stock trading and markets chapter 2.3-2.4 chapter 3

TRANSCRIPT

Stock Trading and Markets

Chapter 2.3-2.4

Chapter 3

Learning Objectives

Describe key characteristics of different types of equity securities and equity indexes

Describe how securities are issued and traded

Describe the mechanics and risk of margin trading and perform relevant calculations

Describe the mechanics and risk of short selling and perform relevant calculations

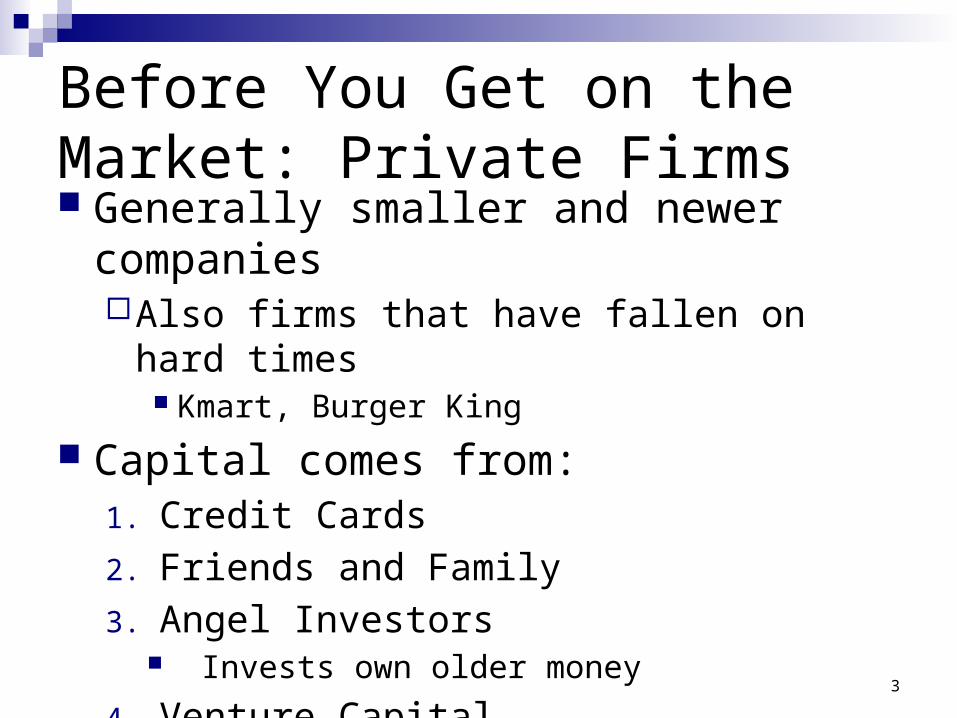

Before You Get on the Market: Private Firms Generally smaller and newer companies

Also firms that have fallen on hard times Kmart, Burger King

Capital comes from:1. Credit Cards

2. Friends and Family

3. Angel Investors Invests own older money

4. Venture Capital Limited Partnerships, provide money and experience

3

Going Public: IPO Initial Public Offering:

When a private firm is made public The general public is now able to invest in the

firm Generally happens when a firm needs more

money than it can raise from VC’sOr when the market is “hot”

4

Primary Market: IPOs & SEOs The firm raises capital from the public by sell

newly issued securities Firms use an underwriter (IB) to sell securities

Firm receives proceeds from the saleUnderwriter receives feesInvestors receive shares

Must file a Prospectus Description of firm and securities offered

Road Show

Relationship Between Issuer, Underwriters, & the Public

Problems With the Basic IPO Underpricing

IPO shares priced too low→The firm is “leaving money on the table”

Winner’s CurseBecause on underpricing IPO’s are a great S.T. betHowever, underwriters determine who can invest

Favor Bank: Giving preferential treatment to big customers So if you aren’t a big customer and you get an IPO

allocation, is it likely to be any good?

