state of the global chemical industry · confidential. © 2018 ihs markittm.all rights reserved....

TRANSCRIPT

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

State of the Global

Chemical IndustryStrong market conditions continue as risks

factors threatening global growth emerge

APIC Marketing Seminar

20 August 2018 | Kuala Lumpur, Malaysia

Mark Eramo

Vice President, Global Business Development,

IHS Markit [email protected]

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Consumer

products

Oil

Gas

Coal

Renewable

Olefins

Aromatics

Chlor-alkali

Others

Commodities

Differentiated

commodities

Technical

specialties

Formulated

products /

performance

materials

Natural

resources

Chemical

intermediates

Base

chemicals

IHS Markit integrated analysis starts with

understanding energy and consumer markets!

Refined

products

& natural

gas liquids

Retail Chemical industry value chainUpstream / Downstream

NGL’s

Naphtha

Fuel Oils

Gasoline

Diesel

Transportation , Packaging

Construction , Recreation

Industrial , Medical

Pharmaceutical , Personal care

Textiles , Electronics

Aerospace , Business equipment

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

How do investors find the right balance in an ultra-competitive global market as intense public

scrutiny of fossil fuels, chemicals and plastics reaches new heights?

Global Energy & Chemicals Trilemma

3

➢ Achieve the economic and human-

kind benefits of investment in energy

and chemical value-chains

➢ Providing a sustainable approach to

the consumption of natural resources

along with sound environmental

stewardship

➢ Be responsive to societal demands

for a healthy and clean environment to

live.

Environment

Economics

Society

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Environment

Economics

Society

The petrochemical industry “trilemma”

4

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Agenda

>Energy & feedstocks

>Supply & demand outlook

> Industry earnings & market sentiments

Key trends influencing chemicals &

refining for the 2020s

State of the industry

Final Remarks

• Trade Policy

• Sustainability focus turns to plastics

• Evolution of refinery/petchem integration

• Heavy vs light feedstocks

5

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Combination of high crude prices and stable natural gas is attractive for

North America energy and gas-based chemical investments

0

3

7

10

13

17

20

0

20

40

60

80

100

120

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

USGC Natural Gas

Brent Crude

Global crude oil vs. USGC natural gas

Source: IHS Markit © 2018 IHS Markit

$/B

arr

el, C

rud

e

$ /

MM

Btu

, N

atu

ralG

as

6

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

North America gas-based energy advantage will continue to attract new chemical

investments in most value-chains through crude oil market cycles

0

200

400

600

800

1,000

1,200

1,400

MiddleEast

N America SE Asia WestEurope

NE Asia

Dolla

rs p

er

Metr

ic T

on

Methanol ECU Ethylene Propylene

2013 Production cost - high crude oil environment

Source: IHS Markit © 2018 IHS Markit

0

200

400

600

800

1,000

1,200

1,400

MiddleEast

N America SE Asia WestEurope

NE Asia

Dolla

rs p

er

Metr

ic T

on

Methanol ECU Ethylene Propylene

2016 Production cost - low crude oil environment

Source: IHS Markit © 2018 IHS Markit

Annual Brent Crude Price = $110/bbl Annual Brent Crude Price = $43/bbl

7

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Chemicals & plastics prices rise and fall with crude oil

0

500

1,000

1,500

2,000

2,500

3,000

Select Base Chemical Spot Price Trends

Source: IHS Markit © 2018 IHS Markit

US

$ /

Metr

ic T

on

0

500

1000

1500

2000

2500

3000

Select Commodity Plastics Spot Price Trends

Source: IHS Markit © 2018 IHS Markit

US

$ /

Metr

ic T

on

Various plastics regional spot prices

including PE, PP, PS, ABS, PVC

Base chemical regional spot prices

including ethylene, propylene, and benzene ABS

PVC

8

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

While the economic forecast is strong, it is more than just the economy that will

drive strong up-cycle conditions from a supply-demand perspective

Delayed capacity additions

enables demand growth to

balance markets

Economic and price volatility

causing lower inventory and

tight supply chains

Positive economic growth results

in acceleration of demand growth

Growth supported by low market

prices that enable substitution

Real GDP **

Percent change 2016 2017 2018 2019 2020

World 2.6 3.3 3.3 3.1 2.9

United States 1.5 2.3 3.0 2.7 1.7

Canada 1.4 3.0 2.2 2.3 2.2

Eurozone 1.8 2.6 2.1 1.7 1.6

United Kingdom 1.8 1.7 1.2 1.1 1.4

China 6.7 6.9 6.7 6.3 6.1

Japan 1.0 1.7 1.1 1.0 0.4

India* 7.1 6.7 7.1 7.3 7.2

Brazil -3.5 1.0 1.7 2.5 2.9

Russia -0.2 1.5 1.8 1.7 1.8

** July 2018 IHSM Economics & Country Risks forecast

9

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

0

1

2

3

4

5

6

7

Ethylene Propylene(PG/CG)

