volatility. downloads today’s work is in: matlab_lec04.m functions we need today: simsec.m,...

TRANSCRIPT

Volatility

Downloads

Today’s work is in: matlab_lec04.m

Functions we need today: simsec.m, simsecJ.m, simsecSV.m

Datasets we need today: data_msft.m

Homework 1

function r=simsec(mu,sigma,T);x=randn(T,1); for t=1:T; r(t,1)=exp(mu+sigma*x(t))-1;end;

Simulate Simple Process

>>data_msft;>>subplot(2,1,1); hist(msft(:,4),[-.2:.01:.2]);>>sigma=std(msft(:,4)); >>mu=mean(msft(:,4))-.5*sigma^2;

T=length(msft); >>r=simsec(mu,sigma,T);>>disp([mean(msft(:,4)) mean(r)]);>>disp([std(msft(:,4)) std(r)]);>>disp([skewness(msft(:,4)) skewness(r)]);>>disp([kurtosis(msft(:,4)) kurtosis(r)]);>>subplot(2,1,2); hist(r,[-.2:.01:.2]);

Compare simulated to actual

Mean, standard deviation, skewness match well

Kurtosis (extreme events) does not match well

Actual has much more mass in the tails (fat tails)

This is extremely important for option pricing!

CLT fails when tails are “too” fat

ModellingVolatility

How to make tales fatter? Add jumps to log normal distribution to

make tails fatter Jumps also help with modeling default Make volatility predictable: Stochastic volatility, governed by state

variable ARCH process (2003 Nobel prize, Rob

Engle)

Jumps

R(t)=exp(µ+σ*X(t)+J(t)) J(t)=J1 with p1, J2 with p2, 0 with 1-p1-p2

>>nlow=sum(msft(:,4)<-.1);>>nhigh=sum(msft(:,4)>.1);>>[T a]=size(msft);>>p1=nlow/T; p2=nhigh/T; >>J1=-.15; J2=.15;

Simulating Jumps

function r=simsecJ(mu,sigma,J1,J2,p1,p2,T);x=randn(T,1); y=rand(T,1);for t=1:T; if y(t)<p1; J(t)=J1; elseif y(t)<p1+p2; J(t)=J2; else J(t)=0; end; r(t)=exp(mu+sigma*x(t)+J(t))-1;end;

Simulating Jumps

>>r=simsecJ(mu,sigma,J1,J2,p1,p2,T);>>disp([mean(msft(:,4)) mean(r)]);>>disp([std(msft(:,4)) std(r)]);>>disp([skewness(msft(:,4)) skewness(r)]);>>disp([kurtosis(msft(:,4)) kurtosis(r)]);>>subplot(2,1,2); hist(r,[-.2:.01:.2]); %Note that kurtosis of simulated now

matches actual

Stochastic Volatility

Suppose volatility was not constant, but changed through time and was predictable

This is very realistic, volatility tends to be much higher during recessions than expansions; high volatility tends to predict high volatility

