the emerging risk environment in china dr. guangping (peter g.) zhang deputy director general china...

Post on 21-Dec-2015

213 views

TRANSCRIPT

The Emerging Risk Environment in China

Dr. Guangping (Peter G.) ZhangDeputy Director General

China Banking Regulatory CommissionShanghai Bureau

Asia-Pacific Finance and Development CenterJune 18, 2008

Major Contents Risk Management Instruments in ChinaOn-shore Products

FX Forwards (Merchant & Inter-bank), FX Swaps, Bond Forwards, IRS, Stock Warrants

Off-shore Products Foreign CNY Derivatives

Non-deliverable Forwards (NDF), Non-deliverable Options (NDO), Non-deliverable IRS (NIRS),H share stocks, Index futures and Options

Risk Management Supervision & Related Issues BASEL II Implementation Difficulties for Risk Management Practices in China Lack of Options Market and Implied Volatilities Low Liquidities of OTC Products Product Design & Pricing

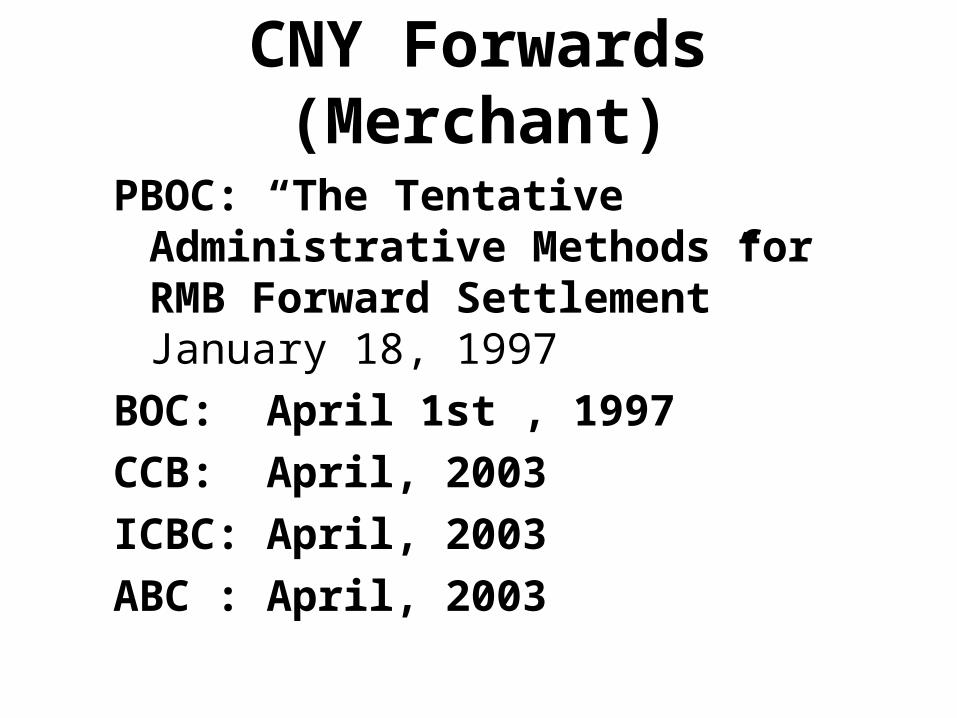

CNY Forwards (Merchant)

PBOC: “The Tentative Administrative Methods for RMB Forward Settlement” January 18, 1997

BOC: April 1st , 1997

CCB: April, 2003

ICBC: April, 2003

ABC : April, 2003

China Foreign Exchange Trade Center (CFETCS)

China Foreign Exchange Trade Center (CFETCS) was authorized to trade CNY forwards on August 15, 2005

CNY/USDCNY/JPYCNY/HKDCNY/Euro

China Foreign Exchange Trade Center (CFETCS)

Trading has not been active at CFETCS,Trading turnover in

1Q2006 RMB3420 million (430 million USD); 2Q2006 RMB7210 million (900 million USD)3Q2006 RMB31.5 billion (3.98 biillion USD)4Q2006 8.75 billion USD1Q2007 5.323 billion USD 2Q2007 5.347 billion USD3Q2007 4.323 billion USD4Q2007 7.391 billion USD2006 $14.06 billion; 2007 $22.384 billion

