w acuaf t ial upda e - american academy of actuaries 1991 actuarial update.pdf · t ial upda te...

TRANSCRIPT

WeAcuaft ial UpdateVOLUME 20 NUMBER 9

In t

2

his issue

From the President

3 Letters to the Editor

7 Economic Assumptionsfor Pension Plans

Checklist of AcademyStatements

Annual StatementChanges

Long-term Care

5 8Insurance-A NewFederal Presence

1 O A.M. Best ReleasesInsolvency Study

10 Name Change for CAPPApproved

1 1 Medicaid Task ForceReleases Report

1 ] Academy Speaks out

12 Standards Outlook

EnclosuresIncluded in this month's issue ofThe Update are the following :

• Government Relations Watch

• In Search Of . . .

• ASB Boxscore

0 ASB Hearing Memorandum

• 1992 Enrolled ActuariesMeeting Exhibit Brochure

AMERICAN ACADEMY OF ACTUARIES SEPTEMBER 1991

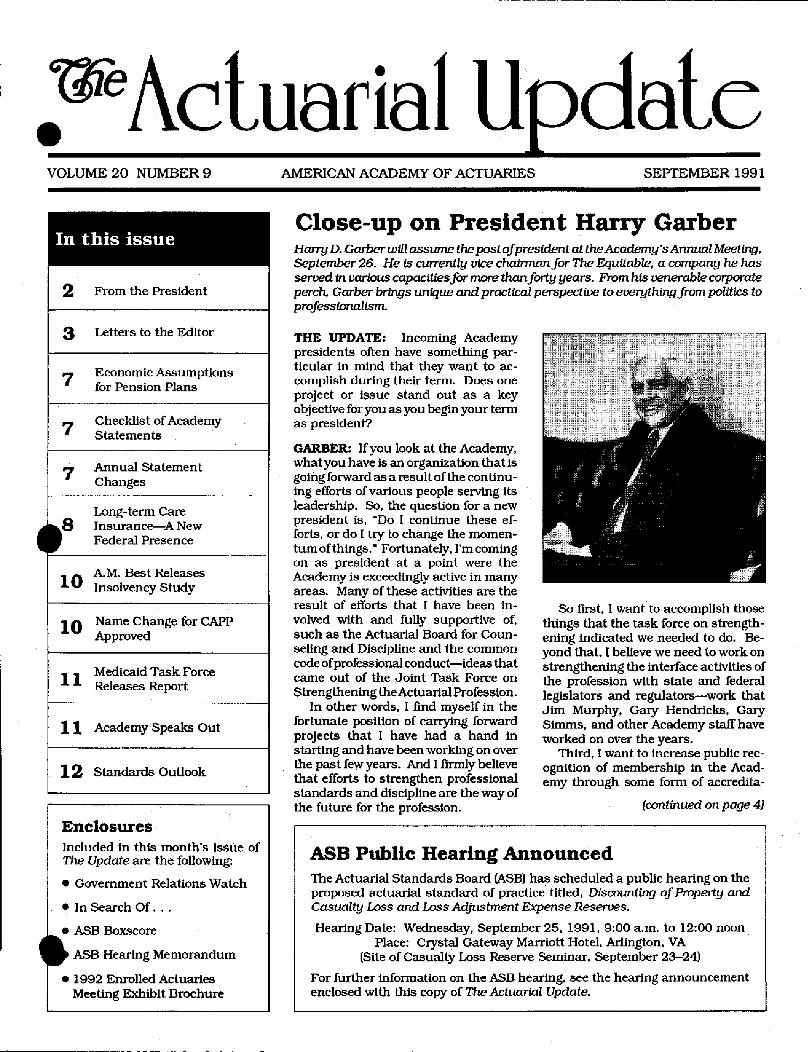

Close-up on President Harry GarberHarry D. Garber will assume the post ofpresident at theAcademy'sAnnual Meeting,September 26 . He is currently vice chairman for The Equitable, a company he hasserved in various capacities for more than forty years. From his venerable corporateperch, Garber brings unique and practical perspective to everything from politics toprofessionalism.

THE UPDATE: Incoming Academypresidents often have something par-ticular in mind that they want to ac-complish during their term. Does oneproject or issue stand out as a keyobjective for you as you begin your termas president?

GARBER: If you look at the Academy,what you have is an organization that isgoing forward as a result of the continu-ing efforts of various people serving Itsleadership. So, the question for a newpresident is, "Do I continue these ef-forts, or do [ try to change the momen-tum of things ." Fortunately, I'm comingon as president at a point were theAcademy is exceedingly active in manyareas. Many of these activities are theresult of efforts that I have been In-volved with and fully supportive of,such as the Actuarial Board for Coun-seling and Discipline and the commoncode of professional conduct-ideas thatcame out of the Joint Task Force onStrengthening theActuarial Profession .

In other words, I find myself in thefortunate position of carrying forwardprojects that I have had a hand instarting and have been working on overthe past few years. And I firmly believethat efforts to strengthen professionalstandards and discipline are the way ofthe future for the profession .

So first, I want to accomplish thosethings that the task force on strength-ening indicated we needed to do . Be-yond that. [ believe we need to work onstrengthening the interface activities ofthe profession with state and federallegislators and regulators-work thatJim Murphy, Gary Hendricks, GarySimms, and other Academy staff haveworked on over the years .

Third, I want to increase public rec-ognition of membership in the Acad-emy through some form of accredita-

(continued on page 4)

ASB Public Hearing AnnouncedThe Actuarial Standards Board (ASB) has scheduled a public hearing on theproposed actuarial standard of practice titled, Discounting of Property andCasualty Loss and Loss Adjustment Expense Reserves.

Hearing Date : Wednesday, September 25, 1991, 9 :00 a.m. to 12:00 noonPlace: Crystal Gateway Marriott Hotel, Arlington, VA

(Site of Casualty Loss Reserve Seminar, September 23-24)

For further information on the ASB hearing, see the hearing announcementenclosed with this copy of The Actuarial Update .

2

of Actuaries

PresidentMavis A. Walters

President-ElectHarry D. Garber

Vice PresidentsRobert H. DobsonCharles E. FarrDaniel J. McCarthyMichael A. Waiters

SecretaryRichard H. Snader

TreasurerThomas D. Levy

Executive Vice PresidentJames J. Murphy

Executive Office1720 [ Street, N.W. 7th FloorWashington, D .C. 20006(202) 223-8196FAX (202) 8724948

Membership AdministrationWoodfield Corporate Center475 N. Martingale RoadSchaumburg, Illinois 60173-2226(708) 706-3513

ChairpersonCommittee on PublicationsRoland E. KingEditorE. Toni MulderExecutive EditorErich ParkerAssociate EditorsGary D. LakeStephen A. MeskinCharles Barry H. WatsonManaging EditorJeanne CaseyContributing EditorKen KrehbielProduction ManagerRenee Cox

American Academy of Actuaries1720 1 Street, N .W 7th FloorWashington, D.C. 20006Statements of fact and opinion in this publication,Including editorials and letters to thee editor, are madeon the responsibility of the authors alone and do notnecessarily imply or represent the position of theAmerican Academy of Actuaries, the editors, or themembers of the Academy.

Harry D. Garber

The Quality Movementand Our Profession

Improvement in the quality and reli-ability of products has been a key focusfor industrial companies in NorthAmerica over the past fewyears and willcontinue to be one in the years ahead.The quality movement is being em-braced, as well, by service and financialcompanies. Although the actuarialprofession has undertaken many im-portant initiatives to bolster its publicrepute in recent years, these steps havelacked an all-encompassing theme anda coherent theory. I believe the qualitymovement provides such a central fo-cus. It should be adopted by the profes-sion as the organizing approach to In-creased professionalism .

Quality is a worthy goal. Recogni-tion of the actuarial profession as onethat preaches and achieves high qual-ity will be beneficial not only to theprofession as it pursues its public in-terface goals, but also to individualactuaries in their relationships withemployers and clients.

