taxation - accounting technicians ireland · taxation . republic of ireland. sample paper 3 . ......

TRANSCRIPT

Taxation Republic of Ireland Sample Paper 3 2017 / 2018 Questions and Suggested Solutions Finance Act 2016

Sample Paper 3 Updated 2018 Examinations Page 2 of 20

NOTES TO USERS ABOUT SAMPLE PAPERS

Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance to students and their teachers regarding the style and type of question, and their suggested solutions, in our examinations. They are not intended to provide an exhaustive list of all possible questions that may be asked and both students and teachers alike are reminded to consult our published syllabus (see www.AccountingTechniciansIreland.ie) for a comprehensive list of examinable topics. There are often many possible approaches to the solution of questions in professional examinations. It should not be assumed that the approach adopted in these solutions is the only correct approach, particularly with discursive answers. Alternative answers will be marked on their own merits. This publication is copyright 2017 and may not be reproduced without permission of Accounting Technicians Ireland. © Accounting Technicians Ireland, 2017.

INSTRUCTIONS TO CANDIDATES

PLEASE READ CAREFULLY For candidates answering in accordance with the law and practice of the Republic of Ireland. In this examination paper the € symbol may be understood and used by candidates in the Republic of Ireland to indicate the Euro. Candidates should answer the paper in accordance with the appropriate provisions up to and including the Finance Act 2016. The provisions of the Finance Act 2017 should be ignored. Allowances and rates of taxation, to be used by candidates, are set out in a separate booklet supplied with the examination paper. Answer ALL THREE questions from Section A. Answer ANY TWO of the three questions from Section B. If more than TWO questions are answered in section B, then only the first two questions, in the order filed, will be corrected. Candidates should allocate their time carefully. All workings should be shown. All figures should be labeled as appropriate e.g. €s, units etc. Answers should be illustrated with examples, where appropriate. Question 1 begins on Page 2 overleaf. The following inserts are enclosed with the paper: • Tax Reference Material • Multiple choice Answer Sheet (Question 1)

Sample Paper 3 Updated 2018 Examinations Page 4 of 20

SECTION A

Answer ALL THREE questions in this section

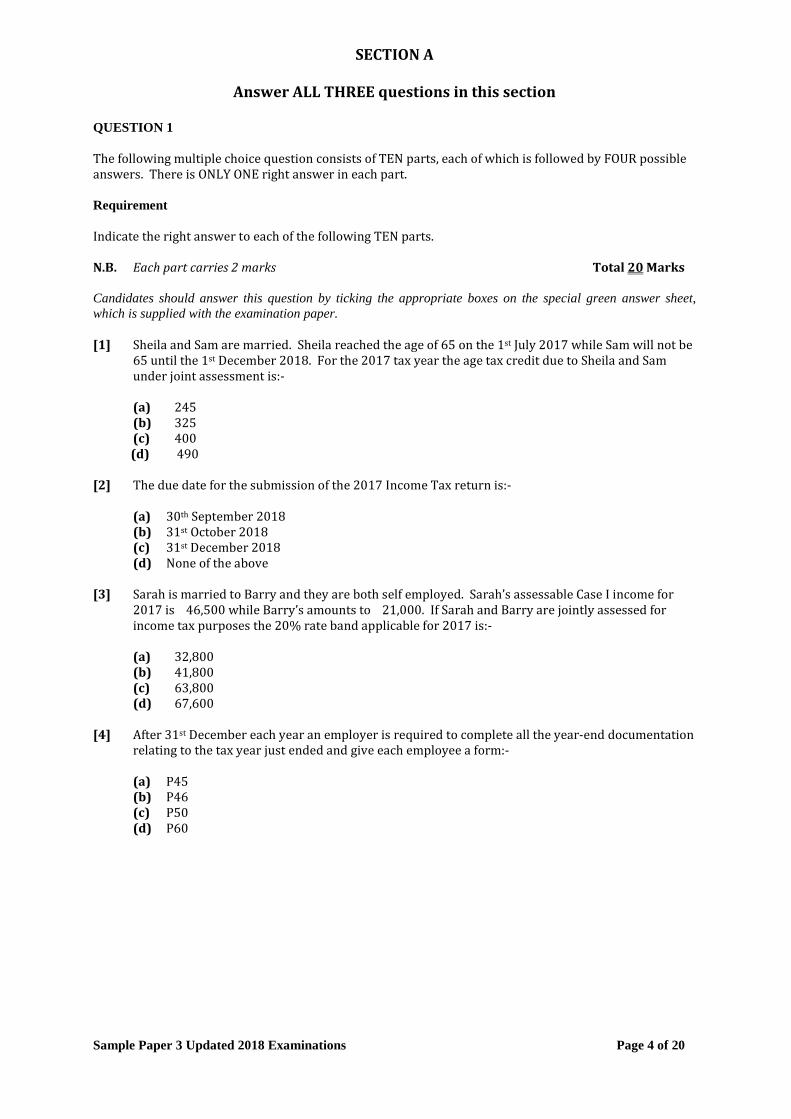

QUESTION 1 The following multiple choice question consists of TEN parts, each of which is followed by FOUR possible answers. There is ONLY ONE right answer in each part. Requirement Indicate the right answer to each of the following TEN parts. N.B. Each part carries 2 marks Total 20 Marks Candidates should answer this question by ticking the appropriate boxes on the special green answer sheet, which is supplied with the examination paper. [1] Sheila and Sam are married. Sheila reached the age of 65 on the 1st July 2017 while Sam will not be

65 until the 1st December 2018. For the 2017 tax year the age tax credit due to Sheila and Sam under joint assessment is:-

(a) €245 (b) €325 (c) €400 (d) €490

[2] The due date for the submission of the 2017 Income Tax return is:-

(a) 30th September 2018 (b) 31st October 2018 (c) 31st December 2018 (d) None of the above

[3] Sarah is married to Barry and they are both self employed. Sarah’s assessable Case I income for 2017 is €46,500 while Barry’s amounts to €21,000. If Sarah and Barry are jointly assessed for income tax purposes the 20% rate band applicable for 2017 is:-

(a) €32,800 (b) €41,800 (c) €63,800 (d) €67,600

[4] After 31st December each year an employer is required to complete all the year-end documentation

relating to the tax year just ended and give each employee a form:-

(a) P45 (b) P46 (c) P50 (d) P60

Sample Paper 3 Updated 2018 Examinations Page 5 of 20

QUESTION 1 (Cont’d.)

