separate financial statements - sygnity financial statements in... · 2011 program ... mr raimondo...

TRANSCRIPT

SEPARATE FINANCIAL STATEMENTS in accordance with the International Financial Reporting Standards for the fiscal year commenced October 1, 2015 and ended September 30, 2016

9 grudnia 2013

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

Warsaw, December 16, 2016

Jan Maciejewicz

Roman Durka

Jakub Leśniewski

President of the Management Board

Vice-President of the Management Board

Vice-President of the Management Board for Finance

……………………………

……………………………

……………………………

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

Table of contents

Separate statement of comprehensive income .................................................................................................................. 5

Separate balance sheet ................................................................................................................................................... 6

Separate statement of changes in equity .......................................................................................................................... 7

Separate statement of cash flows .................................................................................................................................... 8

Supplemental information ............................................................................................................................................... 9

1. General information ........................................................................................................................................... 9

1.1 Sygnity S.A. ........................................................................................................................................... 9

1.2 Supervisory Board .................................................................................................................................. 9

1.3 Management Board .............................................................................................................................. 10

1.4 Auditor ................................................................................................................................................ 10

2. Basis for preparation of the financial statements ................................................................................................ 11

3. Basic accounting principles ............................................................................................................................... 13

3.1 Application of the new standards, changes to standards and interpretation ............................................. 13

3.2 Changes to accounting principles and to data presentation ..................................................................... 14

3.3 Relevant accounting principles .............................................................................................................. 14

4. Financial risk management ............................................................................................................................... 26

4.1 Financial risk factors............................................................................................................................. 26

4.1.1 Market risk .................................................................................................................................... 26

4.1.2 Credit risk ...................................................................................................................................... 26

4.1.3 Liquidity risk .................................................................................................................................. 27

4.2 Capital risk management ...................................................................................................................... 28

5. Important estimates and accounting assessments ............................................................................................. 29

6. Information on operating segments .................................................................................................................. 30

7. Approval of financial statements for the fiscal year 2014/2015 ........................................................................... 30

8. Sales revenues ................................................................................................................................................ 31

9. Costs by type and cost of goods and services sold ............................................................................................. 31

10. Other operating revenues ................................................................................................................................. 32

11. Other operating expenses ................................................................................................................................ 32

12. Financial revenues ........................................................................................................................................... 33

13. Financial expenses ........................................................................................................................................... 33

14. Income tax ...................................................................................................................................................... 33

14.1 Tax burden .......................................................................................................................................... 33

14.2 Effective tax rate reconciliation ............................................................................................................. 34

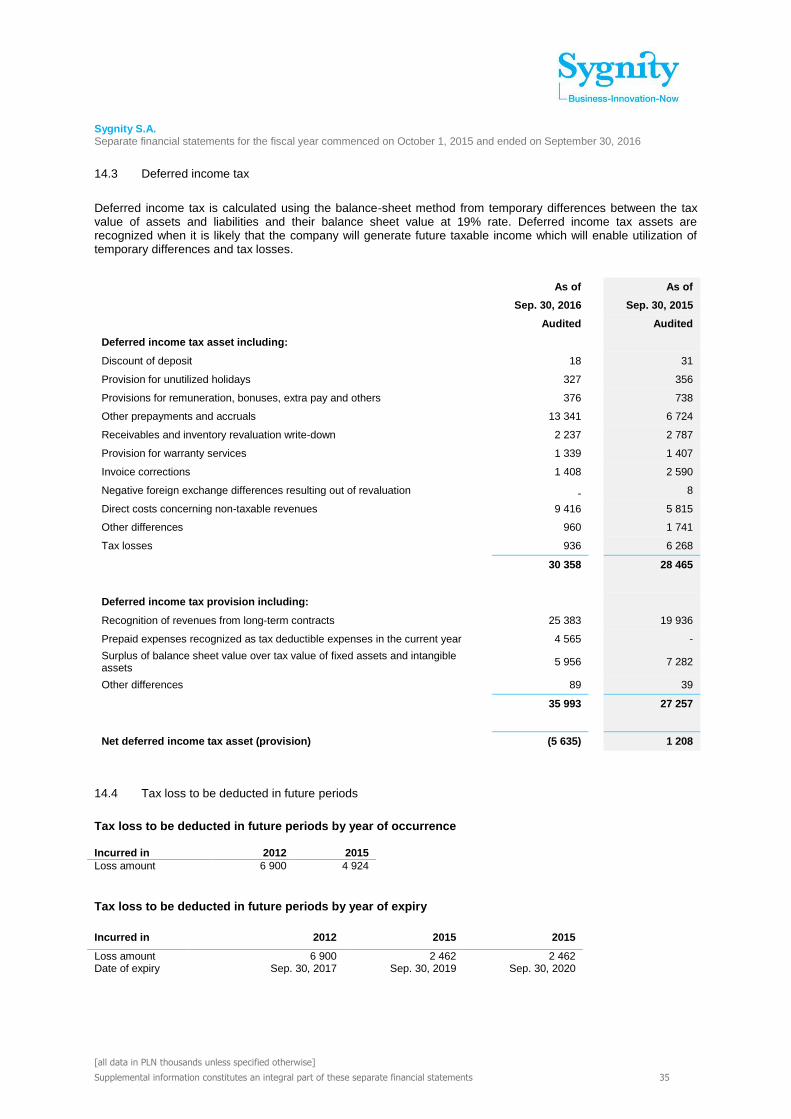

14.3 Deferred income tax............................................................................................................................. 35

14.4 Tax loss to be deducted in future periods .............................................................................................. 35

14.5 Tax settlements ................................................................................................................................... 36

15. Loss per share ................................................................................................................................................. 36

16. Tangible fixed assets ....................................................................................................................................... 37

17. Intangible assets ............................................................................................................................................. 39

18. Goodwill impairment test .................................................................................................................................. 41

19. Investments in codependent entities ................................................................................................................. 42

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements

4

20. Shares and interests in subsidiaries................................................................................................................... 43

21. Financial assets ............................................................................................................................................... 45

22. Inventory ........................................................................................................................................................ 45

23. Trade receivables and other receivables ............................................................................................................ 46

24. Long-term contracts......................................................................................................................................... 48

25. Cash and cash equivalents ............................................................................................................................... 49

26. Equity ............................................................................................................................................................. 49

26.1 Share capital ......................................................................................................................................... 49

Shareholder structure ...................................................................................................................................... 49

Treasury shares ............................................................................................................................................... 49

26.2 Shares of Sygnity S.A. held by Members of Management Board and Members of Supervisory Board ........... 50

26.3 Other capital items ................................................................................................................................ 51

27. Employee share schemes ................................................................................................................................. 51

2011 Program ................................................................................................................................................. 51

2013 Program ................................................................................................................................................. 51

28. Interest-bearing bank credits and loans ............................................................................................................ 52

29. Bond liabilities and other financial liabilities ....................................................................................................... 53

30. Provisions........................................................................................................................................................ 55

31. Trade liabilities and other liabilities ................................................................................................................... 56

