relationship between corporate governance...

TRANSCRIPT

CHAPTER – 6

RELATIONSHIP BETWEEN CORPORATE GOVERNANCE VARIABLES AND LISTING

PERFORMANCE OF INDIAN IPOs

IPO provides an opportunity to the issuing company to tap wider pool of public funds in

order to provide capital for its future growth. Its inherent nature of penetrating into public

pockets breaking the private arenas and the unique setting characterized by information

asymmetry has always grabbed attention of researchers and academicians. IPO pricing,

timing and performance have been three primary issues which have been dominant areas

of research in this field. Pricing of IPOs, however, remains the most contentious issue.

Two anomalies related to pricing issues are (1) high initial returns (or underpricing) and

(2) long run underperformance (Ching-Yi Lin, 2005). Where IPO underprcing reduces

the initial owners’ wealth, long run underperformance results in a wealth loss to all

shareholders.

Underpricing though used interchangeably with the initial returns, remains the common

terminology used in IPO literature (e.g., Ritter, 1998). Greater the extent of underpricing,

higher will be the initial returns. IPO underpricing, which refers to stock returns

experienced during the initial trading day in the secondary market, reduces the capital

received by an IPO firm through IPO process (Lin and Chuang, 2011) and is regarded as

a direct wealth transfer from founders and initial shareholders to new external investors

(Filatotchev and Bishop, 2002).

This performance indicator is unique to the IPO context and represents the difference

between investment banker's initial valuation of the firm and stock market's valuation of

firm at the end of first day of public trading and hence is referred to as money that initial

shareholders "leave on the table" (e.g., Tully, 1999). As noted by Certo, et al. (2001b),

underpricing captures both wealth creation for first-day investors and lost (unretained)

wealth for initial shareholders who sold their equity to the investment banker at a price

below its value in investor market at the end of first day of trading. Economic magnitude

of IPO underpricing is formidable and the phenomenon is globally pervasive.

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

151

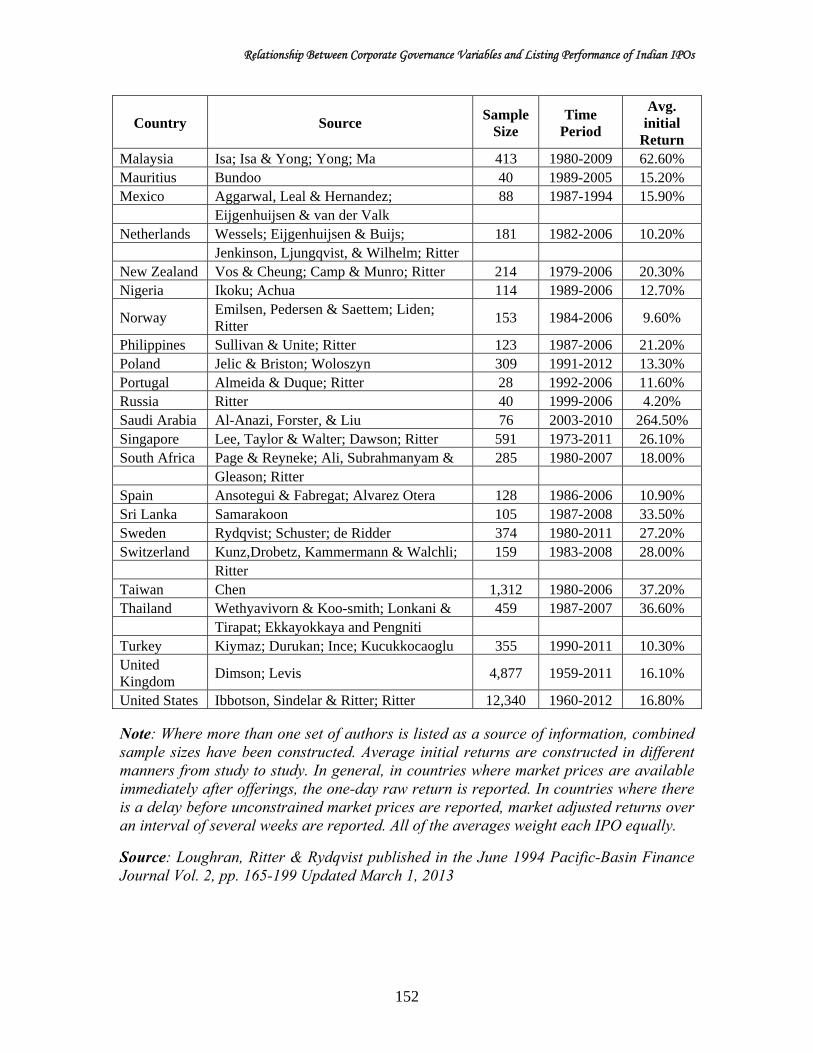

Table 6.1: Equally Weighted Average Initial Returns for 50 Countries

Country Source Sample

Size Time

Period

Avg. initial

Return Argentina Eijgenhuijsen & van der Valk 20 1991-1994 4.40% Australia Lee, Taylor & Walter; Woo; Pham; Ritter 1,562 1976-2011 21.80% Austria Aussenegg; Ritter 102 1971-2010 6.30% Belgium Rogiers, Manigart & Ooghe; Manigart 114 1984-2006 13.50% DuMortier; Ritter Brazil Aggarwal, Leal & Hernandez; Saito; 275 1979-2011 33.10% Ushisima Bulgaria Nikolov 9 2004-2007 36.50% Canada Jog & Riding; Jog & Srivastava; 696 1971-2010 6.70% Kryzanowski, Lazrak & Rakita; Ritter Chile Aggarwal, Leal & Hernandez; 65 1982-2006 8.40% Celis & Maturana; Ritter China Chen, Choi, & Jiang; Jia & Zhang 2,102 1990-2010 137.40% Cyprus Gounopoulos, Nounis, and Stylianides; 73 1997-2011 20.30% Chandriotis Denmark Jakobsen & Sorensen; Ritter 164 1984-2011 7.40% Egypt Omran 53 1990-2000 8.40% Finland Keloharju 162 1971-2006 17.20% France Husson & Jacquillat; Leleux & Muzyka; 697 1983-2010 10.50% Paliard & Belletante; Derrien & Womack; Chahine; Ritter; Vismara Germany Ljungqvist; Rocholl: Ritter; Vismara 736 1978-2011 24.20% Greece Nounis, Kazantzis & Thomas; 373 1976-2011 50.80% Thomadakis, Gounopoulos & Nounis Hong Kong McGuinness; Zhao & Wu; Ljungqvist & 1,259 1980-2010 15.40% Yu; Fung, Gul, and Radhakrishnan; Ritter India Marisetty and Subrahmanyam; Ritter 2,964 1990-2011 88.50% Indonesia Suherman 410 1990-2012 25.70% Iran Bagherzadeh 279 1991-2004 22.40% Ireland Ritter 31 1999-2006 23.70%

Israel Kandel, Sarig & Wohl; Amihud & Hauser;

348 1990-2006 13.80%

Ritter Italy Arosio, Giudici & Paleari; 273 1985-2009 16.40% Cassia, Paleari & Redondi; Vismara Japan Fukuda; Dawson & Hiraki; Hebner & 3,136 1970-2011 40.20% Hiraki; Pettway & Kaneko; Hamao, Packer, & Ritter; Kaneko & Pettway Jordan Al-Ali and Braik 53 1999-2008 149.00% Korea Dhatt, Kim & Lim; Ihm; Choi & Heo; 1,593 1980-2010 61.60% Mosharian & Ng; Cho; Joh; Ritter

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

152

Country Source Sample

Size Time

Period

Avg. initial

Return Malaysia Isa; Isa & Yong; Yong; Ma 413 1980-2009 62.60% Mauritius Bundoo 40 1989-2005 15.20% Mexico Aggarwal, Leal & Hernandez; 88 1987-1994 15.90% Eijgenhuijsen & van der Valk Netherlands Wessels; Eijgenhuijsen & Buijs; 181 1982-2006 10.20% Jenkinson, Ljungqvist, & Wilhelm; Ritter New Zealand Vos & Cheung; Camp & Munro; Ritter 214 1979-2006 20.30% Nigeria Ikoku; Achua 114 1989-2006 12.70%

Norway Emilsen, Pedersen & Saettem; Liden; Ritter

153 1984-2006 9.60%

Philippines Sullivan & Unite; Ritter 123 1987-2006 21.20% Poland Jelic & Briston; Woloszyn 309 1991-2012 13.30% Portugal Almeida & Duque; Ritter 28 1992-2006 11.60% Russia Ritter 40 1999-2006 4.20% Saudi Arabia Al-Anazi, Forster, & Liu 76 2003-2010 264.50% Singapore Lee, Taylor & Walter; Dawson; Ritter 591 1973-2011 26.10% South Africa Page & Reyneke; Ali, Subrahmanyam & 285 1980-2007 18.00% Gleason; Ritter Spain Ansotegui & Fabregat; Alvarez Otera 128 1986-2006 10.90% Sri Lanka Samarakoon 105 1987-2008 33.50% Sweden Rydqvist; Schuster; de Ridder 374 1980-2011 27.20% Switzerland Kunz,Drobetz, Kammermann & Walchli; 159 1983-2008 28.00% Ritter Taiwan Chen 1,312 1980-2006 37.20% Thailand Wethyavivorn & Koo-smith; Lonkani & 459 1987-2007 36.60% Tirapat; Ekkayokkaya and Pengniti Turkey Kiymaz; Durukan; Ince; Kucukkocaoglu 355 1990-2011 10.30% United Kingdom

Dimson; Levis 4,877 1959-2011 16.10%

United States Ibbotson, Sindelar & Ritter; Ritter 12,340 1960-2012 16.80%

Note: Where more than one set of authors is listed as a source of information, combined sample sizes have been constructed. Average initial returns are constructed in different manners from study to study. In general, in countries where market prices are available immediately after offerings, the one-day raw return is reported. In countries where there is a delay before unconstrained market prices are reported, market adjusted returns over an interval of several weeks are reported. All of the averages weight each IPO equally.

