us housing since 2001 · 2017-02-15 · miami var prices rhpi rhpig rhping ... and mortgage rates...

TRANSCRIPT

US Housing since 2001:

What’s different this time?

William Wheaton

Department of Economics

Center for Real Estate

MIT

January, 2017

IAP

HISTORIC PERSPECTIVE: WHAT HAS HAPPENED TO REAL PRICES AND UNIT CONSTRUCTION: 1981-2016

1). - 68 Markets = 68 stories?

- Coastal cities

- Mid West Hinterland

- Sunbelt

2). What to look at?

- Housing prices (constant dollars, FHA repeat sale price index)

- New construction: total building permits

- Long term trends in each

- Recession volatility: historic –vs- 2001/2016

(Ignore Green/Blue)

Coastal markets: Boston

Boston

VAR prices

RHPI RHPIG RHPING

1980 1985 1990 1995 2000 2005 2010 2015

100

150

200

250

300

350

VAR permits

1980 1985 1990 1995 2000 2005 2010 2015

0

2000

4000

6000

8000

10000

12000PRM

PRMG

PRMNG

Coastal markets: LA

LosAngeles

VAR prices

RHPI RHPIG RHPING

1980 1985 1990 1995 2000 2005 2010 2015

100

150

200

250

300

350

400

VAR permits

1980 1985 1990 1995 2000 2005 2010 2015

0

2500

5000

7500

10000

12500

15000

17500

20000PRM

PRMG

PRMNG

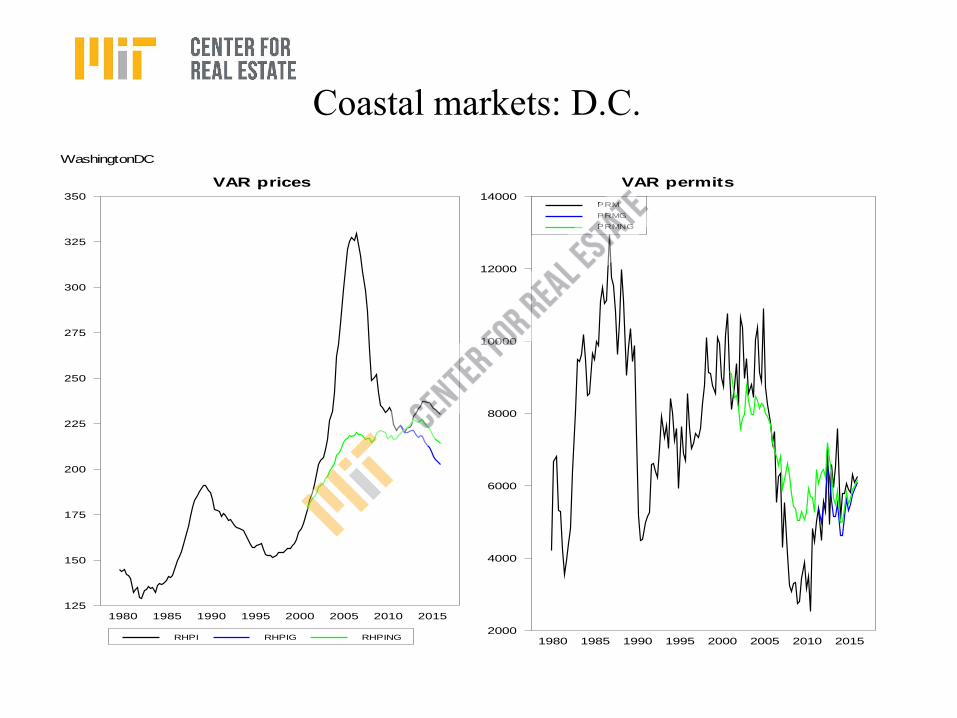

Coastal markets: D.C.

