the outlook for housing in 2015 - arizona · pdf filethe outlook for housing in 2015 jonathan...

TRANSCRIPT

© 2015 Move, Inc. All rights reserved. Do not copy or distribute. 1

THE OUTLOOK FOR HOUSING IN 2015 Jonathan Smoke Chief Economist

Arizona State Association of REALTORS® | March 25, 2015

© 2015 Move, Inc. All rights reserved. Do not copy or distribute. 2

NATIONAL CONTEXT

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

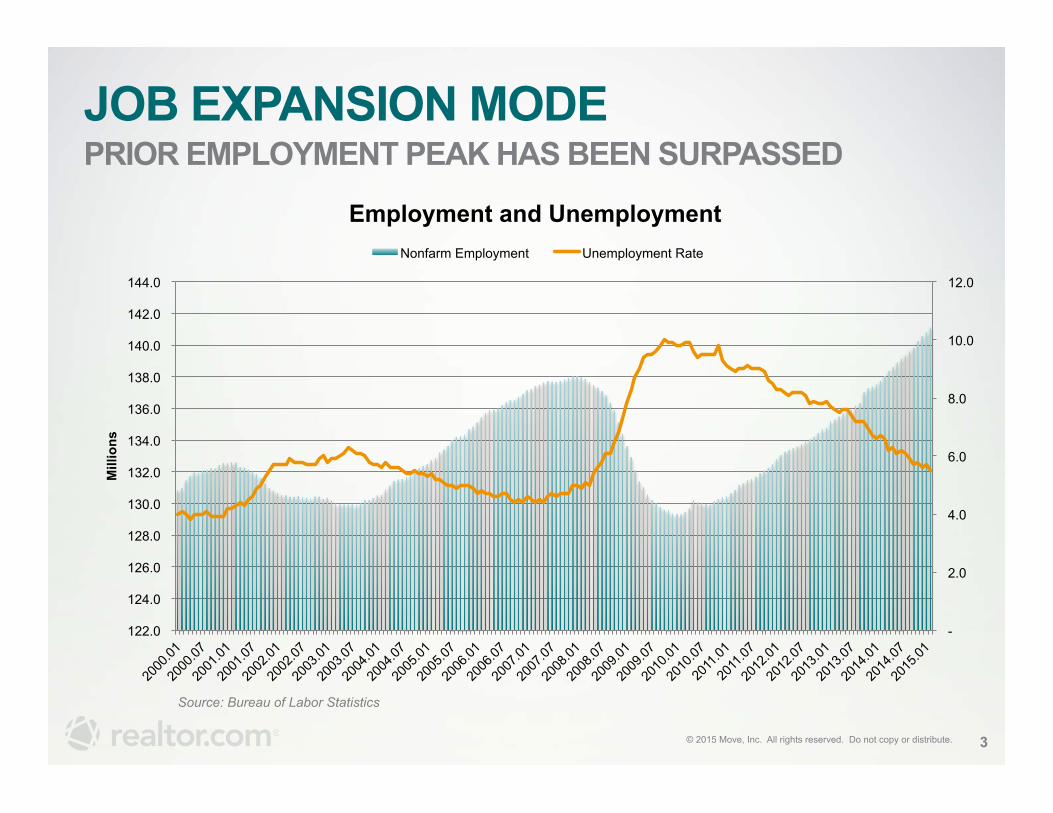

JOB EXPANSION MODE PRIOR EMPLOYMENT PEAK HAS BEEN SURPASSED

3

Source: Bureau of Labor Statistics

-

2.0

4.0

6.0

8.0

10.0

12.0

122.0

124.0

126.0

128.0

130.0

132.0

134.0

136.0

138.0

140.0

142.0

144.0

Mill

ions

Employment and Unemployment Nonfarm Employment Unemployment Rate

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

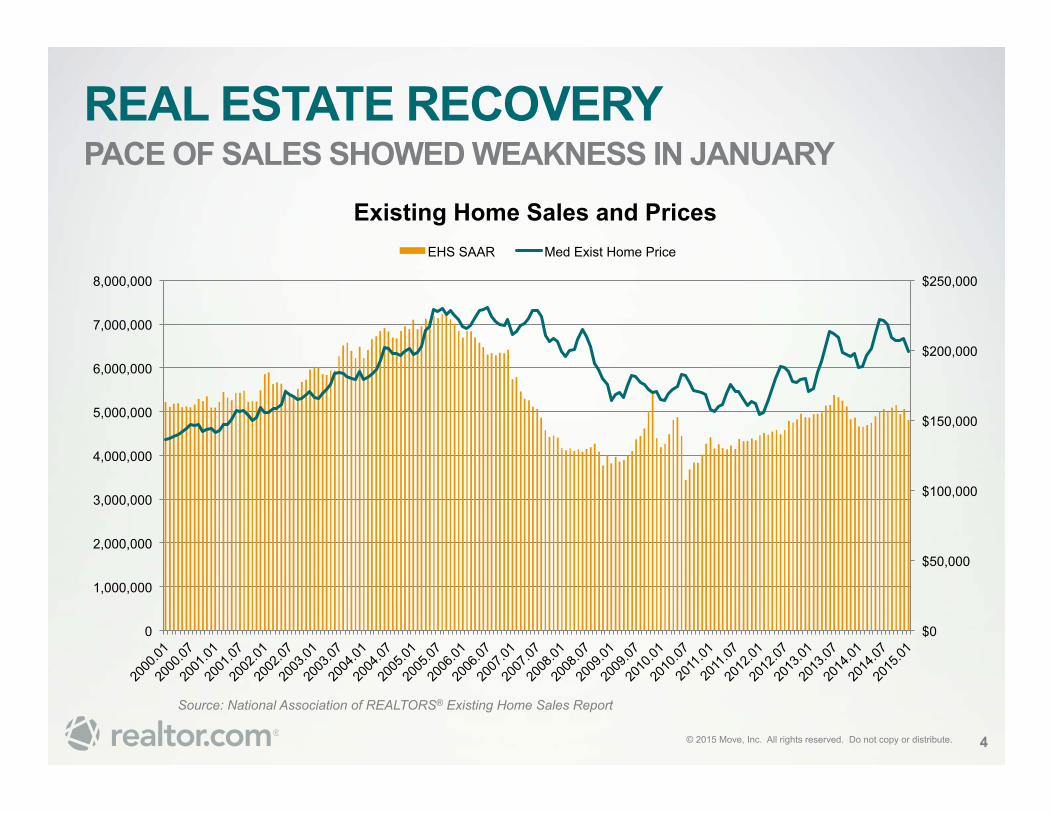

REAL ESTATE RECOVERY PACE OF SALES SHOWED WEAKNESS IN JANUARY

4

Source: National Association of REALTORS® Existing Home Sales Report

$0

$50,000

$100,000

$150,000

$200,000

$250,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Existing Home Sales and Prices EHS SAAR Med Exist Home Price

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

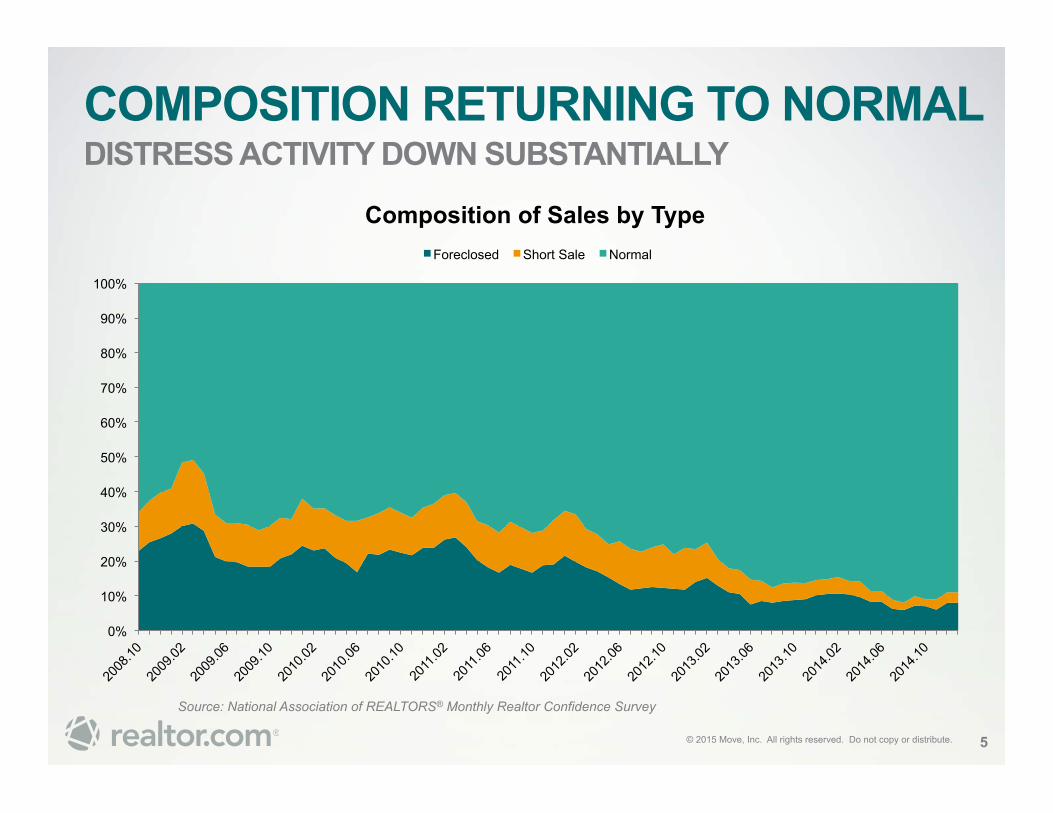

COMPOSITION RETURNING TO NORMAL DISTRESS ACTIVITY DOWN SUBSTANTIALLY

5

Source: National Association of REALTORS® Monthly Realtor Confidence Survey

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Composition of Sales by Type Foreclosed Short Sale Normal

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

INVENTORY IS A CONSTRAINT DEMAND CONTINUES TO EXCEED SUPPLY

6

Source: National Association of REALTORS®, Commerce Department

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2000

.01

2000

.05

2000

.09

2001

.01

2001

.05

2001

.09

2002

.01

2002

.05

2002

.09

2003

.01

2003

.05

2003

.09

2004

.01

2004

.05

2004

.09

2005

.01

2005

.05

2005

.09

2006

.01

2006

.05

2006

.09

2007

.01

2007

.05

2007

.09

2008

.01

2008

.05

2008

.09

2009

.01

2009

.05

2009

.09

2010

.01

2010

.05

2010

.09

2011

.01

2011

.05

2011

.09

2012

.01

2012

.05

2012

.09

2013

.01

2013

.05

2013

.09

2014

.01

2014

.05

2014

.09

2015

.01

Months' Supply of Homes for Sales Existing New

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

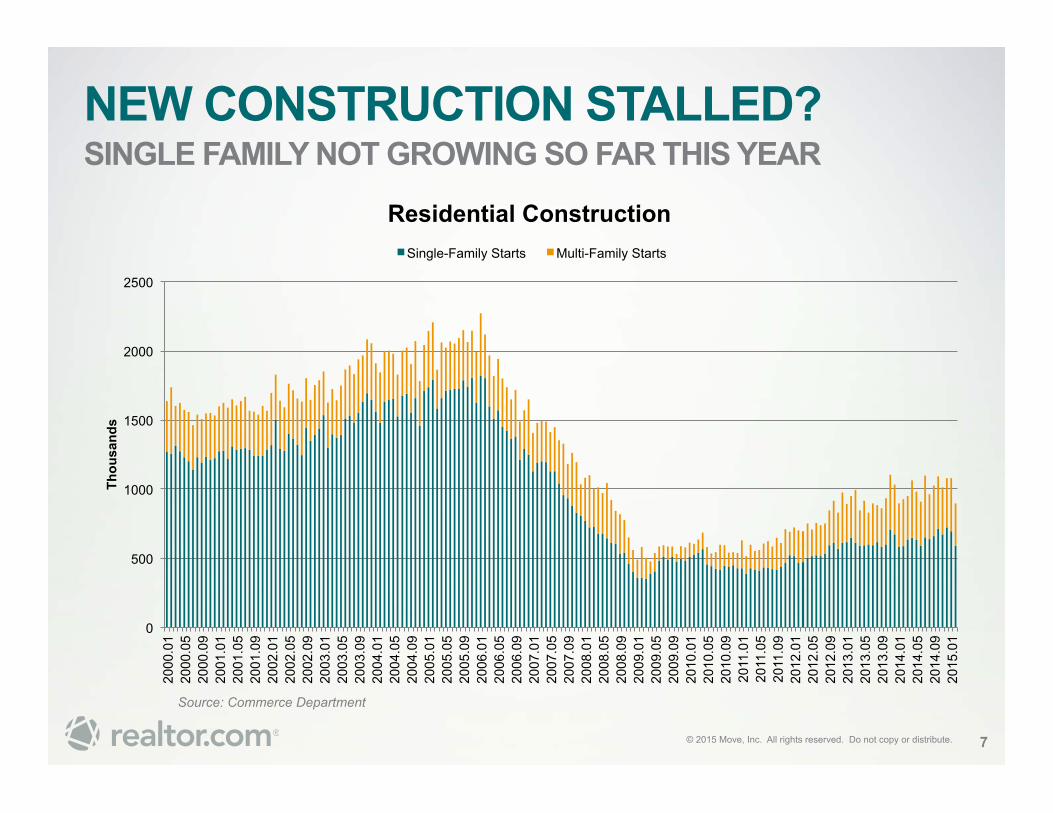

NEW CONSTRUCTION STALLED? SINGLE FAMILY NOT GROWING SO FAR THIS YEAR

7

Source: Commerce Department

0

500

1000

1500

2000

2500

2000

.01

2000

.05

2000

.09

2001

.01

2001

.05

2001

.09

2002

.01

2002

.05

2002

.09

2003

.01

2003

.05

2003

.09

2004

.01

2004

.05

2004

.09

2005

.01

2005

.05

2005

.09

2006

.01

2006

.05

2006

.09

2007

.01

2007

.05

2007

.09

2008

.01

2008

.05

2008

.09

2009

.01

2009

.05

2009

.09

2010

.01

2010

.05

2010

.09

2011

.01

2011

.05

2011

.09

2012

.01

2012

.05

2012

.09

2013

.01

2013

.05

2013

.09

2014

.01

2014

.05

2014

.09

2015

.01

Thou

sand

s

Residential Construction Single-Family Starts Multi-Family Starts

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

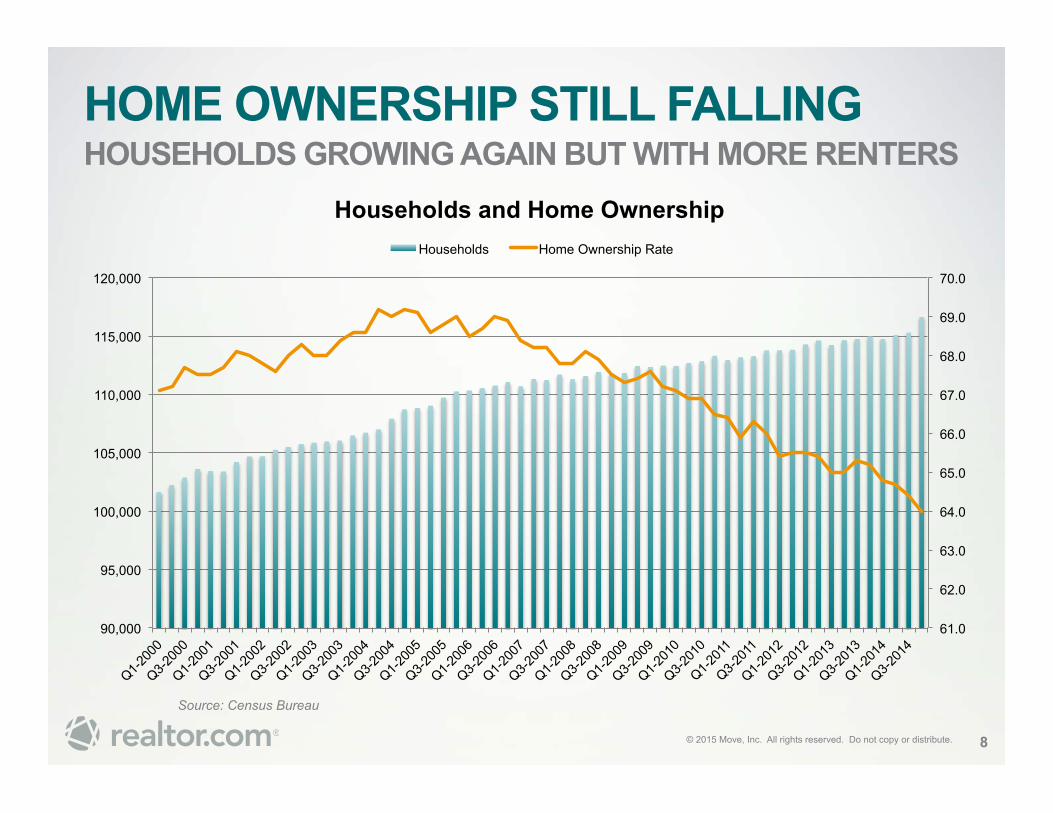

HOME OWNERSHIP STILL FALLING HOUSEHOLDS GROWING AGAIN BUT WITH MORE RENTERS

8

Source: Census Bureau

61.0

62.0

63.0

64.0

65.0

66.0

67.0

68.0

69.0

70.0

90,000

95,000

100,000

105,000

110,000

115,000

120,000

Households and Home Ownership Households Home Ownership Rate

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

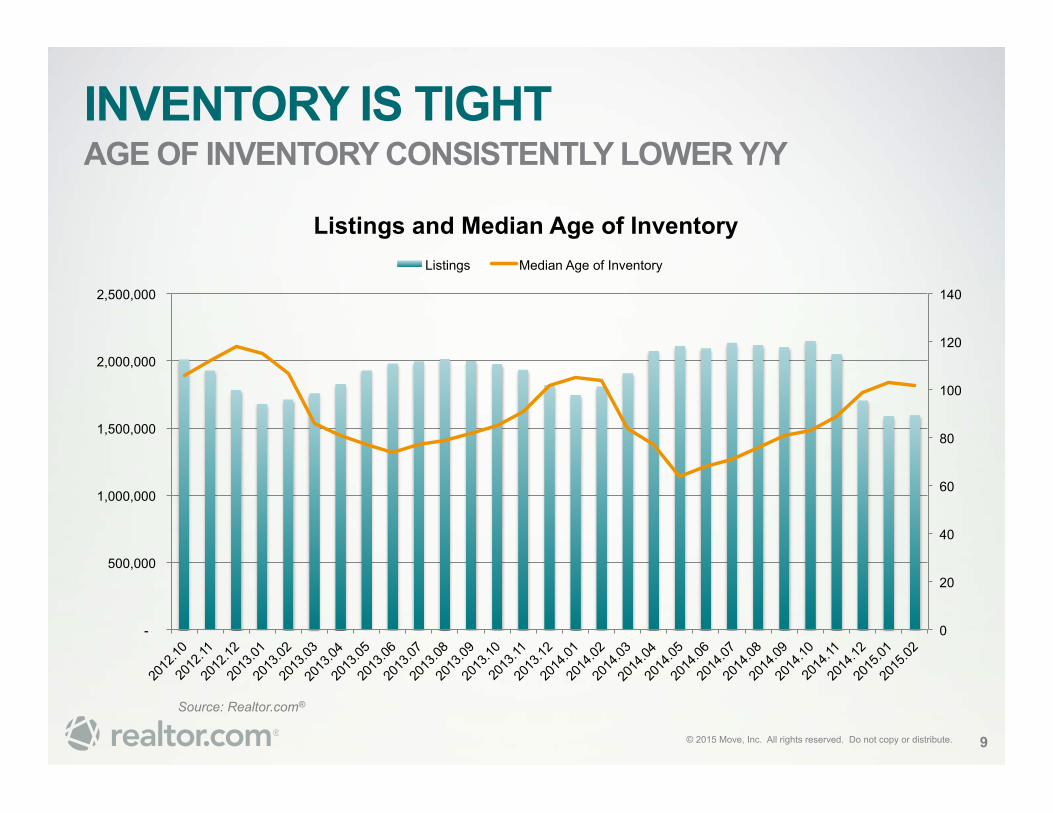

INVENTORY IS TIGHT AGE OF INVENTORY CONSISTENTLY LOWER Y/Y

9

Source: Realtor.com®

0

20

40

60

80

100

120

140

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Listings and Median Age of Inventory Listings Median Age of Inventory