Source: Loughran, Ritter & Rydqvist published in the June 1994 Pacific-Basin Finance Journal Vol. 2, pp. 165-199 Updated March 1, 2013

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

153

Ample evidence has been documented to highlight the existence and extent of

underpricing across different regions. Table 6.1 presents the prevalence of the

positive initial returns as available on the listing day across different countries. The

table elucidates and validates the existence of underpricing across all economies

differing only in extent. A large number of studies have addressed the underpricing

phenomenon and attempted to find explanations to this premium. Several theories

have emerged to explain these positive initial returns such as information asymmetry

(Baron, 1982), winners’ curse hypothesis (Rock, 1986), underwriters’ reputation

theory (Carter and Manaster, 1990) and signaling hypothesis (Allen and Faulhaber,

1989; Grinblatt and Hwang, 1989; Welch, 1989). Although many theories attempt to

unravel the mystery of IPO underpricing, no one convincing common explanation has

sprang up. However, most of the theories revolve around information asymmetry

between issuing firm and other participants in the IPO process. Asymmetric

information is higher for smaller and newer firms and inherent costs make it difficult

to resolve these problems and this increases agency costs which manifest as

underpricing.

6.1 CORPORATE GOVERNANCE AND UNDERPRICING

Due to information asymmetry problem, wherein issuers have better information about

their firm’s future performance than outside investors, the firms adopt varied mechanisms

to signal firm quality and communicate their true value to investors. Rather, at the heart

of signaling theory is information asymmetry (Spence, 1973). This is necessary in the

light of prevailing uncertainty in the minds of investors. Literature on underpricing, much

of which is based on signaling theory, addresses various signals employed by firms to

dispel the apprehensions of investing public. These include retained ownership (Leland

and Pyle, 1977 and Keasey and McGuiness, 1992), underpricing for seasoned issues

(Ibbotson, 1975; Allen and Faulhaber, 1989; Welch, 1989), prestigious underwriters

(Booth and Smith, 1986; Carter and Manaster, 1990; Michaely and Shaw, 1994) reputed

investment bankers (Carter et al., 1998; Paudyal, et al., 1998), auditor reputation (Titman

and Trueman, 1986) and prestige of venture capitalists (Megginson and Weiss, 1991; Da

Silva Rose et al., 2002).

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

154

Despite the extant literature on signaling in context of IPO underpricing, little attention

has been devoted to association between corporate governance attributes and IPO initial

performance particularly in the context of Asian economies (Yong, 2007). This has

emerged as an explanation to underpricing in the times of shift towards qualitative signals

in the backdrop of losing relevance of financial and quantitative information in

communicating credibility of new issue firms. Kim and Ritter (1999) suggested that the

relationship between financial information and equity values is particularly tenuous in the

IPO context. The disturbing regularity of corporate upheavals and financial irregularities

globally have stimulated the growing interest in corporate governance mechanisms. Also,

Yong (2007) shared the view that corporate governance is the new area of IPO research.

Thus corporate governance emerged as an important area and its relevance is constantly

increasing. It is widely accepted that good corporate governance systems are associated

with better corporate value, and is also a key element in corporate competitiveness and

access to capital (Jensen and Meckling, 1979; Shleifer and Vishny, 1997). Sanders and

Boivie (2004) suggest that corporate governance parameters can serve as useful screening

and sorting criteria that influence investors' valuations of the IPO firm when primary

information sources are limited or obscure. Researchers also believe that certain

governance related signals reduce investor anxiety and contribute in reducing extent of

underpricing. Governance attributes as a signaling device lie consistent with the two key

criteria for an effective signal: they are observable and known in advance (i.e. occur prior

to any transaction offer) and are costly for lower quality IPO firms to utilize due to

difficulty in imitation.

6.2 EMPIRICAL EVIDENCE ON UNDERPRICING AND GOVERNANCE

Investigation of corporate governance mechanisms as signals at the time of IPO, thus,

emerges as an important empirical issue in research. IPO provides a unique setting to

evaluate effects of governance as effective monitoring is all the more critical for firms

going public in the face of aggravated agency conflicts (Brennan and Franks, 1997). Very

limited initiatives in this direction have been documented though literature in Indian

context is almost non-existent. The investigation becomes important given the economic

and financial dimension of India and also because the influences of corporate governance

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

155

variables on underpricing are expected to be different in emerging markets owing to

different institutional environments.

Prior efforts in relation to corporate governance and underpricing have been largely

limited to developed economies and other typical areas but developing markets of India

lack this exploration. Few studies have recently attempted to investigate board of

directors and IPO underpricing (listing day performance) using data from the United

States (e.g., Certo et al., 2001; Howton et al., 2001). Evidence from emerging markets is

quite rare, among the few are Chen and Strange (2004), Lin and Chuang (2011), and

Yatim (2011), which use a sample of IPO firms in China, Taiwan and Malaysia,

respectively. The impact of governance measures on performance of IPOs in small

frontier markets of West Africa facing the challenge of adoption of international

governance best practices (Hearn 2011, Hearn 2012) has also been studied. In the light of

the economic significance of Indonesia being the largest economy in Southeast Asia,

Darmadi and Gunawan (2012) explored the influence of corporate governance

mechanisms on initial returns for this emerging market attracting foreign attention and

investments. Chen and Yang (2013) did not find a significant relationship between

underpricing and governance and ownership structure for ChiNext IPOs. On the same

lines, IPO investors on the Alternative Investment Market (London) were found not to

necessarily view the monitoring benefits of board structure and managerial ownership as

important signals of firm quality (Wu and Hsu, 2012). Clearly concentration of past

efforts has been in developed and established economies of US (Certo et al., 2001a; Certo

et al., 2001b; Howton et al., 2001; Dempere, 2007), UK (Filatotchev and Bishop, 2002;

Chahine et al., 2009), France (Chahine, 2004; Mnif, 2009). However, with the vibrancy

in growth of economies, research efforts have been redirected towards growing and

emerging markets of Australia (Ching Yi-Lin, 2005), China (Li, 2005; Li and Naughton,

2007), Indonesia (Darmadi and Gunawan, 2012); Malaysia (Yatim, 2011); Singapore

(Mitchelle et al., 2008) and now it should be India.

With regards to Indian markets, however, literature on information asymmetry problems

at the time of IPO and contribution of governance attributes in mitigating these and

resulting effect on initial pricing performance is rather scant. This issue, therefore, forms

the main focus of present effort.

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

156

6.3 SAMPLE AND METHODOLOGY

The primary objective of this chapter is to examine the relationship between corporate

governance measures (as measured through board structures and ownership variables)

and listing day performance of newly issued securities. Signaling power of these

attributes and how far are they incorporated and relied on in taking the investment

decisions is attempted to be studied.

Sample for this objective is the firms which issued new equity securities between the time

period April 1, 2001 and March 31, 2012 and got them listed on the Bombay Stock

Exchange (BSE). IPO prospectuses prepared and submitted for the purpose of issue is the

source of culling data on corporate governance systems of IPO firms. For information on

market prices of securities and SENSEX values the ACEEQUITY database and BSE

website (www.bseindia.com) were relied on. Additional information about firm attributes

and issue variables was collected using above sources as well as PROWESS and

Capitaline database.

To analyse the relationship between IPO’s initial returns and corporate governance

mechanisms multiple regression analysis has been employed. As a precursor to regression

analysis relationships between underpricing and governance variables have been explored

using ANOVA and t-tests to investigate if the board structures and ownership patterns

differ across return continuum. Variables of interest, i.e., the governance variables for

analysis have been categorized into those relating to board structures and others

indicating ownership patterns. Other than these, firm specific and issue specific variables

have also been included in study to control for their effects on returns. Listing day returns

have been measured as raw returns (unadjusted) and market returns (those adjusted for

market movements with SENSEX as the barometer). The description of variables as

operationalized in the study is provided in Table 6.2.

With the specified objectives and outlined data and sample the chapter proceeds first to

examine and establish the underpricing phenomenon in India, examine the degree and

direction of governance variables to the listing day returns and then checking for

dependency of returns on these attributes.