What does quality entail in the areaof service and professional activity? Inthe United States, the most prestigiousrecognition for quality In business isthe Malcolm Baidrige National QualityAward. Each year, two or three com-panies that best meet certain criteriaare selected as winners of the award .The same criteria are applied to allcompanies . To win the award, compa-nies must demonstrate (1) a knowledgeof customers' requirements and expec-tations, (2) a work force that is bothknowledgeable and dedicated to im-proving the quality of its productsand/or services, (3) a process for con-trolling the quality of the products and/or services, (4) a system for regularlycompiling information on the quality ofproducts and/or services as well ascustomer satisfaction, and (5) a leader-ship that creates and sustains a clearvision of quality values and seeks con-tinuing improvement in quality .

Quality Criteria Applied

I believe the

The Actuarial Update

by and large could be used as a basis forestablishing and executing a quality-based program for the actuarial profes-sion. Specifically, I would suggest thefollowing elements for such a progra

1 . The profession should understandthe customers' requirements and ex-pectations for each of the various actu-arial services to be performed .

2. For each of these different ser-vices, there should be specified qualifi-cation standards and standards ofpractice .

3. Individual actuaries should un-derstand and observe these standards .

4. The profession should havemechanisms in place to ensure thatthese standards are being observed, tomeasure customer satisfaction, and totake any needed corrective action.

5. The profession should continu-ally seek to improve its members' qual-ity performance.

Where Are We Today?

Where does the actuarial professionstand with respect to these criteriatoday? We have well-establishedstandards of professional conduct, andwe have made good progress in definingstandards ofpractice for most actuservices. We have well-developed geral qualification standards. We arecontinuing to fine-tune specific quali-fication standards for particular actu-arial services.

We also have a well-establisheddiscipline process for handling viola-tions ofthe professional code ofconduct.With respect to the reported failures ofsome individuals to observe standardsof practice or qualification standards,however, our discipline process is lessmature. But we are improving as wegain experience. In most cases of pro-fessional misconduct, counseling is abetter response than punishment. Asproposed, the Actuarial Board forCounseling and Discipline would beable to provide this counseling .

Two serious deficiencies remain,however. The first concerns an under-standing of our customers, be theyemployers, clients, regulators, or legis-lators. In many instances, our profes-sion has established standards forvarious actuarial services without con-sulting its customers. For any profes-sional, consulting the customer islogical and reasonable approach toscaring quality. Yet too often it's olooked, maybe because professionalsthink that they know what's best for

Malcolm Baldrige criteria their customers .

September 1991

According to company officials I havetalked with, even design engineers fromcompanies that have won the MalcolmBaldrige Award (e.g., IBM, Rochester,

4Cadillac) often fail to consult cus-ers-and thereby misjudge their

attitudes. The actuarial profession maybe quilty of similar arrogance and/oroversight.

We will never know whether, as aprofession, we are improving our per-formance vis-a-vis customers' expecta-tions, unless we work with our custom-ers. Without doubt, this Is a difficulttask. But, as a profession we mustexercise as much Imagination inbringing customers Into our quality-improvement strategies as we alreadyapply when dealing with new legal andbusiness requirements .

Our second deficiency involves thedegree of control our profession hasover the quality ofworkbeing performedby practicing actuaries. Except forcases submitted through the disciplineprocess, the profession does not knowthe extent to which its standards are

Letters to the -Editor

•ist by Our Own Petard?

I just read Ed Hustead's comments inthe July Update, i .e., "Pension AuditRevisited." In my opinion, Ed is right"on the mark ." The Internal RevenueService's criteria may be, in fact, un-justifiable, but much of what is hap-pening is a direct by-product of theinaction ofpension actuaries as a pro-fession .

Almost six years ago at the annualmeeting ofthe Conference of Actuariesin Public Practice, I commented on,among other things, professional ac-tuaries' responsibilities in measuringfunding adequacy.

The ambivalence of the actuarial pro-fession in adopting minimum fundingstandards has always been a concern tome and many others. Long before ERISAwas enacted in 1974, there wasanobviousneed for minimum funding standards.Pension plan assets clearly were grow-ing rapidly and would soon exceed atrillion dollars, funds supposedly dedi-cated to provide benefitsforemployees.Mdifficult to accept the fact that many

cries today retain a laissez-fairea titude about the need for minimumprofessional and ethical standards morerigorous than those Imposed by ERISA .

being observed. This is inadequatequality assurance fora profession whosewatchword is "quality." In addition todisciplining and counseling individu-als as cases come up, we need tomonitor, in general , how well actuariesare observing the profession's stan-dards. Then, as problems are uncov-ered, we will need to develop and imple-ment new ways to improve theprofession's system for quality control .

Of course, the actions of knowledge-able, responsible professionals are whatultimately determine the reputation ofa profession. The job for the professionis to establish the standards that are tobe met and then to educate its mem-bers about them, to monitor how thestandards are being applied, and, whennecessary, to take corrective action .

We are moving in the right direction .If we apply the precepts of the qualitymovement directly, I believe that theprofession will gain greater recogni-tion. Let's become known as a profes-sion that not only preaches, butachieves, high quality. A

We keep talking but do little : It's nowonder our profession remains virtu-ally invisible when we have refused toadopt our own minimum standardsand principles of practice .

Daniel F. McGinnWhittier, California

Distinguished Service

The actuarial profession has, at longlast, received the ultimate of publicrecognition! The Internal Revenue Ser-vice includes us in its definition of "per-sonal service activity." This term is de-fined as "an activity that involves per-forming personal services in the fields ofhealth, law, engineering, architecture,accounting, actuarial science, per-forming arts, or consulting, or anyothertrade or business In which capital is nota material income-producing factor ."(See page 40, 1990 1040 Forms andInstructions, Package 1040-5, IRS)

One might wonder about the signifi-cance of the order in which the profes-sions are listed, or about the notableabsence of the fields of economics, so-cial sciences , and statistics)

Robert J. MyersSilver Spring, Maryland

3

Colleague ConcursI was distressed to find in the 1991annual report of the Board of Trusteesof the Federal Hospital Insurance (HI)Trust Fund an attack on the profes-sionalism of the chief actuary of theHealth Care Financing Administration(HCFA) by the two public trustees,Stanford G . Ross and David M . Walker.Even though the public trustees haveno actuarial credentials, their statementappears to be calculated to pass judg-ment on the professional judgment ofthe chief actuary and the actuarialprofession .

It takes great courage for the chiefactuary to qualify his certification withregard to the methodology and as-sumptions in the face of this sort ofpressure from "big shot" political ap-pointees .

The public trustees alleged that thechief actuary made "an expression of aprofessional preference outside of thebounds of the legally required actuarialopinion." To the contrary, it is the dutyand responsibility of the chief actuaryto express any legitimate concerns inthe actuarial certification. Indeed, legalcounsel for both HCFAand the TreasuryDepartment have ruled that the chiefactuary's opinion Is proper and withinthe bounds of the statute.

The public trustees have attemptedto trivialize the actuarial certificationand its requirement in the statute bystating:

We have taken great care to reviewthis year's HI annual report. We haveclosely examined and seriously consid-ered the comments noted in the actuarialopinion and concluded that they are notpersuasive and should not have resultedin a qualified actuarial opinion, basedon the applicable statutory requirement.We respect the right of the HCFA ChiefActuary to express his professional viewsregarding any significant actuarialmatters but regret that he, in our view, hasimproperly qualified his actuarial opinion.

I consider the public trustees' state-ment to be an assault on the actuarialprofession. It is noteworthy that themajority of the trustees declined to jointhe two public trustees in their state-ment. Actuaries must be able to accu-rately inform the public of the financialstatus of guaranteed benefits such asSocial Security , life Insurance, pensions,and health insurance, without pressureand political interference .

Gregory SavordBaltimore, Maryland

4

CLOSE-UP ON HARRY GARBER(continuedfrom page 1)

tion. I view this as an opportunisticactivity; that is, the profession mustseize opportunities for public recogni-tion or "accreditation" in the form ofspecific regulations and legislation. Asan example, the valuation actuary con-cept has developed in the life practicearea and is now being implemented bystate regulation . The National Associa-tion of Insurance Commissioners (NAIC)requires that a qualified valuation ac-tuary submit an opinion and now de-fines "qualified actuary" as a memberofthe Academy.

