visit umt online at 10-1 acct125© 2006 umt accounting fundamentals for managers university of...

TRANSCRIPT

Visit UMT online at www.umtweb.edu 10-1ACCT125© 2006 UMT

ACCOUNTING ACCOUNTING FUNDAMENTALS FOR FUNDAMENTALS FOR

MANAGERSMANAGERS

University of Management and Technology1901 North Fort Myer Drive

Arlington, VA 22209Voice: (703) 516-0035 Fax: (703) 516-0985

Website: www.umtweb.edu

Visit UMT online at www.umtweb.edu 10-2ACCT125© 2006 UMT

Carl S. WarrenCarl S. WarrenSurvey of AccountingSurvey of Accounting (2 (2ndnd ed.) ed.)

© 2004 South-Western© 2004 South-Western

10-3Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Task Force Clip Art Task Force Clip Art included in this electronic included in this electronic presentation is used with presentation is used with

the permission of New the permission of New Vision Technology of Vision Technology of

Nepean Ontario, Canada.Nepean Ontario, Canada.

Visit UMT online at www.umtweb.edu 10-4ACCT125© 2006 UMT

Chapter 10Chapter 10

Accounting Systems for Accounting Systems for Manufacturing BusinessesManufacturing Businesses

10-5Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

ContinuedContinuedContinuedContinued

Learning ObjectivesLearning Objectives

1. Distinguish the activities of a manufacturing business from those of a merchandise or service business.

2. Define and illustrate materials, factory labor, and factory overhead costs.

3. Describe accounting systems used by manufacturing businesses.

4. Describe and illustrate a job order cost accounting system.

After studying this After studying this chapter, you should chapter, you should

be able to:be able to:

After studying this After studying this chapter, you should chapter, you should

be able to:be able to:

10-6Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Learning ObjectivesLearning Objectives

5. Use job order cost information for decision making.

6. Diagram the flow of costs for a service business that uses a job order cost accounting system.

7. Describe just-in-time manufacturing.

8. Describe and illustrate the use of activity-based costing in a service business.

10-7Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

1Distinguish the activities of a manufacturing business from those of a merchandise or service business.

Learning ObjectiveLearning Objective

10-8Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

MerchandisingMerchandisingMerchandisingMerchandising

ManufacturingManufacturingManufacturingManufacturing

Reports:Cost of merchandise soldMerchandise inventory

Reports:Cost of goods soldMaterials inventoryWork in process inventoryFinished goods inventory

10-9Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

2Define and illustrate materials, factory labor, and factory overhead costs.

Learning ObjectiveLearning Objective

10-10Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Cost ClassificationsCost Classifications

PeriodPeriodCostsCosts

PeriodPeriodCostsCosts

SellingExpenses

SellingExpenses

AdministrativeExpenses

AdministrativeExpenses

DirectMaterials

DirectMaterials

FactoryOverhead

FactoryOverhead

DirectLabor

DirectLabor

ProductProductCostsCosts

ProductProductCostsCosts

10-11Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Manufacturing CostsManufacturing Costs

1. Enters directly into the product.2. Is significant amount of total product cost.

1. Enters directly into manufacturing the product.2. Is significant amount of total product cost.

Cost other than direct materials cost and direct labor cost incurred in the manufacturing of product.

Direct Materials:Direct Materials:

Direct Labor:Direct Labor:

Factory Overhead:Factory Overhead:

10-12Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

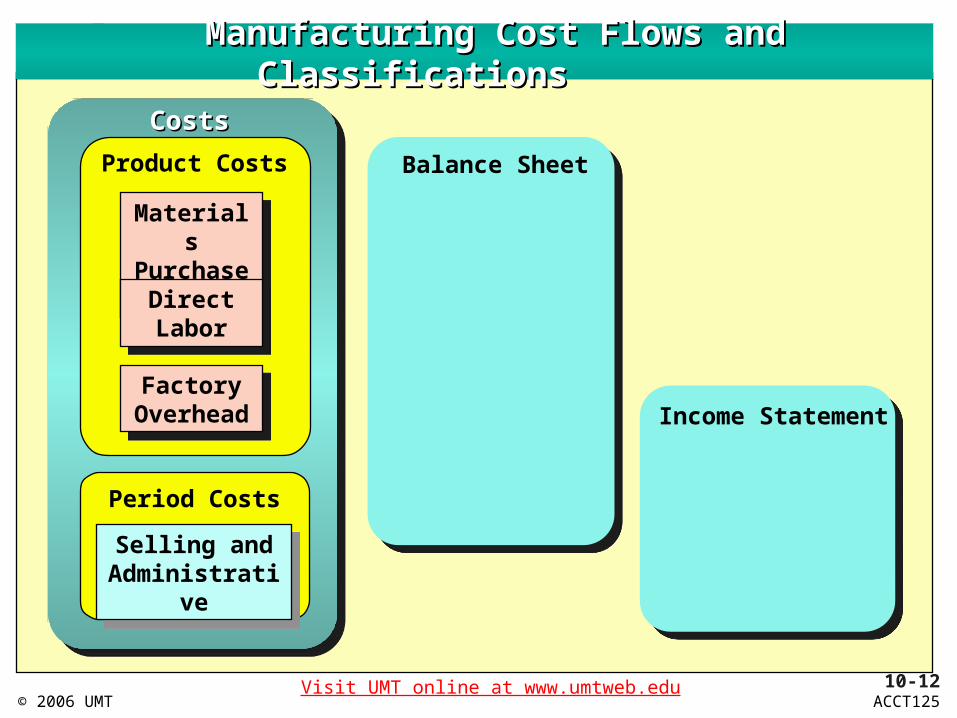

Manufacturing Cost Flows and Classifications Manufacturing Cost Flows and Classifications

Product Costs

MaterialsPurchases

MaterialsPurchases

Period Costs

DirectLabor

DirectLabor

Factory Overhead

Factory Overhead

Selling andAdministrative

Selling andAdministrative

CostsCosts

Balance Sheet

Income Statement

10-13Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

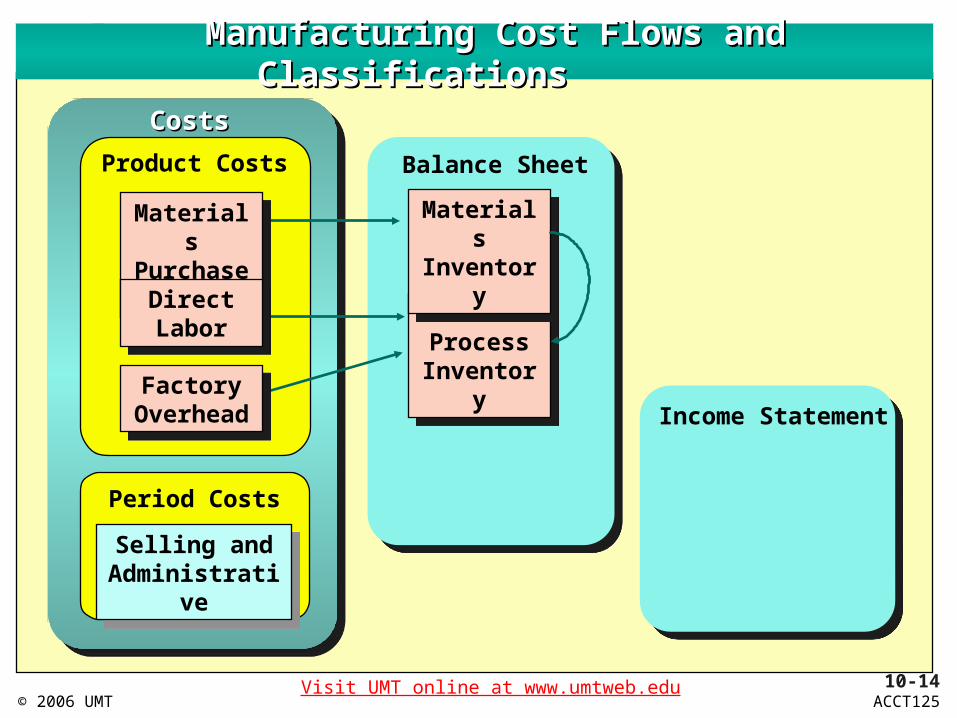

Balance Sheet

MaterialsInventory

MaterialsInventory

Manufacturing Cost Flows and Classifications Manufacturing Cost Flows and Classifications

Product Costs

MaterialsPurchases

MaterialsPurchases

Period Costs

Income Statement

DirectLabor

DirectLabor

Factory Overhead

Factory Overhead

Selling andAdministrative

Selling andAdministrative

CostsCosts

10-14Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Work inProcess

Inventory

Work inProcess

Inventory

Balance Sheet

MaterialsInventory

MaterialsInventory

Manufacturing Cost Flows and Classifications Manufacturing Cost Flows and Classifications

