students’ companion - citn | home · students’ companion ... d thank god is a student in idia...

TRANSCRIPT

Page 1 of 24

THE CHARTERED INSTITUTE OF TAXATION OF NIGERIA (Chartered Institute by Act No. 76 of 1992)

STUDENTS’ COMPANION

OCTOBER 2011 PROFESSIONAL EXAMINATION

PROFESSIONAL 1 OUESTION AND SUGGESTED SOLUTIONS

Page 2 of 24

THE CHARTERED INSTITUTE OF TAXATION OF NIGERIA OCTOBER 2011 PROFESSIONAL EXAMINATION

PROFESSIONAL EXAMINATION 1: REVENUE LAW

INSTRUCTION: ATTEMPT ALL QUESTIONS TIME: 3 HOURS

1 In the course of a forensic audit exercise at Ewejoko Ltd by Kelechi Sofala & Co, a firm of Chartered

Accountants and Tax Practitioners, receipts and legal documents on the lease of the premises presently

occupied by the company and land purchased along Lekki/Epe Road, Lagos were presented to the

Auditors.

You are in the team of Auditors sent to carry out the audit, especially the tax aspects.

a What element of tax will you look for on the receipts and documents? 10 marks

b In the event the appropriate tax had not been paid, what are the legal implications and steps to take

to rectify the omission? 10 marks

(Total: 20 marks)

2 a “I can’t define an elephant, but I know one when I see it.” How helpful is this

aphorism in the definition of tax? 10 marks

b Discuss the canons of interpretation of tax statutes by the courts in Nigeria.

10 marks

(Total: 20 marks)

3 Femabay Oil & Gas Overseas Ltd, a company incorporated in Germany, is engaged in oil exploration in

the riverine area of Ondo State. The company seeks your assistance in preparing its returns for 2011 to the

Federal Inland Revenue Service. What items of chargeable profits and adjustable profits recognised under

the Petroleum Profit Tax Act will you consider germane?

20 marks

4 a What do you understand by the term “Capital Gains Tax”? 5 marks

b What are the challenges of capital gains tax administration in Nigeria. 15 marks

(Total: 20 marks)

5 a There is a clear-cut division of legislative and judicial powers among the tiers of

government in Nigeria. Discuss with reference to tax matters. 15 marks

b What are the functions of a tax system? 5 marks

(Total: 20 marks)

Page 3 of 24

PROFESSIONAL EXAMINATION 1: PERSONAL TAXATION

ATTEMPT ALL QUESTIONS. SHOW ALL WORKINGS TIME: 3 HOURS

1 a In Nigeria, many unregistered businesses (artisans and sole traders) are thriving

But not within the tax net of the Government. This phenomenon should be

checked as a means of boosting revenue and ensuring justice and equity.

Advise the relevant tax authorities on ways of ensuring that all potential tax payers are duly

assessed. 12 marks

b When does an assessment become final and conclusive? 12 marks

c The term “Place of residence” is very significant in personal income tax system.

Define the term “Place of residence”. 4 marks

(Total: 20 mark)

2 Chukwu Garba is married with five children.

Details about his children are as follows:

a Musa is 8 years old.

b Fatimah(unmarried) is in Federal Government College and is 17 years old.

c Funmi is in primary school and is aged 9 years.

d Thank God is a student in Idia Secondary School, Benin City and her age at the last birthday was

14 years.

e Nkechi(unmarried) is an undergraduate in Ambrose Alli University and is aged 18 years.

Other information are as follows:

(i) He took a life insurance policy for which he pays annual premium of N370,000

(ii) He provides for his old age by contributing N25,000 per annum to pension scheme approved by

the Joint Tax Board.

(iii) His aged parents live with him. They have no income of their own. He is an employee on a salary

of N5,700,000.

(iv) Capital sum of his life policy is N4,200,000.

Required:

a Compute his tax for 2009 year of assessment. 10 marks

b In what circumstances can claim for children and dependent relative allowances be approved?

5 marks

c In relation to taxation of a sole trader, what is the difference between adjusted profit for tax

purposes and net profit? 5 marks

(Total: 20 marks)

3 Mr. Cameron Wood is in the employment of God is good Institute of Nigeria. He got to Lagos on January

1, 2010 to assume duties on the following terms:

a Mr. Cameron Wood being a British citizen is to receive £2,500 which is part of his salary in

London less United Kingdom tax.

b The Institute would pay Mr. Wood in Nigeria another N900,000 and this should be subject to

Nigerian income tax.

In view of the double taxation agreement between Nigeria and the United Kingdom, Mr Wood will

be entitled to the double taxation relief on any part of income assessed in Nigeria. The United

Kingdom tax paid on £2,500 is £250. The rate of exchange is N250 to £1.

Mr Wood is entitled to personal allowance, earned income allowance, three children’s allowances

and life assurance premium of N 60,000.

You are required to compute:

(i) Mr. Wood’s chargeable income. 10 marks

Page 4 of 24

(ii) The credit to be given (if any) to Mr. Wood on tax paid on his United Kingdom’s income.

7 marks

(iii) Comment on your computation above. 3 marks

(Total: 20 marks)

4 a Olu, Ade and Oye have been in partnership business for many years. The

Partnership profit and loss account for the year ended 31st December 2009 were given as follows:

N N

Gross profit 7,404,600

Salaries and wages 1,446,000

Partners’ salaries 744,000

Staff loans written off 54,000

Partners’ loans interest 186,000

Interest on capital 37,200

Repairs and maintenance 262,200

Office rent 144,000

Depreciation (fixed appropriation) 52,500

General office expenses 307,200

General provision for doubtful debts 75,000 (3,308,100)

Net profit 4,096,500

Additional information:

Olu Ade Oye Total

N N N N

Salary 312,000 276,000 156,000 744,000

Loan interest 54,000 53,400 78,600 186,000

Interest on capital 7,200 10,500 19,500 37,200

The partners share profit and losses in the ratio of 3:2:1 while capital allowance is

N86,100.

You are required to:

Compute the chargeable income of the partners from partnership business for the purpose of

income tax.

Show all workings.

15 marks

b List any five incomes which are exempted from tax under the tax laws in Nigeria.

5 marks

(Total: 20 marks)

5 On April 12, 2007, Mr. Toulassi Dankwa acquired a house erected on an acre of land at a cost of

N15,000,000. Other expenses of acquisition were N25,000 for legal expenses and valuation fee of

N50,000.

On November 30, 2007, a bungalow was erected on the excess space at a cost of

N 3,000,000. On June 1, 2009, the bungalow was sold to a cousin for N4,000,000. The actual market

value was N5,000,000 and the market value of the rest of the property was N17,000,000.