In the property/casualty practicearea, all states now require loss reserveopinions by qualified actuaries. Thisdevelopment resulted from a publicneed for greater confidence in insurers'ability to meet their financial respon-sibilities . I think that additional oppor-tunities for actuaries' formal recognitionwill arise in other areas as well. I willmake sure that we are looking for suchopportunities, whether or not any hap-pen to come up during my term of office .

THE UPDATE: What opportunities forgreater public recognition do you thinkmight arise?

GARBER: Well, I think one opportunitymight develop in the area of insurancecompany solvency. As a result of anumber of insurance companyinsolvencies, the Congress is now veryinterested in the issue of insurer sol-vency regulation . They are endeavor-ing to find a way to do somethingpositive, whether it's substituting fed-l eral regulation for state regulation,

undergirding state regulation, orwhatever. Some of the models that theCongress, and Representative Dingell'ssubcommittee in particular, is lookingat are the "appointed actuary" approachin the United Kingdom and similardevelopments in Canada . If Congressdecides to follow up with these ideas toany degree, I think that would be anopportunity for us to get further rec-ognition and maybe accreditation forthe profession .

THE UPDATE: When you speak aboutgaining accreditation for the profession,are you specifically thinking in terms offederal recognition?

GARBER: Yes, that's exactly what I'mthinking about. When the Academywas founded, it's original purpose wasto gain federal accreditation for the

profession in the United States. Wewere unable to accomplish that goalback then, and I think it's clear nowthat we won't accomplish it in the broadsense that we had originally hoped. Sowe are focusing rather on gaining rec-ognition for specific actuarial duties.The valuation actuary's role is nowrecognized by state regulators . . Theenrolled actuary designation, createdunder the Employee Retirement IncomeSecurity Act of 1974, was perhaps thefirst instance of a kind of accreditationfor actuaries .

I do think we will end up accom-plishing our goal of gaining federalrecognition more on a need-by-need ortask-by-task basis, rather than by get-ting broad, governmental accreditationfor the whole profession . We'll simplyhave to take every opportunity we'regiven to further institutionalize the roleof the actuary .

THE UPDATE: Do you expect that theActuarial Board for Counseling andDiscipline (ABCD) and the commoncode of professional conduct will helpthe effort to gain federal recognition forthe profession?

GARBER: Yes. Any profession firstneeds to have a body of knowledge withwhich it skillfully serves the public .Second, it needs to have a code ofprofessional conduct. Third, it musthave standards of practice . The fourthrequirement is a discipline process thatensures that members of the profes-sion follow those standards and thecode of conduct. These are the fouressential elements of any profession .

The task force on strengthening theprofession thought that the professionneeded to work harder in the areas ofprofessional conduct and discipline .The problems are that the actuarial

The Actuarial Update

organizations have had their own pro-fessional standards, some have not re-quired their members to follow thestandards of practice issued by theActuarial Standards Board, and ehas had its own code of professioconduct. Also, discipline cases involv-ing members often have not been coor-dinated among the organizations, anddifferences have developed among thevarious organizations in terms of howspecific cases were handled .

Anindividualwho Is amemberoftwoorganizations and violates a standardof practice may well be disciplined verydifferently by the actuarial organiza-tions. I've seen situations where oneorganization concluded that an indi-vidual really did nothing wrong, andtherefore no discipline was required,while the other organization sent a let-ter of warning.

It was thought that the professionneeded to get its act together in thisarea. Those of us on the Joint TaskForce on Professionalism looked intothe problem and concluded that eachorganization should continue to havethe responsibility and the ability todiscipline its own members-thatshould not be taken away by any effortto coordinate the discipline processamong the actuarial organizations .didn't want to have a central authothat could discipline a member of eSociety of Actuaries and tell the Societythat it should throw that member out .However, we thought it was very im-portant to establish a uniform code ofconduct that would require each or-ganization to discipline its members ifthey failed to follow the ASB standardsof practice or the Academy's qualifica-tion standards .

As a practical matter, we thought itimportant to set up one body to inves-tigate cases where discipline might berequired. That's the role oftheABCD aswe've conceived it. The ABCD would bea service arm to each of the organiza-tions by investigating cases. providingcounseling to individuals, and recom-mending disciplinary measures as ap-propriate. However, in the end, anydisciplinary action to be taken would betaken by the organizations and theirboards.

We consider the counseling role oftheABCD very Important. Clearly, whenyou are dealing with a code of conductthe issue is were you lying, stealing, orcheating. These are basic probleone doesn't ordinarily need to do a Icounseling in those instances . Butwhen you get to standards of practice,you have more complex issues. For

September 1991

example, did the individual know that acertain standard of practice existed? Ifthe individual did know about the ap-plicable standard, did he or she under-

d it? Did the individual think thedard meant one thing, when it re-

ly meant something else?Ultimately, counseling is a much

more powerful tool than discipline .Discipline €s what you want to applywhen all else fails . We wanted to havethe ability, when individuals had un-knowingly violated standards , to makesure that they understood what theyshould be doing. If people who knowbetter continue toviolate standards, wecan always resort to punitive actions .But when there 's a huge body of stan-dards that some members may notknow exist, or have never read, or don'trealize apply to the specific situationwith which they are dealing , it's veryImportant to have a means to counselthem. Such a process may also help usto identify possible ambiguity in astandard that the Actuarial StandardsBoard could subsequently clarify .

The establishment of the ABCD willgive us the ability to do those kinds ofthings on a professionwide basis. Therereally are surprisingly few serious dis-cipline cases, and they can be dealt

0 th by the ABCD making a recom-ndation. The membership organi-tions would then take care of any

disciplinary action themselves .

THE UPDATE: At this time, does itlook like all the actuarial organizationswill support the ABCD, as proposed?And what Is the status of the uniformcode of conduct that was exposed to themembership?

GARBER: Each of the other organiza-tions has had a hand in putting theABCD proposal together. The leadershipsof the other organizations are all rep-resented on the Academy's Board ofDirectors. At this point, there is noreason to believe that there will be anymajor problem; in fact, there seems to .be broad support for the ABCD . Evenso, it is not necessary that all of theorganizations actually become a part ofthis process. However, I do think thatit's in theirinterest. I would expect thatthey would all participate eventually.

Meanwhile, the work on the uniformcode of conduct is proceeding as well .Again, the uniform code as drafted does

a

Pt have to be adopted word-for-wordeach organization ; but we do want tove each organization adopt a code

that follows the uniform code's wordingas closely as possible . I believe all the

organizations will adopt the commoncode in principle and thereby requiretheir members to follow the actuarialstandards of practice of the ASB andthe qualification standards of theAcademy.

THE UPDATE: As you mentioned withrespect to public recognition, the valu-ation actuary has now been formallyrecognized by the NAIC. Do you want tocomment a bit on the significance of that?

GARBER; I think it's very importantthat the states come to understand andrespect the profession's ability to disci-pline its own members . I think there'sbeen a certain amount of skepticismabout the Academy's ability to do that .And there seems to have been somereluctance on the part of state regula-tors to identify, for potential disciplin-ary action, those individuals who theybelieve are not living up to the standardsof the profession.

UnderJim Murphy's leadership, theAcademy has begun informal discus-sions with state regulators and par-ticularly with actuaries involved in in-surance regulation at the state level . AtNAIC meetings, Academy representa-tives regularly meet with actuaries fromthe state insurance departments. Iexpect we will be able to cooperate moreclosely and seek the common objectiveof having state regulatory authoritiesrely more on actuaries . This will hap-pen when regulators are more confidentthat the profession itself can ensurethat actuaries will perform in a profes-sional manner .

It's up to the profession to make surethat people who do actuarial work arein fact qualified to undertake that workWe've begun a process of defining whatqualifications are necessary for specifictasks. Continuing education require-ments area part of that .

Another very important part issomething I talk about in my editorial .(See page 2.) Not only must the pro-fession set professional standards andthen counsel and discipline people whoare reported as failing to meet thosestandards, the profession must becomemuch more active in monitoring actu-aries to see whether they are meetingthe standards .

I think that this more proactive ap-proach to professionalism is necessaryif we are going to convince people thatmembers of our profession are trulyaccountable. The Committee on Pro-fessional Responsibility, chaired byPast President James MacGinnitie, istaking this positive approach .

