taxation - accounting technicians ireland · sample paper 2 updated 2018 examinations page 1 of 22....

TRANSCRIPT

Sample Paper 2 Updated 2018 examinations Page 1 of 22

Taxation Republic of Ireland Sample Paper 2 2017 / 2018 Questions and Suggested Solutions Finance Act 2016

Sample Paper 2 Updated 2018 examinations Page 2 of 22

NOTES TO USERS ABOUT SAMPLE PAPERS

Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance to students and their teachers regarding the style and type of question, and their suggested solutions, in our examinations. They are not intended to provide an exhaustive list of all possible questions that may be asked and both students and teachers alike are reminded to consult our published syllabus (see www.AccountingTechniciansIreland.ie) for a comprehensive list of examinable topics. There are often many possible approaches to the solution of questions in professional examinations. It should not be assumed that the approach adopted in these solutions is the only correct approach, particularly with discursive answers. Alternative answers will be marked on their own merits. This publication is copyright 2017 and may not be reproduced without permission of Accounting Technicians Ireland. © Accounting Technicians Ireland, 2017.

Sample Paper 2 Updated 2018 examinations Page 3 of 22

INSTRUCTIONS TO CANDIDATES

PLEASE READ CAREFULLY For candidates answering in accordance with the law and practice of the Republic of Ireland. In this examination paper the € symbol may be understood and used by candidates in the Republic of Ireland to indicate the Euro. Candidates should answer the paper in accordance with the appropriate provisions up to and including the Finance Act 2016. The provisions of the Finance Act 2017 should be ignored. Allowances and rates of taxation, to be used by candidates, are set out in a separate booklet supplied with the examination paper. Answer ALL THREE questions from Section A. Answer ANY TWO of the three questions from Section B. If more than TWO questions are answered in section B, then only the first two questions, in the order filed, will be corrected. Candidates should allocate their time carefully. All workings should be shown. All figures should be labeled as appropriate e.g. €s, units etc. Answers should be illustrated with examples, where appropriate. Question 1 begins on Page 2 overleaf. The following inserts are enclosed with the paper: • Tax Reference Material • Multiple choice Answer Sheet (QUESTION 6)

Sample Paper 2 Updated 2018 examinations Page 4 of 22

SECTION A Answer ALL THREE questions in this section

QUESTION 1 Sally is a self-employed florist and has been in business for a number of years. Sally has prepared accounts for the year ended 31st December 2017 but she is unsure of the correct tax treatment for certain items. The accounts as prepared are as follows: Accounts for the year ended 31st December 2017 Notes € €

Sales ................................................................................ 135,416 Opening stock ................................................................. 7,850

Purchases ........................................................................ (1) 75,450 83,300 Closing stock .................................................................. 9,156 Cost of sales .................................................................... 74,144 Gross Profit ..................................................................... 61,272 Add Rent received .................................................................. 5,400 Discount received for prompt payment........................... 145 Interest earned................................................................. 120 5,665 66,937 Less Wages ............................................................................. (2) 40,400 Light and heat ................................................................. (3) 8,150 Legal fees ........................................................................ (4) 1,185 Telephone ....................................................................... (5) 3,105 Depreciation.................................................................... 1,150 Discount allowed ............................................................ 200 Refund of deposit for let apartment ................................ 500 Entertainment/promotion ................................................ (6) 1,240 Motor expenses ............................................................... (7) 13,300 Insurance ......................................................................... (8) 2,610 Book keeping costs ......................................................... 850 Loan repayments ............................................................. (9) 3,700 Sundry (all allowable)..................................................... 875 77,265 Net profit/(loss) (10,328)

Sample Paper 2 Updated 2018 examinations Page 5 of 22

QUESTION 1 (Cont’d.) NOTES (1) The purchases figure includes €2,300 in respect of a new cash register purchased in August 2017. (2) Wages € Sally paid herself €200 per week as a wage...................................................... 10,400 Wages paid to full time staff by cheque ............................................................ 21,600 PAYE/PRSI/USC for employees paid to the Revenue ..................................... 4,800 Preliminary tax payment for Sally .................................................................... 3,600 40,400

Sally set up a direct debit with her bank for the payment of PAYE/PRSI/USC. Form P35 was completed in January 2017 and a balance of PAYE/PRSI/USC amounting to €850 was paid with the submission of the return. This figure has not been included in the accounts as Sally was unsure of the correct treatment of this item.

(3) Light and heat

Sally rents out an apartment which is situated over the shop. Separate bills are not available for the shop and apartment but Sally estimates that 30% of the light and heat refers to the apartment.