On January 1, 2010, Mr. Toulassi Dankwa sold the rest of the property for N18,000,000 after incurring the

following expenses.

a Improvement before sale 250,000

Page 5 of 24

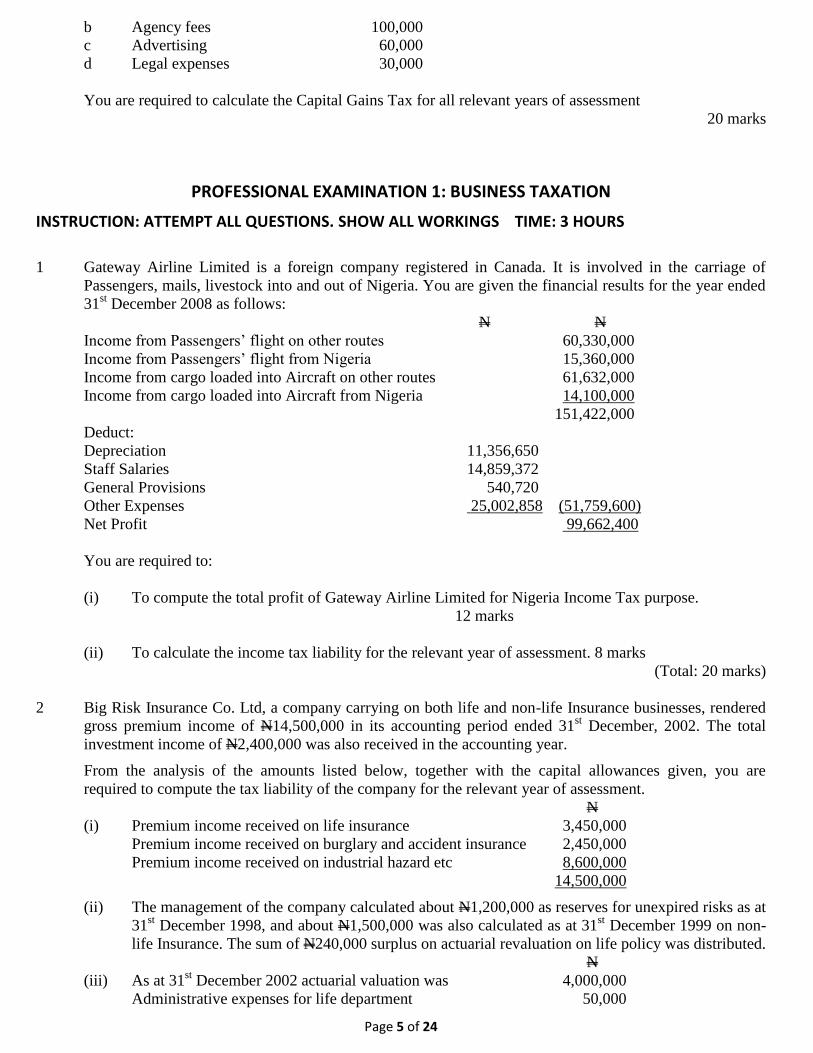

b Agency fees 100,000

c Advertising 60,000

d Legal expenses 30,000

You are required to calculate the Capital Gains Tax for all relevant years of assessment

20 marks

PROFESSIONAL EXAMINATION 1: BUSINESS TAXATION

INSTRUCTION: ATTEMPT ALL QUESTIONS. SHOW ALL WORKINGS TIME: 3 HOURS

1 Gateway Airline Limited is a foreign company registered in Canada. It is involved in the carriage of

Passengers, mails, livestock into and out of Nigeria. You are given the financial results for the year ended

31st December 2008 as follows:

N N

Income from Passengers’ flight on other routes 60,330,000

Income from Passengers’ flight from Nigeria 15,360,000

Income from cargo loaded into Aircraft on other routes 61,632,000

Income from cargo loaded into Aircraft from Nigeria 14,100,000

151,422,000

Deduct:

Depreciation 11,356,650

Staff Salaries 14,859,372

General Provisions 540,720

Other Expenses 25,002,858 (51,759,600)

Net Profit 99,662,400

You are required to:

(i) To compute the total profit of Gateway Airline Limited for Nigeria Income Tax purpose.

12 marks

(ii) To calculate the income tax liability for the relevant year of assessment. 8 marks

(Total: 20 marks)

2 Big Risk Insurance Co. Ltd, a company carrying on both life and non-life Insurance businesses, rendered

gross premium income of N14,500,000 in its accounting period ended 31st December, 2002. The total

investment income of N2,400,000 was also received in the accounting year.

From the analysis of the amounts listed below, together with the capital allowances given, you are

required to compute the tax liability of the company for the relevant year of assessment.

N

(i) Premium income received on life insurance 3,450,000

Premium income received on burglary and accident insurance 2,450,000

Premium income received on industrial hazard etc 8,600,000

14,500,000

(ii) The management of the company calculated about N1,200,000 as reserves for unexpired risks as at

31st December 1998, and about N1,500,000 was also calculated as at 31

st December 1999 on non-

life Insurance. The sum of N240,000 surplus on actuarial revaluation on life policy was distributed.

N

(iii) As at 31st December 2002 actuarial valuation was 4,000,000

Administrative expenses for life department 50,000

Page 6 of 24

Salaries for life department staff 200,000

Other allowable expenses for life department 10,000

(iv) Investment income:

Dividend received (net of 5% withholding tax) 1,275,000

Gross interest received on debenture stock 175,000

Interest on fixed deposit in banks 950,000

2,400,000

(v) Total expenses relating to non-life N

Claims 3,550,000

Commissions 1,420,000

Administrative expenses 4,150,000

Depreciation 880,000

10,000,000

(vi) Loss on sale of fixed assets included in administration expenses was N40,000.

(vii) Capital allowances N

Capital allowances b/f 145,000

Initial allowances for the year 450,000

Annual allowances for the year 1,205,000

Balancing allowance 21,000

Balancing charge 31,000

(20 marks)

3 (a) List the powers of Federal Inland Revenue Service Board under the Federal

Inland Revenue Service (Establishment) Act 2007. 5 marks

(b) Define the following terms:

(i) Tax 2 marks

(ii) Taxation 3 marks

(c) List exhaustively the composition of the Federal Inland Revenue Service Board.

10 marks

(Total: 20 marks)

4 Ade Nigeria Limited has been in manufacturing business since January 2004. At the commencement of

the business, the company acquired so many assets among which were two assets that were sold in 2008.

The details of the assets sold are as follows:

ASSET COST SALES CONSIDERATION

N N

Machinery 800,000 2,400,000

Land and Building 1,200,000 4,000,000

In 2009, machinery and land and building were bought for N4,800,000 and

N7,200,000 respectively to replace the ones sold

Required:

(a) Calculate the roll over relief available to Ade Nigeria Limited in respect

of these two classes of assets on the assumption that new assets were bought to replace the old

ones. 15 marks

(b) List five assets disposal, the gains on which capital gains tax would not be chargeable.