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

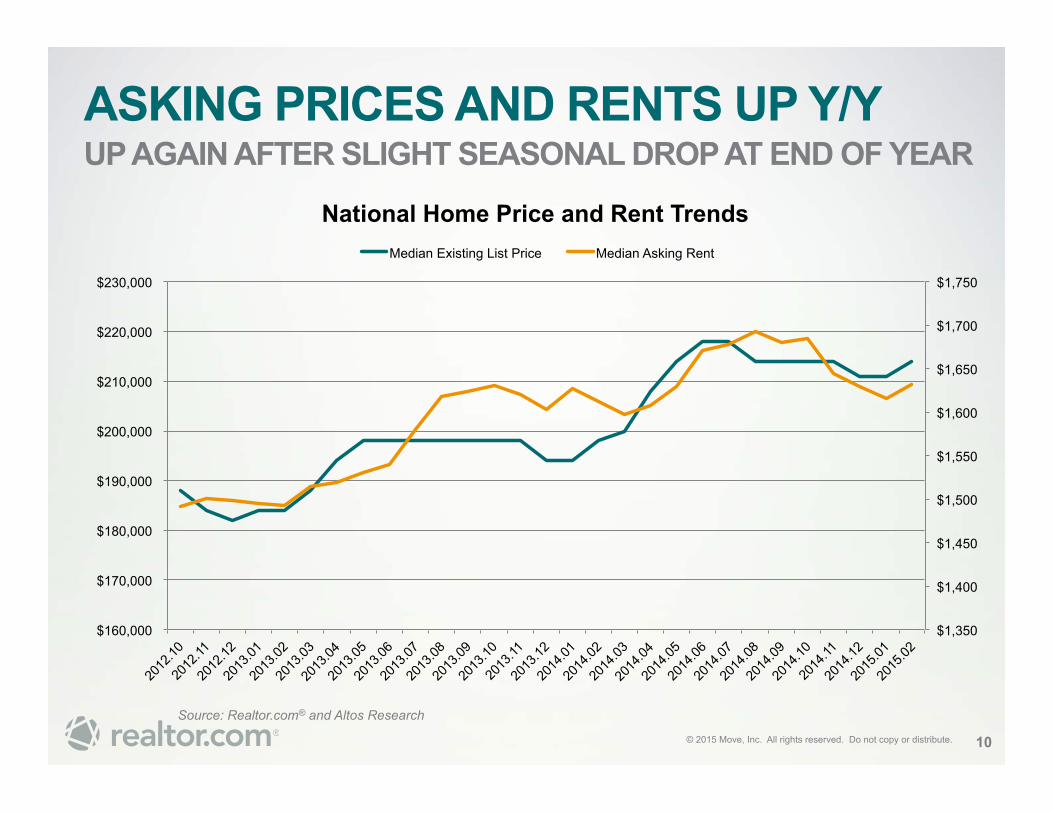

ASKING PRICES AND RENTS UP Y/Y UP AGAIN AFTER SLIGHT SEASONAL DROP AT END OF YEAR

10

Source: Realtor.com® and Altos Research

$1,350

$1,400

$1,450

$1,500

$1,550

$1,600

$1,650

$1,700

$1,750

$160,000

$170,000

$180,000

$190,000

$200,000

$210,000

$220,000

$230,000

National Home Price and Rent Trends Median Existing List Price Median Asking Rent

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

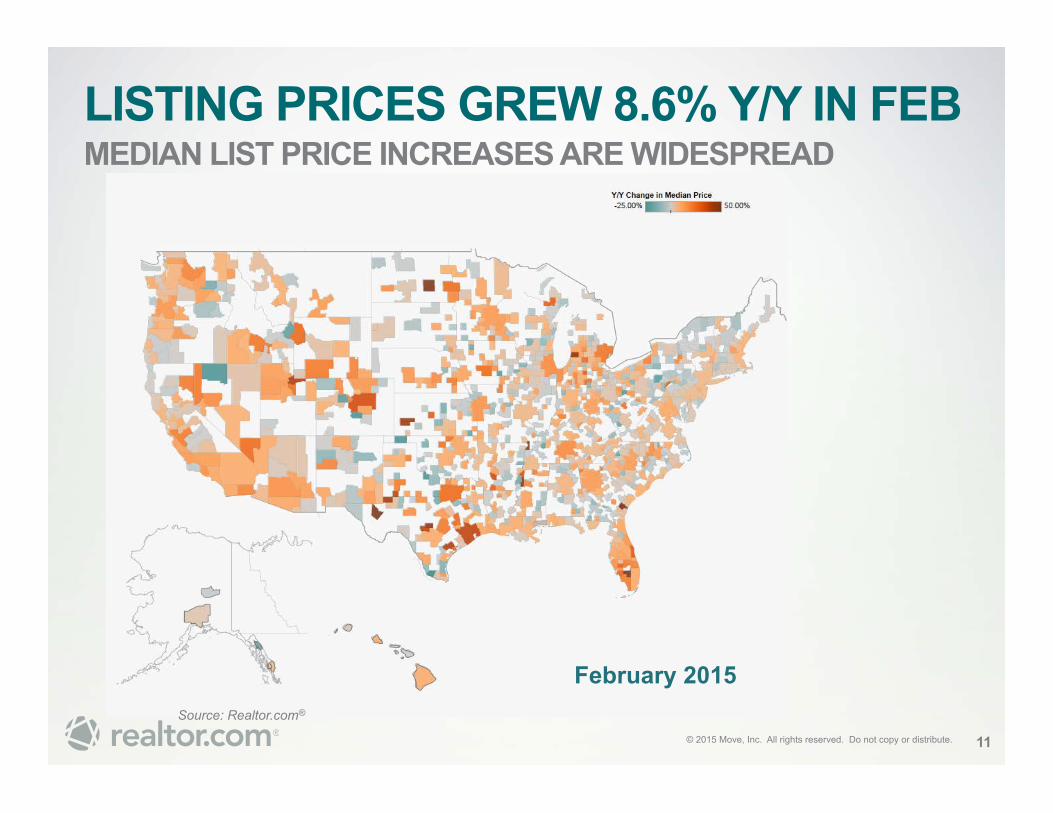

LISTING PRICES GREW 8.6% Y/Y IN FEB MEDIAN LIST PRICE INCREASES ARE WIDESPREAD

11

February 2015 Source: Realtor.com®

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

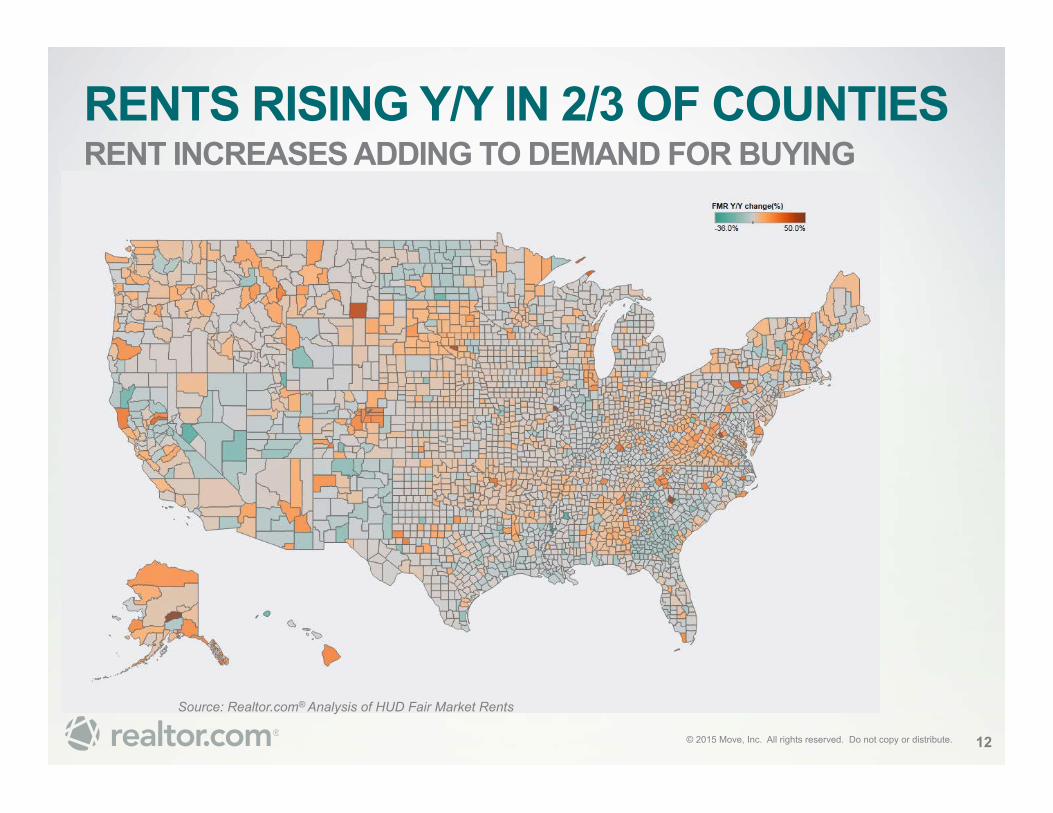

RENTS RISING Y/Y IN 2/3 OF COUNTIES RENT INCREASES ADDING TO DEMAND FOR BUYING

Source: Realtor.com® Analysis of HUD Fair Market Rents

12

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

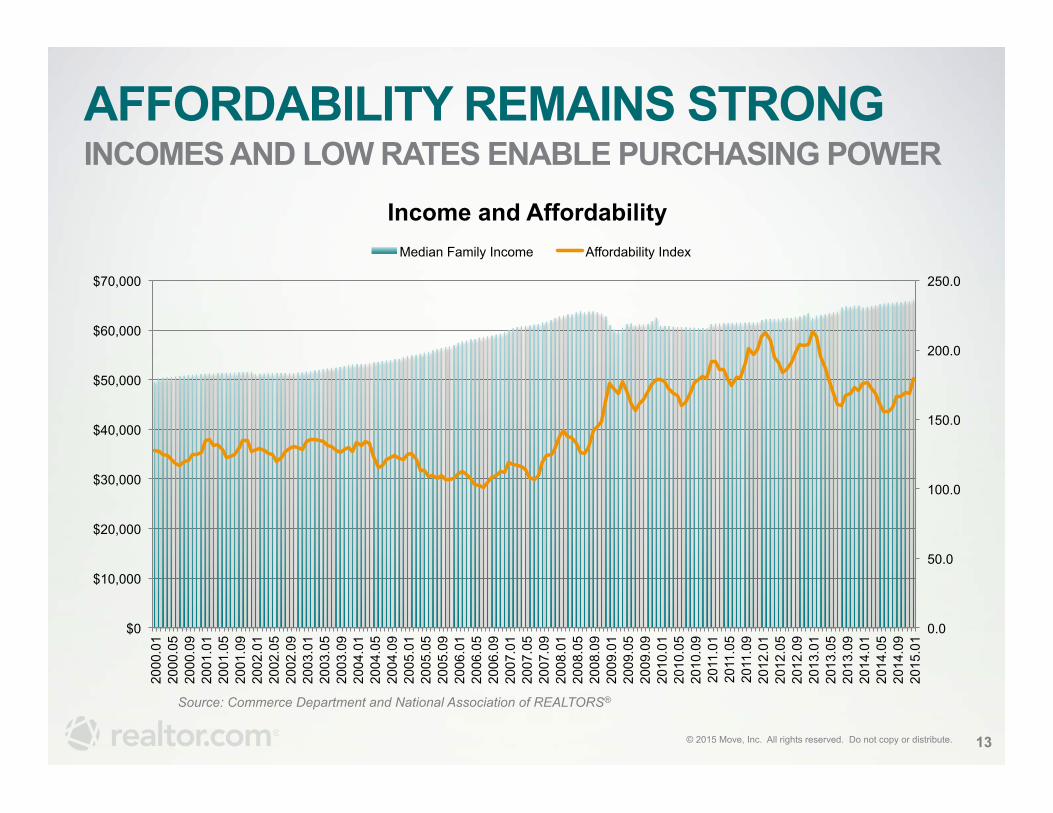

AFFORDABILITY REMAINS STRONG INCOMES AND LOW RATES ENABLE PURCHASING POWER

13

Source: Commerce Department and National Association of REALTORS®

0.0

50.0

100.0

150.0

200.0

250.0

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

2000

.01

2000

.05

2000

.09

2001

.01

2001

.05

2001

.09

2002

.01

2002

.05

2002

.09

2003

.01

2003

.05

2003

.09

2004

.01

2004

.05

2004

.09

2005

.01

2005

.05

2005

.09

2006

.01

2006

.05

2006

.09

2007

.01

2007

.05

2007

.09

2008

.01

2008

.05

2008

.09

2009

.01

2009

.05

2009

.09

2010

.01

2010

.05

2010

.09

2011

.01

2011

.05

2011

.09

2012

.01

2012

.05

2012

.09

2013

.01

2013

.05

2013

.09

2014

.01

2014

.05

2014

.09

2015

.01

Income and Affordability Median Family Income Affordability Index

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

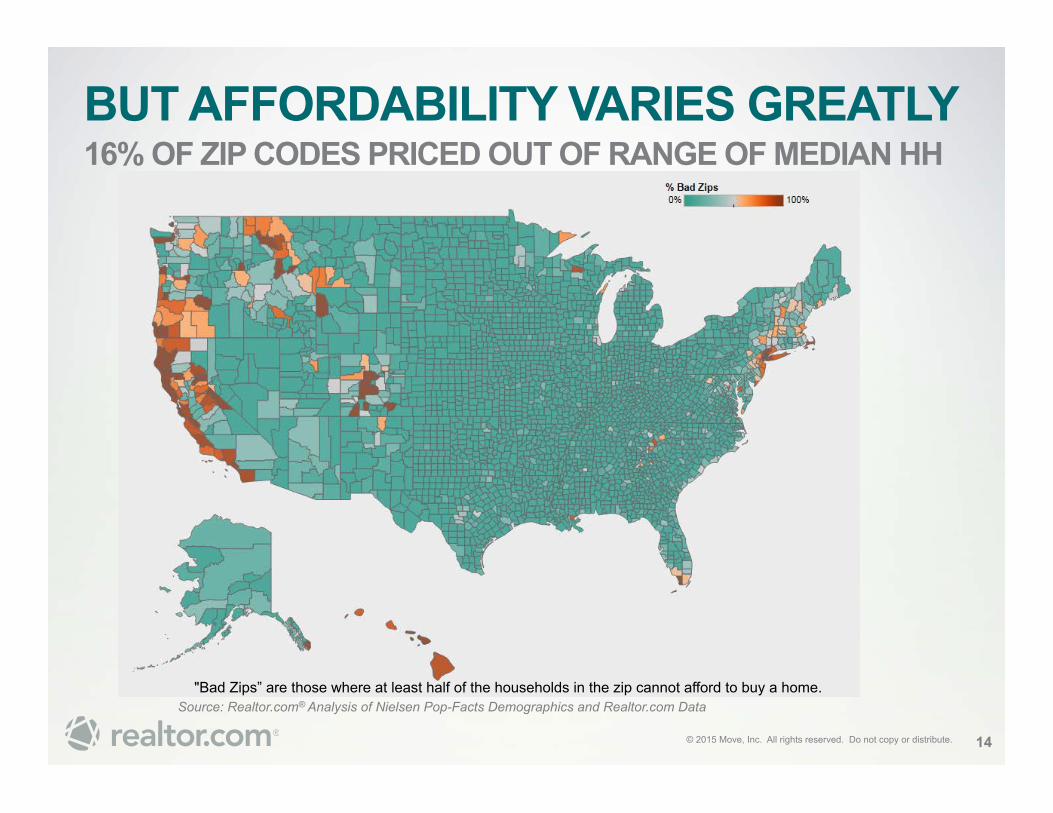

BUT AFFORDABILITY VARIES GREATLY 16% OF ZIP CODES PRICED OUT OF RANGE OF MEDIAN HH

Source: Realtor.com® Analysis of Nielsen Pop-Facts Demographics and Realtor.com Data

14

"Bad Zips” are those where at least half of the households in the zip cannot afford to buy a home.

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

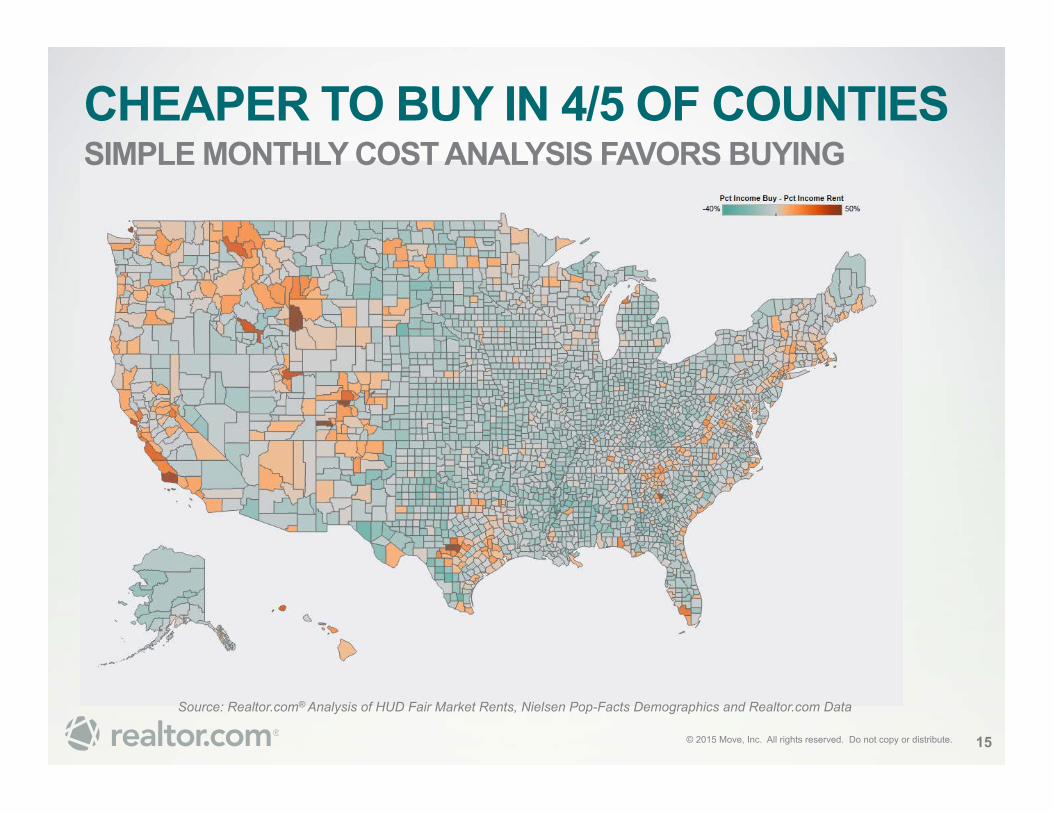

CHEAPER TO BUY IN 4/5 OF COUNTIES SIMPLE MONTHLY COST ANALYSIS FAVORS BUYING

Source: Realtor.com® Analysis of HUD Fair Market Rents, Nielsen Pop-Facts Demographics and Realtor.com Data