(4) Legal fees € Appeal against a rates bill ............................................................................................. 125 Planning permission application for shop extension ..................................................... 950 Solicitor’s letter to debtor regarding late payment ........................................................ 110 1,185

(5) Telephone €

Purchase of new mobile telephone ............................................................................... 440 Insurance cover for mobile telephone ........................................................................... 85 Mobile telephone calls .................................................................................................. 1,350 Land line telephone calls .............................................................................................. 980 Cost of repairing telephone system in the shop ............................................................ 250 3,105 The mobile telephone is used exclusively for business purposes. Private telephone calls on the land line are estimated at 30% and calls regarding the management of the apartment are estimated at 5% of total land line calls.

(6) Entertainment/Promotion €

Cost of taking customers to local golf course (Sally estimates that her turnover increased by 5% as a result of the goodwill generated by this) ......................................................... 560 Staff Christmas party .................................................................................................... 460 Purchase of prizes for customer draw ........................................................................... 220

1,240

Sample Paper 2 Updated 2018 examinations Page 6 of 22

QUESTION 1 (Cont’d.) (7) Motor Expenses €

Lease of a delivery van ................................................................................................. 4,900 Van running expenses (excluding insurance - see note 8 below) ................................. 3,950 Car running costs (excluding insurance - see note 8 below) ......................................... 4,450 13,300

The van was leased from January 2017 and the list price of the van at that time was €26,000. Sally estimates that she uses the van 10% of the time for private purposes. The car is used 30% of the time by Sheila for private purposes.

(8) Insurance € Car insurance ................................................................................................................ 850 Van insurance ............................................................................................................... 550 Public and Employers liability insurance ..................................................................... 960 Apartment insurance ..................................................................................................... 250

2,610

(9) Loan repayments € Term loan repayments .................................................................................................. 2,500 Credit Union loan repayments ...................................................................................... 1,200 3,700

The amount of the term loan was €10,000 and this was used to finance the cost of a new refrigerated display cabinet for the shop. The interest element of the loan repayments amounted to €768. The credit union loan amounted to €5,000 and was used to refurbish the apartment which is let. The interest element included amounts to €424.

Requirement

Compute Sally’s Schedule D, Case I tax adjusted profits for the year ended 31st December 2017. Total 20 Marks

Sample Paper 2 Updated 2018 examinations Page 7 of 22

QUESTION 2 Ciaran and Maeve were married on the 1st July 2017 and are both in their late 20’s. Details of their respective incomes and outgoings for the 2017 tax year are as follows: Ciaran Income Ciaran commenced self-employment as a quantity surveyor on the 1st March 2017. Accounts have been prepared for the year ended 28th February 2017 and these show a tax adjusted profit figure of €41,700. Prior to commencing self-employment, Ciaran was an employee of RTU Ltd and in the period 1st January 2017 to the date of cessation on 11th February 2017 he earned €4,960 with the company. In this period he had €500 deducted from his wages in respect of his contribution to a Revenue approved pension scheme and he also paid €168 PRSI, €269 USC and €612 PAYE. In 2017 Ciaran earned a dividend of €352 from the credit union. This amount was paid gross without the deduction of deposit interest retention tax. Ciaran has a mortgage with Big Bank Plc. The mortgage was taken out in June 2007 when he purchased his first principal private residence. To assist with the loan repayments Ciaran let out two of the bedrooms at a monthly rent of €350 for each room. The rooms were let until the end of May 2017. Outgoings Mortgage interest paid to Big Bank Plc for the year ended 31st December 2017 amounted to €4,000. Mortgage interest relief was allowed at source by Big Bank Plc. In June 2017 Ciaran borrowed €10,000 from the credit union and used the money to finance the cost of a new car. Interest paid on this loan in the year ended 31st December 2017 amounted to €480. Maeve Income Maeve is an employee of AXY Ltd. In 2016 she earned €21,000 and paid PAYE of €560. Requirement (a) Prepare a computation of the amount of tax payable by both Ciaran and Maeve for the 2017 tax year. 12 Marks (b) Explain the difference between exempt supplies and zero rated supplies for VAT purposes and include at

least three examples of each. 8 Marks

Total 20 Marks N.B. For the purposes of answering this question ignore PRSI and the USC

Sample Paper 2 Updated 2018 examinations Page 8 of 22

QUESTION 3 With regard to Income Tax write brief notes on each of the following: (a) Relief for medical expenses. 6 Marks (b) Employee tax credit 6 Marks (c) Dependent relative tax credit 4 Marks (d) Blind persons tax credit 4 Marks Total 20 Marks

SECTION B

Answer TWO of the three questions in section B

QUESTION 4

You have been asked to manage the payroll system of BBA Ltd. Details regarding two employees of the company are as follows:

Sheila Perkins

Sheila commenced employment with BBA Ltd. on the 1st October 2017 and is paid on a monthly basis. The following details are relevant for each of the two months October and November 2017.