That is sigma is replaced by sigma(t)=f(Z(t)) where Z(t) is a random variable

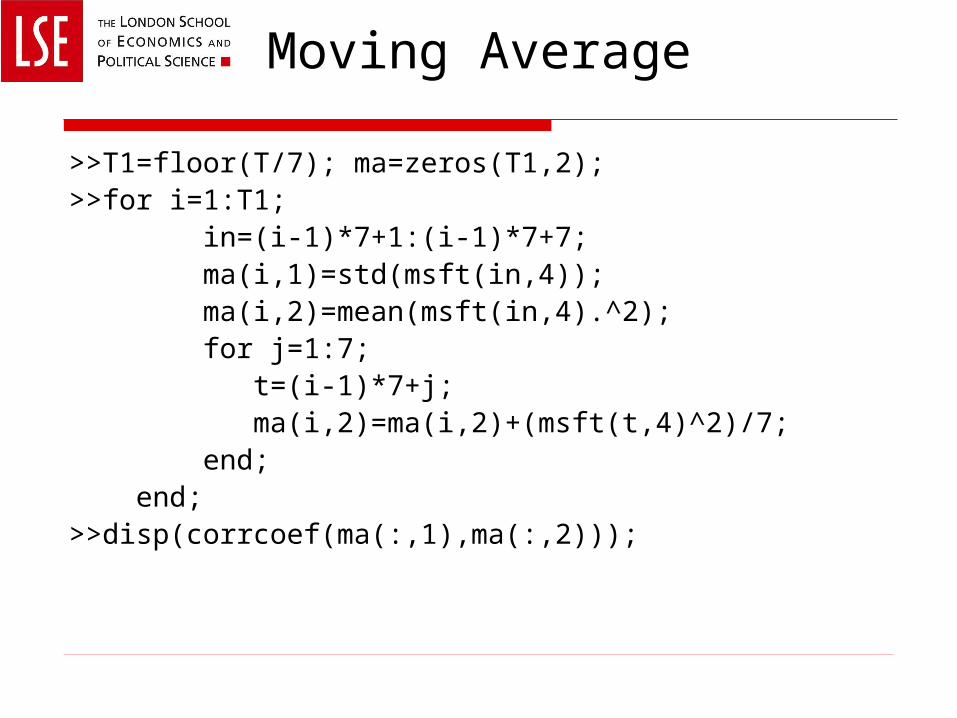

Moving Average

When we have a long time series of data we can calculate the local average a few points around each point in time, this is called a moving average

We will write code to calculate a moving average and use it to analyze stochastic volatility (to be used later as well)

Moving Average

>>T1=floor(T/7); ma=zeros(T1,2);>>for i=1:T1; in=(i-1)*7+1:(i-1)*7+7; ma(i,1)=std(msft(in,4)); ma(i,2)=mean(msft(in,4).^2); for j=1:7; t=(i-1)*7+j; ma(i,2)=ma(i,2)+(msft(t,4)^2)/7; end; end;>>disp(corrcoef(ma(:,1),ma(:,2)));

>>subplot(3,1,1); plot(ma(:,1));>>subplot(3,1,2); plot(ma(:,2));>>WN=exp(randn(T1,1)); subplot(3,1,3); plot(WN);

regress()

regcoef=regress(Y,X) regresses vector time series Y on multiple time series in X

regcoef contains the regression coefficients Y must be Tx1, X must be TxN where N is the

number of regressors If you want a constant in your regression, first

column of X must be all 1’s ie y(t)=A+B*x(t), than Y=[y(1); y(2); … y(T)], X=[1 x(1); 1 x(2); … 1 x(T)] [a1 a2]=regress(Y,X) gives coefficients in a1, and

95% bounds in a2 [a1 a2 a3 a4 a5]=regress(Y,X) gives coefficients

in a1, 95% bounds in a2, R2 in a5(1)

No predictability in WN

>>X=[ones(T1-1,1) WN(1:T1-1,1)];>>Y=WN(2:T1,1);>>[regcoef sterr a3 a4 rsq]=regress(Y,X);>>disp([regcoef sterr]);

Note regcoef(2) is close to zero and sterr(2,:) is not significant disp(rsq(1));

