school finance 101 by ben irwin business manager parkview school district

TRANSCRIPT

School Finance 101

by Ben IrwinBusiness Manager

Parkview School District

2

Components of School Finance

• The WUFAR• Revenue Limits• Equalization Aid• Tax Levy• Equalized Value of Property• Membership• Debt

3

The WUFAR

• School districts in Wisconsin use the Wisconsin Uniform Financial Accounting Requirements (WUFAR) to categorize all of their finances.

• The WUFAR is fund accounting, which separates each revenue and expenditure into a specific fund.

• A majority of school finances are held in the General Fund (Fund 10), but there are also other funds for areas like food service and special education.

4

The WUFAR

5

Revenue Limits

Overview• School districts have a limit

on their revenues they are able to collect each year.

• Money calculated in the revenue limit formula comprises about 85% of a district’s revenue.

• The revenue limit is Equalization Aid plus Property Taxes.

Revenue Limit

Revenue85%

Other Operat-

ing Rev-enue15%

6

Revenue Limits

Tax Levy

Equalization Aid

Revenue Limit

7

Revenue Limits

Key Components• Prior-year aid.• Three-year history of

student membership.• Property values.• Prior-year base revenue per

member.• Allowable per pupil change.

8

Revenue Limits

Year Per Pupil

2005-06 $ 248.48

2006-07 $ 256.93

2007-08 $ 264.12

2008-09 $ 274.68

2009-10 $ 200.00

2010-11 $200.00

2011-12 $ -561.28

2012-13 $ 50.00

Allowable Per Pupil Change• Each year, districts are

allowed to add in a per-pupil increase.

• Traditionally this number was indexed for inflation.

• However, with the recent changes to the law, this number has been limited in recent years.

9

Equalization Aid

Overview• School districts receive

money from the state each year called equalization aid.

• Similar to revenue limits, many factors are involved when calculating equalization aid.

• For most school districts, this is their largest source of revenue.

10

Equalization Aid

Key Components• Property values (more aid

will go to “Property Poor Districts”).

• Prior-year spending.• Membership from

September and January counts.

SpendingEligible costs

MembershipEqualized

Valuation of Property

11

Tax Levy

Revenue Limit Equalization Aid Tax Levy

12

Tax Levy

Overview• Limits are set from the state on how much a district can

tax.• School districts can seek additional taxes through non-

referendum debt and community activities.

13

Mill Rate

• The mill rate is a calculation of taxes per $1,000 of equalized values.

• Useful for comparing school districts, but a poor reflection of what taxpayers will see on their bill.

• Individual tax levies are separated by municipality and then by individual property values.

14

Equalized Value of Property

Overview• Determined by the state

Department of Revenue.• Used to divide property taxes

between municipalities in the district.

• Once we tell each municipality how much they owe the district in taxes, they divide that number among property owners based on assessed values.

2010-2011 Equalized Value

Percent of District Value

2010-2011Avon 18,439,620 4.4%Center 24,115,682 5.8%Magnolia 4,913,144 1.2%Newark 123,226,900 29.5%Plymouth 97,926,100 23.4%Rock 12,652,617 3.0%Spring Valley 34,561,067 8.3%Footville 33,988,300 8.1%Orfordville 68,189,900 16.3%Total District 418,013,330 100.00%

15

Membership

Overview• Outside of state factors, membership will have the largest impact on

school finances.• The revenue limit will use a three-year average of membership from

student counts in September.• Equalization Aid will use September and January counts from last year.