€ Salary per month ......................................................................... 3,750.00

Less Contribution to pension fund per month ............................. 300.00

3,450.00

Sheila left her employment with BBA Ltd. on the 29th November 2017 (week 48 of the 2014 tax year). BBA Ltd. operates a bonus scheme for employees and on leaving her employment Sheila was paid €450 in respect of the bonus due to her for her period of employment. The following details are relevant for the 2017 tax year: Monthly Tax Credit: €268.50 Monthly cut off point: €2,725.00 Month 1 Basis applies The normal rates of USC apply. A month 1 basis also applies to the calculation of USC.

Sample Paper 2 Updated 2018 examinations Page 9 of 22

Padraig Hopkins Padraig has been employed by BBA Ltd. for a number of years and is paid weekly. Details of pay and tax deducted up to week 4 of the 2017 tax year are as follows:

€ Gross Pay .................................................................................... 2,225.00

Tax Deducted .............................................................................. 105.00

Weekly Tax Credit……………………………………………………………. 63.46

Tax Rate Standard

USC Cut Off €231 @1%, €128 @3%, €998 @5.5%

For week 5 Padraig earned €550.00 and was also paid an additional €150.00 in respect of an error made in the calculation of overtime pay due for work done in week 2 of the 2017 tax year.

Requirement

(a) Calculate the take home pay in respect of Sheila Perkins for each of the months of October and

November 2017.

10 Marks

(b) Calculate the tax home pay in respect of Padraig Hopkins for week 5 of the 2017 tax year. 10 Marks

Total 20 Marks

Sample Paper 2 Updated 2018 examinations Page 10 of 22

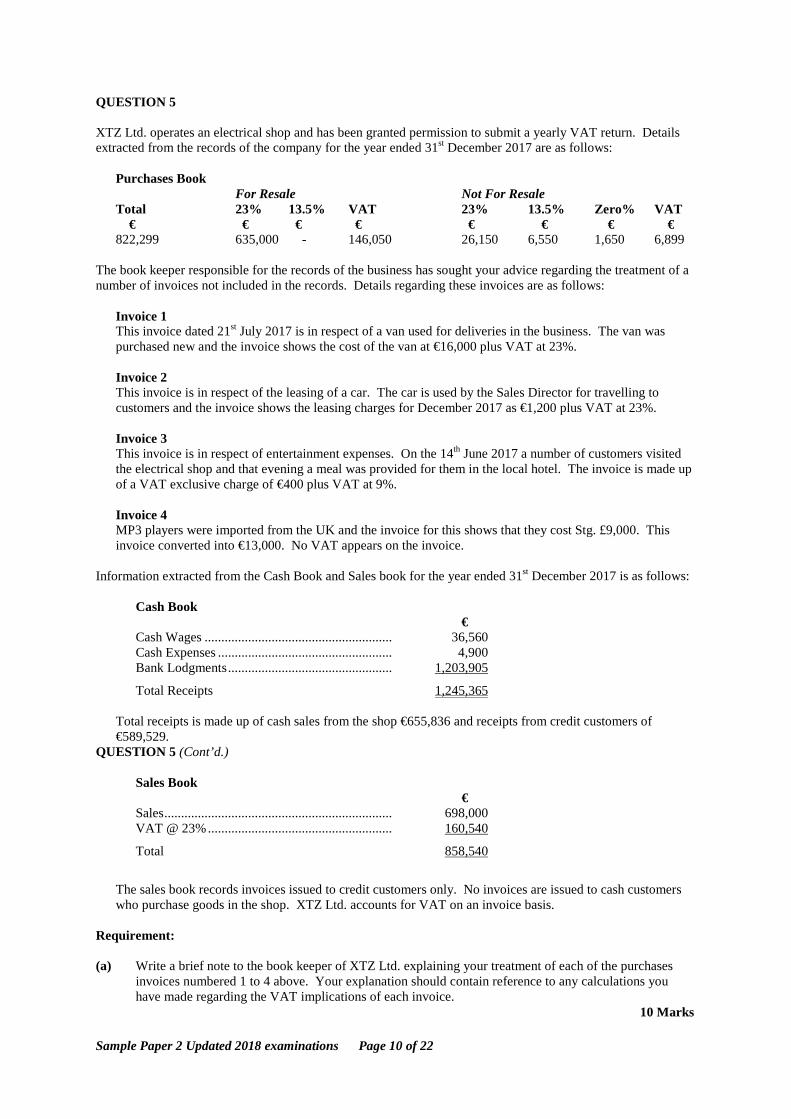

QUESTION 5 XTZ Ltd. operates an electrical shop and has been granted permission to submit a yearly VAT return. Details extracted from the records of the company for the year ended 31st December 2017 are as follows:

Purchases Book For Resale Not For Resale

Total 23% 13.5% VAT 23% 13.5% Zero% VAT € € € € € € € € 822,299 635,000 - 146,050 26,150 6,550 1,650 6,899

The book keeper responsible for the records of the business has sought your advice regarding the treatment of a number of invoices not included in the records. Details regarding these invoices are as follows:

Invoice 1 This invoice dated 21st July 2017 is in respect of a van used for deliveries in the business. The van was purchased new and the invoice shows the cost of the van at €16,000 plus VAT at 23%. Invoice 2 This invoice is in respect of the leasing of a car. The car is used by the Sales Director for travelling to customers and the invoice shows the leasing charges for December 2017 as €1,200 plus VAT at 23%. Invoice 3 This invoice is in respect of entertainment expenses. On the 14th June 2017 a number of customers visited the electrical shop and that evening a meal was provided for them in the local hotel. The invoice is made up of a VAT exclusive charge of €400 plus VAT at 9%. Invoice 4 MP3 players were imported from the UK and the invoice for this shows that they cost Stg. £9,000. This invoice converted into €13,000. No VAT appears on the invoice.

Information extracted from the Cash Book and Sales book for the year ended 31st December 2017 is as follows:

Cash Book € Cash Wages ........................................................ 36,560 Cash Expenses .................................................... 4,900 Bank Lodgments ................................................. 1,203,905

Total Receipts 1,245,365

Total receipts is made up of cash sales from the shop €655,836 and receipts from credit customers of €589,529.

QUESTION 5 (Cont’d.)

Sales Book € Sales .................................................................... 698,000 VAT @ 23% ....................................................... 160,540

Total 858,540

The sales book records invoices issued to credit customers only. No invoices are issued to cash customers who purchase goods in the shop. XTZ Ltd. accounts for VAT on an invoice basis.

Requirement: (a) Write a brief note to the book keeper of XTZ Ltd. explaining your treatment of each of the purchases

invoices numbered 1 to 4 above. Your explanation should contain reference to any calculations you have made regarding the VAT implications of each invoice.

10 Marks

Sample Paper 2 Updated 2018 examinations Page 11 of 22

(b) Compute the VAT payable /refundable for the year ended 31st December 2017. 10 Marks Total 20 Marks QUESTION 6 The following multiple choice question consists of TEN parts, each of which is followed by FOUR possible answers. There is ONLY ONE right answer in each part.

Requirement Indicate the right answer to each of the following TEN parts. N. B. Each part carries 2 marks Total 20 Marks

Candidates should answer this question by ticking the appropriate boxes on the special green answer sheet, which is supplied with the examination paper. [1] Billy’s income for the 2017 tax year amounts to €21,480. He pays €3,000 per annum into a permanent

health insurance scheme. The amount allowable for tax purposes in respect of permanent health insurance for the 2017 tax year amounts to:-

(a) Nil (b) €1,074 (c) €2,148 (d) €3,000

[2] Paul is single and aged 76 years. In the 2017 tax year he earned €4,300 from a pension provided by his

former employer. He was also in receipt of the contributory old age pension for the year which amounted to €13,500 for the year. The total tax payable by Paul for the 2017 tax year amounts to:-

(a) nil (b) €260 (c) €1,910 (d) €2,832

[3] Louise is a self-employed hairdresser. For the 2017 tax year her tax liability amounts to €4,600. If Louise’s income tax return for 2017 was submitted on the 14th December, 2017 the surcharge payable for the late submission of the return is:- (a) nil (b) €156 (c) €230 (d) €460

[4] Investment income which has suffered income tax at source is assessable under:-

(a) Schedule D Case II (b) Schedule D Case III (c) Schedule D Case IV (d) Schedule D Case V

Sample Paper 2 Updated 2018 examinations Page 12 of 22

[5] Seamus is a director of ABC Ltd. and owns 80% of the company’s issued share capital. In month 1 of the 2017 tax year he is due a salary of €1,950. If Seamus pays PRSI under class S the amount of employee PRSI payable in January 2017 amounts to:-

(a) nil (b) €58.50 (c) €78.00 (d) €97.50

[6] Igor moved to Ireland for the first time and commenced employment with RTB Ltd. in week 13 of the 2017 tax year. He has not yet approached the Revenue concerning his tax affairs. If Igor earned €400 in week 13 the PAYE deductible for that week would amount to:-