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

157

Table 6.2: Operationalization of Research Variables for Study of Corporate Governance and Returns

Variables Operationalization Dependent Variable

Underpricing on listing day

1. Raw return- Closing price on the first trading day on the secondary market minus offer price, divided by offer price

2. MAER- Raw return minus the market return as measured by the BSE’s sensitive index

Independent Variables (Board related)Board size Total number of directors on the board

Board committees Inverse of total number of board committees to assist the board

Board independence Percentage of independent directors on the board Women directors Percentage of women directors on the board Age of board Average of the individual age of all board members

Related board members Number of members on the board who are related to each other

Board reputation The total number of board directorships held by non-executive directors at other firms

Independent Variables (Ownership related)

Promoter ownership Percentage of shares held by board of promoters (founders) at the time of issue

Promoter ownership squared

Square term of the percentage of shares held by board of promoters (founders) at the time of issue

Block holder ownership Number of shareholders holding shares more than 10% of total shares to denote concentrated ownership

Top 10 shareholding Percentage of shares owned by the 10 largest shareholders of a firm

Top 10 shareholding squared

Square term of percentage of shares owned by the 10 largest shareholders of a firm

Control Variables (Issue and firm related)

Subscription ratio Number of times the IPO has been subscribed: indicator of over or under subscription

Issue size Logarithm transformation of proceeds received from issuing new shares (in crores)

Listing delay Number of days between close of issue and listing on BSE Issue price The offer price of shares issued through IPO

IPO age Logarithm transformation of number of years between date of incorporation and IPO issue date

Total assets Logarithm transformation of book value of total assets as expressed in crores of rupees

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

158

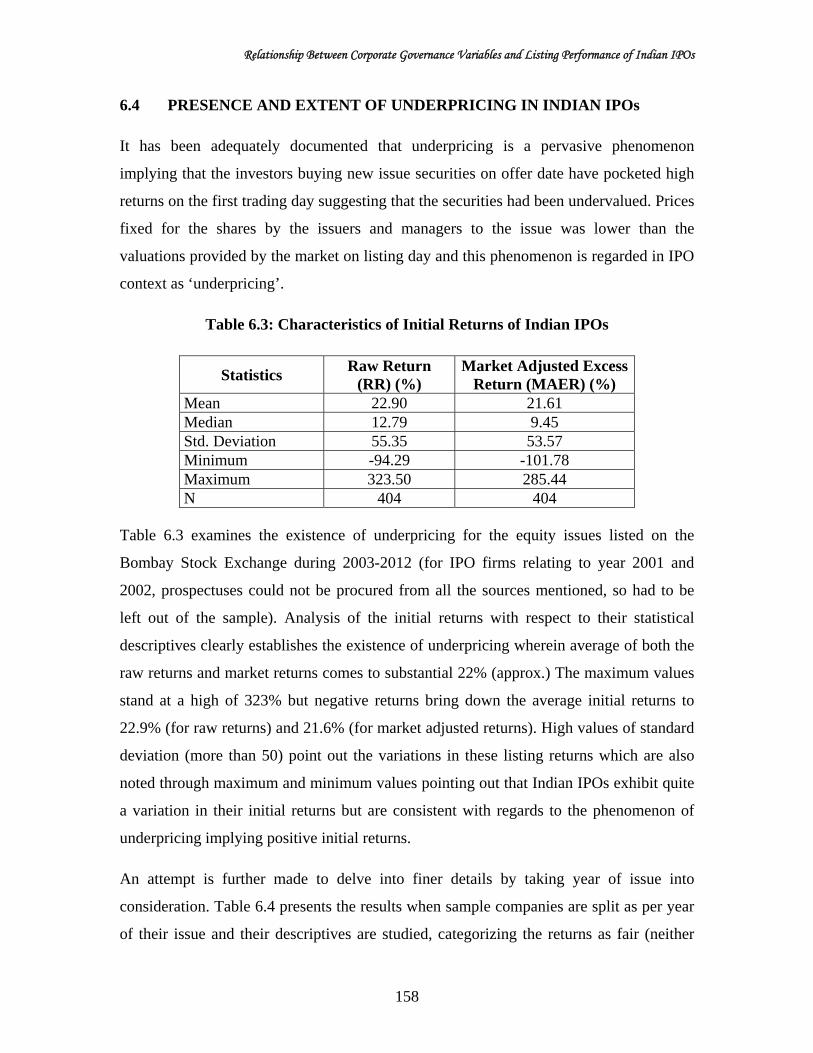

6.4 PRESENCE AND EXTENT OF UNDERPRICING IN INDIAN IPOs

It has been adequately documented that underpricing is a pervasive phenomenon

implying that the investors buying new issue securities on offer date have pocketed high

returns on the first trading day suggesting that the securities had been undervalued. Prices

fixed for the shares by the issuers and managers to the issue was lower than the

valuations provided by the market on listing day and this phenomenon is regarded in IPO

context as ‘underpricing’.

Table 6.3: Characteristics of Initial Returns of Indian IPOs

Statistics Raw Return

(RR) (%) Market Adjusted Excess

Return (MAER) (%) Mean 22.90 21.61 Median 12.79 9.45 Std. Deviation 55.35 53.57 Minimum -94.29 -101.78 Maximum 323.50 285.44 N 404 404

Table 6.3 examines the existence of underpricing for the equity issues listed on the

Bombay Stock Exchange during 2003-2012 (for IPO firms relating to year 2001 and

2002, prospectuses could not be procured from all the sources mentioned, so had to be

left out of the sample). Analysis of the initial returns with respect to their statistical

descriptives clearly establishes the existence of underpricing wherein average of both the

raw returns and market returns comes to substantial 22% (approx.) The maximum values

stand at a high of 323% but negative returns bring down the average initial returns to

22.9% (for raw returns) and 21.6% (for market adjusted returns). High values of standard

deviation (more than 50) point out the variations in these listing returns which are also

noted through maximum and minimum values pointing out that Indian IPOs exhibit quite

a variation in their initial returns but are consistent with regards to the phenomenon of

underpricing implying positive initial returns.

An attempt is further made to delve into finer details by taking year of issue into

consideration. Table 6.4 presents the results when sample companies are split as per year

of their issue and their descriptives are studied, categorizing the returns as fair (neither

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

159

underpriced nor overpriced, no returns), positive (underpriced issues) and negative

(overpriced issues). Of the total IPO companies 263 across all years are underpriced

giving positive returns to investors on the listing day while 141 of the 404 IPOs result in

negative returns.

Table 6.4: Summary Statistics of Year-wise IPO Raw Returns

Year N Mean Median SD Min Max Positive Fair Negative 2003 4 73.34 61.07 58.44 22.90 148.33 4 0 0 2004 20 48.75 37.17 69.71 -89.11 209.71 17 0 3 2005 55 46.07 31.53 63.38 -14.81 323.50 48 0 7 2006 65 27.41 15.80 44.10 -30.12 230.26 47 0 18 2007 98 34.21 15.67 59.92 -42.17 286.25 63 0 35 2008 37 -16.83 -6.64 45.13 -94.29 68.11 14 0 23 2009 20 4.37 1.35 35.99 -58.72 129.25 12 0 8 2010 63 10.89 6.00 35.08 -88.64 103.98 38 0 25 2011 37 3.51 -11.07 55.55 -69.83 153.50 17 0 20 2012 5 6.56 2.80 12.82 -5.00 25.68 3 0 2

The initial unadjusted returns of these IPOs are found to be positive on an average for all

years of sample except for the year 2008 wherein these returns are recorded at -16.83

percent which coincide with the global downturn which did not leave even the Indian

capital market unaffected. Another distinct pattern which emerges is the decreasing initial

returns over time which can be conjectured to the legislative initiatives aiming at

normalizing returns to ensure efficient market mechanisms. Mean returns from these

IPOs as on the listing day show a diluting effect which is elucidated by the decreasing

values (48.75 in 2004 to 10.89 in 2010). The tendency, however, of positive returns of

individual IPOs remains strong to which the very high maximum values stand evidence,

which are way above 100 percent for almost all years. None of the IPOs in any of the

years delivers fair returns or is fairly priced when their offer price and listing day prices

are compared.

Similarly, these returns when adjusted against the returns of the market (i.e. against the

SENSEX values) to calculate MAER also show almost similar results. When checking

for number of positive and negative MAER IPOs, again 263 are underpriced while the

number of overpriced IPOs stands at 141 confirming the existence of a trend of positive

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

160

returns to the investors of IPO (underpricing). Table 6.5 presents a year wise description

of MAER of sample IPO firms which establishes existence of underpricing in Indian

markets. Positive returns accruing to initial investors though are decreasing over time

being negative and minimum in 2008-09 which coincides with the financial hiccups

world over as a fall out of global crisis.

Table 6.5: Summary Statistics of Year-wise IPO Initial Market Adjusted Excess Returns

Year N Mean Median SD Min Max Positive Fair Negative 2003 4 65.40 52.31 54.47 21.61 135.36 4 0 0 2004 20 45.63 30.32 72.15 -101.78 203.38 17 0 3 2005 55 41.55 27.73 59.38 -12.81 277.40 48 0 7 2006 65 23.06 9.70 43.57 -30.32 230.89 47 0 18 2007 98 33.76 15.22 58.00 -28.69 285.44 63 0 35 2008 37 -11.27 -1.03 45.89 -101.55 84.87 14 0 23 2009 20 1.79 -1.25 37.70 -65.66 134.57 12 0 8 2010 63 10.16 4.11 34.84 -85.69 98.19 38 0 25 2011 37 4.48 -6.19 54.81 -75.06 144.52 17 0 20 2012 5 7.75 4.27 13.74 -4.42 29.22 3 0 2

The median values for MAER also show decreasing values indicating a trend of

mitigation of underpricing which is being attempted through tighter norms and stringent

rules for IPO pricing and allied mechanisms. Minimum values here do point out existence

of overpricing but it remains low both in number and quantum as positive returns

dominate as indicated by mean values. High values of standard deviations depict huge

variations with returns varying significantly across mean values but consistency with

regards to positive returns is certain.

Although quantum of underpricing in Indian markets is reclining but it is far from being

non-existent and thus remains a prolific research area. Fairly priced IPOs are a distant

dream (no IPOs in this category) retaining contentiousness of IPO pricing. Thus, research

in this area is continuous with all studies forwarding different explanations to this

pervasive underpricing phenomenon. Initial testing of initial returns of IPO in India

confirm the existence of a phenomena where securities are undervalued before issue and

market valuations as confirmed on listing are higher than these, resulting in high returns

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

161

for first day investors. Underpricing, as found to exist, is investigated henceforth for

meaningful explanations drawn primarily from corporate governance.