Product Costs

MaterialsPurchases

MaterialsPurchases

Period Costs

Income Statement

DirectLabor

DirectLabor

Factory Overhead

Factory Overhead

Selling andAdministrative

Selling andAdministrative

CostsCosts

10-15Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

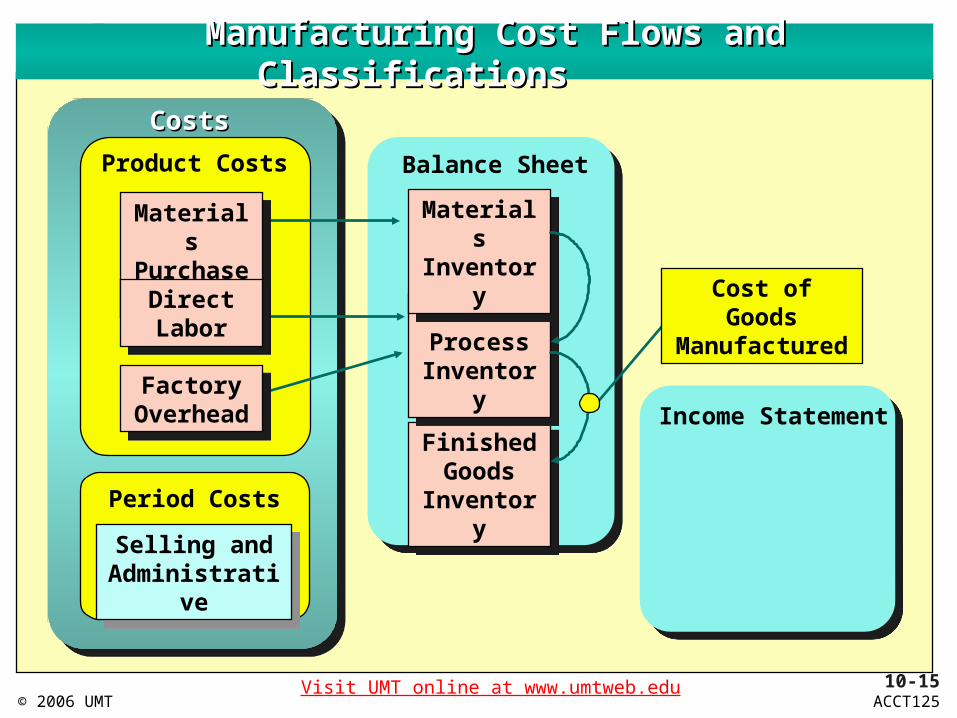

FinishedGoods

Inventory

FinishedGoods

Inventory

Work inProcess

Inventory

Work inProcess

Inventory

Balance Sheet

MaterialsInventory

MaterialsInventory

Manufacturing Cost Flows and Classifications Manufacturing Cost Flows and Classifications

Product Costs

MaterialsPurchases

MaterialsPurchases

Period Costs

Income Statement

DirectLabor

DirectLabor

Factory Overhead

Factory Overhead

Selling andAdministrative

Selling andAdministrative

CostsCosts

Cost of Goods Manufactured

10-16Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Cost of

Goods Sold

Cost ofGoods Sold

FinishedGoods

Inventory

FinishedGoods

Inventory

Work inProcess

Inventory

Work inProcess

Inventory

Balance Sheet

MaterialsInventory

MaterialsInventory

Manufacturing Cost Flows and Classifications Manufacturing Cost Flows and Classifications

Product Costs

MaterialsPurchases

MaterialsPurchases

Period Costs

Income Statement

DirectLabor

DirectLabor

Factory Overhead

Factory Overhead

Selling andAdministrative

Selling andAdministrative

CostsCosts

Product costs flow through the balance sheet to

the income statement

Product costs flow through the balance sheet to

the income statement

10-17Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Selling and

Administrative

Selling andAdministrative

Cost ofGoods Sold

Cost ofGoods Sold

FinishedGoods

Inventory

FinishedGoods

Inventory

Work inProcess

Inventory

Work inProcess

Inventory

Balance Sheet

MaterialsInventory

MaterialsInventory

Manufacturing Cost Flows and Classifications Manufacturing Cost Flows and Classifications

Product Costs

MaterialsPurchases

MaterialsPurchases

Period Costs

Income Statement

DirectLabor

DirectLabor

Factory Overhead

Factory Overhead

Selling andAdministrative

Selling andAdministrative

CostsCosts

Period costs flow directly to the

income statement

Period costs flow directly to the

income statement

10-18Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

3Describe accounting systems used by manufacturing businesses.