5 marks

(Total: 20 marks)

Page 7 of 24

5 (a) Write short notes on the following types and forms of assessment:

i Original assessment. 2 marks

ii Revised/amended assessment. 2 marks

iii Additional assessment. 2 marks

iv Best of judgement (BOJ). 2 marks

v Self assessment. 2 marks

(b) i Discuss the conditions that will make an assessment to be final

and conclusive . 6 marks

ii List two reasons why a back duty assessment could be instituted against a tax payer.

4 marks

(Total: 20 marks)

PROFESSIONAL EXAMINATION 1: INTERNATIONAL TAXATION

INSTRUCTION: ATTEMPT ALL QUESTIONS. SHOW ALL WORKINGS TIME: 3 HOURS

1 The main focus of bilateral tax treaties is the elimination of double taxation and fiscal evasion.

a (i) Define “double taxation” and “fiscal evasion” with respect to International

Taxation.

(ii) Mention two types of double taxation.

(iii) State three ways adopted by a typical tax treaty to eliminate double

taxation. 10 marks

b Mention four methods through which challenges posed by transfer pricing to the determination of

the correct tax liability of an enterprise could be resolved.

10 marks

2 Define the following terms under international tax:

a Contracting states 4 marks

b Competent authority 4 marks

c Treaty shopping 4 marks

d Diplomatic channel 4 marks

e Tax sparing 4 marks

(Total: 20 marks)

3 Mamadu Construction Company Limited engages in irrigation and building construction for many years.

Messrs Dowell and company was appointed as a Tax Consultant to enable the company to understand the

thrust of Value Added Tax particularly as it affects its operation. There has been a dispute as to the

amount of Value Added Tax the company is liable to pay to the Integrated tax office. To assist you in your

assignment as a tax consultant to the company, the following details are made available to your firm.

DATE DETAILS AMOUNT(N)

1/9/08 Bought a Concrete Mixer 333,333

3/9/08 Bought Scaffolding pipes 1,000,000

4/9/08 Bought a Poker Vibrator 233,333

5/9/08 Bought Chippings 45,000

6/9/08 Bought an ½ Trailer load of Granite 65,000

7/9/08 Bought an ½ Trailer load of Gravel 56,000

8/9/08 Bought a Sharp Photocopier 55,000

9/9/08 Bought an Executive Table 17,500

10/9/08 Bought Office Chairs 27,750

Page 8 of 24

14/9/08 Negotiated a contract for 4,500,000

(and received progress payment of N2,250,000 on 4/9/08)

15/9/08 Won a labour only contract for 1, 250,000

(based on Architect valuation, due for payment on 5/9/08

and eventually paid on 28/9/08 was N250,000).

VAT was paid on all the company’s purchases.

You are required to:

a Compute the VAT payable (if any) for the month of September 2008 and

b State when and in what manner VAT payment should be made

(Total: 20 marks)

4 a Why is the concept of “residence” so important in international tax? 5 marks

b Mention the criteria employed as tie breaker under Article 4(2) of a typical double taxation

agreement in the event of dual residence involving an individual.

15 marks

5 a Article (2) allows for the allocation of expenses. List any five (5) of the conditions that must be

satisfied for the allocation of the expenses. 5 marks

b Build co, resident in state B, visits state C a few times in May 2008(In total, for 2 weeks) to

acquire and conclude a contract with client Co; resident in state C, to construct a new office

building for client Co. Build Co. subsequently concludes a contract with specialized company Prep

Co; also resident in state B, to do the preparatory work and lay the foundation for the building at

the designated plot of land in state C. Prep Co. starts to work there on 1st October, 2008, finalises

its part of the project and leaves state C on 31st December, that same year.

Due to heavy rainfall, Build Co. cannot start constructing the building until 1st March, 2009.

In April, 2009, it contacts client Co. because, having completed the building, capacity problem

prevent it from removing its equipment and cleaning up the site. Fortunately, Build Co. has a

100% subsidiary. Anonymous Co; also resident in state B, which is prepared to carry out these

activities. Client Co agrees, so their contract is amended and a new contract is concluded between

Client Co. and Anonymous Co. Build Co. finalises the construction and leaves state C in mid-

September, 2009. Anonymous Co. starts removing the equipment and cleaning the site; finalizing

and leaving state C in mid October of that same year.

Required:

(i) Does Build Co, Prep Co or Anonymous Co have a PE in state C?

(ii) If so, when would they come into existence and when would they end?

15 marks

(Total: 20 marks)

Page 9 of 24

PE 1 REVENUE LAW

SOLUTION TO QUESTION 1

a. The elements of tax appropriate to receipts and land documents, and leases is Stamp Duty. Stamp duties are

duties imposed on instruments.

Section 2 of the Stamp Duties Act defines Instrument as including “every written document” with reference to

instruments of marketable security.

Section 23 (3) captures Conveyance on sale and lease as registerable instruments – see also the Schedule.

Section 58 provides that any contract or agreement under seal or under hand only, for the sale of any equitable

estate or interest in any property whatsoever shall be charged with the same ad valorem duty to be paid by the

purchaser. In the same vein, Section 68 provides that an agreement for a lease, or with respect to the letting of

any lands or tenements, shall be charged with the same duty as if it were an actual lease made for the term and

consideration mentioned in the agreement.

b. In the event the documents are not stamped then the problem of the legal status of the documents will arise.

Today, there is no obligation to stamp a document, unlike a failure to pay income tax. Failure to pay income tax is

an offence.

However, by virtue of section 22 of the Stamp Duty Act, an instrument which is not duly stamped in accordance

with the law in force at the time it was executed shall not be tendered in evidence, except in criminal cases or to

prove fraud, refresh a witnesses’ memory or in bankruptcy.

In revenue case, the relevance of not stamping is as to penalty charge for failing to register the instrument at the

due date.

To avoid accumulation of penal charges, the receipts and lease agreements should be stamped by presenting

them to the Commissioner of Stamp Duties for assessment and stamping.

Penalty may be mitigated or remitted by the Commissioner.

SOLUTION TO QUESTION 2

a There is no universally accepted definition of tax. The Oxford English Dictionary defines tax as a “a compulsory

contribution to the support of government levied on persons, property, income, commodities, transactions etc,

now at a fixed rate mostly proportionate to the amount on which the contribution is levied”, Tiley, in his book,

Revenue Law, criticized this definition as being limited in scope as to the purpose of taxation and tells very little of

the meaning of a tax.