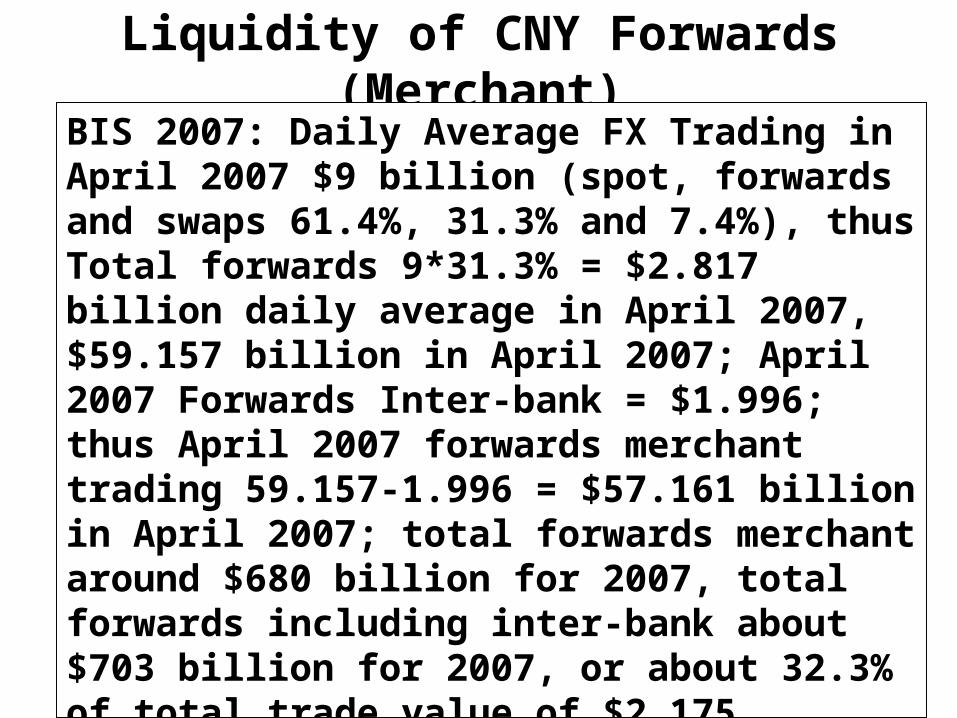

Liquidity of CNY Forwards (Merchant)BIS 2007: Daily Average FX Trading in April 2007 $9 billion (spot, forwards and swaps 61.4%, 31.3% and 7.4%), thusTotal forwards 9*31.3% = $2.817 billion daily average in April 2007, $59.157 billion in April 2007; April 2007 Forwards Inter-bank = $1.996; thus April 2007 forwards merchant trading 59.157-1.996 = $57.161 billion in April 2007; total forwards merchant around $680 billion for 2007, total forwards including inter-bank about $703 billion for 2007, or about 32.3% of total trade value of $2.175 trillion in 2007, compared to international ratio around 150%

