retirement reform october 2012 1. section 1: the problem retirement costs are jacksonville’s...

TRANSCRIPT

Retirement Reform

October 2012

1

Section 1: The Problem

Retirement Costs are Jacksonville’s Fiscal Cliff

An Everywhere Challenge

• Municipalities throughout the nation and throughout the State of Florida are facing significant budget challenges brought on by compounding compensation and benefit obligations that are growing at alarming rates.

Municipalities that fail to take timely action to address the increasing costs associated with compensation and benefits find themselves with budget deficits, layoffs, and the elimination of needed services.

Worse case scenario: Stockton, CA or Central Falls, RI

City Revenue Going Down

• Decline in revenues from FY 11/12 ($958 million) to FY 12/13 ($948 million)

• Passage of Amendment Four could reduce revenue by $7 million in FY 13/14 and $13 million in FY 14/15

City Retirement Costs Going Up

• Just four years ago, the City of Jacksonville spent less than 7% -- $65 million – of its budget on overall pension costs.

• This coming year, the City is projected to spend nearly 16% of its budget – nearly $150 million – on overall pension costs.

• That’s an increase from $65 million to $150 million in just four years with the same size budget.

5

Retirement Reform Priority

• Mayor Brown has made retirement reform the top priority of his second year as mayor.

• His promise: unveil a retirement reform plan by the end of 2012.

• The goal was to have a plan that would respect and protect both hard-working city employees and taxpayers

Retirement Reform Process

• For the Brown Administration, this process started back in June 2011 with the detailed work of then Mayor-elect Brown’s Pension Transition Committee.

• Peyton Administration laid foundation with 2011-400

The Retirement Reform Process, continued

• Those efforts, along with other community analyses, helped to frame up four key questions for our retirement reform initiative:

• (1) What is the scope of the problem?

The Retirement Reform Process, continued

• (2) How have other municipalities dealt with retirement cost challenges?

• (3) What limitations does Florida law place on the reform of retirement benefits?

• (4) What reform plan(s) address the city’s financial needs while meeting the state’s legal requirements?

Retirement Reform Experts

• To help answer those questions, we turned to three experts:

– Attorney Jim Linn of Lewis, Longman, and Walker in Tallahassee

– Actuary Robert Dezube of the Milliman Group to evaluate the PFPF and assist in making reform recommendations

(Milliman is the actuary for the FRS)

Retirement reform experts, continued

• Jeff Williams of the Siegel Group to evaluate the General Employees Pension Plan (GEPP) and assist in making reform recommendations

• Mayor’s Special Adviser on Pensions, Kevin Hyde.

COJ Pension Plans

• Police and Fire Pension Fund (PFPF)

• General Employees Pension Plan (GEPP)– Includes Corrections Employees

12

Specific PFPF Challenges

1. Annual Contributions Skyrocketing

Fiscal Year 10/11: $76.1 million

(8% of overall general fund)