(a) €48 (b) €80 (c) €136 (d) €164

[7] Patricia is single and employed by RRB Ltd. The amount of her weekly tax credit and weekly cut off point are most likely to be:-

Tax Credit Cut Off Point

(a) €31.73 .............................. €650.00 (b) €31.73 .............................. €1,261.54 (c) €63.46 .............................. €650.00 (d) €63.46 .............................. €1,261.54

[8] A trader selling goods only is obliged to register for VAT if his annual turnover for the year exceeds or is likely to exceed:-

(a) €35,000 (b) €37,500 (c) €70,000 (d) €75,000

[9] ATN Ltd. operates an electrical shop in Dundalk. A customer from Northern Ireland has ordered a television which they intend using in their private residence in Belfast. ATN Ltd. has engaged a courier to deliver the television to Belfast. The VAT rate applicable to the sale of the television is:-

(a) 13.5% (b) 23% (c) Zero%, as the goods are being exported (d) Nil, as the transaction is an exempt transaction

Sample Paper 2 Updated 2018 examinations Page 13 of 22

[10] For VAT purposes which of the following is an exempt supply:-

(a) Supply of medical services by a medical doctor (b) Supply of medical equipment (c) Supply of materials to be used to construct an extension to a medical waiting room (d) Supply of accountancy services to a medical doctor