According to Webster’s Dictionary of English Language ‘tax’ means a charge imposed by government authority

upon property, individuals, or transactions to raise money for public purpose. This definition has also been

criticized as imperfect as it hardly help in distinguishing what is a tax from what is not a tax.

Generally, experts seem to agree on a descriptive approach highlighting the characteristics of tax. Thus, a tax is “a

compulsory levy imposed by an organ of government for public purposes

(Per Duff J in Lawson’s case). It has become settled that a tax has the three features set out in the definition:

I. a compulsory levy II. imposed by an organ of government

III. for public purposes. Without prejudice to this definition, fines, toll fees, social security contributions etc. do not fall within tax. That is

why it is not always safe to assert that it is that simple to recognize a tax merely by seeing it. Greater effort must

be put in to test each charge against the settled criteria of tax before reaching a conclusion.

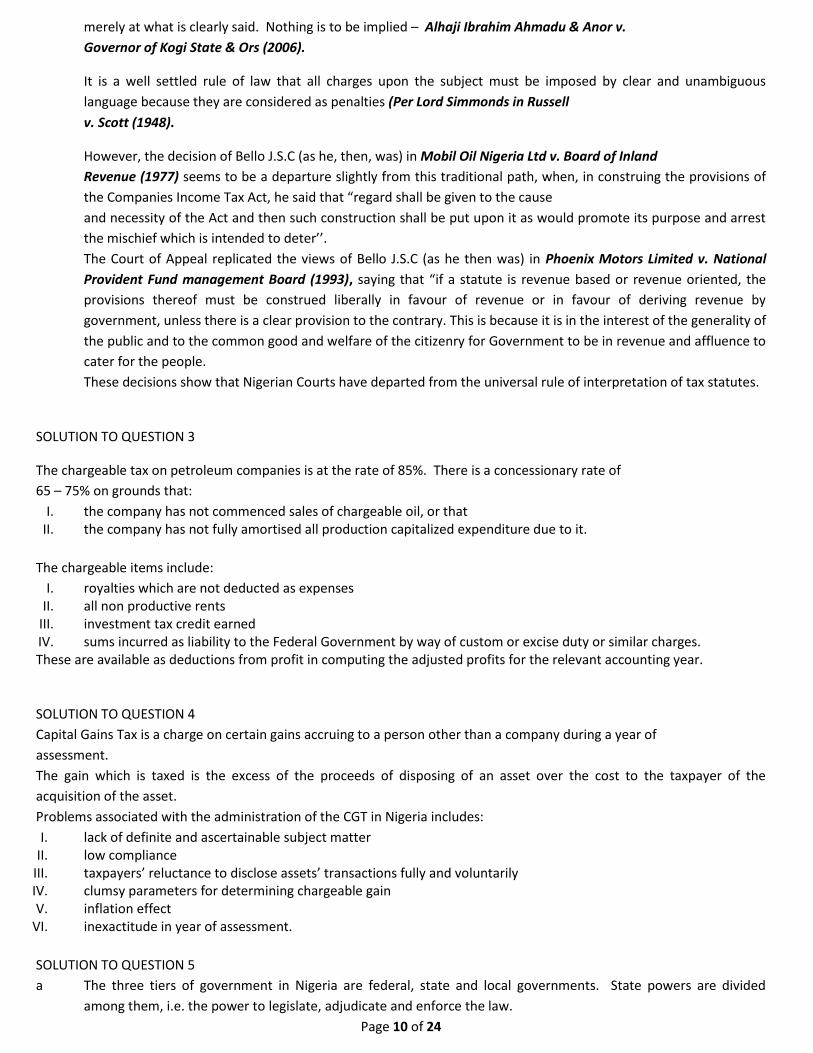

b The Courts interpreted the law. In interpreting tax statutes Courts in Nigeria follow the English

Law Courts. In a tax legislation the courts use the literal rule of interpretation. The courts look

Page 10 of 24

merely at what is clearly said. Nothing is to be implied – Alhaji Ibrahim Ahmadu & Anor v.

Governor of Kogi State & Ors (2006).

It is a well settled rule of law that all charges upon the subject must be imposed by clear and unambiguous

language because they are considered as penalties (Per Lord Simmonds in Russell

v. Scott (1948).

However, the decision of Bello J.S.C (as he, then, was) in Mobil Oil Nigeria Ltd v. Board of Inland

Revenue (1977) seems to be a departure slightly from this traditional path, when, in construing the provisions of

the Companies Income Tax Act, he said that “regard shall be given to the cause

and necessity of the Act and then such construction shall be put upon it as would promote its purpose and arrest

the mischief which is intended to deter’’.

The Court of Appeal replicated the views of Bello J.S.C (as he then was) in Phoenix Motors Limited v. National

Provident Fund management Board (1993), saying that “if a statute is revenue based or revenue oriented, the

provisions thereof must be construed liberally in favour of revenue or in favour of deriving revenue by

government, unless there is a clear provision to the contrary. This is because it is in the interest of the generality of

the public and to the common good and welfare of the citizenry for Government to be in revenue and affluence to

cater for the people.

These decisions show that Nigerian Courts have departed from the universal rule of interpretation of tax statutes.

SOLUTION TO QUESTION 3

The chargeable tax on petroleum companies is at the rate of 85%. There is a concessionary rate of

65 – 75% on grounds that:

I. the company has not commenced sales of chargeable oil, or that II. the company has not fully amortised all production capitalized expenditure due to it.

The chargeable items include:

I. royalties which are not deducted as expenses II. all non productive rents

III. investment tax credit earned IV. sums incurred as liability to the Federal Government by way of custom or excise duty or similar charges. These are available as deductions from profit in computing the adjusted profits for the relevant accounting year.

SOLUTION TO QUESTION 4

Capital Gains Tax is a charge on certain gains accruing to a person other than a company during a year of

assessment.

The gain which is taxed is the excess of the proceeds of disposing of an asset over the cost to the taxpayer of the

acquisition of the asset.

Problems associated with the administration of the CGT in Nigeria includes:

I. lack of definite and ascertainable subject matter II. low compliance

III. taxpayers’ reluctance to disclose assets’ transactions fully and voluntarily IV. clumsy parameters for determining chargeable gain V. inflation effect

VI. inexactitude in year of assessment.

SOLUTION TO QUESTION 5

a The three tiers of government in Nigeria are federal, state and local governments. State powers are divided

among them, i.e. the power to legislate, adjudicate and enforce the law.

Page 11 of 24

The legislative power on tax matters is vested expressly in the National Assembly with respect to personal income

tax, profits tax and capital gains tax by virtue of the 1999 Constitution.

Taxation is under the Exclusive Legislative List implying that only the Federal Government can “impose” these

taxes. The power to “collect” is shared among the three tiers of government.

