 300 300

Profit/ Loss 225 75

Tax * - 22.5

Total Tax for the Group 22.5

* Subject to MAT

150

150

225

225

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

28

Scope

SDT defined to include

• any expenditure in respect of which payment has been made or to be made to a specified person [section 40A(2)(b)];

• any transaction referred to in section 80A;

• any transfer of goods or services referred to in sub-section (8) of section 80-IA;

• any business transacted between the taxpayer and other person as referred to in sub-section (10) of section 80-IA;

• any transaction, referred to in any other section under Chapter VI-A or section 10AA, to which provisions of sub-section (8) or sub-section (10) of section 80-IA are applicable; or

• any other transaction as may be prescribed

Applicability

• Applicable where aggregate amount of transactions exceeds INR 5 crores in a year

• Applicable from FY 2012-13 onwards

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

29

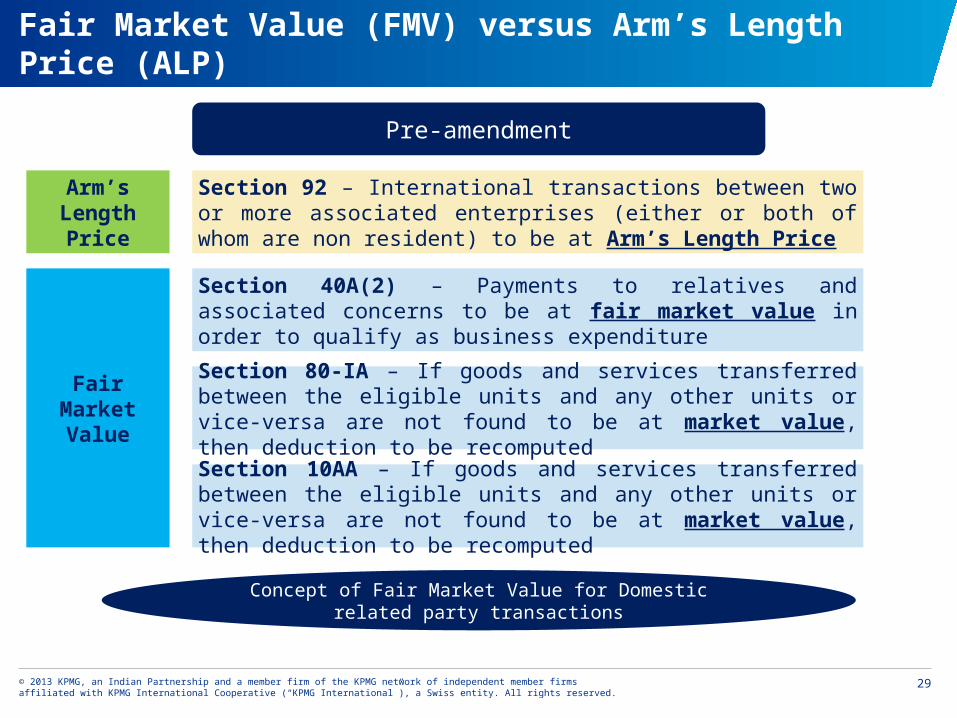

Fair Market Value (FMV) versus Arm’s Length Price (ALP)

Pre-amendment

Arm’s Length Price

Section 92 – International transactions between two or more associated enterprises (either or both of whom are non resident) to be at Arm’s Length Price

Section 40A(2) – Payments to relatives and associated concerns to be at fair market value in order to qualify as business expenditure

Section 80-IA – If goods and services transferred between the eligible units and any other units or vice-versa are not found to be at market value, then deduction to be recomputed

Section 10AA – If goods and services transferred between the eligible units and any other units or vice-versa are not found to be at market value, then deduction to be recomputed

Fair Market Value

Concept of Fair Market Value for Domestic related party transactions

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

30

Fair Market Value (FMV) versus Arm’s Length Price (ALP)

Post-amendment

Arm’s Length Price

Section 92(2) – Where in an international transaction or specified domestic transaction, two or more associated enterprises enter into a mutual agreement or arrangement for the allocation or apportionment of, or any contribution to, any cost or expense incurred or to be incurred in connection with a benefit, service or facility provided or to be provided to any one or more of such enterprises, the cost or expense allocated or apportioned to, or, as the case may be, contributed by, any such enterprise shall be determined having regard to the arm's length price of such benefit, service or facility, as the case may be. Section 92(2A) – Any allowance for an expenditure or interest or allocation of any cost or any income in relation to the specified domestic transaction shall be computed having regards to the arm’s length price

Concept of Arm’s Length Price for Domestic related party transactions

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

31

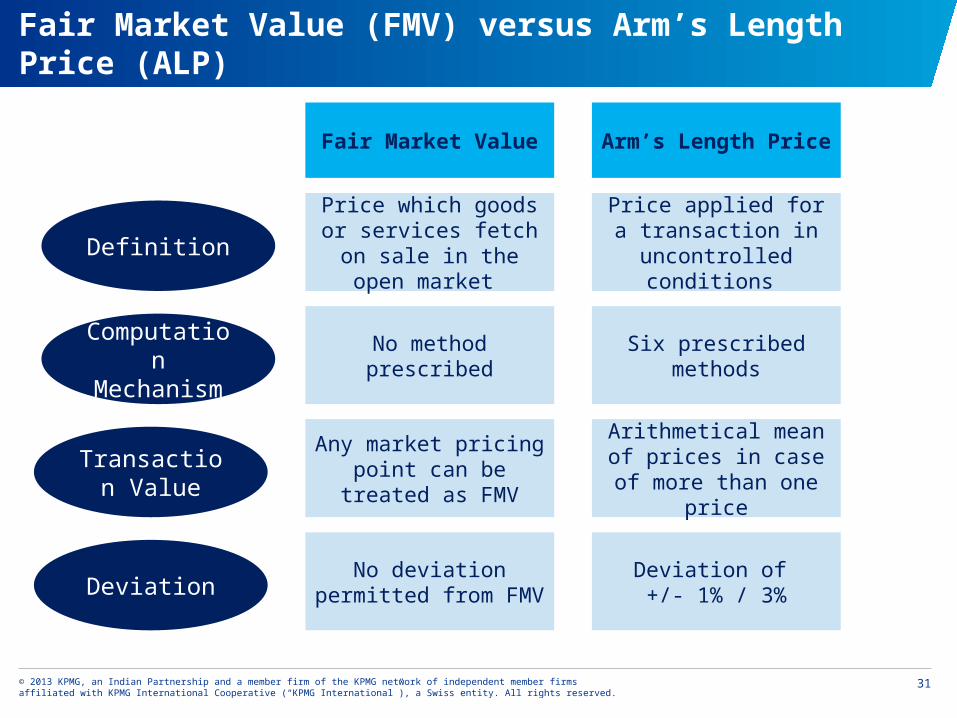

Fair Market Value (FMV) versus Arm’s Length Price (ALP)

Price which goods or services fetch on sale in

the open market

Price applied for a transaction in

uncontrolled conditions

No method prescribed

Any market pricing point can be treated as FMV

No deviation permitted from FMV

Six prescribed methods

Arithmetical mean of prices in case of more

than one price

Deviation of +/- 1% / 3%

Fair Market Value Arm’s Length Price

Definition

Computation Mechanism

Transaction Value

Deviation

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

32

Section 40A(2)(b) – Basics

Section 92BA extends TP to “any expenditure in

respect of which payment has been made or is to

be made to a person referred to in clause (b) of

sub-section (2) of section 40A”

Applies only to ‘expenditure’ in respect of

payments made or to be made to specified

persons

• No impact on income side

Only the entity incurring the expense will need to

complete the prescribed compliances

Expenditure by one group entity is income for

another group entity - arms length analysis may

consider both transacting parties

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

33

Section 40A(2)(b) – Specified Persons

Section 40A(2)(b) - list of persons / entities to be treated as related parties/ specified persons

• Specified persons having substantial interest ( i.e. more than 20% voting power or share in profits)

in taxpayer’s business and vice-versa covered;

• Scope expanded to include sister concerns

Illustrative list of entities / persons that may be included for a corporate taxpayer:

a) Company holds 20% or more equity in the tax payer;

b) Companies whose 20% or more shares are held by such a company that holds more than 20%

equity in the tax payer;

c) Companies in which the tax payer holds 20% or more equity;

d) Directors of tax payer company, and relatives of such Directors;

e) Directors of companies in category (a) above; and relatives of such Directors;

f) If an individual holds 20% or more equity in the tax payer, then relatives of such an individual; all

other companies where such individual is a Director; all other Directors of such a company, and

relatives of all such Directors; etc

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

34

Section 40A(2)(b) – Scope (1/2)

IndividualAssessee

Relatives Sec 40A(2)(b)(i)

Person in whose business / profession

assessee or his relative has substantial interest

Sec 40A(2)(b)(vi)(A)

Persons covered under section 40A(2)(b) – Applicable in case of Individual assessee

“Relative” - in relation to an individual, the husband, wife, brother or sister or any lineal ascendant or descendant of that individual

“Substantial interest” - A person is deemed to have a substantial interest in a business or profession, if,—(a) in a case where the business or profession is carried on by a company, such person is the beneficial owner of shares carrying not less than 20% of voting power; and(b) in any other case, such person is, at any time during the previous year, beneficially entitled to not less than 20 % of profits

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

35

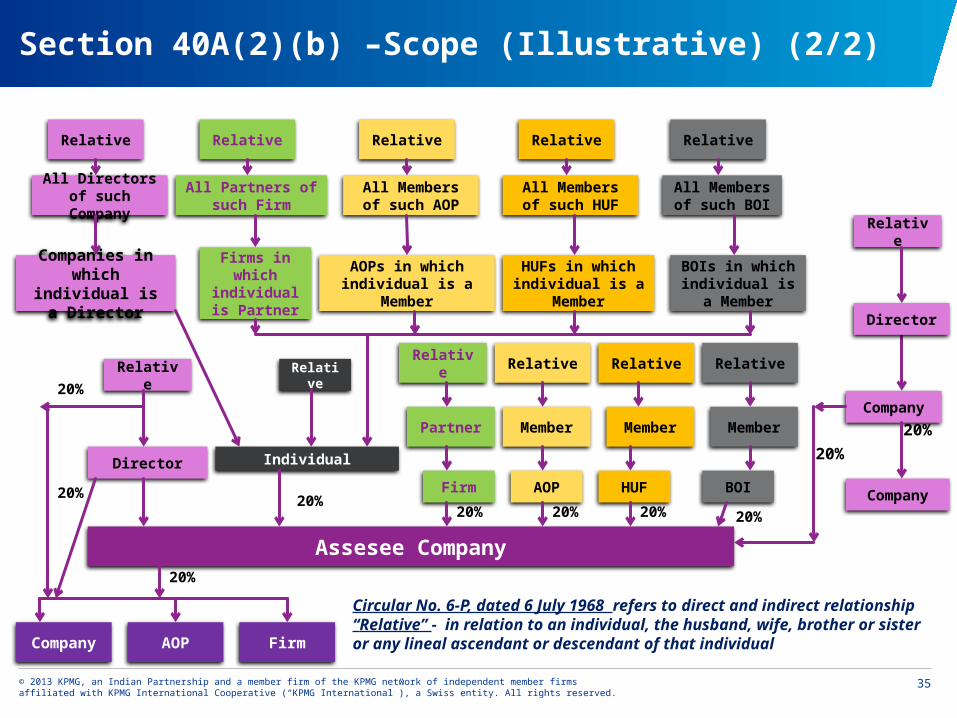

Assesee Company

Company

Company

20%Director

Relative

Individual

Relative

Companies in which

individual is a Director

All Directors of such

Company

20%

AOPs in which individual is a

Member

All Members of such AOP

Firms in which

individual is Partner

All Partners of such Firm

HUFs in which individual is a

Member

All Members of such HUF

Firm AOP HUF

20%

Relative

Company

20%

20%

20%

Relative Relative

Partner

20% 20%

Member Member

Director

Relative

BOI

Relative

Member

20%

All Members of

such BOI

BOIs in which individual is a

Member

AOP Firm

20%

Relative Relative Relative Relative Relative

Circular No. 6-P, dated 6 July 1968 refers to direct and indirect relationship“Relative” - in relation to an individual, the husband, wife, brother or sister or any lineal ascendant or descendant of that individual

Section 40A(2)(b) –Scope (Illustrative) (2/2)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

36

Illustrations

Section 40A(2)(b)(iv)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

37

Illustrations

Section 40A(2)(b)(iv)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

38

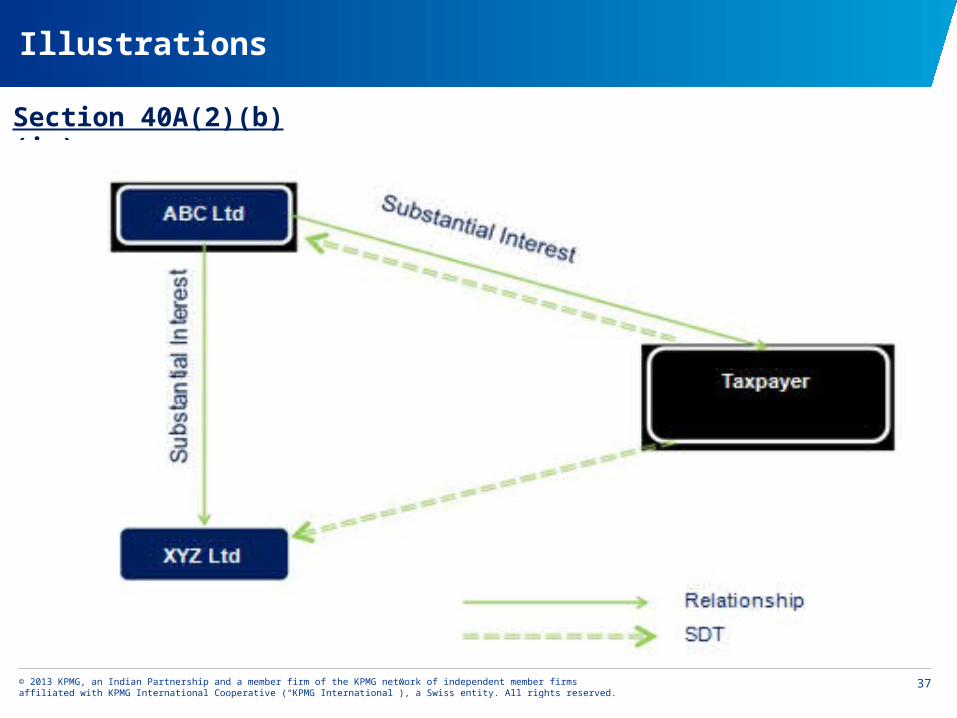

Taxpayer

ABC Ltd Mr. B

Mr. A

Mr. C

Section 40A(2)(b)(v)

