ware youth center -...

TRANSCRIPT

WARE YOUTH CENTER COUSHATTA, LOUISIANA

FINANCIAL STATEMENTS FOR THE YEAR ENDED

JUNE 30.2015

liiSAi Postlethwaite &Netterville

A Professional Accounting Corporation

www.pncpa.com

TABLE OF CONTENTS

PAGE

INDEPENDENT AUDITORS' REPORT 1-2

MANAGEMENT'S DISCUSSION AND ANALYSIS 3-7

FINANCIAL STATEMENTS

Statement of Net Position 8

Statement of Activities 9

Balance Sheet - Governmental Fund 10

Reconciliation of the Governmental Fund Balance Sheet to the Statement of Net Position 11

Statement of Revenues, Expenditures, and Changes in Fund Balances -Governmental Fund 12

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of the Governmental Fimd to the Statement of Acti vities 13

Notes to the Financial Statements 14 - 30

REQUIRED SUPPLEMENTARY INFORMATION

Schedule of Revenues, Expenditures, and Changes in Fund Balances of the Governmental Fund - Budget (GAAP Basis) and Actual 31

Schedule of Proportionate Share of Net Pension Liability 32

Schedule of Employer Contributions 3 3

OTHER SUPPLEMENTARY INFORMATION

Schedule of Compensation, Benefits and Other Payments to Executive Director 34

OTHER REPORTING REQUIRED BY GOVERNMENT AUDITING STANDARDS

Independent Auditors' Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government A uditing Standards 35-36

Schedule of Findings and Questioned Costs 3 7

Summary Schedule of Prior Audit Findings 3 8

iij8i3|i Postlethwaite & Netterville

A Professional Accounting Corporation Associated Offices in Principal Cities of the United States

www.pncpa.com

INDEPENDENT AUDITORS' REPORT

Board of Commissioners Ware Youth Center Coushatta, Louisiana 71019

We have audited the accompanying financial statements of the governmental activities and the major fund of the Ware Youth Center, Louisiana (the Center), as of and for the year ended June 30,2015, and the related notes to the financial statements, which collectively comprise the Center's basic financial statements as listed in the table of contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free fi"om material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating tlie overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities and the major fund of the Center, as of June 30, 2015, and the respective changes in financial position for the year then ended in accordance with accounting principles generally accepted in the United States of America.

-1 -

8550UnitedPlazaBlvd, Suite 1001 • Baton Rouge, LA 70809 • Tel: 225.922.4600 • Fox: 225.922.4611

Other Matters

Accounting principles generally accepted in the United States of America require that the management's discussion and analysis, the budgetary comparison information, the Schedules of Proportionate Share of the Net Pension Liability and the Schedule of the Employer Contributions on pages 3 to 7, 31, 32 and 33, respectively, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management's responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the basic financial statements of the Center. The accompanying Schedule of Compensation, Benefits and Other Payments to the Executive Director on page 34 is presented for the purpose of additional analysis and is not a required part of the basic financial statements.

The Schedule of Compensation, Benefits and Other Payments to the Executive Director is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, this schedule is fairly stated, in all material respects, in relation to the basic financial statements as a whole.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated September 28, 2015 on our consideration of the Center's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Center's internal control over financial reporting and compliance.

September 28, 2015

-2-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

MANAGEMENT'S DISCUSSION AND ANALYSIS JUNE 30,2015

The Management's Discussion and Analysis of the Ware Youth Center's (the Center's) financial performance presents a narrative overview and analysis of the Center's financial activities for the year ended June 30, 2015. This document focuses on the current year's activities, resulting changes, and currently known facts. Please read this document in conjunction with the Center's financial statements, which begin on page 8.

FINANCIAL HIGHLIGHTS

• Revenues exceeded expenses by approximately $652,000 for the year as compared to the prior year when expenses exceeded revenues by approximately $406,000. This improvement was the result of an increase in revenue because of a slight increase in group-home and residential contract rates, combined with a reduction in pension expense attributable to a significant change in the accounting principal as described in footnote 1 to the financial statements, page 18.

• The fund level fmancial statements (see description on page 4) report fund balance of approximately $535,000, an increase of approximately $410,000 from the prior year. This level of fimd balance equals 6.8% of annual expenditures.

OVERVIEW OF THE FINANCIAL STATEMENTS

The following graphic illustrates the minimum requirements for the Center as established by Governmental Accounting Standards Board Statement 34, Basic Financial Statements-and Management's Discussion and Analysis-far State and Local Governments.

These financial statements consist of three sections - Management's Discussion and Analysis (this section), the basic financial statements (including the notes to the fmancial statements), and required supplementary information.

Basic Financial Statements

Government-Wide Financial Statements This annual report consists of a series of financial statements. The Statement of Net Position and the Statement of Activities (on page 8 and 9) provide information about the activities of the Center as a whole and present a longer-term view of the Center's finances. These statements include all assets and liabilities using the accrual basis of accounting, which is similar to the accounting used by most private-sector companies. All of the current year's revenues and expenses are taken into account regardless of when cash is received or paid.

-3-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

MANAGEMENTS DISCUSSION AND ANALYSIS JUNE 30,2015

OVERVIEW OF THE FINANCIAL STATEMENTS (continued)

The Statement of Net Position and the Statement of Activities report the Center's net position and changes in them. The Center's net position, the difference between assets plus deferred outflows, and liabilities plus deferred inflows, is one way to measure the Center's financial health, or financial position. Over time, increases or decreases in the Center's net position are one indicator of whether its financial health is improving or deteriorating.

Fund Financial Statements Fund financial statements start on page 10. The Center utilizes only one fund, its general fund, which is considered to be a governmental fund type. All of the Center's basic services are reported in governmental funds, which focus on how money flows into and out of those funds and the balances left at year end that are available for spending. These funds are reported using an accounting method called modified accrual accounting, which measures cash and all other financial assets that can readily be converted to cash. The governmental fund statements provide a detailed short term view of the Center's general government operations and the basic services it provides. Governmental fund information helps you determine whether there are more or fewer financial resources that can be spent in the near future to finance the Center's activities as well as what remains for future spending.

FINANCIAL ANALYSIS OF THE ENTITY

Statements of Net Position As of Year End

Assets Current and other assets Capital assets, net

Total Assets

Deferred Outflows of Resources

Liabilities Current liabilities Compensated absences payable Net pension liability

Total Liabilities

Deferred Inflows of Resources

Net position Net investment in capital assets Unrestricted

Total Net Position

2015 (Restated)

2014

$ 1,002,203 $ 536,024 10.221.103 10.583.400 11.223.306 11.119.424

1.121.369 1.028.645

467,560 411,327 208,030 206,887

10.156.045 12.803.902 10.831.635 13.422.116

2.135.587 .

10,221,103 10,583,400 riO.843.6501 111.857.4471

$ 1622.5471 S 11.274.0471

-4-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

MANAGEMENT'S DISCUSSION AND ANALYSIS JUNE 30,2015

FINANCIAL ANALYSIS OF THE ENTITY (continued)

Net position of the Center increased by $651,500, or 51% from the previous fiscal year. The increase is the result of revenues exceeding expenses during the fiscal year ended 2015 (See table below).

