© 2015 kpmg llp, a canadian limited liability partnership and a member firm of the kpmg network of...

TRANSCRIPT

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

1

6th Annual Dallas TEI Canadian Tax Luncheon

February 24, 2015

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

2

Agenda

1. CRA UPDATE ON US COMPANIES PROVIDING SERVICES IN CANADA

2. CASE STUDY – INVERSION OF US COMPANY TO CANADA

3. CRA RULINGS UPDATES OF INTEREST

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

3

CRA Update on US Companies Providing Services in Canada

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

4

Topics

1. Carrying on business under domestic law

2. Permanent establishment protection and Treaty-Based Return

3. Regulation 105

4. Regulation 102

5. Recent CRA Technical Interpretation

6. CRA Audit Activity and Experiences

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

5

1. Carrying on business in Canada under Domestic law

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

6

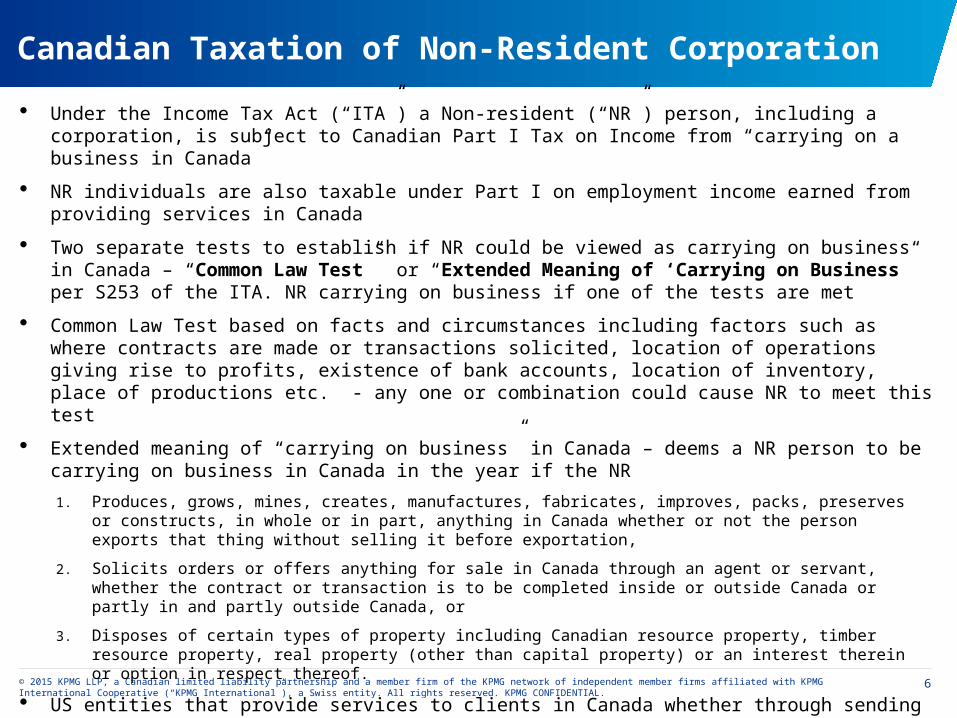

Canadian Taxation of Non-Resident Corporation

· Under the Income Tax Act (“ITA”) a Non-resident (“NR”) person, including a corporation, is subject to Canadian Part I Tax on Income from “carrying on a business in Canada”

· NR individuals are also taxable under Part I on employment income earned from providing services in Canada

· Two separate tests to establish if NR could be viewed as carrying on business in Canada – “Common Law Test” or “Extended Meaning of ‘Carrying on Business” per S253 of the ITA. NR carrying on business if one of the tests are met

· Common Law Test based on facts and circumstances including factors such as where contracts are made or transactions solicited, location of operations giving rise to profits, existence of bank accounts, location of inventory, place of productions etc. - any one or combination could cause NR to meet this test

· Extended meaning of “carrying on business” in Canada – deems a NR person to be carrying on business in Canada in the year if the NR

1. Produces, grows, mines, creates, manufactures, fabricates, improves, packs, preserves or constructs, in whole or in part, anything in Canada whether or not the person exports that thing without selling it before exportation,

2. Solicits orders or offers anything for sale in Canada through an agent or servant, whether the contract or transaction is to be completed inside or outside Canada or partly in and partly outside Canada, or

3. Disposes of certain types of property including Canadian resource property, timber resource property, real property (other than capital property) or an interest therein or option in respect thereof.