WashingtonDC

VAR prices

RHPI RHPIG RHPING

1980 1985 1990 1995 2000 2005 2010 2015125

150

175

200

225

250

275

300

325

350

VAR permits

1980 1985 1990 1995 2000 2005 2010 20152000

4000

6000

8000

10000

12000

14000PRM

PRMG

PRMNG

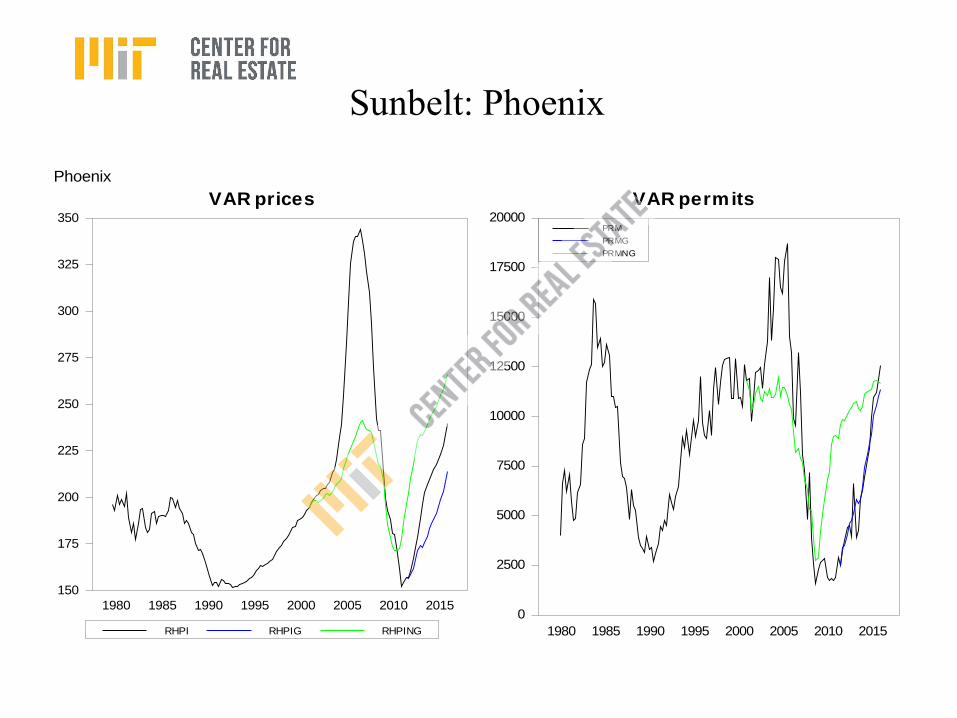

Sunbelt: Phoenix

Phoenix

VAR prices

RHPI RHPIG RHPING

1980 1985 1990 1995 2000 2005 2010 2015

150

175

200

225

250

275

300

325

350

VAR permits

1980 1985 1990 1995 2000 2005 2010 2015

0

2500

5000

7500

10000

12500

15000

17500

20000PRM

PRMG

PRMNG

Sunbelt markets: Miami

Miami

VAR prices

RHPI RHPIG RHPING

1980 1985 1990 1995 2000 2005 2010 2015

100

150

200

250

300

350

400

VAR permits

1980 1985 1990 1995 2000 2005 2010 2015

0

2500

5000

7500

10000PRM

PRMG

PRMNG

Sunbelt markets: Atlanta

Atlanta

VAR prices

RHPI RHPIG RHPING

1980 1985 1990 1995 2000 2005 2010 2015130

140

150

160

170

180

190

200

210

220

VAR permits

1980 1985 1990 1995 2000 2005 2010 20150

2500

5000

7500

10000

12500

15000

17500

20000

22500PRM

PRMG

PRMNG

Midwest markets: Chicago

Chicago

VAR prices

RHPI RHPIG RHPING

1980 1985 1990 1995 2000 2005 2010 2015

100

120

140

160

180

200

220

240

260

VAR permits

1980 1985 1990 1995 2000 2005 2010 2015

0

2000

4000

6000

8000

10000

12000

14000PRM

PRMG

PRMNG

Midwest markets: St. Louis

StLouis

VAR prices

RHPI RHPIG RHPING

1980 1985 1990 1995 2000 2005 2010 2015

140

150

160

170

180

190

200

210

220

VAR permits

1980 1985 1990 1995 2000 2005 2010 2015

500

1000

1500

2000

2500

3000

3500

4000

4500

5000PRM

PRMG

PRMNG

Midwest markets: Kansas City

KansasCity

VAR prices

RHPI RHPIG RHPING

1980 1985 1990 1995 2000 2005 2010 2015150

160

170

180

190

200

210

VAR permits

1980 1985 1990 1995 2000 2005 2010 20150

1000

2000

3000

4000

5000PRM

PRMG

PRMNG

HISTORIC PERSPECTIVE: WHAT HAS HAPPENED TO REAL PRICES AND UNIT CONSTRUCTION: 1981-2016

1). - Strong upward trend in constant $ house prices on the coasts.

- 2001-2011 Volatility greater than past recessions

2). - Much less (or no) price trend in Mid West

- 2001-2011 volatility still much greater.

3). - Little or no price trend in the Sunbelt.

- 2001-2011 volatility enormous, dominating

4). - In all markets, the trend in unit construction is

flat or downward (slower demographic growth?)

- Construction I(0) moves closest with price

levels I(1)

BUT 2001-2016 INCLUDED:

(1) A STRONG ECONOMIC RECOVERY (2001-2006)

(2) THE WORST RECESSION SINCE 1930.