Directo

r

Director Relative

Sub

stan

tial I

nter

est

Illustrations

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

39

Illustrations

Section 40A(2)(b)(vi)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

40

Issue Relating to Indirect Holding

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

41

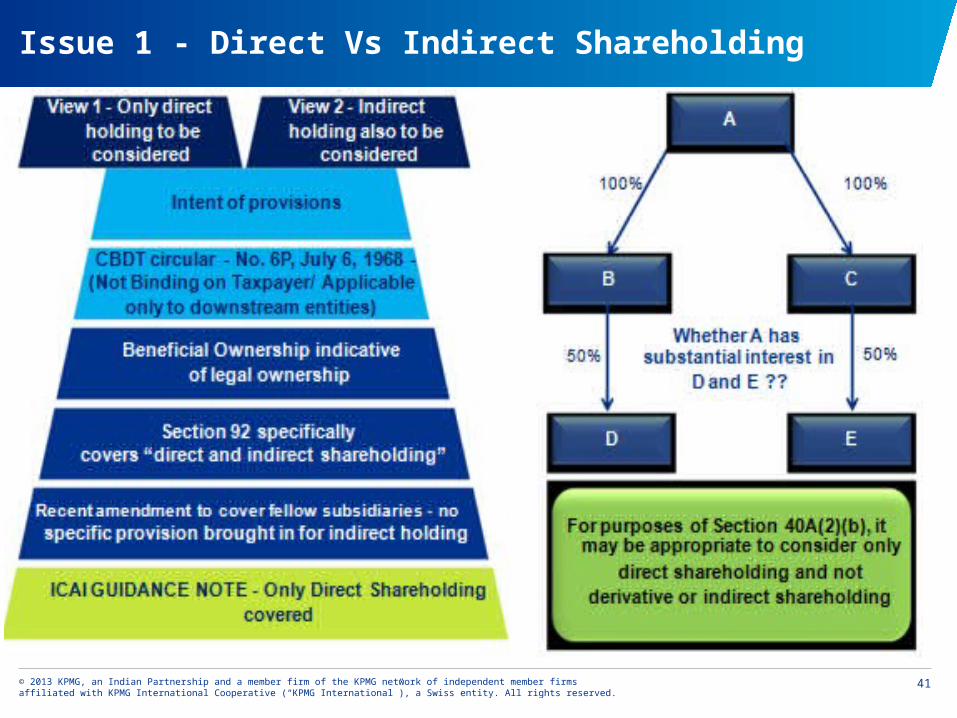

Issue 1 - Direct Vs Indirect Shareholding

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

42

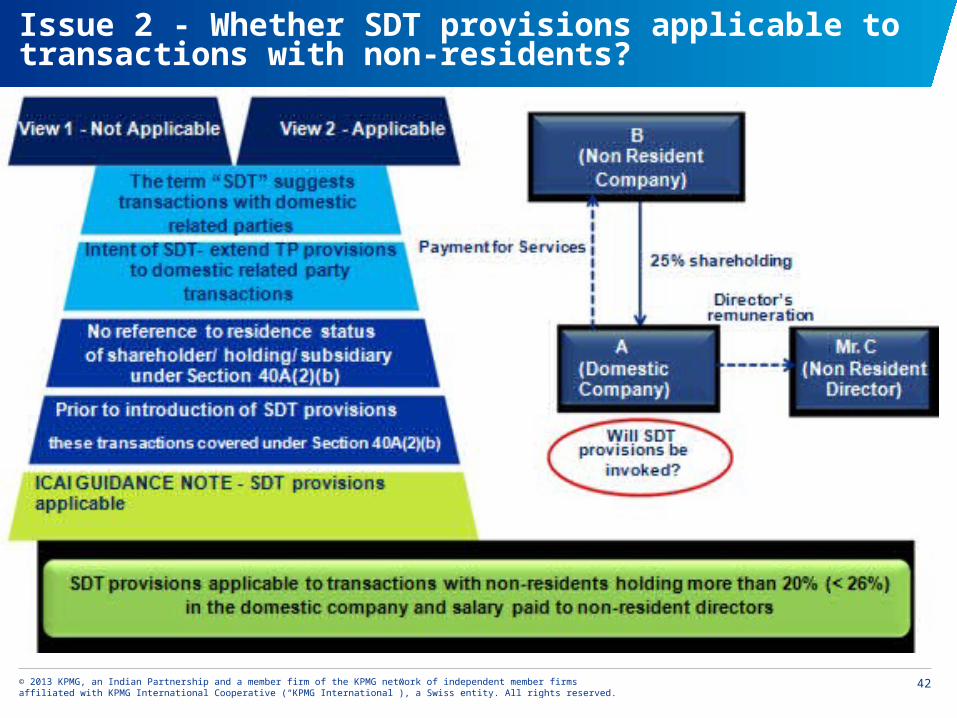

Issue 2 - Whether SDT provisions applicable to transactions with non-residents?

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

43

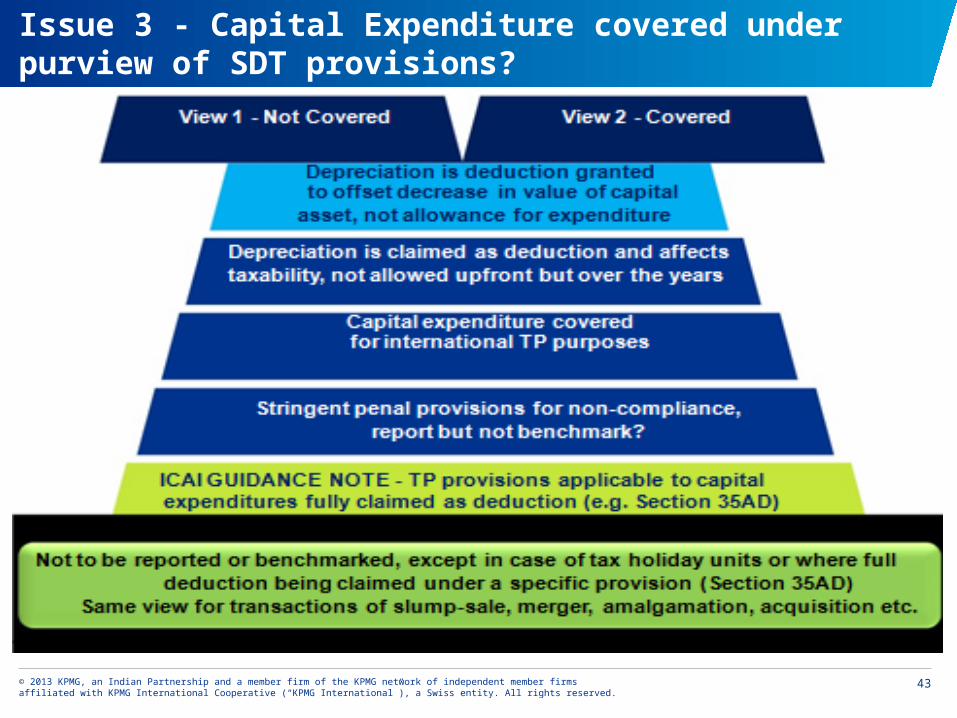

Issue 3 - Capital Expenditure covered under purview of SDT provisions?

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

44

Issue 4 - Period of applicability of SDT to tax holiday units?

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

45

Issue 5 - Whether inter-unit cost allocation is a SDT?

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

46

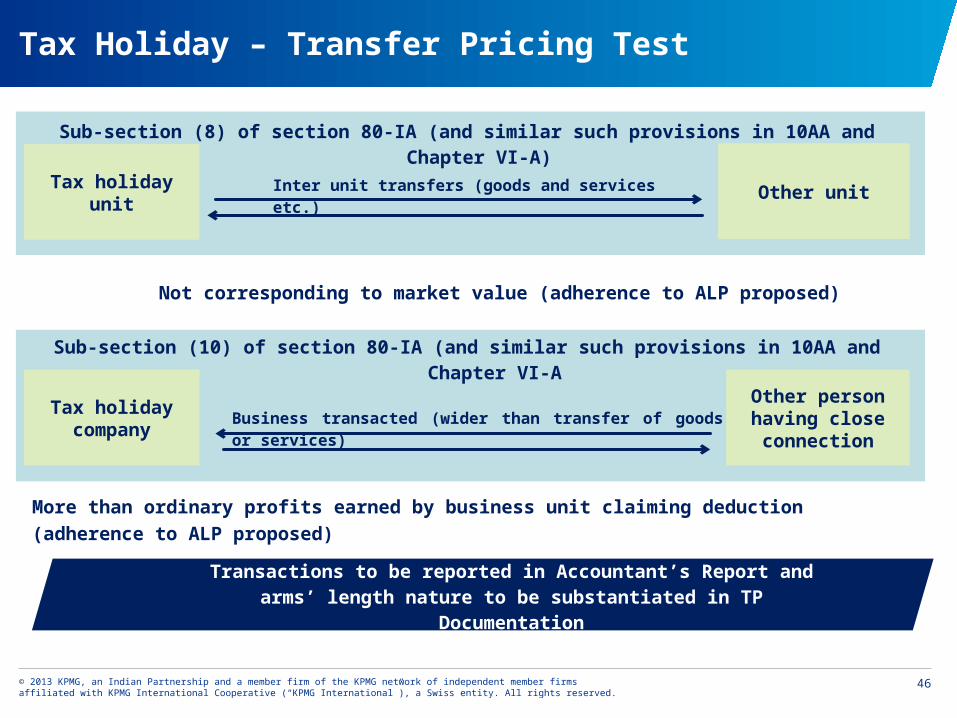

Tax Holiday – Transfer Pricing Test

Tax holiday unit Other unit

Sub-section (8) of section 80-IA (and similar such provisions in 10AA and Chapter VI-A)

Inter unit transfers (goods and services etc.)

Other person having close connection

Tax holiday company

Business transacted (wider than transfer of goods or services)

Sub-section (10) of section 80-IA (and similar such provisions in 10AA and Chapter VI-A

Not corresponding to market value (adherence to ALP proposed)

Transactions to be reported in Accountant’s Report and arms’ length nature to be substantiated in TP Documentation

More than ordinary profits earned by business unit claiming deduction (adherence to ALP proposed)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

47

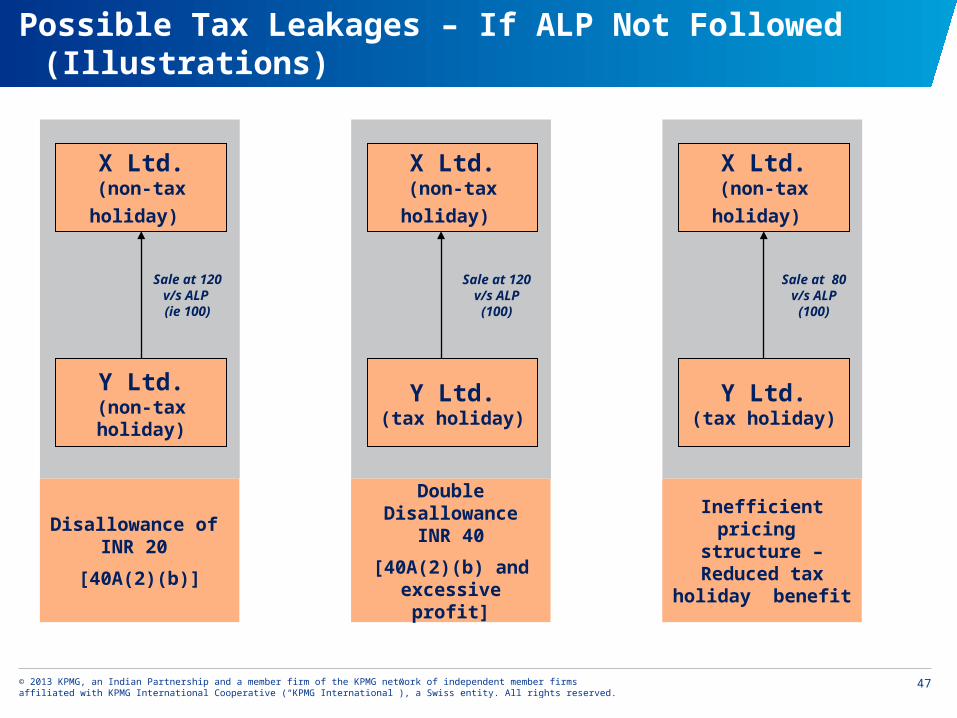

Possible Tax Leakages – If ALP Not Followed (Illustrations)