· US entities that provide services to clients in Canada whether through sending employees or contracting locally generally would be caught under both of the tests and should be “Carrying on business in Canada”.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

7

2. Permanent Establishment Protection and Treaty Based Returns

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

8

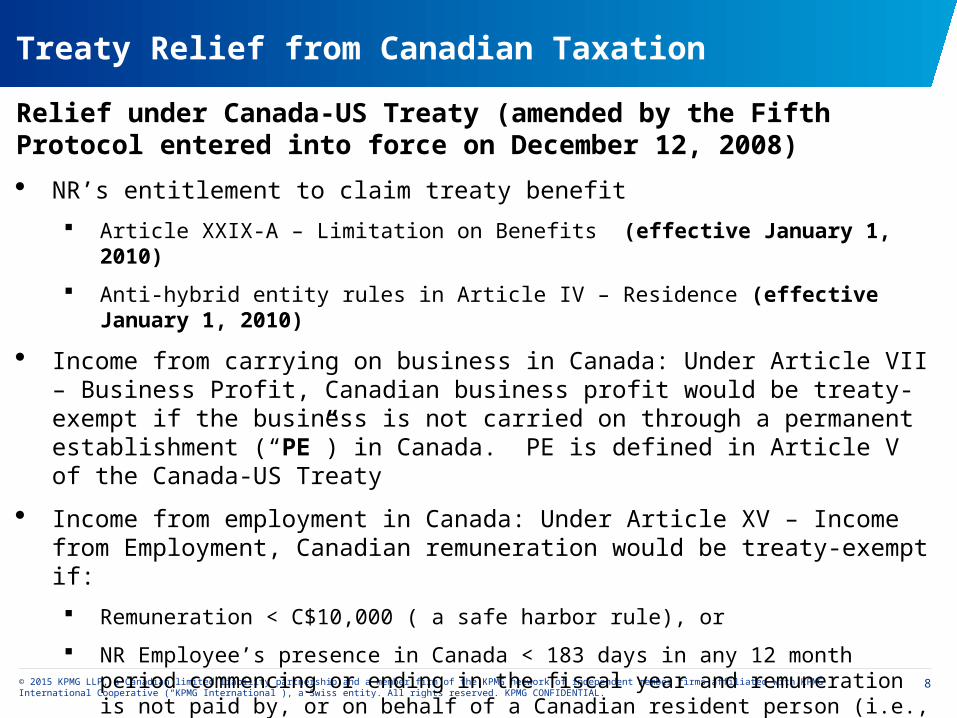

Treaty Relief from Canadian Taxation

Relief under Canada-US Treaty (amended by the Fifth Protocol entered into force on December 12, 2008)

· NR’s entitlement to claim treaty benefit

Article XXIX-A – Limitation on Benefits (effective January 1, 2010)

Anti-hybrid entity rules in Article IV – Residence (effective January 1, 2010)

· Income from carrying on business in Canada: Under Article VII – Business Profit, Canadian business profit would be treaty-exempt if the business is not carried on through a permanent establishment (“PE”) in Canada. PE is defined in Article V of the Canada-US Treaty

· Income from employment in Canada: Under Article XV – Income from Employment, Canadian remuneration would be treaty-exempt if:

Remuneration < C$10,000 ( a safe harbor rule), or

NR Employee’s presence in Canada < 183 days in any 12 month period commencing or ending in the fiscal year and remuneration is not paid by, or on behalf of a Canadian resident person (i.e., not necessary be the NR’s employer) and is not borne by a PE in Canada (i.e., expense is not allowed as a deduction from taxable income).

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

9

NR’s Canadian Tax Filing Requirement

NR corporation – T2 Corporation Income Tax Return (”T2”)

· Required to file a T2 if the NR carries on a business in Canada.

· Treaty-based return must be filed if the NR corporation would otherwise owe Part I tax, but a treaty exempts the corporation from Canadian tax The return is commonly referred to as treaty-based return, which generally includes a T2 jacket and

Schedule 91 – Information concerning claims for treaty-based exemptions

Schedule 97 – Additional information on non-resident corporations in Canada

· Essentially an audit roadmap for CRA to assess activities in Canada.

· Required to disclose information on various types of revenues earned in Canada, information on 5 largest customers, remuneration paid to Canadian resident employees and subcontractors, remuneration paid to, and duration of time spent in Canada by, NR employees and contractors.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

10

Permanent Establishment – Defined in Article V of the Canada-US Treaty

Includes:

· A fixed place of business through which the NR carries on its business in Canada.