[5] Jane earned €80,000 in the first 50 weeks of the 2017 tax year. In week 51 of the same year she

earned €800. If Class A PRSI is applicable to Jane the total amount of PRSI payable to the Revenue for week 51 is:-

(a) Nil (b) €26.92 (c) €32.00 (d) €118.00

[6] Samanta commenced employment with BTT Ltd. in week 23 of the 2017 tax year. Her previous

employment ceased in week 4 of the 2017 tax year. Details extracted from the form P45 supplied by her previous employer shows weekly tax credits of €61.80 and weekly cut off point of €618.20. If Samanta earned €740 in week 23 of the 2017 tax year the PAYE deducted from her pay for that week would amount to:-

(a) €173.58 (b) €148.00 (c) €110.56 (d) €303.40

[7] Simon commenced business as a builder’s providers on the 1st January 2017. In the year ended 31st

December, 2017 his turnover including VAT at 23% amounted to €460,000 and his closing receivables (debtors) were €26,200. If Simon accounts for VAT on a cash receipts basis the amount of VAT due on outputs for the year ended 31st December, 2017 would amount to:-

(a) €54,714 (b) €81,117 (c) €86,016 (d) €99,774

[8] ABC, a VAT registered business cannot claim back VAT on which of the following expenses incurred

in the course of business:-

(a) Petrol (b) Diesel (c) Electricity (d) Purchases

[9] Ciara opened a restaurant in January 2017. Initially the turnover was expected to be €12,000 per

month but in April 2017 Ciara was surprised to find that the turnover for the three months to the end of March fell short of expectations and amounted to €20,000. Ciara is confident that turnover will rise over the coming months and that her original estimate of turnover for the year will be proved right. In these circumstances Ciara is obliged to register for VAT with effect from:- (a) 1st January 2017 (b) 1st April 2017 (c) 1st July 2017 (d) 1st September 2017

[10] The cash receipts basis of accounting for VAT may be used by a person whose annual turnover is

less than:-

(a) €350,000 (b) €500,000 (c) €635,000 (d) All of the above

Sample Paper 3 Updated 2018 Examinations Page 6 of 20

QUESTION 2 Peter has been in business for a number of years and is an electrical contractor. He has prepared accounts for the year ended 31st December 2017 and these are reproduced below: Accounts for the year ended 31st December 2017 Notes € €

Sales .................................................................................................. 595,456 Cost of sales ................................................................................... 441,690

Gross Profit .................................................................................... 153,766

Add Dividends received ..................................................................... 450 Interest earned ............................................................................. 230 680 154,446 Less Employee costs ............................................................................ (1) 68,358 Administrative costs .................................................................. (2) 1,956 Bad debts ........................................................................................ (3) 2,350 Repairs ............................................................................................. (4) 7,210 Motor expenses ............................................................................ (5) 16,790 Advertising and promotion .................................................... (6) 5,100 Legal costs ...................................................................................... (7) 1,880 Interest ............................................................................................ (8) 985 Sundry expenses ......................................................................... (9) 6,300 Office light and heat ................................................................... 1,200 Insurance ........................................................................................ (10) 2,080

114,209 Net profit/(loss) 40,237

NOTES € (1) Employee costs Drawings by Peter ................................................................................................................ 8,250 Wages paid to Peter’s wife who is a book keeper for the business ................ 16,650 Staff wages ............................................................................................................................... 37,498 Bonus to employees ............................................................................................................ 1,800 Christmas party for employees ...................................................................................... 560 Preliminary tax payment for Peter ............................................................................... 3,600 68,358

The bonus to employees is the net amount after deduction of PAYE/PRSI and it was paid at the end of January 2018. The PAYE/PRSI deducted together with employers PRSI amounting to €1,250 in total was paid by Peter to the Revenue in February 2017 and is not included in the figures above.

Sample Paper 3 Updated 2018 Examinations Page 7 of 20

QUESTION 2 (Cont’d.) (2) Administrative costs € Telephone ................................................................................................................................ 1,340 Trade magazines ................................................................................................................... 256 Stationery ................................................................................................................................. 360 1,956

Peter estimates that 30% of the telephone calls are his private calls. The cost of stationery includes €80 in respect of the purchase and postage of Christmas cards to customers.

(3) Bad debts Bad debts written off ........................................................................................................... 2,500

Reduction in general bad debt provision ........................................................... (800) Increase in specific bad debt provision ...................................................................... 560 Solicitor’s letter to debtor regarding bad debts ...................................................... 90 2,350 (4) Repairs € Purchase of new telephone system .............................................................................. 1,560 Constructing new storage facility .................................................................................. 3,750 Repairs to office windows ................................................................................................ 1,550 Repairs to office equipment ............................................................................................. 350 7,210

(5) Motor expenses €

Parking fines ........................................................................................................................... 230 Mileage paid to employees working away from base in accordance with civil service rates ............................................................................................................................ 850 Van running costs ................................................................................................................. 3,850 Van depreciation ................................................................................................................... 3,200 Car expenses ........................................................................................................................... 4,560 Car depreciation .................................................................................................................... 4,100 16,790 One of the employees has the use of the van for private purposes. It is estimated that his private mileage represents approximately 10% of the total miles travelled. The car is used by Peter and originally cost €30,000 when purchased new in 2009. Peter’s private mileage amounts to 25% of the total miles travelled.

(6) Advertising and promotion €

Gifts to customers at Christmas ..................................................................................... 3,200 Diaries ........................................................................................................................................ 600 Radio advertising .................................................................................................................. 1,100 Advertising in local paper regarding sale of boat .................................................. 200

5,100 The Christmas gifts to customers were given to the top ten customers and the cost ranged from €200 to €600 each. Peter is convinced these gifts will help him to get repeat business from these customers. The diaries cost €8 each and contain details of Peter’s business and his contact details. Peter considers this as a cost of advertising.