X Ltd.(non-tax holiday)

Y Ltd.(non-tax holiday)

Sale at 120 v/s ALP (ie 100)

Disallowance of INR 20

[40A(2)(b)]

X Ltd.(non-tax holiday)

Y Ltd.(tax holiday)

Sale at 120 v/s ALP

(100)

Double Disallowance

INR 40

[40A(2)(b) and excessive profit]

X Ltd.(non-tax holiday)

Y Ltd.(tax holiday)

Sale at 80 v/s ALP

(100)

Inefficient pricing structure – Reduced tax holiday benefit

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

48

Domestic Transfer Pricing affecting tax holiday undertakings

Transactions to be reported in Accountant’s Report and arms’ length nature to be substantiated in the TP Documentation

Section Nature of undertaking covered

80IA Undertakings engaged in Developing, operating and maintaining, developing and operating and maintaining infrastructure

facilities Generation/ transmission or distribution of power Reconstruction / revival of power generating plants

80IB Undertakings located/ engaged in Industrially backward districts as notified Scientific research and development Refining mineral oil / commercial production of natural gas Operating cold chain facility for agricultural produce Processing, preservation and packing of meat / meat products or poultry / marine/dairy products Operating and maintaining a hospital of specified capacity

80IC Undertaking located in notified Centre/ Parks/ Areas in Sikkim Himachal Pradesh/ Uttaranchal North –Eastern states

80ID Undertaking engaged in business of hotel / convention centre in specified areas/ districts

10AA Undertakings having a Special Economic Zone unit

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

49

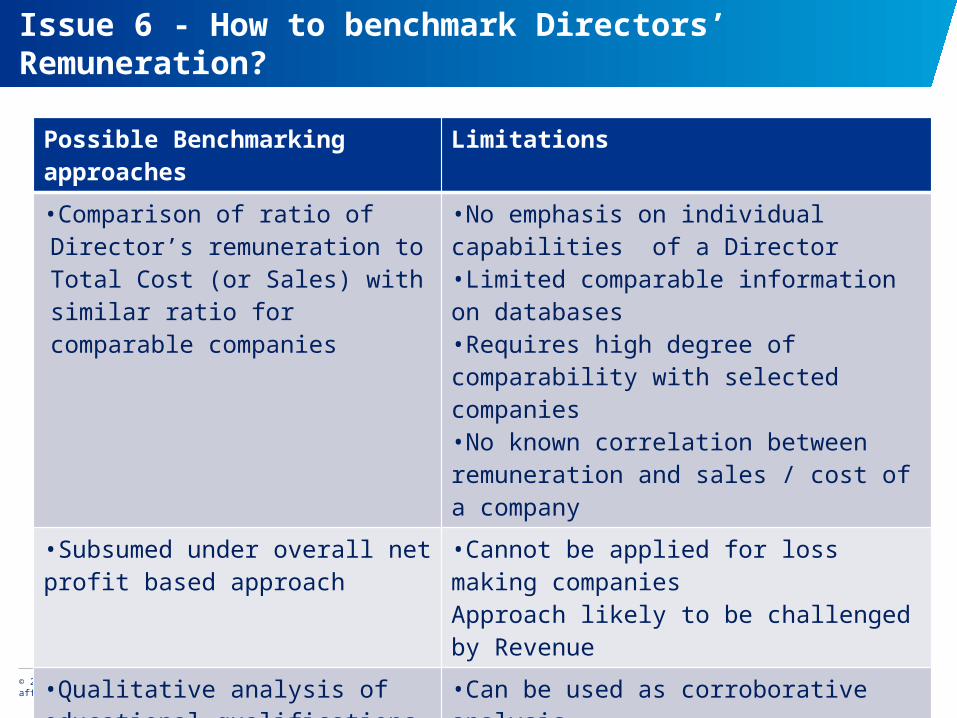

Issue 6 - How to benchmark Directors’ Remuneration?

Possible Benchmarking approaches

Limitations

•Ceilings provided in Companies Act, Central Government approvals, Listing agreement norms, DPE Guidelines, Shareholder and Board of Director resolutions, Remuneration Committee approvals

•Not applicable to private limited companies •Upper ceilings can be challenged by Revenue

•Peer review •Availability of reliable data may be a constraint

•Salary drawn elsewhere, simultaneously or previously

•Generally not available for promoter directors

•External publicly available salary data on HR websites

•Could be unreliable and difficult to obtain •May lead to cherry-picking

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

50

Issue 6 - How to benchmark Directors’ Remuneration?

Possible Benchmarking approaches

Limitations

•Comparison of ratio of Director’s remuneration to Total Cost (or Sales) with similar ratio for comparable companies

•No emphasis on individual capabilities of a Director •Limited comparable information on databases •Requires high degree of comparability with selected companies •No known correlation between remuneration and sales / cost of a company

•Subsumed under overall net profit based approach

•Cannot be applied for loss making companies Approach likely to be challenged by Revenue

•Qualitative analysis of educational qualifications, work experience, etc.

•Can be used as corroborative analysis

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

51

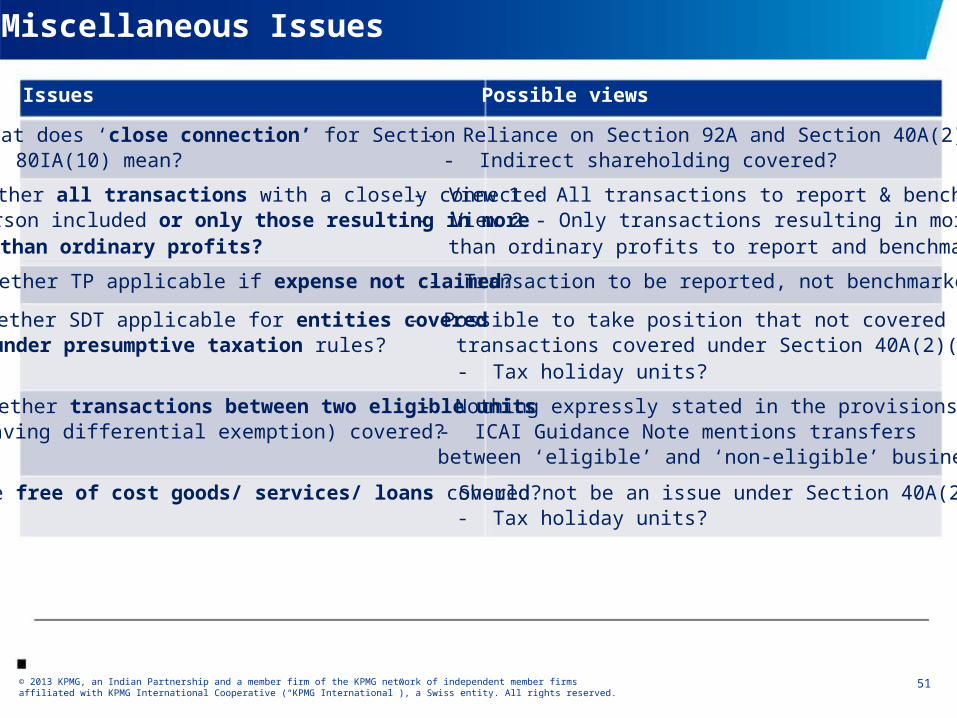

Miscellaneous Issues

Issues Possible views

What does ‘close connection’ for Section - Reliance on Section 92A and Section 40A(2)(b)80IA(10) mean? - Indirect shareholding covered?

Whether all transactions with a closely connected - View 1 - All transactions to report & benchmarkperson included or only those resulting in more - View 2 - Only transactions resulting in morethan ordinary profits? than ordinary profits to report and benchmark

Whether TP applicable if expense not claimed? - Transaction to be reported, not benchmarked?

Whether SDT applicable for entities covered - Possible to take position that not covered forunder presumptive taxation rules? transactions covered under Section 40A(2)(b)

- Tax holiday units?

Whether transactions between two eligible units - Nothing expressly stated in the provisions(having differential exemption) covered? - ICAI Guidance Note mentions transfers

between ‘eligible’ and ‘non-eligible’ business?

Are free of cost goods/ services/ loans covered? - Should not be an issue under Section 40A(2)(b)- Tax holiday units?

Methods for determining ALP

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

53

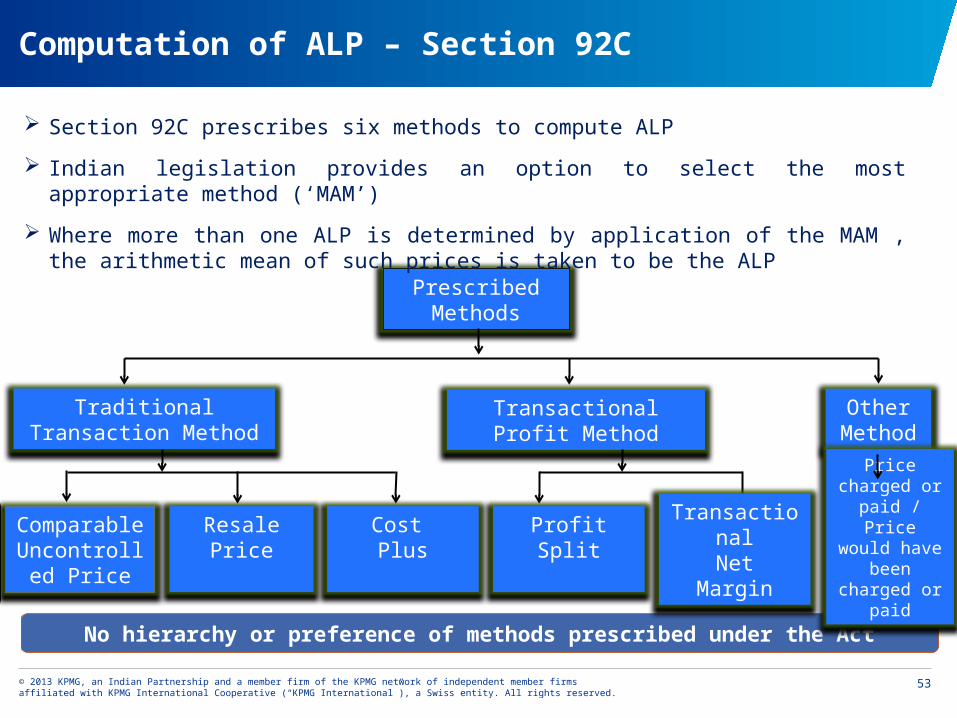

Computation of ALP – Section 92C

Prescribed Methods

Traditional Transaction Method

Transactional Profit Method

ResalePrice

Comparable Uncontrolled

Price

No hierarchy or preference of methods prescribed under the Act

Other Method

Price charged or paid / Price would have

been charged or paid

Section 92C prescribes six methods to compute ALP

Indian legislation provides an option to select the most appropriate method (‘MAM’)

Where more than one ALP is determined by application of the MAM , the arithmetic mean of such prices is taken to be the ALP

Cost Plus

ProfitSplit

TransactionalNet

Margin

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

54

OECD Guidelines Hierarchy

Comparable Uncontrolled Price Method

Most Preferred

Least Preferred

Cost Plus Method

Resale PriceMethod

Transactional Net Margin

Method

Profit Split Method

Traditional Transaction Methods

Transactional Profits Methods

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

55

Order of consideration of methods

The Indian transfer pricing regulations do not prescribe any specific

hierarchy of methods

The OECD guidelines state that traditional transactions methods are

preferable to transactional profit methods (in a situation where both can

be applied in an equally reliable manner).

Further, the OECD guidelines state that the CUP is the “preferred

method”, this should be used in preference to any others

Profit-based methods are often “one-sided” methods that use profits to

make inferences about pricing

• Assumes that profits are largely dependent on transfer prices

• Profit-based methods make sense if - and only if – the assumption

holds and profits are largely dependent on transfer prices

Application of TNMM to a specific tested party breaks down when

factors other than transfer pricing have a material impact on profits

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

56

Selection of Transfer Pricing Methods

Most appropriate method shall be the method best suited to the facts and

circumstances of each particular international transaction and which

provides the most reliable measure of an arm’s length price in relation

to the international transaction

Factors considered for selection of the most appropriate method

• Nature and class of international transaction

• Class of associated enterprise and functions performed

• Availability, coverage and reliability of data

• Degree of comparability between the International transaction

• Extent to which reliable and accurate adjustments can be made

• The nature, extent and reliability of assumptions for application of the

method

Ru

le 10C

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

57

Rule 10B(2) - Comparability Factors

Comparability factors

CharacteristicsDepends on type: tangible,

intangible or service

Functional Analysis

Conduct is best evidence of risk bearing,

should be consistent with control

Economic Circumstances

Geography, size of market, date and time

Contractual termsWhere not written,

deduce from conduct

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

58

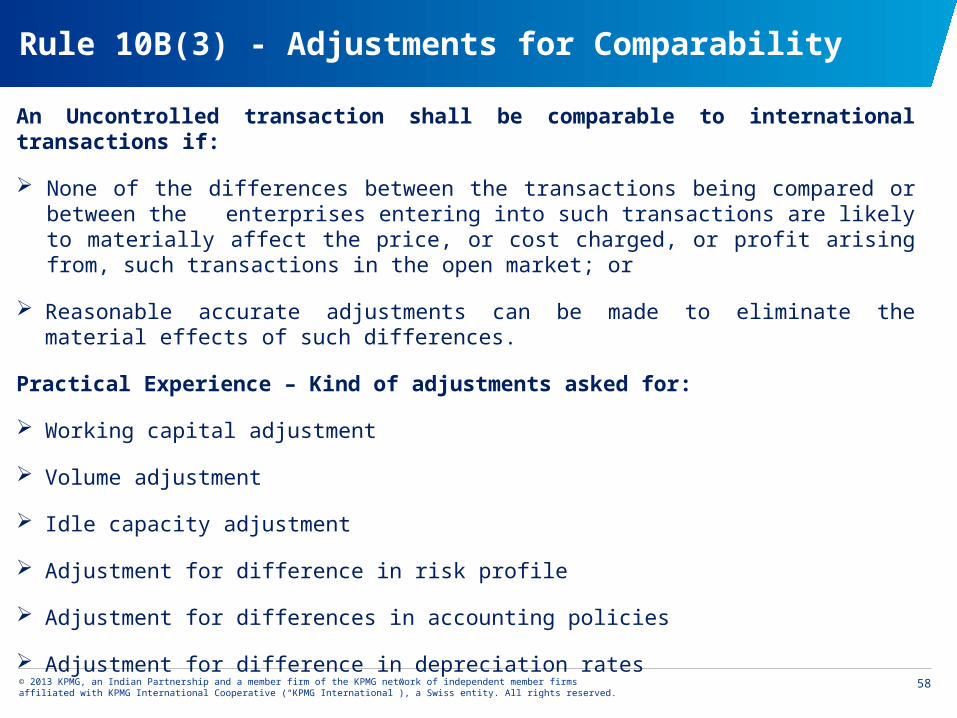

Rule 10B(3) - Adjustments for Comparability

An Uncontrolled transaction shall be comparable to international transactions if:

None of the differences between the transactions being compared or between the enterprises entering into such transactions are likely to materially affect the price, or cost charged, or profit arising from, such transactions in the open market; or

Reasonable accurate adjustments can be made to eliminate the material effects of such differences.

