understanding business value

DESCRIPTION

What is your business worth? There are some fundamental truths about undertaking a business valuation. This essay provides a simple explanation of business valuation methodologies and de-bunks some of the myths surrounding valuation techniques.TRANSCRIPT

Understanding Business ValueBy Kevin Lovewell

Copyright © 2014 Powers Corporate Solutions 2

UNDERSTANDING BUSINESS VALUE

This e-book is copyright. All rights reserved. No part of this document may be copied, used or reproduced (including by making any electronic or digital copy), published or communicated in any form or by any means without the prior permission of the author. With the exception of use for private study, research, criticism or reviews as permitted under the Copyrights Act.

By Kevin Lovewell

Understanding Business Value

Contents

WHAT DOES BUSINESS VALUE REFER TO? 3

A BRIEF HISTORY OF VALUE 3

WHY PERFORM A BUSINESS VALUE EXERCISE 4

VALUATION METHODS 4 The trend is my friend. 5 Valuation based on the physical assets of the business. 5 Book Value 5 Adjusted Book Value 5,6 Valuations based upon Cash Flow 6 Multiple of Earnings or Income Approach 6 Discounted Future Earnings. 6 Discounted cash flow 7 Capitalised Earnings 7

BALANCING RISK AND RETURN. 8

RATIO ANALYSIS 9 Gross Profit Margin % 9 Net Profit Margin % 9 ROCE – Return on Capital Employed 9 Activity Ratio 9

CONCLUSION 10

WOULD YOU LIKE TO KNOW MORE? 10

What is your business worth? There are some fundamental truths about undertaking a business valuation. This essay provides a simple explanation of business valuation methodologies and de-bunks some of the myths surrounding valuation techniques.

UNDERSTANDING BUSINESS VALUE

Copyright © 2014 Powers Corporate Solutions 3

It is generally accepted that the 1830’s heralded the transition from agrarian (farming) society to an industrial economy. As a consequence, the output of machinery became the focus of the economy, society and business. Commerce and industry became economic drivers. In fact by the late 1800’s all the tools used today in the fields of cost accounting and management accounting had been invented. Value was measured in terms of property owned by the business, (Assets less liabilities). Arriving at business value was as simple and straightforward as establishing the value of net assets in the balance sheet of the business. (Also referred to as the owners’ equity)

The 1960’s signaled the transition from the industrial to the intellectual economy. Intellectual refers to activities relating to knowledge, creativity, and collaboration of the workforce that leverage diverse operating systems derived from IP – Intellectual Property, (not ownership per se of the assets of the organisation)

A very good indicator of this transition from Industrial to intellectual economies is that the output of the mind occupies the functionality of the majority of workers today. Nearly eight out of ten workers now produce services - rather than “things.” Even products (tangible goods) are primarily purchased on the basis of intangible explanations such as brand, reputation, service levels etc.

In 2005, Stern School of Business (NYU) completed a study that investigated 3500 companies (This is not a small sample size) The study set out to measure the correlation between “book value”

A brief history of Value

and “capitalisation” over time. (i.e. the value of net assets shown in the balance sheet, and its relationship with the price shareholders were prepared to pay for shares.)

The study established that in 1978, there existed a 95% correlation between the balance sheet and capitalisation. There was a very close relationship, between the balance sheet value and the share value or price.

However by 2005, the correlation had fallen to 28% for the same 3,500 companies. Examined another way, 28% of the companies perceived value was explained by the physical net assets, but a whopping 72% of the “things” that created value were unexplained, not identified, intangible.

Our accounting measurements such as ROCE [Return on Capital Employed], COGS [Cost of Goods Sold] and other familiar metrics explain much less today in our intellectual economy than they did when they were invented for the Industrial economies of the 1800’s

Consequently, it is not surprising that conventional endeavors to uncover “value” are only attempts to make “tangible” what is “intangible”, because increasingly and ultimately the pure financial methods of arriving at the value of a business are virtually meaningless.

1 – Less than 28% of a companies ’ va lue can be found in the financial records of that Company.Stern Business School (NYU) 2005

The value of a business has traditionally been considered to be equal to the sum of the assets or physical resources owned or controlled by the business. Analysts, shareholders and business owners use the financial reports provided by a business to determine with relative confidence what a business is worth.

Another way of contemplating how to arrive at the “value” of a business is to refer to the monetary sum a willing buyer is prepared to pay; and a willing vendor is willing to take for that business. In this context, value of the business is certain and agreed to.