32. Deferred income .............................................................................................................................................. 57

33. Associates and transactions with associates....................................................................................................... 57

34. Compensation of the top management.............................................................................................................. 58

35. Structure of employment .................................................................................................................................. 59

36. Contingent liabilities ......................................................................................................................................... 59

37. Seasonal or periodical nature of operations ....................................................................................................... 60

38. Claims and disputes ......................................................................................................................................... 60

39. Events after the reporting period ...................................................................................................................... 60

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements

5

Separate statement of comprehensive income

Period:

Period:

from Oct. 1, 2015

from Oct. 1, 2014

Note to Sep. 30, 2016

to Sep. 30, 2015

Audited

Audited

Adjusted*

Net revenue from sales

Revenue from sales of products and services 8 337 605

368 612

Revenue from sales of goods and materials 8 59 862

39 910

397 467

408 522

Cost of products, goods and materials sold

Cost of producing the products and services sold 9 (288 830)

(308 686)

Value of goods and materials sold 9 (52 826)

(35 126)

(341 656)

(343 812)

Gross profit on sales

55 811

64 710

Cost of sales 9 (20 472)

(19 273)

Overhead costs 9 (36 810)

(43 707)

Other operating income 10 1 817

3 768

Other operating expenses 11 (303)

(1 618)

Operating profit

43

3 880

Financial income 12 585

373

Financial expenses 13 (4 030)

(4 543)

Result on financial operations

(3 445)

(4 170)

Write-down of joint-venture 19 (344)

-

Loss before tax

(3 746)

(290)

Income tax 14 (6 755)

(3 700)

Net loss

(10 501)

(3 990)

Other comprehensive income

-

-

Revaluation of provision for pension benefits

2

-

Total loss

(10 499)

(3 990)

Basic and diluted loss per share (in PLN) 15 (0.92)

(0.35)

* - adjusted data. For details see note 3.2

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements

6

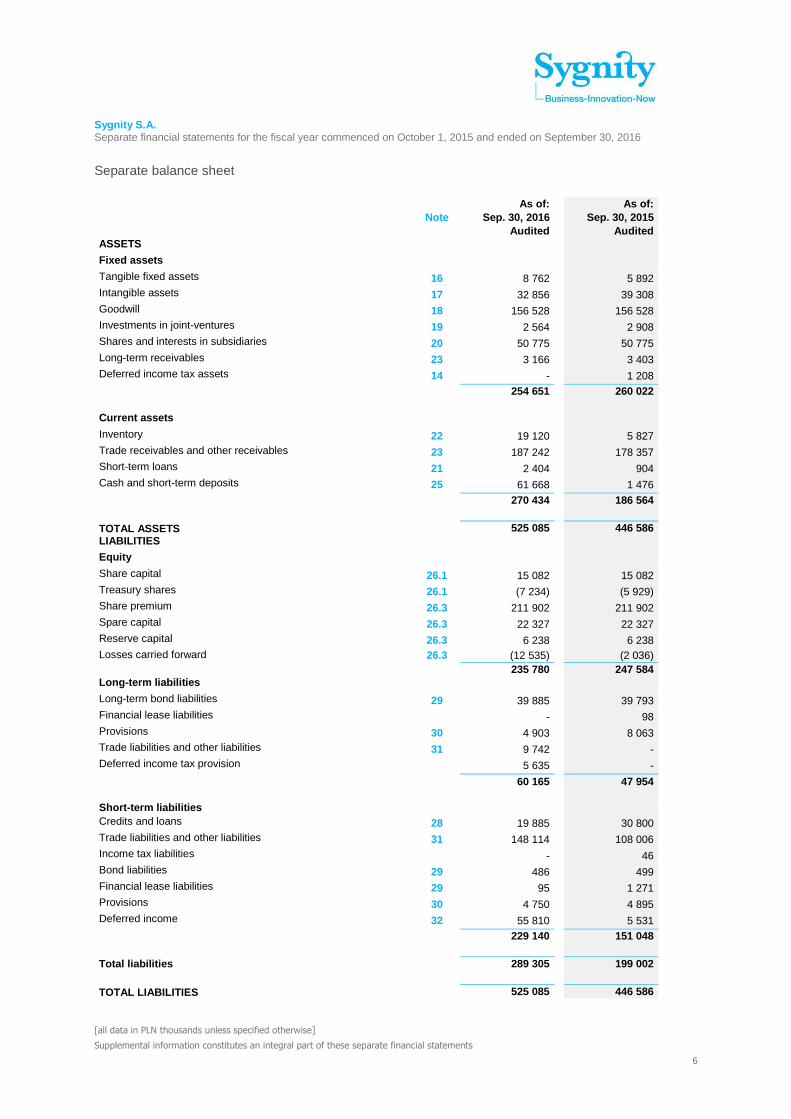

Separate balance sheet

As of:

As of:

Note Sep. 30, 2016

Sep. 30, 2015

Audited

Audited

ASSETS

Fixed assets

Tangible fixed assets 16 8 762

5 892

Intangible assets 17 32 856

39 308

Goodwill 18 156 528

156 528

Investments in joint-ventures 19 2 564

2 908

Shares and interests in subsidiaries 20 50 775

50 775

Long-term receivables 23 3 166

3 403

Deferred income tax assets 14 -

1 208

254 651

260 022

Current assets

Inventory 22 19 120

5 827

Trade receivables and other receivables 23 187 242

178 357

Short-term loans 21 2 404

904

Cash and short-term deposits 25 61 668

1 476

270 434

186 564

TOTAL ASSETS

525 085

446 586

LIABILITIES

Equity

Share capital 26.1 15 082

15 082

Treasury shares 26.1 (7 234)

(5 929)

Share premium 26.3 211 902

211 902

Spare capital 26.3 22 327

22 327

Reserve capital 26.3 6 238

6 238

Losses carried forward 26.3 (12 535)

(2 036)

235 780

247 584

Long-term liabilities

Long-term bond liabilities 29 39 885

39 793

Financial lease liabilities

-

98

Provisions 30 4 903

8 063

Trade liabilities and other liabilities 31 9 742

-

Deferred income tax provision

5 635

-

60 165

47 954

Short-term liabilities

Credits and loans 28 19 885

30 800

Trade liabilities and other liabilities 31 148 114

108 006

Income tax liabilities

-

46

Bond liabilities 29 486

499

Financial lease liabilities 29 95

1 271

Provisions 30 4 750

4 895

Deferred income 32 55 810

5 531

229 140

151 048

Total liabilities

289 305

199 002

TOTAL LIABILITIES

525 085

446 586

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements

7

Separate statement of changes in equity

Share capital

Treasury shares

Share premium

Spare capital

Reserve capital

Retained earnings /

(losses carried

forward)

TOTAL EQUITY

As of October 1, 2014

15 082

(5 560)

211 902

16 090

-

14 429

251 943

Total comprehensive income:

- net loss

-

-

-

-

-

(3 990)

(3 990)

