taxation republic of ireland - accounting technicians … republic of ireland 1st year examination...

TRANSCRIPT

Taxation Republic of Ireland 1st Year Examination

May 2016 Solutions, Examiners Comments & Marking Scheme

Taxation ROI May 2016 1st Year Paper

Page 2 of 20

NOTES TO USERS ABOUT THESE SOLUTIONS

The solutions in this document are published by Accounting Technicians Ireland. They are intended to provide guidance to students and their teachers regarding possible answers to questions in our examinations. Although they are published by us, we do not necessarily endorse these solutions or agree with the views expressed by their authors. There are often many possible approaches to the solution of questions in professional examinations. It should not be assumed that the approach adopted in these solutions is the ideal or the one preferred by us. Alternative answers will be marked on their own merits. This publication is intended to serve as an educational aid. For this reason, the published solutions will often be significantly longer than would be expected of a candidate in an examination. This will be particularly the case where discursive answers are involved. This publication is copyright 2016 and may not be reproduced without permission of Accounting Technicians Ireland. © Accounting Technicians Ireland, 2016.

Page 3 of 20 Taxation (ROI)(TXR) S2016

Accounting Technicians Ireland

1st Year: Summer 2016

Paper: TAXATION (Republic of Ireland)

Monday 16 May 2016

9.30 a.m. to 12.30 p.m.

INSTRUCTIONS TO CANDIDATES

PLEASE READ CAREFULLY

For candidates answering in accordance with the law and practice of the Republic of Ireland. Candidates should answer the paper in accordance with the appropriate provisions up to and including the Finance Act 2014. The provisions of the Finance Act 2015 should be ignored. Allowances and rates of taxation, to be used by candidates, are set out in a separate booklet supplied with the examination paper. Answer ALL THREE questions from SECTION A. Answer ANY TWO of the three questions from Section B. If more than TWO questions are answered in Section B, then only the first two questions, in the order filed, will be corrected. Candidates should allocate their time carefully. All workings should be shown. All figures should be labelled as appropriate e.g. €s, units etc. Answers should be illustrated with examples, where appropriate. Question 1 begins on Page 2 overleaf. The following inserts are enclosed with the paper: Tax Reference Material

Page 4 of 20 Taxation (ROI)(TXR) S2016

SECTION A

Answer ALL THREE questions in this Section. QUESTION 1 The following multiple choice question consists of TEN parts, each of which is followed by FOUR possible answers. There is ONLY ONE right answer in each part.

Requirement Indicate the right answer to each of the following TEN parts. N.B. Each part carries 2 marks Total 20 Marks Candidates should answer this question by ticking the appropriate boxes on the special answer sheet which is contained within the answer booklet. [1] A married individual aged 60 pays rent of €5,000 per annum. The rent relief tax credit available for the

2015 tax year amounts to:

(a) €5,000 (b) €2,400 (c) €1,000 (d) €480

[2] Which of the following does not satisfy the requirement for the payment of preliminary tax for the 2015

tax year:

(a) 90% of the expected liability for 2015. (b) 100% of the expected liability for 2014. (c) 100% of the expected liability for 2013. (d) 105% of the liability for 2013.

[3] Sam is given a loan of €120,000 by his employer on 1 January 2015. The rate of interest on the loan is 3%. He uses the loan towards the purchase of his first house. How much is the annual benefit in kind included in Sam’s Income Tax computation for 2015:

(a) €4,800 (b) €3,200 (c) €1,200 (d) €8,400

[4] John leased a new Volvo (category B CO2 emissions) for use in his business in January 2015. The list price of the car was €48,000 and he paid lease charges of €12,000 in 2015. The amount of the lease charges to be added back in the 2015 adjusted profit computation is:

(a) €6,000 (b) €9,000 (c) €12,000 (d) €15,000

Page 5 of 20 Taxation (ROI)(TXR) S2016

Question 1 cont. [5] Burt stays at home to look after his two boys Sam aged 4 and Mike aged 9. Burt’s only source of income

is rental income of €6,000. Burt’s wife Mary works for ABC Ltd and has a gross annual salary of €62,000 The home carer’s tax credit Burt is entitled to is as follows:

(a) €350 (b) €420 (c) €700 (d) €810

[6] Which of the following persons does not have to register for VAT in Ireland:

(a) Persons whose supplies of taxable services exceed €40,000 in any 12 month period. (b) Persons whose supply of taxable goods is likely to exceed €76,000 in any 12 month period. (c) Person whose sale of a principal private residence is likely to exceed €525,000. (d) Persons whose supplies of goods and services exceed €38,000 in any 12 month period.