Learning ObjectiveLearning Objective

10-19Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

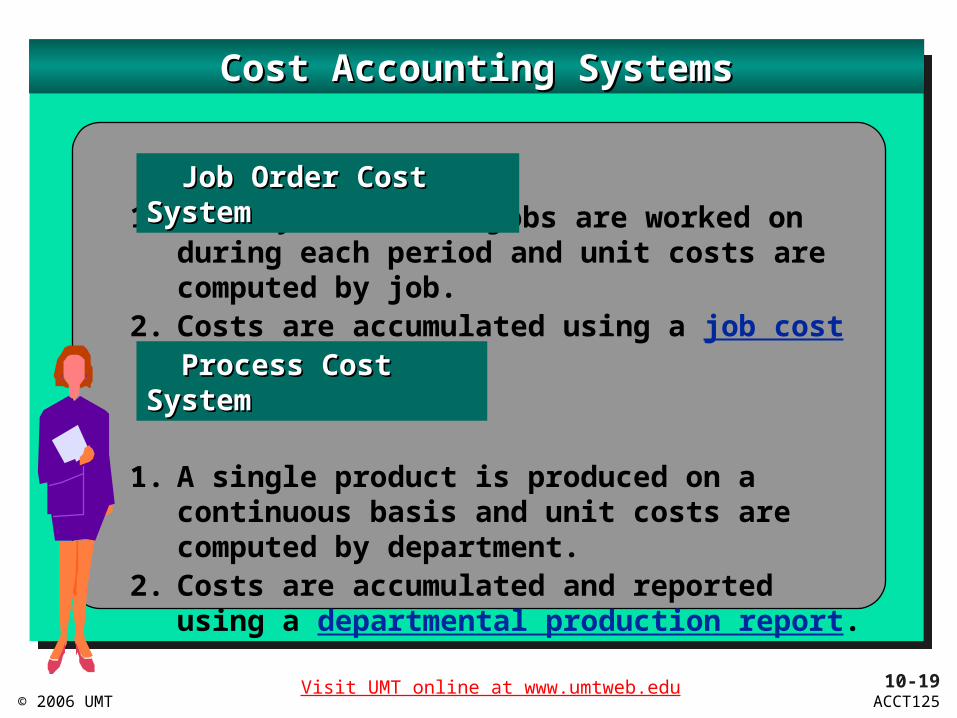

Cost Accounting SystemsCost Accounting Systems

1. Many different jobs are worked on during each period and unit costs are computed by job.

2. Costs are accumulated using a job cost sheet.

1. A single product is produced on a continuous basis and unit costs are computed by department.

2. Costs are accumulated and reported using a departmental production report.

Job Order Cost SystemJob Order Cost System

Process Cost SystemProcess Cost System

10-20Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

4Describe and illustrate a job order cost accounting system.

Learning ObjectiveLearning Objective

10-21Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Materials Information and Cost FlowsMaterials Information and Cost Flows

Job 711,000 units of American History

Balance $ 3,000Direct Materials Direct Labor Factory Overhead

Job 724,000 units of Algebra

Direct Materials Direct Labor Factory Overhead

Materials Requisitions

10-22Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Materials Information and Cost FlowsMaterials Information and Cost Flows

Job 711,000 units of American History

Balance $ 3,000Direct Materials 2,000Direct Labor Factory Overhead

Job 724,000 units of Algebra

Direct Materials $11,000Direct Labor Factory Overhead

Materials Requisitions

10-23Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

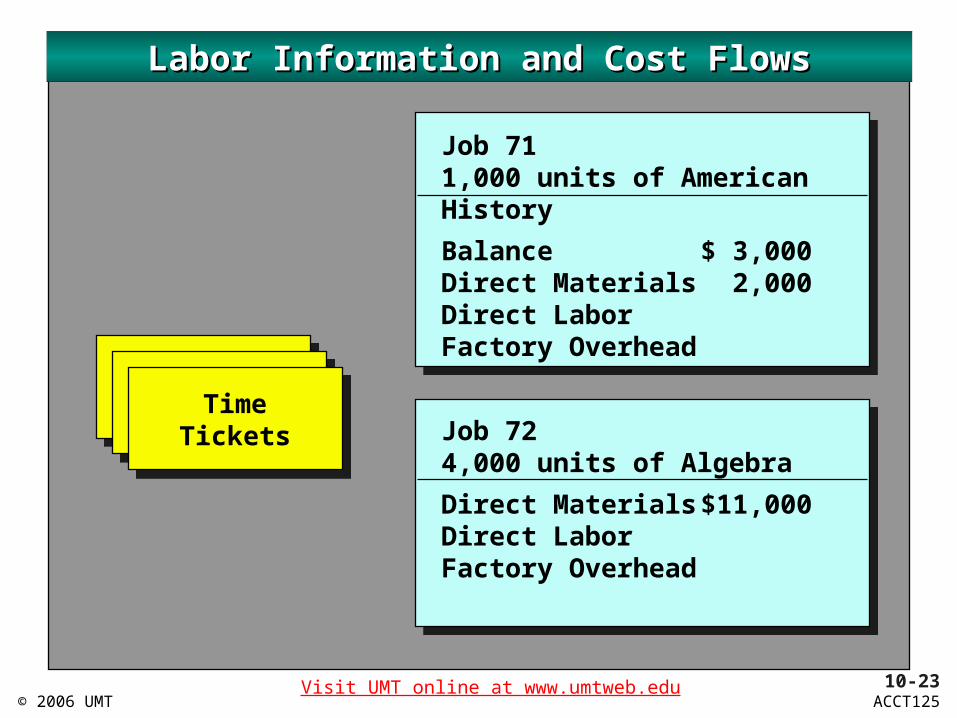

Labor Information and Cost FlowsLabor Information and Cost Flows

Job 711,000 units of American History

Balance $ 3,000Direct Materials 2,000Direct Labor Factory Overhead

Job 724,000 units of Algebra

Direct Materials $11,000Direct Labor Factory Overhead

TimeTickets

10-24Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Labor Information and Cost FlowsLabor Information and Cost Flows