Practical Experience – Kind of adjustments asked for:

Working capital adjustment

Volume adjustment

Idle capacity adjustment

Adjustment for difference in risk profile

Adjustment for differences in accounting policies

Adjustment for difference in depreciation rates

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

59

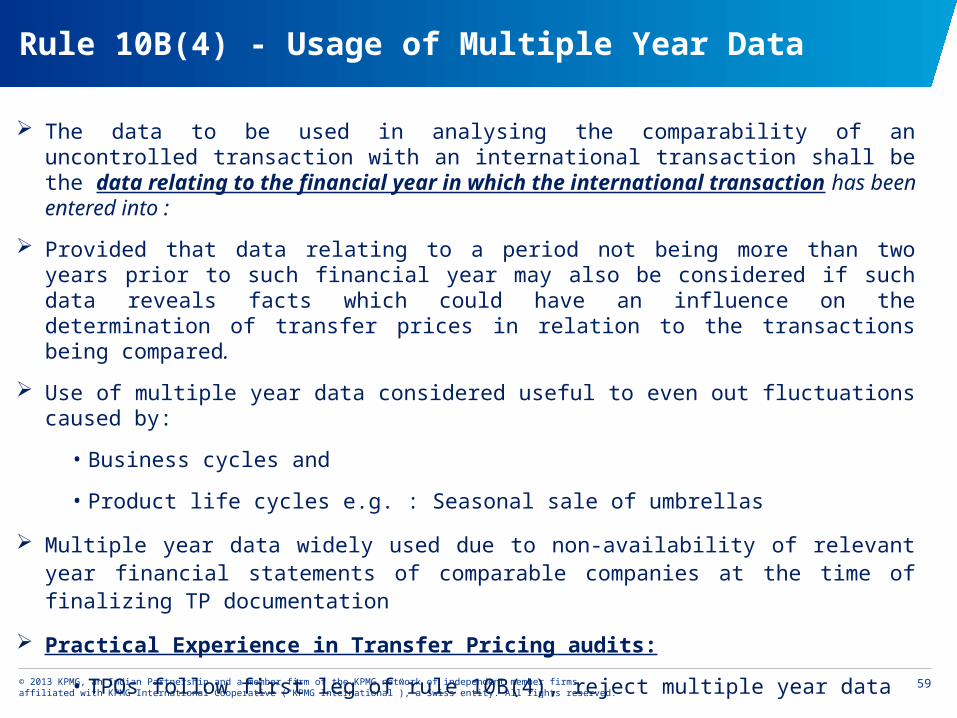

Rule 10B(4) - Usage of Multiple Year Data

The data to be used in analysing the comparability of an uncontrolled transaction with an international transaction shall be the data relating to the financial year in which the international transaction has been entered into :

Provided that data relating to a period not being more than two years prior to such financial year may also be considered if such data reveals facts which could have an influence on the determination of transfer prices in relation to the transactions being compared.

Use of multiple year data considered useful to even out fluctuations caused by:

• Business cycles and

• Product life cycles e.g. : Seasonal sale of umbrellas

Multiple year data widely used due to non-availability of relevant year financial statements of comparable companies at the time of finalizing TP documentation

Practical Experience in Transfer Pricing audits:

• TPOs follow first leg of rule 10B(4), reject multiple year data

• Adopt only data relating to the relevant financial year and undertake adjustments (including the data which was not available at the time of filing of return)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

60

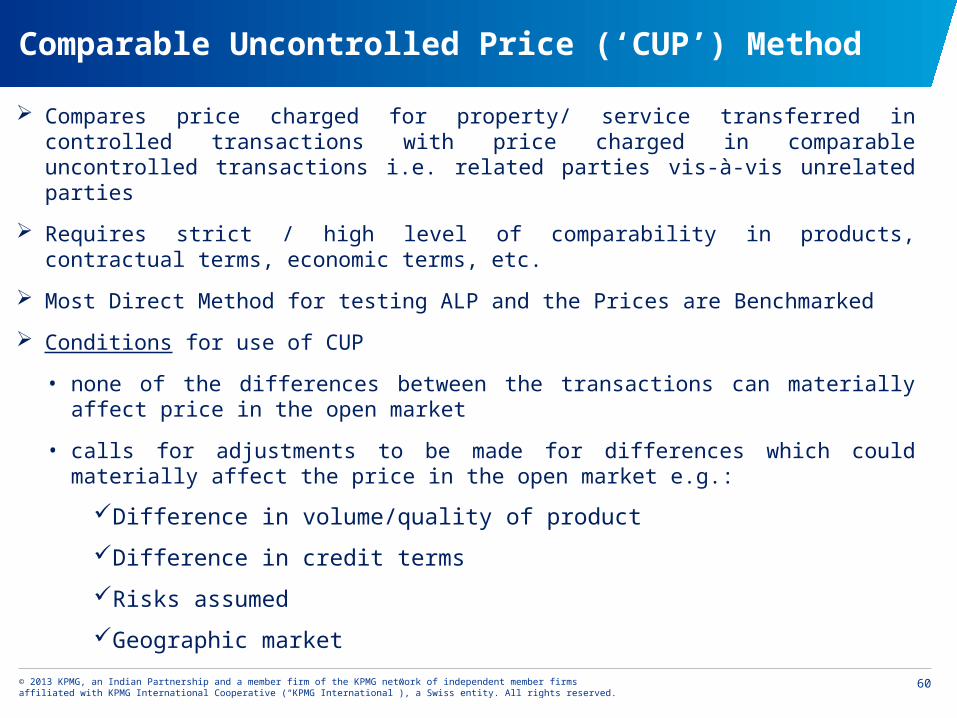

Comparable Uncontrolled Price (‘CUP’) Method

Compares price charged for property/ service transferred in controlled transactions with price charged in comparable uncontrolled transactions i.e. related parties vis-à-vis unrelated parties

Requires strict / high level of comparability in products, contractual terms, economic terms, etc.

Most Direct Method for testing ALP and the Prices are Benchmarked

Conditions for use of CUP

• none of the differences between the transactions can materially affect price in the open market

• calls for adjustments to be made for differences which could materially affect the price in the open market e.g.:

Difference in volume/quality of product

Difference in credit terms

Risks assumed

Geographic market

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

61

CUP Method

Ext

ern

al C

UP

Unrelated Co. Y

Unrelated Co. Z

India

Tra

nsfe

r P

rice Internal CUP

Outside India

(e.g. USA)

India

Subsidiary Co

Parent Co

Unrelated Co. X

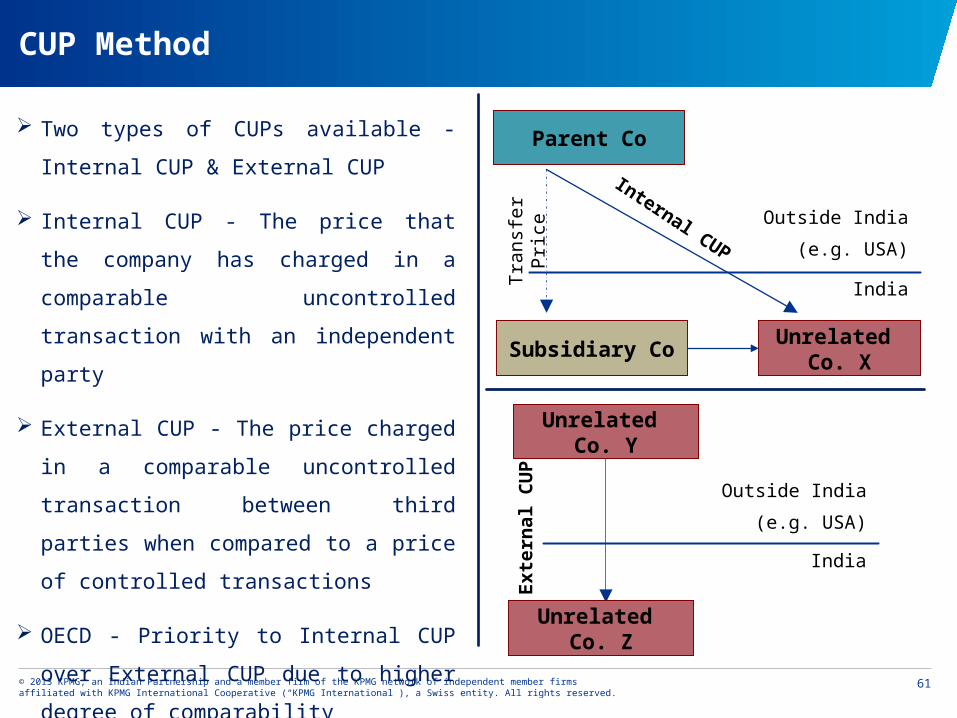

Two types of CUPs available - Internal CUP

& External CUP

Internal CUP - The price that the company

has charged in a comparable uncontrolled

transaction with an independent party

External CUP - The price charged in a

comparable uncontrolled transaction

between third parties when compared to a

price of controlled transactions

OECD - Priority to Internal CUP over

External CUP due to higher degree of

comparability

Outside India

(e.g. USA)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

62

CUP Method – Case Study I

Unrelated Supplier A (Japan)

Unrelated Supplier B (Russia)

Related Supplier Foreign Co. (AUS)

Ind Co. (India)

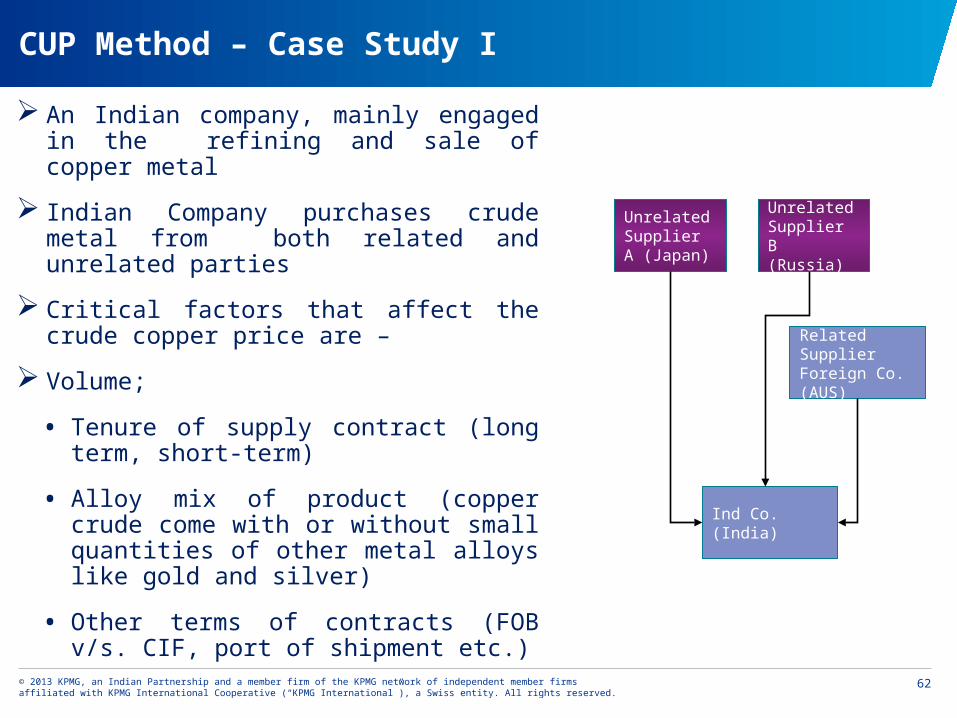

An Indian company, mainly engaged in the refining and sale of copper metal

Indian Company purchases crude metal from both related and unrelated parties

Critical factors that affect the crude copper price are –

Volume;

• Tenure of supply contract (long term, short-term)

• Alloy mix of product (copper crude come with or without small quantities of other metal alloys like gold and silver)

• Other terms of contracts (FOB v/s. CIF, port of shipment etc.)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

63

CUP Method – Case Study I

Criteria Related Party ForCo (Australia)Controlled

Unrelated Party A (Japan)Uncontrolled

Unrelated Party B (Russia)Uncontrolled

Tenure of Contract

Long Term (10 yrs)