[7] Judy is employed by ABC Ltd. and is paid €3,600 per month. Judy’s SRCOP and tax credits are

€2,816.67 and €275 respectively per month. The income tax liability to be deducted from Judy’s salary in January 2015 is:

(a) €720.00 (b) €609.50 (c) €601.66 (d) €445.00

[8] Which of the following transactions is deemed to be a supply for VAT purposes:

(a) Sale of electrical goods in the course of business. (b) Goods provided as security for a loan or debt. (c) The transfer of a business from one VAT registered person to another. (d) Goods supplied free of charge as replacement for original goods under a warranty or guarantee.

[9] Which form must an employer provide to an employee at the end of a tax year:

(a) P45 (b) P60 (c) P30 (d) P35

[10] Pete received a dividend from a UK company in 2015. The dividend voucher showed a Gross dividend of

€1,000, a UK tax credit of €200 and a Net dividend of €800. The amount Peter should include in his Income Tax return in respect of this dividend is:

(a) €1,000 (b) €200 (c) €800 (d) €1,200

Total 20 marks

Page 6 of 20 Taxation (ROI)(TXR) S2016

QUESTION 2 You are Mary Smith and you have recently started with Brown & Co, a firm of accountants and tax advisers. You have been asked to assist in the preparation of a study manual for junior staff who are studying for their Accounting Technician examinations. You are required to write brief notes on each of the following areas to be included in the manual:

(a) Explain the three rules to be applied to the second year of assessment on the commencement of a business.

5 marks

(b) Outline five advantages of electronic filing for practitioners and other customers using the Revenue Online System (ROS).

5 marks

(c) Explain the export of goods to another EU country and the import of goods from an EU country in relation to VAT and outline in detail the Irish VAT position for each.

5 marks

(d) Outline and explain the four conditions to be satisfied for the BIK charge on a car to be reduced by 20%.

5 marks Total 20 Marks

QUESTION 3 Paul and Aileen have been married for the last ten years and are jointly assessed. It is that time of year again when they want to work out their tax liability for 2015. Their income and expenses for 2015 are detailed below. Paul is self-employed for the last 5 years. He prepares accounts to 30 April each year and his tax adjusted profits for the last two years have been as follows: Year ended 30 April 2015 €36,000 Year ended 30 April 2016 €42,000 He has a personal pension scheme and contributed €11,000 to his pension scheme in 2015. Paul is 45 years old. Paul entered into a qualifying deed of covenant in 2014 to pay Mark €5,000 per annum in March each year. Mark is an incapacitated child aged 10 years who is not related to Paul and is his neighbour’s son. Aileen is employed by Happy Days Limited and had a gross salary of €55,000 in 2015 with PAYE deducted of €8,800. Aileen received deposit interest, net of DIRT at 41%, amounting to €1,239 in 2015. She also received a dividend net of dividend withholding tax from BCF Plc amounting to €100. Aileen maintained her widowed mother Mary in 2015. Mary’s only source of income is her pension which amounted to €10,500 in 2015. Aileen carried out renovation to their house in 2014 which qualified for relief under the home renovation incentive scheme. She spent €15,000 (VAT exclusive amount) on external insulation and installing triple glaze windows. Aileen and Paul rented out a room in their house and received €11,000 in gross rent in 2015. They had expenses in relation to the letting of €1,500 (repairs to the room). Requirement Calculate Paul and Aileen’s income tax liability for the 2015 tax year on the basis that joint assessment applies. 20 Marks For the purposes of answering this question you can ignore PRSI and USC. Total 20 Marks

