spring 2015 jp dolphin final capstone project submission

TRANSCRIPT

Historic Review,

Comparative Analysis and

Future Recommendations For

Distributed Renewable Energy

Management Strategies

John-Peter Dolphin

Candidate, Harvard University Masters in Sustainability and

Environmental Management

Spring 2015

i

Abstract

Swanson’s Law has held true and the price of photovoltaic solar panels has dropped

precipitously. In fact, the technology has now reached a tipping point where installing rooftop

solar is within the reach of middle class Americans. The U.S. solar industry already employs

more individuals than the coal and natural gas industries combined, and the number of rooftop

installations in the US is expected to grow more than 600% over the next five years.

The rise of solar will catalyze a stark transition in the electric utility industry on par with

the switch from direct to alternating current. In mass, solar, and other distributed generating

systems, can cause considerable damage to existing electrical infrastructure, which is designed to

facilitate the historic centralized generation service model. In addition to this new bi-directional

flow of energy, distributed solar is extremely variable, with changes in on-site usage as well as

local weather conditions significantly affecting generation. As such and based on the accuracy of

current weather prediction algorithms, distributed generation systems are difficult to incorporate

into demand forecasts. In addition to infrastructure damage and over generation, solar is also

causing a cost shift to non-solar customers. Similar to deregulation and decoupling, this solar

cost shift will significantly impact the financial integrity of the electric utility industry.

This research paper reviews how three geographies, California, Hawaii and Germany, are

handling the growth of distributed solar. Infrastructure integrity as well as government policies

and financial incentives are reviewed. Load profile curves for each jurisdiction are compared,

with utility responses evaluated. Eight key recommendations are made, applicable to not only the

geographies reviewed, but also to any grid operator facing increasing distributed solar

penetration rates.

ii

Acknowledgements

My pursuit of a graduate degree, never mind the successful completion of this research paper,

would not be possible without the love and support of my wife, Rachel Silverman Dolphin. In

good times, and bad, she has been on my side, all while exceling in her own graduate work. I

also have to thank my parents and in-laws for their unbridled emotional and mental support.

Professor George Buckley and Teaching Assistant Sarah Driscoll provided the entire Spring

2015 Capstone cohort with an excellent framework for success and enough positive feedback to

fill the Giant Ocean Tank of the New England Aquarium.

Thank you to all of the professors and administrators, past and present, who helped shape the

Sustainability and Environmental Management program into the cornucopia of opportunity and

new beginnings that it is today.

iii

Table of Contents

Abstract ............................................................................................................................................ i

Acknowledgements ......................................................................................................................... ii

List of Figures ................................................................................................................................ iii

List of Tables ................................................................................................................................. iv

Definition of Terms......................................................................................................................... v

Introduction ..................................................................................................................................... 1

Note on Prior Knowledge Requirements .................................................................................... 2

Background ..................................................................................................................................... 2

The Industrial Revolution Sparks Demand for Electricity ......................................................... 3

The Battle of the Currents ........................................................................................................... 5

Centralized Power with Monopoly Service Territories .............................................................. 7

RTOs and OPEC ......................................................................................................................... 9

Deregulation, Enron, and Decoupling ...................................................................................... 14

Critical Mass and Impacting the Electricity Grid ..................................................................... 21

Methodology ................................................................................................................................. 27

Cases ............................................................................................................................................. 28

California .................................................................................................................................. 29

Hawaii ....................................................................................................................................... 36

Germany .................................................................................................................................... 40

Discussion & Recommendations .................................................................................................. 48

Discussion ................................................................................................................................. 49

Strengths and Weaknesses of the German Electricity Industry ............................................. 50

Energy Storage ...................................................................................................................... 53

A Threatened Business Model ............................................................................................... 57

Forecasting............................................................................................................................. 58

Recommendations ..................................................................................................................... 60

Conclusion ............................................................................................................................. 66

References ..................................................................................................................................... 68

iv

List of Figures

Figure 1 – Competition Abounds In The Early DC Market . ......................................................... 4

Figure 2 – Simplified Diagram Of Electricity Flow, From Generation To Use ............................. 8

Figure 3 – The Ratio Between Elrctricity Demand And Generation Capacity ............................. 12

Figure 4 – Historic Price Of Electricity ........................................................................................ 13

Figure 5 – Wholesale Price Of Electricity In California During Deregulation ............................ 19

Figure 6 – Installed Solar Cost per Watt ...................................................................................... 23

Figure 7 – Levelized Cost of Energy, variety of generating sources ........................................... 25

Figure 8 – Recent and Expect Residential Solar Growth ............................................................ 26

Figure 9 – Organization of NERC Interconnections.................................................................... 30

Figure 10 – California Genration Mix .......................................................................................... 31

Figure 11 – CSI Installed Capacity ............................................................................................... 32

Figure 12 – California's Duck Curve (Cal ISO 2013). ................................................................. 34

Figure 13 – Hawaii Genration Mix ............................................................................................... 37

Figure 14 – Hawaii's Nessie Curve ............................................................................................... 38

Figure 15 – Growth of Renewables in Germany .......................................................................... 42

Figure 16 – Solar Irradiation Rates, United States v. Germany .................................................... 43

Figure 17 – Germany's Extended Nessie Curve ........................................................................... 44

Figure 18 – Map of US Renewable Portfolio Standards............................................................... 51

Figure 19 – Worldwide Energy Storage Installtions .................................................................... 54

Figure 20 – Solar Cost Shift Positive Feedback Loop .................................................................. 58

Figure 21 – R&D by Investor Owned Utilities ............................................................................. 61

Figure 22 – Rooftop Solar Cost Comparision US v. Germany .................................................... 62

List of Tables

Table 1 – Basic Case Study Jurisdiction Comparables ................................................................ 28

v

Definition of Terms

Alternating Current (AC) – An electrical current that oscillates directions with a defined

frequency. The dominant form of electricity used for transmitting electrical energy over large

distances.

Balancing authority – The organization responsible for predicting electricity demand and

insuring generation capacity availability. Generally either the local utility, ISO or RTO.

Base load – Electricity demand or load that rarely if ever subsides; for example, transportation

and water infrastructure demands. Because of its constant nature, specific generating facilities,

also called base load power plants, are designed to serve this load. Base load power plants, such

as nuclear power plants, are incapable of quickly varying generation rates.

Demand response – A method of matching electricity supply with grid demand by having high

use customers strategically reduce demand, rather than by increasing electricity generation.

Direct Current (DC) – An electrical current that flows in a single direction. Used primarily by

in home appliances and machinery, requiring a transformer when using electricity from the grid.

Distributed Generation (DG) – Electricity generation that occurs within the distribution grid.

Although on-site generators at hospitals or industrial facilities technically qualify, the use of DG

typically refers to small scale renewable installations, especially rooftop solar.

Distribution grid – Low voltage electrical infrastructure used to safely distribute electricity

from substations through neighborhoods and to the final point of use.

Eastern Interconnection – The connection of electrical networks that stretches from the eastern

seaboard, north into Canada and as far west as the Rocky Mountains.

Electricity grid – Also known simply as “the grid,” the combination of distribution and

transmission networks that relay electricity between generation and points of use.

European Energy Exchange (EEX) – A wholesale electricity market that connects generating

plants throughout the European Union, providing reliability and connecting demand with the

most efficient source of generation.

Frequency – The rate of oscillation of alternating current, typically 60 hertz in the United States.

Changes to this rate can cause super positioning as well as constructive and destructive

interference, all of which can have devastating effects to electrical equipment.

Grid operator – Umbrella term which refers to the local utility, ISO or RTO in charge of

activities including demand forecasting, generation scheduling, and infrastructure maintenance.

May or may not also be the jurisdiction’s balancing authority.

vi

Independent System Operator (ISO) – A third party organization typically established by a

state government to oversee the jurisdiction’s wholesale electricity market. An ISO typically

owns no infrastructure and its revenue is separated from the amount of electricity sold.

Peak load – The highest electricity demand of either a day, season or year. Peak load often

coincides with extreme weather events. Specific power plants, known as peaker plants, typically

serve this load and are normally designed with minimal lead time requirements and increased

ramping flexibility. Peaker plants are generally not as economically efficient to operate and often

have some of the highest emission rates.

Point of use – Overarching term meant to signal the location of energy consumption by any

customer class including homes, businesses and industrial locations.

Ramp rate – How quickly a power plant can change its generation. Because of their very nature,

the incorporation of variable energy sources, such as solar and wind, can require ramping by

other generating facilities in order to meet consistent demand requirements.