15

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

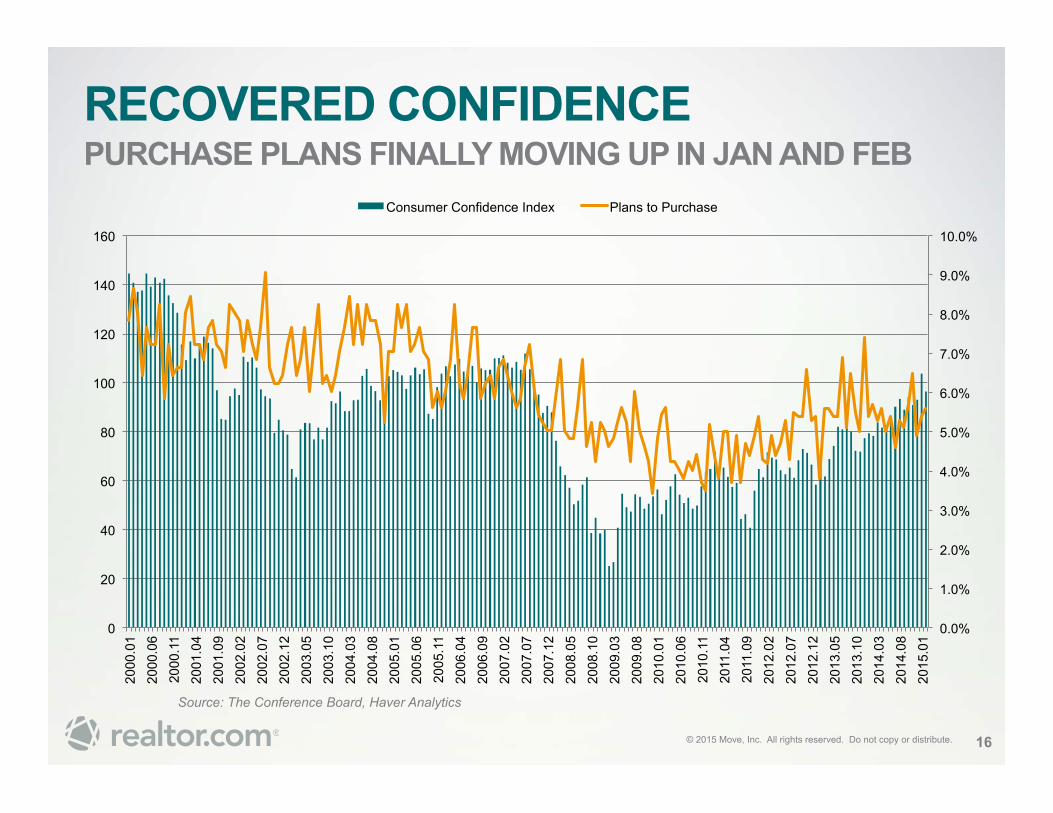

RECOVERED CONFIDENCE PURCHASE PLANS FINALLY MOVING UP IN JAN AND FEB

16

Source: The Conference Board, Haver Analytics

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

0

20

40

60

80

100

120

140

160

2000

.01

2000

.06

2000

.11

2001

.04

2001

.09

2002

.02

2002

.07

2002

.12

2003

.05

2003

.10

2004

.03

2004

.08

2005

.01

2005

.06

2005

.11

2006

.04

2006

.09

2007

.02

2007

.07

2007

.12

2008

.05

2008

.10

2009

.03

2009

.08

2010

.01

2010

.06

2010

.11

2011

.04

2011

.09

2012

.02

2012

.07

2012

.12

2013

.05

2013

.10

2014

.03

2014

.08

2015

.01

Consumer Confidence Index Plans to Purchase

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

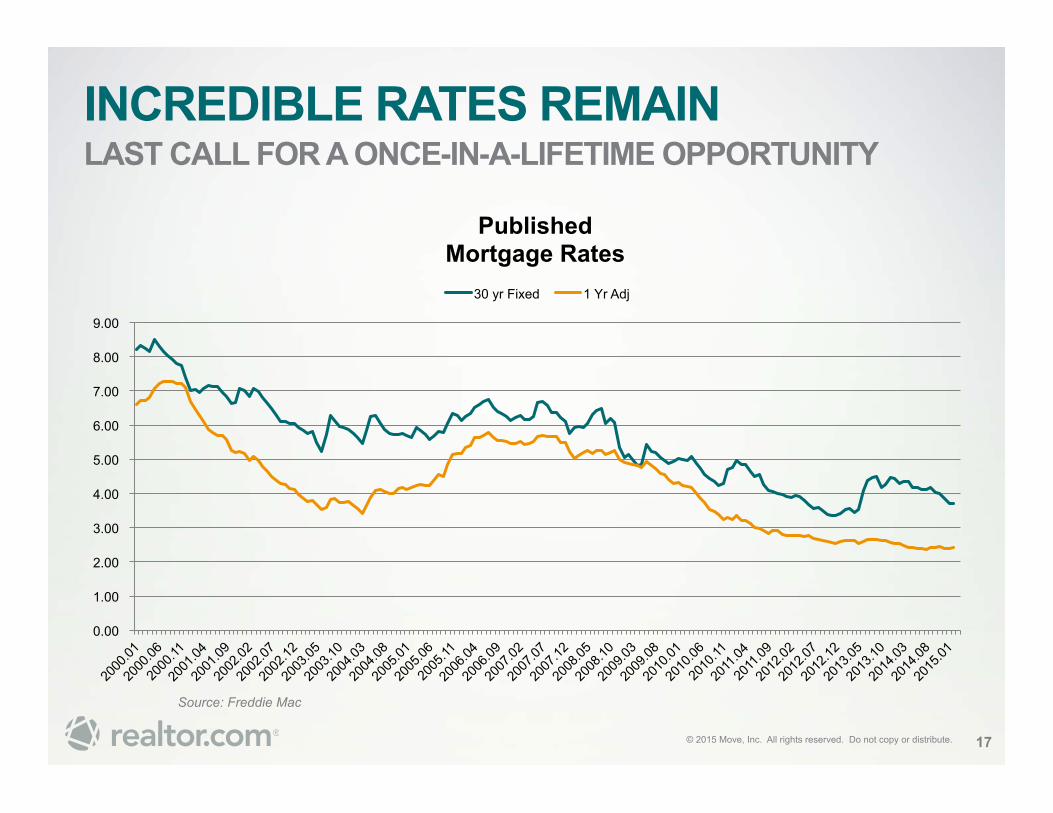

INCREDIBLE RATES REMAIN LAST CALL FOR A ONCE-IN-A-LIFETIME OPPORTUNITY

17

Source: Freddie Mac

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

Published Mortgage Rates

30 yr Fixed 1 Yr Adj

© 2015 Move, Inc. All rights reserved. Do not copy or distribute. 18

DEMAND DRIVERS

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

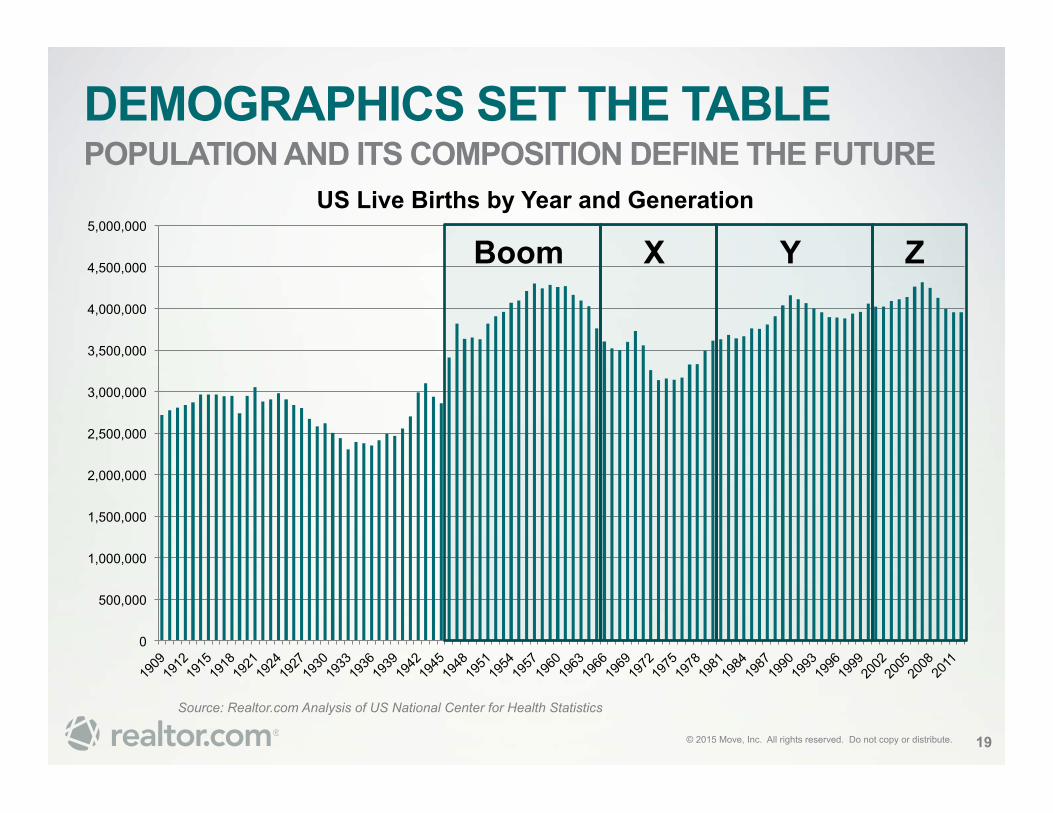

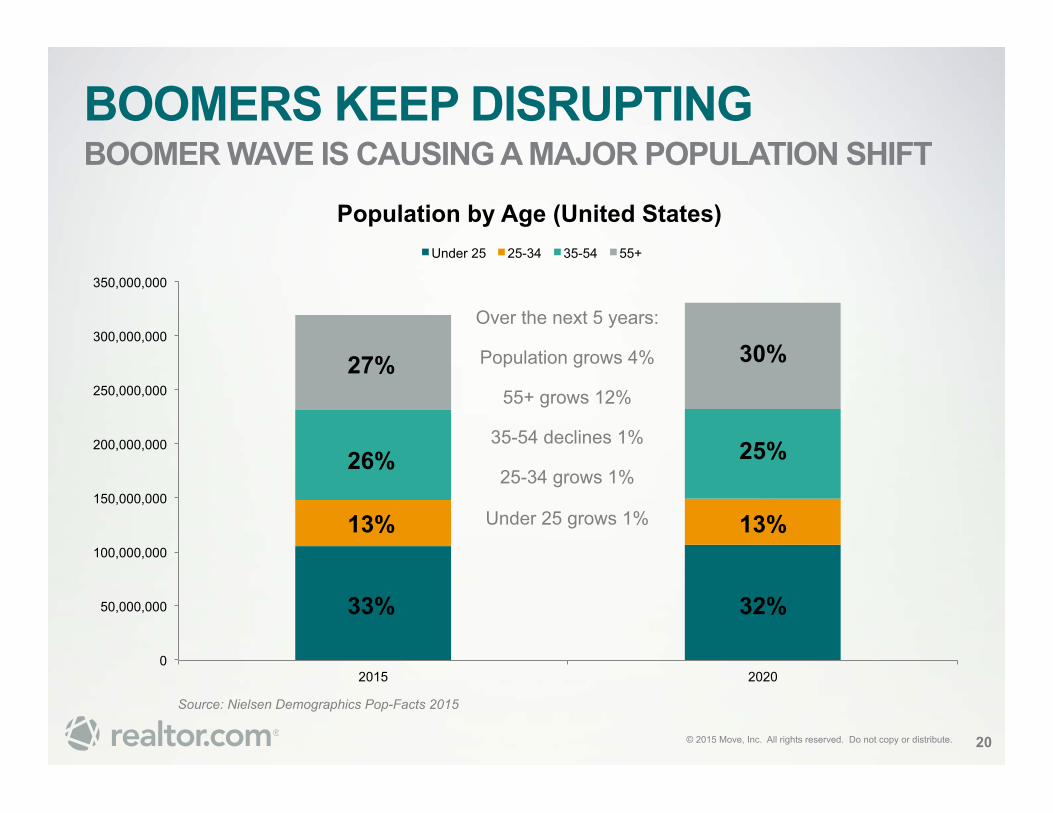

DEMOGRAPHICS SET THE TABLE POPULATION AND ITS COMPOSITION DEFINE THE FUTURE

19

Source: Realtor.com Analysis of US National Center for Health Statistics

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

US Live Births by Year and Generation

Boom X Y Z

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

2015 2020

Population by Age (United States) Under 25 25-34 35-54 55+

BOOMERS KEEP DISRUPTING BOOMER WAVE IS CAUSING A MAJOR POPULATION SHIFT

20

Source: Nielsen Demographics Pop-Facts 2015

Over the next 5 years:

Population grows 4%

55+ grows 12%

35-54 declines 1%

25-34 grows 1%

Under 25 grows 1%

27%

26%

13%

33%

30%

25%

13%

32%

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

EMPLOYMENT BEGETS OPPORTUNITY BEST YEAR FOR GROWTH IN 25-34 EMPLOYMENT SINCE ’87

21 Source: Bureau of Labor Statistics, Realtor.com® Analysis

0.0

2.0

4.0

6.0

8.0

10.0

12.0 25-34 Unemployment Overall Unemployment

← First Millennial Turns 25

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

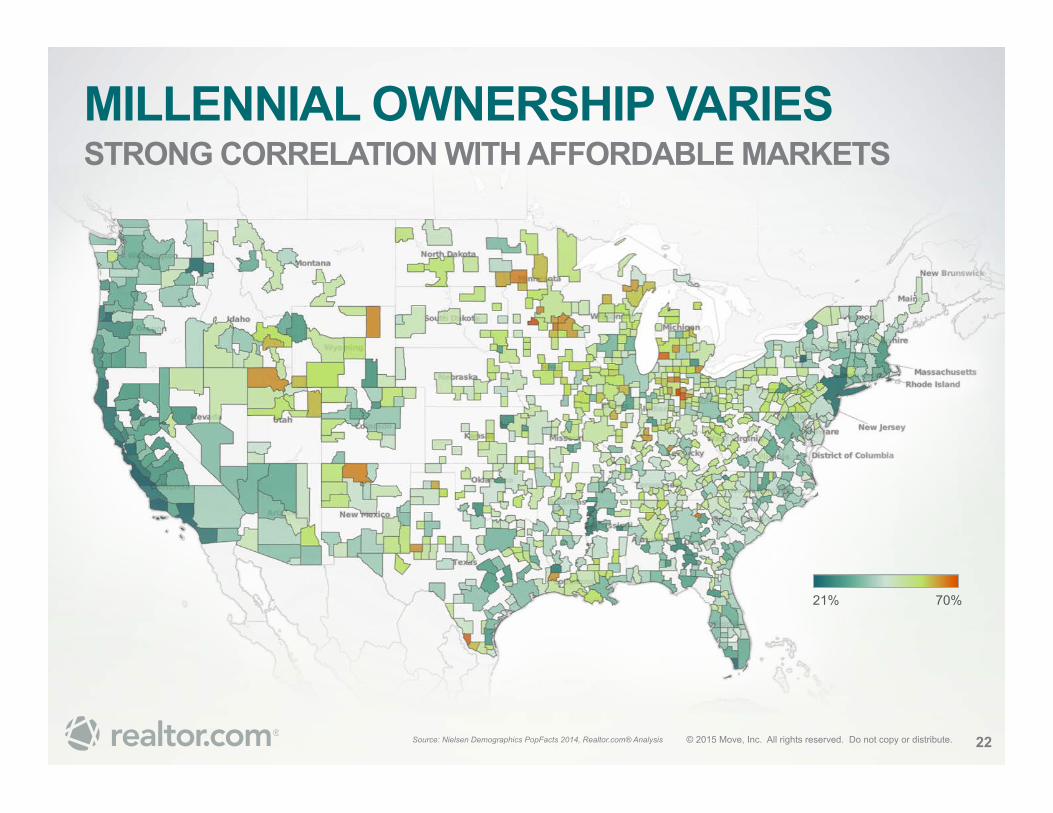

MILLENNIAL OWNERSHIP VARIES STRONG CORRELATION WITH AFFORDABLE MARKETS

22 Source: Nielsen Demographics PopFacts 2014, Realtor.com® Analysis

21% 70%

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

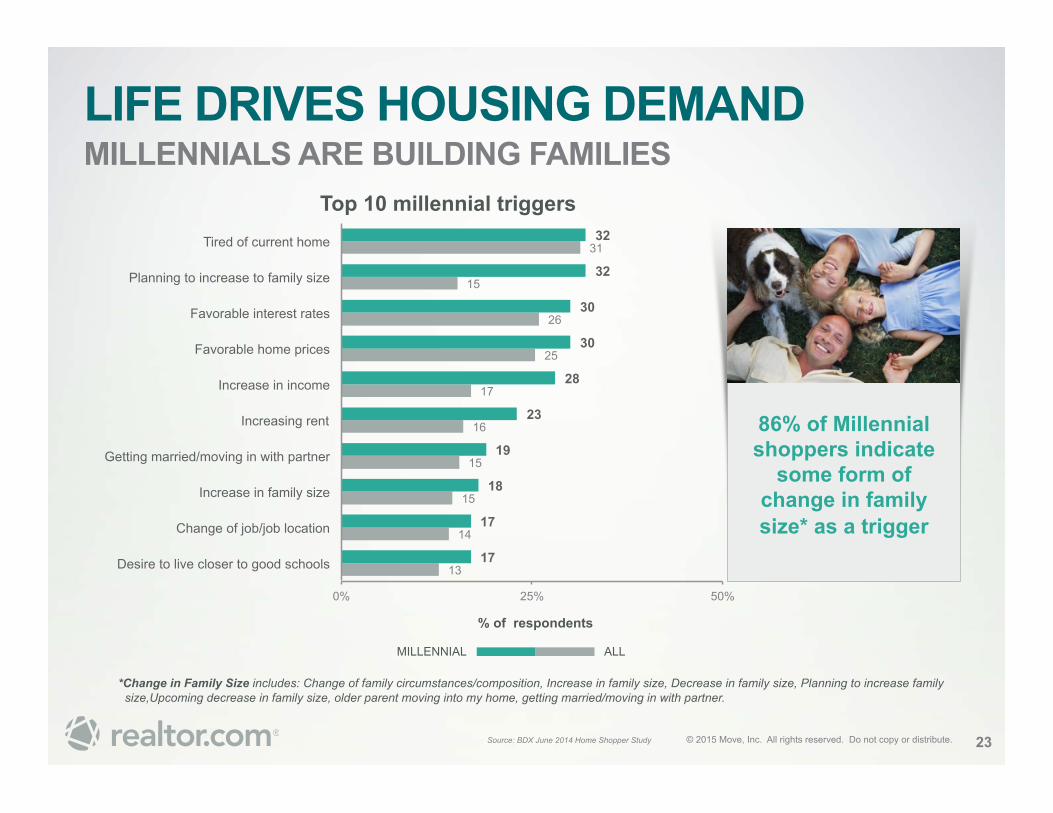

13

14

15

15

16

17

25

26

15

31

17

17

18

19

23

28

30

30

32

32

0% 25% 50%

Desire to live closer to good schools

Change of job/job location

Increase in family size

Getting married/moving in with partner

Increasing rent

Increase in income

Favorable home prices

Favorable interest rates

Planning to increase to family size

Tired of current home

% of respondents

Top 10 millennial triggers

LIFE DRIVES HOUSING DEMAND MILLENNIALS ARE BUILDING FAMILIES

86% of Millennial shoppers indicate

some form of change in family size* as a trigger

*Change in Family Size includes: Change of family circumstances/composition, Increase in family size, Decrease in family size, Planning to increase family size,Upcoming decrease in family size, older parent moving into my home, getting married/moving in with partner.