5

In sum, there Is a whole web ofthings that are being developed to bol-ster professionalism. All of these efforts,I believe, are designed to help the profes-sion to get greaterpublic recognition . Ofcourse, public recognition In turn givesthe profession a greater responsibility forassuring that It's members are living upto professional standards and aretherefore worthy of that recognition .

THE UPDATE: Do you think that allthe necessary structures are therewithin theAcademy to accomplish whatyou want to in the year ahead?

GARBER: Well, the practice councilswere established to make sure that wewere coordinating our response to pub-lic issues and continually identifyingthe issues that the profession shouldaddress.

But that alone is not enough . Forexample, if the Casualty PracticeCouncil identifies particular issues thatare Important to actuaries in the ca-sualty practice area and such issuesrequire research, It is also importantthat the council connects with the Ca-sualtyActuarlal Society in order to fundand conduct that research . In addition,if there are public issues developingthat are apt to be very important to thecasualty practitioners, we need to passthat Information on to the CasualtyActuarial Society, so that it can plan itseducational and communications ac-tivities . I would hope that the practicecouncils will coordinate all of theseactivities. The profession must prepareIts members for whatever they have todo as a result of the public policy issues .And we must be sure that the professionis prepared with the information that itneeds to bring to the legislators and regu-lators as they formulate public policy.

THE UPDATE: So you would under-score the current philosophy behind theAcademy's government information pro-gram, which is "getting information fromthose who have it to .those who need it ."

GARBER: Yes, I want to emphasizethat, because some of our, membersmay not understand what we are tryingto do. The Society ofActuaries still has,as part of its constitution, a prohibitionabout expressing opinions on publicissues. Some actuaries may think thatif we shouldn't express an opinion onpublic policy, that we ought not to getinvolved in regulatory or other legisla-tive matters . However, it's clear to methat we must have a role . What is

(continued overleaf)

6

lacking most in the legislative arena isreal Information. Too much legislationis based on anecdotal information .People who can bring real informationto the process are very valuable . Ourrole is not to try to persuade policymakers but to inform them so thatbetter decisions can be made .

THE UPDATE: Do you think that theAcademy's government informationprogram Is working optimally in thisrespect, or could it be doing more?

GARBER: The challenge for the pro-gram, It seems to me, is to be able todetermine what is prompting certainlegislation. If you're going to providehelpful information to the debate, youneed to know what problem prompted theproposed legislation in the first place. It'snot always clear at the beginning .

If research is required on a problem,you are really a couple years away frombeing able to provide the informationand technical guidance required. That'swhy being able to anticipate legislativeissues is so important.

The government Information pro-gram appears, at least for now, to bemeeting the needs for information inWashington. I don't have the sensethat we are under-resourced. But we'llhave to evaluate the program as timegoes on. We're still in the developmentprocess.

It's very important to establish ourcredibility and to have policy makersbecome more reliant on us . That's notsomething that you can do simply bythrowing more people into the job .Government relations Is such a peoplebusiness. Individual people have tobuild the organization's credibility. It'sInitially Jim Murphy and GaryHendricks that policy makers come toview as credible. Only as their personalcredibility Is established will policymakers see the Academy as credible.

THE UPDATE: You apparently have agood deal of credibility on the Hill your-self. When you testify, members ofCongress seem genuinely interested inwhat you have to say . Could you talk abit about your own experience In thelegislative arena?

GARBER: For about five years, upuntil the fall of last year, my corporateresponsibilities involved governmentrelations . Specific issues I've been in-volved with on the federal level includetax issues , employee benefits issues,and McCarran-Ferguson. Demutual-ization was my principle focus at thestate level. I've also been involved to

some degree with housing issues. And,since my youth, I've always had a greatinterest in history and politics-someof my family were involved in politics .

As a vice chairman of a company,with a strong technical background,I've been able to work with members ofCongress on broad issues as well aswith their staffs on more technicalmatters. I can move back and fortheasily between the two levels, whereasmost people don't have the opportunityto do that. With my actuarial back-ground, I have a fundamental under-standing of businesses, and I amtherefore able to provide legislators withinformation and an understanding thatmany people involved in lobbying don'thave. They know the party line, but theyreally don't have the ability to talk withfundamental knowledge about howbusinesses work.

Government relations is interesting .You always have to take into accountthat the members' main job is to get re-elected. They get re-elected by servingtheir constituents ; if their constituentsbelieve that they are well served, themembers are re-elected . So, in everydiscussion it's important to know notonly what it is that you want to achieve,but to tie it in with whatever the mem-ber is looking to achieve. It's not enoughto just go in and give your story ; youreally have to understand where themember is coming from and what angleis most likely to Influence the member.It's like dealing with any sales situa-tion. You have got to know what aclient is looking for. And if you'reworking with congressional staffs, youhave to determine what their problemsare and how you can help them .

THE UPDATE: You mentioned thatmembers of your family have been inpolitics . Perhaps that gives you par-ticular sensitivity to how old pols needto satisfy their constituencies! Couldyou tell us a bit about your family'spolitical side?

GARBER: Family members on mymother's side were very Involved inDemocratic Party politics. Mygrandfa-ther was the clerk of the House duringthe Wilson Administration. In fact,during the 1924 Democratic Conven-tion I think he wielded the gavel. I don'tremember the exact title he had ; essen-tiallyhe was parliamentarian . Thatwasthe convention that went over 100 bal-lots to get a nominee .

I also had an uncle who ran forlieutenant governor, and my motherwas a Democratic Committeewoman .With this exposure, I Inherited a life-

The Actuarial Update

long interest In politics and history.

THE UPDATE: Where did you grow up?And what led you to become an actuary?

GARBER: I'm orginally from Detroiwent to Yale and graduated in 1950.joined The Equitable in 1950, and I'velived in New York ever since. Strangelyenough, I still don't feel part of NewYork. It's a place where I live, but I don'thave a strong association with It.

I came to New York because, when Igraduated, we were in the 1949-1950recession, and there weren't that manyjobs available. There were a lot ofcompanies looking for actuaries,though, In fact, The Equitable hirednine people that year.

I had a degree In math, and once I'dbegun toworkatThe Equitable, I startedtaking the actuarial exams. I servedbriefly in the Navy from 1952 to 1954,although I never got out of the UnitedStates: I served in Rochester, NewYork, and Lincoln, Nebraska. Afterthat, I came back to The Equitable, andI've been there ever since .

The last time I had a full-time actu-arial position was 1963, before I wasasked to head up the largest computerproject that The Equitable has everundertaken. I did that for severalyearsand became head of all systems aeties. Then I got Involved in torporactivities, ran the individual businessfor The Equitable for a couple of years,and then became The Equitable's firstchief financial officer in 1981 . Eventu-ally I was elected vice chairman and gotinvolved with government relations workfor The Equitable .

THE UPDATE: Does any recent expe-rience or opportunity you've had standout in your mind as particularly chal-lenging and rewarding?

GARBER. Very much so . One of mypersonal goals has been to complete aplan for the demutualization of TheEquitable. A few years back, a group ofNew York company people, which In-cluded actuaries and lawyers, workedwith representatives of the New YorkInsurance Department to develop ademutualization law. We Incorporatedinto this law many of the ideas developedby the Society of Actuaries' task force ondemutualization, which I chaired .

This is an example of how research .in this case research by the Society ofActuaries, was going on at the stime that legislators were examininproblem. We were able to draw on t ht

and help develop a law that Ifeel very proud of. It's basically sound

September 1991

law. The real fun forme now is applyingthe law to my company as we seek todemutualize .

So taking theoretical findings to theIslative arena, and then to the realId-that's very challenging and very

tisfying. The process of developingthe demutualization law was ideal-companies working with regulators . Ittook a long time; there was a lot of giveand take, a lot of argumentation. But inthe end, we had a law that everyone feltquite comfortable with. As we gothrough the process ofdemutualizationat The Equitable, the fundamentalswritten into the law are holding up verywell. The whole process will probablytake two to three years. We startedabout this time last year and hope tofinish about this time next year .

