the application of exploratory data analysis (eda) …raw.rutgers.edu/docs/wcars/28wcars/28wcars...

TRANSCRIPT

The Application of Exploratory Data Analysis

(EDA) in Auditing

Qi Liu Ph.D. Candidate (A.B.D.)

Dept. of Accounting & Information Systems

Rutgers University

28th WCARS

November 9, 2013

Outline

Introduction

An overview of EDA concept

EDA in Auditing

An application of EDA in auditing – A credit card retention case

Future Research

2

Motivation

Audit is a data intensive process; data analysis plays an important role

in audit process.

Current data analysis approaches used in auditing process focus on

validating predefined audit objectives, which can not discover unaware

risks from the data.

EDA is often linked to detective work, and one of its objectives is to

identify outliers.

Even though some EDA techniques have been used in some auditing

procedures, EDA has never been systematically employed in auditing.

Contribution

This research contributes to the auditing literature by taking the first cut

to use exploratory data analysis in auditing and illustrate a real-world

application in audit process.

3

Introduction

Definition of EDA

Exploratory data analysis (EDA) is a data analysis approach emphasizing

on pattern recognition and hypothesis generation.

4

Exploratory Data Analysis (EDA) Confirmatory Data Analysis (CDA)

Reasoning Type Inductive Deductive

Goal Pattern Recognition and Hypothesis

generation

Estimation, Modeling, Hypothesis testing

Applied Data Observation Data (data collected without

well-defined hypothesis)

Experimental data (data collected through

formally designed experiments)

Techniques Descriptive Statistics, Data Visualization,

Clustering Analysis, Process Mining…

Traditional statistical techniques of

inference, significance, and confidence

Advantages • No assumptions required

• Promotes deeper understanding of the

data

• Precise

• Well-established theory and methods

Disadvantages • No conclusive answers

• Difficult to avoid bias produced by

overfitting

• Required unrealistic assumptions

• Difficult to notice unexpected results

Confirmatory Data Analysis (CDA) is a widely used data analysis approach

emphasizing on experimental design, significance testing, estimation, and

prediction (Good, 1983).

5

EDA vs CDA

Since 1980s, EDA has been applied to diversified disciplines such as interior

design, marketing, industrial engineering, and geography (Chen et al., 2011;

Nayaka and Yano, 2010; Koschat and Sabavala, 1994; Wesley et al., 2006; De

Mast and Trip, 2007, 2009) .

A framework to apply EDA in practical problem solving issues include: (1)

display the data; (2) identify salient features; (3) interpret salient features (De

Mast and Kemper, 2009).