· Generally includes a place of management, a branch, an office, a factory etc.

· A building site or construction or installation project constitutes a PE if it lasts more than 12 months.

· An enterprise is deemed to provide services through a PE (“Service PE”) where:

The services are performed in Canada by an individual who is present in Canada for periods > 183 days in any 12 month period, and, during that period(s), >50% of the gross active business revenues of the enterprise consists of income derived from the services performed in Canada by that individual; or

The services are provided in Canada for > 183 days in any 12 month period with respect to the same/connected project for customers who are either resident of Canada or maintain a PE in Canada and the services are provided in respect of that PE.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

11

NR’s Canadian Tax Filing Requirements & Penalties

NR individual – T1 Personal Income Tax Return (“T1”)

· Required to file a T1 where the NR:

owes tax under Part I for the year

· No requirement to file treaty-based T1 return to claim treaty benefits

· However, treaty-based T1 return has to be filed in order to claim refund of taxes previously withheld on behalf of the NR individual

Penalties for failure to file

5% of unpaid Part I tax liability, plus 1% of unpaid Part I tax liability for each complete month (maximum 12) for which the return was not filed

· Additional penalty for repeated failure to file

· Minimum penalty for NR corporation - $25/day, minimum $100, maximum $2,500

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

12

Withholding Tax and Regulation 105/102

· Withholding taxes are imposed to ensure collection of taxes from NR:

Business Income from Rendering Services in Canada – S. 153(1)(g) and Reg. 105 require that amount be withheld from payment made to a NR in respect of services rendered in Canada (other than remuneration paid to a NR employee)

Employment Income – S.153(1)(a) and Reg. 102 require that amount be withheld from remuneration payment made to a NR employee in respect of an office or employment services rendered in Canada

· Payor is required to withhold and remit to the CRA

· Reg 102/105 withholding is not a tax, but a payment on account of the NR’s overall Canadian income tax liability (i.e., a tax instalment paid on behalf of the NR)

· NR’s actual tax liability is determined when the NR’s Canadian income tax return is filed and assessed

• Generally, withholding is required regardless of whether the NR is liable for Canadian tax, unless a withholding tax waiver has been obtained.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

13

3. Regulation 105

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

14

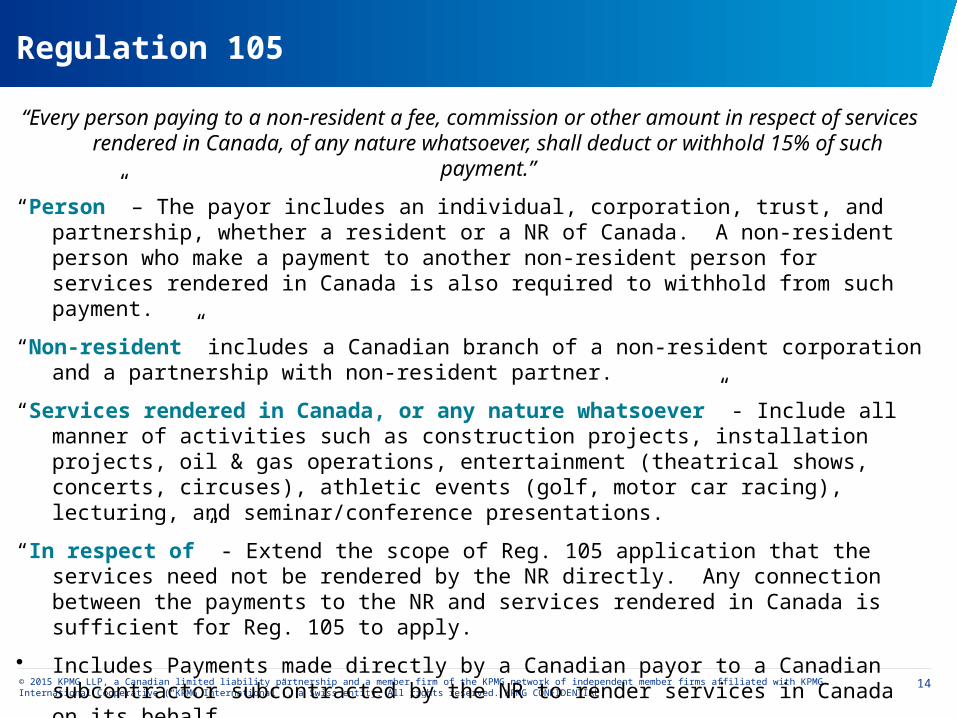

Regulation 105

“Every person paying to a non-resident a fee, commission or other amount in respect of services rendered in Canada, of any nature whatsoever, shall deduct

or withhold 15% of such payment.”