I think my experience shows thatyou can take the base of knowledge youhave as a professional and build on it bydoing new and different things . Youwant to have a firm knowledge base,but you don't want to be so rooted therethat you are limited inwhat you can do.Being an actuary is a fine career path;however, there's a lot more you can do,just by building on that base of knowl-edge and being open to opportunities .i

*Septembu Cheek1st of

Academy Statements0 PS-91 C-10 Response to Okla-homa Department's Inquiry onTrendingTechniques in Ratemaking

U PS-91H-6 Comments on Com-munity Rating and Small GroupHealth Insurance Reform

Check the public statement(s) thatyou would like to receive and sendyour request to the Academy'sWashington office .

Ann ialSta t0M9es

At Its June 1991 meeting. theNational Association ofInsuranceCommissioners (NAIC) BlanksTask Force adopted changes tothe 1991 annual statement. No-tice of these changes in their de-tail and supporting documenta-tion is available upon request from

ffhd ' ington o ice.s Wasemy0 the AcaPlease reference "NAIC AnnualStatement Changes for 1991"when making your request .

EConomiCAsst mptionsfor Pension Plansby Silvio Ingul

The Actuarial Standards Board's (ASB)Pension Committee has been hard atwork drafting a standard of practice onselecting economic assumptions forpension plans. The committee anticipatesthat the proposed standard will be ap-proved for exposure at the October 1991ASB meeting. Once the proposed stan-dard is approved for exposure . all of youwill have the opportunity to comment .

Since this standard strikes at thecore of what pension actuaries do, thePension Committee especially urgespension practitioners to review theproposed standard and send theircomments to the ASB . The committeeneeds to hear both what practitionersthink is right and what they think iswrong with the proposed standard .

This standard on selecting economicassumptions will be the first in a seriesof standards dealing with pension as-sumptions that the ASB Pension Com-mittee hopes to develop. The committee'sultimate goal is to develop a set of stan-dards covering all actuarial assumptionsused to perform pension valuations.

TheASB has undertaken this projectfor several reasons. The first, andprobably the most important reason, isthat no formal guidelines for settingactuarial assumptions for pensionplans currently exist. Other groups,such as the Internal Revenue Service(IRS) and the Financial AccountingStandards Board (FASB), have taken itupon themselves to promulgate re-quirements. It is thought that if ourprofession had a formal set of standards,the IRS and the FASB might recognizeour standards and be less inclined toimpose new regulations and standardson us. Another reason for the proposedstandard is to prevent abuse with re-spect to setting assumptions .

Preview of Proposed Standard

The proposed standard is designed tobe flexible. As with all ASB standardsof practice, actuaries may deviate fromthe standard as long as they disclosewhy they deviated from the standardand what the effect of the deviation is .

The proposed standard provides gen-eral guidance for setting economic assump-tions . Depending upon the particular valu-ation being performed, any specific rulesconcerning setting assumptions for cer-tain types of valuations [e .g., for purposes

7

of internal Revenue Code Section 412 orStatement ofFinancial Accounting Stan-dards (SFAS) No. 87), would also need tobe considered by the actuary .

The standard emphasizes settingassumptions on an explicit rather thanimplicit basis. The use of select andultimate assumptions may becomemore prevalent. This is especially im-portant when interest rates are highand therefore there is a higher riskassociated with reinvestment.

The standard discusses economicassumptions such as inflation, invest-ment return, salary inreases, and gov-ernment indexes . The assumptionsshould be selected in a consistent man-ner. For example, the same underlyinginflation rate should be used for boththe interest and salary assumptions .

The standard stresses that whilepast experience is important . greateremphasis should be placed on the long-term expectations .

The importance of the asset mix inselecting the interest assumption isdiscussed, as are other considerations,such as the plan's funded status, theasset valuation method, and taxes. Thestandard describes the methodologyfor determining economic assumptionsfrom a combination of elements, i .e . .the "building-block approach ." Thestandard includes the concept of look-ing at the rate of return in three compo-nents, the pure rate (i .e., net of taxes andinflation), inflation, and the tax premium .

One thing the standard does notattempt to do is set a defined range forwhat is to be considered reasonable .The committee discussed the issue . Itdecided that any attempt to define arange of reasonableness could divertthe practitioner from going through ananalytical process in setting the assump-tions, something the committee consid-ers very important. Setting a definedrange could also lead to abuses if therange were simply used as a safe harbor .

Finally, the standard has a second-ary purpose. Users of actuarial com-munications such as pension valua-tions need to understand the views andprinciples that guide actuaries in set-ting economic assumptions .

I hope this brief article has piquedyour interest and will start the discus-sion process a little earlier than theactual exposure date. The ASB and itsPension Committee want to hear fromyou. We want this standard to repre-sent a general consensus within ourprofession, not just the views of theASB and the Pension Committee,

Ingut is a member of the Pension Corn-mtttee of theASB.

8

Long-Term Care Insurance-A NewFederal Presence?

by Gary D. Hendricks

Up until now, private insurance hascome under the states' petview almostexclusively. Medicare supplementalpolicies (i.e., Medigap) and the deter-mination of what constitutes a life in-surance contract are notable excep-tions; these are areas where the federalgovernment has the last word . It nowseems clear that Congress is going toextend the federal presence into a newarea and set consumer-protectionstandards for private long-term care(LTC) Insurance. Several bills intro-duced this year would set federalstandards for LTC policies-what theyshould cover, how they should bemarketed-as well as stipulate how thefederal standards should be imple-mented by the states .

Current Legislation

Last year, several congressional com-mittees, including the House Commit-tee on Energy and Commerce, heldhearings on current practices in privateLTC insurance. As a result of thosehearings, the 102nd Congress is nowconsidering bills that would imposefederal standards on long-term carepolicies.

In February, Representative J . RoyRowland (D-GA), a member of HouseCommittee on Energy and Commerce,introduced the first of these bills, H .R.1205. His bill did not actually set forthfederal standards, instead it called forthe Secretary of Health and HumanServices to undertake a study andsubmit proposed federal standards forcongressional consideration. SinceFebruary, three other bills have beenset before Congress, each of whichwould, in fact, establish federal stan-dards for LTC policies .

In April, Representative Ron Wyden(D-OR) introduced H .R. 1916. On thesame day, Senator David Pryor (D-AR)introduced a companion Senate bill, S .846. Pryor Is an influential member ofthe Senate Finance Committee andChairman of Senate Special Committeeon Aging. In May, Representative TerryL. Bruce (D-IL) Introduced H .R. 2378 .The Wyden. Pryor, and Bruce bills

are all serious proposals . When intro-duced, Wyden's bill had six cospon-sors, five Democrats and one Republi-can-all are important members of the

House. Pryor's companion Senate billhas the strong support of a number ofhis Senate collegues including MajorityLeader George Mitchell. Bruce's billoriginally had six cosponsors . It Islikely that one of these bills, or a com-promise bill, will be enacted during the102nd Congress, which is nearing theend of its first session .

The Wyden/Pryor bill is similar tothe more recent Bruce bill, but thereare some important differences, both inthe means for implementing the stan-dards and in the standards themselves .

Implementing Federal Standards

The Wyden/Pryor bill adopts the ap-proach that the Omnibus Budget Rec-onciliation Act of 1990 (OBRA 90) tooktoward Implementing federal standardsfor Medicare supplementary policies .Under the bills, the National Associa-tion of Insurance Commissioners (NAIC)is required within twelve months ofenactment to promulgate a model lawand regulation for the states to imple-ment. If the NAIC fails to meet itsdeadline, the Secretary of Health andHuman Services is charged with de-veloping the modeflaw and regulationwithin the following twelve months .

The Secretary of Health and HumanServices is also charged with deter-mining whether a state has establisheda program that meets the federalstandards. If a state fails to gain theapproval of the Department of Healthand Human Services, no new LTCpolicies maybe issued in the state, andthe state will be denied federal Medic-aid funds. In addition, persons whooffer a policy for sale in a state that hasnot complied with the federal standardsare subject to a civil penalty not toexceed $25,000 for each violation . Thesame civil penalty applies to issuerswho violate any of the specific standardsset forth in the law and regulations .