However, why do we confront this transparently simple question of “business value” with expensive and time consuming analysis? Why the requirement for licensed experts with their complex legal disclaimers? And why is such a significant amount of research and due diligence needed to determine what a business is worth?

What does Business Value refer to?

Copyright © 2014 Powers Corporate Solutions 4

UNDERSTANDING BUSINESS VALUE

Having stated that financial metrics are less than effective in determining value, why then provide an explanation of how to use them?

When we view the statistics freely available in respect of company buyouts, and transfers it is not surprising that we find 80% of mergers and acquisitions do not add value. In fact 50% of them actually destroy value. (Big bucks for consultants – less than impressive returns for shareholders). This is one main reason that we embark upon business valuation exercises. There will always be a role for establishing what is a fair value, due to the constant flow of businesses changing hands; Someone has to make the decision “What is a fair price!”

The fact is, estimating your business value is necessary for a few more reasons.

• The growing frequency of disputes between owners ending up in courts! (Such as marriage break-ups, partnership dissolution, shareholders discontent).

• How to answer “Is my business worth more now than last year”?

• What should I insure my business for?

• What is my capacity/ability to borrow funds?

• What should I set as my asking price if I want to sell my business?

• What should I set as my offering price if I want to buy a business

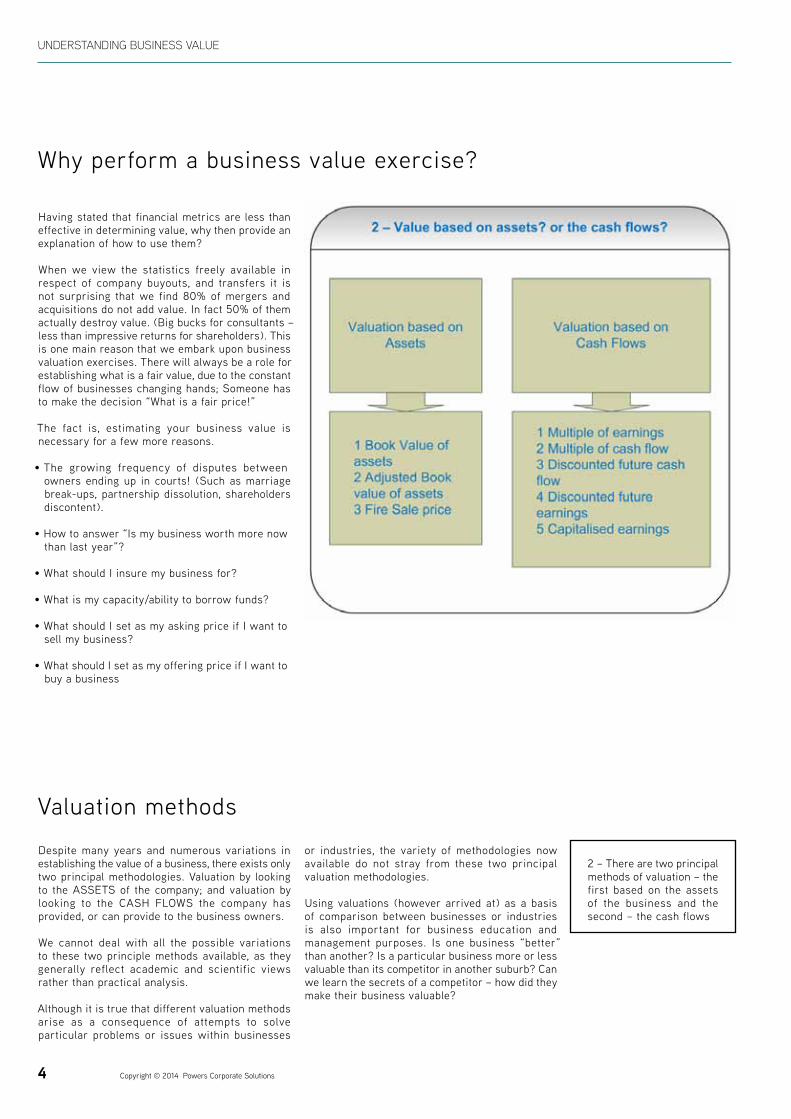

Why perform a business value exercise?

