xerox investor handout - amazon web...

TRANSCRIPT

Xerox Investor Handout

Xerox Strategy Overview / Quarter 3 2014 Results

Forward-Looking Statements

This presentation contains "forward-looking statements" as defined in the Private Securities Litigation Reform Act of 1995. The words

“anticipate,” “believe,” “estimate,” “expect,” “intend,” “will,” “should” and similar expressions, as they relate to us, are intended to identify

forward-looking statements. These statements reflect management’s current beliefs, assumptions and expectations and are subject to a

number of factors that may cause actual results to differ materially. These factors include but are not limited to: changes in economic

conditions, political conditions, trade protection measures, licensing requirements and tax matters in the United States and in the foreign

countries in which we do business; changes in foreign currency exchange rates; actions of competitors; our ability to obtain adequate

pricing for our products and services and to maintain and improve cost efficiency of operations, including savings from restructuring

actions and the relocation of our service delivery centers; the risk that multi-year contracts with governmental entities could be

terminated prior to the end of the contract term; the risk in the hiring and retention of qualified personnel; the risk that unexpected costs

will be incurred; the risk that subcontractors, software vendors and utility and network providers will not perform in a timely, quality

manner; our ability to recover capital investments; the risk that our Services business could be adversely affected if we are unsuccessful

in managing the start-up of new contracts; development of new products and services; our ability to protect our intellectual property

rights; our ability to expand equipment placements; the risk that individually identifiable information of customers, clients and employees

could be inadvertently disclosed or disclosed as a result of a breach of our security; service interruptions; interest rates, cost of

borrowing and access to credit markets; reliance on third parties, including subcontractors, for manufacturing of products and provision

of services; our ability to drive the expanded use of color in printing and copying; the outcome of litigation and regulatory proceedings to

which we may be a party; and other factors that are set forth in the “Risk Factors” section, the “Legal Proceedings” section, the

“Management’s Discussion and Analysis of Financial Condition and Results of Operations” section and other sections of our Quarterly

Reports on Form 10-Q for the quarters ended March 31, 2014 and June 30, 2014 and our 2013 Annual Report on Form 10-K filed with

the Securities and Exchange Commission. The Company assumes no obligation to update any forward-looking statements as a result of

new information or future events or developments, except as required by law.

2

Our Message to You: Xerox is…

3

• Well-positioned and investing to grow in attractive services markets

• Applying innovation to lead transition of BPO to automated, analytics-driven outsourcing

• Executing to improve Services performance and consistency

• Leading in attractive areas of document technology while delivering strong

profitability and cash flow

• Disciplined in our capital allocation with focus on delivering shareholder value

• On a journey to be the most sought after customer partner and place to work

in our industry

Xerox Strategy

Apply technology and innovation to transform the way people work and live

Drive Operational Excellence Across Our Businesses

Innovate to

Differentiate Our

Offerings

Leverage Brand

Strength and Market

Position

Profitably Grow

Services in Attractive

Markets

Lead in Document

Technology

Engage, Develop and Support Our People

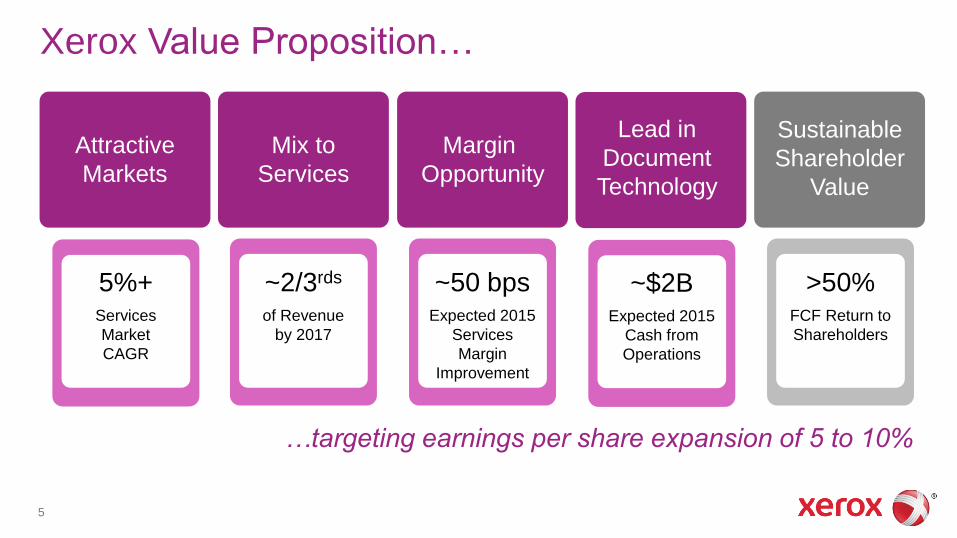

Xerox Value Proposition…

…targeting earnings per share expansion of 5 to 10%

Mix to

Services

~2/3rds

of Revenue

by 2017

Attractive

Markets

5%+ Services

Market

CAGR

Margin

Opportunity

~50 bps Expected 2015

Services

Margin

Improvement

Sustainable

Shareholder

Value

>50% FCF Return to

Shareholders

Lead in

Document

Technology

~$2B Expected 2015

Cash from

Operations

5

Document Technology

Document Technology Strategy

7

Grow in

Developing

Markets

Innovate in All

We Do

Market focused strategy underpinned by operational excellence and talented workforce

Operational Excellence, Global Delivery and Economy of Scale

Engage, Develop and Support Our People

Lead in

Managed Print

Services

Channel

Expansion and

Market Reach

Lead in Graphic

Communications

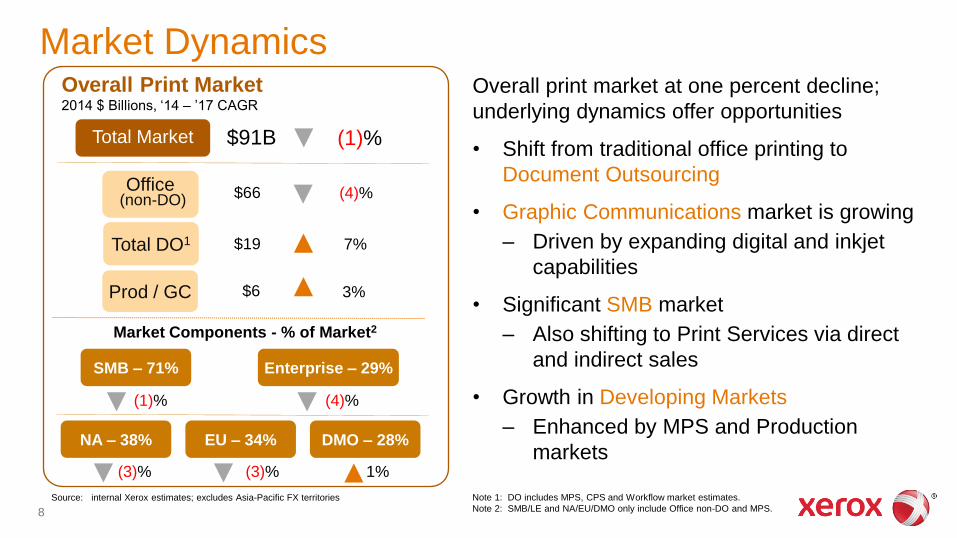

Market Dynamics

8

Overall print market at one percent decline;

underlying dynamics offer opportunities

• Shift from traditional office printing to

Document Outsourcing

• Graphic Communications market is growing

– Driven by expanding digital and inkjet

capabilities

• Significant SMB market

– Also shifting to Print Services via direct

and indirect sales

• Growth in Developing Markets

– Enhanced by MPS and Production

markets

Source: internal Xerox estimates; excludes Asia-Pacific FX territories

Overall Print Market 2014 $ Billions, ‘14 – ’17 CAGR

Office (non-DO)

Total DO1

Prod / GC

(4)%

7%

3%

$66

$19

Total Market $91B (1)%

SMB – 71% Enterprise – 29%

(1)% (4)%

$6

NA – 38% DMO – 28%

(3)% 1%

EU – 34%

(3)%

Note 1: DO includes MPS, CPS and Workflow market estimates.

Note 2: SMB/LE and NA/EU/DMO only include Office non-DO and MPS.

Market Components - % of Market2

WW 1H14 Equipment Sale Revenue Share %

Xerox has been the leader

for 19 consecutive quarters

Technology Advances Sustain Industry Leadership

Sustained Market Share Leadership

Industry Recognition

Gold Ink Awards Europe Digital Press Award

Magic Quadrant for Managed Print Services,

Worldwide

IDC MarketScape WW MPS & Document

Services Hardcopy Vendor Analysis

2014 Quocirca MPS Landscape

A leader in The Forrester Wave™:

Managed Print Services

Xerox Corporation Mobile Print Solution 2

Outstanding Enterprise Mobile Print Solution

Xerox Corporation 2014 Document Imaging Solutions

Line of the Year

9

IDC: Published September 2014

Forrester: Published Q2 2012, Forrester Research, Inc.

Gartner: Published October 21, 2013 by Ken Weilerstein, Sharon McNee, Elizabeth Kim. Gartner does not endorse any vendor, product or service depicted in its research publications, and does not advise

technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner's research organization and should not be construed

as statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.

Xerox

21 17

14

11

[------- Competitors -------]

Market Leading Portfolio – SMB and Large Enterprise Broadest Portfolio of Print and Document Outsourcing Capabilities will enable MPS growth with the market and increased share of SMB market

15 New Workflow Offerings in 2014

Workflow Integration for Mobile and Cloud

Industry Leading Security

Cost Control and Sustainability

IT Enablers

ConnectKey®

Xerox® WorkCentre®

7845/7855

Xerox® WorkCentre®

5945/5955

Xerox® Color

C60/70

Xerox®

WorkCentre®

6655

Xerox® WorkCentre®

7220/7225

Xerox® WorkCentre®

7970

Xerox® WorkCentre® 3655

Xerox® WorkCentre®

5865/5875/5890

19 New Technology Offerings in 2014

ConnectKey®

ConnectKey®

ConnectKey®

ConnectKey®

ConnectKey®

ConnectKey®

10

Market Leading Portfolio – Graphic Communications Broadest Portfolio of Graphic Communications Offerings

to capture increased share of color growth and inkjet opportunity within the 50 trillion total production pages

Web-to-print

Variable Data Cross Media

Pre-press Color Management

Automation

7 New Workflow Offerings in 2014

Xerox® 8250 Production Printer

Xerox® Color J75 Press

Xerox® Color 800/1000 Presses

Xerox ® Versant 2100 Press

Xerox® Reference®

Xerox® CiPress® 500

Xerox® CiPress® 325

Xerox® eVolution® 150 /250

Xerox® iGen® 150 Digital Press

Xerox® Compact®

4 New Technology Offerings in 2014

11

Demonstrated Operational Excellence Across Value Chain…

Global Reach

Direct Sales Capability

Extensive Channels and

Partnerships

Broad Customer Relationships Sales Excellence and Productivity

Global Service

Remote Connectivity and Diagnostics

Global Delivery Center

Automation

Offering Innovation

Offshoring and Right-shoring

…drives sustained market share and strong operating margin.

Global Delivery

Manufacturing Productivity

Global Sourcing

Product Cost and Portfolio Simplification

RD&E Efficiency and Alignment

Infrastructure Optimization 20%

45%

31%

4%

SAG

Equipment

Post Sale

& Managed

Services

Over $9B of

Addressable Spend1

% of Total

RD&E

Note 1: Includes operating expenses for Document Technology and Document Outsourcing.

12

Services

Services Strategy…

Manage Our

Portfolio of

Businesses

Grow

Globally

Transform the

Way We Work

Deliver

Operational

Excellence

Use Analytics

to Increase

Value

14

Engage, Develop and Support Our People

...will drive revenue growth and margin improvement.