Statements of Activities For the Year Ended

2015 2014 Program revenues

Charges for services $ 910,743 $ 897,238 Operating and capital grants and contributions 6,886,739 6,619,654

Expenses Public safety (•7.583.0851 (8,299,375)

Subtotal (214,397) (782,483)

General revenues 437.103 376.104 Change in net position (after re-statement of beginning net position) $ 651.500 $ f406.379I

The Center's total revenues increased by approximately $340,000 or 5% from the previous year. The total cost of all programs and services decreased by approximately $716,000 from the previous year. The favorable trend in revenues is due primarily to increased contract rates for group home and residential residents. The reduction reported in expenses is primarily due to the implementation of new accounting standards which changed the way pension costs are recognized. See the explanation of the current year adoption of Governmental Accounting Standards Board Statement No. 68 within the New Accounting Standards Section of footnote 1 to the financial statements.

CAPITAL ASSET AND DEBT ADMINISTRATION

Capital Assets

At the end of 2015, the Center had $10,221,103, net of accumulated depreciation, invested in a broad range of capital assets (See table below). This amount represents a net decrease (including additions and retirements) of $362,297 or 3.42% from the previous year and is attributable primarily to depreciation expense.

Capital Assets at Year End (Net of Accumulated Depreciation)

Land Buildings and building improvements Automobiles and equipment

Total

2015 2014 $ 175,017 $ 175,017

9,785,230 10,155,027 260.856 253.356

$ 10.221.103 $ 10.583.400

-5-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

MANAGEMENT'S DISCUSSION AND ANALYSIS JUNE 30,2015

CAPITAL ASSET AND DEBT ADMINISTRATION (continued)

Long Term Liability

The Center had $208,030 in compensated absences payable (annual leave) at year end compared to $206,887 at the previous year end, an increase of $1,143 or .5%. In accordance with a new accounting standard, the Center recorded pension liabilities of $10,156,045 and $12,803,902 as of June 30, 2015 and 2014, respectively. This liability represents the Center's proportionate share of the Net Pension Liabilities of the Louisiana State Employees Retirement System (LASERS) and the Teachers Retirement System of Louisiana (TRSL). Long term liabilities are summarized below:

Outstanding Long-term Liabilities at Year End

2015 2014 Compensated absences payable $ 208,030 $ 206,887 Pension liability 10.156.045 12.803.902 Totals $ 10.364.075 $ 13.010.789

There were no borrowings undertaken during the year.

VARIATIONS BETWEEN ORIGINAL AND FINAL BUDGETS

Actual revenues were consistent with the final budget, coming in approximately $200,000 more than the budgeted amounts.

Actual expenditures were consistent with the final budget, coming in approximately $209,000 less than the budgeted amounts.

The original budget was not amended during the year.

ECONOMIC FACTORS AND NEXT YEAR'S BUDGET

The Center's elected and appointed officials considered the following factors and indicators when setting next year's budget, rates, and fees. These factors and indicators include;

1) Intergovernmental revenues 2) Charges for services 3) Interest income

The Ware Youth Center does not expect any significant changes in next year's budget as compared to the current year.

-6-

WARE YOITTH CENTER COUSHATTA, LOUISIANA

MANAGEMENT'S DISCUSSION AND ANALYSIS JUNE 30,2015

CONTACTING THE WARE YOUTH CENTER'S MANAGEMENT

This financial report is designed to provide our citizens, taxpayers, customers, investors and creditors with a general overview of the Center's finances and to show the Center's accountability for the money it receives. If you have questions about this report or need additional financial information, contact Kenneth Loftin, Executive Director, Rt. 1 Box 6000, Coushatta, Louisiana 71019.

-7-

WARE YOUTH CENTER

COUSHATTA. LOUISIANA STATEMENT OF NET POSITION

JUNE 30.2015

2015 ASSETS Current Assets

Cash and cash equivalents Accounts receivable, net Prepaid Expenses

Noncurrent Assets Capital Assets, net Utility Deposits

Total Assets

DEFERRED OUTFLOWS OF RESOURCES Deferred amounts related to pension liability

Total deferred outflows of resources

LIABnJTIES Current Liabilities

Accounts payable and accruals Non-current Liabilites

Compensated absences payable Net pension liability

Total Liabilities

$ 606,381 333,685

61,382

10,221,103 755

11,223,306

1,121,369

1,121,369

467,560

208,030 10,156,045

10,831,635

DEFERRED INFLOWS OF RESOURCES Deferred amounts related to pension liability

Total deferred outflows of resources

NET POSITION Net investment in capital assets Unrestricted (deficit)

Total Net Position

2,135,587

2,135,587

10,221,103 (10,843,650)

$ (622,547)

The accompanying notes are an integral part of these financial statements.

-8-

WARE YOUTH CENTER

COUSHATTA. LOUISIANA STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30.2015

Program Revenues

Expenses Charges for

Services

Operating Grants and

Contributions

Capital Grants and

Contributions Function/Program Activities Governmental Activities: Public Safety

General Revenues Fines, forefeitures and fees Interest and Investment Income Royalties and leases Miscellaneous

Total General Revenues

Change in Net Position

Net Position, Begirming of Year (Restated)

Net Position, End of Year

$ 7,583,085 $ 910,743 $ 6,886,739 $

Net (Expense) Revenue and

Changes in Net Position

214,397

323,666 118

20,494 92,825

437,103

651,500

(1,274,047)

$ (622,547)

The accompanying notes are an integral part of these financial statements.

-9-

WARE YOUTH CENTER COUSHATTA. LOUISIANA GOVERNMENTAL FUND

BALANCE SHEET JUNE 30.2015

2015

ASSETS Cash and cash equivalents $ 606,381 Accounts Receivable 333,685 Prepaid Expenses 61,3 82 Utility Deposit 755

Total Assets $ 1,002,203

LIABILITIES AND FUND BALANCE Accounts payable and accruals $ 467,560

Total Liabilities 467,560

FUND BALANCES Nonspendable

Prepaid Expenses 61,3 82 Utility Deposits 755

Unassigned 472,506 Total Fund Balances 534,643

Total Liabilities and Fund Balances $ 1,002,203

The accompanying notes are an integral part of these financial statements.

-10-

WARE YOUTH CENTER COUSHATTA. LOUISIANA

RECONCILIATION OF THE GOVERNMENTAL FUND BALANCE SHEET TO THE STATEMENT OF NET POSITION

JUNE 30.2015

Total Fund Balances for Governmental Funds $ 534,643

Amounts reported to governmental activities in the statement of net position are different because;

Capital assets used in governmental activities are not financial resources and therefore are not reported in the funds. These assets consist of:

Land $ 175,017 Buildings and building improvements, net of $4,504,886 in accumulated depreciation 9,785,230 Automobiles and equipment, net of $589,978 in accumulated depreciation 260,856

Total Capital Assets 10,221,103

The government-wide financial statements must accrue expenses as the obligation is incurred, whereas governmental funds do not recognize an expense or liability for long-term liabilities until they are due. These liabilities consist of:

Compensated absences payable $ (208,030) Net pension liability (10,156,045)

(10,364,075) Deferred outflows of resources represent the consumption of net position that applies to a future period and will not be recognized as an outflow of resources on the government-wide financial statements until then. Deferred inflows of resources represent the acquisition of net position that applies to a future period and will not be recognized as an inflow of resources on the government-wide financial statements until then. A cost-sharing employer is required to recognize pension expense and report deferred outflows of resources and deferred inflows of resources related to pensions for its proportionate shares of collective pension expense and collective deferred outflows of resources and deferred inflows of resources related to pensions. These deferrals consist of:

Deferred pension contributions $ 1,121,369 Deferred amounts related to changes in net pension liability (2,135,587)

(1,014,218)

Total Net Position of Governmental Activities $ (622,547)

The accompanying notes are an integral part of these financial statements.