Allocation of part of net profit of previous year for the spare capital and reserve capital

-

-

-

6 237

6 238

(12 475)

-

Share buyback

-

(369)

-

-

-

-

(369)

As of September 30, 2015

15 082

(5 929)

211 902

22 327

6 238

(2 036)

247 584

As of October 1, 2015

15 082

(5 929)

211 902

22 327

6 238

(2 036)

247 584

Total comprehensive income:

- net loss

-

-

-

-

-

(10 501)

(10 501)

- revaluation of provision for retirement benefits

-

-

-

-

-

2

2

Share buyback

-

(1 305)

-

-

-

-

(1 305)

As of September 30, 2016

15 082

(7 234)

211 902

22 327

6 238

(12 535)

235 780

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 8

Separate statement of cash flows

Period:

Period:

from Oct. 1, 2015

from Oct. 1, 2014

Note to Sep. 30, 2016

to Sep. 30, 2015

Audited

Audited

Cash flows from operating activities

Loss before tax

(3 746)

(290)

Adjustments for:

97 148

(12 733)

Depreciation 9 16 126

14 382

Interest income and expenses

3 416

4 236

Profits on investing operations

(252)

(2 392)

Other adjustments

-

(98)

Change in working capital *

77 858

(28 861)

Net cash generated from operating activities

93 402

(13 023)

Income tax paid

(3 256)

(2 846)

90 146

(15 869)

Cash flows from investing activities

Inflow from sales of tangible fixed assets and intangible assets

-

100 Purchase of tangible fixed assets and intangible assets

(6 942)

(3 426)

R&D expenses

(5 824)

(8 852)

Expenses for purchase of shares and interests

-

(1 085)

Loans granted

(1 500)

(330)

Loans repaid

-

7

(14 266)

(13 586)

Cash flows from financing activities

Expenses for purchase of shares and interests

(1 305)

(369)

Inflows from issue of debt securities 29 -

40 000

Expenses for redemption of debt securities 29 -

(40 000)

(Repayments) / inflows from credits and loans taken on

(10 915)

26 775

Repayment of financial lease liabilities

(456)

(1 810)

Interest paid

(3 012)

(3 231)

(15 688)

21 365

Total net cash flows

60 192

(8 090)

Cash at the beginning of the period

1 476

9 566

Cash at the end of the period

61 668

1 476

*Change in working capital

Change in provisions

(5)

(2 434)

Change in inventory

(13 293)

5 542

Change in receivables

(8 648)

(3 670)

Change in liabilities

49 433

(31 852)

Change in prepayments and accruals

50 371

3 553

Total

77 858

(28 861)

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 9

Supplemental information

1. General information

1.1 Sygnity S.A.

Sygnity S.A. (the “Parent company”, “Entity”, “Sygnity”, “Issuer” or “Company”) is a joint stock company incorporated in Poland, with its registered seat in Warsaw, ul. Franciszka Klimczaka 1, entered into the register of entrepreneurs of the National Court Register kept by the Regional Court, 13th Economic Division of the National Court Register, under KRS number KRS 0000008162. The Company has been assigned the REGON statistical number 190407926. The Company has been established for an indefinite term. Company’s fiscal year commences October 1, and ends September 30. The core business of the Company is software, and IT consultancy and related business. The Company’s offering includes the following IT services:

Software development and implementation,

IT projects consultancy,

Integration of IT systems,

Outsourcing services,

Hardware delivery and installation,

Construction of local and wide area computer networks (LAN and WAN),

Software, network and hardware maintenance services,

Training services.

The Company has been established for an indefinite term. The Company's shares have been listed at the Warsaw Stock Exchange since 1995.

1.2 Supervisory Board

As of September 30, 2016 the Supervisory Board consisted of the following members:

Mr Tomasz Sielicki - Chairman of the Supervisory Board

Mr Kristof Zorde - Vice-Chairman of the Supervisory Board

Mr Piotr Rymaszewski - Member of the Supervisory Board

Mr Piotr Skrzyński - Member of the Supervisory Board

Mr Ryszard Wojnowski - Member of the Supervisory Board

On November 16, 2016 the Extraordinary General Meeting of Shareholders appointed the Supervisory Board for a new three year-long term in office, consisting of the following members who were not replaced as on the day of preparation of these financial statements:

Mr Raimondo Eggink - Chairman of the Supervisory Board

Ms Beata Gessel - Kalinowska vel Kalisz - Member of the Supervisory Board

Mr Tomasz Sielicki - Vice-Chairman of the Supervisory Board

Mr Piotr Skrzyński - Member of the Supervisory Board

Mr Mariusz Bogdan Tokarski - Member of the Supervisory Board

Mr Paweł Zdunek - Member of the Supervisory Board

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 10

1.3 Management Board

As of the day of publication of these financial statements the Management Board of the Company was composed of:

Mr Jan Maciejewicz - President of the Management Board

Mr Roman Durka - Vice-President of the Management Board

Mr Jakub Leśniewski - Vice-President of the Management Board for Finance

During the fiscal year ended September 30, 2016 following changes to the composition of the Management Board occurred:

Between October 1, 2015 and February 12, 2016 the Company's Management Board was as follows:

Mr Janusz R. Guy - President of the Management Board

Mr Jakub Leśniewski - Vice-President of the Management Board for Finance

Ms Magdalena Bargieł - Vice-President of the Management Board for HR

Mr Roman Durka - Vice-President of the Management Board

Mr Bogdan Zborowski - Vice-President of the Management Board for Sales

On February 12, 2016 the Company's Supervisory Board adopted the resolution to appoint Mr Jan Maciejewicz as the Vice-President of the Management Board for the current term and adopted resolutions appointing the following persons as members of the Management Board of the Company:

Mr Janusz R. Guy as President of the Management Board;

Ms Magdalena Bargieł as Vice-President of the Management Board for HR;

Mr Roman Durka as Vice-President of the Management Board;

Mr Jakub Leśniewski as Vice-President of the Management Board for Finance;

Mr Jan Maciejewicz as Vice-President of the Management Board;

for the new common three year term of office that commenced on the day of the General Meeting of Shareholders approving the financial statements for the fiscal year ended September 30, 2015, i.e. on March 24, 2016. On March 24, 2016, on the day the General Meeting of Shareholders that approved the financial statements for the fiscal year ended September 30, 2015 was held the term in office of Mr Bogdan Zborowski as Member of the Management Board has expired. On May 30, 2016 the Supervisory Board of the Company has made a decision to recall Mr Janusz R. Guy – President of the Management Board and Ms Magdalena Bargieł – Vice-President of the Management Board for HR from their positions in the Management Board. At the same time the Supervisory Board of the Company has on May 30, 2016 decided to appoint Mr Jan Maciejewicz, then the Vice-President of the Management Board, as the President of the Management Board of Sygnity. The above listed changes to the Management Board of the Company have no influence on the duration of the present common term of office of the Management Board of Sygnity.

1.4 Auditor

PricewaterhouseCoopers Sp. z o. o.