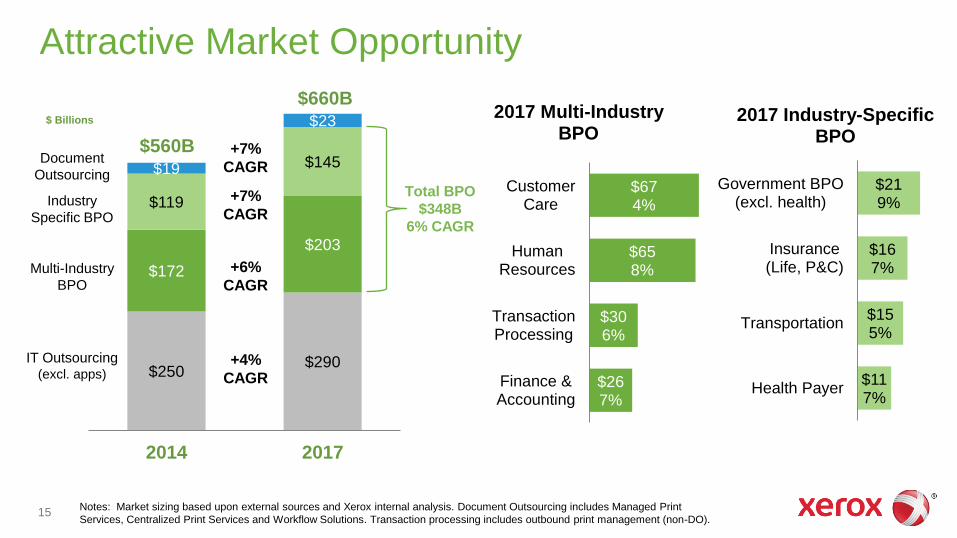

$250 $290

$172

$203

$119

$145 $19

$23

2014 2017

Attractive Market Opportunity

$26 7%

$30 6%

$65 8%

$67 4%

Finance &Accounting

TransactionProcessing

HumanResources

CustomerCare

2017 Multi-Industry BPO

Notes: Market sizing based upon external sources and Xerox internal analysis. Document Outsourcing includes Managed Print

Services, Centralized Print Services and Workflow Solutions. Transaction processing includes outbound print management (non-DO).

$ Billions

$560B

$660B

IT Outsourcing (excl. apps)

Industry

Specific BPO

Multi-Industry

BPO

Document

Outsourcing

+4%

CAGR

+7%

CAGR

+6%

CAGR

+7%

CAGR

$11 7%

$15 5%

$16 7%

$21 9%

Health Payer

Transportation

Insurance(Life, P&C)

Government BPO(excl. health)

2017 Industry-Specific BPO

Total BPO

$348B

6% CAGR

15

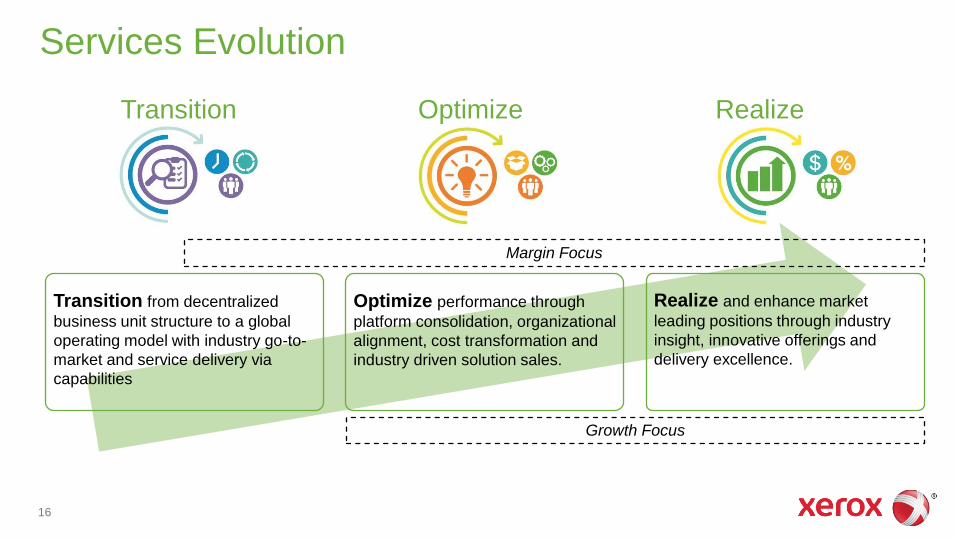

Services Evolution

Optimize Realize

Transition

16

Transition from decentralized

business unit structure to a global

operating model with industry go-to-

market and service delivery via

capabilities

Optimize performance through

platform consolidation, organizational

alignment, cost transformation and

industry driven solution sales.

Realize and enhance market

leading positions through industry

insight, innovative offerings and

delivery excellence.

Margin Focus

Growth Focus

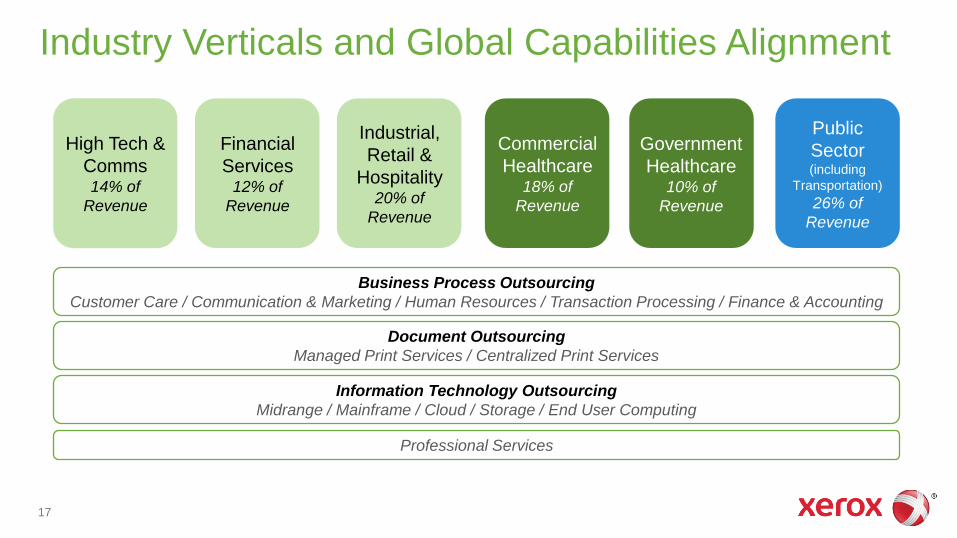

Industry Verticals and Global Capabilities Alignment

Financial

Services 12% of

Revenue

High Tech &

Comms 14% of

Revenue

Industrial,

Retail &

Hospitality 20% of

Revenue

Commercial

Healthcare 18% of

Revenue

Government

Healthcare 10% of

Revenue

Public

Sector (including

Transportation)

26% of

Revenue

Document Outsourcing

Managed Print Services / Centralized Print Services

Information Technology Outsourcing

Midrange / Mainframe / Cloud / Storage / End User Computing

Business Process Outsourcing

Customer Care / Communication & Marketing / Human Resources / Transaction Processing / Finance & Accounting

Professional Services

17

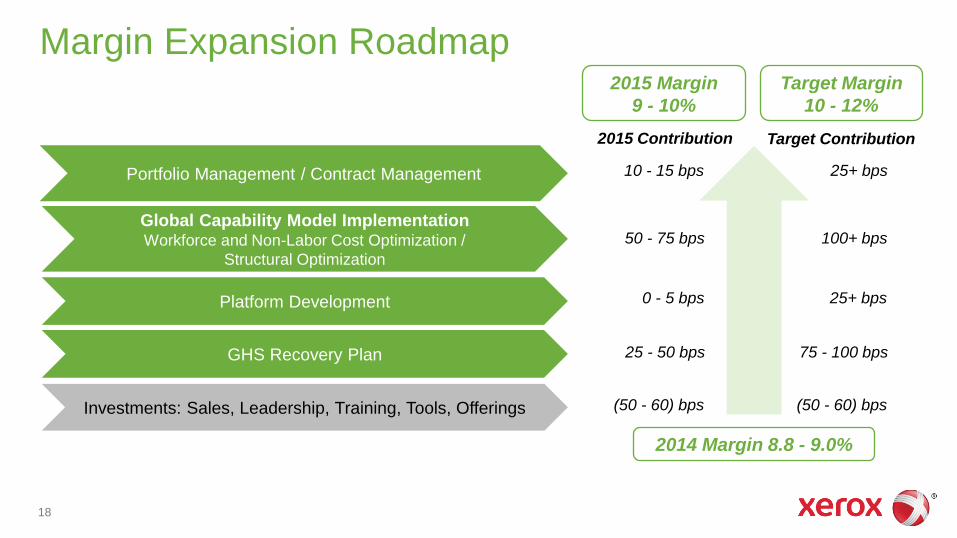

Margin Expansion Roadmap

GHS Recovery Plan

Global Capability Model Implementation Workforce and Non-Labor Cost Optimization /

Structural Optimization

Portfolio Management / Contract Management

18

2014 Margin 8.8 - 9.0%

Target Margin

10 - 12%

Investments: Sales, Leadership, Training, Tools, Offerings

10 - 15 bps

2015 Margin

9 - 10%

25+ bps

2015 Contribution Target Contribution

50 - 75 bps 100+ bps

25 - 50 bps 75 - 100 bps

(50 - 60) bps (50 - 60) bps

Platform Development 0 - 5 bps 25+ bps

Revenue Growth Acceleration Levers…

Acquisitions More Rapid

Growth Outside

the U.S.

Industry

Verticals /

Cross Selling /

Signings

Acceleration

New Large

Contract Yield

Reduced

Large Contract

Run-offs

...will drive revenue growth back to target model.

19

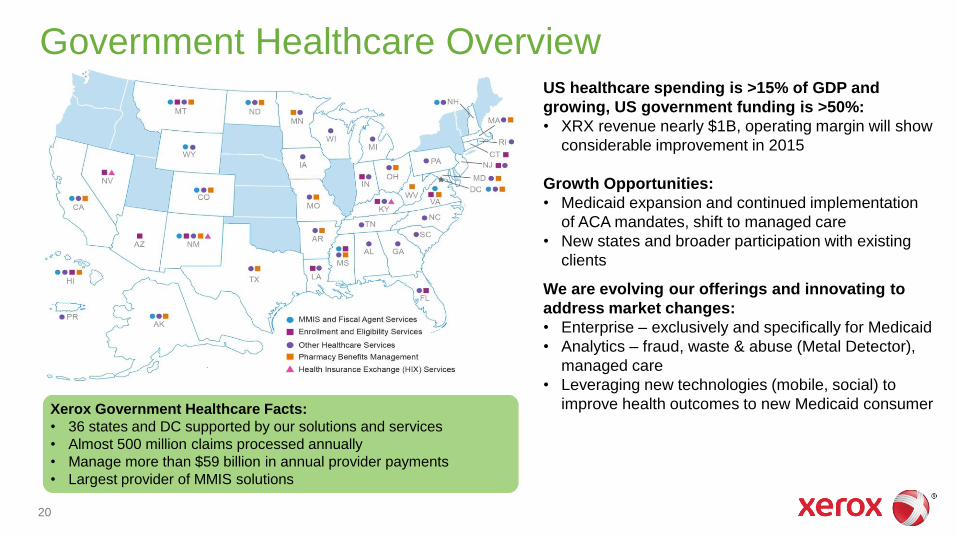

Government Healthcare Overview

Xerox Government Healthcare Facts:

• 36 states and DC supported by our solutions and services

• Almost 500 million claims processed annually

• Manage more than $59 billion in annual provider payments

• Largest provider of MMIS solutions

US healthcare spending is >15% of GDP and

growing, US government funding is >50%:

• XRX revenue nearly $1B, operating margin will show

considerable improvement in 2015

Growth Opportunities:

• Medicaid expansion and continued implementation

of ACA mandates, shift to managed care

• New states and broader participation with existing

clients

We are evolving our offerings and innovating to

address market changes:

• Enterprise – exclusively and specifically for Medicaid

• Analytics – fraud, waste & abuse (Metal Detector),

managed care

• Leveraging new technologies (mobile, social) to

improve health outcomes to new Medicaid consumer

20

Commercial Healthcare Overview

The global healthcare market is ~$48 billion, 7%

CAGR

• XRX revenue in excess of $1B, operating margin

and annual growth above target model

Healthcare Mega Trends:

Shift to consumer model, changing payment and risk

model, increasing care and quality measurement

Our Growth Strategy:

• Leverage core scale-based services

• Accelerate growth in vertical specific services

• Build and acquire new capabilities

We are evolving our offerings and innovating to

address market changes:

• Analytics – Juvo, Digital Assistant, managed care

and fraud, waste & abuse

• Technology – Atrial Fibrillation Image Processing

Patient Becoming key

decision maker

21

Xerox Commercial Healthcare Facts:

• 2/3 of US insured patients are touched by XRX

• 1,900+ hospitals served

• 100% of top 20 US managed healthcare plans are clients

• Industry leader in size/capability across a number of key categories

Transportation Overview

The global transportation market is ~$13 billion,

5% CAGR

• XRX revenue nearly $1B, operating margin above

target model

Global Transportation Mega Trends:

Urbanization, changing demographics, always

connected, new business models

Our Growth Strategy – Urban Mobility: Series of

interrelated solutions designed to satisfy mobility

needs of mega cities, businesses and their citizens

today and in the future

We are evolving our offerings and innovating to

address market changes:

• Parking – Merge® A smart grid for parking

• Electronic Tolling – Xerox Vehicle Passenger

Detection System™

Xerox Transportation Facts:

• US Industry leader across several offerings, also high global ranking

and industry recognition for leadership in excellence and innovation

• 35 countries host our transportation solutions worldwide

• $5 billion in electronic toll payments processed annually

• 37 billion public transit transactions managed annually

22

Human Resources Outsourcing and Consulting

The global HRS BPO market is ~$65 billion, 8% CAGR

• XRX revenue over $1B, operating margin and growth

varies by business area

Global HRS Mega Trends:

Private exchanges, focus on employee productivity, shift

to defined contribution versus defined benefit, employee

engagement, Business/Learner centric solutions

HRS and Professional Services Capabilities:

• Learning

• Buck Consulting

• Total Benefits and HR Outsourcing

We are evolving our offerings and innovations to

address market changes:

• Private Healthcare Exchange – RightOpt®

• BPaaS solutions – fully integrated SaaS applications

• Data Analytics – diagnostic, prescriptive and

predictive

• Learning Hub – integrated learning platform

23

Xerox HR Services Facts:

• Over 2,000 clients with 9M+ employees and retirees served

• Global footprint across 72 countries; addressing 23 languages

• 5M+ Learners supported globally

• Highly ranked by industry analysts across all major offerings

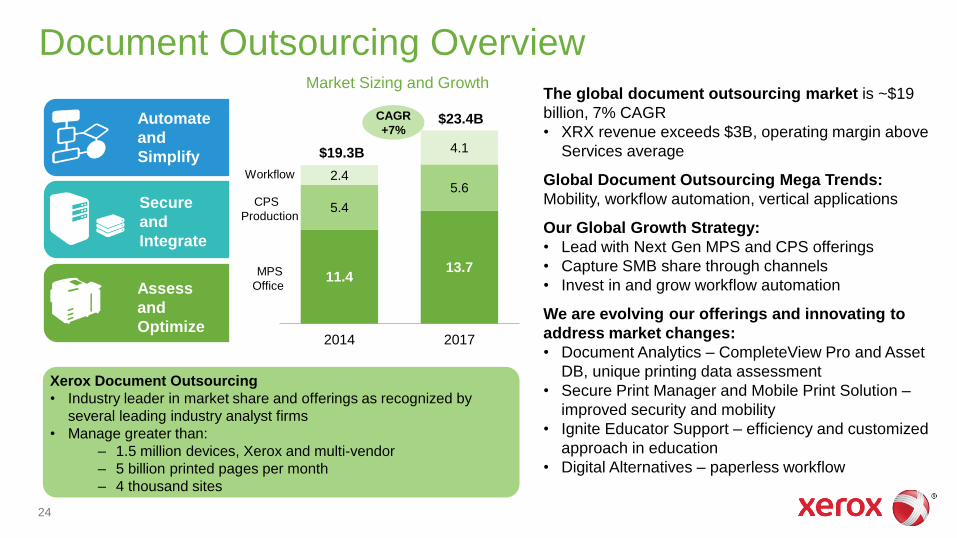

Document Outsourcing Overview

11.4 13.7

5.4

5.6 2.4

4.1

2014 2017

CAGR

+7%

$19.3B

$23.4B

Xerox Document Outsourcing

• Industry leader in market share and offerings as recognized by

several leading industry analyst firms

• Manage greater than:

– 1.5 million devices, Xerox and multi-vendor

– 5 billion printed pages per month

– 4 thousand sites

The global document outsourcing market is ~$19

billion, 7% CAGR

• XRX revenue exceeds $3B, operating margin above

Services average

Global Document Outsourcing Mega Trends:

Mobility, workflow automation, vertical applications

Our Global Growth Strategy:

• Lead with Next Gen MPS and CPS offerings

• Capture SMB share through channels

• Invest in and grow workflow automation

We are evolving our offerings and innovating to

address market changes:

• Document Analytics – CompleteView Pro and Asset

DB, unique printing data assessment

• Secure Print Manager and Mobile Print Solution –

improved security and mobility

• Ignite Educator Support – efficiency and customized

approach in education

• Digital Alternatives – paperless workflow

Automate

and

Simplify

Secure

and

Integrate

Assess

and

Optimize

Market Sizing and Growth

CPS

Production

24

MPS

Office

Workflow

Financial Overview

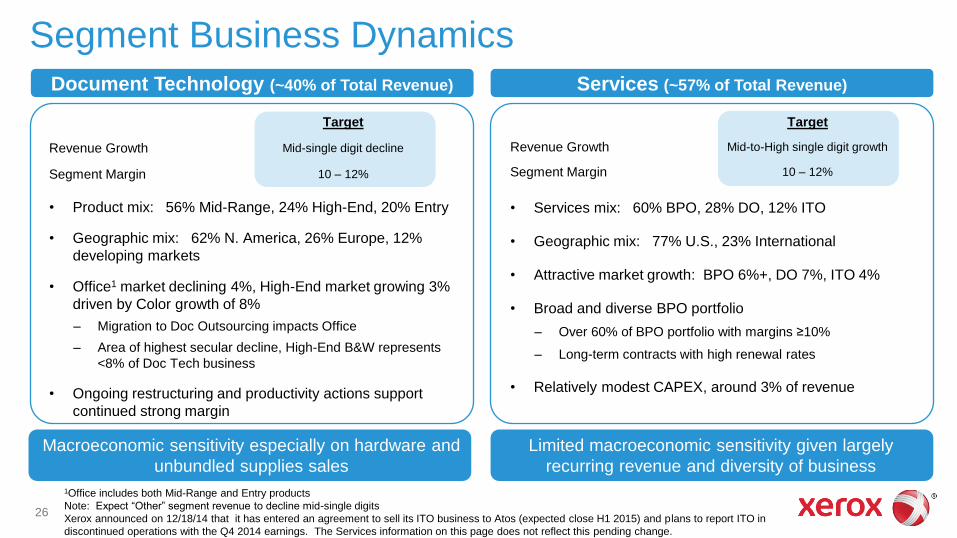

Segment Business Dynamics

Target

Revenue Growth Mid-to-High single digit growth

Segment Margin 10 – 12%

• Services mix: 60% BPO, 28% DO, 12% ITO

• Geographic mix: 77% U.S., 23% International

• Attractive market growth: BPO 6%+, DO 7%, ITO 4%

• Broad and diverse BPO portfolio

– Over 60% of BPO portfolio with margins ≥10%

– Long-term contracts with high renewal rates

• Relatively modest CAPEX, around 3% of revenue

Services (~57% of Total Revenue) Document Technology (~40% of Total Revenue)

Macroeconomic sensitivity especially on hardware and

unbundled supplies sales

Limited macroeconomic sensitivity given largely

recurring revenue and diversity of business

1Office includes both Mid-Range and Entry products

Note: Expect “Other” segment revenue to decline mid-single digits

Xerox announced on 12/18/14 that it has entered an agreement to sell its ITO business to Atos (expected close H1 2015) and plans to report ITO in

discontinued operations with the Q4 2014 earnings. The Services information on this page does not reflect this pending change.

Target

Revenue Growth Mid-single digit decline

Segment Margin 10 – 12%

26

• Product mix: 56% Mid-Range, 24% High-End, 20% Entry

• Geographic mix: 62% N. America, 26% Europe, 12%

developing markets

• Office1 market declining 4%, High-End market growing 3%

driven by Color growth of 8%

– Migration to Doc Outsourcing impacts Office

– Area of highest secular decline, High-End B&W represents

<8% of Doc Tech business

• Ongoing restructuring and productivity actions support

continued strong margin

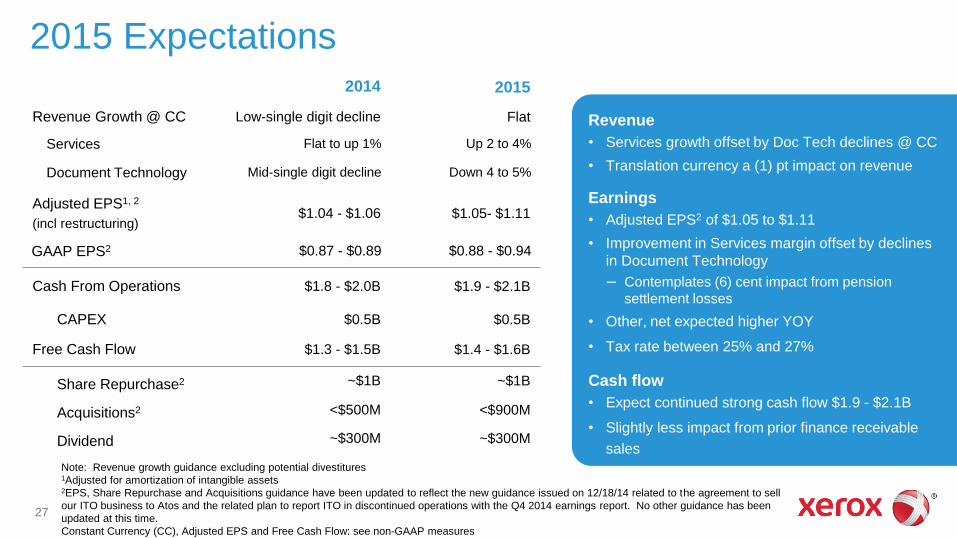

2015 Expectations

Note: Revenue growth guidance excluding potential divestitures 1Adjusted for amortization of intangible assets 2EPS, Share Repurchase and Acquisitions guidance have been updated to reflect the new guidance issued on 12/18/14 related to the agreement to sell

our ITO business to Atos and the related plan to report ITO in discontinued operations with the Q4 2014 earnings report. No other guidance has been

updated at this time.

