the importance of internal controls lgc resource april 2014

TRANSCRIPT

The Importance of

Internal Controls

LGC Resource April 2014

WHAT ARE INTERNAL CONTROLS?

Processes effected by an entity’s management and other personnel designed to provide assurance regarding the achievement of objectives relating to operations, reporting, and compliance.

COSO (Committee of Sponsoring Organizations) of the Treadway Commission

Control Environment The control environment is the core of any system of

internal control.

It sets the tone for the entire organization.

Factors include: ethical values competence of employees at all levels managements’ operating style and attitude

toward controls

Risk Assessment Risks are INTERNAL and EXTERNAL events

that threaten the accomplishment of objectives. Process of identifying, evaluating, and deciding

how to manage these events….. What is the likelihood of the event occurring? What would be the impact if it were to occur? How do we reduce the risk?

Consideration of Fraud

Control Activities Control Activities consist of the specific policies

and procedures put in place to mitigate the risk of error, noncompliance, and fraud.

(physical inventory count, segregation of duties, authorization of activities, proper backup procedures)

Communication & Information Adequate information must be captured,

identified, and communicated on a timely basis.

Just a reminder…….

ACTIONS SPEAK LOUDER THAN WORDS

MonitoringMonitoring occurs in the course of

everyday operations, it includes regular management & supervisory activities and other actions personnel take in performing their duties.

Simple Definition Internal controls are common sense

procedures that address:

What could go wrong? What steps should be taken to prevent

those events from happening?

Personal Internal Control System

Locking your car when you leave it in the parking lot

Comparing your receipts to your credit card statement

Keeping your banking PIN confidential

Why are Internal Controls Important?

They can catch small mistakes before they become big problems.

They protect employees by removing opportunities for innocent mistakes or intentional fraud.

Why are Internal Controls Important?

Protect the strong from temptation Protect the weak from opportunity Protect the innocent from false accusation

From Once upon Internal Control by James Ulvog, CPA

Opportunity

Pressure Rationalization

FRAUD TRIANGLE

FRAUD

$208,830

$202,345

$177,630

FRAUD

Frauds discovered in the recent years. Committed by one person Trusted employee Internal controls were either nonexistent or

not monitored

Effective IS Controls Proper back-up procedures

Section 10-7-121, TCA, requires that records maintained electronically be copied to a storage media daily. Storage media more than one week old shall be stored at a location other than at the building where the original is maintained

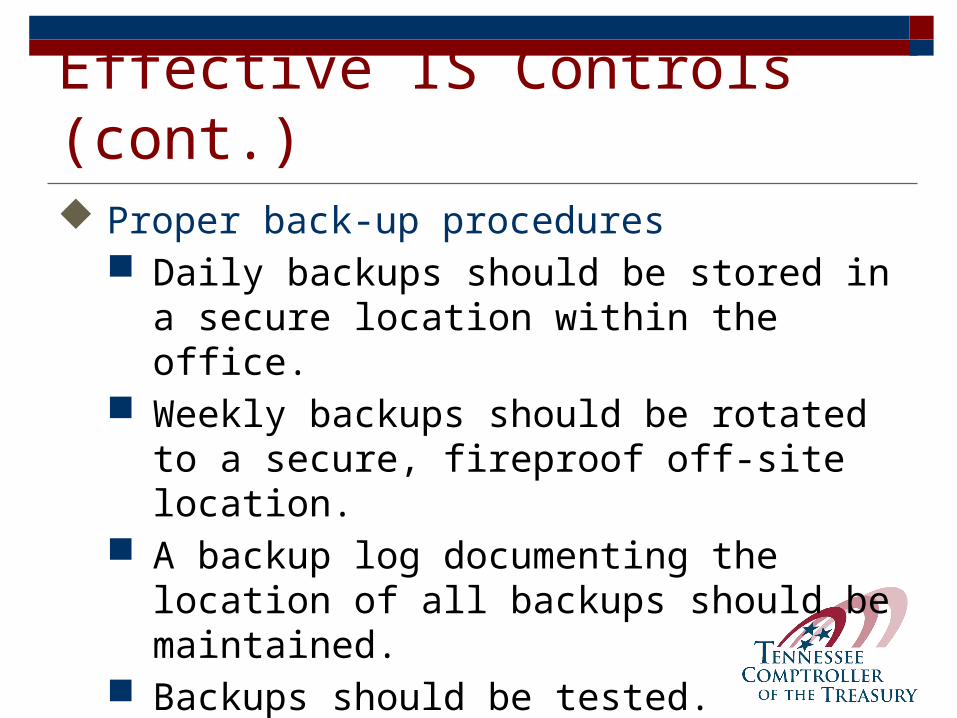

Effective IS Controls (cont.) Proper back-up procedures

Daily backups should be stored in a secure location within the office.