7

Cost of an IPO

DRK, Inc., has just sold 250,000 shares in an initial public offering. The underwriter’s explicit fees were $120,000. The offering price for the shares was $100, but immediately upon issue, the share price jumped to $150.How much did the underwriter make?How much did the IPO cost DRK?

Secondary Market Investors trade previously issued securities

among themselvesThis is the market we generally think/talk about

Firm does not receive any of the profitsIf the firm is not engaged in these

transactions then does the firm care about what happens? Why?

9

Types of Equity Securities Preferred stock: Claim to a perpetual stream of firm’s cash

No vote Fixed dividends, given priority over common, but after debt Taxed like common stock (not tax-deductible)

Corporate tax exclusions on 70% of dividends earned

Common stock: represents Ownership of the company Common equity has a claim to any residual cash Limited Liability

Financial Markets: Goals Ideally: facilitate low-cost investment

Provide liquidity by minimizing time and cost associated with trading Bringing buyers and sellers to a single location Promoting price continuity Reduce information costs associated with investing

Reality: These are publicly traded companies, so____________

Basic Order Type Market Order: Executed immediately at best price

Bid: price at which dealer will buy security Ask: price at which dealer will sell security

Price-contingent Order: Buy/sell at specified price or better Limit buy/sell order: specifies price at which investor will

buy/sell Will only transact at the specified price

Stop order: becomes a market order once a specified price is reached

Will be filled at best possible price, which maybe above or below the specified price

What do we know? What is uncertain?

Price-Contingent Orders

Limit Book Example Consider the following limit order book for a share of

stock. The last trade in the stock occurred at a price of $50.

What price will a market buy order (100 shares) be filled? What price is the next market buy order be filled at? Does a dealer what to increase or decrease his inventory?

Limit Buy Orders Limit Sell Orders

Price Shares Price Shares

$49.75 500 $50.25 100

$49.50 800 $51.50 100

$49.25 500 $54.75 300

$49.00 200 $58.25 100

$48.50 600

Trading Costs

Bid Represents offers to buy Investors “sell to the bid.”

Ask Represent offers to sell. Investors buy at the ask

In an efficient market trades will generally happen between the bid and ask (mid point)

1. Brokerage Commission: fee paid to broker for making trade2. Spread: Difference between the bid and asked prices

This is one way to profit from making a market

Types of Markets Direct search

Buyers and sellers must search for each other No intermediaries

Brokered markets (Housing) Brokers (intermediary) search out buyers and sellers

Dealer markets (NASDAQ) Investors transact with a dealers who has an inventory of

assets from which they buy and sell Auction markets (NYSE)

Traders converge at one place to trade Electronic communication networks (ECNs)

Computer systems that can automatically execute orders Play an increasingly important role in our financial system

Rise of ECNs 1969: Instinet (first ECN) established 1975: Elimination of fixed commissions (No more easy money)

1994: NASDAQ Scandal (Dealers avoided odd 1/8) SEC instituted new order-handling rules, Include ECN quotes ECNs given ability to register as stock exchanges

2000: Emergence of NASDAQ Stock Market 2006: NYSE acquires ECN renamed NYSE Arca 2007: Reg NMS

All exchanges linked electronically Required to honor quotes from other exchanges Broker needs to find best price available

U.S. Markets The New York Stock Exchange

The largest U.S. stock exchange as measured by the value of the stocks listed on the exchange

Automatic electronic trading runs side-by-side with traditional broker/specialist system Response to 1987 crash SuperDot : Electronic order-routing system DirectPlus: Fully automated execution for small orders Specialists: Handle large orders and maintain orderly trading