The Bruce bill's approach to imple-mentation differs from that found inthe Wyden/Pryor bill. First, the Sec-retary of Health and Human Services,not the NAIL, is charged with promul-gating a regulation to implement thefederal standards. The NAIC is men-tioned only as a consultant in the pro-cess. Second. the Bruce bill containstighter implementation deadlines . The

The Actuarial Update

Department of Health and Human Ser-vices is charged with developing aregulation within six months of anyfederal standards' enactment ; statesthat do not complywithin twelve monmaybe sanctioned. Asunderthebill, the Department of HealthHuman Services is charged with de-termining whether states are in com-pliance .

Proposed Federal Requirements

Both the Wyden/Pryor and Bruce billsinclude a long list of federal standards .Most are very similar, even identical .But, here again, there are some im-portant differences .

Consumer Information : Both theWyden and Bruce bills require con-sumer access to complaint files on LTCpolicies and access to the considerableinformation that companies are requiredto file periodically with each state in-surance department.

The Wyden bill requires state infor-mation filings on the number of LTCpolicies in force, the most recent pre-mium rates, and premium trends forthe previous five years. Also requiredare lapse rates, replacement rates, andrescission rates by agent, and clairry~denied as a percentage of claims smitted .

The Bruce bill includes an equallyextensive but somewhat different list ofinformation . Significantly, the Brucebill makes no reference to reporting onan agent-by-agent basis .

Policyholder Rights : Under both theWyden and Bruce bills, new policy-holders are guaranteed a thirty-dayfree trial during which they can cancelthe policy. If the applicant returns thepolicy or coverage is denied during thethirty days, all premiums must be re-funded. All policies are guaranteedrenewable and cannot be cancelled bythe issuer except for nonpayment ofpremiums or material misrepresenta-tion by the policyholder. The Bruce billqualifies this, however, stating that thepolicy is guaranteed renewable "if thepolicy has not been in effect for 5 years ."

Both bills give policyholders greaterrights by limiting contestability. Underthe Wyden bill, policies cannot becancelled or benefits denied based onfraud or misrepresentation at the timeof issue unless the issuer providesinsured with notice of such fraumisrepresentation within six monthsissue. The Bruce bill would lengthenthe notice period to one year .

September 1991

Both bills also give policyholders theright to an explanation when benefitsare denied and require the issuer toprovide information on the reasons for

ial within sixty days .th bills require guaranteed con-

tinuation and conversion rights forgroup policies. Conversions must bemade to policies with the same orequivalent benefits and cannot requireevidence of insurability. Neither of thebills place restrictions on the premiumsthat can be charged to those who opt toconvert when they terminate coverageunder the group policy.

Preexisting conditions: Policies mayexclude preexisting conditions fromcoverage, but only for the first sixmonths of the policy, and replacementpolicies cannot exclude preexistingconditions at all . Neither can theyrequire any additional waiting period ifany waiting periods under the originalpolicy were already satisfied .

Group replacements must take theentire group without exclusions forconditions that were covered under theoriginal policy. However, underwritingis permitted to the extent that a newpolicy includes coverages that were notincluded in the original policy.

lhefit Standards: The Wyden billrequires that all policies provide for atleast twelve consecutive months ofbenefits. The Bruce bill takes a strongerposition and prohibits a dollar limita-tion on the maximum amount of ben-efits that may be paid under the policy.

Both bills place similar restrictionson conditions that can be used to limitbenefits. For example, both state thata long-term care policy may not con-dition or limit eligibility for one benefitto the need for or receipt of any otherbenefit. Both bills also set minimumstandards for home health care andwould not allow policies to restrict suchbenefits to the need for registerednurses, for example . The Bruce bill issomewhat more explicit by definingdirectly what benefits must include .For example, the bill states that "homehealth care services shall includehomemaker services, assistance withactivities of daily living, and respitecare services ."

Both bills provide that in determin-ing benefits, other than nursing facility

efits, all policies are required to usetional assessments and to specifylevel of functional impairment that

must be reached before obtaining LTCbenefits . Each policy must also provide

policyholderswho dispute the Insurer'sassessment a means to appeal.

Inflation protection: Both the Wydenand Bruce bills require limited protec-tion against inflation and includeidentical provisions . Each policy mustinclude a specified annual percentageincrease ofat least 5% in dollar paymentlevels and maximum payment limits .

Under Wyden's proposal, all policiesmust also specify a limit on the annualpercentage increase in premiums. TheBruce bill is silent in this area .

Nonforfeiture: Wyden's bill requiresthat, if policies lapse after some periodof time (to be determined by the NAIC inits model law and regulation), thepolicies must specify what benefitsthen become available. Available ben-efits must be a percentage of the ben-efits otherwise available at term, or insome other form to be determined bythe NAIC .

The Bruce bill is more explicit . If apolicy lapses after five or more years,the policy must provide benefits equalto at least 30% of the benefits otherwiseavailable at term. Moreover, thespecified percentage is to increaseabove 30% in a manner to be determinedby regulation from the Department ofHealth and Human Services .

Prior rate approval: Both bills requireprior approval of rates by the states .The Wyden bill would require proposedincreases in rates to be accompaniedby an actuarial memorandum. TheBruce bill does not require an actuarialmemorandum but would require thatthe rate increase be based on soundactuarial standards as recognized inregulations . Both bills would requirean opportunity for public commentbefore rates are approved by the states .

Sales Practices: The Wyden bill in-cludes a general requirement regardingduty of good faith and fair dealing andprohibits a number of sales practices,for example, twisting, high-pressuretactics, cold-lead advertising, sale toMedicaid-eligibles, and sale ofduplicateservice-benefit policies . Agents whopractice illegal sales techniques can getfive years in jail and be fined $25,000for each violation. The Bruce bill is notnearly so specific, except with regard toduplicate coverage.

Under the Wyden bill, insurers mustprovide an outline of coverage for newissues and for renewals, and they mustuse standard terminology and uniform

9

format for presenting the outline ofcoverage. The outline of coverage mustinclude (1) a description of principalbenefits; (2) a statement of principalexclusions, reductions, and limitations ;(3) a statement of terms under whichthe policy may be continued or dis-continued; (4) terms for conversion orcontinuation; (5) a reservation of theright to change premiums and a state-ment of the percentage limit on anuualpremium increases ; (6) a statement ofthe value of the policy (to be determinedin .regulations) ; (7) information on na-tional average costs for nursing facili-ties and home health care, and infor-mation (in graphic form) on the value ofthe policy's benefits as compared tosuch national average costs ; and (8)graphic information on the projectedeffect of inflation on the value ofbenefitsduring a twenty-year period .

The Bruce bill, on the other hand,does not outline these details. Rather,the bill states that such an outline ofcoverage shall be based on the NAIC'sLTC Insurance Model Regulation ofDecember 1990 . Neither does the Brucebill require an outline of coverage forpolicy renewals .

The Wyden bill restricts first-yearcompensation for newly issued policiesto no more than 200% of compensationfor the second and subsequent years .The Bruce bill does not restrict com-pensation .

New Trend in Regulation?

The potential, ifnot certain, move towardfederal standards for LTC policies isitself a significant regulatory develop-ment. It is also important because itmay signify a new model for the regu-lation of Insurance products . Thishybrid model combines federal stan-dards with state enforcement and splitssetting standards from setting rates-responsibilities that have traditionallybeen connected . The Wyden/PryorandBruce bills also highlight a more subtleunderlying debate on who will developfuture regulations. Will the NAIC con-tinue to be the predominant promul-gator of model regulations or, as in theBruce bill, will regulations increasinglycome directly from federal agencies?The Bruce bill may well be an indicatorofa change In Congress's basic attitudeaboutwho should be in the driver's seatregarding insurance regulation .

Hendricks is chiefeconomist and direc-tor of government information for theAcademy .

10

A.M. Best ReleasesInsolvency Studyby Jeanne Casey

A recent report released by A.M. BestCompany Is intended to till what Bestcalls the "information void" plaguinglegislative debates on insurer solvencyregulation. Best's Insolvency Study :Property/Casualty Insurers, 1969-1990, is billed as "the most comprehen-sive study to date on the scope, magni-tude and characteristics of the 372property/casualty insolvencies thatoccurred from 1969 to 1990 ." It cer-tainly compiles some interesting data .