Regional Transmission Organization (RTO) – Typically a self-organized group of

neighboring utilities who interconnect electricity networks in order to continue to meet customer

needs during times of increased demand or maintenance.

Photovoltaics solar (PV solar) – A type of solar panel, typically made of silicon, that generates

electricity through the transfer of electrons between metalloids, rather than through the use of

thermal energy.

Smart meter – Onsite equipment that measures electricity consumption at intervals as short as

every minute and relays such information to the grid’s operator via a wireless radio network.

Substation – A critical piece of the electricity grid that steps down high voltage electricity from

the transmission grid to voltages usable on the distribution grid.

Transmission grid – Network of high tension, high voltage electrical wires that transmits

electricity from large centralized power plants to substations, typically using AC.

Variable energy source - Electricity generating systems that depend on natural conditions,

rather than fuel, for power. As such, their generation varies when weather conditions change.

Watt (W) – Standard unit of measure for electricity. 1,000 watts is abbreviated as kW, a MW is

1 million watts and a GW is 1 billion watts. A single CFL lightbulb uses about 12 watts in an

hour or 12Wh, and the average U.S. home uses about 900 kWh of electricity per month. The

average centralized power plant has a generation capacity of between 1 – 1.5 MWhs.

Western Interconnection – The connection of electrical networks that stretches from Baja,

Mexico to British Columbia, Canada and east to the Rocky Mountains.

1

Introduction

Electricity serves as a critical cornerstone of modern life, used in everything from the

cultivation and curation of our food, extending education beyond the confines of the classroom,

improving land, air and sea transportation as well as, supporting emergency services including

police and fire. Electricity is so integrated into our modern lives that society sometimes takes it

for granted, forgetting the impact centralized power plants can have on communities and the

environment.

Increased awareness regarding these impacts, combined with technological

advancements, and associated cost reductions, have led to distributed renewable energy

technologies, especially rooftop photovoltaic (PV) solar, becoming increasingly popular.

However, the modern electricity grid and nearly everything associated with it, including utility

business models and regulatory language, were not designed for the bi-directional flow of

electricity from these new distributed generating assets. Faced with a new market landscape, but

few new tools, many utilities choose to essentially ignore output from small scale installations,

which they believe to be negligible (St. John, 2013).

While this output was negligible 15 years ago, distributed PV solar installation costs have

continued to plummet, and consequently installed generating capacity has continued to grow

(QER, 2015). California alone now exceeds 2 GWs of installed PV capacity, or approximately

7% of peak demand. (Cal ISO, 2013b; CPUC, 2015). Although no longer cost prohibitive, legacy

infrastructure systems, outdated regulations and threatened business models have suppressed the

continued growth of distributed renewable energy systems. Furthermore, failures in forecasting

technology prevent electric utilities from accurately incorporating distributed renewable energy

2

into generation plans. Because of this, utilities over-generate, essentially negating any positive

environmental or health benefits created by the distributed energy (MIT, 2011).

This report will assess the impacts that distributed generation (DG) has had on the

German electricity market, where nearly 70% of peak demand is met by solar power (Wirth,

2015). Based on third party and governmental reviews of this jurisdiction, the policies,

technologies and equipment used to successfully manage this level of distributed solar PV

penetration will be accessed against the infrastructure and regulatory environments of California

and Hawaii. These two locations are currently the largest markets for distributed PV solar in the

United States by capacity and penetration rate, respectively.

Note on Prior Knowledge Requirements

A technical understanding of electrical power systems and electricity generation, i.e.

voltage, frequency, reactive power, etc., are not required to understand the recommendations

made by this research paper. However, if a reader would like to learn more about these

fundamental topics, The Future of the Electric Grid provides an accessible, yet thorough,

overview of the topic (MIT, 2011). A historical account of the growth and transformation of the

electricity industry does, however, provide an important backdrop to the legacy systems,

operating standards and regulations of today. As such, the Background section of this report

includes a chronological overview of the foundation, growth, regulation and evolution of the

electricity industry.

Background

The saying “Thomas Edison would recognize today’s electricity grid” is widely used to

highlight the slow moving nature of the electricity industry (LaMonica, 2014). For several

reasons, including utility companies’ service territory monopolies which eliminate competition

3

and therefore innovation, the sentiment of the saying is true; the use of Edison, however, is

anachronistic. The electricity industry in general, and especially the electricity grid, has evolved

significantly since the early twentieth century. To begin, Edison’s direct current technology lost

to Nikola Tesla’s alternating current (EIA, 2000). Alternating current allows for centralized

power plants, leading to the radial array electricity grid of today (MIT, 2011). Rising costs, along

with increasing environmental awareness, have however led to a return to on-site direct current

generation, this time in the form of rooftop solar PV arrays (DOE, 2015). The penetration rate of

solar PV systems is now reaching a critical mass and beginning to negatively impact

infrastructure and reduce system wide efficiencies (MIT, 2011). This historical perspective is

critical to understanding why the modern electrical grid is designed and operated in the way it is

today.

The Industrial Revolution Sparks Demand for Electricity

While electricity as we know it has been experimented with since the mid-1700s, it was

not until the invention of the reciprocating steam engine during the Industrial Revolution that

electricity’s potential was realized (NAE, 2015). In addition to enabling railroad transportation,

the steam engine revolutionized manufacturing and allowed factories, previously dependent on

water wheels for mechanical power, to be located more strategically. These first closed circuit

systems were initially limited to facilities that could afford on-site generators, which required

significant fuel and labor. Electricity generation continued in this on-site manner until the first

commercial power plant, the Edison Electric Light Station, was built in 1882 (NAE, 2015). The

attraction of electric lights in storefront windows helped to expose the marvel of electricity to the

masses, and combined with safety campaigns lambasting the use of open flames, these and other

efforts led to increased demand for electricity in residential applications (ibid). This increased

4

demand led to an explosion of electricity and lighting companies. By 1907 there were forty-five

electricity companies operating in Chicago, with similar numbers in other major cities (Crews,

1998). An open market meant that while one resident received power from Company A, their

neighbor on the left might receive service from Company B, and their neighbor on the right from

Company C. Soon overhead electric lines crisscrossed even small cities, see Figure 1.

Although revolutionary, electricity service from the power company was both unreliable

and expensive. As a result many manufacturing facilities maintained their own on-site generation

capabilities, and those that didn’t often used batteries (EIA, 2000). Although they had minimal

capacity when compared to today’s devices, these batteries aimed to provide the same service

that modern day data centers and manufacturing centers require: a bridge power supply that helps

Figure 1 – Pratt, Kansas 1911. With no defined service territories and minimal regulations,

providing electricity to businesses and residents was a wide open market, even in small

town America (Cassingham, 2011).

5

overcome interruptions and protects equipment from drastic changes in frequency (EIA, 2000;

Schröder, 2012). So how did the decentralized, minimally regulated, unreliable, open market of

Edison’s time evolve into the electricity industry of today?

The Battle of the Currents

While Edison may have been instrumental in creating demand for electricity through

advancements to the incandescent lightbulb, creating a matching supply of electricity was not a

problem the world renowned inventor could effectively overcome. Hindsight and modern

electrical engineering principles demonstrate that there were two main reasons why Edison’s

direct current (DC) electricity grid failed: voltage drop and economies of scale.

Aluminum, steel and copper are the standard materials used in electrical wiring (MIT,

2001). Each material has a different conductivity, which can be simplified as the friction endured

by electricity as it travels along the length of a material (MIT, 2001). This “friction” decreases

electricity’s voltage, or the total available power. The further that electricity travels along a wire,

the more resistance is endured and increasing amounts of voltage is lost (MIT, 2011). This

voltage drop required early DC power plants to be located within approximately 1 mile of the

electrical load, otherwise the amount of resistance endured would create too much of a voltage

drop to service customer load (NAE, 2015).

This required DC generating plants, as well as the associated infrastructure to be

replicated several times throughout a city. Furthermore, electrical use cases that required more

powerful electricity than the standard 12V lightbulb necessitated DC power plants to have a

completely separate generator and distribution system (NAE, 2015). Comparatively high voltage

alternating current endures less resistance over the same electrical wire, allowing it to be sent

great distances with minimal voltage losses (MIT, 2001). This high voltage AC is then stepped

6

down through a transformer to a voltage that is useful for the customer (MIT, 2001). This step

down process allows for large centralized plants, which benefit from economies of scale, to be

built in strategic locations some distance away from the end user. High voltage alternating

current can also be stepped down to different levels. This allows one generating facility to

provide power to both manufacturing and residential applications through the same distribution

grid.