Taxation ROI May 2016 1st Year Paper

Page 7 of 20 Taxation (ROI)(TXR) S2016

SECTION B

Answer TWO of the three questions in Section B. QUESTION 4 You are employed as a trainee accounting in the firm Monahan & White Accountants and have recently started to assist with payroll calculations for clients. Details regarding two employees of AB Solutions Ltd. are as follows: Kevin Byrne Kevin has been employed by AB Solutions Ltd for the last ten years and he is paid on a monthly basis. For the month of July 2015 he earned €4,250 gross. In addition to his salary Kevin has been provided with a number of benefits as follows: A bicycle for cycling to and from work each day. This costs AB Solutions Ltd €800 when they purchased it for Kevin in April 2015. Subsidised canteen meals which are provide to all employees. Kevin estimates this saves him €120 per month on food. Kevin is employed in the engineering department and AB Solutions Ltd paid his annual subscription to Engineers Ireland Ltd amounting to €1,200. Gym membership of €65 per month. The month 1 basis applies. Kevin has a monthly SRCOP of €3,150 and a monthly tax credit of €275. His USC monthly cut off point is €1,001. Sally Jones Sally is a third year student in University in Dublin studying hospitality. As part of her degree she has to undertake a six weeks work placement. Sally started with AB Solutions on 9th March 2015 and finished on the 17th April 2015. Each week Sally was paid €350. Sally gave AB Solutions her PPS number and understood as she had no other income for the year she would not pay tax. Required:

(a) Calculate the take home pay for Kevin Byrne for the month of July 2015. You are required to briefly explain your treatment of the benefits provided by AB Solutions Ltd. 8 marks

(b) Calculate the total take home pay for Sally Jones for the six weeks of her work placement.

6 marks

(c) Outline three employer’s obligations under the PAYE system. 3 marks

(d) Outline two examples where an individual would be exempt from USC. 3 marks

Total 20 Marks

Taxation ROI May 2016 1st Year Paper

Page 8 of 20 Taxation (ROI)(TXR) S2016

QUESTION 5

Bob runs his own furniture design business. The total invoices issued to his customers during 2015 amounted to €180,000 excluding VAT at 23%. To date Bob has received in €147,600 including VAT from customers on foot of these invoices. He incurred the following costs in relation to his business in 2015:

Purchases/ Expenses €

Purchase of goods for resale 35,670

Purchase of van 7,800

Hotel and meals costs to attend a trade fair 2,500

Telephone 1,450

Electricity 630

Diesel for van 2,400

Repair and servicing the van 1,400

All of the purchases costs are inclusive of VAT at 23% with the exception of electricity and repairs (13.5%) and

hotel costs (9%).

Bob also pays a cleaner €2,000 per month.

Requirement

(a) Calculate Bob’s VAT liability for 2015 assuming Bob operates on the cash receipts basis. 10 Marks

(b) Bob plans on taking one of his custom designed tables and chairs he made in the business for his own

use. Outline the VAT treatment if any for Bob as a result of this gift. 5 Marks

(c) Explain the difference between exempt and zero rated supplies, giving examples of each and outlining

the VAT implications of each. 5 Marks

Total 20 Marks

Taxation ROI May 2016 1st Year Paper

Page 9 of 20 Taxation (ROI)(TXR) S2016

QUESTION 6 Sally Jones runs a hair salon in Tallaght in Dublin. She has been in business for the last fifteen years and has the following results for the year ended 31 December 2015: Accounts for the year ended 31st December 2015 Notes € €

Sales ................................................................................ 102,256

Add Dividends received (net) ................................................. 1,279 Rental income ................................................................ 8,750

Gross Profit ..................................................................... 112,285

Less Employee costs ............................................................... (1) 22,789 Administrative costs ....................................................... (2) 4,500 Miscellaneous ................................................................. (3) 2,750 Subscriptions and Donations .......................................... (4) 2,650 Insurance ......................................................................... (5) 2,890 Advertising and promotion ............................................. (6) 2,260 Professional Fees ............................................................ (7) 1,100 Profit on disposal of non-current assets .......................... (8) (450) Depreciation.................................................................... 1,200 Light and Heat ................................................................ (9) 4,500 Loan repayments ............................................................. (10) 3,400

47,589 Net profit/(loss) 63,696

NOTES € (1) Employee costs Staff salaries ..................................................................................................... 4,525 Drawings ........................................................................................................... 10,780 Income Tax payment for Sally .......................................................................... 5,200 Pension contribution for Sally .......................................................................... 2,284

22,789

When Sally submitted the December P30 she paid the PAYE/PRSI of €1,540 out of her personal bank account. This is not included in the figures above.