Long Term (8 yrs)

Short Term (2 yrs)

Volume during year under consideration

2200 MT 3000 MT 9000 MT

Alloy Mix 0.5% Gold, 1% silver

1% Gold, 1% silver

None

Port of shipment

Australia Japan Russia

Price (per MT) INR 29,500 (applicable for entire year)

INR 32,000 (applicable for entire year)

INR 28,500 (applicable for entire year)

Other Terms FOB basis CIF basis FOB basis

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

64

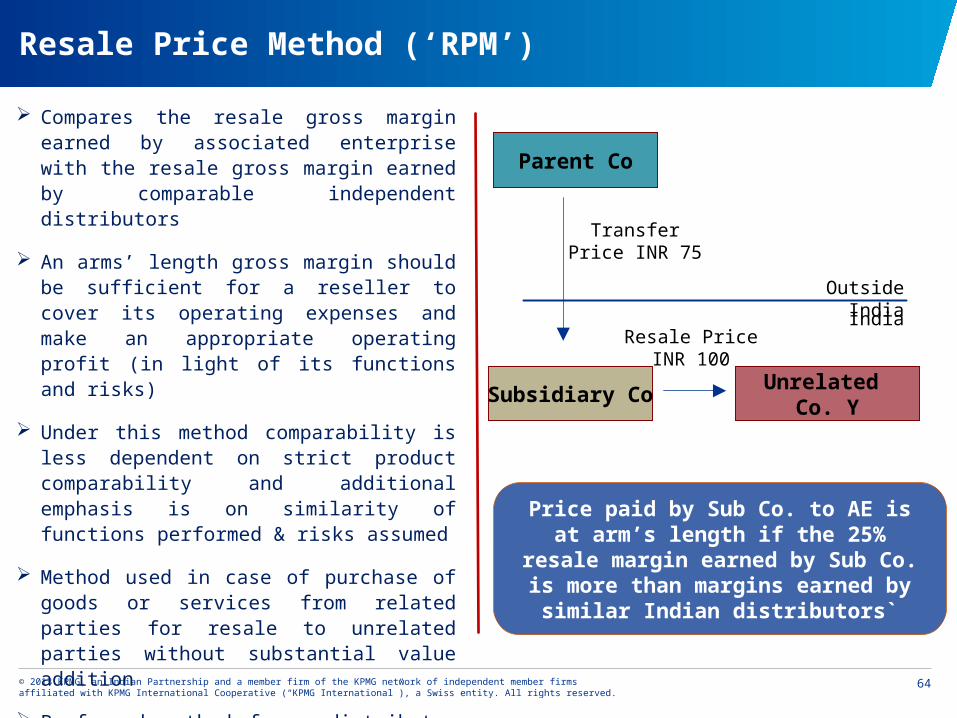

Resale Price Method (‘RPM’)

Price paid by Sub Co. to AE is at arm’s length if the 25% resale margin earned by Sub Co. is more than margins earned by

similar Indian distributors`

Transfer Price INR 75

Resale Price INR 100

Subsidiary Co

Parent Co

Unrelated Co. Y

Outside India

India

Compares the resale gross margin earned by associated enterprise with the resale gross margin earned by comparable independent distributors

An arms’ length gross margin should be sufficient for a reseller to cover its operating expenses and make an appropriate operating profit (in light of its functions and risks)

Under this method comparability is less dependent on strict product comparability and additional emphasis is on similarity of functions performed & risks assumed

Method used in case of purchase of goods or services from related parties for resale to unrelated parties without substantial value addition

Preferred method for a distributor buying purely finished goods from a group company (if no CUP available)

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

65

RPM – Case Study I

Independent third party in India

End Customer

Foreign Manufacturer

Related party in India

COGS = INR 150Resale Price = INR 200

Gross Profit Margin = 50/200 = 25%

Transfer Price = ??

Resale Price = INR150

ALP= 150 – (150*25%) =112. 50

Sale to independent third party at INR 150 and sale to end customer by third party at INR 200

Sale to end customer by related party at INR 150

Particulars Amount

Gross Profit 50 i.e. (200-150)

Gross Margin 25% i.e. (50/200)

Arm’s Length Purchase Cost 112.50 i.e. [150 – (25% 0f 150)]

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

66

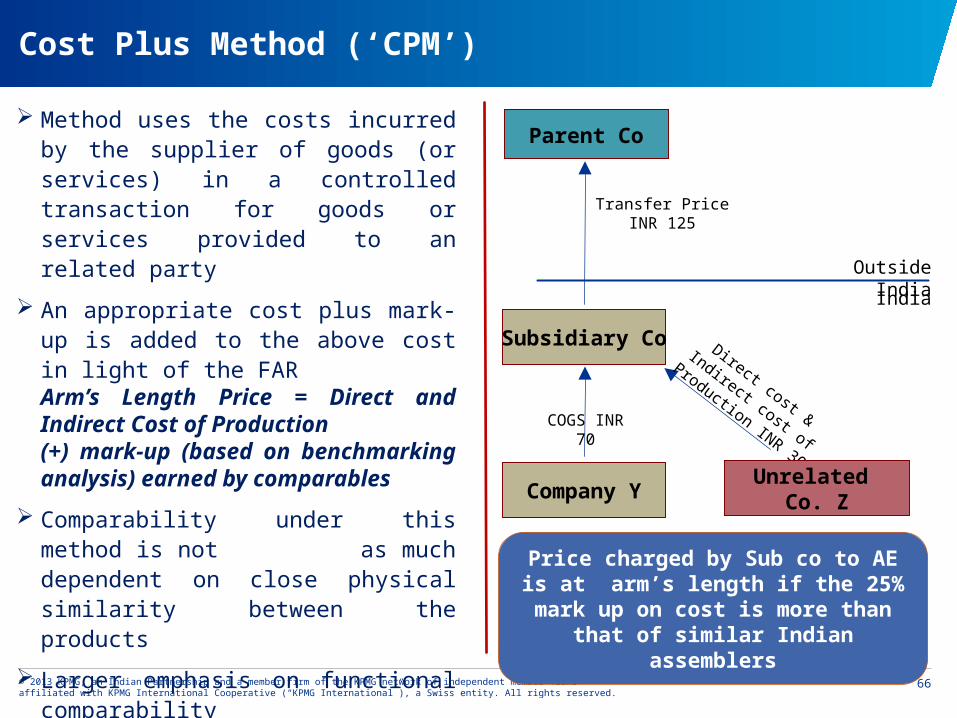

Cost Plus Method (‘CPM’)

Price charged by Sub co to AE is at arm’s length if the 25% mark up on

cost is more than that of similar Indian assemblers

Transfer Price INR 125

Direct cost & Indirect cost

of Production INR 30COGS INR 70

Outside India

India

Subsidiary Co

Parent Co

Unrelated Co. ZCompany Y

Method uses the costs incurred by the supplier of goods (or services) in a controlled transaction for goods or services provided to an related party

An appropriate cost plus mark-up is added to the above cost in light of the FAR Arm’s Length Price = Direct and Indirect Cost of Production (+) mark-up (based on benchmarking analysis) earned by comparables

Comparability under this method is not as much dependent on close physical similarity between the products

Larger emphasis on functional comparability

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

67

CPM – Case Study

B Ltd. derives technology support from

A Ltd.

(20 percent of normal GP)

Marketing Risks associated withservices rendered to customers other than A Ltd(10 percent of normal GP)

B Ltd. offered one month’s credit to A Ltd.(1.5 percent GP)D

IFF

ER

EN

CE

S

A Ltd. (AE)

100 man-hours @ INR2,000 per man-hourTotal Costs incurred(INR 175,000) C Ltd

(Third Party)

B Ltd. – Software Development +onsite and offsite consultancy services

@ INR 3,000 perman-hour

GP margin earned oncosts 40 %

B Ltd

Arm’s Length Price for

transaction between

B Ltd and A Ltd?

Pro

visi

on

of

serv

ice

s

Provision of services

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

68

CPM – Case Study – contd…

Direct and Indirect Costs (INR) 175,000

G.P. mark-up in comparable uncontrolled transaction (A) 40 %

Less:

Adjustment for Technology Support from A Ltd. (20% of 40%) (8%)

Risk adjustment – no market risk as regard trades with A Ltd. (10% of 40%) (4%)

Sub-total (B) 12%

Add:

Cost of credit to A Ltd. 1.5%

Sub-total (C) 1.5%

Arm’s length GP mark-up = (A) – (B) + (C) 29.50%

Arm’s length Income (INR) 226,625

Increased Income INR (226,625 – 200,000) 26,625

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

69

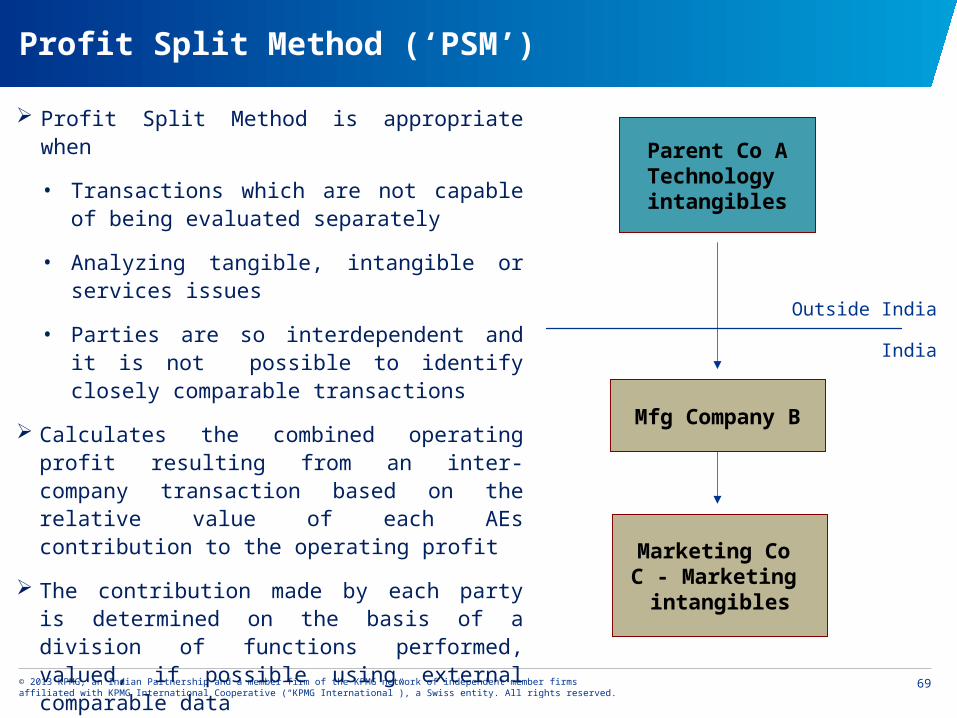

Profit Split Method (‘PSM’)

India

Outside India

Mfg Company B

Parent Co ATechnology intangibles

Marketing Co C - Marketing

intangibles

Profit Split Method is appropriate when

• Transactions which are not capable of being evaluated separately

• Analyzing tangible, intangible or services issues

• Parties are so interdependent and it is not possible to identify closely comparable transactions

Calculates the combined operating profit resulting from an inter-company transaction based on the relative value of each AEs contribution to the operating profit

The contribution made by each party is determined on the basis of a division of functions performed, valued, if possible using external comparable data

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

70

Transactional Net Margin Method (‘TNMM’) (1/2)

Subsidiary Co BNet margin 5%

Parent Co A

Unrelated CosNet margin 3%

Unrelated Cos

India

Outside India

Usually regarded as an indirect and one-sided method, but is most widely adopted

Applicable for any type of transaction and often used to supplement analysis under other methods

Most frequently used method in India, due to

Lack of availability of comparable uncontrolled prices and

Lack of gross margin data required for application of the cost plus method/ resale price method

Examines net operating profit from transactions as a percentage of a certain base

Operating margin should be compared to operating margin earned by same enterprise on uncontrolled transaction – Internal TNMM

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

71

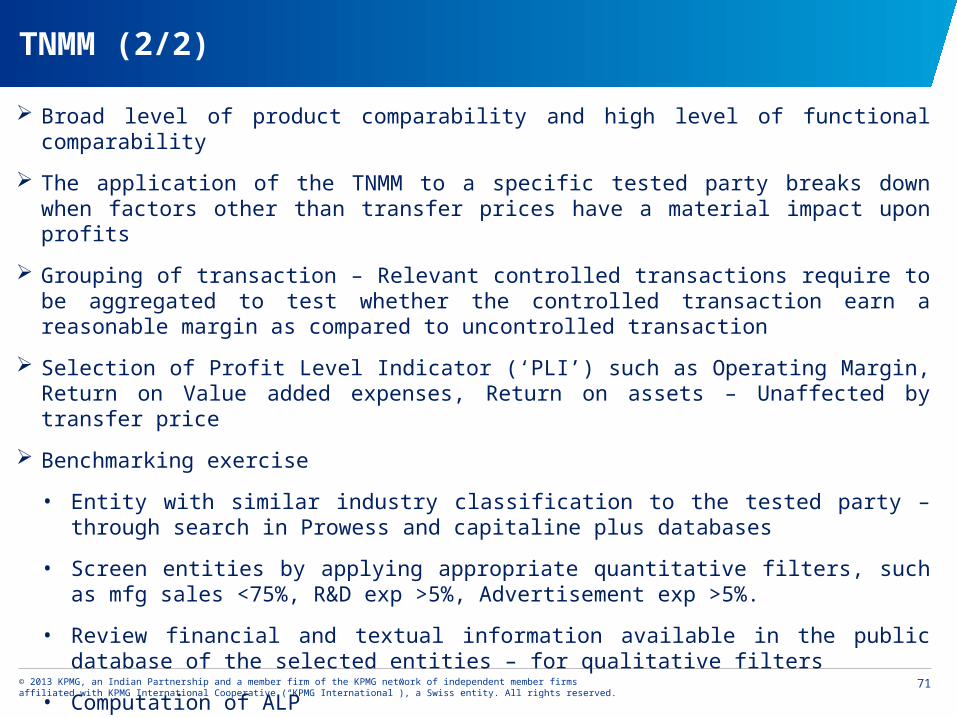

TNMM (2/2)

Broad level of product comparability and high level of functional comparability

The application of the TNMM to a specific tested party breaks down when factors other than transfer prices have a material impact upon profits

Grouping of transaction – Relevant controlled transactions require to be aggregated to test whether the controlled transaction earn a reasonable margin as compared to uncontrolled transaction

Selection of Profit Level Indicator (‘PLI’) such as Operating Margin, Return on Value added expenses, Return on assets – Unaffected by transfer price

Benchmarking exercise

• Entity with similar industry classification to the tested party – through search in Prowess and capitaline plus databases

• Screen entities by applying appropriate quantitative filters, such as mfg sales <75%, R&D exp >5%, Advertisement exp >5%.