Al. Armii Ludowej 14

00-638 Warszawa

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 11

2. Basis for preparation of the financial statements

These separate annual financial statements were drawn up in compliance with the International Financial Reporting Standards ("IFRS") approved by the EU. The IFRS include standards and interpretations approved by the International Accounting Standards Board (IASB) and the International Financial Reporting Interpretations Committee (IFRIC).

The separate financial statements were drawn up in accordance with the historical cost principle, except for derivative financial instruments and financial assets held for sale which are measured at fair value.

Preparation of separate financial statements compliant with IFRS requires application of relevant accounting estimates. Furthermore, it requires the Management Board to use its own judgment while applying the adopted accounting principles. Issues which require a more thorough judgment, more complex issues, as well as assumptions and estimates relevant for the separate financial statements have been presented in Note 5. These separate financial statements should be read in combination with the consolidated financial statements for the fiscal year ended on September 30, 2016.

These annual separate financial statements were drawn up on going concern assumption. The Management Board of the Company has drawn-up the Company’s cash flow plan for the next fiscal year commencing on October 1, 2016 and ending on September 30, 2017, that takes into account the access to sources of financing allowing funding, implementation and maintenance of large scale IT projects, timely settlement of liabilities and continuing growth of the Entity. Management Board expects the Company to be capable of settling all its liabilities: repayment of interests, credit, loan and bond installments, as well as accounts due to the suppliers when due. As of the date of these interim condensed consolidated financial statements, the Company has met the terms and conditions for continuation of credit agreements in regard to covenants and other liabilities resulting out of the credit agreements and bonds issued.

Pursuant to the resolution of the Extraordinary General Meeting of Shareholders of the Company of November 28, 2014 Management Board of Sygnity S.A obtained consent for execution of the short- and medium-term bond issue program, which will be carried out in a period not extending beyond December 31, 2017. Maximum Program value is 100 000. In addition, the Management Board of the Company intends to refinance the debt or extend the existing lines of credit with the banks for subsequent term.

Due to formal requirements, including those concerning the use of prudent valuation principle and going concern principle, the Management Board points to the following issues. The Company is a party to external financing agreements for a total amount of 52 851 (of which 39 885 are long-term bond liabilities due on December 19, 2017 and 13 685 is the debt in renewable credits maturing on March 31, 2017) as of the balance sheet date (see notes 28 and 29), subject to covenants concerning, among others, its financial results.

Changes in valuations of long-term contracts (see notes 23 and 24) may influence (both positively and negatively) the financial result and profitability of the Company. In the negative case they may result in breach of covenants of credit agreements and bond issue agreements, which in turn may result in increased costs of financing, necessity to renegotiate financing terms and conditions or the liabilities being called in for immediate repayment, thus may constitute significant uncertainty as to continuation of business by the Company in foreseeable future. The valuations of long-term contracts and their performance in subsequent reporting periods depends on many factors, including external factors, beyond the Parent company’s control.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 12

With respect to one of such contracts being performed by the Company the Ordering Party (a public sector client) declared that it will not be continuing the already commenced work in the initially agreed scope. As a result, the Company is currently in the process of negotiating the way of contract termination as well as potential participation in execution of the renewed project in a new formula, the final result of which cannot be clearly determined as of the date of drawing up these financial statements. Considering the valuation of the contract on the balance sheet date (not yet invoiced receivables for work items resulting from long-term contracts in amount of 16 715) the Management Board of the Company – to its best knowledge of the status of the negotiations in progress and based on review of rights and obligations of the parties resulting out of their agreement – adopted various scenarios taking into account the probabilities of occurrence of results of contract settlement. Due to the ongoing negotiations, the real final valuation of the contract may differ from the one disclosed in these financial statements.

Concerning another key contract, there are also negotiations in progress with respect to changes to the method of its execution, thus the future valuation of this contract may differ from the one disclosed in these statements. Moreover, during performance of this contract the Management Board of the Company decided to formulate and put forward claims against a subcontractor for a maximum amount of 37 000. Based on negotiations being conducted with the supplier and contract analysis the Management Board assesses that the amount likely to be recovered through settlement or litigation is approximately 18 000. The cost budget of this project takes into account the adjustment for this amount.

In the opinion of the Management Board the described events that potentially may form grounds for establishment of a valuation write-down of estimated receivables require an ongoing analysis from the point of view of their impact on Company’s financial standing, however as of the day of drawing up these statements in the opinion of the Management Board of the Company no premises occurred that would substantiate the need to perform write-downs for the abovementioned long-term contracts. Regardless of the above the Company, taking into account the results of such analysis and the market situation as well as standpoints of the contracting parties shall consider commencing measures to assure undisturbed functioning of the Company. Unless the circumstances described above as significant uncertainty occur, in the opinion of the Management Board all covenants and obligations resulting from under the credit agreements and bonds issues will continue to be met in the foreseeable future. These statements do not account for any adjustments related to lack of possibility to continue business operations, as in the opinion of the Management Board the statements should be drawn-up on going concern principle. In the opinion of the Management Board the working capital of the Company and possibilities to renegotiate current agreements or obtaining alternative sources of financing allow for assuring continuation of its business and maintaining liquidity for at least 12 months following the date of preparation of these financial statements. These separate financial statements of Sygnity S.A. cover data for the period of 12 months ended September 30, 2016 and as of September 30, 2016, contain comparable data for the period of 12 months ended September 30, 2015 and as of September 30, 2015. Financial data contained in these financial statements are stated in Polish zlotys (“PLN"), and all values are in PLN thousands, unless otherwise specified. These financial statements were approved for publication by the Management Board on December 16, 2016.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 13

3. Basic accounting principles

3.1 Application of the new standards, changes to standards and interpretation

In these financial statements the Company has for the first time applied the new and amended standards and interpretations applicable to financial statements for fiscal years commencing January 1, 2015 and beyond:

a) Improvements to IFRS 2011-2013

b) Defined benefits plans: Employee contributions - Amendments to IAS 19

c) Improvements to IFRS 2010-2012

In these financial statements the Company did not decide on early adoption of the following new and amended standards and interpretation, which entered into force for financial statements for the fiscal years commenced on January 1, 2016:

a) Annual amendments to IFRS 2012-2014

b) Amendments to IFRS 11 concerning acquisition of interest in joint operations

c) Amendments to IAS 16 and IAS 38 on depreciation

d) Amendments to IFRS 10, IFRS 12 and IAS 28 on "Investment entities: Applying the Consolidation

Exception"

e) Amendments to IAS 27 on equity method in separate financial statements

f) Amendments to IAS 1

In these financial statements the Company did not decide on early adoption of the following published standards, interpretations or amendments to existing standards before their entry into force: a) IFRS 9 "Financial instruments: Classification and measurement and hedge accounting"

b) IFRS 15 - "Revenue from Contracts with Customers"

c) Amendments to IFRS 10 and IAS 28 “Sales or contribution of assets between the investor and its

associate or joint venture”

d) IFRS 16 ”Leases”

e) Amendments to IAS 12 “Recognition of deferred tax assets for unrealised losses”

f) Amendments to IAS 7 “Disclosure initiative”

g) Amendments to IFRS 2 “Classification and valuation of share-based payment transactions”

Assessment of influence of the above amendments on the financial statements:

In the opinion of the Management Board application by the Company of the new or amended standards and

interpretations did not have significant influence on the financial statements of the Company.