6

Current Applications of EDA

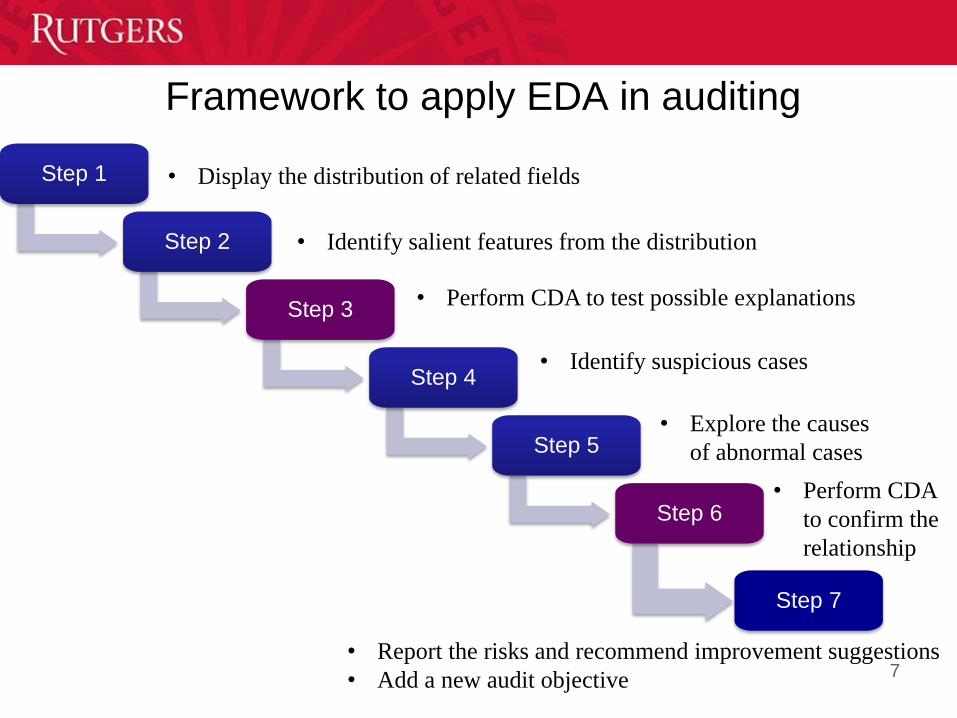

Framework to apply EDA in auditing

7

Step 1

Step 2

Step 3

Step 4

Step 5

Step 6

Step 7

• Display the distribution of related fields

• Identify salient features from the distribution

• Perform CDA to test possible explanations

• Identify suspicious cases

• Explore the causes

of abnormal cases

• Perform CDA

to confirm the

relationship

• Report the risks and recommend improvement suggestions

• Add a new audit objective

8

Purpose

Demonstrate the benefits of applying EDA in audit process

Provide a real example to support the proposed guidelines

Scenario: Clients call the bank asking for a reduction of their card fees. Bank

representatives offer discounts to clients to retain their accounts.

Objectives: identify the situations of loss of revenue in the negotiation of

fees caused by bank representatives, as b:

bank representatives offer higher discounts than allowed

bank representatives usually offer the highest allowable discounts without

putting enough efforts to negotiate lower discounts

bank representatives offer discounts without any negotiation with the

clients

Credit Card Retention Case

Data Description

9

Data (Retention Dataset) Selected Attributes

Each record represents a

customer call

195,694 records

162 fields

Time frame: January, 2012

Original fee (VLR_ANUIDADE_G)

Actual fee (_Valor da Anuidade de Saída)

Agent identification (Funcional do Agente)

Supervisor identification (Funcional do

Supervisor)

Location of the customer service center

(Polo de Atendimento)

Call duration (Tempo de Atendimento de

Retenti)

Data Preprocess

Discount Calculation

Applied EDA techniques

Descriptive Statistics

Data Visualization

Data Transformation

Methodology

10

Bank policy allows bank representatives to offer discounts up to 100% of

the annuity to retain the customer

Results Analysis (1/8)