(2) Administrative costs € Telephone bills ................................................................................................ 2,200 New photocopier for the office ......................................................................... 1,200 Magazines for the salon .................................................................................... 500 Stationery ......................................................................................................... 600 4,500

Sally has agreed that 25% of the calls on the telephone bill relate to the phone in the rented house. (3) Miscellaneous €

Taxation ROI May 2016 1st Year Paper

Page 10 of 20 Taxation (ROI)(TXR) S2016

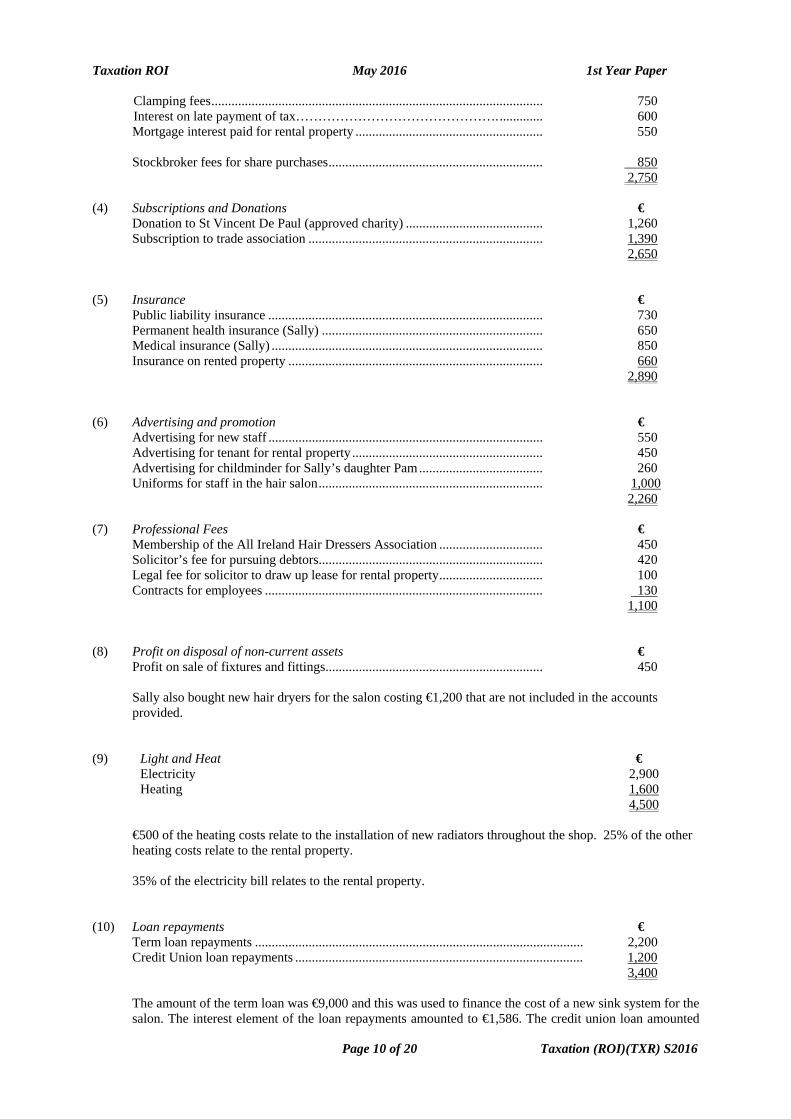

Clamping fees ................................................................................................... 750 Interest on late payment of tax………………………………………. ............. 600 Mortgage interest paid for rental property ........................................................ 550 Stockbroker fees for share purchases ................................................................ 850 2,750 (4) Subscriptions and Donations € Donation to St Vincent De Paul (approved charity) ......................................... 1,260 Subscription to trade association ...................................................................... 1,390 2,650 (5) Insurance €

Public liability insurance .................................................................................. 730 Permanent health insurance (Sally) .................................................................. 650 Medical insurance (Sally) ................................................................................. 850 Insurance on rented property ............................................................................ 660 2,890