-11 -

WARE YOUTH CENTER COUSHATTA. LOUISIANA

STATEMENT OF REVENUES. EXPENDITURES. AND CHANGES IN FUND GOVERNMENTAL FEND

FOR THE YEAR ENDED JUNE 30 2015

REVENUES Intergovernmental Charges for Services Fines, forfeitures and fees Interest and Investment Income Royalties and Leases Miscellaneous

Total Revenues

2015 6,885,391 910,743 323,666

118 20,494 92,825

8,233,237

EXPENDITURES Personal Services Travel Operating Services Supplies Professional Services Capital Outlay

Total Expenditures

5,814,771 12,205

930,699 757,436 198,666 109,514

7,823,291

Excess of Revenues over Expenditures 409,946

Fund Balance, Beginning of Year 124,697

Fund Balance, End of Year $ 534,643

The accompanying notes are an integral part of these statements.

-12-

WARE YOUTH CENTER COUSHATTA. LOUISIANA

RECONCILIATION OF THE STATEMENT OF REVENUES. EXPENDITURES. AND CHANGES IN FUND BALANCE OF THE GOVERNMENTAL

FUND TO THE STATEMENT OF ACTIVITIES

Net Change in Fund Balance- Total Governmental Funds $ 409,946

Amounts reported for govermnental activites in the statement of activities are different because:

Governmental funds report capital outlays as expenditures. However, in the statement of activites the cost of those assets is allocated over their estimated useful lives and reported as depreciation expense. This is the amount by which depreciation ($471,812) exceeds capital outlays ($109,514) in the current period. (362,298)

Some expenses reported in the statement of activities, such as compensated absences, do not require the use of current financial resources and therefore are not reported as expenditures in governmental funds. (1,142)

In the government-wide financial statements, a cost-sharing employer is required to recognize an allocated portion of pension expense and amortization of deferred outflows of resources and deferred inflows of resources of the pension plans in which it participates. The expense reflects benefits being earned rather than contributions paid to the plan. The fund financial statements recognize pension costs based on funding obligations and when the contributions are due. The difference is reflected as a reduction of expense. 604,994

Change in Net Position of Governmental Activities $ 651,500

The accompanying notes are an integral part of these statements.

-13-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POT JCIES

The Ware Youth Center (the Center) was created by Act 833 of the 1986 Legislature, which enacted Part XI-A of Chapter 7 of Title 15 of the Louisiana Revised Statutes of 1950 to be comprised of RS. 15: 1097 through 1097.5 to establish and provide for the purposes and functions of the Ware Youth Center for the parishes of Bienville, Claiborne, DeSoto, Natchitoches, Red River, Sabine, and Webster. The Center's funding is provided by enabling legislation, which grants the power to levy taxes, incur debt and issue bonds, and by RS. 15: 1095.6, which provides for the imposition of court costs in certain juvenile and criminal proceedings in all courts within the area of its jurisdiction. Act 147 of the 1991 Legislature amended and reenacted RS. 15: 1097 through 1097.2 and enacted Subpart G of Part XI of Chapter 7 of Title 15 of the Louisiana Revised Statutes of 1950, comprised of RS. 15: 1099.1 through 1099.7 which authorized any parish governing authority having a youth center and any juvenile detention authority to enter into a lease or lease-purchase contract for construction, operation, and maintenance of a youth center within the parish and authorized other parishes to enter into participation agreements with a parish having a youth center to sublease space and house juveniles at the center.

Act 147 amended the territorial jurisdiction of the Ware Youth Center to include the parishes of Claiborne, DeSoto, Natchitoches, Red River, Sabine, and Webster. However, Act 147 allowed Bienville and Claiborne Parishes to withdraw from membership and participation in the Center during the period beginning September 1, 1991 and ending December 31, 1991. These parishes elected to withdraw from participation in the Center. At June 30, 2014, the parishes of DeSoto, Natchitoches, Red River, Sabine and Webster were included in the territorial jurisdiction of the Ware Youth Center.

The purpose of the Center is to assist and afford opportunities to pre-adjudicatoiy and post-adjudicatory children who enter the juvenile justice system to become productive, law-abiding citizens of the community, parish, and state by the establishment of rehabilitative programs within a structured environment and to provide physical facilities and related services for children throughout the parishes belonging to the Center including the housing, care, supervision, maintenance, and education of juveniles under the age of seventeen years, and for juveniles seventeen years of age and over who were under seventeen years of age when they committed an alleged offense.

Basis of Presentation

The accompanying financial statements have been prepared in accordance with accoimting principles generally accepted in the United States of America as prescribed by the Governmental Accounting Standards Board (GASB). These principles are found in the Codification of Governmental Accomting and Financial Reporting Standards, published by the GASB. GASB is the accepted standard setting body for establishing governmental accounting principles and reporting standards that are generally accepted in the United States of America.

The Center's basic financial statements consist of the government-wide statements and the fund financial statements.

Government-wide Financial Statements

The government-wide financial statements consist of the Statement of Net Position and the Statement of Activities and are reported using the economic resources measurement focus and the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows.

-14-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

1. STJMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued!

Fund Financial Statements

Governmental Fund:

The governmental fund financial statements (the Fund Balance Sheet and Statement of Revenues, Expenditures and Changes in Fund Balance) are presented using the current financial resources measurement focus and the modified accrual basis of accounting. Under the modified accrual basis of accounting, revenues are recognized when they become measurable and available to fund current operations. The Center considers all revenues reported in the governmental funds to be available if the revenues are collected within sixty days after year-end. Expenditures are recognized when the related fund liability is incurred, except for principal and interest on long-term debt which is recognized when due.

The governmental fund financial statements provide information about the Center's governmental fimd. The emphasis of fimd financial statements is on the major governmental funds. As of June 30, 2015 the Center had one major governmental fund as follows:

• General fund - accounts for the general operations of the Center that are funded through unrestricted funding sources. The General Fund is always a major fimd.

Budgetarv Accounting

Formal budgetary accounting is employed as a management control. The Center prepares and adopts a budget prior to July 1 of each year for its general fimd in accordance with Louisiana Revised Statutes. The operating budget is prepared based on prior years ' revenues and expenditures and the estimated increase therein for the current year, using the modified accrual basis of accounting. The Ware Youth Center amends its budget when projected revenues are expected to be less than budgeted revenues by five percent or more and/or projected expenditures are expected to be more than budgeted amounts by five percent or more. All budget appropriations lapse at year end.

Cash and Cash Equivalents

Cash and cash equivalents are considered to be cash on hand, demand deposits, interest bearing demand deposits, and short-term investments with original maturities of three months or less from the date of acquisition.

Investments

Investments are limited by Louisiana Revised Statute and the Ware Youth Center's investment policy. Under state law, the Center may invest in obligations of the U. S. Treasuiy and U. S. Agencies, or certificates of deposit, certain corporate bonds, and other high grade debt securities. Investments are carried at fair market value as of the balance sheet date.