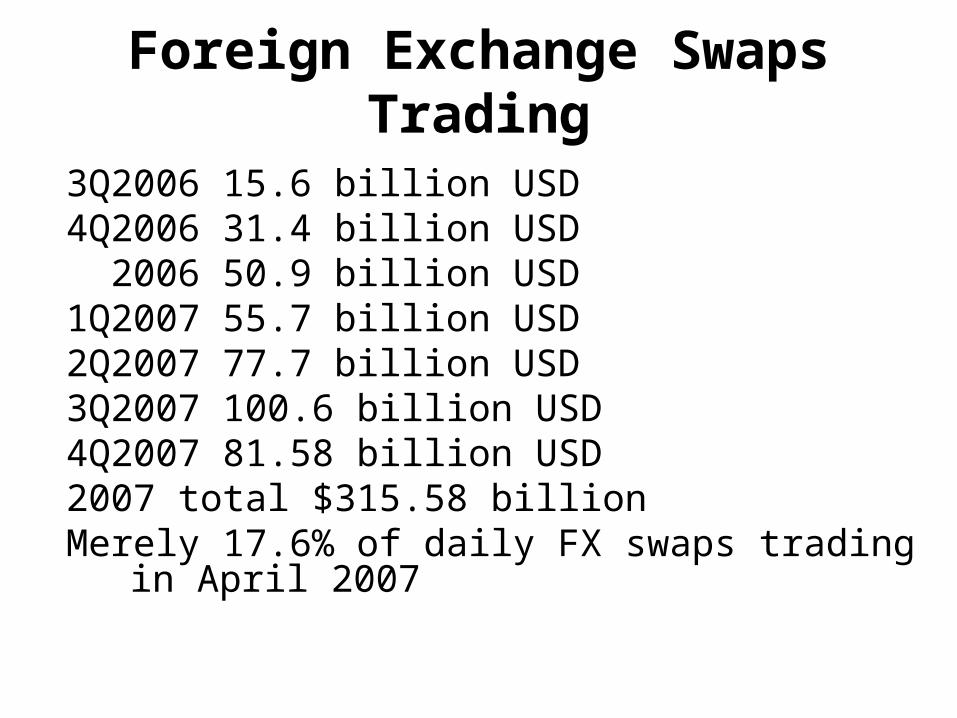

Foreign Exchange Swaps Trading

3Q2006 15.6 billion USD4Q2006 31.4 billion USD 2006 50.9 billion USD1Q2007 55.7 billion USD 2Q2007 77.7 billion USD3Q2007 100.6 billion USD4Q2007 81.58 billion USD2007 total $315.58 billionMerely 17.6% of daily FX swaps trading

in April 2007

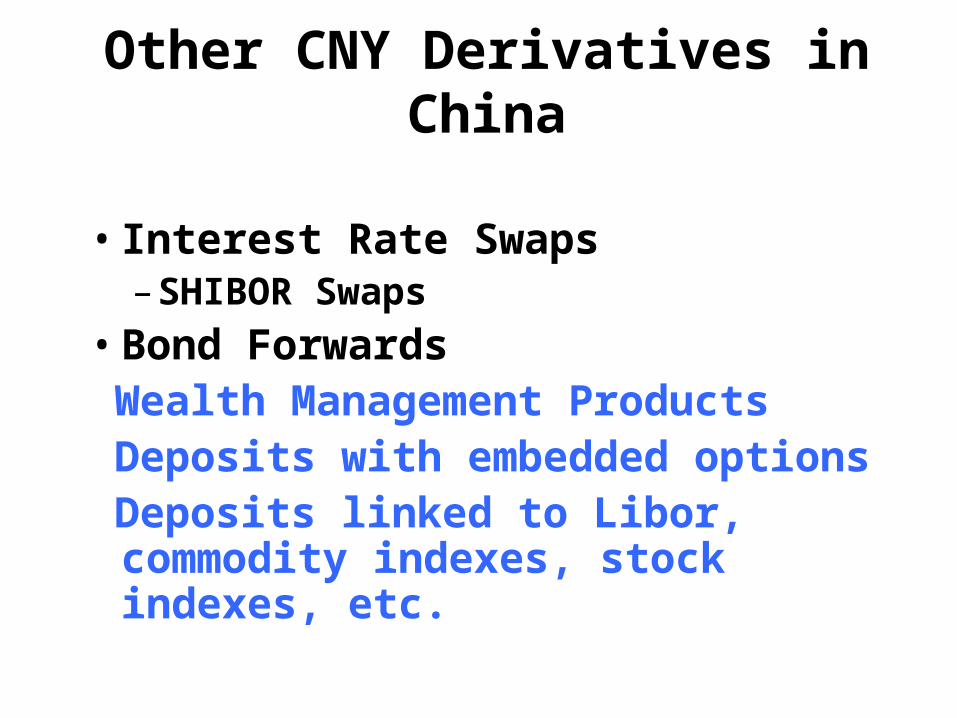

Other CNY Derivatives in China

• Interest Rate Swaps– SHIBOR Swaps

• Bond Forwards Wealth Management Products Deposits with embedded options Deposits linked to Libor, commodity

indexes, stock indexes, etc.

