visiÓn de lloydvisiÓn de … · forum mediasegur: alternativas para afrontar la crisis...

TRANSCRIPT

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 1 -

VISIÓN DE LLOYD’S PARA AFRONTARVISIÓN DE LLOYD S PARA AFRONTAR LA CRISIS

Beatriz Ramírez

Directora del Área Legal, Lloyd’s Iberia

20 Diciembre, 2011.

Lloyd’s

Claves

Índice

Dos ejemplos:

→ Riesgos emergentes

→ Agencias de suscripción

Conclusiones

© Lloyd’s

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 2 -

LLOYD’S Es el mercado lider de seguros especializados en el mundo

© Lloyd’s

De un café…

Primera referencia conocida al café de Edward Lloyd en Tower

© Lloyd’s

yStreet(London Gazette 18-21 February 1688)

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 3 -

1688

aseguramiento de barcos y cargas

© Lloyd’s

… a todo tipo de seguros y retos…1887 1911 19691906

© Lloyd’s

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 4 -

PIPER ALPHA1988

EXXON VALDEZ1989

HURACANES1989

ASBESTOS1980s- 1990s

© Lloyd’s

Plan R&R para gestionar las reclamaciones anteriores a 1992.

Lloyd’s sobrevivió, pero sin entender bien los nuevos riesgos a los que se enfrentaba el mercado.

De la Reconstrucción.. a la Renovación

Se carecían de standards de actuación y la gestión era pobre

Se aceptan miembros corporativos

© Lloyd’s

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 5 -

2001 – Lloyd’s sufre importantes pérdidas por los ataques terroristas

Del 11/Sept al huracán Katrina

al World Trade Center

2001 – Regulación sobre Lloyd’s pasa a la Financial Services Authority (FSA)

2002 – Nueva estructura de Franquicia

© Lloyd’s

2005 – Huracanes Katrina, Rita y Wilma.

Catástrofes 2010 - 2011Reclamaciones netas del mercado y pérdidas netas publicadas

Market Lloyd’s (net)