Sample Paper 3 Updated 2018 Examinations Page 8 of 20

QUESTION 2 (Cont’d.) (7) Legal costs €

Planning application for extension to business premises .................................. 850 Unfair dismissal claim by employee ............................................................................. 320 Health and safety statement ............................................................................................ 560 Contracts for employees .................................................................................................... 150

1,880 (8) Interest € Business bank overdraft .................................................................................................... 150 Term loan for office extension ........................................................................................ 560 Interest charged by suppliers ......................................................................................... 75 Late payment of PAYE/PRSI/USC ................................................................................. 200

985

(9) Sundry expenses € Goods taken by Peter for his own use ......................................................................... 900 Accountancy fees .................................................................................................................. 5,400 6,300

20% of the accountancy fees refer to the production of figures submitted to the bank as part of Peter’s application for a home loan mortgage.

(10) Insurance The total bills for the year amounted to €2,600. Peter deducted 20% from the bills on the basis that this amount relates to insurance for non business items.

Requirement Compute Peter’s Schedule D, Case I tax adjusted profits for the year ended 31st December 2017. Total 20 Marks

Sample Paper 3 Updated 2018 Examinations Page 9 of 20

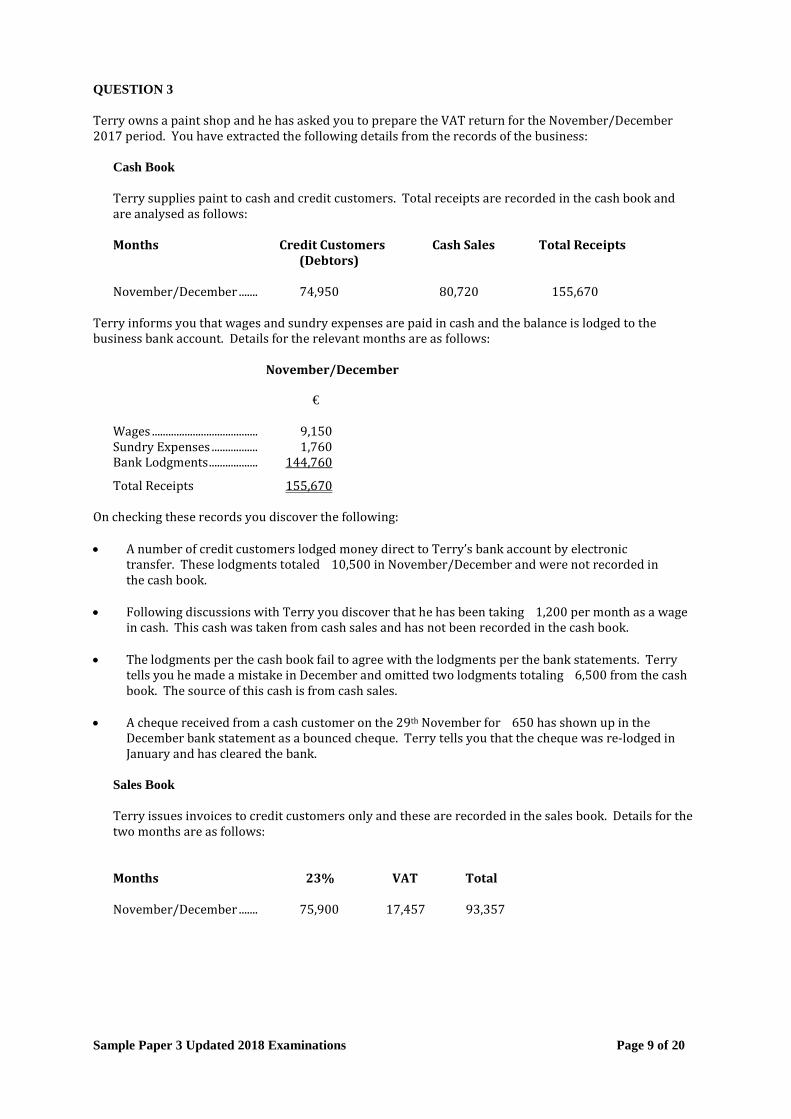

QUESTION 3 Terry owns a paint shop and he has asked you to prepare the VAT return for the November/December 2017 period. You have extracted the following details from the records of the business:

Cash Book Terry supplies paint to cash and credit customers. Total receipts are recorded in the cash book and are analysed as follows: Months Credit Customers Cash Sales Total Receipts (Debtors) € € € November/December ....... 74,950 80,720 155,670

Terry informs you that wages and sundry expenses are paid in cash and the balance is lodged to the business bank account. Details for the relevant months are as follows: November/December

€

Wages ....................................... 9,150 Sundry Expenses ................. 1,760 Bank Lodgments .................. 144,760

Total Receipts 155,670 On checking these records you discover the following: • A number of credit customers lodged money direct to Terry’s bank account by electronic

transfer. These lodgments totaled €10,500 in November/December and were not recorded in the cash book.

• Following discussions with Terry you discover that he has been taking €1,200 per month as a wage

in cash. This cash was taken from cash sales and has not been recorded in the cash book. • The lodgments per the cash book fail to agree with the lodgments per the bank statements. Terry

tells you he made a mistake in December and omitted two lodgments totaling €6,500 from the cash book. The source of this cash is from cash sales.

• A cheque received from a cash customer on the 29th November for €650 has shown up in the

December bank statement as a bounced cheque. Terry tells you that the cheque was re-lodged in January and has cleared the bank.

Sales Book Terry issues invoices to credit customers only and these are recorded in the sales book. Details for the two months are as follows: Months 23% VAT Total € € € November/December ....... 75,900 17,457 93,357