Sample Paper 2 Updated 2018 examinations Page 14 of 22

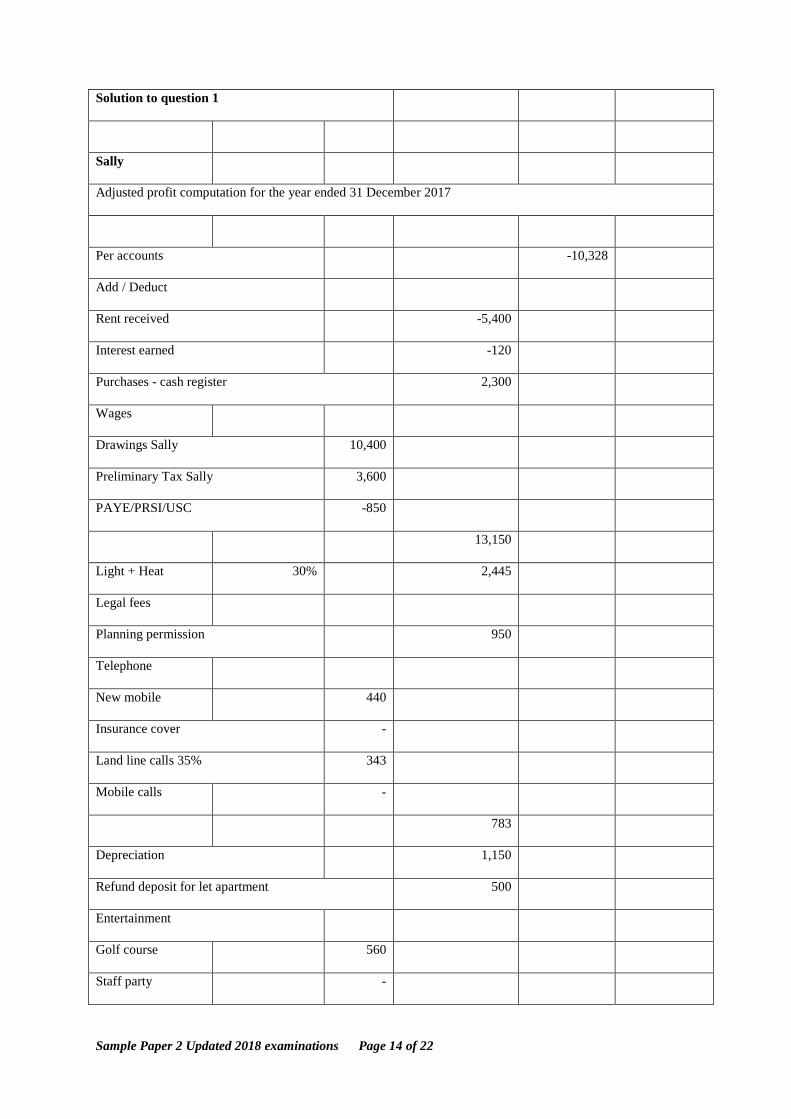

Solution to question 1

Sally

Adjusted profit computation for the year ended 31 December 2017

Per accounts -10,328

Add / Deduct

Rent received -5,400

Interest earned -120

Purchases - cash register 2,300

Wages

Drawings Sally 10,400

Preliminary Tax Sally 3,600

PAYE/PRSI/USC -850

13,150

Light + Heat 30% 2,445

Legal fees

Planning permission 950

Telephone

New mobile 440

Insurance cover -

Land line calls 35% 343

Mobile calls -

783

Depreciation 1,150

Refund deposit for let apartment 500

Entertainment

Golf course 560

Staff party -

Sample Paper 2 Updated 2018 examinations Page 15 of 22

Customer draw -

560

Motor expenses

Lease van 10% 490

Van running costs 395

Car running costs 30% 1,335

2,220

Insurance

Car 30% 255

Van 10% 55

Apartment 250

560

Loan repayments

Term loan (2,500-768) 1,732

Credit union loan 1,200

2,932

22,030

Adjusted Profit 11,702

Sample Paper 2 Updated 2018 examinations Page 16 of 22

Solution to Question 2

Income Tax Computation for 2017

Ciaran and Maeve

Ciaran Maeve

Case 1 41,700 x 10/12 34,750

Sch E 4,960 Sch E 21,000

Pension 500

4,460

Case V Exempt 0

Case III 352

39,562 21,000

Tax Tax

33,800 20% 6,760 21,000 20% 4,200

5,762 40% 2,304.80

39,562 9,064.80

Tax Credits Tax credits

Single 1,650 1,650

PAYE + earned 1,650 1,650

3,300 3,300

5,764.80 900

Paid PAYE 612 560

5,152.80 340

Sample Paper 2 Updated 2018 examinations Page 17 of 22

Notes Mortgage interest relief is allowed at source and not included in the Income Tax computation. No relief is due on the interest paid on the car loan. b) Exempt supplies

The main difference between exempt supplies and zero rated supplies is exempt supplies are not allowed register for VAT and cannot either charge VAT or claim back VAT on any of their purchases.

Certain goods and services are exempt from VAT. These include most financial services, insurance services, postal services, national broadcasting, education, medical, dental, optical, hospital services.

A person supplying only exempt goods or services is not entitled to register for VAT and is therefore not entitled to any input credit for VAT suffered on business purposes.

Zero rated

If you supply zero rated goods or services you are entitled to register for VAT and charge 0% VAT and you can claim back VAT on your purchases as you are VAT registered.

This rate applies to certain goods and services e.g. oral medicines, certain books, certain foodstuff, children’s clothing and footwear and certain medical equipment.

It applies to goods exported to business customers in the EU and customers in non-EU countries.

One important distinction between zero rated and exempt is where a person supplies zero rated goods or services it may be obliged to register for VAT. This in turn allows it to claim an input credit for all VAT paid on goods and services purchased by the business. Where a business or company supplies an exempt service it is not an accountable person and is not entitled to register for VAT. Therefore it cannot claim credit for VAT paid on goods and services received in the course of business.

Single assessment

Ciaran 5,764.80

Maeve 900

6,646.80

Sample Paper 2 Updated 2018 examinations Page 18 of 22

Solution to Question 3

(a) Relief for Medical Expenses Available in respect of unreimbursed medical expenses. Qualifying expenditure includes visits to and treatment in a hospital or approved nursing home, physiotherapy, orthopedic or similar treatment provided by a doctor, transport by ambulance, medicines and drugs supplied on prescription by a medical practitioner. Routine ophthalmic or dental care is not eligible for relief. Relief is in respect of expenditure incurred by the taxpayer, for himself or on behalf of anyone else. Relief is granted by way of a tax credit at 20% with the exception of nursing home charges which are allowed at the taxpayer’s marginal rate of tax. Forms used in claiming relief are forms Med 1 and Med 2.

(b) Employee tax credit

An annual tax credit for 2017 of up to €1,650 is granted to an individual and/or spouse, who are in receipt of emoluments to which PAYE is applied. This is dependent on the individual having Schedule E emoluments of at least €8,250 (8,250 @ 20% = 1,650). If the taxpayer’s emoluments are less than €8,250, the tax credit is restricted to the amount of the emoluments multiplied by the standard rate of tax. Anti-avoidance provisions exclude from the relief emoluments paid by a company to a proprietary director or to the spouse of such a director. Also excluded are emoluments paid by a self-employed individual or by a partnership in which the individual is a partner to the spouse of the individual. A proprietary director is a director of a company who is the beneficial owner of or able to control directly or indirectly more than 15% of the ordinary share capital of the company.