Because of these benefits, AC was chosen to power the World’s Fair in Chicago and

shortly thereafter the Niagara Falls hydro-electric plant also chose to employ AC (EIA, 2000).

Edison, who had invested significantly in direct current, did not readily admit defeat; driven by

pride and the desire for profit, Edison conducted a media blitz which lambasted AC as dangerous

and orchestrated, among other things, the invention of the electric chair, which was built to use

alternating current (EIA, 2000). Economic realities of centralized power production overpowered

Edison’s efforts and AC became the standard in the US and around the world.

Over the course of just 50 years the proximity relationship between man and power, both

mechanical and electrical, came full circle. Pre-Industrial Revolution manufacturing centers were

located along rivers, in order to take advantage of the natural power of flowing water. Thanks to

the steam engine, DC electricity could be generated locally or onsite and factories were moved to

cities, which were more strategic locations given the proximity to labor and transportation

networks. Centralized AC power plants then moved electricity generation out of the city center

and back to the water, which is used to help cool the plants’ generators (Botkin & Keller, 2010).

As previously mentioned, this research paper will discuss how rooftop solar is now bringing

customer-located DC power generation back.

7

Centralized Power with Monopoly Service Territories

Economies of scale played a critical role in the War of the Currents and again in the

creation of utility service territories as they are known today. As shown in Figure 1, the urban

electricity market was flooded with competition in the late nineteenth and early twentieth

century. Direct current required generation to occur within just a few miles of consumption, and

as a result an entire electric company’s operations were often within the purview of a municipal

government. However, the Great Depression brought a steep decline in demand for electricity.

Many electric utilities declared bankruptcy, selling off both their customer bases and the metal in

their overhead power lines, in order to help pay off debts (EIA, 2000). As a result, the utilities

that survived often had operations that extended beyond municipal and sometimes state

boundaries, undermining the authority and bearing of local regulations. With local laws no

longer enough to control these large utilities, and a great sense of distrust in unregulated

industries due to the stock market crash, The Public Utilities Holding Company Act of 1935

granted the Securities and Exchange Commission regulatory authority over utilities (MIT, 2011).

As part of this regulation and despite the aversion to large corporations, it was widely

recognized that a geographically based natural monopoly was a more efficient use of

infrastructure. It was at this time that both natural gas pipeline companies and electric utilities

were granted exclusive service territories and exceptions from the Sherman Antitrust Act (MIT,

2011). As part of the negotiations leading up to this legislation, utility representatives agreed to

not resist or impede the efforts of the Bureau of Reclamations, the Tennessee Valley Authority

(TVA) and the Rural Electrification Administration (REA) (EIA, 2000). These government

agencies created large generation sites, including the Hoover, Cooley and Bonneville dams,

providing low cost electricity to rural and Western markets. Utility representatives, whose

8

businesses served mainly large East Coast municipalities, bartered away what they saw as

perpetually small, rural markets.

Government and commercial systems alike, utilized large centralized AC power plants.

These plants were both more efficient, i.e. more affordable for the consumer, and more reliable

than previous DC plants, eliminating the need for manufacturing facilities to continue to own and

operate onsite generating facilities or battery storage devices. Figure 2 provides a basic overview

of the infrastructure involved in transmitting high voltage AC power from a centralized plant to

end users. Moving from left to right, a centralized power plant generates high voltage AC

electricity, which in turn is sent over transmission lines. Because of this potentially dangerous

voltage level, transmission lines have clearly defined easements and are strung above the tree

line. Community lines are the prototypical electricity lines one might see on a residential street

and are often also referred to as distribution or overhead lines. Before electricity can be sent

along local community lines, a decrease in voltage must be made. This decrease is completed at a

local sub-station; substations can reduce the electric flow from upwards of 65kV all the way

down to the standard 120V utilized by modern day home appliances (EIA, 2000).

Figure 2 – Simplified diagram of electricity flow, from generation to use

9

Community lines can be arranged in either radial, grid or hybrid arrays. Radial arrays

reach outward like the branches of a tree. With only one connection to a central source of

electricity, outer service areas are vulnerable to an interruption in operation closer to the center;

true radial arrays are rare due to their vulnerability (EIA, 2000). Grid arrays traverse a given area

in a checkerboard type pattern; such systems minimize the number of customers impacted by any

one incident through extreme redundancy with a multitude of alternative routes available if any

interruption occurs (ibid). Hybrid arrays combine the two in what can be most accurately

described as a spider web type fashion. Hybrid arrays allow for an effective level of redundancy

without requiring extensive amounts of infrastructure (ibid). The presence of one array type or

another depends significantly on the geographic conditions and history of development.

RTOs and OPEC

Between the Great Depression and the end of the twentieth century, technological

advancements continued to improve the efficiency of centralized plants. However, this 70 year

period brought with it significant changes in how utilities operated and the demands of the

customers they served.

During World War II and for approximately the ten years after, electricity demand was

dominated by factories and manufacturing facilities. Demand was predictable and consistent, and

the limited number of large customers allowed for utilities to have direct relationships with their

most important clients. It was at this time that demand response relationships first developed;

scheduled maintenance, extreme weather or unexpected grid demands would occasionally

exceed a local utility’s generation capacity. Rather than force a brownout, or worse, rolling

blackouts on all customers, strapped local utilities would request that industrial facilities reduce

10

production or cut a shift short. In exchange, utilities offered these industrial customers reduced

rates, and lauded them for putting the needs of the community above their own.

While these mutually beneficial relationships between industrial customers and utilities

continue to this day, there were and will continue to be times when industrial users of electricity

prefer not to reduce demand. For example, ahead of an impending quarterly manufacturing

quota, or in the middle of a sensitive production run. While formal demand response contracts

exist today, locking industrial users into specific curtailments, historically such contracts were

not common-place and in many instances plant managers chose not to reduce electricity use

when requested (EIA, 2000). The combination of increased grid demand due to suburbanization

and increasingly stalwart industrial customers put local electric utilities in a difficult position.

Should the local utility build a power plant that would only be utilized to meet peak demand for a

few hours every year? Even if the answer is yes, constructing a power plant is a multi-year

process, what was a utility to do in the interim? In order to most efficiently meet peak demand

requirements, many local utilities began to connect their electrical grid with that of a neighboring

utility. “Because different utilities often had standardized on different transmission voltages,

mergers and interconnections between adjacent utilities often required—and often still require—

transformers to link lines with different voltages. These transformers produce losses” (MIT,

2011, p. 238). Despite these losses, the marginal cost of these connections is generally lower

than building a rarely used “peaker plant,” and consequently these types of connections between

otherwise vertically integrated utilities with service territory monopolies began to arise with

increased frequency during the 1950s. This happened to such an extent that by 1962, nearly the

entire Eastern Seaboard of the United States was connected.

11

Interconnection brought reliability, but it also brought the potential for domino effect

destruction. This was the case in 1965 when a transmission line’s safety relay was tripped and set

in motion a cascade of overwhelmed electricity grids. In addition to affecting power availability

in Ontario, which was the site of the original infrastructure failure, the resulting blackout covered

the vast majority of New York (including Manhattan), New Jersey, Connecticut, Rhode Island,

Vermont, New Hampshire and Maine; all in all, 30 million people were without power (NBC,

1965).

In response to the blackout, and with the hopes of preempting increased regulation, the

electric utility industry formed the North American Electric Reliability Council (NERC). The

council created voluntary operating standards and worked communally to address reliability and

capacity issues. Side Note: Following a similar overloading event in 2003, affecting 55 million

people across 9 states and provinces, the Federal Energy Regulatory Commission (FERC)

directed that all NERC standards, previously voluntary, were mandatory (MIT, 2011). Because

all systems are not the same, NERC moved to establish Regional Transmission Organizations

(RTOs). Where interconnected utilities previously primarily relied on one another during times

of excess demand, RTOs coordinate generation capacity, maintenance, and related issues on a

daily basis.

While RTOs helped to improve resiliency, they did little to reduce the cost of generation.

Incremental technological advancements were made during the time period, but they could not

compete with the rising costs of fuel leading up to and following the OPEC Oil Embargo. While

many associate the OPEC Embargo with gasoline rationing during the winter of 1973, the utility

industry was hit just as hard and perhaps for a longer period of time. In 1973, 30% of the total

energy (BTUs) consumed in the US was attributable to gasoline, almost entirely by the

12

transportation industry; however, 47% of total energy consumption was from oil and similarly

was almost entirely attributable to electricity generation (EIA, 1979). Limited domestic supplies,

either pumped dry or abandoned due to the previously cheap availability of Middle Eastern oil,

escalated the problem.