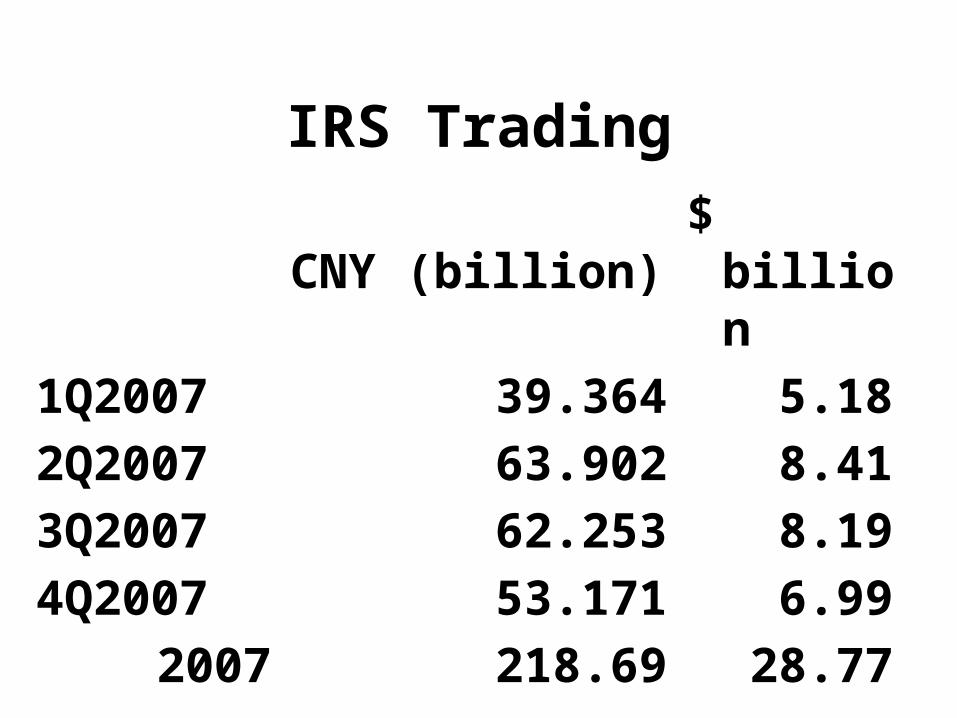

IRS Trading

CNY (billion) $ billion

1Q2007 39.364 5.18 2Q2007 63.902 8.41 3Q2007 62.253 8.19 4Q2007 53.171 6.99

2007 218.69 28.77

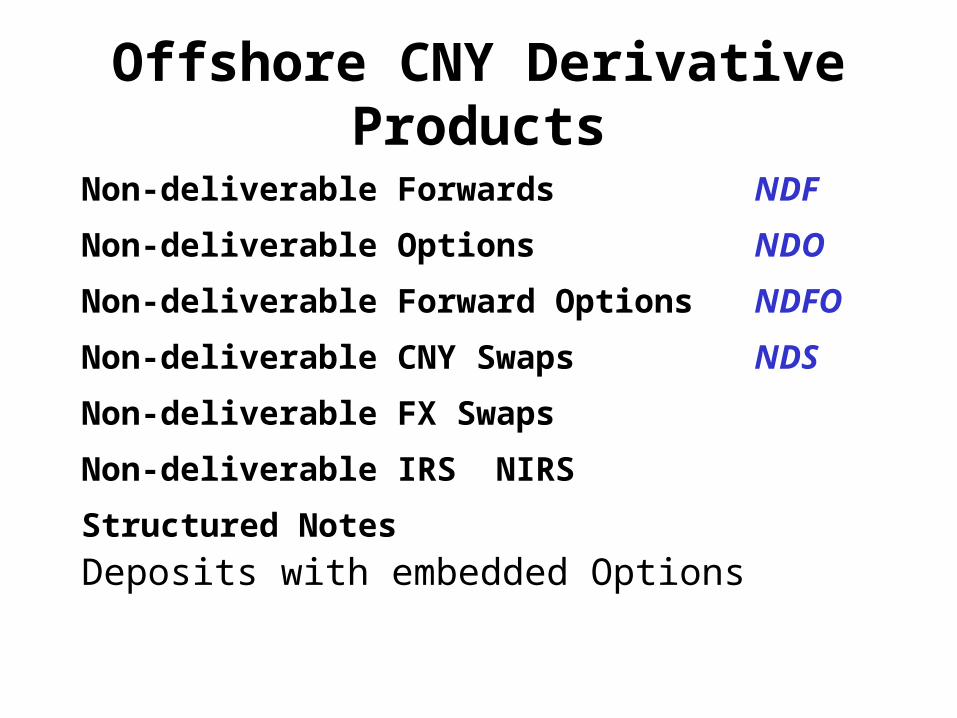

Offshore CNY Derivative Products

Non-deliverable Forwards NDF

Non-deliverable Options NDO

Non-deliverable Forward Options NDFO

Non-deliverable CNY Swaps NDS

Non-deliverable FX Swaps

Non-deliverable IRS NIRS

Structured Notes