Source: BDX June 2014 Home Shopper Study 23

ALL MILLENNIAL

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

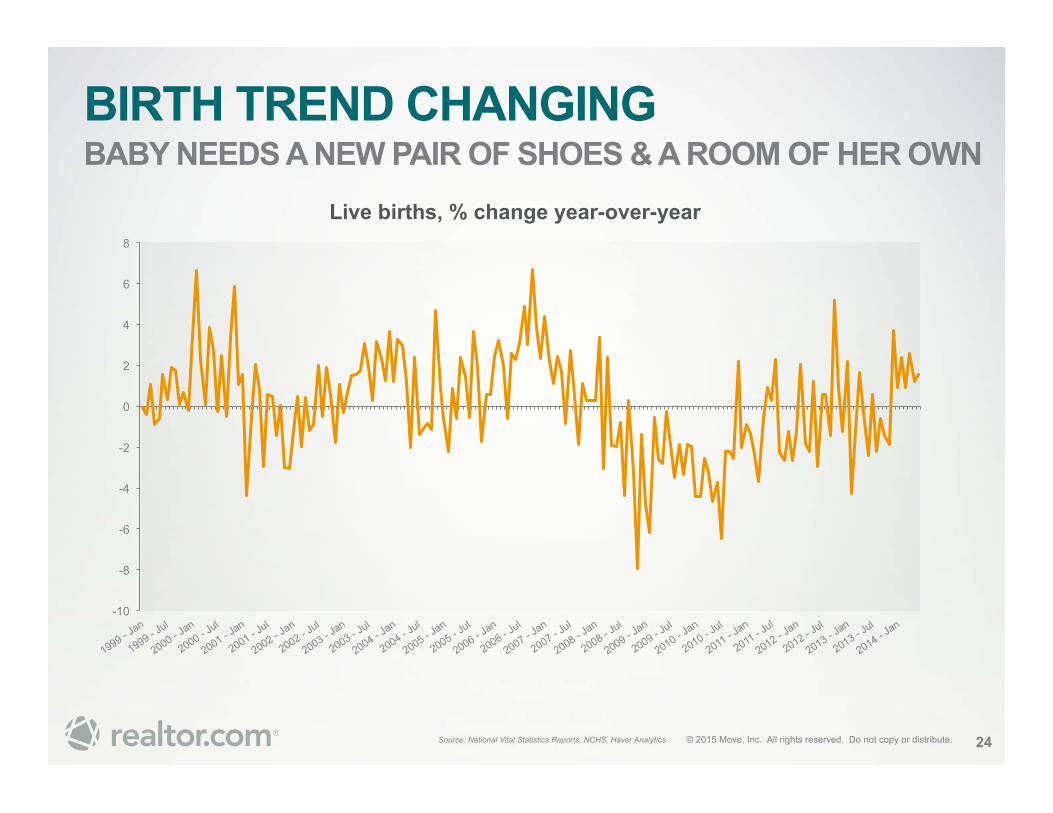

BIRTH TREND CHANGING BABY NEEDS A NEW PAIR OF SHOES & A ROOM OF HER OWN

24

-10

-8

-6

-4

-2

0

2

4

6

8

Live births, % change year-over-year

Source: National Vital Statistics Reports, NCHS, Haver Analytics

© 2015 Move, Inc. All rights reserved. Do not copy or distribute. 25

WE COULD DO MORE

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

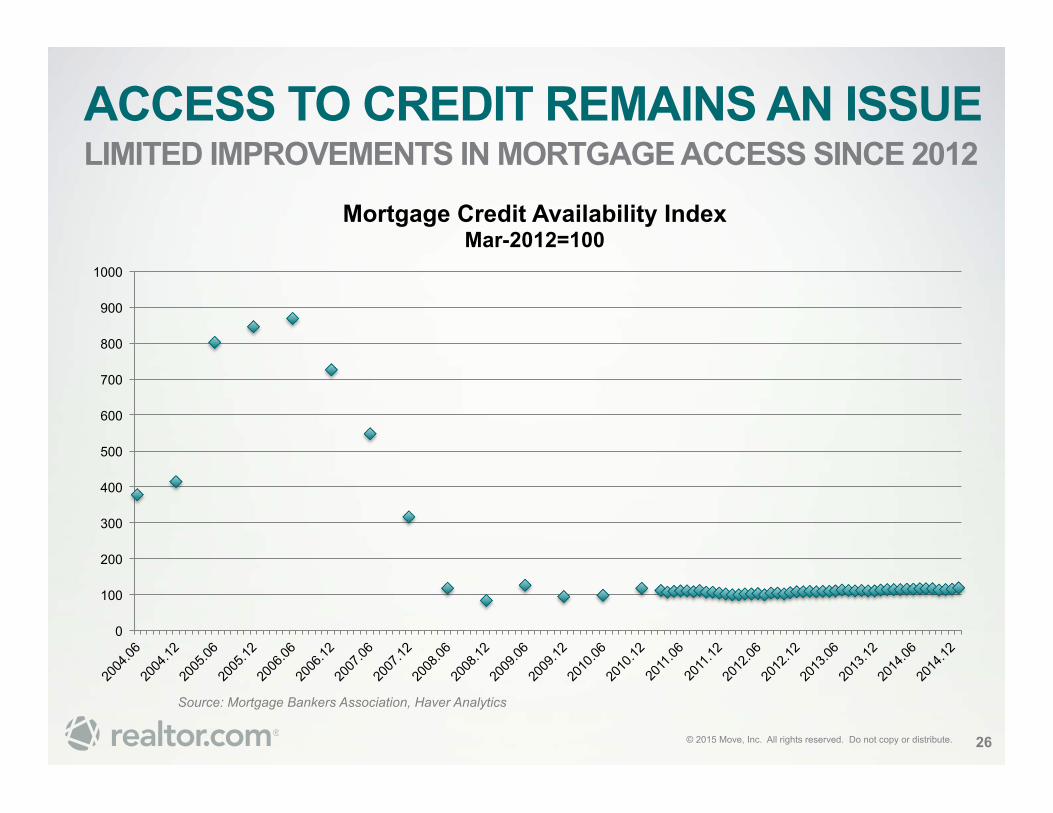

ACCESS TO CREDIT REMAINS AN ISSUE LIMITED IMPROVEMENTS IN MORTGAGE ACCESS SINCE 2012

26

Source: Mortgage Bankers Association, Haver Analytics

0

100

200

300

400

500

600

700

800

900

1000

Mortgage Credit Availability Index Mar-2012=100

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

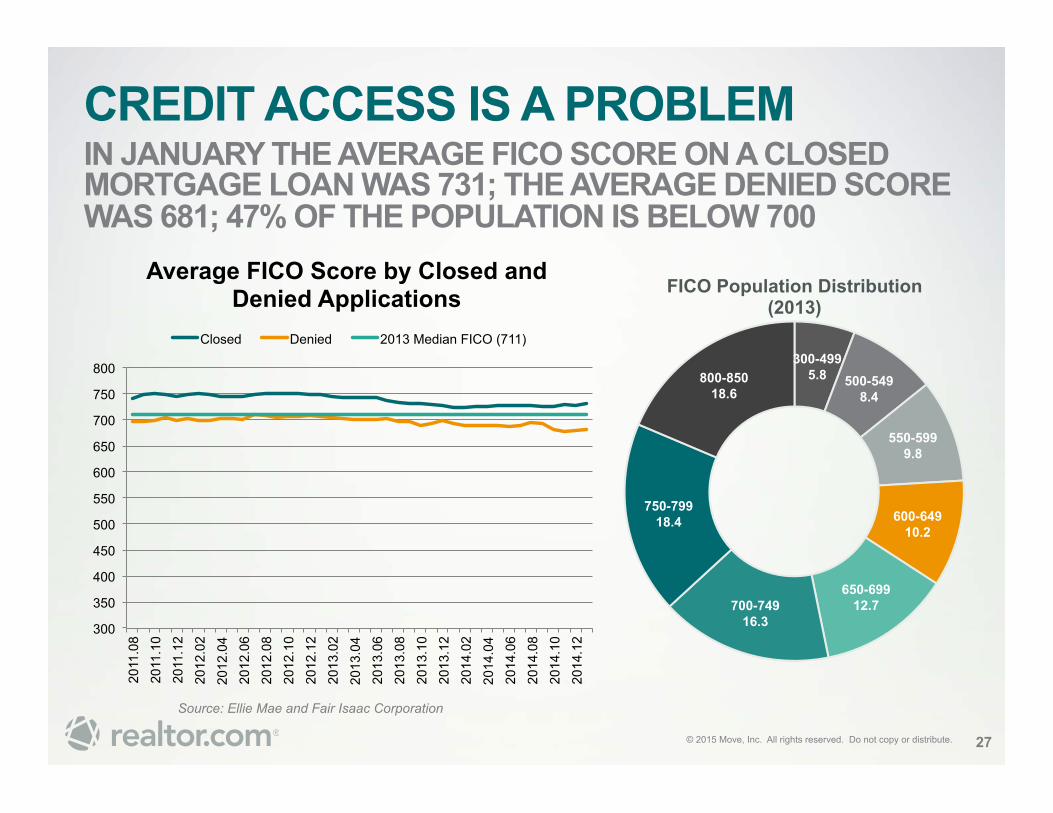

CREDIT ACCESS IS A PROBLEM IN JANUARY THE AVERAGE FICO SCORE ON A CLOSED MORTGAGE LOAN WAS 731; THE AVERAGE DENIED SCORE WAS 681; 47% OF THE POPULATION IS BELOW 700

27

Source: Ellie Mae and Fair Isaac Corporation

300-499 5.8 500-549

8.4

550-599 9.8

600-649 10.2

650-699 12.7 700-749

16.3

750-799 18.4

800-850 18.6

FICO Population Distribution (2013)

300

350

400

450

500

550

600

650

700

750

800

2011

.08

2011

.10

2011

.12

2012

.02

2012

.04

2012

.06

2012

.08

2012

.10

2012

.12

2013

.02

2013

.04

2013

.06

2013

.08

2013

.10

2013

.12

2014

.02

2014

.04

2014

.06

2014

.08

2014

.10

2014

.12

Average FICO Score by Closed and Denied Applications

Closed Denied 2013 Median FICO (711)

© 2015 Move, Inc. All rights reserved. Do not copy or distribute. 28

KEY FACTORS COMING TOGETHER MORE DEMAND AND RECOVERY IN FIRST-TIME BUYERS

• More jobs • Millennials reaching tipping point of key 25-34 year range • More households • More life events

• Mortgage rates at near-historical lows but will go up • Qualification standards should loosen in a risk-appropriate way • New conventional 3% down payment mortgages • Lower FHA insurance premiums

• This is the perfect year to list

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

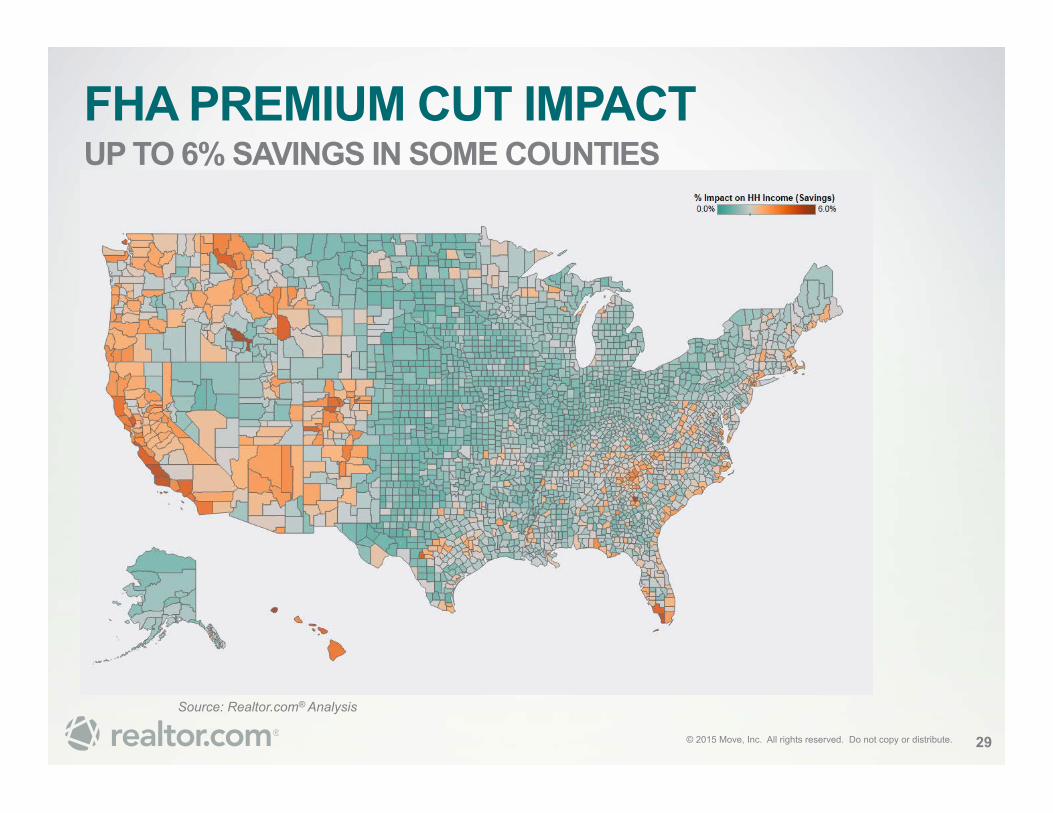

FHA PREMIUM CUT IMPACT UP TO 6% SAVINGS IN SOME COUNTIES

Source: Realtor.com® Analysis

29

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

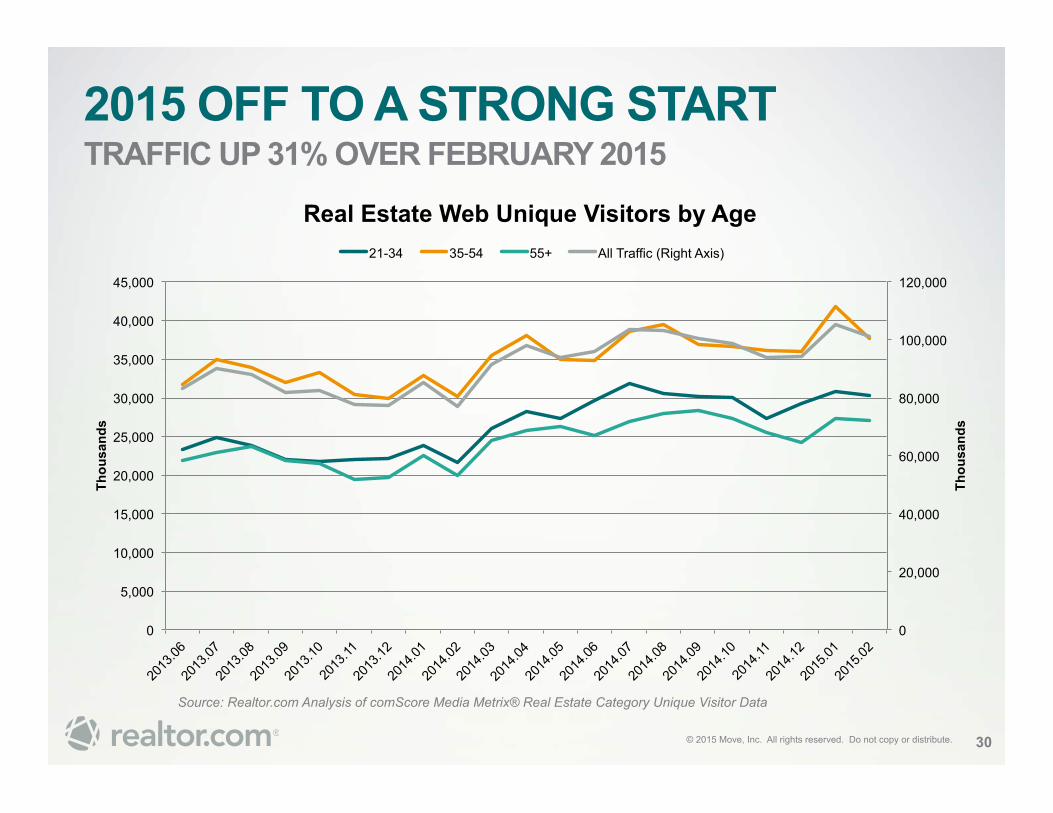

2015 OFF TO A STRONG START TRAFFIC UP 31% OVER FEBRUARY 2015

30

Source: Realtor.com Analysis of comScore Media Metrix® Real Estate Category Unique Visitor Data

0

20,000

40,000

60,000

80,000

100,000

120,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Thou

sand

s

Thou

sand

s

Real Estate Web Unique Visitors by Age 21-34 35-54 55+ All Traffic (Right Axis)

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

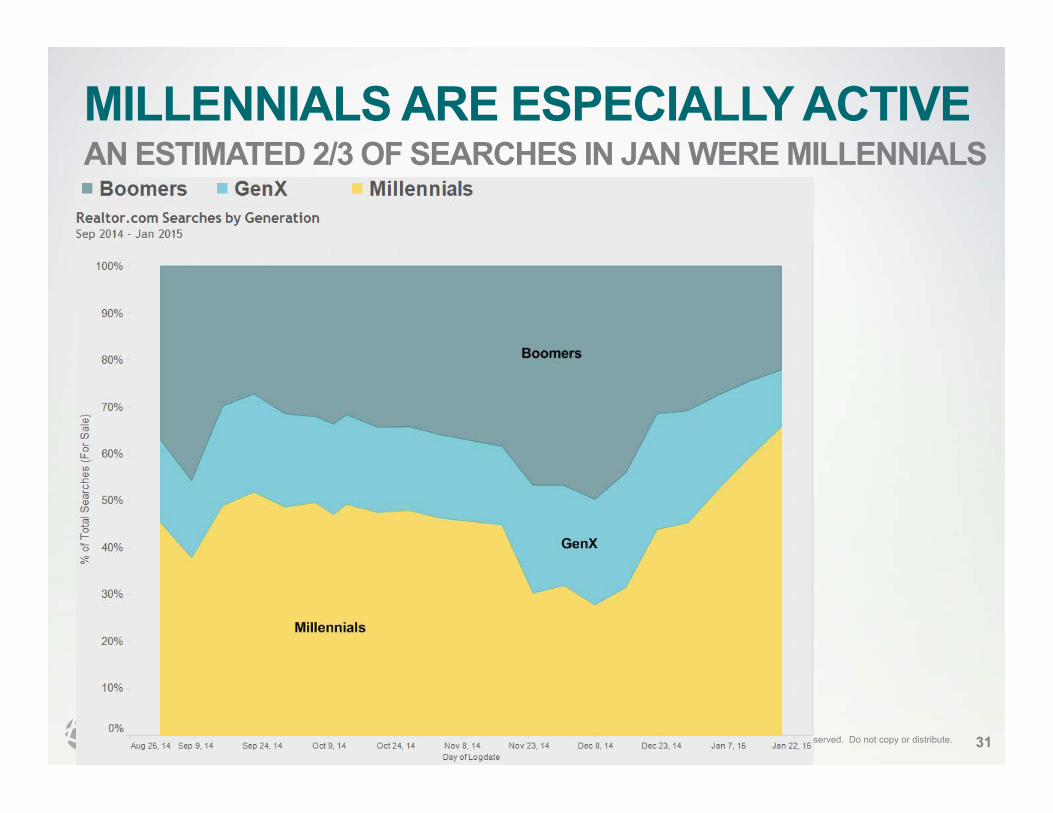

MILLENNIALS ARE ESPECIALLY ACTIVE AN ESTIMATED 2/3 OF SEARCHES IN JAN WERE MILLENNIALS

31

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

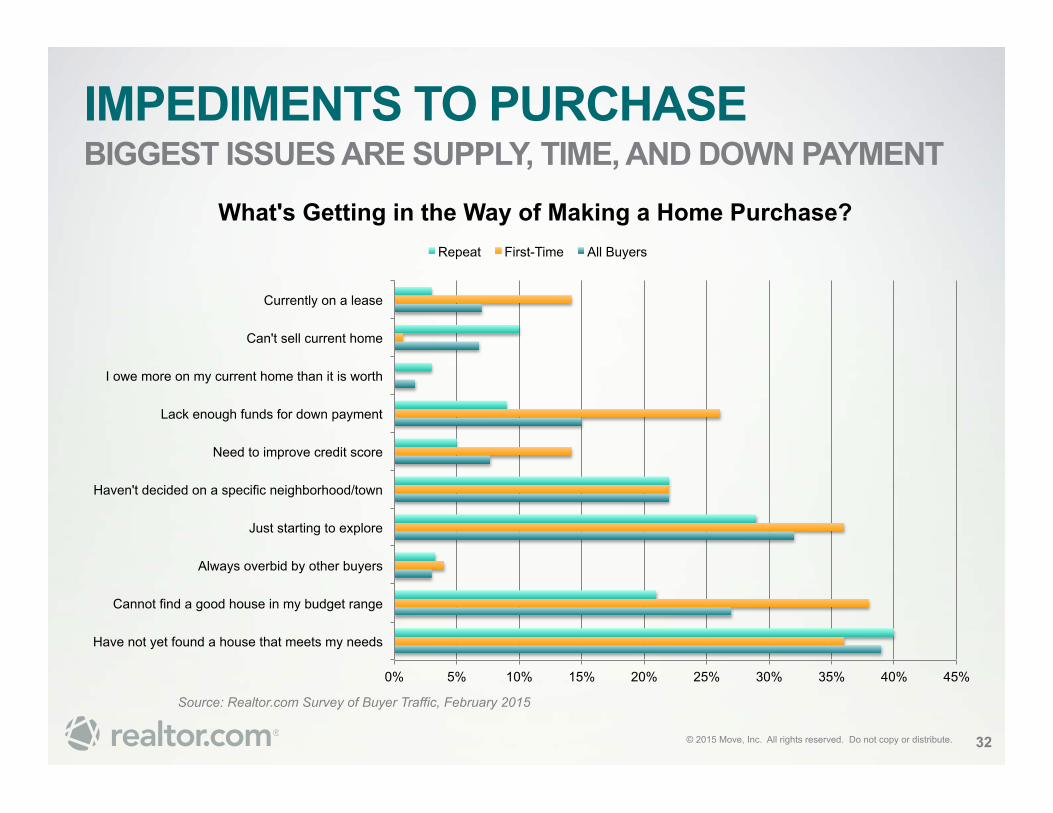

IMPEDIMENTS TO PURCHASE BIGGEST ISSUES ARE SUPPLY, TIME, AND DOWN PAYMENT

32

Source: Realtor.com Survey of Buyer Traffic, February 2015

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Have not yet found a house that meets my needs