Receivables

All receivables are reported at their gross value and, where applicable, are reduced by the estimated portion that is expected to be uncollectible.

- 15-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30, 2015

1- SUMMARY OF SIGNIFICANT ACCOUNTING POETCTES fcontinuedl

Bad Debts

Uncollectible accounts receivable are recognized as bad debts through the establishment of an allowance account at the time information becomes available which would indicate the uncollectibility of the particular receivable. At June 30,2014, $0 was considered to be uncollectible.

Capital Assets

Capital assets are carried at historical costs. Depreciation of all exhaustible capital assets used by the Center is charged as an expense against operations in the Statement of Activities. Capital assets net of accumulated depreciation are reported on the Statement of Net Position. Depreciation is computed using the straight line method over the estimated useful life of the assets, generally 20 to 40 years for buildings and building improvements and 5 to 10 years for moveable property. Expenditures for maintenance, repairs and minor renewals are charged to earnings as incurred. Major expenditures for renewals and betterments are capitalized.

Compensated Absences

The Center employees earn annual leave at various rates depending on the number of years in service. The maximum amount of annual leave that may be accumulated by each employee is 160 hours. Upon termination, an employee is compensated for up to 160 hours of unused annual leave at the employee's hourly rate of pay at the time of termination.

Restricted Net Position

In the government-wide financial statements, equity is classified as net position and displayed in three components:

1. Net investment in capital assets - consists of capital assets including restricted capital assets, net of accumulated depreciation and reduced by the outstanding balances of any bonds, mortgages, notes, or other borrowings that are attributed to the acquisition, construction, or improvement of those assets.

2. Restricted net position - net position with constraints placed on the use either by a) external groups such as creditors, grantors, contributors, or laws or regulations of other governments; or b) law through constitutional provisions or enabling legislation.

3. Unrestricted - all other net position is reported in this category.

-16-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

1- SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continuedl

Fund Balance

In the fund financial statements, governmental fund equity is classified as fund balance and displayed in five components:

1. Nonspendable - amounts that cannot be spent either because they are in nonspendable form or because they are legally or contractually required to be maintained intact.

2. Restricted - amounts constrained to specific purposes by either a) creditors, grantors, contributors, or the laws or regulations of other governments, or b) constitutional provisions or enabling legislation.

3. Committed - amounts constrained to specific purposes by the governmental entity at its highest level of decision-making authority (Board of Commissioners). These amounts cannot be used for any other purposes unless the government takes the same highest level action to remove or change the constraint.

4. Assigned - amounts that do not meet the criteria to be classified as restricted or committed that are intended to be used for specific purposes as established by the Board of Commissioners or its management to which the Board of Commissioners has delegated the authority to assign amounts for specific purposes.

5. Unassigned - all other spendable amounts.

The Board of Commissioners establishes (and modifies or rescinds) fund balance commitments and assignments by passage of an ordinance or resolution.

The Center typically uses restricted fund balances first, followed by committed, assigned and unassigned funds when an expenditure is incurred for purposes for which amounts in any of these fund balance classifications could be used.

Deferred Outflows/Inflows of Resources

The statement of financial position reports a separate section for deferred outflows and (or) deferred inflows of financial resources. Deferred outflows of resources, represents a consumption of net position that applies to a future period(s) and so will not be recognized as an outflow of resources (expense^xpenditure) until then. Deferred inflows of resources represents an acquisition of net position that applies to a future period(s) and so will not be recognized as an inflow of resources until that time.

Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

-17-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES rcontinuedJ

Pension Plans

The Ware Youth Center is a participating employer in two defined benefit pension plans (plans) as described in Note 6. For purposes of measuring the Net Pension Liability, deferred outflows of resources and deferred inflows of resources related to pensions, and pension expense, information about the fiduciary net position of each of the plan, and additions to/deductions from each plans' fiduciary net position have been determined on the same basis as they are reported by each of the plans. For this purpose, benefit payments (including refunds of employee contributions) are recognized when due and payable in accordance with the benefit terms. Investments have been reported at fair value within each plan.

Current Year Adoption of New Accounting Standard and Restatement of Net Position

The Ware Youth Center adopted Government Accoimting Standards Board (GASB) Statement Number 68 -Accomting and Financial Reporting for Pensions - an amendment of GASB Statement No. 27, and Statement Number 71 - Pension Transition for Contributions Made Subsequent to the Measurement Date - an amendment of GASB Statement No. 68. Because these pronovmcements were required to be implemented retroactively, all prior periods presented have been restated. The net effect to the entity-wide Statement of Net Position for the prior year that resulted from the adoption of GASBs 68 and 71 is as follows:

Governmental Activities

Total Net Position, June 30,2014 as previously reported $ 10,501,210

Net Pension Liability at June 30, 2014 (12,803,902)

Deferred Outflow of Resources 1,028,645

Total Net Position, June 30,2014, Restated $ (1,274,047)

-18-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

2. DEPOSITS WITH FINANCIAL INSTITUTIONS AND INVESTMENTS

Cash and cash equivalents include demand deposits at local financial institutions with a canying value of $274,851 at June 30,2015. Deposits in financial institutions can be exposed to custodial credit risk. Custodial credit risk is the risk that in the event of a financial institution failure, the Center's deposits may not be returned to them. To mitigate this risk, state law requires deposits to be secured by federal deposit insurance or the pledge of securities owned by the fiscal agent financial institution. As of June 30,2015, the Center's bank balance of these deposits was fully collateralized through FDIC insurance as well as bank owned securities pledged on behalf of the Center, and therefore was not exposed to custodial credit risk.

Cash and cash equivalents also include investments in the Louisiana Asset Management Pool (LAMP), a local government investment pool in the amount of $331,635. LAMP is administered by LAMP, Inc., which is a nonprofit corporation organized under the laws of the State of Louisiana which was formed by an initiative of the State Treasurer, representatives from various organizations of local government, the Government Finance Officers Association of Louisiana, and the Society of Louisiana CPA's. Only local governments having contracted to participate in LAMP have an investment interest in its pool of assets. The primary objective of LAMP is to provide a safe environment for the placement of public funds in short-term, high quality investments. LAMP investments are restricted to securities issued, guaranteed, or backed by the U.S. Treasury, the U.S. government or one of its agencies, enterprises, or instrumentalities, as well as repurchase agreements collateralized by those securities. The dollar weighted average portfolio maturity of LAMP assets is restricted to not more than 90 days, and consists of no securities with maturity in excess of 397 days. LAMP is designed to be highly liquid to give its participants immediate access to their account balances.

This investment pool has not been assigned a custodial risk category since the Center has not issued securities, but rather owns an undivided beneficial interest in the assets of this pool.

Credit Risk. The state investment pool (LAMP) operates in accordance with state laws and regulations. The Center's investment in LAMP was rated AAAm by Standard & Poor's.