U.S. Markets• NASDAQ

• Lists about 3,000 firms• Originally, NASDAQ was primarily a dealer

market with a price quotation system• Today, NASDAQ’s Market Center offers a

sophisticated electronic trading platform with automatic trade execution

• Large orders may still be negotiated through brokers and dealers

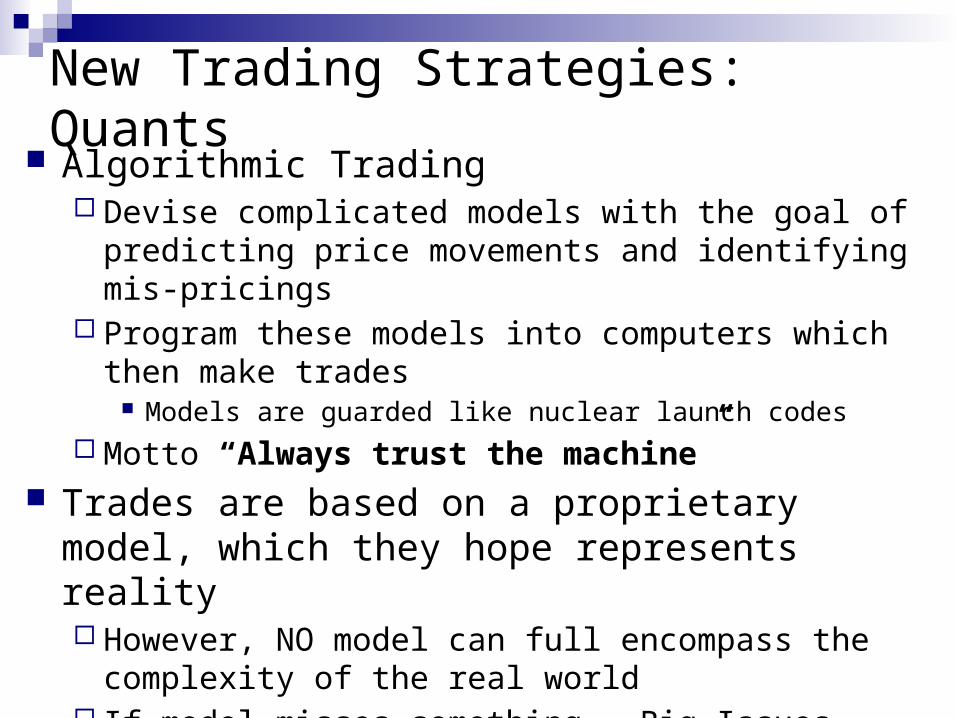

New Trading Strategies: Quants Algorithmic Trading

Devise complicated models with the goal of predicting price movements and identifying mis-pricings

Program these models into computers which then make trades Models are guarded like nuclear launch codes

Motto “Always trust the machine” Trades are based on a proprietary model, which they hope

represents reality However, NO model can full encompass the complexity of the

real world If model misses something → Big Issues

New Trading Strategies: HFT High-Frequency Traders: Special class of algorithmic trading HTF claims to uses computer programs to make very

rapid trading decisions (with very short order execution time) in order to compete for very small profits

Alternative: NMS requires brokers to look for the best prices available across multiple markets HFT set small orders in all markets, looking for big orders Once they detect a large order they rush to the other exchanges,

Front Running the larger order Transact with the large order initiator at a profit