The Management Board of the Company is analyzing the expected influence of adoption of the standards not used so far, however at the present stage it does not seem that adoption of these standards, except for IFRS 15 – “Revenue from Contracts with Customers”, would have a significant influence on Company’s financial statements.

In the opinion of the Management Board of the Company the IFRS 15 will have a significant influence on the financial statements as the model of recognizing the revenue from contracts with clients changes. As on the date of preparation of these financial statements the Company has not completed its analysis of influence of the new standard.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 14

3.2 Changes to accounting principles and to data presentation

In the fiscal year ended September 30, 2016 the Company has not made any changes to the accounting

principles and to data presentation except for a change of classification of part of overhead expenses and cost of

producing the products and services sold to cost of sales to better reflect the amounts of costs of the Company as

per where they occur.

As the result of change of classification of part of overhead expenses and cost of producing the products and

services sold to cost of sales, the overhead expenses in the fiscal year ended September 30, 2015 decreased by

1 034, cost of producing the products and services sold decreased by 385 and the cost of sales plus the sum of

the above two amounts, namely 1 419.

There were no other changes of accounting principles, presentation of items in the separate balance sheet and the separate statement of comprehensive income with respect to the status as on September 30, 2015.

3.3 Relevant accounting principles

The key accounting principles applied when drawing up these separate financial statements are presented below. These principles were applied in all presented periods on continuous basis, unless specified otherwise.

3.3.1 Functional and reporting currency

The functional and reporting currency of these annual separate financial statements is the Polish zloty (PLN).

Exchange rates used for the

purposes of balance sheet valuation Average arithmetic exchange rates for

individual fiscal years were

Currency Sep. 30, 2016 Sep. 30, 2015

fiscal year commenced Oct. 1,

2015 and ended Sep. 30, 2016

fiscal year commenced Oct. 1,

2014 and ended Sep. 30, 2015

EUR 4.3120 4.2386 4.3348 4.1707

USD 3.8558 3.7754 3.9268 3.6419

3.3.2 Measurement of foreign currency denominated items

Foreign currency denominated transactions are converted into the functional currency at the rate prevailing on the transaction date. Foreign exchange gains and losses under settlement of those transactions and resulting from balance sheet valuation of foreign currency denominated assets and liabilities are recognized accordingly in the profit and loss account.

Foreign exchange gains and losses relating to financing activities are recognized in the profit and loss account in the "Financial revenues" or "Financial expenses" items. All other foreign exchange profits or losses are recognized in the profit and loss account in the “Other operations” item.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 15

3.3.3 Investments in subsidiaries, associates and jointly controlled entities

Subsidiary entities are all entities (including special purpose vehicles) in relation to which the Company has the right to manage their financial and operating policies, which is usually accompanied by possession of the number of shares / interest granting over half of the total number of voting rights, unless such ownership does not provide the control. While assessing whether the Company controls a given entity the existence and effect of potential voting rights which can be exercised at a given time or changed for shares/interest are taken into account. Investments in subsidiary entities are recognized at their purchase price less possible impairment write-offs.

Associated entities are those entities on which the Company can exert significant influence but has no control over. Typically this is equivalent to having between 20% and 50% of voting rights at the General Meeting of the Company. The investments in the associates are recognized in the balance sheet at their purchase price less possible impairment write-offs.

Jointly controlled entities are joint ventures requiring appointment of a legal person, partnership or any other entity wherein every partner to the joint venture holds interest. The interest of the Company in such joint-venture is recognized in the balance sheet at value of contribution.

3.3.4 Fixed assets, current assets and offsetting

Assets the realization of which is expected within 12 months following the balance sheet date are recognized as current assets. The other assets are recognized as fixed assets. Neither assets, liabilities, revenue or expenses are offset unless this is allowed by a standard or an interpretation.

3.3.5 Tangible fixed assets

Buildings, machinery and equipment, means of transportation and other fixed assets are recognized at their purchase price/cost of producing less any subsequent depreciation and all impairment write-downs and plus any improvements made. Land is recognized at its purchase price and not subsequently depreciated.

Expenditures for improvements are recognized in the balance sheet value of the fixed asset or as a separate fixed asset (where appropriate) only when it is likely that this will result in economic benefit to the Company, while the costs of the asset can be reliably measured. The balance sheet value of replaced parts is removed from the balance sheet. All other expenditures incurred for repairs and maintenance are posted to the profit and loss account in the financial period in which they were incurred.

Depreciation is applied to the purchase price or the cost of producing the asset concerned, less the residual value of that asset and plus the amount of improvements made to the asset concerned. The depreciation rates used reflect the useful lifetime of the tangible fixed assets. Depreciation is calculated using the straight-line method. The depreciation rates for particular groups of tangible fixed assets are:

- computer sets and servers: 20% - 30%

- facsimiles, copiers and similar office equipment: 10% - 20%

- other technical equipment: 10%

- telephone exchanges: 10%

- means of transportation: 14% - 33%

- buildings and structures: 10% - 20%

The residual value, useful lifetime and method of depreciation of assets are reviewed on annual basis and, if required – adjusted, effective at the beginning of the next fiscal year.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 16

A given tangible fixed asset may be removed from the balance sheet following its disposal or in the event when no economic benefits resulting from further use of that asset are expected. All profits or losses resulting from removal of a given tangible fixed asset from the balance sheet are recognized in the profit and loss account in the period when it was written-off.

In the event the balance sheet value of a fixed asset exceeds its estimated recoverable value, its balance sheet value is immediately reduced to the recoverable value ("Impairment of non-financial assets"). Impairment write-downs on non-financial assets are recognized in other operating costs, while reversal of write-downs is recognized in other operating income.

3.3.6 Impairment of non-financial assets

Assets with unspecified useful lifetime, such as goodwill, are not subject to depreciation, but are tested on an annual basis for possible impairment. Assets subject to depreciation are tested for impairment whenever any events or changed circumstances indicate a possibility of failure to realize their balance sheet value. A loss due to impairment is recognized in the amount by which the balance sheet value of a given asset exceeds its recoverable value. The recoverable value is the higher of: the assets’ fair value less cost to sell, or the usable value. For the purposes of impairment tests assets are grouped at the lowest level with reference to which separate cash flows (cash generating units) may be identified. Non-financial assets, other than goodwill, in relation to which impairment has been determined earlier on, are assessed as of each balance sheet date for premises indicating the possibility of reversal of a given write-down.