In addition to scarcity inflated fuel costs, utilities also faced a continually increasing

demand for electricity, as outlined by Figure 3.

. Compounding double digit increases in demand were experienced each year between

1950 and 1973 (EIA, 2015b). In the three years leading up to the Oil Embargo, electricity

demand increased by 30%, 49% and 46%, respectively (EIA, 2015b). Faced with rising demand

Figure 3 –The ratio between supply and demand has stayed very stable over the last 65 years, save for

three influential events (Derived from EIA, 2015b).

13

and limited supply from both domestic and foreign sources, electricity prices began to increase.

As shown in Figure 4 in the years following the OPEC Oil Embargo of 1973, electricity prices

rose by as much as 35% (MIT, 2011, p. 237). In order to help reign in rising costs, as well as

diversify the electricity industry in hopes of protecting it from future international market

manipulations, Congress passed a series of pieces of legislation beginning with the Public

Utilities Regulatory Policies Act (PURPA) (EIA, 2000). PURPA aimed to add market

coordinated cost minimizing functions to a regulated monopoly space and did so by requiring

local utilities to buy power from non-utility power generators at “avoided costs,” effectively

creating the wholesale market for electricity (MIT, 2011, p. 238). This required the creation of a

third party purchasing authority, a role filled by Independent System Operators (ISOs). Whereas

RTOs are self-organized industry association aimed at insuring adequate supply during periods

of maintenance and high demand, ISOs are independent third party organizations that operate

Figure 4 – During the time of Edison, electricity cost as much as $5 per kWh (MIT, 2011, p.

235). The transition to centralized plants and alternating current significantly reduced costs,

and following the recovery from the Great Depression electricity prices have dropped

significantly (MIT, 2011, p. 237).

14

above the utilities with the goal of insuring generation efficiency. While ISOs play an important

role in forecasting system wide demand as well as scheduling and dispatching generation assets,

they do not own any power plants or transmission infrastructure, nor do they operate at the

distribution level of the electricity grid. This lack of ownership helps to insure efficient operation

and shortly after initial implementation the PURPA created ISO structure was deemed a success.

The combination of behind the scenes competition with a consumer facing monopoly was lauded

“as the benchmark for market design – the textbook ideal that should be the target for policy

makers” (MIT, 2011, p. 239). Following its successful implementation in the United States

historic revision to electricity markets were made all across the globe, most notably in Chile and

the United Kingdom (ibid).

Deregulation, Enron, and Decoupling

As previously mentioned the original intent behind PURPA was to create wholesale

electricity markets. The underlying ideology behind the legislative change was that opening up

the utility markets to competition would help to drive down the price of electricity (Weare,

2003). This was certainly the thought process in California, where electricity rates were “on

average 50 percent higher than the rest of the U.S.” (PBS, 2001). Deregulation was a step beyond

the creation of ISOs; in theory a free market would aggressively identify waste without the need

for an overseeing body. Each jurisdiction implemented deregulation in its own manner; for

example, Pennsylvania created a wholesale market, but does not allow independent energy

traders, who did not directly own generating assets, to participate (MIT, 2001). Because of the

number of companies and individuals affected, the size of the financial ramifications, and the

impact on international policy, California’s deregulation process will be the focus of this section.

15

Determining the underlying cause of the California Energy Crisis is beyond the scope of

this research paper. This paper will, however, outline several of the coinciding factors that

affected and allowed for manipulation of the California electricity market. These factors become

increasingly important as distributed energy generation capacities continue their penetration

beyond first adopters and further into the general population.

With an ISO already in place, and electricity prices still unreasonably higher than the rest

of the country, California was one of the first states to pursue almost complete deregulation

(Weare, 2003). This “almost” is an important caveat as traditional utilities were not allowed to

change rates charged to residential customers, despite the fact that the utility would be facing

variable costs depending on market pricing, fuel costs, etc. A wholesale market requires

suppliers other than the pre-existing vertically integrated utilities. Because it takes several years

to build a power plant, the first step in deregulation in California was the forced sale of 40% of

California investor owner utilities’ (IOUs) generation capacity (Weare, 2003) . Under Assembly

Bill (AB) 1890 power plants were sold at auction, with minimal requirements relating to industry

knowledge or ability to effectively operate the generating facility (ibid). Several out of state

investment companies purchased power plants (ibid). One issue that would add another layer to

the Energy Crisis is that many of these purchasing companies owned and operated assets outside

of the state. Similar to the transition from municipal to state utilities, these new companies no

longer came under the exclusive jurisdiction of prior regulators, in this case the California

Public Utilities Commission as all previous state utilities had, instead they fell under the

jurisdiction of the Federal Energy Regulatory Commission (Weare, 2003). Another subtle, but

important, variable that contributed to the energy crisis was reduced new generating capacity

construction. As previously outlined by Figure 3, electricity generating capacity traditionally

16

tracked growth in electricity demand. While the OPEC crisis reduced the ratio of demand to

supply, uncertainty regarding deregulations during the 1990s reversed this trend as many utilities

were wary to invest in a large power plant that they could be forced to sell, at a potential loss,

before recovering their investment (Weare, 2003).

One of the key components of California's AB 1890 that differed from other deregulation

schemes was that it forbade utilities from signing extended power purchase agreements and

instead forced utilities to make all purchases in the day ahead and spot market (Weare, 2003). By

emphasizing these short term markets, the CPUC shifted power producers’ focus from continued

long term operation to short term profit maximization. Seeking this short term profit

maximization, independent power producer (IPP) began to manipulate the wholesale market in

May of 2000. One way this was achieved was through unscheduled maintenance (Weare, 2013).

After accepting bids from the day ahead market, power producers who owned multiple

generating facilities would inform the Cal ISO that one of their facilities required unscheduled

maintenance (ibid). Unscheduled maintenance carried no penalty and would flood the spot

market, which was intended to only cover slight variations in demand from Cal ISO’s forecasts,

with immediate demand requirements (ibid). These last minute requests artificially inflated the

wholesale price of electricity leading to higher revenues for power producers.

Another market manipulation method used by independent power producers was over

scheduled transmission lines (Weare, 2003). With the state's electricity transmission

infrastructure built by previously vertically integrated monopolies, there was very little need for

interconnection. In fact, there was only one transmission line that connected the northern and

southern halves of the state, named Path 15. Recognizing this vulnerability, power producers

would intentionally bid on generation requirements on the other side of the interconnection. A

17

coordinated bidding process eventually led to the maximum capacity passing through the

transmission line; this allowed IPPs to tack on “congestion charges” on top of their day ahead

bid. This eliminated the availability of generating capacity from the other side of Path 15 to serve

spot market needs. As a result, the spot market was separated into two separate markets, allowing

independent power producers located on either side of Path 15 to charge even higher prices, and

leaving traditional utilities with no recourse (ibid).

AB 1890 included a tariff on electricity produced outside of California (Weare, 2003). In

theory, this allowed in-state power producers to charge comparatively lower prices, making their

electricity more attractive, with the intended purpose of encouraging in-state operation and job

creation (ibid). However, IPPs participated in electricity laundering schemes that would obscure

the original source of the electricity generated (ibid). Their goal was to make it seem that

electricity was actually coming from out of state, increasing the sales price. A simplified

explanation of the convoluted accounting schemes used does not do justice to the lengths IPPs

went to in order to scheme the wholesale market (Weare, 2003). In short, IPPs purchased,

bundled, resold, split, rebundled and then resold generation quotas dozens of times (ibid).

California’s deregulation process did not require separation between upstream and

downstream non-utility actors (Weare, 2003). As such, divisions of the same company were

allowed to purchase generation rights from one another, as discussed previously in regards to

energy laundering. Several IPPs also owned and operated natural gas supply pipelines and

extended this corporate nepotism to the purchase of natural gas (ibid). These companies,

including Enron, manipulated the underlying cost of natural gas in order to affect the price of

electricity, costs that were recuperated when they were eventually passed onto the local utility.

18

In order to drive prices even higher, independent power producers on several occasions

chose not to completely match all demand purchase requests. Because electricity cannot be

efficiently stored, these gaps between supply and demand would lead to brown and black outs

(Weare, 2003). Utilities, who were legally obligated to serve customers in their service territory,

would then be forced to bid even higher in the whole sale markets, in hopes of attracting

generation capacity that previously had not participated (ibid).

Market manipulation is not completely to blame, as the newly created regulatory

structure exaggerated suppliers’ power and left electricity purchasers with imperfect competition

and no reasonable alternatives. Rises in wholesale market prices, outlined in Figure 5, could not

be passed along to consumers, who were protected by a rate freeze (Weare, 2003). With no

consumer price signal attached to the peaks in the wholesale market, demand for electricity

increased as individuals and companies moved to incorporate computers and other electronics

into the daily operation of homes and businesses. During the ten years between 1990 and 2000,

electricity demand in the state increased on average approximately 1.5% annually (ibid, p. 16).