• Review financial and textual information available in the public database of the selected entities – for qualitative filters

• Computation of ALP

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

72

Summary of Methods

Methods Product Comparability

Functional Comparability Approach Remarks

CUP Very High Medium Prices are benchmarked

Very difficult to apply as very high degree of comparability required

RPM High Medium GPM (on sales) benchmarked

Difficult to apply as high degree of comparability required

CPM High High GPM (on costs) benchmarked

Difficult to apply as high degree of comparability required

PSM Medium Very High Profit Margins Complex Method, sparingly used

TNMM Medium Very High Net Profit Margins

Most commonly used Method

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

73

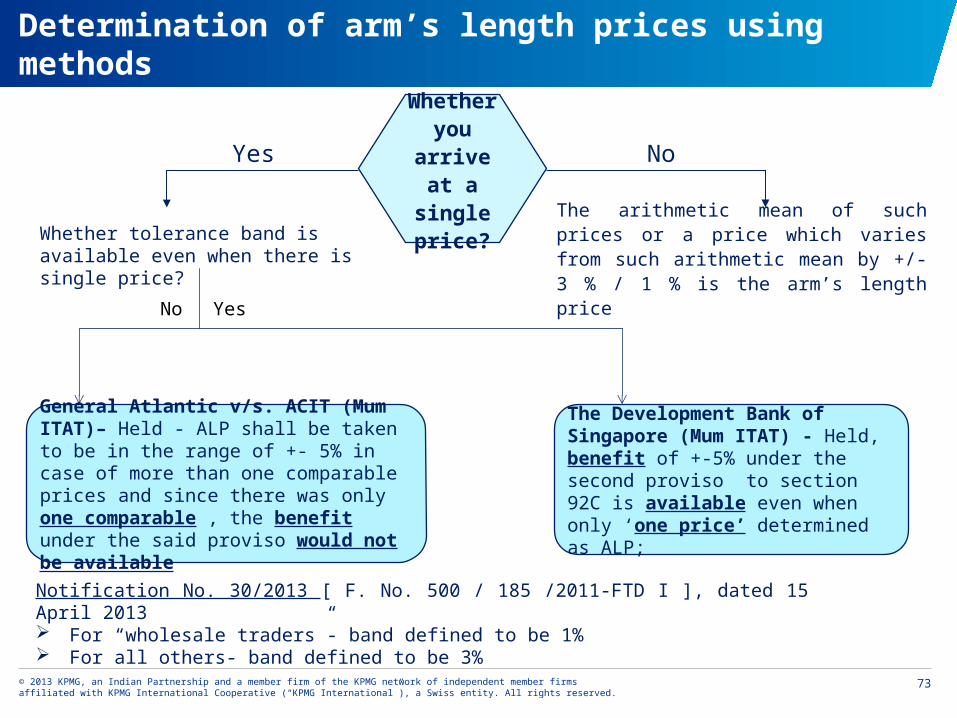

Determination of arm’s length prices using methods

Whether you arrive at a single

price? The arithmetic mean of such prices or a price which varies from such arithmetic mean by +/- 3 % / 1 % is the arm’s length price

Yes No

Notification No. 30/2013 [ F. No. 500 / 185 /2011-FTD I ], dated 15 April 2013 For “wholesale traders”- band defined to be 1% For all others- band defined to be 3%

Whether tolerance band is available even when there is single price?

General Atlantic v/s. ACIT (Mum ITAT)– Held - ALP shall be taken to be in the range of +- 5% in case of more than one comparable prices and since there was only one comparable , the benefit under the said proviso would not be available

The Development Bank of Singapore (Mum ITAT) - Held, benefit of +-5% under the second proviso to section 92C is available even when only ‘one price’ determined as ALP;

No Yes

Transfer Pricing Documentation

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

75

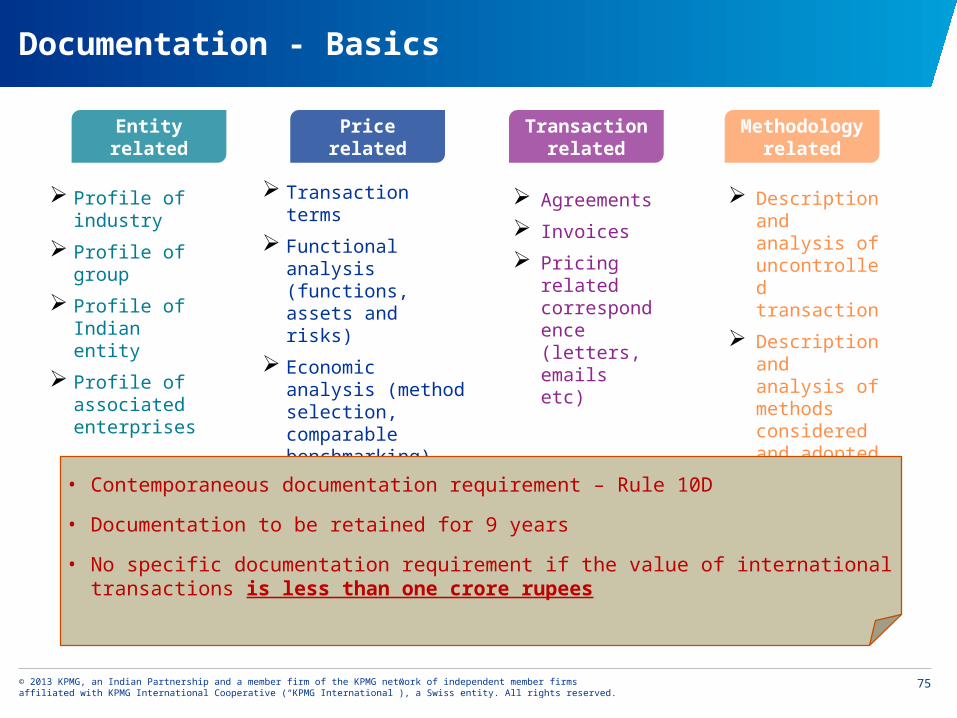

Documentation - Basics

Profile of industry

Profile of group

Profile of Indian entity

Profile of associated enterprises

Transaction terms

Functional analysis (functions, assets and risks)

Economic analysis (method selection, comparable benchmarking)

Forecasts, budgets, estimates

Agreements

Invoices

Pricing related correspondence (letters, emails etc)

Description and analysis of uncontrolled transaction

Description and analysis of methods considered and adopted

Methodology related

• Contemporaneous documentation requirement – Rule 10D

• Documentation to be retained for 9 years

• No specific documentation requirement if the value of international transactions is less than one crore rupees

Transaction related

Price relatedEntity related

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

76

Entity Related Documentation

Corporate Background

Understanding taxpayer’s business, including its legal structure and the terms of its contracts, is fundamental to transfer pricing analysis

The documentation must start with a basic analysis of who does what and in what legal capacity

Identify the related parties to cross-border transactions

Shareholding pattern viz. name of the shareholder and % of shareholding

Determine the parties’ legal status (subsidiary or branch) and

Whether the relationship is as agent or principal

Profile of the taxpayer and multinational group/ associated enterprises should be properly documented

An understanding obtained in this phase will help carrying out Industry analysis

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

77

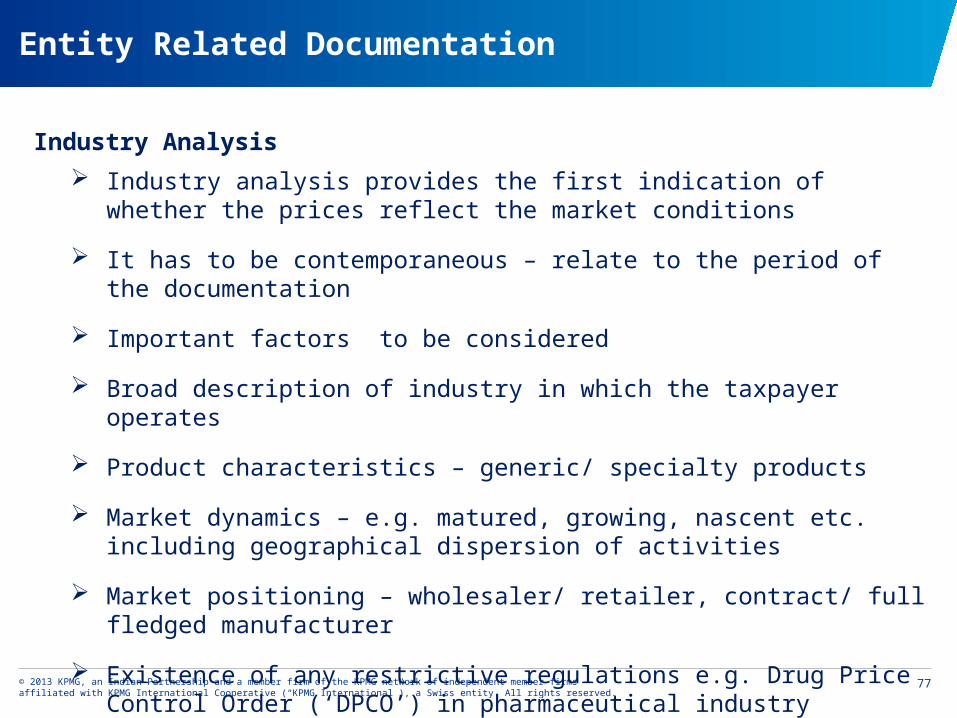

Entity Related Documentation

Industry Analysis

Industry analysis provides the first indication of whether the prices reflect the market conditions

It has to be contemporaneous – relate to the period of the documentation

Important factors to be considered

Broad description of industry in which the taxpayer operates

Product characteristics – generic/ specialty products

Market dynamics – e.g. matured, growing, nascent etc. including geographical dispersion of activities

Market positioning – wholesaler/ retailer, contract/ full fledged manufacturer

Existence of any restrictive regulations e.g. Drug Price Control Order (‘DPCO’) in pharmaceutical industry

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

78

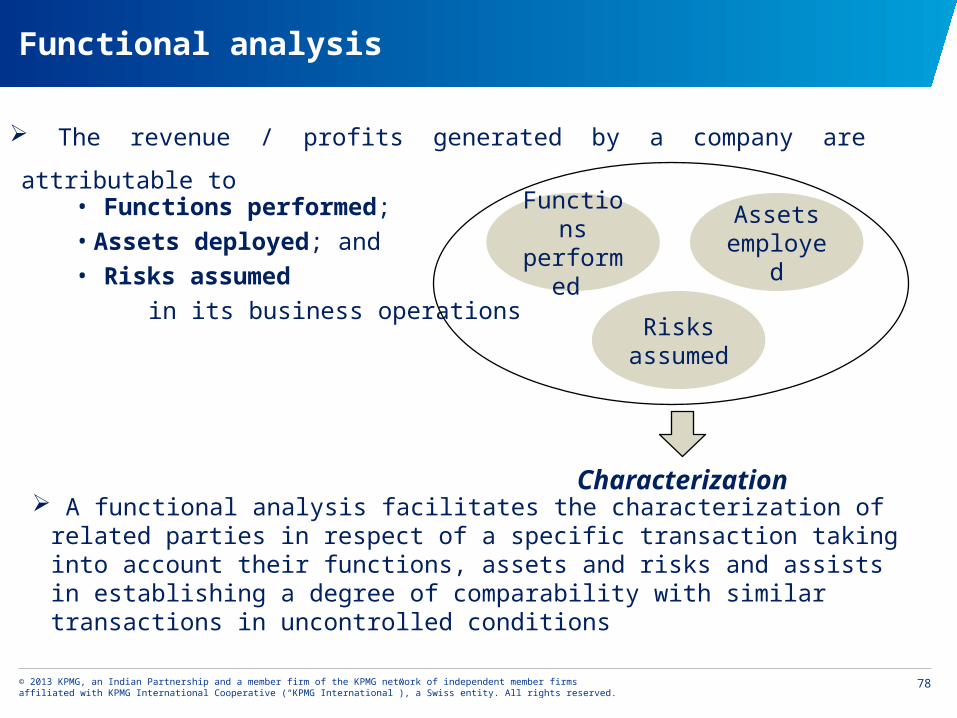

Functional analysis

The revenue / profits generated by a company are attributable to • Functions performed; • Assets deployed; and • Risks assumed

in its business operations

Functions performed

Assets employed

Characterization A functional analysis facilitates the characterization of related parties in respect of

a specific transaction taking into account their functions, assets and risks and assists in establishing a degree of comparability with similar transactions in uncontrolled conditions