6.5 COMPARISON OF IPO FIRMS WITH POSITIVE AND NEGATIVE

INITIAL RETURNS

Indian IPOs have been found to be generating positive returns for initial investors as

established from the listing day returns. This implies that on an average the IPO

valuations of securities are found to be lower than the valuations of securities by the

markets on listing in stock exchange which helps the investors of IPO to pocket positive

returns. Listing day returns of the IPOs though on an average have been positive but

negative returns also exist. To get deeper insights into behavior of initial returns, they are

segregated as positive returns (underpriced IPOs) and as IPOs with negative returns to

find out if these two types of firms vary with respect to governance characteristics and

firm variables. Do these two categories of firms differ from each other on the basis of

variables of interest when measured using raw returns and market adjusted returns is

attempted to be investigated in this section.

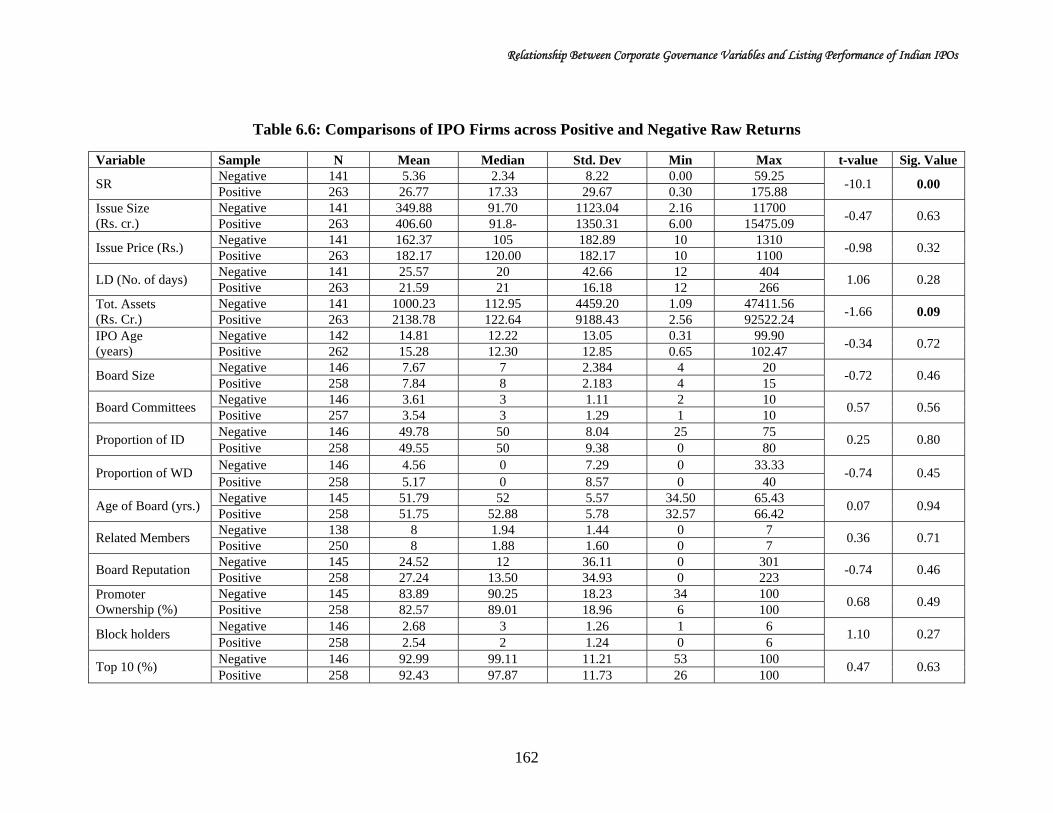

Table 6.6 presents details of both types of firms on governance parameters as well as

other control variables differentiated on the basis of raw returns i.e. unadjusted listing day

prices. Each of the variables included for analysis is explored for underpriced and

overpriced IPOs to see if there lies a significant difference among these firms in relation

to each of the parameters. Firm variables included in study are subscription ratio, issue

size, issue price, listing delay, total assets and age of IPO firm due to their inherent

potential to influence the returns. It is therefore attempted to check if, on account of these

variables the firms generating positive and negative returns vary or are similar.

The subscription ratio, indicating number of times the issue has been subscribed

(oversubscribed), shows significantly different values for firms with positive returns and

those generating negative first day returns. IPOs which are overpriced have mean

subscription ratio of 5.36 in contrast to 26.71 times for underpriced IPOs. A striking

difference is also observed for maximum values of these two classes on account of

subscription ratio which stands at an astoundingly high ratio of 175 for positive returns

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

162

Table 6.6: Comparisons of IPO Firms across Positive and Negative Raw Returns

Variable Sample N Mean Median Std. Dev Min Max t-value Sig. Value

SR Negative 141 5.36 2.34 8.22 0.00 59.25

-10.1 0.00 Positive 263 26.77 17.33 29.67 0.30 175.88

Issue Size (Rs. cr.)

Negative 141 349.88 91.70 1123.04 2.16 11700 -0.47 0.63

Positive 263 406.60 91.8- 1350.31 6.00 15475.09

Issue Price (Rs.) Negative 141 162.37 105 182.89 10 1310

-0.98 0.32 Positive 263 182.17 120.00 182.17 10 1100

LD (No. of days) Negative 141 25.57 20 42.66 12 404

1.06 0.28 Positive 263 21.59 21 16.18 12 266

Tot. Assets (Rs. Cr.)

Negative 141 1000.23 112.95 4459.20 1.09 47411.56 -1.66 0.09

Positive 263 2138.78 122.64 9188.43 2.56 92522.24 IPO Age (years)

Negative 142 14.81 12.22 13.05 0.31 99.90 -0.34 0.72

Positive 262 15.28 12.30 12.85 0.65 102.47

Board Size Negative 146 7.67 7 2.384 4 20

-0.72 0.46 Positive 258 7.84 8 2.183 4 15

Board Committees Negative 146 3.61 3 1.11 2 10

0.57 0.56 Positive 257 3.54 3 1.29 1 10

Proportion of ID Negative 146 49.78 50 8.04 25 75

0.25 0.80 Positive 258 49.55 50 9.38 0 80

Proportion of WD Negative 146 4.56 0 7.29 0 33.33

-0.74 0.45 Positive 258 5.17 0 8.57 0 40

Age of Board (yrs.) Negative 145 51.79 52 5.57 34.50 65.43

0.07 0.94 Positive 258 51.75 52.88 5.78 32.57 66.42

Related Members Negative 138 8 1.94 1.44 0 7

0.36 0.71 Positive 250 8 1.88 1.60 0 7

Board Reputation Negative 145 24.52 12 36.11 0 301

-0.74 0.46 Positive 258 27.24 13.50 34.93 0 223

Promoter Ownership (%)

Negative 145 83.89 90.25 18.23 34 100 0.68 0.49

Positive 258 82.57 89.01 18.96 6 100

Block holders Negative 146 2.68 3 1.26 1 6

1.10 0.27 Positive 258 2.54 2 1.24 0 6

Top 10 (%) Negative 146 92.99 99.11 11.21 53 100

0.47 0.63 Positive 258 92.43 97.87 11.73 26 100

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

163

IPOs. Higher subscription ratio is indicative of higher demand which then is translated

into better performance. Thus, on account of number of times IPO is subscribed the two

categories of firms significantly differ making this characteristic an important

distinguishing feature. Firms with positive returns have been found to have a higher

subscription ratio on an average than those with negative returns.

For issue size, which represents the total value of shares offered through the IPO, the

mean values are found to be higher for firms generating positive returns but the

differences are not statistically significant. Though median values and maximum

values along with other descriptives show a difference but they fail the test of

statistical significance giving inference that issue size and issue price of securities of

issuing firms are not a basis of distinction between firms with positive and negative

returns. Time gap between the close of issue and listing of securities on BSE, called

as listing delay, is 22 days on an average for positive returns firms while it stands as

26 days for firms with negative returns. Minimum value though stands at 12 for both

categories but the maximum is found as high as 404 days for overpriced IPOs.

However, these differences again are not statistically significant. IPO age also

displays the same behavior but the differences lack statistical validity. Total assets

value of IPO firms at the time of IPO is also studied for both these types of firms and

these are found to be significantly higher for firms with positive returns (at 10% level

of significance) standing at a mean value of 2139 crores. Huge differences are also

observed in maximum values which are almost double the value of assets of

overpriced IPOs for firms with positive returns. It can be deduced that total asset base

of underpriced firms are significantly higher than other firms as computed at the time

of IPO.

On account of governance attributes, the return typology is found to hold no

significance as the little differences found lack statistical significance. Ratio of

independent directors, board committees, age of board members assume almost equal

mean values across all firms and do not bring out any significant differences among

firms with positive and negative returns. Firms with more reputed directors, larger

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

164

board size, and more women as directors on board leave more money on the table, i.e.

are underpriced but this hypothesis lacks statistical significance as seen from the

insignificant values for these variables in Table 6.6. With regards to ownership

variables also, the results do not conform to test of statistical validity though lower

percentage of promoter ownership, lower number of block holders and lower

percentage of shares retained by top 10 owners is seen for firms generating positive

returns to IPO investors but statistical insignificance again remains an issue.

Differences are noted for sample firms on these governance variables but they are not

found to be significant enough to qualify as differentiating criteria between firms

ensuring positive returns and negative returns for the investors. On the whole

differences in means for the categorized firms exist only on account of subscription

ratio, total assets and not on account of corporate governance measures.

Similar exploration is done for MAER wherein, again firms are classified as those with

positive returns and others which deliver negative returns to investors as measured on

the listing day. Results for the analysis have been presented in Table 6.7 which

includes all firm variables, issue variables and the governance proxies considered in

the study.