Fiscal Year 12/13: 121.3 million

(Nearly 13% of overall general fund)13

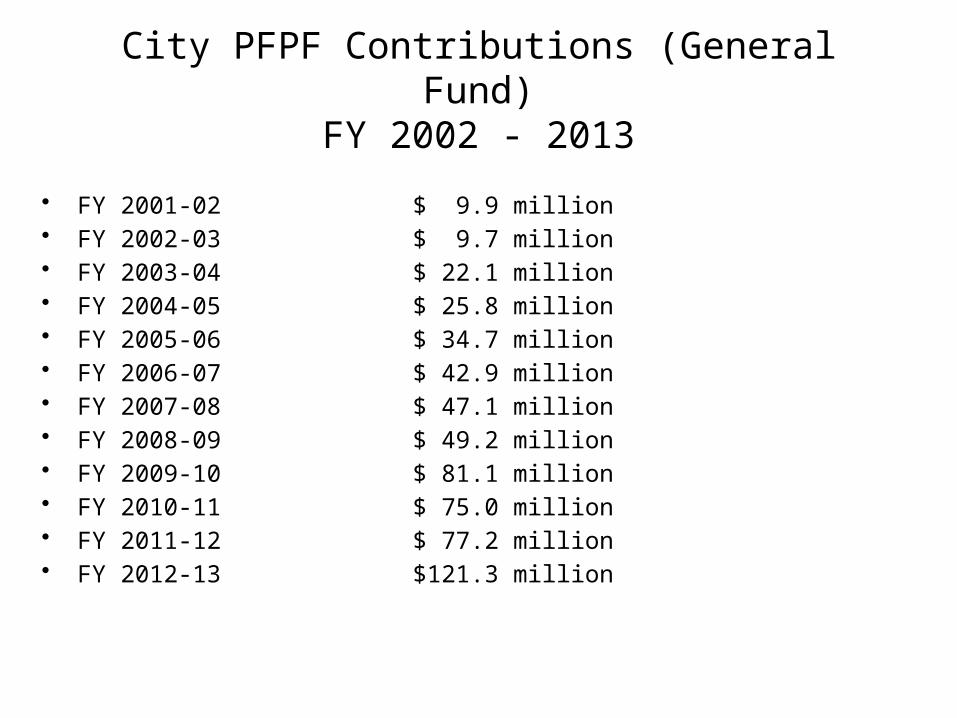

City PFPF Contributions (General Fund)FY 2002 - 2013

• FY 2001-02 $ 9.9 million• FY 2002-03 $ 9.7 million

• FY 2003-04 $ 22.1 million• FY 2004-05 $ 25.8 million• FY 2005-06 $ 34.7 million• FY 2006-07 $ 42.9 million• FY 2007-08 $ 47.1 million

• FY 2008-09 $ 49.2 million• FY 2009-10 $ 81.1 million• FY 2010-11 $ 75.0 million• FY 2011-12 $ 77.2 million• FY 2012-13 $121.3 million

2. PFPF Significantly Underfunded

Unfunded Actuarial Liability (UAAL)

Actuarial accrued liability (value of benefits)Minus Net assets available for benefits

= Unfunded Actuarial Accrued Liability(bigger number means bigger problem)

15

Increase in UAAL

16

Oct. '03 Oct. '06 Oct. '08 Oct.'110

200

400

600

800

1000

1200

1400

1600

UAAL

UAAL

Pension Report Card Grade for PFPF

“F”Source:

Tough Choices Facing Florida’s Government

November 2011 – based on 2009 data

Leroy Collins Institute

Reason: Plan was less than 50% funded

17

The Cost of Inaction

• If the COJ takes no action – PFPF benefits stay the same and we rely on the same assumptions as to rate of return on investments (7.75%) – we will continue to underfund the PFPF while steadily increasing general fund contributions.

18

Pension Cost Components

1. Normal Cost – annual cost of current benefits, without unfunded actuarial accrued liability (UAAL) payment

2. UAAL Amortization Payment

[UAAL = assets minus liabilities = debt]

Actuarial losses Plan improvements

19

Projected Contributions Under Status Quo

Series1

Ser

ies1

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000Recommended City Contribution

Employer Normal Cost UAL Amortization

Rec

om

men

ded

Cit

y C

on

trib

uti

on

20

Projected Contribution Trend Under Status Quo

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 2041 2042 2043

$131.988592678547

143.692067587921

151.237350722791

157.576115797781

164.236671915082

168.970155450913

174.770992826171

178.558166201967

182.206836908616

189.708469789908

197.905458469548

207.483951489574

216.409428958765

225.615866887931

235.229451182178

219.098779726701

218.173690968736

228.731009320338

239.422960101416

250.534861966086

261.178883362744

273.628030493931

254.055111616427

264.723645423725

277.662088750207

268.828768194505

280.999368055187

248.946694703623

258.944081011062

271.872870185172

173.551680029456

25

75

125

175

225

275

Projection of Recommended City Contribution

Rec

om

men

ded

Cit

y C

on

trib

uti

on

(m

illi

on

s)

21

Projected UAAL Trend Under Status Quo

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 2041

$1409.751559

1547.8581325075

1596.97753295733

1626.42896692502

1648.36191782071

1662.21071158632

1674.00548338176

1681.54180070885

1684.77503845628

1685.41940338664

1684.23499462661

1676.88613756517

1662.71678881147

1639.68031091436

1607.98280260022

1564.17796534424

1509.86347715342

1469.19781050781

1429.66367647966

1379.25991012934

1315.17560436186

1237.9079725199

1147.1677120877

1040.36801798699

949.976820060985

846.062597465711

725.914892821803

610.630948122993

478.989967552525

375.696503525346

259.70832845356

100

300

500

700

900

1,100

1,300

1,500

1,700

Projection of Unfunded Actuarial Accrued Liability ($ mil-lions)

UA

AL

($

mil

lio

ns)

22

Key Status Quo Data Points

• Retirement benefits stay the same• Rate of return remains at 7.75%• Anticipated FY 2013 Contribution: $122m• Recommended COJ Contributions:

– FY 2014: $144 million– FY 2015: $151 million– FY 2016: $158 million– FY 2017: $164 million– FY 2018: $169 million– FY 2019: $175 million

23

Bottom Line for Next Budget

• If nothing changes – benefits stay the same, the assumed rate of return stays the same – the City will devote an additional $22 million in general fund revenue to the PFPF (yet still be under-funding).