Apart from the taxes listed in the Exclusive List, the State and the Federal Governments can impose other taxes

pursuant to the Concurrent List. In exercise of their powers on the residual list States have imposed taxes on their

subjects and also exercised their power to collect.

In judicial matters, only the Federal High Court has jurisdiction over revenue matters. However,

State High Courts also have jurisdiction over taxes imposed by the State in exercise of its powers under the

concurrent and residual list.

b The functions of a tax system are:

I. to raise revenue to meet government expenditure

II. to redistribute wealth

III. to exert control; moral and economic

PE 1 PERSONAL TAXATION

SOLUTION TO QUESTION 1

(a) T he following are some suggestions as to the ways the tax authorities can ensure that all the potential

tax payers are duly assessed.

1. There should be intensive direct assessment drive by the tax authorities. This can be achieved by

achieving that all the locations where businesses are operating are visited and tax enumeration

carried out.

2. The tax authorities should ensure that the companies which award contracts to all such business

are made to quote their TIN (Taxpayer Identification Number) on their headed papers.

3. Any company that awards contract to a business entity that did not indicate its tax registration

numbers should be penalised and made to pay some tax based on the value of cotract awarded to

such businesses

4. Every student who is going to be admitted into a higher school must provide the tax clearance

certificate of his parent or guardian.

5. Filling of annual returns by business names to the Corporate Affairs Commission should be made

compulsory for such businessess to continue to remain in business.The Tax Clearance Certificate

as well as a clear indication of the tax file number.

(b) Assessment becomes final and conclusive where no valid objection or appeal has been lodged within

the time limit. It is also applicable where an assessment is made or agreed to revise or determine on

appeal has not been the subject of further appeal within the time allowed.

(c) In relation to an individual , “place of residence” means a place available for his domestic use in Nigeria

on relevant day, and does not include any hotel , rest house or other place at which he is temporarily

lodging unless no more permanent place is available for his use on that day.

Page 12 of 24

SOLUTION TO QUESTION 2

CHUKWU GARUBA

Computation of Tax liability for 2009 year Assessment

N N

Salary 5,700,000 Deduct Relief:

Personal Allowance 1,145,000

Children Allowance 10, 000

Dependent Relative Allowance 4,000

Life Assurance Policy 370,000

Pension contribution 25,000 1,554, 000

4,146,000

Tax Payable

N 1ST N30,000 at 5% 1,500 Next N 30,000 at 10% 3,000 Next N50,000 at 15% 7,500 Next N50,000 at 20% 10,000 Next N3,986,000 at 25% 996,500 1,018,500

(b)

i. Children Allowance

Children allowance is claimed on annual basis on children maintained by the claimant in the

preceeding year under the following conditions:

- The children must not exceed 4 in number

- The child must not exceed the age of 16

- If the child is aged above 16, then he/she must either be attending full time educational

institution or be apprenticed to a trade.

ii. Dependent Relative Allowance

It is claimed by the claimant on

- An aged or widowed parents maintained in the preceding year

- The aged parent must not earn a total income that exceed N600 per annum

- The number of dependents must not exceed 2

(c) The difference between adjusted profit and net profit is the fact that the net profit arise from accounting

entries where all expenses is deemed to have been incurred by the sole trader. Conversely, adjusted

profit seeks to be the difference between taxable income and allowable expenses only. This account for

why adjustments are made on the net profit to be able to arrive at the adjusted profit. This requires

adding back non –allowable expenses and deducting non-taxatble incomes

SOLUTION TO QUESTION 3

(a) Computation of Mr. Cameron WOOD‟S chargeable income for 2010 Assessment year

N N

Salary paid in london 625.000

Page 13 of 24

Salary paid in Nigeria 900,000 Less reliefc: Personal (5000 †20% ×1525,000) 310,000 Children (2,500 × 3) 7 500 Life assurance 60,000 ( 377,500 Chargeable income 1,147,500 Income Rate Tax

On 1st 30,0000 5% 1, 500 Next 30,000 10% 3000 Next 50,000 15% 7500 Next 50,000 20% 10,000 Next 987,500 25% 246,875 268, 875

Rate of Nigerian tax 268,875 = 17.64% 1,525,000

Tax payable on N625,000 at the Nigerian rate of 17.64% is N110,250 since United Kingdom tax is

N62,500. The credit to be given to Mr. Green is N62,500. The credit to be given cannot exceed the

foregn tax paid.

SOLUTION TO QUESTION 4

OLU, ADE AND OYE

Partnership computation of Adjusted Profit for the 2010 Year of Assessment

N N

Profit per Accounts 4,096,500

Add back:

Depreciation 52,500

Provision for doubtful debts 75,000

Staff loan written off 54,000

Partner Salaries 744,000

Partner loan interest 186,000

Interest on capital 37,200 1,148,700

Adjusted Partnership Profit 5,245,200

Less capital Allowance 86,100

5,159, 100

Page 14 of 24

Computation of Partners‟ Income

Olu ½ ADE ½ OYE ½

N N N N

Partner SalarIes 744,000 312,000 276,000 156,000

Loan Interest 186,000 54,000 53,400 78,600

Interest on Capital 37,200 7 200 10,500 19,500

Share of Profit 4,191,900 2, 095,950 1,397,300 698,650

Total I ncome 5, 159, 100 2,469,150 1,737,200 952,750

Working‟, share of profit

N N

Total Income 5,159,100

Less Partner Salaries 744,000

Loan interest 186,000

Interest on capital 37,200 967,200

4, 191, 900

Share of Profit

Olu 3/6 x 4,191,900 = 2,095,950

Ade 2/6 x 4,191,900 = 1,397,300

Oye 1/6 x 4,191,900 698, 650

4,191,9000

(b) The following five income are exempted from tax

1. The salary, allowances ,pension and gratuity of the President

2. The income of a statutory or registered building society or statutory or registered friendly society

other than income from any business carried on by the society.

3. Income accruing to or derived by an exempt organisation other than from any business.

4. The income of a public corporation or institution exempted from tax under any enactment.

5. Income of an individual entitled to priviledges under the diplomatic immunities.

6. Interest dividend or

(a) Any other income of an approved units trust scheme or mutual fund

(b) Any other income payable under an approved unit trust scheme or mutual fund to a holder of

that scheme.

Page 15 of 24

SOLUTION TO QUESTION 5

Mr. Toulassi Donkwa

Computation of Capital Gains Tax Liability for year 2007 Tax year

N

Sale Proceed 5,000,000

Less cost of acquistion

A, 5000 X 18,075 000 A + B X C 5000 + 17,000

4,108,000

Capital Gains 892,000

Capital Gains Tax liability N89,200

Note;

(1) Total cost of the property

Cost of whole property N15,000,000

Incidental expenses 75,000

Cost of construction on open space 3,000,000

18,075,000

(11) The sale to the cousin is a connected person transaction.Consequently, the higher of the actual

sales and marker value is used for the computation.