HOW MUCH VOLATILITY IS EXPLAINED BY THOSE?

1). - Estimate a VAR model with house price growth and new construction (both variables stationary)

2). - Make the VAR conditional on local job growth and Mortgage rates (the 2 most important economic drivers of housing in the literature).

3). - # lags (SBIC test) generally 5-7.

4). - Back test: Use the model to dynamically forecast prices and construction, beginning in 2001 and extending to 2016 – using actual employment growth and mortgage rates in each market. (green line).

Repeat for recovery starting in 2011 (blue line).

Phoenix VAR forecast Errors in price changes: Phoenix

VAR prices

RHPI RHPIG RHPING

1980 1985 1990 1995 2000 2005 2010 2015

150

175

200

225

250

275

300

325

350

VAR permits

1980 1985 1990 1995 2000 2005 2010 2015

0

2500

5000

7500

10000

12500

15000

17500

20000PRM

PRMG

PRMNG

RESULTS1). - In all markets forecast prices rise upward (at bit)

from 2001 to 2006 as local economies improve from the 2001 recession. On average the forecast rise is 8% versus an actual rise of 41%!

2). - In virtually all markets forecast prices drop from 2007 to 2011, but on average by only 5% as a sharp drop in mortgage rates help cushion that impact of severe job losses. The actual drop is 42%!

3). - From 2011 to today forecast prices rise an average 10% as opposed to a 12% actual recovery.

4). - Construction errors tend to follow price errors

5). - Forecast 2016 price levels on average are 14% ahead of 2001, actual are 11%.

The forecast misses all the volatility: the “Bubble”

Question #1: where is the “bubble” biggestAbsolute value forecast error: |2006-2001| + |2011-2006|

Largest Smallest

Miami 2.18429

LosAngeles 2.02762

FortLauderdale1.81099

Orlando 1.6072

WestPalmBeach1.42981

LasVegas 1.36861

Tampa 1.33156

Tucson 1.32317

Phoenix 1.2671

OrangeCounty1.25254

SanDiego 1.24643

Ventura 1.20361

Dallas 0.23586

FortWorth 0.22419

Cleveland 0.19361

Buffalo 0.185464

Tulsa 0.17275

Raleigh 0.16647

Cincinnati 0.16511

Columbus 0.16302

Greensboro 0.16022

Louisville 0.15486

Dayton 0.14657

Pittsburgh 0.12142

Indianapolis0.04112

(“CANFLAZ”)

Hypothesis #1: purchase of 2nd or Investment (speculative)

homes fed demand (Condos excluded)

Source: Loan Performance, Torto Wheaton Research

0 10 20 30 40 50

Nation

San Diego

Sacramento

Riverside

Miami

Tampa

Phoenix

Orlando

Las Vegas

Fort Myers

Atlantic City

1999

2005

Investment and 2nd Home Loans as Share of New Loans, %

The simple statistics are suggestive: prices appreciate

more where second home buying is on the rise.

y = 0.0273x + 14.536

R2 = 0.4201

0

20

40

60

80

100

-1,000 0 1,000 2,000 3,000

2002-2005 cumulative change in shares

of investment and 2nd home loans, BPS

2002-2005 Cumulative change in HPI, %

How important was Speculation in the US

Housing Crisis?

1). “Speculation” is the purchase of additional housing units mainly for investment rather than use. Chinese “store of value”

2). 2nd homes can be calculated from Census Vacancy data:

= URE (Usual Residence Elsewhere) + Seasonal+ Occasional Use + other. These are “vacant” units not on the market.

3). This calculation has grown from 8% of owned units in 1978 to 16% in 2008 = 200k annual increase.

4). Post 1998 mortgage interest on 2nd homes became fully tax deductible. Helping home ownership or speculation?

5). Foreign exchange matters. Low dollar generates foreign purchases of US condos in anticipation of a recovery?

6). Four states: Florida, California, AZ, N.V. “CANFLAZ” contributed disproportionately to the Boom/Bust: 51% of foreclosures, 20% of pop. These are US second home havens.

But 1996-2007 “Bubble” and subsequent “bust” also mirrored

an unprecedented rise/fall in home ownership. Did the Rising

ownership share fuel house prices or reverse?

The ownership – Price nexus

• High house price levels make ownership less

affordable, but rising prices lower the annual

cost of owning, stimulating ownership.

• Low house prices makes houses affordable, but

falling house prices generate strategic defaults,

foreclosures, falling ownership.

• Willen (2016). Increase in ownership rate up to

2007 occurred almost uniformly across all

income groups! Not a low income phenomena.

• Did it rise equally in all locations?

CANFLAZ homeownership rose/fell 2x US!