3. ACCOUNTS RECEIVABLE

The following is a summary of accounts receivable by type of entity at Jime 30, 2015:

State of Louisiana $ 50,965 Police Juries and other local governments 278,776 Other 3.944

Total S 333.685

- 19-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

4. CAPITAL ASSETS

A summary of Ware Youth Center's capital assets at June 30, 2015 follows:

Capital Assets, not depreciated Land Total Capital Assets, not depreciated

Capital Assets, being depreciated Buildings and building improvements

Less accumulated depreciation Total buildings and building improvements

Automobiles and equipment Less accumulated depreciation:

Total automobiles and equipment

Total Capital Assets being depreciated

Total Capital Assets, net

Balance Balance June 30.2014 Additions Retirements June 30.2015

$ 175.017 $ - S - $ 175.017 175,017 175,017

14,263,147 26,969 14,290,116 14.108.1201 G96.7761 14.504.8861 10,155,027 (369,797) 9,785,230

881,045 82,536 (103,747) 859,834 1627.6891 175.0361 103.747 1589.9781 253,356 7,500 260,856

10.408.383 1416.3241 10.046.086

10.583.400 1362.2971 10.221.103

Depreciation expense of $471,812 was charged to the public safety function within the statement of activities.

5. ACCOUNTS PAYABLE AND ACCRUALS

The following is a summary of accounts payable at June 30, 2015:

Class of Pavables Vendor Payroll liabilities

Total

$ 172,077 295.483

$ 467.560

-20-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

6. COMPENSATED ABSENCES

At June 30, 2015, employees of the Center had accumulated $208,030 in annual leave benefits, which were computed in accordance with GASB Codification Section C 60. The following is a summary of the changes in accumulated annual leave benefits for the year ended June 30, 2015.

Compensated absences payable, begirming of year $ 206,887 Additions 141,891 Deletions (140.7481 Compensated absences payable, end of year $ 208.030

7. DEFINED BENEFIT PENSION PLANS

The Ware Youth Center (the Center) is a participating employer in two cost-sharing defined benefit pension plans. These plans are administered by two public employee retirement systems, the Teachers' Retirement System of Louisiana (TRSL) and the Louisiana State Employees' Retirement System (LASERS). Article X, Section 29(F) of the Louisiana Constitution of 1974 assigns the authority to establish and amend benefit provisions of these plans to the State Legislature. Each system is administered by a separate board of trustees and all Systems are component units of the State of Louisiana.

Each of the Systems issues an annual publicly available financial report that includes financial statements and required supplementary information for the system. These reports may be obtained by writing, calling or downloading the reports as follows:

TRSL: LASERS 8401 United Plaza Blvd. 8401 United Plaza Blvd. P. O. Box 94123 P. O. Box 44213 Baton Rouge, Louisiana 70804- Baton Rouge, Louisiana 70804-9123 4213 (225)925-6446 (225)925-0185 www.trsl.orgwww.lasersonline.org

The Center implemented Government Accounting Standards Board (GASB) Statement 68 on Accoimting and Financial Reporting for Pensions and Statement 71 on Pension Transition for Contributions Made Subsequent to the Measurement Date - an Amendment of GASB 68. These standards require the Center to record its proportional share of each of the pension plans' Net Pension Liability deferred outflows of resources, deferred inflows of resources, pension expense and to report the following disclosures:

Plan Descriptions:

Teachers' Retirement System of Louisiana fTRSLI

The Teachers' Retirement System of Louisiana (TRSL) is the administrator of a cost-sharing multiple employer defined benefit plan. The plan provides retirement, disability, and survivor benefits to employees who meet the legal definition of a "teacher" as provided for in LRS 11:701. The Center has participants in TRSL's Regular Plan. Eligibility for retirement benefits for this plan and the calculation of retirement benefits are provided for in LRS 11:761. Most members are eligible to receive retirement benefits 1) at the age of 60 with 5 years of creditable service, 2) at the age of 55 with at least 25 years of creditable service, or 3) at any age with at least 30 years of creditable service. Retirement benefits are calculated by applying a percentage ranging from 2% to 3% of final average salary multiplied by years of service. Final average salary is based upon the member's highest successive 36 months (hi^est successive 60 months for members employed after January 1, 2011).

-21 -

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

7. DEFINED BENEFIT PENSION PLANS fContinMedl

In lieu of terminating employment and accepting a service retirement, an eligible member can begin participation in the Deferred Retirement Option Program (DROP) on the first retirement eligibility date for a period not to exceed the 3rd anniversary of retirement eligibility. Delayed participation reduces the three year participation period. During participation, benefits otherwise payable are fixed, and deposited in an individual DROP account. Upon termination of DROP, the member can continue employment and earn additional accruals to be added to the fixed pre-DROP benefit. Upon termination of employment, the member is entitled to the fixed benefit, an additional benefit based on post-DROP service (if any), and the individual DROP account balance which can be paid in a lump sum or an additional annuity based upon the account balance.

Under LRS 11:778, members who have suffered a qualified disability are eligible for disability benefits if employed prior to January 1, 2011 and have five or more years creditable service, or if employed on or after January 1, 2011 and attained at least 10 years of creditable service. Members employed prior to January 1, 2011 receive disability benefits equal to IW/o of his average compensation multiplied by his years of creditable service, but not more than 50% of his average compensation subject to statutory minimums. Members employed on or after January 1, 2011 receive disability benefits equal to the regular retirement formula without reduction by reason of age.

Survivor benefits are provided for in LRS 11:762. In order for survivor benefits to be paid, the deceased member must have been in state service at the time of death and must have a minimum of five years of service credit, at least two of which were earned immediately prior to death, or must have had a minimum of twenty years of service credit regardless of when earned. Survivor benefits are equal to 50% of the benefit to which the member would have been entitled if he had retired on the date of his death using a factor of IV2V0 regardless of years of service or age, or $600 per month, whichever is greater.

Louisiana State Employees' Retirement System (LASERSI

The Louisiana State Employees' Retirement System (LASERS) is the administrator of a cost-sharing multiple employer defined benefit pension plan to provide retirement, disability, and survivor's benefits to eligible state employees and their beneficiaries as defined in LRS 11:411-414. The Center has participants in this plan who began service under the LASER plan and later transferred to employment with the Center. The age and years of creditable service required in order for a member to receive retirement benefits are established by LRS 11:441 and vary depending on the member's hire date, employer and job classification. The substantial majority of members may retire with full benefits at any age upon completing 30 years of creditable service and at age 60 upon completing 10 years of creditable service. Additionally, members may choose to retire with 20 years of service at any age, with an actuarially reduced benefit. The computation of retirement benefits are provided for in LRS 11:444. The basic annual retirement benefit for members is equal to a percentage (between 2.5% and 3.5%) of average compensation multiplied by the number of years of creditable service.

The State Legislature authorized LASERS to establish a Deferred Retirement Option Plan (DROP). When a member enters DROP, their status changes from active member to retiree even though they continue to work and draw their salary for a period of up to three years. The election is irrevocable once participation begins. During DROP participation, accumulated retirement benefits that would have been paid to each retiree are separately tracked. For members who entered DROP prior to January 1, 2004, interest at a rate of one-half percent less than the System's realized return on its portfolio (not to be less than zero) will be credited to the retiree after participation ends. At that time, the member must choose among available alternatives for the distribution of benefits that have accumulated in the DROP account. Members who enter DROP on or after January 1, 2004, are required to participate in LASERS Self-Directed Plan (SDP) which is administered by a

-22-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

7. PEFTNED BENEFIT PENSION PLANS IContinuedJ

third-party provider. The SDP allows DROP participants to choose from a menu of investment options for the allocation of their DROP balances. Participants may diversify their investments by choosing from an approved list of mutual funds with different holdings, management styles, and risk factors. Members eligible to retire and who do not choose to participate in DROP may elect to receive at the time of retirement an initial benefit option (IBO) in an amount up to 36 months of benefits, with an actuarial reduction of their future benefits. For members who selected the IBO option prior to January I, 2004, such amount may be withdrawn or remain in the IBO account earning interest at a rate of one-half percent less than the System's realized return on its portfolio (not to be less than zero). Those members who select the IBO on or after January 1, 2004, are required to enter the SDP as described above.