With regards to subscription ratio the results are on the same lines as in case of raw

returns as discussed above making it an important and significant point of distinction

between the two categories of firms. All other firm variables and those relating to IPO

fail to bring about a statistically significant difference among underpriced and

overpriced IPOs though variation in mean values is noted. Except for listing delay and

issue size firms with negative returns have mean values lower for variables including

subscription ration, issue price, total assets and IPO age than the underpriced firms

highlighting the strong credentials which enable firms to sustain the costs associated

with underpricing of issue. The insignificant values for these variables, however, show

that the firms are almost similar on these accounts and do not present discernible

differences.

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

165

Table 6.7: Comparisons of IPO Firms across Positive and Negative MAERs

Variable Sample N Mean Median Std. Dev Min Max t-value Sig. Value

SR Negative 147 5.95 2.35 8.71 0.00 59.25

-8.19 0.00 Positive 257 26.85 17.25 30.20 0.30 175.88

Issue Size (Rs. cr.)

Negative 147 389.91 91.70 1209.21 2.16 11700 0.02 0.98

Positive 257 387.69 91.90 1324.86 6.00 15475.09

Issue Price (Rs.) Negative 147 163.07 106.50 181.55 10 1310

-1.09 0.27 Positive 257 184.72 120 188.61 10 1032

LD (No. of days) Negative 146 25.46 20 42.08 12 404

1.05 0.29 Positive 258 21.60 21 16.33 12 266

Tot. Assets (Rs. Cr.)

Negative 148 1167.31 108.62 5908.83 1.09 61500.78 -1.23 0.21

Positive 256 2078.80 122.64 8812.21 2.56 92522.24 IPO Age (years)

Negative 148 14.15 12.22 10.97 0.31 70.45 -1.02 0.30

Positive 256 15.51 12.30 13.84 0.65 102.47

Board Size Negative 147 7.63 7 2.38 4 20

-1.00 0.31 Positive 252 7.86 8 2.18 4 16

Board Committees Negative 147 3.56 3 1.08 2 10

-0.00 0.99 Positive 251 3.57 3 1.31 1 10

Proportion of ID Negative 147 49.27 50 7.85 25 75

-0.72 0.47 Positive 252 49.93 50 9.49 0 80

Proportion of WD Negative 147 5.09 0 7.71 0 33.33

0.14 0.88 Positive 252 4.97 0 8.42 0 40

Age of Board (yrs.) Negative 147 51.76 52.38 5.79 34.50 65.43

-0.08 0.93 Positive 251 51.81 52.71 5.65 32.57 66.42

Related Members Negative 142 2.01 2 1.46 0 7

1.16 0.24 Positive 241 1.82 2 1.57 0 6

Board Reputation Negative 146 25.83 13 39.29 0 301

-0.17 0.85 Positive 252 26.48 12 33.21 0 182

Promoter Ownership (%)

Negative 146 85.47 92.38 17.39 34 100 1.91 0.05

Positive 252 81.80 87.15 19.11 6 100

Block holders Negative 147 2.67 3 1.25 1 6

0.91 0.36 Positive 252 2.56 2 1.25 0 6

Top 10 (%) Negative 147 94.03 99.42 10.43 59 100

1.66 0.09 Positive 252 92.07 97.47 11.86 26 100

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

166

Moving on to the governance factors, as in case of raw returns, mean values for board

committees, percentage of independent directors, age of board and number of block

holders display no differences among the two types of firms. Women directors on an

average show a higher value for firms with negative MAER, a result which lies in

contradiction to those seen for raw returns but this higher value does not stand the test of

statistical significance and so no concrete conclusions can be drawn. Same are the results

for number of board committees constituted in the IPO firm to help board members

discharge their responsibilities and number of shareholders holding more than 10% of

total shares (block holders). Number of members on board and other directorships of

these members expressed as board reputation are found to be higher in case of

underpriced IPO firms highlighting that larger and reputed boards are afforded by these

firms which generate positive returns for IPO investors. Ownership variables as

represented by promoter ownership and ownership in the hands of top 10 shareholders

show significant results implying that differences exist among underpriced and

overpriced issues on account of these two components. Promoter holding in these

underpriced issues is lower than the other firms reflecting the fact that there is more

dilution of control by such firms and hence their ability to stand the control and cost

issues. Ownership concentration levels for such firms are also low indicating a trend of

dispersed ownership taken positively by the markets as reflected from the positive returns

on the listing day. Other than these ownership parameters, none of the governance

attributes are found to have significant values when comparing the mean values of firms.

On the whole, when comparing firms with positive and negative returns the mean

differences are found to be significant only for subscription ratio and total assets (in case

of raw returns) getting to the conclusion that firms do differ on account of this ratio. For

corporate governance variables, the differences on various parameters are not found to be

significant except for promoter and block holder ownership. The differences among

underpriced and overpriced firms on account of governance mechanisms are not found to

be significant which means that these mechanisms do not bring about significant changes

in returns. Underpriced firms are not found to be governance wise different from those

with negative returns and the reasons for differences in returns lie in factors other than

these. Corporate governance preparedness of IPO firms is not solely responsible for

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

167

concrete and substantial differences in these firms when compared for means on the basis

of listing day returns. Taking the study of IPO returns further, the need for which is

highlighted from results above, governance attributes considered in the study are

individually studied against the positive and negative returns for further insight.

6.6 ANALYSIS OF GOVERNANCE VARIABLES ACROSS LISTING RETURNS

The present section attempts to find explanations to the underpricing phenomenon

using corporate governance attributes measured through board structures and ownership

variables. Within this broader objective it also becomes pertinent to analyze the

behavior and response of listing day prices to these governance attributes. The returns

on listing day are measured through two variables: the raw returns or unadjusted returns

which are measured as a difference between listing price and offer price and dividing

by offer price. As a variant, these returns are adjusted for market movements as

represented by SENSEX values on these two dates to be regarded as MAER- the

market adjusted excess returns.

For this section, raw returns and market adjusted returns on the listing day are segregated

as positive and negative returns and how they respond to each of the governance

attributes is studied. Positive returns imply the IPOs being underpriced while overpriced

IPOs result in negative returns. Each of the governance variables included in the study

have been studied for their association with positive and negative returns and overall

returns.

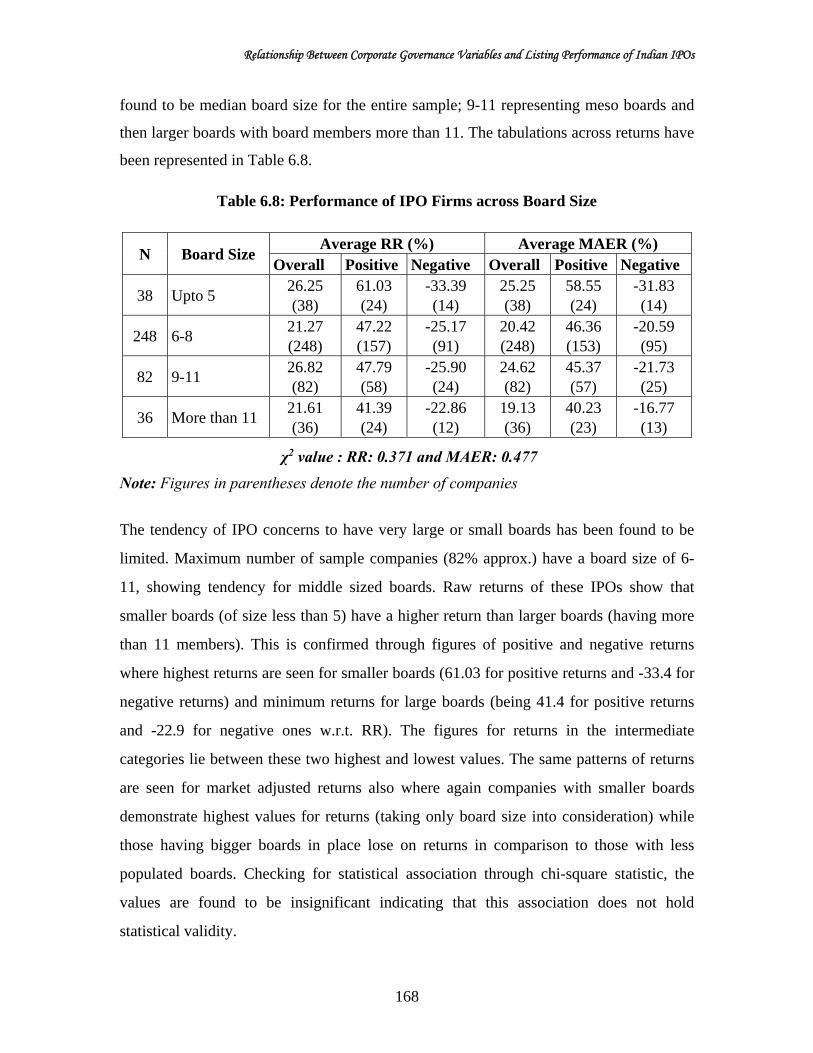

6.6.1 Board Size and Initial Returns

Board size, indicating the total number of directors on board of company is a very

important board characteristic. The researchers have not been able to reach a consensus

with regards to most appropriate board size. There is, for example, some evidence that

smaller boards are more beneficial (e.g., Yermack, 1996). While, there is also support for

larger boards being more effective (Alexander et al., 1993).

To understand the relationship between board size and returns, board size is categorized

into four classes: up to 5 denoting smaller boards; 6-8 medium sized boards where 8 was

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

168

found to be median board size for the entire sample; 9-11 representing meso boards and

then larger boards with board members more than 11. The tabulations across returns have

been represented in Table 6.8.