(But state/local ownership data too thin for further

analysis)

60

61

62

63

64

65

66

67

68

69

70

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

US CANVFLAZ (simple average)

Homeownership rate, %

Hypothesis #2: Homeownership movement suggests

Credit “availability” expanded/contracted (LTV, DTI,

documentation requirements...)

0

100

200

300

400

500

600

700

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

0

4

8

12

16

20

24

28

Subprime Loan Origiations

Subprime as % of Total Originations

Subprime Originations as % Total Mortgage Debt Outstanding

$ Billions Percent

Evidence of credit relaxation in

the conforming loan market

• Fraction of conforming home purchase loans with

LTV>80%: 1998 (55%),2004 (65%), 2009 (72%).

• Fraction of conforming home purchase loans with

DTI>40%: 1998 (25%), 2004 (40%), 2009 (40%).

• Subprime loan market has loans with credit

standards way below the conforming market and

its market share rose significantly until it

collapsed in 2008.

What about the recovery since 2011?

• On average prices have increased 12% (constant

dollars) 22% in current dollars since 2011.

• The 2001 back test forecast predicted 10%

(constant $) recovery. Pretty close

• A back test from 2011 predicted 9% also not bad

• Job growth and continued low rates over the last 5

years well predicts the house price recovery so far

• Looking beyond 2016, what will happen to jobs

and rates? And then what is the model missing?

Since 2012: A once-in-a-lifetime opportunity! But

future Rents fall (new construction) and rates will rise

Negative factors for a post 2016 model forecast

3.0

4.5

6.0

7.5

9.0

10.5

12.0

13.5

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

P/R and i*P/R Ratios, 2013q2=1 30-year fixed mortgage rate, %

P/R ratio

i*P/R ratio

Mortgage rate

Sources: BLS, FHFA, CBRE EA.

Housing starts have been way below household formation

and total demand (+ 2nd homes & demolitions) for 8 years.

Inevitable construction recovery also limits future prices

1997-2008

6.5 Mil

Historic Equilibrium: 222,000 excess units (=demolitions + second homes )

Future Job growth contrained • Job growth is increasingly constrained post 2016

– Aging means a labor force that grows at less than 1%

yearly (<100k new jobs/month becomes the new

steady state, full employment normal)

– The prospect of Immigration reform limits job

growth significantly from farm workers to H1B

programmers.

– As we near full a employment rate (95.2%) these

factors dominate the cyclic changes in labor force

participation.

– Limit further price recovery

What about household formation?

• Household formation from 2008-2016 is only

65% of what it was prior to the Recession.

– Huge increase in millennials (age 20-35) living at

home (27% in 2010 versus 15% in 1980).

– Increase in doubling up (economic hardship and

rising rents)

– This despite: increases in divorce, singledom and

aging (all boost headship rates, FRB study)

– Household formation data is difficult nationally

and non-existent at local market level.

Outside the model

…and home ownership?

• Home Ownership fallen almost 6% since 2007

• Permanent change in tenure “preference”, fear of

asset loss, love of no commitment, job insecurity?

• Millennials never married rate soared to 62%

from 32% (1980). Singles rent.

• Extreme foreclosures, households left with no

equity after recession so moving requires renting.

• “Outside the model” because difficult to get local

market data on ownership

1). A recovery in Household Formation

- 2000-2007 Household formation averages: 1,285,000 yearly

- From 2008-2015 averages: 780,000

- It has to return to 1,200,000 range plus make up for lost formation of 2m during the downturn!

- Economists in accord that it will recover

2). A permanent shift in ownership/tenure choice?

- Credit standards are relaxing again, mortgages

available with greater flexibility.

- Wages finally starting to improve.

- Unique opportunity argument.

- Millennial issues are temporary, postponing

- They will shortly grow up, marry, move, buy.

Future Prospects

345678910111213141516

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Delinquency Rate Transition to foreclosureSource: Mortgage Bankers Association

Mortgage Delinquency leveling off, foreclosures

dropping, recovering equity… all positive

Factors outside model all look positive: household

formation recovers, renter growth declines, # owners surge

Conclusions• Boom/Bust largely unexplained by economic fundamentals

• But post 2011 recovery in prices and Housing construction is well explained by job growth and mortgage rates.

• Future outlook for job growth and rates is all negative.

• Price growth in all markets has recovered to or above pre-boom 2001 levels (constant $), but model forecast beyond 2016 should have price growth slowing – so a long way back to 2007 peak price levels (never?).

• Factors outside of the model, however, generally support stronger price growth: – Pick up/recovery in household formation

– Stabilizing, reviving home ownership rate

– Reductions in negative equity restore mobility

• What have I left out?

Conclusions• Real prices back to or ahead of 2001.

• Long way to go to be back to 2007 levels

• then again if real interest rates rise