Terremoto de Chile $8bn $1.4bn

Nueva Zelanda Darfield $6bn $0.7bn

Nueva Zelanda Lyttelton $14bn $1.4bn

Tohoku $30bn – $40bn $1.95bn

Australia inundaciones /ciclón $5bn $0 65bn

© Lloyd’s

Australia inundaciones /ciclón $5bn $0.65bn

USA Tornados $18bn $0.6bn

Huracán Irene $3bn-$6bn TBA

Fuente: Lloyd’s Informe anual y comunicado de prensa 13/5/2011

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 6 -

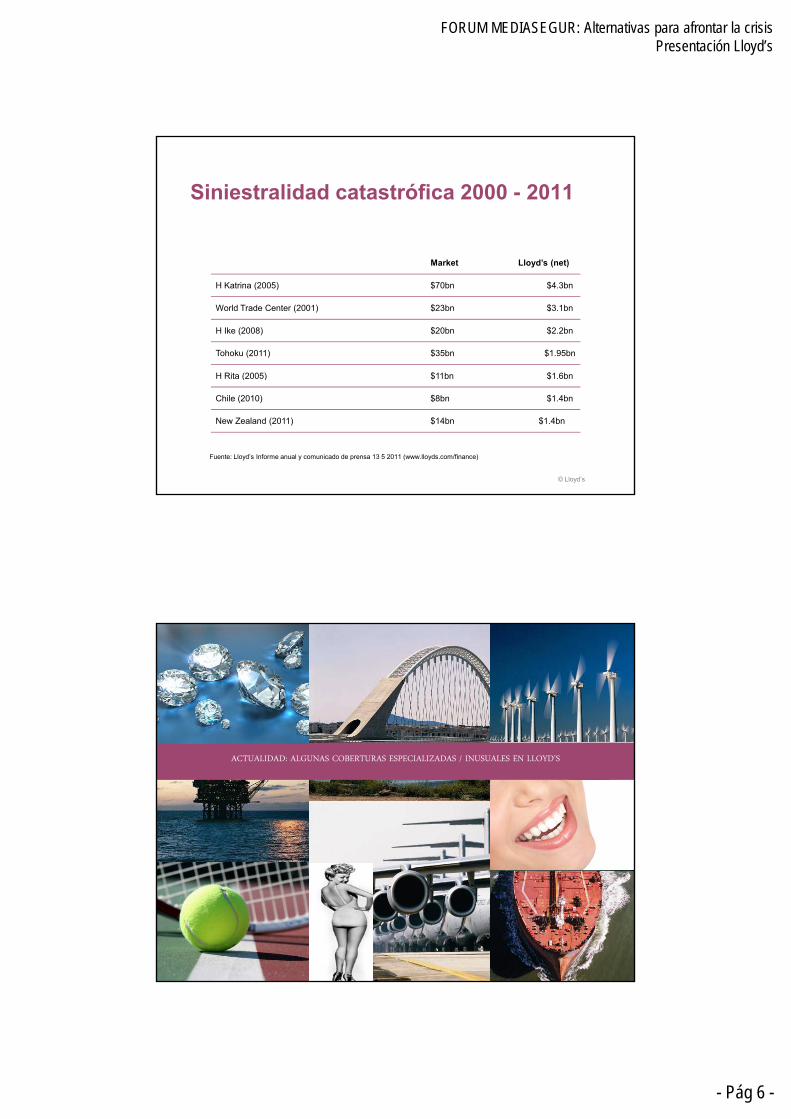

Siniestralidad catastrófica 2000 - 2011

Market Lloyd’s (net)

H Katrina (2005) $70bn $4.3bn

World Trade Center (2001) $23bn $3.1bn

H Ike (2008) $20bn $2.2bn

Tohoku (2011) $35bn $1.95bn

H Rita (2005) $11bn $1 6bn

© Lloyd’s

H Rita (2005) $11bn $1.6bn

Chile (2010) $8bn $1.4bn

New Zealand (2011) $14bn $1.4bn

Fuente: Lloyd’s Informe anual y comunicado de prensa 13 5 2011 (www.lloyds.com/finance)

ACTUALIDAD: ALGUNAS COBERTURAS ESPECIALIZADAS / INUSUALES EN LLOYD’S

© Lloyd’s

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 7 -

Claves

Capacidad extraordinaria para adaptarse a los cambios.

Seguridad y fortaleza económica

Confirmación de ratings A+ (Standard & Poors-Fitch) y A (AM Best)

Constante búsqueda de la innovación en soluciones y estructuras

→ Riesgos emergentes

→ Agencias de suscripción

© Lloyd’s

RIESGOS EMERGENTES

© Lloyd’s

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 8 -

“un riesgo que es percibido como potencialmente importante peroun riesgo que es percibido como potencialmente importante, pero

que no ha sido entendido totalmente o no se ha tenido en cuenta

en términos de seguro”.

© Lloyd’s

Riesgos Emergentes en Lloyd’s

Lloyd’s es un Mercado Especializado

Soluciones innovadoras

Los nuevos tipos de riesgos representan un desafío

Para evitar que se repitan riesgos sistémicos (amianto y polución)

Riesgo Emergente en la mira de todos

© Lloyd’s

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 9 -

Algunos Riesgos EmergentesImpacto del clima que se produce en el espacioNanotecnologíaNanotecnologíaEMF. Campos electromagnéticosPandemiasBiología sintética

© Lloyd’s

Agencias de suscripción

© Lloyd’s

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 10 -

¿Qué es una agencia de suscripción?

Entidad mercantil a la que una entidad aseguradora o reaseguradora leEntidad mercantil a la que una entidad aseguradora o reaseguradora le otorga ciertos poderes o autoridad para, en su nombre y por su cuenta, aceptar y suscribir riesgos, emitir y firmar las pólizas y desarrollar otras labores de administración y de gestión de siniestros.

Coverholders = “agencias de suscripción”

Actualmente reguladas en arts. 86 bis y ter Ley Ordenación y Supervisión Seguros Privados.

© Lloyd’s

Características

► No es un mediador de seguros. Es un apoderado de aseguradora

► Puede operar con más de una aseguradora no española► Puede operar con más de una aseguradora no española.

► Corredor ≠ agencia de suscripción.

► Autorización DGS y cumplimiento de requisitos.

► Registro Administrativo de Agencias de Suscripción.

► Posibilidad de operar en otros países del EEE (pasaporte).