Deposits with embedded Options

CNY NDF-most Popular Product offshoreCame into existence in 1996 before Asian financial crisis, yet liquidity was extremely low

Liquidity began to pick up late in 2002

Trading turnover estimated around US$150- 180 billion in 2003 & 2004!

around US$250 billion in 2005

around US$300 billion in 2006

around US$360 billion in 2007

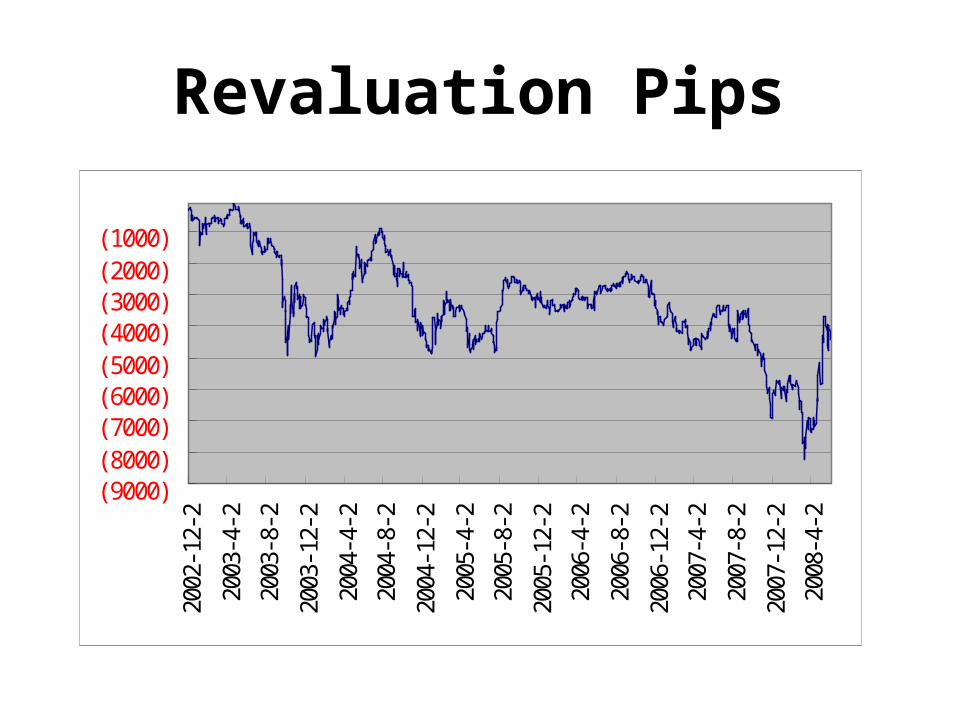

Revaluation Pips

(9000)(8000)(7000)(6000)(5000)(4000)(3000)(2000)(1000)