16

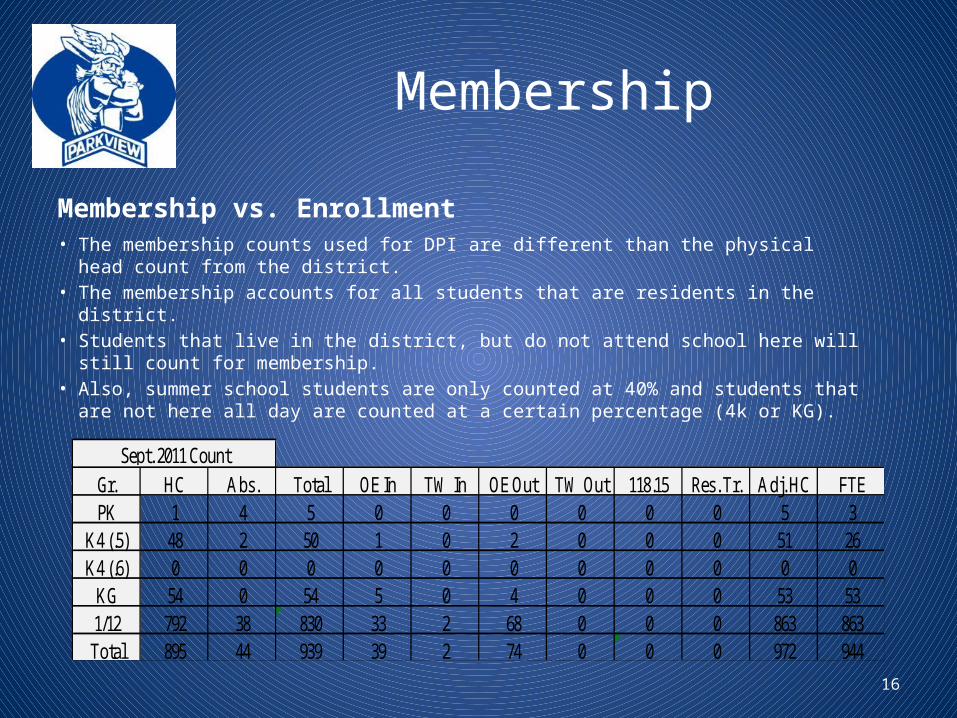

Membership

Membership vs. Enrollment• The membership counts used for DPI are different than the physical head count from

the district.• The membership accounts for all students that are residents in the district.• Students that live in the district, but do not attend school here will still count for

membership.• Also, summer school students are only counted at 40% and students that are not

here all day are counted at a certain percentage (4k or KG).

Gr. HC Abs. Total OE In TW In OE Out TW Out 118.15 Res. Tr. Adj. HC FTEPK 1 4 5 0 0 0 0 0 0 5 3

K4 (.5) 48 2 50 1 0 2 0 0 0 51 26K4 (.6) 0 0 0 0 0 0 0 0 0 0 0

KG 54 0 54 5 0 4 0 0 0 53 531/12 792 38 830 33 2 68 0 0 0 863 863Total 895 44 939 39 2 74 0 0 0 972 944

Sept. 2011 Count

17

Membership

Open Enrollment• Students are allowed to attend a

different school from their resident district if they choose to.

• School districts are still able to count the open enrolled student in their revenue limit and equalization aid count numbers.

• However, districts will pay a large portion of the open enrolled student’s tuition to the district they are attending.

Base Revenue per Member 2011-12 (amount received for each resident

student)$9,643.73

Open Enrollment Tuition 2011-12 (amount that we must pay for each

resident student that attends a different school)

$6,867.00

18

Debt

• School districts can burrow up to $1,000,000 without elector approval (Fund 38) and all of this debt must be repaid within the revenue limit.

• Beyond that, school districts must get voter approval through a referendum (Fund 39).

• When referendum is passed, a school district has the authority to go beyond the revenue limit.

19

Debt

Short-Term Borrowing• Due to the variances in school revenues and expenditures, a lot

of school districts in Wisconsin will short-term borrow each year. • While expenditures are fairly consistent each month, revenues

come in lump sums, which can impact a school district’s cash flow situation.

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun $-

$500,000.00

$1,000,000.00

$1,500,000.00

$2,000,000.00

Revenues