Note, R2 is close to zero

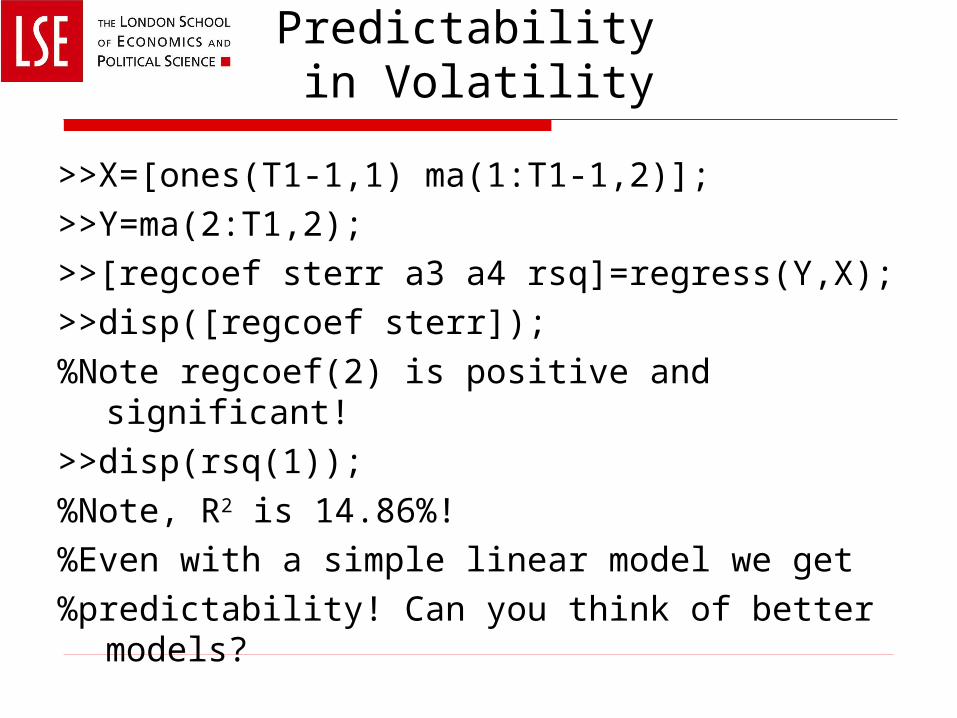

Predictability in Volatility

>>X=[ones(T1-1,1) ma(1:T1-1,2)];>>Y=ma(2:T1,2);>>[regcoef sterr a3 a4 rsq]=regress(Y,X);>>disp([regcoef sterr]);%Note regcoef(2) is positive and significant!>>disp(rsq(1));%Note, R2 is 14.86%!%Even with a simple linear model we get%predictability! Can you think of better models?

Scatter Plot

>>subplot(2,1,1); plot(WN(1:T1-1,1),WN(2:T1,1),'.'); >>subplot(2,1,2); plot(ma(1:T1-1,2),ma(2:T1,2),'.');

Discrete, Markov volatility

sigma(t)=.015 or .025 (daily) When sigma(t)=.015, it will be .015 with

probability .9 tomorrow, and will be .025 with probability .1 tomorrow

When sigma(t)=.025, it will be .025 with probability .9 tomorrow, and will be .015 with probability .1 tomorrow

Transition probability matrix: [.9 .1; .1 .9] This is a 2-state Markov process, it is

predictable, when sigma(t) is high, it is likely to stay high

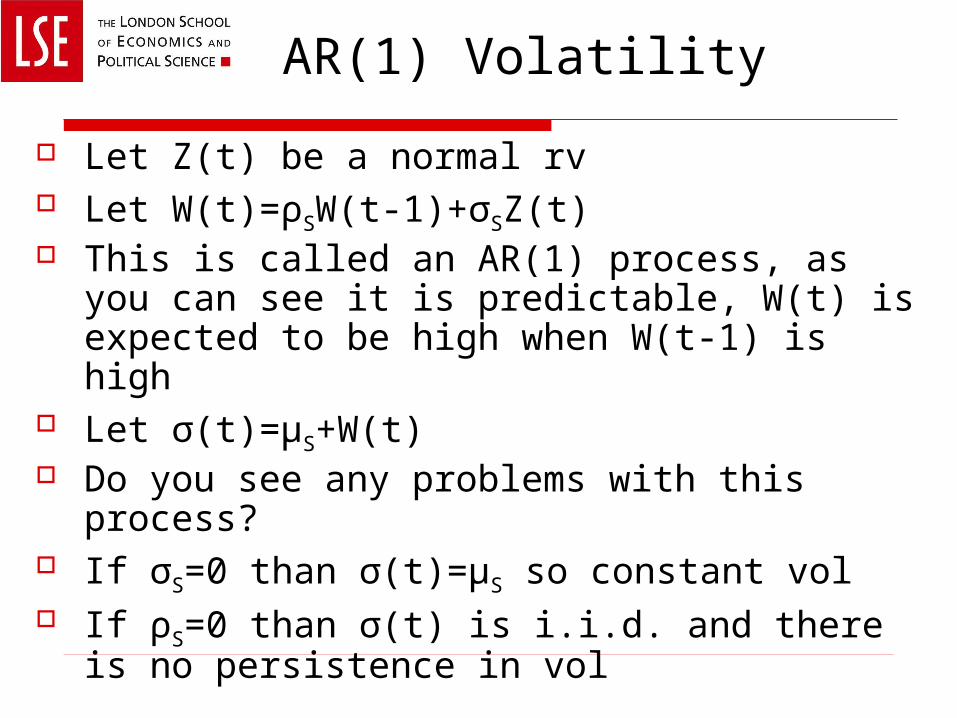

AR(1) Volatility

Let Z(t) be a normal rv Let W(t)=ρSW(t-1)+σSZ(t) This is called an AR(1) process, as you can

see it is predictable, W(t) is expected to be high when W(t-1) is high

Let σ(t)=µS+W(t) Do you see any problems with this process? If σS=0 than σ(t)=µS so constant vol If ρS=0 than σ(t) is i.i.d. and there is no

persistence in vol

Simulating Stochastic Vol

function r=simsecSV(mu,muS,J1,J2,p1,p2,rho,sigmaS,T);x=randn(T,1); y=rand(T,1); z=randn(T+1,1); W(1)=0;J=zeros(T,1); r=zeros(T,1);for t=1:T; W(t+1)=rho*W(t)+sigmaS*z(t+1); sigma(t)=abs(muS+W(t)); if y(t)<p1; J(t)=J1; elseif y(t)<p1+p2; J(t)=J2; else J(t)=0; end; r(t)=exp(mu+sigma(t)*x(t)+J(t))-1;end;