2002

-12-

2

2003

-4-2

2003

-8-2

2003

-12-

2

2004

-4-2

2004

-8-2

2004

-12-

2

2005

-4-2

2005

-8-2

2005

-12-

2

2006

-4-2

2006

-8-2

2006

-12-

2

2007

-4-2

2007

-8-2

2007

-12-

2

2008

-4-2

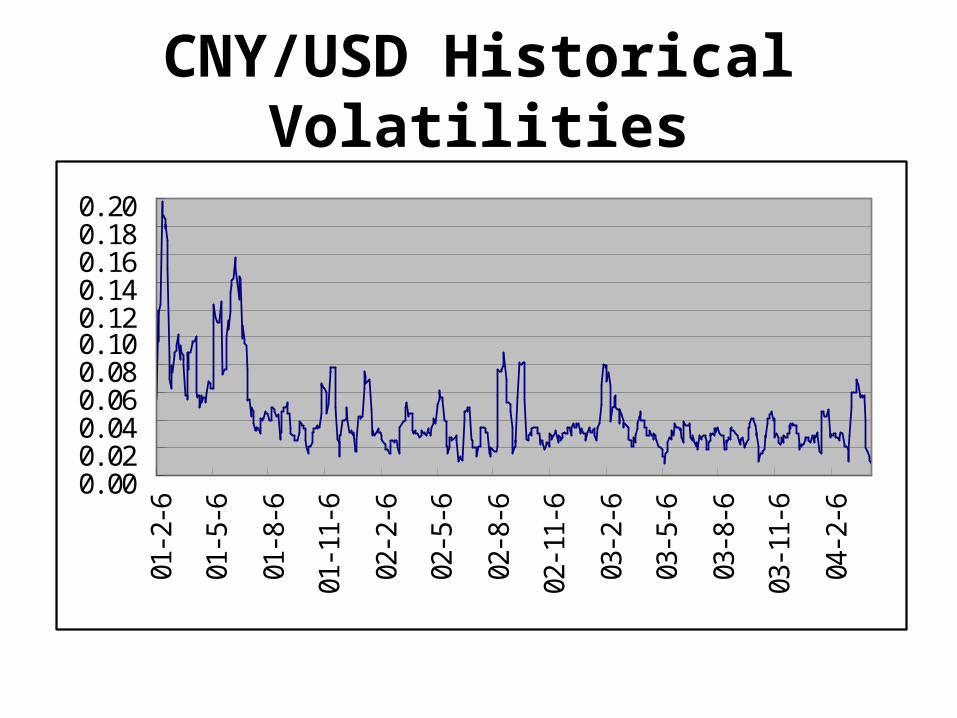

CNY/USD Historical Volatilities

0. 000. 020. 040. 060. 080. 100. 120. 140. 160. 180. 20

01-2

-6

01-5

-6

01-8

-6

01-1

1-6

02-2

-6

02-5

-6

02-8

-6

02-1

1-6

03-2

-6

03-5

-6

03-8

-6

03-1

1-6

04-2

-6

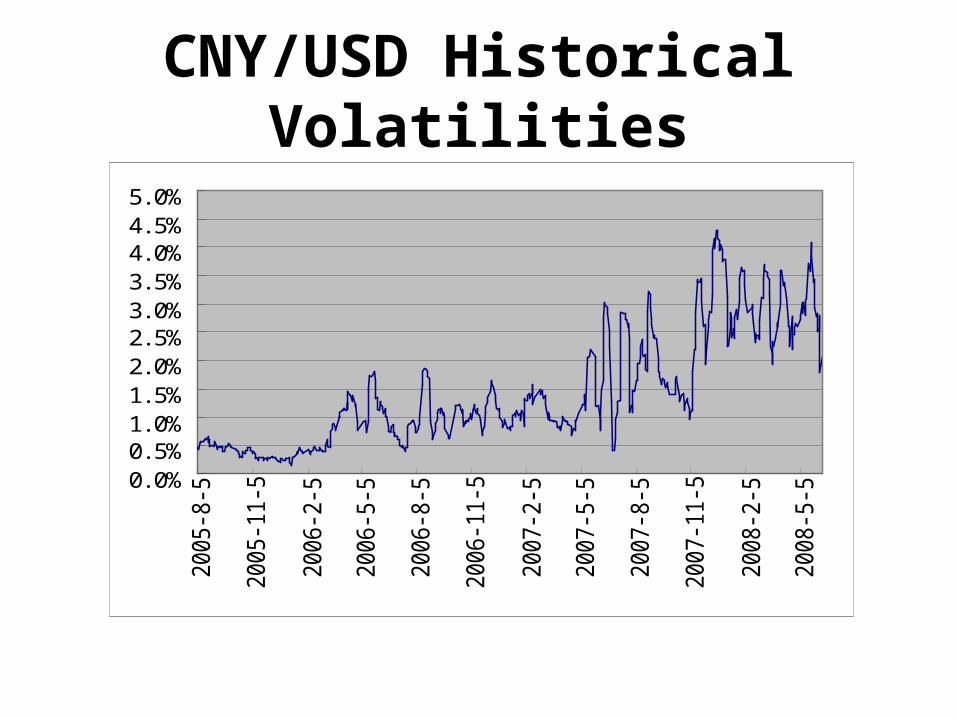

CNY/USD Historical Volatilities

0. 0%0. 5%1. 0%1. 5%2. 0%2. 5%3. 0%3. 5%4. 0%4. 5%5. 0%20

05-8

-5

2005

-11-

5

2006

-2-5

2006

-5-5

2006

-8-5

2006

-11-

5

2007

-2-5

2007

-5-5

2007

-8-5

2007

-11-

5

2008

-2-5

2008

-5-5

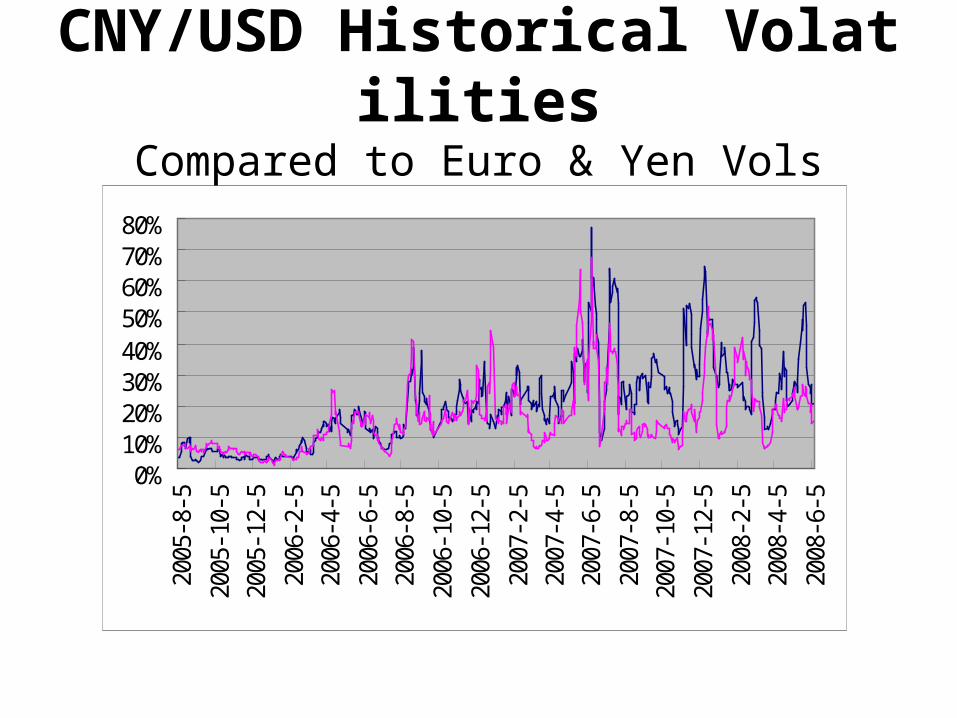

CNY/USD Historical VolatilitiesCompared to Euro & Yen Vols

0%10%20%30%40%50%60%70%80%

2005

-8-5

2005

-10-

5

2005

-12-

5

2006

-2-5

2006

-4-5

2006

-6-5

2006

-8-5

2006

-10-

5

2006

-12-

5

2007

-2-5

2007

-4-5

2007

-6-5

2007

-8-5

2007

-10-

5

2007