Methanol Chlorine Benzene Paraxylene

Avg. 2012 - 2016 2017 Avg. 2018 - 2022

Base Chemical average global demand growth; 2017 estimated total demand

Source: IHS Markit © 2018 IHS Markit

Mill

ion M

etr

ic T

ons

Ethylene and propylene remain in high growth mode; methanol growth stabilizes

152 102

78 73

46 41

Global demand estimate for 2017

10

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Given an assumption of strong economic growth, all measures and analytics show

ethylene / propylene / chlor-alkali, will be supply-constrained

65.0

70.0

75.0

80.0

85.0

90.0

95.0

100.0

2000 2005 2010 2015 2020 2025

Ethylene (Steam Cracker) Propylene (PG/CG) Chlorine

Global Nameplate Capacity Utilization

Source: IHS Markit © 2018 IHS Markit

Perc

ent N

am

epla

te U

tiliz

ation

-20

-10

0

10

20

30

40

50

60

2000 2005 2010 2015 2020 2025

Ethylene Propylene (PG/CG) Chlorine

Global Surplus Capacity as % of Total Demand

Source: IHS Markit © 2018 IHS Markit

Perc

ent of to

tal dem

and

Growth Assumptions Per Year

• Ethylene ~ 6 MM tons

• Propylene ~ 5 MM tons

• Chlorine ~ 2 MM tons

11

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

For chemicals, plant builds either aligned with demand or hydrocarbon supply; lately

global capital investment has trended down - except in the US. Will it continue?

0

20

40

60

80

100

120

0

15

30

45

60

75

90

105

120

135

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Bil

lio

n (

201

4)

$

Milli

on

s o

f To

ns

ROW Americas

Spend

© 2018 IHS MarkitSource: IHS Markit

Capital Spending in the Chemical Industry

12

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

China and North America investment continues at rapid pace along with more

modest growth in other locations

0

50

100

150

200

250

300

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24 26

United States Canada

Saudi Arabia Iran

South Korea Singapore

China India

Total base chemical capacity for select countries

Milli

on

Metr

ic T

on

s

Source: IHS Markit

0

5

10

15

20

25

30

35

40

45

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20 22 24 26

Canada Saudi Arabia

Iran South Korea

Singapore India

Total base chemical capacity for select countries

Milli

on

Metr

ic T

on

s

Source: IHS Markit

Total base chemical capacity includes: ethylene, propylene (PG,CG), methanol, chlorine, benzene, paraxylene

13

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Chemical industry in a sustained and unprecedented peak earnings cycle

• Steady global economic expansion

driving growth across most markets

• Oil volatility, reduced Chinese

reinvestment and a focus on M&A vs

expansions has constrained global

build

• Extended up-cycle is one major

“Harvey-type” event away from

triggering a ‘super-cycle’

• Widening oil to gas differentials

support margin expansion for gas-

based producers like N. America and

the Middle East

• Strong margins or economic pull-

back creates the potential for

overbuild post-2021

-$50

$0

$50

$100

$150

$200

91 93 95 97 99 01 03 05 07 09 11 13 15 17 19 21

Weighted Average EarningsChemical Industry weighted average cash earnings, $/Ton

Source: IHS Markit © 2018 IHS Markit

14

Increased risks in the forecast

• Geo-politics: Iran, NoKo, G8-7-6-?

• Energy volatility

• Govt fiscal policy “mistakes”

• Growing protectionist approach to trade

© 2018 IHS Markit

Industry Strategic Issues …emerging trends that will reshape chemicals and refining

industries in the near term and during the 2020’s

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

From NAFTA to BREXIT to US-China trade relations,

the subject of trade policy has become a primary

concern for future planning

• Global economic growth is steady in 2018 however,

momentum is slowing. Heightened risks could impact

growth, including high oil prices, political uncertainty,

and the potential for regional trade wars.

• Rising trade tensions are occurring at a difficult time

for most emerging markets, many of which have come

under increasing pressure from rising US interest

rates and an appreciating US dollar.

• The timing of the trade war could not be worse, as

monetary stimulus is beginning to wear off, oil prices

are elevated, and political risks are on the rise. Global

growth is beginning to slow, question is, by how

much?

• Regarding US-China trade, the more recent “lists” are

seeing grades of PE and PE finished goods

16

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Sustainability focus turns to plastics with

major media attention

• The most critical issue that will influence the

industry during the decade of the 2020’s.

• Local communities exploring bans on single-use

plastic applications as the issue of plastics waste

in the oceans has become an international media

issue: CNN, Economist, National Geographic's,

BBC

• United Nations “World Environmental Day” had

plastics waste as a central theme.

• The solutions will come from a cooperative,

approach that brings all the stakeholders together

to solve this very complex issue.

• A slowdown (versus history) in growth for

commodity plastics demand must now be

considered in long term forecasting.

“Single use” application bans

Marine waste

European “Circular Economy”

Self imposed corporate bans

17

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Next stage in the evolution of refinery &

petrochemical integration

• Higher fuel efficiency and increased use of

EV’s create a forecast for a declining growth

rate in the demand for refined products.

• Forecast is causing many refining

companies to re-think their petrochemical

strategy.

• Options range from continued but growing

feedstock supply relationships to major

direct investments in the sector.