Table 6.8: Performance of IPO Firms across Board Size

N Board Size Average RR (%) Average MAER (%)

Overall Positive Negative Overall Positive Negative

38 Upto 5 26.25 (38)

61.03 (24)

-33.39 (14)

25.25 (38)

58.55 (24)

-31.83 (14)

248 6-8 21.27 (248)

47.22 (157)

-25.17 (91)

20.42 (248)

46.36 (153)

-20.59 (95)

82 9-11 26.82 (82)

47.79 (58)

-25.90 (24)

24.62 (82)

45.37 (57)

-21.73 (25)

36 More than 11 21.61 (36)

41.39 (24)

-22.86 (12)

19.13 (36)

40.23 (23)

-16.77 (13)

χ2 value : RR: 0.371 and MAER: 0.477

Note: Figures in parentheses denote the number of companies

The tendency of IPO concerns to have very large or small boards has been found to be

limited. Maximum number of sample companies (82% approx.) have a board size of 6-

11, showing tendency for middle sized boards. Raw returns of these IPOs show that

smaller boards (of size less than 5) have a higher return than larger boards (having more

than 11 members). This is confirmed through figures of positive and negative returns

where highest returns are seen for smaller boards (61.03 for positive returns and -33.4 for

negative returns) and minimum returns for large boards (being 41.4 for positive returns

and -22.9 for negative ones w.r.t. RR). The figures for returns in the intermediate

categories lie between these two highest and lowest values. The same patterns of returns

are seen for market adjusted returns also where again companies with smaller boards

demonstrate highest values for returns (taking only board size into consideration) while

those having bigger boards in place lose on returns in comparison to those with less

populated boards. Checking for statistical association through chi-square statistic, the

values are found to be insignificant indicating that this association does not hold

statistical validity.

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

169

Clearly then, listing returns do support the hypothesis of smaller boards (but when seen in

isolation) advocating ease in reaching consensus and less conflicts which generally

emanate from divergent views. The tendency of the companies for middle sized boards

may emerge from the inherent complexities in decision making and necessity of diverse

viewpoints.

6.6.2 Board Committees and Initial Returns

Board committees are included as a part of board structures and are meant to enable

board members perform their fiduciary duties more efficiently and effectively.

Committees are constituted with directors as members and chairpersons for facilitating

and ensuring corporate accountability and enhancing credibility of board structures.

Recognizing their eminence, board committees have been necessitated by law. Clause 49

of the listing agreement in India recommends constitution of mandatory committees

(Audit Committee and Shareholder/ Investors Grievance Committee) and non-mandatory

committee (Remuneration Committee).

Table 6.9: Performance of IPO Firms across Board Committees

N Number of

Board Committees

Average RR (%) Average MAER (%) Overall Positive Negative Overall Positive Negative

23 Less than 3 37.40 (23)

60.86 (17)

-29.07 (6)

33.39 (23)

63.12 (15)

-22.37 (8)

237 3 25.81 (237)

50.07 (160)

-26.97 (77)

25.42 (237)

47.95 (158)

-20.99 (79)

143 More than 3 16.65 (143)

42.07 (85)

-24.05 (58)

14.85 (143)

41.80 (83)

-22.09 (60)

χ2 value : RR: 0.066 and MAER: 0.135

Note: Figures in parentheses denote the number of companies

To analyze the responsiveness of returns to number of committees of board constituted

by the concerned IPO company, board committees are categorized as compulsory (2

which implies less than 3), non-mandatory (3) and voluntary (more than 3) on the lines of

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

170

recommendations of Clause 49. These are then checked for underpriced firms (positive

returns) and overpriced firms (negative returns) against both raw and adjusted returns.

Indian IPO firms are found to have mostly three committees on their boards as have been

specified by the listing agreement’s Clause 49 namely Audit Committee, Shareholder/

Investors Grievance Committee and Remuneration Committee. However, seeing the

facilitations these committees provide to board and decision making, number of firms

having more than 3 board committees is also noticeable (almost 35%). This constitution

of committees is also done in the light of credibility and reliability which they are

supposed to convey to investors. The distribution of returns across various categories of

board committees is presented in Table 6.9 wherein classifications have been provided to

raw returns and market returns.

The overall average raw returns show a declining trend to increase in number of board

committees as they fall down to 17% for more than three committees while they stand at

37% for two board committees, the mandatory number. The split of these returns as

positive and negative also corroborates these results. Amongst the underpriced firms

(those with positive returns), the highest percentage of average returns stands at 61%

which dilutes to 42.07 as the number of board committees increases from two to more

than three. The negative returns also show a decrease as the IPO concerns constitute

voluntary board committees. MAERs when investigated across different number of board

committees also indicate a similar trend reflecting highest returns for firms with only two

committees. Among positive MAERs, returns stand at 42% for more than 3 board

committees while for only two, these returns are as high as 63%. The patterns for

negative MAERs are not very discernible and stand differently from the negative raw

returns for which explanations that can be conjectured are market movements.

With regards to board committees it is, therefore, clear that there definitely lies a

relationship with returns, though inverse. The existence of relationship is confirmed

through significant value of chi-square (0.066) for raw returns and loosely significant for

adjusted returns. IPO concerns are governed largely by the legal compulsions and

potential of the variable to communicate better preparedness on decision making aspect

but this is not commensurate with the listing day returns.

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

171

6.6.3 Board Independence and Initial Returns

Proportion of independent directors on the board has always been a dominating measure

of corporate governance measure. Independent directors are expected to bring expertise

and an independent view to board which can take care of interests of stakeholders and

effective decision making. With the New Companies Act, 2013 clearly defining

independent directors, empowering them and granting supremacy in conducting affairs of

a company, the pertinence of board independence has accentuated. The legal requirement

as per clause 49 of listing agreement provides that where the Chairman of the Board is a

non-executive director, at least one-third of the Board should comprise of independent

directors and in case he is an executive director, at least half of the Board should

comprise of independent directors. Provided that where the non-executive Chairman is a

promoter of the company or is related to any promoter or person occupying management

positions at the Board level or at one level below the Board, at least one -half of the

Board of the company shall consist of independent directors. However, Companies Act,

2013 provides that all listed companies should have at least one-third of the Board as

independent directors. Such other class or classes of public companies as may be

prescribed by the Central Government shall also be required to appoint independent

directors. On the basis of requirements before the implementation of new law,

classifications in this category have been made as less than 50%, exactly 50%, 51-70% to

provide for the requirement of one-third of board strength and more than this percentage

which reflects the voluntary requirement to have more independent directors than

mandated.

The results for percentage of independent directors and their effects in case of

underpriced and overpriced firms have been tabulated in Table 6.10. Maximum

frequency is observed for the proportion of independent directors between half and one

third of total board strength. The number of IPO firms with independent directors less

than 50% stands at 70 (17 percent of total sample) highlighting those not abiding by legal

requirements. This is seen among firms which came out with their IPO in early years of

the sample as non-compliance in new IPOs is almost non-existent. Inducting more than

the mandated numbers of independent directors is not a frequently followed practice,

hardly one percent (4 IPOs) of firms fall in this category.

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

172

Table 6.10: Performance of IPO Firms across Proportion of Independent Directors

N Independent directors (%)

Average RR (%) Average MAER (%) Overall Positive Negative Overall Positive Negative

70 Less than 50% 18.57 (70)

38.24 (46)

-24.16 (24)

16.79 (70)

39.44 (42)

-15.90 (28)

247 50% 21.64 (247)

45.65 (164)

-27.61 (83)

20.31 (247)

45.18 (156)

-21.80 (91)

83 51-70% 30.44 (83)

65.90 (50)

-23.28 (33)

29.76 (83)

57.06 (56)

-26.88 (27)

4 More than 70% 19.43

(4) 28.37

(3) -7.41 (1)

17.07 (4)

25.44 (3)

-8.03 (1)

χ2 value : RR: 0.553 and MAER: 0.287

Note: Figures in parentheses denote the number of companies

Numbers for returns indicate that as the proportion of independent directors increases,

both raw and market returns, on an average, increase till the mandatory requirements

(indicated by 70%) but beyond that the average returns drop down steeply. Breaking

up this return to positive and negative returns, the patterns observed are no different.

When the proportion of board independence increases beyond two-thirds of total

strength, the positive returns fall down to 28.37 from the highest level of 66% (to 25%

from 57% in case of market return). The negative returns, in case of MAER, get all the

more negative till proportion of 70 and then stand at -8% when percentage of

independent directors surpasses 70%. The negative raw returns, however, differ a little

as their upturn is observed at the level of 50% though negative values are minimum for

highest proportion. The chi-square values of 0.553 and 0.287 for RR and MAER

respectively, confirm the lack of significant association between board independence

and returns.

For the relation of independent directors to returns, mandatory level (of two-third)

provides the point of turns to the increasing returns which suddenly fall indicating that

firms with two-thirds of directors as independent deliver maximum returns on the listing

date. Overall, on this account it can be summarized that firms prefer to stick to the

specified mandatory requirement on board independence which is supplemented by good

returns at these points.

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

173

6.6.4 Gender Diversity and Initial Returns

Even in times of women empowerment, presence of women on corporate boards remains

a rarity. It is actually their absence on boards globally which makes news and this indeed

has made gender diversity a widely talked and extensively researched issue. Presence of

women on boards draws theoretical support from agency, resource dependency and

institutional theory and has extant empirical support which necessitates women in

directorial position for financial and non-financial gains. Gender diversity, therefore, has

emerged as an important aspect of board structure and purported to be influential in board

effectiveness.