Job 711,000 units of American History

Balance $ 3,000Direct Materials 2,000Direct Labor 3,500Factory Overhead

Job 724,000 units of Algebra

Direct Materials $11,000Direct Labor 7,500Factory Overhead

TimeTickets

10-25Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

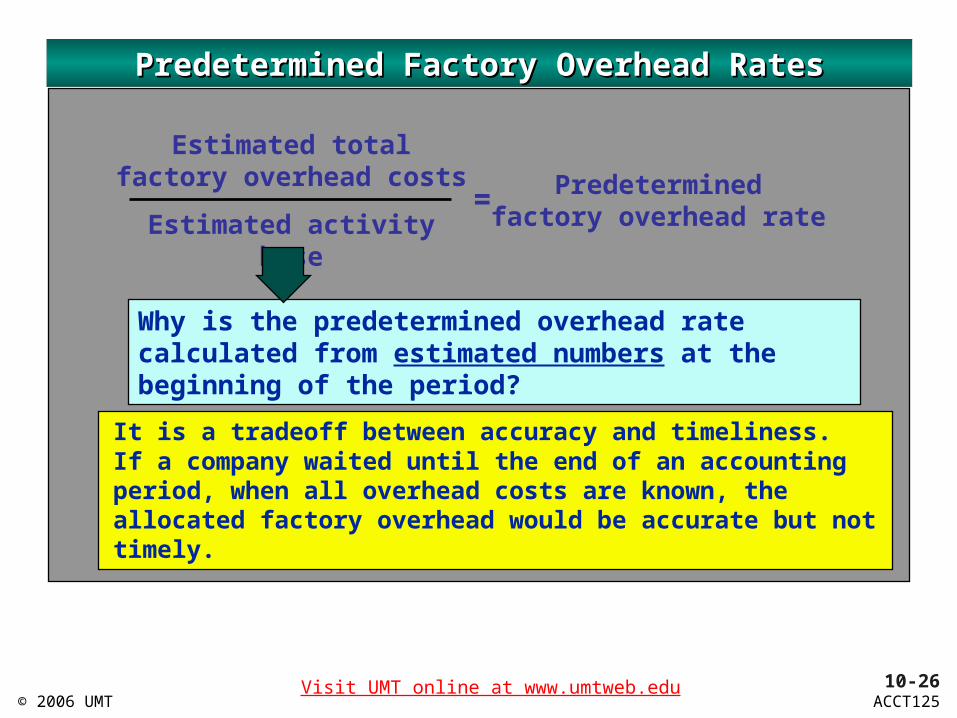

Predetermined Factory Overhead RatesPredetermined Factory Overhead Rates

Activity base examples

Estimated totalfactory overhead costs

Estimated activity base

Predeterminedfactory overhead rate

=

1. Direct labor hours 2. Direct labor dollars 3. Machine hours 4. Direct materials 5. Other

10-26Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Predetermined Factory Overhead RatesPredetermined Factory Overhead Rates

Estimated totalfactory overhead costs

Estimated activity base

Predeterminedfactory overhead rate

=

Why is the predetermined overhead rate calculated from estimated numbers at the beginning of the period?

It is a tradeoff between accuracy and timeliness.If a company waited until the end of an accounting period, when all overhead costs are known, the allocated factory overhead would be accurate but not timely.

10-27Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Predetermined Factory Overhead RatesPredetermined Factory Overhead Rates

Estimated totalfactory overhead costs

Estimated activity basePredetermined

factory overhead rate=

$50,000 estimatedfactory overhead costs

10,000 estimateddirect labor hours

=

10-28Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Predetermined Factory Overhead RatesPredetermined Factory Overhead Rates

Estimated totalfactory overhead costs

Estimated activity basePredetermined

factory overhead rate=

$50,000 estimatedfactory overhead costs

10,000 estimateddirect labor hours

=$5 per directlabor hour

10-29Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Predetermined Factory Overhead RatesPredetermined Factory Overhead Rates

Estimated totalfactory overhead costs

Estimated activity basePredetermined

factory overhead rate=

$50,000 estimatedfactory overhead costs

10,000 estimateddirect labor hours

=$5 per directlabor hour

For each direct labor hour worked, factory overhead applied is $5.