Eligibility requirements and benefit computations for disability benefits are provided for in LRS 11:461. All members with ten or more years of creditable service or members aged 60 or older regardless of date of hire who become disabled may receive a maximum disability benefit equivalent to the regular retirement formula without reduction by reason of age. Hazardous duty persormel who become disabled in the line of duty will receive a disability benefit equal to 75% of final average compensation.

Provisions for survivor's benefits are provided for in LRS 11:471-478. Under these statutes, the deceased member who was in state service at the time of death must have a minimum of five years of service credit, at least two of which were earned immediately prior to death, or who had a minimum of twenty years of service credit regardless of when earned in order for a benefit to be paid to a minor or handicapped child. Benefits are payable to an unmarried child until age 18 or age 23 if the child remains a full-time student. The minimum service requirement is ten years for a surviving spouse with no minor children, and benefits are to be paid for life to the spouse or qualified handicapped child.

Funding Policy

Article X, Section 29(E)(2)(a) of the Louisiana Constitution of 1974 assigns the Legislature the authority to determine employee contributions. Employer contributions are actuarially determined using statutorily established methods on an annual basis and are constitutionally required to cover the employer's portion of the normal cost and provide for the amortization of the unfunded accrued liability. Employer contributions are adopted by the Legislature annually upon recommendation of the Public Retirement Systems' Actuarial Committee (PRSAC).

Contributions to the plans are required and determined by State statute (which may be amended) and are expressed as a percentage of covered payroll. The contribution rates in effect for the year ended June 30, 2015, for the Center and covered employees were as follows:

School System Employees

Teachers' Retirement System:

Regular Plan 28.00% 8.00%

State Employees' Retirement System 37.00% 7.50% - 8.00%

-23-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30, 2015

7. DEFTNED BENEFIT PENSION PLANS (Continued^

The contributions made to the Systems for the past three fiscal years, which equaled the required contributions for each of these years, were as follows:

2015 2014 2013

Teachers' Retirement System: Regular Plan $ 44,140 $ 56,752 $ 54,873

State Employees'Retirement System 1,060,173 974,893 983,602

Pension Liabilities, Pension Expense, and Deferred Outflows of Resources and Deferred Inflows of Resources Related to Pensions

The following schedule lists the Center's proportionate share of the Net Pension Liability allocated by each of the pension plans based on a June 30, 2014 measurement date. The total pension liability used to calculate the Net Pension Liability was obtained from an actuarial valuation as of that date. The Center uses this measurement to record its Net Pension Liability and associated deferred amounts as of June 30, 2015 in accordance with GASB Statement 68. The schedule also includes the proportionate share allocation rate used at June 30,2014 along with the change compared to the June 30, 2013 rate. The Center's proportion of the Net Pension Liability was based on a projection of the Agency's long-term share of contributions to the pension plan relative to the projected contributions of all participating employers, actuarially determined.

Net Pension Rate at June 30, Increase (Decrease) Liability at June 30, 2014 to June 30,2013

Teachers'Retirement System $ 383,713 0.00375% (0.00159)% State Employees'Retirement System 9,772,332 0.15629% (0.01073)%

10,156,045

The following schedule list the Center's recognized pension expense for each plan including amortization of deferred inflows and outflows for the year ended June 30,2015:

Teachers'Retirement System $ (1,646) State Employees' Retirement System 502,313

$ 502,667

-24-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

7. DEFINED BENEFIT PENSION PLANS (Continuedl

At June 30, 2015, the Center reported deferred outflows of resources and deferred inflows of resources related to pensions from the following sources:

Differences between expected and actual experience Net difference between projected and actual earnings on pension plan investments

Changes in proportion and differences between Employer contributions and proportionate share of contributions Employer contributions subsequent to the measurement date

Total

Deferred Outflows of Resources

17,056

1,104,313 1,121,369

Deferred Inflows of Resources

$ (177,805)

(1,285,256)

(672,526)

(2,135,587)

Summary totals of deferred outflows of resources and deferred inflows of resources by pension plan:

Deferred Outflows of Resources

Deferred Inflows of Resources

Teachers' Retirement System State Employees' Retirement System (LASERS)

$ 54,207 $ (204,021)

1,067,162 (1,931,566)

$ 1,121,369 $ (2,135,587)

The Center reported a total of $1,104,313 as deferred outflow of resources related to pension contributions made subsequent to the measurement period of June 30, 2014 which will be recognized as a reduction in Net Pension Liability in the year ended June 30, 2016. The following schedule list the pension contributions made subsequent to the measurement period for each pension plan:

Teachers' Retirement System State Employees' Retirement System (LASERS)

Subsequent Contributions

$ 44,140 1,060,173

$ 1,104,313

-25-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

7. DEFINED BENEFIT PENSION PLANS (ContinBcdJ

Other amounts reported as deferred outflows of resources and deferred inflows of resources related to pensions will be recognized in pension expense as follows:

Year TRSL LASERS Total 2016

2017

2018

2019

(48,488)

(48,488)

(48,488)

(48,490)

(653.215)

(653.216)

(309,073)

(309,073)

(701.703)

(701.704)

(357,561)

(357,563) (193,954) $ (1,924,577) $ (2,118,531)

Actuarial Assumptions

A summary of the actuarial methods and assumptions used in determining the total pension liability for each pension plan as of June 30,2014 are as follows:

Valuation Date

Actuarial Cost Method

Actuarial Assumptions;

Expected Remaining

Service Lives

Investment Rate of Return

TRSL

June 30,2014

Entry Age Normal

5 years

7.75% net of investment expenses

LASERS

June 30,2014

Entry Age Normal

3 years

7.75% per annum.