Cannot find a good house in my budget range

Always overbid by other buyers

Just starting to explore

Haven't decided on a specific neighborhood/town

Need to improve credit score

Lack enough funds for down payment

I owe more on my current home than it is worth

Can't sell current home

Currently on a lease

What's Getting in the Way of Making a Home Purchase? Repeat First-Time All Buyers

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

1. Mortgage rates and home prices are solidly on an upward trajectory

2. Affordability and impact of mortgage options will greatly influence demand

3. Behold the enormous impact of Millennials and Boomers and what that means for demand

4. The real estate market is returning to a normal rhythm—life drives demand but supply impacts the results

REMEMBER THESE THEMES

33

© 2015 Move, Inc. All rights reserved. Do not copy or distribute. 34

THERE IS NO US HOUSING SUCH THING AS A

MARKET

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

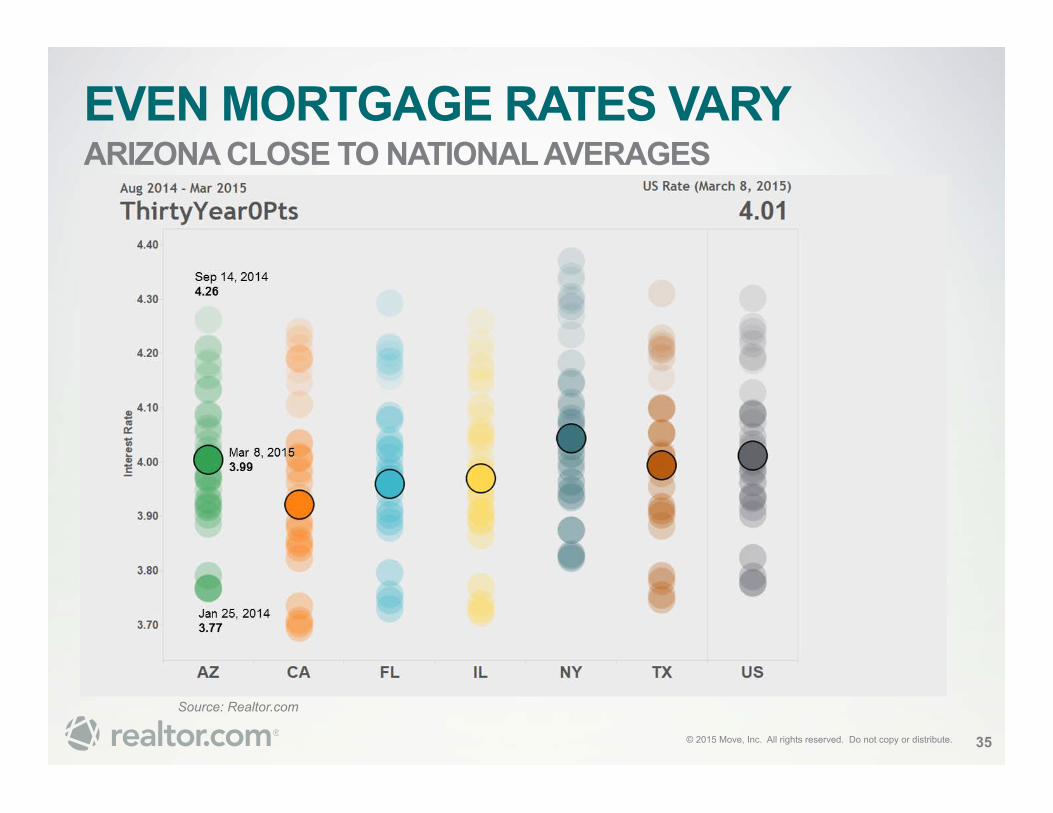

EVEN MORTGAGE RATES VARY ARIZONA CLOSE TO NATIONAL AVERAGES

35

Source: Realtor.com

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

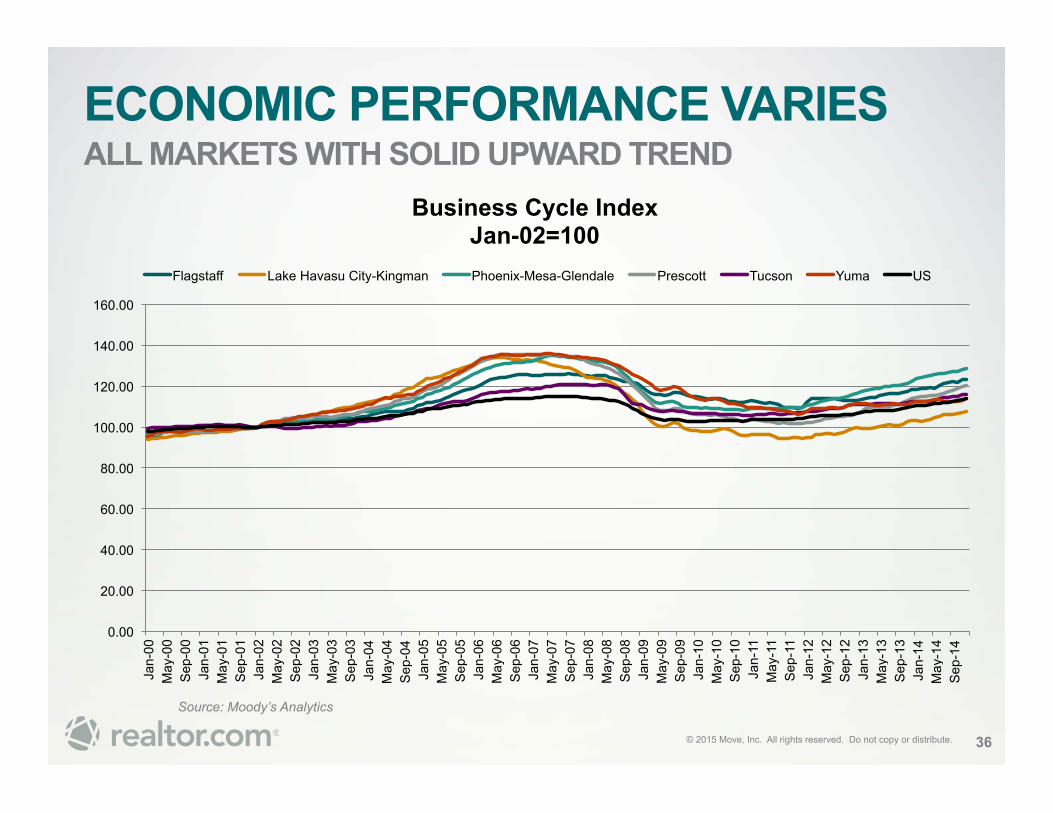

ECONOMIC PERFORMANCE VARIES ALL MARKETS WITH SOLID UPWARD TREND

36

Source: Moody’s Analytics

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

Jan-

00

May

-00

Sep

-00

Jan-

01

May

-01

Sep

-01

Jan-

02

May

-02

Sep

-02

Jan-

03

May

-03

Sep

-03

Jan-

04

May

-04

Sep

-04

Jan-

05

May

-05

Sep

-05

Jan-

06

May

-06

Sep

-06

Jan-

07

May

-07

Sep

-07

Jan-

08

May

-08

Sep

-08

Jan-

09

May

-09

Sep

-09

Jan-

10

May

-10

Sep

-10

Jan-

11

May

-11

Sep

-11

Jan-

12

May

-12

Sep

-12

Jan-

13

May

-13

Sep

-13

Jan-

14

May

-14

Sep

-14

Business Cycle Index Jan-02=100

Flagstaff Lake Havasu City-Kingman Phoenix-Mesa-Glendale Prescott Tucson Yuma US

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

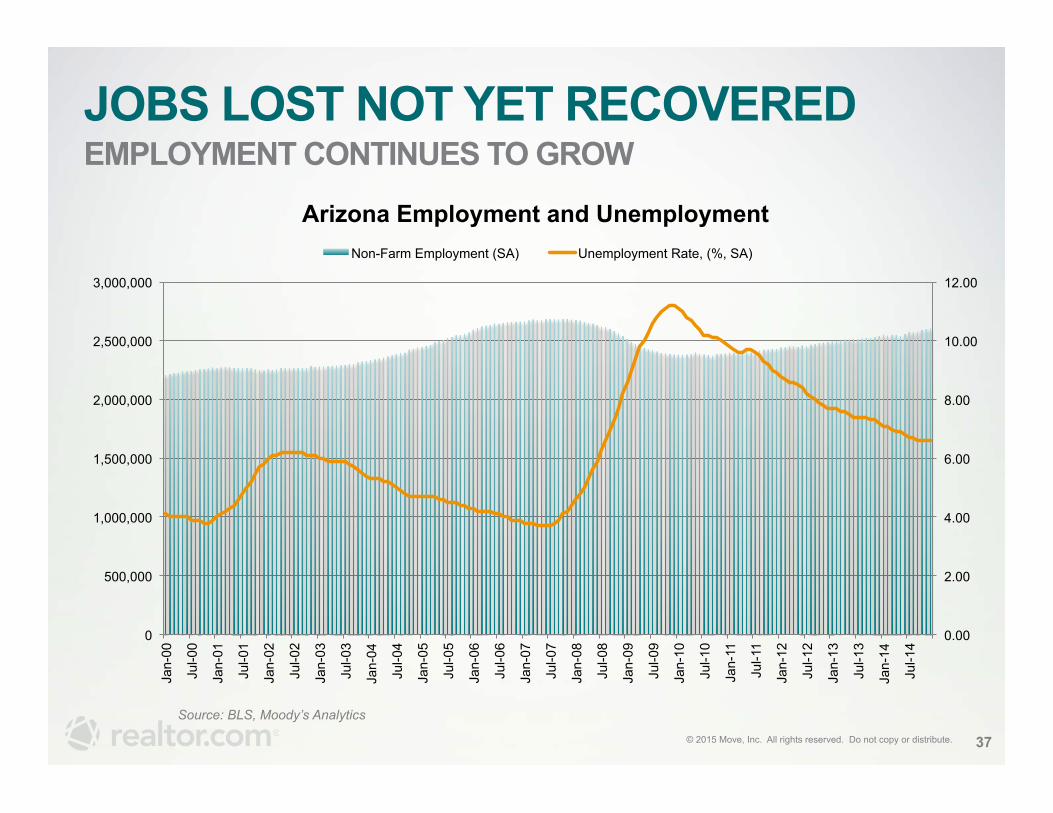

JOBS LOST NOT YET RECOVERED EMPLOYMENT CONTINUES TO GROW

37

Source: BLS, Moody’s Analytics

0.00

2.00

4.00

6.00

8.00

10.00

12.00

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Jan-

00

Jul-0

0

Jan-

01

Jul-0

1

Jan-

02

Jul-0

2

Jan-

03

Jul-0

3

Jan-

04

Jul-0

4

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Arizona Employment and Unemployment Non-Farm Employment (SA) Unemployment Rate, (%, SA)