But this average rate was heavily influence by 4% annual increases in demand between 1998 and

2000, which was coincidently the time period of California’s deregulation. It was during this

same time period that supply was at its lowest (ibid, p. 16). California historically imported 20%

of its electricity from neighboring states, but droughts in the Pacific Northwest limited the

amount of hydroelectricity available to meet California’s increased demand (ibid). Demand also

increased by 6.2% in Nevada and 3.7% in Arizona, leading to limited export availability (ibid, p.

16).

As a result of these and other market variables, the price of electricity on the wholesale

market was 2,000% higher during the winter of 2000 than it had been just a year prior, see Figure

19

5 (Weare, 2003 p. 1). Unable to pass along these increased costs, state utilities lost millions of

dollars. The electricity crisis was at its worse during 2001 when over the course of nine days

there were “a total of 42 hours of outages,” (Weare, 2003, p. 3). The US urban area average is no

more than 5 minutes over the course of an entire year (MIT, 2011, p. 9).

With its income limited and facing unprecedented increases in costs, Pacific Gas &

Electric (PG&E), California’s largest utility, borrowed $13 billion dollars in order to bridge the

gap between rising costs and limited income. With no end to the underlying issues in sight and

the company’s lowest credit rating in history, barring it from borrowing any further at reasonable

rates, PG&E declared bankruptcy (ibid). California’s other large IOUs were also forced to

borrow significantly in order to meet their obligations. A conservative estimate of the financial

Figure 5 - The wholesale price of electricity in California during the period of deregulation. As can be

clearly seen the mere initiation of deregulation in 1998 did not immediately lead to the rise of electricity

prices, in fact prices initially dipped. It was however the confluence of several factors that played a role

the rising price of electricity (Weare, 2003, p. 1).

20

impact of The California Energy Crisis is $40 billion or 3.5% of California’s annual GDP (id, p.

3). In comparison, the most temporally recent crisis, the nationwide Savings and Loan Crisis,

was approximately $100 billion, but only 0.05% of the country’s GDP (ibid, p. 4).

The California state government was forced to intervene and using its emergency powers

shutdown the wholesale electricity market. Criminal charges were filed against IPPs who

colluded to affect wholesale prices, including Enron and its CEO Kenneth Lay. The international

popularity of PURPA legislation came to a screeching halt; no new ISOs have been formed since

the 2001 Energy Crisis (MIT 2011, p. 240). That being said previously established alternative

forms of deregulation including in Texas and New York have been successful in decreasing costs

and providing consumers with increased provider options.

California’s electricity industry required significant reforms, one of which was

decoupling. Decoupling separates a utility’s revenues from the amount of electricity the utility

sells. Instead revenues are based on a percentage of the monetary value of assets under

management. This calculation includes the value of power plants, transmission lines, and the

distribution grid. Electricity usage is estimated and this forecast is used to determine electricity

rates, which in aggregate meet state set revenue levels. Decoupling eliminates the juxtaposition

of promoting customer energy efficiency with utility revenues. In fact, customer energy

efficiency, along with corporate operational efficiency and demand side management can lead to

increased profits as they reduce costs, while leaving revenues unaffected. Decoupling actually

presents electric utilities with a rare opportunity: even when other parts of the economy are doing

poorly, the utility is essentially guaranteed revenues.

Similarly distributed renewables do not affect decoupled utilities’ profits as they simply

reduce demand, just like customer energy efficiency. Decreased demand, whether through

21

efficiency or renewable energy generation, does however effect electricity rate calculations. In

order to recoup the same amount of revenue from a smaller amount of demand, usage rates must

be raised. This phenomenon is known as a “cost shift;” similar to the unintended impacts of

deregulation, cost shifting could potentially impact the utility industry’s financial integrity and is

reviewed in more detail during the California and Discussion sections.

Critical Mass and Impacting the Electricity Grid

Before the California Energy Crisis, the PURPA ISO model was replicated in

Switzerland, where for the first time the right to produce electricity by “non-utility” actors was

extended beyond involvement in wholesale markets and all the way downstream to the consumer

(Perlin, 2013). Just like in the United States, electricity prices in Switzerland rose following the

OPEC Oil Embargo (Perlin, 2013). It was at this time that research into renewable energy

systems, which required no fuel, began to increase (ibid). Markus Real of Zurich was an early

adopter of rooftop PV solar and felt that it was an underappreciated technology, which not only

had the potential to protect consumers from future oil embargos, but also to reduce pollution

(ibid). Mr. Real believed so adamantly in the potential of the technology that in 1987 he started

Project Megawatt (Perlin, 2013). Intended as a social movement more than anything, Project

Megawatt aimed to install 333, three kW solar PV systems on rooftops throughout the capital

city (Perlin, 2013). The combined capacity of all 333 systems was one MW, hence the name. The

core idea of price protection and environmental stewardship resonated with the people of Zurich

and Project Megawatt was able to quickly enroll more than enough homeowners. However, once

the rooftop PV systems were installed, participating homeowners were disappointed with paying

the retail rate for electricity from their local utility, but only being paid an “avoided costs” rate,

which was 600% lower, for the electricity that their rooftop panels generated (ibid). As these

22

early adopters were individuals of influence, they were able to convince the local utility council

that electricity generated on their roofs was just as valuable as the electricity generated by the

utility’s large centralized plant (ibid). Side Note: One key factor in this political success was the

incorporation of local business leaders into Project Megawatt, including the owner of

Switzerland’s largest glass fabrication company, which made glass covers for solar panels. As a

result “net metering” was born, and Project Megawatt’s impact extended well beyond the 333

homes in Zurich, with net metering legislation significantly improving the return on investment

of distributed renewable systems and became the legislative standard in regions with some of the

highest rates of renewable energy generation, including Japan, Germany and California (ibid).

While net metering revolutionized the potential revenue stream for distributed

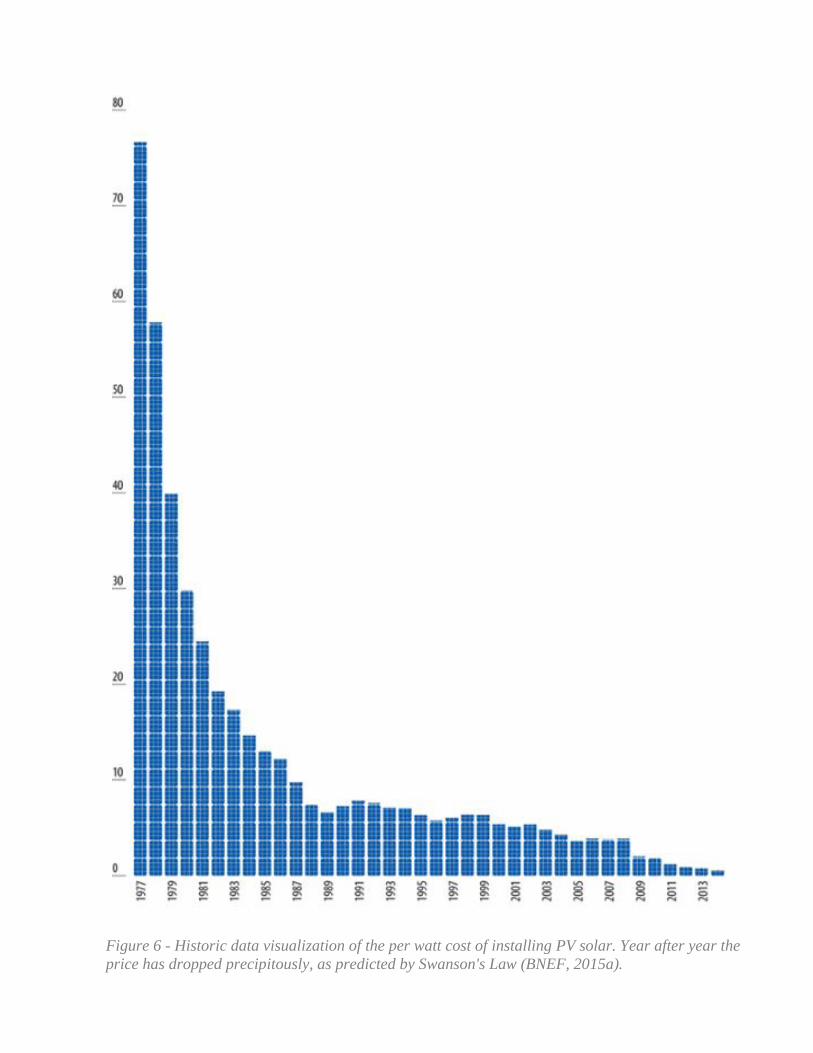

renewables, the core technology was still relatively expensive at approximately $10.00 per watt

in 1987 (BNEF, 2015a). For reference the un-weighted average residential price of electricity in

the United States in 2014 was $0.115 per kWh (EIA, 2015b). However, similar to Moore's Law

regarding the exponential increase in semiconductor computing power, Swanson's Law exists in

regards to the exponential decrease in the per watt cost of PV solar. Historical pricing metrics

outline the validity of this hypothesis, as seen in Figure 6. The per watt cost of utility scale solar

installations is now so low that it has reached "grid parity" in some markets. Grid parity

compares the per watt marginal costs of building a new generating source, such as a traditional

centralized coal, natural gas or nuclear power plant (EIA, 2000). In order to better account for

required operating expenses over the life of a plant, and not just installation costs, a different

metric has been developed: the Levelized Cost of Energy (LCOE). In addition to the cost of fuel,

which renewables do not entail, LCOE takes into account operating labor, maintenance and the