Scope of Insolvencies

Over the past twenty-two years, theproperty/casualty industry has gonethrough two complete underwritingcycles . The Best study compares thenumber of Insolvencies that occurredIn 1975, at the end of one underwritingcycle, with the all-time high number ofinsolvencies in 1985.

In 1975, the industry had twenty-nine insolvencies-this number repre-sents 1 .0% of the total number ofproperty/casualty companies . How-ever, these Insolvencies constituted only0.3% of the industry's total premiumswritten .

In 1985, forty-nine companies be-came insolvent-an increase of 69%over the earlier peak in 1975 . Thesefailed companies represented 1 .4% ofall companies and accounted for 1.0%of the industry's premium. Accordingto Best, "In each of the last 22 years, withthe exception of 1985, the premium vol-ume of insolvencies has been less than0.5% of industry's premium volume ."

Insolvencies by State

Fifty percent of all 372 property/ca-sualty insolvencies for the twenty-two-year period occurred in six states . Forty-seven of these companies were domi-ciled in Texas ; thirty-five in California ;thirty-five in Pennsylvania; thirty inNew York; twenty-two in Illinois ; andeighteen in Florida. These six statescombined have regulatory authority over34% of domestic property/casualtyinsurers.

The percentage of insolvencies pernumber of companies domiciled in astate is, on average, 0.7% per year .Florida and California experiencedhigher than the average failure rate,1 .3% and 1 .6% respectively. On the

other hand, Illinois, which has the mostproperty/casualty companies , has hada relatively low failure rate-0.3% .

State Regulatory Resources

In 1990, the five states with the largestbudgets overall (California, New York,Texas, Florida, and North Carolina) spent52% of all regulatory dollars, althoughthese states only had regulatory author-ityfor a bitmore than 20%ofall life/healthand property/casualty insurers.

Budget dollars per domiciled com-pany spent on insurance regulationranged from $3,000 to $343,000 in1990. AM. Best observed that "largestate budgets, relative to the number ofdomiciled companies, did not neces-sarily correlate with lower failure fre-quency experience ."

Company Characteristics

'Small companies (policyholders' sur-plus of $5 million or less) have accountedfor 63% of the insolvencies over thepast 22 years," reports Best. Middle-sized companies (policyholders surplusof $5 to $50 million) accounted for 34%of the insolvencies; large companies, 3%.

However, when the number ofinsolvencies Is taken as a percentage oftotal companies within each of thesesectors, medium-sized companies haveexperienced the highest failure fre-quency. 0.7%. Small and large compa-nies average failure frequencies were0.6% and 0.1% respectively.

"Although the industry's companiesare almost evenly divided between stockand mutual ownership, stock compa-nies have experienced an average fail-ure frequency more than four timesgreater than that of mutual companies ."Best reports .

Companies that experienced pre-mium growth greater than the industrynorm of 5% to 25% accounted for 81%of all insolvencies .

The report also discussed economicfactors such as inflation and interestrates and their effects on the industryand its underwriting cycle .

Causes of Insolvencies

Together, deficient loss reserves, linkedwith Inadequate product pricing, andrapid growth accounted for 50% of theinsolvencies for which Best was able toidentify primary causes. Alleged fraudwas identified as the cause of insolvencyIn 10% of the cases, as were overstatedassets. Other causes included signifi-cant change in business (9%), reinsurancefailure (7%), catastrophe losses (6%) .

The Actuarial Update

Best concluded that, "with the pos-sible exception of catastrophe losses,all the causes of insolvencies involvedsome form of company mismanagement ."

On the basis of its study, AM . )makes some general recommendatifor improving solvency regulation, in-cluding:

• Regulators should target high-riskcompanies for more frequent reviews .

• Regulators should focus attentionon companies that AM. Best and otherqualified rating agencies have identifiedas high-risk companies .

• Companies that are not rated byqualified rating agencies should beclosely monitored .

• Licensing should require risk-ad-justed capitalization in order to reflectthe degrees of risk associated with dif-ferent lines of business.

• Stiffer fines and penalties shouldbe levied in cases of fraudulent finan-cial reporting .

Best said It did not "expect theIndustry's current underwriting down-turn which began in 1988 to be asprolonged nor as severe as the 1978through 1984 soft cycle ." Rather, Bestexpects the property/casualtyindustry's annual failure frequency topeak at 1.1% ofall companies-that's atotal of 45 insolvencies-in 19921993. The percentage of tnsolvencieeindustry premium volume will remainwell below 1 .0%, Best said.

If you would like to receive a copy of thereport, please contact A .M. Best's cus-tomer service department at (908) 439-2200, ext. 5552.

Look for a story on the changes instorefor the A .M. Best rating sys-tem in an upcoming Update.

Name Changefor CAPP Approved,~""It, As of September 1, theMme Conference of Actuaries

in Public Practice (CAPP)will be called the Confer-

ence of Consulting Actuaries (cm) .The organization's leadership rec-ommended the change because itbelieved that the new name wouldbetter reflect the organization'sfocus on the consulting actuary'perspective . The proposed changwas approved by a membershipvote In May.

September 1991

Medicaid Task ForceReleases Report

ohn Hlemm

Medicaid costs in the aggregate arecurrently growing at an annual rate ofover 25%, with rates in some statesexceeding 50%. These extraordinaryrates of growth have considerably ex-ceeded federal and state budget pro-jections . If this trend continues, by themid- 1990s, combined federal and stateMedicaid spending may surpass Medi-care spending.

As mentioned in the July Update, lastApril the Bush Administration ap-pointed a "swat team" to examine thesubstantial and unexpected increasesin recent spending under the federal-state Medicaid program, which financeshealth care for 27 million low-incomeAmericans. The swat team compriseda joint task force of officials from theDepartment of Health and HumanServices (HHS), Office of Managementand Budget (OMB), and CongressionalBudget Office .

The work of the joint task force,which included on-site visits to nineAges and an independent actuary's

w of the Medicaid budget process,c minted In the report Better Man-agementfor Better Medicaid Estimates,Issued by HHS and OMB on July 10.

The report concludes that about two-thirds of the shortfall in recent Medic-aid budget estimates is attributable tochanges In federal and state legislationand policies that were not anticipatedby budget estimators, for example, theuse of refundable donations and pro-vider-specific taxes to leverage federalfunds. The report asserts that greaterattention to Medicaid estimating at bothfederal and state levels could provideearlier warning of Medicaid trends andminimize the budget "shocks" that haverecently plagued the system .

The report specifically recommendsconsolidating responsibility for federalMedicaid functions within the MedicaidBureau of the Health Care FinancingAdministration (HCFA). It also calls foran expanded role for HCFA, particularlythe Medicaid actuaries, in monitoringand reviewing state Medicaid budgetactivities and developments-including

eking Medicaid policy proposals instate and developing independent-by-state federal Medicaid forecasts

as a check on states' own estimates .Thirdly, it recommends enhancing thefederal-state Medicaid partnership by

providing feedback on the accuracy ofstates' estimates as well as sharingIdeas for improving the estimates .

The task force's recommendationsare now being implemented at HCFAunder very tight time constraints . Thetask force asks that improved datacollection and systems for monitoringstate activities be developed by the endof the year.

The current effort is not the first one

Academy Speaks Out

FASB Gets Comments onPresent Value Accounting

In December 1990, the Financial Ac-counting Standards Board (FASB) re-leased its discussion memorandumPresent Value-Based Measurements inAccounting. Now under considerationby FASB is how and when present-value-based measurements should beused instead of undiscounted mea-surements for accounting purposes .(See related article in the February 1991Update.) The Academy's Committee onProperty and Liability Financial Re-porting, chaired by David G. Hartman,formally commented on the discussionmemorandum in a July 9 letter to theFASB .. The committee also plans totestify at the FASB hearings In lateAugust .

Much of the Academy committee'seight pages of comments focus on theaspect of risk and how best to recog-nize risk in discounted measurements .Currently, property/casualty insurancecompanies usually present their claimliabilities on an undiscounted basis .This practice is recognized undergenerally accepted accounting prin-ciples (GAAP), presumably becausethere Is too much uncertainty in thetiming and amount of loss paymentsfor property/casualty insurers to usepresent-value-based measurementsappropriately.