Sample Paper 3 Updated 2018 Examinations Page 10 of 20

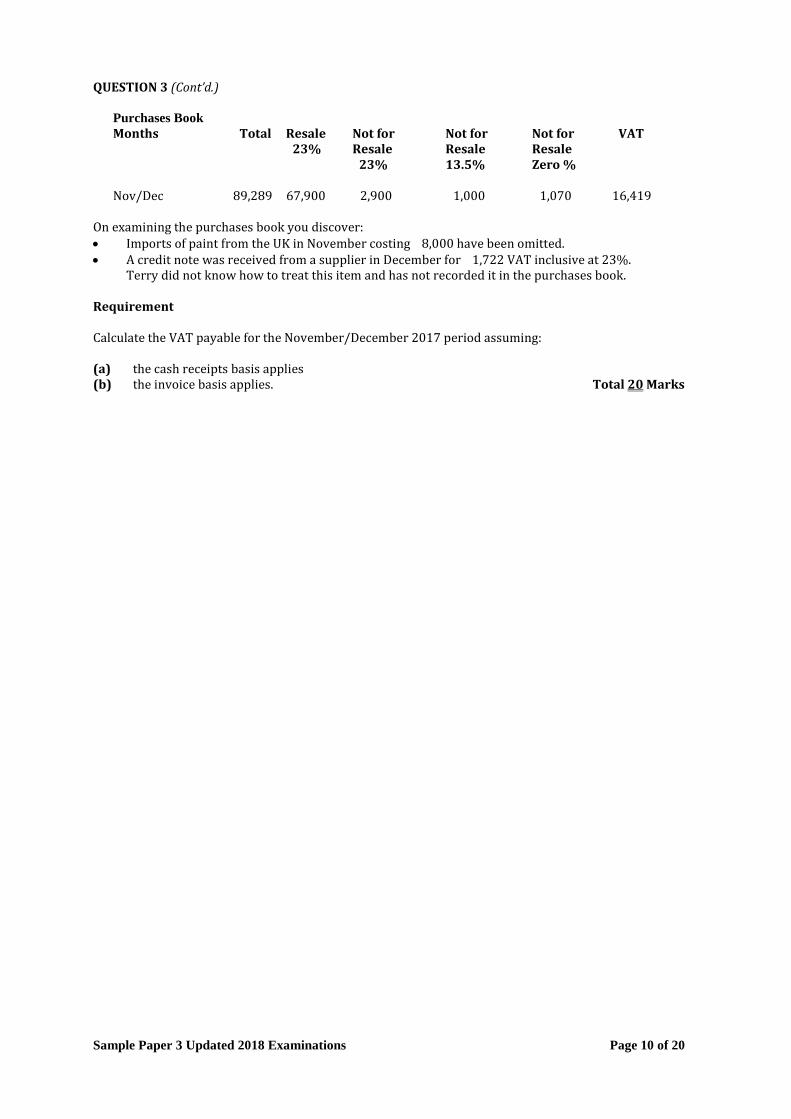

QUESTION 3 (Cont’d.)

Purchases Book Months Total Resale Not for Not for Not for VAT

23% Resale Resale Resale 23% 13.5% Zero %

€ € € € € € Nov/Dec 89,289 67,900 2,900 1,000 1,070 16,419

On examining the purchases book you discover: • Imports of paint from the UK in November costing €8,000 have been omitted. • A credit note was received from a supplier in December for €1,722 VAT inclusive at 23%.

Terry did not know how to treat this item and has not recorded it in the purchases book. Requirement Calculate the VAT payable for the November/December 2017 period assuming: (a) the cash receipts basis applies (b) the invoice basis applies. Total 20 Marks

Sample Paper 3 Updated 2018 Examinations Page 11 of 20

SECTION B

Answer TWO of the three questions in section B

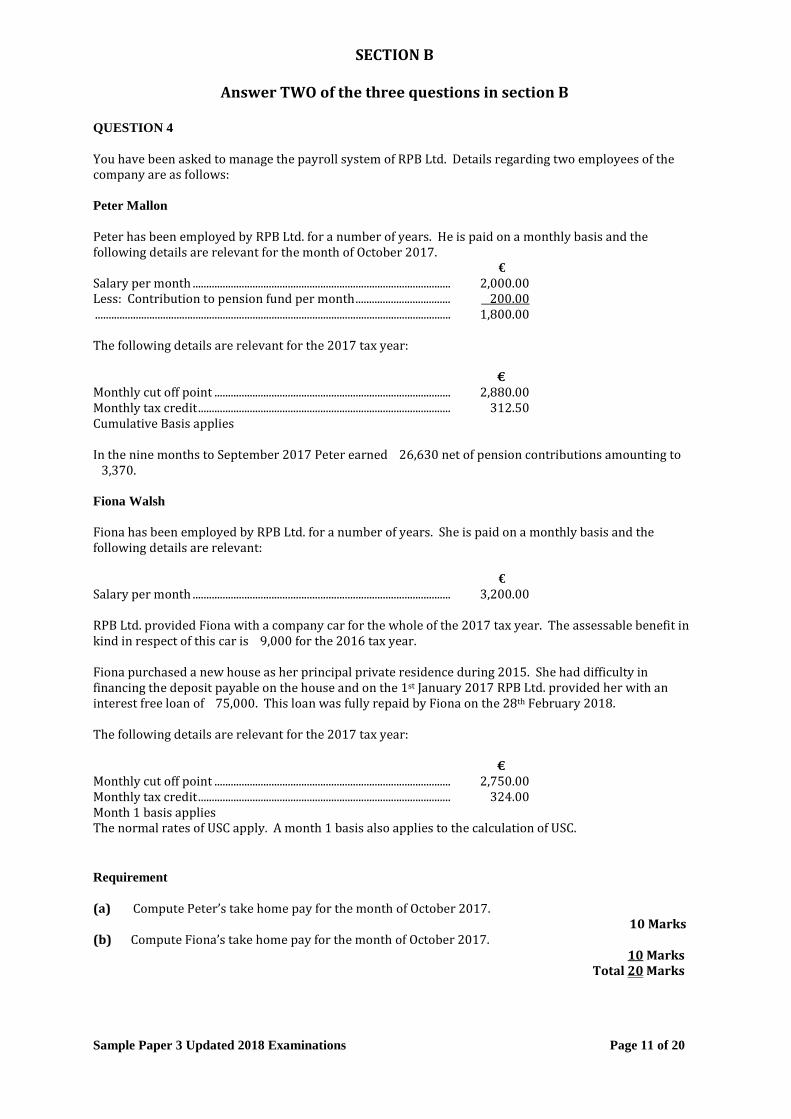

QUESTION 4 You have been asked to manage the payroll system of RPB Ltd. Details regarding two employees of the company are as follows: Peter Mallon Peter has been employed by RPB Ltd. for a number of years. He is paid on a monthly basis and the following details are relevant for the month of October 2017. € Salary per month ............................................................................................... 2,000.00 Less: Contribution to pension fund per month ................................... 200.00 ................................................................................................................................... 1,800.00 The following details are relevant for the 2017 tax year: € Monthly cut off point ....................................................................................... 2,880.00 Monthly tax credit ............................................................................................. 312.50 Cumulative Basis applies In the nine months to September 2017 Peter earned €26,630 net of pension contributions amounting to €3,370. Fiona Walsh Fiona has been employed by RPB Ltd. for a number of years. She is paid on a monthly basis and the following details are relevant: € Salary per month ............................................................................................... 3,200.00 RPB Ltd. provided Fiona with a company car for the whole of the 2017 tax year. The assessable benefit in kind in respect of this car is €9,000 for the 2016 tax year. Fiona purchased a new house as her principal private residence during 2015. She had difficulty in financing the deposit payable on the house and on the 1st January 2017 RPB Ltd. provided her with an interest free loan of €75,000. This loan was fully repaid by Fiona on the 28th February 2018. The following details are relevant for the 2017 tax year: € Monthly cut off point ....................................................................................... 2,750.00 Monthly tax credit ............................................................................................. 324.00 Month 1 basis applies The normal rates of USC apply. A month 1 basis also applies to the calculation of USC. Requirement (a) Compute Peter’s take home pay for the month of October 2017.