23

Figure 6 - Historic data visualization of the per watt cost of installing PV solar. Year after year the

price has dropped precipitously, as predicted by Swanson's Law (BNEF, 2015a).

24

expected useful life of the power plant (EIA, 2000). LCOE has its own faults, as it does not take

into account associated transmission infrastructure costs or end of life recycling and remediation

costs. There are several other metrics, including lifetime system costs, which attempt to consider

either a more holistic approach or a different perspective. While solar may be dependent on feed-

in tariffs or subsidies in order to reach grid parity, or a comparable LCOE, many argue that these

financial appropriations help to take into account externalities not currently considered by the

market (MIT, 2011; QER, 2015; Weare, 2003). Examples of externalities include the human

health and environmental impacts of smokestack exhaust, the greenhouse gas effect of power

plant emissions, and the historic non-monetary subsidies received by the oil and gas industries.

The National Renewable Energy Laboratory tracks LCOE in an open database, called the

Transparent Cost Database, and has developed an interactive tool which allows users to

compare LCOE as well as capital costs, operating costs and capacity factors across generation

technologies. A screen shot of the Transparent Cost Database’s LCOE visualization can be seen

in Figure 7.

No matter the metric, the cost of installing, operating and supporting renewables has

dropped precipitously over the last 30 years; furthermore, these reductions are expected to

continue for renewables whereas traditional generating sources have already matured as

technologies. Economic models suggest that the cost of distributed solar has likely approached a

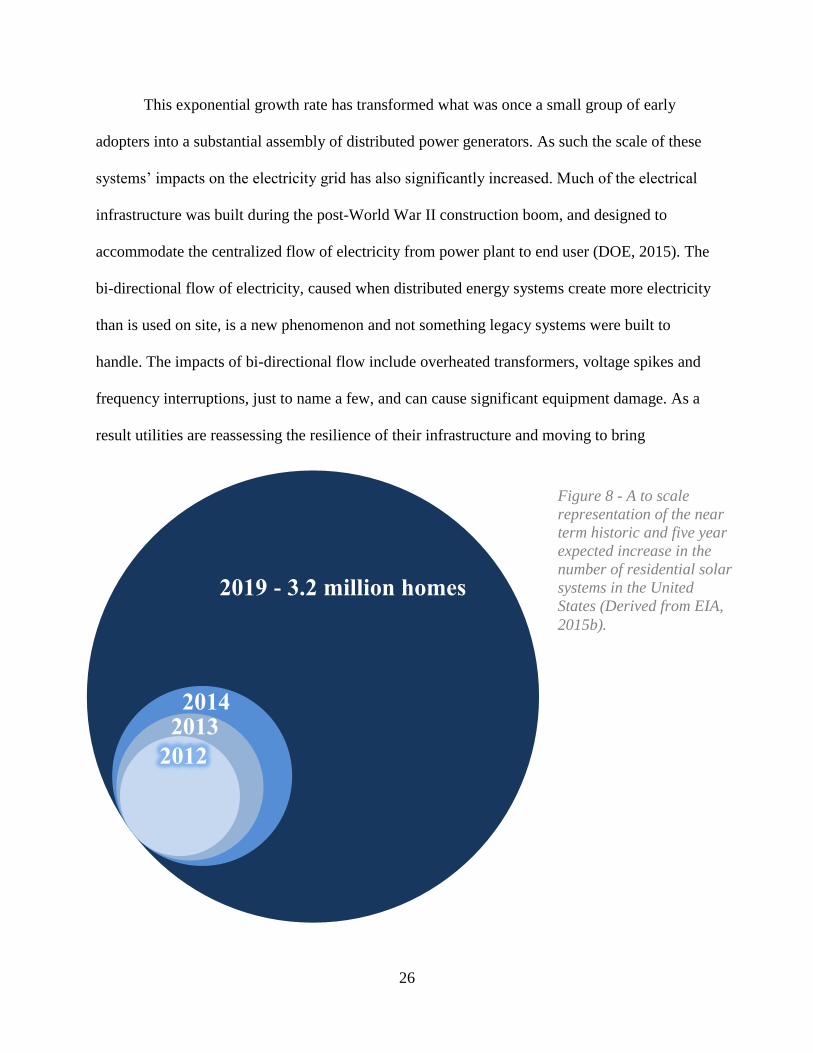

tipping point where in it is now affordable for the general public (BNEF, 2015b). The United

States’ residential solar market has grown by 50% or more for each of the past three years (EIA,

2015b). This rate is expected to continue, with forecasts of 630% market growth over the next 5

years, see Figure 8 (EIA, 2015b). Another way this groeth can be explained is that in 2016 solar

systems will be installed at a rate of one per minute (BNEF, 2015b).

1977: $76.67 per watt

2014: $0.70 per watt

25

Fig

ure 7

- Histo

ric and estim

ated

LC

OE

from

a va

riety of g

enera

ting so

urces. T

he len

gth

of th

e box

plo

ts outlin

es technolo

gy va

riatio

ns a

nd

subsid

y differen

ces (NR

EL

, 2015

).

26

This exponential growth rate has transformed what was once a small group of early

adopters into a substantial assembly of distributed power generators. As such the scale of these

systems’ impacts on the electricity grid has also significantly increased. Much of the electrical

infrastructure was built during the post-World War II construction boom, and designed to

accommodate the centralized flow of electricity from power plant to end user (DOE, 2015). The

bi-directional flow of electricity, caused when distributed energy systems create more electricity

than is used on site, is a new phenomenon and not something legacy systems were built to

handle. The impacts of bi-directional flow include overheated transformers, voltage spikes and

frequency interruptions, just to name a few, and can cause significant equipment damage. As a

result utilities are reassessing the resilience of their infrastructure and moving to bring

2012

2013

2014

Figure 8 - A to scale

representation of the near

term historic and five year

expected increase in the

number of residential solar

systems in the United

States (Derived from EIA,

2015b).

2019 - 3.2 million homes

27

transparency to these unintended, nevertheless significant, infrastructure costs. Distributed solar

does however offer benefits to the electricity grid as well. If strategically located the combination

of distributed systems, batteries and/or demand response can eliminate the need for expensive

transmission infrastructure upgrades (MIT, 2011). Furthermore solar systems generation

overlaps with a significant portion of peak demand and can reduce associated GHG emissions

and air pollution (QER, 2015).

Methodology

This research paper takes a case study approach to assessing how governments and

private utilities have promoted and are incorporating distributed photovoltaic solar into the

electricity grid. Utility structures, renewable penetration rates and infrastructure resiliency are

reviewed for California, Hawaii and Germany. The cases under consideration each bring a

unique perspective, as distributed solar generation is in a different stage of deployment in each

jurisdiction, and are further differentiated as the regulatory atmosphere in each circumstance is

unique. This research paper relies entirely on publically available information; in addition to

aiming to understand the problems faced by utilities, this research attempts to discover strategies,

based on historic successes and failures, that will aid in the continued integration of distributed

renewables into the electricity grid. As the installation costs of renewables continues to drop and

demand for greenhouse gas and pollution free electricity continues to rise, utilities will be faced

with critical decisions regarding how to minimize costs while fully utilizing a growing asset

class.

28

Cases

This research paper reviews three electricity markets: California, Hawaii and Germany.

Although more in depth details will be given in each section, Table 1provides an overview of the

each geography.