-26-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

7. DEFINED BENEFIT PENSION PLANS rContiniiecU

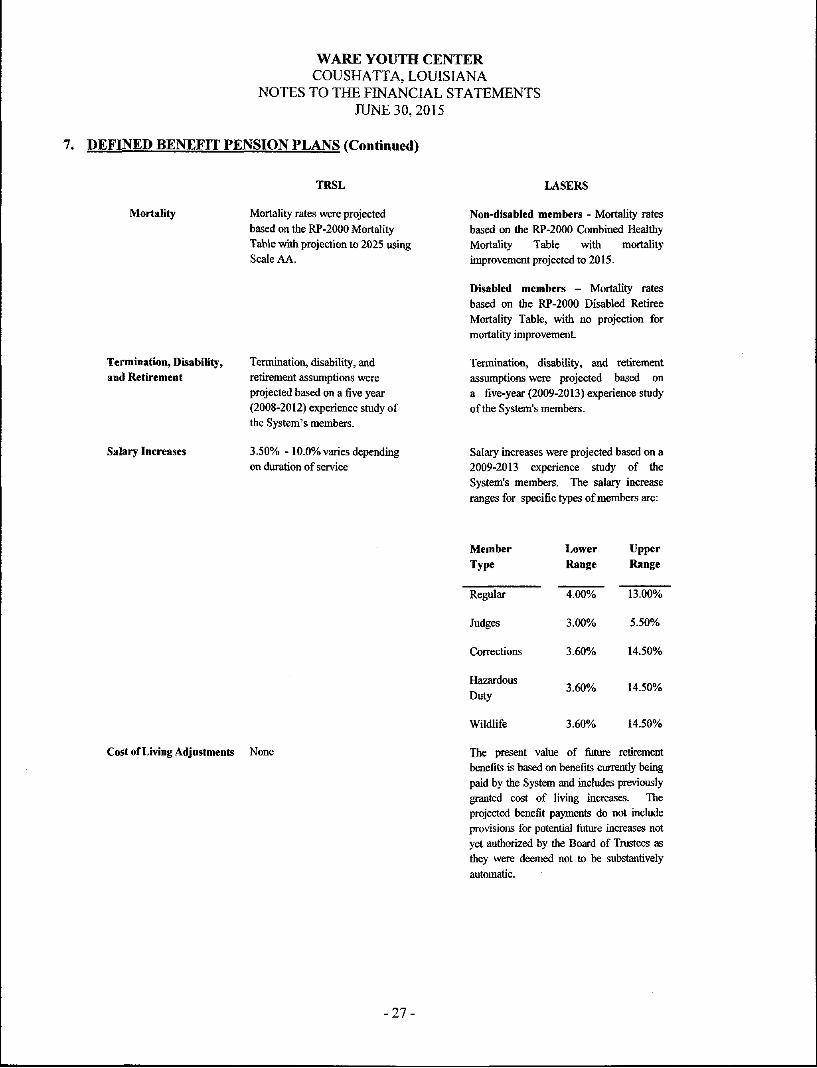

Mortality

Termination, Disability, and Retirement

Salary Increases

TRSL

Mortality rates were projected based on the RP-2000 Mortality Table with projection to 2025 using Scale AA.

Termination, disability, and retirement assumptions were projected based on a five year (2008-2012) experience study of the System's members.

3.50% - 10.0% varies depending on duration of service

LASERS

Non-disabled members - Mortality rates based on the RP-2000 Combined Healthy Mortality Table with mortality improvement projected to 2015.

Disabled members - Mortality rates based on the RP-2000 Disabled Retiree Mortality Table, with no projection for mortality improvement.

Termination, disability, and retirement assumptions were projected based on a five-year (2009-2013) experience study of the System's members.

Salary increases were projected based on a 2009-2013 experience study of the System's members. The salary increase ranges for specific types of members are:

Member Type

Regular

Judges

Corrections

Lower Range

4.00%

3.00%

3.60%

Upper Range

13.00%

5.50%

14.50%

Hazardous Duty

Wildlife

3.60% 14.50%

3.60% 14.50%

Cost of Living Adjustments None The present value of future retirement benefits is based on benefits currently being paid by the System and includes previously granted cost of living increases. The projected benefit payments do not include provisions fra- potential future increases not yet authorized by the Board of Trustees as they were deemed not to be substantively automatic.

-27-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30, 2015

7. DEFINED BENEFIT PENSION PLANS rContinuedl

The following schedule list the methods used by each of the retirement systems in determining the long term rate of return on pension plan investments:

TRSL LASERS

The long-term expected rate of return on pension plan investments was determined using a building-block method in which best-estimate ranges of expected future real rates of return (expected returns, net of pension plan investment expenses and inflation) are developed for each major asset class. These ranges are combined to produce the long-term expected rate of retum by weighting the expected fiiture real rates of retum by the target asset allocation percentage and by adding expected inflation and an adjustment for the effect of rebalancing/diversification.

The long-term expected rate of retum on pension plan investments was determined using a building-block method in which best-estimate ranges of expected future real rates of retum (expected retums, net of pension plan investment expense and inflation) are developed for each major asset class. These ranges are combined to produce the long-term expected rate of retum by weighting the expected future real rates of retum by the target asset allocation percentage and by adding expected inflation and an adjustment for the effect of rebalancing/diversification.

The following table provides a summary of the best estimates of arithmetic/geometric real rates of retum for each major asset class included in each of the Retirement System's target asset allocations as of June 30, 2014:

Target Allocation Long-Term Expected Real Rate of Retum

Asset Class TRSL LASERS TRSL LASERS

Cash - - - 0.50%

Domestic equity 31.0% 27.0% 4.71% 4.69%

International equity 19.0% 30.0% 5.69% 5.83%

Domestic fixed income 14.0% 11.0% 2.04% 2.34%

International fixed income 7.0% 2.0% 2.80% 4.00%

Altematives 29.0% 23.0% 5.94% 8.09%

Global asset allocation - 7.0% - 3.42%

Real assets - - - -

Total 100.0% 100.0% n/a 5.78%

n/a - amount not provided by Retirement System

-28-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30,2015

7. DEFINED BENEFIT PENSION PLANS fContinuedJ

Discount Rate

The projection of cash flows used to determine the discount rate assumed that plan member contributions will be made at the current contribution rate and that sponsor contributions will be made at rates equal to the difference between actuarially determined contribution rates and the member rate. Based on those assumptions, each of the pension plan's fiduciary net position was projected to be available to make all projected future benefit payments of current plan members. Therefore, the long-term expected rate of return on pension plan investments was applied to all periods of projected benefit payments and to determine the total pension liability. The discount rate used to measure the total pension liability for TRSL and LASERS was 7.75 and 7.75, respectively for the year ended June 30,2014.

Sensitivity of the Employer's Proportionate Share of the Net Pension Liability to Changes in the Discount Rate

The following table presents the Center's proportionate share of the Net Pension Liability (NPL) using the discount rate of each Retirement System as well as what the Center's proportionate share of the NPL would be if it were calculated using a discount rate that is one percentage-point lower or one percentage-point higher than the current rate used by each of the Retirement Systems:

1.0% Decrease Current Discount Rate 1.0% Increase

TRSL

Rates 6.75% 7.75% 8.75%

Center's Share of NPL $ 488,714 $ 383,713 $ 294,351

LASERS

Rates 6.75% 7.75% 8.75%

Center's Share of NPL $ 12,533,807 $ 9,772,332 $ 7,431,588

Payables to the Pension Plan

The Center recorded accrued liabilities to each of the Retirement Systems for the year ended June 30, 2015 mainly due to the accrual for payroll at the end of each of the fiscal years. The amounts due are included in liabilities under the amounts reported as accounts, salaries and other payables. The balance due to each for the retirement systems at June 30,2015 is as follows:

TRSL $ 4,860

LASERS 102,470

~$ 107,330

-29-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

NOTES TO THE FINANCIAL STATEMENTS JUNE 30, 2015

8. RISK MANAGEMENT

The Center is exposed to various risks of loss related to torts; theft of, damage to, and destruction of assets: errors and omissions; injuries to employees; and natural disasters. The Center maintains commercial insurance coverage covering each of those risks of loss. Management believes such coverage is sufficient to preclude any significant uninsured losses to the Center.