Constant Currency (CC), Adjusted EPS and Free Cash Flow: see non-GAAP measures

27

2014 2015

Revenue Growth @ CC Low-single digit decline Flat

Services Flat to up 1% Up 2 to 4%

Document Technology Mid-single digit decline Down 4 to 5%

Adjusted EPS1, 2

(incl restructuring) $1.04 - $1.06 $1.05- $1.11

GAAP EPS2 $0.87 - $0.89 $0.88 - $0.94

Cash From Operations $1.8 - $2.0B $1.9 - $2.1B

CAPEX $0.5B $0.5B

Free Cash Flow $1.3 - $1.5B $1.4 - $1.6B

Share Repurchase2 ~$1B ~$1B

Acquisitions2 <$500M <$900M

Dividend ~$300M ~$300M

Revenue

• Services growth offset by Doc Tech declines @ CC

• Translation currency a (1) pt impact on revenue

Earnings

• Adjusted EPS2 of $1.05 to $1.11

• Improvement in Services margin offset by declines

in Document Technology

– Contemplates (6) cent impact from pension

settlement losses

• Other, net expected higher YOY

• Tax rate between 25% and 27%

Cash flow

• Expect continued strong cash flow $1.9 - $2.1B

• Slightly less impact from prior finance receivable

sales

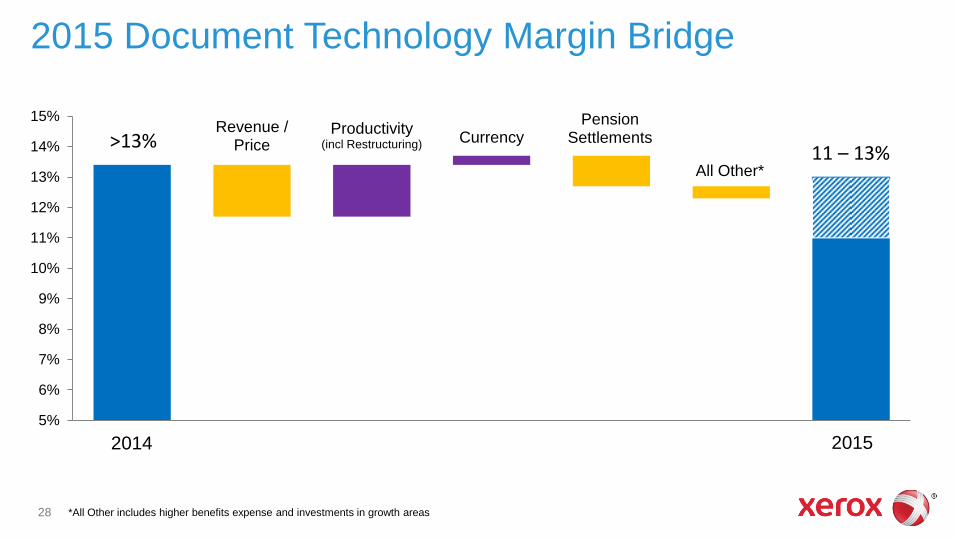

>13% 11 – 13%

Revenue / Price

Productivity (incl Restructuring)

Currency Pension

Settlements

All Other*

5%

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

2014 Productivity inclRestructuring

Pension Settlement 2015

28

2015 Document Technology Margin Bridge

2015 2014

*All Other includes higher benefits expense and investments in growth areas

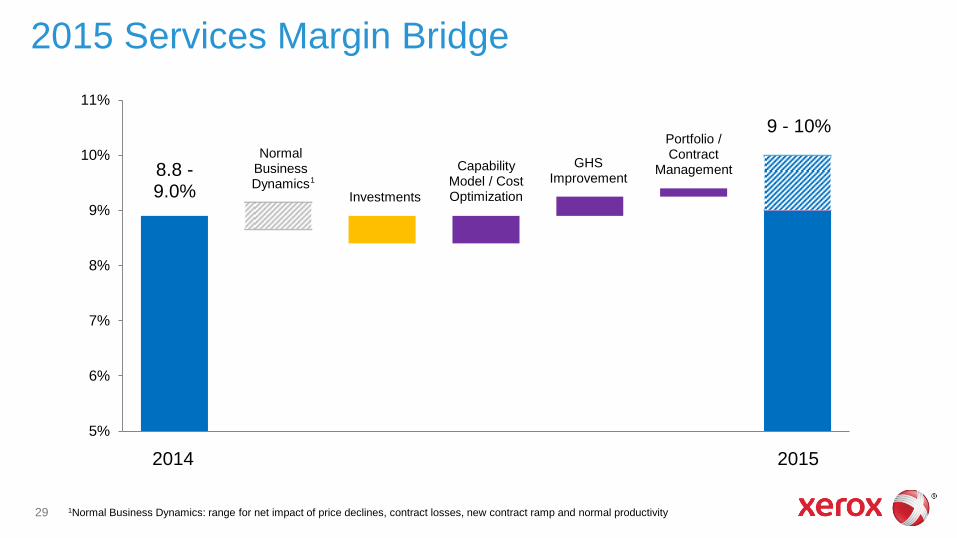

2015 Services Margin Bridge

1Normal Business Dynamics: range for net impact of price declines, contract losses, new contract ramp and normal productivity

8.8 - 9.0%

9 - 10%

Normal Business Dynamics

Investments

GHS Improvement

Portfolio / Contract

Management Capability Model / Cost Optimization

5%

6%

7%

8%

9%

10%

11%

2014 Normal businessdynamics

Investments PortfolioManagement

Govt HealthcareImprovement

Cost Optimization 20152015 2014

29

1

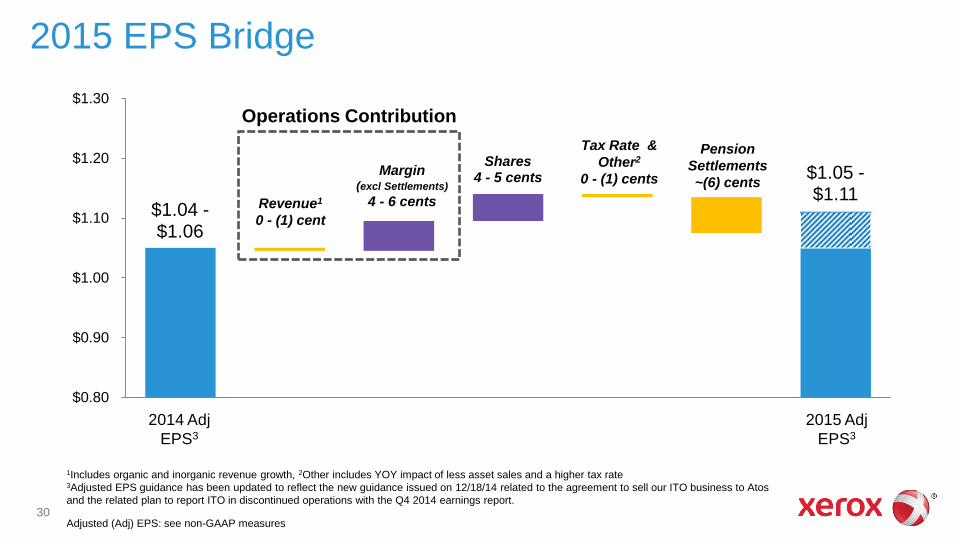

$1.04 - $1.06

$1.05 - $1.11

Shares 4 - 5 cents

$0.80

$0.90

$1.00

$1.10

$1.20

$1.30

2014 Adj EPS RevenueGrowth

Margin exclSettlements

Shares Tax Rate/Other PensionSettlements

2014 Adj EPS

Revenue1

0 - (1) cent

Pension

Settlements

~(6) cents

Tax Rate &

Other2

0 - (1) cents Margin

(excl Settlements)

4 - 6 cents

2015 EPS Bridge

1Includes organic and inorganic revenue growth, 2Other includes YOY impact of less asset sales and a higher tax rate 3Adjusted EPS guidance has been updated to reflect the new guidance issued on 12/18/14 related to the agreement to sell our ITO business to Atos

and the related plan to report ITO in discontinued operations with the Q4 2014 earnings report.

Operations Contribution

30

2014 Adj

EPS3

2015 Adj

EPS3

Adjusted (Adj) EPS: see non-GAAP measures

$0

$100

$200

$300

$400

2012 2013 2014E 2015E

DB Plan Cost DB Settlement Loss DC Plan Cost

$0

$100

$200

$300

$400

$500

2012 2013 2014E 2015E

DB Cash Contribution DB Stock Contribution

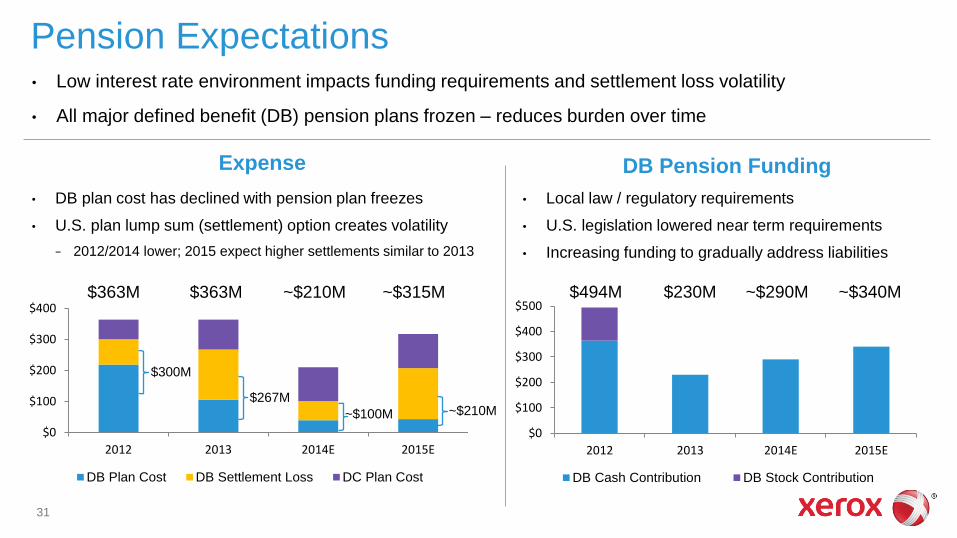

Pension Expectations

Expense DB Pension Funding

• DB plan cost has declined with pension plan freezes

• U.S. plan lump sum (settlement) option creates volatility

− 2012/2014 lower; 2015 expect higher settlements similar to 2013

$230M

• Local law / regulatory requirements

• U.S. legislation lowered near term requirements

• Increasing funding to gradually address liabilities

• Low interest rate environment impacts funding requirements and settlement loss volatility

• All major defined benefit (DB) pension plans frozen – reduces burden over time

~$340M ~$290M $363M ~$210M ~$315M $363M

$300M

$267M

~$100M ~$210M

$494M

31

Cash Flow Dynamics

Continued strong cash flow

2015 reflects moderating impact

from previous Finance Receivable

sales

• Partially offset by higher pension

funding

No Finance Receivable sales

planned in 2015

32

(in billions) 2012 2013 2014 Est. 2015 Est.

Operating Cash Flow (OCF) $2.6 $2.4 $1.8 - $2.0 $1.9 - $2.1

Adjustments:

Cash from F/R Sales $(0.6) $(0.6) - -

Impact from prior F/R Sales - $0.3 ~$0.4 ~$0.3

Underlying OCF* $2.0 $2.1 $2.2 - $2.4 $2.2 - $2.4

Operating Cash Flow Trend

*Underlying OCF is reported OCF adjusted for the impacts of Finance Receivable sales. See non-GAAP measures.

$0

$1

$2

$3

2012 2013 2014E 2015E

OCF Underlying OCF

(in

bill

ion

s)

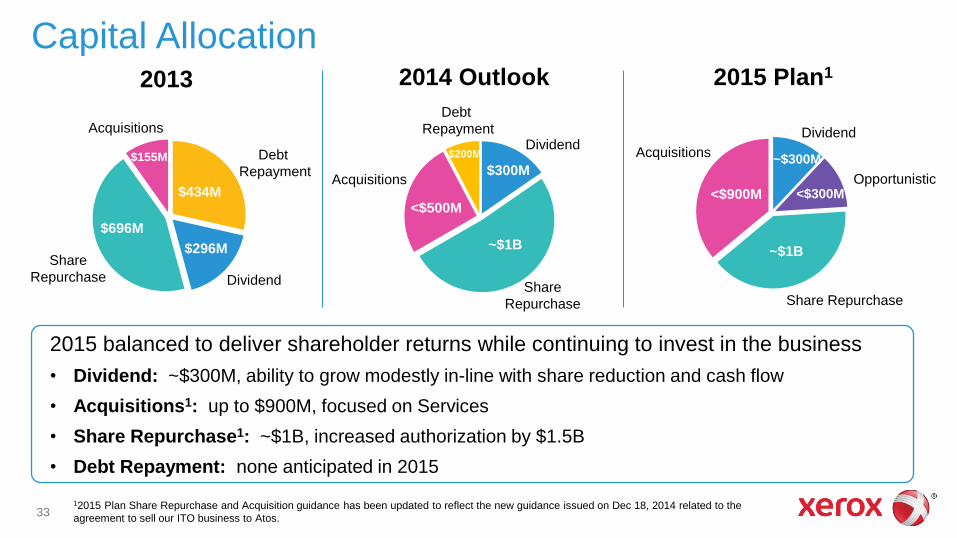

Capital Allocation

2013

2015 balanced to deliver shareholder returns while continuing to invest in the business

• Dividend: ~$300M, ability to grow modestly in-line with share reduction and cash flow

• Acquisitions1: up to $900M, focused on Services

• Share Repurchase1: ~$1B, increased authorization by $1.5B

• Debt Repayment: none anticipated in 2015

2015 Plan1

Opportunistic

Acquisitions

Share Repurchase

Dividend Acquisitions

Dividend

Debt

Repayment

Share

Repurchase

$696M

$296M

$434M

$155M

33

Share

Repurchase

Dividend

Debt

Repayment

Acquisitions

2014 Outlook

~$1B

<$500M

$300M

$200M

~$1B

<$300M <$900M

~$300M

12015 Plan Share Repurchase and Acquisition guidance has been updated to reflect the new guidance issued on Dec 18, 2014 related to the

agreement to sell our ITO business to Atos.