Weekly backups should be rotated to a secure, fireproof off-site location.

A backup log documenting the location of all backups should be maintained.

Backups should be tested.

Effective IS Controls (cont.) Password Maintenance

All users should have a unique login and password. Shared logins should not be used.

Passwords should remain confidential. Passwords should be changed every 90

days. Passwords of former employees should be

immediately disabled.

Effective IS Controls (cont.) Disaster Recovery Planning

Specific steps to follow to restore system Emergency phone numbers of personnel and

vendors Backup storage location Manual procedures to follow until the system

is restored

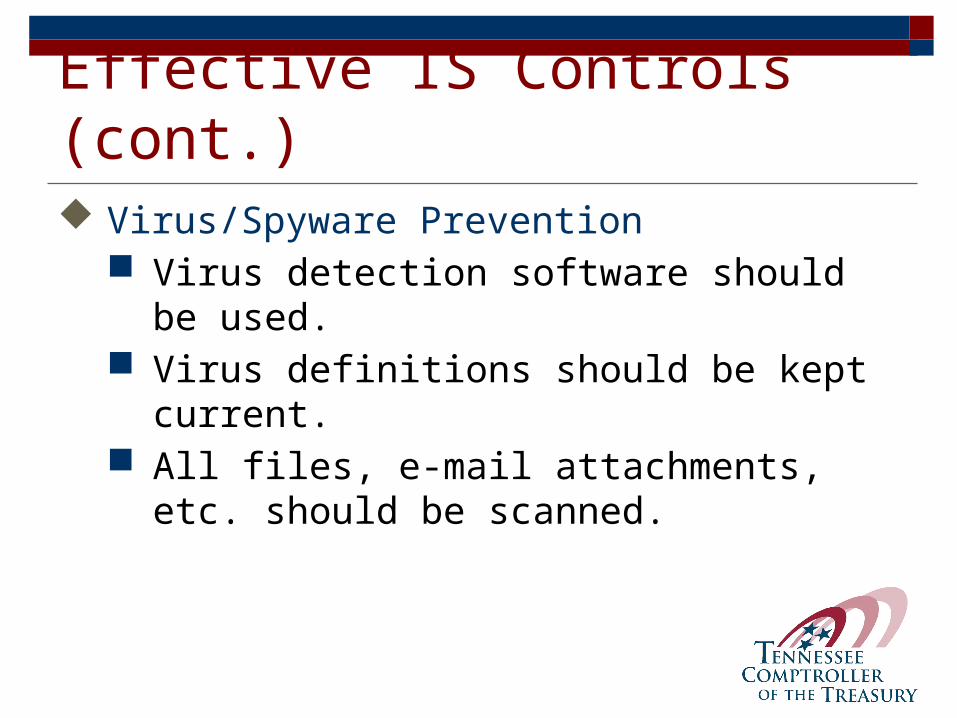

Effective IS Controls (cont.) Virus/Spyware Prevention

Virus detection software should be used. Virus definitions should be kept current. All files, e-mail attachments, etc. should be

scanned.

Effective IS Controls (cont.) Policies and procedures manual

Operating system and application security Start-up/shut down procedures Back-up procedures Hardware software maintenance procedures Daily, monthly, and year-end procedures Output distribution list Hardware disposal policy Virus prevention policy

Effective IS Controls (cont.)

Loading Operating System Updates

Restricting Physical Access to System

Proper Application Controls Adequate audit trail exists. Audit logs are maintained and reviewed.

Audit Logs and Other Reports TnCIS

Delete Log Report Out-of Court Payments Report

Trustee Audit Changes By Date Report Unprorated Receipts Report Maximum Posting Date Report

Fund Offices Payroll Check Change Report Maximum Posting Date Report

Reasons why controls don’t always work: Inadequate knowledge of policies or governing

regulations.

“I didn’t know that!”

Form over substance “You mean I’m supposed to do something besides initial/sign it?”

Inadequate segregation of duties

“We trust ‘A’ who does all of these things”

The “Trusted Employee”Per the ACFE’s 2012 Report to the Nations:

87% of the fraudsters studied had never been charged or convicted of a fraud related offense

84% had never been punished or terminated by an employer for fraud-related conduct

What is Segregation of Duties?In general, the main incompatible duties to be segregated are:

Custody of Assets Authorization or approval of related transactions

affecting those assets Recording or reporting of related transactions

What is Segregation of Duties? No employee should be in a position to both

commit fraud or error and conceal it in their normal course of duties.