(6) Advertising and promotion € Advertising for new staff .................................................................................. 550 Advertising for tenant for rental property ......................................................... 450 Advertising for childminder for Sally’s daughter Pam ..................................... 260 Uniforms for staff in the hair salon ................................................................... 1,000

2,260 (7) Professional Fees €

Membership of the All Ireland Hair Dressers Association ............................... 450 Solicitor’s fee for pursuing debtors ................................................................... 420 Legal fee for solicitor to draw up lease for rental property ............................... 100 Contracts for employees ................................................................................... 130

1,100

(8) Profit on disposal of non-current assets € Profit on sale of fixtures and fittings................................................................. 450

Sally also bought new hair dryers for the salon costing €1,200 that are not included in the accounts provided.

(9) Light and Heat € Electricity 2,900 Heating 1,600 4,500

€500 of the heating costs relate to the installation of new radiators throughout the shop. 25% of the other heating costs relate to the rental property. 35% of the electricity bill relates to the rental property.

(10) Loan repayments € Term loan repayments .................................................................................................. 2,200 Credit Union loan repayments ...................................................................................... 1,200 3,400

The amount of the term loan was €9,000 and this was used to finance the cost of a new sink system for the salon. The interest element of the loan repayments amounted to €1,586. The credit union loan amounted

Taxation ROI May 2016 1st Year Paper

Page 11 of 20 Taxation (ROI)(TXR) S2016

to €4,000 and was used to refurbish the rental property which is let. The interest element included amounts to €278.

Requirement Compute Sally Jones’ Schedule D, Case I tax adjusted profits for the year ended 31st December 2015. Total 20 Marks

Taxation ROI May 2016 1st Year Paper

Page 12 of 20 Taxation (ROI)(TXR) S2016

1st Year Examination: May 2016

Taxation ROI

Suggested Solutions

and Examiner’s Comments

Students please note: These are suggested solutions only; alternative answers may also be deemed to be correct and will be marked on their own merits.

Statistical Analysis – By Question

Question No. 1 2 3 4 5 6

Average Mark (%) 57% 45% 57% 57% 66% 79%

Nos. Attempting 876 865 869 410 560 765

Statistical Analysis - Overall

Pass Rate 76% Average Mark 59% Range of Marks Nos. of Students 0-39 120 40-49 91 50-59 194 60-69 213 70 and over 259 Total No. Sitting Exam 887 Total Absent 228 Total Approved Absent 44 Total No. Applied for Exam 1159

General Comments:

GENERAL COMMENTS ON THE PAPER AS A WHOLE Overall the standard was very good this year with traditional questions like net adjusted profit very well answered. As per previous years the theory questions would benefit from more depth in their answers.

Taxation ROI May 2016 1st Year Paper

Page 13 of 20 Taxation (ROI)(TXR) S2016

Examiner Comments on Question One

Solution 1 Total

Marks Allocated

1 – D 2 2 – C 2 3 – C 2 4 – A 2 5 – A 2 6 – C 2 7 – C 2 8 – A 2 9 – B 2 10–C 2 Total 20 Marks

Question one was well answered overall. In the main, students appeared to either know the answer or not and some candidates scored very highly, others poor scores. Overall the majority of candidates passed this question.

Taxation ROI May 2016 1st Year Paper

Page 14 of 20 Taxation (ROI)(TXR) S2016

Examiner Comments on Question Two

Solution 2 a) Total Marks

Allocated

Commencement

Second Year of Assessment 1. 12 month accounting period ending in second tax year of trading

If there is only one set of accounts finishing in the year, and they are for a full 12 months, then this set of accounts will form the basis period for the second year of assessment. This is the general rule for an ongoing business

2. More than one set of accounts / accounting period less than 12 months

If there is more than one set of accounts, or if there is one set for less than 12 months, then the profits for the 12 months ending on the later of those dates will be assessed.

3. No accounting period ending in the second year of assessment

The final rule for the second year of use is actual.