10 Marks (b) Compute Fiona’s take home pay for the month of October 2017. 10 Marks Total 20 Marks

Sample Paper 3 Updated 2018 Examinations Page 12 of 20

QUESTION 5 Shirley and Patrick have been married for a number of years. Shirley is aged 39 while Patrick is aged 41 years. Details of their respective incomes and outgoings are as follows: Shirley Income Shirley is a self employed chiropodist for a number of years. Tax adjusted profits per accounts are as follows: € Year ended 31st January 2016 ............................................... 38,000 Year ended 31st January 2017 ............................................... 43,000 Year ended 31st January 2018 ............................................... 56,000 In the year ended 31st December 2017 Shirley earned deposit interest with BIG Bank Plc. of €147.50 net of deposit interest retention tax at 39%. In March 2017 Shirley received a dividend of €374.40 in respect of shares held in RTQ Plc. This dividend was in respect of the year ended 31st December 2016. In March 2018 Shirley received a dividend from RTQ Plc. of €416.00 in respect of the year ended 31st December 2017. Both dividends received were paid net of dividend withholding tax at 20%. In November 2017 Shirley purchased a house for letting. She had difficulty finding a suitable tenant and eventually on the 1st March 2017 she let the premises for the first time at a rent of €1,200 per month. The rent is payable on the first day of each month. Outgoings Shirley contributes €1,000 per month to a Revenue approved pension fund. Patrick Income Patrick is an employee of AXY Ltd. His salary for the year ended 31st December 2017 amounted to €30,000. In addition to the salary Patrick was paid a bonus based on sales achieved. In February 2017 he received a bonus for the year ended 31st December 2016 of €1,350 and in February 2017 he received €1,500 for the year ended 31st December 2017. PAYE deducted in 2017 amounted to €3,400.

Sample Paper 3 Updated 2018 Examinations Page 13 of 20

QUESTION 5 (Cont’d.) Patrick is obliged to use his own car while travelling on behalf of AXY Ltd. In 2017 he travelled a total of 60,000 kilometers and 20% of these were for private purposes. Patrick keeps a record of the motor expenses incurred by him and following discussions with his employer he received a payment in respect of business travel in accordance with Civil Service rates. The amount due was paid monthly and amounted to €13,440 in total for 2017. Patrick submitted a claim form to his employer each month detailing the customers he called to and the distance travelled each day for business purposes. Requirement Prepare income tax computations for 2017 in respect Shirley and Patrick on the basis that single assessment applies. Total 20 Marks N.B. For the purposes of answering this question ignore PRSI and the USC

QUESTION 6 [a] Mary has been a self employed hairdresser for a number of years and on the 30th

November 2017 she retired from business. Accounts have been prepared and the tax adjusted profits are as follows:

€ Year ended 31 May 2015 ................................... 29,280 Year ended 31 May 2016 ................................... 27,600 Year ended 31 May 2017 ................................... 30,600 Period to 30 November 2017 (cessation) .. 11,100

Calculate the assessable Schedule D Case 1 income for Mary for the 2015, 2016 and 2017 tax years.

10 Marks (a) Write a brief note on the purpose and content of the Revenue form P45. 5 Marks (b) Write a brief note on the one parent family tax credit. 5 Marks Total 20 Marks

Sample Paper 3 Updated 2018 Examinations Page 14 of 20

These solutions have been amended for the 2018 Examinations Solution to question 1 [1] D [2] B [3] C [4] D [5] D [6] C [7] B [8] A [9] A [10] D