11

Policy-violating bank representatives and negative discounts

0.15%

0.59%

0.69%

1.21%

4.60%

5.71%

15.66%

31.34%

13.39%

15.14%

11.51%

0%

0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00% 35.00%

<0

0-10%

10%-20%

20%-30%

30%-40%

40%-50%

50%-60%

60%-70%

70%-80%

80%-90%

90%-100%

>100%

Dis

co

un

t

Descriptive statistics of discounts

Frequency distribution of discounts

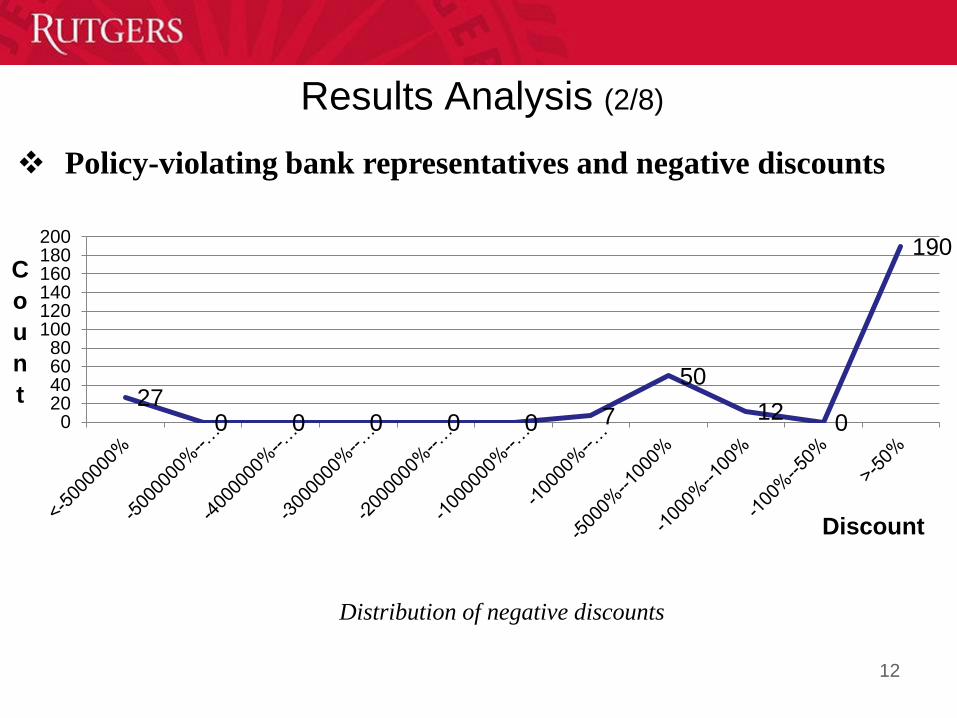

Results Analysis (2/8)

12

Policy-violating bank representatives and negative discounts

27 0 0 0 0 0 7

50

12 0

190

020406080

100120140160180200

C

o

u

n

t

Discount

Distribution of negative discounts

Results Analysis (3/8)

13

Policy-violating bank representatives and negative discounts

New Audit Objective:

Actual fees are recorded correctly.

Original fees reflect the number of cards in an account.

Relationships between negative discounts and original and actual fees

Results Analysis (4/8)

14

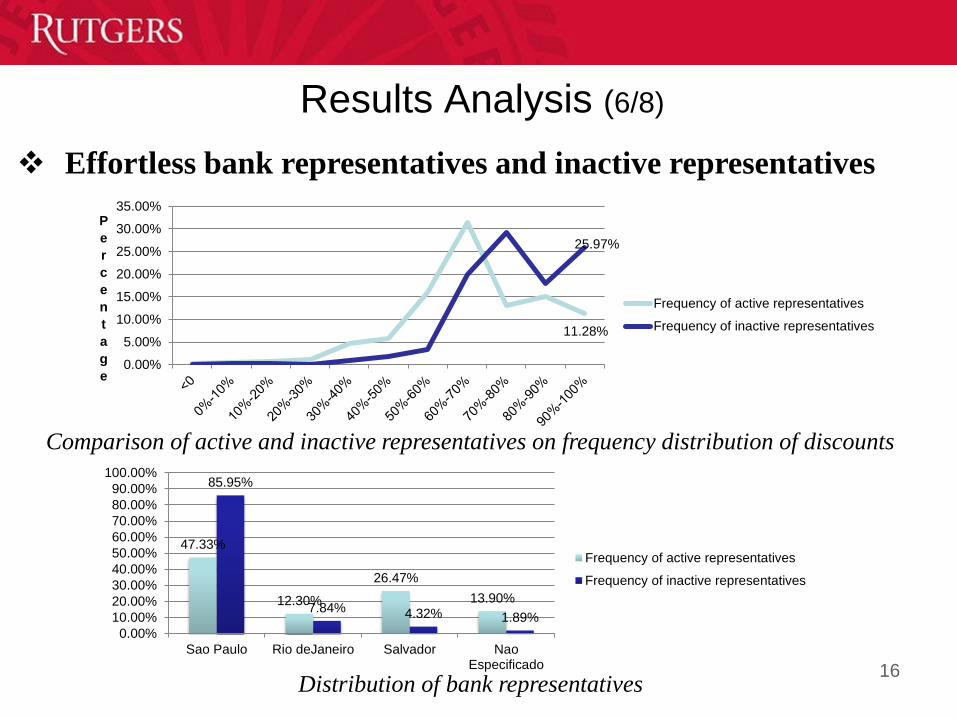

Effortless bank representatives and inactive representatives

Distribution of bank representatives offered 100% discounts in the whole retention data and

the 100% discount subset

Bank representatives who always offer 100% discounts should be considered

not putting enough effort to negotiate with the clients for a lower discount.