3.3.7 Goodwill

The goodwill resulting out of acquisition of a business entity is initially recognized at the price of acquisition being the surplus cost of acquisition of business entities over the share of the acquiring entity in the net fair value of identifiable assets, liabilities and contingent liabilities. Following initial recognition, the goodwill is recognized at purchase price less any accumulated impairment write-downs. Goodwill is tested for possible impairment on an annual basis or more frequently - in case circumstances or changes occur that indicate possible impairment. Goodwill impairment write-downs are irreversible. Profits and losses from sale of the operations belonging to cash generating units to which goodwill has been allocated account for relevant part of the company’s balance sheet value, concerning the sold operations.

In order to carry out a the impairment tests, the goodwill is allocated to cash generating units (CGUs). Allocations are performed for such cash generating units or groups of cash generating units that are expected to benefit from the combination that resulted in the goodwill being generated.

3.3.8 Other intangible assets

Intangible assets acquired within a separate transaction are initially recognized at purchase price. Intangible assets acquired by takeover of an economic entity are initially recognized at fair value as of the takeover date. Following initial recognition the other intangible assets are measured at the cost less amortization write-downs and impairment. The useful life of intangible assets is assessed at the time of initial recognition, and it is deemed definite or indefinite.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 17

Intangible assets with a specific useful life are amortized using the straight-line method throughout their useful life which is reflected in the amortization rates for particular groups of other intangible assets presented below:

cost of completed research and development work: 20% - 50%

concessions, patents, licenses, software and similar values: 5% - 50%

other intangible assets: 10% - 20%

relations with clients: 20%

order book: 50%

product brands: 10%

trademarks: 10% - 20%

Expenditures for research and development are capitalized provided the criteria specified in section "Costs of research and development works" are met.

Useful lifetimes are subject to annual reviews and, if required, adjusted beginning with the next fiscal year.

3.3.9 Research and development expenses

Costs of research and development work are posted to the profit and loss account at the time they are incurred. The costs which may be allocated directly, but are capitalized as part of a product in the form of software, include payroll costs related to research and development work on software and a relevant part of indirect applicable costs. Expenditures made on research and development work performed within a given project are capitalized provided it is possible to determine that:

from the technical point of view it is possible to complete an intangible asset so that it becomes fit for use,

the entity's management intends to complete an intangible asset for use or for sale,

it is possible for a given intangible asset to be used or sold,

it is possible to demonstrate how the intangible asset concerned will be generating likely future economic benefits,

there are appropriate technical, financial and other resources available that are necessary for a given intangible asset to be completed so that it will be fit for use or sale,

it is possible to reliably determine the amount of expenditures incurred in the course of research and development work that may be allocated to that intangible asset.

Following initial recognition of expenditures incurred for research and development work, the cost model requiring assets to be recognized at the purchase price/manufacturing cost less the accumulated amortization and accumulated impairment write-downs is applied. Capitalized costs of research and development work are amortized throughout the foreseeable period of generating revenues from sale of a given project.

The costs of research and development work are assessed for possible impairment of value on an annual basis - if an asset has not been rendered for use yet, or more often - if in the course of the reporting period there is a premise of impairment of value indicating that their balance sheet value may be impossible to recover.

3.3.10 Borrowing costs

In case of incurring borrowing costs concerning qualified assets the Company capitalizes the borrowing costs related directly to purchase, construction or manufacture of a qualified asset component within the cost of production of such an asset component.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 18

3.3.13 Financial instruments

The Company divides its financial assets into the following categories: recognized at fair value in the financial result, loans and receivables, as well as financial assets held for sale. The classification is based on the criterion of the aim of financial asset acquisition. The Management Board specifies the classification of its financial assets at their initial recognition.

Financial assets and liabilities are recognized in the Company’s balance sheet when the Company becomes party to a binding agreement. Financial assets are written-off the books when the rights to obtain cash flow due to them have expired or have been transferred, and the Company has transferred the total risk and all benefits resulting from the ownership title to them. A financial liability is written-off the books when it has been settled, annulled or when it has expired.

Loans and receivables

Loans and receivables are financial assets not included in derivatives, of determined or determinable payments, which are not quoted on any active market. They are included in current assets provided that their maturity date is not longer than 12 months following the balance sheet date, or when it is not longer than the regular operation cycle related to long-term contracts exceeding 12 months. The principles of valuating loans and receivables are presented in the section “Trade receivables and other receivables”.

Financial assets recognized at fair value in the financial result

The Company includes derivative instruments in instruments held for sale. Assets included in that category are current assets if they are sold within 12 months; if they are held for a longer period then they are recognized as fixed assets.

Financial assets held for sale

Financial assets held for sale are financial instruments which are not derivative instruments and are to be included in this category or ones which are not included in any other category. They are considered fixed assets unless the Management Board does not intend to dispose of them within 12 months from the balance sheet date.

Derivative instruments and hedge accounting

Due to its operations, the Company bears financial risks related to changes in currency exchange rates and interest rates. In order to hedge against these risks, the Company applies currency forward contracts. The Company does not apply hedge accounting.

Rules applicable while using derivatives are included in the Company’s risk management policy approved by the Management Board.

Derivatives are included in the category of “marketable” which are initially recognized at fair value and then they are measured at their fair value in the profit and loss account.

Investments in securities

Where a market convention assumes the provision of a security after a precisely defined period of time following the transaction date, investments in securities are recognized in account books and are written-off the books on the date of concluding a purchase or sale transaction. Investments in securities are initially valued at their fair value (plus transaction costs in case of financial assets held for sale).

Investments in securities are classified as valued at their fair value through the financial result or as held for sale and they are measured as of the balance sheet date at their fair value. When securities have been classified as valued at their fair value by the financial result, profits and losses resulting from the change of the fair value will be recognized in the profit and loss account for a given period. In case of assets held for sale, profits and losses resulting from the change of their fair value are recognized directly in capitals until the asset component is sold or the impairment is recognized. Accumulated profits and losses previously recognized in capitals are then transferred to the profit and loss account for a given period.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 19

3.3.14 Impairment of financial assets The Company assesses as of each balance sheet date whether there is objective evidence that the financial assets component or a group of financial assets is impaired.

The policy concerning impairment of receivables and loans is presented in section “Trade receivables and other receivables”. When determining whether securities included in the held for sale category have been impaired, a significant or continuing loss of the fair value of a given security below its cost is taken into consideration. If such evidence exists (in the case of financial assets held for sale), total losses incurred to date – determined as the difference between the purchase price and current fair value, less possible losses due to impairment already recognized in the profit and loss account – are excluded from the equity and recognized in the profit and loss account. The impairment losses already recognized in the profit and loss account and the losses due to capital instruments are not subject to reversal by the financial result.

3.3.15 Inventory Inventory is disclosed at its purchase price or at its production costs not higher than the net sales price. The production costs are made up of direct material costs and, as required, of the direct payroll costs and a justifiable part of indirect costs. Outgoing inventory of materials and goods is valued at actual prices. The net sales price corresponds to the estimated sales price less all costs necessary to complete the production and costs of rendering the inventory saleable or finding a purchaser (i.e. sales and marketing costs, etc.).