Rely heavily on speed, has led to colocation, and private fiber optic lines

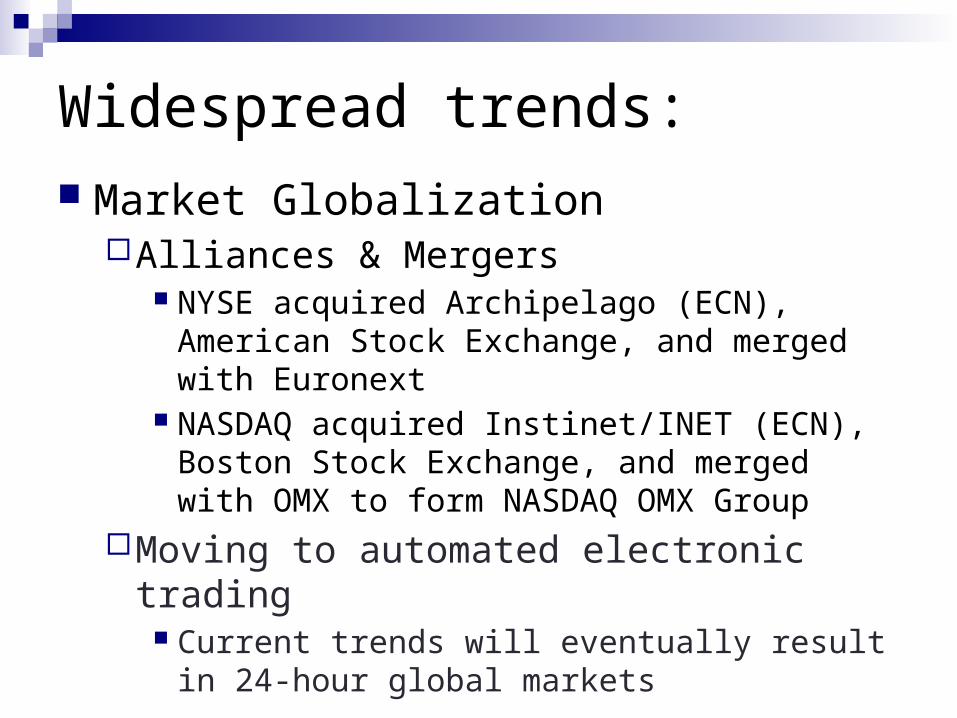

Widespread trends: Market Globalization

Alliances & Mergers NYSE acquired Archipelago (ECN), American Stock

Exchange, and merged with Euronext NASDAQ acquired Instinet/INET (ECN), Boston Stock

Exchange, and merged with OMX to form NASDAQ OMX Group

Moving to automated electronic trading Current trends will eventually result in 24-hour global

markets

Buying on Margin Borrowing part of the total purchase price of a

position using a loan from a brokerInvestor contributes the remaining portion

Margin refers to the percentage or amount contributed by the investor

You are leveraging your position

Margin Terminology Initial Margin Requirement (IMR)

Amount that investor must put up set by Fed (50%) Equity

Position value – Borrowing + Additional cash Maintenance Margin Requirement

Fed says 25%, but brokers generally set at 30%Margin Call triggered when equity hits MMR

Margin CallNotification from broker: put up more cash or position

is liquidated

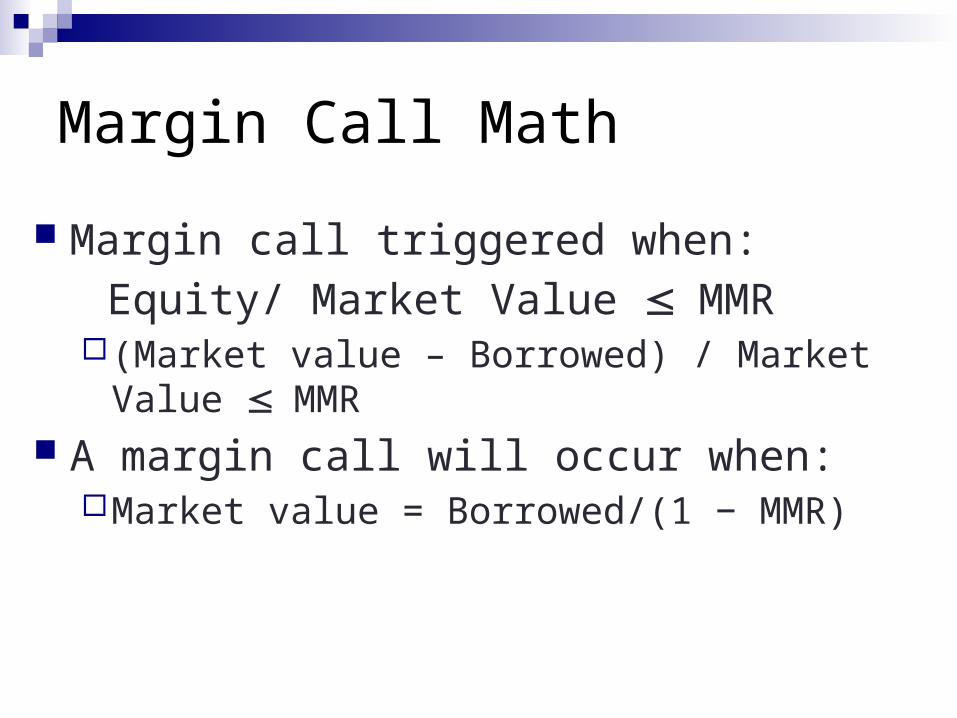

Margin Call Math

Margin call triggered when:

Equity/ Market Value MMR(Market value – Borrowed) / Market Value MMR

A margin call will occur when:Market value = Borrowed/(1 − MMR)

Margin Call Example

We want to purchase 1,000 shares of X Corp, which is currently trading at $70 on MarginIMR is ___ %We have a conservative broker so MMR is 40%What is the market value of our position?How much can we borrow?What is our equity position?

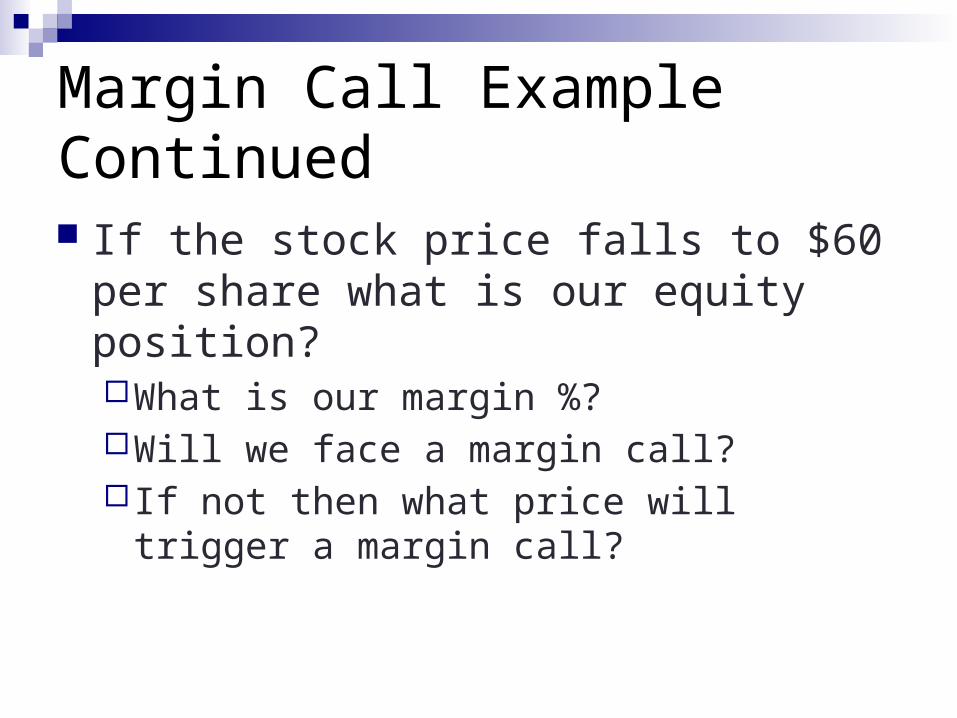

Margin Call Example Continued

If the stock price falls to $60 per share what is our equity position?What is our margin %?Will we face a margin call?If not then what price will trigger a margin call?

Margin Example 2

Steve opens a brokerage account and purchases 100 shares of IBM at $40 per share. He borrows $2,000 from his broker to help pay for the purchase. The interest rate on the loan is 8%.What is Steve’s initial equity position (margin)?If the price rises to $45 at year end what is his

margin? Hint: Don’t forget about interest

What was the return on the investment?