Risks assumed

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

79

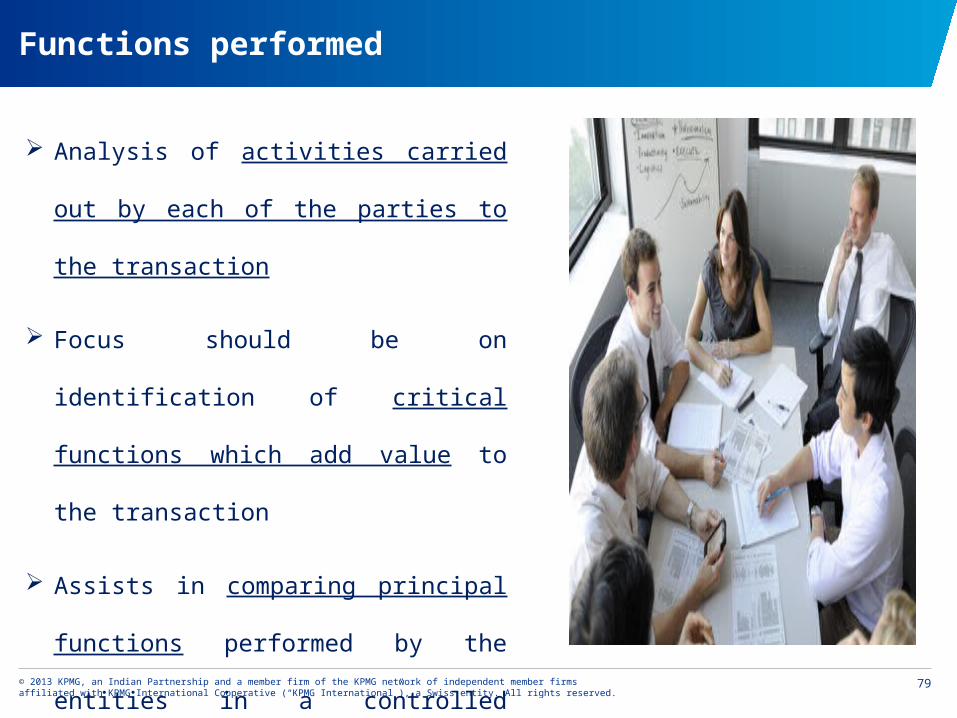

Functions performed

Analysis of activities carried out by each of

the parties to the transaction

Focus should be on identification of critical

functions which add value to the

transaction

Assists in comparing principal functions

performed by the entities in a controlled

transaction with the functions performed in

uncontrolled transactions

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

80

Assets employed

Analysis of the type of assets and their nature needs to be understood

Helps in determination of their contribution to the business process/economic

activity

Facilitates understanding of respective roles played by the entities participating in

the International transaction

Knowledge of assets owned and employed by the entities facilitates determination

of the profit margin to be earned by them

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

81

Risks assumed

Analysis of risks undertaken by each transacting entity

As the risk increases, the expected return should increase

as well

The potential risks are company and industry specific

Only important risks should be described and quantified

Important to distinguish between which entity bears risks

as per legal terms and which one bears as per the

economic substance of the transaction

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

82

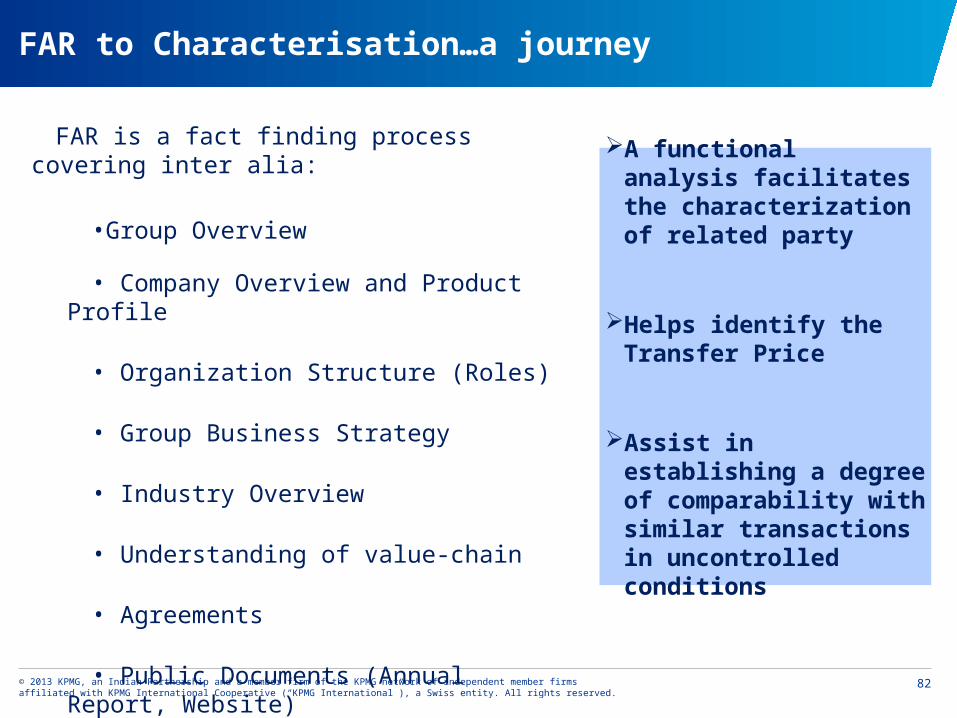

FAR to Characterisation…a journey

FAR is a fact finding process covering inter alia:

•Group Overview

• Company Overview and Product Profile

• Organization Structure (Roles)

• Group Business Strategy

• Industry Overview

• Understanding of value-chain

• Agreements

• Public Documents (Annual Report, Website)

A functional analysis facilitates the characterization of related party

Helps identify the Transfer Price

Assist in establishing a degree of comparability with similar transactions in uncontrolled conditions

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

83

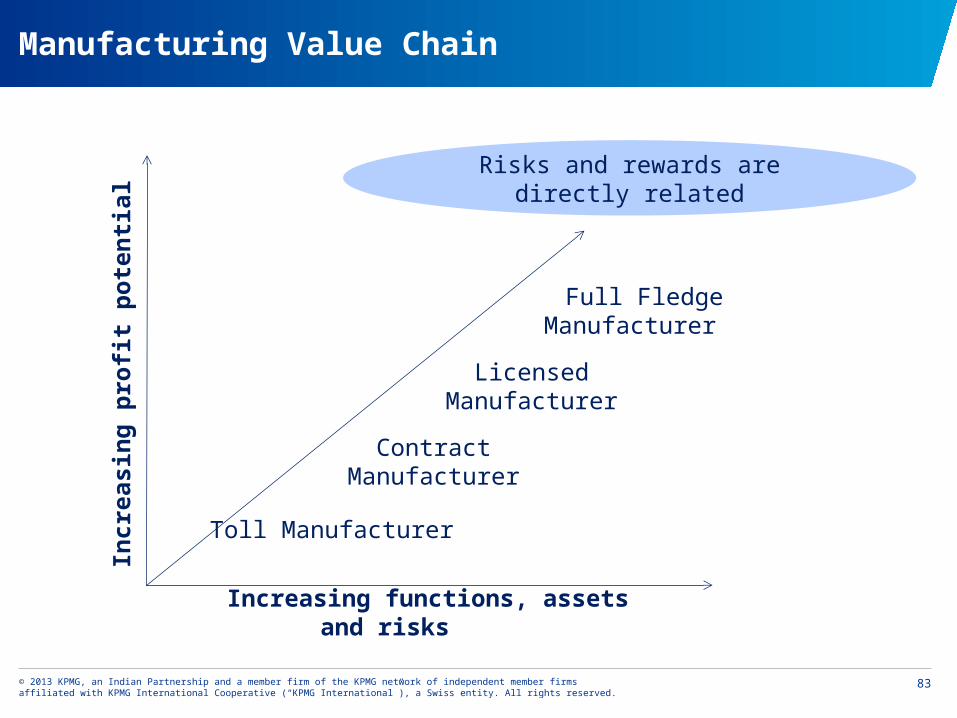

Manufacturing Value Chain

Increasing functions, assets and risks

Risks and rewards are directly related

Toll Manufacturer

Contract Manufacturer

Licensed Manufacturer

Full Fledge Manufacturer

Incr

easi

ng

pro

fit

po

ten

tial

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

84

Price Related Documentation

Economic Analysis

Economic analysis refers to benchmarking the financial parameters of the taxpayer and

comparable companies

Document any adjustments made for differences in functions/ risks borne by the

comparables vis-à-vis taxpayer

Search strategy to be clearly documented

• Selection of Most Appropriate Method (‘MAM’), Tested Party, Profit Level Indicator

• Analysis of internal comparables

• Databases used and applicability of filters used to select comparables

• Search methodology and basis for acceptance / rejection of companies

• Workings of actual application of MAM

Periodic review of TP Policy and TP documentation

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

85

Transaction Related Documentation

Agreements / contracts etc. with AEs or unrelated parties in respect of similar international

transactions

Documents that may be helpful for showing the process of price negotiations with the

related parties such as agreements, invoices, emails/ faxes

Official publications, reports, studies & databases from Government of foreign countries

Research reports & technical publications of institutions of national or international repute

Price publications including stock market quotations or commodity market quotations

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

86

Documentation : Key Points under Rule 10D

Indian TP documentation requirements are staggering

Rule 10D prescribes detailed set of requirements pertaining to

Organizational Structure

Nature of business/industry and market conditions

Controlled transactions

Background documents

Comparability: functions, assets and risk analysis

Selection of transfer pricing method

Application of the transfer pricing method

Assumptions, strategies, policies

Supporting information

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

87

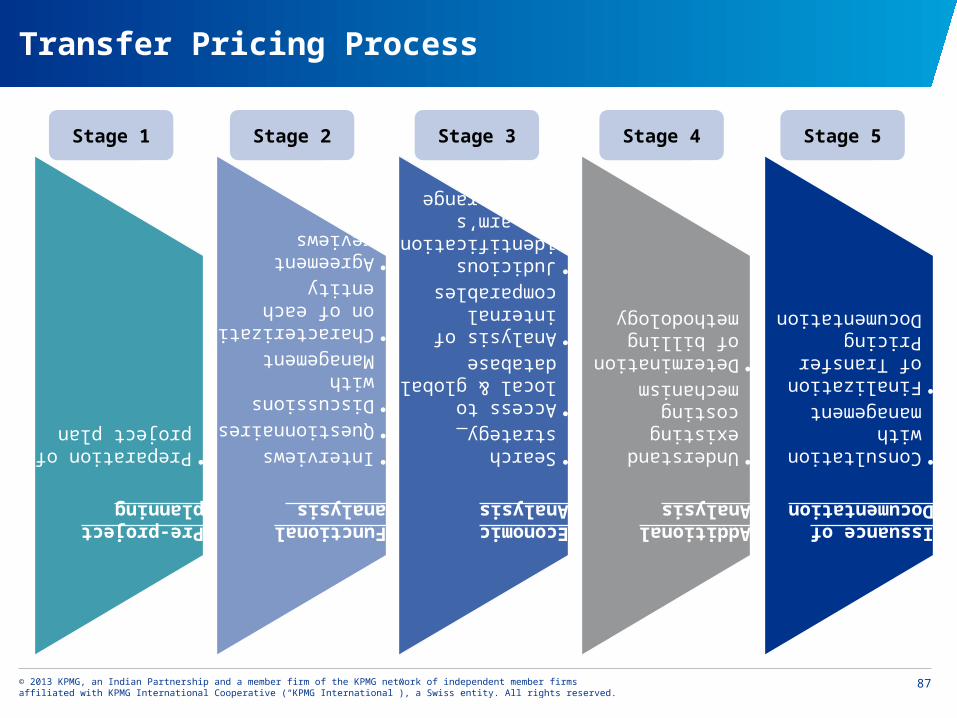

Pre-project planning

•Preparation of project plan

Functional analysis

•Interviews•Questionnaires•Discussions with Management•Characterization of each entity•Agreement reviews

Economic Analysis

•Search strategy •Access to local & global database•Analysis of internal comparables•Judicious identification of arm’s length range

Additional Analysis

•Understand existing costing mechanism•Determination of billing methodology

Issuance of Documentation

•Consultation with management•Finalization of Transfer Pricing Documentation

Stage 1 Stage 2 Stage 3 Stage 4 Stage 5

Transfer Pricing Process

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

88

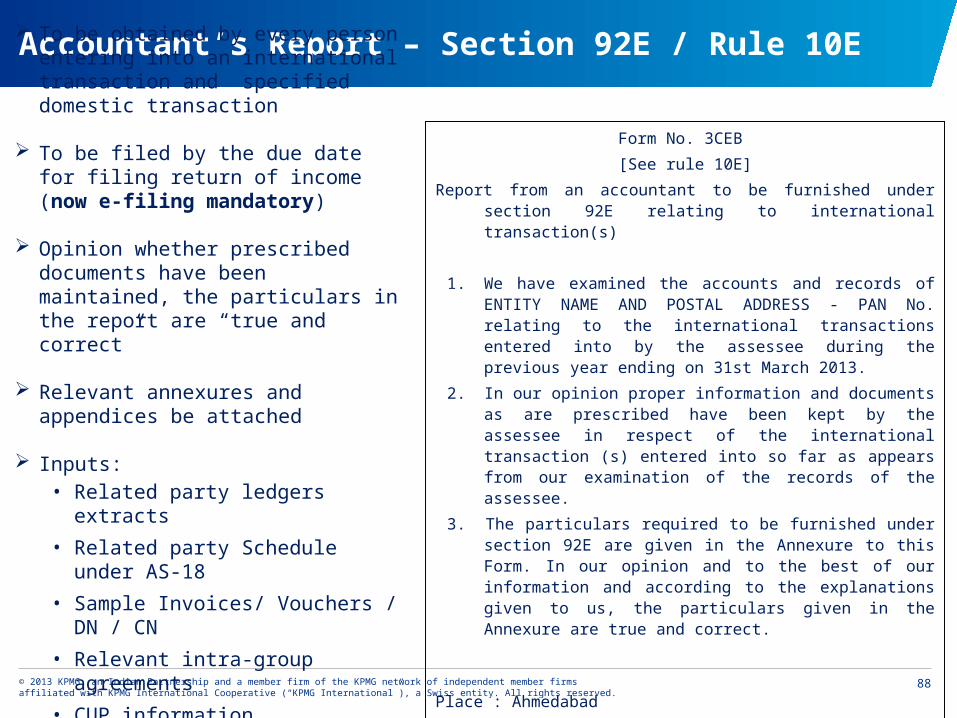

Accountant’s Report – Section 92E / Rule 10E

To be obtained by every person entering into an international transaction and specified domestic transaction

To be filed by the due date for filing return of income (now e-filing mandatory)

Opinion whether prescribed documents have been maintained, the particulars in the report are “true and correct”

Relevant annexures and appendices be attached

Inputs: • Related party ledgers extracts

• Related party Schedule under AS-18

• Sample Invoices/ Vouchers / DN / CN

• Relevant intra-group agreements

• CUP information

Form No. 3CEB

[See rule 10E]

Report from an accountant to be furnished under section 92E relating to international transaction(s)

1. We have examined the accounts and records of ENTITY NAME AND POSTAL ADDRESS - PAN No. relating to the international transactions entered into by the assessee during the previous year ending on 31st March 2013.