Job 71 350 x $5 = $1,750Job 72 500 x $5 = $2,500

Direct FactoryLabor OverheadHours Applied

10-30Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Assigning Factory Overhead to JobsAssigning Factory Overhead to Jobs

Job 711,000 units of American History

Balance $ 3,000Direct Materials 2,000Direct Labor 3,500Factory Overhead

Job 724,000 units of Algebra

Direct Materials $11,000Direct Labor 7,500Factory Overhead

Time TicketsPredetermined

Overhead Rates

10-31Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Assigning Factory Overhead to JobsAssigning Factory Overhead to Jobs

Job 711,000 units of American History

Balance $ 3,000Direct Materials 2,000Direct Labor 3,500Factory Overhead 1,750

Job 724,000 units of Algebra

Direct Materials $11,000Direct Labor 7,500Factory Overhead 2,500

Time TicketsPredetermined

Overhead Rates

10-32Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

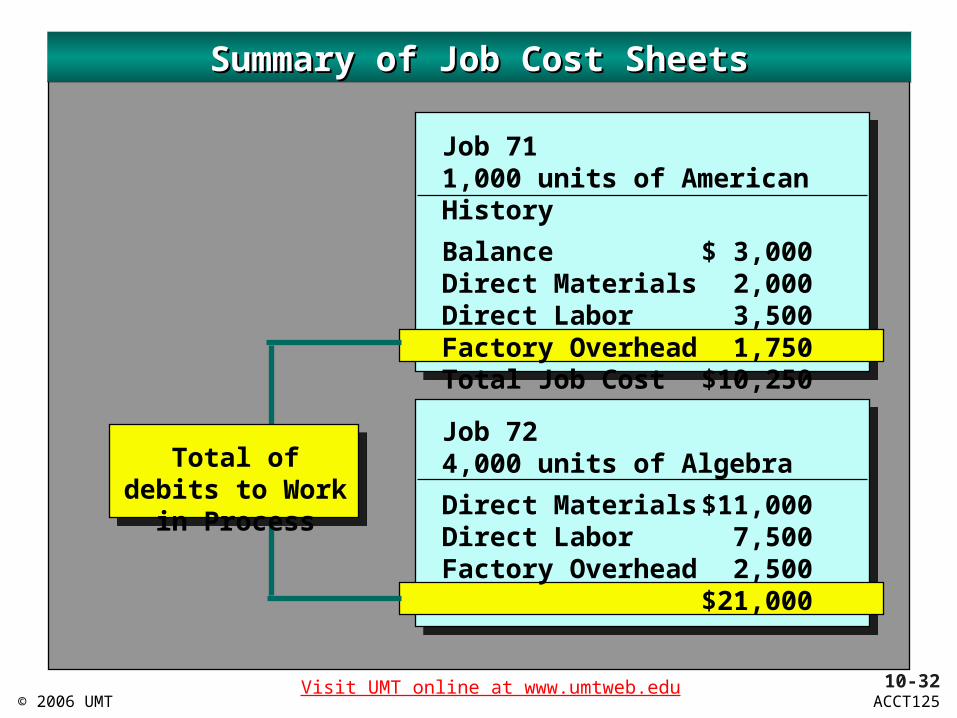

Summary of Job Cost SheetsSummary of Job Cost Sheets

Job 711,000 units of American History

Balance $ 3,000Direct Materials 2,000Direct Labor 3,500Factory Overhead 1,750Total Job Cost $10,250

Job 724,000 units of Algebra

Direct Materials $11,000Direct Labor 7,500Factory Overhead 2,500 $21,000

Total of debits to Work in Process

10-33Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Goodwell PrintersIncome Statement

For the Month Ended December 31, 2004

Sales $28,000

Cost of goods sold 20,150

Gross profit $ 7,850

Selling and admin. expenses:

Sales salaries expense $2,000

Office salaries expense 1,500

Total selling and admin.

expenses 3,500

Income from operations $ 4,350

10-34Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

5Use job order cost information for decision making.

Learning ObjectiveLearning Objective

10-35Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Job 144Item: 200 folding chairs

Materials Quantity

(board feet)Materials

PriceMaterials Amount

Direct materials: WoodDirect materials per chair

1,600 $3.50 $5,600$28

10-36Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Job 163Item: 200 folding chairs

Materials Quantity

(board feet)Materials

PriceMaterials Amount

Direct materials: WoodDirect materials per chair

2,000 $3.50 $7,000$35

10-37Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

6Diagram the flow of costs for a service business that uses a job order cost accounting system.

Learning ObjectiveLearning Objective

10-38Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Wages PayableDirect labor xxxIndirect labor xxx

Factory Overhead

Work in Process Cost of Services

Indirect labor xxxSupplies used xxxApplied overhead (xxx)

Direct labor xxxApplied overhead xxxCompleted jobs (xxx)

Completed jobs xxx

SuppliesUsed xxx

Flow of Costs Through a Service Flow of Costs Through a Service BusinessBusiness

10-39Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

7Describe just-in-time manufacturing.