Sample Paper 3 Updated 2018 Examinations Page 15 of 20

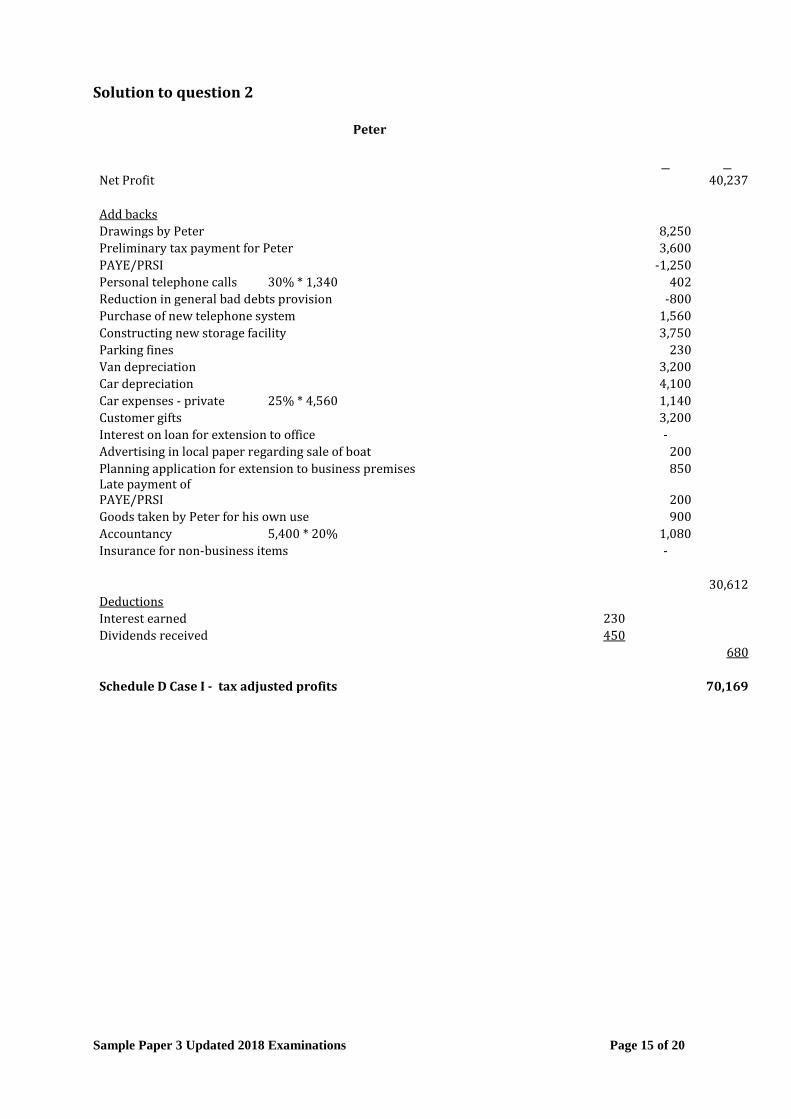

Solution to question 2

Peter € € Net Profit 40,237 Add backs Drawings by Peter 8,250 Preliminary tax payment for Peter 3,600 PAYE/PRSI -1,250 Personal telephone calls 30% * 1,340 402 Reduction in general bad debts provision -800 Purchase of new telephone system 1,560 Constructing new storage facility 3,750 Parking fines 230 Van depreciation 3,200 Car depreciation 4,100 Car expenses - private 25% * 4,560 1,140 Customer gifts 3,200 Interest on loan for extension to office - Advertising in local paper regarding sale of boat 200 Planning application for extension to business premises 850 Late payment of PAYE/PRSI 200 Goods taken by Peter for his own use 900 Accountancy 5,400 * 20% 1,080 Insurance for non-business items - 30,612 Deductions Interest earned 230 Dividends received 450 680 Schedule D Case I - tax adjusted profits 70,169

Sample Paper 3 Updated 2018 Examinations Page 16 of 20

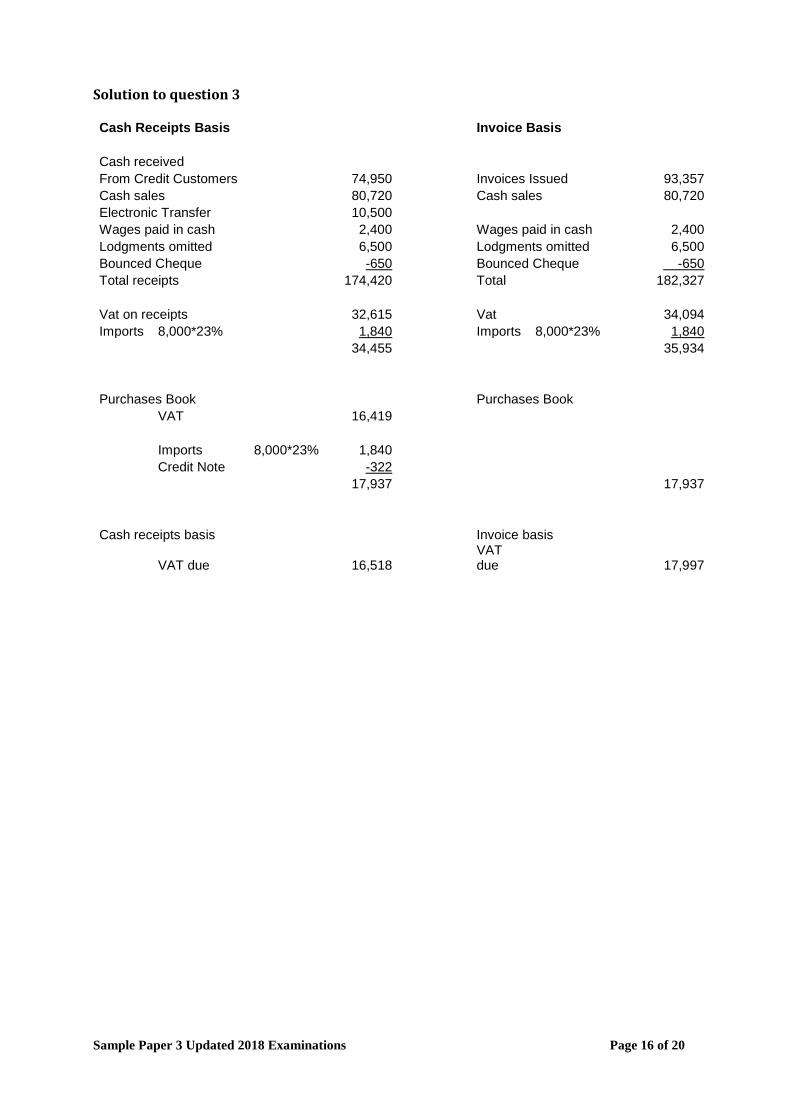

Solution to question 3 Cash Receipts Basis Invoice Basis Cash received From Credit Customers 74,950 Invoices Issued 93,357 Cash sales 80,720 Cash sales 80,720 Electronic Transfer 10,500 Wages paid in cash 2,400 Wages paid in cash 2,400 Lodgments omitted 6,500 Lodgments omitted 6,500 Bounced Cheque -650 Bounced Cheque -650 Total receipts 174,420 Total 182,327 Vat on receipts 32,615 Vat 34,094 Imports 8,000*23% 1,840 Imports 8,000*23% 1,840 34,455 35,934 Purchases Book Purchases Book VAT 16,419 Imports 8,000*23% 1,840 Credit Note -322 17,937 17,937 Cash receipts basis Invoice basis