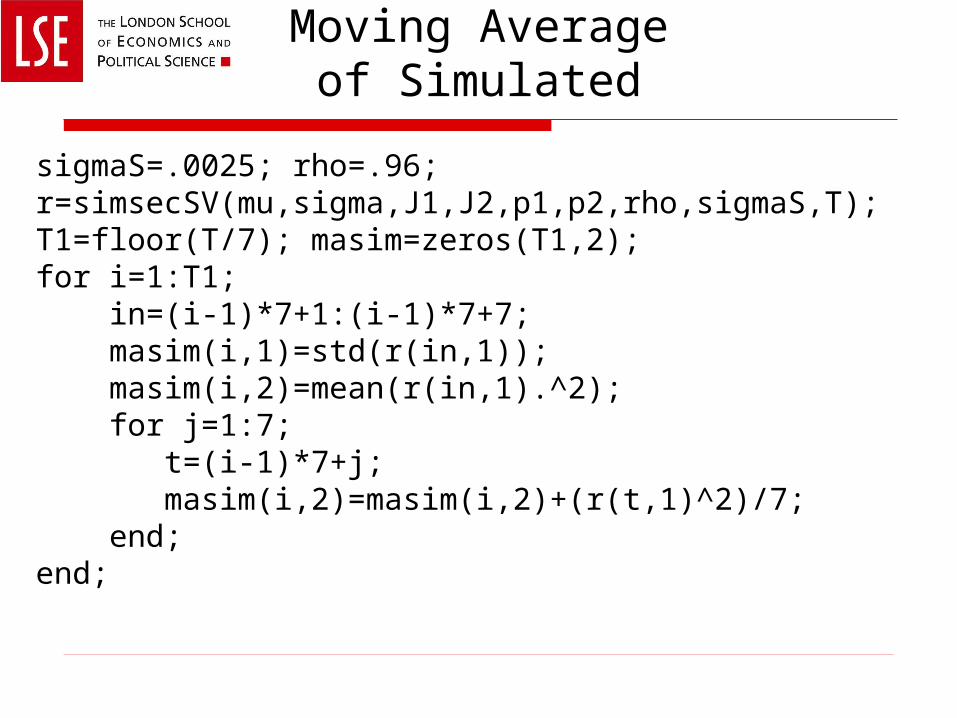

Moving Averageof Simulated

sigmaS=.0025; rho=.96;r=simsecSV(mu,sigma,J1,J2,p1,p2,rho,sigmaS,T);T1=floor(T/7); masim=zeros(T1,2);for i=1:T1; in=(i-1)*7+1:(i-1)*7+7; masim(i,1)=std(r(in,1)); masim(i,2)=mean(r(in,1).^2); for j=1:7; t=(i-1)*7+j; masim(i,2)=masim(i,2)+(r(t,1)^2)/7; end;end;

>>X=[ones(T1-1,1) masim(1:T1-1,1)]; Y=masim(2:T1,1);>>[regcoef sterr a3 a4 rsq]=regress(Y,X);>>disp([regcoef sterr]); disp(rsq(1));>>subplot(2,1,1); plot(ma(:,1))>>subplot(2,1,2); plot(masim(:,1));

OptionalHomework (2)

Use the function from Homework (1) to simulate Microsoft daily returns for a period of a year many times, over and over again

Each time record the total return for the year This is called Monte-Carlo simulation How likely is it that Microsoft loses 30% in one year? How

likely is it to lose 40%? Separate the worst 5% of years from the next 95%. What is

the value lost at the 5% break? This is called Value at Risk, it is a commonly used risk measure

How sensitive is Value at Risk to jump parameters? Jump events are quite rare, do you think they are easy to estimate?

OptionalHomework (3)

Extend the model by adding stochastic volatility, try both the discrete Markov and the AR(1) process (AR(1) case done in class in file simsecSV.m)

How does this change kurtosis and likelyhood of tail events?

Plot a time series of squared Microsoft returns and squared simulated returns (with and without stochastic volatility)

Does it look like high times are followed by high times in the data? In the model with no stochastic vol? In the model with stochastic vol?

Do you see any problems with the AR(1) formulation for volatility?

Does Value at Risk change during high volatility and low volatility times?