Despite many years and numerous variations in establishing the value of a business, there exists only two principal methodologies. Valuation by looking to the ASSETS of the company; and valuation by looking to the CASH FLOWS the company has provided, or can provide to the business owners.

We cannot deal with all the possible variations to these two principle methods available, as they generally reflect academic and scientific views rather than practical analysis.

Although it is true that different valuation methods arise as a consequence of attempts to solve particular problems or issues within businesses

Valuation methods

2 – There are two principal methods of valuation – the first based on the assets of the business and the second – the cash flows

or industries, the variety of methodologies now available do not stray from these two principal valuation methodologies.

Using valuations (however arrived at) as a basis of comparison between businesses or industries is also important for business education and management purposes. Is one business “better” than another? Is a particular business more or less valuable than its competitor in another suburb? Can we learn the secrets of a competitor – how did they make their business valuable?

UNDERSTANDING BUSINESS VALUE

Copyright © 2014 Powers Corporate Solutions 5

The trend is my friend.

Valuation based on the physical assets of the business.

Adjusted Book ValueThere are many valid reasons to argue that book value does not reflect actual or even the realisable value of the assets in question, and consequently the book value should be “adjusted” up or down.

Book ValueBook value represents the application of traditional accounting concepts. The term refers to the purchase or acquisition cost of an asset less any accumulated depreciation for that asset.

However when attempting to determine business value; “Book Value” is expanded to include all assets, less their accumulated depreciation and also less any liabilities. The short hand version is as follows: Assets less Liabilities equals Owners Equity [A – L = OE]. This is also referred to as simply “Equity”.

Benefits of using Book Value or Equity.

• Simple to calculate

• Tangible assets can be touched, sold, used.

Disadvantages

• The assumption that the assets of a company are

Valuation based on the ASSETS of the company is relatively straightforward. This method is the “tried and true” method. As discussed in a previous section, this method is objective, proven and certain. However as also demonstrated, it is prone to significant understatement. As intangible assets become the dominant driver of value inside any business, the valuation method based solely on assets will be less likely to be relied upon by buyers and sellers.

So why do Banks still use this method? Security!.... Banks are very risk averse and they can seldom sell an intangible if called upon to do so as a result of business closure.

In establishing value it is important to compare the results you have with some form of benchmark. This is why we have “rules of thumb” such as “times earnings” mentioned later in this essay; It is also why accountants use ratio analysis that compare the same derived data over multiple time periods, (such as Gross Profit, Net Profit, Return on Equity, return on Capital Employed) These indexes and trends offer very illuminating information about businesses over time as a result of comparing the business you are involved with against historical, or comparative company, or available detail from data collecting companies like the stock exchange, ATO or Australian Bureau of Statistics.

If there is one thing we have learned, it is that we must be optimistic about the future, however the past is (unfortunately or fortunately) a fair barometer of the future in most business cases.

3 – Va l u a t i o n s a re meaningless if performed in isolation - all valuations shou ld be compar i son based – over time or across business / industry.

One very clear trend, is the growth in annual business valuations conducted specifically for Board and management purposes (i.e. internal use). Measuring growth in value for the purposes of improving company performance, changing risk profile and improving cash flow are witness to both the importance of independent, verifiable and consistent valuation processes; and the availability of less costly valuation skills now available in the market.

The price that similar businesses have sold for, or a similar business is worth, may not provide any sound or meaningful support for you, but it remains for you to establish and substantiate a differing opinion; and trends (measurement over time, or measurement across businesses or industries) should form part of the ammunition used.

actually worth the cash that was spent on them can be wildly inaccurate. That’s one reason why we deduct accumulated depreciation.

• We know that the value of the assets owned or held by a company does not reflect true value.

Where this knowledge is useful:

Analysts refer to equity when forming comparative views. Examples are financial and value ratios.

Copyright © 2014 Powers Corporate Solutions 6

UNDERSTANDING BUSINESS VALUE

Adjusted Book Value cont.

For example property (generally but not exclusively) appreciates in value over time. As a consequence, making al lowance for the changes in value (increases and decreases) can be justified in certain circumstances.

Another way of “adjusting” the book value of assets is to reflect the value of “intangibles” such as Goodwill, value of the company brand or patents and copyrights.

A third way of determining adjusted value is to consider what the market may pay at a “salvage” auction. Generally this is much less than even market value – Everybody wants a bargain, this method is also known to many as “Fire – Sale” price.