California Hawaii Germany

Population Served 38.8 million1 1.42 million

1 80.62 Million

2

Service Territory 163,696 mi2 1

4,028 mi2 1

137,903 mi2 2

Total Generation 296,628 Gwh3 9639 Gwh

4 614,000 Gwh

5

from Renewables 18.77%3 13.7%

4 26.2%

5

from Solar 1.8%3 <3%

4 5.7%

5

from Distributed Solar <1%3 <2%

4 4.5%

5

Peak demand met by Solar 7%6 80%

7 69.5%

5

Price* $0.1747/kWh8 $0.3334/ kWh

8 $0.31428/kWh

5

* Residential rate; assumes €1=$1.08

1: (USCB, 2014). 2: (World Bank, 2015). 3: (DBEDT, 2013). 4: (CEC, 2014). 5: (Wirth,

2015). 6: (CPUC, 2015). 7: (Paulos, 2014). 8: (EIA, 2015b).

California Overview:

California’s state government has set clear mandates regarding distributed energy

resource integration, yet utilities have little control over their own energy generation portfolio, as

they have been forced to cede this authority to the Cal ISO (Weare, 2003). California has the

largest installed solar capacity, distributed or otherwise, in the nation (CPUC, 2015). As a result,

grid operators are beginning to encounter a bi-model demand curve (PG&E, 2014). Often called

the Duck curve, the associated bi-directional flow of electricity can negatively impact

infrastructure (Cal ISO, 2013).

Hawaii Overview:

Spurred by the highest electricity rates in the United States, one in nine Hawaiian utility

customers have rooftop solar installed (HECO, 2013; Wesoff, 2014). Faced with dwindling

Table 1 – Basic electrical industry information comparison for each case study jurisdiction

29

profits and strained infrastructure, the local electric company is no longer approving solar

interconnection requests in some areas (St. John, 2014a). This high level of solar penetration

forms a “Nessie Curve,” which has a steep increase in electricity demand following sunset,

similar to the steep slope of the Loch Ness Monster’s neck. Such a quick ramp up in demand is

not only expensive to service, but is also nearly unfeasible with the current infrastructure. (St.

John, 2014b). The utility and the state’s Public Utilities Commission are at odds, with the PUC

calling the Hawaiian Electric Company’s (HECO’s) renewable integration plans “fundamentally

flawed” and a “failure” (HPUC, 2014, p. 28).

Germany Overview:

As the result of the country’s unique feed-in tariffs, Germany exceeds both California in

total installed solar capacity and Hawaii in penetration rate. German utilities have dealt with the

Duck and Nessie curves by focusing on local infrastructure and shifting from a centralized power

production model to a distributed system where the utility acts as an enabler of customer owned

generating assets. Following Fukushima, Germany expedited the decommissioning of a majority

of its nuclear power plants GFNA, 2015. These shutdowns have added flexibility to the

electricity grid and allowed it to actually increase electricity exports to neighboring countries,

while still being able to supply power during a solar eclipse.

California

The California Independent System Operator (Cal ISO or CAISO) is one of the largest

third party grid management organizations in the world and is considered a thought leader in the

space (Weare, 2003). Cal ISO incorporates over 80% of the state of California and works closely

with the state’s utilities, especially the three largest: Pacific Gas & Electric (PG&E), Southern

California Edison (SCE), and San Diego Gas & Electric (SDG&E), all of which are investor

30

owned utilities (IOUs) (Cal ISO, 2015d). Cal ISO forecasts the state’s electricity demand and

then manages the competitive wholesale electricity market in order to properly match this

demand, while insuring transmission lines and other high level infrastructure are not

overburdened (Cal ISO, 2015a). As a result of unique state legislation, utility and Cal ISO

revenues are “decoupled” from both demand forecasts and the amount of electricity generated.

Approximately a quarter of the electricity used in the state is imported from power plants

outside of, but connected to, the Cal ISO grid as part of the Western Interconnection (Cal ISO,

2015a). The Western Interconnection helps to provide Cal ISO and all connected electricity grid

Figure 9 – The electricity grids of the United States and Canada are linked and

subsequently split into three different interconnections governed by eight different regional

councils (NERC, 2013).

31

operators with reliability and the opportunity to service electricity demand outside of their

service territory. The Western Interconnect stretches eastward into parts of Texas, as far south as

Baja, Mexico, and north to encompass the Canadian provinces of British Columbia and Alberta,

see Figure 9 (Cal ISO, 2015b).

Over 1,400 generation facilities, located throughout the Western Interconnection and

owned by more than 100 companies, participate in Cal ISO’s wholesale electricity markets,

which include day ahead, hour ahead and on-demand auctions (Cal ISO, 2015a; Cal ISO, 2015c;

Cal ISO, 2015e). It is Cal ISO’s responsibility to manage these markets while adhering to the

confines of the Renewable Portfolio Standard (RPS) set by the CPUC. The Cal ISO failed to

meet the RPS legislation requirement for 2010, which required that 20% of electricity generated

during that year come from renewable resources (CEC, 2014). The next goal, established by

Senate Bill X1-2, is for 33% of electricity to be renewable in 2020 (CEC, 2014). California’s

Figure 10 - In 2013 California consumed 199,783 GWhs of electricity. The fuel source ratios outline a

clear commitment to low greenhouse gas emission sources (CEC, 2014).

32

electricity generation portfolio is outlined in Figure 10.

In order to meet these renewable energy generation goals California has instituted several

programs, including financial incentives. The Go Solar Campaign is the umbrella name for state

programs designed to incentivize customer owned solar; the largest such program is the

California Solar Initiative (CSI) which has a budget allocation of $2.167 billion over 10 years

(CPUC 2014a). The CSI program, as outlined by Figure 11, contains a stepwise functionality

designed to incentivize a growing capacity of solar given the same amount of funding each year.

Financial payments are made to solar system owners based on monitored system generation

(CPUC 2014a). The incentive, which is a consistent per kWh rate, continues for 20 years.

Incentive rates decrease with each year for new participants (ibid). To date, the CSI program has

Figure 11 – Customer sited solar capacity installed in CA’s IOU territories through the CSI

program, 1993-2013 (CPUC, 2014b).

33

led to the installation of over 2,100 MW of solar capacity at more than 227,000 customer sites

(CPUC, 2014b, p. 8). Other incentive programs include the New Solar Homes Partnership,

designed to benefit low income families, the Emerging Renewables Program, and the Self

Generation Incentive Program (CPUC, 2014a).

The combination of these incentive programs with the continually declining price of solar

has led to California having the largest installed solar capacity in the United States. Other states

look to California with hopes of understanding what their state’s electricity grid may look like in

the future. One unanticipated impact is the solar “cost shift;” in short, solar panels reduce the

overall amount of electricity which utilities can spread their decoupled revenues over. As a

result, the per kWh retail price of electricity rises (E3, 2013). Additionally, because the type of

individuals that install solar panels a) are likely high users of electricity, who pay higher rates

under California’s tiered rate structure; b) own a home on which they can install solar; and c) can

afford the upfront payment solar panels historically required, this “cost shift” has been compared

to a regressive tax (Johnson, 2011). Politicians and disgruntled citizens have condensed the

situation into the middle class, paying for the rich to install solar panels (Johnson, 2011).

Although the rhetoric may be terse, the sentiment is actually not too much of an exaggeration

and might even under sell the scale of the problem. According to a report commissioned by the

CPUC, the current cost shift is approximately 1% of all utility revenues, or $359 million, and

with increased solar installation rates expected over the next several years, the cost shift in 2020

is expected to impact 3.2% of all utility revenues, or $1 billion (E3, 2013).