Table 6.11: Performance of IPO Firms across Levels of Gender Diversity

N No. of

Women directors

Average RR (%) Average MAER (%) Overall Positive Negative Overall Positive Negative

277 0 23.88 (277)

48. 20 (178)

-23.48 (99)

22.38 (277)

46.16 (176)

-22.46 (96)

103 1 20.44 (103)

51.00 (60)

-22.20 (43)

19.47 (103)

51.00 (57)

-19.36 (46)

24 2* 22.26 (24)

33.06 (20)

-29.07 (4)

22.42 (24)

35.08 (19)

-23.14 (5)

χ2 value : RR: 0.723 and MAER: 0.905

Note: Figures in parentheses denote the number of companies * Only one company had three women directors so clubbed in this category only

Maximum number of women directors in sample companies was found to be three which

existed for a single company (Beeyu Overseas Limited) and so for tabulating results here

the company has been clubbed with the third category of 2 directors. The number of

women directors, hence varies between zero and two and for these the average returns

have been studied. As evident from Table 6.11, no discernible relationship can be figured

between these two variables as corroborated by insignificant values for the chi-square test

of association. Average initial returns are found to be almost same for no women

companies and those with two women as directors with a comparatively lesser return for

those with one woman indicating that approach of tokenism would not help convert

concept of gender diversity into returns. In case of underpriced IPOs, the raw returns are

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

174

seen to be increasing and then sharp rise is observed as the number of women increases to

two. For negative raw returns and both positive and negative MAERs, the performance in

terms of return first improves with one woman director and with addition of one more

woman the performance weakens.

For gender diversity the numbers indicate very negligible representation of women on

boards which seems to be an exercise in letter blowing away the spirit. The maximum

number of women not surpassing mark of two is really a matter of concern calling for

remedial measures (like introduced in the Companies Act, 2013 whereby inducting at

least one woman as director on the board has been made mandatory for specified

companies). There definitely lies a relationship with returns, though that emerges clearly

in one section of sample (positive raw returns) but the low numbers can be held

responsible for same. The effect on returns can be purported to be more emphatic and

evident in case of large number of women as directors in companies.

6.6.5 Board Age and Initial Returns

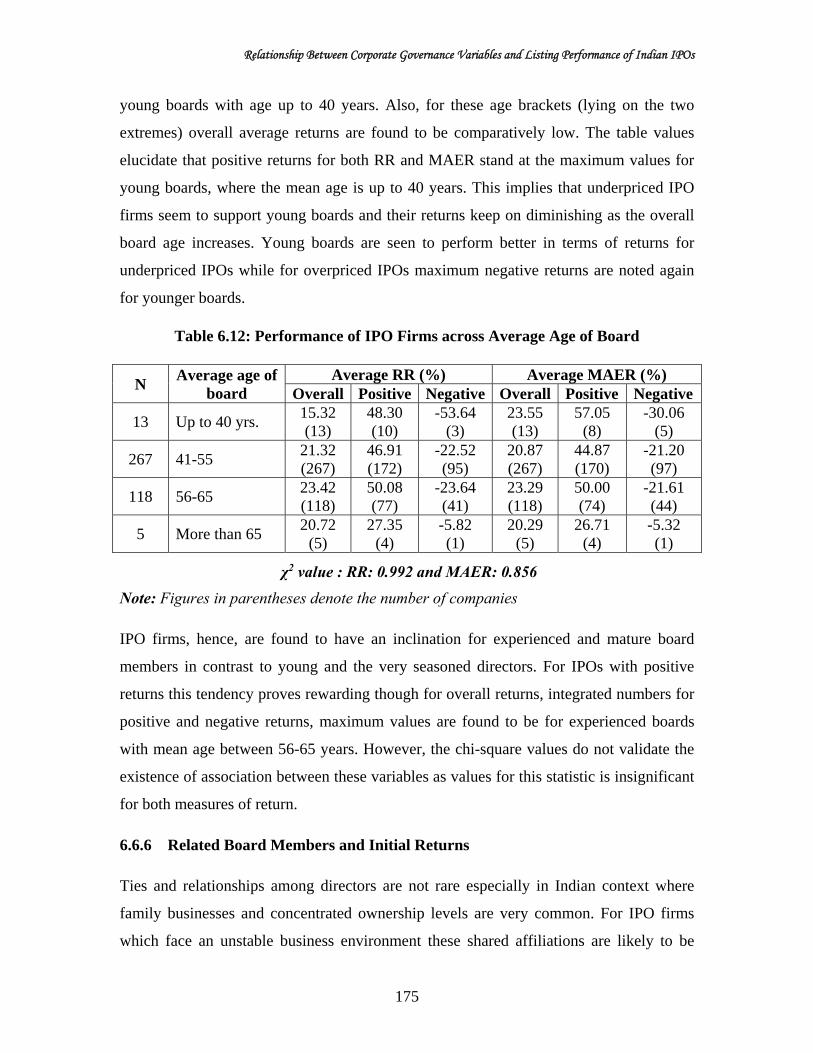

Experience and maturity of board members is expected to lend viability and credibility to

the strategic decisions taken in board rooms which are expected to set the pace for firm’s

growth and development. One of the important factors from where this experience and

maturity emanates is the age of board members. Age of board, as referred here, refers to

average of individual age of each of the board members and is included here being

another measure of board quality. It affects on decision making and therefore its

relationship with returns is analyzed next.

Board age was found to vary between 32 and 66 years. The classifications across this

range have been made as young boards (up to 40 years), experienced boards (41-

55years), mature boards (with mean age in the range of 56 to 65 years) and senior boards

(more than 65 years ripe in age and experience). The age classifications of board are

contrasted with positive, negative and overall returns and the results are presented in

Table 6.12. IPO boards are found to be having directors which are middle aged for their

experience and maturity rather than having very senior directors (boards with average age

of more than 65 years are merely 5 of the total sample) and numbers stand low even for

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

175

young boards with age up to 40 years. Also, for these age brackets (lying on the two

extremes) overall average returns are found to be comparatively low. The table values

elucidate that positive returns for both RR and MAER stand at the maximum values for

young boards, where the mean age is up to 40 years. This implies that underpriced IPO

firms seem to support young boards and their returns keep on diminishing as the overall

board age increases. Young boards are seen to perform better in terms of returns for

underpriced IPOs while for overpriced IPOs maximum negative returns are noted again

for younger boards.

Table 6.12: Performance of IPO Firms across Average Age of Board

N Average age of

board Average RR (%) Average MAER (%)

Overall Positive Negative Overall Positive Negative

13 Up to 40 yrs. 15.32 (13)

48.30 (10)

-53.64 (3)

23.55 (13)

57.05 (8)

-30.06 (5)

267 41-55 21.32 (267)

46.91 (172)

-22.52 (95)

20.87 (267)

44.87 (170)

-21.20 (97)

118 56-65 23.42 (118)

50.08 (77)

-23.64 (41)

23.29 (118)

50.00 (74)

-21.61 (44)

5 More than 65 20.72

(5) 27.35

(4) -5.82 (1)

20.29 (5)

26.71 (4)

-5.32 (1)

χ2 value : RR: 0.992 and MAER: 0.856

Note: Figures in parentheses denote the number of companies

IPO firms, hence, are found to have an inclination for experienced and mature board

members in contrast to young and the very seasoned directors. For IPOs with positive

returns this tendency proves rewarding though for overall returns, integrated numbers for

positive and negative returns, maximum values are found to be for experienced boards

with mean age between 56-65 years. However, the chi-square values do not validate the

existence of association between these variables as values for this statistic is insignificant

for both measures of return.

6.6.6 Related Board Members and Initial Returns

Ties and relationships among directors are not rare especially in Indian context where

family businesses and concentrated ownership levels are very common. For IPO firms

which face an unstable business environment these shared affiliations are likely to be

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

176

valuable by encouraging friendly and co-operative exchanges. Though these can also

destroy rather than create value by creating excessive managerial power leading to

managerial entrenchment. Thus, the importance of this variable as a governance attribute

and its potential effect on IPO returns remains immense. The association of this variable

across returns is tabulated in Table 6.13.

Table 6.13: Performance of IPO Firms across Related Board Members

N Related

members on board

Average RR (%) Average MAER (%)

Overall Positive Negative Overall Positive Negative

128 None 27.85 (128)

45.00 (38)

-12.76 (89)

25.60 (128)

42.14 (90)

-13.57 (38)

109 Two 18.79 (109)

52.82 (63)

-27.82 (46)

18.61 (109)

52.85 (61)

-24.91 (48)

102 2-4 22.57 (102)

51.38 (62)

-22.07 (40)

21.83 (102)

51.88 (59)

-19.42 (43)

49 More than 4 23.71 (49)

34.40 (40)

-26.26 (9)

20.34 (49)

34.88 (36)

-19.93 (13)

χ2 value : RR: 0.628 and MAER: 0.635

Note: Figures in parentheses denote the number of companies

More than two thirds of the sampled IPO firms have related members on the boards and

of these more than half of them have related members more than two indicative of the

trend of inducting family members on the board rather than scouting for options outside.

The instances of having more than four members from the family as directors at the same

time are also found which amount to 12% of the entire sample. Analyzing these numbers

of related members against returns it is found that the listing returns on an average are

lower for boards with two related members than those for boards with all directors

unrelated to each other. Then again, it rises against 2-4 members category and falls for

companies with more than four related members. On the whole the mean listing day

returns are highest for firms where directors have no family ties amongst themselves (RR

of 28% and MAER of 26%) while for those IPOs which are underpriced and generate

positive returns, the maximum value stands against the category of two related directors

being 53% for both raw returns and adjusted returns. For the overpriced IPOs, no evident

trends are discovered. Insignificant values of chi-square here again not only just point

towards lack of association but also indicate the need for further analysis.