Benefits

When consistently applied over time, adjustments

help business owners determine with greater certainty true “realisable value” for assets or classes of assets.

Adjustments can be made for changes in value over time (both appreciation and depreciation). A practical example of these “adjustments” is the willingness of accountants (normally very conservative professionals), to systematically adjust the books to recognise changes in risk, technology, value of the dollar; or for changes in wear and tear of assets.

Disadvantages

Due to the fact that any “adjusting” is based upon opinion, this method is always going to be open to debate and will rarely be accepted by opposing parties.

Valuations based upon Cash Flow

The second category of valuation methods are by reference to valuations based upon the profit making potential of the business – Sometimes referred to as cash flow methods.

Multiple of Earnings or Income Approach Discounted Future Earnings

This method is by far the most well-known and easiest method to understand. It is used by real estate agents and accountants as a “rule of thumb” method for providing guidance. The starting point is to ascertain the profit before tax for a twelve month trading period. The method then multiplies that figure by anything from two times to nine times and even higher.

Example – let’s say a small sandwich bar and lunchtime coffee shop returned a profit of $30,000 for a year. If we used a multiplier of say three times (3 x $30,000) The value of the shop would be $90,000.

This method is simple and straightforward. The debate occurs when owners who want the best sale price attempt to bump up the multiplier to 4, 5 or more. Or alternatively attempt to add back their wages, or Interest, or even suggest that they take most of the money out in cash or consumables so the profit figure should be inflated by these sums.

Disadvantages

The “rule of thumb” is debatable, seldom being accepted without encouragement to take into consideration (once again) the intangibles like location, access to clients, newness etc.Vagueness in interpretation. When dealing with investors who are active in the stock market, this phrase (earnings multiples) has a different meaning, so it is important to be clear on what you mean when you use this expression.

This method approaches valuation by assuming the business will continue to operate, and will year after year make profits (and sometimes losses). Secondly, that these future profits or earnings must reasonably be converted into todays’ monetary equivalent to arrive at a true value as at today.

By adding up or summing al l future period profit(loss) and applying a discount rate to convert the future into todays’ equivalent dollar value, business value can be determined.

Benefits

The method takes into consideration the “time value of money” i.e. any business investor would prefer to have the money today, rather than at some future time. The calculation “compensates” the investor for the time span involved.

The method permits the incorporation of a “risk premium”. For example, as an investor looks further and further into the future there is an increasing risk that the planned future earnings will not happen. The discount rate allows for this uncertainty (or risk) to be built into the valuation.

Disadvantages

The risk premium is a balance of opinion and fact and can be hotly disputed by opposing sides.

5 – first seek to understand the risks to future cash flow…

4 – In 2007 nearly al l v a l ua t i on t ransac t i ons were for formal valuations. By 2011 almost 95% were for va lue improvement knowledge.

Bstar

UNDERSTANDING BUSINESS VALUE

Copyright © 2014 Powers Corporate Solutions 7

Discounted cash flow

As with discounted future earnings, pure (actual) cash flows are estimated to continue to occur in the future, and when converted into todays cash equivalent, can assist in estimating the value of a business.

Benefits This valuation method is generally used when attempting to value new businesses. A company that is presently selling product or services has some accounting evidence to provide certainty in respect of revenue, costs and net profit. A new business however has significant uncertainty in respect for the assumptions made leading up to “profit” Therefore using only cash flow, some of the uncertain assumptions are eliminated

Disadvantages As with Discounted future earnings, the method is based on opinion, and perceptions of risk. The risk can be viewed from the perspective of risk outside the business such as industry risk, or risk of outside events impacting the industry; or risk inside the business. Significant debate can and does occur between parties on exactly how much to “discount” the numbers provided within the cash flow forecasts to cover all the risks.

An example of the application of discounted cash flow using excel spreadsheets is shown in this table.

Capitalised Earnings

Using the “Capitalised Earnings” approach is the most difficult to use, and to explain. However, it is the valuation methodology and process we use when being asked to provide an accountant’s independent valuation report.

“Capitalised Earnings” reflects the position that any business should be generating sufficient profit profits after tax to return the owners investment.

Where successfully applied, we have observed the models use quantitative and qualitative information to determine independently both the risk drivers and the value drivers present.

Firstly it is necessary to work out the rate of return (interest rate) that will be used to reflect the business owner’s risk. Then the earnings are divided by that capitalized rate. The difficulties arrive in explaining the variety of mathematical formulas used for determining the rate, and then how earnings was arrived at!