Computation of Capital Gains Tax Payable for 2008

N N

Sales proceed 18,000,000

Less advertising 60,000

Agency fees 100,000

Legal expenses 30,000

Improvement before sale 250,000 440,000

Net sale Proceed 17,560,000

Less :

Cost of Acquisition (NWI) 13,967,000

Capital Gains 3,593,000

Capital Gains Tax at 10% 359,300

Note: Note working 1

Cost of the remaining part of the asset

Page 16 of 24

N

Total cost of asset 18,075 000

Less: cost of part disposed 4,108,000

Cost of remaining part of asset 13,967,000

PE 1 BUSINESSS TAXATION

SOLUTION TO QUESTION 1

a. GATEWAY AIRLINES LIMITED

Computation of Taxable Profit for 2009 Tax Year

N N

1. Global Income 151,422,000

2. Nigeria Income 29,460,000

3. Global Adjusted Profit:

Net Profit Reported 99,662,400

Add:

Depreciation 11,356,650

General Provision 540,720

11,897,370

Adjusted Profit 111,559,770

b Computation of tax liability

Adjusted Profit

4. Adjusted Profit Ratio = -------------------- x 100

Global Income

111,559,770

= ----------------- x 100

151,422,000 1 = 73.5%

Depreciation

5. Depreciation Ratio = ------------------ x 100%

Global Income

11,356,65O

= ----------------- x 100

151,422,000 1 =7.5%

6. Nigeria Adjusted Profit

=Adjusted Profit Ratio x Nigeria Income

=73.67% x N29,460,000 = 21,703,182

7. Capital Allowance

Page 17 of 24

=Depreciation Allowance x Nigeria Income

=7.5% x N29,460,000 2,209,500

Relieved (2,209,500) (2,209,500)

19,493.682

(a) Taxable {Profit = N19,493,682

(b) Tax Payable at 30% (N19,493,683 x 30%) = N5,848,105 Note:

Nigeria Income is arrived at as follows: N

- Income from Passenger fight from Nigeria 15,360,000 - Income from Cargo Loaded from Nigeria 14,100,000 29,460,000

SOLUTION TO QUESTION 3

BIG RISK INSURANCE CO. LTD

Computation of Tax Liability for 2003 Tax Year

N N

Life Business 1,105,000

Non-Life Business 2,070,000

3,175,000

Add: Balancing Charge 31,000

3,206,000

Initial Allowance 450,000

Annual Allowance 1,205,000

Balancing Allowance 21,000

Capital Allowance 145,000

1,821,000

Relieved (1,821,000) (1,821,000)

Taxable Profit 1,385,000

Tax due at 30% (N1,385,000 x 30%) N415,500

NOTES

(a) Life Business N N

Investment Income:

Interest on Debenture 175,000

Interest on Deposit 950,000

Surplus on actuarial Valuation 240,000

Page 18 of 24

1,365,000

Deduct:

Administrative Cost 50,000

Salaries 200,000

Other 10,000

260,000

Adjusted Profit 1,105,000

I. The dividend income received net of withholding tax is frank investment income which is not to be subjected to further tax.

II. Surplus on actuarial valuation is chargeable to tax when distributed.

(b) Non-Life Business: N N Premium on Burglary 2,450,000

Premium on Industrial Hazards 8,600,000

11,050,000

Provision for Unexpired Risk N N

At the beginning 1,200,000

Accrued Premium 400,000

1,600,000

12,650,000

Provision for Unexpired Risks:

At the End 1,500,000

Claim 3,550,000

Commission 1,420,000

Administrative Expenses 4,110,000

(10,580,000)

(i.e N4,150,000 - N40,000) 2,070,000

Adjusted for loss on sale of fixed assets

Adjusted Profit 2,070,000

SOLUTION TO QUESTION 3

(a) Powers of the Board The Board shall:

I. Provide the general policy guidelines relating to the functions of the service II. Manage and superintend the policies of the service on matters on matters relating to the

administration of the revenue assessment, collection and accounting system under the Act or any enactment or law.

III. Review and approve the strategic plans of the service IV. Employ and determine the term and conditions of service including disciplinary measures of the

employees of the service V. Stipulate remuneration, allowance, benefits and pension of staff and employee in consultation VI. Do such other things which in it‟s opinion are necessary to ensure the efficient performance of the

functions of the ser ice under the Act.

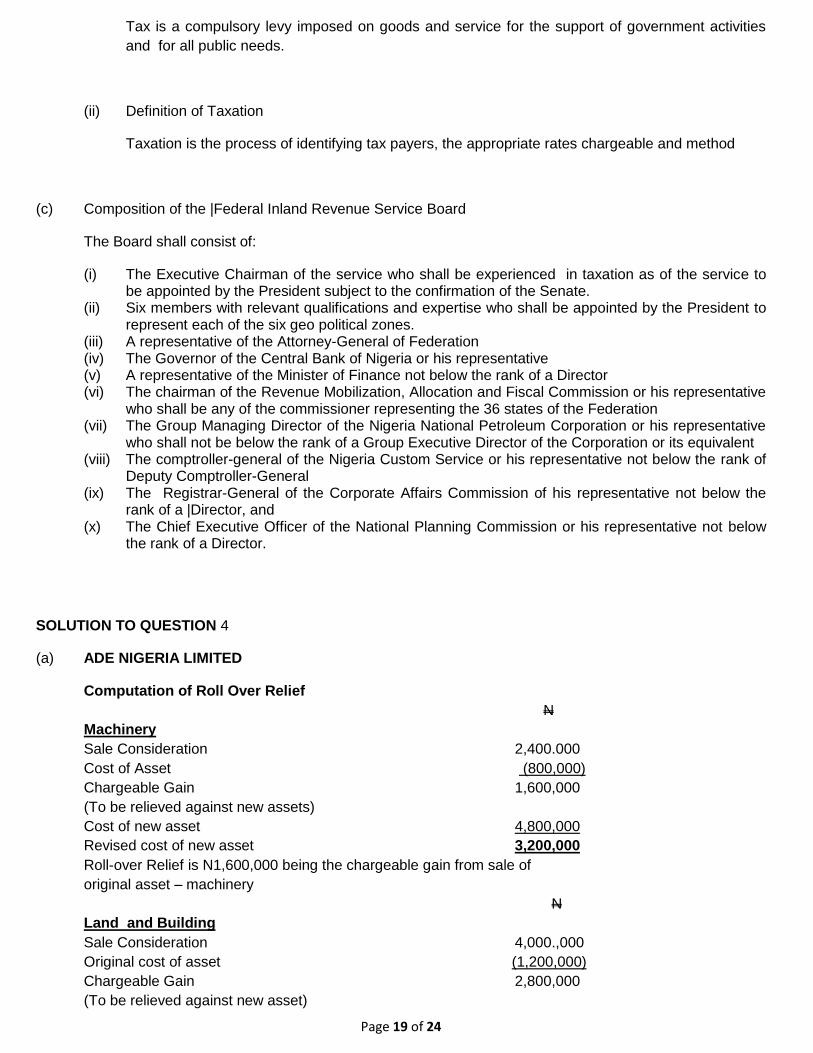

(b) (i) Definition of Tax

Page 19 of 24

Tax is a compulsory levy imposed on goods and service for the support of government activities

and for all public needs.