1.5

1.5

2

b) The main advantages of ROS:

Avoid duplication of effort and reduce compliance costs Reduce paper handling More effective use of time More accurate processing of returns

24 hour, 365 day access to Revenue

Calculation facilities to assist customers Instant knowledge of returns Speedier repayments Faster processing of returns and payments

Any 5, 1 mark each.

c) Cross Border Trade

1) Exports of goods to other EU countries (intra community dispatches) The Irish VAT rate depends on whether or not the customer is registered for VAT in the other EU country. The zero rate can apply to goods supplied to VAT registered persons provided that the Irish supplier obtains and quotes the VAT registration number of the foreign company on the invoice issued. The VAT rate applicable to sales to unregistered persons in other EU countries will be generally the relevant Irish VAT applicable to the item.

This question was the most poorly answered question in the paper with the majority of candidates scoring less than 50% on it. The problem seems to be as in previous years- students failed to write enough on narrative questions. Surprisingly, a lot of students answered the commencement rules poorly. Students were in the main good on ROS and VAT and poor on the rules for BIK reduction for a company car. More study is needed on theory.

Taxation ROI May 2016 1st Year Paper

Page 15 of 20 Taxation (ROI)(TXR) S2016

2) Imports into Ireland from an EU country (intra community acquisitions) Once supplier quotes Irish VAT number of Irish business customer on invoice issued then:

- Supply is charged at the zero rate by the EU supplier - The Irish company will self account for Irish VAT on the acquisition

The net effect of the transaction is nil.

2.5 Marks each d)

BIK reduction company car In order to qualify for the relief the following must apply: - the employee must spend 70% of their time working away from base (this only

applies where business mileage is below the minimum threshold i.e. 24,135 km) - the annual business travel exceeds 8,047 km - The employee must work at least 20 hours per week - The employee must maintain a logbook of daily business travel.

1 1

1.5 1.5

Total 20 Marks

Taxation ROI May 2016 1st Year Paper

Page 16 of 20 Taxation (ROI)(TXR) S2016

Examiner Comments on Question Three

Solution 3 Income Tax Computation

Total Marks

Allocated Paul Schedule D Case I 36,000 1 Less: Pension (36,000-5,000)31,000 x 25% = 7,750

-7,750 1

Less: Covenant -5,000 23,250 1

Aileen Sch D Case IV 2,100 1

Sch D Case V Rent a room relief 0 2

Sch E 55,000 1

Sch F 125 1

€66,050 (42,800+23,250) x 20% 13,210 1

€2,100 x 41% 861 1

€12,325 x 40% 4,930 19,001 1

Less Non-refundable Tax Credits: Personal tax credit 3,300 1

PAYE 1,650 1

Dependent relative 70 1

DIRT €2,100 x 41% 861 1

Renovation (€15,000 x 13.5%)/2 1,013 6,894 2

12,107 Less: Refundable Tax Credits: PAYE deducted 8,800 1

DWT 25 8,825 1

3,282 Add: Tax deducted on covenant 1,000 1

Tax Due 4,282

Total: 20 Marks

This question was in the main well answered. In some areas, students fell down on included pension deduction and the treatment of the covenant. Students often failed to realise that there was not enough income to be taxed at 20% for both spouses combined. The renovation scheme was often deducted in full and not split over two years.

Taxation ROI May 2016 1st Year Paper

Page 17 of 20 Taxation (ROI)(TXR) S2016

Examiner Comments on Question Four

Section B Solution 4 a)

Kevin Byrne Take Home Month 7

Bicycle – exempt once up to maximum of €1,000 and can only be claimed once every five years by employee. Bicycle must be bought by employer and used mainly to travel to and from work. Canteen meals – exempt once provided to all staff Professional membership – exempt once connected with job Gym membership - assessable

Total Marks

Allocated

1

1

0.5

Gross Pay

Gym Total

€4,250 €65 €4,315

0.5 0.5

€ €

Income tax 3,150 x 20% 1,165 x 40%

630 466

0.5 0.5

1,096

Less: Tax credit (275) 0.5

Income Tax (821.00) 0.5

USC

€1,001 x 1.5% = 15.02 0.5

€464 x 3.5% = 16.24 0.5

€2,850 x 7% = 199.50 0.5

Total USC (230.76) PRSI €4,315 x 4% = (172.60) 0.5

Total Tax 1,224.36

Take Home Pay Month 7 (€4,025-

€1,224,36) 3,025.64 0.5

This question was fairly well answered but some students failed to realise that bicycle, canteen meals and professional membership are exempt. For Sally, many students failed to recognise that there is no PRSI.