At least two sets of eyes are required for any

transaction

Example: Movie Theater

What if it’s not possible to properly segregate duties?Use Compensating Controls

Supervisory or other oversight procedures designed to reduce the risk of errors or fraud not being detected

by James Climer @ Climercomics.com

Compensating Controls

EXAMPLES?

Effective Controls- Cash Receipts and DepositsSeparate cash drawers Prenumbered cash receipts- 9-2-103,

TCAStamp checks “for deposit only” as soon

as they are receivedDrawer checkout proceduresDeposit timely- 3 day deposit lawDeposit Receipts Intact

Effective Controls- Cash Receipts and Deposits (cont.)

Deposit slips should be itemizedSign- “You must receive an official

receipt or your transaction is not complete

Segregate Duties- Employees responsible for receipting should NOT also be responsible for posting receipts to the accounting records.

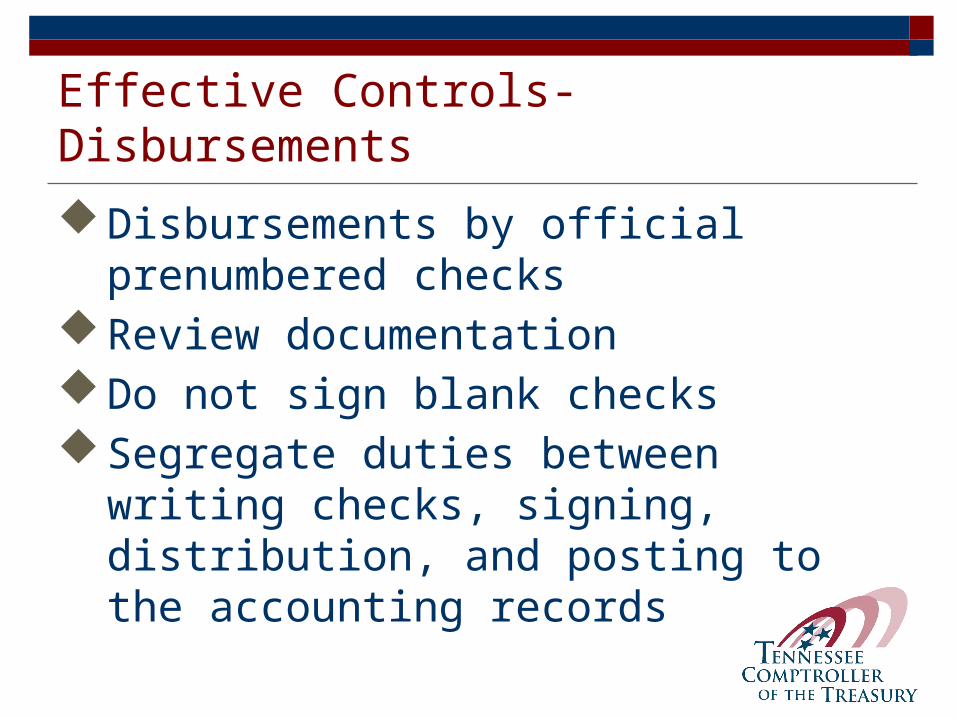

Effective Controls- Disbursements

Disbursements by official prenumbered checks

Review documentationDo not sign blank checksSegregate duties between writing checks,

signing, distribution, and posting to the accounting records

Effective Controls- Bank Reconciliations One employee should be responsible for

opening the bank statement, reviewing it, and initialing.

A separate employee should reconcile the bank statement monthly

Bank reconciliations should be reviewed by an employee not responsible for reconciling the statement.

Effective Controls- Procurement

Establish clear lines of authority for approving purchases before they occur

Purchase orders Verify availability of appropriations before

purchases are approved Payments for purchases should only be made

after documentation that the goods or services were received

Segregate duties between approval, payment and updating the accounting records

Effective controls- Journal Entries (JE’s) Use a standard journal entry form Supervisory review and approval of all journal

entries Segregate duties between preparation of the

JE, Approval of the JE, and posting to the records

Supervisory review that all JE’s were properly posted to the records

More information? Comptroller’s website has internal control

checklists specifically designed for offices such as

Trustee General Sessions and Circuit Court Clerk Clerk and Master Etc.

www.comptroller.tn.gov

www.comptroller.tn.gov

INTERNAL CONTROL CHECKLISTS

Questions?