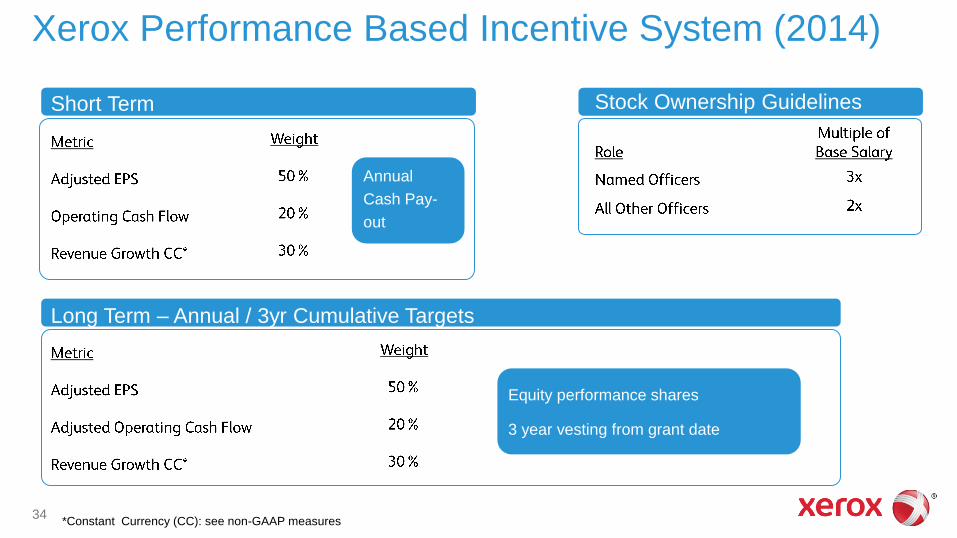

Xerox Performance Based Incentive System (2014)

Short Term Stock Ownership Guidelines

Annual

Cash Pay-

out

34

Long Term – Annual / 3yr Cumulative Targets

Equity performance shares

3 year vesting from grant date

*Constant Currency (CC): see non-GAAP measures

Third-Quarter 2014 Earnings Presentation Ursula Burns Chairman & CEO

Kathy Mikells Chief Financial Officer

October 22, 2014

Xerox Direction

Annuity 85% of Total Revenue

Services 57% of Total Revenue

• Grow revenue

• Generate profits in line with industry’s best

• Strengthen and differentiate the portfolio

• Support customers and our people

• Allocate capital to enhance shareholder

returns

36

Third-Quarter Overview

Adjusted EPS1 of 27 cents, GAAP EPS2 of 22 cents Total revenue of $5.1B, down 2%

Services revenue up 1% or flat CC1; margin of 8.9%

• Revenue growth improves in BPO; offsets decline in ITO

• Margin increased sequentially driven by BPO

Document Technology revenue down 6%; margin of 14.0%

• Profit expansion driven by continued productivity initiatives as well as currency and pension benefits

Operating margin1 of 9.5%, up 10 bps YOY Cash from operations of $595M in Q3, $1.2B YTD

• Share repurchase of $251M in Q3, $730M YTD

• Acquisitions of $25M in Q3, $306M YTD

1Adjusted EPS, Constant Currency (CC) and Operating Margin: see non-GAAP measures

2GAAP EPS from Continuing Operations 37

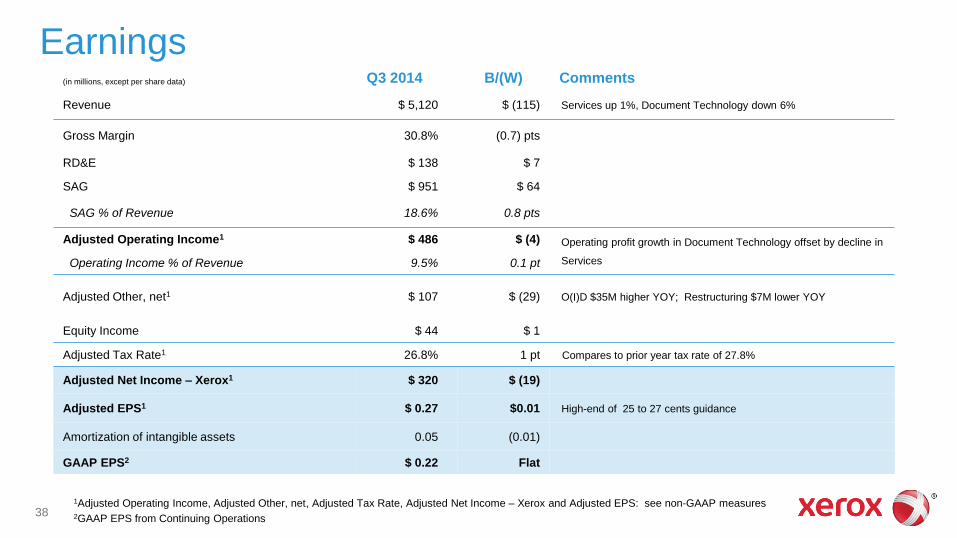

Earnings (in millions, except per share data) Q3 2014 B/(W) Comments

Revenue $ 5,120 $ (115) Services up 1%, Document Technology down 6%

Gross Margin 30.8% (0.7) pts

RD&E $ 138 $ 7

SAG $ 951 $ 64

SAG % of Revenue 18.6% 0.8 pts

Adjusted Operating Income1 $ 486 $ (4) Operating profit growth in Document Technology offset by decline in

Services Operating Income % of Revenue 9.5% 0.1 pt

Adjusted Other, net1 $ 107 $ (29) O(I)D $35M higher YOY; Restructuring $7M lower YOY

Equity Income $ 44 $ 1

Adjusted Tax Rate1 26.8% 1 pt Compares to prior year tax rate of 27.8%

Adjusted Net Income – Xerox1 $ 320 $ (19)

Adjusted EPS1 $ 0.27

$0.01

High-end of 25 to 27 cents guidance

Amortization of intangible assets 0.05 (0.01)

GAAP EPS2 $ 0.22

Flat

1Adjusted Operating Income, Adjusted Other, net, Adjusted Tax Rate, Adjusted Net Income – Xerox and Adjusted EPS: see non-GAAP measures 2GAAP EPS from Continuing Operations

38

Services Segment

BPO revenue up 2%, DO flat and ITO down 3%

Margin up sequentially; short of expectations

Multi-plank strategy progressing

• Re-aligning organization to leverage our scale, gain

efficiencies and improve customer value

Signings

• BPO/ITO renewal rate of 82%

• New business signings2 down 18% YOY and 6% TTM

• Significant deals awarded, not yet signed

Q3 % B/(W) YOY

(in millions) 2014 Act Cur CC1

Total Revenue $2,948 1% Flat

Segment Profit $262 (10)%

Segment Margin 8.9% (1.1) pts

Segment Margin Trend

Revenue Growth Trend (CC1)

Signings (TCV) Q3

Business Process Outsourcing $1.4

Document Outsourcing $0.7

Information Technology Outsourcing $0.2

Total $2.3B

YOY Growth (21)%

TTM Growth (17)%

39 1Constant currency (CC): see non-GAAP measures 2New Business Signings = ARR (Annual Recurring Revenue) + NRR (Non-Recurring Revenue)

Note: Historical data updated to reflect Truckload Management Services divestiture and reclassification to Discontinued Operations

4%

6%

3%

(2)% 0%

1% 0%

(4)%

0%

4%

8%

Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14

9.4%

10.2% 10.0% 9.6%

8.6% 8.6% 8.9%

5%

7%

9%

11%

Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14

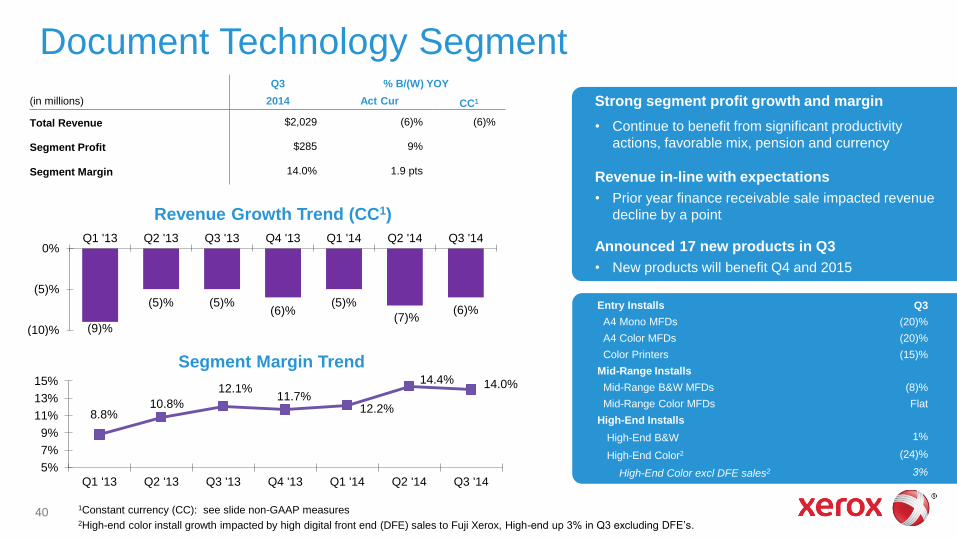

Document Technology Segment

Segment Margin Trend

Revenue Growth Trend (CC1)

Q3 % B/(W) YOY

(in millions) 2014 Act Cur CC1

Total Revenue $2,029 (6)% (6)%

Segment Profit $285 9%

Segment Margin 14.0% 1.9 pts

Strong segment profit growth and margin

• Continue to benefit from significant productivity

actions, favorable mix, pension and currency

Revenue in-line with expectations

• Prior year finance receivable sale impacted revenue

decline by a point

Announced 17 new products in Q3

• New products will benefit Q4 and 2015

Entry Installs Q3

A4 Mono MFDs (20)%

A4 Color MFDs (20)%

Color Printers (15)%

Mid-Range Installs

Mid-Range B&W MFDs (8)%

Mid-Range Color MFDs Flat

High-End Installs

High-End B&W 1%

High-End Color2 (24)%

High-End Color excl DFE sales2 3%

40 1Constant currency (CC): see slide non-GAAP measures 2High-end color install growth impacted by high digital front end (DFE) sales to Fuji Xerox, High-end up 3% in Q3 excluding DFE’s.