(ii) Definition of Taxation

Taxation is the process of identifying tax payers, the appropriate rates chargeable and method

(c) Composition of the |Federal Inland Revenue Service Board

The Board shall consist of:

(i) The Executive Chairman of the service who shall be experienced in taxation as of the service to be appointed by the President subject to the confirmation of the Senate.

(ii) Six members with relevant qualifications and expertise who shall be appointed by the President to represent each of the six geo political zones.

(iii) A representative of the Attorney-General of Federation (iv) The Governor of the Central Bank of Nigeria or his representative (v) A representative of the Minister of Finance not below the rank of a Director (vi) The chairman of the Revenue Mobilization, Allocation and Fiscal Commission or his representative

who shall be any of the commissioner representing the 36 states of the Federation (vii) The Group Managing Director of the Nigeria National Petroleum Corporation or his representative

who shall not be below the rank of a Group Executive Director of the Corporation or its equivalent (viii) The comptroller-general of the Nigeria Custom Service or his representative not below the rank of

Deputy Comptroller-General (ix) The Registrar-General of the Corporate Affairs Commission of his representative not below the

rank of a |Director, and (x) The Chief Executive Officer of the National Planning Commission or his representative not below

the rank of a Director.

SOLUTION TO QUESTION 4

(a) ADE NIGERIA LIMITED

Computation of Roll Over Relief

N

Machinery

Sale Consideration 2,400.000

Cost of Asset (800,000)

Chargeable Gain 1,600,000

(To be relieved against new assets)

Cost of new asset 4,800,000

Revised cost of new asset 3,200,000

Roll-over Relief is N1,600,000 being the chargeable gain from sale of

original asset – machinery

N

Land and Building

Sale Consideration 4,000.,000

Original cost of asset (1,200,000)

Chargeable Gain 2,800,000

(To be relieved against new asset)

Page 20 of 24

Cost of new asset 7,200,000

Revised cost of new asset 4,400,000

Roll-over Relief is N2,800,000 being the chargeable gain from the sale of

original Land and Building.

(b) Capital Gains arising from the following assets disposal will not attract Capital Gains Tax.

I. Any capital gain arising from the disposal of any government security II. Any capital gain arising from the disposal of shares and securities III. Any capital gains from the disposal of a medal won for honour and Gallantry IV. Any capital gains on the disposal of life assurance policies and any Investment under super-

annuation fund scheme V. Any capital gain on the disposal of motor vehicle for private use

VI. Any capital gain on a chattel disposed for not more than N,1000 in any year of assessment VII. Any capital gain given on the disposal of a landed property by a forced acquisition by any

government in Nigeria, provided: (a) the taxpayer has not taken any previous step to dispose the asset by way of entering into

negotiation to sell (b) the taxpayer has not shown any previous intention to dispose off the asset e.g. by way of

advertisement VIII. Any capital gain accruing to local authorities IX. Any capital gains accruing to diplomatic bodies X. Any capital gain accruing to charitable institutions, statutory or registered friendly societies, co-

operative societies or trade unions XI Any capital gain on the disposal of a dwelling house

XII Any chargeable gain by way of compensation for loss of office

SOLUTION TO QUESTION - 5

(a) I. Original Assessment

This is the first assessment raised on a taxpayer in a particular year of assessment. An original

assessment may be the subject of an objection and appeal procedure.

II Revised /Amended Assessment

This is the assessment that is raised to replace an original assessment. The replacement, usually

arise from either a notice of objection or appeal that is successful.

III. Additional Assessment

An additional assessment will usually arise from a back –duty assessment. The additional

assessment is to cover a shortfall in tax that was previously paid.

IV Best of Judgement Assessment (BOJ)

This will usually arise where the taxpayer has either not filed returns or is not even registered for

tax purpose. Where this occurs, the Inspector of Taxes will simply use the best of his judgement

to estimate the assessable profit, capital allowance claimable and the tax payable. A best of

judgement assessment (BOJ) is also subject to objection and appeal procedure.

V. Self Assessment

This was introduced in 1993. It requires the tax payer to display some level of trust. This is

because the taxpayer is expected to complete a standard self assessment form. The typical self

assessment form should contain all the information expected to be found on a normal notice of

Page 21 of 24

assessment. Where a taxpayer files his returns by self assessment, two advantages accrue to the

taxpayer.

(a) The first is that the taxpayer could make payment in installments equally over six months. (b) Secondly, where all the installments are paid on due dates, 1% bonus is deductible on the

sixth installment.

(b) I Conditions that will make an assessment to be final and conclusive.

An assessment is considered final and conclusive where:

(a) No valid objection or appeal has been lodged within the Statutory time limit (b) No further notice has been given of the appeal against a decision of the Appeal

Commissioner or a judge. (c) The amount of total income or profit has been determined on objection or on appeal the

assessment as made to, revised or determined on appeal.

ii. Reasons why a back duty assessment could be instituted against a

taxpayer. Back duty assessment could be instituted on the occurrence of one or more of the

following events.

(a) Errors or omissions in the assessment or collection of taxes due to deliberate intention of the taxpayer

(b) False or doubtful claim of allowance in respect of current or previous years (c) Failure to disclose or include in full any income or earnings in the returns made available to

the tax office (d) Decrease in revenue or profit in the returns filed to the tax office (e) Tax has not been charged and assessed or has been charged or assessed at less than which

ought to have been charged or assessed.

PE 1 INTERNATIONAL TAXATION

SOLUTION TO QUESTION 1

a

I. Double taxation occurs when income is taxed both by the taxpayer‟s country of residence and in another country where the income arises. - The term double taxation means two taxes imposed on the property by the governing body

during the same tax period and for the same taxing purpose

- Double taxation occurs where two or more countries impose similar taxes on the same taxpayer of the same base.

Fiscal evasion simply means a criminal way of evading the payment of tax.