(c) Dependent relative tax credit

The tax credit is €70 for 2017. Conditions which must be satisfied to claim the tax credit for a particular tax year are as follows: -

• The claimant must prove that he maintains at his own expense the dependent relative • The dependent relative must be a relative for his or his wife • The dependent relative must be incapacitated by old age or infirmity from maintaining himself • If the dependent relative is the claimant’s or his wife’s widowed father or mother, relief is granted

whether the widowed parent is incapacitated or not • The tax credit available is granted provided the relative’s income does not exceed an income limit. The

income limit for 2017 is €14,504. • The tax credit may not be claimed in addition to an incapacitated child tax credit by reference to an

incapacitated child being the dependent relative. (d) Blind persons tax credit

The non-refundable tax credit for 2017 is €1,650. If a husband and wife are both blind the tax credit is €3,300. Medical evidence regarding the degree of blindness may be required for submission to the Revenue.

Sample Paper 2 Updated 2018 examinations Page 19 of 22

Solution to question 4

Sheila Perkins

PRSI Class A1

Employee October Employee November

3,750.00 4% 150.00 4,200.00 4% 168.00

PAYE € PAYE €

Pay 3,450 Pay 3,900

2,725 20% 545.00 2,725 20% 545.00

725 40% 290.00 1,175 40% 470.00

3,450 835.00 3,900 1,015.00

Tax Credit 268.50 Tax Credit 268.50

566.50 746.50

USC USC

1,001.00 0.5% 5.00 1,001.00 0.5% 5.00

563.33 2.5% 14.08 563.33 2.5% 14.08