The more risky the business, the industry and even the broader economy, the higher is the required rate of return that should be used.

Similarly the calculation of the “true” income and costs can become quite complex. For example income can be adjusted to reflect “free” cash flow, profit before tax, after tax, or before dividends or after dividends.

The true carrying value of the assets being used to actually earn the revenue is also open for debate. What should or should not be included is dependent upon the bias of the “expert” providing the opinions.

Present Value CALCULATION

The following shows how to calculate the present value of a certain cash flow ($2,000) accruing each year over the next five years

Interest Rate 12%Payment 2,000

Year 0 1 2 3 4 5

Payment 2,000 2,000 2,000 2,000 2,000

Present value factor 100% 89% 80% 71% 64% 57%

PV of payment 1,786 1,594 1,424 1,271 1,135

This sum Now $2,000

Times the PV Factor 0.893

is worth $1785.71 (in twelve months time)

Times the PV Factor 0.797

is worth $1594.39 (in two years time)

Times the PV Factor 0.712

is worth $1423.56 (in three years time)

Times the PV Factor 0.636

is worth $1,271.04 (in four years time)

Times the PV Factor 0.567

is worth $1,134.85 (in five years time)

Receiving the sum of $7209.55 now, is equivalent to receiving $2,000 each year for five years

Copyright © 2014 Powers Corporate Solutions 8

UNDERSTANDING BUSINESS VALUE

Balancing Risk and Return

All business owners confront risks in relation to earning their revenue. Valuations based upon future cash flows feature prominently in the valuation models used. Further, when confronting formal / legal disputes “capitalized earnings” helps in developing an understanding of the “Risks” to future cash flow and assists in presenting a defendable unbiased methodology.

Following, are some simple observations about risk drivers and value drivers that should be considered in the context of working out any valuation.

• There are many things about business customers that are uncertain; Are they happy? Will they come back if ownership of the business changes, if prices are increased, if a competitor opens up in premises close by.

• Operations: The way you operate determines risk, the assets owned or needed by the business. Old equipment such as computers, vehicles, plant that will shortly need to be replaced, or new operational equipment that must be bought soon.

• Verbal agreements: “Hand shake” agreements invariably create a more risky environment, for example for tenancy rights, rights to use something or some process.

• Contracts that will expire soon, - for technology, tenancy and patents again place future cash flows at risk.

• Financial risk includes relative debt levels – irrespective of the sources – (including the business owner who works long hours for minimal wages- who is now a source of credit)

How you assess the risk to future cash flows should be clear. A final word of caution here; don’t rely upon biased data, and performing valuations at least annually helps determine trends.

6 – There are four key ratiosGross Profit, Net Profit, ROCE and Activity ratios.

UNDERSTANDING BUSINESS VALUE

Copyright © 2014 Powers Corporate Solutions 9

Gross Profit Margin %

Net Profit Margin %

Activity Ratio

Calculated from revenue (or sales) less the direct cost of producing the sale, equals gross profit.Gross profit then divided by Sales.

Company A is more profitable than company B. The reasons could be many, however so long as they are comparable, Company A will always be more valuable than Company B – because it makes more money from selling the products it sells.

The Net Profit % is calculated by dividing Net Profit $ by Sales $

The Net Profit – (whether it be “before tax” or “after tax”) is the monies available to be taken by the owners. Net profit is the reason we are in business, so there should be no argument as to the importance of this ratio.

There may be businesses that make better profits than others. There may be valid reasons why a profit figure is low or high, and there might be costs that are included or not included. Still, the actual measurement is an important first step.

Calculated as Sales / Net Assets. This ratio measures how much revenue is gained by the assets needed to gain that revenue.

Company A makes more money, with a smaller investment in assets needed, and provides more cash at the end of the day to the owners.

These examples have been created to highlight two main points.

Comparisons are important – whether it be comparison of a particular companies progress over time – known as trend analysis. Or comparison of two companies, or even comparison with “best practice” “Industry norms” or desired outcomes.Secondly, whatever the derived valuation of a business, it is important to satisfy yourself that the information you have received is meaningful to you.

Company A: produces $1.36 in revenue for every dollar of total capital employed.

Company B only earns $1.07 for every dollar of total capital employed.