“Person” – The payor includes an individual, corporation, trust, and partnership, whether a resident or a NR of Canada. A non-resident person who make a payment to another non-resident person for services rendered in Canada is also required to withhold from such payment.

“Non-resident” includes a Canadian branch of a non-resident corporation and a partnership with non-resident partner.

“Services rendered in Canada, or any nature whatsoever” - Include all manner of activities such as construction projects, installation projects, oil & gas operations, entertainment (theatrical shows, concerts, circuses), athletic events (golf, motor car racing), lecturing, and seminar/conference presentations.

“In respect of” - Extend the scope of Reg. 105 application that the services need not be rendered by the NR directly. Any connection between the payments to the NR and services rendered in Canada is sufficient for Reg. 105 to apply.

• Includes Payments made directly by a Canadian payor to a Canadian subcontractor subcontracted by the NR to render services in Canada on its behalf.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

15

Regulation 105 – Bundled Contracts

Examples of Bundled Contracts (i.e, include components other than Canadian Services):

· Contract for services rendered in Canada and use of property in Canada· Contract for purchase of equipment/software, including installation or training· Royalties for use of computer software, including IT support rendered in Canada· Contract for services rendered in Canada and outside of Canada

Reg. 105 Implication

If the agreement does not provide for a reasonable allocation of purchase price for the Canadian services, the CRA’s administrative policy is that the full contact payment be subject to Reg. 105 withholding

Planning Points· Separate agreement of the payment for Canadian services· Provide for a reasonable allocation for the Canadian services in the same

agreement

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

16

Regulation 105 – Waiver from Withholding

· Waiver application can be made by or on behalf of NR

· NR demonstrates that its ultimate tax liability < Reg. 105 withholdings, either because of treaty protection (i.e. services not provided through a PE (“Treaty-Based Waiver”) or by virtue of estimated income and expenses (“Income and Expense Waiver”)

· Waiver application should be made at least 30 days before

Commencement of services, or

First payment made to the NR

· However, waiver process is cumbersome and impractical and are being denied more and more often.

· Waiver applies prospectively, even if the waiver application is submitted before payments begin.

· Treaty-based waiver may still be denied for US residents under many exceptions as follows:

NR is related to the Canadian payor

NR is providing services of a repetitive nature or multi-year engagements under a single contract

NR has previously been determined to have a PE in Canada

NR is a US LLC that has not “checked the box” to be treated as a corporation

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

17

Regulation 105 – Income and Expense (I&E) Waiver

· Alternative for NR who cannot qualify for a treaty-based waiver

· Reduced withholding based on estimated net income, taxed at the

applicable combined federal and provincial income tax rate for Canadian

resident corporations or individuals.

· Provided very seldom by CRA and has little application in practice.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

18

Regulation 105 – Payor’s Withholding & Remittance Obligations

Withholding – 15% of Gross Payment

· Where the contract between the NR vendor and the payor stipulates that the payment to the NR be net of all required withholding tax, the required withholding tax should be calculated on the gross-up amount

· If the services is rendered in Quebec, a further 9% must be withheld and remitted to Revenue Quebec

· The applicable withholding tax amount can be reduced only if waiver is obtained by NR vendor

· Payor is required to provide NR with T4NR by Feb 28 of following year showing amounts withheld.

Penalties for Failure to Withhold and Remit

· Penalties are severe, so if in doubt, the payor should withhold

10% of the amount not withheld, plus interest, or

20% of the amount not withheld if gross negligence or knowingly failed to withhold

· Subsection 227(8.4) of ITA – Payor has the right to recover amount not withheld from the NR. Consider inclusion of an indemnity clause in the service contract that the vendor be responsible for the Reg. 105 withholding should it arise.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

19

Regulation 105 – NR Vendor’s Canadian Tax Filing Obligation

· Corp. Branch Tax Return- If the NR is considered carrying on business in Canada, and the business is carried on in Canada through a PE

Withheld tax in excess of the actual Canadian tax liability would be refunded with the filing of branch tax return

· Treaty-Based Return – If the NR is resident in a treaty country and is considered carrying on business in Canada but not through a PE in Canada

Required filing for NR corporation. Withheld tax would be refunded with the filing of treaty-based return

· Filing Due Date

Corporation: Six months after the end of the tax year

· Subject to late filing penalty and interest

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

20

4. Regulation 102

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

21

Regulation 102 – Periodic Remuneration Payments

· Every person paying remuneration to NR employees, who provide

services in Canada, is subject to the same withholding, remitting and

reporting requirement as for Canadian resident employees.