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

177

The variable of related board members definitely influences the returns though the kind

of relationship is mixed which is positive at some levels and then tends to turn negative.

Very high number of directors with family ties which each other does not for sure result

in value addition rather tends to erode values which draws its explanation from

‘entrenchment hypothesis’.

6.6.7 Board Reputation and Initial Returns

Interlocking directorate which refers to the practice of members of one corporate board

serving on the boards of multiple corporations, is a common practice. These multiple

directorships where on one side can allow for cohesion and coordinated action on the

other side, work as a reputational signal to the investors on account of competence and

quality of firm management. This director prestige also can lend legitimacy to these new

ventures which resort to various mechanisms to communicate their credibility and

performance potential to investing public.

Table 6.14: Performance of IPO Firms across Board Reputation

N No. of other

directorships Average RR (%) Average MAER (%)

Overall Positive Negative Overall Positive Negative

20 None 0.50 (20)

30.92 (10)

-29.91 (10)

-0.32 (20)

25.70 (11)

-32.12 (9)

159 1-10 26.58 (159)

56.44 (102)

-28.86 (57)

25.94 (159)

53.03 (105)

-26.74 (54)

160 11-50 21.66 (160)

43.73 (106)

-21.65 (54)

19.56 (160)

44.14 (97)

-18.28 (63)

64 More than 50 24.52 (64)

40.58 (45)

-13.51 (19)

23.41 (64)

40.04 (44)

-13.19 (20)

χ2 value : RR: 0.147 and MAER: 0.689

Note: Figures in parentheses denote the number of companies

Board reputation, as it is referred to, has been measured through other directorships of

non-executive directors. On the basis of patterns observed, these have been categorized

from zero to 50, though the highest value observed was 303. A director having no other

directorships is unusual though 20 companies fall in this category which is mostly

companies with practices of in-bred directors. The concentration is seen for other

directorships in the range of a few to fifty which has 79% of the sample values.

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

178

Interlocking directorates prove to build upon value for the IPO firms which are translated

into listing day returns (loosely significant for raw returns as revealed from the chi-square

value of 0.147) because they stand pretty low for companies where directors have no

other directorships as evident from figures in Table 6.14. Maximum returns are found to

be associated with directorships ranging from 1-10 which is highest among other

categories with other directorships greater than 10. This trend is observed both for overall

raw and market returns as well as for segregated returns.

Figures and facts on this variable clarify that other directorships do contribute to

reputation and prestige of boards, the steep increase in values from 0.50 to 26% for raw

returns but as these directorships increase this rise in value starts diluting. When seen

against returns, other directorships must be adopted by concerns but their higher numbers

probably increase doubts as to diversion of focus and commitment on part of directors

with interlocks.

6.6.8 Promoter Ownership and Initial Returns

In addition to the board variables, three ownership variables have also been included as

proxies for corporate governance of firms because Lemmon and Lins (2003) contend that

ownership structure is a fundamental determinant of the extent of agency problems

between insiders and outsiders, which may in turn affect the firm’s valuation. The first

variable included is promoter ownership which reflects the proportion of shares held by

promoters in the firm’s share capital. The relationship between returns and promoter

ownership as pointed out by Morck, Shleifer, and Vishny (1988) depends on 2 opposing

forces: the ‘convergence of interests’ effect (where higher ownership tends to align the

interests of promoters with those of shareholders) and the ‘entrenchment effect’ (which

allows them to entrench themselves and work for self-interests).

Indian firms being primarily family promoted firms have a strong tendency to be owned

and managed by the founders and hence it is attempted to study how this ownership

affects the returns of IPOs on listing day. The results have been tabulated in Table 6.15

wherein ownership of shares by promoters is put into three categories and studied for

positive, negative and overall returns. The clear tendency of high ownership by promoters

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

179

emerges out where almost 93% of the total sample companies have promoter ownership

more than 50% of total capital and highest numbers are seen for more than 75% of the

shares indicating trends of high promoter ownership among Indian IPOs.

Table 6.15: Performance of IPO Firms across Promoter Ownership

N Promoter

ownership (%) Average RR (%) Average MAER (%)

Overall Positive Negative Overall Positive Negative

29 Upto 50% 24.96 (29)

47.94 (19)

-18.70 (12)

26.18 (29)

42.65 (21)

-17.07 (8)

90 51-75% 22.09 (90)

47.63 (61)

-31.62 (29)

21.13 (90)

45.43 (61)

-29.98 (29)

284 More than 75% 23.04 (284)

47.61 (183)

-27.47 (101)

21.40 (284)

47.01 (175)

-19.74 (109)

χ2 value : RR: 0.681 and MAER: 0.146

Note: Figures in parentheses denote the number of companies

The overall raw returns are noted to increase along increased ownership by promoters of

the company while the adjusted returns stand at a maximum where promoter ownership is

the minimum. A clear increasing trend is seen for positive MAERs, i.e. for underpriced

IPOs (the loosely significant value of 0.146 for MAER), where average returns are found

to be increasing with higher levels of promoter ownership which shows

operationalization of the alignment effect. This trend, however, is not consistent across

all categories of returns. In case of overpriced IPOs, as categorized on the basis of

MAERs, the return stands most negative for middle ranges of ownership while least

negative for least promoter ownership levels. When contrasted with negative raw returns

the patterns are not very similar where least negative values are seen for highest

ownership levels. For IPOs with positive raw returns, the higher values stand for lowest

and highest ownership levels which give an indication towards a u-shaped relationship

between ownership and returns.

Indian IPOs are definitely governed by the tendencies of family promoted businesses

resulting in concentrated ownership and high levels of promoter ownership. These levels

definitely influence the returns as on listing day though the relationship does not emerge

out concretely (insignificant values for chi-statistic) hinting at a curvilinear relationship

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

180

where in mix of both direct and relationship exists. The dominance of convergence and/or

entrenchment effect, thus, remains an empirical issue.

6.6.9 Block Shareholders and Initial Returns

Variable block shareholders has been introduced as a measure of concentrated ownership

which is expected to affect the returns under the same principles of ‘alignment of interest’

and ‘entrenchment of interest’. Block shareholders mean the number of shareholders of

the firm owning more than 10 percent of the total shares at the time of IPO. Larger the

number of these block shareholders the more dispersed is the ownership structure of the

firm and vice-versa. The behavior of listing day returns to these block ownership patterns

is attempted to be studied and results are presented in Table 6.16 which shows the largest

IPOs for the intermediate category where the number of block holders stands between 2

and 4.

Table 6.16: Performance of IPO Firms across Number of Block Shareholders

N Number of

block holders Average RR (%) Average MAER (%)

Overall Positive Negative Overall Positive Negative

90 Up to 2 27.71 (90)

48.41 (61)

-15.82 (29)

25.20 (90)

45.12 (61)

-16.71 (29)

285 2-4 21.46 (285)

46.28 (185)

-25.36 (100)

20.20 (285)

45.36 (180)

-22.93 (105)

29 4-6 25.13 (29)

59.56 (17)

-23.63 (12)

24.34 (29)

60.99 (16)

-20.77 (13)

χ2 value : RR: 0.391 and MAER: 0.220

Note: Figures in parentheses denote the number of companies.

For the overall average of returns, both unadjusted and adjusted reveal that for less

number of block holders the returns are maximum, which first decrease and then

increase as the number of these block holders increase. The non-existence of concrete

and clear association between these attributes is confirmed by the insignificant chi-

square values. Among positive returns, maximum return values for raw and market

returns are noted for firms which have higher number of block shareholders. This

implies that larger number of block holders result in more underpricing due to the

tendencies of these block holders to extract private benefits which do not accrue to

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

181

other shareholders. For firms with negative return, these returns again indicate a

relationship wherein returns first decrease and then increase with increase in number of

block holders. The relationship as unraveled for ownership variable above, hints at a

non-linear tendency where the operation of both the entrenchment and alignment

hypothesis exists at different levels.

6.6.10 Ownership by Top 10 Shareholders and Initial Returns

As another measure of ownership and more specifically concentration of ownership,

ownership levels of top 10 owners are included. Cumulative percentage of shares held by

10 largest shareholders would indicate the extent of concentration existing at the time of

IPO. Higher this percentage the more concentrated ownership is believed to be and vice

versa. Claessens and Djankov (1999) find that firm profitability and labour productivity

are positively associated with ownership concentration.

In this direction, IPO firms are classified into categories wherein it is observed that firms

have high concentration levels because largest numbers of IPOs are found to have 85%

and higher equity ownership in hands of the top 10 owners. 130 of the total firms have

ownership at the level of 100% implying that all ownership is limited in the hands of 10

shareholders and the situation seemingly becomes grave when these 10 owners include

promoters and family members. Thus, concentrated ownership is found to be a typical

feature of Indian IPOs.

Table 6.17: Performance of IPO Firms across Ownership by Top 10 Shareholders

N Top 10 owners

(%) Average RR (%) Average MAER (%)

Overall Positive Negative Overall Positive Negative

71 Upto 85% 23.49 (71)

44.31 (49)

-22.87 (22)

22.00 (71)

40.76 (50)

-22.66 (21)

203 85-100% 25.67 (203)

48.34 (139)

-23.58 (64)

23.95 (203)

47.63 (133)

-21.05 (70)

130 Exactly 100% 18.24 (130)

48.50 (75)

-23.01 (55)

17.75 (130)

47.58 (74)

-21.66 (56)

χ2 value : RR: 0.061 and MAER: 0.043

Note: Figures in parentheses denote the number of companies

Relationship Between Corporate Governance Variables and Listing Performance of Indian IPOs

182

The relationship of these levels to returns are presented in Table 6.17 which elucidates

that overall average returns stand at a maximum for intermediate category (26% RR and