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

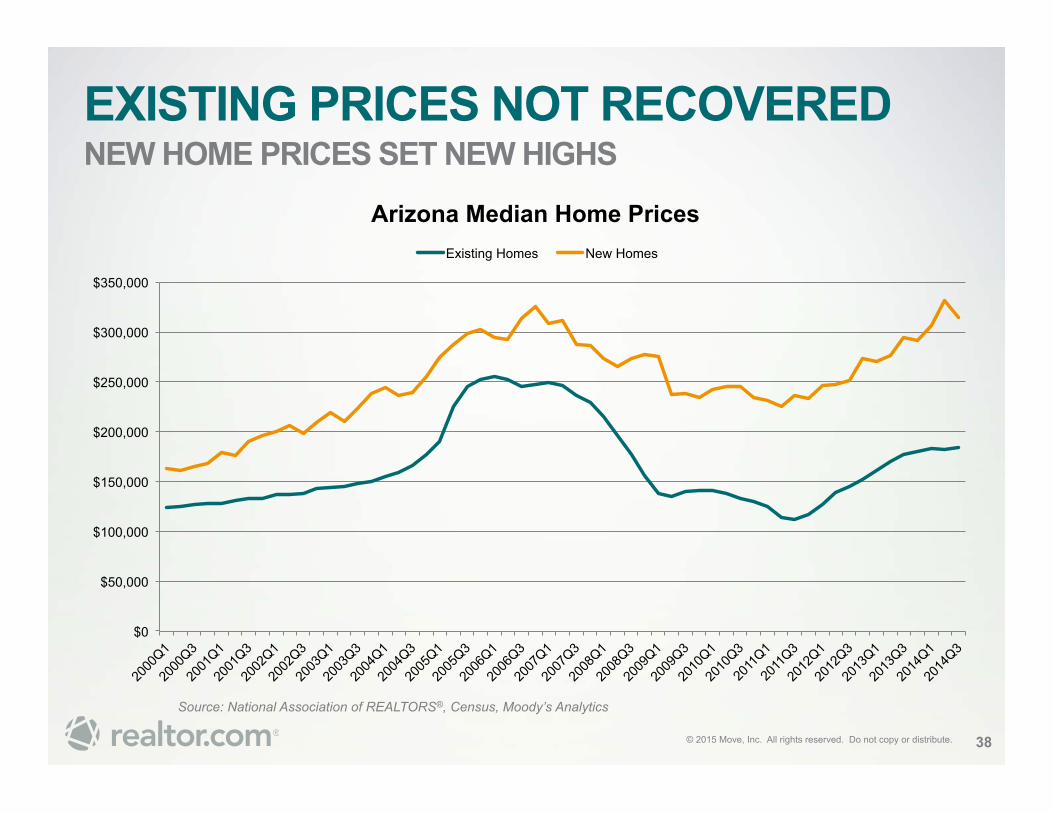

EXISTING PRICES NOT RECOVERED NEW HOME PRICES SET NEW HIGHS

38

Source: National Association of REALTORS®, Census, Moody’s Analytics

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

Arizona Median Home Prices Existing Homes New Homes

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

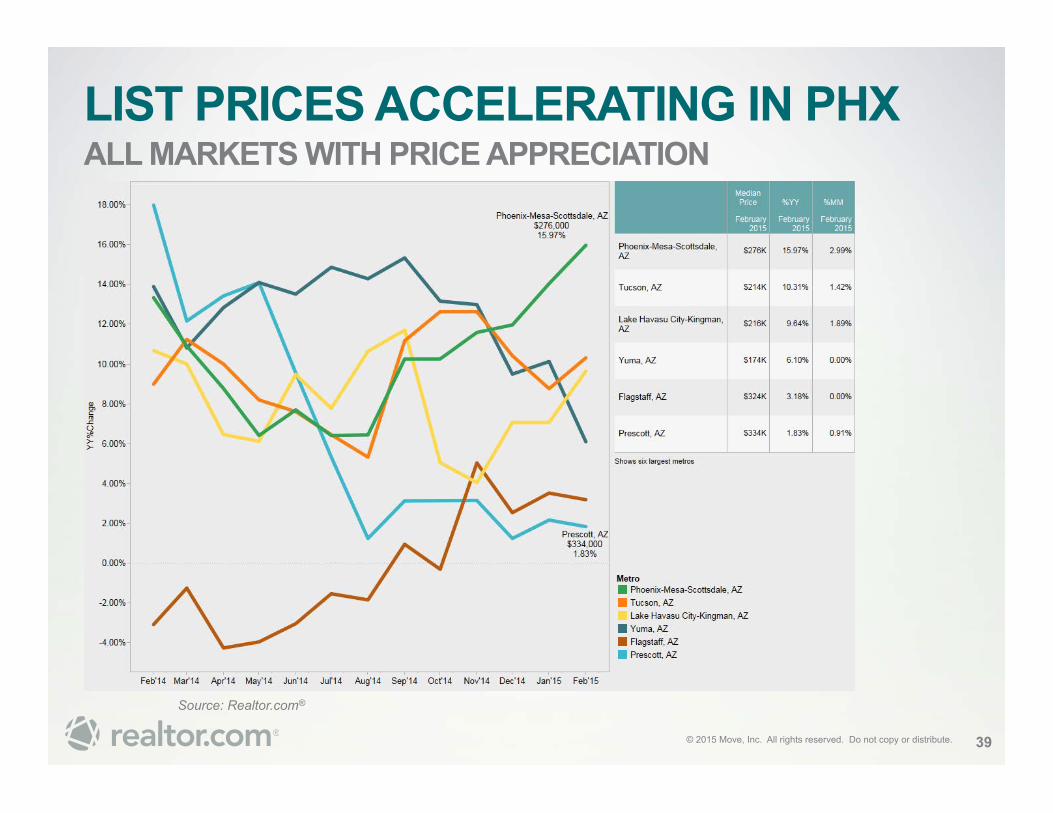

LIST PRICES ACCELERATING IN PHX ALL MARKETS WITH PRICE APPRECIATION

39

Source: Realtor.com®

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

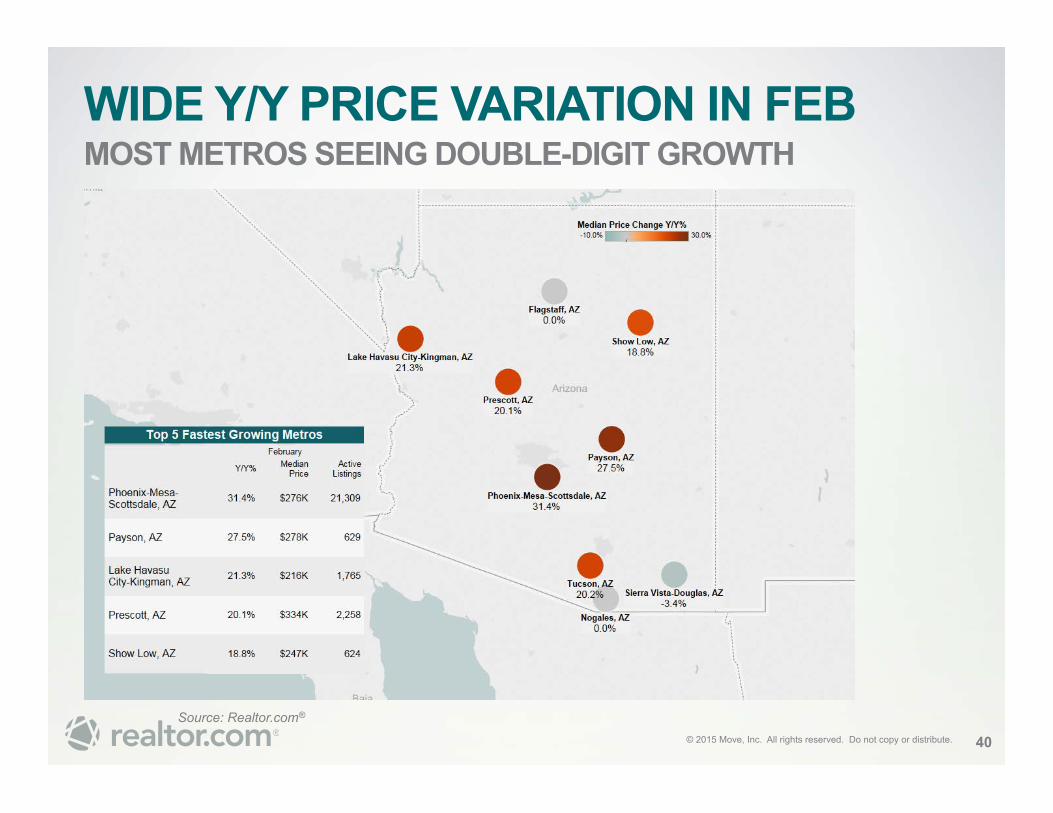

WIDE Y/Y PRICE VARIATION IN FEB MOST METROS SEEING DOUBLE-DIGIT GROWTH

Source: Realtor.com®

40

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

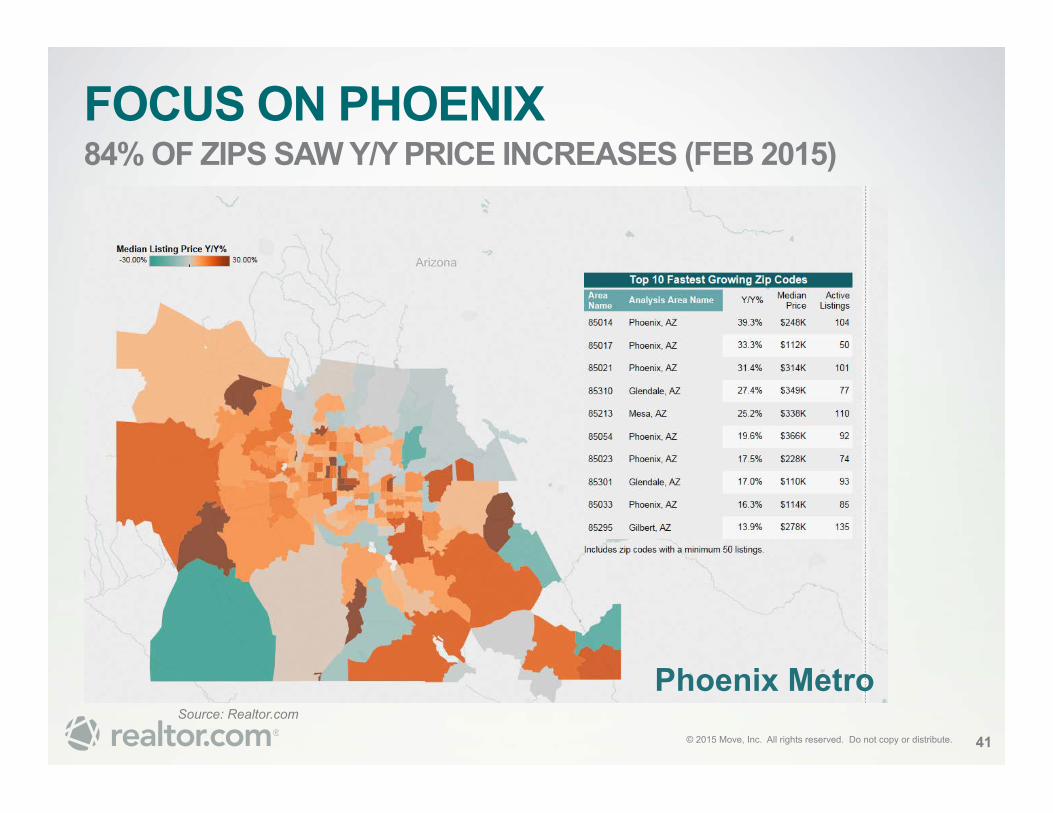

FOCUS ON PHOENIX 84% OF ZIPS SAW Y/Y PRICE INCREASES (FEB 2015)

Source: Realtor.com

41

Phoenix Metro

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

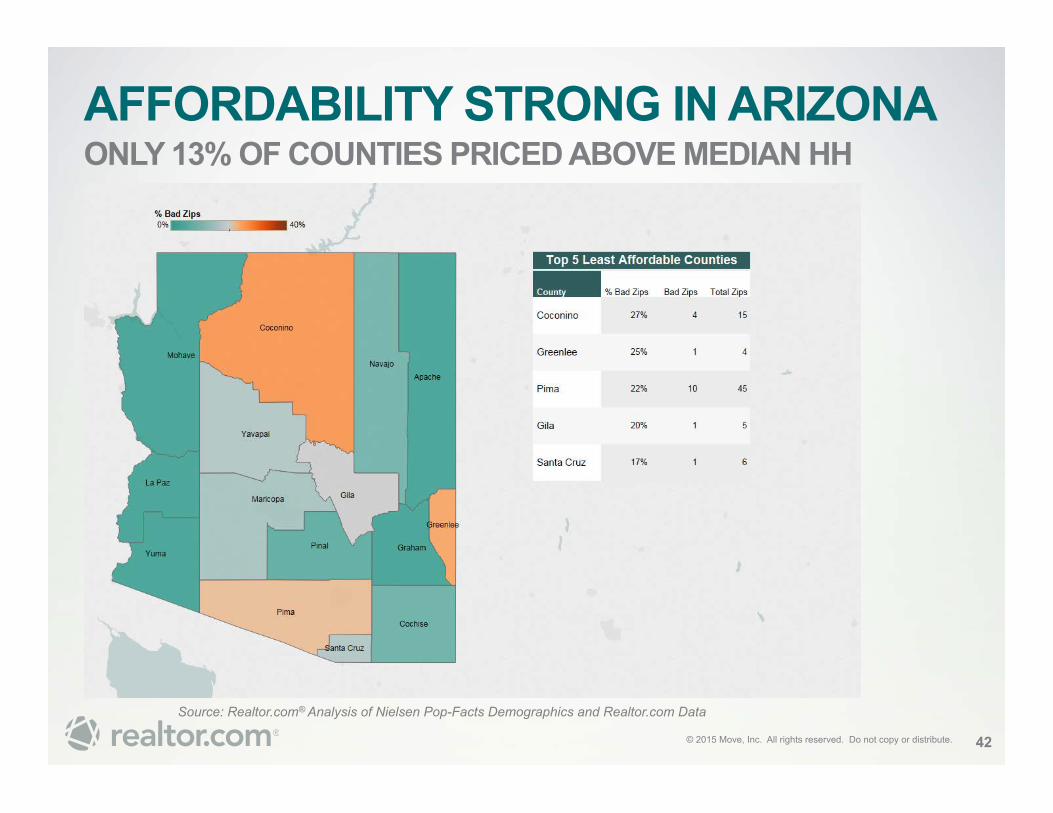

AFFORDABILITY STRONG IN ARIZONA ONLY 13% OF COUNTIES PRICED ABOVE MEDIAN HH

Source: Realtor.com® Analysis of Nielsen Pop-Facts Demographics and Realtor.com Data

42

"Bad Zips” are those where at least half of the households in the zip cannot afford to buy a home.

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

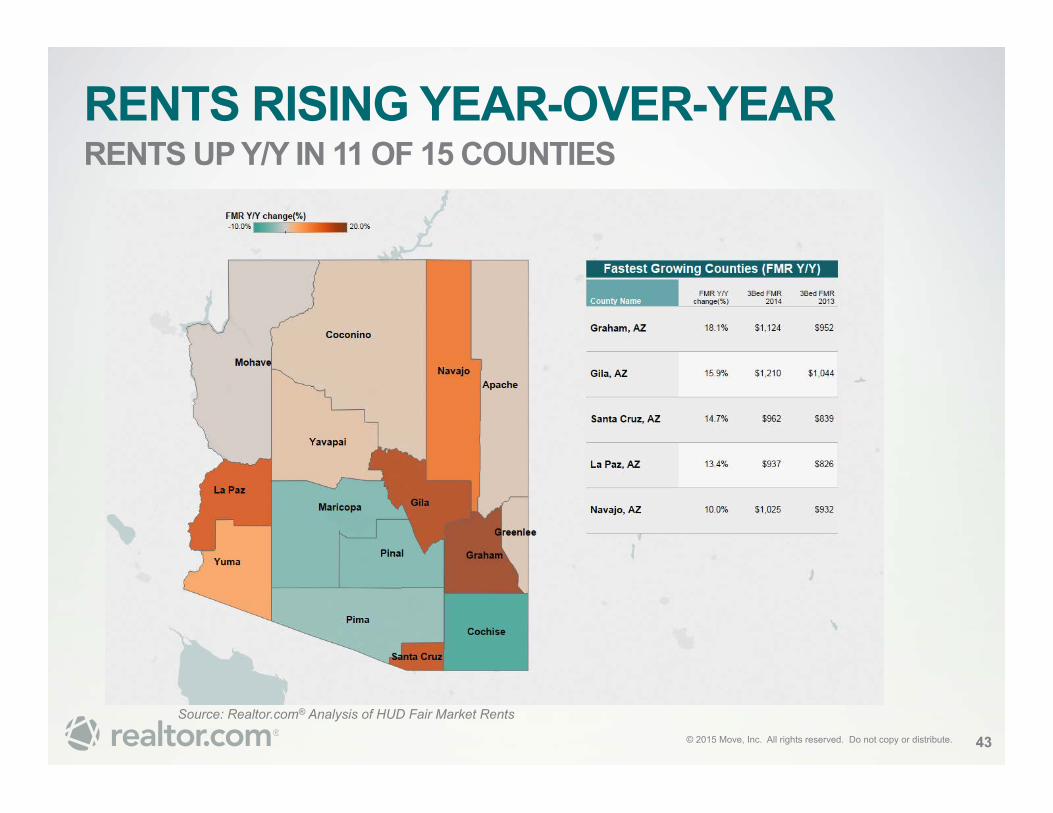

RENTS RISING YEAR-OVER-YEAR RENTS UP Y/Y IN 11 OF 15 COUNTIES

Source: Realtor.com® Analysis of HUD Fair Market Rents

43

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

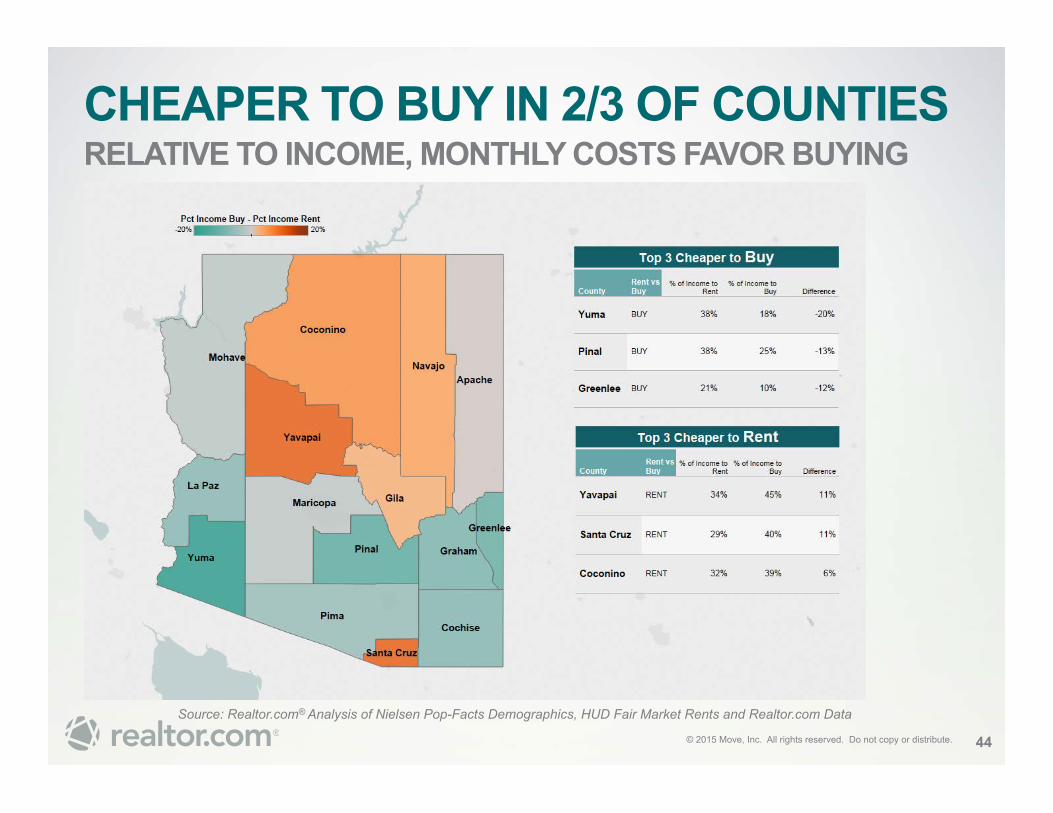

CHEAPER TO BUY IN 2/3 OF COUNTIES RELATIVE TO INCOME, MONTHLY COSTS FAVOR BUYING

Source: Realtor.com® Analysis of Nielsen Pop-Facts Demographics, HUD Fair Market Rents and Realtor.com Data

44

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

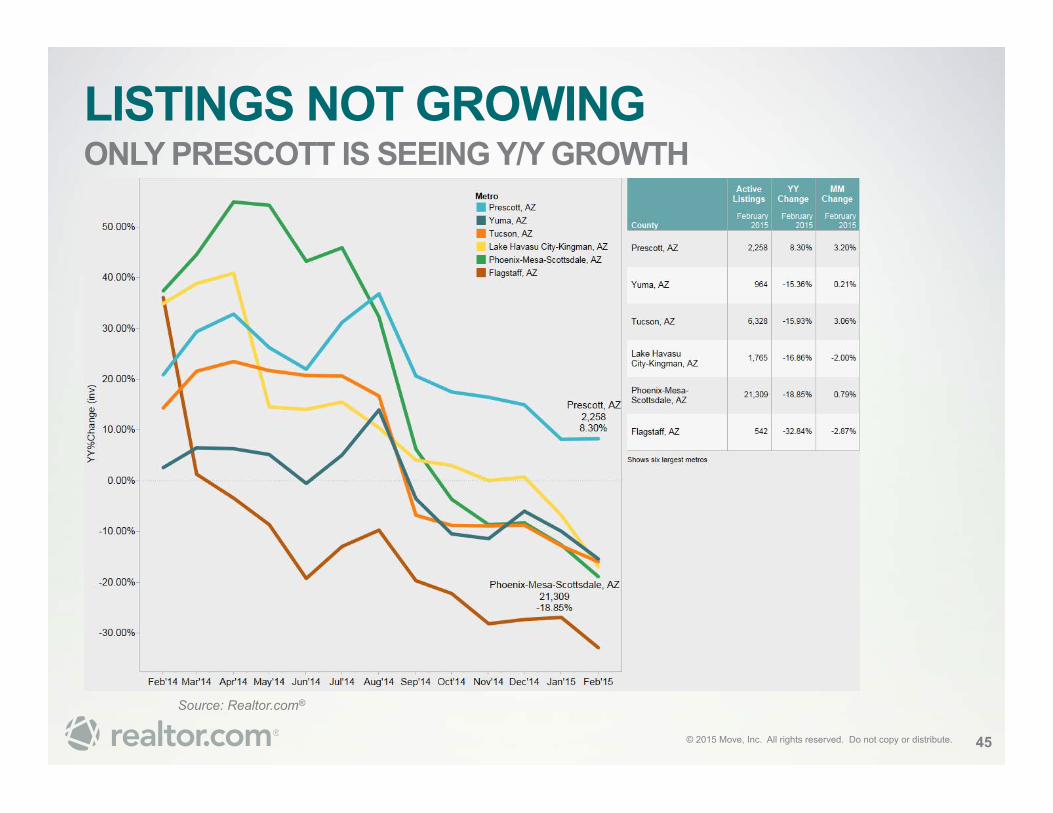

LISTINGS NOT GROWING ONLY PRESCOTT IS SEEING Y/Y GROWTH

45

Source: Realtor.com®

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

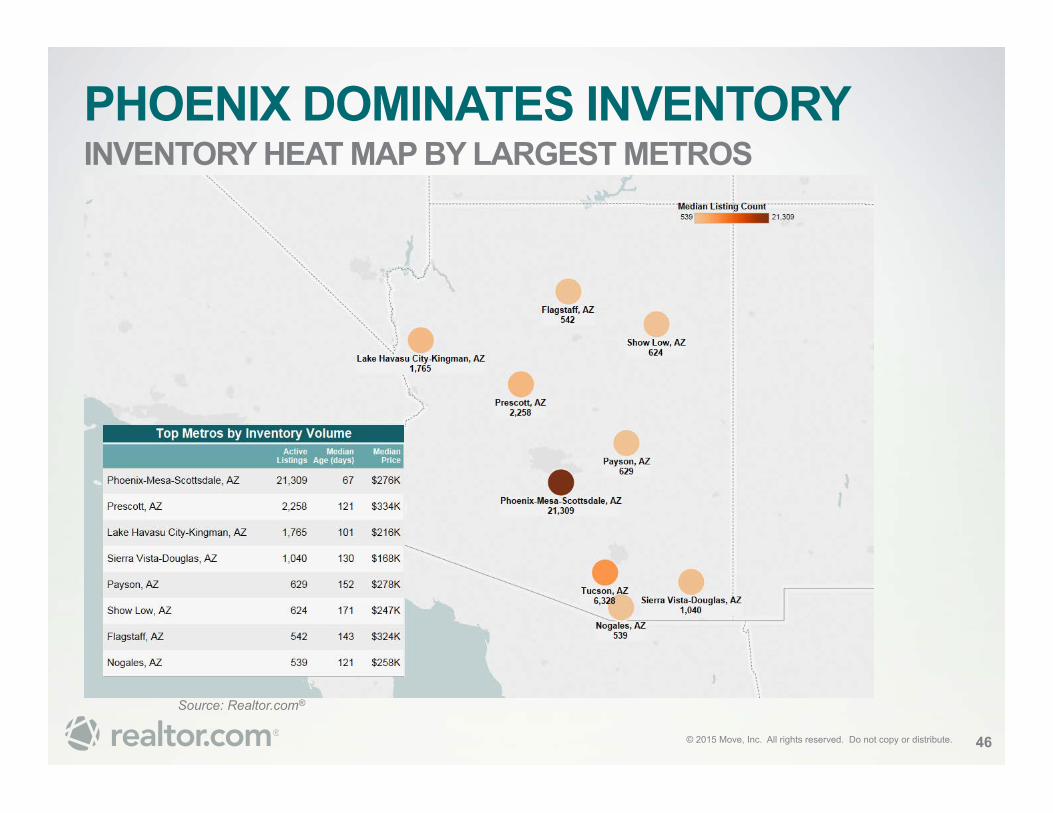

PHOENIX DOMINATES INVENTORY INVENTORY HEAT MAP BY LARGEST METROS

Source: Realtor.com®

46

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

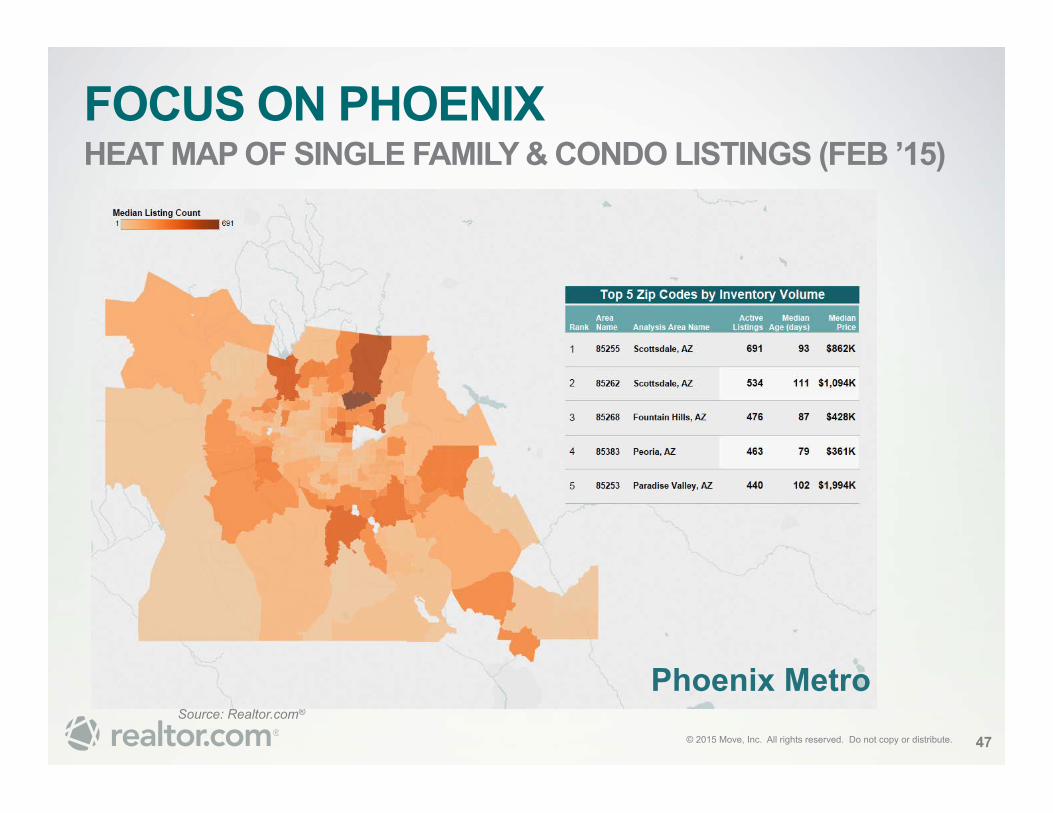

FOCUS ON PHOENIX HEAT MAP OF SINGLE FAMILY & CONDO LISTINGS (FEB ’15)