Taxation ROI May 2016 1st Year Paper

Page 18 of 20 Taxation (ROI)(TXR) S2016

b)

Sally Jones Weeks 1 to 4 Weeks 5 and 6 Total Pay 350.00 350.00 2,100.00 Tax @20% 70.00 70.00 Tax Credit 31.73 0 Tax due 38.27 70.00 293.08 PRSI Class A0 350 x 0% 0 0 0 USC – Emergency Basis €350 x 18% 28.00 28.00 168.00 Take Home Pay Pay 2,100.00 0.5 Mark Income Tax (293.08) 2 Marks PRSI 0 2 Marks USC (168.00 1 Mark Net Pay 1,806,92 0.5 Mark

c) Examples of points

1. Register as an employer with the Revenue Commissioners. 2. Deduct the correct tax from payments made (and benefit given) to employees. 3. Pay this tax over to the Revenue Commissioners.

Any relevant points 1 Mark each d) - an individual whose total income does not exceed €12,012 in a year - Income that is not subject to income tax such as benefits that are exempt from BIK and Department of Social Protection Payments. - income subject to DIRT

Any 2 relevant points, 1.2 Marks each.

Taxation ROI May 2016 1st Year Paper

Page 19 of 20 Taxation (ROI)(TXR) S2016

Examiner Comments on Question Five

Solution 5 a)

Total Marks

Allocated

Purchase of goods

€35,670/123 x 23 = €6,670 1

Purchase of van

€7,800/123 x 23 = €1,459 1

Hotel and meals

No input credit is allowed €0 1

Telephone bills

€1,450/123 x 23 = €271 1

Electricity

€630/113.5 x 13.5 = €75 1

Diesel

€2,400/123 x 23 = €449 1

Repairs

€1,400/113.5 x 13.5 = €167 1

Cleaner

No VAT €0 1

Total input credits €9,091

Output VAT €120,000/1.23 23% = €27,600

1

Input VAT €9,091

Net VAT Payable €18,509 1 b) This is a self-supply. 1 Mark Bob would have claimed an input credit on the materials used to make the table and chairs and he has now taken the product from the business for his own use. 2 Marks Bob must account for VAT on the cost of the materials as if he sold them. 2 Marks

Question 5 was well answered in the main. Some students failed to realise that VAT is not allowable on hotel meals and cleaners.

Taxation ROI May 2016 1st Year Paper

Page 20 of 20 Taxation (ROI)(TXR) S2016

c) Exempt supplies A person supplying exempt goods or services is not entitled to register for VAT and is therefore not entitled to any input credit for VAT suffered on business purposes. Examples financial services, insurance services. 2.5 Marks Zero rated supplies Where a business supplies zero rated goods or services it may be obliged to register for VAT. This in turn allows the business to reclaim VAT on business items purchased. 2.5 Marks

Total 20 Marks Examiner Comments on Question Six

Solution 6 Total Marks

Allocated Profit per accounts 64,696 0.5 Less:

Dividend received 1,279 0.5 Rent received 8,750 10,029 0.5 54,667 Add: Drawings 10,780 0.5 Tax payment 5,200 0.5 Pension 2,284 0.5 P30 (1,540) 1 Photocopier 1,200 1 Telephone 2,200 x 25% = 550 1 Clamping 750 0.5 Interest on late payment Charity Donation SVDP

600 1,260

0.5 0.5

Mortgage 550 1 Stockbroker 850 1 PHI Medical insurance

650 850

0.5 0.5

Rental insurance 660 1 Tenant advertising 450 1 Childminder advertising 260 1 Legal fees lease 100 0.5 Profit on disposal (450) 1 Radiators Depreciation

500 1,200

0.5 0.5

Heating 1,100 x 25% Term loan (2,200-1,586) Credit Union Loan

275 614 1,200

1 1 1

Electricity rental 1,015 1 29,808 Taxable Profits 84,475 or 83,475 Total 20 Marks

This was the best answered question with students scoring very highly here. Some students failed to realise that charitable donations are no longer an allowable deduction. Other students failed to correctly calculate the term ‘loan addback’ but in the main great answers.