9. CLAIMS AND CONTINGENCIES

The Center participates in federal and state programs that are fully or partially funded by grants received from other Governmental units. Expenditures financed by grants are subject to audit by the appropriate grantor government. If expenditures are disallowed due to noncompliance with grant program regulations, the Center may be required to reimburse the grantor government. The Center believes that disallowed expenditures, if any, based on subsequent audits will not have a material effect on any of the governmental fiinds or the overall financial position of the Center.

In the normal course of operations, claims/lawsuits may occur for which insurance has not been obtained. Management believes that such claims/lawsuits, if any, are not expected to have a material impact on the operations of the Center.

10. COMPENSATION PAID TO BOARD MEMBERS

The members of the Board of Commissioners of the Center receive no compensation for their services.

-30-

REQUIRED SUPPLEMENTARY INFORMATION

OTHER SUPPLEMENTARY INFORMATION

WARE YOUTH CENTER COUSHATTA. LOUISIANA

SCHEDULE OF REVENUES. EXPENDITURES AND CHANGES IN FUND BALANCE OF THE GOVERNMENTAL FUND-BUDGET (GAAP) BASIS AND ACTUAL

FOR THE YEAR ENDED JUNE 30J015

Variance REVENUES Original Budget Final Budget Actual

Intergovernmental $ 6,687,711 $ 6,687,711 $ 6,885,391 $ 197,680 Charges for Services 1,000,460 1,000,460 910,743 (89,717) Fines, forfeitures and fees 325,395 325,395 323,666 (1,729) Interest and Investment Income 28 28 118 90 Royalties and Leases 4,694 4,694 20,494 15,800 Miscellaneous 14,332 14,332 92,825 78,493

Total Revenues 8,032,620 8,032,620 8,233,237 200,617

EXPENDITURES Personal Services 5,823,626 5,823,626 5,814,771 8,855 Travel 10,356 10,356 12,205 (1,849) Operating Services 1,130,079 1,130,079 930,699 199,380 Supplies 742,784 742,784 757,436 (14,652) Professional Services and

miscellaneous expense 255,775 255,775 198,666 57,109 Capital Outlay 70,000 70,000 109,514 (39,514)

Total Expenditures 8,032,620 8,032,620 7,823,291 209,329

Excess (Deficiency) of Revenues Over Expenditures - - 409,946 409,946

Fund Balance, Begirming of Year 124,697 124,697 124,697 _

Fund Balance, End of Year $ 124,697 $ 124,697 $ 534,643 $ 409,946

-31-

WARE YOUTH CENTER COUSHATTA. LOUISIANA

SCHEDULE OF PROPORTIONATE SHARE OF THE NET PENSION LIABILITY FOR THE YEAR ENDED JUNE 30,2015 (*)

2015 TRSL LASERS

0.00375% 0.15629%

$383,713 $ 9,772,332

$ 157,643 $ 2,865,332

243.41% 341.05%

63.70% 65.00%

Employer's Proportion of the Net Pension Liability

Employer's Proportionate Share of the Net Pension Liability

Employer's Covered-Employee Payroll

Net Pension Liability as a % of Covered Payroll

Plan Fiduciary Net Position as a Percentage of the Total Pension Liability

This schedule is to be built prospectively. Until a full 10-year trend is compiled, the schedule will show information for those years for which data is available, beginning with EYE June 30, 2015.

* The amounts presented have a measurement date as of the previous fiscal year end.

The Two Retirement Systems reported in this schedule are as follows; TRSL = Teachers' Retirement System of Louisiana LASERS = Louisiana State Employees' Retirement System

-32-

WARE YOUTH CENTER COUSHATTA. LOUISIANA

SCHEDULE OF THE EMPLOYER'S CONTRIBUTIONS FOR THE YEAR ENDED JUNE 30,2015

Contractually Required Contribution' TRSL

$ 44,140

2015 LASERS $ 1,060,173

Contributions in Relation to Contractually Required

Contribution^ 44,140 1,060,173

Contribution Deficiency (Excess)

Employer's Covered Employee Payroll

Contributions as a % of Covered Employee Payroll

$ 157,643

28.00%

$ 2,865,332

37.00%

This schedule is to be build prospectively. Until a full 10-year trend is compiled, the schedule will show information for those years for which data is available, beginning with EYE June 30,2015.

For reference only:

' Employer contribution rate multiplied by employer's covered employee payroll

^ Actual employer contributions remitted to the Plan

^ Employer's covered employee payroll amount for the fiscal year ended June 30, 2015

The Two Retirement Systems reported in this schedule are as follows: TRSL = Teachers' Retirement System of Louisiana LASERS = Louisiana State Employees' Retirement System

-33-

WARE YOUTH CENTER COUSHATTA. LOUISIANA

SCHEDULE OF COMPENSATION BENEFIT AND OTHER PAYMENTS TO EXECUTIVE DHtECTOR

FOR THE YEAR ENDED JUNE 30.2015

Executive Director: Kenneth Loftin

Purpose Amount Salary $ 193,600 Travel 3,150

$ 196,750

-34-

OTHER REPORTING REQUIRED BY GOVERNMENT AUDITING STANDARDS

Postlethwaite & Netterville

A Professional Accounfing Corporotion Associated Offices in Principal Cities of the United States

www.pncpa.com

INDEPENDENT AUDITORS' REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FE^ANCIAL STATEMENTS

PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

Board of Commissioners Ware Youth Center Coushatta, Louisiana 71019

We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the governmental activities and the major fund of Ware Youth Center (the Center), as of and for the year ended June 30, 2015, and the related notes to the financial statements, which collectively comprise the Center's basic financial statements, and have issued our report thereon dated September 28,2015.

Internal Control Over Financial Reporting

In planning and performing our audit of the financial statements, we considered the Center's internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Center's internal control. Accordingly, we do not express an opinion on the effectiveness of Center's internal control.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

-35-

8550 United Ploza Blvd, Suite 1001 • Baton Rouge, LA 70809 • Tel: 225.922.4600 • Fox: 225.922.4611

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Center's financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity's internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity's internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

September 28,2015

-36-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

SCHEDULE OF FINDINGS AND QUESTIONED COSTS FOR THE YEAR ENDED JUNE 30,2015

SECTION #1 SUMMARY OF AUDITORS' RESULTS

FINANCIAL STATEMENTS

1. Type of auditors'report issued: Unmodified

2. Internal control over financial reporting: a. Material weakness(es) identified? No b. Significant deficiency(ies) identified that are not

considered to be material weaknesses? None reported

3. Noncompliance material to financial statements noted? No

SECTION #2

FINANCIAL STATEMENT FINDINGS

NONE

-37-

WARE YOUTH CENTER COUSHATTA, LOUISIANA

SUMMARY SCHEDULE OF PRIOR AUDIT FINDINGS FOR THE YEAR ENDED JUNE 30,2015

Findings - Financial Statement Audit

2014-01 Payroll

Condition:

Status:

2014-02

Condition:

Status

The accountant enters the payroll information in the pajroll system from which payroll direct deposits are generated and initiates the cash transfer from the operating account to the payroll account. He also reconciles the payroll reports to the Time Clock Manager software reports, which detail the time worked by employees. He also reconciles the bank statements. Further, documentation is not maintained evidencing that initial compensation and raise levels for each employee are authorized.

Resolved.

Budget Law

The Center is not publishing a notice of the budget hearing in an official journal. Further, the budget that was prepared did not include the beginning fund balance.

Resolved.

-38-