24

The Rate Debate

• Growing consensus that the assumed rate of return (7.75%) is too optimistic given recent market conditions.

• The State of Florida has worked to utilize more realistic assumptions in the Florida Retirement System (FRS) and urged municipal governments to do the same.

25

More on the Rate Debate

• In September, Florida State Board of Administration Exec. Dir. Ash Williams recommended that the state lower its rate of return from 7.75% to 7.25%.

• PFPF Executive Director John Keane and actuary Jarmon Welch say they want to lower the PFPF rate “in stages”

26

Even More on the Rate Debate

• In September, PFPF provided data from its investment advisers showing an expected actual return of 6.9% over the next 10 years.

• Based on that data, our actuary recommended an assumed rate of return of 6.5% (6.9% minus .4% commission for PFPF investment advisers)

27

The Costs of Inaction with a Realistic Rate of Return

• Adjusting the rate of return from 7.75% to a more realistic 6.9% is a fiscally conservative and prudent step that limits PFPF underfunding.

• But it causes annual COJ contributions to the PFPF to grow substantially

28

Contribution Projection: Same Benefits, New Rate

Series1

Ser

ies1

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000Recommended City Contribution

Employer Normal Cost UAL Amortization

Rec

om

men

ded

Cit

y C

on

trib

uti

on

29

Contribution Trend: Same Benefits, New Rate

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 2041 2042 2043

$167.386839025735

180.502650658775

186.068883245014

190.176838243258

194.460835578562

196.826502339378

200.011056525029

201.320322062845

202.482561479985

206.876633629376

211.731644628432

217.575291665322

222.650141373642

227.752981478701

233.040124393886

218.000023818192

215.09122718186

221.009266281085

226.909364591408

232.939549822709

238.384336365634

244.903185386644

228.871712941804

234.016259418794

240.643069251381

232.607381794007

238.507269991113

215.907755624508

220.503402191614

226.934860254739

119.668180124325

25

75

125

175

225

275

Projection of Recommended City Contribution

30

UAALTrend: Same Benefits, New Rate

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 2041

$1792.792214

1956.473825845

1979.32161309793

1981.43362105029

1976.82126391756

1964.0015478392

1948.75488709375

1928.71807765984

1904.31570426273

1877.04759005481

1847.78871208837

1812.79758254912

1771.75796392981

1723.10715933525

1667.28125412204

1601.45405808997

1527.48601445582

1464.14033485545

1401.53572563605

1330.37123571739

1248.48025131902

1156.74141586976

1055.13399243629

942.101644029654

840.456216171581

729.150985127733

606.505143241036

486.528353826704

355.01153812044

240.604613803267

116.531674660481

250

750

1,250

1,750

2,250

Projection of Unfunded Actuarial Accrued Liability ($ mil-lions)

UA

AL

($

mil

lio

ns)

31

Key Data Points for Same Benefits, New Rate of Return

• Retirement benefits stay the same• Rate of return lowered to 6.9%• Anticipated FY 2013 Contribution: $122m• Recommended COJ Contributions:

– FY 2014: $181 million – FY 2015: $186 million– FY 2016: $190 million– FY 2017: $194 million– FY 2018: $197 million– FY 2019: $200 million

32

COJ Reform Options

• Fundamental Operating Principles

• Utilization of “Freeze” Concept

• The Reform Plan

33

Fundamental Operating Principles

1. Reform will not rely on an increase in the millage rate.

2. Any reform must use realistic assumptions on rate of return and payroll growth.

3. Current retirees will not be affected.

34

Fundamental Operating Principles, continued

4. All current employees will keep what they have already earned but will experience change once the reform plan is implemented.

5. Any reform must reduce the unfunded liability, not merely extend the time for payment. Debt will not pay for debt.

• We will not propose Pension Obligation Bonds or Pension Liability Reduction Bonds

35

The “Plan Freeze”

– The current plan will be “frozen” as of date certain (the “Frozen Plan”).• Employees’ vested benefits as of that date will be

fixed at whatever level the employee was entitled to as of date certain

– Example – employee who had worked 10 years had vested at 30% (10 x 3% yearly) in the plan. Upon retirement the employee is entitled to retirement benefit at 30% of pay.