"As actuaries, we regularly deal withthe practical aspects of decision-mak-ing based on the valuation of 'risky'cash flows or forecasted earningstreams," the committee said . Anychange in the current practice shouldrequire risk to be taken into account ."Adopting a present-value techniquefor the claim liability, without consid-eration ofthe risk associated with claim

I1

to be directed at improving federal over-sight of the Medicaid program, but it isthe first to have the force of an official"swat team" behind it.

Klemm is a supervisory actuary with theHealth Care Financing Administrationand was himself a member of the Med-icaid swat team. Klemm was inter-viewed in, the June 1991 Update .

reserves, results in less reliable finan-cial statements," the committee as-serted .

The committee referred to the Actu-arial Standards Board's proposed ac-tuarial standard of practice titledDiscounting of Property and CasualtyLoss and Loss Adjustment Expense Re-serves, which would require that theactuary "consider the degree of uncer-tainty inherent in loss reserve projec-tions." (See announcement on page 1 .)The committee stated that present-value-based calculations are possibleto do, but as the ASB proposed standardon discounting indicates, "risk must beconsidered when those calculations aremade." In sum, "present-value-basedmeasurement of claim liabilities is anincomplete adjustment to GAAP fi-nancial reporting. Consideration ofuncertainty is also required ."

"There are practical ways to includerisk in present-value-based measure-ments and to handle the theoreticaland implementation issues raised inthe discussion memorandum," thecommittee said . "Assuming that assetsare valued at market value, liabilitiesshould be discounted at a risk-adjustedinterest rate, which is a risk-free rateadjusted downward . The risk-free rateshould consider the term structure ofthe liabilities and the risk adjustmentshould consider the risks in manage-ment's best estimate of that structure ."

If the risk question Is resolved prop-erly," the committee said, it believesthat present-value-based measure-ments can be used when marketplacevalues are unavailable and presentvalue best serves the measurementobjective. The committee will be work-ing with the FASB to ensure that therisk question is properly resolved .

The committee's full statement is avail-able from the Academy's Washingtonoffice. Please request PS-91 C-9 .

12

Standards Outlookby Christine Nickerson

The Actuarial Standards Board's (ASB)agenda far its July meeting illustrates wellthe variety of ASS projects. What followsis a report on the board's recent actions .

LTC Standard AdoptedThe first order of business was a review ofthe proposed flnalversion of a standard forlong-term care insurance. Bartley Munson,chair of the Task Force on Long-TermCare, reviewed the draftwith the ASB . Theboard noted that the proposed standardcontains more background and educa-tional material than some other standards,but decided that such material is appro-priate because long-term care is a newlyemerging area of actuarial practice .

The board spent some time discussingthe section dealing with actuarial as-sumptions and premiums. Munson notedthat it is an important issue for consum-ers. The board emphasized that the stan-dard should make clear that assumptionsmust be consistent with any guaranteesin the terms and provisions of the policy .

Minor changes to the proposed stan-dard were suggested, mostly for purposesof clarification. The board voted unani-mously In favor of adopting the proposalas a standard of practice.

Cash Flow Testing

Douglas Collins, Joint Casualty/Life CashFlow Testing Task Force chairperson,presented the proposed final version ofthe standard, Performing Cash Flow Test-ing for Insurers .

Development of actuarial standards ofpractice in the area of how to performcash flow testing was originally under-taken separately for the life and healthand the property/casualty specialites .The first to be published was ActuarialStandard of Practice No.7, ConcerningCash Flow Testing for Life and HealthInsurance Companies. When the Casu-alty Committee of the ASB undertookdevelopment of a parallel standard, theboard decided there should be a singlestandard on performing cash flow testingthat would apply both to life and healthinsurers and to property/casualty insur-ers. The board therefore appointed a jointcasualty/life task force to draft a new stan-dard applicable to both practice areas .

Upon reviewing the draft of the pro-posed standard, Performing Cash FlowTestingfor Insurers, at the July meeting,the board voiced concern about thestandard's use of the term "hypotheticalassets ." The board asked the task force tohave the standard specify that it is notappropriate for a company to use the

same asset more than once to supportdifferent liabilities. Other clarificationswere also suggested.

The board voted to adopt the proposedstandard, which, when published, willreplace the current version of ActuarialStandard ofPractice No. 7.

Economic Assumptions for Pensions

Also under review at the meeting was anexposure draft of a proposed standard onselecting economic assumptions for pen-sion plans. The previously promulgatedActuarial Standard ofPractice No. 4, Mea-suringPension Obligations, contains somegeneral principles for selecting demo-graphic and economic assumptions .However, in recent years, regulatory andother changes in the pension environ-ment have created a need for more spe-cific and detailed guidance, especially inthe selection of economic assumptions .(See article on page 7 .)

Silvfo ingui, a member of the ASB Pen-sion Committee, presented the draftstandard on economic assumptions to theboard. The ASB reviewed the proposaland decided that, while it contained agreat deal of good material, It was notready for exposure . The board asked thecommittee to rework the document andbring it to the October ASB meeting .

Financial Reporting Standards

When the ASB was established in 1988,it undertook to reformat existing stan-dards of practice into a uniform format .Currently, the Life Committee of the ASBis working on revising and reformattingthe various Financial Reporting Recom-mendations and Interpretations relatedto life insurance . At the July meeting,Life Committee Chairperson HaroldIngraham presented revised versions ofRecommendation 2, Relations with theAuditor, and Recommendation 7, State-ment ofActuarial Opinion for Life Insur-ance Company Annual Statements .

Recommendation 2 was first pub-lished by the Academy in 1974 and wasupdated in 1983. In addition to replacingRecommendation 2, the currently pro-posed revision would also incorporatesome language from Recommendation 3,Actuarial Report and Statement of Actu-arial Opinion. The board reviewed the LifeCommittee's revision of Recommendation2 and voted to release it as an exposuredraft because of significant revisions .

The board also reviewed Recommen-dation 7, Statement of Actuarial OpinionforLiifeInsurance CompanyAnnual State-ments. Recommendation 7 was originallypromulgated by the Academy in 1975, inresponse to the National Association ofInsurance Commissioners' (NAIC) re-quirement that a statement of actuarialopinion on reserves and other actuarial

The Actuarial Update

items accompany the submission of lifeand accident and health annual state-ments to state regulatory authorities .

The board's consideration of the newlyrevised Recommendation 7was cocated by the fact that the NAIC neeadopted a new Standard Valuation Lawand model regulation for the actuarialopinion and memorandum. Because ofthese changes in the law and regulation,the board expressed concern that therevised version would be of decliningvalue when released. Therefore, theASBtook no action on the revised standardand asked the Life Committee to considerfurther how best to address the situation .

SFAS 106 Compliance GuidelineThe board .also reviewed a preliminarydraft of an actuarial compliance guide-line for StatementofFlnancialAccountingStandards (SFAS) No. 106, Employers' Ac-countingfor Postretirement Benefits OtherThan Pensions. The compliance guidelinewould provide guidance on the actuarialcalculations required by SFAS 106 .

Retiree Health Care Committee Chair-person RobertHaver discussed this projectwith the board . He explained the difficultyin drafting such a guideline. Retireewelfare benefit valuations for the purposeof the accruals required by SFAS 106 area new area of practice for actuaries, re-quiring experience and skill usually fin two different areas of practice, penand group health benefits. Haver said ethat the guideline would be aimed atactuaries who are familiar either withpension or group health benefits and whoare starting to do SFAS 106 calculations .The guideline would point out areas thatcould cause problems for a practitionernew to this work as well as give generalguidance. The board supported thecommittee's approach. The committee willcontinue to work on drafting the guideline .

Loss Reserve DiscountingThe board decided to hold a public hear-ing on the proposed loss reserve dis-counting standard on September 25, inconjunction with this year's CasualtyLoss Reserve Seminar. (See announce-ment enclosed with this Update mailing.)

The proposed standard, Discountingof Property and Casualty Lossand LossAdjustment Expense Reserves, was re-leased as a second exposure draft inJanuary 1991, with a comment dead-line of April 30, 1991 . The proposedstandard would define the issues andconsiderations that an actuary shouldtake Into account in determiningcounted property or casualty lossor toss adjustment expense reserve

ickerson is director of the standardsprogram.