Source: Realtor.com®

47

Phoenix Metro

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

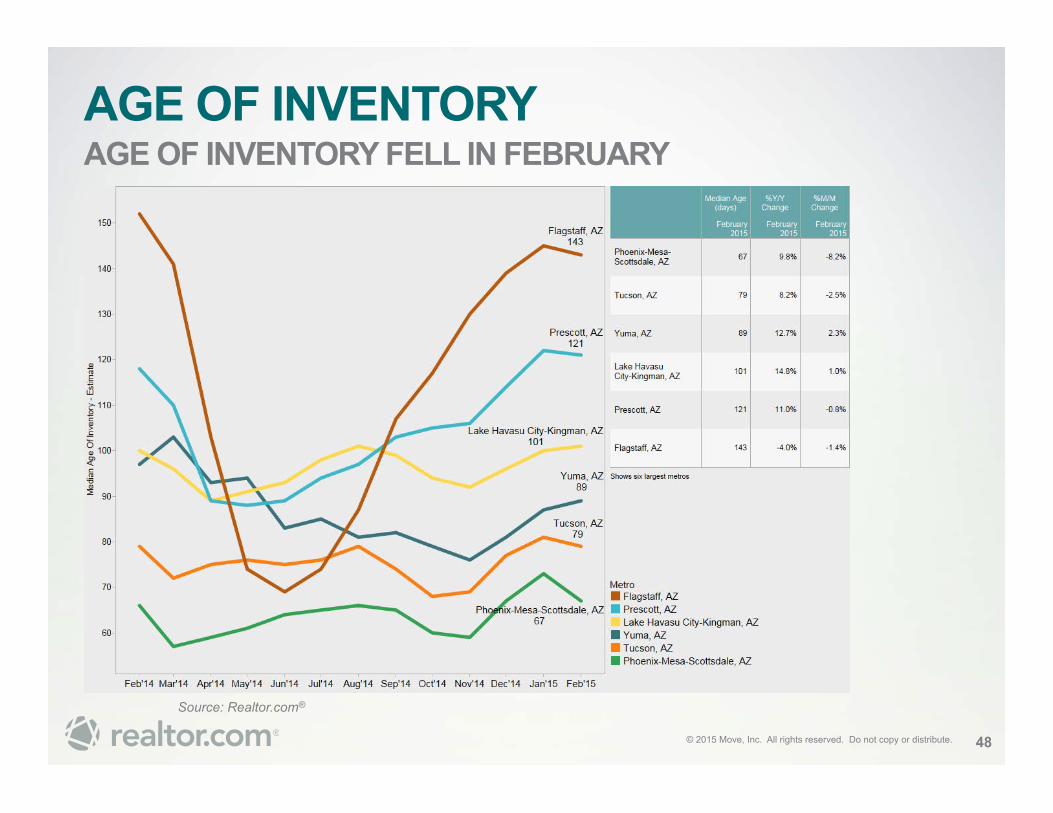

AGE OF INVENTORY AGE OF INVENTORY FELL IN FEBRUARY

48

Source: Realtor.com®

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

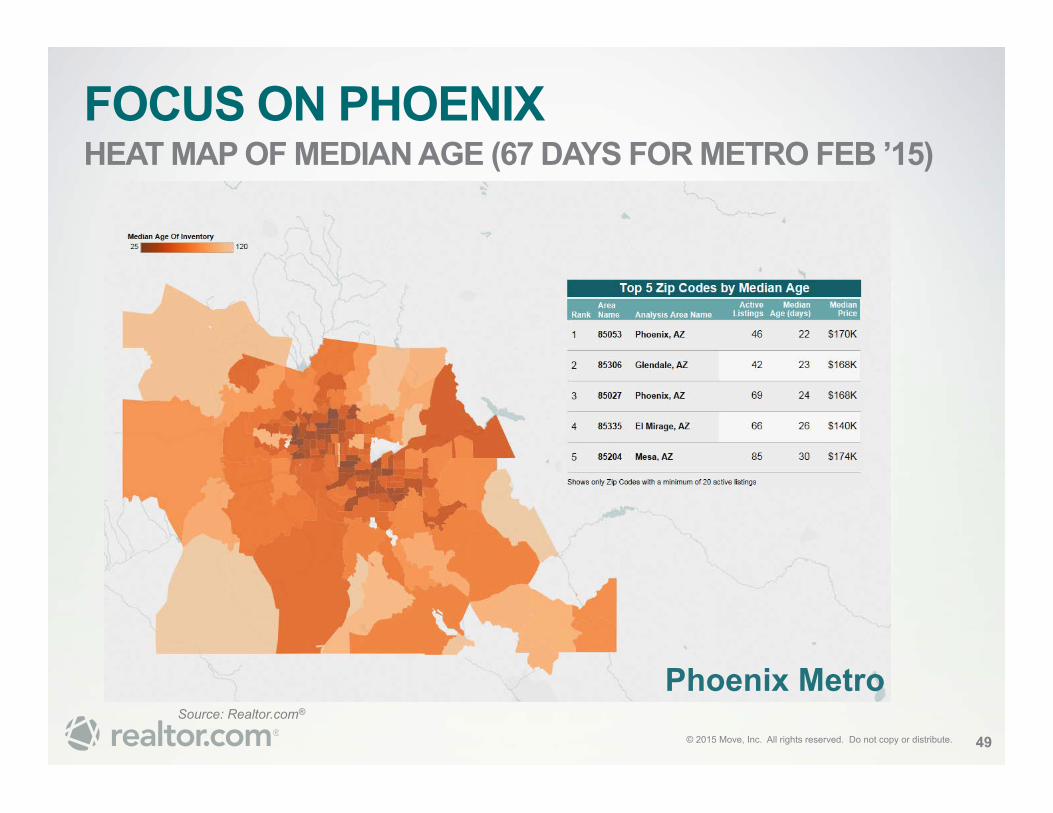

FOCUS ON PHOENIX HEAT MAP OF MEDIAN AGE (67 DAYS FOR METRO FEB ’15)