(9)%

(5)% (5)% (6)%

(5)%

(7)% (6)%

(10)%

(5)%

0%Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14

8.8% 10.8%

12.1% 11.7%

12.2%

14.4% 14.0%

5%

7%

9%

11%

13%

15%

Q1 '13 Q2 '13 Q3 '13 Q4 '13 Q1 '14 Q2 '14 Q3 '14

Cash Flow

41

(in millions) Q3 2014 YTD 2014

Net Income $ 272 $ 830

Depreciation and amortization 349 1,070

Restructuring and asset impairment charges 28 93

Restructuring payments (31) (103)

Contributions to defined benefit pension plans (101) (206)

Inventories (34) (137)

Accounts receivable and Billed portion of finance receivables1 10 (153)

Accounts payable and Accrued compensation 126 38

Equipment on operating leases (81) (204)

Finance receivables1 48 144

Other 9 (166)

Cash from Operations

$ 595 $ 1,206

Cash from Investing

$ (128) $ (574)

Cash from Financing $ (417) $ (1,327)

Change in Cash and Cash Equivalents 8 (749)

Ending Cash and Cash Equivalents $ 1,015 $ 1,015

Cash From Ops $595M, $1.2B YTD

• Underlying Cash from Ops2 $697M

in Q3, $1,543M YTD

Q3 YOY impact from Finance

Receivable sales was $(418)M3

Working capital continues to

improve

CAPEX $112M

Acquisitions $25M

Share Repurchase of $251M and

$77M of Common Stock Dividends

1Accounts receivable includes collections of deferred proceeds from sales of receivables and finance receivables includes collections on

beneficial interest from sales of finance receivables 2See Underlying Cash Flow slide in Appendix 3YOY estimated impact to operating cash flows from prior years finance receivable sales

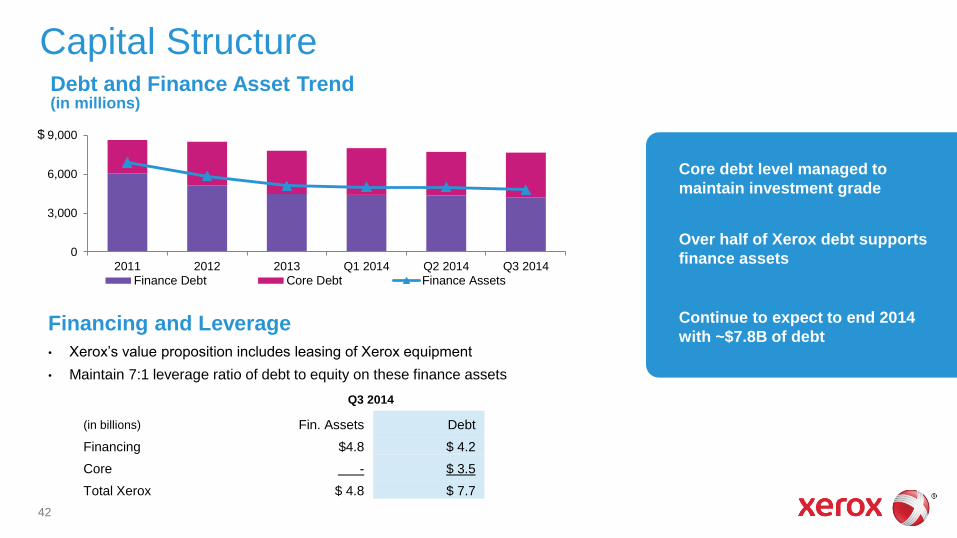

Capital Structure

Core debt level managed to

maintain investment grade

Over half of Xerox debt supports

finance assets

Continue to expect to end 2014

with ~$7.8B of debt

42

Financing and Leverage

• Xerox’s value proposition includes leasing of Xerox equipment

• Maintain 7:1 leverage ratio of debt to equity on these finance assets

Debt and Finance Asset Trend (in millions)

Q3 2014

(in billions) Fin. Assets Debt

Financing $4.8 $ 4.2

Core - $ 3.5

Total Xerox $ 4.8 $ 7.7

0

3,000

6,000

9,000

2011 2012 2013 Q1 2014 Q2 2014 Q3 2014

Finance Debt Core Debt Finance Assets

$

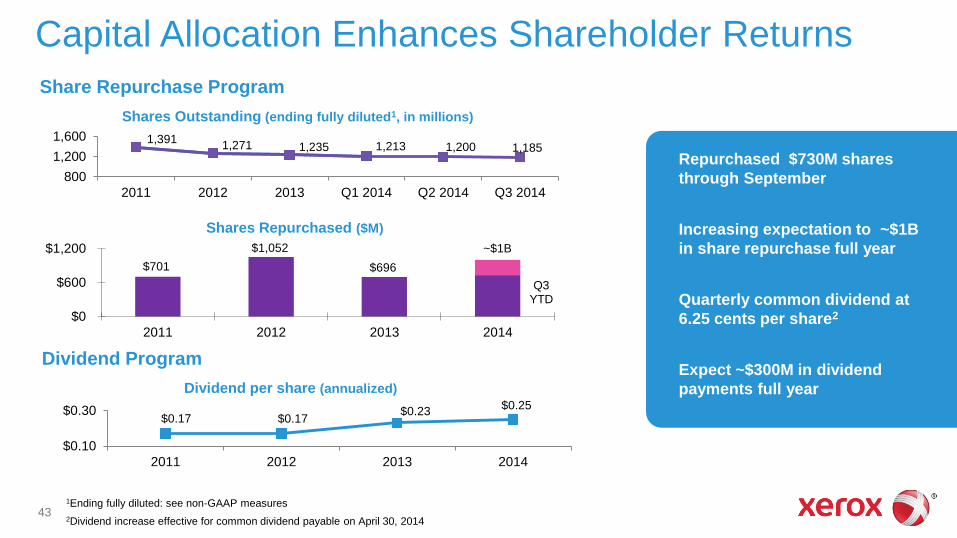

Capital Allocation Enhances Shareholder Returns

Repurchased $730M shares

through September

Increasing expectation to ~$1B

in share repurchase full year

Quarterly common dividend at

6.25 cents per share2

Expect ~$300M in dividend

payments full year

43

Share Repurchase Program

Dividend Program

1Ending fully diluted: see non-GAAP measures

2Dividend increase effective for common dividend payable on April 30, 2014

Shares Repurchased ($M)

Shares Outstanding (ending fully diluted1, in millions)

$0.17 $0.17 $0.23

$0.25

$0.10

$0.30

2011 2012 2013 2014

Dividend per share (annualized)

1,391 1,271 1,235 1,213 1,200 1,185

800

1,200

1,600

2011 2012 2013 Q1 2014 Q2 2014 Q3 2014

$701

$1,052

$696

Q3 YTD

~$1B

$0

$600

$1,200

2011 2012 2013 2014

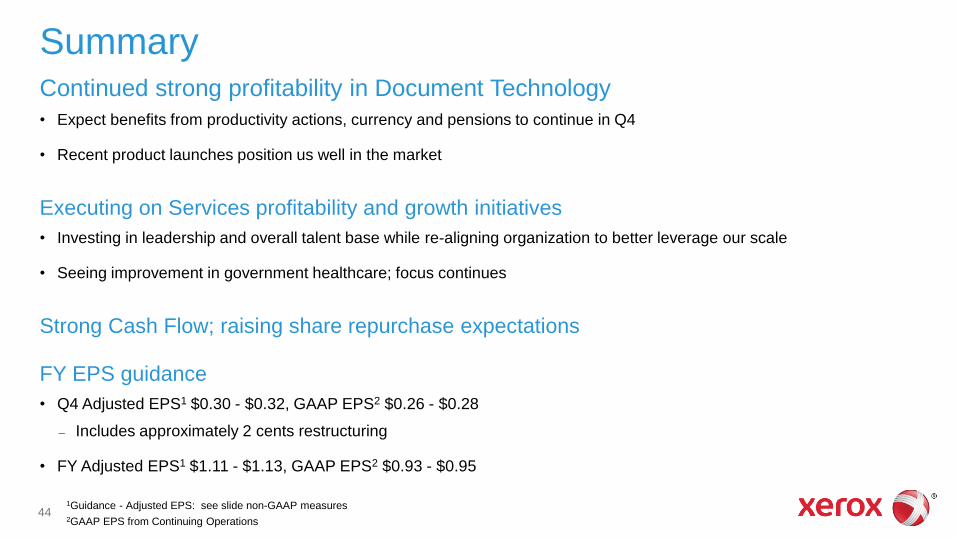

Summary Continued strong profitability in Document Technology

• Expect benefits from productivity actions, currency and pensions to continue in Q4

• Recent product launches position us well in the market

Executing on Services profitability and growth initiatives

• Investing in leadership and overall talent base while re-aligning organization to better leverage our scale

• Seeing improvement in government healthcare; focus continues

Strong Cash Flow; raising share repurchase expectations

FY EPS guidance

• Q4 Adjusted EPS1 $0.30 - $0.32, GAAP EPS2 $0.26 - $0.28

– Includes approximately 2 cents restructuring

• FY Adjusted EPS1 $1.11 - $1.13, GAAP EPS2 $0.93 - $0.95

44 1Guidance - Adjusted EPS: see slide non-GAAP measures

2GAAP EPS from Continuing Operations

Appendix

Revenue Trend

(in millions) FY Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 YTD

Total Revenue $21,634 $5,182 $5,376 $5,235 $5,548 $21,341 $5,099 $5,281 $5,120 $15,500

Growth (1)% (2)% 1% Flat (3)% (1)% (2)% (2)% (2)% (2)%

CC1 Growth Flat (2)% 1% (1)% (4)% (2)% (2)% (3)% (2)% (2)%

Annuity $18,158 $ 4,458 $4,521 $4,424 $4,579 $17,982 $4,384 $4,500 $4,372 $13,256

Growth 1% (1)% 1% Flat (3)% (1)% (2)% Flat (1)% (1)%

CC1 Growth 2% (1)% 1% (1)% (3)% (1)% (2)% Flat (1)% (2)%

Annuity % Revenue

84% 86% 84% 85% 83% 84% 86% 85% 85% 86%

Equipment $3,476 $724 $855 $811 $969 $3,359 $715 $781 $748 $2,244

Growth (10)% (11)% 1% 1% (4)% (3)% (1)% (9)% (8)% (6)%

CC1 Growth (8)% (11)% 1% Flat (5)% (4)% (2)% (9)% (8)% (7)%

2013 2012

46 1Constant currency: see slide non-GAAP measures

2014

Note: 2012, 2013, Q1 2014 and Q2 2014 are revised to remove business revenues that were reclassified to discontinued operations

Note: Xerox announced on 12/18/14 that it has entered an agreement to sell its ITO business to Atos (expected close H1 2015) and plans to report

ITO in discontinued operations with the Q4 2014 earnings. The Revenue information on this page does not reflect this pending change.

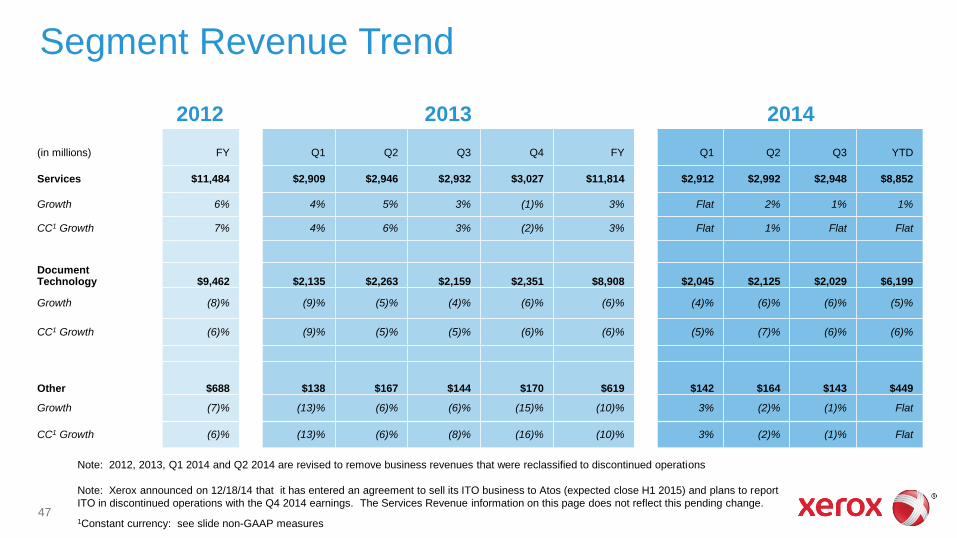

Segment Revenue Trend

(in millions) FY Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 YTD

Services $11,484 $2,909 $2,946 $2,932 $3,027 $11,814 $2,912 $2,992 $2,948 $8,852

Growth 6% 4% 5% 3% (1)% 3% Flat 2% 1% 1%

CC1 Growth 7% 4% 6% 3% (2)% 3% Flat 1% Flat Flat

Document Technology $9,462 $2,135 $2,263 $2,159 $2,351 $8,908 $2,045 $2,125 $2,029 $6,199

Growth (8)% (9)% (5)% (4)% (6)% (6)% (4)% (6)% (6)% (5)%

CC1 Growth (6)% (9)% (5)% (5)% (6)% (6)% (5)% (7)% (6)% (6)%

Other $688 $138 $167 $144 $170 $619 $142 $164 $143 $449

Growth (7)% (13)% (6)% (6)% (15)% (10)% 3% (2)% (1)% Flat

CC1 Growth (6)% (13)% (6)% (8)% (16)% (10)% 3% (2)% (1)% Flat

2013 2012

47

2014

1Constant currency: see slide non-GAAP measures

Note: 2012, 2013, Q1 2014 and Q2 2014 are revised to remove business revenues that were reclassified to discontinued operations

Note: Xerox announced on 12/18/14 that it has entered an agreement to sell its ITO business to Atos (expected close H1 2015) and plans to report

ITO in discontinued operations with the Q4 2014 earnings. The Services Revenue information on this page does not reflect this pending change.