Learning ObjectiveLearning Objective

10-40Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

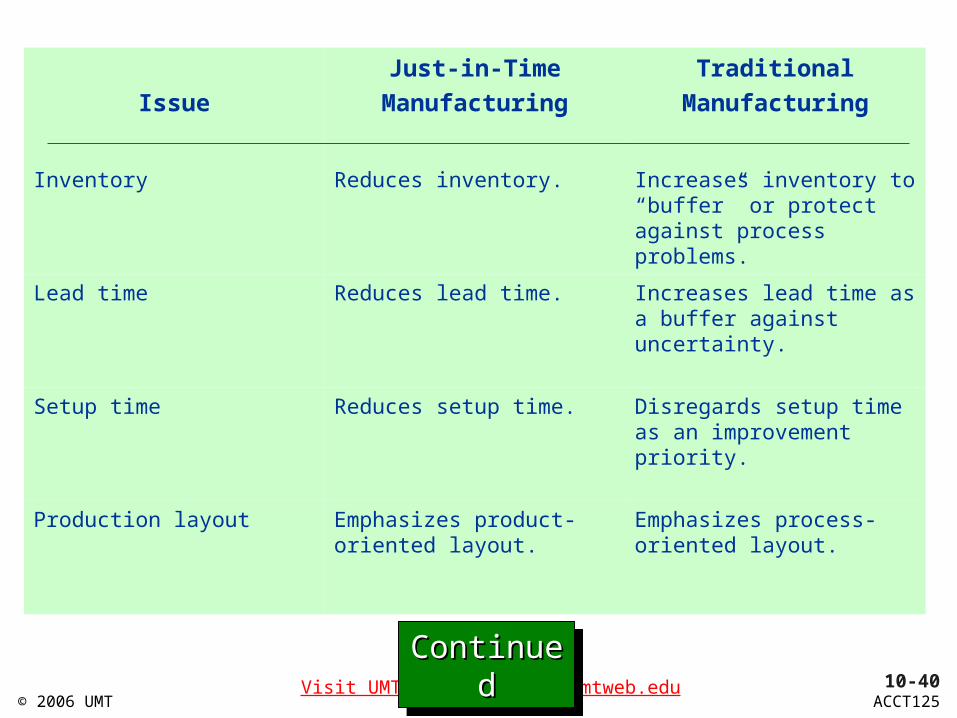

Issue

Just-in-Time

Manufacturing

Traditional

Manufacturing

Inventory Reduces inventory. Increases inventory to “buffer” or protect against process problems.

Lead time Reduces lead time. Increases lead time as a buffer against uncertainty.

Setup time Reduces setup time. Disregards setup time as an improvement priority.

Production layout Emphasizes product-oriented layout.

Emphasizes process-oriented layout.

ContinuedContinuedContinuedContinued

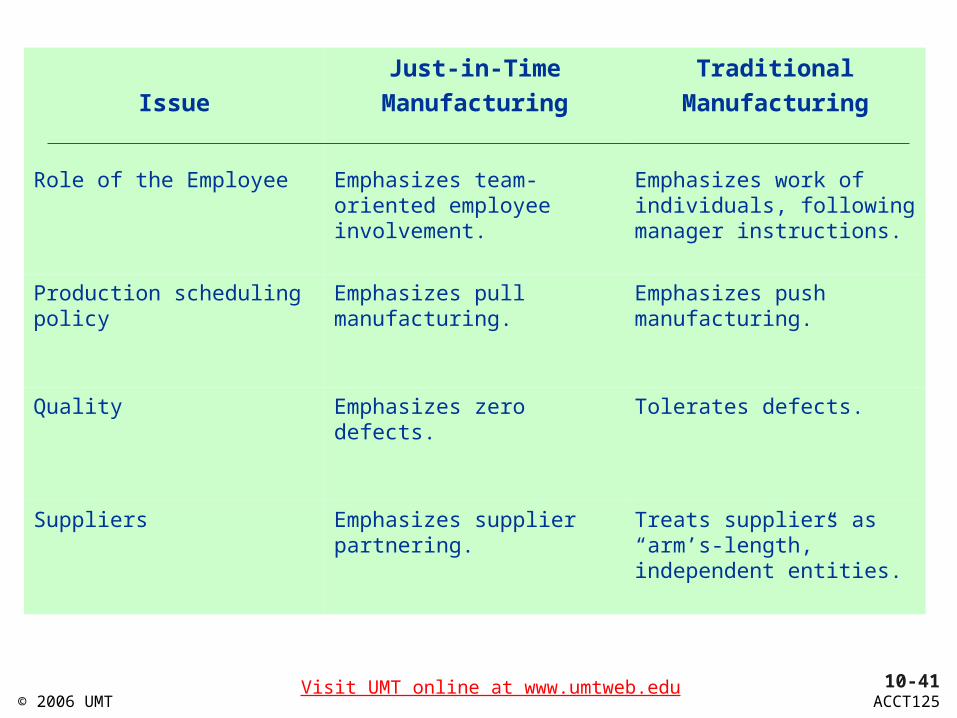

10-41Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Issue

Just-in-Time

Manufacturing

Traditional

Manufacturing

Role of the Employee Emphasizes team-oriented employee involvement.

Emphasizes work of individuals, following manager instructions.

Production scheduling policy Emphasizes pull manufacturing.