· “Person” includes both resident and NR employer

· “Employee” vs. independent contractor – based on the same rules for

resident and NR individual. Director is considered an employee for the

purposes of the Act

· “Remuneration” includes salary, wages, commissions, bonuses, and

taxable benefits (both cash and non-cash such as stock options, mortgage

assistance, cost-of-living allowance and gross up of remuneration to

compensate the employee for Canadian withholding taxes).

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

22

Regulation 102 – Treaty-Based Waiver

· Apply by the employee, or the employer subject to the employee’s

authorization

· NR employee must qualify for treaty relief under the Dependent Personal

Services (or Income from Employment) article of Canada’s tax treaty with

the NR employee’s country of residence

· Waiver will be denied if the NR employee has a balance owing or has not

filed prior year’s T1

· Waivers are difficult and time consuming to obtain and must be obtained

prior to employment services in Canada.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

23

Regulation 102 – Employer’s Obligation

Withholding

· Income tax: at graduated tax rates applicable to Canadian resident employee

· CPP & EI: Same withholding requirement as for resident employee. There may be an exemption based on a reciprocal agreement between Canada and US.

Remittance – Generally, due date is 15th day of the month following the month in which the payment was made

Filing – T4 Summary and Information Slips – Information Return of Remuneration Paid

· Report remuneration paid on an annual basis

· Due date: Last day of February in the year following the year in which the return relates

Penalties

· Failure to withhold - 10% of amount not withheld, plus interest, or if gross negligence or knowingly failed to withhold, 20% of amount not withheld, plus interest

· Failure to file T4: $25 a day, minimum $100, maximum $2,500.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

24

Regulation 102 – NR Employee’s Obligations

Canadian Tax Return Filing

· NR employee must file a Canadian T1 for any year in which the NR individual has

Canadian employment income and has liability for Part I tax

· T1 determines the final tax liability, which may result in either a refund or an

additional tax payment, being the difference between the final tax liability and the

source deductions remitted by the employer

· Filing obligation remains even if a waiver has been obtained

· Due date: Generally, April 30 of the following calendar year

· Failure to file: subject to penalty and interest.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

25

Regulation 102 – Practical Issues

· US employer corporation required to run shadow Canadian payroll – Administrative and cash flow burden to company

· Employees have to file Canadian personal tax returns even if employment income is treaty protected. Additional compliance costs as employer may have to pay for these returns to be filed

· Refund of income taxes remitted technically belongs to the employee – however since employer generally will fund the Canadian withholding tax – mechanism required for employees to pay refund back to employer. This can be an issue if employee is no longer with the company

· Refund is subject to review by CRA and it could open an examination up with respect to individual employees prior to issuing refund

· Many US based companies have ignored payroll requirements in the past on the basis that the burden to company outweighs the risk if caught

· Information on Treaty based return could lead CRA to verify if NR is registered for payroll and making remittances. Heightened area of audit focus for CRA. See subsequent slides for real audit situations.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

26

5. Recent CRA Technical Interpretation

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

27

Recent Reg. 102 CRA Technical Interpretation - TI 2013-0508651E5

· Canadian resident (”Canco”) that hires a US Corporation (“US Co”) to provide services of its employees in Canada could be liable for withholding and remitting income tax on remuneration

· CRA notes that in certain cases it may be unclear who the actual employer is in situations where an employee is temporarily assigned to Canco

· Based on examination of all the facts and circumstances

· Canco could be considered to be the payer even if the employees remain on US Co’s payroll

· US Co could be considered to be paying the remuneration on behalf of Canco

· Canco could be liable in this case for non compliance and unremitted taxes

· Could affect business relationship with customers if they receive a surprise letter or assessment from CRA

· May be prudent to ensure that the action and agreements of both parties make it clear that no employee/ employment relationship exists between Canco and US Co employees.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

28

6. CRA Audit Activity and Experiences

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

29

Recent Client Experience with CRA Audit – Reg. 102

US Co is a C Corp and is eligible for Treaty Benefits under the Canada US Treaty

US Co has been providing services in Canada since 2010 and has filed a Treaty based return every year

In 2013, US Co had two large service contracts in Canada and earned $1.2 Million in service revenues