In addition to this social angst the cost shift is causing, solar is having a significant

impact on how Cal ISO manages electricity production. Electricity demand over the course of

the day typically resembles a sine wave with a peak between 4-6PM and a similar magnitude and

34

length valley around 3AM. Depending on the latitude, solar panels generate their maximum

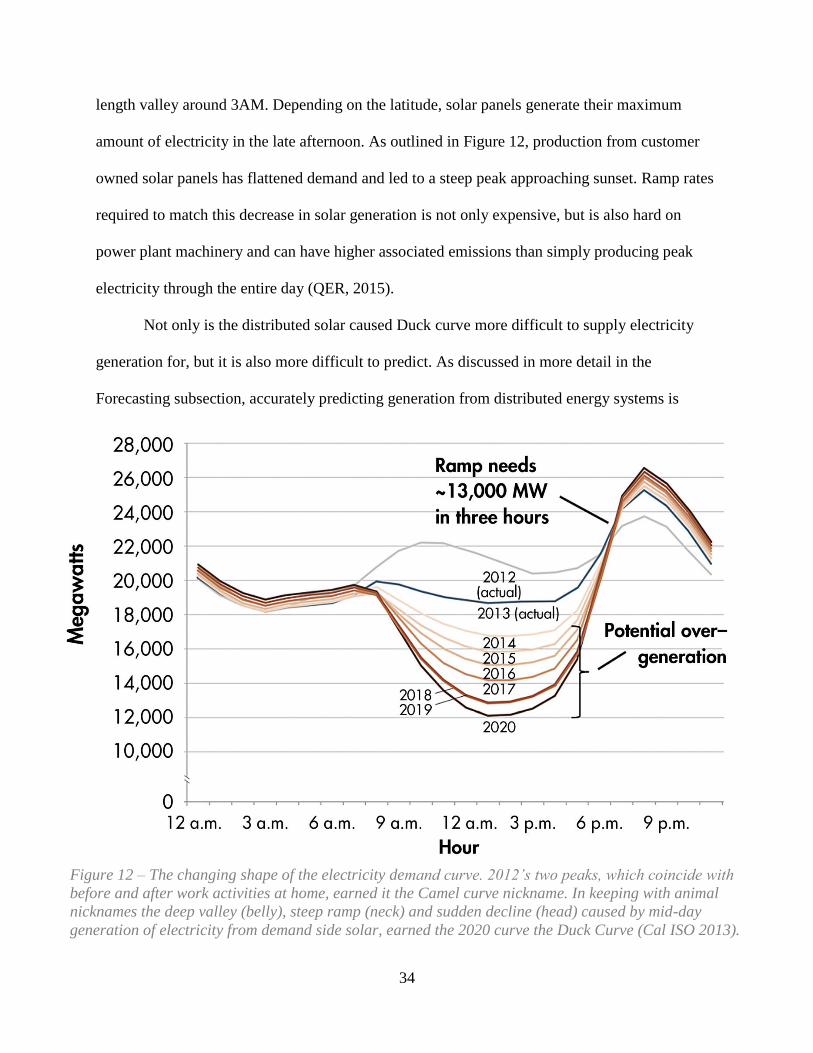

amount of electricity in the late afternoon. As outlined in Figure 12, production from customer

owned solar panels has flattened demand and led to a steep peak approaching sunset. Ramp rates

required to match this decrease in solar generation is not only expensive, but is also hard on

power plant machinery and can have higher associated emissions than simply producing peak

electricity through the entire day (QER, 2015).

Not only is the distributed solar caused Duck curve more difficult to supply electricity

generation for, but it is also more difficult to predict. As discussed in more detail in the

Forecasting subsection, accurately predicting generation from distributed energy systems is

Figure 12 – The changing shape of the electricity demand curve. 2012’s two peaks, which coincide with

before and after work activities at home, earned it the Camel curve nickname. In keeping with animal

nicknames the deep valley (belly), steep ramp (neck) and sudden decline (head) caused by mid-day

generation of electricity from demand side solar, earned the 2020 curve the Duck Curve (Cal ISO 2013).

35

difficult. One of these reasons is that most DG systems are installed “behind the meter,” meaning

grid operators only have insight into the net demand, and not the independent variables of solar

generation and on-site demand (Letendre, 2014, p. v). The ramp rate of solar panels, which can

quickly change the amount of electricity generated due to a passing cloud, adds another layer to

forecasting algorithms. When combined with weather forecasts that are both temporally

inaccurate, and do not have enough locational granularity, the task is almost impossible (ibid).

For these reasons Cal ISO does not currently include DG systems in demand forecasts, although

the organization is working on a pilot algorithm to predict generation; there are no plans to

incorporate the results of this algorithm into demand forecasts (ibid).

One of the final unique characteristics of the California electricity industry to be

discussed as a part of this research paper is the ability of local governments to create public

power agencies (CMUA, 2003). As previously discussed, decoupling bases local utilities’

revenues on assets under management. Via public power agencies, local governments are able to

purchase the electrical infrastructure within their jurisdiction, despite IOUs regulatory protected

service territory monopolies (Eskenazi, 2014). Therefore, the creation of new public power

agencies threatens to decrease future revenues for the state’s IOUs. This purchasing authority

extends beyond standard city governments and includes almost any formal body regardless of its

involvement or expertise in energy generation such as school boards, water districts, and public

transit authorities (Eskenazi, 2014). Based on growing consumer demand for renewable energy,

an increasing number of applications have been submitted to create new public power agencies

(Eskenazi, 2014). While the scale of public power authorities is currently minimal, they could

radically shift the utility landscape and require an increased role from the Cal ISO to maintain

infrastructure and insure reliability (ibid).

36

Hawaii

Where California leads in total installed capacity, Hawaii leads in distributed renewable

penetration: one in nine customers has rooftop solar installed (Wesoff, 2014). Growth in

distributed solar has been fueled by electricity rates at 34 cents per kilowatt hour, which is more

than three times higher than the national average (HECO, 2013). Like many things in the

Hawaiian Islands, much of the cost associated with power production is a result of supply chain

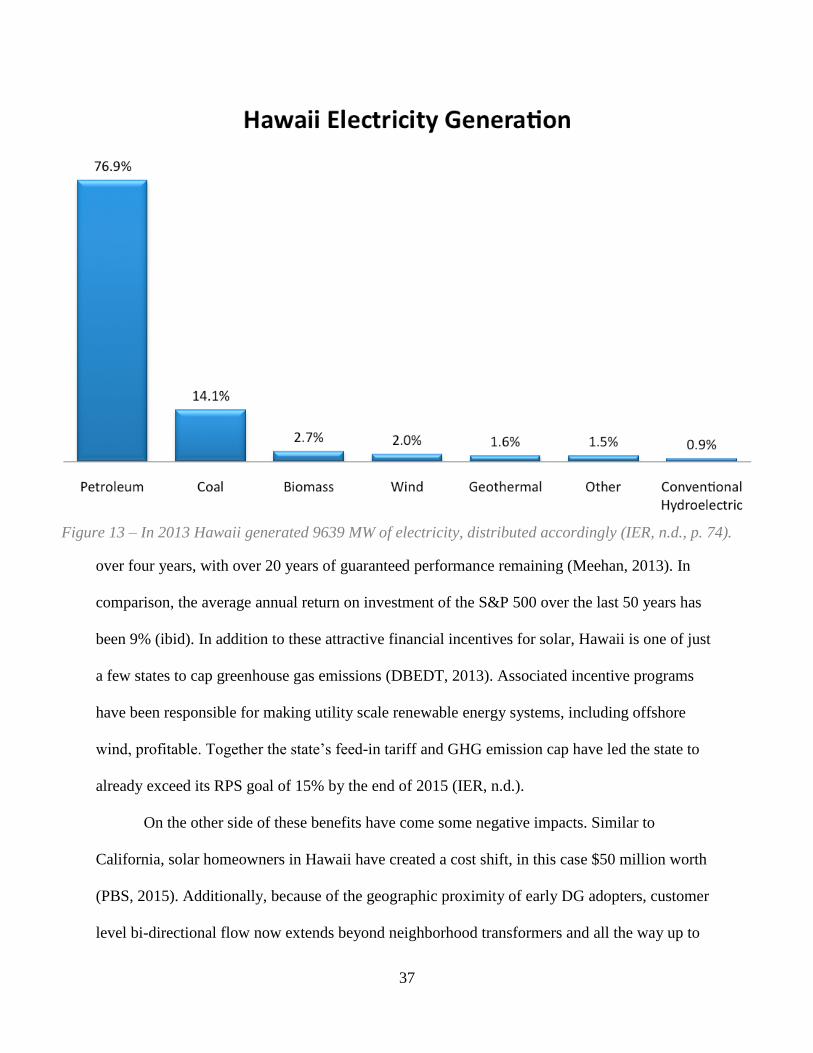

costs, mainly, transporting fuel to the remote islands. As outlined in Figure 13, petroleum

accounts for the overwhelming majority of electricity generated by the HECO, the state’s

electricity conglomerate (IER, n.d.).

Unfortunately, energy generation from petroleum causes significant pollution, including

greenhouse gas emissions. This combination of the high expense and environmental impacts has

made Hawaii a popular market for alternative energy generation systems. Biomass and waste-to-

energy systems experienced early adoption, as legislatures recognized that using part of the

state’s limited space for landfills was a losing proposition. Offshore wind has also seen success,

as the prevailing winds that made Hawaii an important trade waystation continue today. The

distributed energy generation source that has been most popular, however, is solar. Rooftop solar