-12-

5

2008

-2-5

2008

-4-5

2008

-6-5

Appreciation and Further Expectation for RMB

2%4%6%8%

10%12%14%16%18%20%22%24%26%28%30%

2005

-8-1

2005

-10-

1

2005

-12-

1

2006

-2-1

2006

-4-1

2006

-6-1

2006

-8-1

2006

-10-

1

2006

-12-

1

2007

-2-1

2007

-4-1

2007

-6-1

2007

-8-1

2007

-10-

1

2007

-12-

1

2008

-2-1

2008

-4-1

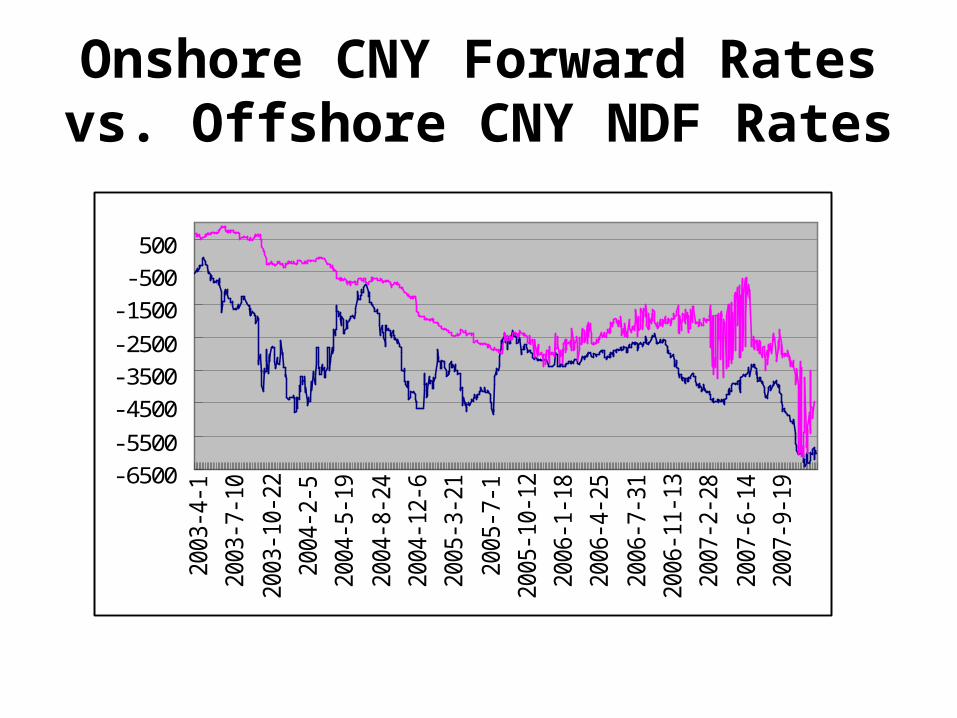

Onshore CNY Forward Rates vs. Offshore CNY NDF Rates

-6500-5500

-4500-3500-2500

-1500-500500

2003

-4-1

2003

-7-1

0

2003

-10-

22

2004

-2-5

2004

-5-1

9

2004

-8-2

4

2004

-12-

6

2005

-3-2

1

2005

-7-1

2005

-10-

12

2006

-1-1

8

2006

-4-2

5

2006

-7-3

1

2006

-11-

13

2007

-2-2

8

2007

-6-1

4

2007

-9-1

9

BASEL II Implementation in China

Major Chinese Banks are Required to Implement BASEL II by 2010

Market Risk Management

Credit Risk Management

Future Market DemandHedging CNY FX Risk

-Steady Growth of Foreign Trade

-Expansion of QDIIs

-International Investments

-Foreign Participation of Domestic Capital Market, Banking Industry

Need to Develop the Options Market

Challenges for Market Risk Management in China

• Construction of reliable Yield Curve

• Interest Rate Liberalization

• Structuring and Pricing Capacity

• Market Risk Management Models (VaR)

Challenges for Market Risk Management in China

• Lack of Exchange Trade Options

• No Implied Volatilities

• Low Liquidity of Existing Products

Comparisons with Indian Rupee Derivatives Markets

Average Daily Trading Value of Foreign Exchange in China & India

Foreign Exchange Trading ($billion)

SpotsOutright

Forwards

Foreign Exchan

ge Swaps

China 9 5.53 2.82 0.67

India 34 14.48 9.35 10.13

China 61.4% 31.3% 7.4%

India 42.6% 27.5% 29.8%

Word 3210 32.6% 11.7% 55.6%

Average Daily IR derivatives in April$ 1 billion in 2004 and $ 3 billion in 2007, India,

---in China

“Exotic Options” 1997(1st),1998(2nd), 2008(3rd)

“Chinese Yuan Derivative Products”(English,400p)

World ScientificOctober 2004 (Peter G. Zhang)

Chinese Yuan Derivative Products

China Financial Press (in Chinese,900p), May 2006;

2nd Edition (around 1300p), April 2008

Thank You!