II. The two types of double taxation are: - economic double taxation - judicial double taxation.

III. The four ways adopted by a typical tax treaty to eliminate double taxation are:

Exemption method - Article 23 (A)

Credit method – Article 23 (B)

Mutual Agreement Procedure - Article 25

Exchange of Information - Article 26

Page 22 of 24

b The four methods through which challenges posed by transfer pricing to the determination of the correct

tax liability of an enterprise could be resolved are:

Comparable uncontrollable method

Resale price method

Cost-plus method

The safe harbor method.

SOLUTION TO QUESTION 2

(a) The two countries that are parties to the bilateral tax treaty are called contracting states.

(b) The term Competent Authority in all the tax treaties between Nigeria and other countries means the

Minister of Finance or his authorized representatives.

(c) Treaty shopping means an analysis of tax treaty provisions to structure an international

transaction or operation so as to take advantage of a particular tax treaty. The term

is normally applied to a situation where a person not resident of either the treaty

countries established an entity in one of the treaty countries in order to obtain treaty

benefits - OECD Definition.

Treating shopping also means shopping for the best tax rates offered by treaty countries in order to carry

out transaction in such a manner to take advantage of those tax rates.

d The Minister of Foreign Affairs is regarded as „‟diplomatic channel‟‟ through which the

Contracting states exchange information.

e Tax sparing is a provision in the treaties Act that seeks to protect the tax incentives

Which the government might have granted to companies as part of the economic

development strategy. The Nigerian government has granted various incentives to

entice Foreign Direct Investment (FDI) into Nigeria. The intention of the government

is that the benefits would accrue to the relevant investor but without a tax sparing provision, such benefit

would be captured by the tax policy of country of residence

of the investor. The income which the government has spared through its incentive

legislations thereby flows, not to the investor directly but to the government of the

country of residence.

SOLUTION TO QUESTION 3

a MAMADU CONSTRUCTION COMPANY LIMITED

Computation of Value Added Tax payable for September, 2008

Page 23 of 24

N N

Income

Progress payment on 4/9/2008 2,250,000

Progress payment on 28/9/2008 250,000

2,500,000 Output

VAT on income received

5% of N2,500,000 125,000

Direct Expenses

Concrete Mixer 333,333

Scalfolding Pipes 1,000,000

Poker Vibrator 233,333

Chippings 45,000

½ Trailer Load of Granites 65,000

½ Transfer Load of Gravel 56,000

Total Direct Expenses 1,732,666

Cost for 50% contract certified

= 50% of N1,732,666 = 866,333

Input VAT on the 50% direct Expenses:

= 5% of N866,333 = (43,316.65)

VAT Payable to FIRS 81,683,35

NOTES TO SOLUTION ABOVE

(I) Direct Expenses: Given the nature of the work of the taxpayer, it has been

assumed that the cost of the concrete mixer, scalfolding pipes and vibrators

are direct expense as they are written off with the contract. On the other hand

the cost of furniture and sharp photocopier are taken as capital assets acquisition, the VAT of

which is not allowed for deduction.

(2) The VAT Input is appropriate as follows:

= Contract Certified x Direct Expenses x 5%

Total Contract

= 2,250,000 x 1,732,666 x 5% = =N=43,316.65

4,500,000

b

The VAT computed in 3 a above must be paid within 21 days following the month of transaction. Consequently, the liability must be settled on or before 21st October 2008.

In remitting the tax, the appropriate VAT Form 002 would be completed and certified by an official of the company. TIN (Tax identification Number) must be well written in the space provide for it in the form.

The tax due is then paid into the designated Bank to which the company is located. The Bank Teller (new E-Ticket) evidencing payment is then filed with the completed VAT Form

002 with the Integrated Tax office (ITO) where treasury receipt will be issued to acknowledge the receipt of the VAT by FIRS.

SOLUTION TO QUESTION 4

a The concept of residence is so important in international tax because tax administrators

need to identify persons and corporate bodies as tax payers. This is the first major task

Page 24 of 24

of any tax administrator. In identifying tax payers under the domestic context, the universally accepted

concept is that of residence rule. Once you are a resident of a particular tax jurisdiction then you are

automatically a taxpayer of that tax jurisdiction.

This reason makes the concept of residence so important in International Taxation.

b The criteria employed as a tie-breaker under Article 4(2) of a typical DTA in the event of

dual residence involving an individual are:

i. He shall be deemed to be a resident of the state in which he has a permanent home available to him; if he has permanent home available to him in both states, he shall be deemed to be resident of the state with which his personal economic relations are chosen (centre of vital interest).

ii. If the state in which he has centre of vital interest cannot be determined or if he does not have a permanent home available to him in either state he shall be deemed to be resident of the state in which he has a habitual abode.

iii. If he has habitual abode in both state or in neither of them he shall be deemed to be resident of the state of which he is a national.

iv. If he is a national of both states or neither of them, the competent authorities of the contracting

states shall settle the question by mutual agreement.

SOLUTION TO QUESTION 5

a The five (5) conditions that must be satisfied for the allocation of expenses are: -

i. That the expenses must have been incurred for the purpose of the business of the PE i.e the burden lies on the Head Office to prove that the expenses are wholly,

exclusively, necessarily and reasonably incurred in earning the profits of the PE.

ii. That the expenses actually incurred and related to the activities of the PE are deductible. iii. That the ordinary expenses which include “executive and administrative expenses” wherever

incurred, for the purpose of the PE are to be allowed as cost. iv. That deductions not allowable for the determination of the profits of the PE include inter-company

royalties, rents and interest on loan, other than bank loan. v. That transfer between the Head Office and PE must be at Arm‟s length, and

vi. That commission and fees for specific services rendered are allowable at costs.

b

i. As regards Build Co. its visit to State C in May 2008 did not constitute a basic rule in PE. These visits also did not count in determining the time the building site lasted in State C as they

preceded the starting date of the building work.

Prep Co. operated as subcontractor to Build Co. in carrying out the preparatory activities for the

project. This time is attributed to Build Co. which means that the calculation of the period for

which Build Co. is active started from 1st October 2008. The temporary interruption of the work

due to heavy rain did not cause the site to cease, and thus, the counting includes these months.

When Build Co. left State C in mid September, the site had lasted 11 ½ months. This is less than

the threshold of 12 months in the OECD model, and so Build Co. would not have a PE in State C.

However, State C may have domestic anti-abuse legislation, under which the artificial

fragmentation of a contract in order to avoid the 12 months period is ignored. If State C did not

consider that this project has been fragmented in this way, and therefore challenged the situation

under this legislation, and the courts in State C accepted this argument on an appeal from Build

Co. against the tax assessment. Build Co. would have passed the 12 months threshold and

therefore have a PE in State C.

ii. Prep Co. has no PE as it stayed below the 12 month threshold. Anonymous Co. also has no PE unless it is also considered to have a PE under the anti-abuse legislation of State C.