20 non resident employees were sent to Canada during the year to provide services. Total remuneration allocated to Canadian services in total was approx. US $ 250,000

Projects were not connected and no employee spent more than 183 days in Canada in any twelve month period

US Co determined not to have a PE in Canada and US employees exempt from Canadian tax under the Treaty

Information disclosed on Treaty return attracted CRA attention and audit commenced

Audit conclusion was no PE but US Co should be remitting taxes in respect of employees providing employment services in Canada, notwithstanding employees are treaty protected

CRA assessed over CAD $ 76,000 for salary withholding tax, penalties and interest

US Co currently assessing whether to simply pay the amounts owing or whether it will require its employees to register and file Canadian returns and recover taxes (interest and penalties non recoverable)

Even if amounts are paid, CRA could request that employees file returns. This could be an issue if employees are no longer with the company

Nevertheless, US Co is now on CRA radar and it, along with its employees, will now have to be compliant moving forward. Exposure to years before 2013 also exists

Not an isolated case. KPMG in Toronto is currently dealing with multiple similar situations.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

30

Recent Client Experience with CRA Audit – Reg. 105

· US Parent is a C Corp and is eligible for Treaty Benefits under the Canada US Treaty. US Parent does not carry on business in Canada.

· Canco is a subsidiary of US Parent. Canco provides certain services to its clients in Canada.

· US Parent entered into a service agreement with an unrelated US company (”US Co”). Pursuant to the agreement Canco can hire US Co directly.

· US Co hired a resident Canadian contractor to provide the services.

· CRA commenced withholding tax audit of Canco and determined that it should be withholding 15% on payments made to US Co even through services were provided by Canadian contractor.

· US Co deemed to be carrying on business in Canada even though it contracts out the work. Canco was assessed over $300,000 in late withholding tax, interest and penalties

· Canco, with the assistance of US Parent, had to go back to US Co to recover the withholding tax.

· US Co now has to file a treaty based return to recover the withholding tax.

· In this situation US Parent is an important customer of US Co and as such US Co complied. This may not always be the case and significant business relationship issues could arise. Therefore it is best to deal with these matters upfront and to be compliant from the beginning of any agreement.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

31

Case Study – Inversion of US Company to Canada

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

32

Tim HortonsCanada

Burger KingUSA

Publicly TradedCommon Shareholders

Canada

Case Study – Inversion of US Company to Canada

Publicly TradedCommon Shareholders

U.S.

Various Subsidiaries

Various Subsidiaries

Before Inversion (simplified chart):

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

33

Case Study – Inversion of US Company to Canada

· Burger King Worldwide Inc. (“Burger King”), a publicly traded Delaware Corporation and Tim Hortons Inc., a publicly traded Canadian corporation, entered into an arrangement agreement and plan of merger in August 2014.

· Former Burger King shareholders own approximately 76% of the combined entity following the merger.

· Both Burger King and Tim Hortons, through a series of transactions became wholly owned subsidiaries of an Ontario limited partnership (“ Red LP”).

· RBI Holdings, a new Canadian publicly traded company became the GP of Red LP and majority interest partner by votes and value.

· Former Tim Hortons and Burger King common shareholders received common shares of RBI Holdings.

· Former Burger King shareholders received exchangeable units of Red LP as part of the transaction subject to certain elections being made.

· RBI Holdings entitled to distributions from Red LP that generally correspond to dividends and distributions paid by RBI Holdings on its common and preferred shares.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

34

RBI HoldingsCanada

Burger KingUSA

Case Study – Inversion of US Company to Canada

Publicly TradedUS & Canada

(former Tim Hortons & Burger KingCommon Shareholders)

PartnershipOntario

(former Burger KingCommon Shareholders

Exchangeable Units)

After Inversion (simplified organization chart):

Tim HortonsCanada

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

35

Case Study – Inversion of US Company to Canada

Observation:

US anti-inversion tax rules that might otherwise deem RBI (a Canadian public

company) to be a full US taxpayer are NOT applicable due to substantial Canadian

business activity.

Result:

1. Access Canada treaty network to reduce withholding taxes.

2. Ability to leverage Burger King with tax-effective financing.

3. Canada income tax rate is approx. 10% lower than US income tax rate.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

36

CRA Rulings Updates of Interest

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

37

CRA Ruling – Affiliated Company Loss Transfer

Structure Prior to Transactions

USCo 1Public NYSE

USCo 2

Lossco

U.S.