– Employee will not accrue any additional benefits under the frozen plan for subsequent years of service

36

After the “Plan Freeze”

• A new plan will be implemented from a date certain going forward

• Employees will begin accruing benefits under the new plan or all service after the Frozen Plan fixed date.

• The new plan will have different benefits from what was available in the Frozen Plan

• This approach is not unique – the most effective way to achieve meaningful savings on a short and long term basis

37

The Plan: Maintain Defined Benefit (DB) model but reform benefit package

– Working with our experts, we crafted a reform package that we believe will credibly:

• Fund COJ pension obligations• Control costs short and long term• Comply with law to retain Chapter funds• Reduce UAAL

38

Current System vs. DB Reforms

Benefit-by-Benefit Comparison

39

Benefit CapCURRENT JAX

POLICE OFFICERS &

FIREFIGHTERS

2011-400 PROPOSED CHANGES

None None Cap of $99,999

40

Normal Retirement AgeCURRENT JAX

POLICE OFFICERS &

FIREFIGHTERS

2011-400 PROPOSED CHANGES

20 years 55/10 years or

65/5<10yrs

60 years of age AND 27

years of work

41

Employee Contribution

CURRENT JAX POLICE

OFFICERS & FIREFIGHTERS

2011-400 PROPOSED CHANGES

7% 8% 14%

42

Benefit Accrual RateCURRENT JAX

POLICE OFFICERS &

FIREFIGHTERS

2011-400 PROPOSED CHANGES

3% (for 20yrs); then 2% for cap

at 80%

2.8% (for 25yrs); then 2% for cap

at 80%

1.667% with a cap at 50%

43

COLACURRENT JAX

POLICE OFFICERS &

FIREFIGHTERS

2011-400 PROPOSED CHANGES

3%, 3mos. after DROP

3%, 24 mos. after

separation

Elimination, if not

accrued

44

DROPCURRENT JAX

POLICE OFFICERS &

FIREFIGHTERS

2011-400 PROPOSED CHANGES

DROP Eligibility at

20 yrs

Delay DROP Eligibility to

25 yrs

Elimination

45

Average Final Contribution

CURRENT JAX POLICE

OFFICERS & FIREFIGHTERS

2011-400 PROPOSED CHANGES

Avg. last 24 mos.

(52 pay pds.)