Emphasizes push manufacturing.

Quality Emphasizes zero defects. Tolerates defects.

Suppliers Emphasizes supplier partnering.

Treats suppliers as “arm’s-length,” independent entities.

10-42Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

8Describe and illustrate the use of activity-based costing in a service business.

Learning ObjectiveLearning Objective

10-43Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

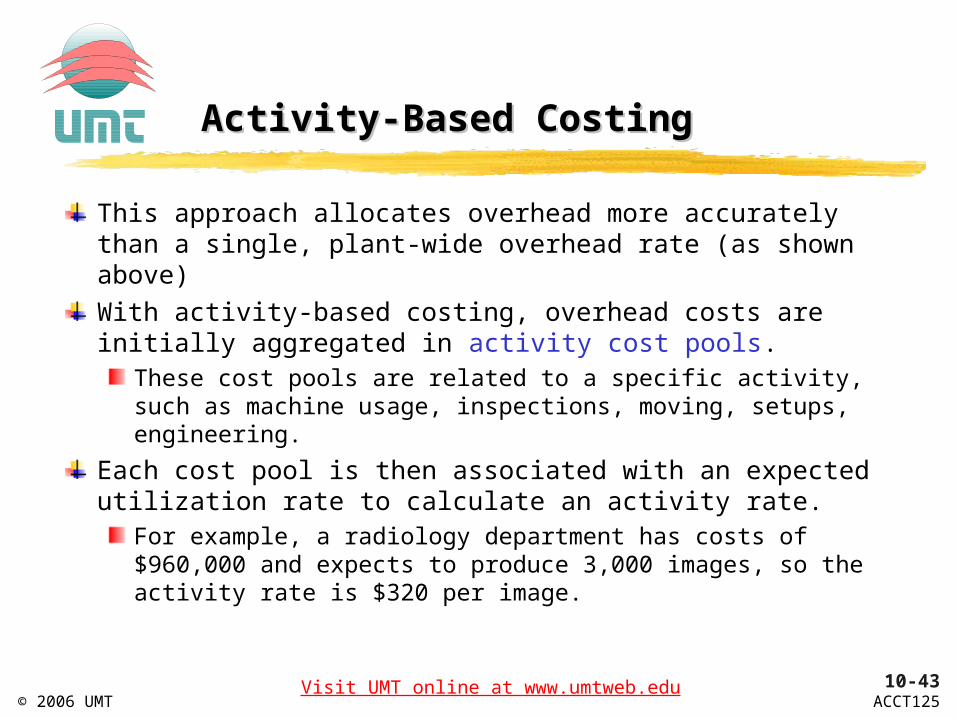

Activity-Based CostingActivity-Based Costing

This approach allocates overhead more accurately than a single, plant-wide overhead rate (as shown above)

With activity-based costing, overhead costs are initially aggregated in activity cost pools.

These cost pools are related to a specific activity, such as machine usage, inspections, moving, setups, engineering.

Each cost pool is then associated with an expected utilization rate to calculate an activity rate.

For example, a radiology department has costs of $960,000 and expects to produce 3,000 images, so the activity rate is $320 per image.

10-44Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Activity

Activity-Base

Usage

Activity

Rate =

Activity

Cost

Admitting 1 admission $180 per admission = $ 180

Radiological testing 2 images 320 per image = 640

Operating room 4 hours 200 per hour = 800

Pathological testing 1 specimen 120 per specimen = 120

Dietary and laundry 7 days 150 per day = 1,050

Total $2,790

Activity-Based CostingActivity-Based Costing

Mary Wilson was a patient in the hospital. The hospital overhead associated with her stay includes the following:

10-45Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

Activity-Based CostingActivity-Based Costing

Note that only those activities that affected Mary are charged to her bill.

Patient activity costs also may be combined with direct costs, such as drugs and supplies, for reporting with the revenues earned for each patient.

The result is a customer-based profitability report.

Such reports can be used by management to guide decisions on pricing or service delivery.

These reports also may be useful in determining if services for a given patient were remarkable in some way.

In the following illustration, Birini appears to have received a remarkable number of services relative to the revenue.

10-46Visit UMT online at www.umtweb.eduACCT125© 2006 UMT

HOPEWELL HOSPITALCustomer (Patient) Profitability Report

For the Period Ending December 31, 2004Adcock,

Kim

Birini,

Brian

Conway,

Don

Wilson, Mary

Revenues $9,500 $21,400 $5,050 $3,300

Less patient costs:

Drugs and supplies $ 400 $1,000 $ 300 $ 200

Admitting 180 180 180 180

Radiological testing 1,280 2,560 1,280 640

Operating room 2,400 6,400 1,600 800

Pathological testing 240 600 120 120

Dietary and laundry 4,200 14,700 1,050 1,050

Total patient costs $8,700 $25,440 $4,530 $2,990

Income from operations $ 800 $(4,040) $ 520 $ 310