• Current assets being built in China and

others in the planning stages, seek to enter

the petrochemical market with significant

scale.

000

300

600

900

1200

2010 2015 2020 2025 2030 2035 2040

Petrochemicals products Refined products

Index of base chemicals and refined products growth

Source: IHS Markit ©2018 IHS Markit

Petrochemicals and refined products markets, cumulative

Milli

on

To

ns

Petrochemicals forecasts to grow at a multiple above

GDP, as economies expand and urbanization increases.

Refined products growth is forecast to flatten by 2030.

18

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

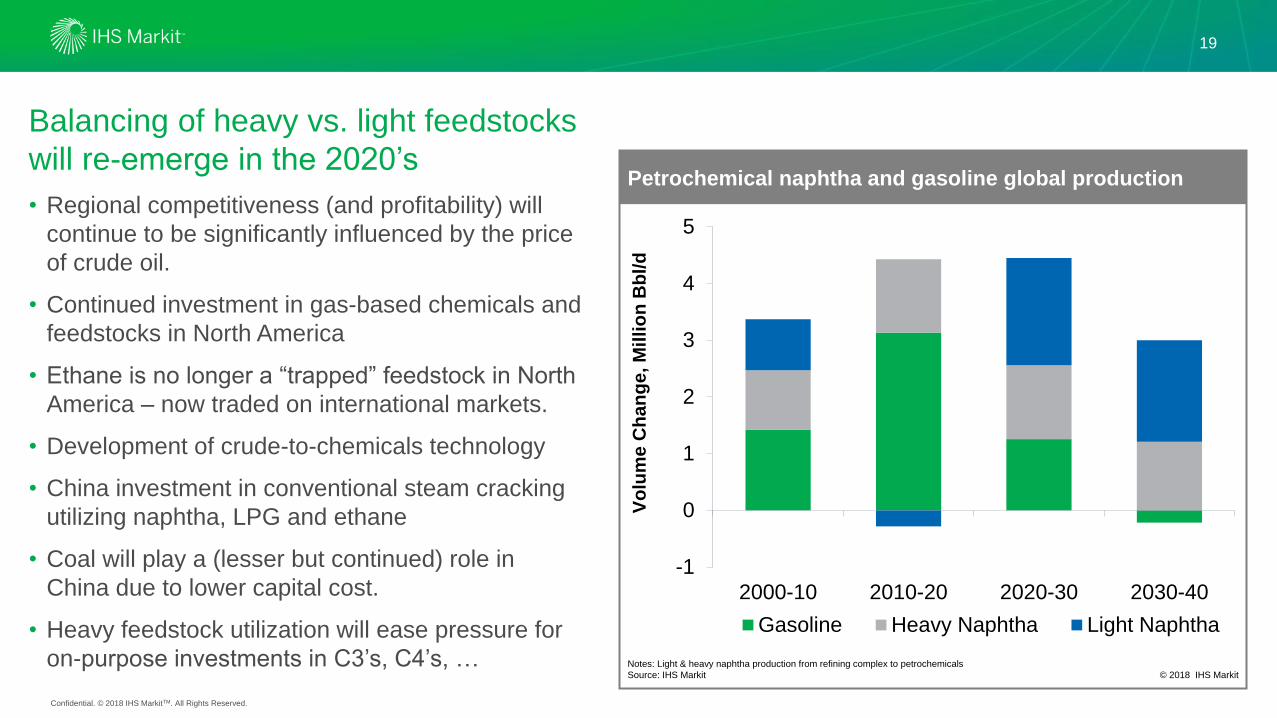

Balancing of heavy vs. light feedstocks

will re-emerge in the 2020’s

• Regional competitiveness (and profitability) will

continue to be significantly influenced by the price

of crude oil.

• Continued investment in gas-based chemicals and

feedstocks in North America

• Ethane is no longer a “trapped” feedstock in North

America – now traded on international markets.

• Development of crude-to-chemicals technology

• China investment in conventional steam cracking

utilizing naphtha, LPG and ethane

• Coal will play a (lesser but continued) role in

China due to lower capital cost.

• Heavy feedstock utilization will ease pressure for

on-purpose investments in C3’s, C4’s, …

-1

0

1

2

3

4

5

2000-10 2010-20 2020-30 2030-40

Gasoline Heavy Naphtha Light Naphtha

Petrochemical naphtha and gasoline global production

Notes: Light & heavy naphtha production from refining complex to petrochemicals

Source: IHS Markit

Vo

lum

e C

han

ge, M

illi

on

Bb

l/d

© 2018 IHS Markit

19

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

➢ Chemical industry will likely carry strong

profit momentum into the 2020’s.

➢ Strong demand and limited supplies are

driving an extended upcycle to record length.

➢ The degree of risks to the forecast is rising

with higher crude prices, currency

fluctuations, rising interest rates, and trade

tariffs that could escalate into a “trade war”.

➢ Sustainability issues from carbon to plastics

will remain top priorities .

➢ Chemical industry must take the offensive

when addressing sustainability issues to

demonstrate fact-based and common sense

solutions that benefit all of society.

20