Avg. of last 5 Avg. of last 5

46

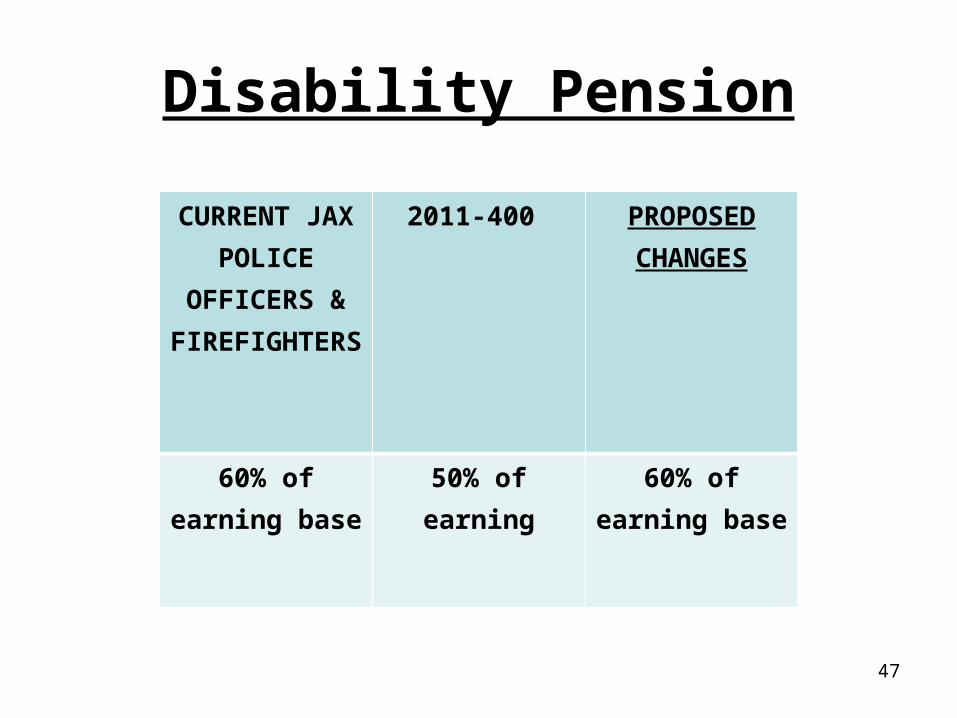

Disability Pension

CURRENT JAX POLICE

OFFICERS & FIREFIGHTERS

2011-400 PROPOSED CHANGES

60% of earning base

50% of earning 60% of earning base

47

Pensionable Wages

CURRENT JAX POLICE

OFFICERS & FIREFIGHTERS

2011-400 PROPOSED CHANGES

No Change No change Exclude Shift and

Differentials

48

DB Reform: City Contribution

Series1

Ser

ies1

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000 Recommended City Contribution

Employer Normal Cost UAL Amortization

Rec

om

men

ded

Cit

y C

on

trib

uti

on

49

DB Reform: Contribution Trend

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 2041 2042 2043

$122.01693773701

132.55643683876

137.836745694657

141.8908824993

146.389019485776

148.809400206101

152.844296298488

154.502302698852

155.734103292209

160.408151822953

165.441387213858

171.312267391898

176.685699199932

182.164368830316

187.787799604363

172.700630039021

169.516540184567

175.133781505044

180.68262812511

186.215456880396

191.19818714156

197.192459961254

180.538055599325

185.119347982805

190.797766693428

182.024579065869

187.170664772476

163.751390442552

167.617129177925

173.427825595508

74.2812923069966

25

75

125

175

225

Projection of Recommended City Contribution

Rec

om

men

ded

Cit

y C

on

trib

uti

on

Per

cen

tag

e

50

DB Reform: UAAL Trend

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 2041

$1718.7969089796

1837.99806229353

1862.15603390413

1867.82865011105

1867.13038202144

1859.93539286967

1850.31541096349

1838.86597676982

1823.94672478459

1807.68802179634

1790.22904891674

1768.03317418271

1740.24860078333

1705.34681422736

1663.25093676401

1612.91077247144

1553.16622755123

1505.7030668633

1458.18386361747

1401.34058430827

1335.48429452039

1259.23718845455

1172.86885965878

1075.09105589148

988.369498278328

892.198312734641

784.435600829684

679.696311084713

563.970294028003

466.324850432603

359.465933850165

100

300

500

700

900

1,100

1,300

1,500

1,700

1,900

Projection of Unfunded Actuarial Accrued Liability ($ mil-lions)

UA

AL

($

mil

lio

ns)

51

Key Data Points for DB Reform (Level Percent of Pay)

• Retirement benefits modified in DB model• Rate of return lowered to 6.9%• Anticipated FY 2013 Contribution: $122m• Recommended COJ Contributions:

– FY 2014: $133 million– FY 2015: $138 million– FY 2016: $142 million– FY 2017: $146 million– FY 2018: $149 million– FY 2019: $153 million

52

Bottom Line for Next Budget

• Let’s look at this in two ways.

• If we simply compare this to how much we are slated to pay next year under the status quo, $133 million is $11 million less than $144 million.

• But that $133 million means we are not underfunding the plan.

53

More on Next Budget

• And $133 million is $48 million less than $181 million.

• If we make the rate of return more realistic without changing benefits, we would have to spend $181 million next year to fully fund our obligations.

• If we use more realistic assumptions, modify DB benefits, and use the level percentage of payroll approach, COJ will save $48 million and still fully

fund plan.54

What Does $48 Million Mean?

• $48 million means the jobs of 800 City of Jacksonville employees if you assume an average compensation amount of $60K (salary + benefits).

• $48 million means approximately the combined FY 2013 budgets for Public Libraries and Parks & Recreation.

55

Retirement Reform Process

• We haven’t negotiated directly with the Police and Fire Pension Fund or with the General Employees Pension Plan because the law says that employee benefits should be negotiated with unions.

• Judicial decisions hold that retirement benefits are a mandatory subject of collective bargaining with unions.

56

More Retirement Reform Process

• And in the contracts that they signed and that City Council overwhelmingly ratified, several unions agreed that they would sit down with the City and discuss retirement reform.

• That process starts this week with meetings with four

COJ employee unions.

57

Schedule of Meetings

• Monday, 10/29: FOP

• Tuesday, 10/30: AFSCME

• Wednesday, 10/31: FOP

• Thursday, 11/1: LIUNA and JSA

58

Retirement Reform Resources

• Web Page at www.coj.net

• Fact Sheet

• Employee Q&A

• Side-by-Side

• Links to studies59