ROCE – Return on Capital EmployedThe ratio ROCE is one of the most dynamic ratios used in business analysis. It links the Balance Sheet and the Profit and Loss, measuring the operational effectiveness between them both. The ratio shows the relationship between Earnings (or more simply Net Profit – or when used by accountants various other “adjusted” bottom lines) and the Assets used to actually achieve the earnings.

Irrespective of the type of industry you occupy, the ROCE should be at least equal to the average interest rate, or if used, the WACC. The ratio is arrived at as follows. Net Profit / ((Current Assets

– Current Liabilities) + Non- Current Assets).

A B

Sales $45,000 $45,000

Less COGS $26,000 $35,000

Gross Profit $19,000 $10,000

Gross Profit Margin 42% 22%

A B

Sales $45,000 $45,000

Less COGS $26,000 $35,000

Gross Profit $19,000 $10,000

Gross Profit Margin 42% 22%

Expenses $8,000 $7,000

Net Profit $11,000 $3,000

Net Profit Margin 24% 7%

A B

Net Profit $11,000 $3,000

Balance Sheet Assets $45,000 $55,000

Balance Sheet Liabilities $12,000 $13,000

Balance Sheet Net Assets $33,000 $42,000

Calculated ROCE 33% 7%

A B

Sales $45,000 $55,000

Balance Sheet Net Assets $33,000 $42,000

Activity Ratio $1.36 $1.07

Ratio AnalysisThere are many financial ratios available – entire text books full. Over years we have distil led the available rations down to a handful, and we offer four key ratios, and explain their importance to business valuation.

Copyright © 2014 Powers Corporate Solutions 10

UNDERSTANDING BUSINESS VALUE

Conclusion

When assisting business owners determine how much their business is worth we first seek to understand the future risks confronting the business. As discussed we use both quantifiable and qualitative knowledge – backed up by court tested risk and value profiling. The valuation methodologies we use are dominated by the methods that utilise future cash flows and we look specifically at Capitalised Value when performing formal valuations – again because they are defendable in courts of law. We use many financial ratios to supplement our knowledge and guide decisions but have offered just four key ratios, and explained their importance.

The essential ingredient when conducting a business valuation exercise is the clear identification of exactly what is being valued. It is important to understand if it is the business, the assets within

7 – Don’t pay for what you don’t understand

WOULD YOU LIKE TO KNOW MORE?

INTRODUCING KEVIN LOVEWELL – MR BUSINESS PLAN

Would you like more help from Kevin Lovewell - Mister Business Plan?

If you have read this e-book and you need more – there are solutions and services provided by my company that you should know about.

We produce business valuations using a patented (BCRC)* methodology that contains processes designed to accurately determine the value of a business. This patented methodology uses quite complex mathematical formulae and guides the creation of defendable profit multiples – producing our capitalisation rate, plus the most appropriate risk variables and business risk drivers for the business cash flow profile.

Boards of Directors, Business owners, solicitors and advisors have been using these valuations to improve financial performance and drive future cash flows and as the basis for sound decisions in a range of negotiations

(*The BStar Business Capitalisation Rate Calculator or BCRC and all trade marks and copyrights are owned by BStar Pty Ltd)

We have been business planners and strategists for many years. We have written business plans for very large companies and for the not so large companies. My workbook “Writing a Successful Business Plan” was developed for larger organisations seeking to create a special identity and unique path.

Other programs available are workshops for inventors – where we deal with the components

of creativity, the thinking skills and practical steps needed within start-ups and even re-start ups.

Whilst I mostly concentrate on research and development consul tancy projects , p lac ing inventions into the marketplace, and helping entrepreneurs fund their new enterprises, I am able to take on private client work, and commence new projects throughout the year.

To reach me:Email [email protected]: 07 3906 2838Or use the link on the website to find information, help, and access to e-books, papers and blogs

www.powers.net.au

the business, the proprietorship, future profits, or future cash flows that are being used to estimate

“business value”.

Just as important is the fact that all methodologies are opinion based, despite the very complex mathematical structures that might be used. The key or primary assets that create value in our economy are now the “intangible assets” such as people, processes, customers, and innovations. These things are difficult to measure and manage – but not impossible. A 2004 KPMG Study of fortune 500 companies revealed that the companies voted

“best to work for” based on those companies attitude and care for employees and customers, were valued significantly above the market or equivalent businesses, some by as much as 50%.

Copyright © 2014 Powers Corporate Solutions