VAT due 16,518 VAT due 17,997

Sample Paper 3 Updated 2018 Examinations Page 17 of 20

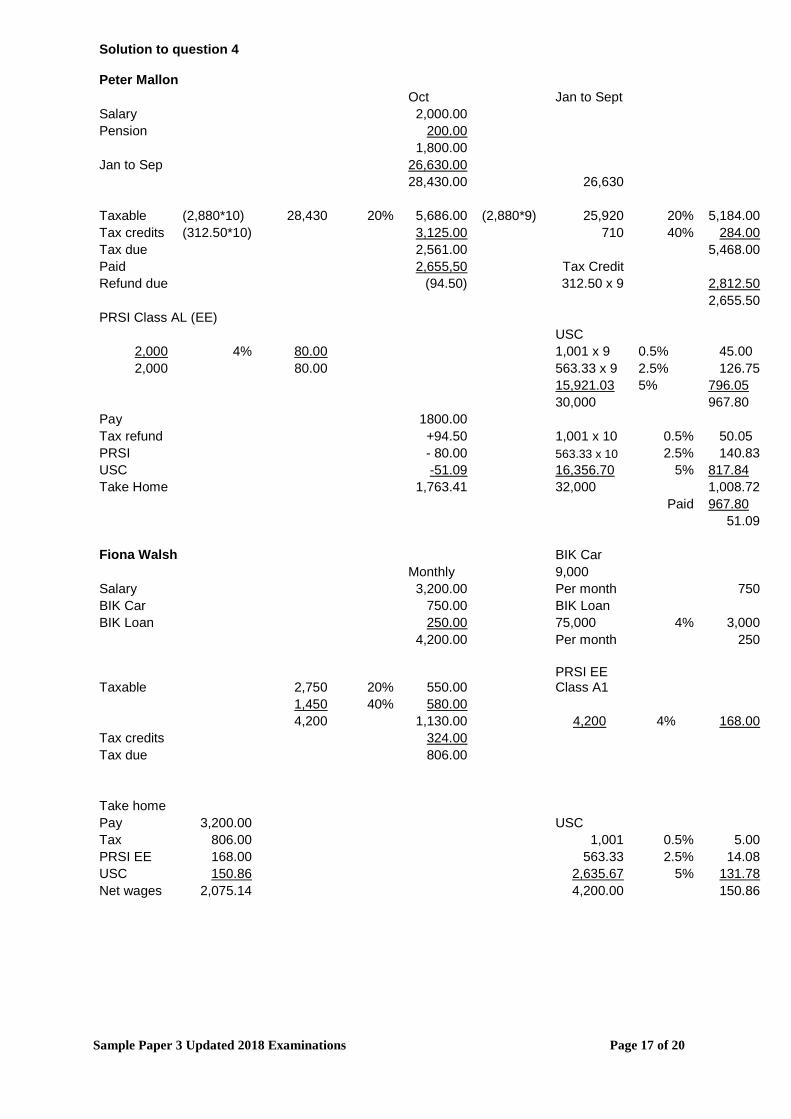

Solution to question 4 Peter Mallon Oct Jan to Sept Salary 2,000.00 Pension 200.00 1,800.00 Jan to Sep 26,630.00 28,430.00 26,630 Taxable (2,880*10) 28,430 20% 5,686.00 (2,880*9) 25,920 20% 5,184.00 Tax credits (312.50*10) 3,125.00 710 40% 284.00 Tax due 2,561.00 5,468.00 Paid 2,655,50 Tax Credit Refund due (94.50) 312.50 x 9 2,812.50 2,655.50 PRSI Class AL (EE)

USC 2,000 4% 80.00 1,001 x 9 0.5% 45.00 2,000 80.00 563.33 x 9 2.5% 126.75

15,921.03 5% 796.05 30,000 967.80 Pay 1800.00 Tax refund +94.50 1,001 x 10 0.5% 50.05 PRSI - 80.00 563.33 x 10 2.5% 140.83 USC -51.09 16,356.70 5% 817.84 Take Home 1,763.41 32,000 1,008.72 Paid 967.80 51.09 Fiona Walsh BIK Car Monthly 9,000 Salary 3,200.00 Per month 750 BIK Car 750.00 BIK Loan BIK Loan 250.00 75,000 4% 3,000 4,200.00 Per month 250

Taxable 2,750 20% 550.00 PRSI EE Class A1

1,450 40% 580.00 4,200 1,130.00 4,200 4% 168.00 Tax credits 324.00 Tax due 806.00 Take home Pay 3,200.00 USC Tax 806.00 1,001 0.5% 5.00 PRSI EE 168.00 563.33 2.5% 14.08 USC 150.86 2,635.67 5% 131.78 Net wages 2,075.14 4,200.00 150.86

Sample Paper 3 Updated 2018 Examinations Page 18 of 20

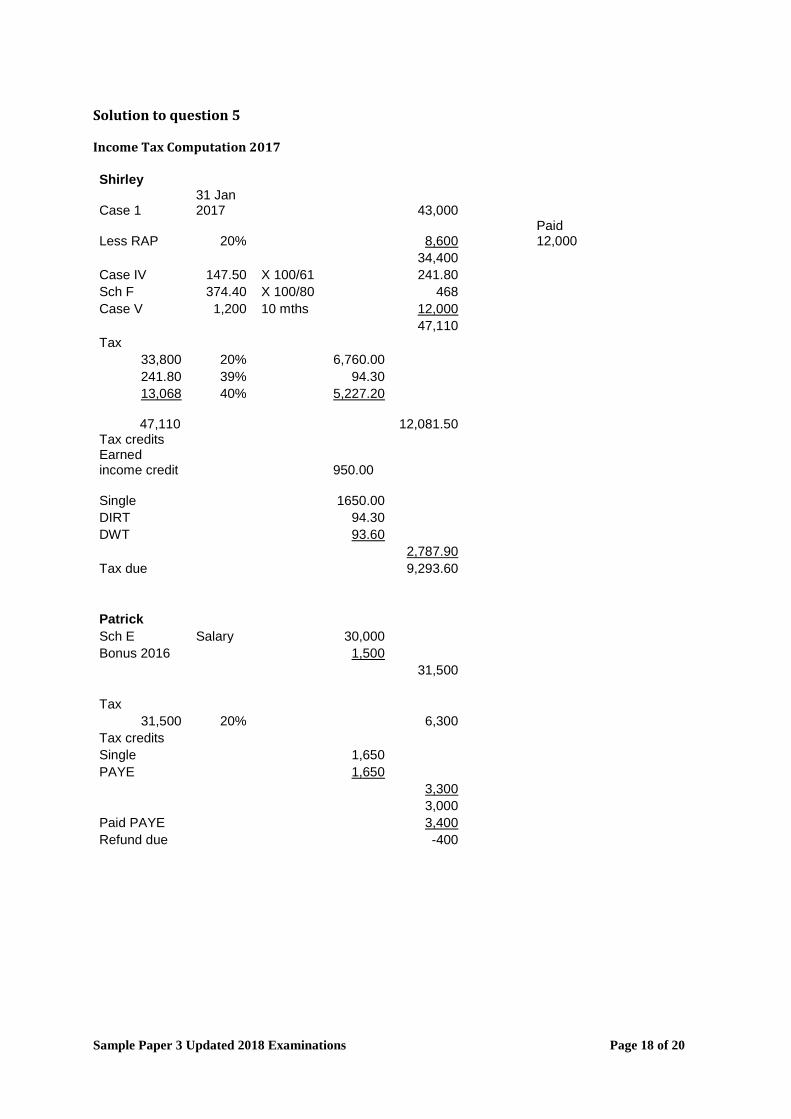

Solution to question 5 Income Tax Computation 2017 Shirley

Case 1 31 Jan 2017 43,000

Less RAP 20% 8,600 Paid 12,000

34,400 Case IV 147.50 X 100/61 241.80 Sch F 374.40 X 100/80 468 Case V 1,200 10 mths 12,000 47,110 Tax