Metrics Reference – Q3 YTD

Entry Installs YTD

A4 Mono MFDs (22)%

A4 Color MFDs (7)%

Color Printers (3)%

Mid-Range Installs

Mid-Range B&W MFDs (15)%

Mid-Range Color MFDs 1%

High-End Installs

High-End B&W (10)%

High-End Color1 (14)%

YTD

Business Process Outsourcing $5.5

Document Outsourcing $2.0

Information Technology Outsourcing $0.5

Total $8.0B

Signings Growth YOY (22)%

Signings Growth TTM (17)%

YTD

Digital MIF 2%

Color MIF 12%

Digital Pages (3)%

Color Pages 5%

Color Revenue (CC2) (2)%

YTD

Renewal Rate (BPO and ITO) 75%

Signings and Renewal Rate Install, MIF and Page Growth

Installs, color revenue, pages and MIF include both the Document Technology and Services segments. Color revenue and color pages reflect

revenue and pages from color capable devices. 1High-end color install growth impacted by high digital front end (DFE) sales to Fuji Xerox, High-end up 5% YTD excluding DFE’s. 48 2Constant currency: see slide non-GAAP measures

Underlying Cash Flow

49

1Represents cash that would have been collected had we not sold finance receivables. Net of collections on beneficial interest.

2Underlying OCF is reported OCF adjusted for the impacts of Finance Receivable sales: see slide non-GAAP measures

Estimated

(in millions) Q1 2014 Q2 2014 Q3 2014 FY 2014 Q1 2013 Q2 2013 Q3 2013 FY 2013

Operating Cash Flow (OCF) $286 $325 $595 $1,206 $1.8 - $2.0B ($87) $533 $961 $1,407 $2.4B

Adjustments:

Cash From F/R Sales - - - - - - - ($384) ($384) $(0.6)B

Impact from prior F/R Sales1 $123 $112 $102 $337 $0.4B $89 $58 $68 $215 $0.3B

Underlying OCF2$409 $437 $697 $1,543 $2.2 - $2.4B $2 $591 $645 $1,238 $2.1B

YTD 2014 YTD 2013

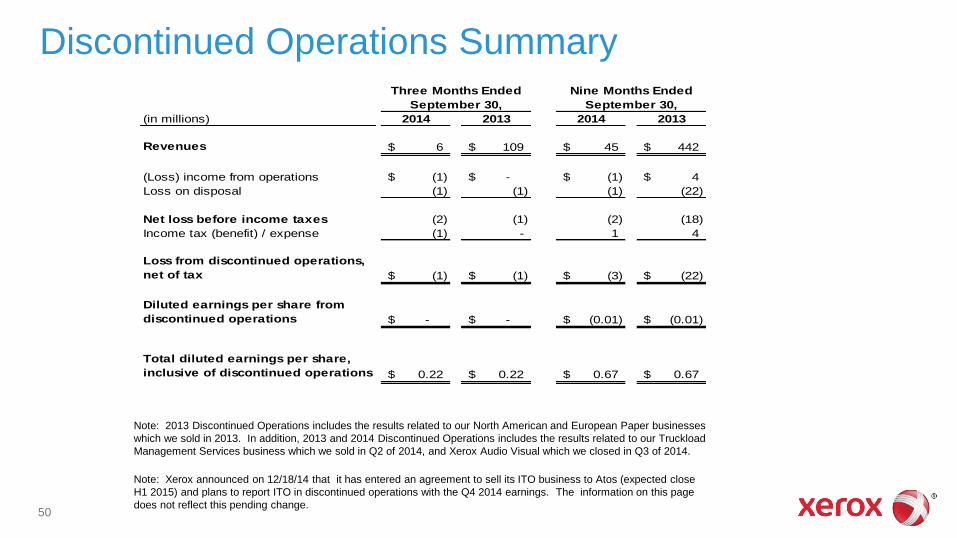

Discontinued Operations Summary

50

Note: 2013 Discontinued Operations includes the results related to our North American and European Paper businesses

which we sold in 2013. In addition, 2013 and 2014 Discontinued Operations includes the results related to our Truckload

Management Services business which we sold in Q2 of 2014, and Xerox Audio Visual which we closed in Q3 of 2014.

(in millions) 2014 2013 2014 2013

Revenues 6$ 109$ 45$ 442$

(Loss) income from operations (1)$ -$ (1)$ 4$

Loss on disposal (1) (1) (1) (22)

Net loss before income taxes (2) (1) (2) (18)

Income tax (benefit) / expense (1) - 1 4

Loss from discontinued operations,

net of tax (1)$ (1)$ (3)$ (22)$

Diluted earnings per share from

discontinued operations -$ -$ (0.01)$ (0.01)$

Total diluted earnings per share,

inclusive of discontinued operations 0.22$ 0.22$ 0.67$ 0.67$

Three Months Ended Nine Months Ended

September 30, September 30,

Note: Xerox announced on 12/18/14 that it has entered an agreement to sell its ITO business to Atos (expected close

H1 2015) and plans to report ITO in discontinued operations with the Q4 2014 earnings. The information on this page

does not reflect this pending change.

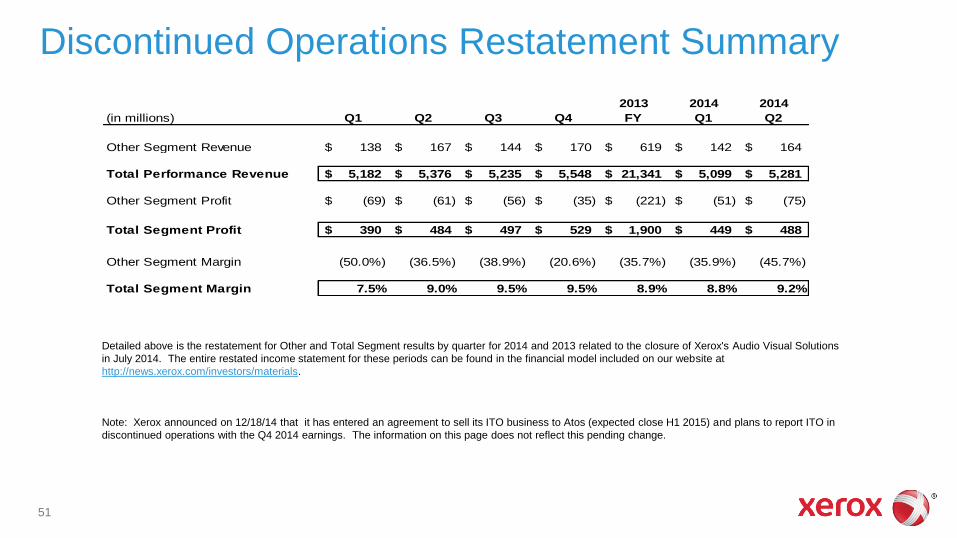

Discontinued Operations Restatement Summary

51

Detailed above is the restatement for Other and Total Segment results by quarter for 2014 and 2013 related to the closure of Xerox's Audio Visual Solutions

in July 2014. The entire restated income statement for these periods can be found in the financial model included on our website at

http://news.xerox.com/investors/materials.

2013 2014 2014

(in millions) Q1 Q2 Q3 Q4 FY Q1 Q2

Other Segment Revenue 138$ 167$ 144$ 170$ 619$ 142$ 164$

Total Performance Revenue 5,182$ 5,376$ 5,235$ 5,548$ 21,341$ 5,099$ 5,281$

Other Segment Profit (69)$ (61)$ (56)$ (35)$ (221)$ (51)$ (75)$

Total Segment Profit 390$ 484$ 497$ 529$ 1,900$ 449$ 488$

Other Segment Margin (50.0%) (36.5%) (38.9%) (20.6%) (35.7%) (35.9%) (45.7%)

Total Segment Margin 7.5% 9.0% 9.5% 9.5% 8.9% 8.8% 9.2%

Note: Xerox announced on 12/18/14 that it has entered an agreement to sell its ITO business to Atos (expected close H1 2015) and plans to report ITO in

discontinued operations with the Q4 2014 earnings. The information on this page does not reflect this pending change.

Non-GAAP Measures

53

“Adjusted Earnings Measures”: To better understand the trends in our business, we believe it is necessary to adjust the following amounts determined

in accordance with GAAP to exclude the effects of certain items as well as their related income tax effects.

• Net income and Earnings per share (“EPS”)

• Effective tax rate

In 2014 and 2013, we adjusted for the amortization of intangible assets. The amortization of intangible assets is driven by our acquisition activity which

can vary in size, nature and timing as compared to other companies within our industry and from period to period. Accordingly, due to the incomparability

of acquisition activity among companies and from period to period, we believe exclusion of the amortization associated with intangible assets acquired

through our acquisitions allows investors to better compare and understand our results. The use of intangible assets contributed to our revenues earned

during the periods presented and will contribute to our future period revenues as well. Amortization of intangible assets will recur in future periods.

We also calculate and utilize an Operating income and margin earnings measure by adjusting our pre-tax income and margin amounts to exclude certain

items. In addition to the amortization of intangible assets, operating income and margin also exclude Other expenses, net as well as Restructuring and

asset impairment charges. Other expenses, net is primarily comprised of non-financing interest expense and also includes certain other non-operating

costs and expenses. Restructuring and asset impairment charges consist of costs primarily related to severance and benefits for employees pursuant to

formal restructuring and workforce reduction plans. Such charges are expected to yield future benefits and savings with respect to our operational

performance. We exclude these amounts in order to evaluate our current and past operating performance and to better understand the expected future

trends in our business.

“Constant Currency”: To better understand trends in our business, we believe that it is helpful to adjust revenue to exclude the impact of changes in the

translation of foreign currencies into U.S. dollars. We refer to this adjusted revenue as “constant currency.” Currencies for developing market countries

(Latin America, Brazil, Middle East, India, Eurasia and Central-Eastern Europe) that we operate in are reported at actual exchange rates for both actual

and constant revenue growth rates because (1) these countries historically have had volatile currency and inflationary environments and (2) our

subsidiaries in these countries have historically taken pricing actions to mitigate the impact of inflation and devaluation. Management believes the constant

currency measure provides investors an additional perspective on revenue trends. Currency impact can be determined as the difference between actual

growth rates and constant currency growth rates.

Non-GAAP Financial Measures

54

“Free Cash Flow”: To better understand the trends in our business, we believe that it is helpful to adjust cash flows from operations to exclude amounts

for capital expenditures including internal use software. Management believes this measure gives investors an additional perspective on cash flow from

operating activities in excess of amounts required for reinvestment. It provides a measure of our ability to fund acquisitions, dividends and share

repurchase. It also is used to measure our yield on market capitalization. A reconciliation of this non-GAAP financial measure and the most directly

comparable measure calculated and presented in accordance with GAAP is set forth in the slide entitled “2014 Guidance”.