3.3.16 Trade receivables and other receivables Trade receivables and other receivables are initially recognized at fair value, and then, once they have been decreased by impairment write-downs they are recognized at adjusted acquisition price (amortized cost) with application of the effective interest rate. Impairment write-downs are made when there is objective evidence that the Company will not be able to receive all its receivables in accordance with the original settlement terms and conditions. In order to measure receivables at amortized cost, the debtor's major financial problems, probability of its insolvency or financial reorganization, as well as its failure to settle or delayed settlement of liabilities are taken into account, and these are recognized as indicators of trade receivable impairment. The amount of the write-downs is equal to the difference between the balance sheet value of a given asset and its value measured at amortized cost. The write-down amount is recognized in the profit and loss account. The balance sheet value of a given asset is decreased by revaluation write-downs, and the loss amount is posted to the profit and loss account (sales expenses). In case of bad trade receivable it is written off the account of provisions for trade receivables. Amounts recovered later after being written off are credited to the cost of sales item in profit and loss account.

Contract receivables The Company recognizes among assets within trade receivables, in the "Uninvoiced receivables from clients resulting from agreements" item the amounts due from clients for contract deliverables, with respect to all contracts in progress, in case of which the costs incurred – plus the recognized profits (less the recognized losses) – exceed the invoiced amounts.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 20

3.3.17 Deferred income Deferred income is accounted for while observing the prudence principle and accrual principle. In particular the deferred income includes the equivalent of amounts received or due from the trading partners for deliverables that shall be provided in future reporting periods.

The Company recognizes among deferred income within the "Deferred income" item an amount due to clients for

contract deliverables, with respect to all contracts in progress, in case of which the amounts invoiced exceed the

costs recognized.

3.3.18 Cash and cash equivalents Cash and short-term deposits recognized in the balance sheet include cash at the banks and on hand, as well as short-term deposits with the original maturity date of maximum three months. Balance of cash and cash equivalents recognized in the statement of cash flow consists of cash and cash equivalents specified above. Balances of un-repaid overdraft facilities are recognized in the balance sheet in the credits and loans item.

3.3.19 Assets held for sale Fixed assets or groups of assets classified as assets held for sale are measured at their balance sheet value or fair value less sales expenses, whichever is lower.

3.3.20 Equity

Equity of the Company is recognized at nominal value in accordance with the principles stipulated in legal regulations and the provisions set forth in the Articles of Association.

Share capital of the Company is recognized in the amount specified in the Articles of Association and entered in a court register.

Marginal costs related directly to issue of new shares or options are recognized in equity as a decrease of proceeds from the issue.

3.3.21 Share-based payments

Some employees of the Company may receive additional compensation in the form of share options, due to which employees provide services in exchange for shares or rights to shares ("transactions settled with equity instruments").

The cost of transactions settled with employees through equity instruments is measured by reference to the fair value as of the date the rights were granted. The fair value is determined by an independent valuer. No conditions concerning performance/results, besides those related to the price of shares of the Company ("market conditions") are taken into account at measurement of transactions settled with equity instruments.

The cost of transactions settled with equity instruments is recognized in the profit and loss account including a corresponding increase in equity within the period in which the conditions concerning performance/results, ending on the date the employees acquire full rights to benefits ("date of acquisition of rights"), are met. A cumulated cost recognized due to transactions settled with equity instruments as of each balance sheet date until the date of acquisition of the rights reflects the passage of time of acquisition of the rights and the number of options to which the rights will eventually be acquired – according to the opinion of the Management Board of the Company. No costs are recognized due to options the rights to which have not been finally acquired except for options the acquisition of which depends on market conditions, which are treated as acquired regardless of meeting market conditions provided all other conditions concerning performance are met.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 21

In case of a change to the conditions of allocation of options settled with equity instruments, as a minimum such costs are recognized as if these conditions had not changed. Furthermore, costs due to each increase in value of a transaction as a result of such a change, measured as of the date the change was implemented, are recognized.

The dilutive effect of issued shares is taken into account in determination of profit per share as additional dilution of shares.

3.3.22 Employee benefits

Pursuant to the company compensation schemes, the employees of the Company have right to a retirement severance pay. Retirement severance pay is a one-time payment made upon retirement. The amount of the retirement severance pay depends on the employment tenure and average compensation of the employee concerned. The Company creates a provision for future liabilities due to retirement severance pay in order to allocate the costs to the period which they refer to. Pursuant to IAS 19, retirement severance pays are programs of defined benefits after the period of employment. The current value of these liabilities as of each balance sheet date is calculated by an independent actuary. Liabilities accrued are equal to the discounted payments which will be made in the future, considering staff churn, and they refer to the period before the balance sheet date. Demographic information as well as information on staff churn is based on historical data. Profits and losses due to actuarial calculations are recognized in the profit and loss account and in other comprehensive income.

The Company pays contributions to national retirement schemes under defined contribution plans. Contributions to defined contribution plans are recognized as costs in the profit and loss account in the period they concern.

3.3.23 Provisions Provisions are established when the Company has an effective liability (legal or commonly expected) resulting from past events, and when it is likely that fulfilling this liability will lead to the need to spend the resources related to economic benefits and when it is possible to estimate the amount of this liability in a reliable manner.

When the influence of value of money over time is significant, the amount of the provision is determined by discounting the expected future cash flows to the present value, with the application of a gross discount rate reflecting present market valuations of value of money and possible risk related to a given liability. If the method consisting of discounting has been applied, the increase of provisions in time is recognized as borrowing costs.

3.3.24 Leases Company as a lessee

Financial lease agreements which generally transfer to the Company all risk and benefits resulting from possessing the leased object, are recognized in the balance sheet as of the date of commencement of lease as the lower of the two following values: the fair value of the tangible asset constituting a lease object or the present value of minimum lease charges. Lease charges are divided into financial costs and reduction of balance of liabilities due to lease, in a manner allowing for determining a fixed interest rate on the remaining liability to be paid. Financial expenses are recognized directly in the profit and loss account.

Fixed assets used pursuant to financial lease agreements are depreciated over either: estimated economic useful lifetime of the fixed asset or the term of lease, whichever is shorter.

Lease agreements, pursuant to which the lessor generally retains all the risk and benefits resulting from possessing the lease object, are considered as operating lease agreements. Lease charges due to operating lease agreements and further lease installments are recognized as costs in the profit and loss account by a straight-line method throughout the term of lease.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 22

Company as a lessor

Lease agreements, pursuant to which the Company generally retains all the risk and benefits resulting from possessing the lease object, are considered as operating lease agreements. Conditional lease charges are recognized as income in the period when they become due.

3.3.25 Financial liabilities and equity instruments Financial liabilities and equity instruments are classified on the basis of their economic contents resulting from the concluded agreements. An equity instrument is an agreement giving the right to participate in the Company’s assets less all liabilities.

3.3.26 Equity instruments Equity instruments issued by the Company are recognized in the value of the revenues less direct issuance costs.