Short Sales Sale of shares not owned by investor but borrowed

through broker with intention to replace laterPurpose: To profit from a decline in the price of a

stock or security Mechanics

Borrow stock through a dealerSell it and deposit proceeds and margin in an accountClosing out the position: Buy the stock and return to

the party from which it was borrowed

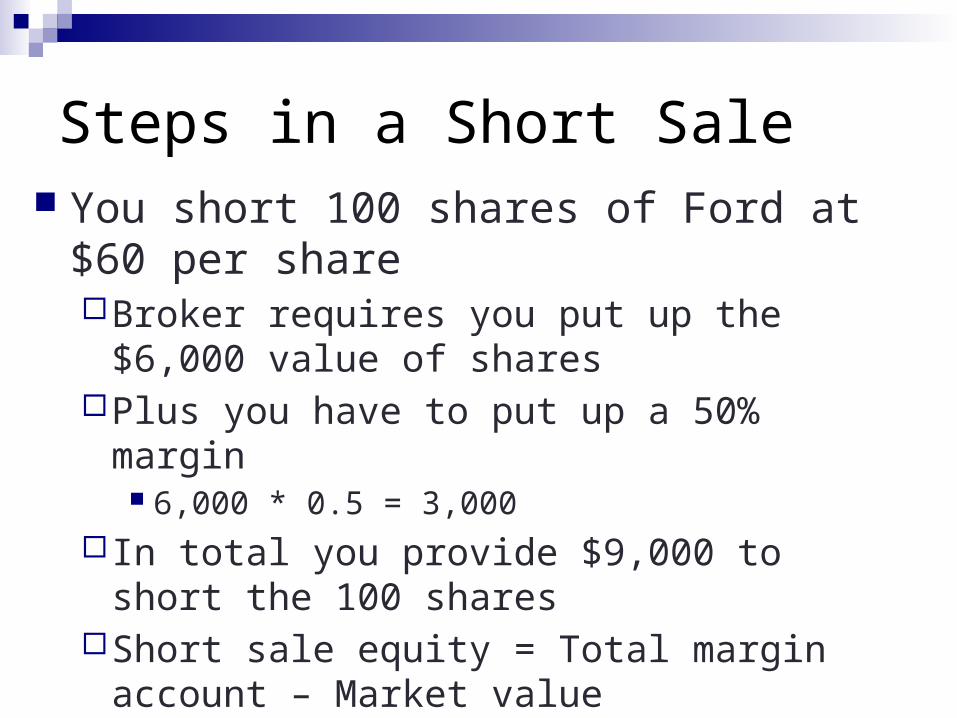

Steps in a Short Sale You short 100 shares of Ford at $60 per share

Broker requires you put up the $6,000 value of shares

Plus you have to put up a 50% margin 6,000 * 0.5 = 3,000

In total you provide $9,000 to short the 100 sharesShort sale equity = Total margin account – Market

value 3,000 = 9,000 – 6,000

Short Sale Math Maintenance margin for short sale of stock with price >

$16.75 is 30% market value 30% x $6,000 = $1,800

You have $1,200 excess margin What price triggers a margin call?

Hint: When equity = (.30 x Market value) Total margin account – MV = (MMR * MV) MV = Total Margin Account / (1+MMR)

Short Example Bill opened an account to short-sell 1,000

shares of Ford at $40 per share. The initial margin requirement was 50%. A year later, the price of Ford has risen from $40 to $50, and the stock has paid a dividend of $2 per share.

How much margin remains in the account? What is the short margin %? What is his rate of return?

Long & Short Cash Flows

Purchase of Stock

Time Action Cash Flow*

0 Buy share − Initial price

1 Receive dividend, sell share Ending price + Dividend

Profit = (Ending price + Dividend) – Initial price

Short Sale of Stock

Time Action Cash Flow*

0 Borrow share; sell it + Initial price

1 Repay dividend and buy share to replace share originally borrowed

− (Ending price + Dividend)

Profit = Initial price – (Ending price + Dividend)

*Note: A negative cash flow implies a cash outflow.

Margin Example 3

Sara opens a brokerage account and purchases 300 shares of Google for $50/share. She borrows $5,000 from her broker for the purchase. The interest rate on the loan is 10%.

What is Sara’s initial margin? If at the end of the year the price has fallen to

$40 what is her margin? Hint: What does she owe the broker?

What is her rate of return?