“Underlying Cash Flow”: To better understand the trends in our business, we believe that it is helpful to adjust cash flows from operations for the cash

flow impacts from our sales of finance receivables. The sale of finance receivables has a significant impact on operating cash flows in the period of sale

as well as on collections in subsequent periods due to the long term nature of these receivables. In addition to providing a better understanding of the

underlying trends in cash flows from operations, management believes this measure gives investors an additional perspective on comparing and

analyzing the year-over-year changes in our cash flows as well as the impacts of these sales on cash flows in the period. A reconciliation of this non-

GAAP financial measure and the most directly comparable measure calculated and presented in accordance with GAAP is set forth in the slide entitled

“Underlying Cash Flows”.

Management believes that these non-GAAP financial measures provide an additional means of analyzing the current periods’ results against the

corresponding prior periods’ results. However, these non-GAAP financial measures should be viewed in addition to, and not as a substitute for, the

Company’s reported results prepared in accordance with GAAP. Our non-GAAP financial measures are not meant to be considered in isolation or as a

substitute for comparable GAAP measures and should be read only in conjunction with our consolidated financial statements prepared in accordance

with GAAP. Our management regularly uses our supplemental non-GAAP financial measures internally to understand, manage and evaluate our

business and make operating decisions. These non-GAAP measures are among the primary factors management uses in planning for and forecasting

future periods. Compensation of our executives is based in part on the performance of our business based on these non-GAAP measures.

Unless otherwise noted, reconciliations of these non-GAAP financial measures and the most directly comparable measures calculated and presented in

accordance with GAAP are set forth on the following slides.

Non-GAAP Financial Measures

55

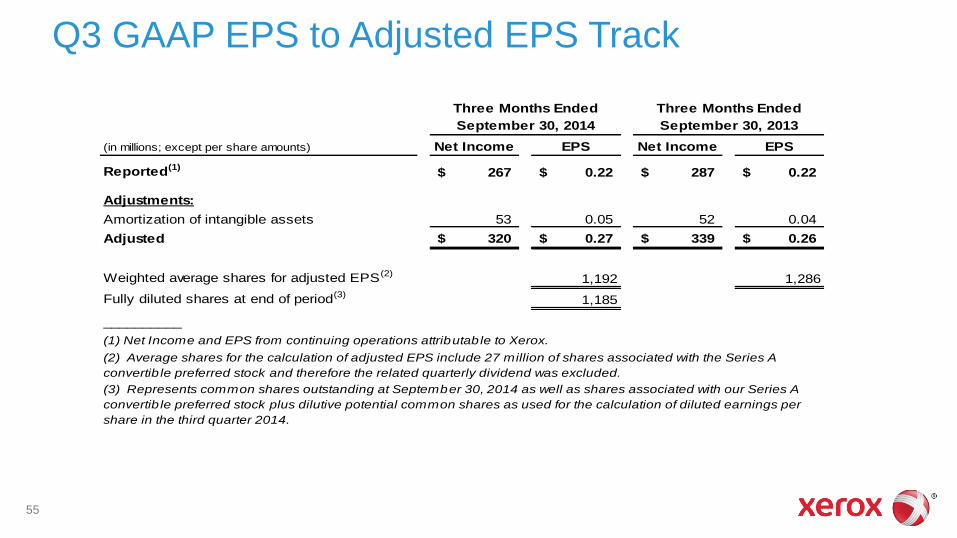

Q3 GAAP EPS to Adjusted EPS Track

(in millions; except per share amounts) Net Income EPS Net Income EPS

Reported(1)267$ 0.22$ 287$ 0.22$

Adjustments:

Amortization of intangible assets 53 0.05 52 0.04

Adjusted 320$ 0.27$ 339$ 0.26$

Weighted average shares for adjusted EPS(2)1,192 1,286

Fully diluted shares at end of period(3)1,185

__________

(1) Net Income and EPS from continuing operations attributable to Xerox.

(2) Average shares for the calculation of adjusted EPS include 27 million of shares associated with the Series A

convertib le preferred stock and therefore the related quarterly dividend was excluded.

(3) Represents common shares outstanding at September 30, 2014 as well as shares associated with our Series A

convertib le preferred stock plus dilutive potential common shares as used for the calculation of diluted earnings per

share in the third quarter 2014.

Three Months Ended Three Months Ended

September 30, 2014 September 30, 2013

56

GAAP EPS to Adjusted EPS Guidance Track

Q4 2014 FY 2014

GAAP EPS from Continuing Operations $0.26 - $0.28 $0.93 - $0.95

Adjustments:

Amortization of intangible assets 0.04 0.18

Adjusted EPS $0.30 - $0.32 $1.11 - $1.13

Note: GAAP and Adjusted EPS guidance includes anticipated restructuring

Earnings Per Share Guidance

57

Q3 Adjusted Operating Income/Margin

(in millions) Profit Revenue Margin Profit Revenue Margin

Reported pre-tax income (1)300$ 5,120$ 5.9% 334$ 5,235$ 6.4%

Adjustments:

Amortization of intangible assets 85 83

Xerox restructuring charge 28 35

Other expenses, net 73 38

Adjusted Operating Income/Margin 486$ 5,120$ 9.5% 490$ 5,235$ 9.4%

_______________

(1) Profit and Revenue from continuing operations attributable to Xerox.

September 30, 2014 September 30, 2013

Three Months Ended Three Months Ended

58

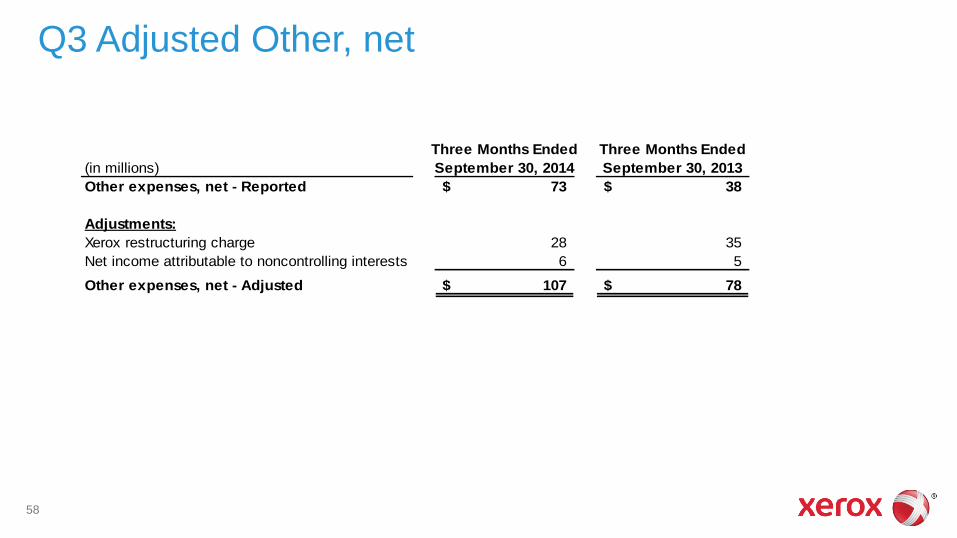

Q3 Adjusted Other, net

Three Months Ended Three Months Ended

(in millions) September 30, 2014 September 30, 2013

Other expenses, net - Reported 73$ 38$

Adjustments:

Xerox restructuring charge 28 35

Net income attributable to noncontrolling interests 6 5

Other expenses, net - Adjusted 107$ 78$

59

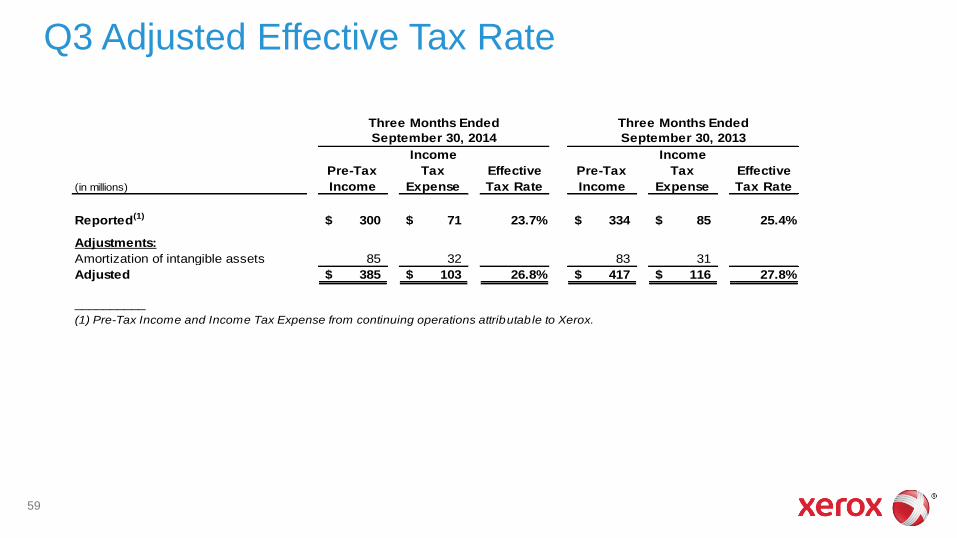

Q3 Adjusted Effective Tax Rate

(in millions)

Pre-Tax

Income

Income

Tax

Expense

Effective

Tax Rate

Pre-Tax

Income

Income

Tax

Expense

Effective

Tax Rate

Reported(1) 300$ 71$ 23.7% 334$ 85$ 25.4%

Adjustments:

Amortization of intangible assets 85 32 83 31

Adjusted 385$ 103$ 26.8% 417$ 116$ 27.8%

__________

Three Months Ended Three Months Ended

September 30, 2014 September 30, 2013

(1) Pre-Tax Income and Income Tax Expense from continuing operations attributable to Xerox.

60

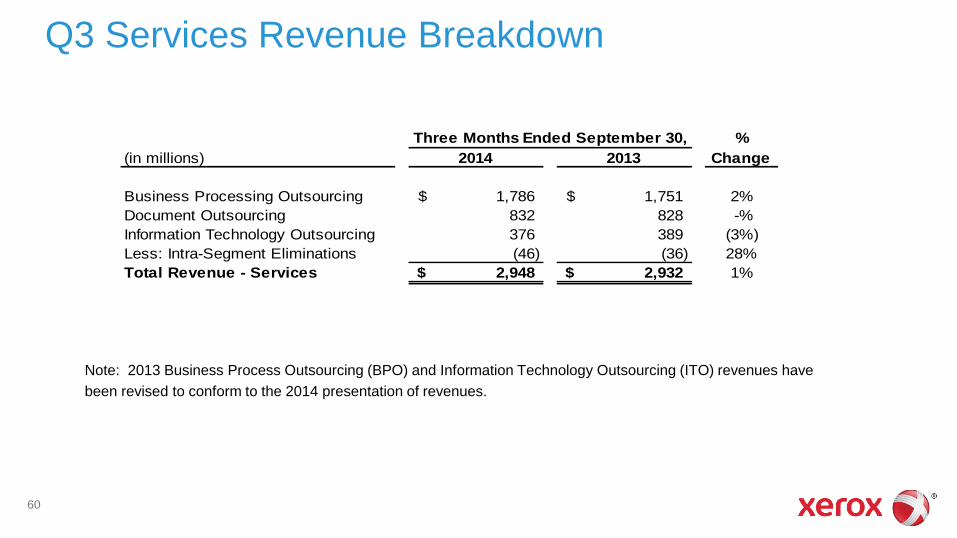

Q3 Services Revenue Breakdown

Note: 2013 Business Process Outsourcing (BPO) and Information Technology Outsourcing (ITO) revenues have

been revised to conform to the 2014 presentation of revenues.

%

(in millions) 2014 2013 Change

Business Processing Outsourcing 1,786$ 1,751$ 2%

Document Outsourcing 832 828 -%

Information Technology Outsourcing 376 389 (3%)

Less: Intra-Segment Eliminations (46) (36) 28%

Total Revenue - Services 2,948$ 2,932$ 1%

Three Months Ended September 30,

©2014 Xerox Corporation. All rights reserved. Xerox® and Xerox Design® are trademarks of Xerox Corporation in the United States and/or other countries.