3.3.27 Bank credits and loans

At the moment of the initial recognition, all bank credits and loans are recognized at fair value, less the costs of obtaining a credit or loan. After the initial recognition, interest-bearing credits and loans are further valued in accordance with a depreciated cost (adjusted purchase price), using the effective interest rate method. When determining a depreciated cost (adjusted purchase price), costs of obtaining a borrowing or credit, as well as discounts or bonuses gained while settling liabilities are taken into consideration.

3.3.28 Trade liabilities

Trade liabilities are the obligations to pay for goods and services acquired from suppliers in the course of the enterprise's regular business activities. Trade liabilities are classified as short-term liabilities if the payment date falls within one year (or in the course of regular business activity cycle of an enterprise, if longer). Otherwise, liabilities are recognized as long-term.

Trade liabilities in the initial recognition are disclosed at fair value, whereas subsequently they are disclosed at depreciated cost, using the effective interest rate method.

Trade liabilities include accrued expenses in the amount of likely liabilities due in the current reporting period

when the liability amount may be reliably estimated. Accrued expenses have a lower probability of turning into

expense than liabilities. Accrual adjustments are performed with observance of prudence principle and on accrual

basis.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 23

3.3.29 Revenues Revenues are recognized in the amount in which it is likely that the Company will gain economic benefits related to a given transaction, and when the amount of income may be valued in a reliable way. Revenues are shown after deduction of value added tax, refunds, rebates and discounts.

Multi-element contracts

Sales of products and services are based mainly on contacts concluded on standard terms and conditions; however, the Company also enters into multi-element contracts which require the Management Board to perform a detailed analysis and interpretation in order to ensure appropriate recognition in the financial statements. Appropriate recognition of revenues resulting from multi-element contracts consists of assessment whether the delivered products and services should be accounted for as individual elements for which revenue is recognized independently or the contract should be recognized as an inseparable whole. In case of separation of independent elements within the sales contract, the contract price is allocated to its particular elements, based on their relative fair value. Changes in price allocations between contract elements may have influence on the date of revenue recognition, but not on the total amount of revenue recognized in the contract.

Consortium agreements

The Company recognizes the total revenue due to a consortium agreement, also with regard to other consortium members, if its participation in the consortium was significant in terms of the risks incurred and benefits obtained.

Long-term contracts

The aim of valuation of a long-term IT implementation contract is to determine the value of revenues to be

recognized with regard to progress of work. The Company performs valuation applying the degree of progress

method. Application of this method results in recognition of revenues proportionally to the incurred costs, which as

a result allows for maintaining a constant aggregate margin on the contract, provided that the contract is not a

loss generating contract.

Progress of contract is recognized as ratio between costs incurred until the balance sheet date and total contract

costs (total contract costs cover costs incurred until the balance sheet date and currently expected costs to

complete the contract). Revenues corresponding to contract progress as of the balance sheet date are

recognized by multiplying the progress ratio by the total planned revenues from the contract.

If the incurred costs less estimated losses and plus profits recognized in the profit and loss account exceed by

their percentage progress the percentage progress of invoiced sales, the resulting difference of amount of non-

invoiced sales is presented in the assets of the balance sheet in the other receivables under the “Uninvoiced long-

term contracts receivables” as part of trade receivables.

Loss generating contracts

A loss generating contract is a contract in which total contract revenue is lower than total costs.

When it is highly likely that total costs of contract performance would exceed total revenues from the agreement,

the estimated loss is recognized as a cost for the period in which it was discovered by establishing a provision for

contract losses. The amount of provision and/or relevance of its presence is reviewed as of each subsequent

balance sheet date, until completion of the contract.

The value of provisions established for losses is recognized in the “long-term IT contracts valuation” category of

liabilities”.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 24

Methods of contract completion progress measurement

To determine degree of contract completion, the Company applies such methods that allow for determination of

progress of work in reliable manner. Depending on the nature of contract, these methods may include:

determination of proportion of contract costs incurred for work performed until the balance sheet date

compared to the estimated total contract costs,

measurement of the work performed, or

comparison of physically performed work against the contract deliverables.

When the degree of contract completion is determined on basis of incurred contract costs, such costs include only

these contract costs that reflect the work completed so far. Examples of costs, which should not be included, are

as follows:

costs of future activities related to the agreement, e.g. costs of materials purchased to complete the

project, which as of the valuation date, have been not installed or utilized in any other way yet;

advance payments to subcontractors for work to be performed under the contract.

If the degree of progress of service, expected total costs of its performance or the result cannot be reliably

determined as of the balance sheet date, then:

revenues are recognized only up to the amount of contract costs incurred in the given reporting period,

however not exceeding the costs that are likely to be covered in the future by the client,

contract costs shall be recognized as costs of the period in which they were incurred.

The percentage progress method is applied cumulatively in each accounting period with respect to the then

current estimates of revenues and contract costs. The effects of changes to estimates of contract revenues or

costs are recognized in the current accounting period.

Sales of goods

Revenue from sales of goods primarily consists of revenues from sales of computer hardware. Revenues are recognized if a significant risk and benefits resulting from the ownership title to products have been transferred to the purchaser and when the revenue amount may be valued in a reliable way.

Sale of licenses and software

Revenues are recognized if a significant risk and benefits resulting from the ownership title to products have been transferred to the purchaser and when the amount of revenue may be valued in a reliable way. Revenues from sales of third party licenses (from the Company's business partners) and own licenses are recognized when all the rights and obligations related to the product have been transferred to the client, and the client has accepted and confirmed receipt of the license or software.

Implementation services

Revenues are recognized in accordance with the degree of progress of a given service; most often this is the revenue resulting from long-term contracts settled in time. Detailed information on the revenue recognition has been provided in the paragraph "Long-term contracts”.

Maintenance services

Revenues from maintenance services consist of revenues from fixed remuneration contracts for provision of maintenance services for hardware and software. These revenues are usually recognized in the period in which relevant services were provided.

Sygnity S.A. Separate financial statements for the fiscal year commenced on October 1, 2015 and ended on September 30, 2016

[all data in PLN thousands unless specified otherwise]

Supplemental information constitutes an integral part of these separate financial statements 25

Revenues from lease

Revenues from lease of investment real-estates are recognized using the straight-line method for the entire term

of lease for open agreements.

3.3.30 Dividends

Dividends are recognized when shareholders obtain the rights to acquire them. Dividend payouts to shareholders of the Company recognized as liability in the financial statements of the Company during the period then they were approved by the shareholders of the Company.

3.3.31 Interest income

Interest income is recognized proportionally to the period of time by an effective interest rate.

3.3.32 Income tax

Income tax for a reporting period includes current and deferred income tax. Tax is recognized in the profit and loss account, except for the scope in which it relates directly to items included in the comprehensive statement of income or in equity.

In such a case tax is also recognized in the other comprehensive income or in equity respectively. Current tax charges are calculated pursuant to tax provisions in force or those actually introduced as of the balance sheet date. The Management Board carries out a periodic review of calculations of tax liabilities in relation to situations in which relevant tax regulations are subject to interpretation, establishing potential provisions for the amounts payable to tax authorities.