CANADAProfitco

GPco 1Subco GPco 2

LP 1Manufacturing

Financing

LP 2

$286M tax lossIn 2013

Taxable incomeIn 2013 of $260M

99.9% 0.1% 1%

99%

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

38

CRA Ruling – Affiliated Company Loss Transfer Facts of Note

· LossCo and ProfitCo related by virtue of both being indirectly controlled by

USCo 1

· LP 1 units held as capital property

· Both LP 2 and LossCo carry on active businesses in Canada

· No transactions with persons unrelated to LossCo outside ordinary cause

of business.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

39

CRA Rulings – Affiliated Company Loss Transfer Transactions – Prior to December 31, 2014

· Lossco incorporates a new NSULC (“Newco”)

· Lossco continues from Ontario into Nova Scotia

· Profitco transfers shares of Subco to Lossco for preferred shares of

Lossco. Redemption price = FMV of preferred shares $3Billion. Parties

elect to transfer at adjusted cost base (“ACB”) for tax purposes.

· Lossco and Subco amalgamate to form Amalco

· Partnership Agreement of LP1 is amended so that income is only allocated

to parties of LP that are partners at fiscal year-end (December 31)

· LP1 allocates 99% of its income earned from LP 2 to Amalco. Amalco

shelters this income from Canadian tax with 2013 Lossco non-capital loss

carry forward.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

40

CRA Ruling – Affiliated Company Loss TransferStructure at December 31, 2014

USCo 1Public NYSE

Amalco Profitco

GPco 1 GPco 2

LP 1 LP 2

$286M tax lossCarry forward

99.9% of incomePick up

0.1% 1%Newco

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

41

CRA Affiliated Company Loss Transfer2015 Unwind Transactions

· Not desirable for Amalco and LP 1 to combine operations due to LP 1’s highly leverage leasing model

· Amalco transfers LP units to Newco for common shares. Parties elect for the transaction to occur at ACB

for tax purposes

· Amalco transfers Newco to Profitco for preferred shares. FMV and redemption amount of preferred shares

should equal FMV of Lossco preferred shares issued in the loss transfer transaction

· Profitco and Lossco cross redeem preferred shares for notes which are subsequently cancelled

· Newco is liquidated in Profitco on a tax-free basis

Rulings and Result

· Profitco is once again the majority interest partner in LP1 and the group has made effective use of tax

losses by using Lossco / Amalco’s loss carry forward against LP1’s income.

· Deemed dividends arising on cross redemptions will not be recharacterized as taxable capital gains

· Amalco will be a member of LP1 continuously until December 31, 2014

· GAAR will not apply.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

42

CRA Affiliated Company Loss Transfer Final Structure After Unwind

USCo 1Public NYSE

Profitco

GPco 2ULC

LP 1

LP 2

99.9%

0.1%

1%

Amalco

USCo 2

U.S.

CANADA

GPco 1ULC

99%

100% 100%

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

43

Favorable CRA Ruling on Inbound Loan Restructuring

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

44

Initial Structure

Facts:

1. Forco is a publicly owned LLC and is treated as a corporation for U.S. tax purposes.

2. Forco is not a “qualifying person” as per Article 29-A of the Canada – U.S. treaty (“the Treaty”).

3. ForOpco, an LLC that is wholly owned by Forco, carries on a business in the U.S..

4. USco, a wholly owned subsidiary of Forco, is a U.S. resident and regarded as a corporation under the U.S. tax laws.

5. USco is not a “qualifying person” as per Article 29-A of the Treaty.

6. Forco and USco do not file a consolidated U.S. tax return.

7. Dutchco is a Dutch resident corporation that is disregarded under the U.S. tax laws and is wholly owned by Forco.

8. ULC is a Canadian resident corporation that is disregarded under the U.S. tax laws and is wholly owned by Dutchco. ULC carries on a business in Canada that is the same business as the U.S. business carried on by ForOpco.

9. Dutchco borrowed funds from Forco (“Dutchco Note”) and loaned to ULC (“ULC Note”) on an interest-bearing basis.

Result:

· The interest payments made by ULC to Dutchco would be subject to Canadian Part XIII withholding tax of 10% (pursuant to the Canada – Netherlands treaty).

Interest-bearing loan to ULC(ULC Note)

100%100%

Dutchco

ForOpco USco

ULC

100%

Netherlands

U.S.