0

100

200

300

400

500

600

700

86

156

390

954

790

654

290

557

290

666

195

238

290

507

790

522

890

633

291

252

190

448

791

266

699

959

790

013

290

072

290

670

498

564

187

098

795

239

090

839

790

891

490

192

790

535

590

933

990

007

891

178

691

397

491

192

790

796

491

158

590

858

690

960

292

395

199

798

190

797

290

901

292

170

891

536

195

048

890

469

999

055

999

809

991

188

791

185

490

572

090

787

191

491

291

190

690

858

5

F

r

e

q

u

e

n

c

y

Bank Representatitves ID

Frequency in total Frequency in 100% discount subset

Results Analysis (5/8)

15

Effortless bank representatives and inactive representatives

Descriptive statistics of frequency distribution of bank representatives

Inactive

representatives

32%

Supervisor

3%

35% Active

representatives

65%

Distribution of bank representatives

Results Analysis (6/8)

16

Effortless bank representatives and inactive representatives

Comparison of active and inactive representatives on frequency distribution of discounts

Distribution of bank representatives

11.28%

25.97%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%P

e

r

c

e

n

t

a

g

e

Frequency of active representatives

Frequency of inactive representatives

47.33%

12.30%

26.47%

13.90%

85.95%

7.84% 4.32% 1.89%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

Sao Paulo Rio deJaneiro Salvador NaoEspecificado

Frequency of active representatives

Frequency of inactive representatives

Results Analysis (7/8)

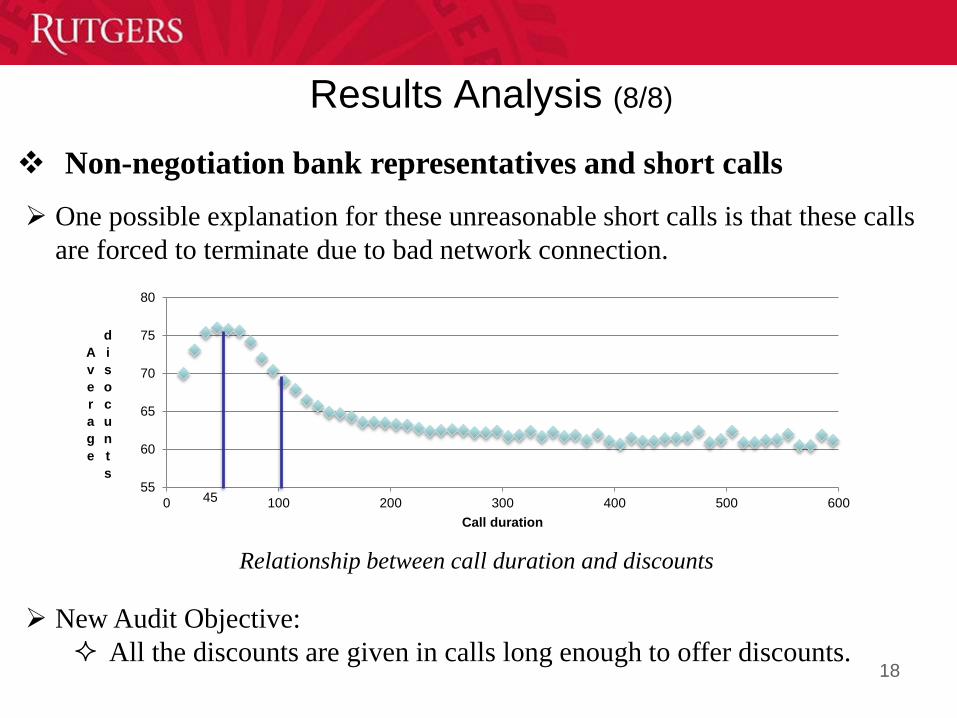

17

Non-negotiation bank representatives and short calls

Frequency distribution of call duration less than 600 seconds

Bank representatives who offer a discount without negotiation usually related

to short call duration

Descriptive statistics of call duration

One possible explanation for these unreasonable short calls is that these calls

are forced to terminate due to bad network connection.

New Audit Objective:

All the discounts are given in calls long enough to offer discounts.

Results Analysis (8/8)

18

Non-negotiation bank representatives and short calls

Relationship between call duration and discounts

45 55

60

65

70

75

80

0 100 200 300 400 500 600

A

v

e

r

a

g

e

d

i

s

o

c

u

n

t

s

Call duration

Future research directions

Demonstrate the application of EDA in the audit of financial

statement related business cycle.

Demonstrate the application of EDA in other types of auditing.

Extend current framework to continuous auditing environment.

Explore the application of other EDA technologies in auditing.

Explore the most suitable EDA techniques for each audit

procedure.

19

Thank You!

20