2,185.67 5% 109.28 2,635.67 5% 131.78

3,750.00 128.36 4,200.00 150.86

Take Home Pay October November

Pay 3,750.00 3,750.00

Bonus - 450.00

3,750.00 4,200.00

Pension 300.00 300.00

3,450.00 3,900.00

Tax 566.50 746.50

Sample Paper 2 Updated 2018 examinations Page 20 of 22

PRSI 150.00 168.00

USC 128.36 150.86

844.86 1,065.36

Take home 2,605.14 2,834.64

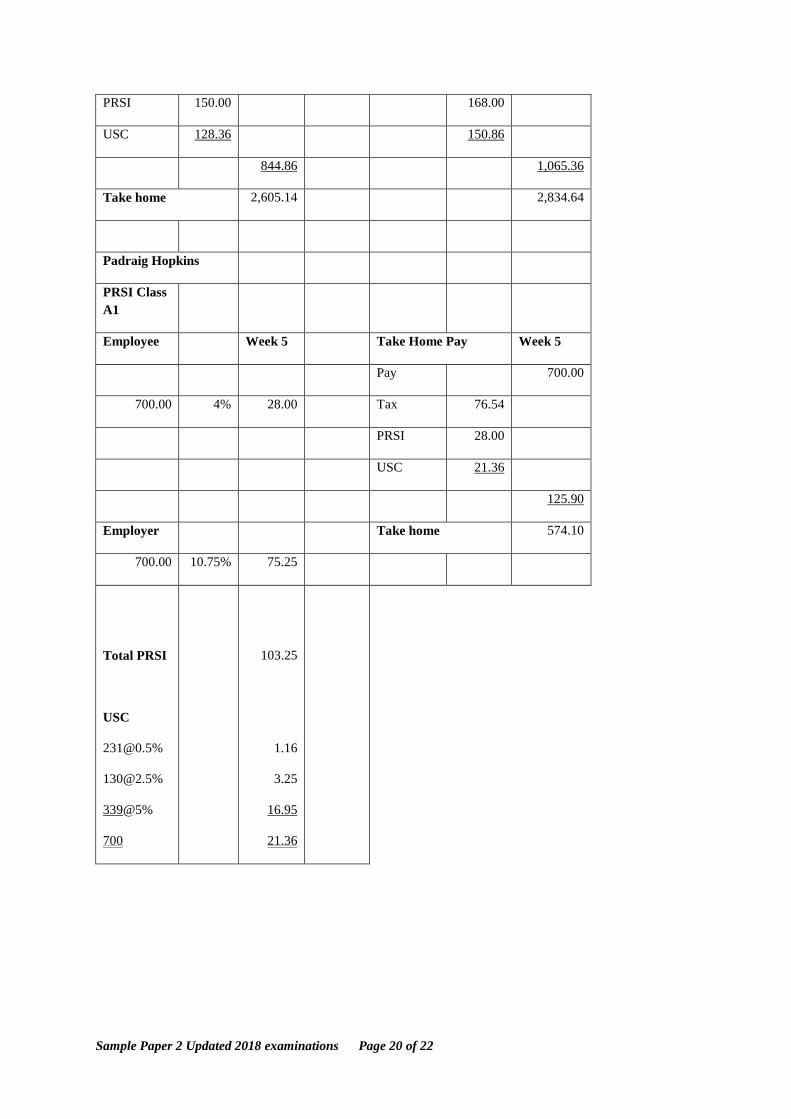

Padraig Hopkins

PRSI Class A1

Employee Week 5 Take Home Pay Week 5

Pay 700.00

700.00 4% 28.00 Tax 76.54

PRSI 28.00

USC 21.36

125.90

Employer Take home 574.10

700.00 10.75% 75.25

Total PRSI

USC

339@5%

700

103.25

1.16

3.25

16.95

21.36

Sample Paper 2 Updated 2018 examinations Page 21 of 22

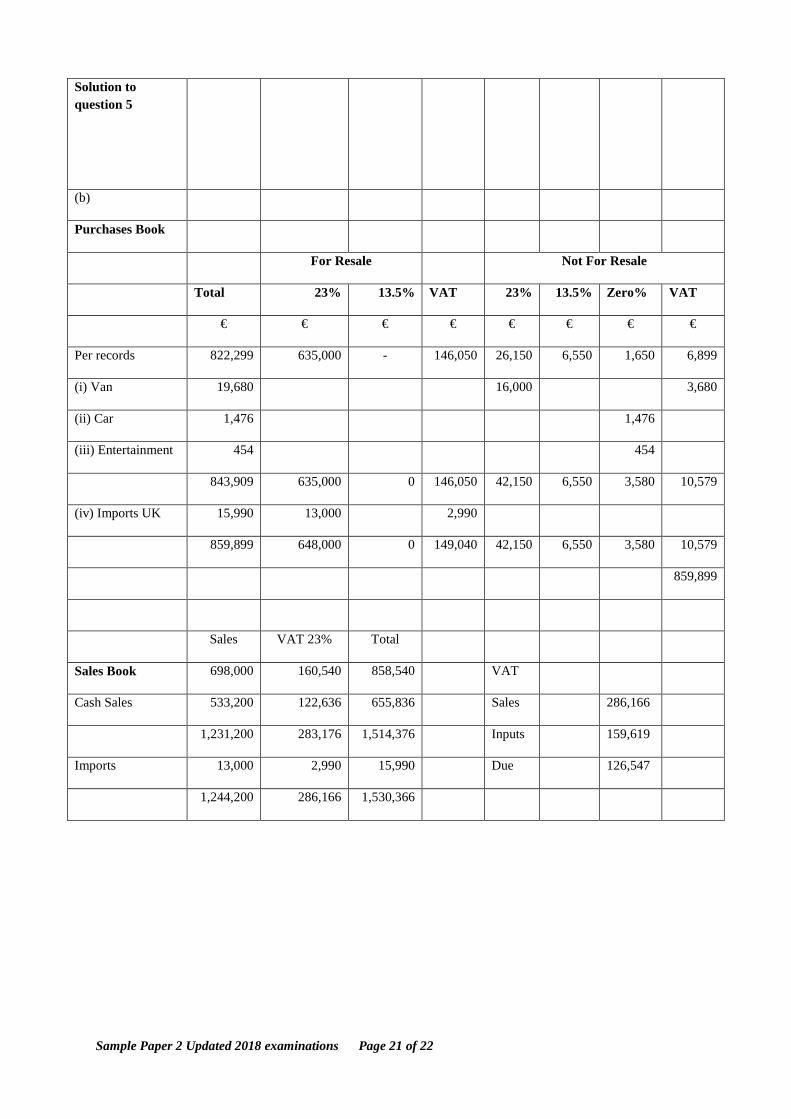

Solution to question 5

(b)

Purchases Book

For Resale Not For Resale

Total 23% 13.5% VAT 23% 13.5% Zero% VAT

€ € € € € € € €

Per records 822,299 635,000 - 146,050 26,150 6,550 1,650 6,899

(i) Van 19,680 16,000 3,680

(ii) Car 1,476 1,476

(iii) Entertainment 454 454

843,909 635,000 0 146,050 42,150 6,550 3,580 10,579

(iv) Imports UK 15,990 13,000 2,990

859,899 648,000 0 149,040 42,150 6,550 3,580 10,579

859,899

Sales VAT 23% Total

Sales Book 698,000 160,540 858,540 VAT

Cash Sales 533,200 122,636 655,836 Sales 286,166

1,231,200 283,176 1,514,376 Inputs 159,619

Imports 13,000 2,990 15,990 Due 126,547

1,244,200 286,166 1,530,366

Sample Paper 2 Updated 2018 examinations Page 22 of 22

Solution to question 6

[1] (c)

[2] (a)

[3] (c)

[4] (c)

[5] (C)

[6] (d)

[7] (c)

[8] (d)

[9] (b)

[10] (a)