Canada

Canadian business

Interest-bearing loan to Dutchco (Dutchco Note)

Interest (Canadian withholding tax applies)

Forco

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

45

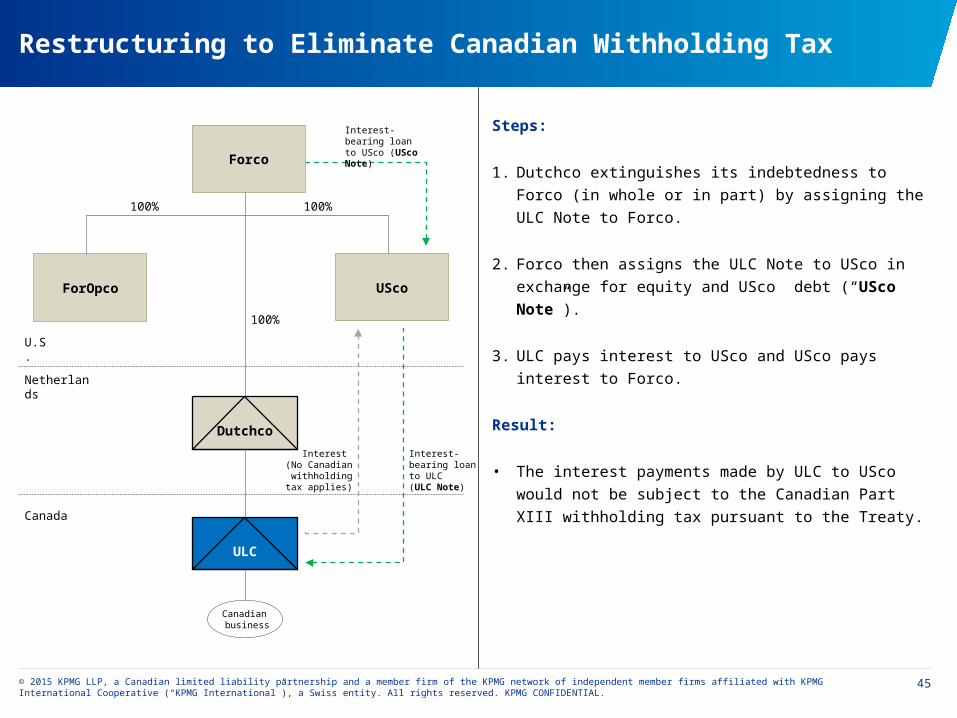

Restructuring to Eliminate Canadian Withholding Tax

Steps:

1. Dutchco extinguishes its indebtedness to Forco (in whole or in

part) by assigning the ULC Note to Forco.

2. Forco then assigns the ULC Note to USco in exchange for

equity and USco debt (“USco Note”).

3. ULC pays interest to USco and USco pays interest to Forco.

Result:

• The interest payments made by ULC to USco would not be

subject to the Canadian Part XIII withholding tax pursuant to

the Treaty.Interest-bearing loan to ULC(ULC Note)

100%100%

Dutchco

ForOpco USco

ULC

100%

Netherlands

U.S.

Canada

Canadian business

Interest-bearing loan to USco (USco Note)

Forco

Interest (No Canadian

withholding tax applies)

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

46

Issues Considered by the CRA

1. Whether Article IV(7)(b) of the Treaty would apply to deny the treaty benefits:

a) After the restructuring, the interest payments will be made by ULC to USco and USco will include it in its income for U.S. tax purposes.

b) Per the CRA, the U.S. tax treatment to USco of the interest payment would be the same if ULC were treated as a corporation for U.S. tax purposes.

c) Therefore, Article IV(7)(b) will not apply.

2. Whether the Limitation on Benefits (“LoB”) clause of the Treaty would apply to deny the treaty benefits:

d) Per the CRA, the LoB clause should not apply as USco would qualify under the active trade or business test.

e) The CRA has not elaborated on the underlying reasons supporting its view in this regard.

f) However, the fact that a person related to USco (i.e. ForOpco) is engaged in an active conduct of a U.S. trade or business may have formed basis for the CRA’s opinion.

g) Additionally, presumably the U.S. trade or business in this case would be substantial relative to the Canadian business activity.

h) Under the active trade or business test, the entitlement to the treaty benefits applies only on a particular item of income in question.

i) Treaty relief will not be granted automatically in the next instance of a cross-border flow of income need to reassess the applicability of the active trade or business test each time an item of income is received by a non-qualifying person.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

47

Thank you

Presentation by:

Ryan Friedman, Tax Partner

416-228-7140

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. KPMG CONFIDENTIAL.

48

KPMG CONFIDENTIAL

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2015 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.