33,800 20% 6,760.00 241.80 39% 94.30 13,068 40% 5,227.20

47,110 12,081.50

Tax credits Earned income credit 950.00

Single 1650.00

DIRT 94.30 DWT 93.60 2,787.90 Tax due 9,293.60 Patrick Sch E Salary 30,000 Bonus 2016 1,500 31,500 Tax

31,500 20% 6,300 Tax credits Single 1,650 PAYE 1,650 3,300 3,000 Paid PAYE 3,400 Refund due -400

Sample Paper 3 Updated 2018 Examinations Page 19 of 20

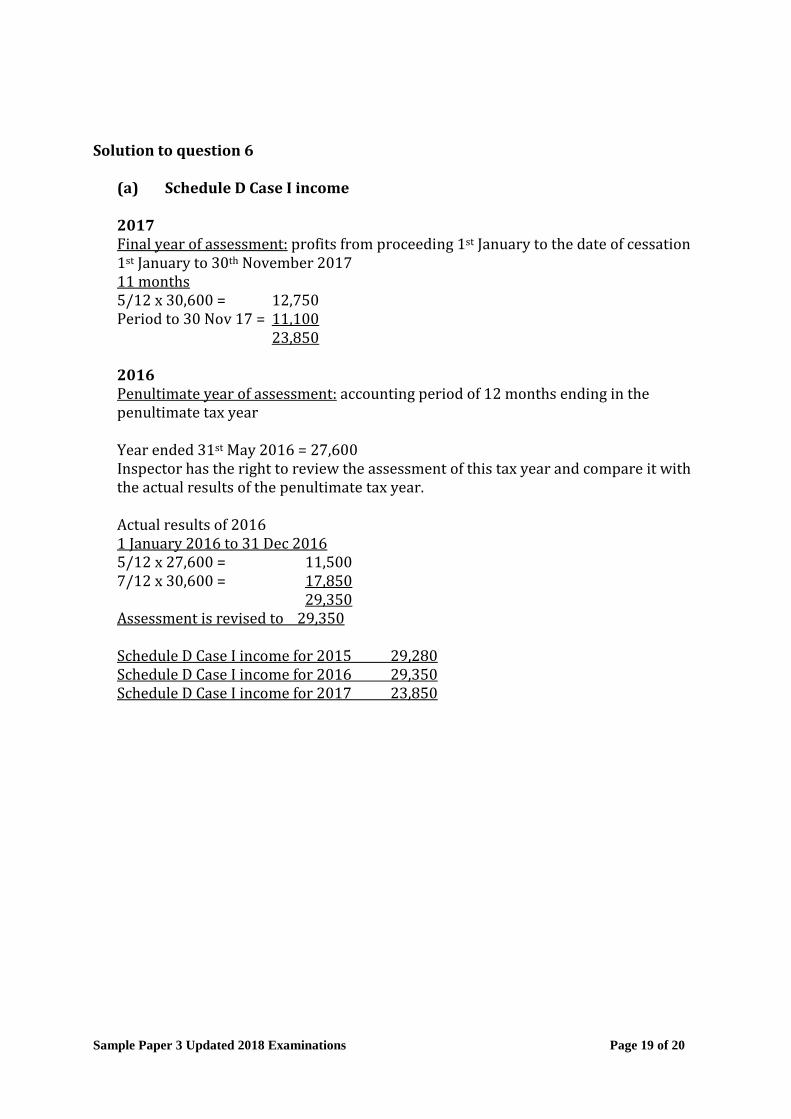

Solution to question 6

(a) Schedule D Case I income 2017 Final year of assessment: profits from proceeding 1st January to the date of cessation 1st January to 30th November 2017 11 months 5/12 x 30,600 = 12,750 Period to 30 Nov 17 = 11,100 23,850 2016 Penultimate year of assessment: accounting period of 12 months ending in the penultimate tax year Year ended 31st May 2016 = 27,600 Inspector has the right to review the assessment of this tax year and compare it with the actual results of the penultimate tax year. Actual results of 2016 1 January 2016 to 31 Dec 2016 5/12 x 27,600 = 11,500 7/12 x 30,600 = 17,850 29,350 Assessment is revised to €29,350 Schedule D Case I income for 2015 €29,280 Schedule D Case I income for 2016 €29,350 Schedule D Case I income for 2017 €23,850

Sample Paper 3 Updated 2018 Examinations Page 20 of 20

(b) Purpose and content of Revenue form P45 When an employee leaves employment or dies while in employment the employer is obliged to complete a form P45. It is possible to file form P45 using the Revenue Online Service (ROS). Form P45 contains details of pay, tax, USC, PRSI and LPT deducted to date employment ceases. It also contains information concerning the tax credits, standard rate cut off point and USC cut off points of the employee.

(c) One parent family tax credit

The one parent family tax credit for 2017 is €1,650. To qualify for the one parent family tax credit, an individual must satisfy the following conditions: -

The individual (who may be a widow, widower, separated parent or unmarried person) must not be entitled to a married persons tax credit for the particular tax year in question; and

The individual must have at least one child (under 18 years or if over 18 years, a child undergoing full-time education or vocational training, or an incapacitated child) who resides with him/her for the whole or part of the tax year.

No relief is granted to an unmarried couple who are living together as man and wife. The tax credit is granted in addition to the incapacitated child tax credit, if applicable and

remains constant at €1,650 irrespective of the number of dependent children that the taxpayer maintains.

The tax credit is not affected by the amount of the child’s income.