Source: Realtor.com®

49

Phoenix Metro

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

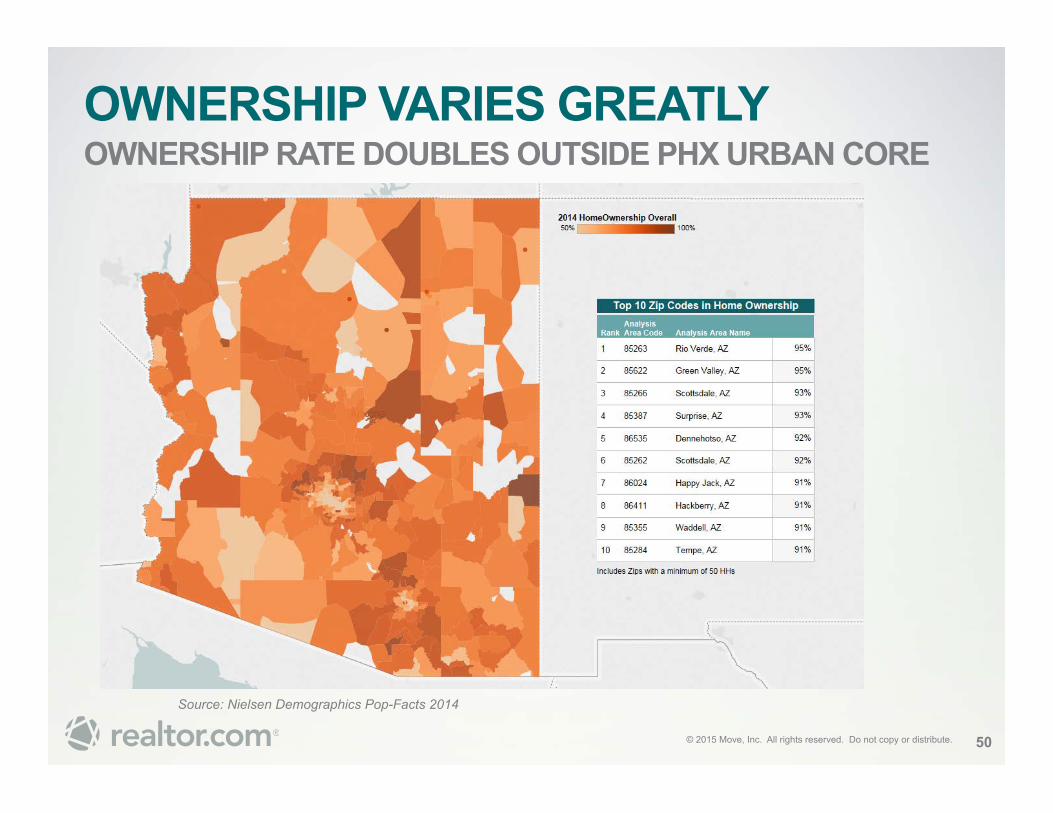

OWNERSHIP VARIES GREATLY OWNERSHIP RATE DOUBLES OUTSIDE PHX URBAN CORE

Source: Nielsen Demographics Pop-Facts 2014

50

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

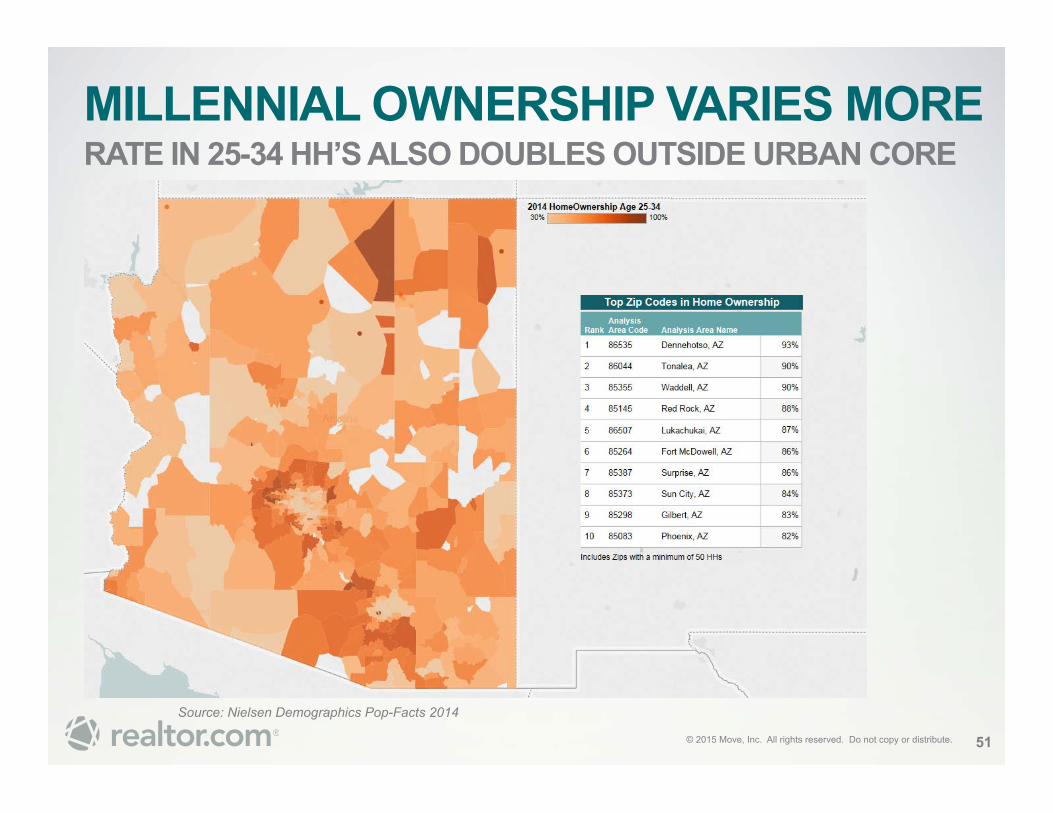

MILLENNIAL OWNERSHIP VARIES MORE RATE IN 25-34 HH’S ALSO DOUBLES OUTSIDE URBAN CORE

Source: Nielsen Demographics Pop-Facts 2014

51

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

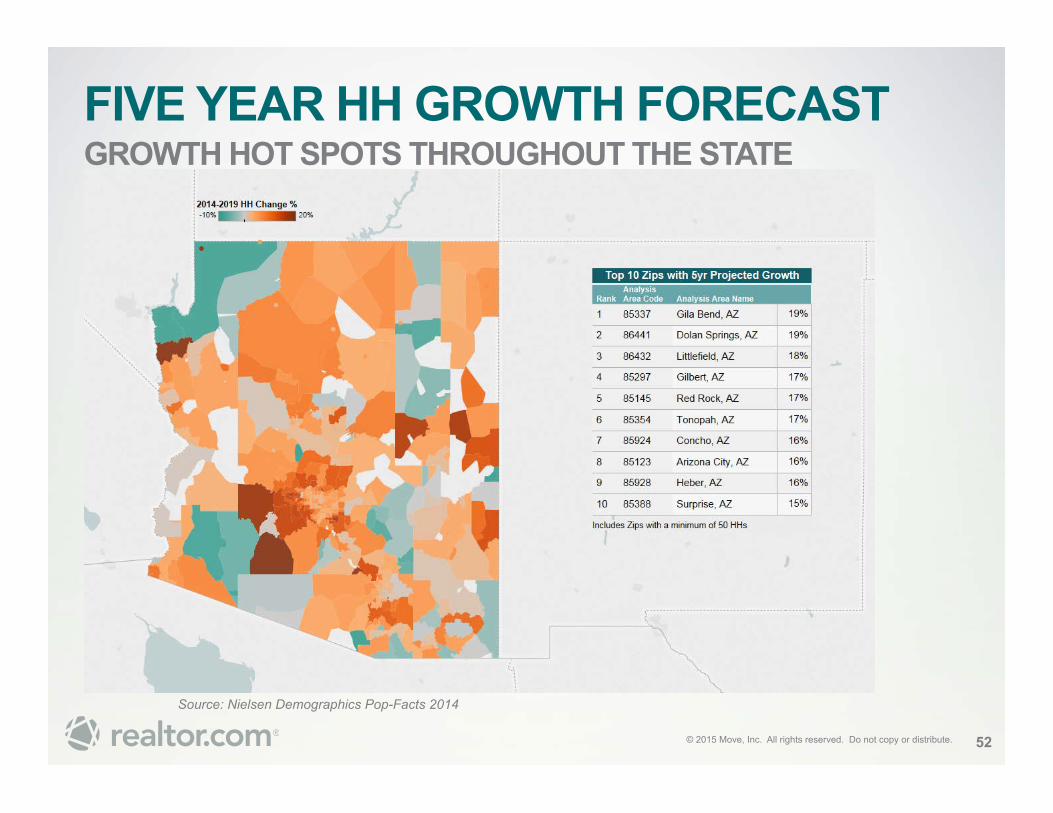

FIVE YEAR HH GROWTH FORECAST GROWTH HOT SPOTS THROUGHOUT THE STATE

Source: Nielsen Demographics Pop-Facts 2014

52

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

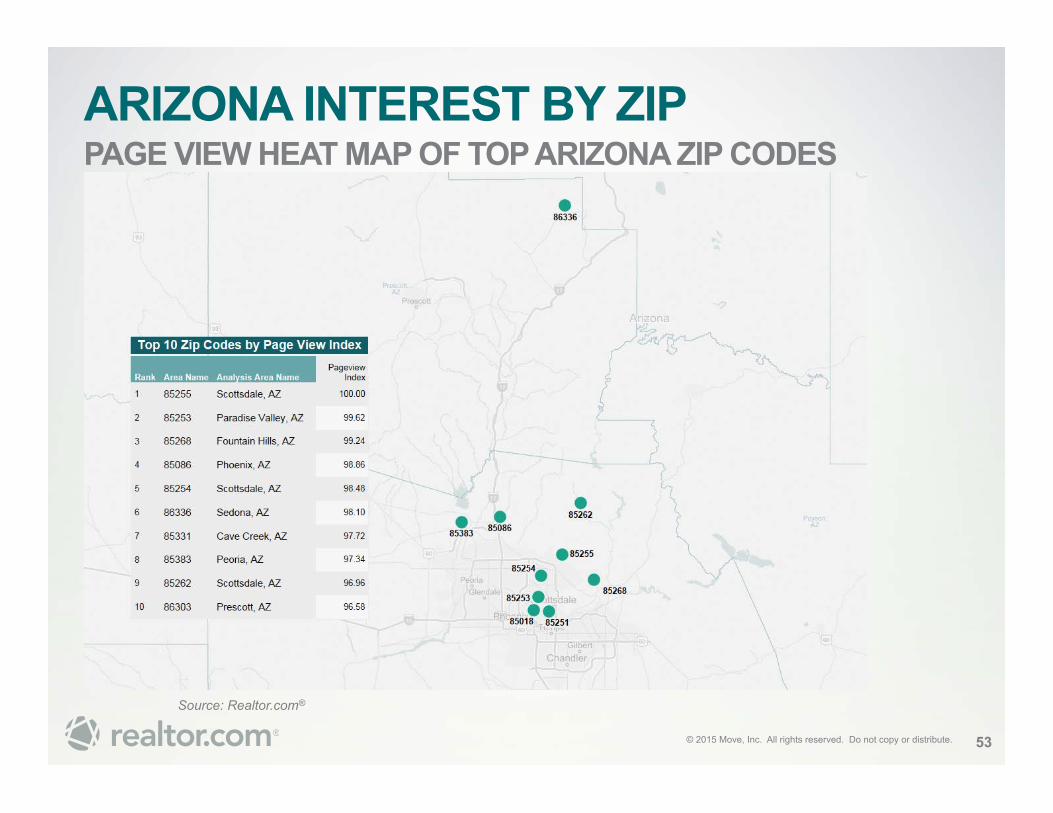

ARIZONA INTEREST BY ZIP PAGE VIEW HEAT MAP OF TOP ARIZONA ZIP CODES

Source: Realtor.com®

53

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

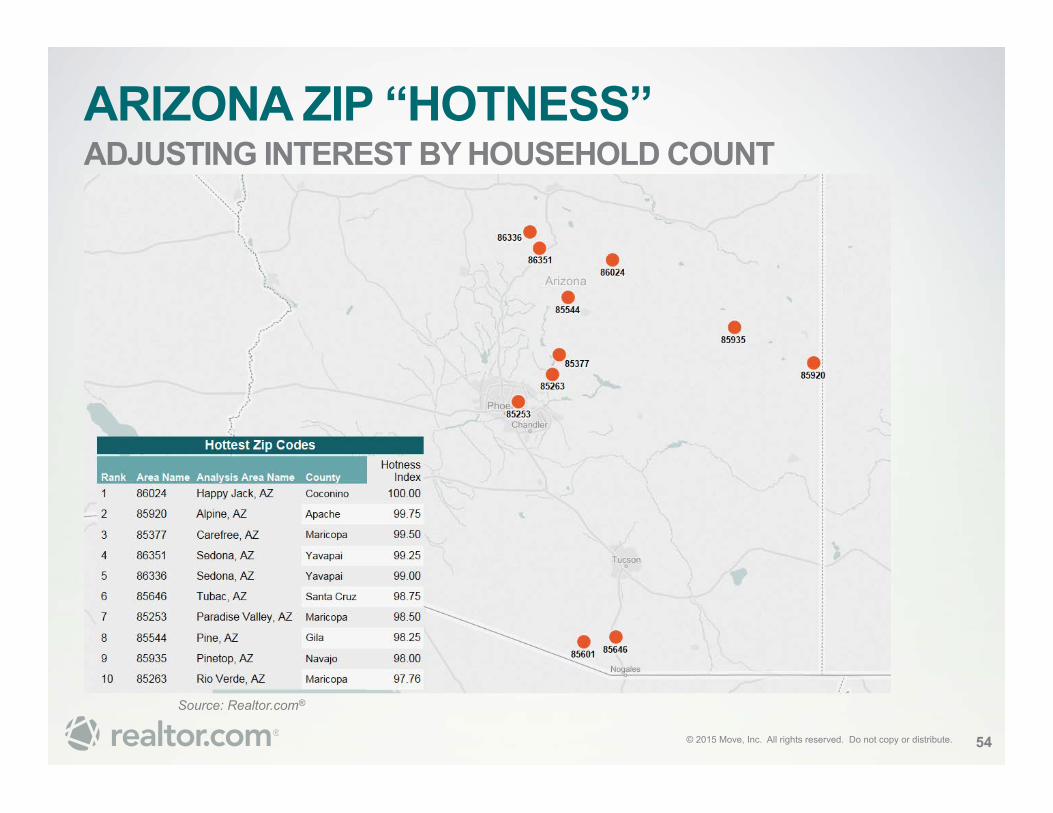

ARIZONA ZIP “HOTNESS” ADJUSTING INTEREST BY HOUSEHOLD COUNT

Source: Realtor.com®

54

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

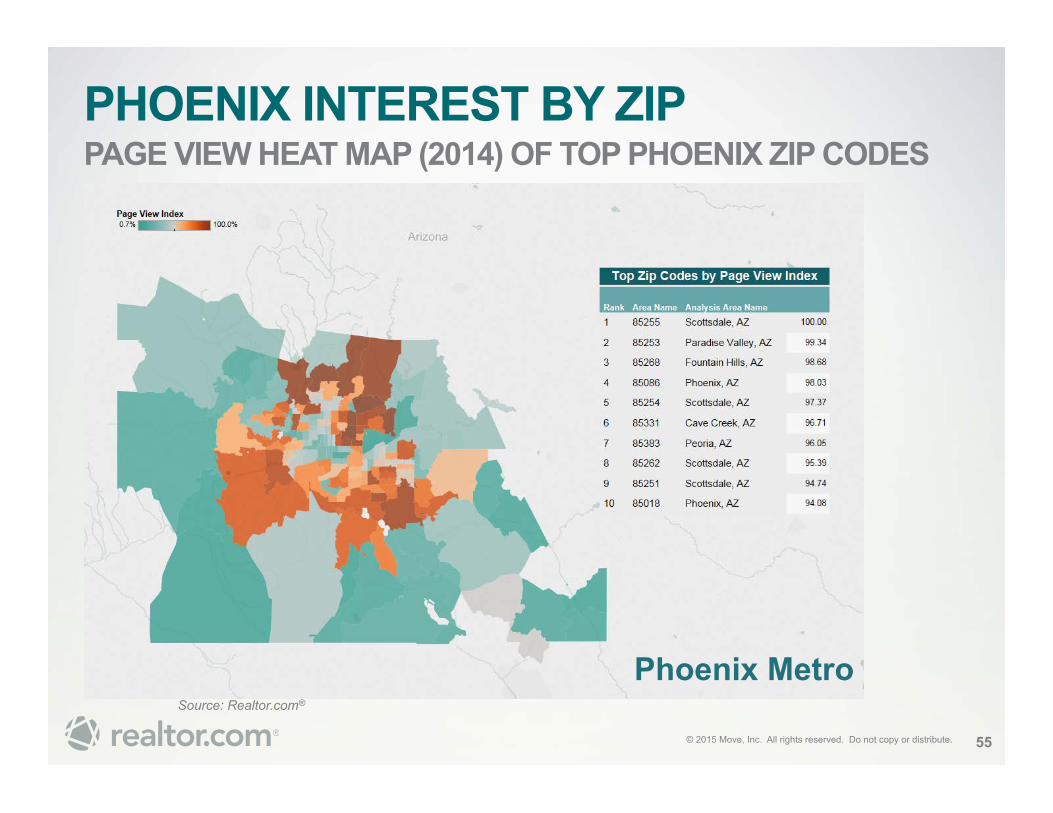

PHOENIX INTEREST BY ZIP PAGE VIEW HEAT MAP (2014) OF TOP PHOENIX ZIP CODES

Source: Realtor.com®

55

Phoenix Metro

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

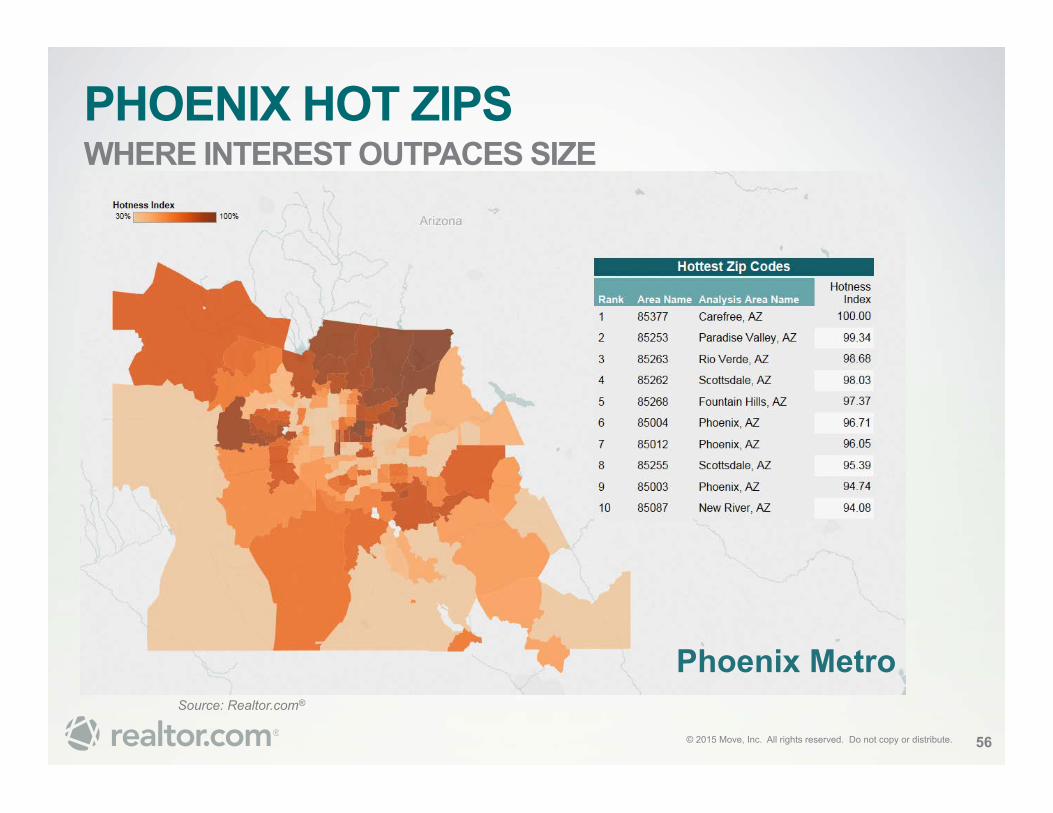

PHOENIX HOT ZIPS WHERE INTEREST OUTPACES SIZE

Source: Realtor.com®

56

Phoenix Metro

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

2015 2020

Population by Age (Arizona) Under 25 25-34 35-54 55+

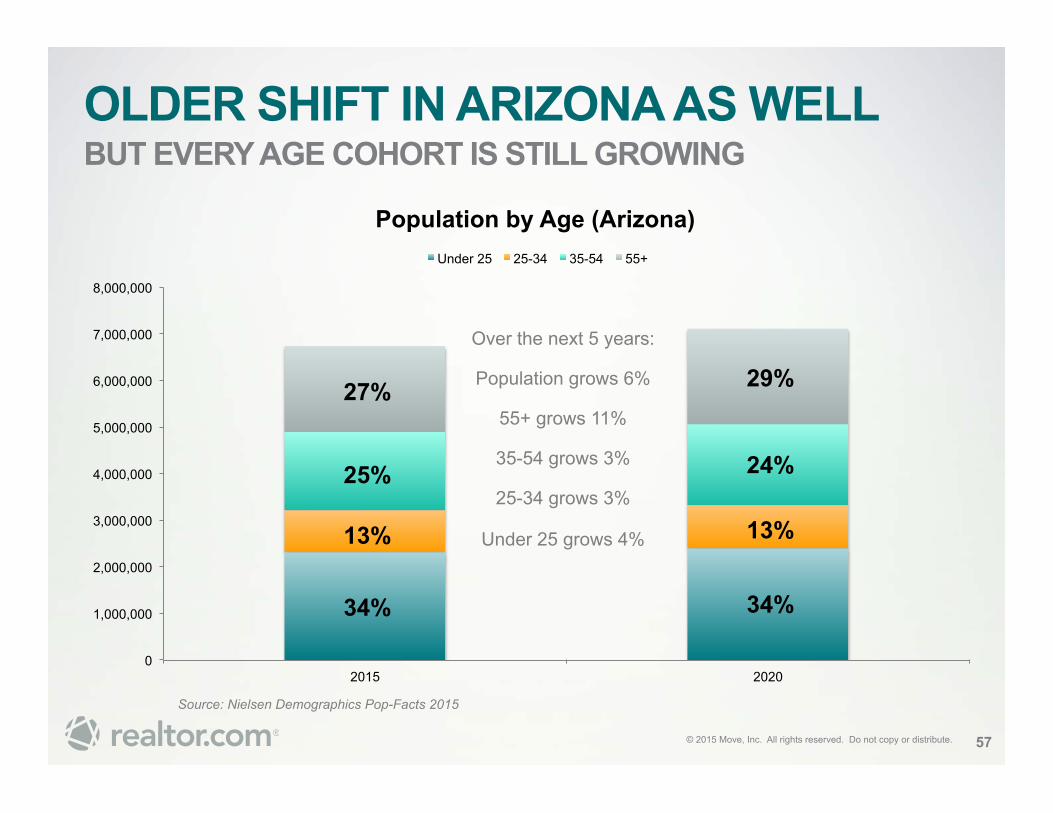

OLDER SHIFT IN ARIZONA AS WELL BUT EVERY AGE COHORT IS STILL GROWING

57

Source: Nielsen Demographics Pop-Facts 2015

27%

25%

13%

34%

29%

24%

13%

34%

Over the next 5 years:

Population grows 6%

55+ grows 11%

35-54 grows 3%

25-34 grows 3%

Under 25 grows 4%

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

GROWTH SHOULD NOT BE A SURPRISE MOST SEARCHED “HOW MUCH DOES [X] COST?” BY STATE

Source: Fixr.com

58

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

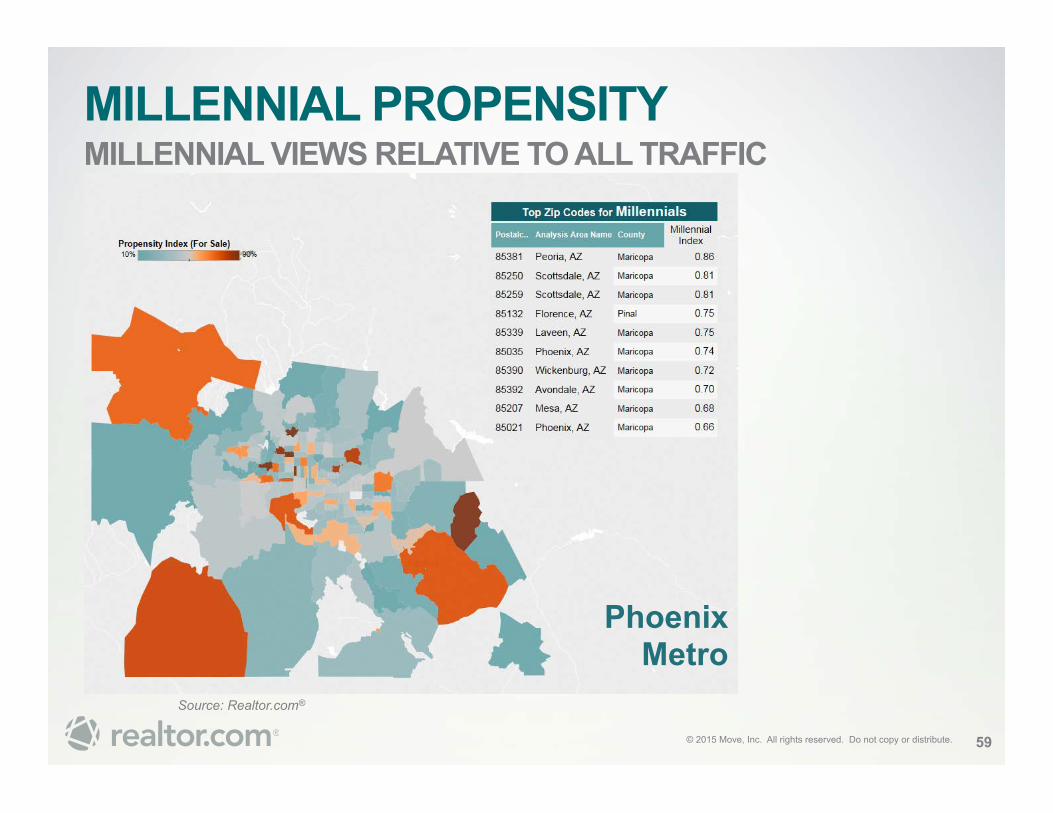

MILLENNIAL PROPENSITY MILLENNIAL VIEWS RELATIVE TO ALL TRAFFIC

Source: Realtor.com®

59

Phoenix Metro

© 2015 Move, Inc. All rights reserved. Do not copy or distribute.

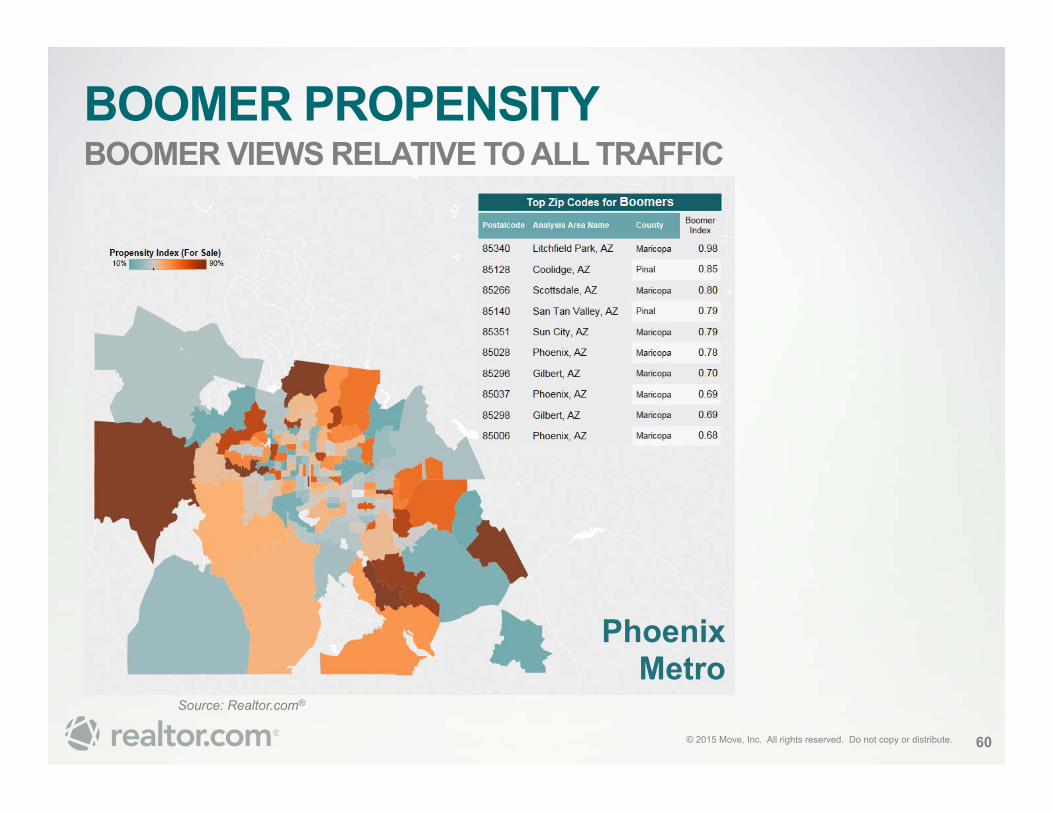

BOOMER PROPENSITY BOOMER VIEWS RELATIVE TO ALL TRAFFIC

Source: Realtor.com®

60

Phoenix Metro

© 2015 Move, Inc. All rights reserved. Do not copy or distribute. 61

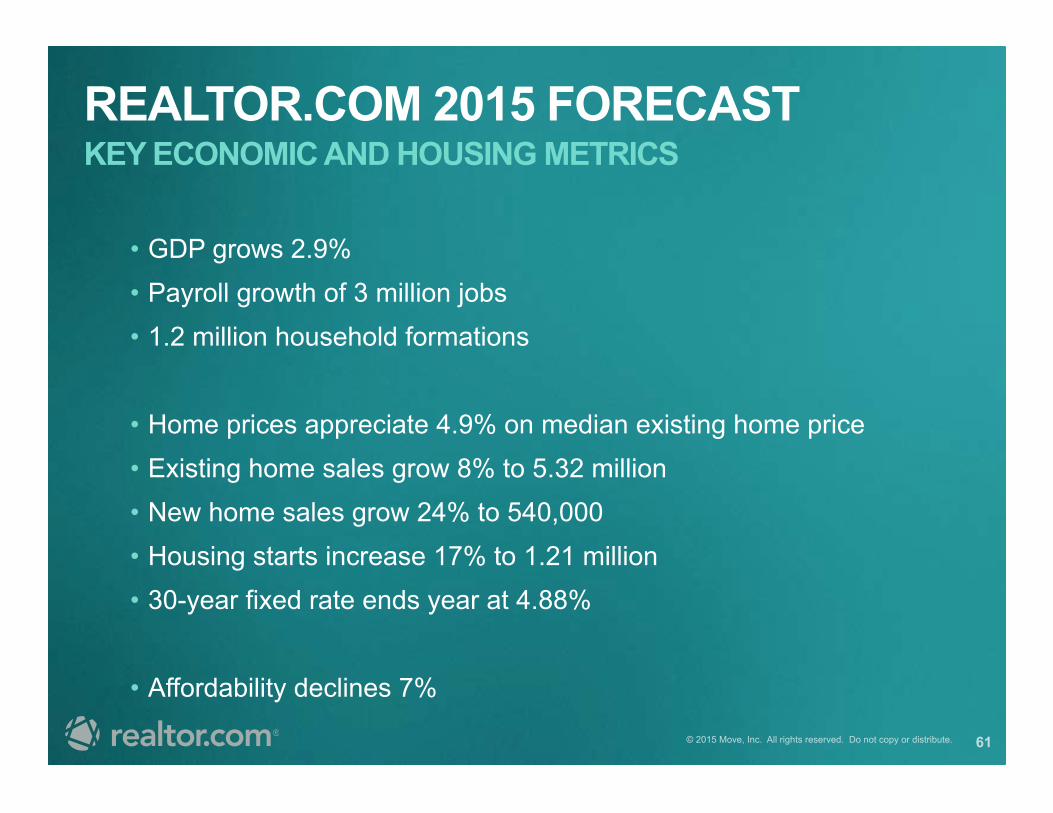

REALTOR.COM 2015 FORECAST KEY ECONOMIC AND HOUSING METRICS

• GDP grows 2.9% • Payroll growth of 3 million jobs • 1.2 million household formations

• Home prices appreciate 4.9% on median existing home price • Existing home sales grow 8% to 5.32 million • New home sales grow 24% to 540,000 • Housing starts increase 17% to 1.21 million • 30-year fixed rate ends year at 4.88%

• Affordability declines 7%

© 2015 Move, Inc. All rights reserved. Do not copy or distribute. 62

Jonathan Smoke Chief Economist

realtor.com®

[email protected] @SmokeonHousing 703.634.9193

THANK YOU

© 2015 Move, Inc. All rights reserved. Do not copy or distribute. 63