© Lloyd’s

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 11 -

Agencias de Suscripción / Coverholders

Madrid

SERVICE COMPANIES

Madrid

110

Núm. Coverholders

RC 15COVERHOLDER POR RAMOS

MTA 9

DAÑOS 6

MOTOR 2

S d t il d l i A di

© Lloyd’s

See detailed classes in Appendix

Fuente: Market Intelligence calculation based on Lloyd’s Delegated Authorities, (Mayo 2011)

17 Coverholders/agencias suscripción y 3 “service companies”

Búsqueda de productos con éxito en otros mercados

Canales de distribución (corredores)

Conclusiones

Lloyd’s es un mercado de seguros solvente y estable.

Adaptación y constante búsqueda de la innovación.

Seguridad y fortaleza económica

Riesgos emergentes: anticipación, análisis y preparación.

Las agencias de suscripción son un modo de distribución innovador.

© Lloyd’s

FORUM MEDIASEGUR: Alternativas para afrontar la crisisPresentación Lloyd’s

- Pág 12 -

DisclaimerThe information contained in this presentation is being provided on a confidential basis and should not be made available to the general public, the mediaor any third party without the express prior written consent of Lloyd’s. This information is not intended for distribution to, or use by, any person or entity inany jurisdiction or country where such distribution or use would be contrary to local law or regulation. It is the responsibility of any person communicatingthe contents of this document or communication, or any part thereof, to ensure compliance with all applicable legal and regulatory requirements.

The content of this presentation does not represent a prospectus or invitation in connection with any solicitation of capital. Nor does it constitute an offerto sell securities or insurance, a solicitation or an offer to buy securities or insurance, or a distribution of securities in the United States or to a U.S. person,or in any other jurisdiction where it is contrary to local law. Such persons should inform themselves about and observe any applicable legal requirement.

Lloyd’s has provided the material contained in this presentation for general information purposes only. Lloyd’s accepts no responsibility and shall not beliable for any loss which may arise from reliance upon the information provided.

This presentation includes forward-looking statements. These statements reflect Lloyd's current expectations and projections about future events andfinancial performance, both with respect to Lloyd's in particular and the insurance, reinsurance and financial and services sectors in general. All forward-looking statements address matters that involve risks, uncertainties and assumptions because they relate to events and depend on circumstances that willoccur in the future and which are beyond the control of Lloyd’s. Based on a number of factors, actual results could vary materially from those anticipatedby the forward-looking statements. These factors include, but are not limited to, the following:

(a) rates and terms and conditions of policies may vary from those anticipated;(b) actual claims paid and the timing of such payments may vary from estimated claims and estimated timing of payments, taking into account the

preliminary nature of such estimates;(c) claims and loss activity may be greater or more severe than anticipated, including as a result of natural or man-made catastrophic events;(d) competition on the basis of pricing, capacity, coverage terms or other factors may be greater than anticipated, or Lloyd's products could become

uncompetitive in light of changes in market conditions;(e) reinsurance placed with third parties may not be fully recoverable, or may not be paid on a timely basis, or such reinsurance from creditworthy

reinsurers may not be available or may not be available on commercially attractive terms;(f) developments in the financial and capital markets may adversely affect investments of capital and premiums, or the availability of equity capital or( ) p p y y p p , y q y p

debt;(g) changes in legal, regulatory, tax or accounting environments in relevant countries may adversely affect (i) Lloyd's ability to offer its products or

attract capital, (ii) claims experience, (iii) financial return, or (iv) competitiveness;(h) mergers, consolidations, divestitures and other transactions by third parties could adversely affect Lloyd's, including but not limited to changes in

the distribution or placement of risks due to increased consolidation of insurance and reinsurance brokers; or(i) economic contraction or other changes in general economic conditions could adversely affect (i) the market for insurance generally or for certain

products offered by Lloyd's, or (ii) other factors relevant to Lloyd's performance.

The foregoing list of factors is not comprehensive, and should be read in conjunction with other cautionary statements that are included herein orelsewhere. Lloyd’s cautions readers to consider carefully such factors. Any forward-looking statements speak only as of the date they are made. Lloyd'sundertakes no obligation to update or revise any forward-looking statement, whether as a result of new information, future developments or otherwise.

© Lloyd’s