2. In our opinion proper information and documents as are prescribed have been kept by the assessee in respect of the international transaction (s) entered into so far as appears from our examination of the records of the assessee.

3. The particulars required to be furnished under section 92E are given in the Annexure to this Form. In our opinion and to the best of our information and according to the explanations given to us, the particulars given in the Annexure are true and correct.

Place : Ahmedabad

Date : For XYZ Co.

Chartered Accountants

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

89

CBDT vide notification 86/2013 dated 01 November

2013, notified Cyprus under Section 94A of the

Income Tax Act, 1961 for not providing information

to Indian Income Tax Authorities

This notification would have far reaching

implications on entities of India having

transactions with any person in Cyprus

Cyprus : Notified Jurisdictional Area u/s 94A

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

90

Brief implications of the same are as follows : -

• Applicability of TP : If an assessee enters into

a transaction where one of the parties to the

transaction is a person located in Cyprus, then

all the parties to the transaction shall be deemed

to be AE and the transactions shall be deemed

to be an international transaction. Consequently,

all TP provisions will apply;

• Payment to Financial Institution : Assessee

needs to furnish an authorization under Form

10FC to financial institution to provide relevant

information to tax authorities while claiming

deduction in respect of any payment made to

any financial institution in Cyprus;

Cyprus : Notified Jurisdictional Area u/s 94A

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

91

• Conditions for deductibility : Assessee needs to

maintain and furnish information as prescribed

under Rule 21AC(5) in order to avail deduction in

respect of any other expenditure or allowance from

the transaction with a person located in Cyprus;

• Unexplained Receipts : Onus is now on assessee

to satisfactorily explain source of money if received

from person in Cyprus;

• Higher withholding rate : Any payment made to a

person located in Cyprus shall be liable for

withholding tax at 30 per cent or a rate prescribed in

the Act, whichever is higher

Cyprus : Notified Jurisdictional Area u/s 94A

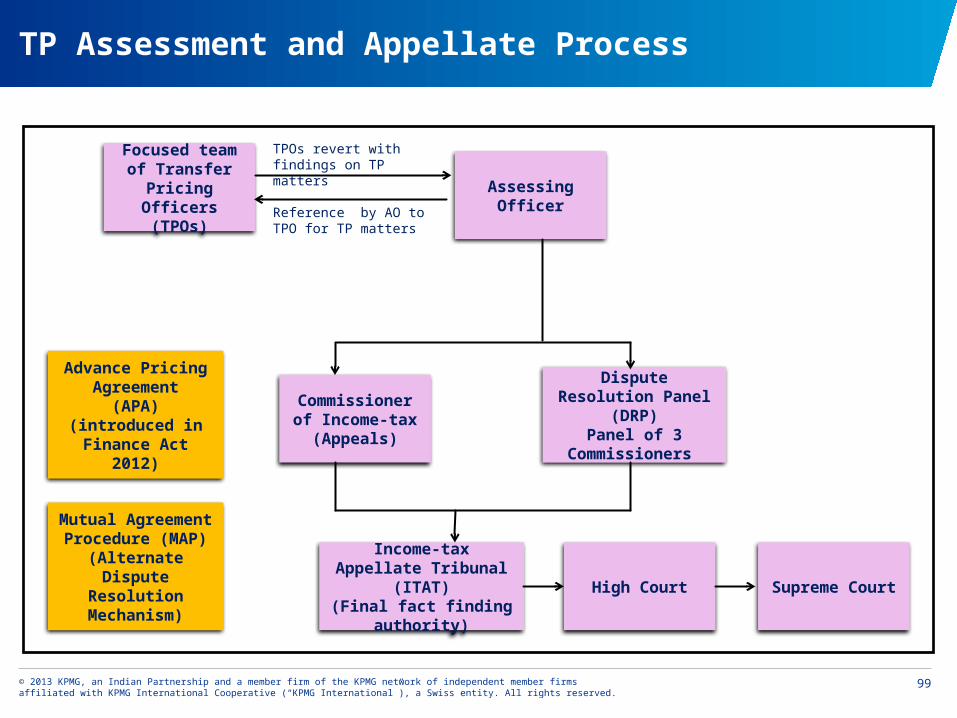

Transfer Pricing Assessment

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

93

Key Audit Triggers

Consistent losses / low margins of the assessee attributable to inter-company transactions

Significant changes in profitability of the assessee and its AEs

High Royalty / Technical fee payouts, Cost recharges, Management Fees, Cost allocations

Net losses incurred by routine distributors

Low mark-ups for services

Application of Ratio’s such as ROCE / Berry ratio / cash profit instead of net margins

Significant Advertisement and marketing spends by manufacturing / distribution companies

Use of foreign comparables

Substantial increase in transfer pricing audits and disputes across the Globe , India is no exception….

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

94

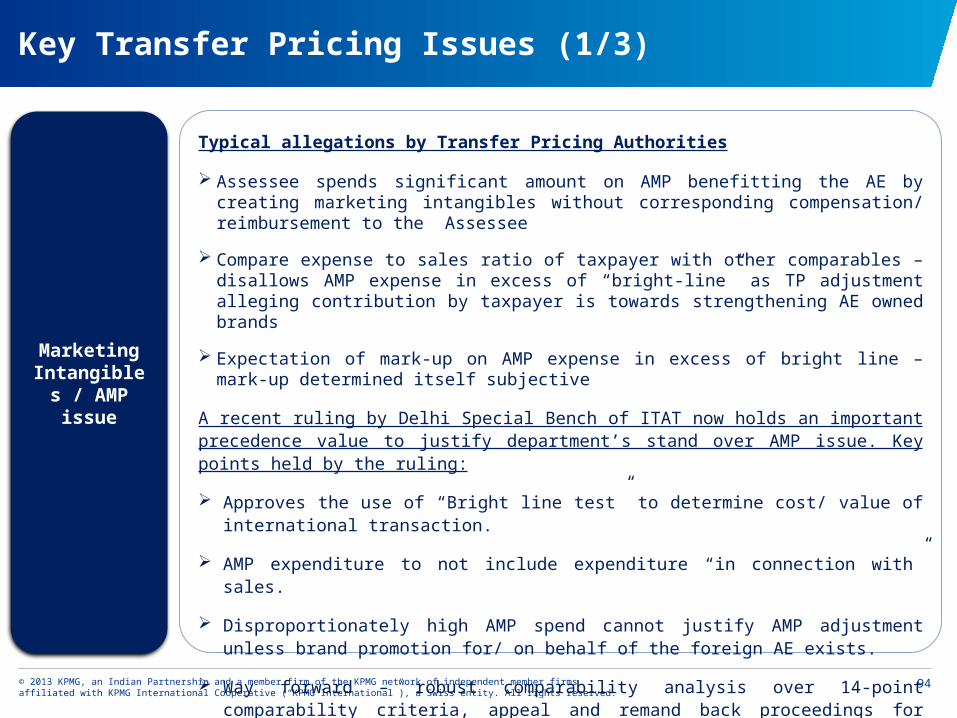

Key Transfer Pricing Issues (1/3)

Marketing Intangibles / AMP issue

Typical allegations by Transfer Pricing Authorities

Assessee spends significant amount on AMP benefitting the AE by creating marketing intangibles without corresponding compensation/ reimbursement to the Assessee

Compare expense to sales ratio of taxpayer with other comparables – disallows AMP expense in excess of “bright-line” as TP adjustment alleging contribution by taxpayer is towards strengthening AE owned brands

Expectation of mark-up on AMP expense in excess of bright line – mark-up determined itself subjective

A recent ruling by Delhi Special Bench of ITAT now holds an important precedence value to justify department’s stand over AMP issue. Key points held by the ruling:

Approves the use of “Bright line test” to determine cost/ value of international transaction.

AMP expenditure to not include expenditure “in connection with” sales.

Disproportionately high AMP spend cannot justify AMP adjustment unless brand promotion for/ on behalf of the foreign AE exists.

Way forward – robust comparability analysis over 14-point comparability criteria, appeal and remand back proceedings for prior year disputes, APA for subsequent years

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

95

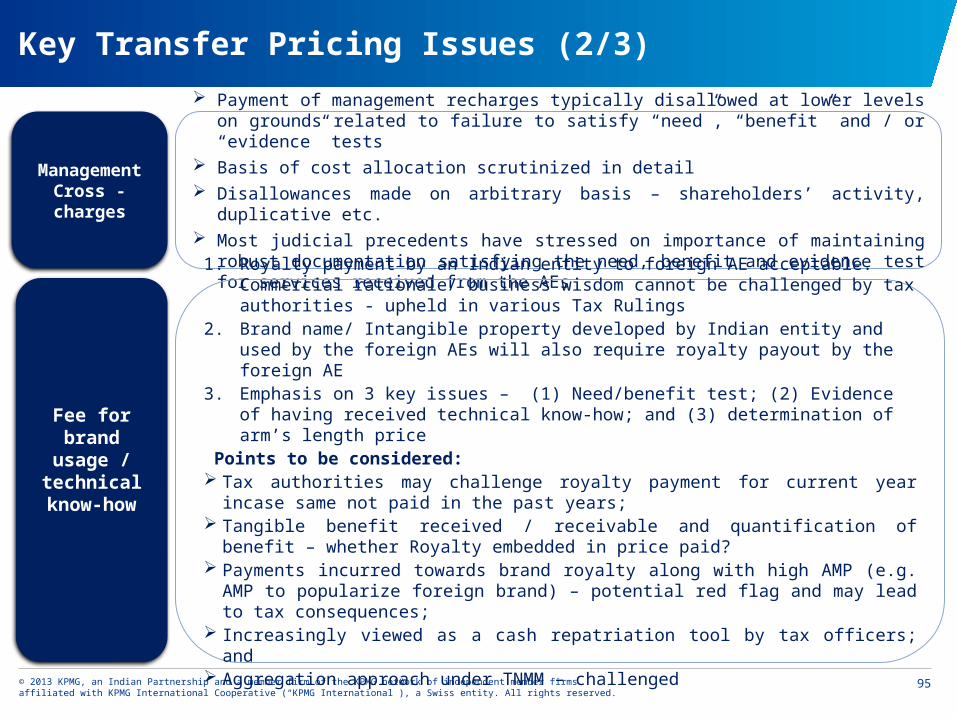

Key Transfer Pricing Issues (2/3)

Management Cross -charges

Fee for brand

usage / technical know-how

Payment of management recharges typically disallowed at lower levels on grounds related to failure to satisfy “need”, “benefit” and / or “evidence” tests

Basis of cost allocation scrutinized in detail Disallowances made on arbitrary basis – shareholders’ activity, duplicative etc. Most judicial precedents have stressed on importance of maintaining robust documentation

satisfying the need, benefit and evidence test for services received from the AEs

1. Royalty payment by an Indian entity to foreign AE acceptable. Commercial rationale/ business wisdom cannot be challenged by tax authorities - upheld in various Tax Rulings

2. Brand name/ Intangible property developed by Indian entity and used by the foreign AEs will also require royalty payout by the foreign AE

3. Emphasis on 3 key issues – (1) Need/benefit test; (2) Evidence of having received technical know-how; and (3) determination of arm’s length price

Points to be considered: Tax authorities may challenge royalty payment for current year incase same not paid in the

past years; Tangible benefit received / receivable and quantification of benefit – whether Royalty

embedded in price paid? Payments incurred towards brand royalty along with high AMP (e.g. AMP to popularize

foreign brand) – potential red flag and may lead to tax consequences; Increasingly viewed as a cash repatriation tool by tax officers; and Aggregation approach under TNMM – challenged

© 2013 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

96

Key Transfer Pricing Issues (3/3)

TP adjustments being made on account of under valuation of shares where Foreign parent has made investments in an Indian subsidiary

Typical FactsForeign parent company infuses share capital in the Indian

subsidiary (at face value or at certain value per share arrived using DCF or other valuation methodology)

The Revenue takes a position that the shares have been issued to the Holding Company at an undervalued price / less that the fair market value of the shares;